Guide To Intelligent Data Analysis

User Manual:

Open the PDF directly: View PDF ![]() .

.

Page Count: 399 [warning: Documents this large are best viewed by clicking the View PDF Link!]

- Preface

- Contents

- Symbols

- Introduction

- Practical Data Analysis: An Example

- Project Understanding

- Data Understanding

- Principles of Modeling

- Data Preparation

- Finding Patterns

- Clustering

- Hierarchical Clustering

- Prototype-Based Clustering

- Density-Based Clustering

- Self-organizing Maps

- Association Rules

- Deviation Analysis

- Hierarchical Clustering

- Notion of (Dis-)Similarity

- Prototype- and Model-Based Clustering

- Density-Based Clustering

- Self-organizing Maps

- Frequent Pattern Mining and Association Rules

- Deviation Analysis

- Finding Patterns in Practice

- Further Reading

- References

- Finding Explanations

- Finding Predictors

- Evaluation and Deployment

- Appendix A Statistics

- Terms and Notation

- Descriptive Statistics

- Probability Theory

- Inferential Statistics

- Appendix B The R Project

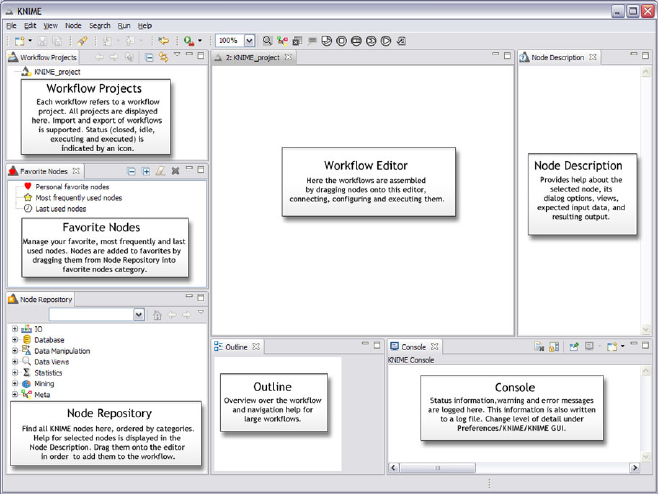

- Appendix C KNIME

- References

- Index

Michael R. Berthold rChristian Borgelt r

Frank Höppner rFrank Klawonn

Guide to Intelligent

Data Analysis

How to Intelligently Make

Sense of Real Data

Prof. Dr. Michael R. Berthold

FB Informatik und

Informationswissenschaft

Universität Konstanz

78457 Konstanz

Germany

Michael.Berthold@uni-konstanz.de

Dr. Christian Borgelt

Intelligent Data Analysis &

Graphical Models Research Unit

European Centre for Soft Computing

C/ Gonzalo Gutiérrez Quirós s/n

Edificio Científico-Technológico

Campus Mieres, 3aPlanta

33600 Mieres, Asturias

Spain

christian.borgelt@softcomputing.es

Prof. Dr. Frank Höppner

FB Wirtschaft

Ostfalia University of Applied Sciences

Robert-Koch-Platz 10-14

38440 Wolfsburg

Germany

f.hoeppner@ostfalia.de

Prof. Dr. Frank Klawonn

FB Informatik

Ostfalia University of Applied Sciences

Salzdahlumer Str. 46/48

38302 Wolfenbüttel

Germany

f.klawonn@ostfalia.de

Series Editors

David Gries

Department of Computer Science

Upson Hall

Cornell University

Ithaca, NY 14853-7501, USA

Fred B. Schneider

Department of Computer Science

Upson Hall

Cornell University

Ithaca, NY 14853-7501, USA

ISSN 1868-0941

ISBN 978-1-84882-259-7 e-ISSN 1868-095X

e-ISBN 978-1-84882-260-3

DOI 10.1007/978-1-84882-260-3

Springer London Dordrecht Heidelberg New York

British Library Cataloguing in Publication Data

A catalogue record for this book is available from the British Library

Library of Congress Control Number: 2010930517

© Springer-Verlag London Limited 2010

Apart from any fair dealing for the purposes of research or private study, or criticism or review, as per-

mitted under the Copyright, Designs and Patents Act 1988, this publication may only be reproduced,

stored or transmitted, in any form or by any means, with the prior permission in writing of the publish-

ers, or in the case of reprographic reproduction in accordance with the terms of licenses issued by the

Copyright Licensing Agency. Enquiries concerning reproduction outside those terms should be sent to

the publishers.

The use of registered names, trademarks, etc., in this publication does not imply, even in the absence of a

specific statement, that such names are exempt from the relevant laws and regulations and therefore free

for general use.

The publisher makes no representation, express or implied, with regard to the accuracy of the information

contained in this book and cannot accept any legal responsibility or liability for any errors or omissions

that may be made.

Cover design: VTeX, Vilnius

Printed on acid-free paper

Springer is part of Springer Science+Business Media (www.springer.com)

Preface

The main motivation to write this book came from all our problems to find suitable

material for a textbook that would really help us to teach the practical aspects of data

analysis together with the needed theoretical underpinnings. Many books out there

tackle either one or the other of these aspects (and, especially for the latter, there are

some fantastic text books out there), but a book providing a good combination was

nowhere to be found.

The idea to write our own book to address this shortcoming arose in two different

places at the same time—when one of the authors was asked to review the book

proposal of the others, we quickly realized that it would be much better to join

forces instead of independently pursuing our individual projects.

We hope that this book helps others to learn what kind of challenges data analysts

face in the real world and at the same time provides them with solid knowledge

about the processes, algorithms, and theories to successfully tackle these problems.

We have put a lot of effort into balancing the practical aspects of applying and using

data analysis techniques while making sure at the same time that we did not forget

to also explain the statistical and mathematical underpinnings behind the algorithms

beneath all of this.

There are many people to be thanked, and we will not attempt to list them all.

However, we do want to single out Iris Adä who has been a tremendous help with

the generation of the data sets used in this book. She and Martin Horn also deserve

our thanks for an intense last minute round of proof reading.

Konstanz, Germany Michael R. Berthold

Oviedo, Spain Christian Borgelt

Braunschweig, Germany Frank Höppner and Frank Klawonn

v

Contents

1 Introduction ................................ 1

1.1 Motivation.............................. 1

1.1.1 Data and Knowledge . . ................... 2

1.1.2 Tycho Brahe and Johannes Kepler .............. 4

1.1.3 Intelligent Data Analysis .................. 6

1.2 The Data Analysis Process . . . ................... 7

1.3 Methods, Tasks, and Tools . . . ................... 11

1.4 HowtoReadThisBook....................... 13

References . ............................. 14

2 Practical Data Analysis: An Example .................. 15

2.1 TheSetup .............................. 15

2.2 Data Understanding and Pattern Finding .............. 16

2.3 ExplanationFinding......................... 20

2.4 PredictingtheFuture......................... 21

2.5 Concluding Remarks ......................... 23

3 Project Understanding .......................... 25

3.1 DeterminetheProjectObjective................... 26

3.2 AssesstheSituation ......................... 28

3.3 DetermineAnalysisGoals...................... 30

3.4 Further Reading ........................... 31

References . ............................. 32

4 Data Understanding ........................... 33

4.1 Attribute Understanding ....................... 34

4.2 Data Quality ............................. 37

4.3 DataVisualization.......................... 40

4.3.1 Methods for One and Two Attributes . . . ......... 40

4.3.2 Methods for Higher-Dimensional Data . . ......... 48

4.4 CorrelationAnalysis......................... 59

vii

viii Contents

4.5 Outlier Detection ........................... 62

4.5.1 Outlier Detection for Single Attributes . . ......... 63

4.5.2 Outlier Detection for Multidimensional Data ........ 64

4.6 MissingValues............................ 65

4.7 A Checklist for Data Understanding ................. 68

4.8 Data Understanding in Practice ................... 69

4.8.1 Data Understanding in KNIME ............... 70

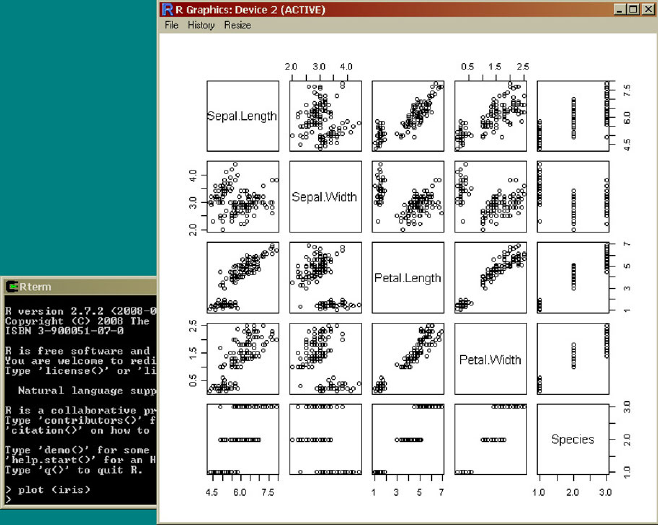

4.8.2 Data Understanding in R .................. 73

References . ............................. 78

5 Principles of Modeling .......................... 81

5.1 Model Classes ............................ 82

5.2 Fitting Criteria and Score Functions ................. 85

5.2.1 Error Functions for Classification Problems ......... 87

5.2.2 Measures of Interestingness ................. 89

5.3 Algorithms for Model Fitting . ................... 89

5.3.1 ClosedFormSolutions ................... 89

5.3.2 GradientMethod....................... 90

5.3.3 CombinatorialOptimization................. 92

5.3.4 Random Search, Greedy Strategies, and Other Heuristics . 92

5.4 Types of Errors ............................ 93

5.4.1 Experimental Error . . ................... 94

5.4.2 SampleError......................... 99

5.4.3 Model Error .........................100

5.4.4 AlgorithmicError ......................101

5.4.5 Machine Learning Bias and Variance . . . .........101

5.4.6 Learning Without Bias? ...................102

5.5 Model Validation ...........................102

5.5.1 TrainingandTestData....................102

5.5.2 Cross-Validation.......................103

5.5.3 Bootstrapping ........................104

5.5.4 Measures for Model Complexity ..............105

5.6 Model Errors and Validation in Practice ...............111

5.6.1 ErrorsandValidationinKNIME ..............111

5.6.2 ValidationinR........................111

5.7 Further Reading ...........................113

References . .............................113

6 Data Preparation .............................115

6.1 SelectData..............................115

6.1.1 Feature Selection . . . ...................116

6.1.2 Dimensionality Reduction ..................121

6.1.3 Record Selection .......................121

6.2 CleanData..............................123

6.2.1 Improve Data Quality . ...................123

Contents ix

6.2.2 MissingValues........................124

6.3 ConstructData............................127

6.3.1 Provide Operability . . ...................127

6.3.2 Assure Impartiality . . ...................129

6.3.3 MaximizeEfficiency.....................131

6.4 Complex Data Types .........................134

6.5 DataIntegration ...........................135

6.5.1 VerticalDataIntegration...................136

6.5.2 Horizontal Data Integration .................136

6.6 Data Preparation in Practice . . ...................138

6.6.1 Data Preparation in KNIME .................139

6.6.2 Data Preparation in R . ...................141

References . .............................142

7 Finding Patterns .............................145

7.1 HierarchicalClustering .......................147

7.1.1 Overview...........................148

7.1.2 Construction.........................150

7.1.3 VariationsandIssues.....................152

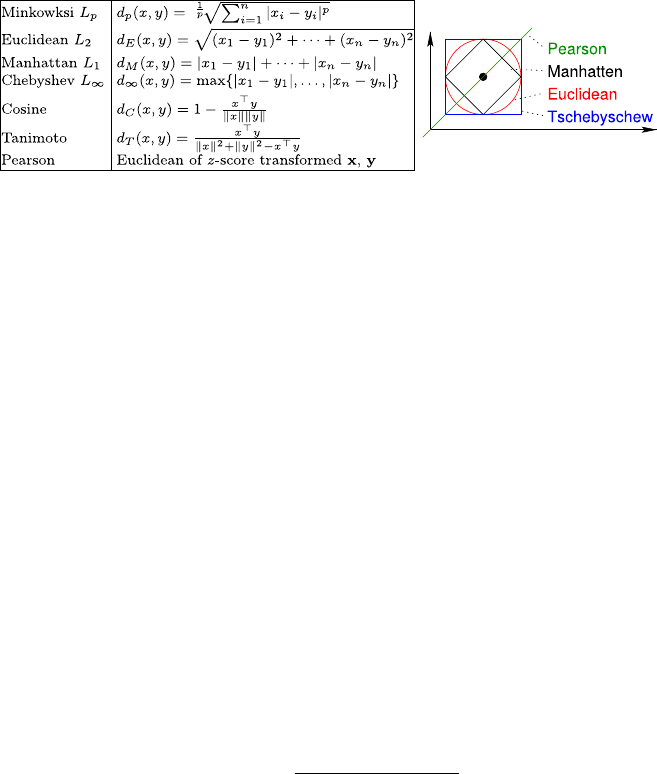

7.2 Notionof(Dis-)Similarity......................155

7.3 Prototype- and Model-Based Clustering ...............162

7.3.1 Overview...........................162

7.3.2 Construction.........................164

7.3.3 VariationsandIssues.....................167

7.4 Density-BasedClustering ......................169

7.4.1 Overview...........................170

7.4.2 Construction.........................171

7.4.3 VariationsandIssues.....................173

7.5 Self-organizingMaps ........................175

7.5.1 Overview...........................175

7.5.2 Construction.........................176

7.6 Frequent Pattern Mining and Association Rules . .........179

7.6.1 Overview...........................179

7.6.2 Construction.........................181

7.6.3 VariationsandIssues.....................187

7.7 DeviationAnalysis..........................194

7.7.1 Overview...........................194

7.7.2 Construction.........................195

7.7.3 VariationsandIssues.....................197

7.8 FindingPatternsinPractice .....................198

7.8.1 FindingPatternswithKNIME................199

7.8.2 FindingPatternsinR ....................201

7.9 Further Reading ...........................203

References . .............................204

xContents

8 Finding Explanations ...........................207

8.1 DecisionTrees............................208

8.1.1 Overview...........................209

8.1.2 Construction.........................210

8.1.3 VariationsandIssues.....................213

8.2 Bayes Classifiers ...........................218

8.2.1 Overview...........................218

8.2.2 Construction.........................220

8.2.3 VariationsandIssues.....................224

8.3 Regression..............................229

8.3.1 Overview...........................230

8.3.2 Construction.........................231

8.3.3 VariationsandIssues.....................234

8.3.4 TwoClassProblems.....................242

8.4 Rulelearning.............................244

8.4.1 Propositional Rules . . ...................245

8.4.2 Inductive Logic Programming or First-Order Rules .....251

8.5 FindingExplanationsinPractice ..................253

8.5.1 FindingExplanationswithKNIME.............253

8.5.2 UsingExplanationswithR .................255

8.6 Further Reading ...........................257

References . .............................258

9 Finding Predictors ............................259

9.1 Nearest-Neighbor Predictors . . ...................261

9.1.1 Overview...........................261

9.1.2 Construction.........................263

9.1.3 VariationsandIssues.....................265

9.2 Artifical Neural Networks . . . ...................269

9.2.1 Overview...........................269

9.2.2 Construction.........................272

9.2.3 VariationsandIssues.....................276

9.3 Support Vector Machines . . . ...................277

9.3.1 Overview...........................278

9.3.2 Construction.........................282

9.3.3 VariationsandIssues.....................283

9.4 Ensemble Methods ..........................284

9.4.1 Overview...........................284

9.4.2 Construction.........................286

9.4.3 Further Reading .......................289

9.5 FindingPredictorsinPractice....................290

9.5.1 FindingPredictorswithKNIME ..............290

9.5.2 UsingPredictorsinR ....................292

References . .............................294

Contents xi

10 Evaluation and Deployment .......................297

10.1Evaluation ..............................297

10.2DeploymentandMonitoring.....................299

References . .............................301

A Statistics ..................................303

A.1 TermsandNotation .........................304

A.2 DescriptiveStatistics.........................305

A.2.1 TabularRepresentations...................305

A.2.2 Graphical Representations ..................306

A.2.3 Characteristic Measures for One-Dimensional Data ....309

A.2.4 Characteristic Measures for Multidimensional Data ....316

A.2.5 Principal Component Analysis ...............318

A.3 Probability Theory ..........................323

A.3.1 Probability ..........................323

A.3.2 Basic Methods and Theorems ................327

A.3.3 Random Variables . . . ...................333

A.3.4 Characteristic Measures of Random Variables .......339

A.3.5 Some Special Distributions .................343

A.4 InferentialStatistics .........................349

A.4.1 Random Samples . . . ...................350

A.4.2 ParameterEstimation ....................351

A.4.3 Hypothesis Testing . . . ...................361

B The R Project ...............................369

B.1 InstallationandOverview ......................369

B.2 Reading Files and R Objects . . ...................370

B.3 R Functions and Commands . . ...................372

B.4 Libraries/Packages ..........................373

B.5 R Workspace .............................373

B.6 FindingHelp.............................374

B.7 Further Reading ...........................374

C KNIME ..................................375

C.1 InstallationandOverview ......................375

C.2 BuildingWorkflows .........................377

C.3 ExampleFlow ............................378

C.4 RIntegration.............................380

References ...................................383

Appendix A . . . .............................383

Appendix B . . . .............................383

Index ......................................385

Symbols

A,Aiattribute, variable [e.g., A1=color,A2=price,A3=category]

ωa possible value of an attribute [e.g., ω=red]

Ω, dom(·) set of possible values of an attribute

[e.g., Ω1=Ωcolor =dom(Ai)={red,blue,green}]

Aset of all attributes [e.g., A={color,price,category}]

mnumber of considered attributes [e.g., 3]

xa specific value of an attribute [e.g., x2=xprice =4000]

Xspace of possible data records [e.g., X=ΩA1×···×ΩAm]

Dset of all records, data set, D⊆X[e.g., D={x1,x2,...,xn}]

nnumber of records in data set

xrecord in database [e.g., x=(x1,x

2,x

3)=(red,4000,luxury)]

xAattribute Aof record x[e.g., xprice =4000]

x2,A attribute Aof record x2

DA=vset of all records x∈Dwith xA=v

Ca selected categorical target attribute [e.g., C=A3=category]

ΩCset of all possible classes [e.g., ΩC={quits,stays,unknown}]

Ya selected continuous target attribute [e.g., Y=A2=price ]

Ccluster (set of associated data objects) [e.g., C⊆D]

cnumber of clusters

Ppartition, set of clusters {C1,...,Cc}

pi|jmembership degree of data #j to cluster #i

[pi|j]membership matrix

d.distance function, metric (dE: Euclidean)

[di,j ]distance matrix

xiii

Chapter 1

Introduction

In this introductory chapter we provide a brief overview over some core ideas of

intelligent data analysis and their motivation. In a first step we carefully distinguish

between “data” and “knowledge” in order to obtain clear notions that help us to work

out why it is usually not enough to simply collect data and why we have to strive

to turn them into knowledge. As an illustration, we consider a well-known example

from the history of science. In a second step we characterize the data analysis pro-

cess, also often referred to as the knowledge discovery process, in which so-called

“data mining” is one important step. We characterize standard data analysis tasks

and provide a brief catalog of methods and tools to tackle them.

1.1 Motivation

Every year that passes brings us more powerful computers, faster and cheaper stor-

age media, and higher bandwidth data connections. Due to these groundbreaking

technological advancements, it is possible nowadays to collect and store enormous

amounts of data with amazingly little effort and at impressively low costs. As a

consequence, more and more companies, research centers, and governmental in-

stitutions create huge archives of tables, documents, images, and sounds in elec-

tronic form. Since for centuries lack of data has been a core hindrance to scientific

and economic progress, we feel compelled to think that we can solve—at least in

principle—basically any problem we are faced with if only we have enough data.

However, a closer examination of the matter reveals that this is an illusion. Data

alone, regardless of how voluminous they are, are not enough. Even though large

databases allow us to retrieve many different single pieces of information and to

compute (simple) aggregations (like average monthly sales in Berlin), general pat-

terns, structures, and regularities often go undetected. We may say that in the vast

amount of data stored in some databases we cannot see the wood (the patterns)

for the trees (the individual data records). However, it is most often exactly these

patterns, regularities, and trends that are particularly valuable if one desires, for

example, to increase the turnover of a supermarket. Suppose, for instance, that a

M.R. Berthold et al., Guide to Intelligent Data Analysis,

Texts in Computer Science 42,

DOI 10.1007/978-1-84882-260-3_1, © Springer-Verlag London Limited 2010

1

2 1 Introduction

supermarket manager discovers, by analyzing the sales and customer records, that

certain products are frequently bought together. In such a case sales can sometimes

be stimulated by cleverly arranging these products on the shelves of the market (they

may, for example, be placed close to each other, or may be offered as a bundle, in

order to invite even more customers to buy them together).

Unfortunately, it turns out to be harder than may be expected at first sight to ac-

tually discover such patterns and regularities and thus to exploit a larger part of the

information that is contained in the available data. In contrast to the overwhelm-

ing flood of data there was, at least at the beginning, a lack of tools by which raw

data could be transformed into useful information. Almost fifteen years ago John

Naisbett aptly characterized the situation by saying [3]: “We are drowning in in-

formation, but starving for knowledge.” As a consequence, a new research area has

been developed, which has become known under the name of data mining. The goal

of this area was to meet the challenge to develop tools that can help humans to find

potentially useful patterns in their data and to solve the problems they are facing

by making better use of the data they have. Today, about fifteen years later, a lot of

progress has been made, and a considerable number of methods and implementa-

tions of these techniques in software tools have been developed. Still it is not the

tools alone, but the intelligent composition of human intuition with the computa-

tional power, of sound background knowledge with computer-aided modeling, of

critical reflection with convenient automatic model construction, that leads intelli-

gent data analysis projects to success [1]. In this book we try to provide a hands-on

approach to many basic data analysis techniques and how they are used to solve data

analysis problems if relevant data is available.

1.1.1 Data and Knowledge

In this book we distinguish carefully between data and knowledge. Statements like

“Columbus discovered America in 1492” or “Mister Smith owns a VW Beetle” are

data. Note that we ignore whether we already know these statements or whether

we have any concrete use for them at the moment. The essential property of these

statements we focus on here is that they refer to single events, objects, people, points

in time, etc. That is, they generally refer to single instances or individual cases. As a

consequence, their domain of application and thus their utility is necessarily limited.

In contrast to this, knowledge consists of statements like “All masses attract

each other” or “Every day at 7:30 AM a flight with destination New York departs

from Frankfurt Airport.” Again, we neglect the relevance of these statements for

our current situation and whether we already know them. Rather, we focus on the

essential property that they do not refer to single instances or individual cases but are

general rules or (physical) laws. Hence, if they are true, they have a large domain of

application. Even more importantly, though, they allow us to make predictions and

are thus highly useful (at least if they are relevant to us).

We have to admit, though, that in daily life we also call statements like “Colum-

bus discovered America in 1492” knowledge (actually, this particular statement is

1.1 Motivation 3

used as a kind of prototypical example of knowledge). However, we neglect here

this vernacular and rather fuzzy use of the notion “knowledge” and express our re-

grets that it is not possible to find a terminology that is completely consistent with

everyday speech. Neither single statements about individual cases nor collections of

such statements qualify, in our use of the term, as knowledge.

Summarizing, we can characterize data and knowledge as follows:

data

•refer to single instances

(single objects, people, events, points in time, etc.)

•describe individual properties

•are often available in large amounts

(databases, archives)

•are often easy to collect or to obtain

(e.g., scanner cashiers in supermarkets, Internet)

•do not allow us to make predictions or forecasts

knowledge

•refers to classes of instances

(sets of objects, people, events, points in time, etc.)

•describes general patterns, structures, laws, principles, etc.

•consists of as few statements as possible

(this is actually an explicit goal, see below)

•is often difficult and time-consuming to find or to obtain

(e.g., natural laws, education)

•allows us to make predictions and forecasts

These characterizations make it very clear that generally knowledge is much more

valuable than (raw) data. Its generality and the possibility to make predictions about

the properties of new cases are the main reasons for this superiority.

It is obvious, though, that not all kinds of knowledge are equally valuable as any

other. Not all general statements are equally important, equally substantial, equally

significant, or equally useful. Therefore knowledge has to be assessed, so that we

do not drown in a sea of irrelevant knowledge. The following list (which we do not

claim to be complete) lists some of the most important criteria:

criteria to assess knowledge

•correctness (probability, success in tests)

•generality (domain and conditions of validity)

•usefulness (relevance, predictive power)

•comprehensibility (simplicity, clarity, parsimony)

•novelty (previously unknown, unexpected)

In the domain of science, the focus is on correctness, generality, and simplicity

(parsimony) are in the focus: one way of characterizing science is to say that it is

the search for a minimal correct description of the world. In economy and industry,

however, the emphasis is placed on usefulness, comprehensibility, and novelty: the

main goal is to gain a competitive edge and thus to increase revenues. Nevertheless,

neither of the two areas can afford to neglect the other criteria.

4 1 Introduction

1.1.2 Tycho Brahe and Johannes Kepler

We illustrate the considerations of the previous section with an (at least partially)

well-known example from the history of science. In the sixteenth century studying

the stars and the planetary motions was one of the core areas of research. Among its

proponents was Tycho Brahe (1546–1601), a Danish nobleman and astronomer, who

in 1576 and 1584, with the financial help of King Frederic II, built two observatories

on the island of Ven, about 32 km north-east of Copenhagen. He had access to the

best astronomical instruments of his time (but no telescopes, which were used only

later by Galileo Galilei (1564–1642) and Johannes Kepler (see below) to observe

celestial bodies), which he used to determine the positions of the sun, the moon,

and the planets with a precision of less than one angle minute. With this precision

he managed to surpass all measurements that had been carried out before and to

actually reach the theoretical limit for observations with the unaided eye (that is,

without the help of telescopes). Working carefully and persistently, he recorded the

motions of the celestial bodies over several years.

Stated plainly, Tycho Brahe collected data about our planetary system, fairly

large amounts of data, at least from the point of view of the sixteenth century. How-

ever, he failed to find a consistent scheme to combine them, could not discern a

clear underlying pattern—partially because he stuck too closely to the geocentric

system (the earth is in the center, and all planets, the sun, and the moon revolve

around the earth). He could tell the precise location of Mars on any given day of

the year 1582, but he could not connect its locations on different days by a clear

and consistent theory. All hypotheses he tried did not fit his highly precise data. For

example, he developed the so-called Tychonic planetary system (the earth is in the

center, the sun and the moon revolve around the earth, and the other planets revolve

around the sun on circular orbits). Although temporarily popular in the seventeenth

century, this system did not stand the test of time. From a modern point of view we

may say that Tycho Brahe had a “data analysis problem” (or “knowledge discov-

ery problem”). He had obtained the necessary data but could not extract the hidden

knowledge.

This problem was solved later by Johannes Kepler (1571–1630), a German as-

tronomer and mathematician, who worked as an assistant of Tycho Brahe. Contrary

to Brahe, he advocated the Copernican planetary system (the sun is in the center,

the earth and all other planets revolve around the sun in circular orbits) and tried

all his life to reveal the laws that govern the motions of the celestial bodies. His ap-

proach was almost radical for his time, because he strove to find a mathematical de-

scription. He started his investigations with the data Tycho Brahe had collected and

which he extended in later years. After several fruitless trials and searches and long

and cumbersome calculations (imagine: no pocket calculators), Kepler finally suc-

ceeded. He managed to combine Tycho Brahe’s data into three simple laws, which

nowadays bear his name: Kepler’s laws. After having realized in 1604 already that

the course of Mars is an ellipse, he published the first two of these laws in his work

1.1 Motivation 5

“Astronomia Nova” in 1609 [6] and the third law ten years later in his magnum opus

“Harmonices Mundi” [4,7]:

1. The orbit of every planet (including the earth) is an ellipse,

with the sun at a focal point.

2. A line from the sun to the planet sweeps out equal areas

during equal intervals of time.

3. The squares of the orbital periods of any two planets relate to each other

like the cubes of the semimajor axes of their respective orbits:

T2

1/T 2

2=a3

1/a3

2, and therefore generally T∼a3

2.

Tycho Brahe had collected a large amount of astronomical data, and Johannes Ke-

pler found the underlying laws that can explain them. He discovered the hidden

knowledge and thus became one of the most famous “data miners” in history.

Today the works of Tycho Brahe are almost forgotten—few have even heard his

name. His catalogs of celestial data are merely of historical interest. No textbook on

astronomy contains excerpts from his measurements—and this is only partially due

to the better measurement technology we have available today. His observations and

precise measurements are raw data and thus suffer from a decisive drawback: they

do not provide any insight into the underlying mechanisms and thus do not allow us

to make predictions. Kepler’s laws, on the other hand, are treated in basically all as-

tronomy and physics textbooks, because they state the principles according to which

planets and comets move. They combine all of Brahe’s observations and measure-

ments in three simple statements. In addition, they permit us to make predictions:

if we know the location and the speed of a planet relative to the sun at any given

moment, we can compute its future course by drawing on Kepler’s laws.

How did Johannes Kepler find the simple astronomical laws that bear his name?

How did he discover them in Tycho Brahe’s long tables and voluminous catalogs,

thus revolutionizing astronomy? We know fairly little about his searches and efforts.

He must have tried a large number of hypotheses, most of them failing. He must have

carried out long and cumbersome computations, repeating some of them several

times to eliminate errors. It is likely that exceptional mathematical talent, hard and

tenacious work, and a significant amount of good luck finally led him to success.

What we can be sure of is that he did not possess a universally applicable procedure

or method to discover physical or astronomical laws.

Even today we are not much further: there is still no silver bullet to hit on the right

solution. It is still much easier to collect data, with which we are virtually swamped

in today’s “information society” (whatever this popular term actually means) than

to discover knowledge. Automatic measurement instruments and scanners, digital

cameras and computers, and an abundance of other automatic and semiautomatic

devices have even relieved us of the burden of manual data collection. In addition,

database and data warehouse technology allows us to store ever increasing amounts

of data and to retrieve and to sample them easily. John Naisbett was perfectly right:

“We are drowning in information, but starving for knowledge.”

It took a distinguished researcher like Johannes Kepler several years (actually

half a lifetime) to evaluate the data that Tycho Brahe had collected—data that from

6 1 Introduction

a modern point of view are negligibly few and of which Kepler actually analyzed

closely only those about the orbit of Mars. Given this, how can we hope today to

cope with the enormous amounts of data we are faced with every day? “Manual”

analyses (like Kepler’s) have long ceased to be feasible. Simple aids, like the visual-

ization of data in charts and diagrams, even though highly useful and certainly a first

and important step, quickly reach their limits. Thus, if we refuse to surrender to the

flood of data, we are forced to develop and employ computer-aided techniques, with

which data analysis can be simplified or even automated to some degree. These are

the methods that have been and still are developed in the research areas of intelligent

data analysis, knowledge discovery in databases and data mining. Even though these

methods are far from replacing human beings like Johannes Kepler, especially since

a mindless application can produce artifacts and misleading results, it is not entirely

implausible to assume that Kepler, if he had been supported by these methods and

tools, could have reached his goal a little earlier.

1.1.3 Intelligent Data Analysis

Many people associate any kind of data analysis with statistics (see also Ap-

pendix A, which provides a brief review). Statistics has a long history and originated

from collecting and analyzing data about the population and the state in general.

Statistics can be divided into descriptive and inferential statistics.Descriptive

statistics summarizes data without making specific assumptions about the data,

often by characteristic values like the (empirical) mean or by diagrams like his-

tograms. Inferential statistics provides more rigorous methods than descriptive

statistics that are based on certain assumptions about the data generating random

process. The conclusions drawn in inferential statistics are only valid if these as-

sumptions are satisfied.

Typically, in statistics the first step of the data analysis process is to design the

experiment that defines how data should be collected in order to be able to carry out

a reliable analysis based on the obtained data. To capture this important issue, we

distinguish between experimental and observational studies.Inanexperimental

study one can control and manipulate the data generating process. For instance,

if we are interested in the effects of certain diets on the health status of a person,

we might ask different groups of people to stick to different diets. Thus we have a

certain control over the data generating process. In this experimental study, we can

decide which and how many people should be assigned to a certain diet.

In an observational study one cannot control the data generating process. For

the same dietary study as above, we might simply ask people on the street what they

normally eat. Then we have no control about which kinds of diets we get data and

how many people we will have for each diet in our data.

No matter whether the study is experimental or observational, there are usually

independence assumptions involved, and the data we collect should be representa-

tive. The main reason is that inferential statistics is often applied to hypothesis test-

ing where, based on the collected data, we desire to either confirm or reject some

1.2 The Data Analysis Process 7

hypothesis about the considered domain. In this case representative data and certain

independencies are required in order to ensure that the test decisions are valid.

In contrast to hypothesis testing, exploratory data analysis is concerned with

generating hypotheses from the collected data. In exploratory data analysis there

are no or at least considerably weaker model assumptions about the data generating

process. Most of the methods presented in this book fall into this category, since

they are mostly universal methods designed to achieve a certain goal but are not

based on a rigorous model as in inferential statistics.

The typical situation we assume in this book is that we already have the data.

They might not have been collected in the best way, or in the way we would have

collected them had we been able to design the experiment in advance. Therefore,

it is often difficult to make specific assumptions about the data generating process.

We are also mostly goal-oriented—that is, we ask questions like “Which customers

will yield the highest profit”?—and search for methods that can help us to answer

such questions or to solve our problems.

The opportunity of analyzing large business databases that were initially col-

lected for completely different purposes came with the availability of powerful tools

and technologies that can process and analyze massive amounts of data, so-called

data mining techniques. A few years ago some people seemed to believe that with

just the right data mining tool at hand any kind of desired knowledge could be

squeezed out of a given database automatically with no or only little human inter-

ference. However, practical experience demonstrates that every problem is different

and a full automatization of the data analysis process is simply impossible. Today

we understand by knowledge discovery in databases (KDD) an interactive “pro-

cess of identifying valid, novel, potentially useful, and ultimately understandable

patterns in data” [3]. This process consists of multiple phases, and the data mining

or modeling step became just a single step in it. That is, after a period of time where

powerful tools were (sometimes) naively applied to the data, the “intelligent ana-

lyst” is brought back into the loop. As a consequence, the KDD process differs not

so much anymore from classical statistical data analysis (except where the lacking

principled data acquisition takes its toll). To emphasize that every project is different

and therefore intelligence is required to make the most out of the already gathered

data, we use the term intelligent data analysis, which was coined by David Hand

[1,5] (and is used today almost synonymously with the KDD process).

In this book we strove to provide a comprehensive guide to intelligent data anal-

ysis, outlining the process and its phases, presenting methods and algorithms for

various tasks and purposes, and illustrating them with two freely available software

tools. In this way we hope to offer a good starting point for anyone who wishes to

become more familiar with the area of intelligent data analysis.

1.2 The Data Analysis Process

There are at least two typical situations in which intelligent data analysis may help

us to find solutions to certain problems or provide answers to questions that arise.

8 1 Introduction

In the first case, the problem at hand is by no means new, but it is already solved as

a matter of routine (e.g., approval of credit card applications, technical inspection

during quality assurance, machine control by a plant operator, etc.). If data has been

collected for the past cases together with the result that was finally achieved (such

as poor customer performance, malfunction of parts, etc.), such historical data may

be used to revise and optimize the presently used strategy to reach a decision. In

the second case, a certain question arises for the first time, and only little experi-

ence is available, or the experience is not directly applicable to this new question

(e.g., starting with a new product, preventing abuse of servers, evaluating a large

experiment or survey). In such cases, it is supposed that data from related situations

may be helpful to generalize the new problem or that unknown relationships can be

discovered from the data to gain insights into this unfamiliar area.

What if we have no data at all? This situation does not occur literally in prac-

tice, since in most cases there is always some data. Especially in businesses huge

amounts of data have been collected and stored for operational reasons in the past

(e.g., billing, logistics, warranty claims) that may now be used to optimize vari-

ous decisions or offer new options (e.g., predicting customer performance, reducing

stock on hand, tracking causes of defects). So the right question should be: How do

we know if we have enough relevant data? This question is not answered easily. If

it actually turns out that the data is not sufficient, one option is to acquire new data

to solve the problem. However, as already pointed out in the preceding section, the

experimental design of data acquisition is beyond the scope of this book.

There are several proposals about what the intelligent data analysis process

should look like, such as SEMMA (an acronym for sample, explore, modify, model,

assess used by SAS Institute Inc.), CRISP-DM (an acronym for CRoss Industry

Standard Process for Data Mining as defined by the CRISP-DM consortium) [2],

or the KDD-process [3](see[8] for a detailed comparison). In this book, we are

going to follow the CRISP-DM process, which has been developed by a consortium

of large companies, such as NCR, Daimler, and SPSS, and appears to be the most

widely used process model for intelligent data analysis today.

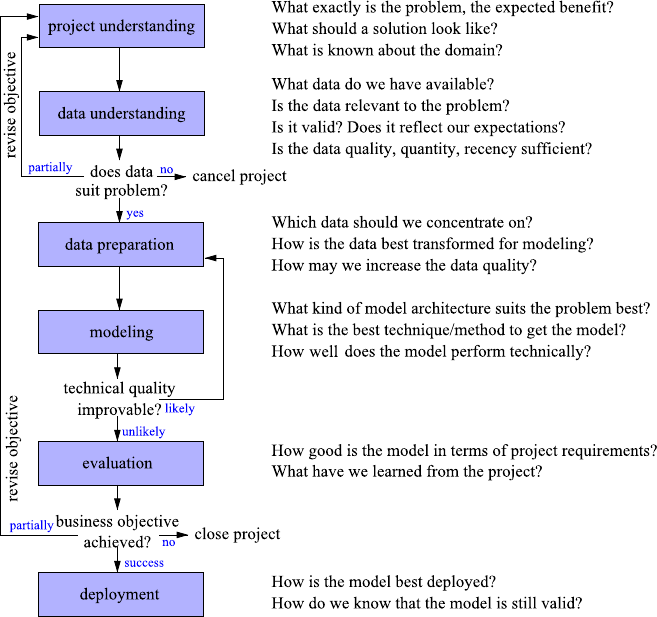

CRISP-DM consists of six phases as shown in Fig. 1.1. Most of these phases are

usually executed more than once, and the most frequent phase transitions are shown

by arrows. The main objective of the first project understanding step (see Chap. 3)

is to identify the potential benefit as well as the risks and efforts of a successful

project, such that a deliberate decision on conducting the full project can be made.

The envisaged solution is also transferred from the project domain to a more techni-

cal, data-centered notion. This first phase is usually called business understanding,

but we stick to the more general term project understanding to emphasize that our

problem at hand may as well be purely technical in nature or a research project

rather than economically motivated.

Next we need to make sure that we will have sufficient data at hand to tackle

the problem. While we cannot know this for sure until the end of the project, we

at least have to convince ourselves that there is enough relevant data. To achieve

this, we proceed in the data understanding phase (see Chap. 4) with a review of

the available databases and the information contained in the database fields, a visual

1.2 The Data Analysis Process 9

Fig. 1.1 Overview of the CRISP-DM process together with typical questions to be asked in the

respective phases

assessment of the basic relationships between attributes, a data quality audit, an in-

spection of abnormal cases (outliers), etc. For instance, outliers appear to be abnor-

mal in some sense and are often caused by faulty insertion, but sometimes they give

surprising insights on closer inspection. Some techniques respond very sensitively

to outliers, which is why they should be treated with special care. Another aspect is

empty fields which may occur in the database for various reasons—ignoring them

may introduce a systematic error in the results. By getting familiar with the data,

typically first insights and hypotheses are gained. If we do not believe that the data

suffices to solve the problem, it may be necessary to revise the project’s objective.

So far, we have not changed any field of our database. However, this will be re-

quired to get the data into a shape that enables us to apply modeling tools. In the

data preparation phase (Chap. 6) the data is selected, corrected, modified, even

new attributes are generated, such that the prepared data set best suits the prob-

lem and the envisaged modeling technique. Basically all deficiencies that have been

identified in the data understanding phase require special actions. Often the outliers

10 1 Introduction

and missing values are replaced by estimated values or true values obtained from

other sources. We may restrict the further analysis to certain variables and to a se-

lection of the records from the full data set. Redundant and irrelevant data can give

many techniques an unnecessarily hard time.

Once the data is prepared, we select and apply modeling tools to extract knowl-

edge out of the data in the form of a model (Chaps. 5and 7–9). Depending on

what we want to do with the model, we may choose techniques that are easily in-

terpretable (to gain insights) or less demonstrative black-box models, which may

perform better. If we are not pleased with the results but are confident that the model

can be improved, we step back to the data preparation phase and, say, generate new

attributes from the existing ones, to support the modeling technique or to apply

different techniques. Background knowledge may provide hints on useful transfor-

mations that simplify the representation of the solution.

Compared to the modeling itself, which is typically supported by efficient tools

and algorithms, the data understanding and preparation phases take considerable

part of the overall project time as they require a close manual inspection of the data,

investigations into the relationships between different data sources, often even the

analysis of the process that generated the data. New insights promote new ideas

for feature generation or alter the subset of selected data, in which case the data

preparation and modeling phases are carried out multiple times. The number of

steps is not predetermined but influenced by the process and findings itself.

When the technical benchmarks cannot be improved anymore, the obtained re-

sults are analyzed in the evaluation phase (Chap. 10) from the perspective of the

problem owner. At this point, the project may stop due to unsatisfactory results, the

objectives may be revised in order to succeed under a slightly different setting, or

the found and optimized model may be deployed.

After deployment, which ranges from writing a report to the creation of a soft-

ware system that applies the model automatically to aid or make decisions, the

project is not necessarily finished. If the project results are used continuously over

time, an additional monitoring phase is necessary: during the analysis, a number of

assumptions will be made, and the correctness of the derived model (and the deci-

sions that rely on the model) depends on them. So we better verify from time to time

that these assumption still hold to prevent decision-making on outdated information.

In the literature one can find attempts to create cost models that estimate the costs

associated with a data analysis project. Without going into the details, the major key

factors that remained in a reduced cost model derived from 40 projects were [9]:

•the number of tables and attributes,

•the dispersion of the attributes (only a few vs. many values),

•the number of external data sources,

•the type of the model (prediction being the most expensive),

•the attribute type mixture (mixture of numeric and nonnumeric), and

•the familiarity of the staff with data analysis projects in general,

the project domain in particular, and the software suites.

1.3 Methods, Tasks, and Tools 11

While there is not much we can do about the problem size, the goal of this book is

to increase the familiarity with data analysis projects by going through each of the

phases and providing first instructions to get along with the software suites.

1.3 Methods, Tasks, and Tools

Problem Categories Every data analysis problem is different. To avoid the effort

of inventing a completely new solution for each problem, it is helpful to think of

different problem categories and consider them as building blocks from which a

solution may be composed. These categories also help to categorize the large num-

ber of different tools and algorithms that solve specific tasks. Over the years, the

following set of method categories has been established [3]:

•classification

Predict the outcome of an experiment with a finite number of possible results

(like yes/no or unacceptable/acceptable/good/very good). We may be interested

in a prediction because the true result will emerge in the future or because it is

expensive, difficult, or cumbersome to determine it.

Typical questions: Is this customer credit-worthy? Will this customer respond to

our mailing? Will the technical quality be acceptable?

•regression

Regression is, just like classification, also a prediction task, but this time the value

of interest is numerical in nature.

Typical questions: How will the EUR/USD exchange rate develop? How much

money will the customer spend for vacation next year? How much will the ma-

chine’s temperature change within the next cycle?

•clustering,segmentation

Summarize the data to get a better overview by forming groups of similar cases

(called clusters or segments). Instead of examining a large number of similar

records, we need to inspect the group summary only. We may also obtain some

insight into the structure of the whole data set. Cases that do not belong to any

group may be considered as abnormal or outliers.

Typical questions: Do my customers divide into different groups? How many op-

erating points does the machine have, and what do they look like?

•association analysis

Find any correlations or associations to better understand or describe the inter-

dependencies of all the attributes. The focus is on relationships between all at-

tributes rather than focusing on a single target variable or the cases (full record).

Typical questions: Which optional equipment of a car often goes together? How

do the various qualities influence each other?

•deviation analysis

Knowing already the major trends or structures, find any exceptional subgroup

that behaves differently with respect to some target attribute.

Typical questions: Under which circumstances does the system behave differ-

ently? Which properties do those customers share who do not follow the crowd?

12 1 Introduction

The most frequent categories are classification and regression, because decision

making always becomes much easier if reliable predictions of the near future are

available. When a completely new area or domain is explored, cluster analysis and

association analysis may help to identify relationships among attributes or records.

Once the major relationships are understood (e.g., by a domain expert), a deviation

analysis can help to focus on exceptional situations that deviate from regularity.

Catalog of Methods There are various methods in each of these categories to

find reliable answers to the questions raised above. However, there is no such thing

as a single gold method that works perfectly for all problems. To convey some idea

which method may be best suited for a given problem, we will discuss various meth-

ods in Chaps. 7–9. However, in order to organize these chapters, we did not rely on

the problem categories collected above, as some methods can be used likewise for

more than one problem type. We rather used the intended task of the data analysis

as a grouping criterion:

•finding patterns (Chap. 7)

If the domain (and therefore the data) is new to us or if we expect to find interest-

ing relationships, we explore the data for new, previously unknown patterns. We

want to get a full picture and do not concentrate on a single target attribute yet.

We may apply methods from, for instance, segmentation, clustering, association

analysis, or deviation analysis.

•finding explanations (Chap. 8)

We have a special interest in some target variable and wonder why and how it

varies from case to case. The primary goal is to gain new insights (knowledge)

that may influence our decision making, but we do not necessarily intend au-

tomation. We may apply methods from, for instance, classification, regression,

association analysis, or deviation analysis.

•finding predictors (Chap. 9)

We have a special interest in the prediction of some target variable, but it (possi-

bly) represents only one building block of our full problem, so we do not really

care about the how and why but are just interested in the best-possible prediction.

We may apply methods from, for instance, classification or regression.

Available Tools As already mentioned, the key to success is often the proper com-

bination of data preparation and modeling techniques. Data analysis software suites

are of great help as they reduce data formatting efforts and ease method linking.

There is a long list of commercial and free software suites and tools, including the

following classical products:

•IBM SPSS PASW Modeler (formerly Clementine)

Clementine was the first commercial data mining workbench in 1994 and is a

commercial product from SPSS, now IBM.

http://www.spss.com/

•SAS Enterprise Miner

A commercial data mining solution from SAS.

http://www.sas.com/

1.4 How to Read This Book 13

•The R-project

R is a free software environment for statistical computing and graphics.

http://www.r-project.org/

•Weka

Weka is a popular open-source collection of machine learning algorithms, initially

developed by the University of Waikato, New Zealand.

http://www.cs.waikato.ac.nz/ml/weka/

For an up-to-date list of software suites see, for instance,

http://www.kdnuggets.com/software/suites.html

Although the choice of the software suite has considerable impact on the project

time (usability) and can help to avoid errors (because some of them are easily spot-

ted using powerful visualization capabilities), the suites cannot take over the full

analysis process. They provide at best an initial starting point (by means of analysis

templates or project wizards), but in most cases the key factor is the intelligent com-

bination of tools and background knowledge (regarding the project domain and the

utilized tools). The suites exhibit different strengths, some focus on supporting the

human data analyst by sophisticated graphical user interfaces, graphical configura-

tion and reporting, while others are better suited for batch processing and automati-

zation.

In this book, we will use R, which is particularly powerful in statistical tech-

niques, and KNIME (the Konstanz Information Miner1), which is an open-source

data analysis tool that is growing in popularity due to its graphical workflow editor

and its ability to integrate other well-known toolkits.

1.4 How to Read This Book

In the next chapter we will take a glimpse at the intelligent data analysis process by

looking over the shoulder of Stan and Laura as they analyze their data (while only

one of them actually follows CRISP-DM). The chapter is intended to give an im-

pression of what will be discussed in much greater detail throughout the book. The

subsequent chapters roughly follow the CRISP-DM stages: we analyze the problem

first in Chap. 3(project understanding) and then investigate whether the available

data suits our purposes in terms of size, representativeness, and quality in Chap. 4

(data understanding). If we are confident that the data is worth carrying out the anal-

ysis, we discuss the data preparation (Chap. 6) as the last step before we enter the

modeling phase (Chaps. 7–9). As already mentioned, data preparation is already

tailored to the methods we are going to use for modeling; therefore, we have to in-

troduce the principles of modeling already in Chap. 5. Deployment and monitoring

is briefly addressed in Chap. 10. Readers who, over the years, have lost some of

their statistical knowledge can (partially) recover it in Appendix A. The statistics

1Available for download at http://www.knime.org/.

14 1 Introduction

appendix is not just a glossary of terms to quickly look up details but also serves as

a book within the book for a few preparative lessons on statistics before delving into

the chapters about intelligent data analysis.

Most chapters contain a section that equips the reader with the necessary infor-

mation for some first hands-on experience using either R or KNIME. We have set-

tled on R and KNIME because they can be seen as extremes on the range of possible

software suites: R is a statistical tool, which is (mostly) command-line oriented and

is particularly useful for scripting and automatization. KNIME, on the other hand,

supports the composition of complex workflows in a graphical user interface.2Ap-

pendices Band Cprovide a brief introduction into both systems.

References

1. Berthold, M., Hand, D.: Intelligent Data Analysis. Springer, Berlin (2009)

2. Chapman, P., Clinton, J., Kerber, R., Khabaza, T., Reinartz, T., Shearer, C., Wirth, R.: Cross

Industry Standard Process for Data Mining 1.0, Step-by-step Data Mining Guide. CRISP-DM

consortium (2000)

3. Fayyad, U.M., Piatetsky-Shapiro, G., Smyth, P., Uthurusamy, R. (eds.): Advances in Knowl-

edge Discovery and Data Mining. AAAI Press/MIT Press, Menlo Park/Cambridge (1996)

4. Feynman, R.P., Leighton, R.B., Sands, M.: The Feynman Lectures on Physics. Mechanics, Ra-

diation, and Heat, vol. 1. Addison-Wesley, Reading (1963)

5. Hand, D.: Intelligent data analysis: issues and opportunities. In: Proc. 2nd Int. Symp. on Ad-

vances in Intelligent Data Analysis, pp. 1–14. Springer, Berlin (1997)

6. Kepler, J.: Astronomia Nova, aitiologetos seu physica coelestis, tradita commentariis de

motibus stellae martis, ex observationibus Tychonis Brahe. (New Astronomy, Based upon

Causes, or Celestial Physics, Treated by Means of Commentaries on the Motions of the Star

Mars, from the Observations of Tycho Brahe) (1609); English edition: New Astronomy. Cam-

bridge University Press, Cambridge (1992)

7. Kepler, J.: Harmonices Mundi (1619); English edition: The Harmony of the World. American

Philosophical Society, Philadelphia (1997)

8. Kurgan, L.A., Musilek, P.: A survey of knowledge discovery and data mining process models.

Knowl. Eng. Rev. 21(1), 1–24 (2006)

9. Marban, O., Menasalvas, E., Fernandez-Baizan, C.: A cost model to estimate the effort of data

mining process (DMCoMo). Inf. Syst. 33, 133–150 (2008)

2The workflows discussed in this book are available for download at the book’s website.

Chapter 2

Practical Data Analysis: An Example

Before talking about the full-fledged data analysis process and diving into the details

of individual methods, this chapter demonstrates some typical pitfalls one encoun-

ters when analyzing real-world data. We start our journey through the data analysis

process by looking over the shoulders of two (pseudo) data analysts, Stan and Laura,

working on some hypothetical data analysis problems in a sales environment. Being

differently skilled, they show how things should and should not be done. Through-

out the chapter, a number of typical problems that data analysts meet in real work

situations are demonstrated as well. We will skip algorithmic and other details here

and only briefly mention the intention behind applying some of the processes and

methods. They will be discussed in depth in subsequent chapters.

2.1 The Setup

Disclaimer The data and the application scenario used in this chapter are fictional.

However, the underlying problems are motivated by actual problems which are en-

countered in real-world data analysis scenarios. Explaining particular applicational

setups would have been entirely out of the scope of this book, since in order to un-

derstand the actual issue, a bit of domain knowledge is often helpful if not required.

Please keep this in mind when reading the following. The goal of this chapter is

to show (and sometimes slightly exaggerate) pitfalls encountered in real-world data

analysis setups and not the reality in a supermarket chain. We are painfully aware

that people familiar with this domain will find some of the encountered problems

strange, to say the least. Have fun.

The Data For the following examples, we will use an artificial set of data sources

from a hypothetical supermarket chain. The data set consists of a few tables, which

have already been extracted from an in-house database:1

1Often just getting the data is a problem of its own. Data analysis assumes that you have access to

the data you need—an assumption which is, unfortunately, frequently not true.

M.R. Berthold et al., Guide to Intelligent Data Analysis,

Texts in Computer Science 42,

DOI 10.1007/978-1-84882-260-3_2, © Springer-Verlag London Limited 2010

15

16 2 Practical Data Analysis: An Example

•Customers: data about customers, stemming mostly from information collected

when these customers signed up for frequent shopper cards.

•Products: A list of products with their categories and prices.

•Purchases: A list of products together with the date they were purchased and the

customer card ID used during checkout.

The Analysts Stan and Laura are responsible for the analytics of the southern and

northern parts, respectively, of a large supermarket chain. They were recently hired

to help better understand customer groups and behavior and try to increase revenue

in the local stores. As is unfortunately all too common, over the years the stores

have already begun all sorts of data acquisition operations, but in recent years quite

a lot of this data has been merged—however, still without a clear picture in mind.

Many other stores had started to issue frequent shopping cards, so the directors of

marketing of the southern and northern markets decided to launch a similar program.

Lots of data have been recorded, and Stan and Laura now face the challenge to fit

existing data to the questions posed. Together with their managers, they have sat

down and defined three data analysis questions to be addressed in the following

year:

•differentiate the different customer groups and their behavior to better understand

their impact on the overall revenue,

•identify connections between products to allow for cross selling campaigns, and

•help design a marketing campaign to attract core customers to increase their pur-

chases.

Stan is a representative of the typical self-taught data analysis newbie with little

experience on the job and some more applied knowledge about the different tech-

niques, whereas Laura has some training in statistics, data processing, and data anal-

ysis process planning.

2.2 Data Understanding and Pattern Finding

The first analysis task is a standard data analysis setup: customer segmentation—

find out which types of customers exist in your database and try to link them to

the revenue they create. This can be used later to care for clientele that are re-

sponsible for the largest revenue source or foster groups of customers who are

under-represented. Grouping (or clustering) records in a database is the predomi-

nant method to find such customer segments: the data is partitioned into smaller

subsets, each forming a more coherent group than the overall database contains. We

will go into much more detail on this type of data analysis methods in Chap. 7.For

now it suffices to know that some of the most prominent clustering methods return

one typical example for each cluster. This essentially allows us to reduce a large

data set to a small number of representative examples for the subgroups contained

in the database.

2.2 Data Understanding and Pattern Finding 17

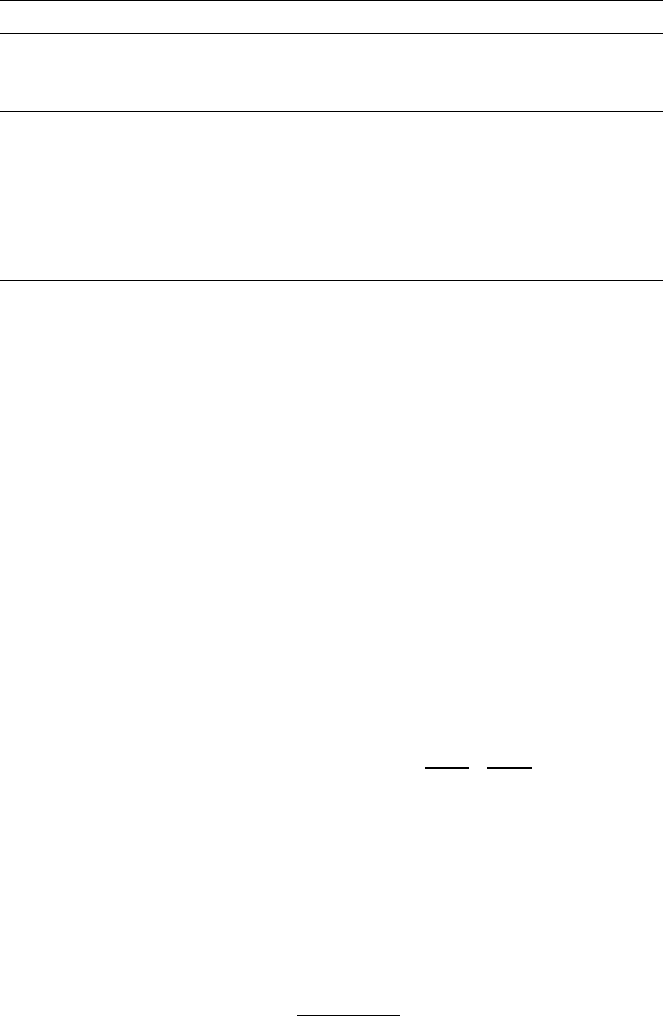

Table 2.1 Stan’s clustering

result Cluster-id Age Customer revenue

146.5€1,922.07

239.4€11,162.20

339.1€7,279.59

446.3€419.23

539.0€4,459.30

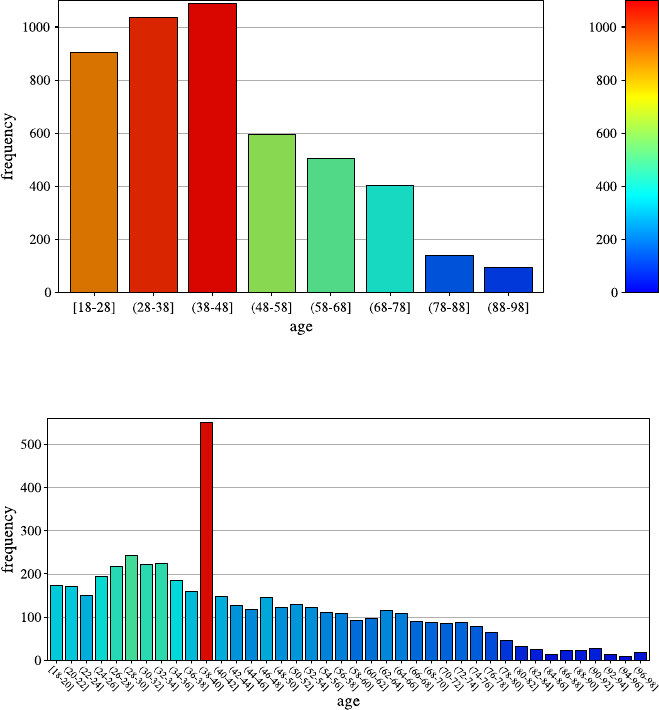

The Naive Approach Stan quickly jumps onto the challenge, creates a dump of

the database containing customer purchases and their birth date, and computes the

age of the customers based on their birth date and the current day. He realizes that

he is interested in customer clusters and therefore needs to somehow aggregate the

individual purchases to their respective “owner.” He uses an aggregating operator in

his database to compute the total price of the shopping baskets for each customer.

Stan then applies a well-known clustering algorithm which results in five prototyp-

ical examples, as shown in Table 2.1.

Stan is puzzled—he was expecting the clustering algorithm to return reasonably

meaningful groups, but this result looks as if all shoppers are around 40–50 years

old but spend vastly different amount of money on products. He looks into some of

the customers’ data in some of these clusters but cannot seem to find any interesting

relations or any reason why some seem to buy substantially more than others. He

changes some of the algorithm’s settings, such as the number of clusters created, but

the results are similarly uninteresting.

The Sound Approach Laura takes a different approach. Routinely she first tries

to understand the available data and validates that some basic assumptions are in fact

true. She uses a basis data summarization tool to report the different values for the

string attributes. The distribution of first names seems to match the frequencies she

would expect. Names such as “Michael” and “Maria” are most frequent, and “Rose-

marie” and “Anneliese” appear a lot less often. The frequencies of the occupations

also roughly match her expectations: the majority of the customers are employ-

ees, while the second and third groups are students and freelancers, respectively.

She proceeds to checking the attributes holding numbers. In order to check the age

of the customers, she also computes the customers’ ages from their birth date and

checks minimum and maximum. She spots a number of customers who obviously

reported a wrong birthday, because they are unbelievably young. As a consequence,

she decides to filter the data to only include people between the ages of 18 and 100.

In order to explore the data more quickly, she reduces the overall customer data set

to 5,000 records by random sampling and then plots a so-called histogram, which

shows different ranges of the attribute age and how many customers fall into that

range. Figure 2.1 shows the result of this analysis.

This view confirms Laura’s assumptions—the majority of shoppers is middle

aged, and the number of shoppers continuously declines toward higher age groups.

18 2 Practical Data Analysis: An Example

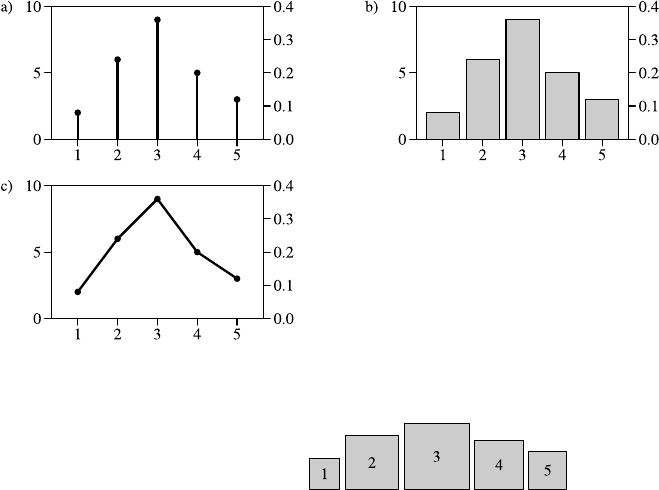

Fig. 2.1 A histogram for the distribution of the value of attribute age using 8 bins

Fig. 2.2 A histogram for the distribution of the value of attribute age using40bins

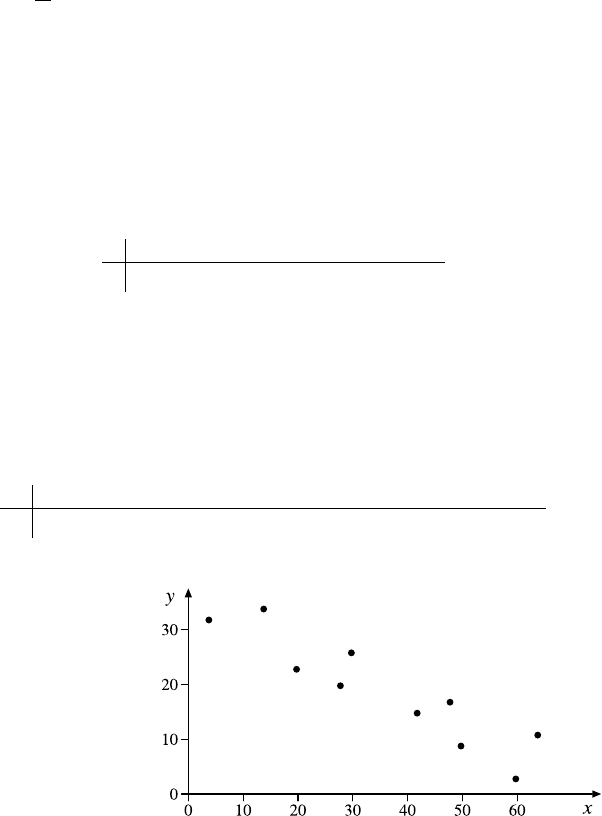

She creates a second histogram to better inspect the subtle but strange cliff at around

age 48 using finer setting for the bins. Figure 2.2 shows the result of this analysis.

Surprised, she notices the huge peak in the bin of ages 38–40. She discusses this

observation with colleagues and the administrator of the shopping card database.

They have no explanation for this odd concentration of 40-year-old people ei-

ther. After a few other investigations, a colleague of the person who—before his

retirement—designed the data entry forms suspects that this may have to do with

the coding of missing birth dates. And, as it turns out, this is in fact the case: forms

where people entered no or obviously nonsensical birth dates were entered into the

form as zero values. For technical reasons, these zeros were then converted into the

Java 0-date which turns out to be January 1, 1970. So these people all turn up with

the same birth date in the customer database and in turn have the same age after the

2.2 Data Understanding and Pattern Finding 19

Table 2.2 Laura’s clustering

result Cluster Age Avg. cart price Avg. purchases/

month

175.3€19.- 5.6

242.1€78.- 7.8

338.1€112.- 9.3

430.6€16.- 4.8

544.7€45.- 3.7

conversion Laura performed initially. Laura marks those entries in her database as

“missing” in order to be able to distinguish them in future analyses.

Similarly, she inspects the shopping basket and product database and cleans up a

number of other outliers and oddities. She then proceeds with the customer segmen-

tation task. As in her previous data analysis projects, Laura first writes down her

domain knowledge in form of a cognitive map, indicating relationships and depen-

dencies between the attributes of her database. Having thus recalled the interactions

between the variables of interest, she is well aware that the length of customer’s

history and the number of overall shopping trips affect the overall basket price, and

so she settles on the average basket price as a better estimator for the value of a

particular customer. She considers also distinguishing the different product cate-

gories, realizing that those, of course, also potentially affect the average price. For

the first step, she adds the average number of purchases per month, another indicator

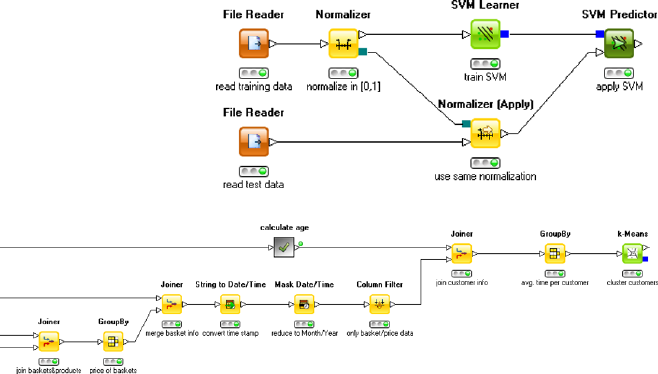

for the revenue a customer brings in. Data aggregation is now a bit more complex,

but the modern data analysis tool she is using allows her to do the required join-

ing and pivoting operations effortlessly. Laura knows that clustering algorithms are

very sensitive to attributes with very different magnitudes, so she normalizes the

three attributes to make sure they all three contribute equally to the clustering result.

Running the same clustering algorithm that Stan was using, with the same setting

for the number of clusters to be found, she gets the result shown in Table 2.2.

Obviously, there is a cluster (#1) of older customers who have a relatively small

average basket price. There is also another group of customers (#4) which seems

to correlate to younger shoppers, also purchasing smaller baskets. The middle-aged

group varies wildly in price, however. Laura realizes that this matches her assump-

tion about family status—people with families will likely buy more products and

hence combine more products into more expensive baskets, which seems to explain

the difference between clusters #2/#3 and cluster #5. The latter also seem to shop

significantly less often. She goes back and validates some of these assumptions by

looking at shopping frequency and average basket size as well and also determines

the overall impact on store revenues for these different groups. She finally discusses

these results with her marketing and campaign specialists to develop strategies to

foster the customer groups which bring in the largest chunk of revenue and develop

the ones which seem to be under-represented.

20 2 Practical Data Analysis: An Example

2.3 Explanation Finding

The second analysis goal is another standard shopping basket analysis problem: find

product dependencies in order to better plan campaigns.

The Naive Approach Stan recently read in a book on practical data analysis how

association rules can find arbitrary such connections in market basket data. He runs

the association rule mining algorithm in his favorite data analysis tool with the de-

fault settings and inspects the results. Among the top-ranked generated rules, sorted

by their confidence, Stan finds the following output:

’foie gras’ (p1231) <- ’champagne Don Huberto’ (p2149),

’truffle oil de Rossini’ (p578) [s=1E-5, c=75%]

’Tortellini De Cecco 500g’ (p3456)’

<- ’De Cecco Sugo Siciliana’ (p8764) [s=1E-5, c=60%]

He quickly infers that this representation must mean that foie gras is bought when-

ever champagne and truffle oil are bought together and similarly for the other rule.

Stan knows that the confidence measure cis important, as it indicates the strength

of the dependency (the first rule holds in 3 out of 4 cases). He considers the sec-

ond measure of frequency sto be less important and deliberately ignores its fairly

small value. The two rules shown above are followed by a set of other, similarly lux-

ury/culinary product-oriented rules. Stan concludes that luxury products are clearly

the most important products on the shelf and recommends to his marketing man-

ager to launch a campaign to advertise some of the products on the right side of

these rules (champagne, truffle oil) to increase the sales of the left side (foie gras).

In parallel, he increases orders for these products, expecting a recognizable increase

in sales. He proudly sends the results of his analysis to Laura.

The Sound Approach Laura is puzzled by those nonintuitive results. She reruns

the analysis and notices the support values of the rules extracted by Stan—some

of the rules Stan extracted have indeed a remarkably high confidence, and some

do almost forecast shopping behavior. However, they have very low support values,

meaning that only a small number of shopping baskets containing the products were

ever observed. The rules that Stan found are not representative at all for his customer

base. To confirm this, she runs a quick query on her database and sees that, indeed,

there is essentially no influence on the overall revenue.

She notices that the problem of low support is caused by the fact that Stan ran

the analysis on product IDs, so in effect he was forcing the rules to differentiate

between brands of champagne and truffle oil. She reruns the analysis based on the

product categories instead, ranks them by a mix of support and confidence, and finds

a number of association rules with substantially higher support:

tomatoes <- capers, pasta [s=0.007, c=32%]

tomatoes <- apples [s=0.013, c=22%]

Laura focuses on rules with a much higher support measure sthan before and also

realizes that the confidence measure cis significantly higher than one would expect

2.4 Predicting the Future 21

by chance. The first rule seems to be triggered by a recent fashion of Italian cooking,

whereas the apple/tomato-rule is a known aspect.

However, she is still irritated by one of the rules discovered by Stan, which has