CPA A1.3 ADVANCED FINANCIAL REPORTING Study Manual

User Manual:

Open the PDF directly: View PDF ![]() .

.

Page Count: 452 [warning: Documents this large are best viewed by clicking the View PDF Link!]

- Financial Reporting Study Manual Cover Contents and Syllabus RO'Neill 8 08 12

- Study Unit Title Page

- 1 Regulatory and Conceptual Framework of Accounting 17

- Structure of IASC Foundation 18

- Development of an IFRS 20

- The Regulatory Framework 20

- 2 IAS 1 (Revised) – Presentation of Financial Statements 29

- Introduction 30

- 6 IAS 20 – Accounting for Government Grants & Disclosure of Government Assistance 81

- 8 IAS 40 – Investment Properties 103

- Assets with Both Tangible and Intangible Elements 124

- Website Development Costs 124

- Questions 124

- Objective 128

- Definitions 128

- Measurement 128

- Valuation Methods 130

- Disclosure 130

- 22 IFRS 5 – Non-Current Assets Held For Sale and Discontinued Operations 303

- 24 IAS 18 – Revenue 325

- 25 IAS 32, IAS 39, IFRS 7 – Financial Instruments 331

- Study Unit Title Page

- 27 IFRS 1 – First Time Adoption of International Financial Reporting Standards 361

- 28 IAS 34 – Interim Financial Reporting 365

- 29 IAS 41 – Agriculture 369

- 30 IFRS 8 – Operating Segments 377

- 31 Purchase of Own Shares and Distributable Profits 385

- Financial Reporting Study Manual Study Unit 1-16 RO'Neill 8 08 12 doc

- Study Unit 1

- The Regulatory and Conceptual Frameworks of Accounting

- A. Structure of IASC Foundation

- The IASC Foundation

- SAC

- IASB

- IFRIC

- a. INTRODUCTION

- B. objective

- D. components of financial statements

- E. financial review by management

- F. structure, content and reporting

- Example 1 – Statement of Financial Position

- i. statement OF COMPREHENSIVE INCOME

- A. Objective

- B. Definition

- C. Recognition

- D. Initial Measurement

- E. Subsequent Expenditure

- F. Measurement after Recognition

- G. Derecognition

- H. Depreciation

- I. Disclosure

- A. OBJECTIVE

- Income Statement

- Statement of Financial Position

- A. Definition

- B. Accounting Treatment

- C. Borrowing Costs Eligible for Capitalisation

- D. Commencement of Capitalisation

- E. Cessation of Capitalisation

- F. Suspension of Capitalisation

- G. Interest Rates

- H. Disclosure

- A. DEFINITION

- A. Introduction

- B. Definitions

- C. Recognition

- D. Accounting Treatment

- E. Repayment of Government Grants

- F. Disclosure

- G. Sundry Matters

- A. INTRODUCTION

- IAS 17 – Leases

- A. Introduction

- B. Types of Leases

- C. Accounting Treatment of Leases

- D. Detailed Treatment of Finance Leases

- E. Payments In Advance

- F. Recording Finance and Operating Leases in the Books of the Lessor

- G. Disclosure Requirements for Lessees

- H. Disclosure Requirements for Lessors

- I. Sale And Leaseback Transactions

- A. Objective

- B. Exclusions

- C. Definition

- D. Recognition and Initial Measurement

- E. Subsequent Measurement

- F. Cost Model

- G. Fair Value Model

- H. Cost Model vs. Fair Value Model

- I. Transfers

- J. Owner-Occupied Property and Investment Property

- K. Disposals

- L. Disclosure

- A. OBJECTIVE

- A. Objective

- B. Exclusions

- C. Definition

- D. Accounting Treatment

- E. Acquisition by Government Grant

- F. Exchange of Assets

- G. Internally Generated Goodwill

- H. Internally Generated Intangible Assets

- I. Research

- J. Development

- K. Measurement of Intangible Assets After Recognition

- L. Cost Model

- M. Revaluation Model

- N. Useful Life

- O. Disposals and Retirements

- P. Disclosure Requirements

- Q. Assets with Both Tangible and Intangible Elements

- R. Website Development Costs

- S. Questions

- A. OBJECTIVE

- B. EXCLUSIONS

- C. DEFINITION

- D. ACCOUNTING TREATMENT

- E. ACQUISITION BY GOVERNMENT GRANT

- F. EXCHANGE OF ASSETS

- G. INTERNALLY GENERATED GOODWILL

- H. INTERNALLY GENERATED INTANGIBLE ASSETS

- I. RESEARCH

- J. DEVELOPMENT

- K. MEASUREMENT OF INTANGIBLE ASSETS AFTER RECOGNITION

- L. COST MODEL

- M. REVALUATION MODEL

- N. USEFUL LIFE

- O. DISPOSALS AND RETIREMENTS

- P. DISCLOSURE REQUIREMENTS

- A. Objective

- B. Definitions

- C. Measurement

- D. Valuation Methods

- E. Disclosure

- A. OBJECTIVE

- A. Objective

- B. Provisions

- C. Definitions

- D. Restructuring

- E. Onerous Contract

- F. Contingent Liabilities

- G. Contingent Assets

- H. Disclosures

- I. Revision and Examination Practice Question

- A. OBJECTIVE

- If a group of items is being measured, it is the “expected value”.

- A. Objective

- B. Definition

- C. Dividends

- D. Updating Disclosures

- E. Disclosure

- F. Going Concern Considerations

- A. OBJECTIVE

- A. Introduction

- B. Definitions

- C. Accounting Policies

- D. Changes in Accounting Policies

- E. Disclosures

- F. Limitations of Retrospective Application

- G. Changes in Accounting Estimates

- H. Correction of Prior Period Errors

- I. Questions

- a. Applying the new accounting policy to transactions, other events and conditions occurring after the date as at which the policy is changed, and

- b. Recognising the effect of the change in the accounting estimate in the current and future periods affected by the change.

- C. ACCOUNTING POLICIES

- Accounting policies are determined by applying relevant IFRS or IFRIC and considering any relevant implementation guidance issued by the IASB.

- Where there is no IFRS or Interpretation that addresses a specific transaction, event or condition, then management should exercise judgement in developing and applying an accounting policy that results in information that is relevant and reliable.

- Reliable information should:

- In this regard, when exercising such judgement, management should refer to (in this order):-

- a. The requirements and guidance of the IFRS’s and IFRIC’s dealing with similar and related issues

- b. The definitions, recognition criteria and measurement concepts for assets, liabilities and expenses in the framework

- D. CHANGES IN ACCOUNTING POLICIES

- The standard highlights two types of event that do not result in the change of an accounting policy:

- In the case of non-current tangible fixed assets, a move to revaluation accounting will not result in a change of accounting policy under IAS 8 but a revaluation as per IAS 16.

- If a change in accounting policy is required by a Standard or Interpretation, then any transitional arrangements contained therein must be followed. If no such transitional arrangements are provided or an accounting policy is being changed voluntarily...

- (Prospective application is not allowed unless it is impracticable to determine the cumulative effect).

- The following disclosures are required for a change in an accounting policy:-

- 1. Reason for the change

- 2. Amount of the adjustment for the current period and for each period presented

- 3. Amount of the adjustments required for the periods prior to those disclosed in the financial statements

- 4. The fact that comparative information has been restated

- The entity should also disclose the impact of new IFRS that have been issued but have not yet come into force.

- G. CHANGES IN ACCOUNTING ESTIMATES

- It is acknowledged that the use of reasonable estimates is an essential part of the preparation of financial statements and consequently does not undermine their reliability. By their nature, these estimates may have to be revised periodically if the ...

- It is important, then, to realise that the revision of an estimate is not an error nor does it relate to prior periods.

- The effect of a change in an accounting estimate should be included in the period of the change if the change affects that period only or the period of the change and future periods if the change affects both. Any corresponding changes in assets and l...

- H. CORRECTION OF PRIOR PERIOD ERRORS

- Errors can normally be corrected through the income statement of the period when uncovered unless the errors are material. In the event that the errors uncovered relate to a previous period and they are classed as material, then it is necessary to cor...

- Only where it is impracticable to determine the cumulative effect of an error on prior periods can an entity correct the error prospectively.

- The following disclosures are required for errors uncovered:-

- 1. Nature of the prior period error

- 2. For each period, the amount of the correction (for each line item affected and, where applicable, the basic and diluted earnings per share)

- 3. The amount of the error at the beginning of the earliest prior period presented

- 4. In retrospective restatement is impracticable for a particular prior period, the circumstances that led to the existence of that condition and a description of how and from when the error has been corrected. Subsequent periods need not repeat these disc•

- A. Introduction

- B. Definitions

- C. Control

- D. Exemptions from the Requirement to Prepare Consolidated Financial Statements

- E. Accounting Dates

- F. Accounting Policies

- G. Cessation of Control

- H. Disclosure – IAS 27

- I. Acquisition Costs

- J. Mechanics and Techniques

- A. INTRODUCTION

- A. Introduction

- B. Determining the Fair Value of Net Assets

- C. Inter-Company Inventory Profit

- D. Inter-Company Profit on Sale of a Non-Current Asset

- E. Inter-Company Debts

- F. Preference Shares in a Subsidiary Company

- G. Loan Notes in a Subsidiary Company

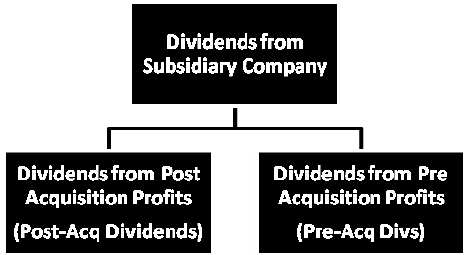

- H. Inter-Company Dividends

- I. Acquisitions of Subsidiary During the Year

- Consolidated Statement of Financial Position H Ltd Group

- Consolidated Statement of Financial Position H Limited Group

- Inter-Company Account

- I. ACQUISITIONS OF SUBSIDIARY DURING THE YEAR

- A. Investments in Associates and Interests in Joint Ventures

- B. Equity Method of Accounting

- C. Disclosure Requirements

- D. Mechanics and Techniques

- E. Transactions Between Group and Associate

- F. Interests in Joint Ventures

- G. Disclosure

- Financial Reporting Study Manual Study Unit 17-19 RO'Neill 8 08 12 doc

- A. Introduction

- B. Non-Controlling Interest

- C. Profit and Loss - Balance Forward in Subsidiary

- D. Inter-Company Profits

- E. Dividends

- F. Transfers to Reserves

- G. Debit Balance on Income Statement at Acquisition

- H. Sales and Cost of Sales

- I. Debenture Interest

- J. Acquisition of Subsidiary During the Year

- K. Revision and Examination Practice Questions

- L. Associate Companies in the Income Statement

- M. Goodwill on Acquisition of an Associate

- Consolidated Income Statement

- A. Introduction

- E. Cash Flow Statements and Overseas Transactions

- A. INTRODUCTION

- E. CASH FLOW STATEMENTS AND OVERSEAS TRANSACTIONS

- A. Objective

- B. Definitions

- C. Operating Activities

- D. Investing Activities

- E. Financing Activities

- F. Reporting Cash Flows From Operating Activities

- G. Worked Examples

- H. Disposal of a Tangible Non-Current Asset

- I. Taxation

- J. Dividends

- K. Worked Example

- L. Consolidated Cash Flow Statements

- M. Limitations of the Cash Flow Statement

- N. Advantages of the Cash Flow Statement

- O. Surmounting a Cash Shortage

- Financial Reporting Study Manual Study Unit 20-28 RO'Neill 8 08 12 doc

- A. Objective

- B. Definitions

- C. Contracts

- D. Contract Costs

- E. Contract Revenue

- F. Recognition of Costs and Revenues

- G. Measuring Outcome Reliably

- H. Stage of Completion

- I. Presentation

- J. Disclosures

- K. Further Definitions

- A. OBJECTIVE

- A. Explanatory Note

- B. Scope

- C. Definitions

- D. Number of Shares

- E. Measurement of Basic Earnings Per Share

- F. Changes in Capital Structure

- G. Presentation and Disclosure

- H. Retrospective Adjustments

- I. Fully Diluted Earnings Per Share

- J. Share Warrants and Options

- K. Contingently Issuable Shares

- L. Convertible Bonds/Loan Stock

- M. Dilutive/Anti-Dilutive Potential Ordinary Shares

- Example 1

- Example 2

- Example 3

- Example 4

- Example

- Example

- Example

- Number of Shares

- I. FULLY DILUTED EARNINGS PER SHARE

- A. Objective

- A. OBJECTIVE

- B. ASSETS HELD FOR SALE - DEFINITION

- IAS 18 – Revenue

- A. The Timing of Revenue Recognition

- B. Recognition

- C. Critical Event –V– Accretion Approach

- D. IAS 18 Revenue - Introduction

- E. Sale of Goods

- F. Rendering of Services

- G. Interest, Royalties and Dividends

- H. Disclosure

- Liabilities and Equity

- Compound Financial Instruments

- Interest, Dividends, Losses and Gains

- Disclosure of Financial Instruments

- Terms

- Information to be Disclosed

- A. Introduction

- B. Interested Parties

- C. Profitability Ratios

- D. Liquidity Ratios

- E. Investment Ratios

- F. Limitations of Ratio Analysis

- G. Other Measures of Business Operations

- H. Worked Example

- I. Revision and Examination Practice Questions

- A. INTRODUCTION

- B. INTERESTED PARTIES

- C. PROFITABILITY RATIOS

- D. LIQUIDITY RATIOS

- E. INVESTMENT RATIOS

- F. LIMITATIONS OF RATIO ANALYSIS

- G. OTHER MEASURES OF BUSINESS OPERATIONS

- A. Introduction

- B. Accounting Policies

- C. Exemptions and Exceptions

- D. Comparative Information

- IAS 34 – Interim Financial Reporting

- A. Introduction

- B. Minimum Components of an Interim Financial Report

- C. Selected Explanatory Notes

- D. Periods for which Interim Financial Statements are Required to be Presented

- E. Materiality

- F. Seasonal or Uneven Revenue and Costs

- Financial Reporting Study Manual Study Unit 29-34 RO'Neill 8 08 12 doc

- Study Unit 29

- IAS 41 – Agriculture

- Contents

- A. Introduction

- F. DISCLOSURE

- Purchase of Own Shares and Distributable Profits

- B. Distributable Profits

- A. PURCHASE OF OWN SHARES

- 1. Premium on redemption 10,000 x RWF0.22 = RWF2,000

- A distribution is defined as every description of distribution of a company’s assets to members (shareholders) of the company whether in cash or otherwise, with the exception of:

- Calculation of Distributable Profit

- Financial Reporting Study Manual Study Unit 35 RO'Neill 8 08 12 doc

CPA

Certified Public Accountant Examination

Stage: Advanced 1.3

Subject Title: Financial Reporting

Study Manual

BLANK

Page 1

© iCPAR

All rights reserved.

The text of this publication, or any part thereof, may not be reproduced or transmitted in any form or

by any means, electronic or mechanical, including photocopying, recording, storage in an information

retrieval system, or otherwise, without prior permission of the publisher.

Whilst every effort has been made to ensure that the contents of this book are accurate, no

responsibility for loss occasioned to any person acting or refraining from action as a result of any

material in this publication can be accepted by the publisher or authors. In addition to this, the authors

and publishers accept no legal responsibility or liability for any errors or omissions in relation to the

contents of this book.

INSTITUTE OF

CERTIFIED PUBLIC ACCOUNTANTS

OF

RWANDA

ADVANCED 1.3

FINANCIAL REPORTING

First Edition 2012

This study manual has been fully revised and updated

in accordance with the current syllabus.

It has been developed in consultation with experienced lecturers.

Page 2

BLANK

Page 3

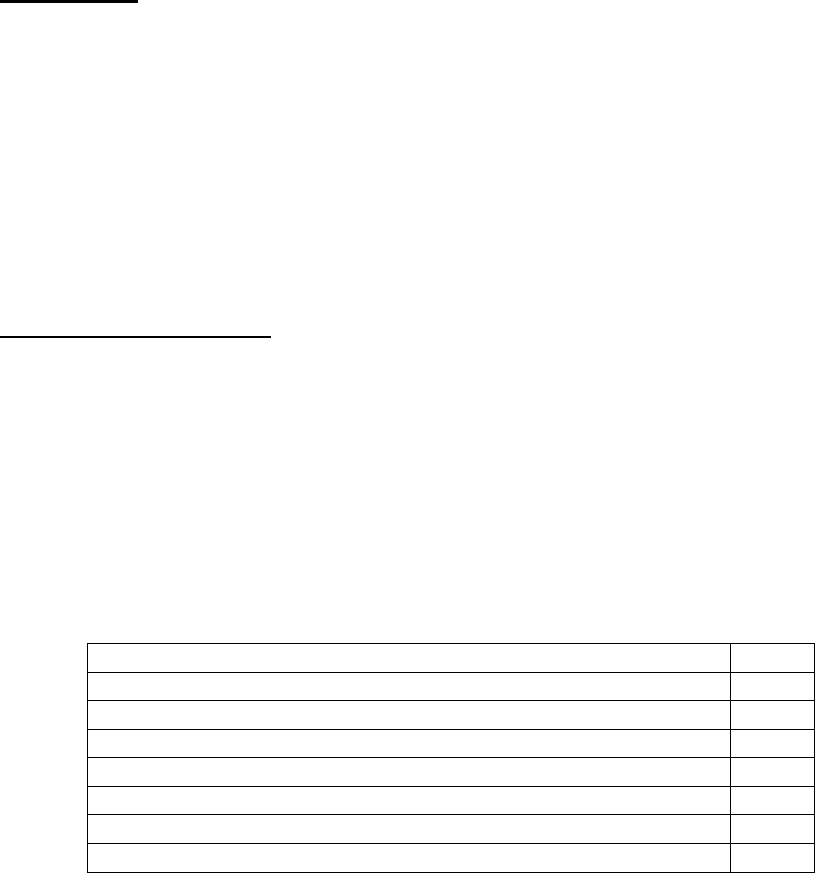

CONTENTS

Study Unit Title Page

Introduction to Course 13

1 Regulatory and Conceptual Framework of Accounting 17

Structure of IASC Foundation 18

Development of an IFRS 20

The Regulatory Framework 20

The Conceptual Framework 21

The Framework for the Preparation and Presentation of

Financial Information 22

Commonly Used Concepts in Financial Reporting 27

2 IAS 1 (Revised) – Presentation of Financial Statements 29

Introduction 30

Objective 30

Purpose of Financial Statements 30

Components of Financial Statements 30

Financial Review by Management 31

Structure, Content and Reporting 31

Sundry Matters 32

Statement of Financial Position Format 33

Statement of Comprehensive Income 36

Information to be Presented on Face of Income Statement or in the Notes 37

Statement of Changes in Equity 38

Disclosure of Significant Accounting Policies 39

3 IAS 16 – Property, Plant & Equipment 41

Objective 42

Definition 42

Recognition 42

Initial Measurement 43

Subsequent Expenditure 45

Measurement after Recognition 46

Derecognition 50

Depreciation 50

Disclosure 52

Page 4

Study Unit Title Page

4 IAS 36 – Impairment of Assets 55

Introduction 56

Definitions 57

Calculating an Impairment Loss 58

Recognition of Impairment Losses in the Financial Statements 59

Cash Generating Units 62

Reversal of Impairment Losses 69

Disclosures 70

Example 71

5 IAS 23 – Borrowing Costs 75

Definition 76

Accounting Treatment 76

Borrowing Costs Eligible for Capitalisation 76

Commencement of Capitalisation 77

Cessation of Capitalisation 77

Suspension of Capitalisation 77

Interest Rates 78

Disclosure 80

6 IAS 20 – Accounting for Government Grants & Disclosure of

Government Assistance 81

Introduction 82

Definitions 82

Recognition 83

Accounting Treatment 83

Repayment of Government Grants 85

Disclosure 86

Sundry Matters 86

7 IAS 17 – Leases 89

Introduction 90

Types of Leases 90

Accounting Treatment of Leases 91

Detailed Treatment of Finance Leases 91

Payments in Advance 97

Recording Finance and Operating Leases in the Books of the Lessor 98

Disclosure Requirements for Lessees 99

Disclosure Requirements for Lessors 100

Sale and Leaseback Transactions 101

Page 5

Study Unit Title Page

8 IAS 40 – Investment Properties 103

Objective 104

Exclusion 104

Definition 104

Recognition and Initial Measurement 104

Subsequent Measurement 105

Cost Model 105

Fair Value Model 106

Cost model Vs Fair Value Model 107

Transfers 108

Owner-Occupied Property and Investment Property 110

Disposals 110

Disclosure 111

9 IAS 38 – Intangible Assets 113

Objective 115

Exclusions 115

Accounting Treatment 116

Acquisition by Government 117

Exchange of Assets 117

Internally Generated Goodwill 117

Internally Generated Intangible Assets 117

Research 118

Development 118

Measurement of Intangible Assets After Recognition 119

Cost Model 120

Revaluation Model 120

Useful Life 121

Disposals and Retirements 122

Disclosure Requirements 122

Assets with Both Tangible and Intangible Elements 124

Website Development Costs 124

Questions 124

10 IAS 2 – Inventories 127

Objective 128

Definitions 128

Measurement 128

Valuation Methods 130

Disclosure 130

Page 6

Study Unit Title Page

11 IAS 37 – Provisions, Contingent Liabilities & Contingent Assets 133

Objective 134

Provisions 134

Definitions 134

Restructuring 137

Onerous Contract 137

Contingent Liabilities 138

Contingent Assets 138

Disclosure 139

12 IAS 10 – Events After The Reporting Period 141

Objective 142

Definition 142

Dividends 144

Updating Disclosures 144

Disclosure 144

Going Concern Considerations 144

13 IAS 8 – Accounting Policies, Changes in Accounting Estimates and

Errors 145

Introduction 146

Definition 146

Accounting Policies 147

Changes in Accounting Policies 147

Disclosures 149

Limitations of Retrospective Application 149

Changes in Accounting Estimates 150

Correction of Prior Period Errors 151

Questions

14 Consolidated Financial Statements 1

– Introduction to the Consolidated Statement of Financial Position 153

Introduction 154

Control 155

Exemptions from the Requirement to Prepare Consolidated

Financial Statements 155

Accounting Dates 157

Accounting Policies 157

Cessation of Control 157

Disclosure – IAS 27 157

Acquisition Costs 158

Mechanics and Techniques 160

Page 7

Study Unit Title Page

15 Consolidated Financial Statements 2

– Advanced Consolidated Statement of Financial Positions 165

Introduction 166

Determining the Fair Value of Net Assets 166

Inter-Company Inventory Profit 168

Inter-Company Profit on Sale of a Non-Current Asset 169

Inter-Company Debts 170

Preference Shares in Subsidiary Company 173

Loan Notes in a Subsidiary Company 174

Inter-Company Dividends 174

Acquisitions of Subsidiary During the Year 179

16 Consolidated Financial Statements 3

– Associates and Joint Ventures 189

Investments in Associates and Interests in Joint Ventures 190

Equity Method of Accounting 190

Disclosure Requirements 191

Mechanics and Techniques 192

Transactions Between Group and Associate 194

Interests in Joint Ventures 195

Disclosure 197

17 Consolidated Financial Statements 4

– Consolidated Income Statements 203

Introduction 204

Non-Controlling Interest 205

Profit and Loss – Balance Forward in Subsidiary 206

Inter-Company Profits 208

Dividends 210

Transfers to Reserves 215

Debit Balance on Income Statement at Acquisition 216

Sales and Costs of sales 217

Debenture Interest 218

Acquisition of Subsidiary During the Year 218

Revision and Examination Practice Questions 220

Associate Companies in the Income Statement 225

Goodwill on Acquisition of an Associate 228

18 IAS 21 – The Effects of Changes in Foreign Exchange Rates 235

Introduction 236

Functional and Presentation Currencies 236

Accounting for Individual Transactions 237

Translating the Financial Statements of Foreign Operation 242

Cash Flow Statements and Overseas Transactions 244

Page 8

Study Unit Title Page

19 Cash Flow Statements 245

Objective 247

Definitions 247

Operating Activities 247

Investing Activities 248

Financing Activities 248

Reporting Cash Flows from Operating Activities 249

Worked Examples 251

Disposal of a Tangible Non-Current Asset 257

Taxation 258

Dividends 259

Worked Example 259

Limitations of the Cash Flow Statement 271

Advantages of the Cash Flow Statement 271

Surmounting a Cash Shortage 272

20 IAS 11 – Construction Contracts 273

Objective 274

Definitions 274

Contracts 274

Contract Costs 275

Contract Revenue 275

Recognition of Costs and Revenues 276

Measuring Outcome Reliably 276

Stage of Completion 276

Presentation 277

Disclosures 282

Further Definitions 282

21 IAS 33 – Earnings Per Share 283

Explanatory Note 284

Scope 284

Definitions 284

Number of Shares 285

Measurement of Basic Earnings Per Share 286

Changes in Capital Structure 287

Presentation and Disclosure 292

Retrospective Adjustments 293

Fully Diluted Earnings Per Share 293

Share Warrants and Options 294

Dilutive/Anti-Dilutive Potential Ordinary Shares 298

Page 9

Study Unit Title Page

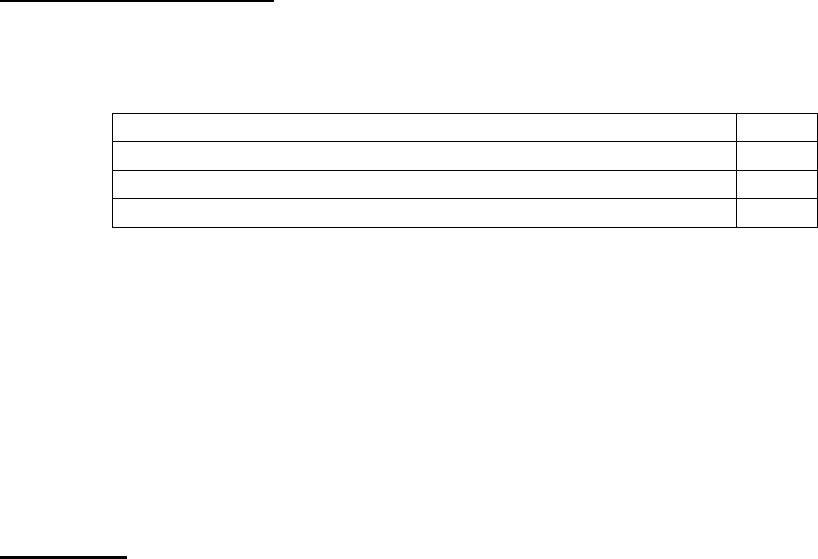

22 IFRS 5 – Non-Current Assets Held For Sale and Discontinued

Operations 303

Objective 304

Assets Held for Sale – Definition 304

Assets Held For Sale – Measurement 305

Assets Held For Sale – Presentation 306

Assets Held For Sale – Miscellaneous Points 306

Discontinued Operations – Definition 307

Discontinued Operations – Presentation 308

23 IAS 12 – Income Taxes 311

Introduction 312

Current Tax 312

Deferred Tax 313

Calculation of Deferred Tax 314

Why Account for Deferred Tax? 317

Deferred Tax Liabilities and Assets 318

Tax Rate 319

Further Specific Examples 319

Disclosure Requirements 321

24 IAS 18 – Revenue 325

The Timing of Revenue Recognition 326

Recognition 326

Critical Event v Accretion Approach 326

IAS 18 Revenue - Introduction 327

Sale of Goods 328

Rendering of Services 328

Interest, Royalties and Dividends 328

Disclosure 329

25 IAS 32, IAS 39, IFRS 7 – Financial Instruments 331

IAS 32 – Financial Instruments: Presentation 332

IAS 39 – Financial Instruments: Recognition and Measurement 336

IFRS 7 – Financial Instruments: Disclosures 339

Page 10

Study Unit Title Page

26 Analysing Financial Information 343

Introduction 344

Interested Parties 345

Liquidity Ratios 350

Investment Ratios 355

Limitations of Ratio Analysis 358

Other Measures of Business Operations 358

27 IFRS 1 – First Time Adoption of International Financial Reporting

Standards 361

Introduction 362

Accounting Policies 362

Exemptions and Exceptions 363

Comparative Information 364

28 IAS 34 – Interim Financial Reporting 365

Introduction 366

Minimum Components of an Interim Financial Report 366

Selected Explanatory Notes 367

Periods for which Interim Financial Statements are

Required to be Presented 368

Materiality 368

Seasonal or Uneven Revenue and Costs 368

29 IAS 41 – Agriculture 369

Introduction 370

Definitions 370

Recognition and Measurement 371

Gains and Losses 373

Government Grants 374

Disclosure 374

30 IFRS 8 – Operating Segments 377

Introduction 378

Definition 378

Reportable Segments 379

Disclosing Segmental Information 380

Drawbacks to Segmental Reporting 381

Page 11

Study Unit Title Page

31 Purchase of Own Shares and Distributable Profits 385

Purchase of Own Shares 386

Distributable Profits 389

32 IAS 19 – Employee Benefits 393

Introduction 394

Short-Term Employees Benefits 394

Post Employment Benefit Plans 396

Accounting for Pension Plans 397

The 10% Corridor Rule 405

Settlement and Curtailments 409

Past Service Costs 411

Other Long-Term Employee Benefits 411

Termination Benefits 412

Disclosure 413

IAS 26 – Accounting and Reporting by Retirement Benefit Plans 414

33 IAS 24 – Related Party Disclosures 417

Objective 418

Impact on the Financial Statements 418

Definitions 419

Disclosure Requirements 420

34 IFRS 2 – Share Based Payment 423

Introduction 424

Arguments Against Accounting for Share Based Payments 424

Accounting for Share Based Transactions 424

Disclosures 430

Example 430

35 IPSAS

36 Reporting for Various Entities

Social and Environmental Accounting and Reporting

Government Sector Financial Reporting

Accounting for Inflation

Page 12

BLANK

Page 13

INTRODUCTION TO THE COURSE

Stage: Advanced Level 1

Subject Title: A1.3 Advanced Financial Reporting

Aim

The aim of this subject is to ensure that students apply the appropriate judgement and

technical ability in the preparation and interpretation of financial statements for

complex business entities. Students must also be able to evaluate and communicate the

impact of current issues and developments in financial reporting to those who may not

have that technical expertise.

Advanced Financial reporting as an Integral Part of the Syllabus

By using a case study approach Advanced Financial reporting develops the technical

skills acquired in Financial Accounting and Financial reporting to ensure that students

can view financial reporting in its broadest context.

Learning Outcomes

On successful completion of this subject students should be able to:

• Apply and explain the acquisition method of accounting and related disclosure

requirements in financial statements and notes.

• Interpret and apply international financial reporting standards (including

reference to IPSAS) and interpretations adopted by the IASB selecting the

appropriate accounting treatment for transactions and events

• Analyse and evaluate financial statements.

• Write detailed reports, tailored to the technical understanding of the different

user groups.

• Evaluate and discuss the main accounting issues currently facing the

professional accountant in the field of financial accounting.

• Demonstrate appropriate professional judgement and ethical sensitivity.

Page 14

Syllabus:

1. Legislation

• Company Law relating to the preparation of all financial statements

2. Preparation of Financial Statements (Including

Consolidated Financial Statements)

• Statutory financial statements for incorporated entities

• Consolidated financial statements.

• Re-Construction & Re- Organisation

• Effects of Inflation

• Social Responsibility Accounting

• Environmental Accounting

3. International Financial Reporting

• An in depth knowledge of all technical pronouncements currently in issue with

particular reference to their application to practical situations (including

reference to the public sector).

• Current issues in financial reporting

• International Accounting Standards and International Financial Reporting

Standards

- (Revised) Presentation of Financial Statements

- Property, Plant & Equipment

- Impairment of Assets

- Borrowing Costs

- Accounting for Government Grants & Disclosure of Government

Assistance

- Leases

- Investment Properties

- Intangible Assets

- Inventories

- Provisions, Contingent Liabilities & Contingent Assets

- Events after the Balance Sheet Date

- Accounting Policies, Changes in Accounting Estimates & Errors

- The effects of changes in Foreign Exchange Rates

- Cash Flow Statements

- Construction Contracts

- Earnings Per Share

- Non Current Assets

- Income Taxes

- Revenue

- Financial Instruments

- First time adoption of

- Interim Financial Reporting

- Agriculture

- Operating Segments

Page 15

- Employee Benefits

- Related Party Disclosures

- Share Based Payment

4. Analysis, Evaluation and Interpretation of Financial

Statements

• Ratio analysis and cash flow analysis.

• Critical appraisal of financial statements; and

• Interpretation of financial statements and preparation of reports thereon.

Page 16

BLANK

Page 17

Study Unit 1

The Regulatory and Conceptual Frameworks of Accounting

Contents

______________________________________________________________________

A. Structure of IASC Foundation

______________________________________________________________________

B. Development of an IFRS

______________________________________________________________________

C. The Regulatory Framework

D. The Conceptual Framework

___________________________________________________________________________

E. The Framework for the Preparation and Presentation of Financial Information

___________________________________________________________________________

F. Commonly Used Concepts in Financial Reporting

___________________________________________________________________________

Page 18

A. STRUCTURE OF THE IASC FOUNDATION

In 1999, in a move that reflected the growing importance of international accounting

standards, the board of the International Accounting Standards Board (IASB) recommended

and later adopted a new constitution and structure.

As a result, the International Accounting Standards Committee Foundation was established in

the USA in 2001. An independent not-for-profit organisation, it is governed by 22 IASC

Foundation Trustees, who are required to have a comprehensive understanding of

international issues relevant to accounting standards for use in the world’s capital markets.

The main objectives of the IASC are:

• To develop a single set of understandable and enforceable global accounting standards

which of are high quality

• To require high quality, transparent and comparable information in financial statements

to help users in making economic decisions.

• To promote the use and application of these standards.

• To bring about convergence of national accounting standards and international

accounting standards.

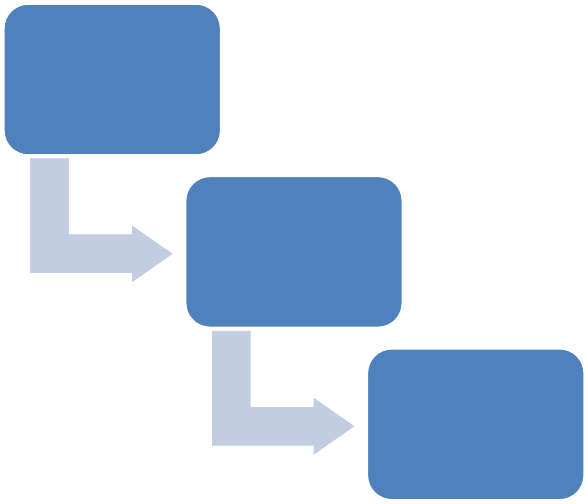

The IASC Foundation has a number of subsidiary bodies:

• The International Accounting Standards Board (IASB)

• The International Financial Reporting Interpretations Committee (IFRIC)

• The Standards Advisory Council (SAC)

IASB

SAC

IFRIC

The IASC

Foundation

Page 19

The IASB

The IASB is made up of 14 members and has the same objectives as the IASC Foundation. It

has sole responsibility for issuing International Financial Reporting Standards (IFRS’s),

following rigorous and open due process. The IASB cannot enforce compliance with its

standards and therefore it relies upon the co-operation of national standard setters.

All the most important national standard setters are represented on the IASB and their views

are taken into account so that a consensus is reached. These national standard setters can also

issue discussion papers and exposure drafts for comment in their own countries so that the

views of all preparers and users of financial statements can be represented.

With all the major national standard setters now committed to the international convergence

project, the IASB aims to develop a single set of understandable and enforceable, high quality

worldwide accounting standards.

The SAC

THE Standards Advisory Council provides a forum for experts from different countries and

different business sectors with an interest in international financial reporting to offer advice

when drawing up new standards. Its main objective is to give advice to the Trustees and the

IASB on agenda decisions and work priorities and on the major standard-setting projects.

The IFRIC

This committee has taken over the work of the previous Standing Interpretations Committee.

In reality, it is a compliance body whose role is to provide rapid guidance on the application

and interpretation of international accounting standards where contentious or divergent

interpretations have arisen.

It operates an open due process in accordance with its approved procedures. Its

pronouncements (known as SICs and IFRICs) are important because financial statements

cannot be described as being in compliance with IFRSs unless they also comply with the

interpretations.

Other Bodies

The IASB has enhanced its reputation and credibility even further by developing its

relationship with the International Organisation of Securities Commissions (IOSCO). This is

a very influential organisation of the world’s stock exchanges.

In 1995, the then International Accounting Standards Committee agreed to develop a core set

of standards which, when endorsed by IOSCO, would be used as an acceptable basis for

cross-border listings. This was achieved in 2000, arguably making the international

accounting standards the first steps towards global accounting harmonisation. Furthermore,

since 2005, as part of its harmonisation process, the European Union requires all listed

companies in all member states to prepare their consolidated financial statements using

IFRSs.

National standard setters (such as the UK’s Accounting Standards Board and The USA’s

Financial Accounting Standards Board) have a role to play in the formulation of international

accounting standards. Seven of the leading national standard setters work closely with the

Page 20

IASB, which the IASB sees as a “partnership” between the IASB and the national standard

setters, as they work towards the convergence of accounting standards worldwide. Often the

IASB will ask members of national standard setting bodies to work on particular projects in

which those countries have greater experience or expertise. Many countries that are

committed to closer integration with IFRSs will publish domestic standards equivalent (if not

identical) to IFRSs on a concurrent timescale.

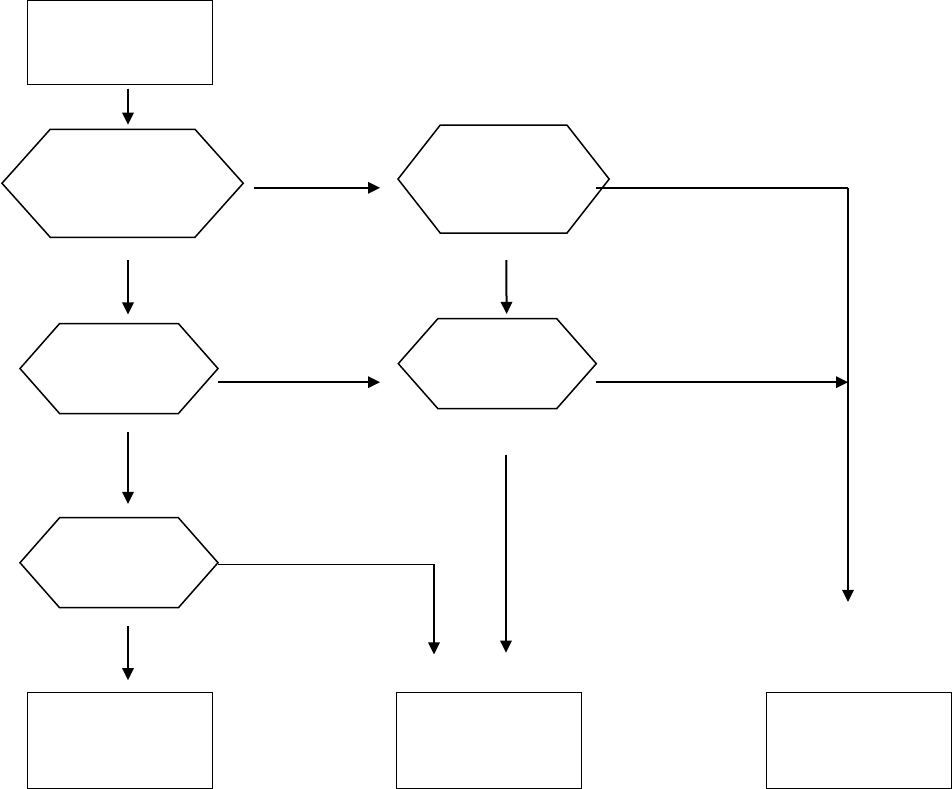

B. DEVELOPMENT OF AN IFRS

As mentioned above, the IASB is responsible for the development and publication of

international accounting standards. The standard requires the votes of at least eight of the

fourteen IASB members. The procedure is as follows:

1. The IASB (advised by the SAC) identifies a subject and appoints an advisory

committee to advise on the issues relevant to the subject area. If the subject matter is

complex and of high importance, the IASB may publish Discussion Documents for

public comment.

2. Following the receipt and review of comments, the IASB then develops and publishes

an Exposure Draft for public comment. The Exposure Draft is a draft version of the

intended subject. The normal comment period for both the Discussion document and the

Exposure Draft is ninety days.

3. After the review of any comments received, an International Financial Reporting

Standard (IFRS) is issued. The IASB also publishes a Basis for Conclusions, which

explains how it arrived at its conclusions and helps users to apply the standard in

practice. Sometimes, the IASB will conduct public hearings at which the proposed

standards are openly discussed and occasionally, field tests are conducted to ensure that

proposals are practical and workable around the world.

It is important to note that the IASC Foundation, the IASB and the accountancy profession

itself does not have the power to enforce compliance with the IFRSs. However, some

countries do adopt the IFRSs as their local standards, with others ensuring that there is no

significant difference between their standards and IFRs. Over the last decade or so, the profile

and status of the IASB has increased with the result being a commensurate increase in the

persuasive force of the IFRSs globally.

C. THE REGULATORY FRAMEWORK

The purpose of a regulatory framework is to regulate both the format and content of financial

statements. Accounting disclosure is regulated through a combination of:

• National company law and EU directives

• Stock exchange rules

• IFRS

Page 21

Accounting standards by themselves would not be a sufficient regulatory framework. Legal

and market regulations are also required to ensure the full regulation of both the preparation

and publication of financial statements.

A regulatory framework is desirable for the following reasons:

• Financial statements are based on principles and rules that can vary significantly from

country to country are prepared for users. There is also a wide range of users of these

financial statements (for example, investors, lenders, customers, government).

Preparation of accounts based on different principles makes it difficult, if not

impossible, for investors to analyse and interpret the information. A regulatory

framework would ensure consistency in financial reporting.

• The information needs to be comparable, as without this quality the credibility of the

financial reports would be undermined. This could have a negative impact on

investment. A regulatory framework would increase the users understanding of and

confidence in the financial statements.

• Increasingly, globalisation has resulted in trans-national financing, foreign direct

investment and securities trading. Thus, a single set of rules for the measurement and

recognition of assets, liabilities, income and expenses is required.

• A regulatory framework would also regulate the behaviour of companies towards their

investors, protecting the users of the financial statements. It would help ensure that the

financial statements give a true and fair view of the company’s financial performance

and position.

D. THE CONCEPTUAL FRAMEWORK

A conceptual framework can be defined as a coherent system of interrelated objectives and

fundamental principles. It is framework which prescribes the nature, function and limits of

financial accounting and financial statements. It can be thought of as an outline of the

generally accepted principles which form the theoretical foundation for financial reporting.

The IASB follows the principles-based approach to financial reporting (as opposed, say, to

the rules-based approach favoured by the FASB in the USA).

The establishment of these principles provide the basis for both the development of new

accounting standards and an appraisal of the standards already in issue.

There are a number of arguments in favour of having a conceptual framework:

• It allows both accounting standards and generally accepted accounting practice (GAAP)

to be developed in line with agreed principles. It would be extremely difficult to attempt

to address all technical issues that would satisfy the needs of every user.

• It helps avoid a situation where accounting standards are developed in an ad hoc and

piecemeal fashion, as a kneejerk response to specific problems and/or abuses. This sort

of “fire-fighting” can lead to inconsistencies between different accounting standards.

Page 22

• The conceptual framework enables critical issues to be addressed. For example, until

relatively recently, no accounting standard contained a definition of basic terms such as

“asset” or “liability”.

• With certain types of transactions becoming more and more complex over the years, a

conceptual framework aids accountants and auditors to deal with transactions not

covered per se by an accounting standard. It can give guidance of the general principles

on how transactions should be recorded and presented in the financial statements.

• Where a conceptual framework exists, an issue not yet covered by an accounting

standard can be dealt with temporarily by providing an interim approach until a specific

standard is issued.

• It is believed that standards that are based on principles are more difficult to circumvent

than a rules-based approach (the “cookbook” approach).

• It makes it less likely that the standard setting process can be influenced or even

hijacked by vested interests, for example large corporations or business sectors. This

enhances the credibility of the IFRSs and the accounting profession.

E. THE FRAMEWORK FOR THE PREPARATION AND PRESENTATION OF

FINANCIAL INFORMATION

The “Framework for the Preparation and presentation of Financial Information” (or simply,

“The Framework”) is a conceptual accounting framework that sets out the concepts and

principles that underpin the preparation and presentation of financial statements for external

users. It applies to the financial statements of both private and public entities.

The purpose of the framework is to:

• Assist the IASB in its role of developing future accounting standards and reviewing

existing IFRSs/IASs.

• Assist the IASB by providing a basis for reducing the number of alternative accounting

treatments permitted by the IFRSs

• Assist national standard setting bodies in developing national standards.

• Assist those preparing financial statements to apply IFRSs and also to deal with areas

where there is no relevant standard

• Assist auditors when they are forming an opinion as to whether financial statements

conform with IFRSs

• Assist users of financial statements when they are trying to interpret the information in

financial statements which have been prepared in accordance with IFRSs

• Provide information to other parties that are interested in the work of the IASB

Page 23

The Framework identifies the users of financial statements, and their main information needs,

to be:

• Investors: concerned about the risk and return of their investments.

• Employees: concerned about risks to their continuing employment and remuneration

• Lenders: concerned about the entities ability to service and repay loans and interest

• Suppliers and other trade creditors: concerned about whether they will be paid in

full and on time

• Customers: concerned about the ability of the entity to continue in business

• Governments and their agencies: concerned about taxation national statistics etc.

• The public: concerned about local economy, environmental issues, employment

opportunities etc.

The Framework has seven chapters:

1. The objective of financial statements

2. Underlying assumptions

3. The qualitative characteristics of financial statements

4. The elements of financial statements

5. Recognition of the elements of financial statements

6. Measurement of the elements of financial statements

7. Concepts of capital and capital maintenance

The salient points of each chapter will be outlined here.

Objective of financial statements

According to the Framework, the objective of financial statements is to provide information

about the financial position, performance and changes in financial position of an enterprise

that is useful to a wide range of users in making economic decisions.

The Framework points out that financial statements prepared for this purpose should meet the

common needs of most users, whilst also showing the results of the stewardship and

accountability of management. It is important to remember that the information is based on

historical information. However, if the information is reliable, its predictive value (i.e. its use

in assessing future performance) is greatly enhanced. Users can then use this information in

making their economic decisions.

Underlying assumptions

The Framework makes reference to two specific underlying assumptions:

(a) Accruals basis of accounting

Transactions are recognised when they occur and are recorded and reported in the

accounting periods to which they relate, regardless of the timing of the cash flows

arising from these transactions.

Page 24

(b) Going concern

Financial statements are prepared (normally) on the assumption that an enterprise is a

going concern and will continue in operation for the foreseeable future. If it is

management’s intention to liquidate (or significantly reduce the scale of its operations)

the accounts would have to be prepared on a different basis (e.g. the “break-up basis)

and this would have to be disclosed.

The qualitative characteristics of financial information

The Framework identifies four qualitative characteristics (all are subject to a threshold quality

of materiality):

(a) Relevance

Information provided by financial statements needs to be relevant. Information that is

relevant has predictive and confirmatory value. Information is considered relevant if :

• It has the ability to influence the economic decisions of users: and

• It is provided in time to influence those decisions

(b) Reliability

Information that is reliable can be depended upon to present a faithful representation

and is neutral, error free, complete and prudent. It also depends on the concept of

substance over form, because by applying this concept, users will see the economic

reality of transactions.

(c) Comparability

Users must be able to:

• Compare the financial statements of an entity over time to identify trends in its

financial position and performance

• Compare the financial statements of different entities to evaluate their relative

financial performance and financial position

In order to achieve this, there must be both consistency and adequate disclosure. Users

must be informed of the accounting policies employed in the preparation of the

financial statements as well as any changes in those policies in the period and the

effects of such changes. Furthermore, to compare the performance of the entity over

time, it is important that the financial statements show comparative information for the

preceding period(s).

(d) Understandability

It is assumed that users have a reasonable knowledge of business and economic

activities and are willing to study the information provided with reasonable diligence.

For information to be understandable, users needs to be able to perceive its significance.

Information that is relevant and reliable should not be excluded from the financial

statements simply because it is difficult for some users to understand.

Page 25

The elements of financial statements

The Framework provides definitions of the elements of financial statements. When applied

with the recognition criteria, the definitions provide guidance on how and when the financial

effect of transactions or events should be recognised in the financial statements.

(a) Assets

Assets are resources controlled by the entity as a result of past events, from which

future economic benefits are expected to flow to the entity.

(b) Liabilities

Liabilities are an entity’s obligations to transfer economic benefits, as a result of past

transactions and/or events.

(c) Equity Interest

Equity interest is the residual amount found be deducting all liabilities of the entity

from all of the entity’s assets.

(d) Income

Income is an increase in economic benefits during the accounting period in the form of

inflows or enhancements of assets or decrease in liabilities that result in increases in

equity (other than those relating to contributions from equity participants).

This definition follows a statement of financial position approach rather than the more

traditional income statement approach to recognising income>

(e) Expenses

Expenses are decreases in economic benefits during the accounting period in the form

of outflows or depletions of assets or incurring of liabilities that result in decreases in

equity (other than those relating to contributions from equity participants).

Recognition of the elements of financial statements

Recognition is the depiction of an element in words and by monetary amount in the financial

statements.

In order to be recognised in the financial statements, an item must meet the definition of an

element (see above). In addition, the Framework has two other criteria which must be met

before it can be recognised:

(a) It is probable that any future economic benefit associated with the item will flow to or

from the enterprise; and

(b) The item has a cost or value that can be measured with reliability.

Measurement of the elements of financial statements

Once an item meets the above criteria and is to be recognised in the financial statements, it is

necessary to decide on what basis it is to be measured. The item must, of course, have a

monetary value attached to it. The Framework outlines four measurement bases that are

frequently used in reporting; historic cost, current cost, realisable value, and present value. It

Page 26

mentions that historic cost is the most commonly adopted , although often within a

combination of bases, for example valuing inventories at the lower of cost and realisable

value or impairing a receivable to the present value of the amount considered collectible.

(a) Historic cost

Assets are recorded at cash paid at the date of acquisition. Liabilities are recorded at the

amount of proceeds received in exchange for the obligation (e.g. loan notes) or the

amount of cash expected to be paid to satisfy the liability (e.g. taxation).

(b) Current cost

Assets are recorded at cash that would have to be paid to acquire the same or equivalent

asset. Liabilities are carried at the undiscounted amount of cash required to settle the

obligation.

(c) Realisable value

Assets are recorded at cash that would be obtained by selling the asset in an orderly

disposal. Liabilities are carried at their settlement values (i.e. the undiscounted amounts

of cash expected to be paid to satisfy the liabilities in the normal course of business.

(d) Present Value

Assets are recorded at the present discounted value of future net cash flows that the item

is expected to generate in the normal course of business. Liabilities are carried at the

present discounted value of the future net cash outflows that are expected to be required

to settle the liabilities in the normal course of business.

Concepts of capital maintenance

The Framework refers to two concepts of capital; the financial concept of capital and the

physical concept of capital. The great majority of enterprises adopt the financial concept of

capital, which deals with the net assets of the entity. The physical concept of capital may be

more applicable where the users of the financial information are more concerned with the

operating capability of the enterprise.

The needs of the user should determine the most appropriate basis to adopt.

(a) Financial concept

A profit is earned if the financial amount of the net assets at the end of the period is

greater than that at the beginning of the period (excluding any distributions to and

contributions from the owners). Financial capital maintenance is measured in either

nominal monetary units or units of constant purchasing power.

(b) Physical concept

A profit is earned if the physical productive capacity (operating capacity) of the

enterprise (or the resources needed to achieve that capacity) at the end of the period is

greater than at the beginning of the period (excluding any distributions to and

contributions from the owners).

Page 27

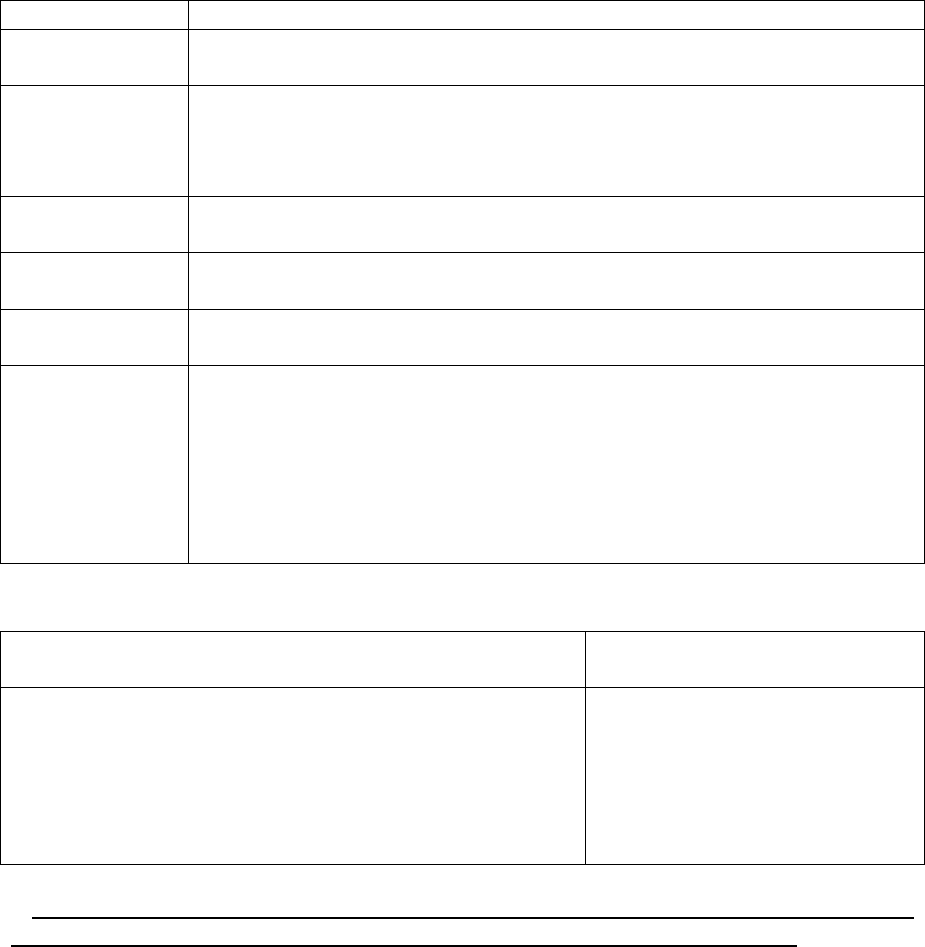

F. COMMONLY USED CONCEPTS IN FINANCIAL REPORTING

Though the Framework mentions two accounting policies that underpin the financial

statements of the company, other concepts can be employed too, to varying degrees:

Prudence

Cautious presentation of the entity's financial position. Profits

are recognised only when realised while losses are provided for

as soon as they are foreseen

Consistency

There is similar accounting treatment of like items within each

accounting period and from one period to the next

Entity

That the accounts recognise the business as a distinct separate

entity from its owners

Money Measurement

Accounts only deal with those items to which a monetary value

can be attributed

Materiality

If omission, misstatement or non disclosure affects the view

given, item is material and disclosure is required

Substance over Legal

Form

Recognises economic substance from legal form e.g. assets

acquired on hire purchase

Stable Monetary Unit

That the value of the monetary unit used is consistent over time

Accounting Periods

Accounts are prepared for discrete time periods

Page 28

BLANK

Page 29

Study Unit 2

IAS 1 (Revised) – Presentation of Financial Statements

Contents

_____________

A. Introduction

_____________

B. Objective

_____

C. Purpose of Financial Statements

_____

D. Components of Financial Statements

_____

E. Financial Review by Management

_____

F. Structure, Content and Reporting

______

G. Sundry Matters

______

H. Statement of Financial Position Format

______________________________________________________________________

I. Statement of Comprehensive Income

_____

J. Information to be Presented on Face of Income Statement or in the Notes

_____

K. Statement of Changes in Equity

______

L. Disclosure of Significant Accounting Policies

_____

M. Question / Solution

______

Page 30

A. INTRODUCTION

IAS 1 (Revised) was published in September 2007. It introduced a number of changes, the

main ones being as follows:

• The titles of the main financial statements were amended to Statement of Changes in

Position, Statement of Comprehensive Income and Statement of Cash Flows

• To present all non-owner changes in equity (comprehensive income) either in one

statement of comprehensive income or a separate income statement and statement

showing other comprehensive income

• To present a statement of financial position at the beginning of the earliest comparative

period when the entity applies a prior period adjustment.

The intention of the revision is to improve the quality of the information provided to users by

aggregating information in the financial statements on the basis of shared characteristics.

B. OBJECTIVE

The objectives of IAS 1 are to:

1. Provide the formats for the presentation of Financial Statements, such as Income

Statement and Statement of Financial Position.

2. Ensure that the Financial Statements are comparable year on year for the entity and

comparable to competitors.

3. Set out the disclosure required by management relating to the judgements they have

made in selecting the entity’s accounting policies.

4. Set out the disclosure to be made in relation to estimating uncertainty at the Statement

of Financial Position date, in particular where there is a significant risk of causing a

material adjustment to the carrying amounts at which assets and liabilities will be

presented in the next financial year.

C. PURPOSE OF FINANCIAL STATEMENTS

The objective of general purpose financial statements is to provide information about the

financial position of an entity. General purpose financial statements are those intended to

serve users who do not have the authority to demand financial reports tailored for their own

needs.

Financial statements also show the results of management’s stewardship of the entity’s

resources.

D. COMPONENTS OF FINANCIAL STATEMENTS

A complete set of financial statements should include:

Page 31

• A statement of financial position at the end of the period,

• A statement of comprehensive income for the period,

• A statement of changes in equity for the period

• Statement of cash flows for the period, and

• Notes, comprising a summary of accounting policies and other explanatory notes.

When an entity applies an accounting policy retrospectively or makes a retrospective

restatement of items in its financial statements, or when it reclassifies items in its financial

statements, it must also present a statement of financial position as at the beginning of the

earliest comparative period.

An entity may use titles for the statements other than those stated above. For example, an

entity may continue to use the previous title of Statement of Financial Position and cash flow

statement.

E. FINANCIAL REVIEW BY MANAGEMENT

In addition to the Financial Statements identified in Section D above, management may

present a Financial Review outside of the Financial Statements. The Financial Review

explains the main features of the entities financial performance and financial position as well

as the main areas of uncertainty. This Financial Review typically includes:

(a) An outline of the main factors affecting performance including changes in the business

environment in which the entity operates. How the entity has reacted to those changes

and the effect.

(b) Entity’s policy for investment and its dividend policy.

(c) How the entity is financed.

(d) Any resources that the entity uses that are not disclosed on the Statement of Financial

Position in accordance with IFRS’s.

Other reports which may be included are:

(a) Environmental Reports – Particularly in industries where environmental issues are of

significance.

(b) Value Added Statements.

Any reports provided in addition to the Financial Statements are outside the scope of the

IAS’s.

F. STRUCTURE, CONTENT AND REPORTING

• The financial statements shall be identified clearly and distinguished from other

information.

• The financial statements should show:

− The name of the reporting entity

Page 32

− The Statement of Financial Position date or the period covered by the income

statement

• The currency in which the financial statements are presented

• The level of rounding used in presenting amounts e.g. RWF’000, RWFm or the like.

• The financial statements shall be presented at least annually.

G. SUNDRY MATTERS

Fair Presentation and Compliance with IFRSs

The financial statements must "present fairly" the financial position, financial performance

and cash flows of an entity. Fair presentation requires the faithful representation of the effects

of transactions, other events, and conditions in accordance with the definitions and

recognition criteria for assets, liabilities, income and expenses set out in the Framework. The

application of IFRSs, with additional disclosure when necessary, is presumed to result in

financial statements that achieve a fair presentation.

IAS 1 requires that an entity whose financial statements comply with IFRSs make an explicit

and unreserved statement of such compliance in the notes. Financial statements shall not be

described as complying with IFRSs unless they comply with all the requirements of IFRSs

(including Interpretations).

Inappropriate accounting policies are not rectified either by disclosure of the accounting

policies used or by notes or explanatory material.

IAS 1 acknowledges that, in extremely rare circumstances, management may conclude that

compliance with an IFRS requirement would be so misleading that it would conflict with the

objective of financial statements set out in the Framework. In such a case, the entity is

required to depart from the IFRS requirement, with detailed disclosure of the nature, reasons,

and impact of the departure

Going Concern

An entity preparing IFRS financial statements is presumed to be a going concern. If

management has significant concerns about the entity's ability to continue as a going concern,

the uncertainties must be disclosed. If management concludes that the entity is not a going

concern, the financial statements should not be prepared on a going concern basis, in which

case IAS 1 requires a series of disclosures.

Accruals Basis of Accounting

IAS 1 requires that an entity prepare its financial statements, except for cash flow

information, using the accrual basis of accounting.

Consistency of Presentation

The presentation and classification of items in the financial statements shall be retained from

one period to the next unless a change is justified either by a change in circumstances or a

requirement of a new IFRS.

Page 33

Materiality and Aggregation

Each material class of similar items must be presented separately in the financial statements.

Dissimilar items may be aggregated only if they are individually immaterial.

Materiality has been defined as follows: “Omissions or misstatements of items are material if

they could, individually or collectively, influence the economic decisions of users taken on the

basis of the Financial Statements. Materiality depends in the size and nature of the omission

or misstatement judged in the circumstances. The size or nature of the item, or a combination

of both, could be the determining factor.”

Offsetting

Assets and liabilities, and income and expenses, may not be offset unless required or

permitted by a Standard or an Interpretation.

Comparative Information

IAS 1 requires that comparative information shall be disclosed in respect of the previous

period for all amounts reported in the financial statements, both face of financial statements

and notes, unless another Standard requires otherwise.

If comparative amounts are changed or reclassified, various disclosures are required.

H. STATEMENT OF FINANCIAL POSITION FORMAT

It is important before attempting a Statement of Financial Position to clearly understand the

split between current and non-current assets and liabilities

Current Assets

An asset shall be classified as current when it satisfies any of the following criteria:

(a) It is expected to be realised or is intended for sale or use in the entity’s normal operating

cycle;

(b) It is held primarily for the purpose of being traded;

(c) It is expected to be realised within 12 months after the Statement of Financial Position

date, or

(d) It is cash or a cash equivalent (as defined by IAS 7 Cash Flow Statements)

All other assets shall be classified as non-current.

Current Liabilities

A liability shall be classified as current when it satisfies any of the following criteria:

(a) It is expected to be settled in the entity’s normal operating cycle;

(b) It is held primarily for the purpose of being traded;

(c) It is due to be settled within 12 months after the Statement of Financial Position date.

All other liabilities shall be classified as non-current liabilities.

Page 34

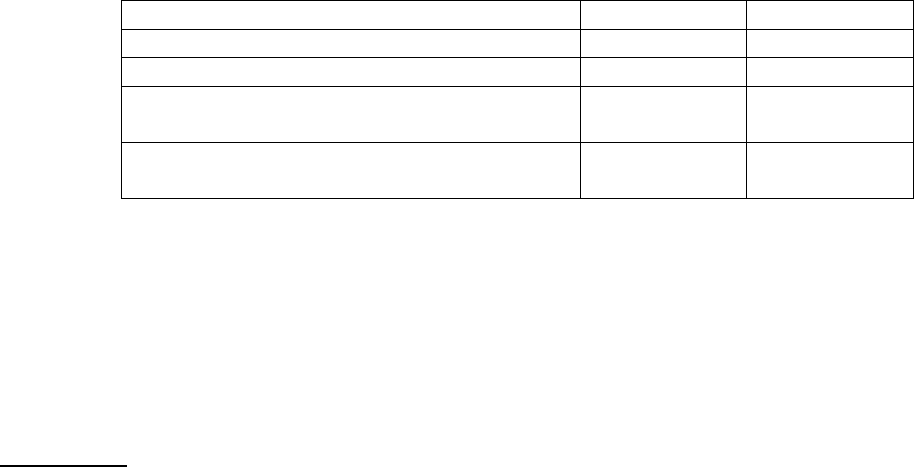

EXAMPLE OF A STATEMENT OF FINANCIAL POSITION

ABC LTD

STATEMENT OF FINANCIAL POSITION AS AT 31ST DECEMBER 2009

RWFm

RWFm

Assets

Non-Current Assets

Property

150

Plant and Equipment

78

Intangible Assets

22

Investments

30

280

Current Assets

Inventories

81

Trade Receivables

76

Prepayments

4

Cash and Cash Equivalents

22

183

Total Assets

463

Equity and Liabilities

Shareholders’ Equity

Share Capital

100

Share Premium

20

Revaluation Reserve

35

Retained Earnings

97

Total Equity

252

Non-Current Liabilities

Long-Term Borrowings

150

Long-Term Provisions

10

Total Non-Current Liabilities

160

Current Liabilities

Trade Payables

35

Accruals

4

Income Tax Payable

12

Total Current Liabilities

51

Total Equity and Liabilities

463

Page 35

Example 1 – Statement of Financial Position

The following information is available about the balances of ALP, a limited liability

company.

Balances at 31st May 2010

RWF

Non-Current

Assets

- Cost

500,000

- Accumulated Depreciation

100,000

Cash at Bank

95,000

Issued Share Capital – Ordinary Shares of RWF1 each

200,000

Inventory

125,000

Trade Payables

82,000

Retained Earnings

292,500

10% Loan Notes

150,000

Trade Receivables

112,000

Loan Note Interest Owing

7,500

REQUIREMENT:

Prepare the Statement of Financial Position of ALP as at 31st May 2010 using the format IAS

1 – Presentation of Financial Statements.

ALP Limited

Statement of Financial Position as at 31st May 2010

Assets

RWF

RWF

Non-Current Assets:

Cost

500,000

Less Accumulated Depreciation

(100,000)

400,000

Current Assets

Inventory

125,000

Trade Receivables

112,000

Cash at Bank

95,000

332,000

Total Assets

732,000

Equity and Liabilities

Shareholders’ Equity

Share Capital

200,000

Retained Earnings

292,500

492,500

Non-Current Liabilities

10% Loan Notes

150,000

Current Liabilities

Trade Payables

82,000

Accruals

7,500

89,500

Total Current Liabilities

239,500

Total Liabilities

Page 36

Total Equity and Liabilities

732,000

I. STATEMENT OF COMPREHENSIVE INCOME

IAS 1 allows a choice of two presentations of comprehensive income:

1. A statement of comprehensive income showing total comprehensive income; OR

2. An income statement showing the realised profit or loss for the period PLUS a

statement showing other comprehensive income.

Total comprehensive Income is the realised profit or loss for the period, plus other

comprehensive income.

Other comprehensive income is income and expenses that are not recognised in profit or loss.

That is, they are recorded in reserves rather than as an element of the realised profit for the

period. For example, other comprehensive income would include a change in revaluation

surplus.

Statement of Comprehensive Income

The recommended pro-forma layout is as follows:

PQR

Statement of Comprehensive Income for the Year Ended 31st December 2009

RWF’000

Revenue X

Cost of sales (X)

Gross profit X

Administrative expenses (X)

Profit from operations X

Finance costs (X)

Investment income X

Profit before tax X

Income tax expense (X)

Profit for the year X

Other Comprehensive Income

Gain/Loss on revaluation of PPE X

Gain/Loss on available for sale investments X

Total comprehensive income for the year X

Income Statement Plus Statement of Comprehensive Income

The recommended pro-forma layout is as follows:

Page 37

PQR

Income Statement for the year ended 31st December 2009

RWF’000

Revenue X

Cost of sales (X)

Gross profit X

Administrative expenses (X)

Profit from operations X

Finance costs (X)

Investment income X

Profit before tax X

Income tax expense (X)

Profit for the year X

A recommended format for the presentation of other comprehensive income is as follows:

PQR Other Comprehensive Income for the year ended 31st December 2009

RWF’000

Profit for the Year X

Other comprehensive income

Gain/Loss on revaluation of PPE X

Gain/Loss on available for sale investments X

Total comprehensive income for the year X

J. INFORMATION TO BE PRESENTED EITHER ON THE FACE OF THE

INCOME STATEMENT OR IN THE NOTES

When items of income and expense are material, their nature and amount shall be disclosed

separately. Examples of these would include:

(a) The write down of inventories to net realisable value

(b) The write down of property, plant and equipment to recoverable amount

(c) Gains/losses on disposal of property, plant and equipment

(d) Gains/losses on disposal of investments

(e) Legal settlements

An entity shall not present any items of income and expenses as extraordinary items. The

description extraordinary items was used in the past to represent income and expenses arising

from events outside the ordinary activities of the business. IAS 1 has therefore abolished this

classification of items.

Page 38

Example – Income Statement Function of Expenditure Method

Set out below are details from the financial records of Watt Limited:

RWFm

Distribution Costs

5,470

Interest Costs

647

Cost of Sales

18,230

Sales Revenue

44,870

Income Tax Expense

1,617

Administration Expenses

9,740

REQUIREMENT:

Prepare the Income Statement

SOLUTION:

Watt Limited - Income Statement for the year ended 31st March 2009

RWFm

Sales Revenue

44,870

Cost of Sales

18,230

Gross Profit

26,640

Administration Expenses

(9,740)

Distribution Costs

(5,470)

Profit from Operations

11,430

Interest Costs

(647)

Profit Before Tax

10,783

Income Tax Expense

(1,617)

Net Profit for the Year

9,166

K. STATEMENT OF CHANGES IN EQUITY

An entity shall present a statement of changes in equity showing on the face of the statement:

(a) Profit or loss for the period

(b) Each item of income and expense for the period that is recognised directly in equity e.g.

a revaluation surplus on the revaluation of property

(c) The effects of changes in accounting policies and correction of errors recognised in

accordance with IAS8

(d) The amounts of transactions with equity holders e.g. issue of shares, any premium

thereon and dividends to equity holders.

(e) The balance of retained earnings (accumulated profit) at the start of the year, changes

during the year and the balance at the end of the year.

(f) The balance on each reserve account at the start of the year, changes during the year and

the balance at the end of the year.

Therefore, the statement of changes in equity provides a summary of all changes in equity

arising from transactions with owners, including the effect of share issues and dividends.

Other non-owner changes in equity are disclosed in aggregate only.

Page 39

Statement of Changes in Equity

Essentially the statement of changes in equity presents in a columnar format all the changes

which have affected the various equity balances of share capital and reserves.

Share Share Revaluation Retained

Total

Capital Premium Reserve Earnings

Equity

RWF RWF RWF RWF

RWF

Balance at 1.1.09 X X X X

X

Change in accounting

policy (X)

(X)

__ ___ ___ ____ ___

Restated Balance X X X X

X

Issue of shares X X X

Revaluation gain X

X

Transfer (X) X -

Profit for the year X

X

Dividends (X) (X)

__ ___ ___ ____ ____

Balance at 31.12.09 X X X X X

__ ___ ___ ____ _____

L. DISCLOSURE OF SIGNIFICANT ACCOUNTING POLICIES

An entity shall disclose the significant accounting policies used in preparing the financial

statements.

Page 40

BLANK

Page 41

Study Unit 3

IAS 16 – Property, Plant and Equipment

Contents

___________________________________________________________________________

A. Objective

___________________________________________________________________________

B. Definition

___________________________________________________________________________

C. Recognition

___________________________________________________________________________

D. Initial Measurement

___________________________________________________________________________

E. Subsequent Expenditure

___________________________________________________________________________

F. Measurement after Recognition

___________________________________________________________________________

G. Derecognition

___________________________________________________________________________

H. Depreciation

___________________________________________________________________________

I. Disclosure