Pic R1020 Best Practices Guide

User Manual: R1020

Open the PDF directly: View PDF ![]() .

.

Page Count: 49

Disclaimer

All users of the information contained in this document understand

and agree that IFTA, Inc. is not responsible for the accuracy of the

information provided to IFTA, Inc. by the person or persons that

prepared the materials herein. All information contained in this

document is provided to IFTA, Inc. by the responsible party or parties

and IFTA, Inc. does not alter the information provided or

independently confirm the accuracy of the information provided. The

sole responsibility of the accuracy of the data lies solely with the

person or persons who prepared the materials.

This document was prepared by the IFTA Audit Committee as a tool

to assist member jurisdictions in conducting IFTA audits. Member

jurisdictions are in no way required to implement the practices

contained herein by the IFTA Governing Documents. Suggested

changes or additions should be addressed to the IFTA Audit

Committee.

BEST PRACTICES AUDIT GUIDE

Section TABLE OF CONTENTS Page

i May 2006

I. Introduction 1

II. Eligibility / Exemptions 1

A. Vehicles 1

B. Fleet 2

III. Licensee Responsibilities 2

A. Distance Records 2

B. Fuel Records 3

C. Trip / Temporary Permits 5

D. Monthly / Quarterly Summaries 5

E. Supporting Information for IVDRs 6

F. Lessor Responsibility 6

G. Program Compliance Reviews 7

H. Records Retention 8

IV. General Accounting and Auditing Standards 8

A. Standards 8

B. Audit Responsibilities 9

V. Audit Plan 9

A. Audit Selection and Assignment 9

B. Audit Preparation 9

1. Audit Package and Permanent Office File Review 9

2. Audit Period Determination 10

3. Selection of Representative Sample Period 10

4. Audit Notification 10

VI. Conducting the Audit 11

A. Background 11

1. Understanding the Emphasis of the Audit 11

2. Pre-Audit Conference 11

3. Understanding of Fleet and Lease Agreements 15

B. Determining Quality of Source Documents 16

1. Nature of Evidence 16

2. Verifying Equipment List 17

3. Distance Recaps 17

4. Computerized Distance System 17

5. Fuel Records 20

BEST PRACTICES AUDIT GUIDE

Section TABLE OF CONTENTS Page

ii May 2006

6. Inadequate Records 21

C. Sampling 22

1. Types of Sampling 22

2. Sample Size 23

3. Sampling Source Documents 23

4. Accountable Distances 24

5. Practical Aspects of Sampling 24

6. Some Pointers Regarding Sampling 24

7. Evaluating Sampling Results 26

8. Projecting Errors 27

D. Distance / Fuel Verification 28

1. Testing the Distance / Fuel Recorded on the Licensee’s System 28

2. Accuracy of the Distance and Fuel Information on the IVDRs 29

3. Relevance and Frequency of Differences in IVDR Distances / Fuel 29

4. Tracing IVDRs to the Recaps 31

5. Testing the Accuracy of the Licensee’s Recaps / Schedules 31

6. Relevance and Frequency of Recap Differences 31

7. Odometer Readings 32

8. Distance and Fuel Adjustments 32

9. Isolated Errors 33

10. Sampling vs. Full Audit of Records 33

11. Determining Audited Distance and Fuel 34

E. Equipment Verification 35

F. Audit Results 35

1. Determining Results 35

2. Exit Conference and Audit Finalization 36

G. Audit Report and Working Paper File 38

1. Audit Report 38

2. Working Papers 39

3. Permanent Audit File 40

4. Indexing Working Papers 41

5. General Working Paper Preparation 41

6. Review of the Audit 43

7. Netting of Audit Adjustments 44

8. Communications with Other Jurisdictions 44

BEST PRACTICES AUDIT GUIDE

Page 1 of 45 May 2006

I. INTRODUCTION

IFTA - Section Reference: R130, R140, R150, R305, R1310, A100, R600, R610, R620,

R625, R630, R635, R640, R800, R810.100, R810.200, R820, R830.100, R830.200, R840

The focus of the International Fuel Tax Agreement (IFTA) audit program should be to

determine if the licensee is in compliance with the terms of the agreement and with

jurisdictional statutes.

The IFTA is a multijurisdictional fuel tax agreement that simplifies the reporting of fuel taxes

by interjurisdictional motor carriers. The IFTA establishes a single uniform system for

administering and collecting fuel consumption taxes from interjurisdictional carriers. Under

IFTA, motor carriers register with their base jurisdiction, and receive credentials, which allow

them to travel through other IFTA member jurisdictions. Carriers then file a single quarterly

return with a single payment to their base jurisdiction that covers all of their travel in other

IFTA member jurisdictions. The base jurisdiction processes the IFTA tax return and

forwards funds to each jurisdiction or requests funds for net fuel taxes.

The base jurisdiction is required to audit the motor carriers representing not only

their own interests, but also the interests of all other member jurisdictions. An audit

program is therefore an important and essential compliance measure and ensures that

proper revenues are being collected by each jurisdiction.

II. ELIGIBILITY / EXEMPTIONS

Eligibility under IFTA:

A. Vehicles - R245.100, R245.200, R245.300, R221, R305

Qualified motor vehicle means a motor vehicle used, designed or maintained for

transportation of persons or property and:

• Having two axles and a gross vehicle weight or registered gross vehicle weight

exceeding 26,000 pounds or 11,797 kilograms, or

• Having three or more axles regardless of weight, or

• Is used in combination, when the weight of such combination exceeds 26,000

pounds or 11,797 kilograms gross vehicle or registered gross vehicle weight.

Qualified motor vehicle does not include recreational vehicles.

Any person based in a member jurisdiction operating a qualified motor vehicle(s) in two

or more member jurisdictions is required to license under this Agreement, except as

indicated in IFTA Articles of Agreement, Sections R310, and R500.

BEST PRACTICES AUDIT GUIDE

Page 2 of 45 May 2006

B. Fleet

Fleet means one or more vehicles.

Under IFTA, a carrier may be registered in more than one base jurisdiction if its

operations in each jurisdiction meet the criteria for IFTA licensing and reporting.

When a carrier has several fleets, which would otherwise be based in two (2) or more

IFTA jurisdictions, the commissioners of the affected jurisdictions may allow the

consolidation of the fleets for reporting purposes. The carrier must apply to each

jurisdiction for permission to consolidate the fleets.

Exemptions under IFTA - R830.100, R830.200

• All vehicles under 26,000 pounds or 11,797 kilograms gross vehicle weight, or

• Trailers, those vehicles not used for propulsion

• Those vehicles traveling only intra-jurisdictionally, regardless of weight, or

• Recreational vehicles

Also, each jurisdiction may designate exempt vehicles (as well as miles and/or fuel) i.e.

municipal vehicles, farm vehicles. A list of the jurisdictional exemptions may be perused

at the IFTA, Inc. website.

Exempt fuel and/or distance must be included in total reported fuel and/or distance in

determining the MPG. Refer to each jurisdictional exemption to determine how to claim

the exemption. (See IFTA Articles of Agreement sections R1000 and R1100)

• A Licensee who qualifies as an IFTA carrier, but does not wish to participate in the

IFTA

• Program must obtain fuel tax permits to travel through member jurisdictions.

III. LICENSEE RESPONSIBILITIES - R700

Every licensee shall maintain records to substantiate information reported on the quarterly

tax returns. Operational records shall be maintained or be made available for audit in the

base jurisdiction. Recordkeeping requirements shall be specified in the IFTA Procedures

manual.

A. Distance Records - P540.100, P540.100.005 - -.015, P540.200, P540.200.005 - -.050

Licensees shall maintain detailed distance records, which show operations on an

individual-vehicle basis.

The Operational records shall contain, but not be limited to:

• Taxable and non-taxable usage of fuel;

• Distance traveled for taxable and non-taxable use; and

• Distance recaps for each vehicle for each jurisdiction in which the vehicle operated.

BEST PRACTICES AUDIT GUIDE

Page 3 of 45 May 2006

An acceptable distance accounting system is necessary to substantiate the information

reported on the tax return filed quarterly or annually. A licensee’s system, at a minimum,

must include distance data on each individual vehicle for each trip and be recapitulated

in monthly fleet summaries. Supporting information should include:

• Date of the trip (starting and ending)

• Trip origin and destination

• Route of travel (may be waived by the base jurisdiction)

• Beginning and ending hub odometer/odometer reading of the trip (may be waived by

the jurisdiction)

• Total trip miles/kilometers

• Miles/kilometers by jurisdiction

• Unit number or vehicle identification number

• Vehicle fleet number

• Licensee’s name, and

• May include additional information at the discretion of the base jurisdiction.

B. Fuel Records - P550.100, P550.200, P550.300, P550.400.005 - -.025, P560.100,

P560.200, P560.300.005 - -.035, P570.100, P570.200, P570.300, P570.400.005 - -.025,

P570.500, R1000.100, R1000.200, R1010, 100, R1010.200, R1010.300, R1020.100,

R1020.200, R1020.300

The licensee must maintain complete records of all motor fuel purchased, received, and

used in the conduct of its business.

Separate totals must be compiled for each motor fuel type,

Retail fuel purchases and bulk fuel purchases are to be accounted for separately.

The fuel records shall contain but not be limited to:

• The date of each receipt of fuel

• The name and address of the person from whom purchased or received

• The number of gallons or liters received

• The type of fuel, and

• The vehicle or equipment into which the fuel was placed.

Retail purchases must be supported by receipt or invoice, credit card receipt, automated

vendor generated invoice or transaction listing or microfilm/microfiche of the receipt or

invoice. Receipts that have been altered or indicate erasures are not accepted for tax-

paid credits unless the licensee can demonstrate the receipt is valid.

BEST PRACTICES AUDIT GUIDE

Page 4 of 45 May 2006

Receipts for retail fuel purchases must identify the vehicle by the plate or unit number or

other licensee identifier, as distance traveled and fuel consumption may be reported only

for vehicles identified as part of the licensee’s operation. An acceptable receipt or

invoice must include, but shall not be limited to, the following:

• Date of purchase

• Seller’s name and address

• Number of gallons or liters purchased

• Fuel type

• Price per gallon or liter or total amount of sale

• Unit numbers, and

• Purchaser’s name (see R1010.300 of the IFTA Articles of Agreement)

Bulk fuel is normally delivered into storage facilities maintained by the licensee, and fuel

tax may or may not be paid at the time of delivery. Original delivery tickets and/or

receipts must be retained by the licensee. Receipts that have been altered or indicate

erasures are not accepted for tax-paid credits unless the licensee can demonstrate the

receipt is valid. Bulk inventory reconciliations must be maintained. For withdrawals from

bulk storage, records must be maintained to distinguish fuel placed in qualified vehicles

from other uses. To obtain credit for withdrawals from licensee-owned, tax-paid bulk

storage, the following records must be maintained:

• Date of withdrawal

• Number of gallons or liters

• Fuel type

• Unit number, and

• Purchase and inventory records to substantiate that tax was paid on all bulk

purchases.

Upon application by the licensee, the base jurisdiction may waive the requirement of unit

numbers for fuel withdrawn from the licensee’s own bulk storage and placed in its

qualified motor vehicles. The licensee must show that adequate records are maintained

to distinguish fuel placed in qualified vs. non-qualified motor vehicles for all member

jurisdictions.

To obtain credit for tax-paid purchases, the licensee must retain a receipt, invoice, credit

card receipt, or automated vendor generated invoice or transaction listing, showing

evidence of such purchases and taxes paid. These records may be kept on microfilm,

microfiche, or other computerized or condensed record storage system which meets the

BEST PRACTICES AUDIT GUIDE

Page 5 of 45 May 2006

legal requirement of the base jurisdiction. Licensees are not required to submit proof of

tax-paid purchases with their tax returns. Receipts that have been altered or indicate

erasures are not accepted for tax-paid credits unless the licensee can demonstrate that

the receipt is valid.

The retail purchase of fuel which is placed into the fuel tank of a qualified vehicle, and

upon which tax has been paid to a jurisdiction shall qualify as a tax-paid retail fuel

purchase. The receipt must show evidence that tax was paid directly to the applicable

jurisdiction or at the pump. Specific requirements for these receipts are outlined in the

IFTA Procedures Manual section P560. No member jurisdiction shall require evidence

of such purchases beyond what is specified in the Procedures Manual. In the case of a

lessee/lessor agreement, receipts for tax-paid purchases may be in the name of either

the lessee or the lessor provided a legal connection can be made to the reporting party.

Storage fuel is normally delivered into fuel storage facilities by the licensee and fuel tax

may or may not be paid at the time of delivery. Motor fuel which is placed into the fuel

tank of a qualified motor vehicle from a licensee’s own bulk storage, and upon which tax

has been paid to the jurisdiction where the bulk fuel storage tank is located, shall be

considered a tax-paid bulk fuel purchase. The licensee’s records must identify the

quantity of fuel taken from the licensee’s own bulk storage and placed in its qualified

motor vehicles. Record keeping requirements for tax-paid bulk fuel purchases are

provided in IFTA Procedures Manual, section P570.

C. Trip Permits - R315, R263, R650

In lieu of motor fuel tax licensing under this Agreement, persons may elect to satisfy

motor fuels use tax obligations on a trip-by-trip basis.

Temporary Permit: Means a permit issued by the base jurisdiction or its agent to be

carried in a qualified vehicle in lieu of display of the permanent annual decals. A

temporary permit is valid for a period of 30 days to give the carrier adequate time to affix

the annual permanent decals. The base jurisdiction may charge an administrative fee to

the licensee to cover the cost of issuance. Temporary permits must be vehicle specific

and show the expiration date. The temporary permit need not be displayed but shall be

carried in the vehicle.

D. Monthly / Quarterly Summaries - P540.100.015

Licensees shall maintain detailed distance records, which show operations on an

individual vehicle basis. The operational records shall contain, but not be limited to,

distance recaps for each vehicle for each jurisdiction in which the vehicle operated.

BEST PRACTICES AUDIT GUIDE

Page 6 of 45 May 2006

E. Supporting Information for IVDRs (Individual Vehicle Distance Records) - A540.-

.200

The information recorded on the IVDRs must be accurate and legible. The distance

figures to be entered on IVDRs can be obtained from various sources such as odometer

and/or hubodometer readings, DOT logs, provincial/state maps, a standard distance

guide or a household goods distance guide, a computer software or a global positioning

system (GPS) as long as the method used is accurate and consistent. The primary

concern is that the percentage of total distance allocated to affected jurisdictions is

accurate. Licensees should accumulate IVDRs and prepare monthly/quarterly recaps. -.

It must be stressed that distance figures supported by IVDRs can be used in numerous

areas where a licensee is required to file some type of distance report, such as IRP

registration applications, third structure taxes, -fuel usage, - etc.

A540.400 If the base jurisdiction utilizes a distance reporting software program to verify

the records of the licensee, it shall be used as an audit tool. The auditor must use

discretion when verifying the licensee’s records. Documentation such as trip records,

odometer readings and other records used by the licensee to substantiate its actual

distance records must be considered by the auditor in determining an acceptable

distance reporting system.

F. Lessor Responsibility - R230, R233, R510.100.005 - -.010, R510.200, R520.100,

R520.200, R530.100, R530.200, R540

Lessor - means the party granting the use of equipment, with or without a driver, to

another.

Lessee - means the party acquiring the use of equipment, with or without a driver, from

another.

Short-term leases. In the case of a short-term motor vehicle rental, by a lessor

regularly engaged in the business of leasing or renting motor vehicles without drivers, for

compensation, to licensees or other lessees of 29 days or less, the lessor will report and

pay the fuel use tax unless the following two conditions are met,

1. The lessor has a written rental contract which designates the lessee as the party

responsible for reporting and paying the fuel use tax; and

2. The lessor has a copy of the lessee’s IFTA fuel tax license which is valid for the term

of the rental.

Long-term leases. A lessor regularly engaged in the business of leasing or renting

motor vehicles without drivers, for compensation, to licensees or other lessees may be

BEST PRACTICES AUDIT GUIDE

Page 7 of 45 May 2006

deemed to be the licensee, and such lessor may be issued a license if an application

has been properly filed and approved by the base jurisdiction.

In the case of a household goods carrier using independent contractors, agents or

service representatives, under intermittent leases, the party liable for motor fuel use tax

shall be the:

1. Lessee (carrier) when the qualified motor vehicle is being operated under the

lessee’s jurisdictional operating authority. The base jurisdiction, for purposes of this

Agreement, shall be the base jurisdiction of the lessee (carrier) regardless of the

jurisdiction in which the qualified motor vehicle is registered, for vehicle registration

purposes, by the lessor or lessee.

2. The lessor (independent contractor, agent or service representative) when the

qualified motor vehicle is being operated under the lessor’s jurisdictional operating

authority. The base jurisdiction, for purposes of this agreement, shall be the base

jurisdiction of the lessor, regardless of the jurisdiction in which the qualified motor

vehicle is registered for vehicle registration purposes.

Independent Contractors:

Short-term leases: In the case of a carrier using independent contractors under short-

term leases of 29 days or less, the trip lessor will report and pay all fuel taxes.

Long-term leases: In the case of a carrier using independent contractors under long-

term leases (30 days or more) the lessor and lessee will be given the option of

designating which party will report and pay fuel use tax. In the absence of a written

agreement or contract, or if the document is silent regarding responsibility for reporting

and paying fuel use tax, the lessee will be responsible for reporting and paying fuel use

tax. If the lessee (carrier) through a written agreement or contract assumes

responsibility for reporting and paying fuel use taxes, the base jurisdiction, for purposes

of this Agreement, shall be the base jurisdiction of the lessee, regardless of the

jurisdiction in which the qualified motor vehicle is registered for vehicle registration

purposes by the lessor. No member jurisdiction shall require the filing of such leases but

such leases shall be made available upon request of any member (see IFTA Procedures

Manual section P520).

G. Program Compliance Reviews - P1210, P1230

Member jurisdictions shall permit periodic program compliance reviews to be performed

to assure they are in compliance with the provisions of the Agreement. At the expense

of the member jurisdictions conducting such reviews, they will be performed after the

BEST PRACTICES AUDIT GUIDE

Page 8 of 45 May 2006

first year of implementation of the Agreement. The expenses of such reviews may be

paid through the International Fuel Tax Association if funds are available. Beginning

January 1, 1997, the Program Compliance Reviews will be conducted according to a

schedule developed by IFTA, Inc. Jurisdictions will be required to participate in their

appropriate share of program compliance reviews each year. No member jurisdiction will

be required to participate in more than two compliance reviews per year.

H. Records Retention - P510.100, P510.200, P510.300, P550.100, P550.200, P550.300

The licensee is required to preserve the records upon which the quarterly tax return is

based for four years from the return due date or filing date, whichever is later, plus any

time period included as a result of waivers or jeopardy assessments. Failure to provide

records demanded for audit purposes extends the four year record retention requirement

until the records are provided. Records may be kept on microfilm, microfiche or other

computerized or condensed record storage system acceptable to the base jurisdiction.

The licensee must maintain complete records of all motor fuel purchased, received, and

used in the conduct of its business. Separate totals must be compiled for each motor

fuel type. Retail fuel purchases and bulk fuel purchases are to be accounted for

separately.

Records may be kept on microfilm, microfiche, or other computerized or condensed

records storage system which meets the requirements of the base jurisdiction.

IV. GENERAL ACCOUNTING AND AUDITING STANDARDS

A. Standards - A510, A210.100, A210.200, A210.300, A220.100, A220.200

For an audit to be acceptable to all member jurisdictions, it must be conducted in a

professional manner and the results be clearly documented. Standard terminology is to

be used in reporting audit findings. Acceptable audit standards provide that several

procedures may be employed. However, it is necessary that each audit reflect adequate

information necessary to satisfy the commissioners of the various member jurisdictions.

The examination is to be performed by a person or persons having adequate technical

training and proficiency in auditing. In all matters relating to the assignment, an

independent mental attitude is to be maintained by the auditor. The independent auditor

must be without bias with respect to the licensee under audit to ensure the impartiality

necessary for the dependability of the findings. However, this independence does not

imply the attitude of a prosecutor, but rather a judicial impartiality that recognizes an

obligation to fairness. Due professional care is to be exercised in performing the

examination and preparing the report. The auditor is to make a proper study and

BEST PRACTICES AUDIT GUIDE

Page 9 of 45 May 2006

evaluation of the licensee's internal accounting controls to determine their reliability and

the extent to which auditing procedures are to be restricted. The work is to be

adequately planned, and assistants, if any, are to be properly supervised.

B. Audit Responsibilities - A410.100, A410.200, A410.300, A410.400, A410.500,

A420.100, A420.200, A420.300, A420.400

Member jurisdictions are responsible for the staffing of auditors who meet the

qualifications of the jurisdiction's personnel guidelines. Member jurisdictions are

responsible for proper training of audit and audit supports staffs in audit planning and

procedures. Member jurisdictions are responsible for the actions of their auditors.

Member jurisdictions should allow auditors to discuss any discrepancies with licensees.

Member jurisdictions should allow auditors to make preliminary recommendations to

licensees. Auditors must give all licensees equal consideration. There must be no

preferential treatment given. Auditors should audit all licensees under a uniform

program unless special circumstances dictate otherwise. Auditors should conduct

themselves in a manner, which would promote cooperation and good relations between

the base jurisdiction and the licensee.

V. AUDIT PLAN

A. Audit selection and assignment - A310, A320.100, A320.200, A320.300

The base jurisdiction must complete audits of an average of 3% per year of the IFTA

accounts reported by that jurisdiction on the annual report from the previous year. This

count includes carriers who are registered and report no activity.

At least 15% of the audits shall involve low distance accounts, 25% shall involve high

distance accounts, while the remaining 60% will cover accounts of any size.

B. Audit Preparation

Any preparation that can be done prior to arriving at the licensee’s place of business

should be done. This will reduce the time needed to conduct the audit at the licensee’s

office.

1. Audit Package and Permanent Office File Review:

a. Past audits and areas of discrepancies.

b. IRP application and equipment list.

c. Consider sending out a pre-audit questionnaire.

d. Review IFTA application.

e. Review number of decals issued each year in the audit period.

BEST PRACTICES AUDIT GUIDE

Page 10 of 45 May 2006

f. Review reported returns for:

i. Constant or extreme MPG/KPL

ii. Large fluctuations in distance or fuel

iii. Size of operation

iv. Number of jurisdictions traveled

v. Non-IFTA distances

vi. Calculation errors

vii. Seasonal fluctuation

viii. Review billing and refunds

ix. Tax paid fuel

g. Other related information.

2. Audit Period Determination

The audit period will cover at least one registration year, and up to four registration

years.

3. Selection of Representative Sample Period for Testing Purposes - A530,

A530.100, A530.200, A530.300, A530.400

Unless a specific situation dictates, all audits will be conducted on a sampling basis.

Sample period(s) must be representative of the licensee’s operations. Sample

period(s) may be different for member jurisdictions due to seasonal operations. The

licensee should be allowed input into sample selection if legitimate reasons exist. An

agreement, that the sampling methodology is appropriate, should be signed by the

licensee and the auditor.

4. Audit Notification - A610.100, A610.200, A610.300, A620.100, A620.200

At least 30 days prior to conducting a routine audit, the licensee should be contacted

in writing and advised of the approximate date that an audit is to be conducted and

the time period the audit will cover. The notification will provide the licensee the

opportunity to make the required records available and provide assurance the

tentative schedule is acceptable. For purposes of documentation and to avoid

misunderstanding, a copy of the notification letter should be incorporated into the

audit file detailing the tentative audit date and the documentation the licensee is

required to furnish. For just cause, notification requirements may be waived. All pre-

audit contact should be confirmed in writing. Jurisdictions may contact each other

prior to the audit to obtain pertinent information. Copies of correspondence between

the licensee and member jurisdictions that have a bearing on a tax liability and

BEST PRACTICES AUDIT GUIDE

Page 11 of 45 May 2006

special instructions that may affect the audit should be forwarded to the base

jurisdiction.

VI. CONDUCTING THE AUDIT

A. Background

1. Understanding the Emphasis of the Audit - A520

The audit emphasis should be placed on the evaluation of the licensees’ distance

and fuel recording system to determine if the system can be relied upon.

Based on the study and evaluation of internal controls, along with other relevant

factors, the auditor needs to determine the nature and extent of procedures

necessary to test the system or controls.

The auditor can draw an unbiased sample of source documents of distance and fuel

records and follow them through the accounting system to check the reliability of the

recording system. The uses of a random, systematic, or haphazard selection

process are acceptable. Summary/recap records must be available to trace the

source documents for trips for a particular vehicle through the accounting system into

the proper reports. Summaries/recaps may be prepared on a monthly or, at

minimum, a quarterly basis.

If summaries/recaps are not available, the auditor may request that the licensee

compile such recaps, or choose to compile the information him/herself, depending on

the number of vehicles.

Once the degree of reliance on the accounting system is established and supported

by test results, the auditor can determine the extent of additional testing required.

Additional testing should verify that the data reported accurately reflect the data

recorded in the licensee's distance and fuel accounting system.

2. Pre-audit Conference - A630

The auditor should hold a pre-audit conference with the licensee. The purpose of

this meeting is to explain the audit and to gain an understanding of the licensee’s

distance and fuel reporting system, equipment registration system (including leased

vehicles, owner-operated vehicles, non-IFTA equipment), and internal control

structure. A Pre-Audit Questionnaire may be used at this time or prior to the

commencement of the pre-audit conference.

In addition, the pre-audit conference should outline the licensee’s operation, audit

procedures, records to be examined, sample period, sampling procedures, etc. The

BEST PRACTICES AUDIT GUIDE

Page 12 of 45 May 2006

licensee and auditor(s) should determine who has the responsibility for the final

acceptance of audit findings and who should be involved in the exit conference.

During the interviews, talk to the people involved with processing the information,

explain the audit process, and discuss the unique aspects of their business. During

all discussions, remember to think about the best and most efficient approach to

auditing the licensee's records. Consider management philosophy and control

methods, competence of personnel, other influences on the distance and fuel

reporting system, such as payroll, and your audit objectives.

Many licensees will not understand what is required of them during the audit

process. Take this opportunity to educate them.

Some factors to review when conducting the pre-audit conference are as follows:

a. Licensee’s Operations:

i. Determine what the licensee's business is.

ii. Determine the organizational structure of the company.

b. General Information:

i. Identify whom to talk to about obtaining records, discussing errors, attending

closing conferences.

ii. Determine what the working hours of the office are and the individuals' work

schedules.

c. Records: (A540, A550)

i. Determine if the requested records are available for audit. For record

keeping requirements, review Section III of this manual.

ii. Determine if the licensee has complete records for the periods under audit.

iii. Determine whether the records are maintained in a timely fashion. Determine

whether the information contained on the IVDR’s is sufficient to allow the

audit of reported distance and fuel.

iv. Review pertinent lease agreements to determine the licensee’s responsibility.

v. Discuss whether distance is reported by odometer readings (or other type

measure), by routes, or by standard distance chart (including maps). (If

odometer/hub odometer is not used, how is total distance accurately

determined?)

vi. Discuss whether fuel is reported based on fuel receipts, fuel invoices, bulk

fuel withdrawals, or some other process.

vii. Review how the records are kept; determine whether they are turned in after

BEST PRACTICES AUDIT GUIDE

Page 13 of 45 May 2006

each trip, weekly, or monthly.

viii. Determine how trips and/or trip sheets are numbered; i.e., pre-numbered,

numbered by the driver, same as shipment number, numbered upon

completion of trip.

ix. Determine how the licensee records and reports distance and fuel when a trip

overlaps months/quarters.

d. Internal Controls: (A640)

i. Make inquiries about the system by interviewing personnel involved with the

reporting process.

ii. Walk through the system - trace one or two IVDR’s through the process.

iii. Determine the extent of automation within the licensee’s system of record

keeping;

iv. Determine if the distance and fuel reporting system is a stand-alone system

or integrated with the company's financial or other systems.

v. Determine if a review or edit is performed of the IVDR’s and distance and fuel

compiled, including who does the review and whether the review is

documented.

vi. Determine if a review or edit is performed of the monthly or quarterly

summaries, including who does the review and whether the review or edit is

documented.

vii. If edits are performed, obtain a pre-edit version of the documentation.

viii. Determine if a third party (service agent, accountant, etc.) prepares the IFTA

tax return.

ix. Determine if there have been any changes in the record keeping or reporting

system during the audit period. (If there has been a change, you will want to

sample the system before and after the change.)

e. Gathering Information about the System:

i. Information about a licensee's record keeping system is obtained through

discussion with the personnel involved in order to find out each individual’s

role in the system and their knowledge. This is an important step and is

accomplished by exercising professional judgment in evaluating the

information obtained. The auditor has a responsibility to report any

weaknesses to the licensee.

ii. The auditor should identify the strengths and weaknesses of the licensee’s

BEST PRACTICES AUDIT GUIDE

Page 14 of 45 May 2006

system to determine the nature and extent of auditing procedures employed:

• Strengths – A strength is a control or a procedure the auditor intends to

rely upon to reduce testing. For example, if the auditor believes that

controls for assigning distance and fuel among the jurisdictions are

adequate the auditor can reduce, not eliminate, the testing.

• Weaknesses - A weakness in the system can be defined as the absence

of a control, which makes the auditor's expectations of error greater than

would normally be found in a system with adequate internal control.

iii. Internal control evaluation guides or questionnaires may be used as a

reminder to list points to be considered.

f. Walk-Through of the System:

i. The auditor should select one or more documents of each transaction type

and follow some action through the entire accounting process.

ii. As part of the walk-through, the auditor should ask to review each point

where some action is taken, such as a check of clerical accuracy, a review, or

an approval. Example; if an individual is to have initialed or signed the

document before passing it along to another department, the auditor may

ascertain that this was done by inquiring whether the initials or the signature

appearing on the documents is that of the employee being interviewed. The

auditor may observe how the current documents, flowing through the control

system, are being handled by the individual interviewed. The auditor may

also check on information received by asking each individual to describe the

work being done under the prescribed procedures.

The walk-through enables the auditor to obtain a better understanding of the

detailed operations.

g. Document the System:

i. Has the system been audited before?

ii. Documentation of the system can range from identifying source documents to

a narrative or flow chart.

Documentation of working papers is discussed in more detail later in this

chapter. Flow-charting could be used.

It is important during each of these steps, to consider all possible error types,

determine the controls, which should detect the errors, and decide if the

licensee’s procedures contain those controls.

BEST PRACTICES AUDIT GUIDE

Page 15 of 45 May 2006

It is at this point that the auditor must determine whether the system can be

audited, determine the scope of the audit, and establish specific audit

procedures.

iii. If the auditor has determined that the licensee’s record keeping system is

sufficient to enable good records to be maintained, the auditor must next

determine if the individual records are sufficient for audit.

One of the auditing standards of fieldwork is that sufficient competent

evidential matter is to be obtained to afford a reasonable basis to support the

accuracy of the report filed by the licensee.

3. Understanding of the Fleet and Lease Agreements - R510-R540

The auditor should have acquired a clear understanding of the licensee’s fleet(s)

during the opening conference.

The auditor needs to know the number of vehicles in a licensee’s fleet and if the

licensee has any lease agreements with owner-operators. The lease agreements

need to be examined.

Short-term leases. In the case of a short-term motor vehicle rental, by a lessor

regularly engaged in the business of leasing, or renting motor vehicles with or

without drivers, for compensation to licensees or other lessees of 29 days or less,

the lessor will report and pay the fuel use tax unless the following two conditions are

met:

a. The lessor has a written rental contract which designates the lessee as the party

responsible for reporting and paying the fuel use tax; and

b. The lessor has a copy of the lessee’s IFTA fuel tax license which is valid for the

term of the rental.

Long-term leases: A lessor regularly engaged in the business of leasing or renting

motor vehicles without drivers for compensation to licensees or other lessees may be

deemed to be the licensee, and such lessor may be issued a license if an application

has been properly filed and approved by the base jurisdiction.

In the case of a household goods carrier using independent contractors, agents, or

service representatives, under intermittent leases, the party liable for motor fuel use

tax shall be:

a. The lessee (carrier) when the qualified motor vehicle is being operated under the

lessees’ jurisdictional operating authority. The base jurisdiction for purposes of

this Agreement shall be the base jurisdiction of the lessee (carrier), regardless of

BEST PRACTICES AUDIT GUIDE

Page 16 of 45 May 2006

the jurisdiction in which the qualified motor vehicle is registered for vehicle

registration purposes by the lessor or lessee;

b. The lessor (independent contractor, agent or service representative) when the

qualified motor vehicle is being operated under the lessor’s jurisdictional

operating authority. The base jurisdiction for purposes of this Agreement shall be

the base jurisdiction of the lessor, regardless of the jurisdiction in which the

qualified motor vehicle is registered for vehicle registration purposes.

Short-term leases. In the case of a carrier using independent contractors under

short-term/trip leases of 29 days or less, the trip lessor will report and pay all fuel

taxes.

Long-term leases. In the case of a carrier using independent contractors under

long-term leases (30 days or more) the lessor and lessee will be given the option of

designating which party will report and pay fuel use tax. In the absence of a written

agreement or contract, or if the document is silent regarding responsibility for

reporting and paying fuel use tax, the lessee will be responsible for reporting and

paying fuel use tax. If the lessee (carrier) through a written agreement or contract

assumes responsibility for reporting and paying fuel use taxes, the base jurisdiction

for purposes of this Agreement shall be the base jurisdiction of the lessee,

regardless of the jurisdiction in which the qualified motor vehicle is registered for

vehicle registration purposes by the lessor.

No member jurisdiction shall require the filing of such leases but such leases shall be

made available upon request of any member (see IFTA Procedures Manual, Section

P520).

The auditor also needs to understand the methods used to arrive at the distance and

fuel recorded on IVDR’s, (i.e., odometers, map distance, a software package, fuel

invoices, fuel receipts, bulk fuel withdrawal records, etc.). The methods used by the

licensee will affect the test procedures.

B. Determining Quality of Source Documents

Most of the auditor's work in determining the accuracy of the IFTA quarterly report

consists of obtaining and evaluating distance, fuel, and equipment records.

1. Nature of Evidence

There are several types of records that may be used as evidence during the audit.

They consist of trip records, vehicle maintenance records, driver daily logs,

employee time cards or earning records, maintenance records, dispatch reports, bills

BEST PRACTICES AUDIT GUIDE

Page 17 of 45 May 2006

of lading, cash disbursement records, cash receipt records, leases, titles, and reports

filed with the jurisdictions, fuel receipts, fuel invoices, and bulk fuel withdrawal

records.

2. Verifying Equipment List

The auditor needs to determine that all qualified vehicles are included on the

equipment list.

The equipment list for fuel tax should also be examined as it may differ from the

equipment list for IRP. The auditor must be sure to compare both equipment lists

against the licensee's records carefully and completely.

3. Distance Recaps - P540

The auditor should request the licensee’s summaries to support the quarterly IFTA

tax report. This is a necessary starting point since it will help determine if the auditor

is working with the records that were used to prepare the report.

The auditor should verify enough summaries and recaps to determine if the quarterly

returns are being filed properly. The auditor must also verify that the total distances

and tax paid credit gallons have been properly allocated to the various jurisdictions.

If the testing of the summaries to the report is unsatisfactory, consider expanding the

sample. Any difference between the summaries and the IFTA tax return should be

considered an error.

For IFTA, a quarterly summary is required for each quarter in the audit period. The

summary must show the total and jurisdictional distance and fuel for the total fleet

and for each vehicle in the fleet.

4. Computerized Distance System - P610 - P670

If a licensee is using a computerized distance system, they still have to maintain

individual trip reports to support the route the vehicle actually traveled. A

computerized distance summary is not acceptable as the sole source document.

On board recording devices, vehicle tracking systems or other electronic data

recording systems may be used (at the option of the carrier) in lieu of or in addition to

handwritten trip reports for fuel tax reporting. Other equipment monitoring devices

that transmit data or may be interrogated as to vehicle location or travel may be used

to supplement or verify handwritten or electronically generated trip reports. Any

device or electronic system used in conjunction with a device shall meet the

requirements stated in this Section. On-board recording or vehicle tracking devices

BEST PRACTICES AUDIT GUIDE

Page 18 of 45 May 2006

may be used in conjunction with manual systems or in conjunction with computer

systems.

All recording devices must meet the requirements stated in IFTA Procedures

manual, Section P640 and P660.

When the device is to be used alone, printed reports must be produced which

replace handwritten trip reports. The printed trip reports shall be retained for audit.

Vehicle and fleet summaries which show miles and kilometers by jurisdiction must

then be prepared manually. The entire system must meet the requirements stated in

IFTA Procedures Manual, Sections P640, P650, and P660. If the printed reports will

not be retained for audit, the system must have the capability of producing, upon

request, the reports indicated in IFTA Procedures Manual, Section 640. When the

computer system is designed to produce printed trip reports, vehicle and fleet

summaries which show miles and kilometers by jurisdiction must also be prepared.

To obtain information needed to verify fleet distance and to prepare the “Individual

Vehicle Distance Report,” the device must collect the following data on each trip:

date of trip (starting and ending); trip origin and destination (location code is

acceptable); routes of travel or latitude/longitude positions used in lieu thereof (may

be waived by the base jurisdiction). If latitude/longitude positions are used, they

must be accompanied by the name of the nearest town, intersection or cross street.

If latitude/longitude positions are used, jurisdiction crossing points must be calculated

or identified; beginning and ending odometer or hubodometer reading of the trip

(may be waived by the base jurisdiction); total trip distance; distance by jurisdiction;

power unit number or vehicle identification number; vehicle fleet number and

licensee’s name. Optional trip data (may be included at the discretion of the base

jurisdiction) driver ID or name and intermediate trip stops. For purposes of fuel tax

reporting, the device must collect the following data: date of purchase; seller’s name

and address (vendor code acceptable); number of gallons or liters purchased; fuel

type ( may be referenced from vehicle file); price per gallon or liter or total amount of

sale (required only for purchases from vendors); unit number and purchaser’s name

(in the case of lessee/lessor agreement, receipts will be accepted in either name,

provided a legal connection can be made to reporting party).

For purposes of bulk fuel tax, the device must collect, in addition, the following data:

date of withdrawal; number of gallons or liters; fuel type; unit number and purchase

and inventory records to substantiate that tax was paid on all bulk purchases.

BEST PRACTICES AUDIT GUIDE

Page 19 of 45 May 2006

The following reports may be prepared by an electronic computer system –that

accepts data from on-board recording or vehicle tracking devices rather than the

recording device itself. The system shall be able to produce the following reports: an

Individual Vehicle Distance Record (IVDR) report for each trip that includes the

information required in IFTA Procedures Manual, Section P640. (Note: this report

may be more than one page); monthly, quarterly and annual summaries of vehicle

trips by vehicle number showing miles or kilometers by jurisdiction; monthly,

quarterly and annual trip summaries by fleet showing the number of miles or

kilometers by jurisdictions.

Exceptions that identify all edited data, omissions of required data (see IFTA

Procedures Manual, Section P640), system failures, non-continuous life-to-date

odometer readings, travel to noncontiguous jurisdictions and trips where the location

of the beginning trip is not the location of the previous trip must be identified.

In cases where speed/rpm sensors or odometer/speedometer interface devices are

providing pulse inputs to the on-board computer, the system will record the

calibration factors used in calculating mileage at time of download from the vehicle to

the base computer. The fleet shall also keep accurate records of all Engine Control

Module calibrations.

The carrier must obtain a certificate from the manufacturer certifying that the design

of the on-board recording or vehicle tracking device has been sufficiently tested to

meet the requirements of this provision. The on-board recording or vehicle tracking

device and associated support systems must be, to the maximum extent practicable,

tamper-proof and must not permit altering of the information collected. Editing the

original information collected will be permitted. All editing must be identified and both

the edited and original data must be recorded and retained

The on-board recording or vehicle tracking device shall warn the driver visually

and/or audibly that the device has ceased to function. The device must time and

date stamp all data recorded. The device must not allow data to be overwritten

before the data has been extracted. The device shall warn the driver visually and/or

audibly that the device’s memory is full and can no longer record data. The device

must automatically update a life-to-date odometer when the vehicle is placed in

motion or the operator must enter the current vehicle odometer reading when the on-

board recording or vehicle tracking device is connected to the vehicle. The device

must provide a method for the driver to confirm that the entered data is correct (e.g.

BEST PRACTICES AUDIT GUIDE

Page 20 of 45 May 2006

a visual display of the entered data that can be reviewed and edited by the driver

before the data is finally stored).

It is the carrier’s responsibility to recalibrate the on-board recording device on

mechanical or electronic installations when the tire size changes, the vehicle drive-

train is modified or any modifications are made to the vehicle which affect the

accuracy of the on-board recording device. The device must be maintained and

recalibrated in accordance with the manufacturer’s specifications. A record of

recalibrations must be retained for the audit retention period. It is the carrier’s

responsibility to maintain a second copy (back-up copy of the electronic files either

electronically or in paper form) for the audit retention period. At the data transfer. It

is the carrier’s responsibility to assure its drivers are trained in the use of the

computer system. Drivers shall be required to note any failures of the on-board

recording or vehicle tracking device and to prepare manual trip reports of all

subsequent trip information until the device is again operational. It is the carrier’s

responsibility to assure the entire record-keeping system meets the requirements of

IFTA. It is suggested that the carrier contact the base jurisdiction IFTA Audit Section

for verification of audit compliance prior to implementation.

5. Fuel records:

The retail purchase of fuel which is placed into the fuel tank of a qualified motor

vehicle, and upon which tax has been paid to a jurisdiction, shall qualify as a tax-paid

retail fuel purchase. The receipt must show evidence of tax paid directly to the

applicable jurisdiction or at the pump. Specific requirements for those receipts are

outlined in the IFTA Procedures Manual, Section P560. No member jurisdiction shall

require evidence of such purchases beyond what is specified in the Procedures

Manual. In the case of a lessee/lessor agreement, receipts for tax-paid purchases

may be in the name of either the lessee or the lessor provided a legal connection can

be made to the reporting party. Retail purchases must be supported by a receipt or

invoice, credit card receipt, automated vendor generated invoice or transaction

listing, or microfilm/microfiche of the receipt or invoice. Receipts that have been

altered or indicate erasures are not accepted for tax-paid credits unless the licensee

can demonstrate the receipt is valid. Receipts for retail fuel purchases must identify

the vehicle by plate or unit number or other licensee identifier, as distance traveled

and fuel consumption may be reported only for vehicles identified as part of the

licensee’s operation. An acceptable invoice or receipt must include, but shall not be

BEST PRACTICES AUDIT GUIDE

Page 21 of 45 May 2006

limited to, the following: date of purchase; seller’s name and address; number of

gallons or liters purchased; fuel type; price per gallon or liter or total amount of sale;

unit numbers; and purchaser’s name (see R1010.300 of the IFTA Articles of

Agreement)

Bulk fuel is normally delivered into fuel storage facilities by the licensee and fuel tax

may or may not be paid at the time of delivery. Motor fuel which is placed into the

fuel tank of a qualified motor vehicle from a licensee’s own bulk storage, and upon

which tax has been paid to the jurisdiction where the bulk fuel storage tank is

located, shall be considered a tax-paid bulk fuel purchase. The licensee’s records

must identify the quantity of fuel taken from the licensee’s own bulk storage and

placed in its qualified motor vehicles. Record-keeping requirements for tax paid bulk

fuel purchases are provided in IFTA Procedures Manual, Section P570.

Original delivery tickets and/or receipts must be retained by the licensee. Receipts

that have been altered or indicate erasures are not accepted for tax-paid credits

unless the licensee can demonstrate the receipt is valid. Bulk fuel inventory

reconciliations must be maintained. For withdrawals from bulk storage, records must

be maintained to distinguish fuel placed in qualified motor vehicles from other uses.

To obtain credit for withdrawals from licensee-owned, tax paid bulk storage, the

following records must be maintained: date of withdrawal; number of gallons or liters;

fuel type; unit number; and purchase and inventory records to substantiate that tax

was paid on all bulk purchases. Upon application by the licensee, the base

jurisdiction may waive the requirement of unit numbers for fuel withdrawn from the

licensee’s own bulk storage and placed in its qualified motor vehicles. The licensee

must show that adequate records are maintained to distinguish fuel placed in

qualified vs. non-qualified motor vehicles for all member jurisdictions.

6. Inadequate Records – A550, R1210-R1230, R1270

If the licensee’s records are lacking or inadequate to support any report filed by the

licensee or to determine the licensee’s tax liability, the base jurisdiction shall have

authority to estimate the fuel use upon (but is not limited to) factors such as the

following:

a. Prior experience with the licensee.

b. Licensees with similar operations.

c. Industry averages.

d. Records available from fuel distributors.

BEST PRACTICES AUDIT GUIDE

Page 22 of 45 May 2006

e. Other pertinent information the auditor may obtain or examine.

Unless the auditor finds substantial evidence to the contrary by reviewing the above,

in the absence of adequate records, a standard of 4.00 MPG/1.7KPL will be used.

When tax paid fuel documentation is unavailable, all claims for tax paid fuel will be

disallowed.

C. Sampling – A530

It is not always necessary to conduct an audit of all of the records maintained for the

licensee’s vehicles. The vehicles to be audited can be chosen by using a sampling

method. Representative samples must be selected from the population. Sampling

introduces an element of risk into auditing. The auditor continually decides how

extensive the procedures must be to avoid excessive risk. The auditor considers the

effectiveness of systems of internal control, the number and size of items to be tested,

and the probabilities that groups of items, numbers of vehicles, total distances, distance

allocation, total fuel, or tax paid credit gallons will be misstated in significant amount. As

with materiality, judgment plays an important role in determining the acceptable risk.

Non-statistical sampling is the standard approach used by IFTA auditors. The auditor

determines a sample size and evaluates the results of the sample based on the sound

reasoning and judgment of the auditor. This differs from statistical sampling in that

sampling risk is not measured.

Regardless of what sampling methodology used, the auditor should discuss the

proposed sample with the licensee in accordance with IFTA A530.

1. Types of Sampling:

There are several approaches for non-statistical sampling, including haphazard,

random, systematic, judgmental, and block.

a. Haphazard sampling - Items have been selected without regard to size, source,

or other attributes. This is an attempt by the auditor to select a sample without

bias. For IFTA auditors, this is the most common method used to select units for

testing.

b. Random sampling - Each unit in the population has an equal chance of being

selected, without bias. This can be accomplished by using a random number

table or a computer program, which generates random numbers. It is likely that

the licensee's vehicle numbering system will be unique for internal purposes and

not consistent with random number tables or computer software. Therefore, it

may be necessary to number the vehicles starting with 1, in order to use a table

BEST PRACTICES AUDIT GUIDE

Page 23 of 45 May 2006

or computer to generate the sample.

c. Systematic sampling - Auditor selects every "nth" item. When an auditor is in

the field, systematic selection is a convenient method of selecting a sample, as

long as the population is in random order.

d. Judgmental sampling - The sample is selected based on the sound reasoning

and judgment of the auditor. For IFTA auditors, this method is common when

there are unusual relationships, and the auditor feels errors could exist in a

specific area.

e. Block sampling - Items are selected in a sequence. For IFTA auditors, this is

the most common method used. The sequence is usually three consecutive

months within a quarter.

2. Sample Size:

IFTA does not have any quantitative guidelines established when selecting the

number of vehicles for the sample size. The size of the sample will depend upon the

results of the auditor's preliminary review of the factors such as:

a. The internal control of the licensee's overall accounting system.

b. The internal control of the licensee's reporting system.

c. Flow of paperwork within the licensee's system.

d. System of calculating distances.

e. System of calculating total fuel consumption.

f. System of reporting tax paid credit gallons.

g. Record retention system.

h. Consistency of reporting systems.

- (R1310): The base jurisdiction shall audit its licensees on behalf of all member

jurisdictions. The auditor should make every effort to choose a sample period in

which all jurisdictions through which the licensee traveled is represented.

When selecting the different vehicles from the months selected for audit, try to get a

cross-section (i.e. a representative sample). If you are confident that the sample is

valid, do not be concerned if the sample does not represent distances in all IFTA

jurisdictions. You may request distance information for a specific unit and time

period to review to at least validate that distance not represented within the sample is

correct.

BEST PRACTICES AUDIT GUIDE

Page 24 of 45 May 2006

3. Sampling Source Documents - A520

It is suggested, but not required, that fleet miles/kilometers be verified to source

documentation for at least three representative quarters. To determine if the

licensees distance accounting system properly accumulates all distance generated

by units identified to the licensee’s operation, not less than three representative

months should be selected for audit with respect to computations of jurisdiction

distance via routes traveled and to assure that all miles/kilometers are reported into

the system.

The most effective method of tracing distance from IVDRs to the summaries is

through a method of sequential audit. Using this method, the auditor tracks the

beginning trip sheet odometer’s readings and/or location to the ending of the period

trip sheet. This catches the most common error, failure to include deadhead or inter-

jurisdiction distances. For example, deadhead distances might not be properly

accounted for if the end of the prior trip is Tucson and the next trip starts in Phoenix.

A540.400. If the base jurisdiction uses a distance reporting software program to

verify the records of the licensee, it shall be used as an audit tool. The auditor must

use discretion when verifying the licensee’s records. Documentation such as trip

records, odometer readings, and other records used by the licensee to substantiate

its actual distance records must be considered by the auditor in determining an

acceptable distance reporting system.

4. Accountable Distances - P710

The IFTA tax return shall cover the previous calendar quarter and shall include the

following information: total distance traveled during the reporting period by qualified

motor vehicles in the licensee’s fleet, regardless of whether the miles or kilometers

are taxable or non-taxable by a jurisdiction.

5. Practical Aspects of Sampling

In conducting the sampling program, the auditor should also consider the following

practical aspects:

a. If you selected 15 vehicles for testing and have tested eight vehicles and found

no errors, consider discontinuing testing - what is the risk of error?

b. If you select a sample and find errors, consider whether the errors are isolated or

reoccurring. A recurring error should be projected over the audit period.

c. If there is a situation where isolated errors are occurring, discontinue sampling

and audit in detail for the isolated errors. Do not include isolated errors in the

BEST PRACTICES AUDIT GUIDE

Page 25 of 45 May 2006

sample projection.

d. If you selected a sample and found errors, consider whether the error factor is

reasonable. Sit down with the licensee and discuss the problems. Try to get

acceptance from the licensee that they will accept the projection of the sample

error factor over the entire population. It is not always necessary to expand your

sample.

6. Some Pointers Regarding Sampling

a. Sample periods should be chosen in such a manner as to prevent biased results.

b. Sample period may be adjusted to accommodate the licensee’s reporting

system(s) or record retention design(s) as long as the results remain

representative, valid, and reliable.

c. A sample size is acceptable, providing the auditor documents the procedure

used to secure the items in the sample. (size recommendations in table “j”)

d. The auditor is to consider the effects of multiple weight classes as well as long

haul vs. local in regard to the design and selection of the sample period or

sample items.

e. The auditor is to consider the effects of multiple operating divisions and/or fleets,

which may have different vehicle types and reporting systems, in regard to the

design and selection of the sample period or sample items.

f. Sampling periods may be changed, modified, and deleted at the auditor's

discretion based upon documentation and the licensee’s environment (internal

control, distance reporting system, and record retention).

g. The licensee may request the sample period be changed because of some

extraordinary event (fact). This request may be allowed, but the auditor would

have to audit the "exception period" as well as the new period. An error in the

exception period may be isolated to that period. If the exception period could not

be audited, the auditor should provide an explanation and possibly isolate the

effect of unacceptable record keeping.

h. Any sampling procedure that deviates from the examination of all items in a

sample period must be documented as to the reason for the deviation and for the

new sampling procedure.

i. The auditor should use solid professional judgment and common sense in

applying sample period results in the audit situation.

BEST PRACTICES AUDIT GUIDE

Page 26 of 45 May 2006

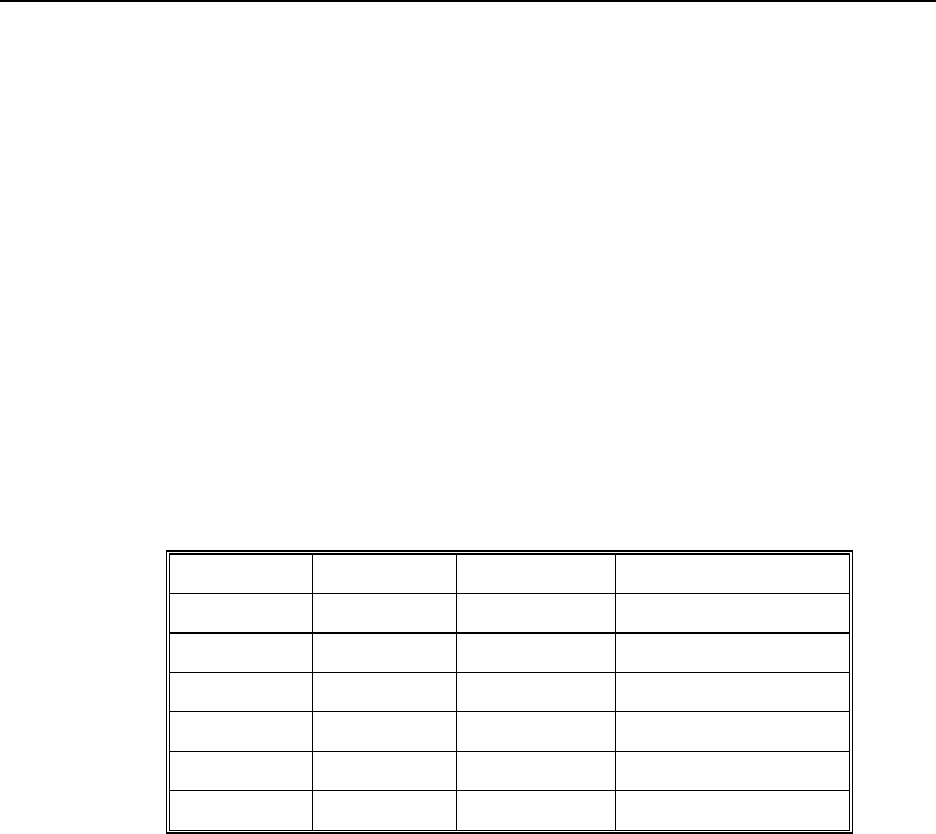

j. General idea of the sample size to be chosen:

Fleet Size Sample Size

1,000 + units 30 +

1,000 units 20-30

500 units 15-20

100 units 10-15

50 units 6-8

10 units 2-3

When selecting the sample size, the auditor should consider the effectiveness of

systems of internal control, the number and size of items to be tested, number of

vehicles, total distances, etc. Auditor’s judgment plays an important role in

determining the risk accepted.

7. Evaluating Sampling Results

After the audit procedures have been performed for the sample periods, the auditor

must evaluate the results to determine whether the findings should be projected over

the audit period (recurring errors).

Below is a list of several commonly occurring errors to look for during the audit

process.

a. Incorrect time period (distance year) reported

b. Total distance reported does not match odometer readings

c. Failure to record deadhead or bobtail distances

d. Failure to record base jurisdiction distances

e. Failure to operate interjurisdictionally

f. Clerical errors in distance calculations/reporting

g. Errors in transcribing distance/fuel from IVDR to recap, including:

• General transcription errors

• Picking up route number rather than distance

• IVDR distance not included on recap

• Some IVDR's missing

• Page of driver's notebook missing

• IVDR does not break out distance by jurisdiction

• Vehicle eliminated from fleet and not reflected in distance figures

BEST PRACTICES AUDIT GUIDE

Page 27 of 45 May 2006

• All log sheets not available at end of month and person in office estimates

distance for remaining timeframe

• Pick up 250 miles for trip as South Carolina when should be 160 in North

Carolina and 90 in South Carolina

• Pick up wrong jurisdiction from IVDR - especially similar names, such as New

York and New Jersey

• Odometer gaps - beginning odometer reading does not agree with prior

ending odometer reading

• Increasing all distance by a percentage to make sure enough distance is

reported

• Origin, destination and, possibly, fuel stops are identified and the route is run

via software without log consideration.

• Trip locations are identified via technology but route is adjusted by a quality

control editor.

• IRP distance does not match IFTA distance.

• Fuel purchase allocated to the wrong jurisdiction.

• Fuel units reported in dollars rather than gallons/liters.

• Non-taxed fuel reported as tax paid.

Analyzing and isolating errors will help the auditor focus on possible problems.

There are two major reasons for the analysis:

8. Projecting Errors

When the auditor uncovers errors during the audit, there are several courses of

action that can be taken.

a. Isolate the reason for the error and, using the facts and circumstances of that

particular situation, estimate the error. For example, if the reason for the error is

that base jurisdiction distance is not reported, determine the interjurisdictional

distance per day, week, or trip. Then, determine the applicable number of days,

weeks, or trips and multiply to arrive at the total error.

b. If the sample results can be representative of the population, project the error

based on sample results. For instance, if distance for one vehicle is omitted from

the application and it runs a similar route throughout the year, use your three-

month sample, and project the results to each quarter in the audit period.

c. If the sample is not representative of the population, expand the sample size to

an extent that is representative of the population up to 100%. However, if

BEST PRACTICES AUDIT GUIDE

Page 28 of 45 May 2006

relatively minor errors or isolated errors are noted, it might not be necessary to

expand sample.

d. If an isolated non-recurring error is noted, do not project sample results, but use

the actual error amount.

e. If the type of error that is occurring cannot be determined, expand the audit in the

particular area. The auditor can then determine the total error or better project

the error based on facts and circumstances. For instance, if the error is an end-

of-month cut-off, expand the audit to cover the end-of-month cut-off problem.

f. Use the sample error to project the error in the population.

g. If errors are minor, consider them immaterial.

h. If a type of error can reoccur due to a lack of internal control, but that type of

error can occur in non-sampled vehicles in other jurisdictions or at other

distances, the zeroing out of refunds should be considered.*

When the auditor uses sampling as an audit tool, and if any errors are projected to

the population, the projection may result in significant distance discrepancies and tax

recalculation. If a member jurisdiction disagrees with the audit, it may request

additional information, including the working papers, to determine whether the base

jurisdiction audit is sufficient to support the refund/assessment request.

If determined through audit that the system does not have the checks and balances

to support compliance, positive variances could be posted, but negative variances

could be zeroed. *

* IFTA does not have specific provisions for or against this type of adjustment. The

theory that an audit should make the licensee whole should only be applicable when

acceptable documentation is maintained. In cases where internal controls are

lacking or source documents do not give sufficient indication of the movement of the

vehicles or auditor creation of distances is necessary, rewarding the licensee with a

refund from any jurisdiction should be discouraged.

D. Distance / Fuel Verification

1. Testing the Distance / Fuel Recorded on Licensee's System

Examine the selected IVDRs to determine if:

a. They contain all basic information required.

b. Trip distance recorded is reasonably accurate and properly allocated among all

jurisdictions. A distance program can be used as a tool to determine the

accuracy of the reported distance.

BEST PRACTICES AUDIT GUIDE

Page 29 of 45 May 2006

c. Vehicle movement is continuous (odometer readings are sequential, preceding

trip destination is same as next trip's origin).

d. No unusual time lapses exist between recorded trips.

e. They contain fuel purchase information.

f. Fuel receipts are attached.

g. Fuel receipts contain all of the required information.

h. Bulk fuel withdrawals are documented.

i. Fuel receipts/invoices are compiled in some other system.

As the auditor reviews licensee distance and fuel records, situations will be

encountered where audited figures differ from those reported. These differences

need to be discussed with the licensee to determine why the difference occurred.

2. Accuracy of the Distance and Fuel Information on the IVDR's

The distance and fuel on an IVDR (which should include routes of travel) must be

verified by the auditor. There are several ways to verify these distances.

a. Odometer or hub odometer.

b. Sources of distance information:

i. Official jurisdiction highway map.

ii. Household goods carriers' distance record book.

iii. Automated distance software systems.

iv. Commercial road atlas.

The fuel purchases and tax paid credit gallons on an IVDR, or monthly fuel summary,

must be verified by the auditor. To verify fuel purchases and tax paid credit gallons:

a. Review original fuel receipts

b. Review original vendor invoices (These should list vehicle specific fuel

purchases)

c. Review Bulk fuel withdrawal records and reconciliations

3. Relevance and Frequency of Differences in IVDR Distances / Fuel

One of the main functions of the audit will be to determine the relevance and

frequency (isolated or recurring) of the differences found in the IVDR distances/fuel,

and to decide if the application of changes to a licensee's system as a whole is

warranted.

Factors that may cause differences between reported and audited distance and fuel

that should be reviewed during the audit, might include:

a. Failure to include all deadhead and interjurisdictional distances:

BEST PRACTICES AUDIT GUIDE

Page 30 of 45 May 2006

i. Beginning odometer reading does not agree with previous trip ending

reading.

ii. Different locations for one trip's end point and the next trip's beginning.

b. Missing IVDR's:

i. Unexplained period of time or distances;

ii. Valid IVDR not entered in monthly recaps.

c. IVDR does not include all necessary information:

i. Distance by jurisdiction not broken out;

ii. In-city delivery/local area distance not noted.

d. Inaccurate distance data on the IVDRs:

i. Broken or miss-calibrated odometers.

ii. Distances according to recorded routes do not match map distances

iii. The licensee and auditor may be using different automated distance systems.

iv. Obviously estimated or rounded distances.

e. Inaccurate fuel information:

i. Missing fuel receipts.

ii. Fuel receipts allocated to the wrong jurisdiction.

iii. Fuel receipts discovered for purchases in jurisdictions with no reported

distance.

iv. No bulk fuel withdrawal records or reconciliation.

v. Non-IFTA vehicles fueled from bulk fuel storage.

vi. No fuel purchases documented for a vehicle that has reported distance

traveled.

vii. Review resulting MPG/KLM for each vehicle to make sure they are

reasonable. Extremely high or low MPG/KLM may indicate errors in reporting

fuel.

When the audited distance for an individual jurisdiction is different from the

jurisdiction's distance recorded on the IVDR, the auditor needs to consider whether

the licensee dropped or picked up any loads within the jurisdiction or if travel was

straight through a jurisdiction. It may not be possible to determine this from the

IVDR. If a licensee traveled across a jurisdiction and made no stops, the distance

recorded for that jurisdiction should be at least the minimum map distance for the

particular route taken.

If the test results in numerous errors and irregularities, the auditor might consider

BEST PRACTICES AUDIT GUIDE

Page 31 of 45 May 2006

expanding the sample or testing a second sample, if there is doubt about the sample

being representative of the population.

If the test does not reveal any material differences, and the sample was

representative of the population, the auditor can place reliance on the licensee's