CENTRAL MACHINERY 95288 27 VISHAL RATHORE

User Manual: CENTRAL MACHINERY 95288

Open the PDF directly: View PDF ![]() .

.

Page Count: 8

et

International Journal on Emerging Technologies 4(1): 169-176(2013)ISSN No. (Print): 0975-8364

ISSN No. (Online): 2249-3255

Energy Audit on Earth Moving Industry

Vishal Rathore*, Amitesh Paul ** and Rajesh Singhadiya***

Department of Mechanical Engineering,

*Research Scholar, SSSIST, Sehore, (M.P.)

**Head of Department, SSSIST, Sehore, (M.P.)

***Energy Auditor, (M.P.)

(Received 05 May, 2013, Accepted 15 June, 2013)

ABSTRACT: Energy auditing has been conducted to the Liu Gong India Pvt. Ltd., Pithampur Dhar

(M.P.) to estimate the Energy consumed in a day, week and monthly. The Energy Auditing for a day is the

index of the consumption which normalizes the situation of Energy crisis by providing the conservation

schemes. Any organization so called bulk consumer of electrical energy propose to adopt suitable

technology or scheme of energy conservation to minimize. The unwanted power shutdown either

incidentally or by load shedding.

Energy auditing has been a part and parcel of every consumer of any form of which energy is exhaustible

and inexhaustible in nature. In olden days their practice used to exploitation of energy only when it is

available for example during crops harvesting wind blow in one direction was very essential for that they

used wait overnight whenever wind blows little heavily harvesting process used to be done. Also they used

select the season for harvesting exclusively for this purpose because ample labours were also available

there will not rain and sufficient sun is available people will not be having any work in the field. That is

how energy by nature was used by formers. Now we are being literate energy being used without

bothering its existence further. Energy auditing is one tool through which balancing of demand and

supply is determined and the positive mismatch cannot be compensated either by organic way or it might

be difficult task. Aim of performing this project is to conserve and utilize the energy which is in the form

Compressed Air & Electrical Energy, which would be used efficiently, effectively and regularly without

any shortage for the future requirement of the industry.

Keywords: Conservation, Feasibility, Recommendations, Payback Period

I. INTRODUCTION

Company: LiuGong India, an arm of the leading

China’s machinery company, Guangxi LiuGong

Machinery Co., Ltd. (LiuGong) having

manufacturing experience for more than 50 years, is

quite optimistic about its future in India.

Presently LiuGong India with its registered office in

Delhi and has its regional offices in metros, logistic

centre in Chennai and the manufacturing plant in

Pithampur in Madhya Pradesh. LiuGong India Plant is

a milestone for Chinese companies in India &

China, covers 44 acres fully equipped with the latest

machines, equipments with the latest technology and

having the fully operational capacity of R&D-

Manufacturing-Sales-Service-Parts, which will

produce 2,000 units wheel loaders and excavators

annually in first phase and other products of the

company will be launched in the coming

phases. LiuGong will have 3 phases in Pithampur

plant attaining FDI investment of around Rs 500 crore

in future.

Energy auditing in a integral part of energy

conservation and energy management is also part and

parallel of conservation. Damage and supply gap is

large energy to lead to similar natural defects. Energy

disaster such as Tsunami and earth quake. The next

generation generating yet to come will be completely

light blind. It is because power never be available

after this disaster and not ever rehabilitate the

reconstruction of buildings. To avoid the energy

calamity proposed auditing report use the innovative

energy utilization schemes through which the

ferocious of situation might blindness can be

eradicated.

The primary objective of the energy audit is to

determine ways to reduce energy consumption per

unit of product output or to lower operating costs. The

energy audit provides a benchmark, or reference

point, for managing and assessing energy use across

the organization and provides the basis for ensuring

more effective use of energy.

Rathore, Paul and Singhadiya 170

The energy audit would give a positive orientation to

the energy cost reduction, preventive maintenance,

and quality control programs which are vital for

production and utility activities. Such an audit

program will help to keep focus on variations that

occur in the energy costs, availability, and reliability

of supply of energy, help decide on the appropriate

energy mix, identify energy conservation

technologies, retrofit for energy conservation

equipment, etc

II. METHODOLOGY

The energy audit uses existing or easily obtained data.

• Determine energy consumption in the organization

• Estimate the scope for saving

• Identify the most likely (and easiest areas) for

attention

• Identify immediate (especially no-cost/low-cost)

improvements/savings

• Set a reference point

Identify areas for more detailed study/measurement

Methodology of this work is concentrated on two

important things that need to be developed in order to

investigate the performance of the Compressor &

Electricity Data which is the location of measurement

points and it devices, and experiment set-up.

III. DATA ANALYSIS

There are three Reciprocating compressors, in the

plant. All the compressors have the same capacity

with same technical specification. During the energy

audit of compressed air system, team was conducted

following test:

•Free Air Delivery (FAD) test.

•Loading & unloading

Compressor Specification :

S.No

Parameter

Compressor ID (RSD/SF1/Utility/PM/3800285)

1

Make

ELGI

2

Type

Compressor

3

Product Type

GA-11P

4

Serial No.

PNE-1102021

5

Free Air Delivery (M3/hr)

115.56

6

Maximum Final Presser (Bar)

7.5

5

Motor (KW)

11

6

Receiver Capacity (Liter)

500

7

Cooling

Air

Motor Detailed

1

Make

Semens

2

Type

Induction Motor

3

Power (kW)

11

4

Phase

3

5

RPM

2950

6

Frequency (Hz)

50

7

Voltage (V)

420

8

Current (A) Loading/Unloading

21.5/12.4

9

Cos Ø

0.84

10

Rated Specific power consumption( kW/M3/hr)

0.0952

*Note-: WLU = Wheel Loader Unit, MGU = Motor Grader Unit

Rathore, Paul and Singhadiya 171

Sr.

No

Air compressor reference

Units

Value for

Shot

Blasting

Unit

Value for

Paint Line &

Testing

Value for

WLU &

MGU

1

Receiver volume plus volume of pipeline

(total volume)

m³

0.5114

0.5

1.00855

2

Receiver temperature

°C

35

35

35

3

Initial receiver pressure (P1)

kg/cm2

0

0

0.1

4

Final receiver pressure (P2)

kg/cm2

7.3

6.5

7

5

Time taken to fill receiver from P1 to P2 (T)

min

2.22

2.09

3.52

6

Atmospheric pressure (Po)

kg/cm2

1.01

1.01

1.01

Free Air Delivery Test :

S.NO.

CALCULATION

FOR

FAD = (P2 - P1/ Po) × (V/T) × {(273+

t1) / (273 + t2)}

Result

(Nm3/

min)

VOLUMETRIC

EFFICIENCY (%)

=( Actual FAD

delivered / Rated

FAD) × 100

Result

(%)

1

Shot Blasting Unit

=(7.3 –0/ 1.01) × (0.5114/ 2.22) ×

{(273+ 27) / (273 + 35)}

1.62

(1.62/1.93) ×100

83

2

Paint Line & Testing

=(6.5 –0/ 1.01) × (0.5/ 2.09) × {(273+

27) / (273 + 35)}

1.5

(1.50/1.93) ×100

77.67

3

WLU & MGU

( Assembly Line)

=(7 –0.1/ 1.01) × (1.00855/ 4.0) ×

{(273+ 27) / (273 + 35)}

1.677

(1.677/1.93) ×100

86

Leakage Test :

Compressor

Value for Shot

Blasting Unit

Value for Paint Line & Testing

Value for Wheel loader &

Motor Grader Unit

Load time (t1)

Min 0.82

Min 0.76

Min 0.5

Unload time (t2)

Min 8.58

Min 2.26

Min 5.25

S.NO.

CALCULATION

FOR

% Leakage = {(t1/ (t1+ t2)} ×100

Result

(%)

% Leakage x

FAD (m³/day)

Leakage in

One Shift

(8x60)

(m³/day)

1

Shot Blasting Unit

{0.82/(0.82+8.58)} ×100

8.72

0.1413

68

2

Paint Line & Testing

{0.77/(0.77+2.26)} ×100

25

0.3812

182.976

3

WLU & MGU

( Assembly Line)

{0.5/(0.5+5.25)} ×100

8.7

0.1458

70.031

Rathore, Paul and Singhadiya 172

Reduce Leakage & Wastage By Awareness & Preventive Maintenance.

S.NO.

Location

% of

Leakage

Targeted % Reduction

Working

Hours/Day

Expected Energy

Saving (Kwh/Yr)

1

Shot Blasting Unit

25

20

17

14,698

2

Paint Line Unit

8.7

3

8

1045

3

Wheel Loader &

Motor Grader Unit

8.7

3

8

1037

4

Total

16,780

Expected Energy Saving= 16,780 kWh/Year.

Expected Saving @ Rs.7/- per kWh= 1, 17,460/-

Expected Investment = Nil

Simple Payback Period =Immediate

Suggestion for Energy Efficiency In Compressed

Air System

•Reduced Compressor delivery pressure,

wherever possible to save energy.

•Provide extra air receivers at point of high

cycle air demand which permits operation

without extra compressor capacity.

•Compressed air leakage of 40-50% is not

uncommon. Carry out periodic leak tests

to estimate the quantity of leakage.

•Compressed air piping layout should be

made preferably as ring main to provide

desired pressure to all users.

•A smaller dedicated compressor can be

installed at load point located far off from

the central compressor house, instead o

supplying air through lengthy pipelines.

•Pneumatic equipment should not be

operated above the recommended

operating pressure as this not only wastes

energy but can also lead to excessive wear

of equipment’s components which leads to

further energy wastage.

•Pneumatic tools such as drill and grinders

consume about 20 times more energy then

motor driven tools. Hence they have to be

used efficiently. Whenever possible, they

should be replaced with electrically

operated tools.

•If pressure requirement for process are

widely different (e.g. 3 bar to 7 bars), it is

advisable to have two separate compressed

air system.

IV. ELECTRICITY DATA

LiuGong India Pvt. Ltd. (Motor Grader Unit,

Canteen & Campus Lightening Area) has

presently taken the power supply from MPMKVV.

Co. Ltd with the help of 33 KV Industrial urban

feeders under tariff 2110 HV- 3.1 with Contracted

Maximum Demand (CMD) is 76 KVA.

Electrical Energy Consumption and Bills:

The analysis of the electricity bill was done by

using latest tariff schedule for HV-3.1 33 KV

Industrial (Urban) feeder. The tariff schedule is

given in appendix 3.1.

Electricity billing is following manner under tariff schedule HV- 3.1.

PARTICULARS

UNITS

VALUE

Demand charges

Rs./kVA

Rs. 335/-

Energy Charges

Rs./kWh

Rs. 4.70/-

Low PF Surcharges (+)

1% to 2% on Energy charges etc. for every

point

As per PF recorded below 0.90 and

applicable

PF Rebate (-)

1% to 5% on Energy charges rebate

As per Pf recorded above 0.95

TOD surcharges (+)

Rs/kWh

Rs. 5.405/-

TOD rebate (-)

Rs/kWh

Rs. 4.35/-

CESS (duty)@ 15 %

Rs/kWh

Rs. 0.405/-

Meter rent

Rs/month

Rs. 2000/-

Rate per unit

Rs/kWh

Rs. 7.0./-

Rathore, Paul and Singhadiya 173

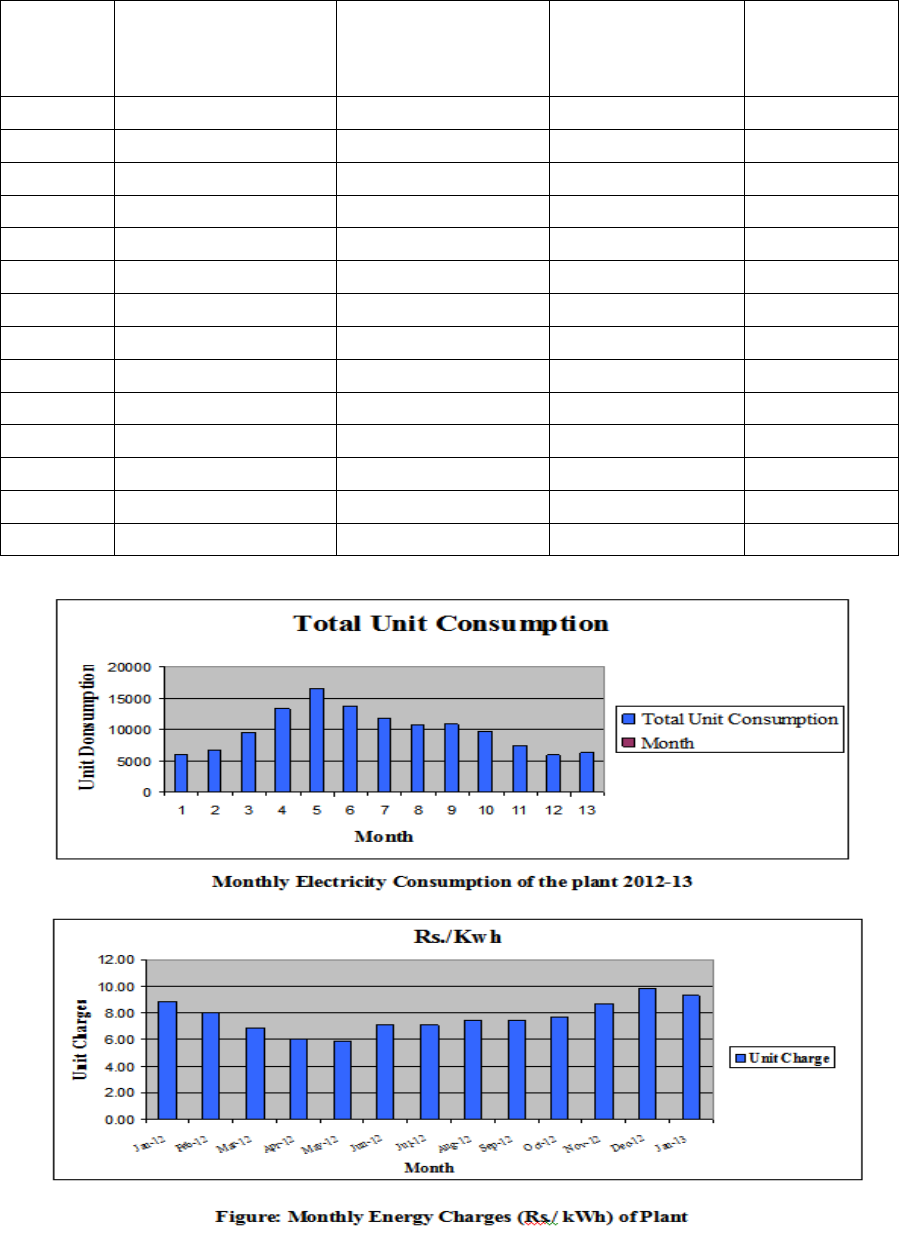

Monthly Electricity Consumption of the Plant 2012-2013.

Sr. No.

Month & Year

Total Unit

Consumption (kwh)

Total Amount

Rs./Kwh

1

1-Jan-2012

5890

52047.00

8.84

2

1-Feb-2012

6620

53062.00

8.02

3

1-Mar-2012

9430

64736.00

6.86

4

1-Apr-2012

13990

84920.00

6.07

5

1-May-2012

16600

97919.00

5.90

6

1-Jun-2012

13750

97607.00

7.10

7

1-Jul-2012

11690

83041.00

7.10

8

1-Aug-2012

10690

79661.00

7.45

9

1-Sep-2012

10780

80239.00

7.44

10

1-Oct-2012

9620

74327.00

7.73

11

1-Nov-2012

7300

63069.00

8.64

12

1-Dec-2012

5910

57740.00

9.77

13

1-Jan-2013

6290

58525.00

9.30

Total

1,28,560

9,46,893.00

7.71

Rathore, Paul and Singhadiya 174

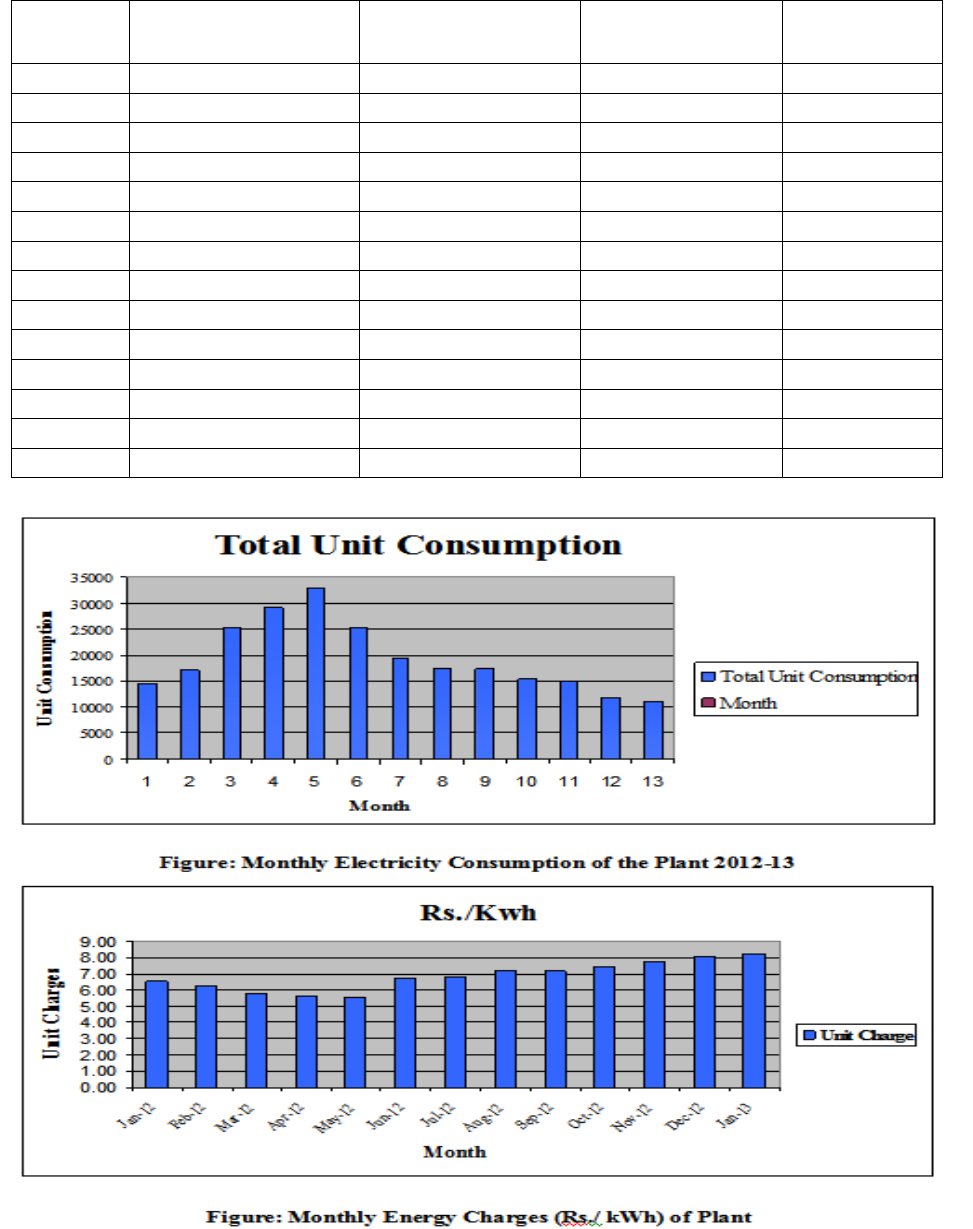

V. ELECTRICITY DATA

LiuGong India Pvt. Ltd. (Wheel Loader, office

Building, and Trading Unit & Testing Unit) has

presently taken the power supply from

MPMKVV.CO. Ltd. with the help of 33KV

Industrial urban feeder under tariff 2110 HV-3.1 with

Contracted Maximum Demand (CMD) is 105 KVA.

Monthly Electricity Consumption of the Plant 2012-2013.

Sr. No.

Month & Year

Total Unit

Consumption (kwh)

Total Amount

Rs./Kwh

1

1-Jan-2012

14515

95288.00

6.56

2

1-Feb-2012

17170

107566.00

6.26

3

1-Mar-2012

25435

145628.00

5.73

4

1-Apr-2012

29235

164468.00

5.63

5

1-May-2012

32995

182750.00

5.54

6

1-Jun-2012

25300

169238.00

6.69

7

1-Jul-2012

19400

132012.00

6.80

8

1-Aug-2012

17440

124688.00

7.15

9

1-Sep-2012

17220

122884.00

7.14

10

1-Oct-2012

15425

114265.00

7.41

11

1-Nov-2012

14940

111653.00

7.47

12

1-Dec-2012

11875

95604.00

8.05

13

1-Jan-2013

11100

90986.00

8.20

Total

252050

1657030.00

6.82

Rathore, Paul and Singhadiya 175

Energy Conservation Measure with Cost Economics

Demand Side Management

By Discarding 76KVA Feeder (Demand Side Management)

During the Energy Audit last 13 month electricity bill was analysis in the following table :

Sr.

No

.

Month &

Year

Actual KVA

Consumption

Total

Consumptio

n (KVA)

Billing KVA

(90% of CD)

Total

Billing

(KVA)

Difference

(KVA)

=

Billing - Actual

Additional

Fixed

Charge

(Rs./KVA)

paid on

90% CD

MPE57804

(105 KVA)

MPE56284

(76 KVA)

MPE57804

(105 KVA)

MPE56284

(76 KVA)

1

1-Jan-2012

21

24

45

95

68

163

118

39530/-

2

1-Feb-2012

23

28

51

95

68

163

112

37520/-

3

1-Mar-2012

25

38

63

95

68

163

100

28000/-

4

1-Apr-2012

34

51

85

95

68

163

78

33500/-

5

1-May-2012

28

55

83

95

68

163

80

26800/-

6

1-Jun-2012

35

52

87

95

68

163

76

25460/-

7

1-Jul-2012

27

44

71

95

68

163

92

30820/-

8

1-Aug-2012

28

36

64

95

68

163

99

33165/-

9

1-Sep-2012

28

39

67

95

68

163

96

32160/-

10

1-Oct-2012

32

42

74

95

68

163

89

29815/-

11

1-Nov-2012

33

28

61

95

68

163

102

34170/-

12

1-Dec-2012

26

21

47

95

68

163

116

38860/-

13

1-Jan-2013

26

22

48

95

68

163

115

38525/-

Total

1273

422305/-

VI. OBSERVATION

•As per the rule of minimum demand charges

90% of the CD, plant is paying fixed charges

(Rs. 335/KVA) on 95 KVA per month for

MPE57804 (105 KVA).

•Similarly pant is paying fixed charges (Rs.

335/KVA) on 68 KVA per month

MPE56248 (76 KVA)

•Total amount paid by plant Rs. 4,22,305/- in

last year on additional pay on 1273 KVA

VII. RECOMMENDATION

It is Recommended to management take the action

for permanent disconnect the 76KVA Contract

Demand feeder & shift all load on MPE57804 (105)

Feeder.

Saving Calculation

•Expected Demand Saving = 1018KVA Per

year

•Expected Money Saving = Rs. 3, 41, 030 /-

Per year

Suggestion for Energy Saving through Power

Consumption

•All Interior walls should be painted using

Enameled paint which would reflect light.

•All Air conditional rooms should be Air light

and doors should be Hydraulic closing

system. Outside air entry in to the air

conditioned room is not hygienic.

•Provision can be made for cooled water

storage facility wherever possible attached

AC room, so that multipurpose utilization of

AC to cool the water will reduce the power

consumption by 30% .

•Replacement of CRT monitor by LCD

monitor not only gives the cost benefit

interns of energy saving but also play a

significant role of radiations due high

potential .when CRT is used high voltage

level handling by CRT at HT electrodes

may emit harmful radiations beyond the

screen which affect the vision.

Rathore, Paul and Singhadiya 176

•Human being get in touch for trouble

shooting may receive great risk of

deadly shock if they touch the charged

body which is normally charged up to

10000volts (approximately). In LCD

monitor all such problems can be

minimized.

•Energy saving by replacing LCD desktop

with LAPTOP illustrate the benefit s in

terms of portability, space saving,

maintenance cost of desktop computers

and additional cost of peripherals. Also

cost of damage and other electrical

problems. Critical space management and

cost involved can be removed. Wiring for

LAN and labour cost can also be

prevented.

•Unnecessary power consumption by

negligence of user and system

administrator for not switching off

while leaving the office will have more

vulnerability for damage due to short

circuit and heavy voltage due to lightning

.

•It is recommended to replace fluorescent

lamps by CFL which are handy by

construction and possibility of breakage is

less. Installation is easy and the labour

charge required for replacement of burnt

tubes and defected choke lamps is a costly

affair. Disposal of burnt tubes will disturb

the habitat place of both human being and

animals. The release of krypton and argon

gases is more dangerous, it may lead to

ecological imbalance if it in mass

destruction.

•Switch off the photocopier machine at the

main outlet itself when not in use or in

other words machine should not be kept in

stand by and sleep mode which consumes

power.

VIII. CONCLUSION

The Proposed project gives strong warning to the

consumer not only in terms of the energy bills also

the energy crisis in the near future to all sectors of

people and in this project the recommendations

reduces the around 15-20% of the energy and 25-

30% of cost reduction excluding some issues takes

more payback period and some are economically

not fit will also be taken in to account in a long run.

There is a scope of improvement to include the

advanced lighting scheme to reduce further 10% of

the cost.

REFERENCES

[1]. Handbook of Bureau of Energy Audit,

Organization of Govt. of India

[2]. www.energymanagertraining.com

[3]. www.google.com

[4]. Website of Liu Gong India Pvt. Ltd.

[5]. Working manual on energy auditing by the

Asian productivity organization(apo) and national

productivity council (npc) in new Delhi, India,

[6]. Efficient Use of Electricity In Industries- Devki

Energy Consultancies Pvt. Ltd., Vadodara

[7]. Free guide to achieving financial success as an

energy auditor by Energy audit Institute- DAVV

(Indore).