FISERV OOC 7127 04

User Manual: 7127-04

Open the PDF directly: View PDF ![]() .

.

Page Count: 11

7127-04 Wisconsin (04/08)

1

Unum Life Insurance Company of America

2211 Congress Street

Portland, Maine 04122

(207) 575-2211

TAX QUALIFIED NURSING HOME INSURANCE OR QUALIFIED LONG TERM CARE

INSURANCE

OUTLINE OF COVERAGE

FOR THE EMPLOYEES OF

FISERV, INC. - #133398

Group Master Policy/Certificate Form Number GLTC04/CLTC04

Caution: If you must complete an Application for Long Term Care Insurance which includes

evidence of insurability, the issuance of a long term care insurance certificate will be based on your

responses to the questions on your application. You retained a copy of your Application for Long

Term Care Insurance when you applied. If your answers are incorrect or untrue, the company may

have the right to deny benefits or rescind your coverage. The best time to clear up any questions is

now, before a claim arises! If, for any reason, any of your answers are incorrect, contact Unum at this

address: Unum Life Insurance Company, 2211 Congress Street, Portland, Maine 04122.

If nursing home insurance coverage is purchased:

THE WISCONSIN INSURANCE COMMISSIONER HAS ESTABLISHED

MINIMUM STANDARDS FOR NURSING HOME INSURANCE. THE POLICY

MEETS THOSE STANDARDS.

THE POLICY COVERS CERTAIN TYPES OF NURSING HOME CARE. THIS

POLICY DOES NOT COVER HOME HEALTH CARE. THERE MAY BE

LIMITATIONS ON THE SERVICES COVERED. READ YOUR CERTIFICATE

CAREFULLY.

FOR MORE INFORMATION ON LONG-TERM CARE SEE THE "GUIDE TO

LONG-TERM CARE" GIVEN TO YOU WHEN YOU APPLIED FOR COVERAGE

UNDER THE POLICY. THE POLICY'S BENEFITS ARE NOT RELATED TO

MEDICARE.

7127-04 Wisconsin (04/08)

2

If long term care insurance coverage is purchased:

THE WISCONSIN INSURANCE COMMISSIONER HAS ESTABLISHED

MINIMUM STANDARDS FOR LONG-TERM CARE INSURANCE. THE POLICY

MEETS THOSE STANDARDS.

THE POLICY COVERS CERTAIN TYPES OF NURSING HOME AND HOME

HEALTH CARE SERVICES. THERE MAY BE LIMITATIONS ON THE

SERVICES COVERED. READ YOUR CERTIFICATE CAREFULLY.

FOR MORE INFORMATION ON LONG-TERM CARE SEE THE "GUIDE TO

LONG-TERM CARE" GIVEN TO YOU WHEN YOU APPLIED FOR COVERAGE

UNDER THE POLICY. THE POLICY'S BENEFITS ARE NOT RELATED TO

MEDICARE.

1.

The policy is a group policy which is issued in the state of Wisconsin.

2. PURPOSE OF OUTLINE OF COVERAGE. This outline of coverage provides a very brief

description of the important features of the policy. You should compare this outline of coverage

to outlines of coverage for other policies available to you. This is not an insurance contract,

but only a summary of coverage. Only the group policy contains governing contractual

provisions. This means that the group policy sets forth in detail the rights and

obligations of both you and the insurance company. Therefore, if you purchase this

coverage, or any other coverage, it is important that you READ YOUR CERTIFICATE

CAREFULLY!

3. FEDERAL TAX CONSEQUENCES. The policy for long term care insurance is intended to be

a federally tax-qualified long term care insurance contract under Section 7702B(b) of the

Internal Revenue Code of 1986, as amended and may qualify you for federal and state tax

benefits.

4. TERMS UNDER WHICH THE CERTIFICATE MAY BE CONTINUED IN FORCE OR

DISCONTINUED

a. RENEWABILITY - THE CERTIFICATE IS GUARANTEED RENEWABLE. This means you

have the right, subject to the terms of the policy to continue your coverage as long as

premium for your coverage is paid on time. Unum cannot change any of the terms of the

policy on its own, except that, in the future, IT MAY INCREASE THE PREMIUM YOU PAY.

7127-04 Wisconsin (04/08)

3

b. CONTINUATION OF COVERAGE. If your group long term care coverage ends for reasons

other than non-payment of premium or your choice to have premium payments stopped for

your coverage, you may elect continuation of coverage. This means that the same

coverage you had under this plan can continue on a direct billed basis. If you are already

direct billed, your coverage will automatically transfer to continued coverage. Election for

continued coverage must be made within 60 days of the date your group coverage would

otherwise end. Any premium that applies must be paid directly to Unum by you for any

coverage to be continued.

c. WAIVER OF PREMIUM. We will waive payment of premium for your coverage during any

period of time that you are receiving benefits under the policy. However, premium

payments will not be waived if you are only receiving Respite Care or Additional Care

Benefits.

5. TERMS UNDER WHICH THE COMPANY MAY CHANGE PREMIUMS. WE HAVE A LIMITED

RIGHT TO CHANGE PREMIUMS. We reserve the right to change any and all premiums. Any

change in premium must apply to all similar policies issued on this policy form and in the state

in which the policy is or certificates are sitused. Premiums cannot be increased because of any

change in the age or health of the persons covered under the policy. We cannot discontinue

the policy except where required by law or as a result of non-payment of premium.

6. TERMS UNDER WHICH THE CERTIFICATE MAY BE RETURNED AND PREMIUM

REFUNDED.

a. You may cancel your coverage for any reason within 30 days after it is delivered to you or

your representative. Simply return your certificate, within 30 days of its receipt, to us. If this

is done, your certificate will be canceled from the beginning and all premiums paid for your

coverage will be refunded.

b. If you die while insured under the policy, we will refund any pro rata portion of any premium

paid covering the period after your death. We will make the refund within 30 days after we

receive written notice of your death. Payment will be made to your estate.

7. THIS IS NOT MEDICARE SUPPLEMENT COVERAGE. If you are eligible for Medicare, review

the Guide to Health Insurance for People with Medicare available from the insurance company.

Neither Unum nor its agents represent Medicare, the federal government or any state

government.

8. LONG TERM CARE COVERAGE. Policies of this category are designed to provide coverage

for one or more necessary or medically necessary diagnostic, preventive, therapeutic,

rehabilitative, maintenance, or personal care services, provided in a setting other than an acute

care unit of a hospital, such as in a nursing home, in the community or in the home.

7127-04 Wisconsin (04/08)

4

The policy provides coverage in the form of a fixed dollar indemnity benefit if you are

Chronically Ill and you are receiving care while confined in a Long Term Care Facility. If the

policy includes coverage for Professional Home and Community Care or Total Choice Home

Care and you elect such coverage, we will pay you a benefit if you choose to receive care at

home or in the community. Coverage is subject to the policy limitations, benefit maximums and

elimination period requirements.

9. BENEFITS PROVIDED BY THE POLICY. Refer to the attached SUMMARY OF BENEFITS

for the benefits available under the Policyholder’s plan.

Eligibility for the Payment of Benefits

You will be eligible for a benefit if, on or after the effective date of your coverage and while your

coverage is in effect, you become Chronically Ill.

Conditions for Payment of Benefits

To receive benefits under the policy, the following conditions must be met:

you must satisfy the Elimination Period, if applicable;

you must be receiving Qualified Long Term Care Services;

the treatment for your Chronic Illness must be provided pursuant to a written Plan of Care;

and

we must approve your claim.

You must also provide us with a Licensed Health Care Practitioner’s Certification that you are

unable to perform (without Substantial Assistance from another individual) two or more

Activities of Daily Living for a period of at least 90 days, or that you require Substantial

Supervision by another individual to protect you from threats to your health or safety due to

Severe Cognitive Impairment. You will be required to submit a Licensed Health Care

Practitioner’s Certification every 12 months.

Limitations on Payment of Benefits

We will not pay benefits in excess of any coverage amounts you choose or for coverages that

you have not elected. Benefits paid will reduce your Lifetime Maximum Benefit and will no

longer be available once your Lifetime Maximum has been reached. We will not pay benefits

for Qualified Long Term Care Services you receive during the Elimination Period, except as

described in the Respite Care Benefit and the Additional Care Benefit provisions. The policy

only pays benefits if you are receiving Qualified Long Term Care services.

LTC Facility Benefit Payment

You must give us proof that you are receiving Qualified Long Term Care Services in a LTC

Facility before a LTC Facility Monthly Benefit is paid. If you are eligible for benefits for a period

of less than one month, we will pay you 1/30th of the monthly benefit for each day that you are

Chronically Ill and receiving Qualified Long Term Care Services in a LTC Facility. (Refer to the

OPTIONAL BENEFITS PROVIDED BY THE POLICY section of this Outline of Coverage for

information on benefit payments for home care).

7127-04 Wisconsin (04/08)

5

Additional Care Benefit:

Once you are eligible for a benefit payment, you will have access to Additional Care designed

to assist you in living at home or in other residential housing. You do not need to complete

your Elimination Period for an Additional Care Benefit payment to begin. The Additional Care

must be:

appropriate for your Chronic Illness and conform with generally accepted medical

standards;

provided pursuant to a written Plan of Care;

recommended by a Licensed Health Care Practitioner; and

approved by us prior to receipt of Additional Care.

Bed Reservation Benefit

If you are receiving a LTC Facility Monthly Benefit and your stay in the facility is interrupted due

to a stay in an acute care facility, or due to a temporary absence and a charge is made to

reserve your LTC Facility accommodations, you will be eligible for a Bed Reservation Benefit.

We will pay you 1/30th of the LTC Facility Monthly Benefit for each day you are absent from the

LTC Facility:

up to 90 days per calendar year if your absence is due to a stay in an acute care facility; or

up to 30 days per calendar year for a temporary absence not related to a stay in an acute

care facility.

In no event will the maximum number of Bed Reservation days exceed 90 days per calendar

year. Bed Reservation Benefit payments will reduce your Lifetime Maximum Benefit and will no

longer be available once your Lifetime Maximum Benefit has been reached. If your stay in a

LTC Facility is interrupted while you are satisfying your Elimination Period, such days will be

used to help satisfy your Elimination Period.

Respite Care Benefit

If you are Chronically Ill and receiving Respite Care but you are not receiving a LTC Facility

Monthly Benefit (or a Home Care Monthly Benefit if your coverage includes a home care

benefit) you will be eligible to receive a Respite Care Benefit. The Respite Care Benefit you will

receive is equal to 1/30th of your LTC Facility Monthly Benefit for each day you have Respite

Care for up to 21 days each calendar year. You do not need to complete your Elimination

Period for Respite Care payments to begin and the days you are receiving Respite Care will

count toward satisfying your Elimination Period.

7127-04 Wisconsin (04/08)

6

Words That Have A Special Meaning

Activities of Daily Living (ADLs) are bathing, dressing, toileting, transferring, continence and

eating.

Additional Care means special services; equipment or caregiver training designed to assist you

in living at home or in other residential housing. Additional Care may include:

assistance in locating long term care providers and caregivers in your area (this service is

also available even if you are not eligible for benefits);

a visit from a Licensed Health Care Practitioner who will develop your Plan of Care;

a visit from a home safety expert who will assess your residence and offer suggestions for

increased personal safety;

purchase or rental of a medical alert service;

purchase or rental of durable medical equipment;

home modifications for your support; or

caregiver training.

Chronic Illness and Chronically Ill means you are unable to perform, without Substantial

Assistance from another individual, two or more Activities of Daily Living; or you require

Substantial Supervision by another individual to protect you from threats to your health and

safety due to Severe Cognitive Impairment.

Elimination Period means the number of days during which you are Chronically Ill and you are

receiving services appropriate for your Chronic Illness, but no benefit is payable.

Lifetime Maximum Benefit means the total dollar amount of benefits that will be paid under the

policy, excluding any Additional Care Benefit.

Long Term Care (LTC) Facility means a facility (such as a nursing home, an assisted living

facility, a hospice facility, a rehabilitation facility, an Alzheimer’s facility or a residential care

facility) that is licensed by the appropriate federal or state agency to engage primarily in

providing care and services sufficient to support your needs resulting from Chronic Illness.

Plan of Care means a written plan prescribed by a Licensed Health Care Practitioner, based

upon an assessment that evaluates your level of functional capacity.

Qualified Long Term Care Services means necessary diagnostic, preventive, therapeutic,

curing, treating, mitigating and rehabilitative services and maintenance or personal care

services that are required by you.

Respite Care means short-term or periodic Qualified Long Term Care Services which are

required to maintain your health or safety and to give temporary relief to your primary caregiver

from his or her caregiving duties.

7127-04 Wisconsin (04/08)

7

Severe Cognitive Impairment means a severe deterioration or loss in your short or long term

memory; your orientation as to person, place, or time; or your deductive or abstract reasoning

as reliably measured by clinical evidence and standardized tests. Such loss can result from a

sickness, injury, advanced age, Alzheimer’s disease or irreversible or similar form of dementia.

Substantial Assistance means stand-by or hands-on assistance without which you would not be

able to safely and completely perform the ADL. Stand-by assistance means the presence of

another person within arm’s reach of you while you are performing the ADL. Hands-on

assistance means physical assistance (minimal, moderate or maximal) without which you

would not be able to perform the ADL.

Substantial Supervision means continual supervision (which may include cueing by verbal

prompting, gestures or other demonstrations) by another individual for the purpose of protecting

you from threats to your health or safety.

OPTIONAL BENEFITS PROVIDED BY THE POLICY -- EACH OF THE FOLLOWING

OPTIONAL BENEFITS IS AVAILABLE UNDER THE POLICYHOLDER’S PLAN. OPTIONAL

BENEFITS MAY BE AVAILABLE AT AN ADDITIONAL COST TO YOU. YOU MAY ALSO

REFER TO THE ATTACHED SUMMARY OF BENEFITS TO DETERMINE AVAILABLE

OPTIONAL BENEFITS.

Home Care Options:

Professional Home and Community Care Benefit:

If your coverage includes the Professional Home and Community Care Benefit, we will pay

1/30th of the Home Care Monthly Benefit you elected for each day you receive Professional

Home and Community Care Services. Professional Home and Community Care Services may

be provided anywhere other than a LTC Facility, an acute care facility or other location

excluded by the policy. You must provide written proof indicating the number of days you

received Professional Home and Community Care Services before a benefit is paid.

Professional Home and Community Care Services means Qualified Long Term Care Services

provided to you for at least one hour or more per day by or through a Licensed Home Health

Care Agency; by a Licensed Health Care Professional; or in an Adult Day Care Facility.

Professional Home and Community Care Services include nursing care; physical, respiratory,

and occupational or speech therapy; homemaker services; hospice care; or other services

pursuant to your Plan of Care.

Included in the Professional Home and Community Care Benefit is an International Benefit.

You may be eligible to receive International Benefits if you become Chronically Ill and are

receiving Qualified Long Term Care Services while traveling outside of the United States, its

territories or possessions, or Canada. International Benefits will be paid on an indemnity basis.

7127-04 Wisconsin (04/08)

8

Total Choice Home Care Benefit:

If your coverage includes the Total Choice Home Care Benefit, we will pay 1/30th of the Home

Care Monthly Benefit you elected for each day you receive Total Choice Home Care Services.

Total Choice Home Care Services may be provided anywhere other than a LTC Facility, an

acute care facility or other location excluded by the policy.

Total Choice Home Care Services means Qualified Long Term Care Services provided to you

by anyone, including a Family Member, by or through a Licensed Home Health Care Agency;

by a Licensed Home Health Care Professional; in an Adult Day Care Facility; or by an informal

caregiver. Total Choice Home Care Services include nursing care; physical, respiratory, and

occupational or speech therapy; homemaker services; hospice care; or other services pursuant

to your Plan of Care.

Included in the Total Choice Home Care Benefit is an International Benefit. You may be

eligible to receive International Benefits if you become Chronically Ill and are receiving Qualified

Long Term Care Services while traveling outside of the United States, its territories or

possessions, or Canada. International Benefits will be paid on an indemnity basis.

Inflation Protection and Benefit Increase Options:

5% Compound Inflation Protection:

If your coverage includes this option, your LTC Facility Monthly Benefit will increase each year

on the Coverage Effective Date by 5% of your LTC Facility Monthly Benefit in effect on that

date. Increases will be automatic and will occur regardless of your health and whether or not

you are eligible for or are receiving benefit payments. Your premium will not increase due to

automatic increases in your LTC Facility Monthly Benefit.

10. LIMITATIONS AND EXCLUSIONS

We will not provide benefits for:

a Chronic Illness caused by war or any act of war, whether declared or undeclared, that

occurs while your coverage is in force.

a Chronic Illness caused by intentionally self-inflicted injuries or attempted suicide, while

sane.

a Chronic Illness caused by the commission of a crime for which you have been convicted

under law, or caused by your attempt to commit a crime under law caused by the

participation in a felony, riot, or insurrection.

a Chronic Illness caused by alcoholism or drug addiction, alcohol abuse, drug addiction or

drug abuse including, but not limited to, prescription or non-prescription drugs, except when

taken as ordered by a Physician and drug addiction.

any period of time while you are Chronically Ill and you are confined in a hospital, other than

if you are confined to a LTC Facility that is a distinctly separate part of a hospital. This

exclusion does not apply to those periods covered under the Bed Reservation Benefit.

any period of time that you are Chronically Ill and you are outside the United States, its

territories or possessions or Canada for 30 consecutive days or longer if a home care

benefit is not selected.

7127-04 Wisconsin (04/08)

9

THE POLICY MAY NOT COVER ALL THE EXPENSES ASSOCIATED WITH YOUR LONG TERM

CARE NEEDS.

11. RELATIONSHIP OF COST OF CARE AND BENEFITS. Because the cost of long term care

services will likely increase over time, you should consider whether and how the benefits of this

plan may be adjusted.

If the plan provides an Inflation Protection or Benefit Increase Option and you have

chosen the option, your LTC Facility Monthly Benefit will increase each year on the

Coverage Effective Date. Increases will be automatic and will occur regardless of your

health and whether or not you are Chronically Ill. Your premium will not increase due to

the automatic increases in your LTC Facility Monthly Benefit.

After your coverage is in force, you will be allowed to increase your coverage based on

the benefits available under the Policyholder’s plan. To do so, you must complete a new

benefit election form and a Long Term Care Insurance Application. No increased or

additional coverage will become effective unless we approve your Long Term Care

Insurance Application for such change. Premiums for your coverage may be adjusted

due to changes or increase in your coverage based on your age on the date you apply to

change or increase your coverage.

12. ALZHEIMER’S DISEASE AND OTHER ORGANIC BRAIN DISORDERS.

The policy provides for coverage of Severe Cognitive Impairment. Severe Cognitive

Impairment is not related to the inability to perform ADLs. Rather, Severe Cognitive Impairment

means that you have lost the ability to reason and suffer a decrease in awareness, intuition and

memory. Examples of Severe Cognitive Impairment are: Alzheimer’s disease, multi-infarct

dementia, brain injury, brain tumors, irreversible dementia or other such structural alterations of

the brain.

13. PREMIUM

The initial premium charges will be figured at the premium rates as shown on the attached pages.

Unum may change the premium rates when the terms of the policy are changed.

14. ADDITIONAL FEATURES

Medical underwriting may be required.

Eligibility and Participation

You are eligible for the plan if you are: an Active Employee of the Policyholder and your

Family Members.

RIGHT OF APPEAL

You have the right to appeal any claim decision. Your appeal must be in writing and must be

sent to us within 90 days of your denial notice.

7127-04 Wisconsin (04/08)

10

We will notify you in writing if a claim or any part of a claim is denied. The denial letter will

state:

the specific reason(s) for the denial with reference to the applicable Policy provision(s);

a description of any additional material or information that is necessary to complete the

claim;

an explanation of why the additional material or information is necessary;

a statement describing your access to documents;

a statement describing your appeal and legal rights to bring suit; and

the name, address and telephone number of the individual designated by us to

administer your appeal.

If you are not satisfied with the reason for the denial, you or your authorized representative may

ask to have the claim reviewed by us. Your appeal must be in writing and should include all

supporting materials or information that will help us to review the claim. We will review your

appeal and all new information submitted, and notify you or your representative of our decision

within 30 days of receiving the appeal. If special circumstances require an extension of time for

processing, you will be notified of the reasons for the extension and the date by which we

expect to make a decision. A decision shall be made no later than 120 days following receipt of

the initial request for review. We can extend the time periods if we have not received needed

information from you. In some cases, we may request that you provide additional information

to assist in the review.

You or your authorized representative may request copies of those documents that are relevant

to your claim.

15. CONTACT THE STATE SENIOR HEALTH INSURANCE ASSISTANCE PROGRAM IF YOU

HAVE GENERAL QUESTIONS REGARDING LONG TERM CARE INSURANCE. CONTACT

US IF YOU HAVE SPECIFIC QUESTIONS REGARDING YOUR LONG TERM CARE

INSURANCE CERTIFICATE.

7127-04 Wisconsin (04/08)

11

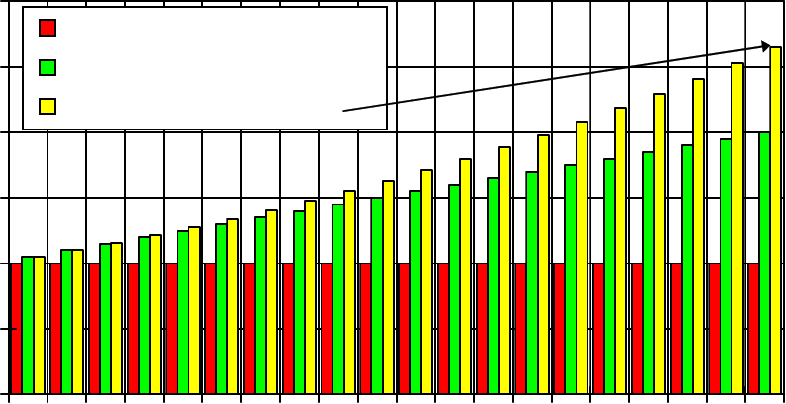

Monthly Premium Based On the Following:

Issue Age 65

LTC Facility with Professional Home and Community Care (50%)

90 Day Elimination Period

Lifetime Maximum Benefit Period

Monthly Premium Without Inflation Protection: $253.12

Monthly Premium With 5% Compound Inflation Protection: $440.42

Premium will remain level; it will not increase due to automatic increases in benefit amounts.

Long Term Care

Comparison of Benefits for Simple and Compound

Inflation Protection

0

1000

2000

3000

4000

5000

6000

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

Policy Year

Monthly

Dollar

Amount

No Inflation

5% Simple Benefit Increase

5% Compound Inflation