A Guide To Community Shared Solar: Utility, Private, And Nonprofit Project Development (Book), Powered By SunShot, U.S. Departme PV

User Manual:

Open the PDF directly: View PDF ![]() .

.

Page Count: 76

- A Guide to Community Shared Solar: Utility, Private, and Non pro˜t Project Development

- ACKNOWLEDGEMENTS

- TABLE OF CONTENTS

- Section 1: Introduction

- Section 2: Community Shared Solar Project Models

- Section 3: Emerging State Policies to Support Community Shared Solar

- Section 4: Tax Policies and Incentives

- Section 5: Securities Compliance

- Section 6: Getting Started

- Section 7: Resources

- Appendix A

- Appendix B

- For more information,

A Guide to

Community Shared Solar:

Utility, Private, and Nonprot Project Development

ACKNOWLEDGEMENTS

This guide is an updated version of the original Guide to Community Solar, published November 2010

(see www.nrel.gov/docs/fy11osti/49930.pdf), which was developed for the National Renewable Energy

Laboratory by Northwest Sustainable Energy for Economic Development, Keyes and Fox, Stoel Rives, and

the Bonneville Environmental Foundation. This guide builds on the research and writing from the Northwest

Community Solar Guide, published by Bonneville Environmental Foundation and Northwest SEED.

AUTHORS

Jason Coughlin, Jennifer Grove, Linda Irvine, Janet F. Jacobs, Sarah Johnson Phillips, Alexandra Sawyer,

Joseph Wiedman

REVIEWERS AND CONTRIBUTORS

Dick Wanderscheid, Bonneville Environmental Foundation; Stephen Frantz, Sacramento Municipal

Utility District; David Brosch, University Park Community Solar, LLC; Lauren Suhrbier, Clean Energy

Collective; Marc Romito, Tucson Electric Power; Ellen Lamiman, Energy Solutions

GRAPHIC DESIGN

Lynnae Burns, Bonneville Environmental Foundation

Available online at: www.osti.gov/bridge

Published May 2012

NOTICE

This report was prepared as an account of work sponsored by an agency of the United States government.

Neither the United States government nor any agency thereof, nor any of their employees, makes any

warranty, express or implied, or assumes any legal liability or responsibility for the accuracy,

completeness, or usefulness of any information, apparatus, product, or process disclosed, or represents

that its use would not infringe privately owned rights. Reference herein to any specic commercial

product, process, or service by trade name, trademark, manufacturer, or otherwise does not necessarily

constitute or imply its endorsement, recommendation, or favoring by the United States government or any

agency thereof. The views and opinions of authors expressed herein do not necessarily state or reect

those of the United States government or any agency thereof. As with the rst version of this guide, the

case studies have been provided by the program developers and have not been independently veried by

the authors or the U.S. Department of Energy (DOE).

SPONSORS

This report was made possible through funding from the DOE SunShot Initiative. To learn more, please

visit www.energy.gov/sunshot.

This document is not legal or tax advice or a legal opinion on specic facts or circumstances. The contents

are intended for informational purposes only. The authors are solely responsible for errors and omissions.

Prepared for NREL Subcontract No. AGG-2-22125-01

TABLE OF CONTENTS

SECTION 1: INTRODUCTION .............................................................................................................. 2

Purpose ......................................................................................................................................................... 2

How to Use This Guide ................................................................................................................................. 2

Why “Community Shared” Solar? ................................................................................................................. 3

Definition of Key Terms ................................................................................................................................. 4

SECTION 2: COMMUNITY SHARED SOLAR PROJECT MODELS................................................... 6

Comparison of Models .................................................................................................................................. 7

Utility-Sponsored Model ................................................................................................................................ 8

Special Purpose Entity (SPE) Models ......................................................................................................... 15

Nonprofit Model ........................................................................................................................................... 27

Summary of Benefit Allocation Options by Model ....................................................................................... 32

SECTION 3: EMERGING STATE POLICIES TO SUPPORT COMMUNITY SHARED SOLAR ....... 33

Group Billing ................................................................................................................................................ 33

Virtual Net Metering .................................................................................................................................... 34

Joint Ownership .......................................................................................................................................... 37

SECTION 4: TAX POLICIES AND INCENTIVES ............................................................................... 38

Business Energy Investment Tax Credit (“Commercial ITC”) ..................................................................... 39

Modified Accelerated Cost Recovery System (MACRS) ............................................................................ 39

Tax Credit Bonds ........................................................................................................................................ 40

Federal Grants ............................................................................................................................................ 41

State and Local Tax Considerations ........................................................................................................... 41

Interactions Among State and Federal Incentives ...................................................................................... 43

SECTION 5: SECURITIES COMPLIANCE ......................................................................................... 44

SECTION 6: GETTING STARTED ...................................................................................................... 47

SECTION 7: RESOURCES ................................................................................................................. 52

Organizations & Institutions ........................................................................................................................ 52

Publications & Online Tools ........................................................................................................................ 53

APPENDIX A ....................................................................................................................................... 55

Business Formation And Types: Special Project Entities For Community Shared Solar Projects ............. 62

APPENDIX B ....................................................................................................................................... 63

Introduction to IREC’s Community Renewables Model Program Rules ..................................................... 63

IREC’s Community Shared Renewables Model Program Rules ................................................................ 68

2

SECTION 1: INTRODUCTION

PURPOSE

In communities across the United States, people are seeking alternatives to conventional energy sources.

Whether they aim to increase energy independence, hedge against rising fuel costs, cut carbon emissions,

or provide jobs, people are looking to community-scale renewable energy projects for solutions. Falling

costs and creative new financing models have made solar projects—including community shared solar

projects—more financially feasible.

This guide is a resource for those who want to develop community shared solar projects, from community

organizers or solar energy advocates to government officials or utility managers. By exploring the range

of incentives and policies while providing examples of operational community shared solar projects, this

guide will help communities plan and implement successful energy projects. In addition, by highlighting

some policy best practices, this guide suggests changes in the regulatory landscape that could

significantly boost community shared solar installations across the nation.

HOW TO USE THIS GUIDE

The information in this guide is organized around three sponsorship models: utility projects, special

purpose entity projects, and nonprofit projects. The guide begins with examples of the three project

sponsorship models, discussing the legal and financial implications of each model. This is followed by a

discussion of state policies that encourage community shared solar. The guide then reviews some of the

tax and financing issues that impact community shared solar projects. While the guide cannot offer legal

or tax advice, the authors hope to provide an outline of the legal hurdles that every project organizer

should consider. Finally, Section 6, Getting Started provides readers with practical tools and tips for

planning their own projects. The Appendices provide a more detailed comparison of business structures

suitable for special purpose entities pursuing solar projects and the Interstate Renewable Energy

Council’s Model Community Renewables Program Rules.

As with the first version of this guide, the case studies have been provided by the program sponsors

or developers and have not been independently verified by the authors or by NREL. Please contact

the program sponsor for further information.

This guide cannot possibly describe all available incentives or cite all the examples of community shared

solar efforts nationwide. For information regarding the most recent developments, see Section 7, Resources.

Introduction

3

SECTION 1: INTRODUCTION

WHY “COMMUNITY SHARED” SOLAR?

For the purpose of this guide, “community shared solar” is defined as a solar-electric system that provides

power and/or financial benefit to multiple community members. Community shared solar advocates

recognize that the on-site solar market comprises only one part of the total market for solar energy. A

2008 study by the National Renewable Energy Laboratory (NREL) found that only 22 to 27% of

residential rooftop area is suitable for hosting an on-site photovoltaic (PV) system.1 Community options

expand access to solar power for renters, those with shaded roofs, and those who choose not to install a

residential system on their home for financial or other reasons. As a group, ratepayers and tax payers fund

solar incentive programs. Accordingly, as a matter of equity, solar energy programs should be designed in

a manner that allows all contributors to participate.

This guide focuses on projects designed to increase access to solar energy and to reduce up-front costs for

participants. Secondary goals met by many community shared solar projects include:

Improved economies of scale

Optimal project siting

Increased public understanding of solar energy

Local job generation

Opportunity to test new models of marketing, project financing, and service delivery.

Creative mechanisms to foster greater solar energy project deployment are not limited to those described

in this guide. Readers may be interested in investigating the following efforts that employ some elements

of community shared solar:

Volume purchasing efforts, such as those in Portland, OR (Solarize Portland!) and nationwide

(One Block Off the Grid)

Solar services co-ops such as Cooperative Community Energy, CA

Utility-owned distributed generation on customer rooftops, such as the Arizona Public Service

Community Power Project.

1 Supply Curves for Rooftop Solar PV-Generated Electricity for the United States, National Renewable Energy Laboratory, Nov. 2008.

www.nrel.gov/docs/fy09osti/44073.pdf .

4

SECTION 1: INTRODUCTION

DEFINITION OF KEY TERMS

The following terms are defined in the context of community shared solar.

Renewable Energy Certificates (RECs, carbon offsets, or green tags): A renewable energy facility

produces two distinct products. The first is electricity. The second is the package of environmental

benefits resulting from not generating the same electricity—and emissions—from a conventional gas or

coal-fired power plant. These environmental benefits can be packaged into a REC and sold separately

from the electrical power. A REC represents the collective environmental benefits, such as avoided

mercury, carbon dioxide (CO2), and other environmentally harmful pollutants, as a result of generating

one megawatt-hour (MWh) of renewable energy.

In most cases, RECs are sold on a per MWh basis. However, some project organizers choose to sell all

future rights to RECs up front, on a per-installed-watt basis, effectively capturing an installation rebate

and forgoing any future revenue from REC sales.

Net metering: Most on-site renewable energy systems use net metering to account for the value of the

electricity produced when production is greater than demand. Net metering allows customers to bank this

excess electric generation on the grid, usually in the form of kilowatt-hour (kWh) credits during a given

period. Whenever the customer’s system is producing more energy than the customer is consuming, the

excess energy flows to the grid and the customer’s meter “runs backwards.” This results in the customer

purchasing fewer kilowatt-hours from the utility, so the electricity produced from the renewable energy

system can be valued at the retail price of power. Most utilities have a size limit for net metering.

Community shared solar project organizers should be sure to check before assuming participants in a

community shared solar system can net meter. It may be that some alternative arrangement, such as group

billing or joint ownership, is used to account for the value of the electricity produced by a community

shared solar project.

Tax appetite: Individuals and businesses can reduce the amount of taxes owed by using tax credits. For a

tax credit to have any value, though, the individual or business must actually owe taxes. If the individual

or business is tax exempt or does not have sufficient income to need tax relief, the tax credits have no

value. Individuals or businesses that can use tax credits to reduce the amount they owe in taxes are said to

have a “tax appetite.” For example, public and nonprofit organizations are tax exempt, and therefore, do

not have a tax appetite. In addition, taxpaying entities might be eligible to use tax-based incentives, but

have insufficient tax appetite to make full use of them.

Investment Tax Credit (ITC): Section 48 of the Internal Revenue Code defines the federal ITC. The

ITC allows commercial, industrial, and utility owners of PV systems to take a one-time tax credit

equivalent to 30% of qualified installed costs. There is also a federal residential renewable energy tax

credit (Internal Revenue Code Section 25D), but the residential tax credit requires that the PV system be

installed on a home the taxpayer owns and uses as a residence, thus it would rarely, if ever, be applicable

to community shared solar projects.

5

SECTION 1: INTRODUCTION

Power purchase agreement (PPA): A PPA is an agreement between a wholesale energy producer and a

utility under which the utility agrees to purchase power. The PPA includes details such as the rates paid for

electricity and the time period during which it will be purchased. Sometimes, the term PPA or “third-party

PPA” is used to describe the agreement between the system owner and the on-site system host, under

which the host purchases power from the system. This arrangement is not explicitly allowed in all states; in

some states, it may subject the system owner to regulation as a utility. To avoid confusion, in this guide, a

PPA refers only to an agreement by a utility to purchase power from the solar system owner.

Solar services agreement (SSA): A solar services agreement is an agreement between the system owner

and the system site host, for the provision of solar power and associated services. The system owner

designs, installs, and maintains the system (a set of solar services) and signs an agreement with the host to

continue to provide maintenance and solar power. The agreement is sometimes referred to as a PPA, but

in this guide, we use the term SSA to indicate that the agreement between the system owner and the

system site host is more than a power purchase: it is an agreement that the system owner will provide

specific services to ensure continued solar power.

Securities: A security is an investment instrument issued by a corporation, government, or other

organization that offers evidence of debt or equity. Any transaction that involves an investment of money

in an enterprise, with an expectation of profits to be earned through the efforts of someone other than the

investor, is a transaction involving a security. Community shared solar organizers must be sure to comply

with both state and federal securities regulations, and avoid inadvertently offering a security. For more

information on securities, see Section 4, Tax Policies and Incentives.

Photo from United Power’s Sol Partners Installation, Colorado

6

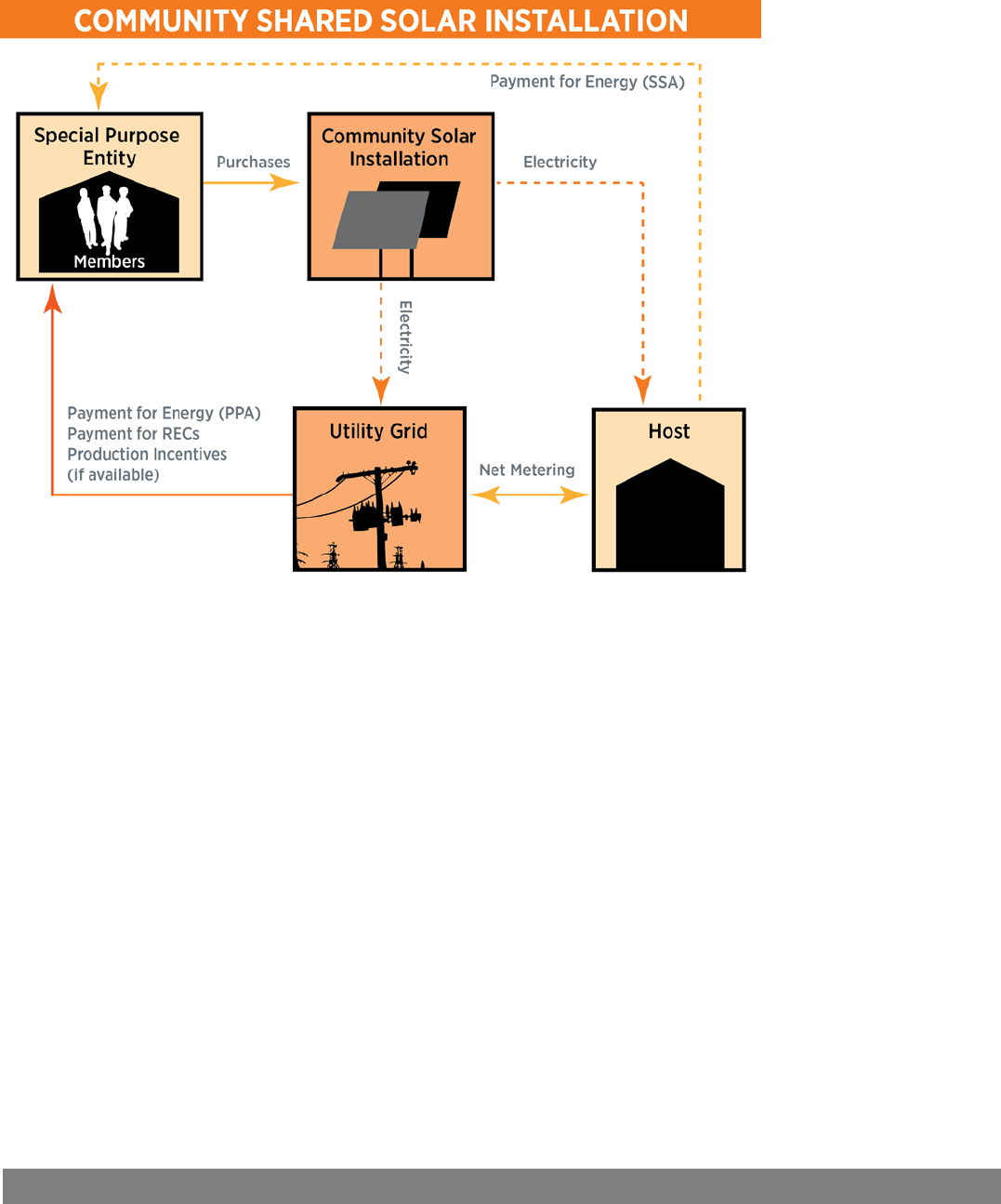

SECTION 2: COMMUNITY SHARED SOLAR PROJECT

MODELS

People have many reasons for organizing or participating in a community shared solar project. Just as

their motives vary, so do the possible project models, each with a unique set of costs, benefits,

responsibilities, and rewards. This section reviews several project models:

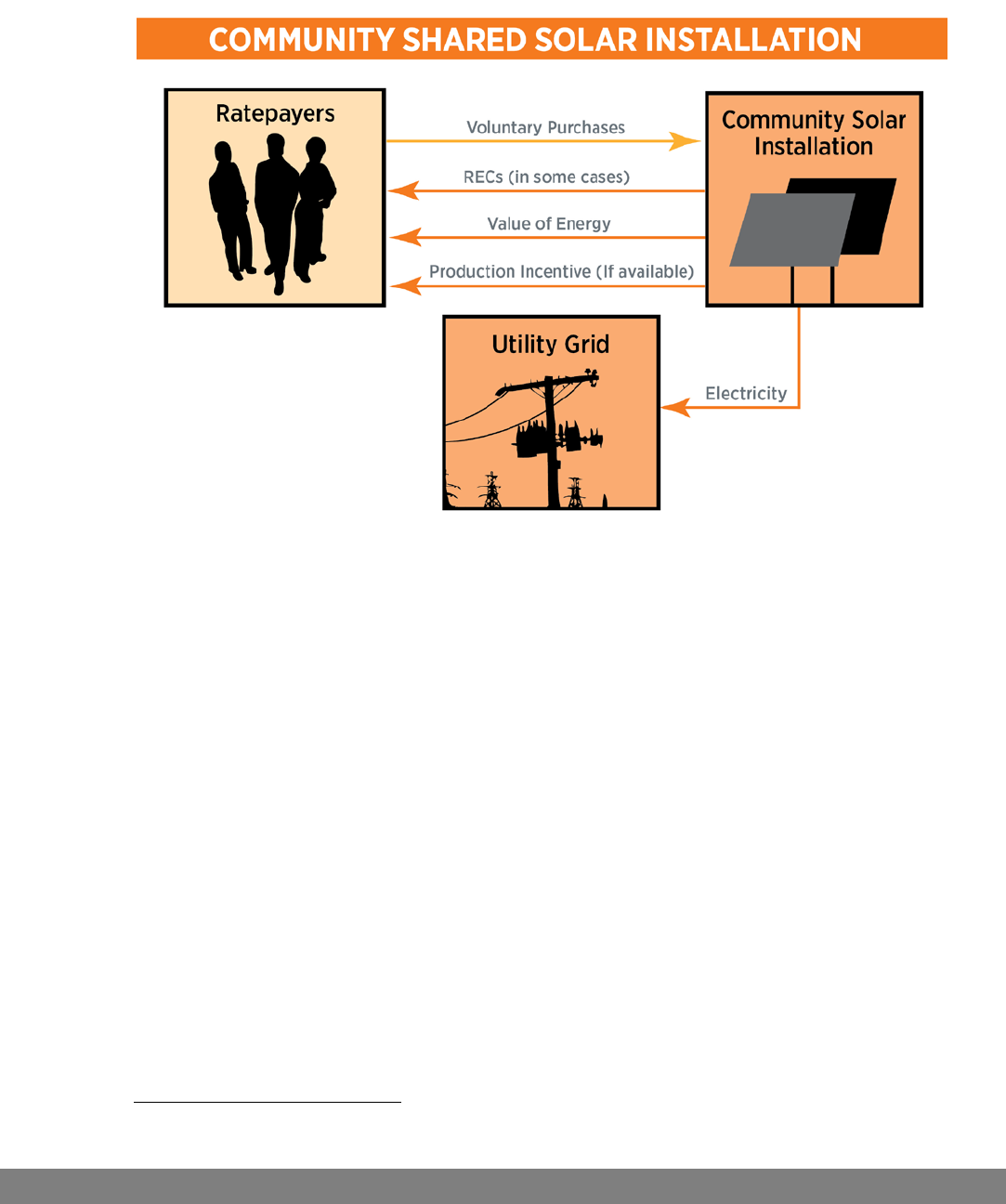

Utility-Sponsored Model: A utility owns or operates a project that is open to voluntary ratepayer

participation.

Special Purpose Entity (SPE) Model: Individuals join in a business enterprise to develop a

community shared solar project.

Nonprofit Model: A charitable nonprofit corporation administers a community shared solar project

on behalf of donors or members.

The authors of this guide illustrate pros and cons of different sponsorship models, as well as variations

within project models, so that project planners can select the model and variations that best suit their

situation and goals. Before selecting a project model, every planner should consider the issues below.

Allocation of Costs and Benefits: Who will pay to plan, construct, and operate the solar system?

Who will have rights to benefits, including the electricity produced, RECs, revenue from electricity

sales, tax benefits, other incentives, and ownership of the project’s assets (such as the solar system

itself)?

Financial and Tax Considerations: Will money be raised through a solar fee on electricity bills, by

equity or debt financing of a business entity, through charitable donations, or other options? What

kind of tax implications will there be for participants—e.g., will the project generate taxable income

for participants? Will it generate tax credits or deductions for participants?

Other Legal Issues: How will the project design address securities regulation, utilities regulation,

business regulation, and the complexity of agreements between various project participants?

The chart on the following page compares aspects of the three sponsorship models.

Community Shared Solar Project Models

7

SECTION 2: COMMUNITY SHARED SOLAR PROJECT MODELS

COMPARISON OF MODELS

Utility Special Purpose Entity Nonprofit

Owned By Utility or third party SPE members Nonprofit

Financed By Utility, grants,

ratepayer subscriptions

Member investments,

grants, incentives

Memberships, donor

contributions, grants

Hosted By Utility or third party Third party Nonprofit

Subscriber

Profile

Electric rate payers

of the utility Community investors Donors, members

Subscriber

Motive

Offset personal

electricity use

Return on investment;

offset personal

electricity use

Return on investment;

philanthropy

Long-term

Strategy

of Sponsor

Offer solar options;

add solar generation

(possibly for Renewable

Portfolio Standard)

Sell system to host;

retain for electricity

production

Retain for electricity

production for life of

system

Examples

• Sacramento Municipal

Utility District –

SolarShares Program

• Tucson Electric Power –

Bright Tucson Program

• University Park

Community Solar, LLC

• Clean Energy

Collective, LLC

• Island Community

Solar, LLC

• Winthrop Community

Solar Project

• Solar for Sakai

8

SECTION 2: COMMUNITY SHARED SOLAR PROJECT

MODELS

UTILITY-SPONSORED MODEL

For communities desiring to organize a community shared solar project, the local electric utility is a good

place to start. First of all, utilities are likely to have the legal, financial, and program management

infrastructure to handle organizing and implementing a community shared solar project. Second, many

utilities are actually governed by the member customers and can be directed to pursue projects on

members’ behalf. Fully one-fourth of Americans own their own electric power company through co-ops,

or city- or county-owned utilities.2 In general, publicly owned utilities have taken the lead in deploying

community shared solar projects. Even when the utility is investor-owned or privately held, it may wish

to expand customer choice with an option for community shared solar power.3

OVERVIEW

In most utility-sponsored projects, utility customers participate by contributing either an up-front or

ongoing payment to support a solar project. In exchange, customers receive a payment or credit on their

electric bills that is proportional to 1) their contribution and 2) how much electricity the solar project

produces. Usually, the utility or some identified third party owns the solar system itself. The participating

customer has no ownership stake in the solar system. Rather, the customer buys rights to the benefits of

the energy produced by the system. Note that utility-sponsored community shared solar programs differ

from traditional utility “green power” programs in that “green power” programs sell RECs from various

renewable energy resources and generally do not act as a hedge against rising electric costs; utility

community shared solar programs sell energy or rights to energy from specific solar installations, with or

without the RECs, at a rate that is generally locked in for a period of many years.

Utility-sponsored programs can help make solar power more accessible by decreasing the amount of the

purchase required, and by enabling customers to purchase solar electricity in monthly increments. Both

Sacramento Municipal Utility District’s SolarShares and Tucson Electric Power’s Bright Tucson

programs allow customers to participate in community shared solar on a monthly basis.

2 Growing a Green Economy for All: From Green Jobs to Green Ownership, The Democracy Collaborative, June 2010, p. 22.

www.community-wealth.org/_pdfs/news/recent-articles/07-10/report-warren-dubb.pdf.

3 ITC tax benefits may not be readily accessible to for-profit utilities, due to the normalization accounting rules.

9

SECTION 2: COMMUNITY SHARED SOLAR PROJECT MODELS

TAX AND FINANCE ISSUES FOR UTILITY-SPONSORED PROJECTS

A utility project’s ability to use tax incentives depends on the individual utility’s characteristics. Electric

co-ops, municipal utilities and public utility districts are exempt from federal income taxes, and thus,

cannot benefit from federal tax incentives, like the ITC and depreciation. However, the utility can make

use of Clean Renewable Energy Bonds (CREBs) that are not available to the for-profit investor-owned or

privately held utilities.

Since 2008, investor-owned utilities have been eligible to use the commercial ITC on qualifying public

utility property. And as taxpaying entities, the utilities may have the tax appetite to make use of them.

However, normalization accounting rules limit regulated utilities’ flexibility in maximizing the value of

these tax benefits compared to other private developers. Normalization rules require regulated utilities to

spread the benefits of investment tax credits throughout the useful life of the solar project in the rate-

making process. The utility’s incentive for investment is the difference between the value it receives from

the tax credit up front and the value it passes on to customers over time (i.e., the time value of money).

Private developers have the flexibility to pass on the benefits of the ITC sooner, which can give them a

price advantage over utility solar projects.4

4 P. Alvarez and B. Hodges. (2009). “Buying Into Solar.” Public Utilities Fortnightly. p. 57.

10

SECTION 2: COMMUNITY SHARED SOLAR PROJECT

MODELS

Other legal issues for utility-sponsored projects include the following:

Securities Compliance. In designing mechanisms for customer participation in solar projects,

utilities must be careful to comply with state and federal securities regulations. This requires

carefully considering what benefit a customer-participant receives in exchange for a financial

contribution to the project and how the project is marketed. For example, customer participants may

be offered ownership stakes in the solar system itself or just the rights to certain benefits from the

energy produced (such as credit on their electric bills, RECs, or access to a special electric rate).

However, regardless of how the program is marketed, depending on your state, the receipt of credits

on electric bills or other benefits may constitute a return on an investment and fall within the blue

sky laws (state laws that regulate the offering and sale of securities).

Allocation of Incentives. In addition to federal tax incentives, a utility-sponsored project might be

eligible for various state incentive programs that provide cash benefits or savings to the project. The

utility must consider whether and how these incentives will be passed on to customer participants and

the tax implications of how the incentives are handled. For example, in Washington State, participants

in a utility-sponsored program are eligible for production incentives. While the state Department of

Revenue has ruled that the incentive is not taxable, the IRS has not ruled definitively on whether

subsidies for solar PV in community shared solar installations are taxable income, although the

precedent is that subsidies for energy conservation measures are not taxable.5

RECs. Customer participants in utility-sponsored projects often desire to claim the environmental

benefits of using solar energy. Participants can only make such a claim if they receive RECs or the

utility retires the RECs on the participants’ behalf. If the utility keeps the RECs for any reason,

including Renewable Portfolio Standard compliance, only the utility can make environmental claims

related to the solar system. The utility-sponsored project should consider and make explicit how

RECs are allocated.

From a participant perspective, the tax implications are minimal. Bill credits for the value of electricity

are not generally taxed; at the same time, participants in a utility-sponsored project are not eligible for the

federal investment tax credit. The relative ease of participating in a utility-sponsored project may offset

some of the foregone tax incentives available under other community shared solar ownership models.

EXAMPLES OF UTILITY-SPONSORED PROJECTS

The following examples highlight some of the project options available to those planning a utility-

sponsored project.

5 26 USC 136 states that subsidies from public utilities for energy conservation measures are not taxable. For example, Washington State’s

production incentive was ruled to be not income. See http://apps.leg.wa.gov/WAC/default.aspx?dispo=true&cite=458-20.

11

SECTION 2: COMMUNITY SHARED SOLAR PROJECT MODELS

Sacramento Municipal Utility District (SMUD): SolarShares Program

SMUD’s SolarShares Program allows

customers who cannot or choose not to

acquire PV systems of their own to

purchase solar power directly from

SMUD while achieving net metering

benefits comparable to behind-the-meter

PV. SMUD buys the output of local,

community-scale photovoltaic systems

under 20-year PPAs and then resells the

solar power to participating customers.

Bill credits equivalent to the amount of

energy the customer buys from the

SolarShares system are credited to the

customer through virtual net metering

and are equivalent in value to the bill

credits received by a customer with behind-the-meter PV—i.e., full retail price per kWh. The program is

subsidized with SB16 surcharge funds, which allows SMUD to sell the power for less than the PPA

purchase price. SMUD retains the renewable energy credits and is able to count up to 25 MW of

SolarShares projects toward its 125-MW SB1 goal. SolarShares’ business goals are to make solar benefits

available to all SMUD ratepayers, to contribute to achieving SMUD’s 125-MW SB1 goal, and to gather

pricing and marketing experience that could lead to a sustainable solar enterprise for SMUD beyond the

current, mandated incentive program.

SolarShares began in mid-2008 with a 1-MW system constructed by enXco at a leased site in Wilton. The

system has thus far produced an average 1,745 MWh per year, of which about 86% has been sold to

SolarShares participants. Intensified marketing in Q4 2011 succeeded in moving the percentage sold

toward the program’s 95% goal. The program has maintained stable enrollment of around 600 customers

throughout its three-year life, with most dropouts attributable to customers moving out of the District.

Market research conducted in mid-2009 confirmed that most SolarShares customers are satisfied with the

program (75% positive responses) and would recommend it to others (85% positive responses).

6 SB1 is the California Solar Initiative, a state mandate requiring all California electric utilities to offer a 10-year program of declining incentives

for customer-sited PV. It expires at the end of 2016.

Photo from Stephen Frantz, Sacramento Municipal Utility District

12

SECTION 2: COMMUNITY SHARED SOLAR PROJECT

MODELS

Customers pay a fixed monthly fee, based on both their average electricity consumption and the amount

of PV to which they want to subscribe (from 0.5 to 4 kW). SMUD is exploring the marketing advantages

of changing this pricing structure to a flat fixed fee per kWh, allowing customers to purchase in packets

of 1,000 kWh/year. Once enrolled, customers are locked in at the fixed monthly fee, for as long as they

wish to participate. They receive monthly kWh credits for the estimated output of their solar subscription.

Although customers currently pay a premium for solar energy, the effective rate for solar is locked in

when they enroll, which maintains the ability of solar to act as a hedge against future price increases.

SMUD is making plans for expansion of up to 25 MW by the end of 2016. An RFP for a second

megawatt was released in Q3 2011, and the next 1-MW project is scheduled for completion in Q3 2012.

The PPA price for the second MW will be blended with the price for the original system to yield a lower

participation fee for both existing and new program subscribers. Depending on market response to the

second project, SMUD will probably seek to expand the program by larger increments in the future (the

enabling legislation caps projects at 5 MW each).

Program Highlights

• System Owner: enXco, with SMUD purchasing 100% of the output under a 20-year PPA

• Installed Capacity: 1 MW

• Participant Agreement: Customers pay a fixed monthly fee in return for a kWh credit. Credit varies

monthly, as solar output varies, so a 12-month consecutive commitment is requested.

• Electricity: The estimated kWh generated by a customer’s share is netted against the customer’s

consumption at home, at the full retail rate.

• RECs: Retained by SMUD

• Number of Participants: Approximately 600

Financial Details

• Installed Cost: NA

• Capital Financing: Handled by third party, enXco

• Tax Credits: 30% federal business investment tax credit taken by enXco, depreciation taken by enXco

• Estimated Annual Cost: Varies by customer size and array size. Output from a 0.5-kW share for the

small user will cost $129/year at 2012 prices. As the price for non-solar energy rises, a participant

could eventually realize monthly savings on their solar purchase.

For more information: Stephen Frantz, sfrantz@smud.org, (916) 732-5107, www.smud.org/

13

SECTION 2: COMMUNITY SHARED SOLAR PROJECT MODELS

Tucson Electric Power: Bright Tucson Community Solar Program

In 2011, Tucson Electric Power launched its Bright Tucson Community Solar Program to create

opportunities for customers unable to install traditional distributed solar power. Through the program,

customers have the opportunity to purchase solar power in “blocks” of 150 kWh per month. Program

participants can choose to purchase some or all of their energy through the program. Each purchased

block replaces the charges for an equivalent amount of conventional power. At current rates, the solar

block is more expensive by about two cents per kWh, but program blocks are exempt from two

surcharges applied to other electric usage. Both these surcharges are adjusted annually to reflect changing

energy costs, so the benefit of avoiding them could increase over time. The solar block rate is locked in

for 20 years under rules approved by the Arizona Corporation Commission (ACC), offering TEP

customers a way to hedge against future rate increases. While blocks purchased through the program will

still be subject to non-fuel rate changes, the blocks will not be affected by changes to the base energy rate

or renewable energy surcharges.

Tucson Electric Power offers an online solar calculator to help potential participants determine how many

blocks to purchase to offset the desired quantity of household electricity use. If the solar energy purchased

through the program exceeds actual usage during a monthly billing period, the excess is carried forward

to the next billing period as a credit. Any credit remaining after the September billing period will be paid

in full as a credit on the next bill.

Photo from Marc Romito, Tucson Electric Power

14

SECTION 2: COMMUNITY SHARED SOLAR PROJECT

MODELS

The first source of solar power for the Bright Tucson Community Solar Program is a 1.6-MW single-axis

tracking PV array located in The Solar Zone at the University of Arizona Science and Technology Park.

TEP is expanding the program as demand requires through utility-owned systems and power purchase

agreements. Currently, program participants have purchased 2.1 MW of community shared solar.

The following details pertain specifically to the first Bright Tucson Community Solar Program solar

source, a 1.6-MW single-axis tracking PV array, unless otherwise noted.

Program Highlights

• System Owner: Tucson Electric Power

• System Host: University of Arizona Science and Technology Park

• Installed Capacity: 1.6-MW single-axis tracking PV array

• Participant Agreement: Customers pay a fixed monthly fee per solar block in return for a

150-kWh credit. Any credit remaining after the September billing period will be paid in full

as a credit on the next bill.

• Electricity: Each 150-kWh block replaces the charges for an equivalent amount of

conventional power at a rate that currently adds $3 per month to the customer’s electric bill.

• RECs: Retained by TEP

• Number of Participants: 564 (six are commercial; includes all program solar sources)

Financial Details

• Installed Cost: $4/watt

• Capital Financing: Utility financed

• Tax Credits: For 1.6-MW single-axis tracking array, TEP used levelized ITC. For 2-MW

dual-axis tracking array, owner took the Treasury Grant (in lieu of ITC).

• Estimated Annual Cost: $36/year for a monthly 150-kWh block. As the price for non-solar

energy rises, participants could eventually realize monthly savings on their solar purchase.

For more information: Marc Romito, mromito@tep.com, www.tep.com/Renewable/Home/Bright

OTHER COMMUNITY SHARED SOLAR PROJECTS

United Power, CO; City of Ellensburg, WA; Florida Keys Electric Co-op, FL; Seattle City Light, WA;

St. George, UT; City of Ashland, OR; Coming Soon: San Diego Gas & Electric, CA

15

SECTION 2: COMMUNITY SHARED SOLAR PROJECT MODELS

SPECIAL PURPOSE ENTITY (SPE) MODELS

To take advantage of the tax incentives available to commercial solar projects, organizers may choose to

structure a project as a business. In most states, there is a range of business entities that could be suitable

for a participant-owned community shared solar project. (Please see Appendix A for more in-depth

descriptions of these business entities.) The main challenges in adapting these commercial solar structures

for community shared projects include:

Fully using available tax benefits when community investors have a limited tax appetite,

including a lack of passive income

Maintaining the community project identity when engaging non-community-based

tax-motivated investors

Working within limits on the number of unaccredited investors if the project is to be

exempt under securities laws.

OVERVIEW

When a group chooses to develop a community shared solar project as a special purpose entity, it assumes

the significant complexity of forming and running a business. The group must navigate the legal and

financial hurdles of setting up a business and raising capital, and comply with securities regulation. In

addition, it must negotiate contracts among the participant/owners, the site host and the utility; set up

legal and financial processes for sharing benefits; and manage business operations.

Given the complexity of forming a business, it is not surprising that many special purpose entities

pursuing community shared solar are organized by other existing business entities with legal and financial

savvy. Solar installation companies such as My Generation Energy in Massachusetts have successfully

created LLCs to purchase solar installations funded by groups of investors. Although this expands the

market for solar, the benefits are limited to a small group of tax-motivated investors. In an alternative

model, the Clean Energy Collective in Colorado has created a business structure under which

participation is offered to an unlimited number of utility customers.

16

SECTION 2: COMMUNITY SHARED SOLAR PROJECT

MODELS

TAX AND FINANCE ISSUES FOR SPECIAL PURPOSE ENTITY PROJECTS

Federal income tax benefits offer significant value for solar projects, but can be challenging for

community shared projects to use effectively. Making use of tax credits or losses (from depreciation)

requires significant taxable income. Moreover, passive investors in a community shared solar project

(investors who do not take an active role in the company or its management) can only apply the ITC to

passive income tax liability. As discussed below, most investors in a community shared solar project will

likely be passive investors, and few will have passive income. As a result, most individuals cannot fully

use federal tax benefits. In this section, we describe the major limitations on using federal tax benefits and

outline potential financing structures that accommodate those limitations. However, the descriptions here

do not account for the many nuances that might apply to individual projects.

17

SECTION 2: COMMUNITY SHARED SOLAR PROJECT MODELS

Passive Activity Rules

IRS “passive activity” rules are a major challenge for community-based renewable energy investors

trying to use federal tax benefits. In most cases, an individual’s investment in a community shared solar

project will be considered a passive investment. Passive activity rules allow tax credits or losses generated

from passive investment to be used to offset only passive income.7

Most individuals primarily have non-passive income, which includes salaries, wages, commissions, self-

employment income, taxable social security, and other retirement benefits. Non-passive income also

includes portfolio income, such as interest, dividends, annuities, or royalties not derived in the ordinary

course of a business. While portfolio income may seem passive, the IRS specifically excludes it from the

category of passive income.

Passive income can only be generated by a passive activity. There are only two sources for passive

income: a rental activity or a business in which the taxpayer does not materially participate.

“Participation” generally refers to work done in connection with an activity in which the taxpayer owns

an interest. To “materially” participate in the trade or business activity (in this case, operation of a solar

project) an individual must participate on a regular, continuous, and substantial basis in the operations of

the activity. This is a high standard that participants likely will not be able to meet. That means most

participants will be passive investors, limited to applying federal tax benefits to passive income. The

community shared solar project itself likely will not generate sufficient income to make full use of the

ITC or depreciation benefits, at least not in the early years of a project. Therefore, a project intending to

rely on federal tax benefits will have to seek participation of an investor with a larger tax appetite.

At-Risk Limitations

In addition to passive activity rules, at-risk rules limit the amount of losses one can claim from most

activities. Specifically, one can only claim losses equivalent to one’s amount of risk in the activity. The

“at-risk” amount generally is the amount of cash and property one contributes to the activity. In addition,

any amount borrowed for use in the activity is at-risk, as long as the borrower is personally liable for

repayment of the loan or the loan is secured with property not used for the activity. Money contributed

from a non-recourse loan is not considered “at-risk.”

7 For a list of IRS material participation tests and other details about passive activity and at-risk rules, see IRS Publication 925, available at:

www.irs.gov/pub/irs-pdf/p925.pdf.

18

SECTION 2: COMMUNITY SHARED SOLAR PROJECT

MODELS

Securities Regulation

Securities regulations are a major factor in financing structures for the SPE model. To reduce the burden

of securities compliance, many small projects seek a private placement exemption to registration

requirements. Qualifying for such an exemption requires limiting who can invest in the project (based on

assets or income for individuals) and how such an offering can be conducted. The practical effect is to

limit the number of middle-income individuals who can invest in a community shared solar project. If a

project is designed to produce electricity proportional to the amount used by the participants, securities

issues will effectively limit the size of a project. For example, private placement exemption limits the

number of “unaccredited” investors to 35 or fewer.8 A 1-MW solar facility, in contrast, could serve far

more participants, perhaps 300 to 500. Therefore, project developers must carefully consider how to

reconcile their financing mechanism with the size of their project, the number of participants, and type of

participants.

Potential Financing Structures

Special purpose entities need to plan their financing structures carefully. Structures that effectively use

the ITC can be complex and tend to mimic the structures used by larger commercial solar projects. For a

community SPE, potential financing structures that maximize federal tax incentives include:

Self-financing: This is the simplest option for a community SPE is to finance the project with equity

invested by community members. However, in order to fully use federal tax benefits, the SPE needs

to have enough community investors that have sufficient tax appetite to use federal tax incentives.

Given the passive loss rules and the at-risk limitations discussed above, this is not a realistic goal for

community groups consisting of individuals who lack other sources of passive income. That means

the project organizers will likely have to make the project economically viable without full use of

federal tax incentives (difficult without aid from a state or local incentive of similar value), or will

have to use one of the more complex structures such as a flip or a sale/leaseback (described below).

This need not take away from the community ownership, if the project can find even one community

member with the financial resources and tax appetite to participate as the primary tax investor.

Flip Structure: In this scenario, the community SPE partners with a tax-motivated investor in a new

special purpose entity that owns and operates the project. Initially, most of the equity comes from the

tax investor and most of the benefit (as much as 99%) would flow to the tax investor. When the tax

investor has fully monetized the tax benefits and achieved an agreed-upon rate of return, the

allocation of benefits and majority ownership (95%) would “flip” to the community SPE (but not

within the first five years). After the flip, the community SPE has the option to buy out all or most of

the tax investor’s interest in the project at the fair market value of the tax investor’s remaining

interest. Note that the numbers provided here reflect IRS guidelines on flip structures issued for wind

projects claiming the federal production tax credit. Similar rules potentially could apply to solar

projects claiming the ITC.

8 To be considered an accredited investor, an individual must have either: 1) a net worth of more than $1 million or 2) an annual income of

$200,000 ($300,000 jointly with a spouse) in each of the most recent two years and a reasonable expectation of having the same income level

in the current year.

19

SECTION 2: COMMUNITY SHARED SOLAR PROJECT MODELS

Sale/Leaseback: In this scenario, the community SPE (as the developer of the project, the site host,

or both) installs the PV system, sells it to a tax investor and then leases it back. As the lessee, the

community SPE is responsible for operating and maintaining the solar system and has the right to

sell or use the power. In exchange for use of the solar system, the community lessee makes lease

payments to the tax investor (the lessor). The tax investor has rights to federal tax benefits generated

by the project and the lease payments. The community SPE may have the option to buy back the

project at 100% fair market value after the tax benefits are exhausted.

There are numerous complex legal, financial, and tax issues associated with all of these financing

structures. These descriptions do not cover these issues completely. For more information on financing

structures, see Section 7, Resources.

EXAMPLES OF SPECIAL PURPOSE ENTITY PROJECTS

The following examples represent two possible approaches: a volunteer-led LLC and a business

enterprise that partners with utilities to deliver solar to customers. These special purpose entities are

structured as LLCs. Although there has been much interest in the possibility of structuring a community

shared solar enterprise as a cooperative (co-op), in fact, co-ops are not exempt from the complex

securities issues and project organizers have tended to choose to do business as LLCs.9 Several rural

electric co-ops that deliver electricity to customer/members have started community shared solar

programs, but the programs are peripheral to the function as consumer co-ops for the distribution of

electricity. As in the previous edition of this guide, the descriptions of the programs in the following

pages have been provided by the program sponsors or developers and have not been independently

verified by the authors or by DOE.

9 Tangerine Power, LLC, based in Washington State has created a business model for a solar power co-op and has launched the Edmonds

Community Solar Cooperative.

20

SECTION 2: COMMUNITY SHARED SOLAR PROJECT

MODELS

University Park Community Solar LLC, Maryland

The volunteer founders of University Park

Community Solar spent more than two

years crafting the legal and financial

aspects of their business model. With

expert consultation, including help from a

state senator to change the Maryland net

metering law, the volunteers formed a

member-managed LLC that will return

their investment in five to six years. Within

the group, there are both active and passive

investors.

A 22-kW system was installed on the roof

of a local church in May 2010. The LLC

will pass benefits to its members based on

revenue from several sources: electricity

sold to the church and grid, the auction of RECs, federal tax incentives, and depreciation. The LLC and

the Church signed a 20-year agreement detailing the provision of electricity, access to the solar array,

maintenance, insurance, and other issues. The host has an option to purchase the system before the 20-

year term is up.

To assist in establishing the LLC, the group received pro bono help from the Maryland Intellectual

Property Legal Resource Center and paid approximately $12,000 for other legal and accounting expertise.

The founders note that initial accounting and legal fees could overwhelm any return to members. Going

forward, they plan to handle the accounting and tax paperwork in house as much as possible.

The LLC organizers were careful to obtain legal advice on how to gain an exemption from state and

federal SEC filing requirements. The organizers are not all “accredited” investors. In addition, the

organizers were required to create lengthy disclosure documents to ensure that investors were fully

informed of the risks. Their attorneys advised them to pursue an exemption that restricted them in several

aspects, including having fewer than 35 unaccredited investors, keeping the offering private, and limiting

membership within the state of Maryland. See Section 5, Securities Compliance, for information about

securities compliance and private placement exemptions.

Photo from David Brosch, University Park Community Solar, LLC

21

SECTION 2: COMMUNITY SHARED SOLAR PROJECT MODELS

Project founders are looking to expand the model beyond the first site. Additional host sites in Maryland

and other states are being explored, including schools, nonprofits, and places of worship. Furthermore, the

LLC has offered to share legal and accounting documents with groups around the nation to facilitate the

model’s replication. The first successful replication was completed in December 2011 by Greenbelt

Community Solar, LLC in Greenbelt, Maryland.

Program Highlights

• System Owner: University Park Community Solar, LLC

• System Host: Church of the Brethren, University Park, MD

• Installed Capacity: 22 kW

• Participant Agreement: LLC passes net revenues (after expenses) and tax credits to members

• Electricity: LLC sells power to the church below retail rate; rate escalates approximately 3.5%/year;

church net meters and annual net excess generation is compensated by the utility

• RECs: LLC is working to auction RECs independently

• Number of Participants: 35 LLC Members

Financial Details

• Installed Cost: $5.90/watt

• Capital Financing: Project financed with member investments

• Tax Credits: $39,000 ITC (taken as the 1603 Treasury Grant in lieu of a tax credit)

• Grants: $10,000 from state of MD

• MACRS: Will depreciate 85% of cost over six years

• Annual Income from Power Sales: $3,300 in the first year, rising 3.5%/year

• Estimated Annual Income from REC Sales: $7,000 (28 RECs at $250 per MWh)

For more information: David Brosch, davidcbrosch@comcast.net, (301) 779-3168,

www.universityparksolar.com

22

SECTION 2: COMMUNITY SHARED SOLAR PROJECT

MODELS

Clean Energy Collective, LLC, Colorado

The Clean Energy Collective (CEC) provides a member-owned model that enables individuals to directly

own panels in a community shared solar farm. The CEC works closely with local utilities to create

community-scale solar projects that combine the on-bill credits of a utility-owned project with the

equivalent tax benefits and rebates of an individually owned solar project. While the 30% investment tax

credit is not directly available to individuals who participate in the project, the cost to participate is

adjusted to reflect the value of the tax credits. For projects initiated in 2011 or earlier, the CEC took the

1603 Treasury Grant, instead of the ITC, as the initial owner of the array. Portions of the array were then

sold to customers at discounted costs (reducing the cost by the proportioned Treasury Grant amount).

Customers could not take a tax credit on their purchase because the grant had been taken by the CEC.

Both parties are subject to recapture over the first five years if the resulting system is then sold to a

disqualified or non-taxpaying entity. Creating this proprietary project model, with ownership, tax and

legal considerations, proved challenging.

When individuals purchase panels in the solar farm, the utility credits them for the electricity produced at

or above the retail rate using the CEC’s RemoteMeter™ software system. The purchase price is as low as

$535, depending on location, available rebates, and RECs. For example, in the first project, CEC sold the

rights to all future RECs up front on a per-watt basis, offsetting a portion of the installed cost. The

benefits of ownership are transferable. If an owner moves within the service territory, the bill credits

follow them; if an owner moves out of the territory, the owner can resell ownership to another utility

customer or back to the CEC at fair market value, or donate the property to a nonprofit.

Photo from Lauren Suhrbier, The Clean Energy Collective, LLC

23

SECTION 2: COMMUNITY SHARED SOLAR PROJECT MODELS

The owners must be customers of the electric utility in which the community array is located and their

purchase is limited to the number of panels they need to offset 120% of their yearly electric use. These rules

ensure that benefits directly accrue to the local utility customers rather than outside investors. The CEC is

the management company representing the community owners and maintaining the solar arrays. In order to

provide “utility-grade” long-term power to the utility, a percentage of the monthly power credit value and

the initial sale price goes toward funding insurance, operations, and maintenance escrows.

The first CEC project is a 78-kW array in the Holy Cross Energy service territory. The CEC leased the

land, sold the project to customers, and negotiated a PPA with Holy Cross Energy. The PPA rate paid by

Holy Cross will escalate as regular utility rates increase. CEC’s RemoteMeter™ system automatically

calculates monthly bill credits for customer accounts and integrates directly with the utility’s billing

system to apply the credits.

In 2011, the CEC completed three more projects, bringing its installed project portfolio to 2.5 MW.

Project Highlights – First Project: Mid Valley Metro Solar Array

• System Owner: Individuals and businesses in Holy Cross Energy utility territory

• System Host: CEC leases site from the Mid Valley Metropolitan District

• Installed Capacity: 78 kW

• Participant Agreement: Minimum $725 purchase (a single panel after rebates and incentives).

Panel owners receive monthly credits for the value of the electricity produced for 50 years.

• Electricity: CEC, as agent for its customers, has a PPA with Holy Cross Energy to purchase the

power produced. Customers receive the resulting monetary credit on their monthly electric bill.

• RECs: Holy Cross Energy purchased rights to RECs for $500/kW installed (paid up front).

• Number of Participants: 18 customers

Financial Details – First Project

• Installed Cost: $466,000 or $6/watt (Cost to customers: $3.15/watt, includes all rebates, RECs and

credits taken by the CEC)

• Capital Financing: Project built with internal CEC private capital, which is paid back as individuals

buy in to the project

• Federal Tax Credit: CEC takes the 1603 Treasury Grant and passes the savings to the customer

• Rebates: $1/watt plus $0.50/watt for rights to the RECs from Holy Cross Energy

• Estimated Annual Income from Power Sales: $15,444 ($198/kW), rising as regular rates rise

• Simple Payback: 13.1 years

24

SECTION 2: COMMUNITY SHARED SOLAR PROJECT

MODELS

Project Highlights – Subsequent Three Projects

• System Owner: Individuals, businesses, and educational institutions in various Colorado

utility territories

• System Host: CEC leases sites from government and private entities

• Installed Capacity: 858 kW, 1.1 MW, and 498 kW

• Participant Agreement: Minimum purchase ranges from $535 to $756 (a single panel after rebates

and incentives). Panel owners receive monthly credits for the value of the electricity produced.

• Electricity: CEC, as agent for its customers, has a PPA with the utility to purchase the power

produced, or has an established rate tariff. Customers receive the resulting monetary credit on their

monthly electric bill.

• RECs: Utilities purchased rights to RECs for $500/kW installed (paid up front).

• Number of Participants: 400, 500, and 200

Financing Details – Subsequent Three Projects

• Installed Cost: $6/watt, $6/watt, $5.30/watt (cost to customers as low as $3/W includes all rebates,

RECs and credits taken by the CEC)

• Capital Financing: Projects built with bridge loan financing from JP Morgan Chase and internal

CEC private capital

• Federal Tax Credit: CEC takes the 1603 Treasury Grant and passes the savings to the customer

• Rebates: $1.25/watt to $1.58/watt, including up-front sale of RECs

• Estimated Annual Income from Power Sales: $172,000, $220,000 and $78,300. Rising as regular

rates rise

• Simple Payback: 12.5 to 15.5 years

For more information: Lauren Suhrbier, Lauren@easycleanenergy.com, (970) 319-3939,

www.easycleanenergy.com

25

SECTION 2: COMMUNITY SHARED SOLAR PROJECT MODELS

Island Community Solar, LLC, Washington

Inspired by the passage of Washington State’s

generous production incentive for community

shared solar projects (WAC 458-20-273), a group

of solar enthusiasts developed a project in their

community on Whidbey Island, Washington.

Working closely with the local Port District and

the utility, Puget Sound Energy, they developed a

one-acre “P-Patch” for solar farmers on Port

property at Greenbank Farm. The P-Patch consists

of six separately metered plots, each capable of

hosting approximately 25 kW of ground mounted

solar panels. The solar farmers pay rent to the Port

and sell power directly to the grid. When the acre

is fully built out, it will generate almost enough to

match the on-site annual consumption.

In order to capture the investment tax credit, the Whidbey Island group chose to form an LLC, Island

Community Solar (ICS). ICS obtained exemption from securities filing requirements under the Federal

Intrastate Offering Exemption (Rule 147) and a Washington Small Offering Exemption (WAC 460-44A-

504), which prohibits advertising and limits the number of unaccredited investors. After preparing

extensive disclosure documents, ICS raised $430,000 from 36 local members. ICS built 50 kW in two

phases, completing the installation in January 2012.

ICS projects a positive return on investment over the ten year lease period. The 1603 Treasury Grant

enabled the LLC to monetize the investment tax credit. Although most members do not have sufficient

tax appetite to use the passive losses from depreciation, they will earn a return from the state production

incentive and power sales to the utility.

It may be difficult to replicate or expand this project without policy changes. The expiration of the 1603

Treasury Grant makes it unlikely that the members will be able to monetize future tax credits, because

most lack the tax appetite. The sunset of the Washington State production incentive in June 2020 means

that every subsequent project has a shorter window of opportunity to earn incentives. Finally, the avoided

cost of the power generated is dropping. The utility’s PPA rates for 2012 are lower than in 2011, due to

many factors including downward pressure on electric prices from an abundance of natural gas, and the

discarding of an assumed future cost for carbon.

Photo from Linda Irvine, Island Community Solar LLC

26

SECTION 2: COMMUNITY SHARED SOLAR PROJECT

MODELS

Project Highlights

• System Owner: Island Community Solar, LLC

• System Host: Port of Coupeville’s Greenbank Farm

• Installed Capacity: 50 kW; estimated Production: 52,930 kWh/year

• Participant Agreement: Members receive distributions, profits, and losses in proportion

to capital contributions; passive loss limitations apply.

• Electricity: Sold to the utility through a 10 year PPA, escalating 2.5% annually

• RECs: Retained by the owner; no market for solar RECs in WA

• Number of Participants: 36

Financial Details

• Installed Cost: $410,000 installation; $8,000 legal; $5,400/year insurance

• Capital Financing: 100% owner equity

• Federal Tax Credit: $123,000 1603 Treasury Grant

• Incentives: Production Incentive of $1.08/kWh until June 30, 2020

• Estimated Annual Income: $56,840 (production incentive); $4,128 (power sales)

• Estimated Annual Expenses: $10,000

• Simple Payback: 7.2 years

For more information: Linda Irvine, linda@nwseed.org, www.nwseed.org

27

SECTION 2: COMMUNITY SHARED SOLAR PROJECT MODELS

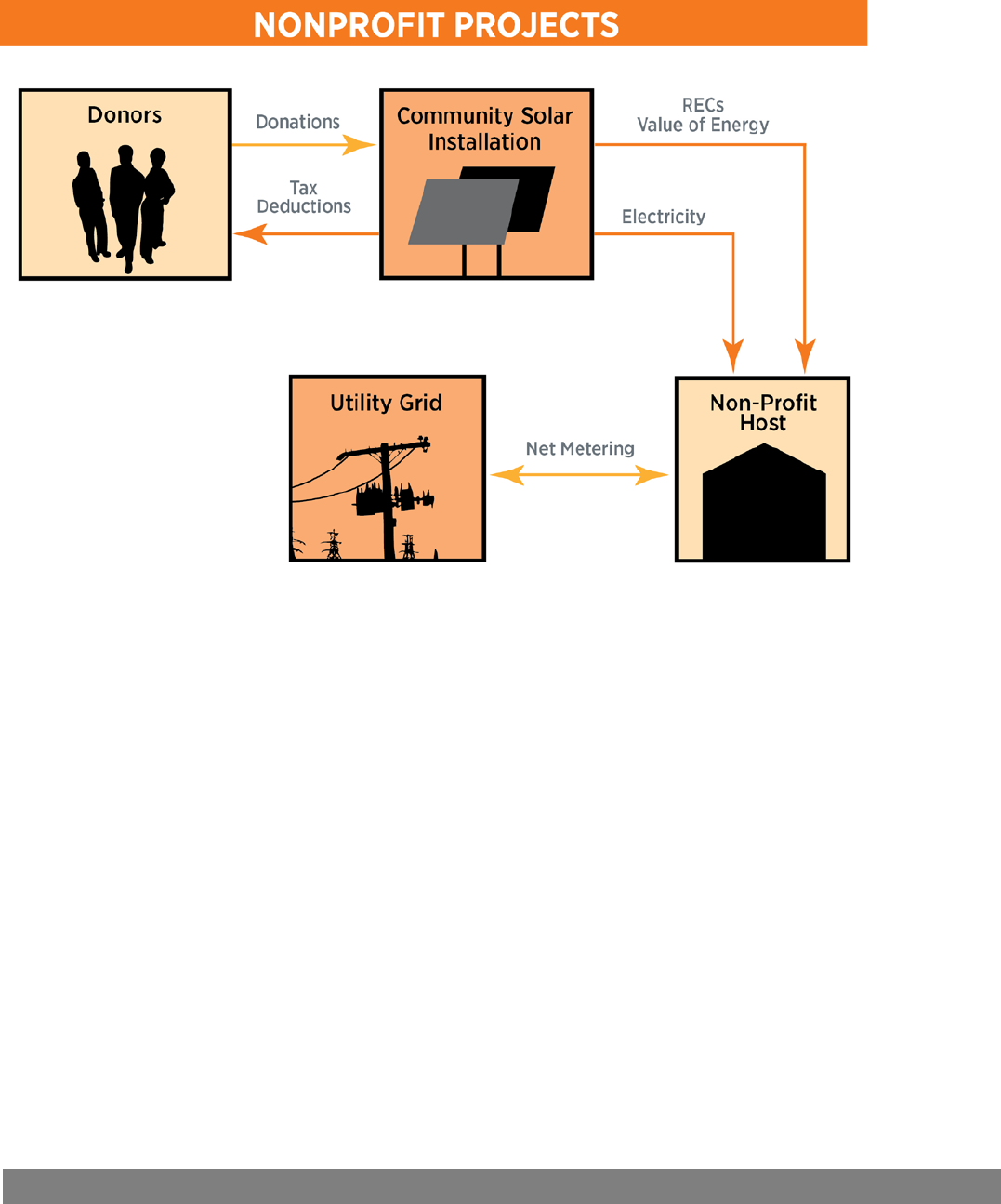

NONPROFIT MODEL

Nonprofits may engage with community

shared solar projects in at least two ways:

they may organize and administer a

community shared solar project that shares

benefits with participating members or they

may solicit donations for a solar project.

While this second option is not strictly

“community shared solar,” in that the donors

do not share directly in the benefits of the

solar installation, the donors do share indirectly, by lowering energy costs for their favored nonprofit and

demonstrating environmental leadership. In addition, with emerging state policies such as virtual net

metering and group billing, there may be possibilities for nonprofit project sponsors to share benefits with

their donor/members. In a variation on nonprofit ownership, a nonprofit may partner with a third-party

for-profit entity, which can own and install the system and take the tax benefits. This model has been

deployed successfully in the California Multifamily Affordable Housing program and at other nonprofit

locations throughout the country.10

OVERVIEW

Nonprofit organizations such as schools and churches are partnering with local citizens to develop

community shared solar projects. Under this model, supporters of the nonprofit organization help finance

the system through tax-deductible donations or direct investment in the project. The second option

requires that the nonprofit comply with state and federal securities regulations. While the nonprofit is not

eligible for the federal commercial ITC, it may be eligible for grants or other sources of foundation

funding that would not otherwise be available to a business. An example of this model is the “Solar for

Sakai” project on Bainbridge Island, Washington, in which a community nonprofit raised donations for a

solar installation, and in turn, donated the installation to a local school.

10 The Portland Habilitation Center Northwest, a nonprofit organization, partnered with U.S. Bancorp Community Development Corporation,

which will own and finance an 870 kW system to provide energy to the nonprofit.

If a nonprofit were to return some benefit

to donors, (for example, a portion of

production incentives or a share of

electric savings) this would constitute a

“quid pro quo” contribution and the donor

could not deduct their entire contribution.

28

SECTION 2: COMMUNITY SHARED SOLAR PROJECT

MODELS

TAX AND FINANCE ISSUES FOR NONPROFIT PROJECTS

As non-taxpaying entities, nonprofit organizations typically are not eligible for tax incentives. However,

donors to a nonprofit project can receive a tax benefit in the form of a tax deduction. The IRS allows

taxpayers who itemize deductions to deduct verifiable charitable contributions made to qualified

organizations. Of course, a tax deduction is much less valuable than a tax credit. For example, a $100 tax

credit reduces taxes owed by $100 while a $100 tax deduction reduces taxes owed by $25 for a taxpayer

in the 25% federal bracket.

Donors can deduct their contributions to a community shared solar project if the project sponsor obtains tax-

exempt status as a charitable organization under the Internal Revenue Code (26 U.S.C. § 501(c)(3)). Section

501(c)(3) organizations must be organized and operated exclusively for exempt purposes such as charitable,

religious, educational, or scientific purposes. Section 501(c)(3) organizations may not be operated for the

benefit of private interests and are restricted in how much time they can devote to lobbying activities. The

Application for Recognition of Exemption under Section 501(c)(3) is IRS Form 1023.

29

SECTION 2: COMMUNITY SHARED SOLAR PROJECT MODELS

Winthrop Community Solar Project, Washington

Following the 2010 launch of Okanogan

County Electric Cooperative’s (OCEC)

first community shared solar project, co-

op members who had been unable to

participate were eager to develop another

community shared solar project.

Project design and management was

handled by Energy Solutions, who

solicited the Town of Winthrop as project

host and the Partnership for a Sustainable

Methow (PSM) as project administrator.

As a nonprofit with a mission to initiate,

encourage, and support activities that

foster long-term sustainability and

wellbeing in the Methow Valley

community, PSM was eligible for a Nonprofit Notification of Claim of Exemption from the Washington

State Division of Securities. This exemption allowed PSM to offer ownership in the community shared

solar project to members, contributors, or participants in the organization, or to relatives of community

members. In early 2011, the opportunity to participate was announced through local press, radio, and the

PSM website. Applications were processed on a first come, first served basis, ultimately attracting 49

investors to fully fund the community shared solar project in just six weeks. Investment levels ranged

from $500 to $15,000, with investors participating at all levels.

Participating investors were not eligible to claim the 30% federal investment tax credit, which is

unavailable to nonprofits and other entities that do not pay taxes. However, the high state production

incentive for community shared solar projects using Washington-made materials partially made up for the

loss of the tax credit. When the production incentive expires in June 2020, project ownership will be

transferred to the Town of Winthrop.

Program Highlights

• System Owner: Participating OCEC members

• System Administrator: Partnership for a Sustainable Methow

• System Host: Town of Winthrop

• Installed Capacity: 22.8-kW ground mounted array

• Participant Agreement: Ownership purchased in $500 increments up to $15,000. Investors sign an

ownership contract with PSM, which receives owners’ investments, pays bills, and distributes

production incentive to owners through June 2020. System ownership will then transfer to the

project host, the Town of Winthrop.

Photo from Ellen Lamiman, Energy Solutions

30

SECTION 2: COMMUNITY SHARED SOLAR PROJECT

MODELS

• Electricity: Net metering benefits accrue to Town of Winthrop (host), production incentive benefits

accrue to participating OCEC members (owners)

• RECs: Remain with participating OCEC members

• Number of Participants: 49 investors

Financial Details

• Installed Cost: $200,000 or $8.77/watt (cost to investors $9.64/watt, includes insurance,

bookkeeping, and administration costs)

• Capital Financing: Project financed with owner investments, secured prior to construction

• Tax Credits: None; federal tax credit cannot be claimed if project is not a business venture or is not

placed on an owner’s residential property.

• Grants: None

• Rebates: None

• Estimated Annual Payment to Participants: $72 per $500 of investment

• Estimated ROI: 30% by June 2020

For more information: Ellen Lamiman, elamiman@silicon-energy.com, (425) 320-6063,

www.sustainablemethow.net

31

SECTION 2: COMMUNITY SHARED SOLAR PROJECT MODELS

Photo from Joe Deets, Community Energy Solutions

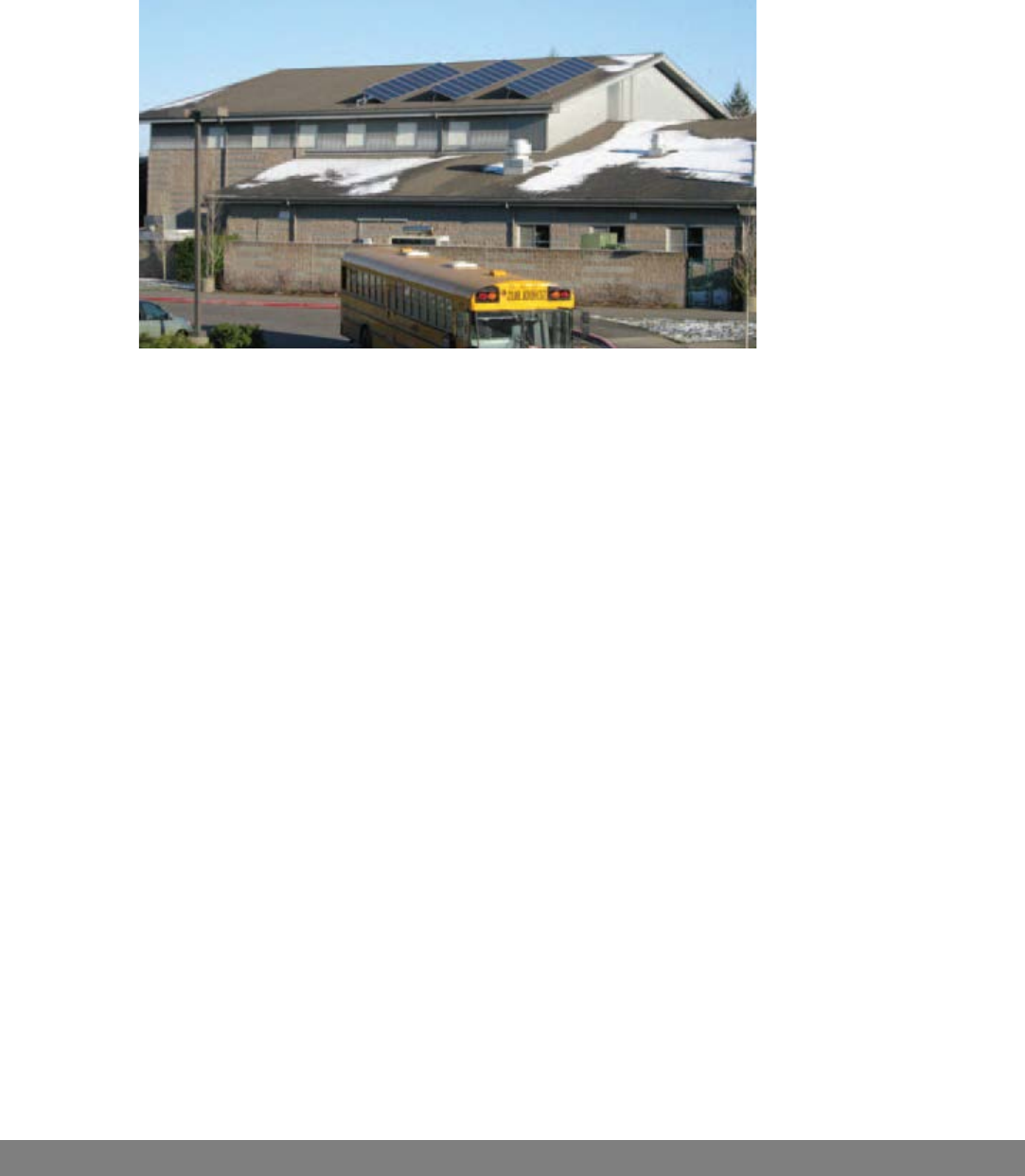

Solar for Sakai, Bainbridge Island, Washington

Community Energy Solutions, a nonprofit organization on Bainbridge Island, Washington, led the effort

to raise funds for a solar installation at Sakai Intermediate School. Twenty-six community organizations

or individuals made tax-deductible donations to Community Energy Solutions. The school owns the PV

system and all of the resulting power and environmental attributes.

Program Highlights

• System Owner: Sakai Intermediate School

• Installed Capacity: 5.1 kW

• Electricity: Net metered

Financial Details

• Installed Cost: $50,000 or $9.80/watt (not including energy curriculum and monitoring)

• Grants: $25,000 from utility (Puget Sound Energy)

• Donations: $30,000 through Community Energy Solutions

• Production Incentive: $0.15/kWh from state of WA

32

SECTION 2: COMMUNITY SHARED SOLAR PROJECT

MODELS

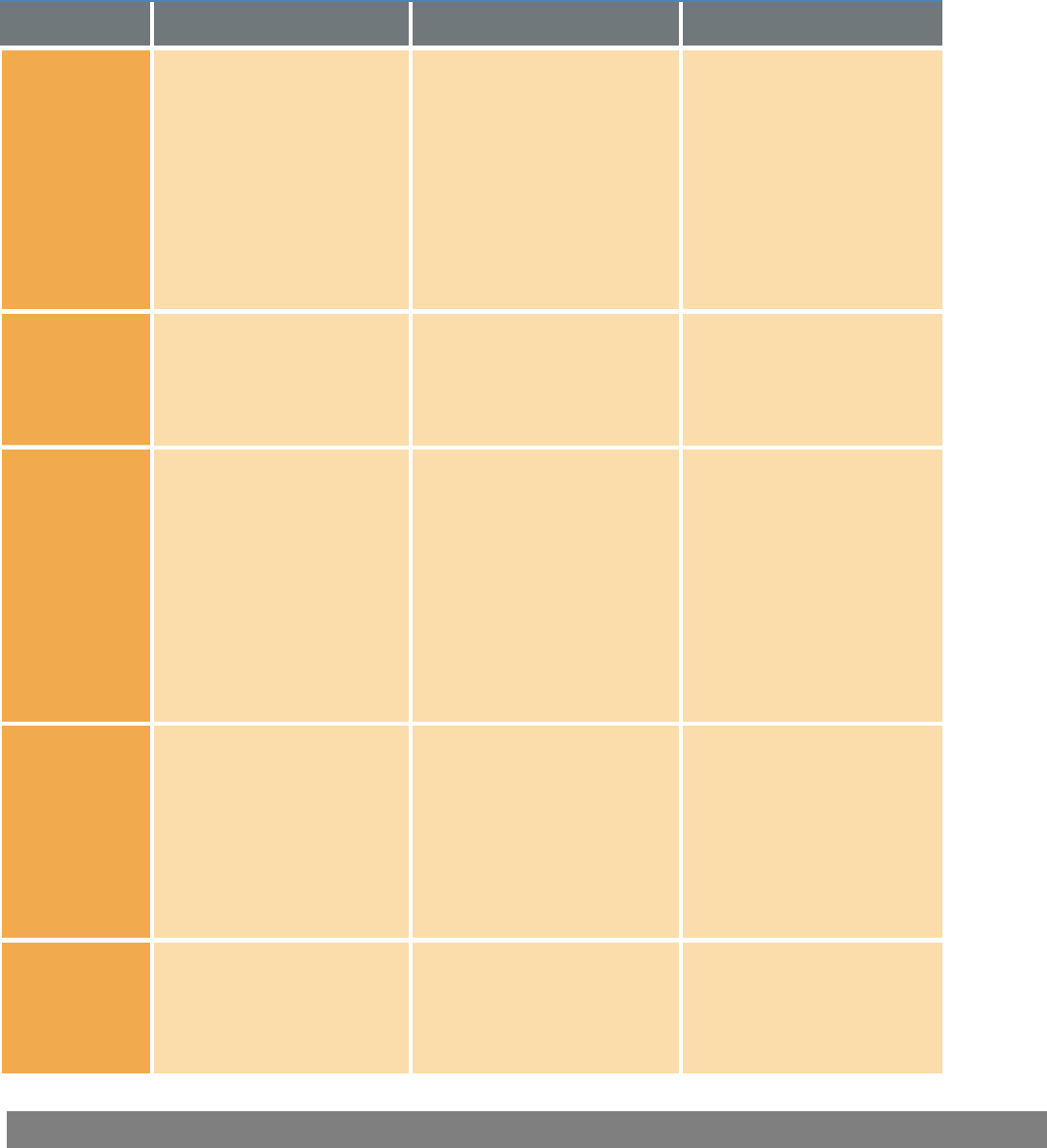

SUMMARY OF BENEFIT ALLOCATION OPTIONS BY MODEL

As evidenced by the examples above, there are many options for allocating the benefits of community

shared solar within each sponsorship model. The following chart summarizes the most common options.

Utility Special Purpose Entity Nonprofit

Electricity from

Solar System

• Participants receive an

estimated or actual kWh

credit for their portion of

project (virtual net

metering)

• Participants receive a

monetary credit for the

value of production for

their portion of the project

• SPE sells the electricity to

the utility (PPA)

• SPE sells the electricity to

the system host (SSA)

• SPE assigns kWh to utility

accounts per agreement

with utility (virtual net

metering)

• Electricity from the system

is netted against SPE

members’ group bill

• Nonprofit owner uses

on-site and net meters

• Nonprofit owner assigns

to utility accounts per

agreement with utility

(virtual net metering)

• Electricity from the

system is netted against

a group bill

Renewable

Energy

Credits

• Assigned to participants

• Retired on participants’

behalf

• Retained by the utility

• Rights to RECs sold

up front

• RECs sold on an

ongoing basis

• Retained for participants

• Rights to RECs sold

up front

• RECs sold on an

ongoing basis

• Retained for nonprofit

Federal Tax

Credits and

Deductions

• Neither the commercial

ITC nor the residential

renewable energy tax

credit is available to

participants

• If the utility has a tax

appetite, it may use the

commercial ITC

• Normalization accounting

rules will impact the value

of the ITC for regulated

utilities

• SPE can pass benefits of

Commercial ITC through to

participants

• Only of use if participants

have a tax appetite for

passive income offsets

• Project donors can deduct

the donation on their taxes

• Nonprofits are not eligible

for federal tax credits

Accelerated

Depreciation

(MACRS)

• Not available to

participants

• An investor-owned utility

may be able to use

MACRS, provided they

own the system

• To qualify for MACRS,

regulated utilities must use

normalization accounting

• SPE passes depreciation

benefits through to the

participants, subject to

passive activity rules

• Not useful to nonprofits

State and

Utility Rebates

and Incentives

• Utility may qualify and use

rebates/incentives to buy

down the project costs;

benefits are indirectly

passed on to participants

• SPE may qualify and use

rebates/incentives to buy

down the project costs or

pass through to participants

• Nonprofit may qualify and

use rebates/incentives to

buy down the project costs

33

SECTION 3: EMERGING STATE POLICIES TO SUPPORT COMMUNITY SHARED SOLAR

Over the last several years, a number of states have expanded their successful on-site solar programs by

instituting policies that encourage innovative community shared solar programs. While each of these state

programs varies considerably, a number of themes are emerging. For example, all of the current state-

level programs require the solar array and the group members to be located within the same utility service

territory. Other requirements to participate in “group” ownership benefits vary, but may include a cap on

system size, proof of partial ownership, or limits on the type of ratepayers that can participate. Billing

methods also vary; some programs offer one aggregate bill for the entire group, whereas others assign a

pro-rated monetary credit on each member’s bill.

State-level community shared solar policies can be grouped based on how the benefits of community

shared solar are distributed. In general, there are three broad categories: group billing, virtual net

metering, and joint ownership.

GROUP BILLING

Group billing arrangements operate much like master metering in a multi-unit residential or commercial

building. Under master metering, a landlord receives a single electric bill for all electricity usage within a

building, including tenant load. The landlord then determines how to assign energy costs to individual