Twelfth Five Year Plan_vol 2.indb MW 185 12fyp Vol2

User Manual: MW 185

Open the PDF directly: View PDF ![]() .

.

Page Count: 438 [warning: Documents this large are best viewed by clicking the View PDF Link!]

Twelfth Five Year Plan

(2012–2017)

Economic Sectors

Volume II

Copyright © Planning Commission (Government of India) 2013

All rights reserved. No part of this book may be reproduced or utilised in any form or by any means, electronic or mechanical,

including photocopying, recording or by any information storage or retrieval system, without permission in writing from the Planning

Commission, Government of India.

First published in 2013 by

SAGE Publications India Pvt Ltd

B1/I-1 Mohan Cooperative Industrial Area

Mathura Road, New Delhi 110 044, India

www.sagepub.in

SAGE Publications Inc

2455 Teller Road

Thousand Oaks, California 91320, USA

SAGE Publications Ltd

1 Oliver’s Yard, 55 City Road

London EC1Y 1SP, United Kingdom

SAGE Publications Asia-Pacific Pte Ltd

33 Pekin Street

#02-01 Far East Square

Singapore 048763

Published by Vivek Mehra for SAGE Publications India Pvt Ltd, Phototypeset in 11/13pt Minion Pro by RECTO Graphics, Delhi and

printed at Saurabh Printers, New Delhi.

Library of Congress Cataloging-in-Publication Data

India. Planning Commission

Twelfth fi ve year plan (2012/2017)/Planning Commission, Government of India.

Volumes cm

1. India—Economic Policy—1991–92. Finance, Public—India. I. Title.

HC435.3.I39 338.954009’0512—dc23 2013 2013009870

ISBN: 978-81-321-1368-3 (PB)

The SAGE Team: Rudra Narayan, Archita Mandal, Rajib Chatterjee and Dally Verghese

Twelfth Five Year Plan

(2012–2017)

Economic Sectors

Volume II

Planning Commission

Government of India

Thank you for choosing a SAGE product! If you have any comment,

observation or feedback, I would like to personally hear from you.

Please write to me at contactceo@sagepub.in

—Vivek Mehra, Managing Director and CEO,

SAGE Publications India Pvt Ltd, New Delhi

Bulk Sales

SAGE India offers special discounts for purchase of books in bulk.

We also make available special imprints and excerpts from our

books on demand.

For orders and enquiries, write to us at

Marketing Department

SAGE Publications India Pvt Ltd

B1/I-1, Mohan Cooperative Industrial Area

Mathura Road, Post Bag 7

New Delhi 110044, India

E-mail us at marketing@sagepub.in

Get to know more about SAGE, be invited to SAGE events, get on

our mailing list. Write today to marketing@sagepub.in

This book is also available as an e-book.

YZ

Contents

List of Figures vii

List of Tables viii

List of Boxes xii

List of Acronyms xiv

List of Annexures xxv

12. Agriculture 1

13. Industry 51

14. Energy 130

15. Transport 195

16. Communication 258

17. Rural Development 286

18. Urban Development 318

19. Other Priority Sectors 362

Figures

12.1 Growth and Fluctuations in GDP Agriculture and Allied 2

12.2 All India Average Real Daily Wage Rate at 2011–12 Prices (` Per Day) 9

13.1 Contribution of Manufacturing to GDP Very Low in India 52

13.2 India and Global Manufacturing States 52

13.3 New Approach to Industrial Policy 55

13.4 Focus on Sectors as well as Cross-cutting Issues 59

13.5 Strategy for Land Issues 81

13.6 Description of Land Acquisition Process 83

13.7 Two Connected ‘Tracks’ for Implementation and Systems’ Improvement 101

13.8 Capability Map 102

14.1 Exploration Blocks awarded in NELP Rounds 172

14.2 Renewable Power Capacities, Top Five Countries, 2010 183

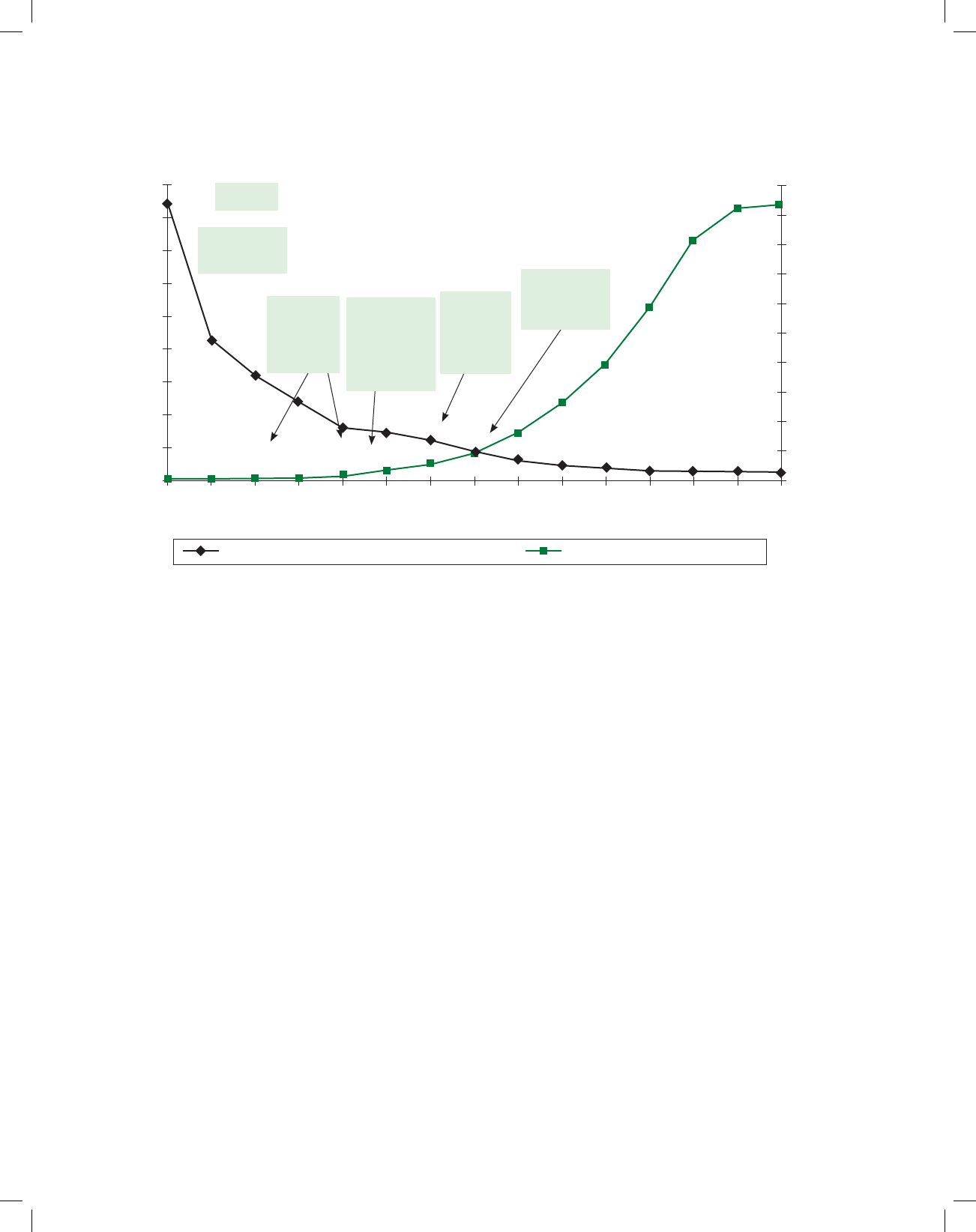

14.3 Cost of Renewable Energy Technologies Per MW 185

15.1 Existing and Proposed Thermal Power Plants on National Waterways 232

15.2 National Waterway-2 234

15.3 Kaladan Multimodal Transit Transport Project 234

16.1 Telephone Subscribers Growth during 2007–12 259

16.2 Distribution of Urban and Rural Subscribers 260

16.3 Number of Telephone and Broadband Connections 260

16.4 Mobile Tariff Trends V/s Growth in Mobile Subscribers in India (1999–2012) 261

17.1 Access to Household Amenities in Rural India (2001 to 2011) 303

17.2 Households by Type of Latrine Facility in Rural India in 2001 304

17.3 Households by Type of Latrine Facility in Rural India in 2011 304

17.4 PURA Transaction Structure 312

17.5 Institutional Structure for PURA 314

18.1 Sources of Increase in Urban Population 319

18.2 Key Constitutes of India’s Urban Future 324

Tables

12.1 Growth Rate of Agricultural and Allied Sectors 1

12.2 Some Weather Details 3

12.3 Averages and Standard Deviations of Annual Growth Rates of GSDP from Agriculture and

Allied Sectors

4

12.4 Growth of Output, Inputs and Productivity 6

12.5 Gross Capital Formation (GCF) in Agriculture, Forestry and Fishing (2004–05 prices) 8

12.6 Average Annual Growth Rates in Yields Per Hectare 10

12.7 Public Sector Capital Formation and Subsidies to Agriculture (Centre and States) 13

12.8 Real Prices of Agricultural Produce 17

12.9 Demand and Supply of Food Commodities during the Twelfth Plan 18

12.10 Expenditure on Agricultural Research and Education 30

12.11 Outlays and Expenditure of MoA and Its Three Departments (DAC, DAHDF and DARE) 47

12.12 Gross Budgetary Support (Department-wise) 50

12.13 Comparison of States Outlay and Expenditure for Eleventh and Twelfth Plan 50

13.1 Rate of Growth of GDP at Factor Cost at 2004–05 Prices (Per cent) 53

13.2 GCF in Industry 53

13.3 Employment by Sector 54

13.4 Processes that Enable Learning 62

13.5 Manufacturing Ecosystem Infrastructure 62

13.6 Registered MSMEs—Manufacturing 85

13.7 Definition of MSME 85

13.8 Manufacturing GDP by Sector and Employment Projections 96

13.9 Key Variables and Assumptions 105

13.10 Ministry/Department-wise Twelfth Five Year Plan (2012–17) Outlays Industry Sector 129

14.1 Energy Intensity for Total Primary Energy* 130

14.2 Energy Intensity 131

14.3 Household Access (%) 132

14.4 Trends in Supply of Primary Commercial Energy 133

14.5 Share of Each Fuel in Total Energy Production and Consumption 134

14.6 Installed Capacity Addition during the Eleventh Plan (in MW) 136

14.7 Mode-wise/Sector-wise Break-up of Generation 137

14.8 All-India Cumulative Generating Capacity (as on 31 March 2012) (in MW) 137

14.9 Planned Manufacturing Capacity MW Per Annum 139

14.10 Cumulative Achievement of Transmission Lines at the End of the Eleventh Plan 140

14.11 Aggregate Technical and Commercial Los ses of State Power Utilities (within State) 141

14.12 Viability of Major State Utilities Not Improving (Excluding Delhi and Odisha) 142

14.13 Details of Year-wise Progress Achieved on Restructured APDRP (as on 31 March 2012) 142

Tables ix

14.14 Status on RGGVY Progress during the Tenth and the Eleventh Plan 143

14.15 Outlay/Expenditure: Centre, States and UTs (` Crore) 146

14.16 Sector-wise and Mode-wise Capacity Addition (Provisional) during the Twelfth Plan (MW) 146

14.17 Changing Structure of Fuel for Electricity 147

14.18 Status of Hydro Electric Potential Development 148

14.19 Fuel Requirement during 2016–17 149

14.20 Transmission Line at the End of the Twelfth Plan Period 150

14.21 Inter-Regional Flow of Power at the End of Twelfth Plan Period 151

14.22 Details of Coal and Lignite Production 160

14.23 Inventory of Coal and Lignite Reserves as on 1 April 2012 160

14.24 Accretion of Coal Reserves 161

14.25 Coal Washing Capacity by the end of Eleventh Plan Period 162

14.26 Financial Performance of the Coal Sector 165

14.27 Coal Demand during the Twelfth Plan 165

14.28 Coal Production 166

14.29 Share of Underground Production in Total Production 167

14.30 Price Comparison of Domestic Coal with other Countries 167

14.31 Consumption of Petroleum Products 171

14.32 Physical Performance of Petroleum and Natural Gas Sector 172

14.33 Share of Overseas Hydrocarbon Production 173

14.34 Under-Recoveries on Petroleum Products 174

14.35 Demand of Petroleum Products 176

14.36 Projection of Crude Oil Production in the Twelfth Plan 176

14.37 Natural Gas Demand for Twelfth Five Year Plan 176

14.38 Projection of Natural gas production in Twelfth Plan (BCM) 177

14.39 Breakup of the Exploration Programme for the Twelfth Plan 177

14.40 Likely Under-Recoveries on Petroleum* Products 178

14.41 Projected Refining Capacity during Twelfth Plan (MMTPA) 178

14.42 R&D Expenditure by Major Oil and Gas Companies 180

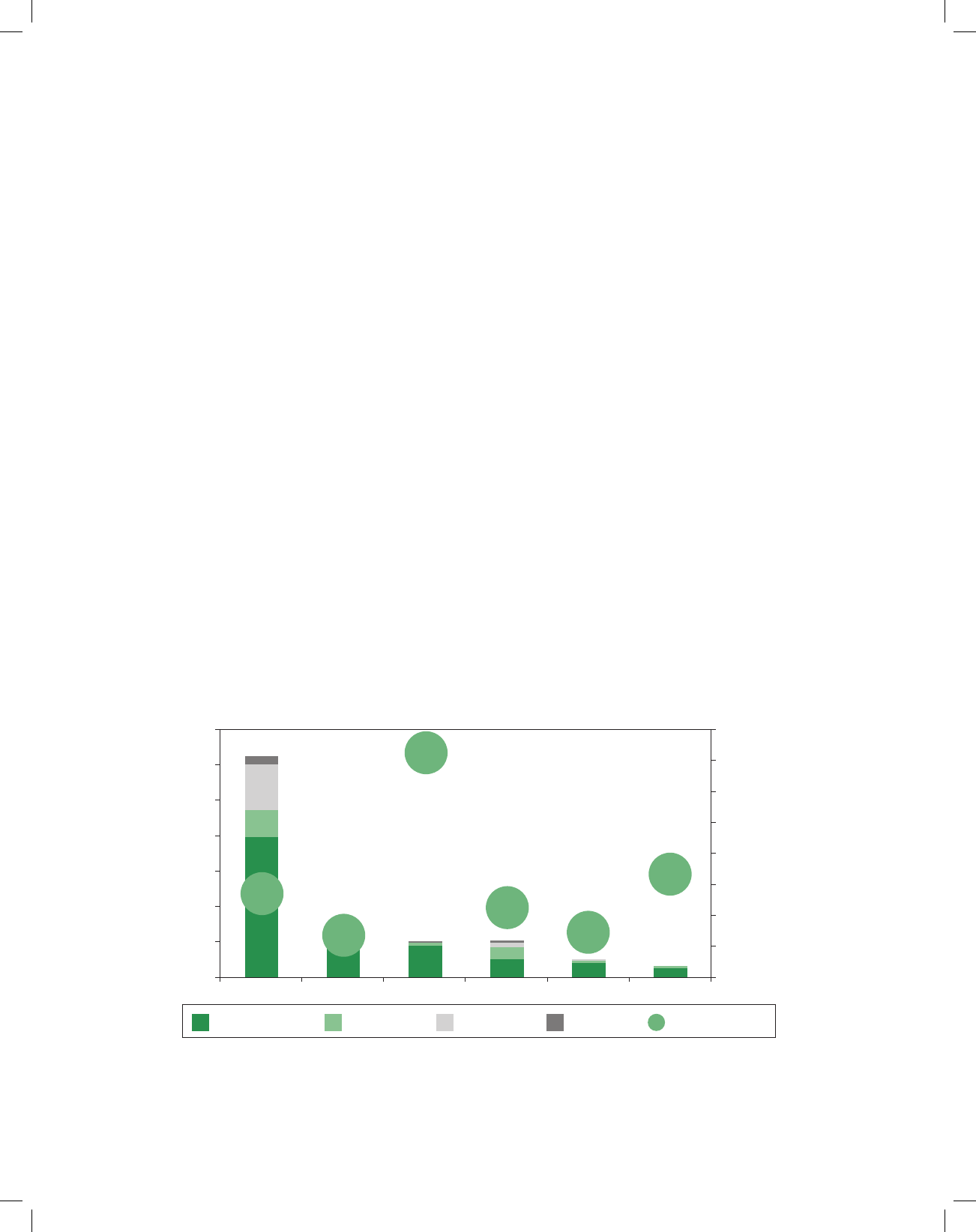

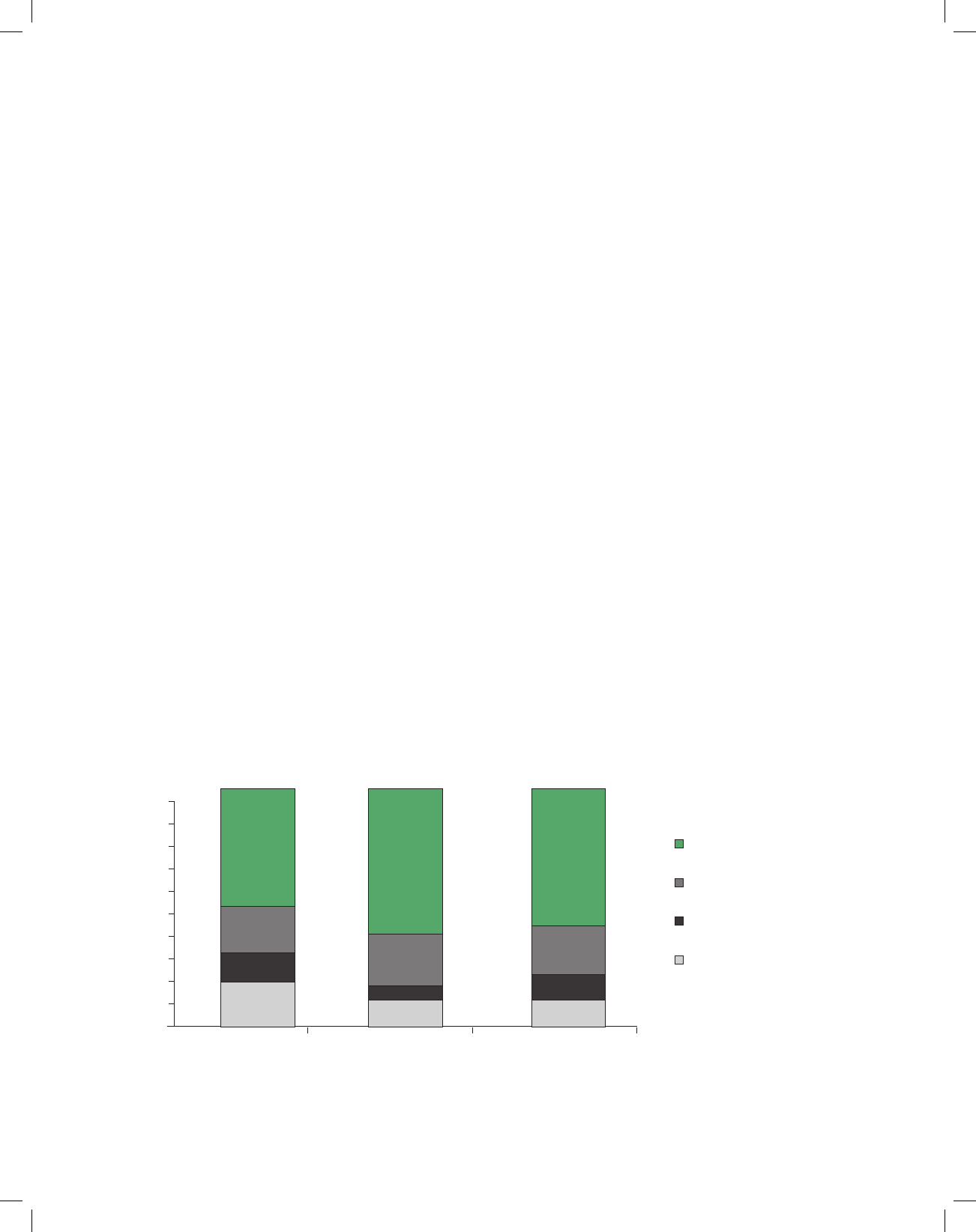

14.43 Eleventh Plan Power Capacity Addition through Grid Interactive Renewable Power 185

14.44 Cost of Power for Various Renewable Energy Sources 186

14.45 Power Capacity Addition through Off Grid Renewable Power 186

14.46 Eleventh Plan Financial Allocations and Expenditure: MNRE 187

14.47 Indicative Twelfth Five Year Plan Outlay for the Various Ministries/Departments in the

Energy Sector

190

15.1 CO2 Emissions from Various Transport Modes 196

15.2 Overview of Financial Position of the Indian Railways 199

15.3 Investment in Railways during Eleventh Plan 200

15.4 Performance of Freight Business during Eleventh Five Year Plan 201

15.5 Performance of Passenger Business during Eleventh Five Year Plan 201

15.6 Losses in Passenger Services 201

15.7 Capacity Creation during Eleventh Plan 202

15.8 Throw Forward of Infrastructure Projects as on 1 April 2012 202

15.9 Rolling Stock Performance during Eleventh Plan 203

15.10 Productivity Performance 203

15.11 Benchmarking Indian Railways with Chinese and Russian Railways 204

15.12 Traffic Projections 206

x Tables

15.13 Passenger Traffic Projections for Twelfth Plan 207

15.14 Projection of Originating PKM for Twelfth Plan 207

15.15 Creation of Fixed Assets during the Twelfth Plan 209

15.16 Rolling Stock Requirement during the Twelfth Plan 210

15.17 Passenger Service Yields in some Major Economies 213

15.18 Freight Yields in some Major Economies 213

15.19 Physical Achievements under NHDP during the Eleventh Five Year Plan 215

15.20 Progress of NHDP up to 30 April 2012 216

15.21 Physical Progress of Non-NHDP NHs during Eleventh Five Year Plan 217

15.22 State Roads Progress during the Eleventh Plan 218

15.23 Physical Progress–PMGSY (as on 31 March 2012) 219

15.24 Financial Progress (as on 31st March, 2012) 219

15.25 Habitation Coverage–Bharat Nirman (as on 31 March 2012) 220

15.26 Cumulative Physical Progress under Bharat Nirman (up to March 2012) 220

15.27 Targets for the Twelfth Plan 223

15.28 Projected Road Freight and Passenger Traffic 225

15.29 Financial Performance of the Shipping Sector in the Eleventh Plan 227

15.30 Estimated Requirements of Additional Vessels and Investment 228

15.31 Eleventh Plan Projection and Achievements of Traffic and Capacity by Major Ports 237

15.32 Commodity Wise Capacity Creation by Major Ports during Eleventh Plan 237

15.33 Traffic Handled at Major and Non-Major Ports during Eleventh Plan 238

15.34 Trend of the Productivity Parameters during Eleventh Plan 238

15.35 Year-wise Awards during Eleventh Plan under PPP 238

15.37 Commodity wise Capacity by the end of Twelfth Plan 239

15.36 Major Ports wise Traffic/Capacity Projections by End of Twelfth Plan 239

15.38 Commodity Wise Traffic by the End of Twelfth Plan (2016–17) 240

15.39 Growth Projections for the Twelfth Five Year Plan: Passenger and Cargo Traffic Forecasts 243

15.40 Investment Requirements during the Twelfth Plan 243

15.41 Comparison of ATF Prices in India with Competing Hubs 245

15.42 Flights/Week 247

15.43 Ministry/Department–wise Twelfth Five Year Plan (2012–17) Outlays for Transport Sectors 251

16.1 Targets and Achievements 267

16.2 Key Targets for the Twelfth Plan for the Electronics and IT-ITeS Industry 268

17.1 Overview of MGNREGA Performance, 2006–12 287

17.2 (A) Average Daily Wage Rates for Agricultural Labour: Male 289

17.2 (B) Seasonality of MGNREGA Employment Provided during 2010–11 290

17.3 Additional List of Permissible Works Under MGNREGA 291

17.4 Wage Payment Cycle under MGNREGA 294

17.5 Accountability Matrix for Delays in Wage Payments under MGNREGA 295

17.6 Phasing of the National Rural Livelihoods Mission 299

17.7 Investments in Rural Drinking Water, 1951–2012 300

17.8 Access to Household Amenities in Worst Performing States in Terms of Toilet Facilities in

Rural India, 2011 (Percentage of Rural Households)

303

17.9 Percentage of Households with No Latrine Facilities in Rural India, 2011 304

17.10 Total Sanitation Campaign, Physical Progress, Eleventh Plan 305

17.11 Total Sanitation Campaign, Financial Progress, Eleventh Plan 305

17.12 Major Increase in Unit Cost Support for IHHLs during the Twelfth Plan 305

17.13 IAY-Financial Performance during Eleventh Plan (2007–08 to 2011–12) 307

Tables xi

17.14 Physical Performance of IAY During Eleventh Plan (2007–08 to 2011–12) 307

17.15 Convergence of IAY with other Rural Infrastructure 308

17.16 Scheme for Purchase of Home Site and Incentive for Additional Target under IAY 308

17.17 Infrastructure and Amenities to be Provided, Operated and Maintained under PURA

Project by Private Developer in the Twelfth Plan

313

17.18 NSAP Progress in the Eleventh Plan 314

17.19 Physical and Financial Progress of NSAP Components, Eleventh Plan 315

18.1 Physical and Financial Progress under JNNURM (March 2012) 323

18.2 Estimates of Urban Transport Investments by HPEC 344

18.3 Requirement of CAPEX 344

18.4 Investments under JNNURM 349

18.5 Investment Requirement Estimates by HPEC 350

18.6 Requirement of CAPEX as per Working Group 350

19.1 Construction Sector-Macro Aggregates 362

19.2 Flow of Bank Credit to Construction Sector 371

19.3 Flow of FDI in Construction Activities (including Roads and Highways) 371

19.4 Alternative growth scenarios of tourism 376

19.5 Performance of Handloom Sector during the Eleventh Plan Period 397

19.6 Performance of Handicrafts Sector during the Eleventh Plan Period 402

Boxes

13.1 Examples of Weak Domestic Standards Leading to Influx of Sub-standard Products in the

Country

61

13.2 Dwindling Indian Capital Goods Industry 68

13.3 Strategies for Highest Overall Impact 98

13.4 Key Recommendations for Manufacturing 99

13.5 Key Recommendations 122

13.6 Key Recommendations 125

14.1 Achievements in Power Sector during the Eleventh Plan 136

14.2 Recommendations of Task Force on Open Access 145

14.3 Perform, Achieve and Trade Mechanism 157

15.1 Containerisation In Railways 207

15.2 Business Models for Passenger and Rail Freight Logistics: The JR East and Deutsche Bahn

Ways

208

15.3 Dedicated Freight Corridors (DFCs) – A Game Change for the Indian Rail Sector 209

15.4 New Generation Locomotives 210

15.5 Public-Private Partnership (PPP) in Railways 212

15.6 Key Message from Reports on Railways: The Need for Organisational Reforms 214

15.7 Financing of National Highway Development Programme (NHDP) 216

15.8 Engineering, Procurement, Construction (EPC) Contract 217

15.9 Innovations by some State Governments 223

15.10 Introduction of Electronic Toll Collection (ETC) 225

15.11 Coal Transport to Farakka through Power Station – A Break through for IWT 233

15.12 Development of Airports During the Eleventh Plan 242

15.13 GAGAN—The Indian Satellite Based Augmentation System (SBAS) for Air Navigation

Services (ANS)

244

16.1 Spectrum Trading 263

16.2 Twelfth Plan Targets for the Telecommunication Sector 264

16.3 Key Achievements (as on 31 March 2012) 267

17.1 New Guidelines Strengthen Demand-driven Character of MGNREGA 293

17.2 Limitations of SGSY 298

18.1 Vision of Our Cities 320

18.2 State of Service Delivery—Key Indicators 321

18.3 Transforming Public Transport in Cities 324

18.4 Harmonising the Role of Parastatals with Elected Municipal Bodies 326

18.5 Strategic Densification—International Examples 330

18.6 Recommendation of Isher Ahluwalia Committee on Financial Devolution to ULBs 332

18.7 PPP in Urban Sector under JNNURM 333

Boxes xiii

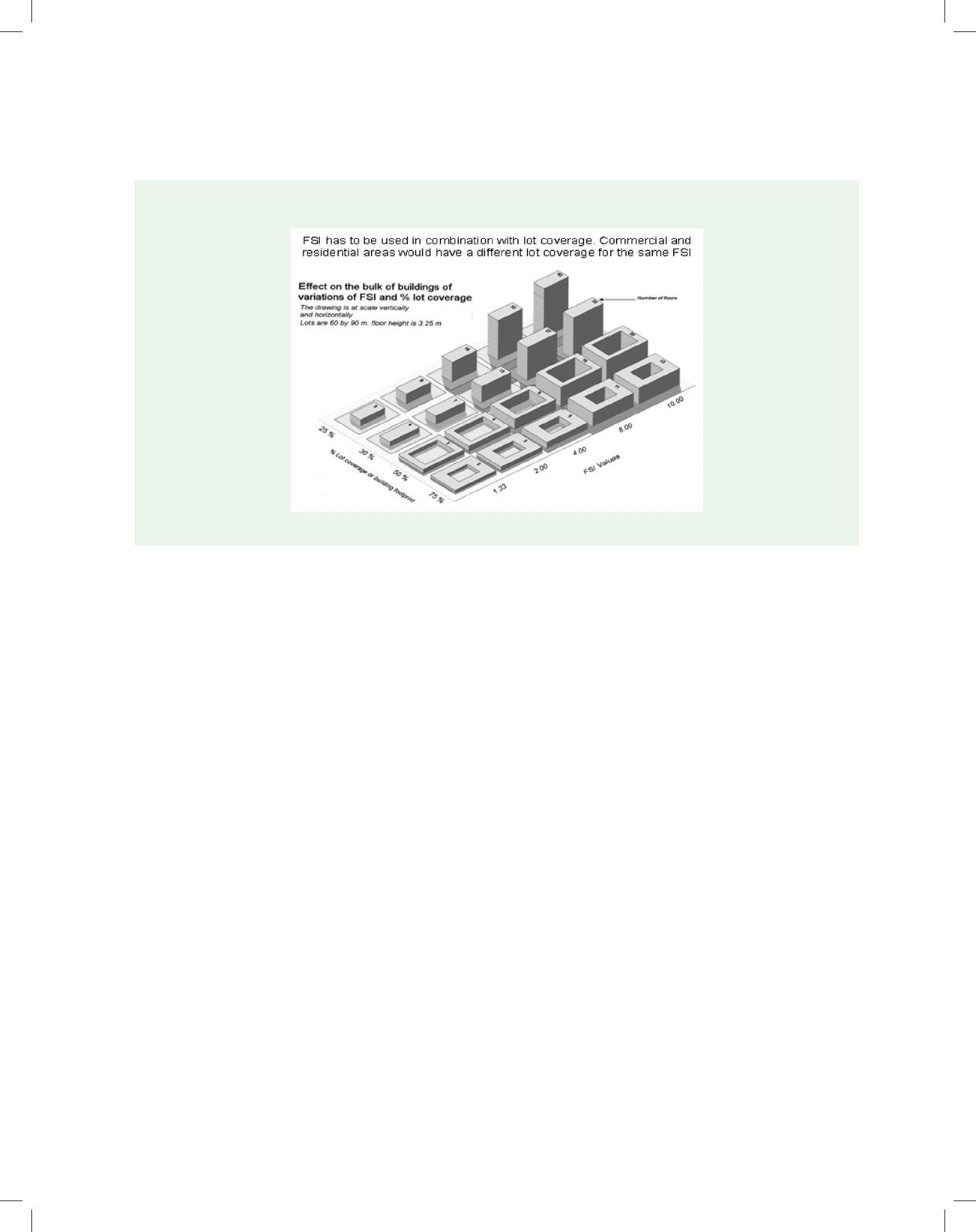

18.8 FSI and Coverage Areas Can be Combined to Increase Densities 338

18.9 Metro—A Transformational Approach to Public Transport 341

18.10 Reforms and Desired Outcomes Related to Water Supply and Sanitation 348

18.11 Reforms under JNNURM Comprehensive List of Reforms in Urban Sector 355

18.12 Major Schemes for Urban Renewal at a Glance 358

19.1 Financing Instruments for Affordable Housing 374

19.2 Popular Choice by Design! 399

19.3 Twelfth Plan Interventions for Handlooms 401

19.4 Twelfth Plan Schemes for Handicrafts 404

19.5 Upturn in India’s Sporting Performance 410

Acronyms

2G/3G/4G Second Generation/Third

Generation/Fourth Generation

AAI Airport Authority of India

AAY Antodaya Anna Yojana

ACA Additional Central Assistance

ACC Artisan Credit Card

ACS Average Cost of Supply

ADB Asian Development Bank

ADC Access Deficit Charges

ADDA Asansol Durgapur Development

Authority

AES Acute Encephalitis Syndrome

AI Artificial Insemination

AIBP Accelerated Agriculture Benefit

Programme

AIC Agricultural Insurance Corporation

AIR All India Radio

AIU Association of Indian Universities

AL Arable Land

AML Anti-Money Laundering

AMM Abandoned mine methane

AMPC Automated Mail Processing Centre

ANM Auxiliary Nurse Midwife

AnSI Anthropological Survey of India

AOC Agreement of Collaboration

APL Above Poverty Line

APMC Agriculture Produce Marketing

Committee

APMSS Andhara Pradesh Mahila Samakhya

APO Assistant Programme Officer

ARPU Average Revenue Per User

ARR Average Revenue Realised

ARYA Attracting & Retaining Youth in

Agriculture

ASHA Accredited Social Health Activist

ASI Archaeological Survey of India

ASPIRE Agriculture Science Pursuit for

Inspired Research Excellence

ASSOCHAM Associated Chamber of Commerce

ATC Air Traffic Control

ATF Automatic Transmission Fluid

ATFC Agriculture Technology Forecast

Centre

ATls Administrative Training Institutes

ATMAs Agriculture Technology

Management Agency

ATS Apprentice Training Scheme

B.P.Ed. Bachelor of Physical Education

BAF Batch Annealing Furnace

BC Business Correspondent

BCM Billion cubic metres

BDOs Block Development Officers

BE Budgetary Estimate

BEE Bureau of Energy Efficiency

BEML Bharat Earth Movers Ltd.

BFDAs Brackish water Farmers

Development Agencies

BFO Business Facilitation Officer

BHEL Bharat Heavy Electricals Ltd.

BIPP Biotechnology Industry Partnership

Programme

BIRAP Biotechnology Industry Research

Assistance Programme

BIS Bureau of Indian Standards

BLY Bachat Lamp Yojana

BMPTC Building Material and Technology

Promotion Council

BORL–Bina Bharat Oman Refineries Limited

BOT Build-Operate-Transfer

BPCL Bharat Petroleum Corporation

Limited

BPL Below Poverty Line

BPO Branch Post Office/ Business

Process Outsourcing

BPR Business Process Re-engineering

BRCs Block Resource Centres

Acronyms xv

BRO Border Roads Organisation

BRT Bus Rapid Transit

BSUP Basic Services to the Urban Poor

BTKM Billion Tonne Kilometre

BU Billion Unit

BWA Broadband Wireless Access

C&AG Comptroller & Auditor General

CA Conservation Agriculture

CACP Commission for Agriculture Costs

& Prices

CAG Comptroller and Auditor General

CAGR Compound Annual Growth Rate

Cal/Kg Calorie/ kilogramme

capex Capital expenditure

CBDT Central Board of Direct Taxation

CBM Coal bed Methane

CBOs Community Based Organisations

CBRM Capacity Building and Reform

Management

CCDA Coal Conservation and

Development Act

CCL Central Coalfields Limited

CCRF Code of Conduct for Responsible

Fisheries

C-DAP Comprehensive District Agriculture

Plants

C-DOT Centre for Development of

Telematics

CDP City Development Plans

CEA Central Electricity Authority

CEF Citizen Engagement Framework

CEIG Chief Electrical Inspectorate to

Govt. of India

CERC Central Electricity Regulatory

Commission

CERT Computer Emergency Response

Team

CERT–In Indian Computer Emergency

Response Team

CETP Common Affluent Treatment Plan

CeWiT Centre for Excellence in Wireless

Technology

CFI Construction Federation of India

CFSI Children Film Society of India

CFT Cluster Facilitation Team/

Combating of Financing of

Terrorism

CGD City Gas Distribution

CGP Cluster of Gram Panchayats

CGRF Consumer Grievance Redressal

Forum

CH4. CO Methane, Carbon Monoxide

CHPs Coal Handling Plants

CIDC Construction Industry Development

Council

CII Confederation of Indian Industry

CLCSS Credit Linked Capital Subsidy

Scheme

CM Confederation of Indian Industries

CMA Counter Magnet Area

CMM Coal mine methane

CMPDIL Central Mine Planning and Design

Institute

CMSA Community Managed Sustainable

Agriculture

CNG Compressed natural gas

CPCB Central Pollution Control Board

CPCL Chennai Petroleum Corporation

Limited

CPE Customer Premises Equipment

CPIAL or

CPIIW

Consumer Price Index for

Agricultural Labour/Consumer

Price Index for Industrial Workers

CPIS Coconut Palm Insurance Scheme

CPMG Chief Post Master General

CPPs Captive power plants

CPWD Central Public Works Department

CREDAI Confederation of Real Estate

Developers’ Associations of India

CRPs Community Resource Persons

CRRI Central Road Research Institute

CRRI-In Indian Computer Emergency

Response Team

CSC Cluster Stimulation Cell/Common

Services Centre

CSIR Council for Scientific and Industrial

Research

CSO Central Statistical Office/Civil

Society Organisation

CSR Corporate Social Responsibility

CSS Centrally Sponsored Scheme

CST Central Sales Tax/Concentrating

Solar Technology

CTL Coal to liquid

CUF Capacity Utilisation Factor

CVO Chief Vigilance Officer

xvi Acronyms

C-WET Centre for Wind Energy Technology

CWG Common Wealth Games

DAC Department of Agriculture &

Cooperation

DAE Department of Atomic Energy

DAHDF Department of Animal Husbandry,

Dairying & Fisheries

DALY Disability Adjusted Life Years

DAP Diammonium Phosphate

DARE Department of Agricultural

Research & Education

DAS Digital Addressable System

DAVP Directorate of Advertisement and

Visual Publicity

DBT Department of Bio-technology

DCI Dredging Corporation of India

DD Doordarshan

DeitY Department of Electronics and

Information Technology

DEMU/

MEMU

Diesel-Electric Multiple Unit/

Mainline Electric Multiple Unit

DFC Dedicated Freight Corridor

DFP Directorate of Field Publicity

DGCA Directorate General of Civil Aviation

DGH Director General of Hydrocarbons

DGPS Differential Global Positioning

System

DIPP Department of Industrial Policy and

Promotion

DIPP Department of Industrial Policy and

Promotion

DoP Department of Posts

DoT Department of Telecommunication

DP Development Plan

DPC District Programme Coordinator

DPRs Detailed Project Reports

DPSU Defence Public Sector Undertaking

DRDA District Rural Development Agency

DRDO Defence Research & Development

Organisation

DRI Differential Rate of Interest

DRM Digital Radio Mondiale

DSM Demand side management

DSS Decision Support System

DST Department of Science &

Technology

DTC Direct Tax Code

DTH Direct to Home

DWDM Dense Wavelength Division

Multiplexing

E&P

companies

Exploration and Production

Companies

EBP

Programme

Ethanol Blended Petrol Programme

ECB External Commercial Borrowing

ECBC Energy Conservation Building Code

ECO Local Cable Operators

EDGE Enhanced Data for Global Evolution

EDMC Electronic Design and

Manufacturing Cluster

EDS Electronics Delivery of Services

EEZ Exclusive Economic Zone

EFC Expenditure Finance Committee

eFMS Electronic Fund Management

System

EIAs End Implementing Agencies

EIL Engineers India Limited

EM Entrepreneur’s Memorandum

EMC Electronics Manufacturing Cluster

EMMC Electronic Media Monitoring

Centre

EMSC Environmental Measures and

Subsidence Control scheme

EMU Electric Multiple Unit

EOL Essar Oil Ltd

EPC Engineering Procurement and

Construction

ERP Enterprise resource planning

ESDM Electronics System Design &

Manufacturing

ETP Effluent Treatment Plant

EWS Economically Weaker Sections

EXIM Export Import

FAB Fabrication Unit

FAO Food and Agriculture Organisation

FAR Floor Area Ratio

FDI Foreign Direct investment

FFDAs Fish Farmers Development

Agencies

FICCl Federation of Indian Chamber of

Commerce & Industry

FM Frequency Modulation

FMD Foot & Mouth Disease

FO/LSHS Furnace oil/Low Sulphur Heavy

Stock

FOLD Forum of Load Dispatchers

Acronyms xvii

FoR Forum of Regulators

FPOs Farmer Producer Organisation

FPS Fair Price Shop

FRBM Fiscal Responsibility and Budget

Management Rules

FSA Fuel Supply Agreement

FSI Floor Space Index

FSRU Floating Storage & Regasification

units

FTA Free Trade Agreement

FTII Films and Television Institute of

India

FYP Five Year Plan

GAIL Gas Authority of India Ltd

GBI support Generation based incentive support

GBS Gross Budgetary Support

GCF Gross Capital Formation

GCV Gross calorific value

GDP Gross Domestic Product

GIPCL Gujarat Industries Power Company

Ltd

GIS Geographical Information System

GKMS Gramin Krishi Mausam Seva

GMO Genetically Modified Organisms

GOI Government of India

GoI-UNDP Government of India-United

Nations Development Programme

GPR Ground Penetrating Radar

GPS Global Positioning System

GPs Gram Panchayats

GQ Golden Quadrilateral

GRIHA Green Rating for Integrated Habitat

Assessment

GSDP Gross State Domestic Product

GSI Geological Survey of India

GSM Global System for Mobile

Communication

GST Goods and Services Tax

GT Gross Tonne

GTO/IGBT Gate Turn Off (Thyrister)/lnsulated

Gate Bipolar Transistor

GW GigaWatt

HD High Definition

HDTV High Definition Television

HEC Heavy Engineering Corporation

HEIs Higher Educational Institutions

HEMM Heavy earth moving machinery

HITS Headend In The Sky

HMCP Hardware Manufacturing Cluster

Park

HMEL Hindustan Mittal Energy Limited

HMT Hindustan Machine Tools

HPCL Hindustan Petroleum Corporation

Limited

HPEC High Powered Expert Committee

HPOs Head Post Offices

HPT High Power Transmitter

HRD Human Resource Development

HRSS High Resolution Seismic Survey

HS Herorrhagic Septicemia

HSIL High Surge Impedance Loading

HTLS High Temp. Low Sag

HTREL High-tech Reconnaissance &

Exploration Licences

HUDCO Housing and Urban Development

Corporation

HUMS Indian Institutes of Urban

Management

I&B Information & Broadcasting

IAAS Integrated Agro-Meteorological

Advisory Service

IAASTD International Assessment of

Agricultural Knowledge, Science &

Technology for Development

IAP Integrated Action Plan

IAY Indira Awaas Yojana

IBF Indian Broadcasting Foundation

IBIN India Backbone Implementation

Network

IBM Indian Bureau of Mines

IBP Indian Broadcasting Foundation

IBS In Building Solutions

IC Integrated Circuit

ICAR Indian Council of Agricultural

Research

ICD Inland Container Depot

ICF Integrated Coach Factory

ICMR Indian Council of Medical Research

ICRIS Integrated Coal Resource

Information System

ICT Information and Communication

Technology

ICTE Information, Communication

Technology and Electronics

IDA International Development

Association

xviii Acronyms

IEBR Internal and Extra Budgetary

Resources

IEC Information Education and

Communication

IFFI International Film Festival of India

IGNDPS Indira Gandhi National Disability

Pension Scheme

IGNOAPS Indira Gandhi National Old Age

Pension Scheme

IGNWPS Indira Gandhi National Widow

Pension Scheme

IHHL Individual Household Latrine

IHSDP Integrated Housing & Slum

Development Programme

IIDS Integrated Infrastructural

Development Scheme

IIFCL India Infrastructure Finance

Company Limited

IIHT Indian Institute of Handloom

Technology

IIIT Indian Institute of Information

Technology

IIPA Indian Institute of Public

Administration

IISc Indian Institute of Science

IIT Indian Institute of Technology

IIUMs Indian Institutes of Urban

Managements

ILCS Integrated Low Cost Sanitation

Scheme

ILRIS Integrated Lignite Resource

Information System

IMD Indian Meteorological Department

IMEI International Mobile Equipment

Identity

IMIS Integrated Management

Information System

IMPCC Inter Media Publicity Coordination

Committee

IMT International Mobile

Telecommunications

INDIPEX India International Philatelic

Exhibition

IOCL Indian Oil Corporation Limited

IP Intellectual Property/Internet

Protocol

IPM Integrated Pest Management

IPR Intellectual Property Rights

IPTV Internet Protocol Television

IPV 4/IPV 6 Internet Protocol version 4/Internet

Protocol version 6

IRDA Insurance Regulatory Development

Authority

IRDP Integrated Rural Development

Programme

ISO Indian Standard Organisation

ISPRL Indian Strategic Petroleum Reserve

Ltd

ISRO Indian Space Research Organisation

ISSHUP Interest Subsidy Scheme for

Housing the Urban Poor

IT Information Technology

ITA-1 Information Technology

Agreement-1

ITI Indian Telephone Industries

ITIs Industrial Training Institutes

IT-ITeS Information Technology-and

Information Technology enabled

Service

IVRS Interactive Voice Response System

IWAI Inland Waterways Authority of

India

IWT Inland Waterways Transport

JE Japanese Encephalitis

JLGs Joint Liability Groups

JMP Joint Monitoring Programme

JNNURM Jawaharlal Nehru National Urban

Renewal Mission

JNNUSM Jawaharlal Nehru National Solar

Mission

JRDA Jharia Rehabilitation and

Development Authority

JV Joint Venture

JWGs Joint Working Groups

KCC Kisan Credit Card

Kgoe/US$ Kilograms of Oil Equivalent/US

Dollar

KVIC Khadi & Village Industries

Corporation

KVK Krishi Vigayan Kendra

KVs Kendriya Vidyalayas

kW Kilo Watt

Kwh Kilowatt hour

L. km Line kilometre

Acronyms xix

LAD Least Assured Depth

LARR Land Acquisition and Rehabilitation

and Resettlement Bill, 2011

LBFL Local Bodies Finance List

LCO Local Cable Operators

LDBs Livestock Development Boards

LDC Land Development Corporation

LDO Light Diesel Oil

LEED Leadership in Energy &

Environmental Design

LHB Linke Holfmann Busch

LIGs Low Income Group

LNCPE Laxmibai National College of

Physical Education

LNG Liquefied natural gas

LPG Liquefied Petroleum Gas

LPT Low Power Transmitter

LR Land Readjustment

LTCCS Long Term Cooperative Credit

Structure

LTE Long Term Evolution

LWE Left Wing Extremism

M&A Mergers and Acquisitions

M.P.Ed. Master of Physical Education

MA Moving Average

MANAGE National Institute for Agriculture

Extension and Management

MAT Minimum Alternative Tax

Mbps Megabits per second

MCCL Mahanadi Coalfields Limited

MCS Monitoring, Control and

Surveillance

MDI Management Devolution Index

MDRR Mines and Minerals (Development

and Regulation) Bill, 2011

MEA Ministry of External Affairs

MES Minimum Economic Size

MFIs Microfinance Institutions

MGNREGA Mahatma Gandhi National Rural

Employment Guarantee Act

MGNREGS Mahatma Gandhi National Rural

Employment Guarantee Scheme

MGR Merry-Go-Round

MHz/GHz Mega Hertz/Giga Hertz

MIS Management Information System

MITI Ministry of International Trade and

Industry, Japan

MMBTU Million Metric British Thermal Unit

MM-III Mini Mission III

MMP Mission Mode Project

MMSCMD Million Metric Standard Cubic

Metre Per Day

MMT Million Metric Tonnes

MMTOE Million tones oil equivalent

MMTPA Million Metric Tonne Per Annum

MNAIS Modified National Agricultural

Insurance Scheme

MNRE Ministry of New and Renewable

Energy

MoA Ministry of Agriculture

MoC Ministry of Coal

MoHUPA Ministry of Housing and Urban

Poverty Alleviation

MoP Ministry of Power

MoP&NG Ministry of Petroleum and Natural

Gas

MoRD Ministry of Rural Development

MoRTH Ministry of Roads Transport &

Highways

MoSPI Ministry of Statistics & Programme

Implementation

MOT Multi-organisation Team/ Muriate

of Potash

MoU Memorandum of Understanding

MoUD Ministry of Urban development

MPCs Metropolitan Planning Committees

MRP Maximum Retail Price

MRPL Mangalore Refinery and

Petrochemicals Limited

MS Motor spirit

MSE-CDP Cluster Development Programme of

the M/o MSME

MSEFC Micro & Small Enterprise

Facilitation Councils

MSIPS Modified Special Incentive

Programme Scheme

MSME Micro, Small & Medium Enterprise

MSMED Act MSME Development Act, 2006

MSP Minimum Support Price

MT Million Tonnes

MTA Mid-term Appraisal

MTEE Market Transformation for Energy

Efficiency

MTOE Million tons of oil equivalent

MW Medium Wave/Megawatt

MWe Megawatt electrical

xx Acronyms

MWp. Megawatt Peak

NABARD National Bank for Agriculture and

Rural Development

NABFINS NABARD Financial Services

NAC Non Agricultural use of Land

NADA National Anti-Doping Agency

NAIS National Agricultural Insurance

Scheme

NAPCC National Action Plan on Climate

Change

NARS National Agriculture Research System

NATRIP National Automotive Testing and

R&D Infrastructure Project

NAVA National Audio-Visual Archives

NBA News Broadcasters Association/

Nirmal Bharat Abhiyan

NBECI National Bio Energy Corporation of

India

NBFCs Non-Banking Finance Companies

NBS Nutrient Based Subsidy

NCC National Cadet Corps

NCP National Competition Policy

NCR National Capital Region

NCTE National Council of Teacher

Education

NDDB National Dairy Development Boards

NDP National Dairy Plant

NDTL National Dope Test Laboratory

NE North East

NEF National Electricity Fund

NEGP National e-Governance Plan

NERUDP North Eastern Region Urban

Development Programme

NELP New Exploration Licensing Policy

NER North Eastern Region

NFAP National Frequency Allocation Plan

NFBS National Family Benefit Scheme

NFDB National Fisheries Development

Board

NFDC National Film Development

Corporation

NFSA National Food Security Act

NFSB National Food Security Bill

NFSM National Food Security Mission

NGN Next Generation Network

NGO Non-Governmental Organisation

NGP Nirmal Gram Puraskar

NGRCA National Gender Resources Centre

in Agriculture

NGRI National Geophysical Research

Institute

NHAI National Highway Authority of India

NHB National Horticulture Board/

National Housing Bank

NHDP National Highway Development

Programme

NHM National Horticulture Mission

NIA Net irrigated area

NICRA National Initiative on Climate

Resilient Agriculture

NIMZ National Investment and

Manufacturing Zone

NIPER National Institute of Pharmaceutical

Education & Research

NIS National Institute of Sports

NISC National Institute of Sports

Coaching

NISSM National Institute of Sports Science

and Sports Medicine

NIUA National Institute of Urban Affairs

NKN National Knowledge Network

NLCPR Non-Lapsable Central Pool of

Resources

NLP Natural Language Processing

NMCC National Manufacturing

Competitiveness Council

NMCP National Manufacturing

Competitiveness Programme

NMEEE National Mission for Enhanced

Energy Efficiency

NMSA National Mission for Sustainable

Agriculture

NMSH National Mission on Sustainable

Habitat

NMT Non-Motorised Transport

NOCL Nagarjuna Oil Corporation Limited

NOFN National Optical Fibre Network

NPBB National Programme for Bovine

Breeding

NPBBD National Programme for Bovine

Breeding and Dairy

NPCBB National Project for Cattle & Buffalo

Breeding

NPFAI National Playfields Association of

India

Acronyms xxi

NPFP National Physical Fitness

Programme

NPK Nitrogen Phosphorous & Potash

NPM Non-Pesticidal Management of

Pests

NPMSH&F National Project on Management of

Soil Health & Fertility

NPS New Pension Scheme/ New Pricing

Scheme

NPYAD National Programme for Youth and

Adolescent Development

NRAA National Rained Area Authority

NRDWP National Rural Drinking Water

Programme

NREGS National Rural Employment

Guarantee Scheme

NRL Numaligarh Refinery Limited

NRLM National Rural Livelihood Mission

NSAP National Social Assistance

Programme

NSD National School of Drama

NSDC National Skill Development

Corporation

NSDF National Skill Development Fund

NSF National Sports Federation

NSIC National Small Industry Corporation

NSNIS Netaji Subhas National Institute of

Sports

NSS National Sample Survey/National

Service Scheme

NSSO National Sample Survey Office/

National Sample Survey

Organisation

NTDPC National Transport Development

Policy Committee

NTKM Net Tonne Kilometre

NTP National Telecom Policy

NTPC National Thermal Power

Corporation

NTS National Institute of Sports

NUHHP National Urban Housing and

Habitat Policy

NULM National Urban Livelihoods

Mission

NURTA National Urban Rail Transit

Authority

NUSP National Urban Sanitation Policy

NVG National Voluntary Guidelines on

Soc., Env., & Eco Responsibility for

Business

NVs Navodaya Vidyalayas

NYC National Youth Corps

NYKs Nehru Yuva Kendras

O&M Operation & Maintenance

O+OEG Oil and oil equivalent gas

OBCs Other Backward Classes

ODF Open Defecation Free

OFB Ordinance Factory Board

OIL Oil India Limited

OMCs Oil Marketing Companies

OMS Output per man shift

OMT Operate-Maintain-Transfer

ONGC Oil and Natural Gas Corporation

Limited

OVL ONGC Videsh Ltd

oya Year on Year Average

PACS Primary Agriculture Cooperative

Society

PAPU Pan African Postal Union

PAT Perform, Achieve & Trade

PATM Perform, Achieve and Trade

Mechanism

PCB Pollution Control Board

PCU Policy Coherence Unit

PDAs Pension Distribution Agencies

PEARL Peer Experience and Reflective

Learning

PHPDT Peak Hour Peak Direction Traffic

PIB Public Information Bureau

PIC Public Information Campaign

PKM Passenger Kilometre

PLB Public Land Banks

PLI Postal Life Insurance

PMEGP Pradhan Mantri Employment

Guarantee Programme

PMGSY Pradhan Mantri Grameen Sadak

Yojna

PNG Piped natural gas

PNGRB Petroleum and Natural Gas

Regulatory Board

POL Petroleum, Oil and Lubricants

POLIF Post Office Life Insurance Fund

POs Post Offices

POSOCO Power System Operation

Corporation Limited

xxii Acronyms

PPAC Petroleum Planning and Analysis

Cell

PPAs Power purchase agreement

PPP Public–Private Partnership

PPPP People Private–Public Partnership

PPPIAD Public–Private Partnership

for Integrated Agricultural

Development

PPVFRA Protection of Plant Variety &

Farmers Rights Authority

PRGF Partial Risk Guarantee Fund

PRIs Panchayati Raj Institutions

Provi. Provisional

PSB Public Service Broadcaster

PSCs Production Sharing Contracts

PSUs Public Sector Undertakings

PTA Preferential Trade Agreement

PURA Provision of Urban Amenities in

Rural Areas

PWD Public Works Department

PWSS Piped Water Supply System

PYD Programme for Youth Development

PYKKA Panchayati Yuva Khel aur Krida

Abhiyan

R&D Research and Development

R&M AND LE Renovation & Modernisation and

Life Extension

R&R Rehabilitation and Resettlement

R/P ratios Reserves-to-Production ratio

R–APDRP Restructured Accelerated Power

Development and Reforms

Programme

RAY Rajiv Awas Yojana

RBCs Rural Building Centres

RCUES Regional Centres of Urban and

Environment Studies

RDF Rural Development Flexi-fund

RDSO Research Design and Standards

Organisation

RE bonds Renewable Energy bonds

RE Revised Expenditure

READY Rural Entrepreneurship &

Awareness Development Yojana

REC Renewable Energy Certificate

RFD Result Framework Document

RFID Radio Frequency Identification

RGGVY Rajiv Gandhi Grameen

Vidyutikaran Yojana

RGNIYD Rajiv Gandhi National Institute of

Youth Development

RHF Rural Housing Fund

RIA Regulatory Impact Analysis

RIDF Rural Infrastructure Development

Fund

RIL Reliance Industries Limited

RIL-KG Reliance Industries Limited-Krishna

Godavari Basin

RIS River Information System

RITES Rail India Techno Economic

Services

RKVY Rashtriya Krishi Vikas Yojana

RMSA Rashtriya Madhyamik Shiksha

Abhiyan

ROB/RUB Road Over Bridge/ Road Under

Bridge

RoW Right of Way

RPLI Rural Postal Life Insurance

RPO Renewable Purchase Obligation

RPOLIF Rural Post Office Life Insurance

Fund

RRTS Regional Rapid Transit System

RTE Right to Education

RUDSETIs Rural Development and Self-

Employment Training Institutes

S&DD Song and Drama Division

S&L Standards and Labelling

SAD Special Additional Duty

SAGES Goaf edge supports

SAMETIs State Agriculture Management

Extension & Training Institutions

SARDP-NE Special Accelerated Road

Development Programme for the

North East

SAT Sports Authority of India

SAU/SAUs Social Audit Unit/State Agricultural

Universities

SBD Standard bid documents

SCCL Singareni Collieries Company

Limited

SCs Scheduled Castes

SCSP Scheduled Castes Sub-Plan

SDO Standard Developing Organisations

SDTV Standard Definition Television

SEB State Electricity Board

SEBI Securities & Exchange Board of India

SECC Socio-Economic and Caste Census

Acronyms xxiii

SECF Contribution to State Energy

Conservation Fund

SFAC Small Farmers Agribusiness

Consortium

SFCs State Finance Commissions

SGSY Swarnajayanti Gram Swarozgar

Yojana

SHBs State Housing Boards

SHGs Self-Help Groups

SIBRI Small Industry Business Research

Initiatives

SITP Scheme for Integrated Textile Park

SJSRY Swarna Jayanti Sahari Rozgaar

Yojana

SKO Superior Kerosene Oil

SLNA State-Level Nodal Agency

SLSC State Level Sanctioning Committee

SME Small and Medium Enterprise

SOC Soil Organic Carbon

SOE State Owned Enterprise

SOP Standard Operating Producer

SoRs Schedule of Rates

SPTLs State Pesticide Testing Laboratory

SPV Special Purpose Vehicle

SRFTI Satyajit Ray Film and Television

Institute

SRI System of Rice Intensification

SSA Sarva Shiksha Abhiyan

STB Set Top Box

STL Short term liabilities

STOA Short-Term Open Access

STs Scheduled Tribes

STU/CTU State Transmission Utilities/Central

Transmission Utility

SW Short Wave

SWAN State Wide Area Network

TCF Trillion cubic feet

TCIL Telecommunications Consultants

India Ltd

TCoE Telecom Centres of Excellence

TDB Technology Development Board

TDR Transfer of Development Rights

TDRs Tradable Development Rights

TDSAT Telecom Disputes Settlement

Appellate Tribunal

TEC Telecom Engineering Centre

TFP Total Factor Productivity

TISCO Tata Iron and Steel Company

Limited

TMNE (NE) Technology Mission for North

Eastern Region

TNUDF Tamil Nadu Urban Development

Fund

TOD Time of Day

TOPS Terrestrial Observation &

Prediction System

TPDS Targeted Public Distribution System

TPSs Town Planning Schemes

TQM Total Quality Management

TSC Total Sanitation Campaign

TSDO Telecom Standards Development

Organisation

TSP Telecom Service Provider/Tribal

Sub-Plan

TUFS Technology Upgradation Fund

Scheme

UC Utilization Certificate

UCG Underground Coal Gasification

UGC University Grants Commission

UHV Useful heat value

UID Unique Identification

UID Unique Identification—AADHAR

UIDSSMT Urban Infrastructure Development

for Small & Medium Towns

UIG Urban Infrastructure and

Governance

UK United Kingdom

ULBs Urban Local Bodies

ULIP Unit Linked Insurance Plan

UMPPs Ultra Mega Power Projects

UMTA Unified Metropolitan Transport

Authority

UNICEF United Nations Children’s Fund

UPU Universal Postal Union

USA United States of America

USEPA United States Environment

Protection Agency

USHA Urban Statistics for HR and

Assessments

USIS Urban Sport Infrastructure

USOF Universal Service Obligation Fund

UT Urban Transport

VAS Value Added Services

VAT Value Added Tax

VCFEE Venture Capital Fund for Energy

Efficiency

VFX Visual Effects

VGF Viability Gap Funding

xxiv Acronyms

VLFM Visionary Leadership for

Manufacturing

VLPT Very Low Power Transmitter

VoIP Voice Over Internet Protocol

VUs Vehicle Units

VWSC Village Water and Sanitation

Committee

WBCIS Weather Based Crop Insurance

Scheme

WDM-PON Wavelength Division Multiplexed

Passive Optical Network

WHO World Health Organisation

WiPS Wireless Intrusion Prevention

System

WRDA Warehouse Regulatory &

Development Authority

WSCs Weavers’ Service Centres

WTO World Trade Organisation

XGPON Next Generation Gigabit Passive

Optical Network

Annexures

13.1 Manufacturing GDP by Sector and Employment Projections 105

13.2 Sector-wise Recommendations 106

13.3 Twelfth Five Year Plan (2012–17) Outlays (GBS) for Industry Sector 129

14.1 Eleventh Plan Physical Progress of RGGVY Projects under Implementation 191

14.2 Sectoral Coal Demand/Off-take for Annual Plan 2012–13 192

14.3 Annual Plan 2012–13—Company-wise Production—Ministry of Coal 193

14.4 Physical Targets of Renewable Programme for the Twelfth Plan 194

15.1 Central Road Sector Outlay and Expenditure-At Current Price for Eleventh Plan 252

15.2 Plan-wise Addition to NH Length 254

15.3 Achievement on National Highways 254

15.4 National Highways Development Project Phase I to VII 255

15.5 Physical Performance of Air India Limited during Eleventh Plan Period 256

15.6 Financial Performance of Air India Ltd. during the Eleventh Plan Period 256

15.7 Financial Performance of Airports Authority of India during Eleventh Plan Period 257

15.8 Financial Performance of Pawan Hans Helicopters Ltd. during Eleventh Plan Period 257

16.1 Twelfth Five Year Plan (2012–17) Outlays for the Ministry of Communications and IT and

Ministry of Information and Broadcasting

285

INTRODUCTION

12.1. Although agriculture now accounts for only

14 per cent of Gross Domestic Product (GDP), it

is still the main source of livelihood for the major-

ity of the rural population. As such rapid growth of

agriculture is critical for inclusiveness. Important

structural changes are taking place within the sec-

tor and there are definite signs of improved per-

formance. Agricultural growth has accelerated

compared to the Tenth Plan and diversification

is proceeding (Table 12.1). The National Sample

Survey Organisation (NSSO) data brings out that

rural labourers are shifting to non-agricultural work,

tightening the labour market in agriculture and put-

ting pressure on farm wages. However, dependence

on agriculture remains unchanged among the rural

self-employed whose average farm size continues to

12

Agriculture

decline with population growth. This is also an age-

ing, more feminised population, whose educated

young members are less likely to want to stay in

farming. The viability of farm enterprise, mostly

small farms, must therefore be a special area of

Plan focus in the Twelfth Plan. The Plan must also

focus on other priorities such as resource-use effi-

ciency and technology to ensure sustainability of

natural resources, adaptation to climate change and

improvements in total factor productivity.

RECENT TRENDS: PERFORMANCE AND

POINTERS

GDP Growth

12.2. The average of annual growth rates of GDP in

agriculture and allied sectors during the Eleventh

TABLE 12.1

Growth Rate of Agricultural and Allied Sectors

(in percentage)

Plan Share of Agriculture in the

Economy

Growth Rate of Agriculture

and Allied Sectors

Growth Rate of Total

Economy

(All Figures based on 2004–05 prices)

Ninth Five Year Plan 23.4 2.5 5.7

Tenth Five Year Plan 19.0 2.4 7.6

Eleventh Plan (2007–08 to 2011–12)

2007–08 16.8 5.8 9.3

2008–09 15.8 0.1 6.7

2009–10 14.6 0.8 8.6

2010–11 (2nd RE) 14.5 7.9 9.3

2011–12 (Rev Est.) 14.1 3.6 6.2

Eleventh Plan Average 15.2 3.7 8.0

Source: Central Statistical Office, New Delhi Press Release dated 7th Feb, 2013.

2 Twelfth Five Year Plan

Five Year Plan is now placed at 3.7 per cent. This is

short of the target of 4 per cent but is significantly

better than the achievement of 2.4 per cent in the

Tenth Plan. Failure to reach the target growth is

one reason for the high inflation in prices of food

and other primary commodities that persist despite

the recent slowdown in overall GDP growth.

Consequently, although the overall GDP growth tar-

get of the Twelfth Plan has been revised down since

the Approach Paper, the growth target for agricul-

ture is maintained at 4 per cent.

12.3. A natural question which arises is whether the

target of 4 per cent is attainable in view of past short-

falls. Although growth trends and targets are subject

to high errors due to weather variability (for exam-

ple, the Eleventh Plan average was pulled down by

two successive bad harvests in 2008–09 and 2009–

10), there is reason for cautious optimism because

the turn-around that began after 2004 appears to be

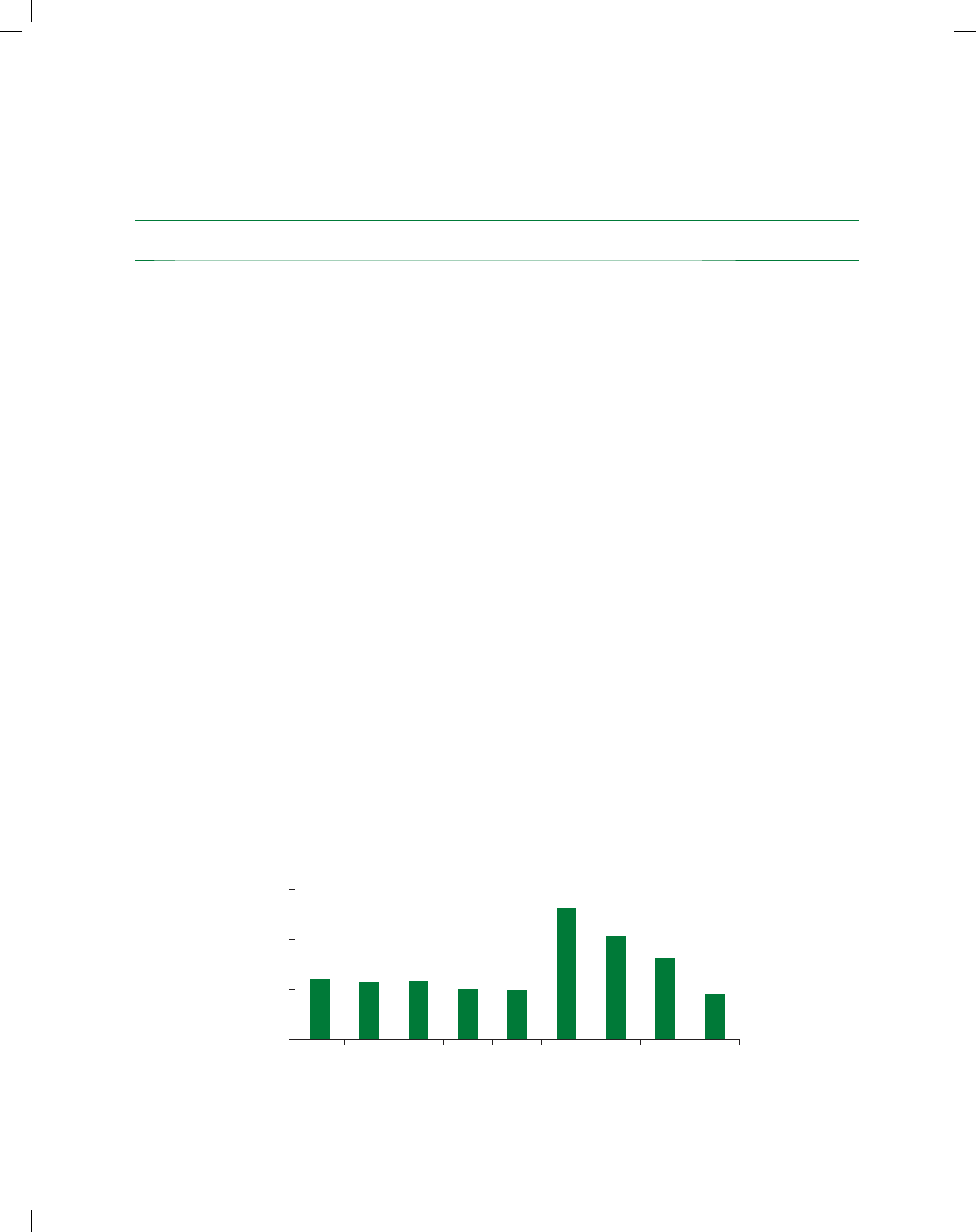

maintaining its momentum. Figure 12.1 plots aver-

ages and standard deviations of annual growth rates

over moving five-year periods, a trend of the growth

averages and also annualised five-year growth rates

based on five-year moving averages. All these show

growth still trending up and variability reducing.

The Eleventh Plan growth rate based on five-year

moving averages is at 3.6 per cent, the highest for any

five-year period ever and, significantly, growth vari-

ability has also reduced to lowest ever.

12.4. The reduction in variability is important since

claims of acceleration or deceleration make sense

only when variability is low. Also, it is a measure

of how well the system is able to cope with inevita-

ble bouts of aberrant weather and yet maintain the

growth momentum. It should be noted that agri-

cultural growth was positive in 2009–10 despite the

worst drought in nearly 40 years. More generally,

whereas earlier periods saw at least one and normally

two years of negative growth in every five year, there

has not been a single year of negative growth of agri-

culture and allied sectors after 2002–03.

12.5. The magnitude of secular decline in growth

variability over the last 30 years is also important.

This is now less than a third of its peak. A major

role must have been played by the increase in irriga-

tion from about 20 per cent of arable area in 1981

to 35 per cent today, based mainly on groundwa-

ter. However, since water tables have fallen and

temperatures risen, the extent of variability decline

is surprisingly large. Even assuming zero variabil-

ity on irrigated land, this implies that variability on

rain-fed land must have reduced very substantially.

Clearly factors such as a more diversified agriculture,

1.0

2.0

3.0

4.0

5.0

6.0

1976–77

1981–82

1986–87

1991–92

1996–97

2001–02

2006–07

2011–12

2.0

4.0

6.0

8.0

10.0

12.0

Average of annual growth rates 5 yr MA Std dev of annual growth rates (axis 2)

FIGURE 12.1: Growth and Fluctuations in GDP Agriculture and Allied

Agriculture 3

extended information reach and investments both

on-farm and in watershed development, appear to

have enabled better responses to depleting natural

resources and weather risk. Although there is con-

siderable scope to improve each of these factors fur-

ther, it is a matter of satisfaction that developments

in these areas are having a positive effect.

The Climate Challenge

12.6. The climate challenge facing agriculture needs

to be taken seriously. Table 12.2 shows a distinct

trend towards both drier and warmer weather, par-

ticularly during the last three Plan periods. Rainfall

in context of agriculture has traditionally been

discussed in terms of the monsoon (that is, June–

September) but annual precipitation is probably

much more relevant now since the dominance of

Kharif crops has reduced. Viewed in this perspec-

tive, it is noteworthy that each of the last three Plan

periods has recorded lower mean rainfall and higher

rainfall variability compared to the immediately pre-

vious period. Three (2008, 2009 and 2011) of the

five Eleventh Plan years had annual rainfall below

95 per cent of long period average, as compared

to only five in the previous 15 years. Temperature

conditions have deteriorated even more. Periods

prior to 1997 can be considered normal, but warm-

ing has increased at an accelerating pace since then.

The Eleventh Plan period contained the two warm-

est years (2010 and 2009) ever recorded since 1900.

Even the coolest year (2008) during these five years

was the thirteenth warmest in the last 110 years.

State-wise performance

12.7. The Mid-term Appraisal of the Eleventh Plan

(MTA) had noted that the recovery in agriculture

after 2004 was associated with clear signs of renewed

dynamism in rain-fed areas. Table 12.3, presents

state-wise averages and standard deviations of

annual growth rates of Gross State Domestic Product

(GSDP) from agriculture and allied activities for four

separate periods since 1981–82. It clearly shows the

following:

1. The all-States average and median growth rates

of GSDP recovered beyond levels before mid-

1990s, to reach near 4 per cent in the period

after 2004–05, this also happened individually in

many states, particularly those with large rain-

fed areas. The states with best performance were

Jharkhand, Chhattisgarh, Manipur, Tripura,

Mizoram, Rajasthan, Gujarat, Maharashtra,

Karnataka and Andhra Pradesh, all with above 5

per cent growth.

2. Despite more difficult weather conditions, all

except few hill states managed substantial reduc-

tion of growth variability (measured by standard

deviation of annual growth rates) during 2005–

12 as compared to the past.

TABLE 12.2

Some Weather Details

1951/52 to

1967/68

1968/69 to

1980/81

1981/82 to

1990/91

1991/92 to

1996/97

1997/98 to

2001/02

2002/03 to

2006/07

2007/08 to

2011/12

Annual Rainfall (cm)

Mean 122.5 118.7 120.1 121.0 118.5 113.7 111.7

Standard Deviation 12.5 10.2 11.5 7.2 8.3 9.4 10.0

Monsoon Rainfall (cm)

Mean 91.9 88.8 88.8 90.0 87.8 83.9 86.6

Standard Deviation 10.1 9.6 11.0 6.5 5.5 7.9 9.7

Annual Temperature anomaly from normal (°C)

Mean 0.04 –0.03 0.09 0.19 0.34 0.56 0.65

Standard Deviation 0.28 0.24 0.03 0.10 0.22 0.11 0.26

Source: Climate bulletins and other publications of the India Meteorological Department.

4 Twelfth Five Year Plan

TABLE 12.3

Averages and Standard Deviations of Annual Growth Rates of GSDP from Agriculture and Allied Sectors

Average of Annual Growth Rates Standard Deviation of Annual Growth Rates

1981–82

to

1993–94

1994–95

to

1999–2000

2000–01

to

2004–05

2005–06

to

2011–12

1981–82

to

1993–94

1994–95

to

1999–2000

2000–01

to

2004–05

2005–06

to

2011–12

Andhra Pradesh 3.9 2.8 4.7 5.0 10.0 13.8 9.7 6.5

Arunachal Pradesh 9.3 –0.8 1.6 5.0 9.7 8.5 7.2 7.8

Assam 2.5 0.2 –0.1 4.1 4.8 2.7 1.4 2.2

Bihar 1.1 3.1 7.4 3.3 12.9 22.7 24.1 11.9

Chhattisgarh 4.9 –2.1 4.6 7.3 10.5 10.5 35.3 9.1

Gujarat 8.8 5.2 9.1 5.5 53.5 27.0 24.2 10.4

Haryana 4.5 2.1 2.7 4.2 12.2 7.0 3.5 5.7

Himachal Pradesh 2.8 0.3 8.0 1.5 12.4 2.1 6.2 9.7

Jammu & Kashmir 1.3 5.2 3.6 0.7 11.2 5.7 3.8 2.9

Jharkhand 1.1 4.3 5.0 8.0 12.9 7.2 19.6 5.1

Karnataka 4.5 4.1 –2.9 5.1 8.7 5.7 15.1 6.8

Kerala 3.2 1.9 1.7 –0.2 6.4 4.9 2.4 3.4

Madhya Pradesh 4.9 1.6 2.2 4.4 10.5 3.4 27.1 4.7

Maharashtra 5.7 3.1 1.6 5.3 17.3 10.1 6.9 11.5

Manipur 2.8 2.1 5.8 5.9 3.6 6.2 6.9 4.4

Meghalaya 1.1 7.2 4.8 3.3 11.2 6.2 2.1 2.2

Mizoram 0.1 5.7 4.8 5.9

Nagaland 14.1 2.5 9.7 2.3

Odisha 2.6 0.0 3.5 3.1 18.6 11.0 16.4 2.5

Punjab 4.9 2.5 1.8 1.8 4.6 4.4 2.6 1.6

Rajasthan 5.9 5.5 10.9 5.5 26.5 14.4 44.9 10.1

Sikkim –1.2 6.5 3.4 11.1 1.0 2.4

Tamilnadu 5.8 1.8 –0.5 4.6 12.7 9.6 14.0 7.0

Tripura 2.5 3.7 4.0 5.7 7.1 5.7 11.4 5.6

Uttar Pradesh 2.8 3.5 1.0 2.8 3.2 5.2 1.8 1.4

Uttarakhand 2.8 2.4 3.3 2.0 3.2 3.5 4.9 4.3

West Bengal 5.3 4.1 2.4 2.6 9.2 4.3 4.0 3.4

Sum of GSDP of:

All above states

3.4

(3.4)

2.5

(3.3)

2.1

(1.7)

3.8

(3.7)

5.8

(5.1)

5.2

(4.6)

6.5

(6.1)

2.8

(2.5)

High irrigation states 3.8 3.2 1.7 2.7 3.1 3.8 2.1 0.9

Medium irrigation states 2.9 1.8 3.1 4.2 9.8 9.1 8.5 3.0

Low irrigation states 3.6 2.8 1.5 4.5 5.6 4.7 9.1 5.3

High productivity states 4.1 2.9 2.5 2.1 3.9 3.1 2.2 0.8

Mid productivity states 3.0 2.4 2.1 3.7 4.0 6.6 4.5 2.3

Low productivity states 3.6 2.6 2.5 5.1 11.0 6.4 16.7 5.4

Across States:

Median 3.6 2.5 3.5 4.2 10.5 6.2 6.9 5.1

Standard deviation 2.2 2.3 3.7 1.9

Note: Figures in brackets use corresponding national GDP agriculture and allied (2004–05 prices) data. High irrigation refers to the

GSDP sum over Haryana, Punjab, Uttar Pradesh and West Bengal (Net irrigated area (NIA)/Arable land (AL) > 55 per cent in 2008–09).

Low irrigation (NIA/AL < 30 per cent) refers to Assam and North-East, Chhattisgarh, Himachal Pradesh, Jharkhand, Karnataka, Kerala,

Maharashtra, Rajasthan and Uttarakhand. Medium refers to the rest. High productivity states (present GSDP/AL > `70,000/hectare

at 2004–05 prices) are Tripura, West Bengal, Kerala, Himachal Pradesh, Punjab, J&K and Haryana. Low productivity (GSDP/AL <

`35,000) states are Rajasthan, Meghalaya, Madhya Pradesh, Chhattisgarh, Maharashtra, Odisha, Jharkhand, Karnataka and Gujarat.

The rest are Middle productivity. The 1980–81 series gives data only for undivided Bihar, MP and UP; these have been split using

1993–94 ratios to get GSDP for new States.

Agriculture 5

3. The variation in performance across States sug-

gests that State-level responses and implementa-

tion play a very significant role in determining

agricultural performance. However, to the extent

that available technology limits potential growth,

it will be difficult to maintain high growth rates

where productivity has increased close to poten-

tial levels. This is relevant because the Eleventh

Plan strategy gave much greater flexibility to

States and focused more on yield gaps within

existing technology, rather than emphasising

new technologies and supporting these. The

growth acceleration since 2005 has therefore

been much stronger in states with lower pro-

ductivity and less irrigation. This suggests that

the strategy may be correcting the past relative

neglect which caused rain-fed farming, covering

over 60 per cent of arable land, to perform well

below potential.

12.8. It is a matter of concern that the recent growth

revival has been weak in areas with high land pro-

ductivity, not only in relatively more irrigated states

such as Punjab, Haryana, Uttar Pradesh and West

Bengal that had green revolution success, but also

in less irrigated states such as Kerala, Himachal

Pradesh and Jammu & Kashmir where high produc-

tivity reflects a high-value cropping pattern based on

horticulture. These States together contribute about

35 per cent of national agricultural output from 20

per cent of arable land, but none of them have been

able to surpass growth rates achieved in the past.

Even Gujarat, a low productivity state that sustained

near 10 per cent growth for almost a decade through

better water use and rapid adoption of Bt cotton

hybrids, slowed down perceptibly in the Eleventh

Plan as Bt adoption saturated and yields reached a

plateau. Clearly, growth is more difficult to acceler-

ate at higher productivity levels without new tech-

nology, particularly if past patterns of growth have

taken a toll on natural resources.

OUTPUTS, INPUTS AND PRODUCTIVITY

12.9. The Eleventh Plan had made four conscious

choices. First, with technology fatigue evident, it

funded research better but emphasised on getting

more from existing technology. Second, since one

size does not fit all, it decentralised plan funds to

encourage initiatives at State and lower levels. Third,

aware of low public investment and food security

needs, it increased Centre’s spending on these, par-

ticularly in disadvantaged regions. Fourth, noting

farmer distress, it tried to focus not just on pro-

duction but also on farm incomes, stressing service

delivery and suggesting encouragement of group

activity with land and tenancy reforms put back on

the agenda. Compared to the original green revo-

lution that built on the best, this strategy sought to

deliver faster growth, that is, more inclusive, more

stable and less concentrated spatially. Nonetheless,

there is a wide demand for a ‘second green revolu-

tion’ with more irrigation and better crop-specific

technologies, with some even claiming that Bt cot-

ton has been the only recent success. The Twelfth

Plan accepts the proposition that a greater techni-

cal thrust is needed, and the strategy for agriculture

should take this into account

12.10. In order to provide a snapshot of the Eleventh

Plan performance and give indication of what the

Twelfth Plan should do differently, long-run data

on growth of output by sub-sector and also rates of

growth of input use and productivity are presented

in Table 12.4. Since performance is almost invari-

ably discussed in the context of well-defined policy

periods, those chosen for this table are same as in the

Eleventh Plan document: (i) Pre-Green Revolution

(1951–52 to 1967–68); (ii) Green Revolution proper

(1968–69 to 1980–81); (iii) Wider technology cover-

age (1981–82 to 1990–91) when focus shifted from

intensification of Green Revolution in best areas

to its spread to new areas; (iv) Early liberalisation

period (1991–92 to 1996–97) when relative prices

became an additional focus, both because agriculture

was expected to gain from reduced trade protection

to industry and also with Minimum Support Prices

(MSP) used for active growth promotion rather than

just passive price support. The other three periods in

the table are subsequent Plan periods: (v) Ninth Plan

(1997–98 to 2001–02); (vi) Tenth Plan (2002–03 to

2006–07) and (vii) Eleventh Plan (2007–08 to 2011–

12). For each of these periods, the average of annual

growth rates is presented for each variable chosen.

12.11. As noted above, growth of agricultural GDP

at 3.3 per cent was short of the 4 per cent target for

6 Twelfth Five Year Plan

TABLE 12.4

Growth of Output, Inputs and Productivity

(period averages of annual growth rates)

Pre-Green

Revolution

Green

Revolution

Wider

Coverage

Early

Liberalisation

Ninth Plan Tenth Plan Eleventh

Plan

1951/52 to

1967/68

1968/69 to

1980/81

1981/82 to

1990/91

1991/92 to

1996/97

1997/98 to

2001/02

2002/03 to

2006/07

2007/08 to

2011/12

I. Value of Output (2004–05 prices)

Cereals 4.2 3.4 3.5 2.4 1.5 1.0 3.0

Pulses 3.0 0.7 3.4 0.8 0.3 1.8 4.2

Oilseeds 3.2 1.8 7.4 4.4 –2.5 7.4 4.5

Sugars 3.3 4.1 4.2 2.4 9.4 1.7 2.2

Fibres 4.4 2.5 5.3 6.5 –5.6 15.1 10.7

Non-horticulture crops 3.2 2.7 3.0 2.1 1.7 2.1 2.8

Horticulture 2.6 4.2 3.1 5.7 3.8 2.6 4.7

All Crops 3.0 3.0 3.0 3.1 2.3 2.1 3.4

Livestock 1.0 3.3 4.8 4.0 3.6 3.6 4.8

Crops and Livestock 2.5 3.0 3.3 3.3 2.6 2.5 3.8

Fishing 4.7 3.1 5.7 7.1 2.7 3.3 3.6

Forestry 1.7 –0.2 0.3 0.3 2.7 1.3 2.3

Agriculture and allied 2.3 2.4 3.0 3.1 2.6 2.4 3.6

II. Value of Intermediate Inputs (2004–05 prices)

Seed 1.5 1.1 2.3 1.6 –0.6 1.4 4.1

Feed of livestock 1.9 4.0 0.1 0.9 3.9 0.7 3.3

Organic manure 0.0 1.3 0.7 0.5 1.6 2.9 3.3

Fertilisers and pesticides 18.2 9.3 8.7 2.0 3.9 4.8 6.7

Diesel oil 26.0 13.1 8.7 4.3 5.1 5.1 5.8

Electricity 18.5 15.2 12.9 14.4 –4.1 2.6 8.0

All inputs crops and

livestock

2.4 4.5 2.2 1.9 3.0 2.5 4.4

Inputs for fishing 4.6 3.3 5.4 6.5 2.7 1.5 3.5

Inputs for forestry 1.7 –0.2 0.1 0.3 2.6 1.3 2.3

All inputs Agriculture and

allied

2.3 3.9 2.1 1.9 3.0 2.4 4.3

III. Gross Value Added (2004–05 prices)

Crops and Livestock 2.7 2.7 3.7 3.7 2.5 2.5 3.5

Fishing 4.7 3.0 5.8 7.2 2.7 3.6 3.7

Forestry 1.7 –0.2 0.4 0.3 2.8 1.3 2.3

Agriculture and allied 2.5 2.4 3.5 3.7 2.5 2.4 3.3

IV. Factor Inputs into Agriculture

Land (Gross cropped area) 1.3 0.4 0.8 0.3 –0.1 0.6 0.3

Labour 1.8 1.1 0.5 2.3 0.3 0.5 –1.5

Net Fixed Capital Stock 2.3 3.6 2.8 3.1 3.4 4.7 6.0

Of which: Public 3.9 2.0 1.4 2.3 3.6

Private 1.4 4.3 5.1 6.6 7.5

V. Partial Factor Productivities (2004–05 prices)

Land productivity 1.2 2.0 2.7 3.3 2.6 1.8 3.1

Labour productivity 0.7 1.4 3.0 1.4 2.2 1.8 4.8

Capital productivity 0.2 –1.1 0.7 0.6 –0.9 –2.4 –2.7

Note: Cropped Area from Ministry of Agriculture, Land use statistics; Labour is agricultural employment from Census till 1971 and

NSSO (weekly status) from 1972–73; all other data are from Central Statistical Office (CSO): National Accounts 2004–05 prices.

Agriculture 7

agricultural GDP but was faster than that in the

Tenth or the Ninth Plan, though lower than the

period from 1981–82 to 1996–97. The growth rates

for individual crops shown in Table 12.4 are for

gross value of output and not value added, but they

present a valid basis for inter-period comparisons.

1. Growth of total value of output in agriculture

proper (crops and livestock) during the Eleventh

Plan averaged 3.8 per cent per year which was

the highest among all seven periods considered.

2. Total non-horticulture crop output grew mar-

ginally faster than target (2.8 per cent against

2.7 per cent target) mainly because of foodgrains

(3.1 per cent actual against 2.3 per cent target),

oilseeds (4.5 per cent against 4 per cent) and

fibres (10.7 per cent against 5 per cent).

3. Horticulture at 4.7 per cent was only marginally

short of the 5 per cent target.

4. Growth of output from livestock (4.8 per cent)

was again highest amongst all the periods consid-

ered but this performance, and even more, so for

fishing (3.6 per cent), fell short of the ambitious

6 per cent target set for these two sub-sectors.

5. Growth of forestry was expectedly slower, pull-

ing down the growth of total value of output in

agriculture and allied to 3.6 per cent, but this

too was the highest among all the seven periods

considered.

12.12. Growth in intermediate inputs has acceler-

ated steadily reaching 4.3 per cent per annum dur-

ing the Eleventh Plan, which was much higher than

growth of output and over twice the growth rate of

intermediate input use during 1981–97. The more

rapid growth in input use explains why despite the

faster growth of the gross value of output during

the Eleventh Plan at 3.6 per cent than in the period

1981–82 to 1996–97 (about 3.0 per cent), GDP in

agriculture (which is a value added concept) grew

more slowly. In other words, agricultural growth

became more input intensive in the Eleventh Plan.

This suggests the need to re-look policies relating to

inputs, especially fertiliser and power.

12.13. Policies towards input use need to distinguish

between traditional inputs such as seed, feed and

organic manure and modern inputs such as chemical

fertiliser, pesticides and farm power. With low seed

replacement, underfed farm animals and soils short

of organic carbon, projections by working groups for

the Twelfth Plan suggest that past growth of these tra-

ditional inputs should be improved upon. However,

these working groups also project lower growth of

‘modern’ inputs than observed during the Eleventh

Plan. For example, 2016–17 requirements of chemi-

cal fertiliser and farm power are placed at levels that

imply annual growth for both fertilisers and ‘mod-

ern’ energy at about 4.5 per cent. These exceed cor-

responding the Eleventh Plan projections but are

much less than the Eleventh Plan actual. Reduced fer-

tiliser and fuel subsidies would be consistent with the

desired moderation in trend of these inputs. Restraint

is also needed on pesticides use which rose sharply in

the Eleventh Plan after years of being subdued.

12.14. In parallel with high growth of intermediate

inputs, there was acceleration in growth of the net

capital stock in agriculture and allied sectors during

the Eleventh Plan. As shown in Table 12.4 (item IV),

Net Fixed Capital Stock in agriculture expanded at

6.0 per cent per year, much faster than in the pre-

vious two Plans. The public component of capi-

tal stock increased by 3.6 per cent while the private

component increased at 7.5 per cent per year, both

showing acceleration compared to the previous

two Plans. However, public investment in agricul-

ture, which was stepped up very substantially in the

last three years of the Tenth Plan, stagnated in the

Eleventh Plan (Table 12.5). This was mainly because

of a large shortfall in planned investment in irriga-

tion. As a result a key part of the Eleventh Plan strat-

egy to achieve 4 per cent agricultural growth which

was to increase public investment in agriculture to

4 per cent of agricultural GDP and thereby achieve

growth of public sector capital stock in agriculture at

least equal to the required 4 per cent growth of total

capital stock has not fructified. Clearly, to attain 4

per cent agricultural growth in the Twelfth Plan will

require firmer commitment to ensure realisation of

this unattained the Eleventh Plan objective.

12.15. Private investment in agriculture has accel-

erated over the past three Plans. Private investment

8 Twelfth Five Year Plan

TABLE 12.5

Gross Capital Formation (GCF) in Agriculture, Forestry and Fishing (2004–05 prices)

Year GDP from Agriculture

and Allied

2004–05 Prices

GCF in Agriculture and Allied at

2004–05 Prices

GCF in Agriculture as Per Cent of

GDP from Agriculture

Public

Sector

Private

Sector

Total Public

Sector

Private

Sector

Total

1 2 345678

Tenth Plan

2002–03 5,17,559 10,299 63,215 73,514 2.0 12.2 14.2

2003–04 5,64,391 12,683 57,238 69,921 2.3 10.1 12.4

2004–05 5,65,426 16,187 59,909 76,096 2.9 10.6 13.4

2005–06 5,94,487 19,940 66,664 86,604 3.5 11.2 14.6

2006–07 6,19,190 22,987 69,070 92,057 3.7 11.2 14.9

Eleventh Plan

2007–08 6,55,080 23,257 82,484 1,05,741 3.6 12.6 16.1

2008–09 6,55,689 20,572 1,06,555 1,27,127 3.1 16.3 19.4

2009–10 6,62,509 22,719 1,08,420 1,31,139 3.4 16.4 19.8

2010–11 7,09,103 21,500 1,20,754 1,42,254 3.0 17.0 20.1

Source: Central Statistical Office National Accounts Division.

averaged 15.6 per cent of agricultural GDP in the first

four years of the Eleventh Plan as against expected

12 per cent. The main driver of this was a large

relative price shift in favour of agriculture, show-

ing that farmers respond to price incentives. If cal-

culated in current price terms rather than constant,

private investment averaged 13 per cent of agri-

cultural GDP—only slightly higher than expected.

Nonetheless, total capital stock in agriculture grew