THE INSTITUTE OF CAT L2.3 MANAGEMENT ACCOUNTING Study Manual

User Manual:

Open the PDF directly: View PDF ![]() .

.

Page Count: 454 [warning: Documents this large are best viewed by clicking the View PDF Link!]

- Study Unit Title Page

- Some More Terminology 30

- 4 Materials and Stock Control 51

- 5 Labour 91

- Methods of Remuneration 93

- 7 Job Costing/Batch Costing 155

- 9 Process Costing 1 183

- Application and General Principles 184

- 17 Cost Book Keeping 429

- INTRODUCTION TO the COURSE

- A. NATURE AND FUNCTIONS OF COST ACCOUNTING

- b. COST ACCOUNTING COMPARED WITH FINANCIAL ACCOUNTING

- c. THE ROLE OF COST ACCOUNTING IN A MANAGEMENT INFORMATION SYSTEM

- B. BASIC COSTING METHODS

- C. COST CENTRES AND COST UNITS

- D. SUPERIMPOSED PRINCIPLES AND TECHNIQUES

- E. SOME MORE TERMINOLOGY

- F. DIFFERENCE BETWEEN ABSORPTION AND MARGINAL COSTING SYSTEMS

- A. Introduction

- A. INTRODUCTION AND DEFINITIONS

- B. ACCOUNTING FOR MATERIALS

- C. OUTLINE OF PROCEDURES

- Ordering Stock

- Receiving Stock

- Issuing Stock

- Storing Stock

- Stock Levels

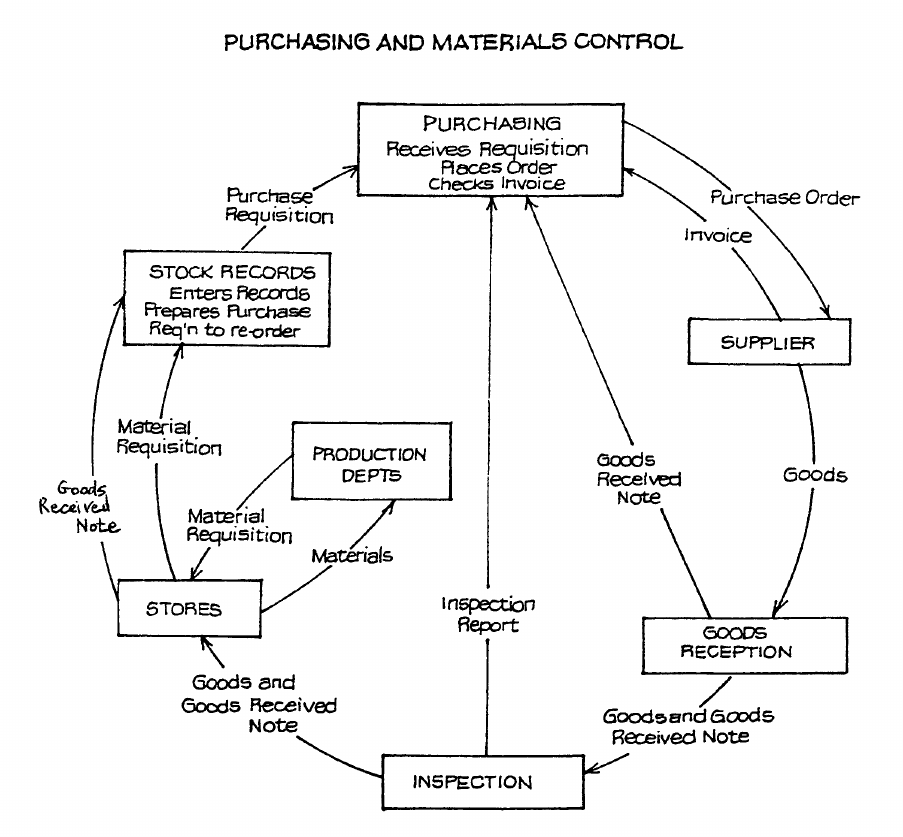

- D. ORGANISATION AND DOCUMENTATION OF PURCHASING

- F. PROCEDURE IN THE ACCOUNTS DEPARTMENT

- G. THE STOREKEEPER AND STORES ISSUES

- H. STOCK LEVELS

- I. ECONOMIC ORDER QUANTITY

- J. STOCK TURNOVER

- K. ACCOUNTING RECORDS REQUIRED FOR MATERIALS

- L. STOCKTAKING

- M. THE PRICING OF MATERIAL ISSUES

- N. OBSOLETE, DORMANT AND SLOW-MOVING STOCK

- A. METHODS OF REMUNERATION

- B. TIME RATES

- C. INCENTIVE SCHEMES

- D. PIECE-RATEs

- E. DIFFERENTIAL PIECE-RATE SYSTEMS

- F. PREMIUM BONUS SCHEMES

- G. GROUP BONUS SCHEMES

- H. PERFORMANCE-RELATED PAY

- I. PROFIT SHARING AND CO-PARTNERSHIP

- J. NON-MONETARY INCENTIVES

- K. MEASUREMENT OF THE EFFICIENCY OF LABOUR

- L. LABOUR TURNOVER

- M. RECORDING LABOUR COSTS

- Time Recording Methods

- N. INDIRECT LABOUR

- O. TREATMENT OF OVERTIME

- P. SUMMARY

- A. EXAMPLES OF EXPENSES

- B. NOTIONAL EXPENSES

- C. CAPITAL EQUIPMENT

- D. INTRODUCTION TO OVERHEAD COSTS

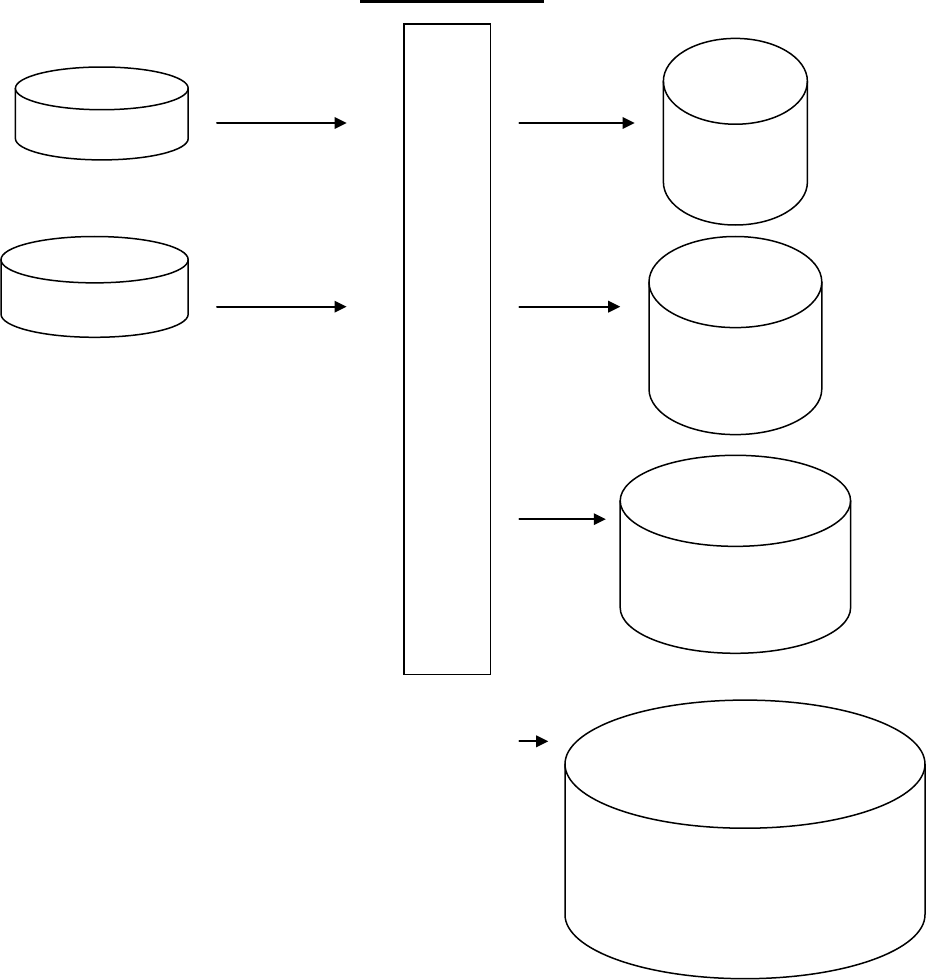

- E. OVERHEAD ALLOTMENT

- Dept 1

- Dept 2

- Service Centre

- General Overhead Cost Centre

- F. OVERHEAD ABSORPTION

- G. THE USE OF PREDETERMINED ABSORPTION RATES

- H. TREATMENT OF ADMINISTRATION OVERHEAD

- I. TREATMENT OF SELLING AND DISTRIBUTION OVERHEAD

- J. ACTIVITY-BASED COSTING

- A. INTRODUCTION

- B. FACTORY JOB COSTING

- A. APPLICATION AND GENERAL PRINCIPLES

- B. BUILDING UP PROCESS COSTS

- C. Examples of Process Costing

- Example 1: Demonstration of Process Accounts and Stock Accounts When the Value of Opening and Closing Work-in-Progress is Given

- Example 2: Introduction to “Equivalent Units” - Work-in-Progress at End of Period Only

- Example 3: Work-in-Progress at Both Beginning and End of the Period: FIFO Method

- Example 4: Work-in-Progress at Both Beginning and End of Period: Average Method

- Essential Differences Using FIFO and Average Methods

- Example 5: Alternative Layout Where a Process Other Than the First is Involved - The layout is shown below.

- D. Losses in process costing – normal losses and abnormal losses

- A. OPERATING COSTING

- B. PROCESS COSTING INVOLVING BOTH LOSSES AND WORK-IN-PROGRESS

- A. INTRODUCTION

- B. LIMITATION OF ABSORPTION COSTING

- C. FIXED, VARIABLE AND SEMI-VARIABLE COSTS

- D. DEFINITION OF MARGINAL COST

- E. THE MARGINAL COST EQUATION: TERMINOLOGY OF MARGINAL COSTING

- F. USES OF MARGINAL COSTING

- G. ARGUMENTS AGAINST MARGINAL COSTING

- I. worked example

- J. when production is constant but sales fluctuate

- K. when sales are constant but production fluctuates

- L. marginal and absorption costing compared

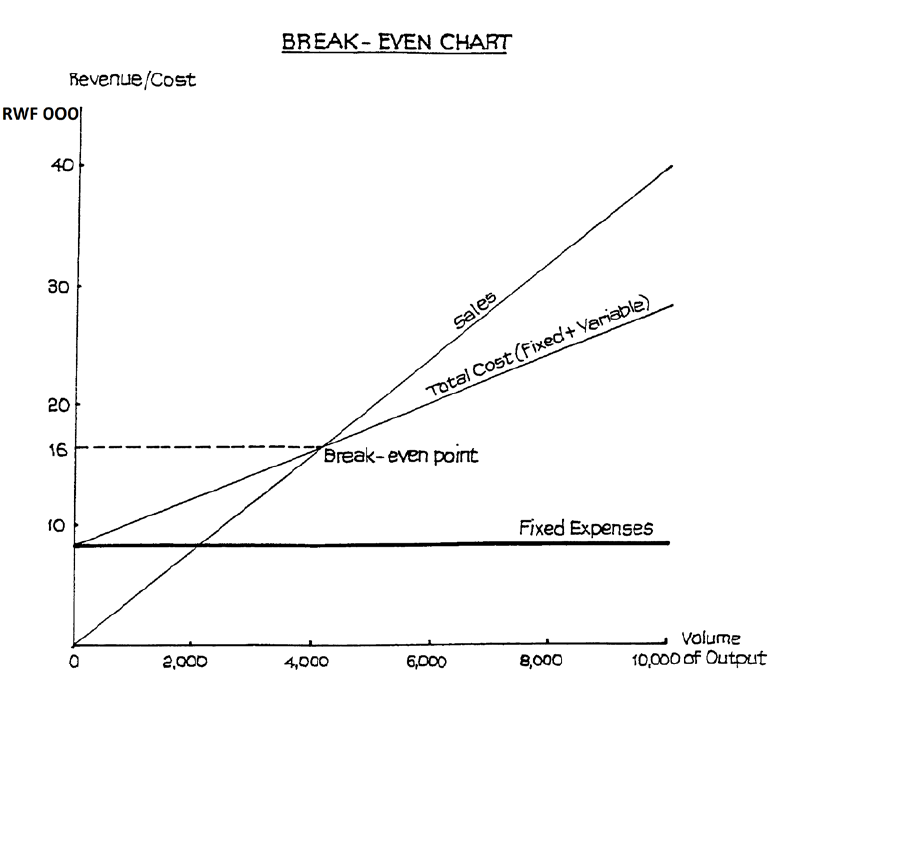

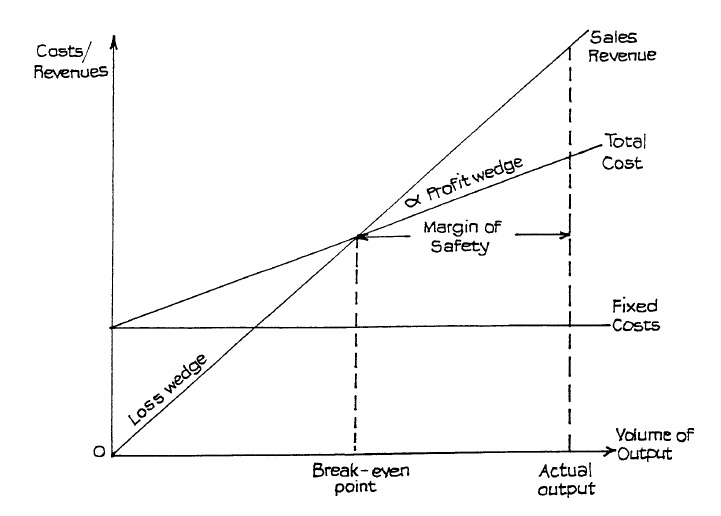

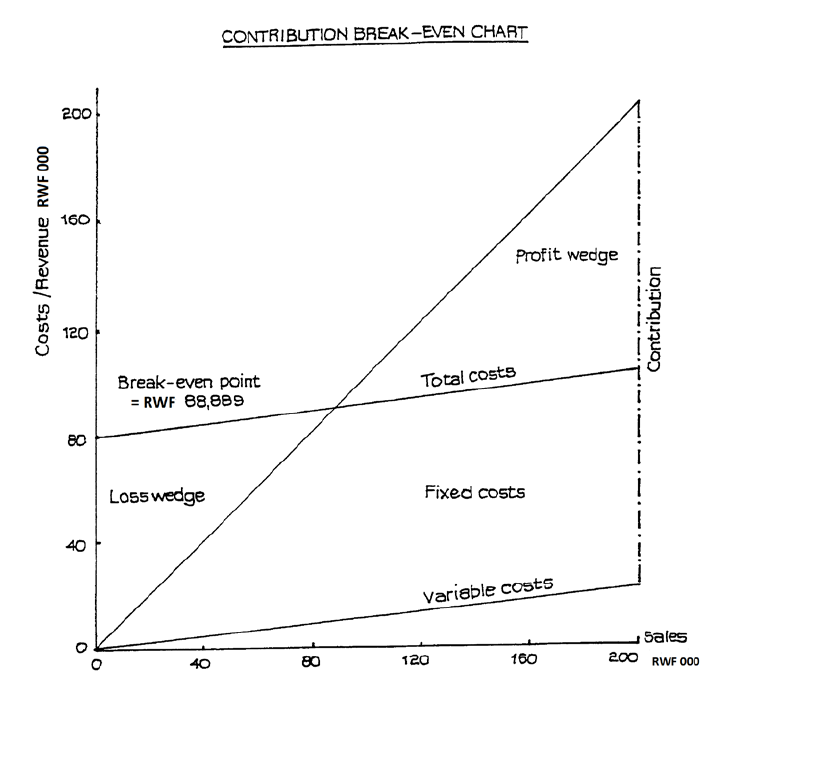

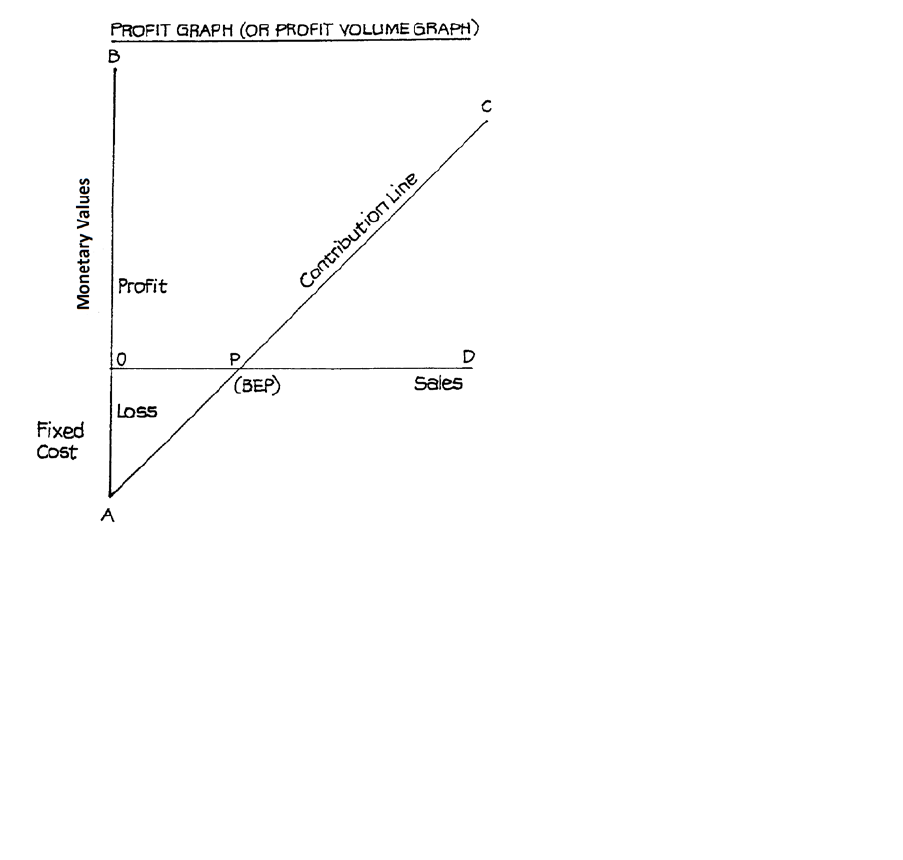

- A. BREAK-EVEN ANALYSIS

- B. BREAK-EVEN CHART

- C. THE PROFIT VOLUME GRAPH

- D. USE OF THE PROFIT VOLUME GRAPH FOR MORE THAN ONE PRODUCT

- E. THE PROFIT/VOLUME OR CONTRIBUTION/SALES RATIO

- F. MARGINAL PROFIT AND LOSS ACCOUNT

- It should be clear that over several periods taken together such that stock at the beginning of the first period and at the end of the last period was nil, the absorption and marginal costing methods would give the same total profit, but the amount of...

- A. INTRODUCTION

- Relevant costs for decision making purposes are:

- Maximum sales demand (units) 120 160 110

- a. introduction

- b. types of standard cost and system

- c. setting standards

- d. types of variance

- e. the standard hour

- f. measures of capacity

- g. limitations of standard costing

- H. purpose of variance analysis

- I. MEANING and possible causeS OF variances

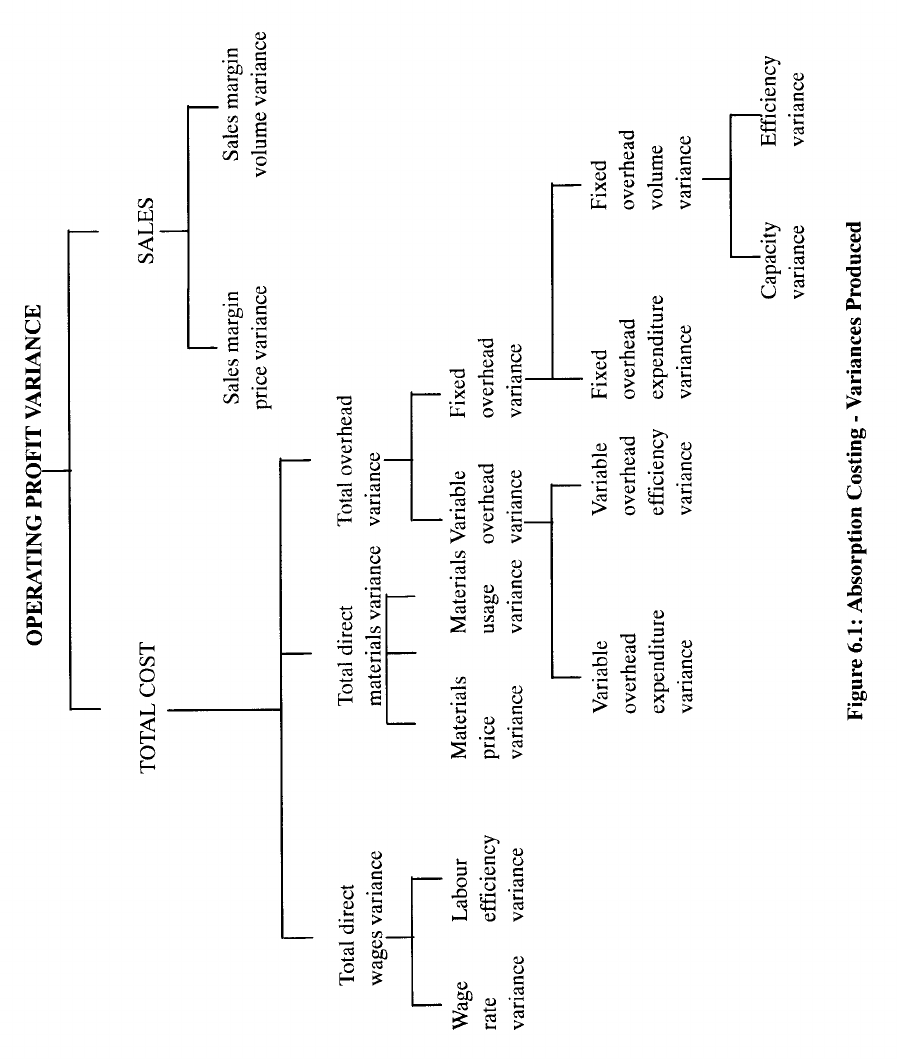

- Scheme of Analysis: Absorption Costing

- Variance Calculations

- (a) Direct Materials

- (b) Direct Labour

- (c) Variable Overheads

- (i) Variable Overhead Expenditure Variance

- (ii) Variable Overhead Efficiency Variance

- (d) Fixed Overheads

- (i) Fixed Overhead Expenditure Variance

- (ii) Fixed Overhead Volume Variance

- (iii) Fixed Overhead Capacity Variance

- (iv) Fixed Overhead Efficiency Variance

- (e) Sales Variances

- (i) Sales Margin Price Variance

- (ii) Sales Margin Volume Variance

- Summary of Variances

- Analysing Variances: Marginal Costing

- Comparing Variances Resulting Under Absorption and Marginal Costing

- J. relationships between variances and investigation of their causes

- K. planning and revision variances

- L. worked example

- a. definitions

- B. advantages of budgetary control systems

- C. types of budget

- D. preparation of budgets

- E. Control mechanism

- f. Flexible budgets

- G. Behavioural implications

- h. Budgeting and long-term objectives

- I. Public Sector Budgets

- a. FUNCTIONAl budgets

- B. master budgets

- C. cash budget

- D. flexible budgets

- E. zero-base budgeting (zbb)

- F. Budgetary control and standard costing - behavioural considerations

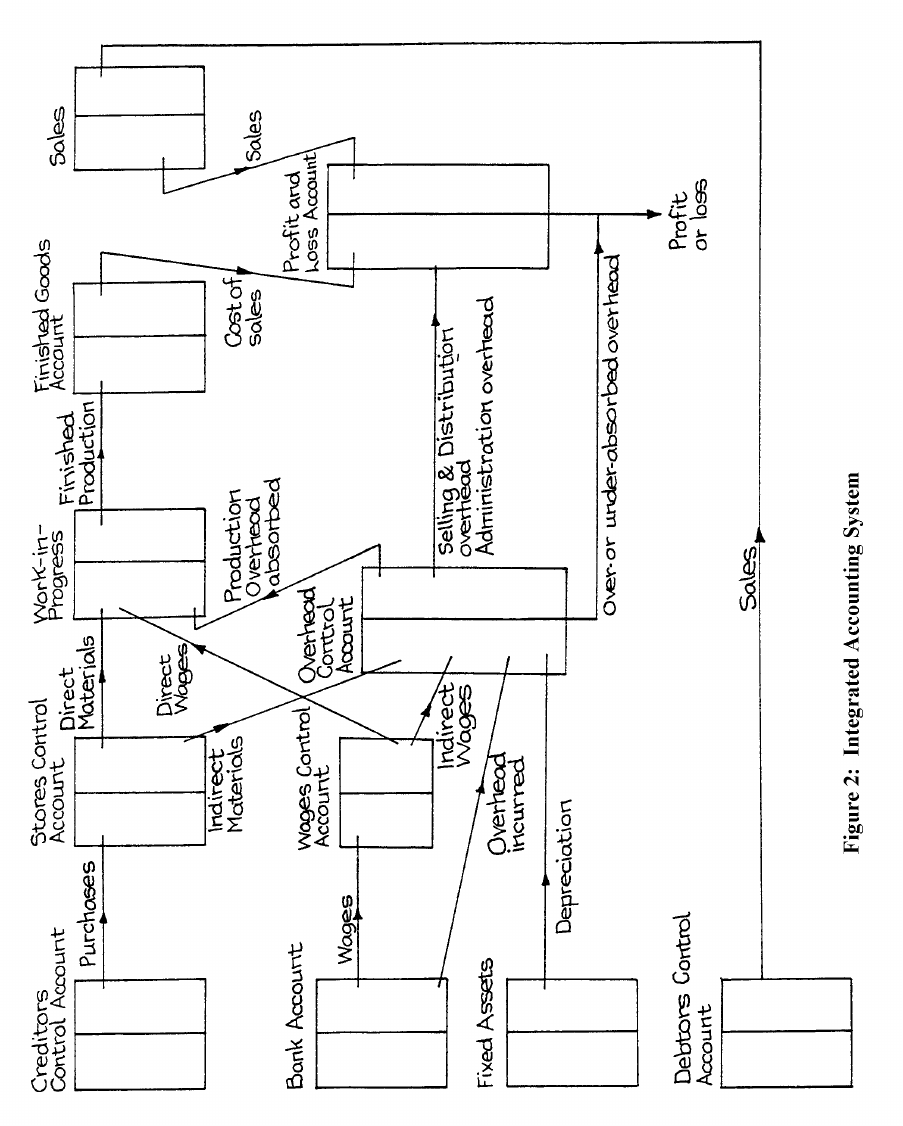

- A. COST ACCOUNTING SYSTEMS

- B. INTEGRATED OR INTEGRAL SYSTEMS

- KEY Management Accounting TERMS

CAT

Certified Accounting Technicians Examination

Stage: Level L2.3

Subject Title: Management Accounting

Study Manual

BLANK

F2.1 MANAGEMENT ACCOUNTING

Page 1

© CPA Ireland

All rights reserved.

The text of this publication, or any part thereof, may not be reproduced or transmitted in any

form or by any means, electronic or mechanical, including photocopying, recording, storage

in an information retrieval system, or otherwise, without prior permission of the publisher.

Whilst every effort has been made to ensure that the contents of this book are accurate, no

responsibility for loss occasioned to any person acting or refraining from action as a result of

any material in this publication can be accepted by the publisher or authors. In addition to

this, the authors and publishers accept no legal responsibility or liability for any errors or

omissions in relation to the contents of this book.

INSTITUTE OF

CERTIFIED PUBLIC ACCOUNTANTS

OF

RWANDA

LEVEL 2

L2.3 MANAGEMENT ACCOUNTING

First Edition 2012

This study manual has been fully revised and

updated in accordance with the current

syllabus. It has been developed in

consultation with experienced lecturers.

F2.1 MANAGEMENT ACCOUNTING

Page 2

BLANK

F2.1 MANAGEMENT ACCOUNTING

Page 3

Contents

Study Unit Title Page

Introduction to Your Course 9

1 Introduction to Cost Accounting

13

Nature and Functions of Cost Accounting 14

Cost Accounting Compared with Financial Accounting 16

The Role of Cost Accounting in a Management Information System 17

2 Principles of Costing 19

The Elements of Cost 20

Basic Costing Methods 25

Cost Centres and Cost Units 26

Superimposed Principles and Techniques 28

Some More Terminology 30

Difference Between Absorption and Marginal Costing Systems 30

3 Cost Behaviour Patterns 35

Introduction 36

Fixed Costs 36

Variable Costs 37

Semi-Variable Costs 38

Step Costs 38

The Linear Assumption of Cost Behaviour 44

Accountant’s v’s Economist Model 45

Factors Affecting the Activity Level 45

Cost Behaviour and Decision Making 46

Cost Variability and Inflation 46

4 Materials and Stock Control 51

Introduction and Definitions 53

Accounting for Materials 54

Outline of Procedures 55

Organisation and Documentation of Purchasing 59

Receiving Department 65

Procedure in the Accounts Department 67

The Storekeeper and Stores Issues 69

Stock Levels 71

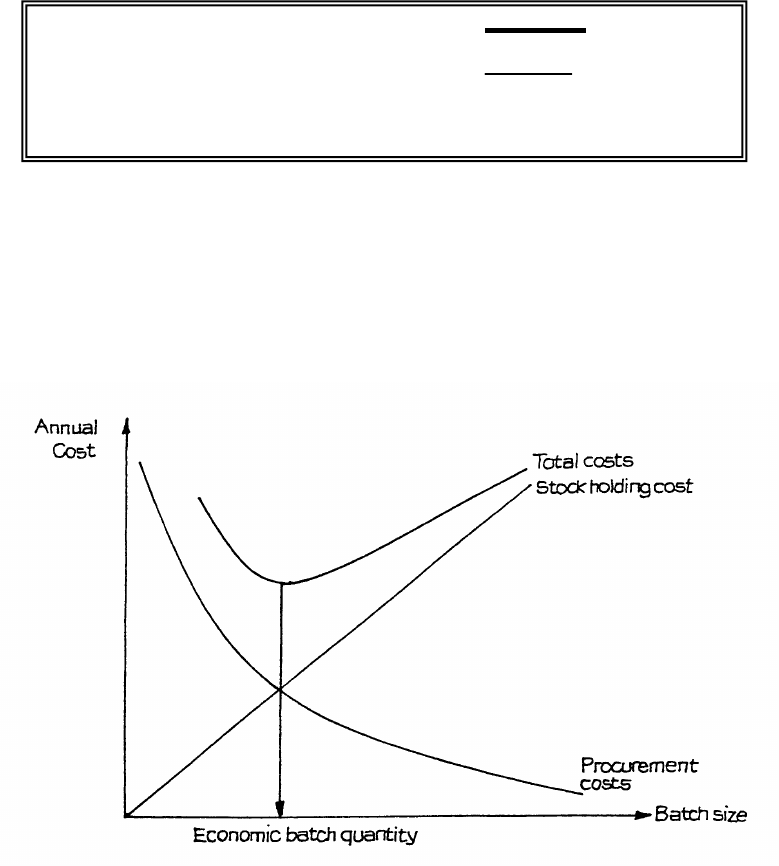

Economic Order Quantity 73

Stock Turnover 76

Accounting Records Required for Materials 76

Stocktaking 77

The Pricing of Material Issues 81

Obsolete, Dormant and Slow-Moving Stock 87

Just-In-Time (JIT) 88

F2.1 MANAGEMENT ACCOUNTING

Page 4

Contents

Study Unit Title Page

5 Labour 91

Methods of Remuneration 93

Time Rates 94

Incentive Schemes 97

Straight Piece-Rate Systems 99

Differential Piece-Rate Systems 100

Premium Bonus Schemes 101

Group Bonus Schemes 103

Performance-Related Pay 104

Profit Sharing and Co-Partnership 105

Non-Monetary Incentives 107

Measurement of the Efficiency of Labour 108

Labour Turnover 109

Recording Labour Costs 111

Indirect Labour 112

Treatment of Overtime 114

Summary 115

6 Overheads and Activity Based Costing

117

Examples of Expenses 118

Notional Expenses 118

Capital Equipment 120

Introduction to Overhead Costs 121

Overhead Allotment 125

Overhead Absorption 132

The Use of Predetermined Absorption Rates 138

Treatment of Administration Overhead 141

Treatment of Selling and Distribution Overhead 141

Activity-Based Costing 143

7 Job Costing/Batch Costing

155

Introduction 156

Factory Job Costing 157

Introduction to Batch Costing 170

Calculation of Cost per Unit 171

Production Line Information 171

Batch Production vs Continuous Production 171

Example 172

Economic Batch Quantity 173

F2.1 MANAGEMENT ACCOUNTING

Page 5

Contents

Study Unit Title Page

8 Service Costing 175

Introduction 176

Service Cost Units 176

Cost Collection & Cost Sheets 177

Internal Service Activities 177

Examples 178

9 Process Costing 1 183

Application and General Principles 184

Elements of Process Costing 185

Examples of Process Costing 186

Losses in Process Costing 201

10 Process Costing 2 207

Operating Costing 208

Process Costing Involving Both Losses and Work-in-Progress 212

11 Marginal v Absorption Costing 223

Introduction 224

Limitation of Absorption Costing 224

Fixed, Variable and Semi-Variable Costs 227

Definition of Marginal Cost 229

The Marginal Cost Equation: Terminology of Marginal Costing 229

Uses of Marginal Costing 231

Arguments Against Marginal Costing 236

Assumptions of Marginal Costing 237

Worked Example 238

When Production is Constant but Sales Fluctuate 242

When Sales are Constant but Production Fluctuates 247

Marginal and Absorption Costing Compared 250

12 Breakeven Analysis 257

Break-Even Analysis 258

Break-Even Chart 262

The Profit Volume Graph 270

Use of the Profit Volume Graph for More Than One Product 272

The Profit/Volume or Contribution/Sales Ratio 277

Marginal Profit and Loss Account 282

F2.1 MANAGEMENT ACCOUNTING

Page 6

Contents

Study Unit Title Page

13 Decision Making 289

Introduction 290

The Practical Use of Relevant Costs 291

Market Vulnerability Analysis 304

Continue/Close Down Decisions 305

Marginal Costing in Decision Making 306

Decision Making Involving a Single Limiting Factor 313

14 Standard Costing and Variance Analysis 319

Introduction 321

Types of Standard Cost and System 322

Setting Standards 323

Types of Variance 330

The Standard Hour 331

Measures of Capacity 332

Limitations of Standard Costing 334

Purpose of Variance Analysis 334

Meaning and Possible Causes of Variances 335

Relationships Between Variances and Investigation of Causes 351

Planning and Revision Variances 358

Worked Example 360

15 Budgets - Planning and Control 363

Definitions 364

Advantages of Budgetary Control Systems 367

Types of Budget 368

Preparation of Budgets 369

Control Mechanism 375

Flexible Budgets 379

Behavioural Implications 381

Budgeting and Long-term Objectives 382

Public Sector Budgets 382

16 Preparation, Techniques and Considerations of Budget 387

Functional Budgets 388

Master Budgets 389

Cash Budget 400

Flexible Budgets 408

Zero-base Budgeting (ZBB) 420

Budgetary Control and Standard Costing – Behavioural Considerations 425

F2.1 MANAGEMENT ACCOUNTING

Page 7

Contents

Study Unit Title Page

17 Cost Book Keeping 429

Cost Accounting Systems 430

Integrated or Integral Systems 431

Glossary Key Terms 441

F2.1 MANAGEMENT ACCOUNTING

Page 8

BLANK

F2.1 MANAGEMENT ACCOUNTING

Page 9

INTRODUCTION TO THE COURSE

Stage: Level 2

Subject Title: L2.3 Management Accounting

Aim

The aim of this subject is to ensure that students develop a knowledge and understanding of

the various cost accounting principles, concepts and techniques appropriate for planning,

decision-making and control and the ability to apply these techniques in the generation of

management accounting reports.

Learning Outcomes

On successful completion of this subject, students should be able to:

• Explain the relative strengths and weaknesses of alternative cost accumulation

methods and discuss the value of management accounting information.

• Calculate unit costs applying overhead using both absorption costing and activity

based costing principles.

• Apportion and allocate costs to units of production in job, batch and process costing

systems, for the purpose of stock valuation and profit measurement.

• Identify and explain cost behaviour patterns and apply cost-volume profit analysis.

• Define and use relevant costs in a range of decision-making situations.

• Prepare and present budgets for planning, control and decision-making.

• Compute, interpret and investigate variances.

• Demonstrate communication skills including the ability to present quantitative and

qualitative information, together with analysis, argument and commentary, in a form

appropriate to the intended audience.

F2.1 MANAGEMENT ACCOUNTING

Page 10

Syllabus:

1. The Role of the Management Accountant

• The nature and scope of management accounting.

• The relationship between management accounting and financial accounting.

• Cost classifications.

• The role of the Management Accountant in a modern business environment including

the recognition of possible ethical issues that may arise.

2. Cost Accumulation Systems

• Accounting for materials: stock valuation approaches (FIFO; LIFO and AVCO);

EOQ; JIT concepts.

• Accounting for labour: remuneration methods; incentive schemes; productivity,

labour turnover and labour performance reports.

• Accounting for Overheads: absorption costing and activity based costing (ABC)

approaches to overheads.

3. Costing Methods

• Job and batch costing.

• Process costing for single products and the use of equivalent units calculations under

both FIFO and Weighted Average accounting systems.

• Process costing ledger accounts including normal and abnormal loss/gain.

• The role of costing in non-manufacturing sectors.

• Marginal costing and the importance of contribution for decision-making.

• Comparison of marginal costing and absorption costing approaches.

4. Information for Decision Making

• Cost behaviour patterns and identification of fixed/variable elements in a cost using

High/Low method.

• Break-even analysis and the importance of contribution.

• Break-even chart preparation and interpretation.

• Calculation of break-even point, margin of safety and target profit.

• Limitations of Cost Volume Profit Analysis.

• Relevant costing principles including committed, sunk and opportunity costs.

• Relevant costs in decision-making.

• Decision making with a single limiting factor/constraint.

• Qualitative factors relevant to specific decisions.

F2.1 MANAGEMENT ACCOUNTING

Page 11

5. Information for Planning and Control

• The role of budgeting including alternative budgeting systems (Fixed, flexible,

incremental and Zero Based Budgeting (ZBB)).

• Behavioural and motivational issues in the budgetary process.

• Functional and subsidiary budgets.

• Standard costing: role and procedures for standard setting including different types of

standards.

• Variance analysis: the calculation and interpretation of basic sales/cost variances.

Reconciliation reports. The inter-relationship and possible causes of variances. (Fixed

overhead capacity and efficiency variances are not examinable.)

F2.1 MANAGEMENT ACCOUNTING

Page 12

BLANK

F2.1 MANAGEMENT ACCOUNTING

Page 13

Study Unit 1

Introduction to Cost Accounting

Contents

A. Nature and Functions of Cost Accounting

B. Cost Accounting Compared with Financial Accounting

C. The Role of Cost Accounting in a Management Information System

F2.1 MANAGEMENT ACCOUNTING

Page 14

A. NATURE AND FUNCTIONS OF COST ACCOUNTING

What Is “Cost Accounting”?

The Chartered Institute of Management Accountants, in its publication, “Terminology of

Management and Financial Accountancy”, defines cost accounting as:

“.... that part of management accounting which establishes budgets and standard costs,

and the actual costs of operations, processes, departments or products and the analysis of

variances, profitability or social use of funds.”

This involves participation in and with management to ensure that there is effective:

• Formulation of plans to meet objectives (long-term planning)

• Formulation of short-term operation plans (budgeting/profit planning)

• Corrective action to bring future actual transactions into line (financial control)

• Recording of actual transactions.

What Cost Accounting Provides for the Organisation

(a) Additional Financial Information

When cost accounting was first used, its main purpose was to provide additional

information concerning the financial operations of an organisation. For the majority of

firms, this is still considered as its main purpose. It usually implies historical costing and

the production of regular detailed statements and statistics.

(b) Control Information

A more modern concept of cost accounting is that its purpose is to assist management by

providing them with control information.

This usually demands more from the cost accountant. He or she will still produce

statistical statements, but will be required to analyse and interpret these statements.

Comparisons will be made with “budgets” and “standards”, and the cost accountant will

probably use the exception system of reporting, advising management only where action

is required.

F2.1 MANAGEMENT ACCOUNTING

Page 15

(c) Management Tool

Cost accounting has often been likened to a tool in the hands of management. Consider

what this means:

(i) It must be the right tool. The cost accountant, in consultation with management,

must agree what information is required and when; the cost of providing it will also

have to be taken into consideration. The question must also be asked, is complete

accuracy necessary? Will an approximation within given limits be of more value, if

it can be provided swiftly?

Any system of costing must be tailored to suit the organisation which it serves. In

many cases simple historical cost accounting will be sufficient; in others a more

sophisticated system may be necessary.

(ii) The tool must be capable of doing the job. The cost accountant must ensure that the

facts and figures produced provide management with the information they require,

in an easily assimilated form.

Do not forget that manufacturing conditions and markets will change over the years,

and the cost accounting system may need to be adapted to suit changing needs. A

new system may need to be designed and introduced.

(iii) It is management who use the tool, and the extent of its success will depend upon the

degree of efficiency with which it is used.

Objects of a Cost Accounting System

Different firms will use cost accounting for different purposes. Nevertheless, every system

will involve some of the objectives listed below.

(a) Cost Control

This will be assisted by:

(i) Finding out the cost of each product (or service), process and department - costs

must be ascertained in phase with manufacturing activity, enabling remedial action

to be taken quickly when it is required.

(ii) Comparing the costs with budget, standard or past performance figures to indicate

the degree of efficiency attained.

(iii) Analysing the variances from budget and identifying the person or department

responsible so that prompt, remedial action may be taken.

(iv) Disclosing to what extent production facilities are used and indicating the amount

and cost of idle and waiting time.

F2.1 MANAGEMENT ACCOUNTING

Page 16

(v) Presenting the information suitably to management, in such a form as to guide them

in taking any necessary action.

(b) Advice to Management in the Formulation of Policy

This will include:

(i) Provision of information to assist in the regulation of production and the systematic

control of the organisation.

(ii) Provision of special investigations and reports. These might deal with such matters

as:

− Whether to manufacture a part or to sub-contract another firm.

− The advisability of installing new machinery.

− The effect of increased or reduced production volumes on profitability.

(c) Advice on the Effects of Management Policy

This will be disclosed through reports (both regular reports and those following special

investigations).

(d) Estimating and Price Fixing

Figures will be provided from standards or past results as the basis for future estimates.

Cost is an important factor in price fixing, but it is not the only one. Demand and

competitive activity are also crucial. Therefore a firm’s profitability may depend largely

on its ability to control costs in ways described in (a) above.

B. COST ACCOUNTING COMPARED WITH FINANCIAL

ACCOUNTING

You will be familiar already with the end-products of financial accounting, namely the

balance sheet and the profit and loss account. These are valuable documents for

management, the first giving the position of a company or firm at a specific time, the second

showing the results of the company’s operations over a specific period of time. The books of

account from which the profit and loss account and balance sheet are derived are also of

value, since they provide a record of every transaction.

Despite the value of the financial accounts, it was their inadequacy which gave rise to the

introduction of costing and the development of costing techniques. The financial accounts

show primarily external transactions (sales, purchases, borrowing, etc.) and the profit for the

organisation as a whole. Management requires detailed knowledge of the cost of each

product or unit, of each department or process to show how the profit was built up and the

F2.1 MANAGEMENT ACCOUNTING

Page 17

relative profitability of each section of the business. Cost accounting has now become an

essential factor of every business.

It is of interest that in recent years “integrated accounts” (see later in this study unit) have

grown in popularity. Integrated accounts are merely the combining of the financial and cost

accounts into one set of books. We seem to have come full circle, from the separation of the

financial and cost accounts, through the development of costing, to the joining together of the

two systems into one integral system. Of course, in many businesses increasing

computerisation has assisted this development.

C. THE ROLE OF COST ACCOUNTING IN A

MANAGEMENT INFORMATION SYSTEM

Product Analysis

Only the very simplest form of organisation does not need a cost accounting system, and even

in this case some “cost accounting” would be done, but the simplicity of the business renders

a special system unnecessary.

In a more complex organisation, results can be analysed in depth. The cost of each process or

operation which goes to make up the final product can be ascertained, as can the cost of the

various “service” departments (stores, tool room, power house, etc.).

Investigating Costs

The cost accountant would not be satisfied merely to ascertain the figures, however. Perhaps

costs can be reduced, and/or revenues, and/or production increased.

The cost accountant will consult the sales manager. It may be that increases in price will

result in a decrease in sales. Moreover, financial considerations are not the only ones to be

borne in mind.

By pursuing such enquiries, the cost accountant is achieving the second function of costing,

that is, cost control. It should be stated here that it is not the cost accountant’s job to make

executive decisions, but merely to express the management’s policy in terms of money, and

to indicate where efficiency may be increased.

Guiding Management Policy

A most important side to the cost accountant’s work is providing information to management

at all levels. His or her job is to advise management of the financial effects of alternative

policies. He or she is an adviser only; it is for the manager to make policy decisions. Thus

the cost accounting system will justify itself only when the information it produces is used by

management. (Management accountants are part of “Management” and make use of both

cost accounting information and financial accounting information for their involvement in

management decisions.)

F2.1 MANAGEMENT ACCOUNTING

Page 18

Non-Financial Considerations

Clearly therefore, before management can make decisions, they require information on which

to arrive at the decisions and cost accounting information is one part of the required

information. Other matters need to be considered which are frequently of a non-financial

nature, however. These might include:

(a) position in the market;

(b) environmental considerations;

(c) legal constraints;

(d) staff qualifications and training needs

F2.1 MANAGEMENT ACCOUNTING

Page 19

Study Unit 2

Principles of Costing

Contents

_______________________________________________________________

A. The Elements of Cost

_______________________________________________________________

B. Basic Costing Methods

_______________________________________________________________

C. Cost Centres and Cost Units

_______________________________________________________________

D. Superimposed Principles and Techniques

_______________________________________________________________

E. Some More Terminology

_______________________________________________________________

F. Difference Between Absorption and Marginal Costing Systems

_______________________________________________________________

F2.1 MANAGEMENT ACCOUNTING

Page 20

A. THE ELEMENTS OF COST

The expenditure we are considering in our cost accounting is, of course, the same expenditure

(subject to certain considerations which will be mentioned) as that which is dealt with in the

financial accounts. It is merely that we are looking at it in a different way. Whereas the

financial accounts are normally concerned only with the nature of the expense, e.g. whether it

is wages, lighting and heating, etc., the cost accounts are concerned with the purpose of the

expense, e.g. whether the wages are in respect of, say, manufacturing or distribution, and if

manufacturing, whether they are in respect of labour directly or indirectly concerned with the

product, and so on.

Make sure that you clearly UNDERSTAND, and then REMEMBER, the following

classifications.

Labour, Materials and Expenses

All expenditure can be classified into three main groups - labour, materials and expenses.

Each of the expenses may be subdivided into one of two categories:

(a) Items directly applicable to the product, i.e. direct.

(b) Items which cannot be directly applied to the product, i.e. indirect.

The total of indirect materials, indirect labour and indirect expenses is called overhead.

Fixed and Variable Costs

There is a further subdivision of costs which we may briefly note here (and about which I

will say more later), and that is between fixed costs and variable costs. Fixed costs are those

which remain constant (in total) over a wide range of output levels, while variable costs are

those which vary (in total) more or less according to the level of output. This division is of

great significance, and we shall be dealing with it later. Observe, now, that by its very nature

“prime cost” consists of variable items only, while the various overhead categories may

contain some of each kind.

(a) Examples of fixed costs: rent, rates, insurance, depreciation of buildings, management

salaries.

(b) Examples of variable costs: raw materials, commission on sales, piece-work earnings.

F2.1 MANAGEMENT ACCOUNTING

Page 21

Definitions

Here are some definitions in this connection, which you must understand clearly:

(a) Direct Labour Cost

This is the cost of remuneration for employees’ efforts applied directly to a product or

saleable service which can be identified separately in product costs.

Examples of direct labour, as defined above, would include the costs of employing

bricklayers, machine operators, bakers, miners, bus drivers. There is no doubt as to

where you would charge these labour costs. Doubt would arise, however, with a truck

driver’s wage in a factory. His wage cannot be charged direct to any product, as he is

helping many departments and operators. Therefore, his wage would have to be

classified as indirect. In a few exceptional circumstances it may be established that the

truck driver is employed only to transport materials for the manufacture of one product.

If this were the case, his wage could be charged direct to the product, and he would be

as much a direct worker as the operator who is using the materials.

(b) Direct Materials Cost

This is the cost of materials entering into and becoming constituent elements of a

product or saleable service and which can be identified separately in product cost. The

following materials fall within this definition:

(i) All materials specially purchased for a particular job, order or process.

(ii) All materials requisitioned from the stores for particular production orders.

(iii) Components or parts produced or purchased and requisitioned from the finished

goods store.

(iv) Material passed from one operation to another.

We must consider here the term “raw material”. In many cases the raw material of one

industry or process is the finished product of another. Thus leather in the form of hides

constitutes the finished product of a tannery but the raw material of a footwear factory;

while carded wool, the product of the carding process, becomes the raw material of the

hardening section.

(c) Direct Expenses

These are costs, other than materials or labour, which are incurred for a specific product

or saleable service.

Direct expenses are not encountered as often as direct materials or labour costs. An

example would be electric power to a machine, provided that the power is metered and

the exact consumption by the machine is known. We can then charge the cost of power

direct to the job. More often, however, we will know only the electricity bill for the

whole factory, so this will be an indirect expense.

F2.1 MANAGEMENT ACCOUNTING

Page 22

Another example of a direct expense is a royalty payment to the inventor of a product.

(d) Prime Cost

This is the total cost of direct wages, direct material and direct expenses.

(e) Overhead

Overhead is the total cost of indirect labour, indirect materials and indirect expenses.

Examples of indirect materials include oils, cotton waste and grease. Examples of

indirect labour include the costs of employing maintenance workers, oilers, cleaners

and supervisors. Examples of indirect expenses include lighting, rent and

depreciation.

Overheads may be divided into four main groups:

(i) works or factory expense;

(ii) administration expense;

(iii) selling expense;

(iv) distribution expense.

An Example from the Confectionery Industry

The cost of production of most commodities is made up mainly of the cost of the raw

materials of which they are manufactured and the cost of labour which is employed making

them, i.e. wages.

F2.1 MANAGEMENT ACCOUNTING

Page 23

RWF RWF RWF

To Direct Materials Consumed:

(1) Flour

Opening Stock 2,080

Purchases 5,720

7,800

Less:

Closing Stock 990

Part-Finished Goods 300 1,290 6,510

(2) Gelatine

Opening Stock 1,720

Purchases 3,180

4,900

Less:

Closing Stock 55

Part-Finished Goods 60 115 4,785

(3) Sugar and Other Materials

Opening Stock 5,040

Purchases 10,920

15,960

Less:

Closing Stock 4,985

Part-Finished Goods 360 5,345 10,615

COST OF RAW MATERIALS USED 21,910

To Direct Labour 3,720

To Direct Expense -

PRIME COST 25,630

To Factory Overhead 6,650

FACTORY COST (COST OF PRODUCTION) RWF32,280

F2.1 MANAGEMENT ACCOUNTING

Page 24

To this total of factory cost will be added administration, selling and distribution expenses, to

arrive at a figure of total cost, to which will be added profit to give the selling price. (This

method of costing is known as Absorption Costing - see later.)

The example given above is of a “process” industry in which the product passes from one

process to the next. Unless production is shut down completely at the end of each accounting

period, which would be most uneconomical, there will at all times be some product “in the

pipeline” at various stages of completion which will be credited against the charges for the

period in question and become the opening charge for the subsequent period. These opening

and closing adjustments are always necessary.

An Example from the Photographic Industry

Let us now consider a business which manufactures cameras, where the amount of labour

involved in manufacture is small compared with the amount of precision machinery which is

necessary for the manufacture of efficient apparatus. In such an industry, costs arising from

the depreciation and obsolescence of machinery may be of much greater importance

compared with the cost of materials and labour than they were in the case of the

confectionery manufacturing company. These charges which are related only indirectly to

output are said to constitute indirect expenditure, as against materials and labour and other

similar items which constitute direct expenditure.

In addition to depreciation, all the charges incurred in the general offices (such as salaries of

managers, rent and rates) together with the expenses involved in marketing the product (such

as advertising and carriage) must be included in the indirect expenses. You will appreciate,

therefore, that in order to give a reflection of the cost of production for each unit of output,

accounts must be prepared to show the allocation of these indirect expenses as well as the

direct expenses (provided it is intended to follow Absorption Costing methods rather than

Marginal Costing - see later).

F2.1 MANAGEMENT ACCOUNTING

Page 25

B. BASIC COSTING METHODS

The basic costing method employed by an organisation must be devised to suit the methods

by which goods are manufactured or services are provided. The choice is between specific

order costing, service/function costing and continuous operation/ process costing.

Specific Order Costing

This costing method is applicable where the work consists of separate contracts, jobs or

batches, each of which is authorised by a special order or contract.

The subdivisions of specific order costing are:

(a) Job Costing

This applies where work is undertaken to a customer’s special requirements. Each

“job” is of comparatively short duration. Throughout the manufacturing process, each

job is distinct from all other jobs. Examples of industries using job costing are:

building maintenance, certain types of engineering (e.g. manufacture of special purpose

machines) and printing.

(b) Batch Costing

This is a form of specific order costing which applies where similar articles are

manufactured in batches, either for sale, or for use within the undertaking. In most

cases the costing is similar to job costing.

(c) Contract Costing

This applies when work of long duration is undertaken to customers’ special

requirements, e.g. builders, civil engineers, etc.

In job costing, costs of each job (or batch) can be separately identified.

Continuous Operation/Process Costing

This is the basic costing method applicable where goods or services are produced by a

sequence of continuous or repetitive operations or processes to which costs are charged

before being averaged over the units produced during the period. This procedure is widely

used, for example, in the chemicals industry.

Service/Function Costing

This is the method used for specific services or functions, e.g. canteens, maintenance and

personnel. These may be referred to as service centres, departments or functions.

F2.1 MANAGEMENT ACCOUNTING

Page 26

C. COST CENTRES AND COST UNITS

Cost Centre

A cost centre is a location, function or item of equipment in respect of which costs may be

ascertained and related to cost units for control purposes. A cost centre may be a productive

department, an individual machine, a service department such as stores serving the productive

departments, etc.

Cost Unit

This is a quantitative unit of product or service in relation to which costs are ascertained. For

instance, in paint manufacture, costs would be ascertained “per litre of paint”. The litre of

paint is therefore the cost unit.

Examples of cost units in other activities are:

Accounting Account maintained

Brewing Barrel of beer racked

Brickmaking 1,000 bricks

Building industry Complete job or contract

Cable manufacture 1,000 yards (or m) of cable

Canteen Employee or meal served

Chemicals industry Per gram, kg, etc. depending on relative quantity

produced

Power station Kilowatt/hours

Gravel or sand pits Cubic yard/metre extracted

Hospitals Per patient-day, or per bed-week

Invoicing Per 100 or 1,000 invoices

Liquids Gallon, litre

Maintenance Operating hour or value of asset

Metal plating Square foot/metre

Police service Per 1,000 population or per constable-day

Printing Ream or 1,000 copies

Public transport Miles run, passenger-mile, 100-seat mile or fare-stage

Purchasing Per order placed, or value of materials

Sales order department Per enquiry, or value of sales made

Sales representative Per call or value of sales made

School Per pupil-day or per examination passed

Steam 1,000 lbs steam raised

Storage Tonne of material, gallon or litre of liquid, value of

materials

Street cleaning 1,000 population, or mile of road

Street lighting Lamp or mile of road

Timber 1,000 cu. ft, board-foot, etc.

F2.1 MANAGEMENT ACCOUNTING

Page 27

Typing Space, line typed or standard document typed

Water supply 1,000 population or 1,000 gallons produced

Window cleaning per window or 100 sq. yds

Profit Centre

A profit centre is a location or function in respect of which both expenditure and income may

be attributable. A profit centre may be a division of the business or a specific function within

the organisation. In order that true profitability may be assessed, it is necessary to install

procedures to transfer-charge all relevant costs and revenue to the profit centre. Ideally, the

net costs of all central operating areas should be allocated, on an agreed basis, to profit

centres.

The development of the profit centre concept means that profit centres have come to act as a

focal point for the collation of cost centres and the provision of useful high-level management

information.

Examples of profit centres in the financial services industry are:

− UK clearing banking

− Merchant banking

− Credit card operations

− Corporate banking

− International banking.

F2.1 MANAGEMENT ACCOUNTING

Page 28

D. SUPERIMPOSED PRINCIPLES AND TECHNIQUES

Whichever costing method is in use (a choice which will be largely dictated by the

production method), there is a choice of principles and techniques which may be adopted in

presenting information to management. These are introduced briefly here, and we will study

some of them in detail later.

Absorption Costing

This principle involves all costs, including the costs of selling and administration, being

allotted to cost units. Total overheads are “absorbed”, via the method thought most

appropriate.

Marginal Costing

This is a principle whereby variable costs only are charged to cost units, and the fixed cost

attributable to the relevant period is written off in full against the “contribution” for that

period, contribution being the difference between total sales value and total variable costs. At

this stage therefore, remember when using marginal costing, do NOT attempt to apportion

fixed costs to individual cost units.

Actual Cost Ascertainment

This is the ascertainment of costs in retrospect, after they have been incurred. It is also

known as historical costing.

Variance Accounting

This is a technique whereby the planned activities of an undertaking are quantified in

budgets, standard costs, standard selling prices and standard profit margins. These are then

compared with the actual results, and note is taken of the differences, i.e. the “variances”, for

subsequent examination.

Differential Costing

This is a technique used in the preparation of “ad hoc” information, in which only cost and

income differences between alternative courses of action are taken into consideration. In

other words, any costs which would be incurred whatever decision were taken, are ignored.

Incremental Costing

This is another technique used in the preparation of “ad hoc” information. Here

consideration is given to a range of graduated or stepped changes in the level or nature of

F2.1 MANAGEMENT ACCOUNTING

Page 29

activity, and the additional costs and revenues likely to result from each degree of change are

presented.

Uniform Costing

This is the use by several undertakings of the same costing system (i.e. the same basic

method, specific order costing or operation costing, and the same superimposed principles

and techniques, e.g. absorption costing rather than marginal costing). Uniform costing

enables the results of the various organisations concerned to be compared. In many

industries, a trade association advises member firms on costing methods, and collects data

from them, which is then circulated to member firms so that they can see how they compare

with other firms in the industry. Strict anonymity is, of course, maintained.

To recapitulate at this stage, a reminder of the total cost structure, within the context of

Absorption Costing, can be represented as follows:

Direct Labour Prime

Direct Materials Cost Works, Factory

Direct Expenses or Production

Cost

Factory Overheads Total

Cost

Admin. Overheads

Selling Overheads Selling

Distribution Overheads Price

Profit

Figure 3

F2.1 MANAGEMENT ACCOUNTING

Page 30

E. SOME MORE TERMINOLOGY

Controllable and Uncontrollable Costs

Sometimes reference is made to costs being either “controllable” or “uncontrollable”. As we

have seen already, costs are charged or allocated to cost centres. Each cost centre has an

officer in control. Costs are said to be “controllable” when the costs charged can be

influenced by the actions of this person in charge. Where they cannot, they are of course

“uncontrollable” costs. Sometimes controllable costs are referred to as “managed costs”.

Avoidable and Unavoidable Costs

“Avoidable costs” are the specific costs of part of an organisation which would be avoided if

that part or sector/activity did not exist. Another term for this is “relevant costs”. It follows,

therefore, that “unavoidable costs” are those that are unaffected by a particular decision. As

they are in fact irrelevant to the decision, they are also known as “irrelevant costs”.

F. DIFFERENCE BETWEEN ABSORPTION AND

MARGINAL COSTING SYSTEMS

We have already looked at the broad divisions between Absorption and Marginal Costing

systems but we have not yet considered them in detail. This we will do later in the course. In

the meantime, let us consider a case which may indicate more clearly the difference.

F2.1 MANAGEMENT ACCOUNTING

Page 31

A company manufactures three products, A, B and C, and in the year makes a profit of

RWF70,000, as follows:

RWF

Total Sales 600,000

Variable Labour 160,000

Variable Material 240,000

Variable Overhead 30,000

Fixed Overhead 100,000

Net Profit 70,000

It is decided to analyse these figures between Products A, B and C. The company uses

absorption costing and apportions (or spreads) fixed overhead in proportion to the sales value

of Products A, B and C. (We have not yet covered the methods of getting a proportion of

overhead costs into costs; this follows later in the course.)

The figures now become:

Total A B C

RWF RWF RWF RWF

Sales 600,000 250,000 200,000 150,000

Variable Labour 160,000 70,000 45,000 45,000

Variable Material 240,000 100,000 60,000 80,000

Variable Overhead 30,000 15,000 10,000 5,000

Fixed Overhead 100,000 41,666 33,334 25,000

Net Profit 70,000 23,334 51,666 (5,000)

Management considers the situation. It decides to stop manufacturing C, since it is producing

a net loss of RWF5,000. Sales of A and B cannot be increased because of market conditions.

However, as a result of dropping C, fixed overheads will reduce to RWF90,000. The staff

formerly employed on the production of C were temporary and have been sacked.

Management congratulates itself and looks forward to an improved net profit situation.

F2.1 MANAGEMENT ACCOUNTING

Page 32

To their dismay the following results arise:

Total A B

RWF RWF RWF

Sales 450,000 250,000 200,000

Variable Labour 115,000 70,000 45,000

Variable Material 160,000 100,000 60,000

Variable Overhead 25,000 15,000 10,000

Fixed Overhead 90,000 50,000 40,000

Net Profit 60,000 15,000 45,000

Despite their efforts, profits are actually reduced by RWF10,000!

The reason for this should be fairly obvious. If we consider the situation in terms of financial

accounting, we have lost RWF20,000 gross profit which C produced (RWF150,000 sales less

RWF130,000 cost of sales) which in turn could have been available to cover, in part, the

expenses of the company. This is basically the approach followed by marginal costing.

Instead of referring to “gross profit”, the term “contribution” is used, that is, the contribution

made towards covering overheads or fixed costs.

If a marginal costing approach had been taken to the initial figures for Products A, B and C,

these would have read as follows:

Total A B C

RWF RWF RWF RWF

Sales 600,000 250,000 200,000 150,000

Variable Labour 160,000 70,000 45,000 45,000

Variable Material 240,000 100,000 60,000 80,000

Variable Overhead 30,000 15,000 10,000 5,000

430,000 185,000 115,000 130,000

Sales less

Variable Costs

(CONTRIBUTION) 170,000 65,000 85,000 20,000

Fixed Overhead 100,000

Net Profit 70,000

F2.1 MANAGEMENT ACCOUNTING

Page 33

Note, no attempt has been made to spread the fixed overhead cost of RWF100,000 between

Products A, B and C. Provided the total contribution is greater than fixed overhead, a net

profit will result. Obviously, if the contribution in total can be increased (by increased sales

prices or variable costs reductions) a higher net profit will result.

In this case we have studied, it is in fact the very spreading of fixed overhead costs between

Products A, B and C which lead management to think that C was making an overall loss. For

some particular reason, it was decided to allocate fixed overheads to Products A, B and C in

direct proportion to their sales value. Suppose instead it had been decided to allocate them in

direct proportion to the variable overheads incurred by A, B and C. This would have resulted

in fixed overhead of RWF50,000 being allocated to A, RWF33,334 to B and RWF16,666 to

C, with the result that the overall net profit of RWF70,000 would have been split between A

RWF15,000, B RWF51,666 and C RWF3,334. In this case, the management might not have

been tempted to cancel C!

Clearly, the basis on which fixed overheads are allocated is most important in the decision

areas of sales levels, production levels, etc. Advocates of marginal costing consider that, at

best, such allocation of fixed overheads is fairly arbitrary and can only confuse, so it is better

not to attempt it.

We will return to this later in the course but at this point it must be stated that absorption

costing is still widely practised and indeed in some areas is ideal for the needs which exist.

In monopolistic situations, in local and in central government, it can be, and is, used

extensively. In such circumstances cost management often centres on comparisons of total

cost in one period of time with another period of time. Provided the same method of

allocating fixed overheads is used in the periods being compared, then such cost comparisons

are still valid, particularly as the information is required for comparison purposes only and

not for changes in levels of production/services decisions.

F2.1 MANAGEMENT ACCOUNTING

Page 34

BLANK

F2.1 MANAGEMENT ACCOUNTING

Page 35

Study Unit 3

Cost Behaviour Patterns

Contents

A. Introduction

B. Fixed Costs

C. Variable Costs

D. Semi-Variable Costs

E. Step Costs

F. The Linear Assumption of Cost Behaviour

G. Accountants vs Economist Model

H. Factors Affecting the Activity Level

_______________________________________________________________

I. Cost Behaviour and Decision Making

_______________________________________________________________

J. Cost Variability and Inflation

F2.1 MANAGEMENT ACCOUNTING

Page 36

A. INTRODUCTION

As we saw earlier in this study unit, costs can be divided either into direct and indirect costs,

or variable and fixed costs.

Direct costs are variable, that is the total cost varies in direct proportion to output. If, for

instance, it requires RWF10 worth of material to make one item it will require RWF20 worth

to make two items and RWF100 worth to make ten items and so on.

Overhead costs, however, may be either fixed, variable or semi-variable.

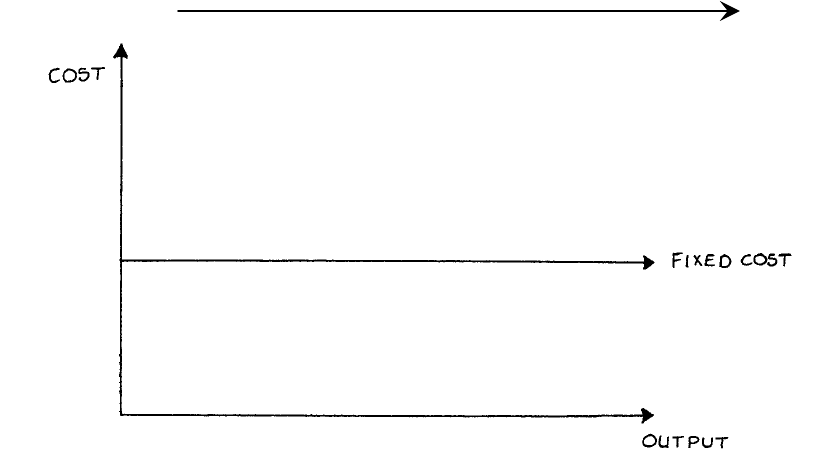

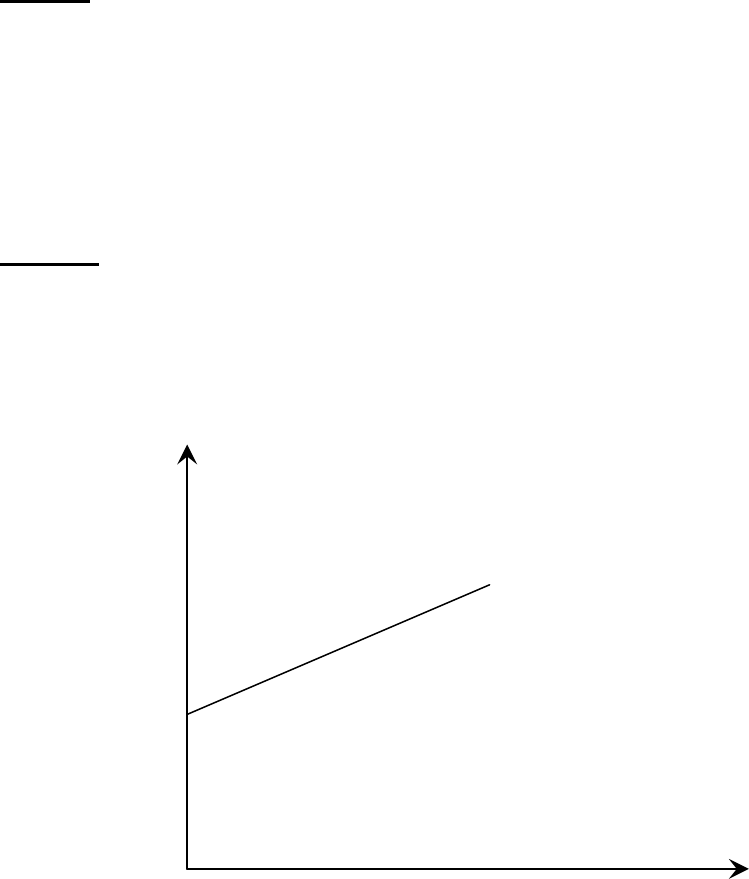

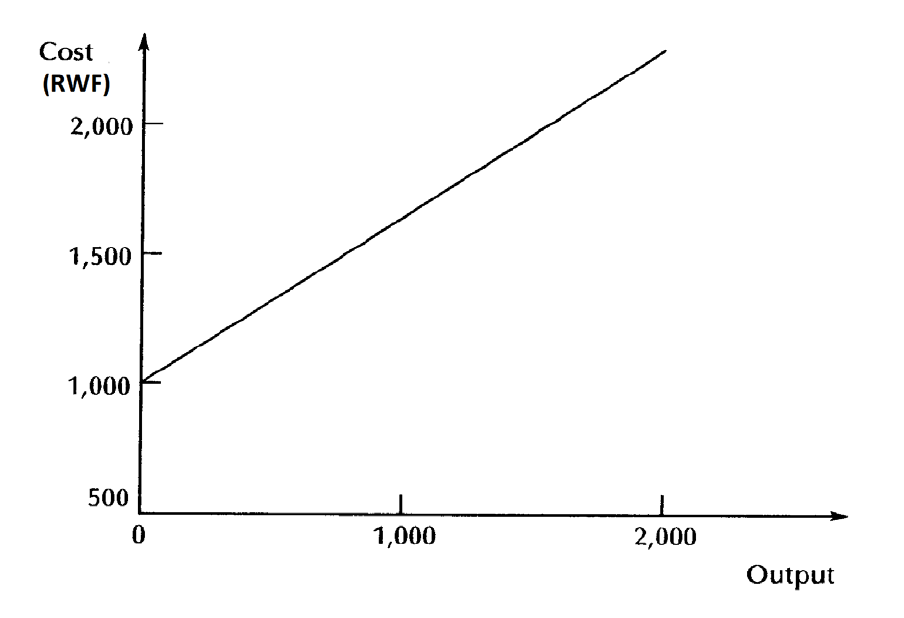

B. FIXED COST

A fixed cost is one which can vary with the passage of time but, within limits, tends to

remain fixed irrespective of the variations in the level of output. All fixed costs are overhead.

Examples of fixed overhead are: executive salaries, rent, rates and depreciation.

A graph showing the relationship of total fixed cost to output appears in Figure 4.

Figure 4

Please note the words “within limits” in the above description of fixed costs. Sometimes this

is referred to as the “relevant range”, that is the range of activity level within which fixed

costs (and variable costs) behave in a linear fashion.

F2.1 MANAGEMENT ACCOUNTING

Page 37

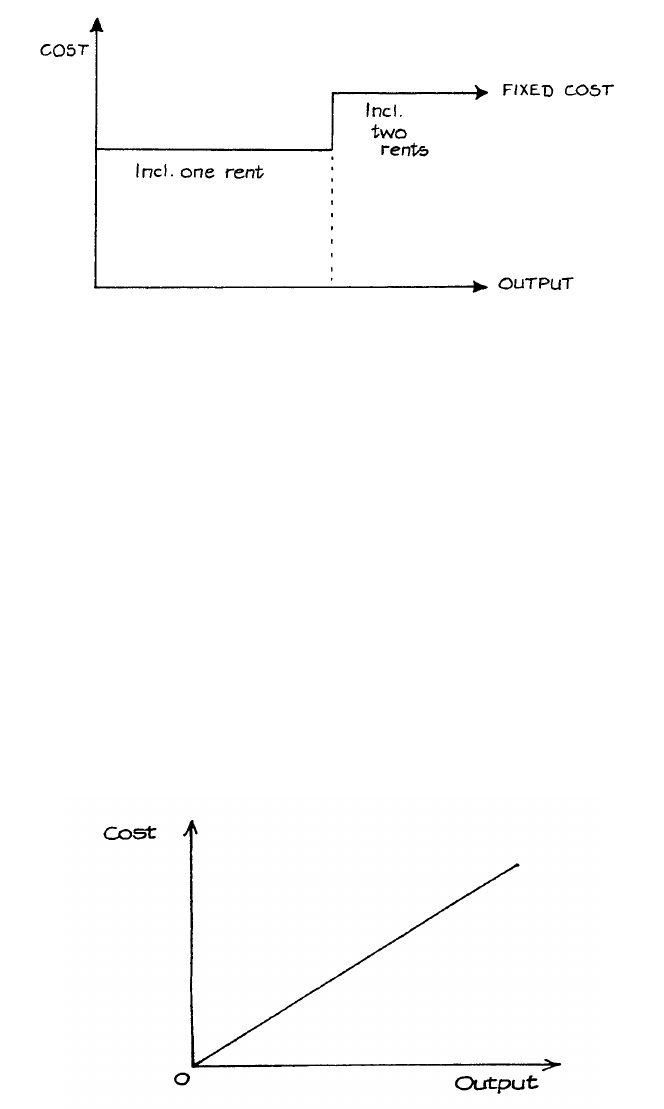

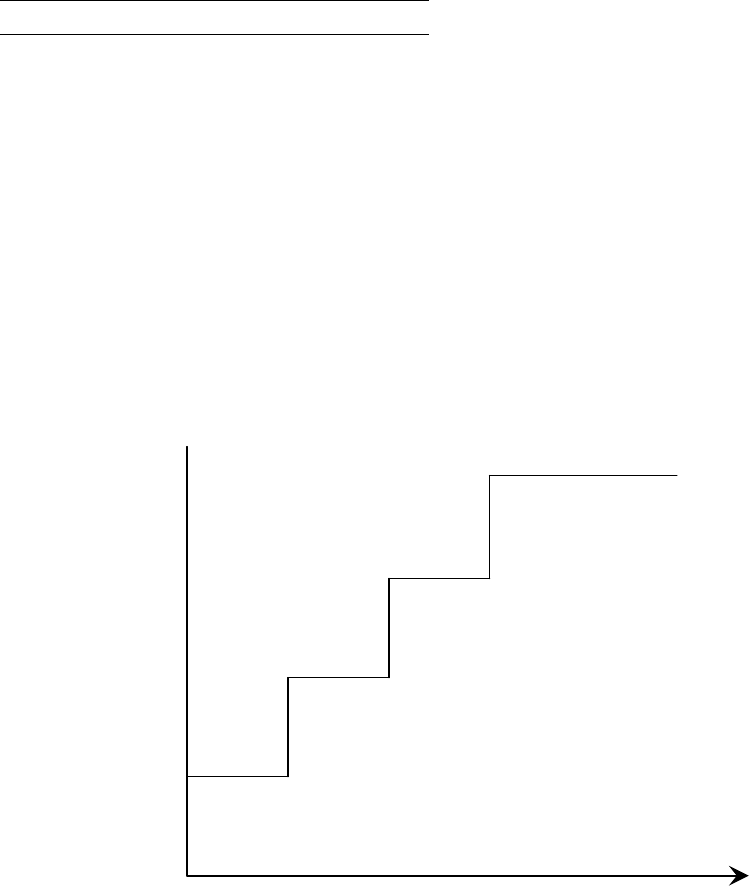

Suppose an organisation rents a factory. The yearly rent is the same no matter what the

output of the factory is. If business expands sufficiently, however, it may be that a second

factory is required and a large increase in rent will follow. Fixed costs would then be as in

Figure 5.

Figure 5

A cost with this type of graph is known as a step function cost for obvious reasons.

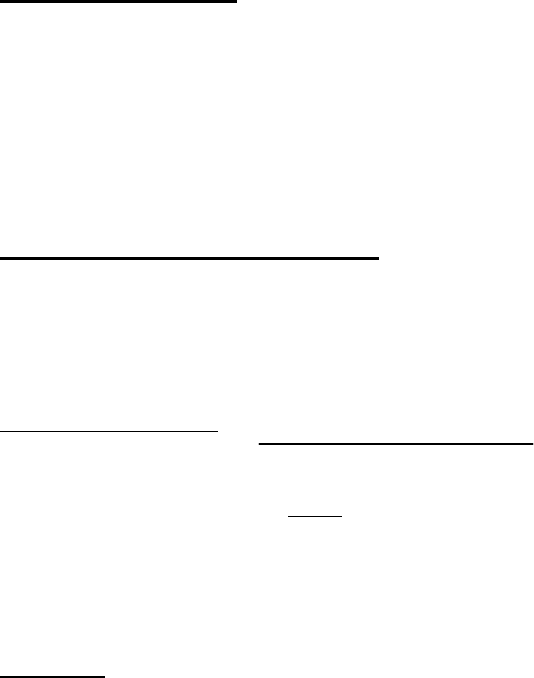

C. VARIABLE COST

This is a cost which tends to follow (in the short term) the level of activity in a business.

As already stated, direct costs are by their nature variable. Examples of variable overhead

are: repairs and maintenance of machinery; electric power used in the factory;

consumable stores used in the factory.

The graph of a variable cost is shown in Figure 6.

Figure 6

F2.1 MANAGEMENT ACCOUNTING

Page 38

D. SEMI-VARIABLE (OR SEMI-FIXED) COST

This is a cost containing both fixed and variable elements, and which is thus partly affected

by fluctuations in the level of activity.

For examination purposes, semi-variable costs usually have to be separated into their fixed

and variable components. This can be done if data is given for two different levels of output.

Example

At output 2,000 units, costs are RWF12,000.

At output 3,000 units, costs are RWF17,000.

Therefore for an extra 1,000 units of output, an extra RWF5,000 costs have been incurred.

This is entirely a variable cost, so the variable component of cost is RWF5 per unit.

Therefore at the 2,000 units level, the total variable cost will be RWF10,000. Since the total

cost at this level is RWF12,000, the fixed component must be RWF2,000. You can check

that a fixed component of RWF2,000 and a variable component of RWF5 per unit gives the

right total cost for 3,000 units.

E. STEP COST

RWF

Total Cost

F2.1 MANAGEMENT ACCOUNTING

Page 39

Level of Activity

Example: Rent can be a step cost in certain situations where accommodation requirements

increase as output levels get higher.

A Step Cost

Many items of cost are a fixed cost in nature within certain levels of activity.

Semi-Variable Costs

This is a cost containing both fixed and variable components and which is thus partly affected

by fluctuations in the level of activity (CIMA official DFN).

Example: Running a Car

• Fixed Cost is Road Tax and insurance.

• Variable cost is petrol, repairs, oil, tyres-all of these depend on the number of miles

travelled throughout the year.

RWF

Total Cost

Level of Activity

A method of splitting semi-variable costs is the High – Low method.

F2.1 MANAGEMENT ACCOUNTING

Page 40

High – Low method

Firstly, examine records of cost from previous period. Then pick a period with the highest

activity level and the period with the lowest level of activity.

• Total Cost of high activity level minus total cost of low activity level will equal variable

cost of difference in activity levels.

• Fixed Costs are determined by substitution

Example of High - Low Method

Highest level 10,000 units, cost of RWF4,000

Lowest Level activity level 2,000 units cost of RWF1,600

Variable Cost Element: (RWF4,000 - RWF1,600)

10,000 units – 2,000 units

= 2,400

8,000

∴ = RWF 0.30 per unit

Fixed Cost (under high level figure)

RWF4,000 – (10,000 x RWF 0.30)

= RWF1,000

Scattergraphs

Information about two variables that are considered to be related in some way can be plotted

on a scattergraph. This is simply a graph on which historical data can be plotted. For cost

behaviour analysis, the scattergraph would be used to record cost against output level for a

large number of recorded “pairs” of data.

Then by plotting cost level against activity level on a scattergraph, the shape of the resulting

figure might indicate whether or not a relationship exists.

In such a scattergraph, the y axis represents cost and the x axis represents the output or

activity level.

One advantage of the scattergraph is that it is possible to see quite easily if the points indicate

that a relationship exists between the variables, i.e. to see if any correlation exists between

them.

F2.1 MANAGEMENT ACCOUNTING

Page 41

Positive correlation exists where the values of the variables increase together (for example,

when the volume of output increases, total costs increase).

Negative correlation exists where one variable increases and the other decreases in value

Some illustrations:

1. Weight and height in humans

Weight

Positive Linear Correlation

x x x

x x

x

x x

x x

x x

Height

2. Sales of Scarves and temperature

Sales x x x Negative Linear Correlation

x x x

x x x

x x x

x x x

x x x

Temperature

F2.1 MANAGEMENT ACCOUNTING

Page 42

3. Sugar Imports and Mining Production

Imports

x x x

x x x x x

x x x x x No Correlation

x x x x x x

x x x x x x x x

x x x x x x

x x x

x x x x

Mining Production

A scattergraph can be used to make an estimate of fixed and variable costs, by drawing a

“line of best fit” through the band of points on the scattergraph, which best represents all the

plotted points.

The above diagrams contain the line of best fit. These lines have been drawn using

judgement. This is a major disadvantage, as drawing the line “by eye”. If there is a large

amount of scatter, different people may draw different lines.

Thus, as a technique, it is only suitable where the amount of scatter is small or where the

degree of accuracy of the prediction is not critical.

However, it does have an advantage over the high-low method in that all points on the graph

are considered, not just the high and low point.

Regression Analysis

This is a technically superior way to identify the “slope” of the line. It is also known as

“Least Squares Regression”. This statistical method is used to predict a linear relationship

between two variables. It uses all past data (not just the high and low points) to calculate the

line of best fit.

The equation of the regression line of y on x is of the form:

y = a + bx

F2.1 MANAGEMENT ACCOUNTING

Page 43

In other words, if we are trying to predict the cost (y) from an activity (x), it is necessary to

calculate the values of a and b from given pairs of data for x and y. The following formulae

are used:

a = Σy - bΣx

n n

b = nΣxy - ΣxΣy

nΣx2 – (Σx)2

where “n” is the number of pairs of x and y values. (The symbol “Σ” means

‘the sum of’)

Thus, in order to calculate “a”, it is necessary to calculate “b” first.

Example

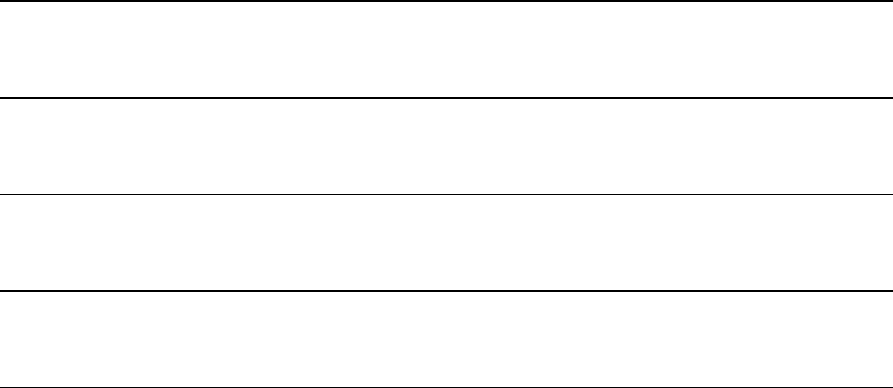

The following is the output of a factory and the cost of production over the last 5 months:

Output (‘000 units)

Cost (RWF’000)

January

20

82

February

16

70

March

24

90

April

22

85

May

18

73

(i) Determine a formula to show the expected level of costs for any given volume of

output

(ii) Prepare a budget for total costs if output is 27,000 units

Solution:

Let x = output

Let y = costs

n = 5 (5 pairs of x & y values)

Construct a table as follows: (in ‘000)

x

y

xy

x2

y2

20

82

1,640

400

6,724

16

70

1,120

256

4,900

24

90

2,160

576

8,100

22

85

1,870

484

7,225

18

73

1,314

324

5,329

Σx = 100

Σy = 400

Σxy = 8,104

Σx2 = 2,040

Σy2 = 32,278

F2.1 MANAGEMENT ACCOUNTING

Page 44

b = nΣxy - ΣxΣy = 5(8,104) – (100)(400)

nΣx2 – (Σx)2 5(2,040) – (100)2

b = 2.60

a = Σy - bΣx = 400 – 2.6(100)

n n 5 5

a = 28 (or 28,000)

Thus, the formula for any given level of output is:

y = RWF28,000 + RWF2.60x

where

y = total cost (in RWF’000)

x = output (in ‘000 units)

If output is 27,000 units, then total cost (y) will be:

y = RWF28,000 + RWF2.60(27,000)

y = RWF98,200

F. THE LINEAR ASSUMPTION OF COST BEHAVIOUR

1. Cost are assumed to be either fixed, variable or semi-variable within a normal range of

output.

2. Fixed and variable costs can be estimated with degrees of probable accuracy. Certain

methods maybe used to access this (High-Low method).

3. Costs will rise in a straight line/linear fashion as the activity increases.

F2.1 MANAGEMENT ACCOUNTING

Page 45

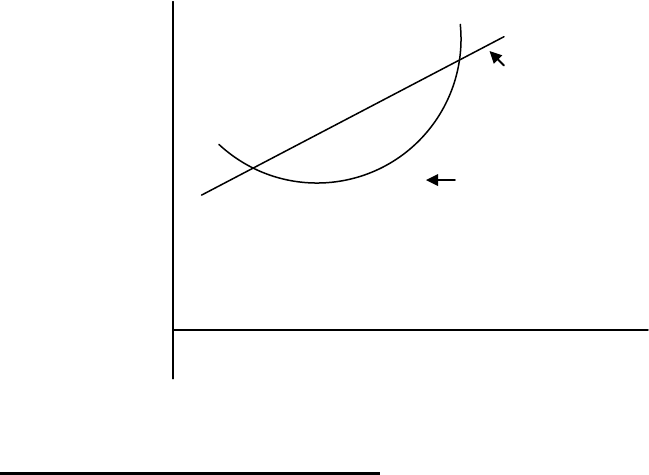

G. ACCOUNTANTS - V’S – ECONOMIST MODEL

RWF

Total Cost

Activity

Assumptions of Above Diagram

The accountants state that the linear assumption of cost behaviour is linear because:

1. The linear cost (straight line) is only used in practice within normal ranges of output

‘Relevant Range of Activity’.

The term ‘Relevant Range’ is used to refer to the output range at which the firm expects

to be operating in the future.

2. It is easier to understand than Economists’ cost line.

3. The fixed and variable costs are easier to use.

4. The relevant range and the costs estimated by the economists and the accountants will

not be very different.

H. FACTORS AFFECTING THE ACTIVITY LEVEL

1. The economic environment.

2. The individual firm – its staff, their motivation and industrial relations.

3. The ability and talent of management.

4. The workforce (unskilled, semi-skilled and highly skilled).

5. The capacity of machines.

6. The availability of raw material.

Economists Cost Lines Curvilinear

Accountants Cost Line is Linear (Straight)

F2.1 MANAGEMENT ACCOUNTING

Page 46

I. COST BEHAVIOUR AND DECISION MAKING

Factors to Consider:

1. Future plans for the company.

2. Current competition to the company.

3. Should the selling price of a single unit be reduced in order to attract more customers.

4. Should sale staff be on a fixed salary or on a basic wage with bonus/commission.

5. Is a new machine required for current year.

6. Will the company make the product internally or buy it.

For all of the above factors, management must estimate costs at all levels and evaluate

different courses of action. Management must take all eventualities into account when

making decisions for the company.

Example of things management would need to know is fixed costs do not generally change as

a result of a decision unless the company have to rent an additional building for a new job

etc.

J. COST VARIABILITY AND INFLATION

Care must be taken in interpreting cost data over a period of time if there is inflation. It may

appear that costs have risen relative to output, but this may be purely because of inflation

rather than because the amount of resources used has increased.

If a cost index, such as the Retail Price Index, is available the effects of inflation can be

eliminated and the true cost behaviour pattern revealed.

It is essential for the index selected to be relevant to the company; if one of the many Central

Statistical Office indices is not appropriate, it may be possible for the company to construct

one from its own data.

F2.1 MANAGEMENT ACCOUNTING

Page 47

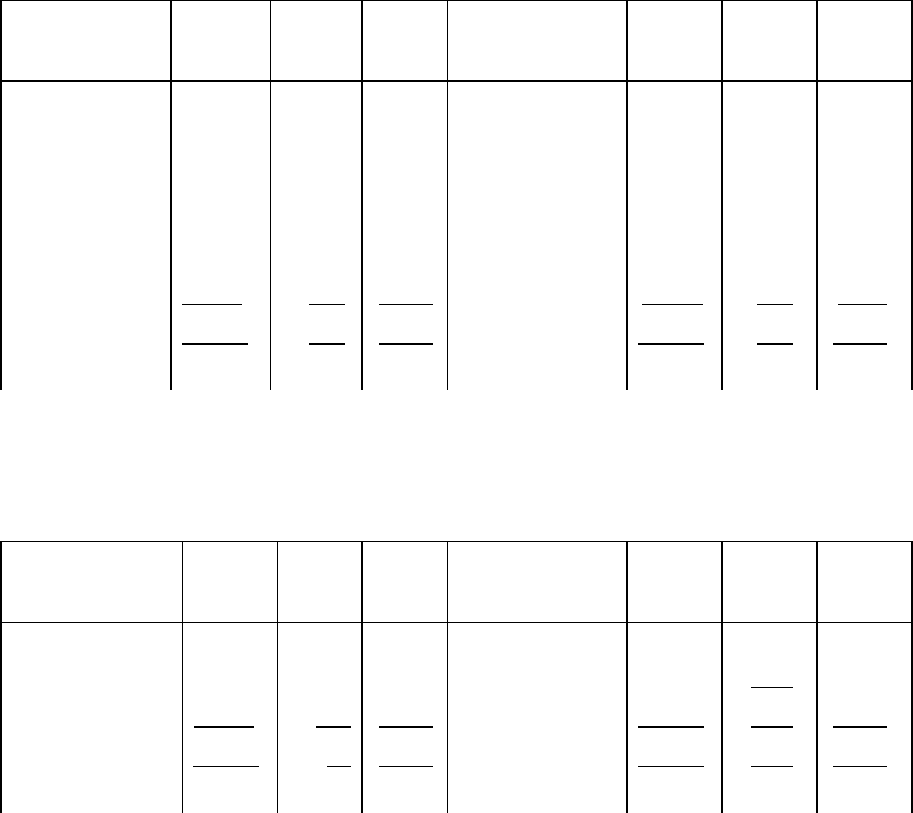

Consider the following example, which deals with the relationship between production output

and the total costs of a single-product company, taken over a period of four years:

Year Output Total Costs

(tonnes) RWF

1 2,700 10,400

2 3,100 11,760

3 3,700 14,880

4 4,400 20,700

Suppose that we have the above information, together with the cost indices as follows:

Year Cost Index

1 100

2 105

3 120

4 150

5 175 (estimated)

If our estimated output for Year 5 is 5,000 tonnes, how may we calculate the estimated total

costs?

First, we have to convert the costs of the four years’ production to Year 1 cost levels, by

applying the indices as follows:

Conversion Cost at

Year Actual Cost Factor Year 1 Level

RWF RWF

1 10,400 1 10,400

2 11,760 100/105 11,200

3 14,880 100/120 12,400

4 20,700 100/150 13,800

F2.1 MANAGEMENT ACCOUNTING

Page 48

Secondly, we must split the adjusted costs into their fixed and variable elements. This is

done by examining the difference or movement between any two years, for example:

Production Adjusted Cost

Year 1 2,700 tonnes RWF10,400

Year 4 4,400 tonnes RWF13,800

We observe that an increase of 1,700 tonnes gives a rise in costs of RWF3,400. The variable

cost is therefore RWF2 per tonne.

Now by deducting the variable cost from the adjusted cost in any year, we can ascertain the

level of fixed cost. For example, in Year 4, the variable cost @ RWF2 per tonne would be

4,400 × RWF2 = RWF8,800. If we deduct this figure from the total adjusted cost

RWF13,800, we are left with the fixed cost total of RWF13,800 – RWF8,800 = RWF5,000.

This fixed cost is, of course, expressed in terms of Year 1 cost level. In real terms, the fixed

costs (those costs which do not vary with changes in volume) will increase over the four years

in proportion to the cost index.

We now see that the yearly total costs, adjusted to Year 1 cost levels, may be split into the

fixed and variable elements as follows:

Production Fixed Variable Total

Year (tonnes) RWF @ RWF2 tonne RWF

1 2,700 5,000 5,400 10,400

2 3,100 5,000 6,200 11,200

3 3,700 5,000 7,400 12,400

4 4,400 5,000 8,800 13,800

5 (est’d) 5,000 5,000 10,000 15,000

Finally, by applying the cost index for each year to the total costs at Year 1 cost levels, we

may complete our forecast:

F2.1 MANAGEMENT ACCOUNTING

Page 49

Total Cost at

Year Year 1 Levels Cost Index Actual Cost

RWF RWF

1 10,400 100 10,400

2 11,200 105 11,760

3 12,400 120 14,880

4 13,800 150 20,700

5 (est’d) 15,000 175 26,250

Limitations

This forecast of RWF26,250 for the total costs in Year 5 is, of course, subject to many

limitations. The method of calculation assumes that all costs are either absolutely fixed or are

variable in direct proportion to the volume of production. In practice, as we have seen, it is

usually found that “fixed” costs will tend to rise slightly in steps, while the variable costs will

usually rise less steeply at the higher levels of output, because of the economies of scale.

Also, our forecast will only be as accurate as our forecast of the cost index for Year 5. This is

as difficult to predict as the Retail Price Index, which is influenced by changes in the price of

each item in the “shopping basket”.

The analysis of cost behaviour in this way is thus useful as a guide to management, provided

we remember that:

(a) It assumes a linear (or “straight line”) relationship between volume and cost.

(b) Costs will be influenced by many other factors, such as new production methods or new

plant.

(c) Inflation will have a varying effect on different items of cost.

This subject of cost behaviour is fundamental to many aspects of cost accounting.

F2.1 MANAGEMENT ACCOUNTING

Page 50

BLANK

F2.1 MANAGEMENT ACCOUNTING

Page 51

Study Unit 4

Materials and Stock Control

Contents

A. Introduction and Definitions

B. Accounting for Materials

C. Outline of Procedures

D. Organisation and Documentation of Purchasing

E. Receiving Department

F. Procedure in the Accounts Department

G. The Storekeeper and Stores Issues

H. Stock Levels

I. Economic Order Quantity

J. Stock Turnover

K. Accounting Records Required for Materials

F2.1 MANAGEMENT ACCOUNTING

Page 52

Contents (continued)

L. Stocktaking

M. The Pricing of Material Issues

N. Obsolete, Dormant and Slow-Moving Stock

_______________________________________________________________

O. Just-In-Time (JIT)

_______________________________________________________________

F2.1 MANAGEMENT ACCOUNTING

Page 53

A. INTRODUCTION AND DEFINITIONS

You have so far in your studies learned how cost accounting differs from financial

accounting, how we can set up double entry cost accounts, how expenditure can be

categorised into cost elements, and the nature of these cost elements, and we have touched on

the two accounting techniques of absorption costing and marginal costing.

We are now going to examine the first element of cost - material. Before we do so, however,

you should study carefully the following definitions of the various kinds of materials stock:

(a) Raw Materials

This is unprocessed stock awaiting conversion into saleable products. Remember that

the finished product of one process or industry is often the raw material of the next

process or another industry.

(b) Bulk Materials

These are materials not in unit form, i.e. they cannot be counted but must be measured

by weight, volume, bars, tubes or sheets. Such materials are not suitable for the work

in hand without any change in form.

(c) Part-Finished Stock

This is work-in-progress which has not reached the stage of completion as a part or

component.

(d) Finished Goods

These are manufactured goods, ready for sale or despatch, e.g. to a customer or agent.

They may also be known as manufactured stock or completed stock, and represent

work-in-progress which has been completed and transferred physically, and by entry in

the accounts, from the manufacturing department to the warehouse.

(e) Finished Parts

These are items or component parts which are in store and are awaiting either final

assembly or sale as spares.

(f) Scrap Material

This is discarded material which has some recovery value and which is usually either

disposed of without further treatment (other than reclamation and handling), or

reintroduced into the production process in place of raw material.

(g) Indirect Materials

These are materials which cannot be identified as part of the product, e.g. material for

the machine which makes the product.

(h) Consumable Stores

This term refers to certain direct materials, such as lubricants, waste, cleaning

materials, etc.

F2.1 MANAGEMENT ACCOUNTING

Page 54

B. ACCOUNTING FOR MATERIALS

Accounting for materials is every bit as important as accounting for cash.

Waste

Adequate control is necessary to guard against the many forms of waste which occur, such as

carelessness, pilfering, breakages, breaking bulk materials into small lots, overstocking, etc.

Overstocking

This causes loss by wasting space and congesting the stores; physical deterioration through

evaporation, shrinkage, damp or rust; obsolescence, so that space is wasted by out-of-date

material; and loss of interest on capital needlessly locked up.

Inefficient purchasing may result in direct financial loss by buying in the wrong markets or at

the wrong time, and in indirect loss by holding up the work on account of the failure to secure

deliveries at the required time.

Advantages of Accounting for Materials

The advantages of stores (material) accounting may be summarised briefly as follows:

(a) A check on the honesty of staff is provided.

(b) Differences are detected, investigated and prevented in the future.

(c) Production is not held up for lack of materials.

(d) Overstocking is avoided.

(e) Systematic buying is facilitated.

(f) Obsolete stocks are detected and dealt with.

(g) Wastage due to various causes can be measured.

(h) In the event of a fire which damages materials in stores but not the relative records, or

of a burglary, there is evidence available to produce to the insurance company in

connection with the amount of the claim.

F2.1 MANAGEMENT ACCOUNTING

Page 55

C. OUTLINE OF PROCEDURES

We shall now briefly outline the procedures necessary in the purchase, receipt, storage, issue

and transfer of materials.

Stock Control

Ordering Stock

Receiving Stock

Issuing Stock

Stock Levels

Storing Stock

F2.1 MANAGEMENT ACCOUNTING

Page 56

Buying

(a) Requests for the purchase of materials should always be made to the purchasing officer,

who can co-ordinate the requirements of several departments.

(b) The purchasing officer should maintain records so that the best possible terms can be

obtained for the goods required. (This will usually mean best possible price, but

occasionally it may be necessary to accept a higher price, for instance to obtain speedier

delivery.)

(c) Official order forms should be issued by the purchasing department and copies should

be raised as follows:

(i) To supplier.

(ii) To goods inward area to facilitate checking on arrival of goods.

(iii) Copy retained to check supplier’s invoice when it arrives.

(iv) Additional copies may be raised according to the requirements of the business, but the

number should be kept to a minimum.

Receipt

All goods should be introduced into the organisation through a designated and controlled

area. The material should be inspected by a competent official, who should prepare, in

duplicate, a goods received note. One of these forms should be passed to the purchasing

department for comparison with the copy of the order form and the invoice when it comes to

hand. The second copy will be passed to the storeman, who will enter details on the bin card

when receiving the goods. (Bin cards are more fully described in the next study unit.)

It is common for a firm supplying goods to require a signature of an authorised official of the

recipient organisation. Such procedures obviously improve the internal controls within the

supplier but often the recipient is acknowledging that he has received the goods, in full, in

good condition. In many cases the necessary testing and checking will take some time so it is

usual to sign the delivery note and add the word “unexamined”. This provides satisfactory