EVPA Measuring And Managing Impact A Practical Guide

User Manual:

Open the PDF directly: View PDF ![]() .

.

Page Count: 140 [warning: Documents this large are best viewed by clicking the View PDF Link!]

EUROPEAN VENTURE PHILANTHROPY ASSOCIATION JUNE 2015

A PRACTICAL

GUIDE TO

MEASURING

AND MANAGING

IMPACT

EUROPEAN VENTURE PHILANTHROPY ASSOCIATION

2A PRACTICAL GUIDE TO MEASURING AND MANAGING IMPACT

EUROPEAN VENTURE PHILANTHROPY ASSOCIATION

www.fsc.org

©1996 Fore st StewardshipCouncil

Cert no.SA-COC-001530

Mixed Sources

Product groupfromwell-managed

forestsand othercontrolle dsources

Published by the European Venture Philanthropy Association

This edition June 2015

Copyright © 2015 EVPA

Email: info@evpa.eu.com

Website: www.evpa.eu.com

Creative Commons Attribution-Noncommercial-No Derivative Works 3.0.

You are free to share – to copy, distribute, display, and perform the work

– under the following conditions:

• Attribution: You must attribute the work as

A PRACTICAL GUIDE TO MEASURING AND MANAGING IMPACT

Copyright © 2015 EVPA.

• Non commercial: You may not use this work for commercial purposes.

• No Derivative Works: You may not alter, transform or build upon this work.

• For any reuse or distribution, you must make clear to others the licence

terms of this work.

Authors: Dr Lisa Hehenberger, Anna-Marie Harling, Peter Scholten

Design and typesetting: Pitch Black Graphic Design The Hague/Berlin

ISBN 9789082316087

This publication is supported under the EU Programme for Employment and

Social Innovation “EaSI” (2014–2020).

For more information see: http://ec.europa.eu./social/easi

The information contained in this publication does not necessarily reect the position

or opinion of the European Commission.

With the nancial support of the European Commission.

JUNE 2015 3

A PRACTICAL

GUIDE TO

MEASURING

AND MANAGING

IMPACT

DR. LISA HEHENBERGER, ANNAMARIE HARLING AND PETER SCHOLTEN | JUNE 2015

EVPA is grateful to:

Acanthus Advisers, Adessium

Foundation, BMW Foundation

and Omidyar Network for their

structural support

EVPA is grateful to:

Fondazione CRT for the support

of its Knowledge Centre

4A PRACTICAL GUIDE TO MEASURING AND MANAGING IMPACT

EUROPEAN VENTURE PHILANTHROPY ASSOCIATION

JUNE 2015 5

Preface

Executive Summary

Part 1:

Introduction and Overview

1.0 Introduction and Overview

1.1 Background

1.2 How is social impact currently

measured by social investors and

venture philanthropists?

1.3 Five-step framework

1.4 Methodology

1.5 Denition of social impact

Part 2:

The Impact Measurement Process

2.0 Step 1: Setting Objectives

2.1 What?

2.2 How to?

2.3 Practical tips

2.4 Recommendations for managing

impact

2.5 Worked Example

3.0 Step 2: Analysing Stakeholders

3.1 What?

3.2 How to?

3.3 Practical tips

3.4 Recommendations for managing

impact

3.5 Worked Example

4.0 Step 3: Measuring Results:

Outcome, Impact and Indicators

4.1 What?

4.2 How to?

4.3 Practical tips

4.4 Recommendations for managing

impact

4.5 Worked Example

6

14

28

29

30

30

31

33

34

36

37

37

37

46

46

46

48

48

49

54

54

55

57

57

60

70

70

71

76

76

78

84

85

85

86

86

87

93

93

94

95

101

102

103

109

116

121

126

132

133

137

5.0 Step 4: Verifying & Valuing Impact

5.1 What?

5.2 How to?

5.3 Practical tips

5.4 Recommendations for managing

impact

5.5 Worked Example

6.0 Step 5: Monitoring & Reporting

6.1 What?

6.2 How to?

6.3 Practical tips

6.4 Recommendations for managing

impact

6.5 Worked Example

7.0 Managing Impact

8.0 Conclusions

Part 3:

Case studies

9.1 Case Study:

Ferd Social Entrepreneurs investing

in The Scientist Factory

9.2 Case Study:

Impetus Trust investing in Blue Sky

9.3 Case Study:

Oltre Venture investing in PerMicro

9.4 Case Study:

Esmée Fairbairn Foundation investing

in Social Impact Partnership

(developed and run by Social Finance)

9.5 Case Study:

Auridis investing in Papilio

Part 4:

Appendices

10.0 Glossary of Terms

11.0 Sources

TABLE OF CONTENTS

6A PRACTICAL GUIDE TO MEASURING AND MANAGING IMPACT

EUROPEAN VENTURE PHILANTHROPY ASSOCIATION

Preface

JUNE 2015 7

PREFACE

Introduction to the second edition from Lisa Hehenberger,

Research & Policy Director of EVPA

This is the second edition of A Practical Guide to Measuring and Managing Impact

(“the Guide”), rst published in 2013. In what follows, we will provide a brief update of

the uptake of the Guide, the remaining challenges that practitioners face, the contribution

of the guide to policy work, and nally what EVPA’s future plans are in terms of research

on impact measurement and management.

When we started developing the Guide in 2011, we responded to the need of EVPA members

for more clarity in terms of impact measurement. We had noticed that the problem was not

the lack of information, but rather the absence of guidance in how to make sense of the

information on impact measurement. Therefore, we engaged in a meta-analysis of almost

1,000 different approaches as included in resources such as the TRASI database1 curated

by the US-based “Foundation Center”. From these approaches, EVPA, informed by the

convening of an Expert Group of twenty-seven venture philanthropy and social invest-

ment practitioners, consultants, academics and representatives of other organisations

involved in impact measurement, selected the most commonly used approaches and then

further distilled these approaches into a ve step process. The objective was to derive the

commonalities between various approaches to come up with clear recommendations on

how to measure impact.

We discovered during the process that the most important aspect of impact measurement

is not the actual value or numbers you obtain from the exercise, but the integration of

an impact approach in the organisation so that impact becomes an integral part of the

entire management or investment process. By undertaking and learning from the process

of measuring impact, an organisation can work more effectively towards achieving societal

impact. That is why we moved from working on just measuring to also managing impact.

Uptake of the Guide and recent developments

The EVPA guide has been well received, with over 2,000 copies downloaded since its

launch in April 2013 and more than 500 hard copies distributed. It has been translated

to Swedish, Spanish and French. As shown by the results of EVPA’s 4th Industry Survey2,

an increasing number of organisations are using the ve steps of impact measurement

outlined in the Guide.

1. http://trasi.foundationcenter.org/

2. Hehenberger, L., Boiardi, P.,

Gianoncelli, A., (2014), “European

Venture Philanthropy and social

investment 2013/2014 – The EVPA

Survey”, EVPA.

8A PRACTICAL GUIDE TO MEASURING AND MANAGING IMPACT

EUROPEAN VENTURE PHILANTHROPY ASSOCIATION

PREFACE

Additionally, the survey shows that the large majority of respondents are measuring

outcomes and trying to assess the impact of its activities, pointing to the importance the

practice has for VP/SI practitioners, and their increased sophistication in the use of the

practice.

The objective of our best practice research is to increase the effectiveness of practitioners and

we see the results as encouraging, although direct attribution to EVPA’s work is difcult

to claim. Many challenges remain for both funders and investees who still consider impact

measurement a complex and technical practice. However, we do believe that the Guide and

the dissemination and policy work around it have contributed to raising awareness for the

topic of impact measurement and management in our sector.

EVPA and its members are being recognised as important actors in the practice of impact

measurement. EVPA’s work on impact measurement is being referenced in the European

Commission’s Standard3 on impact measurement, and we have participated in and contrib-

uted to the report4 produced by the Working Group on Impact Measurement of the taskforce

on social impact investment established by the G8.

In terms of the European Standard, when the Guide was in its nal stages, the European

Commission set up it Sub-group on Impact Measurement to advise the Commission on

the topic. EVPA participated in the sub-group (and in GECES) and presented the ve steps

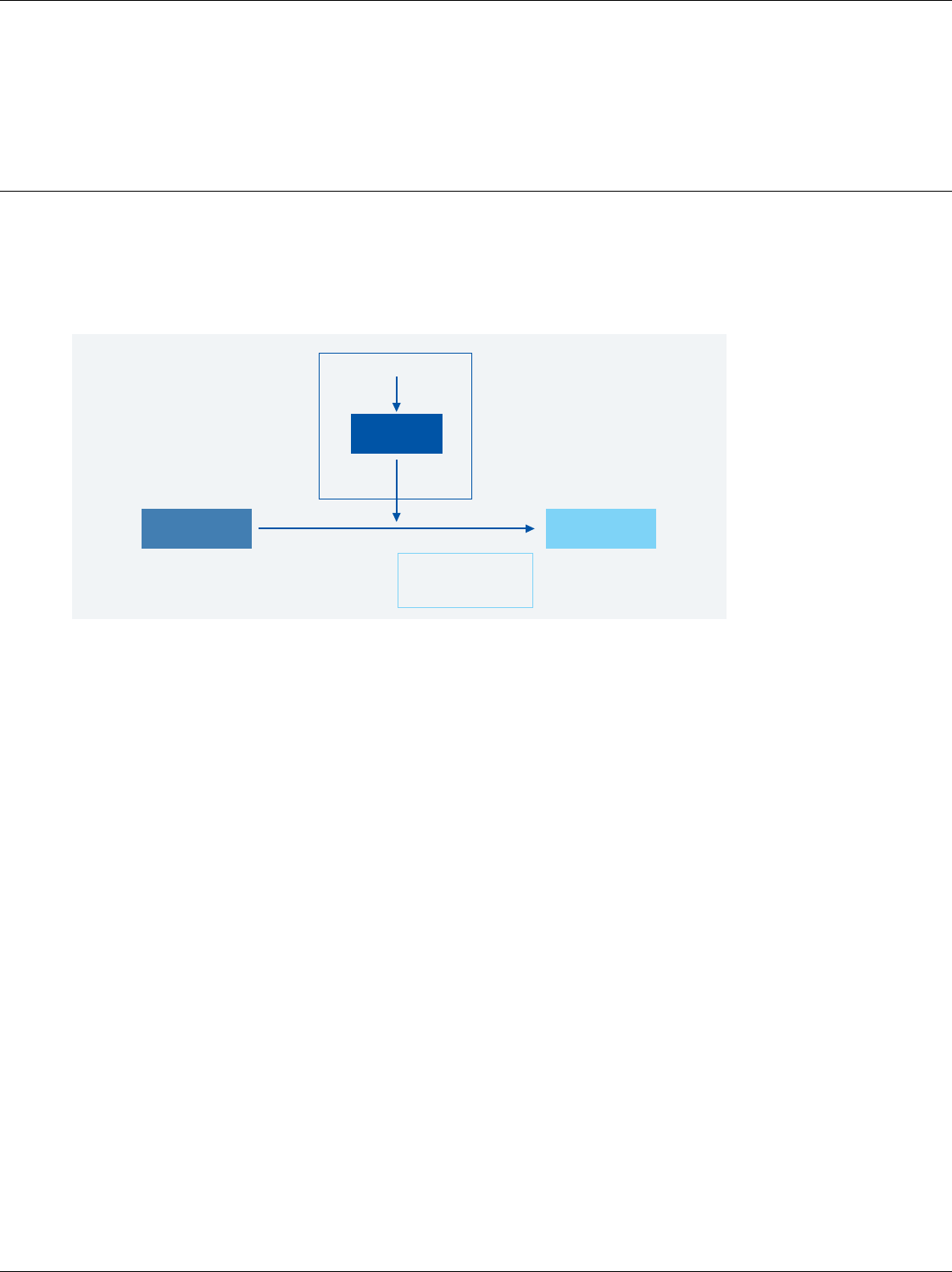

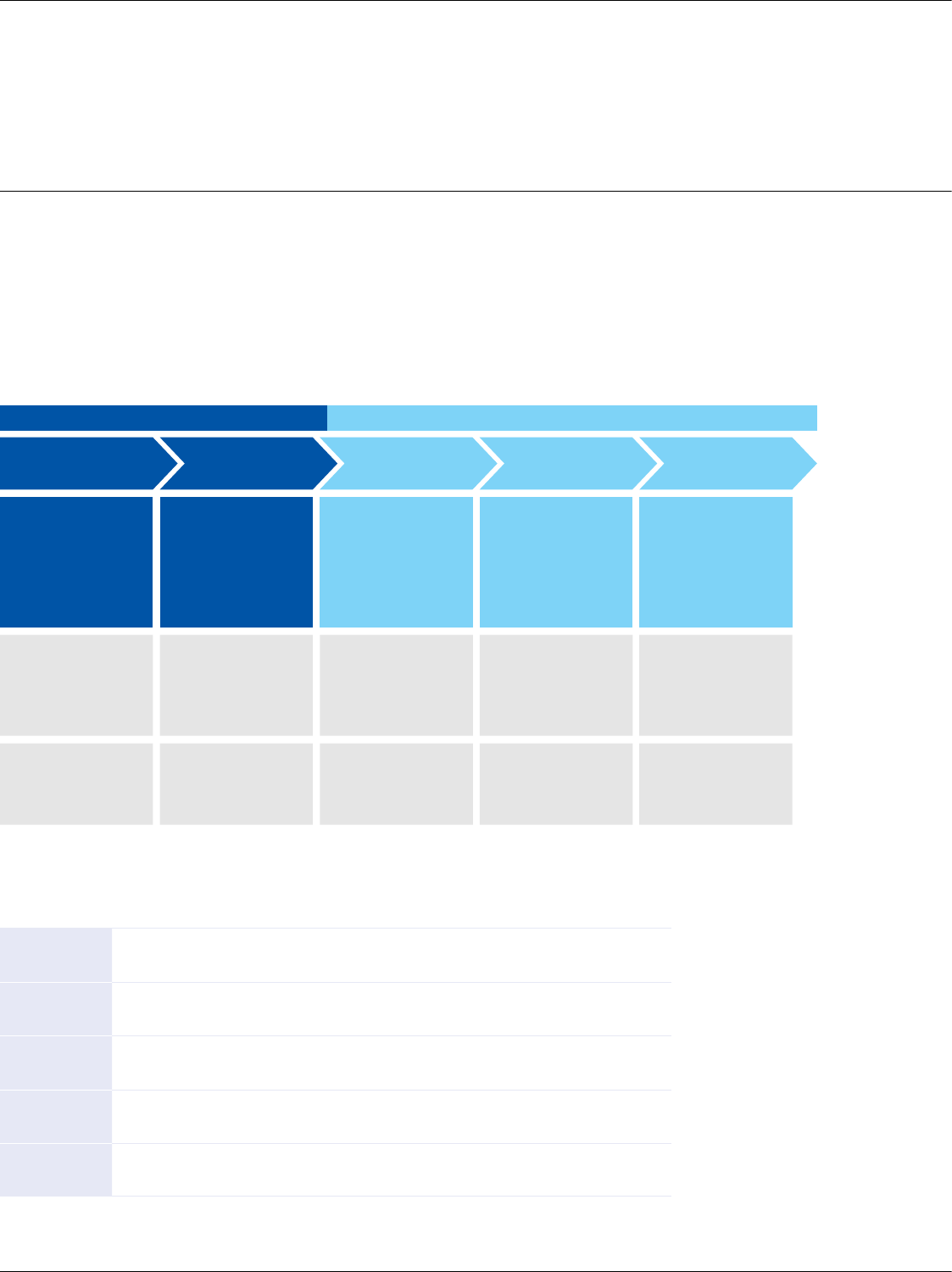

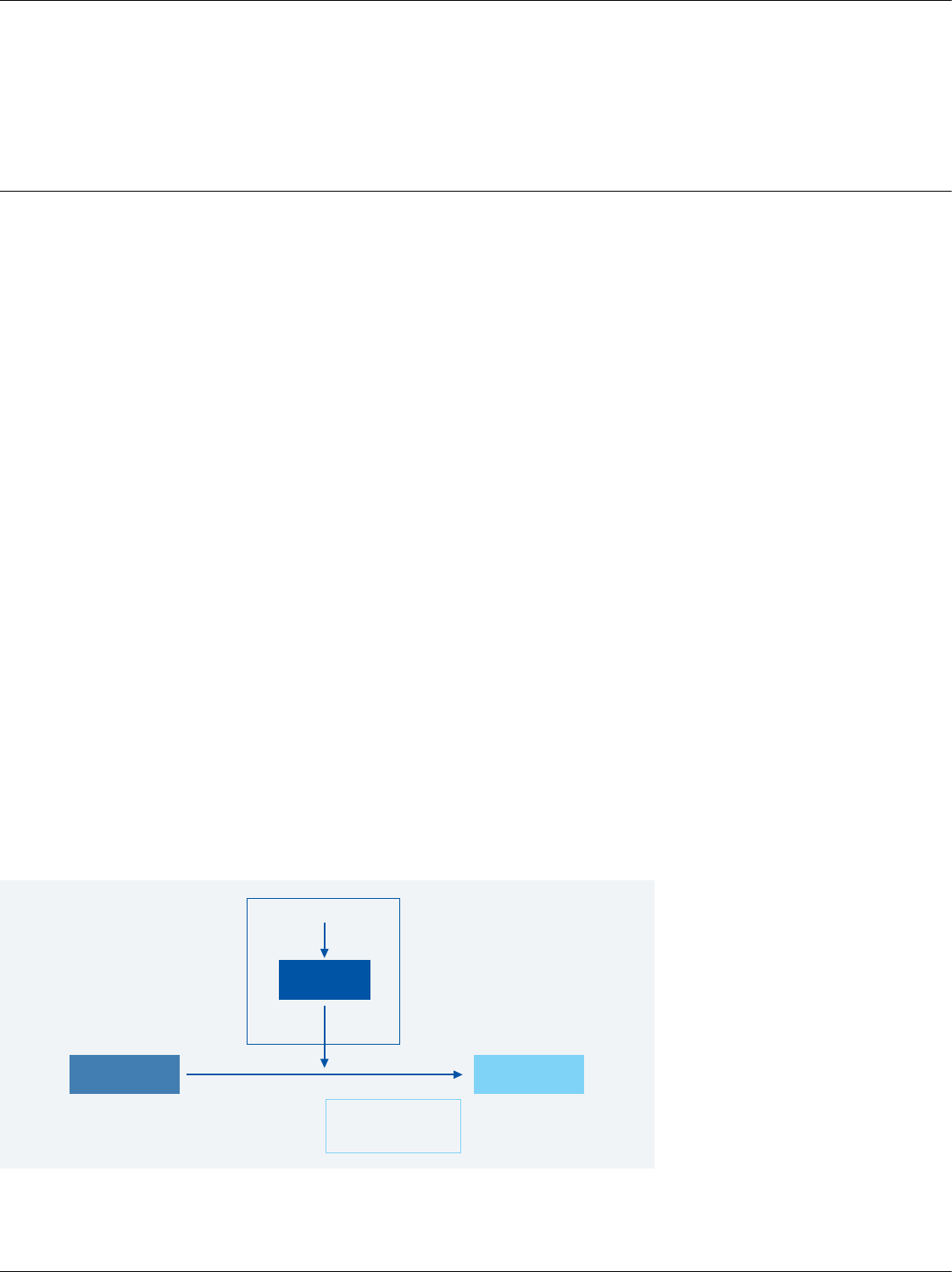

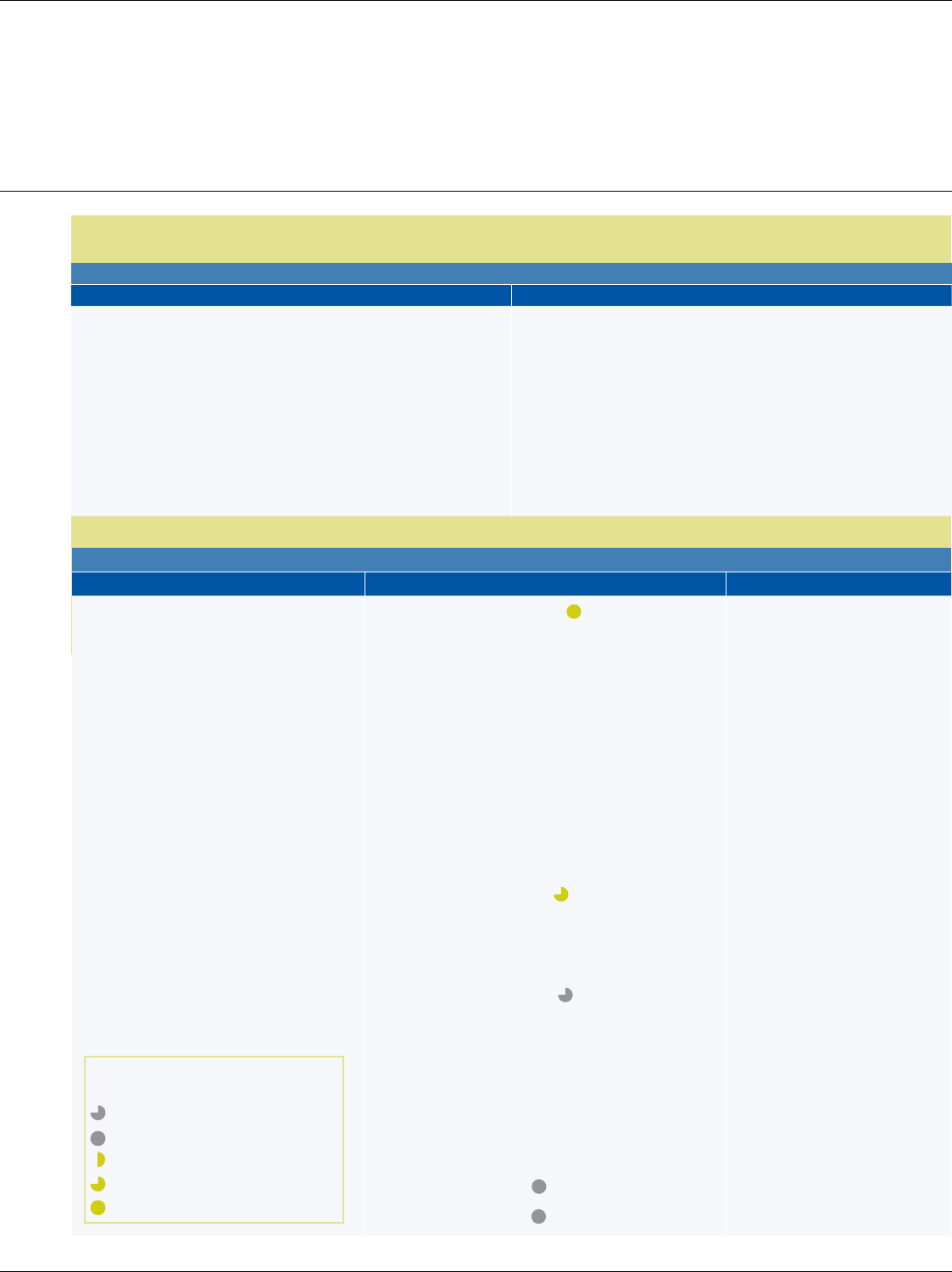

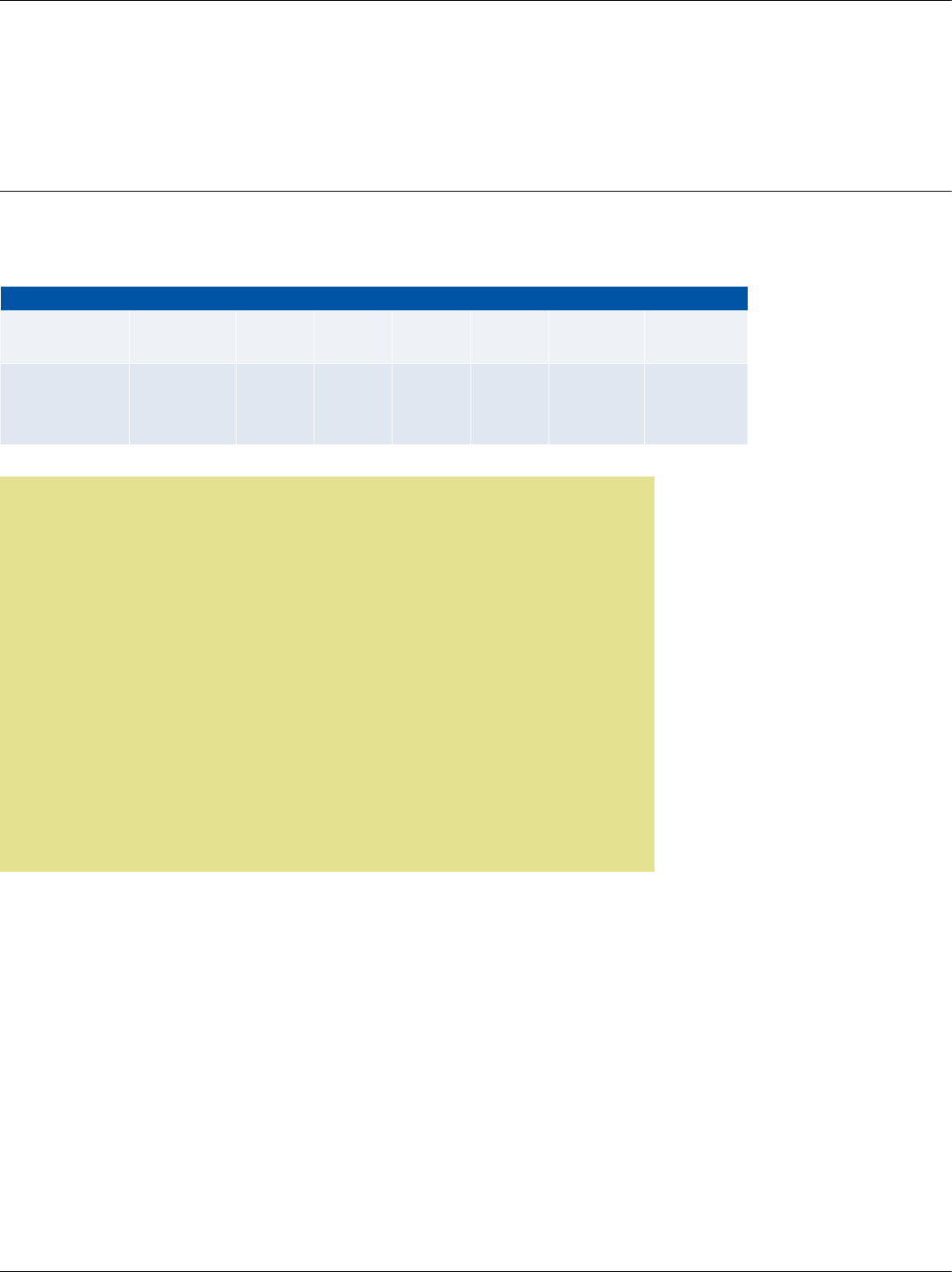

Outputs Outcomes Impact

84 87

70

Objectives of social impact

measurement by %

of respondents

n=91

multiple choice

numbers in %

3. http://europa.eu/rapid/

press-release_IP-14-696_

en.htm?locale=EN

4. http://www.

socialimpactinvestment.org/

reports/Measuring%20Impact%20

WG%20paper%20FINAL.pdf

% of VPOs that perform

each step of societal

impact measurement

FYs 2011 and 2013

2013 n=92

2011 n=57

numbers in %

0 20 40 60 80 100

84

72

Step 5

72

72

Step 4

90

88

Step 3

73 79

Step 2

90

86

Step 1

JUNE 2015 9

PREFACE

of the Guide during one of the meetings. The experts in the Sub-group agreed that the

European Standard of Impact Measurement should be set at the process level (adopting

EVPA’s ve steps) and not at the indicator level (indicators can only be standardised at

social sector level and they have to be chosen in accordance with relevance to the social

organisation measuring impact). The European Standard was formally adopted in June

20145 and the report can be downloaded for free6.

Another important development for our sector has been the study conducted by the

Working Group on Impact Measurement (WGIM) of the Taskforce on Social Impact Invest-

ment established by the G8. The WGIM was composed of experts from the G8 countries

(later to be G7) as well as representatives of the European Commission and OECD. WGIM

built on the work of both EVPA and GECES, and extended it by including specic steps for

data collection and data analysis.

Considering the uptake of the Guide and its contribution to European and Global standards

as outlined above, we are condent that the Guide reects best practice globally as it

currently stands today. Core principles that have come out of these work streams, and that

will guide our work on impact measurement going forward, are as follows:

•Impact measurement has to be relevant to the organisation measuring so that it becomes

part of their management system and helps them improve their work to achieve greater

impact.

•Impact measurement also needs to be proportionate to the organisation at hand, keeping

in mind that it is a means towards an end, not an end in itself.

Attempts are being made at standardising social impact measurement indicators, across

social sectors and on broad levels, leaving room for some local adaptation at project-level.

Several databases (e.g. IRIS, Global Value Exchange) exist that have collected key perfor-

mance indicators commonly used. Reporting standards are already being developed by

social investors in cooperation with investees in many parts of Europe (e.g. Social Reporting

Standard in Germany). New and more sophisticated tools (e.g. Sinzer, PULSE) have been

created and are being developed to support practitioners in measuring and managing

impact.

Next steps for EVPA

Although the eld has come a long way since EVPA held its rst workshop on performance

measurement in 2007, EVPA members are still in need of additional training and guidance

on impact measurement. The lack of benchmarking measures, the absence of standards in

terms of evidence needed, and the lack of data of the impact of funders on their investees

are a few frequently mentioned issues. We particularly see the need to make the research

even more hands-on, practical and relevant with concrete case studies that run through

the impact measurement process in a VPO. Furthermore, EVPA’s guide should be seen as

5. http://europa.eu/rapid/

press-release_IP-14-696_

en.htm?locale=EN

6. http://ec.europa.eu/social/main.

jsp?catId=738&langId=en&pubId

=7735&type=2&furtherPubs=yes

10 A PRACTICAL GUIDE TO MEASURING AND MANAGING IMPACT

EUROPEAN VENTURE PHILANTHROPY ASSOCIATION

PREFACE

an evolving document that incorporates new developments and provides up-to-date and

practical guidance. Therefore, we have decided to invest further in research on the topic.

Concretely, the next steps include conducting and writing a number of in-depth case studies

to be published in a separate report on how to measure and manage impact in practice, to

be further developed as training material.7 This research will provide VP/SI practitioners

with practical real-life and in-depth cases of how impact measurement can be performed.

The exploratory case studies will help us revise the Guide in 2016, based on ndings

regarding what works/what doesn’t work and what organisations are struggling with

using the ve steps proposed in our Guide. The case studies are not a means for EVPA to

“prove” its 5-steps, but a way to reect on what organisations are struggling with when

measuring impact. We also aim to include, where relevant, any new, upcoming method-

ologies in impact measurement and emergent issues (e.g. how to evaluate outcomes, issue

of proportionality, levels of evidence needed and use of control groups, measurement

standards that allow comparability, etc.).

Other plans include developing a micro-site on impact measurement, to develop a

community of practice, making research on impact measurement a process of continuous

learning that builds on existing knowledge and on the experiences of VP/SI organisa-

tions. The micro-site will help EVPA collect knowledge and best practices around the topic

and make it available for practitioners in a user-friendly way. Through the community of

practice we will also collect experiences and practical cases to help EPVA and its members

upgrade and revise the learnings.

It is our aim that the research on impact measurement and management will allow us to

provide even more practical guidance that will facilitate the work of VP/SI practitioners

and the investees they support. We also intend to build on EVPA’s reputation as a leading

actor in terms of setting standards in the VP and Social Investment industry, and thus

reduce problems of multiple standards in impact measurement that increase the work

of both investor and investee. And we should never lose track of the overall purpose of

impact measurement; to help both funders and investees work towards greater impact –

while being relevant and proportionate.

Lisa Hehenberger

Research and Policy Director, EVPA

7. A shortened and simplified

version of the case studies will

then be used for training purposes

at a later stage.

JUNE 2015 11

PREFACE

Introduction from Daniela Barone Soares,

Chief Executive of Impetus Trust

What’s Impact Measurement for? Ask a social purpose organisation (SPO), and they’ll tell

you it helps them prove that what they do makes an impact, gives funders reassurance that

their money is well-spent, and provides the stories and case studies they need for further

fundraising. They might add at the end that the data helps them rene and improve their

programmes, and inform their decision-making.

Venture Philanthropy Organisations (VPOs), like Impetus, work for a social sector where

the work of impact measurement is driven by the need to extract maximum value from our

nite resources. Where SPOs stop doing things that don’t work, even if funders love that

project. Where new projects are explicitly based on learnings from previous work, and bear

the imprint of past successes and failures.

“Managing impact” might not be a phrase to set the world on re but we believe the

benets of embedding the concept across the social sector would be transformational – and

immediately tangible. SPOs are often experts in the needs of their beneciaries, but lack

the data on their own activities to make informed resource allocation decisions, or build an

organisation that really plays to its own strengths. Data doesn’t just reveal impact – it is a

prerequisite for making impact. It’s also the mother and father of innovation. Innovation

isn’t just about ‘new’; it has to be about ‘better’. Data reveals where an SPO could do better,

and tells them when they’ve got there.

This Practical Guide to Measuring and Managing Impact is a timely resource with a wealth

of much-needed information for Venture Philanthropy Organisations (VPOs), and the SPOs

they back. It’s one of the many reasons we’re proud to partner with the EVPA Knowledge

Centre, because sharing best practice is an essential part of the development of our sector.

VPOs are in a strong position to take impact measurement and management practice to the

next level. Collecting relevant data, and crucially putting it to good use, is a key challenge

for SPOs. Our unrestricted funding backs the unglamorous, but essential, work of building

capacity. And we’re in it for the long haul: we know this sort of organisational change

cannot happen overnight, and we don’t expect short-term projects to do the trick.

At Impetus, we are committed to building this capacity in the organisations we support.

We build relationships of trust that allow us to push our organisations to achieve more than

they might have thought possible. Our deep understanding of the sector is complemented

by the private sector expertise we bring in, and our long-term engagement means that

support packages can see an SPO right through the process of nding out what to measure,

collecting the data, and putting in place the virtuous circle that connects performance data

to performance improvement.

12 A PRACTICAL GUIDE TO MEASURING AND MANAGING IMPACT

EUROPEAN VENTURE PHILANTHROPY ASSOCIATION

PREFACE

And of course we are an SPO too! We are acutely aware that we have a duty to expend the

resources entrusted to us for maximum impact, and that we only identify impact through

data. We need to know what wouldn’t have happened without us – whether that be more

lives changed, improved cost-efciency, greater sustainability, or all of the above, in the

organisations we support. This is undoubtedly difcult to measure. But we are committed

to nding better, and more useful ways to do so; we know our own funders value this

information, but rst and foremost we are doing it to ensure that, year on year, we do what

we do better. This guide helps us on our journey.

A nal word: managing impact is not about removing risk, as this is often the partner of

innovation. We believe SPOs should be intelligent risk takers, with venture philanthropy

providing the ultimate risk capital. Data allows you to know when you are taking a risk,

as well as whether it pays off. And when the “pay off” can mean changing the lives of

thousands, or even millions, we all need to know about it.

Daniela Barone Soares

Chief Executive, Impetus Trust

JUNE 2015 13

PREFACE

Name Organisation

Brad Presner Acumen Fund

Ken Ito Asian Venture Philanthropy Network

Claudia Leissner Auridis

Bettina Windau Bertelsmann Stiftung

Richard Kennedy CAN Breakthrough

Camilla Backström Charity Rating / NAYA AB

Nalini Tarakeshwar CIFF

Uli Grabenwarter EIF

Iana Petkova /

Gina Crane

Esmée Fairbairn Foundation

Emeline Stievenart ESSEC Business School

Rosien Herweijer European Foundation Centre

Øyvind Sandvold FERD Social Entrepreneurs

Fabrizio Ferraro IESE Business School

Anne Holm Rannaleet IKARE / EVPA Board

Meredith Niles Impetus Trust

Filipe Santos INSEAD

Sarah Gelfand IRIS / GIIN

Thomas Kagerer LGT Venture Philanthropy

Eva Varga NESsT

Lorenzo Allevi Oltre Venture

Emma Lane Spollen One Foundation

Pieter Oostlander Shaerpa

Alex Nicholls Skoll Centre for Social

Entrepreneurship

Marlon Van Dijk Social Evaluator

Claire Coulier Social Impact Analyst Association

Jeremy Nicholls SROI Network

Sophie Robin Stone Soup / ESADE Business School

Expert Group composition

EVPA is grateful for the contribution of the following Expert

Group to the development of this manual.

This list refers to the experts’ afliations at the time the rst

edition of the report was published in April 2013.

14 A PRACTICAL GUIDE TO MEASURING AND MANAGING IMPACT

EUROPEAN VENTURE PHILANTHROPY ASSOCIATION

Executive summary

JUNE 2015 15

EXECUTIVE SUMMARY

8. We use investment through-

out as including the range of

nancing instruments from

grants, loans and equity.

This manual is targeted specically at venture philanthropy organisations and social investors

(“VPO/SI”), and more generally at impact investors, foundations and any other funders

interested in generating a positive impact on society. Throughout the document, we use

the term “VPO/SI” to refer to such social sector funders. The rst objective of the manual

is to create a roadmap or guidebook to help VPO/SIs navigate through the current maze of

existing methodologies, databases, tools and metrics on social impact measurement. There-

fore, we do not take a stand to recommend a particular tool, but rather have attempted to

distil best practice from the various ways of measuring and managing social impact. The

second objective is to trigger a movement towards best practice when it comes to measuring

and managing impact. We would like the manual to become a working document that

evolves with new versions over time as our industry knowledge develops.

The manual should be useful both for beginners in impact measurement, who are consid-

ering how to get started, and for more advanced investors who are struggling with how to

better integrate an impact focus into everyday investment management decisions. Within

the VPO/SI, the person (or team) assigned to measure impact will be the natural reader/

user of the manual, but we also recommend executive directors, boards of directors and

investment managers to use the manual as a reference for key decisions on topics such as

resource allocation, deal selection and investment management. The manual uses plenty

of real-life examples from VPO/SIs as well as ve longer case studies that were developed

by the impact measurement initiative (IMI) Expert Group members. The manual does not

consider how to measure nancial impact but focuses solely on social impact (using a

broad denition of social that may also include environmental or cultural).

Our starting point has been to devise a process of Impact measurement for a VPO/SI wanting

to measure the impact of their investment8 in a Social Purpose Organisation (“SPO”). The

guide focuses on two levels: how to measure and manage the impact of specic investments

(level of SPO) and how the VPO/SI itself contributes to that impact (level of VPO/SI).

This process is the “how to” of impact measurement and is often what is most needed by

venture philanthropy organisations and social investors in general to get started. Analysis

of existing methodologies for impact measurement and the experience of working together

with VPO/SIs showed that most methods and tools to measure impact share a general

framework.

16 A PRACTICAL GUIDE TO MEASURING AND MANAGING IMPACT

EUROPEAN VENTURE PHILANTHROPY ASSOCIATION

EXECUTIVE SUMMARY

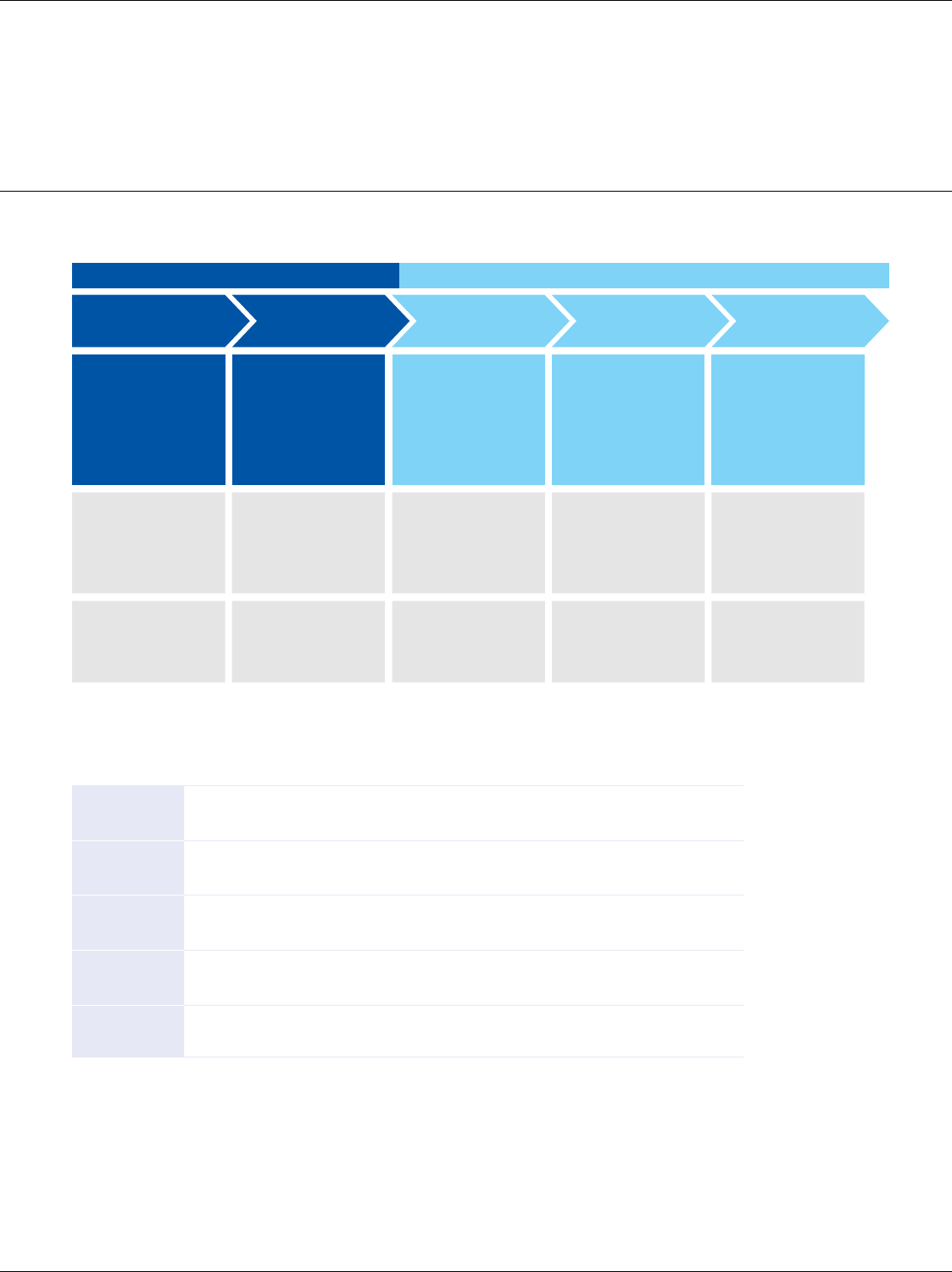

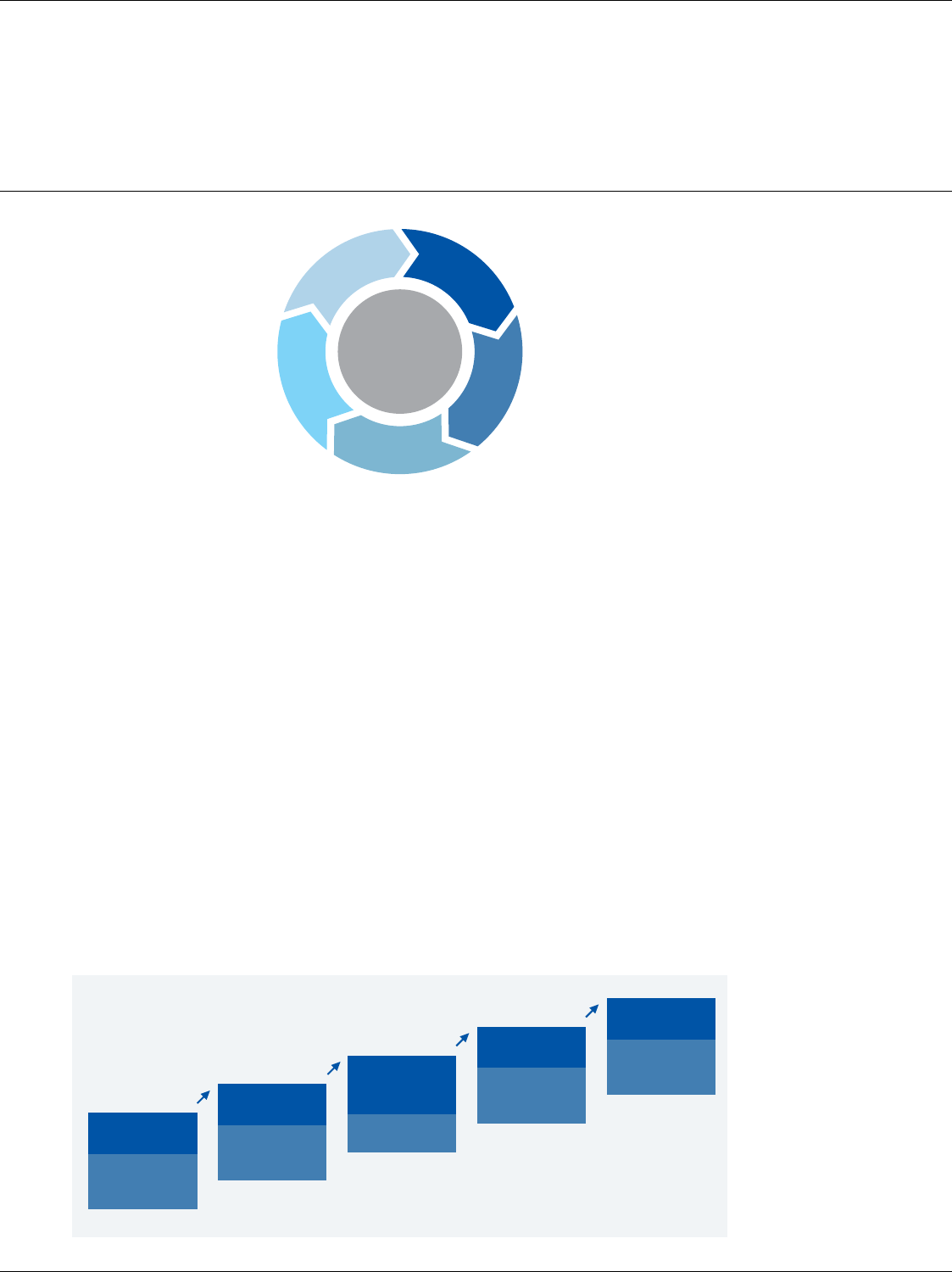

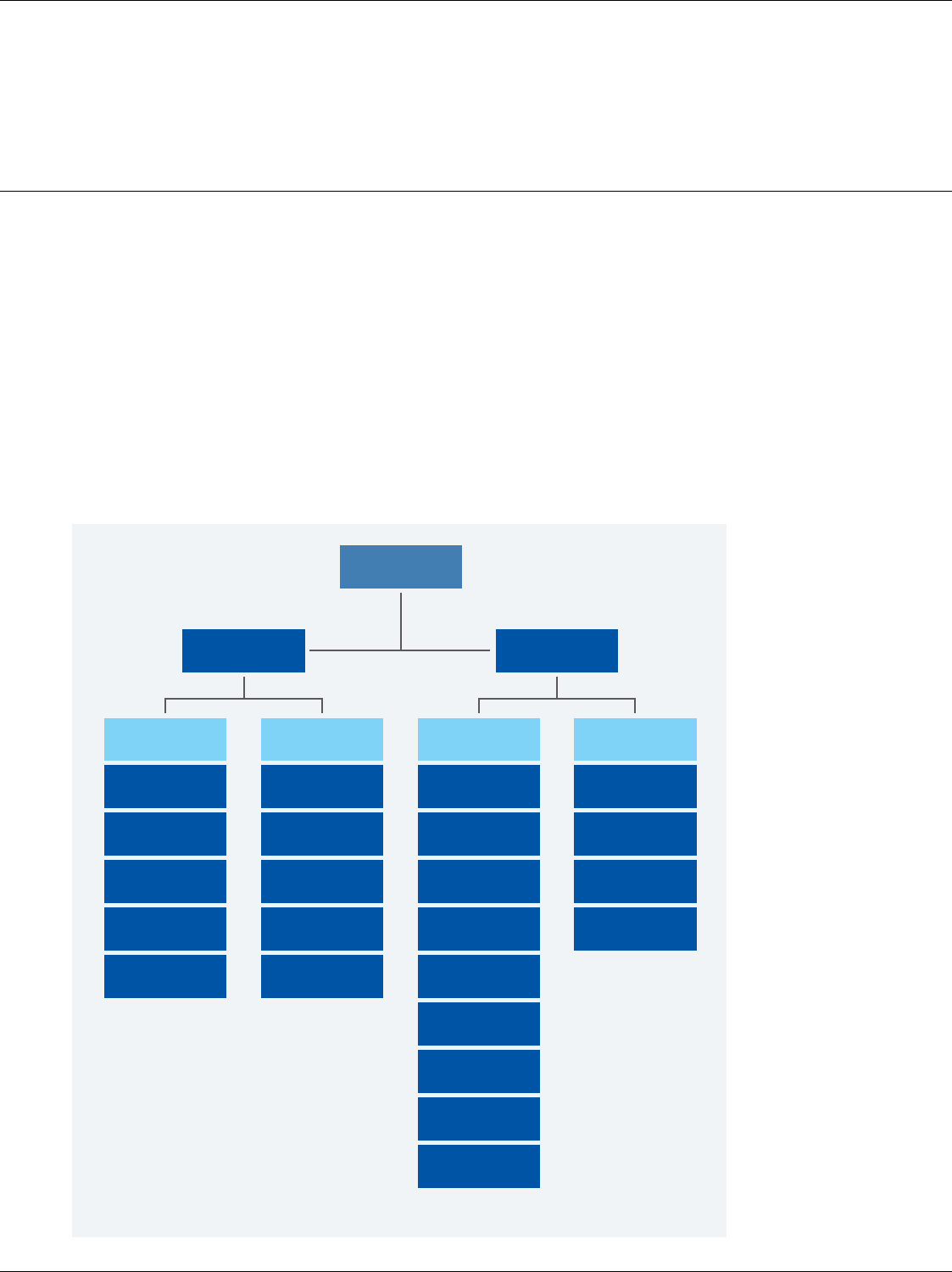

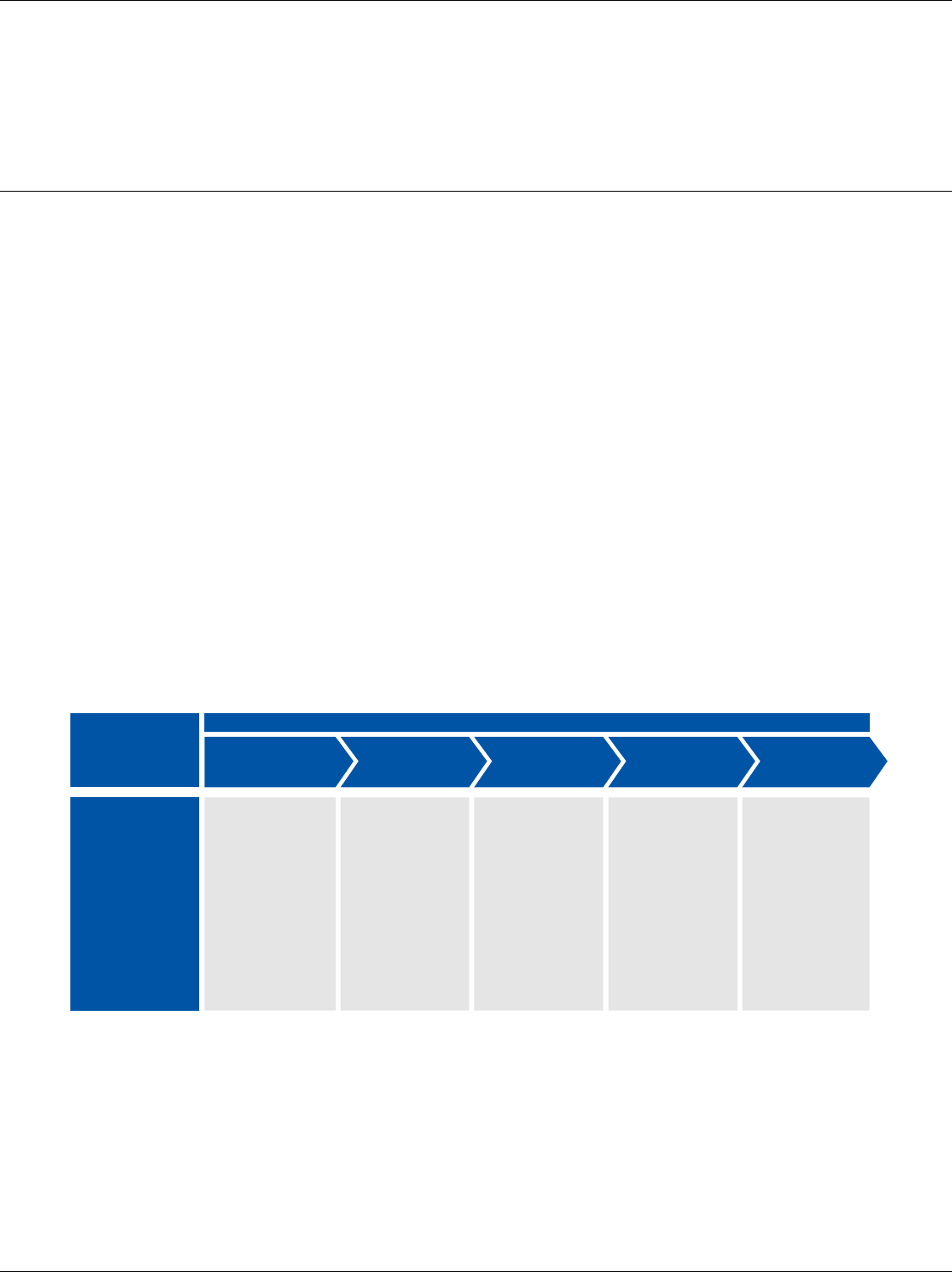

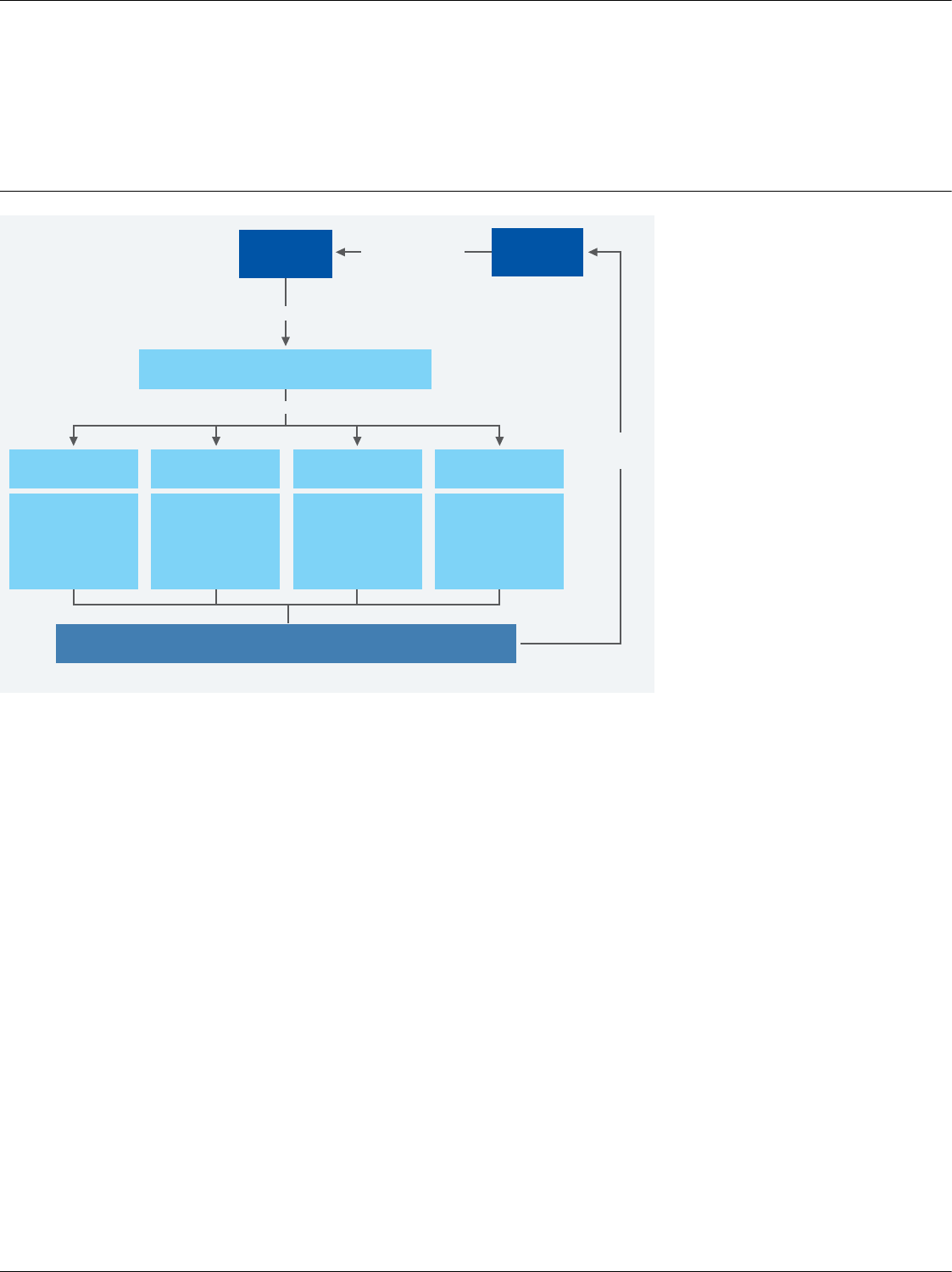

We represent the framework as having ve steps as shown in the following diagram:

The steps are presented in sequential order and we recommend that VPO/SIs go through

the steps in this order. However within the process it is possible to go back to steps and

revise them as you gain more information and more familiarity with the process. Some

VPO/SIs may nd it useful to go through each of the steps at a theoretical level before

implementing them in practice.

The goal of impact measurement is to manage and control the process of creating social

impact in order to maximise or optimise it (relative to costs). Managing impact occurs

continuously and is facilitated by integrating impact measurement in the investment

management process. It is important to identify what may need to change within the

investment management process so that you are able to maximise social impact. That is

why Managing Impact is the core of the impact measurement process. For each step in

the process, one should consider how this relates to the everyday work of funding and

building stronger social purpose organisations.

The impact value chain was the starting point for the denitions used in this manual as it

clearly sets out the differences between inputs, outputs, outcome and impacts.

The 5 steps of social

impact measurement

Source: EVPA

Managing

Impact

5

.

M

o

n

i

t

o

r

i

n

g

4

.

V

e

r

i

f

y

i

n

g

&

3

.

M

e

a

s

u

r

i

n

g

2

.

A

n

a

l

y

s

i

n

g

a

n

d

R

e

p

o

r

t

i

n

g

V

a

l

u

i

n

g

I

m

p

a

c

t

R

e

s

u

l

t

s

S

t

a

k

e

h

o

l

d

e

r

s

1

.

S

e

t

t

i

n

g

O

b

j

e

c

t

i

v

e

s

JUNE 2015 17

EXECUTIVE SUMMARY

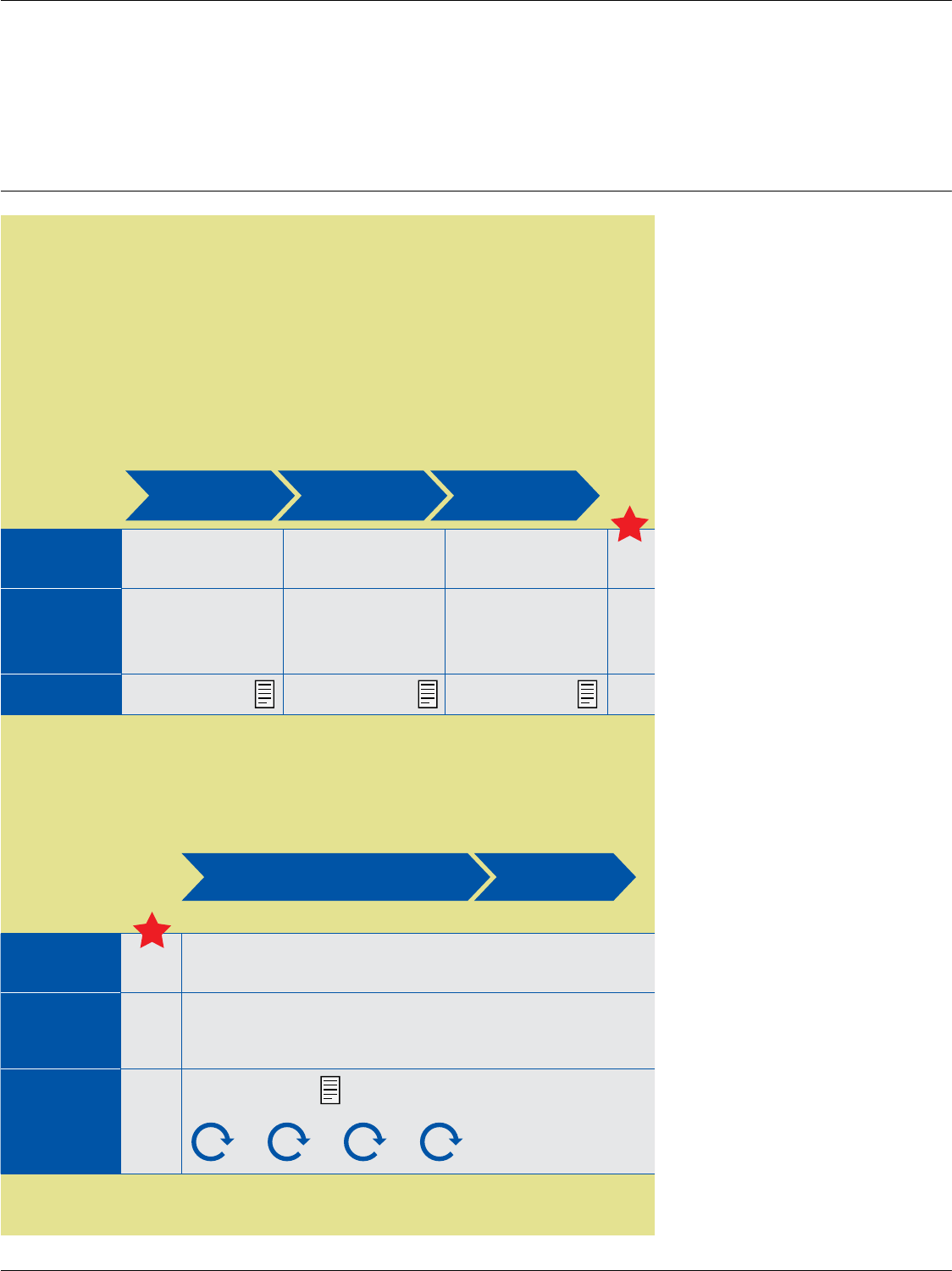

The Impact Value Chain

Source: Elaborated by EVPA from Rockefeller Foundation Double Bottom Line Project

In this manual, the following denitions are used:

To accurately (in academic terms) calculate social impact, you need to adjust outcomes for:

(i) what would have happened anyway (“deadweight”); (ii) the action of others (“attribution”);

(iii) how far the outcome of the initial intervention is likely to be reduced over time (“drop

off”); (iv) the extent to which the original situation was displaced elsewhere or outcomes

displaced other potential positive outcomes (“displacement”); and for unintended conse-

quences (which could be negative or positive).

Inputs: all resources, whether capital or human, invested in the activities of the

organisation.

Activities: the concrete actions, tasks and work carried out by the organisation to

create its outputs and outcomes and achieve its objectives.

Outputs: the tangible products and services that result from the organisation’s

activities.

Outcomes: the changes, benets, learnings or other effects (both long and short term)

that result from the organisation’s activities.

Social

Impact:

the attribution of an organisation’s activities to broader and longer-term

outcomes.

SPO’s Planned Work SPO’s Intended Results

4. Outcomes 5. Impact2. Activities1. Inputs 3. Outputs

Resources (capital,

human) invested in

the activity

€, number of people

etc.

Development &

implementation of

programs, building

new infrastructure

etc.

Number of people

reached, items sold,

etc.

Effects on target

population e.g.

increased access to

education

Attribution to changes

in outcome. Take

account of alternative

programs e.g. open air

classes

€50k invested, 5 people

working on project

Land bought, school

designed & built

New school built with

32 places

Students with

increased access to

education: 8

Students with access

to education not

including those with

alternatives: 2

Tangible products

from the activity

Changes resulting

from the activity

Outcomes adjusted

for what would have

happened anyway,

actions of others &

for unintended

consequences

Concrete actions of

the SPO

18 A PRACTICAL GUIDE TO MEASURING AND MANAGING IMPACT

EUROPEAN VENTURE PHILANTHROPY ASSOCIATION

EXECUTIVE SUMMARY

EVPA’s recommendation for measuring social impact is to calculate outcomes while

acknowledging (and if possible adjusting for) those factors that contribute to increasing

or decreasing the impact of the organisation; rather than aiming to calculate very specic

impact numbers.

In what follows, we provide a quick glance at the recommended impact measurement

process as detailed in the manual.

Step 1: Setting Objectives

This step includes dening the scope of the VPO/SI’s impact measurement and setting

objectives. Setting objectives is a vital step in any impact measurement process and needs

to be considered at both the level of the VPO/SI and the investee SPO. Often VPO/SIs do

not spend enough time upfront considering their own impact objectives and why they

want to measure impact, which later makes it difcult to take decisions regarding what is

relevant and what is not when faced with scarce resources.

The more specic the objectives the better the impact measurement that can be prepared

For a VPO/SI, objectives should be set at two levels:

(i) Level of the VPO/SI.

On the rationale and scope of impact measurement, the VPO/SI should aim to answer ve

questions upfront:

a. What is your motivation for measuring social impact?

There are many different purposes for using impact measurement and these could each

imply different target audiences and outlook.

b. What resources can you dedicate to impact measurement?

Resources to be considered include nancial, human, technological and time.

c. What type of SPOs are you working with?

The maturity i.e. the stage of development of the SPO will potentially limit the type of

information that the SPO can provide to you.

d. What level of rigour do you require in your impact analysis?

Depending on how accountable you expect your investees to be, you can increase the

rigour of your analysis and thereby reduce the risk of any impact claims made.

e. What is your time frame for measuring impact?

The time period over which you measure impact should be determined by the most

important outcomes and estimated length of time required to achieve them. But in

practice there may be internal or external pressures to invest for a certain period of time.

Depending on your timeframe, you will be able to draw either very specic or more

general conclusions about the impact of the SPO.

JUNE 2015 19

EXECUTIVE SUMMARY

Recommendations for managing impact:

•A VPO/SI must formulate its overarching social problem or issue so as to choose

investments in SPOs that can contribute to solving that social issue.

•Understanding the current and expected social impact of an SPO early in the decision-

making process is extremely valuable: it creates a common understanding of the

impact of an organisation; allows the VPO/SI and SPO to “speak the same language”;

and facilitates assessment of achievement of impact at later stages. A VPO/SI should

convince the SPO of the value of impact measurement, provide assistance where

possible and dene with them the responses to the essential questions to help them

express their objectives.

•Decisions have to be made about the amount of time and resources that a SPO should

dedicate to impact measurement.

On its impact objectives, the VPO/SI should aim to answer these questions:

a. What is the overarching social problem or issue that the VPO/SI is trying to solve?

This can be more or less difcult depending on how broad or focused your approach

but a clearly articulated response is necessary to be able to choose investments that can

contribute to solving the social issue that the VPO/SI is addressing.

b. What objective does the VPO/SI want to achieve?

Looking at your overall objectives and the relationship to be built with investees.

c. What are the expected outcomes?

The VPO/SI should evaluate the expected outcome of its investment in the SPO, i.e. the

expected outcome of the SPO and how the VPO/SI expects to contribute to achieving

that outcome. It is important to consider potential unintended consequences of the

VPO/SI’s activities.

(ii) Level of the SPO.

At a minimum you should answer these questions about the SPO:

a. What is the social problem or issue that the SPO is trying to solve?

The response should include information about the nature and magnitude of the

problem or opportunity; which populations are affected; whether the matter is changing

or evolving as well as in what way it is changing or evolving.

b. What activities are the SPO undertaking to solve the social problem or issue?

This should include a description of exactly what the SPO is doing to try to effect a change.

c. What resources or inputs (as per the impact value chain) does the SPO have and need

to undertake its activities?

This should include the time, talent, technology, equipment, information and other assets

available to conduct the activities, as well as the VPO/SI’s contribution to helping the

SPO to solve the issue.

d. What are the expected outcomes?

This should include what the SPO must achieve to be considered successful and will form

the basis of the milestones against which the SPO will be measured. It is also important

to consider the unintended consequences of the SPO’s activities.

20 A PRACTICAL GUIDE TO MEASURING AND MANAGING IMPACT

EUROPEAN VENTURE PHILANTHROPY ASSOCIATION

EXECUTIVE SUMMARY

Step 2: Analysing Stakeholders

VPO/SI investments generate value for a variety of stakeholders. A stakeholder is dened

as, “Any party effecting and/or affected by the activities of the organisation.”

This is an important step because the VPO/SI needs:

•To understand the expectations of the stakeholders, their contribution to and the potential

impact the SPO’s work will have on them.

•The co-operation of the main stakeholders in the impact measurement process.

Applying to both the VPO/SI and SPO level, there are two aspects to stakeholder analysis:

(i) Stakeholder identication; which includes stakeholder mapping (direct and indirect

contributors and beneciaries), stakeholder selection (using concepts such as materi-

ality, accountability and relevancy) and analysis of stakeholder expectations.

(ii) Stakeholder engagement; which includes communicating with the selected stakeholders

and is vital to be able to understand their expectations and, later in the process, verify

if their expectations have been met. This is described in more detail in Step 4.

Step 3: Measuring Results: Outcomes, Impact and Indicators

This step again occurs at two levels:

•VPO/SI level: its own outputs, outcomes, impact and indicators as per its own objectives

(theory of change etc); impact measurement at a portfolio level; impact of the VPO/SI’s

work on the SPO.

•SPO level: transforming its objectives into measurable results via outputs, outcomes,

impact and indicators.

To transform the objectives set in Step 1 into measureable results a VPO/SI and SPO must

consider outputs, outcomes, impact and indicators. For a VPO/SI, it is not sufcient to

just consider the impact achieved by the SPO, it is also important to assess the impact of

the work of the VPO/SI on the SPO. Outputs are directly related to the activities of the

organisation i.e. what is done to try and make a change in the base case, hence these are

Recommendations for managing impact:

•A VPO/SI must get the buy-in of key stakeholders (donors/investors, staff/human

resources, SPOs) to the impact objectives of the VPO so that their expectations are

managed and their contributions are aligned.

•Engagement with a VPO/SI’s key stakeholders should happen upfront and any major

changes in the impact objectives should be properly communicated.

•When a VPO/SI makes an investment in a SPO, stakeholder analysis should be

included during the due diligence phase. As the investment period proceeds, it is

advisable to regularly get back to these stakeholders to verify that their expectations

are being met (more details on how to do this in Step 4).

•Consider upfront when would be the appropriate time to revisit stakeholder analysis

together with the SPO (e.g. change to outcomes being achieved, major new funding

streams, new business lines, policy changes).

JUNE 2015 21

EXECUTIVE SUMMARY

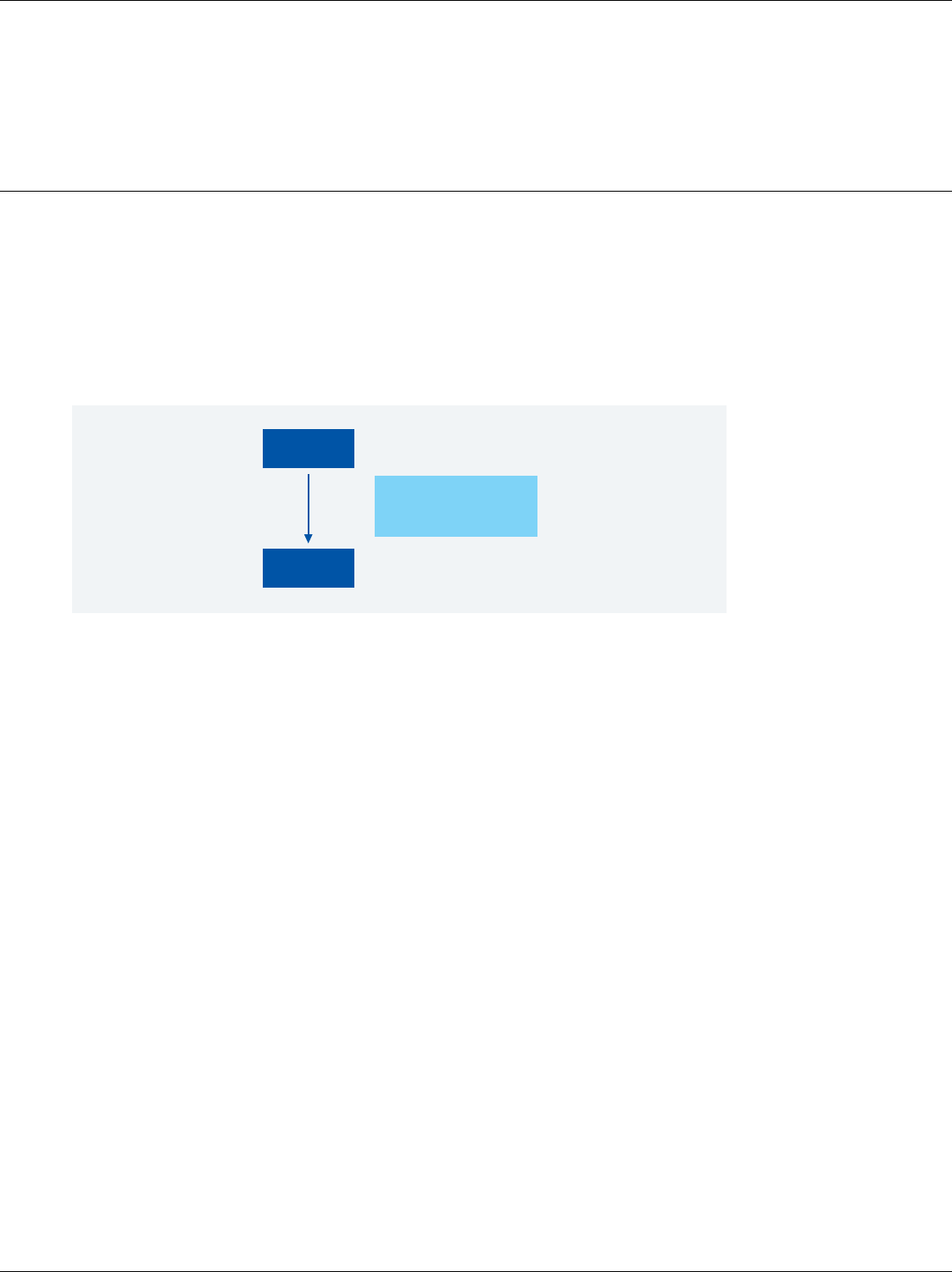

Internal vs external focus:

the use of outputs,

outcomes or impacts

generally easier to measure. Outcomes and impacts are related to the expected and unex-

pected effects of the activities of the organisation, hence they are outside the scope of the

organisation’s activities (but within their scope in terms of accountability) and generally

more difcult to measure.

Indicators are used to show progress towards or away from outputs or outcomes. If output

indicators are required these should be sourced as much as possible from public databases

such as IRIS, Global Value Exchange or other databases. If these output indicators point in

the same direction as the outcome you are targeting or if there exists independent research

showing that specic outputs do result in specic outcomes then some may also be used

as outcome indicators. If not we recommend the following process to select outcome indi-

cators:

(i) Dene outcomes as change statements, target statements or benchmark statements.

(ii) Select outcomes: you may have a list of outcome statements but you must select those

outcomes that are most important, material, useful and feasible (in achievement not in

measurement).

(iii) Select indicators i.e. identify two to three factors that provide measurable evidence

for a sub-optimal situation. There are four aspects to a good indicator:

a. Indicators should generally be aligned with the purpose of the organisation, although

if a potential unintended outcome has been identied, relevant indicators for this

out-come may by denition not be aligned with the purpose of the organisation.

b. Indicators should be “SMART”.

c. Indicators should be clearly dened so they can be reliably measured and ideally

comparable with those used by others.

d. More than one indicator should be used, with preference for two or three.

Impact itself is a technical and often academic discussion including concepts such as drop

off, displacement, deadweight and attribution. The rationale for this guide is to remove the

complexity around the issue and provide practical guidance.

Base Case Changed Case

Outcomes

Impacts

External Focus

Internal Focus

Outputs

Inputs

Organisation

Source: EVPA

22 A PRACTICAL GUIDE TO MEASURING AND MANAGING IMPACT

EUROPEAN VENTURE PHILANTHROPY ASSOCIATION

EXECUTIVE SUMMARY

The ability of an organisation to measure impact will depend on the sector and geography

in which it is operating. The propensity of European governments to move towards pay for

performance contracts means the measurement of impact is becoming more important for

those organisations active in these areas. However, for many organisations, access to inde-

pendent statistics and the creation of control groups in order to assess displacement, dead-

weight, drop off and attribution is not possible due to the expense and specialist skill-set

to carry them out. In these cases we encourage organisations to measure impact by calcu-

lating outcomes and acknowledging those factors that may mean that the outcomes are not

equal to the impact i.e. can increase or decrease impact. In some cases it may be possible to

think about some evidence as to what a control group may look like and could be used for

comparison purposes, for example based on research of comparable situations elsewhere.

Step 4: Verifying & Valuing Impact

In this step, we need to verify whether the claim we make on having positive social impact

is true, and if so, to what extent (i.e. to what value). The responses to these questions will

allow us to rene the target outcomes and associated indicators, creating a positive

feedback loop in the impact measurement process. This step also helps identify the

impacts with the highest social value, which can help an organisation focus their resources

towards those initiatives that create most impact on society.

Again, this step needs to occur at two levels: both at the level of the VPO/SI as well as at

the level of the SPO.

Recommendations for managing impact:

•For a VPO it is not enough to just consider the impact achieved by the SPO, it is also

important to assess the impact of the work of the VPO/SI on the SPO.

•The denition of portfolio level indicators may be required to measure how well a

VPO/SI has achieved its objectives as an organisation.

•The VPO/SI should ask the SPO to focus on those indicators that are directly related

to the SPO’s theory of change and hence in line with their operational process. Any

additional indicators required for the VPO/SI to satisfy its impact measurement needs

should be collected by the VPO/SI.

•The expected outputs, outcome and impact, and the corresponding indicators should

be dened before the investment is made and agreed upon by the VPO/SI and the

SPO.

•Clarify at the beginning of the relationship (i.e. during due diligence and within deal

structuring) who is responsible for measuring what. This can evolve over time and

should be reviewed on an annual basis.

JUNE 2015 23

EXECUTIVE SUMMARY

The VPO/SI must verify (or at least record) the non-nancial assistance provided to their

investees. They should then conrm with the investees that this assistance was in fact

valued. It may also be necessary for VPO/SIs to verify at regular intervals that the expecta-

tions of other stakeholders (donors/investors and human resources) are met so that correc-

tive actions can be undertaken if necessary.

At the level of the SPO, it is important to verify whether the outcomes make sense for the

stakeholder i.e. if the outcomes were realised during the timeframe and in the quantities

expected.

Verifying impact can be done via:

•Desk research: conrming whether the trends detected and interpreted by the SPO can

be triangulated with other data (external research reports, databases, government statis-

tics etc.);

•Competitive analysis: comparing the results of the SPO with other comparable organisa-

tions in terms of similar issues, geographies and populations targeted;

•Interviews / focus groups: asking neutral questions to a representative sample of your

key stakeholders. This format can be particularly useful when the VPO/SI is assessing

the value of its non-nancial assistance to the SPO. However it is recommended that a

neutral party conduct these interviews so as to ensure SPOs are comfortable providing

the most truthful responses).

The next step is to understand if the outcome was important i.e. of value to the stakeholder.

Numerous techniques and methodologies exist for measuring value created. We have

chosen not to list all the possible techniques preferring instead to cite certain useful refer-

ences. Two general categories can be identied: qualitative and quantitative (monetisation).

•Qualitative: storytelling, client satisfaction surveys, participatory impact assessment

groups, progress out of poverty index.

•Quantitative (monetisation): techniques for valuing e.g. perceived value / revealed pref-

erence and Value Game or techniques for cost / benet analysis e.g. cost-saving methods

and quality adjusted life years calculations.

Whether you select a quantitative or qualitative technique or a combination of both for

valuing impact will depend on your rationale for measuring impact in the rst place. For

example, often governments tend to prefer quantitative approaches whereas the general

public may prefer qualitative methods.

24 A PRACTICAL GUIDE TO MEASURING AND MANAGING IMPACT

EUROPEAN VENTURE PHILANTHROPY ASSOCIATION

EXECUTIVE SUMMARY

Step 5: Monitoring & Reporting

The nal step in the impact measurement process involves monitoring – tracking progress

against (or deviation from) the objectives dened in the rst step and made concrete

through the indicators set in the third step; and reporting – transforming data into present-

able formats that are relevant for key stakeholders. Monitoring and reporting are iterative

processes that go hand in hand because what is monitoring to one stakeholder is reporting

to another e.g. when a VPO/SI is monitoring the progress of an investee SPO, that SPO is

reporting relevant data to the VPO/SI. As in the other steps we must consider the process

at two levels: the VPO/SI and SPO.

(i) Monitoring

Once an organisation has decided on the indicators to be measured and veried that they

make sense to the key stakeholders, they need to start collecting data in a systematic way.

In practice, the type of system may be considered upfront but we urge organisations to

go through the impact measurement process at least theoretically prior to setting up the

system to understand the type of information that needs collection.

The VPO/SI should be collecting and analysing data on:

•Specic indicators that measure its progress towards reaching its overarching social

objectives.

•Time invested and/or € provided in non-nancial support to its investees.

•The investee SPOs, according to the objectives and indicators previously dened.

There is also a need to evaluate if the SPO is effectively monitoring its activities and

outcomes e.g. are the selected indicators appropriate (providing a balanced picture of the

situation and picking up potentially positive and negative aspects) and if the VPO/SI has a

role to play in improving the impact measurement practices of the investee

Recommendations for managing impact:

•Perform this step at the beginning of an investment (as part of the due diligence), at

least once during the investment period (to check that the impact is achieved and

valued) and again at the time of exit (as a way to check that the desired impact has

been achieved and makes sense).

•Make clear assignments between the SPO and VPO/SI about who is responsible for

which parts of the verifying and valuing process.

•Unless you verify whether you have created value through your support of the SPO,

you cannot credibly make that statement.

•VPO/SIs should use independent studies to assess the value they provide to the

SPOs as directly questioning investees may be a delicate matter, resulting in them not

always providing truthful answers.

•VPO/SIs should verify at regular intervals that the expectations of other stake-

holders (donors/investors and human resources) are met so that corrective action

can be undertaken if necessary.

JUNE 2015 25

EXECUTIVE SUMMARY

Recommendations for managing impact:

•To remove a reliance on and/or culture of “gut feeling”, VPO/SIs should work with

the SPO to develop an impact monitoring system that can be integrated into the

management processes of the organisation.

•Check whether the system the SPO already works with is sufcient to meet your

requirements – if not, a VPO/SI should be prepared to contribute to improving it

through pro-bono partners or other resources (although generally this support doesn’t

extend to the actual data collection). The objective should be a system that is of value

to the SPO as a management tool.

•The cost to support and maintain a SPO’s impact monitoring system (including

personnel time and costs) should be part of the SPO’s budget and hence part of the

negotiation with the investor in order to decide how costs should and/or could be split.

•When working with very early stage SPOs and helping them develop business plans,

integrate requirements on impact measurement at this stage.

•Agree on reporting requirements upfront with SPO and co-investors to eliminate the

burden of multiple reporting on the SPO.

•Manage expectations about frequency and level of detail for reporting, and the way

SPOs report; will they just report on numbers or also on verication (and if so, with

what frequency).

The SPO needs to evaluate the outcomes or impacts that are being achieved through the

activities of its organisation and the practical lessons that can be learned from the results.

With this information it is then possible to decide what actions are needed to increase

impact.

(ii) Reporting

Once the data has been collected and analysed, an organisation needs to consider how

to present this information. The purpose of reporting affects the information that should

be included. Depending whether the focus is on an internal or an external audience, the

various stakeholders may require different types of reports. The stakeholder analysis

conducted in Step 2 should guide the development of reporting, considering the stake-

holders’ multiple objectives.

One of the challenges of the social sector is that each SPO needs to report in different ways

to each funder. Some initiatives (e.g. Social Reporting Standard) are trying to overcome this

problem, but there is still a problem of lack of standardisation that leads to inefciencies.

26 A PRACTICAL GUIDE TO MEASURING AND MANAGING IMPACT

EUROPEAN VENTURE PHILANTHROPY ASSOCIATION

EXECUTIVE SUMMARY

Managing Impact

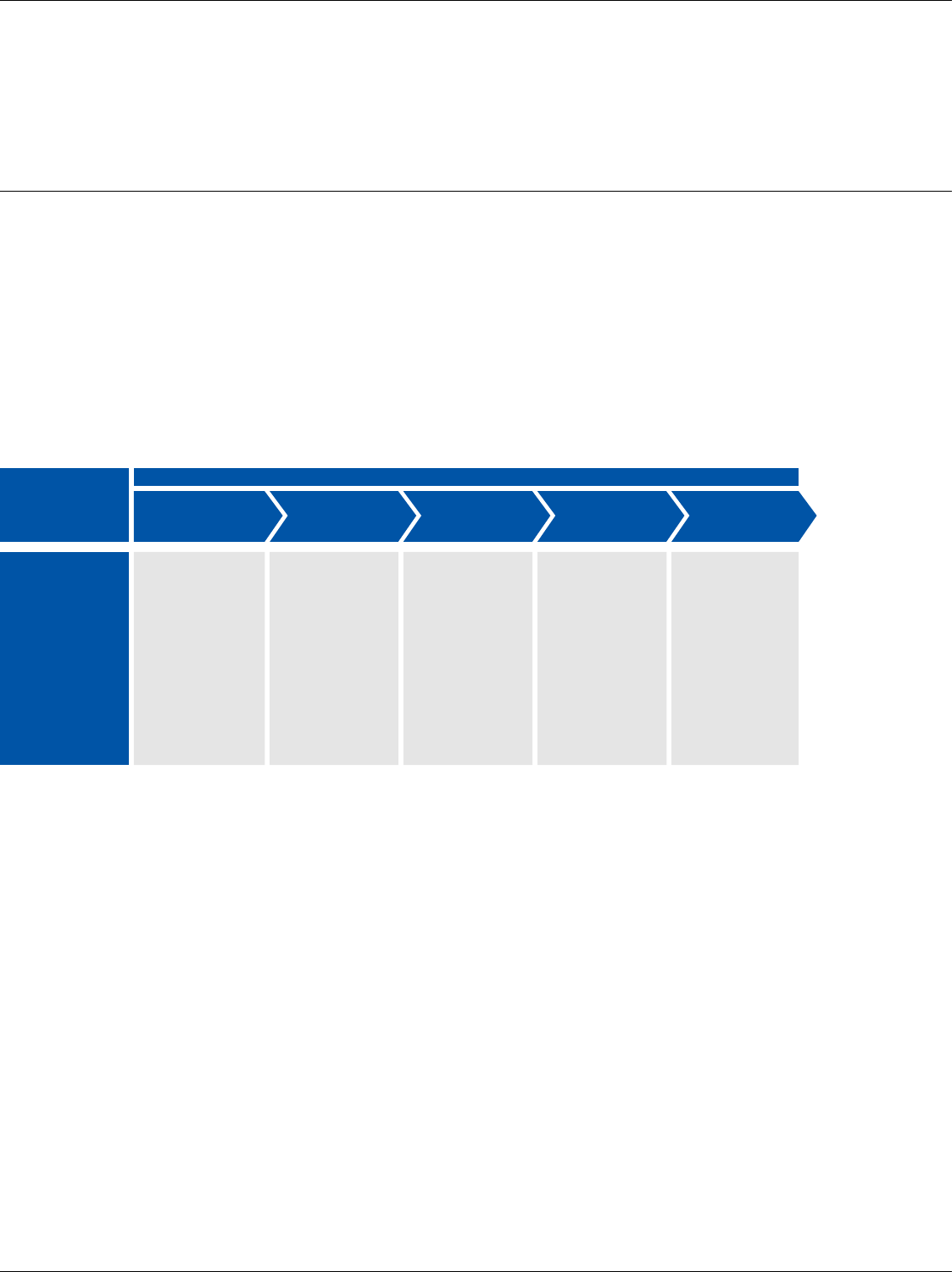

The impact measurement process outlined in the ve steps should allow the VPO/SI to

better manage the impact generated by its investments. To manage impact, the VPO/SI

should continuously use the impact measurement process to identify and dene correc-

tive actions if the overall results deviate from expectations. It will also have become clear

that impact measurement is very closely aligned to your investment management process.

Given most VPO/SIs are aiming to maximise impact, the corrective actions taken may

apply as much to the investment management process as to impact measurement itself.

Managing impact in the investment process

Assess whether invest-

ment opportunity fits

with VPO/SI strategy

by asking questions

detailed in setting

objectives.

Decide on the

overarching social

impact objectives

of the VPO/SI –

these will guide the

investment process.

Dig deeper into

questions asked in

setting objectives.

Perform stakeholder

analysis.

Verify and value

expected results.

Map outputs, out-

comes and impacts

and decide on key

indicators against

which progress will

be measured.

Decide on monito-

ring and reporting

content and frequency

and assign responsi-

bilities.

Regularly assess

impact results against

key indicators.

Verify and value

reported results at

regular intervals.

Revise indicators

if significant changes

are made in the

business and impact

model.

Investment

management Exit

Due diligence

(detailed screening)

Deal

screening

Investment

strategy Deal

structuring

Investment process

Perform thorough

analysis of impact

results against

objectives –

verifying

and valuing

reported

results.

JUNE 2015 27

28 A PRACTICAL GUIDE TO MEASURING AND MANAGING IMPACT

EUROPEAN VENTURE PHILANTHROPY ASSOCIATION

PART 1:

Introduction

and Overview

JUNE 2015 29

INTRODUCTION AND OVERVIEW

1.0 Introduction and Overview

This manual is targeted specically at venture philanthropy organisations and social investors

(“VPO/SI”), and more generally at impact investors, foundations and any other funders

interested in generating a positive impact on society. Throughout the document, we use the

term “VPO/SI” to refer to such social sector funders.

The rst objective of the manual is to assist investors in improving the way they measure

impact, providing practical tips and recommendations for how it works in real-life situations.

For that purpose, the manual is a roadmap or guidebook to help VPO/SIs navigate through

the current maze of existing methodologies, databases, tools and metrics on social impact

measurement. The manual does not recommend a particular tool, but rather attempts to distil

best practice from the various ways of measuring and managing social impact. The manual

should be useful both for beginners in impact measurement, who are considering how to get

started, and for more advanced investors who are struggling with how to better integrate an

impact focus into everyday investment management decisions. The manual does not consider

how to measure nancial impact but focuses solely on social impact (using a broad denition

of social that may also include environmental or cultural impact). The second objective is to

trigger a movement towards best practice when it comes to measuring and managing impact.

We would like the manual to become a working document that evolves with new versions

over time as our industry knowledge develops.

The manual focuses on two levels, how to measure the impact of specic investments and

how the VPO/SI itself contributes to that impact. It focuses on devising a process of impact

measurement for a VPO/SI evaluating the impact of their investment in a SPO. This process

is the “how to” of impact measurement and is often what is most needed by VPO/SIs to get

started. The ultimate goal is for impact to become an integral part of the investment manage-

ment process. Within the VPO/SI, the person (or team) assigned to measure impact will be

the natural reader/user of the manual, but we also recommend executive directors, boards of

directors and investment managers use the manual as a reference for key decisions on topics

such as resource allocation, deal selection and investment management.

In order to ensure the inclusion of the opinions and experiences of various stakeholders, EVPA

convened an Expert Group consisting of twenty-seven venture philanthropy practitioners,

consultants, academics and representatives of other organisations involved in impact measure-

ment. We have beneted greatly from the collaboration of these experts who freely and enthu-

siastically contributed their time and knowledge to the development of this document. The

members of the Expert Group are listed in the preface and we are extremely grateful to them.

The manual uses plenty of real-life examples from VPO/SIs as well as ve longer case studies

that were developed by the impact measurement initiative (IMI) Expert Group members. In

this version of the manual, we also include the feedback received during the workshop we

organised on the topic with 80 participants and individual feedback collected during a consul-

tation period of around three months following the publication of the rst draft.

30 A PRACTICAL GUIDE TO MEASURING AND MANAGING IMPACT

EUROPEAN VENTURE PHILANTHROPY ASSOCIATION

INTRODUCTION AND OVERVIEW

This practical guide is presented through a framework of ve steps that an investor should

go through when measuring impact. The process nishes with a section on managing

impact that attempts to integrate the elements of impact measurement into the investment

process. We have stayed away from set methodologies and instead tried to provide specic

recommendations and practical examples. Five concrete and detailed case studies are

provided to further show how real VPO/SIs are dealing with impact measurement. These

cases studies are examples of the current state of the eld and show how VPO/SIs are

addressing the challenges they face in measuring impact. Finally, the document provides a

glossary and additional resources.

1.1 Background

Venture philanthropy (VP) works to build stronger investee organisations with a social

purpose (SPOs) by providing them with both nancial and non-nancial support in order

to increase their social impact. Although we use the word social we include impacts that

maybe social, environmental or cultural. The venture philanthropy approach includes both

the use of social investment (equity and debt instruments) and grants. The key character-

istics of venture philanthropy include high engagement, organisational capacity-building,

tailored nancing, non-nancial support, involvement of networks, multi-year support

and performance measurement.

An integral part of the VP approach is the measurement of performance; placing emphasis

on good business planning, measurable outcomes, achievement of milestones and nancial

accountability and transparency. The focus of this manual is social impact measurement.

1.2 How is social impact currently measured by social investors and venture

philanthropists?

The rationale for undertaking this impact measurement initiative was inspired by the

out-come of a workshop on impact measurement organised by EVPA in June 2011, and

the results of the 2011 EVPA Survey of European VPO/SIs, collecting data on 50 VPO/SIs

based in Europe with investments in Europe and abroad. The general opinion that came

out of the workshop was that there was a strong need for further direction on how to

approach impact measurement.

The second annual EVPA survey of Venture Philanthropy and Social Investment in Europe9,

released on 1st March 2013, collecting data on 61 VPO/SIs also reinforced the importance

of social impact measurement.

The key highlights of the survey with respect to impact measurement were as follows:

•There is increased attention to measuring social impact: The focus on social impact measure-

ment increased, with 90% of respondents measuring social impact on at least an annual

basis during the investment period. Although impact measurement still occurs less

frequently than nancial performance measurement.

9. Hehenberger, L.; Harling,

A., (2013), “European Venture

Philanthropy and Social Investment

2011/2012”, EVPA.

JUNE 2015 31

INTRODUCTION AND OVERVIEW

•VPO/SIs still focus on outputs more than outcomes or impact: The objectives of the impact

measurement system are, in the majority of cases (84%), still based on output measures.

Nevertheless we saw an increase in the percentage of VPO/SIs attempting to measure

changes in outcome or impact.

•Increase in budget assigned to impact measurement: In scal year 2011, the average annual

budget for measuring social impact was just over €63k (compared to €18k in 2010), with

a median spend of €15k.

•Lack of standardisation indicates a high degree of fragmentation in the use of impact measurement

tools and systems: In line with last year’s survey a majority of VPO/SIs (73%) indicated that

they were not using a standardised tool to measure social impact. Among those that did

use such a tool, the most frequently mentioned were Social Evaluator and SROI, although

a quarter of people did say they were using IRIS indicators or theory of change. Interest-

ingly, when asked whether they used one of the steps of the 5-step process developed

herein, between 70-90% of respondents used each of the steps.

•Impact measurement is not fully integrated into the decision-making process: 53% never or only

sometimes take the social performance into account before releasing new funds.

•Impact measurement does not inform employee compensation: Only 12% of the VPO/SIs

include social performance in the compensation schemes for their own staff.

The outcome of the workshop and the results of the EVPA Industry Survey 2011/2012 rein-

forced EVPA’s opinion that there was a need for additional clarity and guidance on impact

measurement.

1.3 Five-step framework

Analysis of existing resources on impact measurement and the experience of working

with VPO/SIs showed that most methods and tools to measure impact share a general

framework. This general framework was the starting point for the discussions on impact

measurement.

We see the framework as having ve steps, which will be explored in greater detail in the

main body of the manual (Part 2). Each of the ve steps applies to the VPO and how it

should consider its own impact, as well as to the SPO. The ve steps are as follows:

1. Setting Objectives: setting the scope of the impact analysis (why and for whom), the level

(portfolio of social investments/individual social enterprise) and what the desired social

change is. Objectives should be set at:

•Level of VPO/SI (dening scope of impact measurement and the overarching social

objectives the VPO/SI wants to achieve)

•Level of investee (social issue to be solved, inputs/activities, expected outcomes)

32 A PRACTICAL GUIDE TO MEASURING AND MANAGING IMPACT

EUROPEAN VENTURE PHILANTHROPY ASSOCIATION

INTRODUCTION AND OVERVIEW

2. Analysing Stakeholders: ranking the multitude of potential stakeholders in order of

priority, weighing their contribution to the completeness of the analysis against the

resources required, and analysing their inputs (if any), activities and potential outputs.

•Level of VPO/SI (employees, board of directors, investors / donors)

•Level of investee (direct and indirect contributors and beneciaries)

3. Measuring Results – Outcome, Impact and Indicators: measuring the output, outcome and

impact10 that derive from your activity for the key stakeholders, and understanding how

different types of indicators can be used to map the social result of the social enterprise’s

and VPO/SI’s work.

•Level of VPO/SI (based on the objectives of VPO/SI, you can map results and consider

portfolio level indicators)

•Level of investee (outputs, outcomes, impact and indicators relating to the objectives of

the SPO)

4. Verifying & Valuing Impact: verifying that the impact is not too subjective and whether

it indeed was valued by the key stakeholders – considering quantitative and/or

qualitative methods (by calculating the social value of an investment or otherwise) and

comparing the results of the work against relevant benchmarks.

•Level of VPO/SI (was non nancial support provided to investees, valued by the

investee etc.)

•Level of investee (verifying and valuing impact for key stakeholders)

5. Monitoring & Reporting: collecting data and devising a system to store and manage the

data as well as integrating this information into overall operations and reporting the

data to relevant stakeholders.

•Level of VPO/SI (what systems are required to collect, store and manage data, reporting

formats)

•Level of investee (collection, management and reporting requirements for the SPO)

The manual presents the steps in a sequential order and we recommend that VPO/SIs go

through the steps in this order. However within the process it is possible to go back to steps

and revise them as you gain more information and more familiarity with the process. Some

VPO/SIs may nd it useful to go through each of the steps at a theoretical level before

implementing them in practice. For example it may be difcult for the SPO to engage with

certain stakeholders on a frequent basis, therefore in practice you may need to gain the

information required for Steps 2 and 4 at the same time.

Working through impact measurement it will become clear that each step also has ramica-

tions for the investment management process. Given VPO/SIs are interested in maximising

impact it is important to identify what may need to change within the investment manage-

ment process so you are indeed able to maximise impact. Within this manual we call this

managing impact. For each step in the process, the VPO/SI should consider how it relates to

the everyday work of funding and building stronger social purpose organisations.

10. The definition of these terms

are explored in section 1.5.

JUNE 2015 33

INTRODUCTION AND OVERVIEW

1.4 Methodology

EVPA proposed a ve-step process for how to measure social impact based on our own

research on impact measurement and the practical experience of working with VPO/SIs

that measure impact. A brief description of the contents of the ve-step process was circu-

lated to the Expert Group in the spring of 2012. Between April and July of 2012, six webinars

were held, each webinar related to a particular step in the process (plus an introductory

session). The members of the Expert Group were divided into ve working groups and

asked to prepare a presentation, including a case study on a particular step. The experiences

and discussions among the participants in these webinars have served to adjust and edit

the frame-works put forward in this manual to ensure it is well grounded in the practice

of EVPA members and other social investors. The data gathered from the Expert Group

members was complemented with more in-depth interviews with selected VPO/SIs.

The rst draft of A Practical Guide to Measuring and Managing Impact was released for

consultation in November 2012 and the 80 participants of EVPA’s impact measurement

workshop provided initial feedback. Between November 2012 and March 2013 additional

feedback was garnered from VPO/SI practitioners in order to improve the guide. The

timeline of the Impact Measurement Initiative is shown below.

The 5 steps of social

impact measurement

Source: EVPA

Managing

Impact

5

.

M

o

n

i

t

o

r

i

n

g

4

.

V

e

r

i

f

y

i

n

g

&

3

.

M

e

a

s

u

r

i

n

g

2

.

A

n

a

l

y

s

i

n

g

a

n

d

R

e

p

o

r

t

i

n

g

V

a

l

u

i

n

g

I

m

p

a

c

t

R

e

s

u

l

t

s

S

t

a

k

e

h

o

l

d

e

r

s

1

.

S

e

t

t

i

n

g

O

b

j

e

c

t

i

v

e

s

Webinar

Series

April – July

2012

Case Study

Development

April – August

2012

1st Draft

Manual &

Workshop

November 2012

Consultation

Period

November 2012

– March 2013

“Version 1.0”

Manual

April 2013

Timeline of the Impact

Measurement Initiative

34 A PRACTICAL GUIDE TO MEASURING AND MANAGING IMPACT

EUROPEAN VENTURE PHILANTHROPY ASSOCIATION

INTRODUCTION AND OVERVIEW

Inputs: all resources, whether capital or human, invested in the activities of the

organisation.

Activities: the concrete actions, tasks and work carried out by the organisation to

create its outputs and outcomes and achieve its objectives.

Outputs: the tangible products and services that result from the organisation’s

activities.

Outcomes: the changes, benets, learnings or other effects (both long and short term)

that result from the organisation’s activities.

Social

Impact:

the attribution of an organisation’s activities to broader and longer-term

outcomes.

1.5 Denition of social impact

There is currently a large amount of discussion and debate around social impact meas-

urement. However, before diving into the topic it is important to agree the denitions of

certain frequently used words in the impact measurement dialogue.

The impact value chain has become a popular starting point for dening social impact as it

clearly sets out the differences between inputs, outputs, outcome and social impacts.

The impact value chain was also the starting point for the denitions used in this manual.

Based on the discussions in the Expert Group, EVPA has agreed the following denitions:

The Impact Value Chain

Source: Elaborated by EVPA from Rockefeller Foundation Double Bottom Line Project

SPO’s Planned Work SPO’s Intended Results

4. Outcomes 5. Impact2. Activities1. Inputs 3. Outputs

Resources (capital,

human) invested in

the activity

€, number of people

etc.

Development &

implementation of

programs, building

new infrastructure

etc.

Number of people

reached, items sold,

etc.

Effects on target

population e.g.

increased access to

education

Attribution to changes

in outcome. Take

account of alternative

programs e.g. open air

classes

€50k invested, 5 people

working on project

Land bought, school

designed & built

New school built with

32 places

Students with

increased access to

education: 8

Students with access

to education not

including those with

alternatives: 2

Tangible products

from the activity

Changes resulting

from the activity

Outcomes adjusted

for what would have

happened anyway,

actions of others &

for unintended

consequences

Concrete actions of

the SPO

JUNE 2015 35

INTRODUCTION AND OVERVIEW

To accurately (in academic terms) calculate social impact you need to adjust outcomes for:

(i) what would have happened anyway (“deadweight”); (ii) the action of others (“attribution”);

(iii) how far the outcome of the initial intervention is likely to be reduced over time (“drop

off”); (iv) the extent to which the original situation was displaced elsewhere or outcomes

displaced other potential positive outcomes (“displacement”); and for unintended conse-

quences (which could be negative or positive).

EVPA’s recommendation for measuring social impact is to calculate outcomes while

acknowledging (and if possible adjusting for) those factors that contribute to increasing

or decreasing the impact of the organisation, rather than aiming to calculate very specic

impact numbers. This is a general recommendation however we accept that there are

certain organisations (for example those who interact with government for pay for perfor-

mance type contracts) that may be required to produce more scientically accurate social

impact numbers.

As with all denitions, they are most effectively demonstrated through the use of an

example11. Let us look at an investment in an organisation that focuses on increasing access

to education for primary school age children in developing countries. We have introduced

the key factors from the case in the impact value chain above to illustrate the difference

between input, out-put, outcome and impact.

The theory of change for this organisation is that lack of access to education is a key factor

in preventing the poor from moving out of poverty. Hence to increase access to education

the organisation builds educational infrastructure in developing countries. Its inputs are

the money invested and the people employed to build the educational infrastructure.

Their principal activity (although it may have other complementary ones) is building new

schools. One particular output would be a new school built with places for 32 primary

school children, although the actual outcome with respect to increased access to education

is only 8 as 24 of the other potential primary school children were kept at home to work

on the harvest and do other essential work for the family. In fact, the impact is even less

when adjusting for the change that would have taken place if the SPO had not performed

its activity: of those 8 primary school children, 6 were already receiving some form of

education through open air classes and visiting teachers.

This example shows the importance of understanding the difference between impact,

out-comes and outputs when considering the social impact of a SPO.

11. Elaborated from Grabenwarter &

Liechtenstein, (2011), “In search

of gamma: an unconventional

perspective on impact investing”.

36 A PRACTICAL GUIDE TO MEASURING AND MANAGING IMPACT

EUROPEAN VENTURE PHILANTHROPY ASSOCIATION

PART 2:

The Impact

Measurement

Process

JUNE 2015 37

THE IMPACT MEASUREMENT PROCESS

STEP 1: SETTING OBJECTIVES

In the following sections, we will go through each step in the impact measurement process.

For each step, we will explain what it means, how the step is implemented at two levels

(i) at the level of the Investor, the VPO/SI, and (ii) at the level of the Investee, the SPO itself;

provide concrete recommendations and illustrate by using a real-life example. The reason

why the manual contemplates two levels is because a VPO/SI achieves impact indirectly

by investing in a SPO that is solving a particular social issue. A VPO/SI needs to consider

both levels and how to achieve an appropriate alignment between the two.

2.0 Step 1: Setting Objectives

2.1 What?

This step includes the denition of the scope of impact measurement by the VPO/SI and

then the setting of objectives. Setting objectives may appear an intuitively simple task but

in practice there is often confusion. Without a clear understanding of objectives it is difcult

to proceed with the impact measurement process and this can lead to overburdening the

SPO and even the VPO/SI with excessive data collection requests.

The more specic the objectives the better the impact measurement can be prepared. Objec-

tives should be set at two levels:

(i) At the level of the VPO/SI; and

(ii) At the level of the SPO

2.2 How to?

Level of VPO/SI

Before thinking about measuring the social impact of an investee, VPO/SIs should dene

the scope of their impact measurement and set their own objectives in terms of impact and

their relationships with the SPOs. Our conversations with VPO/SIs have highlighted that