CPA I1.4 AUDITING Study Manual

User Manual:

Open the PDF directly: View PDF ![]() .

.

Page Count: 201 [warning: Documents this large are best viewed by clicking the View PDF Link!]

- I1 4 Auditing Standard Cover sheet PW formatted V2 110412 RO'Neill 26 07 12

- I1 4 Auditing Copyright PW Formatted V2 110412 RO'Neill 26 07 12

- I1 4 Auditing Course contents PW formatted V2 110412 RO'Neill 26 07 12

- I1 4 Auditing Aims Objectives Syllabus of Auditing PW Formatted V2 11 04 12 RO'Neill 26 07 12

- I1 4 Auditing Unit 1 PW formatted V2 110412 RO'Neill 26 07 12

- I1 4 Auditing Unit 2 PW formatted V2 110412 RO'Neill 26 07 12

- I1 4 Auditing Unit 3 PW Formatted V2 110412 R'ONeill 26 07 12

- I1 4 Auditing Unit 4 PW Formatted V2 110412 RO'Neill 26 07 12

- I1 4 Auditing Unit 5 PW formatted V2 110412 RO'Neill 26 07 12

- I1 4 Auditing Unit 6 PW formatted V2 110412 RO'Neill 26 07 12

- The Entity's Risk Assessment Process

- B. Information Systems, Including the Related Business Processes, Relevant to Financial Reporting and Communication

- Specific examples of controls would include:

- Approval and control of documents through signing off or pre-numbering,

- Checking the arithmetical accuracy of records,

- Reviewing control accounts for large or unusual items,

- Reconciling figures,

- Matching figures or documents,

- Limiting physical access to assets and records,

- Matching physical existence to book records and other external data,

- Segregating duties such as custody of assets from initiation of transactions to recording of transactions to review of transactions.

- Limitations of Internal Control

- D. ASSESSING THE RISK OF MATERIAL MISSTATEMENT

- I1 4 Auditing Unit 7 PW formatted V2 110412 RO'Neill 26 07 12

- I1 4 Auditing Unit 8 PW formatted V2 110412 RO'Neill 26 07 12

- Selecting All Items (100% examination)

- Selecting Specific Items

- Audit Sampling

- Sample Size

- Selecting Items for Testing to Gather Audit Evidence

- Selecting the audit sample

- Audit Conclusions and Reporting

- If adequate disclosure is made in the financial statements, the auditor should express an unqualified opinion but modify the auditor's report by adding an emphasis of matter paragraph that highlights the existence of a material uncertainty and draws a...

- Acknowledgment by Management of its Responsibility for the Financial Statements

- Representations by Management as Audit Evidence

- Documentation of Representations by Management

- Action if Management Refuses to Provide Representations

- Determining the Need to Use the Work of an Expert

- Competence and Objectivity of the Expert

- Scope of the Expert's Work

- Evaluating the Work of the Expert

- Reference to an Expert in the Auditor's Report

- I1 4 Auditing Unit 9 PW formatted V2 110412 RO'Neill 26 07 12

- I1 4 Auditing Unit 10 PW formatted V2 110412 RO'Neill 26 07 12

- I1 4 Auditing Unit 11 PW formated V2 110412 RO'Neill 26 07 12

CPA

Certified Public Accountant Examination

Stage: Intermediate Level I1.4

Subject Title: Auditing

Study Manual

INSIDE COVER - BLANK

Page 1

INTRODUCTION

© CPA Ireland

All rights reserved.

The text of this publication, or any part thereof, may not be reproduced or transmitted in any

form or by any means, electronic or mechanical, including photocopying, recording, storage

in an information retrieval system, or otherwise, without prior permission of the publisher.

Whilst every effort has been made to ensure that the contents of this book are accurate, no

responsibility for loss occasioned to any person acting or refraining from action as a result of

any material in this publication can be accepted by the publisher or authors. In addition to

this, the authors and publishers accept no legal responsibility or liability for any errors or

omissions in relation to the contents of this book.

INSTITUTE OF

CERTIFIED PUBLIC ACCOUNTANTS

OF

RWANDA

INTERMEDIATE I1

I1.4 AUDITING

First Edition 2012

This study manual has been fully revised and updated

in accordance with the current syllabus.

It has been developed in consultation with experienced lecturers.

Page 2

INTRODUCTION

BLANK

Page 3

CONTENTS

CONTENTS

Study

Unit

Title

Page

Introduction to Your Course

7

1

Introduction

13

Assurance

14

Levels of Assurance

14

The Audit Function

15

Types of Audits

15

The Limitations of an Audit

16

The need for Regulation

17

Methodology of an Audit

18

ISA 200

19

2

The Auditor and the Audit Environment

21

Audit Opinion

22

Role of the Auditor

23

Relationships & Responsibilities

23

The Audit Profession

24

International Standards on Auditing

25

Corporate Governance

28

Codes of Best Practice

29

3

Auditors Legal, Ethical & Professional Responsibilities – Part 1

35

Professional & Ethical Responsibilities

36

Statutory Responsibilities & Rights

43

Appointment of Auditors

44

Resignation & Removal of Auditors

44

Auditor Duties & Rights

46

4

Auditors Legal, Ethical & Professional Responsibilities – Part 2

49

Auditor’s responsibilities in relation to fraud and for the entities

compliance with Laws & Regulations

50

Auditor’s responsibilities defined by case law arising from negligence

and Related exposure and consequences

55

Pre-Appointment Procedures

58

5

Audit Planning and Supervision

65

Materiality

67

Audit Risk and its Components

69

Audit Strategies

71

Knowledge of the entity and its environment

76

Response to assessed risks of material misstatement

79

Documentation

85

Audit Supervision and Review

88

Page 4

CONTENTS

Study

Unit

Title

Page

6

Internal Control – Assessing Control Risk & Tests of Control

91

Internal Control

92

Information Systems, including the Related Business Process relevant

to Financial reporting and communication

95

Control Activities

95

Assessing the Risk of Material Misstatement

97

Tests of Control

98

Assessment of impact on audit strategy

100

The recording of control systems

100

Audit Programmes

102

7

Financial Statement items – Substantive Procedures

115

Assertions

116

Specific Audit Procedures

116

Balance Sheet items

119

Profit & Loss items

137

Assessment of Misstatements

139

Impact on Audit Reporting

140

8

Audit Execution – Other Considerations

141

Sampling

142

Analytical Review

144

Going Concern

146

Subsequent Events

150

Accounting Estimates

153

Commitments & Contingencies

154

Management Representations

156

Use of Experts

158

Opening Balances

161

Comparatives

163

9

Computer Information Systems

167

Entity computer systems and controls

168

Computer Assisted Audit Techniques (CAAT’s)

175

10

Audit Reporting

179

Review Considerations

180

Reporting on audited financial statements

183

Key concepts

185

Basic element of report

186

Modified Reports

188

Circumstances giving rise to modified reports

190

Auditors’ responsibilities before and after date of audit report

191

Auditors’ responsibilities for other documents

191

Page 5

CONTENTS

Study

Unit

Title

Page

11

Public Sector Auditing

195

The role of the Office of the Auditor General (OAG)

196

The Legal Environment in which the OAG and auditees function

196

Specific considerations for public sector auditing

198

The role of INTOSAI

198

Page 6

INTRODUCTION

BLANK

Page 7

INTRODUCTION

INTRODUCTION TO THE COURSE

Stage: Intermediate 1

Subject Title: I1.4 Auditing

Aim

The aim of this subject is to introduce students to the concepts and principles of the audit

process and to develop their understanding of its application in the context of the legal,

regulatory and ethical framework of the profession.

Auditing as an Integral Part of the Syllabus

Auditing is an essential foundation subject for the subsequent study of Audit Practice and

Assurance Services at Advanced 2 Stage. It is also an essential component for the study of

Advanced Financial reporting at Advanced 2 Stage. In carrying out the audit of an entity’s

financial statements there is a critical need to identify the source, and test the treatment of

financial statement items (period transactions and year-end balances) and disclosures, to

ensure compliance with generally accepted accounting practice. The subjects: Financial

Accounting and Financial Reporting will provide students with this necessary knowledge.

Introduction to Law, Company Law, Taxation and Information Systems will increase

students’ awareness of other matters that an auditor must consider in the audit process.

Learning Outcomes

On successful completion of this subject students should be able to:

• Interpret and discuss the legal, regulatory and ethical framework within which the

auditor operates.

• Differentiate and explain the respective responsibilities of directors and auditors.

• Explain the nature, purpose and scope of an audit and discuss and defend the role of

the auditor.

• Apply and explain the process relating to the acceptance and retention of professional

appointments, to include the purpose and content of engagement letters.

• Devise an overall audit strategy and develop an audit plan.

• Supervise and review the various stages of the audit process.

• Outline the nature of internal controls and the procedures required to evaluate control

risk relating to specific accounting systems, in order to identify internal controls and

weakness within the systems.

• Distinguish between Tests of Control and Substantive Procedures.

• Design and apply the appropriate audit tests to include in the audit programme.

• Carry out analytical procedures and assess the implications of the outcome.

Page 8

INTRODUCTION

• Explain the significance, purpose and content of management letters and management

representations.

• Explain the distinction between an internal and external audit.

• Apply and discuss audit sampling.

• Demonstrate the outcome and implications of subsequent event reviews.

• Plan and describe the audit of computer information systems.

• Draw appropriate conclusions leading to the formulation of the auditor’s opinion.

• Apply and explain the basic component elements of the Auditor’s Report.

• Identify and analyse matters that impact on the wording of Modified

Reports differentiating between matters that do not affect the auditor’s opinion and

matters that do affect the auditor’s opinion.

• Recognise ethical issues, discuss, escalate or resolve these as appropriate within the

Institute’s ethical framework, demonstrating integrity, objectivity, independence and

professional scepticism.

Page 9

INTRODUCTION

Syllabus:

1. The Auditor and the Audit Environment

• The Statutory Audit: need, objective, focus, nature and structure. Public interest,

expectations, interrelationships between auditor, directors (management) and

shareholders and other users of financial statements, including their respective

roles and the auditor’s duties to these parties.

• The Rwandan audit profession and ICPAR: organisation and regulation.

• International Standards on Auditing (ISAs) and other technical pronouncements

issued by APB: nature, formulation, issuance and compliance enforcement.

• The audit implications of International Accounting Standards (IFRS/IAS):

understanding and basis for application.

• Directors’ responsibilities versus auditor’s responsibilities for financial statements

and internal controls; distinction between external and internal audit.

• Corporate governance.

2. Auditor’s Legal, Ethical and Professional Responsibilities

• Professional ethical responsibilities:

- IFAC Code of Ethics.

• Statutory responsibilities and rights:

- Key responsibilities derived from International Standards on Auditing (ISAs).

- Auditor’s responsibility in relation to fraud and for the entity’s compliance

with laws and regulations.

- Auditor’s responsibilities defined by case law arising from alleged negligence

(financial statements misstated) and related exposure and consequences

- Pre-appointment procedures: client assessment (including management

integrity) and completion of engagement letter.

3. Audit Planning and Supervision

• Materiality: nature (quantitative and qualitative), determination, impact and use

throughout different phases of the audit.

• Audit risk and its components (inherent, control and detection risks):

interrelationships, evolution as audit progresses and impact on nature, timing and

extent of audit work.

• Audit strategies (risk based auditing, tests of control, substantive procedures,

combined procedures, audit around and through computerised systems) and their

impact on the conduct of the audit.

• Knowledge of the entity and its environment: business, risks, management, and

accounting systems.

• Nature, extent and timing of audit procedures in response to assessed risks of

material misstatement, sufficient and appropriate audit evidence, types of audit

evidence, general audit techniques (enquiry, observation, inspection, analysis,

computation, confirmation).

• Audit planning memo, audit programmes and working papers.

• Audit supervision and review.

Page 10

INTRODUCTION

4. Audit Execution: Internal Control, Assessing Control Risk and Tests

of Control

• Entity’s control environment and control procedures, objectives, limitations,

attributes.

• Auditor’s and management’s respective responsibilities.

• Internal control descriptions (flowcharts, narrative descriptions, walkthroughs)

and internal control assessments (ICEs/ICEQs).

• Broad approach to internal controls, components of internal controls, limitations

of internal control.

• Assessing the Risk of Material Misstatement, Internal Controls assessment and

Tests of Control for the following major systems: sales, purchases, payroll, cash

receipts and disbursements, inventory.

• Audit Programmes for Tests of Control.

• Final Assessment of Control Risk.

• Management letter reporting and assessment of impact on audit strategy.

5. Audit Execution: Financial Statement Items Substantive Procedures.

• Application of specific substantive procedures to test the following categories of

assertions:

- Assertions relating to classes of transactions and events;

- Assertions relating to account balances;

- Assertions relating to presentation and disclosure.

• Audit of statements of financial position, validation procedures, applied in audit

of: - Tangible fixed assets.

- Inventory.

- Accounts receivable, prepayments & sundry debtors.

- Investments and market securities.

- Bank and cash balances.

- Accounts Payable, accruals & sundry creditors, provisions for

liabilities.

- Debenture loans and bank borrowings.

- Capital and Reserves, Equity.

• Audit of statements of comprehensive Income account, validation procedures,

applied in audit of:

- Revenues and expenses.

- Sales/purchases.

- Wages and salaries.

- Other statement of comprehensive income account items.

• Understanding of IFRS/IAS concerning above items.

• Misstatements / aggregation / assessment / impact on audit reporting.

Page 11

INTRODUCTION

6. Audit Execution: Other Considerations

• Sampling methods: decision to use, judgemental versus statistical (MUS)

sampling methods for controls and financial statement items, sample selection and

assessment.

• Analytical review: nature and use (financial statements/data) throughout audit.

• Going concern and its impact throughout the different phases of the audit.

• Subsequent events.

• Accounting estimates.

• Commitments and contingencies.

• Management representation letters.

• Use of experts.

7. Audit Execution: Computer Information Systems (Cis) Auditing

• Entity’s computer systems and controls:

- Computer systems: general applications of e-commerce and impact on control

and audit work, key computer processes including data organisation and

access, network and electronic transfers and transaction processing

modes, key computer system hardware and software, including XBRL

(eXtensible Business Reporting Language.

- Key computer system general controls: design and implementation, data

integrity, privacy and security, system program changes, system access and

disaster recovery plans.

- Key computer system application controls: transactions input, processing and

output, master-file changes.

• Computer Assisted Audit Techniques (CAATs):

- Nature (computer software including expert systems and test data),

- Purpose (testing, administration),

- Application and related audit concerns (integrity and security of CAATs, audit

planning considerations).

8. Audit Reporting

• Reporting on Audited Financial Statements.

• Key concepts: opinion, true and fair view, materiality, statutory requirements.

• Basic elements of the Auditor’s Report.

• Modified Reports, differentiating between

- Matters that do not affect the auditor’s opinion, and

- Matters that do affect the auditor’s opinion.

• Circumstances giving rise to Modified Reports:

- Limitations on Scope.

- Disagreements with management.

• Auditor’s responsibility before and after the date of the Auditor’s Report.

• Auditor’s responsibility for other information in documents (e.g. Annual Report)

containing audited financial statements.

Page 12

INTRODUCTION

9. Public sector auditing

• The role of the OAG

• The legal environment in which the OAG and auditees function

• Specific considerations for public sector auditing

• The role of INTOSAI

Page 13

UNIT 1 - INTRODUCTION

Study Unit 1

Introduction to Auditing

Contents

A. Assurance

B. Levels of Assurance

C. The Audit Function

D. Types of Audits

E. The Limitations of an Audit

F. The need for Regulation

G. Methodology of an Audit

H. ISA 200

Page 14

UNIT 1 - INTRODUCTION

INTRODUCTION

There has been a huge growth in information that is available today in all aspects of business.

The use of the internet has made access to information relatively easy and more and more

information is been required in all areas, not just financial. For example, take a look at the

Bank of Kigali annual report.

This growth in information has led to a need for assurance as to the quality and reliability of

that information so that users can make informed decisions based on the information that is

available to them.

A. ASSURANCE

The International Standards on Auditing (ISA) glossary of terms gives a definition of an

assurance engagement as “one in which a practitioner expresses a conclusion designed to

enhance the degree of confidence of the intended users other than the responsible party about

the outcome of the evaluation or measurement of a subject matter against criteria.”

In practice, this could be an auditor expressing an opinion to the shareholders of a company

on a set of financial statements prepared by management as to whether they have been

prepared in a true and fair manner in accordance with accounting standards and relevant

company law.

An audit is a type of assurance engagement.

B. LEVELS OF ASSURANCE

Various levels of assurance may be given but this depends very much on (1) the individual

engagement, (2) the criteria applied and (3) the subject matter. The glossary of terms refers

to two types but I will refer to three:

• Reasonable level of assurance – subject matter materially conforms to criteria; i.e.

accounts give a true and fair view having regard to the accounting standards and law,

such as carried out in an audit. This can also be known as a positive expression.

• Limited level of assurance – no reason to believe that subject matter does not

conform to criteria. Essentially, a negative form of expression. Expect to see this in a

review engagement. A review engagement is another type of assurance engagement.

• Absolute assurance - Can never be given. There are inherent limitations of an audit

that affect the auditor’s ability to detect material misstatements in a set of financial

statements.

Page 15

UNIT 1 - INTRODUCTION

C. THE AUDIT FUNCTION

What is an audit?

An audit is an exercise, of which the objective is to enable an independent auditor to express

an opinion on whether a set of financial statements has been prepared in a true and fair

manner and in accordance with an identified financial reporting framework.

An audit is an exercise the objective of which is:

• to enable an independent auditor to express an opinion,

• on whether a set of financial statements,

• are prepared, in a true and fair manner,

• in accordance with an identified financial reporting framework.

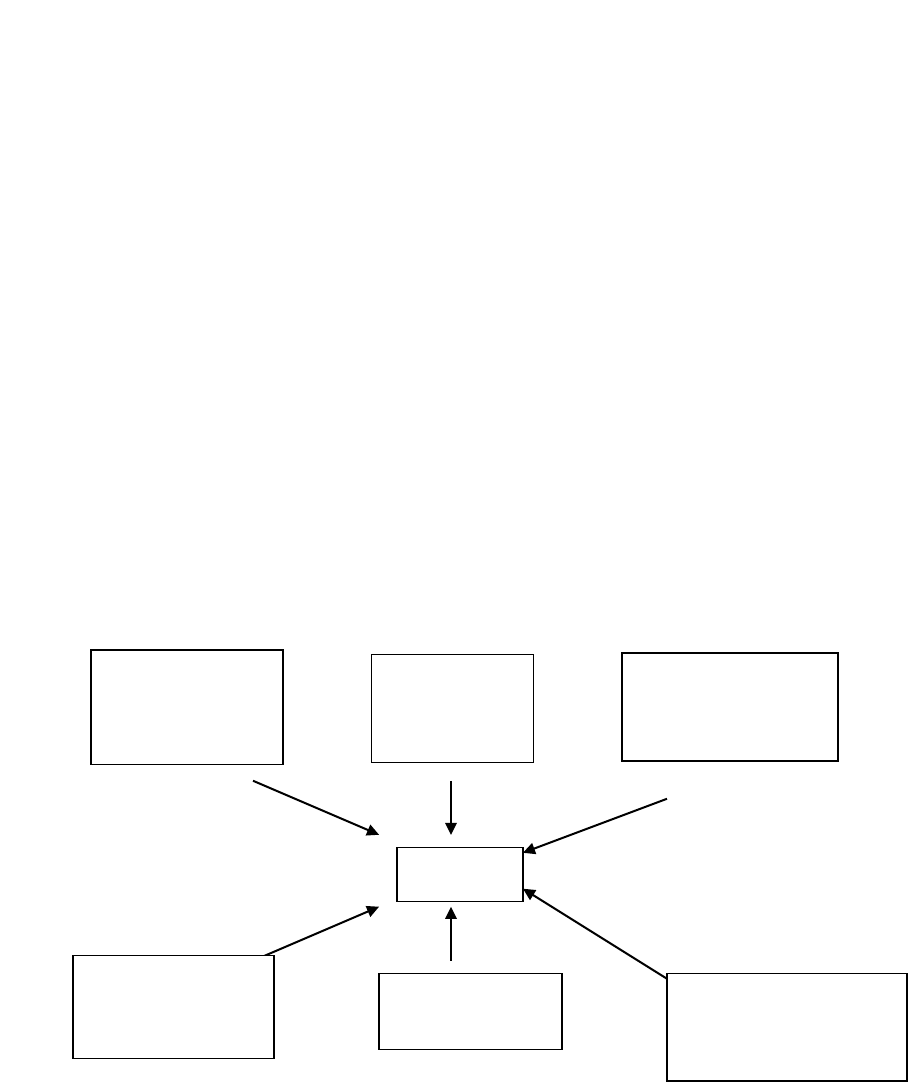

Overview of Syllabus and audit

D. TYPES OF AUDITS

• Statutory audits as required by companies’ legislation.

• Non-statutory audits preferred by interested parties rather than being required by law.

For example, charities, societies, public interest companies

• Small entity audits.

A statutory audit is an independent examination of a company’s financial statements in order

to verify that the accounts have been prepared in accordance with company law and

International Financial Reporting standards (IFRS) .

Not all companies however, are required to have an audit. Audit exemption guidelines exist

within certain jurisdictions.

Legal &

Regulatory

environment

Internal controls &

financial

statements

Ethics

AUDIT

Corporate

Governance &

current issues

Risk Assessment

& Audit process

Reporting

Page 16

UNIT 1 - INTRODUCTION

Small companies depending on the jurisdiction could possibly avail of the audit exemption

because:

• The cost may outweigh the benefit.

• Small companies are generally owner managers, so no distinction between

shareholders and managers.

• Many small companies lack a system of internal controls.

• Their use of basic books of record.

However, small companies can opt to have an audit carried out specifically where the

potential users of financial statements may expect it.

There are arguments for and against small company audits.

For

Against

Reassurance given by audited accounts for

shareholders not involved in management.

Where shareholders are part of management,

the whole audit exercise may not appear to

be value for money.

Audited accounts provide a good indication

of a fair valuation for shares particularly

unquoted shares.

An audit provides management with an

independent check on the accuracy of their

financial statements. Also, some auditors do

provide decent management letters.

In reality, a more focused systems review or

similar consultancy report would be of more

benefit to management.

Employees can gain comfort from audited

accounts as to their job security and for

wage negotiations.

In reality, I don’t think this actually

happens.

Bank managers often rely on audited

accounts when reviewing security in the

event of granting a loan.

More importantly though, a bank manager

may want to see a good credit history in a

company’s transactions with the bank.

Suppliers can gain assurance from audited

accounts when giving credit to customers.

On the contrary, the accounts might be out

of date and the customer could be

experiencing difficulties. Might be more

appropriate to get relevant credit references.

Revenue can rely on audited accounts to

back up tax returns.

In reality, revenue accepts sets of accounts

prepared by independent accountants.

E. THE LIMITATIONS OF AN AUDIT

• Not every item is checked. In fact, only test checks are carried out by auditors. It

would be impractical to examine all items within a class of transactions or account

balance. Hence, it is not really possible to give absolute assurance.

• Auditors depend on representations from management and staff. Collusion can

mitigate some good controls such as division of duties. There is always the

possibility of collusion or misrepresentation for fraudulent purposes.

Page 17

UNIT 1 - INTRODUCTION

• Evidence gathered is persuasive rather than conclusive. It often indicates what is

probable rather than what is certain. Take for example vouching a bank statement. It

only shows you that one account. Are there others?

• Auditing is not purely an objective exercise. Judgements have to be made in a

number of areas. The view in financial statements is itself based on a combination of

fact and judgement. For example, valuing stock in a grain silo or valuing jewellery.

• The timing of an audit. Significant credit notes after the year-end can alter a true and

fair view. Problems arise whether you audit too early or too late.

• An unqualified audit opinion is not a guarantee of a company’s future viability, the

effectiveness and efficiency of management, nor that fraud has not occurred in the

company. Profit margins can differ from firm to firm yet both could have a clean

audit report.

So are there any benefits of an audit? Yes, there are.

• The shareholders of a company are given an independent opinion as to the true and

fair view of the accounts that have been prepared by management.

• The use made by third parties such as suppliers and banks of the accounts as

confidence in the performance of a company.

• Auditors themselves can use the knowledge accumulated during the course of the

audit to provide additional services to the company such as the provision of

consultancy services or a management letter showing weaknesses in the business and

recommendations to alleviate such weaknesses in the future.

• While not responsible for detecting fraud, the very fact that an audit is carried out and

may uncover evidence of fraud, can help to mitigate against such risks.

• Managers in some firms may be removed from day to day transactions especially

regarding remote locations and an audit can allay fears of fraud or simple bad book-

keeping

F. THE NEED FOR REGULATION

Where there is reduced confidence in the markets and this leads to business failure, this in

turn leads to instability. As a result there is increased demand for regulation.

There has been regulation in the markets since the introduction of the concept of limited

liability. The requirement for audited financial statements is a way to protect the owners of a

business from unscrupulous management and also prevent the abuse of the limited liability

status. Standards used are a form of self-regulation. Company law is regulation, where self-

regulation doesn’t appear to be working.

Enron raised serious questions about self- regulation. In response the Sarbanes-Oxley Act

of 2002 was passed in the USA. This set up improved corporate governance including

Page 18

UNIT 1 - INTRODUCTION

enhanced internal controls and improved levels of auditor independence. This has led to

attempts to strengthen regulation in a number of other countries too.

The conduct of audits is covered by:

1. A code of ethics

2. International Standards on Auditing

3. Company Law.

In addition, Auditors are regulated by a number of different bodies, for example:

• The International Auditing and assurance standards board (IAASB)

• The Government

• Professional Accountancy bodies such as ICPAR

G. METHODOLOGY OF AN AUDIT

1. Determine the scope and the audit approach.

Legislation and the auditing standards lay down the scope for statutory audits. An auditor

should prepare a plan for his audit.

2. Ascertain the system and controls.

Discuss the accounting system and the flow of documents with all the relevant personnel

in the company. Document all your notes. Some auditors do flow charts, narrative notes

and/or internal control questionnaires. Get to know the client’s business. Confirm that

you have recorded the system accurately by carrying out walkthrough tests.

3. Assess the system and internal controls.

Evaluate the system as it is, to weigh up its reliability and draw up a plan to test its

effectiveness. At this stage you could draw up a letter to management recommending any

improvements you consider from your findings. In addition, what you have learned here

may influence the type of further audit testing you may carry out later on.

4. Test the system and internal controls.

Above, you evaluated the controls that are in place. Now you need to test that they were

effective, Compliance tests will cover many more transactions than the walkthrough tests.

You need to carry out a representative sample through the accounting period.

If you can establish that the controls are indeed effective, you can reduce the amount of

detailed testing later on. However, if the controls turn out to be ineffective, then more

substantive tests will need to be carried out.

5. Test the financial statements.

This section covers the substantive testing which has been described earlier. You are

effectively trying to stand over the figures in the financial statements. Substantive tests

are audit procedures performed to detect material misstatements. Remember, if you think

Page 19

UNIT 1 - INTRODUCTION

that any error you might find in a class of transactions will not be significant, then there is

little point carrying out the substantive test.

6. Review the financial statements.

After all the testing has been done and the evidence gathered, you should review the

accounts as to their overall reliability making a critical analysis of the content and

presentation.

7. Express an opinion.

You need to evaluate all the evidence you have gathered and express an opinion on a set

of accounts by way of a written audit report.

You may, in addition, write a management letter which can set out improvements you

recommend or to place on record specific points in connection with the audit.

H. ISA 200

ISA 200 International standards on auditing) 200: objective and general principles

governing an audit of financial statements sets out what audits are all about.

• The auditor should comply with the code of ethics for professional accountants issued

by the International Federation of Accountants (IFAC) and the ethical pronouncements

issued by the auditor’s relevant professional body.

• The auditor should conduct an audit in accordance with International Standards of

Auditing and should plan and perform an audit with an attitude of professional

scepticism.

• ISA 200 also makes a very important point in that while the auditor is responsible for

forming and expressing an opinion on the financial statements, the responsibility for

preparing and presenting those financial statements lies with the management.

• Furthermore, the auditor does not have any responsibility with regard to the prevention

and detection of fraud. Again, that lies with the management.

Page 20

UNIT 2 – THE AUDITOR AND THE AUDIT

ENVIRONMENT

BLANK

Page 21

UNIT 2 – THE AUDITOR AND THE AUDIT

ENVIRONMENT

Study Unit 2

The Auditor and the Audit Environment

Contents

A. Audit Opinion

B. Role of the Auditor

C. Relationships & Responsibilities

D. The Audit Profession

E. International Standards on Auditing

F. Corporate Governance

G. Codes of Best Practice

Page 22

UNIT 2 – THE AUDITOR AND THE AUDIT

ENVIRONMENT

THE AUDITOR AND THE AUDIT ENVIRONMENT

The Statutory Audit

The Companies Acts depending on the applicable jurisdiction shall require that the majority

of all companies must have an audit carried out. An exemption exists for small companies

depending on the applicable jurisdiction.

In addition to qualifying as a small company the following would need consideration

depending on the applicable jurisdiction:

• Company must be a private company

• Company must not be a bank or insurance entity

• Company must not be part of a group

• All filing requirements within the applicable jurisdiction are kept up to date.

A. AUDIT OPINION

The objective of an audit is for an independent auditor to express an opinion on a set of

financial statements.

The key opinion is whether the accounts give a true and fair view. Unfortunately, there is

no formal definition as it is not laid out in Company law. However, it is generally accepted

that a set of accounts can only give a true and fair view if they are not factually incorrect and

present information in an impartial way that is clearly understood by the reader.

It could also be argued that in order to ensure that a set of accounts gives a true and fair view,

an auditor should have regard for Company Law and Accounting Standards pertaining to

those financial statements and that he himself has carried out the audit in accordance with the

relevant regulatory pronouncements, codes of ethics and Auditing Standards.

Aside from the key opinion, there are a number of other issues that the auditor needs to report

on and these should be laid out by the companies’ acts.

These are matters of opinion and matters of fact.

Matters of opinion:

1. Have proper accounting records been kept?

2. Is the information in the directors’ report consistent with that given in the financial

statements?

3. Does a financial situation exist which may require an Special Meeting?

4. Have the accounts been prepared in accordance with the provisions of the companies’

acts?

Page 23

UNIT 2 – THE AUDITOR AND THE AUDIT

ENVIRONMENT

Matters of fact:

1. Has the auditor received all the information and explanations he deems necessary for

the purposes of his audit?

2. Do the financial statements agree with the books of account?

The statutory audit opinion is given by way of a written standard audit report addressed to the

shareholders of a company. The report should be signed and dated by the auditor.

B. THE ROLE OF THE AUDITOR

The auditor is the independent person that gives his opinion on a set of financial statements.

He does not provide absolute assurance. In other words he does not say the “accounts are

correct”. Audits have their limitations.

However, this is often misunderstood by users of accounts who seem to wrongly accuse the

auditor of shortcomings especially where there are infamous business failures or perceived

wrong doing. This is known as the “expectation gap”.

The expectation gap exists because the role and duties of the auditor which are recommended

to be laid out by the companies acts, codes of ethics and auditing standard could be different

from the perceived role of the auditor by the general public and even company directors

themselves. For example, it is believed that the auditor should find all errors whether

unintentional or intentional such as fraud.

C. RELATIONSHIPS AND RESPONSIBILITIES

There are a number of stakeholders interested in financial statements from the shareholders to

management, customers to suppliers, revenue authorities to bank managers, and even future

investors.

The audit report is prepared by the auditor for the shareholders on the actions of the

management (directors).

The auditor has no legal duty to report to management or anyone else in respect of the

financial statements. However, in practice other parties do read the audit report and often

rely on the assurance given by the auditors.

Key issues:

• Management are responsible for the preparation and presentation of the accounts

• Management are responsible for the prevention and detection of fraud within a

company

Page 24

UNIT 2 – THE AUDITOR AND THE AUDIT

ENVIRONMENT

• Management are responsible for safeguarding the assets of a company

• The auditor is responsible for expressing an opinion on a set of accounts prepared by

management.

D. THE AUDIT PROFESSION

Depending on the jurisdiction it would be recommended to set up an Accounting

Supervisory Authority together with an Auditing Authority. Its role would be to supervise the

practice of auditing and accounting in the relevant country.

Previously, each professional accounting body supervised their own members, however more

recently Independent Supervisory Authorities are being established in countries e.g. in

Ireland (IAASA)

The main functions of an Auditing and Accounting Supervisory Authority would be:

• To supervise how each body regulates its own members

• To promote adherence to the highest possible professional standards

• To monitor the accounts of companies to ensure compliance with companies

legislation.

Each professional body will regulate and monitor its own members. Each body will issue its

own code of ethics. By and large the codes of ethics are very similar.

Persons carrying out audits must have the permission of the relevant authorities. It is strongly

recommended that all auditors have to be registered. Members of recognised bodies such as

CPA, ACCA and Chartered Accountants are registered auditors if they have practising and

auditing certificates from their respective bodies.

The Institute of Certified Public Accountants of Rwanda (ICPAR) is the Professional

Accountancy Organization (PAO) mandated by law number 11/2008 to regulate the

Accounting profession in the Republic of Rwanda. ICPAR is the only authorized by law to

register and grant practising certificates to Certified Public Accountants (CPAs) in Rwanda.

Certified Public Accountant Certificate holders that are registered as members of ICPAR are

entitled to the CPA( R ) designation.

The Institute operates in the public interest including promotion of financial reporting,

auditing and ethical standards.

The practising audit firms in Rwanda are very small in size and need capacity building with

respect to quality of audit.

Page 25

UNIT 2 – THE AUDITOR AND THE AUDIT

ENVIRONMENT

E. INTERNATIONAL STANDARDS ON AUDITING

Readers of information need assurance as to the reliability of that information. In addition,

they will want to know that this reliability will not vary from one set of company accounts to

another. In order to ensure this, an auditor audits a set of accounts in accordance with

common standards.

There is a need then for auditors to be regulated so that all auditors follow the same

standards. One of the main points of IAS200 (objective and general principles governing an

audit of financial statements) is that auditors must follow the international standards of

auditing in the exercise of an audit.

The International standards of auditing (ISAs) are produced by the International Auditing and

Assurance Standards Board (IAASB), which is part of the International Federation of

Accountants (IFAC). The IFAC is a global organisation for the accounting profession.

The intention is that the standards issued will improve the degree of uniformity of auditing

practices, both in a standardised approach to the audit and a standard reporting format.

Only in exceptional circumstances, can an auditor judge if it is necessary to depart from an

auditing standard in order to achieve the objective of an audit. The auditor would need to be

able to justify his actions.

ISAs need only be applied to material matters. What is material is not defined in law but it is

generally accepted that something is material if its omission or misstatement could influence

the economic decisions of users of financial statements. Materiality can be based on value,

e.g. large amounts are more likely to be material than small ones, though sometimes they may

also be material by nature, for example if it exposes inappropriate decision-making within an

organisation possibly based on favouritism or personal bias.

ISAs are mandatory in some jurisdictions for the audit of company’s accounts.

Setting Standards - The Process:

• The IAASB identifies new developments,

• The IAASB appoints a task force to draft a standard,

• Consultation takes place,

• An “exposure draft” is produced, essentially a draft standard issued welcoming

comments from the profession and any other interested party,

• The taskforce considers comments and may make amendments,

• The Standard is finalised and formally approved by the IAASB.

Page 26

UNIT 2 – THE AUDITOR AND THE AUDIT

ENVIRONMENT

International standards of Auditing

Glossary of terms

ISQC 1

ISA 200

Objective and general principles governing an audit of financial statements

ISA 210

Terms of audit engagements

ISA 220

Quality control for audits of historical financial information

ISA 230

(Revised) Audit Documentation

ISA 240

The auditor's responsibility to consider fraud in an audit of financial statements

ISA 250

Consideration of laws and regulations in an audit of financial statements

ISA 260

Communication of audit matters with those charged with governance

ISA 265

Communicating deficiencies in internal control to those charged with

governance

ISA 300

Planning an audit of financial statements

ISA 315

Obtaining an understanding of the entity and its environment and assessing the

risks of material misstatement

ISA 320

Audit materiality

ISA 330

The auditor's procedures in response to assessed risks

ISA 402

Audit considerations relating to entities using service organisations

ISA 450

Evaluation of misstatements identified during the audit

ISA 500

Audit evidence

ISA 501

Audit evidence - additional considerations for specific items

ISA 505

External confirmations

ISA 510

Initial engagements - opening balances and continuing engagements - opening

balances

ISA 520

Analytical procedures

ISA 530

Audit sampling and other means of testing

ISA 540

Audit of accounting estimates

ISA 545

Auditing fair value measurements and disclosures

ISA 550

Related parties

ISA 560

Subsequent events

ISA 570

Going concern

ISA 580

Management Representations

ISA 600

Using the work of another auditor

ISA 610

Considering the work of internal audit

ISA 620

Using the work of an expert

ISA 700

The auditor's report on financial statements

ISA 705

Modifications to opinions in the Independent Auditor’s Report

ISA 706

Emphasis of matter paragraphs and other matter paragraphs in the Independent

Auditor’s Report

ISA 710

Comparatives

ISA 720

(Revised) Section A - Other Information in Documents Containing Audited

Financial Statements; Section B -

The Auditor's Statutory Reporting

Responsibility in Relation to Directors’ reports

Page 27

UNIT 2 – THE AUDITOR AND THE AUDIT

ENVIRONMENT

International Accounting Standards, International Financial Reporting Standards and

International Public Sector Accounting Standards)

The auditor needs to express an opinion on a set of accounts as to whether they give a true

and fair view. In order to give a true and fair view, a set of accounts should have regard for

the provisions of company law and international accounting standards. Private sector

standards are known as International Financial Reporting Standards (IFRSs). There are public

sector equivalents, largely based on the IFRSs, known as International Public Sector

Accounting Standards (IPSASs).

The IFRSs are shown below (older Standards which have not been replaced by a more recent

IFRS are still called International Accounting Standards (IASs).

The private sector Standards in issue are shown below:

IAS 1

Presentation of Financial Statements

IAS 2

Inventories

IAS 7

Statement of Cash Flows

IAS 8

Accounting Policies, changes in Accounting Estimates and Errors

IAS 10

Events After the Reporting Period

IAS 11

Construction contracts

IAS 12

Income Taxes

IAS 16

Property, Plant and Equipment

IAS 17

Leases

IAS 18

Revenue

IAS 19

Employee Benefits

IAS 20

Accounting of Government Grants and Disclosure of Assistance

IAS 21

The Effects of Changes in Foreign Exchange Rates

IAS 23

Borrowing Costs

IAS 24

Related Party Disclosures

IAS 26

Accounting and Reporting by Retirement Benefit Plans

IAS 27

Consolidated and Separate Financial Statements

IAS 28

Investments in Associates

IAS 31

Interests in Joint Ventures

IAS 32

Financial Instruments: Presentation

IAS 33

Earnings per Share

IAS 34

Interim Financial Reporting

IAS 36

Impairment of Assets

IAS 37

Provisions, Contingent Liabilities and Contingent Assets

IAS 38

Intangible Assets

IAS 39

Financial Instruments: Recognition and Measurement

IAS 40

Investment Property

IAS 41

Agriculture

IFRS 1

First Time Adoption of International Financial Reporting Standards

IFRS 2

Share - Based Payment

IFRS 3

Business Combinations

Page 28

UNIT 2 – THE AUDITOR AND THE AUDIT

ENVIRONMENT

IFRS 5

Non-current Assets Held for Sale and Discontinued Operations

IFRS 7

Financial Instruments: Disclosures

IFRS 8

Operating Segments

F. CORPORATE GOVERNANCE

A string of high profile scandals and frauds in the 1980’s and the 1990’s forced the adoption

of voluntary codes of best practice in many countries (for example the UK) to enforce good

practice by directors and to communicate the adherence to good practice by management to

the shareholders. These Codes could be applied globally.

It was vital that companies were managed well i.e. there was good corporate governance.

It would be recommended to bring in many aspects of good corporate governance into

company law.

For example: The Cadbury report defines Corporate Governance as:

“The system by which companies are directed and controlled”.

Why is good corporate governance important?

Shareholders and managers are usually separate in a company and it is important that the

management of a company deals fairly with the investment made by the owners.

Corporate governance is about ensuring that public companies are managed effectively for

the benefit of the company and its shareholders.

In smaller companies, generally, shareholders are fully informed about the management of

the business as they are the directors themselves. However, in large companies the day to

day running of a company is the responsibility of the directors. Shareholders only get a look-

in at the Annual Meeting.

In addition, auditors only report on the truth and fairness of financial statements. They do not

report on how the shareholders’ investment is being managed and whether their investment is

subject to fraud.

Why does the need for good corporate governance come about?

• Unscrupulous management ignoring distinction between company’s money and their

own,

• Management manipulating share price for personal gain,

Page 29

UNIT 2 – THE AUDITOR AND THE AUDIT

ENVIRONMENT

• Management disguising poor results and mismanagement,

• Management extracting funds from company and raising finance fraudulently.

• Management inefficiencies in decision-making and internal control systems (these

might not be deliberate but are still problematic for shareholders)

Authority

Good corporate governance can be enforced by law (Sarbanes Oxley in the US) and/or by

agreement through codes of best practice.

So what does good corporate governance entail?

• Effective management

• Support /oversight of management by non-exec directors with sufficient experience

• Fair appraisal of performance

• Fair remuneration and benefits

• Fair financial reporting

• Sound systems of internal control

• Constructive relationship with directors

G. CODES OF BEST PRACTICE

Two prominent codes have been formed in the UK and are considered best practice in

modern times and could be applied internationally.

For example: The Rwandan Stock Exchange commenced operations in January 2008 and has

presently four listed companies, namely:-

1. Balirwa

2. KCB

3. NMG

4. BOK

In Rwanda these codes could be applied as “Codes of Best Practice”

• The Cadbury report

• The Combined code

The Cadbury Report

The Cadbury report was issued in 1992. Its terms of reference considered:

• The responsibilities of executive and non-executive directors and the frequency, clarity

and form in which information should be provided to shareholders.

Page 30

UNIT 2 – THE AUDITOR AND THE AUDIT

ENVIRONMENT

• The case for audit committees, their composition and role.

• The responsibilities of auditors and the extent and value of the audit.

• The links between auditors, shareholders and the directors.

The Cadbury report was aimed at directors of all UK PLCs, however directors of all

companies are encouraged to apply the code. Directors should state in the financial

statements, normally through the director’s report, whether they comply with the code and

must give any reasons for non-compliance.

The Cadbury report covered a number of areas including the board of directors, non-

executive directors, executive directors and the audit function. Some of the provisions

include:

Board of Directors

• They should meet on a regular basis.

• They should have clearly accepted divisions of responsibilities, so no one person has

complete power.

• The posts of chairman and CEO should be separate.

• Decisions which require a single signature or several signatures need to be laid out in a

formal schedule and procedures must be put in place to ensure that the schedule is

followed.

Non-executive directors

• They are not involved in the day to day running of the company and should bring their

independent judgment to bear in the affairs of the company. Such affairs may include

key appointments and standards of conduct.

• There should be no business or financial connection between the company and the non-

executive directors other than fees and a shareholding.

• Their fees should reflect the time they spend on the business.

• They should not participate in share option schemes or pension schemes.

• Appointments of non-executive directors should be for a specific term and automatic

re-appointment is discouraged.

• Procedures should exist whereby they may take independent advice.

• A remuneration committee consisting of non-executive directors should decide on the

level of pay for executive directors.

Executive directors

• They run the company on a day to day basis and should have service contracts in place

of not more than three years in length, unless approved by the shareholders.

• Directors’ emoluments should be fully disclosed in the accounts and should be analysed

between salary and performance based pay.

Page 31

UNIT 2 – THE AUDITOR AND THE AUDIT

ENVIRONMENT

Audit

• The code states that the audit is the cornerstone of corporate governance. It is an

objective and external check on the stewardship of management.

• Some flaws exist in the framework for auditing, such as choices in accounting

treatments, poor links between shareholders and auditors, price competition between

audit firms and the “expectations gap” between auditors and the public.

• Disclosing fees for audit in the financial statements should safeguard against the threat

of objectivity where auditors offer other services to their audit clients.

• Formal guidelines concerning audit rotation should be drawn up by the accounting

profession.

• The accountancy profession should be involved in setting criteria for the evaluation of

internal control.

• There is a need for auditors to report on going concern. This is now reflected in

auditing standards.

The Combined Code

For example the UK stock exchange issues guidance on a regular basis. In 1998 it issued the

combined code. This combined key guidance from various reports including the Cadbury

report into the one code.

Some of its principles included which can be adopted globally are:

• Every company should have an effective board.

• There should be clear divisions of responsibilities at board level.

• There should be an appropriate balance of executive and non-executive directors.

• A formal procedure for appointments to the board should exist.

• The board should receive timely information in order to discharge its duties.

• All directors should maintain and upgrade their skills and knowledge.

• There should be an annual evaluation of its own performance.

• All directors should be submitted to re-election at appropriate time intervals.

• There should be appropriate levels of remuneration that are sufficient to attract, retain

and motivate individuals of the necessary quality required.

• A significant portion of pay should be performance related.

• A formal procedure for the fixing of pay levels should exist and no director should have

a hand in fixing his/her own pay.

• The board should present a balanced assessment of the company’s performance.

• The board should implement a good system of internal control.

• The board should have meaningful communication with the shareholders and should

use the Annual Meeting to communicate with investors.

For example, the UK Stock exchange rules require that the annual report includes a statement

of how a company has applied the principles of the combined code and must disclose whether

there has been compliance with those principles. Auditors should review this statement.

Page 32

UNIT 2 – THE AUDITOR AND THE AUDIT

ENVIRONMENT

Although the UK stock exchange rules require the code to be complied with, there is no

statutory duty for companies to do so. It is in fact a voluntary code.

This allows for flexibility in its application although shareholders will be aware of the

position due to the disclosure requirements.

In addition, being a voluntary code allows companies to opt out to the detriment of their

shareholders and there are companies while unlisted companies should be encouraged to

apply the codes.

Making the code obligatory may create an excessive burden of requirement especially for

smaller companies.

Audit Committees

Audit committees are generally made up of non-executive directors. They are perceived to

increase confidence in financial reports.

A number of recommendations contained in the combined code are:

• Audit committee should comprise at least three non-executive directors (two for smaller

companies).

• Its main role and responsibilities should be clearly set out in written terms of reference.

• The committee should be provided with sufficient resources to undertake its duties.

Role and responsibilities

• To monitor the integrity of the financial statements and other formal announcements.

• To review the internal financial controls and the company’s control and risk

management systems.

• To monitor and review the effectiveness of the internal audit function.

• To make recommendations regarding the appointment of external auditors and their

remuneration.

• To monitor and review the external auditor’s independence and objectivity.

• To develop and implement policy on the engagement of the external auditor in other

non-assurance services.

Advantages of an audit committee

• Provides an independent point of contact for the external auditor, particularly in the

event of disagreements.

• Can create a climate of discipline and control.

Page 33

UNIT 2 – THE AUDITOR AND THE AUDIT

ENVIRONMENT

• Increased confidence in the credibility and objectivity of financial reports, by

increasing the quality of the financial reporting and enabling the non-executive

directors to contribute an independent judgment.

• Internal auditors can report directly to the committee thereby providing a greater degree

of independence from management.

• The existence of such a committee should make the executive directors more aware of

their duties and responsibilities.

• Can act as a deterrent to fraud or illegal acts by executive directors.

Disadvantages of an audit committee

• Can be difficult to source sufficient non-executive directors with the necessary

competence to be effective.

• Auditors may not raise issues of judgment where there are formalised reporting

procedures.

• Costs may increase.

• Findings are generally not made public, so it is not always clear what they actually do.

Internal control effectiveness

Internal control is an essential tool in having good corporate governance and impacts

significantly on the audit approach that might be taken.

The directors of a company are responsible for putting in place an effective system of

internal control. An effective system of internal control will help management safeguard the

assets of a company, prevent and detect fraud and therefore, safeguard the shareholders’

investment.

In addition, it helps ensure reliability of reporting and compliance with laws. The use of the

word ‘help’ denotes the fact that there are inherent limitations in any system of internal

controls and as such there can be no such thing as absolute assurance.

The directors need to set up internal control procedures and need to monitor these to ensure

that they are operating effectively.

The system of internal control will reflect the control environment which depends a lot on the

attitude of the directors towards risk.

The combined code recommends that the board of directors report on their review of internal

controls. This assessment should cover the changes in risks which the company faces and its

ability to respond to these changes, the scope and quality of management’s monitoring of risk

and internal control and the extent and frequency of reports to the board. It should also assess

the significant controls, failings and weaknesses that might have a material impact on the

accounts.

Page 34

UNIT 2 – THE AUDITOR AND THE AUDIT

ENVIRONMENT

Auditors should assess the review carried out by the directors. They should assess whether

the company’s summary of the process of review is supported by documentation prepared by

the directors and that it reflects that process.

This review is not as defined as an audit. Therefore, it is only possible to give limited

assurance. For this reason, the auditors are not expected to assess whether the director’s

review covers all risks and controls and whether the risks are satisfactorily addressed by the

internal controls.

In order to avoid any misunderstandings, a paragraph is inserted into the audit report setting

out the scope of the auditor’s role.

Auditors should bring to the attention of directors any material weaknesses they find in the

system of internal control.

In order to monitor and assess the system of internal controls as to their reliability and

effective operation, a company may set up an internal audit department to carry out the

internal audit function.

There are significant differences between the external audit and internal audit functions.

1. An internal auditor is an employee of the company. Therefore, under applicable

company law, the internal auditor is precluded from acting as the external auditor of a

company.

2. External auditors are required by appropriate laws to belong to a recognised body,

which guarantees their appropriate qualification, adherence to technical standards and

overall competence. The internal auditor on the other hand requires no formal

training.

3. Unlike the external auditors, who are appointed at the Annual Meeting by the

shareholders of a company, the internal auditor is hired by the management of the

company. In turn this means he can be dismissed by the directors or other senior

managers, subject only to normal employment rights.

4. The primary objective of the external auditor is laid down by the applicable

companies’ acts, whereas the internal auditor’s objectives are dictated by the

management of the company. As a result, management can place limitations on the

scope of the internal auditor’s work. While some of his work may be similar to that

of the external auditor, more of it could relate to areas such as value for money.

Page 35

UNIT 3 – AUDITORS LEGAL, ETHICAL & PROFESSIONAL RESPONSIBILITIES – Part 1

I1.4 Auditing

Study Unit 3

Auditors Legal, Ethical & Professional Responsibilities –

Part 1

Contents

A. Professional & Ethical Responsibilities

B. Statutory Responsibilities & Rights

C. Appointment of Auditors

D. Resignation & Removal of Auditors

E. Auditors Duties & Rights

Page 36

UNIT 3 – AUDITORS LEGAL, ETHICAL & PROFESSIONAL RESPONSIBILITIES – Part 1

I1.4 Auditing

AUDITOR’S LEGAL, ETHICAL & PROFESSIONAL

RESPONSIBILITIES PART 1

A. PROFESSIONAL AND ETHICAL RESPONSIBILTIES

ISA 200 sets out the general principles of an audit. The auditor should comply with the code

of ethics for professional accountants issued by the International Federation of Accountants.

Accountants require ethics because people rely on them for their expertise in specific areas.

Both the International Federation of Accountants (IFAC) and the Institute of Certified

Public Accountants of Rwanda (ICPAR) have issued a code of ethics of which the

fundamental principles of both associations are very similar.

Both identify-

• Fundamental principles of ethical behaviour

• Potential threats to those principles

• Possible safeguards to counter those threats.

If the code of ethics is contravened, members may face disciplinary proceedings which could

result in a fine, censorship, suspension or withdrawal of membership and with it possibly the

right to practice.

The fundamental principles are as follows:

• Integrity. A member should be straightforward and honest in all professional and

business relationships.

• Objectivity. A member should not allow bias, conflict of interest or undue influence

of others to override professional or business judgements.

• Professional competence and due care. A member has a continuing duty to

maintain professional knowledge and skill at the level required to ensure that a client

or employer receives competent professional service. If you are not up to the task,

you shouldn’t take it on.

• Confidentiality. A member should respect the confidentiality of information

acquired as a result of professional and business relationships and should not disclose

any such information to third parties without proper and specific authority unless

there is a legal or professional right or duty to disclose. Any information acquired

should not be used for the personal advantage of the member or third parties.

• Professional behaviour. A member should comply with relevant laws and

regulations and should avoid any action that discredits the profession.

Page 37

UNIT 3 – AUDITORS LEGAL, ETHICAL & PROFESSIONAL RESPONSIBILITIES – Part 1

I1.4 Auditing

The circumstances in which members operate may give rise to specific threats to compliance

with the fundamental principles. However, it is impossible to define every situation that

creates such threats and to specify the appropriate mitigating action.

The Institute of Certified Public Accountants of Rwanda ( ICPAR) conceptual framework

requires each member to identify, evaluate and address threats to compliance. ICPAR – Code

of Ethics – Part A 100.2

If the threats are significant, then you need to identify and apply safeguards to eliminate the

risk or to reduce it to an acceptable manner.

If no appropriate safeguards are available, then you need to eliminate the activities causing

the threat or decline the engagement or discontinue it as the case may be.

It would be recommended to follow the relevant ethical pronouncements which the

International Federation of Accountants (IFAC) outlines together with the auditor’s relevant

professional body.

ETHICAL STANDARDS

1. Integrity, Objectivity and Independence

2. Financial, business, employment and personal relationships

3. Long association with the audit engagement

4. Fees, remuneration and evaluation policies, litigation, gifts and hospitality

5. Non-Assurance Services provided to an Assurance Client

Integrity, Objectivity and Independence

An auditor should establish documented policies and procedures designed to ensure that in

relation to each audit engagement, the audit firm and anyone in a position to influence the

conduct and outcome of the audit should act with integrity, objectivity and independence.

The leadership of the audit firm should take responsibility for establishing a good control

environment within the firm.

Independence needs to be considered at all stages of the audit process.

The audit partner should ensure that the directors of an entity are informed of all matters that

affect an auditor’s objectivity and independence.

An auditor needs to be, and seen to be, independent. They must have independence of mind

and independence in appearance. It is a fundamental principle.

Independence is a state of mind that permits the provision of an opinion without being

affected by influences that compromise professional judgement, allows an individual to act

with integrity and exercises objectivity and professional judgement.

Page 38

UNIT 3 – AUDITORS LEGAL, ETHICAL & PROFESSIONAL RESPONSIBILITIES – Part 1

I1.4 Auditing

An auditor needs to avoid facts and circumstance that are so significant that a reasonable and

informed third party would reasonably conclude an auditor’s integrity, objectivity or

professional scepticism had been compromised.

Public confidence in the operation of capital markets and in the conduct of public interest

entities depends upon the credibility of the opinions and reports issued by auditors.

What are the possible threats to independence?

Integrity, objectivity and independence are the principal types of threats.

• Self- interest.

A financial interest in a client, undue dependence on fees, close business relationship,

concern over losing a client, potential employment with client or loans from client;

anything which may cause the auditor to be reluctant to make decisions during an

audit.

• Self -review.

Reporting on the operation of financial systems after you were involved in their

design and implementation. Preparation of the accounts which are now being audited.

• Management threat.

Making judgements and taking decisions which are the responsibility of management,

such as changing journal entries, approving transactions or preparing source

documents. This can be linked to self- review.

• Advocacy.

Acting as a legal advocate for a client in litigation or promoting shares in the

company.

• Familiarity.

Allowing close personal relationships to develop with client personnel through long

association or a family relationship. The auditor may not be sufficiently questioning

of the client point of view. Accepting gifts of significant value is also a sign of

excessive familiarity.

• Intimidation.

Threat of replacement due to disagreement, perhaps you want to qualify the accounts.

Possible Safeguards to independence

Safeguards that may eliminate or reduce threats to an acceptable level fall into two general

categories:

1. Safeguards created by the profession, legislation or regulation and

2. Safeguards in the work environment whether within the auditor’s own systems and

procedures or within the client company.

Page 39

UNIT 3 – AUDITORS LEGAL, ETHICAL & PROFESSIONAL RESPONSIBILITIES – Part 1

I1.4 Auditing

The first category includes:

• Educational, training and experience requirements for entry into the profession.

• The existence of a clear and robust Code of Ethics

• Continuing professional development requirements.

• Corporate governance regulations and Professional standards.

• Professional or regulatory monitoring and disciplinary procedures.

The second category would include for example:

Firm wide safeguards

• Documented policies and procedures to implement and monitor quality control of

engagements.

• Documented policies regarding identification of threats, their evaluation and

application of safeguards.

• Policies and procedures to enable identification of interests and relationships between

auditor and client.

• Monitoring the fee income received.

• Timely communication of a firm’s policies and procedures to all staff and appropriate

training thereof.

• A suitable disciplinary mechanism to promote compliance with policies.

Possible Engagement specific safeguards

• Involving an additional professional accountant to review the work done.

• Consulting independent third parties.

• Disclosing the nature of services provided and extent of fees charged to those charged

with client governance.

• Rotating senior audit team personnel.

Possible Safeguards within client systems and procedures

• Persons other than management ratify auditor appointment.

• Client has competent employees with experience to make decisions.

• The client has a corporate governance structure that provides appropriate oversight

and communications regarding the firm’s service.

International standard on quality control (ISQC 1) sets out the standards and provides

guidance regarding a firm’s responsibilities for its system of quality control for audits.

• The firm should establish a system of quality control designed to provide it with

reasonable assurance that the firm and its personnel comply with professional

standards and regulatory and legal requirements.

Page 40

UNIT 3 – AUDITORS LEGAL, ETHICAL & PROFESSIONAL RESPONSIBILITIES – Part 1

I1.4 Auditing

• The firm’s system of quality control should include policies and procedures

addressing elements such as leadership responsibilities, ethical requirements,

acceptance and continuance of client engagements, human resources, engagement

performance and monitoring.

• The quality control policies and procedures should be documented and communicated

to the firm’s personnel.

Confidentiality

There is a duty of confidence to the client. Confidentiality ensures that all information

necessary for the audit is given to the auditor. However, there are several exceptions noted.

The principle is twofold. One, you should refrain from disclosing any information acquired

without proper authority to do so unless there exists a legal or professional right or duty to

disclose.

Secondly, you should refrain from using any information acquired for your own personal

advantage or that of a third party.

A member should maintain confidentiality even in a social environment and even needs to

comply with the principle even after the end of the professional relationship.

Exceptions when members may be required to disclose:

• Disclosure permitted by law and authorised by client.

• Disclosure by applicable law e.g. production of documents during course of legal

proceedings or disclosure to appropriate public authorities of infringements of law

that have come to light - EG: money laundering, Theft and Fraud Offences and a Duty

to report where books of account have not been kept.

• Professional duty or right to disclose when not prohibited by law, such as to comply

with quality assurance reviews, to respond to an inquiry by an institute, to protect the

professional interests of a member in legal proceedings or to comply with technical

standards and ethics.

Under ISA 250 consideration of laws and regulations in an audit of financial statements, if

auditors become aware of a suspected or actual occurrence of non-compliance with law and

regulation which give rise to a statutory right or duty to report, they should report it to the

proper authority immediately.

Page 41

UNIT 3 – AUDITORS LEGAL, ETHICAL & PROFESSIONAL RESPONSIBILITIES – Part 1

I1.4 Auditing

Areas of controversy

Independence

• Multiple services

Many audit firms are moving away from their traditional roles and are offering a

wider variety of work to their clients. Audit is sometimes even seen as a loss leader in

gaining other lucrative work.

Having more legislation in this area could restrict clients and limit opportunities for

further business and any synergies found in the auditor also providing additional

services would be lost.

Note, in the USA, SEC guidance suggests that an auditor is not independent in

relation to a listed company if they provide certain non-assurance services, such as

bookkeeping, internal audit, management or human resources functions.

• Specialist services

Services such as valuation of intangible assets, property or unquoted investments were

carried out by a firm who are also a company’s auditors can lead to a self- review

threat. A firm should not therefore audit a client’s accounts which include specialist

work carried out by them.

• Second opinions

Second opinions are acceptable but not if the current auditors are pressurised to accept

the second opinion. In order to avoid this, there should be constant communication

between the two auditors.