Trust Funds A Guide For Real Estate Brokers And Salespersons Cal BRE

User Manual:

Open the PDF directly: View PDF ![]() .

.

Page Count: 30

- RE13 - Rev 2-2014.pdf

- Trust Funds

- GENERAL INFORMATION

- TRUST FUND BANK ACCOUNTS

- Other Accounting Systems and Records

- RECORDING PROCESS

- RECONCILIATION OF ACCOUNTING RECORDS

- DOCUMENTATION REQUIREMENTS

- ADDITIONAL REQUIREMENTS - DOCUMENTS

- AUDITS AND EXAMINATIONS

- SAMPLE TRANSACTIONS

- Questions and Answers Regarding Trust Fund Requirements and Record Keeping

- SUMMARY

State of California

Bureau of Real Estate

TRUST FUNDS

A Guide for Real Estate

Brokers and Salespersons

RE 13 (Rev.1/2014)

CONTENTS

TOPIC PAGE NUMBER

GENERAL INFORMATION 1

Trust Funds and Non-Trust Funds 1

Why a Trust Account? 1

Trust Fund Handling Requirements 1

Identifying the Owner(s) of Trust Funds 2

TRUST FUND BANK ACCOUNTS 2

General Requirements 2

Trust Account Withdrawals 3

Interest-Bearing Accounts 3

Commingling Prohibited 4

Trust Fund Liability 5

Summary – Maintaining Trust Account Integrity 5

ACCOUNTING RECORDS 6

General Requirements 6

Columnar Records 6

Record of All Trust Funds Received and Paid Out – Trust Fund Bank Account 6

Separate Record for Each Beneficiary or Transaction 7

Record of All Trust Funds Received – Not Placed in Broker’s Trust Account 7

Separate Record for Each Property Managed 7

OTHER ACCOUNTING SYSTEMS AND RECORDS 7

Journal 8

Cash Ledger 8

Beneficiary Ledger 8

RECORDING PROCESS 8

RECONCILIATION OF ACCOUNTING RECORDS 8

Purpose 8

Reconciling the Bank Account Record With the Bank Statement 9

Reconciling the Bank Account Record With the Separate Beneficiary or Transaction Records 9

Unexplained Trust Account Overages 9

Suggestions for Reconciling Records 9

DOCUMENTATION REQUIREMENTS 10

Activities and Related Documents 10

ADDITIONAL REQUIREMENTS – DOCUMENTS 10

Person Signing Contract to be Given Copy 10

AUDITS AND EXAMINATIONS 11

SAMPLE TRANSACTIONS 11

QUESTIONS AND ANSWERS REGARDING

TRUST FUND REQUIREMENTS AND RECORD KEEPING 18

SUMMARY 18

TRUST FUND RECORD KEEPING EXHIBITS 19

Trust Funds

Real estate brokers and salespersons receive trust funds in the normal course of doing business. They receive these funds on behalf of

others, thereby creating a fiduciary responsibility to the funds’ owners. Brokers and salespersons must handle, control and account for

these trust funds according to established legal standards. While compliance with these standards may not necessarily have a direct

bearing on the financial success of a real estate business, non-compliance can result in unfavorable business consequences. Improper

handling of trust funds is cause for revocation or suspension of a real estate license, not to mention the possibility of being held

financially liable for damages incurred by clients.

This publication discusses the legal requirements for receiving and handling trust funds in real estate transactions as set forth in the

Real Estate Law and the Regulations of the Real Estate Commissioner. It describes the requisites for maintaining a trust fund bank

account and the precautions a licensee should take to ensure the integrity of the account. It explains and illustrates the trust fund record

keeping requirements under the Business and Professions Code and the Commissioner’s Regulations.

The discussions and examples in this publication involve real property sales and property management trust account transactions.

Other types of real estate activities involving trust funds, although subject to the same laws and regulations, may also have to comply

with additional legal and regulatory requirements. While these other types of transactions may require records significantly different

from those illustrated, the record keeping fundamentals still apply.

GENERAL INFORMATION

Trust Funds and Non-Trust Funds

Since trust funds must be handled in a special manner, a licensee must be able to distinguish trust funds from non-trust funds. Trust

funds are money or other things of value that are received by a broker or salesperson on behalf of a principal or any other person, and

which are held for the benefit of others in the performance of any acts for which a real estate license is required. Trust funds may be

cash or non-cash items. Some examples are cash, a check used as a purchase deposit (whether made payable to the broker or to an

escrow or title company), a personal note made payable to the seller, or even an automobile’s “pink slip” given as a deposit.

The discussions in this publication pertain to real estate trust funds received by licensees, and not to non-trust funds such as real estate

commissions, general operating funds, and rents and deposits from broker-owned real estate. These other types of funds, as long as not

commingled with trust funds, are not subject to the Real Estate Law and Commissioner’s Regulations. It should be noted, however,

that under certain circumstances the California Bureau of Real Estate (CalBRE) does have the jurisdiction to look into transactions

involving non-trust funds.

Why a Trust Account?

A trust account is set up as a means to separate trust funds from non-trust funds. Although it can certainly be argued that keeping trust

funds in a trust account will not prevent a dishonest broker from misusing the funds, separating client’s funds from the broker’s own

funds provides a better physical and accounting control over the trust funds.

An important reason for designating a trust fund depository as a trust account is the protection afforded principals’ funds in situations

where legal action is taken against the broker or if the broker becomes incapacitated or dies. A broker who holds and properly

accounts for trust funds in a true trust account will be able to successfully prevent or defend the freezing of trust funds pending

litigation against the broker or during probate.

Trust funds also have better insurance protection if deposited into a trust account. The general counsel of the FDIC, in an opinion in

1965, held that funds of various owners which are placed in a custodial deposit (trust account) in an insured bank will be recognized

for insurance purposes to the same extent as if the owners’ names and interests in the account are individually disclosed on the records

of the bank, provided the trust account is specifically designated as custodial and the name and interest of each owner of funds in the

account are disclosed on the depositor’s records. Each client with funds deposited in a trust account maintained with a federally

insured bank is insured by the FDIC up to $250,000, as opposed to just $250,000 for the entire account, as long as the regulatory

requirements are met.

Trust Fund Handling Requirements

A typical trust fund transaction begins with the broker or salesperson receiving trust funds from a principal in connection with the

purchase or lease of real property. According to Business and Professions Code Section 10145, trust funds received must be placed

into the hands of the owner(s) of the funds, into a neutral escrow depository, or into a trust account maintained pursuant to

Commissioner’s Regulation 2832 not later than three business days following receipt of the funds by the broker or by the broker’s

salesperson.

2

An exception to this rule is when a check is received from an offeror in connection with an offer to purchase or lease real property. As

provided under Commissioner’s Regulation 2832, a deposit check may be held uncashed by the broker until acceptance of the offer if

the following conditions are met:

1. the check by its terms is not negotiable by the broker, or the offeror has given written instructions that the check shall not be

deposited or cashed until acceptance of the offer; and

2. the offeree is informed, before or at the time the offer is presented for acceptance, that the check is being held.

If the offer is later accepted, the broker may continue to hold the check undeposited only if the broker receives written authorization

from the offeree to do so. Otherwise, the check must be placed, not later than three business days after acceptance, into a neutral

escrow depository or into the trust fund bank account or into the hands of the offeree if both the offeror and offeree expressly so

provide in writing.

According to Business and Professions Code Section 10145, a real estate salesperson who accepts trust funds on behalf of the broker

under whom he or she is licensed must immediately deliver the funds to the broker or, if directed to do so by the broker, place the

funds into the hands of the broker’s principal or into a neutral escrow depository or deposit the funds into the broker’s trust fund bank

account.

A neutral escrow depository, as used in Business and Professions Code Section 10145, means an escrow business conducted by a

person licensed under Division 6 (commencing with Section 17000) of the Financial Code or by any person described in subdivisions

(a)(1) and (a)(3) of Section 17006 of the Financial Code.

Identifying the Owner(s) of Trust Funds

A broker must be able to identify who owns the trust funds and who is entitled to receive them, since these funds can be disposed of

only upon the authorization of that person. The person entitled to the funds may or may not be the person who originally gave the

funds to the broker or the salesperson. In some instances the party entitled to the funds will change upon the occurrence of certain

events in the transaction. For example, in a transaction involving an offer to buy or lease real property or a business opportunity, the

party entitled to the funds received from the offeror (prospective buyer or lessor) will depend upon whether or not the offer has been

accepted by the offeree (seller or landlord).

Prior to the acceptance of the offer, the funds received from the offeror belong to that person and must be handled according to his/her

instructions. If the funds are deposited in a trust fund bank account, they must be maintained there for the benefit of the offeror until

acceptance of the offer. Or, as discussed in the previous section, if the offeror wishes, his/her check may be held uncashed by the

broker as long as he/she gives written instructions to the broker to do so and the offeree is informed before or at the time the offer is

presented for acceptance that the check is being so held.

After acceptance of the offer, the funds shall be handled according to instructions from the offeror and the offeree as follows:

• An offeror’s check held uncashed by the broker before acceptance of the offer may continue to be held uncashed after acceptance

of the offer, only upon written authorization from the offeree. [Commissioner’s Regulation 2832(d)]

• The offeror’s check may be given to the offeree only if the offeror and offeree expressly so provide in writing. [Commissioner’s

Regulation 2832(d)]

• All or part of an offeror’s purchase money deposit in a real estate sales transaction shall not be refunded by an agent or subagent

of the seller without the express written permission of the offeree to make the refund.

TRUST FUND BANK ACCOUNTS

General Requirements

Trust funds, such as a purchase money deposit check, received by a licensee that are not forwarded directly to the broker’s principal or

to a neutral escrow depository or for which the broker does not have authorization to hold uncashed must be deposited to the broker’s

trust fund bank account. (Business and Professions Code Section 10145)

Business and Professions Code Section 10145 and Commissioner’s Regulation 2832 require that a trust account meet the following

criteria:

1. designated as a trust account in the name of the broker as trustee;

2. maintained with a bank or recognized depository located in California; and

3. not an interest-bearing account for which prior written notice can, by law or regulation, be required by the financial institution as

a condition to withdrawal (except as noted in the discussion below of “Interest-Bearing Accounts”).

3

A broker may have an out-of-state trust account if the account is insured by the Federal Deposit Insurance Corporation (FDIC) and is

used to service first loans for the types of note owners/investors specified in Section 10145(a)(2) of the Business and Professions

Code.

Trust Account Withdrawals

According to Commissioner’s Regulation 2834, withdrawals from the trust account may be made only upon the signature of one or

more of the following:

1. the broker in whose name the account is maintained;

2. the designated broker-officer if the account is in the name of a corporate broker;

3. if specifically authorized in writing by the broker, a salesperson licensed to the broker, who has enter into a written agreement

pursuant to Section 2726; or

4. if specifically authorized in writing by the broker who is a signatory of the trust account, an unlicensed employee of the broker

covered by a fidelity bond at least equal to the maximum amount of trust funds to which the employee has access at any time.

No arrangement under which a person named in items 3 or 4 is authorized to make withdrawals from a broker’s trust fund relieves an

individual broker or the broker-officer of a corporate broker licensee from responsibility or liability as provided by law in handling

trust funds in the broker’s custody.

Interest-Bearing Accounts

A trust fund bank account normally may not be interest-bearing. A broker may, however, at the request of the owner of trust funds, or

of the principals to a transaction or series of transactions from whom the broker has received trust funds, deposit the funds into an

interest-bearing account in a bank or savings and loan association if all of the following requirements of Business and Professions

Code Section 10145(d) are met:

1. The account is in the name of the broker as trustee for a specified beneficiary or specified principal of a transaction or series of

transactions.

2. All of the funds in the account are covered by insurance provided by an agency of the federal government.

3. The funds in the account are kept separate, distinct, and apart from funds belonging to the broker or to any other person for whom

the broker holds funds in trust.

4. The broker discloses the following information to the person from whom the trust funds are received and to any beneficiary

whose identity is known to the broker at the time of establishing the account:

the nature of the account;

how the interest will be calculated and paid under various circumstances;

whether service charges will be paid to the depository and by whom; and

possible notice requirements or penalties for withdrawal of funds from the account.

5. No interest earned on funds in the account shall inure directly or indirectly to the benefit of the broker or to any person licensed to

the broker, even if the funds’ owners would permit such an arrangement.

6. In an executory sale, lease, or loan transaction in which the broker accepts funds in trust to be applied to the purchase, lease, or

loan, the parties to the contract shall have specified in the contract or by collateral written agreement the person to whom interest

earned on the funds is to be paid or credited.

The only other situation where a real estate broker is allowed to deposit trust funds into an interest-bearing account occurs when the

broker is acting as an agent for a financial institution which is the beneficiary of a loan. In this case the broker may, pursuant to

Commissioner’s Regulation 2830.1, deposit and maintain funds received from or for the account of an obligor (borrower) into an

interest-bearing trust account in a bank or savings and loan association in order to pay interest on an impound account to the obligor in

accordance with Section 2954.8 of the Civil Code, as long as the following requirements are met:

1. The funds received from or for the account of the obligor are for the future payment of property taxes, assessments or insurance

relating only to a property containing a one-to-four family residence.

2. The account is in the name of the broker as trustee.

3. All of the funds in the account are covered by insurance provided by an agency of the federal government.

4. All of the funds in the account are funds held in trust by the broker for others.

4

5. The broker discloses to the obligor how interest will be calculated and paid.

6. No interest earned on the trust funds shall inure directly or indirectly to the benefit of the broker or to any person licensed to the

broker.

Commingling Prohibited

Funds belonging to a licensee may not be commingled with trust funds. Commingling is strictly prohibited by the Real Estate Law. It

is grounds for the revocation or suspension of a real estate license pursuant to Business and Professions Code Section 10176(e).

Commingling occurs when:

1. Personal or company funds are deposited into the trust fund bank account. Except for what is provided in Section 2835 of the

Commissioner’s Regulations as noted below, this is a violation of the law even if separate records are kept.

2. Trust funds are deposited into the licensee’s general or personal bank account rather than into the trust fund account. In this case

the violation is not only commingling, but also handling trust funds contrary to Business and Professions Code Section 10145. It

is also grounds for suspension or revocation of a license under Business and Professions Code Section 10177(d).

3. Commissions, fees, or other income earned by the broker and collectible from the trust account are left in the trust account for

more than 25 days from the date they were earned.

A common example of commingling is depositing rents and security deposits on broker-owned properties into the trust account. As

these funds relate to the broker’s properties, they are not trust funds and, therefore, may not be deposited into the trust fund bank

account. Likewise, the broker may not make mortgage payments and other payments on broker-owned properties from the trust

account even if the broker reimburses the account for such payments. Conducting personal business through the trust account is

strictly prohibited and is a violation of the Real Estate Law.

Commissioner’s Regulation 2835 provides that the following situations do not constitute “commingling” for purposes of Business and

Professions Code Section 10176(e):

(a) The deposit into a trust account of reasonably sufficient funds, not to exceed $200, to pay service charges or fees levied or

assessed against the account by the bank or financial institution where the account is maintained.

(b) The deposit into a trust account maintained in compliance with item (d) below of funds belonging in part to the broker’s principal

and in part to the broker when it is not reasonably practicable to separate such funds, provided the part of the funds belonging to

the broker is disbursed not later than 25 days after the deposit and there is no dispute between the broker and the broker’s

principal as to the broker’s portion of the funds. When the right of a broker to receive a portion of trust funds is disputed by the

broker’s principal, the disputed portion shall not be withdrawn until the dispute is settled.

(c) The deposit into a trust account of broker-owned funds in connection with mortgage loan activities as defined in subdivision (d)

or (e) of Section 10131 of the Business and Professions Code or when making, collecting payments on, or servicing a loan which

is subject to the provisions of Section 10240 of the Business and Professions Code provided:

(1) The broker meets the criteria of Section 10232 of the Business and Professions Code.

(2) All funds in the account which are owned by the broker are identified at all times in a separate record which is distinct from

any separate record maintained for a beneficiary.

(3) All broker-owned funds deposited into the account are disbursed from the account not later than 25 days after their deposit.

(4) The funds are deposited and maintained in compliance with item (d) below.

(5) For this purpose, a broker shall be deemed to be subject to the provisions of Section 10240 of the Business and Professions

Code if the broker delivers the statement to the borrower required by Section 10240.

(d) The trust fund account into which the funds are deposited is maintained in accordance with the provisions of Section 10145 of the

Business and Professions Code and the Commissioner’s Regulations.

To summarize, a real estate broker’s personal funds may be in the trust account in the following two specific instances:

1. Up to $200 to cover checking account service fees and other bank charges such as check printing charges and service fees on

returned checks. Trust funds may not be used to pay for these expenses. (The preferred practice, however, is for the broker to

have the bank debit his/her own personal account for any trust account fees and charges.)

2. Commissions, fees, and other income earned by a broker and collectible from trust funds may remain in the trust account for a

period not to exceed 25 days. Regulation 2835 recognizes that it may not always be practical to disburse the earned income

immediately upon receipt. For instance, a property management company may find it too burdensome to collect its management

5

fee every time a rent check is received and deposited to the trust account. Therefore, as long as the broker disburses the fee from

the trust account within 25 days after deposit there is no commingling violation. Note, however, that income earned shall not be

taken from trust funds received before depositing such funds into the trust bank account. Also, under no circumstances may the

broker pay personal obligations from the trust fund bank account even if such payments are a draw against commissions or other

income. The broker must issue a trust account check to himself/herself for the total amount of the income earned, adequately

documenting such payment, and then pay personal obligations from the proceeds of that check.

Trust Fund Liability

Trust fund liability arises when funds are received from or for the benefit of a principal. The aggregate trust fund liability at any one

time for a trust account with multiple beneficiaries is equal to the total positive balances due to all beneficiaries of the account at the

time. Note that beneficiary accounts with negative balances are not deducted from other accounts when calculating the aggregate trust

fund liability.

Funds on deposit in the trust account must always equal the broker’s aggregate trust fund liability. If the trust account balance is less

than the total liability a trust fund shortage results. Such a shortage is in violation of Commissioner’s Regulation 2832.1, which states

that the written consent of every principal who is an owner of the funds in the account shall be obtained by a real estate broker prior to

each disbursement if such a disbursement will reduce the balance of the funds in the account to an amount less than the existing

aggregate trust fund liability of the broker to all owners of the funds. Conversely, if the trust account balance is greater than the total

liability, there is a trust fund overage and the broker may be in violation of Business and Professions Code Section 10176(e) for

commingling.

A trust fund discrepancy of any kind is a serious violation of the Real Estate Law. Many real estate licenses have been revoked after a

CalBRE audit disclosed a trust account shortage. To ensure that the balance of the trust account always equals the trust fund liabilities,

a broker should implement the following procedures:

l. Deposit intact and in a timely manner to the trust account all funds that are not forwarded to escrow or to the funds’ owner(s) or

which are not held uncashed as authorized. This practice, required under Commissioner’s Regulation 2832, lessens the risk of the

funds being lost, misplaced, or otherwise not deposited to the trust account. A licensee is accountable for all trust funds received

whether or not they are deposited. CalBRE auditors have seen numerous cases where trust funds received were properly recorded

on the books but were never deposited to the trust account.

2. Maintain adequate supporting papers for any disbursement from the trust account. Record the disbursement accurately in both the

Bank Account Record and the Separate Beneficiary Record. The broker must be able to account for all disbursements of trust

funds. Any unidentified disbursement will cause a shortage.

3. Disburse funds from a beneficiary’s account only when the disbursement will not result in a negative or deficit balance (negative

accountability) in the account. Many trust fund shortages are caused by disbursements to a beneficiary in excess of funds received

from or for account of that beneficiary. The excess disbursements are, in effect, paid out of funds belonging to other beneficiaries.

A shortage occurs because the balance of the trust fund bank account, even if it is a positive balance, is less than the broker’s

liability to the other beneficiaries.

4. Ensure that a check deposited to the trust fund account has cleared before disbursing funds against that check. This applies, for

example, when a broker who has deposited an earnest money check for a purchase transaction has to return the funds to the buyer

because the offer is rejected by the seller. A trust fund shortage will result if the broker issues the buyer a trust account check and

the buyer’s deposit check bounces or for some reason fails to clear the bank.

5. Keep accurate, current and complete records of the trust account and the separate record for each beneficiary. These records are

essential to ensure that disbursements are correct.

6. On a monthly basis, reconcile the cash record with the bank statement and with the separate record for each beneficiary or

transaction.

Summary - Maintaining Trust Account Integrity

In summary, to maintain the integrity of the trust fund bank account, a broker must ensure that:

1. his/her personal or general operating funds are not commingled with trust funds;

2. the balance of the trust fund account is equal to the broker’s trust fund liability to all owners of the funds; and

3. the trust fund records are in an acceptable form and are current, complete and accurate.

6

ACCOUNTING RECORDS

General Requirements

An important aspect of the broker’s fiduciary responsibility to the client is the maintenance of adequate records to account for trust

funds received and disbursed. This is true whether the funds are deposited to the trust fund bank account, sent to escrow, held

uncashed as authorized under Commissioner’s Regulation 2832, or released to the owner(s) of the funds. These records:

1. provide a basis upon which the broker can prepare an accurate accounting for clients.

2. state the amount of money the broker owes the account beneficiaries at any one time. (This is especially important when there are

a large number of transactions.)

3. prove whether or not there is an imbalance in the trust account. Some brokers audited by CALBRE have disagreed that their trust

accounts had a shortage or an overage in the amount disclosed by the audit, but could not provide documentation to support their

position.

4. guarantee that beneficiary funds deposited in the trust account will be insured up to the maximum FDIC/NCUSIF, etc. insurance

coverage.

There are two types of accounting records that may be used for trust funds: columnar records in the formats prescribed by

Commissioner’s Regulations 2831 and 2831.1; and records other than columnar that are in accordance with generally accepted

accounting practices which include details specified in subdivision (a) of the Regulations and are in a format that will readily enable

tracing and reconciliation in accordance with Section 2831.2. Regardless of the type of records used, they must include the following

information:

1. all trust fund receipts and disbursements, with pertinent details, presented in chronological sequence;

2. the balance of the trust fund account, based on recorded transactions;

3. all receipts and disbursements affecting each beneficiary’s balance, presented in chronological sequence; and

4. the balance owing to each beneficiary or for each transaction.

Either manually produced or computerized accounting records are acceptable. The type and form of records appropriate to a particular

real estate operation as well as the means of processing transactions will depend on factors such as the nature of the business, the

number of clients, the volume of transactions, and the types of reports needed. For example, manual recording on columnar records

might be satisfactory for a broker handling a small number of transactions, while a computerized system might be more appropriate

and practical for a large property management operation.

Columnar Records

A broker may decide to use the columnar records prescribed by Commissioner’s Regulations 2831 and 2831.1. The records required

will depend on whether the trust funds received are deposited to the trust account or are forwarded to an escrow depository or to the

owner of the funds. These records are:

1. Columnar Record of All Trust Funds Received and Paid Out - Trust Fund Bank Account (CALBRE form RE 4522);

2. Separate Record for Each Beneficiary or Transaction (CALBRE form RE 4523); and

3. Record of All Trust Funds Received - Not Placed in Broker’s Trust Account (CALBRE form RE 4524).

The first two records are required when trust funds are received and deposited to the trust fund bank account.

The third record is required when trust funds received are not deposited to the trust account, but are instead forwarded to the

authorized person(s).

If the trust fund account involves clients’ funds from rental properties managed by the broker, the Separate Record for Each Property

Managed (CALBRE form RE 4525) may be used in lieu of the Separate Record for Each Beneficiary or Transaction.

A broker who has an escrow division pursuant to Financial Code Section 17006(a)(4) must keep the above mentioned records for

escrow funds. (Commissioner’s Regulation 2951)

Record of All Trust Funds Received and Paid Out - Trust Fund Bank Account

This record is used to journalize all trust funds deposited to and disbursed from the trust fund bank account. At a minimum, it must

show the following information in columnar form: date funds were received; name of payee or payor; amount received; date of

deposit; amount paid out; check number and date; and the daily balance of the trust account.

7

All transactions affecting the trust account are entered in chronological order on this record regardless of payee, payor or beneficiary.

If there is more than one trust fund bank account, a different columnar record must be maintained for each account, pursuant to

Commissioner’s Regulation 2831.

Separate Record for Each Beneficiary or Transaction

This record is maintained to account for funds received from or for the account of each beneficiary, or for each transaction, and

deposited to the trust account. With this record, the broker can ascertain the funds owed to each beneficiary or for each transaction.

The record must show the following in chronological order: date of deposit; amount of deposit; name of payee or payor; check

number; date and amount; and balance of the individual account after posting transactions on any date.

A separate record must be maintained for each beneficiary or transaction from whom the broker received funds that were deposited to

the trust fund bank account. If the broker has more than one trust account, each account must have its own set of beneficiary records

so that they can be reconciled with the individual trust fund bank account record required by Commissioner’s Regulation 2831.2.

Record of All Trust Funds Received - Not Placed in Broker’s Trust Account

This record is used to keep track of funds received and not deposited to a trust fund bank account. In this situation, the broker is

handling the funds and must keep records of same. Examples are:

1. earnest money deposits forwarded to escrow;

2. rents forwarded to landlords; and

3. borrowers’ payments forwarded to lenders.

This record must show the date funds were received, the form of payment (check, note, etc.), amount received, description of property,

identity of the person to whom funds were forwarded, and date of disposition. Trust fund receipts are recorded in chronological

sequence, while their disposition is recorded in the same line where the corresponding receipt is recorded.

Transaction folders usually maintained by a broker for each real estate sales transaction showing the receipt and disposition of

undeposited checks are not acceptable alternatives to the Record of Trust Funds Received But Not Deposited to the Trust Fund Bank

Account.

An exception to this record keeping requirement is provided in Commissioner’s Regulation 2831(e), which states that a broker is not

required to keep records of checks made payable to service providers, including but not limited to escrow, credit and appraisal

services, when the total amount of such checks for any transaction does not exceed $1,000. However, a broker shall retain for three

years copies of receipts issued or obtained in connection with the receipt and distribution of such checks and, upon request of CalBRE

or the maker of the checks, a broker must account for the receipt and distribution of the checks.

Separate Record for Each Property Managed

This record is similar to, and serves the same purpose as, the Separate Record for Each Beneficiary or Transaction. It does not have to

be maintained if a separate record is already used for a property owner’s account. The Separate Record for Each Property Managed is

useful when the broker wants to show some detailed information about a specific property being managed.

OTHER ACCOUNTING SYSTEMS AND RECORDS

A broker may use trust fund records not in the columnar form as prescribed by Commissioner’s Regulations 2831 and 2831.1. Such

records must be in accordance with generally accepted accounting principles and must include detail specified in subdivision (a) of

these Regulations and be in a format that will readily enable tracing and reconciliation in accordance with Section 2831.2. Whether

prepared manually or by computer, they must include at least the following:

1. A journal to record in chronological sequence the details of all trust fund transactions.

2. A cash ledger to show the bank balance as affected by the transactions recorded in the journal. The ledger is posted in the form of

debits and credits. (In some cases the cash ledger may be combined with the journal.)

3. A beneficiary ledger for each of the beneficiary accounts to show in chronological sequence the transactions affecting each

beneficiary’s account, as well as the balance of the account.

To comply with generally accepted accounting principles, there must be one set of journal, cash ledger, and beneficiary ledger for

each trust fund bank account.

8

Journal

A journal is a daily chronological record of trust fund receipts and disbursements. A single journal may be used to record both the

receipts and the disbursements, or a separate journal may be used for each. To meet minimum record keeping requirements, a journal

must:

1. Record all trust fund transactions in chronological sequence.

2. Contain sufficient information to identify the transaction such as the date, amount received or disbursed, name of or reference to

payee or payor, check number or reference to another source document of the transaction, and identification of the beneficiary

account affected by the transaction.

3. Correlate with the ledgers. For example, it should show the same figures that are posted, individually or in total, in the cash ledger

and in the beneficiary ledgers. The details in the journal must be the basis for posting transactions on the ledgers and arriving at

the account balances.

4. Show the total receipts and total disbursements regularly, at least once a month.

Cash Ledger

The cash ledger shows, usually in summary form, the periodic increases and decreases (debits and credits) in the trust fund bank

account and the resulting account balance. It can be incorporated into the journal or it can be a separate record, for example a general

ledger account. If a separate record is used, the postings must be based on the transactions recorded in the journal. The amounts posted

on the ledger must be those shown in the journal.

Beneficiary Ledger

A separate beneficiary ledger must be maintained for each beneficiary or transaction or series of transactions. This ledger shows in

chronological sequence the details of all receipts and disbursements related to the beneficiary’s account, and the resulting account

balance. It reflects the broker’s liability to a particular beneficiary. Entries in all these ledgers must be based on entries recorded in the

journal.

RECORDING PROCESS

Keeping complete and accurate trust fund records is easier when specific procedures are regularly followed. The following procedures

may be useful in developing a record keeping routine:

1. Record transactions daily in the trust fund bank account and in the separate beneficiary records.

2. Use consistently the same specific source documents as a basis for recording trust fund receipts and disbursements. (For example,

receipts pertaining to real estate resales will be recorded based on the Real Estate Contract and Receipt for Deposit form, and

disbursements will always be recorded based on the checks issued from the trust account or debit notices from the bank.)

3. Calculate the account balances on all applicable records at the time entries are made.

4. Reconcile the records monthly to ascertain that transactions are properly recorded on both the bank account record and the

applicable subsidiary records.

5. Reconcile the trust records to the trust account bank statement on a monthly basis to ascertain that amounts per the bank are in

agreement with amounts per the trust fund records.

6. If more than one trust fund bank account is maintained, keep a different set of properly labeled columnar records (cash record and

beneficiary record) for each account.

RECONCILIATION OF ACCOUNTING RECORDS

Purpose

The trust fund bank account record, the separate beneficiary or transaction record, and the bank statement are all interrelated. Any

entry made on the bank account record must have a corresponding entry on a separate beneficiary record. By the same token, any

entry or transaction shown on the bank statement must be reflected on the bank account record. This applies to columnar as well as to

other types of records.

9

The accuracy of the records is verified by reconciling them at least once a month. Reconciliation is the process of comparing two or

more sets of records to determine whether their balances agree. It will disclose whether the records are completed accurately.

For trust fund record keeping purposes, two reconciliations must be made at the end of each month:

1. reconciliation of the bank account record (RE 4522) with the bank statement; and,

2. reconciliation of the bank account record (RE 4522) with the separate beneficiary or transaction records (RE 4523).

Reconciling the Bank Account Record With the Bank Statement

The reconciliation of the bank account record with the bank statement will disclose any recording errors by the broker or by the bank.

If the balance on the bank account record agrees with the bank statement balance as adjusted for outstanding checks, deposits in

transit, and other transactions not yet included in the bank statement, there is more assurance that the balance on the bank account

record is correct. Although this reconciliation is not required by the Real Estate Law or the Commissioner’s Regulations, it is an

essential part of any good accounting system.

Reconciling the Bank Account Record With the Separate Beneficiary or Transaction Records

This reconciliation, which is required by Commissioner’s Regulation 2831.2, will substantiate that all transactions entered on the bank

account record were posted on the separate beneficiary or transaction records. The balance on the bank account record should equal

the total of all beneficiary record balances. Any difference should be located and the records corrected to reflect the correct bank and

liabilities balances. Commissioner’s Regulation 2831.2 requires that this reconciliation process be performed monthly except in those

months when there is no activity in the trust fund bank account, and that a record of each reconciliation be maintained. This record

should identify the bank account name and number, the date of the reconciliation, the account number or name of the principals or

beneficiaries or transactions, and the trust fund liabilities of the broker to each of the principals, beneficiaries or transactions.

Unexplained Trust Account Overages

When a broker performs a reconciliation pursuant to Commissioner’s Regulation 2831.2, the broker may find an unexplained overage.

An unexplained overage is defined as funds in a real estate broker’s trust account which exceed the aggregate trust fund liability of

such account where the broker is unable to determine the ownership of such excess funds.

Unexplained trust account overages are trust funds and unless the broker can establish the ownership of such funds, the funds must be

maintained in the broker’s trust fund account or in a separate trust fund account established to hold such funds.

Unexplained trust account overages may not be used to offset or cover shortages that may exist otherwise in the broker’s trust account.

A broker must keep a separate record of unexplained trust account overages including a separate subsidiary ledger to record the

potential trust fund liability. Such records must include the date of recording and the date on which such funds became an unexplained

trust account overage. A broker holding unexplained trust account overages must perform a monthly reconciliation of such funds in

accordance with Commissioner’s Regulation 2831.2.

Suggestions for Reconciling Records

The following is a general discussion on how to perform the trust account reconciliations.

1. Before performing the reconciliations, record all transactions up to the cut-off date in both the bank account record and the

separate beneficiary or transaction records.

2. Use balances as of the same cut-off date for the two records and the bank statement.

3. For the bank account reconciliation, calculate the adjusted bank balance from the bank statement and from the bank account

record. (Brokers commonly err by calculating the adjusted bank balance based solely on the bank statement, ignoring the bank

account record. While they may know the correct account balances, they may not realize their records are incomplete or

erroneous.)

4. Keep a record of the two reconciliations performed at the end of each month, along with the supporting schedules.

5. Locate any difference between the three sets of accounting records. A difference can be caused by:

• not recording a transaction

• recording an incorrect figure

• erroneous calculations of entries used to arrive at account balances

• missing beneficiary records

• bank errors.

10

DOCUMENTATION REQUIREMENTS

Activities and Related Documents

In addition to accounting records, the Bureau of Real Estate requires that the broker maintain all documents prepared or obtained in

connection with any real estate transaction handled. Here is a list of typical activities and the corresponding documentation.

Activity Documentation

1. Receiving trust funds in the form of:

• Purchase deposits from buyers

• Rents and security deposits from tenants

• Other receipts

• Real estate purchase contract and receipt for deposit,

signed by the buyer

• Collection receipts

• Collection receipts

2. Depositing trust funds

• Bank deposit slips

3. Forwarding buyers’ checks to escrow

• Receipt from title/escrow company and copy of check

4. Returning buyers’ checks

• Copy of buyer’s check signed and dated by buyer,

signifying buyer’s receipt of check

5. Disbursing trust funds

• Checks issued

• Supporting papers for the checks, such as invoices,

escrow statements, billings, receipts, etc.

6. Receiving offers and counteroffers from buyers and

sellers

• Real estate purchase contract and receipt for deposit,

signed by respective parties

• Agency disclosure statement

• Transfer disclosure statement

7. Collecting management fees from the trust fund bank

account

• Property management agreements between broker and

property owners. (Note: If only one trust fund check is

issued for management fees charged to various

property owners, there should be a schedule or listing

on file showing each property and amount charged,

and the total amount, which should agree with the

check amount.)

• Cancelled checks

8. Reconciling bank account record with separate

beneficiary records

• Record of reconciliation

ADDITIONAL REQUIREMENTS - DOCUMENTS

The following is an additional requirement of the Real Estate Law and the Commissioner’s Regulations relating to the preparation and

management of real estate transaction documents.

Person Signing Contract to be Given Copy

Under Business and Professions Code Section 10142, any time a licensee prepares or has prepared an agreement authorizing or

employing that licensee to perform any acts for which a real estate license is required or when the licensee obtains the signature of any

person to any contract pertaining to such services or transaction, the licensee must deliver a copy of the agreement to the person

signing it at the time the signature is obtained. Examples of such documents are listing agreements, real estate purchase contract and

receipt for deposit forms, addenda to contracts, and property management agreements.

11

AUDITS AND EXAMINATIONS

Because of the importance of trust fund handling, the Commissioner has an ongoing program of examining brokers’ records. As

necessary, audited licensees are made aware of deficiencies in trust fund handling and record keeping. If an audit discloses actual trust

fund imbalances or money handling procedures which may cause monetary loss, appropriate disciplinary proceedings may be

initiated.

Section 10148 of the Business and Professions Code provides that a real estate broker shall retain for three years copies of all listings,

deposit receipts, canceled checks, trust records, and other documents executed by or obtained by the broker in connection with any

transaction for which a real estate broker license is required. The retention period shall run from the date of the closing of the

transaction or from the date of the listing if the transaction is not consummated. After notice, such books, accounts and records shall

be made available for examination, inspection and copying by the Commissioner or a designated representative during regular

business hours, and shall, upon the appearance of sufficient cause, be subject to audit without further notice, except that such audit

shall not be harassing in nature.

SAMPLE TRANSACTIONS

To demonstrate the record keeping requirements discussed above, we have simulated trust account records for typical real estate

transactions occurring over a thirty-day period. To set the stage, let us assume that James Adams, a real estate broker, owns and

operates a one-man real estate office specializing in residential sales and property management. Broker Adams has one trust fund bank

account. We will look at the trust account activity for this office for the month of May, 2013.

The use of columnar records to record these transactions is illustrated in Exhibits 1 - 10 at the end of this publication. As previously

discussed, a broker may use other types of records as long as they meet generally accepted accounting standards.

2013 TRANSACTIONS

May 1 Opened a trust account with First County Bank, and deposited $100 of his own money to cover bank service charges.

May 1 Entered into agreements to manage the following rental properties:

Address

Owner’s Name

a) 1538 South Ave.

Anycity, CA

T. Eddie

b) 3490 Tower St.

Anycity, CA

L. Stewart

.

c) 9152 High Way

Anycity, CA

W. Allen

d) 2351-2353 Kingstone Way

Anycity, CA

S. Manly

e) 7365 Meadow Circle

Anycity, CA

J. Bird

12

May 3 Deposited the following rents received from tenants of managed properties:

Property.

Tenant’s Name

Rent Received

a) 1538 South Ave.

B. Hamms

$1,700

b) 3490 Tower St., Unit 1

R. Robertson

$700

c) 2351 Kingston Way

I. Warren

$1,250

TOTAL

$3,650

May 6 Received a $5,000 check payable to broker from Mr. and Mrs. Dennis White as deposit for their offer to buy a house at

615 Lake Drive, Anycity, owned by Mr. and Mrs. Richard J. Jensen. Buyers’ offer instructed broker to hold the check

uncashed until their offer was accepted by the Jensens.

May 6 Received and deposited $2,250 from T. Sundance representing rent of $1,250 for May 5 to 30, and $1,000 security deposit

for 7365 Meadow Circle.

May 6 Was notified by the Jensens that they accepted the offer on their property.

May 6 Deposited the $5,000 check from Mr. and Mrs. White.

May 8 Obtained an exclusive listing to sell a six-plex at 915 Galaxy St., Anycity, owned by R. Jays.

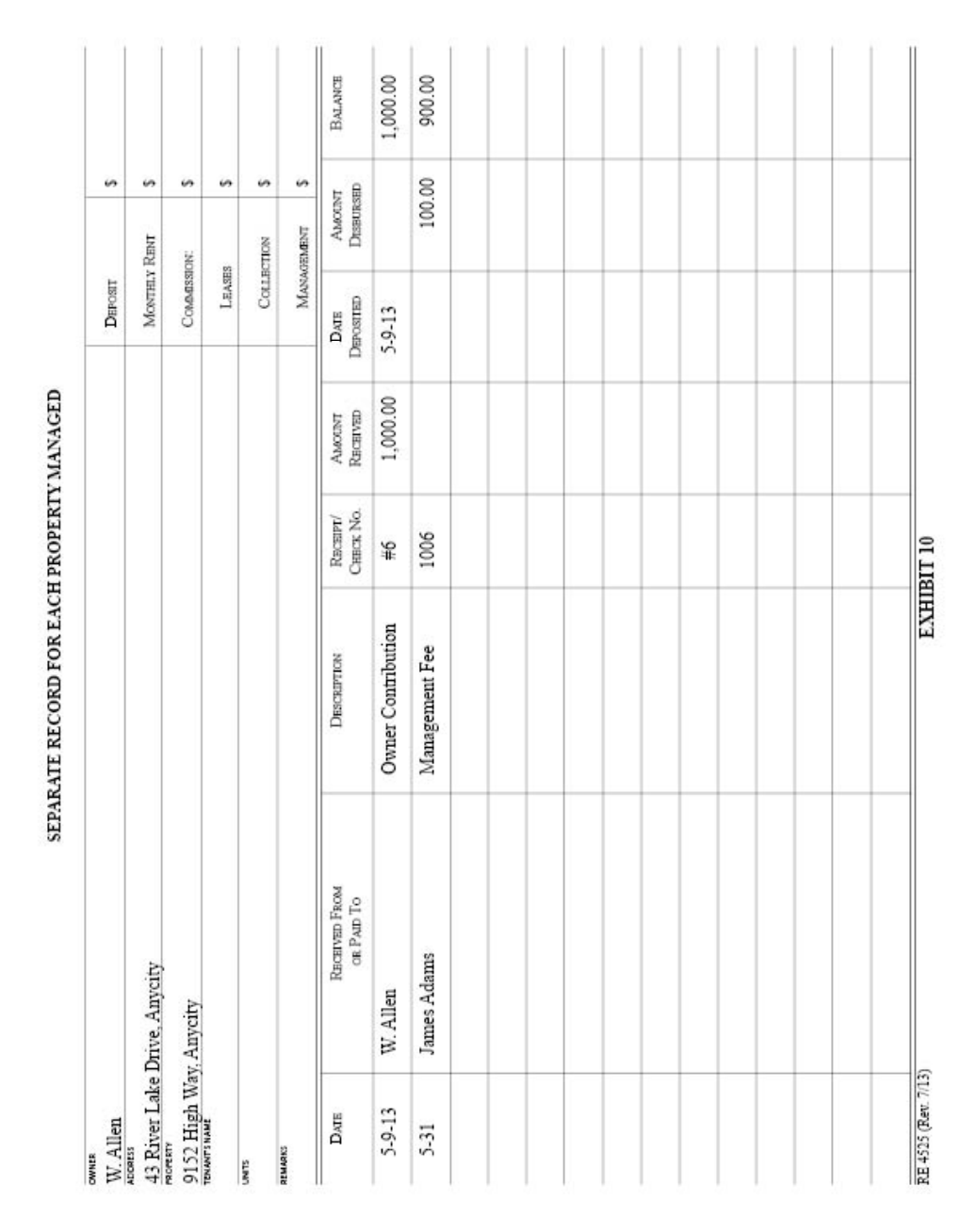

May 9 Received $1,000 from W. Allen, owner of 9152 High Way, to cover anticipated expenses for the property. Amount was

deposited the same day.

May 10 Issued the following checks to pay for various expenses connected with the managed properties:

Check No.

Payee

Purpose

Amount

1001

ABC Mortgage Co.

Mortgage payment for 1538 South Ave.

$1,300

1002

Anycity Treasury

Utilities for 1538 South Ave.

135

1003

Professional Cleaners

Cleaning for 3490 Tower St.

125

1004

Mr. Handyman

Minor repairs on 2351 Kingston

95

TOTAL $1,655

May 14 Received a $4,000 check from B. Sun, payable to Title Escrow Company, with an offer to buy the 915 Galaxy property.

May 15 Received R. Jays’ acceptance of the buyer’s offer on 915 Galaxy Street.

May 16 Delivered the $4,000 check from B. Sun to Title Escrow Company.

May 20 Issued check number 1005 for $5,000 to First Title Co. for account of Mr. and Mrs. White, buyers of the 615 Lake Drive

property.

May 22 Received an offer and a $3,000 check as deposit from R. Olive to buy a single family house at 31009 Technology Street

owned by T. Evans.

May 24 Returned R. Olive’s check after seller rejected the offer.

May 31 Charged property management fees to the following accounts and issued check number 1006 for $590 payable to himself:

Property Owner

Management Fee

T. Eddie

$170

L. Stewart

70

W. Allen

100

S. Manly

125

J. Bird

125

Total $590

May 31 Sent statement of account to each owner of the managed properties.

13

Background Information

James Adams keeps four types of columnar records:

1. Record of all Trust Funds Received and Paid Out - Trust Fund Bank Account (hereinafter referred to as “Bank Account

Record”). This record is required under Commissioner’s Regulation 2831 for each trust account a broker has.

2. Record of all Trust Funds Received - Not Placed in Broker’s Trust Account (hereinafter referred to as “Record of

Undeposited Receipts”). This is required under Commissioner’s Regulation 2831.

3. Separate Record For Each Beneficiary or Transaction (hereinafter referred to as “Separate Beneficiary Record”). This is

required under Commissioner’s Regulation 2831.1.

4. Separate Record For Each Property Managed (hereinafter referred to as “Separate Property Record”). This serves the same

purpose as the Separate Beneficiary Record.

To illustrate the recording process, listed below are the entries made on the books by James Adams as well as the documents prepared

or obtained as support for each transaction. The actual entries are shown on the forms/exhibits at the end of this publication.

Note that:

• Each entry to any record shows all the pertinent information of the transaction, such as the date, name of payee, name of

payor, amount, check number, etc.

• The daily bank balance is computed and posted on the Account Record after recording the transactions.

• The balance owing to the client is computed and posted on the Beneficiary Record or Separate Property Record, after posting

transactions.

• Any entry made on the Bank Account Record has a corresponding entry on a Beneficiary Record or a Separate Property

Record, and vice versa.

• All records except the Record of Undeposited Receipts show entries in chronological sequence regardless of transaction type.

The Record of Undeposited Receipts shows the disposition of a trust fund in the same line as the receipt is entered, rather

than in chronological sequence.

Step-By-Step Narrative of Trust Account Entries

(Actual recording shown in Exhibits 1 - 10)

Transaction

Date

Documentation Entries

May 1

Deposit slip prepared by

broker.

Record the deposit on:

1. The Bank Account Record. Balance is $100. (Exh. 1)

2. A newly prepared Separate Beneficiary for James Adams. Balance is $100.

(Exh. 2)

May 1

Management agreements

signed by property owners

and broker.

No entries needed since there was no receipt nor disbursement of trust funds.

May 3

Collection receipts Nos. 2, 3

and 4 issued to B. Hamns, R.

Robertson, and I. Warren,

respectively.

Record the $3,650 receipt on:

1. The Bank Account Record. New balance is $3,750. (Exh. 1)

2. Newly prepared Separate Beneficiary Records for:

T. Eddie - balance is $1,700 (Exh. 4)

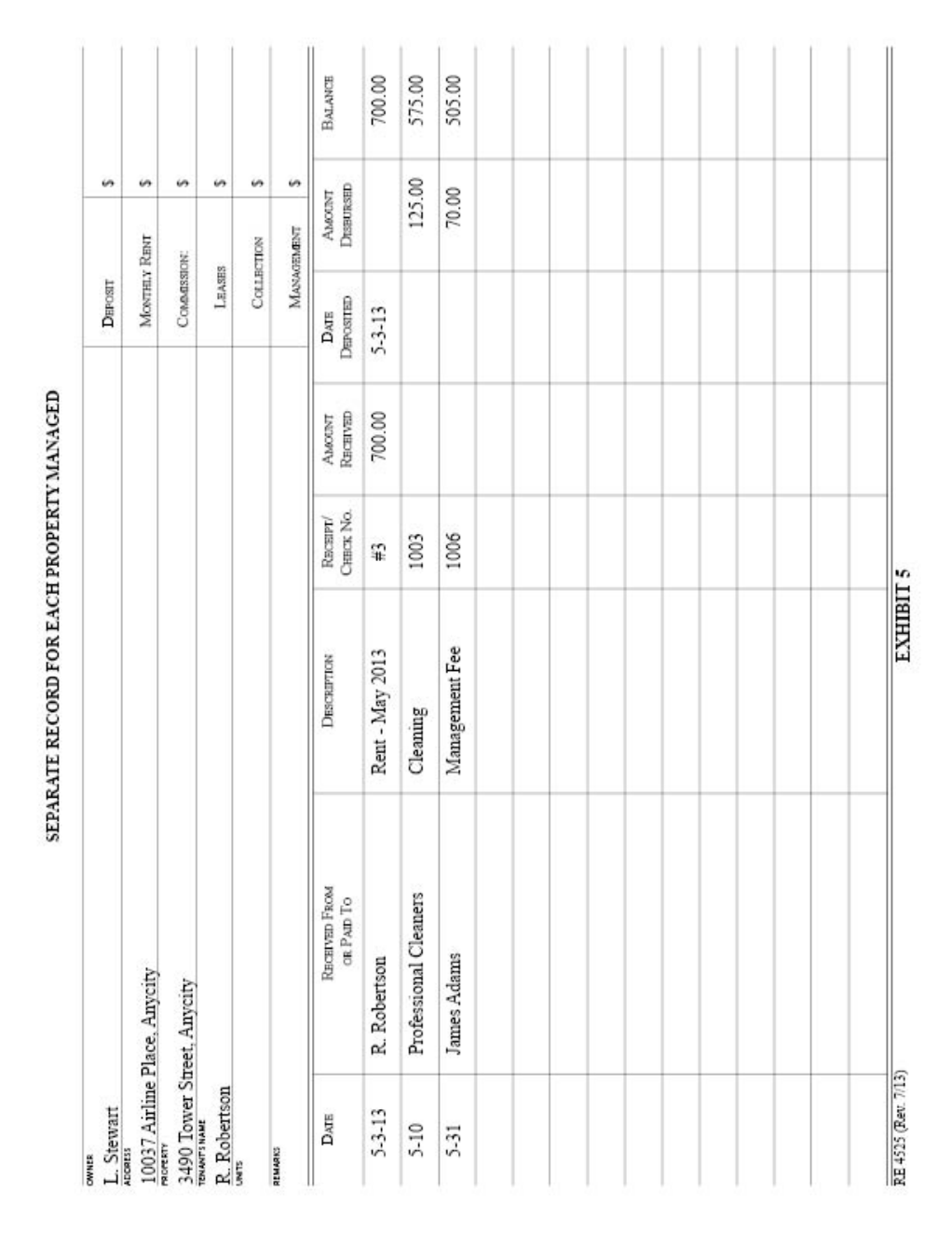

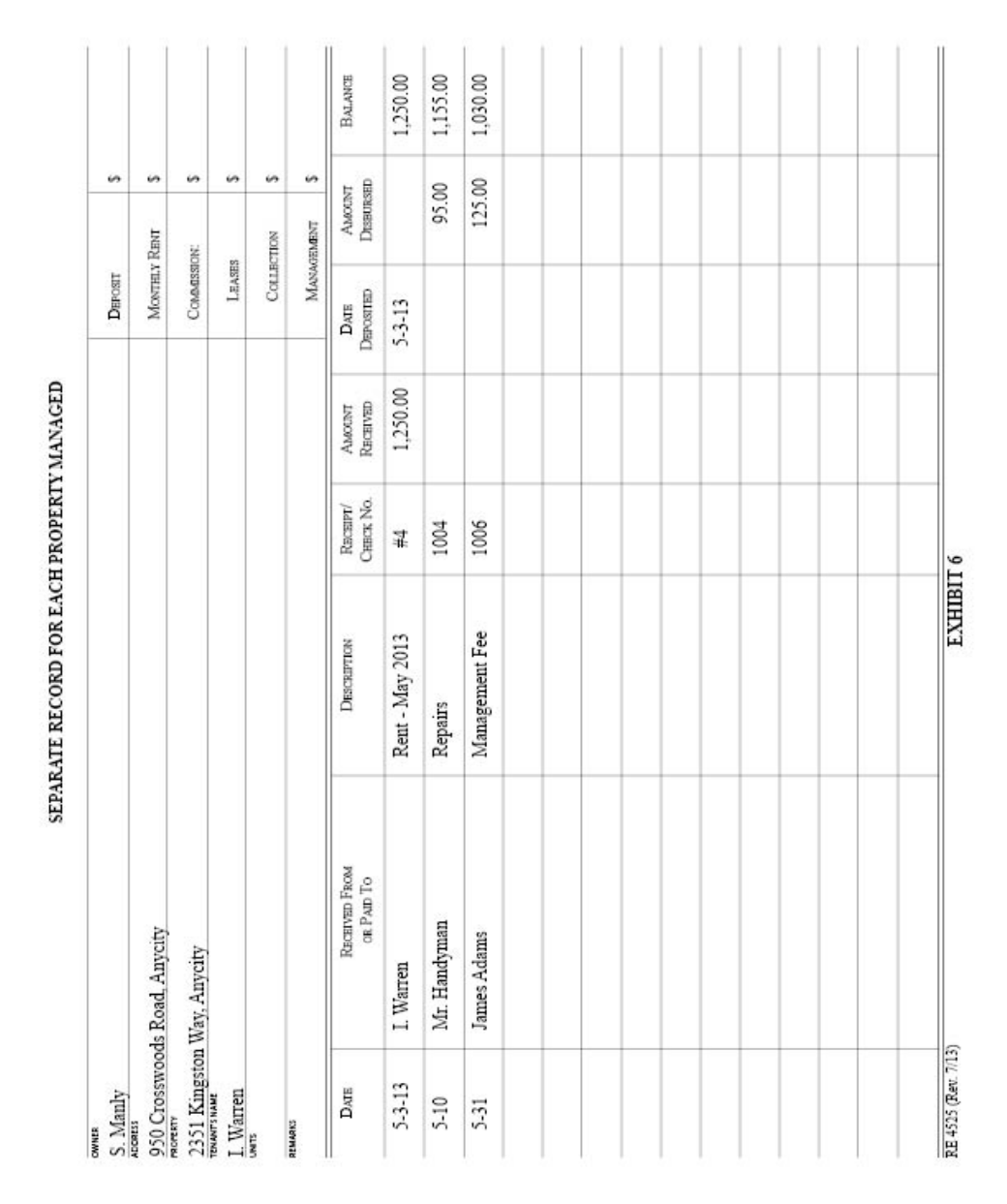

L. Stewart – bal. is $700 (Exh. 5)

S. Manly - balance is $1,250 (Exh. 6)

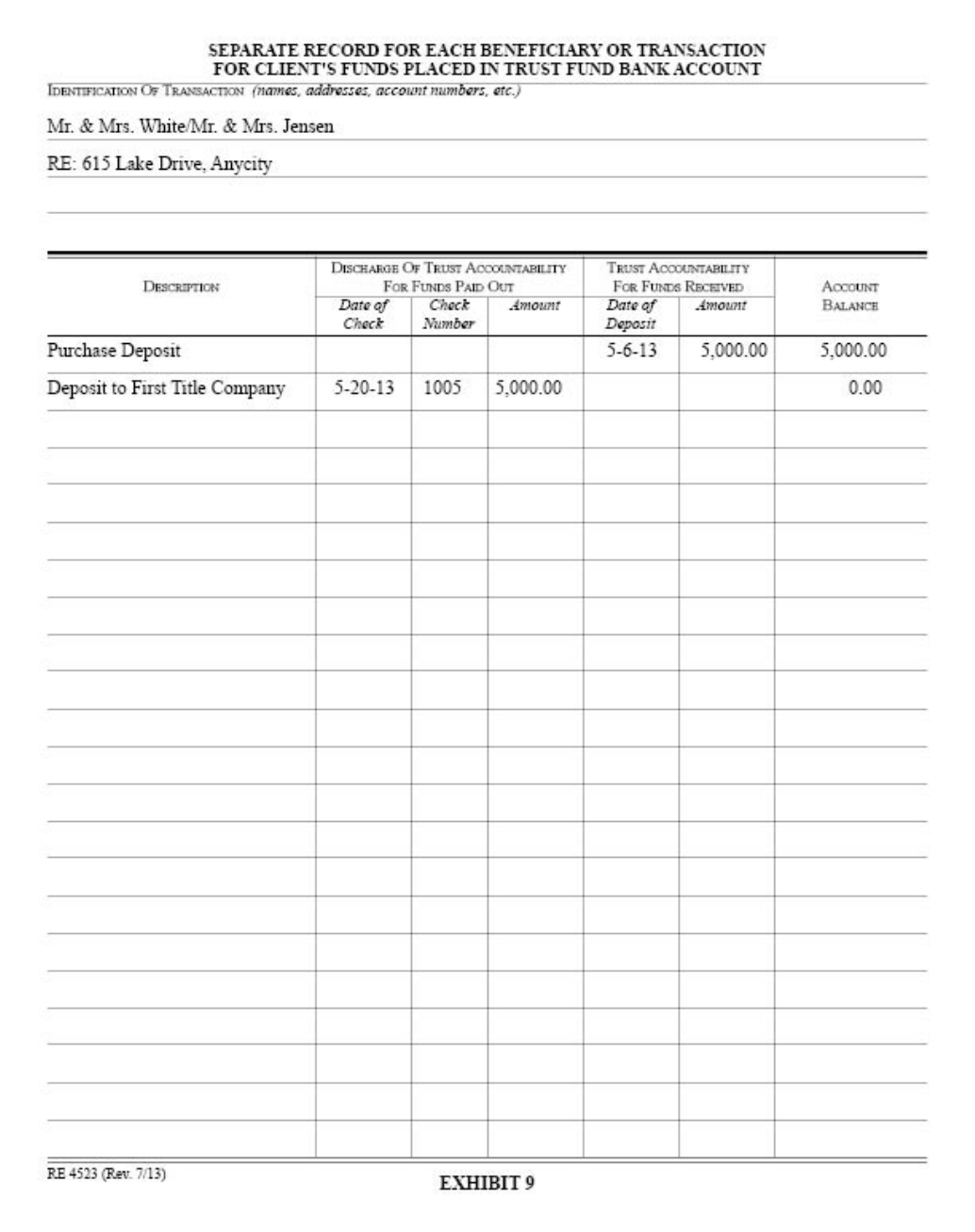

May 6

Real Estate Purchase

Contract and Receipt for

Deposit signed by Mr. and

Mrs. White. Collection

receipt No. 1 issued to the

Whites.

Enter transaction on the Record of Undeposited Receipts. (Exh. 3)

No Separate Beneficiary Record is necessary since the check was not deposited.

14

Transaction

Date

Documentation Entries

May 6

Collection receipt No. 5

issued to T. Sundance.

Receipt showed that $1,250

of the $2,250 was for rent

and the other $1,000 was for

security deposit.

Record the $2,250 deposit on:

1. The Bank Account Record. (Exh. 1)

2. Separate Beneficiary Records for:

J. Bird - Sundance’s Security Deposit, bal. is $1,000. (Exh. 7)

J. Bird - balance is $1,000. (Exh. 8)

(Since security deposits will be accounted to the tenant in the future, James

Adams keeps a separate record for deposits. Total liability to the owner is the

sum of the two records - one for security deposits, another for rents and other

transactions.)

May 6

Real Estate Contract and

Receipt for trust funds were

received for Deposit signed

by Mr. and Mrs. Jensen.

No entries were made since no trust funds were received or disbursed.

May 6

Deposit receipt prepared by

broker.

Record $5,000 deposit on:

1. Bank Account record. New balance is $11,000. (Exh. 1)

2. A newly prepared Separate Beneficiary Record - Mr. and Mrs. White/Mr.

and Mrs. Jensen. Account balance is $5,000. (Exh. 9)

3. Record of Undeposited Receipts. (Exh. 3) Shows disposition of check

previously entered on the record.

May 8

Exclusive Listing Agreement

signed by sellers and broker.

May 9

Collection receipt No. 6

issued to W. Allen.

Record receipt on:

1. The Bank Account Record. New balance is $12,000. (Exh. 1)

2. A newly prepared Separate Beneficiary Record - W. Allen. Balance is

$1,000. (Exh. 10)

May 10

Checks issued by broker.

Supporting papers for each

check.

Record disbursements on:

1. Bank Account Record. New Balance is $10,345. (Exh. 1)

2. Separate Beneficiary Records for:

T. Eddie - New balance is $265. (Exh. 4)

L. Stewart - New balance is $575. (Exh. 5)

S. Manly - New balance is $1,155. (Exh. 6)

May 14

Real Estate Purchase

Contract and Receipt for

Deposit signed by B. Sun.

Record receipt on the Record of Undeposited Receipts. (Exh. 3)

May 15

Real Estate Purchase

Contract and Receipt for

Deposit signed by R. Jays.

No entry was needed since there was no receipt or disbursement of funds.

May 16

Receipt issued by Title

Escrow Company.

Note disposition of check on the Record of Undeposited Receipts. (Exh. 3)

May 20

Check issued by broker.

Receipt issued by First Title

Company.

Record disbursements on the:

1. Bank Account Record. New balance is $8,345. (Exh. 1)

2. Separate Beneficiary Record - Mr. and Mrs. White/Mr. and Mrs. Jensen.

New balance is $0. (Exh. 9)

May 22

Real Estate Purchase

Contract and receipt for

Deposit signed by R. Olive.

15

Transaction

Date

Documentation Entries

May 24

Real Estate Purchase

Contract and Receipt for

Deposit rejected by T.

Evans.

Post the return of check on the Record of Undeposited Receipts. (Exh. 3)

May 31

List showing the breakdown

of the check amount,

showing the charge to each

owner.

(NOTE: A list is necessary

as support for a check

disbursement chargeable to a

number of beneficiaries.

Posting the entries on the

separate records without

such a list is not sufficient.)

Record disbursements on the:

1. Bank Account Record. New balance is $7,755. (Exh. 1)

2. Separate Beneficiary Records for:

New

Owners Balance

T. Eddie $95

L. Stewart $505

W. Allen $900

S. Manly $1,030

J. Bird $1,125

After recording the daily transactions, the next step in the trust fund accounting process is the reconciling of records at the end of the

month. James Adams prepared reconciliation schedules by comparing the bank balance on the Bank Account Record with the bank

statement balance (the bank reconciliation) and also with the total of the Separate Beneficiary Records balances (the reconciliation

report).

The bank statement and reconciliations are shown on the next two pages.

16

FIRST COUNTY BANK STATEMENT

MAIN BRANCH

5 Main Avenue

ANYCITY, CA 90002

PAGE 1 of 1

DATE OF THIS STATEMENT: 05/31/13

JAMES ADAMS

TRUST ACCOUNT

8310 ORANGE AVENUE

ANYCITY, CA 90002

CHECKING ACCT. 123456 CUSTOMER SINCE 1995

SUMMARY: PREVIOUS STATEMENT BALANCE ON 04/30/13 00.00

TOTAL OF 5 DEPOSITS FOR ................................................. 12,000.00

TOTAL OF 4 CHECKS FOR.................................................... 6,560.00

TOTAL OF 1 OTHER DEBIT FOR ......................................... 7.00

STATEMENT BALANCE ON 05/31/13 .................................. 5,433.00

CHECKS/ CHECKS

OTHER CHECK DATE

DEBITS NUMBER POSTED AMOUNT

1001 5/14 1,300.00

1002 5/16 135.00

1003 5/16 125.00

1005 5/21 5,000.00

OTHER

DEBITS

DATE

POSTED AMOUNT

05/31 SERVICE CHARGE 7.00

DEPOSITS/ DEPOSITS

OTHER DATE

CREDITS POSTED AMOUNT

5/1 100.00

5/6 3,650.00

5/6 2,250.00

5/6 5,000.00

5/9 1,000.00

DAILY

BALANCE DATE AMOUNT DATE AMOUNT

5/1 100.00 5/16 10,440.00

5/6 11,000.00 5/21 5,440.00

5/9 12,000.00 5/31 5,433.00

5/14 10,700.00

17

James Adams

Bank Reconciliation

First County Bank

May 31, 2013

Balance per bank statement, 5/31/13 .................................... $5,433.00

Add deposits in transit .......................................................... -0-

Less outstanding checks:

check #1004 ........................................... $95.00

#1006 ..................................................... 590.00 <685.00>

Adjusted bank balance, 5/31/13 ............................................ $4,748.00

Balance per books, 5/31/13................................................... $4,755.00

Less May bank service charge .............................................. <7.00>

Adjusted balance, 5/31/13 .................................................... $4,748.00

James Adams

Reconciliation Report

First County Bank

Account No. 123456

May 31, 2013

Beneficiary Balance

James Adams (Broker) ......................................................... $93.00

W. Allen ............................................................................... 900.00

J. Bird ................................................................................... 1,000.00

J. Bird ................................................................................... 1,125.00

T. Eddie ................................................................................ 95.00

S. Manly ............................................................................... 1,030.00

L. Stewart ............................................................................. 505.00

Total per subsidiary records.................................................. $4,748.00

(Agrees with bank account record balance.)

18

Questions and Answers Regarding Trust Fund Requirements and Record Keeping

Q. Are security deposits on rental units the property of the owner or should they be held in trust by the broker for the tenant?

A. They are trust funds. As such, control and disbursement of the security deposits are at the instruction of the property owner.

Q. Am I permitted to wait until checks deposited to my trust account have cleared before I issue a trust check to fund a customer’s

check?

A. Although the Real Estate Law is silent on this, good business practice dictates that you wait until a customer’s check deposited to

your trust account has cleared prior to the issuing of your trust check as a refund.

Q. How should I handle an earnest money check which is to be deposited into escrow upon acceptance of the offer?

A. Such a check may be held until the offer is accepted and then placed in escrow but only when directed to do so by the buyer,

provided you disclose to the seller the fact the check is being held in uncashed form. In such cases, it is good practice to include

such a provision in the deposit receipt. You must keep a columnar record of the receipt of the check, the name of the escrow

company and the date the check was forwarded to the escrow.

Q. As a broker-owner of rentals, do I have to put security deposits in a trust account?

A. Money you receive on your own property is received as a principal, not as an agent. As such, these are not trust funds and should

not be placed in the trust account.

Q. Must I keep a deposit receipt signed only by the buyer and rejected by the seller?

A. Yes. Such a record must be maintained for three years.

Q. May I maintain one trust fund account for both collections from my property management business and deposits on real estate

sales transactions?

A. Since property management funds usually involve multiple receipt of funds and several monthly disbursements, it is suggested that

separate trust fund accounts be maintained for property management funds and earnest money deposits. However, all trust funds

can be placed in the same trust fund account as long as separate records for each trust fund deposit and disbursement are

maintained properly and the account is not an interest-bearing account.

Q. If the buyer and seller decide to go directly to escrow and the buyer makes out a check to the escrow company and hands it

directly to the escrow clerk, do I have to maintain any records of this check?

A. No. You must maintain records only of trust funds which pass through your hands for the benefit of a third party.

Q. How long must I keep deposit receipts?

A. Deposit receipts must be maintained for three years.

SUMMARY

We might say this publication presents the three R's of trust funds: Responsibility, Requirements, and Records.

It is a real estate broker’s responsibility to protect clients’ funds at all times and keep clients fully informed of the nature and

disposition of all trust funds.

To aid brokers in carrying out this responsibility, the Real Estate Commissioner’s Regulations include requirements concerning trust

funds. A real estate broker also needs to meet other requirements from a practical business point of view. To protect clients’ funds

adequately and in the business-like fashion expected, the broker must keep accurate records.

19

20

21

22

23

24

25

26

27

28