535348 TMI Distribution Guide Annual Plan Only

User Manual:

Open the PDF directly: View PDF ![]() .

.

Page Count: 24

1

TD Insurance

Travel Medical Insurance

Annual Plan

Distribution Guide

Name of Insurance Product

Travel Medical Insurance Annual Plan Coverage

Type of Insurance Product

Group Travel Insurance

Name and Address of Insurer:

TD Life Insurance Company

P.O. Box 1

Toronto Dominion Centre

Toronto, Ontario M5K 1A2

Phone: 1-888-788-0839

Name and Address of the Administrator:

Allianz Global Assistance

P.O. Box 277

Waterloo, Ontario N2J 4A4

Phone: 1-800-293-4941

416-977-2039

Fax: 519-742-9471

Name and Address of the Distributor:

The Toronto-Dominion Bank

P.O. Box 1

TD Centre

Toronto, Ontario M5K 1A2

Responsibility of the Autorité des marchés financiers

The Autorité des marchés financiers does not express an opinion on the quality of the product

offered in this guide.

The Insurer alone is responsible for any discrepancies between the wording of the guide and the policy.

2

Table of Contents

Section

Page

Introduction................................................................................................................................................. 3

Nature of the Coverage ................................................................................................................................ 3

Right to Examine the Certificate ..................................................................................................................... 3

Section 1: Summary of Annual Plan Benefits ............................................................................................... 3

Section 2: Eligibility – Who Can Apply for Coverage? ................................................................................... 4

Eligibility Requirements ................................................................................................................................ 4

What Coverage Options are Available? ........................................................................................................... 4

When is a Medical Questionnaire Required?.................................................................................................... 5

How to Apply for a Top-up of Your Annual Plan ................................................................................................ 5

Section 3: Medical Emergency Coverage ..................................................................................................... 5

What to Do in a Medical Emergency ............................................................................................................... 5

Medical Emergency Insurance Limitations ....................................................................................................... 5

Medical Emergency Benefits ......................................................................................................................... 6

Section 4: Exclusions That Apply to All Benefits .......................................................................................... 8

Pre-Existing Condition Exclusion.................................................................................................................... 8

Medical Emergency Insurance Exclusions ....................................................................................................... 9

Section 5: General Information about this Coverage ................................................................................... 11

Your Obligations as an Insured Person ......................................................................................................... 11

Medical Emergency Coverage Period ........................................................................................................... 11

Covered Risk ............................................................................................................................................ 12

Automatic Extension of Certificate in the Event of a Medical Emergency ............................................................ 12

When Your Certificate Terminates ................................................................................................................ 12

How to Renew Your Annual Plan ................................................................................................................. 12

How to Contact Our Administrator ................................................................................................................ 12

Proof of Insurance ..................................................................................................................................... 13

Section 6: How to Make a Claim ................................................................................................................ 13

Medical Emergency Claim........................................................................................................................... 13

If You report the claim immediately ............................................................................................................... 13

If You do not report the claim immediately ..................................................................................................... 14

Section 7: Premiums and Cancellation and Right to Examine/Rescind of Coverage...................................... 14

Premiums ................................................................................................................................................. 14

Cancelling and Right to Examine/Rescind Your Annual Plan ............................................................................ 14

Section 8: General Conditions................................................................................................................... 15

Access to Medical Care .............................................................................................................................. 15

Benefit Payments ...................................................................................................................................... 15

Coordination of Benefits with Other insurance ................................................................................................ 15

Currency .................................................................................................................................................. 15

Group Policy ............................................................................................................................................. 15

Legal Action Limitation Period...................................................................................................................... 15

Misrepresentation of Facts Other than Your Health/Medical Information ............................................................. 15

Proof of Loss and Timely Reporting .............................................................................................................. 15

Relationship Between Us and the Group Policyholder ..................................................................................... 15

Review and Medical Examination ................................................................................................................. 16

Subrogation .............................................................................................................................................. 16

Insurer’s Reply .......................................................................................................................................... 16

Appeal of an Insurer’s Decision and Recourse ............................................................................................... 16

Similar Products ........................................................................................................................................ 16

Referral to the Autorité des marchés financiers .............................................................................................. 16

Section 9: Definitions ............................................................................................................................... 16

3

Introduction

This Distribution Guide describes TD Annual Plan Travel Medical Insurance, underwritten by TD Life Insurance

Company (“We”, “Us”, “Our”) under the Group Policy TI002 issued to The Toronto-Dominion Bank (the “Policyholder”

or “TD Canada Trust”). Allianz Global Assistance provides administrative and adjudication services under the Group

Policy. It will help You make a knowledgeable decision about the type of coverage that best suits Your needs without

the presence of an insurance advisor.

All benefits under the Certificate are subject in every respect to the Group Policy which alone constitutes the

agreement under which benefits will be provided. The principal provisions of the Group Policy affecting Insured

Persons are summarized in the Certificate. The Group Policy is on file at the office of the Policyholder and upon

request, You are entitled to examine and receive a copy of the Group Policy.

Terms in italic throughout this Distribution Guide are defined in the “Definitions” section.

Nature of the Coverage

Medical Emergency

We will pay a benefit if an Insured Person suffers a Medical Emergency during a Covered Trip.

Right to Examine the Certificate

You have ten (10) days from the date You purchase the Certificate to notify Us if You wish to cancel coverage. If You

cancel coverage within this 10 day period, You will receive a full refund of any premiums paid, provided You have not

departed on a Covered Trip, and no claims have been initiated.

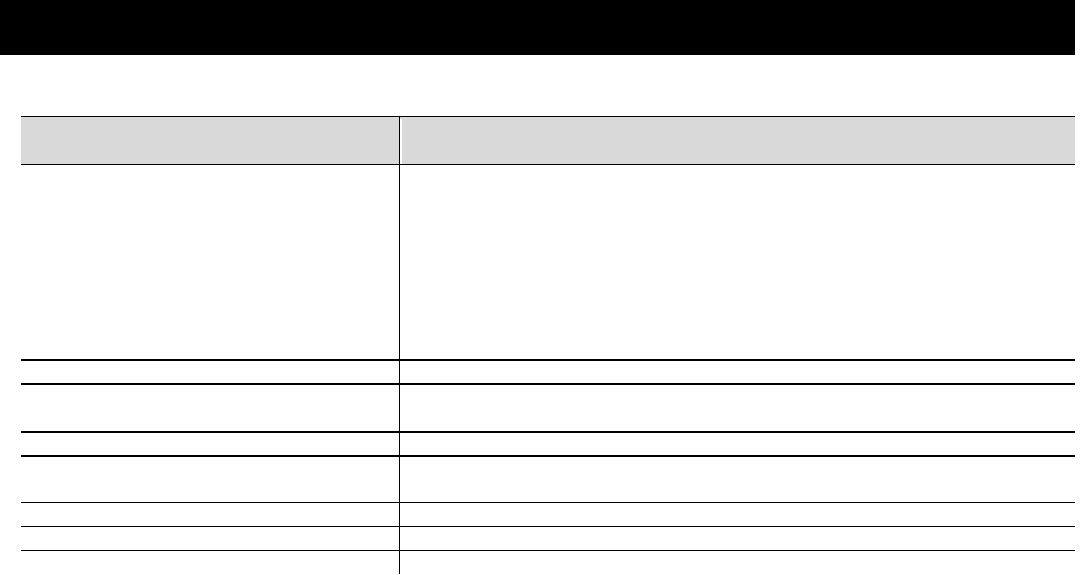

Se ction 1:

Summary of Annual Plan Be ne fits

For complete details of coverage, please refer to the applicable sections within this Distribution Guide.

Coverage

Maximum Benefit Payable

(per Insured Person per Covered Trip)

Medical Emergency coverage and other

benefits including:

Hospital benefit

Physician's bills

Diagnostic services

Ambulance

Medical appliances

Emergency return home

Up to $5,000,000 per Insured Person per Covered Trip with no overall

maximum per Policy Year.

Private duty nursing

Up to $5,000

Professional fees (Physiotherapist,

Chiropractor, etc.)

Up to $300 per profession

Accidental dental

Up to $2,000

Bedside Companion benefit

Round trip economy air fare and up to $1,500 for meals and

accommodation for a Bedside Companion.

Travelling Companion benefit

One-way economy air fare

Vehicle return

Up to $1,000

Return of deceased

Up to $5,000

4

Se ction 2:

Eligibility – Who Can Apply for Cov e rage ?

You can apply for insurance by completing an Application online at tdinsurance.com, or over the telephone with Our

Administrator, from 8 a.m. to 9 p.m. ET, Monday to Saturday, toll-free at 1-800-293-4941 or 416-977-2039.

You can also apply for top-up coverage by calling Our Administrator at the 24-Hour Assistance line and completing an

Application by telephone. The telephone number is 1-800-359-6704 from Canada or the United States, or from any

other countries, You can call collect at 416-977-5040.

Eligibility Requirements

You may apply for Annual Plan Coverage if You are:

at least 18 years old on the Effective Date of Your Annual Plan, if You are purchasing either the 9-day, 17-day, or

30-day plan options; or

18 to 84 years old on the Effective Date of Your Annual Plan, if You are purchasing the 60-day plan option; and

a Resident of Canada; and

covered under a GHIP; and

a TD Bank Group customer, or the Spouse or Dependent Child of a TD Bank Group customer; and

in Canada when You buy the coverage; and

have answered medical questions to determine whether You are eligible for this coverage (when required as part of

the application process); and

You purchase the insurance no earlier than 240 days before the Effective Date of Your Annual Plan.

What Coverage Options are Available?

There are three coverage options available under the Annual Plan: Single Coverage, Couple Coverage and Family

Coverage.

1. Single Coverage

You may apply for Single Coverage for yourself, or on behalf of Your Dependent Child(ren) who are travelling

without either You or Your Spouse if:

You specify in Your Application that the Certificate is to cover the Dependent Child(ren) instead of You; and

Your Dependent Child(ren) meet(s) the Eligibility Requirements above, except that:

- they do not have to be TD Bank Group customers; and

- they can be under 18 years old.

2. Couple Coverage

You may apply for coverage under the Annual Plan on behalf of Your Spouse or a Travelling Companion under

Couple Coverage if:

You name Your Spouse or Travelling Companion in Your Application; and

You and Your Spouse or Travelling Companion meet the Eligibility Requirements above, except that:

- they do not have to be a TD Bank Group customer; and

- if Your Travelling Companion is Your Dependent Child, then he or she may be under 18 years old.

3. Family Coverage

You may apply for coverage under the Annual Plan for Your Spouse and Your Dependent Child(ren) under Family

Coverage if:

You name Your Spouse and/or Dependent Child(ren) in Your Application; and

they meet the Eligibility Requirements above, except that:

- they do not have to be TD Bank Group customers; and

- Your Dependent Child(ren) is/are travelling with You or Your Spouse; and

- Your Dependent Child(ren) may be under 18 years old.

NOTE: Couple Coverage and Family Coverage are not available when a medical questionnaire is required as part of

Your application process. To find out if a medical questionnaire is required, refer to "When is a Medical Questionnaire

Required?" below.

5

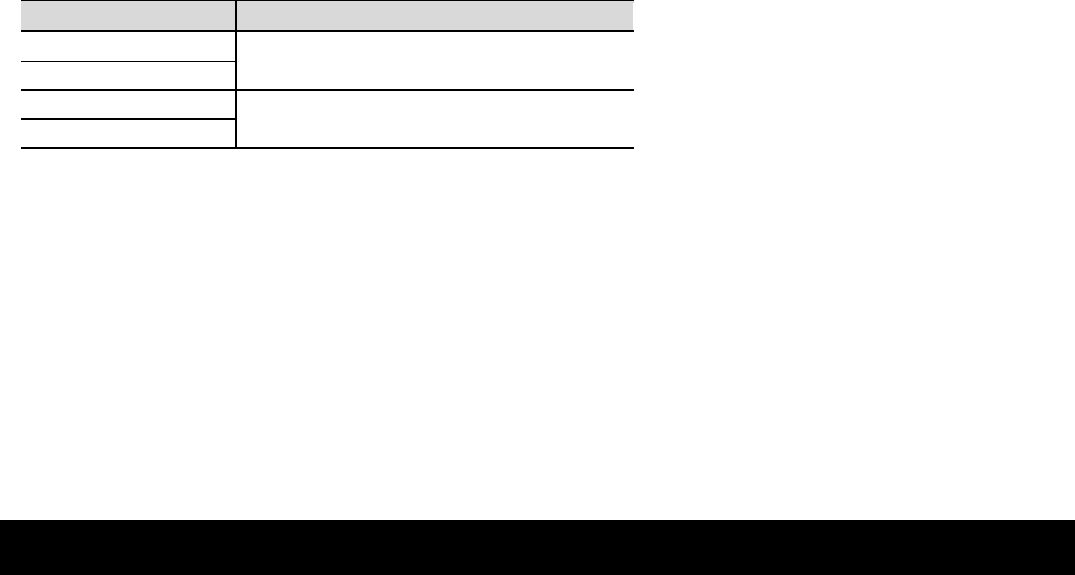

When is a Medical Questionnaire Required?

Depending on Your age and the Annual Plan option You choose, some customers will need to answer a medical

questionnaire to determine if insurance can be provided. In these cases, the premium for coverage will be based on

the answers to the medical questions. Some applicants may not qualify for coverage based on their responses to the

medical questions. The following table explains when a medical questionnaire will need to be completed.

Annual Plan Option

Medical Questionnaire is required for:

9-day plan

All applicants 65 years of age and older

17-day plan

30-day plan

All applicants 55 years of age and older

60-day plan

How to Apply for a Top-up of Your Annual Plan

If You already have a TD Travel Medical Insurance Annual Plan, and You are planning a trip that will last more than

the maximum number of days allowed for a Covered Trip under Your Annual Plan option, You can apply for top-up

coverage, if each Insured Person meets the applicable Eligibility Requirements above, except that:

You do not have to be in Canada when You purchase this top-up of coverage; and

You can apply either before or after You depart on Your trip if:

- no Insured Person has suffered a Medical Emergency before You apply for this top-up of coverage; and

- You apply before 11:59 p.m. ET on the last day of Your Covered Trip (please note that the date of departure

counts as one full day); and

- the Covered Trip is from one (1) day up to 212 days but not longer than the maximum number of days allowed

under Your GHIP for travel outside of Canada; and

- You pay the required premium for the top-up coverage.

Any top-up is subject to approval by Our Administrator.

Se ction 3:

M edical Em ergency Cov e rage

What to Do in a Medical Emergency

In a Medical Emergency, You must call Our Administrator immediately, or as soon as is reasonably possible. If not,

benefits will be limited as described below under “Medical Emergency Insurance Limitations” Some expenses will only

be covered if Our Administrator approves them in advance.

You can get help 24 hours a day, seven days a week by calling:

from Canada or the U.S., toll-free, 1-800-359-6704; or

from other countries, 416-977-5040, collect.

Our Administrator will verify whether coverage is in effect and, if so, will direct the Insured Person to the nearest

appropriate medical facility. Our Administrator will arrange for direct payment to the medical service provider wherever

possible, and manage the Medical Emergency from the initial report through to its conclusion.

If a direct payment cannot be arranged, the Insured Person may be asked to pay for services and then submit a claim

for reimbursement of eligible expenses.

NOTE: All payments and payment guarantees are subject to the terms, conditions, limitations and exclusions of the

Certificate.

Medical Emergency Insurance Limitations

1. Medical Emergency Treatment requires pre-approval

You must notify Our Administrator before obtaining Medical Emergency Treatment so that We may:

confirm coverage

provide pre-approval of Treatment

6

If it is medically impossible for You to call prior to obtaining Medical Emergency Treatment, We ask You to call

within 48 hours, or as soon as possible, or have someone call on Your behalf. Otherwise, if You do not call Our

Administrator before You obtain Medical Emergency Treatment, Your Maximum Benefit Payable will be reduced to

80% of Your medical expenses covered under this insurance, to a maximum of $30,000.

2. Failure to meet the requirement to be covered by a GHIP

You must be covered under the GHIP of Your province or territory of residence prior to and for the entire duration

of the Covered Trip. It is Your responsibility to check that You do have this coverage. There is no coverage under

the Certificate if You do not have a valid GHIP.

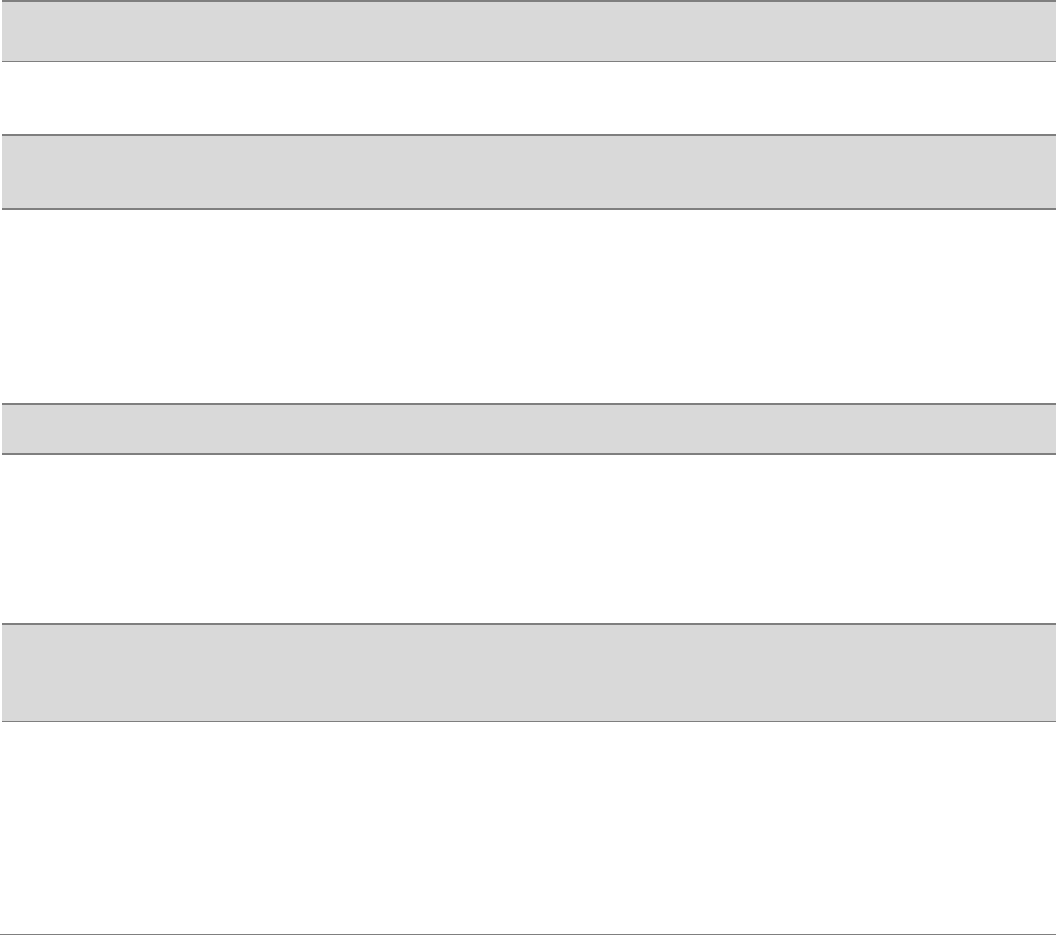

Medical Emergency Benefits

We will pay a Medical Emergency benefit for eligible Medical Emergency expenses if an Insured Person suffers a

Medical Emergency during the Medical Emergency Coverage Period for a Covered Trip.

Eligible Medical Emergency expenses include:

Medical Emergency Coverage up to $5,000,000 per Covered Trip. No overall maximum per Policy Year.

Hospital benefit

Attendance at a Hospital or appropriate medical facility for Treatment as an inpatient,

outpatient, and emergency basis, when approved in advance by Our Administrator.

Physicians’ bills

Fees charged by a Physician, when required as part of Treatment for a Medical

Emergency, and approved in advance by Our Administrator.

Private duty nursing

Up to $5,000 for services performed and supplies deemed necessary by a registered

nurse; including medically necessary nursing supplies.

Diagnostic services

Charges for diagnostic tests, laboratory tests and X-rays which are prescribed by the

treating Physician, and approved in advance by Our Administrator if the tests involve:

magnetic resonance imaging (MRI); or

computerized axial tomography (CAT) scans; or

sonograms; or

ultrasounds; or

any invasive diagnostic procedures, including angioplasty.

Ambulance

Charges for emergency ambulance service to the nearest approved Hospital.

Air ambulance

Charges for emergency air ambulance only if Our Administrator determines that the

Insured Person’s physical condition precludes the use of any other means of

transportation; and:

makes the determination before the service is provided; and

pre-approves the service; and

arranges for the service.

Prescriptions

Reimbursement of prescription drugs required as part of emergency Treatment while in

Hospital.

NOTE: Vitamins and patent, proprietary and experimental drugs are excluded.

Professional fees

Up to a maximum of $300 per profession for expenses incurred as a result of a covered

Medical Emergency which requires Treatment by a licensed physiotherapist, chiropractor,

chiropodist, podiatrist or osteopath, if:

Treatment is required for the immediate relief of an acute symptom, and that,

according to a Physician, cannot be delayed until You return to Your province or

territory of residence; and

Treatment is ordered by a Physician during a Covered Trip and received by a licensed

professional as described under this benefit.

7

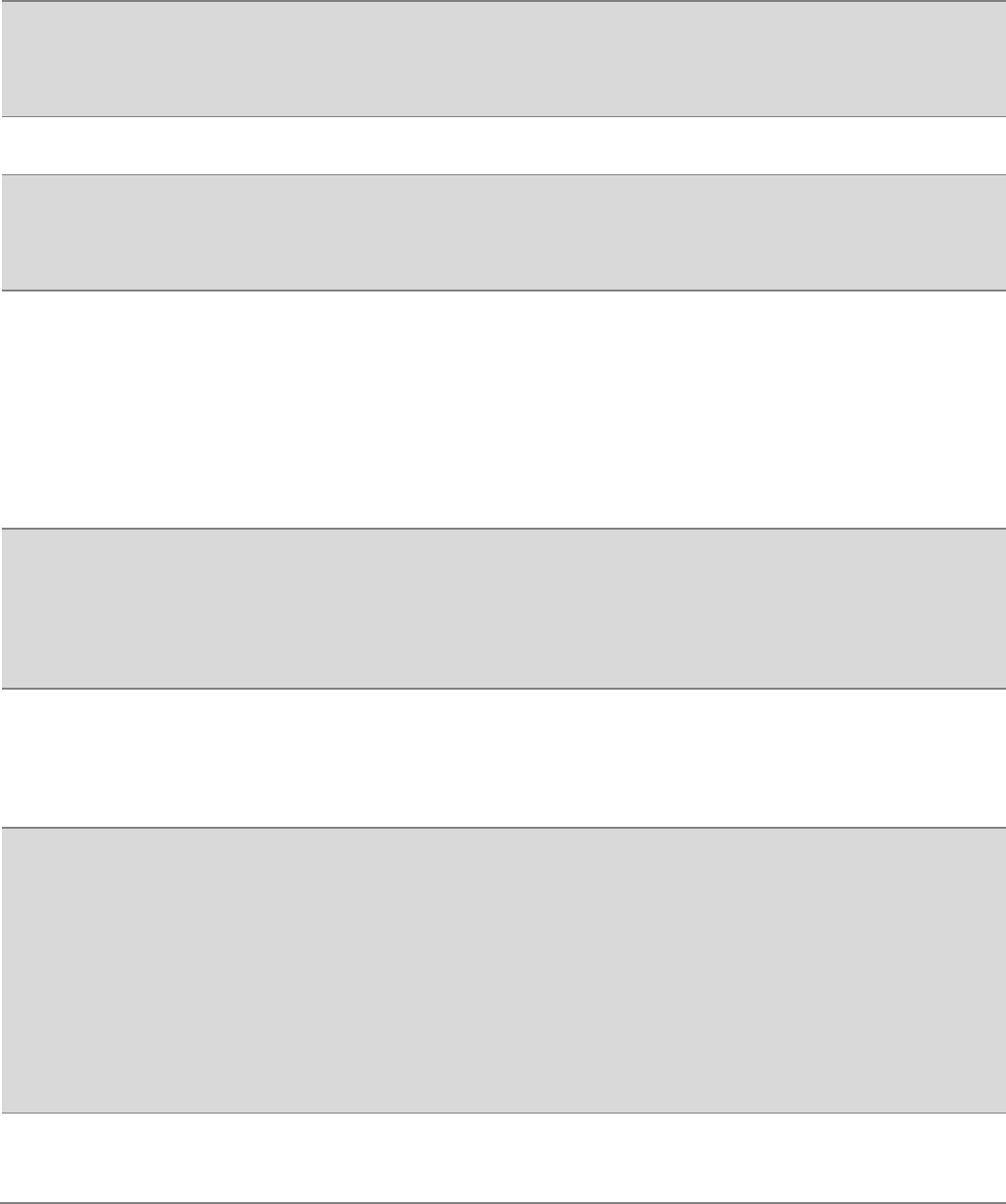

Accidental dental

Up to $2,000 for dental Treatment that is:

required during a Medical Emergency Coverage Period; and

necessary because of a blow to natural or permanently installed teeth which occurs as

a result of a Medical Emergency.

Emergency relief of

dental pain

Treatment for emergency relief of dental pain is covered up to a maximum of $200.

Medical appliances

The cost of casts, crutches, trusses, braces, slings, splints, medical walking boots, and/or

the rental cost of a wheelchair or walker, if:

prescribed by a Physician; and

required because of a Medical Emergency.

Emergency return

home

The cost of a one-way economy fare and, if required to accommodate a stretcher, a

second one-way economy fare, if:

as a result of a Medical Emergency, Our Administrator determines that an Insured

Person should return to Canada; and

Our Administrator approves the transportation in advance.

NOTE: We will also pay the expenses for a qualified medical attendant to accompany

You to Your province or territory of residence if recommended by the attending Physician

during Your Medical Emergency and approval is granted by Our Administrator in

advance.

Bedside Companion

benefit

The cost of one round-trip economy airfare from Your Bedside Companion’s province or

territory of residence, and up to $150 per day, to a maximum of $1,500 for food and

accommodation, if:

You are Hospitalized because of a covered Medical Emergency and are expected to

remain Hospitalized for at least three (3) consecutive days; and

Our Administrator approves this benefit in advance.

Travelling Companion

benefit

The cost of a single one-way economy airfare for a Travelling Companion to return to his

or her place of departure, if:

an Insured Person has a covered Medical Emergency that makes it necessary for the

Travelling Companion to stay beyond their scheduled return date; and

Our Administrator approves the travel in advance.

Meals and

accommodation

up to $350 per day to a maximum of $3,500, for Your :

- commercial accommodations and meals; and

- essential telephone calls and internet usage fees; and

- taxi fares (or rental car in lieu of taxi fares);

if, upon a Physician’s discretion You, or Your Travelling Companion, are relocated to

receive medical attention, for a Medical Emergency covered under this insurance; or

You are delayed beyond Your return date in order to receive Medical Emergency

Treatment; or

Your Travelling Companion requires Medical Emergency Treatment for any Medical

Condition covered under this insurance.

NOTE: Subject to pre-authorization from Our Administrator.

Incidental Hospital

expenses

Up to $50 per day to a maximum of $500, for Your incidental Hospital expenses

(telephone calls, television rental, parking), while You are Hospitalized for at least 48

hours.

8

Return and escort of

Dependent Children

If Dependent Children are travelling with You or join You during Your Covered Trip and

You are Hospitalized for more than 24 hours or You must return to Your province or

territory of residence because of Your Medical Emergency covered under this insurance,

this insurance covers:

the lesser of the cost of a one-way economy air fare on a commercial flight via the

most cost effective route for the return of those Dependent Children to their province or

territory of residence or the cost incurred to change the return date of existing air fare

on a commercial flight; and

the cost of a return economy air fare via the most cost effective route on a commercial

flight for an escort, if the airline requires that the Dependent Children be escorted.

Vehicle return

Up to $1,000 toward the cost of returning an Insured Person’s vehicle to his or her home

or the nearest vehicle rental agency, if:

the Insured Person is unable to return the vehicle because of a Medical Emergency;

and

Our Administrator arranges for the return of the vehicle.

Return of deceased

Up to $5,000 toward the cost of preparation and transportation home of a deceased

Insured Person if death results from a covered Medical Emergency; or

the burial or the cremation of an Insured Person’s remains where their death occurred;

and

one round-trip economy airfare, if:

- an Immediate Family Member is required to identify or obtain release of the

deceased; and

- Our Administrator approves the transportation in advance.

NOTE: The cost of a burial casket or urn is not covered.

Se ction 4:

Exclusions T hat Apply to All Be ne fits

Pre-Existing Condition Exclusion

Your Pre-existing Condition exclusion is determined by the answers provided by You, when You completed Your

Application for insurance and, where applicable, the medical questionnaire (depending on Your age and the Annual

Plan option You choose). To be eligible for benefits under the Certificate, a Pre-Existing Condition must be Stable for

a specified period of time before Your Departure Date. The following table explains which Pre-Existing Condition

exclusion and stability period applies to You. Where applicable, refer to Your Declaration of Coverage to find Your rate

category.

9 Day & 17 Day Annual Plans options

Your Age

Rate Category

Pre-Existing Condition exclusion that applies to You:

Under the

age of 65

No Rate

Category

We will not pay for any Medical Emergency expenses or benefits incurred directly

or indirectly as a result of Your Medical Condition or related condition (whether or

not the diagnosis has been determined), if at any time in the 90 days before You

depart on Your Covered Trip, Your Medical Condition or related condition has not

been Stable, other than a Minor Ailment.

Age 65 and

older

Rate Category

A and B

We will not pay for any Medical Emergency expenses or benefits incurred directly

or indirectly as a result of Your Medical Condition or related condition (whether or

not the diagnosis has been determined), if at any time in the 90 days before You

depart on Your Covered Trip, Your Medical Condition or related condition has not

been Stable, other than a Minor Ailment.

Rate Category

C, D and E

We will not pay for any Medical Emergency expenses or benefits incurred directly

or indirectly as a result of Your Medical Condition or related condition (whether or

not the diagnosis has been determined), if at any time in the 180 days before You

depart on Your Covered Trip, Your Medical Condition or related condition has not

been Stable, other than a Minor Ailment.

9

30 Day & 60 Day Annual Plans options

Your Age

Rate Category

Pre-Existing Condition exclusion that applies to You:

Under the

age of 55

No Rate

Category

We will not pay for any Medical Emergency expenses or benefits incurred directly

or indirectly as a result of Your Medical Condition or related condition (whether or

not the diagnosis has been determined), if at any time in the 90 days before You

depart on Your Covered Trip, Your Medical Condition or related condition has not

been Stable, other than a Minor Ailment.

Age 55 and

older

Rate Category

A and B

We will not pay for any Medical Emergency expenses or benefits incurred directly

or indirectly as a result of Your Medical Condition or related condition (whether or

not the diagnosis has been determined), if at any time in the 90 days before You

depart on Your Covered Trip, Your Medical Condition or related condition has not

been Stable, other than a Minor Ailment.

Rate Category

C, D and E

We will not pay for any Medical Emergency expenses or benefits incurred directly

or indirectly as a result of Your Medical Condition or related condition (whether or

not the diagnosis has been determined), if at any time in the 180 days before You

depart on Your Covered Trip, Your Medical Condition or related condition has not

been Stable, other than a Minor Ailment.

Medical Emergency Insurance Exclusions

In addition to the exclusion outlined above, under "Pre-Existing Condition Exclusion," the Certificate does not cover

any Treatment, services, or expenses of any kind caused directly or indirectly as a result of the following:

1. A child born during the Covered Trip

We will not pay any expenses or benefits with respect to Your child born during a Covered Trip.

2. Abuse of alcohol, drug, or intoxicants

We will not pay any expenses or benefits with respect to:

any Medical Condition, including symptoms of withdrawal, arising from, or in any way related to, Your chronic

use of alcohol, drugs or other intoxicants whether prior to or during Your Covered Trip; or

any Medical Condition arising during Your Covered Trip from, or in any way related to, the abuse of alcohol,

drugs or other intoxicants.

3. Claims related to expectant mother’s complications of pregnancy, or delivery

We will not pay any expenses or benefits with respect to:

routine pre-natal or post-natal care; or

pregnancy, delivery or complications of either arising nine (9) weeks before the expected date of delivery or

anytime, after delivery.

4. Failure to transfer to an appropriate facility for Treatment

We reserve the right to transfer an Insured Person to an appropriate medical facility, or to his or her province or

territory of residence, for further Treatment in consultation with the Insured Person’s treating Physician. Refusal to

comply with an arranged transfer will release Us from any liability to pay any expenses incurred after the

scheduled transfer date.

5. Hazardous activities

We will not pay any expenses or benefits with respect to an accident that occurs while You are participating in any

non-standard sport or activity involving a high level of risk, such as those indicated below, but not limited to:

parasailing, hang-gliding and paragliding; or

parachuting and sky diving; or

bungee jumping; or

mountaineering; or

cave exploration; or

amateur scuba diving, unless You hold at least a basic scuba diving license from a certified school; or

any airborne activity in any aircraft other than a passenger aircraft that holds a valid certificate of airworthiness.

10

6. Illegal act

We will not pay any expenses or benefits with respect to Your committing or attempting to commit a criminal

offence or illegal act, including driving while impaired or over the legal limit.

7. Inaccurate evidence of insurability

We will not pay any expenses or benefits with respect to Your failure to provide accurate and complete evidence of

insurability as described under "Your Obligations as an Insured Person," in Section 5.

8. Intentional self-inflicted injury

We will not pay any expenses or benefits with respect to intentional self-inflicted injury, suicide or attempted

suicide (whether or not the Insured Person is aware of the result of their actions), regardless of the Insured

Person's state of mind.

9. Medical Emergency occurring outside the Coverage Period

We will not pay a benefit with respect to a Medical Emergency that occurs before the Medical Emergency

Coverage Period begins or after it ends. For example, no benefit will be paid with respect to a Medical Emergency

that occurs after 11:59 p.m. ET on the last day of a Covered Trip, if You have not purchased top-up coverage for

the trip.

NOTE: The day of departure counts as a full day for this purpose.

10. Mental disorders

We will not pay any expenses or benefits with respect to any mental, nervous or emotional disorders, including any

Medical Emergency arising from these disorders.

11. Misrepresentation

This Certificate is issued on the basis of information in Your application (including answers to the medical

questionnaire, if required). When completing the application and answering the medical questions, Your answers

must be complete and accurate. In the event of a claim, We will review Your medical history. If any of Your

answers are found to be incomplete or inaccurate:

Your coverage will be null and void

Your claim will not be paid

We will refund Your premium

12. Non-compliance with prescribed medical Treatment

We will not pay any expenses or benefits with respect to any Medical Condition that is the result of You not

following medical Treatment as prescribed to You, including prescribed medication.

13. Non-emergency services

We will not pay expenses and benefits with respect to non-emergency, experimental or elective Treatment (e.g.

cosmetic surgery, chronic care, rehabilitation including any expenses for directly or indirectly related

complications).

14. Ongoing Medical Emergency Treatment (investigations, Treatment and surgery) requires pre-approval

After Your Medical Emergency Treatment has started, Our Administrator must assess and approve additional

medical Treatment. If You undergo a medical investigation, obtain Treatment or surgery that is not pre-approved,

expenses and benefits will not be paid under the Certificate. This includes invasive testing or surgery (e.g. cardiac

catheterization, other cardiac procedures, transplant and MRI).

15. Payment of benefit prohibited by Canadian law

We will not pay a benefit where the payment of the benefit is prohibited by Canadian law or where Canada has

signed a treaty or agreed to a sanction prohibiting such payment.

16. Professional sports or racing

We will not pay any expenses or benefits with respect to Your participation in professional sports or any organized

racing or speed contests.

17. Recurrence or ongoing Treatment once Medical Emergency has ended

We will not pay any expenses or benefits relating to the continued Treatment, recurrence or complication of a

Medical Condition or related condition, following Medical Emergency Treatment during Your trip, if Our

Administrator determines that Your Medical Emergency has ended.

11

18. Travel advisories

We will not pay any expenses or benefits for Your Medical Emergency or related Medical Condition, if the reason

for Your Medical Emergency or related Medical Condition is associated in any way with a written formal travel

warning of ‘Avoid all non-essential travel’ or of ‘Avoid all travel’ issued before Your Departure Date by the

Canadian Government, advising Canadians not to travel to the country, region or city of Your trip.

19. Travel against medical advice

We will not pay any expenses or benefits incurred after Your Physician advised You not to travel.

20. Travelling when Treatment could be expected

We will not pay any expenses or benefits relating to:

any Medical Condition or related condition if the purpose of Your trip is to obtain or receive a diagnosis, medical

Treatment, surgery, investigation, palliative care, alternative therapy, as well as any directly or indirectly-related

complication; or

any Medical Condition for which it was reasonable, prior to departure, to expect Treatment or Hospitalization

during Your trip; or

any symptoms evident that it would be reasonable to expect You to investigate in the three (3) months prior to

Your departure on a Covered Trip.

21. War

We will not pay any expenses or benefits relating to a Medical Condition incurred as a result of:

an act of war, whether declared or undeclared; or

hostile or warlike action in time of peace or war; or

insurrection; or

a riot, civil disorder or civil war; or

rebellion; or

revolution; or

hijacking.

Se ction 5:

Ge ne ral Information about this Cov e rage

Your Obligations as an Insured Person

Failure to disclose impacts Your benefits

The Certificate is voidable by Us and no benefits will be paid if a person who applies to be insured and completes a

medical questionnaire as part of the Application:

fails to disclose all Medical Conditions, current medications, prescribed medications and periods of Hospitalization in

response to the medical questions; or

fails to fully, completely and accurately answer the medical questions.

The Certificate and all coverage hereunder is voidable by Us even if:

the failure to disclose or misrepresentation relates only to the amount of premium that should have been paid; or

any failure to disclose or misrepresentation does not relate to the cause of any claim.

NOTE: We may investigate the answers provided to the health questions in the Application at any time, including at the

time of claim.

Medical Emergency Coverage Period

The Medical Emergency Coverage Period for the Annual Plan begins when the Insured Person departs on a Covered

Trip and ends on the earlier of:

the date the Insured Person returns from the Covered Trip; or

if You do not have top-up coverage, 11:59 p.m. ET on the last day of Your Covered Trip; or

11:59 p.m. ET on the last day of Your top-up coverage shown in the most recent Declaration of Coverage; or

the date the Certificate terminates.

12

Covered Risk

We will pay a Medical Emergency benefit if an Insured Person suffers a Medical Emergency during the Medical

Emergency Coverage Period for a Covered Trip.

We will pay for the Reasonable and Customary Charges for eligible Medical Emergency expenses up to the Maximum

Benefit Payable as described in the section “Summary of Annual Plan Benefits”, less any amounts payable or

reimbursable under:

a GHIP;

any group or individual health plans; OR

any insurance policies.

Automatic Extension of Certificate in the Event of a Medical Emergency

If an Insured Person is suffering from a Medical Emergency on the date the Medical Emergency Coverage Period

would end for any reason except cancellation of the Certificate, the Medical Emergency Coverage Period is

automatically extended to 72 hours immediately following the end of the Medical Emergency:

for that Insured Person; and

for any other Insured Person if:

- that other Insured Person has extended his or her trip past his or her scheduled return date because of the first

Insured Person’s Medical Emergency; and

- Our Administrator has approved a Travelling Companion benefit for that other Insured Person.

When Your Certificate Terminates

If You do not renew Your Annual Plan, it will terminate on Your Anniversary Date.

How to Renew Your Annual Plan

Your Annual Plan will automatically renew on the Anniversary Date if:

You provided instructions to renew automatically; and

We have a valid credit card on file on Your Anniversary Date; and

no Insured Person under the Certificate is required to complete a medical questionnaire on the Anniversary Date;

and

We receive and accept the renewal premium.

To renew an Annual Plan, You can contact Our Administrator before Your Anniversary Date to arrange for payment at

1-800-293-4941 (toll-free) or at 416-977-2039 from 8 a.m. to 9 p.m. ET, Monday to Saturday.

If there have been any changes to the insurance coverage, We will send You a new Certificate; otherwise, Your most

recent Certificate will continue to apply. If You wish to cancel Your insurance, You can do so as described "Section 7:

Cancelling Your Annual Plan."

How to Contact Our Administrator

1. 24-hour Emergency Assistance Number

To report a Medical Emergency, or to apply for top-up coverage, call Our Administrator 24 hours a day, seven

days a week:

from the U.S. or Canada, 1-800-359-6704;

from elsewhere, call collect, 416-977-5040.

2. Customer Service

To obtain a claim form, cancel Your insurance or for general inquiries, call Our Administrator from 8 a.m. to 9 p.m.

ET, Monday to Saturday, toll-free at 1-800-293-4941 or 416-977-2039 or send Your request to:

Re: TD Insurance Travel Medical Insurance

Allianz Global Assistance

P.O. Box 277

Waterloo, Ontario N2J 4A4

Fax: 519-742-9471

13

Proof of Insurance

Your proof of insurance is the Declaration of Coverage document that is provided to You when You complete Your

Application for coverage. If You do not receive Your proof of insurance before You depart on Your Covered Trip, You

must contact Our Administrator immediately.

You will have coverage once You complete the following steps:

applicants meet the Eligibility Requirements for insurance under Section 2; and

apply for insurance; and

if required, You provide Us with accurate and complete evidence of insurance. See "When is a Medical

Questionnaire Required" in Section 2, and "Your Obligations as an Insured Person" above; and

pay the required premium at time of enrollment.

Once this is complete, You will receive Proof of Insurance.

Se ction 6:

How to M ake a Claim

IMPORTANT NOTE: You must report Your claim and provide supporting documentation to Our Administrator as soon

as possible, but no later than one (1) year after the date it occurred.

Medical Emergency Claim

A Medical Emergency should always be reported immediately, as described in Section 3 under "What to Do in a

Medical Emergency," or benefits will be limited.

To make an Medical Emergency claim, as part of the requirements under Section 8: General Conditions ("Proof of loss

and timely reporting"), We will need documentation to substantiate the claim, including but not limited to the following:

proof of payment by You and by any other benefit plan; and

the original itemized receipts for all bills and invoices; and

proof of travel (including departure and return dates); and

medical records including complete diagnosis by the attending Physician or documentation by the Hospital, which

must support that the Treatment was medically necessary; and

proof of the accident if You are submitting a claim for dental expenses resulting from a Medical Emergency; and

Your historical medical records (if We determine applicable).

If You report the claim immediately

If Our Administrator guarantees or pays eligible expenses on behalf of an Insured Person, then You and, if applicable,

the Insured Person must sign an authorization form allowing Our Administrator to recover those expenses:

from the Insured Person’s GHIP; and

from any health plan or other insurance; and

through rights You may have against other insurers or other parties (see Section 8: General Conditions, under

“Subrogation”).

If Our Administrator pays eligible expenses that are covered under other insurance or another plan, You and the

Insured Person (if applicable) must help Our Administrator to seek reimbursement as required.

The Insured Person must also provide evidence of the actual departure date from his or her province or territory of

residence. If requested, an Insured Person must confirm any return dates to his or her province or territory of

residence.

NOTE: If Our Administrator makes an advance payment for expenses that are later discovered to be ineligible under

the Certificate, the Insured Person must reimburse Us.

14

If You do not report the claim immediately

In a Medical Emergency, You must call Our Administrator immediately, or as soon as is reasonably possible. If not,

benefits will be limited as described under “Medical Emergency Insurance Limitations” in Section 3. If an Insured

Person incurs eligible Medical Emergency expenses without first contacting Our Administrator for assistance and claim

management, he or she must first submit receipts and other proof to:

GHIP; and

then to any group or individual health plan(s) and/or insurer(s).

Eligible Medical Emergency expenses not covered by a GHIP or other plan or insurance must be submitted to Our

Administrator with proof of:

claim, receipts and payment statements

the actual departure date from Your province or territory of residence (Proof includes, but not limited to, a flight

itinerary, gas receipts or toll-road receipts)

See Section 5 under “How to Contact Our Administrator,” for information on how to get a claim form.

Se ction 7:

Pre miums and Cance llation and Right to Examine /Re scind of Cov e r age

Premiums

Premiums will be based on:

the age of the oldest person to be insured under Your Certificate as of:

- the Effective Date of Your Certificate; or

- if applicable, the Anniversary Date on which Your Certificate is renewed; and

the medical information provided when You apply (where applicable); and

Our pricing that is in effect at the time of Your Application; and

Your coverage type (Single, Couple, Family).

NOTE: Please note that premium rates can be changed without notice.

Cancelling and Right to Examine/Rescind Your Annual Plan

You have ten (10) days from the date You purchase the Certificate to cancel coverage and receive a full refund of any

premium paid. All requests for cancellation of the Annual Plan must be made to Our Administrator, in writing or by

phone (see "How to Contact Our Administrator," in Section 5). The following explains how and when cancellations may

take place.

by phone – cancellation will be effective on the date of Your call; or

by written, mailed request – cancellation will be effective on the post-marked date of Your request.

When Can You Cancel

Premium Refund/Fees

No later than ten (10) days from the date You purchase

this Certificate.

Full refund

After ten (10) days from the date You purchase this

Certificate

No refund

15

Se ction 8:

General Conditions

Unless the Certificate or the Group Policy states otherwise, the following conditions apply to Your coverage.

Access to Medical Care

TD Life, TD Bank Group, Our Administrator and their affiliates are not responsible for the availability, quality or results

of any medical Treatment or transport, or for the failure of any Insured Person to obtain medical Treatment.

Benefit Payments

This Certificate contains provisions removing or restricting the right of the Insured Person to designate

persons to whom or for whose benefit money is to be payable. This means that under the Group Policy, neither

You nor any Insured Person has the right to choose a beneficiary who will receive any benefits payable under the

Certificate. Benefits are payable to You or, on Your behalf, to Your medical service provider.

Coordination of Benefits with Other insurance

All of Our policies are excess insurance, meaning that any other sources of recovery You have will pay first, and this

insurance policy will be the last to pay. The total benefits payable under all Your insurance, including the Certificate,

cannot be more than the actual expenses for a claim. If an Insured Person is also insured under any other insurance

certificate or policy, We will coordinate payment of benefits with the other insurer.

In no case will We seek to recover against employment related plans if the lifetime maximum for all in-country and

out-of-country benefits is $50,000 or less. If the lifetime maximum for all in-country and out-of-country benefits is

over $50,000, We will coordinate benefits only above this amount.

Currency

All amounts shown are in Canadian currency.

Group Policy

All benefits under the Certificate are subject in every respect to the Group Policy, which alone constitutes the

agreement under which benefits will be provided. The principal provisions of the Group Policy affecting Insured

Persons are summarized in the Certificate. The Group Policy is on file at the office of the Policyholder and upon

request, You are entitled to receive and examine a copy of the Group Policy.

Legal Action Limitation Period

Every action or proceeding against an insurer for the recovery of insurance money payable under the contract is

absolutely barred unless commenced within the time set out in the Insurance Act (for actions or proceedings governed

by the laws of Alberta and British Columbia), The Insurance Act (for actions or proceedings governed by the laws of

Manitoba), the Limitations Act, 2002 (for actions or proceedings governed by the laws of Ontario), or other applicable

legislation. For those actions or proceedings governed by the laws of Quebec, the prescriptive period is set out in the

Civil Code of Quebec.

Misrepresentation of Facts Other than Your Health/Medical Information

We will not pay any expenses or benefits if You, any person insured under the Certificate or anyone acting on Your

behalf attempts to deceive Us or makes a fraudulent, false or exaggerated claim.

Proof of Loss and Timely Reporting

If You are making a claim, You must complete and send Our Administrator the appropriate claim forms, together with

written proof of loss (e.g. original invoices and tickets, medical and/or death certificates as described in Section 6: How

to Make a Claim) as soon as possible. In every case, You must report Your claim within one (1) year from the date of

the accident or the date the claim arises.

Relationship Between Us and the Group Policyholder

TD Life Insurance Company is affiliated with The Toronto-Dominion Bank (“TD Bank”).

16

Review and Medical Examination

When a claim is being processed, We will have the right and the opportunity, at Our own expense, to review all

medical records related to the claim and to examine the Insured Person medically when and as often as may be

reasonably required.

Subrogation

There may be circumstances where another person or entity should have paid You for a loss but instead We paid You

for the loss. If this occurs, You agree to co-operate with Us so We may demand payment from the person or entity who

should have paid You for the loss. This may include:

transferring to Us the debt or obligation owing to You from the other person or entity; or

permitting Us to bring a lawsuit in Your name; or

if You receive funds from the other person or entity, You will hold it in trust for Us; or

acting so as not to prejudice any of Our rights to collect payment from the other person or entity.

We will pay the costs for the actions We take.

Insurer’s Reply

Once We have approved the claim, We will notify You and payment will be made within 60 days after receipt of the

required claim forms and written proof of loss.

Once the required proof has been received and the claim has been approved, payment will be made by the Insurer

within 30 days.

If the claim has been denied, We will inform You of the claim denial reasons within 60 days after receipt of the required

claim forms and written proof of loss.

Appeal of an Insurer’s Decision and Recourse

If Your claim is refused, You can appeal this decision by submitting new information to the Insurer. You may also

consult the Autorité des marchés financiers or Your own legal advisor.

Similar Products

Other travel insurance products may be offered by other insurance companies.

Referral to the Autorité des marchés financiers

For more information about the Insurer’s obligation and the distributor’s obligation to You, the customer, You can

contact the Autorité des marchés financiers at:

Autorité des marchés financiers

Place de la Cité, Tour Cominar

2640 Laurier Blvd., 4th Floor

Quebec, Quebec G1V 5C1

Telephone Numbers

Toll free: 1-877-525-0337

Quebec: 418-525-0337

Montreal: 514-395-0337

Fax: 418-525-9512

Internet: http://www.lautorite.qc.ca

Se ction 9:

De finitions

In this Distribution Guide, the following words and phrases shown in italics have the meanings shown below. As You

read through the Distribution Guide, You may need to refer to this section to ensure You have a full understanding of

Your coverage, limitations and exclusions.

17

Administrator

Means the company We select to provide medical and claims assistance, claims

payment, administrative and adjudication services under the Group Policy.

Anniversary Date

Means the date one (1) year from Your Effective Date and, if You renew Your Certificate,

subsequent anniversaries of Your Effective Date.

Application

Means the series of questions that form Your application and are submitted:

on Your behalf when You apply by telephone; or

when You apply online; and

the series of medical questions that form part of Your Application if You apply by

telephone and Your answers to those questions.

The Application which is used to determine Your eligibility for insurance, also includes the

questions asked and answers given in connection with requests to top-up a Coverage

Period or increase coverage. The Application is part of Your insurance contract and is

used to process Your request for insurance.

Bedside Companion

Means a person of Your choice who is required at Your bedside while You are

Hospitalized during Your trip.

Certificate

Means the Certificate of Insurance.

Certificate Holder

Means the TD Bank Group customer who has applied, and has been accepted for

coverage under the Annual Plan.

Coverage Period

Means the period of time between Your Departure Date and the day You actually return

from Your Covered Trip. In the event of a Medical Emergency, Your Coverage Period will

be extended up to 72 hours immediately following the end of the Medical Emergency.

Covered Trip

Means a trip:

made by an Insured Person outside the Insured Person’s province or territory of

residence; and

that begins and ends while the Annual Plan is in effect; and

that lasts no longer than:

- nine (9) consecutive days under the 9-day plan; or

- seventeen (17) consecutive days under the 17-day plan; or

- thirty (30) consecutive days under the 30-day plan; or

- sixty (60) consecutive days under the 60-day plan.

Declaration of

Coverage

Means the document You receive when You apply for new or additional coverage under

the Group Policy, which includes Your Certificate number and confirms the coverage You

have purchased.

Departure Date

Means the date the Insured Person left their home province or territory.

Dependent Child(ren)

Means Your natural, adopted, or step-children who are:

unmarried; and

dependent on You for financial maintenance and support; and

- under 22 years of age, or

- under 26 years of age and attending an institution of higher learning, full-time, in

Canada; or

- mentally or physically handicapped.

NOTE: A Dependent Child does not include a child born while the child’s mother is

outside her province or territory of residence during the Covered Trip and as such, the

child will not be insured with respect to that trip.

18

Effective Date

Means the date Your Certificate takes effect and is the date shown in Your Application or

Your most recent Declaration of Coverage.

GHIP ("Government

Health Insurance

Plan")

Means a Canadian provincial or territorial government health insurance plan.

Group Policy

Means the Group Policy No. TI002 issued by Us for the The Toronto-Dominion Bank.

Hospital

Means:

An institution that is licensed as an accredited hospital, and is staffed and operated for

the care and Treatment of in-patients and out-patients. Treatment must be supervised

by Physicians and there must be registered nurses on duty 24 hours a day. A

laboratory and an operating room must also exist on the premises or in facilities

controlled by the establishment.

A hospital is not an establishment used mainly as a clinic, extended or palliative care

facility, rehabilitation facility, addiction treatment centre, convalescent, rest or nursing

home, home for the aged or health spa.

Hospitalized or

Hospitalization

Means to be an inpatient in a Hospital.

Immediate Family

Member

Means an Insured Person’s:

Spouse, parents, step-parent, grandparents, natural or adopted children, step-children

or legal ward, grandchildren, brothers, sisters, step-brothers, step-sisters, aunts,

uncles, nieces, nephews; and

mother-in-law, father-in-law, brothers-in-law, sisters-in-law, sons-in-law, daughters-in-

law; and

the Insured Person’s Spouse’s grandparents, brothers-in-law and sisters-in-law.

Insured Person

Means a person:

who is eligible to be insured under the Certificate; and

who was named in the Application; and

for whom the required premium has been paid; and

on whom insurance has been issued under the Certificate.

Medical Condition

Means any injury, illness, or disease; complication of pregnancy within the first thirty-one

(31) weeks of pregnancy; a mental or emotional disorder, including acute psychosis that

requires admission to a Hospital.

Medical Emergency

Means a sudden and unforeseen sickness or injury that requires immediate Treatment. A

Medical Emergency no longer exists when the evidence reviewed by Our Administrator

indicates that no further Treatment is required at destination or You are able to return to

Your province/territory of residence for further Treatment.

Minor Ailment

Means any sickness or injury which does not require:

the use of medication for a period greater than fifteen (15) days; or

more than one (1) follow up visit to a Physician, Hospitalization, surgical intervention, or

referral to a specialist; or

which ends at least fourteen (14) consecutive days prior to the Departure Date of the

trip.

NOTE: A chronic condition or complications of a chronic condition are not considered a

Minor Ailment.

19

Physician

Means a medical doctor licensed to prescribe and administer medical Treatment where

the medical services are provided and who is not You or Your Immediate Family Member

or Your Travelling Companion.

Policy Year

Means the period beginning on Your Effective Date and ending with the Anniversary Date

one (1) year later and, if You renew Your Annual Plan, subsequent one (1) year periods,

as applicable.

Pre-Existing

Condition

Means any Medical Condition, that exists prior to Your Departure Date.

Reasonable and

Customary Charges

Means charges incurred for goods and services that are comparable to what other

providers charge for similar goods and services in the same geographical area.

Resident of Canada

and/or Canadian

Resident

Is any person who:

has lived in Canada for a total of 183 days within the last year (the 183 days do not

have to be consecutive); or

is a member of the Canadian Forces.

Spouse

Means:

the person who the Insured Person is legally married to; or

the person the Insured Person has lived with for at least one (1) year and publicly refer

to as his or her domestic partner.

Stable

Means that for any Medical Condition or related condition, other than a Minor Ailment, for

which there have been:

No new symptoms, or more frequent or severe symptoms; or

No new test results showing a deterioration; or

No Hospitalizations; or

No new Treatment, no new medical management, no new prescribed medication; or

No change in Treatment, no change in medical management, no change in prescribed

medication; or

No pending surgery, referrals to a specialist, or other Treatment.

NOTE: The following exceptions are considered Stable:

the routine adjustment of Coumadin, warfarin or insulin (as long as they are not newly

prescribed or stopped) and there has been no change in Your Medical Condition; or

a change from a brand name medication to a generic brand medication of the same

dosage.

Travelling Companion

Means any person who travels with You during the Covered Trip and who is sharing

transportation and/or accommodation with You (to a maximum of three people including

You).

Treatment, or Treated

Means a procedure prescribed, performed or recommended by a Physician or other

authorized healthcare professional for a Medical Condition. Treatment includes but is not

limited to prescribed medication, investigative testing or surgery.

You, Your and Yours

Mean the person(s) named as the Insured Person(s) on Your most recent Declaration of

Coverage, for which insurance coverage was applied and the appropriate premium has

been received by Us.

We, Us, Our and Ours

Mean TD Life Insurance Company.

20

This is the end of the Distribution Guide.

21

NOTICE OF RESCISSION OF AN INSURANCE CONTRACT

NOTICE GIVEN BY A DISTRIBUTOR

Section 440 of the Act respecting the distribution of financial products and services

THE ACT RESPECTING THE DISTRIBUTION OF FINANCIAL PRODUCTS AND SERVICES GIVES YOU

IMPORTANT RIGHTS.

The Act allows you to rescind the insurance contract you have just signed when signing another contract, without

penalty, within 10 days of its signature. To do so, you must give the insurer notice by registered mail within that

time frame. You may use the model below for this purpose.

Despite the rescission of the insurance contract, the first contract entered into will remain in force. Caution, it is

possible that you may lose advantageous conditions as a result of the rescission of this insurance contract; contact

your distributor or consult your contract.

After the expiry of the 10-day delay, you may rescind the insurance at any time; however, penalties may apply.

For further information, contact the Autorité des marchés financiers at (418) 525-0337 or 1-877-525-0337.

NOTICE OF RESCISSION OF AN INSURANCE CONTRACT

To: TD Life Insurance Company P.O. Box 1 TD Centre

Toronto, Ontario

M5K 1A2

Date: ________________________________________ ______________________________________

(date of sending of notice) Certificate #

Pursuant to section 441 of the Act respecting the distribution of financial products and services, I hereby rescind the

insurance certificate issued under group master policy no.:TI002.

Entered into on: __________________________________ In: ________________________________________

(date of signature of contract) (place of signature of contract)

______________________________________________ ______________________________________________

(name of client) (signature of client)

The distributor must first complete this section.

This document must be sent by registered mail.

Sections 439, 440, 441, 442 and 443 of the Act are printed on the back of this notice.

22

439. A distributor may not subordinate the making of a contract to the making of an insurance contract with the insurer

specified by the distributor.

The distributor may not exercise undue pressure on the client or use fraudulent tactics to induce the client to purchase

a financial product or service.

440. A distributor that, at the time a contract is made, causes the client to make an insurance contract must give the

client a notice, drafted in the manner prescribed by regulation, stating that the client may cancel the insurance contract

within 10 days of signing it.

441. A client may cancel an insurance contract made at the same time as another contract, within 10 days of signing it,

by sending notice by registered or certified mail.

Where such an insurance contract is cancelled, the first contract retains all its effects.

442. No contract may contain provisions allowing its amendment in the event of cancellation or termination by the

client of an insurance contract made at the same time.

However, a contract may provide that the cancellation or termination of the insurance contract will entail, for the

remainder of the term, the loss of the favourable conditions extended because more than one contract was made at

the same time.

443. A distributor that offers financing for the purchase of goods or services and that requires the debtor to subscribe

for insurance to guarantee the reimbursement of the loan must give the debtor a notice, drawn up in the manner

prescribed by regulation, stating that the debtor may subscribe for insurance with the insurer and representative of the

debtor’s choice provided that the insurance is considered satisfactory by the creditor, who may not refuse it without

reasonable grounds. The distributor may not subordinate the making of the contract of credit to the making of an

insurance contract with the insurer specified by the distributor.

No contract of credit may stipulate that it is made subject to the condition that the insurance contract subscribed with

such an insurer remain in force until the expiry of the term, or subject to the condition that the expiry of such an

insurance contract will entail forfeiture of term or the reduction of the debtor’s rights.

The rights of the debtor under the contract of credit shall not be forfeited when the debtor cancels, terminates or

withdraws from the insurance contract, provided that the debtor has subscribed for insurance with another insurer that

is considered satisfactory by the creditor, who may not refuse it without reasonable grounds.

23

24

535348 (1017)