315 960 000 AMBIT Ar 06

User Manual: 315-960-000

Open the PDF directly: View PDF ![]() .

.

Page Count: 52

Annual Report 2006

Park Meadows, Kensington, Gauteng

Contents

Page

Executive Summary 1

Directorate & Administration 2 - 3

Chairman & Chief Executive Officer's Report 4 - 9

Corporate Governance Review 10 - 11

Unitholders' Diary 12

Analysis Of Linked Unitholders 13

Directors' Responsibility For & Approval Of The Annual Financial Statements 14

Independent Auditor’s Report 15

Annual Financial Statements

Directors' Report 16 - 17

Balance Sheets 18

Income Statements 19

Statements Of Changes In Equity 20

Cash Flow Statements 21

Notes To The Annual Financial Statements 22 - 39

Property Portfolio 40 - 41

Notice Of Annual General Meeting 42 - 44

Proxy Form 45 - 46

Directors’ Traditional Income Statement & Balance Sheet 47 - 49

This report together with additional information on the

property portfolio is available at: www.ambitprops.co.za

Annual Report 2006

1

Executive Summary

PROFILE

Ambit Properties Limited (Ambit or The Company) is a property loan stock company which listed on the JSE Securities Exchange South

Africa (JSE) in the Financials – Real Estate sector on 4 February 2004. (Share Code: ABT, ISN: ZAE000051645).

The market capitalisation of the company as at 30 September 2006 was R606 million.

The Group (Ambit and its subsidiary, Whirlprops 37 (Proprietary) Limited) has an investment in a property portfolio of 27 properties and

an investment in Oryx Properties Limited (Oryx), a property loan stock company listed on the Namibian Stock Exchange.

INVESTMENT STRATEGY, OBJECTIVES AND PROSPECTS

To provide investors with sustainable and growing income, and the associated capital appreciation, from an investment portfolio of retail,

office and industrial properties. To maintain the existing high quality of the portfolio and expand it with property acquisitions largely in the

major metropolitan areas which offer good rental growth prospects. Ambit will also continue to seek investment opportunities in selected

neighbouring countries.

HIGHLIGHTS

30 September 2006 30 September 2005

(Restated)

• Distribution (cents per unit) 29,60 27,50

• Income yield on unit price at beginning of year 9,2% 12,6%

• Weighted average headline earnings (cents per unit) 32,24 31,30

• Weighted average earnings (cents per unit) 77,20 77,91

• Number of properties 27 29

• Value of property portfolio (R) 824 550 000 671 000 000

• Oryx investment (R) 110 927 000 82 944 000

• Net asset value including distribution yet to be paid (cents per unit) 326 275

• Linked units in issue 186 482 837 173 814 215

• Market price (cents per unit) 325 323

• (Discount)/premium to net asset value (0,3%) 17,5%

• Borrowings (R) 315 960 000 267 199 000

• Interest bearing borrowings as a percentage of long-term assets 33,8% 35,5%

2

Directorate & Administration

From top left to right

R D Jeffery, R R Emslie, N B S Harris, D L Brown, F Uys, J H Beare, I N Mkhari and W H Raffinetti

Directors of Ambit Properties Limited

(Registration number: 2001/007003/06)

as at 30 September 2006 and at the date of this report are:

D L Brown (59)

(FRICS, MIV (SA)) # *

Non-executive independent Chairman

He has 38 years experience in commercial real estate focused

principally on development, leasing and asset management. He was

previously the managing director of Equity Estates (Proprietary)

Limited, until his retirement earlier this year.

N B S Harris (64)

(FRICS) #

Chief Executive Officer

Executive director

He has over 40 years experience in property. He was a director of

Marriott Property Services (Proprietary) Limited. He is a director of

Oryx Properties Limited (listed on the Namibian Stock Exchange),

is a past president of the South African Property Owners Association

and is chairman of the South African Board of the Royal Institution

of Chartered Surveyors.

J H Beare (52)

(BComm, CA(SA)) # • (C)

Non-executive independent director

He has 18 years experience in the property industry. He is the

managing director of Beare Holdings (Proprietary) Limited which is

extensively involved in property investment, development and

administration. He was a business service partner of Pim Goldby

(now Deloitte & Touche).

R R Emslie (48)

(BComm (Hons), CA (SA))

Non-executive director

He has 19 years banking experience with Absa Bank Limited with

senior appointments in both ACMB and the Business Bank. In August

2004 he was appointed as an executive director of the Absa Group.

He is a director of Paramount Property Fund Limited.

Annual Report 2006

3

R D Jeffery (61)

Alternate director to R R Emslie

(MBA)

Non-executive director

He has 41 years banking experience including 11 years experience

in commercial property finance. He is a general manager within the

Business Banking Services Division of Absa Bank Limited heading up

the Commercial Property Finance Department. He is a director of

Paramount Property Fund Limited.

I N Mkhari (32)

(BA Soc. Science) *

Non-executive independent director

Ipeleng is the Chief Investment Officer of Motseng Investment

Holdings (Proprietary) Limited. In 1998 she founded Phosa Iliso

CCTV; the first black woman-owned and managed CCTV business

in South Africa. She later co-founded Motseng Investment Holdings

and is a shareholder of Motseng Investment Holdings. She is a

director of all Motseng group subsidiaries, Kap International and

Marriott Property Fund Managers Limited.

F Uys (59)

(BA, BComm (Hons), MComm)

(Namibian) •

Non-executive independent director

His experience includes being the managing director of Metje &

Ziegler Limited from 1996 to 2004, of TransNamib Limited from

1989 to 1996 and a senior executive of the Trencor Group from

1970 to 1989. He founded the Road Transport Association in

Namibia in 1976 and acted as chairman until 1980. He has served

on various Government and advisory bodies in Namibia as well as

in South Africa. He was chairman of the Namibian Stock Exchange

from 1999 to 2001. He has been the chairman of FP du Toit Transport

(Proprietary) Limited since 1999, is the chairman of Intercape Ferreira

Mainliner (Proprietary) Limited and is a director of Oryx Properties

Limited.

# Member of the Investment Committee

• Member of the Risk, Audit and Compliance Committee

* Member of the Remuneration Committee

(C) Chairman of relevant sub-committee

Administration

Ambit has changed its registered office and as from 1 December

2006, the registered office is:

Ambit Properties Limited

First Floor, 4 Fricker Road

Illovo, 2196

P O Box 618, Melrose Arch, 2076

Company secretary and manager

Ambit Management Services (Proprietary) Limited

First Floor, 4 Fricker Road

Illovo, 2196

P O Box 618, Melrose Arch, 2076

Trustee

Steinway Trustees (Proprietary) Limited

The Manor House

14 Nuttall Gardens

Morningside

Durban, 4001

P O Box 37957, Overport, 4067

Commercial bank

Absa Bank Limited

Business Banking Services

Palazzo Towers West

Monte Casino Boulevard

Fourways, 2055

P O Box 782991, Sandton, 2146

Merchant bank

Grindrod Bank Limited

Building Three, First Floor, North Wing

Commerce Square, 39 Rivonia Road

Cnr Helling Road, Sandton

PO Box 78011, Sandton, 2146

Auditors

Deloitte & Touche

Deloitte & Touche Place

2 Pencarrow Crescent

La Lucia, Durban, 4001

P O Box 243, Durban, 4000

Transfer secretary

Computershare Investor Services 2004 (Proprietary) Limited

70 Marshall Street

Johannesburg, 2001

P O Box 61051, Marshalltown, 2017

Sponsors

Exchange Sponsors (Proprietary) Limited

Building Three, First Floor, North Wing

Commerce Square, 39 Rivonia Road

Cnr Helling Road, Sandton

PO Box 78011, Sandton, 2146

4

Chairman & Chief Executive Officer’s Report

Ambit has performed well for the year under review providing investors with steady income growth. Ambit’s distributable earnings for the financial year

ended 30 September 2006 amounts to R55,2million or 29,6 cents per unit (cpu) which shows growth of 7,6% over the 2005 distribution (2005: 27,5cpu).

The second half distribution of 15,6cpu shows growth of 11,4% over the first half year distribution of 14,0cpu.

1. ECONOMIC REVIEW

The economy continued the sound 4% growth of the past few years and at last job creation was positive.

Inflation remained within the Reserve Bank target of 3 – 6%, albeit edging towards the upper end of the band. Consumer spending continued to grow,

but this was tempered by the 0,5% interest rate increases in June and August. However, the weakening of the Rand against the major currencies will

have a positive impact on exports.

Business confidence ended the period under review at the same positive levels at which it commenced the year.

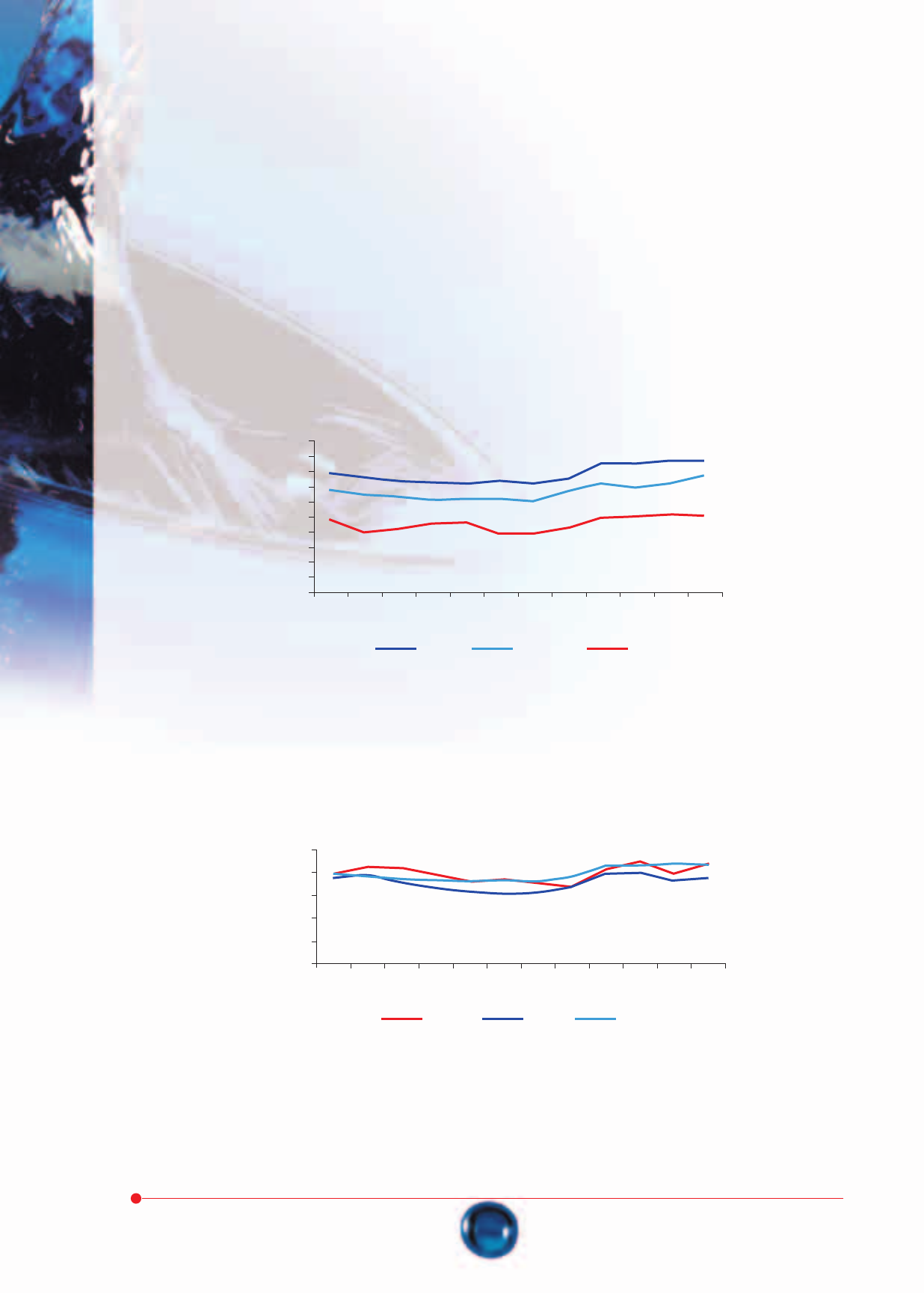

2. LISTED PROPERTY

The listed property sector started the period under review as a favoured asset class, with the strong investor demand driving the South African Property

Index (SAPY) index well below the benchmark Government long bond yields (the R153).

By May 2006, the SAPY index reached a peak of 465 from which it rapidly retreated 25% over the next 2 months following the global re-rating of

the emerging markets and the Reserve Bank increase in interest rates.

However, the underlying property fundamentals had not changed and ongoing growth in distributions from the sector soon had investors recognising

the over sold situation and returning to this asset class. By the end of September 2006 the index had recovered to 408, within 12% of its May high.

10

9

8

7

6

5

4

3

2

1

0

Oct

05

Nov

05

Dec

05

Jan

06

Feb

06

Mar

06

Apr

06

May

06

Jun

06

Jul

06

Aug

06

Sep

06

R153 ECPIX

ZAR/USD

The market capitalisation of the sector commenced the period under review at R45 billion and, by the end of September 2006, stood at R57 billion.

Oct

05

Nov

05

Dec

05

Jan

06

Feb

06

Mar

06

Apr

06

May

06

Jun

06

Jul

06

Aug

06

Sep

06

10

8

6

4

2

0

AMBIT J253 R153

Annual Report 2006

5

The consistent income return from each of the major sectors over the last few years is clearly demonstrated and it is this which forms the foundation

of distribution growth to unitholders.

Ambit, with an income return of 11,5%, outperformed the listed fund index income return of 11% for the 2005 period, but marginally lagged the

growth index of 20,8% with 17,4%. This gave Ambit a total return of 30,8% for the year.

4. REVIEW OF FINANCIAL RESULTS

Ambit has performed steadily for the year under review, with distributions showing 7,6% growth over 2005. The core property portfolio showed a

15% growth in value over 2005.

The financial statements have been prepared in accordance with International Financial Reporting Standards (IFRS) for the first time in the current year,

and IFRS 1 (First time adoption of IFRS) has been applied. The adoption of IFRS has not resulted in any adjustments to the amounts reported previously

in the annual financial statements for the year ended 30 September 2005 or to the opening IFRS balance sheet at 1 October 2004. However, a change

in accounting interpretation of IAS 32 has resulted in the reclassification of share premium to debenture premium and in the amortisation of the resultant

debenture premium. This will increase earnings over the life of the debentures, and the Group has elected to transfer the amount to non-distributable

reserves in order not to affect distributions. This has had the effect of increasing earnings by R1,8 million or 0,99 cents per weighted number of units

in the current year (2005: R1,2 million or 0,72 cents) and increasing the opening balance of non-distributable reserves in 2005 by R0,7 million.

70 000

60 000

50 000

40 000

30 000

20 000

10 000

0

Oct

05

Nov

05

Dec

05

Jan

06

Feb

06

Mar

06

Apr

06

May

06

Jun

06

Jul

06

Aug

06

Sep

06

Rand (Billions)

Source: Inet and Catalyst

Listed Property Market Capitalisation

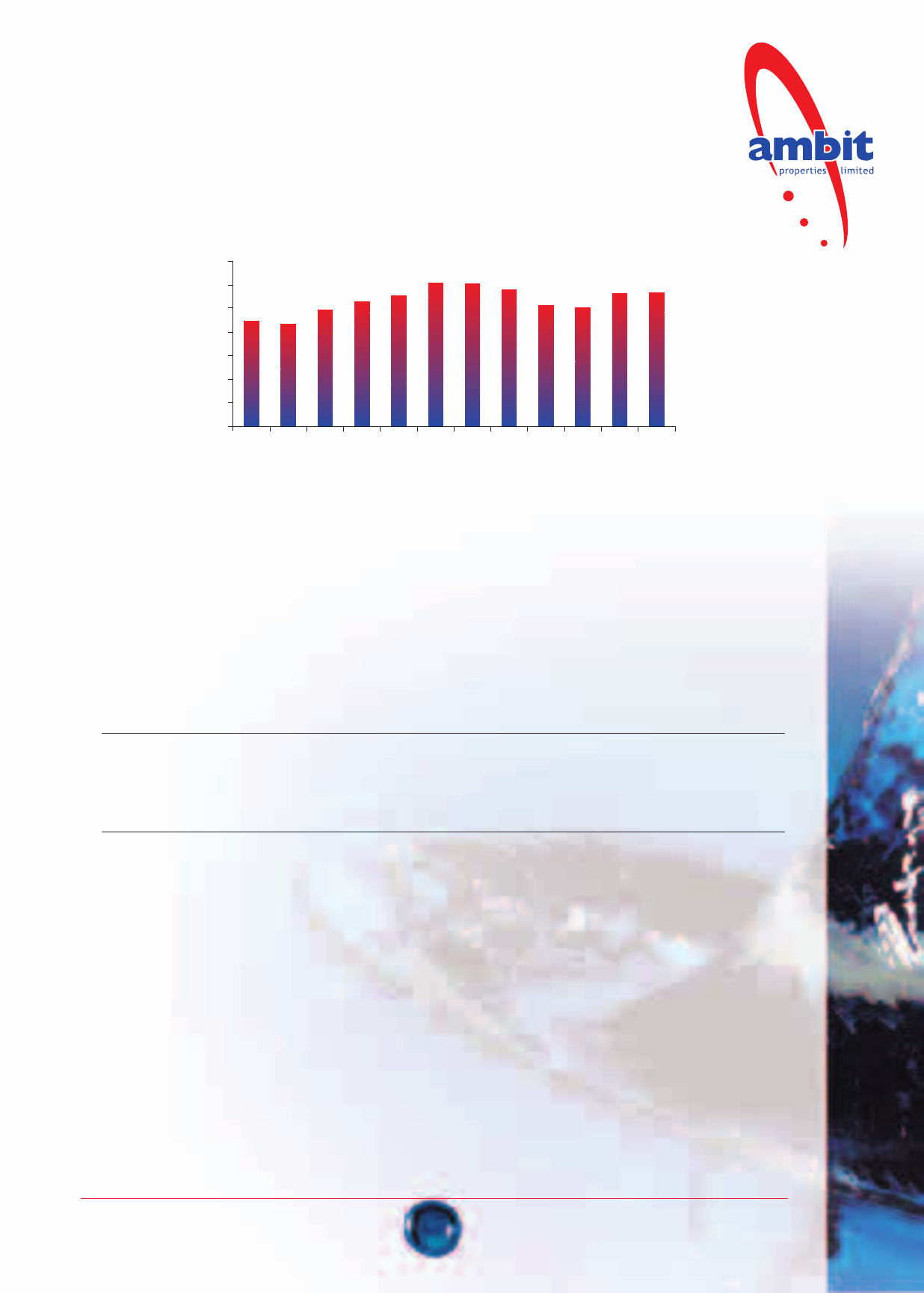

3. THE PROPERTY MARKET

The strong economic conditions have had a substantial impact on the commercial property market. Demand for retail space has continued, only being

satisfied by further new centres being brought to the market.

According to SAPOA’s statistics, vacancies in A grade offices in the popular decentralised office nodes have halved from about 7% to 3,5%.

Industrial and warehousing demand in all popular areas has virtually filled the available space and there is pressure on remaining vacant land from end

users and developers.

Rentals are rising in both the office and industrial sectors driven by demand and increasing building costs, which have risen substantially over the past

two years.

The Investment Property Data Bank (IPD), which measures direct property returns, and at December 2005 reflected a database of R81 billion (2005:

R74,7 billion), recorded a total return of 30,1% for 2005. The retail and industrial sectors were the top performers as can be seen below.

Total return (%) 2002 2003 2004 2005

Retail 11,0 17,3 26,2 33,0

Office 5,0 8,9 16,6 24,5

Industrial 8,8 17,7 24,4 33,1

All Property 9,6 15,3 23,4 30,1

Income return (%)

Retail 9,0 9,7 9,9 9,5

Office 10,3 10,9 10,7 10,9

Industrial 12,3 13,6 13,6 12,4

All Property 9,8 10,5 10,6 10,3

Source: IPD

6

Chairman & Chief Executive Officer’s Report (continued)

4. REVIEW OF FINANCIAL RESULTS (continued)

In terms of IAS 17: Leases, rental income is recognised on the straight line basis. The directors believe that the straight line basis is inappropriate and

this method of accounting does not add value to users of financial statements. The cash flows inherent in the leases and the straight line adjustment

are separately disclosed in the financial statements in order to assist users to calculate growth trends.

5. AMBIT UNIT PRICE

Ambit's unit price has shown very little growth over the 12 month period (325 cents at 30 September 2006, versus 323 cents at 30 September 2005).

This is due to the fall in the price of listed property stocks in June 2006. Ambit’s historic yield on its price at 30 September 2006 was 8,7%, versus

the SAPY index of 7,4%.

The volatility of 2006 resulting from the seemingly insatiable retail investment demand for listed property in the first half of 2006, and the corrective

interest rate increases thereafter, can be seen from the graph below. Ambit’s high of 435cpu in May, the low of 285cpu only two months later and

the year-end price of 325cpu clearly indicate just how the market over-reacted in June and July.

Oct

05

Nov

05

Dec

05

Jan

06

Feb

06

Mar

06

Apr

06

May

06

Jun

06

Jul

06

Aug

06

Sep

06

500

400

300

200

(Cents per unit)

During the year under review, 51% of Ambit's listed units were traded which represents a total value of R322,9 million.

6. THE PROPERTY PORTFOLIO

At year-end, the portfolio comprised 27 quality properties, with a rentable area of 154 029m

2

.

6.1 Geographic and sectoral profile

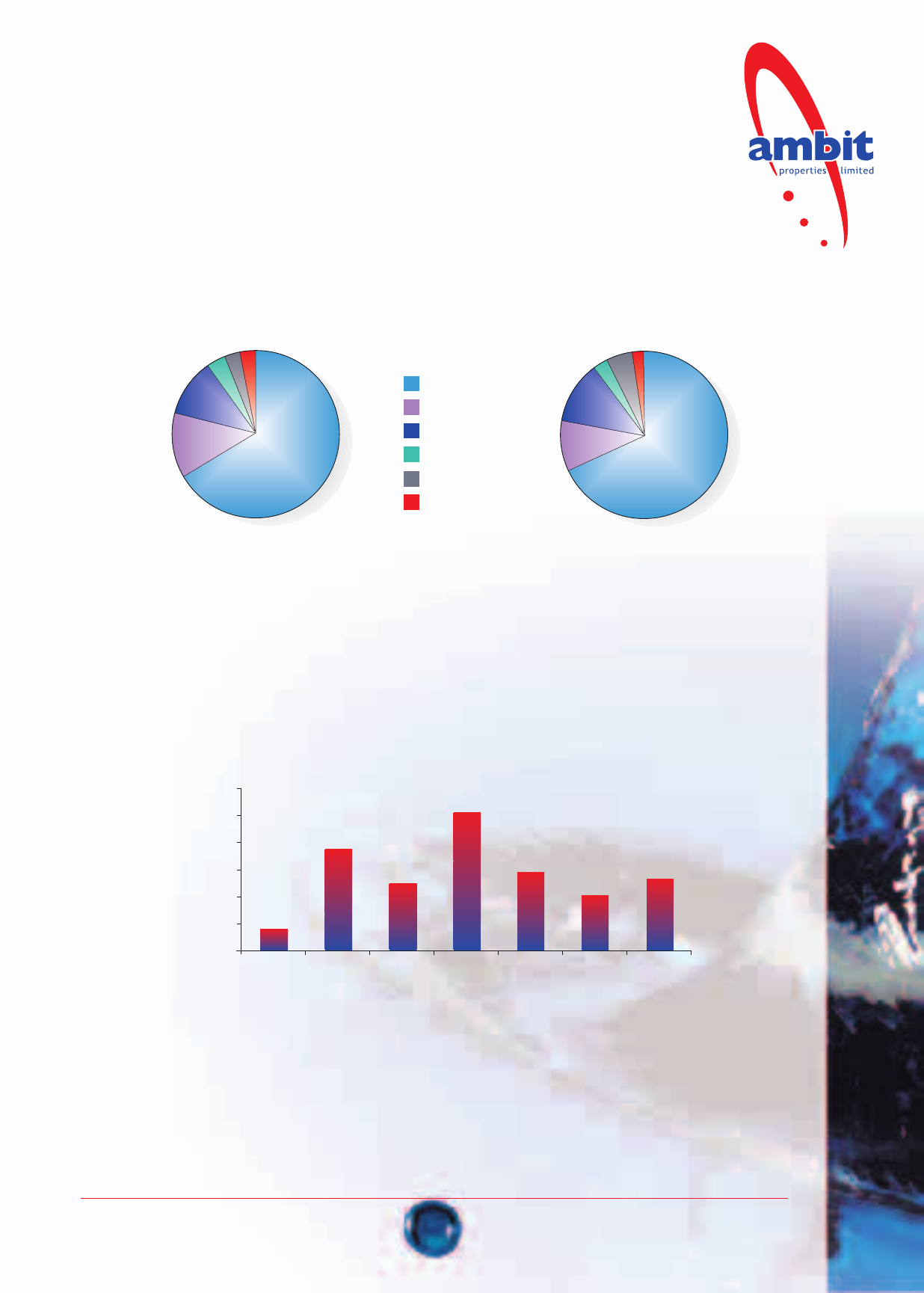

6.1.1 Sectoral spread

Ambit listed with a sectorally diversified property portfolio with a bias towards retail properties. It is management’s intention to maintain a spread

across the 3 major sectors of the commercial property market. The major sectors of the market operate on slightly different cycles of demand

and rental growth and thus at times opportunities arise in each sector for investment acquisitions which show good growth potential.

The sectoral spread of Ambit’s portfolio is set out below. All amounts exclude straight line adjustments.

By income By value

By value, retail has increased from 57% in 2005 to 59% in 2006 and income contribution increased by 3% as a result of the acquisition of

Lowveld Lifestyle Centre.

21%

24%

55%

Retail

Office

Industrial

18%

23%

59%

Annual Report 2006

7

6.1.2 Geographic Spread

Ambit’s strategy is to predominantly invest in properties located in the major metropolitan areas and this strategy has been maintained.

The geographic spread is set out below.

By income By value

66%

3%

13%

3%

4%

11% Gauteng

Pietermaritzburg

Durban

Cape Town

Nelspruit

East London

The acquisition of the Lowveld Lifestyle Centre in Nelspruit has marginally reduced the exposure to Gauteng by value by 3% from last year

to 68% this year-end.

6.2 Lease structure, vacancies and expiry profile

During the period under review, leases in respect of 14,6% by rental value (13 783m

2

) of the portfolio fell due for renewal and of these, 74%

by rental value (9 919m

2

) were successfully renewed. The space that was vacated was substantially re-let as can be seen in the continuing high

occupancy levels.

The vacancy is low at 3,80% by rental value (3,5% by area, 5 310m

2

) and is marginally above the levels at the end of last year of 3 981m

2

(2,6%). The bulk of this vacancy (3 766m

2

) is in the office portfolio where the prospects of leasing are encouraging.

6.3 Lease expiry profile

The lease expiry profile determined by rental value is reflected below:

30%

25%

20%

15%

10%

5%

0%

Vacant 2007 2008 2009 2010 2011 2012+

4%

19%

13%

26%

14%

10%

14%

The favourable lease expiry profile continues with no more than 26% of the portfolio's contractual income falling due for renewal in a particular

year. The increase in expiries in 2009 is a result of a number of 3-year leases being concluded during 2006. During 2007, the bulk of the

renewals lie within the office sector.

6.4 Operating costs

The operating costs of the buildings represent 25,3% of the gross rental income. These costs include all property related expenses without

netting off recoveries, include property management fees, but exclude the asset management fees of the portfolio and interest on borrowings.

Last year these costs represented 25,9% and in 2004 were 25,1% showing that the costs are being consistently maintained.

Of the total expenditure (excluding rates, municipal charges, collection commission and insurance) the value of procurement paid to black

owned companies increased from 35% in 2005 to 50% at year-end and is in line with the target Ambit set in 2004.

68%

2%

10%

5%

3%

12%

8

Chairman & Chief Executive Officer’s Report (continued)

6.5 Acquisitions

During the year Ambit took transfer of a building leased to Absa in Roodepoort on a 5-year lease at a price of R22,5 million on a forward yield

of 11,1%.

Lowveld Lifestyle Centre in Nelspruit was acquired at a cost of R43,2 million on a forward yield of 9,1%. This retail/ lifestyle centre is anchored

by Wetherleys and is 79% let to national companies or their franchisees.

In July 2006, Ambit acquired 50% of a property in Old Main Road, Pinetown, jointly with a subsidiary of Highpine Properties (Proprietary)

Limited, a company concentrating on retail property investment in the Pinetown area, at a joint cost of R28,3 million. The co-owners intend

to redevelop the site to create a shopping centre which will benefit from the site’s prime location between Pinecrest Shopping Centre and

the taxi terminus.

The development will be undertaken during 2007 but is presently let and is income producing.

6.6 Disposals

The five properties which Ambit contracted to sell in the 2005 financial year, were transferred in January 2006. These realised a post capital

gains tax profit of R1,0 million.

6.7 Portfolio revaluation

The portfolio was valued by independent valuers, CB Richard Ellis, as at 30 September 2006.

The valuation reflects a portfolio value of R824,6 million. The core portfolio (excluding additions and disposals) showed an increase in value

of 15% over the year.

7. INVESTMENT IN ORYX PROPERTIES LIMITED

Oryx comprises a quality portfolio of well tenanted investment properties, principally located in Windhoek.

Oryx again produced excellent results, with distributions amounting to 78 cents for the year ended 30 June 2006, showing an 11% growth over the

previous year's distributions. Realisable net asset value increased to 859 cents per unit (2005: 721cpu). During the year, Oryx completed its development

of Phase II of Maerua Mall. The expanded Maerua Complex (39 800m

2

of retail space) is fully tenanted and is trading well. At its year-end, Oryx had

a portfolio of 17 properties with an open market value of N$560,6 million and a vacancy of 1%.

During the year Oryx undertook a rights issue, which, although slightly dilutionary to Ambit in 2006, due to the prepayment of distributions, offered

a sound yield for 2007 and beyond. Ambit followed its rights and applied for further units, thereby increasing its stake marginally to 30,6% (2005:

30,5%). At the date of this report Oryx was trading at 820 cents, which is 4,5% below its realisable net asset value. It therefore continues to offer

sound investment value to Ambit.

2-4 Golf Course Drive, Mount Edgecombe, Durban

Annual Report 2006

9

7. INVESTMENT IN ORYX PROPERTIES LIMITED (continued)

Oryx is classified as an associate to Ambit. Ambit's share of the retained earnings of Oryx for the year was R12,5 million. This, combined with the

rights issue and increased unitholding, has taken Ambit's holding in Oryx to R110,9 million and represents 11,9% of Ambit's investment portfolio.

8. FUNDING ARRANGEMENTS

As at year-end Ambit had interest bearing borrowings of R316 million largely with ABSA and Nedbank who are Ambit's long-term financiers. This

reflects a long-term borrowings to long-term asset ratio of 33,8% (2005: 35,5%). During March 2006, Ambit renegotiated the interest rates on its

facilities and reduced the cost of variable borrowings by 50 basis points and fixed borrowings by 80 basis points.

At year-end, R183,7 million (58%) of the debt was on fixed interest contracts (2005: R145 million or 54%). Ambit's average cost of debt at year-end

was 9.7% p.a. (2005: 10,2% p.a.). The fixed and floating debt structure is set out in Note 14 to the financial statements. Management and the board

will continue to actively manage the funding and interest rate risk.

9. BLACK ECONOMIC EMPOWERMENT (BEE)

During the year management engaged in discussions to introduce an identified BEE group. However, these were terminated following differences

between the shareholders of the management Company, Ambit Management Services (Proprietary) Ltd (AMS). The Board and management are

committed to concluding a meaningful transaction with an appropriate BEE group during 2007.

10. MANAGEMENT COMPANY

In August 2006, Absa Bank Limited acquired the rights to the remaining 50% interest in AMS held by Marriott Corporate Property.

The AMS staff who were seconded from Marriott undertook to manage the year-end accounting, audit and the preparation of the financial statements.

AMS has recruited new staff and resources and will relocate its offices to 4 Fricker Road, Illovo from 1 December 2006.

11. PROSPECTS

The fundamentals of the underlying property market continue to firm notwithstanding the recent interest rate increases and the prospects of further

increases in the next 12 months. Office and industrial rentals are increasing which will provide income growth from the existing portfolio when leases

are renewed.

Ambit’s strategy is to increase its property portfolio to in excess of R1,5 billion and its market capitalisation to in excess of R1 billion during the next

year and management expects to be able to make announcements of acquisitions in the near future. There is no change to the strategy of owning

quality properties in good growth nodes.

Nick Harris has been requested and has accepted to remain on as the Chief Executive Officer of the Group until the end of June 2007 to manage

the transition of AMS and to conclude and bed down the initial tranches of the anticipated growth of the asset base.

During the first half of 2007, the Board will be appointing a new Chief Executive Officer to ensure a smooth handover.

We would like to express our appreciation to management and in particular to those seconded to AMS from Marriott for their dedication and hard

work in what, for some of them, has been a difficult period. We would also thank the non-executive directors for their support, experience and advice

during the past year.

D L Brown N B S Harris

Chairman Chief Executive Officer

23 November 2006 23 November 2006

10

Corporate Governance Review

30 September 2006

The board of directors is committed to the implementation of good corporate governance within the group and endorses the principles of openness,

integrity, accountability and transparency. The board has adopted and applied the Code of Corporate Practices and Conduct as set out in the King II Report.

The Board is of the opinion that the Group currently complies with all the significant requirements as set out in the King II report and the Listings Requirements

of the JSE Limited.

In doing so, the directors recognise the need to conduct the enterprise with integrity in accordance with generally acceptable corporate policies. This

includes timely, relevant and meaningful reporting to its unitholders and other stakeholders; and providing a proper and objective perspective of Ambit.

The directors have accordingly established mechanisms and policies appropriate to the Group's business in keeping with its commitment to the best practices

in corporate governance in order to ensure compliance with the King II Report. The directors will review these from time to time.

BOARD OF DIRECTORS AND ITS SUB-COMMITTEES

The board of directors consists of an executive director and five non-executive directors, four of whom are independent non-executives and hence the

majority of the board comprises independent non-executives. These non-executive directors bring to the Group a wide range of skills and experience

that enable them to contribute an independent view and to exercise objective judgement in matters requiring directors' decisions. The chairman is a non-

executive director, whose role is independent from the executive director.

The executive director holds a service contract. All non-executive directors are subject to retirement by rotation and re-election by Ambit unitholders at

least once every three years in accordance with the Articles of Association.

All new appointments to the board are done on a consensus basis between board members, subject to unitholder approval.

The board, which meets at least quarterly, retains full and effective control over the Group and service providers. The board has established a number of

committees to give detailed attention to its responsibilities and which operate within defined, written terms of reference. These are the investment committee,

the remuneration committee and the risk, audit and compliance committee, and the compositions thereof are set out on pages 2 and 3.

79 Hyde Park Lane, Hyde Park, Gauteng

Annual Report 2006

11

The board has approved a Board Charter to regulate how the business is to be conducted by the board in accordance with the principles of good corporate

governance.

During the period under review, directors who did not attend all 5 board meetings were J Zidel (1 absence), F Uys (1 absence) and I N Mkhari (2 absences).

INVESTMENT COMMITTEE

The board has established an investment committee, which is responsible to the board for monitoring and supervising the Group's strategic investment

objectives and implementing the board's instructions as to acquisitions, disposals and the structuring of borrowings.

REMUNERATION COMMITTEE

The board has established a remuneration committee, which reviews the remuneration of the executive director and recommends non-executive directors’

fees.

RISK, AUDIT AND COMPLIANCE COMMITTEE

The board has established a risk, audit and compliance committee whose primary objectives are to provide the board with additional assurance regarding

the efficacy and reliability of the financial information used by the directors and to assist them in the discharge of their duties. The committee provides

comfort to the board that adequate and appropriate financial and operating controls are in place, that significant business, financial and other risks have been

identified and are being suitably managed and that satisfactory standards of governance, reporting and compliance are in operation. The committee is

responsible for setting the principles for recommending the use of the external auditors for non-audit services, and any significant non-audit work must be

approved by this committee. The committee has formal terms of reference for their responsibilities and the Board is of the opinion that these responsibilities

have been satisfied for the year under review.

Due to its size (one direct employee), Ambit does not have an internal audit function. Management and the Risk, Audit and Compliance Committee review

the internal controls, processes and systems of the Group and it’s service providers.

Within this context, the board is responsible for the Group's systems of internal financial and operational control.

DIRECTORS' DEALINGS

The group operates a policy of prohibiting dealings by directors and certain other managers in periods immediately preceding the announcement of its

interim and year-end financial results and at any other time deemed necessary by the board.

RISK MANAGEMENT

The objective of risk management is to identify, assess, manage and monitor the risks to which the business is exposed. This is a board responsibility. Ambit

pursues active management policies designed to minimise the impact of risk.

With the assistance of expert risk consultants, risks have been assessed and appropriate insurance cover provided for all material risks above pre-determined,

self-insured limits. Levels of cover are re-assessed annually.

DIRECTORS' RESPONSIBILITY

The directors are responsible for the preparation of the annual financial statements, as set out on pages 16 to 39, which fairly represent the state of affairs

of the Group at the end of the financial year.

GOING CONCERN

The directors are of the opinion that the Company and the Group have adequate resources to continue in operation for the foreseeable future and the

annual financial statements and Group annual financial statements have accordingly been prepared on a going concern basis.

D L Brown J H Beare

Chairman Chairman – Risk, audit and compliance committee

23 November 2006 23 November 2006

12

Unitholders’ Diary

Financial year-end 30 September

Annual general meeting 21 February 2007

Distribution plan dates in respect of the financial year ending 30 September 2007:

Financial period Declaration date Record date Payment date

1st half to

31 March 2007 18 May 2007 7 June 2007 11 June 2007

2nd half to

30 September 2007 9 November 2007 30 November 2007 3 December 2007

Park Meadows, Kensington, Gauteng

Annual Report 2006

13

Analysis Of Linked Unitholders

30 September 2006

Number of % of Number of % of

unitholders unitholders units held issued units

Size of holding

1 – 10 000 699 46,94 3 640 819 1,95

10 001 – 25 000 432 29,01 7 654 281 4,10

25 001 – 50 000 176 11,82 6 771 823 3,63

50 001 – 100 000 86 5,78 6 464 015 3,47

100 001 – 500 000 64 4,30 14 823 169 7,95

500 001 – 1 000 000 14 0,94 10 401 439 5,58

`Over 1 000 000 18 1,21 136 727 291 73,32

1 489 100,00 186 482 837 100,00

Type of unitholders

Corporates and investment companies 74 4,97 93 252 379 50,01

Individuals and private companies 1 184 79,52 68 817 124 36,90

Nominee holders and trusts 168 11,28 14 685 002 7,87

Pension and provident funds 63 4,23 9 728 332 5,22

1 489 100,00 186 482 837 100,00

Significant unitholders

Unitholders invested in 5% or more of the company

Redefine Income Fund 43 660 824 23,41

Absa 39 150 567 20,99

Marriott 21 381 327 11,47

Oasis Asset Management 10 218 610 5,48

114 411 328 61,35

Unitholder spread

Held by public 1 482 99,53 103 895 568 55,72

Held by non-public

– directors 4 0,27 500 000 0,26

– unitholders with more than 10% unitholding 3 0,20 82 087 269 44,02

1 489 100,00 186 482 837 100,00

Units traded

Number of units traded 92 200 304

Units traded as a percentage of issued capital 51,44%

JSE price history

12 month high (cents) 435

12 month low (cents) 285

14

Directors’ Responsibility For &

Approval Of The Annual Financial Statements

for the year ended 30 September 2006

The directors are responsible for the preparation and integrity of the annual financial statements and the related information included in the annual report.

In order for the board to discharge its responsibilities, management has developed and continues to maintain a system of internal control. The board has

ultimate responsibility for the system of internal controls and reviews its operation, primarily through the risk, audit and compliance committee.

The internal controls include a risk-based system of internal accounting and administrative controls designed to provide reasonable but not absolute assurance

that assets are safeguarded and that transactions are executed and recorded in accordance with generally accepted business practices and the Group's

policies and procedures. These controls are implemented by trained, skilled personnel with appropriate segregation of duties, are monitored by management

and the risk, audit and compliance committee and include a comprehensive budgeting and reporting system operating within an appropriate control

framework.

The external auditors are responsible for reporting on the annual financial statements, and their unmodified opinion is included on page 15. The annual

financial statements are prepared in accordance with International Financial Reporting Standards and incorporate disclosures in line with the accounting

philosophy of the Group. They are based on appropriate accounting policies consistently applied, except where otherwise stated, and are supported by

reasonable and prudent judgements and estimates.

The directors believe that the Group will be a going concern in the year ahead. Accordingly, in preparing the annual financial statements and Group annual

financial statements, the going concern basis has been adopted.

The annual financial statements for the year ended 30 September 2006 as set out on pages 16 to 39 were approved by the board of directors on

23 November 2006 and are signed on its behalf by:

D L Brown J H Beare

Chairman Chairman – Risk, audit and compliance committee

23 November 2006 23 November 2006

Declaration By Secretary

The Secretary certifies that the Company has lodged with the Registrar of Companies all such returns as are required of a public company, in terms of

Section 268G(d) of the Companies Act No 61 of 1973, as amended, and that all such returns are true, correct and up to date.

Ambit Management Services (Proprietary) Limited

Company Secretary

23 November 2006

Annual Report 2006

15

Independent Auditor’s Report

TO THE MEMBERS OF AMBIT PROPERTIES LIMITED

We have audited the annual financial statements and Group annual financial statements of Ambit Properties Limited set out on pages 16 to 39 for the year

ended 30 September 2006. These financial statements are the responsibility of the Company's directors.

Our responsibility is to express an opinion on these financial statements based on our audit.

We conducted our audit in accordance with International Standards on Auditing. Those standards require that we plan and perform the audit to obtain

reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence

supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates

made by management, as well as evaluating the overall financial statement presentation. We believe that our audit provides a reasonable basis for our

opinion.

In our opinion, the financial statements fairly present, in all material respects, the financial position of the Company and of the Group at 30 September

2006, and the results of their operations and cash flows for the year then ended in accordance with International Financial Reporting Standards and in the

manner required by the Companies Act in South Africa.

Deloitte & Touche

Registered Auditors

Per GD Kruger

Partner

23 November 2006

2 Pencarrow Crescent

La Lucia Ridge Office Estate

Durban

National Executive: GG Gelink – Chief Executive, AE Swiegers – Chief Operating Officer, GM Pinnock – Audit, DL Kenney – Tax,

L Geeingh – Consulting, MG Crisp – Financial Advisory, L Bam – Strategy, CR Beukman – Finance, TJ Brown – Clients

& Markets, SJC Sibisi – Public Sector and Corporate Social Responsibility, NT Mtubu – Chairman of the Board, J Rhynes

– Deputy Chairman of the Board

Regional Leader: GC Brazier

16

Directors’ Report

30 September 2006

NATURE OF BUSINESS

Ambit Properties Limited is a property investment company and is listed on the JSE under the “Financials – Real Estate” sector.

The Group derives its income from a portfolio of investment properties in the retail, office and industrial sectors and an investment in Oryx Properties

Limited, a Namibian property investment company listed on the Namibian Stock Exchange.

ISSUED SHARE CAPITAL

As at 30 September 2006 there were 186 482 837 linked units in issue (2005: 173 814 215), each comprising one ordinary share of 1 cent and one

unsecured variable rate debenture of 180 cents. In order to fund the acquisition of the Lowveld Lifestyle Centre in Nelspruit, 12 668 622 units were issued

on 13 April 2006 at a price of 341 cents. An additional 14 cents per unit was received in respect of the interim distribution subsequently paid.

FINANCIAL REVIEW 2006 2005

(restated)

cents cents

Weighted average headline earnings per linked unit 32,24 31,30

Weighted average earnings per linked unit 77,20 77,91

Distribution per linked unit 29,60 27,50

International Financial Reporting Standards (IFRS) were adopted for the first time in the current year, and the adoption thereof has not resulted in any

changes to the reported numbers. However, a change in accounting interpretation has resulted in the share premium being reclassified to debenture

premium and amortised over the life of the debenture. Details are reflected in Notes 6 and 13.

SUBSIDIARY

Details of the Company's subsidiary are reflected in Note 8. The profit after tax of the subsidiary which is attributable to Ambit amounts to R11,2 million

(2005: R10,4 million).

ASSOCIATE

Details of the Company's associate are reflected in Note 9.

DIRECTORATE

Details of the directors are set out on pages 2 and 3 of this report. The composition of the board, together with changes from 1 October 2006 to the

date of this report, are set out below:

Director Date appointed Date resigned

D L Brown (Chairman)

N B S Harris *

C J Ewin 16/08/2006

J H Beare

I N Mkhari

F Uys

R R Emslie

J Zidel 07/02/2006 03/05/2006

R D Jeffrey (alternate)

2006 2005

Director Salaries Directors’ fees Salaries Directors’ fees

R'000 R'000 R'000 R'000

D L Brown (Chairman) – 95 – 95

N B S Harris * 1 061 – 920 –

– salary 861# – 795# –

– bonus 200 – 125 –

C J Ewin – 48 – 65

J H Beare – 90 – 90

R R Emslie – 50 – 12,5

N P Mageza – – – 37,5

I N Mkhari – 50 – 50

F Uys – 65 – 65

J Zidel – 13 – –

1 061 411 920 415

* Executive

The executive director holds a service contract until 30 June 2007.

No other directors have service contracts.

# The executive director's salary is deducted off asset management fees paid to Ambit Management Services (Proprietary) Limited.

Annual Report 2006

17

DIRECTORS' INTERESTS

The joint beneficial interests of directors in the equity of the company as at 30 September 2006 was 0,26% (500 000 units) and can be analysed as follows:

Director Direct beneficial Indirect beneficial Total

Linked units % Linked units % Linked units %

2006

D L Brown (Chairman) 50 000 0,02 – – 50 000 0,02

N B S Harris * 25 000 0,01 25 000 0,01 50 000 0,02

F Uys 200 000 0,11 – – 200 000 0,11

R D Jeffery (alternate) * 200 000 0,11 – – 200 000 0,11

R R Emslie * – – – – – –

500 000 0,26

2005

D L Brown (Chairman) 50 000 0,03 – – 50 000 0,03

N B S Harris * 25 000 0,01 25 000 0,01 50 000 0,03

C J Ewin * 210 000 0,12 – – 210 000 0,12

F Uys 200 000 0,12 – – 200 000 0,12

R D Jeffery (alternate) * 200 000 0,12 – – 200 000 0,12

R R Emslie * – – – – – –

710 000 0,42

* These directors have insignificant indirect interests in Ambit as a result of having insignificant interests in either Absa Bank Limited or RMBT Holdings

Limited as shareholders.

In April 2006, Ambit acquired 50% of 17-19 and 21-35 Old Main Road, Pinetown in conjunction with Pinespring Properties (Proprietary) Limited, a wholly

owned subsidiary of Highpine Properties (Proprietary) Limited, a company in which Mr J H Beare has an interest.

BORROWINGS

The directors are authorised to borrow funds up to an amount not exceeding 60% of the directors' bona fide valuation of the consolidated total assets of

the Company and its subsidiaries. The Group's interest bearing borrowings at 30 September 2006 are disclosed in Note 14 to the annual financial statements.

ACQUISITIONS, IMPROVEMENTS AND DISPOSALS

Refer to paragraphs 6.5 to 6.7 of the Chairman and CEO's report.

POST BALANCE SHEET EVENTS AND GOING CONCERN

Other than the acquisitions and disposals referred to above, the directors are not aware of any material post balance sheet events and are of the opinion

that the Group has adequate resources to continue in operation for the foreseeable future. The financial statements have accordingly been prepared on a

going concern basis.

MANAGEMENT BY THIRD PARTY

Ambit has a service agreement with Ambit Management Services (Proprietary) Limited (AMS), the rights to which are 100% held by Absa Bank Limited,

in respect of the property asset management, property management and the financial accounting and reporting of the company. During August 2006,

Marriott Property Services (Proprietary) Limited disposed of the rights to its 50% share in the management company to Absa Bank Limited.

COMPANY SECRETARY

The company secretary is Ambit Management Services (Proprietary) Limited, whose business and postal address is as follows:

Postal: Business:

P.O. Box 618 First Floor, 4 Frikker Road

Melrose Arch Illovo

2076 2196

D L Brown N B S Harris

Chairman Chief Executive Officer

23 November 2006 23 November 2006

18

Balance Sheets

30 September 2006

Group Company

Notes 2006 2005 2006 2005

(restated) (restated)

R'000 R'000 R'000 R'000

ASSETS

Non-current assets

Investment properties 7 809 329 659 288 673 558 538 896

– At valuation 824 550 671 000 686 350 548 600

– Straight line adjustment (15 221) (11 712) (12 792) (9 704)

Investment in associate company 9 110 927 82 944 83 998 68 480

Rental receivable – straight line adjustment 14 551 11 437 12 122 9 429

Total non-current assets 934 807 753 669 769 678 616 805

Current assets

Trade and other receivables 6 446 9 679 5 048 9 273

– Trade and other receivables 5 776 9 404 4 378 8 998

– Rental receivable – straight line adjustment 670 275 670 275

Cash and cash equivalents 10 56 128 28 929 56 620 28 839

Interest in subsidiary company 8 – – 93 652 92 931

Total current assets 62 574 38 608 155 320 131 043

TOTAL ASSETS 997 381 792 277 924 998 747 848

EQUITY AND LIABILITIES

Capital and reserves

Share capital 11 1 865 1 738 1 865 1 738

Non-distributable reserves 12 190 886 107 386 134 873 75 039

Distributable reserves/ (in deficit) 364 330 (1 966) (1 999)

Total capital and reserves 193 115 109 454 134 772 74 778

Non-current liabilities

Debentures 13 335 669 312 866 335 669 312 866

Debenture premium 6,13 49 586 31 094 49 586 31 094

Interest bearing borrowings 14 315 960 267 199 315 960 267 199

Deferred taxation liability 15 64 499 36 433 51 666 28 175

Total non-current liabilities 765 714 647 592 752 881 639 334

Current liabilities

Trade and other payables 9 087 9 890 7 880 8 395

Current tax liabilities 367 308 367 308

Linked unitholders for distribution 29 098 25 033 29 098 25 033

Total current liabilities 38 552 35 231 37 345 33 736

TOTAL EQUITY AND LIABILITIES 997 381 792 277 924 998 747 848

Annual Report 2006

19

Income Statements

for the year ended 30 September 2006

Group Company

Notes 2006 2005 2006 2005

(restated) (restated)

R'000 R'000 R'000 R'000

REVENUE 103 620 99 448 86 844 81 177

– Rental – cash flows inherent in leases 16 99 813 93 530 83 458 76 154

– Rental – straight line adjustment 3 807 5 918 3 386 5 023

Property expenses 17 (25 239) (24 229) (21 432) (20 486)

NET RENTAL INCOME FROM PROPERTIES 78 381 75 219 65 412 60 691

Interest income 18 2 040 2 373 14 571 15 816

Debenture interest and dividend income from associate company 9 9 868 8 338 9 868 8 338

Amortisation of debenture premium 6 1 776 1 191 1 776 1 191

Finance costs (23 902) (25 992) (23 902) (25 992)

Administrative expenses 19 (5 266) (4 484) (5 250) (4 252)

Other expenses 20 (2 026) (1 708) (2 026) (1 750)

OPERATING PROFIT 60 871 54 937 60 449 54 042

Change in fair value of investment properties 93 450 87 495 78 095 73 905

– As per valuations 97 257 93 413 81 481 78 928

– Straight line adjustment (3 807) (5 918) (3 386) (5 023)

Profit on disposal of investment properties 72 711 72 711

Share of associate company's after tax profits 6, 9 12 465 12 972 – –

PROFIT BEFORE TAXATION AND DISTRIBUTION

TO UNITHOLDERS 166 858 156 115 138 616 128 658

Debenture interest – linked unitholders (55 199) (47 799) (55 199) (47 799)

PROFIT BEFORE TAXATION 111 659 108 316 83 417 80 859

Taxation 21 (28 125) (26 509) (23 550) (22 446)

PROFIT ATTRIBUTABLE TO LINKED UNITHOLDERS 83 534 81 807 59 867 58 413

Cents Cents Cents Cents

EARNINGS PER LINKED UNIT (weighted) 22 77,20 77,91 64,03 63,84

EARNINGS AND DILUTED EARNINGS PER SHARE (weighted) 22 46,48 49,18 33,31 35,11

DISTRIBUTION PER LINKED UNIT 22 29,60 27,50 29,60 27,50

20

Non-

Share Share Distributable distributable

capital premium reserves reserves Total

R'000 R'000 R'000 R'000 R'000

GROUP

Balance at 30 September 2004 as previously reported 1 583 26 284 257 24 952 53 076

Prior year adjustment:

Reclassification to debenture premium – (26 284) – – (26 284)

Amortisation of debenture premium – – 700 – 700

Transfer of amortisation to non-distributable reserves – – (700) 700 –

Restated balance at 30 September 2004 1 583 – 257 25 652 27 492

Shares issued during the period 155 – – – 155

Net profit attributable to linked unitholders – – 81 807 – 81 807

As previously reported – – 80 616 – 80 616

Prior year adjustment:

Amortisation of debenture premium – – 1 191 – 1 191

Transfer to non-distributable reserves (restated) – – (81 734) 81 734 –

Balance at 30 September 2005 1 738 – 330 107 386 109 454

Shares issued during the year 127 – – – 127

Net profit attributable to linked unitholders – – 83 534 – 83 534

Transfer to non-distributable reserves – – (83 500) 83 500 –

Balance at 30 September 2006 1 865 – 364 190 886 193 115

COMPANY

Balance at 30 September 2004 as previously reported 1 583 26 284 289 15 130 43 286

Prior year adjustments:

Share of associates retained earnings – – (1 492) – (1 492)

Reclassification to debenture premium – (26 284) – – (26 284)

Amortisation of debenture premium – – 700 – 700

Transfer of amortisation to non-distributable reserves – – (700) 700 –

Restated balance at 30 September 2004 1 583 – (1 203) 15 830 16 210

Shares issued during the period 155 – – – 155

Net profit attributable to linked unitholders – – 58 413 – 58 413

As previously reported – – 70 194 – 70 194

Prior year adjustments:

Share of associates retained earnings – – (12 972) – (12 972)

Amortisation of debenture premium – – 1 191 – 1 191

Transfer to non-distributable reserves (restated) – – (59 209) 59 209 –

Balance at 30 September 2005 1 738 – (1 999) 75 039 74 778

Shares issued during the year 127 – – – 127

Net profit attributable to linked unitholders – – 59 867 – 59 867

Transfer to non-distributable reserves – – (59 834) 59 834 –

Balance at 30 September 2006 1 865 – (1 966) 134 873 134 772

Statements Of Changes In Equity

for the year ended 30 September 2006

Annual Report 2006

21

Cash Flow Statements

for the year ended 30 September 2006

Group Company

Notes 2006 2005 2006 2005

R'000 R'000 R'000 R'000

OPERATING ACTIVITIES

Cash generated by operating activities 23 70 105 63 450 58 853 48 758

Interest received and income from associate 11 908 10 711 24 439 24 154

Finance costs (23 902) (25 992) (23 902) (25 992)

Distributions paid to linked unitholders 24 (51 134) (49 286) (51 134) (49 286)

Cash inflow/ (outflow) from operating activities 6 977 (1 117) 8 256 (2 366)

INVESTING ACTIVITIES

Acquisition of investment properties (80 431) (44 800) (80 431) (44 800)

Improvements to investment properties (1 172) (8 592) (1 148) (7 677)

Proceeds on disposal of investment properties 25 382 32 011 25 382 32 011

(Increase)/ decrease in loan to subsidiary – – (721) 444

Acquisition of holding in associate company (15 518) (4 136) (15 518) (4 136)

Cash outflow from investing activities (71 739) (25 517) (72 436) (24 158)

FINANCING ACTIVITIES

Linked units issued 43 200 35 000 43 200 35 000

Share issue expenses – (268) – (268)

Interest bearing borrowings raised/ (repaid) 48 761 (8 455) 48 761 (8 455)

Cash inflow from financing activities 91 961 26 277 91 961 26 277

Increase/ (decrease) in cash and cash equivalents 27 199 (357) 27 781 (247)

Cash and cash equivalents at beginning of year 28 929 29 286 28 839 29 086

CASH AND CASH EQUIVALENTS AT END OF THE YEAR 10 56 128 28 929 56 620 28 839

Scottsville Mall, Durban Road, Pietermaritzburg

22

Notes To The Annual Financial Statements

30 September 2006

1. GENERAL INFORMATION

Ambit Properties Limited (the Company) is a public company listed on the JSE and is incorporated in South Africa. The address of its registered office

and principal place of business is disclosed in the introduction to the annual report. The principal activities of the Company and its subsidiary (the Group)

are described in the Directors’ Report

2. ADOPTION OF NEW AND REVISED INTERNATIONAL FINANCIAL REPORTING STANDARDS

In the current year, the Group has adopted all of the new and revised Standards and Interpretations issued by the International Accounting Standards

Board (the IASB) and the International Financial Reporting Interpretations Committee (IFRIC) of the IASB that are relevant to its operations and effective

for accounting periods beginning on or before 1 October 2005. The adoption of IFRS has not resulted in any adjustment to the amounts reported

previously in the annual financial statements for the year ended 30 September 2005.

3. ACCOUNTING POLICIES

The annual financial statements have been prepared in accordance with International Financial Reporting Standards. The accounting policies used in

the preparation of the financial statements are consistent with those applied in the prior year, with the exception of accounting for the premium on

units issued as disclosed under Debentures in Note 3.10 below and the Company’s carrying value of its investment in associate as described in note

3.4 below.

The principal accounting policies are set out below :

3.1 Basis of consolidation

The consolidated financial statements incorporate the results and financial position of the Company and all its subsidiaries, which are defined

as entities over which the Group has the ability to exercise control so as to obtain benefits from their activities. The results of subsidiaries are

included from the effective dates of acquisition and up to the effective dates of disposal. All inter-company transactions and balances between

Group companies are eliminated.

The accounting policies of the subsidiaries are consistent with those of the holding company.

3.2 Business combinations

The purchase method of accounting is used to account for the acquisition of subsidiaries by the Group. The cost of an acquisition is measured

as the aggregate fair value of the underlying assets acquired, equity instruments issued and liabilities incurred or assumed at the date of exchange,

plus costs directly attributable to the acquisition. Identifiable assets acquired and liabilities and contingent liabilities assumed in a business combination

are measured initially at their fair values at the acquisition date, irrespective of the extent of any minority interest. The excess of the cost of

acquisition over the fair value of the Group's share of the identifiable net assets acquired is recorded as goodwill and is tested for impairment

on an annual basis.

If the cost of acquisition is less than the fair value of the net assets of the subsidiary acquired, the difference is recognised directly in the income

statement. An impairment loss recognised for goodwill is not reversed in a subsequent period. On disposal of a subsidiary, attributable goodwill

is included in the determination of the profit or loss on disposal.

3.3 Investment in subsidiaries

Investments in subsidiaries are recognised at cost less accumulated impairment losses.

3.4 Investment in associates

Associates are those companies, which are not subsidiaries or joint ventures, over which the Group exercises significant influence. Results of

associates are accounted for in the Group using the equity method of accounting, except when the investment is classified as held for sale, in

which case it is accounted for under IFRS 5: Non-Current Assets Held for Sale and Discontinued Operations. Any losses of associates are

brought to account until the investment in, and loans to, such associates are written down to a nominal amount. Thereafter losses are accounted

for only insofar as the Group is committed to providing financial support to such associates. The carrying value of investments in associates

represents the cost of each investment including unamortised goodwill, the share of post acquisition retained earnings or losses and other

movements in reserves. Equity accounted income represents the Group’s proportionate share of the associate’s post-acquisition accumulated

profit after accounting for dividends declared by those entities. Any significant movements between the year-end of associates and the Group

are accounted for. Where a Group entity transacts with an associate of the Group, profits and losses are eliminated to the extent of the Group’s

interest in the associate. Undistributed equity accounted earnings may be transferred to non-distributable reserves.

In the company the investment in associate is held at cost in accordance with IAS 27. The effects of this change in accounting policy are set

out in Note 6 below.

3.5 Investment properties

Investment properties are properties held to earn rental income and appreciate in capital value based on the increase in rental

income.

Annual Report 2006

23

3. ACCOUNTING POLICIES (continued)

Investment properties are initially recognised at cost and are stated at their fair value at each reporting date. Gains or losses arising

from changes in the fair values are reflected in the income statement in the period in which they arise. Unrealised gains are

transferred to a non-distributable reserve in the statement of changes in equity. Unrealised losses are transferred against a non-

distributable reserve to the extent that the decrease does not exceed the amount held in the non-distributable reserve. On

disposal of investment properties, the difference between the net disposal proceeds and the carrying value is charged or credited

to the income statement and then transferred from / to non-distributable reserves. Buildings are not depreciated.

Properties purchased by the company and settled by issuing linked units are recorded at the fair value of the properties acquired,

unless that fair value cannot be reliably estimated. If the entity cannot reliably estimate the fair value of the property, the entity

shall measure the value of the equity issued, and the corresponding increase in equity, indirectly, by reference to the fair value

of the equity instruments granted in terms of IFRS2: Share Based Payments. This excludes purchases of properties which are

regarded as business combinations as described in 3.2 above.

Buildings under development are carried at cost as property, plant and equipment and are transferred to investment property

upon completion.

3.6 Capitalisation of interest

Where the Group undertakes a major development or refurbishment of a property, interest is capitalised to the cost of the

property concerned during the construction period. Capitalisation of interest is suspended during extended periods in which

active development is interrupted.

3.7 Assets held for sale

Properties held for sale are classified as assets for sale and are measured at the lower of the assets’ previous carrying amount

and the fair value less costs to sell.

3.8 Taxation

Income tax expense comprises the sum of current tax payable, Secondary Tax on Companies and deferred taxation. Tax currently

payable is based on the taxable profit for the year. Taxable profit differs from accounting profit as it excludes income or expenses

that are taxable or deductible in other years and it excludes items never deductible or taxable.

Deferred taxation is provided for using the balance sheet liability method, based on temporary differences. Temporary differences

are differences between the carrying amounts of assets and liabilities for financial reporting purposes and their taxation bases.

Deferred taxation is charged to the income statement except to the extent that it relates to a transaction that is recognised directly

in equity, or a business combination that is an acquisition. A deferred taxation asset is recognised to the extent that it is probable

that future taxable profits will be available against which the associated unused tax losses and deductible temporary differences

can be utilised. Deferred taxation assets are reduced to the extent that it is no longer probable that the related tax benefit will

be realised. Deferred taxation assets and liabilities are only set off when there is a legally enforceable right to set off current tax

assets and liabilities.

Deferred taxation assets and liabilities are not recognised if the temporary difference arises from goodwill, or from the initial

recognition (other than business combinations) of other assets and liabilities in a transaction which effects neither the taxable profit

nor the accounting profit.

Deferred taxation is raised at the company tax rate on all temporary differences, including those arising from the revaluation of

properties. When a property is earmarked for future sale, deferred taxation is computed using the capital gains tax rate.

3.9 Impairment (excluding goodwill)

The carrying amount of the Group's assets is reviewed at each balance sheet date to determine whether there is any indication

of impairment. An impairment loss is recognised in profit or loss whenever the carrying amount of an asset exceeds its recoverable

amount, which is the higher of an asset's net selling price and value in use. Where an impairment loss is subsequently reversed,

the carrying amount of the asset is increased to the extent that the increased carrying amount does not exceed the original carrying

amount. A reversal of impairment loss is recognised immediately in profit or loss.

3.10 Financial instruments

A financial asset or financial liability is recognised on the balance sheet for as long as the group is party to the contractual provisions

of the instrument.

Cash and cash equivalents

Cash and cash equivalents comprise cash on hand, deposits held on call with banks and investments in money market instruments,

net of bank overdrafts where legal set-off is permissible.

24

Notes To The Annual Financial Statements (continued)

30 September 2006

3. ACCOUNTING POLICIES (continued)

Trade receivables

Trade and other receivables originated by the Group are held at amortised cost, using the effective interest rate method, after

deducting accumulated impairment losses. Receivables with no fixed maturity are held at cost.

Receivable- straight line basis adjustment

Rental income is recognised on the straight-line basis. Future rentals receivable over the lease period as a result of escalations

are recorded at the differential between the cash received inherent in the lease agreements and the smoothed revenue.

Investments

Financial instruments are initially measured at cost, including directly attributable transaction costs. Subsequent to the initial recognition these

instruments are measured as follows:

• Held-to-maturity investments are held at amortised cost using the effective interest rate method after deducting accumulated impairment

losses.

• Held-for-trading and available-for-sale financial assets are held at fair value.

Gains or losses on Available-for-sale financial assets and Held-for-trading financial assets and liabilities are recognised in net profit for the

year.

Financial liabilities and equity

Financial liabilities and equity instruments issued by the Group are classified according to the substance of the contractual arrangements entered

into and the definitions of a financial liability and an equity instrument. An equity instrument is any contract that evidences a residual interest in

the assets of the Group after deducting all of its liabilities. The accounting policies adopted for specific financial liabilities and equity instruments

are set out below.

Equity instruments

Equity instruments issued by the Company are recorded at the proceeds received, net of direct issue costs.

Debentures

Debentures are recognised at original cost less principal repayments. The premium arising on the issue of linked units is split between the

premium relating to the share and the premium relating to the debenture. The debenture premium is amortised over the remaining life of

the debenture (i.e. to 2029) and the resultant income may be transferred to non-distributable reserves.

Interest bearing borrowings

Interest bearing borrowings are initially measured at fair value, and are subsequently measured at amortised cost, using the effective interest

rate method. Amounts repayable in the next twelve months are classified as current borrowings.

Trade payables

Trade payables are carried at the fair value of the consideration to be paid in the future for goods or services that have been received or supplied

and invoiced or formally agreed with the supplier.

Financial guarantee contracts

Financial guarantee contracts are accounted for as insurance contracts and are initially recorded at cost. Subsequently, they are valued in terms

of IAS 37: Provisions, Contingent Liabilities and Contingent Assets.

3.11 Provisions

Provisions are recognised when the Group has a present legal or constructive obligation as a result of past events, for which it is probable that

an outflow of economic benefits will occur, and where a reliable estimate can be made on the settlement amount of the obligation.

3.12 Revenue recognition

Revenue comprises gross rental income, including all recoveries from tenants. Variable operating cost recoveries are recognised on the accrual

basis. Rental income and fixed operating cost recoveries are recognised on the straight line basis in accordance with IAS 17: Leases. The difference

between the rental income recognised on a cash flow/ accrual basis and the straight line basis is transferred to/ from non-distributable reserves.

Interest income is recognised at the effective rates of interest on a time related basis.

Dividend income and debenture interest are recognised when the right to receive them is established.

3.13 Leases

Investment properties leased out under operating leases are reflected as investment properties on the balance sheet. Where there are fixed

incrementals in rental, the income is recognised on a straight line basis in terms of IAS 17: Leases.

Annual Report 2006

25

3. ACCOUNTING POLICIES (continued)

3.14 Deferred expenses

Deferred expenses comprise tenant installation costs and letting commissions which are amortised on a straight line basis over the lease period

to which they relate. These are currently included in accounts receivable due to the immaterial size thereof.

3.15 Distributions

In terms of the Debenture Trust Deed the interest entitlement on each debenture shall be not less than 90% of the net earnings of the company

before providing for debenture interest, depreciation, amortisation and taxes and before taking into account any revaluation surpluses or deficits

and income transferred to any non-distributable reserves, but after provision for funding cost, whether interest or dividend in nature.

3.16 Segment reporting

On a primary basis the group operates in the following segments:

• Retail

• Office

• Industrial

• Corporate

On a secondary basis the group reports on geographical locations as follows:

• Gauteng

• Pietermaritzburg

• Durban

• Other

3.17 Changes in accounting policy

Where there has been a change in accounting policy, all comparative numbers are retrospectively adjusted.

4. CRITICAL ACCOUNTING ESTIMATES AND JUDGEMENTS

Estimates and judgments are continually evaluated and are based on historical experience as adjusted for current market conditions and other factors.

4.1 Critical accounting estimates and assumptions

The Group makes estimates and assumptions concerning the future. The resulting accounting estimates will, by definition, seldom equal the

related actual results. The estimates and assumptions that have a significant risk of causing a material adjustment to the carrying amounts of assets

and liabilities within the next financial year are discussed below.

(a) Estimate of fair value of investment properties

The best evidence of fair value is current prices in an active market for similar leases and other contracts. In the absence of such information,

the Group determines the amount within a range of reasonable fair value estimates. In making its judgement, the Group considers

information from a variety of sources including:

i) current prices in an active market for properties of different nature, condition or location (or subject to different lease or other

contracts), adjusted to reflect those differences;

ii) recent prices of similar properties in less active markets, with adjustment to reflect any changes in economic conditions since the date

of the transactions that occurred at those prices; and

iii) discounted cash flow projections based on reliable estimates of future cash flows, derived from the terms of any existing lease and

other contracts and (where possible) from external evidence such as current market rents for similar properties in the same location

and condition, and using discount rates that reflect current market assessments of the uncertainty in the amount and timing of the

cash flows.

(b) Principal assumptions for management’s estimation of fair value

If information on current or recent prices is not available, the fair values of investment properties are determined using discounted cash

flow valuation techniques. The Group uses assumptions that are mainly based on market conditions existing at each balance sheet date.

The principal assumptions underlying management’s estimation of fair value are those related to: the receipt of contractual rentals, expected

future market rentals, maintenance requirement and appropriate discount rates. These valuations are regularly compared to actual market

yield data, and actual transactions by the Group and those reported by the market.

The expected future market rentals are determined with reference to current market rentals for similar properties in the same location

and condition.

26

Notes To The Annual Financial Statements (continued)

30 September 2006

4. CRITICAL ACCOUNTING ESTIMATES AND JUDGEMENTS (continued)

4.2 Critical judgments in applying the Group’s accounting policies

Allocation of share premium and debenture premium

The Group has determined, in terms of the requirements of accounting standards, that the linked unit premium should be classified as debenture

premium and not share premium. Debenture premium will be amortised over the minimum contractual period of the debentures, namely

the remaining portion of 25 years from February 2004.

Non-distributable reserves

The Group transfers all capital profits and unrealised profits to non-distributable reserves.

In addition, balances arising due to accounting anomalies are transferred to non-distributable reserves at the discretion of the directors and these

currently comprise:

- straight line adjustments to rental income and fair value adjustments to investment properties

- deferred taxation on fair value adjustments to investment properties

- amortisation of debenture premium

5. NEW ACCOUNTING STANDARDS AND IFRIC INTERPRETATIONS

Certain new additional accounting standards and IFRIC interpretations have been published that are mandatory for accounting periods beginning on

or after 1 January 2006. These new standards and interpretations have not been early adopted by the Group. The directors do not expect that the

adoption of the standards and interpretations will have a material impact on future financial statements. The standards and interpretations in issue, but

not yet effective, that are relevant to the Group are:

IFRS 7: Financial Instrument Disclosures

IFRIC 10: Interim Reporting and Impairment

6. PRIOR YEAR ADJUSTMENTS

The accounting policy for the premium arising on the issue of linked units has been changed. This used to be accounted for as share premium but is

now accounted for as debenture premium in terms of IAS 32. The full amount of share premium has therefore been transferred to debenture premium

and is being amortised over the period until 2029. The prior year figures have been restated. The effect of the change in policy on the Group results

is as follows:

Gross Tax Net

R’000 R’000 R’000

Increase in profit for the year 2005 1 191 - 1 191

2006 1 776 - 1 776

The additional profit has been transferred to a non-distributable reserve through the statement of changes in equity.

The above has had the effect of increasing earnings by R1,8 million or 0,99 cents per weighted number of units in the current year (2005: R1,2 million

or 0,72 cents).

Balance sheet effect: 2006 2005

R’000 R’000

Debenture premium as previously reported - -

Reclassification from share premium 32 985 26 284

Premium arising on current year unit issues 20 268 6 701

Amortisation (3 667) (1 891)

Debenture premium closing balance 49 586 31 094

In accordance with IAS 27, the share of associate’s reserves is no longer accounted for in the Company, and is only accounted for in the Group financial

statements. The effect of this change in policy on the Company results is as follows:

Gross Tax Net

R’000 R’000 R’000

Decrease in profit for the year 2005 12 972 - 12 972

2006 12 465 - 12 465

The effect on the Company’s balance sheet is as follows: 2006 2005

R’000 R’000

Investment in associate as previously reported 110 927 82 944

Removal of share of associate’s retained earnings (26 929) (14 464)

Investment in associate as restated 83 998 68 480

Annual Report 2006

27

Group Company

2006 2005 2006 2005

(restated) (restated)

R'000 R'000 R'000 R'000

7. INVESTMENT PROPERTIES

Carrying value at beginning of the year 659 288 549 706 538 896 443 819

– At valuation 671 000 555 500 548 600 448 500

– Straight line adjustment (11 712) (5 794) (9 704) (4 681)

Acquisition of Investment properties 80 431 44 800 80 431 44 800

Disposals (25 310) (31 305) (25 310) (31 305)

Improvements to investment properties 1 172 8 592 1 148 7 677

Fair value adjustment

– At valuation 97 257 93 413 81 481 78 928

– Straight line adjustment (3 509) (5 918) (3 088) (5 023)

Carrying value at end of the year 809 329 659 288 673 558 538 896

Reconciliation to valuation:

Add: cumulative straight line adjustments 15 221 11 712 12 792 9 704

Investment properties at valuation 824 550 671 000 686 350 548 600

Property descriptions are detailed on pages 40 and 41 of this report.

The property portfolio is subject to mortgage bonds in favour of Absa Bank

Limited and Nedcor Bank Limited as detailed in Note 14.

The cost of the investment properties is R604 million (2005: R547 million)

and they were valued by CB Richard Ellis (Pty) Ltd, independent valuers.

These fair values were approved by the directors, and the ranges of discount

and capitalisations rates in the respective sectors were as follows:

Sector Discount rates Terminal capitalisation rates

% %

Retail 13,5 to 16,0 9,0 to 12,0

Industrial 14,5 to 16,3 10,0 to 13,0

Office 15,5 to 16,5 11,0 to 13,0

8. INTEREST IN SUBSIDIARY COMPANY

Issued share %

capital Holding

R

Whirlprops 37 (Pty) Ltd (incorporated in South Africa) 100 100

Shares at cost – –

Loans 93 652 92 931

Less: Current portion (93 652) (92 931)

Long term portion – –

Directors' valuation 139 102 112 946