EMV Integrator's Guide V 15.2 Oct 2015

EMV%20Integrator's%20Guide%20V%2015.2%20Oct-2015

User Manual:

Open the PDF directly: View PDF ![]() .

.

Page Count: 120 [warning: Documents this large are best viewed by clicking the View PDF Link!]

- EMV Integrator’s Guide

- Release Notes

- Table of Contents

- List of Tables

- List of Figures

- Chapter 1: Overview

- Chapter 2: EMV Processing Overview

- Chapter 3: EMV Development Overview

- Chapter 4: EMV Terminal Interface

- 4.1 EMV Terminal to Card Communication

- 4.2 EMV Data Elements

- 4.3 Contact Transaction Flow

- 4.3.1 Tender Processing

- 4.3.2 Card Acquisition

- 4.3.3 Application Selection

- 4.3.4 Initiate Application Processing

- 4.3.5 Read Application Data

- 4.3.6 Offline Data Authentication

- 4.3.7 Processing Restrictions

- 4.3.8 Cardholder Verification

- 4.3.9 Terminal Risk Management

- 4.3.10 Terminal Action Analysis

- 4.3.11 Card Action Analysis

- 4.3.12 Online Processing

- 4.3.13 Issuer Authentication

- 4.3.14 Issuer-to-Card Script Processing

- 4.3.15 Completion

- 4.3.16 Card Removal

- 4.4 Contactless Transaction Flow

- 4.4.1 Pre-Processing

- 4.4.2 Discovery Processing

- 4.4.3 Application Selection

- 4.4.4 Initiate Application Processing

- 4.4.5 Read Application Data

- 4.4.6 Card Read Complete

- 4.4.7 Processing Restrictions

- 4.4.8 Offline Data Authentication

- 4.4.9 Cardholder Verification

- 4.4.10 Online Processing

- 4.4.11 Completion

- 4.4.12 Issuer Update Processing

- 4.5 EMV Receipts

- Chapter 5: EMV Parameter Interface

- Appendix

EMV Integrator’s Guide

Version 15.2

October 2015

Notice EMV Integrator’s Guide V 15.2

22015 Heartland Payment Systems, Inc., All Rights Reserved–HPS Confidential: Sensitive

Notice

THE INFORMATION CONTAINED HEREIN IS PROVIDED TO RECIPIENT “AS IS” WITHOUT

WARRANTY OF ANY KIND, EXPRESS OR IMPLIED, INCLUDING BUT NOT LIMITED TO, THE

IMPLIED WARRANTIES OF MERCHANTABILITY AND FITNESS FOR A PARTICULAR

PURPOSE, OR WARRANTY OF TITLE OR NON-INFRINGEMENT. ALL SUCH WARRANTIES

ARE EXPRESSLY DISCLAIMED.

HEARTLAND PAYMENT SYSTEMS SHALL NOT BE LIABLE FOR ANY DIRECT, INDIRECT,

SPECIAL, INCIDENTAL, OR CONSEQUENTIAL DAMAGES RESULTING FROM THE USE OF

ANY INFORMATION CONTAINED HEREIN, WHETHER RESULTING FROM BREACH OF

CONTRACT, BREACH OF WARRANTY, NEGLIGENCE, OR OTHERWISE, EVEN IF

HEARTLAND PAYMENT SYSTEMS HAS BEEN ADVISED OF THE POSSIBILITY OF SUCH

DAMAGES. HEARTLAND PAYMENT SYSTEMS RESERVES THE RIGHT TO MAKE

CHANGES TO THE INFORMATION CONTAINED HEREIN AT ANY TIME WITHOUT NOTICE.

THIS DOCUMENT AND ALL INFORMATION CONTAINED HEREIN IS PROPRIETARY

HEARTLAND PAYMENT SYSTEMS INFORMATION. UNDER ANY CIRCUMSTANCES,

RECIPIENT SHALL NOT DISCLOSE THIS DOCUMENT OR THE SYSTEM DESCRIBED

HEREIN TO ANY THIRD PARTY WITHOUT PRIOR WRITTEN CONSENT OF A DULY

AUTHORIZED REPRESENTATIVE OF HEARTLAND PAYMENT SYSTEMS. IN ORDER TO

PROTECT THE CONFIDENTIAL NATURE OF THIS PROPRIETARY INFORMATION,

RECIPIENT AGREES:

(A) TO IMPOSE IN WRITING SIMILAR OBLIGATIONS OF CONFIDENTIALITY AND

NONDISCLOSURE AS CONTAINED HEREIN ON RECIPIENT’S EMPLOYEES AND

AUTHORIZED THIRD PARTIES TO WHOM RECIPIENT DISCLOSES THIS

INFORMATION (SUCH DISCLOSURE TO BE MADE ON A STRICTLY NEED-TO-KNOW

BASIS) PRIOR TO SHARING THIS DOCUMENT AND

(B) TO BE RESPONSIBLE FOR ANY BREACH OF CONFIDENTIALITY BY THOSE

EMPLOYEES AND THIRD PARTIES TO WHOM RECIPIENT DISCLOSES THIS

INFORMATION.

RECIPIENT ACKNOWLEDGES AND AGREES THAT USE OF THE INFORMATION

CONTAINED HEREIN SIGNIFIES ACKNOWLEDGEMENT AND ACCEPTANCE OF THESE

TERMS. ANY SUCH USE IS CONDITIONED UPON THE TERMS, CONDITIONS AND

OBLIGATIONS CONTAINED WITHIN THIS NOTICE.

THE TRADEMARKS AND SERVICE MARKS RELATING TO PRODUCTS OR SERVICES OF

HEARTLAND PAYMENT SYSTEMS OR OF THIRD PARTIES ARE OWNED BY HEARTLAND

PAYMENT SYSTEMS OR THE RESPECTIVE THIRD PARTY OWNERS OF THOSE MARKS,

AS THE CASE MAY BE, AND NO LICENSE WITH RESPECT TO ANY SUCH MARK IS EITHER

GRANTED OR IMPLIED.

To verify existing content or to obtain additional information, please call or email your assigned

Heartland Payment Systems contact.

EMV Integrator’s Guide V 15.2 Release Notes

2015 Heartland Payment Systems, Inc., All Rights Reserved–HPS Confidential: Sensitive 3

Release Notes

Version 15.2 Release Notes

Version Release Date Revisions

1.0 07/15/2014 New document.

1.1 07/31/2014 Clarification updates.

1.2 11/21/2014 Portico updates.

1.2.1 12/19/2014 Removed references regarding preliminary and subject to change.

15.1.1 06/02/2014 Identified corrections and clarification updates.

15.2 10/30/2015 Restructured and applied updates.

Release Notes EMV Integrator’s Guide V 15.2

42015 Heartland Payment Systems, Inc., All Rights Reserved–HPS Confidential: Sensitive

EMV Integrator’s Guide V 15.2 Table of Contents

2015 Heartland Payment Systems, Inc., All Rights Reserved–HPS Confidential: Sensitive 5

Table of Contents

Chapter 1: Overview ................................................................................................................. 13

Introduction ...........................................................................................................................................13

Document Purpose ...............................................................................................................................13

Audience ...............................................................................................................................................13

Payment Application Data Security Standards (PA-DSS) .....................................................................14

Chapter 2: EMV Processing Overview.................................................................................... 15

Introduction ...........................................................................................................................................15

EMV Migration.......................................................................................................................................16

Enhanced Security ...........................................................................................................................16

Card Brand Mandates......................................................................................................................16

Fraud Liability Shifts.........................................................................................................................17

PCI Audit Waivers ............................................................................................................................17

EMV Specifications ...............................................................................................................................17

Contact Specifications......................................................................................................................18

Contactless Specifications ...............................................................................................................18

Heartland Host Specifications ..........................................................................................................19

EMV Online vs. Offline ..........................................................................................................................19

Card Authentication .........................................................................................................................19

Cardholder Verification.....................................................................................................................20

Authorization ....................................................................................................................................20

Full vs. Partial EMV Transactions and Flow..........................................................................................20

Full vs. Partial Transaction Flow ......................................................................................................21

Full vs. Partial Credit Transactions ..................................................................................................22

Full vs. Partial Debit Transactions....................................................................................................22

Chapter 3: EMV Development Overview................................................................................. 23

EMV Terminals ......................................................................................................................................23

Contact Devices ...............................................................................................................................23

Contactless Devices.........................................................................................................................23

Letters of Approval ...........................................................................................................................24

EMV Solutions.......................................................................................................................................24

Integrated.........................................................................................................................................24

Standalone .......................................................................................................................................24

EMV Certifications.................................................................................................................................25

Test Requirements ...........................................................................................................................25

Test Plans ........................................................................................................................................26

VISA Smart Debit/Credit (VSDC) Testing ...................................................................................26

MasterCard Terminal Integration Process (M-TIP) Testing .........................................................26

Table of Contents EMV Integrator’s Guide V 15.2

62015 Heartland Payment Systems, Inc., All Rights Reserved–HPS Confidential: Sensitive

American Express Integrated Circuit Card Payment Specification (AEIPS) Testing ...................27

Discover D-Payment Application Specification (D-PAS) Testing.................................................27

Test Tools .........................................................................................................................................28

Test Environments............................................................................................................................29

Test Process.....................................................................................................................................29

EMV Support .........................................................................................................................................30

Chapter 4: EMV Terminal Interface ......................................................................................... 31

EMV Terminal to Card Communication .................................................................................................31

Application Protocol Data Units (APDUs).........................................................................................31

Tag, Length, Value (TLV) Data Objects ............................................................................................32

Kernel Application Programming Interface (API) .............................................................................32

EMV Data Elements ..............................................................................................................................33

Data Conventions.............................................................................................................................33

Terminal Data ...................................................................................................................................34

Card Data.........................................................................................................................................44

Issuer Data.......................................................................................................................................52

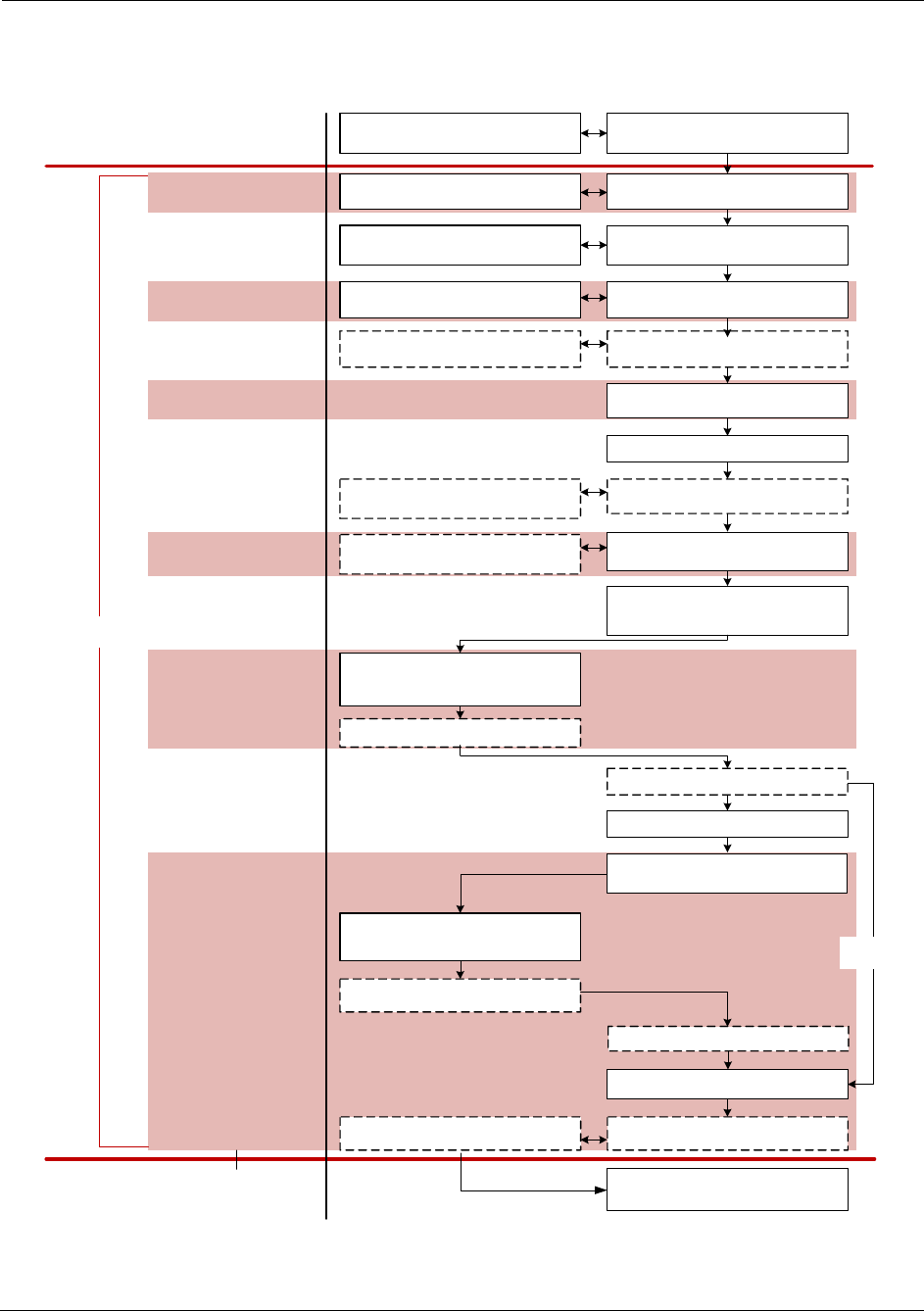

Contact Transaction Flow......................................................................................................................52

Tender Processing ...........................................................................................................................54

Card Acquisition ...............................................................................................................................54

Card Swipe .................................................................................................................................54

Fallback Processing....................................................................................................................55

Application Selection........................................................................................................................56

Available AIDs.............................................................................................................................58

Debit AIDs...................................................................................................................................59

Initiate Application Processing .........................................................................................................59

Read Application Data .....................................................................................................................60

Offline Data Authentication...............................................................................................................60

Processing Restrictions....................................................................................................................61

Cardholder Verification.....................................................................................................................61

PIN Support ................................................................................................................................62

Terminal Risk Management..............................................................................................................63

Terminal Action Analysis ..................................................................................................................63

Card Action Analysis ........................................................................................................................64

Online Processing ............................................................................................................................64

Offline Authorization....................................................................................................................65

Deferred Authorization (Store-and-Forward)...............................................................................65

Forced Acceptance (Stand-In) ....................................................................................................66

Issuer Authentication........................................................................................................................67

Issuer-to-Card Script Processing .....................................................................................................68

Completion .......................................................................................................................................68

EMV Integrator’s Guide V 15.2 Table of Contents

2015 Heartland Payment Systems, Inc., All Rights Reserved–HPS Confidential: Sensitive 7

Card Removal ..................................................................................................................................69

Contactless Transaction Flow ..............................................................................................................69

Pre-Processing ................................................................................................................................71

Discovery Processing.......................................................................................................................71

Application Selection........................................................................................................................71

Initiate Application Processing .........................................................................................................72

Path Determination .....................................................................................................................72

Terminal Risk Management ........................................................................................................72

Terminal Action Analysis .............................................................................................................72

Card Action Analysis...................................................................................................................72

Read Application Data .....................................................................................................................72

Card Read Complete .......................................................................................................................73

Processing Restrictions....................................................................................................................73

Offline Data Authentication ..............................................................................................................73

Cardholder Verification.....................................................................................................................73

Online Processing ............................................................................................................................73

Completion.......................................................................................................................................74

Issuer Update Processing ................................................................................................................74

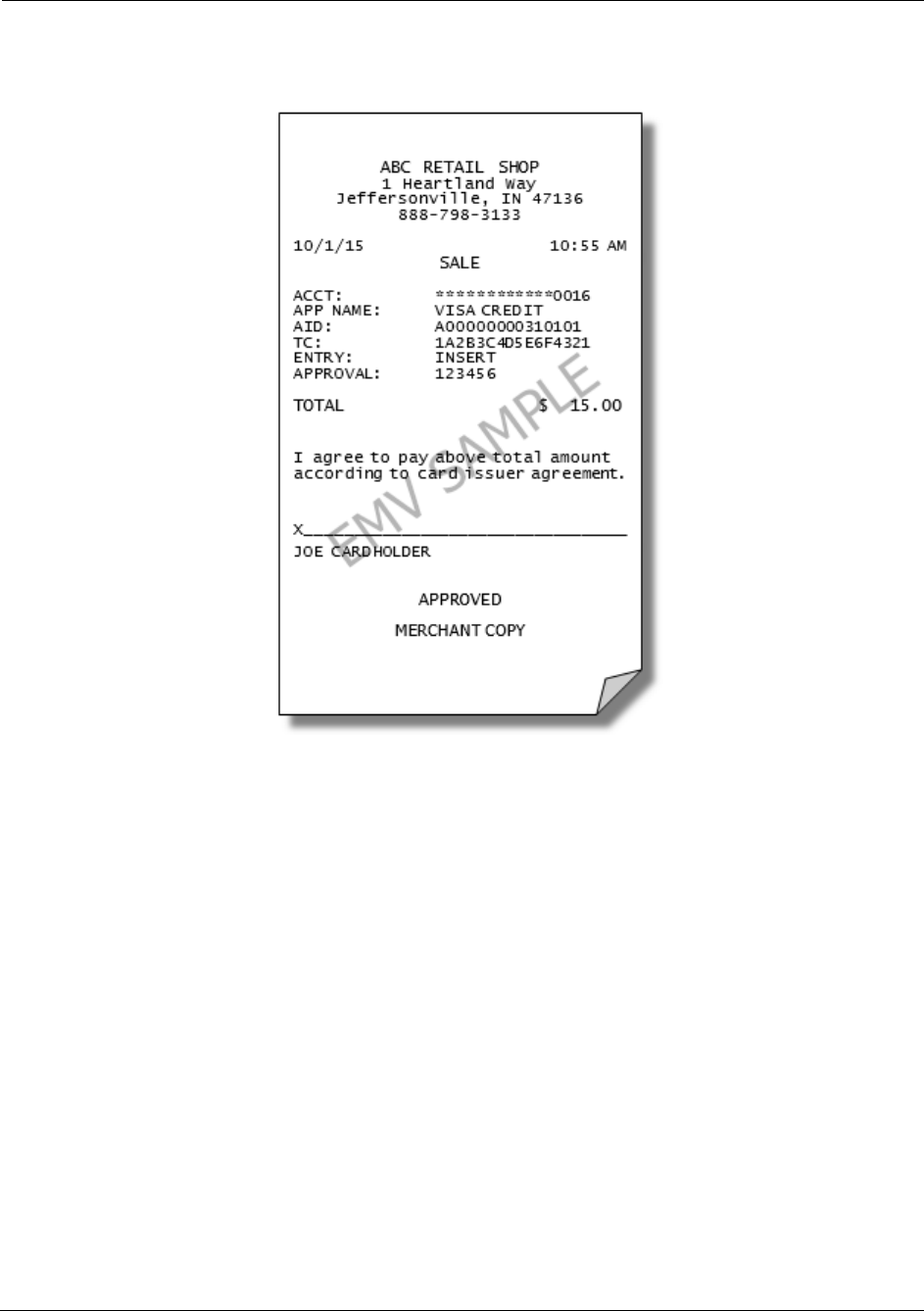

EMV Receipts........................................................................................................................................74

Approval Receipts ............................................................................................................................74

Decline Receipts ..............................................................................................................................76

Chapter 5: EMV Parameter Interface....................................................................................... 77

Introduction ...........................................................................................................................................77

Exchange ..............................................................................................................................................78

POS 8583..............................................................................................................................................78

NTS .......................................................................................................................................................79

Z01 ........................................................................................................................................................79

Portico ...................................................................................................................................................79

SpiDr .....................................................................................................................................................80

Appendix .................................................................................................................................. 81

EMV PDL Data Examples .....................................................................................................................81

Table of Contents EMV Integrator’s Guide V 15.2

82015 Heartland Payment Systems, Inc., All Rights Reserved–HPS Confidential: Sensitive

EMV Integrator’s Guide V 15.2 List of Tables

2015 Heartland Payment Systems, Inc., All Rights Reserved–HPS Confidential: Sensitive 9

List of Tables

2-1 Key Security Features.................................................................................................................16

2-2 Liability Shifts ..............................................................................................................................17

2-3 Contact Specifications ................................................................................................................18

2-4 Contactless Specifications ..........................................................................................................18

2-5 Heartland Host Specifications.....................................................................................................19

2-6 Card Authentication ....................................................................................................................19

2-7 Cardholder Verification ...............................................................................................................20

2-8 Authorization...............................................................................................................................20

2-9 Full vs. Partial EMV Transactions and Flow ...............................................................................20

2-10 Full vs. Partial Transaction Flow .................................................................................................21

2-11 Full vs. Partial Credit Transactions .............................................................................................22

2-12 Full vs. Partial Debit Transactions ..............................................................................................22

3-1 Integrated Solutions ....................................................................................................................24

3-2 VSDC Testing .............................................................................................................................26

3-3 M-TIP Testing .............................................................................................................................26

3-4 AEIPS Testing.............................................................................................................................27

3-5 D-PAS Testing ............................................................................................................................27

3-6 Test Environments ......................................................................................................................29

3-7 Test Process ...............................................................................................................................29

4-1 Command APDU Format ............................................................................................................31

4-2 Response APDU Format ............................................................................................................31

4-3 Data Conventions .......................................................................................................................33

4-4 Terminal Data .............................................................................................................................34

4-5 Card Data....................................................................................................................................44

4-6 Issuer Data..................................................................................................................................52

4-7 Tender Processing......................................................................................................................54

4-8 Fallback Processing....................................................................................................................55

4-9 Application Selection...................................................................................................................56

4-10 Supported Application Methods ..................................................................................................56

4-11 Offline Data Authentication .........................................................................................................60

4-12 Processing Restrictions ..............................................................................................................61

4-13 Cardholder Verification ...............................................................................................................61

4-14 PIN Support ................................................................................................................................62

4-15 Terminal Risk Management ........................................................................................................63

4-16 Terminal Action Analysis.............................................................................................................63

4-17 Online or Offline Disposition .......................................................................................................68

4-18 Contact EMV Flow Differences ...................................................................................................71

4-19 Card Verification .........................................................................................................................73

4-20 Receipt Requirements ................................................................................................................74

5-1 EMV PDL Tables ........................................................................................................................77

A-1 EMV PDL Data Examples...........................................................................................................81

List of Tables EMV Integrator’s Guide V 15.2

10 2015 Heartland Payment Systems, Inc., All Rights Reserved–HPS Confidential: Sensitive

EMV Integrator’s Guide V 15.2 List of Figures

2015 Heartland Payment Systems, Inc., All Rights Reserved–HPS Confidential: Sensitive 11

List of Figures

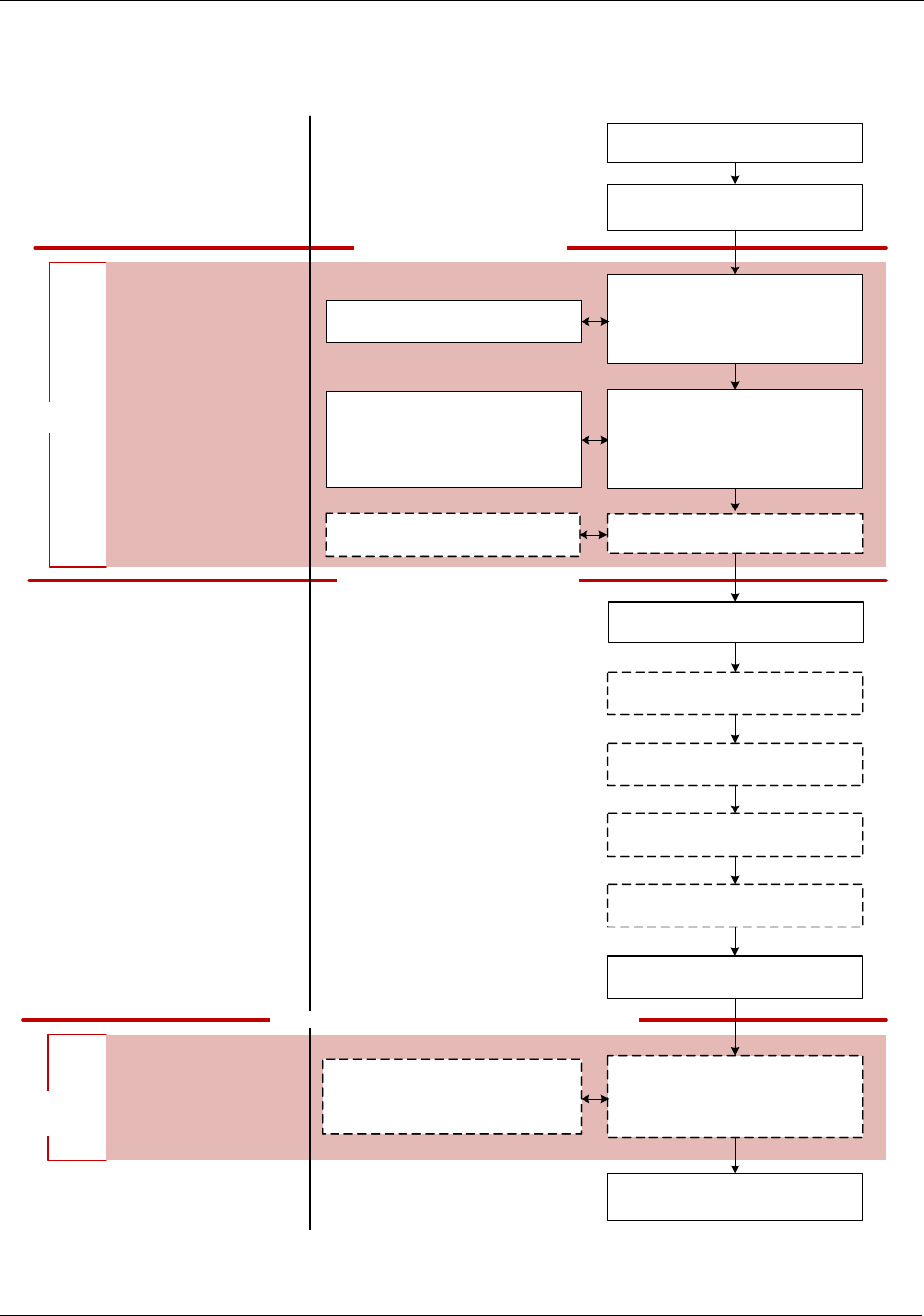

4-1 Contact Transaction Flow ...........................................................................................................53

4-2 Contactless Transaction Flow.....................................................................................................70

4-3 EMV Receipt Example ................................................................................................................75

List of Figures EMV Integrator’s Guide V 15.2

12 2015 Heartland Payment Systems, Inc., All Rights Reserved–HPS Confidential: Sensitive

EMV Integrator’s Guide V 15.2 1: Overview

2015 Heartland Payment Systems, Inc., All Rights Reserved–HPS Confidential: Sensitive 13

Chapter 1: Overview

1.1 Introduction

Heartland Payment Systems, Inc. (Heartland) is a leading third-party provider of payment card

transaction processing, providing the following services:

• Host Network transaction services

• Bank Card, Fleet, Debit and Private Label card processing

• Mobile and e-commerce solutions

• Settlement processing

1.2 Document Purpose

The purpose of this document is to provide an overview of integrating EMV chip card technology

on a POS system and interfacing to Heartland Payment Systems payment processing systems.

1.3 Audience

This document is intended for integrators who wish to develop EMV-capable POS solutions and

interface them with Heartland’s hosts for payment processing. It provides guidelines and

recommendations for that effort.

1: Overview EMV Integrator’s Guide V 15.2

14 2015 Heartland Payment Systems, Inc., All Rights Reserved–HPS Confidential: Sensitive

1.4 Payment Application Data Security

Standards (PA-DSS)

The Payment Card Industry (PCI) Security Standards Council (SSC) has released the Payment

Application Data Security Standards (PA-DSS) for payment applications running at merchant

locations. The PA-DSS assist software vendors to ensure their payment applications support

compliance with the mandates set by the Bank Card Companies (VISA, MasterCard, Discover,

American Express, and JCB).

In order to comply with the mandates set by the bank card companies, Heartland Payment

Systems:

• Requires that the account number cannot be stored as plain, unencrypted data to meet PCI

and PA-DSS regulations. It must be encrypted while stored using strong cryptography with

associated key management processes and procedures.

Note: Refer to PCI DSS Requirements 3.4–3.6* for detailed requirements regarding

account number storage. The retention period for the Account Number in the

shadow file and open batch must be defined and at the end of that period or when

the batch is closed and successfully transmitted, the account number and all other

information must be securely deleted. This is a required process regardless of the

method of transmission for the POS.

• Requires that, with the exception of the Account Number as described above and the

Expiration Date, no other Track Data is to be stored on the POS if the Card Type is a:

VISA, including VISA Fleet; MasterCard, including MasterCard Fleet; Discover, including

JCB, UnionPay, Carte Blanche, Diner's Club, and PayPal; American Express; Debit or

EBT. This requirement does not apply to WEX, FleetCor, Fleet One, Voyager, or Aviation

cards; Stored Value cards; Proprietary or Private Label cards.

• Recommends that software vendors to have their applications validated by an approved

third party for PA-DSS compliance.

• Requires all software vendors to sign a Non-Disclosure Agreement / Development

Agreement.

• Requires all software vendors to provide evidence of the application version listed on the

PCI Council’s website as a PA-DSS validated Payment Application, or a written certification

to Heartland testing to Developer's compliance with PA-DSS.

• Requires that all methods of cryptography provided or used by the payment application

meet PCI SSC’s current definition of ‘Strong Cryptography’.

*Refer to www.pcisecuritystandards.org for the PCI DSS Requirements document and further

details about PA-DSS.

EMV Integrator’s Guide V 15.2 2: EMV Processing Overview

2015 Heartland Payment Systems, Inc., All Rights Reserved–HPS Confidential: Sensitive 15

Chapter 2: EMV Processing Overview

2.1 Introduction

In 1996, Europay, MasterCard, and VISA first published the “EMV” specifications for the use of

chip cards for payment. EMV® is now a registered trademark of EMVCo, LLC, an organization

jointly owned and operated by American Express, Discover, JCB, MasterCard, UnionPay, and

VISA.

EMVCo manages, maintains, and enhances the EMV Integrated Circuit Card Specifications to

help facilitate global interoperability and compatibility of payment system integrated circuit cards

and acceptance devices. EMVCo maintains and extends specifications, provides testing

methodology, and oversees the testing and approval process.

The EMV Specifications provide a global standard for credit and debit payment cards based on

chip card technology. Payment chip cards contain an embedded microprocessor, a type of small

computer that provides strong security features and other capabilities not possible with traditional

magnetic stripe cards.

Chip cards are available in two forms, contact and contactless.

• For contact, the chip must come into physical contact with the chip reader for the payment

transaction to occur.

• For contactless, the chip must come within sufficient proximity of the reader (less than 4

cm) for the payment transaction to occur. Some cards may support both contact and

contactless interfaces, and non-card form factors such as mobile phones may also be used

for contactless payment.

Heartland recommends that vendors become familiar with general EMV processing prior to initial

implementation at Heartland. A good overview of EMV is available from EMVCo at:

http://www.emvco.com/best_practices.aspx?id=217.

2: EMV Processing Overview EMV Integrator’s Guide V 15.2

16 2015 Heartland Payment Systems, Inc., All Rights Reserved–HPS Confidential: Sensitive

2.2 EMV Migration

2.2.1 Enhanced Security

EMV is designed to significantly improve consumer card payment security by providing features

for reducing fraudulent transactions that result from counterfeit and lost and stolen cards. Due to

increased credit card breaches, this enhanced security has become a significant necessity.

The key security features are:

2.2.2 Card Brand Mandates

Effective April 2013, acquirer processors and sub-processor service providers are required to

support merchant acceptance of EMV chip transactions.

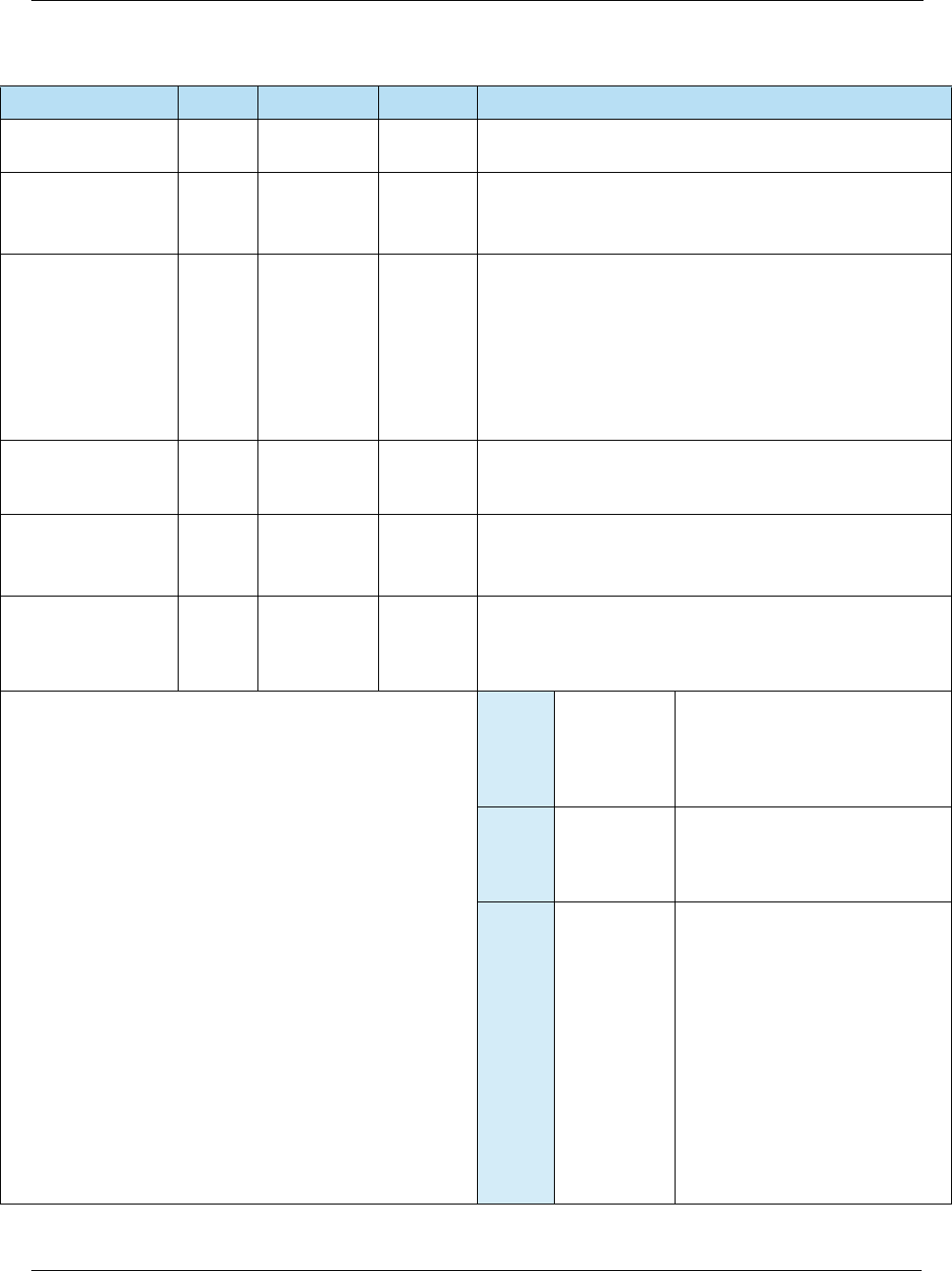

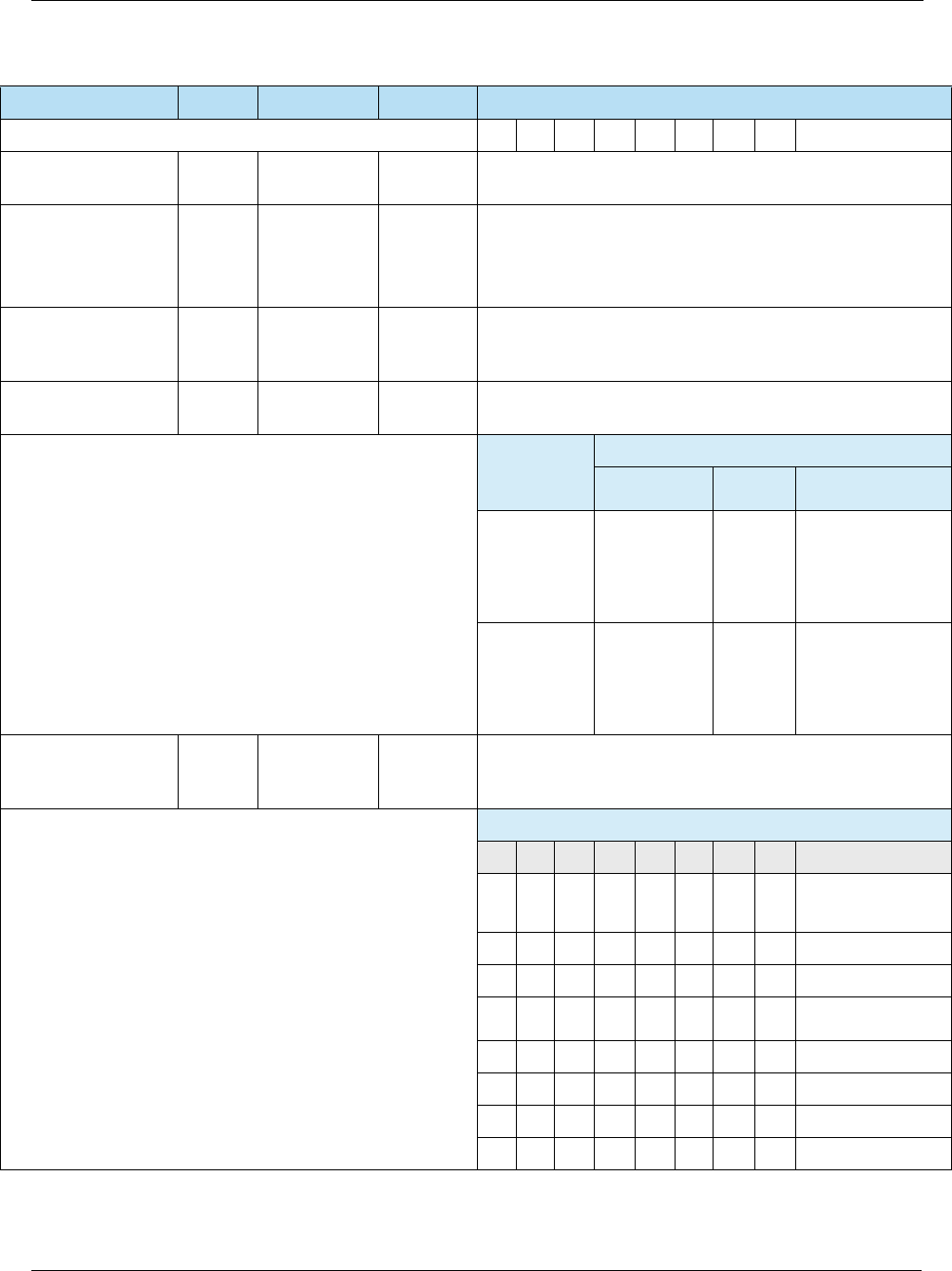

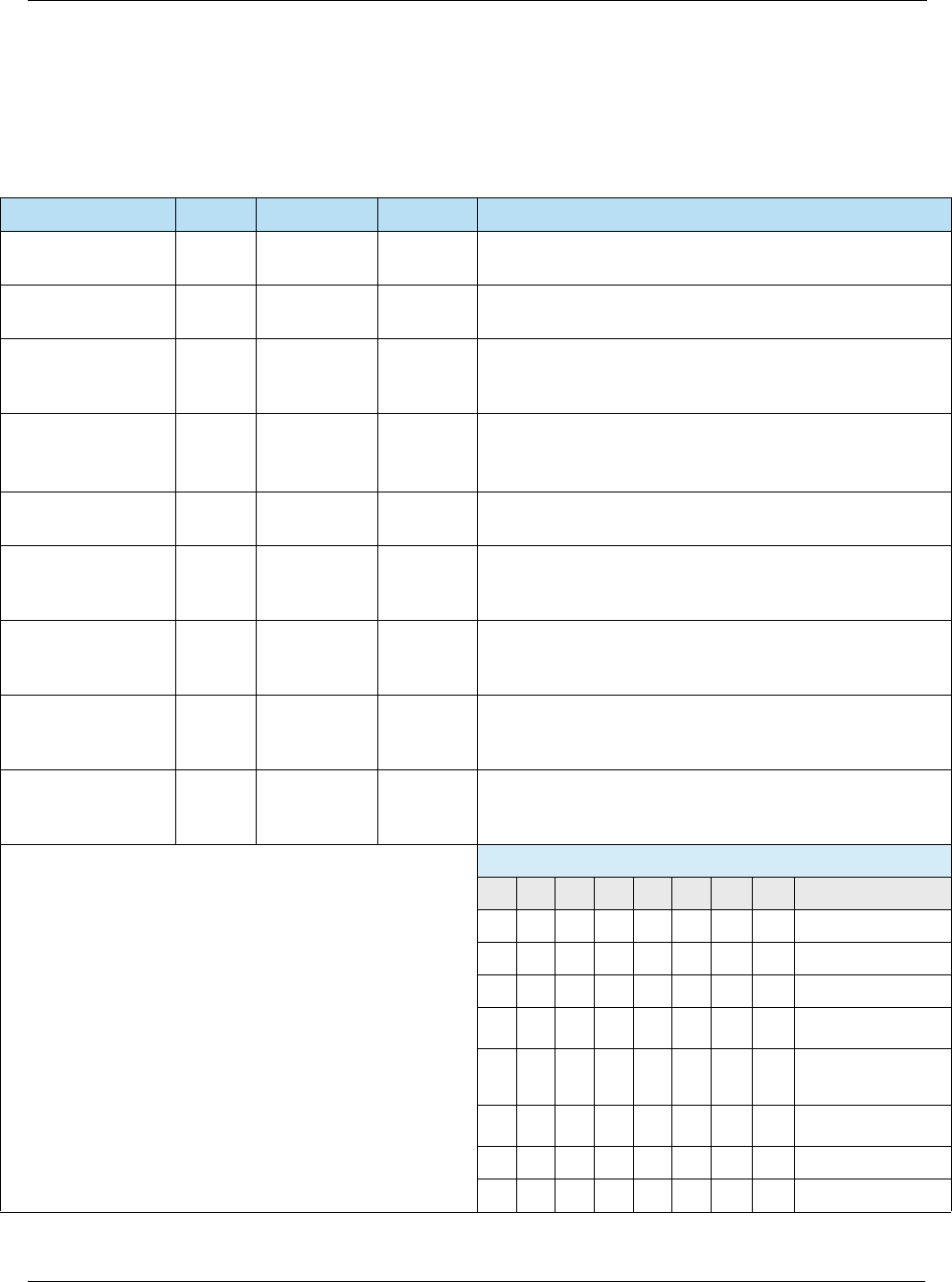

Table 2-1 Key Security Features

Key Security Feature Description

Card Authentication The terminal can authenticate the legitimacy of the card by using a

public-key infrastructure (PKI) and Rivest, Shamir, and Adleman (RSA)

cryptography to validate signed data from the card. The issuer can

authenticate the legitimacy of the card by validating a unique cryptogram

generated by the card for each payment transaction. These features will

help protect against counterfeit fraud.

Risk Management EMV introduces localized parameters to define the conditions under which

the issuer will permit the chip card to be used and force transactions online

for authorization under certain conditions such as offline limits being

exceeded.

Transaction Integrity Payment data such as purchase and cashback amounts are part of the

cryptogram generation and authentication processing, which will help

ensure the integrity of this data across authorization, settlement, and

clearing.

Cardholder Verification More robust cardholder verification processes and methods such as online

PIN (verified online by issuer) and offline PIN (verified offline by card) will

help protect against lost and stolen fraud.

EMV Integrator’s Guide V 15.2 2: EMV Processing Overview

2015 Heartland Payment Systems, Inc., All Rights Reserved–HPS Confidential: Sensitive 17

2.2.3 Fraud Liability Shifts

Effective October 2015 (or October 2017 for automated fuel dispensers), a merchant that does

not support EMV assumes liability for counterfeit card transactions.

There are two types of liability shifts:

2.2.4 PCI Audit Waivers

Effective October 2012, the card brands will waive PCI DSS compliance validation requirements

if the merchant invests in contact and contactless chip payment terminals. For example, VISA’s

Technology Innovation Program (TIP) provides PCI audit relief to qualifying merchants (Level 1

and Level 2 merchants that process more than 1 million VISA transactions annually) when 75

percent of the merchant’s VISA transactions originate at a dual-interface EMV chip-enabled

terminal. MasterCard offers a similar program.

2.3 EMV Specifications

This document provides guidelines for EMV integration, but it does not contain all the EMV

requirements. It should be used in conjunction with the following documents:

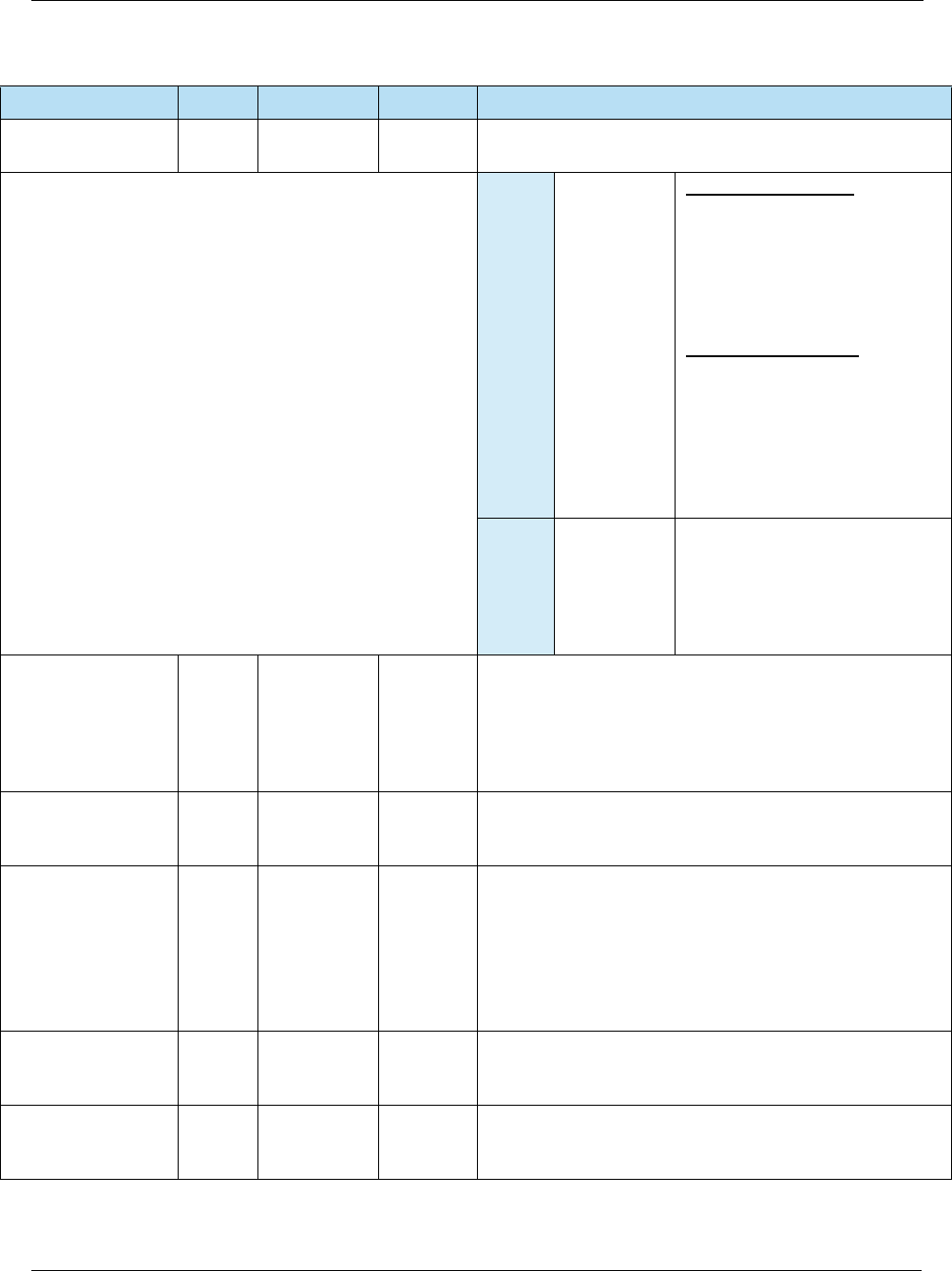

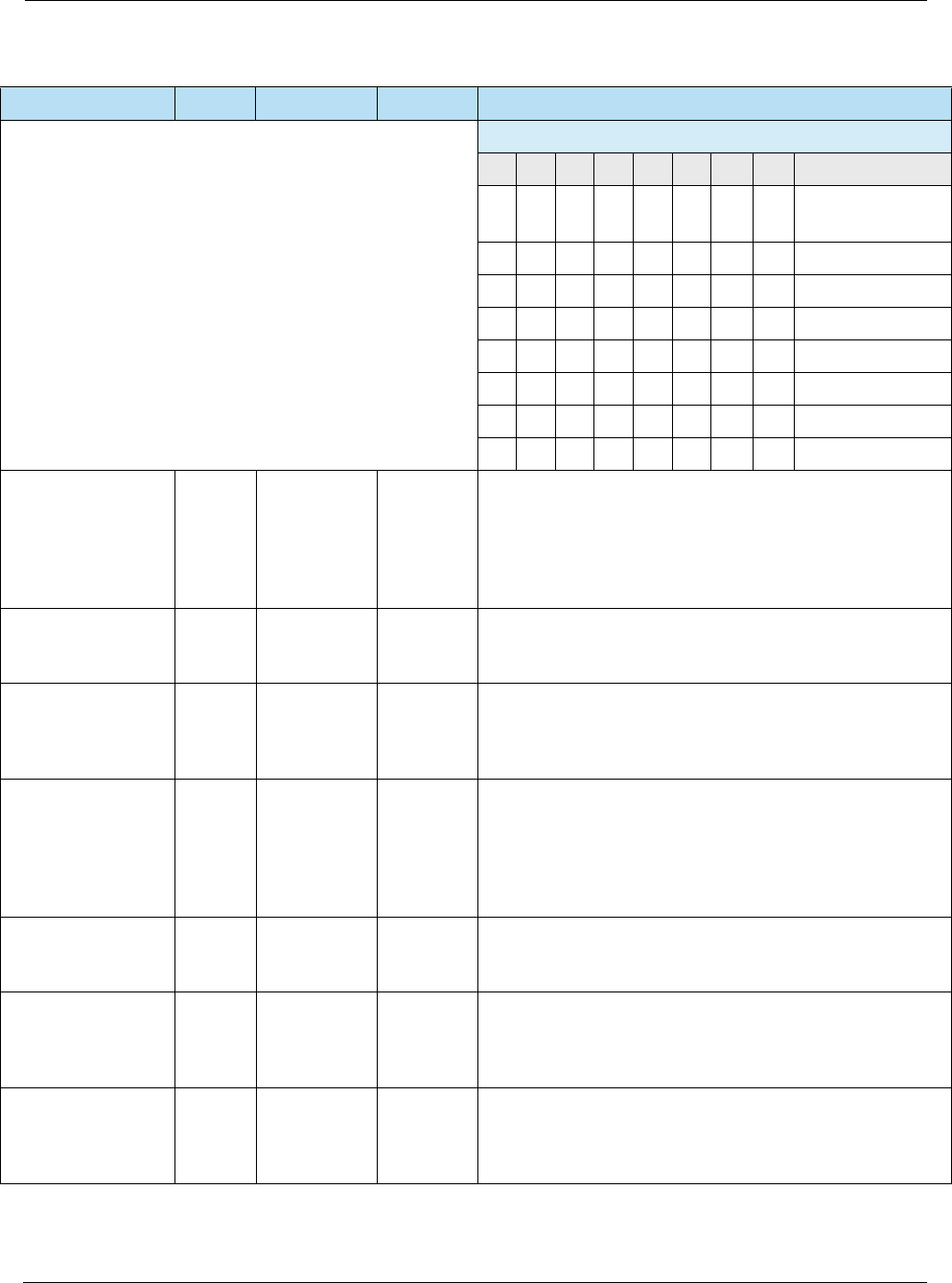

Table 2-2 Liability Shifts

Liability Shift Description

Chip Liability Shift An issuer may charge back a counterfeit fraud transaction that occurred at a

non-EMV POS terminal if the valid card issued was a chip card.

Chip/PIN Liability Shift An issuer may charge back a lost or stolen fraud transaction that occurred at

an EMV POS terminal that was not PIN-capable if the card involved was a

PIN-preferring chip card. A PIN-preferring chip card is defined as an EMV chip

card that has been personalized so that a PIN CVM option (online PIN or

offline PIN) appears in the card’s CVM list with a higher priority than the

signature option.

2: EMV Processing Overview EMV Integrator’s Guide V 15.2

18 2015 Heartland Payment Systems, Inc., All Rights Reserved–HPS Confidential: Sensitive

2.3.1 Contact Specifications

For EMV contact card acceptance, device manufacturers and payment application developers

must adhere to the following specifications:

2.3.2 Contactless Specifications

For EMV contactless card acceptance, device manufacturers and payment application

developers must adhere to the following specifications:

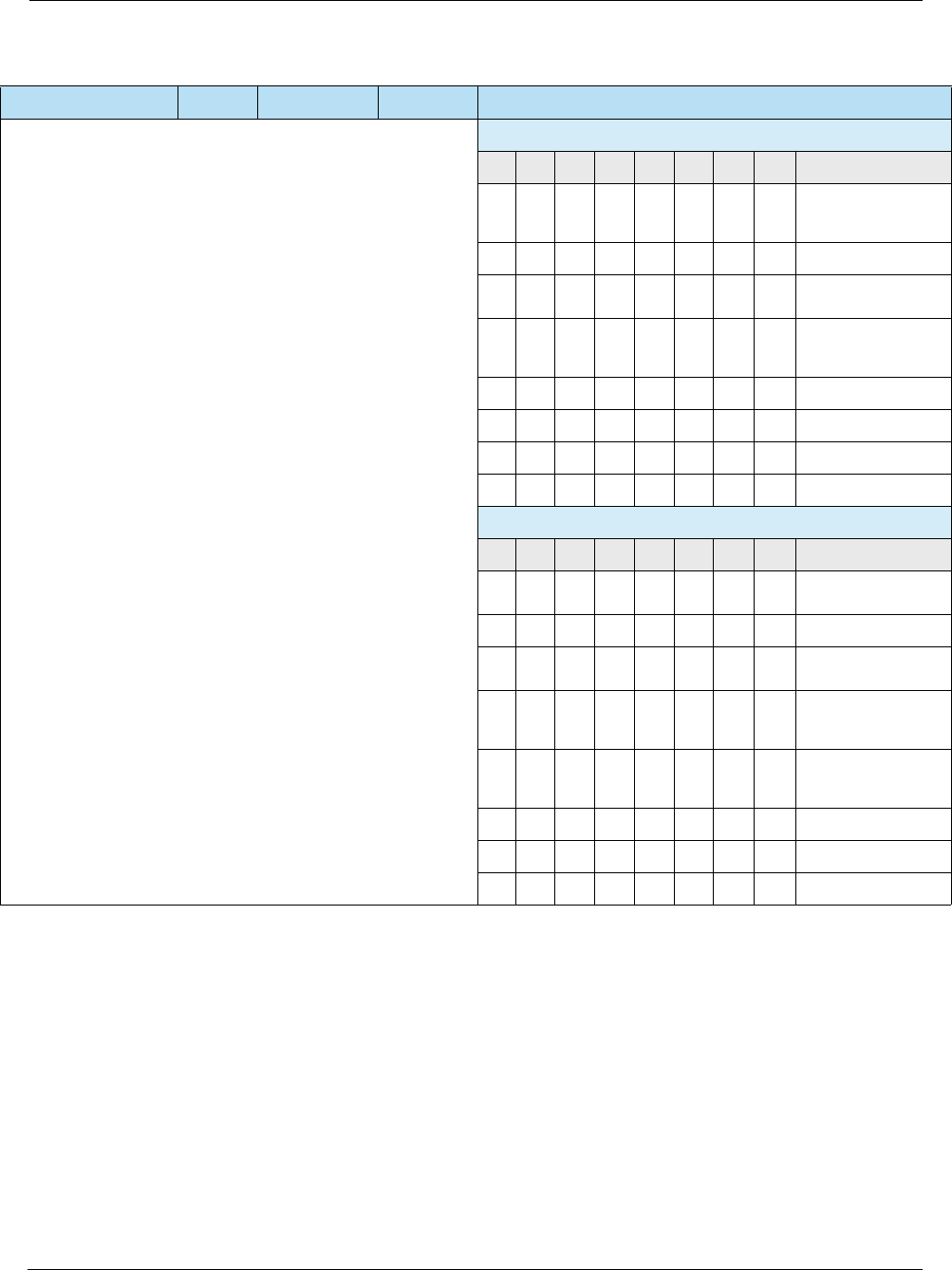

Table 2-3 Contact Specifications

Source Specification

EMVCo • EMV Specifications v4.3 (Nov 2011) –

http://www.emvco.com/specifications.aspx?id=223

– Book 1: Application Independent ICC to Terminal Interface Requirements

– Book 2: Security and Key Management

– Book 3: Application Specification

– Book 4: Cardholder, Attendant, and Acquirer Interface Requirements

VISA • Transaction Acceptance Device Guide v3.0 (May 2015)

• Integrated Circuit Card Specification v1.5 (May 2009)

MasterCard • U.S. Market Terminal Requirements (April 2014)

American Express • AEIPS Terminal Implementation Guide v4.3 (April 2015)

• AEIPS Terminal Technical Manual v4.3 (April 2015)

Discover • Contact D-PAS Acquirer Implementation Guide v3.0 (Jan 2015)

• D-PAS Terminal Specification v1.0 (Jun 2009)

Table 2-4 Contactless Specifications

Source Specification

EMVCo • EMV Contactless Specifications v2.5 (Mar 2015) –

http://www.emvco.com/specifications.aspx?id=21

– Book A: Architecture and General Requirements

– Book B: Entry Point

– Books C [C-1, C-2, C-3, C-4, C-5, C-6, C-7]: Kernel Specifications

– Book D: Contactless Communication Protocol

VISA • Transaction Acceptance Device Guide v3.0 (May 2015)

• Contactless Payment Specification v2.1 (May 2009)

MasterCard • U.S. Market Terminal Requirements (Apr 2014)

• Contactless Reader Specification v3.1 (Jun 2015)

American Express • Contactless NFC Terminal Implementation Guide v1.0 (Mar 2014)

• Expresspay Terminal Specification v3.0 (Feb 2012)

EMV Integrator’s Guide V 15.2 2: EMV Processing Overview

2015 Heartland Payment Systems, Inc., All Rights Reserved–HPS Confidential: Sensitive 19

2.3.3 Heartland Host Specifications

Information given in this document for each network platform is meant to be an overview only.

The latest version of these Heartland platform specifications should be used for complete

message requirements and formats:

2.4 EMV Online vs. Offline

In the magstripe world, the term “offline” is often associated with certain types of transactions that

may occur when host communications are down, such as voice authorization, deferred

authorization (i.e. store and forward), and forced acceptance (i.e. merchant/acquirer stand-in).

Those same transactions can still occur in the EMV world as well, but there are several additional

uses of the term “offline” for EMV.

2.4.1 Card Authentication

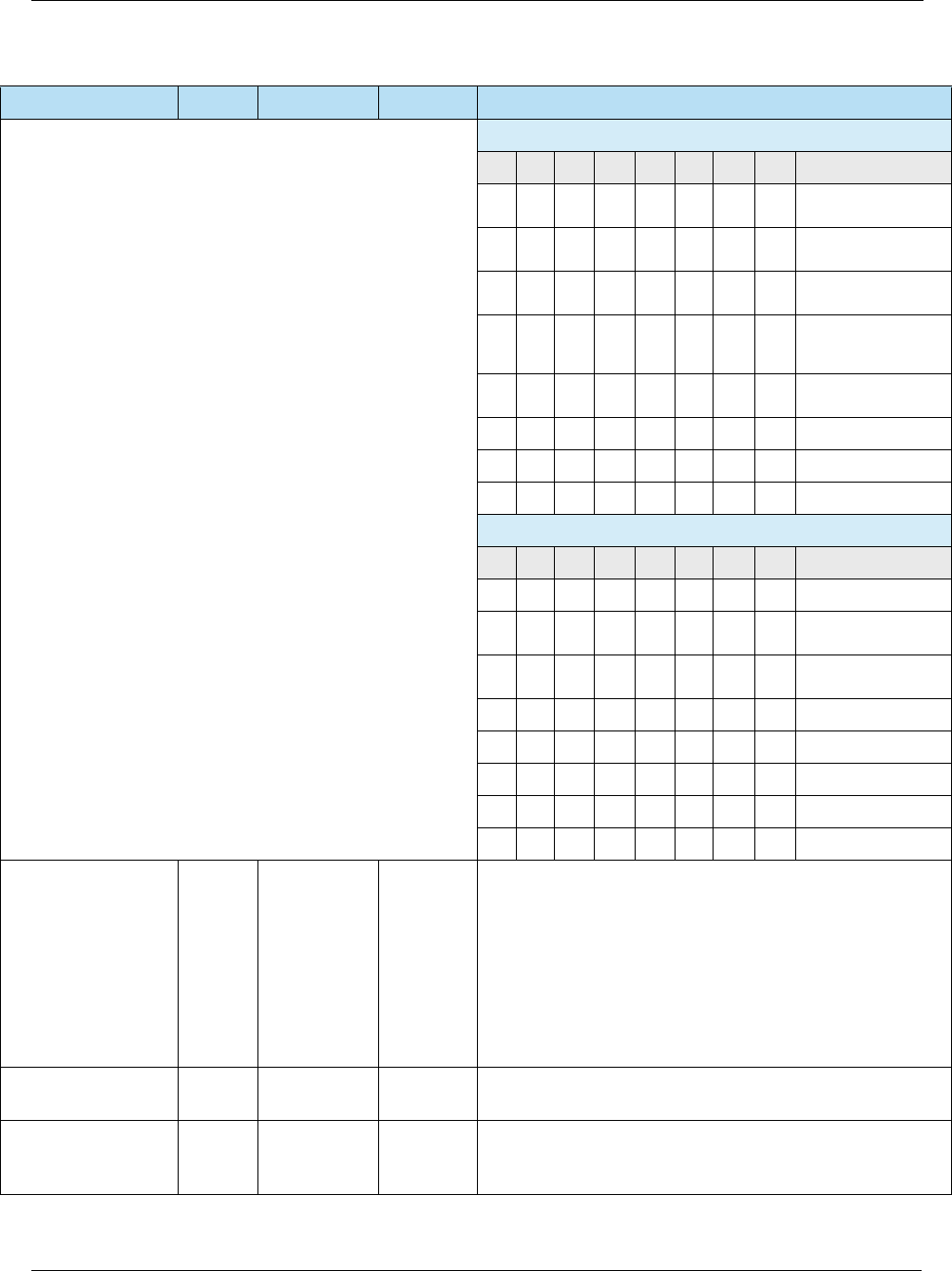

Discover • Contactless D-PAS Acquirer Implementation Guide v1.0

• Contactless D-PAS Terminal Application Specification v1.0

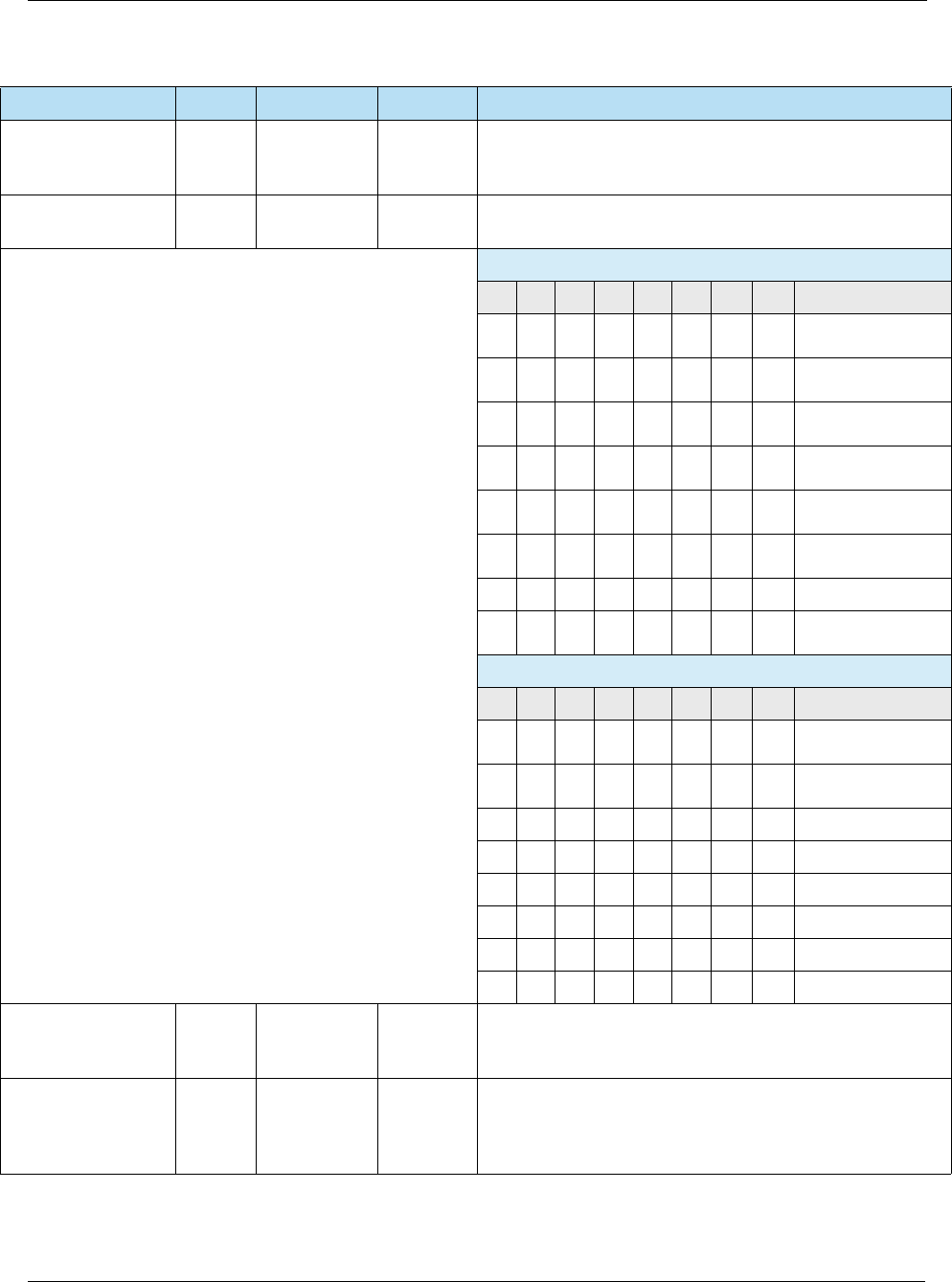

Table 2-5 Heartland Host Specifications

Platform Specification

Exchange • Exchange Host Specifications

Portico • Portico Developer Guide

NWS • Z01 Specifications

• POS 8583 Specifications

• SpiDr Specifications Developer’s Guide

VAPS • Network Terminal Specifications (NTS)

• POS 8583 Specifications

• SpiDr Specifications Developer’s Guide

Table 2-6 Card Authentication

Online Card Authentication vs. Offline Card Authentication

The transaction is sent online to an issuer who

authenticates the CVV in the track data for swiped

transactions, or CVV2 on the back of the card for

manually entered transactions.

The card may be authenticated offline by the terminal

using a PKI and RSA cryptography to verify that

certain static and/or dynamic data elements have been

digitally signed by the legitimate card issuer.

Table 2-4 Contactless Specifications

Source Specification

2: EMV Processing Overview EMV Integrator’s Guide V 15.2

20 2015 Heartland Payment Systems, Inc., All Rights Reserved–HPS Confidential: Sensitive

2.4.2 Cardholder Verification

2.4.3 Authorization

2.5 Full vs. Partial EMV Transactions and Flow

EMV POS solutions typically support both “full” EMV transactions and “partial” EMV transactions

as follows:

Table 2-7 Cardholder Verification

Online Cardholder Verification vs. Offline Cardholder Verification

The transaction is sent online to an issuer who

verifies that the online PIN or AVS data is correct.

An offline PIN may be securely stored on the card, so

the PIN entered on the PIN entry device may be sent

to the card in plaintext or enciphered format to be

validated by the card.

Table 2-8 Authorization

Online Authorization vs. Offline Authorization

The transaction is sent online to an issuer who

approves or declines the transaction.

Based on the amount of the transaction, and the risk

management criteria established by the card and the

terminal, a transaction may be approved or declined by

the card on behalf of the issuer, either with or without

attempt to go online to the issuer.

Table 2-9 Full vs. Partial EMV Transactions and Flow

EMV Transaction Description

Full EMV Transactions Transactions such as Purchases and Pre-Authorizations where the

full EMV transaction flow (i.e. the interaction between the card and

terminal) is performed and the card participates in the authorization

decision, whether online or offline.

Partial EMV Transactions Transactions such as Returns and Reversals where the EMV

transaction flow is only partially performed to the extent necessary to

get the card data from the chip and the card does not participate in

the authorization decision.

EMV Integrator’s Guide V 15.2 2: EMV Processing Overview

2015 Heartland Payment Systems, Inc., All Rights Reserved–HPS Confidential: Sensitive 21

2.5.1 Full vs. Partial Transaction Flow

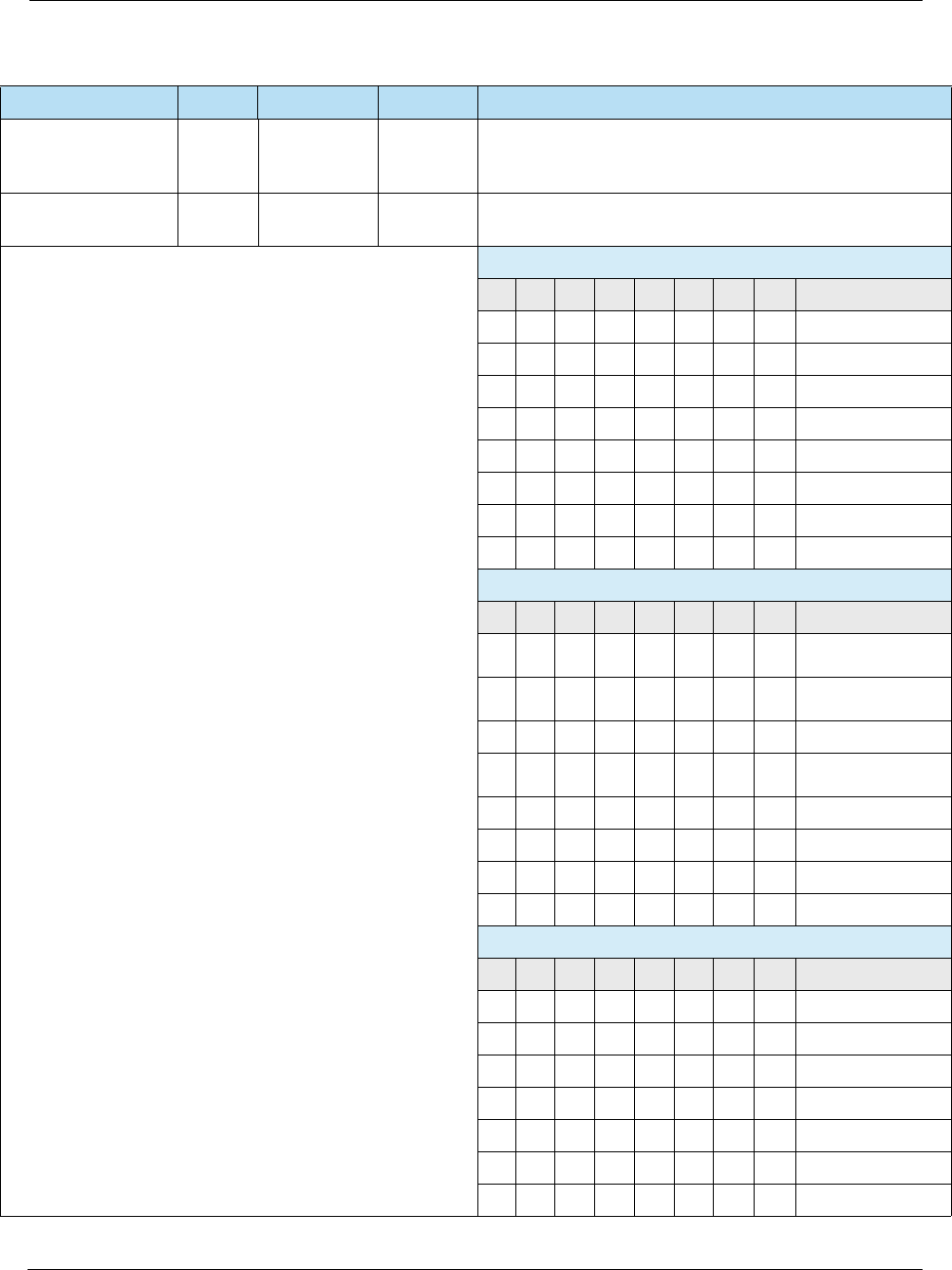

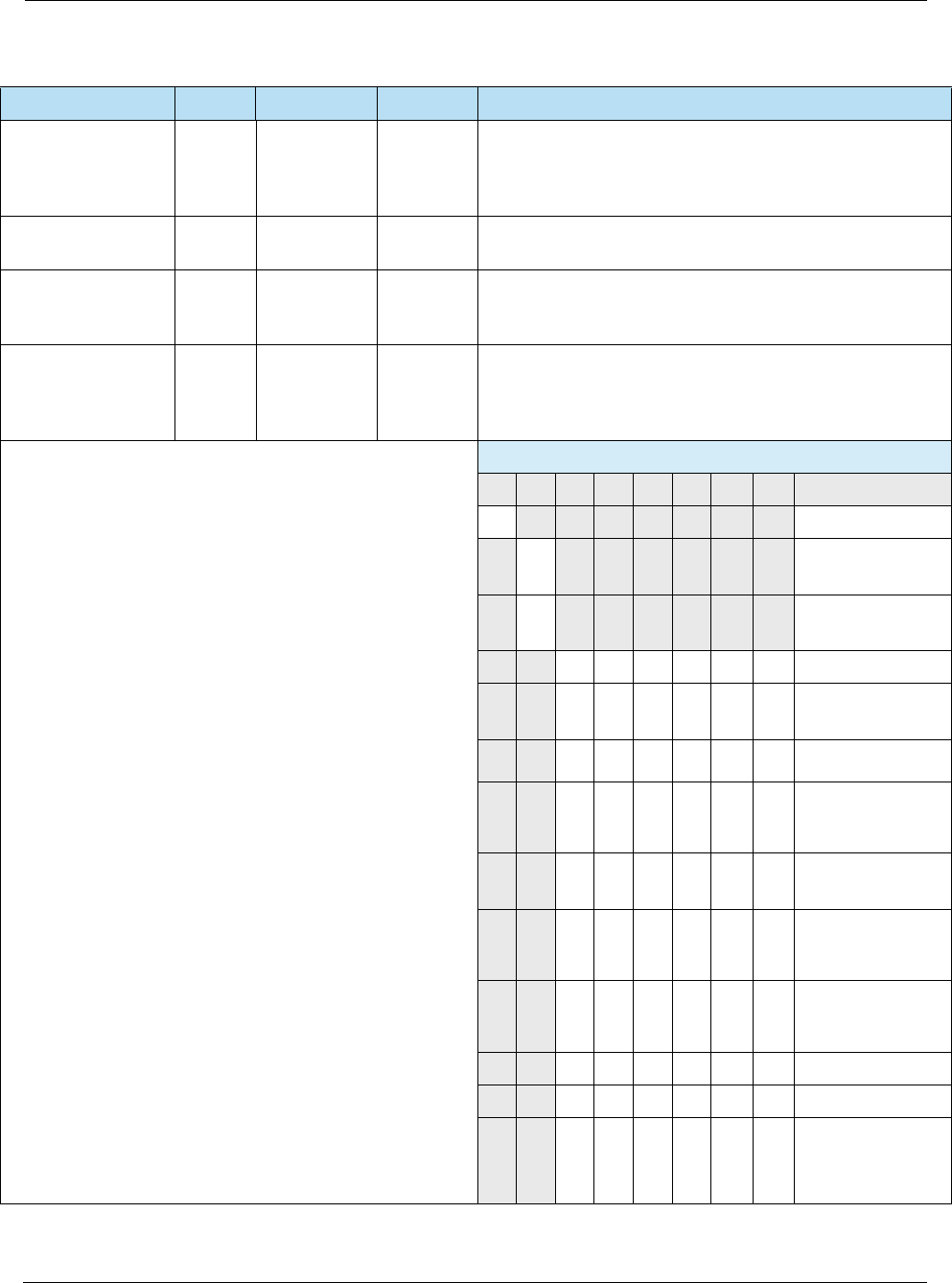

Table 2-10 Full vs. Partial Transaction Flow

EMV Transaction Step Full

EMV

Partial

EMV Notes

Card Acquisition

Card is inserted or tapped.

Application Selection

Initiate Application Processing

Read Application Data

Offline Data Authentication

Processing Restrictions

Cardholder Verification

Terminal Risk Management

Terminal Action Analysis

For partial EMV transactions, the terminal requests an AAC

at 1st GENERATE AC to terminate card usage.

Card Action Analysis

For partial EMV transactions, the card always returns an

AAC.

Online Processing

Issuer Authentication

Completion

Issuer Script Processing

Card Removal

Prompt to remove card if it was inserted.

2: EMV Processing Overview EMV Integrator’s Guide V 15.2

22 2015 Heartland Payment Systems, Inc., All Rights Reserved–HPS Confidential: Sensitive

2.5.2 Full vs. Partial Credit Transactions

2.5.3 Full vs. Partial Debit Transactions

Table 2-11 Full vs. Partial Credit Transactions

EMV Transactions Full

EMV

Partial

EMV Notes

Online Purchase ARQC received at 1st GENERATE AC.

Offline Purchase Advice

Full for EMV offline approvals where TC received at 1st

GENERATE AC or after failed host communications at 2nd

GENERATE AC.

Partial for voice authorizations if PAN obtained from chip.

Pre-Authorization

Incremental Authorization No chip data should be sent.

Completion No chip data should be sent.

Cash Advance

Bill Payment

Card Verify

Purchase Return To obtain PAN from chip if needed.

Void PAN and chip data from original authorization should be sent.

Reversal on Timeout PAN and chip data from original authorization should be sent.

Offline Decline Advice AAC received at 1st GENERATE AC or due to failed Issuer

Authentication at 2nd GENERATE AC.

Table 2-12 Full vs. Partial Debit Transactions

EMV Transactions Full

EMV

Partial

EMV Notes

Online Purchase ARQC received at 1st GENERATE AC.

Purchase Return ARQC received at 1st GENERATE AC.

Void PAN and chip data from original authorization should be sent.

Reversal on Timeout PAN and chip data from original authorization should be sent.

Offline Decline Advice AAC received at 1st GENERATE AC or due to failed Issuer

Authentication at 2nd GENERATE AC.

EMV Integrator’s Guide V 15.2 3: EMV Development Overview

2015 Heartland Payment Systems, Inc., All Rights Reserved–HPS Confidential: Sensitive 23

Chapter 3: EMV Development Overview

3.1 EMV Terminals

In order to develop an EMV POS solution, an approved EMV transaction acceptance device

must be used. In this document all such devices, whether they are a countertop terminal,

multi-function PIN pad, multi-lane signature capture device, automated fuel dispenser module,

etc., will be referred as a 'terminal'.

3.1.1 Contact Devices

For EMV contact card acceptance, use any terminal if all of the following criteria apply:

• Contains an EMVCo Level 1 Contact approved Interface Module (IFM) evaluated against

the EMV ICC Specifications, Book 1 v4.0 or later.

• Contains a MasterCard Terminal Quality Management (TQM) approved IFM.

• Is running an EMVCo Level 2 Contact approved application kernel evaluated against the

EMV ICC Specifications v4.3 or later.

• Contains a PCI PTS 2.x, 3.x or 4.x approved PIN Entry Device (PED) or Encrypting PIN

Pad (EPP), if you plan to support PIN.

3.1.2 Contactless Devices

For EMV contactless card acceptance, use any terminal if all of the following criteria apply:

• Contains an EMVCo Level 1 Contactless approved Proximity Coupling Device (PCD)

evaluated against the EMV Contactless Specifications, Book D v2.1 or later.

• Contains a MasterCard TQM approved PCD.

• Is running a VISA approved payWave application kernel evaluated against the VISA

Contactless Payment Specification v2.1.1 or later.

• Is running a MasterCard approved PayPass application kernel approved against the

MasterCard Contactless Reader Specification v3.0.3 or later.

• Is running an American Express approved Expresspay application kernel evaluated

against the Expresspay Terminal Specification v3.0 or later.

• Is running a Discover approved D-PAS application kernel evaluated against the

Contactless D-PAS Terminal Payment Application v1.0 or later.

• Contains a PCI PTS 2.x, 3.x or 4.x approved PED or EPP, if you plan to support PIN.

REQUIREMENT An EMV POS Solution cannot be certified unless the EMVCo Level 1 and Level 2 Letters of

Approval for your terminal(s) of choice are current and not about to expire.

3: EMV Development Overview EMV Integrator’s Guide V 15.2

24 2015 Heartland Payment Systems, Inc., All Rights Reserved–HPS Confidential: Sensitive

3.1.3 Letters of Approval

The EMVCo and PCI approval numbers and/or Letters of Approval (LoAs) can be obtained from

their respective websites:

•http://www.emvco.com/approvals.aspx?id=83

•https://www.pcisecuritystandards.org/approved_companies_providers/approved_pin_trans

action_security.php

The other approval numbers and/or LoAs can be obtained from the device supplier or

manufacturer.

3.2 EMV Solutions

The type of EMV POS solution to be developed is an important consideration as this will

determine the level of expertise needed, the amount of time it will take and whether a full EMV

certification will be required.

3.2.1 Integrated

Integrated solutions typically involve an Electronic Cash Register (ECR) that is connected to a

terminal containing the EMV kernel and providing all EMV functionality including card acquisition

and PIN entry.

3.2.2 Standalone

Standalone solutions consist of a terminal that runs the POS software, contains the EMV kernel

and provides all EMV functionality. PIN entry occurs on an internal or external PIN pad and if

contactless is supported, the reader may be integrated into the terminal or be a separate device.

A standalone solution is in scope for PCI and full EMV certification.

Table 3-1 Integrated Solutions

Integrated Solution Description

Fully Integrated The terminal provides the EMV functionality, but the ECR still handles

card data and host communication. Therefore, it is in scope for PCI and

full EMV certification.

Semi-Integrated The terminal not only provides the EMV functionality, but also handles the

host communication, so the ECR does not see the card data. Therefore,

the ECR is not in scope for PCI or full EMV certification. Only a minimal

EMV validation script must be run for semi-integrated solutions.

EMV Integrator’s Guide V 15.2 3: EMV Development Overview

2015 Heartland Payment Systems, Inc., All Rights Reserved–HPS Confidential: Sensitive 25

3.3 EMV Certifications

Magstripe swiped and key entered transactions will continue to be certified directly through

Heartland per the existing processes already in place. However, EMV requires additional

certifications. Each card brand has its own proprietary chip applications that run on EMV cards

bearing their brand. For that reason, each card brand has its own certification requirements that

must be met and submitted for approval.

3.3.1 Test Requirements

The card brand certification requirements must be met for each distinct POS configuration that

will be deployed, which is defined by a unique combination of:

• The kernel software, which includes the Level 2 Contact Application Kernel and/or Level 2

Contactless Application Kernel (payWave, PayPass, Expresspay, etc.).

• The terminal application software, which includes the payment application software and

the terminal-to-acquirer communication software.

• The specific terminal configuration, which includes use of a particular EMVCo Level 2

approved kernel configuration for the specific Terminal Type, Terminal Capabilities and

other relevant terminal parameter settings.

• The complete connection path from the terminal to the card brand.

The card brand certification requirements must be met when any of the following occurs:

• A particular POS configuration is deployed for the first time.

• A major upgrade is made to an already deployed POS configuration.

• The terminal hardware and software is upgraded and the change is major according to the

EMVCo Type Approval Bulletin No. 11 (http://www.emvco.com/approvals.aspx?id=108).

Note: Replacing the IFM with another approved IFM is not considered a major change.

• A contact terminal is upgraded to support contactless transactions.

• The terminal application software is upgraded to support additional payment related

functionality such as the partial approval, purchase with cash back, purchase with gratuity,

cardholder application selection, etc.

• The Level 2 kernel configuration is modified.

• The terminal is upgraded to support an additional AID.

• The acquirer modifies its network in such a way that it affects the transaction message

mapping between the POS and the acquirer host that interfaces with the card brand

networks.

• The card brand requests it, for instance, in the scope of the ad-hoc resolution of a field

interoperability issue.

REQUIREMENT If an EMV POS Solution supports multiple kernel configurations, multiple certifications

will be required, one for each kernel configuration that will be used in production.

3: EMV Development Overview EMV Integrator’s Guide V 15.2

26 2015 Heartland Payment Systems, Inc., All Rights Reserved–HPS Confidential: Sensitive

3.3.2 Test Plans

The following card brand test plans must be executed for full EMV certifications:

•VISA Smart Debit/Credit (VSDC) Testing

•MasterCard Terminal Integration Process (M-TIP) Testing

•American Express Integrated Circuit Card Payment Specification (AEIPS) Testing

•Discover D-Payment Application Specification (D-PAS) Testing

3.3.2.1 VISA Smart Debit/Credit (VSDC) Testing

3.3.2.2 MasterCard Terminal Integration Process (M-TIP)

Testing

Table 3-2 VSDC Testing

Test Plan Description

Acquirer Device Validation Toolkit (ADVT) User

Guide v6.1

Up to 32 test cases for EMV contact card acceptance.

qVSDC Device Module Test Cases v2.1 Up to 89 test cases for EMV contactless card acceptance.

Required for stand-alone contactless readers.

Optional for dual-interface (contact and contactless)

integrated readers.

Contactless Device Evaluation Toolkit (CDET) User

Guide v2.1

Up to 15 test cases for general contactless card acceptance.

Table 3-3 M-TIP Testing

Test Plan Description

M-TIP 2.0 Build 215 – M-TIP Subset Up to 175 test cases for EMV contact card acceptance.

M-TIP 2.0 Build 215 – Field Interoperability Subset Up to 89 test cases for EMV contact card acceptance.

M-TIP 2.0 Build 215 – Contactless Subset 6 Up to 23 test cases for EMV contactless card acceptance.

M-TIP 2.0 Build 215 – Contactless Subset 8 Up to 268 test cases for EMV contactless card acceptance.

EMV Integrator’s Guide V 15.2 3: EMV Development Overview

2015 Heartland Payment Systems, Inc., All Rights Reserved–HPS Confidential: Sensitive 27

3.3.2.3 American Express Integrated Circuit Card Payment

Specification (AEIPS) Testing

3.3.2.4 Discover D-Payment Application Specification

(D-PAS) Testing

Table 3-4 AEIPS Testing

Test Plan Description

Global AEIPS Terminal Test Plan v6.0 Up to 34 test cases for EMV contact card acceptance.

Global Expresspay EMV Terminal End-to-End Test

Plan v1.5

Up to 25 test cases for EMV contactless card acceptance.

Table 3-5 D-PAS Testing

Test Plan Description

Contact D-PAS Acquirer-Terminal End-to-End Test Plan

v1.3

Up to 52 test cases for EMV contact card acceptance.

Contactless D-PAS Acquirer-Terminal End-to-End Test

Plan v1.2

Up to 33 test cases for EMV contactless card

acceptance.

3: EMV Development Overview EMV Integrator’s Guide V 15.2

28 2015 Heartland Payment Systems, Inc., All Rights Reserved–HPS Confidential: Sensitive

3.3.3 Test Tools

To successfully execute the test plans, you need the following:

1. The appropriate test cards.

2. A means of capturing, logging and validating the interaction between the terminal and

cards.

One method to accomplish this is to order all of the required physical test cards from a company

such as FIME, along with their Smartspy tools for logging the interaction. However, because

there are hundreds of different test cases and test cards and the requirements often change for

both, this approach is prohibitively impractical and expensive. Heartland recommends

purchasing test tools instead.

Many EMV test tools are available on the market today that remove the need for physical test

cards and rudimentary card spies. These tools emulate all the required test cards, facilitate

execution of the test cases, capture the interaction between the terminal and the cards in a

readable format, clearly indicate pass/fail results of the test cases and log the results in the

format required for submission to the card brands.

You may use any test tool if it has been approved for use by a card brand for the purpose of

meeting that brand’s certification requirements. Each card brand maintains a list of approved test

tools that have been verified to properly emulate the test cards and execute the test cases

required for certification.

The following tools are approved by all four card brands for both contact and contactless EMV

testing:

• ICC Solutions’ ICCSimTmat Test Manager

• UL Transaction Security’s Collis Brand Test Tool

You may choose to purchase either of these tools or any other tools approved for use by one or

more card brands. Heartland uses the Collis Brand Test Tool for testing our internally developed

applications. If you choose to purchase Collis, Heartland can apply knowledge and expertise of

that tool toward facilitating your testing.

EMV Integrator’s Guide V 15.2 3: EMV Development Overview

2015 Heartland Payment Systems, Inc., All Rights Reserved–HPS Confidential: Sensitive 29

3.3.4 Test Environments

Heartland currently has two EMV test environments:

It is essential that you work with POS Integrations to insure you are pointed to the correct test

environment based on the type of testing you are executing.

3.3.5 Test Process

You will need to work with our POS Integrations team to understand and follow their current

certification procedures. The following is only a high-level overview of the process:

Table 3-6 Test Environments

Test Environment Description

Pre-certification This environment is used for executing the card brand test cases to

ensure a 100% pass rate prior to moving to certification. This

environment can also be used for generic EMV and non-EMV testing

where certain dollar amounts trigger fixed responses from the host.

Certification This environment is used for executing the card brand test cases for

submission to the card brands for formal certification.

Table 3-7 Test Process

Test Process Description

Certification Setup A certification analyst will provide you with the appropriate certification request

forms. Once those are returned and processed, the POS Integrations team will set

up the required test accounts, point them to the appropriate environments, provide

you with the corresponding credentials and provide test scripts as follows:

•VISA – No script available. You must configure your test tool according to

configuration being certified and it will specify test case applicability.

•MasterCard – We provide a TSE file that contains your script and must be

imported into your test tool.

•American Express – We provide access to the AMEX Test System (ATS) which

contains your script.

•Discover – We provide a spreadsheet from UL that contains your script.

Card Brand Pre-Certification Execute all card brand test cases in our pre-certification environment to ensure a

100% pass rate prior to moving to certification. Our certification analyst may request

your terminal logs and transaction receipts if needed to help resolve issues.

Class B Certification Execute the non-EMV test script provided by our certification analyst. The analysts

will review the results and provide their analysis. Errors are corrected and test

cases re-executed if necessary.

3: EMV Development Overview EMV Integrator’s Guide V 15.2

30 2015 Heartland Payment Systems, Inc., All Rights Reserved–HPS Confidential: Sensitive

3.4 EMV Support

Our POS Integrations team is available from 9:00 AM to 5:00 PM Eastern to support EMV testing

and can be reached at EMVDevSupport@e-hps.com.

Card Brand Certification Execute all card brand test cases in our certification environment. The following

actions must be completed depending on card brand:

•VISA – Export XML file for upload to Chip Compliance Reporting Tool (CCRT).

•MasterCard – Export TSEZ file containing terminal logs and validation, host

logs and validation and receipts.

•American Express – Complete user validations and upload terminal logs in

ATS.

•Discover – Indicate results and add comments as needed in provided

spreadsheet.

Card Brand Submission A certification analyst will ensure that all test cases have been completed then

submit the results to the card brands for approval. The turnaround time for the card

brands to review, approve and return a Letter of Approval is typically 10-15

business days.

REQUIREMENT Your terminal(s) of choice must have EMVCo Level 2 approved kernel configurations that

match each of the configurations specified in your certification request forms.

Table 3-7 Test Process (Continued)

Test Process Description

EMV Integrator’s Guide V 15.2 4: EMV Terminal Interface

2015 Heartland Payment Systems, Inc., All Rights Reserved–HPS Confidential: Sensitive 31

Chapter 4: EMV Terminal Interface

4.1 EMV Terminal to Card Communication

4.1.1 Application Protocol Data Units (APDUs)

The terminal talks to the Integrated Circuit Card (ICC) using Application Protocol Data Unit

(APDU) command-response pairs, which have the following formats:

• Command APDU Format

• Response APDU Format

Where...

•SW1 SW2 = ‘9000’ (Success)

•SW1 SW2 = ‘6xxx’ (Failure)

Table 4-1 Command APDU Format

Code Description Length

CLA Class of instruction 1

INS Instruction code 1

P1 Instruction parameter 1 1

P2 Instruction parameter 2 1

Lc Number of bytes present in command data field 0 or 1

Data String of data bytes send in command (= Lc) var.

Le Maximum number of data bytes expected in data field of

response

0 or 1

Table 4-2 Response APDU Format

Code Description Length

Data String of data bytes received in response var. (= Lr)

SW1 Command processing status 1

SW2 Command processing qualifier 1

4: EMV Terminal Interface EMV Integrator’s Guide V 15.2

32 2015 Heartland Payment Systems, Inc., All Rights Reserved–HPS Confidential: Sensitive

4.1.2 Tag, Length, Value (TLV) Data Objects

Data objects are BER-TLV coded, as defined in ISO/IEC 8825:

• The Tag field consists of one or more consecutive bytes. It indicates a class, a type, and a

number. EMV tags are coded on one or two bytes.

• The Length field consists of one or more consecutive bytes that indicate the length of the

following value field.

– If bit 8 of the most significant byte of the length field is set to 0, the length field consists

of only one byte. Bits 7 to 1 code the number of bytes of the value field, for lengths from

1 to 127.

– If bit 8 of the most significant byte of the length field is set to 1, the subsequent bits 7 to

1 code the number of subsequent bytes in the length field. The subsequent bytes code

an integer representing the number of bytes in the value field. Two bytes are necessary

to express lengths from 128 to 255.

• The Value field indicates the value of the data object. If L = ‘00’, the value field is not

present.

4.1.3 Kernel Application Programming Interface (API)

Your terminal will come with a Software Development Kit (SDK) that provides an extraction

layer/library built on top of the EMVCo Level 2 contact approved kernel application that allows

your payment application to run EMV transactions. Discussion of the specific functions/methods

that are part of the SDKs provided by the device manufacturers is outside of the scope of this

document, although the intent of this document is to provide the background needed to

successfully utilize any API.

EMV Integrator’s Guide V 15.2 4: EMV Terminal Interface

2015 Heartland Payment Systems, Inc., All Rights Reserved–HPS Confidential: Sensitive 33

4.2 EMV Data Elements

4.2.1 Data Conventions

The following sections describe the TLV data objects that come from the terminal, card, and

issuer. The Value column uses the following format conventions:

Table 4-3 Data Conventions

Value Description

a Alphabetic data elements contain a single character per byte. The permitted characters are alphabetic

only (a to z and A to Z, upper and lower case).

an Alphanumeric data elements contain a single character per byte. The permitted characters are

alphabetic (a to z and A to Z, upper and lower case) and numeric (0 to 9).

ans Alphanumeric Special data elements contain a single character per byte. The permitted characters and

their coding are shown in the Common Character Set table in Annex B of Book 4.

There is one exception: The permitted characters for Application Preferred Name are the non-control

characters defined in the ISO/IEC 8859 part designated in the Issuer Code Table Index associated with

the Application Preferred Name.

b These data elements consist of either unsigned binary numbers or bit combinations that are defined

elsewhere in the specification.

Binary example: The Application Transaction Counter (ATC) is defined as “b” with a length of two

bytes. An ATC value of 19 is stored as Hex '00 13'.

Bit combination example: Processing Options Data Object List (PDOL) is defined as “b” with the

format shown in section 5.4.

cn Compressed numeric data elements consist of two numeric digits (having values in the range Hex '0'–

'9') per byte. These data elements are left justified and padded with trailing hexadecimal 'F's.

Example: The Application Primary Account Number (PAN) is defined as “cn” with a length of up to ten

bytes. A value of 1234567890123 may be stored in the Application PAN as Hex '12 34 56 78 90 12 3F

FF' with a length of 8.

n Numeric data elements consist of two numeric digits (having values in the range Hex '0' – '9') per byte.

These digits are right justified and padded with leading hexadecimal zeroes. Other specifications

sometimes refer to this data format as Binary Coded Decimal (“BCD”) or unsigned packed.

Example: Amount, Authorised (Numeric) is defined as “n 12” with a length of six bytes. A value of

12345 is stored in Amount, Authorised (Numeric) as Hex '00 00 00 01 23 45'.

var. Variable data elements are variable length and may contain any bit combination. Additional information

on the formats of specific variable data elements is available elsewhere.

4: EMV Terminal Interface EMV Integrator’s Guide V 15.2

34 2015 Heartland Payment Systems, Inc., All Rights Reserved–HPS Confidential: Sensitive

4.2.2 Terminal Data

The following data comes from the terminal, payment application, or parameter management

system:

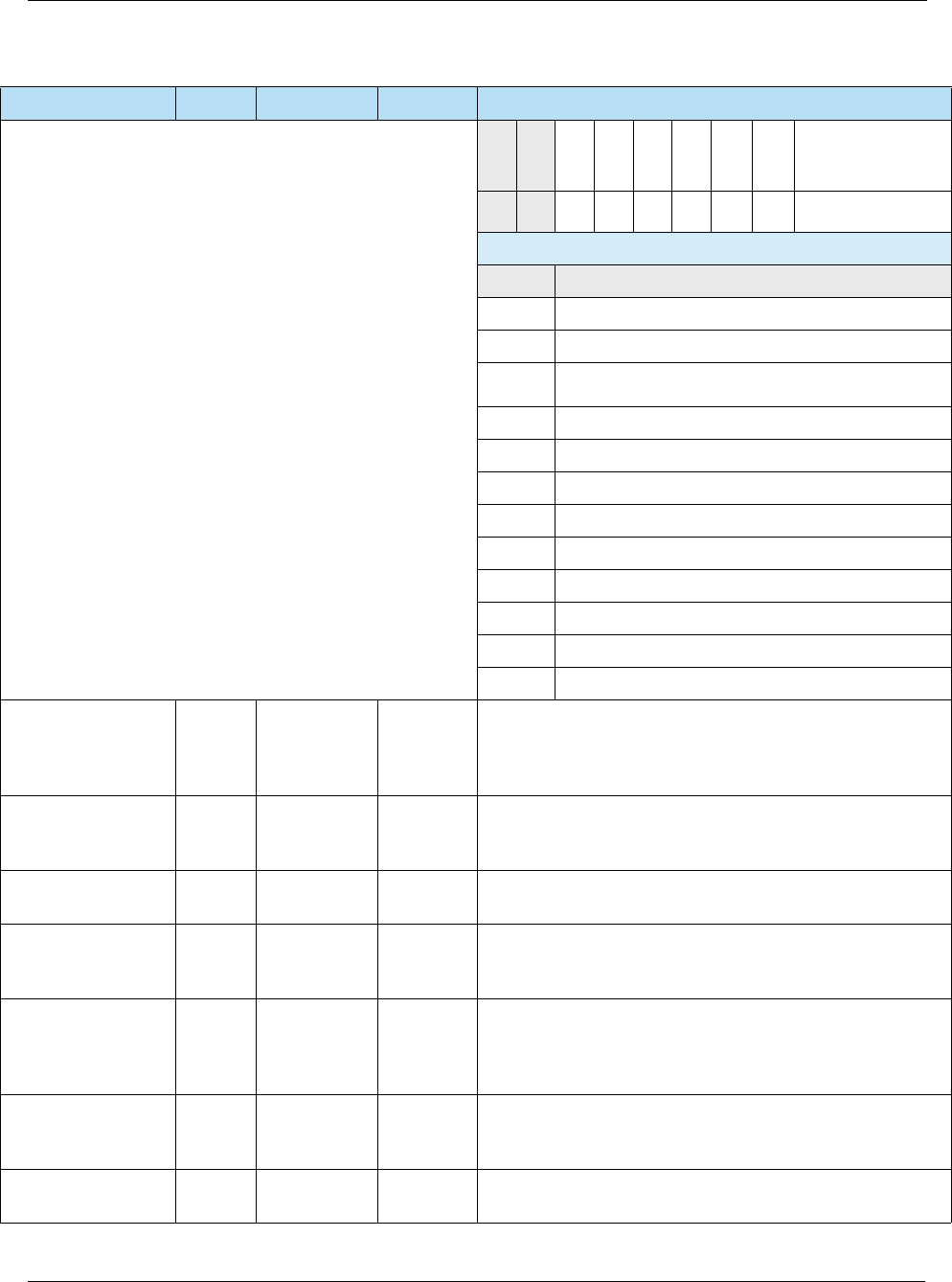

Table 4-4 Terminal Data

Name Tag Length Value Description

ADDITIONAL

TERMINAL

CAPABILITIES

‘9F40’ 5 b Indicates the data input and output capabilities of the

terminal.

Byte 1 – Transaction Type Capability

b8 b7 b6 b5 b4 b3 b2 b1 Meaning

1xx x x x x xCash

x 1 x x x x x x Goods

xx1x xxx xServices

x x x 1 x x x x Cashback

x x x x 1 x x x Inquiry

xxxx x1x xTransfer

xxxx xx1 xPayment

xxxx xx x 1Administrative

Byte 2 – Transaction Type Capability

b8 b7 b6 b5 b4 b3 b2 b1 Meaning

1 x x x x x x x Cash Deposit

x0x x x x x xRFU

xx0x xxx xRFU

xxx0xxx xRFU

xxxx0xx xRFU

xxxx x0x xRFU

xxxx xx0 xRFU

xxxx xx x 0RFU

EMV Integrator’s Guide V 15.2 4: EMV Terminal Interface

2015 Heartland Payment Systems, Inc., All Rights Reserved–HPS Confidential: Sensitive 35

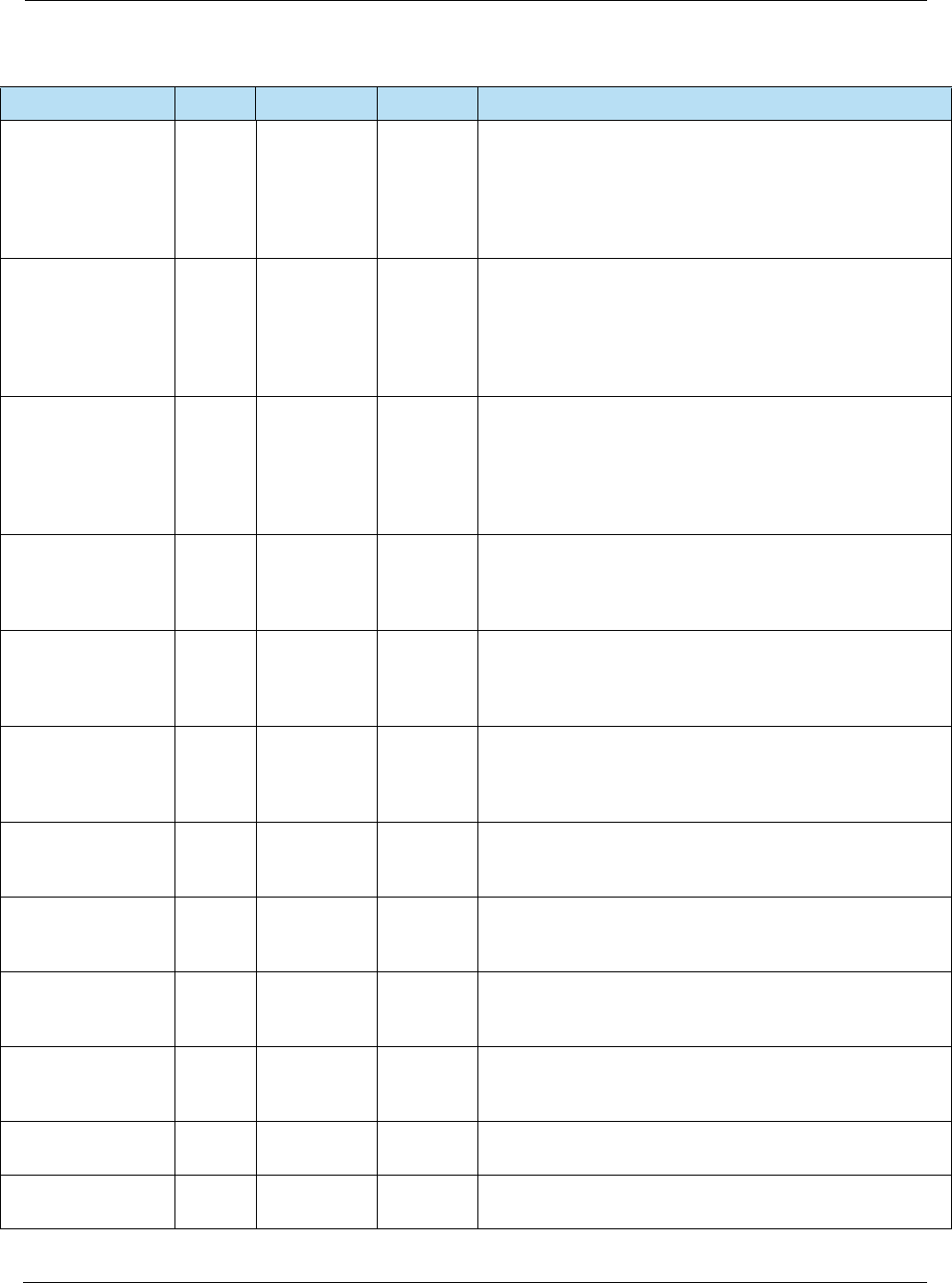

Byte 3 – Terminal Data Input Capability

b8 b7 b6 b5 b4 b3 b2 b1 Meaning

1 x x x x x x x Numeric keys

x 1 x x x x x x Alphabetic and special

character keys

x x 1 x x x x x Command keys

x x x 1 x x x x Function keys

xxxx0xx xRFU

xxxx x0x xRFU

xxxx xx0 xRFU

xxxx xx x 0RFU

Byte 4 – Terminal Data Output Capability

b8 b7 b6 b5 b4 b3 b2 b1 Meaning

1 x x x x x x x Print, attendant

x 1 x x x x x x Print, cardholder

x x 1 x x x x x Display, attendant

x x x 1 x x x x Display, cardholder

xxxx0xx xRFU

xxxx x0x xRFU

x x x x x x 1 x Code table 10

x x x x x x x 1 Code table 9

Byte 5 – Terminal Data Output Capability

b8 b7 b6 b5 b4 b3 b2 b1 Meaning

1 x x x x x x x Code table 8

x 1 x x x x x x Code table 7

x x 1 x x x x x Code table 6

x x x 1 x x x x Code table 5

x x x x 1 x x x Code table 4

x x x x x 1 x x Code table 3

x x x x x x 1 x Code table 2

xxxxxxx1

Code table 1

AMOUNT,

AUTHORIZED

(NUMERIC)

‘9F02’ 6 n 12 Authorized amount of the transaction (excluding

adjustments).

Table 4-4 Terminal Data (Continued)

Name Tag Length Value Description

4: EMV Terminal Interface EMV Integrator’s Guide V 15.2

36 2015 Heartland Payment Systems, Inc., All Rights Reserved–HPS Confidential: Sensitive

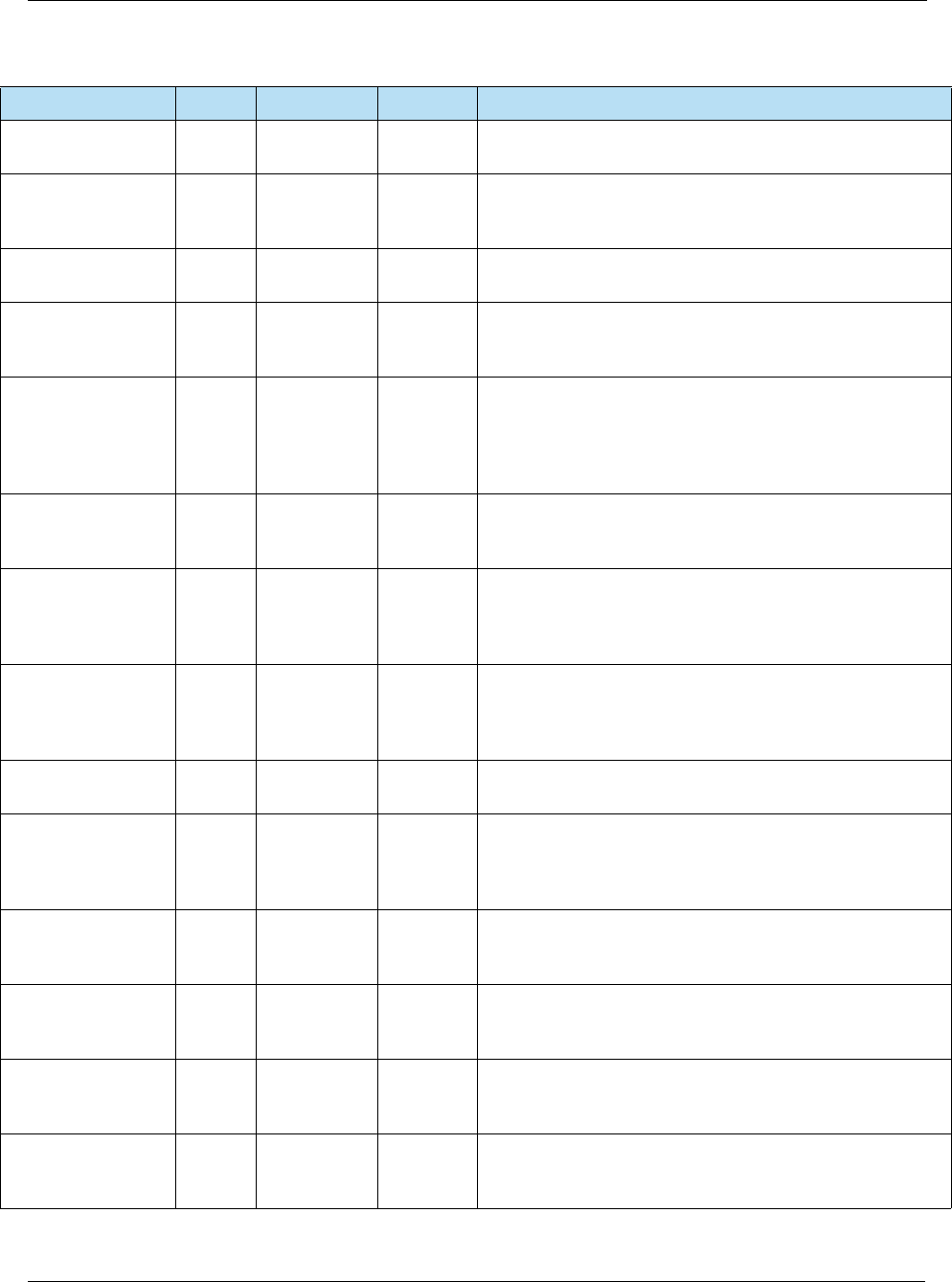

AMOUNT, OTHER

(NUMERIC)

‘9F03’ 6 n 12 Secondary amount associated with the transaction

representing a cashback amount.

APPLICATION

IDENTIFIER (AID) -

TERMINAL

‘9F33’ 3 b Identifies the application as described in ISO/IEC 7816-5.

Consists of the Registered Application Provider Identifier

(RID) + a Proprietary Application Identifier Extension (PIX).

APPLICATION

SELECTION

INDICATOR

— At the

discretion of

the terminal.

The data is

not sent

across the

interface

See

length

For an application in the ICC to be supported by an

application in the terminal, the Application Selection

Indicator indicates whether the associated AID in the

terminal must match the AID in the card exactly, including

the length of the AID, or only up to the length of the AID in

the terminal.

There is only one Application Selection Indicator per AID

supported by the terminal.

APPLICATION

VERSION

NUMBER

‘9F09’ 2 b Version number assigned by the payment system for the

application.

AUTHORISATION

RESPONSE CODE

(ARC)

‘8A’ 2 an 2 Code that defines the disposition of a message.

For online transactions, the terminal should generate the

value as follows:

CARDHOLDER

VERIFICATION

METHOD (CVM)

RESULTS

‘9F34’ 3 b Indicates the results of the last CVM performed.

Byte 1 CVM

Performed

Last CVM of the CVM List

actually performed by the

terminal: One-byte CVM Code of

the CVM List as defined in Book 3

('3F' if no CVM is performed).

Byte 2 CVM

Condition

One-byte CVM Condition Code of

the CVM List as defined in Book 3

or ‘00’ if no actual CVM was

performed.

Byte 3 CVM Result Result of the (last) CVM

performed as known by the

terminal:

• '0' = Unknown (for example,

for signature)

• '1' = Failed (for example, for

offline PIN)

• '2' = Successful (for example,

for offline PIN)

or set to ‘1’ if no CVM Condition

Code was satisfied or if the CVM

Code was not recognized or not

supported.

Table 4-4 Terminal Data (Continued)

Name Tag Length Value Description

EMV Integrator’s Guide V 15.2 4: EMV Terminal Interface

2015 Heartland Payment Systems, Inc., All Rights Reserved–HPS Confidential: Sensitive 37

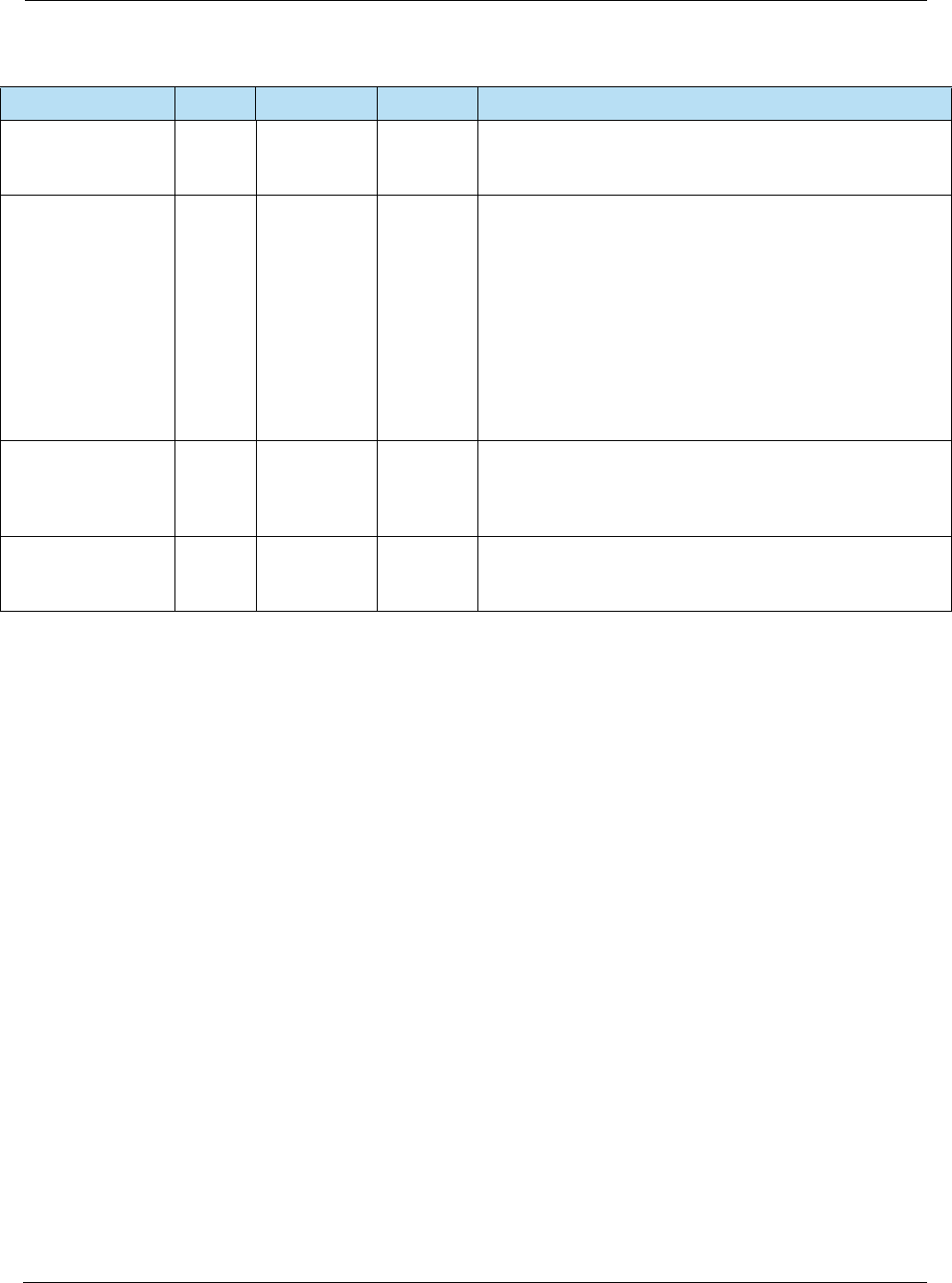

CERTIFICATION

AUTHORITY

PUBLIC KEY

CHECK SUM

— 20 b A check value calculated on the concatenation of all parts of

the Certification Authority Public Key (RID, Certification

Authority Public Key Index, Certification Authority Public

Key Modulus, Certification Authority Public Key Exponent)

using SHA-1.

CERTIFICATION

AUTHORITY

PUBLIC KEY

EXPONENT

— 1 or 3 b Value of the exponent part of the Certification Authority

Public Key.

CERTIFICATION

AUTHORITY

PUBLIC KEY

INDEX

‘9F22’ 1 b Identifies the certification authority’s public key in

conjunction with the RID.

CERTIFICATION

AUTHORITY

PUBLIC KEY

MODULUS

—N

CA

(up to 248)

b Value of the modulus part of the Certification Authority

Public Key.

DEFAULT

DYNAMIC DATA

AUTHENTICATION

DATA OBJECT

LIST (DDOL)

— var. b DDOL to be used for constructing the INTERNAL

AUTHENTICATE command if the DDOL in the card is not

present.

DEFAULT

TRANSACTION

CERTIFICATE

DATA OBJECT

LIST (TDOL)

— var. b TDOL to be used for generating the TC Hash Value if the

TDOL in the card is not present.

ENCIPHERED

PERSONAL

IDENTIFICATION

NUMBER (PIN)

DATA

— 8 b Transaction PIN enciphered at the PIN pad for online

verification or for offline verification if the PIN pad and IFD

are not a single integrated device.

INTERFACE

DEVICE (IFD)

SERIAL NUMBER

‘9F1E’ 8 an 8 Unique and permanent serial number assigned to the IFD

by the manufacturer.

Table 4-4 Terminal Data (Continued)

Name Tag Length Value Description

4: EMV Terminal Interface EMV Integrator’s Guide V 15.2

38 2015 Heartland Payment Systems, Inc., All Rights Reserved–HPS Confidential: Sensitive

ISSUER SCRIPT

RESULTS

‘9F5B’ var.

(up to 20)

b Indicates the result of the terminal script processing.

Byte 1 SCRIPT

RESULT

Most significant nibble: Result of

the Issuer Script processing

performed by the terminal:

• '0' = Script not performed

• '1' = Script processing failed

• '2' = Script processing

successful

Least significant nibble:

Sequence number of the Script

Command

• '0' = Not specified

• '1' to 'E' = Sequence number

from 1 to 14

• 'F' = Sequence number of 15

or above

Byte

2-5

SCRIPT

IDENTIFIER

Script Identifier of the Issuer

Script received by the terminal, if

available, zero filled if not.

Mandatory if more than one

Issuer Script was received by the

terminal.

MAXIMUM

TARGET

PERCENTAGE TO

BE USED FOR

BIASED RANDOM

SELECTION

— 1 n 2 Value used in terminal risk management for random

transaction selection.

This is the desired percentage of transactions “just below”

the floor limit that will be selected to go online.

POINT-OF-SERVIC

E (POS) ENTRY

MODE

‘9F39’ 1 n 2 Indicates the method by which the PAN was entered,

according to the first two digits of the ISO 8583:1987 POS

Entry Mode.

TARGET

PERCENTAGE TO

BE USED FOR

RANDOM

SELECTION

— 1 n 2 Value used in terminal risk management for random

transaction selection.

For transactions with amounts less than the Threshold

Value for Biased Random Selection, the terminal shall

generate a random number from 1 to 99, and if this number

is less than or equal to this value, the transaction shall be

selected to go online.

TERMINAL

ACTION CODE

(TAC) – DEFAULT

‘FFC6’ 5 b Specifies the acquirer’s conditions that cause a transaction

to be rejected if it might have been approved online, but the

terminal is unable to process the transaction online.

TERMINAL

ACTION CODE

(TAC) – DENIAL

‘FFC7’ 5 b Specifies the acquirer’s conditions that cause the denial of a

transaction without attempt to go online.

Table 4-4 Terminal Data (Continued)

Name Tag Length Value Description

EMV Integrator’s Guide V 15.2 4: EMV Terminal Interface

2015 Heartland Payment Systems, Inc., All Rights Reserved–HPS Confidential: Sensitive 39

TERMINAL

ACTION CODE

(TAC) – ONLINE

‘FFC8’ 5 b Specifies the acquirer’s conditions that cause a transaction

to be transmitted online.

TERMINAL

CAPABILITIES

‘9F40’ 3 b Indicates the data input and output capabilities of the

terminal.

Byte 1 – Card Data Input Capability