Your Retirement Benefit—How It Is Figured 211948C 10070 10

User Manual: 211948C

Open the PDF directly: View PDF ![]() .

.

Page Count: 2

(over)

Your Retirement Benefit: How It Is Figured

Your Retirement Benefit:

How It Is Figured YEARS

2010

As you make plans for your retirement, you

may ask, “How much will I get from Social

Security?” There are several ways you can find

out. Social Security sends a yearly Social Security

Statement to everyone age 25 or older who has

paid Social Security taxes and has not yet received

benefits. You should receive a Statement about

three months before your birthday each year.

You also can request a Statement online at

www.socialsecurity.gov/onlineservices. Or, you

can request a Statement by calling Social Security

and asking for a form SSA-7004, Request for Social

Security Statement. You can use the Retirement

Estimator at www.socialsecurity.gov/estimator to

find out how much you might receive.

Many people wonder how their benefit is

figured. Social Security benefits are based on

your lifetime earnings. Your actual earnings are

adjusted or “indexed” to account for changes in

average wages since the year the earnings were

received. Then Social Security calculates your

average indexed monthly earnings during the 35

years in which you earned the most. We apply a

formula to these earnings and arrive at your basic

benefit, or “primary insurance amount” (PIA).

This is how much you would receive at your full

retirement age—65 or older, depending on your

date of birth.

On the back of this page is a worksheet you

can use to estimate your retirement benefit if

you were born in 1948. It is only an estimate;

for specific information, talk with a Social

Security representative.

Factors that can change the amount of

your retirement benefit

•

•

You choose to get benefits before your full

retirement age. You can begin to receive

Social Security benefits as early as age 62,

but at a reduced rate. Your basic benefit will

be reduced by a certain percentage if you

retire before reaching full retirement age.

You are eligible for cost-of-living benefit

increases starting with the year you become

age 62. This is true even if you do not get

benefits until your full retirement age or even

age 70. Cost-of-living increases are added to

your benefit beginning with the year you reach

62 up to the year you start getting benefits.

•

•

You delay your retirement past your full

retirement age. Social Security benefits are

increased by a certain percentage (depending

on your date of birth) if you delay

receiving benefits until past your full

retirement age. If you do so, your benefit

amount will be increased until you start

taking benefits or you reach age 70.

You are a government worker with a

pension. If you also get or are eligible for a

pension from work where you did not pay Social

Security taxes (usually a government job), a

different formula is applied to your average

indexed monthly earnings. To find out how the

Windfall Elimination Provision (WEP) affects

your benefits, go to www.socialsecurity.gov/

gpo-wep and use the WEP online calculator. You

also can review the WEP fact sheet to find out

how your benefit is figured. Or, you can contact

Social Security and ask for Windfall Elimination

Provision (Publication No. 05-10045).

You may find a more detailed explanation about

how your retirement benefit is calculated in the

Annual Statistical Supplement, 2008, Appendix D.

The publication is available on the Internet at

www.socialsecurity.gov/policy/docs/statcomps/

supplement or you can order a paper copy by

writing to the Government Printing Office, P.O.

Box 371954, Pittsburgh, PA 15250-7954.

Contacting Social Security

For more information and to find copies of

our publications, visit our website at

www.socialsecurity.gov or call toll-free,

1-800-772-1213 (for the deaf or hard of hearing,

call our TTY number, 1-800-325-0778). We treat

all calls confidentially. We can answer specific

questions from 7 a.m. to 7 p.m., Monday through

Friday. We can provide information by automated

phone service 24 hours a day.

We also want to make sure you receive

accurate and courteous service. That is why we

have a second Social Security representative

monitor some telephone calls.

YEARS

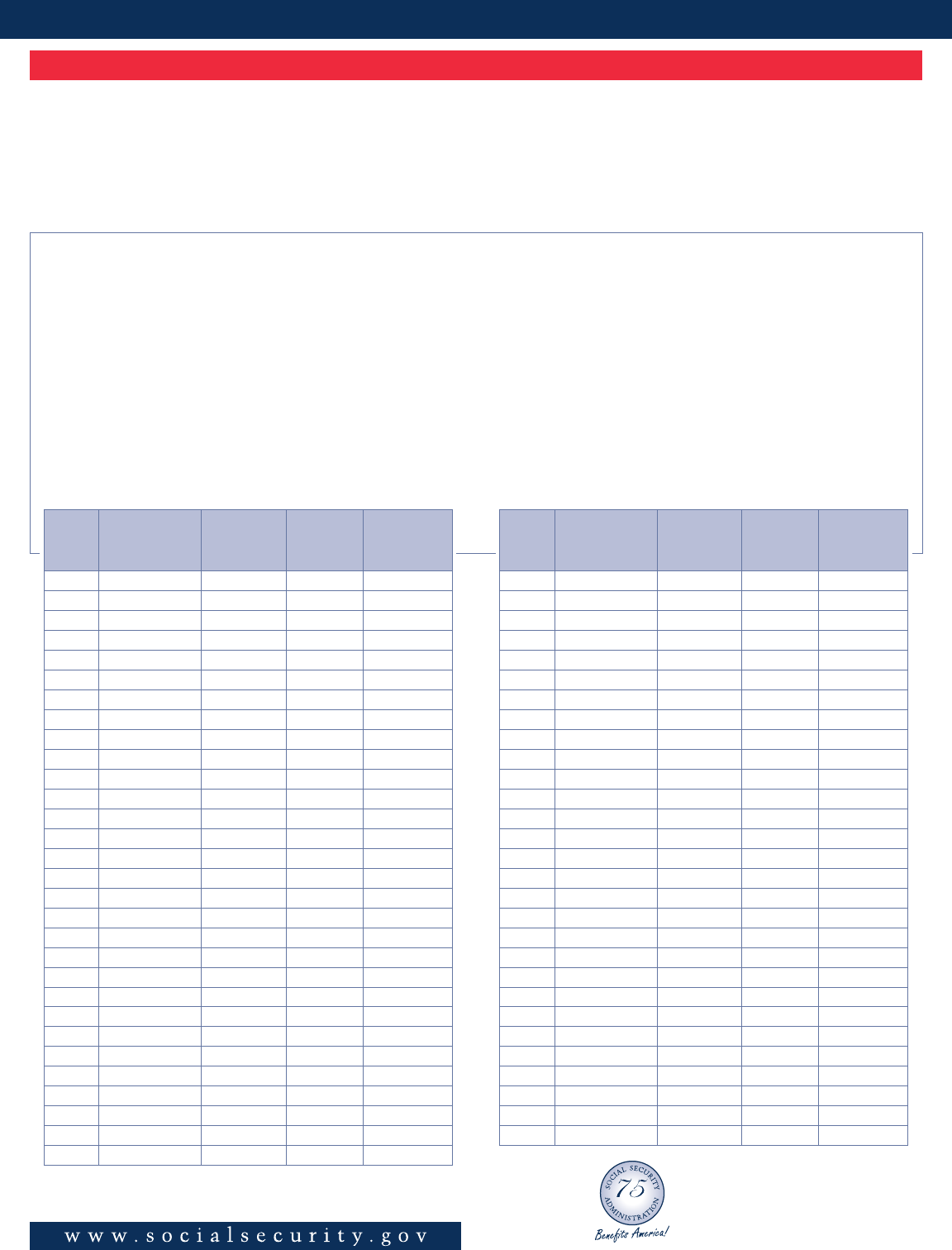

Estimating your Social Security retirement benefit

For workers born in 1948 (people born in 1948 become age 62 in 2010 and are eligible for a benefit)

This worksheet shows how to estimate the Social Security monthly retirement benefit you would be eligible

for at age 62 if you were born in 1948. It also allows you to estimate what you would receive at age 66, your

full retirement age, excluding any cost-of-living adjustments for which you may be eligible. If you continue

working past age 62, your additional earnings could increase your benefit. People born after 1948 can use this

worksheet, but their actual benefit may be higher due to additional earnings and benefit increases. If you were

born before 1948, please go online at www.socialsecurity.gov or contact us for your worksheet.

Step 1: Enter your actual earnings in Column B, but

not more than the amount shown in Column A. If

you have no earnings, enter “0.”

Step 2: Multiply the amounts in Column B by the

index factors in Column C, and enter the results in

Column D. This gives you your indexed earnings,

or the approximate value of your earnings in

current dollars.

Step 3: Choose from Column D the 35 years with the

highest amounts. Add these amounts. $_________

Step 4: Divide the result from Step 3 by 420 (the

number of months in 35 years). Round down to the

next lowest dollar. This will give you your average

indexed monthly earnings. $_________

Step 5: a. Multiply the first $761 in Step 4 by 90%.

$_________

b. Multiply the amount in Step 4 over $761 and

less than or equal to $4,586 by 32%. $_________

c. Multiply the amount in Step 4 over $4,586 by 15%.

$_________

Step 6: Add a, b and c from Step 5. Round down

to the next lowest dollar. This is your estimated

monthly retirement benefit at age 66, your full

retirement age. $_________

Step 7: Multiply the amount in Step 6 by 75%.

This is your estimated monthly retirement benefit

if you retire at age 62. $_________

Year

A.

Maximum

earnings

B.

Actual

earnings

C.

Index

factor

D.

Indexed

earnings

1951 $3,600 14.77

1952 3,600 13.90

1953 3,600 13.17

1954 3,600 13.10

1955 4,200 12.52

1956 4,200 11.70

1957 4,200 11.35

1958 4,200 11.25

1959 4,800 10.72

1960 4,800 10.32

1961 4,800 10.11

1962 4,800 9.63

1963 4,800 9.40

1964 4,800 9.03

1965 4,800 8.87

1966 6,600 8.37

1967 6,600 7.93

1968 7,800 7.42

1969 7,800 7.01

1970 7,800 6.68

1971 7,800 6.36

1972 9,000 5.79

1973 10,800 5.45

1974 13,200 5.15

1975 14,100 4.79

1976 15,300 4.48

1977 16,500 4.23

1978 17,700 3.92

1979 22,900 3.60

1980 25,900 3.30

Year

A.

Maximum

earnings

B.

Actual

earnings

C.

Index

factor

D.

Indexed

earnings

1981 29,700 3.00

1982 32,400 2.84

1983 35,700 2.71

1984 37,800 2.56

1985 39,600 2.46

1986 42,000 2.39

1987 43,800 2.24

1988 45,000 2.14

1989 48,000 2.06

1990 51,300 1.97

1991 53,400 1.90

1992 55,500 1.80

1993 57,600 1.79

1994 60,600 1.74

1995 61,200 1.67

1996 62,700 1.60

1997 65,400 1.51

1998 68,400 1.43

1999 72,600 1.36

2000 76,200 1.29

2001 80,400 1.26

2002 84,900 1.24

2003 87,000 1.21

2004 87,900 1.16

2005 90,000 1.12

2006 94,200 1.07

2007 97,500 1.02

2008 102,000 1.00

2009 106,800 1.00

Social Security Administration

SSA Publication No. 05-10070

ICN 467100

Unit of Issue - HD (one hundred)

January 2010 (Destroy Prior Edition)