FAC1501 Study Guide

User Manual:

Open the PDF directly: View PDF ![]() .

.

Page Count: 388 [warning: Documents this large are best viewed by clicking the View PDF Link!]

1

2

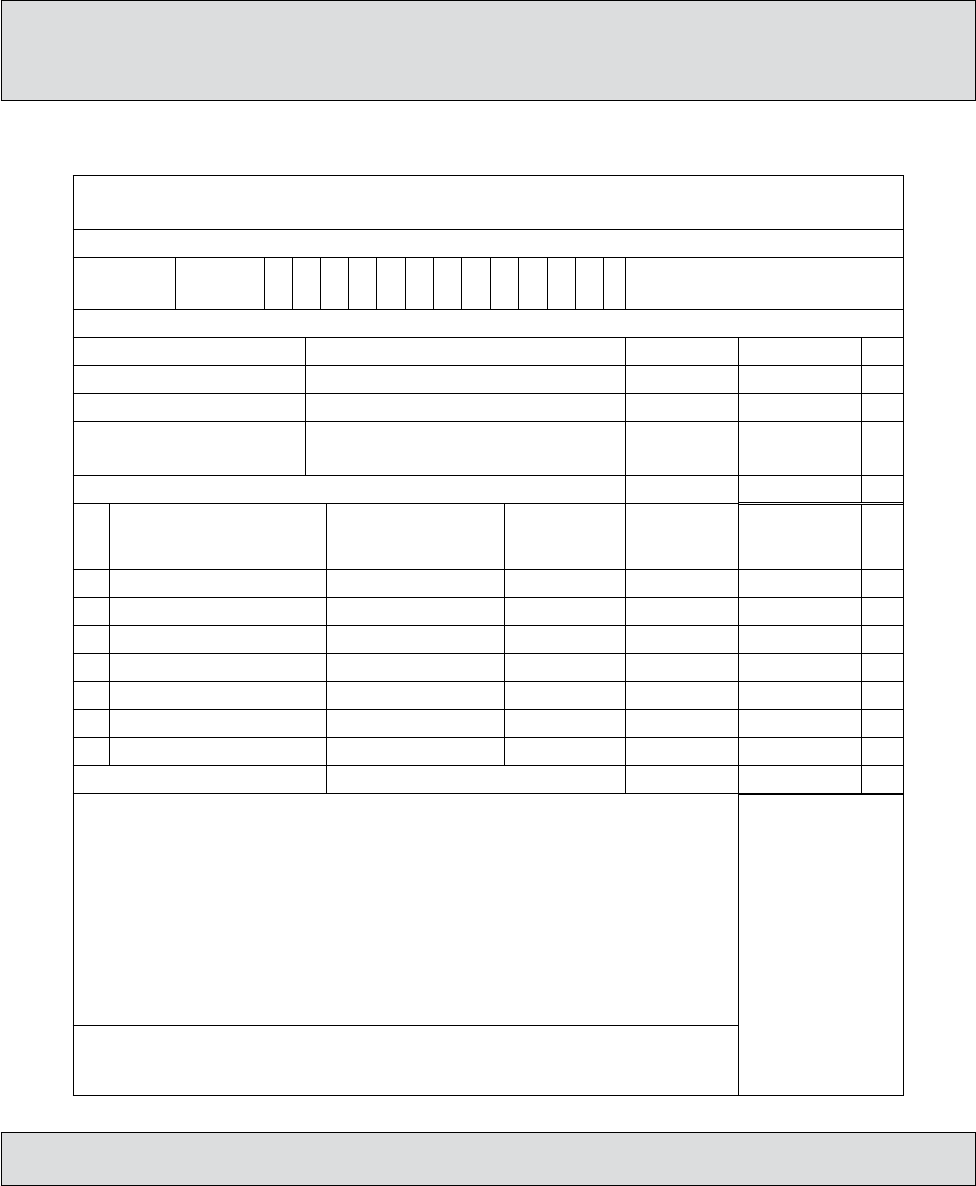

© 2017 University of South Africa

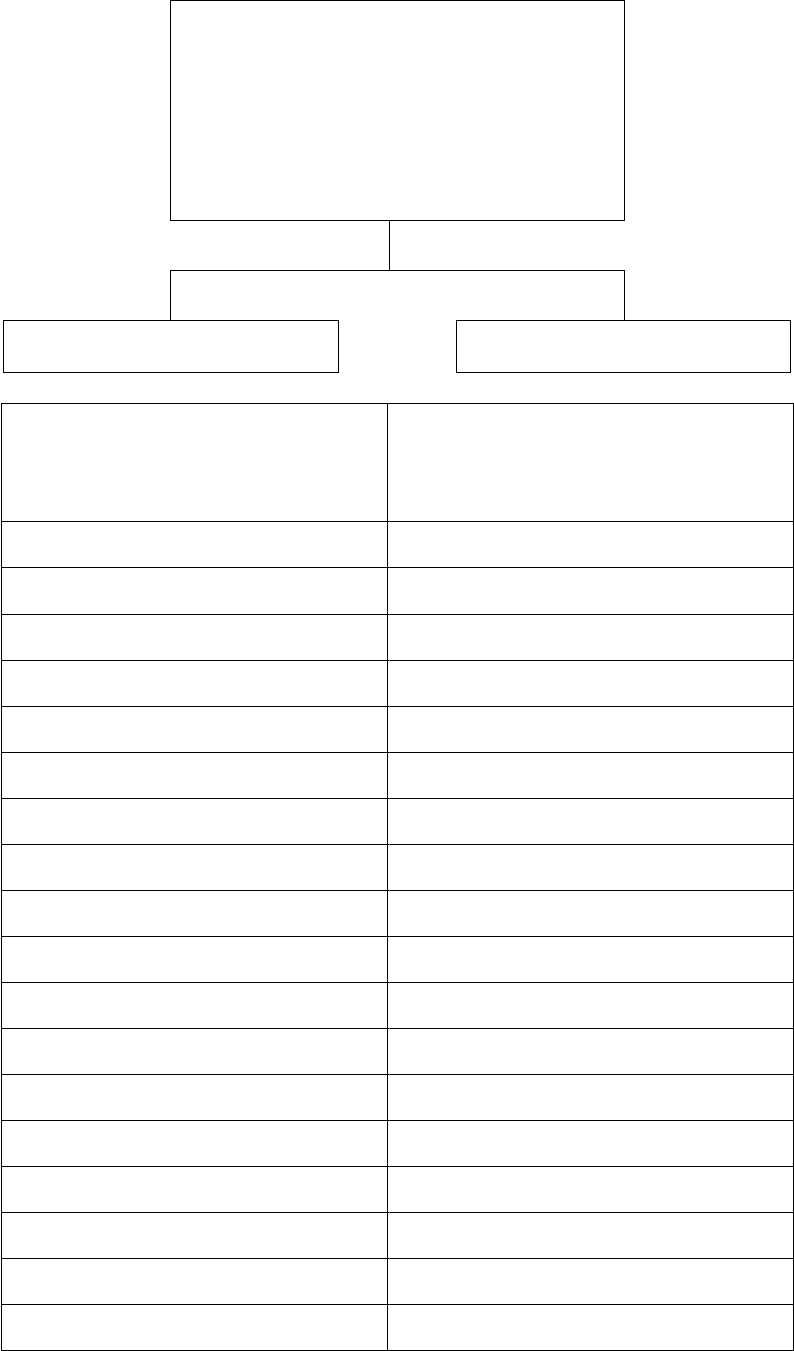

All rights reserved

Printed and published by the

University of South Africa

Muckleneuk, Pretoria

FAC1501/1/2018

70548943

InDesign

FAC1501

Introductory Financial

Accounting

3

INTRODUCTORY

FINANCIAL ACCOUNTING

iv

Preface

4CONTENTS Page

5LEARNING UNIT 1: THE NATURE AND PURPOSE OF FINANCIAL ACCOUNTING 1

6LEARNING UNIT 2: THE ACCOUNTING EQUATION: FINANCIAL POSITION 9

7LEARNING UNIT 3: THE ACCOUNTING EQUATION: FINANCIAL PERFORMANCE 35

8LEARNING UNIT 4: BUSINESS DOCUMENTS: CASH TRANSACTIONS 61

9LEARNING UNIT 5: THE RECORDING OF CASH TRANSACTIONS 115

10LEARNING UNIT 6: CREDIT TRANSACTIONS 191

11LEARNING UNIT 7: INVENTORY 235

12LEARNING UNIT 8: BANK RECONCILIATION STATEMENTS 259

13LEARNING UNIT 9: TRIAL BALANCE 279

14LEARNING UNIT 10: FINAL ACCOUNTS 297

15LEARNING UNIT 11: FINANCIAL STATEMENTS OF A SOLE TRADER 331

FAC1501

LEARNING UNIT 1

Introductory Financial

Accounting

THE NATURE AND

PURPOSE OF

FINANCIAL ACCOUNTING

1

2

FAC1501/1

2OVERVIEW

Learning outcomes ������������������������������������������������������������������������������������������������������������������������������ 2

Key concepts ��������������������������������������������������������������������������������������������������������������������������������������� 2

Assessment criteria ����������������������������������������������������������������������������������������������������������������������������� 3

1�1 Introduction ��������������������������������������������������������������������������������������������������������������������������������� 3

1.2 Whatisnancialaccounting? ����������������������������������������������������������������������������������������������������� 3

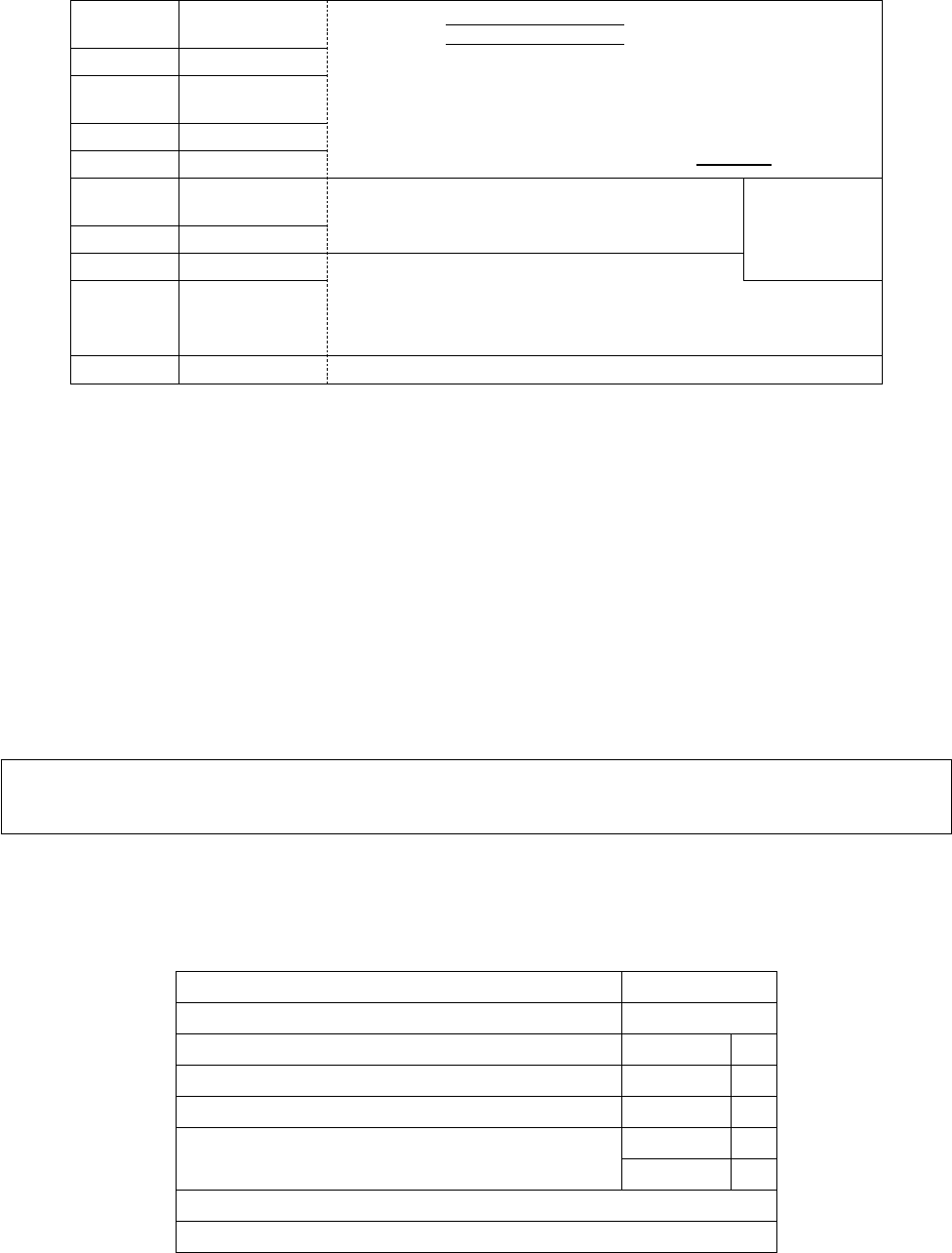

1.3 Theobjectiveofnancialaccounting ������������������������������������������������������������������������������������������ 4

1.4 Thenatureofnancialaccounting ���������������������������������������������������������������������������������������������� 4

1.5 InternationalFinancialReportingStandards(IFRSs)������������������������������������������������������������������ 5

1.6 Theobjectiveofnancialstatements ������������������������������������������������������������������������������������������ 6

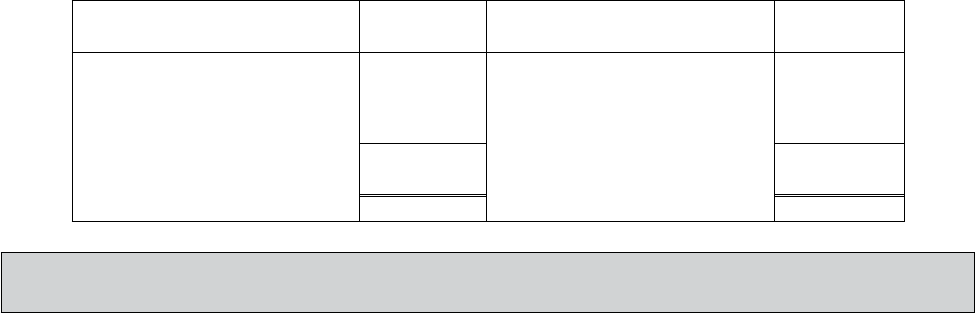

1.7 Usersofnancialstatements ������������������������������������������������������������������������������������������������������6

1.8 Exercisesandsolutions �������������������������������������������������������������������������������������������������������������� 7

Self-assessment ���������������������������������������������������������������������������������������������������������������������������������� 8

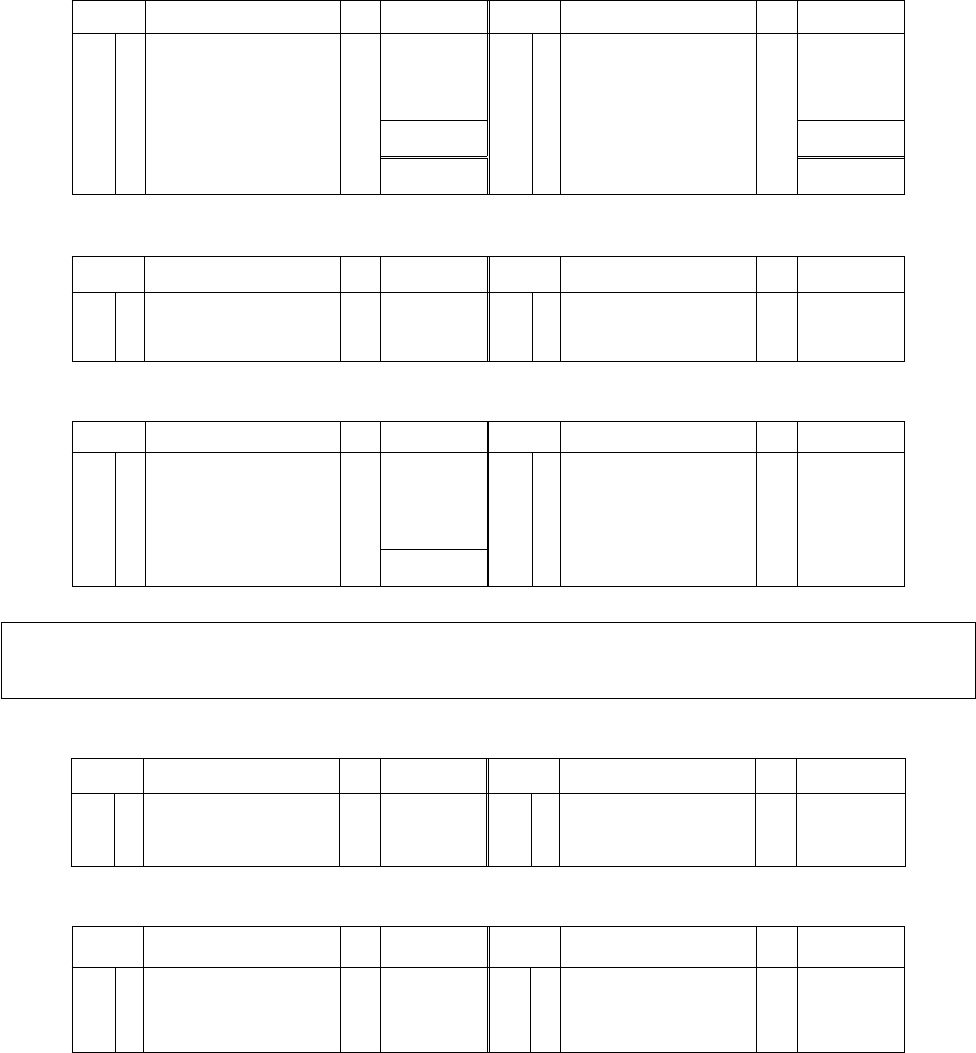

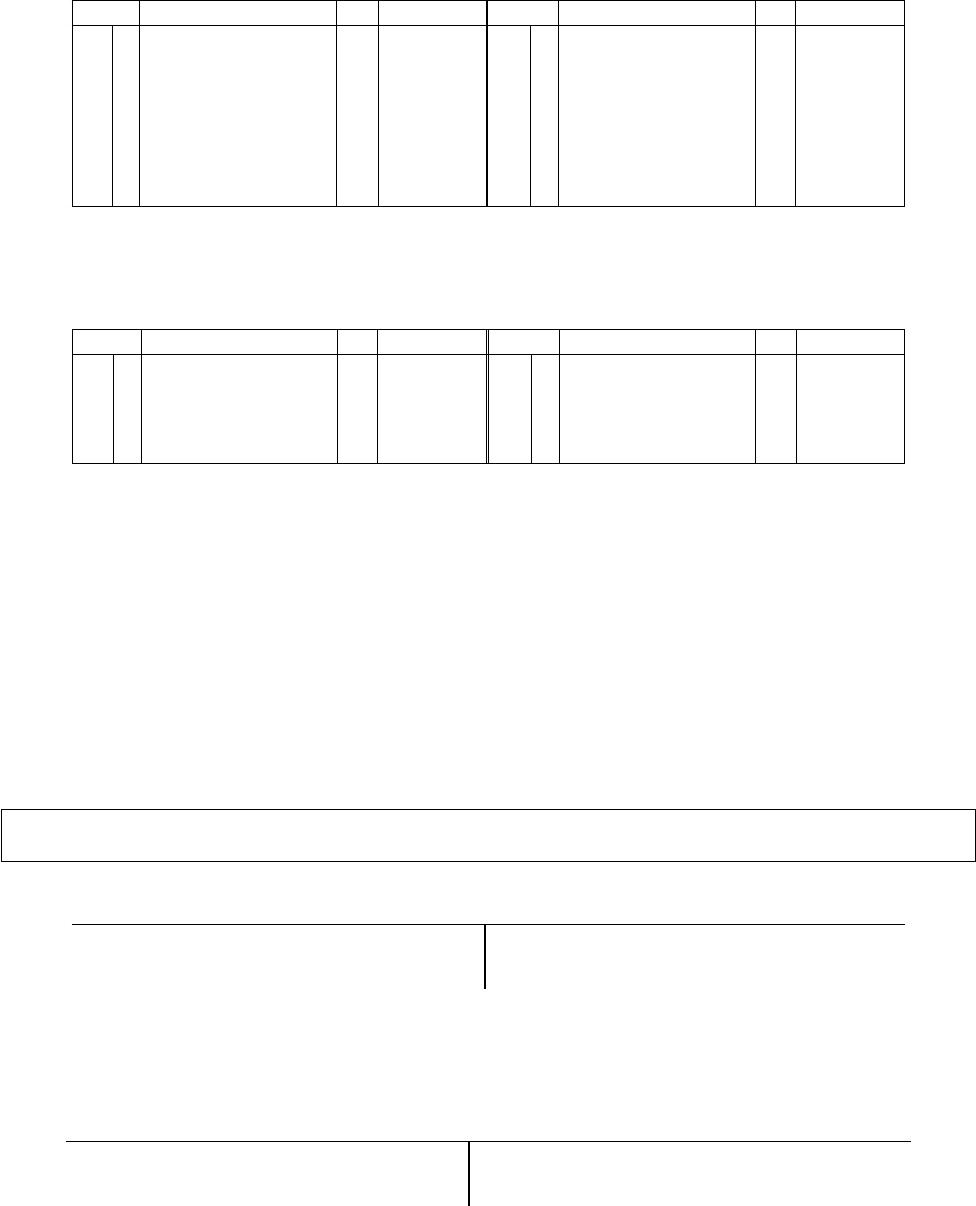

LEARNING OUTCOMES

1Afterstudyingthislearningunityoushouldbeableto:

1

zdenenancialaccounting

zexplaintheobjectiveofnancialaccounting

zexplainthenatureofnancialaccounting

zlistthestepsinvolvedinthenancialaccountingcycle

zexplainthedifferencebetweennancialaccountingandbookkeeping

zexplaintheacronymIFRSs

zidentifytheusersofnancialaccountinginformationinthenancialstatementsandthereasons

whytheyneedthenancialinformation

1

1

KEY CONCEPTS

zTransaction

zFinancialaccounting

zObjectiveofnancialaccounting

zFinancialaccountingcycle

zBookkeeping

zInternationalFinancialReportingStandards(IFRSs)

zUsersofnancialstatements

3

FAC1501/1

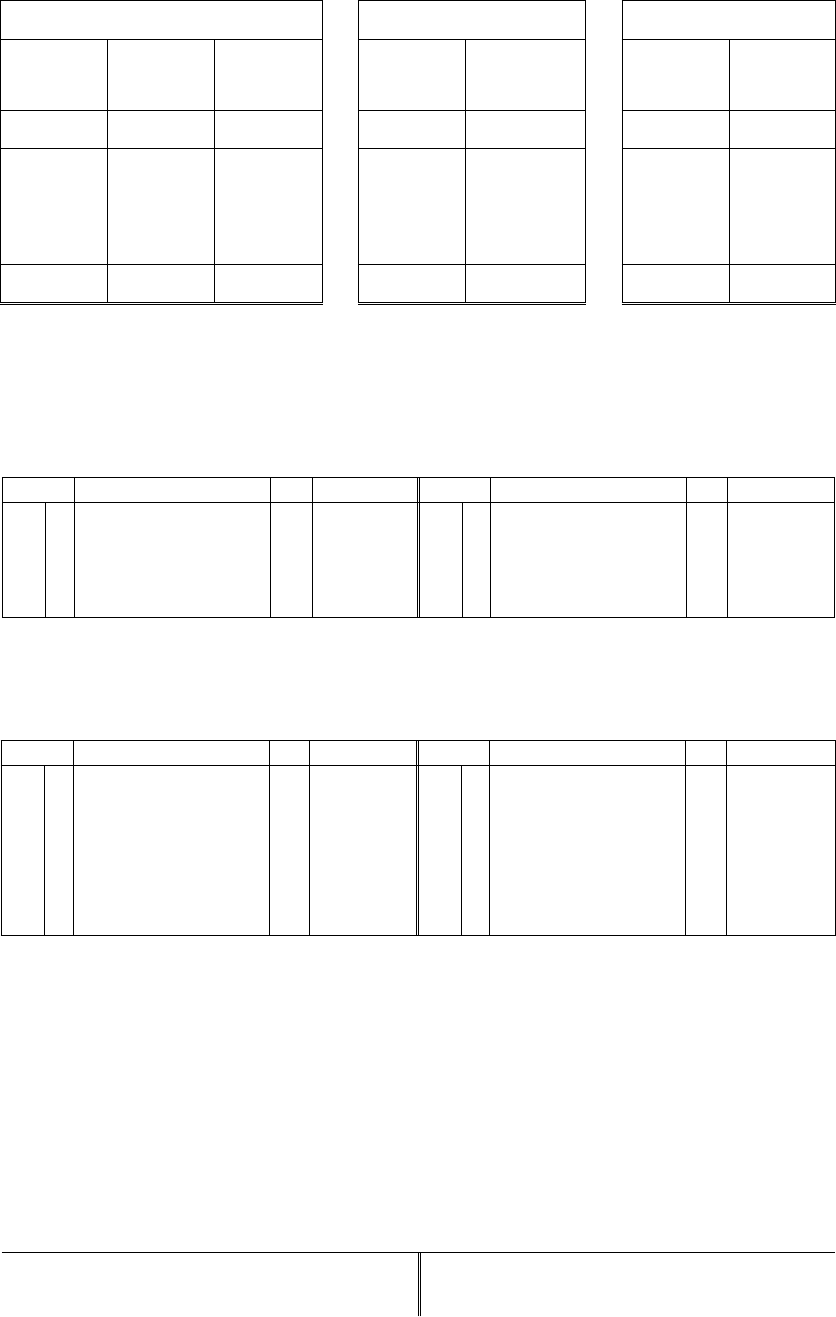

ASSESSMENT CRITERIA

zTheconcept“nancialaccounting”isexplained.

zThenatureandobjectiveofnancialaccountingisexplained.

zThespecicandgeneralfunctionsofnancialaccountingareexplained.

zTheprocessingofbasictransactionsisexplained.

z

ThemeaningofInternationalFinancialReportingStandards(IFRSs)and

itsapplicationtothepreparationandpresentationofnancialinformation

areexplained.

zTheoverallobjectiveofnancialstatementstomeettheneedsoftheusersof

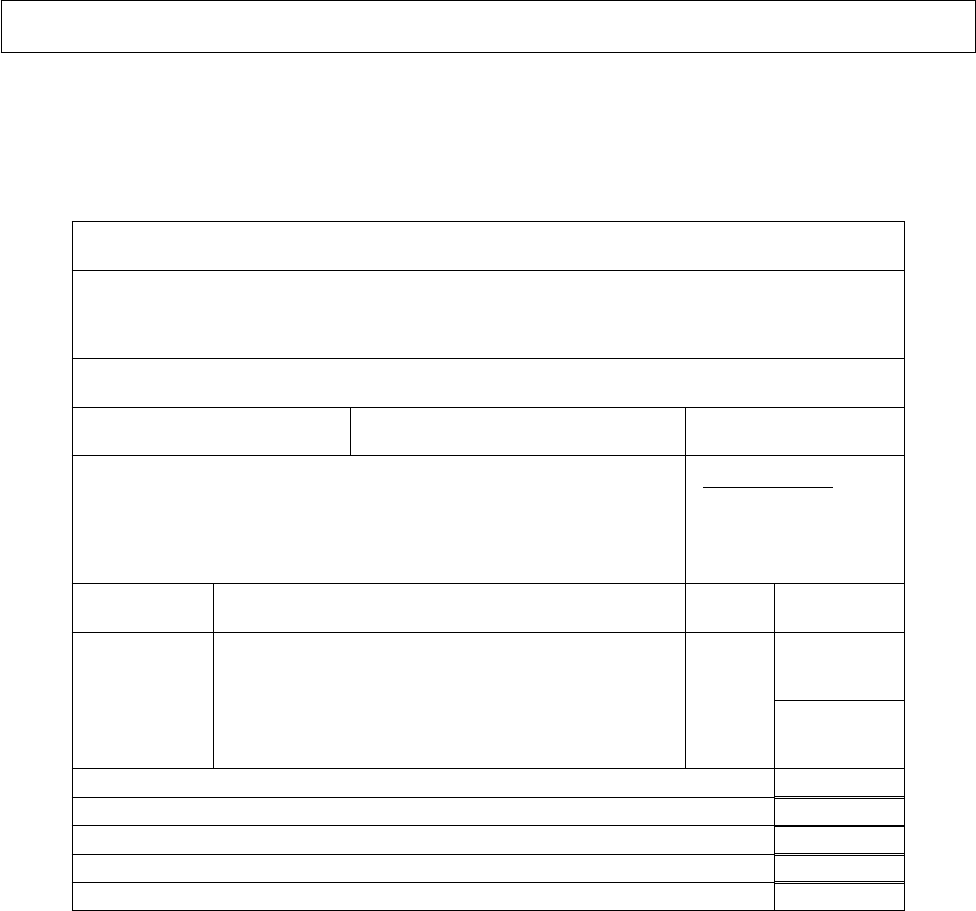

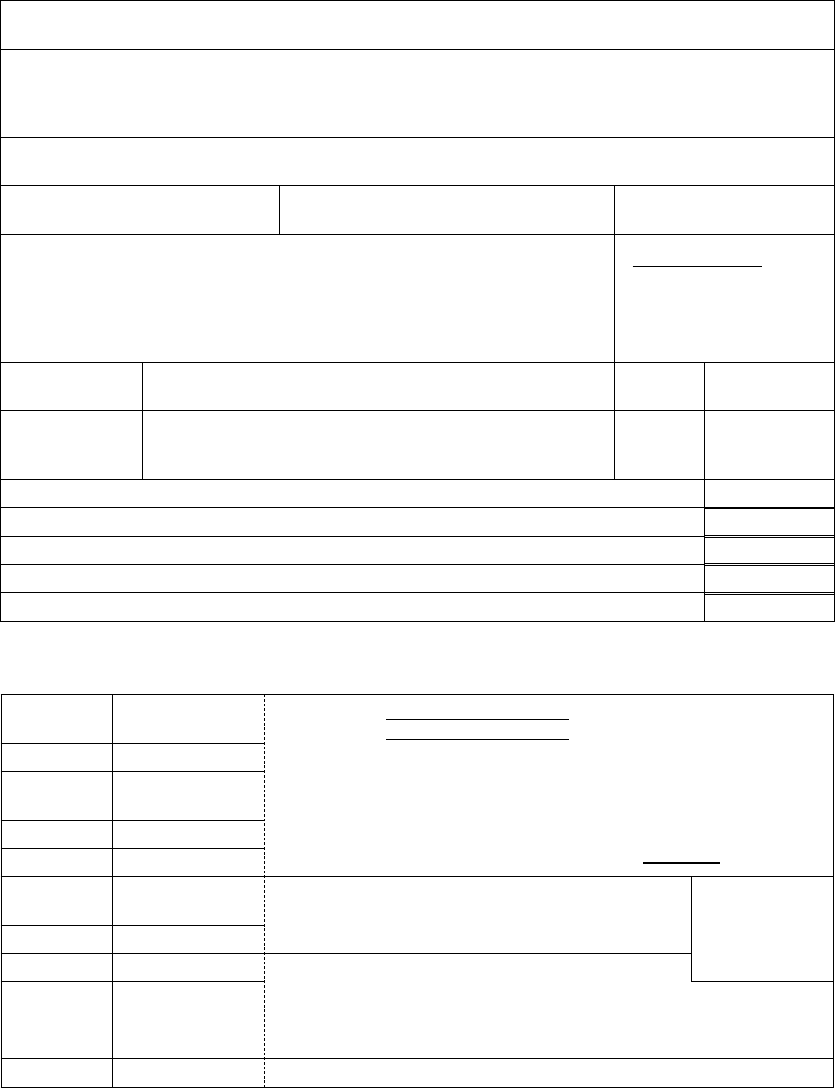

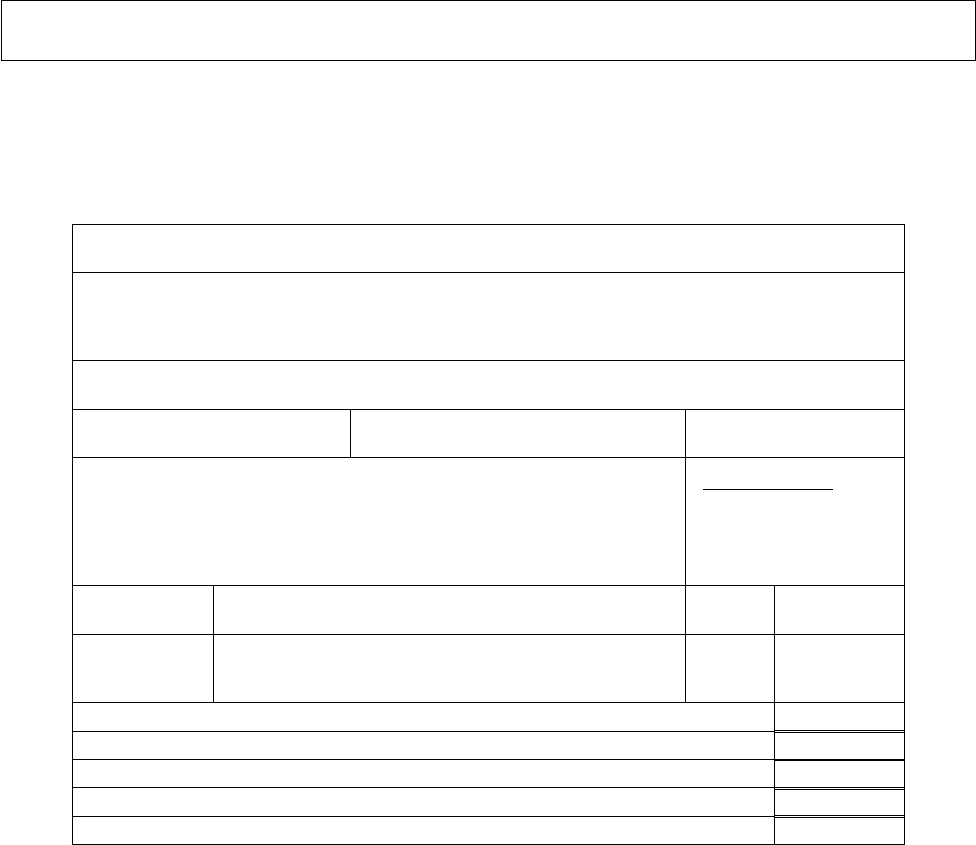

nancialinformationisexplained.

z

Informationusefultotheusersofnancialinformationisdeterminedaccording

tothespecicusers’needs.

1.1 INTRODUCTION

2Every dayall overtheworld literallymillionsoftransactions takeplace.A transaction isan action

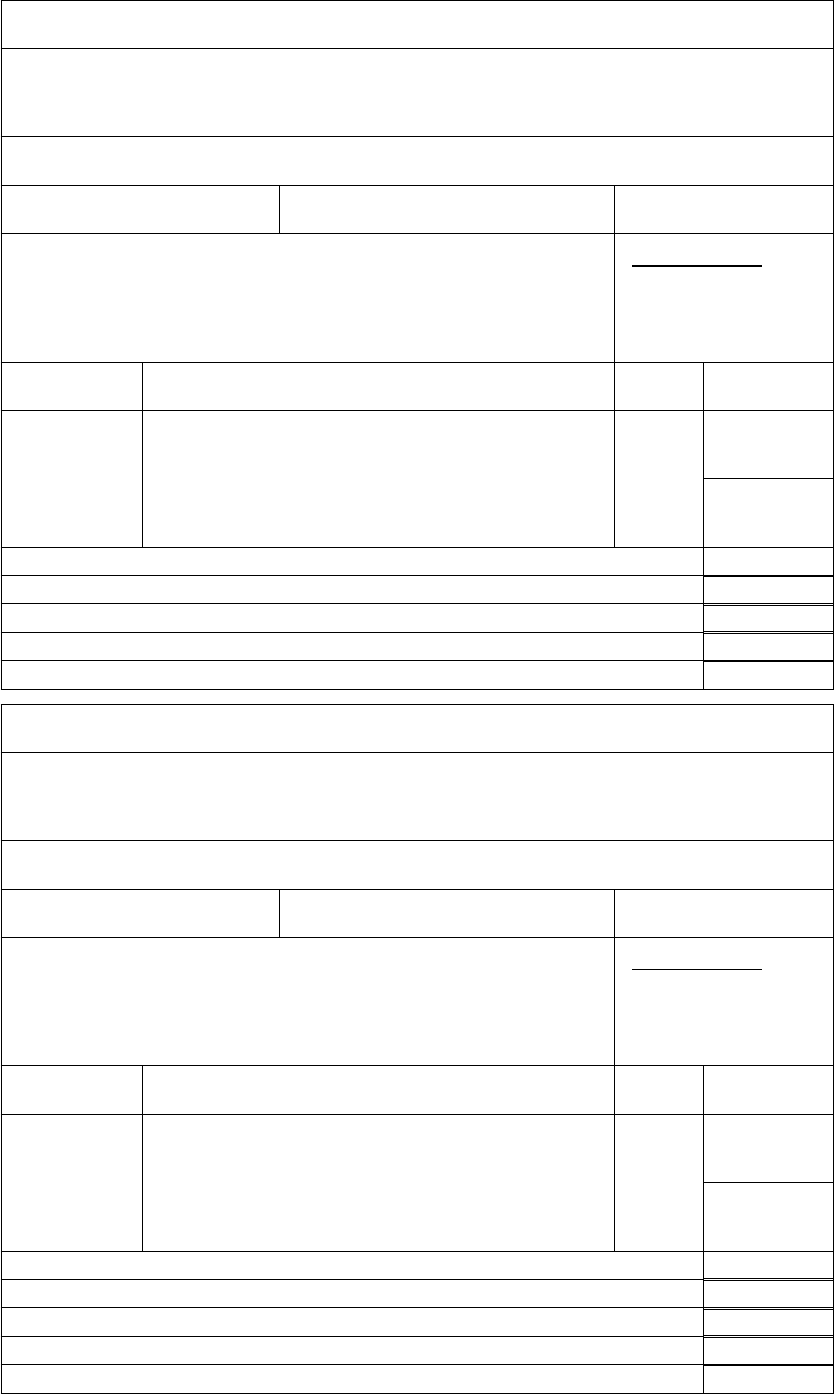

wheremoneyispaidandinreturnanitemorservice,thatthebuyerneeds,isobtained.Thinkabout

buyingaloafofbread–somethingthatmostofusdoonadailybasis.Forusasindividualsitisquite

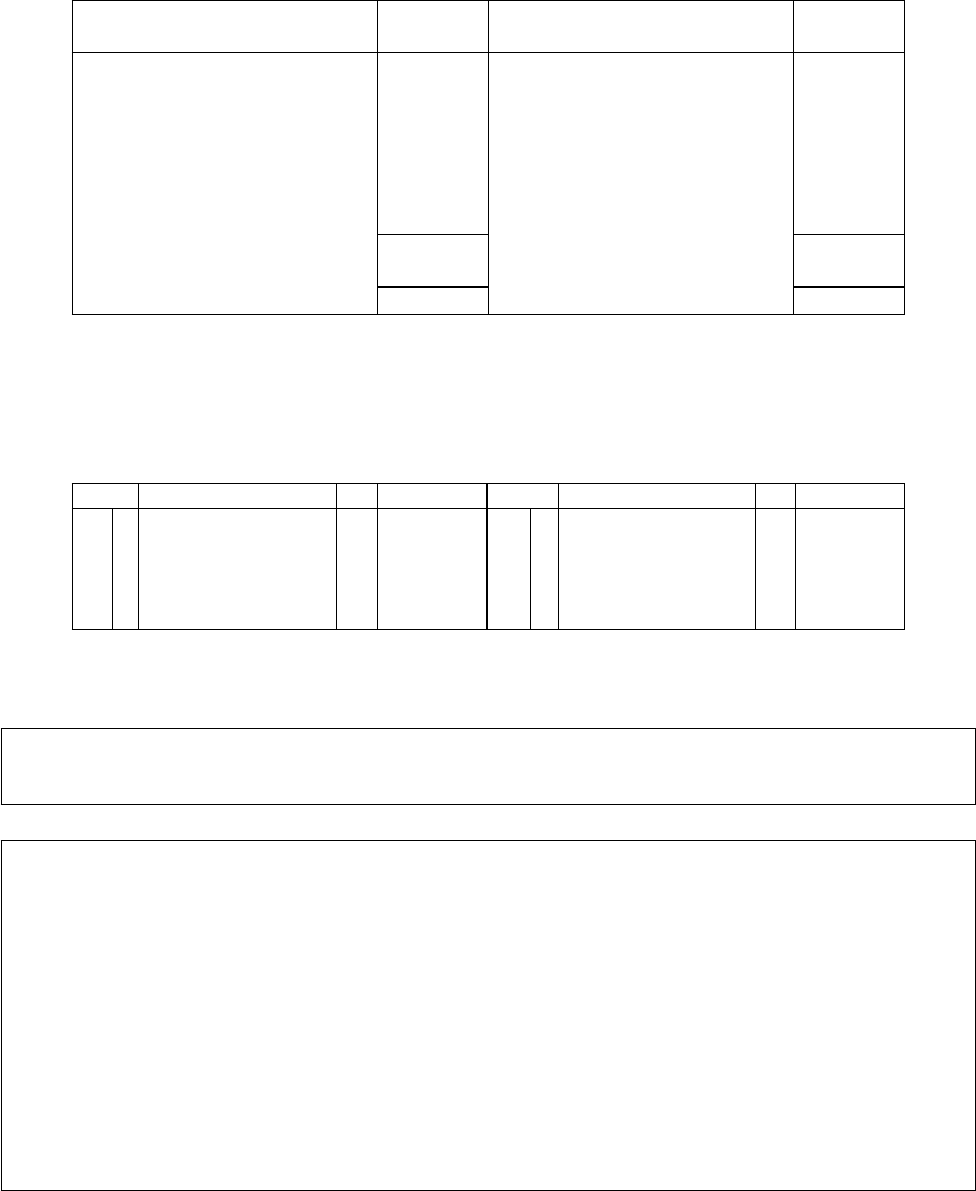

easytorememberwhattransactionsweconcludedforaparticularday,butforabigentity,itwouldbe

impossibletoknowwhattransactionstookplaceduringadayifproperrecordswerenotkept.Itwould

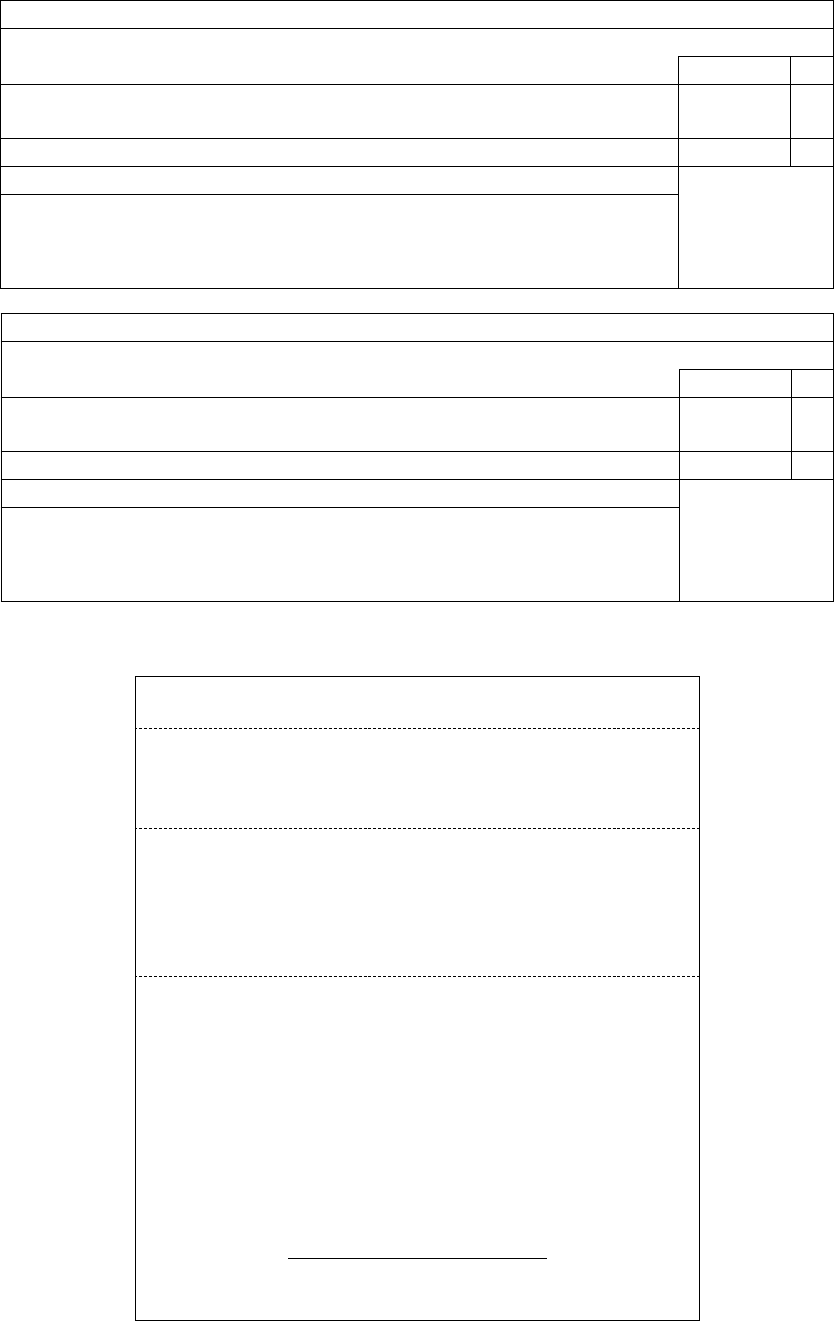

evenbecomeimpossibleforanindividualtorememberwhattransactionswereconcludedamonth

agoifhe/shedoesnothaveaproperrecordkeepingsysteminplace.

1.2 WHAT IS FINANCIAL ACCOUNTING?

3Financialaccountingcanbedenedastheorderlyandsystematicidenticationandrecordingofthe

monetaryvaluesofnancialtransactionsofanindividualorbusinessentity,andthereportingofthe

resultsofthesetransactions byway ofthe preparationandpresentationof nancialstatementsto

enabletheuserstousetheinformationobtainedinthesenancialstatementsasabasisfordecision-

making.Financialaccountingisaspecialisedmethodusedtocommunicatenancialinformationabout

an entity and its activities to those persons or entities that have an interest in the activities of the entity�

4Financialaccountingisaprocessthatinvolvesthreeactivities,namely:

z

Identication–selectingthoseeventsthatareevidenceofeconomicactivity(transactions)relevant

totheparticularentity.

zRecordingthemonetaryvalueoftheeconomicevents(transactions)soastoprovideapermanent

historyofthenancialactivitiesoftheentity.Recordingconsistsofkeepingachronologicaldiary

ofmeasuredeventsinanorderlyandsystematicmanner.Recordingimpliesthateconomicevents

arealsoclassiedandsummarised.

zThe third activity encompasses the communication of the recorded information to interested users�

Theinformationiscommunicatedthroughthepreparationanddistributionofaccountingreports,

themostcommonofwhichareknownasnancialstatements,thatconsistof:

— astatementofnancialposition;

— astatementofprotorlossandothercomprehensiveincome;

— astatementofchangesinequity;

— astatementofcashows;

—

notes,comprisingofasummaryofsignicantaccountingpoliciesandotherexplanatorynotes.

5Anentitydoesnotnecessarilyrefertobusinessentities.Itcanalsorefertoaneducationalinstitution,

areligiousinstitutionoraprivatehousehold.

4

FAC1501/1

NOTE:

Donotbeconcernedifyoudonotunderstandalltheterminologyonthefollowingfewpages,as

theywillallbeexplainedinlearningunits1and2.

1.3 THE OBJECTIVE OF FINANCIAL ACCOUNTING

6Theobjectiveofnancialaccountingistoenabletheusersofnancialinformationtoascertainreadily

whatthenancialresultsandnancialpositionoftheentityis.Withthisstatementwemean:

(a) Didtheentitytradeataprotorloss?

(b)

Whatwastheincomeoftheentityandwhatweretheexpensesincurredinproducingthatincome?

(c) Howmuchdoestheentityowetootherentities?

(d) Howmuchdocustomersowetotheentity?

(e) Whatisthenatureandamount(invalue)ofthevariouskindsofpropertyandotherassetsthe

entitypossesses?

(f) Whatistheamountoftheentity’scapital(equity)?

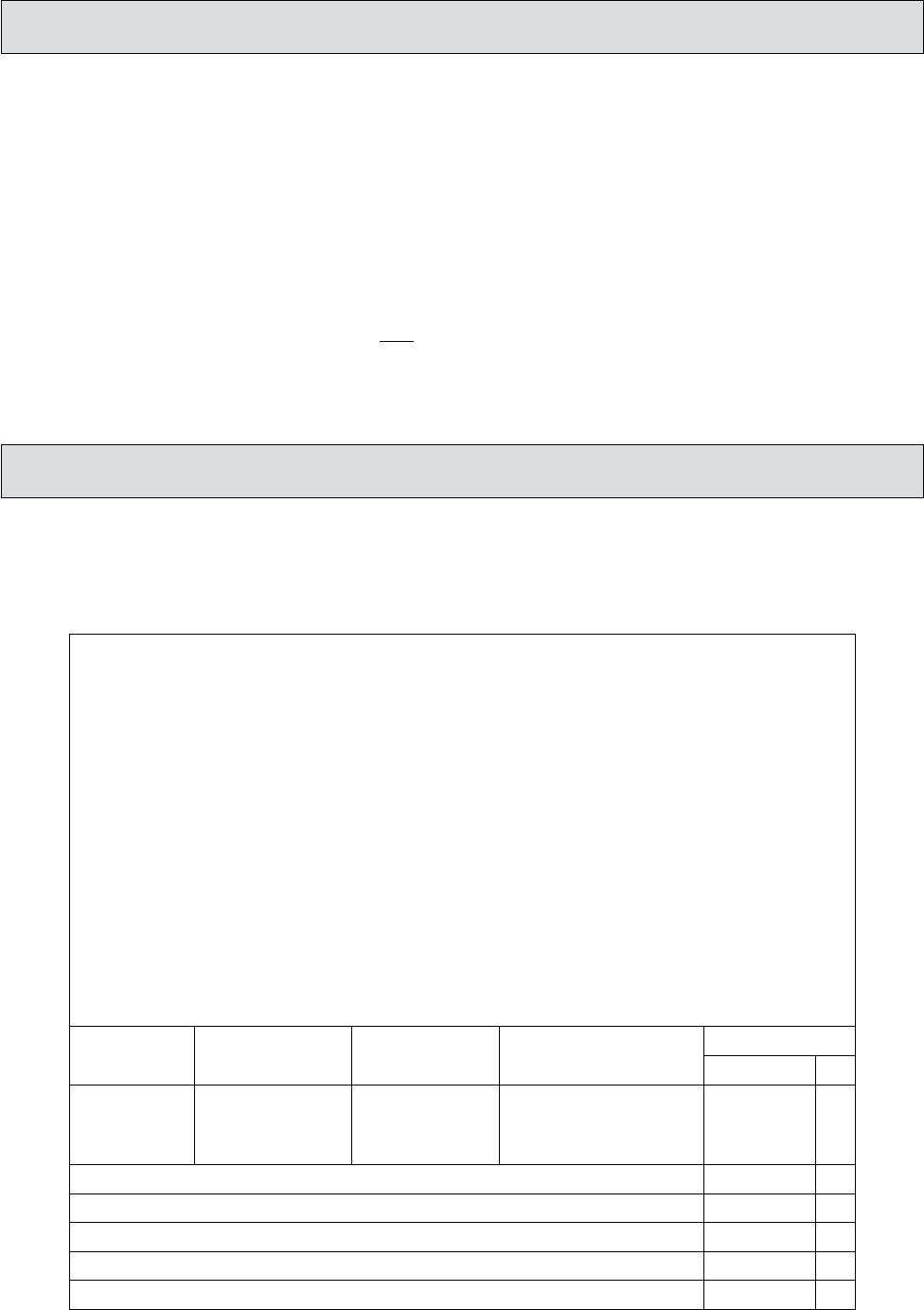

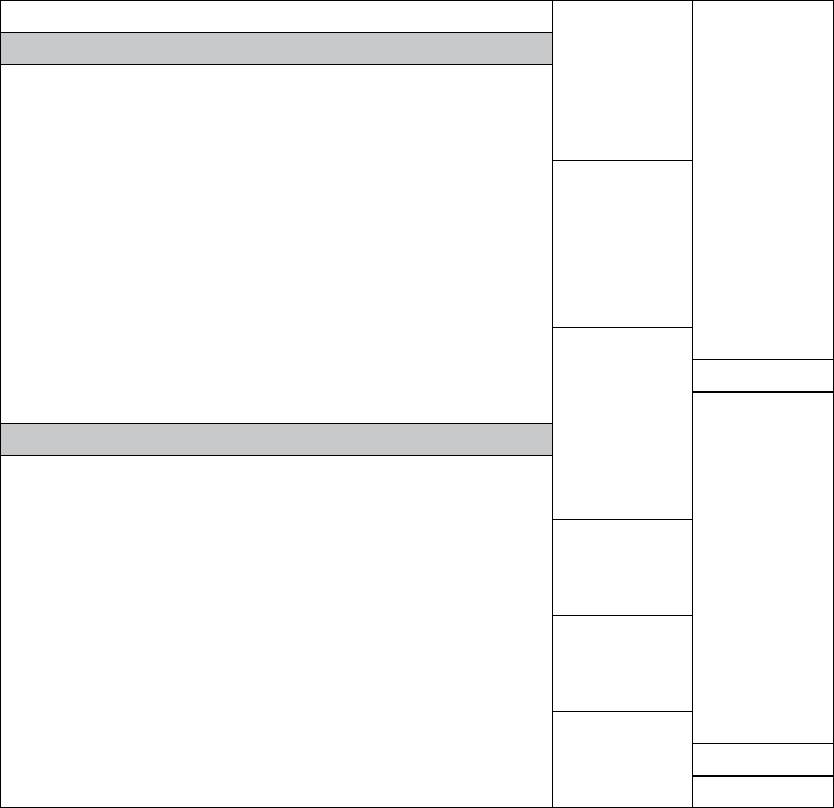

1.4 THE NATURE OF FINANCIAL ACCOUNTING

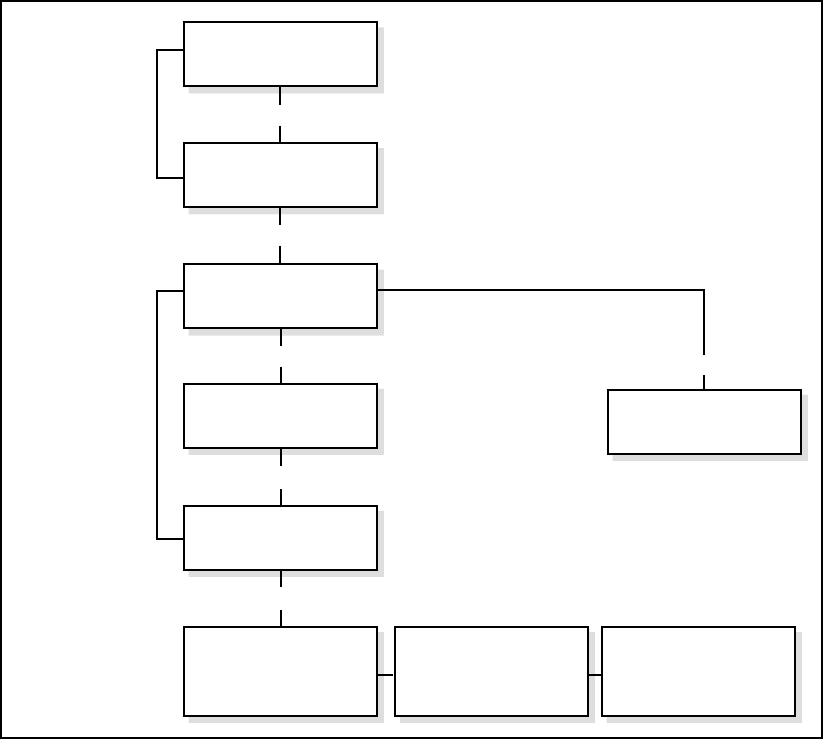

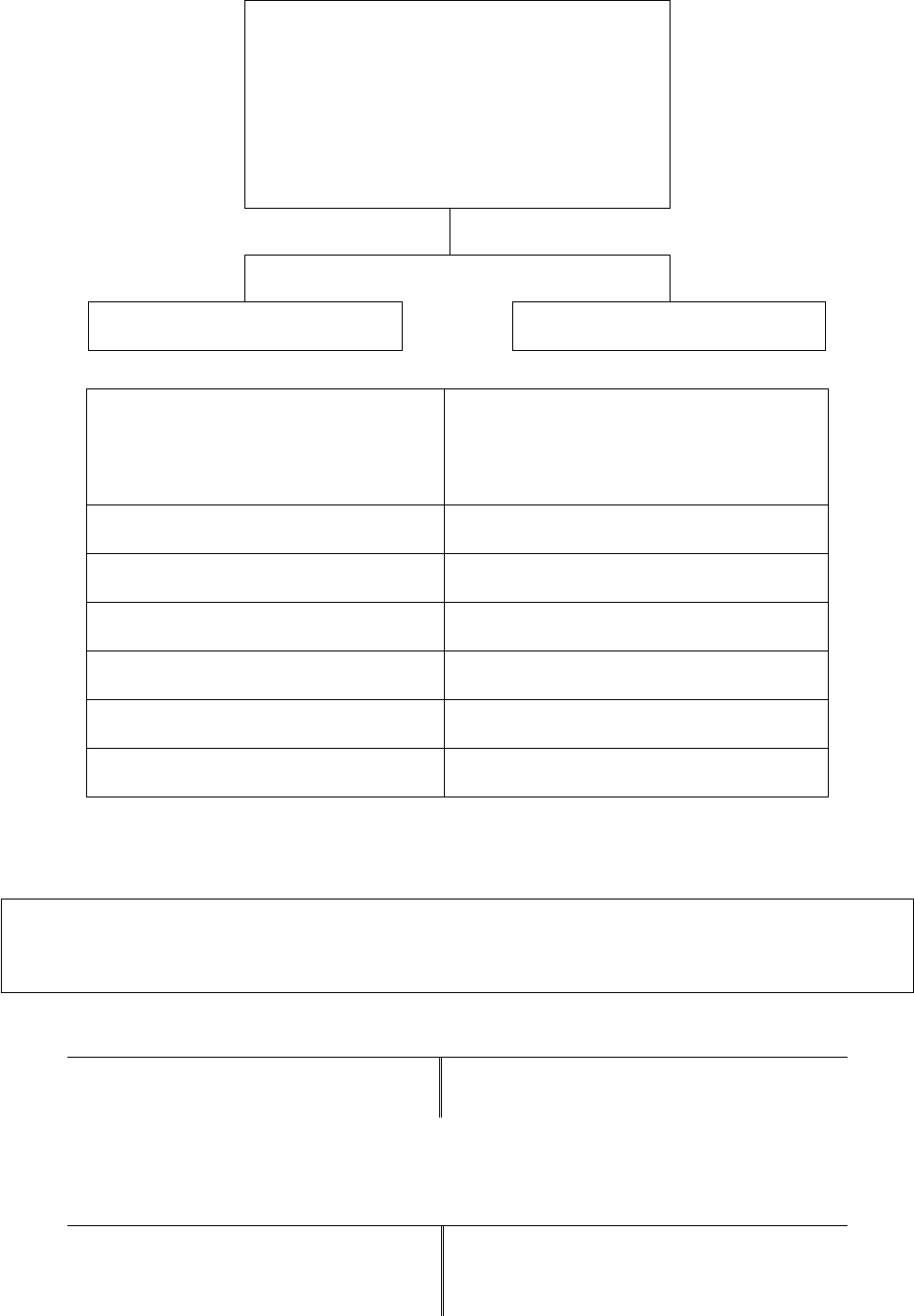

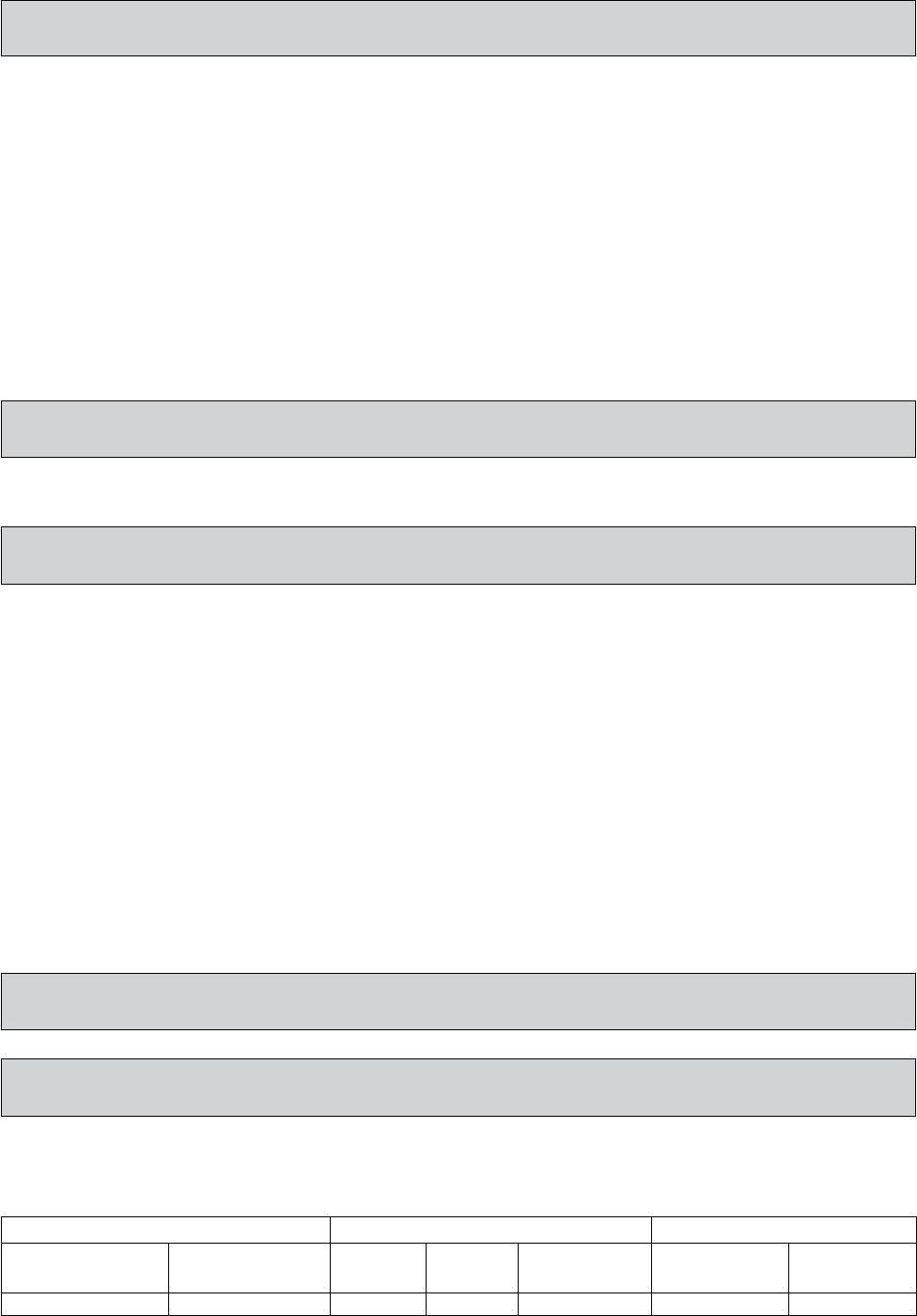

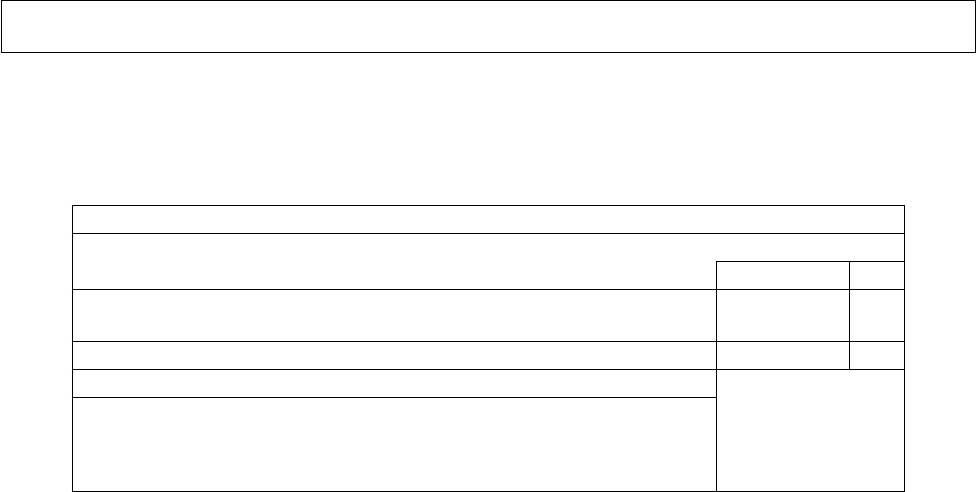

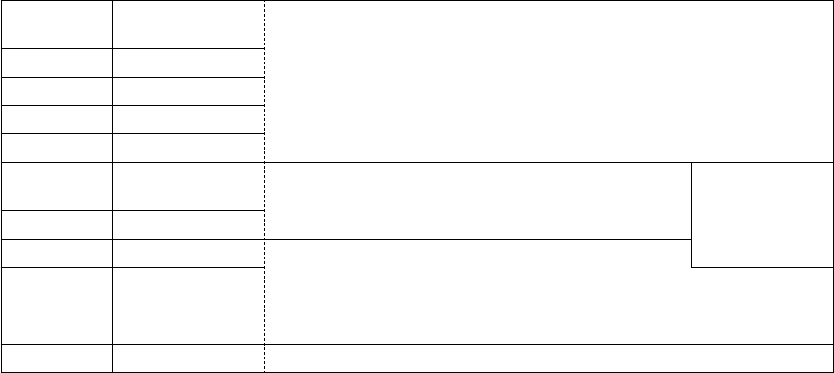

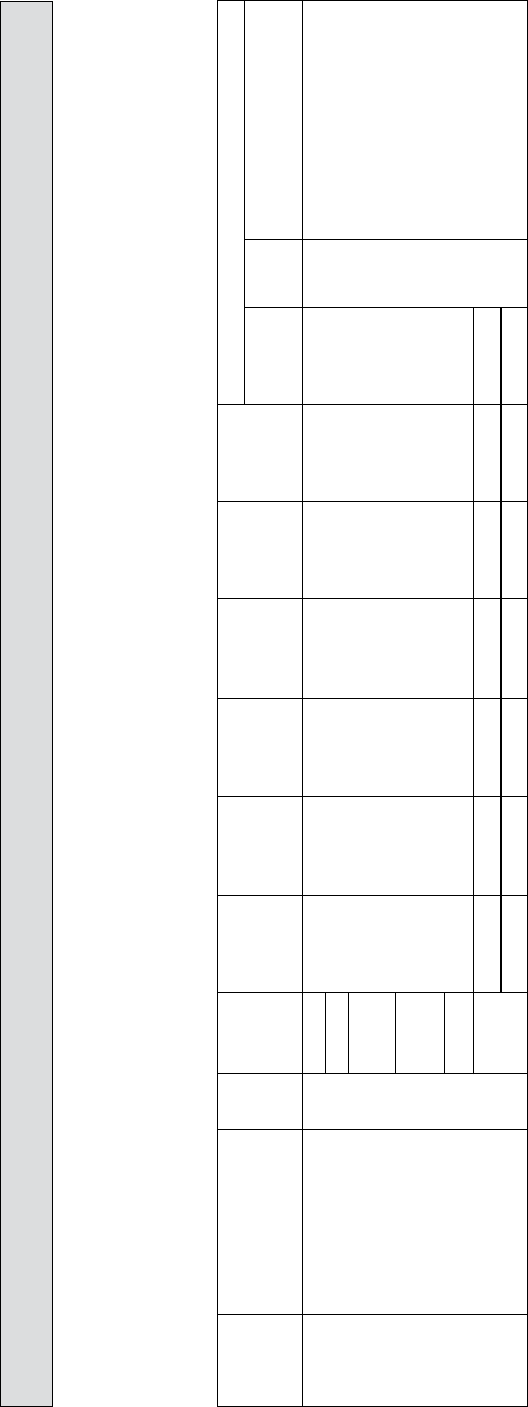

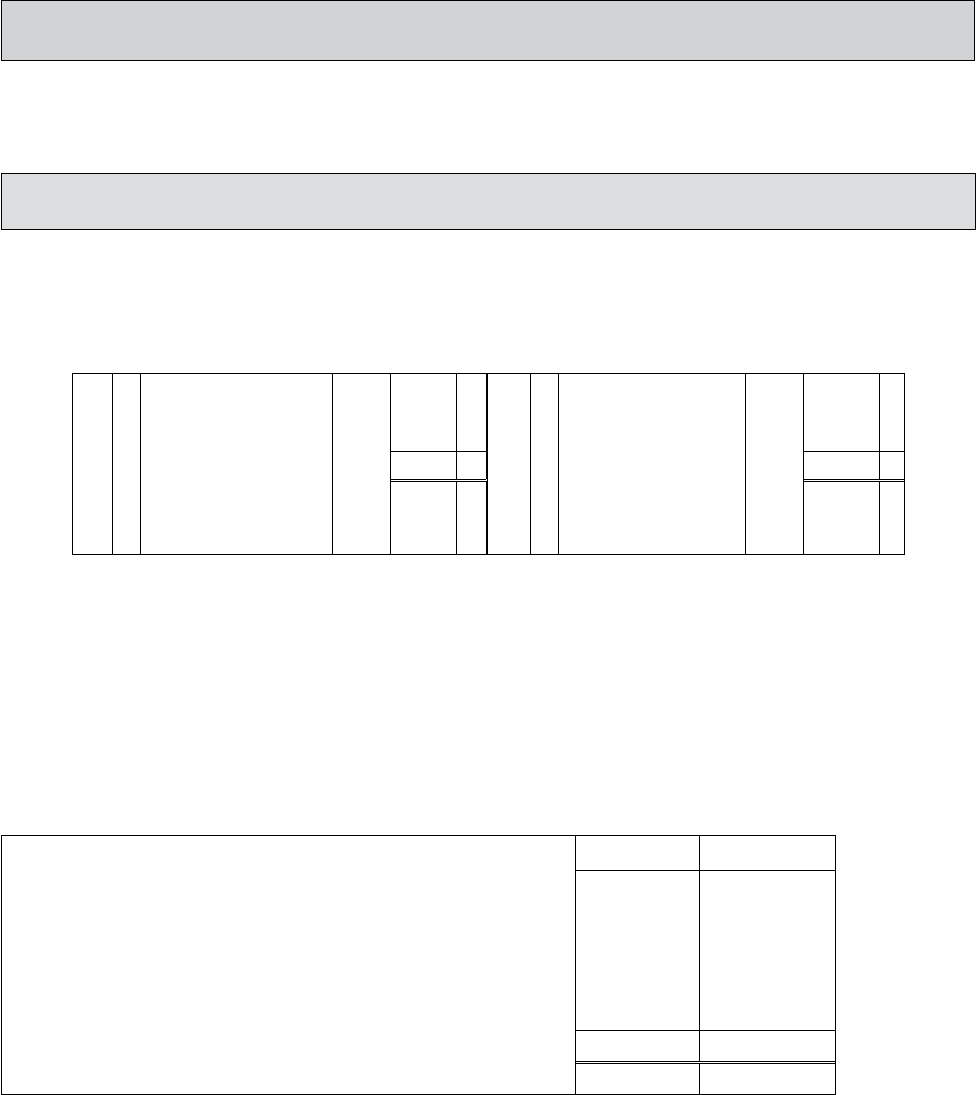

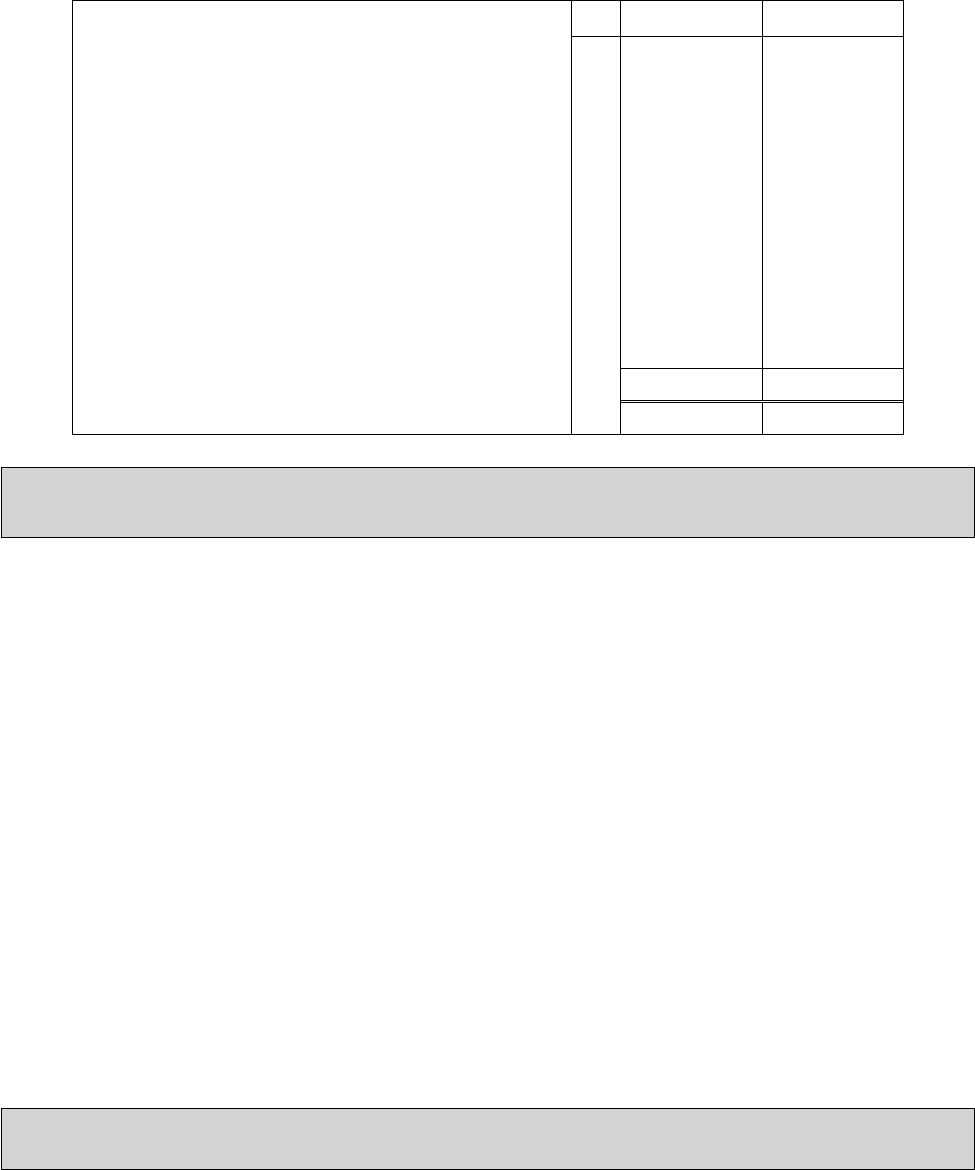

7Financial accounting functions as an information system: far-reaching decisions are taken on the

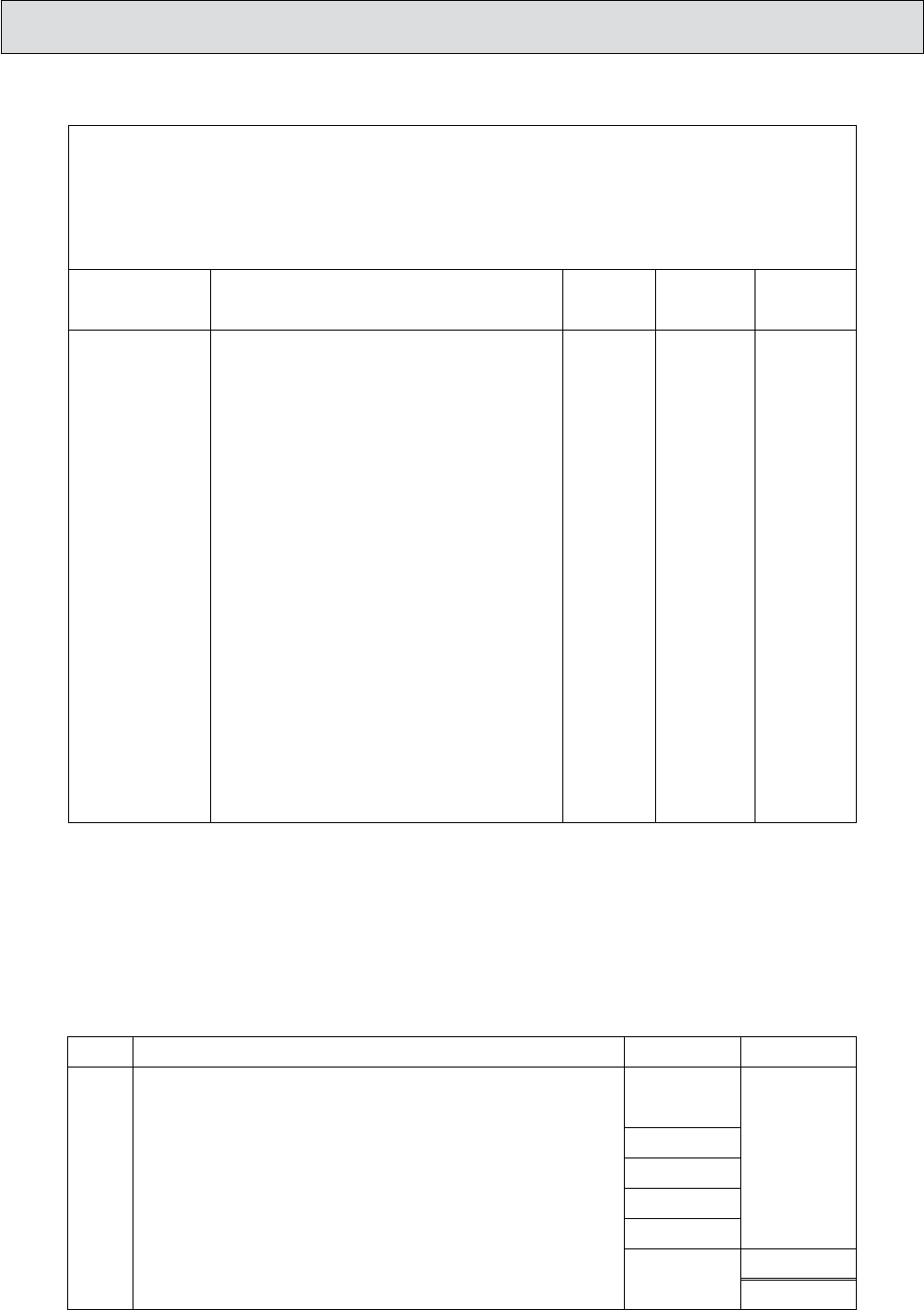

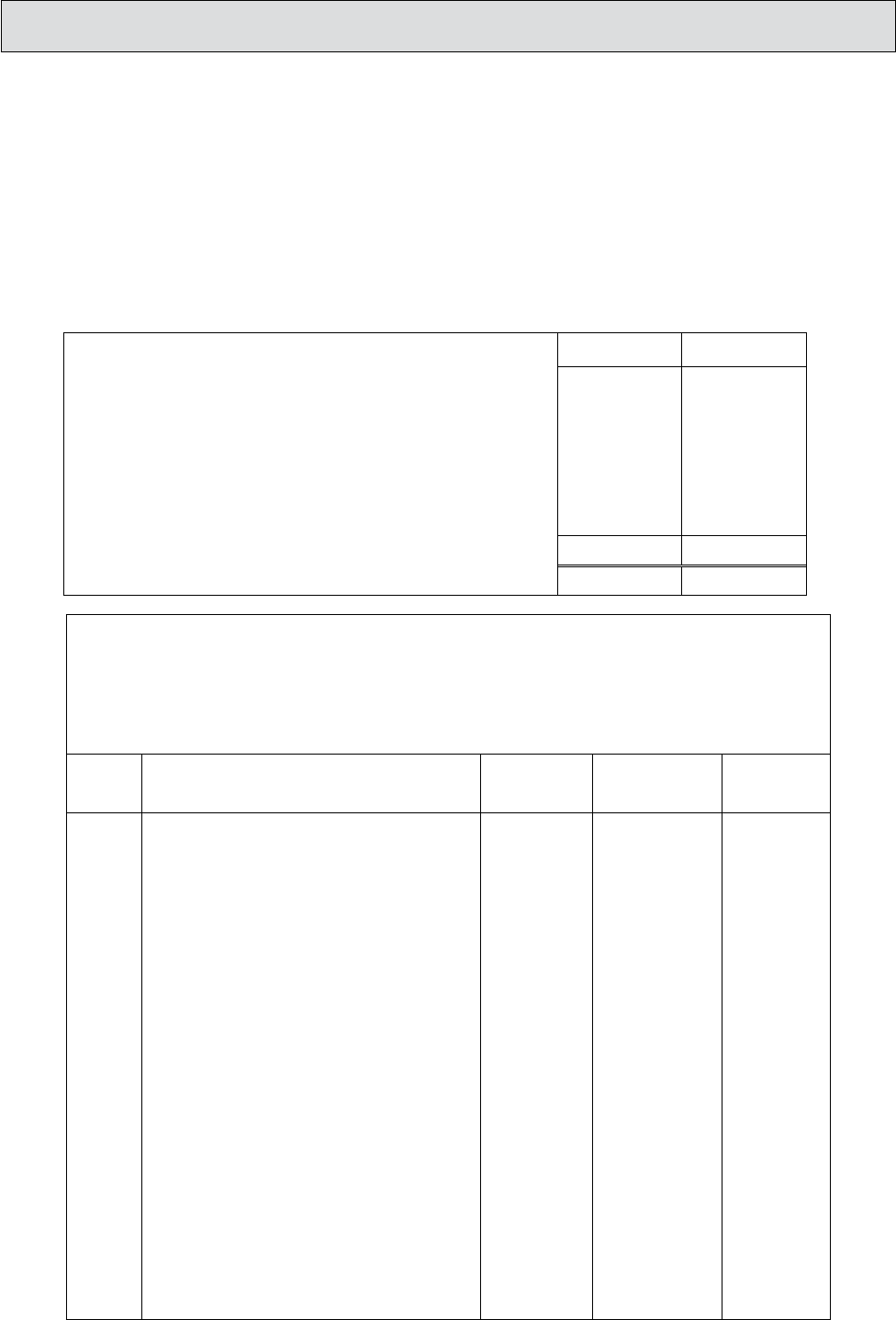

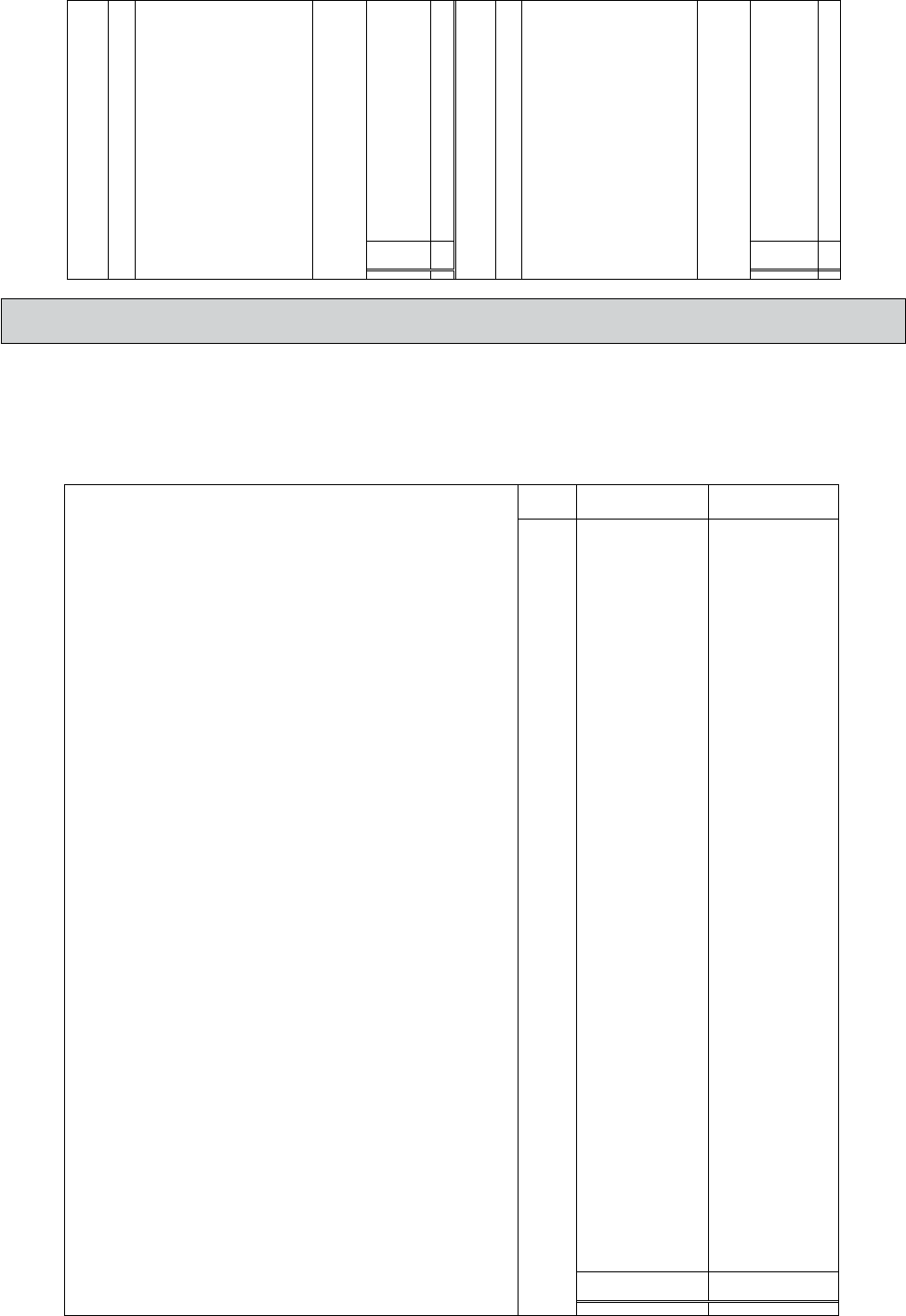

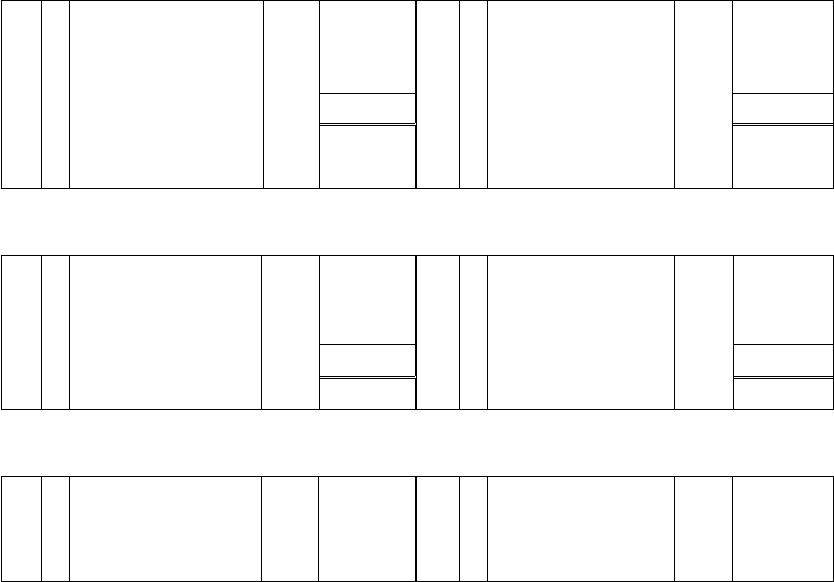

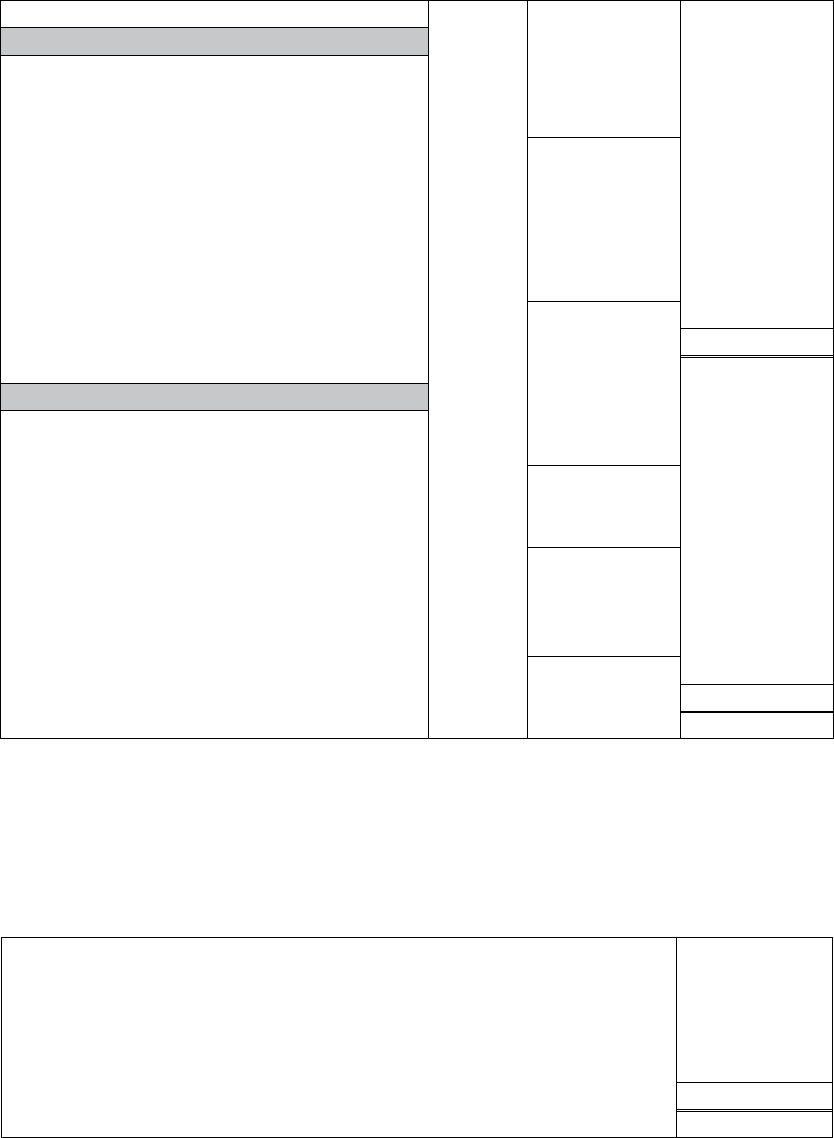

basisoftheresultsreportedinnancialstatementsandbusinesstransactionshavetobemeasured,

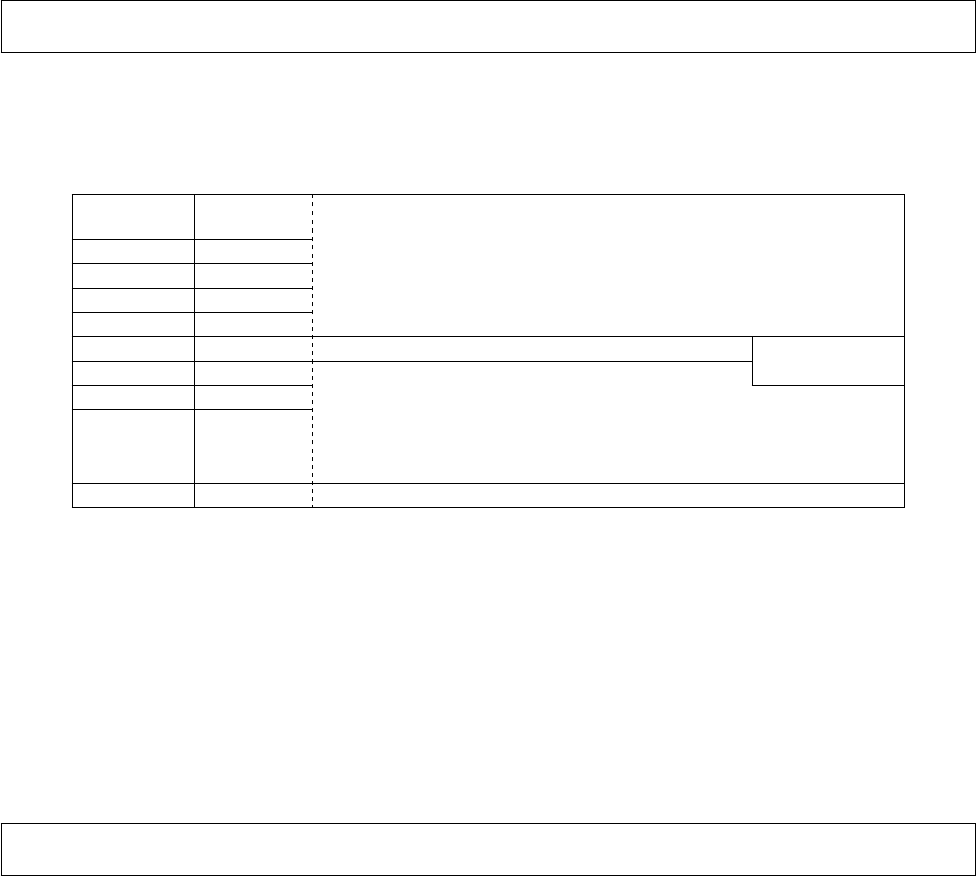

classied, summarised and recorded continuously. We call these actions the nancial accounting

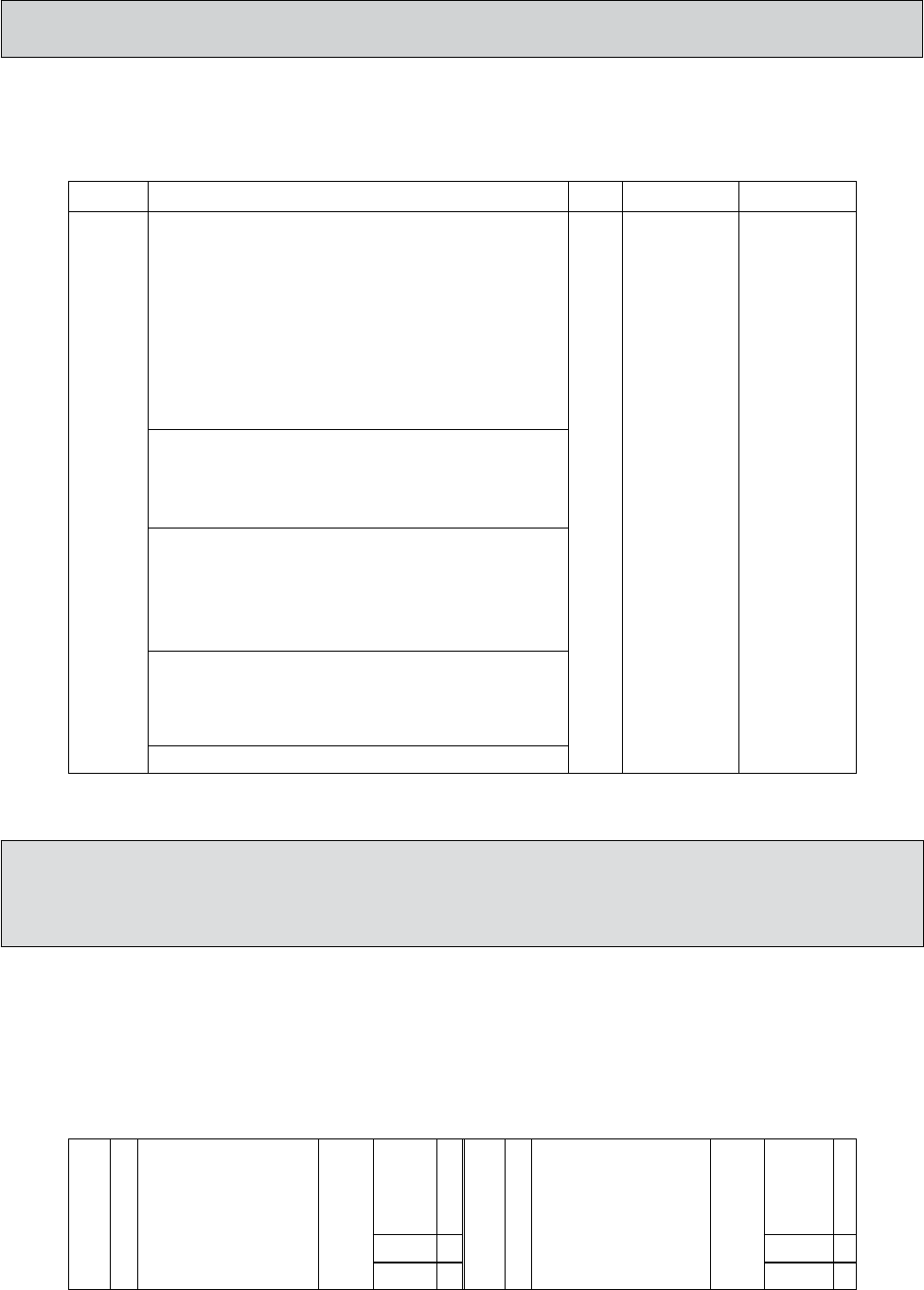

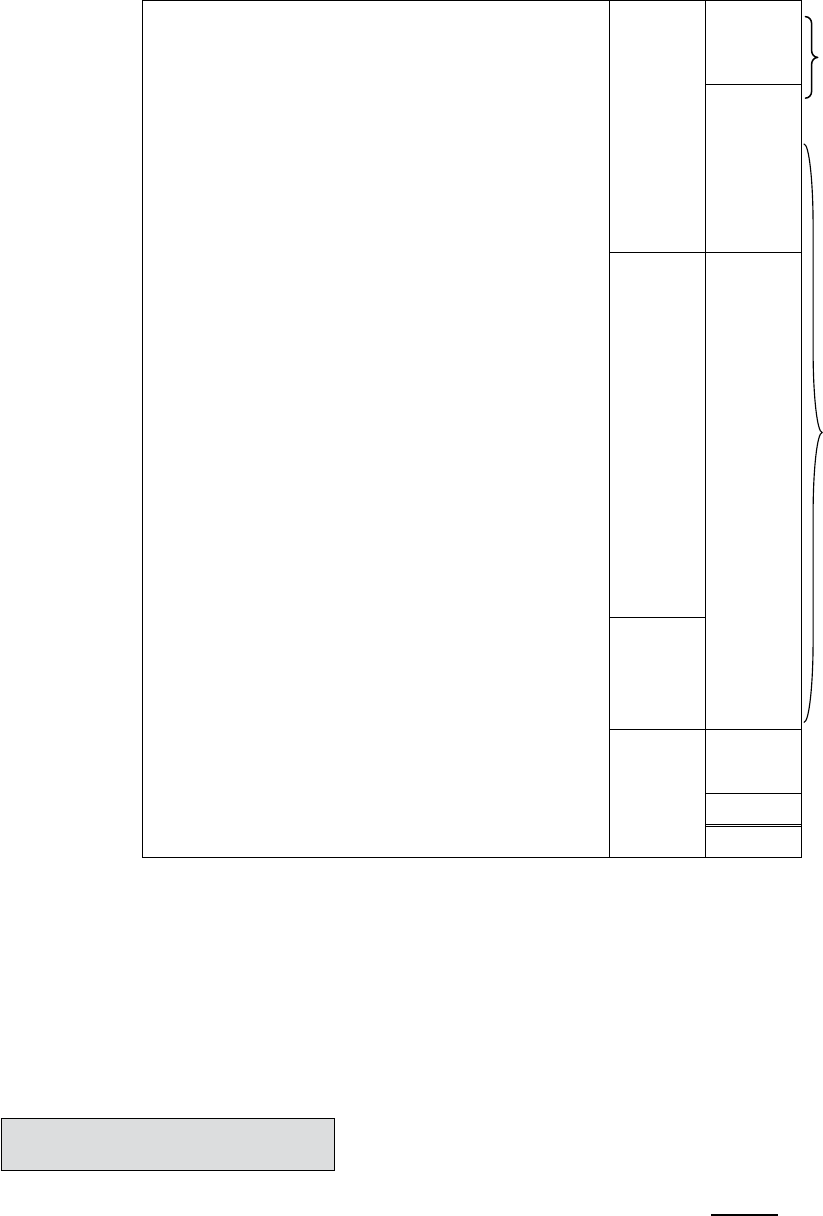

cycle.Thiscycleisdemonstratedinthefollowingdiagram.

5

FAC1501/1

8Diagram 1: The nancial accounting cycle

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25Financialaccountingisthesystematicrecordingofthenancialtransactionsofanentityinsucha

mannerthatanyinformationrequiredbytheentityisreadilyavailable.Thesystematicrecordingof

thenancialinformationiscalledanancialaccountingcycle,whichconsistsoftheelementslisted

in diagram 1�

26Theprocessingstageentailstherecordingoftransactionsandthisprocessisknownasbookkeeping.

Theultimategoaloftheinputstageandtheprocessingstageistopreparenancialstatements.

1.5 INTERNATIONAL FINANCIAL REPORTING STANDARDS (IFRSS)

27Itwouldbeproblematicifeachentitykeptindividualisedrecordsofitstransactionsasthiswouldmake

itdifculttocomparetheperformanceofanentitywiththoseofothersimilarentities.Topreventthis

fromhappening,thenancialaccountingprofessionhasstandardisedthewayinwhichentitiesare

requiredtokeeprecordoftheirtransactions.

28In South Africa the recording and reporting of nancial information are governed by international

nancial reporting standards as set by the Financial Reporting Standards Council (FRSC) in

South Africa. The purpose of these nancial accounting standards will to a great extent ensure

that the same type of transaction is recorded by different entities in more or less the same way.

This will eventually ensure that the nancial statements of different entities conducting the

TRANSACTION

DATA

SOURCE

DOCUMENTS

SUBSIDIARY

JOURNALS

GENERAL

LEDGER

SUBSIDIARY

LEDGERS

TRIAL

BALANCES

FINANCIAL

STATEMENTS

AN A LYSI S

AND

INTERPRETATION

DECISIONMAKING

BY

MANAGEMENT

record on

prepare

post to

extract

prepare

update

INPUT

OUTPUT

PROCESSING

6

FAC1501/1

same type of business are comparable and that an entity’s nancial statements will also be

comparabletothosepreparedinpreviousyears.

29InSouthAfricawehavetocomplywithInternationalFinancialReportingStandards(IFRSs)whichcan

beregardedasthe“rulesfornancialaccounting”.

1.6 THE OBJECTIVE OF FINANCIAL STATEMENTS

30Theobjectiveofnancialstatementsistoprovideinformationaboutthenancialposition,performance

andchangesinthenancialpositionofanentitythatisusefultoawiderangeofusersinmaking

economic decisions�

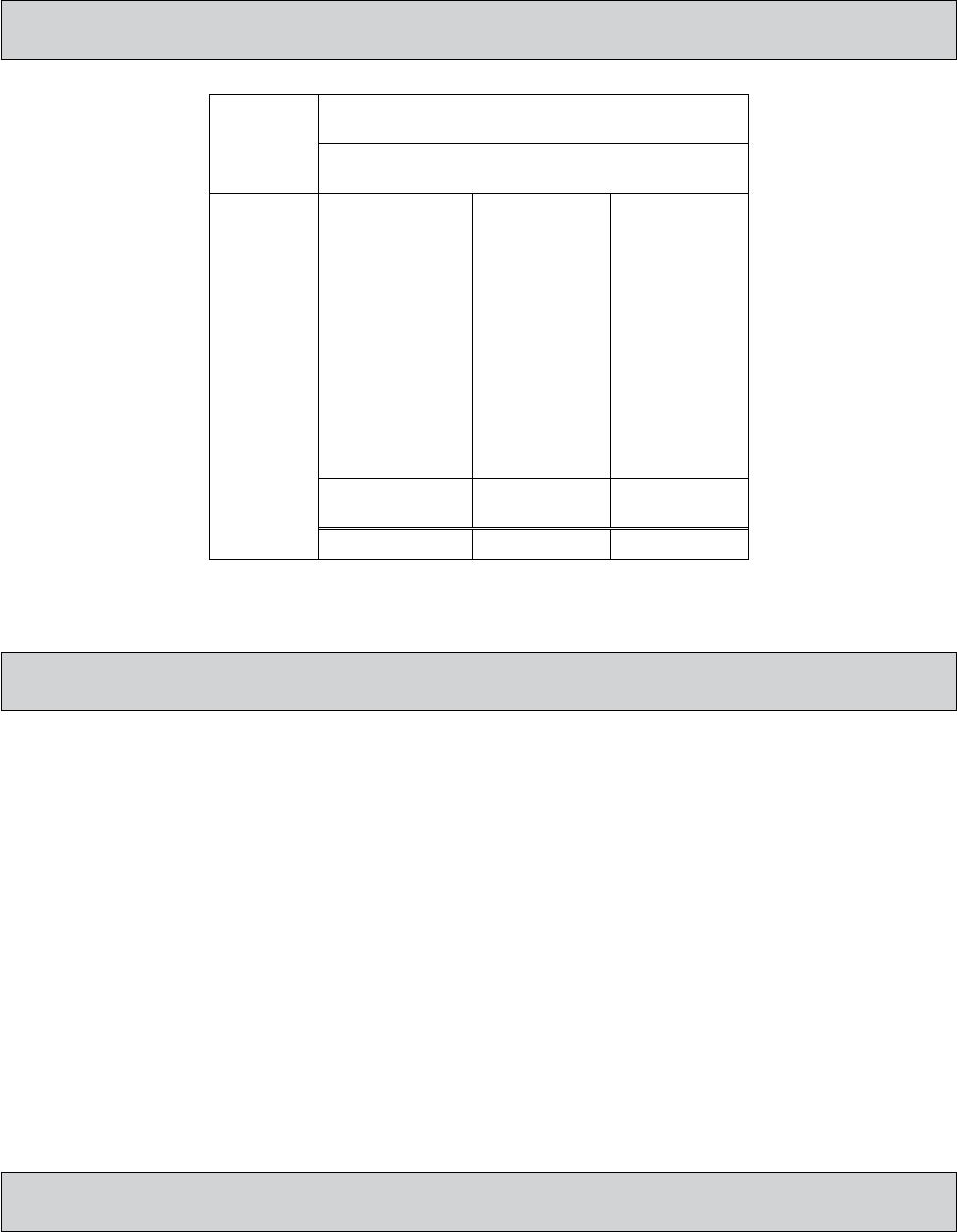

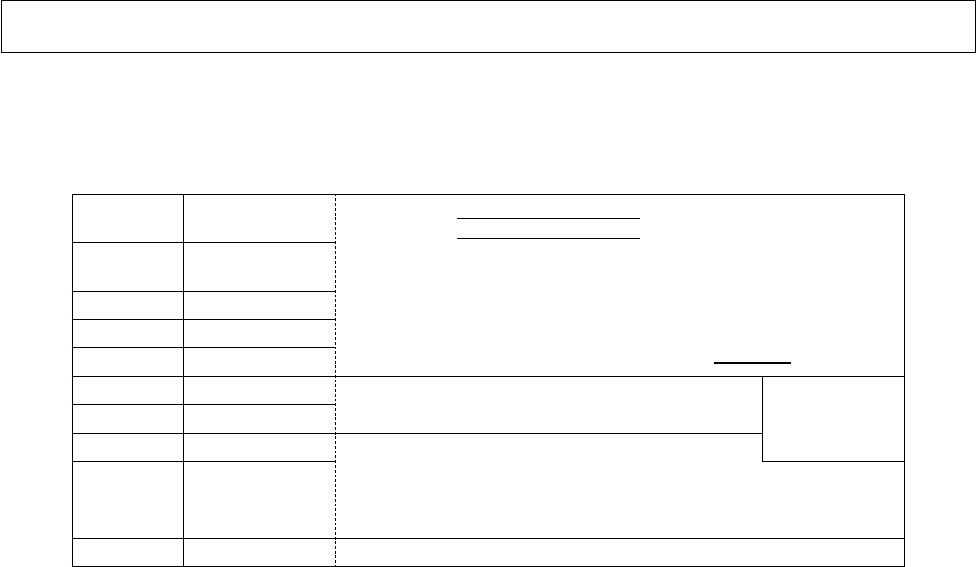

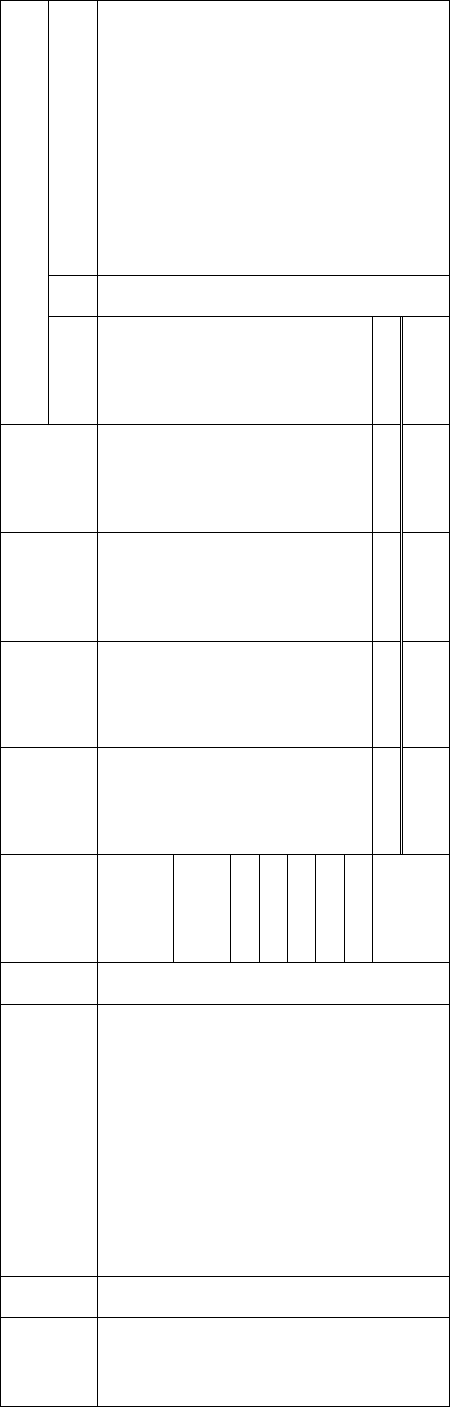

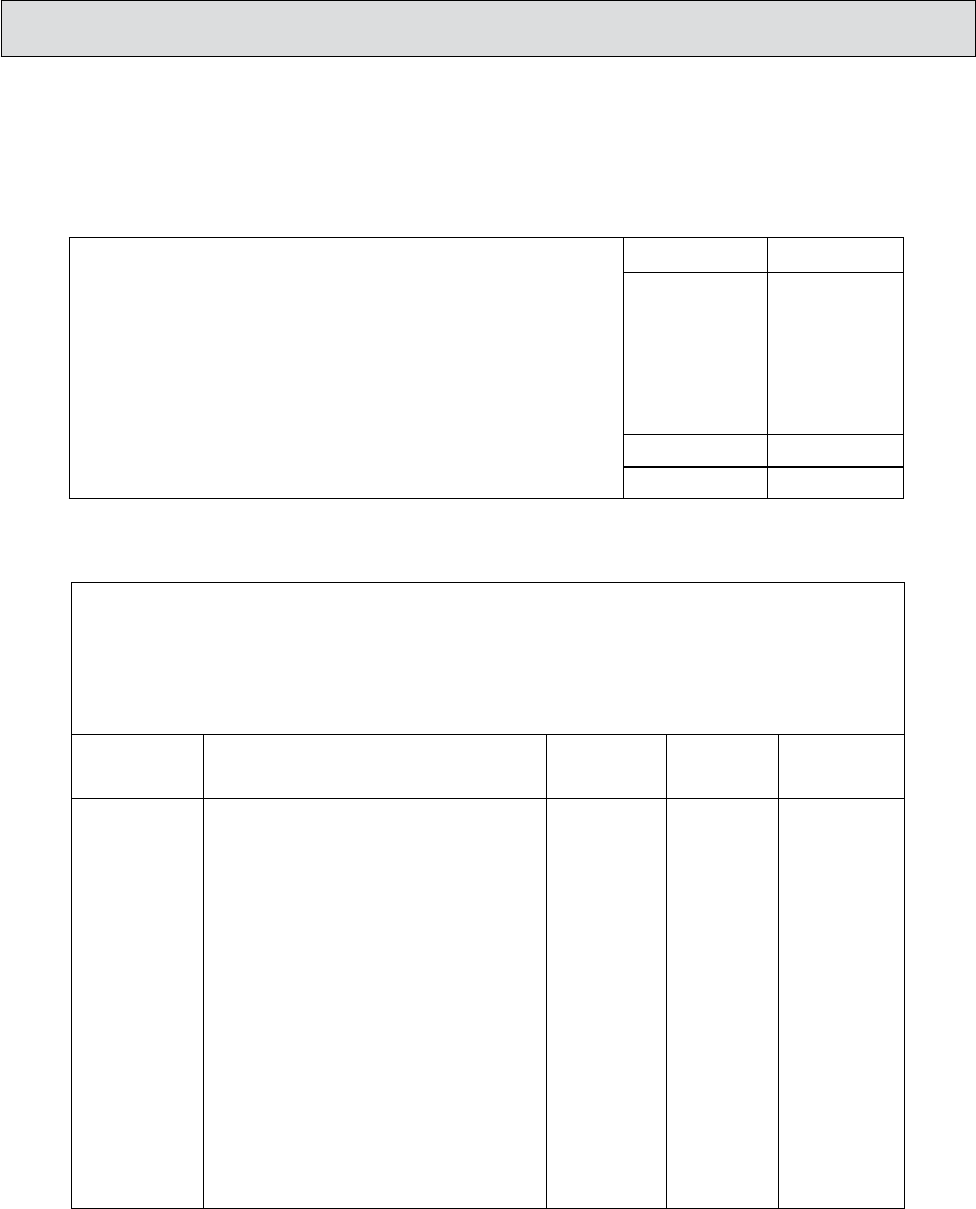

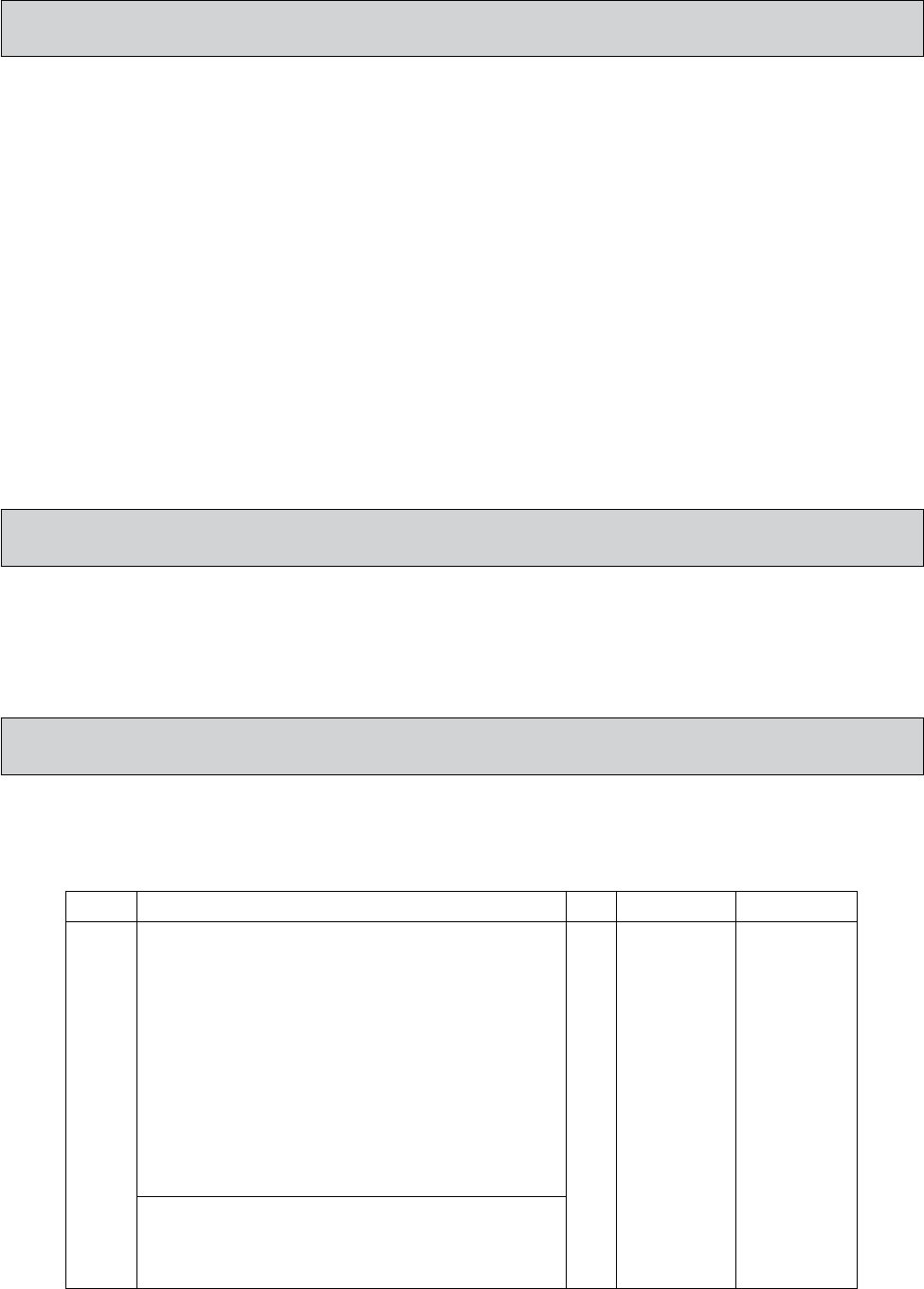

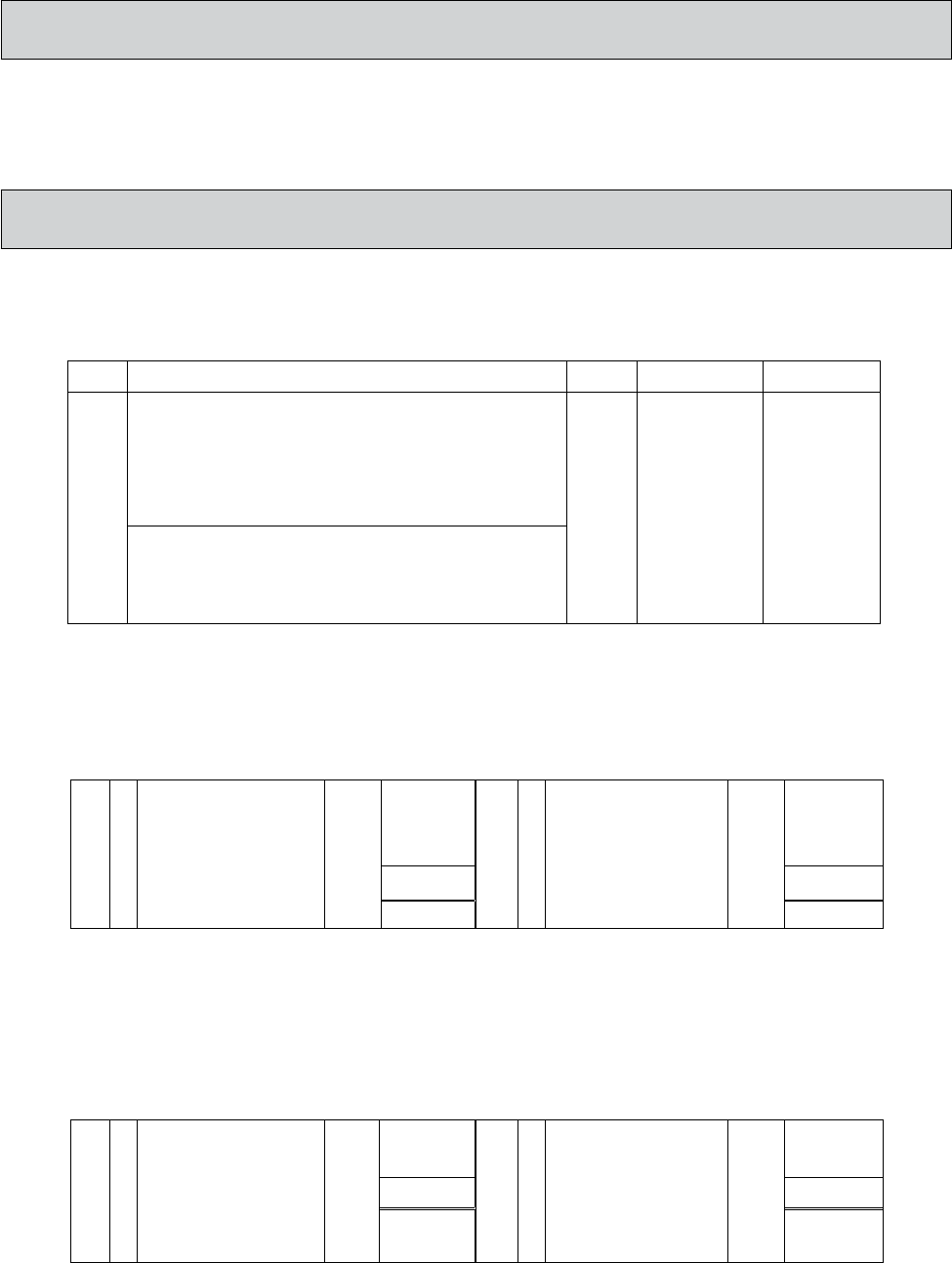

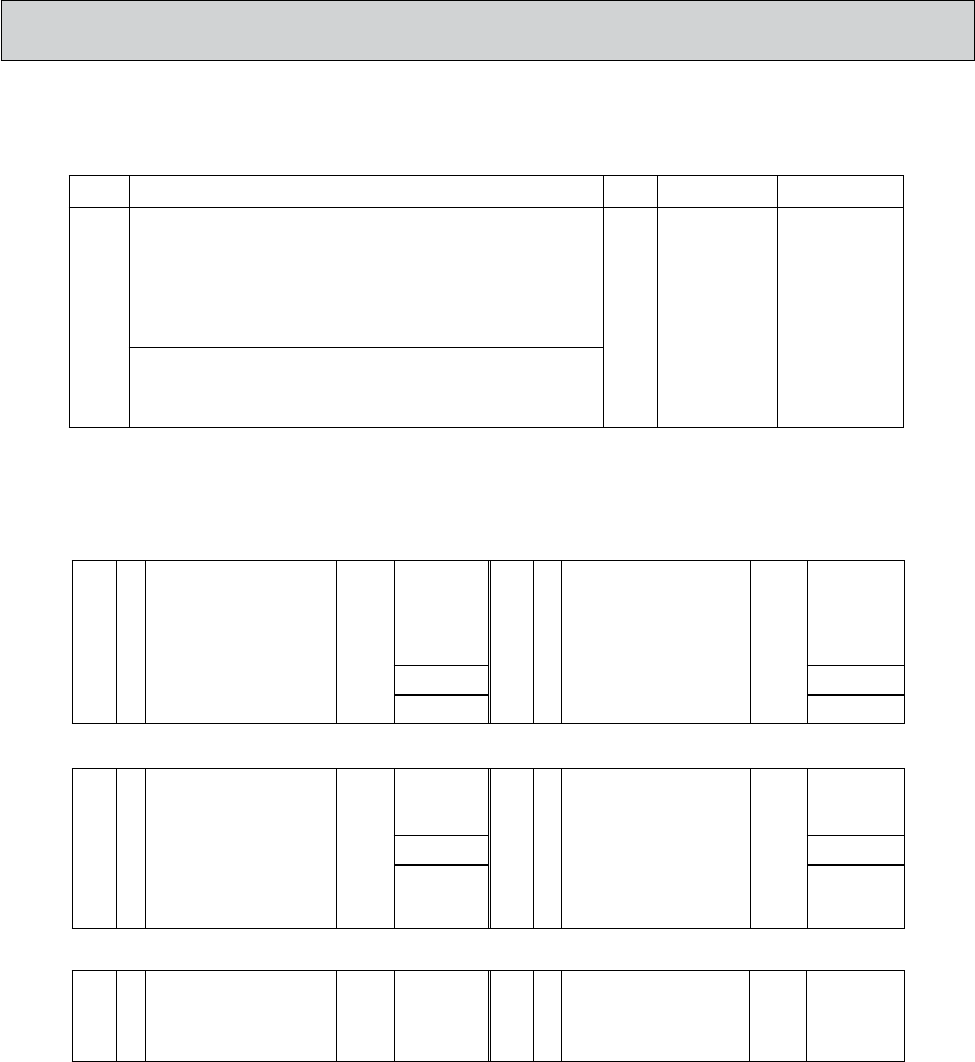

1.7 USERS OF FINANCIAL STATEMENTS

31Financial statements are prepared and presented at least once a year and are directed towards

thecommoninformationneedsofawiderangeofusers.

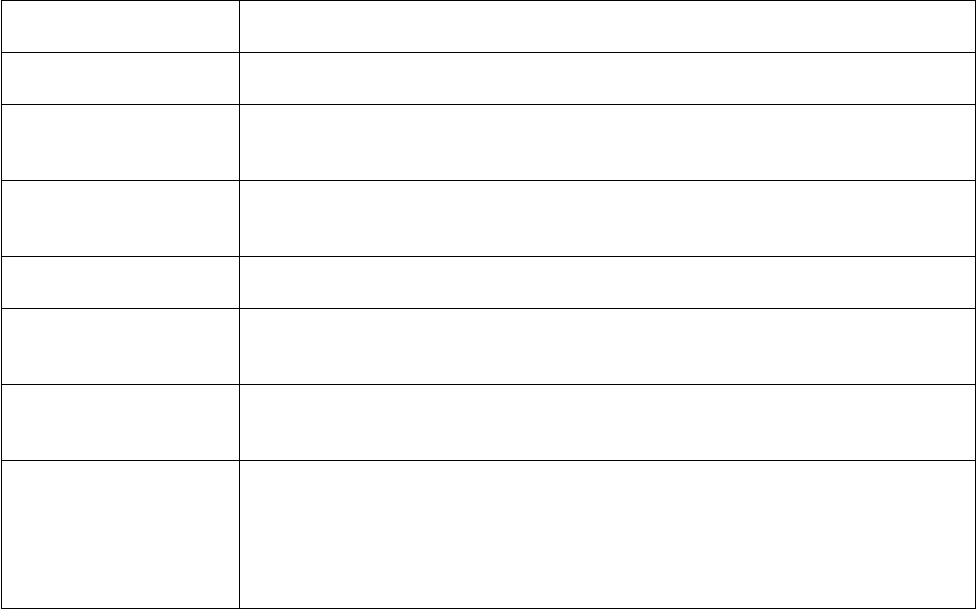

32Thefollowingcategoriesofusers,andtheirneedforaccountinginformation,havebeenidentied:

User Information needs

Clients toassesstheabilityoftheentitytocontinueasagoingconcern.

Employees toassesstheabilityoftheiremployertoprovidestableemploymentand

remuneration�

Government toregulateactivitiesoftheenterprise,compilestatisticsanddetermine

resourceallocationandtaxpolicies.

Investors toassesstheriskandreturnonaninvestmentintheenterprise.

Lenders to assess the ability of the enterprise to pay interest on a loan and to

repayloans.

Suppliers and other

creditors

toassesstheabilityoftheenterprisetopayamountsowing

Management ●planning,thatisdeterminingfutureactionstobetaken;

or

●exercising control, that is evaluating the current situation and taking

corrective steps

33Althoughemployeesareconsideredtobepartoftheorganisation,theydonothavethesame,unlimited

access to the accounting records of the entity�

7

FAC1501/1

1.8 EXERCISES AND SOLUTIONS

3REQUIRED

Answerthefollowingquestions:

(a) Whatisatransaction?

(b) Howwillyoudenenancialaccounting?

(c) Whatistheobjectiveofnancialaccounting?

(d) Whatisthenatureofnancialaccounting?

(e) Listthestepsinthenancialaccountingcycle.

(f) Whatdoesbookkeepingentail?

(g) WhatdoesIFRSsstandfor?

(h) Listthecategoriesofusersofnancialaccountinginformation.

(i) Namethereasonswhymanagementneednancialaccountinginformation.

(j) Whatistheobjectiveofnancialstatements?

4SOLUTION

(a) Atransactionisanactionwheremoneyispaidand,inreturn,anitemorservice,thatthebuyer

needs is obtained�

(b) Financialaccountingistheorderlyandsystematicidenticationandrecordingofthemonetary

valuesofnancialtransactionsofanindividualorbusinessentity,andthereportingoftheresults

ofthesetransactionsbywayofthepreparationandpresentationofnancialstatementstoenable

theuserstousetheinformationasabasisfordecisionmaking.

(c)

Toenabletheusersofnancialinformationtoascertainreadilywhatthenancialresultsand

nancialpositionoftheentityis.

(d) ● toidentifyeventsthatareevidenceofeconomicactivityrelevanttotheparticularentity,

ztorecordthemonetaryvalueofeconomiceventssoastoprovideapermanenthistoryofthe

nancialactivitiesoftheentity,

zto communicate the recorded information to interested users�

(e) Transactions source documents journalsgeneralledgerandsubsidiaryledgerstrial

balancesnalaccountsandnancialstatements

(f) Bookkeepingisthesystematicrecordingoftransactions.

(g) InternationalFinancialReportingStandards.

(h) ● Clients

zEmployees

zGovernment

zInvestors

zLenders

zSuppliersandothercreditors

zManagement

(i) Information to be used for decisions directed at

zplanning,thatisdeterminingfutureactionstobetaken,or

zexercisingcontrol,thatisevaluatingthecurrentsituationandtakecorrectivesteps.

8

FAC1501/1

(j)

Theobjectiveofnancialstatementsistoprovideinformationaboutthenancialposition,

performanceandchangesinthenancialpositionofanentitythatisusefultoawiderangeof

usersinmakingeconomicdecisions.

5SELF-ASSESSMENT

34After you have worked through this learning unit, are you

ableto:

zdenenancialaccounting?

zexplaintheobjectiveofnancialaccounting?

zexplainthenatureofnancialaccounting?

zlistthestepsinvolvedinthenancialaccountingcycle?

zexplainwhattheacronymIFRSsstandsfor?

zlisttheusersofnancialstatements?

z

explain what information different users of nancial

statementswillbeinterestedin?

zexplainthemainobjectiveofnancialstatements?

J

J

J

J

J

J

J

J

K

K

K

K

K

K

K

K

L

L

L

L

L

L

L

L

35IfyouhavemarkedallJyoumaycontinuetothenextlearningunit.

36IfyouhavemarkedanyK you have to revisethatspecicsection.

37IfyouhavemarkedanyL you have to re-studythatspecicsection.

FAC1501

Introductory Financial

Accounting

THE ACCOUNTING

EQUATION: FINANCIAL

POSITION

LEARNING UNIT 2

1

10

FAC1501/1

2OVERVIEW

Learning outcomes ���������������������������������������������������������������������������������������������������������������������������� 10

Key concepts ������������������������������������������������������������������������������������������������������������������������������������� 10

Assessment criteria ��������������������������������������������������������������������������������������������������������������������������� 11

2�1 Introduction ���������������������������������������������������������������������������������������������������������������������������� 11

2�2 Types of business entities ������������������������������������������������������������������������������������������������������ 11

2�3 South African forms of business ownership ��������������������������������������������������������������������������� 12

2�4 Characteristics of a sole trader ���������������������������������������������������������������������������������������������� 12

2.5 Theelementsofnancialstatements ������������������������������������������������������������������������������������� 13

2�6 The double-entry principle ����������������������������������������������������������������������������������������������������� 14

2�7 The accounting equation: Financial position �������������������������������������������������������������������������� 14

2.8 Thestatementofnancialposition ����������������������������������������������������������������������������������������� 23

2�9 Exercises and solutions ��������������������������������������������������������������������������������������������������������� 30

Self-assessment �������������������������������������������������������������������������������������������������������������������������������� 34

LEARNING OUTCOMES

1After studying this learning unit you should be able to:

1

zlist the basic business forms found in South Africa

zexplain the characteristics of a sole trader

zunderstand the accounting equation concerning assets, equity and liabilities

zexplaintheeffectsofnancialaccountingentriesconcerningassets,equityandliabilitiesonthe

accounting equation

zprepare entries in general ledger accounts for assets, equity and liabilities

zprepareastatementofnancialpositionforaserviceentity.

1

KEY CONCEPTS

zServiceentity

zRetailing entity

zManufacturing entity

zForms of business

zSole trader

zDouble-entry principle

zT-account

zDebit

zCredit

zAccounting equation

zAssets

zLiabilities

zEquity

11

FAC1501/1

zIncome

zExpenses

zStatementofnancialposition

zBalancing off of accounts

zDebtors

zCreditors

ASSESSMENT CRITERIA

z

The processing of accounting information by different types of business entities

becauseofthedifferenceinoperatingactivitiesisexplained.

zThe form of business ownership according to the capital needs of an entity

is explained�

zThe characteristics of a sole trader are explained�

zTheelementsofthegeneralpurposenancialstatementsareexplained.

zAccountingterminologyisexplainedandexamplesoftheirusearegiven.

zThe principle of debits and credits are explained�

zBusiness transactions concerning assets, liabilities and equity are explained

with reference to appropriate examples�

z

Accounting policy is demonstrated according to the right methods and procedures

when recording in the accounting equation format and in the ledger accounts�

zAssets,liabilitiesandequityaredenedandclassiedforrecognitioninthe

statementofnancialposition.

2.1 INTRODUCTION

2In the previous learning unit you learned that nancial accounting is an information system

that communicates nancial information to the users of nancial accounting information. But who

exactlyneedstokeepnancialaccountingrecords?Theanswertothisquestionissimple:everybody

who earns an income!

3Theaveragesalaryearnerneedsaccommodation,food,clothes,andhastopay(forexample)the

telephone account, school fees and groceries� They would possibly open a clothing account and pay

theschoolfeesinmonthlyinstalments.Salaryearnerswouldalsohaveabankaccountintowhich

theirsalariesaredepositedeverymonth.Howwouldtheybeabletokeeptrackofwhathasbeenpaid,

whattheystilloweandhowmuchmoneytheyhaveleftwithoutsomeformofnancialaccounting

system?

2.2 TYPES OF BUSINESS ENTITIES

4Theprocessingofnancialaccountinginformation(thatis,bookkeeping)willbedeterminedbythe

operatingactivitiesofanentityandshouldbeadaptedtoprovidetheinformationthatisapplicableto

thespecicoperatingactivities.Theoperatingactivitiesofanentityarethoseactivitiesfromwhichit

triestomakeaprot.Theobjectiveofeveryentityistoearnaslargeaprotaspossible.

5Let’s consider the following example:

6Mr Bongile Sithole, a qualied electrician, has his own business which he runs from his home.

Mr B Sithole trades as BS Electrical and installs electrical cables and repairs electrical faults� In order

forhimtodeliverhisservicesheneedshistools.Hisclientsmustsupplyanycablingorwiringrequired

forthejob,whichtheybuyfromthehardwarestore.Thehardwarestorebuystheseitemsfroman

engineering company that manufactures them�

12

FAC1501/1

zMr Bongile Sithole therefore runs

— a commercial entity

— which sells

— aservicetohisclients.

zThe hardware store is

— a commercial entity

— which buys and sells

— goods to their customers�

7Commercial entities can be retail entities that will sell goods to the public, or whole salers that only sell

goods to retailer entities�

zThe engineering entity is

— a manufacturing entity

— which manufactures and sells

— goods to their customers�

8Eachofthesetypesofentitieswillmakeuseofnancialaccountingrecordsthataresuitabletotheir

ownneeds.Theminimuminformationthatmustbeavailablefromthesenancialaccountingrecords

isprescribedbyInternationalFinancialReportingStandards(IFRSs).

2.3 SOUTH AFRICAN FORMS OF BUSINESS OWNERSHIP

9Mr Bongile Sithole’s entity, the hardware store entity as well as the engineering entity may be conducted

in one of a number of business forms� In order to start any business, money is needed� This money

is referred to as capital� Some types of businesses require more capital than others� For example,

the engineering entity would need machines, an electrician would need his toolbox and the hardware

store will need hardware inventory. The amount of capital needed to start and continue business

operationswouldlargelyinuencetheform of the business�

10Fornancialaccountingpurposeswedistinguishbetweenthefollowingformsofbusinessownership:

zsole traders

zpartnerships

zclose corporations

zcompanies

11In South Africa two types of companies can be formed, namely a prot company and a non-

protcompany.

12Inthismoduleyouwillconcentrateonthenancialaccountingrecordsrequiredbydifferentoperating

activities(thatissalesandservices)ofasoletraderandwewillnotventureintoanyaspectsofthe

other forms of business ownership�

2.4 CHARACTERISTICS OF A SOLE TRADER

z

This entity belongs to one person only� In the case of BS Electrical the entity belongs to

Mr Bongile Sithole�

zIt is suitable for smaller types of entities that do not need big amounts of capital to start�

13

FAC1501/1

zAlldecisionsregardingtheentityaretakenbytheownerandalltheprotsandlossesaccrueto

theowner.MrBongileSitholewilltakealldecisionsregardingBSElectricalandalltheprotand

losses will accrue to him as owner�

zMr Bongile Sithole is the sole owner and disposer of the assets of the business�

zThe sole trader is not a legal entity distinct from its owner� Mr Bongile Sithole will conclude any

contracts applicable to his entity in his own name and he will be liable in his personal capacity for

the debts of the entity�

zAsthesoletraderisnotalegalentity,theprotsoftheentitywillbetaxedinthehandsofthe

owner.MrBongileSitholewilldeclaretheprotsinhispersonalincometaxreturnandhewillbe

taxed on the amount�

zIfMr.BongileSitholedies,theentityceasestoexist.Ifthebusinessactivitiesaretakenoverby

someone else, a new sole trader entity comes into being�

13To be able to do Mr Bongile Sithole’s books it is necessary to look at the accounting equation�

2.5 THE ELEMENTS OF FINANCIAL STATEMENTS

14Everyentityimplementsanancialaccountingsystemaccordingtotheminimumnancialaccounting

standards and practices when it draws up nancial statements that are used in making economic

decisions.Financialstatementswillreectthenancialeffectsoftransactionsbygroupingtheminto

broad classes according to their economic characteristics, namely assets, equity, liabilities, income

andexpenses.Assets,equity,liabilities,incomeandexpensesarecalledtheelementsofnancial

statements�

15Theelementsdirectlyrelatedtothemeasurementofnancialpositionatagiventimeinthestatement

ofnancialpositionareassets,liabilitiesandequity.

Assets are all the resources controlled by the entity (whether they are owned by the entity

or not), for example land and buildings, vehicles, furniture, equipment, trading inventory,

debtors, bank and petty cash.

Remember, not all assets controlled by the entity are owned by the entity� If, for

example,theentityboughtavehicleoncredit,itdoesnotbelongtotheentityuntilthenalinstalment

is paid�

Liabilities are the debts of the entity (all the money owed to third parties), for example

long-term loans, mortgage bonds, bank overdrafts and creditors.

Equity refers to the amount that the owner invested in the entity and is made up mainly of

capital. It is an indication of the assets that actually belong to the owner and is referred to

as the owner’s net worth.

Prot or loss is frequently used as a measure of performance. The elements directly related

to the measurement of nancial performance for a period in the statement of prot or loss and

othercomprehensiveincomeareincomeandexpenses.

Income less expenses = prot for the year

14

FAC1501/1

Income is the income earned by the entity through its normal everyday business activities

for the nancial accounting period (normally a year), for example sales, rent income,

interest income and credit losses recovered.

Expenses are the running expenses of the entity for the nancial accounting period

(normally a year) necessary to earn the income, for example purchases, rent expenses,

telephone expenses, water and electricity, salaries and wages.

16To be able to record transactions correctly it is necessary to have a look at the process of

recording transactions�

2.6 THE DOUBLE-ENTRY PRINCIPLE

17Bookkeepingisthepartofnancialaccountingthatisconcernedwiththerecordingoftransactions.

The transactions are recorded in an account�

An account consists of a left-hand side and a right-hand side and is presented in a “T”

format. The left-hand side is referred to as the debit side and the right-hand side is

referred to as the credit side. The name of the “T” account is written across the centre at

the beginning of each account.

This can be illustrated as follows:

Dr (debit side) ……. Account (credit side) Cr

Left-hand side (LHS) Right-hand side (RHS)

18For each asset, liability, equity, expense and income there will be a “T” account in the books of the

entity� All these “T” accounts together are called the general ledger�

19Thedouble-entryprincipleprovidesalogicalmethodofrecordingtransactions.Inusingthedouble-

entrysystemthemonetary(moneyvalue)ofeachtransactionmustbeenteredonthedebitsideof

one ledger account as well as on the credit side of another ledger account� The entry in one ledger

account refers to the corresponding entry in the other ledger account�

20Astheentriesinthetwoledgeraccountshavebeenenteredonoppositesides,theuseofthedouble

entry system allows for cross references� Each transaction is entered in two separate accounts on

opposite sides, and it is therefore possible to check and control the arithmetical and accounting

accuracy of the work� If each transaction is recorded so that the debit and credit entries are equal, the

same sum of all the debits to the account must equal the sum of all the credits� This can be explained

by way of the accounting equation�

2.7 THE ACCOUNTING EQUATION: FINANCIAL POSITION

21The logical method of recording transactions by way of the accounting equation is used to process

transaction data� Transactions may:

zaffect assets and/or equity and/or liabilities�

zgenerateincomeorgiverisetoexpenditure

15

FAC1501/1

22The accounting equation states that:

ASSETS = EQUITY + LIABILITIES

A = E + L

23OR

EQUITY = ASSETS – LIABILITIES

E = A – L

The equity equals all the assets in the entity less all the claims against those assets (li-

abilities).

24The accounting equation is a mathematical equation that should always balance. The nancial

position of an entity is indicated by this equation�

25Fortheaccountingequationtoalwaysbalanceitrequirestheinvolvementoftwoaccountsforeach

transaction� The accounting equation is, therefore, based on the double-entry accounting system�

Basic requirements for the accounting equation:

zA minimum of two accounts must be used for each transaction.

zThe equation must remain in balance after each transaction. In other words the debit

side (A) is equal to the credit side (E + L).

26Consider the following example of transactions that affect assets and/or equity and/or liabilities:

27Before the entity starts to do business, the accounting equation will look like this:

Debit side =Credit side

A = E + L

Possessions the entity

owns

=Amounts owed to the

owner of the entity

+Amounts owed

to third parties

What the entity owns = What the entity owes

0 = 0

Note that the recording of transactions is done from the point of view of the business en-

tity independent from its owner, Mr Bingole Sithole.

16

FAC1501/1

28Everyentityforwhichseparatenancialrecordsarekeptisanancialaccountingentity.Itisextremely

importanttoseetheentityasseparatefromitsowner:transactionsenteredintobytheentityhaveto

bedealtwithfromthepointofviewoftheentitywhosebooksarebeingdone.

29Transaction 1:

30Mr Bingole Sithole, a qualied electrician, started a small service business, BS Electrical on

1January20.6.HedecidedtodepositR40000intheentity’sbankaccounttostartthebusiness.

31Explanation:

32TheentityreceivedR40000incashandthemoneywasdepositedinabankaccountopenedinthe

name of the entity� It cannot be Mr B Sithole’s bank account� The entity must have its own bank

account.Themoney(bankaccount)isanassetbecauseitisaresourcecontrolledbytheentity(itcan

beusedbytheentitytodobusiness).Theassetsincreasedbecauseitwas“0”beforethistransaction.

Theownerdepositedthemoneyintotheentity’sbankaccount.Anyamountreceivedfromtheowner

is called capital and this increases equity� The entity now owes Mr B Sithole R40 000� Both the left-

handsideoftheequation(A)andtheright-handsideoftheequation(E+L),nowequalsR40000.

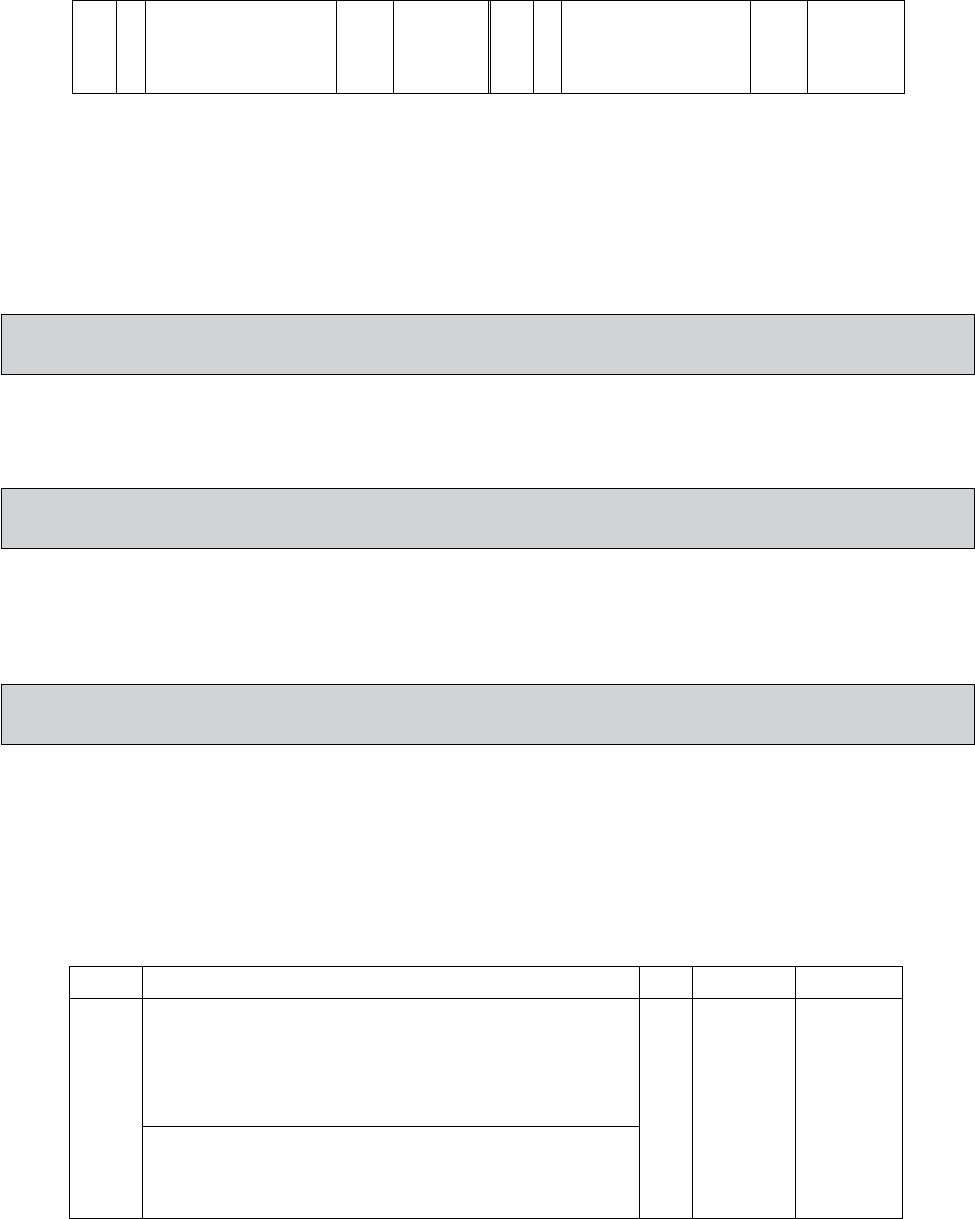

33The effect of this transaction on the accounting equation can be illustrated as follows:

A = E + L

Bank Capital

R R R

+ 40 000 =+ 40 000 +–

NOTE:

The plus sign shows an increase of an element of the accounting equation and a minus shows a

decrease in an element of the accounting equation�

34Transaction 2:

35On 1 January 20�6 BS Electrical bought a toolbox and tools to be used by Mr B Sithole on credit from

Big Builders for R7 000�

36Explanation:

37Tools and equipment are a resource controlled by the entity (it can be used by the entity to do

business).Itisanasset,sotheassetsincreased.TheentityowedmoneytoBigBuilders,acreditor,

so the liabilities would increase�

A creditor is a person or entity to which the entity, BS Electrical, owes money. This debt is

usually paid back within one year.

38

17

FAC1501/1

39The effect of this transaction on the accounting equation can be illustrated as follows:

A = E + L

Bank Tools and

equipment

Capital Big Builders

(creditor)

R R R R

+ 40 000 + 40 000

+ 7 000 + 7 000

40 000 7 000 = 40 000 + 7 000

40Transaction 3:

41On1January20.6BSElectricalboughtaladderfromLadders(Pty)Ltdandpaidforitbycheque,

R1 200�

42Explanation:

43Money(bankaccount)isaresourcecontrolledbytheentity(itcanbeusedbytheentitytodobusiness).

Assets decreased because money was paid by the entity� Tools and equipment, another resource

controlledbytheentity(itcanbeusedbytheentitytodobusiness),increased,thusassetsincreased.

AssetsincreasedanddecreasedwithR1200,leavinguswithanileffect.Theleft-handsideofthe

equation(A)=right-handsideoftheequation(E+L)[R47000=R40000+R7000].

44The effect of this transaction on the accounting equation can be illustrated as follows:

A = E + L

Bank Tools and

equipment

Capital Big Builders

(creditor)

R R R R

+ 40 000 + 40 000

+ 7 0 0 0 + 7 000

- 1 200 + 1 200

38 800 + 8 200 = 40 000 + 7 000

45Transaction 4:

46On 1 January 20�6 BS Electrical borrowed R50 000 from Uni Bank at an interest rate of 10% per

annumrepayableover60months.TheR50000wastransferredtothebankaccountoftheentity.

47Explanation:

48The money received from Uni Bank increased the bank account. Bank is an asset and therefore

theassetsincreasedwiththemoneyreceivedfromUniBank.Theentity however owedUniBank

18

FAC1501/1

R50000.Thisisanobligation(liability)topayandtheliabilitiesincreased.Theleft-handsideofthe

equation(A)=theright-handsideoftheequation(E+L)[R97000=R40000+R57000].

BS Electrical owes Uni Bank, who provided the long-term loan, the money. Uni Bank is a

creditor (nancing creditor) of BS Electrical. This long-term debt is usually not paid back

within one year (in this case it will only be paid back over a period of 5 years (60 months)).

The effect of this transaction on the accounting equation can be illustrated as follows:

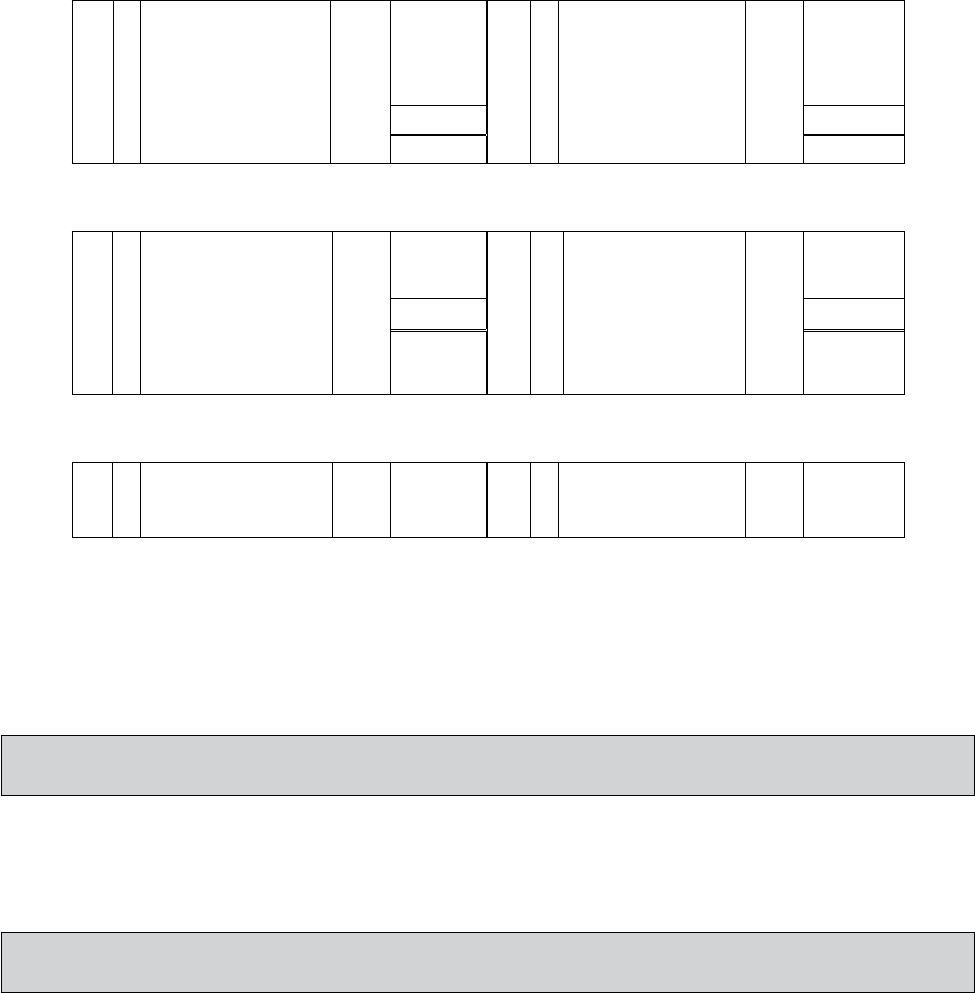

A = E + L

Bank Tools and

equipment

Capital Big Builders

(creditor)

Uni Bank

(long-term

loan)

R R R R R

+ 40 000 + 40 000

+ 7 000 + 7 000

–1200 + 1 200

+ 50 000 + 50 000

+ 88 800 + 8 200 =+ 40 000 ++ 7 000 + 50 000

49The following rules can be applied:

Dr (debit side) Asset accounts (credit side) Cr

+(increase) –(decrease)

Dr (debit side) Liability accounts (credit side) Cr

–(decrease) +(increase)

Dr (debit side) Equity account (credit side) Cr

–(decrease) +(increase)

50For you as a learner of nancial accounting the reality is that the double-entry rules are not

one of those concepts that you can try to understand – you have to learn them!

When analysing a transaction, the following four questions need to be asked:

zWhich two accounts are involved in the transaction?

zDo the accounts form part of assets, equity or liabilities?

zDid the assets, equity or liabilities increase or decrease?

zWhich one of the accounts must be debited and which one must be credited?

19

FAC1501/1

51Let’s consider the transactions of BS Electrical again:

52Transaction 1:

53Mr Bingole Sithole, a qualied electrician, starts a small service business, BS Electrical, on

1January20.6.HedecidedtodepositR40000intheentity’sbankaccounttostartthebusiness.

54The effect of this transaction on the accounting equation can be illustrated as follows:

A = E + L

Bank Capital Liabilities

R R R

+ 40 000 = + 40 000 + –

55Explanation (detailedexplanationoftheaccountingequationtransaction1):

561. Bank account (an asset) increased; and must therefore be debited.

Dr (debit side) Assets (credit side) Cr

+(increase) –(decrease)

572. Capital account (equity) increased; and must therefore be credited.

Dr (debit side) Equity (credit side) Cr

–(decrease) +(increase)

58The above transaction will be recorded in the ledger accounts as follows:

(a) The debit-side of the bank account:

Dr Bank 1Cr

Date Details Fol RDate Details Fol R

20�6

Jan 1Capital (name of

account to be

credited)

40 000

59A few things to remember:

zThedateofthetransaction(date).Thetransactiontookplaceon1January20.6.

zA description of the other account affected by the transaction to make cross-referencing easier

(details).Theaccounttobedebitedisbankaccountandtheaccounttobecreditediscapitalaccount.

zCross-referencingtothefolionumberoftheotheraccountaffected(fol).(Itwillbediscussedina

laterlearningunit.)

20

FAC1501/1

zRecordingtheamountofthetransaction.TheamountofthetransactionisR40000.(Bankaccount

isdebitedwithR40000,andcapitalaccountiscreditedwithR40000.)

(b) The credit-side of the capital account:

Dr Capital 2Cr

Date Details Fol RDate Details Fol R

20�6

Jan 1 Bank (name of

account to be

debited)

40 000

60Debit side = Credit side = R40 000

61Transaction 2:

62On 1 January 20�6 BS Electrical bought a toolbox and tools to be used by Mr Bingole Sithole on credit

from Big Builders for R7 000�

63The effect of this transaction on the accounting equation can be illustrated as follows:

A = E + L

Bank Tools and

equipment

Capital Big Builders

(creditor)

R R R R

+ 40 000 + 40 000

+ 7 000 + 7 000

40 000 7 000 = 40 000 + 7 000

64Explanation (detailedexplanationoftheaccountingequationtransaction2):

651. Tools and equipment account (an asset) increased and must therefore be debited.

Dr (debit side) Assets (credit side) Cr

+(increase) –(decrease)

662. Big Builders’ account (a liability) increased and must therefore be credited.

Dr (debit side) Liabilities (credit side) Cr

–(decrease) +(increase)

67

21

FAC1501/1

68The above transaction will be recorded in the ledger accounts as follows:

(a) The debit-side of the tools and equipment account:

Dr Tools and equipment 3Cr

Date Details Fol RDate Details Fol R

20�6

Jan 1 Big Builders (name

of account to be

credited)

7 000

(b) The credit-side of Big Builders’ account:

Dr Big Builders 4Cr

Date Details Fol RDate Details Fol R

20�6

Jan 1 Tools and equipment

(name of account

to be debited)

7 000

69Debit side = Credit side = R7 000

70Transaction 3:

71On1January20.6BSElectricalboughtaladderfromLadders(Pty)Ltdandpaidforitbycheque,

R1 200�

72The effect of this transaction on the accounting equation can be illustra ted as follows:

A = E + L

Bank Tools and

equipment Capital Big Builders

(creditor)

R R R R

+ 40 000 + 40 000

+ 7 000 + 7 000

– 1 200 + 1 200

+ 38 800 + 8 200 =+ 40 000 ++ 7 000

73Explanation (detailedexplanationoftheaccountingequationtransaction3):

741. Tools and equipment account (an asset) increased and must therefore be debited.

Dr (debit side) Assets (credit side) Cr

+(increase) –(decrease)

22

FAC1501/1

752. Bank account (an asset) decreased and must therefore be credited.

Dr (debit side) Assets (credit side) Cr

+(increase) –(decrease)

76The above transaction will be recorded in the ledger accounts as follows:

77(a) The debit-side of the tools and equipment account:

78Youwillhaveonlyoneledgeraccountforeachasset,liabilityandequityitem.Usethesametoolsand

equipment account as created in transaction 2�

Dr Tools and equipment 3Cr

Date Details Fol RDate Details Fol R

20�6

Jan 1Big Builders

Bank (name of

account to be

credited)

7 000

1 200

79(b) The credit-side of the bank account:

80Use the same bank account created in transaction 1�

Dr Bank 1Cr

Date Details Fol RDate Details Fol R

20�6

Jan 1Capital 40 000

20�6

Jan 1Tools and equipment

(name of account to

be debited)

1 200

81Transaction 4:

82On 1 January 20�6 BS Electrical borrowed R50 000 from Uni Bank at an interest rate of 10% per

annumrepayableover60months.TheR50000wastransferredtothebankaccountoftheentity.

83The effect of this transaction on the accounting equation can be illustrated as follows:

A = E + L

Bank Tools and

equipment

Capital Big Builders

(creditor)

Uni Bank

(long-term

loan)

R R R R R

+ 40 000 + 40 000

+ 7 000 + 7 000

– 1 200 + 1 200

+ 50 000 + 50 000

+ 88 800 + 8 200 =+ 40 000 ++ 7 000 + 50 000

23

FAC1501/1

84Explanation (detailedexplanationoftheaccountingequationtransaction4):

851. Bank account (an asset) increased and must therefore be debited.

Dr (debit side) Assets (credit side) Cr

+(increase) –(decrease)

2. Long-term loan: Uni Bank account (a liability) increased and must therefore be credited.

Dr (debit side) Liabilities (credit side) Cr

–(decrease) +(increase)

86The above transaction will be recorded in the ledger accounts as follows:

(a) The debit-side of the bank account:

87Use the same bank account created in transaction 1 and used in transaction 3�

Dr Bank 1Cr

Date Details Fol RDate Details Fol R

20�6

Jan 1Capital account

Long-term loan:

Uni Bank (name of

account to be

cre dited)

40 000

50 000

20�6

Jan 1 Tools and equipment 1 200

(b) The credit-side of the long-term loan: Uni Bank account:

Dr Long-term Loan: Uni Bank 5Cr

Date Details Fol RDate Details Fol R

20�6

Jan 1 Bank (name of

account to be

debited)

50 000

88The accounting equation is, therefore, based on the double-entry accounting system, and is used for

preparing the statement of nancial position at a specic point in time�

2.8 THE STATEMENT OF FINANCIAL POSITION

89The statement of nancial position reects the nancial position of an entity in terms of the basic

accounting equation on a specic date.Itisastatementofbalancesataspecicdate.

90

24

FAC1501/1

91ThestatementofnancialpositionofBSElectricalpreparedasat1January20.6isasfollows:

BS ELECTRICAL

STATEMENT OF FINANCIAL POSITION AS AT 1 JANUARY 20.6

ASSETS REQUITY AND LIABILITIES R

Bank 88 800 Capital 40 000

Tools and equipment 8 200 Creditor 7 000

Long-term loan 50 000

97 000 97 000

92Atthisstageitisnecessarytohavealookatthewaysassetscanbeused:

z

Some assets are used time and time again in the business to earn an income� The tools and

equipmentusedbyMrBingoleSitholeareexamplesofsuchassets.Theseassetsareclassied

as non-current assets�

z

Someassetshaveashortlifespan,andcontinuallychangeinvalueinthenormalcourseofbusiness,

forexample,moneyinthebank.Theseassetsareclassiedascurrent assets�

93

25

FAC1501/1

94Let’shavealookatthedifferencebetweennon-currentassetsandcurrentassets.

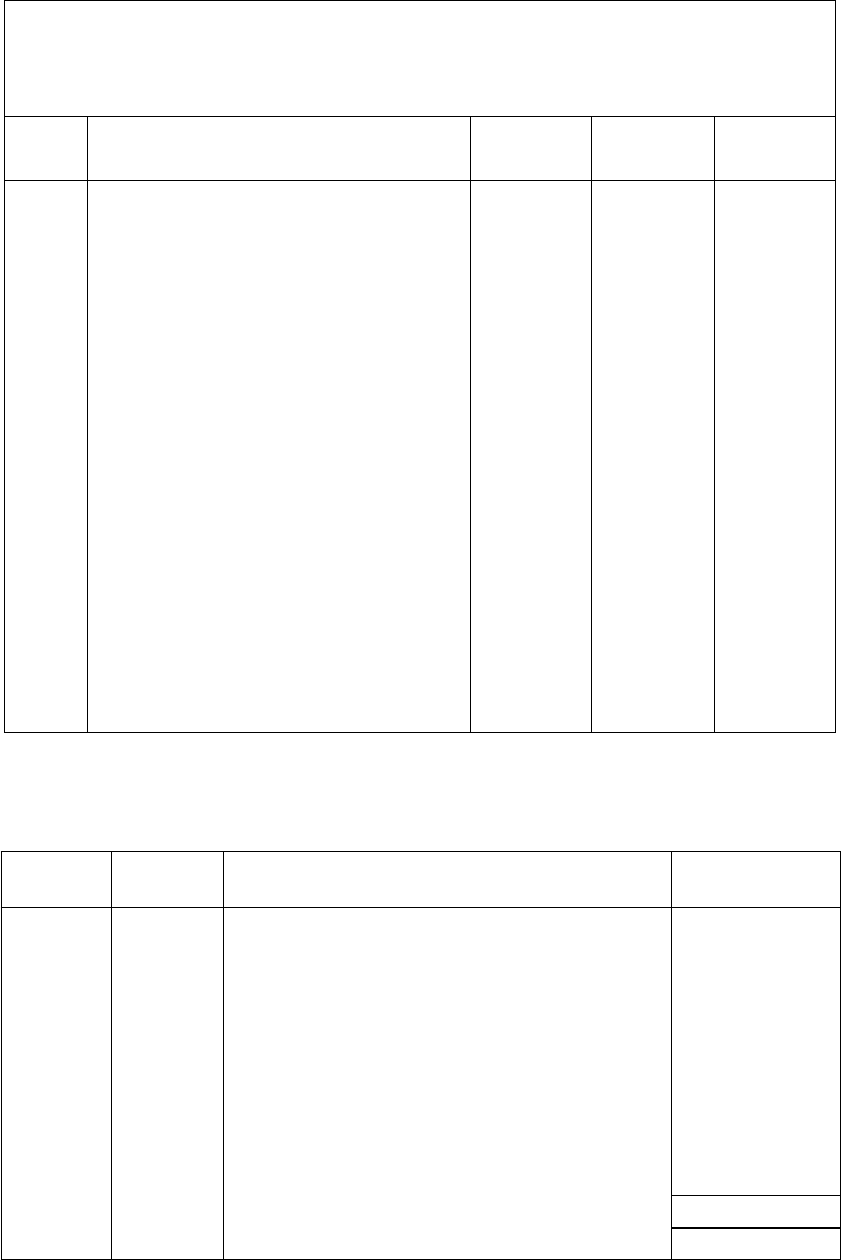

ASSETS

Assets are resources controlled (used)

by the entity, as a result of past events

(asset was bought), and from which

future economic benets (income) are

expected to ow to the entity.

CURRENT NON-CURRENT

An asset shall be classied as

current when it satises any of the

following criteria:

All other assets (thus being assets

that are not classied as current

assets will be classied as non-

current).

zItisexpectedtobeconvertedinto

money(realised),orisintendedfor

sale or consumption, in the entity’s

normal operating cycle�

Non-current assets include tangible,

intangible and nancial assets of a

long-term nature. (In this module we

will only concern ourselves with tan-

giblenon-currentassets.)

zIt is held primarily for the purpose

of being traded�

It is not the intention of the entity to

sell non-current assets, but to use

theseassetsoverthelong-terminits

business operations to earn an

income�

z

It is expected to be converted

into money (realised) within

twelvemonthsofthestatementof

nancialpositiondate.

Non-current assets are those assets

with a useful life of longer than one

year�

Examples of current assets are: Examples of non-current assets are:

zTradinginventories

zConsumable stores on hand

zDebtors(tradereceivables)

zAccrued income

zPre-paid expenses

zBank(positivebalance)

zCashoat

zPetty cash

zLand and buildings

zVehicles

zFurniture

zEquipment

zMachinery

26

FAC1501/1

95Liabilities can also be non-current or current, depending on when the liability must be settled:

z

Someliabilitiesarepayablemorethanoneyearafternancialyearend,thatis,theyarenotpayable

withinthenextnancialyear.Theseliabilitiesareclassiedasnon-current liabilities�

zLiabilitiespayablewithinthenextnancialyearareclassiedascurrent liabilities.

96Let’shavealookatthedifferencebetweencurrentandnon-currentliabilities:

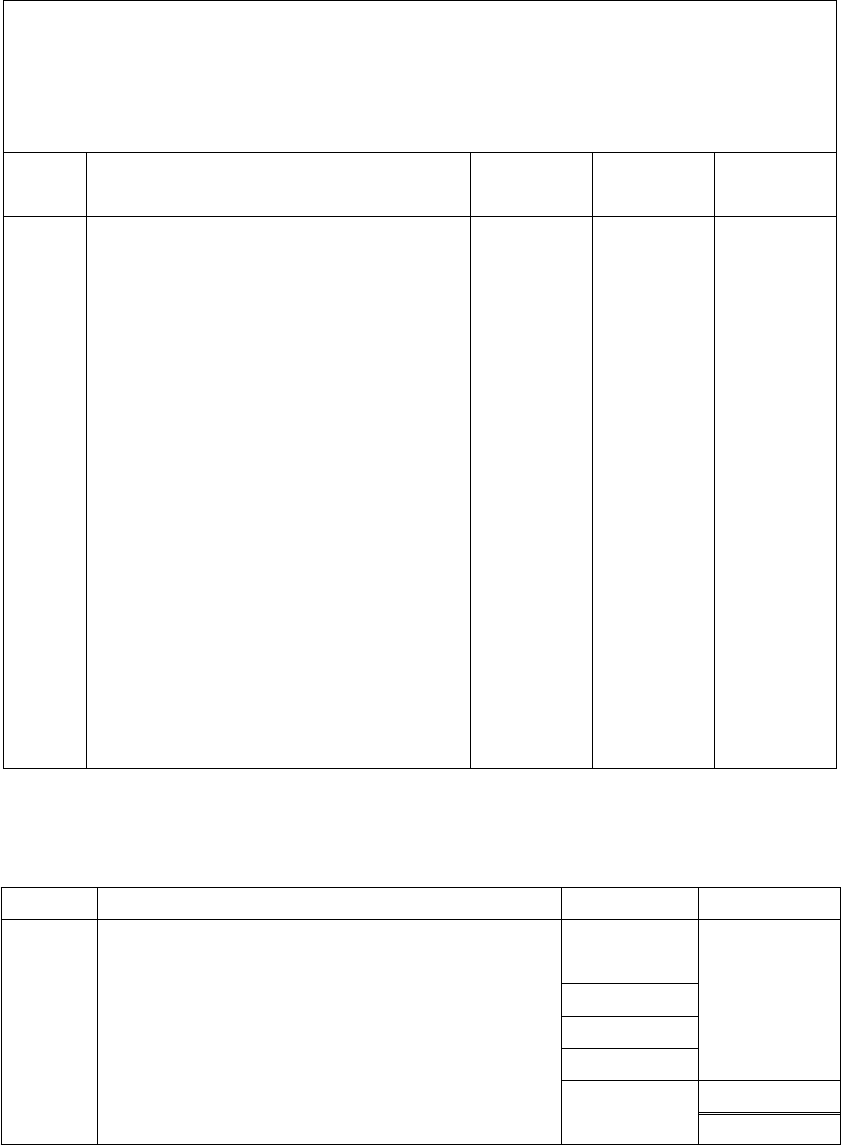

LIABILITIES

Liabilities are present obligations

(debts) of an entity as a result of past

events (borrowing or purchasing) and

represent a potential outow of cash

(payment) from the entity.

CURRENT NON-CURRENT

A liability shall be classied as

current when it satises any of the

following criteria:

All other liabilities (thus being liabili-

ties that are not classied as current

liabilities will be classied as non-

current).

zIt is expected to be settled in the

entity’s normal operating cycle

(usuallyoneyear).

Are long-term debts, and have to be

settled after one year of the statement

ofnancialpositiondate.

z

It is held primarily for the purpose

of being traded�

zItisduetobesettledwithintwelve

months after the statement of

nancialpositiondate.

Examples of current liabilities are: Examples of non-current liabilities are:

zCreditors(tradepayables)

zBankoverdrafts

z

Current portion of long-term

borrowings

zShort-term borrowings

zAccrued expenses

zIncomereceivedinadvance

zLong-term loans

zMortgage

zDebentures

27

FAC1501/1

97AccordingtotheseprinciplesthecorrectstatementofnancialpositionforBSElectricalisasfollows:

BS ELECTRICAL

STATEMENT OF FINANCIAL POSITION AS AT 1 JANUARY 20.6

ASSETS REQUITY AND LIABILITIES R

Non-current assets

Tools and equipment

Current assets

Bank

8 200

88 800

Equity

Capital

Non-current liabilities

Long-term loan

Current liabilities

Creditor

40 000

50 000

7 000

Total assets 97 000 Total equity and liabilities 97 000

98Therulesthatneedtobefollowedwhenthedouble-entryaccountingisappliedcanbederivedfrom

thestatementofnancialposition.(Thecorrectverticalformatwillbediscussedlater.)

99To summarise the ledger accounts in the general ledger:

Dr Bank 1Cr

Date Details Fol RDate Details Fol R

20�6

Jan 1Capital

Long-term loan:

Uni Bank

40 000

50 000

20�6

Jan 1 Tools and equipment 1 200

100The bank account has transactions on the debit side and the credit side� To determine what the net

resultis(iehowmuchmoneyisleftinthebankaccount)theaccountmustbebalanced.

An account with entries on both the debit and the credit sides, have to be balanced (to

balance is to nd the nal amount on the account).

To balance the bank account:

z

Add the debit side of the bank account and write down the total in pencil: R40 000 +

R50 000 = R90 000.

zAdd the credit side of the bank account and write down the total in pencil: R1 200.

zThe debit total of the bank account is more than the credit total. To make the two sides

equal the credit side needs an amount of R90 000 – R1 200 = R88 800. This is the balancing

amount and is recorded on the side of the T-account that is the smallest, in this case,

the credit side. It is shown as a balance c/d.

z

The account is then totalled (the biggest total in pencil, that is the debit side total of

R90 000) and the balance is b/d on the debit side.

zThe bank has a debit balance because the entity has an amount of R88 800 left in the

bank account – which represents an asset of the entity.

28

FAC1501/1

Dr Bank 1Cr

Date Details Fol RDate Details Fol R

20�6

Jan

Feb

1

1

Capital

Long-term loan:

Uni Bank

40 000

50000

20�6

Jan

1

31

Tools and equipment

Balance

c/d

1 200

88 800

90 000 90 000

Balance b/d 88 800

Dr Capital 2Cr

Date Details Fol RDate Details Fol R

20�6

Jan 1Bank 40 000

Dr Tools and equipment 3Cr

Date Details Fol RDate Details Fol R

20�6

Jan 1 Big Builders

Bank

7 000

1 200

8 200

To balance an account with only debit transactions, you only have to add the debit side,

that is, R7 000 + R1 200 = R8 200. If there is only one amount in an account it is left as is.

Dr Big Builders 4Cr

Date Details Fol RDate Details Fol R

20�6

Jan

1

Tools and equipment

7 000

Dr Long-term loan: Uni Bank 5Cr

Date Details Fol RDate Details Fol R

20�6

Jan 1Bank 50 000

29

FAC1501/1

101According to the balances on the ledger accounts in the general ledger of the assets,

liabilitiesandequity,itcanberecognisedinthestatementofnancialpositionasfollows:

BS ELECTRICAL

STATEMENT OF FINANCIAL POSITION AS AT 1 JANUARY 20.6

ASSETS Note R

Non-current assets 8 200

Tools and equipment 8 200

Current assets 88 800

Bank 88 800

Total assets 97 000

EQUITY AND LIABILITIES

Equity 40 000

Capital 40 000

Non-current liabilities 50 000

Long-term loan: Uni Bank 50 000

Current liabilities 7 000

Creditor(BigBuilders) 7 000

Total equity and liabilities 97 000

102Thestatementofnancialpositionisnowshowninitsverticalformatandthisisthecorrectformat

that must be used in future.

30

FAC1501/1

2.9 EXERCISES AND SOLUTIONS

3EXERCISE 1

(a) Denetheconceptofanaccountingentity.

(b) Describethenancialpositionofanentityintermsoftheaccountingequation.

(c) Explain the nature of

(i) assets

(ii) equity

(iii) liabilities

(d) Nametwosourcesofnancing.

(e) Whatismeantbythedouble-entryprinciple?

4SOLUTION: EXCERCISE 1

(a) Anaccountingentityisanyentityforwhichseparatenancialrecordsarekept.

(b) ASSETS = EQUITY + LIABILITIES

(c) (i) Assetsarethepossessionsoftheentity.

(ii) Equity is the interest which the owner has in the business and which the entity therefore

owes to him�

(iii) Liabilitiesarecreditors’interestorinterestsofpartiesotherthantheowner(s).Liabilitiesare

therefore the debts of the entity�

(d) Theownerandcreditors.

(e) Inprincipleitmeansthateverytransactionhasadualeffectontheelementsoftheaccounting

equationandthataftereverytransactiontheaccountingequationmust remain in balance�

5EXERCISE 2

103TheassetsofMaxiServicesamounttoR30000anditsliabilities(creditors)toR5000.

6REQUIRED

Calculate the equity�

7SOLUTION: EXCERCISE 2

104Usetheaccountingequation.Theamountswhicharegivenaresubstitutedfortheappropriatesymbol

andthevalueoftheunknownsymboliscalculated.

105A = E + L

106E = A – L

107E = R30 000 – R5 000

108E = R25 000

31

FAC1501/1

8EXERCISE 3

109TTomistheownerofZebraServiceswhichoffersacarpetcleaningservice.On30November20.6

ZebraServicesownsequipmentamountingtoR100000.ClientsoweR40000forservicesrendered

andZebraServicesowesR20000toasupplierforpartspurchased.ZebraServicesalsohasR10000

in cash in the bank�

9REQUIRED

Show the accounting equation and determine the equity�

10SOLUTION: EXCERCISE 3

110Step 1: Identify the assets:

111 Equipment = R100 000

112 Debtors = R40 000

113 Cash = R10 000

114Step 2: Identify the liabilities:

115 Creditors control = R20 000

116Substitute these amounts into the equation:

117A = E + L

118E = A – L

119E = R(100000+40000+10000) – R20000

120E = R150 000 – R20 000

121E = R130 000

32

FAC1501/1

122ZebraService’snancialpositioncanalsobepresentedintheformofastatementofnancialposition

as follows:

ZEBRA SERVICES

STATEMENT OF FINANCIAL POSITION AS AT 30 NOVEMBER 20.6

ASSETS REQUITY AND LIABILITIES R

Equipment

Debtors

Cash in bank

100 000

40 000

10 000

Equity

Creditors

130 000

20 000

150 000 150 000

11EXERCISE 4

Calculatethemissingguresusingtheaccountingequation:

R

(a) Bank = 4 000

Vehicles = 5 000

Equipment = 7 000

Equity = ?

(b) Equity = 150 000

Loan = 50 000

Bank = ?

Machinery = 190 000

(c) Bank = 5 000

Debtors = 15 000

Buildings = 100 000

Furniture = 40 000

Creditors = 50 000

Equity = ?

(d) Equity = 60 000

Loan = 10 000

Creditors = 6 000

Assets = ?

33

FAC1501/1

12SOLUTION: EXCERCISE 4

(a) A = E + L

E = A – L

E = R(4000+5000+7000) – R0

E = R16 000

(b) A = E + L

R190 000 + Bank = R150 000 + R 50 000

Bank = R200 000 – R190 000

Bank = R 10 000

(c) A = E + L

E = A – L

E = R(5000+15000+100000+40000) – R50000

E = R160 000 – R50 000

E = R110 000

(d) A = E + L

A = R60000 + R(10000+6000)

A = R76 000

34

FAC1501/1

13SELF-ASSESSMENT

123After you have worked through this learning unit, are you

able to:

z

classify the different elements of financial state-

mentscorrectly?

zdeneanasset?

zdenealiability?

zdeneincome?

zdeneexpenses?

z

explainthedifferencebetween(andgiveexamplesof)

non-currentassetsandcurrentassets?

z

explainthedifferencebetween(andgiveexamplesof)

non-currentliabilitiesandcurrentliabilities?

z

explainthedifferencebetween(andgiveexamplesof)

incomeandexpenses?

z

list the rules for debiting and crediting different type of

accountsconcerningassets,equityandliabilities?

z

correctlyclassifyanygivenaccountconcerningassets,

equityandliabilities?

z

correctlyenteranygiventransactionconcerningassets,

equityandliabilitiesintotheaccountingequation?

z

correctly apply the accounting equation to any given

transactionconcerningassets,equityandliabilities?

z

correctlyenteranygiventransactionconcerningassets,

equityandliabilitiesintheledgeraccounts?

zprepareastatementofnancialposition?

J

J

J

J

J

J

J

J

J

J

J

J

J

J

K

K

K

K

K

K

K

K

K

K

K

K

K

K

L

L

L

L

L

L

L

L

L

L

L

L

L

L

IfyouhavemarkedallJ you may continue to the next learning unit �

124IfyouhavemarkedanyKyouhavetorevisethatspecicsection.

125IfyouhavemarkedanyLyouhavetore-studythatspecicsection.

FAC1501

Introductory Financial

Accounting

THE ACCOUNTING

EQUATION: FINANCIAL

PERFORMANCE

LEARNING UNIT 3

1

36

FAC1501/1

2OVERVIEW

Learning outcomes ���������������������������������������������������������������������������������������������������������������������������� 36

Key concepts ������������������������������������������������������������������������������������������������������������������������������������� 36

Assessment criteria ��������������������������������������������������������������������������������������������������������������������������� 37

3�1 Introduction ���������������������������������������������������������������������������������������������������������������������������� 37

3�2 The accounting equation: Financial performance ������������������������������������������������������������������ 37

3�3 The trial balance �������������������������������������������������������������������������������������������������������������������� 46

3.4 Theprotorlossaccount ������������������������������������������������������������������������������������������������������� 47

3.5 Thestatementofprotorlossandothercomprehensiveincome ����������������������������������������� 50

3�6 Summary �������������������������������������������������������������������������������������������������������������������������������� 51

3�7 Exercises and solutions ���������������������������������������������������������������������������������������������������������53

Self-assessment �������������������������������������������������������������������������������������������������������������������������������� 60

LEARNING OUTCOMES

1After studying this learning unit you should be able to:

1

zunderstand the accounting equation concerning income and expenses

zexplaintheeffectsofnancialaccountingentriesconcerningincomeandexpensesontheac-

counting equation

zprepare entries in general ledger accounts of income and expenses

zprepareatrialbalanceforaserviceentity

zprepareaprotorlossaccountforaserviceentity

zprepareastatementofprotorlossandothercomprehensiveincomeforaserviceentity

KEY CONCEPTS

zIncome

zExpenses

zDebtors

zTrial balance

zProtorlossaccount

zStatementofprotorlossandothercomprehensiveincome

37

FAC1501/1

ASSESSMENT CRITERIA

zBusiness transactions concerning income and expenses are explained with

appro priate examples�

z

Accounting policy is demonstrated according to the right methods and procedures

when recording in the accounting equation format and in the ledger accounts�

z

Expensesandincomeandgainsandlossesaredenedandclassiedfor

recognitioninthestatementofprotorlossandothercomprehensiveincome.

3.1 INTRODUCTION

2Theobjectiveofeveryentityistoearnaslargeaprotaspossible.Itisthereforenecessarytodetermine

thenancialperformanceoftheentitybycalculatingthenancialresultoveraspecicperiod.

3.2 THE ACCOUNTING EQUATION: FINANCIAL PERFORMANCE

3Thenancialresultofanentityismeasuredintermsoftheprotorlosswhichtheentityhasmade

overaspecicperiod.Thisperiodisknownasthenancialperiodandisusuallyoneyear.

An entity makes a prot when the income it has earned from its business activities is more

than the expenditure it has incurred in generating or producing that income.

An entity makes a loss when the expenditure it has incurred in generating or producing

income is more than the income it has earned.

PROFIT/LOSS FOR THE YEAR = INCOME – EXPENSES

4Anentitymustearnanincometobeabletopayitsexpenses.Protfortheyearistheowner’sreward

forthecapitalinvestedandtheentrepreneurialspiritshown.

Prot (gains) or income is credited because it increase the equity (capital) amount owed to

the owner of the entity. If equity increases the account must be credited.

Dr (debit side) Capital (credit side) Cr

– (decrease) + (increase)

5Thefollowingrulecanbeappliedtoprot/income:

Dr (debit side) Prot/income (credit side) Cr

Always credited

– (decrease) + (increase)

38

FAC1501/1

INCOME

Prot/income is the increase in

economic benets of an entity during an

accounting period which results in an

increase in equity. Such an increase can

be the result of an increase in assets or

a decrease in liabilities.

REVENUE PROFIT/GAINS

Revenue earned from the entity’s

normal activities (daily operating

activities),forexample:

Gains are increases in economic

benets, which do not arise from the

normal activities of the entity, for

example:

zfees earned zprotonsaleofnon-currentasset

zsales

zinterest income

zrental income

zcommission income

zcreditlossesrecovered

6Expenses are incurred to earn income�

Losses or expenses are debited because it decreases the equity (capital) amount owed

to the owner of the entity. If equity decreases the losses or expense accounts must be

debited.

Dr (debit side) Capital (credit side) Cr

– (decrease) + (increase)

7Thefollowingrulecanbeappliedtolosses/expenses:

Dr (debit side) Losses/expenses (credit side) Cr

Always debited

+ (increase) – (decrease)

39

FAC1501/1

EXPENSES

Losses/expenses are the outow of

economic benets (payments/losses)

during the accounting period, which

results in a decrease in equity. Such a

decrease can be the result of a decrease

in assets or an increase in liabilities.

EXPENSES LOSSES

Expenses are incurred in the normal

courseoftheentity’sactivities.They

arisefromthegenerationofincome,

for example:

Losses are decreases in economic

benets, which do not arise from

the normal activities of the entity, for

example:

zCost of sales zLoss on sale of non-current asset

zRental expenses

zInterest expenses

zWages and salaries

zAdvertising

zCredit losses

zInsurance

zRepairs and maintenance

zTelephone expenses

zWater and electricity

zPostage

zRates and taxes

zStationery

zConsumables

zPackingmaterials

zBankcharges

zDepreciation

zAdministrativeexpenses

40

FAC1501/1

8Let’sconsiderafewmoretransactionsofMrBingoleSitholeforthe20.6nancialyearthatgenerate

incomeorgiverisetoexpenditure.Thenancialyearendsannuallyon31December.

9Transaction 5:

10MrBingoleSitholerenderedaserviceon15January,forcash,toaclientfortheamountofR60000.

11Explanation:

12Received money for services rendered, therefore the bank account (an asset)

increases and must be debited�

Dr (debit side) Assets (credit side) Cr

+ (increase) – (decrease)

13Servicesrenderedarean income that increases the prot for the year.Therefore,equity increased

and services rendered account must be credited� You will now see that the double entry principle

has been adhered too�

Dr (debit side) Prot/income (credit side) Cr

– (decrease) + (increase)

14The effect of the transaction on the accounting equation can be illustrated as follows:

A=E+L

Bank Tools and

equipment

Capital Income/

expenditure

Big Builders

(creditor)

Uni Bank

(long-term

loan)

R R R R R R

88 800 8 200 40 000 7 000 50 000

+ 60 000 + 60 000

148 800 8 200 =40 000 60 000 +7 000 50 000

15

41

FAC1501/1

16The above transaction will be recorded in the ledger accounts as follows:

171. The debit-side of the bank account:

Dr Bank 1Cr

Date Details Fol RDate Details Fol R

20�6

Jan

1

15

Capital

Long-term loan: Uni

Bank

Servicesrendered

(account to be

credited)

40 000

50 000

60 000

20�6

Jan 1 Tools and equipment 1 200

182. The credit-entry in the services rendered account:

Dr Services rendered 2Cr

Date Details Fol RDate Details Fol R

20�6

Jan 15 Bank(account to be

debited)

60 000

19Transaction 6:

20MrBingoleSitholerenderedaserviceon16January,oncredit,toMBeautyfortheamountofR20000.

21Explanation:

22ClientsoweBSElectricalmoney.Theseclientsarecalleddebtors(resourcecontrolledbytheentity),as

aresultofpastevents(renderingofservices),andfromwhichfutureeconomicbenetsareexpected

(moneytobereceived).Therefore,itisanasset.Assets increased and M. Beauty (a debtor) must

be debited�

A person who owes money to the entity is a debtor (asset).

Dr (debit side) Assets (credit side) Cr

+ (increase) - (decrease)

23Services rendered is an income that increases the prot for the year. Therefore, equity

increased and services rendered account must be credited�

Dr (debit side) Prot/income (credit side) Cr

– (decrease) + (increase)

24

42

FAC1501/1

25The effect of the transaction on the accounting equation can be illustrated as follows:

A = E + L

Bank Tools and

equipment

M. Beauty

(debtor)

Capital Income/

expenditure

Big

Builders

(creditor)

Uni Bank

(long-term

loan)

R R R R R R R

88 800 8 200 40 000 7 000 50 000

+ 60 000 + 60 000

+ 20 000 + 20 000

148 800 8 200 20 000 =40 000 80 000 +7 000 50 000

26The above transaction will be recorded in the ledger accounts as follows:

271. The debit-side of M Beauty’s account:

Dr M. Beauty 6 Cr

Date Details Fol RDate Details Fol R

20�6

Jan 16 Servicesrendered

(account to be

credited)

20 000

282. The credit-entry in the services rendered account:

Dr Services rendered 7Cr

Date Details Fol RDate Details Fol R

20�6

Jan 15

16

Bank

M.Beauty(account

to be debited)

60 000

20 000

29Transaction 7:

30On28Januarythebusiness’stelephoneaccountforJanuarywaspaidbycheque,R1200.

31Explanation:

32Telephone expenses is an expense that decreases the prot for the year. Therefore, equity

decreased and the telephone expense account must be debited�

Dr (debit side) Losses/expenses (credit side) Cr

+ (increase) – (decrease)

43

FAC1501/1

33Paidmoneyforthetelephoneaccount,thereforethebank account (an asset) decreases and must

be credited� To complete the double entry the appropriate expense account must be debited�

Dr (debit side) Assets (credit side) Cr

+ (increase) – (decrease)

34The effect of the transaction on the accounting equation can be illustrated as follows:

A = E + L

Bank Tools and

equipment

M Beauty

(debtor)

Capital Income/

expenditure

Big

Builders

(creditor)

Uni Bank

(long-term

loan)

R R R R R R R

88 800 8 200 40 000 7 000 50 000

+60000 + 60 000

+ 20 000 +20000

–1200 –1200

147600 8 200 20000 =40 000 78800 +7 000 50 000

35The above transaction will be recorded in the ledger accounts as follows:

361. The entry on the debit-side of the telephone expenses account:

Dr Telephone expenses 8Cr

Date Details Fol RDate Details Fol R

20�6

Jan 28 Bank(account to be

credited)

1 200

372. The credit-entry in the bank account:

Dr Bank 1Cr

Date Details Fol RDate Details Fol R

20�6

Jan

1

15

Capital

Long-term loan: Uni

Bank

Servicesrendered

40 000

50 000

60 000

20�6

Jan 1

28

Tools and equipment

Telephone expenses

(account to be

debited)

1 200

1 200

38

44

FAC1501/1

39Transaction 8:

40On31Januarythereceptionist’ssalaryforJanuarywaspaidbycheque,R6000.

41Explanation:

42Salaries account is an expense that decreases the prot for the year. Therefore, equity

decreased and salaries account must be debited�

Dr (debit side) Losses/expenses (credit side) Cr

+ (increase) – (decrease)

43Paid the salary of the receptionist, therefore the bank account (an asset) decreases and must

be credited. To complete the double entry the appropriate expense account must be debited.

Dr (debit side) Assets (credit side) Cr

+ (increase) – (decrease)

44The effect of the transaction on the accounting equation can be illustrated as follows:

A = E + L

Bank Tools and

equipment

M. Beauty

(debtor)

Capital Income/

expenditure

Big

Builders

(creditor)

Uni Bank

(long-term

loan)

R R R R R R R

88800 8 200 40 000 7 000 50 000

+60000 + 60 000

+ 20 000 + 20 000

–1200 – 1 200

–6000 – 6 000

141600 8 200 20000 =40 000 72 800 +7 000 50 000

45The above transaction will be recorded in the ledger accounts as follows:

461. The debit-side of the salaries account:

Dr Salaries 9Cr

Date Details Fol RDate Details Fol R

20�6

Jan 31 Bank(account to be

credited)

6 000

47

45

FAC1501/1

482. The credit-entry in the bank account:

Dr Bank 1Cr

Date Details Fol RDate Details Fol R

20�6 20�6

Jan

1

15

Capital

Long-term loan: Uni

Bank

Servicesrendered

40 000

50 000

60 000

Jan

1

28

31

Tools and equipment

Telephone expenses

Salaries (account to

be debited)

1 200

1 200

6 000

49Asummaryofalltheledgeraccountsinthegeneralledger,attheendofJanuary20.6areasfollows:

50Thebankaccountmustbebalancedoff.

51BS ELECTRICAL

52GENERAL LEDGER

Dr Bank 1Cr

Date Details Fol RDate Details Fol R

20�6

Jan

Feb

1

15

1

20�6

Jan

1

28

31

Capital

Long-term loan: Uni

Bank

Servicesrendered

40 000

50 000

60 000

Tools and equipment

Telephone expenses

Salaries

Balance

c/d

1 200

1 200

6 000

141 600

150 000 150 000

Balance

b/d

141 600

Dr Capital 2Cr

Date Details Fol RDate Details Fol R

20�6

Jan 1 Bank 40 000

Dr Tools and equipment 3Cr

Date Details Fol RDate Details Fol R

20�6

Jan 1 Big Builders

Bank

7 000

1 200

8 200

53

46

FAC1501/1

Dr Big builders 4Cr

Date Details Fol RDate Details Fol R

20�6

Jan 1 Tools and equipment 7 000

Dr Long-term loan: Uni Bank Account 5Cr

Date Details Fol RDate Details Fol R

20�6

Jan 1Bank 50 000

Dr M Beauty 6 Cr

Date Details Fol RDate Details Fol R

20�6

Jan 16 Servicesrendered 20 000

Dr Services rendered 7Cr

Date Details Fol RDate Details Fol R

20�6

Jan 15

16

Bank

MBeauty

60 000

20 000

Dr Telephone expenses 8Cr

Date Details Fol RDate Details Fol R

20�6

Jan 28 Bank 1 200

Dr Salaries 9Cr

Date Details Fol RDate Details Fol R

20�6

Jan 31 Bank 6 000

54Theledgeraccountsinthegeneralledgernumberedfrom1to6areassetaccounts,liabilityaccounts

andequityaccounts.Thesebalanceswillappearinthestatementofnancialposition.Theledger

accountsinthegeneralledgernumberedfrom7to9areallincome/protaccountsandexpense/loss

accounts� The arithmetical correctness of the recording of transactions in the general ledger must be

testedonaregularbasis.Thisusuallytakesplaceoncealltransactionsuptoandincludingacertain

date(inthiscase for the monthof January)have been recordedin the general ledger and before

anynalnancialstatementsareprepared.Atrialbalancewillbecompiledtocheckthearithmetical

correctness of the recording of transactions in the general ledger�

3.3 THE TRIAL BALANCE

55The total of all the debit balances on the ledger accounts should be equal to the total of all the

credit balances on the ledger accounts, because all the transactions should have been recorded

47

FAC1501/1

inaccordance withthedouble-entryprinciple.Todeterminewhetherthisisso,the balancesofall

accountsaredeterminedandrecordedinastatementknownasthetrialbalance.

A trial balance is a list of all the balances of all the accounts in the general ledger on a

particular date.

56The names and balances are recorded in the trial balance in the order in which they appear in the

general ledger� There are two columns in which debit balances and credit balances are recorded� The

naltotalsofthetwocolumnsshouldalwaysbethesame.

BS ELECTRICAL

TRIAL BALANCE AS AT 31 JANUARY 20.6

Debit Credit

R R

Bank 141 600

Capital 40 000

Tools and equipment 8 200

Big Builders 7 000

Long-termloan:UniBank 50 000

M.Beauty 20 000

Servicesrendered 80 000

Telephone expenses 1 200

Salaries 6 000

177 000 177 000

57Theerrorswhichmayberevealedbyatrialbalancewillbediscussedindetailinalaterlearningunit.

Thedebitbalancestotalisequaltothecreditbalancestotalandtheprotorlossaccountcannow

be compiled�

3.4 THE PROFIT OR LOSS ACCOUNT

58IfMrBingoleSitholewantstodetermineafteronemonthwhetheritisworthwhileforhimtocarryon

thebusiness,theprot/incomeaccountsandlosses/expenseaccountsmustbeclosedofftotheprot

orlossaccountsothattheprotforthemonthcanbecalculated.

59Thenancialresultofanentityismeasuredintermsoftheprotorlosswhichtheentityhasmade

overaspecicperiod.Thisperiodisknownasthenancial period and is usually one year�

At the end of the nancial period (usually a year) all expense/loss accounts and income/

prot accounts of a service entity must be closed off to a prot or loss account which

forms the basis for the preparation of a statement of prot or loss and other comprehen-

sive income.

60

48

FAC1501/1

61Explanation of the transfer of income to the prot or loss account:

62Tocloseofftheservicesrenderedaccount(income),theservices rendered account must be debited

withR80000,whichisequaltothetotaloftheamountsonthecreditside(R60000+R20000).There

is no total on the debit side� To balance off the ledger account the total amount of R80 000 will be

entered on the debit side� The name of the account that must be credited to complete the double-entry

isprotorlossaccount.Theservicesrenderedaccountwillnowbalanceoff.

63The prot or loss account is credited with R80 000� This is done to adhere to the double-

entry principle�

Dr Services rendered 7Cr

Date Details Fol RDate Details Fol R

20�6

Jan 31 Protorloss(account

to be credited)

80 000

20�6

Jan 15

16

Bank

M.Beauty

60 000

20 000

80 000 80 000

64Explanation of the transfer of expenditure to the prot or loss account:

65Tocloseoffthetelephoneexpenseaccount(anexpense),thetelephone expenses account must be

credited withR1200whichisequaltothetotalamountonthedebitside,R1200.Thereisnobalance

onthetelephoneexpenseaccountbecausethetotalamountistakentotheprotorlossaccount.

66The p ro t or loss account is debited with R1 200� This is done to adhere to the double-entry principle�

Dr Telephone expenses 8Cr

Date Details Fol RDate Details Fol R

20�6

Jan 28 Bank 1 200

20�6

Jan 31 Protorloss(account

to be debited)

1 200

1 200 1 200

67Thesameprincipleisapplicabletotheclosingoffofthesalariesaccount(anexpense)totheprotor

loss account�

68ThesalariesaccountmustbecreditedwithR6000,thetotaloftheamountonthedebitside,R6000.

Thereisnobalanceonthesalariesaccountbecausethetotalamountistakentotheprotorloss

account�

69The p ro t o r lo ss ac c ount is debited with R6 000� This is done to adhere to the double-entry principle�

70

49

FAC1501/1

Dr Salaries 9Cr

Date Details Fol RDate Details Fol R

20�6

Jan 31 Bank 6 000

20�6

Jan 31 Protorloss(account

to be debited)

6 000

6 000 6 000

71Theprotorlossaccountisanalaccountinthegeneralledgerandthestatementofprotorlossand

othercomprehensiveincomeisoneofthenancialstatementsanentityhastoprepare.Itusesthe

sameinformation,buttheoneisanaccountwhiletheotherisastatement(nodebitsideorcreditside).

72The prot or loss account is as follows:

Dr Prot or loss 10 Cr

Date Details Fol RDate Details Fol R

20�6 20�6

Jan 31 Telephone expenses

(account to be

credited)

Salaries (account to

be credited)

Capital(Protforthe

month) (account to

be credited)

1 200

6 000

72 800

Jan 31 Servicesrendered

(account to be

debited)

80 000

80 000 80 000

73Anentitymakesaprotwhentheincomeithasearnedismorethantheexpenditureithasincurred

ingeneratingorproducingthatincome.BSElectricalhasmadeaprotforthemonthbecausethe

incomeearned,R80000,ismorethantheexpensesincurredingeneratingtheincome,R1200+

R6000=R7200.Theincomeearned(prot)isR80000–R7200=R72800.

To calculate the prot or loss for the month (the same as calculating the

balance c/d):

zAdd the debit side of the prot or loss account and write down the total in pencil: R1 200

+ R6 000 = R7 200.

z

Add the credit side of the prot or loss account and write down the total in pencil: R80 000.