THE INSTITUTE OF CAT L2.1 FINANCIAL ACCOUNTING Study Manual

User Manual:

Open the PDF directly: View PDF ![]() .

.

Page Count: 357 [warning: Documents this large are best viewed by clicking the View PDF Link!]

- 50

- The Statement of Comprehensive Income

- 52

- The Statement of Financial Position

- 103

- Control Accounts

- 6

- 122

- The Cash Book and Bank reconciliation Statement

- 125

- Bank Reconciliations Questions / Solutions

- 127

- Questions / Solutions

- 133

- Suspense Accounts

- 8

- 134

- Suspense Accounts

- 134

- Example

- 135

- Errors not affecting the Trial Balance

- 135

- Questions / Solutions

- 145

- IAS 1 – Presentation of Financial Statements

- 9

- IAS 8 – Accounting Policies, Changes in Accounting Estimates & Errors

- 11

- 170

- 170

- Accounting Policies

- 171

- Changes in Accounting Policies

- 171

- Disclosure – Change in Accounting Policies

- 172

- Changes in Accounting Estimates

- 172

- Disclosure – Changes in Accounting Estimates

- 172

- Errors

- 173

- Disclosure – Prior Period Errors

- 217

- IAS 17 – Leases

- 18

- 255

- Company Accounts

- 21

- 299

- IAS 7 – Cash Flow Statements

- 23

- 300

- Cash Management

- INTRODUCTION TO THE COURSE

- A. INTRODUCTION

- B. THE OBJECTIVE OF FINANCIAL STATEMENTS

- C. USERS OF FINANCIAL STATEMENTS

- Creditors

- D. STEWARDSHIP AND ECONOMIC DECISIONS

- O. THE ACCOUNTING PROFESSION AND THE ROLE OF THE ACCOUNTANT

- P. INTERNAL AND EXERNAL AUDITORS

- Q. INTERNAL CONTROL SYSTEMS

- Study Unit 2

- Regulatory & Non-Regulatory Framework

- Rwandan Stock Exchange

- Disadvantages of Standards

- True and Fair

- Framework for the Presentation and Preparation of Financial Statements

- The Purpose of the Framework

- Stage 1: Setting the agenda

- Stage 2: Project planning

- Stage 3: Development and publication

- Stage 4: Development and publication of an exposure draft

- Stage 5: Development and publication of an IFRS

- Procedures after an IFRS is issued

- C. THE REGULATORY FRAMEWORK – STATUTORY

- A. BOOKS OF ORIGINAL ENTRY/BOOKS OF PRIME ENTRY/BOOKS OF FIRST ENTRY

- Sales Day Book

- Cash Receipt Book

- Purchases Day Book

- Cheque Payments Book

- B. NOMINAL LEDGER

- C. DOUBLE ENTRY

- D. THE ACCOUNTING EQUATION

- E. THE STATEMENT OF COMPREHENSIVE INCOME

- Statement of Comprehensive Income for year ended 31st December, 20X0

- EXERCISE: PLB LIMITED

- Non-current Assets

- Current Assets

- Current Liabilities

- Long-Term Liabilities

- Capital

- Effects of incorrect treatment

- EXAMPLE

- Question: MR A. Igwe.

- EXERCISE 1

- EXERCISE 2

- Mr A. Igwe. : Pro Forma Solution

- Mr A. Igwe : Solution

- BSB Ltd: Solution

- Exercise 1: Solution

- PTT Limited: Pro Forma Solution

- A. ACCRUALS AND PREPAYMENTS

- B. QUESTIONS/SOLUTIONS

- B. TRADE RECEIVABLES, BAD DEBTS RECOVERED AND PROVISION FOR BAD DEBTS

- C. OTHER PROVISIONS

- D. PROVISIONS FOR DISCOUNTS ALLOWED

- ___________________________________________________________________________

- D. QUESTIONS/SOLUTIONS

- E. Accounting for VAT

- A. THE CASH BOOK AND BANK RECONCILIATION STATEMENTS

- B. BANK RECONCILIATIONS STATEMENTS QUESTIONS/SOLUTIONS

- C. QUESTIONS/SOLUTIONS

- A. SUSPENSE ACCOUNTS

- B. EXAMPLE

- C. ERRORS NOT AFFECTING THE TRIAL BALANCE

- D. QUESTION/SOLUTION

- E. THE JOURNAL

- F. QUESTIONS/SOLUTIONS

- A. OBJECTIVE

- C. COMPONENTS OF FINANCIAL STATEMENTS

- D. FINANCIAL REVIEW BY MANAGEMENT

- E. STRUCTURE, CONTENT AND REPORTING

- H. EXAMPLE 1 – STATEMENT OF FINANCIAL POSITION

- I. THE STATEMENT OF COMPREHENSIVE INCOME

- J. FUNCTION OF EXPENDITURE METHOD

- A. INTRODUCTION

- B. DEFINITIONS

- C. MEASUREMENT

- D. DISCLOSURE

- E. METHODS OF COSTING

- A. INTRODUCTION

- B. DEFINITIONS

- C. ACCOUNTING POLICIES

- D. CHANGES IN ACCOUNTING POLICIES

- E. DISCLOSURE – CHANGES IN ACCOUNTING POLICY

- F. CHANGES IN ACCOUNTING ESTIMATES

- G. DISCLOSURE – CHANGES IN ACCOUNTING ESTIMATES

- H. ERRORS

- I. DISCLOSURE OF PRIOR PERIOD ERRORS

- A. OBJECTIVE

- B. DEFINITIONS

- C. RECOGNITION AND MEASUREMENT

- D. DIVIDENDS

- E. GOING CONCERN

- F. DISCLOSURE

- A. OBJECTIVE

- B. DEFINITIONS

- C. DEPRECIATION

- D. ACCOUNTING FOR DEPRECIATION

- E. DISPOSAL OF PROPERTY, PLANT AND EQUIPMENT

- G. RECOGNITION AND MEASUREMENT

- H. DISCLOSURE

- I. EXAMPLES

- Reducing Balance

- Straight Line Method

- Solution – Question 2

- 3,000

- 3,000

- COST

- (300)

- (300)

- DEPRECIATION Y/E 31.12.X0

- 2,700

- 2,700

- NET BOOK VALUE 31.12.X0

- (270)

- (300)

- DEPRECIATION Y/E 31.12.X1

- 2,430

- 2,400

- NET BOOK VALUE 31.12.X1

- (243)

- (300)

- DEPRECIATION Y/E 31.12.X2

- 2,187

- 2,100

- NET BOOK VALUE 31.12.X2

- (219)

- (300)

- DEPRECIATION Y/E 31.12.X3

- 1,968

- 1,800

- NET BOOK VALUE 31.12.X3

- (196)

- (300)

- DEPRECIATION Y/E 31.12.X4

- 1,772

- 1,500

- NET BOOK VALUE 31.12.X4

- Reducing Balance

- Straight Line Method

- 1,200

- 1,200

- PROCEEDS

- (1,772)

- (1,500)

- NET BOOK VALUE

- (572)

- (300)

- PROFIT/(LOSS) ON DISPOSAL

- A. OBJECTIVE

- B. DEFINITIONS

- C. RECOGNITION AND MEASUREMENT

- D. SALE OF GOODS

- F. INTEREST, ROYALTIES AND DIVIDENDS

- G. DISCLOSURE

- A. OBJECTIVE

- B. BASIC CONCEPTS

- C. DEFINITIONS

- D. TYPES OF GRANT AVAILABLE

- E. ACCOUNTING TREATMENT

- F. DISCLOSURE

- G. REPAYMENT OF GOVERNMENT GRANTS

- H. GRANT RECOGNITION

- A. OBJECTIVE

- B. DEFINITIONS

- C. RECOGNITION

- D. MEASUREMENT

- E. CHANGES IN PROVISIONS

- F. USES OF PROVISIONS

- G. APPLICATIONOF THE RECOGNITION AND MEASUREMENT RULES

- I. EXAMPLES - RECOGNITION

- A. OBJECTIVE

- B. DEFINITION

- C. RECOGNITION AND PRESENTATION

- D. DISCLOSURE

- IAS 12 requires the following disclosures:

- A. OBJECTIVE

- B. CLASSIFICATION OF LEASES

- C. ACCOUNTING BY LESSEES

- D. DISCLOSURE: LESSEES – FINANCE LEASE

- E. DISCLOSURES: LESSEES – OPERATING LEASE

- A. PREPARING FINANCIAL STATEMENTS FOR DIFFERENT FORMS OF BUSINESS ENTITY

- B. SOLE TRADER ACCOUNTS - INTRODUCTION

- C. TWO APPROACHES IN PREPARING ACCOUNTS

- D. DOUBLE ENTRY APPROACH

- E. QUESTION/SOLUTION

- F. SINGLE ENTRY APPROACH

- G. QUESTION/SOLUTION

- H. USE OF RATIOS

- Goods cost RWF10,000. Gross Profit Percentage is 20%. What is the selling price?

- Goods sold for RWF10,000. Mark-up is 10%. What is the cost price

- I. QUESTION/SOLUTION

- A. INTRODUCTION – STATEMENT OF COMPREHENSIVE INCOME

- B. DIVIDENDS

- C. TRANSFER TO RESERVE

- D. STATEMENT OF FINANCIAL POSITION

- See Chapter 9 IAS 1 for details on the layout of Statement of Financial Position.

- E. SHARE CAPITAL

- F. CORPORATION TAX / INCOME TAX EXPENSE

- H. ULTRA VIRES

- I. RETURNS, STATUTORY BOOKS, DIRECTORS’ REPORTS, NOTICES, RESOLUTIONS AND ACCOUNTS TO BE FILED

- Directors’ Report

- Disclosure Requirements for Employees

- Disclosure Requirements for Directors’ Emoluments

- A. INTRODUCTION

- B. PREPARATION OF LIMITED COMPANY ACCOUNTS

- C. SAMPLE QUESTION/SOLUTION

- D. QUESTIONS/SOLUTIONS

- A. INCOME AND EXPENDITURE ACCOUNTS INTRODUCTION

- B. SOURCES OF INCOME

- C. EXPENDITURE

- D. STATEMENT OF FINANCIAL POSITION

- E. QUESTION/SOLUTION

- RECEIPTS

- A. CASH MANAGEMENT

- B. OBJECTIVE

- C. OPERATING ACTIVITIES

- D. INVESTING ACTIVITIES

- E. FINANCING ACTIVITIES

- F. REPORTING CASH FLOWS FROM OPERATING ACTIVITIES

- G. WORKED EXAMPLES

- Cash Flow Statement - Indirect Method

- H. DISPOSAL OF A TANGIBLE NET ASSET

- I. TAXATION

- J. DIVIDENDS

- K. WORKED EXAMPLE

- A. GENERAL

- B. RATIOS ON RETURN ON CAPITAL

- C. RATIOS ON PROFITABILITY

- D. RATIOS OF ACTIVITY

- E. RATIOS OF LEVERAGE/GEARING

- F. RATIOS OF LIQUIDITY

- G. LIMITATIONS OF RATIO ANALYSIS

- H. SUMMARY

- I. CHECKLIST

Page 0

Page 0

1

BLANK

Page 1

© iCPAR

All rights reserved.

The text of this publication, or any part thereof, may not be reproduced or transmitted in any

form or by any means, electronic or mechanical, including photocopying, recording, storage

in an information retrieval system, or otherwise, without prior permission of the publisher.

Whilst every effort has been made to ensure that the contents of this book are accurate, no

responsibility for loss occasioned to any person acting or refraining from action as a result of

any material in this publication can be accepted by the publisher or authors. In addition to

this, the authors and publishers accept no legal responsibility or liability for any errors or

omissions in relation to the contents of this book.

INSTITUTE OF

CERTIFIED PUBLIC ACCOUNTANTS

OF

RWANDA

Level 2

L2.1 FINANCIAL ACCOUNTING

First Edition 2012

This study manual has been fully revised and updated

in accordance with the current syllabus.

It has been developed in consultation with experienced lecturers.

Page 2

BLANK

Page 3

Contents

Study Unit

Title

Page

Introduction to the Course

9

SECTION 1: GENERAL FRAMEWORK OF ACCOUNTING

1

General Framework of Accounting

13

Introduction

14

The Objective of Financial Statements

14

Users of Financial Statements

14

Stewardship and Economic Decisions

16

The Qualitative Characteristics of Financial Information

17

Components of Financial Statements

18

The Statement of Financial Position

18

The Statement of Comprehensive Income

18

The Statement of Changes in Equity

18

The Cash Flow Statement

19

Elements of Financial Statements

19

Recognition in Financial Statements

20

Measurement in Financial Statements

20

The Historical Cost Convention/System

21

The Accounting Profession and the Role of the Accountant

21

Internal and External Auditors

23

Internal Control Systems

25

2

Regulatory & Non Regulatory Framework

29

Generally Accepted Accounting Policies (GAAP)

30

The Regulatory Framework – Non Statutory

30

The Regulatory Framework – Statutory

38

SECTION 2: BOOK-KEEPING

3

Double Entry, Trial Balance, Statement of Financial Position

41

Books of Original Entry

42

Nominal Ledger

47

Double Entry

49

The Accounting Equation

49

The Statement of Comprehensive Income

50

The Statement of Financial Position

52

The Effects of Transaction on a Statement of Financial Position

53

Capital Expenditure and Revenue Expenditure

62

Questions / Solutions

63

Page 4

Study Unit

Title

Page

4

Accruals and Prepayment

81

Accruals and Prepayments

82

Questions / Solutions

85

5

Trade Receivables, Bad Debts and Provisions

89

Provisions

90

Trade Receivables, Bad Debts, Bad Debts Recovered and Provisions

90

Other Provisions

94

Provisions for Discounts Allowed

95

Provisions for Discounts Received

96

Questions / Solutions

99

6

Control Accounts

103

Control Accounts

104

Trade Receivables Control Account

105

Trade Payables Control Account

107

Questions / Solutions

108

Accounting for VAT

114

7

Bank Reconciliation Statements

121

The Cash Book and Bank reconciliation Statement

122

Bank Reconciliations Questions / Solutions

125

Questions / Solutions

127

8

Suspense Accounts

133

Suspense Accounts

134

Example

134

Errors not affecting the Trial Balance

135

Questions / Solutions

135

The Journal

137

Questions / Solutions

139

SECTION 3: ACCOUNTING TREATMENT OF IDENTIFIED

IAS’S

9

IAS 1 – Presentation of Financial Statements

145

Objective

147

Purpose of Financial Statements

147

Components of Financial Statements

147

Financial Review by Management

147

Structure, Content and Reporting

148

Definitions

148

Statement of Financial Position Format

148

Example 1 – Statement of Financial Position

150

The Statement of Comprehensive Income

151

Function of Expenditure Method

151

Page 5

Study Unit

Title

Page

Nature of Expenditure Method

151

Changes in Inventories of Finished Goods and Work in Progress

152

Raw Materials and Consumables Used

152

Information to be presented either on the face of the Statement of

Comprehensive Income or in the notes

153

Statement of Changes in Equity

155

Statement of Recognised Income and Expense

156

Disclosure of Significant Accounting Policies

156

Questions / Solutions

157

10

IAS 2 – Inventories

163

Introduction - Inventories

164

Definitions

164

Measurement

165

Disclosure

165

Methods of Costing

166

11

IAS 8 – Accounting Policies, Changes in Accounting Estimates &

Errors

169

Introduction

170

Definitions

170

Accounting Policies

170

Changes in Accounting Policies

171

Disclosure – Change in Accounting Policies

171

Changes in Accounting Estimates

172

Disclosure – Changes in Accounting Estimates

172

Errors

172

Disclosure – Prior Period Errors

173

12

IAS 10 – Events after the Reporting Period

175

Objective

176

Definitions

176

Recognition & Measurement

176

Dividends

177

Going Concern

177

Disclosure

177

13

IAS 16 – Property, Plant and Equipment

179

Objective

180

Definitions

180

Depreciation

180

Accounting for Depreciation

181

Disposal of Property, Plant and Equipment

185

Ledger Accounts and Journal Entries

185

Recognition & Measurement

188

Disclosure

190

Page 6

Study Unit

Title

Page

Examples

190

14

IAS 18 - Revenue

195

Objective

196

Definitions

196

Recognition & Measurement

196

Sale of Goods

197

Rendering of Services

197

Interest, Royalties and Dividends

197

Disclosure

197

15

IAS 20 – Government Grants

199

Objective

200

Basic Concepts

200

Definitions

200

Types of Grant Available

201

Accounting Treatment

201

Disclosure

203

Repayment of Grants

203

Grant Recognition

204

16

IAS 37 – Provisions, Contingent Liabilities and Contingent Assets

205

Objective

206

Definition

206

Recognition

207

Measurement

207

Changes in Provisions

208

Uses of Provisions

208

Application of Recognition and Measurement Rules

208

Disclosure

209

Examples – Recognition

210

17

IAS 12 – Income Taxes

213

Objective

214

Definition

214

Recognition and Presentation

214

Disclosure

214

18

IAS 17 – Leases

217

Objective

218

Classification of Leases

218

Accounting by Lessees

219

Disclosure: Lessees – Finance Leases

219

Disclosure: Lessees – Operating Leases

220

Page 7

Study Unit

Title

Page

SECTION 4: PREPARATION OF FINANCIAL STATEMENTS

FOR DIFFERENT FORMS OF BUSINESS ENTITY

19

Sole Traders

221

Preparing Financial Statements for Different Forms of Business Entity

222

Sole Trader Accounts - Introduction

223

Two Approaches in Preparing Accounts

224

Double Entry Approach

224

Question / Solution

228

Single Entry Approach

231

Question / Solution

231

Use of Ratios

233

Question / Solution

234

20

Company Accounts 1

239

Introduction – Statement of Comprehensive Income

240

Dividends

241

Transfer to Reserve

241

Statement of Financial Position

241

Share Capital

241

Corporation Tax / Income Tax Expense

242

Issue of Shares

243

Ultra Vires

249

Returns, Statutory Books, Director’s Reports, Notices, Resolutions and

Accounts to be Filed

250

Ethical Obligations of Company Directors

254

21

Company Accounts

255

Introduction

256

Preparation of Limited Company Accounts

269

Sample Questions / Solutions

270

Questions / Solutions

275

22

Income and Expenditure

291

Introduction – Income and Expenditure Accounts

292

Sources of Income

292

Expenditure

295

Statement of Financial Position

295

Question / Solution

295

Page 8

Study Unit

Title

Page

SECTION 5: INTERPRETATION OF FINANCIAL

STATEMENTS

23

IAS 7 – Cash Flow Statements

299

Cash Management

300

Objective

300

Operating Activities

300

Investing Activities

301

Financing Activities

301

Reporting Cash Flows from Operating Activities

301

Worked Examples

304

Disposal of a Tangible Net Asset

310

Taxation

311

Dividends

311

Worked Example

311

24

Ratio Analysis & Interpretation of Financial Statement

315

General

316

Ratios on Return on Capital

317

Ratios of Profitability

317

Ratios of Activity

319

Ratios of Leverage / Gearing

322

Ratios of Liquidity

323

Limitations of Ratio Analysis

325

Summary

325

Checklist

326

25

Manufacturing Accounts

329

General

330

Divisions of Costs

330

Worked Example

331

26

IPSAS – International Public Sector Accounting Standards

335

Introduction

336

IPSAS 1

338

IPSAS 2

339

IPSAS 12

340

IPSAS 3

341

IPSAS 14

342

IPSAS 17

343

IPSAS 31

346

IPSAS 16

347

IPSAS 19

348

IPSAS 9 & 23

349

Page 9

Page 10

INTRODUCTION TO THE COURSE

Stage: Level 2

Subject Title: L2.1 Financial Accounting

Aim

The aim of this subject is to ensure that students understand how role, function and basic

principles of financial accounting and to prepare accounts for basic reporting entities in

accordance with International Financial Reporting standards (IFRSs) Students should have an

ability to analyse and interpret financial statements.

Learning Outcomes

On successful completion of this subject students should be able to:

• An understanding of the influence of legislation and accounting together with the standard

setting process.

• Be able to recognise and comment on relevant ethical issues relevant to business owners,

managers and accountants.

• The ability to prepare accounts from incomplete records, partnerships, limited companies,

together with an understanding of the importance of cash to a business and to prepare cash

flow statements for limited companies.

• The ability to use ratio analysis as a technique in decision making and performance

evaluation.

• The ability to analyse and interpret financial statements

Page 11

Syllabus:

1. Conceptual and regulatory framework

• Influence of legislation and accounting standards on the production of published accounting

information for organisations

• Impact of legislation on the preparation and reporting of financial statements

• Roles of the International Accounting Standards Board, The Standards Advisory

Council and the International Financial Reporting Interpretations Committee

• Application of International Accounting Standards and International Financial

Reporting Standards to the preparation and presentation of financial statements

• Framework for the Preparation and Presentation of Financial Statements

- The objective of financial statements

- Underlying Assumptions

- Qualitative characteristics of financial statements

- Elements of financial statements

• Standard setting process

- Standard setting process

- Accounting standards and the law on Published Accounts

- The role of the stock exchange

• Internal and external auditors and ethical issues for the Accounting Technician

- Role and duties of internal and external auditors

- Internal control systems

- Ethical issues and responsibilities accruing

• Content and application of specified accounting standards

- Presentation of Financial Statements

- Inventories

- Cash Flow Statements

- Accounting policies, change in accounting estimates and errors

- Events after the Reporting Period

- Income taxes (excluding deferred tax)

- Property, Plant and Equipment

- Leases (Lessee accounting only)

- Accounting for Government Grants and Disclosure of Government Assistance

- Provisions, Contingent Liabilities and Contingent Assets

• Professional ethical issues relevant to business owners, managers and accountants

- Understanding and application of ethical issues

• Government accounting

- General Introduction to Government Accounting

- The IPSAS regime and the public sector

Page 12

2. Financial statements

• Financial statements for limited companies for internal and external purposes

- Preparation of financial statements for limited companies

- Differences between a sole trader and a limited company

- Accounting records of a limited company

- Capital structure of a limited company

- Share premium account

- Dividends

- Reserves

- Practical application of IAS/IFRS requirements

• Disclosure and filing requirements for limited companies

- Format and filing requirements

- Wording and layout of a Statement of Comprehensive Income (Statement of

Comprehensive Income) and Statement of financial Position (Statement of Financial

Position)

- Size criteria for companies

- Disclosure Requirements

- Split of turnover

- Details regarding staff numbers and remuneration

- Movement in non-current assets

- Details of taxes owing

• Cash flow statements for limited companies and an understanding of the importance of

cash to the business entity

- Preparation of cash flow statements in accordance with the IFRS regime

- Importance of cash to a business entity

- Preparation of reports on the interpretation of a Cash flow statement

• The accounts of manufacturing businesses

- Classification of costs

- Work in Progress

- Preparation of the manufacturing account

• Preparation of accounts from incomplete records

- Incomplete records

- Preparation of accounts from incomplete records

3. Interpretation of financial statements

• Ratio Analysis of accounting information

- Broad categories of ratios

- Profitability and return on capital employed

- Long term solvency and stability

- Short term solvency and liquidity

- Efficiency

- Shareholders' investment ratios

• Interpretation of Financial Statements and explanation of ratios used

- Interpretation of Financial Statements

- Explanation of information provided by ratios

- Limitations of ratio analysis

• Preparation of reports for the users of accounting information as a tool in the

decision making process

- Preparation of reports in a professional manner

- Ratio analysis in the decision making process

Page 13

BLANK

Page 14

Study Unit 1

The General Framework of Accounting

Contents

A. Introduction

B. The Objective of Financial Statements

C. Users of Financial Statements

D. Stewardship and Economic Decisions

E. The Qualitative Characteristics of Financial Information

F. Components of Financial Statements

G. The Statement of Financial Position

H. The Statement of Comprehensive Income

I. The Statement of Changes in Equity

J. The Cash Flow Statement

K. Elements of Financial Statement

L. Recognition in Financial Statements

M. Measurement in Financial Statements

N. The Historical Cost Convention/System

O. The Accounting Profession and the Role of the Accountant

Page 15

A. INTRODUCTION

Financial accounting is a branch of economics. It involves gathering, recording, summarising

and presenting information to the various users of financial information.

B. THE OBJECTIVE OF FINANCIAL STATEMENTS

The objective of financial statements is to provide information about the financial position,

performance and changes in financial position of an entity that is useful to a wide range of

users in making economic decisions.

Financial position reveals information about the economic resources that an entity controls,

its financial structure, its liquidity and solvency and its ability to change. This information is

contained in the Statement of Financial Position. Changes in financial position are revealed

in a Cash Flow Statement.

Financial Performance means the return obtained on the resources which the entity controls.

This information can be extracted from the profit and loss account. In International

Accounting the profit and loss account is referred to as the Statement of Comprehensive

Income.

The Reporting Entity

Financial Statements report on all of the activities and resources under the control of the

entity that has prepared them whether it is a sole trader, a club or society or a limited

company.

C. USERS OF FINANCIAL STATEMENTS

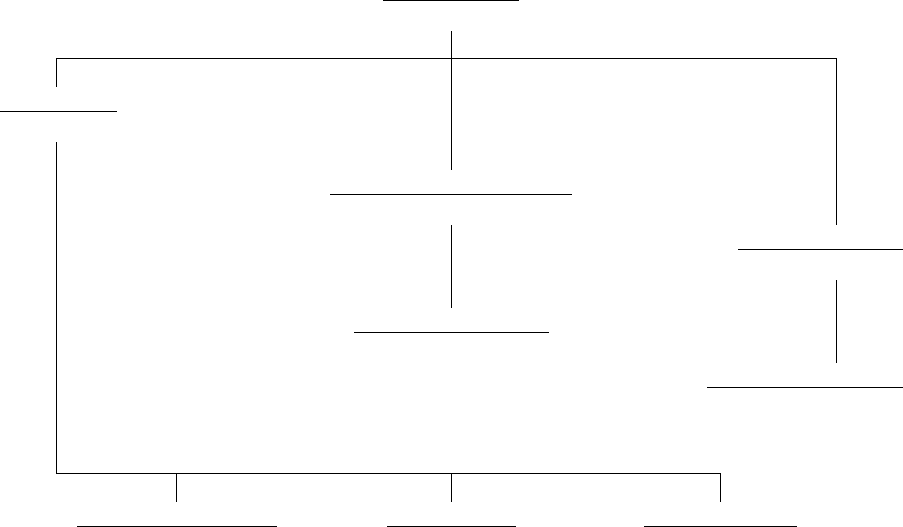

Users of financial statements include the following:

(a) Existing and potential shareholders

Information is required in relation to profit, dividends, trends and prospects in

connection with share price.

(b) Loan Creditors

Information is required in relation to liquidity and to highlight the risk of non-payment.

(c) Business Contact Group i.e. suppliers, customers, competitors and merger/acquisition

situations. Information is required to ensure ability to pay debts, continuity of supply

and trade information.

(d) Analysts and investors

Information on performance, trends and prospects is required for clients

(e) Government

Information is required as a base for taxation and to ensure compliance with company

law

(f) Employees

Information about employment security and to assist with collective pay bargaining

(g) Public

Page 16

Any member of the public may require details of the contribution to the local and

national economy made by the company and the environmental impact.

The objective of accounting is to provide sufficient information to meet the needs of the

various users at the lowest possible cost. There are two branches of accounting, that reflect

the internal and external users of accounting information. Management accounting is

concerned with the provision of information to people within the organisation to help them

make better decisions and improve the efficiency and effectiveness of existing operations,

whereas financial accounting is concerned with the provision of information to external

parties outside the organisation. As such, management accounting could be called internal

accounting and financial accounting could be called external accounting.

Differences between management accounting and financial accounting

The major differences between these two branches of accounting are:

• Legal requirements. There is a statutory requirement for public limited companies to

produce annual financial accounts regardless of whether or not management regards

this information as useful. Management accounting is entirely optional and

information should only be produced if it is considered that the benefits from the use

of the information by management exceed the cost of collecting it.

• Focus on individual parts or segments of the business. Financial accounting reports

describe the whole of the business whereas management accounting focuses on small

parts of the organisation i.e. profitability of products, services etc. Management

accounting information measures the economic performance of decentralised

operating units, such as divisions and departments

• Generally accepted accounting principles. Financial accounting statements must be

prepared to conform with the legal requirements and the generally accepted

accounting principles established by the regulatory bodies. These requirements are

essential to ensure the uniformity and consistency that is needed for external financial

statements. Outside users need assurance that external statements are prepared in

accordance with generally accepted accounting principles so that the inter-company

and historical comparisons are possible. In contrast, management accountants are not

Users of Financial

Statements

Creditors

Employers

Government

Investors

Public

Employees

Page 17

required to adhere to generally accepted accounting principles when providing

managerial information for internal purposes. Instead, the focus is on the serving

management’s needs and providing information that is useful to managers relating to

their decision-making, planning and control functions.

• Time dimension. Financial accounting reports what has happened in the past in an

organisation, whereas management accounting is concerned with future information

as well as past information. Decisions are concerned with future events and

management therefore requires details of expected future costs and revenues.

• Report frequency. A detailed set of financial accounts is published annually and less

detailed accounts are published semi-annually. Management requires information

quickly. Consequently, management accounting reports on various activities may be

prepared at daily, weekly or monthly intervals.

D. STEWARDSHIP AND ECONOMIC DECISIONS

Stewardship entails the safekeeping and proper use of an entity’s resources and their efficient

and profitable use. Existing investors assess management’s stewardship in order to decide

whether to seek a change in management or to change the level of their shareholding in the

entity.

Ethical Issues for Management

Ethical behaviour is an important element of stewardship. Increased accountability and legal

frameworks across the globe now require that businesses take stock of their actions. Ethical

debates in business are not new, however, and the area is large and often hard to quantify.

Business ethics are moral principles that guide how a business behaves and they are the

foundation of lasting business success. When a business practices ethical decision-making

they are practising the values of a democratic society within the workplace. Therefore a

business that places emphasis on ethics provides an environment that promotes honest

working practices. This is especially important in a world that has recently witnessed mass

corporate failures and questionable accounting practices. It is therefore important that

businesses apply appropriate values, ethics and attitudes.

Businesses or other corporate structures will usually have their own statement of business

principles or a code, which sets out their core values and standards. This statement of

principle or code enables the application of a common code of basic values that all persons

within the organisation can agree on. It forces employers and companies to adhere to high

standards of performance by not only following company law legislation but also by “doing

the right thing.” A business ethical code emphasises the importance of applying moral values

to company decisions. It is also important to realise that a code will apply to all members of

the organisation regardless of their position in the company. However, a higher expectation is

placed on qualified professionals such as accountants, who are held in a position of trust

which is damaged by unscrupulous behaviour or poor practice.

Page 18

The advantages of ethical behaviour include:

Higher revenues – demand from positive consumer support

• Improved brand and business awareness and recognition

• Better employee motivation and recruitment

• New sources of finance – e.g. from ethical investors

The disadvantages claimed for ethical business include:

• Higher costs – e.g. sourcing from Fairtrade suppliers rather than lowest price

• Higher overheads – e.g. training & communication of ethical policy

• A danger of building up false expectations

E. THE QUALITATIVE CHARACTERISTICS OF FINANCIAL

INFORMATION

In deciding what information should be included in financial statements, when it should be

included and how it should be presented, the aim is to ensure that financial statements yield

useful information. Financial information is useful if it is:

Relevant

-

If it has the ability to influence the economic decisions of users and is

provided in time to influence those decisions

Reliable

-

Reliability is characterised by:

• Faithful representation

• Substance over form recognition of the economic substance of a

transaction over its legal form

• Neutrality - free from bias

• Prudence - a degree of caution in making estimates in conditions

of uncertainty

• Completeness - an omission can cause information to be false or

misleading

Comparable

-

It enables users to discern and evaluate similarities in, and differences

between, the nature and effects of transactions and other events over

time and across different reporting entities.

Understandable

-

Its significance can be perceived by users who have a reasonable

knowledge of business and economic activities and accounting and a

willingness to study with reasonable diligence the information

provided.

If a conflict arises between these characteristics, a trade-off needs to be found that still

enables the objective of financial statements to be met. For example, if the information that

is the most relevant is not the most reliable and vice versa, it will usually be appropriate to

use the item of information that is the most relevant of those that are reliable.

Financial information with the above characteristics will be most useful to the users of

financial statements. In deciding whether to present financial information separately in the

financial statements the accountant must assess the information’s ability to influence

Page 19

economic decisions it is considered to be material and should be presented separately in the

financial statements.

F. COMPONENTS OF FINANCIAL STATEMENTS

The primary financial statements are currently:

(a) Trading Profit and Loss Account/the Statement of Comprehensive Income

(b) A Statement of Changes in Equity

(c) The Statement of Financial Position

(d) The Cash Flow Statement

Notes to these primary financial statements are used to amplify and explain the primary

statements. The notes on primary financial statements form an integral part of the financial

statements.

G. THE STATEMENT OF FINANCIAL POSITION

This is a financial statement of the assets, liabilities and ownership interests drawn up at a

particular point in time. This point in time for the annual financial statement is referred to as

the entity’s year end.

H. THE STATEMENT OF COMPREHENSIVE INCOME (PROFIT &

LOSS)

The Statement of Comprehensive Income details the trading results for the period. It details

the Revenue earned and the expenses incurred.

I. THE STATEMENT OF CHANGES IN EQUITY

A statement of changes in equity shows the following items:

• Net profit/loss for the period

• Gains/losses recognised directly in equity e.g. surplus on revaluation of land and

buildings

• Cumulative effect of changes in accounting policy and the correction of fundamental

errors (per IAS 8, which will be dealt with in a later chapter)

• Capital transactions with owners, for example, dividend payments share issue.

• Accumulated profit/loss

− At start of the year

− Movement for year

− At end of year

• Reconciliation between carrying amount at the start and end of the year for:

Page 20

− Each class of equity

− Share premium

− Each reserve

J. THE CASH FLOW STATEMENT

This statement shows the increase or decrease in the amount of cash/cash equivalents the

entity has generated since the previous year end.

K. ELEMENTS OF FINANCIAL STATEMENTS

Financial statements need to reflect the effects of transactions and other events on the

reporting entity’s financial performance and financial position. This involves a high degree

of classification and aggregation. Order is imposed on this process by specifying and

defining the classes of items – the elements – that encapsulate the key aspects of the effects

of those transactions and other events. The main elements and their definitions are as

follows:

• Assets – a resource controlled by an entity as a result of past events from which future

economic benefits are expected to flow. Assets are broken down between current assets

and non-current assets (formerly known as fixed assets).

• Liabilities – present obligations of the entity arising from past events, settlement of

which is expected to result in an outflow of resources embodying economic benefits.

Liabilities are broken down between current liabilities and non-current liabilities.

• Equity – the residual interest in the assets of the entity after deducting all its liabilities.

• Income – increases in economic benefits in the form of inflows of assets or decreases of

liabilities that result in increases in equity.

• Expenses – decreases in economic benefits in the form of outflows of assets or

incurrence of liabilities that result in decreases in equity.

Assets

Future Economic Benefits – If an item does not generate future economic benefits it is

not an asset. There must be evidence that cash will be received in the future.

Controlled by an Entity – Though ownership is not essential control is a vital element.

Control means the ability to restrict use.

Past Transactions or Events – The transaction or event must be in the past before an

asset can arise. Access to economic benefits obtained after the Statement of Financial

Position date cannot constitute an asset.

Liabilities

Obligations – These may be legal or constructive. A legal obligation derives from a

contract, legislation or other operation of law. A constructive obligation derives from

the entity’s actions e.g. refunds to dis-satisfied customers.

Page 21

Transfer of Economic Benefits – This normally represents a transfer of cash but could

involve the exchange of an asset e.g. trade in of a motor vehicle.

Obligations that are not expected to result in a transfer of economic benefits e.g. the

guarantee of a loan, are referred to as contingent liabilities

Past Transactions or Events – The transaction or event must be in the past.

L. RECOGNITION IN FINANCIAL STATEMENTS

The objective of financial statements is achieved to a large extent by showing in the primary

financial statements, in words and by a monetary amount, the effects that transactions and

other events have on the elements. This process is known as recognition.

For example, if the effect of a transaction is to create a new asset or liability or to add to an

existing asset or liability, that new asset or liability or addition will be recognised in the

Statement of Financial Position if there is sufficient evidence that it exists and it can be

measured reliably enough as a monetary amount. A gain or loss will be recognised at the

same time, unless there has been no change in the total net assets or the whole of the change

is the result of capital contributions or distributions.

M. MEASUREMENT IN FINANCIAL STATEMENTS

In order that an asset or liability can be recognised, it needs to be assigned a monetary

carrying amount. Two measurement bases could be used for this purpose:

• Historical Cost – which is the lower of cost and recoverable amount (as defined below)

Or

• Current Value – which is the lower amount of replacement cost and recoverable amount.

Most assets and liabilities arise from arm’s length transactions. In such circumstances and

regardless of the measurement basis used, the carrying amount assigned on initial recognition

will be the transaction cost.

The carrying amounts derived from the two bases will usually change after initial recognition,

making it necessary to decide which basis to use. The approach adopted by many entities

involves measuring some Statement of Financial Position categories at historical cost and

some at current value. Although this is often referred to as the modified historical cost basis,

it is more accurately referred to as the mixed measurement system.

It is envisaged that the measurement basis used for a category of assets or liabilities will be

determined by reference to factors such as the objective of financial statements, the nature of

the assets or liabilities concerned and the particular circumstances involved. It is also

envisaged that a separate decision as to the appropriate measurement basis will be taken for

each Statement of Financial Position category. That decision will need to be kept under

review as accounting thought, access to markets, and circumstances change.

Page 22

Whatever the measurement base chosen, the carrying amount may need to be changed from

time to time. This process is known as re-measurement.

• When historical cost measure is used, re-measurements are necessary to ensure that

items are stated at the lower of cost and recoverable amount.

• When a current value is used, re-measurements are necessary to ensure that items are

stated at up to date current value.

Re-measurements will be recognised only if there is sufficient evidence that the monetary

amount has changed and the new amount can be measured with sufficient reliability.

Recoverable amount is the higher of realisable value and value in use. Realisable value is the

amount that could be obtained by selling the asset in an orderly disposal. Value in use is the

present discounted value of the future cash flows obtainable as a result of an asset’s

continued use, including those resulting from its ultimate disposal.

N. THE HISTORICAL CONVENTION/SYSTEM

Conventionally, financial accounts are based on historical cost – which is assets/liabilities

recorded in the Statement of Financial Position at their cost of acquisition. Expenses are

charged against revenues in determining profit based upon historic cost of assets used in

generation of the revenues.

Advantages of Historical Cost Accounting:

(a) Consistent with fundamental accounting concepts

(b) Objective and the information it produces is easily verified.

(c) Simple and inexpensive to record the information.

(d) Easily understood by the users of financial statements.

Disadvantages of Historical Cost Accounting:

(a) Assets values unrealistic, in particular land and buildings.

(b) Comparisons over time meaningless.

(c) Maintenance of the physical substance of business ignored.

O. THE ACCOUNTING PROFESSION AND THE ROLE OF THE

ACCOUNTANT

Professional independence is a concept fundamental to the accountancy profession. It is

essentially an attitude of mind characterised by integrity and an objective approach to

professional work. A practising member should both be and appear to be, in each

professional assignment he undertakes, free of any interest, which might be regarded,

whatever its actual effect, as being incompatible with objectivity. The fact that this is self-

evident in the exercise of the reporting function must not obscure its relevance in respect of

other professional work. Accountants cannot avoid external pressures on their integrity and

objectivity in the course of their professional work, but they are expected to resist these

pressures. They must, in fact, retain their integrity and objectivity in all phases of their

Page 23

practice and, when expressing "opinions" on financial statements avoid involvement in

situations that would impair the credibility of their independence in the minds of reasonable

people familiar with the facts.

The accountancy profession exists to ensure that all interested parties entitled to knowledge

of certain facts have those facts presented objectively. That is the essence of high

professional standards and is as appropriate to the accountant in commerce and industry as to

the accountant in public practice. Anything, which tends to impair or might appear to impair

objectivity, in relation to any particular assignment or client must cast grave doubt on the

propriety of the accountant acting in the assignment for the client in question. Examples of

undesirable financial involvement are

• An accountant should not make a loan to a client or guarantee a client’s overdraft

• A loan should not be accepted from a client

• An accountant should not give advice to a client, where such advice, if acted upon

would result in receipt of commission by the accountant, unless the client is made aware

of the receipt of such commission

It is undesirable that a practice should derive too great a part of its professional income

from one client or group of connected clients. A practice, therefore, should endeavour

to ensure that the recurring fees paid by one client or group of connected clients do not

exceed 10% of the gross fees of the practice or, in the case of a member practising part-

time, 10% of his gross earned income. It is recognised that a new practice seeking to

establish itself or an old practice running itself down may well not, in the short term, be

able to comply with this criterion. If a member is dependent for his income on the

profits of any one office within a practice and the gross income of that office is regularly

dependent on one client or a group of connected clients for more than 10% of its gross

fees, a partner from another office of the practice should take final responsibility for

any report made by the practice on the affairs of that client.

The conduct towards which an accountant should strive is embodied in six broad principles

stated as affirmative Ethical Principles:-

1. Independence, Integrity and Objectivity

An accountant should maintain his/her integrity and objectivity and, when engaged in

the practice of public accounting, be independent of those he/she serves

2. Competence and Technical Standards

An accountant should observe the profession's technical standards and strive continually

to improve this competence and the quality of his/her services

3. Responsibilities to Clients

An accountant should be fair and candid with his/her clients and serve them to the best

of his/her ability, with professional concern for their best interests, consistent with

his/her responsibilities to the public

4. Responsibilities to Colleagues

An accountant should conduct himself/herself in a manner, which will promote co-

operation and good relations among members of the profession

5. Other Responsibilities and Practice

Page 24

An accountant should conduct himself/herself in a manner, which will enhance the

stature of the profession and its ability to serve the public

6. Responsibility of Members Not In Practice

An accountant not in practice must uphold the standards and etiquette of the profession

The foregoing Ethical Principles are intended as a broad guideline. They constitute the

philosophical foundation upon which the professional conduct of accountants is based.

P. INTERNAL AND EXERNAL AUDITORS

The role and function of external auditors

Financial statements are used for a variety of purposes and decisions. For example, financial

statements are used by owners to evaluate management’s stewardship, by investors for

making decisions about whether to buy or sell securities, by credit rating services for making

decisions about credit worthiness of entities, and by bankers for making decisions about

whether to lend money. Effective use of financial statements requires that the reader

understand the roles of those responsible for preparing and auditing financial statements.

Financial statements are the representations of management. When using management’s

statements, the reader must recognize that the preparation of these statements requires

management to make significant accounting estimates and judgments, as well as to determine

from among several alternative accounting principles and methods those that are most

appropriate within the framework of generally accepted accounting standards.

In contrast, the auditor’s responsibility is to express an opinion on whether management has

fairly presented the information in the financial statements. In an audit, the financial

statements are evaluated by the auditor, who is objective and knowledgeable about auditing,

accounting, and financial reporting matters.

During the audit, the auditor collects evidence to obtain reasonable assurance that the

amounts and disclosures in the financial statements are free of material misstatement.

However, the characteristics of evaluating evidence on a test basis, the fact that accounting

estimates are inherently imprecise, and the difficulties associated with detecting

misstatements hidden by collusion and careful forgery, prevent the auditor from finding every

error or irregularity that may affect a user’s decision.

The auditor also evaluates whether audit evidence raises doubt about the ability of the client

to continue as a going concern in the foreseeable future. However, readers should recognize

that future business performance is uncertain, and an auditor cannot guarantee business

success.

Through the audit process, the auditor adds credibility to management’s financial statements,

which allows owners, investors, bankers, and other creditors to use them with greater

confidence.

Page 25

The auditor expresses his assurance on the financial statements in an auditor’s report. The

report, which contains standard words and phrases that have a specific meaning, conveys the

auditor’s opinion related to whether the financial statements fairly present the entity’s

financial position and results of operations. If the auditor has reservations about amounts or

disclosures in the statements, he modifies the report to describe the reservations.

The auditor’s report and management’s financial statements are only useful to those who

make the effort to understand them.

Auditor’s duties

Auditors duties include:-

• Duty to provide an Audit Report – report to the members of the company on the

financial statements examined by them. The auditors’ report must be read at the

general meeting and should be made available to every member of the company.

• Duty to report failure to maintain proper books of account – where auditors form

the opinion that the company being audited is disobeying, or has disobeyed its

obligations to maintain proper books of account, they are obliged to serve notice on

the company informing it of that opinion. The auditors may report this to the Office

of the Registrar General (ORG)

• Duty to exercise Professional Integrity – Auditor is under a duty to carry out the

audit with professional integrity. In preparing their report, they must exercise skill,

car and caution of a reasonably competent, careful and cautious auditor.

Duties and responsibilities of Internal Auditor

Internal auditing is an independent, objective assurance and consulting activity designed to

add value and improve an organisation’s operations. It helps an organization accomplish its

objectives by bringing a systematic, disciplined approach to evaluate and improve the

effectiveness of risk management, control and governance processes.

Independence is established by the organisational and reporting structure. Objectivity is

achieved by an appropriate mind-set. The internal audit activity evaluates risk exposures

relating to the organization's governance, operations and information systems, in relation to:

Effectiveness and efficiency of operations.

Reliability and integrity of financial and operational information.

Safeguarding of assets.

Compliance with laws, regulations, and contracts.

Based on the results of the risk assessment, the internal auditors evaluate the adequacy and

effectiveness of how risks are identified and managed in the above areas. They also assess

other aspects such as ethics and values within the organisation, performance management,

communication of risk and control information within the organization in order to facilitate a

good governance process.

Page 26

The internal auditors are expected to provide recommendations for improvement in those

areas where opportunities or deficiencies are identified. While management is responsible for

internal controls, the internal audit activity provides assurance to management and the audit

committee that internal controls are effective and working as intended.

An effective internal audit activity is a valuable resource for management and the board or its

equivalent, and the audit committee due to its understanding of the organisation and its

culture, operations, and risk profile. The objectivity, skills, and knowledge of competent

internal auditors can significantly add value to an organization's internal control, risk

management, and governance processes. Similarly an effective internal audit activity can

provide assurance to other stakeholders such as regulators, employees, providers of finance,

and shareholders.

Q. INTERNAL CONTROL SYSTEMS

Internal control systems are control procedures put in place by the management of an

organisation to ensure efficient and effective operation of its activities, so as to meet the

organisation's objectives.

The importance of internal control and risk management

A company’s system of internal control has a key role in the management of risks that are

significant to the fulfilment of its business objectives. A sound system of internal control

contributes to safeguarding the shareholders’ investment and the company’s assets.

Internal control facilitates the effectiveness and efficiency of operations, helps ensure the

reliability of internal and external reporting and assists compliance with laws and regulations.

Effective financial controls, including the maintenance of proper accounting records, are an

important element of internal control. They help ensure that the company is not unnecessarily

exposed to avoidable financial risks and that financial information used within the business

and for publication is reliable. They also contribute to the safeguarding of assets, including

the prevention and detection of fraud.

A company’s objectives, its internal organisation and the environment in which it operates

are continually evolving and, as a result, the risks it faces are continually changing. A sound

system of internal control therefore depends on a thorough and regular evaluation of the

nature and extent of the risks to which the company is exposed. Since profits are, in part, the

reward for successful risk-taking in business, the purpose of internal control is to help

manage and control risk appropriately rather than to eliminate it.

Page 27

Maintaining a sound system of internal control

Responsibilities

The board of directors is responsible for the company’s system of internal control. It should

set appropriate policies on internal control and seek regular assurance that will enable it to

satisfy itself that the system is functioning effectively. The board must further ensure that the

system of internal control is effective in managing risks in the manner which it has approved.

In determining its policies with regard to internal control, and thereby assessing what

constitutes a sound system of internal control in the particular circumstances of the company,

the board’s deliberations should include consideration of the following factors:

the nature and extent of the risks facing the company;

the extent and categories of risk which it regards as acceptable for the company to

bear;

the likelihood of the risks concerned materialising;

the company’s ability to reduce the incidence and impact on the business of risks that

do materialise; and

the costs of operating particular controls relative to the benefit thereby obtained in

managing the related risks.

It is the role of management to implement board policies on risk and control. In fulfilling its

responsibilities, management should identify and evaluate the risks faced by the company for

consideration by the board and design, operate and monitor a suitable system of internal

control which implements the policies adopted by the board.

All employees have some responsibility for internal control as part of their accountability for

achieving objectives. They, collectively, should have the necessary knowledge, skills,

information and authority to establish, operate and monitor the system of internal control.

This will require an understanding of the company, its objectives, the industries and markets

in which it operates, and the risks it faces.

Elements of a sound system of internal control

An internal control system encompasses the policies, processes, tasks, behaviours and other

aspects of a company that, taken together: facilitate its effective and efficient operation by

enabling it to respond appropriately to significant business, operational, financial, compliance

and other risks to achieving the company’s objectives.

Page 28

This includes:

safeguarding of assets from inappropriate use or from loss and fraud, and ensuring

that liabilities are identified and managed;

ensuring the quality of internal and external reporting. This requires the maintenance

of proper records and processes that generate a flow of timely, relevant and reliable

information from within and outside the organisation;

ensuring compliance with applicable laws and regulations, and also with internal

policies with respect to the conduct of business.

A company’s system of internal control will reflect its control environment which

encompasses its organisational structure. The system will include:

control activities;

information and communications processes; and

processes for monitoring the continuing effectiveness of the system of internal

control.

The system of internal control should:

be embedded in the operations of the company and form part of its culture;

be capable of responding quickly to evolving risks to the business arising from factors

within the company and to changes in the business environment; and

include procedures for reporting immediately to appropriate levels of management

any significant control failings or weaknesses that are identified together with details

of corrective action being undertaken.

A sound system of internal control reduces, but cannot eliminate, the possibility of poor

judgement in decision-making; human error; control processes being deliberately

circumvented by employees and others; management overriding controls; and the occurrence

of unforeseeable circumstances.

A sound system of internal control therefore provides reasonable, but not absolute, assurance

that a company will not be hindered in achieving its business objectives, or in the orderly and

legitimate conduct of its business, by circumstances which may reasonably be foreseen. A

system of internal control cannot, however, provide protection with certainty against a

company failing to meet its business objectives or all material errors, losses, fraud, or

breaches of laws or regulations.

Reviewing the effectiveness of internal control

Page 29

Responsibilities

Reviewing the effectiveness of internal control is an essential part of the board’s

responsibilities. The board will need to form its own view on effectiveness after due and

careful enquiry based on the information and assurances provided to it.

Management is accountable to the board for monitoring the system of internal control and for

providing assurance to the board that it has done so.

The role of board committees in the review process, including that of the audit committee, is

for the board to decide and will depend upon factors such as the size and composition of the

board; the scale, diversity and complexity of the company’s operations; and the nature of the

significant risks that the company faces. To the extent that designated board committees carry

out, on behalf of the board, tasks that are attributed in this guidance document to the board,

the results of the relevant committees’ work should be reported to, and considered by, the

board. The board takes responsibility for the disclosures on internal control in the annual

report and accounts.

Page 30

Study Unit 2

Regulatory & Non-Regulatory Framework

Contents

A. Generally Accepted Accounting Principles (GAAP)

B. The Regulatory Framework – Non Statutory

C. The Regulatory Framework – Statutory

Page 31

A. GENERALLY ACCEPTED ACCOUNTING PRINCIPLES (GAAP)

The phrase Generally Accepted Accounting Principles is a technical accounting term that

encompasses the conventions, rules and procedures necessary to define accepted accounting

practice at a particular time. It includes not only broad guidelines of general application, but

also detailed practices and procedures. These conventions, rules and procedures provide a

standard by which to measure financial presentations.

GAAP includes the requirements of the Companies Acts and accounting standards. It also

includes acceptable accounting treatments whether or not they are set out in law and

accounting standards.

Sources of GAAP

The main sources of GAAP are:

(a) Company Law

(b) International and Local Accounting Standards

(c) Stock Exchange Requirements

(d) The International Framework for the preparation and presentation of financial

statements.

(e) Any other generally accepted concepts and principles e.g. the money measurement

concept.

B. THE REGULATORY FRAMEWORK – NON STATUTORY

Accounting rules and regulations in certain jurisdictions for example (Ireland, UK) are

governed by a Financial Reporting Council (FRC). The FRC (UK & Ireland) has two

divisions – the Accounting Standards Board (ASB) and the Review Panel. There are 25

members on the council plus some observers, comprising a chairman and three deputy

chairmen. Member representation is from both users and preparers and from auditors and

drawn from three broad establishments – the accountancy profession, the financial

community and the world of business and administration at large. The council meets

approximately three times a year.

The main functions of a Financial Reporting Council (FRC) are to:

• Provide funding for its two divisions – the ASB and the Review Panel.

• Enforce compliance with standards currently in issue and in particular to the Review

Panel – it is the FRC which takes companies to court to enforce changes to accounts

where a company has refused to make changes recommended by the review panel.

• Set a general work programme for the ASB.

• Give guidance to the ASB and the Review Panel to ensure their work is carried out

efficiently and economically.

• Provide a forum for public debate and support of accounting standards.

Prior to the creation of the FRC (UK & Ireland) accounting rules and regulations were

governed by the Accounting Standards Committee (ASC). In total the ASC issued 25

Page 32

Statements of Standard Accounting Practice (SSAP) covering such areas as stocks and long

term contracts research and development and post Statement of Financial Position events.

In Rwanda: The Companies Act, Law No 7/2009 of 27/4/2009 Relating to Companies

(Article 254 and others) mandates the application of International Accounting Standards with

regard to financial reporting by the registered companies. At present, the banks and other

financial institutions are required by the National Bank of Rwanda to follow IFRS. The

newly established ICPAR has been legally mandated to prepare accounting and auditing

standards consistent with IFRS and ISA respectively.

International Accounting Standards Board (IASB): In April 2001 the International

Accounting Standards Board was formed to take over the work of the International

Accounting Standards Committee (IASC).

The International Accounting Standards Committee was set up in 1973. The role of this body

was to formulate and publish accounting standards to be observed in the presentation of

financial statements and to promote their world-wide acceptance and observance and to work

for the improvement and harmonisation of regulations, accounting standards and procedures

relating to the presentation of financial reporting.

Objectives of the IASB

The objectives of the IASB are set out in its mission statement:

• “To develop, in the public interest a single set of high quality, understandable and

enforceable global accounting standards that require high quality transparent and

comparable information in financial statements.”

• To promote the use of rigorous application of these standards.

• To work actively with actual standard-setters to achieve conveyance of accounting

standards around the world.

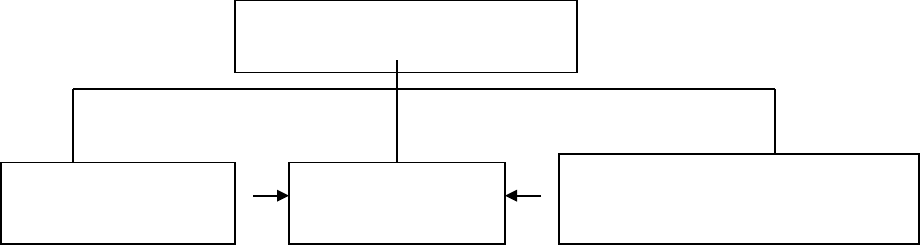

Structure

Foundation Trustees

These are 19 individuals from different geographical and functional backgrounds.

Among their functions are the appointment of the Council, The Board and The Interpretation

Committee. Also they monitor the effectiveness of the IASB, secure funding and approve

budgets and have responsibility for constitutional change.

IASC Foundation

19 Trustees

Standards Advisory

Council (SAC)

IASB

14 Members

International financial Reporting

Interpretations Committee (IFRIC)

Page 33

IASB

This comprises 14 members (12 full time) who are appointed by the trustees for an initial

term of three to five years. The Board’s responsibilities include:

• Develop and publish discussion documents for public comment

• Prepare and issue exposure drafts

• Setting up procedures for reviewing comments received on documents published for

comment

• Preparation and issue of International Accounting Standards

Standards Advisory Council (SAC)

About 45 members make up the Standards Advisory Council. It meets in public at least three

times a year with the Board. It advises the Board on agenda decisions and priorities.

International Financial Reporting Interpretations Committee (IFRIC)

The committee is made up of accounting experts from different countries. The objective of

IFRIC is to develop conceptually sound and practicable interpretations of International

Accounting Standards to be applied on a global basis.

These interpretations are developed for financial reporting issues not specifically addressed

by the International Accounting Standard and where unsatisfactory conflicting interpretations

of a standard have developed. These pronouncements have the same force as an International

Accounting Standard.

Discussion Documents

The IASB develops and publishes discussion documents. These represent a study of a

financial reporting issue. They present alternative solutions to the issue under consideration

and set out arrangements and implications relative to each. Following the receipt of

comments IASB develops and publishes on Exposure Draft.

Exposure Draft

An exposure draft is a proposed accounting standard. The IASB invites comments thereon.

After a reasonable time period, normally 120 days, an accounting standard is produced.

International Accounting Standards/International Financial Reporting Standards

The International Accounting Standards Committee (IASC) produced accounting standards

called International Accounting Standards (IAS). It has published 41 International

Accounting Standards some of which are no longer in force.

The International Accounting Standards Board, which took over from the IASC produces

accounting standards called International Financial Reporting Standards IFRS. To date it has

produced five of these.

Rwandan Stock Exchange

Public limited companies (Ltd) are required to observe requirements as set by the Rwandan

Stock Exchange. Most of its requirements are covered by compliance with company law.

Statements of Recommended Practice (SORPs)

Statements of Recommended Practice are developed in the public interest and set out current

best accounting practice. The primary aims in issuing SORPs are to narrow the areas of

Page 34

difference and variety in the accounting treatment of the matters with which they deal and to

enhance the usefulness of published accounting information. SORPs are issued on subjects

on which it is not considered appropriate to issue an accounting standard at the time.

SORPs may be developed and issued by the Accounting Standards Board or they may be

developed and issued by an "industry" group which is representative of the industry

concerned for the purpose of the developing SORPs specific to that industry and is

recognised as such by the ASR. Such SORPs are sent for approval and franking by the ASB

and are referred to as "franked SORPs". Before approving and franking a franked SORP, the

ASB will review the proposed statement and the procedures involved in its development.

Although SORPs are not mandatory, entities falling within their scope are encouraged to

follow them and to state in their accounts that they have done so. They are also encouraged

to disclose any departure from the recommendations and the reasons for it. The provisions

need not be applied to immaterial items.

Advantages of Standards

(a) Provide the accounting profession with a manual of useful working rules

(b) Forces improvements in the quality of the work of the accountant

(c) Strengthen the accountant's resistance against pressure from directors to use an

accounting policy which may be suspect

(d) Ensure that the users of financial statements get more complete and clearer information

on a consistent basis from period to period

(e) Help in the comparison users may make between the financial statements of one

organisation and another

(f) Direct financial statements towards establishing the economic truth of the entity's

performance

Disadvantages of Standards

(a) The working rules are bureaucratic and lead to rigidity

(b) The quality of the work is restricted because firms and industries differ and change, as

do the environments within which they operate. Standards, which are based on

averages, lead to rigidity and reduce the scope for professional judgements.

(c) Official acceptance reduces the accountant's strength to resist the application of an

inappropriate standard when the directors wish to follow it

(d) Users are likely to think that the financial statements produced using accounting

standards are infallible

(e) Although providing formulae, standards are still low for the figures used as inputs are

selected with some subjectivity, which reduces the possible benefits of comparison

between firms, when the input base may not be known

(f) They have been derived through social or political pressures which may reduce the

freedom and lead to manipulation of the profession

(g) They impair the development of critical thought

(h) The more standards there are the more costly the financial statements are to produce

Page 35

True and Fair

True relates to the correctness of an item in the financial statements. Fair is a judgmental

characteristic relating to the description and measurement of an item in the financial

statements. Consider the following sentence: A motor vehicle cost RWF15,000,000 and its

expected useful life is five years, the cost of RWF15,000,000 can be verified, it is true,

however the useful life of five years is an estimate which can be regarded as fair. If the

expected life was stated as 50 years this would not be regarded as fair.

Compliance with accounting standards is taken as the best indication that the financial

statements show a true and fair view.

Framework for the Presentation and Preparation of Financial Statements

An accounting standard-setter’s conceptual framework or statement of principles describes

the accounting model that it uses as the conceptual underpinning for its work. The Statement

describes the standard-setter’s views on:

• The activities that should be reported on in financial statements

• The aspects of those activities that should be highlighted

• The attributes that information needs to have if it is to be included in the financial

statements

• How information should be presented in those financial statements

The Purpose of the Framework

The framework documents can have a variety of roles. The main role of the Framework is to

provide conceptual input into the IASB’s work on the preparation and appraisal of accounting