IDirect_DrReddys_Q4FY15 4065R DRREDLAB 20150513

User Manual: 4065R

Open the PDF directly: View PDF ![]() .

.

Page Count: 15

May 13, 2015

ICICI Securities Ltd | Retail Equity Research

Result Update

Higher R&D, adverse product mix hit margins

• Revenues grew 11.2% YoY to | 3870.4 crore (I-direct estimate:

| 3993 crore) mainly on account of 15% growth in US formulation

sales to | 1715.4 crore

• EBITDA margins declined 111 bps YoY to 21.3% vs. I-direct estimate

of 26%. The delta was mainly due to higher R&D spend, change in

product mix and currency fluctuation. EBITDA in absolute terms

increased 5.7% to | 825.6 crore vs. I-direct estimate of | 1038.2 crore

• Net profit increased 7.7% to | 518.8 crore vs. I-direct estimate of

| 755.9 crore. The miss was on account of lower operational income

and higher finance expenses

Global generics to piggyback on strong, sustainable US traction

The global generics (GG) segment is expected to grow at a CAGR of 17%

in FY15-17E driven by strong US traction, which is likely to grow at a

CAGR of ~19% during the same period. DRL has developed a knack for

exclusivity/FTF launches on a fairly continuous basis in the US. We expect

this trend to continue further. However, the focus has now shifted to

more unique launches like OTC, complex generics, controlled releases,

etc. The US traction is also likely to nullify European slowdown. The US

pipeline includes 220 filed ANDAs including 68 pending approvals.

Russia CIS becomes volatile; India to provide more stability

Global generics (ex US, Europe) are likely to grow at a steady CAGR of

~17% in FY15-17E driven by growth in India as the Russian performance

remains volatile. These two markets are more or less identical in nature

(branded generics and OTC) with similar growth potential and similar

kinds of risks. DRL is well versed with the dynamics in Russia by virtue of

being an early mover. However, the recent currency volatility and political

unrest have caused disturbances in an otherwise safe market for the

company. For India, growth is expected to be largely from launches in the

oncology and biosimilars space besides an improvement in productivity

of the enhanced field force.

Portfolio realignment eminent

We envisage a fall in share of low margin/high risk segments such as

PSAI and European generics (especially Betapharm), going ahead. Thus,

growth in FY15-17E is likely to emanate from more productive and

sustainable segments such as US and India. Similarly, in terms of product

offering, we envisage more launches in the fields of injectables, OTC,

complex/limited competition products & biosimilars, besides legacy

generics.

US franchisee looks promising; India growth likely to sustain

US and India together hold the key for global generics growth as well as

DRL’s overall growth. Among them, the US is the main catalyst with a

pending product portfolio of 68 ANDAs, which includes 43 Para IVs and

13 FTFs. The company is investing heavily in R&D to bring more and

complex generics and limited competition products, mainly from the non-

oral category, which is likely to take care of sustained US growth for the

next two or three years. India is showing promising growth as well with a

recalibrated approach and the recent acquisition (UCB’s India business)

bodes well for the future. Russia, Europe and PSAI segments, however,

continue to pose challenges for being lumpy and volatile. We have

ascribed a target of | 3949 based on 22x FY17E EPS of | 179.5.

Rating matrix

Rating : Buy

Target : | 3949

Target Period : 12-15 months

Potential Upside : 13%

What’s Changed?

Target Changed from | 3332 to | 3949

EPS FY16E Changed from | 151 to 150.9

EPS FY17E Changing from | 185.1 to | 179.5

Rating Changed from Hold to Buy

Quarterly Performance

Q4FY15 Q4FY14 YoY (%) Q3FY15 QoQ (%)

Revenue 3,870.4 3,480.9 11.2 3,843.1 0.7

EBITDA 825.6 781.3 5.7 980.2 -15.8

EBITDA (%) 21.3 22.4 -111 bps 25.5 -417 bps

Net Profit 518.8 481.7 7.7 574.6 -9.7

Key Financials

(|crore) FY14 FY15 FY16E FY17E

Revenues 13217.0 14818.9 17291.5 19438.4

EBITDA 3312.7 3482.7 4065.1 4667.0

Net Profit 2151.3 2099.0 2562.6 3048.2

EPS (|) 126.7 123.6 150.9 179.5

Valuation summary

FY14 FY15 FY16E FY17E

PE (x) 27.5 28.2 23.1 19.4

Target PE (x) 31.2 31.9 26.2 22.0

EV to EBITDA (x) 14.8 13.9 11.7 9.8

Price to book (x) 5.3 4.4 3.7 3.0

RoNW (%) 23.7 19.3 19.6 19.4

RoCE (%) 19.2 18.1 20.2 21.3

Stock data

Particular

Market Capitalisation

Debt (FY15)

Cash & cash equivalents (FY15)

EV

52 week H/L 3808/2250

Equity capital | 85.0 crore

Face value | 5

| 59800 crore

Amount

| 59280 crore

| 3635 crore

| 3114 crore

Price performance (%)

1M 3M 6M 1Y

Dr Reddy's Labs -8.7 4.1 0.8 27.4

Sun Pharma -15.2 2.8 4.8 54.8

Lupin -11.0 8.1 22.9 82.3

Dr Reddy’s Laboratories (DRREDD) | 3485

Research Analyst

Siddhant Khandekar

siddhant.khandekar@icicisecurities.com

Mitesh Shah

mitesh.sha@icicisecurities.com

Nandan Kamat

nandan.kamat@icicisecurities.com

ICICI Securities Ltd | Retail Equity Research

Page 2

Variance analysis

Q4FY15 Q4FY15E Q4FY14 Q3FY15

Y

oY (%) QoQ (%) Comments

Revenue 3,870.4 3,993.0 3,480.9 3,843.1 11.2 0.7 The growth was mainly driven by 14.6% growth in the US and 15.7% growth in

India.

Raw Material 1,089.6 958.3 927.7 961.7 17.4 13.3 Raw material cost increase was mainly due to adverse product mix, inventory

write-off in the US and currency fluctuation

Other manufacturing expenses 658.8 678.8 561.0 646.2 17.4 1.9

SGNA 794.5 878.5 835.1 857.5 -4.9 -7.3

R & D cost 514.4 447.2 398.5 431.6 29.1 19.2 R&D cost as percentage of sales increased 184 bps to 13.3% on account of

planned scale up in overall R&D spend and filing of three NDAs

Write down of Intangible assets 0.0 0.0 0.0 0.0 0.0 0.0

Write down of goodwill 0.0 0.0 0.0 0.0 0.0 0.0

Other (income)/expenses -12.5 -8.0 -22.6 -34.1 NA NA

Total Expenditure 1,296.4 1,317.7 1,211.0 1,255.1 7.1 3.3

EBITDA 825.6 1,038.2 781.3 980.2 5.7 -15.8

EBITDA (%) 21.3 26 22.4 25.5 -111 bps -417 bps Fall in margins was mainly on account of increase in R&D spend, change in

product mix and currency volatility in the emerging markets

Depreciation 213.7 195.9 195.6 257.4 9.3 -17.0

Finance (income)/ expenses 23.3 -42.0 -16.4 -101.3 LP LP

Share of pr/(loss) to equity investee 4.4 5.0 4.8 4.7 -9.7 -6.2

Tax 74.2 133.4 125.2 254.1 -40.8 -70.8

Net Profit 518.8 755.9 481.7 574.6 7.7 -9.7 Increase in profit was mainly in line with lower operational performance

Key Metrics

North America formulations 1715.4 1945.3 1496.4 1681.9 14.6 2.0 Growth was on account of acquiring of Habitrol brand and increased market

shares in key products. Delta vis-à-vis estimates was on account of lower-than-

expected injectable sales

Europe formulations 234.1 147.2 177.4 194.7 32.0 20.2 Growth was mainly due to new CNS products launches in UK and Germany's

non tender business

India formulations 474.4 459.3 410.1 432.8 15.7 9.6 The growth was mainly on the back of volume expansion in focused brands and

new launches (three products)

Russia & Other CIS formulations 328.9 341.6 451.9 476.6 -27.2 -31.0 The decline was mainly on account of depreciation of Rouble and higher base.

On a constant currency basis, Russia grew 3% YoY

RoW markets formulations 346.5 382.2 196 383.2 76.8 -9.6 Growth was mainly due to robust growth in Venezuela on continuous volume

uptick

PSAI segment 741.5 630.5 664.1 611.2 11.7 21.3 Strong growth on the back of lower base

Proprietary products & Others 29.6 86.8 85.1 89.76 -65.2 -67.0

Source: Company, ICICIdirect.com Research

Change in estimates

(| Crore) Old New % Change Old New % Change

Revenue 17,036.9 17,291.5 1.5 19,538.3 19,438.4 -0.5

EBITDA 4,091.1 4,065.1 -0.6 4,789.3 4,667.0 -2.6

EBITDA Margin (%) 24.0 23.5 -50 bps 24.5 24.0 -50 bps

PAT 2,582.8 2,562.6 -0.8 3,143.6 3,048.2 -3.0

EPS (|) 152.1 150.9 -0.8 185.1 179.5 -3.0

FY16E FY17E

Source: Company, ICICIdirect.com Research

Assumptions

Comments

Growth (%) FY14 FY15 FY16E FY17E FY16E FY17E

North America formulations 73.4 17.1 23.9 15.0 20.0 22.0 We have reduced our US growth assumption due to higher base on account of

Habitrol acqusition and slow product approvals

Europe formulations -15.6 3.0 -0.7 -0.9 -0.5 -1.0

India formulations 21.5 13.7 21.3 16.7 15.0 15.0

Russia & Other CIS formulations 49.5 -10.6 0.9 5.0 0.9 5.0

RoW markets formulations 88.5 77.4 35.3 25.0 30.0 25.0

PSAI segment 0.7 6.2 1.7 2.0 1.7 2.0

Proprietary products & Other 13.1 -19.4 2.0 2.0 2.0 2.0

Current Earlier

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research

Page 3

Company Analysis

Established in 1984, Dr Reddy’s Laboratories (DRL) is one of India’s

pedigreed players with a firm footing in the US and other export markets.

DRL has deep rooted product and market knowledge across therapies.

Like Cipla, DRL also recognised the importance of having good

manufacturing practices (GMP) accreditation in the eighties and

eventually got USFDA approval (first of its kind approval for a formulation

facility in India) in 1987. The company owns 22 manufacturing facilities

and four developing centres across the globe. The facilities have been

approved by various agencies like the USFDA, WHO-Geneva, UKMHRA,

TGA-Australia, MCC-South Africa, DMA Denmark, Brail ANVISA, among

others. Over the years, along with generics, the company also established

itself in the field of discovery of new chemical entities (NCEs) but with

little success.

DRL’s business can be classified into three broad segments- 1) global

generics (GG), 2) pharmaceutical services and active ingredients (PSAI)

and 3) proprietary products (PP). GG (81% of revenues) includes branded

and unbranded prescription and over-the-counter (OTC) products

business. It also includes the operations of the biologics business. This

segment comprises formulation sales to regulated markets of the US,

Europe and emerging markets such as Russia/CIS, India and RoW.

PSAI (17% of revenues) consists of the active pharmaceutical ingredients

(API) business and custom pharmaceutical services (CPS) business. PP

(2% of revenues) consists of NCEs, differentiated formulations and

dermatology focused specialty business operated through Promius

Pharma.

DRL is one of the few Indian companies to foray into new drug discovery

& development (NDDS) and new chemical entity (NCE) research. The

company started research operations in 1992 through a non profit

organisation, Dr Reddy’s Research Foundation, which was later merged

into the company. Despite being an early entrant, the company is yet to

taste success in it. DRL is also the first Indian company to out-license

molecules to big pharma companies.

DRL has spent around 8-9% of the turnover on R&D in the last four years

but this figure is likely to touch 10-11%, going ahead. Beside ANDAs, it

has also filed 10 new drug applications (NDAs) in the 505 b (2) route that

are awaiting approval.

We expect revenues to grow at 15% CAGR to | 19438 crore in FY15-17E,

on the back of growth in the GG segment. This, in turn, will be driven by

the US. The GG is likely to grow at a CAGR of 17% to | 16544 crore

during the same period. On the other hand, the PSAI segment is likely to

slow down, mainly on the back of 1) higher internal consumption and 2)

pricing pressure/order uncertainty in the API and CPS segments,

respectively. The PSAI segment is likely to register 2% CAGR to | 2640

crore in FY15-17E.

ICICI Securities Ltd | Retail Equity Research

Page 4

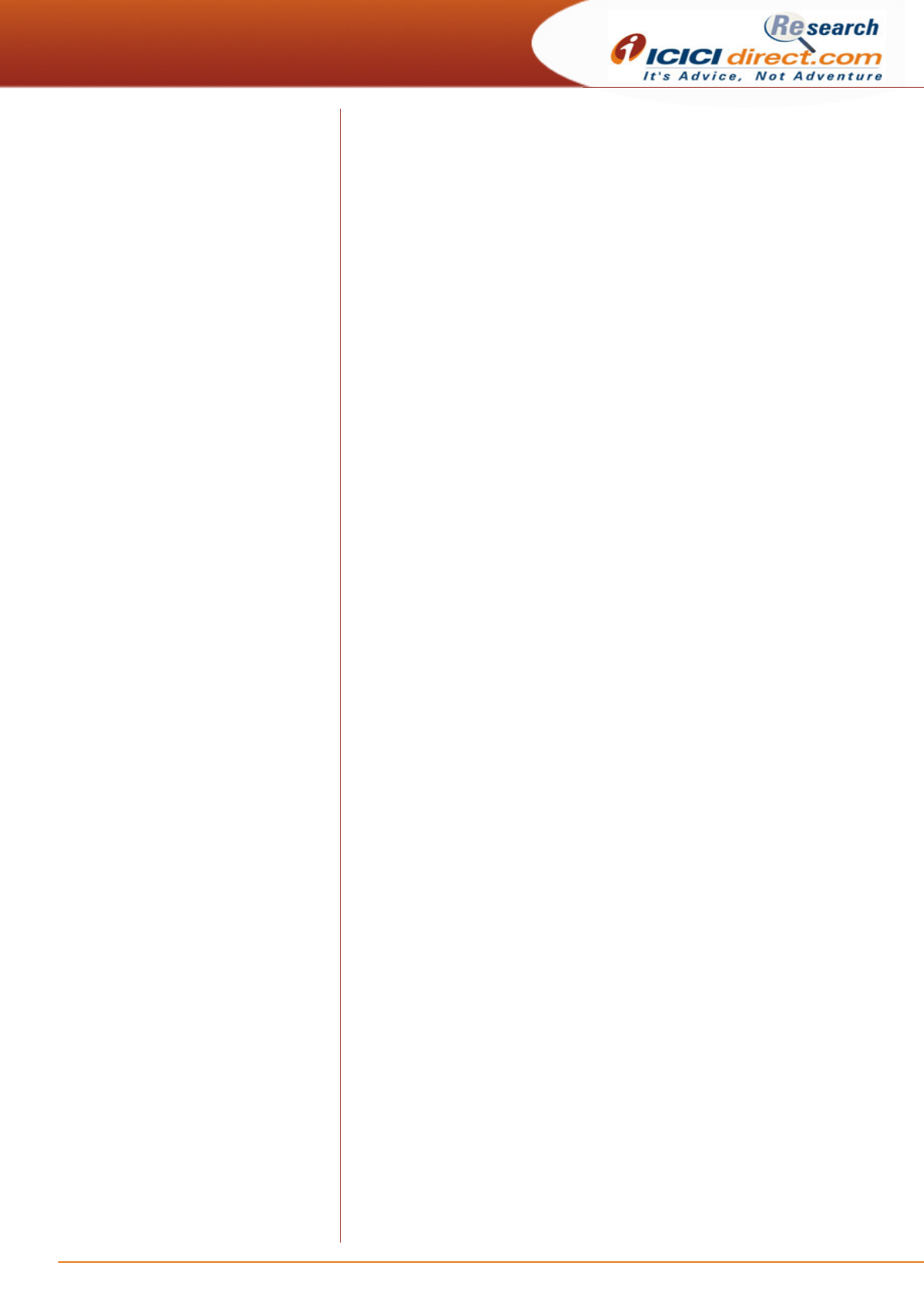

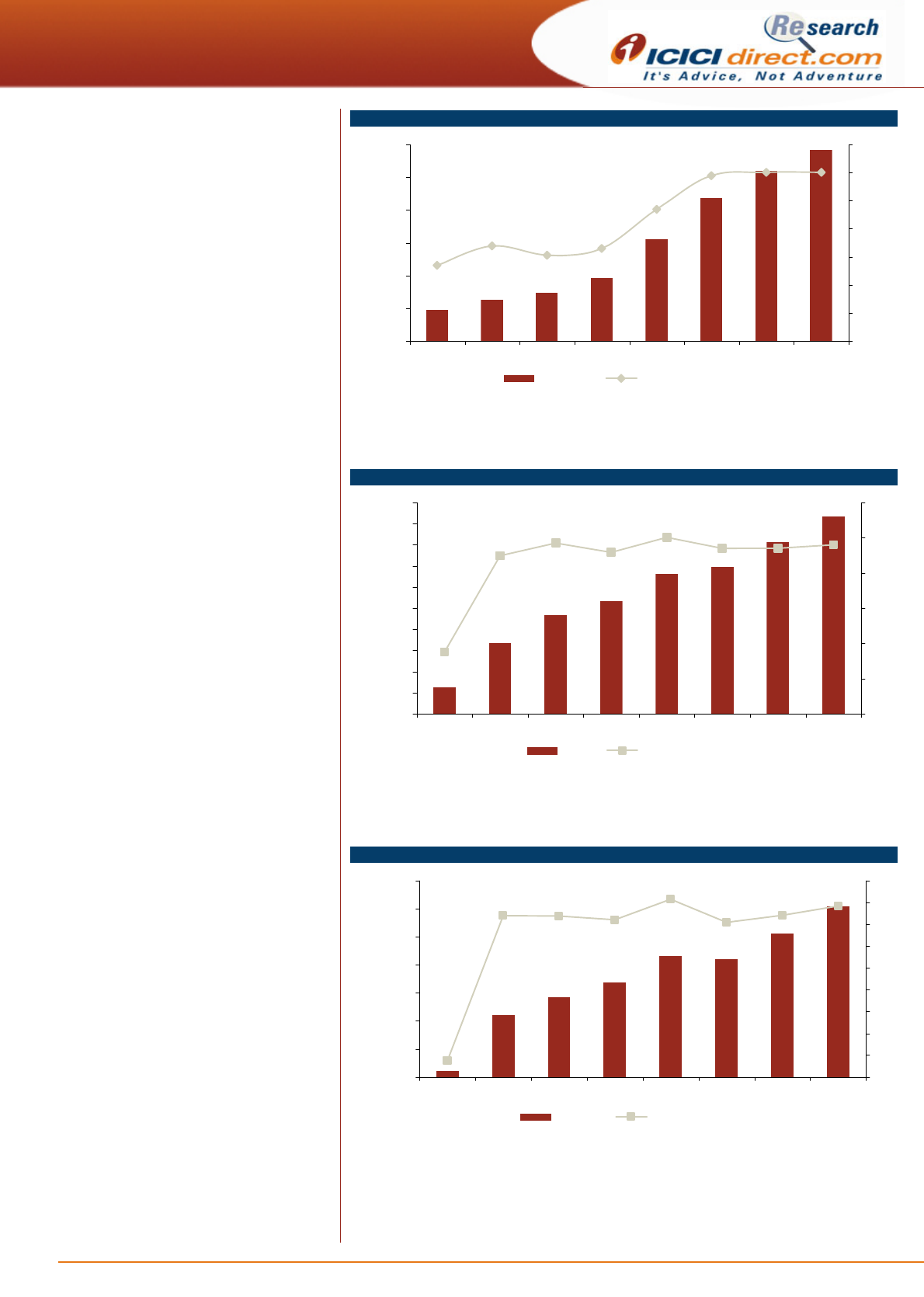

Exhibit 1: Revenues to grow at CAGR of 15% in FY15-17E

7027.7 7469.3

9673.7

11626.6

13217.0

14818.9

17291.5

19438.4

0

4000

8000

12000

16000

20000

24000

FY10 FY11 FY12 FY13 FY14 FY15 FY16E FY17E

(| crore)

Revenues

Source: Company, ICICIdirect.com Research

Exhibit 2: Geography wise revenue break-up

(| crore) FY10 FY11 FY12 FY13 FY14 FY15 FY16E FY17E

North America 1681.7 1899.6 3188.9 3784.6 5530.3 6473.4 8018.7 9221.5

Europe 963.8 843.1 825.9 771.6 697.0 718.1 713.1 706.8

India 1015.8 1169.0 1293.1 1456.0 1571.3 1787.0 2167.6 2530.2

Russia & Other CIS 911.9 1085.8 1326.0 1690.8 1981.9 1771.4 1787.5 1876.9

RoW 287.3 336.5 390.4 553.3 735.9 1305.7 1766.9 2208.6

Global Generics 4860.5 5334.0 7024.3 8256.3 10516.4 12055.7 14453.8 16544.0

North America 367.3 317.0 427.2 574.4 435.4 460.5 469.7 479.1

Europe 665.2 702.0 842.4 1200.7 877.0 945.2 955.8 974.9

India 264.6 261.9 358.6 463.8 378.7 441.1 450.0 459.0

RoW 743.3 683.8 753.1 831.3 706.3 698.8 712.8 727.0

PSAI 2040.4 1964.7 2381.3 3070.2 2397.4 2545.7 2588.3 2640.0

Prop. Products & Others 126.8 170.5 268.2 300.1 303.3 244.6 249.5 254.4

Total 7027.7 7469.2 9673.8 11626.6 13217.1 14845.9 17291.5 19438.4

Source: Company, ICICIdirect.com Research

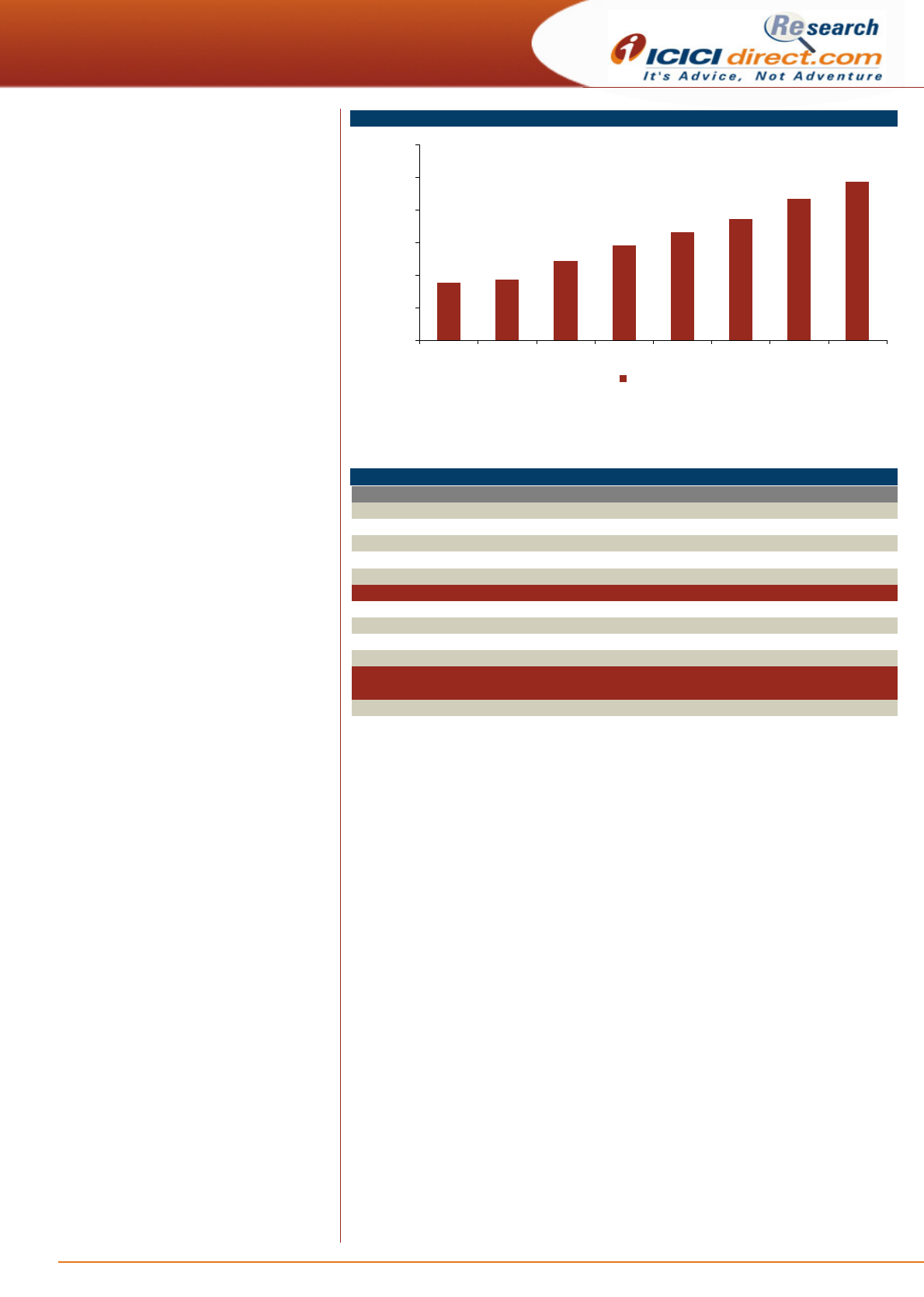

US remains in sweet spot; banking on capabilities and capacity

The US contributes more than 98% of North American sales while the

remaining sales are from Canada. DRL has four USFDA approved

formulations facilities including two in the US. The company operates in

the prescriptions (Rx) and OTC segments in the US market. The sales are

channelled through drug stores, drug wholesalers, health maintenance

organisations and pharmacy chains. DRL is also an authorised supplier to

the US government. After establishing itself in the US generics space, the

focus was shifted to the first to file (FTFs) and AG space.

From FY08 onwards, DRL started filing limited competition/niche products

like injections, controlled releases and complex generics in the US market

in order to reduce the dependence on plain generics. DRL also owns one

of the largest over the counter (OTC) product portfolios in the US.

DRL has a strong product pipeline of 220 ANDAs with 68 pending

approvals. Of these, 43 are Para IVs while 13 have first to file (FTF) status.

Beside ANDAs, DRL has also filed seven NDAs through the 505 b (2)

route, which are awaiting approval. We expect the company to file 18-20

ANDAs every year, going ahead. Going by the future pipeline, (we expect

DRL to launch eight to 10 products per annum, which includes at least

two or three complex products every year besides plain vanilla generic

and FTF opportunities. We expect sales from North America to grow at a

CAGR of 19% in FY15-17E.

ICICI Securities Ltd | Retail Equity Research

Page 5

Exhibit 3: North America sales to be driven by robust pipeline

1681.7 1899.6

3188.9

3784.6

5530.3

6473.4

8018.7

9221.5

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

FY10 FY11 FY12 FY13 FY14 FY15 FY16E FY17E

(| crore)

North America

Source: Company, ICICIdirect.com Research

India: Field force expansion, niche forays to drive growth

DRL ranks seventeenth (in terms of market share, AIOCD, April, 2015)

with a market share of 2.16%. The acute-chronic ratio currently stands at

70:30. Gastrointestinal (GI) is the largest therapeutic group and the

company ranks fifth in this therapeutic group. In many other therapies,

however, it remains a marginal player. The only therapeutic category,

where it holds No. 1 position is anti-neoplastics (oncology), which as a

therapy remains an important but untapped opportunity. To bolster the

domestic franchise, DRL has almost doubled the MR strength from 2250

in FY09 to ~4300 as of today. In order to push domestic growth, DRL has

forayed into the complex biosimilars space, which till date has not

witnessed much crowding. At the same time, these products have not

witnessed the expected traction either. It launched the first biosimilar

oncology product Filgrastim under the brand name Grafeel in 2001. Again

in 2007, it launched another oncology product Rituximab, a biosimilar of

Roche’s blockbuster Mabthera under the brand name Reditux. Overall, it

has launched four biosimilars till date including these two.

Exhibit 4: New launches, improved MR productivity to drive domestic growth

1015.8 1169.0 1293.1

1456.0 1571.3

1787.0

2167.6

2530.2

0

400

800

1200

1600

2000

2400

2800

FY10 FY11 FY12 FY13 FY14 FY15 FY16E FY17E

(| crore)

India

Source: Company, ICICIdirect.com Research

Another interesting high growth/low penetration space for DRL is

oncology. It owns the branded portfolio of products such as Capibine

(Capecitabine), Docetere (Docetaxel) and Cytogem (Gemcitabine).We

expect Indian formulations to grow at a CAGR of 19% in 2015-17E. As per

the management, the NLEM 2011 impact is confined to just ~3-5% of

domestic sales.

ICICI Securities Ltd | Retail Equity Research

Page 6

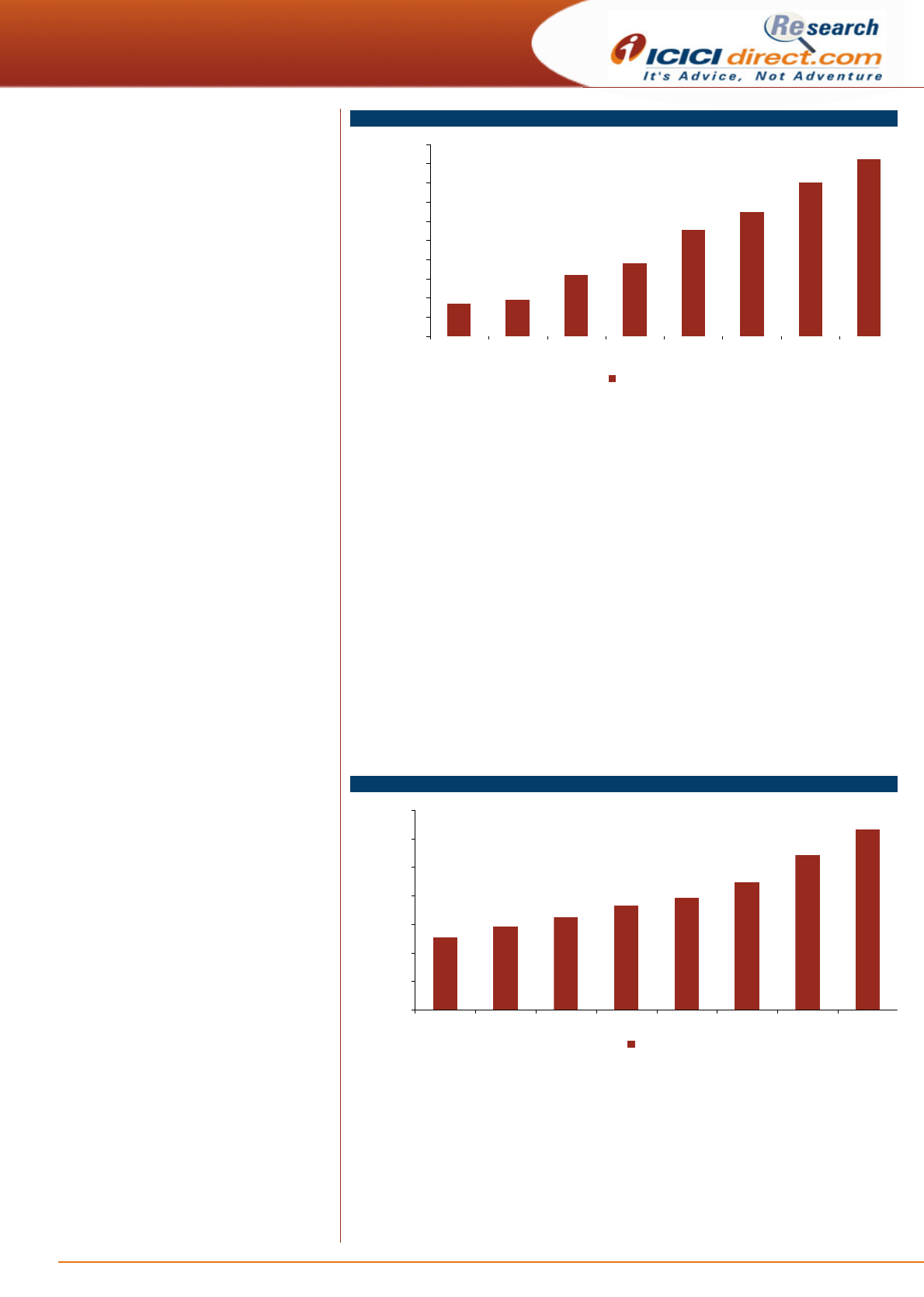

Russia & CIS - banking on experience; region of late has become volatile

DRL was the first Indian entrant in Russia and the CIS, dating back to

1992. Early entry into these markets has helped the company to get hold

of the changing dynamics of these high potential but notoriously volatile

territories. The CIS segment includes countries such as Ukraine, Belarus,

Kazakhstan and Uzbekistan. Russia comprises ~83% of the overall Russia

& CIS (RCIS) segment.

DRL has consolidated its position in the Russian market by focusing on

select therapies such as pain management, anti-infectives, gastro-

intestinal, respiratory, oncology and cardiovascular encompassing

prescription, OTC and hospital sales. The top four brands: Nise, Omez,

Ketorol and Cetrine constituted ~60% of overall Russian sales.

DRL has also struck in-licensing deals with other Indian companies such

as Cipla and Torrent. However, due to the political unrest and sanctions

due to Ukrainian invasion, the region has lost its safe haven status for DRL

besides Rouble volatility. We expect sales from Russia CIS to grow at a

CAGR of 3% in FY15-17E.

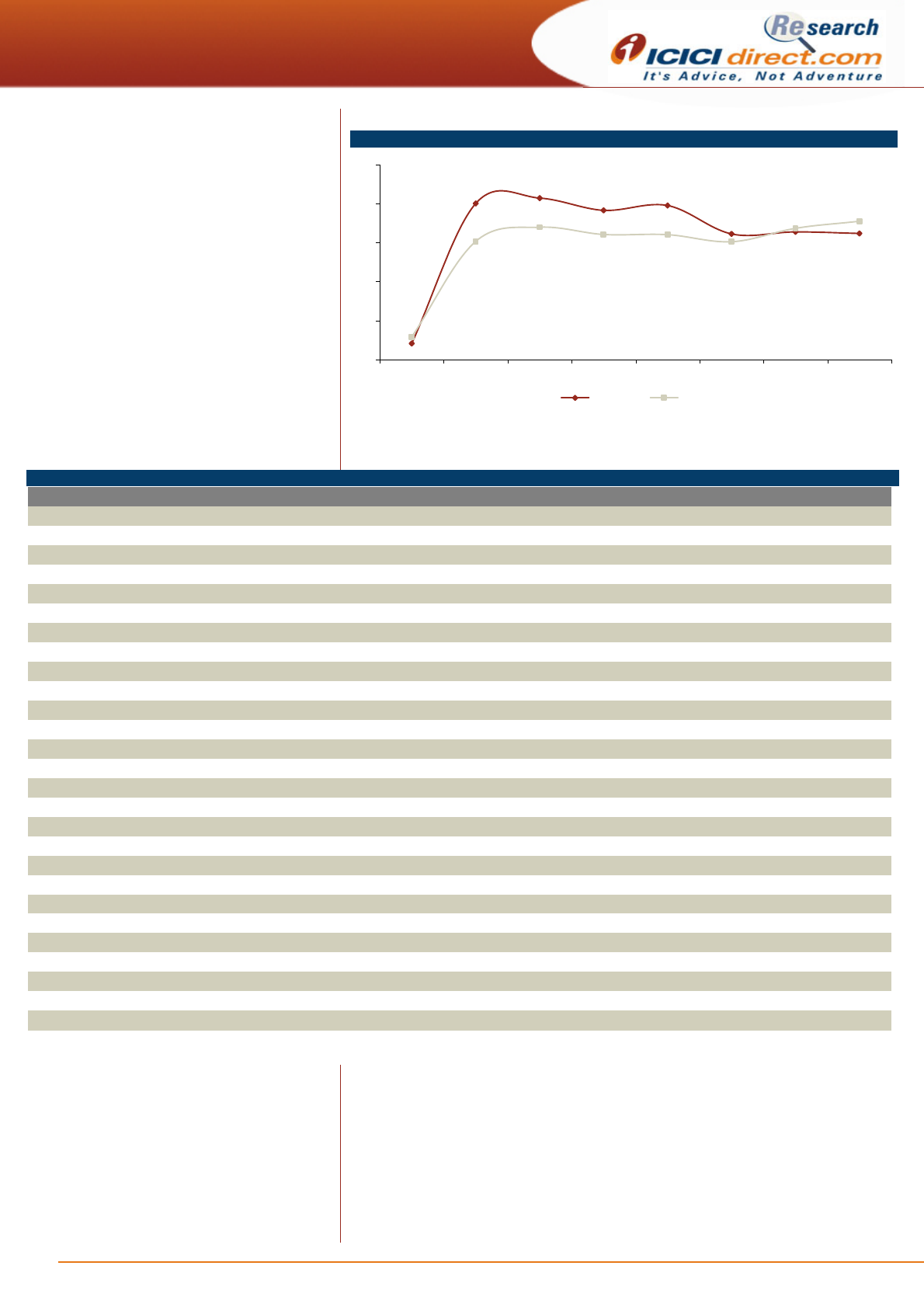

Exhibit 5: Russia & CIS to witness tempered growth due to regional issues

911.9

1085.8

1326.0

1690.8

1981.9

1771.4 1787.5 1876.9

0

500

1000

1500

2000

2500

FY10 FY11 FY12 FY13 FY14 FY15 FY16E FY17E

(| crore)

Russia & Other CIS

Source: Company, ICICIdirect.com Research

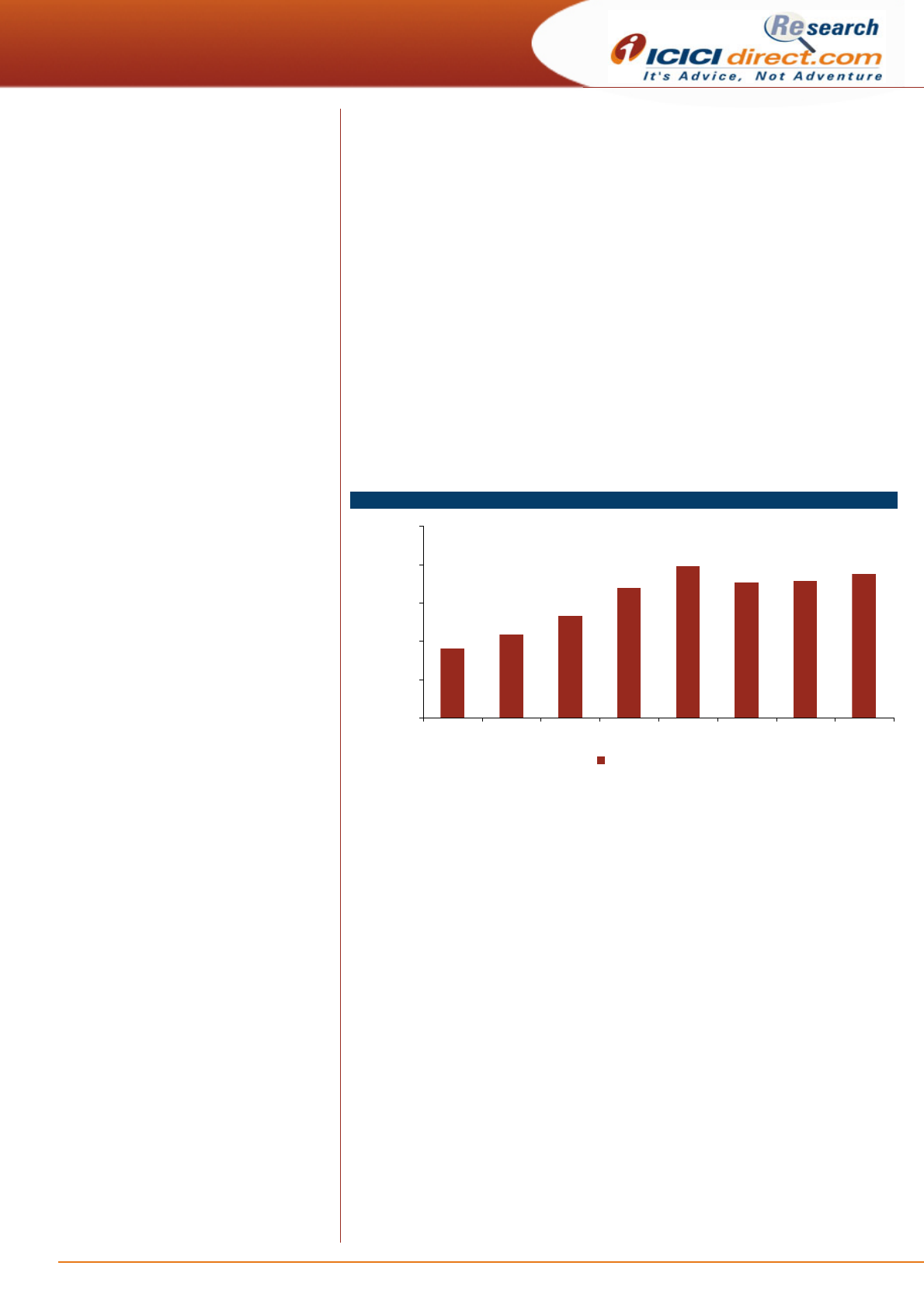

R&D cost to increase further

Dr Reddy’s is one of the few Indian companies to foray into new drug

discovery & development (NDDS) and new chemical entity (NCE) research

with a focus on therapies like dermatology, anti-inflammatory and anti-

infectives from CVS and diabetics. DRL is also the first Indian company to

launch biosimilars in the domestic market.

The R&D cost is expected to be ~12% of turnover in FY16 mainly due to

higher spend in (i) complex generic including injectables and (ii)

biosimilars and novel drug discovery.

ICICI Securities Ltd | Retail Equity Research

Page 7

Exhibit 6: R&D cost to go up due to complex generics and biosimilars

379.3 506.0 591.1

767.4

1240.2

1744.8

2075.0

2332.6

5.4

6.8 6.1 6.6

9.4

11.8 12.0 12.0

0

400

800

1200

1600

2000

2400

FY10 FY11 FY12 FY13 FY14 FY15E FY16E FY17E

(| crore)

0

2

4

6

8

10

12

14

(%)

R & D cost R & D cost (% of revenues)

Source: Company, ICICIdirect.com Research

Exhibit 7: Higher R&D cost likely to restrict improvement in EBITDA margins

616.8

1677.7

2346.5

2666.1

3312.7 3482.7

4065.1

4667.0

8.8

22.5

24.3 22.9

25.1 23.5 23.5 24.0

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

FY10 FY11 FY12 FY13 FY14 FY15 FY16E FY17E

(| crore)

0

5

10

15

20

25

30

EBITDA EBIDTDA Margins(%)

Source: Company, ICICIdirect.com Research

Exhibit 8: Net profit to grow at CAGR of 21% in FY14-17E on high base

1104.0

1426.2

1677.6

2151.3 2099.0

2562.6

3048.2

106.8

1.5

14.8 14.7 14.4

16.3

14.8 15.7

14.2

0

500

1000

1500

2000

2500

3000

3500

FY10 FY11 FY12 FY13 FY14 FY15 FY16E FY17E

(| crore)

0

2

4

6

8

10

12

14

16

18

Net Profit Net Profit Margins (%)

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research

Page 8

Exhibit 9: Trends in return ratios

2.5

24.0 24.8

19.3 19.6 19.4

18.2

20.4

18.1

21.3

23.0

23.7

3.5

19.2

19.2

20.2

0

6

12

18

24

30

FY10 FY11 FY12 FY13 FY14 FY15 FY16E FY17E

RoNW (%) RoCE (%)

Source: Company, ICICIdirect.com Research

Exhibit 10: Trend in quarterly financials

| Crore Q4FY12 Q1FY13 Q2FY13 Q3FY13 Q4FY13 Q1FY14 Q2FY14 Q3FY14 Q4FY14 Q1FY15 Q2FY15 Q3FY15 Q4FY15 YoY (%) QoQ (%)

Revenues 2658.4 2540.6 2880.9 2865.2 3340.0 2844.9 3357.5 3533.8 3480.9 3517.5 3587.8 3843.1 3870.4 11.2 0.7

(inc)/dec in SIT & WIP 13.7 -123.4 -75.1 -45.4 107.8 -118.8 -100.8 -33.6 -77.8 -69.3 -123.8 -127.0 264.5

Raw Material 844.0 902.8 959.9 943.7 1030.0 943.9 986.7 890.7 1005.5 853.6 968.8 1088.6 825.1 -17.9 -24.2

Other manufacturing exp. 403.6 407.2 465.6 478.1 517.6 517.8 524.7 537.5 561.0 648.8 644.2 646.2 658.8 17.4 1.9

Cost of Revenues 1261.4 1186.5 1350.4 1376.3 1655.5 1343.0 1410.6 1394.7 1488.7 1433.2 1489.2 1607.9 1748.4 17.4 8.7

% of Revenues 47.4 46.7 46.9 48.0 49.6 47.2 42.0 39.5 42.8 40.7 41.5 41.8 45.2 241 bps 333 bps

Gross Profit 1397.0 1354.1 1530.5 1488.8 1684.6 1501.9 1946.9 2139.1 1992.2 2084.4 2098.6 2235.2 2122.1 6.5 -5.1

Gross Profit Margins (%) 52.6 53.3 53.1 52.0 50.4 52.8 58.0 60.5 57.2 59.3 58.5 58.2 54.8 -241 bps -333 bps

SGNA 581.1 698.0 663.7 718.9 722.9 718.1 800.4 815.3 835.1 880.7 871.6 857.5 794.5 -4.9 -7.3

% of Revenues 21.9 27.5 23.0 25.1 21.6 25.2 23.8 23.1 24.0 25.0 24.3 22.3 20.5 -346 bps -179 bps

R & D cost 174.1 156.4 175.8 202.5 232.6 243.0 300.9 297.9 398.5 387.5 411.3 431.6 514.4 29.1 19.2

% of Revenues 6.6 6.2 6.1 7.1 7.0 8.5 9.0 8.4 11.4 11.0 11.5 11.2 13.3 184 bps 206 bps

Other (income)/expense -19.9 -21.8 -39.6 -23.3 -163.2 -37.6 -63.7 -17.7 -22.6 -18.5 -26.6 -34.1 -12.5 -44.6 -63.3

% of Revenues -0.7 -0.9 -1.4 -0.8 -4.9 -1.3 -1.9 -0.5 -0.7 -0.5 -0.7 -0.9 -0.3 33 bps 56 bps

Total Expenditure 2100.8 2019.1 2219.0 2274.5 2447.9 2266.5 2448.1 2490.1 2699.7 2682.9 2745.6 2862.9 3044.8 12.8 6.4

% of Revenues 79.0 79.5 77.0 79.4 73.3 79.7 72.9 70.5 77.6 76.3 76.5 74.5 78.7 111 bps 417 bps

EBITDA 557.6 521.5 661.8 590.7 892.1 578.5 909.3 1043.7 781.3 834.7 842.2 980.2 825.7 5.7 -15.8

EBITDA Margins (%) 21.0 20.5 23.0 20.6 26.7 20.3 27.1 29.5 22.4 23.7 23.5 25.5 21.3 -111 bps -417 bps

Depreciation 140.5 129.7 137.6 138.2 149.4 161.3 173.3 179.3 195.6 187.2 195.7 257.5 213.7 9.3 -17.0

EBITA 417.1 391.8 524.2 452.5 742.7 417.2 736.0 864.4 585.7 647.5 646.5 722.7 612.0 4.5 -15.3

Finace (income)/exp. -8.2 21.2 -37.1 9.7 -39.8 7.0 -29.1 -1.5 -16.4 -48.1 -42.1 -101.3 23.3 -242.2 -123.0

Share of pr./(loss) 1.1 1.9 2.8 3.1 2.5 3.6 4.4 4.7 4.8 5.3 5.1 4.7 4.4 -9.7 -6.2

EBT 426.4 372.5 564.2 446.0 785.0 413.7 769.5 870.6 606.9 700.9 693.7 828.6 593.0 -2.3 -28.4

Tax 83.7 36.5 156.7 82.7 214.1 52.8 79.3 252.1 125.2 150.5 119.6 254.1 74.2 -40.8 -70.8

Tax % 19.6 9.8 27.8 18.5 27.3 12.8 10.3 29.0 20.6 21.5 17.2 30.7 12.5

Net Profit 342.7 336.0 407.4 363.3 570.9 360.9 690.2 618.5 481.7 550.4 574.1 574.5 518.8 7.7 -9.7

% of Revenues 12.9 13.2 14.1 12.7 17.1 12.7 20.6 17.5 13.8 15.6 16.0 14.9 13.4

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research

Page 9

SWOT Analysis

Strengths – A seasoned player in the US generic space with a proven

track record. A strong US pipeline with many FTF/limited competition

products. The largest Indian player in Russia/CIS.

Weakness – The PSAI and European businesses remain a drag on

margins and growth. Higher R&D spends in future are expected to put

pressure on current margins. The Russian region has also become volatile

and unpredictable due to political unrest.

Opportunities - The US generics space has scope for complex/limited

competition products. The biosimilars space across the globe. Indian

franchise is still pretty small for a player of DRL’s calibre.

Threats - Increased USFDA scrutiny across the globe regarding cGMP

issues and consolidation in the US pharmacy space. Its Srikakulam API

plant has recently received Form 483 from the USFDA with nine

observations.

Conference call highlights

• DRL expects four or five meaningful USFDA approvals in FY16

• The company expects to complete the acquisition of UCB’s

domestic portfolio by Q1FY16

• The company has completed the site transfer and updated the

USFDA for gNexium API from Srikakulam facility (that received

Form 483 observations) to other API plant

• The company has registered balance sheet translation loss in

Venezuela to the tune of US$14 million in FY15 due to the

prevalence of three-tier currency system in Venezuela. DRL has

applied SIMADI rate of VEF193/US$ to translate its net monetary

assets, other than those which qualify for the CENCOEX rate of

VEF6.3/US$. This has been included in the financial income (net)

• The company expects its R&D cost at ~12% in FY16E. DRL

spends 60% of its R&D on generics & APIs and the remaining on

proprietary and biosimilar products

• The company has hedged US$440 million of cash flow (40-60% of

US forecasted cash flow) for the next 18 months and US$291

million of balance sheet in the range of | 60-64.5/US$. It has also

hedged Russian cash flows of RUB 1760 million (~30% of

forecasted cash flow) at the rate of | 1.16/RUB for FY16

• In Q4FY15, it filed and launched one product each in the US. Till

date, the company is awaiting 68 ANDA approvals, which

includes 43 Para IV filings comprising 13 products with FTF status.

Total ANDA filings stood at 220

• The company filed eight DMFs in Europe in Q4FY15. Global

cumulative DMF filings have reached 735

• The injectable business contribution was ~US$280 million (~27%

of total US sales) in FY15

• The OTC business contributed 36% in FY15 in Russia’s total sales

ICICI Securities Ltd | Retail Equity Research

Page 10

Valuation

The miss was on the back of slower US growth and negative Russian

growth. With Russia now struggling, the US and India together hold the

key for global generics growth as well as DRL’s overall growth. Among

them, the US is the main catalyst with a pending product portfolio of 68

ANDAs, which include 43 Para IVs and 13 FTFs. The company is investing

heavily in R&D to bring more and complex generics and limited

competition products mainly from non-oral category, which is likely to

take care of sustained US growth for the next two or three years. India is

showing promising growth as well with a recalibrated approach. On the

flip side, Russia has become a new matter of concern besides Europe and

the PSAI segment. We have ascribed a target price of | 3949 based on

22x FY17E EPS of | 179.5.

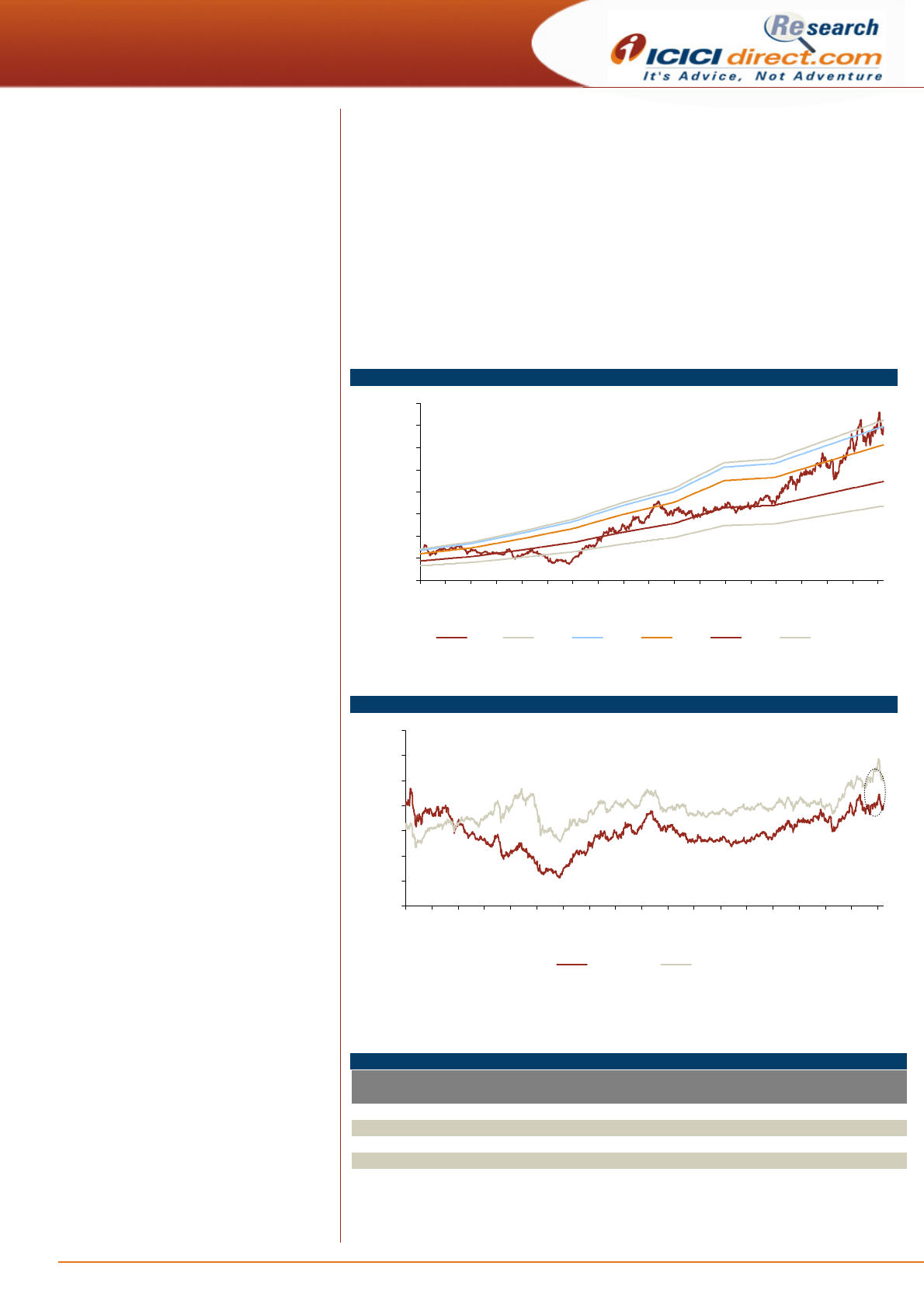

Exhibit 11: One year forward PE

0

500

1000

1500

2000

2500

3000

3500

4000

Mar-06

Sep-06

Mar-07

Sep-07

Mar-08

Sep-08

Mar-09

Sep-09

Mar-10

Sep-10

Mar-11

Sep-11

Mar-12

Sep-12

Mar-13

Sep-13

Mar-14

Sep-14

Mar-15

(|)

Price 21.0x 20.2x 17.7x 12.9x 9.7x

[

Source: Company, ICICIdirect.com Research

Exhibit 12: One year forward PE of company vs. BSE Healthcare Index

0

5

10

15

20

25

30

35

Mar-06

Sep-06

Mar-07

Sep-07

Mar-08

Sep-08

Mar-09

Sep-09

Mar-10

Sep-10

Mar-11

Sep-11

Mar-12

Sep-12

Mar-13

Sep-13

Mar-14

Sep-14

Mar-15

(x)

Dr Reddy's CNX Pharma

21.5% Discount

Source: Company, ICICIdirect.com Research

Exhibit 13: Valuation

Revenues Growth EPS Growth P/E EV/EBITDA RoNW RoCE

(| crore) (%) (|) (%) (x) (X) (%) (%)

FY14 13217 13.7 126.7 28.1 22.3 14.8 23.7 19.2

FY15 14819 12.1 123.6 3.2 22.8 13.9 19.3 18.1

FY16E 17291 16.7 150.9 16.6 18.7 11.7 19.6 20.2

FY17E 19438 12.4 179.5 14.9 15.7 9.8 19.4 21.3

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research

Page 11

Company snapshot

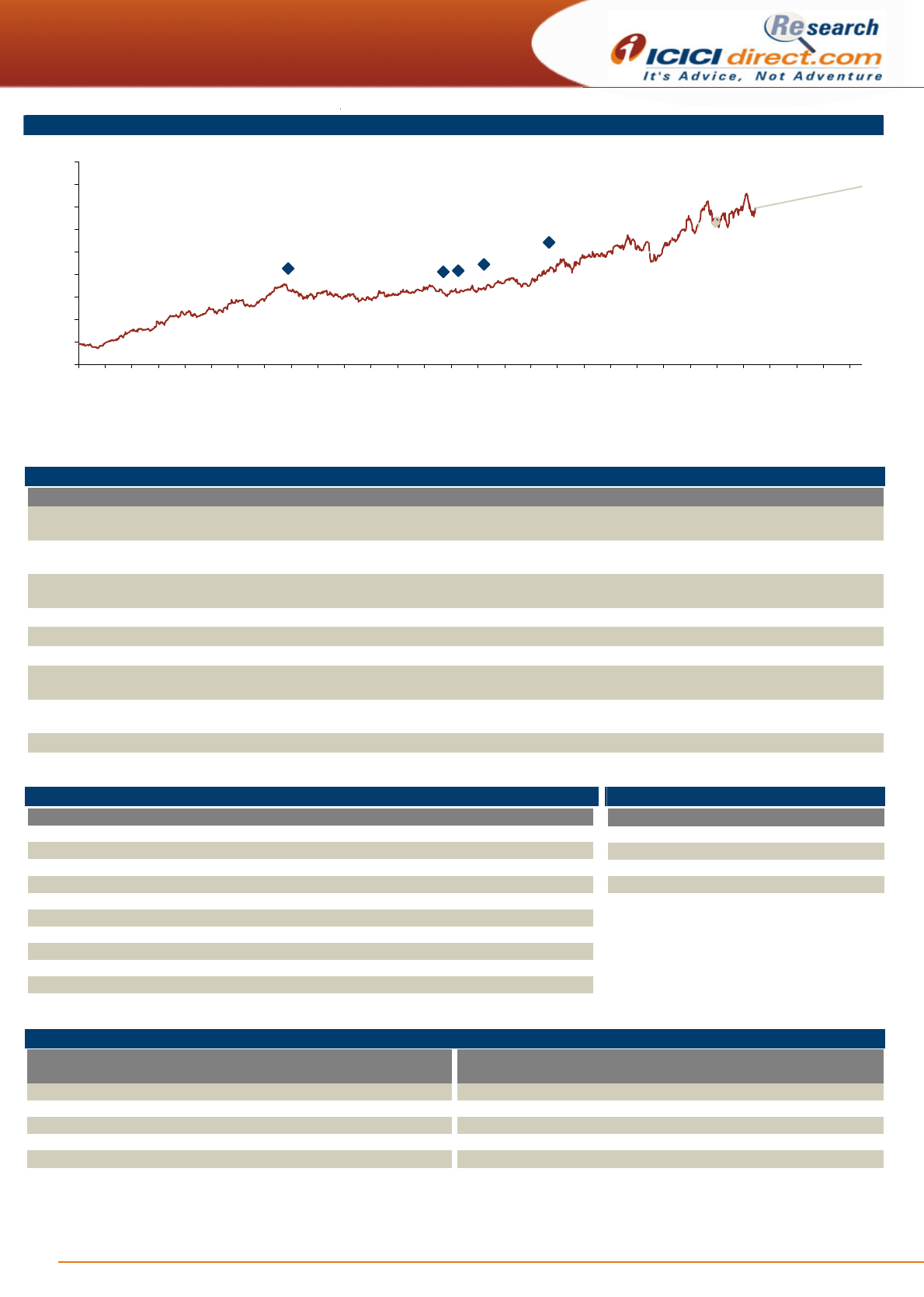

Target Price:| 3949

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

Jan-09

Apr-09

Jul-09

Oct-09

Jan-10

Apr-10

Jul-10

Oct-10

Jan-11

Apr-11

Jul-11

Oct-11

Jan-12

Apr-12

Jul-12

Oct-12

Jan-13

Apr-13

Jul-13

Oct-13

Jan-14

Apr-14

Jul-14

Oct-14

Jan-15

Apr-15

Jul-15

Oct-15

Jan-16

Apr-16

Source: Bloomberg, Company, ICICIdirect.com Research

Key events

Date Event

Jun-09 Announces a partnership with GSK to develop and market select products across emerging markets outside India. Under the tie-up, GSK will have access to more

than 100 branded products of DRL

Nov-10 Acquires GSK’s US oral penicillin facility and product portfolio. Under the agreement, GSK will transfer rights for Augmentin and Amoxil brands in the US market

Dec-10 Enters into licensing of technology transfer, manufacturing and marketing agreement with R-Pharm of Russia. The collaboration is in the area of high-technology and

will work on a profit sharing model

Jun-12 Dr Reddy’s and Merck Serono sign an agreement to co-develop and commercialise a portfolio of biosimilars compounds in oncology

Jul-12 USFDA lifts import alert for chemical manufacturing facility at Cuernavaca, Mexico

Oct-12 Acquires Netherland based specialty injectable company OctoPlus NV

Jun-13 Dr Reddy’s and Fujifilm Corporation call off their joint venture. The JV was started in July 2011 for developing and launching generic drugs in the Japanese market

Dec-14 Dr. Reddy's Labs closed the acquisition of Habitrol brand, an over-the-counter nicotine replacement therapy transdermal patch, from Novartis for a consideration of

US$ 80 million

Apr-15 Enters a €118 million (| 800 crore) definitive agreement to acquire a select portfolio of established products from UCB in India

Source: Company, ICICIdirect.com Research

Top 10 Shareholders Shareholding Pattern

Rank Name Latest Filing Date % O/S Position (m)

n

Change (m)

1 Dr Reddys Holdings Pvt. Ltd. 31-Mar-15 23.32 39.7 0.0

2 Commonwealth Bank of Australia 31-Dec-13 8.54 14.6 14.6

3 First State Investment Management (UK) Limited 31-Mar-15 8.45 14.4 0.0

4 OppenheimerFunds, Inc. 31-Mar-15 4.27 7.3 0.8

5 BlackRock Institutional Trust Company, N.A. 31-Mar-15 3.08 5.3 0.7

6 Abu Dhabi Investment Authority 31-Mar-15 2.09 3.6 -0.1

7 Capital World Investors 31-Mar-15 1.68 2.9 2.9

8 Life Insurance Corporation of India 31-Mar-15 1.65 2.8 -0.5

9 Franklin Templeton Asset Management (India) Pvt. Ltd. 31-Mar-15 1.59 2.7 0.6

10 Capital Research Global Investors 31-Dec-14 1.40 2.4 0.0

(in %) Mar-14 Jun-14 Sep-14 Dec-14 Mar-15

Promoter 25.5 25.5 25.5 25.5 25.5

FII 34.3 35.3 38.4 38.5 38.9

DII 6.3 5.4 5.4 5.7 5.4

Others 33.9 33.8 30.7 30.3 30.2

Source: Reuters, ICICIdirect.com Research

Recent Activity

Investor name Value Shares Investor name

V

alue Shares

Commonwealth Bank of Australia 596.68m 14.55m Investec Asset Management Ltd. -56.00m -1.28m

Capital World Investors 160.46m 2.86m Norges Bank Investment Management (NBIM) -34.58m -0.67m

OppenheimerFunds, Inc. 46.83m 0.84m Life Insurance Corporation of India -28.24m -0.50m

BlackRock Institutional Trust Company, N.A. 38.47m 0.69m J.P. Morgan Asset Management (Hong Kong) Ltd. -23.45m -0.45m

Franklin Templeton Asset Management (India) Pvt. Ltd. 34.91m 0.62m Schroder Investment Management (Hong Kong) Ltd. -16.08m -0.30m

Buys Sells

Source: Reuters, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research

Page 12

.

Financial summary

Profit and loss statement | Crore

(Year-end March) FY14 FY15E FY16E FY17E

Revenues 13217.0 14818.9 17291.5 19438.4

Growth (%) 36.6 12.1 16.7 12.4

Cost of Revenues 5636.9 6278.7 7217.6 8016.6

Gross Profit 7580.2 8540.2 10073.9 11421.9

Gross Profit Margins (%) 57.4 57.6 58.3 58.8

SGNA 3168.8 3404.4 3977.0 4470.8

R & D cost 1240.2 1744.8 2075.0 2332.6

Intangible write down 0.0 0.0 0.0 0.0

Goodwill write down 0.0 0.0 0.0 0.0

Other (income)/expense -141.6 -91.7 -43.2 -48.6

Total Expenditure 9904.4 11336.2 13226.4 14771.4

EBITDA 3312.7 3482.7 4065.1 4667.0

Growth (%) 41.2 5.1 16.7 14.8

EBITDA Margins (%) 25.1 23.5 23.5 24.0

Depreciation 709.5 854.0 880.8 908.9

PBIT 2603.2 2628.7 3184.3 3758.1

Finance Income 167.4 79.6 163.0 188.1

Finance Expenses 127.4 30.4 82.0 58.2

Net Finace (income)/expenses -40.0 -49.2 -81.0 -129.9

Profit/(loss) of ERI* 17.4 19.5 20.0 20.0

EBT 2660.6 2697.4 3285.4 3908.0

Tax 509.4 598.4 722.8 859.8

Net Profit 2151.3 2099.0 2562.6 3048.2

Growth (%) 50.8 -2.4 22.1 19.0

EPS (|) 126.7 123.6 150.9 179.5

Source: Company, ICICIdirect.com Research

Cash flow statement | Crore

(Year-end March) FY14 FY15E FY16E FY17E

Net Profit/(Loss) 2151.3 2099.0 2562.6 3048.2

Add: Depreciation 709.5 854.0 880.8 908.9

(Inc)/Dec in current assets -659.8 -1261.3 -1359.5 -1181.7

Inc/ (Dec) in Current Liailities 46.8 238.8 438.3 446.2

CF from Operating activities 2247.7 1930.4 2522.3 3221.7

(Inc)/Dec in Goodwill -23.5 0.0 0.0 0.0

(Purchase)/Sale of Liq. Inves. -812.0 0.0 0.0 0.0

Fixed Assets -1414.6 -970.2 -1200.0 -1200.0

Deferred Tax -164.1 20.0 20.0 20.0

Inc/(Dec) in MI -2.0 0.0 0.0 0.0

(Inc)/Decin Other Investments 20.9 0.0 0.0 0.0

Others 52.3 -66.6 11.1 9.7

CF from Investing activities -2343.0 -1016.8 -1168.9 -1170.3

Equity Shares 0.2 0.0 0.0 0.0

Inc/(Dec) in Share Premium 33.9 0.0 0.0 0.0

Dividend and Dividend Tax -298.5 -338.3 -378.2 -378.2

Debt 806.4 -839.5 -901.1 -792.0

Other components of equity

-124.7 25.2 0.0 0.0

Inc/(Dec) in Debenture Reserve -171.1 0.0 0.0 0.0

Adjustment Retained earnings 170.6 0.0 0.0 0.0

Others 10.0 0.0 0.0 0.0

CF from Financial activities 426.7 -1152.7 -1279.3 -1170.2

Net Cash flow 331.5 -239.1 74.1 881.2

Cash at the beginning 513.6 845.1 605.9 680.1

Cash 845.1 605.9 680.1 1561.3

Source: Company, ICICIdirect.com Research

Balance sheet | Crore

(Year-end March) FY14 FY15E FY16E FY17E

Equity Capital 85.1 85.1 85.1 85.1

Net Networth 8995.0 10780.8 12965.3 15635.3

Total share holder funds 9080.1 10865.9 13050.3 15720.4

Total Debt 4474.2 3634.7 2733.6 1941.6

Minority Interest 0.0 0.0 0.0 0.0

Deferred tax liabilities 274.4 314.4 354.4 394.4

Non current Liabilities & other 187.5 138.1 160.3 179.6

Total Liabilities 14016.2 14953.0 16298.6 18236.0

Gross Block 10335.4 11335.4 12635.4 13935.4

Acc.Depreciation 5433.6 6217.4 7098.2 8007.1

Net Bock 4901.8 5118.0 5537.2 5928.3

CWIP 667.5 567.5 467.5 367.5

Total Fixed Assets 5569.3 5685.5 6004.7 6295.8

inves in eq. acc. investees 80.6 80.6 80.6 80.6

Other investments-non current 0.0 0.0 0.0 0.0

Liquid Investments 2508.3 2508.3 2508.3 2508.3

Goodwill 342.8 342.8 342.8 342.8

Deferred tax assets 605.4 625.4 645.4 665.4

other non current assets 49.5 66.7 77.8 87.5

Inventories 2399.2 2842.0 3316.2 3727.9

Trade Receivables 3303.7 4060.0 4737.4 5325.6

Derivative financial instruments 55.4 55.4 55.4 55.4

Other current assets 1263.0 1325.3 1533.1 1714.9

Cash & Cash Equivalents 845.1 605.9 680.1 1561.3

Total Current Assets 7866.4 8888.6 10322.2 12385.0

Trade Payables 1050.3 1218.0 1421.2 1597.7

Derivative financial instruments 30.5 30.5 30.5 30.5

Bank overdraft 0.0 0.0 0.0 0.0

provision 281.9 311.2 363.1 408.2

other current liabilities 1643.4 1685.2 1868.3 2093.0

Total Current Liabilities 3006.1 3244.9 3683.2 4129.4

Net Current Assets 4860.3 5643.7 6639.0 8255.6

Total Assets 14016.2 14953.0 16298.6 18236.0

Source: Company, ICICIdirect.com Research

Key ratios

FY14 FY15E FY16E FY17E

Per Share Data (|)

EPS 126.7 123.6 150.9 179.5

Cash EPS 168.4 173.9 202.7 233.0

BV 534.6 639.8 768.4 925.6

Cash per Share 197.4 183.4 187.7 239.6

DPS 15.0 17.0 19.0 19.0

Operating Ratios

Gross Profit Margins 57.4 57.6 58.3 58.8

EBITDA margins 25.1 23.5 23.5 24.0

PBT margins 19.7 17.7 18.4 19.3

Net Profit margins 16.3 14.2 14.8 15.7

Return Ratios

RoE 23.7 19.3 19.6 19.4

RoCE 19.2 18.1 20.2 21.3

RoIC 26.0 23.3 25.2 27.2

V

aluation Ratios

P/E 22.3 22.8 18.7 15.7

EV / EBITDA 14.8 13.9 11.7 9.8

EV / Revenues 3.7 3.3 2.7 2.4

Market Cap / Revenues 3.6 3.2 2.8 2.5

Revenues / Equity 1.5 1.4 1.3 1.2

Price to Book Value 5.3 4.4 3.7 3.0

Dividend yield 11.8 13.8 12.6 10.6

Turnover Ratios

Inventory Days 66 70 70 70

Debtor days 91 100 100 100

Creditor days 29 30 30 30

Asset turnover ratio (x times) 2.2 2.5 2.7 2.9

Solvency Ratios

Debt / Equity 0.5 0.3 0.2 0.1

Debt/EBITDA 1.4 1.0 0.7 0.4

Current Ratio 2.6 2.7 2.8 3.0

Quick Ratio 1.8 1.9 1.9 2.1

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research

Page 13

ICICIdirect.com coverage universe (Healthcare)

ICICIdirect Healthcare coverage Universe

I-Direct CMP TP Rating M Cap

Code (|) (|) (| Cr) FY14 FY15E FY16E FY14 FY15E FY16E FY14 FY15E FY16E FY14 FY15E FY16E FY14 FY15E FY16E

Ajanta Pharma AJAPHA 1247 1488 BUY 11001.3 26.5 38.3 45.6 47.1 32.6 27.4 29.9 21.6 18.2 44.9 40.6 38.1 39.4 32.8 28.9

Apollo Hospitals APOHOS 1239 1455 BUY 17274.6 22.8 26.8 36.8 54.4 46.3 33.7 27.1 24.0 17.0 11.6 12.0 15.5 10.6 11.5 14.2

Aurobindo Pharma AURPHA 1322 1303 BUY 38690.2 47.3 57.4 70.5 28.0 23.1 18.7 19.8 16.4 13.3 24.1 23.4 24.4 31.3 31.6 28.6

Biocon BIOCON 431.8 447 HOLD 8654.9 20.7 20.1 22.5 35.1 29.2 32.4 21.2 21.1 18.0 12.2 10.7 11.7 13.7 15.2 12.4

Cadila Healthcare CADHEA 1650 1634 HOLD 33850.1 39.2 51.1 66.2 42.0 32.3 24.9 29.9 22.4 17.4 15.9 19.0 21.7 23.4 24.6 25.4

Cipla CIPLA 664.1 648 HOLD 53441.1 17.3 15.9 21.7 38.4 41.7 30.5 25.4 23.0 18.5 15.5 14.2 17.6 13.8 11.3 14.2

Dr Reddy's Labs DRREDD 3469 3949 BUY 59232.6 126.7 123.6 150.9 27.4 28.1 23.0 17.9 17.0 14.6 19.2 18.1 20.2 23.7 19.3 19.6

Glenmark Pharma GLEPHA 869.1 824 HOLD 23629.7 20.0 21.5 34.0 43.4 40.4 25.6 19.9 21.5 14.2 16.0 17.1 23.5 18.3 17.4 22.8

Indoco Remedies INDREM 325 375 BUY 2998.7 6.3 9.5 13.3 51.7 34.2 24.4 25.4 17.3 13.3 16.6 21.8 28.1 12.6 16.4 19.4

Ipca Laboratories IPCLAB 653.1 622 HOLD 8260.1 37.9 25.6 31.8 17.2 25.5 20.5 10.8 14.3 13.7 27.6 16.1 17.8 24.4 14.7 16.0

Jubilant Life Sciences VAMORG 170 138 SELL 2716.1 6.8 -6.5 20.0 24.9 -26.3 8.5 6.6 11.9 5.8 10.1 4.5 7.6 4.2 -3.5 7.6

Lupin LUPIN 1748 1866 BUY 78804.8 41.0 53.6 60.4 42.7 32.6 29.0 27.1 21.4 18.8 34.5 33.4 31.9 26.5 27.1 24.5

Natco Pharma NATPHA 2077 1354 HOLD 6918.5 30.3 32.5 44.9 58.5 54.6 39.5 39.9 33.1 26.7 15.3 16.7 18.7 14.1 13.5 16.1

Sun Pharma SUNPHA 949.7 1036 BUY 229025.2 29.0 34.8 39.9 32.7 27.3 23.8 23.6 22.9 19.6 32.4 31.2 28.8 27.0 25.3 23.1

Torrent Pharma TORPHA 1179 1165 HOLD 20001.7 39.2 47.2 50.4 30.1 25.0 23.4 21.2 18.9 15.1 28.5 21.4 26.7 34.9 32.4 28.0

Unichem Laboratories UNILAB 199.8 214 HOLD 1817.9 18.7 7.2 14.1 10.7 27.6 14.1 10.1 17.2 10.3 15.7 7.2 13.5 20.7 7.5 13.9

RoNW (%)

Company

EPS (|) PE(x) EV/EBITDA (x) RoCE (%)

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research

Page 14

RATING RATIONALE

ICICIdirect.com endeavours to provide objective opinions and recommendations. ICICIdirect.com assigns

ratings to its stocks according to their notional target price vs. current market price and then categorises them

as Strong Buy, Buy, Hold and Sell. The performance horizon is two years unless specified and the notional

target price is defined as the analysts' valuation for a stock.

Strong Buy: >15%/20% for large caps/midcaps, respectively, with high conviction;

Buy: >10%/15% for large caps/midcaps, respectively;

Hold: Up to +/-10%;

Sell: -10% or more;

Pankaj Pandey Head – Research pankaj.pandey@icicisecurities.com

ICICIdirect.com Research Desk,

ICICI Securities Limited,

1st Floor, Akruti Trade Centre,

Road No 7, MIDC,

Andheri (East)

Mumbai – 400 093

research@icicidirect.com

ICICI Securities Ltd | Retail Equity Research

Page 15

ANALYST CERTIFICATION

We /I, Siddhant Khandekar, CA INTER and Mitesh Shah, MS (finance), Nandan Kamat MBA Research Analysts, authors and the names subscribed to this report, hereby certify that all of the views expressed

in this research report accurately reflect our views about the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific

recommendation(s) or view(s) in this report.

Terms & conditions and other disclosures:

ICICI Securities Limited (ICICI Securities) is a full-service, integrated investment banking and is,

inter alia,

engaged in the business of stock brokering and distribution of financial products. ICICI Securities is

a wholly-owned subsidiary of ICICI Bank which is India’s largest private sector bank and has its various subsidiaries engaged in businesses of housing finance, asset management, life insurance, general

insurance, venture capital fund management, etc. (“associates”), the details in respect of which are available on www.icicibank.com.

ICICI Securities is one of the leading merchant bankers/ underwriters of securities and participate in virtually all securities trading markets in India. We and our associates might have investment banking

and other business relationship with a significant percentage of companies covered by our Investment Research Department. ICICI Securities generally prohibits its analysts, persons reporting to analysts

and their relatives from maintaining a financial interest in the securities or derivatives of any companies that the analysts cover.

The information and opinions in this report have been prepared by ICICI Securities and are subject to change without any notice. The report and information contained herein is strictly confidential and

meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without

prior written consent of ICICI Securities. While we would endeavour to update the information herein on a reasonable basis, ICICI Securities is under no obligation to update or keep the information current.

Also, there may be regulatory, compliance or other reasons that may prevent ICICI Securities from doing so. Non-rated securities indicate that rating on a particular security has been suspended

temporarily and such suspension is in compliance with applicable regulations and/or ICICI Securities policies, in circumstances where ICICI Securities might be acting in an advisory capacity to this

company, or in certain other circumstances.

This report is based on information obtained from public sources and sources believed to be reliable, but no independent verification has been made nor is its accuracy or completeness guaranteed. This

report and information herein is solely for informational purpose and shall not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial

instruments. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. ICICI Securities will not treat recipients as customers by virtue of their

receiving this report. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific

circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment

objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. The recipient should independently evaluate

the investment risks. The value and return on investment may vary because of changes in interest rates, foreign exchange rates or any other reason. ICICI Securities accepts no liabilities whatsoever for any

loss or damage of any kind arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors are advised to see Risk Disclosure Document to understand the

risks associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to

change without notice.

ICICI Securities or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment

in the past twelve months.

ICICI Securities or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in

respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction.

ICICI Securities or its associates might have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the companies mentioned

in the report in the past twelve months.

ICICI Securities encourages independence in research report preparation and strives to minimize conflict in preparation of research report. ICICI Securities or its analysts did not receive any compensation

or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither ICICI Securities nor Research Analysts have any

material conflict of interest at the time of publication of this report.

It is confirmed that Siddhant Khandekar, CA INTER and Mitesh Shah, MS (finance), Nandan Kamat MBA, Research Analysts of this report have not received any compensation from the companies

mentioned in the report in the preceding twelve months.

Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions.

ICICI Securities or its subsidiaries collectively or Research Analysts do not own 1% or more of the equity securities of the Company mentioned in the report as of the last day of the month preceding the

publication of the research report.

Since associates of ICICI Securities are engaged in various financial service businesses, they might have financial interests or beneficial ownership in various companies including the subject

company/companies mentioned in this report.

It is confirmed that Siddhant Khandekar, CA INTER and Mitesh Shah, MS (finance), Nandan Kamat MBA, Research Analysts do not serve as an officer, director or employee of the companies mentioned in

the report.

ICICI Securities may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report.

Neither the Research Analysts nor ICICI Securities have been engaged in market making activity for the companies mentioned in the report.

We submit that no material disciplinary action has been taken on ICICI Securities by any Regulatory Authority impacting Equity Research Analysis activities.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution,

publication, availability or use would be contrary to law, regulation or which would subject ICICI Securities and affiliates to any registration or licensing requirement within such jurisdiction. The securities

described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and

to observe such restriction.