CRS222_Financial_Analysis_Of_Systems_Integrators_Aug89 CRS222 Financial Analysis Of Systems Integrators Aug89

CRS222_Financial_Analysis_Of_Systems_Integrators_Aug89 CRS222_Financial_Analysis_Of_Systems_Integrators_Aug89

User Manual: CRS222_Financial_Analysis_Of_Systems_Integrators_Aug89

Open the PDF directly: View PDF ![]() .

.

Page Count: 33

FINANCIAL

ANALYSIS

OF

SYSTEMS

INTEGRATORS

CRS 0222

-For

Internal Use

Only-

By

Richard

D.

Buchanan

DTN

264-3663

Prepared

for Chris Sullilvan

CSS

August

1989

CONSULTING

and

RESEARCH

SERVICE

Andrea

Schulman, ManagerlEditor

MK01·11K11

DTN

264-6911

Martha Brunelle, Production

Editor

mamDama

Copyright 1989

by

Digital Equipment Corporation

All

rights reserved

FINANCIAL ANALYSIS

OF

SYSTEMS INTEGRATORS

TABLE OF CONTENTS

PURPOSE

AND METHODOLOGY

EXECUTIVE SUMMARY . . . . . .

.2

.3

SYSTEMS INTEGRATION: AN OVERVIEW. .

.4

Federal and Commercial Sectors Contrasted . . 6

Commercial Sector Segments

............................

7

FINANCIAL ANALYSIS

..................................

8

The Size of

the

U.S. Systems Integration Market: Input's Estimates . 9

Estimates of U.S. Systems Integration Market Growth . . . . .

.10

Input's Market

Share

Estimates for The U.S.

SI

Market . . .

.13

The Size of

the

U.S. Systems Integration Market: Computer

Systems News' Estimates . . . . . . 17

Top

50

Systems Integrators . 19

Hardware Vendors

..

. . 20

Systems Integrators . . . . . . 21

Integration Facilitators . . . . 22

VENDOR PROFILES

...........................

. . . . . . .

23

IBM Corp.. . . . . . . . . . . . .

.23

Electronic Data Systems, Corp.

.24

Anderson Consulting . . . . . . . . . . 25

AT&T.

. . . . . . . . . . . . .

.26

Bolt Beranek and Newman . .

.27

Computer

Task

Group, Inc. . . 28

Litton Industrial Automation Group . 29

SHL

System

House. Inc. . . . . .

.30

U nysis Corp.

..

. . . . . . . . . . 31

Digital Equipment Corporation .

.32

* * * CONSULTING and RESEARCH SERVICE * * *

- - For Internal Use Only - -

FINANCIAL ANALYSIS OF SYSTEMS INTEGRATORS

PURPOSE AND METHODOLOGY

Managers of CSS contracted with Consulting and Research Service for research into

the

cost of sales for systems

in~ators.

The

researcher was asked

to

examine

the

pubHcly

available financial records of systems integrators

as

well as secondary sources available

from third-party

market

research firms. In addition

to

reporting

the

results of these

financial analyses,

it

was hoped

that

such comparisons might reveal patterns indicative of

the structure of this emerging industry, allowing Digital managers to more effectively plan

their competitive strategy.

Information was derived from three sources: publicly available financial reports such as

Annual reports and 10Ks; Third

party

market research reports such

as

Input's report on

Systems Integration and trade press sources, most notably Computer Systems News'

Systems Integration whitepaper.

Brief familiarity with

the

systems integration literature reveals a bewildering variety of

estimates as

to

the

size and growth

rate

of

the

overall systems integration market. Many

of these estimates differ by a factor of two or three. This is

true

not only of

the

industry

revenues and profits but of

the

number of competitors and

the

size of the workforce they

employ. .

The primary reason for these diverse estimates is

that

the

term

systems integration

means dramatically different things to different analysts. Some analysts distinguish be-

tween systems services and programming and strictly hardware integration. Information

systems design and auditing

as

practiced by

the

Big Eight accounting firms is

yet

a third

definition of systems integration. Depending upon where

the

line is drawn, estimates of

the size of

the

systems integration

market

can vary dramatically. Compounding

the

prob-

lem is

the

paucity of information available from third-party market research firms on

how

their estimates have been reached. Unlike some other areas of computer

market

research,

systems integration

data

gathering has

not

been tested over time. This lack of testing can

lead to douhle-counting

or

undercounting of revenues and headcounts.

Another important factor which explains

the

diverse market size estimates is

the

unavail-

ability of disaggregated financial reports. Because the systems integration function is only

now

beginning

to

be recognized as a distinct business, many of

the

primary competitors

have never divisionalized these groups. The integration function may

be

the result of a

collaboration between diverse groups within a corporation, and revenues

are

not recog-

nized

as

"systems integration" revenues as such.

It

is definitely

the

case

that

many firms

have no real idea of what revenues they receive from N systems integration" services, or

how

many of their personnel are involved.

Despite these facts,

data

gathered

by

industry experts using consistent methodologies is

roughly comparable.

The

primary sources of information for this report rely heavily on

Input Corporation's Systems Integration Service, and on

the

special report on Systems

Integration prepared by Computer Industry News. While their overall estimates of

the

size

of

the

market differ, comparisons between competitors can be made within each group's

data.

* * * CONSULTING and RESEARCH SERVICE *

- - For Internal Use Only - -

* *

2

FINANCIAL ANALYSIS OF SYSTEMS INTEGRATORS

EXECUTIVE SUMMARY

Systems Integration is only recently being recognized as a distinct business comprised of

a variety of services, skills and technologies which have traditionally been spread through-

out

most

business organizations. The forces which are driving

the

growth of systems

integration

are

fundamental, worldwide economic changes coincident with

the

emergence

of new, cost effective computing

and

communication technologies.

The relative youth of

the

systems integration function makes measurement of revenues

and

costs difficult since

many

firms do

not

disaggregate

their

financial

statements

to

reflect

the

work done by systems integrators. This difficulty is compounded by

the

fact

that

definitions of systems integration vary widely.

The size of

the

systems integration market in

the

United

States

is variously estimated to

be

between $4.8

and

$6

billion. Growth rates overall are expected

to

be

in

the

range of

25% between 1988 and 1993,

but

rates of growth are different in

the

two primary sectors;

government spending growth is likely to average 19%, while commercial spending growth

is likely to average

300/0.

Overall spending on systems integration in

the

U.S. is expected

to

reach $14.7 billion by 1993.

Profiles of major systems integrators and analysis of their financial

statements

suggests

that

systems integration is a capital intensive business dominated by large firms

that

are

able

to

afford

the

significant investments in software development

and

contract manage-

ment

that

the

business demands. Buying behavior of customers, especially their aversion

to risk when faced with a major investment of strategic importance, also contributes

to

the

advantage

that

well established, financially strong, reputable firms have when bidding

against smaller competitors. The business entails significant barriers to

the

entry of com-

petitors, which

are

likely

to

remain for

the

foreseeable future.

* * * CONSULTING and RESEARCH SERVICE *

- - For Internal Use Only - -

* *

3

FINANCIAL ANALYSIS OF SYSTEMS INTEGRATORS

OVERVIEW OF THE SYSTEMS INTEGRATION FUNCTION

Systems

Integration is only recently beginning

to

be recognized

as

a distinct business.

From

a

marketing

perspective,

the

systems integration function is developing its own

identity, which

can

be defined in

terms

of

the

marketing

mix. Definable Products

are

being recognized

by

potential customers who choose

them

based upon Price, Distribution

and

Prom,otional attributes.

This was

not

always

the

case. Formerly, customers depended upon hardware vendors,

internal MIS managers

or

perhaps

their

accountants

to

recommend and possibly imple-

ment

information systems.

The

complexity

of

the

task

led initially

to

a centralized MIS approach. This solution

proved

to

be inappropriate for

many

decentralized organizations

and

for those businesses

whose operations required geographic

and

information

system

autonomy.

The

availability of

cost

effective alternatives

to

the

centralized mainframe encouraged

the

proliferation of diverse and,

at

times, internally inconsistent information systems.

Support

for

these

multiple

systems

came from professional service firms

that

were hired

to

provide

programming

and

system

design services

at

the

time of initial

startup

or conversion. This

relieved central MIS of

the

need

to

employ large staffs

to

support

the

irregular work-flow,

but

left

the

door open for

the

acquisition of disparate computer systems and software

packages.

Systems

integration

as

a distinct function handled

by

third-party contractors

is-

emerging

to

solve this constellation of technological

and

organizational problems.

The

growing importance of

systems

integration, especially in

the

commercial sector, re-

flects fundamental changes in

the

economic

and

organizational climate for large scale

computing.

Integration of

the

world economy

has

forced businesses to link operations

and

information

systems

for coordination of operations

and

financial strategies

and

to

achieve

the

econo-

mies of scale demanded by ...

Increased international competition. The diffusion of economic power

that

has accompa-

nied large scale economic development in

the

third

world

and

especially in Asia.

has

been

encouraged by a fundamental shift in

the

importance

of

the

traditional

Factors

of

Production.

The

relative importance of Physical Resources, Manpower, Capital, and Managerial Talent

has

changed such

that

Capital

and

Managerial

Talent

(especially

the

talented exploitation

of information),

can

overcome

the

limitations imposed by Physical Resources

and

raw

Manpower. Businesses

as

well

as

governments

are

recognizing

that

the

strategic

use

of

information is a critical success factor for

the

achievement of their goals.

Investments

in

computing resources

are

driven by

attempts

to

marshal

the

critical mass

of

information

required for strategic decision making.

* * * CONSULTING and RESEARCH SERVICE *

- - For Internal Use Only - -

* *

4

FINANCIAL ANALYSIS OF SYSTEMS INTEGRATORS

Ironically,

the

rapid development of computing technologies has often served

to

undercut

the

success of any particular organization's computing strategy. Shortened Computer

Product Life Cycles have left many computer customers with unintegrated computing

systems

and

with organizational problems

that

distract from

the

organization's fundamen-

tal

mission. Computers

are

expected by customers

to

be a means to

an

end,

not

an

end in

themselves. Increasingly, corporations

are

turning

to

third parties

to

manage their inter-

nal computing resources, allowing managers

to

address themselves

to

fundamental busi-

ness problems.

Kodak Company, recently hired Businessland, Inc.

to

manage Kodak's personal computer

operations, and Kodak managers are seeking third-party integrators to manage

DP

and

telecommunications functions as

well.

This is coincident with Kodak's desire, like

that

of

many modern corporations, to concentrate

their

resources and managerial

talent

on their

core business, photography.

"Such thinking

puts

Kodak in

the

vanguard of a movement reshaping

the

computer

industry. Hardware

and

software companies

that

have simply pushed

the

technology as

hard and

as

fast

as

they

could

are

finding

that

it

is

not

enough ... " 1 " Companies

are

getting increasingly bogged down running their own systems, and they

are

increasingly

willing

to

pay

the

price to be relieved of

these

headaches, which show no sign of dimin-

ishing." 2

The Federal Government was the first major organization to embrace systems integration

as

a solution to these problems. This

market

was

the

largest source of systems integration

revenues in 1988

but

a drastic decrease in government spending

will

allow commercial

systems integration revenues to surpass government market revenues during 1989.3

The differences between

the

Federal government

market

and

the

commercial

market

are

significant in

terms

of

the

buying behavior of

the

customers~

the

expertise of

the

vendors.

the

methods of doing business and

the

prospects for

market

growth. Because of these

differences, analysis of relative competitive

strength

of systems integration vendors

must

consider

the

proportion of their revenues derived from each sector. While

the

technological/systems design

task

may

be

similar, the marketing

task

is quite different.

1 "Computer Firms Find

That

Service is

What

Sells, Not Fancier Hardware"; Wall

Street

Journal; August 15, 1989; pp. 1; col.

6.

2 Naomi Karton, Computer Consultant; Quoted in "Computer Firms Find Service

..

",

ibid.

3 "Systems Integration- A Competitive Analysis"; Input, December 1988.

* * * CONSULTING and RESEARCH SERVICE *

- - For Internal Use Only - -

* *

5

FINANCIAL ANALYSIS OF SYSTEMS INTEGRATORS

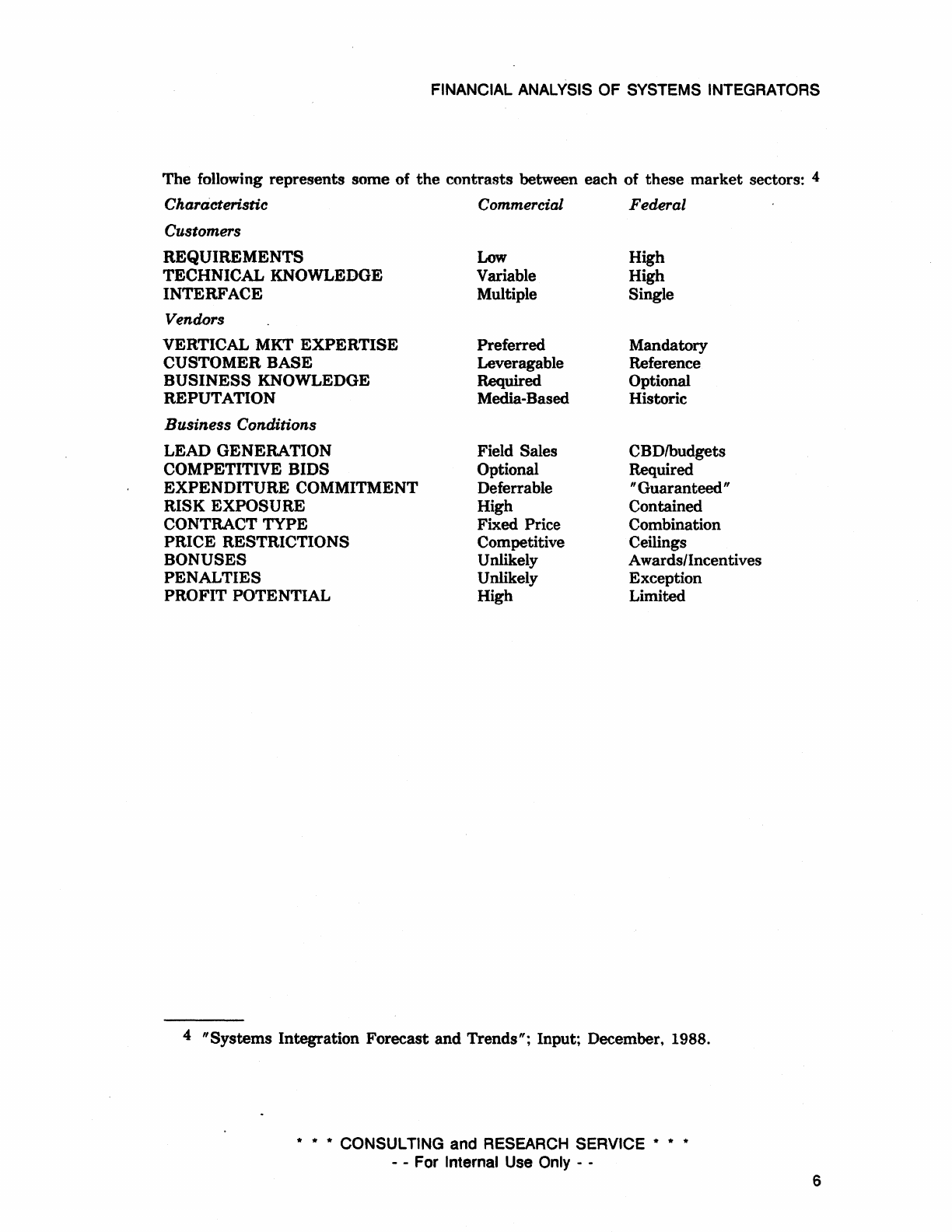

The following represents some of

the

contrasts between each of these

market

sectors: 4

Characteristic Commercial Federal

Customers

REQUIREMENTS

Low

High

TECHNICAL KNOWLEDGE Variable High

INTERFACE Multiple Single

Vendors

VERTICAL MKT

EXPERTISE

Preferred Mandatory

CUSTOMER BASE Leveragable Reference

BUSINESS

KNOWLEDGE Required Optional

REPUTATION Media-Based Historic

Business Conditions

LEAD GENERATION Field Sales CBDlbudgets

COMPETITIVE BIDS Optional Required

EXPENDITURE COMMITMENT Deferrable

II

Guaranteed"

RISK EXPOSURE High Contained

CONTRACT TYPE Fixed Price Combination

PRICE RESTRICTIONS Competitive Ceilings

BONUSES Unlikely Awards/Incentives

PENALTIES Unlikely Exception

PROFIT POTENTIAL High Limited

4 "Systems Integration Forecast and Trends"; Input; December, 1988.

* * * CONSULTING and RESEARCH SERVICE * * *

- - For Internal Use Only - - 6

FINANCIAL ANALYSIS OF SYSTEMS INTEGRATORS

The Commercial Sector

The commercial

market

for

systems

integration is divided, by Input, into

thirteen

industry

sectors:

The Four Largest Segments

•

State

and

Local

Government

•

Discrete

Manufacturing

•

Banking

and

Finance

•

Retail

Distribution

A:dditional Segments

• Process

Manufacturing

•

Insurance

• Wholesale

Distribution

•

Utilities

• Telecommunications

• Medical

• Services

•

Transportation

•

Other

* * * CONSULTING and RESEARCH SERVICE *

- - For Internal Use Only - -

* *

7

FINANCIAL ANALYSIS OF SYSTEMS INTEGRATORS

FINANCIAL ANALYSIS

The Size

of

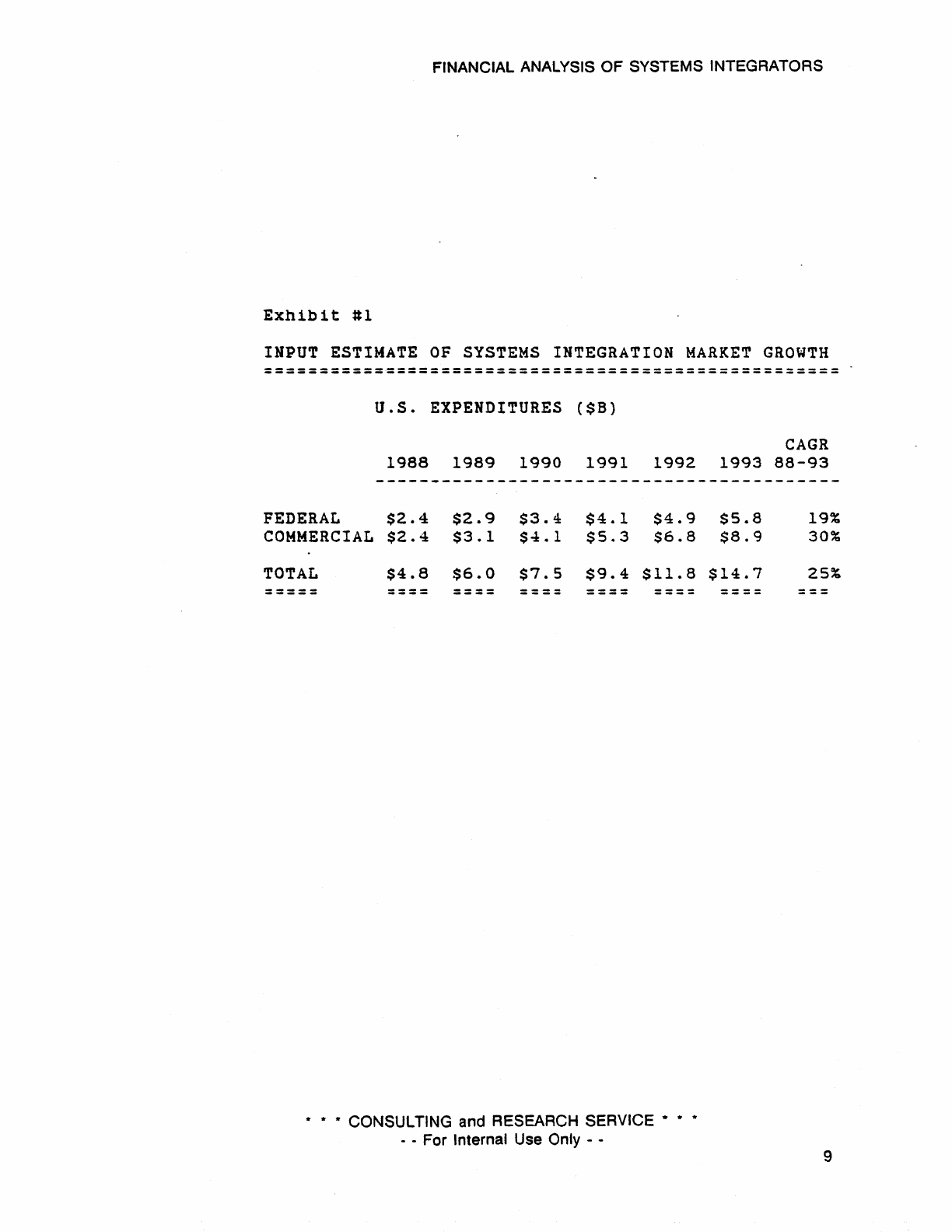

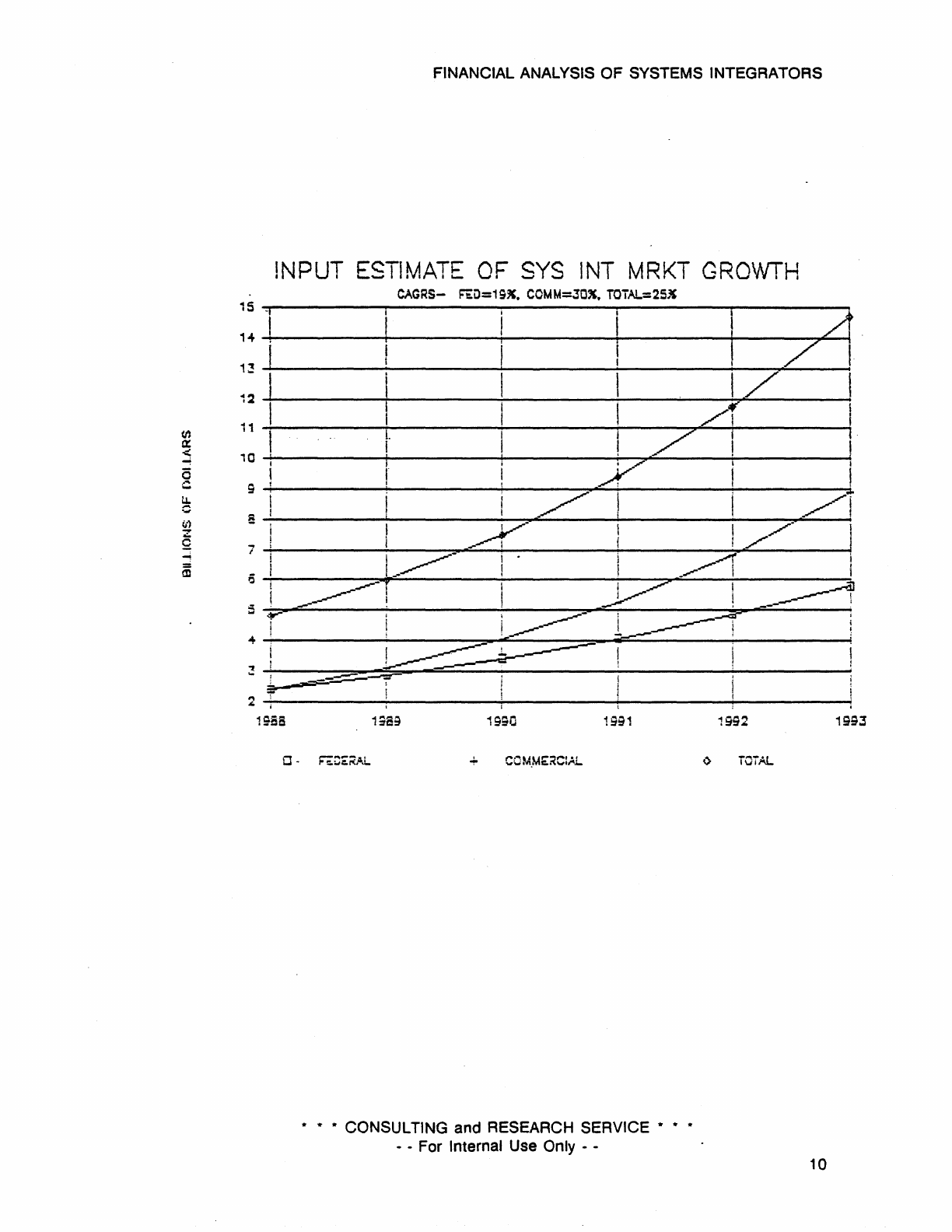

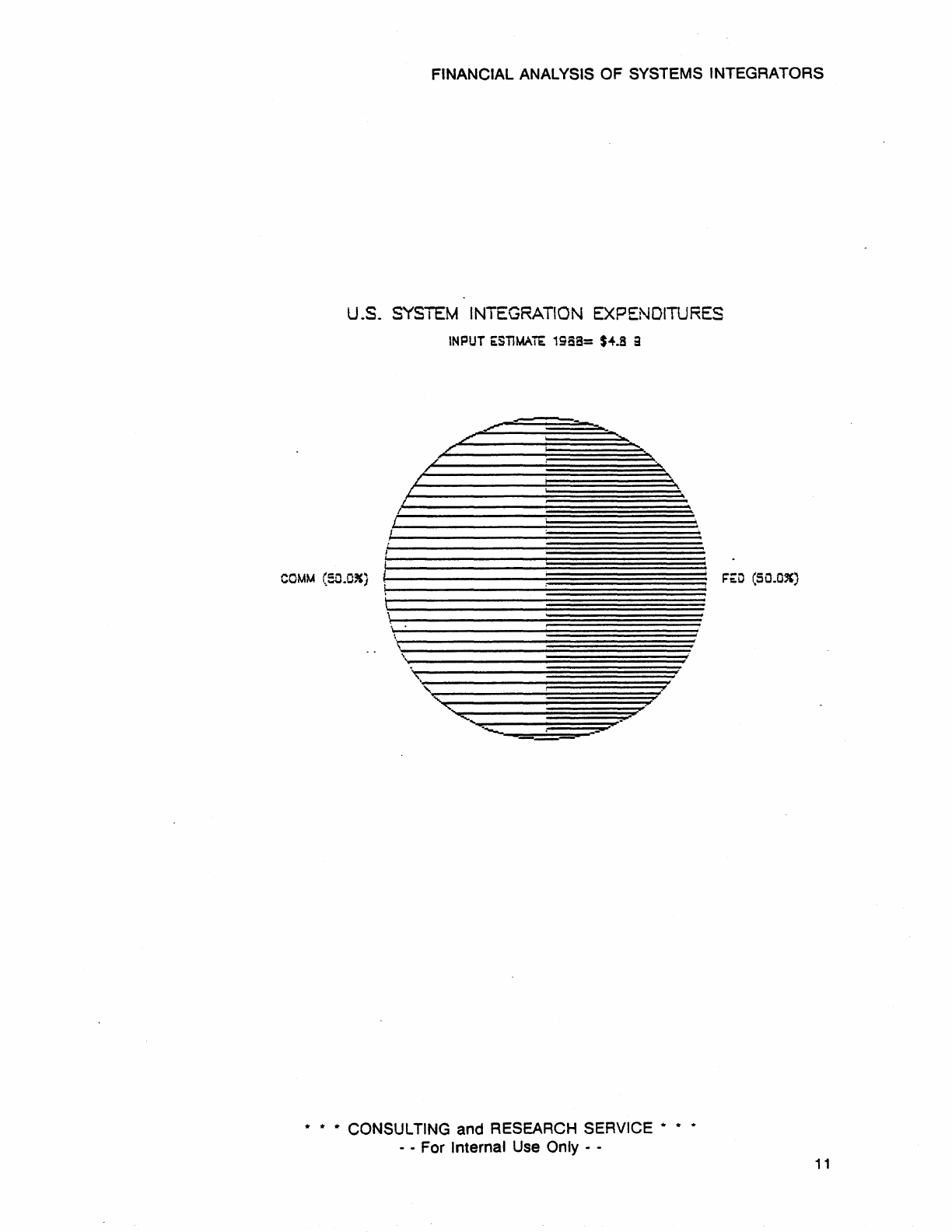

the U.S. Systems Integration Market;

Exhibit

II

details Input's estimates of

the

total size of the U.S. Systems Integration

Market. Exhibits 12, 13 and 14 portray these same data graphically.

Input estimates

the

entire U.S. expenditure on systems integration

to

have been $4.8

billion in 1988, approximately evenly divided between Commercial and Federal

Government sectors. Growth rates for the two sectors differ significantly. Input estimates

that

the

commercial segment will grow

at

a cumulative annual growth

rate

(CAGR)

of 30%

between 1988

and

1993, while

the

government sector

will

average

190/0

over

the

same

period.

For

the U.S. systems integration market as a whole, Input forecasts a 25% CAGR.

1r

1r

* CONSULTING and RESEARCH SERVICE

1r

* *

- - For Internal Use

Only

- - 8

FINANCIAL ANALYSIS OF SYSTEMS INTEGRATORS

Exhibit

#1

INPUT ESTIMATE

OF

SYSTEMS

INTEGRATION

MARKET

GROWTH

----------------------------------------------------

----------------------------------------------------

u.S.

EXPENDITURES

($8)

CAGR

1988

1989

1990

1991 1992

1993

88-93

FEDERAL

$2.4

COMMERCIAL

$2.4

TOTAL

$4.8

-----

-----

$2.9

$3.4

$3.1

$4.1

$6.0

$7.5

----

----

$4.1

$4.9

$5.3

$6.8

$9.4

$11.8

----

---

-

* CONSULTING and RESEARCH SERVICE *

- - For Internal Use Only - -

$5.8

$8.9

$14.7

--

--

19%

30%

25%

9

<t)

a::

<

0

c

~

ii)

Z

Q

-!

m

15

-I

1~

1~

I

i

J

12

11

10

9

S

i

0

5

...

FINANCIAL ANALYSIS OF SYSTEMS INTEGRATORS

!NPUT

ESTIMATE

OF

SYS

INT

MRKT

GROWTH

CAGRS-

!='iLl=1;".

COMM=JOX.

TOTAL=25~

L

I

I

I~--

~-

,.--

i .

!

t/

,

!

71

.;;-

/,

./

I

I

.~

1.---.::

I

3

~----~=-~=---==--------------~----------~--------~

~~::;:::-::..-------

-;=--

2

~'----------~!----------~--------~----------~--------~

1988

19;0

1·~"'1

.~~.

11

11 11

CONSULTING and RESEARCH SERVICE

11

11

11

- - For Internal Use Only - -

1992

1993

~

iCTAL

10

FINANCIAL ANALYSIS OF SYSTEMS INTEGRATORS

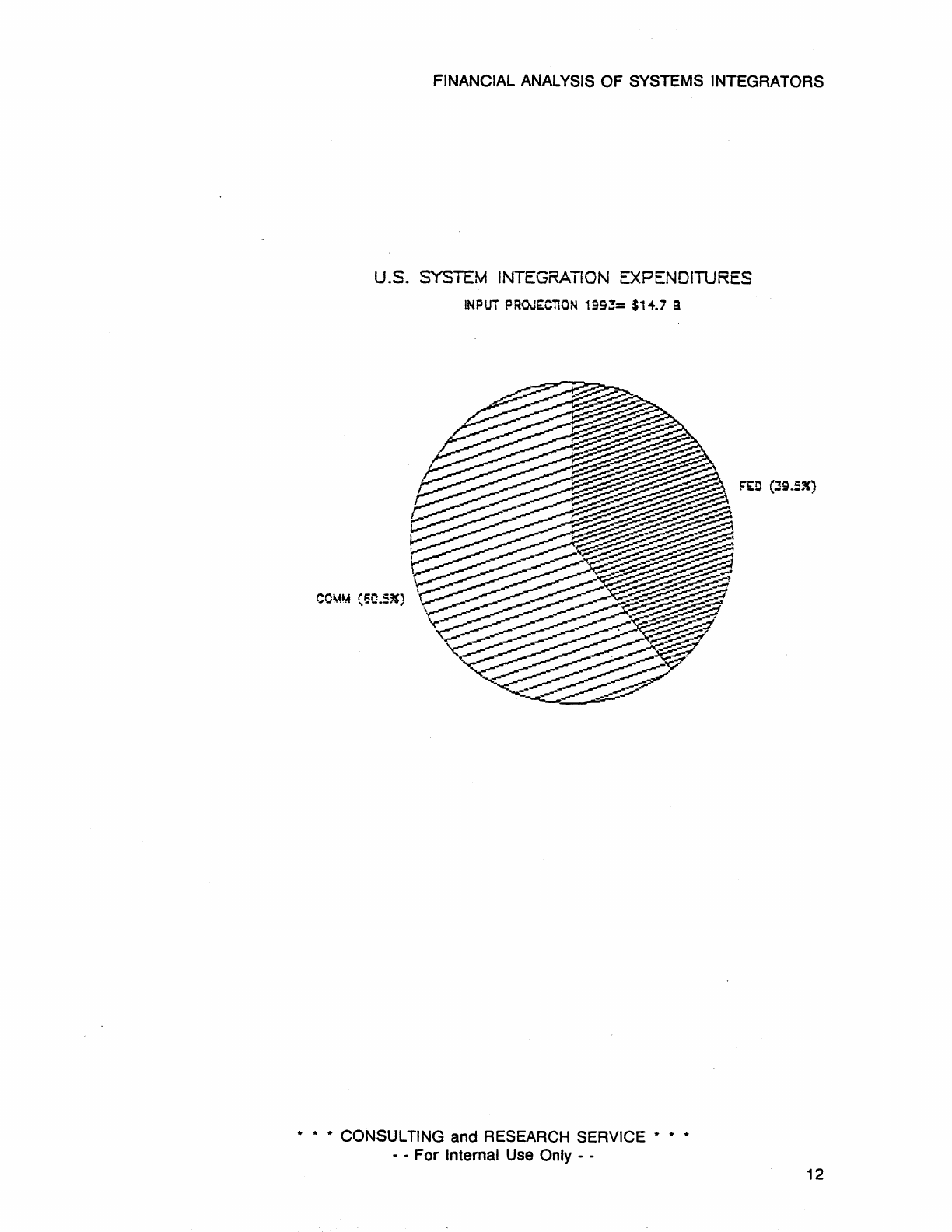

u.s. SYSTEM INTEGRATION EXPENDITURES

CCMM

(SO.03()

I

\

i

\

\ \

INPUT

6:SiiMAiE:

19B8= $

....

8 a

,.

\ "

===

.,

.,

.,

CONSULTING and RESEARCH SERVICE

.,

- - For Internal Use Only - -

1='6:0

(SO.OX)

11

FINANCIAL ANALYSIS

OF

SYSTEMS INTEGRATORS

U.S.

SYSTEM

INTEGRATION EXPENDITURES

INPUi

PROJECTION

1993=

$1

+.7 B

* * * CONSULTING and RESEARCH SERVICE * * *

- - For Internal

Use

Only - -

12

FINANCIAL ANALYSIS OF SYSTEMS INTEGRATORS

U.S.

Systems

Integration;

Input's

Market

Share

Estimates

Exhibit

115

details

Input's

estimates of

the

1988 U.S. systems integration

market

shares

enjoyed by

the

fifteen

top

competitors, together with

the

portion of their systems integra-

tion revenues derived from commercial and federal government contracts. In this exhibit,

the

competitors

are

ranked

by

level of total systems integration revenue.

Note

that

the

percentage

market

share rankings

are

dominated by IBM and

EDS

with

21

% and 13% shares respectively, while other competitors trail significantly. Note

that

Digital's

share

of

the

overall systems integration

market

is estimated by Input to be only

3.5% of

the

total.

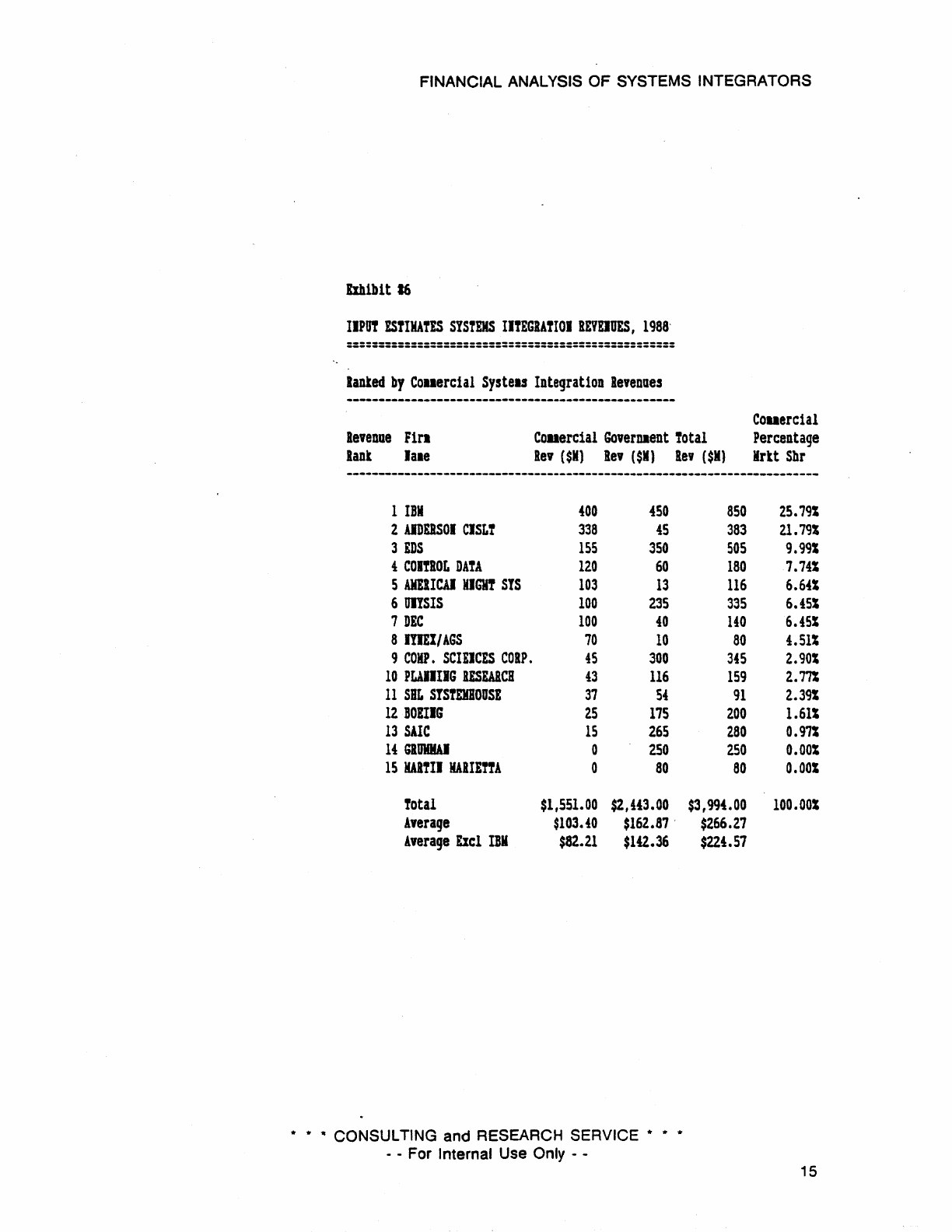

Exhibit

116

details

Input's

estimates of

the

1988 U.S. commercial systems integration

market. In this exhibit,

the

competitors have been reordered

to

reflect their commercial

market

share rankings. Here again, IBM dominates with a 26%

market

share, Anderson

Consulting shows a 22%

share

and EDS drops to number three with a 9.9% share. The

distribution of revenues is still highly concentrated

by

this ranking. Digital's share of this

portion of

the

market is estimated

to

be 6.5%.

Exhibit

117

details

Input's

estimates of

the

1988 Federal Government systems integration

market. The competitors have been reordered according

the

Federal Government

market

shares. The distribution is significantly wider

than

the

commercial sector, with

the

top five

competitors garnering roughly 65% of

the

revenues. Digital's share of

the

government

systems integration

market

is estimated

to

be

1.60/0.

The differences in industry concentration suggested by

the

comparisons between

the

com-

mercial and government sectors highlights the contrasts between

the

markets previously

described.

* * * CONSULTING and RESEARCH SERVICE *

- - For Internal Use Only - -

* *

13

FINANCIAL ANALYSIS OF SYSTEMS INTEGRATORS

ExhIbIt

15

IIPI!

ESfIIA!ES

SYSTEMS

IITEGlAfIOI

lEVEIUES,

1988

===================================================

laDied

by

fatal

Systels

Integration

leveDoes

---------------------------------------------------

le,enoe

Fin

COllercia1

GoverDient

Total

Percentage

Rank

lale

Re,

($11)

Re,

($II)

lev

($11)

IIrtt

Shr

-------------------------------------------------------------------------

1

IBI

400

450

850

2

EDS

155

350

505

3

AlOERSOI

ClSLf

338

45

383

4

CaMP.

SCIEICES

CORP.

45

300

345

5 mSIS

100

235

335

6

SAlC

15

265

280

7

GRUWI

0

2.S0

250

8

BOEIIG

25

175

2.00

9

COI!IOL

DAfA

120

60

180

10

PLAlIIIG

RESEARCH

43

116

159

11

DEC

100

40

UO

12

AKElICAI

HIGHT

SIS

103

13

116

13

SBL

SYStEKBOUSE

37

5.

91

14

IYUI/AGS

70

10

80

15

IAI!I)

HAIIE!!A

0

80

80

fotal

$1,551.00

$2,443.00

$3,994.00

Average

$103.40

$162.87

Average

Exc1

IBI

$82.21

$142.36

* * * CONSULTING and RESEARCH SERVICE *

- - For Internal Use Only - -

$266.27

$224.57

21.28%

12.64%

9.591

8.64%

8.391

7.0lS

6.261

S.OlS

4.511

3.981

3.511

2.901

2.28S

2.00S

2.00S

100.00S

14

FINANCIAL ANALYSIS OF SYSTEMS INTEGRATORS

bhlbtt

16

IIPD!

EStlKATES

SYSTEMS

IltEGIATIOI

RIVElUES,

1988-

===================================================

lanted

by

COllerclal

Systels

Integrat10n

Revenues

---------------------------------------------------

Couerclal

levenue

Firl

COllercial

GQvernaent

Total

Percentage

lani

laae

lev

($11)

Rev

($11)

Rev

($1)

IIrit

Sbr

-------------------------------------------------------------------------

1

IBII

400

450

2

AlDERSOI

CISL!

338

45

3

EDS

155

350

4

COUIOL

DATA

120

60

5

AMEllCA)

liGHT

SIS

103

13

6

UlYSIS

100

235

7

DEC

100

40

8

ImI/AGS

70

10

9

COMPo

StIllCES

CORP.

45

300

10

PLAt.IIG

RESEARCH

43

116

11

SIL

SIStEKBOOSE

37

54

12

BOIIlG

25

175

13

SAlt

15

265

14

GlMAI

0

250

IS

HAITII

HAIIETTA

0

80

Total

$1,551.00

$2,U3.00

Average

$103.40

$162.87

'

Average

£Iel

IBM

$82.21

$142.36

* *

iI

CONSULTING and RESEARCH SERVICE * * *

- - For Internal Use Only - -

850

25.791

383

21.

79%

505

9.991

180

7.741

116

6.641

335

6.451

140

6.451

80

4.511

345

2.901

159

2.771

91

2.391

200

1.611

280

0.971

250

0.001

80

0.001

$3,994.00

100.001

$266.27

$224.57

15

FINANCIAL ANALYSIS OF SYSTEMS INTEGRATORS

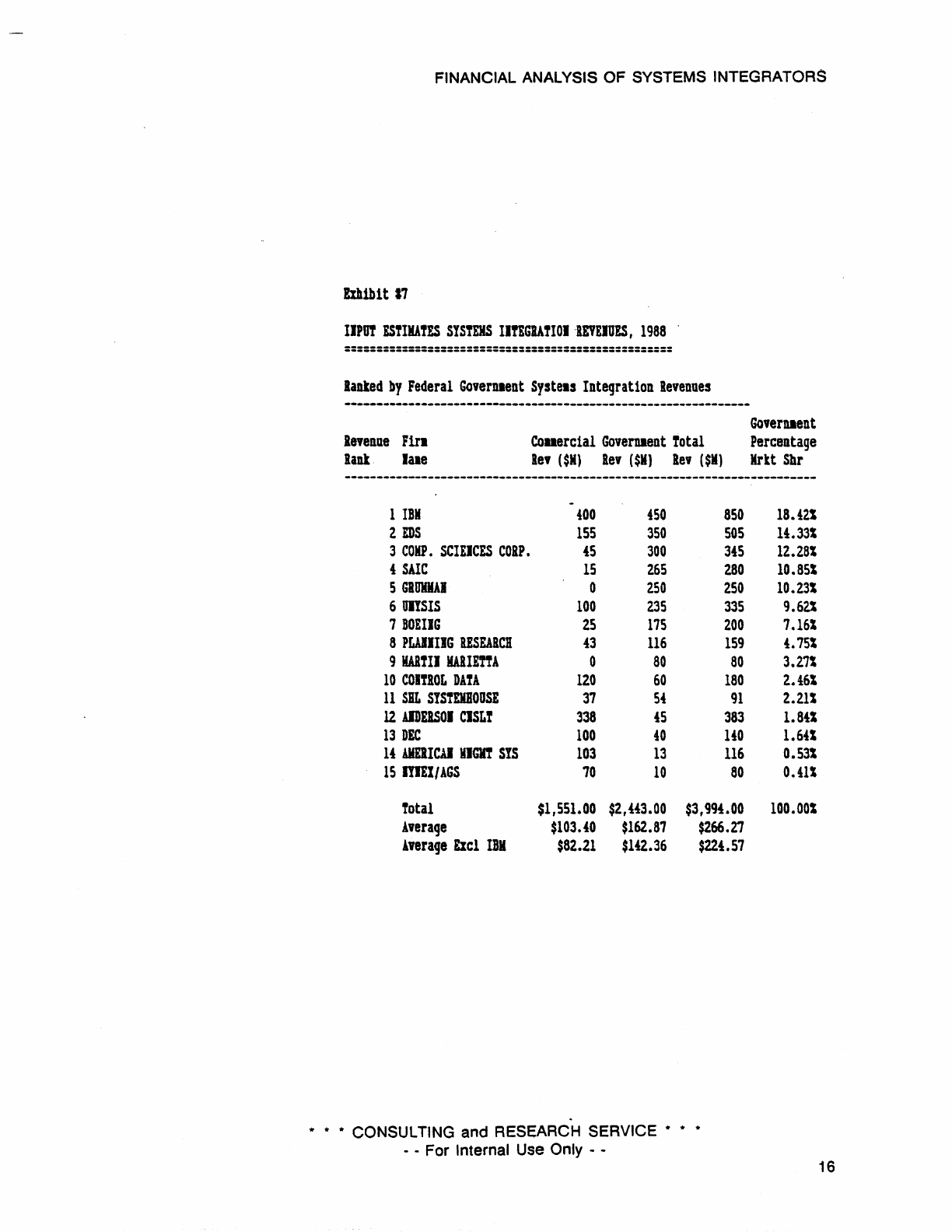

Exhib1t

11

IIPUT

ESTIMATES

SYSTEMS

IITEGIATIOI

-IEVEIDES,

1988

===================================================

lanked

by

Federal

GoverDient

Syste.s

Integrat10n

levenues

GoverDient

Betenue

Fira

lank

lale

eollerc1al

Governaent

Total

Percentage

Rev

($Kl

lev

($K)

lev

($K)

Hrit

Shr

1

IBM

400

450

850

2

EnS

155

350

505

3

COIIP.

SCIEICES

COIP.

45

300

345

4

SAlC

15

265

280

5

GBUlUIAI

0

250

250

6

mSIS

100

235

335

7

BOEIIG

25

175

200

8

PLAlIIIG

RESEARCH

43

116

159

9

HAlTII

HAIIErT!

0

80 80

10

COITROr.

DATA

120

60

180

11

SiL

SYSfEKBOOSE

37

54

91

12

AlDEBSOI

ClSLT

338

45

383

13

DEC

100

40

liO

U

AMElICAI

OGlft

SIS

103

13

116

IS

IYIEI/AGS

70

10

80

Total

$1,551.00

$2,!43.00

$3,994.00

Average

$103.40

$162.87

$266.2.7

Average

£Icl

IBI

$82.21

$U2.36

$224.57

......

CONSULTING and RESEARCH SERVICE

......

- - For Internal Use Only - -

18.42S

14.33S

12.28S

10.85S

10.23S

9.62%

7.16S

4.75S

3.27S

2.46S

2.21S

1.84S

1.64S

0.531

O.41S

100.00S

16

FINANCIAL ANALYSIS OF SYSTEMS INTEGRATORS

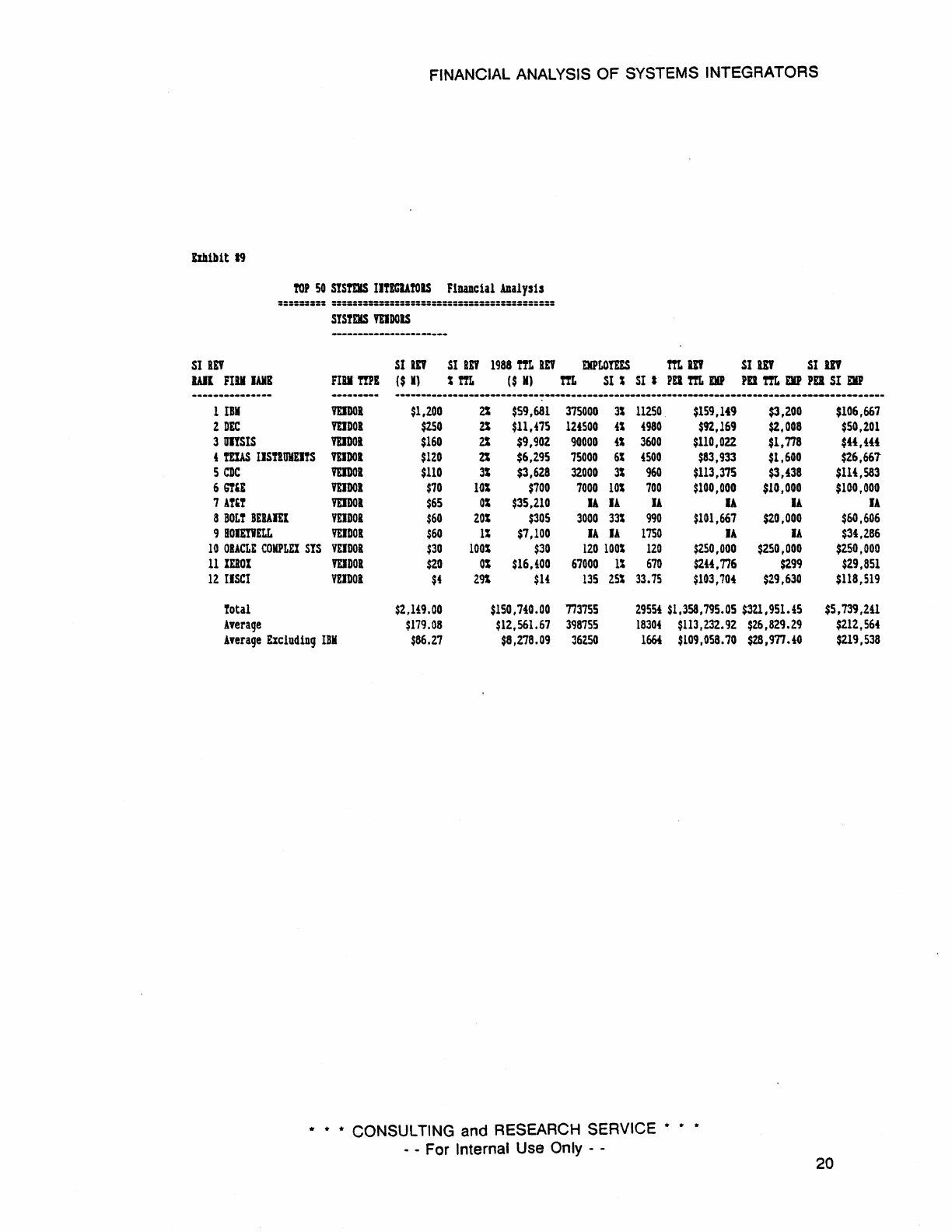

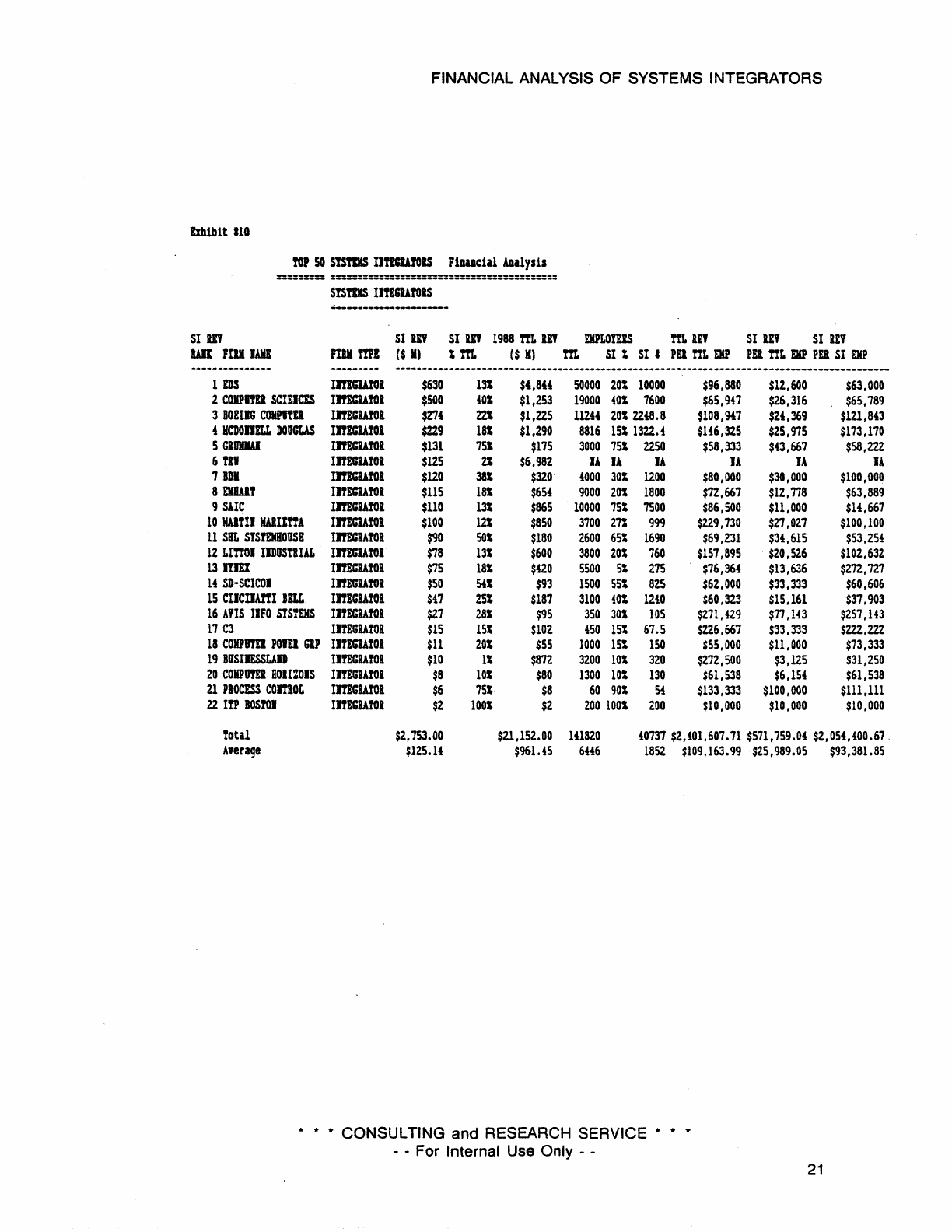

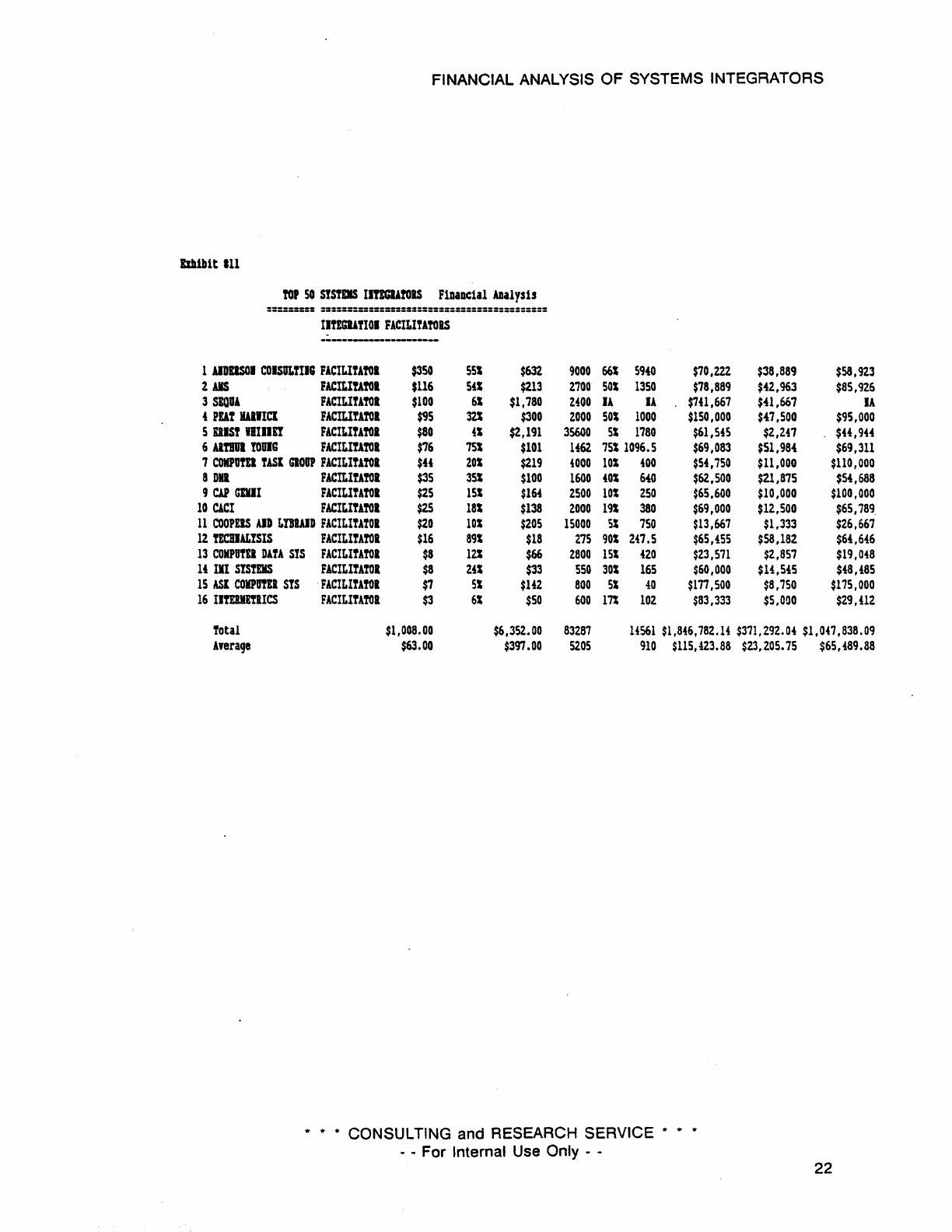

The Size

of

the U.S. Systems integration Market; Computer Systems News' Estim,ates

Computer

Systems

News'

Systems

Integrators whitepaper, published in May

of

1989

provides interesting details

on

the

Top 50

Systems

Integrators

in

the

United

States.

Based upon mailed questionnaires,

the

data

includes information on employee head counts

as

well as revenues. This

data

enables calculation of a useful statistic;

Systems

Integration

Revenue

per

Systems Integration Employee. This statistic is

the

only available information

on

efficiency

or

costs.

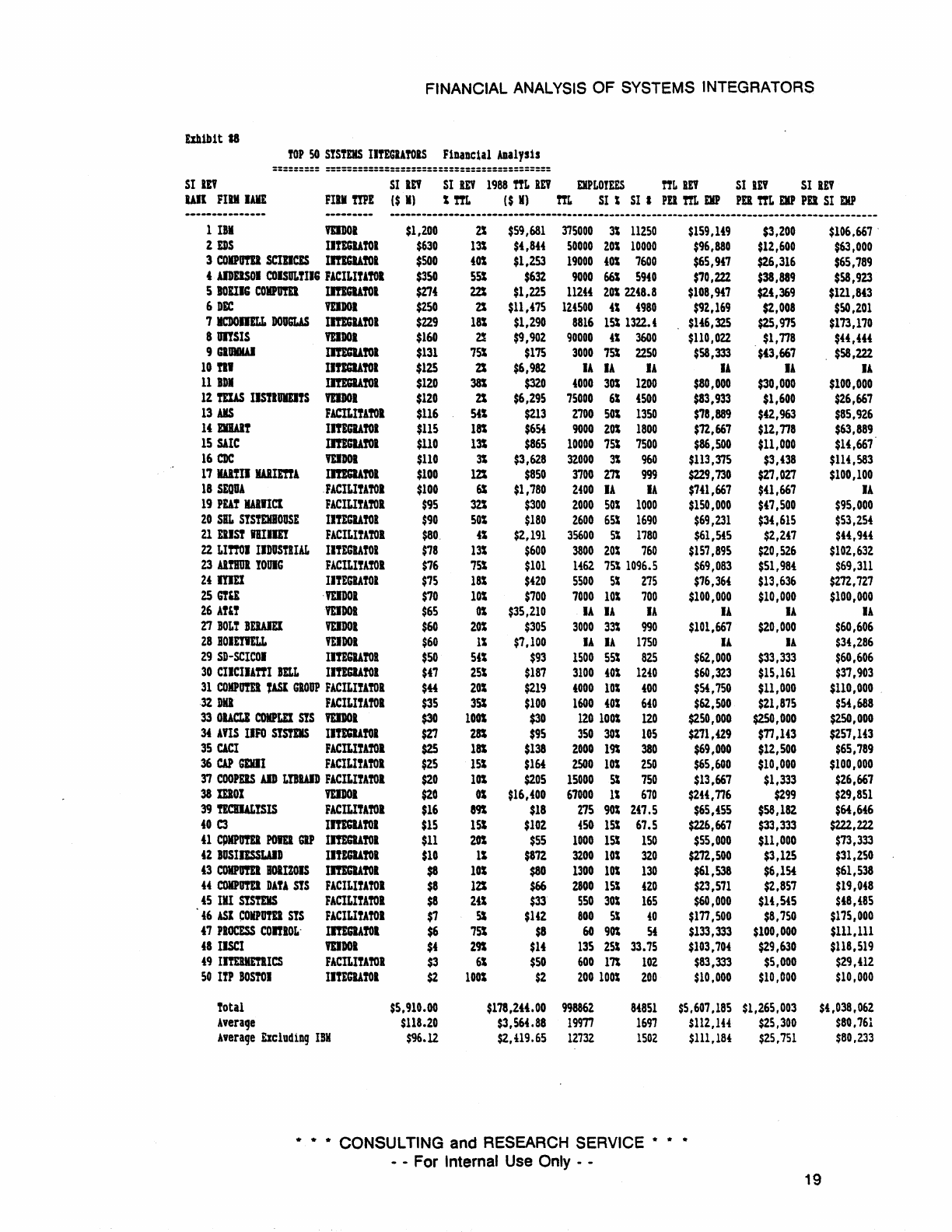

Exhibit

#8

ranks

the

Top 50 systems integrators by

total

systems

integration revenue.

The

estimated

amounts

of revenue differ significantly from those

estimated

by Input. This

is a result of

the

difference in definition

and

accounting

standards

previously alluded to.

The

Top 50

systems

integrators garnered $5.9 billion

in

revenues during 1988 according

to

Computer

System

News. This compares to

the

$4.8 billion

estimated

by Input. The

amounts

of

systems

integration revenue

attributed

to each firm also differ considerably.

Despite

these

discrepancies

the

top

systems integrators appear in both lists.

Computer

Systems

News distinguished competitors

by

type. Vendors

are

those firms

whose primary business mission is hardware sales. Facilitators, typically

the

Big

Eight

accounting firms, sell expertise

in

accounting information systems

and

auditing, with

systems

integration

as

a means

to

promote those services. Integrators,

per

se, have

identified

SI

to

be

their

primary business mission.

Exhibits

#9

through

# 11 detail some of

the

contrasts

among

these

three

segments.

Note first

the

differences in

the

number of competitors: twenty-two integrators, sixteen

facilitators,

and

twenty-two integrators.

Excluding IBM's systems integration revenue

of

over $1 billion,

the

average 1988

SI

revenue for each

segment

was: $63 million for facilitators, $86.27 million for vendors

and

$125.14 million for integrators. Average

SI

revenue per

SI

employee was

estimated

to

be

$212,564 for hardware vendors, $93,381 for integrators

and

$65,499 for facilitators. These

segment

averages compare

to

the

overall (Top

50~

SI

revenue

per

SI

employee

statistic

of

$80,761.

These statistics point

to

a fundamental fact about

the

systems

integration business. While

the

market

is growing quickly

and

while

systems

integration is generally considered

to

be

more profitable

than

pure professional services (10% margins vs services' 6%),

it

is very

capital intensive.

It

does

not

require investment in manufacturing plants like

the

hardware

business

but

most

systems integration firms fund software development programs.

testing

facilities and training programs. Project development costs

and

costs for bidding on con-

tracts

are

significant, amounting

to

up

to

4% of a given

contract's

value, according

to

Mark Hodges of G2 Research. 5

5 "Big Business Dominates

Systems

Integration Sector";

John

Moore;

Systems

Integration whltepaper; Computer

Systems

News; May 1989.

* * * CONSULTING and RESEARCH SERVICE *

- - For Internal Use Only - -

* *

17

FINANCIAL ANALYSIS

OF

SYSTEMS INTEGRATORS

By

contrast

with

the

systems integrators' 10%

to

12% margins. hardware manufacturers

typically receive margins on equipment in excess of 25%. This fact may account for

the

higher average

SI

revenue per employee enjoyed

by

the

vendor segment.

* * * CONSULTING and RESEARCH SERVICE *

- - For Internal Use

Only

- - * *

18

FINANCIAL ANALYSIS OF SYSTEMS INTEGRATORS

Elh1b1t

18

TOP

50

SYSTElIS

I1TEGIATOlS

F1nancla1

Ana1ys1s

=========

==========:::=:===========================

SI

lEV

51

lEY

51

lEY

1988

TTL

iEY

ElPLOtEES

nLiEY

SI

lEY

SI

iEV

un

FlU

lAKE

FIlII

mE

($

11)

tm.

($

If) ttL

SI

t;

51

I

PEl

TTL

DP

PEl.

TTL

ElP

PEl

SI

EYP

---------------

-------------------------------------------------------------------------------------------

1

III

YUDOI

$1,200

2t

$59,681

315000

31

11250

2

IDS

IITEGlAtol

$630

131

$4,844

50000

201

10000

3

COlPum

SCIDCES

ImGUTOI

$500

40t

$1,253

19000

401

7600

•

UDDSOI

COISULTlle;

FACILITATOR

$350

551

$632

9000

661

5940

5

BOElle;

COlPum

ImGbTOI

$274

m

$1,225

112U

2012248.8

6

DEC

YUDOl

$250

2t $ll,475

124500

U

4980

7

ICDOIIELI.

DOUGLAS

ImGlATOI

$229

18t

$1,290

8816

1511322.4

8

mSls

YDDOl

$160

2S

$9,902

90000

41

3600

9

GllDOIAI

IftEGWOI

$131

751

$175

3000

75t

2250

10

ft.

IITIGIATOI

$lZS

2S

$6,982

IA

Ii

IA

11

BDI

ImGlATOI

$120

381

$320

4000

301

1200

12

TEW

IIS'lIUIDTS

YDDOR

$120

2t

$6,295

75000

6t

4500

13

!IS

FACILItAtoR

$116

Sfl

$213

2700

50S

1350

UawT

I1fEGlAtol

$115

181

$654

9000

20t

1800

IS

SAlC

ImGIAtOI

$110

131

$865

10000

75t;

7500

16

CDC

'fEIIGI

$110

3S

$3,628

32.000

3S

960

17

lAUD

mImA

ImGlATOI

$100

121

$850

3700

2"

CJCJ9

18

SEOUA

FACILITATOR

$100

6S

$1,780

2fOO

IA

IA

19

PEAT

WIICl

FACILITATOR

$95

32t

$300

2.000

50S

1000

20

SBL

SYSTEHBOUSE

IIBGlAtol

$90

SOt

$180

2600

65S

1690

2.1

rusr

DIIm

FACILITATOR

$80.

4S

$2,191

35600

5%

1180

22

LITTOI

IIDUStiIAL

II!EGlATOI

$78

13t

$600

3800

20S

760

23

Al!ll1Jl

YOUIG

FACILItAtOR

$76

751

$101

1462

751

1096.5

24

mEl

I1BGlAfOl

$75

181

$420

5500

5S

275

ZS

CUE

·mOOl

$70

101

$700

7000

lOt;

700

26

AUT

mOOI

$65

OS

$35,210

IA

n

IA

21

BOLT

BEWEl

'fEID01

$60

20t

$305

3000

33%

990

28

HOlmELL

'fEIDOR

$60

IS

$7,100

IA

Ii

1750

29

SD-SCICOI

I1BGlATOR

$50

541

$93

1500

55S

825

30

CIICIIATrI

BELL

ll!EGlATOl

$47

25t

$187

3100

40%

12.40

31

COJIPom

fASt

GIOUP

FACILIUTOR

$44

201

$219

4000

lOS

400

32

DII

FACILITATOR

$35

351

$100

1600

40S

640

33

OUeLI

COIPLEI

SIS

mOOl

$30

lOGS

$30

120

lOot

120

34

AYIS

lIFO

SISTDS

I1!EGlATOI

$27

28S

$95

350

30t;

105

35

CACI

FACILIU'lOR

$2S

181

$138

2.000

1~

380

36

CAP

GEJIII

FACILIUTOI

$25

lSI

$164

2500

lOS

250

37

COOPEIS

AID

LtBWD

FACILItATOI

$20

lot

$205

15000

St;

750

38

mOl

mDDI

$20

01

$16,400

67000

11

670

39

TECBlALYSIS

FACILI!AtoR

$16

891

$18

275

90t;

2.47.5

400

ImGlATOI

$15

ISS

$102

4SO

15S

67.5

U

CPlIPum

POm

GIP

ImGlATOI

$11

20S

$55

1000

1St;

ISO

42

BUSIJlSSLAID

IIfEGUTOR

$10

IS

$872.

3200

lOS

320

43

COIIPUfEl

BOIIZOIS

ImGIAroR

$8

101

$80

1300

lOS

130

44

COIPOTEl

DATA

SIS

FACILItATOR

$8

121

$66

2800

ISS

420

45

III

mmlS

FACILITATOR

$8

241

$33

550

30S

165

46

ASI

COIfPUTEI

SIS

FACILITAtoR

$7

51

$142

800

5t;

fO

f7

PIOCESS

conlOL'

ImGlATOI

$6

751

$8

60

90s

54

48

IISCI

lEIDOl

$'

291

$1f

135

25t;

33.75

49

ImDmICS

FACILITAtoR

$3

61

$50

600

17S

102

50

ItP

BOSTOI

IIBGIATOR

$2.

IDOl

$2.

ZOO

lOOt;

200

Total

$5,910.00

$178,2.44.00

998862

84851

Average

$118.2.0

$3,564.88

19m

1697

Average

Excluding

IBH

$96.12

$2,419.65

12732

1502

. .

• CONSULTING and RESEARCH SERVICE •

- - For Internal Use Only - -

$159,H9

$3,200

$106,667

.

$96,880

$12,600

$63,000

$65,947

$26,316

$65,189

$70,222

$38,889

$58,923

$108,947

$2!,369

$121,8'3

$92,169

$2,008

$50,201

$146,325

$25,975

$173,170

$110,022

$1,178

$U,4tt

$58,333

$43,667

$58,222

IA

IA

Ii

$80,000

$30,000

$100,000

$83,933

$1,600

$26,667

$78,889

$'2,963

$85,92.6

$12,667

$12,178

$63,889

$86,500

$11,000

$H,667

$113,3'75

$3,438

$1U,583

$229,730

$27,027

$100,100

$141,667

$41,667

IA

$150,000

$41,500

$95,000

$69,231

$34,615

$53,254

$61,5!S

$2.,U7

$44,944

$151,895

$20,526

$102,632

$69,083

$51,984

$69,311

$76,364

$13,636

$2.12,727

$100,000

$10,000

$100,000

IA IA IA

$101,667

$2.0,000

$60,606

U IA

$34,286

$62,000

$33,333

$60,606

$60,323 $15,161

$37,903

$54,750

$11,000

$110,000

$62,500

$21,875

$54,688

$250,000

$250,000

$2.50,000

$271,429

$17,143

$251,143

$69,000

$12,500

$65,789

$65,600

$10,000

$100,000

$13.667

$1,333

$2.6,667

$244,776

$299

$2.9,851

$65,455

$58,182

$64,646

$22.6,667

$33,333

$222,222

$55.000

$11,000

$73,333

$212,500

$3,125

$31,250

$61,538

$6,154

$61,538

$2.3,571

$2,857

$19,Of8

$60,000

$14,545

$48,485

$177

,500

$8,750

$175,000

$133,333

$100,000 $111,111

$103,704

$29,630

$118,519

$83,333

$5,000

$29,412

$10,000

$10,000 $10,000

$5,607,185

$1,265,003

S4,038,062

$112,144

$25,300

$80,761

$111,18!

$25,751

$80.233

• *

19

FINANCIAL ANALYSIS OF SYSTEMS INTEGRATORS

EIh1blt

19

fOP

50

STSms

IItlGUtoRS

Financial

ADal

ysis

:=:::::::

===:===:::=======:==:===:===:=:==:=::==:==

STstE1lS

mOORS

51

lE'f

51

lEV

51

lEY

1988

TTL

lEV

EllPLOms

mm

51

lEY

51

m

Wl

FIll

lAME

FlumE

($

I)

S

HI.

($

JI)

m.

51

S

S1

1

PEl

m.

EJIP

PD

m.

EIIP

PD

51

DIP

---------------

------------------------------------_

....

----------------------------------------------------

1

IBI

VEJDOI

$1,200

2l

$59,681

375000

3S

11250

$159,H9

$3,200

2

DEC

VEIDOI

$250

2S

$11,.75

12i500

is

{980

$92,169

$2,008

3 mSIS

VDDOI

$160

2l

$9,902

90000

{S

3600

$110,022

$l.na

{

rms

I1StIUKEITS

VEIDaI

$iZO

21

$6,295

75000

61

{500

$83,933

$1,600

5

CDC

VDDOR

$110

3S

$3,628

32000

3S

960

$113,375

$3,f38

6

GTn

VEIDaI

$70

lOS

$700

7000

lOS

700

$100,000

$10,000

7

AnT

VEIDOI

$65

OS

$35,210

U

IA

U

IA

IA

8

BOLT

BEIlAHI

VEIDOR

$60

201

$305

3000

331

990

$101,667

$20,000

91l0lmELL

VEIDOI

$60

II

$7,100

IA IA

1750

IA

IA

10

OBACLE

COMPLEX

SIS

VEIDoa

$30

1001

$30

120

laOS

120

$250,000

$250,000

11

lElOl

VElDOI

$20

01

$16,!00

67000

IS

670

$2U,T16

$299

12

IISCI

VEIDOI

U

29%

$U

135

251

33.75

$103,70f

$29,630

Total

$2,149.00

$150,7{0.00

n375S

2955t

$1,358,795.05

$321,951.

45

Average

Average

Excluding

IBJI

$179.08

$12,561.67

398755

1830.

$86.27

$8,278.09

36250

166j

* CONSULTING and RESEARCH SERVICE *

- - For Internal Use Only - -

$113,232.92

$26,829.29

$109,058.70

$28,9n.!0

$106,667

$50,201

$U,Hf

$26,661

$114,583

$100,000

IA

$60,606

$34,286

$250,000

$29,851

$118,519

$S,739,2tl

$212,56.

$219,538

20

FINANCIAL ANALYSIS OF SYSTEMS INTEGRATORS

bh1btt

110

to.

SO

sysms

IlftGUfOlS FiDUcial

ADalysis

========

::::::::::::::::::::::::::::::::::::::::::

SI

lEY

lAB FlU

lAME

._-------------

1

EDS

2

COJIPutD

SCIEICIS

3

BOEIJG

COlIPutD

j

HCDOnEIJ.

DOUGLAS

5

GllIIIAJ

6 Til

7BDt

8

EJlW.T

9SlIC

10

WTII

WIEn!

11

SBL

SYSTEIIIIOUSE

12

LITtoI

IJDUSHIAL

13

ItIEI

14

SD-SClCOI

15

CIICIJAnr

BELL

16

AVIS

liFO

SYStEJlS

17

C3

18

COJIPUTEI

pom

GIP

19

BIJSllESSWD

20

COJIPUTEI

aOIIZOIS

21

PROCESS

comOL

22

In

BOS!OI

Total

A,eraqe

stsms

InEGUtolS

----------------------

SI

m

51

lEY

1988

m

lEY

ElPLOms

TTL

lEi

51

lE'

SI

lEV

FIlii

mE

($

II)

1m.

($ II) m

51

1

51

I

PEl

m.

DIP

PEl

nr.

EKP

PEl

51

m

-------------------------------------------------------------------------------------------

ImGlAfOl

$630

13%

$4,844

50000

201

10000

$96,880

$ll,600

$63,000

llTECUfOl

$500

jOS

$1,253

19000

401

7600

$65,947 $26,316

$65,789

ImGlAfOl

$274

m

$1,225

lllU

201

22{8.8

$108,947

$24,369

$121,843

II!EGlAtol

$229

In

$1,290

8816

15S

1322.{

$146,325

$25,975

$173,170

ImGUfOl

$131

751

$175

3000

75S

2250

$58,333

$43,667 $58,222

IJ!EGlAtol

$125

2S

$6,982

IA

U

IA

U U

IA

ImGlAfOl

$120

381

$320

4000

30S

1200

$80,000

$30,000

$100,000

IITEGlAfOl

$115

l8S

$654

9000

20S

1800

$72,667

$12,718

$63,889

ImGBAfOl

$110

13%

$865

10000

75S

7500

$86,500 $11,000

$14,667

I1TEGlAtol

$100

12S

$850

3700

271

999

$229,130

$27,027

$100,100

ImGlAfOl

$90

50S

$180

2600

65S

1690

$69,231

$34,615

$53,254

llTEGlAfOl·

$78

13S

$600

3800

20S

760

$157,895

$20,526

$102,632

llTEGlAfOl

$75

18S

$420

5500

Sl

275

$76,364

$13,636

$Z72,727

IITEGUfOl

$50

54S

$93

1500

55S

825

$6Z,000

$33,333 $60,606

IITEGlAfOl

$47

25S

$187

3100

40S

1240

$60,323 $15,161

$37,903

IITEGlAtol

$27

28S

$95

350

30S

105

$Z71,429

$77,143

$257,143

IITEGlAfOl

$15

ISS

$102

450

ISS

67.5

$226,667

$33,333

$222,222

IITEGUtol

$11

20S

$55

1000

ISS

150

$55,000

$11

,000

$73,333

llTEGlAfOl

$10

IS

$872

3200

lOS

3Z0

$272,500

$3,125

$31,250

I1TEGIA!01

$8

lOS

$80

1300

IDS

130

$61,538

$6,154

$61,538

IftEGlAfOl

$6

75S

$8

60

90S

54

$133,333 $100,000

$111,111

IITEGlAtol

$2

100S

$2

200

100S

200

$10,000

$10,000

$10,000

$2,753.00

$21,152.00

lU820

40737

$2,401,607.71

$571,759.04

$2,054,400.67 .

$125.14

$961.45

6U6

1852

* CONSULTING and RESEARCH SERVICE *

- - For Internal Use Only - -

$109,163.99

$25,989.05

$93,381.85

21

FINANCIAL ANALYSIS OF SYSTEMS INTEGRATORS

bJl1btt

III

!OP

50

SlstElS

ImGIA!OlS

FiDlDclal

ADal

ys1s

=:==::=:

=:==::==::==::==:==:=:::=::==:==:==:==::=:

IItEGU!IOI

FACILIUTOas

..

--------------------

1

AlDIISOI

COISULtIIG

FACILItAtol

$350

551

$632

9000

661

5940

$70,222

$38,889

$58,923

2 US

FACILItAtol

$116

541

$213

2100

sal

1350

$78,889

$42,963

$85,926

3

SlQUA

FACILItAtol

$100

61

$1,180

2.00

IA

I!

$741,667

$41,667

IA

4

PEl!

BIllet

FACILItAtoR

$95

32S

$300

2000

SOl

1000

$150,000

$47,500

$95,000

5 UIS! IBIIIEt

FACILItAtol

$80

.1

$2,191

35600

51

1780

$61,5.5

$2,2n

$H,9U

6 AI!BIII

toUlG

FACILIntoR

$76

751

$101

H62

751

1096.S

$69,083

$51,984

$69,311

7

COIIPUfEl

!ASI

GaOOP

FACILITAtoR

$44

20S

$219

4000

101

.00

$54,750

$11,000

$110,000

8DD

FACILItAtoR

$35

351

$100

1600

401

640

$62,500

$21,875

$54,688

9

CAP

GlUI

FACILItATOI

$25

lSI

$164

2500

101

Z50

$65,600

$10,000

$100,000

10

CACI

FACILITAtol

$25

181

$138

2000

191

380

$69,000

$12,500

$65,789

11

COOPEIS

AID

LYBWD

FACILItAtOR

$20

IDS

$205

15000

Sl

750

$13,667

$1,333

$26,667

12

fEClIIALYSIS

FACILIUtoR

$16

891

$18

275

90S

247.5

$65,455

$58,182

$64,646

13

COMPutER

DAt'

SIS

FACILIUtoR

$8

121

$66

2800

151

420

$23,511

$2,857

$19,048

14

III

SYStEJIS

FACILItAtoR

$8

241

$33

550

30S

165

$60,000

$14,545

$48,485

15

ASI

COlPUTEI

SIS

FAClLIUfOl

$7

51

$142

800

51

40

$177,500

$8,750

$175,000

16

IlnmtlICS

FACILIUtoR

$3

61

$SO

600

17%

102

$83,333

$5,000

$29,U2

total

$1,008.00

$6,352.00

83287

U561

$1,846,782.14

$371,292.04

$1,047,838.09

Ayerage

$63.00

$397.00

5205

910

CONSULTING and RESEARCH SERVICE

..

- - For Internal Use Only - -

$115,423.88

$23,205.75 $65,489.88

22

FINANCIAL ANALYSIS

OF

SYSTEMS INTEGRATORS

VENDOR PROFILES 6

Company

IBM

Description

Markets

Services

IBM

is

by

far

the

largest

of

the

systems

integrators

with

a

proud

history

of

selling

integrated

computing

solutions

at

the

upper

management,

strategic

level.

Extensive

experience

in

Federal

Government

systems

integration

projects

is

being leveraged

by

changes

in

the

internal

organizational

environment

at

IBM.

The

former

Federal

Systems

Division

has

been

renamed

The

Systems

Integration

Division

as

of

April,

1988.

Very

broad

base

of

target

markets

including Federal,

State

and

Local

Governments,

Legal, Manufacturing,

Insurance,

Health

Care,

Transportation,

Utilities, Banking/Financial, Wholesale/Distribution,

Business

Services,

Education

and

Telecommunications.

Prime

and

Sub-contracting, facilities design

and

management.

hardware

mainte-

nance, software

development

and

maintenance,

network

design,

project

manage-

ment,

requirements

assessment

and

personnel

training.

Sector

Concentration

1988

SI

revenue split:

80%

Federal

20%

Commercial

Typical

Contracts

FAA

Air Traffic Control Modernization: 10 year, $3.6 billion

U.S.

Health

and

Human

Services - 5

year

Ford

Motor

Company

Corporate

DP

infrastructure

design

and

installation

- 3

year,

$500

million

Hospital

Corp

of

America

office

automation

installation -multi-year

View

of

the

Future

Expects

"significant

growth"

in

both

major

sectors

over

the

next

decade.

IBM

will

target

all

major

industries

and

vertical

markets.

6 Sources of information for

this

section include:

_

Computer

Systems

News

whitepaper

on

Systems

Integration

-

Input's

"Systems

Integration

- A

Corporate

Analysis"

-Various articles in

the

Trade

Press

* CONSULTING and RESEARCH SERVICE

,.

- - For Internal Use Only - -

23

FINANCIAL ANALYSIS OF SYSTEMS INTEGRATORS

Company

Electronic

Data

Systems, Corp.

Description

Markets

Services

The

most

significant pioneer in systems integration as a

separate

business.

Considered to be number two

in

SI

revenues by all major analysts. Bought

out

by

OM

in

1984, half

of

EDS'

revenues derive from work for

the

parent

company.

Very broad

base

of

target

markets

including Federal,

State

and

Local

Governments, Legal, Manufacturing, Insurance, Health Care, Transportation,

Utilities, Banking/Financial, Wholesale/Distribution, Business Services,

Education

and

Telecommunications.

Prime

and

Sub-contracting, facilities design

and

management, hardware mainte-

nance, software development

and

maintenance, network design, project manage-

ment,

requirements

assessment

and

personnel training.

Sector Concentration

1988

SI

revenue split: 70% Federal

Typical Contracts

300/0

Commercial

U.S.

Department

of Defense Enrollment Eligibility

and

Reporting

System

-13

years

Army

Standard

Information Management

Systems

-10

years

Navy Inventory Control

System

-8 years

U.S. Air Force Unified LAN Architecture Project - 6 years

Enron

Corporation Enterprise Management Contract -

10

years

View

of

the

Future

Expects

significant growth, especially in

the

commercial sector. Emphasis

on

total

systems

integration combining traditional technological approaches with

after-installation optimization

of

information

systems

usage. Sees their large size

as

providing a competitive advantage because of

signifi~ant

economies of scale.

* * * CONSULTING and RESEARCH SERVICE *

- - For Internal Use Only - -

* *

24

FINANCIAL ANALYSIS OF SYSTEMS INTEGRATORS

Company

Anderson Consulting

Description

Markets

Services

A

separate

unit

of

Arthur

Anderson & Co., one of

the

world's

largest

accounting

firms, Anderson Consulting is

the

locus of

the

parent

firm's

management

con-

sulting business. Considered

by

analysts

to

be number two

or

three

in

SI

reve-

nues

and

enjoying

almost

100/0

of

the

market

for

SI

in

the

U.S. in 1988.

Broad

base

of

target

markets

including Federal,

State

and Local Governments,

Legal, Manufacturing, Insurance,

Health

Care, Transportation, Utilities,

Banking/Financial, Wholesale/Distribution, Education

and

Telecommunications.

Prime

and

Sub-contracting, facilities management, hardware maintenance, soft-

ware development and maintenance, network design, project

management,

re-

quirements

assessment

and

personnel training, business process change.

Sector

Concentration

1988

SI

revenue split: 12% Government

88%

Commercial

Typical

Contracts

Chicago Title

and

Trust

Co. WAN Project -4

years

Boeing Aerospace Factory/Office Integration

System

$2.7 million

U.S. Social Security Administration

Integrated

Financial Administrative

Systems: Subcontract with American Management

Systems

-

$12

million

View of

the

Future

Believes

there

will

be

consolidation within

the

industry

leaving a small

number

of

truly

excellent prime contractors

and

a

host

of

smaller niche

marketers

tar-

geting

specific industries or computing technologies.

Customers

will demand

strategic

solutions from

their

information systems.

* * * CONSULTING and RESEARCH SERVICE *

- - For Internal Use Only - -

* *

25

FINANCIAL ANALYSIS

OF

SYSTEMS INTEGRATORS

Company

AT&T

Description

Markets

Services

A long history of managing systems integration

type

projects for voice networks

would seem

to

make AT&T a natural for computer systems integration prob-

lems. A formal strategy for entering

the

business was not formulated until early

1988 when

the

Systems Integration Division was formed. This division

has

now

been renamed

the

Integrated Communications Systems Division

and

will

concen-

trate

on

network integration solutions.

Federal,

State

and Local Governments, Education, Banking/Finance

Network and Platform Integration

Sector

Concentration

Not Available

Typical

Contracts

Bank of America Network Switching Project -2 years, $3 million

University of Southern California Voice/Data Network -2 years,

$22

million

State

of Wisconsin Voice/Data Network Integration Project -

$200

million

Tenneco Corp. Voice/Data Network Integration Project -2 years,

$10

million

View of

the

Future

Not Available

* * * CONSULTING and RESEARCH SERVICE *

- -

For

Internal Use Only - -

* *

26

FINANCIAL ANALYSIS

OF

SYSTEMS INTEGRATORS

Company

Bolt

Beranek

and

Newman, Inc.

Dese~ption

Markets

Services

Designer

of

integrated voice/data networks for

government

and

commercial

customers.

Federal Government, Banking/Finance, Manufacturing,

Transportation

Prime

and

Sub-contractor. Maintenance, Software Development, Network

Design, Project Management, Requirements Assessment, Personnel Training,

Hardware Development

Sector Concentration

1988

SI

revenue split: 80% Government

20%

Commercial

Typical

Contracts

U.S.

Department

of Defense

Data

Network -

$50

million

SIMNET

-$25 million

View of

the

Future

Customers will demand one point of contact for information

systems

and

those

firms

that

are

able to control

the

quality

and

delivery of

the

critical required

components will have a competitive advantage.

* CONSULTING and RESEARCH SERVICE

'"

- - For Internal Use Only - -

'"

'"

27

FINANCIAL ANALYSIS OF SYSTEMS INTEGRATORS

Company

Computer Task Group

Inc~

Description

Markets

Services

A firm with a

strong

international focus CTG specializes in "strategic business

systems" and real-time automation development for commercial customers.

They also promote their systems migration and documentation services.

Banking/Finance, Business Services, Federal

State

and

Local Governments,

Education, Legal, Manufacturing, Transportation, Utilities, Wholesale/Retail dis-

tribution and Telecommunications.

Prime and Sub-contractor. facilities management, maintenance, software devel-

opment, network design, project management, requirements assessment,

training.

Sector

Concentration

Not Available

Typical

Contracts

USS-Posco Industries - 3 years, $30 million

View

of

the

Future

Expects commercial systems integration market to grow 30% over

the

next five

years. Professional services component

will

grow faster

than

the

systems inte-

gration market

as

a whole.

eTG

sees their concentration in

the

manufacturing

industry as an advantage since they expect especially high growth in this verti-

cal market.

* * * CONSULTING and RESEARCH SERVICE

'"

- - For Internal Use Only - -

*

'"

28

FINANCIAL ANALYSIS OF SYSTEMS INTEGRATORS

Company

Litton Industrial Automation Group

Description

Markets

Services

A division of Litton Industries, LIAG concentrates on

the

manufacturing auto-

mation segment and on emerging areas such

as

optical-based document manage-

ment

systems

and

image processing.

Federal Government, Manufacturing, Telecommunications, Retail.

Transportation, Wholesale/Distribution, Aerospace

and

Automotive

Prime and Subcontractor, Facilities Management, Maintenance, Software

Development, Project Management, Requirements Assessment, Training.

Sector Concentration

1988

SI

revenue split: 80% Government

Typical Contracts

Boeing Aircraft

Co.

-3 years,

$25

million

View

of the Future

20% Commercial

Views systems integration as very important to national competitiveness

and

a

strategic area for concentration of Litton's resources .

... ...

...

CONSULTING and RESEARCH SERVICE

...

':'

-For Internal Use Only - -

...

...

29

FINANCIAL ANALYSIS OF SYSTEMS INTEGRATORS

Company

SHL

Systemhouse, Inc.

Description

Markets

Services

A Canadian

firm

founded in 1974, half of

its

revenues derive from U.S. accounts.

SHL

addresses both

the

government and commercial sectors

and'

provides sys-

tems

planning, design, implementation, operations supports and services.

Broad base of

target

markets including Federal,

State

and Local Governments,

Legal, Manufacturing, Insurance, Health Care, Transportation, Utilities,

Banking/Financial,

Wholesale/Dist~bution,

Education

and

Telecommunications.

Prime and Subcontractor, Facilities Management, Maintenance, Software

Development, Project Management, Requirements Assessment, Training.

Sector Concentration

1988

SI

revenue split: 55% Government 45% Commercial

Typical

Contracts

U.S. Naval Avionics Center Manufacturing Requirements Planning Project -

$23.8

million

PetroCanada -

$25

million

Canadian Federal Government Department of National Defense

View

of

the

Future

Foresees a blurring of data

and

telecommunications industries and has formed

an

alliance with Ameritech

to

exploit this phenomenon. They note

that

50% of

major systems

are

being composed of microcomponents and they feel

that

exper-

tise in this area of growth is a critical success factor. Accordingly, S HL pur-

chased all of

the

Computerland outlets in Canada in

1988

.

... ...

...

CONSULTING and RESEARCH SERVICE

...

- - For Internal Use Only - -

...

...

30

FINANCIAL ANALYSIS OF SYSTEMS INTEGRATORS

Company

Unysis Corp.

Description

Markets

Services

Comprised of

the

merged Burroughs and Sperry computer firms, U nysis offers a

variety of services

to

the

government and commercial segments focusing par-

ticularly on platform integration and network integration.

Very broad base of

target

markets including Federal,

State

and Local

Governments, Legal, Manufacturing, Insurance, Health Care, Transportation,

Utilities, Banking/Financial, Wholesale/Distribution, Business Services,

Education and Telecommunications.

Prime and Sub-contracting. facilities design and management, hardware mainte-

nance, software development and maintenance, network design, project manage-

ment, requirements assessment

and

personnel training.

Sector Concentration

1988

SI

revenue split:

600/0

Government

Typical Contracts

U.

S. Coast Guard -$82 million

40% Commercial

U.S. Navy On-Board DP Systems, 4, 1 year options, $36 million

Department of Labor Unix-based Employee Benefits System-

$10

million

Royal Thai Air Force Air Defense System

View of the

Future

Foresee 25%

to

30% growth in

the

commercial

market

but a slower

rate

of

. growth in

the

government sector.

* * • CONSULTING and RESEARCH SERVICE *

- - For Internal Use Only - -

* *

31

FINANCIAL ANALYSIS OF SYSTEMS INTEGRATORS

Company

Digital Equipment Corporation

Description

Markets

Services

Having offered

SI

service for

the

last

ten

years, a formal

SI

strategy

was dis-

closed only in September of 1988. Enterprise-wide network management sys-

tems

are being devised with

the

active participation of third

party

vendors.

Skills for integration activities are drawn from a large number of different

groups within

the

company,

rather

than

from a central

SI

division.

Federal Government, Banking/Finance, Manufacturing, Telecommunications and

Media.

Prime

and

Subcontractor, Facilities Management, Maintenance, Software

Development, Network Design, Project Management, Requirements

Assessment, Training.

Sector Concentration

1988

SI

revenue split: 40% Government 60% Commercial

Typical Contracts

Boeing Aircraft Co. Factory Control

System

-$54 million

Over 100 systems integration contracts in the pipeline worth

an

estimated $30

million per

year

for the

next

five years.

View

of

the

Future

The

approach of

an

integrated global

market

place and business environment

will make

it

imperative

that

information systems

match

the

business require-

ments

of all types of enterprises. Customers are looking for partners

they

can

trust

so

that

they

can concentrate on their core businesses

and

areas

of

expertise.

* * * CONSULTING and RESEARCH SERVICE *

- - For Internal Use Only - -

..

..

32