Evolution E 908 D DTCPM Sept 2011

User Manual: Evolution e 908 D

Open the PDF directly: View PDF ![]() .

.

Page Count: 56

The Source For DTC Leaders

PERSPECTIVES

Vol. 10, No. 3 September 2011

PRST STD

U.S. Postage

PAID

Permit #108

Lebanon Junction

KY 40150

DTC PERSPECTIVES, INC.

110 Fairview Avenue, Suite 4

Verona, NJ 07044

CHANGE SERVICE

REQUESTED

Branded vs. Unbranded:

Evaluating Tactics to

Reach Digital Consumers

Rx Non-Adherence:

The Silent Epidemic

Find Digital Consumers

In a Sea of Mass Media

Reinvent DTC Marketing

To Meet Demand in an

Anywhere Health World

In This Issue

Nami Choe

Partner, Senior Director,

Consulting with Ogilvy

Healthworld

Bruce Rooke

Chief Creative Officer at

GSW Worldwide

Marketers have the opportunity to modernize DTC,

improving both campaign ROI and consumer reach

67 million readers • 43.4 million uniques 36 million readers • 6.2 million uniques 3.9 million uniques

yesterday

an apple a day is so

PARADE offers Americans practical steps for better living with

a dose of wellness, nutrition, beauty and medical news.

mediakit.parade.com Source: GfK MRI Fall 2010/Spring 2011; Dash is a publisher-defi ned prototype; comScore,

July 2011 (Parade Partners [E], DashRecipes [E], Parade Health [E])

Editor’s Desk ................................................................................................................4

DTC in Brief ..............................................................................................................6, 8

Spending Review ......................................................................................................10

Branded vs. Undbranded Digital Tactics: Reaching and Converting

Relevant Consumers .................................................................................................12

A series from Crossix RxMarketMetrics

Optimizing ROI through Integrated Marketing ..................................................17

Nami Choe, partner, senior director, consulting with Ogilvy Healthworld

It’s Time ‘DTC’ Stood for Something Else ............................................................20

Bruce Rooke, chief creative officer at GSW Worldwide

Medication Non-Adherence: The Health Care Industry’s Silent Epidemic .....22

Todd Steffes, vice president at FICO

Finding Digital Consumers in a Sea of Mass Media ...........................................26

Doug Zabor, executive vice president, and Qi Jiang, vice president of marketing science,

with Phoenix Marketing International

Memo to Digital Pharma Marketers: Don’t Overlook Viable

Content Sources ........................................................................................................32

Tanayia Washington, insights & analytics manager at CONTEXTWEB

What a Wonderful World it Would Be: Developing Relationship

Marketing Programs .................................................................................................36

Louis Winokur, director of analytics at DKI

Anywhere Health: Reinventing Healthcare Marketing in a

Connected World ......................................................................................................41

Jim Walker, director of emerging trends at Cadient Group

Promises and Perils: The Social Stock Market .....................................................44

Jane Chin, Ph.D., author, online authority & former pharma R&D/medical affairs

Marketing and Media Movers ................................................................................48

An update on DTC personnel and company changes within the industry

Contributors’ Page ...................................................................................................49

A closer look at the contributors to this issue of DTC Perspectives

Advertiser Index and Resource Center .................................................................49

Eye on the Hill: The Debt Ceiling is Just the Tip of the Iceberg ......................50

Jim Davidson reports on what to expect in the coming year from Washington

Perspectives on Books: Never Say Die: The Myth and Marketing of

The New Old Age .....................................................................................................52

Reviewed by Robert Ehrlich of DTC Perspectives, Inc.

DTC Perspectives Editorial: The Uncertainty of Healthcare Continues ..........54

Viable Content

Sources

32

Miss an issue, or want to order one from our archives?

Please visit our website www.dtcperspectives.com to view recent

issues of DTC Perspectives magazine, or call Debra Sander at

(973) 973-239-2051 to purchase previous issues.

PERSPECTIVES

September 2011 Vol. 10, No. 3

DTC Perspectives • September 2011 | 3

44

Social

Stock

Market

Relationship

Marketing

36

DTC Perspectives is Published Quarterly By:

DTC Perspectives, Inc.

110 Fairview Avenue, Suite 4

Verona, NJ 07044

Phone # 1-973-239-2051

Postmaster: Please send address changes to the above.

FREE to Qualified Industry Subscribers in the U.S.

Apply online at www.dtcperspectives.com.

Rates for International and Non-Industry

Subscribers:

$72 Per (1 Year) in the U.S.

$96 (1 Year) Outside of U.S.

Back Issues $10 in U.S.

$30 in All Other Countries

©2011 DTC Perspectives, Inc. All rights reserved.

No part of this publication may be reproduced in

any form unless given permission by the publisher.

Good Signs Ahead

A

fter periods of decline, DTC spending appears to be rebounding in the

first half of 2011, reaching $2.16 billion. Data from The Nielsen Com-

pany shows that to be a healthy increase over the prior year, up 7.6

percent. While several big name brands will be going off patent in the next few

years (including Lipitor, Plavix and Cymbalta), DTC Perspectives believes that

spending by new brands entering the market will counter such losses. Thus,

DTC levels will likely grow once again.

Marketers today understand how crucial DTC can be to a brand’s success;

consumers expect brands to be involved with the conversation. With new chan-

nels and methods for reaching and engaging consumers continually emerging,

marketers are embarking upon some very exciting times. DTC marketing is on

the cusp of an evolution that will break the current standards for communicat-

ing with patients. As Bruce Rooke, chief creative officer with GSW Worldwide,

discusses in his article, “DTC is due for some big innovation. … We have the

chance – and responsibility – to respond to the changing landscape with a whole

new vocabulary of action.” (Rooke’s article begins on page 20.)

In this era of constant change, marketers have the opportunity to re-invent

how they promote their brand – from a campaign’s creative and messaging

to how the brand engages with consumers to determining the optimal media

mix. However, improvements made to DTC campaigns would be fruitless if

they were not properly measured and appropriately adjusted when needed. As

advancements in analytics also develop, marketers can more accurately evalu-

ate campaigns and channels to optimize ROI. “Marketers are continuing to

unlock data analytics’ potential in optimizing investment real-time and in a

more targeted way,” detailed Nami Choe, partner, senior director, consulting

with Ogilvy Healthworld. Choe’s article (beginning on page 17) explains “as

we look to the future, with data becoming more available and tracking more

sophisticated, there are opportunities for marketers to understand the impact

of” their marketing efforts.

Progressing to the next level

With the plethora of opportunities created, jumping into the new frontier of

DTC marketing can seem like a daunting undertaking. However, our industry

must push forward to remain relevant and set new benchmarks for DTC. It is

with this goal that we have designed our upcoming fall conference, Marketing to

the Digital Consumer: Pharma Best Practices Present and Future. We hope that you

will join us Oct. 12-13, learning how you can improve current campaigns and

plan for upcoming initiatives in the future marketplace. We will also be induct-

ing our 2011 Hall of Fame class, featuring progressive industry members: Mark

Bard of the Digital Health Coalition, Bill Drummy of Heartbeat Ideas, Joan

Mikardos of Sanofi-Aventis, and Nancy Phelan of Pfizer.

PERSPECTIVES

Robert Ehrlich

Chairman and CEO

DTC Perspectives, Inc.

Christine Franklin

VP, Marketing and Sales

Jennifer Haug

Editor / Design Coordinator

Matt Yavorski

Sales Associate

Molly Diemel

Marketing and Production

Associate

Debra Sander

Office Coordinator

Scott Ehrlich

President

MDPA Division

Amanda Ehrlich

Director, Publishing

MDPA Division

Debra Rennert

Creative Director

James Ticchio

Art Director

Direct Media Advertising

Jennifer Haug

Sincerely,

4 | DTC Perspectives • September 2011

beaconhc.com

At Beacon, it’s all about you...

■ Your brand: we’ll listen to what you have to say

■ Your business: we’ll understand, because we’ve

been there too…in professional, managed markets,

DTC, oncology, and interactive

■ Your budget: we’ll be transparent and avoid surprises

■ Your success: our experienced professionals are ready

to focus on you

Call Adrienne Lee at 908.781.2600 and tell her what

Beacon can do for you or check out our Web site.

It’s all about you.

We have a thing

for ears…

AP-9009 BEACON AD_DTCPersp_2-2011.indd 1 2/25/11 11:20 AM

IN BRIEF

Facebook Policy Change in Effect,

Some Pharmas Shut Down Pages

As Facebook’s policy change requiring the comments feature

to be enabled on most pages went into effect mid-August, some

pharmaceutical companies have decided to close out their pages.

According to a Washington Post report, companies are concerned

with what the open-commenting policy could lead to. Combining

a lack of FDA guidance on social media best practices with con-

cerns about adverse event reporting (AER) and off-label claims,

companies have had to choose between shutting down their pages

or establishing a plan for continual monitoring of Wall comments.

With many of the companies having joined Facebook within the last year and half, the Post explained that some have

chosen to closely monitor their pages themselves or via a third party rather than turning away. Pfizer and Sanofi each told

the newspaper that they plan to keep their pages online, noting that such engagement and feedback they have garnered

outweighs concerns. While currently uncertain of its potential impact, Amgen and Novo Nordisk have decided to simply

“monitor the situation.”

Meanwhile, AstraZeneca, maker of depression treatment Seroquel XR, opted to close its “Take on Depression” page;

Johnson & Johnson also followed suit by shutting down four of its pages – two devoted to ADHD, as well as rheumatoid

arthritis and psoriasis. Johnson & Johnson manufacturers the respective treatments of Concerta, Simponi and Remicade,

and Stelara. As with all pages, marketers can remove any posted comment from their Wall. Pages devoted to Rx products

can still disable the commenting feature entirely.

Rep. Quayle Meets with WKPS Executives

To Discuss Delivery of Health Information

Congressman Ben Quayle (R-Ariz.) met with executives from Wolters Kluwer Pharma Solutions (WKPS) in late

August to discuss the current state of health information in America. The first-term Congressman and son of former

vice president Dan Quayle is eager to learn more about how industry can improve the delivery of health information

and safety. He was treated to a presentation about health information technology by WKPS executives, including joint

presidents Bob Jansen and Michelle Woker, members of the healthcare analytics team, including Cathy Betz, vice pres-

ident of government affairs, and the company’s Arizona lobbyists,

TriAdvocates.

“One of the things we shared with Congressman Quayle is

our conviction that preserving good access to health information

is vitally important to America’s health as a country,” said Bob

Jansen, president of Wolters Kluwer Pharma Solutions’ healthcare

analytics business in a news release. “The Congressman also shares

the conviction that transparent and actionable health information is

in the best interest of public health.”

WKPS is a leading provider of scientific information and ana-

lytics to pharma/healthcare professionals. While the firm is cur-

rently seeking a buyer, they plan to continue as a leader in the

health information space.

Rep. Ben Quayle (center) met with WKPS’ Bob Jansen, president

and chief commercial officer, and Michelle Woker, president and

chief operating officer, to discuss improvements of today’s delivery

of health information.

6 | DTC Perspectives • September 2011

SSI Brings Its 34 Years of Sampling Leadership to Healthcare, with the Broad Reach

and Precise Targeting to Optimize Your Patient, Caregiver and Physician Research!

Your market research drives your most critical business decisions. And the quality of your research depends

on the quality of your sample. That’s why companies around the globe, including 48 of the top 50 market

research fi rms, trust their most important projects to SSI. Now, SSI is bringing the scientifi c rigor that made us

the world’s sampling leader for 34 years to healthcare, with our new access to patients, caregivers, physicians

and allied health professionals. You benefi t from:

• Wide reach across key therapeutic categories, including metabolic

syndrome, respiratory ailments, mental health, lifestyle treatments and more

• Real-time dynamic profi ling to identify and engage precise segments

• Advanced quality processes—from digital fi ngerprinting to third-party

database matches—to ensure data integrity

• A full range of online and offl ine modes—Web, phone, mobile and mixed

access—to optimize reach

You wouldn’t build your products on anything less than solid science—and neither would we. Experience

the difference sampling science can make in the accuracy of your research. Contact Chris DeAngelis at

203-567-7220 or Chris_DeAngelis@surveysampling.com.

info@surveysampling.com | surveysampling.com

Pure Science

Now…the Science of Sampling

Meets the Science of Medicine

Register FREE for

SSI’s New Webinar—

Mapping the Hi-Tech

Consumer

—at

surveysampling.com/hitech

or scan here.

IN BRIEF

Botox Receives FDA Approval

For Seventh Medical Treatment

The FDA has granted Allergan’s Botox approval for the treatment of “urinary inconti-

nence in people with neurologic conditions such as spinal cord injury and multiple sclerosis

who have overactivity of the bladder,” the agency announced in a news release. As

reported by The New York Times’ blogger, Duff Wilson, this is the seventh medical

condition for which Botox has been authorized to treat since premiering in 2002 as a

cosmetic treatment.

According to the FDA, the Botox injection will relax the bladder, resulting in an

“increase in its storage capacity and a decrease in urinary incontinence” for up to 10

months. Company spokeswoman, Caroline Van Hove, told the Times that Botox has

been studied for more than 100 medical conditions, referring to the drug as “a pipe-

line in a vial.” She added that Allergan is also seeking approval for idiopathic urinary

incontinence.

Other Botox indications include treatment for: hyperhidrosis, chronic migraine headaches, and certain muscle stiffness

and contractions. Global sales for the multi-use drug were approximately $1.5 billion in 2010. Seamus Fernandez, an ana-

lyst with Leerink Swann, predicts sales in the region of $40 million for the current bladder treatment and $210 million for

the broader label by 2017, according to a Reuters report.

Lilly Diabetes Collaborates on

Type I and II Awareness Efforts

To further diabetes awareness and support, Eli Lilly has partnered with the American Diabetes Association (ADA) and

award-winning actor/comedian Anthony Anderson on a type 2 diabetes effort; and Disney and Denise Jonas, mother of

Nick from the Jonas Brothers, for a type 1 diabetes initiative. (Nick Jonas has worked with Bayer Diabetes Care in the

fight against juvenile diabetes.)

Continuing its successful Fearless African-American Connected and Empowered (F.A.C.E.) Diabetes campaign, Eli

Lilly teamed with Anthony Anderson on their most recent effort. Anderson, a paid spokesperson, travelled with the phar-

maceutical giant in events “around the United States to raise awareness of the type 2 diabetes epidemic among African

Americans, a population disproportionately affected by the disease. In fact, according to the [ADA], African Americans are

1.8 times more likely to have diabetes than non-Hispanic whites,” Eli Lilly & Co. explained in a news release. The most

recent event took the “Law & Order” actor to the 14th annual Victory Over Diabetes, a free event hosted by the ADA in

Atlanta.

Moving over to Lilly Diabetes’ type 1 efforts, this campaign will target parents and caregivers whose loved ones have

been diagnosed with the condition. Hosted under the Parenting section on Disney’s Family.com website, visitors can

view informational videos and articles, and connect with other caregivers. Disney Publishing Worldwide will also pro-

vide doctor’s offices with custom children’s books geared to various ages and life-stages with diabetes. Additionally, the

partnership has created the Once Upon a Time contest featuring Denise Jonas. Families

can submit a story, poem or essay about their child’s experience with type 1 diabetes.

Selected by an independent panel of judges, the winner will receive a family trip for four

to the 2012 Friends For Life, an annual international conference devoted to children with

the condition.

8 | DTC Perspectives • September 2011

PROVEN SALES LIFT

MEASURABLE ROI

TARGETED MEDIA

Patient-Centric Marketing via

Specialty Point-of-Care Networks

Awareness:

1 million patients are

watching each month

Compliance:

94% of patients are

purchasing products

immediately

Action and Acquisition:

51% of patients are

asking their HCP

PROVEN SALES LIFT

MEASURABLE ROI

TARGETED MEDIA

Patient-Centric Marketing via

Specialty Point-of-Care Networks

Awareness:

1 million patients are

watching each month

Compliance:

94% of patients are

purchasing products

immediately

Action and Acquisition:

51% of patients are

asking their HCP

PROVEN SALES LIFT

MEASURABLE ROI

TARGETED MEDIA

Patient-Centric Marketing via

Specialty Point-of-Care Networks

Awareness:

1 million patients are

watching each month

Compliance:

94% of patients are

purchasing products

immediately

Action and Acquisition:

51% of patients are

asking their HCP

Patient-Centric Marketing Via

Specialty Point-of-Care Networks

Awareness:

Millions of patients are

watching each month1

Action and

Acquisition:

51% of patients are

asking their HCP2

Compliance:

94% of patients are

purchasing products

immediately3

1. Monthly Affidavits, 2010. 2. Deibler Consulting, 2008. 3. Audits & Surveys Worldwide, 2001

ContextMedia owns and

operates a portfolio of the

largest condition-specific

in-office digital networks

For more information, contact:

Shradha Agarwal,

Chief Marketing Officer

312.239.6656

shradha.a@contextmediainc.com

✔ ROI Guarantee

✔ Proven Results

✔ State-of-the-art Technology

✔ Advanced Reporting

1115a-CM_DTC_Ad_7'11.indd 1 7/28/11 11:13 PM

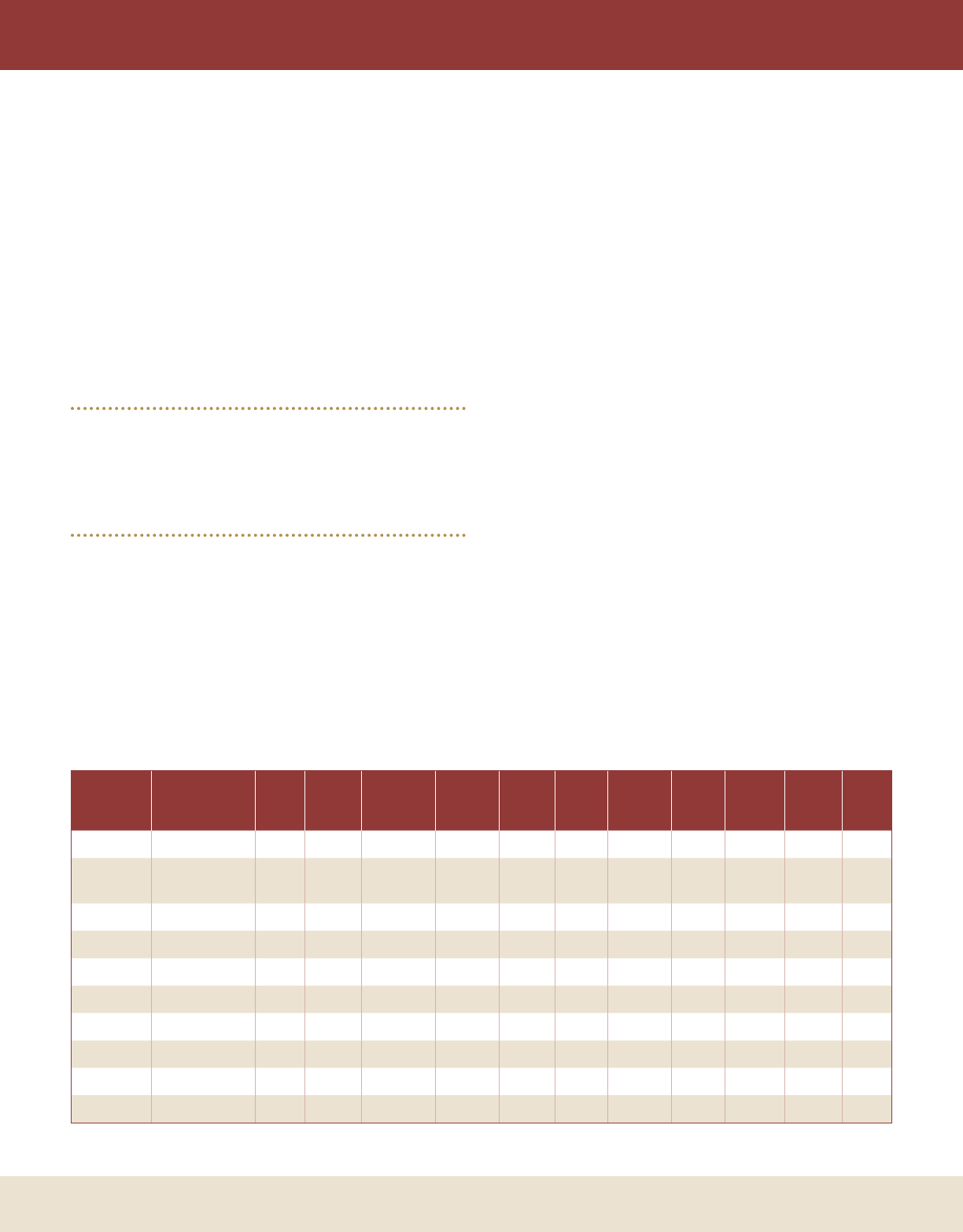

REVIEW

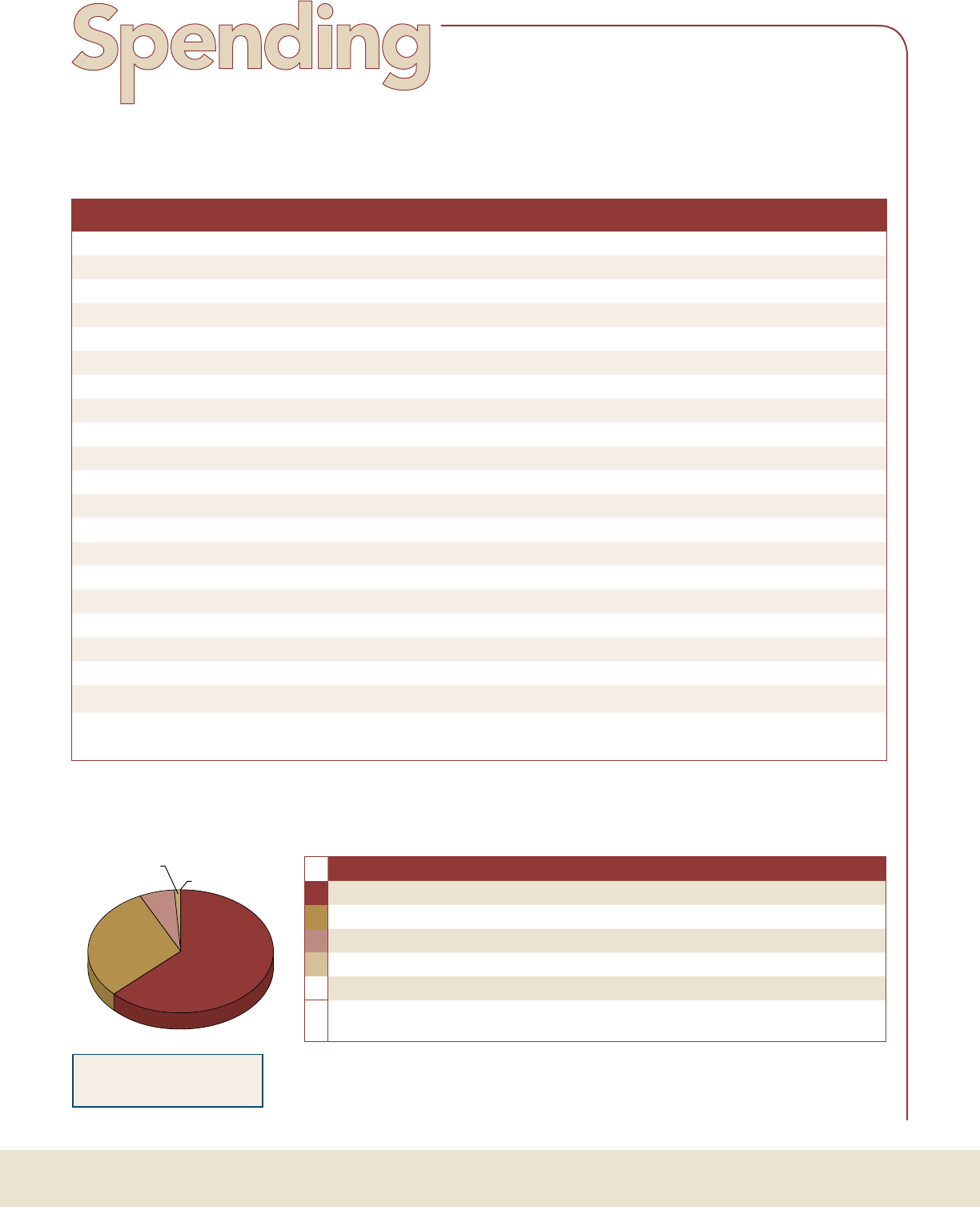

DTC Spending Showing Healthy Signs of Growth at 7.6% in First Half

Five New Brands/Treatment Indications Rank among Top 20 Spenders

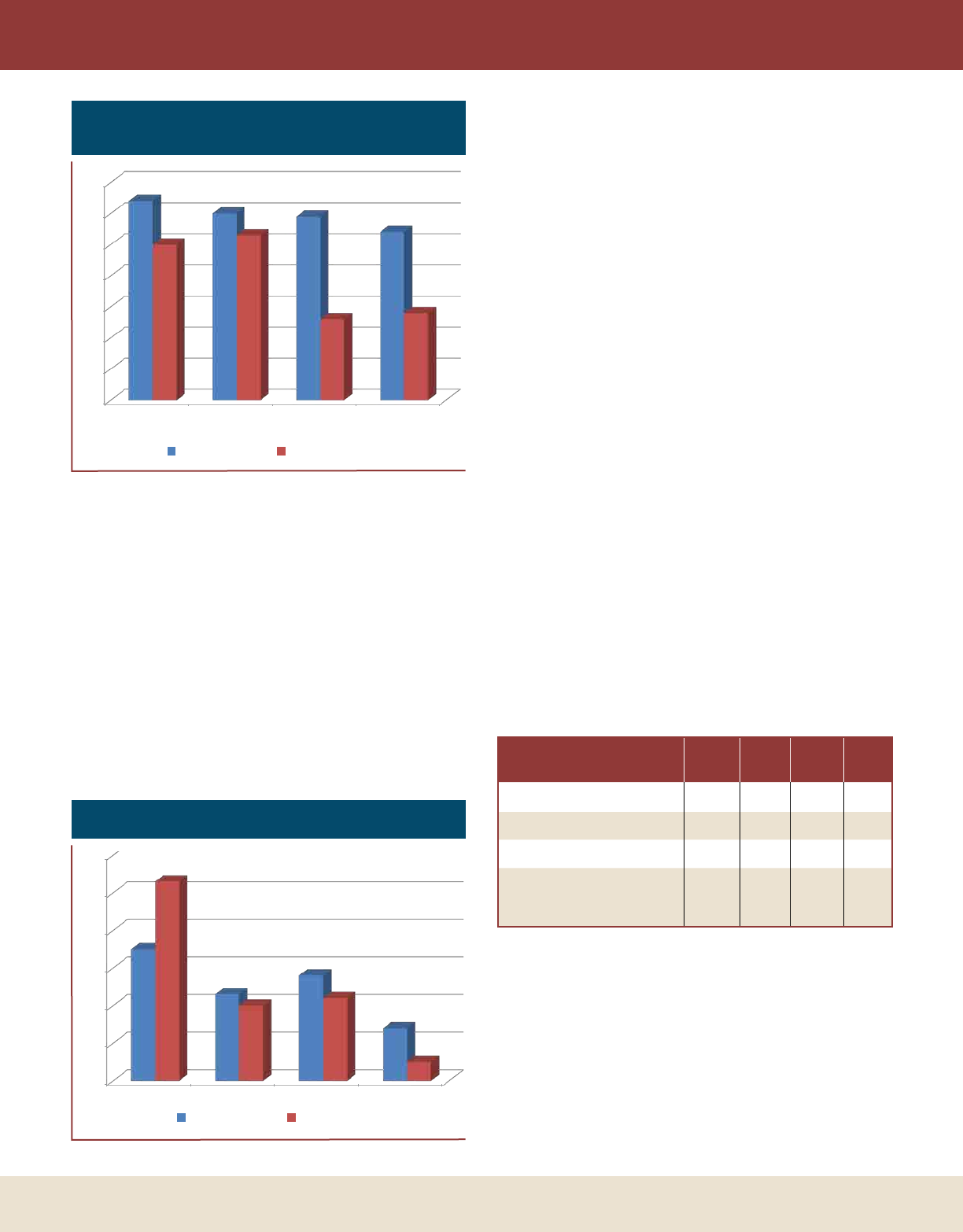

Brand Manufacturer 1H 2010 1H 2011 $ Change % Change

Lipitor Pfizer $141,059,869 $144,924,859 $3,864,990 2.7%

Cymbalta (Pain) Lilly USA $0 $72,541,275 $72,541,275 N/A

Uloric Takeda Pharmaceuticals $244,590 $72,269,377 $72,024,787 29447.2%

Cialis Lilly USA $93,285,343 $71,352,468 -$21,932,875 -23.5%

Celebrex Pfizer $0 $66,677,970 $66,677,970 N/A

Abilify Bristol-Myers/Otsuka America $71,729,538 $63,926,868 -$7,802,670 -10.9%

Seroquel XR AstraZeneca $0 $62,028,290 $62,028,290 N/A

Pristiq Pfizer $77,197,469 $61,367,844 -$15,829,625 -20.5%

Lyrica Pfizer $61,278,288 $59,598,520 -$1,679,768 -2.7%

Cymbalta (Depression) Lilly USA $84,570,291 $56,488,760 -$28,081,531 -33.2%

Viagra Pfizer $44,489,842 $55,443,355 $10,953,513 24.6%

Advair Diskus (Asthma) GlaxoSmithKline $80,361,827 $51,455,379 -$28,906,448 -36.0%

Plavix Sanofi-Aventis/Bristol-Myers $67,918,130 $50,100,266 -$17,817,864 -26.2%

Chantix Pfizer $63,458,544 $49,592,955 -$13,865,589 -21.8%

Enbrel Amgen/Pfizer $4,502,295 $48,351,033 $43,848,738 973.9%

Advair Diskus (COPD) GlaxoSmithKline $55,954,049 $46,280,597 -$9,673,452 -17.3%

Niaspan Abbott Laboratories $5,085,769 $42,912,129 $37,826,360 743.8%

Boniva Genentech/Roche $36,121,712 $42,671,928 $6,550,216 18.1%

Vimovo AstraZeneca $0 $40,800,076 $40,800,076 N/A

Beyaz Bayer HealthCare $0 $39,360,372 $39,360,372 N/A

Total Spending for Top 20 Brands $887,257,556 $1,198,144,321 $310,886,765 35.0%

Total Pharma Spending $2,010,966,227 $2,163,414,680 $152,448,453 7.6%

Media Type 1H 2010 1H 2011 $ Change % Change

65%

Television $1,345,251,695 $1,401,769,069 $56,517,374 4.2%

29%

Magazine $547,455,629 $624,932,017 $77,476,388 14.2%

5%

Newspaper $92,678,960 $117,297,547 $24,618,587 26.6%

1%

Radio $23,663,848 $18,468,477 -$5,195,371 -22.0%

0%

Outdoor $1,916,095 $947,570 -$968,525 -50.5%

Total Pharma

Spending

$2,010,966,227 $2,163,414,680 $152,448,453 7.6%

Source: The Nielsen Company for DTC Perspectives

Nielsen Monitor-Plus is the leader in innovative advertising information services and tracks advertising activity across 18 media types.

For more information, send an e-mail to Marisa Grimes at Marisa.Grimes@nielsen.com.

0%

1%

5%

29%

65%

Television Sees Slight Increase in DTC Promotions

Magazine Segment Gains Market Share

NOTE: Excludes

Internet Advertising

10 | DTC Perspectives • September 2011

His healthcare decisions are influenced by

much more than a visit to his physician.

While physician advice and

prescribing greatly influence

patients, it’s not just physicians

that impact patient behavior.

Patients’ treatment decisions

are also influenced by

information they learn from

other sources, including

patient education programs

and advertising.

By utilizing the most

comprehensive view of patient

behavior and characteristics –

both healthcare- and

consumer-related – SDI can

identify the best venues for

reaching patients and crafting

the most relevant messages.

SDI leads the industry in

providing empirical,

patient-level data to inform

and improve advertising

strategies. We provide insight

on patients’:

• Media preferences

• Advertisement exposure

• Behavior post-exposure

• Attributes and demographics

To learn more, please call

Melissa Leonhauser at

1-800-982-5613 or

visit:www.sdihealth.com/influence

12 | DTC Perspectives • September 2011

Branded Versus

Unbranded Digital Tactics

What to expect in reaching relevant

consumers and converting to brand

C

ampaign planning involves analyzing the tradeoffs

between marketing approaches. In pharmaceuticals,

these decisions grow more complex when choos-

ing not just between channels, but also between branded or

unbranded communications. Marketing decisions become

even murkier considering regulatory compliance requirements

and legal approvals – especially, though not exclusively, with

branded messages. Unbranded messages can often be under-

taken at a lower cost because of the less stringent fair balance

requirements. This results in messages that can be

conveyed in fewer pages, shorter television time,

or smaller display space.

Of course, an unbranded message is typically

not as powerful in driving direct conversion ben-

efit (new patient starts) to a brand. Branded mes-

sages drive the product ethos to patients while

unbranded messages serve to increase disease

awareness and education. While unbranded mes-

saging can grow the size of the market, branded

messaging is necessary to increase a brand’s share

of new patient starts.

The decision as to when and where to use

branded versus unbranded communication can

be challenging in the ever-evolving realm of

digital marketing. Cost considerations aside, one

would hypothesize that branded tactics executed

digitally would more effectively generate conver-

sion to a prescription while unbranded tactics

would hit a wider audience to raise disease or

category awareness and drive a qualified audi-

ence. A meta analysis of branded versus unbrand-

ed digital tactics supports this hypothesis and uncovers

actionable insights into when each should be used along the

continuum of prospect identification, consumer engagement

and conversion to brand use.

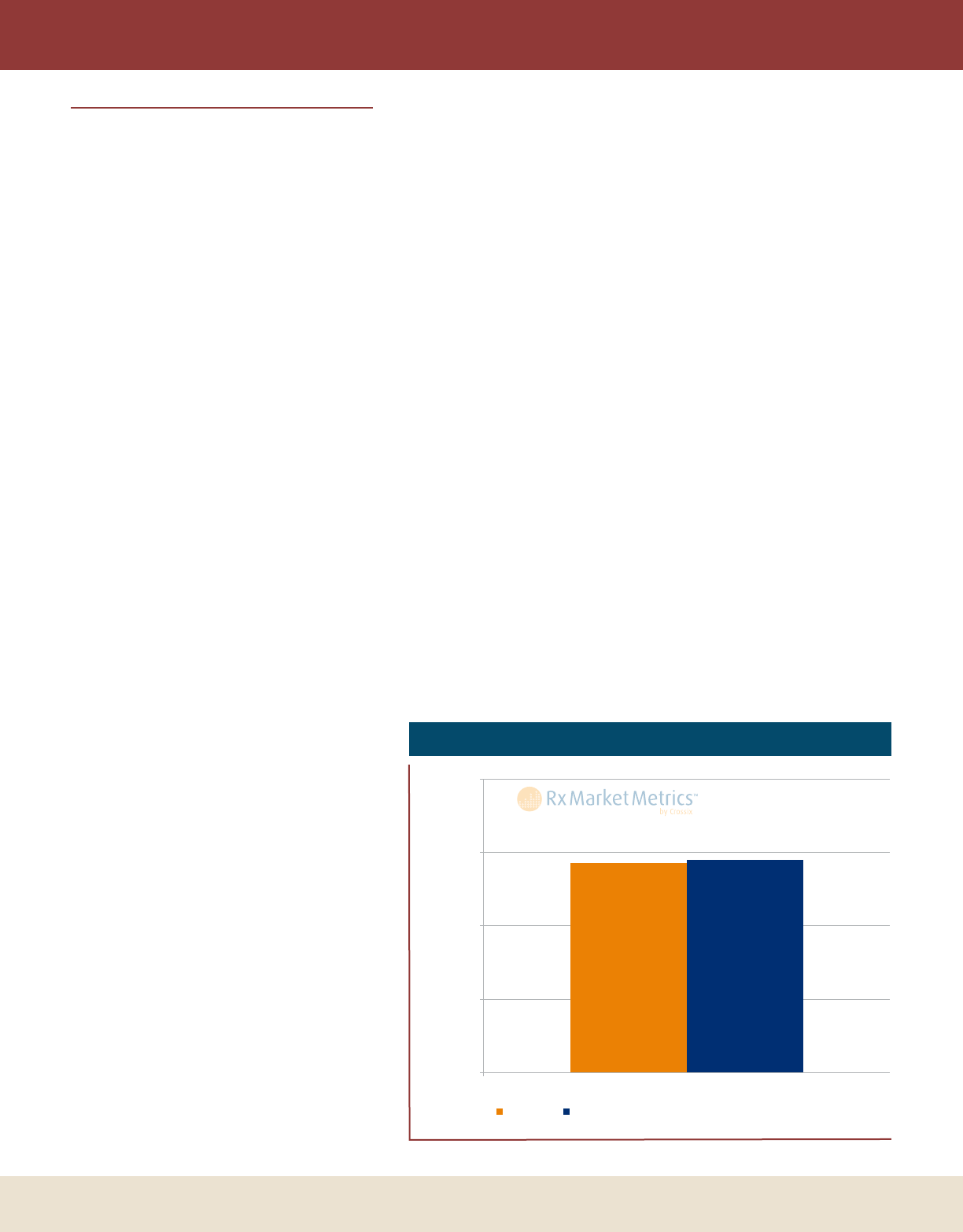

Benchmarking quality

Crossix RxMarketMetrics sheds light on performance dif-

ferences between branded and unbranded tactics using mean-

ingful norms that can help guide brand teams in their planning

efforts. RxMarketMetrics generates these market norms by

An examination of Rx-based benchmarks for branded and unbranded digital tactics demonstrates unique

advantages and disadvantages offered by each. Pharma marketers can leverage the strengths and mitigate

the weaknesses of branded and unbranded tactics by understanding which strategic goals each type of tactic

can best support.

Crossix RxMarketMetrics Series

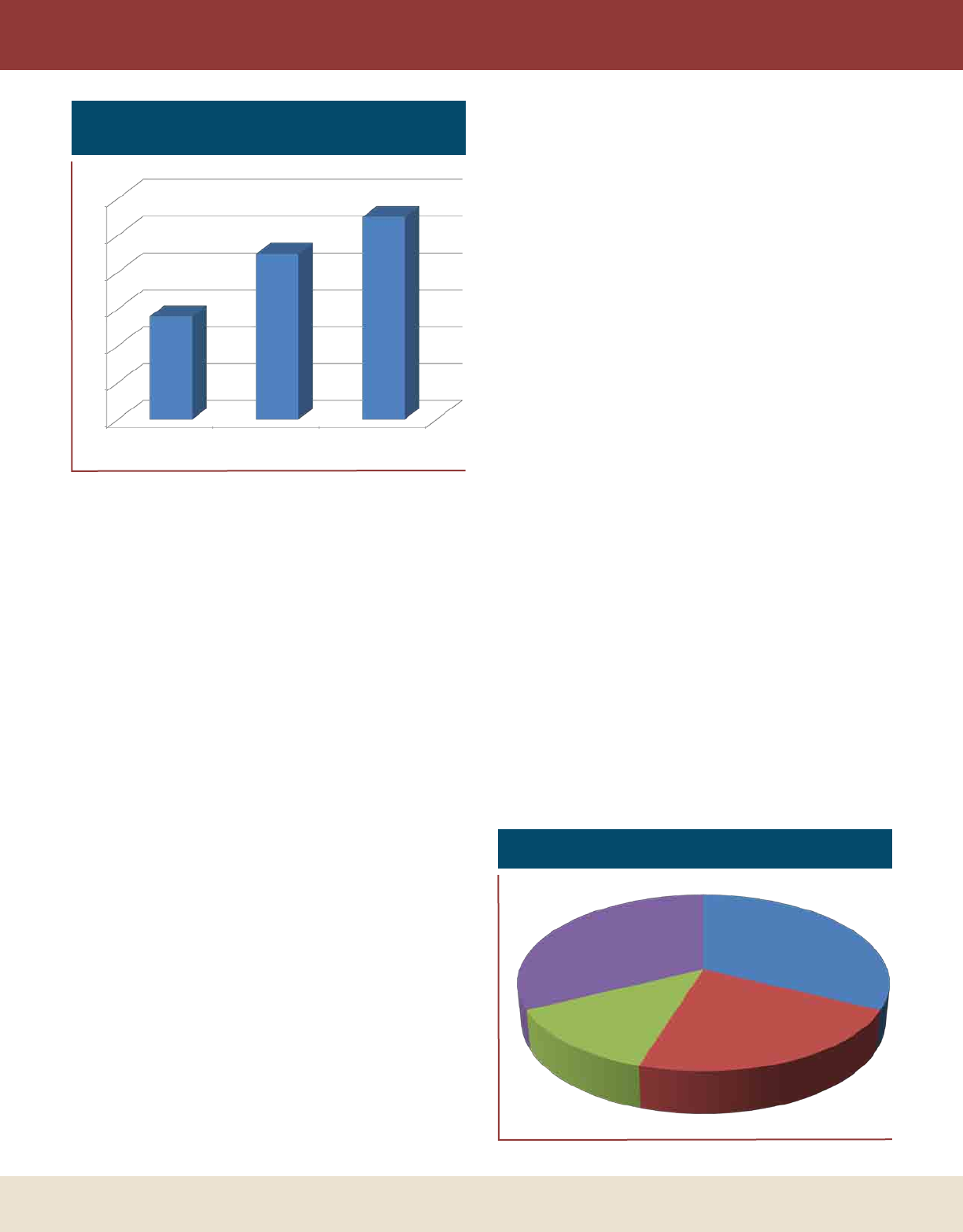

Figure 1: Percentage of Audience Treating in Category

57% 58%

0%

20%

40%

60%

80%

Audience Treating in Category

Branded

Unbranded

% of Audience

Source: Crossix RxMarketMetricsTM March 2011.

DTC Perspectives • September 2011 | 13

BRANDED VS. UNBRANDED

aggregating hundreds of actual Rx matchback

analyses over a broad range of media tactics,

brands and therapeutic categories. RxMarketMet-

rics measures the quality of engaged consumers

through the metric Percentage of Audience Treating

in Category. Audience Treating in Category includes

both existing patients on a specific brand as well as

prospects treating with a competitive therapy. Per-

centage of Audience Treating in Category is a measure

of how well a tactic attracts a relevant audience

likely interested in a brand’s message and, thus,

likely to engage.

Audience vs. prospects

A comparison of quality of engaged audiences

between branded and unbranded tactics across

channels demonstrates meaningful differences in

Rx profile. The median branded tactic generates a

similar share of a qualified audience as the median

unbranded tactic. (See Figure 1.) However, by

drilling down and looking at only those not exist-

ing patients (candidates for conversion), further

insights emerge.

Analysis of the Percentage of Prospects Treating in

Category demonstrates that unbranded tactics drive more quali-

fied prospects than branded tactics. The median unbranded

tactic generates seven percentage points more qualified pros-

pects than the median branded tactic. The lower level gener-

ated from branded tactics is driven by the fact that branded

tactics often attract existing patients treating on the branded

Rx, whereas unbranded drives higher proportion of prospects.

(See Figure 2.)

Based on the median rates, unbranded tactics more effec-

tively drive qualified prospects than branded tactics. However,

this does not necessarily mean that the audience converts at the

same rate as branded. Despite generating a higher rate of Pros-

pects Treating in Category, typical unbranded audiences may not

start at the same point in their treatment decision-making pro-

cess as branded audiences, with implications on effectiveness of

further education and brand-specific messaging.

Branded vs. unbranded conversion

Percentage of Total Conversion Benefit (net of control) quantifies

the time to conversion to a brand Rx realized on a monthly

basis. An examination of two digital tactics, search and web-

site, demonstrates the differences in time to conversion

between audiences engaged with branded tactics and those

engaged with unbranded tactics. In addition to differences

between branded and unbranded tactics in time to conversion,

differences also emerge in absolute conversion rates as well as

the size and scalability of the engaged audience. Among the

top 20 percent of programs, branded tactics drive 1.2x higher

About Crossix RxMarketMetrics

Prescription drug information drawn from Crossix RxMarketMetrics™, market benchmarks for performance of patient

adherence and consumer marketing activities based on thousands of actual Rx analyses including more than 600 consumer

marketing tactics across a broad range of therapeutic categories.

Campaigns included in RxMarketMetrics aggregated for the chronic, lifestyle and specialty/biologic markets and derived

from actual anonymized and aggregated results of consumer marketing campaigns for dozens of leading pharmaceutical

brands ranging from direct response (DR) to general awareness and branding campaigns (GA), and multi-channel, from Web

to Print to TV.

Normative Rx-based measures include conversion rates and curves, retention rates and curves, and Rx patient profiles spe-

cific to the market, channel and tactic. Benchmarks are further broken down by campaign specifics, such as purpose, level of

branding, creative, offer type, response channel and fulfillment stream.

Figure 2: Percentage of Prospects Treating in Category

vs. Existing Patients

46%

11%

53%

5%

0%

20%

40%

60%

80%

Prospects Treating in Category Existing Patients

Branded Unbranded

% of Audience

Source: Crossix RxMarketMetricsTM March 2011.

14 | DTC Perspectives • September 2011

rates of conversion than unbranded tactics. Sometimes branded

communication elements follow unbranded campaigns, poten-

tially mitigating an even larger difference.

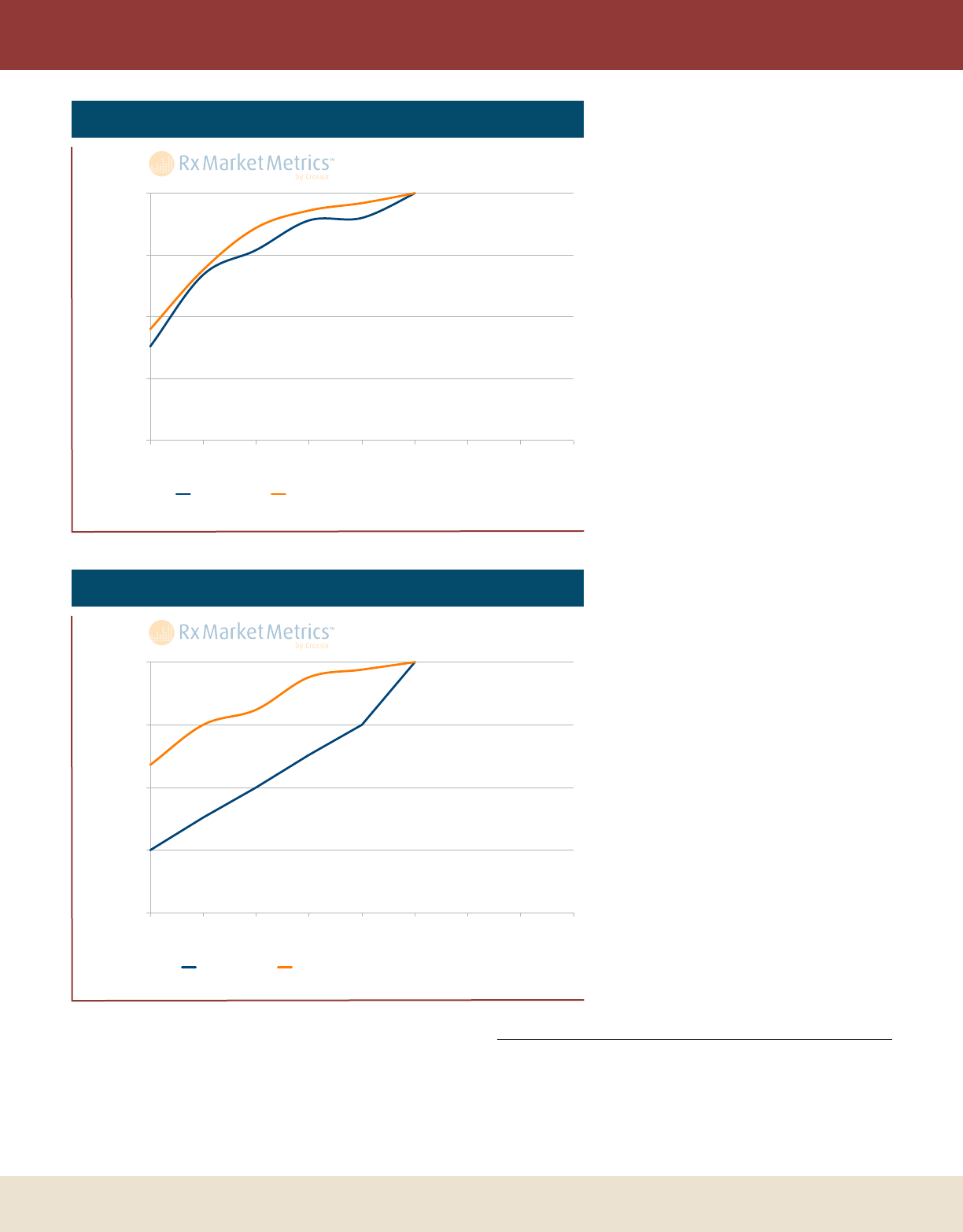

Looking at a six month horizon, we see that the benefit

from branded search shows more quickly with 45 percent of

benefit achieved in just the first month versus 38 percent for

unbranded. Unbranded search share of bene-

fit continues to track comparably with brand-

ed search through the six months, although

at a slightly lower level. (See Figure 3.) An

even larger first month variance appears

when examining branded and unbranded

websites.

Branded websites achieve nearly three-

fifths of the total conversion benefit in just

the first month. It takes unbranded websites

nearly four months to achieve the same share

of benefit – by which point branded websites

have realized over 90 percent of the ben-

efit. (See Figure 4.) A script-in-hand effect

can partially explain this rapid realization of

conversion through both search and branded

websites, wherein visitors to the branded site

have recently received their first Rx and then

proceed to research the product before visit-

ing the pharmacy.

Acting on this information

Brands and agencies typically view

unbranded tactics as a means of casting a

wide net to raise disease awareness, educate

potential patients and grow the size of the

market. RxMarketMetrics demonstrates that

unbranded tactics executed digitally can serve

as a powerful way to attract prospects treat-

ing in category. However, these individuals

convert more slowly and need further sup-

port by branded messages to continue to

move the potential customer from a prospect

to a patient. In considering unbranded cam-

paigns, the lower cost of media, the reduced

regulatory constraints in messaging, and the

broader appeal to higher volume of quali-

fied prospects (wider net) should be weighed

against slower time to conversion and lower

conversion than a similar branded campaign.

The product lifecycle and market share will

often play a major role in considering these

alternatives. Ongoing, granular Rx analysis

of tactics can inform on in-market campaign

performance in near real time.

This is a fourth installment of an ongoing series on Rx market metrics

of various consumer marketing activities. For more information, see the

Crossix RxMarketMetrics™ website (www.rxmarketmetrics.com),

from Crossix Solutions Inc., an Rx-based consumer analytics company

(www.crossix.com).

BRANDED VS. UNBRANDED

Figure 3: Percentage of Total Conversion Benefit – Search

0%

25%

50%

75%

100%

1 2 3 4 5 6 7 8 9

Unbranded

Branded

% of Total Conversion Benefit

Month

Source: Crossix RxMarketMetricsTM March 2011.

Figure 4: Percentage of Total Conversion Benefit – Website

0%

25%

50%

75%

100%

1 2 3 4 5 6 7 8 9

Unbranded Branded

Month

% of Total Conversion Benefit

Source: Crossix RxMarketMetricsTM March 2011.

Providing targeted data driven

solutions for consumer focused

health & lifestyle brands

Call:

Jim Curtis, Chief Revenue Offi cer

jcurtis@remedyhealthmedia.com

212-695-5581

your

remedy

we have

RHM_DTC_Sept_Ad_080111_FINAL.indd 1 8/1/11 10:01 AM

A DTC Perspectives Inc.

Conference

As technology provides exciting new possibilities, Digital DTC

Marketing must push forward, mitigating risks while maximiz-

ing potential gains. Learn how to improve current campaigns

while planning for future initiatives. Hear from 25-plus progres-

sive speakers streamlined over two days:

• Legislative issues you need to be aware of and how to respond

• Accurately evaluate ROI to optimize your digital DTC efforts

• Effective social media programs that secure med/legal approval

• Discover missing pieces in your social media engagement plan

• Improve health communications and brand adoption/loyalty

Marketing to the

Digital Consumer

Phone:

973-239-2051 ext. 221

Online:

www.dtcperspectives.com

under Conferences tab

REGISTER TODAY

Passes starting at $1,995

(includes full access to the conference, events and exhibit hall)

Pharma Best Practices Present and Future

Christopher D. Johnson,

Consumer Brand

Director, AstraZeneca

Todd Kolm

Director Emerging

Channel Strategy,

US Primary Care Consumer

Portfolio, Pfi zer Inc

Matt Giegerich

Chairman & CEO,

Ogilvy CommonHealth

Worldwide

Jane Chin, Ph.D.

Author, online authority

and formerly pharma

R&D/Medical Affairs

Mark Bard

Executive Director and

Co-Founder, Digital

Health Coalition

Raquel Krouse

Sr VP, Prophesee,

Initiative USA

Stu Klein

Interpublic Healthcare

Practice Lead

John Vieira

Senior Director, Marketing

Operations and Strategic

Services, Daiichi Sankyo, Inc.

With Expert Input and Analysis by

Conference Co-Chairs…

Visit www.dtcperspectives.com

for full agenda and details.

Join the

Conversation Now

#DTCDigital

October 12–13, 2011 • Crowne Plaza, Fairfi eld, NJ

Register Now to Hear from Digital Experts:

DTC Perspectives • September 2011 | 17

Optimal ROI is best achieved when the interactions between marketing channels and campaign tactics work

together to increase overall marketing effectiveness. Pharma marketers should focus on three key steps when

measuring integrated campaign ROI: audience type, channel mix, and timing.

by Nami Choe

C

onsumers’ preferences and modes of communication

are diversifying exponentially faster than most contem-

porary marketers can nimbly adapt. By the time mar-

keters collectively acknowledge and begin to understand a new

advent in the industry, another innovation emerges to trans-

form the landscape yet again. (Marketers were still attempt-

ing to unlock mobile’s potential when tablets and new social

media platforms like Foursquare marched into the forum.)

In these circumstances, particularly against the backdrop of

heightened economic pressures, the integrated marketing

approach has regained prominence in industry dialogue with

natural reason. Brands are seeking more structured frameworks

for determining the optimal marketing and media mix.

Marketers must be diligent and fastidious in

their measurement planning to avoid common

pitfalls that inadvertently compromise the

fundamentals of integrated marketing.

The rapidly increasing number of tactics in the media

toolbox yields a complex menu for marketers to select from,

boosting the demand for data-driven analyses and predictive

models to ensure that the final plan will derive the maximum

ROI possible. However, campaign measurement remains

relatively nascent with respect to cross-channel algorithms for

quantifying synergies generated from various media combina-

tions and investment scenarios. Marketers must be diligent and

fastidious in their measurement planning to avoid common

pitfalls that inadvertently compromise the fundamentals of

integrated marketing.

Frequent fluctuations and tightening of budget constraints

during the campaign development process have gener-

ated understandable hesitation to commit to marketing plans

without comprehending how each tactic will contribute to

bottom-line sales and ROI. Internal and agency analytics teams

often collaborate to model multiple investment scenarios to

compare the potential returns associated with various media

mixes.

The challenge with designing predictive models for inte-

grated marketing efforts, though, has been the lack of cross-

channel benchmarks to inform assumptions for lift and return.

Traditionally, third-party vendors specialized in the measure-

ment of a single medium, so most historical data points pertain

to a channel’s independent efficacy, regardless of its relation-

ship with other campaign elements in the consumer’s overall

experience with a brand. Research vendors are making sig-

nificant strides toward centralizing data to expand their breadth

of cross-channel measurement, but a solid and universally

accepted methodology has yet to be introduced. As a result,

the inputs and assumptions for predictive ROI models do not

always account for potential synergies derived from multiple

channels and their cadences.

Optimizing ROI

Through

Integrated

Marketing

18 | DTC Perspectives • September 2011

At the eventual step of minimizing costs to maximize the

ROI output, channels and touches thereby risk omission with-

out the model reflecting the opportunity from its relationship

with other media. In other words, the channels are evaluated,

mixed and matched as independent entities – contrary to the

underlying principles of integrated marketing. Rather than

wait for third-party vendors to release blinded benchmarks

to improve media mix assumptions, marketers should focus

on building their internal repository of cross-channel results

through robust measurement planning that truly reflects the

integration for which their plans strive.

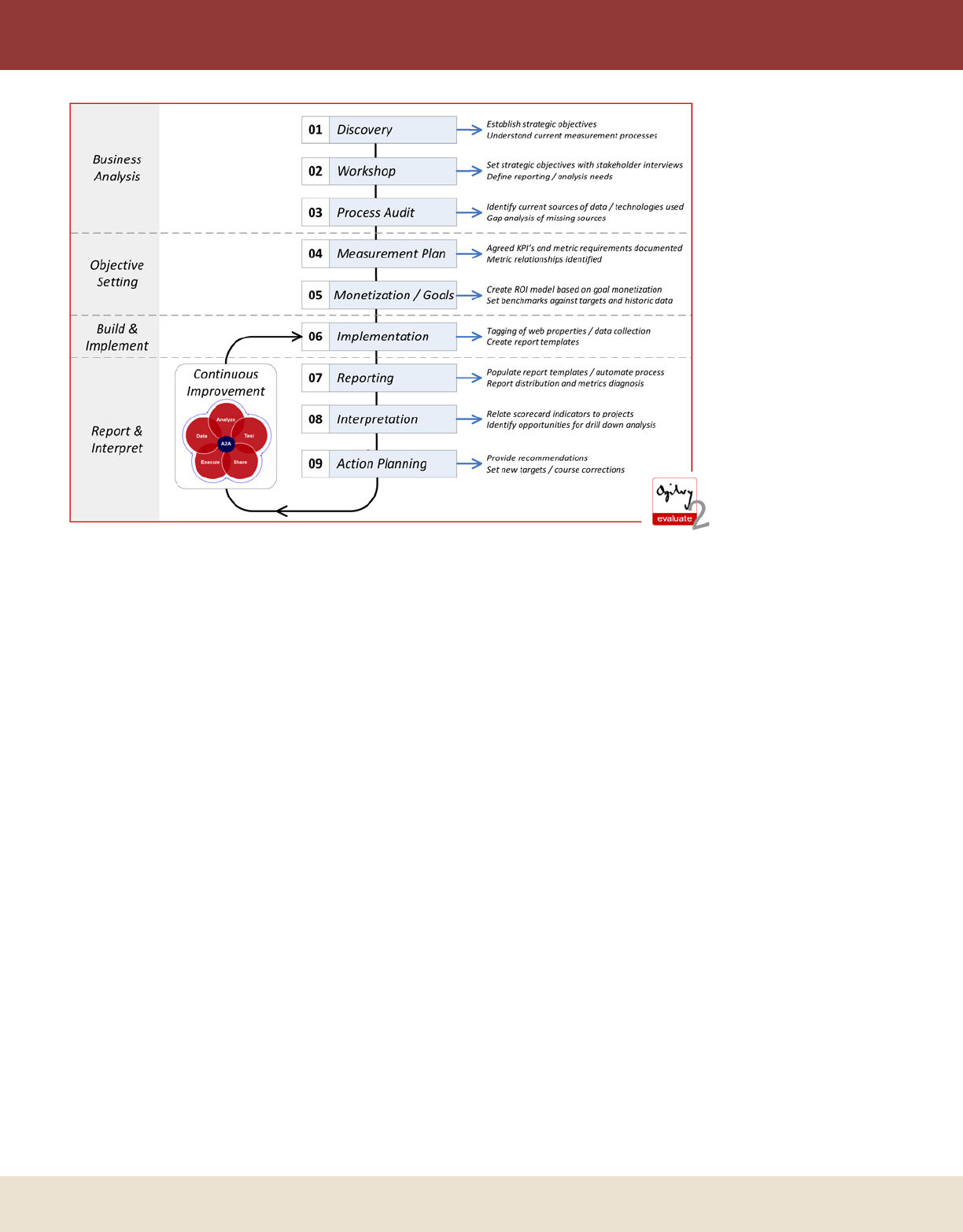

Establish measurement plans

Commence measurement planning before creative

development to ensure that all tactics are tracked prop-

erly. Defining tracking requirements upfront ensures sufficient

time for creative partners and vendors to assist with maximiz-

ing visibility into campaign dynamics. Measurement is too

often an afterthought upon the program’s completion, when

it is too late to implement the appropriate tracking instruments

to address key questions.

The most challenging part of this process is agreeing upon

campaign and tactical objectives. Once key stakeholders are

in agreement, the measurement plan becomes less of a burden

and less time consuming on the analyst without going back

and forth with vendors and marketers. When approached with

discipline and structure, translating objectives into measure-

ment and optimization

plans can be an efficient

process that uncovers data

gaps, minimizes tactical

issues and ultimately keeps

all partners aligned with

marketing goals.

Measurement require-

ments should focus

on enabling tracking

consumer engagement

across multiple chan-

nels. While legal parameters

might limit the granularity

at which consumer activi-

ties may be tracked, generic

source coding can be lever-

aged to identify user paths

and link disparate data

sources. Ideally, marketers

should also consider formal

Media Mix Modeling (an

econometric model which

determines revenue contri-

bution per tactic/program

that accounts for overall

marketing efforts, seasonality and conversion lag times), which

requires substantial campaign setup prior to launch, but can

correlate media exposures/engagement to conversions without

instruments for direct attribution (e.g., source codes and tag-

ging). However, as with any model, it requires marketers to

let ample time for the campaign to make an impact and gather

enough data. Given the need for some level of patience, Media

Mix Modeling is still a particularly attractive solution for mea-

suring DTC campaigns where bridging between consumer

media exposure to actual Rx or product adoption remains a

large gap.

Document key hypotheses/tests in the measure-

ment plan, and allow sufficient time for data to accrue

for statistically significant findings. Data is becoming

increasingly more accessible in real-time, allowing for prompt

in-market optimizations. However, eagerness to optimize has

also led to premature reactions. Adequate sample size is critical

to statistical integrity but is often overlooked when marketers

observe trends only directionally. Rash and frequent optimi-

zations risk dismantling the test plan and might inadvertently

inhibit learnings at the end of the campaign.

Identify connections

Identify key performance indicators (KPIs) that

are aligned with how consumers actually engage with

each channel and across channels. When marketers hold

all tactics against the same objective, the measurement plan

OPTIMIZING ROI

Ogilvy CommonHealth Worldwide’s overall framework for planning, implementing, executing and sustaining

campaign measurement.

Advertise in DTC Perspectives Magazine

Why advertise with us?

• Effi cient Targeting Reach pharmaceutical marketers

for a fraction of the cost than other industry publications

• Engaged Readers Loyal subscribers read us cover-to-

cover, recognizing our content as valuable and relevant to

their business

•Bonus Distribution DTC Perspectives magazine is

also distributed at our DTC National, MDPA & Fall

Conferences

For more information please contact Matt Yavorski at Matt@dtcperspectives.com or 973-239-2051 x224

Value-added packages available for 4 time advertisers.

Opportunity for integrated presence through DTC Perspectives magazine, our website,

e-mails /e-newsletters, and conferences.

REACH THE RIGHT DTC MARKETERS

DTC Perspectives • September 2011 | 19

OPTIMIZING ROI

grows unnecessarily complex and results in channels being

held against unrealistic expectations. The overall objective

of a campaign might be to increase sales, but evaluating all

individual tactics against driving sales would be to overlook

that each channel drives different consumer behaviors toward

conversion. In general, certain tactics are further down the

consumers’ consideration paths and thus produce more direct

attributions to revenue. A common example is the compari-

son between print and SEM. When marketers attempt to hold

print and SEM against the same objective of driving sales,

print typically yields an apparently lower return, prompting

stakeholders to reduce print investment. Instead, the integrated

marketing perspective would suggest that print heightens

awareness and prompts consumer research via SEM.

Focus investment on the select channels that are

truly relevant to the target audience and brand catego-

ry. Some marketers have misinterpreted integrated marketing

as the requirement to create “surround sound” by positioning

the brand in every possible channel – to check all of the pri-

mary media boxes, including TV, print, digital banners, SEM

and social media. However, ROI generally diminishes when

resources are spent unnecessarily or thinly. The measurement

plan also becomes unfocused, as noise from superfluous media

muddles and detracts from evaluating the tactics that were truly

influential to the target audience.

These are exciting times for analytics. Marketers are

continuing to unlock data analytics’ potential in optimizing

investment real-time and in a more targeted way. First step

of successful integration is through the data planning phase

and using data to understand how consumers engage across

most relevant channels. However, as we look to the future,

with data becoming more available and tracking more sophis-

ticated, there are opportunities for marketers to understand

the impact of pulsing versus continued exposure of marketing

efforts.

More research is needed in order to understand how timing

affects the relationship among channels. In addition, further

understanding is needed in integrating the marketing efforts

of different audience types: healthcare professional, patient/

prospect, and pharmacist. Optimal ROI is reached only when

marketers successfully understand and coordinate the relation-

ship of three key factors: audience type, channel mix, and tim-

ing. And it will be the appropriate use and analysis of data that

will enable marketers to achieve this. DTC

Nami Choe is partner, senior director, consulting with Ogilvy

Healthworld. Ogilvy Healthworld is an innovative full service market-

ing agency and a part of Ogilvy CommonHealth Worldwide. Choe

can be reached by telephone at 212-237-4789 or by e-mail at Nami.

Choe@ogilvy.com.

20 | DTC Perspectives • September 2011

I

f change is the Grandmother of Invention (after all, who

do you think begot Necessity?), then the current world

of DTC is like ladies night at the nursing home. There’s a

huge mosh pit of change all around us:

• Almost 75 percent of the biggest DTC spenders will go

generic by the end of 2013. Think about it: Lipitor, Cre-

stor, Plavix, Cymbalta, Viagra, Advair, Boniva, etc. (IMS,

2010)

• There’s been a dramatic shift from mass media to targeted

audience, (e.g., a 23 percent swing from network to cable,

MM&M 2010)

• And, miracle of all miracles, there’s finally a government

agency that admits DTC plays a beneficial role in both

public health and in lowering healthcare costs (The Con-

gressional Budget Committee, May 2011)

Which means DTC is due for some big invention.

In fact, it’d be a shame if we just stood there and kept put-

ting out the same Beauty and the Beast formula of a disease-

stricken patient magically transformed into a walking grin,

interrupted by 32 seconds of fake doctor-patient interaction

while fair balance is read. We have the chance – and respon-

sibility – to respond to the changing landscape with a whole

new vocabulary of action.

What DTC could mean

“Direct to Consumer” says what it is and where it plays.

But effective brands today are built on what they do than what

they are. So imagine if DTC stood for:

D = Do. Do something for consumers beyond dissemi-

nating information. Don’t just stand there at the pulpit and

preach. Add value to your communications by adding utility

to your media. A mobile app (“mHealth”) that empowers a

consumer to do something about their disease, or their care,

can be much more effective in building your brand. Some

other good examples:

1) Is an app that alerts me to when my epinephrine pen

needs replacing worth more than another print ad? It

shows that the brand is actively

engaged in my life, proving its

understanding – not just passively

claiming it.

2) The AllergyManager app (from

Omnaris) gives sufferers an allergy

forecast in their area, along with

information on Omnaris. (But

don’t cheat. Your app has to

be more than just the mobile

version of your website.)

Effective brands are now built on what they do for consumers, rather than what they are. Thus, DTC is

due for some big innovation. By redefining DTC, marketers can truly realize the potential of DTC to

responsibly change consumer healthcare and deliver the coveted: improved outcomes.

by bruCe rooke

It’s Time “DTC”

Stood for

Something Else

DTC Perspectives • September 2011 | 21

3) GoMeals (from Sano-

fi-Aventis) instantly

guides diabetics in

the real world to

what they should eat,

where they can eat,

and helps them watch

what they eat.

4) The Tamiflu cam-

paign* for Roche

where, beyond the

“Happy Feet” danc-

ing penguins, we

gave consumers a

simple mnemonic

to tell the difference

between cold and flu – the F.A.C.T.S. of flu: Fever,

Aches, Chills, Tiredness, and Sudden Symptoms. It gave

caregivers a free diagnostic tool that made them, well,

better caregivers. That’s doing, not just telling.

T = Teach. Equip your consumers to be smarter patients

or more astute caregivers. We love to hide behind the veil of

educating consumers about their health – and then we proceed

to sell in the traditional manner. Let’s truly educate. What if

we walked them through a procedure, step-by-step, fears and

hopes, using a celebrity not as borrowed interest but as the

real consumer (realitylasik.com)? What if we taught men how

to be conversant in controlling uric acid versus medicating

gout pain (Takeda’s Uloric DTC campaign*)? Designer Jacob

Heberlie found the perfect touch in his multiple sclerosis (MS)

animated video series for Dr. Singer’s MS Clinic (mslivingwell.

org) in taking the complex science and therapies and creat-

ing motivating “I get it now” moments for consumers and

caregivers. The year-old GE healthymagination and Howcast

online videos do much of the same (see the case study at how-

cast.com). And the healthymagination/MedHelp app, “I’m

Expecting,” teaches a mom what is going on with her baby

at any given time along the journey. In all of these examples,

smarter consumers equaled more active consumers. And that

teaching leaps over the hurdles and can lead directly to the

brand.

C = Connect. Connect the conversation. Healthcare

decisions are no longer made unilaterally. They include the

consumer (patient), the caregiver(s), the physician, the nurse,

the payer, and the invite list goes on. Plus, under healthcare

reform, team health management will be standard of care

(SOC) at the doctor’s office. So it will take multiple influ-

encers to get to one decision. Which makes connecting that

conversation even more crucial. This doesn’t mean you have

to have the same campaign across all audiences. But it does

mean that somehow in your campaign, you need to inspire

and incentivize a connected conversation. (Yes, beyond the

ol’ “ask your doctor about…”) Besides, you want people talk-

ing about your brand, influencing each other, filling in each

other’s blanks, completing the story – with your brand front

and center.

For example, Eisai realized with Aloxi that the cancer

patient may never speak up about their nausea (for fear of get-

ting reduced, less effective chemo), and the doctor may never

hear the patient complain. So they expanded their campaign

to reach both caregivers and nurses, knowing if they could

connect them, they could create that vital conversation, and

Aloxi would be an important part of the dialogue. The cus-

tomizable e-postcards of Gardasil’s “Tell Someone” campaign*

helped boost awareness from 5 percent to 50 percent. And just

imagine how a Zeo Personal Sleep Coach (www.myzeo.com)

– with all of its tracking data and “ZQ” score – could create

a connected conversation for a branded sleep aid. (Sorry, you

have to imagine it. Hasn’t happened yet.)

So, as you can see, the necessity of change (and the endless

opportunity of digital) has given all of us the chance to make

DTC mean so much more than “Direct to Consumer” (or

“Dull Television Commercials” or even “Diarrhea to Come”).

By redefining DTC to mean Do, Teach, Connect, we can truly

realize the potential of DTC to responsibly change consumer

healthcare and Deliver the Coveted: improved outcomes. DTC

*Denotes campaigns developed by GSW Worldwide.

As chief creative officer, Bruce Rooke provides strategic leadership for

GSW Worldwide’s creative team. His responsibilities include estab-

lishing and implementing standards for creative work and ensuring that

strategic, creative, and branding processes are used consistently across

the agency. Rooke can be reached by e-mail at brooke@gsw-w.com.

REDEFINE DTC

22 | DTC Perspectives • September 2011

Medication

Non-Adherence:

The Health Care Industry’s

Silent Epidemic

In order to increase adherence, marketers need to understand the

consumer behaviors that lead to the original divergence from in-

tended medication use. Based on the FICO Medication Adherence

Score, this article highlights consumer profile examples and explains

the role such generated scores play in the larger pharmaceutical

marketing ecosystem and forecasted scenarios.

by Todd STeffeS

T

he issue of patient adherence to prescription drug regi-

mens hasn’t commanded enough discussion in recent

years, but it has grown into a disturbing trend with sig-

nificant side effects for the health care industry. Not only are

the effects felt by patients, who suffer worse health outcomes

as a result of not taking their medication, but the health care

industry suffers in several ways as well. Chief among these

are increased costs of doing business, providing treatment and

serving patients.

Despite the negative consequences of medication non-

adherence, existing strategies to fight the trend aren’t ade-

quately addressing the problem, and as a result are exposing

patients to greater health risks. The industry as a whole needs

to identify and adopt adherence initiatives that are more pre-

ventative in nature to engage earlier with individuals at risk of

failing to take their medication and keep them on track.

Research shows as many as half of all patients in the U.S.

do not take their medication as prescribed, 31 percent do not

fill prescribed medication, 29 percent stop taking medication

before supply runs out and 24 percent take less than the rec-

ommended dosage1. As you would expect, this has a significant

effect on patient health outcomes; for example, patients with

high blood pressure who do not take medication as prescribed

are more likely to experience complications like coronary

heart disease or stroke. Worst of all, medication non-adher-

ence is estimated to result in around 125,000 premature deaths

in the U.S. each year2.

In addition to detrimental health consequences, non-

adherence adds significant costs to the health care system – the

issue as a whole costs the U.S. health care system $290 billion

each year3, or 13 percent of the total U.S. health care expen-

diture. Furthermore, a 2011 study showed that a non-adherent

patient with high blood pressure spends an average of $3,908

more per year for health care than an adherent patient4. For

congestive heart failure, the additional patient cost is esti-

mated to be $7,823, and for diabetes $3,765. Worse yet, these

social and economic costs are rising, and are likely to continue

unchecked unless current approaches to non-adherence are re-

thought.

Fighting non-adherence today

In recent months, industry leaders have begun to notice

this trend and take action. The National Consumers League

(NCL) and the Surgeon General have announced a three-year

campaign to raise awareness of the importance of medication

adherence. Many prominent health care associations and other

industry leaders are supporting the initiative.

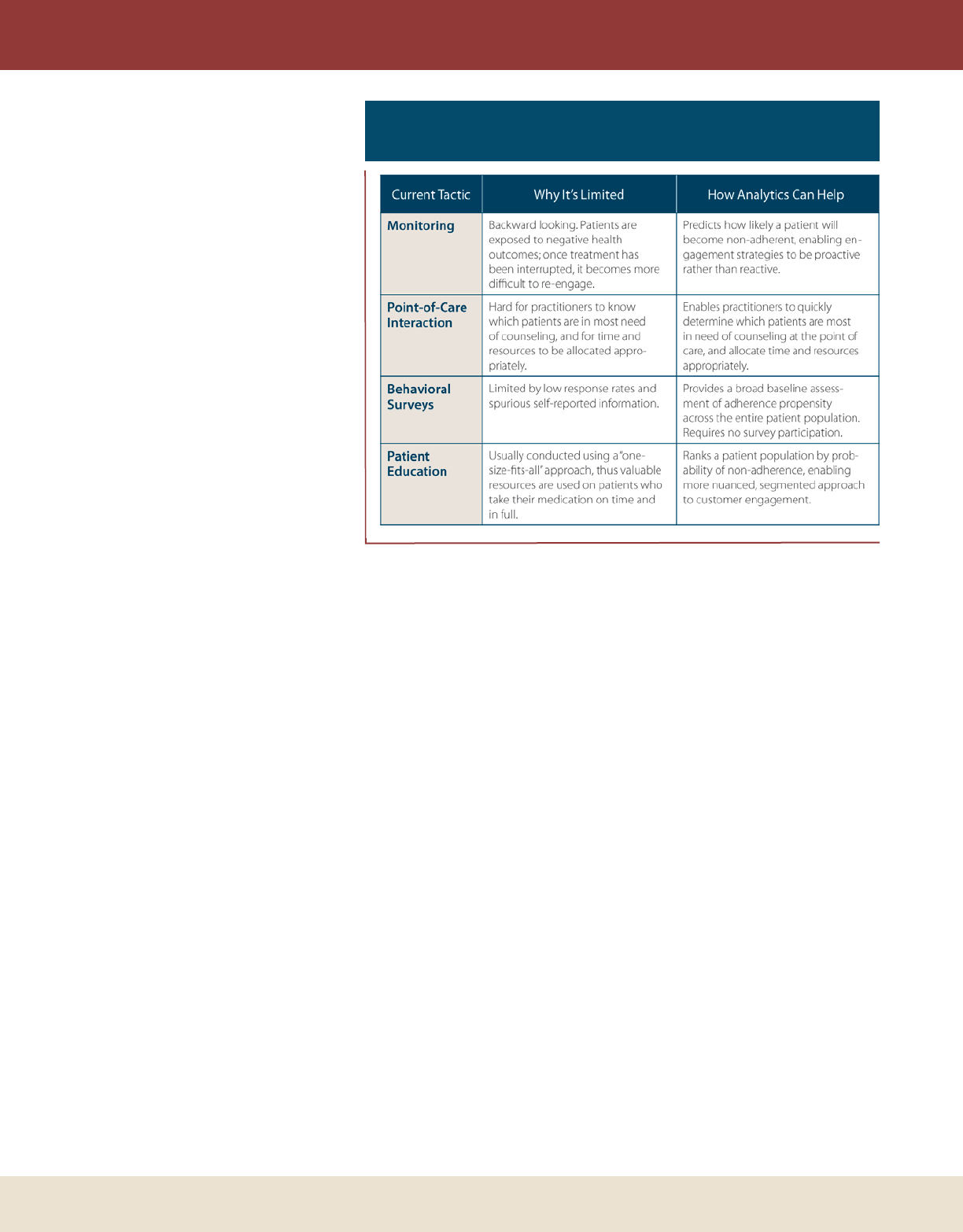

A number of approaches exist today to improve medication

adherence, including (see Figure 1):

• Monitoring: Organizations with access to claims informa-

tion – health care providers and payer organizations – can

monitor patient treatment history and look for gaps.

Unfortunately, this approach only addresses non-adher-

ence after it has occurred, and once treatment has been

stopped it becomes more difficult to re-engage.

• Point-of-care interaction: Health care providers and retail

pharmacies engage in direct communication with patients,

but this is costly and not always accurate. Patients tend to

DTC Perspectives • September 2011 | 23

IMPROVING ADHERENCE

overstate their own prescription usage,

and it’s hard for practitioners to know

which patients are in most need of

counseling. It’s also difficult for these

organizations to decide where their

time and resources are most needed.

• Behavioral surveys: Pharmaceutical

manufacturers have used psychomet-

ric-style surveys to assess current and

future patient adherence behavior.

Though results are useful, responses

often give an incomplete picture of

a patient population because of low

response rates and false or embellished

self-reported information.

• Patient education: Industry organizations

send out mail, e-mails and SMS mes-

sages, and use TV and online channels

to communicate with patients. For

example, pharmaceutical manufactur-

ers like to combine educational mate-

rial with incentives like co-payment

cards to reduce out-of-pocket expenses

for patients. These education strategies can work, but

they are costly because they employ a “one-size-fits-all”

approach and resources are wasted on patients who take

their medication on time and in full.

In sum, there are two primary problems with today’s

approaches to medication non-adherence. First, it’s too late to

impact non-adherence retroactively; it is difficult and costly

to re-engage with a patient and get them back onto their

medication plan after they have already failed to fill a prescrip-

tion. Second, patient engagement strategies need to be more

tailored to specific patient and health condition types, channel-

ing resources to those with the greatest risk of non-adherence.

One-size-fits-all approaches do not effectively accomplish this,

so new solutions are needed to circumvent these challenges

and truly curb medication non-adherence.

Using analytics to focus programs

The use of predictive analytics has emerged as an effective

way to overcome the limitations of current strategies and drive

improved patient medication adherence. These analytic models

can accurately predict who will become non-adherent before

the prescription is written. This could be a real game-changer

in the health care industry – if you can identify which patients

are most at risk of becoming non-adherent, then you can

develop tailored preventative engagement strategies and apply

them to both improve patient health outcomes and save costs.

One approach to do this, like we’ve established with the

new FICO Medication Adherence Score, is to generate a score

early in the course of treatment, when an individual is being

prescribed drugs for the first time. We have learned that it is

important to develop tools that have the greatest flexibility of

application and can be made available to multiple stakeholders.

Leveraging publicly available data sources can provide broad

predictive tools across the entire patient base for enhanced

adherence propensity assessment.

If the score indicates the patient is at higher risk of non-

adherence, a doctor, pharmacy or other organization would

have the opportunity to spend extra time when prescribing the

drugs to emphasize the importance of taking them on time and

in full. After treatment has begun, other intensive engagement

strategies like nurse calls and reminder programs could be used

to reinforce the earlier educational discussions and encourage

adherence. Meanwhile, lower-touch and lower-cost strategies

like e-mails and Web-based educational tools could be used

with lower-risk groups, and co-payment offers could be tai-

lored by risk group as well.

This differentiated approach has the potential to deliver

greater health outcomes and lower costs, compared to tradi-

tional one-size-fits-all approaches. For example, a payer orga-

nization might attempt to improve adherence of new diabetes

patients through a mix of tactics including multiple nurse calls

and counseling sessions – an expensive strategy. Using predic-

tive analytics, the level of nurse interaction could be adjusted

to reflect a patient’s adherence risk ratings; e.g., the com-

pany could reduce levels of nurse outreach to low-risk patients

Figure 1: Solving the Limitations to Current

Non-Adherence Tactics

24 | DTC Perspectives • September 2011

IMPROVING ADHERENCE

(those most likely to adhere) and re-deploy extra resources to

engage higher-risk patients.

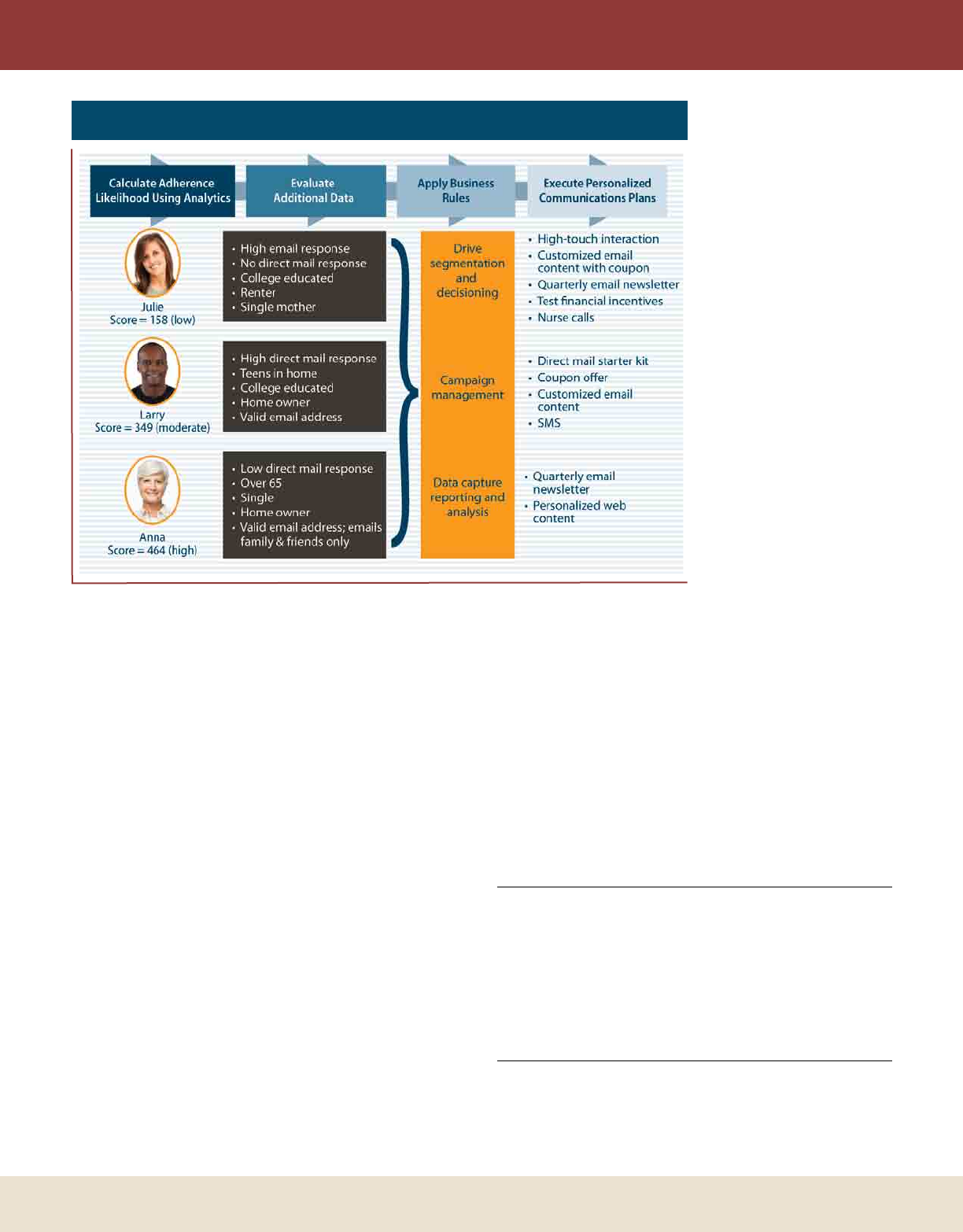

Improving outcomes

By using analytics to predict non-adherence, health care

organizations would have the opportunity to experiment with

the most effective combination of engagement tactics for a

particular patient or group – and then standardize what they

learn to be the best practices. Initiatives such as lifestyle advice

and coaching, e-learning programs, financial incentives and

integrating care management with primary care teams are a

few options at their disposal to encourage patients to play a

more active role in their personal treatment. (See Figure 2.)

These kinds of advanced analytic test-and-learn procedures

are already being deployed successfully in the industry. One

FICO client involved in a multi-year disease management

pilot used this approach to engage and retain diabetes and

chronic heart failure patients. Specifically, the company tested

potential messaging to find which would have the most impact

on patients during the first few seconds of a nurse call. The

messaging was pre-tested in focus groups to gauge audience

understanding and responsiveness, and was tested again in a

nationwide attitudinal survey. Then, analytics were used to

search within this survey information and other available data

sources for groups of patients who respond similarly to specific

engagement tactics. The company used these test-and-learn

results to segment patients

into six groups, and to

develop tailored engagement

strategies for each segment.

Results surpassed original

internal patient enrollment

targets by 17 percent, and

exceeded the program spon-

sor’s target by 36 percent.

Advanced test-and-learn

techniques are particularly

relevant now, as health care

organizations consider the

use of new communica-

tion channels such as mobile

and social media. These

approaches provide an effec-

tive way for organizations to

test patient response to both

old and new engagement

tactics, helping them find the

most effective engagement

strategies more quickly and

cost effectively.

Medication non-adher-

ence has become a significant problem for the health care

industry, inflicting harm on patients through poorer health

outcomes and the health care industry through increased

costs. The problem appears to be worsening, in part because

existing preventative engagement and educational approaches

aren’t identifying high-risk patients until it’s too late. New

analytic-based strategies, however, can play an important role

in improving patient engagement initiatives and ultimately

patient adherence. As these strategies take hold and become a

standard industry practice, the health care system and patients

will both benefit from improved medication adherence rates, a

healthier population and reduced expenditure across the health

care spectrum. DTC

References

1 National Council on Patient Information and Education. “Enhancing Prescrip-

tion Medicine Adherence: A National Action Plan” (2007)

2 Norman G. “It takes more than wireless to unbind healthcare.” Presentation at

Healthcare Unbound Conference (2007)

3 Cutler D. & Everett W. “Thinking Outside the Pillbox: A System-wide

Approach to Improving Patient Medication Adherence for Chronic Disease.”

New England Journal of Medicine, 362, 1553-1555 (2010)

4 Medication Adherence Leads To Lower Health Care Use And Costs Despite

Increased Drug Spending, Health Affairs (2011)

Todd Steffes is a vice president at FICO, and the leader of the com-

pany’s health care business unit. For more information on the FICO

Medication Adherence Score, please visit www.fico.com/adherence.

Steffes can be reached by e-mail at toddsteffes@ fico.com.

Figure 2: Personalized Engagement Tactics

Hall of Fame

It’s Time to Celebrate

the Stars of the Industry

Don’t Miss the Chance to Honor these Individuals in Person!

Attend the DTC Hall of Fame Induction Ceremony on October 12, 2011 at the Crowne

Plaza hotel in Fairfi eld, NJ, all a part of the DTC Perspectives fall conference –

Marketing to the Digital Consumer: Pharma Best Practices Present and Future.

Visit our website at www.dtcperspectives.com,

or call us at 973-239-2051 for more information.

Mark Bard

Executive Director and

Co-Founder

Digital Health Coalition

Bill Drummy

Founder and Chief

Executive Offi cer

Heartbeat Ideas

Joan Mikardos

Senior Director Digital

Center of Excellence

Sanofi -Aventis

Nancy Phelan

Executive Director,

Global Communications

Pfi zer

26 | DTC Perspectives • September 2011

I

s there an ideal media strategy to reach and influence a dig-

ital consumer? Is the answer simply intuitive? And does the

answer vary by the disease category? To attempt to discover

the most definitive answer to these questions requires analysis

of DTC categories that share three characteristics: 1) A large

number of branded options, eight or more, 2) Where most

brands use paid media advertising, and 3) Each category using

all four of the most commonly used media strategies, including

TV, print, online display, and brand website.

Study background

The source of data was selected from Phoenix Healthcare’s

Syndicated DTC monthly tracking studies for the first part of

2011. The trackers deploy a method of accurately measuring

advertising exposure to all forms of media advertising each

month, including all branded websites.

The following selective DTC categories were included, to

which most readers of DTC Perspectives magazine could relate

their brand. Data for the months of January through April

2011 was employed in this article, including 13,000 interviews

which involved 31 brands and 146 creatively different ads. In

total, nearly $300 million dollars was spent on the ads tested

for recall of exposure and call to action:

• Lifestyle: Where the patient will choose to ask for and to

use prescription treatment for their purpose, and has the

majority of influence on brand choice; 58 total: 9 TV, 15

Print, 19 Online, 15 Websites;

• Asymptomatic/chronic: Where the need for prescription

treatment is determined through lab work yet the patient

has influence within large choice of brands; 52 total: 11

TV, 17 Print, 16 Online, 8 Websites;

• Symptomatic/chronic: Where patients have differing choices

through various levels of step therapies and where switch-

ing is patient-driven by efficacy to reduce symptoms; 54

total: 4 TV, 20 Print, 22 Online, 8 Websites.

Finding Digital Consumers in a

Sea of Mass Media

How Digital

Consumers

Respond

to Variable

Media Mixes

Winning the battle to drive patient-initiated brand discussion with doctors can quickly focus on the excitable

digital consumers who are so eager in seeking solutions. Using findings from seven syndicated studies, the

authors look at various media strategies to determine successful tactics for reaching the digital consumer in a

sea of mass media.

by J. douglaS Zabor aNd Qi JiaNg

DTC Perspectives • September 2011 | 27

All respondents were classified into digital consumers and

non-digital consumers to focus the analysis on the former

respondent segment. Since each study is a representative

sample of the generalized potential market for each DTC, the

sample of segment of digital consumers is also considered to be

a random sample of that population (see Figure 1).

Simply put, the study design permitted analysts to 1) Deter-

mine precisely which branded advertisements from any media

source a digital consumer was exposed to, and 2) Correlate

variation in advertising exposure to brand-specific behaviors

recommended by the ads. By measuring how actions vary

among patients based on exposure to different media strategies,

it is possible to determine how one medium (or how one spe-

cific creative version of an ad within one medium) provides a

differential contribution to action.

Unlike any other industry where call to action can be as

creative as the core message concepts, the pharmaceutical

industry call to action is regulated by the FDA. Thus, the effi-

cacy of all pharmaceutical ads can be measured comparatively

on proof that exposure to ad resulted in differential behavior

when compared to audience who were not exposed. Those

“Calls to Action” are defined as:

• Talking to your doctor

• Calling an 800 number

• Visiting the brand’s website

Depending on the media configuration used in the month,

each brand was classified into one of four variations of media

utilization:

• Multi-media: Campaigns with branded ads in at least one

mass media (at least TV or national magazine and radio

or newspaper if used), plus online display and the brand’s

website. A total of 10 brands included.

• Mass media: Campaigns with branded ads in at least one

mass media (at least TV or national magazine and radio or

newspaper if used), plus the brand’s website, but no online

display ads. A total of 7 brands included.

• Digital media: Campaigns using only online display ads plus

the brand’s website. A total of 4 brands included.

• Brand site: Brands with no other media besides the brand’s

website. A total of 10 brands included.

For purpose of this analysis, the term campaign means the

aggregation of all creatively unique messages in all media that

month validated by Competitrack along with the branded

website (see Figure 2).

Importance of digital consumers

A digital consumer, for the purpose of this article, is

defined as someone who used the Internet in the last 30 days

to seek information about signs and symptoms, disease infor-

mation, treatments options, prescription medication options

as well as the use of search for brands, for social feedback on

brands from social media, blogs, and including direct brand

site visits. The size of digital consumer market varies in dif-

ferent disease categories. Specifically, the Asymptomatic and

Chronic category has 28 percent of respondents who are

digital consumers, Lifestyle has 45 percent and Symptomatic

has 55 percent.

The patterns intuitively fit the disease impact on the

individual, with those having aggravating symptoms from

a degenerative disease being the most active consumers

of healthcare information on the Internet. Those with an

asymptomatic chronic condition who are placed on long

MEDIA MIXES

Figure 1: Digital Consumer Segment Size of

DTC Category

0%

10%

20%

30%

40%

50%

60%

Asymptomatic &

chronic

Lifestyle Symptomatic, chronic &

degenerative

28%

45%

55%

Figure 2: Media Campaign Types

Multi-media, 10

Mass only, 7

Digital only, 4

Website only, 10

28 | DTC Perspectives • September 2011

term therapy which a physician reviews only periodically, are

the least active. And the lifestyle market is in-between.

A digital consumer is different than a non-digital consumer

in more important ways to pharmaceutical brands than simply

depending more on the Internet for healthcare decision sup-

port. When comparing among branded ad recallers, digital

consumers are significantly more likely to 1) See their physi-

cian in the last three months, 2) Are aware of more brand

choices by name, 3) Discuss more brands as options for treat-

ment with the physician, and, perhaps most importantly, 4)

Are more likely to initiate a discussion about a brand they saw

an ad for than their non-digital counterparts. In combination,

these behavioral attributes make the digital consumer a highly

desirable target for any brand (see Figure 3).