Discover Contact D PAS: Quick Chip Implementation Guide PAS V1.0 Jul 2016

User Manual:

Open the PDF directly: View PDF ![]() .

.

Page Count: 20

- 1 Introduction

- 2 Overview of Discover Quick Chip

- 3 Discover Quick Chip Transaction Processing

- 3.1 Transaction Amount Selection

- 3.2 Initiate Application Selection

- 3.3 Read Application Data

- 3.4 Offline Data Authentication

- 3.5 Processing Restrictions

- 3.6 Cardholder Verification

- 3.7 Terminal Risk Management

- 3.8 First Terminal Action Analysis

- 3.9 First Card Action Analysis

- 3.10 Second Terminal Action Analysis

- 3.11 Second Card Action Analysis

- 3.12 Online Authorization

- 3.13 Transaction Completion

- 3.14 Issuer Authentication, Card Status Updates and Issuer Scripts

- 3.15 Chip Card Terminals with Non-Zero Floor Limit

- 4 Acquirer and Merchant Certification Requirements

- 5 Issuer Considerations

Proprietary and Confidential

©2016 DFS Services LLC

Discover® Contact D-PAS:

Discover® Quick Chip Implementation

Guide

DISCOVER® FINANCIAL SERVICES

Effective Date: July 12, 2016

Version: 1.0

Discover® Contact D-PAS:

Discover® Quick Chip Implementation Guide

DFS CT D-PAS: QCIG, v1.0 Proprietary and Confidential Page 2 of 20

Date: July 12, 2016 © 2016 DFS Services LLC

DISCLAIMER

This Discover® Contact D-PAS: Discover® Quick Chip Implementation Guide (this “Guide”) provides

implementation guidance to assist Acquirers, Merchants, Issuers and approved network participants with

support for Discover® Quick Chip and is subject to change by Discover at any time without notice to any

party. Neither this Guide nor any other document or communication creates any binding obligation upon

any of the Discover Parties, Acquirers, Merchants, Issuer or any other approved network participant. If

Acquirer, Merchant or third party seeks to support Discover Quick Chip, this Guide identifies Discover’s

requirements with respect to Chip Card Terminal testing and certification services.

This Guide is provided "AS IS" "WHERE IS" and "WITH ALL FAULTS". None of the Discover Parties

(Discover, Diners Club International (DCI), PULSE Network LLC, or any of their affiliates, subsidiaries,

directors, officers or employees) assume or accept any liability for any errors or omissions contained in the

Guide.

The Discover Parties make no representations or warranties of any kind, express or implied, with respect

to the Guide. The Discover Parties specifically disclaim all representations and warranties, including the

implied warranties of merchantability and fitness for a particular purpose. The Discover Parties further

specifically disclaim all representations and warranties with respect to intellectual property subsisting in or

relating to the Guide or any part thereof, including but not limited to any and all implied warranties of title,

non-infringement or suitability for any purpose (whether or not the Discover Parties have been advised,

have reason to know, or are otherwise in fact aware of any information).

The contents of this Guide are proprietary and constitute trade secrets of Discover. This Guide is provided

to Acquirers, Merchants, Issuers and approved network participant for their exclusive use and shall not be

reproduced, published or otherwise disclosed, in whole or in part, to any party outside Discover without the

prior written consent of Discover.

In this Guide, “Discover” and “DFS” refer to DFS Services LLC on behalf of the Discover Parties. Where

used as the operating name for DFS, Discover® means the officers, directors, employees and the network,

systems, and processes, including hardware, software, and personnel, maintained by the Discover Parties

to support Card Issuance and Card Acceptance programs operated by Issuers, Merchants, and Acquirers

for the benefit of Cardholders and Merchants, respectively.

Discover® Contact D-PAS:

Discover® Quick Chip Implementation Guide

DFS CT D-PAS: QCIG, v1.0 Proprietary and Confidential Page 3 of 20

Date: July 12, 2016 © 2016 DFS Services LLC

Table of Contents

1 Introduction ----------------------------------------------------------------------------------------------------------------- 7

1.1 Audience ---------------------------------------------------------------------------------------------------------------- 7

1.2 Scope of the Guide --------------------------------------------------------------------------------------------------- 7

1.3 Organization of this Guide ------------------------------------------------------------------------------------------ 7

1.4 Reference Materials -------------------------------------------------------------------------------------------------- 7

2 Overview of Discover Quick Chip ------------------------------------------------------------------------------------ 9

2.1 Discover Quick Chip versus Standard EMV Transaction Processing ------------------------------------ 9

2.2 Discover Quick Chip Transaction Processing Flow ----------------------------------------------------------- 9

2.3 Other Features of Discover Quick Chip Transactions ------------------------------------------------------ 12

2.3.1 Online Authorization ------------------------------------------------------------------------------------------ 12

2.3.2 Support for Discover Quick Chip by AID ---------------------------------------------------------------- 12

2.3.3 Cash Over Transactions ------------------------------------------------------------------------------------- 12

3 Discover Quick Chip Transaction Processing ----------------------------------------------------------------- 13

3.1 Transaction Amount Selection ----------------------------------------------------------------------------------- 13

3.2 Initiate Application Selection ------------------------------------------------------------------------------------- 13

3.3 Read Application Data --------------------------------------------------------------------------------------------- 13

3.4 Offline Data Authentication --------------------------------------------------------------------------------------- 13

3.5 Processing Restrictions-------------------------------------------------------------------------------------------- 13

3.6 Cardholder Verification -------------------------------------------------------------------------------------------- 13

3.7 Terminal Risk Management -------------------------------------------------------------------------------------- 14

3.8 First Terminal Action Analysis ----------------------------------------------------------------------------------- 14

3.9 First Card Action Analysis ----------------------------------------------------------------------------------------- 14

3.10 Second Terminal Action Analysis ------------------------------------------------------------------------------- 14

3.11 Second Card Action Analysis ------------------------------------------------------------------------------------ 15

3.12 Online Authorization ------------------------------------------------------------------------------------------------ 15

3.13 Transaction Completion ------------------------------------------------------------------------------------------- 15

3.14 Issuer Authentication, Card Status Updates and Issuer Scripts ----------------------------------------- 15

3.15 Chip Card Terminals with Non-Zero Floor Limit ------------------------------------------------------------- 15

4 Acquirer and Merchant Certification Requirements --------------------------------------------------------- 17

4.1 New EMV Deployments ------------------------------------------------------------------------------------------- 17

4.2 Previously-certified Deployments ------------------------------------------------------------------------------- 17

5 Issuer Considerations ------------------------------------------------------------------------------------------------- 19

5.1 Transaction Amount ------------------------------------------------------------------------------------------------ 19

5.2 Issuer Updates to Cards------------------------------------------------------------------------------------------- 19

5.2.1 Issuer Scripts --------------------------------------------------------------------------------------------------- 19

Discover® Contact D-PAS:

Discover® Quick Chip Implementation Guide

DFS CT D-PAS: QCIG, v1.0 Proprietary and Confidential Page 4 of 20

Date: July 12, 2016 © 2016 DFS Services LLC

5.2.2 Card Status Update (CSU) --------------------------------------------------------------------------------- 19

5.3 CVM Selection ------------------------------------------------------------------------------------------------------- 19

5.4 Cardholder Experience -------------------------------------------------------------------------------------------- 20

List of Figures

Figure 1 – Comparison of Standard EMV and Typical Discover Quick Chip Transactions (Signature) .... 10

Figure 2 – Standard EMV versus Discover Quick Chip Transaction Processing Flow .............................. 11

List of Tables

Table 1 – Reference Documents ...................................................................................................................8

Discover® Contact D-PAS:

Discover® Quick Chip Implementation Guide

DFS CT D-PAS: QCIG, v1.0 Proprietary and Confidential Page 5 of 20

Date: July 12, 2016 © 2016 DFS Services LLC

Revision Status

Version Status Date Description

1.0

Release

July 12, 2016

First Release

Discover® Contact D-PAS:

Discover® Quick Chip Implementation Guide

DFS CT D-PAS: QCIG, v1.0 Proprietary and Confidential Page 6 of 20

Date: July 12, 2016 © 2016 DFS Services LLC

[This page is left intentionally blank]

Discover® Contact D-PAS:

Discover® Quick Chip Implementation Guide

DFS CT D-PAS: QCIG, v1.0 Proprietary and Confidential Page 7 of 20

Date: July 12, 2016 © 2016 DFS Services LLC

1 Introduction

This Guide describes the modified D-PAS deployment procedures that are required to implement

Discover Quick Chip.

The objective of Discover Quick Chip is to offer Merchants increased flexibility in connection with

EMV implementation that may help Merchants streamline Chip Card transaction processing on Chip

Card Terminals.

This Guide does not replace any Discover Program Documents, DCI International Operations Manual

[DCI IOM], PULSE Operating Rules and Procedure [PULSE ORP] or the documents referenced

therein. Where applicable, Acquirers, Merchants, Issuers and approved network participants should

refer to the reference documents and other documentation and specifications provided by DFS and

listed in Section1.4 of this Guide. It is assumed that the intended audience is familiar with these

documents.

Discover® is a registered mark of DFS Services LLC (DFS). EMV™ is a registered trademark in the

U.S. and other countries, and is an unregistered trademark in other countries. The registered

trademark is owned by EMVCo.

1.1 Audience

This Guide is primarily for Acquirers that support Discover Quick Chip, and provides information for

Issuers regarding the processing of Discover Quick Chip Transactions.

This Guide may also be used by Acquirer Processors, Merchant Processors, third party processors,

and/or other entities responsible for implementing components and services required to support

Discover Quick Chip.

For the purposes of this Guide, a Merchant is treated the same as an Acquirer, unless otherwise

indicated.

1.2 Scope of the Guide

This Guide highlights the Chip Card Terminal and processing requirements to support Discover

Quick Chip, and to describe the impacts on Issuers and other third parties.

1.3 Organization of this Guide

This Guide is divided into the following sections:

• Section 2: Overview of Discover Quick Chip – provides an overview of how Discover Quick

Chip processing works and how it compares with standard EMV processing.

• Section 3: Discover Quick Chip Transaction Processing – describes the steps in a Discover

Quick Chip Transaction and specific implementation requirements for enabling Discover Quick

Chip Transactions.

• Section 4: Acquirer and Merchant Certification Requirements – outlines the certification

requirements for new EMV deployments, and those previously D-PAS certified.

• Section 5: Issuer Considerations – provides guidance for Issuers to correctly process Discover

Quick Chip Transactions.

1.4 Reference Materials

The documents listed in the following table are referenced in this Guide using the abbreviations

provided. Before using any of these documents, please check for any updates with your DFS

representative.

Discover® Contact D-PAS:

Discover® Quick Chip Implementation Guide

DFS CT D-PAS: QCIG, v1.0 Proprietary and Confidential Page 8 of 20

Date: July 12, 2016 © 2016 DFS Services LLC

Table 1 – Reference Documents

Document

Type

Title

Source

Reference

D-PAS

Documents

Discover Contact D-PAS: Acquirer

Implementation Guide

1 [DFS CT D-PAS: AIG]

Discover Contact D-PAS: Certification Guide

for Issuers and Acquirers

1 [DFS CT D-PAS: CG]

Specifications Discover Contact D-PAS: Terminal

Application Specification

1 [CT D-PAS: TS]

Operating

Regulations

Discover Acquirer Operating Regulations

1

[DN AOR]

DCI International Operations Manual

1

[DCI IOM]

PULSE Operating Rules and Procedure

1

[PULSE ORP]

Agreement Agreement with Discover Party governing

Card Acceptance (the Acquirer Agreement or

Acquirer Processor Agreement, as applicable)

1 [AGR]

EMVCo

Documents

EMV. Integrated Circuit Card Specifications

for Payment Systems, version 4.2. June 2011 2 [EMV 4.2]

Key:

1 = Available from your Implementation Manager.

2 = Available from the EMVCo website: http://www.emvco.com

In the event of a conflict between this Guide and:

• the Agreement, the Agreement shall govern;

• the Operating Regulations generally with respect to Card Issuance or Card Acceptance, the

Operating Regulations shall govern;

• the D-PAS Application Specification with respect to Discover Quick Chip, this Guide shall

govern;

• the D-PAS Certification Guide with respect to testing and certification of Chip Card Terminal

support for Discover® Quick Chip, the D-PAS Certification Guide will govern.

Discover® Contact D-PAS:

Discover® Quick Chip Implementation Guide

DFS CT D-PAS: QCIG, v1.0 Proprietary and Confidential Page 9 of 20

Date: July 12, 2016 © 2016 DFS Services LLC

2 Overview of Discover Quick Chip

As used in this Guide, “Discover Quick Chip” means the Chip Card Terminal implementation option

offered by Discover that uses the modified EMV Transaction flow described below.

Discover Quick Chip reduces the time that a Chip Card is in a Chip Card Terminal by allowing:

• the Chip Card Transaction to start before the Card transaction amount is final; and

• the Chip Card to be removed from the Chip Card Terminal before receipt of the Authorization

Response.

Discover Quick Chip modifies the EMV Transaction flow by enabling certain Transaction processes to

complete after a Chip Card is removed from a Chip Card Terminal. However, it does not change other

standard EMV processes such as Card personalization.

Discover Quick Chip may be implemented for use at any Chip Card Terminal, but is particularly relevant

in environments such as multi-lane retail and quick service restaurants.

2.1 Discover Quick Chip versus Standard EMV Transaction Processing

Discover Quick Chip performs all standard EMV Transaction processes, except post-Authorization

Card processing.

The primary differences between Discover Quick Chip and standard EMV processing are:

• Confirmation of final Card Transaction amount: With Discover Quick Chip, the Chip Card

Terminal is not required to wait for confirmation of the final Transaction amount before

completing Cardholder Verification Method (CVM) processing and requesting data for the online

Authorization from the Chip Card. Instead, a placeholder amount can be used until the actual

amount is known.

Where a placeholder amount is used, all offline CRM processes that use Transaction amounts,

such as profile and CVM selection, are based on the placeholder amount and not the final

Transaction amount.

• Authorization Response: The Chip Card is not required to remain in the Chip Card Terminal

until the Authorization Response is received from the Issuer.

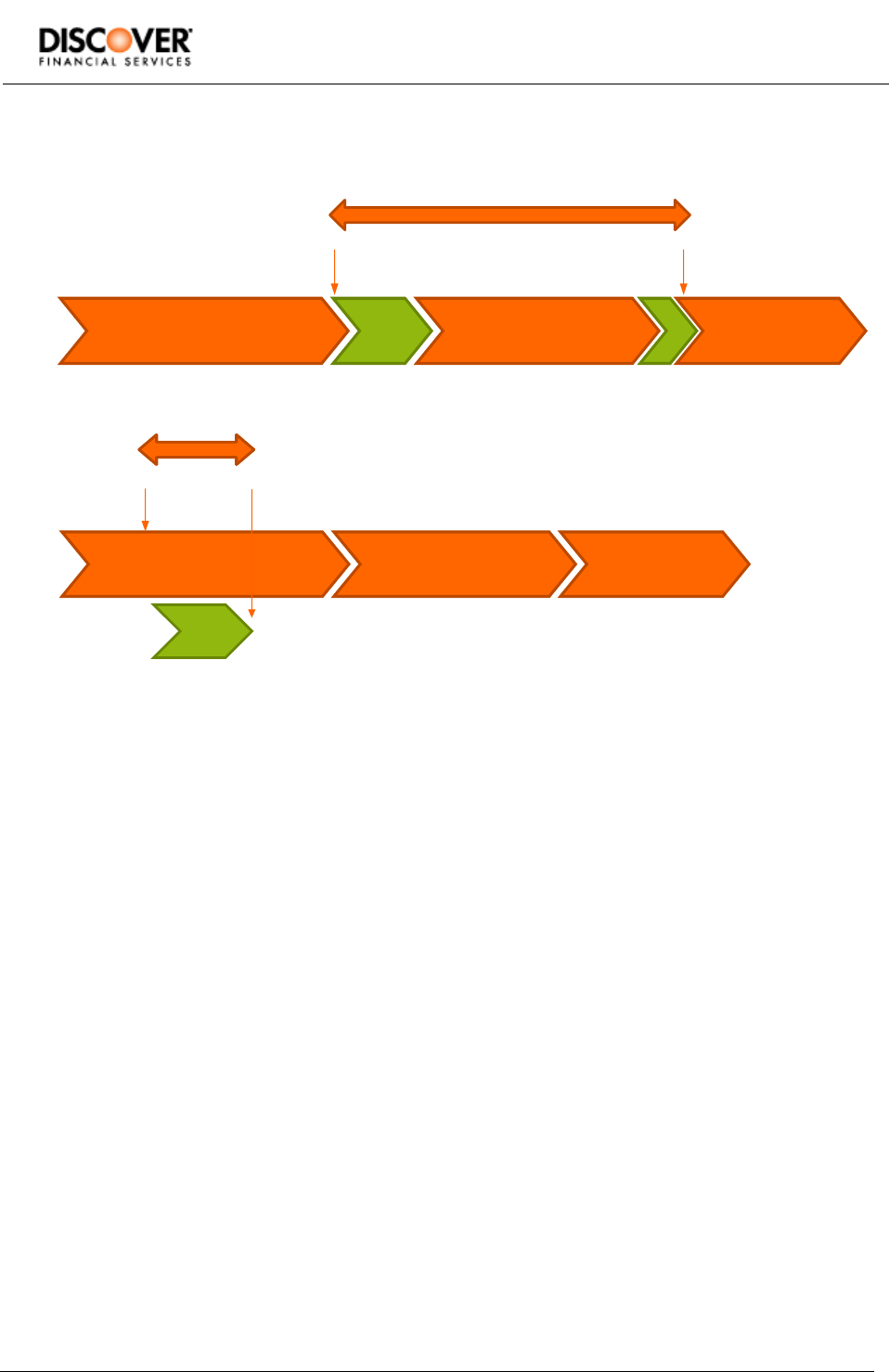

2.2 Discover Quick Chip Transaction Processing Flow

The following Figure shows a comparison between a standard EMV Transaction and a Discover

Quick Chip Transaction, where Signature is the chosen CVM.

Discover® Contact D-PAS:

Discover® Quick Chip Implementation Guide

DFS CT D-PAS: QCIG, v1.0 Proprietary and Confidential Page 10 of 20

Date: July 12, 2016 © 2016 DFS Services LLC

Figure 1 – Comparison of Standard EMV and Typical Discover Quick Chip Transactions

(Signature)

Standard EMV Transaction

Determine transaction amount Online authorization Print + sign

receipt

Determine transaction amount Online authorization Print + sign

receipt

Discover Quick Chip Transaction

Insert Card Remove Card

Card in Reader

Initial EMV

processing

Card

update

Card in Reader

Insert Card Remove Card

Initial EMV processing while

goods are scanned

Placeholder amount used until actual amount known

In a standard EMV Transaction, the final Chip Card Transaction amount is provided to the Chip Card

in order to provide authentication data to the Chip Card Terminal. The Transaction is then processed,

Online Authorization and Card update take place, and a receipt is issued (and signed, if Signature is

the preferred CVM).

In a Discover Quick Chip Transaction, the Chip Card may be inserted into the Chip Card Terminal

and the initial EMV processing carried out at any point while the goods are being scanned. Once the

initial EMV processing is complete and the Card produces a cryptogram for online Authorization, the

Chip Card can be removed from the Chip Card Terminal. Card removal may therefore occur before

the final Transaction amount is known.

For Discover Quick Chip Transactions there are:

• No Card updates

• No final cryptogram

• No possibility of offline approval if online Authorization not possible

• No support at ATMs.

In addition, all offline CRM processes that use Transaction amounts are based on the placeholder

Chip Card Transaction amount, not the final Transaction amount.

The following diagram shows the detailed steps for a standard EMV Transaction. The right hand

column indicates the functions that are performed differently by Chip Card Terminals that support

Discover Quick Chip.

Discover® Contact D-PAS:

Discover® Quick Chip Implementation Guide

DFS CT D-PAS: QCIG, v1.0 Proprietary and Confidential Page 11 of 20

Date: July 12, 2016 © 2016 DFS Services LLC

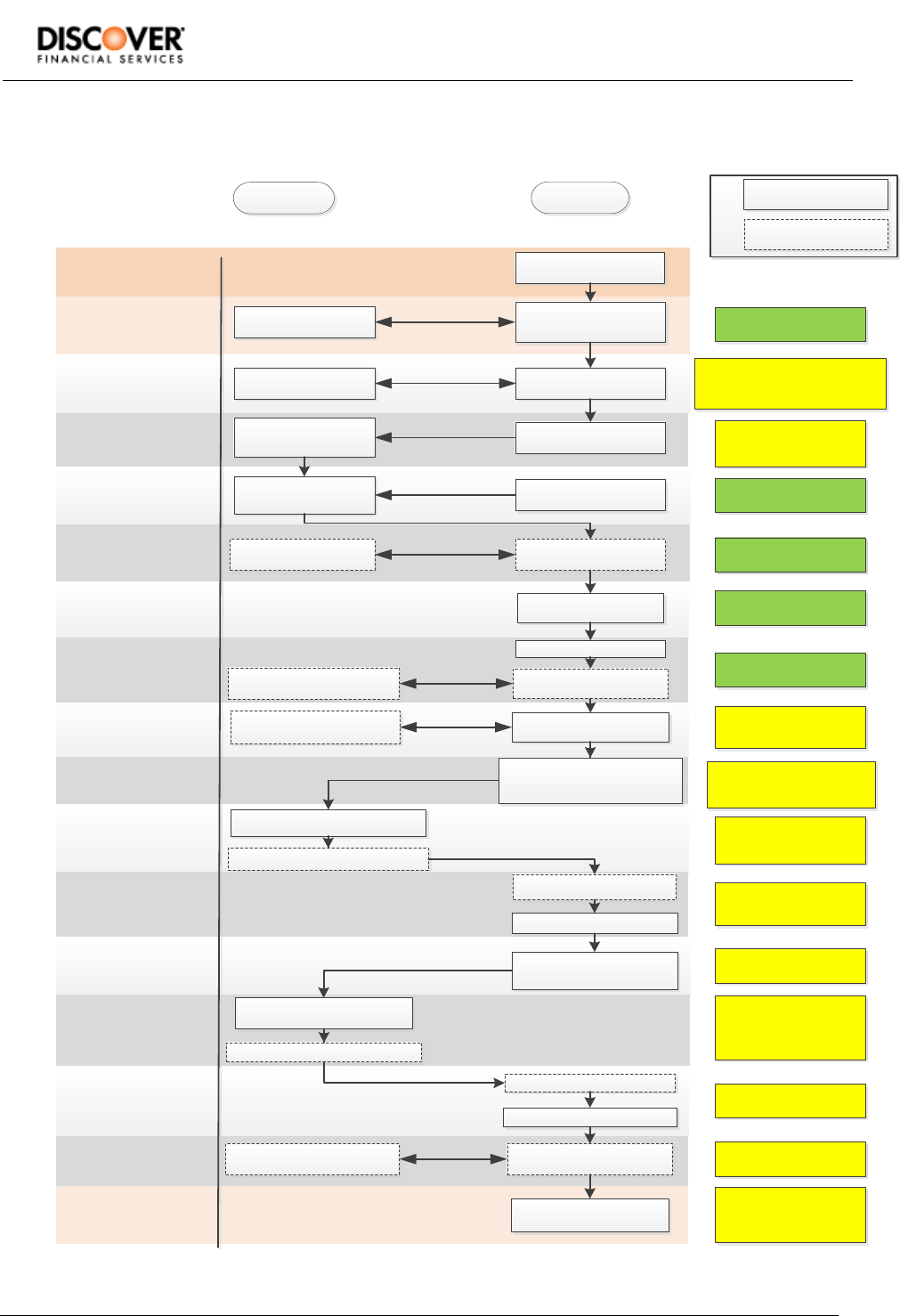

Figure 2 – Standard EMV versus Discover Quick Chip Transaction Processing Flow

Pre-Transaction Processing:

Amount selection

Step 11: Second

Terminal Action

Analysis

Step 14: Issuer to Card

Script Processing

Step 9: First Card Action

Analysis

Step 12: Second Card

Action Analysis

Step 8: First Terminal

Action Analysis

Step 7: Terminal Risk

Management

Step 6: Cardholder

verification

Step 5: Processing

restrictions

Step 4: Offline Data

Authentication

Step 3: Read

Application Data

Step 2: initiate Application

Processing

Step 1: Initiate

Application Selection

Pre-Transaction Processing:

Chip Card Insertion/

Answer to Reset

Requests and stores

application data

Terminal powers up Chip

Card and establishes

communication

Identifies and selects

an application

Initiates Transaction

If SDA or DDA: Terminal

validates chip data

Identifies Transaction

restrictions

Validates Cardholder

Terminal

Chip Card

Provides application

capabilities and

location of data

Provides application data

If DDA: Chip Card

generates security data

If offline PIN: Card provides

PIN-related details & validation

If offline PIN: Terminal

sends PIN to Chip Card

If present: Terminal sends

scripts to Chip Card

If present: Card processes

scripts

Mandatory Process

Optional Process

Key:

Chip Card is inserted

Provides supported

applications

If requested: Card provides risk

management counters

Performs a series of risk

checks

Recommends Transaction be

declined, sent online or approved

Determines if Transaction is

declined, sent online or approved

If CDA: Card generates security data

Step 10: Online

Processing

Step 13: Transaction

Completion

Conclusion of Processing:

Chip Card Deactivation

and Removal

If CDA: Terminal validates

Card

Executes Authorization

Recommends Transaction be

declined or approved

Card determines if Transaction

is to be declined or approved

If CDA: Card generates security data

If CDA: Terminal validates Card

Executes approval or decline

Terminal prints receipt and

deactivates Chip Card

Use final amount if known

or placeholder

If Quick Chip is supported by AID/

BIN range, confirm it is allowed for

the selected application

Transaction must always be

sent online. Terminal requests

ARQC from the Card

Same as standard EMV

Same as standard EMV

Same as standard EMV

Same as standard EMV

Same as standard EMV

Same as standard EMV

Either zero floor limit or

another method to ensure

Transaction is sent online

All decisions are made

online so Card always

returns ARQC

Same as standard EMV, but

not performed until after

completion of EMV process

Always sends ARC of Z3

requesting Card decline

Profile selection cannot

use the Transaction

amount

Card always responds with

AAC with no CDA: Terminal

then prompts for Card

removal

Same as standard EMV, but

card will not return CDA

Not performed

Standard EMV except no

Card deactivation as Card

already been removed

Discover® Contact D-PAS:

Discover® Quick Chip Implementation Guide

DFS CT D-PAS: QCIG, v1.0 Proprietary and Confidential Page 12 of 20

Date: July 12, 2016 © 2016 DFS Services LLC

2.3 Other Features of Discover Quick Chip Transactions

2.3.1 Online Authorization

Discover Quick Chip Transactions are authorized online. If the Issuer does not approve the

Transaction, or if no response to the Authorization Request is received, the Terminal declines the

Transaction.

2.3.2 Support for Discover Quick Chip by AID

Chip Card Terminals may be configured to support Discover Quick Chip by Application Identifier

(AID) to avoid interoperability issues when a Chip Card is presented that does not work with a Quick

Chip Terminal.

2.3.3 Cash Over Transactions

Discover Quick Chip may be used for cash over (‘cash back’) Transactions, subject to the standard

rules in the Agreement [AGR] and Operating Regulations governing these Transactions, and

provided such functionality is supported by the Card settings.

Discover® Contact D-PAS:

Discover® Quick Chip Implementation Guide

DFS CT D-PAS: QCIG, v1.0 Proprietary and Confidential Page 13 of 20

Date: July 12, 2016 © 2016 DFS Services LLC

3 Discover Quick Chip Transaction Processing

This section describes the steps in a Discover Quick Chip Transaction.

3.1 Transaction Amount Selection

Before beginning a Discover Quick Chip Transaction, the Terminal determines whether to use the

final Transaction amount or a placeholder.

• If the actual Transaction amount is known at the time the Card is inserted in the Terminal, the

Discover Quick Chip Transaction is completed using this amount.

• If the actual Transaction amount is not known, a placeholder amount is used.

The placeholder amount is used to generate a cryptogram and is also included in Field 55, Tag 9F02

(Amount, Authorized). The placeholder amount should be greater than the Terminal floor limit to

ensure that all Discover Quick Chip Transactions are sent online for Authorization, unless a certified

proprietary method is used to provide online authorization.

3.2 Initiate Application Selection

DFS recommends that Chip Card Terminals support Discover Quick Chip by AID, with the Terminal

default settings indicating that Discover Quick Chip is not supported.

Before starting a Transaction, the Chip Card Terminal must perform the following steps:

1. Determine which AIDs are supported by both the Card and the Chip Card Terminal.

2. Select the application to be used in the same way as standard EMV, including processing of

the U.S. Common Debit AID if present and applicable.

Application Selection may be performed using either the directory or the “List of AIDs” method,

although the Directory method is recommended to add additional processing efficiency if

supported by the Card.

3. Confirm that Discover Quick Chip is allowed for the selected AID.

If Discover Quick Chip is not allowed, the Transaction must be restarted using the standard

EMV Transaction flow once the final Transaction amount is known. During the Transaction

restart, the Chip Card Terminal should not prompt the user to remove the Card.

3.3 Read Application Data

This step is performed in the same way as standard EMV Transactions.

3.4 Offline Data Authentication

This step is performed in the same way as standard EMV Transactions.

3.5 Processing Restrictions

This step is performed in the same way as standard EMV Transactions.

3.6 Cardholder Verification

Discover Quick Chip may use any of the following CVMs that are available for use in standard EMV

Transactions:

• Online PIN

• Offline PIN

• Signature

• No CVM

Discover® Contact D-PAS:

Discover® Quick Chip Implementation Guide

DFS CT D-PAS: QCIG, v1.0 Proprietary and Confidential Page 14 of 20

Date: July 12, 2016 © 2016 DFS Services LLC

CVMs are processed as follows:

• If PIN is the chosen CVM but the final Transaction amount is not yet known, the PIN entry

device must not display a Transaction amount.

o If Offline PIN is the chosen CVM, the Cardholder is informed of the result by the PIN

entry device.

o If Online PIN is the chosen CVM, the PIN entered is encrypted into a PIN Block for

inclusion in the Authorization Request, in accordance with the Payment Card Industry

PCI PED requirements.

• If Signature is the chosen CVM, the Transaction amount must not be printed or displayed by

the Chip Card Terminal until the Authorization Response is received.

Note: If the CVM list includes rules based on Transaction amount and a placeholder amount is used,

CVM selection is based on the placeholder amount, not the final Transaction amount.

3.7 Terminal Risk Management

This step is performed in the same way as standard EMV Transactions.

The Terminal floor limit should be set to zero to ensure that online Authorization is performed for the

Chip Card Transaction. If the Terminal floor limit is set to an amount other than zero (for example,

the Acquirer or Merchant has implemented non-zero floor limits for non-Discover Quick Chip EMV

Transactions), the Terminal may use a certified proprietary method to ensure that online

Authorization is performed for the Quick Chip Transaction.

3.8 First Terminal Action Analysis

This step is performed in the same way as standard EMV Transactions.

The result should always be that the Terminal requests an Authorization Request Cryptogram

(ARQC) from the Card.

The Transaction amount that is sent to the Card in the GENERATE AC command is either the final

Transaction amount or the placeholder amount (see Section 3.1).

3.9 First Card Action Analysis

This step is performed in the same way as standard EMV Transactions.

The Chip Card may return an ARQC or an Application Authentication Cryptogram (AAC).

The next step depends on the result of the First Card Action Analysis:

• If the Chip Card returns an AAC, the Chip Card Terminal must decline the Chip Card

Transaction and prompt the Cardholder to remove the Card.

• If the Card returns an ARQC, the Terminal stores the ARQC and associated data in preparation

for creating an online Authorization Request, and proceeds to the Second Terminal Action

Analysis step.

3.10 Second Terminal Action Analysis

Unlike a standard EMV Transaction, a Chip Card Terminal that supports Discover Quick Chip

performs the second Terminal and Card Action Analysis steps before requesting online

Authorization.

In the Second Terminal Action Analysis step, the Chip Card Terminal terminates the Discover Quick

Chip Transaction so that the Chip Card can be powered down and removed from the Terminal. It

does this by sending an Authorization Response Code (Tag 8A) with a value of Z3 (Unable to go

online/Offline Declined) to the kernel. The kernel will send a second GENERATE AC command to

the Card containing an Authorization Response Code (ARC) set to Z3.

Discover® Contact D-PAS:

Discover® Quick Chip Implementation Guide

DFS CT D-PAS: QCIG, v1.0 Proprietary and Confidential Page 15 of 20

Date: July 12, 2016 © 2016 DFS Services LLC

Note: The use of Z3 does not mean that the Terminal was actually unable to perform online

Authorization for the Chip Card Transaction. Instead, Z3 is used to force the Chip Card to issue an

AAC and terminate the Chip Card Transaction.

3.11 Second Card Action Analysis

The Card returns an AAC.

The Chip Card Terminal completes standard EMV processing and prompts for the Chip Card to be

removed from the Chip Card Terminal.

3.12 Online Authorization

Online Authorization is required for all Discover Quick Chip Transactions. It is performed by the Chip

Card Terminal once the final Transaction amount is known, and after the Chip Card is removed from

the Terminal.

The amount that was used to generate the ARQC is sent in Field 55, Tag 9F02 (Amount, Authorized)

of the Authorization Request. All other tags in Field 55, as specified in CDOL1, contain the data used

to generate the cryptogram in the First Card Action Analysis step.

The final Transaction amount is sent in Field 4 (Transaction Amount) of the Authorization Request.

If online Authorization is not possible, the Chip Card Transaction must be declined. The Terminal

should display the same message to the Cardholder as it would in other cases where online

Authorization is not possible.

3.13 Transaction Completion

This step is performed in the same way as standard EMV Transactions.

If Signature was the chosen CVM during EMV processing, the Cardholder should be prompted to

sign the receipt or use the electronic signature capture device once the Issuer Authorization has

been received. The receipt can then be printed, showing the final Transaction amount.

The rules for signature verification are the same for Discover Quick Chip as for other signature-based

Chip Card or magnetic stripe Card Transactions. Please refer to the relevant Agreement and

Operating Regulations for details.

3.14 Issuer Authentication, Card Status Updates and Issuer Scripts

Because the Card was withdrawn from the Terminal, it is not available to process Issuer

Authentication (Authorization Response Cryptogram - ARPC), Card Status Updates (CSUs) or Issuer

scripts.

Issuer Authentication is not required for Discover Quick Chip Transactions, because the Transaction

is approved or declined according to the Issuer's decision in the Authorization Response Message.

The Chip Card Terminal application must ignore any Issuer Authentication Data or Issuer Scripts that

appear in the Authorization Response.

3.15 Chip Card Terminals with Non-Zero Floor Limit

This section describes implementation requirements for Chip Card Terminals with a non-zero floor

limit.

If Discover Quick Chip is implemented at a Chip Card Terminal with a non-zero floor limit, one of the

following alternatives must be applied:

• Set the Terminal floor limit to zero for all Transactions

• Set the Terminal floor limit to zero for Discover Quick Chip Transactions, if permitted by the

Terminal application

Discover® Contact D-PAS:

Discover® Quick Chip Implementation Guide

DFS CT D-PAS: QCIG, v1.0 Proprietary and Confidential Page 16 of 20

Date: July 12, 2016 © 2016 DFS Services LLC

• If the floor limit cannot be set to zero, ensure that the placeholder amount exceeds the floor

limit

• Use a certified proprietary mechanism defined by the Terminal vendor to ensure that Discover

Quick Chip Transactions are sent online.

Discover® Contact D-PAS:

Discover® Quick Chip Implementation Guide

DFS CT D-PAS: QCIG, v1.0 Proprietary and Confidential Page 17 of 20

Date: July 12, 2016 © 2016 DFS Services LLC

4 Acquirer and Merchant Certification Requirements

D-PAS Host certification for Acquirers and Merchants is not impacted by Discover Quick Chip. Discover

Quick Chip is certified at the Terminal level.

The Discover Quick Chip Terminal Certification Test Plan contains fewer test cases compared with

standard EMV Chip Card Terminal certification. When Acquirers or Processors choose to support

Discover Quick Chip, they will need to evaluate how to adapt their certification processes to support

the Discover Quick Chip test plan in addition to the existing certification processes for standard EMV.

Merchants and Acquirers can support both Discover Quick Chip and standard EMV processing.

4.1 New EMV Deployments

For deployments of new Chip Card Terminals that will support only Discover Quick Chip

Transactions, DFS has created a streamlined Terminal End-To-End test plan. This test plan contains

fewer test cases than the plan for Chip Card Terminals supporting full EMV functionality.

Please refer to the [DFS CT D-PAS: CG] for details on certification.

4.2 Previously-certified Deployments

Discover Quick Chip does not impact EMVCo Level 1 or 2 approval.

For Chip Card Terminals already certified to support standard EMV, regression testing should be

conducted when implementing Discover Quick Chip. DFS has created a test plan that includes

regression testing and Discover Quick Chip-specific tests that should be performed before Terminal

deployment.

Discover® Contact D-PAS:

Discover® Quick Chip Implementation Guide

DFS CT D-PAS: QCIG, v1.0 Proprietary and Confidential Page 18 of 20

Date: July 12, 2016 © 2016 DFS Services LLC

[This page is left intentionally blank]

Discover® Contact D-PAS:

Discover® Quick Chip Implementation Guide

DFS CT D-PAS: QCIG, v1.0 Proprietary and Confidential Page 19 of 20

Date: July 12, 2016 © 2016 DFS Services LLC

5 Issuer Considerations

Chip Cards issued on any of the Discover AIDs may be used at Discover Quick Chip Terminals. Issuers

do not need to do anything to enable Chip Cards for Discover Quick Chip. However, this section

highlights some potential impacts on Issuers when Chip Cards are used at Discover Quick Chip

Terminals.

5.1 Transaction Amount

The Amount, Authorized (Tag 9F02) value in Field 55 of the Authorization Request Message received

by Issuers may be different from the Transaction amount in Field 4. To prevent problems processing

Discover Quick Chip Transactions, Issuers should confirm that:

• The Amount, Authorized value in Field 55 is used only for cryptogram validation and not for

financial Authorization

• The value in Field 4 of the Authorization Message is used for financial Authorization

• Any mismatch between the Amount, Authorized and Field 4 should not be the sole reason for

declining Authorization Requests for Chip Card Transactions.

Corresponding amounts will also be different in clearing messages that contain Field 55 data. If the

Issuer validates the ARQC in a clearing message, they must do so using the Amount, Authorized

value in Field 55. Any processing that reconciles clearing and Authorization messages must use the

Transaction amounts in other fields and not the Amount, Authorized value.

5.2 Issuer Updates to Cards

This section outlines processing changes applicable to Discover Quick Chip that impact Card update

processing.

5.2.1 Issuer Scripts

Discover Quick Chip Transactions do not support Issuer scripts because the Chip Card is removed

from the Chip Card Terminal before the Authorization Response is received. Issuers therefore

cannot rely on scripts being transmitted to their Cards during every Transaction. As Chip Card

Terminals will vary in support of Discover Quick Chip, Issuers should be aware that their risk

management controls will not be consistently applied.

At a Discover Quick Chip Terminal, all functionality managed with scripting will be affected. Issuers

cannot, therefore, rely on scripts to block Cards that are reported as lost or stolen being supported

at all Chip Card Terminals. Issuers should use the script counter along with the “Issuer Script

Received” and “Issuer Script Failed” indicators in the Card Verification Results (CVR) to determine

when a script was successfully processed by the Card.

5.2.2 Card Status Update (CSU)

Because the Chip Card is removed from a Discover Quick Chip Terminal before receipt of the

Authorization Response, any updates to the Card contained in the CSU (for example, reset of

offline risk management counters, update to PIN Try Counter) will not be processed at Chip Card

Terminals supporting Discover Quick Chip.

Issuers may need to resend the same CSU in multiple subsequent online Authorizations, to ensure

that updates are processed.

5.3 CVM Selection

If the CVM list includes rules based on Chip Card Transaction amount and a placeholder amount is

used, CVM selection is based on the placeholder amount, not the final Transaction amount.

Discover® Contact D-PAS:

Discover® Quick Chip Implementation Guide

DFS CT D-PAS: QCIG, v1.0 Proprietary and Confidential Page 20 of 20

Date: July 12, 2016 © 2016 DFS Services LLC

5.4 Cardholder Experience

As some Merchants may not implement Discover Quick Chip, Cardholder experience will vary from

place to place when using the same Card. This difference may result in call center activity and require

additional customer service representative training.

Issuers may want to make Cardholders aware of the changes that Discover Quick Chip introduces,

and the impact it may have on Chip Card Transactions.