700 Americantower Investorrelations Towers 101 2Q14

User Manual: 700

Open the PDF directly: View PDF ![]() .

.

Page Count: 73

Introduction to the Tower Industry

and American Tower

As of June 30, 2014

Forward Looking Statements

“Safe Harbor” Statement under the Private Securities Litigation Reform Act of 1995: This

presentation contains forward-looking statements concerning our goals, beliefs, strategies,

future operating results and underlying assumptions. Actual results may differ materially from

those indicated by these forward-looking statements as a result of various important factors,

including those described in the appendix attached hereto, Item 1A of our Form 10-Q for the

quarter ended June 30, 2014 under the caption “Risk Factors” and other filings we make with the

SEC. We undertake no obligation to update the information contained in this presentation to

reflect subsequently occurring events or circumstances. Definitions and reconciliations to GAAP

measures are provided at the end of the presentation.

2

The Tower Asset

Section 1

3

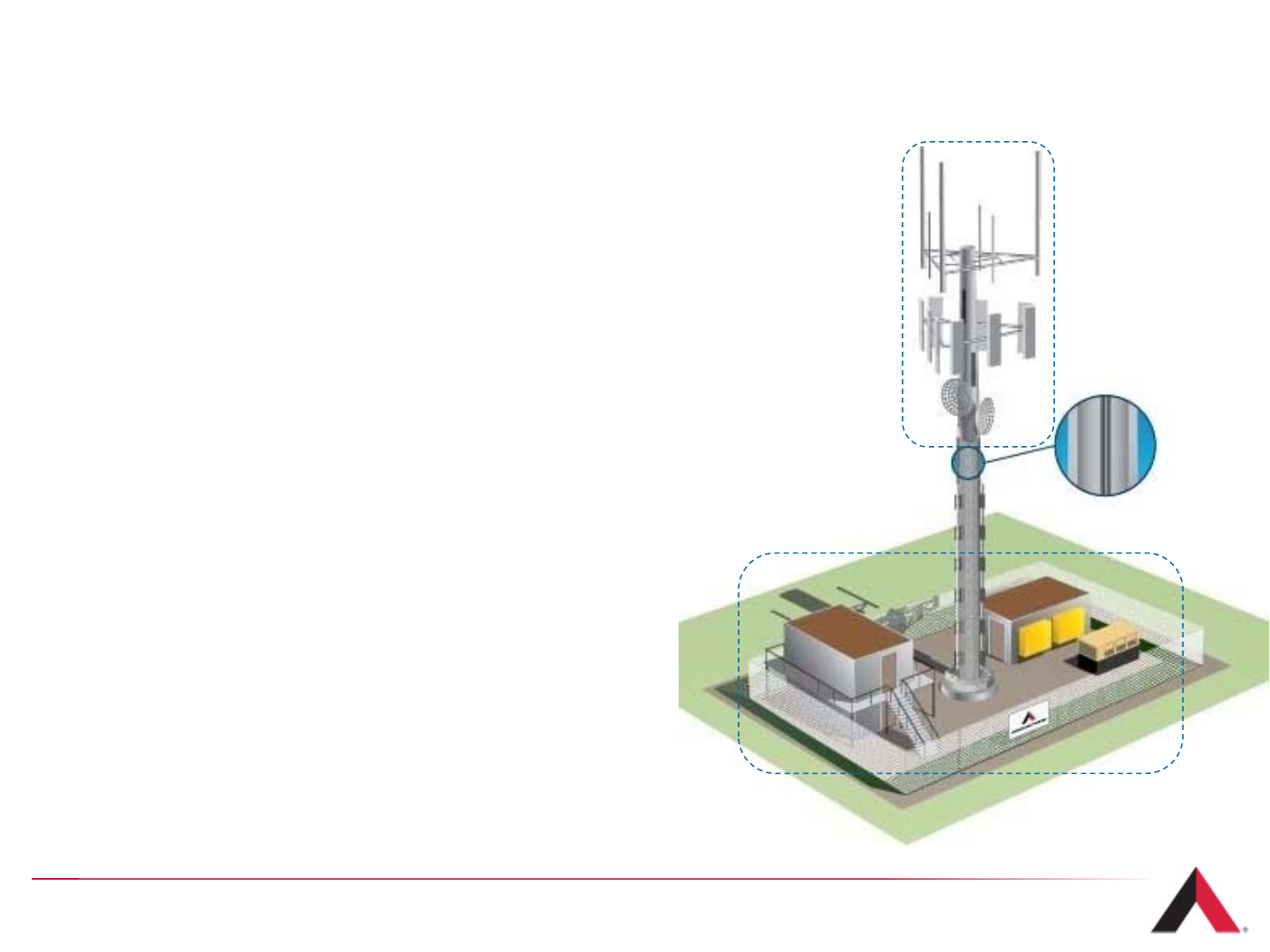

Wireless Tower Basics

What is a tower?

›A vertical structure built on a parcel of land,

designed to accommodate multiple tenants

›Our tenants utilize many different technologies,

including telephony, mobile data, broadcast

television and radio

›Tenants lease vertical space on the tower and

portions of the land underneath for

their equipment

What is found at the tower site?

›Tower company typically owns or leases under

a long-term contract:

›Tower structure

›Ground interest (fee simple or lease)

›Tenant typically owns and operates:

›Equipment, including antenna arrays,

antenna, coaxial cables and base stations

›Equipment shelters

4

Types of Towers

5

Monopole

›100 - 200 feet

›Typical use: telephony

Lattice

›200 - 400 feet

›Also called self-support

›Typical use: telephony

Guyed

›200 - 2,000 feet

›Typical use: television and

radio broadcasting, paging

and telephony

Stealth

›Range in size

›Generally used to maintain

aesthetic quality of area

›Particularly useful in

areas with strict zoning

regulations

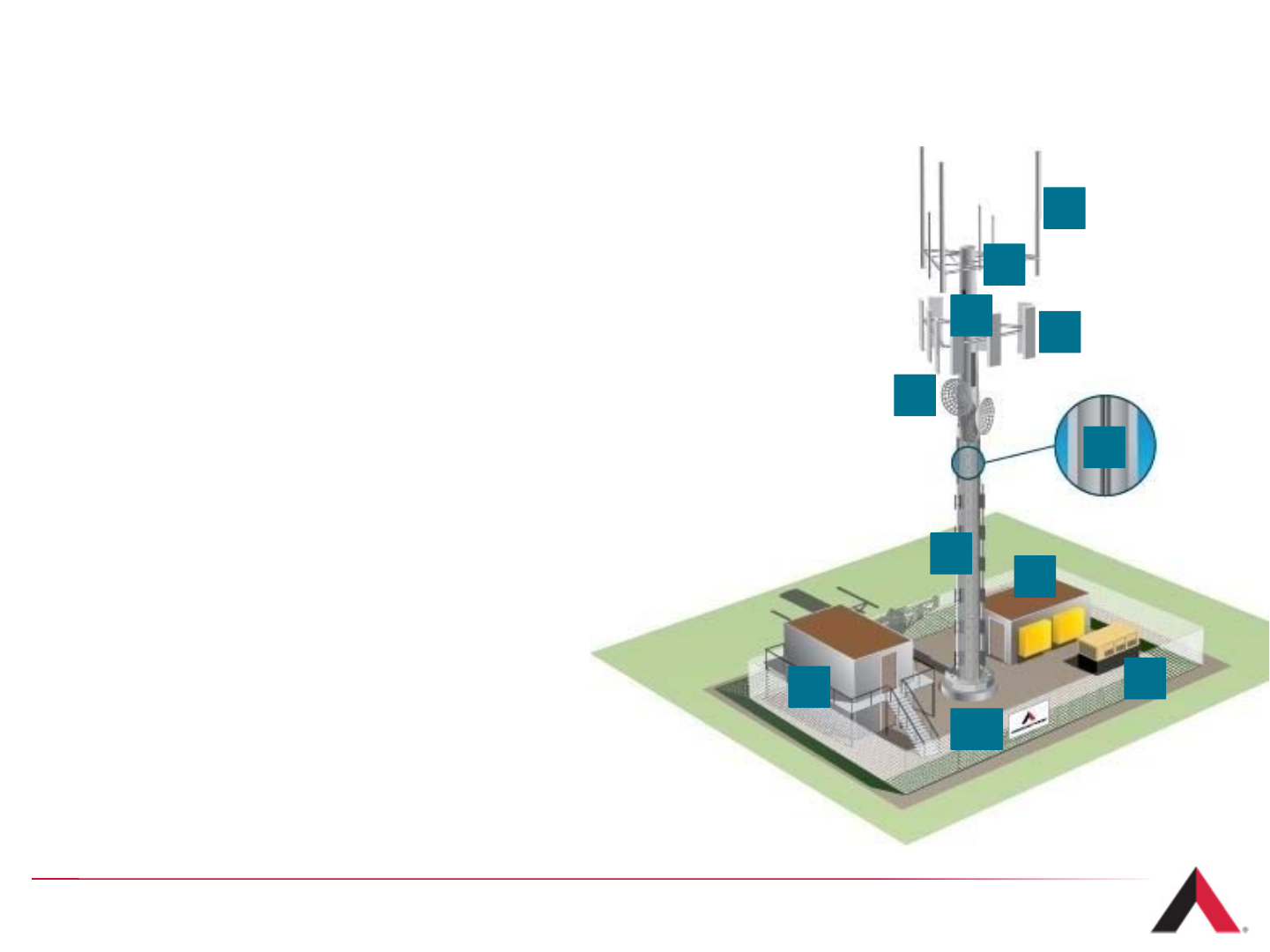

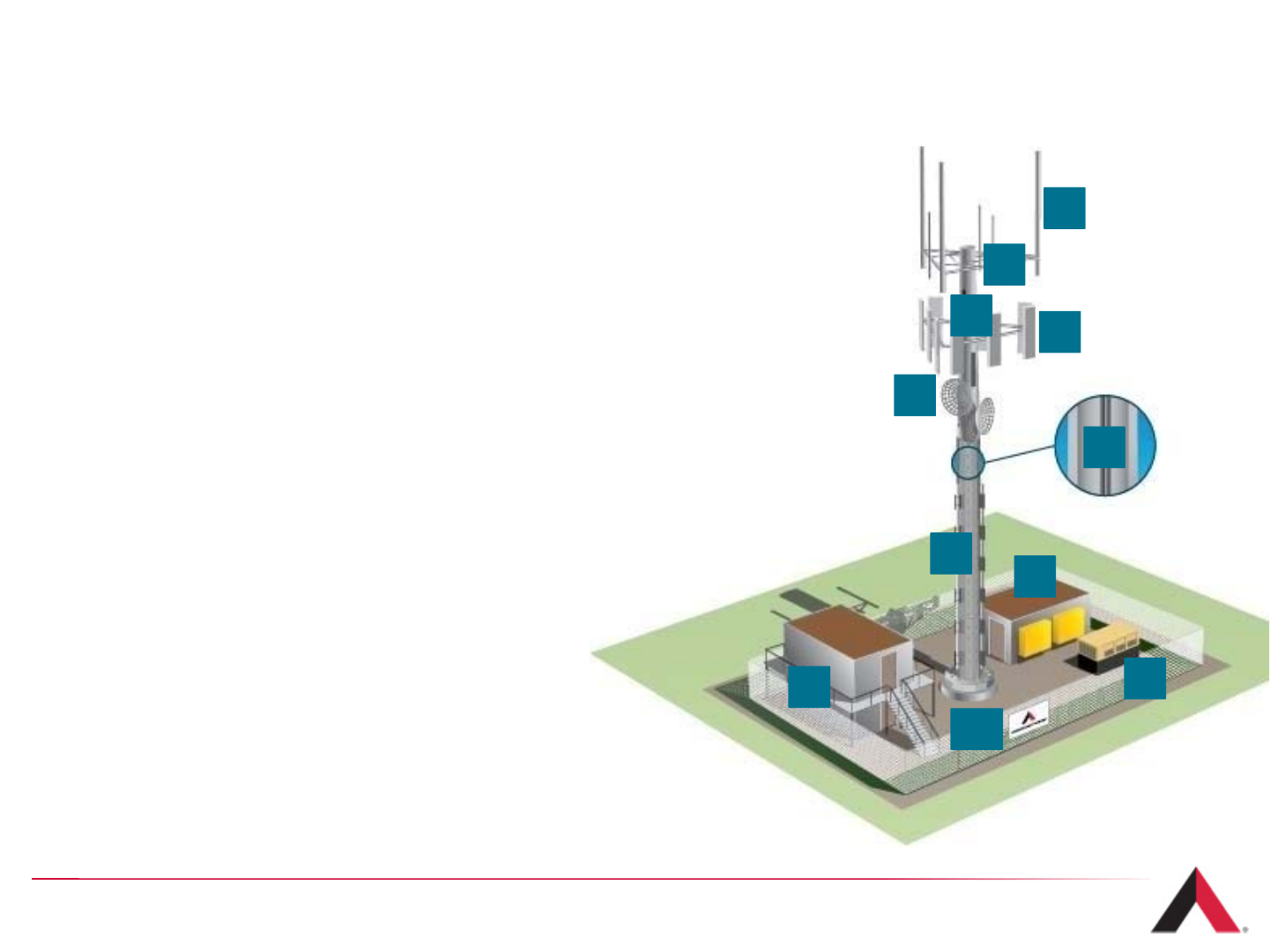

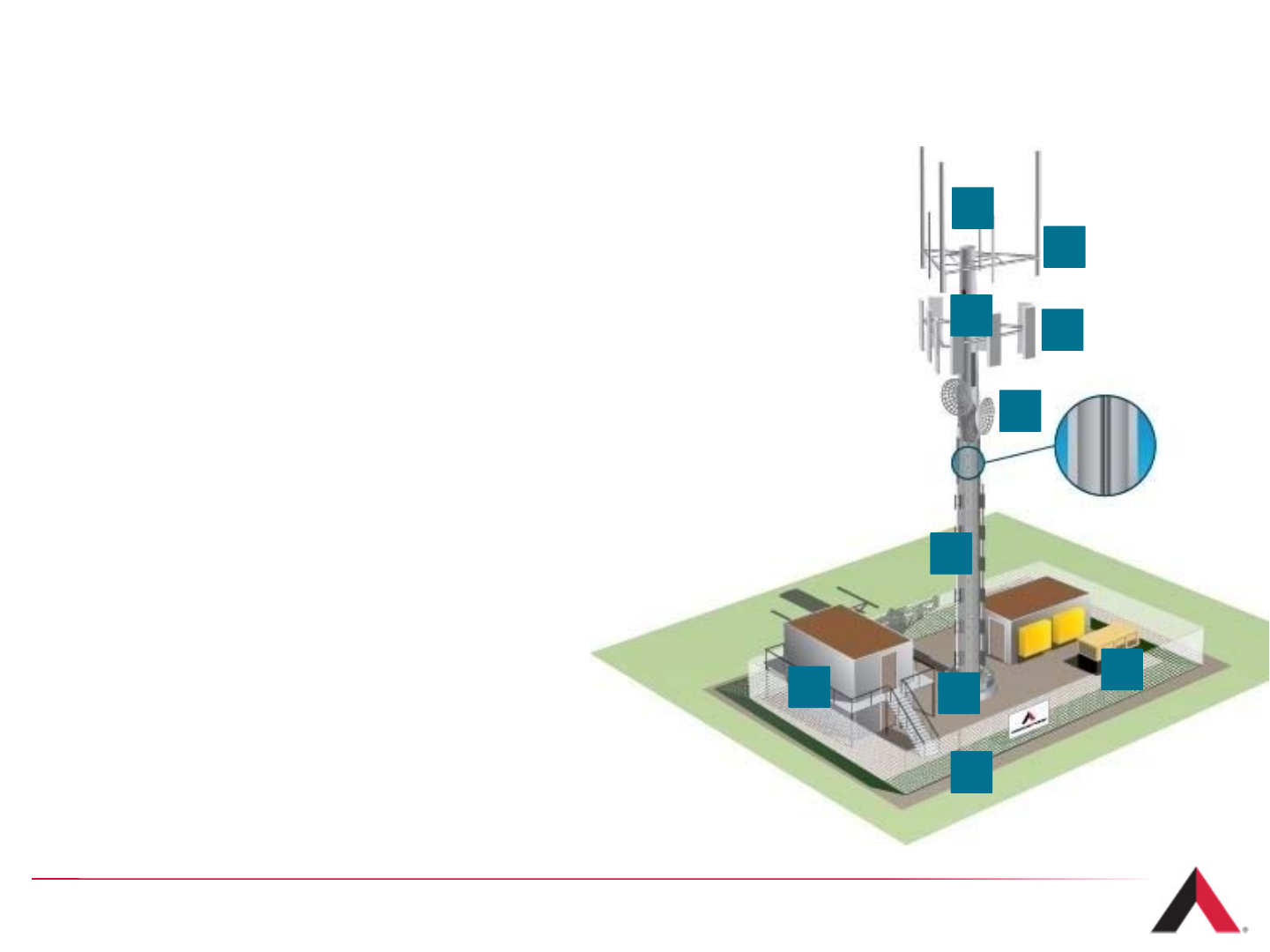

Typical Tower Components

1. Whip Antenna

›A stiff, monopole antenna, usually mounted vertically.

2. Antenna Array

›A platform (typically three sided) where tenants place equipment to provide

signal transmission and reception to a specific area. The number of antennas

necessary per array is determined based on a number of factors, including:

›the number of active subscribers;

›the volume and type of network usage by subscribers

(e.g., average minutes of use, voice versus data);

›the technology being used (e.g.: CDMA, GSM, LTE);

›the type of spectrum currently utilized by the tenant.

3. Port Holes

›Holes cut into the base and top of tower to allow cables

and wiring to pass through the tower structure, from the

base station to the antennas.

4. Panel / Antenna

›Tenant equipment which transmits a signal from the

tower to a mobile device or vice versa.

5. Microwave Dish

›A specific type of antenna, which is used in point-to-point radio, television and

data communications. Also commonly used by wireless carriers for backhaul.

6

1

2

34

5

6

78

9

10

8

Typical Tower Components (continued)

6. Coaxial Cabling (Fiber)

›Transmission lines that carry the signal received from the antenna to the base

station or vice versa.

7. Reinforcement Bars

›Threaded anchors which are used to reinforce towers to add additional

capacity to accommodate further tenants.

8. Shelters

›Buildings at sites used by our tenants to house communications,

radio and network equipment. Some shelters are designed to be stacked

on top of one another to conserve space at smaller sites.

9. Generator

›Gas or diesel powered generators provide emergency backup

power to keep tenant equipment operational during power outages.

AMT has also introduced Backup Power Solution to allow

multiple tenants to use a single generator.

10. Ground Space

›The area within a site where tenants

lease space from the tower company to place

their shelters and generators.

7

1

2

34

5

6

78

9

8

10

Sample Component Ownership Overview

Owned by American Tower

›Tower structure – our tower sites are typically

constructed with the capacity to support

~4 - 5 tenants

›Land parcel owned or operated pursuant to

a long-term lease by American Tower

›Generators are sometimes owned by American Tower

to help facilitate back-up power for the site’s tenants

8

AMT

Owned by Tenants

›Antenna equipment, including

microwave equipment

›Tenant shelters containing

base station equipment and HVAC,

which tenants own, operate and maintain

›Coaxial cable

AMT

TEN

TEN

TEN

TEN

TEN

TEN

AMT

The Business Model

Section 2

9

Recurring Long-Term Revenue Stream

Revenues

Sources

›Multiple tenants lease vertical space on the tower

and portions of the ground for their

communications equipment

›Rental charges are typically based on:

›Property location

›Leased vertical square footage on the tower

›Weight placed on tower from transmission

equipment and backhaul solutions

›Square footage leased on the ground

10

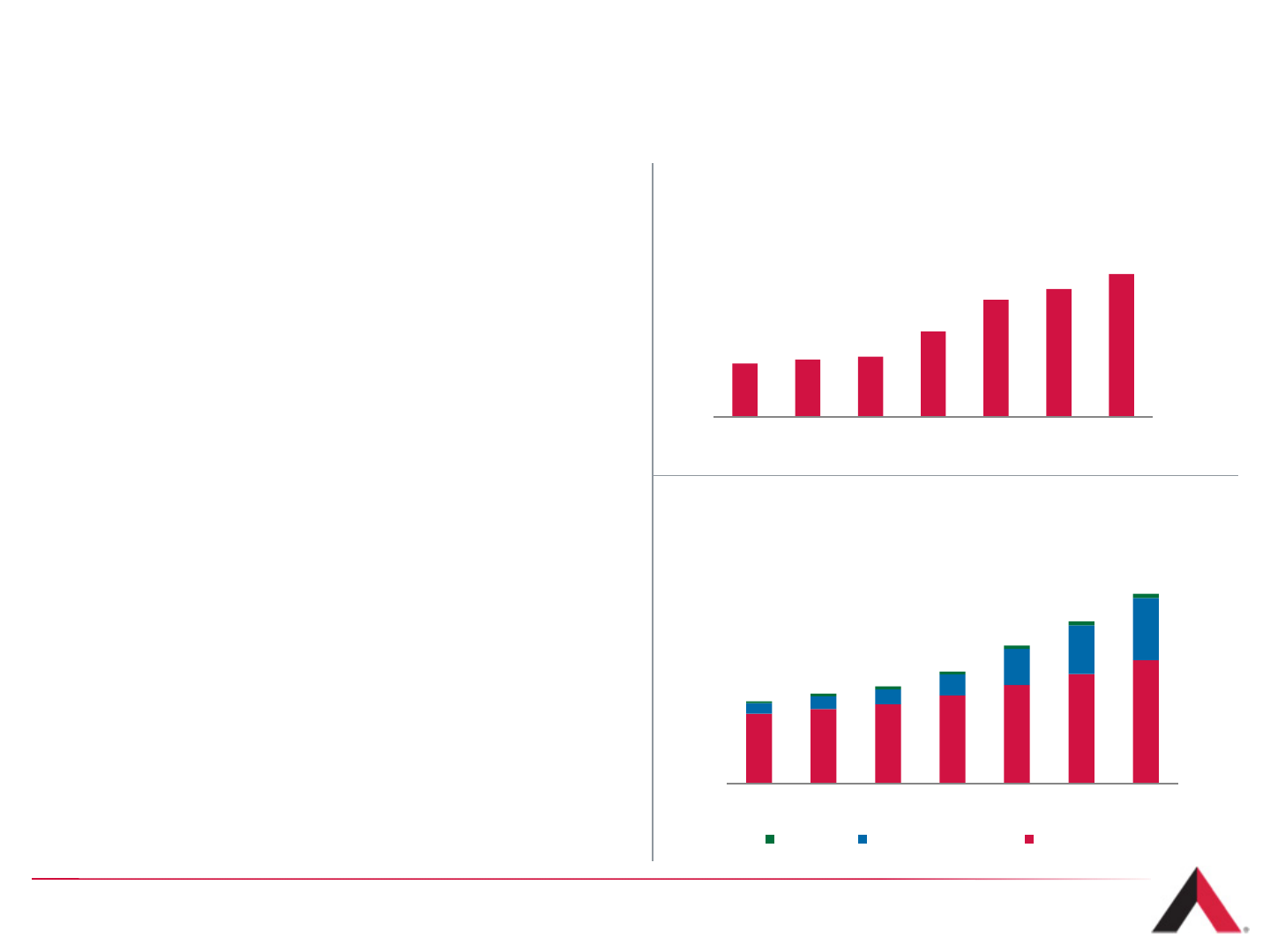

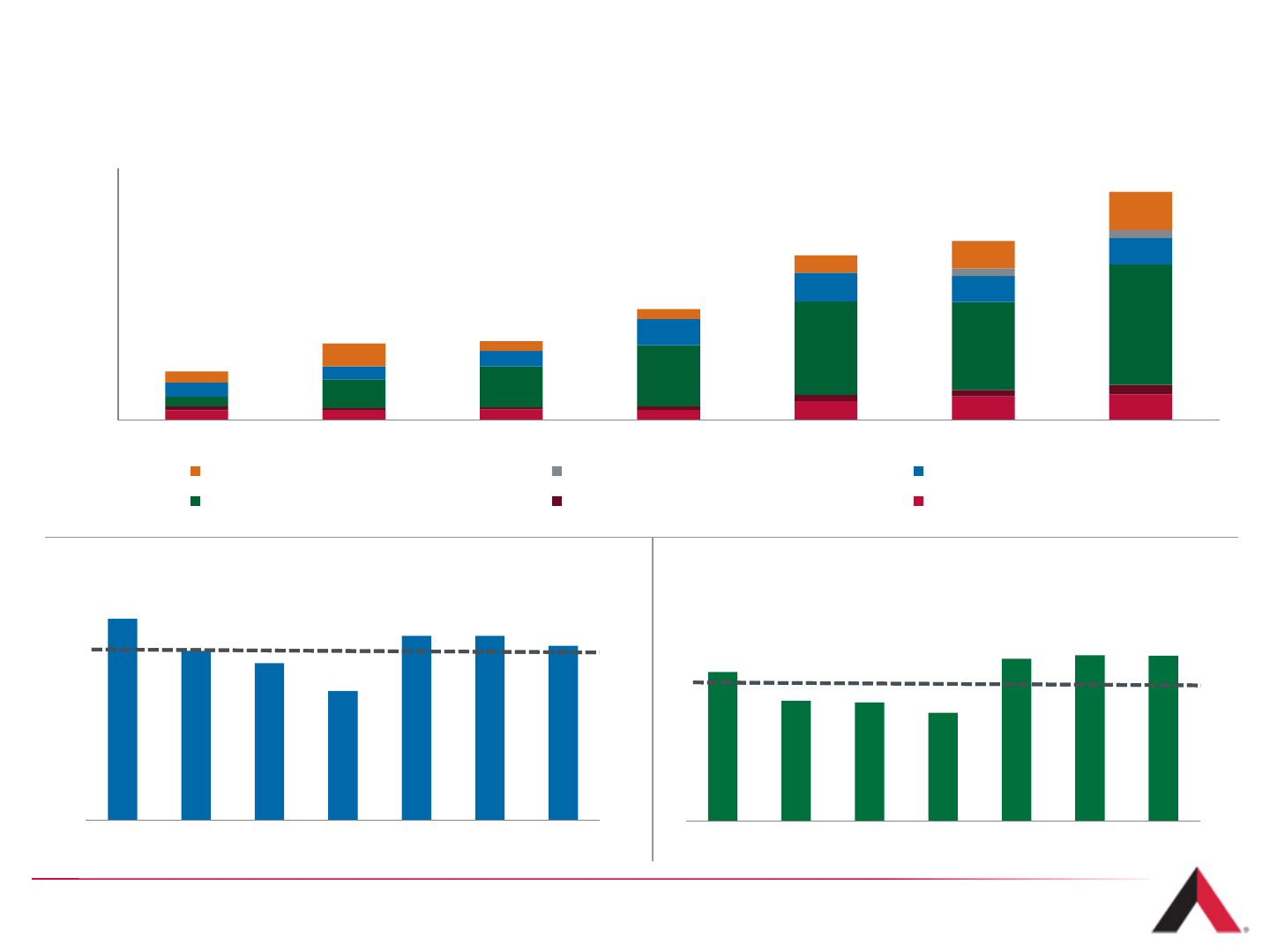

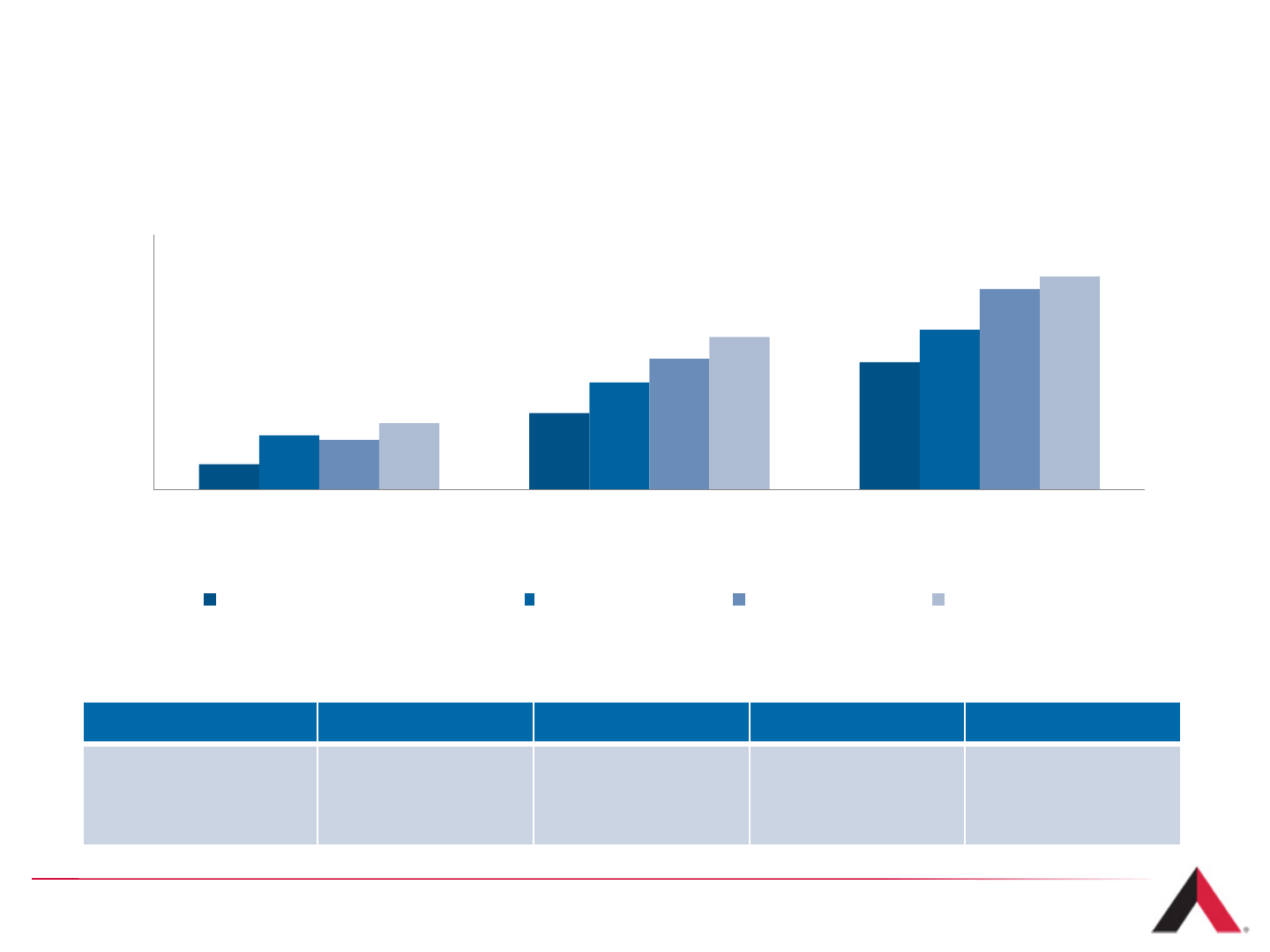

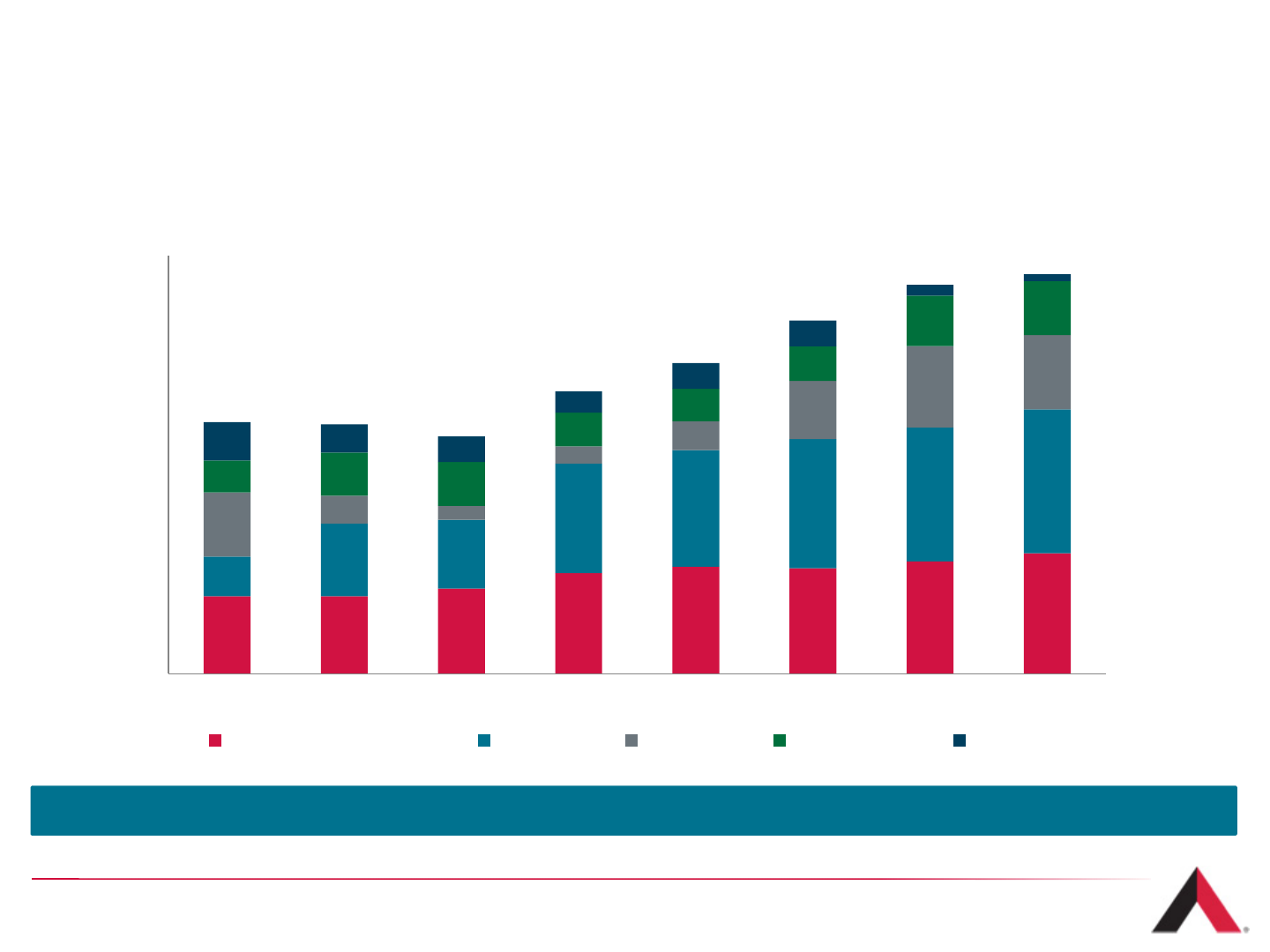

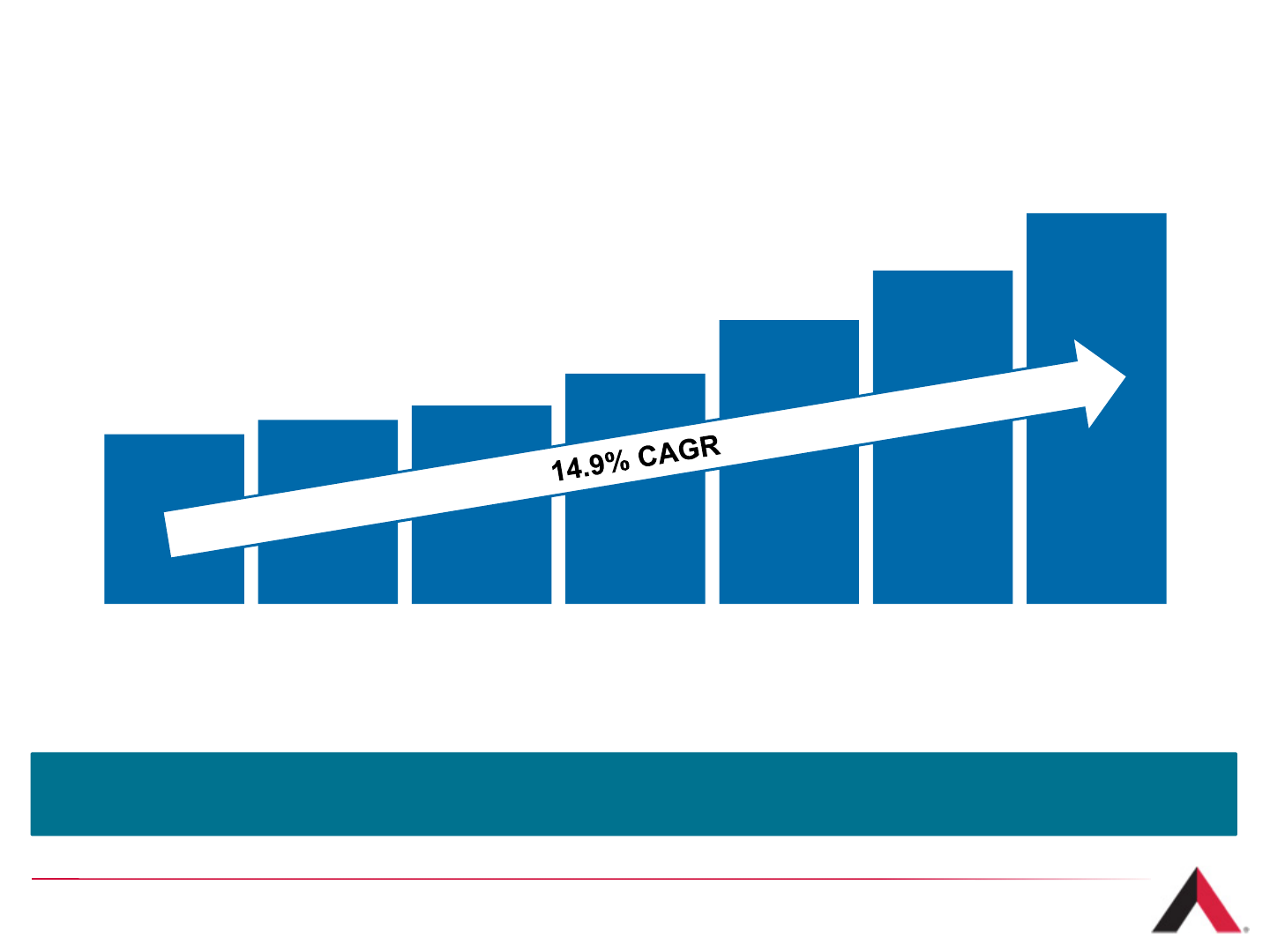

Recurring Long-Term Revenue Stream (Cont.)

11

$8 $9 $10

$14

$19 $20 $23

2007 2008 2009 2010 2011 2012 2013

AMT Non-Cancellable Revenue

Backlog

($ in billions)

2007 2008 2009 2010 2011 2012 2013

Services International R&M Domestic R&M

$1.5 $1.6 $1.7 $2.0 $2.4

$2.9

$3.4

AMT Segment Revenue(1)

($ in billions)

Revenues

Long-Term Customer Leases

›Contracts are typically non-cancellable

›Typical contract terms include an initial term of

10 years with multiple 5-year renewal periods

›Annual lease escalators in the U.S. of

approximately 3%

›Escalations in international markets are

typically based on local inflation rates

›Historically low annual churn of approximately

1 - 2%

(1) “R&M” refers to Rental and Management.

U.S. Operating Cost Structure

Direct Cost of Operations (1)

Sources

›Ground rent

›Monitoring

›Insurance

Land Interest Attributes

›Own ~29% of land under our U.S. sites

›Approximately 68% of sites are on owned land or have a

ground lease with at least 20 years until renewal

›Long-term leases: average remaining ground lease term is

approximately 25 years until final maturity in the U.S.

›Annual lease escalators in the U.S. of approximately

3%

›Selectively purchasing land interests where return

hurdles are met

Fixed Cost Structure of Towers

›Additional tenants result in minimal incremental operating

costs

12

›Real estate taxes

›Utilities and fuel

›Site maintenance

(1) Characteristics as of June 30, 2014

Largely Fixed Operating Cost Structure

International Operating Cost Structure

Direct Cost of Operations (1)

Sources

›Ground rent

›Monitoring

›Insurance

Land Interest Attributes

›Long-term leases: average remaining ground lease term is

approximately ~12 years internationally

›International escalators are typically based on local

inflation indexes

Pass Through

›Our international markets typically pass through a portion

of their operating expenses to the tenant (e.g., ground

rent, fuel)

Fixed Cost Structure of Towers

›Additional tenants result in minimal incremental operating

costs

13

›Real estate taxes

›Utilities and fuel

›Site maintenance

(1) Characteristics as of June 30, 2014

Similar to U.S. Cost Structure but with ability to pass-through expenses to tenant

Low Ongoing Capital Requirements

Capital Expenditure Types:

Revenue-Maintaining Capex:

•Capital Improvements

•Includes spending on lighting systems, fence repairs and ground upkeep. Approximately $500 per tower annually in Latin American

markets, ~$600 in India, ~$700 in EMEA markets and $1,500-$1,750 in the U.S.

•Corporate

•Capital spending primarily on IT infrastructure.

Revenue-Generating Capex:

•Redevelopment

•Capital spending to increase capacity of towers (e.g. height extension, foundation strengthening, etc.).

•Cost is typically shared with the tenant and investment payback period on net capex is typically one to two years.

•Ground Lease Purchases

•Capital spending to purchase land under our sites.

•Discretionary Capital Projects

•Capital spending primarily for the construction of new communications sites and generators

•Start-Up Capital Projects

•Expenditures that are specific to acquisitions and new market launches and that are contemplated in the business cases for these

investments.

14

$-

$100

$200

$300

$400

$500

$600

$700

$800

2007 2008 2009 2010 2011 2012 2013

Redevelopment Start-Up Capital Projects Ground Lease Purchases

Discretionary Capital Projects Corporate Capital Improvements

Historical Capital Spending

15

$1.9

$1.6 $1.5

$1.2

$1.7 $1.7 $1.7

2007 2008 2009 2010 2011 2012 2013

Revenue-Maintaining Capex per Tower

($ in thousands)

Total Capital Expenditures

($ in millions)

3.1%

2.5% 2.4% 2.2%

3.3% 3.4% 3.4%

2007 2008 2009 2010 2011 2012 2013

Revenue-Maintaining Capex

as % of Tower Revenue

Average:

$1.6 Average:

2.9%

Accommodating Additional Tenants

When a tower has reached its initial design capacity, there

remain many ways for us to accommodate future tenant demand.

Redevelopment Capex Examples

1. Height Extension

›Allows for more equipment and more tenants

2. Multiple Antenna Mounting Scenarios

›Options include whips, panels, microwaves and various combinations determined by

internal RF engineering

3. Port Hole Additions

›Additional entry and exit port designs accommodate additional coaxial cables

4. Tower Reinforcements

›Adds structural strength to accommodate additional tenants

5. Strengthened Foundation

›Increases load capacity of the tower

6. Backup Power Generator

›Provided by American Tower, maximizes compound

space

7. Stacked Shelters

›Shelter stacked atop an existing shelter using a steel platform

8. Extended Ground Space

›Where space allows, expanded to accommodate more equipment

16

2

2

3

56

4

8

7

2

1

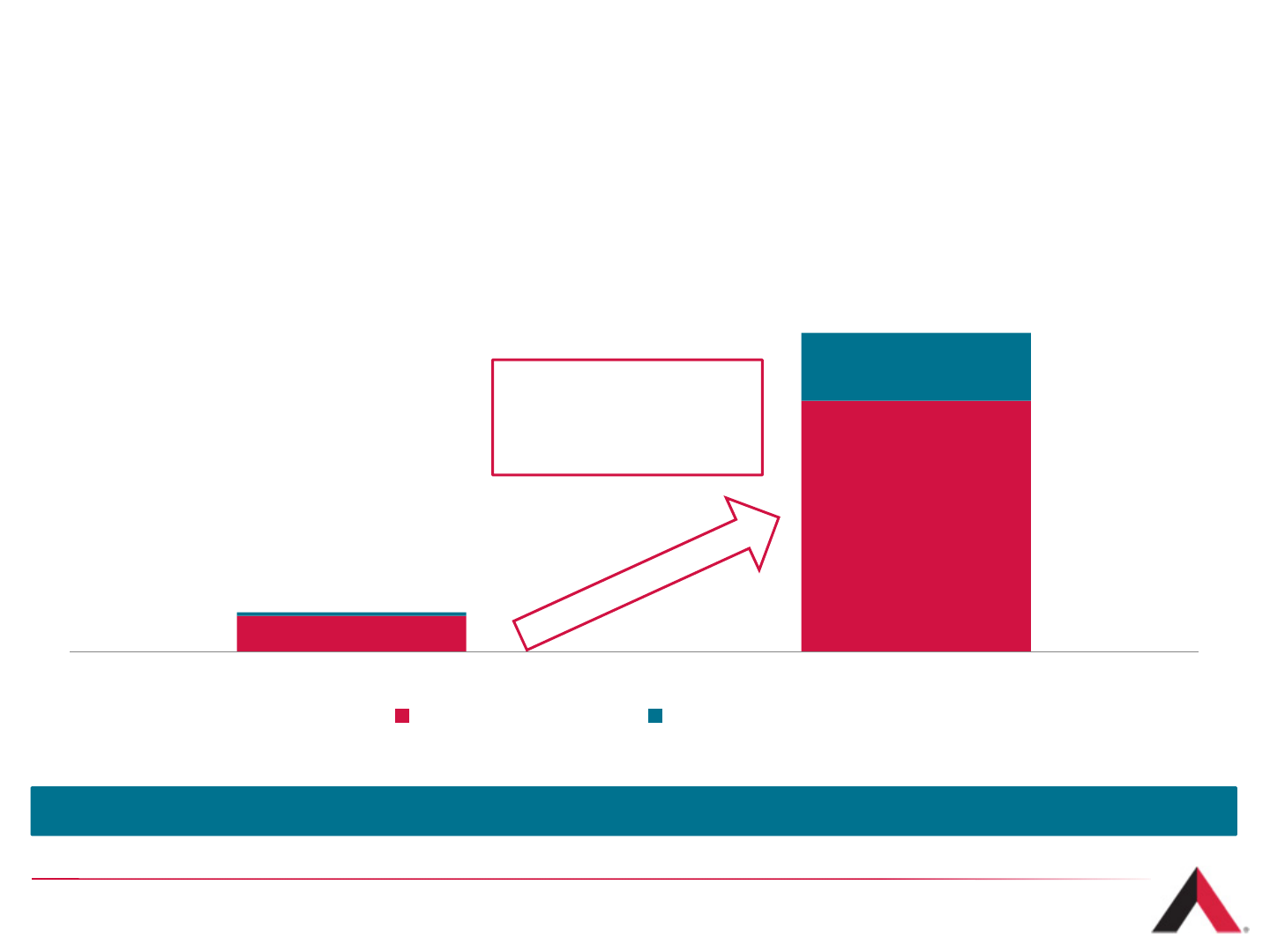

Sample Macro Tower Leasing Scenario

17

Adding tenants, equipment and upgrades results in significantly higher returns, as revenue is

added with minimal incremental cost.

One Tenant Two Tenants Three Tenants

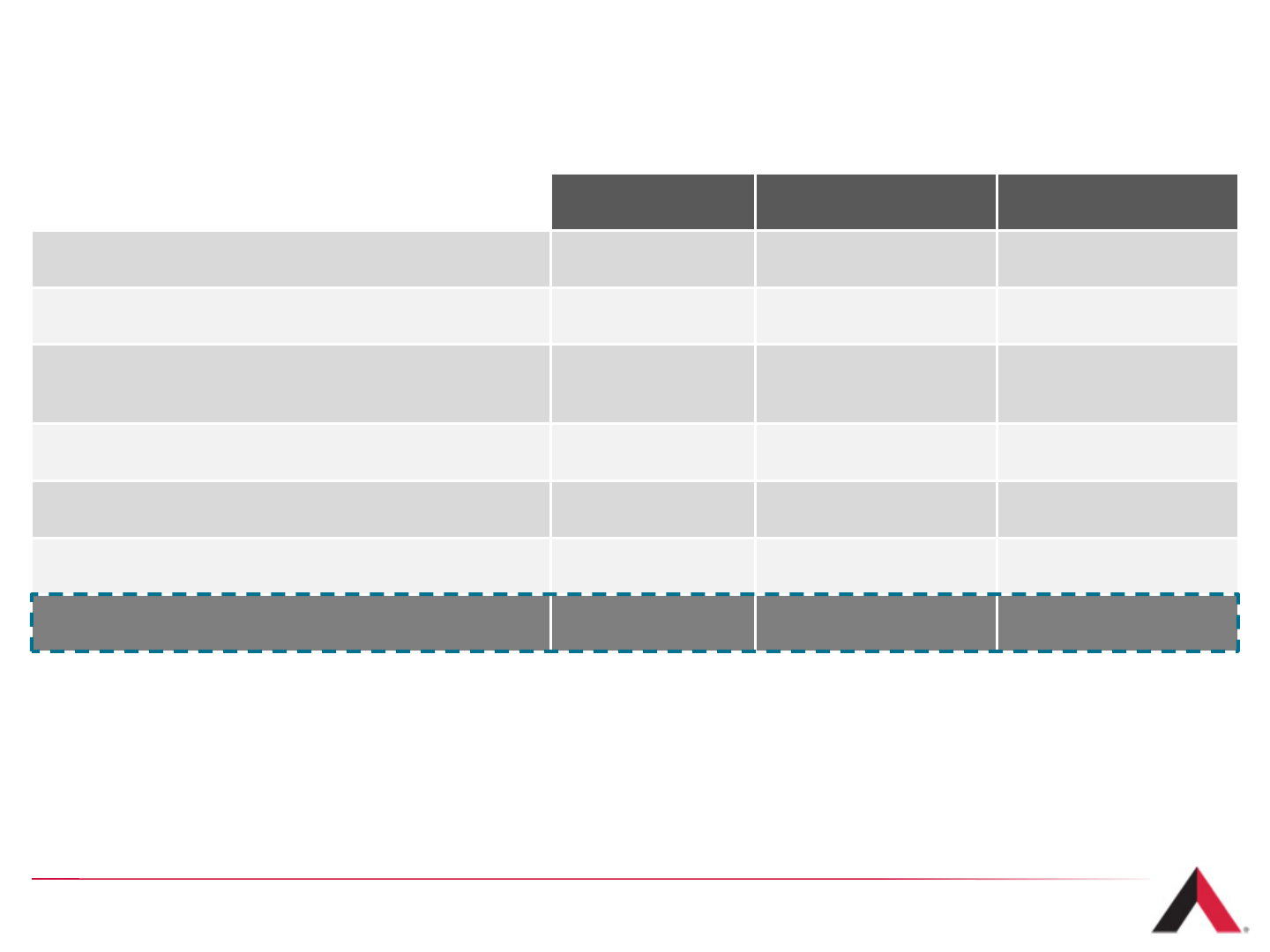

U.S. New Macro Tower Build Economics Drive

Strong ROI(1)

18

(1) For illustrative purposes only. Does not reflect any American Tower financial data.

(2) Calculated as Gross Margin divided by Construction/Upgrade Costs.

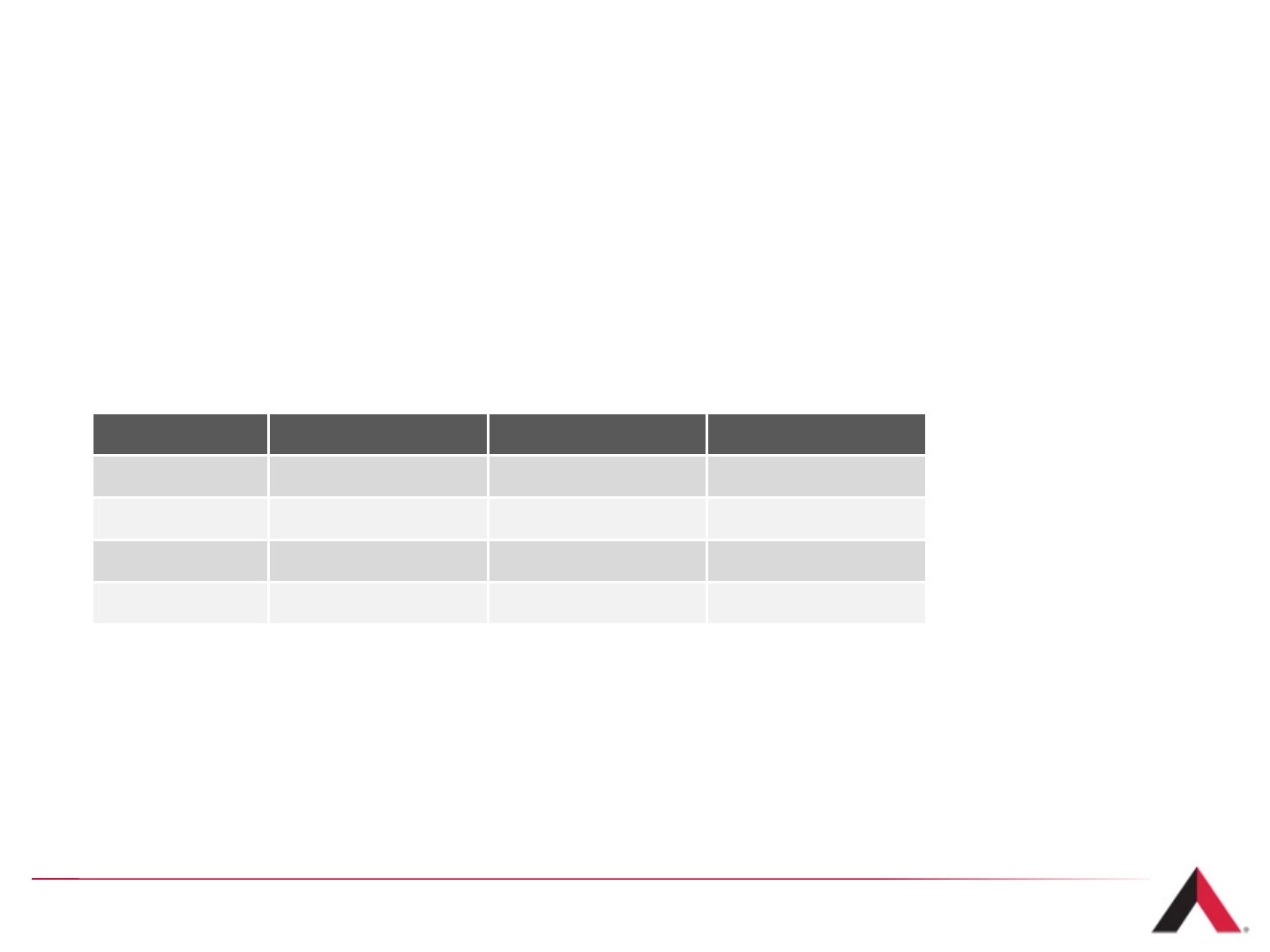

One Tenant Two Tenants Three Tenants

Construction/Upgrade Costs ($ in USD) $250,000 — —

Tenant Revenue $20,000 $40,000 $60,000

Operating Expenses

(including ground rent, utility, monitor) $12,000 $13,000 $14,000

Gross Margin $8,000 $27,000 $46,000

Gross Margin (%) 40% 68% 77%

Gross Margin Conversion Rate (%) – 95% 95%

Return on Investment (2) 3% 11% 18%

International New Tower Build Returns on

Investment Typically Exceed U.S. Returns(1)

19

(1) For illustrative purposes only. Does not reflect any American Tower financial data.

(2) Calculated as Gross Margin divided by Construction/Upgrade Costs.

US LatAm Africa India

Typical Tower

Construction

Cost $225-$275K $125-$150k $150-$175k $30-$50k

3%

11%

18%

9%

17%

25%

8%

21%

31%

10%

24%

33%

0%

5%

10%

15%

20%

25%

30%

35%

40%

One Tenant Two Tenants Three Tenants

Sample Return on Investment(2)

Domestic Market LatAm Africa India

LatAm Africa

Business Model Summary

Numerous factors contribute to the success of the tower business model.

›Secure real estate assets

›Strong recurring cash flow characteristics

›Long-term, non-cancellable lease revenues

›Embedded contractual escalators

›High incremental cash flow margins

›Low maintenance CAPEX

›Financially strong tenant base

›Economies of scale

›Replicate established systems and

processes in new markets

›Ability to add additional assets to existing

markets without a need for significant

increase in overhead

›Barriers to entry

›Location-based business, typically with

significant zoning restrictions

›Capital and time intensive to build meaningful

scale

›Consistent U.S. demand

›$25+ billion in annual CAPEX spending by U.S.

service providers over the last few years(1)

›Rapidly increasing wireless data usage and

adoption of advanced wireless devices

›Strong international demand

›Continued deployment of voice and initial data

networks

›Spectrum auctions and new market entrants

›Demand from new technology overlays

(e.g.: 3G and LTE)

20

(1) Source: Wall Street Research.

Technology Overview

Section 3

21

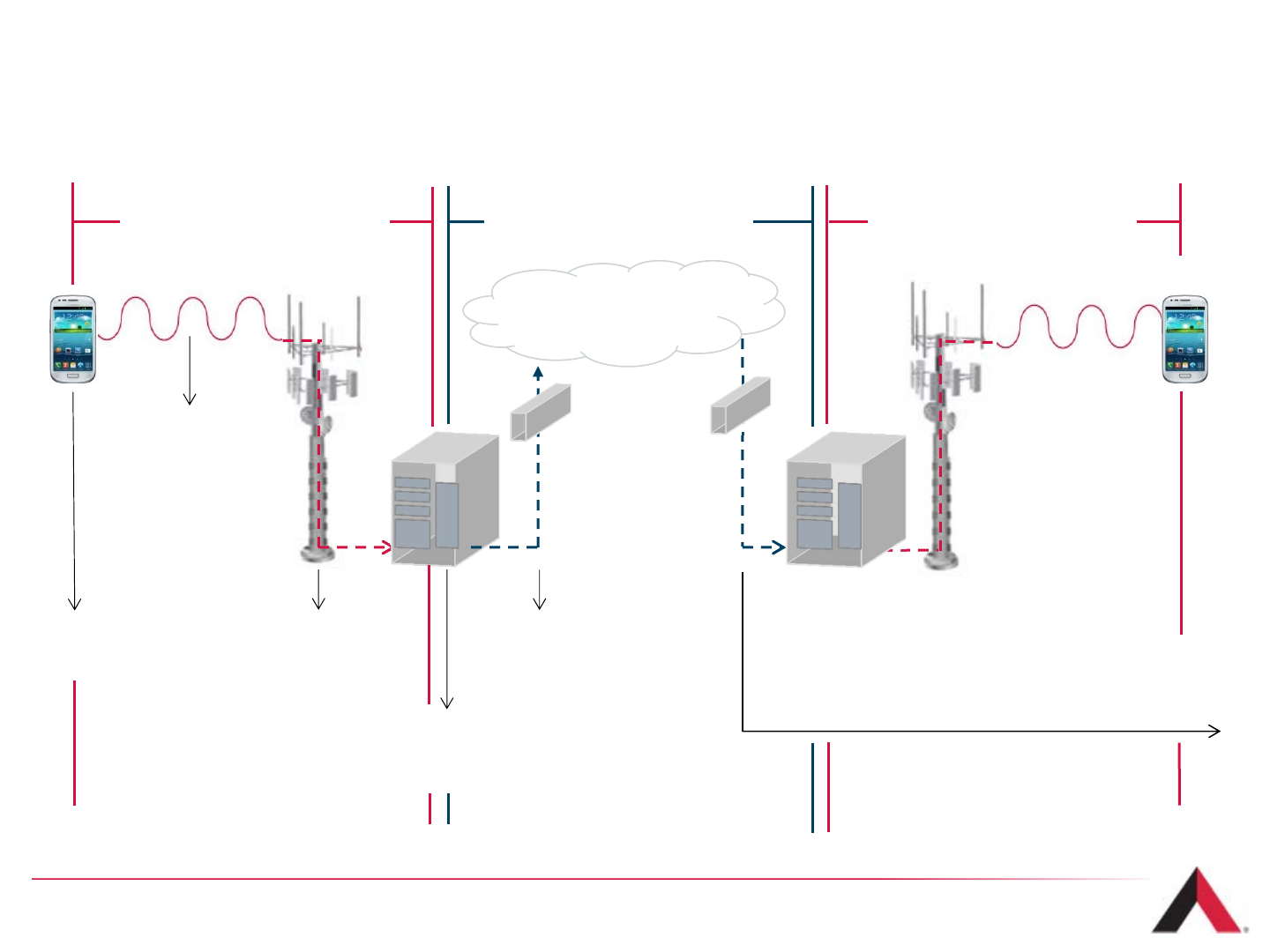

The Mobile Call Sequence

22

7. MOBILE CORE

Call is “switched” and routed

to another tower site closest

to receiving device

1. DEVICE

Call signal starts

at user device

2. SPECTRUM

Call signal travels

via radio wave

spectrum to antenna

on tower

3. TOWER

Spectrum radio waves

travel down tower via

fiber/coaxial cable to

base station 4. BASE STATION

Spectrum radio waves

get translated into

backhaul1

5. BACKHAUL

Call signal travels via

backhaul to market-

level Aggregation

Points

8. PROCESS REVERSES

- Call signal converts from backhaul to spectrum at base station

- Spectrum radio waves travel up fiber/ coaxial cable of tower

- Call signal transmitted from tower antenna via spectrum to device

ANALOGPORTIONOFCALL

[Steps1–4]

DIGITALPORTIONOFCALL

[Steps4–7]

ANALOGPORTIONOFCALL

[Step8]

Wireless Fixed Line Wireless

(1) In some cases the radio has been moved up onto the tower.

6. AGGREGATION

POINTS

Market-level points

that aggregate traffic

before sending on to

the Mobile Core

What is Spectrum?

23

›Spectrum airwaves are licensed to carriers who utilize the spectrum to transmit wireless signals

›The government typically regulates this spectrum and auctions it to wireless carriers for use

›Spectrum is measured in units of “hertz” or Hz

›The three main considerations in evaluating a carrier’s spectrum position include:

1. In which spectrum bands does the carrier hold licenses?

2. How much spectrum (bandwidth) does the carrier have?

3. What type of technology is the carrier deploying on that band of spectrum (i.e. CDMA, HSPA, LTE)?

Spectrum: radio frequency airwaves, needed to transmit analog signals, including wireless

communications signals

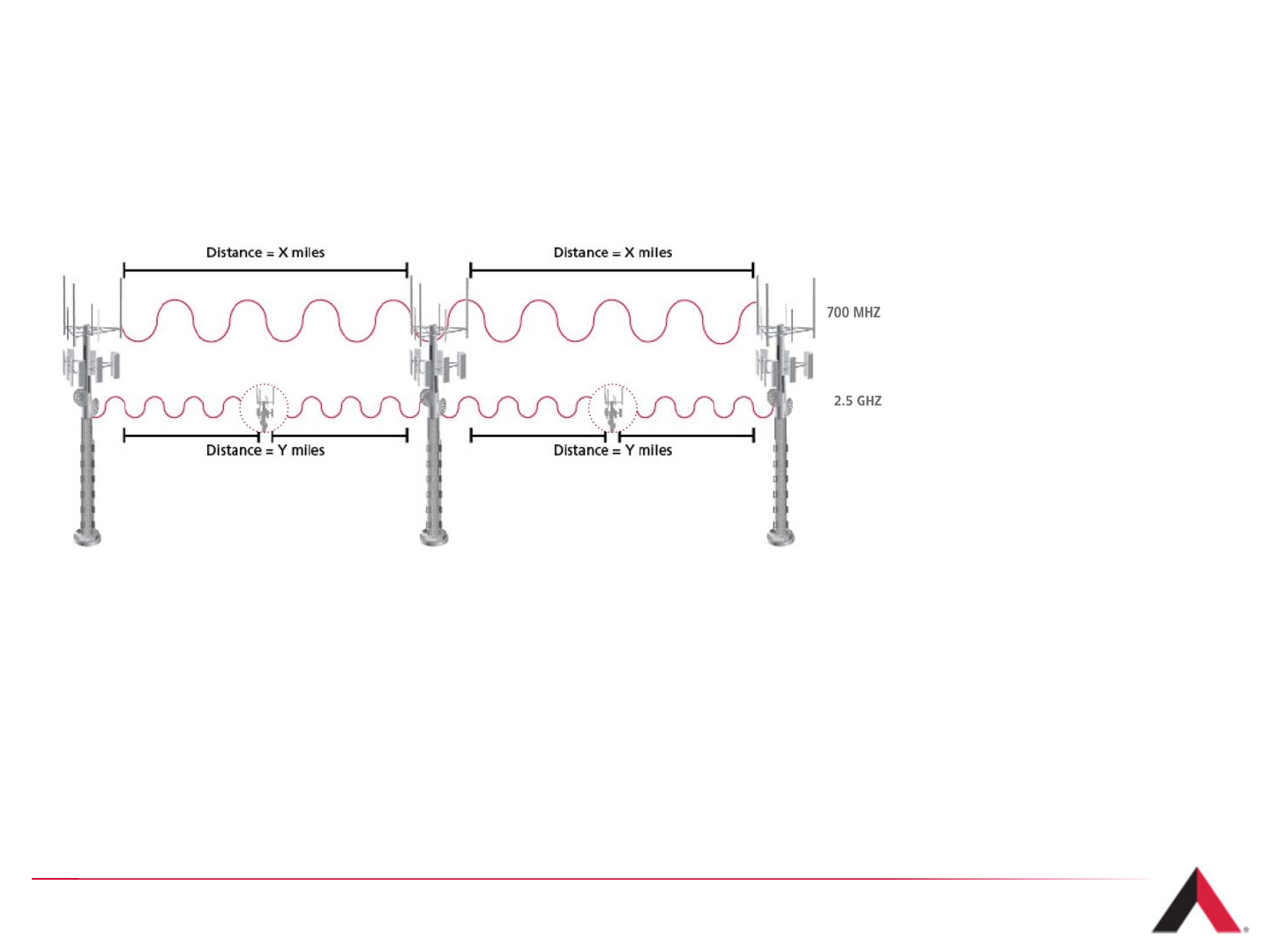

Spectrum Characteristics

›Propagation – radio transmits a signal by driving a current on an antenna; signal

propagates away from antenna as a wave at the speed of light

›Lower-frequency spectrum provides a larger coverage area and better in-building

penetration (“beach front” spectrum)

›Higher-frequency spectrum covers shorter distances (need significantly more cell sites to

get the same level of coverage)

›As spectrum usage increases the distance spectrum can propagate decreases

24

2.5GHz 1.9GHz 1.6GHz 700MHz

(Not to scale)

Radio Spectrum Signal

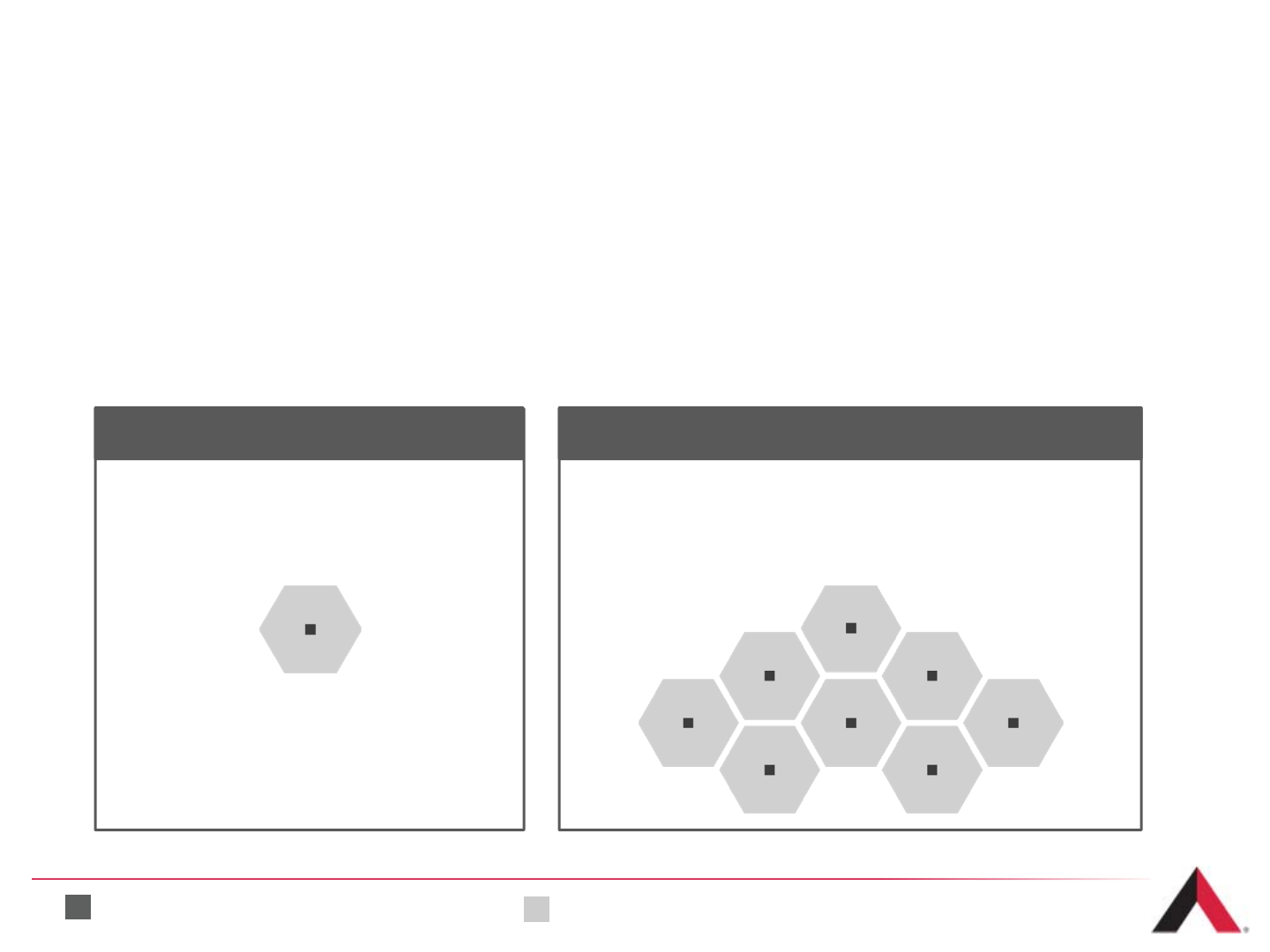

What is a Cell Site?

A cell site is an area within a carrier’s wireless network which is serviced by an

antenna array. Carriers commonly refer to these areas as “rings”.

›Can be located on a tower or alternative structures, such as

rooftops, water towers and church steeples

›One macro tower can support multiple carriers’ cell sites through collocation

25

Cell Site Network

Tower/antenna location Geographic area covered by antenna array

A carrier’s coverage area is dependent upon the

capacity of its equipment and the frequency of

the signal being transmitted.

Cell Site

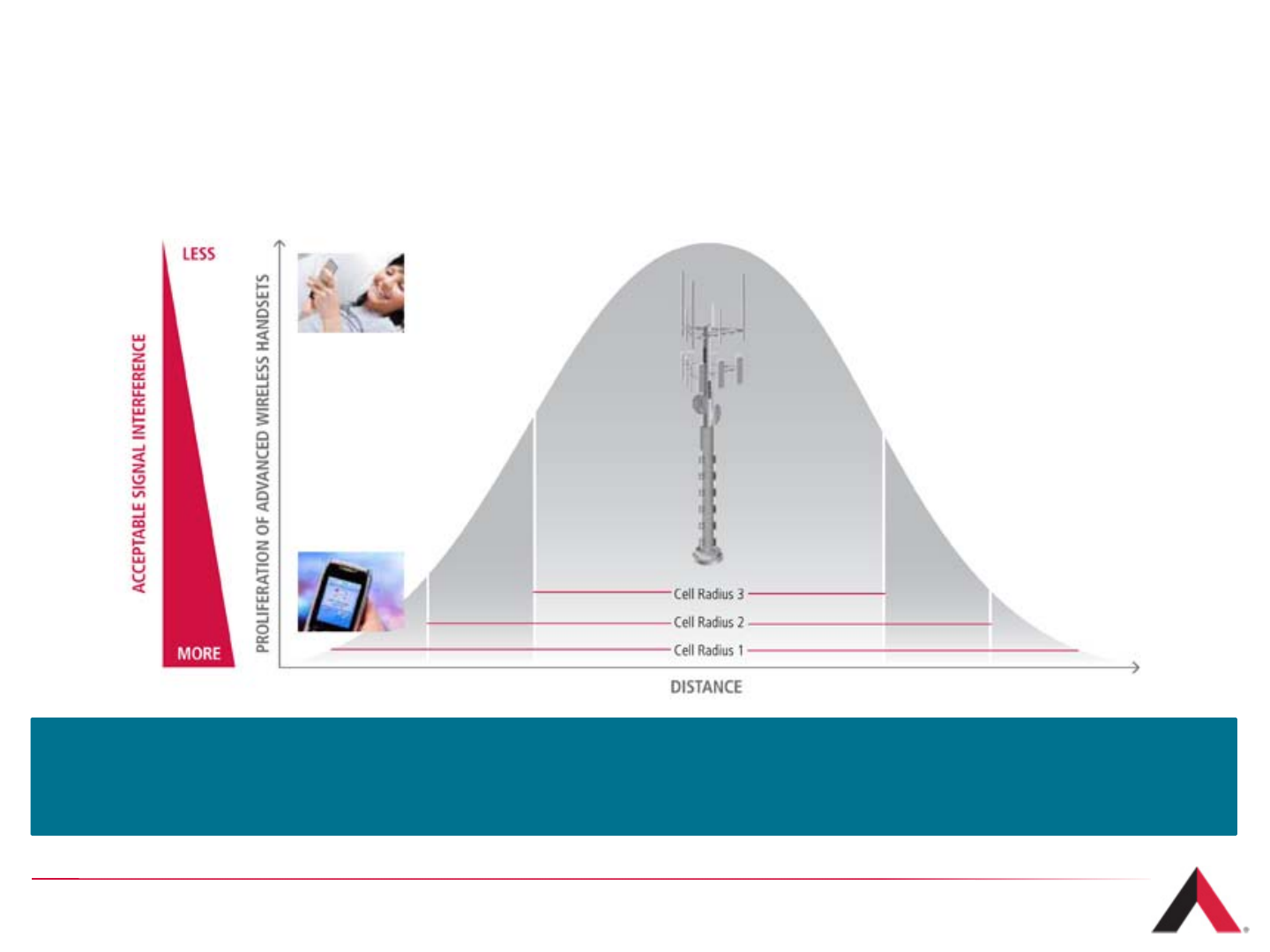

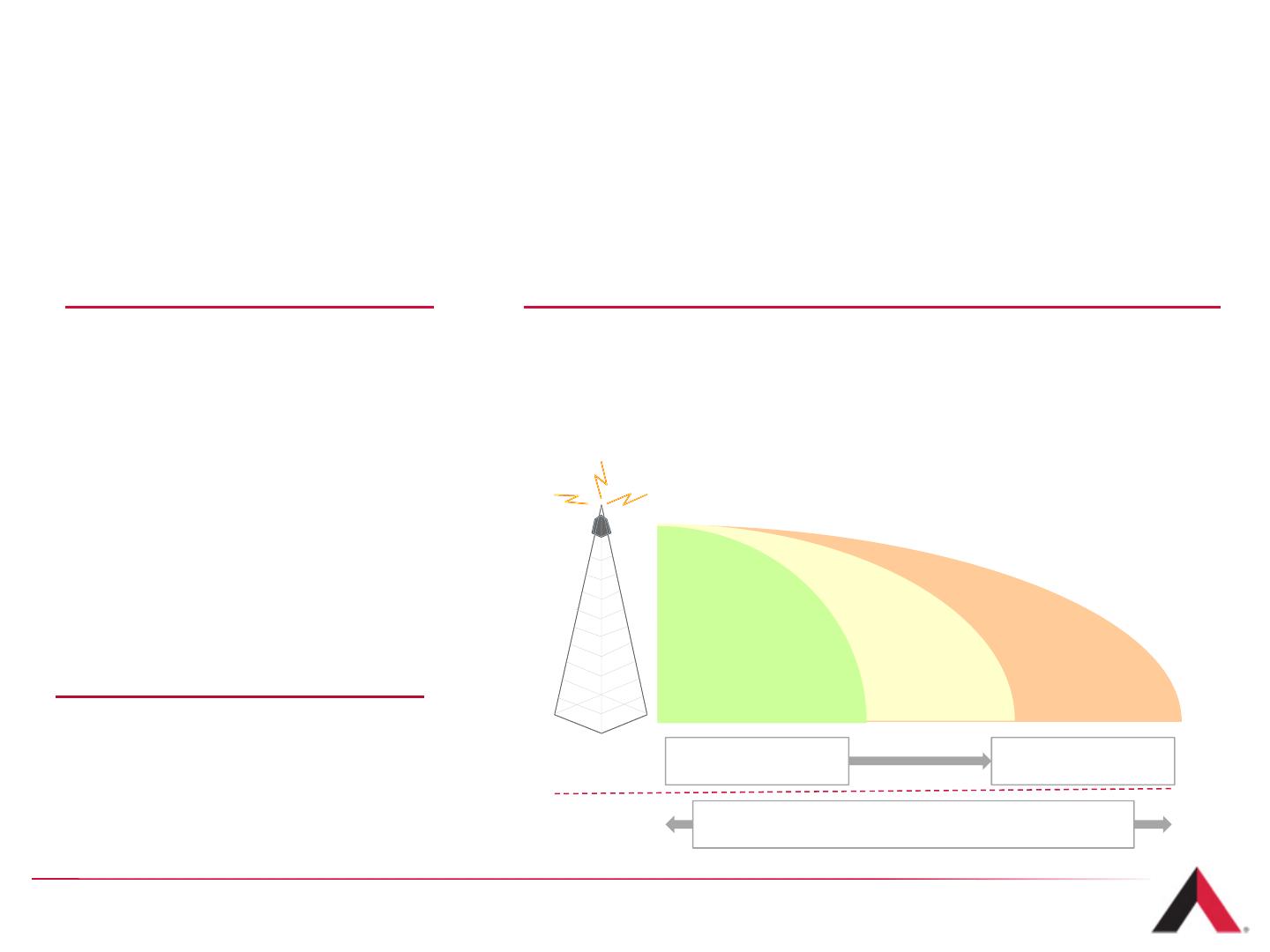

Narrowing Cell Radius

Signal Strength Curve

26

As devices become more advanced, the increasing demand for high-bandwidth applications

and higher quality of service result in a narrower range at which signals can be transmitted. As

a result, carriers are investing in denser networks.

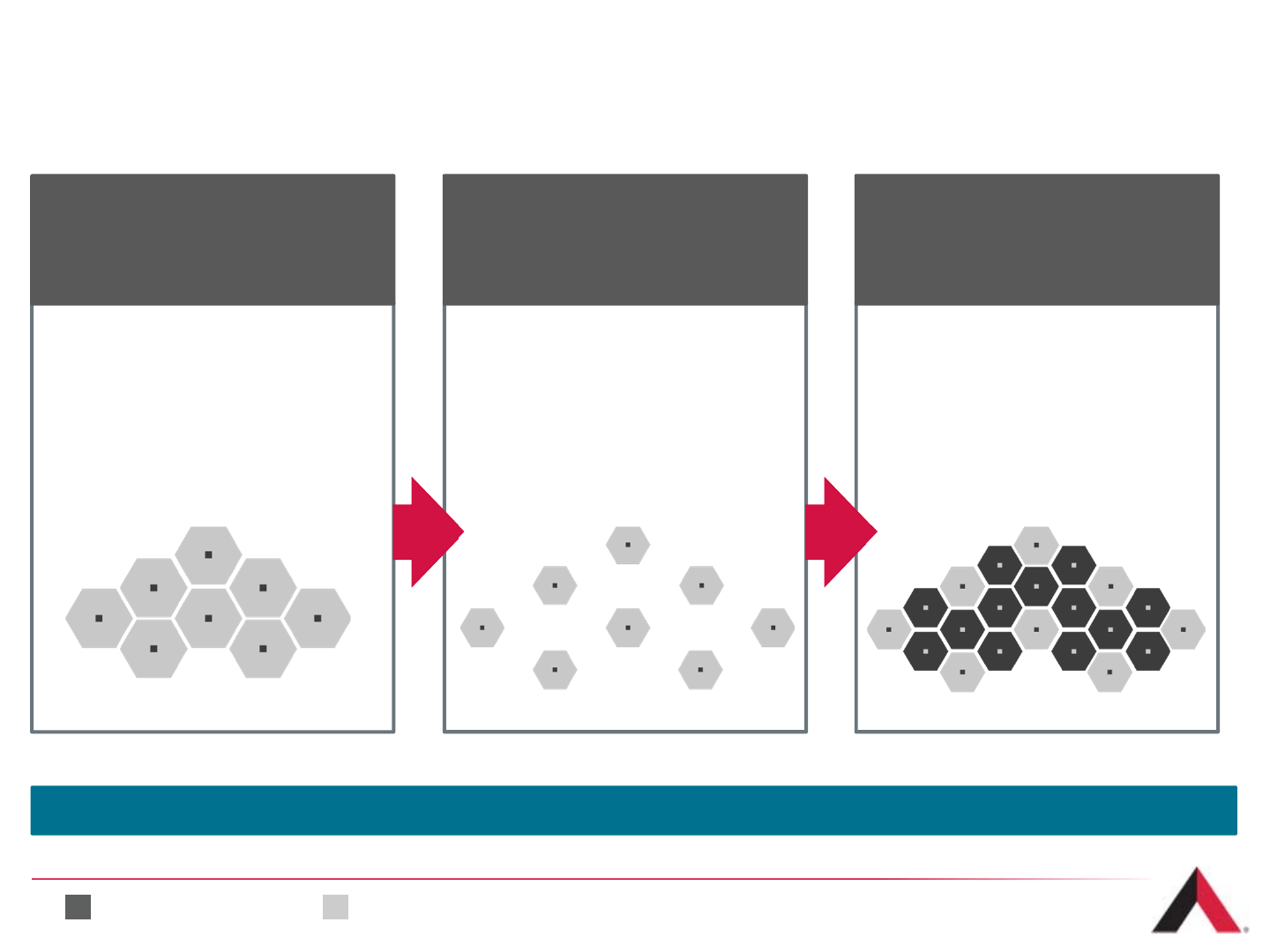

Network Design Evolution

27

New cell site Original cell site

›Quality of voice services

on the rise

›Smartphones introduced

to the market

Network designed for initial

voice and 3G services As data usage rises, the

existing network structure

proves deficient for data

signal propagation

Building new cell sites is

therefore required to create

adequate coverage for

seamless data usage

›Smartphone penetration

on the rise

›New smartphone

handsets introduced

›VoLTE (Voice over LTE)

›Carriers consistently

invest in networks to meet

growing demand

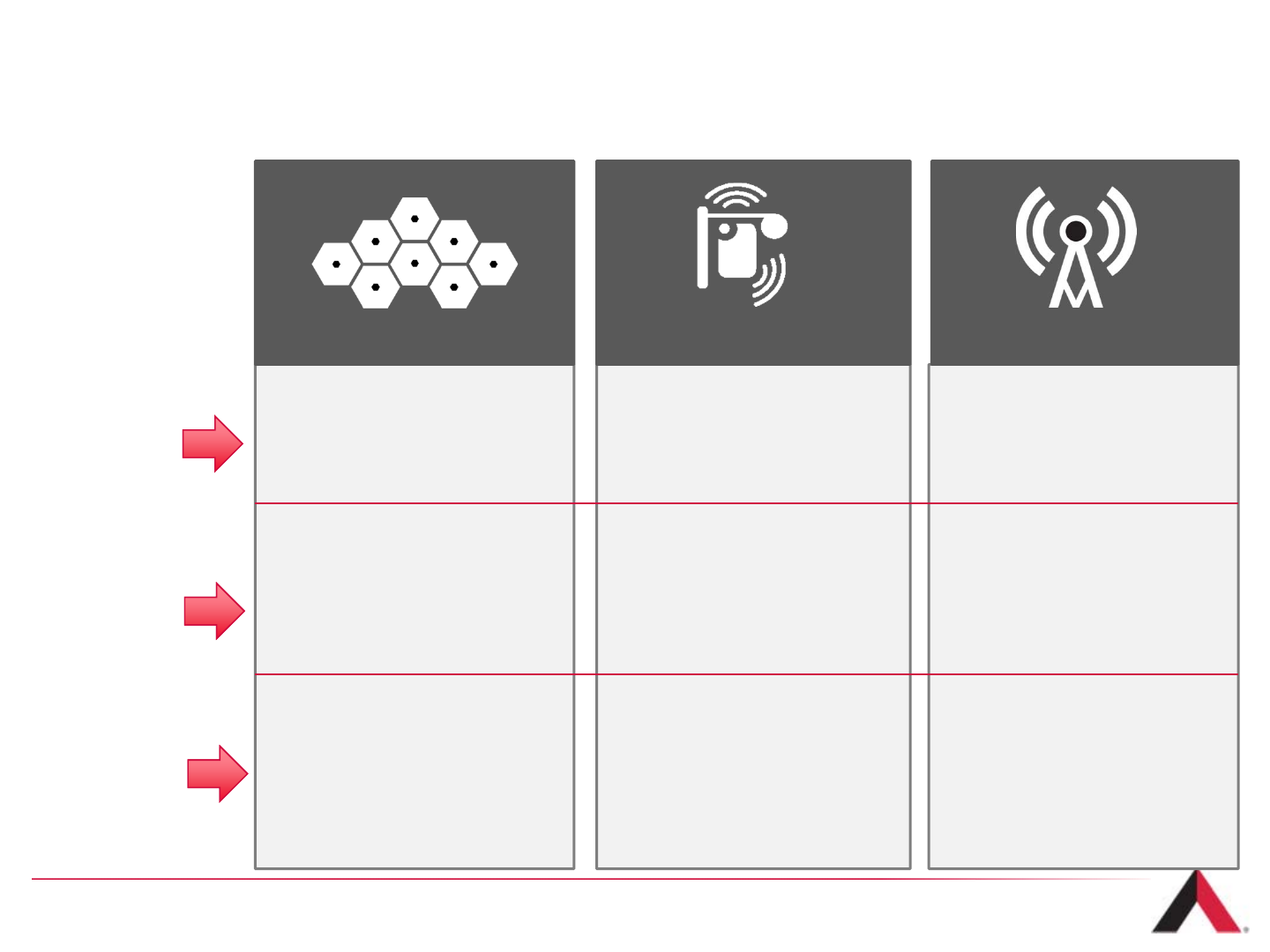

Growing wireless usage results in the need for more cell sites.

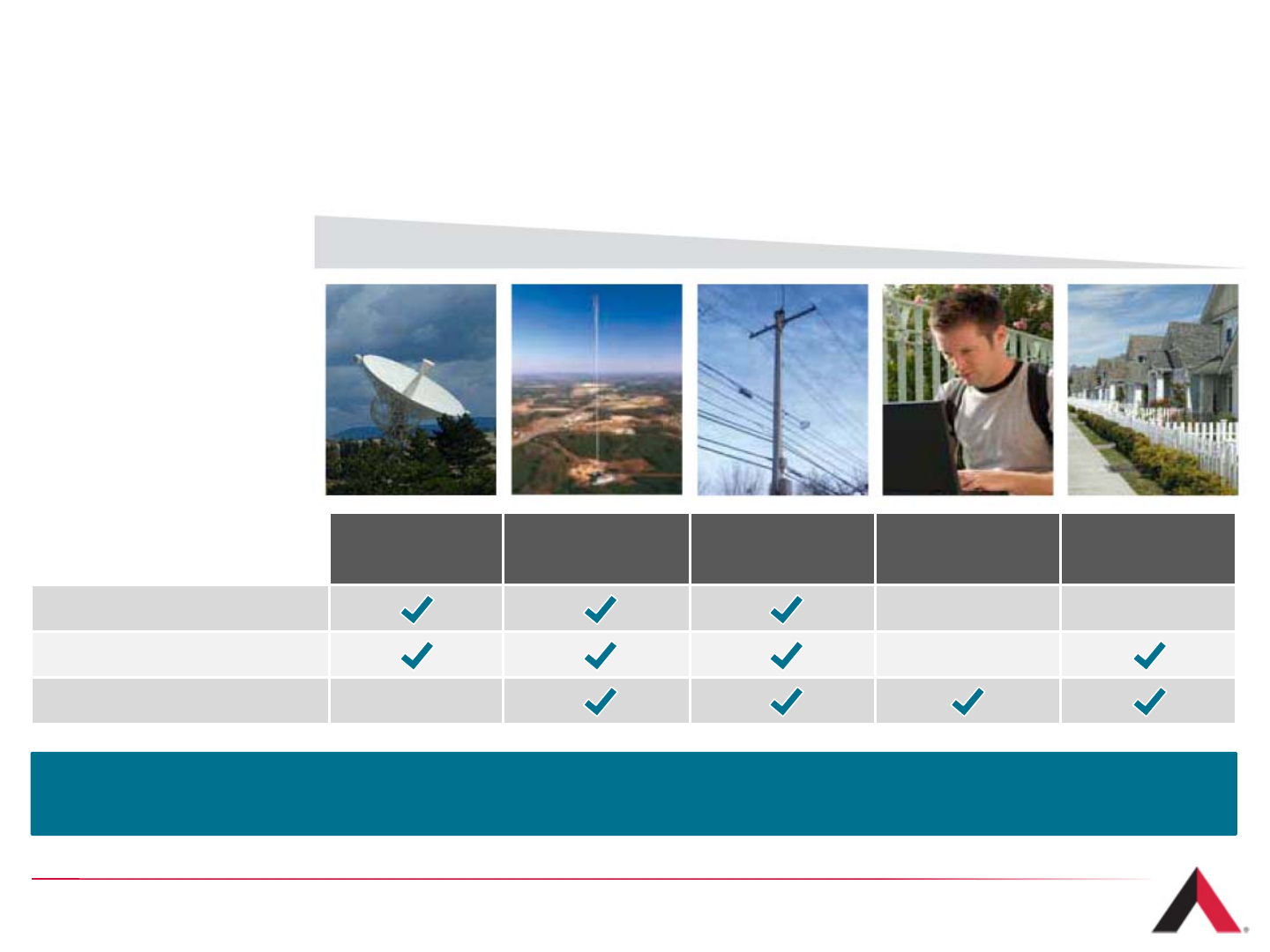

Tower Sites are Preferable in Most Locations

28

Technology Capability

Satellite Tower Sites DAS Network Wi-Fi Small Cell /

Femtocell

Mobility ——

Uses licensed spectrum —

Low latency —

Wide NarrowPopulation Coverage Area

Tower sites continue to be our customers’ preferred solution, as they provide the most

technologically efficient and cost-effective option for coverage and capacity requirements.

Wi-Fi vs. Licensed Spectrum

29

Licensed spectrum allows for exclusive use by licensees with consent of the Federal

Communications Commissions (FCC). Wi-Fi spectrum is unlicensed and it can be used

by any party.

›Disadvantages of using unlicensed Wi-Fi spectrum:

1. Limited Mobility: Unlicensed Wi-Fi spectrum is in the high frequency 2.4 GHz and 5 GHz

bands. This means it is unable to propagate far, requiring significantly more transition

locations to cover an area and limiting its geographic reach.

2. Congestion: Any Wi-Fi capable device is permitted to use unlicensed Wi-Fi spectrum and

as a result, WiFi networks often become congested.

3. Loss of Control: Carriers lose control of their subscribers’ user experience when utilizing

public, unlicensed spectrum.

4. Concentrated in Dense Urban Areas: Because unlicensed spectrum is high frequency and

unable to propagate long distances, it is used predominantly in dense urban areas where

mobility requirements are limited and access points are closer together.

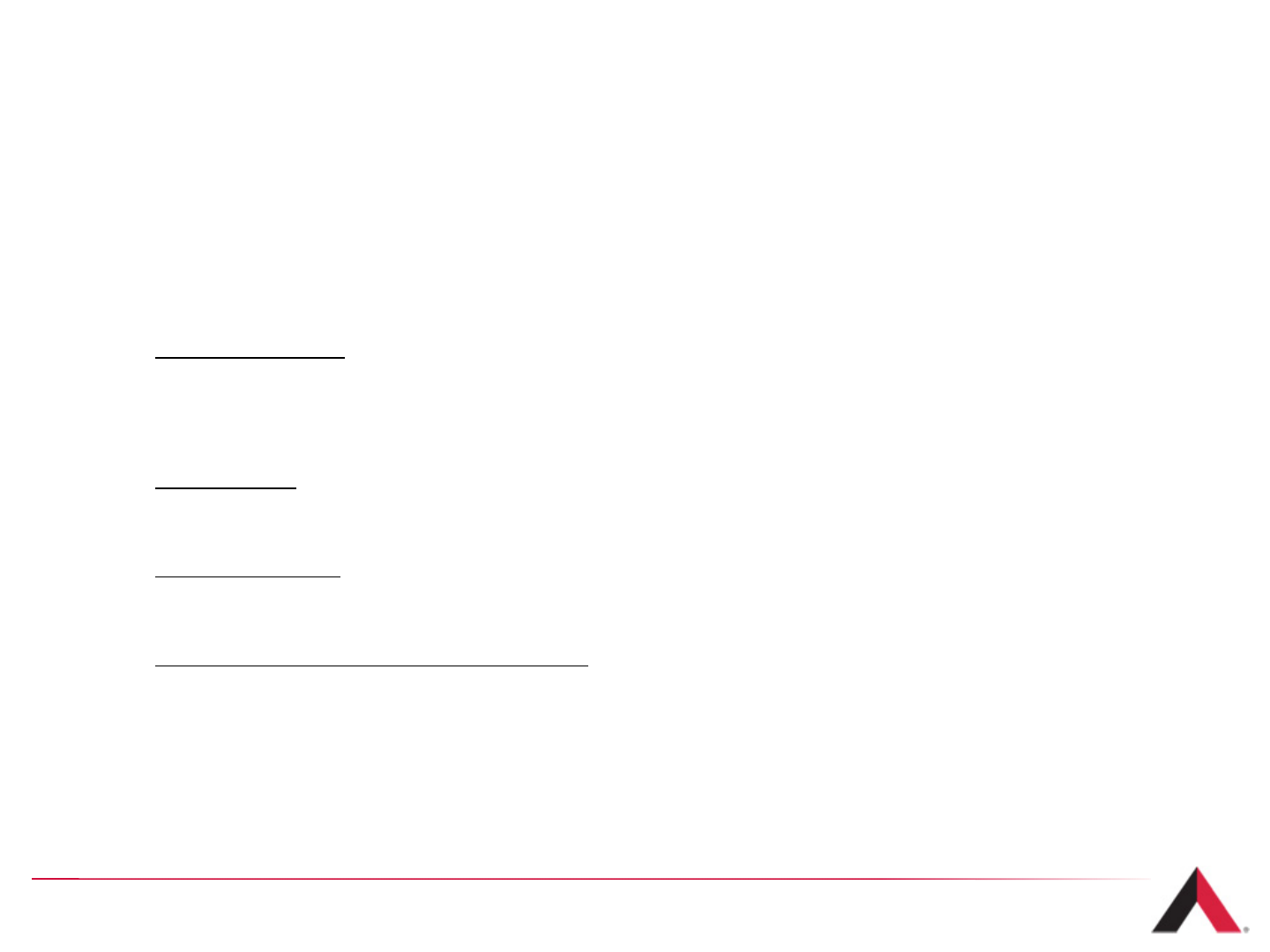

The Morphology View

Morphology is a useful metric to segment tower locations, varying from dense urban

locations to rural locations

Morphologies defined as population density within 1.5km of site location

% of U.S. Area <1% <1% 1% 97%

% of U.S.

Population 3% 13% 54% 30%

Sources: AV&Co. Analysis; U.S. Census Data

Dense Urban Urban Suburban Rural

Population

Density

(pop / sq. km.)

11,500+ 2,900 – 11,500 230 – 2,900 < 230

Tower

Coverage

Radius

(700MHz frequency)

0.7 km 0.9 km 2.5 km 12.6 km

Morphology

Area Typically

Covered >90% >90% 80% ~30%

Example U.S.

84% of the U.S.

population lives

outside of dense

urban and urban

environments

Towers are the preferred solutions in suburban and rural environments

30

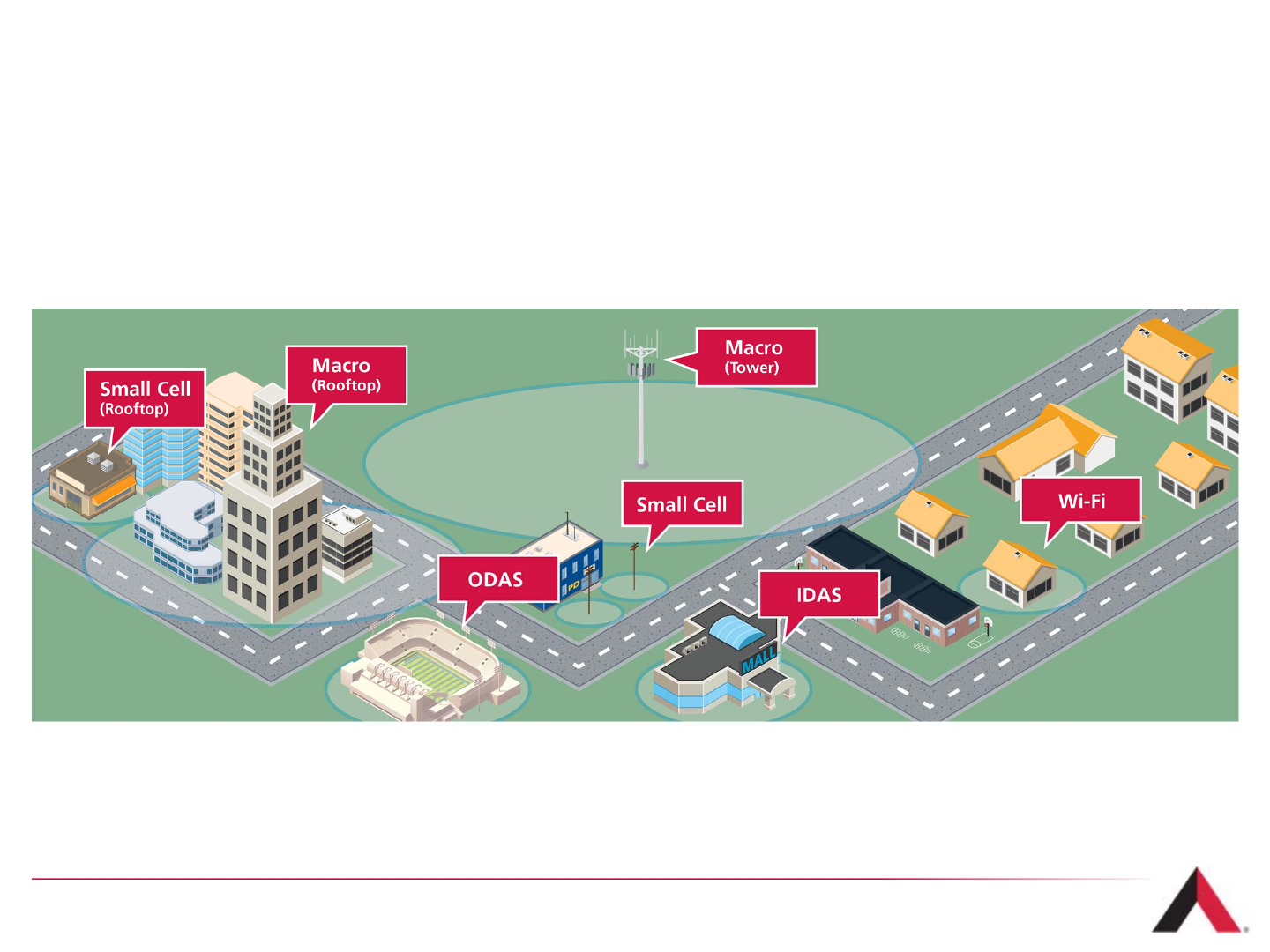

DAS and Rooftops Help Fill the Gaps

31

Indoor DAS

›Provides coverage in indoor

venues, such as malls, casinos

and conference centers

where signals from towers

are insufficient

›Neutral-host networks are

readily accessible to collocation

›AMT is the largest independent

provider of IDAS in the U.S.

Outdoor DAS

›Provides coverage in outdoor

venues, such as racetracks

and stadiums where wireless

usage levels tend to be

extremely concentrated

›Allows for multiple carriers to

leverage single installation

›AMT has partnered with

NASCAR and other venues to

install Outdooor DAS systems

Rooftops

›Predominantly located in dense

urban areas where towers

cannot be installed

›Used in combination with DAS

and Wi-Fi to provide coverage

to concentrated user base

›AMT has access to over 22,000

rooftops throughout the country

Indoor and Outdoor Distributed Antenna Systems (IDAS/ODAS) and Rooftop locations help to

provide coverage in areas where macro tower sites are not available.

Network Design of the Future

Heterogeneous Networks (HetNets)

Network deployments will consist of multiple layers—traditional macro cell towers

provide a blanket of coverage, while underneath this umbrella, a combination of

other technologies are deployed to increase network capacity, particularly in

dense urban areas.

›Macro sites will continue to provide wide area coverage for high mobility users and are the core of

wireless networks

›Multiple solutions including DAS, Rooftops, Wi-Fi and Small Cell networks will complement the coverage

provided by towers

32

U.S. Demand Drivers

Section 4

33

Carrier Lease / Build Decision(1)

›Significant economic incentive exists for carriers to choose a collocation model over building

their own site

›Significant time to market advantage from leasing space on an existing tower site

›Building a site may involve years of work to secure ground interests and zoning approvals

An Example

›Present value of carrier network build-out alternatives

›Carrier Build Scenario

›$225,000 construction cost, $1,250 monthly operating expenses with 3% annual escalator,

9% Weighted Average Cost of Capital (WACC)

›Tower Lease Scenario

›$1,800 monthly lease with 3.5% annual escalator, 9% WACC

34

Term Carrier Build Tower Lease Savings

5 years $286,638 $89,575 $197,062

10 years $333,798 $158,720 $174,359

15 years $368,070 $212,094 $155,976

20 years $394,433 $253,293 $141,140

(1) For illustrative purposes only. Does not reflect any American Tower financial data.

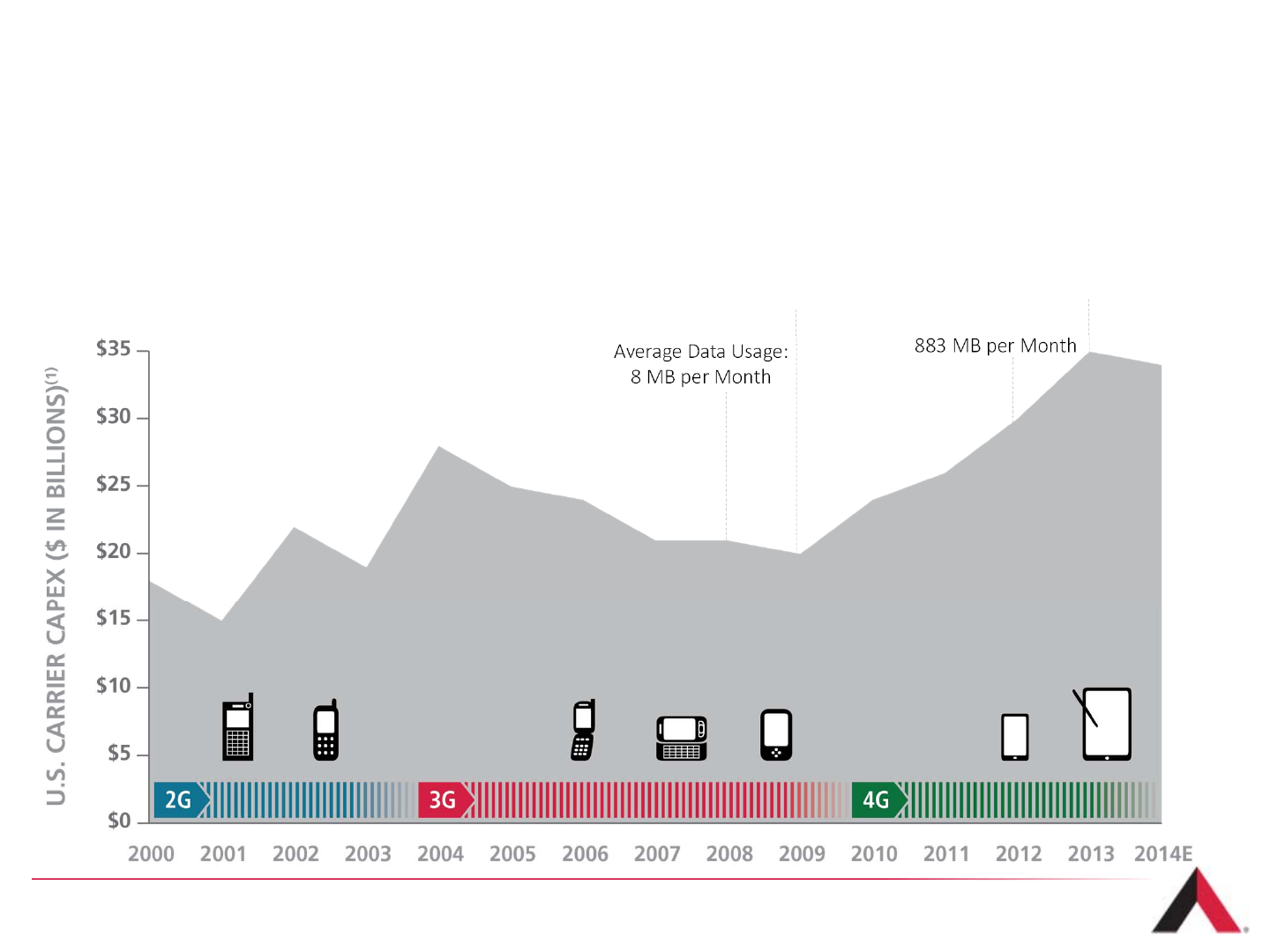

U.S. Wireless Industry Trends

Over the last decade, advancing technology, rising device penetration and

ramping data usage have led to increased levels of carrier capital expenditures.

35

Sources: Wall Street Research and AV & Co. Analysis

AverageDataUsage:

25 MBperMonth

AverageDataUsage:

1,214MBperMonth

AverageDataUsage:

883MBperMonth

AverageDataUsage:

8MBperMonth

21

883

76

1,332

4,556

29

1,214

95

2,014

5,183

Feature Phone Smartphone M2M Module Tablets Laptops

Year End Mobile Data Usage by Device

U.S. Estimates

(MB per Months)

2012

2013

36

Mobile Network Usage

Handset and Data Estimates

Mobile data usage continues to increase as advanced device penetration rises.

Sources: Altman-Vilandrie & Company analysis and Cisco VNI Mobile Forecast, 2012 and 2013.

42X

63X

217X

42X

69X

178X

4G Adoption – Projected Growth

2013 - 2018

13% 7%

62%

41%

26%

52%

2013 2018

Percent of Total Mobile Connections

U.S. Estimates

2G 3G 4G

37

4G connections are expected to grow at a 28% compound annual growth rate between 2013-

2018, while 2G and 3G connections are projected to decline

Source: 2013 Cisco VNI Mobile Forecast Highlights, 2013 - 2018.

3x3x

U.S. Rapid Wireless Data Adoption

Wireless data consumption is forecasted to grow nearly 10x over just five years.

38

(1) 1 petabyte = ~1.049 x 106gigabytes

(2) Macro supplement

Source: 2013 Cisco VNI Mobile Forecast Highlights, 2013 - 2018.

169

1179

17

319

2013 2018

Macro Network Macro Supplement(2)

Macro Network

Traffic Growth:

Nearly 50% CAGR

The vast majority of mobile data traffic continues to be carried over macro tower networks.

U.S. Mobile Data Traffic Forecast

Petabytes per Month(1)

Network Investment by U.S. Carriers (1)

39

(1) Source: Wall Street Research. Capital spending in $ billions.

$-

$5

$10

$15

$20

$25

$30

$35

2007 2008 2009 2010 2011 2012 2013 2014E

Verizon Wireless AT&T Sprint T-Mobile Others

To keep up with the rapid growth in wireless data usage, carriers need to invest in networks.

Annual Wireless Carrier Capital Spending

4G Technology Migration Continues

40

›Several carriers have

substantially completed

initial 4G coverage builds

›Several other carriers

are still focused on

initial deployments

›Emphasis on achieving

nationwide coverage

Current

›Overlay network and fill

in coverage gaps based

on usage trends

›Urban investment

complemented by

suburban deployment

›Emphasis on

augmenting network

capacity

2 - 5 Years

›Full network migration

›Deploy 4G across all cell

sites

›Fill in sites needed

based on usage trends to

continue with capacity

goals

5 - 10 Years

The rollout of 4G in the U.S. is expected to take the better part of a decade and is expected to

result in long-term, solid demand for communications towers.

VoLTE Adoption Requires More Towers

41

Voice service is currently delivered mainly over 2G and 3G networks while data is

transmitted using 4G/LTE networks. Carriers have now deployed or are deploying

“voice over LTE” or VoLTE to move voice transmission to 4G/LTE networks.

Higher spectral efficiency than

2G/3G for delivering voice

Allows 2G/3G spectrum to be

refarmed to LTE

Reduces opex of maintaining distinct

voice and data networks

Potential for higher quality calls

Simultaneous voice and data

possible (not available on CDMA-LTE

phones today)

Increased battery life for LTE-only

phones vs. dual-radio CDMA-LTE

phones

›Increased cellsite densification

compared to LTE data-only networks

•Example: Moving from a network

designed for data-only (i.e. no voice

support at all) to VoLTE on 700 MHz

spectrum could require ~20% more

cell sites

Benefits of VoLTE

Requirements for VoLTE

Why does VoLTE require network densification?

Voice delivered with quality of service requirements (QoS)

has more stringent capacity requirements than “pure-data”

(e.g. browsing) – this is much more pronounced on the typical

cell edge, where a data session can degrade to a point (but a

voice call can’t)

Data

Session:

VoLTE

Session:

Higher throughput, high

efficiency modulation

scheme used

Lower throughput, more

robust (but less efficient)

modulation scheme used

Capacity requirements for a voice call with some minimum QoS don’t

change whether close to cell site or at cell edge

Source: Altman Vilandrie & Company

International Demand Drivers

Section 5

42

Stages of Global Wireless Market Development

43

Source: Altman Vilandrie & Company

(1) Figure above includes assets in Panama which were sold during Q3 2014.

Our International Markets are in diverse stages of wireless technology deployments

Emerging Rapidly Evolving Advanced(1)

›Nationwide wireless voice

coverage build-

outs continue, with many

areas having no access

to reliable service

›Recent and upcoming

spectrum auctions help

to catalyze incremental

network investment

›Recent and upcoming

spectrum auctions help

to catalyze incremental

network investment

International Wireless Markets

Diverse Demand Drivers

44

›Wireless penetration

continues to increase,

and improving network

quality is key for carriers

to add customers

›Increasing penetration

of smartphones and

other wireless devices

xxx

›Exploding mobile

video/gaming usage,

next generation voice

technology over 4G and

connected homes and

vehicles expected to

drive additional demand

›Lack of fixed-line

infrastructure makes

mobile the cost-

effective choice

for communication

›Carriers are continuing to

invest in denser

3G networks as

usage increases with

initial 4G builds

underway

›4G network coverage

build-outs underway with

densification initiatives

expected to accelerate

over next several years

Coverage Technology Wireless Penetration

Emerging

Rapidly

Evolving

Advanced

Additional International Market Information

45

For more detailed information about our international markets, please refer to the “International

Market Overview” presentation located at:

www.americantower.com/corporateus/investor-relations/company-industry-resources

American Tower Overview

Section 5

46

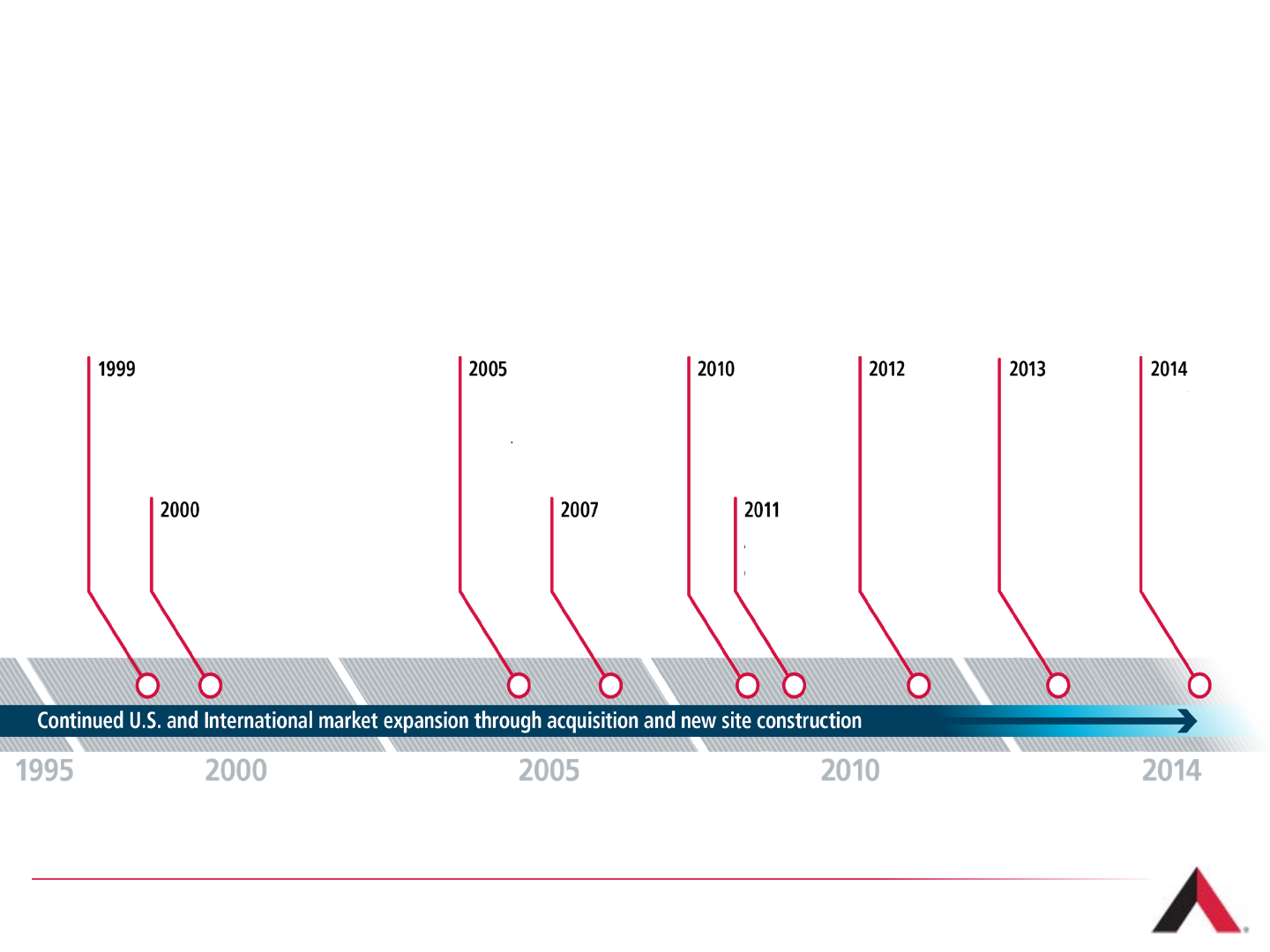

Our History

American Tower (NYSE: AMT) is a leading independent owner, operator and

developer of broadcast and wireless communications real estate.

›Global headquarters located in Boston, Massachusetts

›Global portfolio includes approximately 69,000 owned sites(1)

47

(1) As of June 30, 2014.

American Tower

enters Chile,

Colombia and

Peru

American

Tower enters

Ghana and

South Africa

American Tower

enters Mexico

American Tower

enters Brazil

Merger in the U.S.

with Spectrasite, Inc.

American Tower

enters India

American Tower

begins operating

as a REIT

American

Tower enters

Germany and

Uganda

American Tower

enters Costa

Rica and

Panama

American

Tower acquires

Global Tower

Partners

American

Tower acquires

Richland

Towers

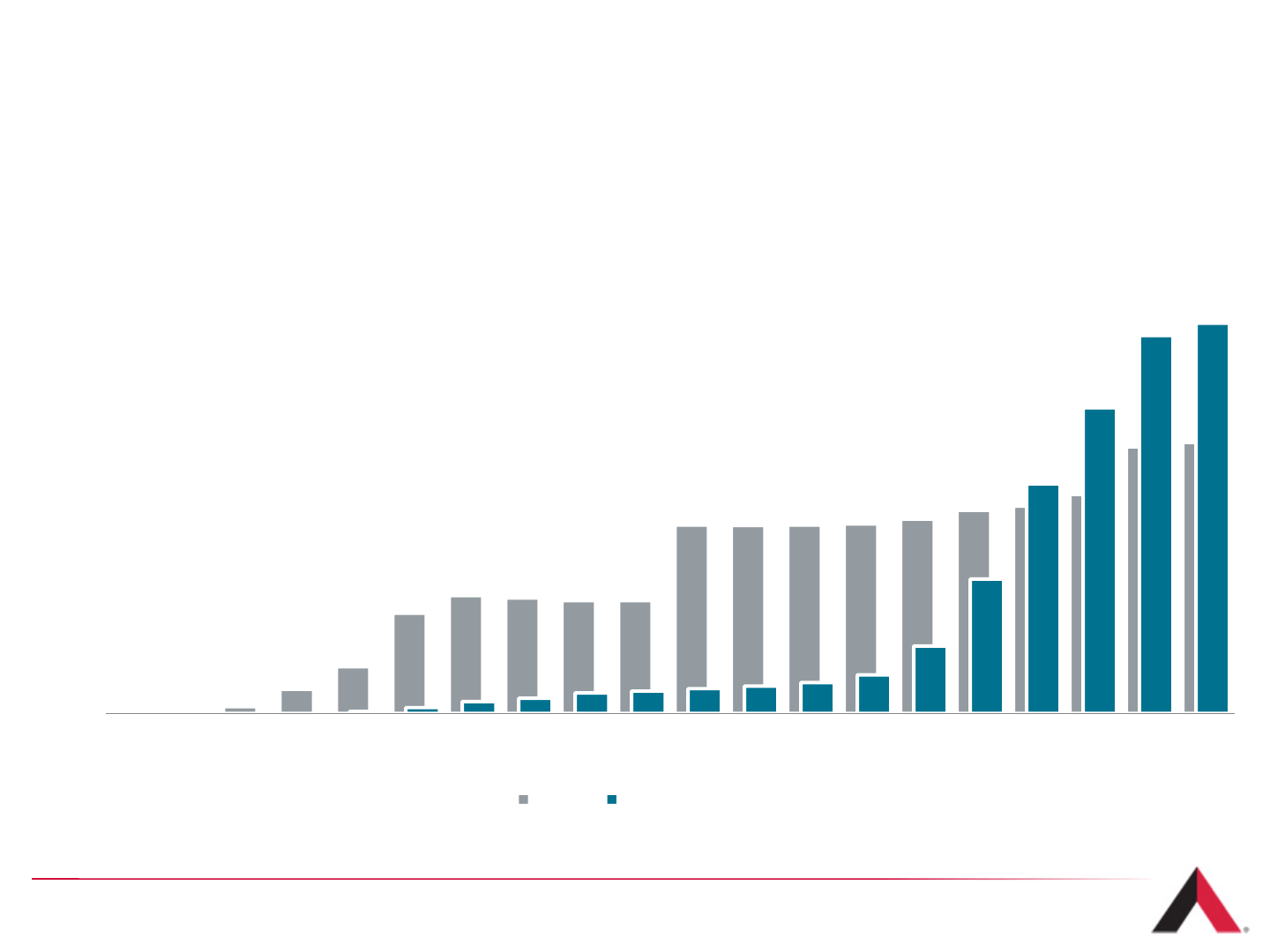

Portfolio of Approximately 69,000 Towers

48

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

U.S. International

Tower Count as of June 30, 2014(1)

(1) Excludes DAS Networks.

Our Global Presence(1)

49

U.S.

Mexico

Colombia

Peru

Chile

Brazil

South Africa

Ghana

Uganda

India

Germany

Costa Rica

Global Tower Count:

2,800+

Global Employees

(1) As of June 30, 2014. Pro Forma for sale of Panama’s assets during Q3 2014.

28,000+

460

8,600+

490+

1,100+

3,500+

6,900+

1,200+

2,000+

1,900+

1,900+

12,000+

69,000+

Total Sites

1,400+

U.S. Employees

12

Countries

Diversification Strategy Driving Strong Organic Growth

50

8% 7% 9% 10%

8%

14% 14%

16%

2011 2012 2013 1H14

Organic

Core Growth

(in Revenue)

›Our top 10 tenants are expected to invest over $40 billion(2) in wireless capex globally during 2014

›Our ~$23 billion of non-cancellable tenant lease revenue represents 7x our 2013 revenue

›Our disciplined investments and portfolio diversification strategy is driving an acceleration of

Organic Core Growth in revenue

~41%

~59%

Communications Sites(1)

~66%

~34%

Revenue(1)

(1) Characteristics for the quarter ended June 30, 2014

(2) Source: Wall Street Research

Domestic International

Definitions are provided at the end of this presentation.

Global Expansion Considerations

Three Pillar Analysis Approach to New Market Expansion

51

Country Wireless Market Opportunity / Counterparty

›Political stability and rule of law

›Solid macro-economic

fundamentals

›Business environment

›Property rights

›Regulatory environment

›Competitive wireless market

›Three or more

wireless carriers

›Stage of wireless maturity

›Voice penetration

›Data network deployments

›Build-to-suit, merger, acquisition

or joint venture

›Evaluate options based on their

economic benefits as well as

structure

›Future potential

investment/expansion within

region

Long-Term Strategy

52

American Tower remains focused on driving AFFO per share growth while increasing

return on invested capital.

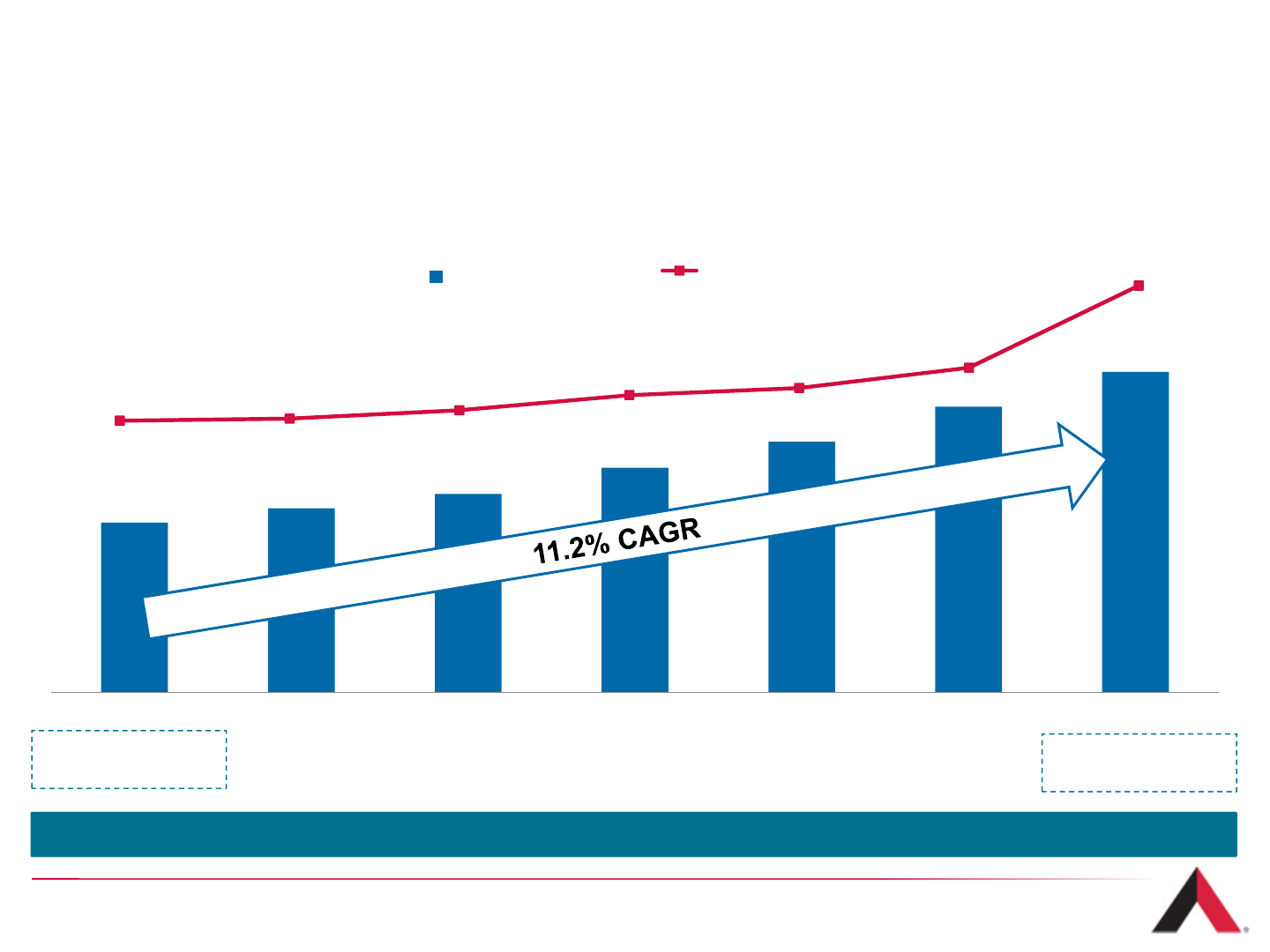

Consistent Revenue Growth

Total Rental & Management Revenue

($ in Millions)

53

$1,426

$3,287

2007 2008 2009 2010 2011 2012 2013

Strong organic core growth and contributions from new assets lead to continued growth in

revenue, both in the U.S. and internationally.

(1)

(1) Reflects the acquisition of Global Tower Partners as of October 1, 2013.

$890 $965 $1,041 $1,178 $1,314

$1,497

$1,680

2007 2008 2009 2010 2011 2012 2013

Operating Profit

19,606

27,739

Tower Count

Strong Domestic Operating Profit Growth

54

Domestic Rental & Management Operating Profit

($ in Millions)

~2.4 Tenants per

Tower ~2.5 Tenants per

Tower

Operating Profit growth has been driven primarily by organic new business commencements.

Definitions are provided at the end of this presentation.

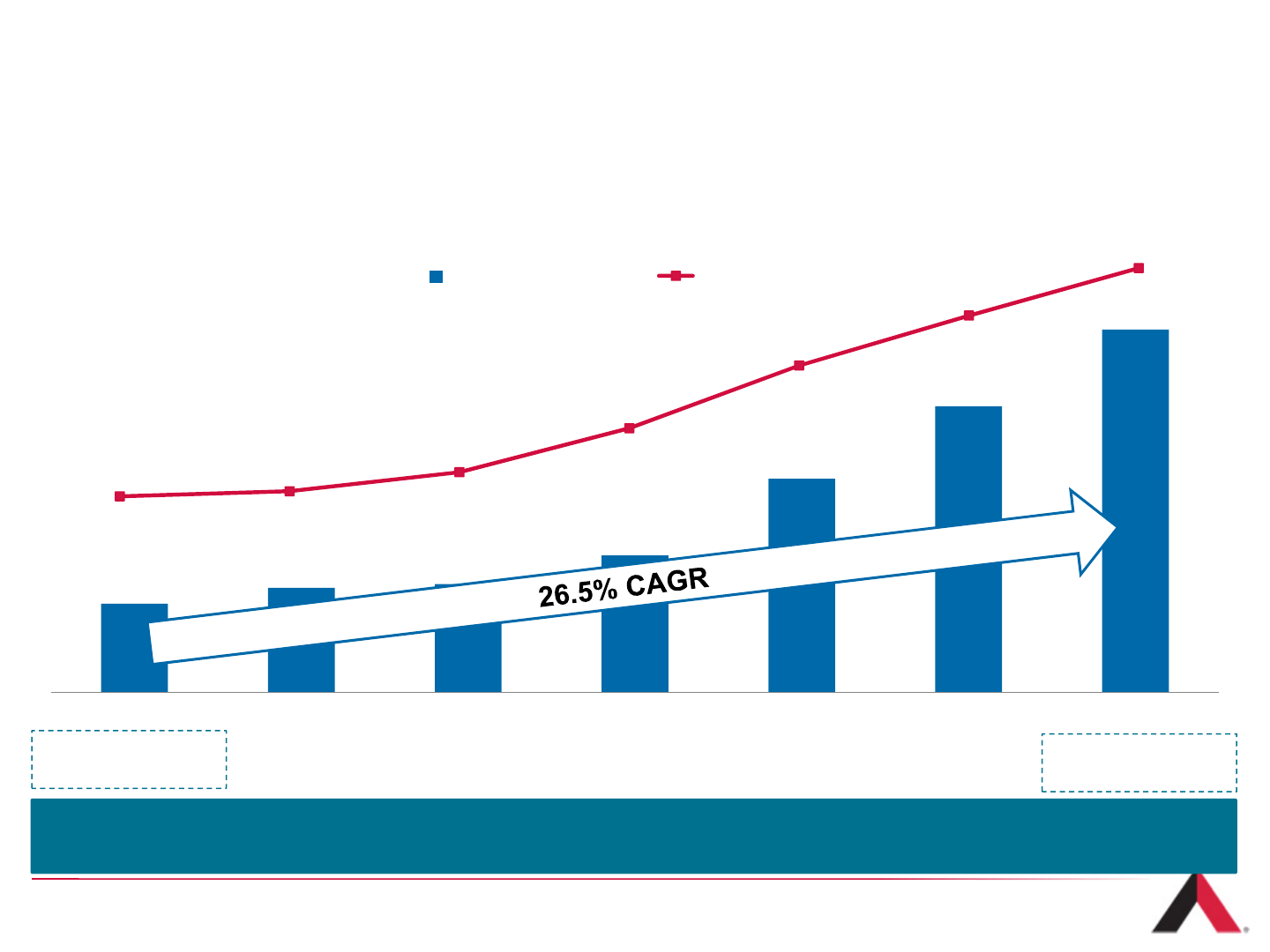

$140 $166 $172 $217

$338

$453

$574

2007 2008 2009 2010 2011 2012 2013

Operating Profit

3,201

39,330

Tower Count

Strong International Operating Profit Growth

55

International Rental & Management Operating Profit

($ in Millions)

~1.8 Tenants per

Tower ~1.6 Tenants per

Tower

Acquisition of primarily single tenant towers positions our international business well for future

organic leasing growth.

Definitions are provided at the end of this presentation.

$979

$2,176

2007 2008 2009 2010 2011 2012 2013

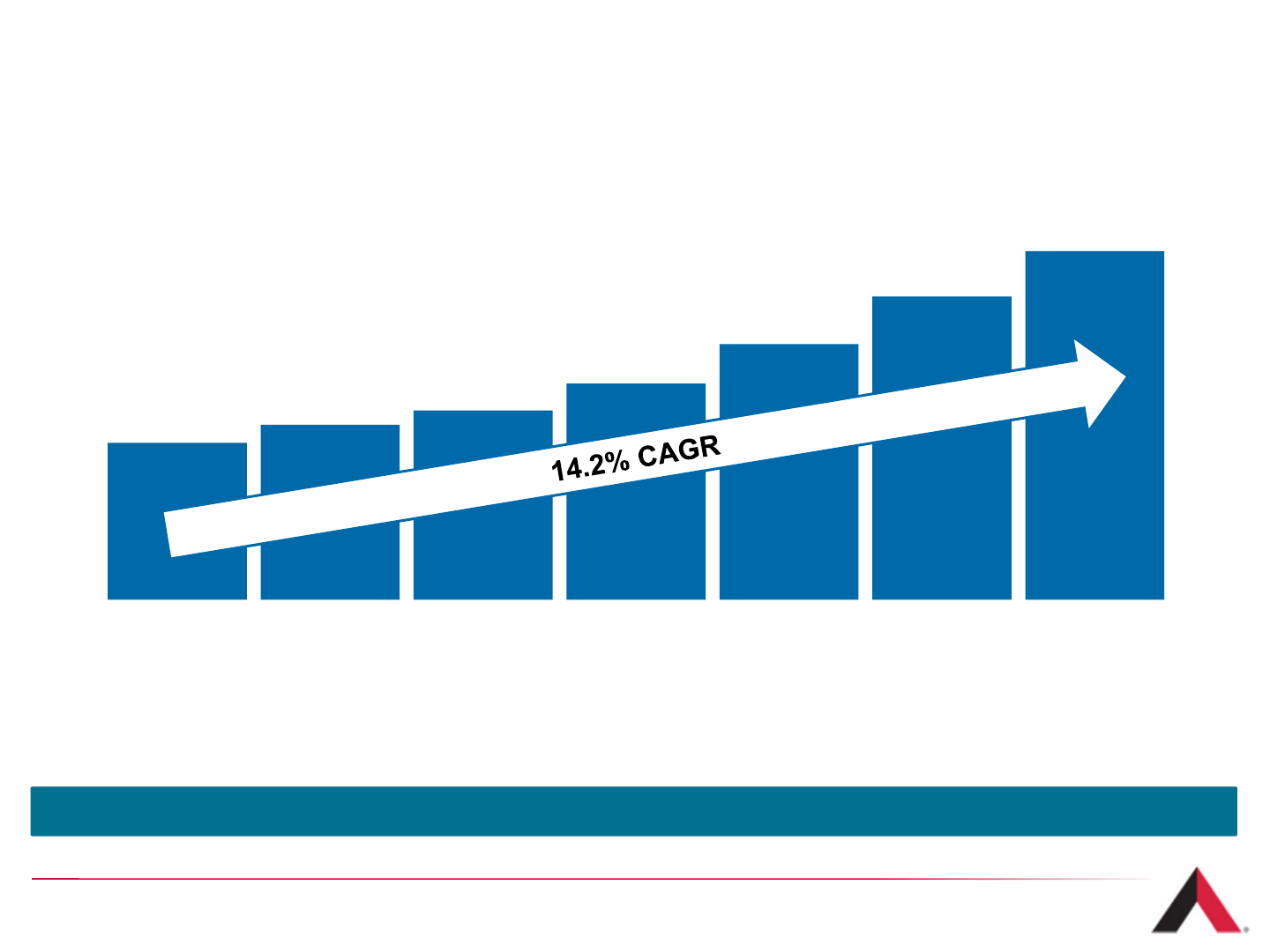

Consistent Adjusted EBITDA Growth

Adjusted EBITDA(1)

($ in Millions)

56

(1) Definitions and reconciliations to GAAP measures are provided at the end of this presentation.

Strong growth with maintenance of high margins

$642

$1,470

2007 2008 2009 2010 2011 2012 2013

Consistent AFFO Growth

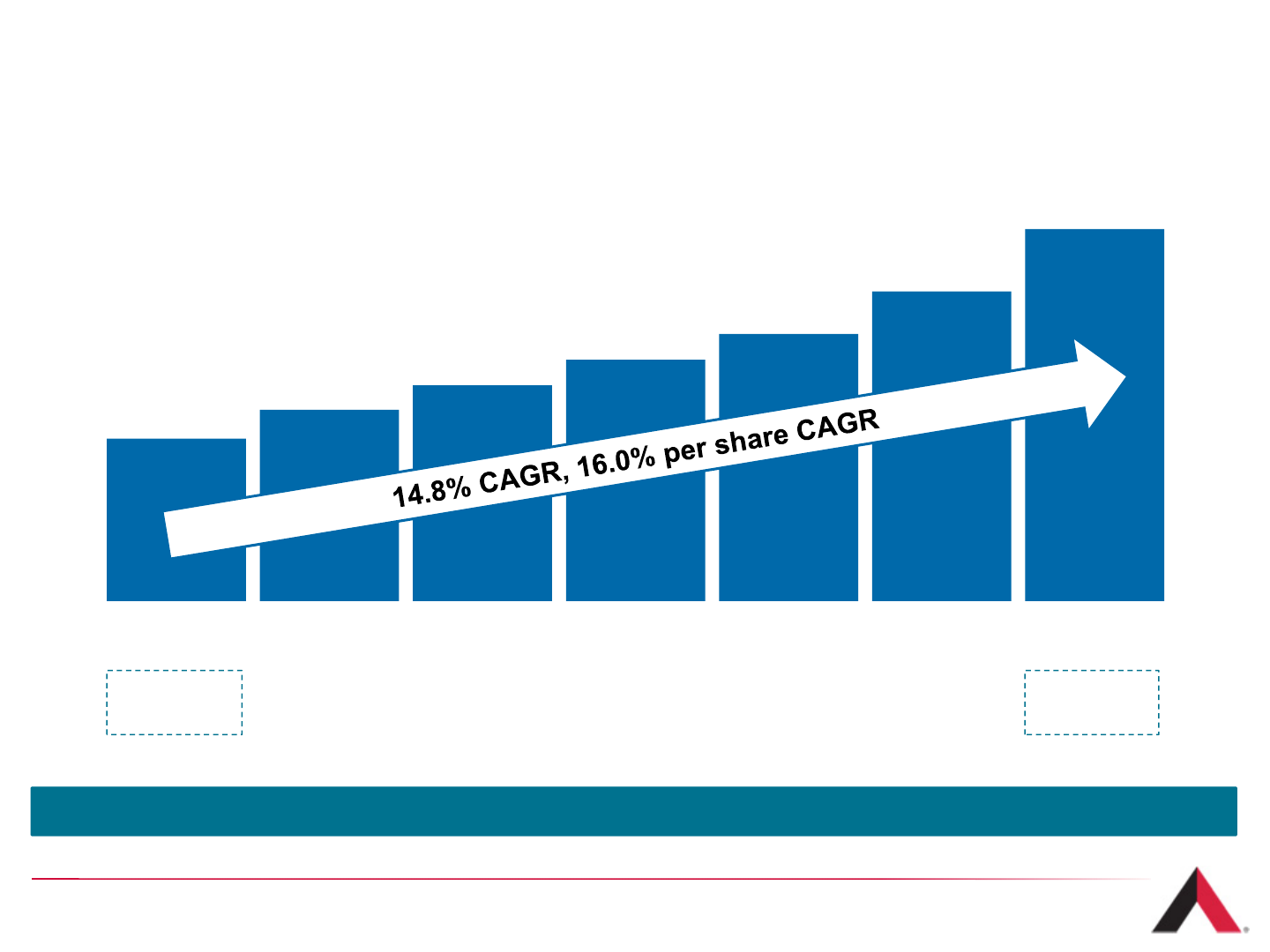

Adjusted Funds From Operations

($ in Millions, except per share amounts)

57

$3.68

Per Share

$1.51

Per Share

Targeting to double 2012 AFFO per Share by 2017

Definitions are provided at the end of this presentation.

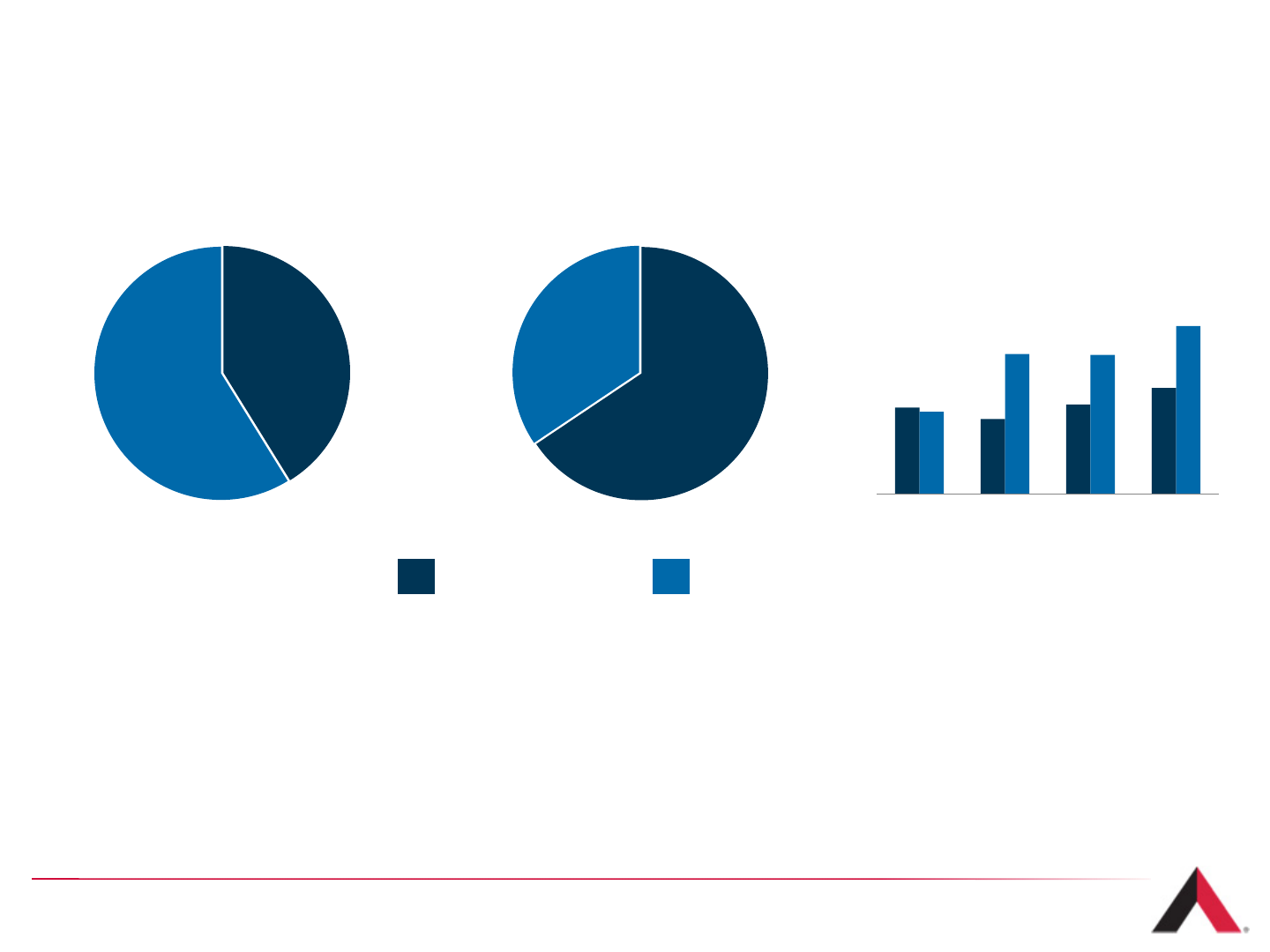

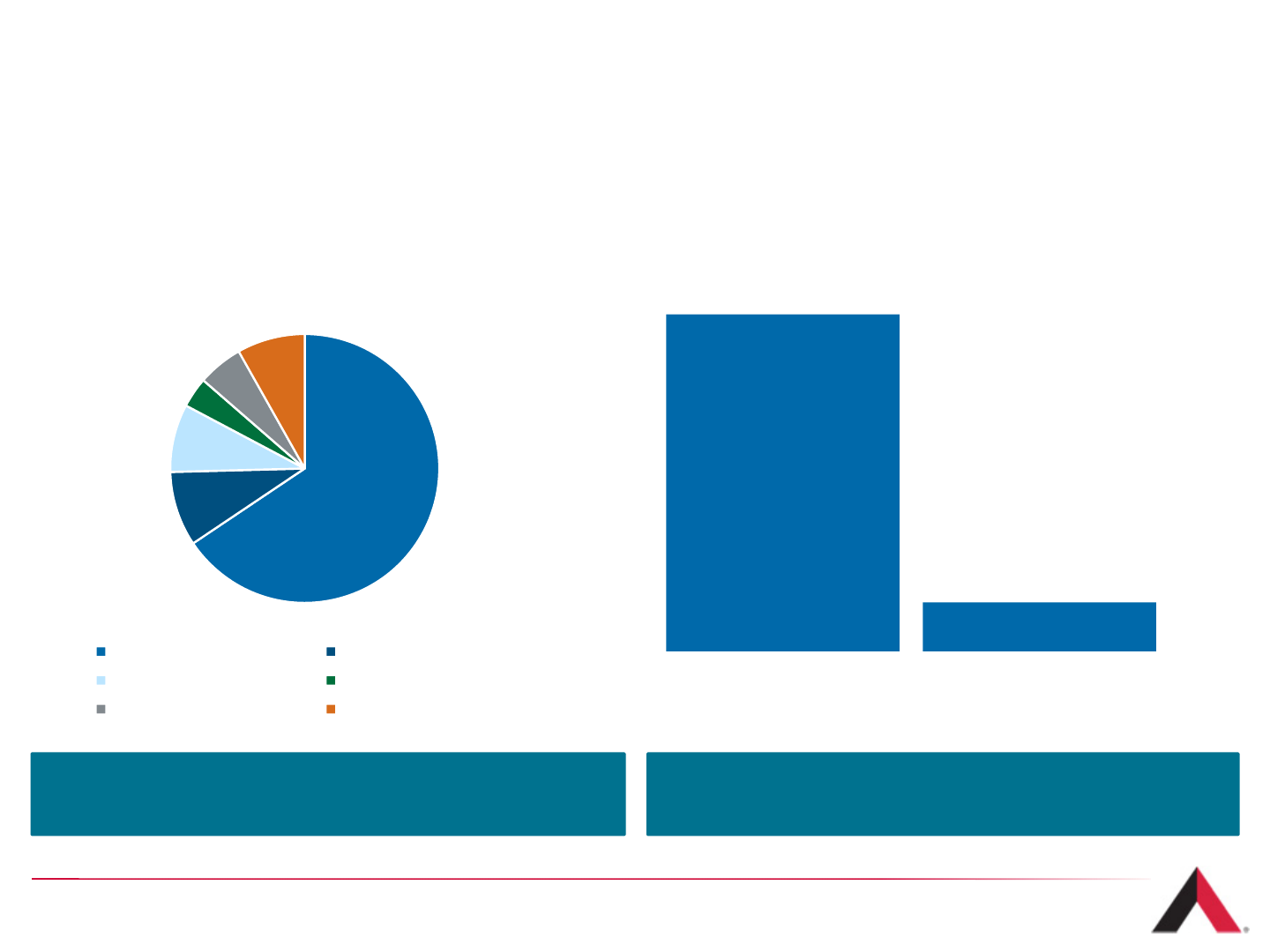

Geographically Diverse, Long-Term Revenue Base

Rental and Management Revenue

by Region(1) Non-Cancellable Tenant Lease Revenue(1)

58

We have diversified our revenue base into

international markets Long-term contracts result in significant,

non-cancellable tenant lease revenue

(1) Characteristics for the quarter ended June 30, 2014.

(2) Includes Chile, Colombia, Peru, Costa Rica and Panama.

(3) Figure above includes assets in Panama which sold during Q3 2014.

66%

9%

8%

4%

5% 8%

Total Revenue by Market

US Mexico

Brazil Other Latin America

India EMEA

~$23B

$3.3B

Non-Cancellable Tenant

Lease Revenue 2013 Rental &

Management Revenue

Non-cancellable

tenant lease

revenue of almost

7x our 2013 rental

& management

segment revenue

(2)(3)

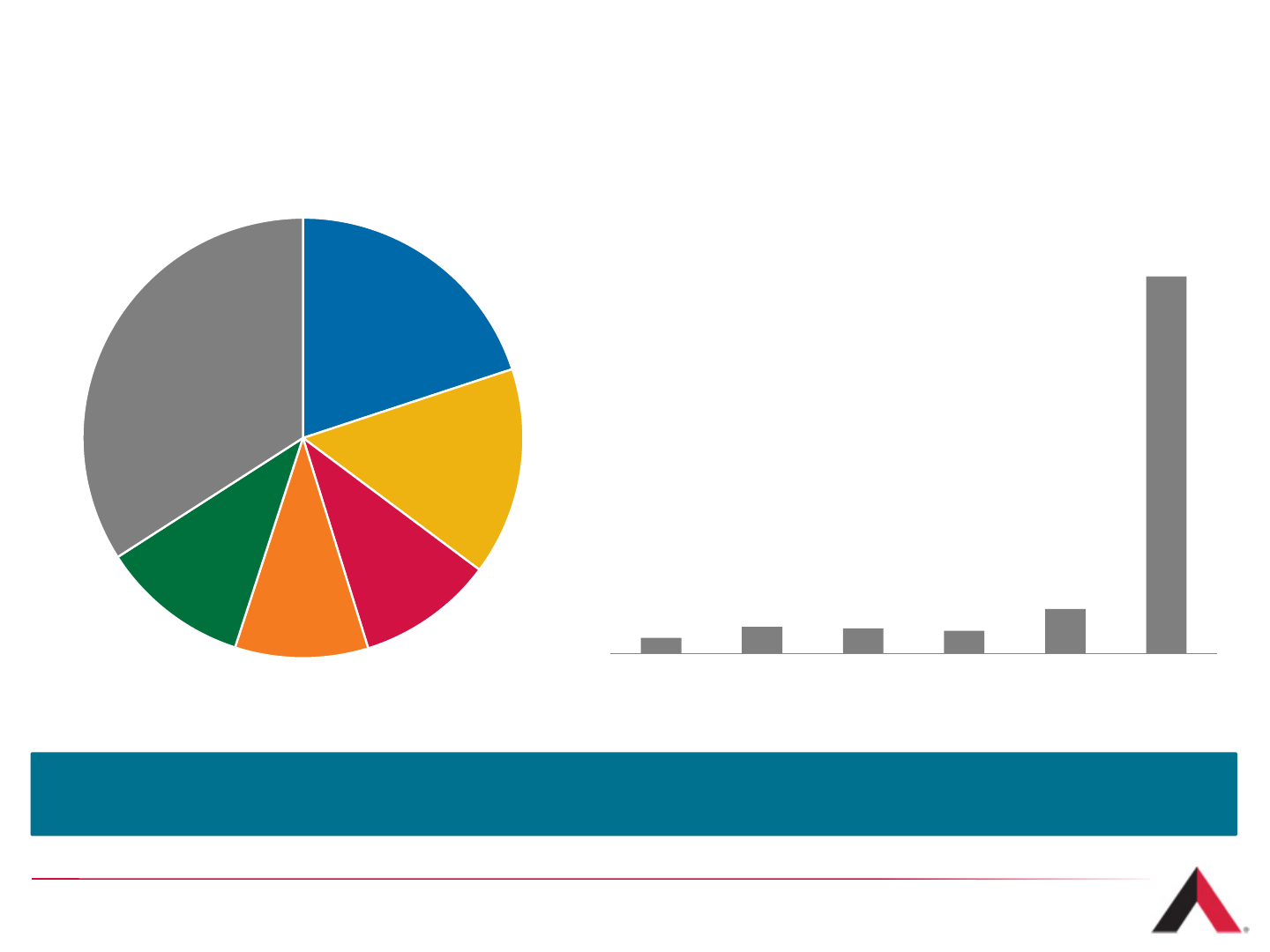

Strong Tenant Profile

Tower Revenue by Customer (1)

59

(1) Characteristics for the quarter ended June 30, 2014.

AT&T

20%

Sprint-Nextel

15%

Verizon

10%

T-Mobile

10%

Other Domestic

11%

International

34%

3% 5% 5% 4% 9%

74%

2014 2015 2016 2017 2018 2019+

Global Tenant Lease Renewal Schedule(1)

~50% from Investment Grade Tenants

American Tower’s customer base includes the leading wireless carriers in the U.S. as well as

a number of large, multinational carriers in our international markets

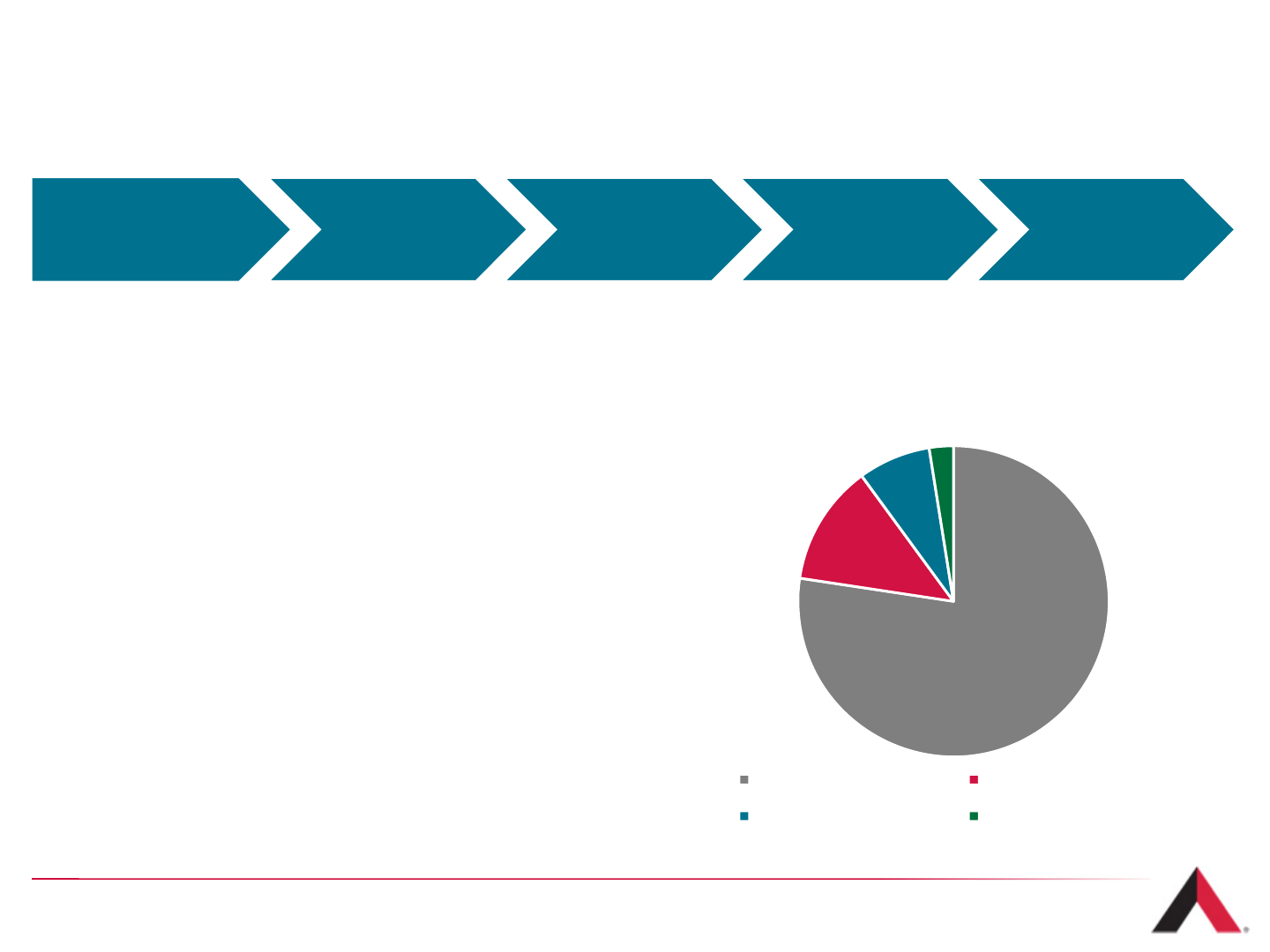

Capital Allocation Priorities

›At least 20% dividend growth expected

›Majority of annual CAPEX budget dedicated

to investing in growth

›Low maintenance capital requirements

›Targeted long-term leverage range continues

to be 3 - 5x

›Consistent deployment of additional capital

towards acquisitions and/or

share repurchases

60

Capital Allocation REIT

Distribution CAPEX Target

Leverage

Range

Opportunistic

Acquisitions

$4,462

$725

$435 $145

Acquisitions Capital Expenditures

REIT Distribution Stock Repurchases

Definitions are provided at the end of this presentation.

2013 Capital Allocation

($ in Millions)

Solid Balance Sheet Position

›Liquidity of ~$3.1 billion as of June 30, 2014

›Expect to de-lever back to within target leverage of 3-5x

range by early 2015

(2) Reflects Net Debt divided by last quarter annualized Adjusted EBITDA.

(3) Pro forma for the $1.5 billion amended and restated revolving credit facility entered into in September 2014, the expiration in September 2014 of the Company’s short-term credit facility entered into in September 2013 and the

Company’s net repayment of $373 million under its 2013 Credit Facility.

Definitions and reconciliations to GAAP measures are provided at the end of this presentation.

4.0x 4.0x 4.1x

5.9x 5.5x 5.0x

1Q13 2Q13 3Q13 4Q13 1Q14 2Q14

Net Leverage Ratio

61

(3)

(2)

(1) Reflects principal balances as of June 30, 2014, pro forma for (i) additional net repayments of $373 million under its 2013 Credit Facility, (ii) the purchase of the $35 million Colombian shareholder loan in July 2014, (iii) the offering of $650 million of senior

notes due 2021 in August 2014, (iv) the repayment in August 2014 of $250 million of securitized notes acquired in connection with the Company’s acquisition of MIP Tower Holdings LLC, (v) the expiration of the Company’s $1 billion short-term credit facility in

September 2014, and (vi) the $1.5 billion amended and restated revolving credit facility entered into in September 2014. Excludes $523 million of other debt, including international loans and capital lease obligations.

$600 $500 $1,000 $1,300 $700 $1,150 $700 $1,000 $1,000

$715 $165

$745 $180

$129

$1,300

$ 410 $ 1,500

$299

$1,590

$1,500

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Debt Maturity Schedule ($ millions) (1)

Unsecured Notes Securitizations Unsecured Bank Debt Other Revolver Availability

The American Tower Difference

Our Vision

To be the premier wireless infrastructure provider in the eyes of our employees, customers and

communities, enabling the deployment of advanced services that make wireless communication

possible everywhere.

Our Mission

›Create a customer-focused team environment where employees are respected

and innovation is a state of mind.

›Deliver the highest level of customer service while providing safe,

compliant and quality tower sites.

›Exceed yearly performance goals to create enduring success.

›Pursue meaningful opportunities to grow and strengthen the Company.

62

Commitment to Corporate Responsibility

63

Philanthropy

We take great pride in how our organization, led by teams of

employees, demonstrates our commitment to the communities

where we live and work.

Ethics

Upholding the highest standard of corporate values is critical to

the success of our business. Starting with our executive management

team, our focus on ethical behavior lays the foundation of our

Company’s culture.

Environmental Responsibility

The promotion of shared infrastructure to customers is fundamentally

green. Internally, our environmental awareness programs, focused on

minimizing the impact of materials used in our daily operations, help

ensure that we are doing our part to care for the environment in our

offices and in the field.

People

American Tower’s diverse teams reach far across the globe and our

employees, no matter where they are, understand that respect,

inclusion, teamwork and communication are the cornerstones of

our organization.

Our Core Principles

›Understand our customers' needs and satisfy them.

Work as a team to build lasting customer relationships by understanding their requirements and

exceeding their expectations.

›Hire good people and empower them.

Place the right people in the right positions, develop their talent and skills and provide

opportunities for them to influence outcomes.

›Focus on solutions, not problems.

Begin with the end in mind and involve the right people. Stay positive and work together for

desired results.

›Do what we say we're going to do.

Set realistic expectations. Communicate clearly. Be accountable for your actions.

›Have fun.

Recognize our success, celebrate together and contribute to a positive work environment.

›Play to win.

Put integrity first. Be competitive. Work together as a team to exceed expectations.

64

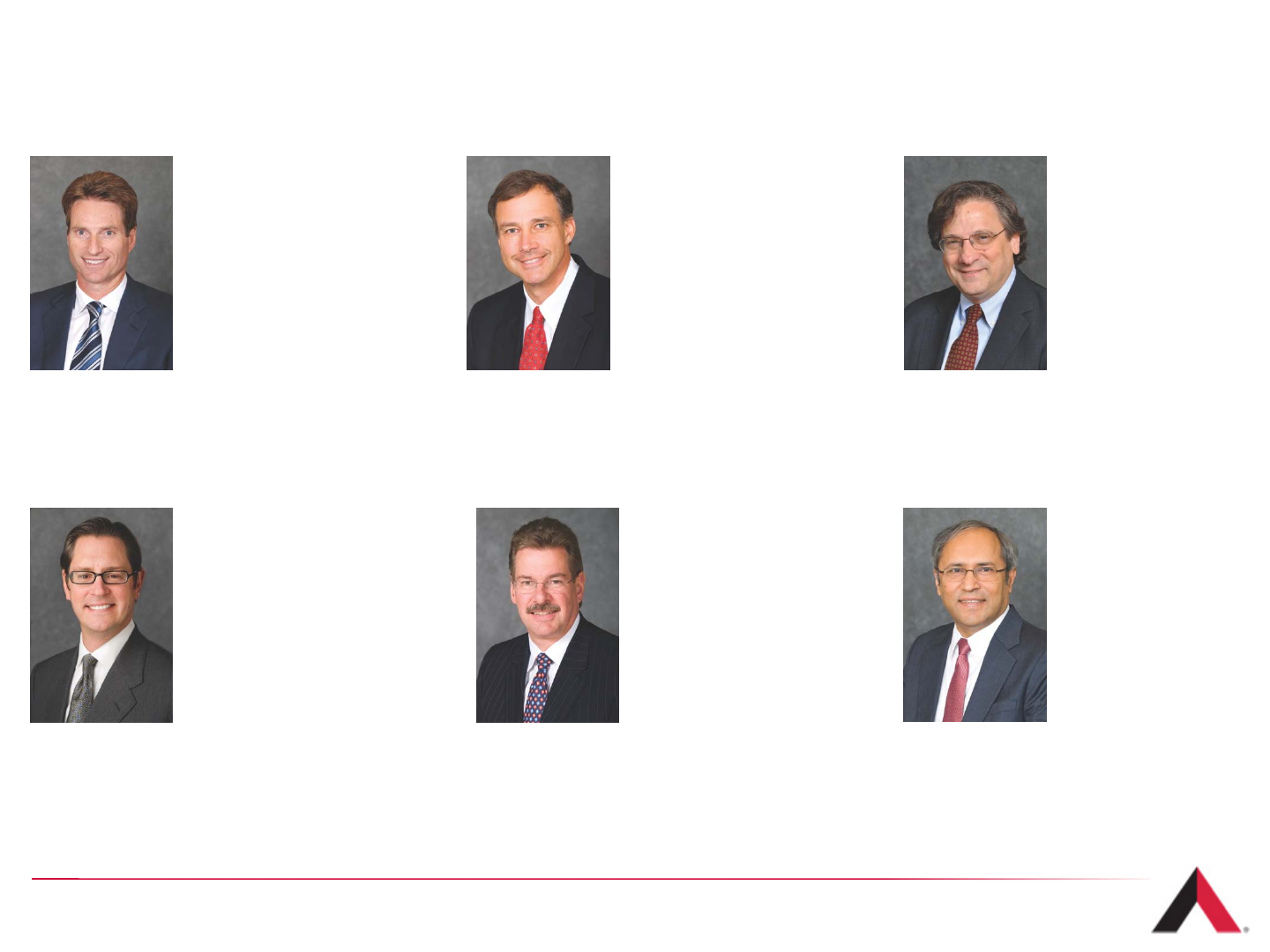

Executive Team

Tom Bartlett

Executive Vice President & Chief

Financial Officer

Ed DiSanto

Executive Vice President, Chief

Administrative Officer & General

Counsel

Hal Hess

Executive Vice President,

International Operations &

President, Latin America &

EMEA

Steven Marshall

Executive Vice President &

President, U.S. Tower Division

Amit Sharma

Executive Vice President

& President, Asia

65

Jim Taiclet

Chairman, President & Chief

Executive Officer

65

Summary

›Strong business model, independent of economic cyclicality

›Leveraging secular growth in global wireless

›High visibility to drivers of revenue and profitability for 2014 and beyond

›Significant investment capacity to fuel strong future growth

›Prudently-maintained balance sheet provides the foundation for future success

›On track to double AFFO/share from 2012 levels by 2017

66

Additional Information

67

For more information on the tower industry and American Tower, please refer to the various

presentations by visiting:

www.americantower.com/corporateus/investor-relations/company-industry-resources

www.americantower.com/corporateus/investor-relations/earnings-materials/index.htm

In addition, please feel free to contact our investor relations team if you have further questions.

Leah Stearns

Vice President,

Investor Relations and Treasurer

617-587-7921

leah.stearns@americantower.com

Igor Khislavsky

Sr. Manager,

Investor Relations

617-587-7915

igor.khislavsky@americantower.com

Kristyn Farahmand

Manager,

Investor Relations

617-375-7545

kristyn.farahmand@americantower.com

Investor Relations Contacts

Margo Williams

Analyst,

Investor Relations

617-375-7589

Margo.williams@americantower.com

Definitions

Adjusted EBITDA: Net income before Income (loss) on discontinued operations, net; Income (loss) from equity method investments;

Income tax provision (benefit); Other income (expense); Loss on retirement of long-term obligations; Interest expense; Interest income; Other

operating income (expense); Depreciation, amortization and accretion; and Stock-based compensation expense.

Adjusted EBITDA Margin: the percentage that results from dividing Adjusted EBITDA by total revenue.

Adjusted Funds From Operations, or AFFO: NAREIT Funds From Operations before (i) straight-line revenue and expense, (ii) stock-

based compensation expense, (iii) the non-cash portion of our tax provision, (iv) non-real estate related depreciation, amortization and

accretion, (v) amortization of deferred financing costs, capitalized interest, debt discounts and premiums and long-term deferred interest

charges, (vi) other income (expense), (vii) loss on retirement of long-term obligations, (viii) other operating income (expense), and

adjustments for (ix) unconsolidated affiliates, and (x) noncontrolling interest, less cash payments related to capital improvements and cash

payments related to corporate capital expenditures.

AFFO per Share: Adjusted Funds From Operations divided by the diluted weighted average common shares outstanding.

Churn: Revenue lost when a tenant cancels or does not renew its lease, and in limited circumstances, such as a tenant bankruptcy,

reductions in lease rates on existing leases.

Core Growth: (Rental and management revenue, Adjusted EBITDA, Gross Margin and Operating Profit) the increase or decrease,

expressed as a percentage, resulting from a comparison of financial results for a current period with corresponding financial results for the

corresponding period in a prior year, in each case, excluding the impact of straight-line revenue and expense recognition, foreign currency

exchange rate fluctuations and material one-time items.

NAREIT FFO: Net income before gains or losses from the sale or disposal of real estate, real estate related impairment charges, real estate

related depreciation, amortization and accretion and dividends declared on preferred stock, and including adjustments for (i) unconsolidated

affiliates and (ii) noncontrolling interest.

NAREIT FFO per Share: Funds From Operations divided by the diluted weighted average common shares outstanding.

Net Leverage Ratio: Net debt (total debt, less cash and cash equivalents) divided by last quarter annualized Adjusted EBITDA.

New Property Core Growth: (Rental and management revenue) the increase or decrease, expressed as a percentage, on the properties

the Company has added to its portfolio since the beginning of the prior period, in each case, excluding the impact of straight-line revenue

and expense recognition, foreign currency exchange rate fluctuations and significant one-time items.

Operating Profit: Gross margin less selling, general, administrative and development expense attributable to the segment, excluding stock-

based compensation expense and corporate expenses. International rental and management segment includes interest income, TV Azteca,

net.

68

Definitions

Operating Profit Margin: Operating profit divided by total revenue.

Organic Core Growth: (Rental and management revenue) the increase or decrease, expressed as a percentage, resulting from a comparison of financial

results for a current period with corresponding financial results for the corresponding period in a prior year, in each case, excluding the impact of straight-

line revenue and expense recognition, foreign currency exchange rate fluctuations, significant one-time items and revenue associated with new properties

that the Company has added to the portfolio since the beginning of the prior period.

Recurring Free Cash Flow: Adjusted EBITDA before straight-line revenue and expense plus interest income less interest expense, cash paid for income

taxes and non-discretionary capital expenditures (redevelopment, capital improvement and corporate capital expenditures).

Recurring Free Cash Flow per Share: Recurring Free Cash Flow divided by the diluted weighted average common shares outstanding.

Segment Gross Margin: segment revenue less segment operating expenses, excluding stock-based compensation expense recorded in costs of

operations; depreciation, amortization and accretion; selling, general, administrative and development expense; and other operating expenses.

International rental and management segment includes interest income, TV Azteca, net.

Segment Gross Margin Conversion Rate: the percentage that results from dividing the change in gross margin by the change in revenue.

Segment Operating Profit: Segment gross margin less segment selling, general, administrative and development expense attributable to the segment,

excluding stock-based compensation expense and corporate expenses. International rental and management segment includes interest income, TV

Azteca, net.

Pass-through Revenues: In several of our international markets we pass through certain operating expenses to our tenants, including in Latin America

where we primarily pass through ground rent expenses, and in India and South Africa, where we primarily pass through fuel costs. We record pass through

as revenue and a corresponding offsetting expense for these events.

Straight-line expenses: We calculate straight-line ground rent expense for our ground leases based on the fixed non-cancellable term of the underlying

ground lease plus all periods, if any, for which failure to renew the lease imposes an economic penalty to us such that renewal appears, at the inception of

the lease, to be reasonably assured. Certain of our tenant leases require us to exercise available renewal options pursuant to the underlying ground lease,

if the tenant exercises its renewal option. For towers with these types of tenant leases at the inception of the ground lease, we calculate our straight-line

ground rent over the term of the ground lease, including all renewal options required to fulfill the tenant lease obligation.

Straight-line revenues: We calculate straight-line rental revenues from our tenants based on the fixed escalation clauses present in non-cancellable

lease agreements, excluding those tied to the Consumer Price Index or other inflation-based indices, and other incentives present in lease agreements with

our tenants. We recognized revenues on a straight-line basis over the fixed, non-cancellable terms of the applicable leases.

69

Reconciliations

70

(Inmillions.Totalsmaynotaddduetorounding.)

RECONCILIATIONOFNETINCOMETOADJUSTED

EBITDA

2007 2008 2009 2010 2011 2012 2013 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14

Netincome $56.6$347.4$247.1$373.6$381.8$594.0$482.2$160.9$84.1$163.2$73.9$193.3$221.7

Loss(income)fromdiscontinuedoperations,net 36.4(111.0) (8.2) (0.0) 0.0$0.0$0.00.00.00.00.00.00.0

Incomefromcontinuingoperations $93.0$236.4$238.9$373.6$381.8$594.0$482.2$160.9$84.1$163.2$73.9$193.3$221.7

Incomefromequitymethodinvestments (0.0) (0.0) (0.0) (0.0) (0.0) ($0.0) $0.00.00.00.00.00.00.0

Incometaxprovision 59.8135.5182.6182.5125.1$107.3$59.519.2(11.4) 15.636.217.621.8

Other(income)expense (20.7) (6.0) (1.3) (0.3) 123.0$38.3$207.5(22.3) 141.729.658.53.716.5

Lossonretirementoflong‐termobligations 35.44.918.21.90.0$0.4$38.735.32.70.00.70.21.3

Interestexpense 235.8253.6249.8246.0311.9$401.7$458.3111.8100.8106.3139.4143.3146.2

Interestincome (10.8) (3.4) (1.7) (5.0) (7.4) ($7.7) ($9.7) (1.7) (1.4) (2.3) (4.2) (2.0) (2.3)

Otheroperatingexpenses 9.211.219.235.958.1$62.2$71.514.35.915.535.913.912.8

Depreciation,amortizationandaccretion 522.9405.3414.6460.7555.5$644.3$800.1185.8184.6184.9244.8245.8245.4

Stock‐basedcompensationexpense 54.654.860.752.647.4$52.0$68.121.017.115.115.024.618.8

ADJUSTEDEBITDA $979.3$1,092.3$1,180.9$1,347.7$1,595.4$1,892.4$2,176.4$524.4$524.0$527.9$600.1$640.5$682.2

Dividedbytotalrevenue $1,456.6 $1,593.5 $1,724.1 $1,985.3 $2,443.5 $2,876.0 $3,361.4 $802.7 $808.8 $807.9 $942.0 $984.1 $1,031.5

ADJUSTEDEBITDAMARGIN 67% 69% 68% 68% 65% 66% 65% 65% 65% 65% 64% 65% 66%

AFFORECONCILIATION (1)

2007 2008 2009 2010 2011 2012 2013 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14

AdjustedEBITDA $979.3$1,092.3$1,180.9$1,347.7$1,595.4$1,892.4$2,176.4$524.4$524.0$527.9$600.1$640.5$682.2

Straight‐linerevenue (69.7) (50.4) (36.3) (105.2) (144.0) (165.8) (147.7) (34.2) (34.4) (37.3) (41.7) (31.2) (33.1)

Straight‐lineexpense 26.727.626.622.331.033.729.77.17.96.38.49.57.9

Cashinterest (227.5) (244.0) (240.4) (237.6) (300.8) (380.6) (435.3) (104.2) (93.4) (99.2) (138.5) (139.9) (143.1)

InterestIncome 10.83.41.75.07.47.79.71.71.42.34.22.02.3

Cashreceived(paid)forincometaxes (2) (35.3) (35.1) (40.2) (36.4) (53.9) (69.3) (51.7) (13.5) (3.6) (6.0) (28.5) (19.1) (16.7)

DividendsDeclaredonpreferredstock ‐‐‐‐‐‐‐‐‐‐‐‐(4.4)

CapitalImprovementCapex (29.2) (32.5) (32.5) (31.4) (60.8) (75.4) (81.2) (15.9) (26.4) (18.7) (20.2) (17.2) (17.2)

CorporateCapex (12.7) (5.6) (8.1) (11.6) (18.7) (20.0) (30.4) (7.5) (9.2) (7.9) (5.8) (5.2) (3.9)

AFFO $642.4$755.8$851.7$952.8$1,055.5$1,222.6$1,469.5$357.8$366.2$367.3$378.2$439.3$473.9

(1) Calculation of AFFO excludes start-up related capital spending in 2012, 2013 and 2014.

(2) 2007 cash tax included in AFFO calculation has been adjusted to exclude a cash tax refund received in 2007 related to the carry back of

certain federal net operating losses.

Risk Factors

71

This presentation contains "forward-looking statements" concerning our goals, beliefs, expectations, strategies, objectives, plans,

future operating results and underlying assumptions, and other statements that are not necessarily based on historical

facts. Examples of these statements include, but are not limited to statements regarding our leverage range, our growth

expectations, including AFFO per share and our REIT distributions, and our expectations regarding the leasing demand for

communications real estate and the wireless industry in general. Actual results may differ materially from those indicated in our

forward-looking statements as a result of various important factors, including: (1) decrease in demand for our communications

sites would materially and adversely affect our operating results, and we cannot control that demand; (2) if our tenants share site

infrastructure to a significant degree or consolidate or merge, our growth, revenue and ability to generate positive cash flows

could be materially and adversely affected; (3) our business is subject to government regulations and changes in current or future

laws or regulations could restrict our ability to operate our business as we currently do; (4) our leverage and debt service

obligations may materially and adversely affect us; (5) if we fail to pay scheduled dividends on our preferred stock, in cash or

common stock, we will be prohibited from paying dividends on our common stock, which may jeopardize our status as a REIT;

(6) increasing competition in the tower industry may materially and adversely affect us; (7) our expansion initiatives involve a

number of risks and uncertainties that could adversely affect our operating results, disrupt our operations or expose us to

additional risk if we are not able to successfully integrate operations, assets and personnel; (8) our foreign operations are subject

to economic, political and other risks that could materially and adversely affect our revenues or financial position, including risks

associated with fluctuations in foreign currency exchange rates; (9) a substantial portion of our revenue is derived from a small

number of tenants, and we are sensitive to changes in the creditworthiness and financial strength of our tenants; (10) we may fail

to realize the growth prospects and cost savings anticipated as a result of our acquisition of MIP Tower Holdings LLC, the parent

company of Global Tower Partners (GTP); (11) new technologies or changes in a tenant’s business model could make our tower

leasing business less desirable and result in decreasing revenues; (12) if we fail to remain qualified as a REIT, we will be subject

to tax at corporate income tax rates, which may substantially reduce funds otherwise available; (13) we may be limited in our

ability to fund required distributions using cash generated through our TRSs; (14) complying with REIT requirements may limit

our flexibility or cause us to forego otherwise attractive opportunities;

Risk Factors

(continued)

72

(15) certain of our business activities may be subject to corporate level income tax and foreign taxes, which reduce our cash

flows and may create deferred and contingent tax liabilities; (16) we may need additional financing to fund capital expenditures,

future growth and expansion initiatives and to satisfy our REIT distribution requirements; (17) if we are unable to protect our

rights to the land under our towers, it could adversely affect our business and operating results; (18) if we are unable or choose

not to exercise our rights to purchase towers that are subject to lease and sublease agreements at the end of the applicable

period, our cash flows derived from such towers will be eliminated; (19) restrictive covenants in the agreements related to our

securitization transactions, our credit facilities and our debt securities could materially and adversely affect our business by

limiting flexibility; (20) we may incur goodwill and other intangible asset impairment charges, which could result in a significant

reduction to our earnings; (21) our costs could increase and our revenues could decrease due to perceived health risks from

radio emissions, especially if these perceived risks are substantiated; (22) we could have liability under environmental and

occupational safety and health laws; and (23) our towers or data centers may be affected by natural disasters and other

unforeseen events for which our insurance may not provide adequate coverage. For additional information regarding factors that

may cause actual results to differ materially from those indicated in our forward-looking statements, we refer you to the

information contained in Item 1A of our Form 10-Q for the quarter ended June 30, 2014. We undertake no obligation to update

the information contained in this presentation to reflect subsequently occurring events or circumstances.

Contact Information

73

Corporate Headquarters

116 Huntington Avenue

Boston, MA 02116

Phone: 617-375-7500

Fax: 617-375-7575

Computershare

P.O. Box 43006

Providence, RI 02940

Phone: 866-201-5087

American Tower Contacts

Transfer Agent