(Bloomberg Financial Series Bloomberg Visual Guide Series) David Wilson To Marke

User Manual:

Open the PDF directly: View PDF ![]() .

.

Page Count: 196 [warning: Documents this large are best viewed by clicking the View PDF Link!]

Visual Guide to

Financial Markets

e Bloomberg Financial Series is meant to serve as the

all-encompassing, yet easy-to-follow, guide on today’s

most relevant nance and trading topics. e content

lives up to the title by being visual; all charts are in

color and presented in a large format for ease of use

and readability. Other visual attributes include con-

sistent elements that function as additional learning

aids for the reader:

■ Key Point sections: Primary ideas and takeaways,

designed to help the reader skim through de ni-

tions and text.

■ De nitions: Terminology and technical concepts

that arise in the discussion.

■ Step-by-Step instructions: Tutorials designed to

ensure that readers understand and can execute

each section of a multi-phase process.

■ Do It Yourself: Worksheets, formulas, and calcula-

tions.

■ Bloomberg Functionality Cheat Sheet: For Bloom-

berg terminal users, a back-of-the-book summary

of relevant functions for the topics and tools

discussed.

For e-reader users, e Bloomberg Financial Series

is available as an enhanced e-book and o ers spe-

cial features, like an interactive Test Yourself section

where readers can test their newly honed knowledge

and skills. e enhanced e-book version includes

video tutorials and special pop-up features. It can be

purchased wherever e-books are sold.

How to Use This Book

Visual Guide to

Financial Markets

David Wilson

BLOOMBERG PRESS

An Imprint of

Copyright © 2012 by David Wilson. All rights reserved.

Published by John Wiley & Sons, Inc., Hoboken, New Jersey.

Published simultaneously in Canada.

Charts reprinted with permission from Bloomberg. Copyright 2011 Bloomberg L.P. All rights reserved.

No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means,

electronic, mechanical, photocopying, recording, scanning, or otherwise, except as permitted under Section 107 or 108

of the 1976 United States Copyright Act, without either the prior written permission of the Publisher, or authorization

through payment of the appropriate per-copy fee to the Copyright Clearance Center, Inc., 222 Rosewood Drive, Danvers,

MA 01923, (978) 750-8400, fax (978) 646-8600, or on the Web at www.copyright.com. Requests to the Publisher for permis-

sion should be addressed to the Permissions Department, John Wiley & Sons, Inc., 111 River Street, Hoboken, NJ 07030,

(201) 748-6011, fax (201) 748-6008, or online at http://www.wiley.com/go/permissions.

Limit of Liability/Disclaimer of Warranty: While the publisher and author have used their best eorts in preparing this

book, they make no representations or warranties with respect to the accuracy or completeness of the contents of this

book and specically disclaim any implied warranties of merchantability or tness for a particular purpose. No warranty

may be created or extended by sales representatives or written sales materials. e advice and strategies contained herein

may not be suitable for your situation. You should consult with a professional where appropriate. Neither the publisher

nor author shall be liable for any loss of prot or any other commercial damages, including but not limited to special,

incidental, consequential, or other damages.

For general information on our other products and services or for technical support, please contact our Customer Care

Department within the United States at (800) 762-2974, outside the United States at (317) 572-3993 or fax (317) 572-4002.

Wiley also publishes its books in a variety of electronic formats. Some content that appears in print may not be available

in electronic books. For more information about Wiley products, visit our web site at www.wiley.com.

Library of Congress Cataloging-in-Publication Data

Wilson, David, 1958 Mar. 28-

Bloomberg visual guide to nancial markets / David Wilson.

p. cm. – (Bloomberg visual guide series)

Includes bibliographical references and index.

ISBN 978-1-118-20423-8 (pbk.); ISBN 978-1-118-22846-3 (ebk); ISBN 978-1-118-23325-2 (ebk); ISBN 978-1-118-26559-8 (ebk);

ISBN 978-1-118-37348-4 (ebk); ISBN 978-1-118-37349-1 (ebk); ISBN 978-1-118-37350-7 (ebk)

1. Finance. 2. Capital market. 3. Investments. I. Title.

HG173.W495 2012

332′.0415 -dc23 2012001524

Printed in the United States of America

10 9 8 7 6 5 4 3 2 1

To Sandy,

who has taught me far more about life and love

than I ever taught her about business and nance.

vii

Contents

Acknowledgments ix

Introduction xi

■ Part I: Direct Investing 1

■ Chapter 1: Overview 3

Quotations 4

Three Rs 6

■ Chapter 2: Government 11

Currencies 12

Quotations 13

Three Rs 15

Bills 18

Quotations 20

Three Rs 21

Notes and Bonds 24

Quotations 26

Three Rs 27

■ Chapter 3: Companies 35

Money Markets 35

Quotations 38

Three Rs 39

Notes and Bonds 42

Quotations 45

Three Rs 46

Stocks 50

Quotations 53

Three Rs 55

■ Chapter 4: Hard Assets 63

Gold 63

Quotations 66

Three Rs 66

Commodities 68

Quotations 70

Three Rs 71

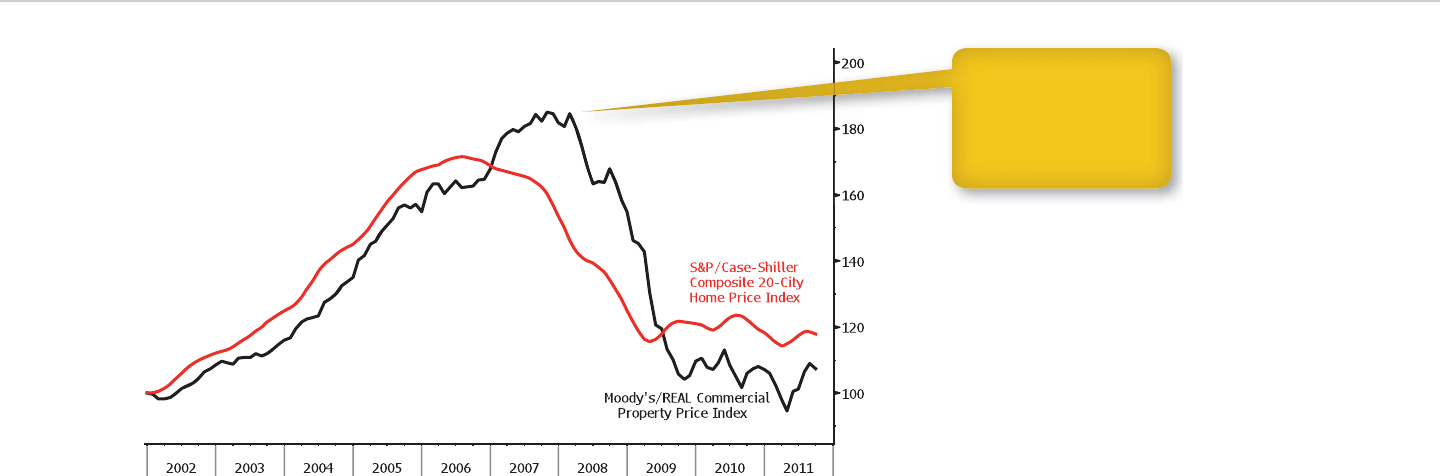

Real Estate 73

Quotations 75

Three Rs 75

■ Chapter 5: Indexes 79

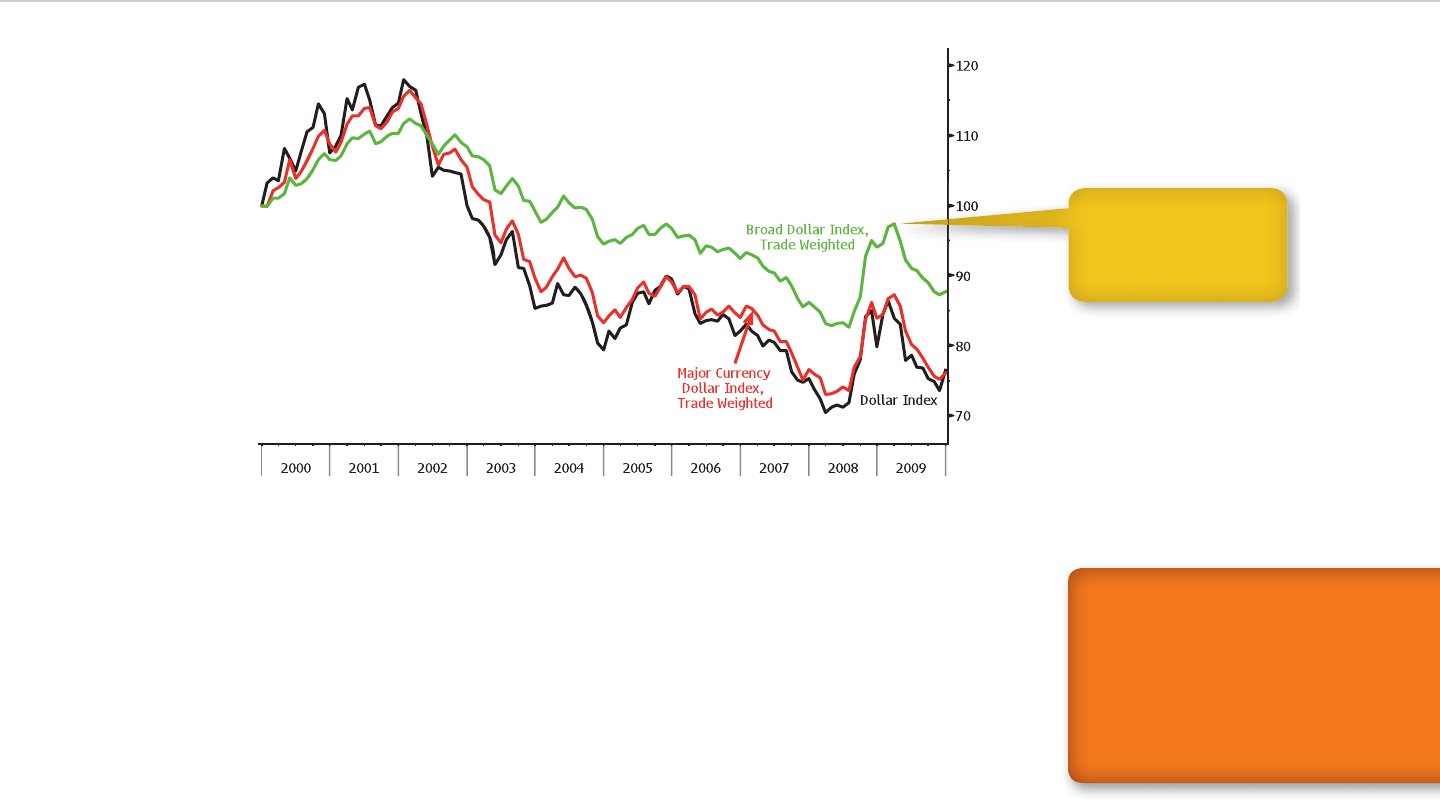

Currency 79

Debt 81

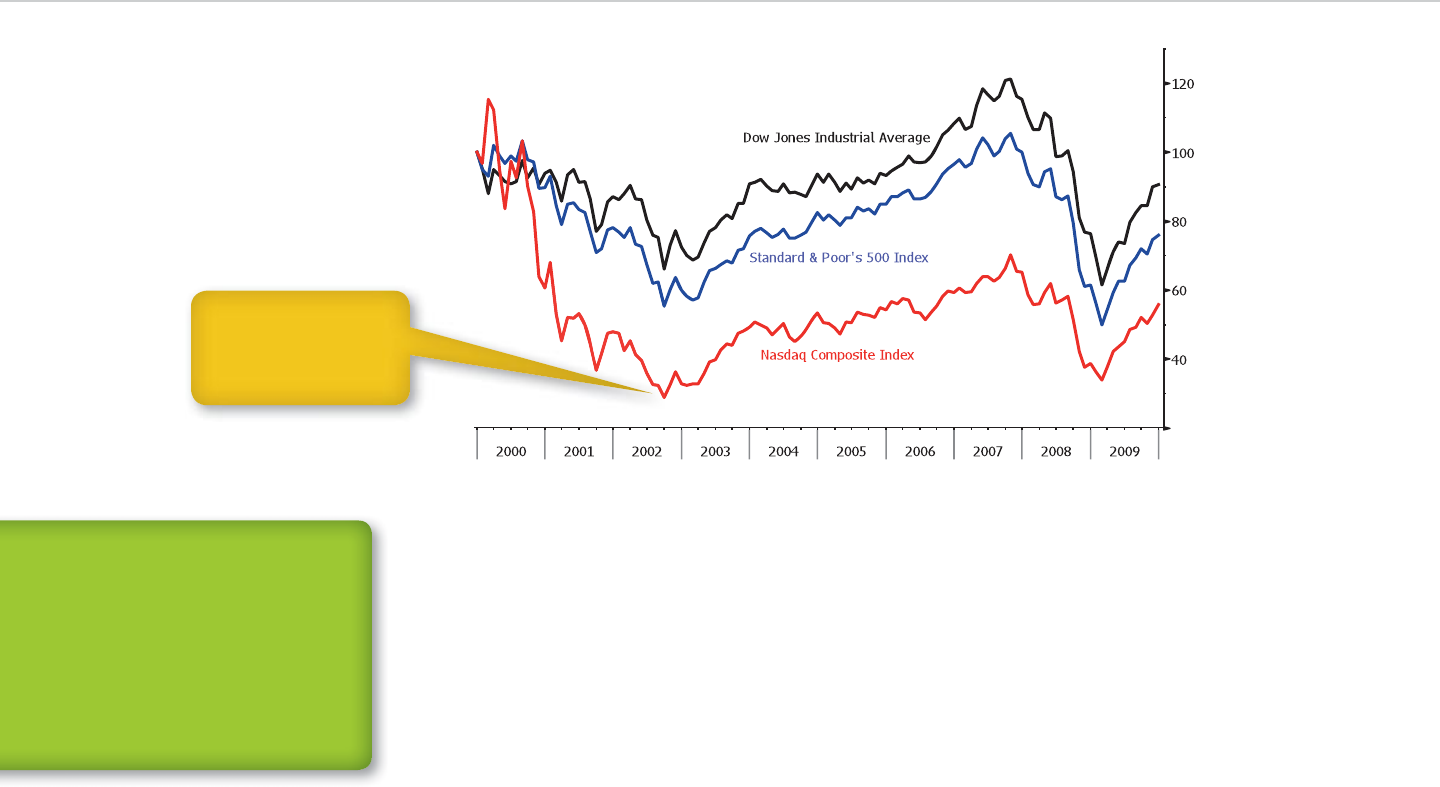

Equity 83

Hard Assets 85

■ Chapter 6: Government Revisited 87

Municipal Bonds 88

Quotations 90

viii ■Contents

Three Rs 91

Mortgage-Backed Securities 93

Quotations 95

Three Rs 95

■ Chapter 7: Companies Revisited 99

Preferred Stock 99

Quotations 100

Three Rs 101

Convertible Securities 103

Quotations 104

Three Rs 105

Bank Loans 106

Quotations 109

Three Rs 109

■ Chapter 8: Hard Assets Revisited 113

Master Limited Partnerships 114

Quotations 115

Three Rs 116

Real Estate Investment Trusts 118

Quotations 120

Three Rs 120

■ Part II: Indirect Investing 123

■ Chapter 9: Overview 125

Quotations 126

Three Rs 127

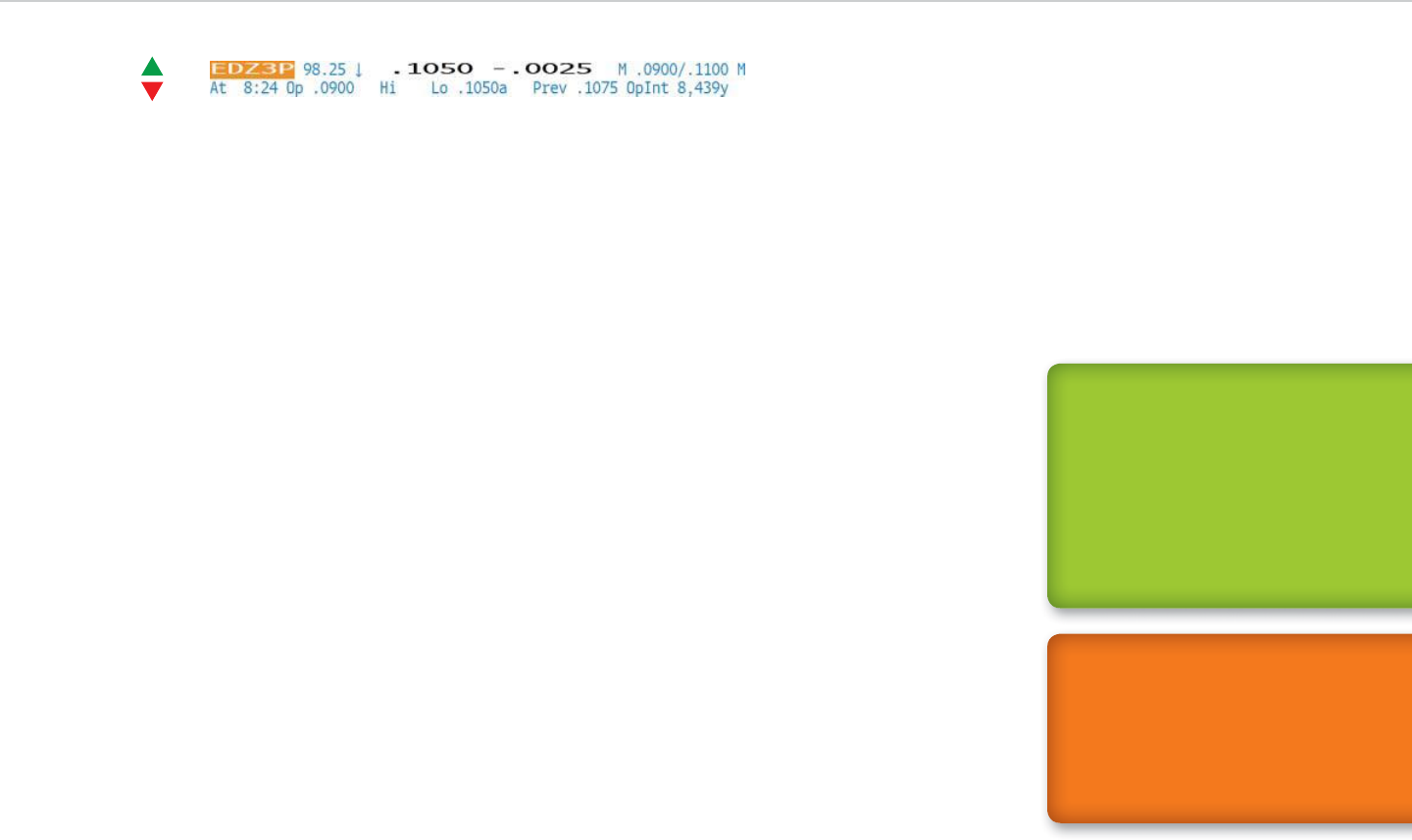

■ Chapter 10: Derivatives 129

Futures and Forwards 129

Quotations 131

Three Rs 134

Options and Warrants 137

Quotations 140

Three Rs 142

Swaps 145

Interest-Rate Swaps 147

Quotations 149

Three Rs 149

Credit Default Swaps 152

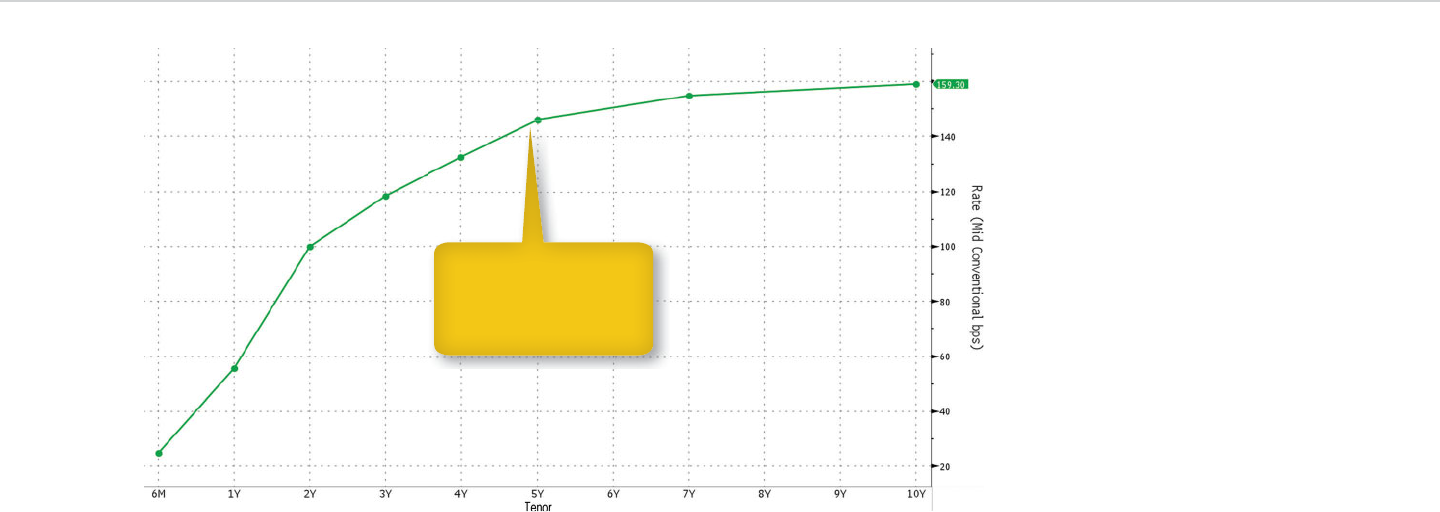

Quotations 153

Three Rs 154

■ Chapter 11: Mutual Funds and Exchange-Traded Funds 159

Quotations 161

Three Rs 162

Alternative Funds 165

Quotations 168

Three Rs 168

■ Chapter 12: Indexes Revisited 173

Futures 173

Options 175

Swaps 176

Funds 177

Appendix: Bloomberg Functionality Cheat Sheet 179

About the Author 181

Index 183

ix

is book is the product of more than two decades

spent learning about and teaching nancial markets

at Bloomberg News even though it was put together

in far less time.

Bloomberg’s editor-in-chief, Matt Winkler,

brought me on board in October 1990. Less than a

year later, he and I started training 25 newly hired

reporters for our Princeton, New Jersey, bureau. We

spent eight weeks in a room with folding tables,

bare floors, and air-conditioning ducts hanging

from the ceiling.

Matt sent me to London the next year to run our

rst European training class, which meant getting my

rst passport. It was a thrill to teach currencies on

the same day that George Soros became the man who

broke the Bank of England, thanks to his hedge fund’s

billion-dollar bet against the British pound.

After serving as the bureau chief in Princeton and

then in New York, I became Bloomberg News’s rst

global training editor in 1994. For the next ve years, I

traveled the world to teach new reporters and editors

about nancial markets, journalism, and the Bloom-

berg terminal. e position was an invaluable learning

experience.

Some of the materials I put together during the

period provided a foundation for this book. Handouts

broke down quotes on securities and commodities

in detail, and you’ll nd similar dissections in most

of the chapters. Another handout highlighted what

you’ll come to know as the three Rs of nancial mar-

kets: returns, risks, and relative value.

e training instinct came ooding back when my

wife and I saw an o -o -Broadway play written by Ken

Jaworowski, a former colleague, in October 2010. e

characters included an economics professor who lec-

tured his students about how the yield curve a ected

the outlook for growth. Afterward, I met the actor

who played the professor and gave him an impromptu

session on the topic, with curves drawn on the back of

a paper placemat. anks, K.J., for the moment.

Matt suggested me as the author of this book, and

I thank him and his chief of sta , Reto Gregori, for

giving me the opportunity. I’m thankful to Stephen

Isaacs, an editor-at-large at Bloomberg Press, and to

Acknowledgments

x■Acknowledgments

Evan Burton, Judy Howarth, and Chris Gage, my edi-

tors at John Wiley & Sons.

Chris Nagi and Nick Baker, who oversee my Chart

of the Day stories for Bloomberg News, let me take

time o as necessary to put the book together. I’m

grateful to them, along with Al Mayers and Anthony

Mancini at Bloomberg Radio, where I serve as stocks

editor, for their support.

Brendan Moynihan and Shin Pei, editors-at-large

for Bloomberg News, read this book in draft form and

provided feedback that helped me improve the n-

ished product. I appreciate their assistance.

I have worked with and trained many other people

at Bloomberg News who deserve thanks. It would take

pages to identify them all, so I hope they will accept

my heartfelt gratitude as a group.

My goal as a nancial journalist has been to tell sto-

ries in a way that my father, William, and my mother,

Evelyn, could understand. ough neither of them

worked in nance, they followed the subject as it

related to our family. ey both have passed away, and

I carry their memory with me always.

e comments of a couple of friends, Runi Sriwar-

dena and Robin Vitale, reinforced the need to keep

things as simple as possible. I’m grateful to them for

the reminder, and I did the best I could to meet that

goal.

Finally, I’d like to thank my wife, Sandy, for her love

and friendship over the years. Little did she know

when we rst met in the mid-1990s at Bloomberg

News that she would end up married to an author.

en again, I didn’t know anyone who shared my at-

titude toward life until she came along.

While I was working on the book, Sandy’s eorts

allowed me to come home and focus on my “night job”

after putting in a full day at the oce. I’m grateful for

her willingness to let me pursue this, and I hope the

results are worth the sacrice.

David Wilson, February 2012

xi

Financial markets are supposed to be complicated.

If they were easier to understand, there wouldn’t

be as much money to go around. Individual investors

wouldn’t need to pay brokers and nancial advisers as

much to manage their nest eggs. ey might be less

inclined to buy high and sell low, ensuring pro ts for

those who do the opposite.

is book is designed to make things simpler. It’s

built around the choices that you have about where to

put your money, an approach that’s more in keeping

with the investment decisions that people make in the

real world.

Look at it this way: If a family member asked you

for some money to start a business, your rst thought

probably wouldn’t be about the kind of securities you

would receive in return. More than likely, it would be

about the person, his or her relationship to you, suc-

cess in life and work, background in business, and

any past requests made for nancial help.

You’ ll nd three basic equivalents of the family

member in nancial markets:

1. Governments, which rely on money from investors

to bridge gaps between spending and taxes. e

bigger the budget de cit, the more borrowing they

need to do.

2. Companies, which raise funds to run and expand

their business and enable owners to buy and sell

their investments.

3. Hard assets, which have a presence that goes be-

yond entries in computer databases or on scraps

of paper. Gold is one example that many investors

favor. Commodities and real estate are others.

After deciding what to invest in, you have to gure

out how to put your money to work. You can invest di-

rectly in governments, companies, and hard assets, and

there’s more than one choice for each. You can make in-

vestments that indirectly re ect their value as well.

Chapter 1 provides an overview of direct investing

and introduces a format used throughout the book.

We’ll begin with the basics, especially the assets and

the markets where they are bought and sold. After

Introduction

that, we’ll dissect a market quotation as it might ap-

pear on a Bloomberg terminal.

We’ll conclude with a review of the three Rs of

financial markets: returns, risks, and relative value.

We’ll go through the components of returns, includ-

ing interest on bonds and dividends on stocks. We’ll

examine the risks that can reduce those returns.

Finally, we’ll look at ways that investors deter-

mine whether an asset is cheap, expensive, or fairly

valued.

Government markets are our next stop in Chap-

ter 2. We’ll start by determining why you’re eectively

making an investment in the government when keep-

ing cash in a bank account or maybe under a mattress.

e answer lies in currencies.

We’ll look at lending money to the government.

You have a choice between buying bills, IOUs that pay

o in no more than a year; notes, which last for as long

as 10 years; and bonds, which raise funds for longer

periods. We’ll tackle bills before moving into notes

and bonds.

Companies compete with the government to raise

money in nancial markets, and Chapter 3 spells out

how. ey can raise funds for a year or less by selling

securities that are similar to government bills. To line

up nancing for longer periods, they can turn to notes

and bonds instead.

Another choice for companies isn’t available to

governments: selling partial ownership, otherwise

known as equity. is chapter explains how investors

can distinguish one company’s shares from another’s.

xii ■Introduction

Hard assets are an alternative to stocks, bonds, and

cash, and Chapters 4 is all about them. Gold comes

rst because many investors consider the precious

metal to be separate from other assets. en we’ll look

at commodities and real estate.

Indexes enable investors to track how well or poor-

ly nancial markets are performing. ese indicators

provide a way for them to assess their own perfor-

mance, or those of the managers working for them.

ey provide a way to invest as well because many

index-based funds are available. Chapter 5 presents

indexes that are based on direct investments.

Chapters 6 through 8 revisit government, compa-

nies, and hard assets to introduce additional markets.

Government debt includes state and local borrowing,

along with many bonds backed by home mortgages.

Companies sell securities that are a cross between

bonds and stocks, and take out bank loans. Inves-

tors can prot from hard assets without having to

own them, and we’ll look at commodity and real es-

tate businesses that provide an added bonus of tax

benets.

e remainder of the book explores indirect invest-

ing, or markets that are one step removed from own-

ership of government IOUs, corporate securities, and

hard assets. Chapter 9 provides an overview of the two

main categories for this type of investing, derivatives

and funds.

Derivatives are covered in more detail in Chapter

10. e value of these contracts is tied to some oth-

er investment, such as a stock, a bond, an interest

Visual Guide to Financial Markets ■xiii

rate, a currency, or an index. We’ll review three basic

types—futures, options, and swaps—and touch on a

few variations as well.

Chapter 11 is all about funds. eir value is based

on investments made by someone else, namely the

manager. We’ll go through mutual funds and ex-

change-traded funds, or ETFs, along with alternative

funds for wealthier investors that are more complex

and costly.

e nal chapter revisits the subject of indexes.

We’ll look at indicators based on derivatives and

funds, and we’ll learn what investors do with them.

at’s a lot to go through, and each chapter could

be developed as its own book. Even so, you’ll be able

to gain a basic knowledge of nancial markets by the

time you’re done. Charts and visual aids show what

each chapter is telling.

With all that in mind, let’s get started.

DIRECT INVESTING

Visual Guide to Financial Markets

by David Wilson

Copyright © 2012 by David Wilson.

3

Overview

Financial markets o er you two basic investment

choices: debt or equity. You can lend money to a

government or company for some amount of time, or

you can buy at least a share of companies and hard

assets.

Debt represents a promise to pay. A borrower is re-

quired to make interest payments, if any, according

to a schedule that’s set when the loan is made. e

borrower eventually has to repay the full amount

and possibly a little extra.

Equity means full or partial ownership. Entire com-

panies are bought and sold in the stock market along

with their shares. Gold, other commodities, and real

estate change hands through markets as well.

Debt payments and equity investments vary from

one market to the next, as you’ll nd out later.

What’s constant is that governments, companies, and

producers of hard assets play a role in these markets

directly. ey are more than names that are attached

to contracts.

Financial markets enable borrowers to nd lenders

and equity owners to locate investors. is rst takes

place in what’s known as the primary market, where

new securities and assets are sold.

Borrowers usually rely on competitive auctions for

fundraising, though some sales are negotiated. Com-

panies can sell stock publicly for the rst time in ini-

tial public o erings (IPOs). ey can sell additional

shares as needed.

Commodity markets that focus on the buying and

selling of raw materials, rather than derivative con-

tracts, can be labeled primary markets. In real estate,

marketplaces for new buildings can be described the

same way.

In secondary markets, investors trade with each

other rather than governments, companies, and own-

ers of hard assets. Most buying and selling happens in

KEY POINT:

Governments and companies

raise money from investors in

primary markets. Investors buy

from and sell to each other in

secondary markets.

4■CHAPTER 1 Overview

conditions. Bottom-up analysis begins by con-

sidering the outlook for a speci c government,

company, or asset.

2. Technical analysis is the study of prices and other

data to determine trading patterns. If a chart shows

that a stock fell to $20 and rebounded twice in six

months, then a technical analyst may conclude

that the next retreat to $20 will attract enough buy-

ers to lead to a rebound. Sales, earnings, and other

fundamental data aren’t part of the picture.

3. Quantitative analysis relies on number crunching.

Financial and trading statistics and other data are

collected and run through mathematical formu-

las programmed into computers. e results are

used to guide investment decisions. e people do-

ing the analysis are known as rocket scientists or

quants, because their work is relatively complex.

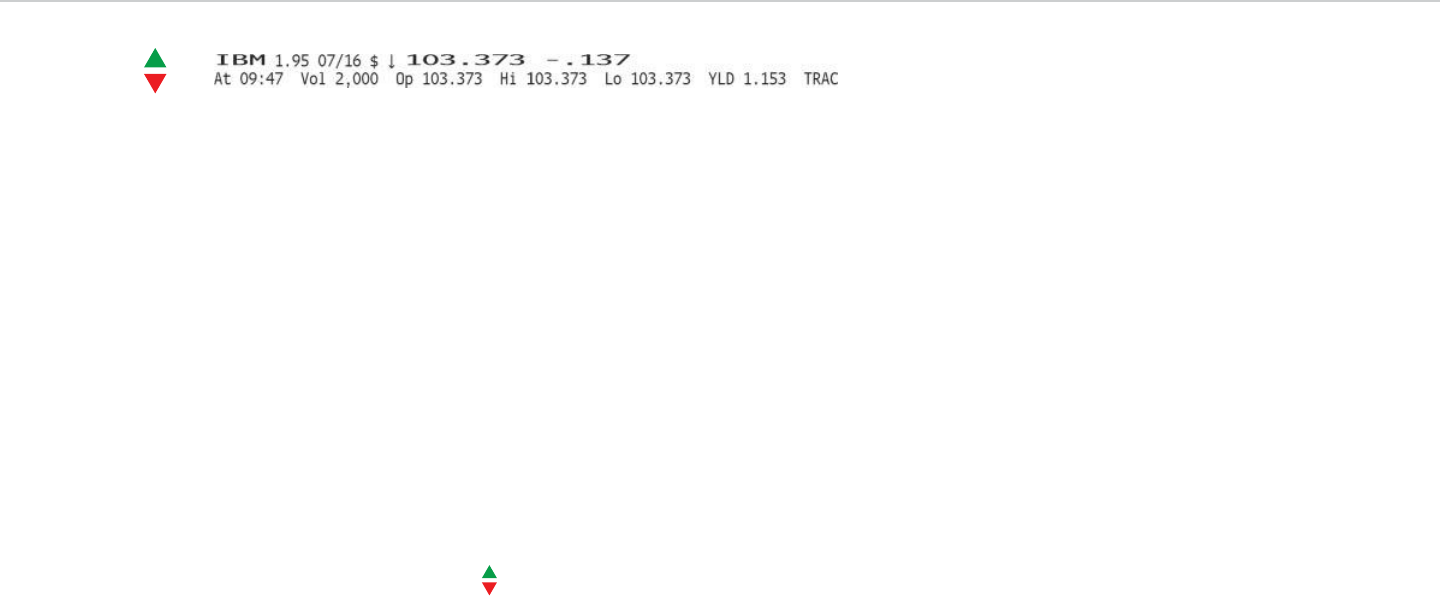

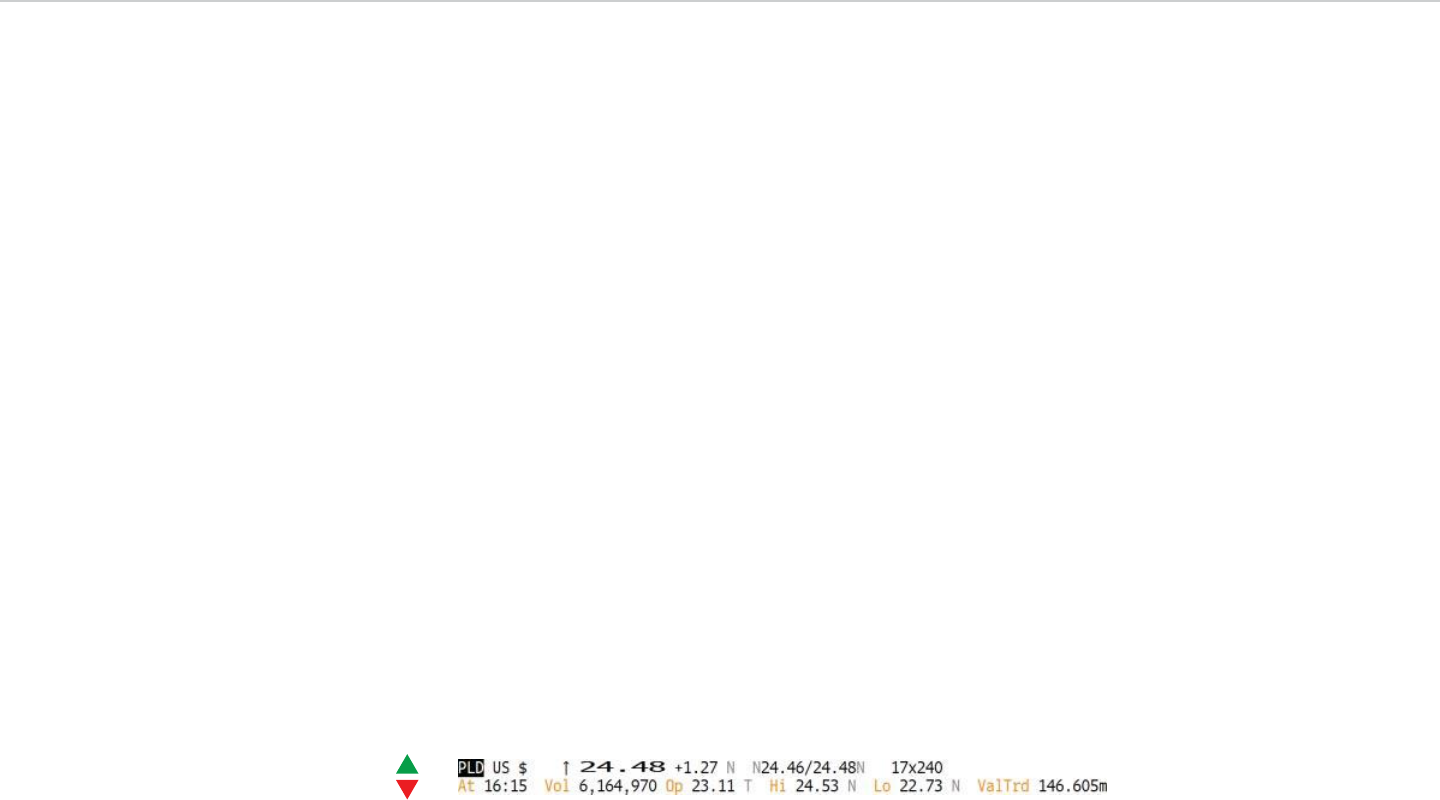

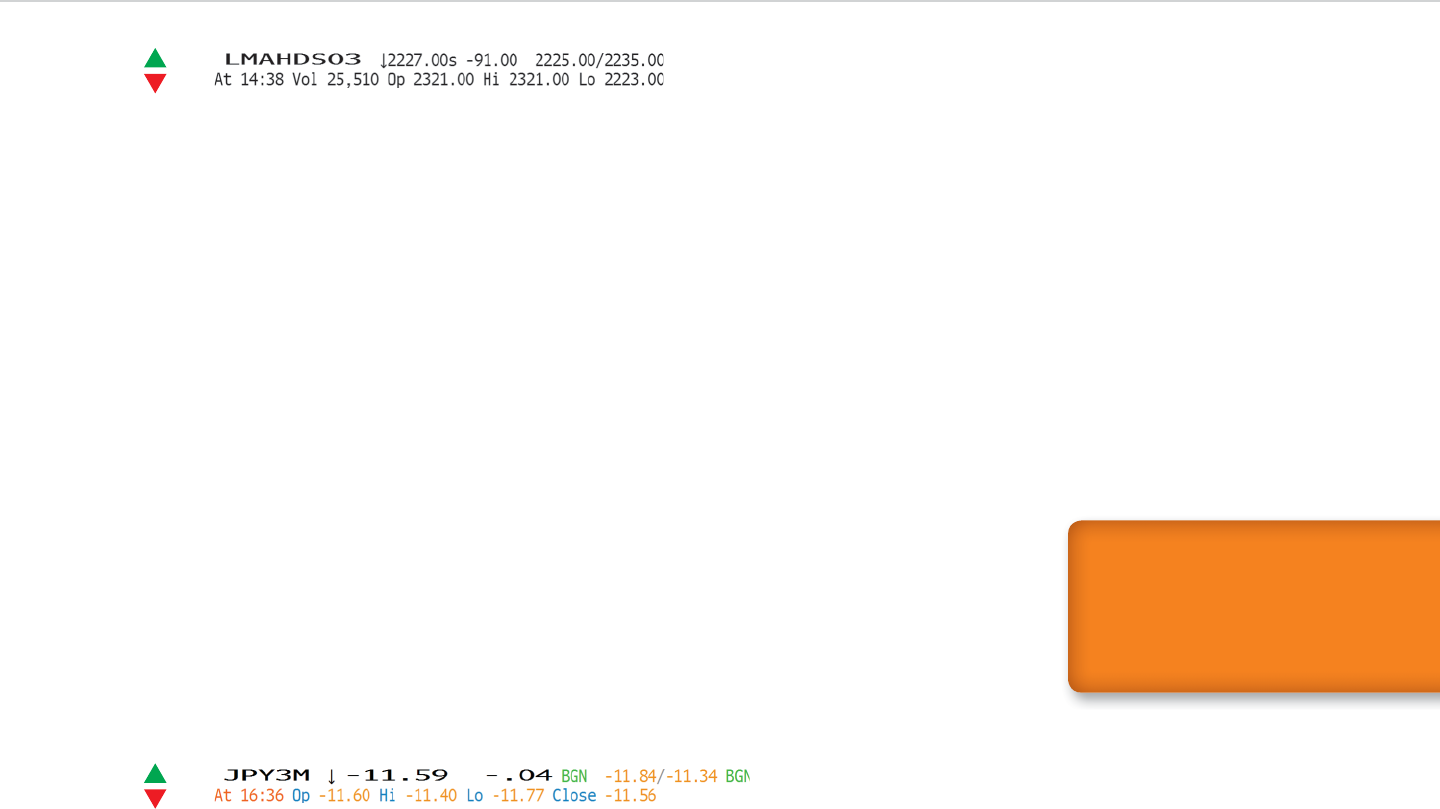

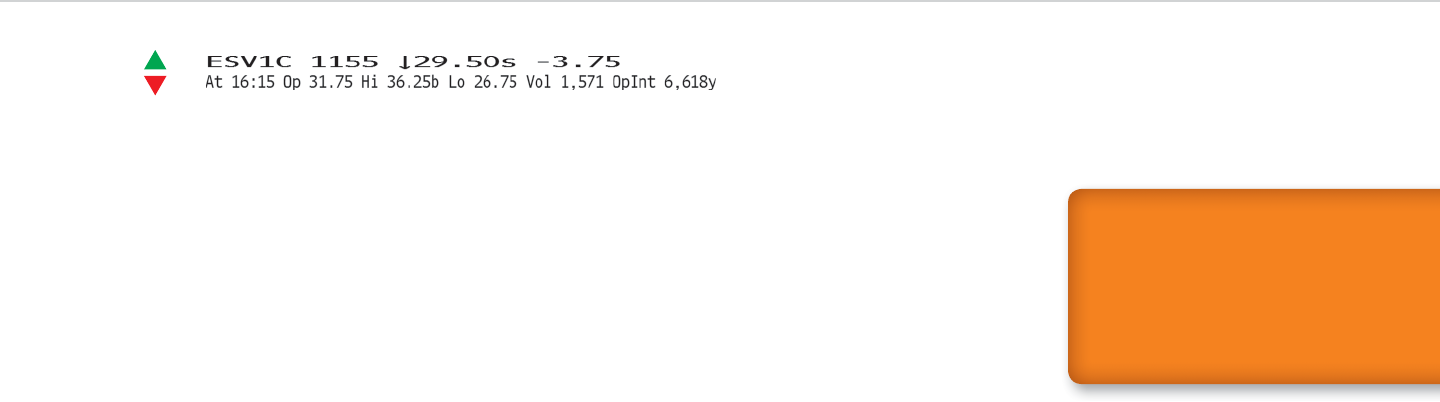

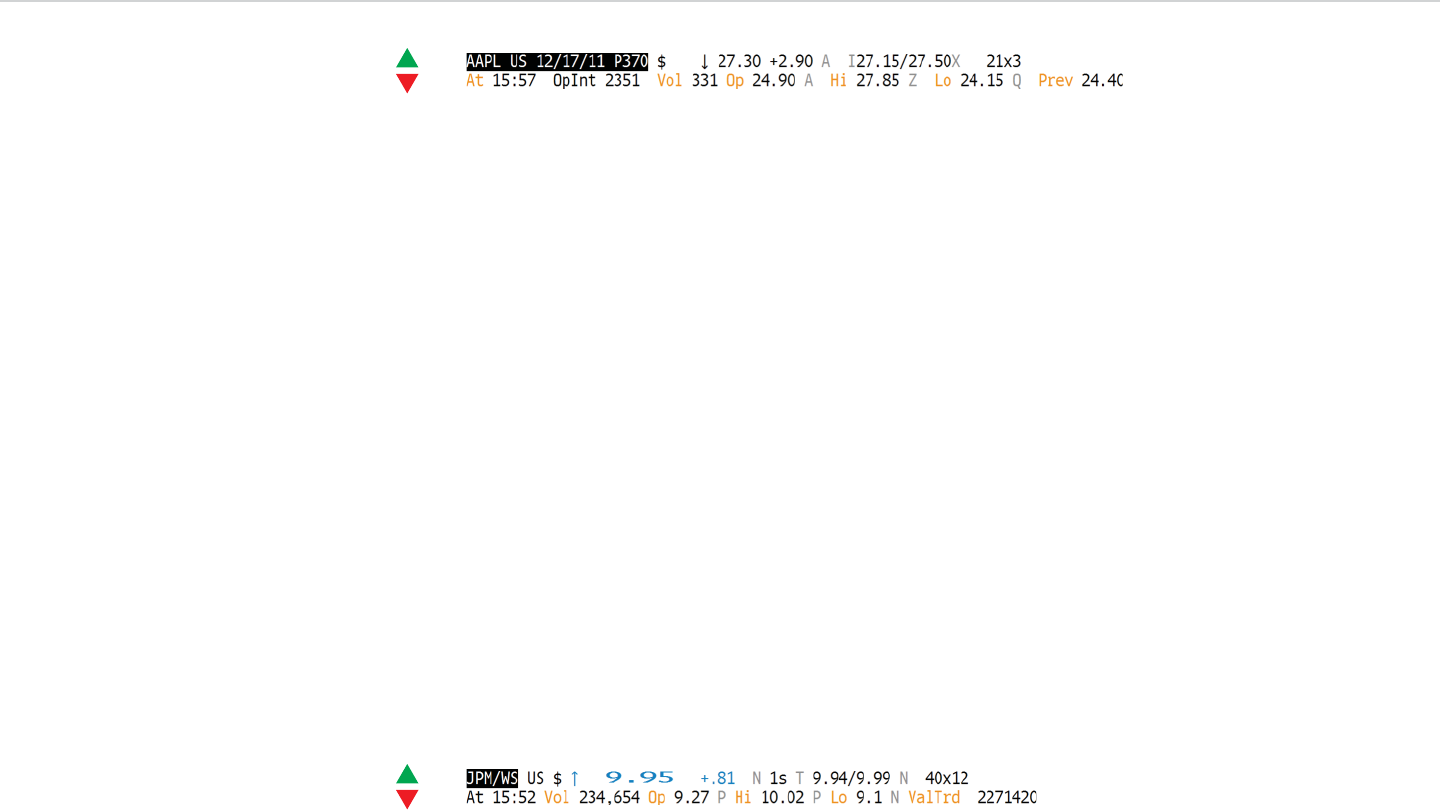

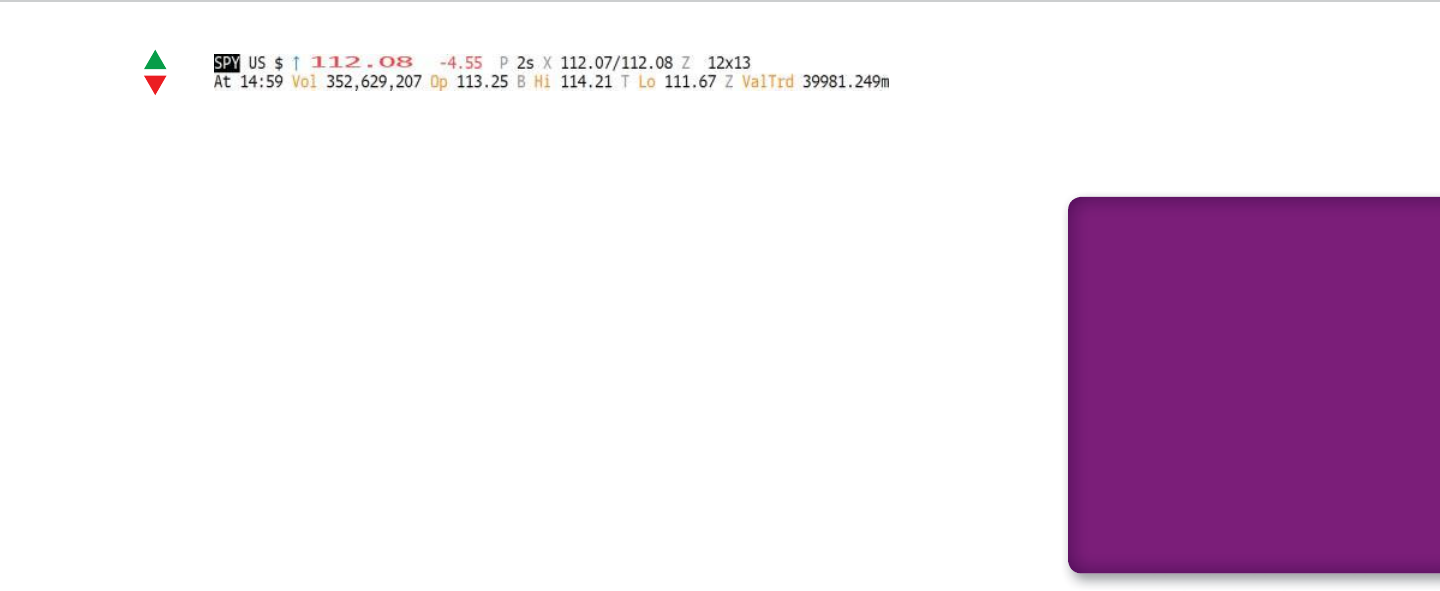

Quotations

Whether you’re looking at governments, companies,

or hard assets, you’ll need to know something about

prices and trading to understand what’s happening to

their value.

e key details vary by market as we’ll learn later.

e data presented in Exhibit 1.1, a stock quotation

these markets if only because they tend to be far big-

ger than primary markets.

e longer the life of a security or asset, the greater

the role of secondary trading. Debt maturing in a few

months is less likely to change hands than a security

with years left until it comes due. Equity has no matu-

rity date by de nition. Gold and other commodities

can be stored inde nitely. Buildings typically last for

decades, and land is eternal.

Investors who own a security or hard asset are said

to have a long position. e holding becomes more

valuable as the price increases. e opposite is a short

position, established by selling a security or asset bor-

rowed from another investor. Anyone with a short po-

sition stands to gain when the price drops, and vice

versa.

ree basic types of analysis help investors decide

whether to go long or short. Some investors rely on

one type, and others combine them in search of in-

vestments most likely to rise or fall.

1. Fundamental analysis focuses on the prospects

for governments, companies, or hard assets. e

analysis can take what’s known as a top-down or

a bottom-up approach. Top-down analysis begins

by looking at overall economic and business

KEY POINT:

There are three main

approaches to market analysis.

Fundamentals provide insight

into a government, company

or hard asset. Technicals

refl ect a security’s price moves.

Quantitative analysis relies on

data.

Exhibit 1.1: An IBM Stock Quote

Visual Guide to Financial Markets ■5

rather get as much money as possible, all other

things being equal.

Ask price: is is the lowest price at which anyone is

willing to sell. It’s known as the oer price. By either

name, it’s the ip side of the bid price, as a buyer

would rather pay as little as possible. e dierence

between the bid and ask prices is known as the bid-

ask spread. e narrower the spread, the easier it

is for investors to buy and sell without moving the

price, and vice versa.

Time: is shows whether the latest price is a rea-

sonable indication of market value. If it’s a minute

or two old, then the answer is probably yes. If it’s an

hour or two old, then maybe not. Times are present-

ed in 24-hour format. is means that a stock price

posted at the close of U.S. stock exchanges, 4 p.m.

Eastern time, would appear as 16:00.

Price range: Opening, high, and low prices for the

day’s trading put the current price in context. How

much have prices moved during the day? Is the cur-

rent price closer to the high or the low? It’s easier

to answer these questions when the data are readily

available. For the same reason, many quotes include

the previous day’s closing price.

for International Business Machines Corp., diers

from what you see in Exhibit 1.2, a quote for one of

IBM’s bonds.

Yet some facts and gures are usually included, no

matter what the security, and they are worth knowing

now. Let’s take a closer look at them.

Security symbol: is code, known as a ticker, is

the rst thing you’ll see in any quote. Some symbols

identify only the original seller or the issuer. Others

include details about the security itself.

Uptick/downtick arrow: e direction of the ar-

row shows the last change, usually in the price. It’s

known as an uptick/downtick arrow because each

price move in a security is called a tick.

Latest price: is is the most basic piece of data

in any quote. It’s usually taken from trades. Some

investments aren’t quoted at a price as we’ll see

later.

Change on the day: By comparing this gure with

the latest price, you’ll know how much the market

value has moved during the day.

Bid price: is is the highest price that anyone is

willing to pay. It’s shown because a seller would

Exhibit 1.2: An IBM Bond Quote

6■CHAPTER 1 Overview

ties in a single market, between market segments, and

among markets as we’ll see again later.

Returns

Price changes usually make the biggest contribution

to returns on an investment. eir e ect depends on

the direction of the move and on whether an investor

owns the security or asset or is betting on a decline.

e rst point is obvious enough. Investors in a

government, company, or hard asset want to make

money. e same goes for anyone who’s betting

against them. e second point refers to whether

someone has a long or short position.

Investors can go long through the primary or sec-

ondary market. Either way, the price they pay for a

security or asset becomes the starting point for deter-

mining their returns.

To go short, investors borrow securities or assets and

sell them as mentioned earlier. e borrowing is usually

conducted in a securities-lending market, where inves-

tors are paid for making their holdings available.

e price of the second transaction, or short sale, is

the basis for calculating returns. If the price declines,

then short sellers can make money by buying back

whatever was sold and by repaying the lender. eir

pro t comes from the gap between the short sale and

market prices. If the security or asset rises, then the

short seller loses.

When we study returns later, we’ll focus on what

investors in governments, companies, and hard assets

will earn. Remember, though, that rising prices don’t

You may have noticed that volume, or the amount

of trading, isn’t part of this list. at’s no accident. Vol-

ume is available mainly for stocks and other securities

that trade on exchanges. For currencies, bonds, and

hard assets, they often are hard to nd or undisclosed.

Three Rs

Now that you have gone this far, it’s time to address a

basic question: What’s in it for me? Put another way,

how would markets for investing in governments,

companies, and hard assets a ect me? To nd the

answer, you have to focus on the three Rs of returns,

risks, and relative value.

e rst two Rs, returns and risks, go together. If

one investment produces higher returns than anoth-

er, then it’s usually riskier as well. Investors who pay

too much attention to the returns can end up su er-

ing unexpected losses when a change in market direc-

tion highlights the risks.

Relative value, the third R, begins with understand-

ing the relationship between the rst two. If the price

of a security or hard asset falls, it’s possible the move

might be temporary and the potential returns may

rise accordingly. It’s also possible the investment has

become more speculative. Returns in the future may

be the same or lower after adjusting for the added risk.

ese kinds of judgments are essential in deter-

mining whether an investment is cheap, expensive, or

fairly priced, the goal of relative-value analysis. ey

can be made for a speci c security, between securi-

STEP-BY-STEP:

REAL RETURN MATH

1. The Standard & Poor’s 500 In-

dex fell 0.003 percent in 2011.

2. Dividends paid during the

year equaled 2.089 percent of

the index’s value.

3. Add price changes and divi-

dends to calculate the nomi-

nal return of 2.086 percent, or

2.1 percent after rounding.

4. Infl ation was 3.4 percent,

based on the change in the

Consumer Price Index (CPI)

for the 12 months ended in

November.

5. Subtract infl ation from the

nominal return to calculate

the real return of minus

1.3 percent.

KEY POINT:

Returns, risks, and relative

value are the three Rs of

investing. Returns are based

on price changes and any

payments that investors

receive. Risks can be general,

specifi c to an investment,

or somewhere in between.

Relative value refers to what’s

cheap, expensive, or fairly

valued.

Visual Guide to Financial Markets ■7

rather than rise. Yet that’s a risk they inevitably

take when they buy securities, commodities, or real

estate.

e short sellers we encountered earlier have the

opposite risk. When their asset’s price increases, the

value of their short position declines, and vice versa.

eir losses can be in nite. Buyers can only lose what

they paid for their holdings plus investment fees and

expenses.

Either way, prices may go in the wrong direction.

is is called market risk. It’s a concern for anyone

who’s invested in a security or market, whether the

holding is direct or indirect.

Another universal risk is the threat that investors

won’t be able to sell an asset at the current market

price because there aren’t enough potential buyers

around. This is known as liquidity risk. The phrase

refers to the ability to raise cash, known as a liquid

asset. Some investments are more liquid than oth-

ers because there’s more trading in them. It’s prob-

ably much easier to sell a 10-year Treasury note,

for example, than a 10-year corporate note. That’s

the case because the government security changes

hands all day, and the company debt might trade

occasionally.

Demand for actively traded securities sometimes

evaporates. Shares of some of the biggest U.S. com-

panies changed hands for as little as one cent a share

on May 6, 2010, when the Standard & Poor’s 500 Index

plunged as much as 10 percent before rebounding.

at’s liquidity risk in the extreme.

lead to gains for everyone invested in a market. Lower

prices don’t hurt everyone either.

We’ll consider what else a ects returns besides

changes in price. Anyone who lends money to govern-

ments and companies typically earns interest. Stocks

often pay dividends. Gold and other commodities

don’t provide either type of payment, which means re-

turns are more closely tied to price moves. Real estate

owners receive lease payments or rental income.

In ation reduces returns by making these pay-

ments less valuable before they are received. Investors

take this e ect into account by tracking real returns,

which are adjusted for in ation. Figures that don’t

have any adjustment are known as nominal returns.

Costs and expenses hurt returns. Buying and sell-

ing securities and hard assets requires the payment of

trading fees. Having someone hold them in an account

adds to the cost. You incur storage and transportation

expense for commodities and maintenance expenses

for real estate. Taxes are imposed on interest and divi-

dend payments and investment gains as a rule.

Because the costs can vary considerably from one

investor to the next, we’ll keep the discussion of them

to a minimum in later chapters. Even so, you should

learn about the tax bene ts that go with investing in

some markets.

Risks

Investors probably wouldn’t bother putting money

into governments, companies, and hard assets if

they knew the prices of their holdings would fall

KEY POINT:

For owners of a security or

hard asset, market risk is the

possibility of a drop in value.

For short sellers, it’s the

opposite.

DEFINITION:

Liquidity

Liquidity is the ease of buying

and selling without causing

price changes.

8■CHAPTER 1 Overview

economy from day to day and by setting benchmark

rates.

Additional moves are made when necessary, as

they were during the 2008 nancial crisis and its af-

termath. e Fed added hundreds of billions of dollars

to the economy through bond purchases, a practice

known as quantitative easing, and started paying in-

terest on funds that banks kept on deposit.

Fiscal policy shapes the way a government takes

in and spends money, which in turn a ects the econ-

omy’s performance. e types of taxes that house-

holds and businesses must pay and the rates they are

charged a ect the revenue side. Outlays are linked to

decisions about national defense, social programs,

and other areas that the government manages.

Policy decisions can explain why the U.S. federal

budget was balanced for part of the 1990s, for instance.

ey can account for the de cits that reached more

than $1 trillion annually during the next decade.

Investors have to concern themselves with cur-

rency risk. Because U.S. stocks and bonds are priced

in dollars, their value is a ected by the dollar’s value

against other currencies. If the dollar is dropping, then

demand from non-U.S. investors may decline, causing

prices to fall.

Currency risk can cut the opposite way as well. A

rising dollar makes U.S. exports more costly to over-

seas buyers, which tends to reduce international trade

and curtail economic growth. Gains in the dollar re-

duce the value of sales and pro ts that U.S. companies

make outside the country.

Risks found outside the markets can trip up inves-

tors in governments, companies, and hard assets as

well. Four of them are worth a closer look.

We’ll start with economic risk, or the possibility

that slower growth or contraction—in the worst case,

a recession or depression—will cut government tax

revenue along with corporate sales and earnings. Risk

exists when growth accelerates, as companies must

pay more for workers or raw materials. Companies

most vulnerable to this risk are known as cyclicals

because their fortunes are closely linked to the econo-

my’s up-and-down cycles.

Political risk is the potential for legislative actions

to deter or prevent governments and companies from

reaching their goals. is risk was especially pro-

nounced for the United States in July and August 2011

when President Barack Obama and Congress were

unable to agree on raising the country’s debt ceiling

until the limit was almost reached.

Policy risk is a speci c type of political risk, which

isn’t limited to the executive and legislative branches.

It’s focused on monetary policy, controlled by the Fed-

eral Reserve (Fed) and other central banks, and s-

cal policy, de ned by taxing and spending decisions

made by the president and Congress.

Monetary policy a ects the amount of funds avail-

able to the economy as well as their cost, otherwise

known as interest rates. e Fed’s version is designed

to meet two goals: containing in ation and maxi-

mizing employment. e central bank pursues these

objectives by adjusting the amount of money in the

KEY POINT:

Currency-market moves

can affect the value of any

investment. When the

dollar is rising, demand for

investments priced in the U.S.

currency tends to increase.

When the dollar is falling,

assets denominated in other

currencies become more

valuable.

Visual Guide to Financial Markets ■9

key detail. Relative-value analysis would help them

decide whether the di erence matters, based on the

potential returns.

e same issue arises when looking at similar se-

curities from di erent entities. Suppose investors

can choose between a three-month government bill

and a corporate security maturing at about the same

time. e company probably will be a riskier bet than

the government. If the corporate security provides

enough additional income to compensate for the

greater risk, it may be worth buying. If not, it’s the

other way around.

Di erent securities from the same entity can be

studied this way. Consider the example of a company

that has publicly traded bonds and shares. It’s possible

to decide which is cheaper by comparing interest pay-

ments on the debt with dividends on the stock even

though the payments aren’t identical.

Relative-value comparisons like these can be ex-

tended to entire markets. ey help investors decide

whether to focus on stocks or bonds, how much cash

to keep on hand, and whether to put money into hard

assets, among other things.

The criteria used to determine what’s cheap, ex-

pensive, and fairly priced vary by market. For bills,

notes, bonds, and other types of debt, interest rates

are important. Though the rates differ, as we’ll

learn later, there’s a common thread to how they are

interpreted. Investors want to know how much they

stand to earn for lending out money, and rates are

the guidepost.

We’ll examine more speci c risks in later chapters.

Credit risk, or the ability of a government or company

to keep up payments on its debt, is one of them. An-

other is business risk, or the threat that a company’s

operations or nances may falter.

Relative Value

U.S. government bills, maturing in one year or less, paid

next to nothing after the Fed began targeting near-zero

interest rates at the end of 2008. Earlier in the 2000s, the

securities rewarded investors with rates of 6 percent or

more. During the 1980s, rates exceeded 10 percent.

e historical comparisons show Treasury debt

is far less lucrative than it used to be. ey provide a

starting point for determining whether the securities

are cheap, expensive, or fairly priced in relative terms.

Similar analysis is done on all the other types of secu-

rities we’ll cover.

History only tells part of the story. Investors have

to determine how much risk there is today for a gov-

ernment, company, or hard asset. en they have to

decide whether the potential returns are high enough

to justify taking that risk.

e opinions of credit-rating services, especially

Standard & Poor’s, Moody’s Investors Service, and

Fitch Ratings, are often part of that process. ese

companies assess the risks that go with debt securi-

ties. eir judgments help shape the views of inves-

tors, for better or worse.

Investors may study two securities that are essen-

tially the same except for the maturity date or another

KEY POINT:

Rating services are private

companies though they are

often called agencies, and

some of them have offi cial

recognition from U.S. and

international regulators.

STEP-BY-STEP:

RISK AND RETURN

1. Suppose a three-month Trea-

sury bill has a 0.1 percent

rate.

2. Suppose a three-month

corporate security has a

0.5 percent rate.

3. Subtract the Treasury bill

rate from the corporate rate,

and what’s left is 0.4 percent.

4. The 0.4 percent is what an

investor gets paid for lend-

ing money to the company,

rather than the government.

5. The investor has to deter-

mine whether the additional

amount is worth the risk.

6. Relative-value analysis

guides the decision-making.

10 ■CHAPTER 1 Overview

Investors in debt securities are concerned with a

borrower’s ability to pay interest on time and repay

the money when it’s due. is leads them to focus on

cash: where it’s coming from, where it’s going, how

much exists, and how fast it’s growing. e less a bor-

rower needs the money, the more secure someone will

be with owning its debt.

Stock investors also concentrate on cash. For one

thing, they’re interested in a company’s ability to pay

dividends. For another, companies with cash can buy

back shares, which can increase returns on the re-

maining stock. ese payouts help determine relative

value as do revenue and earnings, which indicate how

well the business is doing.

Relative-value comparisons are more basic for

hard assets, if only because less data are available. For

commodities, history and supply-demand analysis

play larger roles than they would in securities. ere

aren’t any interest, dividends, and earnings to use in

deciding what’s cheap and expensive.

In real estate, it’s possible to assess value through

comparisons between a property and similar ones

that have been sold recently. That said, the analysis

isn’t as straightforward as finding rates on bonds

or financial ratios for stocks. Real estate doesn’t

change hands that often, so the right numbers can

be elusive.

11

Government

Can you imagine an investment that carries no

risk? No worries about markets, liquidity, or

anything else? What kind of an interest rate would

you expect this investment to provide? Put another

way, what kind of a return would you need to be a

buyer?

For many investors, the answer to the rst two

questions is “yes.” at’s because a risk-free rate is of-

ten used in evaluating returns and in making relative-

value judgments. e rate is theoretical because every

investment carries some risk.

e third and fourth questions can be answered by

looking at the interest rate on three-month Treasury

bills. It’s reasonably close to a risk-free U.S. rate for a

couple of reasons. First, the government can require

many of the more than 300 million Americans to pay

taxes, and the revenue is a source of funds for making

payments on the securities. Second, the government

has the ability to pay with new money.

Other borrowers don’t have the two advantages

working for them. is means government securi-

ties markets are a relatively sure bet for investors. e

three-month period provides an additional margin of

safety as there isn’t much time for risks to surface. e

promise to pay goes with bills, a form of debt. e gov-

ernment can’t sell equity, a riskier type of investment.

Some safety exists in cash, as suggested by the im-

age of people stu ng their money under a mattress

during times of economic turmoil. Government is

responsible for sustaining the value of that cash as it

makes decisions on a country’s borrowing.

Remember, though, that risk-free remains a relative

term. Government debt can lose value as interest rates

rise and in ation accelerates, as do other securities.

Investors who turn over their money for longer peri-

ods can su er bigger losses when rates or in ation go

against them. We’ll explore the risks later in this chap-

ter. For now, let’s take a closer look at currencies.

KEY POINT:

Rates on government securities

are sometimes called risk-free

rates because the debt carries

little risk for investors.

Visual Guide to Financial Markets

by David Wilson

Copyright © 2012 by David Wilson.

12 ■CHAPTER 2 Government

Currencies

We often measure the value of money by how far

it goes at the supermarket, the shopping mall, the

online store, and other retail locations. Another

barometer serves as the foundation for a

multitrillion-dollar market: the amount of a foreign

currency we can purchase.

Money comes in pairs in the foreign exchange mar-

kets. Pairs that include the dollar tend to be watched

most closely. e dollar is a reserve currency, held by

central banks and used internationally to set the price

of goods and services. Because the United States is

the world’s largest economy, there are plenty of dol-

lars crossing borders each day.

Each pair has two values, based on buying or sell-

ing one unit of the currency. ere’s a value, for in-

stance, that shows Japanese tourists en route to the

United States how many dollars they can buy with

their yen. Another exists for the U.S. businessman

going to Tokyo, who has the opposite concern. e

values are mirror images of each other, as shown in

Exhibit 2.1.

Only one of the values in any currency pair is front

and center on traders’ computer screens. Usually, it’s

the amount of another currency you can buy for a dol-

lar. at’s the case with the yen.

There are prominent exceptions. The euro, Eu-

rope’s common currency, is among them. Traders

focus on the number of dollars and cents required

to buy one euro and not the reverse. Others include

British Commonwealth currencies, especially the

British pound and the Australian and New Zealand

dollars.

Currency pairs that exclude the dollar get some

attention. eir exchange rates are called cross rates

because they re ect each currency’s value against

the dollar. is assumes someone will go across the

dollar—buying dollars with one currency and selling

those dollars for the other currency—to complete a

trade. If the dollar trades at 80 yen and the pound is

at $1.60, the pound-yen cross rate is 80 times 1.60, or

128 yen to the pound.

Regardless of the pairing, currency moves can af-

fect economies and nancial markets. A declining

currency makes a country’s goods and services cheap-

er in international markets, and vice versa. is may

encourage more people to visit, like those Japanese

tourists, and to invest in government securities, com-

panies, and hard assets.

Foreign exchange swings can be a double bene t or

a double whammy for investment returns. If a stock or

bond rises, a strengthening of the currency in which

it’s denominated will enhance the gain. If the price

drops, a weaker currency will magnify the loss.

Trillions of dollars changes hands daily in the

global currency markets. e latest available gure

is $4 trillion, taken from an April 2010 survey by the

Bank for International Settlements (BIS). e BIS,

which assists central banks and monetary authorities

worldwide, canvasses them every three years on trad-

ing in currencies and related contracts.

STEP-BY-STEP: FROM

DOLLARS TO YEN

1. Assume the dollar is trading

at 80 yen.

2. The yen’s value is the

inverse, so divide 80 by 100.

3. One yen is equal to 80/100 of

a dollar, or 0.8 cent.

STEP-BY-STEP: FROM

POUNDS TO DOLLARS

1. Assume the pound is trading

at $1.60.

2. The dollar’s value is the in-

verse, so divide 100 by 1.60.

3. One dollar is equal to

100/1.60, or 62.5 pence.

Visual Guide to Financial Markets ■13

currency. You could go to an automated teller ma-

chine (ATM) and withdraw the number of yen you

wanted. You may stop at a bank branch, a foreign-

exchange kiosk at the airport, or a hotel’s front

desk.

If you choose one of these other locations, you’ll

run across a table with three columns. e rst has

the names of currencies, including the dollar. e

second shows how much you would receive in return

for each currency, and the third shows how much you

would have to pay to buy them. e line for the dollar

might look like this: JPY 76.25 78.75.

Practically all this buying and selling takes place

over the counter, or away from exchanges. Banks,

brokers, and other nancial companies connect over

electronic networks to carry out their trading. is

approach means the amount of information available

about foreign exchange trading from day to day is rel-

atively sparse, as we’ll see shortly.

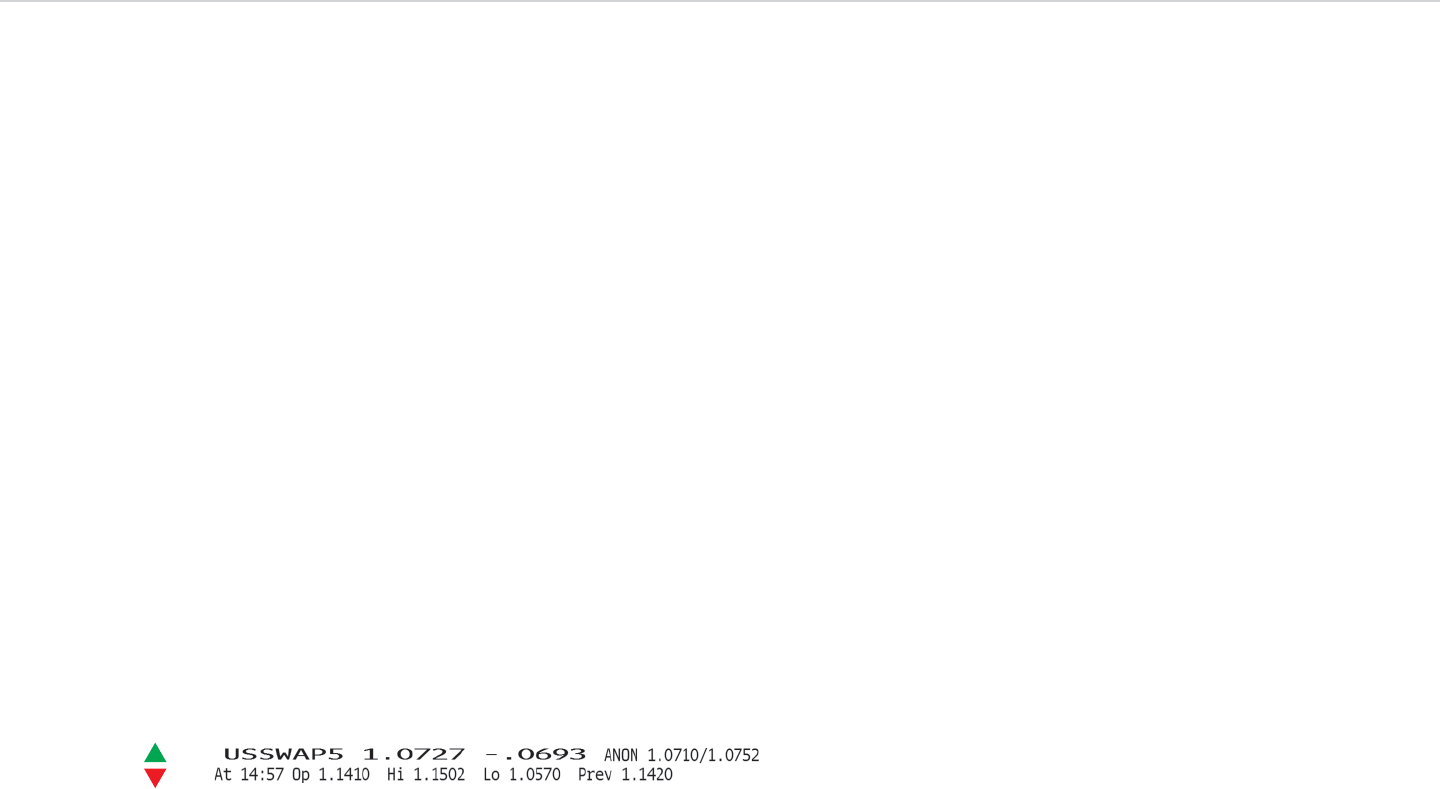

Quotations

Suppose you were that businessman who traveled

to Tokyo from New York and needed to exchange

KEY POINT:

Foreign-exchange quotes

always show the value of one

currency against another.

Moves in the two currencies

over time are mirror images of

each other.

Exhibit 2.1: Dollar’s Value in Yen and Yen’s Value in Dollars

14 ■CHAPTER 2 Government

–.13: Change from the previous day’s last price, re-

corded at 5 p.m. New York time in this case. Curren-

cy markets don’t open and close during the week, as

trading happens worldwide 24 hours a day. e last

price might be based on trading in London, home to

the world’s biggest foreign exchange market, or in

Tokyo, another currency trading hub, for some mar-

ket participants.

BGN 76.32/76.33 BGN: Highest bid and lowest ask

prices, along with the source of each. BGN stands for

Bloomberg generic pricing, which combines quotes

from a number of banks. In other cases, a code for a

speci c bank may appear.

e spread between them is 0.01 yen, far narrower

than the 2.5-yen di erential in our earlier example.

at’s the case because there’s far more currency

bought and sold in the market than at bank branches,

currency kiosks, and hotels.

At 14:32: e second line begins with the time at

which the mid price was recorded. is is as com-

mon as the uptick/downtick arrow in quotes, as

you’ll see later. It’s essential because currency val-

ues, like security prices, are constantly changing.

Op 76.46: Opening price, recorded shortly after

5 p.m. New York time the day before.

e rst number is the bid price, and the second

is the ask, or o er, price. e gap between them,

2.5 yen, is the bid-ask spread. e wider the spread,

the greater the pro ts for a bank, money changer, or

hotel from currency exchange.

Bid and ask prices are all that are disclosed in the

global foreign exchange market. Prices at which cur-

rencies trade aren’t made public, which means there’s

little detail available to show in quotes. Take the Japa-

nese yen as an example (see Exhibit 2.2).

ere’s no way to tell how many yen changed hands

during the day, or the exact price at which dollars were

sold for yen. Let’s nd out what is available.

JPY: e quote’s rst line begins with a three-letter

code for the yen. Each currency has a code. Some of

the more popular ones are EUR for the euro, GBP for

the British pound, CAD for the Canadian dollar, and

CHF for the Swiss franc. When only three letters are

included, the other currency is the dollar. Six-letter

codes are used for cross rates, where the dollar isn’t

involved in the trade. EURJPY, for example, shows

the value of one euro in yen.

76.33: is is the number of yen one dollar will buy.

It’s known as the mid price because it’s halfway be-

tween the bid and ask prices.

KEY POINT:

USD is the three-letter code for

the U.S. dollar. Others include

AUD (Australian dollar), CAD

(Canadian dollar), CHF (Swiss

franc), EUR (euro), and GBP

(British pound), along with JPY

for the yen.

Exhibit 2.2: Yen Quote

Visual Guide to Financial Markets ■15

potential for swings re ects the willingness of gov-

ernments to allow markets to set the value of their

currencies.

Some rates are xed, which means they don’t move.

Argentina, for example, set the value of its peso at $1

between 1991 and 2002. e xing of the exchange

rate helped the country bounce back from years of

economic contraction.

Fixed exchange rates are an example of pegging,

known as linking, in which governments determine

the value of currencies. In other cases, monetary au-

thorities set the range in which the value can uctu-

ate and buy and sell currency to maintain the range.

In 2005, Hong Kong pegged its dollar at HK$7.75 to

HK$7.85 to the U.S. dollar and China let its currency—

the renminbi, denominated in yuan— oat within a

band tied to a basket of currencies.

en there are the freely oating currencies, where

the value is almost entirely determined in markets.

e “almost” is included because central banks occa-

sionally stage what’s known as an intervention. ey

buy and sell currencies when values get too far out of

line for their liking.

Central banks can set lower exchange rates through

currency devaluations. e dollar was last devalued in

1934, when the amount of gold that the U.S. currency

could buy was cut by 41 percent. e pound’s value

tumbled 4 percent on Sept. 16, 1992, when the United

Kingdom withdrew from an agreement that xed its

exchange rate. Several emerging market currencies

have been devalued more recently.

Hi 76.97: High price for the current trading day.

Lo 76.11: Low price for the current trading day.

Close 76.46: Closing price for the previous day. It’s

the basis for the day’s change of –.13, shown in the

rst line.

Three Rs

e Japanese tourists and the U.S. businessman in-

troduced earlier are exchanging currency to cover ex-

penses rather than to turn a pro t. e same might be

said about companies doing business internationally.

ey may need to buy another currency to complete a

purchase or to make an exchange for their local cur-

rency to bring revenue home.

Many investors make foreign exchange trades for

similar reasons. Funds that invest outside their home

country need the local currency to purchase stocks,

bonds, and other assets. Some of these funds trade to

reduce the risk that currency moves will a ect their

pro ts.

Currency speculators have another goal in mind.

They want to make money as one currency rises or

falls in value against another. We’ll look at the three

Rs of returns, risks, and relative value from their

perspective.

Returns

Speculators buy and sell currencies in anticipation

of changes in exchange rates over time. Returns from

making these bets depend on how rates move. e

DEFINITION:

Speculators

Speculators buy and sell to

profi t from changes in market

value.

16 ■CHAPTER 2 Government

Eurodollar rates. Although the name originally referred

to European bank deposits of dollars, the Euro-pre x

has come to mean foreign. ere are Eurodollar rates in

Tokyo and Euroyen rates outside of Japan.

Risks

We’ve seen how market and liquidity risks a ect the

currency market. Anyone buying stocks, bonds, or

hard assets with their money, rather than depositing

the funds in a bank, is more likely to sustain losses.

ey may be large enough to wipe out any gains from

exchange-rate moves.

Political, economic, and policy risks are part of the

territory as well. After all, U.S. paper money says “ e

United States of America” and “Federal Reserve Note.”

is means the president, Congress, and the Fed each

has a role to play in determining its value.

Market-speci c issues also exist, beginning with

interest rate risk. Because money obtained through

the currency market goes into bank deposits, the rate

is set for a certain period. If the central bank raises

rates during that time, the deposit won’t earn as much

money as it might have otherwise. Currency moves

tied to the rate increase may not make up for this lost

opportunity.

In ation risk is another concern. When prices are

rising, the money on a deposit will buy less than it might

have otherwise. If the in ation rate exceeds the deposit

rate, the funds will buy less. Put another way, in ation

reduces the purchasing power of money, whether it’s in

your wallet, your pocketbook, or a bank.

Generally, the daily movements in oating curren-

cies—the dollar, euro, yen, British pound and Swiss

franc, to name a few—re ect what tourists, business-

men, companies, speculators, and others are buying

and selling. is means they provide the greatest po-

tential for returns.

Exchange rate changes aren’t entirely tied to returns

though. Speculators don’t buy currencies and hide

them under a mattress or in a corner o ce. Instead,

they deposit the funds in a bank and earn interest.

Banks dominate currency trading worldwide, so it

makes sense that they would end up with the money.

Deposits are the investment of choice because their

market and liquidity risk is low. is reduces the odds

of investment losses that would cut into returns if the

currency moves the right way.

Put this all together, and it’s understandable that de-

posit rates would a ect the ow of funds into and out of

currencies, as well as their returns. Money tends to ow

into a country as rates increase and ow out as rates fall.

Banks take their lead on what to pay for deposits

from a central bank, such as the Fed. ey’re guided

by a rate that the central bank sets directly. e United

States has a target rate for overnight loans between

banks that’s known as the federal funds rate. e Fed’s

policy makers set the target, and the central bank ad-

justs the amount of money in the banking system each

business day to control the market rate.

Speculators can deposit funds in the country that

printed the money or elsewhere. Interest rates for

deposits made outside the country are known as

KEY POINT:

Governments can directly

affect the value of their

currencies in three ways.

They can establish a fi xed rate

or peg, intervene in foreign-

exchange markets by buying or

selling, or offi cially devalue the

currency.

Visual Guide to Financial Markets ■17

Relative Value

What does the same item cost in di erent locations? e

answer provides a way to determine the value of one cur-

rency against another. McDonald’s Big Mac sandwiches

and Starbucks lattes have been used in these kinds of

comparisons because they’re so widely available.

e analysis is based on the principle that people

should be able to buy goods and services for the same

price anywhere. Economists refer to this as purchas-

ing power parity. Ideally, exchange rates would main-

tain parity, though it doesn’t quite work out that way

in currency markets.

In extreme cases, in ation turns into hyperin a-

tion. Prices rise so far and fast that the increases es-

sentially wipe out a currency’s value. is took place

in Germany after World War I and in several emerging

markets more recently.

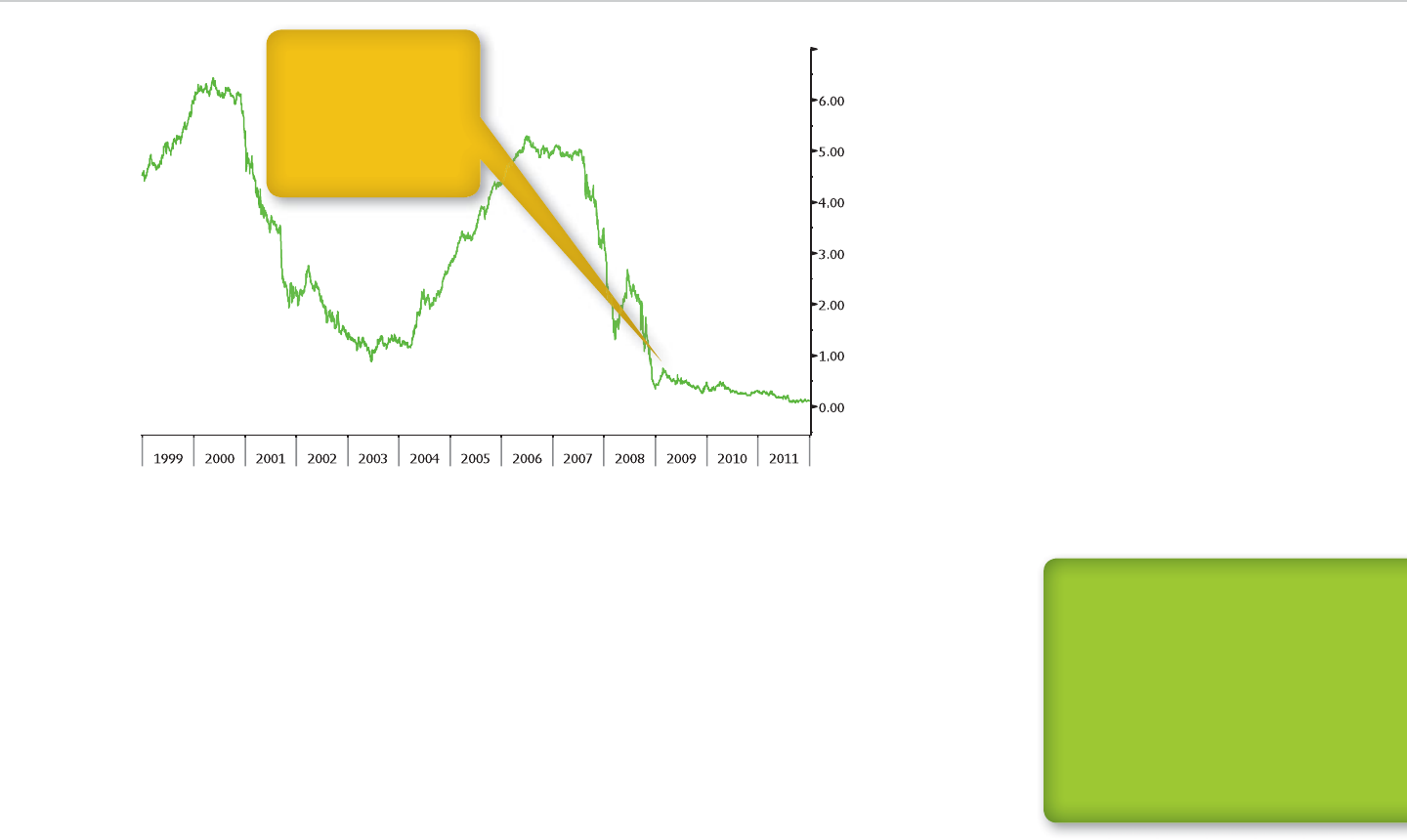

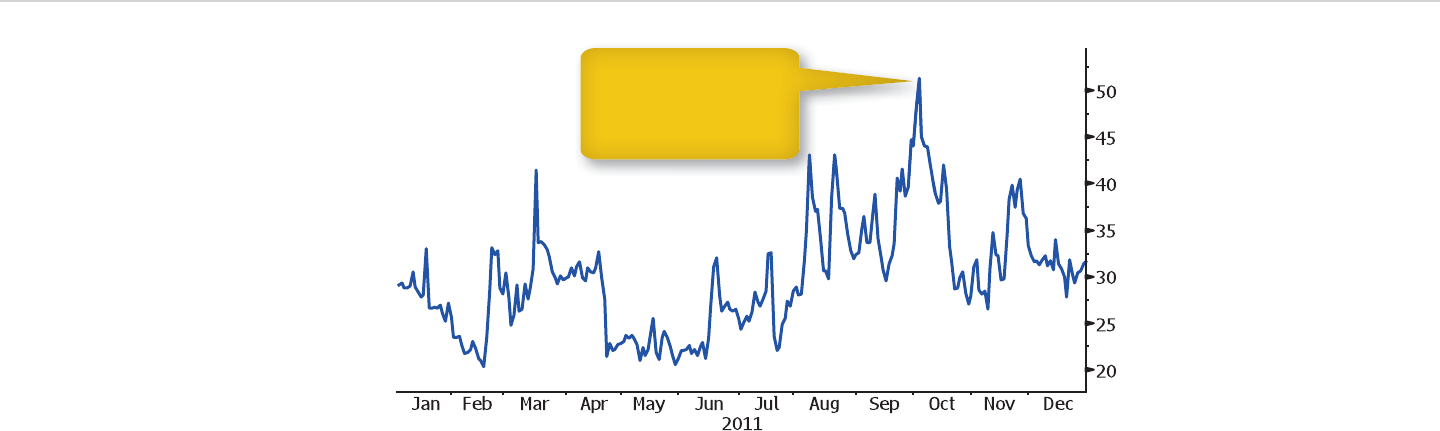

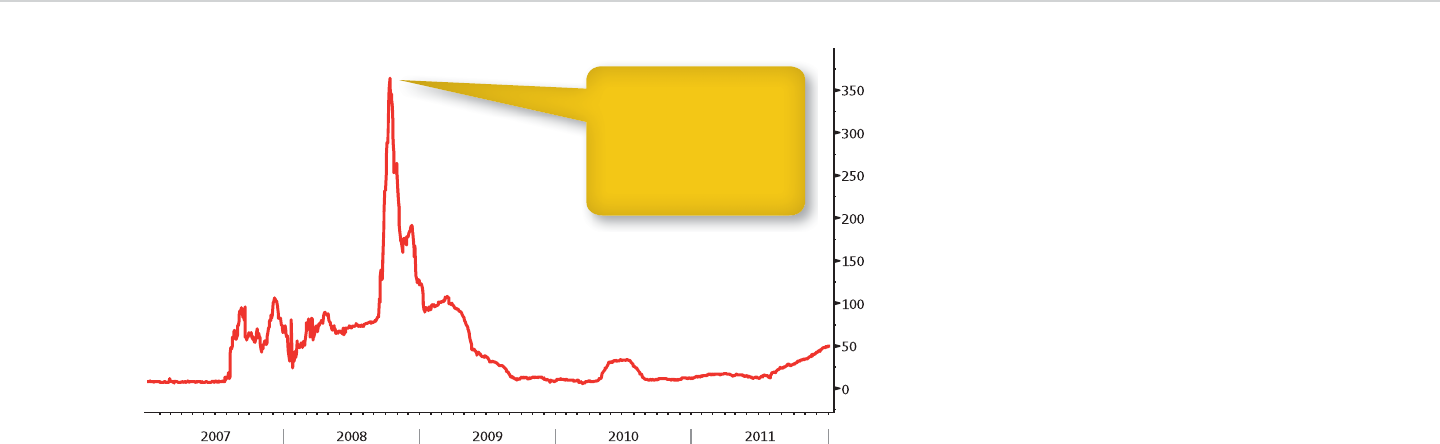

e African country of Zimbabwe provided a worst-

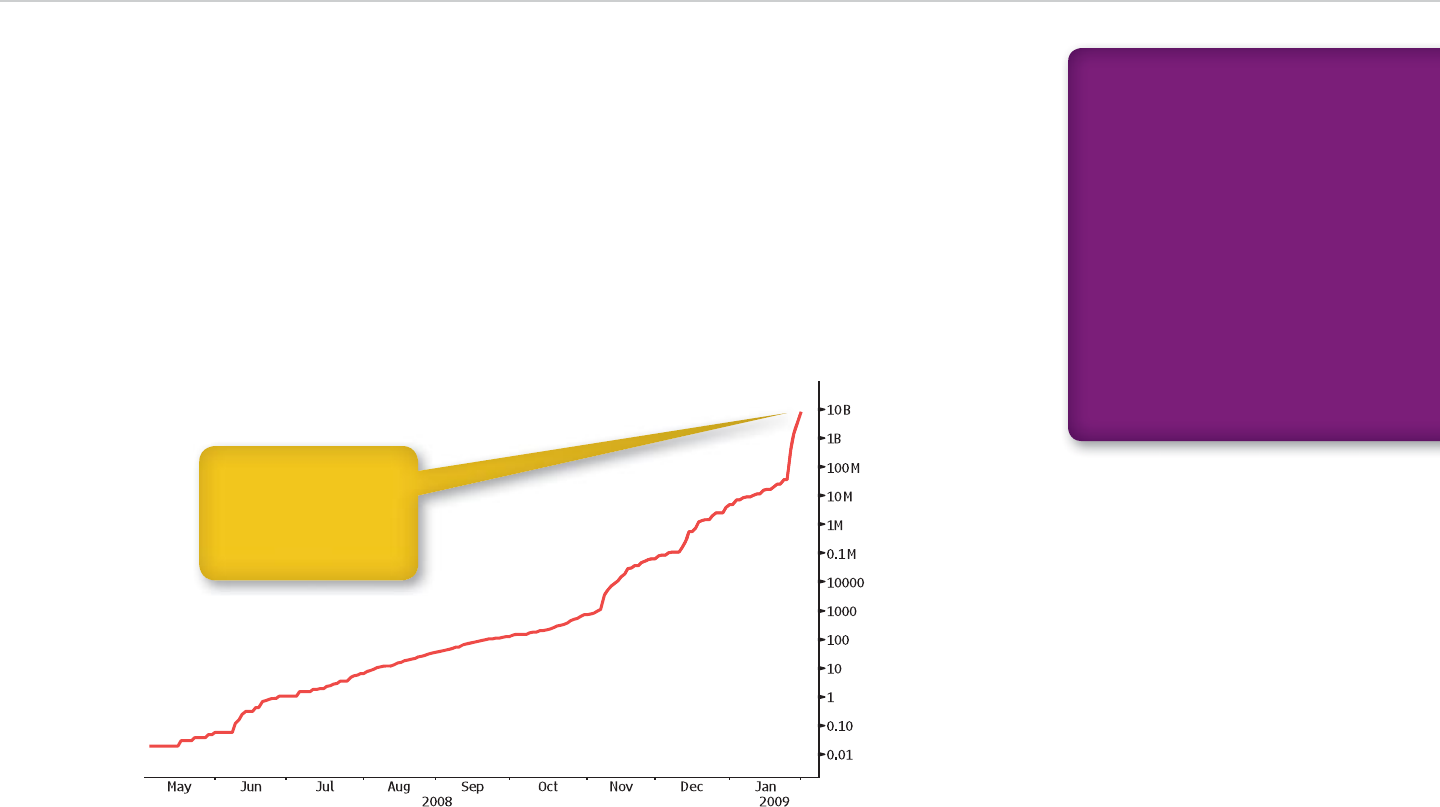

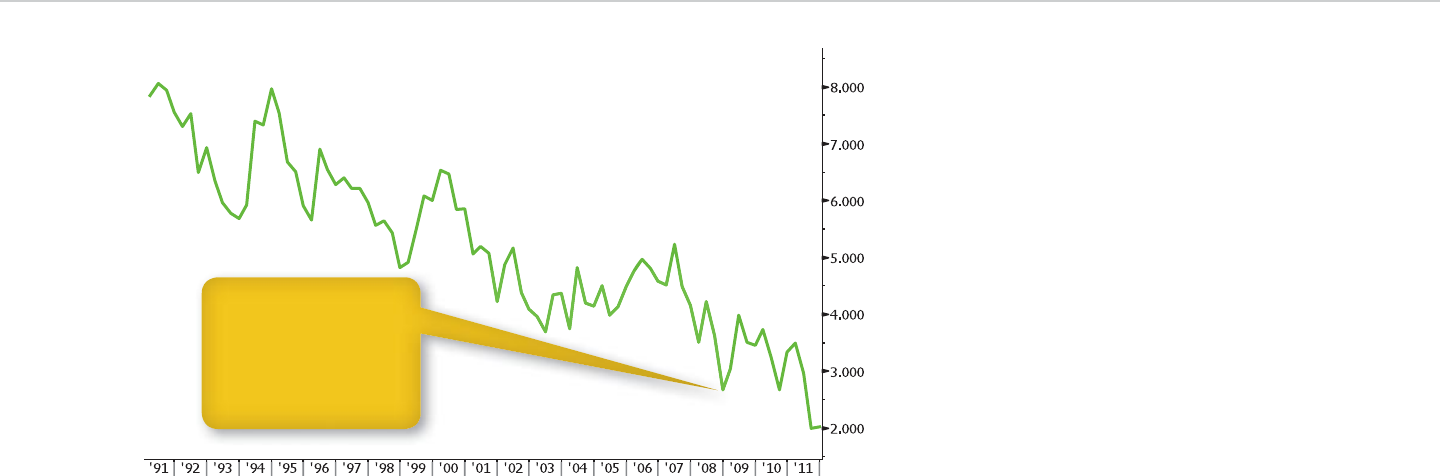

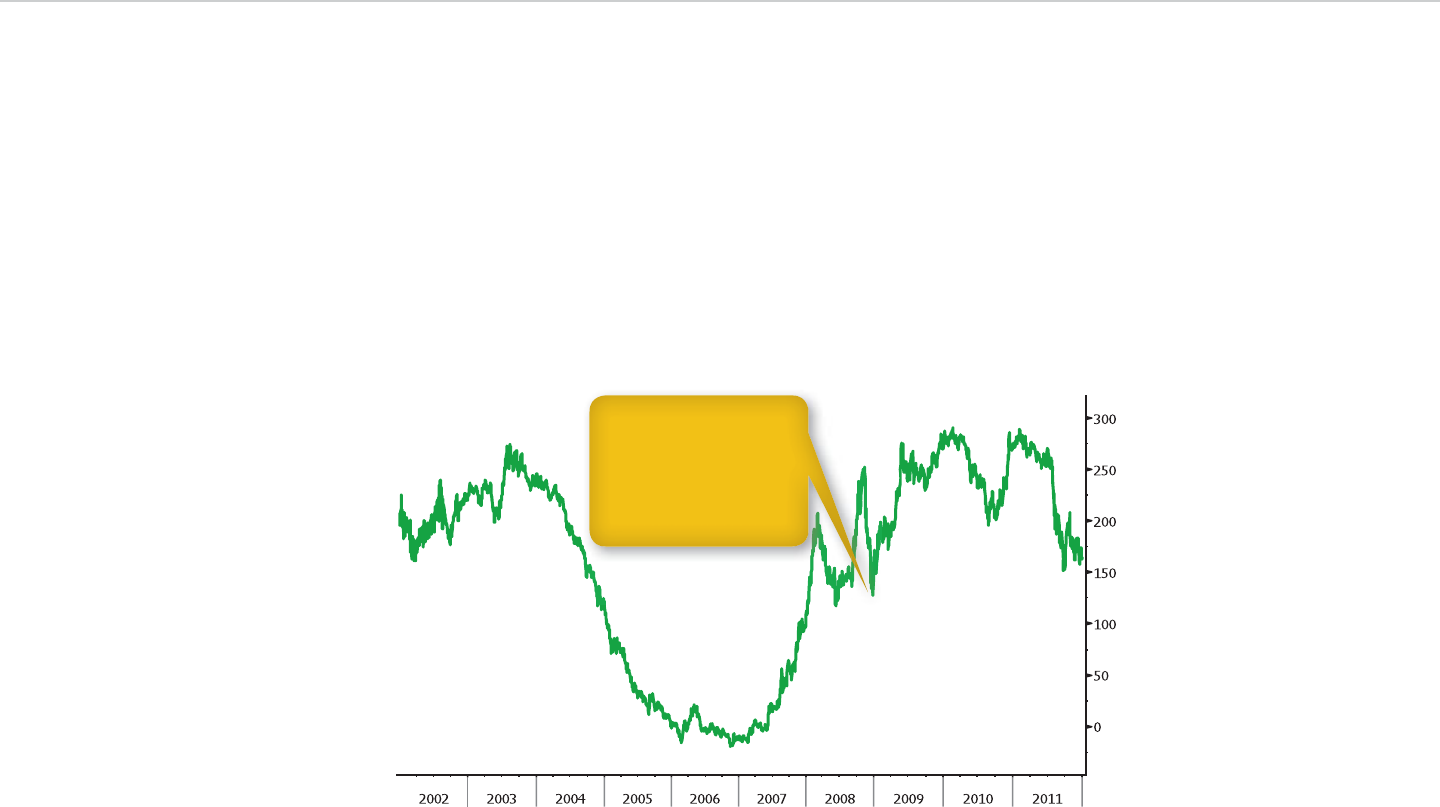

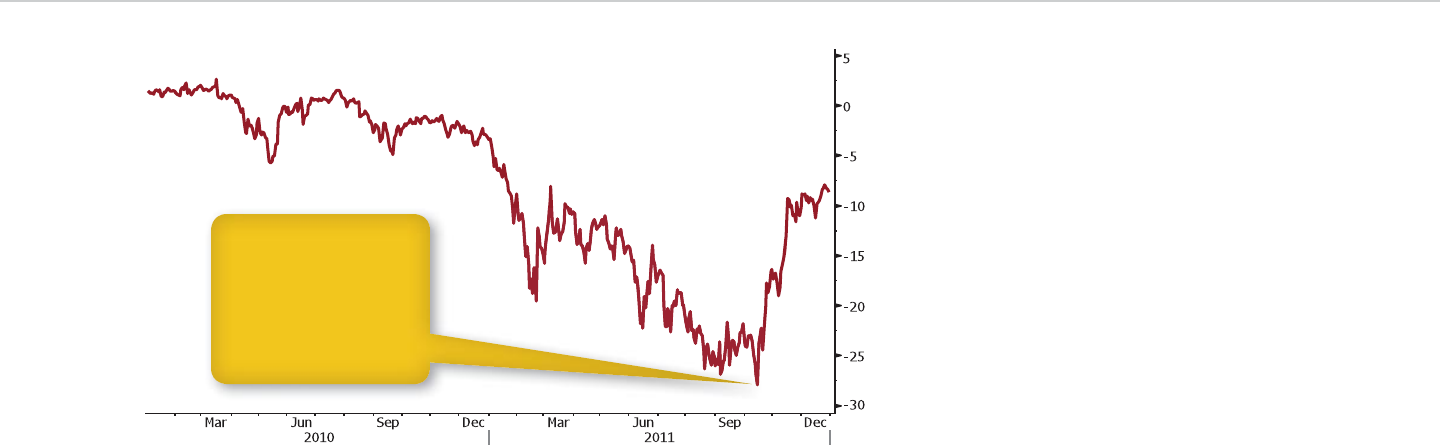

case scenario during the 2000s, as shown in Exhibit 2.3.

Soaring prices prompted Zimbabwe’s central bank to

redenominate its currency, the dollar, multiple times.

e central bank resorted to printing bills with face

values as high as Z$100 trillion before doing away with

the local currency in 2009.

Exhibit 2.3: Number of Zimbabwe Dollars per U.S. Dollar During Hyperinfl ation

The African country’s

central bank issued bills

in denominations as high

as 100 trillion dollars

before the local currency

was abandoned.

1. Assume Big Macs cost $3 at

McDonald’s restaurants in

the United States and

12.5 yuan in China.

2. Divide the Chinese Big Mac

price by the exchange rate to

translate into dollars. If the

yuan is at 6.25 to the dollar,

then the price is 12.5/6.25 = $2.

3. At $2, the Big Mac is

33 percent cheaper in China.

This suggests the yuan is

33 percent undervalued

relative to the dollar.

STEP-BY-STEP:

PURCHASING POWER

18 ■CHAPTER 2 Government

securities we’ll run across later. Companies refer to them

as cash equivalents in nancial statements.

Treasury bills are as safe an investment as you’ll nd

in nancial markets, for a couple of reasons. First, con-

sider the government’s power to impose taxes on tens of

millions of people and millions of companies to pay its

debts. No other borrower is in that position. Second, the

government can create money through the central bank.

If worse came to worst, it would be possible to obtain the

money by cranking up the Fed’s printing presses. at’s

an option no one else has.

e relative safety of government bills is tied to

their maturity date. ere’s less potential for things to

go wrong in a year than there is in ve, 10, or 30 years.

What might happen? We’ll nd out when we examine

the three Rs.

Investors can buy bills in the primary or second-

ary market. e primary market consists of auctions

conducted by the Federal Reserve Bank of New York

(New York Fed) on the Treasury’s behalf. e second-

ary market is run by the largest banks and securities

rms, along with the brokers that connect them.

e Treasury currently sells one-month, three-

month, and six-month bills each week, along with

one-year bills each month. Some banks and securities

rms are required to bid at every auction, ensuring

the government will have buyers for whatever bills are

sold. ese bidders are known as primary dealers, a

title that ts their position within the primary market.

Primary dealers compete at auctions by submitting

bids, based on the interest rate they’re willing to accept.

ere’s another relative-value gauge that was men-

tioned earlier: deposit rates. e gap in rates between

two countries in uences the movement of money be-

tween them, which in turn a ects exchange rates. For

currency speculators, the rate di erential counts for

more than Big Macs and lattes.

Bills

Trillion-dollar budget gaps have to be closed some-

how. e U.S. government has learned this lesson the

hard way in the past few years. Increased spending to

help sustain the country’s economy and uctuations

in tax revenue swelled the federal de cit to more than

$1 trillion annually.

Investors made up the shortfall. e government

stepped up fundraising in the money market, where

money is made available for as long as a year. It leaned

more heavily on the bond market to borrow for two to

30 years.

We’ll visit the government bond market shortly,

so let’s focus on the money market. e U.S. Treasury

sells debt securities maturing in one, three, six, or

12 months on a regular schedule, and for other peri-

ods as needed. ey are known as Treasury bills.

e word “bills” may make you think about the $1, $5,

$10, and $20 bills in your wallet or pocketbook. at’s an

idea worth keeping in mind. Treasury bills play much the

same role as paper money even though the government

doesn’t print and distribute them. Accountants con-

sider them the same as cash, like other money market

DEFINITION:

Treasury bills

Treasury bills are securities

that the U.S. government

sells to borrow funds for a

year or less. Investors and

companies classify them as

cash equivalents.

Visual Guide to Financial Markets ■19

e securities don’t pay interest before they mature,

so the size of the discount has much to do with their

returns, the rst of the three Rs. ey are stated as an-

nual rates for consistency’s sake even for bills matur-

ing in less than a year, as most of them do.

As 2008 ended, discount rates at bill auctions

dropped to almost zero. e decline resulted from

the Fed’s e orts to prop up the U.S. economy through

monetary policy. Put another way, the government

could pay almost nothing to borrow money. Exhibit 2.4

places the borrowing costs in perspective.

e New York Fed then sells the bills at the lowest pos-

sible rate, which translates into the highest price. is

enables the Treasury to borrow as cheaply as possible.

Investors can buy new bills through primary deal-

ers or straight from the Treasury. If they go through

a dealer, the rm’s auction bid will largely determine

what they have to pay. ey can go through Treasury

Direct, a program that lets smaller investors buy secu-

rities at the average rates set in auctions.

ese rates are known as discount rates because

Treasury bills are bought for less than their face value.

Exhibit 2.4: Three-Month Treasury Bill’s High Discount Rate at Auction

Sources: U.S. Treasury, Bloomberg.

The Treasury’s borrow-

ing cost fell to almost

nothing after the Federal

Reserve adopted a target

interest rate near zero.

20 ■CHAPTER 2 Government

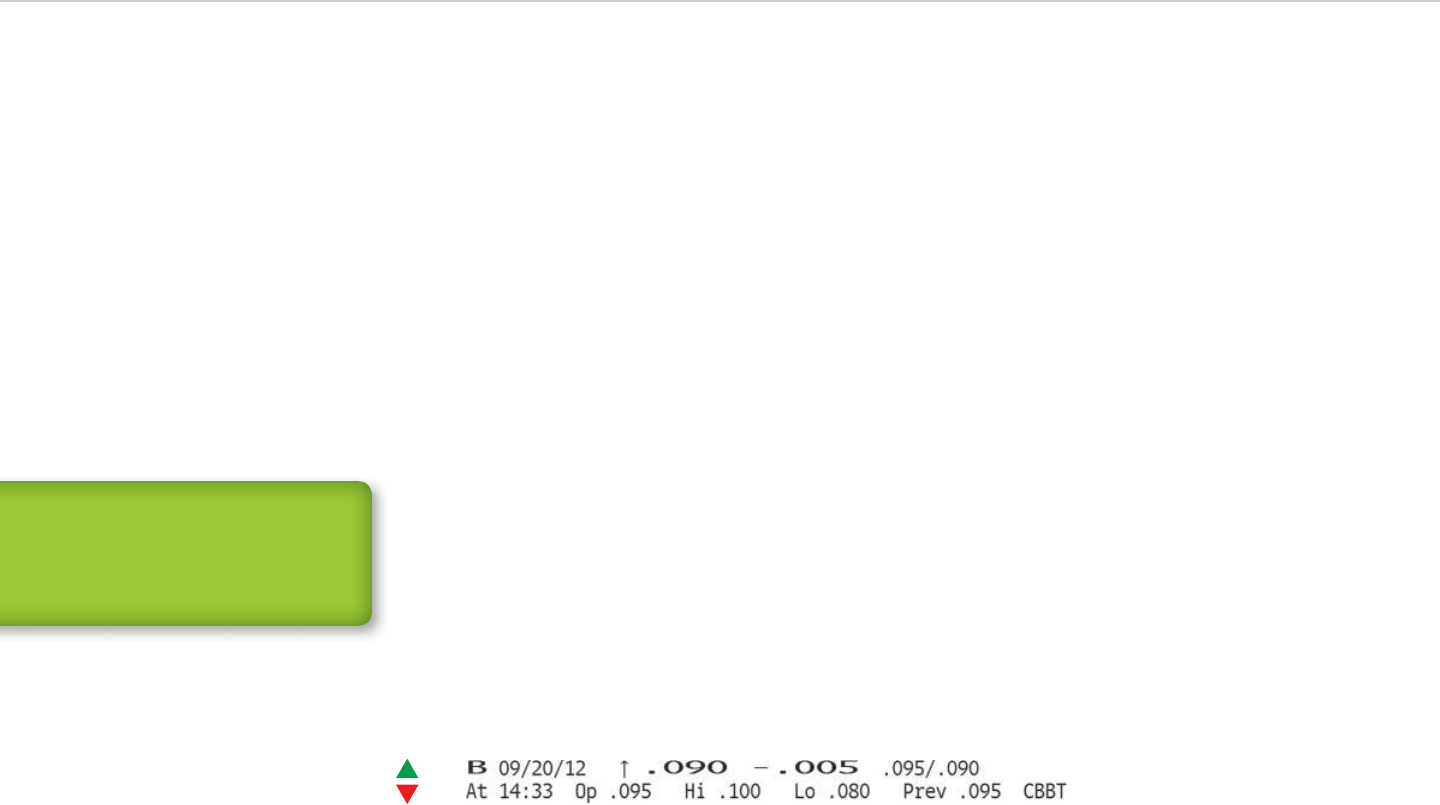

Now that we know what isn’t in Treasury bill

quotes, let’s look at what is (see Exhibit 2.5).

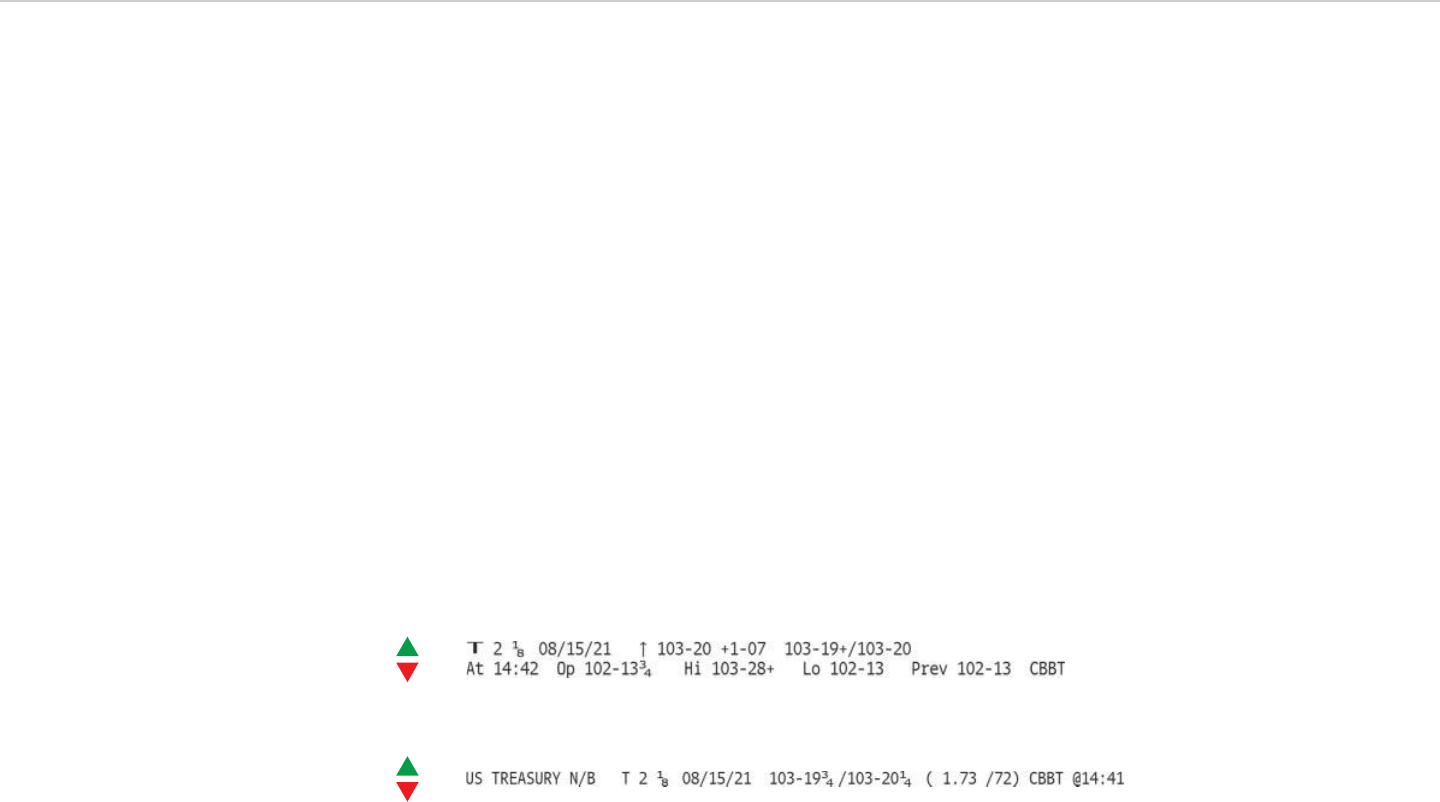

B: Symbol for Treasury bills.

9/20/12: Maturity date, when the holder receives

face value from the Treasury. It’s shown in month/

day/year format.

Up arrow: Direction of the most recent change in

the discount rate. Because the rate moved up, this is

known as an uptick. A down arrow would signify a

decline in the rate, or a downtick. You’ll see arrows

like this in many other quotes.

is uptick/downtick arrow tracks the discount

rate rather than the price. Higher rates mean lower

prices, and vice versa. Keep that in mind, as it’s true

for other types of debt securities.

.090: Discount rate in percentage points. Investors

buying this bill would earn 0.09 point on their in-

vestment by keeping it until the maturity date. at

amounts to nine cents for every $1,000 invested.

Percentages like this are so small that traders and

investors move the decimal point two places to the

right and talk about basis points. Each basis point

amounts to 0.01 percentage point, so the bill’s dis-

count rate is 9 basis points.

Discount rates are the focus in the secondary

market, where the primary dealers and others trade

bills sold at past auctions. ere isn’t an exchange

where the securities are bought and sold. Instead,

trades are made between rms electronically in the

over-the-counter (OTC) market.

Securities rms operate their own electronic trad-

ing networks. Similar systems are provided by inde-

pendent rms, including Bloomberg, which has one

called Bloomberg BondTrader for Treasury bills and

other debt securities.

Dealers may use brokers to carry out trades. Can-

tor Fitzgerald LP, ICAP Plc, and Tullett Prebon Plc

operate three of the biggest brokerages for bills and

other government securities, including the notes and

bonds we’ll study later in this chapter.

Quotations

Prices are nowhere to be found in quotes on Treasury

bills. Instead, they are quoted at discount rates, in

keeping with how they’re sold at auctions. is rate

determines the price that a buyer will pay.

e number or dollar amount of bills traded during

the day won’t be found in quotes either. ey’re omit-

ted because the OTC markets where they trade don’t

make the data widely available.

DEFINITION:

Basis points

Basis points are hundredths of a

percentage point

Exhibit 2.5: A Treasury Bill Quote

Visual Guide to Financial Markets ■21

Returns

Because government bills don’t pay interest before

maturity, their returns depend mainly on the di er-

ence between the purchase price and face value. e

price, in turn, results from the quoted discount rate.

As an example, let’s assume you bought Treasury

bills maturing in one year at a 0.1 percent rate. Based

on how the math works out, you would pay about $999

for every $1,000 face amount of the securities.

ese bills are bound to rise in value as the number

of days to maturity, or the amount of time until that

nal $1,000 payment is due, gets smaller. Changes in

market rates will a ect how and when the increase oc-

curs. In the end, the price will equal $1,000 as long as

the Treasury is paying its debts on time.

Risks

Bills are a type of xed-income security, as the tim-

ing and amount of the payment are preset. Investors

in the securities are taking the same kinds of risks as

they do with government bonds, corporate debt, and

related securities as we’ll see later.

e most basic concern is whether a borrower, in this

instance the government, will be able to pay on time.

is is known as credit risk. e discount rate is a gauge

of the amount of risk that investors see. e higher the

rate, the greater the concern, and vice versa. Bond yields,

which we’ll learn about shortly, play a similar role.

Judging credit risk is the business of credit-rating

services, often called agencies even though they are

.005: Today’s rate change in percentage points. For

the bill, it’s 0.005 point. We might as well move the

decimal point again and refer to the drop as half a

basis point.

.095/.090: Bid and ask rates. e bid rate is higher

because the resulting price will be lower. For the ask

rate, it’s the other way around.

At 14:33: Time of the quote, using the 24-hour clock.

Op .095, Hi .100, Lo .080, Prev .095: Opening, high,

and low rates for the current day and closing rate for

the previous day.

CBBT: Source of the current rate. is is a compos-

ite quote from Bloomberg BondTrader.

Three Rs

Safety comes with a price in the government bill mar-

ket. It’s measured by the potential return, which usually

won’t come close to matching what’s available on other

investments. On the other hand, the risks are relatively

low as well. e United States has paid its debts on time

for decades and isn’t poised to follow companies and

some local governments into bankruptcy court.

e relative safety explains why the rate the United

States pays to borrow has historically been known as a

risk-free rate. e phrase isn’t quite accurate, as noted

earlier, because investors face risks even when the

government’s nances are sound. We’ll explore them

as we go through the three Rs, and learn how investors

nd relative value.

KEY POINT:

The price of a Treasury bill is

less than the face value as long

as the discount rate exceeds

zero. How much less depends

on the rate and the time to

maturity.

1. Start with a value in percent-

age points, such as the .090 in

Exhibit 2.5.

2. Multiply by 100, which is the

same as shifting the decimal

point two places to the right.

3. In this case, .090 × 100 = 9.0,

or 9 basis points. Each basis

point equals 0.01 percentage

point.

STEP-BY-STEP:

BASIS POINTS

22 ■CHAPTER 2 Government

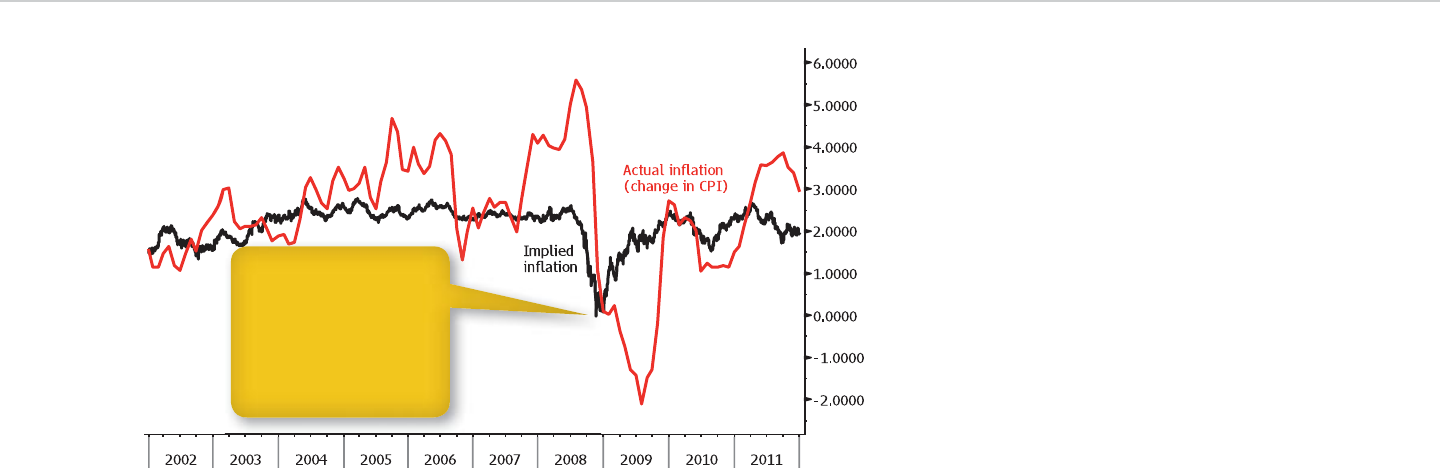

Price Index (CPI), the most widely followed gauge of

in ation, increases at a faster rate. If the pace acceler-

ates, then the risk will rise as well.

Government bills have relatively little risk by com-

parison with other xed-income securities. First, the

government can raise taxes or print more money if

needed to pay its debts. Other borrowers don’t have

those options. at’s why bill rates are often called

risk-free even if that isn’t exactly the case.

Second, the bills mature in no more than a year.

is means there isn’t much time for interest rates or

in ation to cut into the value of the nal payment or

the potential return from reinvesting the money.

Relative Value

Is that 0.1 percent bill in our example, or some other

security like it, worth buying or something to avoid?

We can make relative-value comparisons to help us

answer the question.

Let’s consider how the 0.1 percent rate stacks up

against one-year Treasury bill rates over time. For the

10-year period that ended in 2008, the rate was about

4.5 percent on average. By that standard, the bills earn

next to nothing. en again, the bill rate fell below 1

percent from 2009 onward, which means the gap with

0.1 percent isn’t so wide. Exhibit 2.6 shows the histori-

cal rates.

en you can look at how the discount rate com-

pares with similar rates for three- and six-month bills.

Let’s assume the three-month rate is 0.005 percent,

and the six-month rate is 0.05 percent. is means

companies. Standard & Poor’s, Moody’s Investors

Service, and Fitch Ratings are the three largest services.

ey analyze governments, or sovereigns, and compa-

nies, and they assign ratings to their debt. Although

the borrower usually pays for the ratings, there are

exceptions for sovereign debt. When a government

doesn’t pay, the rating is said to be unsolicited.

Bill ratings start at A-1+ for S&P, P-1 for Moody’s,

and F1+ for Fitch. e companies use fewer tiers, or

levels, than they do for notes and bonds, which we’ll

see later. Only borrowers with high ratings typically

can raise funds in the money market.

Interest rate risk is another concern, as higher rates

translate into lower prices for bills and other debt se-

curities. If the one-year Treasury bill rate in the earlier

example climbed to 0.2 percent the next day from 0.1

percent, the price would fall by about $10 for every

$1,000 face amount. Investors who sell the security or

have to re ect its value in their nancial statements

would su er losses.

Lower rates, on the other hand, pose reinvestment

risk. is refers to the inability to earn as much on a

similar investment when payments are received. e

risk is minimal in our example, because the one-year

bill rate can’t fall too far from 0.1 percent. If the rate

was 1 percent, or perhaps 10 percent, then the risk

would be far greater.

In ation risk, or the threat that price increases will

reduce the buying power of whatever money you re-

ceive, is present as well. is would turn into a reality

in our 0.1 percent example as long as the Consumer

KEY POINT:

MONEY-MARKET RATINGS

Each of the three main credit-

rating services has its own

scale.

S&P uses A-1+, A-1/2/3, B,

B-1/2/3, C, D, Not Rated.

Moody’s uses Prime-1/2/3, Not

Prime.

Fitch uses F1+, F1/2/3, B, C, D,

Not Rated.

Visual Guide to Financial Markets ■23

government, or a company. e borrower might well

be a bigger credit risk than the U.S. government. If that

turns out to be the case, you ought to earn more for

turning over your money.

How much more? e answer provides another

way to judge relative value. Let’s assume the other in-

vestment has a 0.5 percent discount rate. Subtract the

0.1 percent bill rate to calculate the gap between them:

0.4 percentage point. e gure is known as a rate

spread and is expressed in basis points. So, you’ll be

able to earn another 40 basis points for your trouble.

the one-year bill will return 20 times as much if you

tie up your money for four times longer or twice the

amount for investing twice as long. e comparisons

may make the 0.1 percent rate look better.

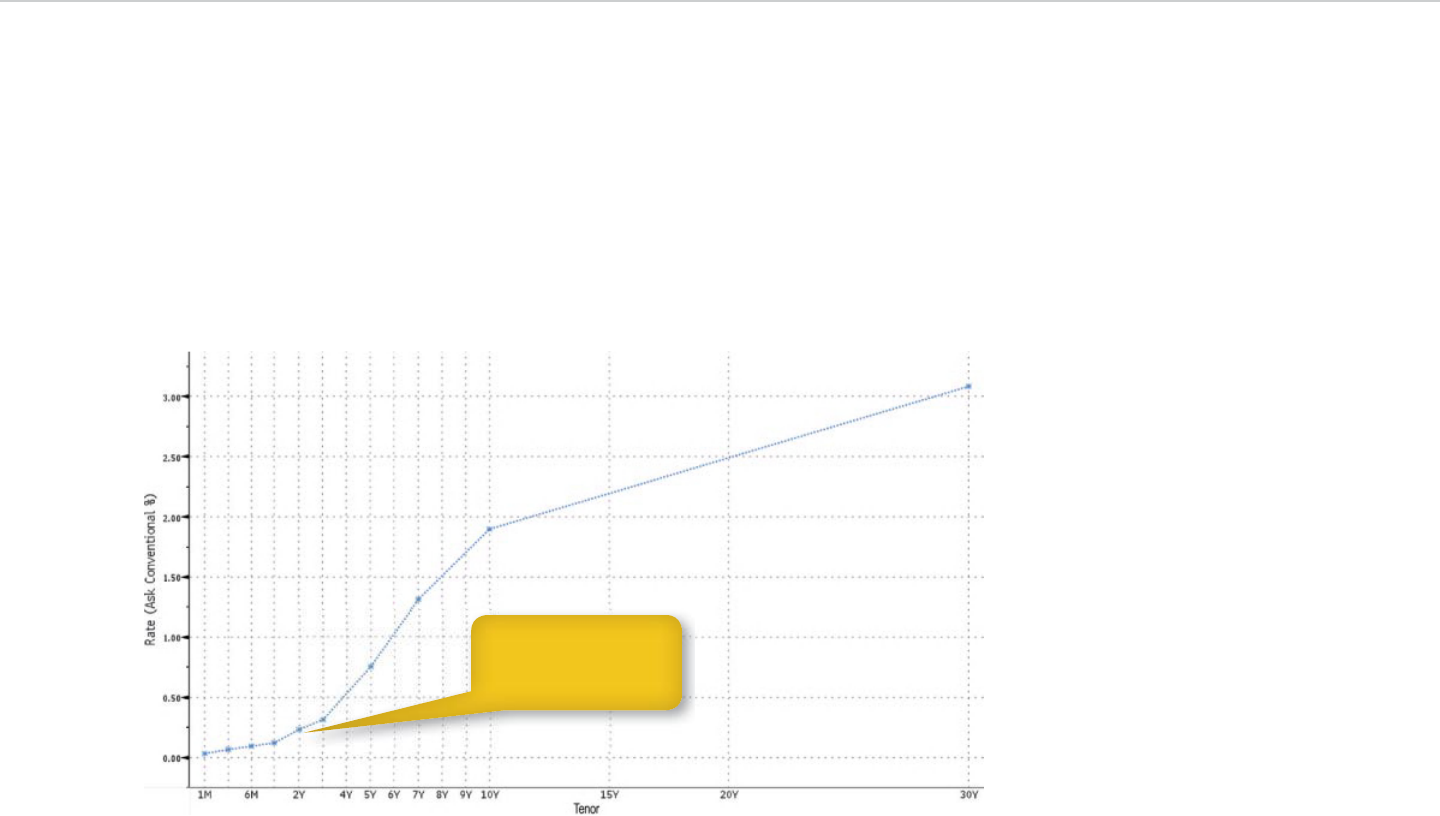

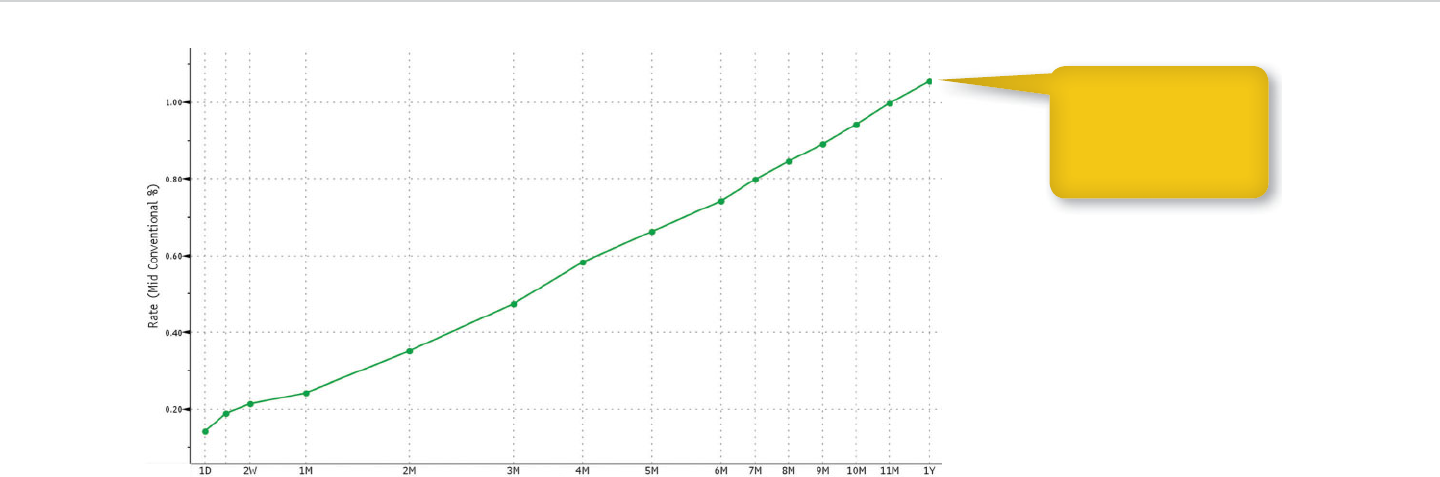

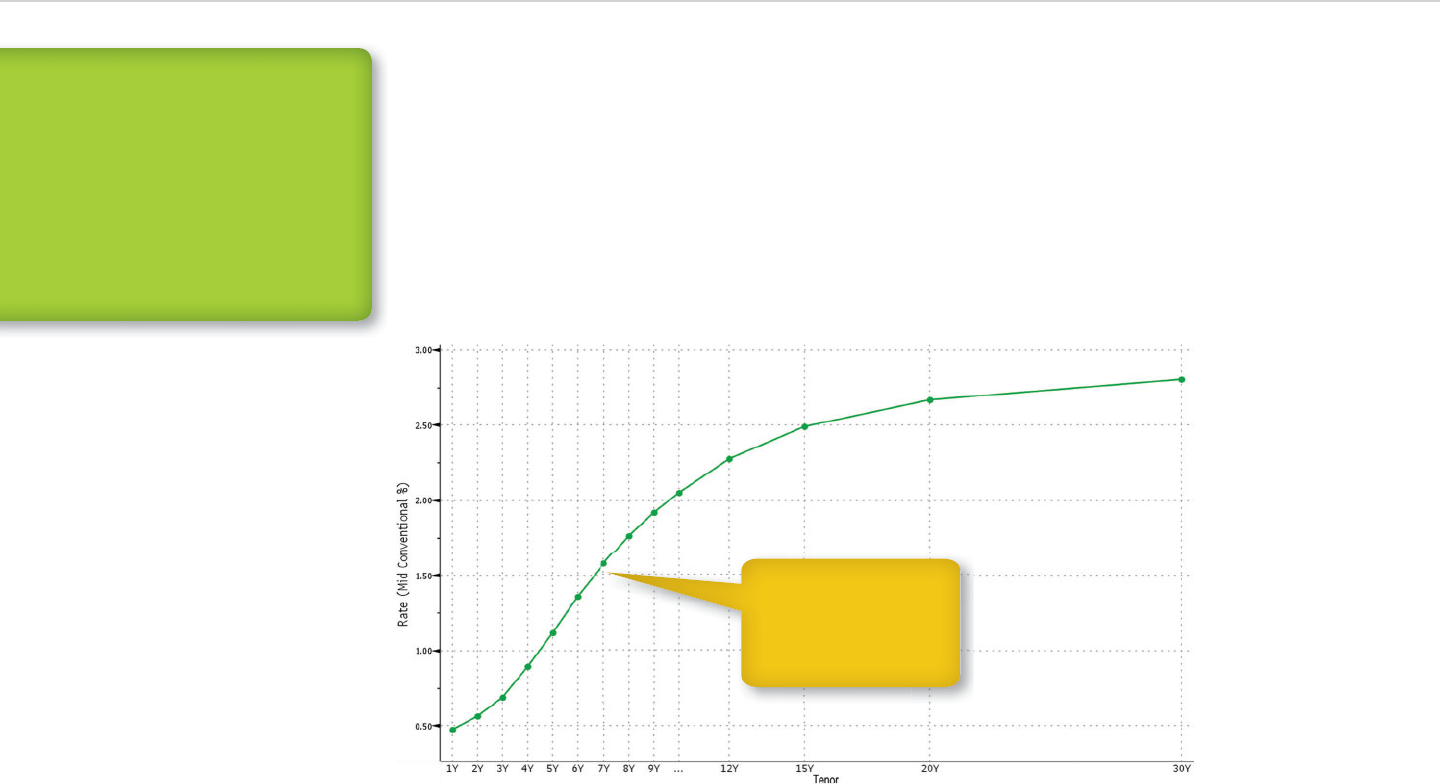

Investors can plot each rate on a graph and con-

nect the dots between them. e result is a rate curve,

used to compare government bills with other types of

securities. We’ll revisit this topic when we run across