PKT C1 511Pkt 14

User Manual: PKT C1

Open the PDF directly: View PDF ![]() .

.

Page Count: 40

2014 Oklahoma

Resident Individual

Income Tax Forms

and Instructions

• Includes Form 511 and Form 538-S

(Oklahoma Resident Income Tax Return

and Sales Tax Relief Credit Form)

This packet contains:

• Instructions for completing the

Form 511: Oklahoma resident

income tax return

• Form 511 income tax form

• Form 538-S: Sales Tax Relief Credit

• Instructions for the direct deposit option

• 2014 income tax tables

Filing date:

• Generally, your return must be

postmarked by April 15, 2015.

For additional information, see the

“Due Date” section on page 4.

•Thisformisalsousedtolean

amended return. See page 6.

Want your refund faster?

• See page 32 for Direct Deposit information.

Oklahoma Taxpayer Access Point

New for 2014!

The Oklahoma Tax Commission is

now offering FREE online ling

of full-year resident Oklahoma

income tax returns through our

OkTAP system. There is no income

limit; check to

to see if you quailfy

at www.tax.ok.gov.

What’s New in the 2014 Oklahoma Tax Packet?

Helpful Hints

• File your return by April 15, 2015. See page 4 for information

regardingextendedduedateforelectronicallyledreturns.

•Ifyouneedtoleforanextension,useForm504andthen

laterleaForm511.

• Be sure to enclose copies of your Form(s) W-2, 1099 or other

withholding statement with your return. Enclose all federal sched-

ules as required.

Table of Contents

2

Before You Begin

You must complete your federal income tax return before begin-

ning your Oklahoma income tax return. You will use the information

entered on your federal return to complete your Oklahoma return.

Remember, when completing your Oklahoma return, round all

amounts to the nearest dollar.

Example:

$2.01 to $2.49 - round down to $2.00

$2.50 to $2.99 - round up to $3.00

•WhencomputingOklahoma’sadditionaldepletion,onlymajoroil

companies are limited to 50% of the net income per well. See the

instructions for Schedule 511-A, line 8 on page 14.

• There is a new deduction for individuals providing foster care.

See the instructions for Schedule 511-C, line C5 on page 17.

• Income from discharge of indebtedness which was added back

to compute your Oklahoma taxable income in tax year 2010 may

be partially deductible. See the instructions for Schedule 511-C,

line C6, #12 on page 18.

Common Abbreviations

Found in this Packet

IRC - Internal Revenue Code

OS - Oklahoma Statutes

OTC - Oklahoma Tax Commission

Sec. - Section(s)

Important:Ifyoulloutanyportionofthe

Schedules 511-A through 511-H or Form 538-S,

you are required to enclose those pages with your

return. Failure to include the pages will result in a

delay of your refund.

Determining Your Filing Requirement ................ 3

ResidenceDened ............................................ 4

Resident Income................................................ 4

Due Date ........................................................... 4

Extensions ......................................................... 4

Who Must File.................................................... 4

Not Required to File........................................... 5

Refunds ............................................................. 5

Net Operating Loss............................................ 5

Estimated Income Tax ....................................... 5

Amended Returns.............................................. 6

Top of Form Instructions .................................... 6-7

Form 511: Select Line Instructions .................... 8-12

When You Are Finished ..................................... 12

Schedule 511-A Instructions .............................. 13-15

Schedule 511-B Instructions .............................. 15-16

Schedule 511-C Instructions .............................. 17-18

Schedule 511-D Instructions .............................. 19

Schedule 511-E Instructions .............................. 19

Schedule 511-F Instructions .............................. 19

Schedule 511-G Instructions ............................. 19

Schedule 511-H Instructions .............................. 19

Contact Information and Assistance .................. 19

Tax Table ........................................................... 20-31

Direct Deposit Information ................................. 32

• The Coal Credit and the Credit for Electricity Generated by Zero-

Emission Facilities may be refundable. See the instructions for

line 29 on page 12 and Forms 577 and 578.

• You may check the status of your refund on our website. For

more information, see All About Refunds on page 5.

Helpful Reminder - TheSchedule511-Cadjustmentsfor

Political Contributions and Interest Qualifying for Exclusion are

no longer available. Both were repealed.

•Besuretosignanddatethereturn.Ifyouarelingajoint

return, both you and your spouse need to sign.

•Afterling,ifyouhavequestionsregardingthestatusofyour

refund, call (405) 521-3160. The in-state toll-free number is (800)

522-8165.

• Do not enclose any correspondence other than those docu-

ments and schedules required for your return.

• Would you like your refund faster? Choose to have your refund

direct deposited into your checking or savings account.

• When you complete the direct deposit section on the Form 511,

verify the routing and account numbers are correct. If the direct

deposit fails to process, your refund will be mailed to you on a

debit card.

2-D Fill-in Forms with Online Calculations

•

Download Forms 24/7

•

View FAQs or Email the OTC a Question

www.tax.ok.gov

Oklahoma Taxpayer

Access Point

Chart A: Federal Filing Requirements for Most People

Chart B: Federal Filing Requirements for Children and Other Dependents

To use this chart, rst nd your ling status. Then read across to nd your age at the end of 2014. You must le a return if

your gross income was at least the amount shown in the last column.

If your Filing Status Is... And your Age Is*... And if your Gross Income Is...**

Single Under65 $10,150

65orolder $11,700

MarriedFilingJoint*** Bothunder65 $20,300

One65orolder $21,500

Both65orolder $22,700

MarriedFilingSeparate Anyage $3,950

HeadofHousehold Under65 $13,050

65orolder $14,600

QualifyingWidow(er) Under65 $16,350

withaDependentChild 65orolder $17,550

single dependents

Were you either age 65 or older or blind?

No.Youmustleareturnifanyofthefollowingapply...

•Yourunearnedincomewasover$1000.

•Yourearnedincomewasover$6,200.

•Yourgrossincomewasmorethanthelarger of:

••$1000,or

••Yourearnedincome(upto$5,850)plus$350.

Yes.Youmustleareturnifanyofthefollowingapply...

•Yourunearnedincomewasover$2,550($4,100if65orolderandblind).

•Yourearnedincomewasover$7,750($9,300if65orolderandblind).

•Yourgrossincomewasmorethanthelarger of:

••$2,550($4,100if65orolderandblind),or

••Yourearnedincome(upto$5,850)plus$1,900($3,450if65orolderandblind).

married dependents

Were you either age 65 or older or blind?

No.Youmustleareturnifanyofthefollowingapply...

•Yourgrossincomewasatleast$5andyourspouselesaseparatereturnanditemizesdeductions.

•Yourunearnedincomewasover$1000.

•Yourearnedincomewasover$6,200.

•Yourgrossincomewasmorethanthelarger of:

••$1000,or

••Yourearnedincome(upto$5,850)plus$350.

Yes.Youmustleareturnifanyofthefollowingapply...

•Yourgrossincomewasatleast$5andyourspouselesaseparatereturnanditemizesdeductions.

•Yourunearnedincomewasover$2,200($3,400if65orolderandblind).

•Yourearnedincomewasover$7,400($8,600if65orolderandblind).

•Yourgrossincomewasmorethanthelarger of:

••$2,200($3,400if65orolderandblind),or

••Yourearnedincome(upto$5,850)plus$1,550($2,750if65orolderandblind).

Ifyourparent(orsomeoneelse)canclaimyouasadependent,usethischarttoseeifyoumustleafederalreturn.

Inthesecharts,unearnedincomeincludestaxableinterest,ordinarydividendsandcapitalgaindistributions.Italsoincludesunemployment

compensation,taxablesocialsecuritybenets,pensions,annuitiesanddistributionsofunearnedincomefromatrust.Earnedincomeincludes

wages,tipsandtaxablescholarshipsandfellowships.Grossincomeisthetotalofyourunearnedandearnedincome.

IfyoudonotmeetthefederallingrequirementsasshownineitherChartAorChartBonthispage,youarenotrequiredtolean

Oklahomataxreturn.Ifyouhavewithholdingormadeestimatedtaxpaymentsyouwouldliketohaverefunded,followtheinstruc-

tionsonpage5,“NotRequiredtoFile”.

*Ifyouturnedage65onJanuary1,2015,youareconsideredtobe65attheendof2014.

**Grossincomemeansalltheincomeyoureceivedintheformofmoney,goods,property,andservicesthatisnotexemptfromfederaltax,includinganyincome

fromsourcesoutsidetheUnitedStatesorfromthesaleofyourmainhome(evenifyoucanexcludepartorallofit).

Donotincludeanysocialsecuritybenetsunless(a)youaremarriedlingseparateandyoulivedwithyourspouseatanytimein2014or(b)one-halfof

yoursocialsecuritybenetsplusyourothergrossincomeandanyfederallytax-exemptinterestismorethan$25,000($32,000ifmarriedlingjointly).If(a)

or(b)applies,seetheinstructionsforFederalForm1040or1040Atogurethetaxablepartofsocialsecuritybenetsyoumustincludeingrossincome.

***Ifyoudidnotlivewithyourspouseattheendof2014(oronthedateyourspousedied)andyourgrossincomewasatleast$3,950,youmustleareturn

regardlessofyourage.

Determining Your Filing Requirement

3

Residence Defined

Resident...

AnOklahomaresidentisapersondomiciledinthisstateforthe

entiretaxyear.“Domicile”istheplaceestablishedasaperson’s

true,xed,andpermanenthome.Itistheplaceyouintendto

returntowheneveryouareaway(asonvacationabroad,busi-

nessassignment,educationalleaveormilitaryassignment).A

domicile,onceestablished,remainsuntilanewoneisadopted.

Part-Year Resident...

Apart-yearresidentisanindividualwhosedomicilewasinOkla-

homaforaperiodoflessthan12monthsduringthetaxyear.

Nonresident...

AnonresidentisanindividualwhosedomicilewasnotinOkla-

homaforanyportionofthetaxyear.

Members of the Armed Forces...

Residencyisestablishedaccordingtomilitarydomicileasestab-

lishedbytheSoldiers’andSailors’CivilReliefAct.

If you were an Oklahoma resident at the time you entered military

service,assignmenttodutyoutsideOklahomadoesnotofitself

changeyourstateofresidence.Youmustleyourreturnasa

residentofOklahomauntilsuchtimeasyouestablishaperma-

nentresidenceinanotherstateandchangeyourmilitaryrecords

(asevidencedbythemilitary’sFormDD2058).Seethespecic

instructionsforSchedule511-C,lineC1-MilitaryPayExclusion.

Whenthespouseofamilitarymemberisacivilianandhasthe

samelegalresidencyasthemilitarymember,thespousemay

retainsuchlegalresidency.Theyleajointresidenttaxreturn

inthemilitarymembers’StateofLegalResidency(ifrequired)

andaretaxedjointlyundernonresidentrulesastheymovefrom

statetostate.Ifthenon-militaryspousedoesnothavethesame

legalresidencyasthemilitarymember,thesameresidencyrules

applyaswouldapplytoanyothercivilian.Thespousewouldthen

complywithallresidencyruleswhereliving.

AnOklahomaresidentlingajointfederalreturnwithanon-

residentspousemayhaveoptionsonhowtoletheOklahoma

return(s).See“FilingStatus”inthe“TopofFormInstructions”on

page7forfurtherinformation.

Who Must File?

Resident...

EveryOklahomaresidentwhohassufcientgrossincometo

requirethelingofafederalincometaxreturnisrequiredtole

anOklahomareturn,regardlessofthesourceofincome.

Ifyoudonothavealingrequirement,buthadOklahomatax

withheld,madeestimatedtaxpayments,qualifyfortheNatural

Disaster Tax Credit, claim earned income credit or other refund-

ablecredits,seethenextsection“NotRequiredtoFile”forfurther

instructions.Ifyouareuncertainaboutyourlingrequirement,

seethechartsonpage3.

Part-Year Resident...

Everypart-yearresident,duringtheperiodofresidency,hasthe

samelingrequirementsasaresident.Duringtheperiodofnon-

residency, an Oklahoma return is also required if the Oklahoma

part-yearresidenthasgrossincomefromOklahomasourcesof

$1,000ormore.UseForm511NR.

Nonresident...

EverynonresidentwithgrossincomefromOklahomasourcesof

$1,000ormoreisrequiredtoleanOklahomaincometaxreturn.

UseForm511NR.

What Is “Resident Income”?

AnOklahomaresidentindividualistaxedonallincomereported

onthefederalreturn,exceptincomefromrealandtangible

personalpropertylocatedinanotherstate,incomefrombusiness

activitiesinanotherstate,orthegains/lossesfromthesalesor

exchangeofrealpropertyinanotherstate.

Note:Residentsaretaxedonallincomefromnon-business

interestanddividends,salaries,commissionsandotherpayfor

personalservicesregardlessofwhereearned.Wagesearned

outsideofOklahomamustbeincludedinyourOklahomareturn,

andcreditfortaxespaidotherstatesclaimedonOklahomaForm

511TX.(SeeForm511,line16)

Due Date

Generally,yourOklahomaincometaxreturnisdueApril15th,the

samedayasyourfederalreturn.However:

• Ifyouleyourreturnelectronically(throughaprepareror

theinternet),yourduedateisextendedtoApril20th.Anypay-

mentoftaxesdueonApril20thmustberemittedelectronically

inordertobeconsideredtimelypaid.Ifthebalancedueonan

electronicallyledreturnisnotremittedelectronically,penalty

andinterestwillaccruefromtheoriginalduedate.

• IftheInternalRevenueCode(IRC)oftheIRSprovidesfor

alaterduedate,yourreturnmaybeledbythelaterduedate

andwillbeconsideredtimelyled.Youshouldwritetheappropri-

ate“disasterdesignation”asdeterminedbytheIRSatthetopof

thereturn,ifapplicable.Ifabillisreceivedfordelinquentpenalty

and interest, you should contact the Oklahoma Tax Commission

(OTC)atthenumberonthebill.

• Iftheduedatefallsonaweekendorlegalholidaywhen

OTCofcesareclosed,yourreturnisduethenextbusinessday.

Yourreturnmustbepostmarkedbytheduedatetobeconsid-

eredtimelyled.

What Is an “Extension”?

Avalidextensionoftimeinwhichtoleyourfederalreturn

automatically extends the due date of your Oklahoma return if no

Oklahomaliabilityisowed.Acopyofthefederalextensionmust

beenclosedwithyourOklahomareturn.Ifyourfederalreturnis

notextendedoranOklahomaliabilityisowed,anextensionof

timetoleyourOklahomareturncanbegrantedonForm504.

90% of the tax liability must be paid by the original due date

of the return to avoid penalty charges for late payment. Inter-

est will be charged from the original due date of the return.

4

Estimated Income Tax

Youmustmakeequal*quarterlyestimatedtaxpaymentsifyou

canreasonablyexpectyourtaxliabilitytoexceedyourwithhold-

ingby$500ormoreandyouexpectyourwithholdingtobeless

than the smaller of:

1. 70%ofyourcurrentyear’staxliability,or

2. Thetaxliabilityshownonyourreturnforthe

precedingtaxableyearof12months.

Taxpayerswhofailtomaketimelyestimatedtaxpaymentsmay

besubjecttointerestonunderpayment.FormOW-8-ES,forling

estimatedtaxpayments,willbesuppliedonrequest.Ifatleast

66-2/3%ofyourgrossincomeforthisyearorlastyearisfrom

farming,estimatedpaymentsarenotrequired.Ifclaimingthis

exception,seeinstructionsforline23.

EstimatedpaymentscanbemadethroughtheOTCwebsiteby

e-checkorcreditcard.Visitthe“OnlineServices”sectionat

www.tax.ok.gov.

*Forpurposesofdeterminingtheamountoftaxdueonanyof

therespectivedates,taxpayersmaycomputethetaxbyplacing

taxableincomeonanannualizedbasis.

SeeFormOW-8-ES-SUP.

Net Operating Loss

ThelossyearreturnmustbeledtoestablishtheOklahoma

NetOperatingLoss(NOL).OklahomaNOLshallbeseparately

determinedbyreferencetoIRCSection172asmodiedby

theOklahomaIncomeTaxActandshallbeallowedwithout

regardtotheexistenceofafederalNOL.Encloseadetailed

scheduleshowingtheoriginandNOLcomputation.Residents

useOklahoma511NOLSchedules. Alsoencloseacopyofthe

federalNOLcomputation.

Fortaxyears2001–2007andtaxyears2009andsubsequent,

theyearstowhichanNOLmaybecarriedshallbedetermined

solelybyreferencetoIRCSection172.Fortaxyear2008,the

yearstowhichanNOLmaybecarriedbackshallbelimitedto

twoyears.

AnNOLresultingfromafarminglossmaybecarriedbackin

accordancewithandtotheextentofIRCSection172(b)(G).

However,theamountoftheNOLcarrybackshallnotexceedthe

lesserof:$60,000,orthelossproperlyshownontheFederal

ScheduleFreducedbyhalfoftheincomefromallothersources

otherthanreectedonScheduleF.Youcanchoosetotreatthe

NOLasifitwerenotafarmingloss.Ifyoumakethischoice,the

carrybackperiodwillbedeterminedbyreferencetoIRCSection

172andtheamountoftheNOLcarrybackwillnotbelimited.

Anelectionmaybemadetoforegothecarrybackperiod.A

writtenstatementoftheelectionmustbepartoftheoriginal

timelyledOklahomalossyearreturn.However,ifyouledyour

returnontimewithoutmakingtheelection,youmaystillmakethe

electiononanamendedreturnledwithinsixmonthsofthedue

dateofthereturn(excludingextensions).Attachtheelectionto

theamendedreturn.Oncemade,theelectionisirrevocable.

TheOklahomaNOL(s)shallbesubtractedonSchedule511-A,

line9.Thereisalsoaspaceprovidedtoenterthelossyear(s).

ThefederalNOL(s)shallbeaddedonSchedule511-B,line4.

Did you have sufcient gross income to require you to le

a federal return?

Yes-YouarerequiredtoleanOklahomareturn.Followthe

instructionsonpages6-19tohelpyoucompleteyourOkla-

homareturn(Form511).

No-Gotostep2.

Did you have any Oklahoma withholding, make Oklahoma

estimated tax payments, qualify for the Natural Disaster

Tax Credit or claim earned income credit or other refund-

able credits?

Yes-Gotostep3.

No-YouarenotrequiredtoleanOklahomareturn(Form

511).Youmaystillqualifytoleforsalestaxrelief,seethe

instructionsonthebackofForm538-S.

You should le an Oklahoma tax return. Complete the

Form 511 as follows:

•FilloutthetopportionoftheForm511accordingtothe

“TopofFormInstructions”onpages6and7.Besureandplace

an‘X’inthebox“NotRequiredtoFile”.

•Completeline1.Entertheamountofyourgrossincome

subjecttothefederallingrequirement.Inmostcasesthiswill

bethesameasyourFederalAdjustedGrossIncome.(Donot

completelines2-19)

•Completelines20through44thatareapplicableto

you.Ifyouqualifyforthefederalearnedincomecredit,you

qualifyfortheOklahomaearnedincomecredit.Enter5%of

thefederalearnedincomecreditonForm511,line28(donot

completeSchedule511-F).

•SignandmailForm511,pages1and2only.Donot

mailpages3and4.Onlysendinpage5ifyouhavecompleted

Schedule511-G.BesuretoincludeyourW-2,1099orother

withholdingstatementtosubstantiateanyOklahomawithholding.

Not Required to File

step one

step two

step three

All About Refunds

Taxpayershavetwoquick,convenientwaystocheckthestatus

oftheirrefundwithouthavingtospeaktoanOTCrepresentative.

Youcancheckyourrefundforthecurrenttaxyearbyoneofthe

followingways:

•VisittheOTCwebsiteatwww.tax.ok.gov and click on

the “CheckonaRefund”link,whichwillleadyoutoourTaxpayer

AccessPoint(OkTAP).Onceonthispage,youwillberequiredto

enterthelastsevendigitsoftheprimarysocialsecuritynumber

onthereturn,theZipCodeonthereturnaswellastheamountof

theanticipatedrefund.

• Call(405)521-3160andenterthesameinformationas

promptedbyourinteractiveautomatedphonesystem.

Note:Ifyourstatushasanapprovaldate,youshouldallowve

tosevenbusinessdaysfromthatdatetoreceiveyourrefund

debitcard,orvebusinessdaysifyouelecteddirectdeposit.

Ifyoudonotchoosetohaveyourrefunddeposited

directlyintoyourbankaccount,youwillreceivea

debitcard.Seepage18forinformationondebit

cardsandpage32formoreinformationondirectdeposit.

Adebitcardordirectdepositarenotyouronlyoptionsto

receiveyourrefund.Iftimelylingyoumayhaveanyamountof

overpaymentappliedtoyournextyear’sestimatedtax.Refunds

appliedtothefollowingyear’sOklahomaestimatedincometax

(atthetaxpayer’srequest)maynotbeadjustedaftertheoriginal

duedateofthereturn.

5

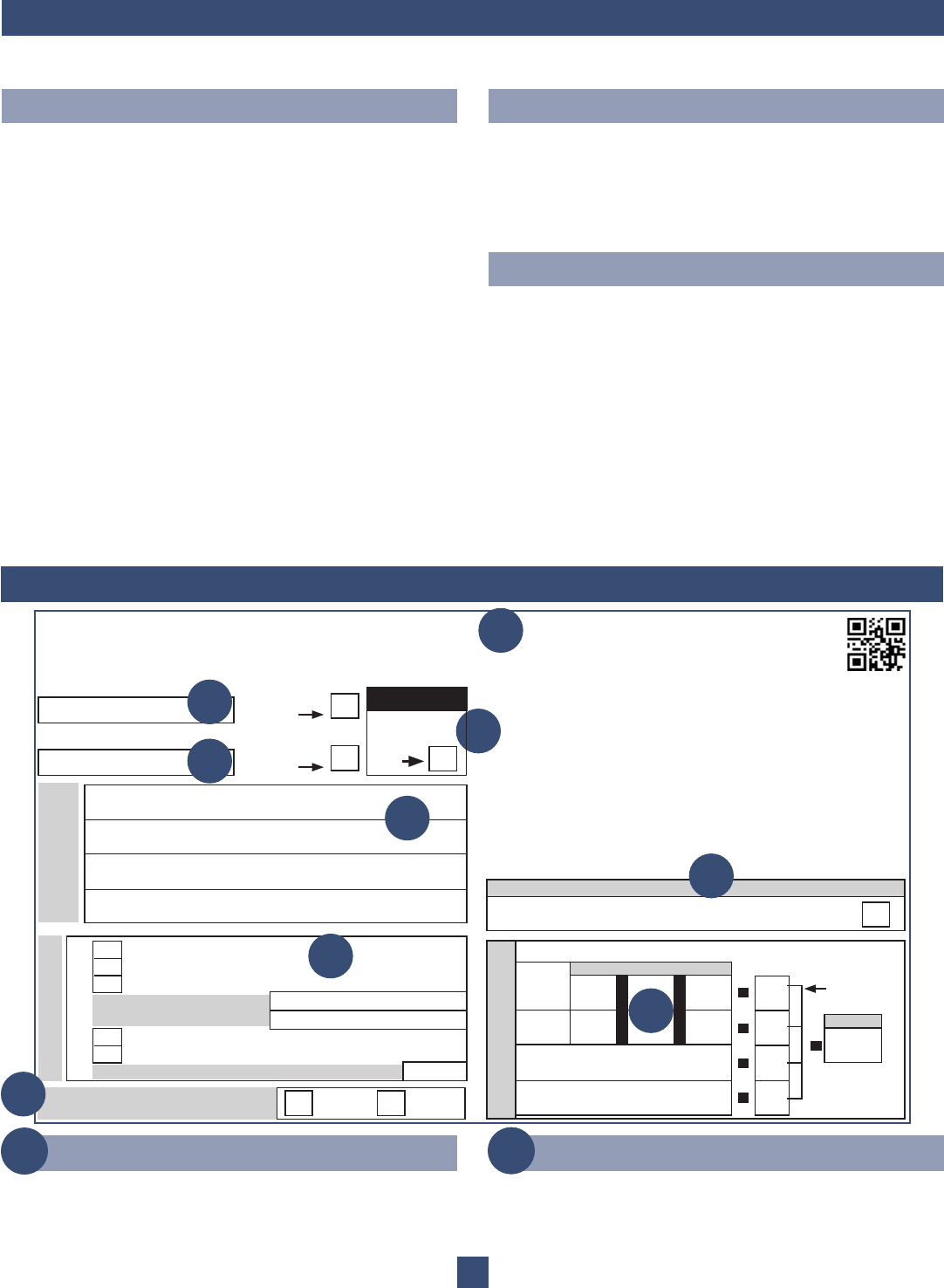

Top of Form Instructions

Amended Returns

Do Not Write in this Space

ASocial Security Number

B

Thebarcodeneartheformnumbercontainsapagenotationsignify-

ingtherstpageofanewreturnforprocessingequipmentuse.The

blankareaisusedforprocessingnotations.Donotwriteinthese

areas.

Enteryoursocialsecuritynumber.Ifyoulemarriedlingjoint,enter

yourspouse’ssocialsecuritynumberinthespaceprovided.Note:

Ifyouarelingmarriedlingseparate,donotenteryourspouse’s

socialsecuritynumberhere.EnterinItemD.

When to File an Amended Return How to Complete an Amended Return

When You Are Finished

Encloseacopyofthefollowingsupportdocuments,ifapplicable.

Failuretoprovidethesupportingdocumentsmaydelaytheprocess-

ingofthereturn.

• Form1040X(AmendedFederalIncomeTaxReturn)orForm

1045(ApplicationforFederalTentativeReturn),

• ProofthatIRShasapprovedtheclaim,suchasthestate-

mentofadjustment,anycorrespondencefromIRS,orthe

depositslipofyourfederalrefund,

• RevenueAgentReport(RAR),CP2000orothernotication

ofanassessmentorachangemadebytheIRS,

• AdditionalFormsW-2or1099notfurnishedwithoriginal

return, and

• Forms,schedulesorotherdocumentationtosubstantiate

anychangemadeontheamendedreturn.

Generally,toclaimarefund,youramendedreturnmustbeled

withinthreeyearsfromthedatetax,penaltyandinterestwerepaid.

Formosttaxpayers,thethreeyearperiodbeginsontheoriginaldue

dateoftheOklahomataxreturn.Estimatedtaxandwithholdings

aredeemedpaidontheoriginalduedate(excludingextensions).

Ifyourfederalreturnforanyyearischanged,anamendedOkla-

homareturnshallbeledwithinoneyear.Ifyouamendyourfederal

return,itisrecommendedyouobtainconrmationtheIRSapproved

yourfederalamendmentbeforelingyouramendedOklahoma

return.FilinganamendedOklahomareturnwithoutsuchIRSconr-

mationmaydelaytheprocessingofyourreturn;however,thismay

benecessarytoavoidtheexpirationofthestatuteoflimitation.

Fileaseparateamendedreturnforeachyearyouareamending.

Noamendedreturnmayencompassmorethanonesingleyear.

Maileachyearsamendedreturninaseparateenvelope.Donot

encloseamendmentsfromdifferentyearsinthesameenvelope.

IfyoudiscoveryouhavemadeanerroronlyonyourOklahomare-

turn,wemaybeabletohelpyoucorrecttheforminsteadoflingan

amendedreturn.Foradditionalinformation,contactourTaxpayer

AssistanceDivisionatoneofthenumbersshownonpage19.

Placean“X”intheAmendedReturncheck-boxatthetopofForm

511,page1.Completetheamendedreturn.Enteranyamount(s)

paidwiththeoriginalreturnplusanyamount(s)paidafteritwasled

online30.Enteranyrefundpreviouslyreceivedoroverpayment

appliedonline32.CompleteSchedule511-H“AmendedReturn

Information”onForm511,page5.

Beginningwithtaxyear2013,theForm511willbeusedtoleanamendedresidentreturn.TheForm511Xwillonlybeusedfortaxyear

2012andprior.Part-yearandnonresidentsuseForm511NR.

6

C

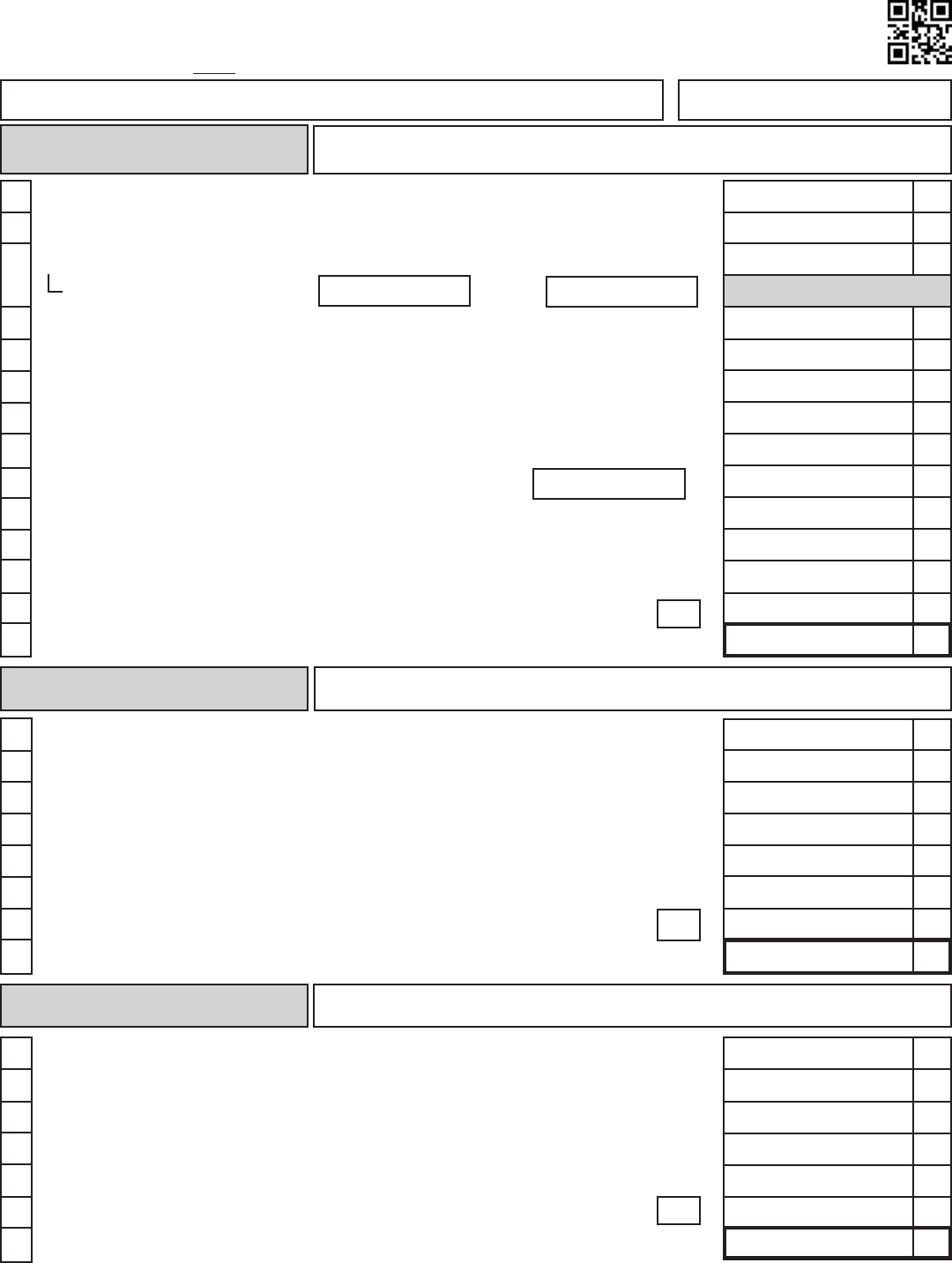

Oklahoma Resident Income Tax Return

Your Social Security Number

Not Required to File

Place an ‘X’ in this box if you do not have sufcient gross

income to require you to le a Federal return. (see instructions)

Name and Address

Please Print or Type

Yourrstname,middleinitialandlastname

Mailingaddress(numberandstreet,includingapartmentnumber,ruralrouteorPOBox)

City,StateandZIP

Ifajointreturn,spouse’srstname,middleinitialandlastname

Regular

Yourself

Spouse

Number of dependent children

Number of other dependents

Add the Totals from

the 4 boxes.

Write the Total

in the box below.

Note: If you may be

claimed as a dependent

on another return,

enter “0” for your

regular exemption.

Total

Exemptions

Place an ‘X’ in this

box if this taxpayer

is deceased

Place an ‘X’ in this

box if this taxpayer

is deceased

Spouse’s Social Security Number

(jointreturnonly)

=

* NOTE:IfclaimingSpecial Exemption,seeinstructionsonpage7of511Packet.

Special Blind

+

*

+

+ + =

=

=

=

Age 65 or Over?

(Please see instructions)

Y o u r s e l f Spouse

Place an ‘X’ in this

box if this is an

amended 511. See

Schedule

511-H.

AMENDED

RETURN!

Form 511

2014

Filing Status

1 Single

2 Marriedlingjointreturn(evenifonlyonehadincome)

3 Marriedlingseparate

• Ifspouseisalsoling,list

nameandSSNintheboxes:

4 Headofhouseholdwithqualifyingperson

5 Qualifyingwidow(er)withdependentchild

•Pleaselisttheyearspousediedinboxatright:

Name:

SSN:

B

B

D

E

G

H

F

A

Not Required to FileAmended Return GC

Exemptions

H

Placean‘X’inthebox,ifyoudonothavesufcientgrossincome

torequireyoutoleafederalreturn,andyouhadOklahomatax

withheld,madeestimatedtaxpayments,qualifyfortheNatural

Disaster Tax Credit, qualify for Oklahoma earned income credit or

otherrefundablecredits.

Finishthetopportionofthereturnbycompletingthe“Exemptions”

section(partHonthediagramonpage6).

Completeline1.Entertheamountofyourgrossincomesubjectto

thefederallingrequirement.Inmostcasesthiswillbethesame

asyourFederalAdjustedGrossIncome.(Donotcompletelines

2-19.)Completelines20through44thatareapplicabletoyou.

IfyouqualifyfortheFederalEarnedIncomeCredit,youqualify

fortheOklahomaEarnedIncomeCredit.Enter5%oftheFederal

EarnedIncomeCreditonForm511,line28(donotcomplete

schedule511-F).

Signandmailthereturn.BesuretoincludeyourW-2,1099

orotherwithholdingstatementtosubstantiateanyOklahoma

withholding.

Note: If you do not have sufcient gross income to require you to le a

federal return and did not have Oklahoma tax withheld, make estimated tax

payments, qualify for the Natural Disaster Tax Credit, qualify for Oklahoma

earned income credit or other refundable credits, do not le an Oklahoma

income tax return (Form 511).

Top of Form Instructions

Totherightoftheword“Yourself”placeanumber“1”inallthe

boxesthatapplytoyou.Nexttotaltheboxes.Thendothesamefor

yourspouseifapplicable.

Exemption Terms

Regular*:Thesameexemptionsasclaimedonyourfederalreturn.

Special:Anadditionalexemptionmaybeclaimedforeach

taxpayerorspousewhomeetsthequalicationsbasedonling

statusandFederalAdjustedGrossIncomelimits**belowand who

is65yearsofageoroveratthecloseofthetaxyear:

(1)Singlereturnwithline1equalto$15,000orless.

(2)Jointreturnwithline1equalto$25,000orless.

(3)Marriedlingseparatereturnwithline1equalto$12,500orless.

(4)Headofhouseholdreturnwithline1equalto$19,000orless.

**Note:IfyourFederalAdjustedGrossIncomeincludesincomefrom

theconversionofatraditionalindividualretirementaccounttoaRoth

individualretirementaccountthisincomeshallbeexcludedindeter-

miningtheFederalAdjustedGrossIncomelimits.

EncloseacopyofyourfederalreturnandForm8606.

Blind:Anadditionalexemptionmaybeclaimedforeachtaxpayeror

spousewhoislegallyblind.

Dependents:Ifclaimingdependents,enterthesamenumberas

onyourfederalreturn.However,ifthenonresidentspousealsohas

anOklahomalingrequirementandislingseparatelyonForm

511NR,thedependencyexemptionswillbeallocatedbetweenthe

resident’sandnonresident’sreturns.

*

NOTE:Ifyoumaybeclaimedasadependentonanotherreturn,

enterzeroforyourregularexemption.YoustillqualifyfortheOkla-

homastandarddeduction.

Sixty-five or Over

F

Placean‘X’inthebox(es)ifyour,oryourspouse’s,ageis65on

orbeforeDecember31,2014.Ifyouturnedage65onJanuary1,

2015,youareconsideredtobeage65attheendof2014.

ThelingstatusforOklahomapurposesisthesameasonthe

federalincometaxreturn,withoneexception.Thisexception

appliestomarriedtaxpayerswholeajointfederalreturnwhere

onespouseisafull-yearOklahomaresident(eithercivilianor

military),andtheotherisafull-yearnonresidentcivilian(non-

military).Inthiscase,thetaxpayersmusteither:

1.FileasOklahomamarriedlingseparate.TheOklahoma

resident,lingajointfederalreturnwithanonresident

civilianspouse,mayleanOklahomareturnasmarriedling

separate.TheresidentwillleonForm511usingthemarried

lingseparateratesandreportingonlyhis/herincomeand

deductions.IfthenonresidentcivilianalsohasanOklahoma

lingrequirement,he/shewillleonForm511NR,usingmarried

lingseparateratesandreportinghis/herincomeanddeductions.

Form574“AllocationofIncomeandDeductions”mustbeled

withthereturn(s).Youcanobtainthisformfromourwebsiteat

www.tax.ok.gov.

-OR-

2.Fileasifboththeresidentandthenonresidentcivilianwere

OklahomaresidentsonForm511.Usethe“marriedlingjoint”

lingstatus,andreportallincome.Ataxcredit(Form511TX)

maybeusedtoclaimcreditfortaxespaidtoanotherstate,if

applicable.Astatementshouldbeattachedtothereturnstating

thenonresidentislingasaresidentfortaxpurposesonly.

IfanOklahomaresident(eithercivilianormilitary)lesajoint

federal return with a nonresident militaryspouse,theyshalluse

thesamelingstatusasonthefederalreturn.Iftheyleajoint

federalreturn,theyshallcompleteForm511NRandincludein

the Oklahoma amount column, all Oklahoma source income of

boththeresidentandthenonresident.

Filing Status

E

Printortypetherstname,middleinitialandlastnameforboth

yourselfandspouse,ifapplicable.Completetheaddressportion

includinganapartmentnumberand/orruralroute,ifapplicable.

Placean‘X’intheboxifyouarelinganamendedreturn.Use

lines30and32toreporttaxpreviouslypaidand/orprevious

overpayments.CompleteSchedule511-H.

Name and Address

D

Ifataxpayerdiedbeforelingareturn,theexecutor,administra-

tororsurvivingspousemayhavetoleareturnforthedecedent.

Placean‘X’intheappropriateboxintheSSNarea.

What About Deceased Taxpayers?

7

Select Line Instructions

Federal Adjusted Gross Income

Enter your Federal Adjusted Gross Income from your federal

return. This can be from any one of the following forms: 1040,

1040A or 1040EZ.

If you do not have an Oklahoma ling requirement, see page 5.

Subtractions

Enter the total from Schedule 511-A, line 14. See Schedule 511-A

instructions on pages 13-15.

Out-of-State Income

This is income from real or tangible personal property or business

income in another state. This includes partnership gains and

gains sustained by S corporations attributable to other states. It is

not non-business interest, installment sale interest, non-business

dividends, salary/wages, pensions, gambling or income from

personal services. (See instructions for line 16.) On line 4a, enter

a brief description of the type of out-of-state income deducted

on 4b. Furnish detailed schedule showing the type, nature and

source of the income and copy of federal return. Documents

submitted should reect to which state(s) the income is attribut-

able. Enclose the other state’s return and/or Schedule K-1, if

applicable.

Additions

Enter the total from Schedule 511-B, line 8. See Schedule 511-B

instructions on pages 15-16.

Adjustments

Enter the total from Schedule 511-C, line 7. See Schedule 511-C

instructions on pages 17-18.

Deductions

Complete line 10 unless you have out-of-state income (Form 511,

line 4). If you have out-of-state income, complete Schedule 511-D

instead of line 10.

• Enter the Oklahoma standard deduction if you did not claim

itemized deductions on your federal return.

If your ling status is “single” or “married ling separate”, your

Oklahoma standard deduction is $6,200.

If your ling status is “head of household”, your Oklahoma

standard deduction is $9,100.

If your ling status is “married ling joint” or “qualifying

widow(er)”, your Oklahoma standard deduction is $12,400.

Note: You qualify for the Oklahoma standard deduction even

when claimed as a dependent on another return.

• If you claimed itemized deductions on your federal return (Form

1040, Schedule A), enter the amount of your allowable itemized

deductions. (Enclose a copy of your Federal Schedule A.)

Exemptions

Complete line 11 unless you have out-of-state income (Form 511,

line 4). If you have out-of-state income, complete Schedule 511-D

instead of line 11.

Oklahoma allows $1,000 for each exemption claimed on the top

of the return.

Total Deductions and Exemptions

If you completed lines 10 and 11, enter the total on line 12. If you

instead completed Schedule 511-D, enter the total from line 5 of

Schedule 511-D.

Oklahoma Income Tax

Using Form 511, line 13, nd your tax in the Tax Table (pages

20-31). Enter the result here unless you used Form 573 “Farm

Income Averaging”. If you used Form 573, enter the amount from

Form 573, line 22, and enter a “1” in the box.

Amounts withdrawn from a Health Savings Account for any

purpose other than those described in 36 OS Sec. 6060.17 and

which are included in your Federal Adjusted Gross Income are

subject to an additional 10% tax. Add the additional 10% tax to

your tax from the tax table* and enter a “2” in the box.

* If you also used Form 573, add the 10% tax to the tax from

Form 573, line 22.

Child Care/Child Tax Credit

Complete line 15 unless your Oklahoma Adjusted Gross Income

(Form 511, line 7) is less than your Federal Adjusted Gross

Income (Form 511, line 1). If your Oklahoma Adjusted Gross In-

come is less than your Federal Adjusted Gross Income, complete

Schedule 511-E to determine the amount to enter on line 15.

If your Federal Adjusted Gross Income is $100,000 or less and you

are allowed either a credit for child care expenses or the child tax

credit on your federal return, you are allowed a credit against your

Oklahoma tax. Your Oklahoma credit is the greater of:

• 20% of the credit for child care expenses allowed by the IRC.

Your allowed federal credit cannot exceed the amount of your

federal tax reported on your federal return.

or

• 5% of the child tax credit allowed by the IRC. This includes

both the nonrefundable child tax credit and the refundable ad-

ditional child tax credit.

If your Federal Adjusted Gross Income is greater than $100,000

no credit is allowed.

Credit for Tax Paid to Another State

If you receive income for personal services from another state,

you must report the full amount of such income on your Okla-

homa return. If the other state also taxes the income, a credit

is allowed on Form 511. Complete Oklahoma Form 511TX and

furnish a copy of the other state(s) return, or Form W-2G if the

taxing state does not allow a return to be led for gambling win-

nings (example: Mississippi).

Note: Taxpayers who have claimed credit for taxes paid to an-

other state on the other state’s income tax return do not qualify to

claim this credit based on the same income.

1

14

2

6

10

8

12

11

15

4

16

More information at www.tax.ok.gov

Oklahoma Tax Law requires you to pay a use tax on

certain items bought out-of-state for use in Oklahoma.

Pay your use tax!

It’s the law.

Use Tax Easy!

8

Other Credits

The amount of other credits as claimed on Form 511CR should

beenteredonthisline.Enterintheboxthenumberthatcorre-

spondswiththecredittowhichyouareentitled.Ifyouqualifyfor

morethanonetypeofcredit,enter“99”inthebox.Seebelowfor

alistofthecreditsavailableonForm511CR.Youcanobtainthis

formfromourwebsiteatwww.tax.ok.gov.

TaxcreditstransferredorallocatedmustbereportedonOTC

Form569.FailuretoleForm569willresultintheaffectedcred-

itsbeingdeniedbytheOTCpursuantto68OSSec.2357.1A-2.

• OklahomaInvestment/NewJobsCredit

Enclose Form 506.

68OSSec.2357.4andRule710:50-15-74.

• Coal Credit

68OSSec.2357.11andRule710:50-15-76.

• CreditforInvestmentinaClean-BurningMotorVehicleFuel

PropertyorInvestmentinQualiedElectricMotorVehicle

Property

68OSSec.2357.22andRule710:50-15-81.

• CreditforQualiedRecyclingFacility

68OSSec.2357.59andRule710:50-15-84.

• SmallBusinessCapitalCredit

Enclose Form 527-A.

68OSSec.2357.60-2357.65andRule710:50-15-86.

• OklahomaAgriculturalProducersCredit

Enclose Form 520.

68OSSec.2357.25andRule710:50-15-85.

• SmallBusinessGuarantyFeeCredit

Enclose Form 529.68OSSec.2357.30.

• CreditforEmployersProvidingChildCarePrograms

68OSSec.2357.26andRule710:50-15-91.

• CreditforEntitiesintheBusinessofProviding

ChildCareServices

68OSSec.2357.27.

• CreditforCommercialSpaceIndustries

68OSSec.2357.13.

• CreditforTourismDevelopmentorQualiedMediaProduc-

tion Facility

68OSSec.2357.34-2357.40.

• OklahomaLocalDevelopmentandEnterpriseZone

IncentiveLeverageActCredit

68OSSec.2357.81.

• CreditforQualiedRehabilitationExpenditures

68OSSec.2357.41andRule710:50-15-108.

• RuralSmallBusinessCapitalCredit

Enclose Form 526-A.

68OSSec.2357.71-2357.76andRule710:50-15-87.

• CreditforElectricityGeneratedbyZero-EmissionFacilities

68OSSec.2357.32A.

• CreditforFinancialInstitutionsMakingLoansunder

theRuralEconomicDevelopmentLoanAct

68OSSec.2370.1.

• CreditforManufacturersofSmallWindTurbines

68OSSec.2357.32BandRule710:50-15-92.

• CreditforQualiedEthanolFacilities

68OSSec.2357.66andRule710:50-15-106.

• PoultryLitterCredit

68OSSec.2357.100andRule710:50-15-95.

• VolunteerFireghterCredit

Enclose the Council on Fireghter Training’s Form.

68OSSec.2385.7andRule710:50-15-94.

• CreditforQualiedBiodieselFacilities

68OSSec.2357.67andRule710:50-15-98.

• FilmorMusicProjectCredit

Enclose Form 562.

68OSSec.2357.101andRule710:50-15-101.

• CreditforBreedersofSpeciallyTrainedCanines

68OSSec.2357.203andRule710:50-15-97.

• CreditforWagesPaidtoanInjuredEmployee

68OSSec.2357.47andRule710:50-15-107.

• CreditforModicationExpensesPaidforanInjuredEmployee

68OSSec.2357.47andRule710:50-15-107.

DryFireHydrantCredit

68OSSec.2357.102andRule710:50-15-99.

• CreditfortheConstructionofEnergyEfcientHomes

68OSSec.2357.46andRule710:50-15-104.

• CreditforRailroadModernization

68OSSec.2357.104andRule710:50-15-103.

• ResearchandDevelopmentNewJobsCredit

Enclose Form 563.

68OSSec.54006andRule710:50-15-105.

• CreditforBiomedicalResearchContribution

68OSSec.2357.45andRule710:50-15-113.

• CreditforEmployeesintheAerospaceSector

Enclose Form 564.

68OSSec.2357.301&2357.304andRule710:50-15-109.

• CreditsforEmployersintheAerospaceSector

Enclose Form 565.

68OSSec.2357.301,2357.302and2357.303andRule

710:50-15-109.

• WireTransferFeeCredit

68OSSec.2357.401andRule710:50-15-111.

• CreditforManufacturersofElectricVehicles

68OSSec.2357.402andRule710:50-15-112.

• CreditforCancerResearchContribution

68OSSec.2357.45andRule710:50-15-113.

• OklahomaCapitalInvestmentBoardTaxCredit

74OSSec.5085.7.

• CreditforContributionstoaScholarship-GrantingOrganization

68OSSec.2357.206andRule710:50-15-114.

• CreditforContributionstoanEducationalImprovementGrant

Organization

68OSSec.2357.206andRule710:50-15-115.

Select Line Instructions

17

9

Select Line Instructions

Oklahoma Use Tax

Everystatewithasalestaxhasacompaniontaxforpurchases

madeoutsidethestate.InOklahoma,thattaxiscalled“usetax”.

IfyouhavepurchaseditemsforuseinOklahomafromretailers

whodonotcollectOklahomasalestaxwhetherbymailorder,

catalog,televisionshoppingnetworks,radio,Internet,phoneor

inperson,youoweOklahomausetaxonthoseitems.Usetax

ispaidbythebuyerwhentheOklahomasalestaxhasnotbeen

collectedbytheseller.IndividualsinOklahomaareresponsible

forpayingusetaxontheirout-of-statepurchases.

Examplesofitemsthataresubjecttosalestaxincludebooks,

compactdiscs,computerequipment,computersoftware,elec-

tronics,clothing,appliances,furniture,sportinggoodsandjewel-

ry.Whenanout-of-stateretailerdoesnotcollectOklahomasales

tax,theresponsibilityofpayingthetaxfallsonthepurchaser.

Usetaxiscalculatedatthesamerateassalestax,whichvaries

bycityandcounty.Thestatesalestaxrateis4.5%(.045)plus

theapplicablecityand/orcountyrates.Ifyoudonotknowthe

exactamountofOklahomausetaxyouowebasedonyourcity

and county sales tax rate, you can either:

1. Usethetaxtableonpage11ormultiplyyour

AdjustedGrossIncomefromline1by0.056%

(.00056),

or

2. Useoneoftheworksheetsbelowtocalculateyour

Oklahomausetax.CompleteWorksheetOneifyou

keptrecordsofallofyourout-of-statepurchases.

CompleteWorksheetTwoifyoudidnotkeeprecords

ofallofyourout-of-statepurchases.

Oklahoma Use Tax - Worksheet #2 (continued)

WorksheetTwohastwoparts.Therstpartisa

calculation of the amount due on items that cost less

than$1,000eachandthesecondpartisacalculation

oftheamountdueonitemsthatcost$1,000ormore

each.TherstcalculationisbasedonaUseTax

Tablethatreectstheestimatedamountofusetax

duebytaxpayerswithvaryingamountsofFederal

AdjustedGrossIncome.Theestimatedamountis

0.056%(.00056)ofFederalAdjustedGrossIncome.If

youbelievethatestimatefromthetableistoohigh

foryourout-of-statepurchases,youmayestimate

whatyouthinkyouowe.

Ifyoupaidanotherstate’ssalesorusetaxonanypurchase,that

amountmaybecreditedagainsttheOklahomausetaxdueon

thatpurchase.

Note: Your use tax worksheets may be reviewed. If it is determined that

you owe more use tax than what is shown on your return, you may be

subject to an assessment for the additional use tax.

20

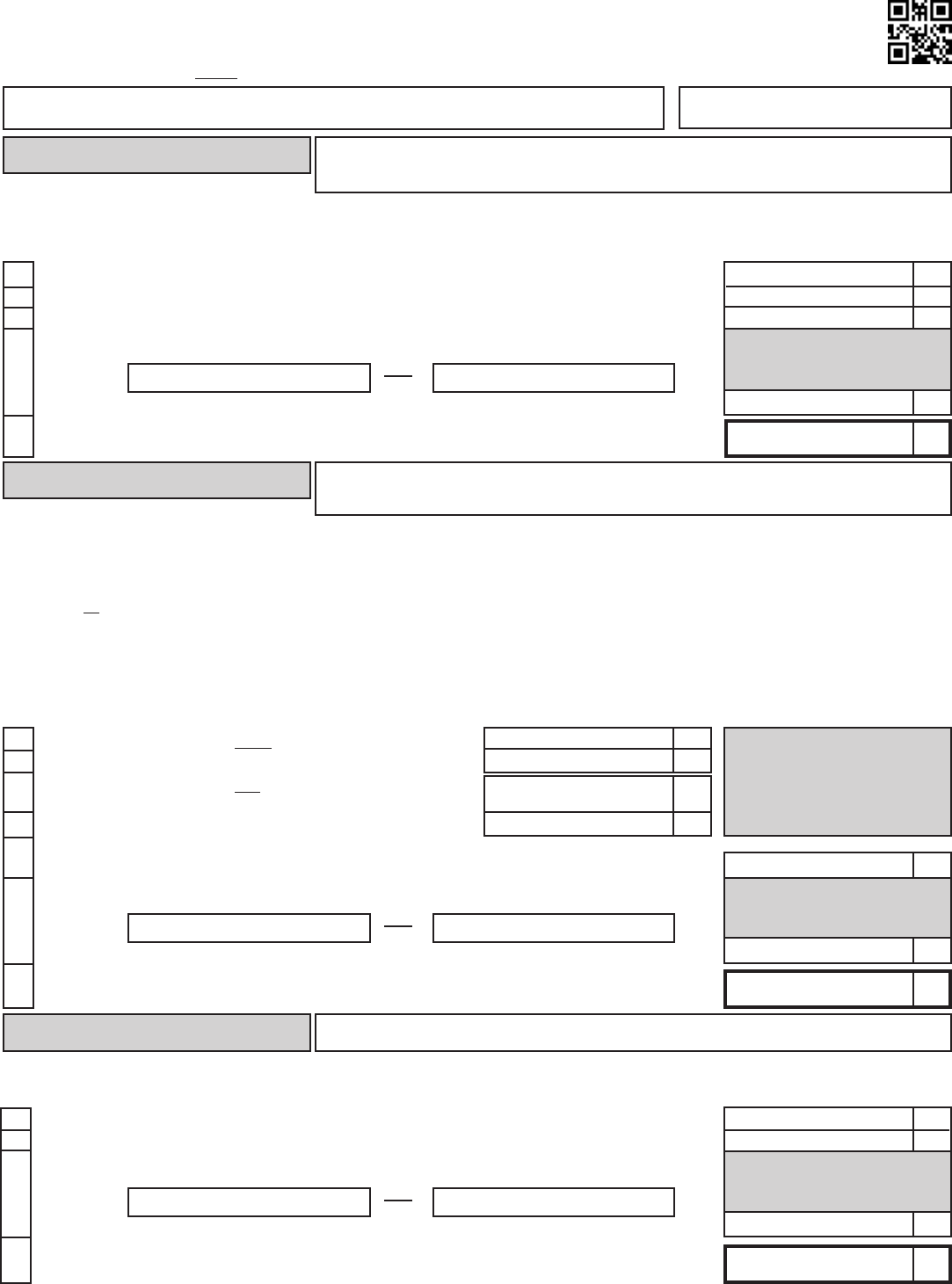

Use Tax Worksheet One

For Taxpayers Who Have Records of All Out-of-State Purchases

1 Enterthetotalamountofout-of-statepurchasesfor1/1/2014through12/31/2014......................

2 Multiplyline1by7%(.07)oryourlocalrate*andentertheamount.............................................

3 Enterthetaxpaidtoanotherstateonthepurchases.Thisamountmaynotexceedthe

amountonline2............................................................................................................................

4 Subtractline3fromline2andentertheresults,roundedtothenearestwholedollar,

hereandonForm511,line20......................................................................................................

1

2

3

4

Use Tax Worksheet Two

For Taxpayers Who Do Not Have Records of All Out-of-State Purchases

1 Purchases of items costing less than $1,000:SeetheUseTaxTableonpage11

toestablishtheusetaxduebasedonyourFederalAdjustedGrossIncome

from Form 511, line 1 ...................................................................................................................

2 Purchases of items costing $1,000 or more: Completelines2aand2bbelowto

calculatetheamountofusetaxowed.

2a Enterthetotalamountofout-of-statepurchases

of$1,000ormorefor1/1/2014through12/31/2014......

2b Multiplyline2aby7%(.07)oryourlocalrate*

and enter the amount ....................................................

3 Addlines1and2bandenterthetotalamountofusetax.............................................................

4 Enterthetaxpaidtoanotherstateonthepurchases.Thisamountmaynotexceedthe...........

amountonline3...........................................................................................................................

5 Subtractline4fromline3andentertheresults,roundedtothenearestwholedollar,

hereandonForm511,line20.....................................................................................................

1

3

4

5

2a

2b

See Page 11 for the

Oklahoma Use Tax Table

*Usetaxiscalculatedthesameassalestax.Yourlocalratewouldbethestatesalestaxrateof4.5%(.045)plustheapplicablecityand/

orcountyratebasedonwhereyoulivedwhenthepurchasewasmade.Theratechartscanbefoundonthewebat:www.tax.ok.gov.

10

Social Security Number (SSN)

TherequestforyourSSNisauthorizedbySection405,Title42,

oftheUnitedStatesCode.Youmustprovidethisinformation.It

willbeusedtoestablishyouridentityfortaxpurposesonly.

Select Line Instructions

Credit for Property Tax Relief

Anyperson65yearsofageorolderoranytotallydisabledper-

son who is head of a household, a resident of and domiciled in

thisstateduringtheentireprecedingcalendaryear,andwhose

grosshouseholdincomeforsuchyeardoesnotexceed$12,000,

mayleaclaimforpropertytaxreliefontheamountofproperty

taxespaidonthehouseholdtheyoccupiedduringthepreceding

calendaryear.Thecreditmaynotexceed$200.Claimmustbe

madeonForm538-H.

Sales Tax Relief/Credit

IfyouarerequiredtoleanOklahomaincometaxreturn,your

returnmustbeledbyApril15th.Anextensionoftimetoleyour

return,includingtheApril20thduedateforelectronicallyled

returns, doesapplytothiscredit.

Toleforsalestaxrelief,youmustbeanOklahomaresidentfor

theentireyear.Yourtotalgrosshouseholdincomecannotexceed

$20,000unlessoneofthefollowingapplies:

• Youcanclaimanexemptionforyourdependent,or

• Youare65yearsofageorolderby12/31/2014,or

• Youhaveaphysicaldisabilityconstitutingasubstantial

handicaptoemployment(provideproof,seeForm538-S).

Ifanyoneoftheabovethreeitemspertainstoyou,yourtotal

grosshouseholdincomelimitisincreasedto$50,000.Filloutand

encloseForm538-Sifyouqualifyforthiscredit.TheForm538-S

isincludedinthispacket.

TheOklahomaDepartmentofHumanServiceswillmakethe

salestaxrefundtopersonswhohavecontinuouslyreceivedaid

totheaged,blind,disabledorMedicaidpaymentsfornursing

homecarefromJanuary1,2014toDecember31,2014.Per-

sonswhohavereceivedtemporaryassistanceforneedyfamilies

(TANF)foranymonthintheyearof2014arenoteligibleforthe

salestaxrefund.

Apersonconvictedofafelonyshallnotbepermittedtolea

claimforsalestaxreliefforanyyearforwhichthatpersonisan

inmateinthecustodyoftheDepartmentofCorrectionsforany

partofthatyear.

Natural Disaster Tax Credit

Thiscreditisforownersofresidentialrealpropertywhosepri-

maryresidencewasdamagedordestroyedinanaturaldisaster

forwhichaPresidentialMajorDisasterDeclarationwasissued,

unlessthenaturaldisasterwasatornadooccurringincalendar

year2012or2013inwhichcaseaPresidentialMajorDisaster

Declarationisnotrequired.Theamountofthecreditisthediffer-

encebetweentheadvalorempropertytaxpaidonsuchproperty

inthetaxyearpriortothedamageordestructionandthetaxpaid

therstyearafterthepropertyisrebuiltorrepaired.Theprimary

residencemustberepairedorrebuiltandusedastheprimary

residencenotlaterthanDecember31,2015,withrespecttothe

calendaryear2012or2013naturaldisasterandnolaterthan36

monthsafteranynaturaldisasteroccurringonorafterJanuary1,

2014.Toclaimthiscredit,Form576mustbeenclosedwithyour

return.

25

26

27

multiply

FederalAGItimes

0.00056

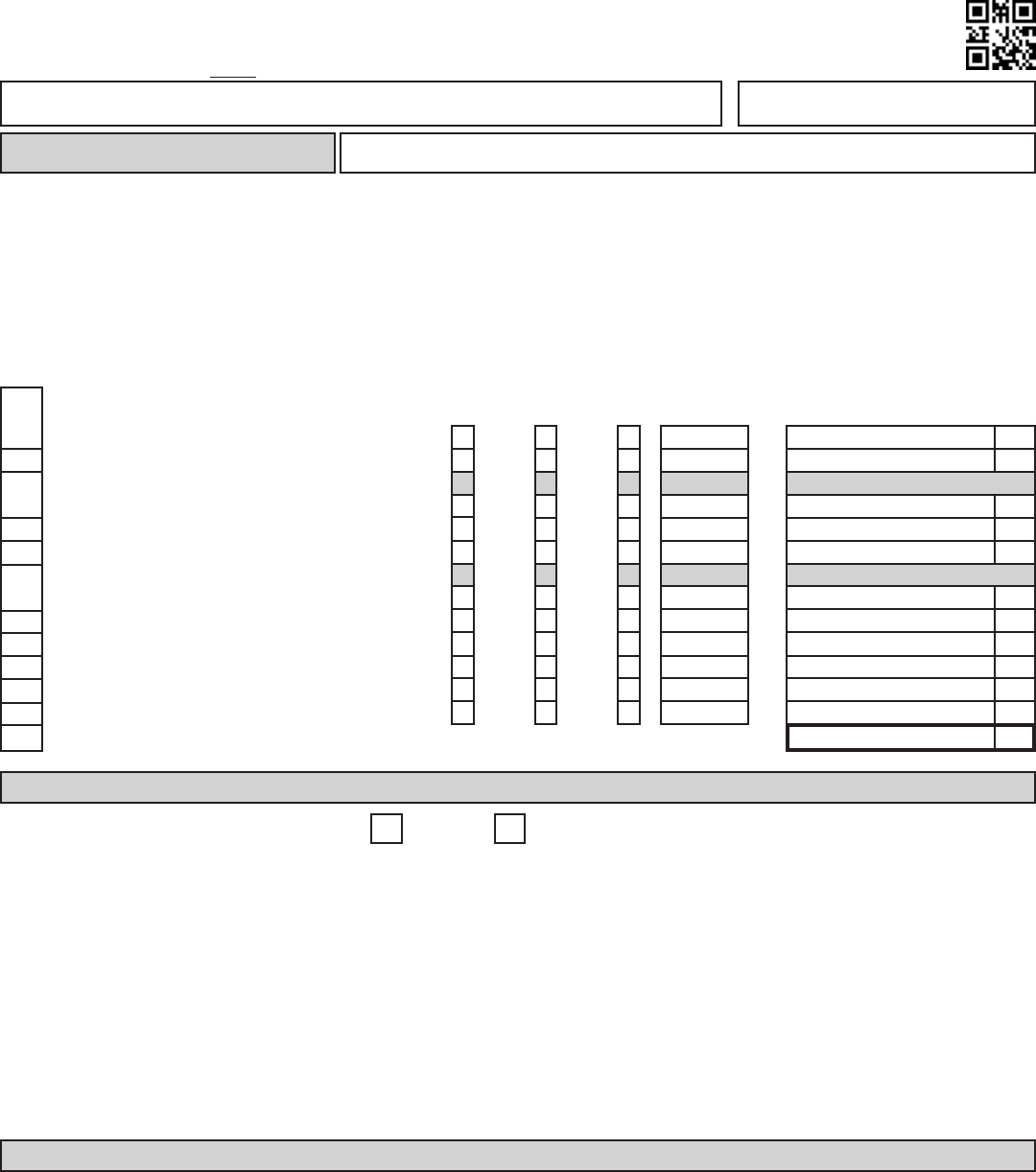

At least But less than

If Federal Adjusted Gross Income

(Form 511, line 1) is: Your Use Tax

Amount is:

Use Tax Table

23

Oklahoma Estimated Tax Payments

EnteranypaymentsyoumadeonyourestimatedOklahoma

incometaxfor2014.Includeanyoverpaymentfromyour2013

returnyouappliedtoyour2014estimatedtax.

Ifatleast66-2/3%ofyourgrossincomethisyearorlastyearis

fromfarming,estimatedpaymentsarenotrequired.Ifclaiming

thisexception,youmustmarktheboxonthislineandenclose a

completecopyofyourfederalreturn.

Forinformationregardingwhoisrequiredtomakeestimatedtax

payments,refertopage5,“EstimatedIncomeTax”.

Payment with Extension

IfyouledOklahomaextensionForm504for2014,enterany

amountyoupaidwiththatform.

24

0 2,090 1

2,090 4,670 2

4,670 6,420 3

6,420 8,170 4

8,170 9,920 5

9,920 11,795 6

11,795 13,545 7

13,545 15,295 8

15,295 17,170 9

17,170 18,920 10

18,920 20,670 11

20,670 22,420 12

22,420 24,295 13

24,295 26,045 14

26,045 27,795 15

27,795 29,670 16

29,670 31,420 17

31,420 33,170 18

33,170 34,920 19

34,920 36,795 20

36,795 38,545 21

38,545 40,295 22

40,295 42,170 23

42,170 43,920 24

43,920 45,670 25

45,670 47,420 26

47,420 49,295 27

49,295 51,045 28

51,045 52,795 29

52,795 54,670 30

54,670 andover

11

Underpayment of Estimated Tax Interest (continued)

Note:NoUnderpaymentofEstimatedTaxInterestshallbeimposed

iftheincometaxliabilityshownonthereturnislessthan$1,000.

Ifyoudonotmeetoneoftheaboveexceptions,youmaycomplete

FormOW-8-PortheOTCwillguretheinterestforyouandsend

youabill.

Ifyouoweunderpaymentofestimatedtaxinterestandyouhavean

overpayment(line34),entertheamountofunderpaymentof

estimatedtaxinterestonthisline(line42)andreducethe

amountyouareapplyingtoestimatedtax(line35)oryourrefund

(line38)bythatsameamount(butnotlessthanzero).Youwillbe

usingyouroverpaymenttopayyourunderpaymentofestimatedtax

interest.Donotencloseapaymentunlessyoustillhaveabalance

dueafterapplyingallofyouroverpayment.

If an amended returnisledbeforetheduedateforlingtheorigi-

nalreturn,includinganyextensions,thetaxshownontheamended

returnisusedtodeterminetheamountofunderpayment.Ifthe

amendedreturnisledaftertheduedate,includingextension,the

taxshownontheamendedreturnwillnotbeusedtocomputethe

amountofunderpayment.

Delinquent Penalty and Interest

Aftertheoriginalduedateofthereturncompute5%penaltyonthe

incometaxdue(line39minusline20).Computeinterestonthe

incometaxdueat1.25%permonthfromtheoriginalduedateofthe

return.Anextensiondoesnotextendthedateforpaymentoftax.

Note:Ifyouhaveavalidextensionoftimetoleyourreturn,

delinquentpenaltyisnotdueif90%ofyourincometaxwaspaidby

theoriginalduedateofthereturn.Delinquentinterestisdueonany

incometaxnotpaidbytheoriginalduedateofthereturn.

Title 68, Oklahoma Statutes, provides that any term used in this

Act shall have the same meaning as when used in a compara-

ble context in the Internal Revenue Code, except when speci-

cally provided for in the Oklahoma Statutes or rules.

Earned Income Credit

Completeline28unlessyourOklahomaAdjustedGrossIncome

(Form511,line7)islessthanyourFederalAdjustedGrossIncome

(Form511,line1).IfyourOklahomaAdjustedGrossIncomeisless

thanyourFederalAdjustedGrossIncome,completeSchedule511-

F*todeterminetheamounttoenteronline28.

Youareallowedacreditequalto5%oftheearnedincomecredital-

lowedonyourfederalreturn.Encloseacopyofyourfederalreturn.

*Note:IfyouarenotrequiredtoleanOklahomareturn,but

youqualifyfortheFederalEarnedIncomeCredit,youqualifyfor

Oklahomaearnedincomecredit.Enter5%oftheFederalEarned

IncomeCredit(donotcompleteSchedule511-F).

Place an “X” in the box(es)online29toreportanycredit

fromForm577orForm578.

IfclaimingtheRefundable Coal Credit,encloseForm577.Any

creditsearned,butnotused,baseduponactivityoccurringonor

afterJanuary1,2014willberefundedat85%ofthefaceamount

ofthecredits.Apass-throughentitythatdoesnotleaclaimfora

direct refund will allocate the credit to one or more of its sharehold-

ers,partnersormembers.

IfclaimingtheRefundable Credit for Electricity Generated by

Zero-Emission Facilities,encloseForm578.Anycreditsgenerat-

ed,butnotused,onorafterJanuary1,2014willberefundedtothe

taxpayerat85%ofthefaceamountofthecredits.Apass-through

entitythatdoesnotleaclaimforadirectrefundwillallocatethe

credittooneormoreofitsshareholders,partnersormembers.

Donations (Original return only)

Schedule511-Gprovidesyouwiththeopportunitytomakeanan-

cialgiftfromyourrefundtoavarietyofOklahomaorganizations.

Notethatthisreducesyourrefundifyouchoosetodonate.The

donationwillbeforwardedtotheappropriateagency.SeeSchedule

511-Gformoreinformation.

PlacethelinenumberoftheorganizationfromSchedule511-Gin

theboxatline36.Ifgivingtomorethanoneorganization,puta“99”

intheboxatline36andattachtheSchedule511-Gshowinghow

youwishthedonationstobedivided.

Amount to be Refunded

Ifyoudonotchoosedirectdepositorthedirectdepositfailsto

process,youwillbeissuedadebitcard.See“AllAboutRefunds”on

page5formoreinformation.

Eastern Red Cedar Revolving Fund (Original return only)

Adonationtothisfundmaybemadeonataxduereturn.Forinfor-

mationregardingthisfund,seeSchedule511-G:Information.

Public School Classroom Support Fund (Original return only)

Adonationtothisfundmaybemadeonataxduereturn.Forinfor-

mationregardingthisfund,seeSchedule511-G:Information.

Underpayment of Estimated Tax Interest

Youwererequiredtomakeestimatedtaxpaymentsifyourincome

taxliabilityexceedsyourwithholdingby$500ormore.Toavoidthe

20%UnderpaymentofEstimatedTaxInterest,timelyledquarterly

estimatedtaxpaymentsandwithholdingarerequiredtobethe

smaller of:

•70%ofthecurrentyeartaxliability,or

•100%ofyourprioryeartaxliability.

TheincometaxliabilityistheOklahomaincometaxduelessall

creditsexceptamountspaidonwithholding,estimatedtaxand

extensionpayments.

Select Line Instructions

28

29

36

43

38

41

42

•Ifyouowetaxes,encloseacheckormoneyorderpayableto

“OklahomaTaxCommission”.YourSocialSecurityNumberandthe

taxyearshouldbeonyourcheckormoneyorderforyourpayment

tobeproperlycredited.Donotsendcash.

•Forinformationregardingelectronicpaymentmethods,visitour

websiteatwww.tax.ok.gov.

•EncloseW-2s,1099sorotherwithholdingstatementstosubstan-

tiatewithholding.

•Do not staple your return.Useapaperclipifnecessary.

•Matherrorsarethemostcommoncauseofarefunddelay.Dou-

blecheckyourcalculations.

•Afterling,ifyouhaveanyquestionsregardingyourrefund,

contactusat(405)521-3160.Thein-statetoll-freenumberis(800)

522-8165.

When You Are Finished...

40

•Donotencloseanycorrespondenceotherthanthosedocuments

andschedulesrequiredforyourreturn.

•Ifforsomereasonyoudonothaveareturnenvelope,mailyour

return,alongwithanypaymentdue,to:

Oklahoma Tax Commission - Income Tax

P.O. Box 26800

Oklahoma City, OK 73126-0800

Important:IfyoulloutanyportionoftheSchedules

511-Athrough511-HorForm538-S,youarerequiredto

enclosethosepageswithyourreturn.Failuretoinclude

thepageswillresultinadelayofyourrefund.

12

Schedule 511-A

Interest on U.S. Government Obligations

Ifyoureportinterestonbonds,notesandotherobligationsofthe

U.S.governmentonyourfederalreturn,thisincomemaybeex-

cludedfromyourOklahomaAdjustedGrossIncomeifadetailed

scheduleisfurnished,accompaniedwith1099sshowingthe

amountofinterestincomeandthenameoftheobligationfrom

whichtheinterestisearned.Iftheincomeisfromamutualfund

whichinvestsinU.S.governmentobligations,enclose docu-

mentationfromthemutualfundtosubstantiatethepercentage

ofincomederivedfromobligationsexemptfromOklahomatax.

InterestfromentitiessuchasFNMAandGNMAdoesnotqualify.

Note:Thecapitalgain/lossfromthesaleofanU.S.Government

Obligationisexempt.EnterexemptgainsonSchedule511-A,

line11andexemptlossesonSchedule511-B,line7.

Social Security

SocialSecuritybenetsthatareincludedintheFederalAdjusted

GrossIncomeshallbesubtracted.Encloseacopyofyourfed-

eralreturn.

Federal Civil Service Retirement in Lieu of

Social Security

Eachindividualmayexclude100%oftheirretirementbenets

receivedfromtheFederalCivilServiceRetirementSystem

(CSRS),includingsurvivorbenets,paidinlieuofSocialSecurity

totheextentsuchbenetsareincludedintheFederalAdjusted

GrossIncome.EnteryourRetirementClaimNumberfromyour

FormCSA1099-RorCSF1099-RintheboxonSchedule511-A,

line3.EncloseacopyofFormCSA1099-RorCSF1099-Rwith

yourreturn.Tobeeligible,such1099-Rmustbeinyourname.

Note:RetirementbenetspaidundertheFederalEmployees

RetirementSystem(FERS)donotqualifyforthisexclusion.

However,forretirementbenetscontainingbothaFERSand

aCSRScomponent,theCSRScomponentwillqualifyforthe

exclusion.ProvidesubstantiationfortheCSRScomponent,

suchasacopyofyourNoticeofAnnuityAdjustment.

Military Retirement

Eachindividualmayexcludethegreaterof75%oftheirretirement

benetsor$10,000,butnottoexceedtheamountincludedinthe

FederalAdjustedGrossIncome.Theretirementbenetsmustbe

fromanycomponentoftheArmedForcesoftheUnitedStates.

Oklahoma Government or Federal Civil Service

Retirement

Eachindividualmayexcludetheirretirementbenetsupto

$10,000,butnottoexceedtheamountincludedintheFederal

AdjustedGrossIncome.(Tobeeligible,youmusthaveretirement

incomeinyourname.)Theretirementbenetsmustbereceived

fromthefollowing:thecivilserviceoftheUnitedStates*, the

OklahomaPublicEmployeesRetirementSystemofOklahoma,

theOklahomaTeacher’sRetirementSystem,theOklahomaLaw

EnforcementRetirementSystem,theOklahomaFireghtersPen-

sion and Retirement System, the Oklahoma Police Pension and

RetirementSystem,theEmployeeretirementsystemscreated

bycountiespursuantto19OSSec.951,theUniformRetirement

SystemforJusticesandJudges,theOklahomaWildlifeConser-

vationDepartmentRetirementFund,theOklahomaEmployment

SecurityCommissionRetirementPlan,ortheEmployeeretire-

mentsystemscreatedbymunicipalitiespursuantto11OSSec.

48-101.EncloseacopyofForm1099-R.

*DonotincludeonthislinetheCSRSretirementbenetsalready

excludedonSchedule511-A,line3.

Note:Anearlydistributionfromaretirementfundduetotermina-

tionofemploymentpriortoyourretirementordisabilitydoesnot

qualifyforthe$10,000retirementincomeexclusion.Generally,

thereisa“1”inbox7ofyourForm1099-Rforthistypeofdis-

tribution.Thisdistributionmayqualifyforthe“OtherRetirement

Income”exclusiononSchedule511-A,line6.

Other Retirement Income

Eachindividualmayexcludetheirretirementbenets,upto

$10,000,butnottoexceedtheamountincludedintheFed-

eralAdjustedGrossIncome.Foranyindividualwhoclaimsthe

exclusionsforgovernmentretireesonSchedule511-A,line5,

theamountoftheexclusiononthislinecannotexceed$10,000

minustheamountsalreadyclaimedonSchedule511-A,line5(if

lessthanzero,enterzero).

Theretirementbenetsmustbereceivedfromthefollowingand

satisfytherequirementsoftheIRC:anemployeepensionbenet

planunderIRCSection401,aneligibledeferredcompensation

planunderIRCSection457,anindividualretirementaccount,

annuityortrustorsimpliedemployeepensionunderIRCSec-

tion408,anemployeeannuityunderIRCSection403(a)or(b),

UnitedStatesRetirementBondsunderIRCSection86,orlump-

sumdistributionsfromaretirementplanunderIRCSection402

(e).EncloseacopyofForm1099-Rorotherdocumentation.

A1

A2

A3

A4

A5

A6

2-D Barcode Information

13

Does Your Form Have One of These?

Ifyourecognizethisbarcodefromyourtaxreturn,yourreturnwaspreparedusingcomputersoftwareutilizingtwo

dimensionalbarcoding.Thismeansyourtaxinformationwillbeprocessedfasterandmoreaccuratelyandyouwill

see your refund faster!

Thespecialmailingaddressfor2-Dincometaxformsis: OklahomaTaxCommission

PostOfceBox269045

OklahomaCity,OK73126-9045

Note:Anyhandwritteninformationwillnotbecapturedwhenareturnisprocessedusingthe2-Dbarcode.

A8

Schedule 511-A continued

A7

U.S. Railroad Retirement Board Benets

AllqualiedU.S.RailroadRetirementBoardbenetsthatare

includedintheFederalAdjustedGrossIncomemaybeexcluded.

Oklahoma Depletion

Oklahomadepletiononoilandgaswellproduction,attheoption

ofthetaxpayer,maybecomputedat22%ofgrossincomede-

rivedfromeachOklahomapropertyduringthetaxableyear.Any

depletiondeductionallowableistheamountsocomputedminus

thefederaldepletionclaimed.IfOklahomaoptionsareexercised,

thefederaldepletionnotusedduetothe65%limitationmay

notbecarriedoverforOklahomapurposes.Acompletedetailed

schedulebypropertymustbefurnished.

Note:Majoroilcompanies,asdenedin52OSSec.288.2,

whencomputingOklahomadepletionshallbelimitedto50%of

thenetincome(computedwithouttheallowancefordepletion)

fromeachproperty.

Leasebonusreceivedisconsideredincomesubjecttodeple-

tion.Ifdepletionisclaimedonaleasebonusandnoincomeis

receivedasaresultofnon-producingproperties,seeSchedule

511-B,line5.

Ifyouhavefederaldepletionbeingcarriedoverintothisyear,see

Schedule511-B,line5.

Oklahoma Net Operating Loss

Entercarryover(s)frompreviousyears.Alsoentertheloss

year(s).ThelossyearreturnmustbeledtoestablishtheOkla-

homaNetOperatingLoss.Seethe“NetOperatingLoss”section

onpage5.AlsoseeSchedule511-B,line4.

Exempt Tribal Income

Ifthetribalmember’sprincipalresidenceison“Indiancountry”as

denedin18U.S.C.Section1151,theincomeearnedonIndian

countrymaybededucted.LegallyacknowledgedIndiancountry

mustbewithinthejurisdictionofthetribeofwhichheorsheisa

member.Allclaimantsmustprovidesufcientinformationtosup-

portthattheserequirementshavebeensatised.

Providethefollowinginformationfortaxyear2014:

a.Acopyofyourtribalmembershipcardorcerticationbyyour

tribeastoyourtribalmembershipduringthetaxyear;and

b.Acopyofthetrustdeed,orotherlegaldocument,whichde-

scribestherealestateuponwhichyoumaintainedyourprincipal

placeofresidenceandwhichwasanIndianallotment,restricted,

orheldintrustbytheUnitedStatesduringthetaxyear.Ifyour

namedoesnotappearonthedeed,orotherdocument,provide

proofofresidenceonsuchproperty;and

c.Acopyofthetrustdeed,orotherlegaldocument,which

describestherealestateuponwhichyouwereemployedor

performedworkorreceivedincomeandwhichwasheldbythe

UnitedStatesofAmericaintrustforatribalmemberoranIndian

tribeorwhichwasallottedorrestrictedIndianlandduringthetax

year.Alsoacopyofemploymentorpayrollrecordswhichshow

youareemployedonthatIndiancountryoranexplanationof

yourworkonIndiancountry;and

A9

A10

Exempt Tribal Income (continued)

d.Anyotherevidencewhichyoubelievesupportsyourclaimthat

youmeetallofthecriteriaforexemptionfromincometax.

Allinformationtosupportyourclaimforrefundmustbeenclosed

with your return.

Gains from the Sale of Exempt Government Obligations

Seethe“note”forSchedule511-A,line1andSchedule511-B,

line1instructions.EncloseFederalScheduleDandForm8949.

Oklahoma Capital Gain Deduction

Youcandeductqualifyinggainsreceivingcapitaltreatmentwhich

areincludedinFederalAdjustedGrossIncome.“Qualifyinggains

receivingcapitaltreatment”meanstheamountofnetcapital

gains,asdenedunderIRCSection1222(11).Thequalifying

gainmust:

1) Beearnedonrealortangiblepersonalpropertylocated

withinOklahomathatyouhaveownedforatleastve

uninterruptedyearspriortothedateofthesale.

2) Beearnedonthesaleofstockorownershipinterestin

anOklahomaheadquarteredcompany,limitedliability

company,orpartnershipwheresuchstockorownership

interesthasbeenownedbyyouforatleasttwouninter-

ruptedyearspriortothedateofthesale.

3) Beearnedonthesaleofrealproperty,tangiblepersonal

propertyorintangiblepersonalpropertylocatedwithin

Oklahomaaspartofthesaleofallorsubstantiallyall

oftheassetsofanOklahomaheadquarteredcompany,

limitedliabilitycompany,orpartnershiporanOklahoma

proprietorshipbusinessenterpriseorownedbytheown-

ersofsuchentityorbusinessenterpriseforaperiodofat

leasttwouninterruptedyearspriortothedateofthesale.

EncloseForm561andacopyofyourFederalScheduleDand

Form(s)8949.

A12

A11

e le

Oklahoma

Go easy on yourself!

14

Low cost or sometimes even no cost...

E-ling your return is simply the speediest,

safest and most secure way to receive your

income tax refund. E-le today and in most

cases you’ll receive your Oklahoma refund in

7-10 days, even faster with direct deposit.

Check us out today to receive a speedy refund!

www.tax.ok.gov

Schedule 511-A continued

A13

Schedule 511-B

State and Municipal Bond Interest

Ifyoureceivedincomeonbondsissuedbyanystateorpolitical

subdivisionthereofthatisexemptfromfederaltaxationbutnot

exemptfromtaxationbythelawsoftheStateofOklahoma,the

totalofsuchincomeshallbeaddedtoFederalAdjustedGross

Income.

1) Incomefromallbonds,notesorotherobligationsissued

bytheStateofOklahoma,theOklahomaCapitalImprove-

mentAuthority,theOklahomaMunicipalPowerAuthority,

theOklahomaStudentLoanAuthority,andtheOklahoma

TransportationAuthority(formerlyTurnpikeAuthority)is

exemptfromOklahomaincometax.Theprotfromthe

saleofsuchbond,noteorotherobligationshallbefree

fromtaxation.

2) IncomefromlocalOklahomagovernmentalobligations

issuedafterJuly1,2001,otherthanthoseprovidedforin

line1,isexemptfromOklahomaincometax.Theexcep-

tionsarethoseobligationsissuedforthepurposeofpro-

vidingnancingforprojectsfornonprotcorporations.Lo-

calgovernmentalobligationsshallincludebondsornotes

issuedby,oronbehalfof,orforthebenetofOklahoma

educationalinstitutions,cities,towns,orcountiesorby

publictrustsofwhichanyoftheforegoingisabeneciary.

3) IncomefromOklahomaMunicipalBondsissuedpriorto

July2,2001,otherthanthoseprovidedforinline1,is

exemptfromOklahomaincometaxonlyifsoprovidedby

thestatuteauthorizingtheirissuance.

4) Incomeonbondsissuedbyanotherstateorpolitical

subdivisionthereof(non-Oklahoma),exemptfromfederal

taxation,istaxableforOklahomaincometax.

Encloseascheduleofallmunicipalinterestreceivedbysource

andamount.Iftheincomeisfromamutualfundwhichinvestsin

stateandlocalgovernmentobligations,enclose documentation

fromthemutualfundtosubstantiatethepercentageofincome

derivedfromobligationsexemptfromOklahomatax.

Note:Iftheinterestisexempt,thecapitalgain/lossfromthesale

ofthebondmayalsobeexempt.Thegain/lossfromthesaleof

astateormunicipalbond,otherthanthoseprovidedforinline1,

isexemptonlyifsoprovidedbythestatuteauthorizingitsissu-

ance.EnterexemptgainsonSchedule511-A,line11andexempt

lossesonSchedule511-B,line7.

Out-of-State Losses

Ifyouincurredlossesfromtheoperationofanout-of-statebusi-

ness,orfromtherentalorsaleofout-of-stateproperty,anysuch

lossesmustbeaddedbacktoFederalAdjustedGrossIncome.

ThisincludespartnershiplossesandlossessustainedbySub-

chapterSCorporationsattributabletootherstates.

B1

Miscellaneous: Other Subtractions

EnterintheboxonSchedule511-A,line13,theappropriate

numberaslistedbelowwhichshowsthetypeofdeduction.Ifyou

areentitledtomorethanonedeductiontype,enterthenumber

“99”.

Enter the number “1” if the following applies:

Royaltyincomeearnedbyaninventorfromaproductdeveloped

andmanufacturedinthisstateshallbeexemptfromincome

taxforaperiodofsevenyearsfromJanuary1oftherstyear

inwhichsuchroyaltyisreceivedaslongasthemanufacturer

remainsinthisstate.Tosupportyourdeductionfurnish:

1) copyofthepatent.

2) copyoftheroyaltyagreementwiththe

manufacturer.

3) copyofregistrationformfromOCAST.(74OSSec.5064.7

(A)(1))

Enter the number “2” if the following applies:

Manufacturer’sexclusion.

(74OSSec.5064.7(A)(2))

Enter the number “3” if the following applies:

SmallBusinessIncubatorexclusion:Exemptionforincome

earnedbythesponsor(74OSSec.5075).Exemptionforincome

earnedbythetenant(74OSSec.5078).

Enter the number “4” if the following applies:

PaymentsreceivedasaresultofaMilitarymemberbeingkilled

inacombatzone:AnypaymentmadebytheUnitedStates

DepartmentofDefenseasaresultofthedeathofamemberof

theArmedForceswhohasbeenkilledinactioninadesignated

combatzoneshallbeexemptfromOklahomaincometaxduring

thetaxableyearinwhichtheindividualisdeclareddeceasedby

theArmedForces.(68OSSec.2358.1A)

Enter the number “5” if the following applies:

IncomeearnedbyanindividualwhoseMilitaryspousewas

killedinacombatzone:Anyincomeearnedbythespouseofa

memberoftheArmedForcesoftheUnitedStateswhohasbeen

killedinactioninadesignatedcombatzoneshallbeexempt

fromOklahomaincometaxduringthetaxableyearinwhichthe

individualisdeclareddeceasedbytheArmedForces.(68OS

Sec.2358.1A)

Enter the number “99” if the following applies:

Allowabledeductionsnotincludedin(1)through(5):Enterany

allowableOklahomadeductionsfromFederalAdjustedGrossIn-

cometoarriveatOklahomaAdjustedGrossIncomethatwerenot

previouslyclaimedunderthisheading“Miscellaneous: Other

Subtractions.”SpecifytypeofsubtractionandOklahomaStatute

authorizingthesubtraction.Enclose a detailedexplanationand

verifyingdocuments.

B2

Need help with the math on your form?

Try using our 2-D ll-in forms

available at

www.tax.ok.gov

15

After ling your individual income tax return,

use OkTAP to check on your refund.

See page 16 for more information.

Where’s My Refund?

Schedule 511-B

B3

B4

B5

Lump-Sum Distributions

Lump-sumdistributionsnotincludedintheFederalAdjusted

GrossIncomeshallbeaddedtotheFederalAGI.Rolloversand

IRAConversionsaretaxedinthesameyearasonthefederal

return.EncloseacopyofForm1099andacompletecopyofthe

federalreturn.

Note:Thelump-sumdistribution,addedbackonthisline,may

qualifyforanexclusionofretirementbenetsfoundonSchedule

511-A.Thedistributionmustbereceivedfromaqualiedplan

andsatisfytherequirementsoftheexclusion.

Federal Net Operating Loss

Entercarryover(s)includedonFederalForm1040.See“NetOp-

eratingLoss”sectiononpage5.AlsoseeSchedule511-A,line9.

Recapture of Depletion Claimed on a Lease

Bonus or Add Back of Excess Federal Depletion

Upontheexpirationofthelease,depletionclaimedmustbe

restoredtoincomeinthecaseofnon-producingproperties.Enter

depletionclaimedonaleasebonusifnoincomewasreceived

fromthepropertyduetoitsleaseexpiration.Acompleteschedule

bypropertymustbefurnished.

Ifthe22%Oklahomaoptionforcomputingdepletionwasusedin

apreviousyearandthe65%federaldepletionlimitationapplied

inthatyear,youmustaddbackanyunusedfederaldepletion

beingcarriedoverfromsuchyearandusedinthecurrentyear’s

federalreturn.Applicablerecaptureisdeterminedonawell-by-

wellbasis.

FortheOklahomaoptionforcomputingdepletionseetheinstruc-

tionsforSchedule511-A,line8.Acompleteschedulebyproperty

mustbefurnished.

Recapture of Contributions to Oklahoma 529 College

Savings Plan and OklahomaDream 529 Account(s)

•Ifanindividualelectstotakearolloveronacontributionwithin

oneyearofthedateofthecontribution,forwhichadeduction

wastakenonthepreviousyear’sreturn,theamountofsuchroll-

overisincludedinincome.Asusedinthisparagraph,“rollover”

meansthetransferoffundsfromtheOklahoma529College

SavingsPlanorOklahomaDream529accountstoanyotherplan

underIRCSection529.

•Anindividualwhomakesanon-qualiedwithdrawalofcon-

tributionsforwhichadeductionwastakenintaxyear2005or

later,suchnon-qualiedwithdrawalandanyearningsthereon

areincludedinincome.Ifanyoftheearningshavealreadybeen

includedinyourFederalAdjustedGrossIncome,donotinclude

thoseearningsagainonthisline.

Miscellaneous: Other Additions

EnterintheboxonSchedule511-B,line7,theappropriatenum-

beraslistedbelowwhichshowsthetypeofaddition.Ifyouhave

morethanoneaddition,enterthenumber“99”.

Enter the number “1” if the following applies:

Lossesfromthesaleofexemptgovernmentobligations:See

the“note”inSchedule511-A,line1andSchedule511-B,line1

instructions.EncloseFederalScheduleDandForm8949.

Enter the number “2” if the following applies:

Ifyouareaswineorpoultryproducerwhohasdeducteddepre-

ciationonanacceleratedbasisonyourOklahomataxreturn

inprevioustaxyears(Schedule511-C),theassetmaybefully

depreciatedforOklahomapurposes.Anydepreciationdeducted

onthisyear’sfederalreturn,afterthedatetheassethasbeen

fullydepreciatedonyourOklahomareturn,mustbeaddedback

toavoidaduplicationofdepreciation.Encloseacopyofthe

federaldepreciationscheduleshowingthedepreciationtakenon

theasset.

Enter the number “3” if the following applies:

IfaqualiedOklahomarenery,ofwhichyouareapartneror

shareholder,electedtoexpensethecostofqualiedrenery

property,suchpropertyisfullydepreciatedforOklahomapur-

poses.ForOklahomapurposesnodepreciationexpensecanbe

takenforthistaxyearonsuchproperty.Enteryourpro-ratashare

ofsuchdepreciation.Includethepartnership’sorcorporation’s

nameandIDNumber.

Enter the number “4” if the following applies:

Youwillhaveanamountonthislineifapass-throughentity,of

whichyouareamember:

• wasrequiredtoadd-backrentsandinterestexpensespaid

toacaptiverealestateinvestmenttrustwhendetermining

Oklahomadistributableincome;or

• wasacaptiverealestatetrustthatwasrequiredtoadd-

backthedividends-paiddeductionwhendetermining

Oklahomadistributableincome.

Enteryourpro-ratashareofsuchadd-back.Includeyourpass-

throughentity’snameandIDnumber.

Enter the number “5” if the following applies:

Enteranyadditionsnotpreviouslyclaimed.Enclose a statement

ofexplanationspecifyingthetypeofadditionandOklahomaStat-

uteauthorizingtheaddition,andverifyingdocuments.

B6

B7

16

www.tax.ok.gov/OkTAP

After ling your

individual income

tax return,

check the status

of your refund by

visiting OkTAP.

You’ll need to provide the last 7 digits of the primary Social Security

Number or Individual Taxpayer Identif ication Number, the ZIP Code

on the return and the exact dollar amount of the refund.

Oklahoma Taxpayer Access Point

Where’s My Refund?

Need a helping hand

ling your taxes?

Visit our website to nd out all the

information on the who, what, when and

where for free income tax assistance

through VITA and TCE programs.

www.tax.ok.gov

Schedule 511-C

C2

C3

C4

C1

C6

C5

continuedonpage18

Military Pay Exclusion

Oklahomaresidentswhoaremembersofanycomponentofthe

ArmedServicesmayexclude100%oftheiractivemilitarypay,

includingReserve&NationalGuardpay,totheextentsuchpay

isincludedintheFederalAdjustedGrossIncome.Retiredmilitary

seeinstructionsforSchedule511-A,line4.

Qualifying Disability Deduction

Ifyouhaveaphysicaldisabilityconstitutingasubstantialhandi-

captoemployment,youmaydeducttheexpenseincurredto

modifyamotorvehicle,home,orworkplacenecessaryto

compensateforthedisability.Encloseascheduledetailingthe

expensesincurredandadescriptionofthephysicaldisability

withdocumentationregardingtheSocialSecurityAdministration

recognitionand/orallowanceofthisexpense.

Qualied Adoption Expense

AnOklahomaresidentmaydeduct“nonrecurringadoption

expenses”nottoexceed$20,000percalendaryear.Expenses

aretobedeductedintheyearincurred.“Nonrecurringadoption

expenses”meansadoptionfees,courtcosts,medicalexpenses,

attorneyfeesandexpenseswhicharedirectlyrelatedtothelegal

processofadoptionofachild.Encloseascheduledescribing

theexpensesclaimed.

Contributions to Oklahoma 529 College Savings Plan