Specifications

- Product Name: Traditional and Simple IRA

- Product Type: Retirement Account

- Provider: EverBank, N.A., World Markets division

- Withdrawal Authorization Form: 314 / 2306T (Rev. 5/2023)

Part 1. IRA Owner

Fill in your personal information, account details, and select the account type (Traditional IRA or SIMPLE IRA).

Part 2. IRA Trustee or Custodian

This section is completed by EverBank, N.A. Fill in the organization details and contact information.

Part 3. Beneficiary or Former Spouse Information

Complete this section if you are a beneficiary or former spouse taking a withdrawal or transferring assets.

Part 4. Withdrawal Information

Specify the total withdrawal amount and withdrawal date. Indicate if this withdrawal will close the IRA.

Part 5. Withholding Election

Determine federal withholding rate and state withholding requirements based on your payment type.

Part 6. Withdrawal Summary

Review penalties, fees, and the net amount paid to you after withholding.

Part 7. Withdrawal Instructions

Assets identified for liquidation will be sold unless otherwise specified in the Special Instructions section.

FAQ

- Q: What is the default federal withholding rate?

A: The default federal withholding rate is 10%, but you can choose a different rate between 0% and 100%. - Q: When should I complete the State Income Tax Withholding Election form?

A: Complete the form for state tax withholding or if you need information specific to your transaction’s state tax implications.

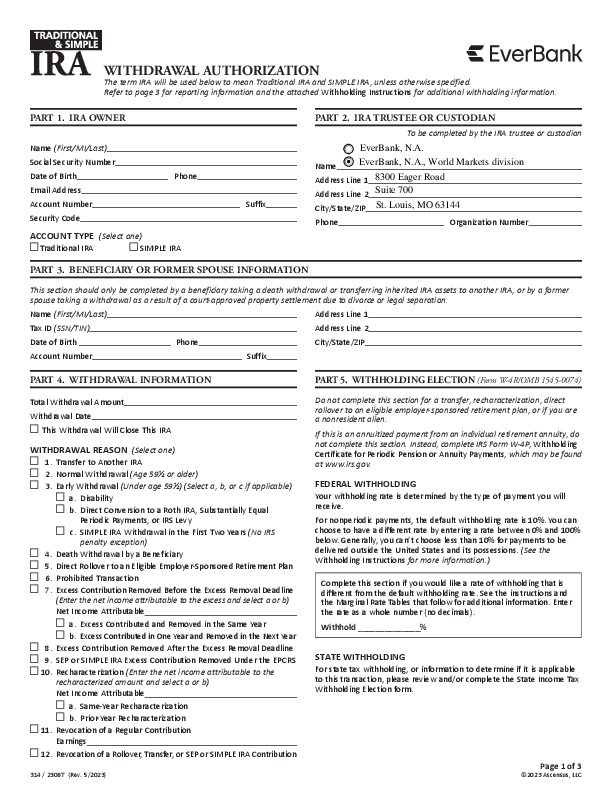

The term IRA will be used below to mean Traditional IRA and SIMPLE IRA, unless otherwise specified.

Refer to page 3 for reporting information and the attached Withholding Instructions for additional withholding information.

PART 1. IRA OWNER

PART 2. IRA TRUSTEE OR CUSTODIAN

To be completed by the IRA trustee or custodian

PART 3. BENEFICIARY OR FORMER SPOUSE INFORMATION

This section should only be completed by a beneficiary taking a death withdrawal or transferring inherited IRA assets to another IRA, or by a former spouse taking a withdrawal as a result of a court-approved property settlement due to divorce or legal separation.

PART 4. WITHDRAWAL INFORMATION

- Total Withdrawal Amount

- Withdrawal Date

This Withdrawal Will Close This IRA

WITHDRAWAL REASON (Select one)

- Transfer to Another IRA

- Normal Withdrawal (Age 59½ or older)

- Early Withdrawal (Under age 59½) (Select a, b, or c if applicable)

- Disability

- Direct Conversion to a Roth IRA, Substantially Equal Periodic Payments, or IRS Levy

- SIMPLE IRA Withdrawal in the First Two Years (No IRS penalty exception)

- Death Withdrawal by a Beneficiary

- Direct Rollover to an Eligible Employer-Sponsored Retirement Plan

- Prohibited Transaction

- Excess Contribution Removed Before the Excess Removal Deadline (Enter the net income attributable to the excess and select a or b) Net Income Attributable

- Excess Contributed and Removed in the Same Year

- Excess Contributed in One Year and Removed in the Next Year

- Excess Contribution Removed After the Excess Removal Deadline

- SEP or SIMPLE IRA Excess Contribution Removed Under the EPCRS

- Recharacterization (Enter the net income attributable to the recharacterized amount and select a or b) Net Income Attributable

- Same-Year Recharacterization

- Prior-Year Recharacterization

- Revocation of a Regular Contribution

Earnings - Revocation of a Rollover, Transfer, or SEP or SIMPLE IRA Contribution

PART 5. WITHHOLDING ELECTION (Form W-4R/OMB 1545-0074)

Do not complete this section for a transfer, recharacterization, direct rollover to an eligible employer-sponsored retirement plan, or if you are a nonresident alien.

If this is an annuitized payment from an individual retirement annuity, do not complete this section. Instead, complete IRS Form W-4P, Withholding Certificate for Periodic Pension or Annuity Payments, which may be found at www.irs.gov.

FEDERAL WITHHOLDING

Your withholding rate is determined by the type of payment you will receive.

For nonperiodic payments, the default withholding rate is 10%. You can choose to have a different rate by entering a rate between 0% and 100% below. Generally, you can’t choose less than 10% for payments to be delivered outside the United States and its possessions. (See the Withholding Instructions for more information.)

Complete this section if you would like a rate of withholding that is different from the default withholding rate. See the instructions and the Marginal Rate Tables that follow for additional information. Enter the rate as a whole number (no decimals).

Withhold ______________%

STATE WITHHOLDING

For state tax withholding, or information to determine if it is applicable to this transaction, please review and/or complete the State Income Tax Withholding Election form.

PART 6. WITHDRAWAL SUMMARY

This section may be completed for informational purposes only.

- Trustee or Custodian Penalties and Fees

- Gross Withdrawal Amount*

- Federal Withholding Amount

- State Withholding Amount

- Net Amount Paid to Recipient

The gross withdrawal amount is the total withdrawal amount in Part 4 after any penalties and fees assessed by the trustee or custodian.

PART 7. WITHDRAWAL INSTRUCTIONS

ASSET HANDLING (Assets identified below will be liquidated immediately unless otherwise specified in the Special Instructions section.)

PAYMENT METHOD

PART 8. SIGNATURES

I certify that I am authorized to receive payments from this IRA and that all information provided by me is true and accurate. I have received a copy of the Withholding Notice Information. No tax advice has been given to me by the trustee or custodian. All decisions regarding this withdrawal are my own, and I expressly assume responsibility for any consequences that may arise from this withdrawal. I agree that the trustee or custodian is not responsible for any consequences that may arise from processing this withdrawal authorization.

- X

Signature of Recipient Date (mm/dd/yyyy) - X

Notary Public/Signature Guarantee (If required by the trustee or custodian) Date (mm/dd/yyyy) - X

Authorized Signature of Trustee or Custodian Date (mm/dd/yyyy)

REPORTING INFORMATION APPLICABLE TO TRADITIONAL IRA AND SIMPLE IRA WITHDRAWALS

You must supply all requested information for the withdrawal so the trustee or custodian can properly report the withdrawal.

If you have any questions regarding a withdrawal, please consult a competent tax professional or refer to IRS Publication 590-B, Distributions from Individual Retirement Arrangements (IRAs), for more information. This publication is available on the IRS website at www.irs.gov or by calling

1-800-TAX-FORM.

WITHDRAWAL REASON

IRA assets can be withdrawn at any time. Most IRA withdrawals are reported to the IRS. IRS rules specify the distribution code that must be used to report each withdrawal on IRS Form 1099-R, Distributions From Pensions, Annuities, Retirement or Profit-Sharing Plans, IRAs, Insurance Contracts, etc.

Transfer to Another IRA. Transfers are not reported on Form 1099-R. Transfers may be made by an IRA owner, beneficiary, or former spouse under a transfer due to a divorce. Inherited IRA assets may only be transferred to another inherited IRA, unless you are a spouse beneficiary.

Normal Withdrawal (Age 59½ or older). If you are age 59½ or older, withdrawals (including required minimum distributions) are reported on Form 1099-R using code 7.

Early Withdrawal (Under age 59½). If you are under age 59½, withdrawals for any reason not listed below are reported on Form 1099-R using code 1.

- Disability. If you are under age 59½ and disabled, withdrawals are reported on Form 1099-R using code 3.

- Direct Conversion to a Roth IRA, Substantially Equal Periodic Payments, or IRS Levy. If you are under age 59½, withdrawals due to direct conversions to a Roth IRA, substantially equal periodic payments, or IRS levy are reported on Form 1099-R using code 2.

- SIMPLE IRA Withdrawal in the First Two Years (No IRS penalty exception). If you are under age 59½ and less than two years have passed since the first contribution to your SIMPLE IRA, withdrawals are reported on Form 1099-R using code S.

- Death Withdrawal by a Beneficiary. Withdrawals by beneficiaries following the death of the original IRA owner are reported on Form 1099-R using code 4. Use code G with code 4 for a surviving spouse beneficiary who elects a direct rollover to an eligible employer-sponsored retirement plan.

- Direct Rollover to an Eligible Employer-Sponsored Retirement Plan. Direct rollovers to eligible employer-sponsored retirement plans (Internal Revenue Code Section (IRC Sec.) 401(a) (e.g., 401(k), profit sharing, money purchase pension plan), annuity plan (IRC Sec. 403(a)), tax-sheltered annuity plan (IRC Sec. 403(b)), or governmental deferred compensation plan (IRC Sec. 457(b)) are reported on Form 1099-R using code G.

Prohibited Transaction. Prohibited transactions as defined in IRC Sec. 4975(c) are reported on Form 1099-R using code 5.

Excess Contribution Removed Before the Excess Removal Deadline. Excess contributions removed before the excess removal deadline (your tax filing deadline, including extensions) must include the net income attributable to the excess.

- If your excess contribution was contributed and removed in the same year, before the excess removal deadline, the withdrawal is reported on Form 1099-R using code 8. If you are under age 59½ also use code 1.

- If your excess contribution was contributed in one year and removed in the next year, before the excess removal deadline, the withdrawal is reported on Form 1099-R using code P. If you are under age 59½ also use code 1.

Excess Contribution Removed After the Excess Removal Deadline. If your excess contribution is removed after the excess removal deadline, the withdrawal is reported on Form 1099-R using code 1 if you are under age 59½ or code 7 if you are age 59½ or older.

SEP or SIMPLE IRA Excess Contribution Removed Under the EPCRS. Excess SEP or SIMPLE IRA contributions removed under the Employee Plans Compliance Resolution System (EPCRS) generally are reported on Form 1099-R using code E.

Recharacterization. A Traditional IRA contribution including the net income attributable may be recharacterized as a Roth IRA contribution up until your tax filing deadline, including extensions.

- Recharacterizations that occur in the same year for which the contribution was made are reported on Form 1099-R using code N.

- Recharacterizations that occur after the year for which the contribution was made are reported on Form 1099-R using code R.

Revocation of a Regular Contribution. Revocations of regular contributions are reported on Form 1099-R using code 8. If you are under age 59½ and earnings on the contribution are distributed, also use code 1.

Revocation of Rollover, Transfer, or SEP or SIMPLE IRA Contribution. Revocations of rollovers, transfers, or SEP or SIMPLE IRA plan contributions are reported on Form 1099-R using code 1 if you are under age 59½ or code 7 if you are age 59½ or older.

WITHHOLDING INSTRUCTIONS (Form W-4R/OMB No. 1545-0074)

General Instructions

Section references are to the Internal Revenue Code.

- Future developments. For the latest information about any future developments related to Form W-4R, such as legislation enacted after it was published, go to www.irs.gov/FormW4R.

Purpose of form. Complete Form W-4R to have payers withhold the correct amount of federal income tax from your nonperiodic payment or eligible rollover distribution from an employer retirement plan, annuity (including a commercial annuity), or individual retirement arrangement (IRA). See below for the rules and options that are available for each type of payment. Don’t use Form W-4R for periodic payments (payments made in installments at regular intervals over a period of more than 1 year) from these plans or arrangements. Instead, use Form W-4P, Withholding Certificate for Periodic Pension or Annuity Payments. For more information on withholding, see Pub. 505, Tax Withholding and Estimated Tax. - Caution: If you have too little tax withheld, you will generally owe tax when you file your tax return and may owe a penalty unless you make timely payments of estimated tax. If too much tax is withheld, you will generally be due a refund when you file your tax return. Your withholding choice (or an election not to have withholding on a nonperiodic payment) will generally apply to any future payment from the same plan or IRA. Submit a new Form W-4R if you want to change your election.

- Nonperiodic payments—10% withholding. Your payer must withhold at a default 10% rate from the taxable amount of nonperiodic payments unless you enter a different rate in the Withholding Election section. Distributions from an IRA that are payable on demand are treated as nonperiodic payments. Note that the default rate of withholding may not be appropriate for your tax situation. You may choose to have no federal income tax withheld by entering “-0-” in the Withholding Election section. See the specific instructions below for more information. Generally, you are not permitted to elect to have federal income tax withheld at a rate of less than 10% (including “-0-”) on any payments to be delivered outside the United States and its territories.

NOTE: If you don’t give Form W-4R to your payer, you don’t provide an SSN, or the IRS notifies the payer that you gave an incorrect SSN, then the payer must withhold 10% of the payment for federal income tax and can’t honor requests to have a lower (or no) amount withheld. Generally, for payments that began before 2024, your current withholding election (or your default rate) remains in effect unless you submit a Form W-4R.

Payments to nonresident aliens and foreign estates. Do not use Form W-4R. See Pub. 515, Withholding of Tax on Nonresident Aliens and Foreign Entities, and Pub. 519, U.S. Tax Guide for Aliens, for more information.

Tax relief for victims of terrorist attacks. If your disability payments for injuries incurred as a direct result of a terrorist attack are not taxable, enter “-0-” in the Withholding Election section. See Pub. 3920, Tax Relief for Victims of Terrorist Attacks, for more details.

2024 Marginal Rate Tables

You may use these tables to help you select the appropriate withholding rate for this payment or distribution. Add your income from all sources and use the column that matches your filing status to find the corresponding rate of withholding. See the instructions for more information on how to use this table.

| 2024 Marginal Rate Tables You may use these tables to help you select the appropriate withholding rate for this payment or distribution. Add your income from all sources and use the column that matches your filing status to find the corresponding rate of withholding. See the instructions for more information on how to use this table. |

|||||

| Single or Married Filing Separately | Married Filing Jointly or Qualifying Surviving Spouse | Head of Household | |||

| Total income over— | Tax rate for every dollar more | Total income over— | Tax rate for every dollar more | Total income over— | Tax rate for every dollar more |

| $0 | 0% | $0 | 0% | $0 | 0% |

| 14,600 | 10% | 29,200 | 10% | 21,900 | 10% |

| 26,200 | 12% | 52,400 | 12% | 38,450 | 12% |

| 61,750 | 22% | 123,500 | 22% | 85,000 | 22% |

| 115,125 | 24% | 230,250 | 24% | 122,400 | 24% |

| 206,550 | 32% | 413,100 | 32% | 213,850 | 32% |

| 258,325 | 35% | 516,650 | 35% | 265,600 | 35% |

| 623,950* | 37% | 760,400 | 37% | 631,250 | 37% |

| * If married filing separately, use $380,200 instead for this 37% rate. | |||||

Specific Instructions

Withholding Election

More withholding. If you want more than the default rate withheld from your payment, you may enter a higher rate in the Withholding Election section.

Less withholding (nonperiodic payments only). If permitted, you may enter a lower rate in the Withholding Election section (including “-0-”) if you want less than the 10% default rate withheld from your payment. If you have already paid, or plan to pay, your tax on this payment through other withholding or estimated tax payments, you may want to enter “-0-”.

- Suggestion for determining withholding. Consider using the Marginal Rate Tables above to help you select the appropriate withholding rate for this payment or distribution. The tables are most accurate if the appropriate amount of tax on all other sources of income, deductions, and credits has been paid through other withholding or estimated tax payments. If the appropriate amount of tax on those sources of income has not been paid through other withholding or estimated tax payments, you can pay that tax through withholding on this payment by entering a rate that is greater than the rate in the Marginal Rate Tables.

The marginal tax rate is the rate of tax on each additional dollar of income you receive above a particular amount of income. You can use the table for your filing status as a guide to find a rate of withholding for amounts above the total income level in the table. - To determine the appropriate rate of withholding from the table, do the following. Step 1: Find the rate that corresponds with your total income not including the payment. Step 2: Add your total income and the taxable amount of the payment and find the corresponding rate.

If these two rates are the same, enter that rate in the Withholding Election section. (See Example 1 below.)

If the two rates differ, multiply (a) the amount in the lower rate bracket by the rate for that bracket, and (b) the amount in the higher rate bracket by the rate for that bracket. Add these two numbers; this is the expected tax for this payment. To get the rate to have withheld, divide this amount by the taxable amount of the payment. Round up to the next whole number and enter that rate in the Withholding Election section. (See Example 2 below.)

If you prefer a simpler approach (but one that may lead to overwithholding), find the rate that corresponds to your total income including the payment and enter that rate in the Withholding Election section.

Examples. Assume the following facts for Examples 1 and 2. Your filing status is single. You expect the taxable amount of your payment to be $20,000. Appropriate amounts have been withheld for all other sources of income and any deductions or credits.

- Example 1. You expect your total income to be $62,000 without the payment. Step 1: Because your total income without the payment, $62,000, is greater than $61,750 but less than $115,125, the corresponding rate is 22%. Step 2: Because your total income with the payment, $82,000, is greater than $61,750 but less than $115,125, the corresponding rate is 22%. Because these two rates are the same, enter “22” in the Withholding Election section.

- Example 2. You expect your total income to be $43,700 without the payment. Step 1: Because your total income without the payment, $43,700, is greater than $26,200 but less than $61,750, the corresponding rate is 12%. Step 2: Because your total income with the payment, $63,700, is greater than $61,750 but less than $115,125, the corresponding rate is 22%. The two rates differ. $18,050 of the $20,000 payment is in the lower bracket ($61,750 less your total income of $43,700 without the payment), and $1,950 is in the higher bracket ($20,000 less the $18,050 that is in the lower bracket). Multiply $18,050 by 12% to get $2,166. Multiply $1,950 by 22% to get $429. The sum of these two amounts is $2,595. This is the estimated tax on your payment. This amount corresponds to 13% of the $20,000 payment ($2,595 divided by $20,000). Enter “13” in the Withholding Election section.

Privacy Act and Paperwork Reduction Act Notice. The IRS asks for the information on this form to carry out the Internal Revenue laws of the United States. You are required to provide this information only if you want to (a) request additional federal income tax withholding from your nonperiodic payment(s) or eligible rollover distribution(s); (b) choose not to have federal income tax withheld from your nonperiodic payment(s), when permitted; or (c) change a previous Form W-4R (or a previous Form W-4P that you completed with respect to your nonperiodic payments or eligible rollover distributions). To do any of the aforementioned, you are required by sections 3405(e) and 6109 and their regulations to provide the information requested on this form. Failure to provide this information may result in inaccurate withholding on your payment(s). Failure to provide a properly completed form will result in your payment(s) being subject to the default rate; providing fraudulent information may subject you to penalties.

Routine uses of this information include giving it to the Department of Justice for civil and criminal litigation, and to cities, states, the District of Columbia, and U.S. commonwealths and territories for use in administering their tax laws. The IRS may also disclose this information to other countries under a tax treaty, to federal and state agencies to enforce federal nontax criminal laws, or to federal law enforcement and intelligence agencies to combat terrorism.

You are not required to provide the information requested on a form that is subject to the Paperwork Reduction Act unless the form displays a valid OMB control number. Books or records relating to a form or its instructions must be retained as long as their contents may become material in the administration of any Internal Revenue law. Generally, tax returns and return information are confidential, as required by section 6103.

The average time and expenses required to complete and file this form will vary depending on individual circumstances. For estimated averages, see the instructions for your income tax return.

If you have suggestions for making this form simpler, the IRS would be happy to hear from you. See the instructions for your income tax return.

State income tax withholding election

Use this form to make a state income tax withholding election. Enter your information using blue or black ink.

- Your information

- Important information

Some state laws may require mandatory state income tax be withheld from withdrawals. If you do not return this form, EverBank, National Association (“EverBank”) is required to withhold state income taxes at the state tax default rate shown on this form.

Other states have voluntary state income tax withholding. Before making an election, be sure to read all notes that may apply to your state of residence.

Mandatory states

State income tax will automatically be withheld at the state tax default. Please complete section 3.

| Arkansas | California | Connecticut | Delaware | District of Columbia | |||

| Iowa | Maine | Massachusetts | Michigan | Nebraska | |||

| North Carolina | Oklahoma | Oregon | Vermont | ||||

| Voluntary states

State income tax will only be withheld if you instruct us to do so. Please complete section 4. |

|||||||

| Alabama | Arizona | Colorado | Georgia | daho | Illinois | ||

| Indiana | Kansas | Kentucky | Louisiana | Maryland | Minnesota | ||

| Mississippi | Missouri | Montana | New Jersey | New Mexico | North Dakota | ||

| Ohio | Pennsylvania | Rhode Island | South Carolina | Utah | Virginia | ||

| West Virginia | Wisconsin | ||||||

| Non-withholding states

State income tax withholding is not allowed. |

|||||||

| Alaska | Florida | Hawaii | Nevada | New Hampshire | |||

| New York | South Dakota | Tennessee | Texas | Washington | |||

| Wyoming | |||||||

Items to keep in mind:

- Payments that are directly transferred to an IRA or directly rolled over to another retirement plan are not subject to state income tax withholding. Therefore, if your payments are being rolled over, no further action is required.

- There may be penalties for not paying enough state income tax during the year.

- State tax withholding rates are always subject to change.

Mandatory state withholding election

Based on your state of legal residence, state income taxes will automatically be withheld from your payment at the rates listed in the charts below, unless you choose one of the available options.

- You can opt out of state withholding.

- If you have elected no federal withholding, state can be elected at any rate.

- You can elect an amount greater than the state default only if federal is being withheld.

- If you have elected no federal withholding, cannot withhold for state.

- You can decline state withholding only if you have elected no federal withholding.

Connecticut only:

When not taking a lump sum of the entire account, I elect:

- No state withholding

- An amount greater than the state-prescribed rate.

Withhold % from the taxable portion of my payment.

- Flat dollar amount of $

- District of Columbia only:

Is the distribution a lump sum of the entire account? ![]() Yes

Yes ![]() No

No

If yes, the mandatory 8.95% will be withheld. If no, the default is 0%.

Iowa only

I am exempt from Iowa withholding from my payment because:

- I am 55 years old (or older); or

- I am disabled and I am receiving retirement income on the basis of a documented disability or I meet federal or state criteria for disability.

Arkansas, Delaware, Maine, Massachusetts, Michigan, Nebraska, North Carolina, Oklahoma,

Oregon, and Vermont

- I elect an amount greater than the state-prescribed rate.

Withhold % from the taxable portion of my payment.

California

- I elect an amount other than the state-prescribed rate.

Arkansas, Delaware, Iowa, Maine, Massachusetts, Michigan, Nebraska, North Carolina, Oklahoma,

Oregon, and Vermont

- In addition to the state-prescribed rate, I elect to withhold an additional amount.

- I choose NOT to have state taxes withheld from my withdrawal or my withdrawal is exempt.

Voluntary state withholding election

| Alabama | Arizona | Colorado | Georgia | Idaho |

| Illinois | Indiana | Kansas | Kentucky | Louisiana |

| Maryland | Minnesota6 | Mississippi | Missouri | Montana |

| New Jersey | New Mexico | North Dakota | Ohio | Pennsylvania |

| Rhode Island | South Carolina | Utah | Virginia | West Virginia |

| Wisconsin |

If you do not select the “Do not withhold” selection or fail to specify a withholding amount or percentage below, EverBank will withhold 6.25%.

Do not withhold (This is the default)

Do not withhold (This is the default)- I elect the following dollar amount or percentage withheld from each payment:

$ or %

Frequency: ![]() One-time distribution

One-time distribution ![]() Recurring periodic payment

Recurring periodic payment

Agreements and certifications

By signing section 6, I understand and agree that EverBank will rely on the veracity and completeness of the information on this form in making the requested account changes. I hereby certify that the information provided on this form and any accompanying documentation is true, complete, and accurate and that I will notify EverBank of any material change in such information or statements.

Under penalties of perjury, I certify that:

- The taxpayer identification number I have given on this form is correct; and

- I am a U.S. citizen or other U.S. person; and

- I am not subject to backup withholding because:

- I am exempt from backup withholding, or

- I have not been notified by the Internal Revenue Service (IRS) that I am subject to backup withholding as a result of a failure to report all interest or dividends, or

- The IRS has notified me that I am no longer subject to backup withholding; and

- The FATCA code(s) entered on this form (if any) indicating that

- I am exempt from FATCA reporting is correct.

Signature

The elections made will become effective with your next available payment. You may revoke this election at any time by completing and submitting a new state income tax withholding election form.

The undersigned agrees that we, EverBank, in our sole discretion, may accept documents that you have signed and sent to us by electronic means, like fax, email, or other file transmittal processes we might offer. By sending us any such document by electronic means, the undersigned agrees that we may rely on it and on the signature, and that the document is binding on the signer even if the original signed document is not delivered to us.

- Account holder Date

Submit

Upload this form and any additional documentation so that we can move forward in the quickest and most secure way. Simply log in to your account at everbank.com and:

- Select the Actions tab

- In the TIAA Documents section, select Upload documents

- Select Files you would like to upload

- Select Folder to upload files to and follow the directions

For bank use only

Verify client Date verified FC number Associate name (Print first & last name)

Documents / Resources

|

EverBank 314 Traditional and Simple IRA Withdrawal Authorization [pdf] Instructions 314, 314 Traditional and Simple IRA Withdrawal Authorization, Traditional and Simple IRA Withdrawal Authorization, Simple IRA Withdrawal Authorization, IRA Withdrawal Authorization, Withdrawal Authorization, Authorization |