CAT L2.3 MANAGEMENT ACCOUNTING Revision Guide

User Manual:

Open the PDF directly: View PDF ![]() .

.

Page Count: 91

- CONTENTS

- REVISION QUESTIONS

- COST BEHAVIOUR PATTERNS

- ANSWER TO REVISION QUESTIONS

- REVISION QUESTION

- Costs of holding large stocks

- LABOUR

- REVISION QUESTION

- 3 marks

- LABOUR

- ANSWER TO REVISION QUESTION

- REVISION QUESTIONS

- ANSWERS TO REVISION QUESTIONS

- 1. CB LIMITED

- REVISION QUESTIONS

- ANSWERS TO REVISION QUESTIONS

- REVISION QUESTIONS

- ANSWERS TO REVISION QUESTIONS

- REVISION QUESTIONS

- ANSWERS TO REVISION QUESTIONS

- [Total: 20 Marks]

- ANSWERS TO REVISION QUESTIONS

- ANSWERS TO REVISION QUESTIONS

- REVISION QUESTION

- ANSWER TO REVISION QUESTION

- REVISION QUESTIONS

- ANSWERS TO REVISION QUESTIONS

- 2. WTT Limited

CAT

Certified Accounting Technicians Examination

Stage: Level 2 L2.3

Subject Title: Management Accounting

Revision Guide

INSIDE COVER - BLANK

Page 1

CONTENTS

Title

Page

Study Techniques

3

Examination Techniques

4

Assessment Strategy

9

Learning Resources

10

Revision Questions and Solutions

10

Page 2

BLANK

Page 3

STUDY TECHNIQUE

What is the best way to manage my time?

• Identify all available free time between now and the examinations.

• Prepare a revision timetable with a list of “must do” activities.

• Remember to take a break (approx 10 minutes) after periods of

intense study.

What areas should I revise?

• Rank your competence from Low to Medium to High for each topic.

• Allocate the least amount of time to topics ranked as high.

• Allocate between 25% - 50% of time for medium competence.

• Allocate up to 50% of time for low competence.

How do I prevent myself veering off-track?

• Introduce variety to your revision schedule.

• Change from one subject to another during the course of the day.

• Stick to your revision timetable to avoid spending too much time on one topic.

Are study groups a good idea?

• Yes, great learning happens in groups.

• Organise a study group with 4 – 6 people.

• Invite classmates of different strengths so that you can learn from one another.

• Share your notes to identify any gaps.

Page 4

EXAMINATION TECHNIQUES

INTRODUCTION

Solving and dealing with problems is an essential part of learning, thinking and intelligence.

A career in accounting will require you to deal with many problems.

In order to prepare you for this important task, professional accounting bodies are placing

greater emphasis on problem solving as part of their examination process.

In exams, some problems we face are relatively straightforward, and you will be able to deal

with them directly and quickly. However, some issues are more complex and you will need to

work around the problem before you can either solve it or deal with it in some other way.

The purpose of this article is to help students to deal with problems in an exam setting. To

achieve this, the remaining parts of the article contain the following sections:

• Preliminary issues

• An approach to dealing with and solving problems

• Conclusion.

Preliminaries

The first problem that you must deal with is your reaction to exam questions.

When presented with an exam paper, most students will quickly read through the questions

and then many will … PANIC!

Assuming that you have done a reasonable amount of work beforehand, you shouldn’t be

overly concerned about this reaction. It is both natural and essential. It is natural to panic in

stressful situations because that is how the brain is programmed.

Archaeologists have estimated that humans have inhabited earth for over 200,000 years. For

most of this time, we have been hunters, gatherers and protectors.

In order to survive on this planet we had to be good at spotting unusual items, because any

strange occurrence in our immediate vicinity probably meant the presence of danger. The

brain’s natural reaction to sensing any extraordinary item is to prepare the body for ‘fight or

flight’. Unfortunately, neither reaction is appropriate in an exam setting.

The good news is that if you have spotted something unusual in the exam question, you have

completed the first step in dealing with the problem: its identification. Students may wish to

Page 5

use various relaxation techniques in order to control the effects of the brain’s extreme

reaction to the unforeseen items that will occur in all examination questions.

However, you should also be reassured that once you have identified the unusual item, you

can now prepare yourself for dealing with this, and other problems, contained in the exam

paper.

A Suggested Approach for Solving and Dealing with Problems in Exams.

The main stages in the suggested approach are:

1. Identify the Problem

2. Define the Problem

3. Find and Implement a Solution

4. Review

1. Identify the Problem

As discussed in the previous section, there is a natural tendency to panic when faced with

unusual items. We suggest the following approach for the preliminary stage of solving and

dealing with problems in exams:

Scan through the exam question

You should expect to find problem areas and that your body will react to these items.

PANIC!!

Remember that this is both natural and essential.

Pause

Take deep breaths or whatever it takes to help your mind and body to calm down.

Try not to exhale too loudly – you will only distract other students!

Do something practical

Look at the question requirements.

Note the items that are essential and are worth the most marks.

Start your solution by neatly putting in the question number and labelling each part of your

answer in accordance with the stated requirements.

Actively reread the question

Page 6

Underline (or highlight) important items that refer to the question requirements. Tick or

otherwise indicate the issues that you are familiar with. Put a circle around unusual items that

will require further consideration.

2. Define the Problem

Having dealt with the preliminary issues outlined above, you have already made a good start

by identifying the problem areas. Before you attempt to solve the problem, you should make

sure that the problem is properly defined. This may take only a few seconds, but will be time

well spent. In order to make sure that the problem is properly defined you should refer back

to the question requirements. This is worth repeating: Every year, Examiner Reports note that

students fail to pass exams because they do not answer the question asked. Examiners have a

marking scheme and they can only award marks for solutions that deal with the issues as

stipulated in the question requirements. Anything else is a waste of time. After you have re-

read the question requirements ask yourself these questions in relation to the problem areas

that you have identified:

Is this item essential in order to answer the question?

Remember that occasionally, examiners will put ‘red herrings’ (irrelevant issues) into the

question in order to test your knowledge of a topic.

What’s it worth?

Figure out approximately how many marks the problem item is worth. This will help you to

allocate the appropriate amount of time to this issue.

Can I break it down into smaller parts?

In many cases, significant problems can be broken down into its component parts. Some parts

of the problem might be easy to solve.

Can I ignore this item (at least temporarily)?

Obviously, you don’t want to do this very often, but it can be a useful strategy for problems

that cannot be solved immediately.

Note that if you leave something out, you should leave space in the solution to put in the

answer at a later stage. There are a number of possible advantages to be gained from this

approach:

1) It will allow you to make progress and complete other parts of the question that you are

familiar with. This means that you will gain marks rather than fretting over something

that your mind is not ready to deal with yet.

Page 7

2) As you are working on the tasks that you are familiar with, your mind will relax and you

may remember how to deal with the problem area.

3) When you complete parts of the answer, it may become apparent how to fill in the

missing pieces of information. Many accounting questions are like jigsaw puzzles: when

you put in some of the parts that fit together, it is easier to see where the missing pieces

should go and what they look like.

3. Find and Implement a Solution

In many cases, after identifying and defining the problem, it will be easy to deal with the

issue and to move on to the next part of the question. However, for complex problems that

are worth significant marks, you will have to spend more time working on the issue in order

to deal with the problem. When this happens, you should follow these steps:

Map out the problem

Depending on your preferred learning style, you can do this in a variety of ways including

diagrams, tables, pictures, sentences, bullet points or any combination of methods. It is best

to do this in a working on a separate page (not on the exam paper) because some of this work

will earn marks. Neat and clearly referenced workings will illustrate to the examiner that you

have a systematic approach to answering the question.

Summarise what you know about the problem

Make sure that this is brief and that it relates to the question requirements. Put this

information into the working where you have mapped out the problem. Be succinct and

relevant. The information can be based on data contained in the question and your own

knowledge and experience. Don’t spend too long at this stage, but complete your workings as

neatly as possible because this will maximise the marks you will be awarded.

Consider alternative solutions

Review your workings and compare this information to the question requirements. Complete

as much of the solution as you can. Make sure it is in the format as stipulated in the question

requirements. Consider different ways of solving the problem and try to eliminate at least one

alternative.

Implement a solution

Go with your instinct and write in your solution. Leave extra space on the page for a change

of mind and/or supplementary information. Make sure the solution refers to your workings

that have been numbered.

Page 8

4. Review

After dealing with each problem and question, you should spend a short while reviewing your

solution. The temptation is to rush onto the next question, but a few moments spent in

reviewing your solution can help you to gain many marks. There are three questions to ask

yourself here:

Have I met the question requirements?

Yes, we have mentioned this already. Examiner Reports over the years advise that failure to

follow the instructions provided in the question requirements is a significant factor in causing

students to lose marks. For instance, easy marks can be gained by putting your answer in the

correct format. This could be in the form of a report or memo or whatever is asked in the

question. Likewise, look carefully at the time period requested. The standard accounting

period is 12 months, but occasionally examiners will specify a different accounting period.

Is my solution reasonable?

Look at the figures in your solution. How do they compare relative to the size of the figures

provided in the question?

For example, if Revenue were 750,000 and your Net Profit figure was more than 1 million,

then clearly this is worth checking.

If there were some extraordinary events it is possible for this to be correct, but more than

likely, you have misread a figure from your calculator. Likewise, the depreciation expense

should be a fraction of the value of the fixed assets.

What have I learned?

Very often in exams, different parts of the solution are interlinked. An answer from one of

your workings can frequently be used in another part of the solution. The method used to

figure out an answer may also be applicable to other parts of your solution.

Conclusion

In order to pass your exams you will have to solve many problems. The first problem to

overcome is your reaction to unusual items. You must expect problems to arise in exams and

be prepared to deal with them in a systematic manner. John Foster Dulles, a former US

Secretary of State noted that: The measure of success is not whether you have a tough

problem to deal with, but whether it is the same problem you had last year. We hope that, by

applying the principles outlined in this article, you will be successful in your examinations

and that you can move on to solve and deal with new problems.

Page 9

ASSESSMENT STRATEGY

Examination Approach

Questions in this examination are structured to ensure that students may demonstrate their

knowledge and understanding of the principles and techniques of cost and management

accounting at an introductory level.

Where appropriate, students are expected to apply and integrate relevant learning from other

syllabi with their learning from the Management Accounting syllabus. This is achieved

through a blend of theoretical and numeric questions, often set in the context of a scenario.

Examination Format

Examination Duration: 3 Hours

The examination is unseen, closed book.

The paper has 6 questions. Questions 1 and 2 are compulsory. Students are required to

answer 3 of the remaining 4 questions. Generally the examination consists of 1

essay/memorandum-type question and 5 computational-type questions. A multiple choice

question may be included as one of the computational questions. Some of the computational

questions may require brief commentary on salient points related to the computations carried

out.

Marks Allocation

Question Marks

1 25

2 (students have a choice part A or B) 15

Choice of 3 questions out of 4 60 (20 marks each)

Total 100

Page 10

LEARNING RESOURCES

Core Texts

Drury, C., Cost and Management Accounting – An Introduction, 7th ed. / Cengage 2011 /

ISBN: 97814032138

Manuals

Institute of Certified Public Accountants of Rwanda – L2.3 Management Accounting

Supplementary Texts and Journals

Lucey, T., /Costing / 7th ed. 2009 / Thomson Learning / ISBN 13-9781844809431 / ISBN

10-1844809439.

C. Drury / Management and Cost Accounting (7th edition) Cengage 2008 / ISBN 13-

9781844805662 / ISBN 10-1844805662.

Horngren, Foster & Datar/ Cost Accounting – A Managerial Emphasis/ Pearson 14th ed 2011

ISBN-10- 0132109174.

Useful Websites (as at date of publication)

www.accountingeducation.com

http://www.icparwanda.com/services.php

Page 11

L2.3 MANAGMENT ACCOUNTING

REVISION QUESTIONS AND SOLUTIONS

Page 12

PRINCIPLES OF COSTING

REVISION QUESTION

1. Answer any one of the following three questions.

(a) Imagine that you and a friend have recently established a small business. You are

the “financial brains” of the business and your friend is the “technical/production

expert”.

Prepare a briefing for your friend setting out the role you will play as the

management accountant in the business. Your answer should make reference to

issues such as:

• The importance of financial information to a business.

• The categories of financial information (Strategic, Tactical and Operational)

and the users of such information.

• The role of the management accountant in the organisation.

You may address any other issue(s) in your briefing, which you feel would be

important to your friend’s understanding of your role in the business.

5 marks

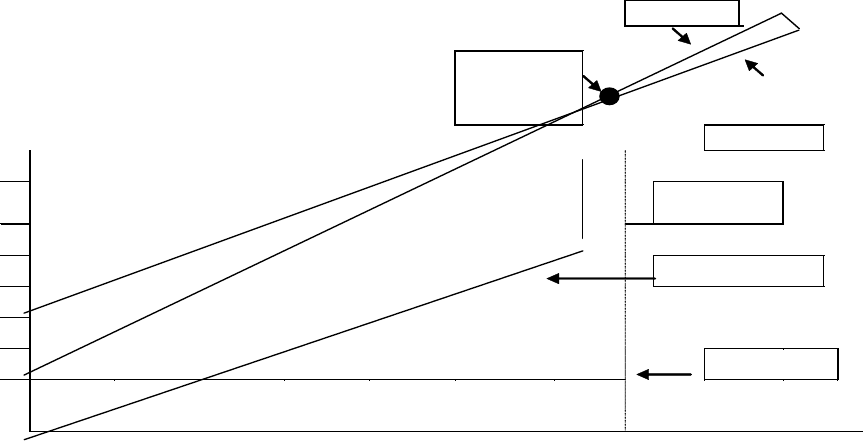

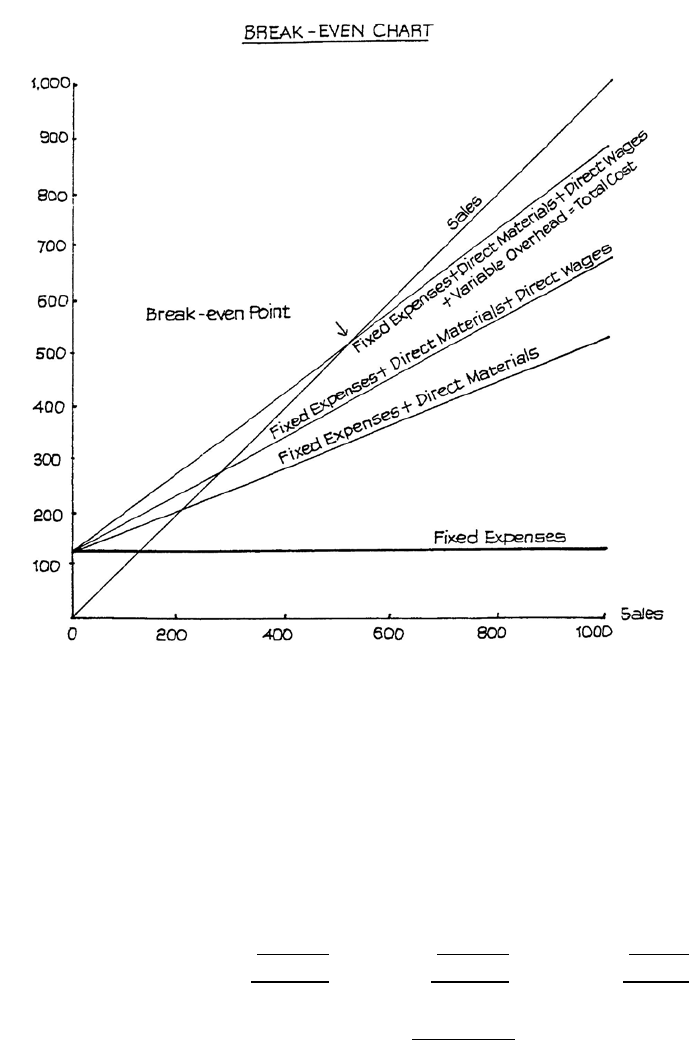

(b) “A graphical representation of cost/volume/profit [CVP] relationships has more

impact than a written statement”.

Briefly outline the major assumptions of CVP analysis.

Using a fictitious example, draw two fully labelled charts, one of which should be

a breakeven chart, which are commonly used in CVP analysis to represent

financial information. Use graph paper to prepare the charts.

5 marks

(c) Outline the principal differences between standard absorption costing and

standard marginal costing and the arguments offered in favour of each method.

Your answer should include a brief numerical example demonstrating the

differences you describe.

5 marks

Page 13

PRINCIPLES OF COSTING

ANSWER TO REVISION QUESTION

1. (a) The answer should address the following general issues:

• A wide range of entities may be interested in the financial activities of a

business- owner/manager, investors, suppliers, customers, banks and tax

authorities. In broad terms, financial information is an essential element in

the process of evaluation, formulation, development and implementation of

strategic plans. It is used for strategic planning purposes, for establishing

selling prices, costs and for product profitability analysis. It is also used for

evaluating performance of individuals and business units.

• Different information is required for different purposes. Information can be

conveniently categorised under three headings. Strategic information, which

is typically used by senior management is characterised as having a broad

focus (particularly looking at the ‘big global picture’ of the external

environment) with a long time frame, typically up to a decade ahead.

Strategic information consists of aggregated data rather than large amounts

of detail. Tactical information, which is typically used by middle

management, is narrower in its focus and has a significantly shorter time

frame (typically up to 1 year). It is more precise than strategic information

and focuses principally on the internal workings of the organisation with

some reference to the external environment. Low level employees use

operational information. It is principally concerned with the efficient use of

resources in order to achieve tactical plans.

• The role of the management accountant is to provide useful information to

assist management in planning, controlling and making decisions. The

management accountant fulfils this role in various ways. In the planning

field, the management accountant is a central figure in the budgeting

process. S/he will also contribute to determining product costs. The

management accountant assists in the control function by monitoring

outcomes of decisions or performance on an ongoing basis. A traditional

example of this is the preparation of periodic variance analysis reports by

means of which management can identify possible difficulties in the

manufacturing process. Management accountants in many world-class

Page 14

companies commonly monitor the quality of output for the purpose of

control.

(b) Assumptions of CVP analysis

• Selling price is constant throughout the entire relevant range.

• Total costs can be separated into fixed and variable components.

• Unit revenues and costs are known with certainty. Costs are linear

throughout the entire relevant range. Both variable cost per and total fixed

costs do not change.

• In multi-product companies, the sales mix remains constant.

• Stock levels do not change.

Candidates should draw the following breakeven chart and one of the other charts

following it:

1. Breakeven chart

Revenues

{Profit

RWFR

WF’00

0

Breakeven

Total costs

80

70

Contributio

n

60

50

Variable costs

40

30

20

Fixed costs

10

500

1000

1500

2000

2500

3000

Output

Page 15

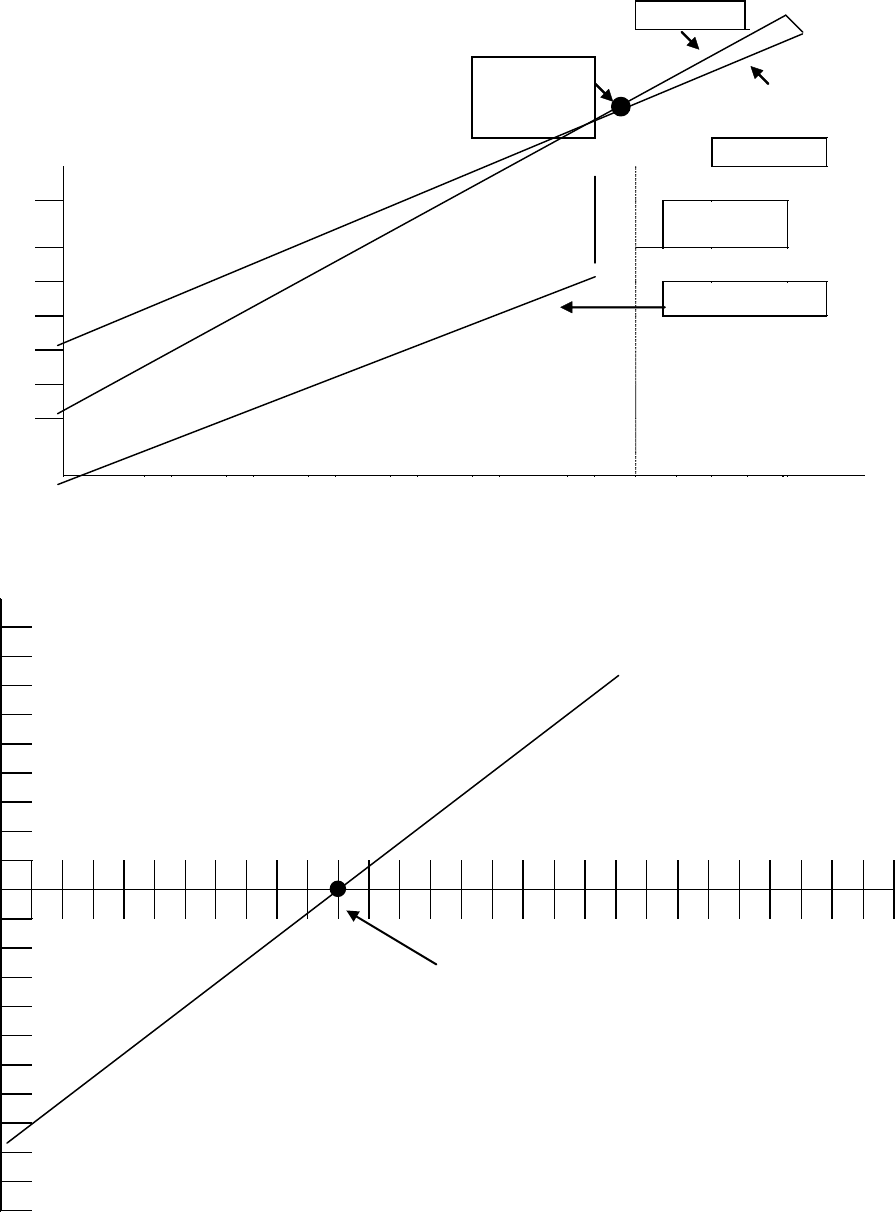

2. Contribution chart

3. Profit / volume chart

Profit/loss

Volume

Breakeven point

Revenues

{Profit

RWFR

WF’00

0

Breakeven

Total costs

80

70

Contributio

n

60

50

Variable costs

40

30

20

10

500

1000

1500

2000

2500

3000

Output

Page 16

(c) Marginal costing and absorption costing

Candidates should identify the following points in their solutions:

• Under absorption costing, all production costs - both fixed and variable- are

attributed to output. Under marginal costing, only variable production costs

are attributed to production, with fixed production costs treated as a period

cost rather than a product cost.

• Proponents of marginal costing argue that absorption of fixed costs is both

illogical and potentially confusing. They argue that it is illogical because

such costs do not accrue as production increases. Rather, they accrue as

time passes. Accordingly, the costs should be treated as a period cost rather

than as a product cost. Furthermore, the technique can be confusing to some

members of management, as it may imply that fixed costs vary in

accordance with production- the greater the level of production, the greater

the level of absorbed overhead and vice-versa. Marginal costing principles

are also considered to be more useful in a short-term decision making

context because they highlight contribution as opposed to profit. Under

absorption costing, short-term profits increase as stock levels are built up.

This may tempt managers to engage in stock building, with the associated

costs and risks of obsolescence and theft.

• Proponents of absorption costing argue that fixed costs are a necessary cost

of production. If such costs are ignored or overlooked, a business is likely

to face losses in the medium to long term. In a seasonal business, where

stock building occurs during periods of low revenues, absorption costing

avoids reporting ‘fictitious losses’ (which would arise under marginal

costing) because the fixed costs would be included as part of stock until the

stock itself is expensed when sold. Additionally, financial reporting

standards mandate the use of absorption costing for the purpose of external

reporting.

• Numerical example:

Candidates are expected to demonstrate their understanding of the impact of

increasing/decreasing and static stocks. This would be achieved by

preparing a three period financial statement for each system, with each

period demonstrating an aspect of the effect of stock movements.

Page 17

COST BEHAVIOUR PATTERNS

REVISION QUESTIONS

1. Answer all parts of this question.

(a) Select the statement that most precisely defines each of the following terms:

(i) A combined cost represents:

(a) Expenditure incurred in previous years which has no impact on

decisions affecting the future.

(b) The forecasted expenditure on acquiring assets of a capital nature.

(c) A future cash outflow that will be incurred regardless of current

decisions.

(d) Any cost which, within certain production limits, does not vary with

the production of goods.

(1 mark)

(ii) The master budget:

(a) Consists of the Capital Expenditure budgets of profit centres only.

(b) Comprises the summarised budgeted Profit & Loss account, budgeted

Balance Sheet and cash budget of the entire company.

(c) Consists of the budgeted Profit & Loss account, budgeted Balance

Sheet and cash budget of Head office only.

(d) Consists of the qualitative Mission Objectives of the entire company.

(1 mark)

(iii) A profit centre is:

(a) A business unit accountable for both costs and revenues.

(b) A committee established by management which is responsible for

overseeing the budgeting process.

(c) The area in a breakeven chart where total revenues exceed total costs.

(d) The sales quantity, expressed in numbers of units sold, after which a

company earns enough to cover total fixed costs.

(1 mark)

Page 18

(iv) The relevant range defines:

(a) The range of variation incorporated into sales forecasts to allow for

uncertainty of demand.

(b) The process of adjusting a budget for a period so that the budgeted

costs for the actual volume of production of the period can be

compared with the actual costs incurred.

(c) The activity levels within which assumptions about cost behaviour in

a breakeven chart remain valid.

(d) The budget period for the short to medium term, usually not

exceeding 12 months.

(1 mark)

(b) “Cost classifications and groupings help to identify relevant and irrelevant costs

and are important for the purposes of cost-volume-profit analysis”.

Explain (with the aid of appropriate diagrams) each of the following patters of

cost behaviour.

• Variable costs

• Fixed costs

• Step costs

• Semi-variable costs. (11 marks)

[Total: 15 marks]

Page 19

COST BEHAVIOUR PATTERNS

ANSWER TO REVISION QUESTIONS

1. (a) (i) c is correct

(ii) b is correct

(iii) a is correct

(iv) c is correct

(b) Main points to be discussed:

Variable costs vary as a function of the level of output or sales. Examples include

raw materials or labour paid on an hourly basis.

Cost

Output

Fixed costs are those costs which are likely to remain unchanged regardless of the

level of output or the particular decision under consideration. The term “fixed”

refers primarily to the short term. Examples of fixed costs include rent, directors

salaries.

Cost

Output

Page 20

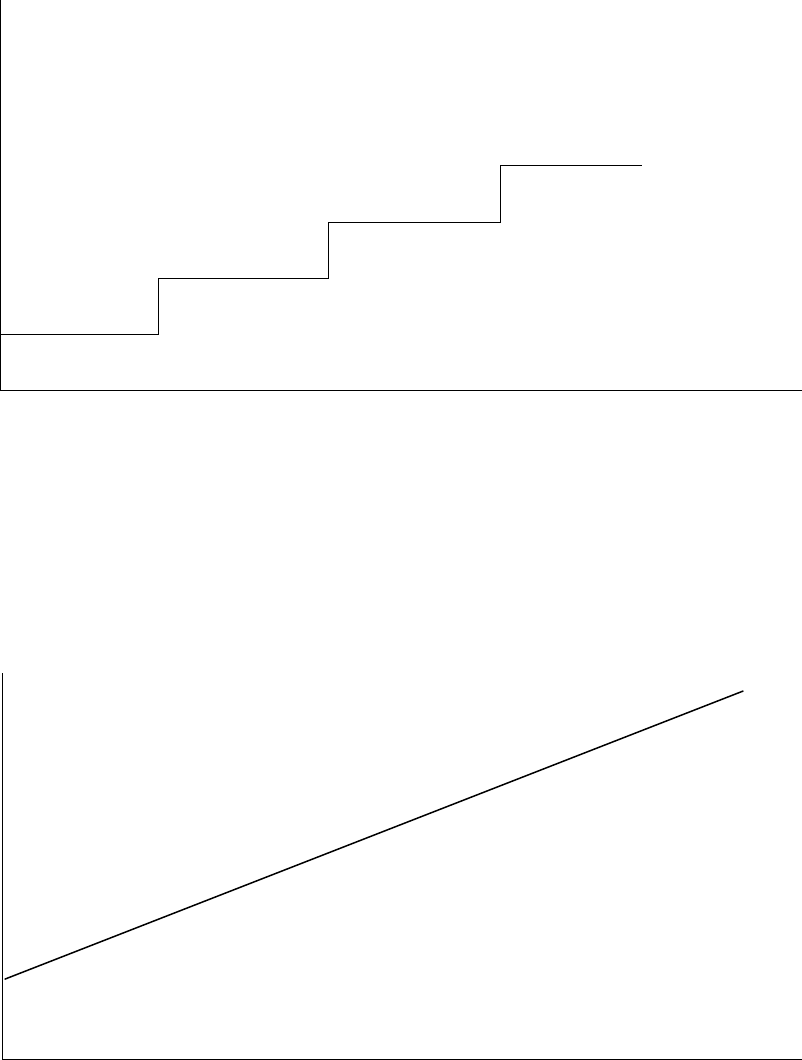

Step costs are costs which change in discrete “steps”. They are similar to variable

costs except that each change in the level of cost is usually caused by a larger

change in input levels than is the case for “true” variable costs. A typical example

would be a supervisors cost – for production of, say, 5,000 units 1 supervisor may

be required; for 5,001 to 10,000 units, a second supervisor may be required etc.

Cost

Output

Semi-variable costs are costs which possess both a fixed and variable cost

component. A typical example is telephone charges which have a fixed rental

charge and a variable unit rate. Note that the starting point is not at the origin as

for normal variable costs.

Cost

Output

Page 21

MATERIALS AND STOCK CONTROL

REVISION QUESTION

1. FN Distribution has recorded the following transactions in respect of raw material

“RM–01” for the month of April 2010:

Date

Details

No. of units

Apr 3

Materials received, RWF12,000

1,500

Apr 8

Materials issued

1,700

Apr 9

Materials received, RWF12,880

1,600

Apr 13

Materials issued

900

Apr 19

Materials issued

450

Apr 26

Materials received, RWF16,000

2,000

Apr 30

Materials issued

300

At the start of April, the company had 1,200 units of RM–01 in stock made up of the

following batches

Remainder of a batch purchased mid March:

200

units costing RWF7.95

each

Full batch received on 30th March:

1,000

units costing RWF7.97

each

REQUIREMENT:

(1) Briefly outline the advantages and disadvantages of the FIFO (First-in, First-out)

method and the LIFO (Last-in, First-out) method of valuing stocks.

(6 marks)

(2) Calculate the total value of each of the material issues in April (and of the

Closing Stocks of RM–01at the end of April using the FIFO method.

(6 marks)

(3) “It is necessary to set off the costs of holding a large stock against the advantages

derived from holding it”. List and briefly explain the typical advantages and

costs of holding large stocks. (8 marks)

[Total: 20 marks]

Page 22

MATERIALS AND STOCK CONTROL

ANSWER TO REVISION QUESTION

1. FN Distribution Ltd

(1) Workings

Supervisors costs.

Total costs 16,000

75 % production 12,000 = RWF150 per production employee

25 % service 4,000 = RWF200 per service employee

Note:

An equally acceptable basis of appropriating the production departments

supervisory overhead would be on the basis of production hours worked.

SOLUTION

Advantages of FIFO

1. Logical – it corresponds to what happens in most businesses as the older

stock is used up first.

2. Easy to understand

3. Generally results in closing stocks being valued at the most current price.

4. Required under SSAP 9.

Disadvantages of FIFO

1. Understates the cost of material issues in times of high inflation.

2. Cumbersome to operate.

3. Can cause some confusion for decision making purposes when the same

material is issued at varying prices.

Advantages of LIFO

1. Stock issues approximate current market price.

2. Decision making may be easier due to 1 above.

Disadvantages of LIFO

1. Cumbersome to operate.

2. Generally would not reflect actual practice in a stockroom.

3. Does not comply with the SSAP 9.

Page 23

(2)

Date

Details

Qty

in

Qty

out

Value (ref)

Cl.

balance

Aug 1

Opening

Balance

1,200

9,560

(1)

9,560

Aug 3

Receipt

1,500

12,000

21,560

Aug 8

Issue

1,700

(13,560)

(2)

8,000

Aug 9

Receipt

1,600

12,880

20,880

Aug 13

Issue

900

(7,200)

(3)

13,680

Aug 19

Issue

450

(3,618)

(4)

10,062

Aug 26

Receipt

2,000

16,060

26,122

Aug 31

Issue

300

(2,415)

(5)

23,707

Workings

1. (200 @ RWF7.95) + (1,000 @ RWF7.97) = RWF9,560

2. RWF9,560 + (500 @ (RWF12,000/ 1,500)) = RWF13,560

3. (900 @ (RWF12,000/1,500)) = RWF7,200

4. (100 @ (RWF12,000/1,500)) + (350 @ (RWF12,880/ 1,600))= RWF3,618

5. (300 @ (RWF12,880/1,600)) = RWF2,415

(3) Advantages of holding large stocks

1. Form a buffer against “stock-outs”.

2. Can enable discounts to be negotiated.

3. In some cases, quality will be more consistent as they originate from a

larger batch rather than from numerous small batches.

4. In times of inflation, large stockholding may provide a competitive edge to

a firm as their stocks will have cost less than stocks bought at current prices

Costs of holding large stocks

a. Large stockholding results in high financing costs.

b. Storage and insurance costs are higher.

c. Risks of obsolescence and theft/pilferage are greater.

d. Spoilage and obsolescence risks increase.

Page - 24 -

LABOUR

REVISION QUESTION

1. Given the following information, calculate for workers (A) to (J) using a Rowan

system:

(a) Time saved;

(b) Earnings (at RWF4 per hour);

(c) Effective hourly rate.

(A) (B) (C) (D) (E) (F) (G) (H) (J)

Time allowed 10 10 10 10 10 10 10 10 10

Time taken 9 8 7 6 5 4 3 2 1

3 marks

Page - 25 -

LABOUR

ANSWER TO REVISION QUESTION

1. You should concentrate on one of the formulae and use it constantly. I prefer the

second (see (c) below).

(a) Time saved:

(A) (B) (C) (D) (E) (F) (G) (H) (J)

1 2 3 4 5 6 7 8 9

(b) Earnings (at RWF4 per hour):

(A) RWF39.60 (D) RWF33.60 (G) RWF20.40

(B) RWF38.40 (E) RWF30.00 (H) RWF14.40

(C) RWF36.40 (F) RWF25.60 (J) RWF7.60

(c) Using the second formula, we find:

Time taken 9 +

Time taken 9 Time saved 1

Time allowed 10

×

× Time rate per hour RWF4

= 9 +

9 1

10

×

× 4 = RWF39.60

Effective hourly rate:

(A) RWF4.40 (D) RWF5.60 (G) RWF6.80

(B) RWF4.80 (E) RWF6 (H) RWF7.20

(C) RWF5.20 (F) RWF6.40 (J) RWF7.60

You should note that the effective hourly rate rises RWF0.40 for every hour

saved. It does not offer any special incentive for exceptional effort.

Page - 26 -

OVERHEADS AND ACTIVITY BASED COSTING

REVISION QUESTIONS

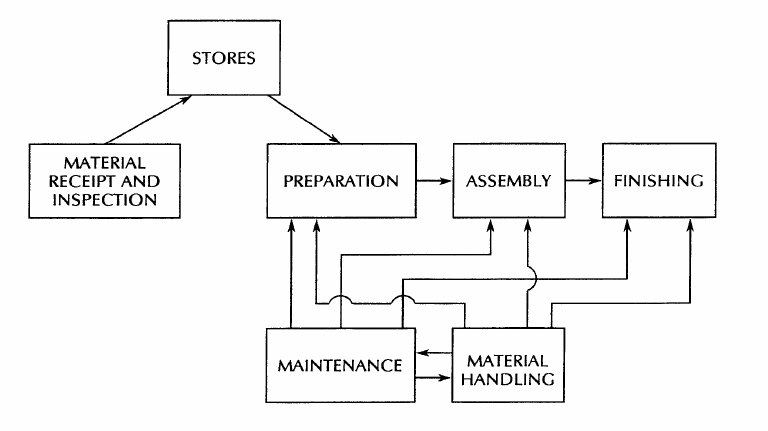

1. TBA Ltd manufactures and sells a range of steam, water and gas valves. The valves are

produced by passing components through a series of production processes -

preparation, assembly and finishing - which are backed up by service functions for

material receipt and inspection, maintenance and material handling.

REQUIREMENT:

(a) (i) Prepare a diagram to illustrate the physical and service flows of the existing

system.

(3 marks)

(ii) Explain the procedure by which product cost accumulation and

responsibility accounting will operate in the system if a traditional

absorption cost approach is used.

(7 marks)

(b) Explain how activity-based costing and the use of cost drivers may help to

improve both product cost data and the effectiveness of responsibility accounting

in TBA Ltd.

(10 marks)

[Total: 20 marks]

2. FVD Limited produces two products - 'Newthings' and 'Oldthings'. Each product uses

similar processes and equipment, but 'Newthings' are produced in large volumes whereas

'Oldthings' are produced in smaller volumes. At present, overheads are apportioned to

products using a traditional absorption costing basis.

You are the cost accountant at FVD Limited and, as a result of the large amount of

discussion in the management literature of Activity Based Costing; you are considering

changing from absorption costing to Activity Based Costing for the purposes of charging

overheads to production.

Page - 27 -

You have decided to prepare a comparison of the product costs using both the current

method and an Activity Based Costing method prior to making a final decision and have

accumulated the following summarised data from next year's budget:

Cost category

RWF

Current basis of

apportionment

Volume related costs

320,000

Machine hours

Purchasing related

costs

156,000

Labour hours

Set-up costs

44,000

Labour hours

520,000

Extracts from the standard cost cards for 'Newthings' and 'Oldthings' show the

following:-

Newthings

Oldthings

Labour hours per unit

3

2

Machine hours per unit

1

1

Budgeted production next year

30,000 units

10,000 units

Number of purchase orders per

annum

170

90

Number of machine set-up per

annum

76

56

REQUIREMENT:

(a) Prepare calculations showing the overheads charged to each product using:

(i) the proposed Activity Based Costing system

(ii) the current (traditional) costing system (12 marks)

(b) "The ABC system recognises that some activities are unrelated to volume by

using allocation bases that are independent of production volume."

Briefly explain how traditional costing systems can result in distorted product

costs using the example of FVD Limited to illustrate your point.

(8 marks)

[Total: 20 Marks]

Page - 28 -

OVERHEADS AND ACTIVITY BASED COSTING

ANSWERS TO REVISION QUESTIONS

1. TBA Ltd.

(a) (i)

Figure 4.1

(ii) Product cost responsibility accounting operates on a system of cost centres.

These cost centres are decided by breaking down the physical operations

under the responsibility of each manager and by attaching costs to product

units as they go through production. An appropriate absorption basis is

decided upon for the overhead costs.

Figure 4.1 illustrates production cost centres (e.g. preparation, assembly,

finishing) and service cost centres (maintenance and material handling).

Labour and overhead costs are allocated to specific cost centres if possible.

Where allocation is not possible an appropriate apportionment will be made (e.g.

maintenance at an apportionment rate per labour-hour and material handling per

unit of, say, 500 valves moved; material receipt and inspection could also be

charged to batches of valves).

Total labour and overhead costs of the production centres, together with

apportioned service centre costs, would then be charged to valve batches. It is

Page - 29 -

likely that this would be based on time spent on each batch of valves in the

appropriate cost centre.

The system can then be controlled by use of standard costing or budgetary control

(both of which we will look at later in the course) through the analysis of

variances.

(b) Activity-based costing links cost to activity and considers that costs incurred

above an acceptable minimum are due to lack of control of activities causing

costs to occur, known as cost drivers.

To take the process of receipt and inspection of material, cost drivers in this

activity could be:

• The relative importance of component inspection (e.g. glassware used in

valves might require a high degree of inspection, whereas moulded plastic

might need just a sampling).

• The bulk of material involved (e.g. it may require four trips to transport

1,000 valves of one size and a single trip to transport 1,000 smaller valves).

Any relationship between the cost drivers and the actual cost of material used is

likely to be simply accidental, so an apportionment using absorption costing

could bear no resemblance to the charge calculated using cost drivers under

activity-based costing. The examples above give illustrations of how this could

occur.

Looking at maintenance charges, these may not be driven by time spent (under

absorption costing), but by type of valve produced - some causing far more wear

on machines than others.

Actually identifying cost drivers can be difficult but, once identified, they are

useful in focusing on activities which cause costs to be incurred. This gives

management a target on which to concentrate when seeking to reduce costs which

are considered to be their responsibility. For instance, machines could be checked

carefully before producing batches of valves which usually cause high machine

maintenance, as a way of reducing breakdown and interruption of production.

Page - 30 -

2. FVD Ltd

(a) (i) Overhead per unit under an Activity Based Costing system

Overhead

Total

overhead

Cost driver

Cost

driver

total

Rate per

cost driver

Volume related

costs

RWF320,000

Total units

40,000

units

RWF8

Purchase related

costs

RWF156,000

Purchase

orders

260 orders

RWF600

Set-up costs

RWF44,000

Set-up qty.

132 set-ups

RWF333.33

∴

the overheads charged to the total units are as follows:

Newthings

Oldthings

Volume related costs

RWF240,000

RWF80,000

Purchase related

costs

RWF102,000

RWF54,000

Set-up related costs

RWF25,000

RWF18,667

RWF367,333

RWF152,667

Overhead per unit

RWF12.24

RWF15.27

Page - 31 -

(ii) Current costing system overheads per unit

Newthings

Oldthings

Total

Total labour hours

90,000

20,000

110,000

Total machine hours

30,000

10,000

40,000

∴the overhead rate per labour hour is RWF1.82 per hour (RWF200,000/110,000

hours) and the overhead rate per machine hour is RWF8 per hour

(RWF320,000/40,000 hours)

The overheads charged to production under this current basis are as follows:

Newthings

Oldthings

Labour

hours

3 hours @ RWF1.82 =

RWF5.46

2 hours @ RWF1.82 = RWF3.64

Machine

hours

1 hour @ RWF8 = RWF 8

1 hour @ RWF8= RWF 8

Overheads

per unit

RWF13.46

RWF11.64

(b) Traditional overhead costing systems use volume-related bases to trace overheads

to production

Many costs of production are not related to volume. These costs are allocated

using an inappropriate base under traditional systems. High-volume products

effectively subsidise the lower volume products.

ABC recognises this by using allocation bases, which are independent of volume.

In the example of FVD Limited, Set-up costs and purchase order costs were

traditionally charged to units using machine hours as a base. This is not an

appropriate base and resulted in Newthings being charged with more overheads

even though they consumed a lower proportion of total resources than Oldthings.

Page - 32 -

JOB COSTING/BATCH COSTING

REVISION QUESTION

1. PAS Limited is a small company which manufactures furniture to order. The company

uses Job costing in determining the costs and profit of each order. At the start of the

financial year, the cost accountant gathered the following information in respect of the

budgeted overheads for each of the three production departments as follows:

Department

Budgeted overheads

Overhead absorption basis

Carving

RWF15,000

1,000 machine hours

Assembly

RWF36,000

6,000 labour hours

Decoration

RWF19,000

1,000 labour hours

Note: These figures are based on normal activity levels.

Selling and distribution overheads are calculated as 20% of factory cost i.e. direct costs

plus production overheads.

The accountant is now calculating the total net profit or loss on a recently completed

order for 100 reproduction regency wardrobes. Details of this order are as follows:

• The selling price of each wardrobe was RWF270

• Materials consumed ……. RWF8,935

• Labour: Carving department 170 hours @ RWF10 per hour

Assembly department 210 hours @ RWF12 per hour

Decoration department 40 hours @ RWF8 per hour

• Machine usage in the carving department totalled 150 hours.

• A fee of RWF500 was paid to an expert furniture historian for consultancy

services provided in respect of the completion of this order.

REQUIREMENT:

(a) Calculate the overhead absorption rates for the production departments.

(3 marks)

(b) Calculate:

(i) The total cost of the batch, clearly identifying Prime Cost, Factory Cost

and Total Cost. (11 marks)

(ii) The unit cost. (3 marks)

(iii) The profit or loss per wardrobe. (3 marks)

[Total: 20 marks]

Page - 33 -

JOB COSTING/BATCH COSTING

ANSWER TO REVISION QUESTION

(a) Overhead absorption rates for each department

Department

Overhead

Budgeted no. of

Absorption units

Rate per

absorption

Carving

RWF15,000

1,000 machine hours

RWF15 per hour

Assembly

RWF36,000

6,000 labour hours

RWF6 per hour

Decoration

RWF19,000

1,000

RWF19 per hour

(b) (i)

Direct costs:

Materials

8,935

Labour-Carving

1,700

- Assembly

2,520

- Decoration

320

Consultancy fee

500

Prime cost

13,975

Production Overheads:

Machine time in carving

2,250

Labour time in assembly

1,260

Labour time in decoration

760

4,270

Factory cost

18,245

Add: 20% for selling/distribution expenses

3,649

Total cost

21,894

(ii)

Unit cost

Total cost of batch as per (a)

RWF21,894

No. of units in batch

100

∴ each unit cost RWF218.94

Page - 34 -

(iii)

Profit per unit

Sales price per unit

RWF270.00

Less:

Cost per unit

RWF218.94

Profit per unit

RWF51.06

Page 35

PROCESS COSTING

REVISION QUESTIONS

1. CB Limited manufactures a range of chemicals and fertilisers for agricultural

purposes.

The manufacture of one of the company’s products, “BeefEmUp”, involves three

distinct processes in which the output from Process 1 is used as the input into Process 2.

Similarly, the output from Process 2 is used as input into Process 3 by which stage the

final product is prepared and then packed for shipping.

The company has established standards for each process as follows:

Process 1 Process 2 Process 3

Normal loss (%)* 5% 5% 10%

Sales value of each unit lost RWF1.83 RWF2.00 RWF4.00

*Note: The normal loss for a process is calculated as a percentage of the units

processed in that process.

The following data is available for August 2011 in respect of each of the processes:

Process 1 Process 2 Process 3

Qty RWF Qty RWF Qty RWF

Units from previous process 1,150 2,980

Materials added 1,200 600 2,010 4,299 600 7,344

Labour incurred 1,500 1,800 900

Overheads incurred 2,000 2,200 600

At the end of process 3, a total of 3,190 fully completed units was transferred to

Finished Goods.

REQUIREMENT:

Prepare each of the Process Accounts for the month of August.

[Total: 15 marks]

Page 36

2. SLR Limited is a company that manufactures a range of tinned soups. The soups are

made by processing raw materials through two distinct processes, Blending and

Flavouring, and a process costing system is in place for the purpose of calculating the

costs of finished output.

Relevant details of each of these processes for the most recent month are as follows:

Blending

Flavouring

Expected output

95% of inputs

90% of inputs

Value of lost liquids per kg

Nil

RWF1

Materials added:

4,000 kgs

RWF11,950

500 kgs

RWF1,000

Labour charged

RWF1,700

RWF555

Machinery time:

@ RWF5 per

hour

300 hours

@ RWF7 per

hour

60 hours

Output

3,700 kgs to Flavouring

3,810 kgs Finished Goods

The total departmental overhead for the month was RWF960 and is absorbed into the

cost of each process using the cost of machinery for each process as a basis.

REQUIREMENT:

(a) Prepare the following accounts for the month:

(i) Blending process account (8 marks)

(ii) Flavouring process account (8 marks)

There are no stocks at either the start or the end of the period.

(b) Briefly outline the common features of most process costing systems. (4 marks)

[Total: 20 marks]

Page 37

PROCESS COSTING 1

ANSWERS TO REVISION QUESTIONS

1. CB LIMITED

Process 1

Units

RWF

Units

RWF

Materials

1,200

600

Normal loss

60

110

Labour

1,500

To process 2

1,150

4,025

Overheads

2,000

Abnormal gain

10

35

1,210

4,135

1,210

4,135

Process 2

Units

RWF

Units

RWF

From Process 1

1,150

4,025

Normal loss

158

316

Materials added

2,010

4,299

Abnormal loss

22

88

Labour

1,800

To process 3

2,980

11,920

Overheads

2,200

3,160

12,324

3,160

12,324

Process 3

Units

RWF

Units

RWF

From Process 2

2,980

11,920

Normal loss

358

1,432

Materials Added

600

7,344

Abnormal loss

32

192

Labour

900

To Finished

Goods

3,190

19,140

Overheads

600

3,580

20,764

3,580

20,764

Page 38

Calculations

Normal Loss units

Calculation

Abnormal loss/(gain) units

Value of good unit

Process

1

5% * 1,200

(1,200 * 95%)–1,150 = (10)

RWF4,100 – RWF110/(1,200 * 95%)

Process

2

5% * (1,150 + 2,010)

(3,169 * 95%) – 2,980 = 22

RWF12,324 – RWF316/(3,160 * 95%)

Process

3

10% * (2,980 + 600)

(3,580 * 90%) – 3,190 = 32

RWF20,764 – RWF1,432/(3,580 * 90%)

Page 39

2.

Blending Account

Details

Units

RWF

Details

Units

RWF

Material

4,000

11,950

Trfr. To Flav.

3,700

15,482

Labour

1,700

Norm. loss

200

---

Machine time

1,500

Abn. Loss

100

418

Overhead

750

4,000

15,900

4,000

15,900

Flavouring Account

Details

Units

RWF

Details

Units

RWF

Ex. Blending

3,700

15,482

Output to Stock

3,810

17,384

Material added

500

1,000

Norm. loss

420

420

Labour

555

Machine time

420

Overhead

210

Ab. Gain

30

137

4,230

17,804

4,230

17,804

Page 40

(b) Common features of process costing systems

Main points covered should include the following:

• Continuous processes are normally a feature of this costing system e.g.

chemicals.

• The output of one process is the input to a subsequent process until a

completed product is made.

• Valuation of Work-in-Process requires a method for valuing homogeneous

units rather than counting individual items.

• Process losses are a standard feature – evaporation, spoilage, spills etc.

• By product or joint products.

Page 41

PROCESS COSTING 2

REVISION QUESTIONS

1. Draw up the process accounts, normal loss account, abnormal loss/gain accounts and

scrap account in the following instance:

Process I Process II Finished Goods

Units going into process 8,000 7,000 6,800

Normal loss 10% 5%

Process I Process II Finished Goods

Cost of process RWF8,000 RWF4,000

Income from sale of

scrap per 100 units RWF4 RWF1

(You may assume that all output from Process I enters Process II.)

There is no work-in-progress at the beginning or end of the period.

(10 Marks)

2. Given the following information show the entries which would appear on Process 4

account for period 8 of the current year, and on the scrap account, abnormal loss/gain

account, and normal loss account.

Value of input to Process 4 RWF9,875

Number of units entering Process 4 9,400

Normal loss percentage 10%

Total process costs RWF4,500

Sales value of loss RWF5 per 100 units

Number of units entering Process 5 8,500

(10 Marks)

Page 42

PROCESS COSTING 2

ANSWERS TO REVISION QUESTIONS

Question 1

Workings

Process I

Input 8,000 units.

Normal loss 800 units, scrap value RWF32.

Expected output 7,200 units

Actual output 7,000 units, i.e. abnormal loss of 200 units.

Cost per unit of normal output = RWF(

8 000, 32

7,200

−

) =

200,7

968,7RWF

Cost of abnormal loss = 200 ×

200,7

968,7RWF

= RWF221

Cost transferred to Process II = 7,000 ×

200,7

968,7RWF

= RWF7,747.

Process II

Input 7,000 units.

Normal loss 350 units, scrap value RWF3.50, say RWF4.

Expected output 6,650 units.

Actual output 6,800 units, i.e. abnormal gain 150 units.

Cost per unit of normal output = RWF(

7 747, + 4,000 4

6,650

−

)

=

650,6

743,11RWF

Value of abnormal gain = 150 ×

11 743

6 650

,

,

= RWF265

Cost transferred to finished goods = 6,800 × RWF

11 743

6650

,

,

= RWF12,008

PROCESS I ACCOUNT

Units RWF Units RWF

Input in units

8,000

Normal loss

800

32

Cost of process

8,000

Abnormal loss

200

221

Process II

account

7,000

7,747

8,000

RWF8,000

8,000

RWF8,000

Page 43

PROCESS II ACCOUNT

Units RWF Units RWF

Input in units

7,000

7,747

Normal loss

350

4

Cost of process

4,000

Finished stock

6,800

12,008

Abnormal gain

150

265

7,150

RWF12,012

7,150

RWF12,012

NORMAL LOSS ACCOUNT

Units RWF Units RWF

Process I

800

32

Abnormal gain

150

2

Process II

350

4

Scrap a/c

800

32

Scrap a/c

200

2

1,150

36

1,150

36

ABNORMAL LOSS ACCOUNT

Units

RWF

Units

RWF

Process I

200

221

Scrap

200

8

Profit and loss

213

200

221

200

221

ABNORMAL GAIN ACCOUNT

Units RWF Units RWF

Normal loss

150

2

Process II

150

265

Profit and loss

263

150

265

150

265

SCRAP ACCOUNT

Units RWF Units RWF

Abnormal waste

200

8

Cash

42

Normal loss

Process I

800

32

Normal loss

Process II

200

2

42

42

Page 44

Question 2

PROCESS NO. 4 ACCOUNT

Units RWF

Value Units RWF

Value

Input

9,400

9,875

Normal loss

940

47

Process cost

4,500

Process No. 5

8,500

14,396

Abnormal gain

account

40

68

9,440

RWF14,443

9,440

RWF14,443

Calculations

(a) Normal output (9,400) less normal waste of 10% (940) = 8,460

Abnormal gain = 40 units.

(b) Normal cost in total = RWF9,875 + RWF4,500 – RWF47

Normal cost per good unit =

8,460

RWF47 RWF4,500 + RWF9,875 −

(c) Value of abnormal gain = Normal unit cost × Abnormal gain in units

=

8,460

RWF47 RWF4,500 + RWF9,875 −

× 40 = RWF68

(d) Value of units transferred to Process 5 = Normal unit cost × Output in units

=

8,460

RWF47 RWF4,500 + RWF9,875 −

× 8,500 = RWF14,396

ABNORMAL GAIN ACCOUNT

Units

RWF

Units

RWF

Normal loss

40

2

Process 4

40

68

Profit and loss

66

40

68

40

68

SCRAP ACCOUNT

Units RWF Units RWF

Normal loss

900

45

Cash

900

45

NORMAL LOSS ACCOUNT

Units RWF Units RWF

Process 4 a/c

940

47

Abnormal gain a/c

40

2

Scrap a/c

900

45

940

47

940

47

Page 45

MARGINAL V ABSORPTION COSTING

REVISION QUESTIONS

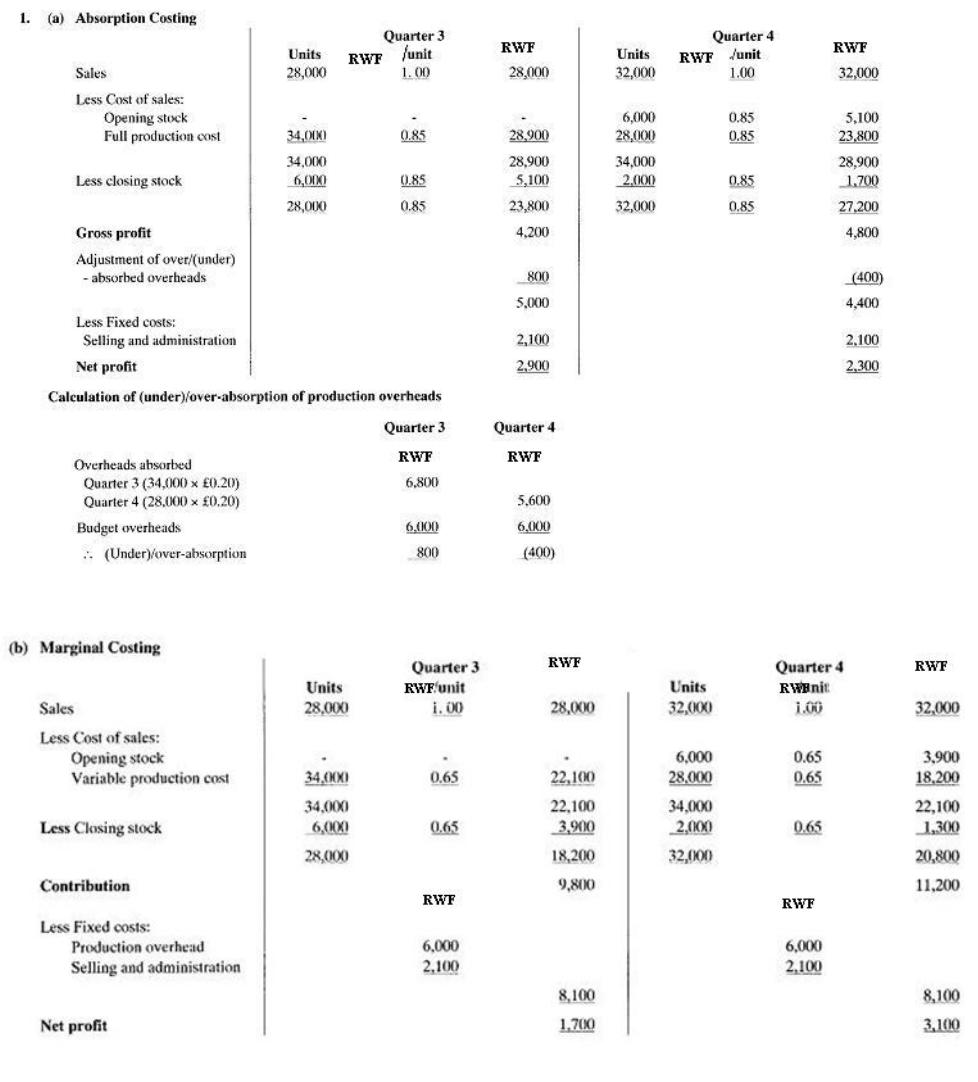

1. The following information is available for XY Ltd, which manufactures a standard

product. Quarterly budget for each of the quarters 3 and 4, Year 1:

RWF

Total

RWF

RWF

Per Unit

RWF

Sales (30,000 units)

30,000

1.00

Production cost of sales:

Variable

19,500

0.65

Fixed overhead

6,000

25,500

0.20

0.85

4,500

0.15

Selling and administration

cost (fixed)

2,100

0.07

Net profit

2,400

0.08

Actual production, sales and stocks in units for quarters 3 and 4, Year 1:

Quarter 3

Quarter 4

Opening stock

-

6,000

Production

34,000

28,000

Sales

28,000

32,000

Closing stock

6,000

2,000

You are required to produce trading and profit and loss accounts for each of the

quarters:

(a) Using absorption costing

(b) Using marginal costing

(10 marks)

2. A manufacturer of leather handbags has been affected by competition from plastic

handbags and is currently operating at between 65 and 70 per cent of maximum

capacity.

The company at present reports profit on an absorption costing basis. The accountant

has been criticised for reporting widely different profits from month to month. He is

proposing to answer these criticisms by reporting differently in order to take into

consideration the impact of the nature of costs (fixed or variable) and, changes due to

seasonal fluctuations in sales volume. This, he hopes, will enable the management to

determine a more positive sales policy.

Page 46

The following information is available from the accounting records:

Standardised cost per unit:

RWF

Direct materials

8.00

Direct labour

7.20

Variable production overheads

3.36

Total variable cost of production

18.56

Fixed production overheads

7.52

Total cost of production

26.08

Fixed production overheads are based on annual budgeted overheads of RWF7,584,000

(RWF632,000 per month) and production volume of 1,008,000 handbags, which

represents 70% of maximum capacity.

There is some small element of flexibility in the fixed overheads, which could be

established at:

Activity level (% of

maximum capacity)

Amount of fixed overheads

RWF000

50 - 70%

632

76 - 90%

648

91 - 100%

656

Fixed overheads actually incurred were the same as budgeted.

Additional information:

March

April

Units sold

87,000

101,000

Units produced

115,000

78,000

Sales price per unit

RWF32

RWF32

Fixed selling costs

RWF120,000

RWF120,000

Fixed administration costs

RWF80,000

RWF80,000

There were no finished goods in stock at 1 March.

REQUIREMENT:

You are required to prepare monthly profit statements for March and April using:

Absorption costing

Marginal costing. (10 Marks)

Page 47

MARGINAL V ABSORPTION COSTING

ANSWERS TO REVISION QUESTIONS

Page 48

Note: You will notice that in this example the net profit in total for the two quarters is not the

same using both methods. This is because there was a net stock increase over the period, an

absorption costing would therefore show a higher profit because of the fixed production

overheads carried forward in stock.

Absorption

Costing

Marginal Costing

Difference - Overheads

Carried Forward in

Stock

RWF

RWF

RWF

Quarter 3 profit

2,900

1,700

1,200

Quarter 4 profit

2,300

3,100

(800)

Total net profit

5,200

4,800

400

Using absorption costing, fixed production overheads carried forward in Quarter 4:

Stock = 2,000 units × RWF0.20

=RWF400

2. (a) Absorption Costing

March

April

RWF000

RWF000

RWF000

RWF000

Sales

2,784.00

3,232.00

Opening stock

Nil

730.24

Direct materials

920.00

624.00

Direct labour

828.00

561.60

Variable production overhead

386.40

262.08

Fixed production overhead

864.80

586.56

2,999.20

2,764.48

Closing stock

(730.24)

(2,268.96)

(130.40)

(2,634.08)

Gross profit

515.04

597.92

Over/(under) absorption

208.80

(45.44)

723.84

552.48

Fixed selling cost

120.00

120.00

Fixed admin. cost

80.00

(200.00)

80.00

(200.00)

Net profit

523.84

352.48

Closing stock calculations:

March: (Units produced 115,000 − Units sold 87,000) × Total unit production

cost RWF26.08

= RWF730,240

Page 49

April: Opening stock 28,000 + Production 78,000 − Sales 101,000 = 5,000

5,000 × RWF26.08 = RWF130,400

Over/under-absorption of fixed production overhead:

Budgeted monthly production = 1 ,008,000/12 = 84,000 = 70% capacity

March production = 115,000 =

115

84

× 70% = 95.8% capacity

So budgeted fixed overheads = RWF656,000

April production = 78,000 so budgeted fixed overheads = RWF632,000

(b) Marginal Costing

March

April

RWF000

RWF000

RWF000

RWF000

Sales

2,784.00

3,232.00

Opening stock

Nil

519.68

Direct materials

920.00

624.00

Direct labour

828.00

561.60

Variable production overhead

386.40

262.08

2,134.40

1,967.36

Closing stock

(based on variable cost)

(519.68)

(1,614.72)

(92.80)

(1,874.56)

Contribution

1,169.28

1,357.44

Fixed costs:

Production overheads

656

632

Selling overheads

120

120

Admin. overheads

80

(856.00)

80

(832.00)

Net profit

313.28

525.44

Page 50

BREAK EVEN ANALYSIS

REVISION QUESTIONS

1. The following figures relate to one year's working in a manufacturing business:

RWF

Fixed overhead 120,000

Variable overhead 200,000

Direct wages 150,000

Direct materials 410,000

Sales 1,000,000

Represent each of these figures on a break-even chart, and determine from the chart the

break-even point.

(3 marks)

2. Production of a chemical product which sells at RWF2.70 per kg usually fluctuates

between 80,000 and 90,000 per month. Costs have been calculated as follows.

Monthly output (kg) 80,000 90,000

RWF RWF

Direct materials 60,000 67,500

Direct wages 72,000 81,000

Production overhead 57,000 58,500

Total production cost 189,000 207,000

The production overhead included in the above costs contains both fixed and variable

elements. The fixed production overhead is expected to remain unchanged up to a

monthly output level of 120,000 kg.

REQUIREMENT:

Calculate:

(a) The fixed overhead cost per month.

(b) The marginal cost per kg.

(c) The total cost if output is increased to 100,000 kg.

(d) The break-even point in kg per month.

(10 marks)

Page 51

3. A sealing compound is manufactured and marketed by Cohesive LTD. The factory has

a production capacity of 10,000,000 litres per annum but is at present working at 40%

capacity.

The compound is sold in 20-litre drums at RWF8.00 each.

The sales manager has suggested reducing the price per drum in order to capture a

larger share of the market. His forecast of sales levels at different prices is:

Price per drum Sales forecast

RWF (drums per annum)

8.00 200,000

7.20 300,000

6.40 400,000

5.60 500,000

Variable costs amount to RWF4.48 per drum whilst fixed costs would be expected to

remain constant at RWF640,000 over the range of output levels under consideration.

REQUIREMENT:

Present in column form a statement showing the forecast profit at each production level

and state which volume should be adopted as the target sales and production level per

annum.

(10 marks)

Page 52

BREAK EVEN ANALYSIS

ANSWERS TO REVISION QUESTIONS

Question 1 Break-even point occurs at RWF500,000 sales value. (See Figure 5.)

Figure 5

Question 2

Units 90,000 80,000 10,000

High Low Difference

RWF RWF RWF

Direct materials 67,500 60,000 7,500

Direct wages 81,000 72,000 9,000

Production overhead 58,500 57,000 1,500

Total 207,000 189,000 18,000

Variable cost per unit

000,10

000,18RWF

= RWF1.80

Page 53

At 80,000 units RWF

Total cost 189,000

Less Variable cost 80,000 × RWF1.80 =144,000

Total fixed cost 45,000

Direct materials cost 60,000

Less Variable cost 80,000 ×

000,10

500,7RWF

(60,000)

Fixed costs NIL

Direct wages cost 72,000

Less Variable cost 80,000 ×

000,10

000,9RWF

(72,000)

Fixed wages cost NIL

Production overhead cost 57,000

Less Variable cost 80,000 ×

000,10

500,1RWF

(12,000)

Fixed production overhead cost RWF45,000

(a) Fixed overhead cost per month = RWF45,000

(b) Marginal cost per kg RWF1.80

(c) Total cost of producing 100,000 kg RWF

Variable cost 100,000 × RWF1.80 180,000

Fixed cost 45,000

RWF225,000

(d) Break-even point in kg

Fixed cost

Contribution per unit

=

RWF1.80) 70.2(

000,45

−RWF

RWF

= 50,000 kg

Page 54

Question 3

Sales units 200,000 300,000 400,000 500,000

Sales unit price RWF8.00 RWF7.20 RWF6.40 RWF5.60

RWF RWF RWF RWF

Total sales 1,600,000 2,160,000 2,560,000 2,800,000

Total variable cost* (896,000) (1,344,000) (1,792,000) (2,240,000)

Contribution 704,000 816,000 768,000 560,000

Fixed costs (640,000) (640,000) (640,000) (640,000)

Profit/(Loss) 64,000 176,000 128,000 (80,000)

* Variable cost per unit = RWF4.48

Sales and production should be set at a target of 300,000 drums.

Page 55

DECISION MAKING

REVISION QUESTIONS

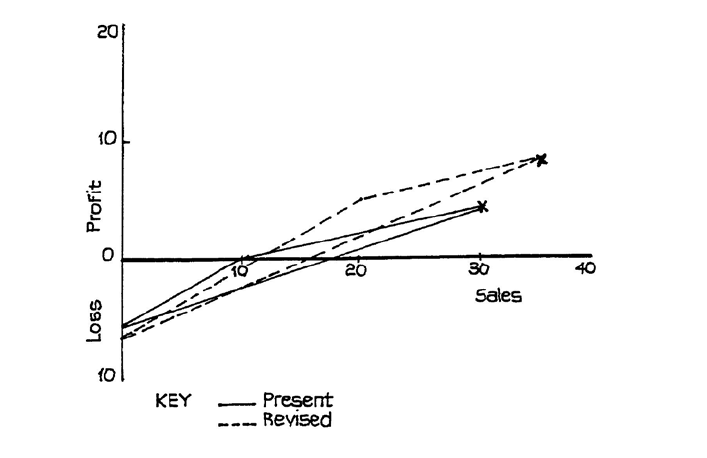

1. (a) Explain what is meant by a break-even chart, and describe its uses.

(b) Illustrate by a graph using the following information:

Sales Variable Cost

RWF RWF

Product A 10,000 4,000

B 5,000 4,000

C 15,000 12,000

RWF30,000 RWF20,000

Fixed expenses RWF6,000

On the same graph, show the effect of eliminating Product B and increasing the

sales of Product A by 100%, with an increase of RWF1,000 in fixed expenses.

(10 marks)

2. CTT Limited is involved in the manufacture of precision engineering machinery. It

Manufactures a substantial proportion of sub-components in-house and is currently

investigating the possibility of sub-contracting the manufacture of a key sub-component

to an outside supplier.

The budgeted annual costs of manufacturing 9,000 units (the annual requirement) of

this component in-house are as follows:

RWF

Direct labour

1,500 hours @ RWF36 per hour

54,000

Direct material

900 kgs @ RWF15 per kg

13,500

Variable overheads

200% direct labour

108,000

Fixed overheads

1,500 hours @ RWF12 per hour

18,000

193,500

Budgeted Fixed Overheads absorbed into this component consist of the following:

RWF

Factory rent (10 year lease)

12,000

Management charges

6,000

18,000

Page 56

If the manufacture of the sub-component is sub-contracted, CTT Ltd will be able to sub-

let the factory space currently used for its manufacture at an annual rent of RWF10,000.

The company will also sell some machinery which would become surplus to

requirements. This machinery has a book value of RWF18,700 and its sale would be

estimated to realise a book loss of RWF2,000.

CTT Ltd will also be able to sell 80kgs of the raw material currently in stock which is

used in the manufacturing process. The company will have the choice of either selling it

to the successful tenderer at a price to be negotiated or else, if no acceptable price is

offered by the successful tenderer, return it to the original supplier at cost less a 15%

restocking charge.

Additionally, two of the four workers currently employed in the manufacture of the

subcomponent would be redeployed within the company but the other two workers will

be made redundant. This will necessitate a redundancy payment of RWF17,000 to each

of these two workers.

The wage of each of the four workers, all of whom are highly skilled and have

considerable accumulated experience, is RWF27,000 per annum. Currently, each of

these workers spends half of his time making the sub-component and the remainder of

his time in the Quality Control department, where the two redeployed workers will now

spend all of their time.

CTT Ltd has prepared a shortlist of the following tenders and has decided that both of

them should be critically evaluated against the costs of in-house production with a view

to making a decision.

• MK Limited has quoted a price of RWF248,000 for the supply of 9,000 units per

annum. It has offered the sum of RWF1,100 for the 80kgs of raw materials. In

addition, it has offered to take on both of the workers due to be made redundant

and will pay each an annual wage of RWF24,000 if its tender is accepted. Both

workers have indicated their agreement to this proposal and, if the tender is

successful, will each receive a concessionary lump-sum payment from CTT

Limited of RWF7,000 instead of a redundancy payment.

• FB Limited has quoted a price of RWF245,000 for the production of 10,000 units

per annum. It has offered the sum of RWF1,000 for the raw materials. FB Ltd

will use its own staff to produce the component but would like to utilise the

machinery and floor space currently used by CTT Ltd for the manufacture of the

Page 57

subcomponent as it believes that such an arrangement would enable it to be better

placed to respond to fluctuations in demand for the sub-component.

The use of these facilities is a key provision of FB Limited tender and is not open

to negotiation. FB Limited has valued the annual use of these facilities at

RWF13,000 and has deducted this sum from the gross value of the tender to

arrive at the quotation of RWF245,000 above.

FB Limited has also agreed to a profit sharing scheme in respect of the 1,000

surplus subcomponents which would be made should the tender be accepted –

2.5% of the sales value of these surplus units will be paid to CTT Limited

annually in arrears. It is expected that these surplus units will be sold for RWF40

each on the open market.

REQUIREMENT:

(a) Determine which of the two external offers gives the lowest price per unit to CTT

Limited.

(18 marks)

(b) On the basis of your calculations in (a), state whether or not the company should

continue to make the sub-component in-house and briefly outline any qualitative

matters relevant to the decision.

(8 marks)

[Total: 26 marks]

Page 58

DECISION MAKING

ANSWERS TO REVISION QUESTIONS

1. Contributions are:

Present Product Sales Variable Cost Contribution

RWF RWF RWF

A 10,000 4,000 6,000

B 5,000 4,000 1,000

C 15,000 12,000 3,000

Revised Product Sales Variable Cost Contribution

RWF RWF RWF

A 20,000 8,000 12,000

B - - -

C 15,000 12,000 3,000

Present fixed expenses are RWF6,000.

Revised fixed expenses are RWF7,000.

Figure 8

From the graph it can be read that:

(a) Present profit is RWF4,000 for sales of RWF30,000.

(b) Revised profit is RWF8,000 for sales of RWF35,000.

(c) Present BEP is RWF18,000.

(d) Revised BEP is RWF16,500 approx.

RWF 000s

Page 59

2. This question must be solved by initially evaluating each tender on the basis that it will

be accepted and comparing the resultant inflows/outflows with the current costs of

making the sub-component in-house.

This question tests the candidate’s ability to identify “relevant” costs and revenues in

the light of the particular terms of each tender, as well as examining candidates

knowledge of typical qualitative factors which impact upon many business decisions.

(a)

Accept

MK Ltd

Tender

Accept

FB Ltd

Tender

Quotation price

RWF248,000

RWF245,000

Sale of raw materials (note 1)

(1,100)

(1,020)

Rental income: (note 2)

(10,000)

None

Sale of machinery: (note 3)

(16,700)

None

Wages saved

(54,000)

(554,000)

Redundancy/lump sum (note 4)

14,000

34,000

Profit sharing: (note 5)

None

(1,000)

Total costs of accepting

180,200

222,980

Number of units

9,000

10,000

Cost per unit

RWF20.02

RWF22.30

Therefore, the offer from MK Ltd is the cheaper of the two tenders.

Notes:

1. Sale of raw materials

If CTT Ltd returns the raw materials to the supplier, it will receive RWF1,020

calculated as follows:

80 kgs @ RWF15 per kg 1,200

Less:

15% restocking charge (180)

Amount received 1,020

When this is compared to the offers from MK Ltd (RWF1,100) and FB Ltd

(RWF1,000), it can be seen that CTT Ltd will sell the material to MK Ltd if its

tender is accepted or else return the materials to the supplier if FB Ltd tender is

successful.

Page 60

2. Rental income

CTT Ltd will be able to sub-let the floor space if MK Ltd is successful; therefore,

the sum of RWF10,000 is shown as income in the above evaluation of that

company’s proposal. However, if FB Ltd succeeds, CTT ltd will not be able to

sub-let the floor space, as it will be used by FB Ltd as part of the overall deal. It

should be noted that, in either case, CTT Ltd will still have to pay the rent. This

sum does not differ under either decision, it has not been shown in the above

evaluation.

1. Sale of machinery

The cash proceeds realised on the sale of the machinery are calculated as follows:

RWF

Book value 18,700

Less

Book loss on disposal (2,000)

16,700

As per note 2, if FB Ltd is successful the machinery will not be sold; therefore, no

proceeds are shown under the evaluation of FB Ltd tender.

2. Redundancy/lump sum costs

Payment to staff if MK Ltd succeeds: 2 staff @ RWF7,000 each = RWF14,000

Payment to staff if FB Ltd succeeds: 2 staff @ RWF17,000 each = RWF34,000

3. Profit sharing

The cash which CTT Ltd will receive under the profit sharing arrangement is

calculated as follows:

1,000 units at RWF40 per unit x 2.5% = RWF1,000

(a) On a purely economic basis, CTT Ltd should not sub-contract the

manufacture of the sub-component to MK Ltd as the relevant (variable) cost

of so doing is approximately RWF0.50 higher (RWF175,500/9,000 =

RWF19.50 present cost per unit). This assumes a one year horizon.

Additionally, there may be other factors which the company might wish to

take into account. These include the following:

Page 61

1. Track record of MK Ltd – is the company a reliable, experienced

supplier?

2. Quality of the component manufactured by MK Ltd – as this is a key

component, it would be of paramount importance that clearly defined

Quality Assurance procedures are installed to ensure top quality.

3. Effect on the morale of staff if two fellow workers are made redundant.

There may be a decline in productivity if staff feel insecure in their

positions.

4. Are there opportunities for CTT Ltd to extract greater economies from

the current production process? Perhaps increased Capital investment

may lower the average unit cost.

5. CTT Ltd should consider the implications of a decision to sub-contract

the manufacture of the component, with special consideration of the

consequences of dependency upon one supplier.

Page 62

STANDARD COSTING AND VARIANCE ANALYSIS

REVISION QUESTION

1. ACM Co Limited manufacture a single product, product W, and have provided you

with the following information which relates to the period which has just ended:

Standard Cost per Batch of Product W

Materials:

Kilos

Price per kilo

RWF

Total

RWF

F

15

4

60

G