FAC1502E1_70539340 3..367 FAC1502 Study Guide

User Manual:

Open the PDF directly: View PDF ![]() .

.

Page Count: 365 [warning: Documents this large are best viewed by clicking the View PDF Link!]

#1997 University of South Africa

Revised edition 2005, 2006, 2007, 2008, 2009, 2010, 2011, 2013, 2014, 2016, 2017

All rights reserved

Printed and published by the

University of South Africa

Muckleneuk, Pretoria

FAC1502/1/2018

70539340

3B2

ACN-Style

CONTENTS

Introduction and overview of the module (v)

Topic A THE BASIC PRINCIPLES AND SPHERES OF ACCOUNTING 1

STUDY UNIT 1: THE NATURE OF ACCOUNTING THEORY, PRINCIPLES,

ACCOUNTING POLICY, PRACTICE AND PROCEDURES 3

STUDY UNIT 2: THE FINANCIAL POSITION 12

STUDY UNIT 3: THE FINANCIAL PERFORMANCE (RESULT) 18

STUDY UNIT 4: THE DOUBLE-ENTRY SYSTEM AND THE ACCOUNTING

PROCESS 22

Topic B COLLECTING AND PROCESSING THE ACCOUNTING DATA OF

ENTITIES 57

STUDY UNIT 5: PROCESSING ACCOUNTING DATA 59

STUDY UNIT 6: ADJUSTMENTS 98

STUDY UNIT 7: THE CLOSING-OFF PROCEDURE, DETERMINING

PROFIT OF AN ENTITY AND PREPARING

FINANCIAL STATEMENTS 116

Topic C ACCOUNTABILITY FOR CURRENT AND NON-CURRENT ASSETS 167

STUDY UNIT 8: CASH AND CASH EQUIVALENTS 169

STUDY UNIT 9: TRADE AND OTHER RECEIVABLES 191

STUDY UNIT 10: INVENTORY 220

STUDY UNIT 11: PROPERTY, PLANT AND EQUIPMENT 230

STUDY UNIT 12: OTHER NON-CURRENT ASSETS 259

Topic D ACCOUNTABILITY FOR CURRENT AND NON-CURRENT LIABILITIES 263

STUDY UNIT 13: CURRENT LIABILITIES 265

STUDY UNIT 14: NON-CURRENT LIABILITIES 277

Topic E ACCOUNTING REPORTING 285

STUDY UNIT 15: FINANCIAL STATEMENTS OF A SOLE

PROPRIETORSHIP 287

STUDY UNIT 16: NONPROFIT ENTITIES 314

STUDY UNIT 17: INCOMPLETE RECORDS 342

FAC1502/1/1/2018 (iii)

Aims of this module

After having studied this module, you should be able to

.apply the basic principles of accounting

.gather, process and record relevant information and prepare basic statement of profit or loss

and other comprehensive income (income statement), statement of changes in equity and

statement of financial position (balance sheet)

.record assets properly and be accountable for assets

.record liabilities properly and be accountable for liabilities

.keep proper records to ascertain the financial performance and financial position of sole

proprietors and non-profit entities

.prepare proper books from incomplete records

NOTE

ALL REFERENCES TO ‘‘ACCOUNTING’’ IN THIS STUDY GUIDE MEANS ‘‘FINANCIAL

ACCOUNTING’’.

(iv)

INTRODUCTION AND OVERVIEW

OF THE MODULE

We would like to welcome you as a student to Module I (FAC1502) of the Accounting I course.

This is the second module of a series of modules presented by the Department of Financial

Accounting at UNISA. The title of this module is Accounting concepts, principles and

procedures.

The courses in the Department of Financial Accounting are presented to degree level (i.e. with

Accounting III as a major subject). This, together with another major and other subjects, will

enable you to obtain either the BCom or BCompt degree. You may, having completed the

BCom or BCompt degree, study further in accounting by studying the BCom/BCompt (honours)

degree and thereafter the MCom/MCompt and DCom/DCompt degrees. This will take quite a

number of years and hard work, but it is possible! The ultimate goal of many students in

accounting is to become accountants and to follow the BCompt route.

Your first milestone will, however, be to master (i.e. to pass) Accounting FAC1502. You must,

therefore, ensure that you understand and know everything contained in this module as

everything is important. It is not only required of you to know it for the examination, but you WILL

need it in future modules or in your everyday walk of life (if you do not study accounting further).

You may ask: Why is it necessary to study accounting? The most important reason will be: To

account for income and expenditure, and for assets and liabilities. You may say: I do not earn

an income or incur expenses, or I do not owe money or own assets. Our question will be in turn:

What about your pocket money, remuneration for work or part time work, your study bursary or

study loan (which is not an income, but a liability) or what about your clothes, books and

stationery you had to buy for your studies? You have to account for the value of all of it. This

does not only apply to your personal case, but especially to the business you own or the

organisation where you work.

Many persons and/or organisations fall into financial difficulties or even go bankrupt and people

land in jail as a result of their lack of knowledge of accounting. We would like to help you to

prevent this.

Now that you know WHY you must study Accounting, what are the aims of the Accounting

FAC1502 module?

Refer again to the Aims of this module, specified above.

FAC1502/1 (v)

Study activities

In this study guide a variety of exercises are given. You should do these exercises by yourself

also and compare your attempt with the solutions given in the study guide. It also contains self-

evaluation questions, to encourage your active participation in the learning process. These are

a combination of reading, studying, doing and thinking activities that are presented in a flexible

manner. This will enable you to absorb the knowledge content of the topic, to practice your

understanding and to direct your thoughts.

This is important because as you encounter these study activities and actually perform them,

you will become directly involved in controlling the extent and the quality of your learning

experience. In short, how much and how well you learn, will depend on the extent of your

progress through the study activities, and the quality of your effort.

In cases where exercises are given, the questions should be answered without reference to

the study material. You should then mark your answer against the answer given in the study

guide. Where your answer differs from that given in the study guide, ask yourself why?, how?,

when?, where? what did I do wrong? If more than 25% is incorrect, try again to answer the

question without referring to the study guide or your previous attempt. Accounting is very much

a practical subject; the more you practice, the better.

Meaning of words

Outcomes are communicated and assessment criteria are phrased in terms of what you should

be able to do. This involves the use of action words, describing what you must do in the

learning activity.

The following list of words includes examples of the action words that you will encounter in this

module. (You need not study this.)

Meaning of action words

WORD MEANING

1 Read So as to obtain a broad and basic background, knowledge or

information; do not study.

2 Read thoroughly Necessary theory that needs to be clearly understood. You may be

assessed on this theory through short questions.

3 Study Learn with the view of gaining the highest level of understanding

and mastery which is necessary for examinations, further study

and/or career.

You will not be required to give a definition of a concept in the

examinations. You will, however be required to apply the theory in

the correct accounting format and to follow the correct steps/

procedures. For example, the layout and terminology to be used in

the preparation of financial statements are prescribed. You may not

use any other formats.

4 Prepare You must make ready or complete what is required on the basis of

previous study.

(vi)

TOPIC A

THE BASIC PRINCIPLES AND SPHERES

OF ACCOUNTING

Learning outcome

The learner should be able to describe, calculate and record the financial performance and

financial position of a sole proprietor, by using the basic accounting equation and the

double-entry system to record the various types of transactions.

1

FAC1502/1

CONTENTS

Study unit Page

1 THE NATURE OF ACCOUNTING THEORY, PRINCIPLES,

ACCOUNTING POLICY, PRACTICE AND PROCEDURES 3

2 THE FINANCIAL POSITION 12

3 THE FINANCIAL PERFORMANCE (RESULT) 18

4THE DOUBLE-ENTRY SYSTEM AND THE ACCOUNTING

PROCESS 22

2

FAC1502/1

STUDY UNIT

1

The nature of accounting theory,

principles, accounting policy, practice

and procedures

Learning outcome

You are able to explain what is meant by the nature of accounting theory, principles,

accounting policy, practice and procedures.

Contents Page

Key concepts 4

1.1 Introduction 4

1.2 What is accounting? 5

1.2.1 Definition 5

1.2.2 The nature of accounting 5

1.3 Universal accounting denominator 6

1.4 Forms of ownership 6

1.5 Users of financial information 6

1.5.1 Investors 7

1.5.2 Employees 7

1.5.3 Lenders 7

1.5.4 Suppliers and other trade payables 7

1.5.5 Customers 7

1.5.6 Government and their agencies 7

1.5.7 Public 7

1.6 The fields of accounting 7

1.6.1 Financial accounting 7

1.6.2 Management accounting 7

3

FAC1502/1

1.7 Accounting principles 8

1.8 Accounting policy 8

1.9 Disclosure of accounting policy 8

1.10 International Financial Reporting Standards (IFRS) 8

1.11 Accounting standards and statements 9

1.11.1 Introduction 9

1.11.2 The Conceptual Framework for Financial Reporting 2010 9

1.11.2.1 The objective of financial statements 9

1.11.2.2 Underlying assumption 9

1.11.2.3 The qualitative characteristics of financial statements 9

1.11.2.4 The elements of financial statements 9

1.11.2.5 Recognition and measurement of the elements of financial

statements 10

1.12 Exercise and solution 10

Self-assessment 11

KEY CONCEPTS

.financial information

.decision making

.nature of accounting

.unit of measurement

.forms of ownership

.fields of accounting

.accounting principles

.international financial reporting standards

.accounting statements

.accounting policy

.going concern

.qualitative characteristics

.elements of financial statements

BEFORE CONTINUING, STUDY TUTORIAL LETTER 101 UP TO THE FIRST ASSIGN-

MENT.

1.1 Introduction

In this module, we introduce you to the concepts, principles and procedures of accounting. The

first two study units are included mainly to give you some background knowledge. At first, the

information may appear to be rather confusing, but if you follow the study guide step by step,

working through all the examples in the prescribed book and exercises in this study guide, the

methods and procedures will become clear. To master this subject, you must get as much

practise as you can – so start early in the semester.

4

FAC1502/1

Over the centuries, accounting developed in conjunction with and as part of the economic

system and it performs an extremely useful and important function in society.

Through the ages, records were always kept by hand, but nowadays computers are being used

increasingly. Whichever method is used, the basic principles remain unchanged, since all

activities in a business are still expressed in terms of money and are recorded. However, it is

necessary to know the procedures used in a manual system in order to understand how a

computerised accounting system works.

Read paragraph 1.1 of the prescribed book.

GOLDEN RULE

Accounting CAN NOT be studied by merely reading/memorising. You need to practise,

practise and practise again!

1.2 What is accounting?

1.2.1 Definition

Study paragraph 1.2 of the prescribed book.

Accounting is therefore a process consisting of the following three activities:

.identifying those events that are evidence of economic activity (transactions) relevant to the

particular business or entity

.recording the monetary value of the economic events (transactions) in order to provide a

permanent history of the financial activities of a business. Recording involves keeping a

chronological diary of measured events in an orderly and systematic manner and classifying

and summarising economic events

.communicating the recorded information to interested users. This information is commu-

nicated through the preparation and distribution of accounting reports, the most common of

which are known as financial statements.

Read paragraphs 1.3 and 1.4 of the prescribed book.

GOLDEN RULE

Accounting records transactions in order to provide useful information for decision making.

1.2.2 The nature of accounting

Accounting is a specialised means of communication which is used to convey a specialised

message about an entity’s finances. The recipient of this specialised message (the user of

financial information) must understand it otherwise the information that is conveyed has no

value.

Accounting uses words and figures to convey financial information to the users of such

information. As you progress with your study of accounting you will become familiar with the

5

FAC1502/1

meaning of these words and figures, which are also known as the concepts, principles and

procedures of accounting. This knowledge will ultimately help you understand the message

contained in financial statements.

Each and every person who is involved in an entity uses financial information to a greater or

lesser degree. Each of us also needs to know something about accounting to manage our

personal financial affairs. Financial resources are limited or scarce, and if we are going to

spend them we must plan properly. Knowledge of accounting is therefore also useful in this

area.

Accounting is therefore a ‘‘language’’ used to convey financial information to interested parties.

Read paragraph 1.7 in the prescribed book thoroughly.

1.3 Universal accounting denominator

The common unit of measurement in accounting is money and in the RSA, the currency is

known as the rand. All an entity’s transactions are converted into monetary values before being

processed. Using money as the common denominator, however, gives rise to two important

limitations:

.Not all events can be expressed in monetary terms.

.The value of money is unstable and is influenced by many economic factors such as

inflation.

1.4 Forms of ownership

The form of a business ownership refers to the way in which a business is owned and

managed – how the original funds for starting the business were raised and how the profits,

losses and risks in the business are divided.

In the RSA, there are four main forms of ownership, namely:

.sole traders

.partnerships

.close corporations

.companies

Apart from these main forms of entities, non-profit entities can also be distinguished.

Study paragraph 1.5 and read paragraph 1.6 thoroughly in the prescribed book.

1.5 Users of financial information

Financial information is required by many users, who analyse the information for various

decision-making purposes. The following are the most common users of this information:

6

FAC1502/1

1.5.1 Investors

1.5.2 Employees

1.5.3 Lenders

1.5.4 Suppliers and other trade creditors

1.5.5 Customers

1.5.6 Government and their agencies

1.5.7 Public

Study paragraphs 1.8 to 1.11 in the prescribed book.

1.6 The fields of accounting

Users of financial information can be subdivided into the following two categories:

.internal users – for example, management and employees

.external users – for example, investors, creditors and government

Two fields of accounting have developed as a result of this distinction between the users of the

information. Financial accounting is concerned with the provision of financial information to

mainly external parties, while management accounting is concerned with the provision of

financial information to people within the entity.

1.6.1 Financial accounting

This field of accounting is concerned with recording transactions and preparing the financial

statements for the entity as a whole. Financial accounting is governed by international financial

reporting standards (IFRS), which consists of external standards which must be adhered to.

These standards ensure the comparability of financial statements between entities.

1.6.2 Management accounting

Management accounting provides financial information for specific purposes. Managers use

this information in their decision making, which leads to the attainment of the objectives of the

entity. Without this financial information, it would be difficult for management to manage

effectively.

In this course we will be concentrating on financial accounting.

Study paragraph 1.12 and read paragraph 1.18 in the prescribed book.

GOLDEN RULE

Financial statements must reveal a fair presentation of the financial position, financial

performance and cash flow of an entity.

7

FAC1502/1

1.7 Accounting principles

In this study unit we turn our attention to the theory of accounting. You may well ask: ‘‘Why?

Accounting is supposed to be a practical subject’’. This is true, but no subject that is logically

structured can exist without a theoretical foundation.

The techniques used in the practice of accounting are based on conceptual and theoretical

ideas. These ideas are generally known as accounting principles.

1.8 Accounting policy

Situations often occur in our everyday lives that are repetitive (ie they are always the same),

but they would each have a different outcome if we were to act differently each time. If we do

not have some kind of guideline on how we should act in such cases, our actions would

probably be inconsistent. Our friends would think we were unreliable. If we lay down a guideline

so that we always act the same way in a particular situation, we can say that we are

determining a policy for our actions, which will result in our actions being consistent.

We encounter precisely the same situation in accounting. Transactions of a repetitive nature

frequently occur, and the requirement of consistency means that an entity has to establish an

accounting policy to determine exactly how such transactions should be treated. Accounting

policy is thus a set of decisions about how the entity will handle the same type of transaction in

order to achieve a consistent result.

1.9 Disclosure of accounting policy

Since an accounting policy represents an entity’s decisions about situations which it could deal

with in various ways, it has to disclose its accounting policy in its financial statements. For

example, an entity has to indicate what basis it has used to deal with the depreciation of

property, plant and equipment.

1.10 International Financial Reporting Standards (IFRS)

This is the next important concept that you will encounter in your accounting studies. For the

sake of conciseness, we will refer to this as IFRS.

If everyone were to develop his or her own language and grammatical rules, communication

would break down. We therefore have generally applicable language and grammar rules.

Accounting, as a specialised medium of communication, has precisely the same problem. If

each entity were to prepare financial reports according to its own accounting rules and its

interpretation of accounting theory and principles, chaos would result in the world of economics

and business.

Afoundation has therefore been developed over the years for the measurement and

disclosure of the results of financial events (transactions).

This foundation is a general framework and encompasses, in broad terms, accounting

concepts, principles, methods and procedures collectively known as IFRS.

In this study guide, we will sometimes disclose more information in the financial statements

than is required by IFRS. This is done to provide more detail and to help you understand

certain concepts.

8

FAC1502/1

1.11 Accounting standards and statements

1.11.1 Introduction

The objective of creating accounting standards for particular issues (eg for the treatment of

taxation in financial statements) is to limit the variety of available accounting practices, but

without striving for strict uniformity or creating a set of rigid rules for all circumstances. The

ultimate aim of accounting standards is to encourage widespread use of particular standards in

financial reporting and to eliminate undesirable alternatives.

1.11.2 The Conceptual Framework for Financial Reporting 2010

Bear in mind that the framework is not a standard. It is a framework ‘‘... which sets out the

objectives and concepts which underlie the preparation and presentation of financial

statements ...’’.

1.11.2.1 The objective of financial statements

Study paragraph 1.9 in the prescribed book again.

1.11.2.2 Underlying assumption

According to the framework, there is one underlying assumption for financial statements.

This is:

(1) the going concern.

Study paragraph 1.13 in the prescribed book.

1.11.2.3 The qualitative characteristics of financial statements

The fundamental qualitative characteristics are:

(1) relevance

(2) faithful representation

Further enhancements to the qualitative characteristics of financial information are:

(1) comparability

(2) verifiability

(3) timeliness

(4) understandability

Study paragraph 1.14 in the prescribed book.

1.11.2.4 The elements of financial statements

GOLDEN RULE

The following are elements of financial statements:

.Elements that measure the financial position (assets = equity + liabilities):

(1) assets

(2) liabilities

(3) equity

9

FAC1502/1

.Elements that measure profitability (profit or loss = increase or decrease in equity):

(4) income

(5) expenses

Study paragraph 1.15 in the prescribed book.

1.11.2.5 Recognition and measurement of the elements of financial statements

Study paragraphs 1.16 to 1.18 in the prescribed book.

1.12 Exercise and solution

We end this study unit with a few revision questions. It is in your own interest to try to answer

these by referring to the study unit or prescribed book.

Exercise

(1) Discuss the nature of accounting.

(2) What is the common unit of measurement in accounting?

(3) Name the four main forms of ownership.

(4) Discuss the different users of financial information.

(5) Differentiate between financial accounting and management accounting.

(6) Name the qualitative characteristics of financial information.

(7) Define the concept of accounting policy.

(8) What is meant by disclosure of accounting policy?

(9) Describe the concept of international financial reporting standards.

(10) Discuss the underlying assumption of financial statements.

(11) Name the fundamental qualitative characteristics of financial statements.

(12) Name the elements of financial statements.

Solution

(1) Refer to paragraph 1.2.2.

(2) The common unit of measurement in accounting is money.

(3) Sole trader

Partnership

Close Corporation

Company

(4) See section 1.5.

(5) See section 1.6.

(6) See section 1.14.3 in the prescribed text book.

(7) See section 1.8 in the study guide.

(8) See section 1.9 in the study guide.

(9) See section 1.10 in the study guide.

(10) See section 1.13 in the prescribed book.

(11) Relevance

Faithful representation

10

FAC1502/1

(12) Assets

Liabilities

Equity

Income

Expenses

SELF-ASSESSMENT

Now that you have studied this study unit, can you:

.describe the importance of financial information as a basis for decision making?

.discuss the different users of financial information and their needs?

.state the different forms of ownership?

.discuss the nature of accounting?

.explain the difference between financial and management accounting?

.name the qualitative characteristics of financial statements?

.explain what is meant by the accounting policy?

.explain what is meant by the disclosure of the accounting policy?

.explain what is meant by the international financial reporting standards?

.explain what is meant by the accounting standards and statements?

11

FAC1502/1

STUDY UNIT

2

The financial position

Learning outcome

Students should be able to describe what the primary purpose of accounting is and what is

understood by the double entry system. They should also be able to calculate the financial

position of an entity and the elements of the basic accounting equation.

Contents Page

Key concepts 12

2.1 Introduction 13

2.2 Accounting entity 13

2.3 Financial position 13

2.4 Net asset value 13

2.5 Application of the basic accounting equation (BAE) 13

2.6 The double-entry system 15

2.7 Revision exercises and solutions 15

2.7.1 Revision exercise 1 15

2.7.2 Revision exercise 2 16

Self-assessment 17

KEY CONCEPTS

.Accounting entity

.Accounting equation

.Financial position

.Assets

.Liabilities

.Equity

.Double-entry

.Net worth

12

FAC1502/1

2.1 Introduction

The primary purpose of accounting is to give information on the financial position and the

financial result of an entity. This study unit deals with the key elements of the financial position.

Read paragraph 2.1 of the prescribed book.

2.2 Accounting entity

Every entity for which separate financial records are kept is an accounting entity. It is extremely

important to see the business as a separate entity from its owners because transactions

entered into by the entity have to be dealt with from the point of view of the entity whose books

are being done.

Study paragraph 1.6 (again) as well as paragraph 2.2 of the prescribed book.

2.3 Financial position

The financial position of the entity is described in terms of assets and interests at a given time.

They are reflected in a statement of financial position, which is essentially an accounting report

on the financial position of an entity. The statement of financial positon communicates relevant

financial information to the owners, creditors and other interested parties.

Study paragraph 2.6 of the prescribed book.

2.4 Net asset value

The difference between the value of assets owned by an entity and the liabilities it has incurred

represents net asset value. If we express this as an equation, then

ASSETS 7LIABILITIES = NET ASSET VALUE

The net asset value represents the portion by which the assets exceed the liabilities. Net asset

value is therefore also called EQUITY.

Study paragraph 2.3 of the prescribed book.

2.5 Application of the basic accounting equation (BAE)

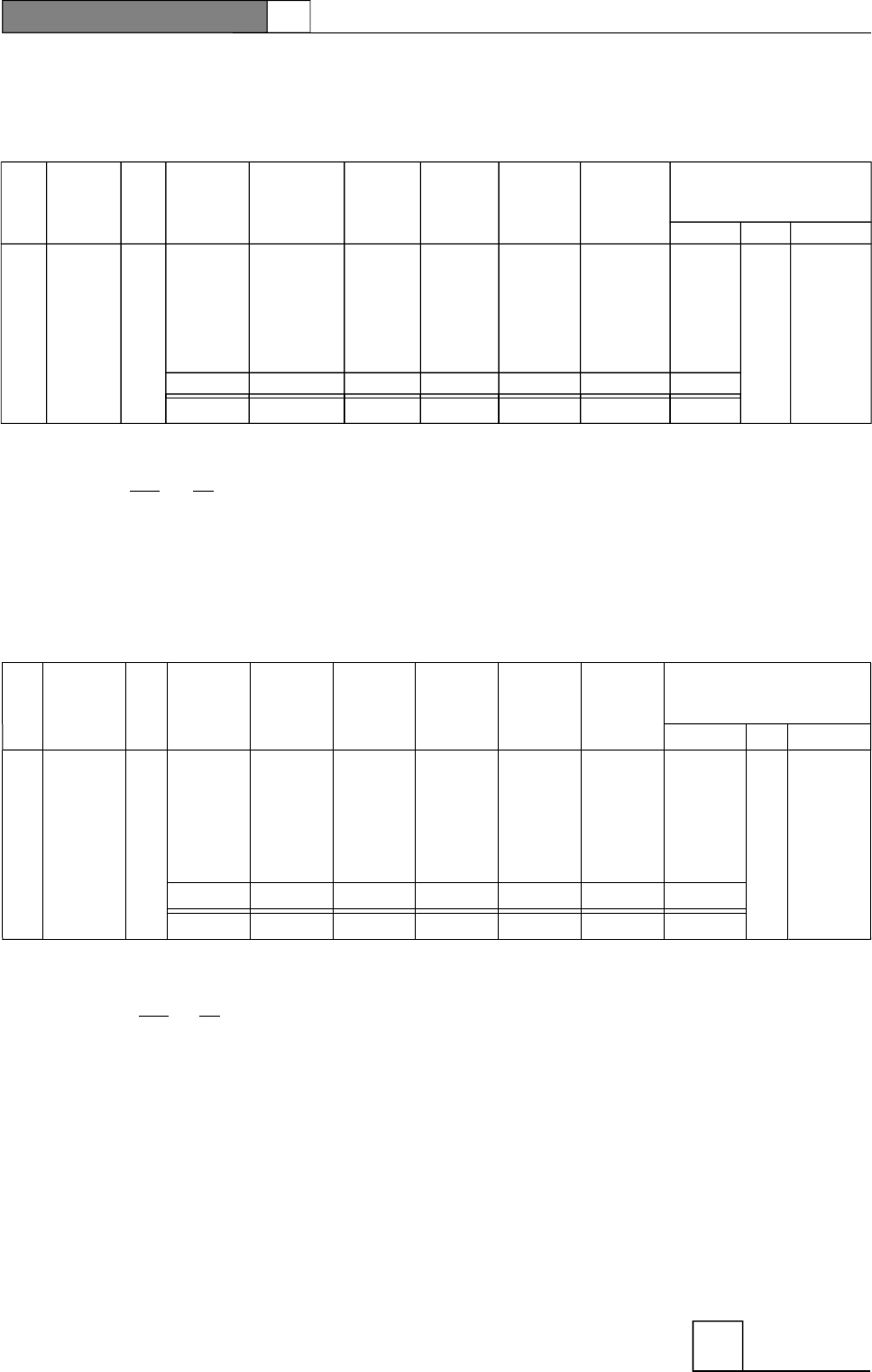

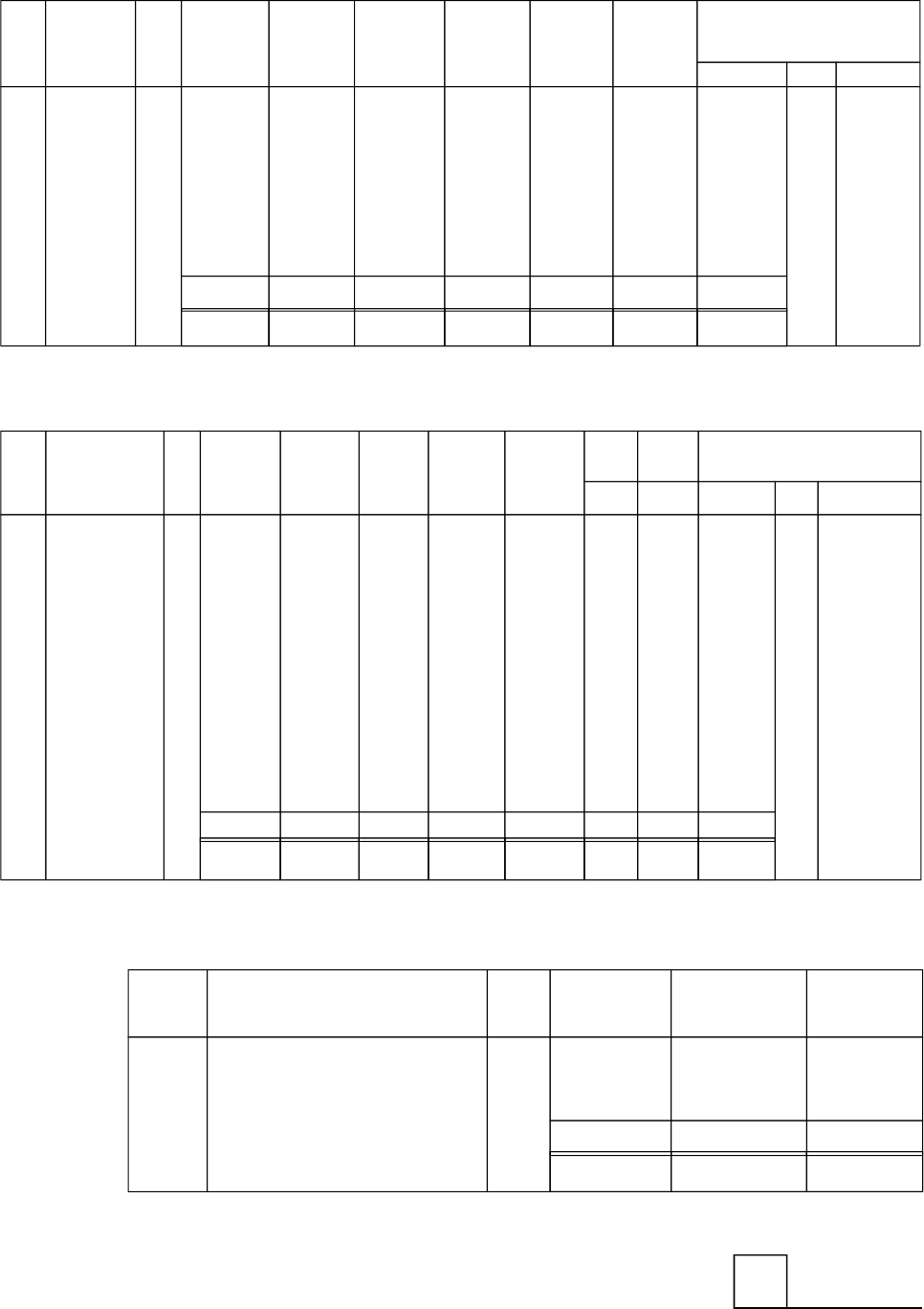

Exercise 1

The assets of Maxi Services amount to R30 000 and its liabilities (creditors) to R5 000.

Calculate the equity.

We use the BAE. The amounts which are given are substituted for the appropriate symbol and

the unknown symbol is calculated.

13

FAC1502/1

A = E + L

E = A – L

= R30 000 7R5 000

= R25 000

Exercise 2

T Tom is the owner of Zebra Services which offers a carpet cleaning service. On

30 November 20.1 Zebra Services owns equipment amounting to R100 000. Clients owe

R40 000 for services rendered and Zebra Services owes R20 000 to a supplier for parts

purchased. Zebra Services also has R10 000 in cash in the bank.

Show the BAE for Zebra Services and determine the equity.

Step 1: Identify the assets

Step 1: Equipment = R100 000

Step 1: Trade receivables = R40 000

Step 1: Cash = R10 000

Step 2: Identify the liabilities

Step 1: Trade payables = R20 000

Substitute these amounts into the equation:

A = E + L

E = A – L

= R(100 000 + 40 000 + 10 000) 7R20 000

= R130 000

Zebra Service’s financial position can also be presented in the form of statement of financial

position (previously known as balance sheet) as follows:

ZEBRA SERVICES

STATEMENT OF FINANCIAL POSITION (BALANCE SHEET) AS AT 30 NOVEMBER 20.1

ASSETS R EQUITY AND LIABILITIES R

Equipment 100 000 Equity 130 000

Trade receivables 40 000 Trade payables 20 000

Cash in bank 10 000

150 000 150 000

14

FAC1502/1

COMMENT

This statement of financial position (balance sheet) is in a basic form. Later we will deal

with statements of financial positions (balance sheets) in more detail.

Study paragraph 2.5 and 2.6 of the prescribed book.

2.6 The double-entry system

The double-entry system is based on the fact that every transaction affects two or more items

in the BAE. In principle it means that each transaction must be recorded in such a way that the

equation remains in balance. The dual effect which each transaction has on the elements of the

BAE is the fundamental principle on which all entries in an accounting system are based.

Study paragraphs 2.4, 2.6 and 2.7 of the prescribed book.

2.7 Revision exercises and solutions

2.7.1 Revision exercise 1

(1) Define the concept of an accounting entity.

(2) Describe the financial position of an entity in terms of the BAE.

(3) Explain the nature of

(a) assets

(b) equity

(c) liabilities

(4) Name two sources of financing.

(5) What is meant by the double-entry system?

Solution: Revision exercise 1

(1) An accounting entity is any entity for which separate financial records are kept.

(2) ASSETS = EQUITY + LIABILITIES

(3) (a) Assets are the possessions of the entity.

(b) Equity is the interest which the owner has in the business and which the entity

therefore owes to him.

(c) Liabilities are creditors’ interests or interests of parties other than the owner(s).

Liabilities are therefore the debts of the entity.

(4) The owner

Trade payables

(5) In principle it means that every transaction has a dual effect on the elements of the BAE

and that after every transaction the BAE must remain in balance.

15

FAC1502/1

2.7.2 Revision exercise 2

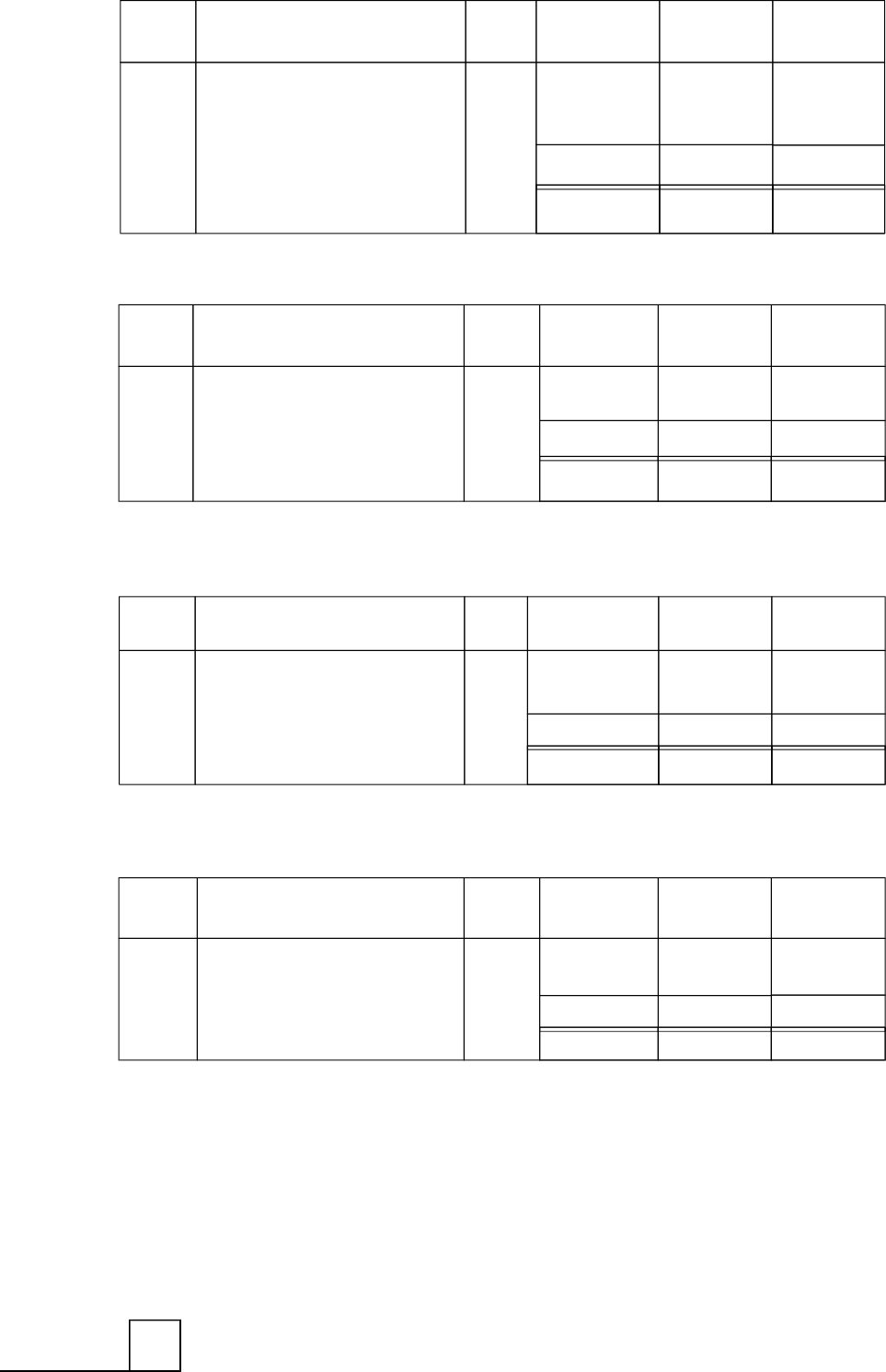

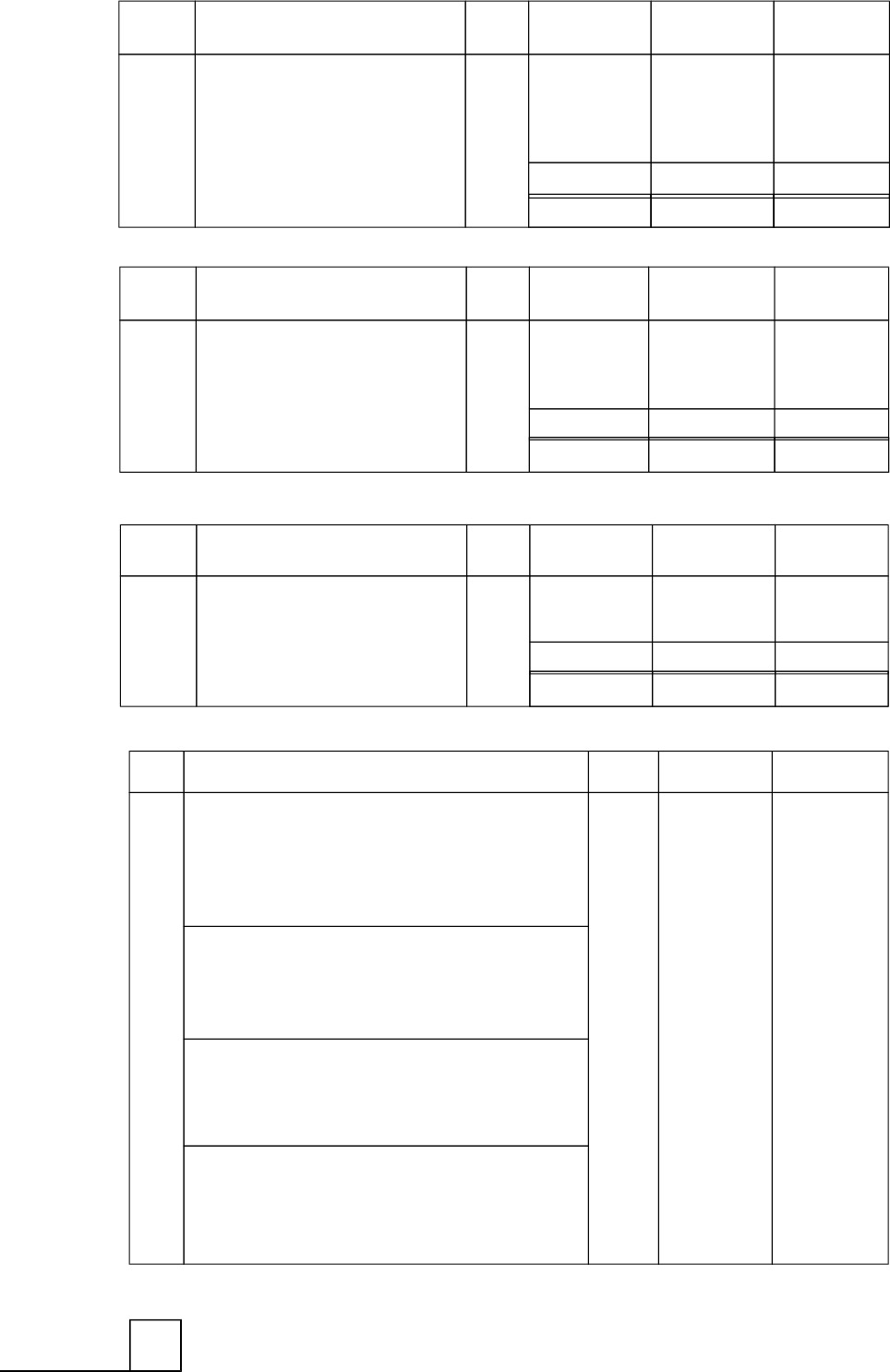

Calculate the missing figures using the BAE.

R

(1) Bank = 4 000

Vehicles = 5 000

Equipment = 7 000

Capital = ?

(2) Capital = 150 000

Loan = 50 000

Bank = ?

Machinery = 190 000

(3) Bank = 5 000

Trade receivables = 15 000

Buildings = 100 000

Furniture = 40 000

Trade payables = 50 000

Capital = ?

(4) Capital = 60 000

Loan = 10 000

Trade payables = 6 000

Assets = ?

Solution: Revision exercise 2

(1) A = E + L

E = A – L

= R(4 000 + 5 000 + 7 000) 7R0

= R16 000

(2) A = E + L

R190 000 + Bank = R(150 000 + 50 000)

R190 000 + Bank = R(150 000 + 50 000) 7R190 000

= R10 000

(3) A = E + L

E = A – L

= R(5 000 + 15 000 + 100 000 + 40 000) 7R50 000

= R160 000 7R50 000

= R110 000

(4) A = E + L

= R60 000 + R(10 000 + 6 000)

= R76 000

16

FAC1502/1

SELF-ASSESSMENT

Now that you have studied this study unit, can you:

.describe the primary purpose of accounting?

.describe an entity?

.describe the financial position of the entity?

.describe the double-entry system?

.calculate the elements of the basic accounting equation?

17

FAC1502/1

STUDY UNIT

3

The financial performance (result))

Learning outcome

Students should be able to apply the concepts of income and expenditure to determine the

gross and net profits (or losses) and the effect thereof on equity.

Contents Page

Key concepts 18

3.1 Introduction 19

3.2 The financial performance (result) 19

3.3 Income 19

3.4 Expenditure 19

3.5 Influence of profit or loss on equity 19

3.6 Statement of profit or loss and other comprehensive income (income

statement) (financial performance) 20

3.7 Statement of changes in equity 20

3.8 Accounting policies and explanatory notes 20

3.9 Revision exercises and solutions 20

3.9.1 Revision exercise 1 20

3.9.2 Revision exercise 2 21

Self-assessment 21

KEY CONCEPTS

.Financial result

.Profit/loss

.Income

.Expenditure

18

FAC1502/1

3.1 Introduction

In paragraph 2.3 we discussed the first component of the primary goal of accounting, which is

to determine the financial position of an entity as it is reflected in the statement of financial

position. In this study unit we discuss the second component of this primary goal, namely the

financial performance of the entity, and indicate how it is reflected in the form of a statement

of profit or loss and other comprehensive income.

Study paragraph 3.1 in the prescribed book.

3.2 The financial performance (result)

The financial result of an entity is measured in terms of the profit or loss which the entity has

made over a specific period, which is referred to as the financial period and which is normally

a year. An entity makes a profit when the income it has earned is more than the expenditure it

has incurred in generating or producing that income. The difference between the income and

expenditure is known as the profit or loss. Profit is the owner’s reward for the capital he or she

has invested and the entrepreneurial spirit he or she has shown. It therefore increases the

equity.

3.3 Income

The objective of every entity is to earn as large an income as possible.

Study paragraph 3.2.1 of the prescribed book.

3.4 Expenditure

Expenditure is incurred to earn income.

Study paragraph 3.2.2 of the prescribed book.

3.5 Influence of profit or loss on equity

Income (profit) increases and expenditure (losses) decreases the owner’s interest.

Study paragraph 3.3 of the prescribed book.

Exercise

The financial position (BAE) of T Payn, an attorney, on 28 February 20.0 is as follows:

A = E + L

R50 000 = R30 000 + R20 000

For the year ended 28 February 20.1 he had the following income and expenditure:

19

FAC1502/1

R

Income received 180 000

Salaries expense 100 000

Administrative costs 20 000

Insurance expense 10 000

Calculate T Payn’s equity on 28 February 20.1.

We use the equation which we discussed in paragraph 2.4 and 4.3:

Profit = Income 7Expenditure

= R180 000 7R(100 000 + 20 000 + 10 000)

= R180 000 7R130 000

= R50 000

E = R30 000 + R50 000

= R80 000

COMMENTS

.Capital plus profit together form the equity of the owner. See the above exercise —

R(30 000 + 50 000) = R80 000.

.Profit is income minus expenditure.

3.6 Statement of profit or loss and other comprehensive

income (income statement) (financial peformance)

The financial performance is measured in the statement of comprehensive income of an entity

(previously known as the income statement).

Study paragraph 3.4 of the prescribed book.

3.7 Statement of changes in equity

Study paragraph 3.5 of the prescribed book.

3.8 Accounting policies and explanatory notes

Study paragraphs 3.6 and 3.7 of the prescribed book.

3.9 Revision exercises and solutions

3.9.1 Revision exercise 1

(1) How is the financial performance (result) calculated in accounting terms? Which financial

report reflects the financial performance?

(2) Give three examples of income.

20

FAC1502/1

(3) Give three examples of expenditure.

(4) How is profit/loss determined for a financial period?

(5) Does a loss increase or decrease the equity of the owner?

Solution: Revision exercise 1

(1) Income minus expenditure. The statement of profit or loss and other comprehensive

income reflects the financial performance.

(2) Refer to paragraph 3.3.

(3) Refer to paragraph 3.4.

(4) Expenditure is subtracted from income. Refer to paragraph 3.2.

(5) A loss decreases equity.

3.9.2 Revision exercise 2

On 28 February 20.2 Alpha Services showed the following income and expenditure for the

financial year.

R

Income received 850 000

Salaries 520 000

Wages 50 000

Telephone expenses 4 000

Stationery 2 000

Interest received 1 000

Insurance 12 000

Calculate the net profit/loss of Alpha Services on 28 February 20.2.

Solution: Revision exercise 2

Income = Income received + Interest received

= R(850 000 + 1 000)

= R851 000

Expenditure = Salaries + Wages + Telephone + Stationery + Insurance

= R(520 000 + 50 000 + 4 000 + 2 000 + 12 000)

= R588 000

Profit = Income 7Expenditure

= R851 000 7R588 000

= R263 000

SELF-ASSESSMENT

Now that you have studied this study unit, can you:

.describe the concept income?

.describe the concept expenditure?

.calculate the profit (or loss)?

.calculate the effect of profit/loss on equity?

21

FAC1502/1

STUDY UNIT

4

The double-entry system and the

accounting process

Learning outcome

Students should be able to analyse and record transactions in the books of an entity and

prepare financial statements.

Contents Page

Key concepts 23

4.1 Introduction 23

4.2 The double-entry system 23

4.3 The effect of transactions on the basic accounting equation (BAE) 24

4.4 Transactions which affect only assets, equity and liabilities 24

4.4.1 Capital contributions 24

4.4.2 Acquisition of loans 25

4.4.3 Purchase of assets for cash 26

4.4.4 Buying assets on credit (debt) 26

4.4.5 Payments to creditors 27

4.4.6 Withdrawals by owner 27

4.5 Transactions which give rise to income and expenditure 28

4.5.1 Income (cash) 28

4.5.2 Expenditure (cash) 29

4.5.3 Income (credit) 29

4.5.4 Expenditure (credit) 30

4.5.5 Payments received from debtors 31

4.6 Summary of transactions 31

4.7 Basic form of a statement of financial position 32

4.8 Revision exercises and solutions 32

4.8.1 Revision exercise 1 32

4.8.2 Revision exercise 2 34

22

FAC1502/1

4.9 The general ledger account 36

4.9.1 Assets 36

4.9.2 Equity and liabilities 36

4.10 Balancing an account 36

4.11 Schematic representation 37

4.12 Recording of transactions in ledger accounts 38

4.13 The general ledger 40

4.14 The trial balance 43

4.15 Preparing financial statements 44

4.15.1 The statement of profit or loss and other comprehensive

income 44

4.15.2 The statement of changes in equity 45

4.15.3 The statement of financial position 46

4.15.4 Notes 47

4.16 Summary 47

4.17 Revision exercises and solutions 48

4.17.1 Revision exercise 1 48

4.17.2 Revision exercise 2 48

4.17.3 Revision exercise 3 49

4.17.4 Revision exercise 4 51

4.17.5 Revision exercise 5 53

Self-assessment 55

KEY CONCEPTS

.Debit and credit .Ledger

.Transactions .Contra account

.Effect on financial position .Folio number

.T-account .Trial balance

4.1 Introduction

We mentioned the double-entry system in paragraph 2.6 in the study guide — read that

paragraph again. To make a double-entry correctly, you need a good working knowledge of the

appropriate names for different things in accounting and particularly the concepts of ‘‘debit’’

and ‘‘credit’’. It is very important that you master this study unit since it explains the foundation

on which the accounting system is built.

Read paragraph 4.1 of the prescribed book.

4.2 The double-entry system

At this stage we are simply using the accounting equation as a teaching aid to explain the

analysis of transactions. The BAE does not form part of a formal accounting system.

To make a double-entry you must:

.Think about what the effect of the transaction is going to be on the BAE, in other words, how

it is going to affect the financial position of the entity.

.Identify the components (accounts) which are involved, that is the components which will

have the desired effect on the equation.

23

FAC1502/1

.Determine which account(s) has/have to be debited and which account(s) has/have to be

credited.

.Be sure that the amount(s) debited are equal to the amount(s) credited.

.Be able to indicate the date of the transaction.

.Indicate the name of the contra ledger account in the account in which you are doing the

entry. The contra account is the other account which is involved in the transaction: the one

account refers to the other.

.Indicate the folio number of the subsidiary journal.

4.3 The effect of transactions on the basic accounting

equation (BAE)

A transaction is an agreed upon transfer of value from one party to another which affects

(changes) the amount, nature or composition of an entity’s assets, liabilities or equity. In other

words it affects the BAE. Entering into a transaction gives rise to the first step in the accounting

cycle, namely the completion of a source document.

Transactions may

.affect assets and/or equity and/or liabilities

.generate income or give rise to expenditure

Study paragraph 4.2 of the prescribed book.

4.4 Transactions which affect only assets, equity and

liabilities

Below we give practical examples of transactions which affect only assets or interests. (A ‘‘+’’

indicates an increase and a ‘‘7’’ indicates a decrease.)

Study paragraphs 4.2.1 to 4.2.4 of the prescribed book.

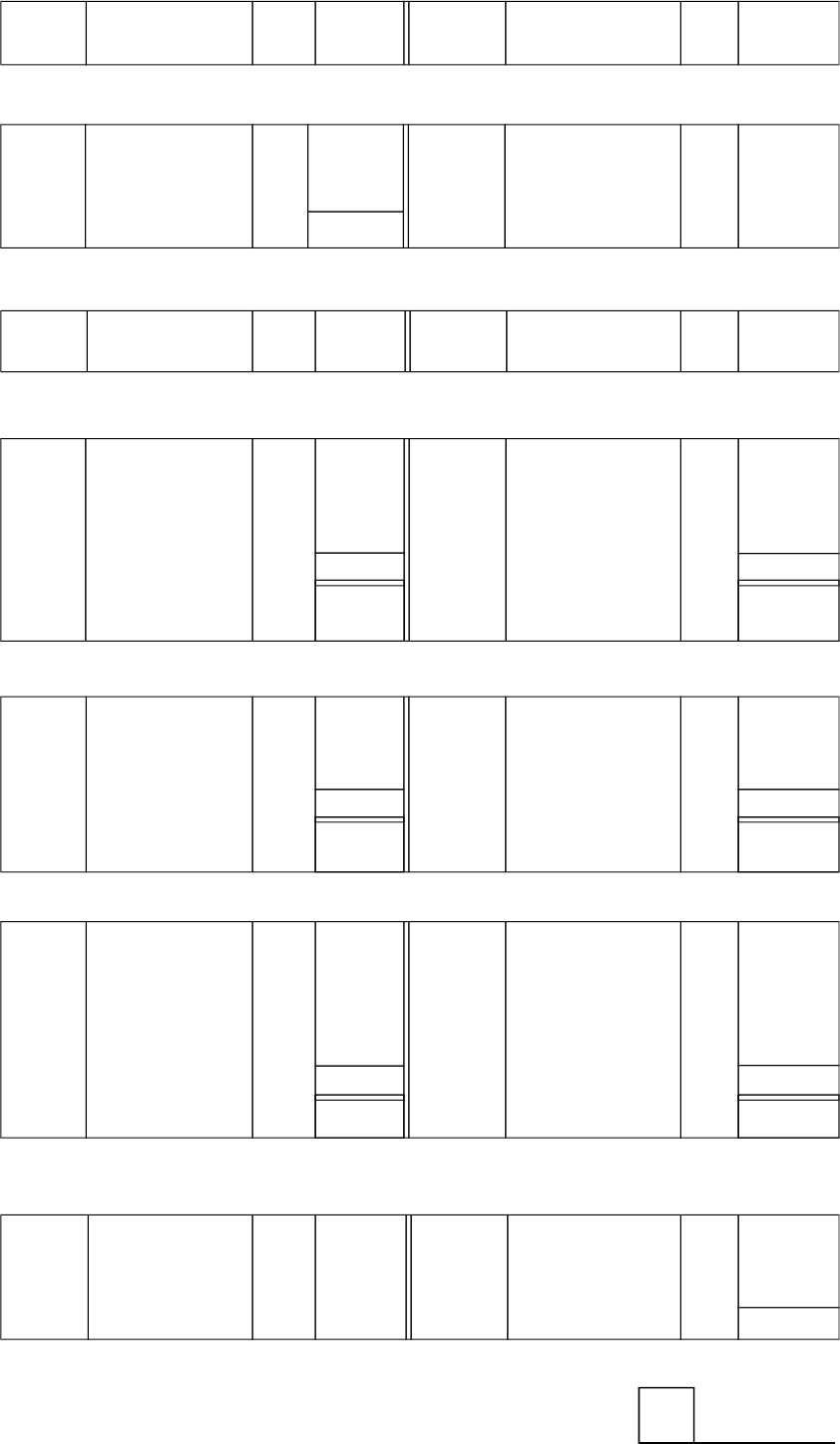

4.4.1 Capital contributions

Transaction

1 Feb 20.1

T Tom decided to start a carpet-cleaning business called Fix-’n-Mat. He

withdrew R130 000 from his personal savings account and deposited it in

Fix-’n-Mat’s bank account.

Analysis (1) The asset ‘‘Bank’’ increases by R130 000 and there is now money in

Fix-’n-Mat’s bank account.

(2) The owner, T Tom, provides Fix-’n-Mat with funds and increases his

interest in Fix-’n-Mat. The equity ‘‘Capital’’ increases by R130 000.

ASSETS =EQUITY +LIABILITIES

Bank Capital

RRR

Previous balances 0 0 0

This transaction + 130 000 + 130 000 0

New balances 130 000 =130 000 +0

24

FAC1502/1

COMMENTS

.In an entity which has not yet entered into any transaction, the elements of the

equation will always be 0.

.The terms ‘‘bank’’ and ‘‘capital’’ in the analysis are actually names of accounts.

.The investment of capital is usually the first transaction.

.Capital may be contributed in the form of cash or any other asset (eg furniture).

‘‘Furniture’’ instead of ‘‘Bank’’ will then increase.

.The BAE balances after the transaction.

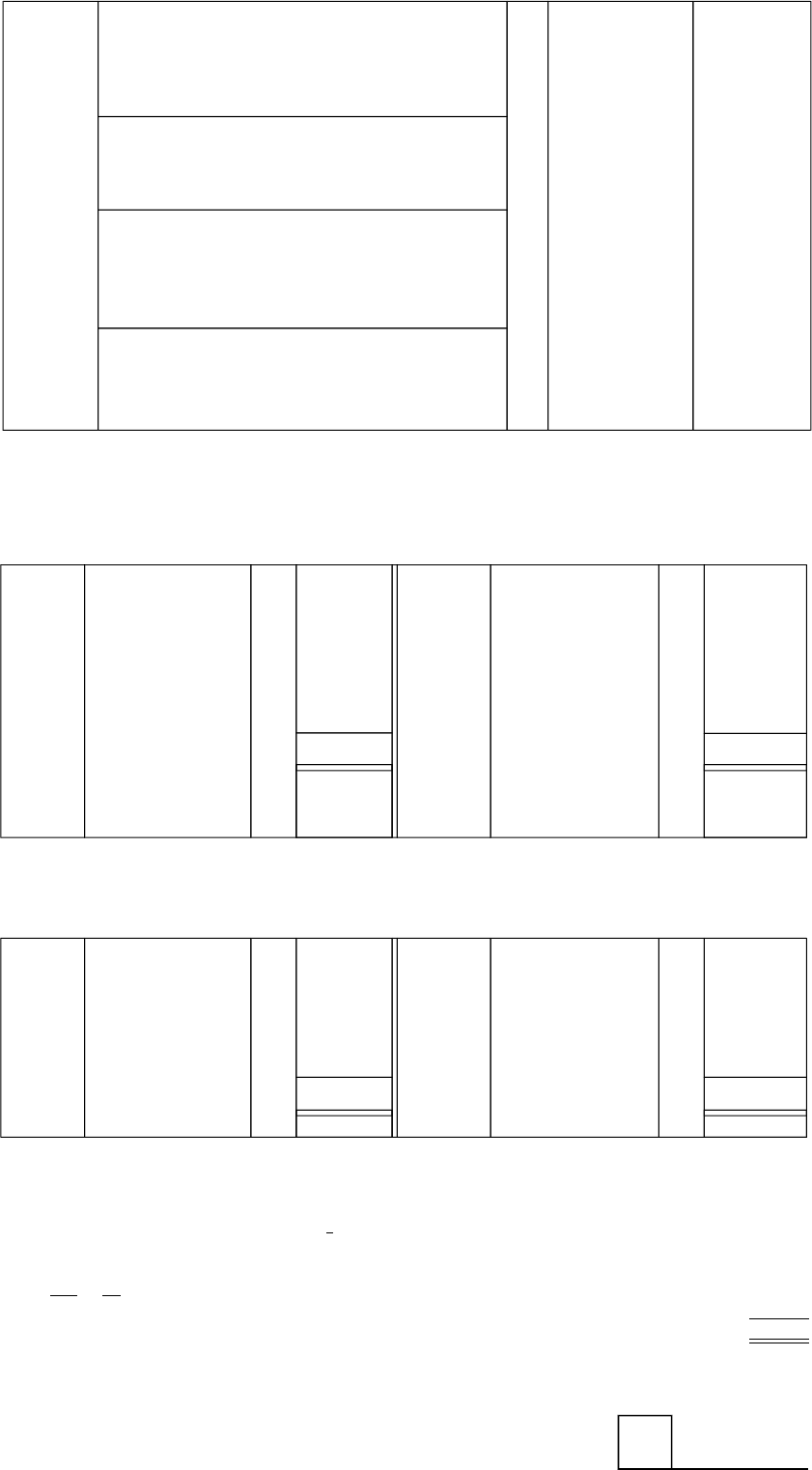

4.4.2 Acquisition of loans

Transaction

2 Feb 20.1

Fix-’n-Mat obtained a loan of R25 000 with a payback period of more than a

year from ABC Bank. The amount was paid into its bank account.

Analysis (1) The asset ‘‘Bank’’ increases by R25 000.

(2) ABC Bank now has a claim against or an interest in Fix-’n-Mat and a

liability, namely a ‘‘Loan: ABC Bank’’, comes into being.

ASSETS =EQUITY +LIABILITIES

Bank Capital Loan:

ABC Bank

RRR

Balances brought

down

130 000 130 000 0

Transaction + 25 000 0 + 25 000

New balances 155 000 =130 000 +25 000

COMMENTS

.The results of the first transaction form the balances which are brought down in this

transaction.

.Liabilities arise when another party or institution supplies funds (make loans) to the

entity.

.Amounts (in this case R25 000) are added to both the left-hand side and the right-

hand side of the BAE.

.The BAE balances after the transaction.

25

FAC1502/1

4.4.3 Purchase of assets for cash

Transaction

6 Feb 20.1

Fix-’n-Mat bought equipment from XY Furnishers for R100 000 and paid by

cheque.

Analysis (1) The asset ‘‘Bank’’ decreases by R100 000 since money has been

withdrawn.

(2) The asset ‘‘Equipment’’ increases.

ASSETS = EQUITY + LIABILITIES

Equip- Loan:

ment Bank Capital

ABC Bank

R R R R

Balances brought down 0 155 000 130 000 25 000

Transaction +100 000 7100 000 0 0

New balances 100 000 55 000 = 130 000 + 25 000

COMMENTS

.Assets now consist of bank and equipment.

.The left-hand side of the equation increases and decreases. One asset is exchanged

for another asset.

.The BAE balances after the transaction.

4.4.4 Buying assets on credit (debt)

Transaction

10 Feb 20.1

Fix-’n-Mat bought furniture for R2 000 on credit from Joc Limited.

Analysis (1) The asset ‘‘Furniture’’ increases by R2 000.

(2) A liability, ‘‘Trade payables’’, comes into being.

EQUITY LIABILITIESASSETS = +

Furniture Equipment Bank Capital Loan:

Trade

ABC pay-

Bank ables

R R R R R R

Balances

brought down 0 100 000 55 000 130 000 25 000 0

Transaction +2 000 0 0 0 0 +2 000

New balances 2 000 100 000 55 000 = 130 000 + 25 000 2 000

26

FAC1502/1

COMMENTS

.Assets may also be bought on credit and a creditor comes into being.

.The transaction is recorded when it is entered into and not when the payment is made.

.The left-hand side and the right-hand side of the BAE increase.

.The BAE balances after the transaction.

4.4.5 Payments to creditors

Transaction

11 Feb 20.1

Fix-’n-Mat paid Joc Limited’s account of R2 000.

Analysis (1) The asset ‘‘Bank’’ decreases by R2 000.

(2) The liability, ‘‘Trade payables’’ (liability), decreases by R2 000.

EQUITY LIABILITIESASSETS = +

Furniture Equipment Bank Capital Loan:

Trade

ABC pay-

Bank ables

R R R R R R

Balances brought

down 2 000 100 000 55 000 130 000 25 000 2 000

Transaction 0 0 72 000 0 0 72 000

New balances 2 000 100 000 53 000 = 130 000 + 25 000 0

COMMENTS

.The left-hand side and the right-hand side of the BAE decrease.

.The BAE balances after the transaction.

4.4.6 Withdrawals by owner

Transaction

12 Feb 20.1

The owner withdrew R1 000 for his own use.

Analysis (1) Fix-’n-Mat’s ‘‘Bank’’ decreases by R1 000.

(2) T Tom’s ‘‘Capital’’ (equity) in Fix-’n-Mat decreases by R1 000.

27

FAC1502/1

EQUITY LIABILITIESASSETS = +

Furniture Equipment Bank Capital Loan:

Trade

ABC pay-

Bank ables

R R R R R R

Balances brought

down 2 000 100 000 53 000 130 000 25 000 0

Transaction 0 0 71 000 71 000 0 0

New balances 2 000 100 000 52 000 = 129 000 + 25 000 0

COMMENTS

.Withdrawals are the opposite of capital contributions and reduce capital. Remember,

withdrawals are not expenditure.

.Where the entity pays personal expenses of the owner’s, it is also treated as a

withdrawal.

.The left-hand side and the right-hand side of the BAE are reduced.

.The BAE balances after the transaction.

4.5 Transactions which give rise to income and expenditure

4.5.1 Income (cash)

Transaction

13 Feb 20.1

Fix-’n-Mat provided services for a client S Silver and received a cheque for

R1 000.

Analysis (1) The asset ‘‘Bank’’ increases by R1 000.

(2) The fee which Fix-’n-Mat earns is an income. Equity therefore

increases by R1 000.

ASSETS = EQUITY + LIABILITIES

Furniture Equipment Bank Capital Income/ Loan: Trade

Expend- ABC pay-

iture Bank ables

R R R R R R R

Balances

brought down 2 000 100 000 52 000 129 000 0 25 000 0

Transaction 0 0 +1 000 0 +1 000 0 0

New balances 2 000 100 000 53 000 = 129 000 1 000 + 25 000 0

28

FAC1502/1

COMMENTS

.Income earned increases the equity. It is the objective of the entity to earn income for

the entrepreneur.

.The left-hand side and the right-hand side of the BAE increase.

.The BAE balances after the transaction.

4.5.2 Expenditure (cash)

Transaction

16 Feb 20.1

Fix-’n-Mat paid wages by cheque, R800.

Analysis (1) The asset ‘‘Bank’’ decreases by R800.

(2) Wages are an expenditure item and the equity decreases by R800.

ASSETS = EQUITY + LIABILITIES

Furniture Equipment Bank Capital Income/ Loan: Trade

Expenditure ABC pay-

Bank ables

R R R R R R R

Balances

brought down 2 000 100 000 53 000 129 000 1 000 25 000 0

Transaction 0 0 7800 0 7800 0 0

New balances 2 000 100 000 52 200 = 129 000 200 + 25 000 0

COMMENTS

.In essence expenditure incurred decreases income and therefore also decreases the

equity.

.The left-hand side and the right-hand side of the BAE decrease.

.The BAE balances after the transaction.

4.5.3 Income (credit)

Transaction

18 Feb 20.1

Fix-’n-Mat provided services worth R6 000 to C Canon on credit.

Analysis (1) C Canon becomes a debtor of Fix-’n-Mat. The asset ‘‘Trade

receivables’’ comes into being and increases by R6 000.

(2) ‘‘Income received’’ are an income item and equity increases by

R6 000.

29

FAC1502/1

ASSETS = EQUITY + LIABILITIES

Income/ Trade

Trade Furniture Equipment Bank Capital Expenditure

Loan:

payables

receivables ABC Bank

R R R R R R R R

Balances brought

down 0 2 000 100 000 52 200 129 000 200 25 000 0

Transaction + 6 000 0 0 0 0 +6 000 0 0

New balances 6 000 2 000 100 000 52 200 = 129 000 6 200 + 25 000 0

COMMENTS

.Organisations or clients who owe money to an entity are known as debtors and arise

from the entity rendering services or goods on credit.

.The left-hand side and the right-hand side of the BAE increase.

.The realisation principle applies here, and the income is shown as having been earned

on 18 February when the service was provided and not when the cash is received.

4.5.4 Expenditure (credit)

Transaction

21 Feb 20.1

Fix-’n-Mat placed an advertisement in a local newspaper for R200.

Payment was due only in 30 days.

Analysis (1) The liability ‘‘Trade payables’’ increases by R200.

(2) ‘‘Advertisements’’ are an expenditure item and the equity decreases

by R200.

ASSETS = EQUITY + LIABILITIES

Income/ Trade

Trade Furniture Equipment Bank Capital Expenditure

Loan:

payables

receivables ABC Bank

R R R R R R R R

Balances brought

down 6 000 2 000 100 000 52 200 129 000 6 200 25 000 0

Transaction 0 0 0 0 0 7200 0 + 200

New balances 6 000 2 000 100 000 52 200 = 129 000 6 000 + 25 000 200

COMMENTS

.Expenditure may also be incurred on credit (for goods/services received).

.The organisations to which money is owed are known as creditors.

.The right-hand side of the BAE increases and decreases.

.The expenditure is shown on 21 February 20.1 and not only when it is paid.

.The BAE balances after the transaction.

30

FAC1502/1

{

{

{

4.5.5 Payments received from debtors

Transaction

28 Feb 20.1

C Canon settled his account in part, R2 000.

Analysis (1) The asset ‘‘Bank’’ increases by R2 000.

(2) The asset ‘‘Trade receivables’’ decreases by R2 000.

ASSETS = EQUITY + LIABILITIES

Income/ Trade

Trade Furniture Equipment Bank Capital Expenditure

Loan:

payables

receivables ABC Bank

R R R R R R R R

Balances brought

down 6 000 2 000 100 000 52 200 129 000 6 000 25 000 200

Transaction 72 000 0 0 + 2 000 0 0 0 0

New balances 4 000 2 000 100 000 54 200 = 129 000 6 000 + 25 000 200

COMMENTS

.This transaction affects assets only.

.The left-hand side of the BAE increases and decreases.

.The BAE balances after the transaction.

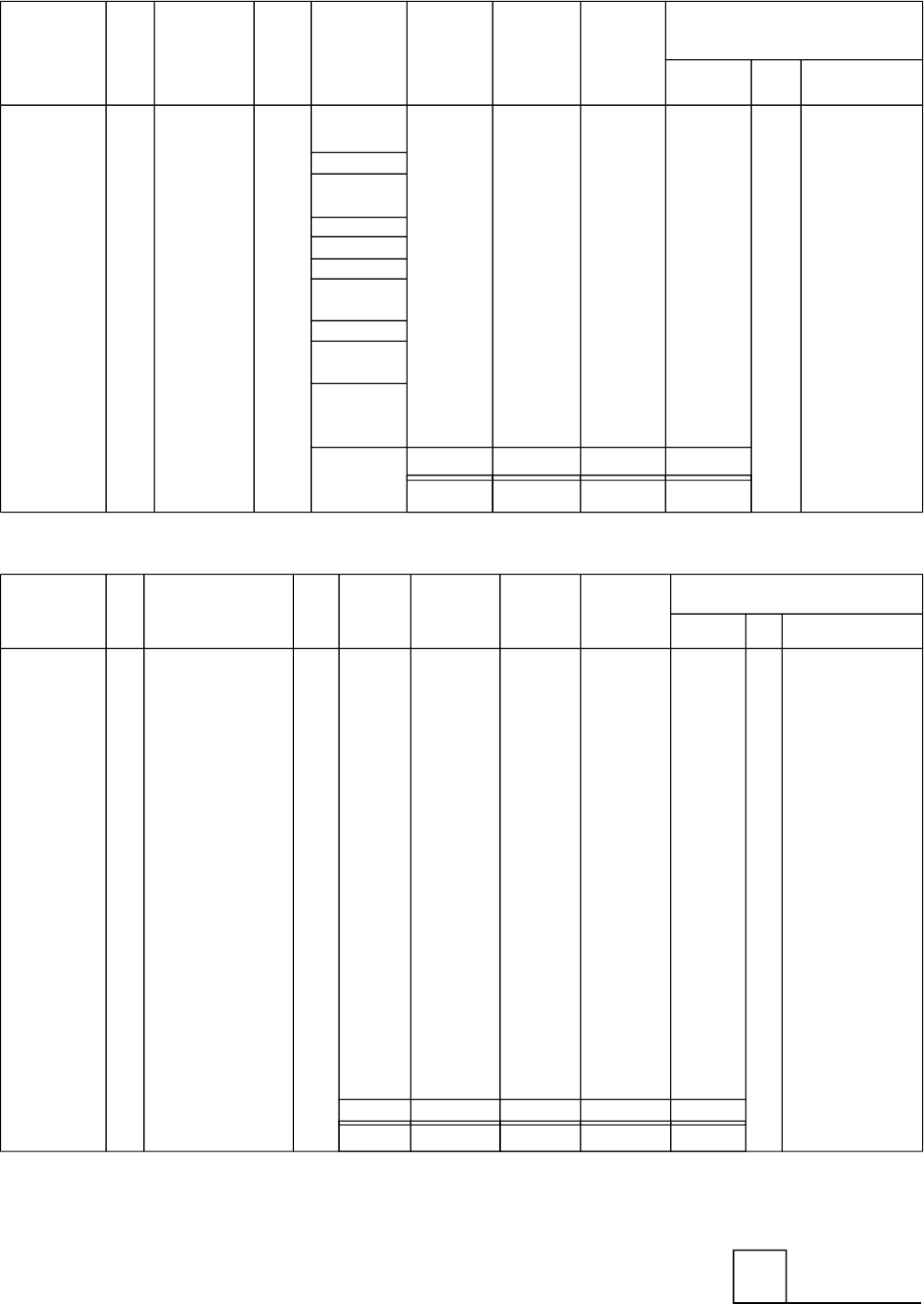

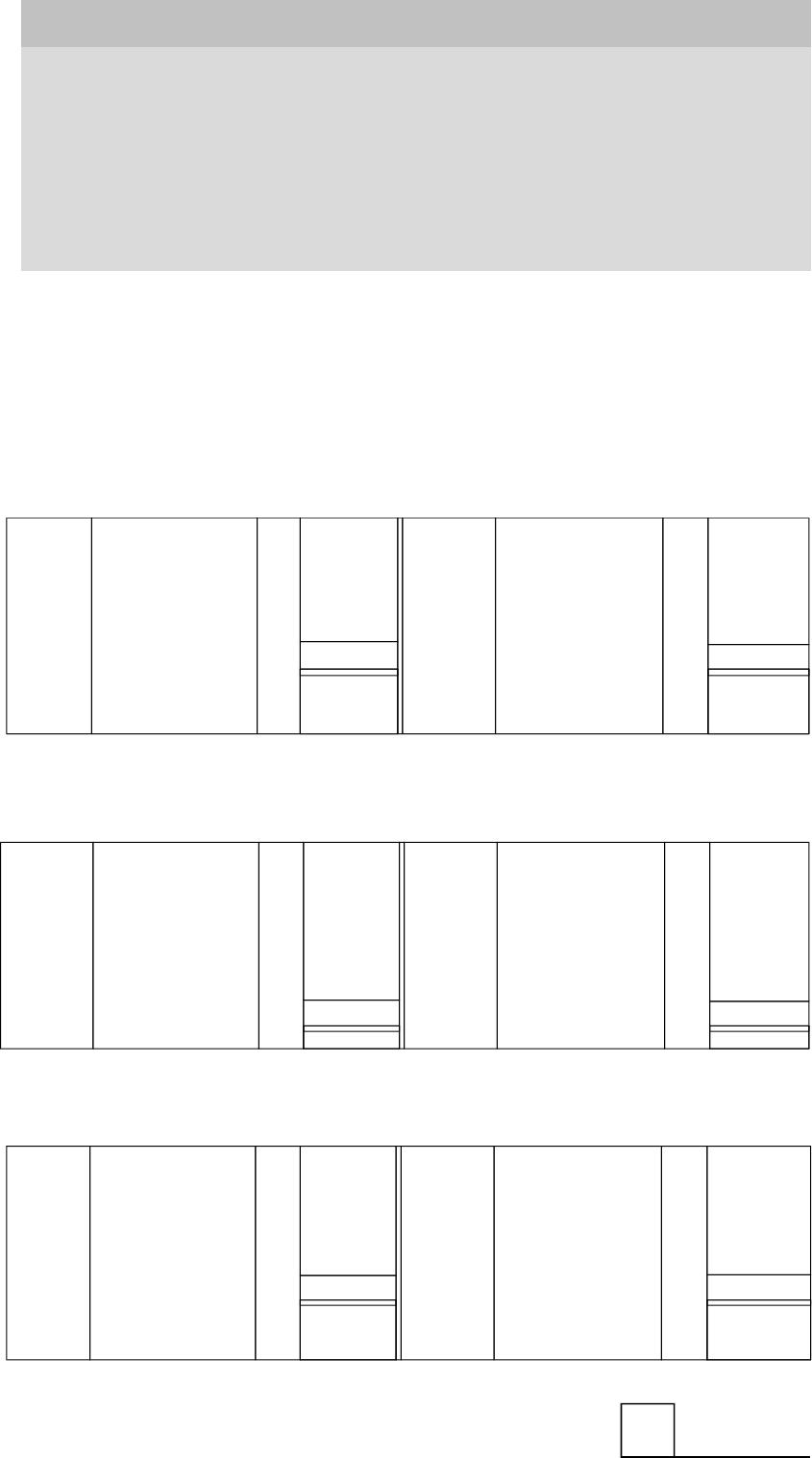

4.6 Summary of transactions

Fix-’n-Mat’s transactions for February 20.1 can now be summarised as follows:

ASSETS = INTERESTS

EQUITY + LIABILITIES

Trade Income/ Loan: Trade

Date receivables Furniture Equipment Bank Capital Expenditure ABC Bank payables

20.1 R R R R R R R R

Feb

1 +130 000 +130 000

2 +25 000 +25 000

6 +100 000 7100 000

10 +2 000 +2 000

11 72 000 72 000

12 71 000 71 000

13 +1 000 +1 000

16 7800 7800

18 +6 000 +6 000

21 7200 +200

28 72 000 +2 000

+4 000 +2 000 +100 000 +54 200 = +129 000 +6 000 + +25 000 +200

160 200 = 135 000 + 25 200

= 160 200

31

FAC1502/1

COMMENT

.Note that these totals correspond to the closing balances in paragraph 4.5.5 above.

4.7 Basic form of a statement of financial position (previously

known as the balance sheet)

Now we are going to prepare a statement of financial position using the totals of the BAE (see

paragraph 4.6). The basic form of the statement of financial position is based on the BAE. You

have already come across a very simple statement of financial position in paragraph 2.5. A

statement of financial position is a report and in essence is a formal presentation of the

elements of the BAE.

FIX-’N-MAT

STATEMENT OF FINANCIAL POSITION AS AT 28 FEBRUARY 20.1

ASSETS Note R

Non-current assets 102 000

Equipment 100 000

Furniture 2 000

Current assets 58 200

Trade and other receivables 4 000

Cash and cash equivalents 54 200

Total assets 160 200

EQUITY AND LIABILITIES

Total equity 135 000

Capital 135 000

Non-current liabilities 25 000

Long-term borrowings 25 000

Current liabilities 200

Trade and other payables 200

Total equity and liabilities 160 200

COMMENTS

.The statement of financial position balances and shows the same totals as the BAE.

.Note the heading — the statement of financial position is prepared to reflect the

financial position on a specific date.

.The withdrawals are subtracted from the capital. As mentioned, withdrawals are not

an expenditure item.

.The equity in the BAE is also R135 000.

4.8 Revision exercises and solutions

4.8.1 Revision exercise 1

D Paulus started a television antenna installation business on 1 June 20.1. The following

transactions took place during the first month:

32

FAC1502/1

{

Transactions:

June 1 Cash in the bank deposited as opening capital, R25 000.

2 D Paulus made his private equipment available to the business, R9 000.

3 Additional equipment purchased and paid for by cheque, R12 000.

4 Installation fees for work done on account for Kannadrift Municipality, R4 200.

6 Vehicle purchased on credit from Virginia Cars Limited, R22 400. This vehicle

was financed by obtaining a loan from Crown Bank at an interest rate of 9% per

annum.

17 Kannadrift Municipality paid R2 200 on their account.

28 Wages paid, R4 000.

29 Cheque drawn for private use, R1 300.

30 Paid R9 000 to Virginia Cars Limited on their account.

Required:

Using the basic accounting equation, analyse the abovementioned transactions as

follows:

NB: (1) Show the effect of each transaction on the basic accounting equation with a plus

sign (+) for an increase and a minus sign (7) for a decrease.

(2) Balance the equation.

Example: On 1 July 20.1 D Paulus received R2 000 in cash for an installation done for Cook

Financing Corporation.

Date Basic accounting equation

A = E + L

20.1 R R R

July 1 + 2 000 + 2 000 0

Solution: Revision exercise 1

D PAULUS

Date Basic accounting equation

A = E + L

20.1 R R R

June 1 + 25 000 +25 000

Jun e 2 + 9 000 + 9 000

Jun e 3 + 12 000

712 000

Jun e 4 + 4 200 + 4 200

Jun e 6 + 22 400 +22 400

Ju ne 17 + 2 200

72 200

Ju ne 28 74 000 74 000

Ju ne 29 71 300 71 300

Ju ne 30 79 000 79 000

Total 46 300 32 900 13 400

46 300

33

FAC1502/1

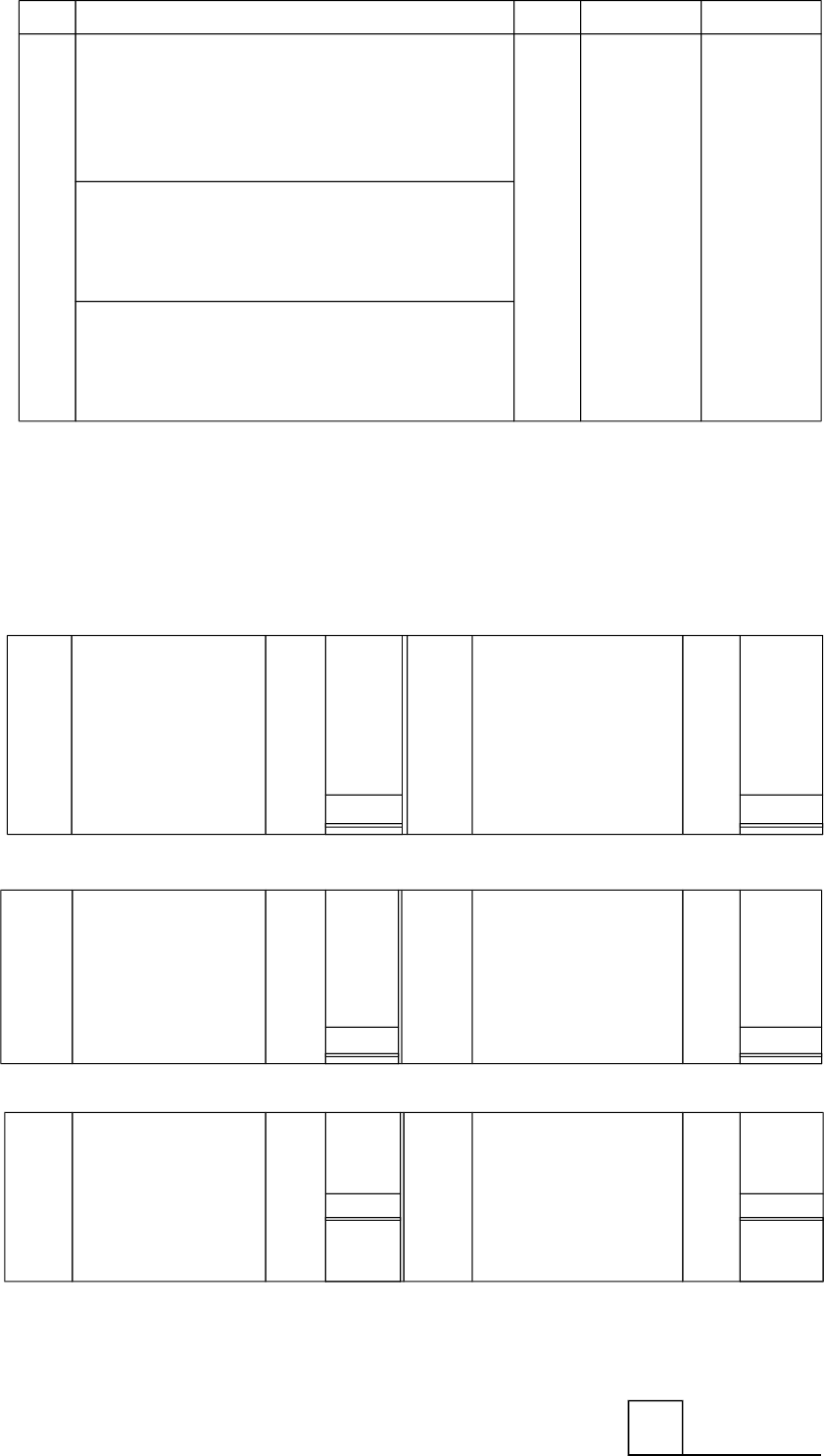

4.8.2 Revision exercise 2

The following transactions during January 20.1 relate to F Fox, an attorney.

Date Transactions Amount

20.1 R

Jan 3 F Fox deposited as opening capital 20 000

Jan Paid rental for January 20.1 2 300

Jan 4 Bought law library on credit from Book Limited 24 000

Jan 5 Bought a computer for cash from Leo Limited 1 700

Jan 6 Provided services for cash 7 200

Jan 9 Debited D Dunn with fees for services rendered 8 318

Jan 10 Leo Limited repaired equipment on credit 100

Jan 13 F Fox drew a cheque for private use 1 234

Jan 18 F Fox received commission on a property transaction 1 350

Jan 29 Paid the following by cheque

i(i) Salaries 8 350

(ii) Leo Limited (on account) 100

Jan 30 Received payment from D Dunn on his account 1 500

Required:

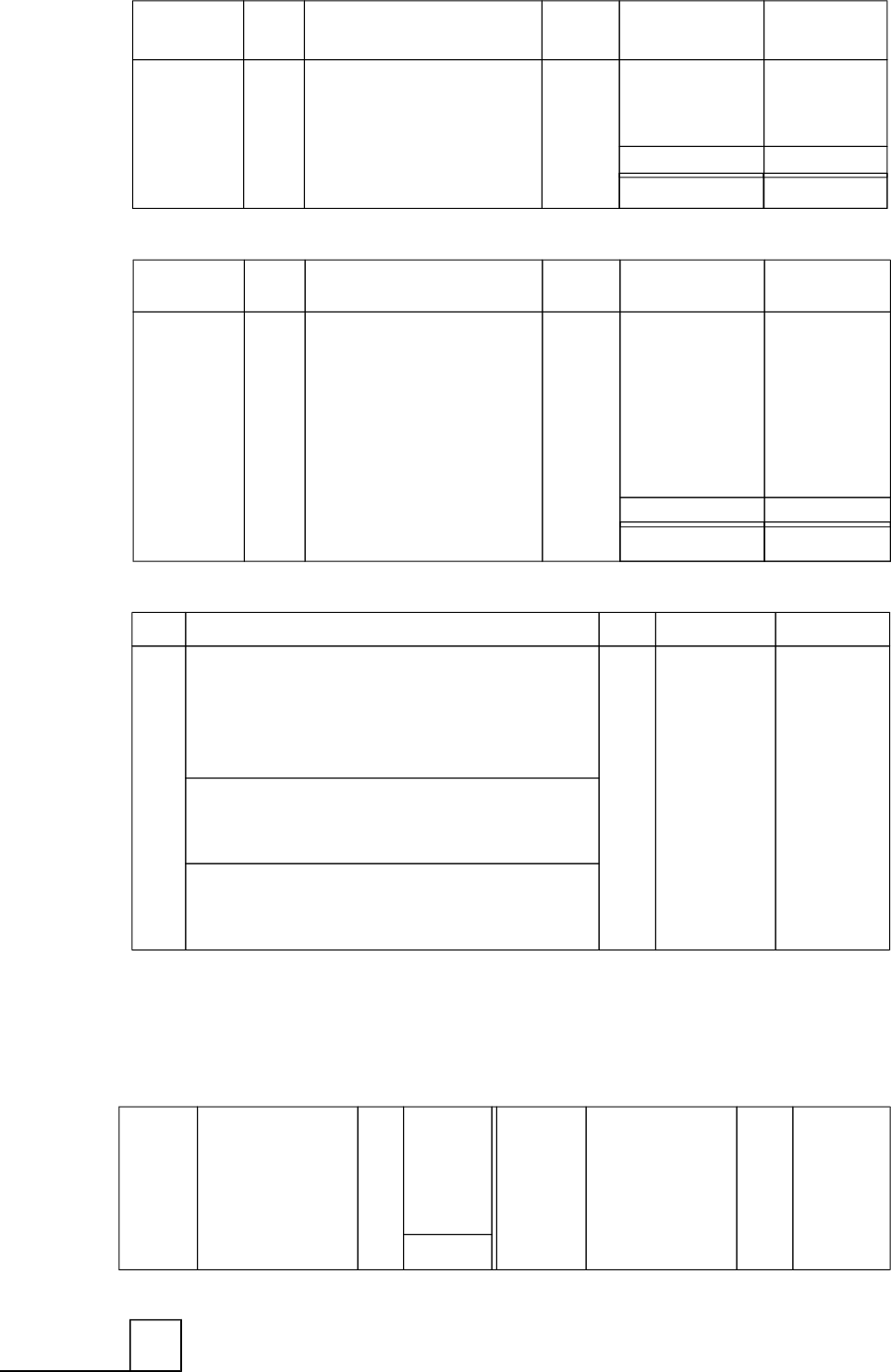

(1) Analyse the above transactions in tabular form as follows:

ASSETS = EQUITY + LIABILITIES

Library Trade Income/

Date and receiv- Bank Capital Expendi- Trade payables

Equip- ables ture

ment

Total = +

(2) Prepare the statement of financial position of F Fox at 31 January 20.1.

34

FAC1502/1

{

{

Solution: Revision exercise 2

F FOX

(1) ACCOUNTING EQUATION

ASSETS =EQUITY +LIABILITIES

Library Trade Income/

Date and receiv- Bank Capital Expendi- Trade payables

Equip- ables ture

ment

20.1 R R R R R R

Jan 3 +20 000 +20 000

72 300 72 300

Jan 4 +24 000 + 24 000

Jan 5 + 1 700 71 700

Jan 6 +7 200 +7 200

Jan 9 +8 318 +8 318

Jan10 7100 + 100

Jan13 71 234 71 234

Jan18 +1 350 +1 350

Jan29 78 350 78 350

7100 7100

Jan30 71 500 +1 500

Total +25 700 +6 818 +16 366 = +18 766 +6 118 + +24 000

R48 884 R48 884

F FOX

(2) STATEMENT OF FINANCIAL POSITION AS AT 31 JANUARY 20.1

ASSETS Note R

Non-current assets 25 700

Equipment 1 700

Library 24 000

Current assets 23 184

Trade and other receivables 6 818

Cash and cash equivalents 16 366

Total assets 48 884

EQUITY AND LIABILITIES

Total equity 24 884

Capital 24 884

Current liabilities 24 000

Trade and other payables 24 000

Total equity and liabilities 48 884

35

FAC1502/1

4.9 The general ledger account

Up to now we have dealt only with asset, liability and equity items appearing in a statement of

financial position or BAE.

We recorded transactions in columns in the summary of the BAE to show their effect on a

specific asset, equity or liability item. We had columns for debtors, furniture, equipment, capital

and so on. But it is impractical to prepare a new equation after every new transaction — just

think what would happen in a business with thousands of transactions! To avoid this we are

now going to open an account in the general ledger for every column of the BAE. We speak of

the general ledger because there are also subsidiary ledgers, which we will explain later.

An account is opened in the general ledger for every asset, liability and equity item. Every

account appears on its own on a page in the ledger and each account is given a number, which

is known as a folio number.

An account is an accounting record in which all transactions relating to a specific item are

recorded.

Study paragraphs 4.3 to 4.3.1 in the prescribed book.

4.9.1 Assets

Study paragraph 4.3.1 in the prescribed book.

4.9.2 Equity and liabilities

Study paragraphs 4.3.2 to 4.3.5 in the prescribed book.

4.10 Balancing an account

With what you have learnt about an account, we now know that an account may have entries

on the debit or the credit side or on both sides.

Study paragraph 4.4 in the prescribed book.

NB:

The closing balance of the previous period becomes the opening balance of the next period.

.c/d = carried down, which indicates the amount to be carried down to the following month

.b/d = brought down, which indicates that the amount has been brought down from the

previous month

36

FAC1502/1

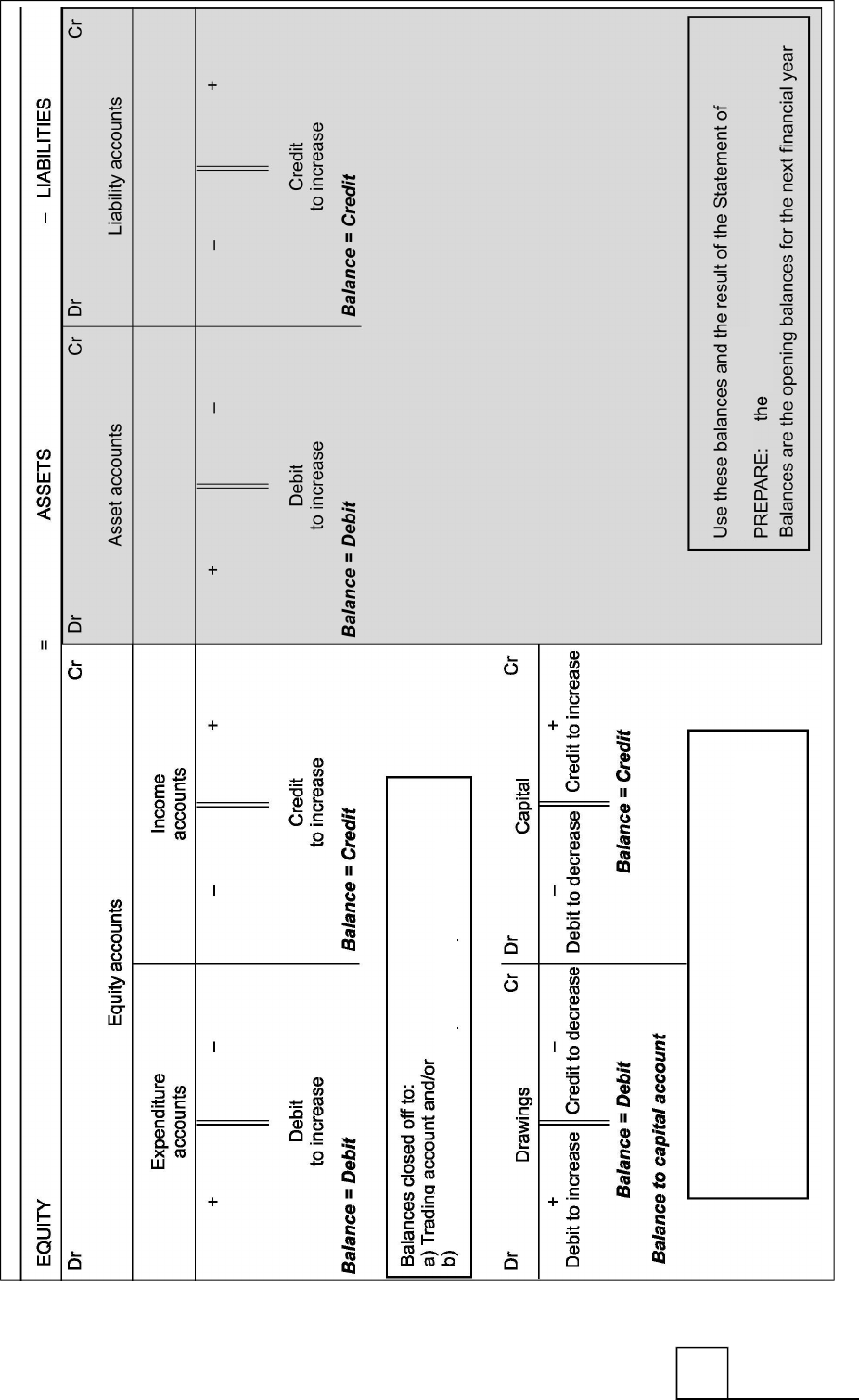

PPRREEPPAARREE:: aa)) SSttaatteemmeenntt ooff pprrooffiitt oorr lloossss aanndd ootthheerr

ccoommpprreehheennssiivvee iinnccoommee

bb)) SSttaatteemmeenntt ooff cchhaannggeess iinn EEqquuiittyy

PPrrooffiitt oorr LLoossss aaccccoouunntt:: PPrrooffiitt ttoo CCaappiittaall aaccccoouunntt

statement of financial position and Notes

in equity to changes

4.11 Schematic representation

37

FAC1502/1

~~

~~

COMMENTS

.The top level of the schematic representation shows the basic accounting equation

(BAE).

.The second level of the schematic representation shows how each of the components

of the BAE becomes part of the account system. The left-hand side of the account is

known as the debit side (Dr) and the right-hand side as the credit side (Cr).

.The total of the amounts on the debit side of an asset account is usually larger than

that on the credit side. The account will therefore usually have a debit balance

(brought down). The total of the amounts on the credit side of a liability account is

usually larger than that on the debit side. The account will therefore usually have a

credit balance (brought down).

.The capital account reflects the equity of the owner at the date of the statement of

financial position. The balance on this account is the result of income, expenditure,

drawings and capital investment. These components are all dealt with separately in

the accounting system.

.Additional capital contributions and income increase equity.

.Drawings and expenditure decrease equity.

.But note: drawings is not an expenditure and therefore does not reduce

the profit.

.The left hand side (Equity section) forms the basis for the preparation of the statement

of profit or loss and other comprehensive income and the statement of changes in

equity.

.The capital (Equity section) and the right hand side (ASSETS and LIABILITIES) form

the basis for the preparation of the statement of financial position.

4.12 Recording of transactions in ledger accounts

When we enter a transaction in a ledger account, we have to ask ourselves: Which accounts

are affected? In answer to this question, we are now going to record the transactions in

paragraphs 4.4 and 4.5 in the ledger accounts (T-accounts).

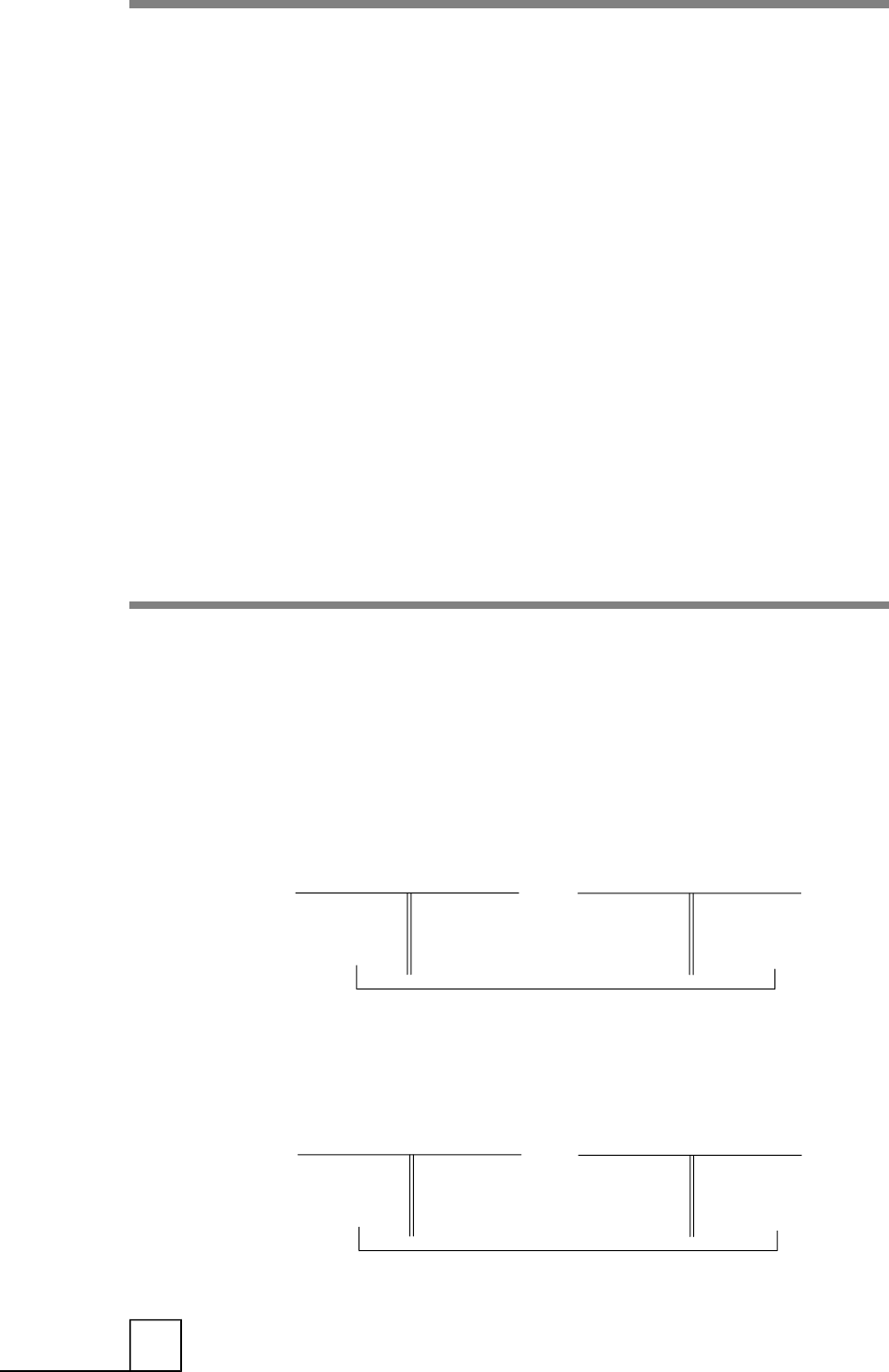

Transaction

(4.4.1)

Bank Capital

130 000 130 000

(4.4.2)

Bank Loan

25 000 25 000

38

FAC1502/1

~~

~ ~

~~

~ ~

~~

~ ~

(4.4.3)

Equipment Bank

100 000 100 000

(4.4.4)

Furniture Trade payables (Joc Ltd)

2 000 2 000

(4.4.5)

Bank Trade payables (Joc Ltd)

2 000 2 000

(4.4.6)

Bank Drawings

1 000 1 000

COMMENT

All drawings by the owner are recorded in a separate account, namely ‘‘Drawings’’, and

not directly in the capital account. Drawings is a disbursement of the profit to the owner

and is not expenses resulting from business operations.

(4.5.1)

Bank Income (fees)

1 000 1 000

(4.5.2)

Bank Wages

800 800

39

FAC1502/1

~ ~

~~

~~

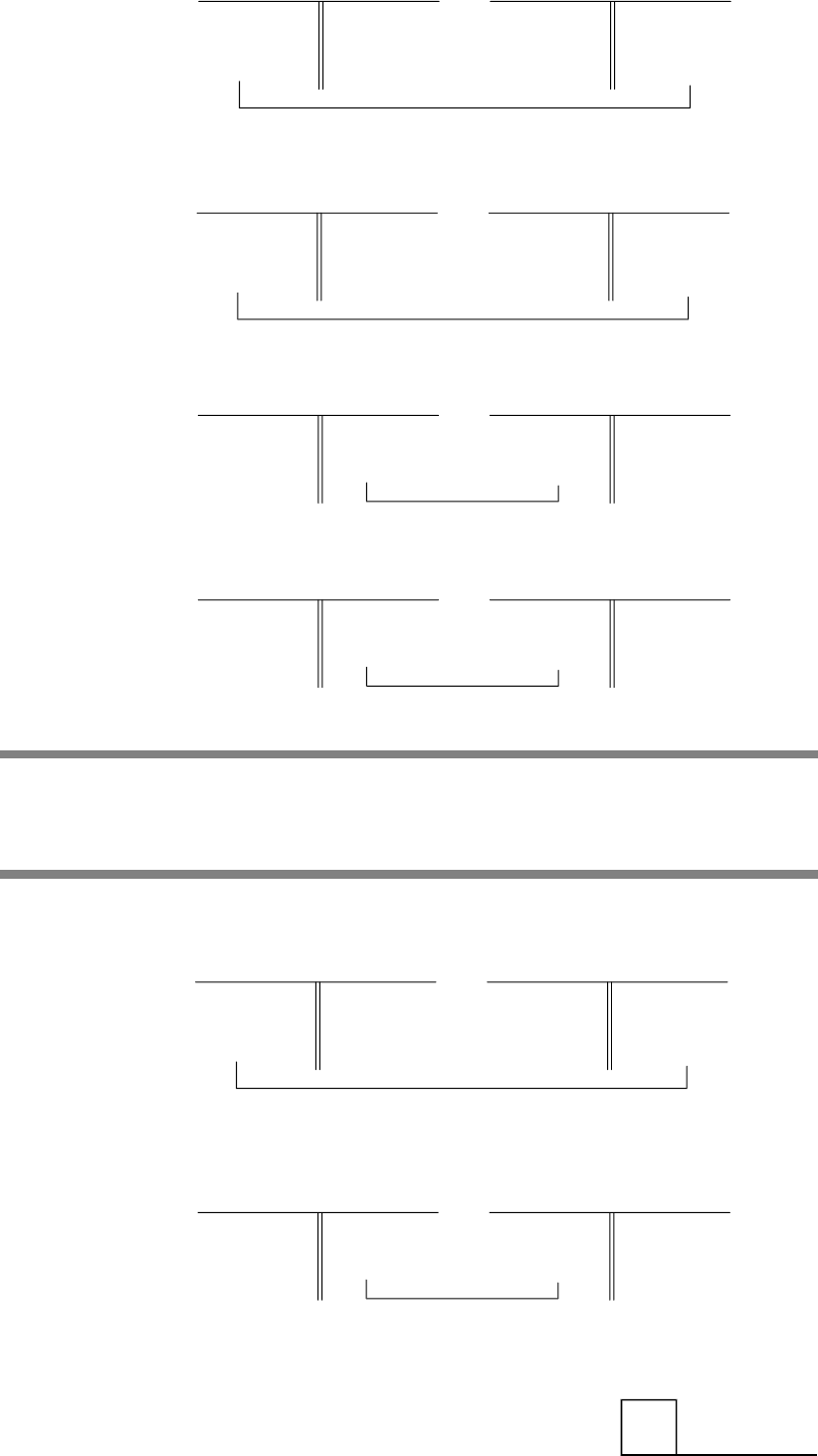

(4.5.3)

Trade receivables (C Canon) Income (fees)

6 000 6 000

(4.5.4)

Trade payables Advertisements

200 200

(4.5.5)

Bank Trade receivables (C Canon)

2 000 2 000

4.13 The general ledger

In the previous example two accounts were opened each time for each transaction. In practice

all transactions which affect, say, bank are summarised in one account for bank. Given the

information we have above, the accounts will take the following form. Each one is closed off

and the balance determined.

GOLDEN RULE

Assets (eg Bank) increase on the Debit (Dr) side and decrease on the Credit (Cr) side of

the account.

Dr Bank Cr

Date Details Fol Amount Date Details Fol Amount

20.1 R 20.1 R

Feb 1 Capital 130 000 Feb 6 Equipment 100 000

Feb 2 Loan:ABC Bank 25 000 Feb 11 Trade payables 2 000

Feb 13 Income received 1 000 Feb 12 Drawings 1 000

Feb 28 Trade receivables 2 000 Feb 16 Wages 800

Feb 28 Balance c/d 54 200

158 000 158 000

20.1

Mar 1 Balance b/d 54 200

40

FAC1502/1

Dr Equipment Cr

20.1 R

Feb 6 Bank 100 000

Dr Furniture Cr

20.1 R

Feb 10 Creditors 2 000

Dr Trade receivables Cr

20.1 R 20.1 R

Feb 18 Income received 6 000 Feb 28 Bank 2 000

Balance c/d 4 000

6 000 6 000

20.1

Mar 1 Balance b/d 4 000

GOLDEN RULE

Equity (eg Capital) and Liabilities (eg Creditors) increase on the credit (Cr) side and

decrease on the debit (Dr) side of the account.

GOLDEN RULE

Income (eg Sales) increases equity and are credited (Cr) to the particular income account.

GOLDEN RULE

Expenses (eg Wages) decreases equity and are debited (Dr) to the particular expense

account.

41

FAC1502/1

Dr Capital Cr

20.1 R

Feb 1 Bank 130 000

Dr Drawings Cr

20.1 R

Feb 12 Bank 1 000

Dr Loan: ABC Bank Cr

20.1 R

Feb 2 Bank 25 000

Dr Trade payables Cr

20.1 R 20.1 R

Feb 11 Bank 2 000 Feb 10 Furniture 2 000

28 Balance c/d 200 21 Advertisements 200

2 200 2 200

20.1

Mar 1 Balance b/d 200

Dr Wages Cr

20.1 R

Feb 16 Bank 800

Dr Advertisements Cr

20.1 R

Feb 21 Creditors 200

Dr Income (fees) Cr

20.1 R

Feb 13 Bank 1 000

18 Debtors 6 000

7 000

42

FAC1502/1

COMMENT

.Note that the details of an item in a ledger account is simply the name of the other

ledger account involved in the transaction. This other ledger account is known as the

contra ledger account.

4.14 The trial balance

Study paragraph 4.5 of the prescribed book.

A trial balance is a list of the balances brought down (b/d) of the accounts in the general ledger

on a specific date.

GOLDEN RULE

The balance ‘‘brought down’’ (b/d) must be used to prepare the trial balance.

The following trial balance has been prepared from the ledger accounts in paragraph 4.13.

FIX-’N-MAT

TRIAL BALANCE AS AT 28 FEBRUARY 20.1

Dr Cr

R R

Bank 54 200

Equipment 100 000

Furniture 2 000

Trade receivables 4 000

Capital 130 000

Drawings 1 000

Loan 25 000

Trade payables 200

Wages 800

Advertisements 200

Income received 7 000

162 200 162 200

GOLDEN RULE

Asset and expense accounts have debit (Dr) balances brought down (b/d) and are entered

on the debit side of the trial balance.

GOLDEN RULE

Equity (capital), liability and income accounts have credit (Cr) balances brought down (b/d)

and are entered on the credit side of the trial balance.

43

FAC1502/1

COMMENTS

.The trial balance balances.

.Note that an account with a debit balance (brought down) is shown on the debit side of

the trial balance and an account with a credit balance (brought down) on the credit

side.

.If we compare the totals of the trial balance with the totals of the columns of the BAE

(see paragraph 4.6), we note the following:

.Capital in the BAE is R129 000. In the trial balance capital, R130 000 (Cr), and

drawings, R1 000 (Dr), are shown separately. This also gives a net total of

R129 000.

.Income less expenditure = R6 000. If the expenses in the trial balance, namely

wages and advertisements with debit balances of R800 and R200 respectively, are

subtracted from the income, namely fees with a credit of R7 000, the net amount is

R(7 000 71 000) = R6 000 credit, which corresponds to the income in the

BAE.

4.15 Preparing financial statements

In this module we deal with the statement of financial position, statement of profit or loss and

other comprehensive income and statement of changes in equity as well as some of the notes.

The statement of cash flows will be dealt with in FAC1601.

As mentioned previously, the trial balance serves as a basis for preparing a statement of profit

or loss and other comprehensive income, statement of changes in equity, and statement of

financial position. The trial balance represents the information in the ledger. The statement of

profit or loss and other comprehensive income shows the entity’s financial result and the

statement of financial position shows its financial position.

Study paragraphs 4.6 and 4.7 of the prescribed book.

4.15.1 The statement of profit or loss and other comprehensive income

We now use the information from the trial balance in paragraph 4.14 above to prepare a

statement of profit or loss and other comprehensive income for Fix-’n-Mat.

FIX-’N-MAT

STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME FOR THE

MONTH ENDED 28 FEBRUARY 20.1

Note R

Revenue 7 000

Distribution, administrative and other expenses (1 000)

Wages 800

Advertisements 200

Profit for the period 6 000

Other comprehensive income for the period —

Total comprehensive income for the period 6 000

44

FAC1502/1

COMMENTS

.Note the title. A statement of profit or loss and other comprehensive income is

prepared for a period ended, not on a certain date.

.The profit for the period as determined in the statement of profit or loss and other

comprehensive income corresponds to the income/expenditure column in the BAE.

.The income and expenditure accounts are called nominal accounts.

GOLDEN RULE

Revenue (comprising income accounts) less expenses result in a profit or loss.

4.15.2 The statement of changes in equity

This statement shows all the changes in equity which have occurred during the financial period.

The purpose of the statement of changes in equity is to reconcile the equity at the beginning of

the financial period with the equity at the end of the financial period. The balance of the equity

at the end of the financial period is then shown in the statement of financial position. Equity will

be discussed in more detail later in this study guide.

FIX-’N-MAT

STATEMENT OF CHANGES IN EQUITY FOR THE MONTH ENDED 28 FEBRUARY 20.1

Capital

R

Balance at 1 February 20.1 130 000

Total comprehensive income for the period 6 000

Drawings (1 000)

Balance at 28 February 20.1 135 000

GOLDEN RULE

The profit increases equity and a loss decreases equity.

COMMENTS

.Note that the statement of changes in equity is prepared for a period ended and not

on a specific date.

.The equity at the end of the month corresponds to the net total in the BAE in paragraph

4.6.

45

FAC1502/1

GOLDEN RULE

The balance at the end of the period on the statement of changes in equity must be the

same as the ‘‘capital’’ reflected in the statement of financial position.

4.15.3 The statement of financial position

Before we prepare a statement of financial position, please refer to paragraph 2.5 and also to

the statement of financial position for Fix-’n-Mat which we compiled in paragraph 4.7.

We will now show the statement of financial position of Fix-’n-Mat in narrative form and in

compliance with IFRS.

FIX-’N-MAT

STATEMENT OF FINANCIAL POSITION AS AT 28 FEBRUARY 20.1

ASSETS Note R

Non-current assets 102 000

Property, plant and equipment 3 102 000

Current assets 58 200

Trade and other receivables 4 000

Cash and cash equivalents (bank) 54 200

Total assets 160 200

EQUITY AND LIABILITIES

Total equity 135 000

Capital 135 000

Total liabilities 25 200

Non-current liabilities 25 000

Long-term borrowings 25 000

Current liabilities 200

Trade and other payables 200

Total equity and liabilities 160 200

COMMENTS

.See paragraph 4.15.4, Notes, for the calculation of property, plant and equipment.

.The total assets of R160 200 corresponds to the total as shown in the BAE in

paragraph 4.6.

.The total equity and liabilities of R160 200 corresponds to the total as shown in the

BAE in paragraph 4.6.

.Words and figures between brackets is for explaining purposes only and do not form

part of any financial statement.

46

FAC1502/1

GOLDEN RULES

.ASSETS are, at this stage, grouped into non-current and current assets.

.Non-current assets do not change often and are used in ordinary business, production

or to render services.

.Current assets change after every operating transaction, thus very often.

.EQUITY (the interest of the owner(s) in the entity) comprise, at this stage, of capital only.

.LIABILITIES comprise, at this stage, non-current and current liabilities

.Non-current liabilities are to be paid after 12 months and do not change often. Current

liabilities are short term, change often and must be repaid within 12 months.

4.15.4 Notes

Additional information on items appearing in the financial statements is given in the notes to the

financial statements.

These explanatory notes are shown after the statement of cash flows. We do not deal with the

statement of cash flows in this module and will therefore show the notes after the statement of

profit or loss and other comprehensive income.

Note number 1 is used to reveal the accounting policies of the business. Now let us prepare the

notes of Fix-’n-Mat.

FIX ’N MAT

NOTES FOR THE MONTH ENDED 28 FEBRUARY 20.1

1. Accounting policy:

The financial statements have been prepared on the historical cost basis and comply with

International Financial Reporting Standards.

2. Revenue represents fees earned for services rendered to clients.

3. Property, plant and equipment Equipment Furniture Total

R R R

Carrying amount: Beginning of period — — —

Cost — — —

Accumulated depreciation — — —

Additions 100 000 2 000 102 000

Depreciation — — —

Carrying amount: End of period 100 000 2 000 102 000

Cost 100 000 2 000 102 000

Accumulated depreciation — — —

No depreciation was written off during this financial period.

4.16 Summary

We began by explaining the financial position (statement of financial position) and financial

performance (statement of profit or loss and other comprehensive income) and then went back

to how we enter into a transaction to set the accounting process in motion.

47

FAC1502/1

4.17 Revision exercises and solutions

4.17.1 Revision exercise 1

(1) Name the three groups of accounts in the general ledger.

(2) What is the difference between the total debits and the total credits of an account called?

(3) How do we test the arithmetical accuracy of transactions in the general ledger?

Solution: Revision exercise 1

(1) .Assets

.Liabilities

.Equity, which includes:

.capital

.drawings

.income

.expenditure

(2) Balance

(3) By preparing a trial balance

4.17.2 Revision exercise 2

List each of the following ledger accounts under one of the categories in the table below.

‘‘Furniture’’ is inserted as an example.

ASSETS EQUITY LIABILITIES

Non-

Non-current Current Expendi- current Current