BAC-06.30.2020 Ex. 99.1

File info: application/pdf · 18 pages · 188.55KB

BAC-06.30.2020 Ex. 99.1

unspecified

Extracted Text

Bank of America Reports Quarterly Earnings of $3.5 Billion, EPS of $0.37 Provision for Credit Losses of $5.1 Billion Includes a $4.0 Billion Reserve Build(A) CET1 Ratio 11.4%, Average Global Liquidity Sources Grew $244 Billion to $796 Billion(B,C)

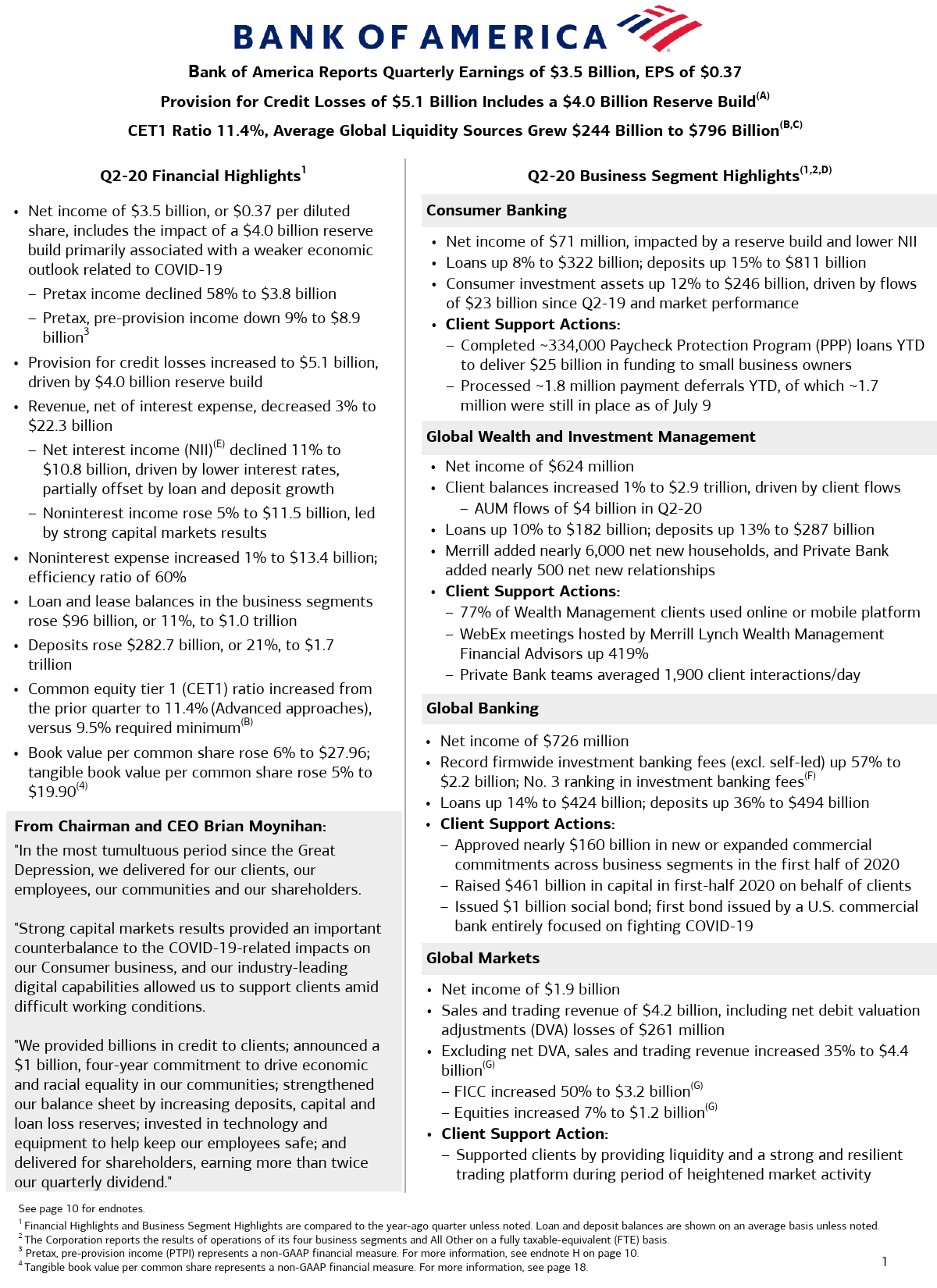

Q2-20 Financial Highlights1

Q2-20 Business Segment Highlights(1,2,D)

� Net income of $3.5 billion, or $0.37 per diluted share, includes the impact of a $4.0 billion reserve build primarily associated with a weaker economic outlook related to COVID-19

� Pretax income declined 58% to $3.8 billion

� Pretax, pre-provision income down 9% to $8.9 billion3

� Provision for credit losses increased to $5.1 billion, driven by $4.0 billion reserve build

� Revenue, net of interest expense, decreased 3% to $22.3 billion � Net interest income (NII)(E) declined 11% to $10.8 billion, driven by lower interest rates, partially offset by loan and deposit growth

� Noninterest income rose 5% to $11.5 billion, led by strong capital markets results

� Noninterest expense increased 1% to $13.4 billion; efficiency ratio of 60%

� Loan and lease balances in the business segments rose $96 billion, or 11%, to $1.0 trillion

� Deposits rose $282.7 billion, or 21%, to $1.7 trillion

� Common equity tier 1 (CET1) ratio increased from the prior quarter to 11.4% (Advanced approaches), versus 9.5% required minimum(B)

� Book value per common share rose 6% to $27.96; tangible book value per common share rose 5% to $19.90(4)

From Chairman and CEO Brian Moynihan:

"In the most tumultuous period since the Great Depression, we delivered for our clients, our employees, our communities and our shareholders.

"Strong capital markets results provided an important counterbalance to the COVID-19-related impacts on our Consumer business, and our industry-leading digital capabilities allowed us to support clients amid difficult working conditions.

"We provided billions in credit to clients; announced a $1 billion, four-year commitment to drive economic and racial equality in our communities; strengthened our balance sheet by increasing deposits, capital and loan loss reserves; invested in technology and equipment to help keep our employees safe; and delivered for shareholders, earning more than twice our quarterly dividend."

Consumer Banking

� Net income of $71 million, impacted by a reserve build and lower NII � Loans up 8% to $322 billion; deposits up 15% to $811 billion � Consumer investment assets up 12% to $246 billion, driven by flows

of $23 billion since Q2-19 and market performance � Client Support Actions:

� Completed ~334,000 Paycheck Protection Program (PPP) loans YTD to deliver $25 billion in funding to small business owners

� Processed ~1.8 million payment deferrals YTD, of which ~1.7 million were still in place as of July 9

Global Wealth and Investment Management

� Net income of $624 million � Client balances increased 1% to $2.9 trillion, driven by client flows

� AUM flows of $4 billion in Q2-20 � Loans up 10% to $182 billion; deposits up 13% to $287 billion � Merrill added nearly 6,000 net new households, and Private Bank

added nearly 500 net new relationships � Client Support Actions:

� 77% of Wealth Management clients used online or mobile platform � WebEx meetings hosted by Merrill Lynch Wealth Management

Financial Advisors up 419% � Private Bank teams averaged 1,900 client interactions/day

Global Banking

� Net income of $726 million � Record firmwide investment banking fees (excl. self-led) up 57% to

$2.2 billion; No. 3 ranking in investment banking fees(F) � Loans up 14% to $424 billion; deposits up 36% to $494 billion � Client Support Actions:

� Approved nearly $160 billion in new or expanded commercial commitments across business segments in the first half of 2020

� Raised $461 billion in capital in first-half 2020 on behalf of clients � Issued $1 billion social bond; first bond issued by a U.S. commercial

bank entirely focused on fighting COVID-19

Global Markets

� Net income of $1.9 billion � Sales and trading revenue of $4.2 billion, including net debit valuation

adjustments (DVA) losses of $261 million � Excluding net DVA, sales and trading revenue increased 35% to $4.4

billion(G) � FICC increased 50% to $3.2 billion(G) � Equities increased 7% to $1.2 billion(G) � Client Support Action: � Supported clients by providing liquidity and a strong and resilient

trading platform during period of heightened market activity

See page 10 for endnotes.

1 Financial Highlights and Business Segment Highlights are compared to the year-ago quarter unless noted. Loan and deposit balances are shown on an average basis unless noted.

2 The Corporation reports the results of operations of its four business segments and All Other on a fully taxable-equivalent (FTE) basis.

3 Pretax, pre-provision income (PTPI) represents a non-GAAP financial measure. For more information, see endnote H on page 10.

4 Tangible book value per common share represents a non-GAAP financial measure. For more information, see page 18.

1

Bank of America Financial Highlights

($ in billions, except per share data) Total revenue, net of interest expense Provision for credit losses Noninterest expense Pretax income Income tax expense Net Income Diluted earnings per share

Three months ended

6/30/2020 $22.3 5.1 13.4 3.8 0.3 3.5 $0.37

3/31/2020 $22.8 4.8 13.5 4.5 0.5 4.0 $0.40

6/30/2019 $23.1 0.9 13.3 9.0 1.6 7.3 $0.74

From Chief Financial Officer Paul Donofrio:

"We strengthened an already strong balance sheet by increasing capital and liquidity and growing deposits. While net charge-offs remained relatively low by historical standards, we added another $4 billion to credit reserves to reflect the current economic outlook. We ended the quarter with record deposits of $1.7 trillion, $242 billion in common equity, and $21 billion in credit reserves that we believe will allow us to continue to be a source of strength for our clients and communities. Our continued focus on Responsible Growth means we are well prepared for the current environment."

Supporting Employees, Clients and Communities

Employees � Extensive steps to help protect and support employees working in our offices, including enhanced cleanings, providing personal protective equipment and installing thousands of wellness barriers

� Special compensation incentives for teammates serving clients in U.S. financial centers, call centers and operation centers

� Expanded employee benefits (no-cost coronavirus testing in U.S.; no-fee Teladoc; enhanced backup childcare, including reimbursement of $100 per day; physical and emotional wellness resources; and vacation and personal day flexibility)

� Dedicated communications and outreach to employees and family members about available resources, including Life Event Services and Employee Assistance Program counseling services

� Employee Relief Fund provides grants to U.S.-based employees experiencing emergency hardships

� 21K+ employees have been reskilled and realigned to serve in new capacities and support our clients

� Committed to no coronavirus-related layoffs in 2020

Clients � Extensive efforts to keep clients safe including enhanced cleanings, personal protective equipment, wellness barriers, physical distancing, virtual client meetings and opening drive-up windows

� Proactive client outreach across all businesses, including: � Millions of letters and emails and placing outbound calls to Consumer and Small Business clients � Thousands of calls, meetings and broadcasts to actively advise and connect with Wealth and Private Bank clients � Proactive guidance and market insight from BofA Global Research and Investment Insights teams

� SBA approved Paycheck Protection Program loans for ~334,000 clients YTD, providing $25 billion in funding to small business owners (avg. of $78K, 99% of loans to businesses with <100 employees)

� Processed more than 16 million Economic Impact Payments YTD, totaling more than $26 billion for clients and non-clients and provided ~$59 billion in unemployment benefits via prepaid debit cards

� Relief available from various fees, including overdraft, nonsufficient funds, monthly maintenance and late charges

Communities and Other � Announced $1 billion, four-year initiative to help drive racial

equality and economic opportunity in communities of color

� Processed ~1.8 million payment deferrals YTD across credit card, auto, mortgage and home equity, of which ~1.7 million were still in place as of July 9

� Announced $25 million commitment to the launch of a new Smithsonian Institution initiative to further how Americans understand, experience and confront issues involving race

� Paused foreclosure sales, evictions and home/auto repossessions

� No negative credit bureau reporting for previously up-to-date clients requesting financial relief

� Committed $100 million to support and address pressing needs � of health crisis, including health care, food and education

� Committed to provide up to $250 million in capital to community development financial institutions (CDFIs) and up to $10 million � in philanthropic grants to help fund CDFI operations

� Issued $1 billion corporate social bond; first bond issued by a U.S. commercial bank entirely focused on fighting COVID-19

Approved nearly $160 billion in new or expanded commercial commitments and raised $461 billion in capital for clients across debt/ equity markets in first half of 2020

Ensuring reliable access for clients' financial needs through 24/7 access to mobile and online banking tools, virtual communication tools, continued access to cash, and ~4,300 financial centers and other bank offices

� Lowered the employee matching gift minimum to $1 and doubled the match for employee donations to 17 organizations focused on racial equality

� Supported clients by providing liquidity and a strong and resilient trading platform during period of heightened market activity

2

Consumer Banking1,2

� Net income of $71 million declined significantly due to COVID-19 impacts:

� higher provision expense for expected credit losses

� lower NII from interest rates

� increased operating costs associated with the health and safety of employees and clients

� Revenue of $7.9 billion decreased 19%, driven by lower NII, as well as lower service charges and card income

� Provision for credit losses increased to $3.0 billion, primarily due to a reserve build associated with a weaker economic outlook related to COVID-19

� Net charge-off ratio improved to 1.05%, compared to 1.24%

� Noninterest expense increased 7% to $4.7 billion, driven by incremental expense to support customers and employees during COVID-19 and investments for business growth and digital capabilities

� Continued investment in financial center and ATM builds/renovations, sales professionals and digital capabilities

Business Highlights(1,3,D)

� Average deposits grew $104 billion, or 15%; average loans grew $25 billion, or 8%, driven by growth in residential mortgages

� Consumer investment assets grew $26 billion, or 12%, to $246 billion, driven by client flows and market performance

� $23 billion of client flows since Q2-19 � 2.9 million client accounts, up 9% YoY � 10 new financial centers opened and 17 renovated in Q2-20

� Combined credit/debit card spend decreased 11%

� 6.6 million Consumer customers enrolled in Preferred Rewards, with 99% retention rate

Digital Usage Continued to Grow1

� 39.3 million active digital banking users, up 5%

� 30.3 million active mobile banking users, up 9% � Digital sales were 47% of all Consumer Banking

sales � 1.8 billion mobile logins in Q2-20 � 11.3 million active Zelle� users, now including small

businesses; sent and received 117 million transfers worth $32 billion in Q2-20, up 79% � Approximately 665,000 digital appointments with a specialist

Financial Results1

($ in millions) Total revenue2 Provision for credit losses Noninterest expense Pretax income Income tax expense Net income

Three months ended

6/30/2020 3/31/2020 6/30/2019

$7,851

$9,129

$9,717

3,024

2,258

947

4,733

4,495

4,412

94

2,376

4,358

23

582

1,068

$71

$1,794

$3,290

Business Highlights(1,3,D)

($ in billions)

Three months ended 6/30/2020 3/31/2020 6/30/2019

Average deposits

$810.7

$736.7

$707.1

Average loans and leases

321.6

316.9

296.4

Consumer investment assets (EOP)

246.1

212.2

219.7

Active mobile banking users (MM)

30.3

29.8

27.8

Number of financial centers

4,298

4,297

4,349

Efficiency ratio

60%

49%

45%

Return on average allocated capital

1

19

36

Total Consumer Credit Card3

Average credit card outstanding balances

$86.2

$94.5

$93.6

Total credit/debit spend

143.3

153.0

161.5

Risk-adjusted margin

8.5%

7.9%

1 Comparisons are to the year-ago quarter unless noted. 2 Revenue, net of interest expense. 3 The consumer credit card portfolio includes Consumer Banking and GWIM.

7.9%

Continued Business Leadership

� No. 1 Consumer Deposit Market Share (Estimated retail consumer deposits based on June 30, 2019 FDIC deposit data)

� No. 1 Small Business Lender (FDIC, Q1-20) � No. 1 Online Banking and Mobile Banking Functionality (Keynova Q2-20

Online Banker ScoreCard; Q1-20 Mobile Banker Scorecard; Javelin 2020 Online and Mobile Banking Scorecards) � No. 1 Home Equity Originator (Inside Mortgage Finance, Home Equity new HELOC commitments, Q1-20) � No. 1 in Prime Auto Credit Distribution of New Originations Among Peers (Experian Autocount; Franchised Dealers; Largest percentage of 680+ Vantage 3.0 originations among key competitors as of April 2020) � No. 1 Digital Checking Account Sales Functionality (Forrester, January 2020) � Named North America's Best Digital Bank (Euromoney, July 2019) � Best Mortgage Lender for First-Time Home Buyers (Nerdwallet, 2020) � 5 Star Ranking Overall - Named a Top Online Stock Broker (Nerdwallet, 2020)

3

Global Wealth and Investment Management 1,2

� Net income of $624 million, down $452 million

� Pretax income declined $599 million, or 42%, to $826 million; pretax margin of 19%

� Pretax, pre-provision income declined $484 million, or 33%, to $1.0 billion(H)

� Revenue of $4.4 billion decreased 10% as lower NII and transactional revenue more than offset the benefits of deposit, loan and AUM growth

� Provision for credit losses increased $115 million to $136 million due to a reserve build associated with a weaker economic outlook related to COVID-19

� Noninterest expense was flat at $3.5 billion

Business Highlights(1,D)

� Total client balances up $29 billion, or 1%, to $2.9 trillion � AUM flows of $4 billion in Q2-20

� Average deposits increased $33 billion, or 13%, to $287 billion; average loans and leases grew $16 billion, or 10%, to $182 billion

Strong Client Growth and Advisor Engagement

� Merrill Lynch Wealth Management � Added nearly 6,000 net new households � WebEx meetings hosted by Financial Advisors up 419% � eCommunications volume up 106% YTD � Client satisfaction with advisors remains high at 93% YTD

� Private Bank � Added nearly 500 net new relationships � Teams averaged 1,900 interactions per day, with clients, up 79% from Q4-19

Digital Usage Continued to Grow

� Secure text messages with GWIM clients up 85% � Total GWIM digital logins up 105% � Merrill Lynch Wealth Management � 77% of clients using an online or mobile platform

across Merrill and Bank of America

� Client usage of MyMerrill mobile app grew 28%

� 39% of checks were deposited through the mobile app, up from 24% in Q2-19

� Private Bank � 77% of clients actively using an online or mobile platform across Private Bank and Bank of America

� 37% YoY growth in active users of the Private Bank mobile app and 15% growth in Private Bank online platform users

� Zelle usage - 94% growth in transactions YoY

Financial Results1

($ in millions) Total revenue2 Provision for credit losses Noninterest expense Pretax income Income tax expense Net income

Three months ended

6/30/2020 3/31/2020 6/30/2019

$4,425

$4,936

$4,900

136 3,463

826 202

189 3,600 1,147

281

21 3,454 1,425

349

$624

$866

$1,076

Business Highlights(1,D)

Three months ended

($ in billions)

6/30/2020 3/31/2020 6/30/2019

Average deposits

$287.1

$263.4

$253.9

Average loans and leases

182.2

178.6

166.3

Total client balances (EOP)

2,927.8

2,658.6

2,898.8

AUM flows

3.6

7.0

5.3

Pretax margin

19%

23%

29%

Return on average allocated

17

23

30

capital

1 Comparisons are to the year-ago quarter unless noted. 2 Revenue, net of interest expense.

Continued Business Leadership

� No. 1 U.S. wealth management market position across client assets, deposits and loans (U.S.-based full-service wirehouse peers based on Q1-20 earnings releases)

� No. 1 in Personal trust assets under management (Industry Q1-20 FDIC call reports)

� No. 1 in Barron's Top 1,200 ranked Financial Advisors (2020) � No. 1 in Forbes' Top Next Generation Advisors (2019) and

Best-in-State Wealth Advisors (2020) � No. 1 in Financial Times Top 401K Retirement Plan Advisers (2019) � No. 1 in Barron's Top 100 Women Advisors (2019) � No. 1 in Forbes' Top Women Advisors (2019) � Digital Wealth Impact Innovation Award for Digital Engagement (AITE

Group, 2020)

4

Global Banking1,2

� Net income decreased $1.2 billion to $726 million

� Pretax income declined $1.6 billion, or 62%, to $995 million

� Pretax, pre-provision income increased $104 million, or 4%, to $2.9 billion(H)

� Revenue of $5.1 billion increased 2%, as higher investment banking fees and portfolio valuations more than offset lower net interest income

� Provision for credit losses increased $1.7 billion to $1.9 billion, primarily due to a reserve build associated with a weaker economic outlook related to COVID-19

� Noninterest expense increased 1% to $2.2 billion

Business Highlights(1,2,D)

� Average deposits increased $131 billion, or 36%, to $494 billion, reflecting client flight to safety, government stimulus and placement of credit draws

� Average loans and leases grew $51 billion, or 14%, to $424 billion, driven by revolver draws at the end of the prior quarter, which have been partially paid down throughout Q2-20

� Record total corporation investment banking fees of $2.2 billion (excl. self-led) increased 57%, driven by increases in advisory, debt and equity underwriting fees � Participated in 9 of the top 10 equity deals and 6 of the top 10 debt deals(F)

Digital Usage Continued to Grow1

� ~500k CashPro� Online users (digital banking platform) across our commercial, corporate and business banking businesses

� CashPro Mobile Active Users increased 50% and logins increased 77% (rolling 12 months, YoY)

� CashPro Mobile Payment Approvals value of $184 billion, with volumes increasing 244% (rolling 12 months, YoY)

� Number of checks deposited via CashPro Mobile up 133%, and dollar volume increased 181% (rolling 12 months, YoY)

� 14 million incoming receivables were digitally matched in last 12 months using Intelligent Receivables, which uses AI to match payments and accounts receivables (May 2020)

� Mobile Wallet adoption for commercial cards grew by 115% YoY (May 2020)

Financial Results1

($ in millions) Total revenue2,3 Provision for credit losses Noninterest expense Pretax income Income tax expense Net income

Three months ended

6/30/2020 3/31/2020 6/30/2019

$5,091

$4,600

$4,975

1,873

2,093

125

2,223

2,321

2,211

995

186

2,639

269

50

713

$726

$136

$1,926

Business Highlights(1,2,D)

Three months ended

($ in billions) Average deposits Average loans and leases

6/30/2020 3/31/2020

$493.9

$382.4

423.6

386.5

6/30/2019 $362.6 372.5

Total Corp. IB fees (excl. selfled)2 Global Banking IB fees2

Business Lending revenue

Global Transaction Services revenue

2.2

1.4

1.4

1.2

0.8

0.7

1.9

2.0

2.1

1.8

2.0

2.2

Efficiency ratio

44%

50%

44%

Return on average allocated capital

7

1

19

1 Comparisons are to the year-ago quarter unless noted. 2 Global Banking and Global Markets share in certain deal economics from investment banking,

loan origination activities, and sales and trading activities. 3 Revenue, net of interest expense.

Continued Business Leadership

� North America's Best Bank for Small to Medium-sized Enterprises (Euromoney, 2020)

� Best Overall Brand Middle Market Banking (Greenwich, 2020) � North America and Latin America's Best Bank for Transaction Services

(Euromoney, 2020) � North America's Best Bank for Financing (Euromoney, 2019) � 2019 Quality, Share and Excellence Awards for U.S. Large Corporate

Banking and Cash Management (Greenwich, 2019) � Relationships with 77% of the Global Fortune 500 and 95% of the U.S.

Fortune 1000 (2019)

5

Global Markets1,2

� Net income of $1.9 billion, increased $849 million, or Financial Results1 81%

� Excluding net DVA, net income increased 96% to $2.1 billion4

� Pretax income increased $1.1 billion, or 75%, to $2.6 billion

� Pretax, pre-provision income increased $1.2 billion, or 82%, to $2.7 billion(H)

� Revenue of $5.3 billion increased 29%, driven by higher sales and trading revenues and investment banking fees, partially offset by the absence of a gain on sale of an equity investment which occurred in Q2-19 � Excluding net DVA, revenue increased 34%4

� Provision for credit losses increased $100 million to $105 million, primarily due to a reserve build associated with a weaker economic outlook related to COVID-19

($ in millions) Total revenue2,3 Net DVA4 Total revenue (excl. net DVA)2,3,4 Provision for credit losses Noninterest expense Pretax income Income tax expense Net income Net income (excl. net DVA)4

Business Highlights(1,2,D)

Three months ended

6/30/2020 3/31/2020 6/30/2019

$5,349

$5,226

$4,144

(261)

300

(31)

$5,610

$4,926

$4,175

105 2,682 2,562

666 $1,896 $2,094

107 2,812 2,307

600 $1,707 $1,479

5 2,675 1,464

417 $1,047 $1,071

� Noninterest expense was flat at $2.7 billion � Average VaR of $81 million5

($ in billions)

Three months ended 6/30/2020 3/31/2020 6/30/2019

Business Highlights(1,2,D)

� Reported sales and trading revenue increased 28% to $4.2 billion

� Excluding net DVA, sales and trading revenue increased 35% to $4.4 billion(G)

� FICC revenue of $3.2 billion increased 50%, driven by strong results across credit-related products, especially in the Americas, as the market rebounded after the March sell-off, as well as a robust performance from macro products due to solid market-making conditions

� Equities revenue of $1.2 billion increased 7%, driven by strong performance in cash and client financing, partially offset by a weaker performance in derivatives

Additional Highlights

� 680+ research analysts covering 3,100+ companies, 1,280+ corporate bond issuers across 55+ economies and 24 industries

Average total assets

$663.1

$713.1

$685.4

Average trading-related assets

467.0

503.1

496.2

Average loans and leases Sales and trading revenue2

74.1

71.7

70.6

4.2

4.6

3.2

Sales and trading revenue (excl. net DVA)2,(G)

Global Markets IB fees2

4.4

4.3

3.3

0.9

0.6

0.6

Efficiency ratio

50%

54%

65%

Return on average allocated

21

19

12

capital

1 Comparisons are to the year-ago quarter unless noted. 2 Global Banking and Global Markets share in certain deal economics from investment banking,

loan origination activities, and sales and trading activities. 3 Revenue, net of interest expense. 4 Revenue and net income, excluding net DVA, are non-GAAP financial measures. See endnote G

on page 10 for more information. 5 VaR model uses a historical simulation approach based on three years of historical data and

an expected shortfall methodology equivalent to a 99% confidence level. Average VaR was $81MM, $48MM and $34MM for Q2-20, Q1-20 and Q2-19, respectively.

Continued Business Leadership

� CMBS Bank of the Year (GlobalCapital US Securitization Awards, 2020) � Derivatives House of the Year (GlobalCapital, 2019; Risk 2020 Award) � Derivatives and Interest Rate Derivatives House of the Year (IFR Awards,

2019) � Most Innovative Bank for Equity Derivatives (The Banker, 2019) � No. 1 Global Research Firm (Institutional Investor, 2019) � No. 1 Global Fixed Income Research Team (Institutional Investor, 2019) � No. 1 Quality Leader for U.S. Fixed Income Overall Trading Quality and

No. 1 for U.S. Fixed Income Overall Service Quality (Greenwich, 2019) � Quality Leader in Global Foreign Exchange Sales and Corporate FX Sales

(Greenwich, 2019) � Share Leader in U.S. Fixed Income Market Share (Greenwich, 2019) � No. 1 Municipal Bonds Underwriter (Refinitiv, 2019)

6

All Other1

� Net income increased to $216 million from $9 million, driven primarily by a $704 million gain on certain mortgage loan sales

� Total corporation effective tax rate of 7% reflects the 11% tax rate expected for the rest of 2020 due to the greater impact of tax credits related to tax-advantaged investments on lower pretax income, as well as the related adjustment to the year-to-date tax rate

Financial Results1

Three months ended

($ in millions) Total revenue2 Provision for credit losses Noninterest expense Pretax loss Income tax expense (benefit)

6/30/2020 $(262) (21) 309 (550) (766)

3/31/2020 $(980) 114 247 (1,341) (848)

6/30/2019 $(503) (241) 516 (778) (787)

Net income (loss)

$216

$(493)

$9

1 Comparisons are to the year-ago quarter unless noted. 2 Revenue, net of interest expense.

Note: All Other consists of asset and liability management (ALM) activities, equity investments, non-core mortgage loans and servicing activities, liquidating businesses and certain expenses not otherwise allocated to a business segment. ALM activities encompass certain residential mortgages, debt securities, and interest rate and foreign currency risk management activities. Substantially all of the results of ALM activities are allocated to our business segments. Equity investments include our merchant services joint venture, as well as a portfolio of equity, real estate and other alternative investments.

7

Credit Quality

Charge-offs

� Total net charge-offs up $24 million, or 2%, from Q1-20 to $1.1 billion

� Consumer net charge-offs decreased $138 million from the prior quarter to $734 million, driven primarily by payment deferrals and government stimulus

� Commercial net charge-offs increased $162 million from the prior quarter to $412 million, driven primarily by commercial real estate and energy

� Net charge-off ratio decreased 1 basis point from the prior quarter to 0.45%

Provision for credit losses � Provision expense increased $356 million from the prior quarter to $5.1 billion � Q2-20 included a reserve build of $4.0 billion primarily due to a weaker economic outlook related to COVID-19

Allowance for credit losses4 � Allowance for credit losses, including unfunded commitments, increased $10.9 billion, or 106%, from 12/31/19 to $21.1 billion

� Allowance for loan and lease losses increased $10.0 billion, or 106%, from 12/31/19 to $19.4 billion, representing 1.96% of total loans and leases

� Nonperforming loans (NPLs) increased $337 million from Q1-20 to $4.4 billion, driven by an increase in commercial NPLs

� Commercial reservable criticized utilized exposure of $26.0 billion increased $8.6 billion, or 167 bps, from Q1-20

� Increases include Retailing, Cruise Lines, Real Estate, Energy, Restaurants and Hotels

Highlights1

Three months ended

($ in millions)

6/30/2020 3/31/2020 6/30/2019

Provision for credit losses

$5,117

$4,761

$857

Net charge-offs Net charge-off ratio2

1,146 0.45%

1,122 0.46%

887 0.38%

At period-end

Nonperforming loans and leases

$4,393

$4,056

$4,187

Nonperforming loan and leases ratio

0.44%

0.39%

0.44%

Allowance for loan and lease losses

$19,389

$15,766

$9,527

Allowance for loan and lease losses ratio3

1.96%

1.51%

1.00%

1 Comparisons are to the year-ago quarter unless noted. 2 Net charge-off ratio is calculated as annualized net charge-offs divided by average

outstanding loans and leases during the period. 3 Allowance for loan and lease losses ratio is calculated as allowance for loan and lease losses

divided by loans and leases outstanding at the end of the period. 4 The Company's adoption of the new CECL accounting standard effective January 1, 2020

measures the allowance based on management's best estimate of lifetime expected credit losses inherent in the Company's lending activities. Prior periods presented reflect measurement of the allowance based on management's estimate of probable incurred credit losses.

Note: Ratios do not include loans accounted for under the fair value option.

See page 10 for endnotes.

8

Balance Sheet, Liquidity and Capital Highlights ($ in billions except per share data, end of period, unless otherwise noted)(B,C)

Ending Balance Sheet Total assets Total loans and leases Total loans and leases in business segments (excluding All Other) Total deposits Average Balance Sheet

Average total assets Average loans and leases Average deposits Funding and Liquidity

Long-term debt Global Liquidity Sources, average(C) Equity Common shareholders' equity Common equity ratio Tangible common shareholders' equity1 Tangible common equity ratio1 Per Share Data Common shares outstanding (in billions) Book value per common share Tangible book value per common share1 Regulatory Capital(B)

CET1 capital Standardized approach Risk-weighted assets CET1 ratio Advanced approaches Risk-weighted assets CET1 ratio Supplementary leverage Supplementary leverage ratio (SLR)

6/30/2020

Three months ended 3/31/2020

6/30/2019

$2,741.7 998.9 973.8

1,718.7

$2,620.0 1,050.8 1,014.7 1,583.3

$2,395.9 963.8 920.5

1,375.1

$2,704.2 1,031.4 1,658.2

$2,494.9 990.3

1,439.3

$2,399.1 950.5

1,375.5

$261.6 796

$242.2 8.8%

$172.4 6.5%

8.66 $27.96

19.90

$256.7 565

$241.5 9.2%

$171.7 6.7%

8.68 $27.84

19.79

$238.0 552

$246.7 10.3%

$176.8 7.6%

9.34 $26.41

18.92

$171.0

$1,475 11.6%

$1,503 11.4%

7.0%

$168.1

$1,561 10.8%

$1,512 11.1%

6.4%

$171.5

$1,467 11.7%

$1,431 12.0%

6.8%

1 Represents a non-GAAP financial measure. For reconciliation, see page 18 of this press release.

9

Endnotes

A

Reserve Build (or Release) is calculated by subtracting net charge-offs for the period from the provision for credit losses recognized in that period. The

period-end allowance, or reserve, for credit losses reflects the beginning of the period allowance adjusted for net charge-offs recorded in that period

plus the provision for credit losses recognized in that period.

B

Regulatory capital ratios at June 30, 2020 are preliminary. The Corporation reports regulatory capital ratios under both the Standardized and Advanced

approaches. The approach that yields the lower ratio is used to assess capital adequacy, which for Common equity tier 1 (CET1) is the Advanced

approaches for the quarter ended June 30, 2020 and the Standardized approach for all other reporting dates presented. Supplementary leverage exposure

at June 30, 2020 excludes U.S. Treasury Securities and deposits at Federal Reserve Banks.

C

Global Liquidity Sources (GLS) include cash and high-quality, liquid, unencumbered securities, inclusive of U.S. government securities, U.S. agency

securities, U.S. agency MBS, and a select group of non-U.S. government and supranational securities, and other investment-grade securities, and are

readily available to meet funding requirements as they arise. It does not include Federal Reserve Discount Window or Federal Home Loan Bank borrowing

capacity. Transfers of liquidity among legal entities may be subject to certain regulatory and other restrictions.

D

We present certain key financial and nonfinancial performance indicators (KPIs) that management uses when assessing consolidated and/or segment

results. We believe this information is useful because it provides management and investors with information about underlying operational performance

and trends. KPIs are presented in Balance Sheet, Liquidity and Capital Highlights and on the Segment pages for each segment.

E

We also measure net interest income on an FTE basis, which is a non-GAAP financial measure. FTE basis is a performance measure used in operating the

business that management believes provides investors a more accurate picture of the interest margin for comparative purposes. We believe that this

presentation allows for comparison of amounts from both taxable and tax-exempt sources and is consistent with industry practices. Net interest income

on an FTE basis was $11.0 billion, $12.3 billion and $12.3 billion for the three months ended June 30, 2020, March 31, 2020 and June 30, 2019,

respectively. The FTE adjustment was $128 million, $144 million and $149 million for the three months ended June 30, 2020, March 31, 2020 and June

30, 2019, respectively.

F

Source: Dealogic as of July 1, 2020.

G

Global Markets revenue and net income, excluding net debit valuation adjustments (DVA), and sales and trading revenue, excluding net DVA, are non-

GAAP financial measures. Net DVA gains (losses) were $(261) million, $300 million and $(31) million for the three months ended June 30, 2020,

March 31, 2020 and June 30, 2019, respectively. FICC net DVA gains (losses) were $(245) million, $274 million and $(30) million for the three months

ended June 30, 2020, March 31, 2020 and June 30, 2019, respectively. Equities net DVA gains (losses) were $(16) million, $26 million and $(1) million for

the three months ended June 30, 2020, March 31, 2020 and June 30, 2019, respectively.

H

Pretax, pre-provision income (PTPI) at the consolidated level is a non-GAAP financial measure calculated by adjusting consolidated pretax income to add

back provision for credit losses. Similarly, PTPI at the segment level is a non-GAAP financial measure calculated by adjusting the segments' pretax

income to add back the provision for credit losses. Management believes that PTPI (both at the consolidated and segment level) is a useful financial

measure as it enables an assessment of the Company's ability to generate earnings to cover credit losses through a credit cycle and provides an

additional basis for comparing the Company's results of operations between periods by isolating the impact of provision for credit losses, which can vary

significantly between periods. For Reconciliations to GAAP financial measures, see page 18 for Total company and below for segments.

(Dollars in millions)

Pretax income Provision for credit losses

Pretax, pre-provision income

Pretax income Provision for credit losses

Pretax, pre-provision income

Pretax income Provision for credit losses

Pretax, pre-provision income

Consumer Banking

$

94

3,024

$ 3,118

Second Quarter 2020

GWIM

Global Banking

Global Markets

$ 826 $ 995 $ 2,562

136

1,873

105

$ 962 $ 2,868 $ 2,667

All Other $ (550)

(21) $ (571)

Consumer Banking $ 2,376

2,258

$ 4,634

First Quarter 2020

GWIM

Global Banking

Global Markets

$ 1,147 $

186 $ 2,307

189

2,093

107

$ 1,336 $ 2,279 $ 2,414

All Other $ (1,341)

114 $ (1,227)

Consumer Banking $ 4,358

947

$ 5,305

Second Quarter 2019

GWIM

Global Banking

Global Markets

$ 1,425 $ 2,639 $ 1,464

21

125

5

$ 1,446 $ 2,764 $ 1,469

All Other $ (778)

(241) $ (1,019)

10

Contact Information and Investor Conference Call Invitation

Investor Call Information

Note: Chief Executive Officer Brian Moynihan and Chief Financial Officer Paul Donofrio will discuss secondquarter 2020 financial results in a conference call at 8:30 a.m. ET today. The presentation and supporting materials can be accessed on the Bank of America Investor Relations website at http://investor.bankofamerica.com.

For a listen-only connection to the conference call, dial 1.877.200.4456 (U.S.) or 1.785.424.1732 (international). The conference ID is 79795. Please dial in 10 minutes prior to the start of the call. Investors can access replays of the conference call by visiting the Investor Relations website or by calling 1.800.934.4850 (U.S.) or 1.402.220.1178 (international) from July 16 through July 25.

Investors May Contact:

Reporters May Contact:

Lee McEntire, Bank of America, 1.980.388.6780 lee.mcentire@bofa.com

Jonathan Blum, Bank of America (Fixed Income), 1.212.449.3112 jonathan.blum@bofa.com

Jerry Dubrowski, Bank of America, 1.646.855.1195 (office) or 1.508.843.5626 (mobile) jerome.f.dubrowski@bofa.com

Bank of America Bank of America is one of the world's leading financial institutions, serving individual consumers, small and middle-market businesses and large corporations with a full range of banking, investing, asset management and other financial and risk management products and services. The company provides unmatched convenience in the United States, serving approximately 66 million consumer and small business clients with approximately 4,300 retail financial centers, including approximately 3,000 lending centers, 2,600 financial centers with a Consumer Investment Financial Solutions Advisor and approximately 2,200 business centers; approximately 16,900 ATMs; and award-winning digital banking with approximately 39 million active users, including approximately 30 million mobile users. Bank of America is a global leader in wealth management, corporate and investment banking and trading across a broad range of asset classes, serving corporations, governments, institutions and individuals around the world. Bank of America offers industryleading support to approximately 3 million small business households through a suite of innovative, easy-to-use online products and services. The company serves clients through operations across the United States, its territories and approximately 35 countries. Bank of America Corporation stock (NYSE: BAC) is listed on the New York Stock Exchange.

Forward-Looking Statements Bank of America Corporation (the "Company") and its management may make certain statements that constitute "forward-looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995. These statements can be identified by the fact that they do not relate strictly to historical or current facts. Forward-looking statements often use words such as "anticipates," "targets," "expects," "hopes," "estimates," "intends," "plans," "goals," "believes," "continue" and other similar expressions or future or conditional verbs such as "will," "may," "might," "should," "would" and "could." Forward-looking statements represent the Company's current expectations, plans or forecasts of its future results, revenues, expenses, efficiency ratio, capital measures, strategy, and future business and economic conditions more generally, and other future matters. These statements are not guarantees of future results or performance and involve certain known and unknown risks, uncertainties and assumptions that are difficult to predict and are often beyond the Company's control. Actual outcomes and results may differ materially from those expressed in, or implied by, any of these forward-looking statements.

11

You should not place undue reliance on any forward-looking statement and should consider the following uncertainties and risks, as well as the risks and uncertainties more fully discussed under Item 1A. Risk Factors of the Company's 2019 Annual Report on Form 10-K and in any of the Company's subsequent Securities and Exchange Commission filings: the Company's potential judgments, claims, damages, penalties, fines and reputational damage resulting from pending or future litigation and regulatory and government actions, including as a result of our participation in and execution of government programs related to the COVID-19 pandemic; the possibility that the Company's future liabilities may be in excess of its recorded liability and estimated range of possible loss for litigation, regulatory, and representations and warranties exposures; the possibility that the Company could face increased servicing, fraud, indemnity, contribution or other claims from one or more counterparties, including trustees, purchasers of loans, underwriters, issuers, monolines, private-label and other investors, or other parties involved in securitizations; the Company's ability to resolve representations and warranties repurchase and related claims, including claims brought by investors or trustees seeking to avoid the statute of limitations for repurchase claims; the risks related to the discontinuation of the London InterBank Offered Rate and other reference rates, including increased expenses and litigation and the effectiveness of hedging strategies; uncertainties about the financial stability and growth rates of non-U.S. jurisdictions, the risk that those jurisdictions may face difficulties servicing their sovereign debt, and related stresses on financial markets, currencies and trade, and the Company's exposures to such risks, including direct, indirect and operational; the impact of U.S. and global interest rates, inflation, currency exchange rates, economic conditions, trade policies and tensions, including tariffs, and potential geopolitical instability; the impact of the interest rate environment on the Company's business, financial condition and results of operations; the possibility that future credit losses may be higher than currently expected due to changes in economic assumptions, customer behavior, adverse developments with respect to U.S. or global economic conditions and other uncertainties; the Company's ability to achieve its expense targets and expectations regarding net interest income, provision for credit losses, net charge-offs, effective tax rate, loan growth or other projections; adverse changes to the Company's credit ratings from the major credit rating agencies; an inability to access capital markets or maintain deposits or borrowing costs; estimates of the fair value and other accounting values, subject to impairment assessments, of certain of the Company's assets and liabilities; the estimated or actual impact of changes in accounting standards or assumptions in applying those standards; uncertainty regarding the content, timing and impact of regulatory capital and liquidity requirements; the impact of adverse changes to total loss-absorbing capacity requirements, stress capital buffer requirements and/or global systemically important bank surcharges; the potential impact of actions of the Board of Governors of the Federal Reserve System on the Company's capital plans; the effect of regulations, other guidance or additional information on the impact from the Tax Cuts and Jobs Act; the impact of implementation and compliance with U.S. and international laws, regulations and regulatory interpretations, including, but not limited to, recovery and resolution planning requirements, Federal Deposit Insurance Corporation assessments, the Volcker Rule, fiduciary standards, derivatives regulations and the Coronavirus Aid, Relief, and Economic Security Act and any similar or related rules and regulations; a failure or disruption in or breach of the Company's operational or security systems or infrastructure, or those of third parties, including as a result of cyber-attacks or campaigns; the impact on the Company's business, financial condition and results of operations from the United Kingdom's exit from the European Union; the impact of any future federal government shutdown and uncertainty regarding the federal government's debt limit; the emergence of widespread health emergencies or pandemics, including the magnitude and duration of the COVID-19 pandemic and its impact on the U.S. and/or global economy, financial market conditions and our business, results of operations and financial condition; the impact of natural disasters, military conflict, terrorism or other geopolitical events; and other matters.

Forward-looking statements speak only as of the date they are made, and the Company undertakes no obligation to update any forward-looking statement to reflect the impact of circumstances or events that arise after the date the forward-looking statement was made.

"Bank of America" and "BofA Securities" are the marketing names used by the Global Banking and Global Markets divisions of Bank of America Corporation. Lending, other commercial banking activities, and trading in certain financial instruments are performed globally by banking affiliates of Bank of America Corporation, including Bank of America, N.A., Member FDIC. Trading in securities and financial instruments, and strategic advisory, and other investment banking activities, are performed globally by investment banking affiliates of Bank of America Corporation ("Investment Banking Affiliates"), including, in the United States, BofA Securities, Inc. and Merrill Lynch Professional Clearing Corp., both of which are registered broker-dealers and Members of SIPC, and, in other jurisdictions, by locally registered entities. BofA Securities, Inc. and Merrill Lynch Professional Clearing Corp. are registered as futures commission merchants with the CFTC and are members of the NFA. Investment products offered by Investment Banking Affiliates: Are Not FDIC Insured � May Lose Value � Are Not Bank Guaranteed. Bank of America Corporation's broker-dealers are not banks and are separate legal entities from their bank affiliates. The obligations of the broker-dealers are not obligations of their bank affiliates (unless explicitly stated otherwise), and these bank affiliates are not responsible for securities sold, offered, or recommended by the broker-dealers. The foregoing also applies to other non-bank affiliates.

For more Bank of America news, including dividend announcements and other important information, visit the Bank of America newsroom at https://newsroom.bankofamerica.com.

www.bankofamerica.com

12

13

Bank of America Corporation and Subsidiaries

Selected Financial Data

(In millions, except per share data)

Summary Income Statement

Net interest income Noninterest income

Total revenue, net of interest expense Provision for credit losses Noninterest expense

Income before income taxes Income tax expense

Net income Preferred stock dividends

Net income applicable to common shareholders

Six Months Ended June 30

2020

2019

$ 22,978 $

24,564

22,115

21,524

45,093

46,088

9,878

1,870

26,885

26,492

8,330

17,726

787

3,067

$

7,543 $

14,659

718

681

$

6,825 $

13,978

Second Quarter

2020

$ 10,848

11,478

22,326

5,117

13,410

3,799

266

$

3,533

249

$

3,284

First Quarter

2020

$

12,130

10,637

22,767

4,761

13,475

4,531

521

$

4,010

469

$

3,541

Second Quarter

2019

$

12,189

10,895

23,084

857

13,268

8,959

1,611

$

7,348

239

$

7,109

Average common shares issued and outstanding Average diluted common shares issued and outstanding

8,777.6 8,813.3

9,624.0 9,672.4

8,739.9 8,768.1

8,815.6 8,862.7

9,523.2 9,559.6

Summary Average Balance Sheet

Total debt securities Total loans and leases Total earning assets Total assets Total deposits Common shareholders' equity Total shareholders' equity

$ 470,638 1,010,835 2,239,406 2,599,557 1,548,766 241,983 265,425

$ 444,077 947,291

2,017,555 2,380,127 1,367,700

244,668 267,101

$ 476,060 1,031,387 2,358,782 2,704,186 1,658,197 242,889 266,316

$ 465,215 990,283

2,120,029 2,494,928 1,439,336

241,078 264,534

$ 446,447 950,525

2,023,722 2,399,051 1,375,450

245,438 267,975

Performance Ratios

Return on average assets Return on average common shareholders' equity Return on average tangible common shareholders' equity (1)

0.58% 5.67 7.97

1.24% 11.52 16.13

0.53% 5.44 7.63

0.65% 5.91 8.32

1.23% 11.62 16.24

Per Common Share Information

Earnings Diluted earnings Dividends paid Book value Tangible book value (1)

$

0.78 $

0.77

0.36

27.96

19.90

1.45 $ 1.45 0.30 26.41 18.92

0.38 $ 0.37 0.18 27.96 19.90

0.40 $ 0.40 0.18 27.84 19.79

0.75 0.74 0.15 26.41 18.92

Summary Period-End Balance Sheet

Total debt securities Total loans and leases Total earning assets Total assets Total deposits Common shareholders' equity Total shareholders' equity Common shares issued and outstanding

June 30 2020

$ 471,861 998,944

2,391,043 2,741,688 1,718,666

242,210 265,637 8,664.1

March 31 2020

$ 475,852 1,050,785 2,265,254 2,619,954 1,583,325 241,491 264,918 8,675.5

June 30 2019

$ 446,075 963,800

2,027,935 2,395,892 1,375,093

246,719 271,408 9,342.6

Credit Quality

Total net charge-offs Net charge-offs as a percentage of average loans and leases outstanding (2) Provision for credit losses

Six Months Ended June 30

2020

2019

Second Quarter

2020

First Quarter

2020

Second Quarter

2019

$

2,268 $

1,878 $

1,146 $

1,122 $

887

0.46%

0.40%

0.45%

0.46%

0.38%

$

9,878 $

1,870 $

5,117 $

4,761 $

857

Total nonperforming loans, leases and foreclosed properties (3) Nonperforming loans, leases and foreclosed properties as a percentage of total loans, leases and foreclosed properties (2) Allowance for loan and lease losses Allowance for loan and lease losses as a percentage of total loans and leases outstanding (2)

For footnotes, see page 14.

June 30 2020

March 31 2020

June 30 2019

$

4,611 $

4,331 $

4,452

0.47%

0.42%

0.47%

$ 19,389 $

15,766 $

9,527

1.96%

1.51%

1.00%

Current period information is preliminary and based on company data available at the time of the presentation.

14

Bank of America Corporation and Subsidiaries

Selected Financial Data (continued)

(Dollars in millions)

Capital Management

Regulatory capital metrics (4): Common equity tier 1 capital Common equity tier 1 capital ratio - Standardized approach Common equity tier 1 capital ratio - Advanced approaches Tier 1 leverage ratio

June 30 2020

March 31 2020

June 30 2019

$ 171,020 $ 168,115 $ 171,498

11.6%

10.8%

11.7%

11.4

11.1

12.0

7.4

7.9

8.4

Tangible equity ratio (5) Tangible common equity ratio (5)

7.3

7.7

8.7

6.5

6.7

7.6

(1) Return on average tangible common shareholders' equity and tangible book value per share of common stock are non-GAAP financial measures. We believe the use of ratios that utilize tangible equity provides additional

useful information because they present measures of those assets that can generate income. Tangible book value per share provides additional useful information about the level of tangible assets in relation to outstanding

shares of common stock. See Reconciliations to GAAP Financial Measures on page 18. (2) Ratios do not include loans accounted for under the fair value option. Charge-off ratios are annualized for the quarterly presentation. (3) Balances do not include past due consumer credit card loans, consumer loans secured by real estate where repayments are insured by the Federal Housing Administration and individually insured long-term stand-by

agreements (fully insured home loans), and in general, other consumer and commercial loans not secured by real estate, and nonperforming loans held for sale or accounted for under the fair value option. (4) Regulatory capital ratios at June 30, 2020 are preliminary. Bank of America Corporation reports regulatory capital ratios under both the Standardized and Advanced approaches. The approach that yields the lower ratio is

used to assess capital adequacy, which for Common equity tier 1 (CET1) is the Advanced approaches for the quarter ended June 30, 2020 and Standardized approach for all other reporting dates presented. (5) Tangible equity ratio equals period-end tangible shareholders' equity divided by period-end tangible assets. Tangible common equity ratio equals period-end tangible common shareholders' equity divided by period-end

tangible assets. Tangible shareholders' equity and tangible assets are non-GAAP financial measures. We believe the use of ratios that utilize tangible equity provides additional useful information because they present

measures of those assets that can generate income. See Reconciliations to GAAP Financial Measures on page 18.

Current period information is preliminary and based on company data available at the time of the presentation.

15

Bank of America Corporation and Subsidiaries

Quarterly Results by Business Segment and All Other

(Dollars in millions)

Total revenue, net of interest expense Provision for credit losses Noninterest expense Net income Return on average allocated capital (1) Balance Sheet Average

Total loans and leases Total deposits Allocated capital (1) Quarter end Total loans and leases Total deposits

Second Quarter 2020

Consumer Banking

GWIM

Global Banking

Global Markets

All Other

$ 7,851 $ 4,425 $ 5,091 $ 5,349 $

(262)

3,024

136

1,873

105

(21)

4,733

3,463

2,223

2,682

309

71

624

726

1,896

216

1%

17%

7%

21%

n/m

$ 321,558 $ 182,150 $ 423,625 $ 74,131 $

810,700

287,109

493,918

45,083

38,500

15,000

42,500

36,000

$ 325,105 $ 184,293 $ 390,108 $ 74,342 $

854,017

291,740

500,918

52,842

29,923 21,387

n/m

25,096 19,149

Total revenue, net of interest expense Provision for credit losses Noninterest expense Net income (loss) Return on average allocated capital (1)

Balance Sheet Average

Total loans and leases Total deposits Allocated capital (1) Quarter end Total loans and leases Total deposits

Consumer Banking

$

9,129 $

2,258

4,495

1,794

19 %

GWIM

First Quarter 2020

Global Banking

Global Markets

4,936 $ 189

3,600 866 23 %

4,600 $ 2,093 2,321

136 1%

5,226 $ 107

2,812 1,707

19 %

All Other

(980) 114 247 (493) n/m

$ 316,946 $ 178,639 $ 386,483 $

736,669

263,411

382,373

38,500

15,000

42,500

71,660 $ 33,323 36,000

$ 317,535 $ 181,492 $ 437,122 $

762,387

282,395

477,108

78,591 $ 38,536

36,555 23,560

n/m

36,045 22,899

Total revenue, net of interest expense Provision for credit losses Noninterest expense Net income Return on average allocated capital (1)

Balance Sheet Average

Total loans and leases Total deposits Allocated capital (1) Quarter end Total loans and leases Total deposits

Consumer Banking

$

9,717 $

947

4,412

3,290

36 %

GWIM

Second Quarter 2019

Global Banking

Global Markets

4,900 $ 21

3,454 1,076

30 %

4,975 $ 125

2,211 1,926

19 %

4,144 $ 5

2,675 1,047

12 %

All Other

(503) (241) 516

9 n/m

$ 296,388 $ 166,324 $ 372,531 $

707,091

253,940

362,619

37,000

14,500

41,000

70,587 $ 31,128 35,000

$ 300,411 $ 168,993 $ 376,948 $

714,289

251,835

358,902

74,136 $ 29,961

44,695 20,672

n/m

43,312 20,106

(1) Return on average allocated capital is calculated as net income, adjusted for cost of funds and earnings credits and certain expenses related to intangibles, divided by average allocated capital. Other companies may define or calculate these measures differently.

n/m = not meaningful

Certain prior-period amounts have been reclassified among the segments to conform to current-period presentation.

The Company reports the results of operations of its four business segments and All Other on a fully taxable-equivalent (FTE) basis.

Current period information is preliminary and based on company data available at the time of the presentation.

16

Bank of America Corporation and Subsidiaries

Year-to-Date Results by Business Segment and All Other

(Dollars in millions)

Total revenue, net of interest expense Provision for credit losses Noninterest expense Net income (loss) Return on average allocated capital (1) Balance Sheet Average

Total loans and leases Total deposits Allocated capital (1) Period end Total loans and leases Total deposits

Consumer Banking

Six Months Ended June 30, 2020

GWIM

Global Banking

Global Markets

All Other

$ 16,980 $ 5,282 9,228 1,865 10%

9,361 $ 325

7,063 1,490

20%

9,691 $ 3,966 4,544

862 4%

10,575 $ 212

5,494 3,603

20%

(1,242) 93

556 (277) n/m

$ 319,252 $ 180,395 $ 405,054 $ 72,896 $

773,685

275,260

438,145

39,203

38,500

15,000

42,500

36,000

$ 325,105 $ 184,293 $ 390,108 $ 74,342 $

854,017

291,740

500,918

52,842

33,238 22,473

n/m

25,096 19,149

Total revenue, net of interest expense Provision for credit losses Noninterest expense Net income (loss) Return on average allocated capital (1)

Balance Sheet Average

Total loans and leases Total deposits Allocated capital (1) Period end Total loans and leases Total deposits

Consumer Banking

$ 19,349 $ 1,921 8,779 6,530 36 %

Six Months Ended June 30, 2019

GWIM

Global Banking

Global Markets

9,720 $ 26

6,887 2,119

30 %

10,130 $ 236

4,478 3,954

19 %

8,326 $ (18)

5,432 2,082

12 %

All Other

(1,135) (295) 916 (26) n/m

$ 294,339 $ 165,369 $ 371,326 $

702,074

257,868

355,866

37,000

14,500

41,000

70,335 $ 31,246 35,000

$ 300,411 $ 168,993 $ 376,948 $

714,289

251,835

358,902

74,136 $ 29,961

45,922 20,646

n/m

43,312 20,106

(1) Return on average allocated capital is calculated as net income, adjusted for cost of funds and earnings credits and certain expenses related to intangibles, divided by average allocated capital. Other companies may define or calculate these measures differently.

n/m = not meaningful

Certain prior-period amounts have been reclassified among the segments to conform to current-period presentation.

Current period information is preliminary and based on company data available at the time of the presentation.

17

Bank of America Corporation and Subsidiaries

Supplemental Financial Data

(Dollars in millions)

FTE basis data (1) Net interest income Total revenue, net of interest expense Net interest yield Efficiency ratio

Six Months Ended June 30

2020

2019

Second Quarter

2020

First Quarter

2020

Second Quarter

2019

$ 23,250 $

24,866 $ 10,976 $

12,274 $

12,338

45,365

46,390

22,454

22,911

23,233

2.09%

2.48%

1.87%

2.33%

2.44%

59.26

57.11

59.72

58.82

57.11

Other Data Number of financial centers - U.S. Number of branded ATMs - U.S. Headcount

June 30 2020 4,298 16,862 212,796

March 31 2020 4,297 16,855 208,931

June 30 2019 4,349 16,561 208,984

(1) FTE basis is a non-GAAP financial measure. FTE basis is a performance measure used by management in operating the business that management believes provides investors with a more accurate picture of the interest margin for comparative purposes. The Corporation believes that this presentation allows for comparison of amounts from both taxable and tax-exempt sources and is consistent with industry practices. Net interest income includes FTE adjustments of $272 million and $302 million for the six months ended June 30, 2020 and 2019, respectively; $128 million and $144 million for the second and first quarters of 2020, respectively, and $149 million for the second quarter of 2019.

Certain prior-period amounts have been reclassified to conform to current-period presentation.

Current period information is preliminary and based on company data available at the time of the presentation.

18

Bank of America Corporation and Subsidiaries

Reconciliations to GAAP Financial Measures

(Dollars in millions, except per share information)

The Corporation evaluates its business based on the following ratios that utilize tangible equity, a non-GAAP financial measure. Tangible equity represents an adjusted shareholders' equity or common shareholders' equity amount which has been reduced by goodwill and intangible assets (excluding mortgage servicing rights), net of related deferred tax liabilities. Return on average tangible common shareholders' equity measures the Corporation's net income applicable to common shareholders as a percentage of adjusted average common shareholders' equity. The tangible common equity ratio represents adjusted ending common shareholders' equity divided by total assets less goodwill and intangible assets (excluding mortgage servicing rights), net of related deferred tax liabilities. Return on average tangible shareholders' equity measures the Corporation's net income as a percentage of adjusted average total shareholders' equity. The tangible equity ratio represents adjusted ending shareholders' equity divided by total assets less goodwill and intangible assets (excluding mortgage servicing rights), net of related deferred tax liabilities. Tangible book value per common share represents adjusted ending common shareholders' equity divided by ending common shares outstanding. These measures are used to evaluate the Corporation's use of equity. In addition, profitability, relationship and investment models all use return on average tangible shareholders' equity as key measures to support our overall growth goals.

See the tables below for reconciliations of these non-GAAP financial measures to the most closely related financial measures defined by GAAP for the six months ended June 30, 2020 and 2019 and the three months ended June 30, 2020, March 31, 2020 and June 30, 2019. The Corporation believes the use of these non-GAAP financial measures provides additional clarity in understanding its results of operations and trends. Other companies may define or calculate supplemental financial data differently.

Six Months Ended June 30

2020

2019

Second Quarter

2020

First Quarter

2020

Second Quarter

2019

Reconciliation of income before income taxes to pretax, pre-provision income Income before income taxes Provision for credit losses

Pretax, pre-provision income

Reconciliation of average shareholders' equity to average tangible shareholders' equity and average tangible common shareholders' equity

Shareholders' equity Goodwill Intangible assets (excluding mortgage servicing rights) Related deferred tax liabilities

Tangible shareholders' equity Preferred stock

Tangible common shareholders' equity

$ 8,330 $ 9,878

$ 18,208 $

17,726 $ 1,870

19,596 $

3,799 $ 5,117 8,916 $

4,531 $ 4,761 9,292 $

8,959 857

9,816

$ 265,425 $ (68,951) (1,648) 759

$ 195,585 $ (23,442)

$ 172,143 $

267,101 (68,951)

(1,750) 805

197,205 (22,433) 174,772

$ 266,316 $ (68,951) (1,640) 790

$ 196,515 $ (23,427)

$ 173,088 $

264,534 $ (68,951)

(1,655) 728

194,656 $ (23,456) 171,200 $

267,975 (68,951)

(1,736) 770

198,058 (22,537) 175,521

Reconciliation of period-end shareholders' equity to period-end tangible shareholders' equity and period-end tangible common shareholders' equity

Shareholders' equity Goodwill Intangible assets (excluding mortgage servicing rights) Related deferred tax liabilities

Tangible shareholders' equity Preferred stock

Tangible common shareholders' equity

$ 265,637 $ (68,951) (1,630) 789

$ 195,845 $ (23,427)

$ 172,418 $

271,408 (68,951)

(1,718) 756

201,495 (24,689) 176,806

$ 265,637 $ (68,951) (1,630) 789

$ 195,845 $ (23,427)

$ 172,418 $

264,918 $ (68,951)

(1,646) 790

195,111 $ (23,427) 171,684 $

271,408 (68,951)

(1,718) 756

201,495 (24,689) 176,806

Reconciliation of period-end assets to period-end tangible assets Assets Goodwill Intangible assets (excluding mortgage servicing rights) Related deferred tax liabilities

Tangible assets

$ 2,741,688 $ 2,395,892

(68,951)

(68,951)

(1,630)

(1,718)

789

756

$ 2,671,896 $ 2,325,979

$ 2,741,688 $ 2,619,954 $ 2,395,892

(68,951)

(68,951)

(68,951)

(1,630)

(1,646)

(1,718)

789

790

756

$ 2,671,896 $ 2,550,147 $ 2,325,979

Book value per share of common stock Common shareholders' equity Ending common shares issued and outstanding

Book value per share of common stock

$ 242,210 $ 8,664.1

$ 27.96 $

246,719 9,342.6

26.41

$ 242,210 $ 8,664.1

$ 27.96 $

241,491 $ 8,675.5

27.84 $

246,719 9,342.6

26.41

Tangible book value per share of common stock Tangible common shareholders' equity Ending common shares issued and outstanding

Tangible book value per share of common stock

$ 172,418 $ 8,664.1

$ 19.90 $

176,806 9,342.6

18.92

$ 172,418 $ 8,664.1

$ 19.90 $

171,684 $ 8,675.5

19.79 $

176,806 9,342.6

18.92

Certain prior-period amounts have been reclassified to conform to current-period presentation. Current period information is preliminary and based on company data available at the time of the presentation.