!! 08 ITEMS1 5

Preview ! 08-ITEMS1-5 Wisconsin Aluminum Foundry Lawn Mower Manuals - Lawn Mower Manuals – The Best Lawn Mower Manuals Collection

User Manual: !! Wisconsin Aluminum Foundry Lawn Mower Manuals - Lawn Mower Manuals – The Best Lawn Mower Manuals Collection

Open the PDF directly: View PDF ![]() .

.

Page Count: 10

1

PART I

ITEM 1. BUSINESS

Briggs & Stratton is the world's largest producer of air cooled gasoline engines for outdoor power equipment.

Briggs & Stratton designs, manufactures, markets and services these products for original equipment

manufacturers (OEMs) worldwide. These engines are aluminum alloy gasoline engines with displacements

ranging from 31 cubic centimeters to 993 cubic centimeters.

Additionally, through its wholly owned subsidiary, Briggs & Stratton Power Products Group, LLC, Briggs &

Stratton is a leading designer, manufacturer and marketer of generators (portable and home standby),

pressure washers, air compressors, snow throwers, lawn and garden powered equipment (riding and walk

behind mowers, tillers, chipper/shredders, leaf blowers and vacuums) and related accessories.

Briggs & Stratton conducts its operations in two reportable segments: Engines and Power Products. Further

information about Briggs & Stratton's business segments is contained in Note 6 of the Notes to Consolidated

Financial Statements.

The Company's Internet address is www.briggsandstratton.com. The Company makes available free of

charge (other than an investor's own Internet access charges) through its Internet website the Company's

Annual Report on Form 10‐K, quarterly reports on Form 10‐Q, current reports on Form 8‐K, and

amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange

Act of 1934, as soon as reasonably practicable after it electronically files such material with, or furnishes

such material to, the Securities and Exchange Commission. Charters of the Audit, Compensation,

Nominating and Governance Committees; Corporate Governance Guidelines and code of business conduct

and ethics contained in the Briggs & Stratton Business Integrity Manual are available on the Company's

website and are available in print to any shareholder upon request to the Corporate Secretary.

Engines

General

Briggs & Stratton's Engines Segment's engines are used primarily by the lawn and garden equipment

industry, which accounted for 84% of the segment's fiscal 2007 engine sales to OEMs. Major lawn and

garden equipment applications include walk‐behind lawn mowers, riding lawn mowers, garden tillers and

snow throwers. The remaining 16% of engine sales to OEMs in fiscal 2007 were for use on products for

industrial, construction, agricultural and other consumer applications, that include generators, pumps and

pressure washers. Many retailers specify Briggs & Stratton's engines on the powered equipment they sell,

and the Briggs & Stratton name is often featured prominently on a product despite the fact that the engine is

only a component.

In fiscal 2007, approximately 28% of Briggs & Stratton's Engines Segment net sales were derived from sales

in international markets, primarily to customers in Europe. Briggs & Stratton serves its key international

markets through its European regional office in Switzerland, its distribution center in the Netherlands and

sales and service subsidiaries and offices in Australia, Austria, Brazil, Canada, China, the Czech Republic,

England, France, Germany, Italy, Japan, Mexico, New Zealand, Poland, Russia, South Africa, Spain, Sweden

and United Arab Emirates. Briggs & Stratton is a leading supplier of gasoline engines in developed countries

where there is an established lawn and garden equipment market. Briggs & Stratton also exports engines to

developing nations where its engines are used in agricultural, marine, construction and other applications.

More detailed information about our foreign operations is in Note 6 of the Notes to Consolidated Financial

Statements.

Briggs & Stratton engines are sold primarily by its worldwide sales force through direct calls on customers.

Briggs & Stratton's marketing staff and engineers in the United States provide support and technical

assistance to its sales force.

Briggs & Stratton also manufactures replacement engines and service parts and sells them to sales and

service distributors. Briggs & Stratton owns its principal international distributors. In the United States the

distributors are independently owned and operated. These distributors supply service parts and replacement

engines directly to independently owned, authorized service dealers throughout the world. These distributors

and service dealers implement Briggs & Stratton's commitment to reliability and service.

2

Customers

Briggs & Stratton's engine sales are made primarily to OEMs. Briggs & Stratton's three largest external

engine customers in fiscal years 2007, 2006 and 2005 were Husqvarna Outdoor Products Group (HOP),

MTD Products Inc. (MTD) and John Deere Power Products. Sales to the top three customers combined were

54%, 51% and 45% of Engines Segment net sales in fiscal 2007, 2006 and 2005, respectively. Under

purchasing plans available to all of its gasoline engine customers, Briggs & Stratton typically enters into

annual engine supply arrangements.

Briggs & Stratton believes that in fiscal 2007 more than 80% of all lawn and garden powered equipment sold

in the United States was sold through mass merchandisers such as Sears Holdings Corporation (Sears), The

Home Depot, Inc. (The Home Depot), Wal‐Mart Stores, Inc. (Wal‐Mart) and Lowe's Companies, Inc.

(Lowe's). Given the buying power of the mass merchandisers, Briggs & Stratton, through its customers, has

continued to experience pricing pressure. Briggs & Stratton expects that this pricing trend will continue in the

foreseeable future. Briggs & Stratton believes that a similar trend has developed for its products in industrial

and consumer applications outside of the lawn and garden market.

Competition

Briggs & Stratton's major domestic competitors in engine manufacturing are Honda Motor Co., Ltd. (Honda),

Kawasaki Heavy Industries, Ltd. (Kawasaki), Kohler Co. (Kohler), and Tecumseh Products Company

(Tecumseh). Several Japanese and Chinese small engine manufacturers, of which Honda and Kawasaki are

the largest, compete directly with Briggs & Stratton in world markets in the sale of engines to other OEMs

and indirectly through their sale of end products.

Briggs & Stratton believes it has a significant share of the worldwide market for engines that power outdoor

equipment.

Briggs & Stratton believes the major areas of competition from all engine manufacturers include product

quality, brand strength, price, timely delivery and service. Other factors affecting competition are short‐term

market share objectives, short‐term profit objectives, exchange rate fluctuations, technology, product support

and distribution strength. Briggs & Stratton believes its product value and service reputation have given it

strong brand name recognition and enhance its competitive position.

Seasonality of Demand

Sales of engines to lawn and garden OEMs are highly seasonal because of consumer buying patterns. The

majority of lawn and garden equipment is sold during the spring and summer months when most lawn care

and gardening activities are performed. Sales of lawn and garden equipment are also influenced by weather

conditions. Engine sales in Briggs & Stratton's fiscal third quarter have historically been the highest, while

sales in the first fiscal quarter have historically been the lowest.

In order to efficiently use its capital investments and meet seasonal demand for engines, Briggs & Stratton

pursues a relatively balanced production schedule throughout the year. The schedule is adjusted to reflect

changes in estimated demand, customer inventory levels and other matters outside the control of Briggs &

Stratton. Accordingly, inventory levels generally increase during the first and second fiscal quarters in

anticipation of customer demand. Inventory levels begin to decrease as sales increase in the third fiscal

quarter. This seasonal pattern results in high inventories and low cash flow for Briggs & Stratton in the

second and the beginning of the third fiscal quarters. The pattern results in higher cash flow in the latter

portion of the third fiscal quarter and in the fourth fiscal quarter as inventories are liquidated and receivables

are collected.

Manufacturing

Briggs & Stratton manufactures engines and parts at the following locations: Auburn, Alabama; Statesboro,

Georgia; Murray, Kentucky; Poplar Bluff and Rolla, Missouri; Wauwatosa, Wisconsin; Chongqing, China; and

Ostrava, Czech Republic. Briggs & Stratton has a parts distribution center in Menomonee Falls, Wisconsin.

In April 2007, the Company announced that it would be discontinuing operations at our Rolla, Missouri facility

in October 2007. Engine manufacturing performed in Rolla will be moving to the Chongqing, China and

Poplar Bluff, Missouri plants.

Briggs & Stratton manufactures a majority of the structural components used in its engines, including

aluminum die castings, carburetors and ignition systems. Briggs & Stratton purchases certain parts such as

3

piston rings, spark plugs, valves, ductile and grey iron castings, zinc die castings and plastic components,

some stampings and screw machine parts and smaller quantities of other components. Raw material

purchases consist primarily of aluminum and steel. Briggs & Stratton believes its sources of supply are

adequate.

Briggs & Stratton has joint ventures with Daihatsu Motor Company for the manufacture of engines in Japan,

with Starting Industrial of Japan for the production of rewind starters in the United States, and The Toro

Company for the manufacture of two‐cycle engines in China.

Briggs & Stratton has a strategic relationship with Mitsubishi Heavy Industries (MHI) for the global distribution

of air cooled gasoline engines manufactured by MHI in Japan under Briggs & Stratton's Vanguard™ brand.

Power Products

General

Briggs & Stratton Power Products Group, LLC's (BSPPG) principal product lines include portable and

standby generators, pressure washers, air compressors, snow throwers and lawn and garden powered

equipment. BSPPG sells its products through multiple channels of retail distribution, including consumer

home centers, warehouse clubs, mass merchants and independent dealers. BSPPG product lines are

marketed under various brands including Briggs & Stratton, Craftsman®, Ferris, Giant Vac, Murray,

Simplicity, Snapper and Troy‐Bilt®.

BSPPG has a network of independent dealers worldwide for the sale and service of snow throwers and lawn

and garden powered equipment.

To support its international business, BSPPG has leveraged the existing Briggs & Stratton worldwide

distribution network.

Customers

Historically, BSPPG's major customers have been Lowe's, The Home Depot and Sears. Other U.S. retail

customers include Tractor Supply Inc., True Value Company, W.W. Grainger, Wal‐Mart and Menards.

Competition

The principal competitive factors in the power products industry include price, service, product performance,

technical innovation and delivery. BSPPG has various competitors, depending on the type of equipment.

Primary competitors include: Honda (portable generators, pressure washers and lawn and garden

equipment), Coleman Powermate Corporation (portable generators), Generac Power Systems, Inc.

(“Generac”) (standby generators), DeVilbiss Air Power Company, a Division of Black & Decker (pressure

washers), Alfred Karcher GmbH & Co. (pressure washers), John Deere (commercial and consumer lawn

mowers), MTD (lawn mowers), the Toro Company (commercial and consumer lawn mowers), and Scag

Power Equipment, a Division of Metalcraft of Mayville, Inc. (commercial lawn mowers).

BSPPG believes it has a significant share of the North American market for portable generators and

consumer pressure washers.

Seasonality of Demand

Sales of BSPPG's products are subject to seasonal patterns. Due to seasonal and regional weather factors,

sales of pressure washers and lawn and garden powered equipment are typically higher during the fiscal

third and fourth quarters than at other times of the year. Sales of portable generators and snow throwers are

typically higher during the first and second fiscal quarters.

Manufacturing

BSPPG's manufacturing facilities are located in Jefferson, Watertown and Port Washington, Wisconsin;

McDonough, Georgia; Munnsville, New York; Newbern, Tennessee; and Qingpu, China. BSPPG also

purchases certain powered equipment under contract manufacturing agreements.

BSPPG plans to close its Port Washington, Wisconsin manufacturing facility during the second quarter of

fiscal 2009. Production will move to the McDonough, Georgia facility.

4

BSPPG manufactures core components for its products, where such integration improves operating

profitability by providing lower costs.

BSPPG purchases engines from its parent, Briggs & Stratton, as well as from Generac, Honda, Kawasaki

and Kohler. BSPPG has not experienced any difficulty obtaining necessary engines or other purchased

components.

BSPPG assembles products for the international markets at its U.S. and China locations and through

contract manufacturing agreements with other OEMs.

Consolidated

General Information

Briggs & Stratton holds patents on features incorporated in its products; however, the success of Briggs &

Stratton's business is not considered to be primarily dependent upon patent protection. The Company owns

several trademarks which it believes significantly affect a consumer's choice of outdoor powered equipment

and therefore create value. Licenses, franchises and concessions are not a material factor in Briggs &

Stratton's business.

For the fiscal years ended July 1, 2007, July 2, 2006 and July 3, 2005, Briggs & Stratton spent approximately

$25.7 million, $28.8 million and $33.5 million, respectively, on research activities relating to the development

of new products or the improvement of existing products.

The average number of persons employed by Briggs & Stratton during fiscal 2007 was 7,666. Employment

ranged from a high of 8,439 in July 2006 to a low of 7,235 in October 2006.

Export Sales

Export sales for fiscal 2007, 2006 and 2005 were $490.7 million (23% of net sales), $527.0 million (21% of

net sales) and $477.4 million (18% of net sales), respectively. These sales were principally to customers in

European countries. Refer to Note 6 of the Notes to Consolidated Financial Statements for financial

information about geographic areas. Also, refer to Item 7A of this Form 10‐K and Note 13 of the Notes to

Consolidated Financial Statements for information about Briggs & Stratton's foreign exchange risk

management.

ITEM 1A. RISK FACTORS

In addition to the risks referred to elsewhere in this Annual Report on Form 10‐K, the following risks, among

others, may have affected, and in the future could affect, the Company and its subsidiaries' business,

financial condition or results of operations. Additional risks not discussed or not presently known to the

Company or that the Company currently deems insignificant may also impact its business and stock price.

Demand for products fluctuates significantly due to seasonality. In addition, changes in the weather

and consumer disposable income impact demand.

Sales of our products are subject to seasonal and consumer buying patterns. Consumer demand in our

markets can be reduced by unfavorable weather, a reduction in disposable income, and other factors. We

manufacture throughout the year although our sales are concentrated in the second half of our fiscal year.

This operating method requires us to anticipate demand of our customers many months in advance. If we

overestimate or underestimate demand during a given year, we may not be able to adjust our production

quickly enough to avoid excess or insufficient inventories, and that may in turn limit our ability to maximize

our potential sales.

We have only a limited ability to pass through cost increases in our raw materials to our customers

during the year.

We generally enter into annual purchasing plans with our largest customers, so our ability to raise our prices

during a particular year to reflect increased raw materials costs is limited.

5

A significant portion of our net sales comes from major customers and the loss of any of these

customers would negatively impact our financial results.

In fiscal 2007, our three largest customers accounted for 36% of our consolidated net sales. The loss of a

significant portion of the business of one or more of these key customers would significantly impact our net

sales and profitability.

Changes in environmental or other laws could require extensive changes in our operations or to our

products.

Our operations and products are subject to a variety of foreign, federal, state and local laws and regulations

governing, among other things, emissions to air, discharges to water, noise, the generation, handling,

storage, transportation, treatment and disposal of waste and other materials and health and safety matters.

New engine emission regulations are being phased in through 2008 by the federal government and the State

of California. We do not expect these changes to have a material adverse effect on us, but we cannot be

certain that these or other proposed changes in applicable laws or regulations will not adversely affect our

business or financial condition in the future.

Foreign economic conditions and currency rate fluctuations can reduce our sales.

In fiscal 2007, we derived approximately 23% of our consolidated net sales from international markets,

primarily Europe. Weak economic conditions in Europe could reduce our sales and currency fluctuations

could adversely affect our sales or profit levels in U.S. dollar terms.

Actions of our competitors could reduce our sales or profits.

Our markets are highly competitive and we have a number of significant competitors in each market.

Competitors may reduce their costs, lower their prices or introduce innovative products that could hurt our

sales or profits. In addition, our competitors may focus on reducing our market share to improve their results.

Disruptions caused by labor disputes or organized labor activities could harm our business.

A portion of our workforce is currently represented by labor unions. In addition, we may from time to time

experience union organizing activities in our non‐union facilities. Disputes with the current labor union or new

union organizing activities could lead to work slowdowns or stoppages and make it difficult or impossible for

us to meet scheduled delivery times for product shipments to our customers, which could result in loss of

business. In addition, union activity could result in higher labor costs, which could harm our financial

condition, results of operations and competitive position.

As of July 1, 2007, we had approximately $384.0 million of long‐term debt. In addition, we have the

ability to incur additional borrowings on our revolving credit facility. This level of debt could

adversely affect our operating flexibility and put us at a competitive disadvantage.

Our level of debt and the limitations imposed on us by the indentures for the notes and our other credit

agreements could have important consequences, including the following:

•we will have to use a portion of our cash flow from operations for debt service rather than for our operations;

•we may not be able to obtain additional debt financing for future working capital, capital expenditures or other

corporate purposes or may have to pay more for such financing;

•some or all of the debt under our current or future revolving credit facilities will be at a variable interest rate,

making us more vulnerable to increases in interest rates;

•we could be less able to take advantage of significant business opportunities, such as acquisition

opportunities, and to react to changes in market or industry conditions;

•we will be more vulnerable to general adverse economic and industry conditions; and

•we may be disadvantaged compared to competitors with less leverage.

The terms of the indentures for the senior notes do not fully prohibit us from incurring substantial additional

debt in the future and our revolving credit facilities permit additional borrowings, subject to certain conditions.

If new debt is added to our current debt levels, the related risks we now face could intensify.

We expect to obtain the money to pay our expenses and to pay the principal and interest on the outstanding

8.875% senior notes, the 7.25% senior notes, the variable rate term notes, the credit facilities and other debt

primarily from our operations. Our ability to meet our expenses thus depends on our future performance,

6

which will be affected by financial, business, economic and other factors. We will not be able to control many

of these factors, such as economic conditions in the markets where we operate and pressure from

competitors. We cannot be certain that the money we earn will be sufficient to allow us to pay principal and

interest on our debt and meet our other obligations. If we do not have enough money, we may be required to

refinance all or part of our existing debt, sell assets or borrow more money. We cannot guarantee that we will

be able to do so on terms acceptable to us. In addition, the terms of existing or future debt agreements,

including the revolving credit facilities and our indentures, may restrict us from adopting any of these

alternatives.

We are restricted by the terms of the outstanding senior notes and our other debt, which could

adversely affect us.

The indentures relating to the senior notes and our revolving credit agreements each include a number of

financial and operating restrictions, which may prevent us from capitalizing on business opportunities and

taking some corporate actions. These covenants could adversely affect us by limiting our ability to plan for or

react to market conditions or to meet our capital needs. These covenants include, among other things,

restrictions on our ability to:

•pay dividends or make distributions in respect of our capital stock or to make certain other restricted

payments;

•incur indebtedness or issue preferred shares;

•create liens;

•make loans or investments;

•enter into sale and leaseback transactions;

•agree to payment restrictions affecting our restricted subsidiaries;

•consolidate, merge, sell or lease all or substantially all of our assets;

•enter into transactions with affiliates; and

•dispose of assets or the proceeds of sales of our assets.

In addition, our revolving credit facility contains financial covenants that, among other things, require us to

maintain a minimum interest coverage ratio and impose a maximum leverage ratio.

Our failure to comply with restrictive covenants under the indentures governing the senior notes and

our revolving credit facilities could trigger prepayment obligations.

Our failure to comply with the restrictive covenants described above could result in an event of default,

which, if not cured or waived, could result in us being required to repay these borrowings before their due

date. If we are forced to refinance these borrowings on less favorable terms, our results of operations and

financial condition could be adversely affected by increased costs and rates.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

ITEM 2. PROPERTIES

The corporate offices and one of Briggs & Stratton's engine manufacturing facilities are located in

Wauwatosa, Wisconsin. Briggs & Stratton also has engine manufacturing facilities in Auburn, Alabama;

Statesboro, Georgia; Murray, Kentucky; Poplar Bluff, Missouri; Ostrava, Czech Republic and Chongqing,

China. These are owned facilities containing approximately 3.1 million square feet of office and production

area. The Company currently leases an engine manufacturing facility in Rolla, Missouri, which contains

approximately 404,000 square feet. Briggs & Stratton also leases warehouse space in the localities of its

engine manufacturing facilities, except China, totaling approximately 619,750 square feet. Additionally, a

service parts distribution center consisting of approximately 335,400 square feet is leased in Menomonee

Falls, Wisconsin.

BSPPG maintains office space and manufacturing facilities in Brookfield, Jefferson, Watertown and Port

Washington, Wisconsin; McDonough, Georgia; Newbern, Tennessee; Munnsville, New York and Qingpu,

China. Of these, the domestic facilities, except Brookfield, Wisconsin, are owned and contain approximately

7

1.5 million square feet. The Brookfield, Wisconsin office space is leased and contains approximately 26,000

square feet. BSPPG also leases warehouse space in Jefferson, Watertown and Fort Atkinson, Wisconsin;

McDonough, Georgia; Grand Prairie, Texas; Greenville, Ohio; Reno, Nevada; and Sherrill and Hamilton, New

York totaling approximately 1.8 million square feet. Additionally, the Qingpu, China facility is leased and

contains approximately 131,000 square feet.

Briggs & Stratton leases approximately 290,000 square feet of space to house its foreign sales and service

operations.

As Briggs & Stratton's business is seasonal, additional warehouse space may be leased when inventory

levels are at their peak. Briggs & Stratton's owned properties are well maintained. Briggs & Stratton believes

that its owned and leased facilities are adequate to perform its operations in a reasonable manner.

ITEM 3. LEGAL PROCEEDINGS

Briggs & Stratton is subject to various unresolved legal actions that arise in the normal course of its

business. These actions typically relate to product liability (including asbestos‐related liability), patent and

trademark matters, and disputes with customers, suppliers, distributors and dealers, competitors and

employees.

On June 3, 2004, eight individuals who claim to have purchased lawnmowers in Illinois and Minnesota filed a

lawsuit (Ronnie Phillips et al. v. Sears Roebuck Corporation et al., No. 04‐L‐334 (20th Judicial Circuit,

St. Clair County, IL)) against the Company and other defendants alleging that the horsepower labels on the

products they purchased were inaccurate. The plaintiffs have amended their complaint several times and

currently seek an injunction, compensatory and punitive damages, and attorneys' fees under various federal

and state laws including the Racketeer Influenced and Corrupt Organization Act on behalf of all persons in

the United States who, beginning January 1, 1994 through the present, purchased a lawnmower containing a

two‐stroke or four‐stroke gasoline combustion engine up to 30 horsepower that was manufactured or sold by

the defendants. On May 31, 2006, the defendants removed the case to the U.S. District Court for the

Southern District of Illinois (No. 06‐412‐DRH). The defendants subsequently filed cross claims against each

other for indemnification and contribution and filed a motion to dismiss the amended complaint. On March

30, 2007, the Court issued an order granting the defendants' motion to dismiss the amended complaint in its

entirety, but the order permits the plaintiffs to refile a complaint after amending several claims. An opinion of

the Court providing more detail concerning its order is expected but has not yet been filed. Two defendants,

MTD Products, Inc. and American Honda Motor Company, have notified the Court that they have reached a

settlement with the putative plaintiff class, but neither defendant's agreement has yet been approved by the

Court.

Although it is not possible to predict with certainty the outcome of these unresolved legal actions or the range

of possible loss, Briggs & Stratton believes the range of possible losses for these unresolved legal actions

will not have a material effect on its financial position.

ITEM 4. SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS

No matters were submitted to a vote of security holders, through the solicitation of proxies or otherwise,

during the three months ended July 1, 2007.

8

Executive Officers of the Registrant

Name, Age, Position Business Experience for Past Five Years

JOHN S. SHIELY, 55

Chairman, President and Chief Executive Officer

(1)(2)(3)

Mr. Shiely was elected to his current position effective

January 2003, after serving as President and Chief

Executive Officer since July 2001 and President and

Chief Operating Officer since August 1994.

TODD J. TESKE, 42

Executive Vice President and Chief

Operating Officer

Mr. Teske was elected to his current position effective

September 2005 after serving as Senior Vice President

and President - Briggs & Stratton Power Products Group,

LLC since September 2003. He previously served as Vice

President and President - Briggs & Stratton Power

Products Group, LLC since February 2003. He also

served as Vice President - Corporate Development from

March 2001 after serving as Controller since October

1998.

JAMES E. BRENN, 59

Senior Vice President and Chief Financial Officer

Mr. Brenn was elected to his current position in October

1998, after serving as Vice President and Controller since

November 1988. He also served as Treasurer from

November 1999 until January 2000.

DAVID G. DEBAETS, 44

Vice President - North American Operations

(Engine Power Products Group)

Mr. DeBaets was elected to his current position effective

September 2007. He has served as Vice President and

General Manager - Large Engine Division since April

2000. He also served as Vice President and General

Manager - Die Cast Components from May 1996 to April

2000.

MARK R. HAZELTINE, 64

Vice President and

Sales Manager - Consumer Products

Mr. Hazeltine was elected to his current position in May

2002, after serving as Vice President and Sales Manager

- Consumer Lawn & Garden since July 1999. He also

served as Sales Manager from February 1995 to June

1999.

ROBERT F. HEATH, 59

Secretary

Mr. Heath was elected to his current position in January

2002. He served as Assistant Secretary from January

2001 to December 2001. In addition, Mr. Heath is Vice

President and General Counsel and has served in these

positions since January 2001. He also served as General

Counsel since December 1997.

HAROLD L. REDMAN, 43

Vice President and President -

Home Power Products Group

Mr. Redman was elected to his current position effective

September 2006. He has served as Vice President and

President - Home Power Products since May 2006. He

also served as Senior Vice President - Sales & Marketing

- Simplicity Manufacturing, Inc. since July 1995.

WILLIAM H. REITMAN, 51

Senior Vice President - Sales &

Customer Support

Mr. Reitman was elected to his current position effective

September 2007, after serving as Senior Vice President

- Sales & Marketing since May 2006, and Vice President

- Sales & Marketing since October 2004. He also served

as Vice President - Marketing since November 1995.

9

DAVID J. RODGERS, 36

Controller

Mr. Rodgers was elected as an executive officer in

September 2007 and has served as Controller since

December 2006. He was previously employed by

Roundy's Supermarkets, Inc. as Vice President -

Controller from September 2005 to November 2006 and

Vice President - Retail Controller from May 2003 to

August 2005. He also was previously employed by Arthur

Andersen LLP and Deloitte & Touche LLP.

THOMAS R. SAVAGE, 59

Senior Vice President - Administration

Mr. Savage was elected to his current position effective

July 1997, after serving as Vice President -

Administration and General Counsel since November

1994. He also served as Secretary from November 1999

to June 2000.

MICHAEL D. SCHOEN, 47

Senior Vice President and President -

International Power Products Group

Mr. Schoen was elected to his current position effective

September 2005 after serving as Vice President -

International Group since July 2001. He was elected an

executive officer in August 2000, after serving as Vice

President - Operations Support since July 1999. He

previously held the position of Vice President -

International Operations since July 1996.

VINCENT R. SHIELY, 47

Senior Vice President and President -

Yard Power Products Group (3)

Mr. Shiely was elected to his current position effective

May 2006, after serving as Vice President and President

- Home Power Products Group since September 2005.

He also served as Vice President and General Manager

- Home Power Products Division October 2004 to

September 2005. He previously served as Vice President

and General Manager - Engine Products Group since

September 2002. He has also served as Vice President

and General Manager - Business Units since December

2001, and as Vice President and General Manager -

Electrical Products Division since October 1998.

CARITA R. TWINEM, 52

Treasurer

Ms. Twinem was elected to her current position in

February 2000. In addition, Ms. Twinem is Tax Director

and has served in this position since July 1994.

JOSEPH C. WRIGHT, 48

Senior Vice President and President -

Engine Power Products Group

Mr. Wright was elected to his current position in May 2006

after serving as Vice President and President - Yard

Power Products Group since September 2005. He also

served as Vice President and General Manager - Lawn

and Garden Division from September 2004 to September

2005. He was elected an executive officer effective

September 2002. He previously served as Vice President

and General Manager - Small Engine Division since July

1997.

(1) Officer is also a Director of Briggs & Stratton. (2) Member of the Board of Directors Executive Committee.

(3) John S. Shiely and Vincent R. Shiely are brothers.

Officers are elected annually and serve until they resign, die, are removed, or a different person is appointed

to the office.

10

PART II

ITEM 5. MARKET FOR THE REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER

MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Briggs & Stratton common stock and its common share purchase rights are traded on the NYSE under the

symbol “BGG”. Information required by this Item is incorporated by reference from the “Quarterly Financial

Data, Dividend and Market Information” (unaudited) on page 52.

Changes in Securities, Use of Proceeds and Issuer Purchases of Equity Securities

Briggs & Stratton did not make any purchases of equity securities registered by the company pursuant to

Section 12 of the Exchange Act during the fourth quarter of fiscal 2007.

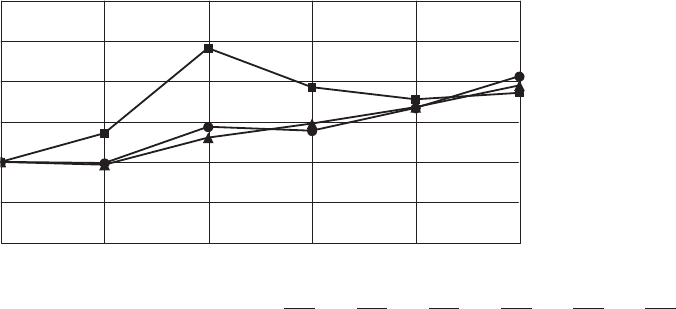

Five‐year Stock Performance Graph

The chart below is a comparison of the cumulative return over the last five fiscal years had $100 been

invested at the close of business on June 30, 2001 in each of Briggs & Stratton common stock, the Standard

& Poor's (S&P) Smallcap 600 Index and the S&P Machinery Index.

6/07

FIVE YEAR CUMULATIVE TOTAL RETURN COMPARISON*

Briggs & Stratton versus Published Indices

$100

$50

$06/02 6/03

6/02 6/03 6/04 6/05 6/06 6/07

JBriggs & Stratton 100.00 135.83 242.40 193.44 178.24 186.34. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

YS&P Smallcap 600 100.00 96.42 130.41 147.95 168.55 195.58. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

FS&P Machinery (diversified) 100.00 98.61 143.97 139.05 167.53 207.08. . . . . . . . . . . . . . . . . . . . . . . . . . . .

* Total return calculation is based on compounded monthly returns with reinvested dividends.

$150

$250

6/05

6/04

$300

6/06

$200