727040 Devondale Murray Goulburn Annual Report 2014

User Manual: 727040

Open the PDF directly: View PDF ![]() .

.

Page Count: 100

We love

dairy foods

Devondale Murray Goulburn

Annual Report 2014

Devondale Murray Goulburn Annual Report 2014

In this Annual Report

2 Performance overview

4 Building a ‘rst choice dairy foods company’

6 MG’s target growth regions

8 From the Chairman

10 Managing Director’s Message

12 Our brands

16 Building world’s best operations

20 Year in Review

26 Board of Directors

28 Executive Leadership Team

30 Corporate Governance Statement

37 Financial Statements

Devondale Murray Goulburn* is Australia’s largest dairy foods

company. In 2013–14, the Company received approximately

3.4 billion litres^, or 37 per cent, of Australia’s milk and generated

sales revenue in excess of $2.9 billion. MG was formed in 1950

and remains 100 per cent dairy farmer controlled, with over

2,500 supplier/shareholders and more than 2,400 employees.

MG is also Australia’s largest dairy food exporter to the major

markets of Asia, the Middle East and North Aica, and the

Americas. MG produces a range of ingredient and nutritional

products, supplies the food service industries globally and its

agship Devondale brand is sold nationally.

* Devondale Murray Goulburn (also MG, the Company or the Co-operative) includes Murray Goulburn Co-operative Co. Limited ABN 23 004 277 089

and subsidiaries. Devondale Murray Goulburn’s Annual Report can be viewed or downloaded om the Company’s website www.mgc.com.au.

^ Includes MG’s majority owned subsidiary, Tasmanian Dairy Products Co Ltd.

Devondale Murray Goulburn Annual Report 2014 1

2008–09

2009–10

2010–11

2011–12

2012–13

2,329,285

2,163,441

2,287,492

2,367,231

2,385,099

2,916,5212013–14

2008–09

2009–10

2010–11

2011–12

2012–13

3,261

2,864

2,827

2,936

3,119*

3,391*2013–14

2008–09

2009–10

2010–11

2011–12

2012–13

746,411

718,542

690,836

739,545

776,634*

784,299*

2013–14

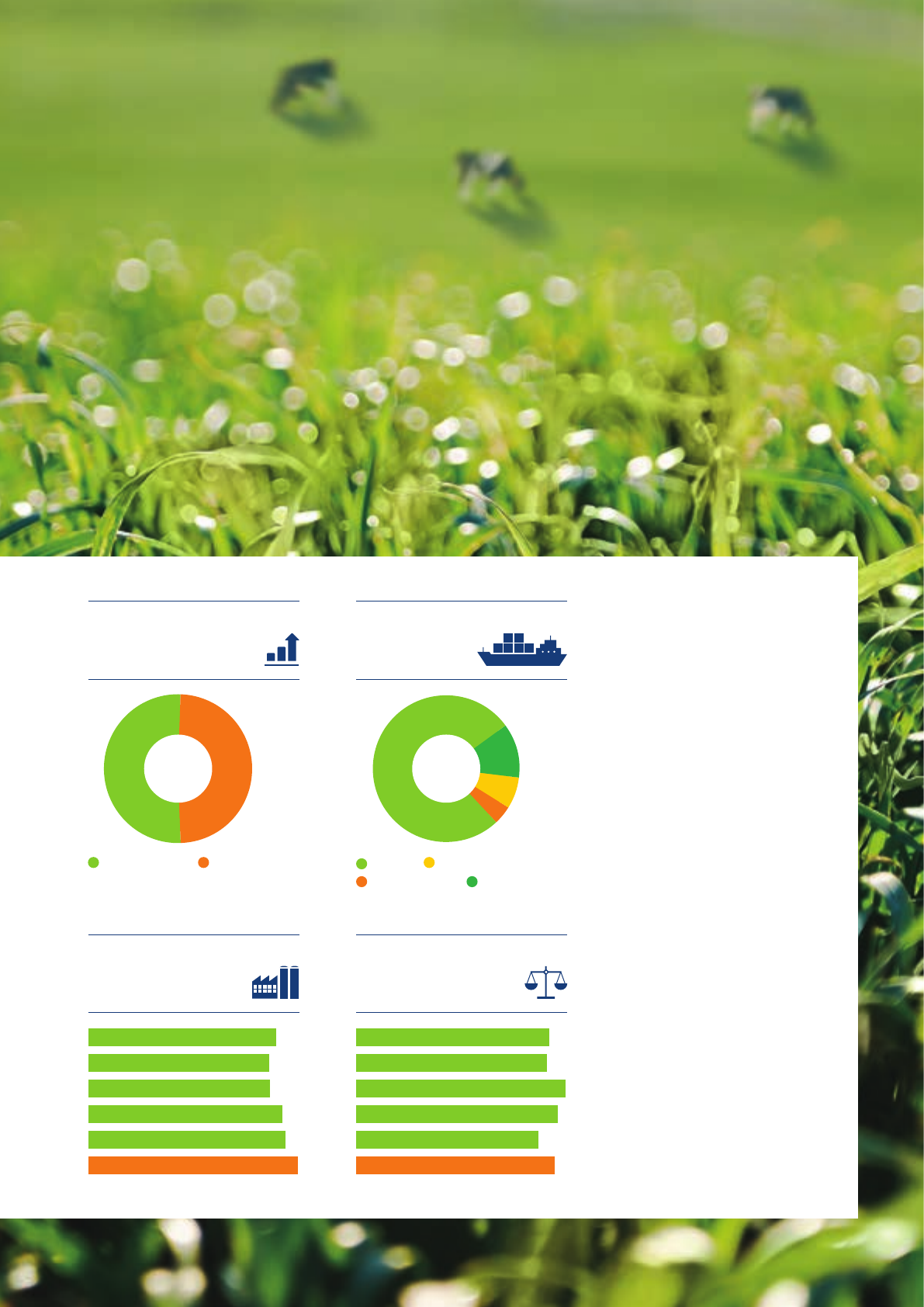

Performance

overview

Strong demand om key markets in Asia and the

Middle East drove prices for world dairy ingredients

to new highs in 2013–14, delivering double digit

revenue growth for MG and a welcome record

nal farmgate milk price for supplier/shareholders.

Year ended

30 June 2014

Year ended

30 June 2013 Change (%)

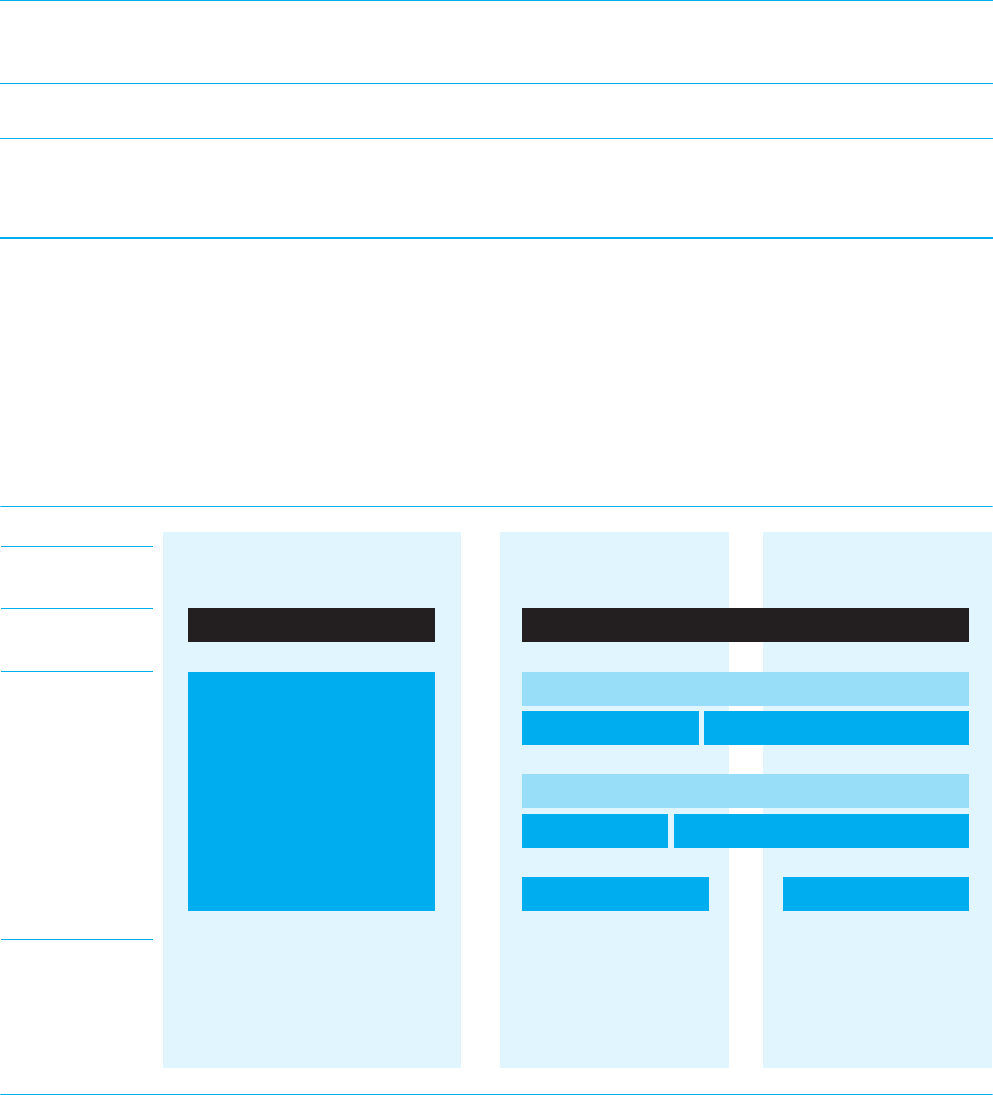

Sales revenue ($ million) 2,917 2,385 22

Reported statutory net prot aer tax ($ million) 29.3 34.9 (16)

Final available milk price ($/kg ms) 6.81 4.97 37

Ordinary dividend declared or paid – per share (cents) 8 8 0

Ordinary dividend declared or paid – total value ($ million) 22.1 21.1 5

Sales revenue

(A$ 000)

Milk intake

(million litres)

Production

(tonnes)

* Includes MG’s majority owned subsidiary, Tasmanian Dairy Products Co Ltd.

2 Devondale Murray Goulburn Annual Report 2014

2008–09

2009–10

2010–11

2011–12

2012–13

727,040

719,003

788,469

759,035

686,487

745,891

2013–14

2008–09

2009–10

2010–11

2011–12

2012–13

1,577,529

1,519,281

1,530,134

1,632,228

1,659,054

1,763,436

2013–14

Asia 77% Middle East/Aica 7%

e Americas 4% Other 12%

Total assets

(A$ 000)

2013–14 Sales revenue

Total revenue

$2.9 billion

(including MG Trading stores)

Equity

(A$ 000)

2013–14 Export volume

Total volume

324,000 tonnes

International 51% Domestic 49%

Devondale Murray Goulburn Annual Report 2014 3

Building a ‘rst choice

dairy foods company’

(i) In order to measure an increase in underlying milk price, rather than use the available milk price paid to suppliers each year, an implied milk price is used, which is based on forecasted

available milk price om FY2012 plus the value of annual dividends. e available milk price targets are normalised for the movements in dairy commodity prices, foreign exchange and

impacts of ination as well as other one o items such as opening inventory.

(ii) Rabobank 2014.

Vision and Strategy 2017

At MG, our goal is to li farmgate returns by at least $1.00 per

kilogram of milk solids(i) by 2017 and drive industry growth.

Our ‘Vision and Strategy 2017’ sets down our plan to get there –

outlining our vision to become a rst choice dairy foods company

for farmers, customers and consumers and our two strategic

focal points: Operational Excellence – our strategy to reshape our

business so that we can become the most ecient supplier of

dairy foods; and Innovation – to drive our shi to higher value

products in the growth categories of nutritional powders, consumer

cheese and dairy beverages.

e strategy recognises that global demand for dairy foods is

strong and growing, particularly in Asia where dairy decit regions

are expected to import an additional 25 billion litres by 2020(ii).

It acknowledges that milk production in Australia has declined

to such an extent that Australia is at risk of losing relevance in

global trade and that farmgate returns need to be higher if MG

is to encourage existing and new supplier/shareholders to grow

milk production once again.

MG intends to invest up to $500 million over the next ve years

to ensure we have the right manufacturing capability and capacity

to respond to the extraordinary growth opportunities ahead for

Australian dairy.

e strategy aims to deliver a $1.00 per kilogram of milk

solids(i) li in farmgate returns to benet our more than 2,500

supplier/shareholders across Australia and cement MG’s position

as Australia’s leading dairy foods company, a co-operative

100 per cent controlled by dairy farmers, dedicated to maximising

the price paid to farmers for their milk. By improving farmgate

returns and farm protability, MG believes farm business owners

will invest and increase milk production. Historically growth

of three per cent per annum has been achievable.

Preserve a

�positive image of�

Australian dairy

Increase

competitiveness

of Australian

dairy farming

Facilitate on-farm�

investment to�grow

milk supply

>3% pa

Australian

milk supply

growth

(equivalent to

incremental EBIT

of ~$300m pa

by FY2017

over FY2012)

$1.00

/kg ms(i)

4 Devondale Murray Goulburn Annual Report 2014

m

a

n

u

f

a

c

t

u

r

i

n

g

S

t

a

t

e

-

o

f

-

t

h

e

-

a

r

t

s

y

s

t

e

m

s

E

ffi

c

i

e

n

t

p

r

o

c

e

s

s

e

s

/

a

n

d

f

o

r

m

a

t

s

R

i

g

h

t

p

r

o

d

u

c

t

s

O

p

e

r

a

t

i

o

n

a

l

E

x

c

e

l

l

e

n

c

e

I

n

n

o

v

a

t

i

o

n

First choice dairy

foods company for

farmers, customers

and consumers

1st

P

r

o

d

u

c

t

s

C

a

t

e

g

o

r

i

e

s

C

h

a

n

n

e

l

s

G

e

o

g

r

a

p

h

i

e

s

s

y

s

t

e

m

s

Our Vision

and Strategy

Operational Excellence

Drive operating excellence

to become the most ecient

supplier of dairy foods.

Innovation

Shi to higher value dairy products

porolio with a focus on nutritional

powders (baby, toddler formula),

consumer cheese and dairy beverages.

5

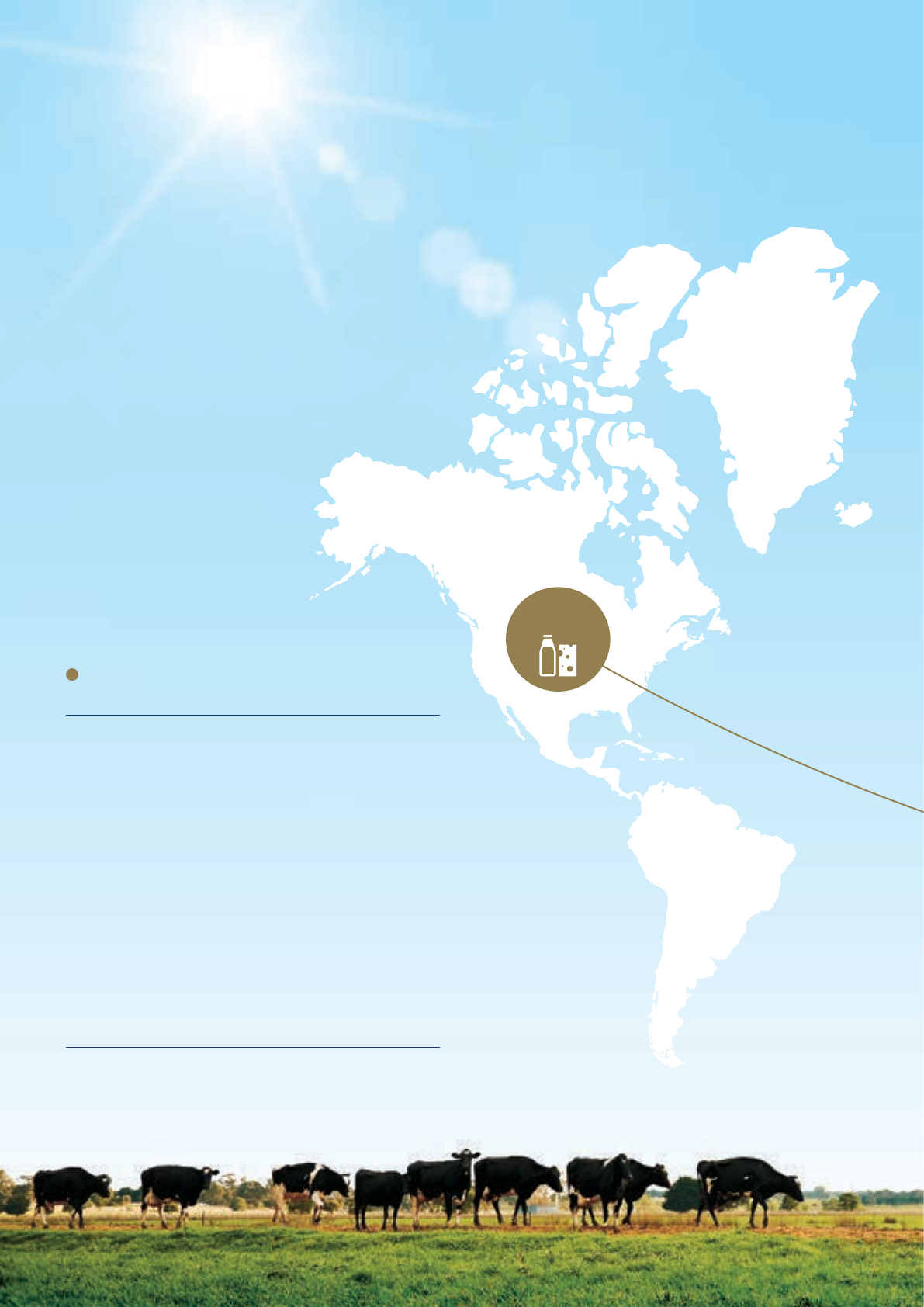

Middle East/

North Aica

China

South East

Asia

Europe

Pacific

Islands

e

Americas

Japan

Devondale Murray Goulburn’s target regions

MG’s target

growth regions

We have our sights set on the growth

markets, particularly South East Asia,

China and the Middle East and North

Aica where the outlook for dairy foods

is strong. MG will ‘look north and go north’,

particularly to Asia, which is expected

to be the growth engine for dairy food

demand for many years to come.

3.4 billion*

litres of milk received

784,299*

tonnes of dairy product produced

324,000

tonnes of dairy product exported

31

countries where MG products are sold

* Includes MG’s majority owned subsidiary, Tasmanian Dairy Products Co Ltd.

6 Devondale Murray Goulburn Annual Report 2014

Middle East/

North Aica

China

South East

Asia

Europe

Pacific

Islands

e

Americas

Japan

Devondale Murray Goulburn Annual Report 2014 7

e past year has been an exceptional

season for Devondale Murray Goulburn’s

supplier/shareholders, who have enjoyed record

farmgate milk prices and excellent seasonal

conditions. 2013–14 was also a milestone year

for MG, as we took decisive action announcing

signicant new inastructure investment,

witnessed further growth in MG’s milk intake

and saw the Co-operative maintain its righul

place as the dairy partner of choice for farmers.

It was an outstanding year for MG. e nal milk price was

$6.81 per kilogram of milk solids on an available weighted

average basis, a 37 per cent increase over last year,

delivering a welcome boost to farm incomes.

e Board declared an unanked nal dividend of eight per cent

on ordinary shares and ve per cent for B and C class preference

shares. For ordinary shares, this equates, for the average

shareholder, to $0.09 per kilogram of milk solids, in addition

to the farmgate milk price paid to supplier/shareholders. In

addition, an unanked special dividend of $0.25 per A class

preference share was paid to A class preference shareholders

as part of the cancellation of those shares.

Total payments to supplier/shareholders(i) for the year were

more than $1.7 billion, representing 61 per cent of MG’s sales(i),

compared to 50 per cent of sales last year. When combining the

nal milk price of $6.81 with the dividend of eight cents per share,

the total return to supplier/shareholders was on average

$6.90 per kilogram of milk solids.

Net prot aer tax was $29.3 million, down om $34.9 million

in the previous year.

Pleasingly, MG’s milk supply grew strongly by eight per cent in

2013–14 to 3.4 billion litres(i), against a backdrop of at Australian

milk production growth of 0.4 per cent(ii). MG’s share of Australia’s

milk pool is now 37 per cent, up om 33 per cent a year ago with

milk supply growing across all regions, particularly in western

Victoria as the region recovers om a poor season in 2013. MG’s

milk supply was also boosted by our entry into the New South Wales

(NSW) milk market – where in our rst 10 months we collected

approximately 100 million litres om new member suppliers.

Investing for future growth

In 2012, the Board endorsed a ve year vision and strategy for

our Co-operative to transform MG and build a ‘rst choice dairy

foods company for farmers, customers and consumers’ –

through achieving operational excellence and driving innovation.

Since then, MG has focused on actioning that strategic plan and

announced a number of investments. ese investments are

being made to upgrade ageing inastructure and ensure we

have world’s best manufacturing capability to meet and serve the

growing needs of international consumers and customers. ey

include the $160 million investment to build our two chilled milk

processing facilities in Melbourne and Sydney; and $19 million

for two new high speed UHT lines at Leongatha – which together

represent the most signicant investment in dairy inastructure

undertaken in Australia for at least a decade.

Dening the right capital structure for MG

Recognising the scale of investment required to reinvigorate

and revitalise MG, in mid-2013 the MG Board announced that

a comprehensive capital structure review would be undertaken

to determine the best way to prudently fund the transformation

of MG’s manufacturing footprint.

MG has identied that capital investments up to $500 million will

be required over the next three to ve years to rejuvenate our

manufacturing and supply chain inastructure.

e capital structure review was instigated to examine the

best way to raise these funds and involved a comprehensive

review of all available options, including: increasing bank debt;

sale and leaseback of assets; retention of prots; raising additional

equity om supplier/shareholders; and raising capital om

external investors.

e review determined that the recommended proposed capital

structure – a funding model that maintains 100 per cent farmer

control, but allows external investors to invest into MG via a

separate, non-voting unit trust – is the most eective and ecient

capital structure for MG to pursue.

From the Chairman

(i) Includes Tasmanian Dairy Products Co Ltd.

(ii) Dairy Australia.

8 Devondale Murray Goulburn Annual Report 2014

Since rst describing the recommended capital structure

at the 2013 Annual General Meeting (AGM), MG has undertaken

an extensive consultation process with MG supplier/shareholders

to discuss the proposal and ensure it meets the needs of the

Co-operative now and into the future. is process has involved

three rounds of supplier consultation meetings across all dairy

regions and feedback om suppliers has resulted in a number

of modications being made to the proposal. A fourth round of

capital structure supplier meetings is planned towards the end

of the 2014 calendar year.

roughout the consultation process with suppliers, a key area

of interest has been how we align the interests of MG supplier/

shareholders and external investors. MG has developed a Farmgate

Milk Price (FMP)/dividend model that retains FMP as the primary

measure of success and aligns higher dividends with higher FMP.

I look forward to further engagement with supplier/shareholders

on the best capital structure for MG and am condent that we will

be in a position to present a nal, recommended capital structure

to supplier/shareholders for approval in the year ahead.

A class preference shares

In early June 2014, we were very pleased that both MG’s

ordinary and A class preference shareholders passed the special

resolutions presented at the meetings of the respective shareholder

groups. Shareholders voted to cancel all the A class preference

shares on issue and pay A class preference shareholders

$1.25 per share in return. e A class preference share was

an old class of share that had been closed to new shareholders

for more than a decade. is class consisted of mainly very

small shareholdings, 20 per cent of which could no longer be

contacted. In these circumstances, the Board’s view was that

a cancellation of the A class preference shares was the right

way forward and represented the best outcome for both A class

preference shareholders and our current supplier/shareholders.

Adding balance sheet strength

During 2013–14, the Company’s balance sheet grew in strength

due in large part to the sale of MG’s stake in Warrnambool Cheese

and Buer Factory Company Holdings Limited (WCB), but also

through the sale and leaseback of the Integrated Logistics Centre

(ILC) at Laverton.

e WCB sale delivered cash proceeds of $93 million and

the sale and leaseback arrangement for the ILC delivered

$93 million in additional cash ow.

ese proceeds were welcome and support MG’s plans to

reinvest in our business, grow market share in Australia and

expand internationally.

While we were disappointed to have missed out on the opportunity

to acquire WCB, the sale of our stake represented an excellent

nancial outcome for the Company and we remain proud of the

role we played in the bidding process, to drive a genuine auction

for these important Australian dairy assets.

Giving back to the community

In addition to the primary role MG plays in supporting

Australia’s dairy farmers through driving farmgate milk prices

higher, the Company also looks for opportunities to support

the broader community.

For the past three years, MG has partnered with Foodbank to

support its work to match the food industry’s surplus food with the

welfare sector’s need. MG donates quality, nutrition-rich products,

primarily UHT milk, that have a real, daily impact on individuals

and communities. During the year, MG donated the equivalent of

761,958 kilograms of dairy foods, which went towards the provision

of more than one million meals to satis the immediate hunger

needs of vulnerable Australians. MG also donated $110,000 to

an industry-funded eort to supply milk to underprivileged families.

In May, we announced a cash contribution of $300,000 to support

the wider Warrnambool community’s eorts to raise $5 million to

build a specialist cancer centre in the western region. e cancer

centre will ensure those ghting cancer in the region will no longer

have to travel long distances for specialist treatment.

A high performing team

In closing I would like to take this opportunity to thank and pay

tribute to the management and sta of MG for the role everyone

has played in this remarkable year for the Company. On behalf

of the Board, I thank you for your service and dedication to the

Co-operative. In particular, I wish to acknowledge and thank

Gary Helou and his management team for their strong leadership.

ere was one change to the composition of the MG Board during

the year. We welcomed new Director Duncan Morris, who was

elected to the Board via the western region, following the retirement

of Don Howard aer 16 years of service. During his time on the

Board, Don oversaw signicant change at MG and in our industry

and was always a passionate advocate for change within MG. We

are indebted to his service.

I also want to thank my fellow Directors for their ongoing support

and dedication to MG in a year when their services were called

on more equently than is usually the case.

Finally, I wish to extend my thanks to you – our supplier/shareholders.

roughout the course of the year we have sought and received

your support as we continue on our path to revitalise and

reinvigorate MG so that we are well placed to take advantage

of the extraordinary opportunities for Australian dairy.

I look forward to welcoming you to the AGM in November.

Philip Tracy

Chairman

Devondale Murray Goulburn Annual Report 2014 9

Managing Director’s Message

At MG, we are commied to delivering a $1.00 per kilogram

of milk solids(i) increase in the farmgate milk price by 2017 and

we are the only Australian dairy foods company to publicly set

such a target.

Having launched MG’s ‘Vision and Strategy 2017’ two years ago

– our ve year plan to drive growth in the farmgate milk price

by becoming a ‘rst choice dairy foods company for farmers,

customers and consumers’ in our chosen markets – we have

made good progress.

Our Vision and Strategy 2017 is grounded in the knowledge that

if Australia is to assume its righul place as a globally relevant

dairying nation, we must grow milk production enabling supply

to meet the rising demand for dairy foods, particularly in

international markets. Most especially, we must ‘look north and

go north’ as Asia is clearly the epicentre driving growth in demand

for high quality dairy foods. Now and into the future MG and

Australian dairy have the prime opportunity to build sustainable

long term growth given our proximity to these markets and

impeccable record as a source of quality, clean and safe food.

is opportunity is too great to pass up.

But we know we can’t just ‘ick the switch’ and double milk

production overnight. It will take investment and a sustained

increase in the farmgate milk price to motivate Australia’s

farmers to invest in their businesses and grow production.

Our Vision and Strategy 2017 is our plan to get there. It has

two critical strategic focal points: Operational Excellence – our

strategy to reshape our business so that we can become the most

ecient supplier of dairy foods; and Innovation – to drive our shi

to higher value products in the growth categories of nutritional

powders, consumer cheese and dairy beverages.

To support our strategy, we have identied capital investments

of $500 million over the next three to ve years to invest in cuing

edge, automated manufacturing technology to drive eciency and

innovation. ese are critical investments to beer connect our

nutritional powders, consumer cheese and dairy beverage supply

chain assets with our target markets.

To fund this level of investment, we reviewed available funding

options and recommended that MG considers a new capital

structure, which maintains our co-operative structure and

100 per cent farmer control and raises external capital via the

issue of units, which would be listed on the Australian Securities

Exchange (ASX). We believe this is an innovative funding structure

to raise non-voting capital, that delivers prot related returns

to external investors, but keeps 100 per cent control in the hands

of MG’s supplier/shareholders.

is approach will diversi MG’s source of investment funds

away om traditional bank debt and deliver MG the nancial

strength, exibility and stability to invest in our growth strategy.

A strong year for MG

Looking at MG’s nancial performance, it was an outstanding

year for the Company. roughout the year, global demand for

dairy foods remained strong and prices for key dairy ingredients

such as whole milk powder stayed at near record levels for an

unprecedented period. ese external factors, combined with our

continued focus on improving performance through reducing costs

and investing to support innovation and value growth, underpinned

the full year result and drove a record high farmgate return.

As is our custom, MG opened early and high, seing a

benchmark for other industry players to follow and giving our

supplier/shareholders condence for the season ahead. e

nal weighted average milk price for the 2013–14 season was

$6.81 per kilogram of milk solids, a 37 per cent increase on

the previous year and a record price for MG.

An unanked nal dividend of eight per cent on ordinary shares

and ve per cent for B and C class preference shares was also

declared. For ordinary shares, this equated on average to

$0.09 per kilogram of milk solids, in addition to the farmgate milk

price paid to supplier/shareholders. An unanked special dividend

of $0.25 per A class preference share was paid to A class

preference shareholders as part of the cancellation of those shares.

It has been a strong year for Devondale

Murray Goulburn and the Australian dairy

industry. Aer a decade of challenges, Australian

dairy roared back to life, spurred on by strong

milk prices, heightened interest in Australia’s

dairy assets and a reinvigorated MG advocating

for industry growth and higher farmgate returns.

(i) In order to measure an increase in underlying milk price, rather than use the available milk price paid to suppliers each year, an implied milk price is used, which is based

on forecasted available milk price om FY2012 plus the value of annual dividends. e available milk price targets are normalised for the movements in dairy commodity prices,

foreign exchange and impacts of ination as well as other one o items such as opening inventory.

10 Devondale Murray Goulburn Annual Report 2014

Total payments to supplier/shareholders(ii) for the year were

more than $1.7 billion, representing 61 per cent of MG’s sales(ii),

compared to 50 per cent of sales last year. When combining the

nal milk price of $6.81 with the dividend of eight cents per share,

the total return to supplier/shareholders was on average

$6.90 per kilogram of milk solids.

MG’s milk supply grew strongly by eight per cent in 2013–14

to 3.4 billion litres(ii), compared to a stagnant total Australian

milk production. Our share of Australia’s milk pool increased

to 37 per cent, up om 33 per cent a year ago with milk supply

growing across all regions, including NSW, South Australia

and Tasmania.

Net prot aer tax was $29.3 million, slightly down om

$34.9 million in the prior year. Our balance sheet was strengthened,

with total equity increasing by $59 million, including a $36 million

gain om the sale of our stake in WCB, which was recognised

directly in equity. As at 30 June 2014, MG had total assets

of $1.76 billion and total equity of $746 million.

Strong revenue growth of 22 per cent to $2.9 billion was delivered

om across our businesses, particularly in international exports

where we saw 30 per cent growth year-on-year to $1.5 billion.

Exports now account for more than 51 per cent of MG’s revenue.

Strong growth was delivered in the strategic segment of nutritional

powders, up 19 per cent, as well as a 77 per cent growth

in international consumer and food service dairy foods.

Our achievements

Across MG, the team continued the foundation work that began in

2012–13 to ensure the Company is well positioned to capitalise on

the signicant opportunities we see ahead for growth in dairy foods.

A year of construction to build two new state-of-the-art chilled

milk processing plants culminated in the ocial opening in July

of the Melbourne plant, with Sydney commencing operation

in early August.

ese facilities are the new home of Devondale’s daily pasteurised

milk brand and the processing base for the groundbreaking

10 year agreement to supply chilled milk for Coles’ private label.

Both sites employ world-leading technology and quality standards

that will assist in positioning MG as the nation’s most ecient

producer of daily pasteurised milk – a market that currently

accounts for around 20 per cent of total Australian milk production.

During the year we also delivered on a number of previously

announced capital investments including $19 million to increase

UHT capacity at Leongatha, $5 million to strengthen our

consumer buer capability at Koroit and $2 million to increase

cheese capacity at Cobram.

With these investments commissioned and operational, our focus

now is on delivery of the three new capital projects announced

in May. Worth a combined $126 million, these projects will further

support transformation of MG’s manufacturing footprint. ey include:

• $74 million investment in consumer cheese at Cobram;

• $38 million in infant nutrition at Koroit and Cobram; and

• $14 million in dairy beverages at Edith Creek.

Together they will deliver world-leading technology with

state-of-the-art automation for processing and packaging a range

of dairy foods destined for Asian and Australian consumers.

Innovation is a central focus. We are investing in our brands

and supply chain to ensure we can navigate a new path to

meet and serve the growing needs of farmers, consumers

and customers for Australian made dairy foods.

At home in Australia, we further strengthened our agship

Devondale brand, with new TV advertisements to support UHT,

consumer cheese and the launch of Devondale Smoothies. ese

eorts have had a clear impact with Devondale being recognised

during the year as a top 15 Australian brand in the annual list of

the nation’s top 100 brands, compiled by Brand Finance Australia.

In international dairy foods, a new team with extensive experience

in Asian markets was recruited to support our retail, food service

and private label business in Asia. is team will be key to building

connectivity into these markets and leveraging the inastructure

investments we are making to customise dairy foods to suit

dierent market and customer requirements. We also launched

Devondale UHT in Vietnam and are on track to introduce a new

consumer convenience UHT oering specically tailored

to China in 2014–15.

Building a safe work environment

Our commitment to building a safe workplace remains a priority.

We have invested signicantly to improve health and safety across

all areas of MG and to ensure that every member of our team has

had safety training so that we build a shared understanding of the

role everyone plays in creating a safe workplace. Since launching

our safety program Goal Zero, last year, we have seen a vast

improvement in our safety record and while I commend the MG

team for this strong turnaround, our goal remains rm – zero

injuries at MG.

In closing, I would like to pay tribute to and thank the incredible

people behind the Company. Firstly, my sincere thanks to our

Chairman, Philip Tracy, and our Board of Directors – whose

experience and counsel I value highly. To the broader MG team,

thank you. I am indebted to you for your passion, hard work and

commitment to the business as we continue our transformation

and pursue growth.

Finally, to the farming families across Australia who support

the co-op ideal and entrust their milk to MG, thank you for

your ongoing support and be assured we remain focused and

commied to driving sustainable growth in the farmgate milk price.

Gary Helou

Managing Director

(ii) Includes Tasmanian Dairy Products Co Ltd.

Devondale Murray Goulburn Annual Report 2014 11

Our brands

Australian milk is predominantly produced

on pasture-based systems where dairy cows

graze esh green pastures every day.

Retail Ingredients and Nutritionals

12 Devondale Murray Goulburn Annual Report 2014

Farm services Joint ventures

Devondale Murray Goulburn Annual Report 2014 13

Who are these caretakers of the

morning, who harvest liquid gold*…

At Devondale Murray Goulburn, we

are a proud co-operative of more than

2,500 Australian dairy farmer/suppliers

who join together each and every day

to produce 37 per cent of Australia’s

nest milk for the world to enjoy.

* Excerpt om Ode to the Dairy Farmer by Robbie Brammall.

14 Devondale Murray Goulburn Annual Report 2014

Devondale Murray Goulburn Annual Report 2014 15

Building world’s

best operations

We have begun the largest investment in

dairy inastructure undertaken in Australia

for more than a decade, as we transform

Devondale Murray Goulburn and pursue

our goal to become the nation’s most

ecient producer of dairy foods.

16 Devondale Murray Goulburn Annual Report 2014

Across MG we are investing in the future of the Australian

dairy industry to deliver higher farmgate returns for our

supplier/shareholders. Several key investment projects were

commissioned during the year and a further $126 million investment

in manufacturing capability and capacity was announced.

MG has commissioned its new world class Melbourne and Sydney

chilled milk processing plants. e plants were designed and built

in around 18 months and utilise the latest in milk processing and

lling technology, operating at high speeds with minimum labour

and energy requirements.

Known as the Devondale Dairy Beverages Centres (Melbourne

and Sydney) the plants use world-leading technology and quality

standards that will assist in positioning MG as the nation’s most

ecient producer of daily pasteurised milk, thereby delivering

strong ongoing returns to MG’s dairy farmer/shareholders.

At Koroit (western Victoria), MG’s investment of $5 million to build

a new retail buer line was commissioned in November 2013 and

is operating at capacity servicing the requirements for Devondale

buer in Australia and international markets. Two new high speed

UHT lines at Leongatha were also commissioned in 2013–14 and

are fully operational.

e year also saw a comprehensive review of MG’s existing

manufacturing footprint. Consequently further investments in key

inastructure were announced to ensure MG has the capability

and capacity it needs to meet growing demand for Australian

made dairy foods, particularly in international markets. ree new

capital projects worth a combined $126 million will be undertaken

at the Company’s existing sites over the next 12 to 18 months and

involve investment in world-leading technology with state-of-the-art

automation for processing and packaging a range of dairy foods

destined for Asian and Australian consumers. e projects

announced were:

• A $74 million investment at Cobram to build a world class

cheese cut and wrap facility to serve Australian and Asian

consumer and food service markets.

• A $38 million investment at Koroit and Cobram to increase

capacity for production of nutritionals for growing international

infant nutrition markets.

• A $14 million investment at Edith Creek to install and commission

a exible small format cup and bole lling line to commercialise

a range of dairy beverage products for consumer markets in

Australia and Asia.

Devondale Murray Goulburn Annual Report 2014 17

Our new Devondale Dairy Beverages

Centres in Melbourne and Sydney

were designed, built and commissioned

in 18 months. The chilled milk facilities

are world-class, featuring complete

end-to-end automation, utilising the latest

milk processing and lling technology

to operate at high speeds with energy

eciency. Each plant is capable of

processing 50,000 litres of milk per

hour and producing 150 million litres

of chilled milk per year.

18 Devondale Murray Goulburn Annual Report 2014

Devondale Murray Goulburn Annual Report 2014 19

Year in Review

Business Operations

In April 2014, Business Operations was formed bringing together

MG’s Operations function and the Ingredients and Nutritionals

business. e newly created Business Operations unit also has

responsibility for ensuring MG’s workplaces are safe and that

MG’s product quality, manufacturing eciency and environmental

practices position MG as the dairy foods supplier of choice with

farmers, customers and consumers.

Building a safe workplace for our people

At MG our approach to safety begins with a belief that in any

circumstance harm and damage can be prevented and that

as an organisation we have a responsibility to do everything

practicable to prevent workplace injury and illness.

Our Goal Zero safety program is designed to drive safety

awareness, improve our health and safety performance and

ultimately eliminate workplace injury across all our workplace

locations including manufacturing sites, MG Trading stores,

eld services and oce locations.

Since launching Goal Zero in 2012–13, MG has invested in

safety training for people across all levels of the organisation and

improved safety procedures and measures across all sites. During

the year, MG’s second ‘stop for safety’ one-hour program was

held focusing on Goal Zero initiatives and to raise awareness and

further identi opportunities to improve safety. A two-day Safety

Leadership Conference was also held for people managers and

compulsory safety training at senior and middle management

levels was rolled out.

is year, these initiatives have supported further signicant

reductions in lost time injury equency rates and lost time injuries

and while we are very pleased with the improvement in our safety

record, MG will not rest until we have zero workplace injuries.

Quality and cost management remain a core focus

In line with MG’s aim to become Australia’s preferred supplier

of dairy foods, Business Operations continuously seeks

opportunities to improve quality, productivity and eciency.

During the year, our drive for greater automation and process

control across operations resulted in further signicant reductions

in both cost and quality claims and led to an additional $50 million

in cost savings being achieved.

Investing in milk collection inastructure

e roll out of owmeters and retractable hoses commenced

at MG during the year, with Gippsland suppliers the rst to have

collections measured by owmeters. e northern and western

regions are scheduled to follow in the second half of 2014.

e introduction of owmeters across the tanker eet brings

MG into line with global industry best practice and delivers a

range of commercial, quality and safety benets, including more

accurate measurement of milk volume, improved sampling and

a safer environment for tanker drivers and suppliers.

MG also invested in 52 new Volvo prime movers and 22 tankers,

which were on the road during the peak season, assisting with

operational eciencies and at the same time delivering improved

safety benets for MG drivers.

Volvos feature market-leading technology, including advanced

electronic braking systems and an electronic stability program

to help prevent the potential for trac accidents and tanker

rollovers. ey also lead the way in cabin strength for driver

safety and are environmentally iendly, complying with ‘Euro 5’

emission standards.

20 Devondale Murray Goulburn Annual Report 2014

A sustainable business into the future

At MG, we maintain a strong commitment to building a sustainable

business, which goes beyond simply ensuring we comply with

relevant legislation.

We want to be industry leaders when it comes to sustainable

performance and have identied 10 key areas to focus our eorts

including: environmental noise, air emissions, odour, surface

water, land and groundwater, waste, energy use, water use,

ora and fauna, and greenhouse gas.

Aspirational targets have been set and during the year MG

continued to see a positive progression towards achieving our

targets. In particular, MG delivered a substantial reduction

in energy consumption and greenhouse gas emissions despite

an increase in production output.

A number of initiatives have driven these positive results

including the impact of a porolio of energy and greenhouse gas

abatement projects, the requirement of sites to reduce energy

by ve per cent per year, the Energy Blitz program and subsequent

eciency activities.

During 2013–14, we continued to be a signatory to the Australian

Packaging Covenant (APC). e APC was established by industry

and government to reduce the impact that packaging has on the

environment, particularly on packaging going to domestic landlls.

Ingredients and Nutritionals

MG’s Ingredients and Nutritionals business is a globally

recognised and respected supplier of bulk and customised dairy

ingredients and nutritional milk powders, primarily in the key

markets of North Asia, South East Asia, Australia, Sri Lanka and

USA. Today, MG is the world’s second largest supplier of dairy

ingredients, with the business accounting for almost half of

MG’s annual revenue.

Strong trading conditions led to price growth across all

commodity groups during the year, largely driven by increased

demand for milk powder om China and buer om Russia.

For MG’s Ingredients and Nutritionals business it was a very

strong year with net sales revenue in 2013–14 up 23 per cent

to $1.6 billion.

MG’s infant nutrition Cobram facility was one of the rst Australian

manufacturers approved by the Chinese authorities to supply

infant formula into China. is followed a comprehensive review

by Chinese authorities of infant formula manufacturers and has

led to tighter regulations around infant nutrition. Our Chinese plant

in Qingdao also received certication, providing MG with both

a premium export range and a locally manufactured range

of infant nutrition products.

MG made good progress towards establishing its reputation

as a reliable supplier of nutritional powders to world-leading

nutritional customers. e investments announced at Cobram and

Koroit to upgrade our powders capability and capacity will also

support MG to capitalise expected growth for nutritional powders.

e MG Ingredients team also continued to leverage long standing

customer relationships and its intimate understanding of customer

needs to develop ideal ingredient solutions for customers.

Devondale Murray Goulburn Annual Report 2014 21

Year in Review

MG Dairy Foods

MG Dairy Foods encompasses all consumer and food service

sales, as well as marketing and innovation, in both domestic and

international markets. e business is charged with taking our

brands to the world.

Dairy Foods Australia

In Australia, where there are multiple dairy companies competing

in a low growth dairy market, trading conditions remain competitive.

In this environment, MG seeks to dierentiate itself om other

dairy companies through maintaining strong relationships with

key customers and investing in brand innovation and marketing

support to drive sales growth.

Despite a challenging trading environment, with continuing food

deation impacting margins and further growth of private labels

leading to deep discounting amongst branded products, MG was

able to deliver double digit net sales revenue and volume growth

in 2013–14. Sales growth was underpinned by the ongoing

strength of MG’s agship Devondale brand, growth across the

Liddells range, increased private label volumes, and continued

strong growth in food service sales.

In the domestic market, MG invested behind its key dairy

brands – Devondale and Liddells – to drive ‘cut through’ with

consumers and to build a point of dierence. For Devondale,

new television advertisements were released to support the

Devondale range of products – om UHT though to cheese

slices and buer. e advertisements use humour to highlight

everyday household challenges, such as running out of milk,

and provide a Devondale solution.

e launch of Devondale Smoothies was an important extension

of the brand. e product is an example of the work MG is doing

to expand and extend the dairy category in Australia to drive

growth. Smoothies were developed in response to research that

showed that consumers, particularly mothers, wanted a great

tasting dairy product for their children that is highly nutritious

and low in sugar.

For Liddells, it was another year of strong sales growth. e brand

continues to resonate with consumers and is now the number one

lactose ee dairy brand in Australia. Given its success, several

brand extensions were launched, including Liddells chilled milk,

cream cheese and cheese shred, with more new products

planned for the year ahead.

Dairy Foods International

Dairy Foods International was established in 2012–13 to drive

growth of MG’s consumer dairy foods business in China,

South East Asia, the Middle East and the Pacic. e business

has focused on developing customised products to meet the

sophisticated needs of consumers and establishing product

distribution for consumers in these regions.

During the year, Devondale UHT milk was relaunched in Vietnam,

supported by a marketing campaign to communicate the unique

benets of Australian milk. In China, where Devondale UHT is an

established brand, sales continue to grow strongly and it is one

of the country’s biggest selling imported milk brands.

New cheese and buer products were also launched in Singapore,

Malaysia and Hong Kong and a dedicated team was recruited

to focus on building MG’s food service business across Asia.

22 Devondale Murray Goulburn Annual Report 2014

8%

increase in MG’s milk intake

37%

of Australia’s total milk supply

20%

growth in MG Trading stores’ sales

Year in Review

Supplier/Shareholder Relations

MG’s Shareholder Relations function oversees milk supply,

commercial raw milk sales and purchases, MG Trading,

shareholder services and corporate aairs.

Milk supply received exfarm increased by eight per cent in

2013–14 to 3.4 billion litres, including the southern milk pool, the

NSW/Sydney region and Tasmania(i). is represents exceptionally

strong growth when compared to Australia’s national milk pool,

which grew by 0.4 per cent and led to MG’s market share growing

by four percentage points. MG now represents 37 per cent of

Australia’s total milk supply.

Importantly, milk supply grew across all supply regions. In northern

Victoria and southern Riverina milk intake was up 1.8 per cent,

Gippsland was 3.3 per cent higher and in the western region,

which includes western Victoria and South Australia, milk supply

grew strongly, up eight per cent on the prior year.

Since announcing MG’s entry into the NSW/Sydney region in

mid-2013, MG has received an overwhelming response om dairy

farmers, with approximately 50 per cent of dairy farm businesses

in the region choosing to join the Co-operative.

MG’s majority owned subsidiary Tasmanian Dairy Products Co Ltd

also continued to grow milk supply in northern Tasmania om its

dedicated group of suppliers.

Improvements to MG’s quality structure

Making high quality and safe dairy foods is vital to MG and milk

quality at the farmgate is an important element of this outcome.

Accordingly, during 2013–14 MG completed a comprehensive

review of our raw milk quality systems, which included feedback

om our supplier consultative groups. e review showed that

the great majority of MG suppliers produce high quality milk for

most of the year. Following the review, the Board and management

recommended changes to the system including a move om ve

quality bands to four, aligning MG’s quality bands with the end use

of suppliers’ milk.

Supporting the Next Generation

MG announced the Next Generation package in 2012–13 to address

some of the key barriers to growth, including access to capital

and skilled labour. In 2013–14, the rst full year of operations

for the package, more than $50 million in investment in dairy

farm businesses has been facilitated with a number of suppliers

accessing one or more of the suite of Next Generation initiatives:

nancial support for young farmers, farming families and new

entrants seeking to grow their business or enter the industry;

access to employment and immigration resources to address

labour market shortages; and leasing partnerships through

MG’s preferred investment providers.

MG Trading

With 23 stores and ve fertiliser stores servicing most of the

south east dairy region, MG Trading is focused on reducing

the cost of farm inputs and supporting increased protability

through providing competitively priced products and services.

Sales om MG Trading stores grew by 20 per cent during the

year to $237 million, on the back of higher farmgate returns,

improved store layouts, an expanded oering and competitive

pricing. MG also opened two new stores – Warragul and Colac

– in the second half of 2013–14, which had a positive impact

on sales growth.

MG Trading continued to develop and enhance its oering during

the year opening new fertiliser depots at Timboon and Katamatite

and launching a tailored dairy farm insurance oer in conjunction

with Marsh Advantage Insurance, and a competitively priced fuel

oer in partnership with Reliance BP.

(i) Includes MG’s majority owned subsidiary Tasmanian Dairy Products Co Ltd.

Devondale Murray Goulburn Annual Report 2014 23

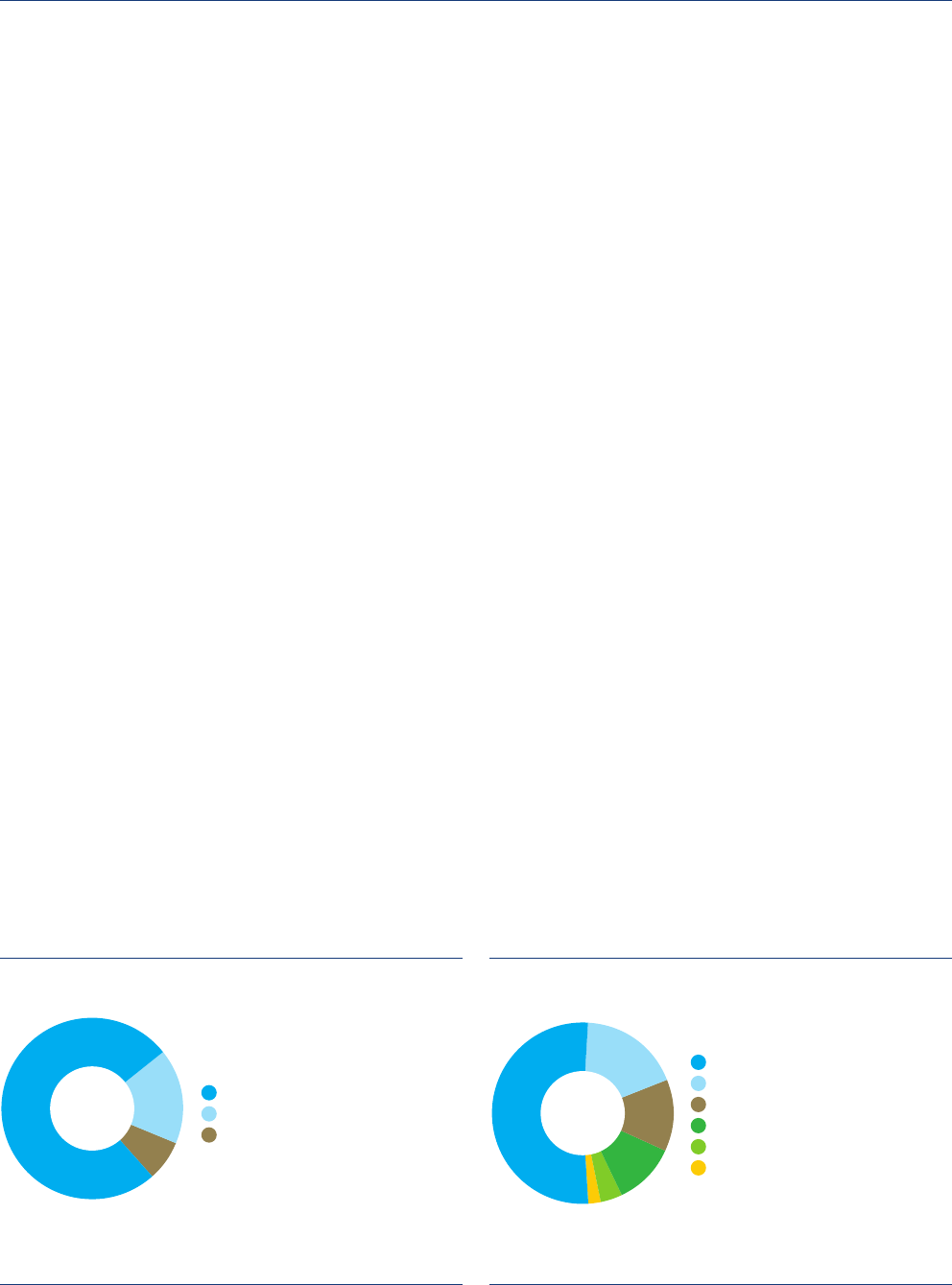

Our People by Location

Note: International count is a manual entry

and wil increase headcount accordingly.

Regional 76%

Metro 17%

International 7%

Organisation by Operation

*Employees of Shareholder Relations and

Business Operations located at FWP are

deemed Corporate.

^ Development and Optimisation, Ingredients

and Nutritionals, PMO and Capital Projects,

Safety and Environmental Sustainability,

Technical Excellence employees are deemed

Business Operations Support

Manufacturing 52%

MG Trading 76%

Logistics 18%

Corporate 11%*

Business Operations Support 4 %^

Field Services 2%

Year in Review

Our People

Ensuring MG people are supported and engaged to maximise

their business contribution is an essential part of MG’s journey

to become a rst choice dairy foods company.

MG’s people related initiatives are focused on accelerating

MG’s ability to leverage its people capability, enhance

performance, achieve operational excellence and facilitate

transformation. MG’s People and Culture function partners

with MG’s business leaders and people to activate and drive

activities that will deliver a high performance organisation.

Supporting our people at work

In 2013–14, further progress was made towards building people

management processes.

A new online plaorm, ‘People Central’ was launched to house

and deliver further eciencies for key people management

processes, including the Company-wide performance management

program. ‘People Central’ facilitates the alignment of key

performance measures throughout the business.

MG’s new online internal information portal was also launched

to improve our ability to share, collaborate and manage information

across multiple sites, geographies and teams. With more than

2,400 people working for MG it is critical that key procedures,

processes and information can be streamlined and accessed

online across distance and time zones.

e ‘Ready, Set, Go’ employee on-boarding and induction program

was introduced to provide new employees with important

information about MG’s business, operations and way of working.

Investing in our people through training and development

continued during the year. In addition to the considerable

investment MG makes to support safety training, Workplace

Behaviours Training, including a Code of Conduct Reesher,

was rolled out for all employees.

Employee engagement

A key focus throughout 2013–14, our employee engagement

was enhanced by the successful renegotiation of our

Transport Enterprise Agreement and a new Greenelds

Enterprise Agreement covering MG’s new Devondale Dairy

Beverages Centres.

We have also put in place a preferred supplier approach for

recruitment, which is generating savings, and our inaugural

talent review was completed, establishing a clear plaorm

to activate our Learning and Development Framework.

* Employees of Shareholder Relations and Business Operations located at FWP are deemed Corporate.

^ Development and Optimisation, Ingredients and Nutritionals, PMO and Capital Projects, Safety and

Environmental Sustainability, Technical Excellence employees are deemed Business Operations Support.

Manufacturing 52%

Logistics 18%

MG Trading 13%

Corporate 11%*

Business Operations Support 4%^

Field Services 2%

Regional 76%

Metro 17%

International 7%

24 Devondale Murray Goulburn Annual Report 2014

ere are more than 2,400

dedicated and passionate people

who make up the MG team, with

76 per cent employed in regional

Australia, providing direct support

to our supplier/shareholders through

the trading stores, eld services,

milk collections and processing.

Devondale Murray Goulburn Annual Report 2014 25

Board of Directors

1. Philip W. Tracy

BEc/BComm, CA, SIA, GAICD

Philip was elected to the Board in 2009 and elected Chairman

in 2011. He is also Chairman of the Remuneration and Nominations

Commiee and a member of the Supplier Relations Commiee.

Philip is a dairy farmer, milking over 2,000 cows at Yanakie

in Gippsland, Victoria. He is a Chartered Accountant and has

a Bachelor of Economics and Commerce and is a graduate

of the Australian Institute of Company Directors.

2. Gary Helou

BE (Hons), MComm, FAICD, FAIM

Gary was appointed as Managing Director in October 2011.

Gary brings experience om a broad range of roles encompassing

the international and domestic food and agricultural industries.

Prior to joining Murray Goulburn, he was Chief Executive Ocer

of SunRice for 11 years. Gary held senior leadership roles

in Hong Kong, Singapore and Indonesia with Pacic Brands

Food Group and Indofood. He has a Chemical Engineering Degree

and a Master of Commerce (Marketing) om the University

of New South Wales.

3. Kenneth W. Jones

Adv. Dip. Ag., MAICD

Kenneth (Ken) was elected to the Board in 2008 and elected

Deputy Chairman in 2011. He is a member of the Compliance

Commiee, Supplier Relations Commiee and Remuneration

and Nominations Commiee.

Ken is a dairy farmer, milking 430 cows at Kergunyah in north

east Victoria. He has an Advanced Diploma in Agriculture and

is a member of the Australian Institute of Company Directors.

4. Natalie Akers

BPPM (Hons), BA, GAICD

Natalie was elected to the Board in 2011. She is a member

of the Compliance Commiee and Supplier Relations Commiee.

Natalie is a dairy farmer, milking 700 cows at Tallygaroopna

in northern Victoria. She has a Bachelor of Public Policy and

Management with honours, a Bachelor of Arts and has completed

the Fairley Leadership Program. Natalie has pursued a professional

career in agriculture, including water policy and dairy research

and development. Natalie is also a graduate of the Australian

Institute of Company Directors.

5. William T. Bodman

BSc (Ag), GAICD

William (Bill) was elected to the Board in 2009 and was joint Deputy

Chairman om 2011 to November 2012. He is a member of the

Finance, Risk and Audit Commiee and Supplier Relations Commiee.

Bill is a dairy farmer, milking 420 cows on two farms at Won Wron

in Gippsland, Victoria. He has a Bachelor of Agricultural Science

Degree om La Trobe University and is a graduate of the

Australian Institute of Company Directors.

6. Peter J.O. Hawkins

BCA (Hons), FAICD, SF Fin, FAIM, ACA (NZ)

Peter was elected to the Board in 2009 as a Special Director.

He is Chairman of the Finance, Risk and Audit Commiee and

a member of the Remuneration and Nominations Commiee.

Peter has had a 41 year career in the banking and nancial

services industry in Australia and overseas at both the highest

levels of management and directorship of major organisations.

He held various senior management and directorship positions

with Australia and New Zealand Banking Group Limited om 1971

to 2005, including Managing Director of ANZ Banking Group (NZ)

Ltd om 1992 to 1995 and was also a director of BHP (NZ) Steel

Limited om 1990 to 1991, ING Australia Limited om 2002

to 2005 and Esanda Finance Corporation om 2002 to 2005.

He is currently a director of Westpac Banking Corporation, Mirvac

Limited Group, Liberty Financial Pty Limited, Treasury Corporation

of Victoria, Clayton Utz and Minerva Financial Group Pty Ltd.

1

4

2

5

3

6

26 Devondale Murray Goulburn Annual Report 2014

7. Michael F. Ihlein

BBus (Acc), FCPA, FAICD, F Fin

Michael (Mike) was elected to the Board in 2012 as a Special

Director. He is Chairman of the Compliance Commiee and

a member of the Remuneration and Nominations Commiee.

Mike is a highly experienced international executive with extensive

knowledge of international business and nance. He held senior

management and directorship positions with Brambles Limited om

2004 to 2009, including Executive Director and Chief Executive

Ocer (2007 to 2009) and Executive Director and Chief Financial

Ocer (2004 to 2007). Mike also held various senior management

and directorship positions with Coca-Cola Amatil Limited, including

Executive Director and Chief Financial Ocer (1997 to 2004)

and Managing Director, Poland (1995 to 1997).

He is currently a director of Scentre Group, CSR Limited, Snowy

Hydro Limited and Chair of the Australian eatre for Young People.

8. Maxwell Jelbart

Maxwell (Max) was elected to the Board in 2012. He is a member

of the Compliance Commiee and Supplier Relations Commiee.

Max is a dairy farmer, milking 1,000 cows at Leongatha South and

350 cows at Caldermeade in Gippsland. He is a Nueld Farming

Scholar, a member of the Nueld Australia Investment Commiee

and a board member of Marcus Oldham College.

9. Edwin Duncan Morris (Duncan Morris)

Dip. Bus. Studies (Accounting), CPA, GAICD

Duncan was elected to the Board in 2013. He is a member

of the Finance, Risk and Audit Commiee and Supplier

Relations Commiee.

Duncan is an accountant and dairy farmer, milking 260 cows

at Cobden, western Victoria. He has spent most of his accounting

career in public practice, primarily aending to the accounting

and taxation needs of dairy farmers. Duncan has had signicant

board experience with local community organisations and is

a graduate of the Australian Institute of Company Directors.

10. Graham N. Munzel

GAICD

Graham was elected to the Board in 2008. He is a member

of the Finance, Risk and Audit Commiee and Supplier

Relations Commiee.

Graham is a dairy farmer, milking 290 cows at Gunbower

in northern Victoria. He is a graduate of the Australian

Institute of Company Directors.

11. John P. Pye

Adv. Dip. Ag., MAICD

John was elected to the Board in 2005. He is Chairman

of the Supplier Relations Commiee and a member of the

Finance, Risk and Audit Commiee and Remuneration and

Nominations Commiee.

John is a dairy farmer, milking 500 cows at Bessiebelle in

western Victoria. He has an Advanced Diploma in Agriculture

and is a member of the Australian Institute of Company Directors.

He is a member of Powercor’s Customer Consultative Commiee

and a former Director of Southern Rural Water Authority

(2002 to 2010).

12. Martin J. Van de Wouw

MAICD

Martin was elected to the Board in 2010. He is a member of

the Compliance Commiee and Supplier Relations Commiee.

Martin is a dairy farmer, milking 280 cows at Princetown in

western Victoria. He has supplied Murray Goulburn for 37 years.

He has completed numerous farm management courses and

is involved with the West Vic Dairy Board and United Dairy

Farmers of Victoria. He is also a member of the Australian

Institute of Company Directors.

7

10

8

11

9

12

Devondale Murray Goulburn Annual Report 2014 27

Executive Leadership Team

1. Gary Helou

BE (Hons), MComm, FAICD, FAIM

Managing Director

Gary Helou was appointed as Managing Director in October 2011.

Gary brings experience om a broad range of roles encompassing

the international and domestic food and agricultural industries.

Prior to joining Murray Goulburn, he was Chief Executive Ocer

of SunRice for 11 years. He held senior leadership roles in Hong

Kong, Singapore and Indonesia with Pacic Brands Food Group

and Indofood.

Gary has a Chemical Engineering Degree and a Master of

Commerce (Marketing) om the University of New South Wales.

2. Brad Hingle

Chief Financial Ocer

Brad Hingle was appointed Chief Financial Ocer in January 2014.

Prior to joining Murray Goulburn, Brad was the Chief Financial

Ocer of SunRice, where he spent 14 years and held a number

of senior roles. Brad has also held senior roles at Deloie Consulting

in Australia as well as at Dunlop Tyres and Mondi Limited in

South Aica. He has studied Cost and Management Accounting.

3. David Mallinson

Dip Bus, PG Cert Finance, MBA, CPA, FNIA, GAICD

Executive General Manager Business Operations

David Mallinson was appointed Executive General Manager

Business Operations in April 2014. David was previously General

Manager Project Management Oce and Capital Projects om

October 2013.

Prior to joining Murray Goulburn David was Fonterra Australia/

New Zealand’s Chief Financial Ocer for six years, having held

various senior roles within the merged business and senior roles

in Bonlac Foods Ltd and United Milk Tasmania. David has also

previously worked for ANZ and Cadbury Schweppes.

David holds various qualications including a Master of Business

Administration om Monash University and he completed

the Executive Development Program at Stanford University

(USA) in 2004.

1 32

28 Devondale Murray Goulburn Annual Report 2014

4. Robert Poole

BAgSci, MBL

Executive General Manager Shareholder Relations

Robert Poole was appointed Executive General Manager

Shareholder Relations in November 2011. Prior to this

appointment Robert was Murray Goulburn’s General Manager

Industry and Government Aairs for three years. Robert has held

a number of senior roles throughout his career including Deputy

Chief Executive Ocer of Australian Dairy Farmers’ Federation,

General Manager of the Australian Dairy Herd Improvement

Scheme and a Regional Manager with Rural Finance Corporation.

In 2011–12 Robert also held leadership roles within the dairy

industry including President of the Australian Dairy Products

Federation and Deputy Chairman of the Australian Dairy

Industry Council.

Robert studied science (Agriculture) at Melbourne University

and was inducted as a Master of Business Leadership at

RMIT University in 2004.

5. Fiona Smith

BSc, LLB, GDipGov, FGIA

Company Secretary and General Counsel

Fiona Smith was appointed Company Secretary and General

Counsel in January 2012.

Prior to joining Murray Goulburn, Fiona was Deputy Company

Secretary at BHP Billiton Limited for four years. She has also

been employed as General Counsel/Company Secretary of Gasnet

Australia, an ASX listed company for seven years and has held

a number of senior legal positions including principal solicitor

with the Australian Government Solicitor. She has over 25 years’

legal experience.

Fiona has a Bachelor of Science and a Bachelor of Laws om the

Australian National University and a Graduate Diploma in Applied

Corporate Governance. Fiona is also a Fellow of the Governance

Institute of Australia.

6. Aditya Swarup

BA (Hons)/Economics, MBA

Executive General Manager Strategy

Aditya Swarup was appointed Executive General Manager

Strategy in 2012.

Aditya has broad experience in strategy consulting and corporate

roles within a broad range of industries including food, agribusiness,

manufacturing and resources across Australia and Asia.

Prior to joining Murray Goulburn, Aditya spent six years at SunRice

as General Manager of Corporate Strategy. Before SunRice, Aditya

spent over eight years in strategy consulting roles, including Monitor

Group and Accenture, advising several large Australian corporates.

Aditya has an MBA om Melbourne Business School, University

of Melbourne (1997) and a Bachelor of Arts (with Honours) and

Economics om the University of Delhi (1991).

4 65

Devondale Murray Goulburn Annual Report 2014 29

1. Introduction

is section of the Annual Report outlines Murray Goulburn’s

governance amework for the year ended 30 June 2014.

Murray Goulburn remains commied to ensuring that its policies

and practices reect a high standard of corporate governance.

e Board considers that Murray Goulburn’s governance

amework and adherence to that amework are fundamental in

demonstrating that the Directors are accountable to shareholders

and are appropriately overseeing the management of risk and the

future direction of the Company.

As an unlisted company, Murray Goulburn is not required

to comply with the ASX Corporate Governance Principles

and Recommendations; however, the Board voluntarily issues

a Corporate Governance Statement to enhance transparency

and communication with stakeholders in relation to the

Company’s corporate governance practices.

Murray Goulburn’s key governance documents, including

the Constitution, Board and Board Commiee Charters and

key policies are available on the Company’s website at

www.mgc.com.au/our-story/governance.

2. Role and Responsibilities of the Board

BOARD

e role of the Board is to represent shareholders, as a whole,

and to promote and protect the interests of the Company. Its

principal objective is to create and enhance shareholder value

but in a manner that is consistent with the co-operative objective

of maximising supplier returns. e Board is accountable to the

shareholders for the Company’s performance and governance.

e Board has adopted a Board Charter, which sets out its

key responsibilities, the maers it has reserved for its own

consideration and decision making and the authority it has

delegated to the Managing Director. e Board’s responsibilities,

as set out in the Board Charter, include:

• the appointment, remuneration and succession planning of the

Managing Director and the Managing Director’s direct reports;

• approval of the corporate strategy, including seing corporate

objectives, performance objectives and approving the annual

operating budget;

• overseeing risk management, internal controls and ethical

and legal compliance, which includes reviewing procedures

to identi the main risks associated with the Company’s

businesses and the implementation of appropriate systems

to manage these risks;

• monitoring corporate performance and implementation

of corporate objectives, strategy and policy;

• approving major capital expenditure, acquisitions and

divestitures, and monitoring capital management;

• monitoring and reviewing management processes aimed

at ensuring the integrity of nancial and other reporting;

• developing and reviewing the Company’s corporate

governance principles and policies; and

• performing such other functions as are prescribed by law.

In addition, the Board has specically reserved certain

maers for its decision, including those set out in the

approved delegations of authority.

DELEGATION TO MANAGEMENT

e Board has delegated to the Managing Director and, through

the Managing Director, to other senior executives, responsibility

for the day-to-day management of the Company’s aairs and

implementation of the corporate objectives, strategy and policy

initiatives. e Managing Director and the broader management

team are required to operate in accordance with Board approved

policies and delegations of authority.

e Managing Director remains accountable to the Board for

the exercise of authority that is delegated. e Board monitors

the decisions and actions of the Managing Director, and the

performance of the Company, to gain assurance that progress

is being made towards the approved corporate objectives and

the delegations of authority are being complied with. e Managing

Director, with the support of management, provides regular

reports to the Board and its Commiees to enable them to

discharge their duties eectively. Senior executives also aend

all scheduled Board meetings, by invitation, where they present,

discuss and provide input on their respective areas of responsibility.

INDEPENDENT PROFESSIONAL ADVICE

e Board and its Commiees may access independent experts

and professional counsel for advice where appropriate and may

invite any person om time to time to aend meetings of the Board.

ACTIVITIES DURING THE YEAR

A key activity of the Board during the year has been governing

the Company having regard to its strategic objectives, as well

as the goal to li farmgate returns and drive industry growth, and

the vision to drive operating excellence and shi to a higher value

dairy products porolio. e Board has focused on the principal

objectives of creating and enhancing shareholder value and

maximising supplier returns. Within this context, the Board

approved various maers, including:

• investments totalling $126 million in consumer cheese

at Cobram ($74 million), infant nutrition at Koroit and

Cobram ($38 million) and dairy beverages at Edith Creek,

Tasmania ($14 million);

• the takeover oer for Warrnambool Cheese and Buer

Factory Company Holdings Limited (WCB) and the subsequent

acceptance of Saputo Inc.’s oer, which ultimately delivered

to the Company cash proceeds of $93 million;

• six step ups in the milk price paid by the Company

throughout the year;

• the opening milk price for nancial year 2015; and

• the proposal to undertake a selective capital reduction and

cancellation of the A class preference shares, which was

ultimately approved by shareholders at the general and

A class preference shareholder meetings held on 6 June 2014.

Importantly, during the year the Board has also overseen

the construction of the two new state-of-the-art chilled milk

processing plants in Melbourne and Sydney, with the plants

ocially opened in July 2014 and August 2014, respectively.

In addition to the above maers, the Board spent a signicant

amount of time considering a potential capital structure to provide

access to equity capital to eectively fund strategic operational

and commercial initiatives to deliver a sustainable increase

Corporate Governance Statement

30 Devondale Murray Goulburn Annual Report 2014

in the annual farmgate milk price, consistent with the Company’s

overarching strategy. e potential capital structure will be the

subject of further Board consideration during nancial year 2015.

3. Structure of the Board

MEMBERSHIP AND MEETINGS

e Board currently has 12 Directors. Of these, nine, including

the Chairman, are elected om the shareholder base (Supplier

Directors), one is the Managing Director and two are

Special Directors.

e Supplier Directors must be current suppliers to the Company

and each must hold at least 10,000 ordinary shares to be eligible

for election.

e Special Directors are selected by taking into account the

skills and competencies that the Board considers are necessary

to augment the direct industry knowledge and other expertise

provided by the Supplier Directors.

During the year, Duncan Morris joined the Board as a Supplier

Director following the annual Director election process undertaken

in accordance with the Company’s Constitution. In eect,

Mr Morris replaced Don Howard, who retired om the Board

aer 16 years as a Supplier Director. As is required with all new

Non-executive Directors, Mr Morris conrmed his acceptance

of the appointment on the standard terms, which are available on

the Company’s website at www.mgc.com.au/our-story/governance.

At the 2012 Annual General Meeting, shareholders approved

various amendments to the Constitution, which included an

increase in the maximum number of Special Directors, giving

the Board the capacity to appoint a third Special Director. During

the year, the Remuneration and Nominations Commiee (with the

assistance of an external recruitment consultant) commenced

identiing potential candidates for this additional directorship

having regard to the skills and experience that would best

complement those held by existing Directors. is process will

continue with a view to the Board appointing a third Special

Director during nancial year 2015.

e Chairman is Philip Tracy and the Deputy Chairman

is Ken Jones. e Chairman and Deputy Chairman are both

Supplier Directors who the Board considers to be independent,

having regard to the guidelines adopted by the Board to assist

in considering independence (as described in Section 4 of this

Corporate Governance Statement).

e Company Secretary, Fiona Smith, is accountable to

the Board, through the Chairman, on all maers to do with

the proper functioning of the Board.

e Directors of the Company, their length of service and

their biographical details are set out on pages 26 to 27.

e Board met 23 times during the year, with 10 scheduled

monthly meetings and 13 ad hoc meetings (predominantly

to consider maers relating to the Company’s takeover oer

for WCB). Details of the number of meetings aended by each

Director are set out in the Directors’ Report on page 40.

At the commencement of each scheduled monthly meeting,

the Board holds a closed session (aended by Non-executive

Directors only), which provides Non-executive Directors with

an opportunity to raise issues in the absence of management.

COMMITTEES

To assist the Board to carry out its responsibilities, the

Board has established a Finance, Risk and Audit Commiee,

a Remuneration and Nominations Commiee, a Compliance

Commiee and a Supplier Relations Commiee.

Other commiees are established om time to time to deal

with specic maers. For example, a commiee was established

in 2013 to specically consider maers relating to the Company’s

capital structure.

Each of the permanent Commiees has a Charter, which sets

out the membership structure, roles and responsibilities and

meeting procedures.

Generally, these Commiees review maers on behalf

of the Board and, as determined by the relevant Charter:

• refer maers to the Board for decision, with

a recommendation om the Commiee; or

• determine maers (where the Commiee acts with delegated

authority), which the Commiee then reports to the Board.

e Company Secretary provides secretarial support

for each Commiee.

ere were a number of changes made to the membership

of each Commiee during the year as a result of the review

undertaken by the Board in December, following the change

in the Board composition.

FINANCE, RISK AND AUDIT COMMITTEE

Role and responsibilities