2012 Publication 502 20502 IRS

User Manual: 20502

Open the PDF directly: View PDF ![]() .

.

Page Count: 35

- Contents

- What's New

- Reminders

- Introduction

- What Are Medical Expenses?

- What Expenses Can You Include This Year?

- How Much of the Expenses Can You Deduct?

- Whose Medical Expenses Can You Include?

- What Medical Expenses Are Includible?

- Abortion

- Acupuncture

- Alcoholism

- Ambulance

- Annual Physical Examination

- Artificial Limb

- Artificial Teeth

- Autoette

- Bandages

- Birth Control Pills

- Body Scan

- Braille Books and Magazines

- Breast Pumps and Supplies

- Breast Reconstruction Surgery

- Capital Expenses

- Car

- Chiropractor

- Christian Science Practitioner

- Contact Lenses

- Crutches

- Dental Treatment

- Diagnostic Devices

- Disabled Dependent Care Expenses

- Drug Addiction

- Drugs

- Eye Exam

- Eyeglasses

- Eye Surgery

- Fertility Enhancement

- Founder's Fee

- Guide Dog or Other Service Animal

- Health Institute

- Health Maintenance Organization (HMO)

- Hearing Aids

- Home Care

- Home Improvements

- Hospital Services

- Insurance Premiums

- Intellectually and Developmentally Disabled, Special Home for

- Laboratory Fees

- Lactation Expenses

- Lead-Based Paint Removal

- Learning Disability

- Legal Fees

- Lifetime Care—Advance Payments

- Lodging

- Long-Term Care

- Meals

- Medical Conferences

- Medical Information Plan

- Medicines

- Nursing Home

- Nursing Services

- Operations

- Optometrist

- Organ Donors

- Osteopath

- Oxygen

- Physical Examination

- Pregnancy Test Kit

- Prosthesis

- Psychiatric Care

- Psychoanalysis

- Psychologist

- Special Education

- Sterilization

- Stop-Smoking Programs

- Surgery

- Telephone

- Television

- Therapy

- Transplants

- Transportation

- Trips

- Tuition

- Vasectomy

- Vision Correction Surgery

- Weight-Loss Program

- Wheelchair

- Wig

- X-ray

- What Expenses Are Not Includible?

- Baby Sitting, Childcare, and Nursing Services for a Normal, Healthy Baby

- Controlled Substances

- Cosmetic Surgery

- Dancing Lessons

- Diaper Service

- Electrolysis or Hair Removal

- Flexible Spending Account

- Funeral Expenses

- Future Medical Care

- Hair Transplant

- Health Club Dues

- Health Coverage Tax Credit

- Health Savings Accounts

- Household Help

- Illegal Operations and Treatments

- Insurance Premiums

- Maternity Clothes

- Medical Savings Account (MSA)

- Medicines and Drugs From Other Countries

- Nonprescription Drugs and Medicines

- Nutritional Supplements

- Personal Use Items

- Swimming Lessons

- Teeth Whitening

- Veterinary Fees

- Weight-Loss Program

- How Do You Treat Reimbursements?

- How Do You Figure and Report the Deduction on Your Tax Return?

- Sale of Medical Equipment or Property

- Damages for Personal Injuries

- Impairment-Related Work Expenses

- Health Insurance Costs for Self-Employed Persons

- COBRA Premium Assistance

- Health Coverage Tax Credit

- How To Get Tax Help

- Index

Userid: CPM Schema: tipx Leadpct: 100% Pt. size: 10 Draft Ok to Print

AH XSL/XML Fileid: Publications/P502/2012/A/XML/Cycle08/source (Init. & Date) _______

Page 1 of 35 10:50 - 10-Dec-2012

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Department of the Treasury

Internal Revenue Service

Publication 502

Cat. No. 15002Q

Medical and

Dental

Expenses

(Including the Health

Coverage Tax Credit)

For use in preparing

2012 Returns

Get forms and other Information

faster and easier by:

Internet IRS.gov

Contents

What's New .............................. 1

Reminders ............................... 1

Introduction .............................. 2

What Are Medical Expenses? ................. 2

What Expenses Can You Include This Year? ..... 2

How Much of the Expenses Can You

Deduct? .............................. 3

Whose Medical Expenses Can You Include? ..... 3

What Medical Expenses Are Includible? ........ 5

What Expenses Are Not Includible? ........... 15

How Do You Treat Reimbursements? ......... 17

How Do You Figure and Report the Deduction

on Your Tax Return? ................... 21

Sale of Medical Equipment or Property ........ 22

Damages for Personal Injuries ............... 24

Impairment-Related Work Expenses .......... 25

Health Insurance Costs for Self-Employed

Persons ............................. 25

COBRA Premium Assistance ................ 26

Health Coverage Tax Credit ................. 27

How To Get Tax Help ...................... 30

Index .................................. 33

What's New

Standard mileage rate. The standard mileage rate al-

lowed for operating expenses for a car when you use it for

medical reasons is 23 cents per mile. See Transportation

under What Medical Expenses Are Includible.

Reminders

Future developments. For the latest information about

developments related to Publication 502, such as legisla-

tion enacted after it was published, go to www.irs.gov/

pub502.

Photographs of missing children. The Internal Reve-

nue Service is a proud partner with the National Center for

Missing and Exploited Children. Photographs of missing

children selected by the Center may appear in this publi-

cation on pages that would otherwise be blank. You can

help bring these children home by looking at the photo-

graphs and calling 1-800-THE-LOST (1-800-843-5678) if

you recognize a child.

Dec 10, 2012

Page 2 of 35 Fileid: Publications/P502/2012/A/XML/Cycle08/source 10:50 - 10-Dec-2012

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Introduction

This publication explains the itemized deduction for medi-

cal and dental expenses that you claim on Schedule A

(Form 1040). It discusses what expenses, and whose ex-

penses, you can and cannot include in figuring the deduc-

tion. It explains how to treat reimbursements and how to

figure the deduction. It also tells you how to report the de-

duction on your tax return and what to do if you sell medi-

cal property or receive damages for a personal injury.

Medical expenses include dental expenses, and in this

publication the term “medical expenses” is often used to

refer to medical and dental expenses.

You can deduct on Schedule A (Form 1040) only the

part of your medical and dental expenses that is more

than 7.5% of your adjusted gross income (AGI). If your

medical and dental expenses are not more than 7.5% of

your AGI, you cannot claim a deduction.

This publication also explains how to treat impair-

ment-related work expenses, health insurance premiums

if you are self-employed, and the health coverage tax

credit that is available to certain individuals.

Pub. 502 covers many common medical expenses but

not every possible medical expense. If you cannot find the

expense you are looking for, refer to the definition of medi-

cal expenses under What Are Medical Expenses.

See How To Get Tax Help near the end of this publica-

tion for information about getting publications and forms.

Comments and suggestions. We welcome your com-

ments about this publication and your suggestions for fu-

ture editions.

You can write to us at the following address:

Internal Revenue Service

Individual and Specialty Forms and Publications

Branch

SE:W:CAR:MP:T:I

1111 Constitution Ave. NW, IR-6526

Washington, DC 20224

We respond to many letters by telephone. Therefore, it

would be helpful if you would include your daytime phone

number, including the area code, in your correspondence.

You can email us at taxforms@irs.gov. Please put

“Publications Comment” on the subject line. You can also

send us comments from www.irs.gov/formspubs/. Select

“Comment on Tax Forms and Publications” under “More

Information.”

Although we cannot respond individually to each com-

ment received, we do appreciate your feedback and will

consider your comments as we revise our tax products.

Ordering forms and publications. Visit www.irs.gov/

formspubs/ to download forms and publications, call

1-800-TAX-FORM (1-800-829-3676), or write to the ad-

dress below and receive a response within 10 days after

your request is received.

Internal Revenue Service

1201 N. Mitsubishi Motorway

Bloomington, IL 61705-6613

Tax questions. If you have a tax question, check the

information available on IRS.gov or call 1-800-829-1040.

We cannot answer tax questions sent to either of the

above addresses.

Useful Items

You may want to see:

Publication

Health Savings Accounts and Other

Tax-Favored Health Plans

Forms (and Instructions)

U.S. Individual Income Tax Return

Itemized Deductions

Health Coverage Tax Credit

What Are Medical Expenses?

Medical expenses are the costs of diagnosis, cure, mitiga-

tion, treatment, or prevention of disease, and the costs for

treatments affecting any part or function of the body.

These expenses include payments for legal medical serv-

ices rendered by physicians, surgeons, dentists, and

other medical practitioners. They include the costs of

equipment, supplies, and diagnostic devices needed for

these purposes.

Medical care expenses must be primarily to alleviate or

prevent a physical or mental defect or illness. They do not

include expenses that are merely beneficial to general

health, such as vitamins or a vacation.

Medical expenses include the premiums you pay for in-

surance that covers the expenses of medical care, and

the amounts you pay for transportation to get medical

care. Medical expenses also include amounts paid for

qualified long-term care services and limited amounts

paid for any qualified long-term care insurance contract.

What Expenses Can You

Include This Year?

You can include only the medical and dental expenses

you paid this year, regardless of when the services were

provided. (But see Decedent under Whose Medical Ex

penses Can You Include, for an exception.) If you pay

medical expenses by check, the day you mail or deliver

the check generally is the date of payment. If you use a

“pay-by-phone” or “online” account to pay your medical

expenses, the date reported on the statement of the finan-

cial institution showing when payment was made is the

date of payment. If you use a credit card, include medical

969

1040

Schedule A (Form 1040)

8885

Page 2 Publication 502 (2012)

Page 3 of 35 Fileid: Publications/P502/2012/A/XML/Cycle08/source 10:50 - 10-Dec-2012

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

expenses you charge to your credit card in the year the

charge is made, not when you actually pay the amount

charged.

If you did not claim a medical or dental expense that

would have been deductible in an earlier year, you can file

Form 1040X, Amended U.S. Individual Income Tax Re-

turn, for the year in which you overlooked the expense. Do

not claim the expense on this year's return. Generally, an

amended return must be filed within 3 years from the date

the original return was filed or within 2 years from the time

the tax was paid, whichever is later.

You cannot include medical expenses that were paid

by insurance companies or other sources. This is true

whether the payments were made directly to you, to the

patient, or to the provider of the medical services.

Separate returns. If you and your spouse live in a non-

community property state and file separate returns, each

of you can include only the medical expenses each ac-

tually paid. Any medical expenses paid out of a joint

checking account in which you and your spouse have the

same interest are considered to have been paid equally

by each of you, unless you can show otherwise.

Community property states. If you and your spouse

live in a community property state and file separate re-

turns or are registered domestic partners in Nevada,

Washington, or California (or a person in California who is

married to a person of the same sex), any medical expen-

ses paid out of community funds are divided equally. Gen-

erally, each of you should include half the expenses. If

medical expenses are paid out of the separate funds of

one individual, only the individual who paid the medical

expenses can include them. If you live in a community

property state and are not filing a joint return, see Publica-

tion 555, Community Property.

How Much of the Expenses

Can You Deduct?

You can deduct on Schedule A (Form 1040) only the

amount of your medical and dental expenses that is more

than 7.5% of your AGI (Form 1040, line 38).

In this publication, the term “7.5% limit” is used to refer

to 7.5% of your AGI. The phrase “subject to the 7.5% limit”

is also used. This phrase means that you must subtract

7.5% (.075) of your AGI from your medical expenses to

figure your medical expense deduction.

Example. Your AGI is $40,000, 7.5% of which is

$3,000. You paid medical expenses of $2,500. You can-

not deduct any of your medical expenses because they

are not more than 7.5% of your AGI.

Whose Medical Expenses

Can You Include?

You can generally include medical expenses you pay for

yourself, as well as those you pay for someone who was

your spouse or your dependent either when the services

were provided or when you paid for them. There are differ-

ent rules for decedents and for individuals who are the

subject of multiple support agreements. See Support

claimed under a multiple support agreement, later under

Qualifying Person.

Yourself

You can include medical expenses that you paid for your-

self.

Spouse

You can include medical expenses you paid for your

spouse. To include these expenses, you must have been

married either at the time your spouse received the medi-

cal services or at the time you paid the medical expenses.

Example 1. Mary received medical treatment before

she married Bill. Bill paid for the treatment after they mar-

ried. Bill can include these expenses in figuring his medi-

cal expense deduction even if Bill and Mary file separate

returns.

If Mary had paid the expenses, Bill could not include

Mary's expenses in his separate return. Mary would in-

clude the amounts she paid during the year in her sepa-

rate return. If they filed a joint return, the medical expen-

ses both paid during the year would be used to figure their

medical expense deduction.

Example 2. This year, John paid medical expenses for

his wife Louise, who died last year. John married Belle

this year and they file a joint return. Because John was

married to Louise when she received the medical serv-

ices, he can include those expenses in figuring his medi-

cal expense deduction for this year.

Dependent

You can include medical expenses you paid for your de-

pendent. For you to include these expenses, the person

must have been your dependent either at the time the

medical services were provided or at the time you paid the

expenses. A person generally qualifies as your dependent

for purposes of the medical expense deduction if both of

the following requirements are met.

1. The person was a Qualifying Child (defined later) or a

Qualifying Relative (defined later), and

2. The person was a U.S. citizen or national or a resident

of the United States, Canada, or Mexico. If your quali-

fying child was adopted, see Exception for adopted

child, later.

Publication 502 (2012) Page 3

Page 4 of 35 Fileid: Publications/P502/2012/A/XML/Cycle08/source 10:50 - 10-Dec-2012

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

You can include medical expenses you paid for an individ-

ual that would have been your dependent except that:

1. He or she received gross income of $3,800 or more in

2012,

2. He or she filed a joint return for 2012, or

3. You, or your spouse if filing jointly, could be claimed

as a dependent on someone else's 2012 return.

Exception for adopted child. If you are a U.S. citizen or

national and your adopted child lived with you as a mem-

ber of your household for 2012, that child does not have to

be a U.S. citizen or national, or a resident of the United

States, Canada, or Mexico.

Qualifying Child

A qualifying child is a child who:

1. Is your son, daughter, stepchild, foster child, brother,

sister, stepbrother, stepsister, half brother, half sister,

or a descendant of any of them (for example, your

grandchild, niece, or nephew),

2. Was:

a. Under age 19 at the end of 2012 and younger than

you (or your spouse, if filing jointly),

b. Under age 24 at the end of 2012, a full-time stu-

dent, and younger than you (or your spouse, if fil-

ing jointly), or

c. Any age and permanently and totally disabled,

3. Lived with you for more than half of 2012,

4. Did not provide over half of his or her own support for

2012, and

5. Did not file a joint return, other than to claim a refund.

Adopted child. A legally adopted child is treated as your

own child. This child includes a child lawfully placed with

you for legal adoption.

You can include medical expenses that you paid for a

child before adoption if the child qualified as your depend-

ent when the medical services were provided or when the

expenses were paid.

If you pay back an adoption agency or other persons

for medical expenses they paid under an agreement with

you, you are treated as having paid those expenses provi-

ded you clearly substantiate that the payment is directly

attributable to the medical care of the child.

But if you pay the agency or other person for medical

care that was provided and paid for before adoption nego-

tiations began, you cannot include them as medical ex-

penses.

You may be able to take a credit for other expen

ses related to an adoption. See the Instructions

for Form 8839, Qualified Adoption Expenses, for

more information.

Child of divorced or separated parents. For purposes

of the medical and dental expenses deduction, a child of

TIP

divorced or separated parents can be treated as a de-

pendent of both parents. Each parent can include the

medical expenses he or she pays for the child, even if the

other parent claims the child's dependency exemption, if:

1. The child is in the custody of one or both parents for

more than half the year,

2. The child receives over half of his or her support dur-

ing the year from his or her parents, and

3. The child's parents:

a. Are divorced or legally separated under a decree

of divorce or separate maintenance,

b. Are separated under a written separation agree-

ment, or

c. Live apart at all times during the last 6 months of

the year.

This does not apply if the child's exemption is being

claimed under a multiple support agreement (discussed

later).

Qualifying Relative

A qualifying relative is a person:

1. Who is your:

a. Son, daughter, stepchild, or foster child, or a de-

scendant of any of them (for example, your grand-

child),

b. Brother, sister, half brother, half sister, or a son or

daughter of any of them,

c. Father, mother, or an ancestor or sibling of either

of them (for example, your grandmother, grandfa-

ther, aunt, or uncle),

d. Stepbrother, stepsister, stepfather, stepmother,

son-in-law, daughter-in-law, father-in-law,

mother-in-law, brother-in-law, or sister-in-law, or

e. Any other person (other than your spouse) who

lived with you all year as a member of your house-

hold if your relationship did not violate local law,

2. Who was not a qualifying child (see Qualifying Child,

earlier) of any taxpayer for 2012, and

3. For whom you provided over half of the support in

2012. But see Child of divorced or separated parents,

earlier, Support claimed under a multiple support

agreement, next, and Kidnapped child under Qualify

ing Relative in Publication 501, Exemptions, Standard

Deduction, and Filing Information.

Support claimed under a multiple support agree-

ment. If you are considered to have provided more than

half of a qualifying relative's support under a multiple sup-

port agreement, you can include medical expenses you

pay for that person. A multiple support agreement is used

when two or more people provide more than half of a per-

son's support, but no one alone provides more than half.

Page 4 Publication 502 (2012)

Page 5 of 35 Fileid: Publications/P502/2012/A/XML/Cycle08/source 10:50 - 10-Dec-2012

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Any medical expenses paid by others who joined you in

the agreement cannot be included as medical expenses

by anyone. However, you can include the entire unreim-

bursed amount you paid for medical expenses.

Example. You and your three brothers each provide

one-fourth of your mother's total support. Under a multiple

support agreement, you treat your mother as your de-

pendent. You paid all of her medical expenses. Your

brothers repaid you for three-fourths of these expenses. In

figuring your medical expense deduction, you can include

only one-fourth of your mother's medical expenses. Your

brothers cannot include any part of the expenses. How-

ever, if you and your brothers share the nonmedical sup-

port items and you separately pay all of your mother's

medical expenses, you can include the unreimbursed

amount you paid for her medical expenses in your medi-

cal expenses.

Decedent

Medical expenses paid before death by the decedent are

included in figuring any deduction for medical and dental

expenses on the decedent's final income tax return. This

includes expenses for the decedent's spouse and de-

pendents as well as for the decedent.

The survivor or personal representative of a decedent

can choose to treat certain expenses paid by the dece-

dent's estate for the decedent's medical care as paid by

the decedent at the time the medical services were provi-

ded. The expenses must be paid within the 1-year period

beginning with the day after the date of death. If you are

the survivor or personal representative making this

choice, you must attach a statement to the decedent's

Form 1040 (or the decedent's amended return, Form

1040X) saying that the expenses have not been and will

not be claimed on the estate tax return.

Qualified medical expenses paid before death by

the decedent are not deductible if paid with a

taxfree distribution from any Archer MSA, Medi

care Advantage MSA, or health savings account.

What if the decedent's return had been filed and the

medical expenses were not included? Form 1040X

can be filed for the year or years the expenses are treated

as paid, unless the period for filing an amended return for

that year has passed. Generally, an amended return must

be filed within 3 years of the date the original return was

filed, or within 2 years from the time the tax was paid,

whichever date is later.

Example. John properly filed his 2011 income tax re-

turn. He died in 2012 with unpaid medical expenses of

$1,500 from 2011 and $1,800 in 2012. If the expenses are

paid within the 1-year period, his survivor or personal rep-

resentative can file an amended return for 2011 claiming a

deduction based on the $1,500 medical expenses. The

$1,800 of medical expenses from 2012 can be included

on the decedent's final return for 2012.

CAUTION

!

What if you pay medical expenses of a deceased

spouse or dependent? If you paid medical expenses for

your deceased spouse or dependent, include them as

medical expenses on your Form 1040 in the year paid,

whether they are paid before or after the decedent's

death. The expenses can be included if the person was

your spouse or dependent either at the time the medical

services were provided or at the time you paid the expen-

ses.

What Medical Expenses Are

Includible?

Following is a list of items that you can include in figuring

your medical expense deduction. The items are listed in

alphabetical order.

This list does not include all possible medical expen-

ses. To determine if an expense not listed can be included

in figuring your medical expense deduction, see What Are

Medical Expenses, earlier.

Abortion

You can include in medical expenses the amount you pay

for a legal abortion.

Acupuncture

You can include in medical expenses the amount you pay

for acupuncture.

Alcoholism

You can include in medical expenses amounts you pay for

an inpatient's treatment at a therapeutic center for alcohol

addiction. This includes meals and lodging provided by

the center during treatment.

You can also include in medical expenses amounts you

pay for transportation to and from Alcoholics Anonymous

meetings in your community if the attendance is pursuant

to medical advice that membership in Alcoholics Anony-

mous is necessary for the treatment of a disease involving

the excessive use of alcoholic liquors.

Ambulance

You can include in medical expenses amounts you pay for

ambulance service.

Annual Physical Examination

See Physical Examination, later.

Artificial Limb

You can include in medical expenses the amount you pay

for an artificial limb.

Publication 502 (2012) Page 5

Page 6 of 35 Fileid: Publications/P502/2012/A/XML/Cycle08/source 10:50 - 10-Dec-2012

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Artificial Teeth

You can include in medical expenses the amount you pay

for artificial teeth.

Autoette

See Wheelchair, later.

Bandages

You can include in medical expenses the cost of medical

supplies such as bandages.

Birth Control Pills

You can include in medical expenses the amount you pay

for birth control pills prescribed by a doctor.

Body Scan

You can include in medical expenses the cost of an elec-

tronic body scan.

Braille Books and Magazines

You can include in medical expenses the part of the cost

of Braille books and magazines for use by a visually im-

paired person that is more than the cost of regular printed

editions.

Breast Pumps and Supplies

You can include in medical expenses the cost of breast

pumps and supplies that assist lactation.

Breast Reconstruction Surgery

You can include in medical expenses the amounts you

pay for breast reconstruction surgery, as well as breast

prosthesis, following a mastectomy for cancer. See Cos

metic Surgery, later.

Capital Expenses

You can include in medical expenses amounts you pay for

special equipment installed in a home, or for improve-

ments, if their main purpose is medical care for you, your

spouse, or your dependent. The cost of permanent im-

provements that increase the value of your property may

be partly included as a medical expense. The cost of the

improvement is reduced by the increase in the value of

your property. The difference is a medical expense. If the

value of your property is not increased by the improve-

ment, the entire cost is included as a medical expense.

Certain improvements made to accommodate a home

to your disabled condition, or that of your spouse or your

dependents who live with you, do not usually increase the

value of the home and the cost can be included in full as

medical expenses. These improvements include, but are

not limited to, the following items.

Constructing entrance or exit ramps for your home.

Widening doorways at entrances or exits to your

home.

Widening or otherwise modifying hallways and interior

doorways.

Installing railings, support bars, or other modifications

to bathrooms.

Lowering or modifying kitchen cabinets and equip-

ment.

Moving or modifying electrical outlets and fixtures.

Installing porch lifts and other forms of lifts (but eleva-

tors generally add value to the house).

Modifying fire alarms, smoke detectors, and other

warning systems.

Modifying stairways.

Adding handrails or grab bars anywhere (whether or

not in bathrooms).

Modifying hardware on doors.

Modifying areas in front of entrance and exit door-

ways.

Grading the ground to provide access to the resi-

dence.

Only reasonable costs to accommodate a home to a

disabled condition are considered medical care. Addi-

tional costs for personal motives, such as for architectural

or aesthetic reasons, are not medical expenses.

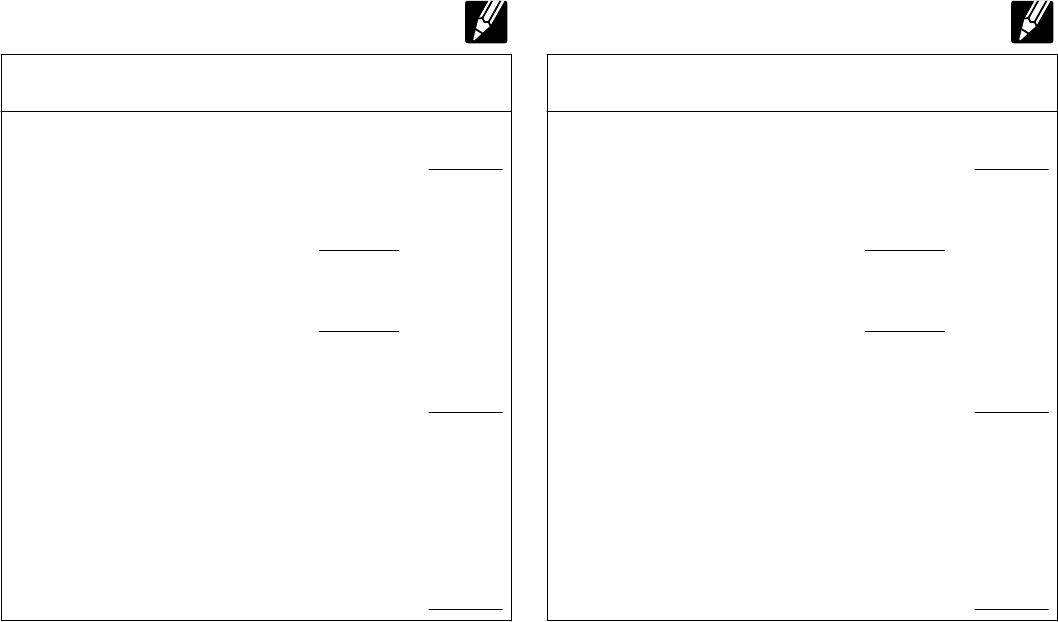

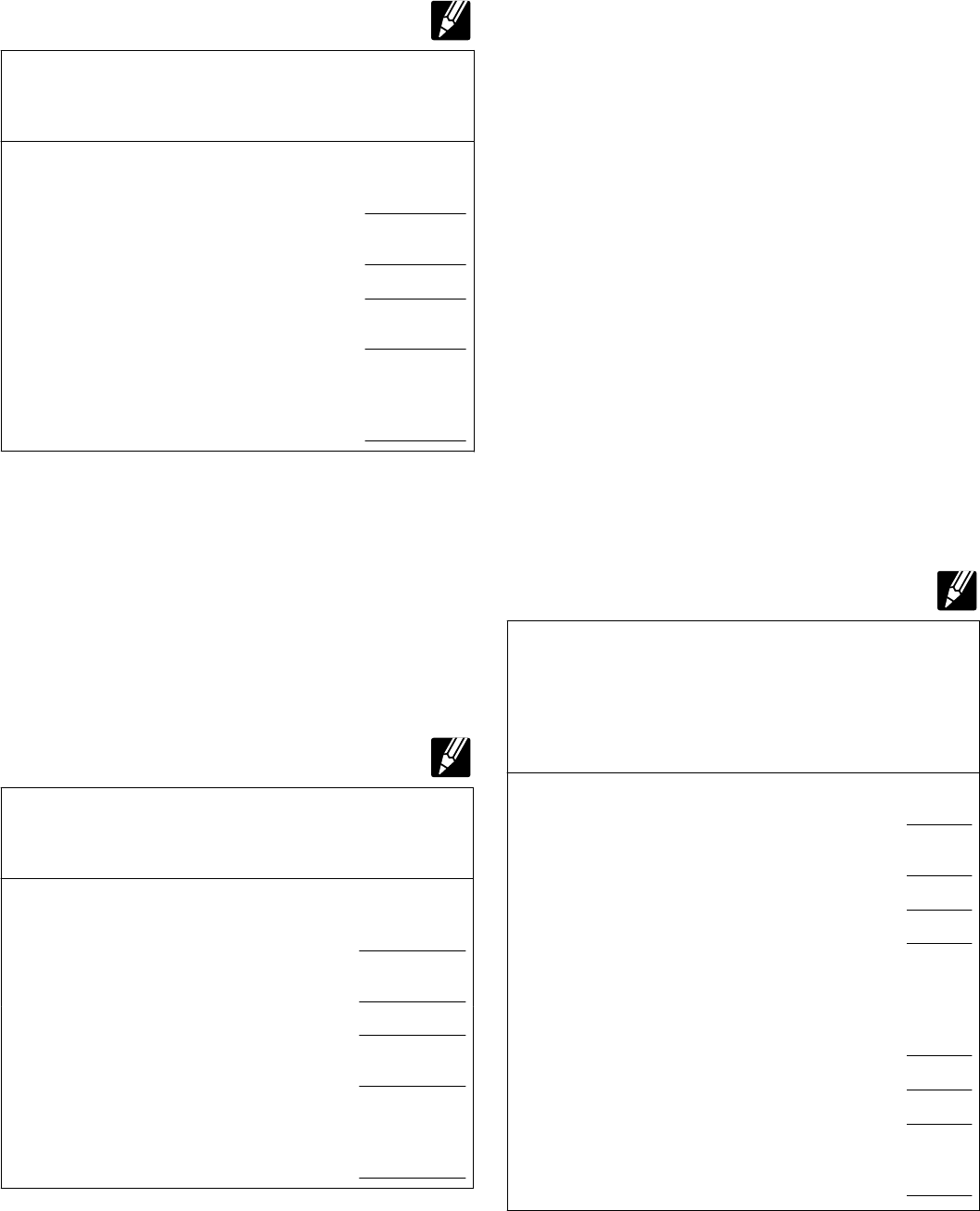

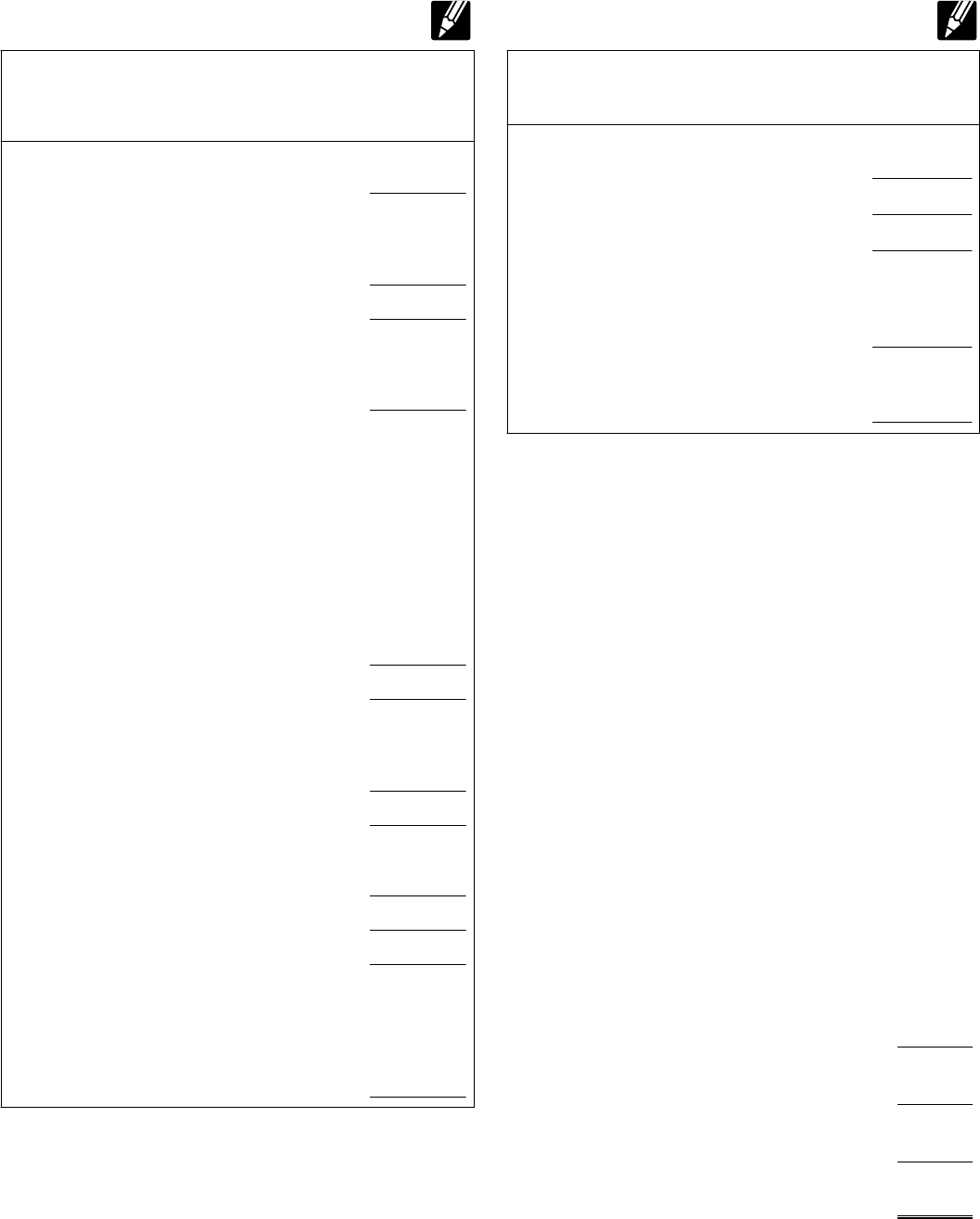

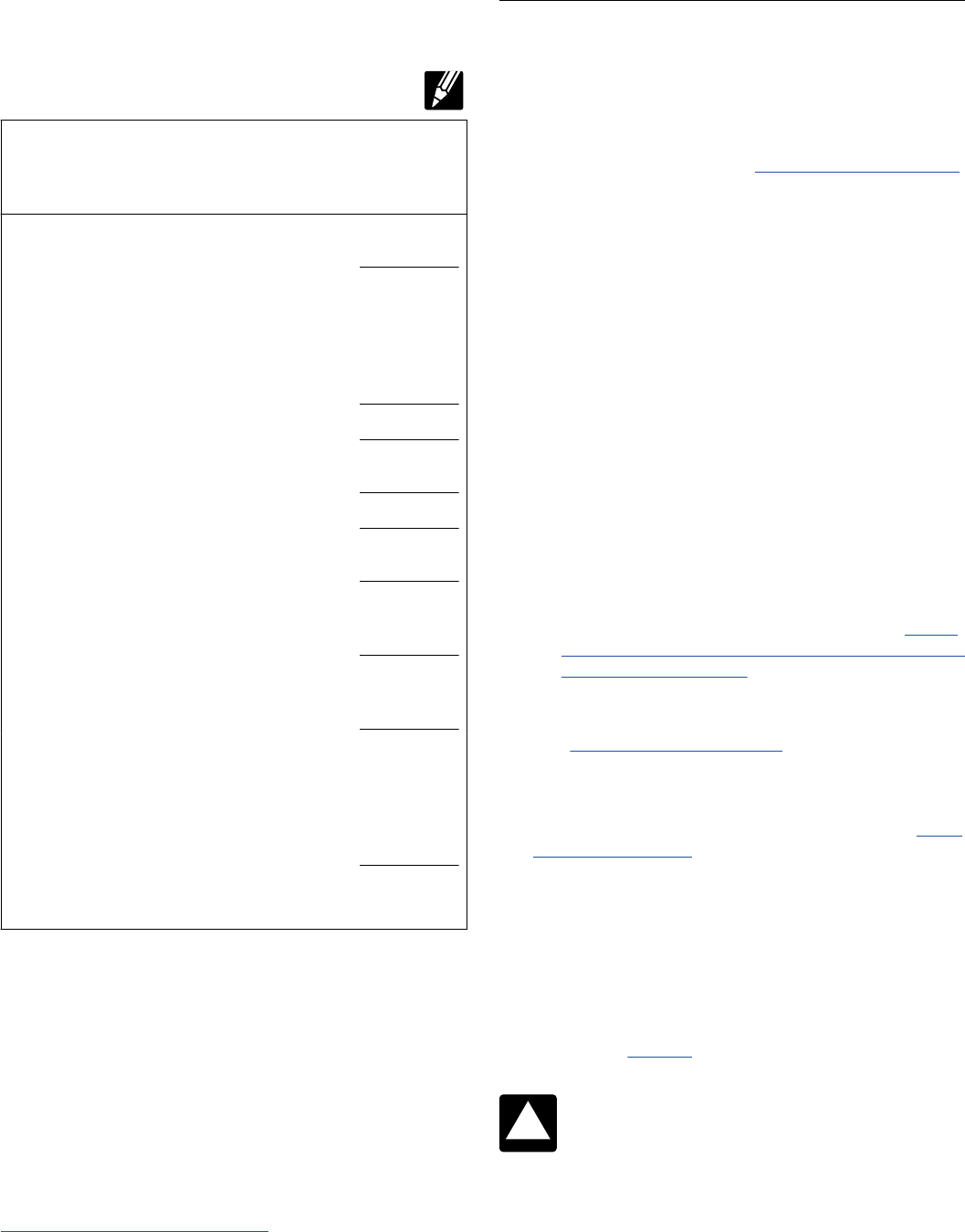

Capital expense worksheet. Use Worksheet A to figure

the amount of your capital expense to include in your

medical expenses.

Page 6 Publication 502 (2012)

Page 7 of 35 Fileid: Publications/P502/2012/A/XML/Cycle08/source 10:50 - 10-Dec-2012

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Capital Expense

Worksheet

Worksheet A.

Keep for Your Records

Instructions: Use this worksheet to figure the amount, if any, of

your medical expenses due to a home improvement.

1. Enter the amount you paid for the home

improvement ......................... 1.

2. Enter the value of your home

immediately after the

improvement .............. 2.

3. Enter the value of your home

immediately before the

improvement .............. 3.

4. Subtract line 3 from line 2. This is the

increase in the value of your home due to

the improvement. ..................... 4.

• If line 4 is more than or equal to line 1,

you have no medical expenses due to the

home improvement; stop here.

• If line 4 is less than line 1, go to line 5.

5. Subtract line 4 from line 1. These are your

medical expenses due to the home

improvement. ........................ 5.

Example. You have a heart ailment. On your doctor's

advice, you install an elevator in your home so that you

will not have to climb stairs. The elevator costs $8,000. An

appraisal shows that the elevator increases the value of

your home by $4,400. You figure your medical expense as

shown in the filled-in example of Worksheet A.

Capital Expense

Worksheet—Illustrated

Worksheet A.

Keep for Your Records

Instructions: Use this worksheet to figure the amount, if any, of

your medical expenses due to a home improvement.

1. Enter the amount you paid for the home

improvement ......................... 1. 8,000

2. Enter the value of your home

immediately after the

improvement .............. 2. 124,400

3. Enter the value of your home

immediately before the

improvement .............. 3. 120,000

4. Subtract line 3 from line 2. This is the

increase in the value of your home due to

the improvement. ..................... 4. 4,400

• If line 4 is more than or equal to line 1,

you have no medical expenses due to the

home improvement; stop here.

• If line 4 is less than line 1, go to line 5.

5. Subtract line 4 from line 1. These are your

medical expenses due to the home

improvement. ........................ 5. 3,600

Operation and upkeep. Amounts you pay for operation

and upkeep of a capital asset qualify as medical expen-

ses, as long as the main reason for them is medical care.

This rule applies even if none or only part of the original

cost of the capital asset qualified as a medical care ex-

pense.

Example. If, in the previous example, the elevator in-

creased the value of your home by $8,000, you would

have no medical expense for the cost of the elevator.

However, the cost of electricity to operate the elevator and

any costs to maintain it are medical expenses as long as

the medical reason for the elevator exists.

Improvements to property rented by a person with a

disability. Amounts paid to buy and install special

plumbing fixtures for a person with a disability, mainly for

medical reasons, in a rented house are medical expen-

ses.

Example. John has arthritis and a heart condition. He

cannot climb stairs or get into a bathtub. On his doctor's

advice, he installs a bathroom with a shower stall on the

first floor of his two-story rented house. The landlord did

not pay any of the cost of buying and installing the special

plumbing and did not lower the rent. John can include in

medical expenses the entire amount he paid.

Car

You can include in medical expenses the cost of special

hand controls and other special equipment installed in a

car for the use of a person with a disability.

Publication 502 (2012) Page 7

Page 8 of 35 Fileid: Publications/P502/2012/A/XML/Cycle08/source 10:50 - 10-Dec-2012

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Special design. You can include in medical expenses

the difference between the cost of a regular car and a car

specially designed to hold a wheelchair.

Cost of operation. The includible costs of using a car for

medical reasons are explained under Transportation,

later.

Chiropractor

You can include in medical expenses fees you pay to a

chiropractor for medical care.

Christian Science Practitioner

You can include in medical expenses fees you pay to

Christian Science practitioners for medical care.

Contact Lenses

You can include in medical expenses amounts you pay for

contact lenses needed for medical reasons. You can also

include the cost of equipment and materials required for

using contact lenses, such as saline solution and enzyme

cleaner. See Eyeglasses and Eye Surgery, later.

Crutches

You can include in medical expenses the amount you pay

to buy or rent crutches.

Dental Treatment

You can include in medical expenses the amounts you

pay for the prevention and alleviation of dental disease.

Preventive treatment includes the services of a dental hy-

gienist or dentist for such procedures as teeth cleaning,

the application of sealants, and fluoride treatments to pre-

vent tooth decay. Treatment to alleviate dental disease in-

clude services of a dentist for procedures such as X-rays,

fillings, braces, extractions, dentures, and other dental ail-

ments. But see Teeth Whitening under What Expenses

Are Not Includible, later.

Diagnostic Devices

You can include in medical expenses the cost of devices

used in diagnosing and treating illness and disease.

Example. You have diabetes and use a blood sugar

test kit to monitor your blood sugar level. You can include

the cost of the blood sugar test kit in your medical expen-

ses.

Disabled Dependent Care Expenses

Some disabled dependent care expenses may qualify as

either:

Medical expenses, or

Work-related expenses for purposes of taking a credit

for dependent care. (See Publication 503, Child and

Dependent Care Expenses.)

You can choose to apply them either way as long as you

do not use the same expenses to claim both a credit and a

medical expense deduction.

Drug Addiction

You can include in medical expenses amounts you pay for

an inpatient's treatment at a therapeutic center for drug

addiction. This includes meals and lodging at the center

during treatment.

Drugs

See Medicines, later.

Eye Exam

You can include in medical expenses the amount you pay

for eye examinations.

Eyeglasses

You can include in medical expenses amounts you pay for

eyeglasses and contact lenses needed for medical rea-

sons. See Contact Lenses, earlier, for more information.

Eye Surgery

You can include in medical expenses the amount you pay

for eye surgery to treat defective vision, such as laser eye

surgery or radial keratotomy.

Fertility Enhancement

You can include in medical expenses the cost of the fol-

lowing procedures to overcome an inability to have chil-

dren.

Procedures such as in vitro fertilization (including tem-

porary storage of eggs or sperm).

Surgery, including an operation to reverse prior sur-

gery that prevented the person operated on from hav-

ing children.

Founder's Fee

See Lifetime Care—Advance Payments, later.

Guide Dog or Other Service Animal

You can include in medical expenses the costs of buying,

training, and maintaining a guide dog or other service ani-

mal to assist a visually impaired or hearing disabled per-

son, or a person with other physical disabilities. In gen-

eral, this includes any costs, such as food, grooming, and

veterinary care, incurred in maintaining the health and vi-

tality of the service animal so that it may perform its duties.

Page 8 Publication 502 (2012)

Page 9 of 35 Fileid: Publications/P502/2012/A/XML/Cycle08/source 10:50 - 10-Dec-2012

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Health Institute

You can include in medical expenses fees you pay for

treatment at a health institute only if the treatment is pre-

scribed by a physician and the physician issues a state-

ment that the treatment is necessary to alleviate a physi-

cal or mental defect or illness of the individual receiving

the treatment.

Health Maintenance

Organization (HMO)

You can include in medical expenses amounts you pay to

entitle you, your spouse, or a dependent to receive medi-

cal care from an HMO. These amounts are treated as

medical insurance premiums. See Insurance Premiums,

later.

Hearing Aids

You can include in medical expenses the cost of a hearing

aid and batteries, repairs, and maintenance needed to op-

erate it.

Home Care

See Nursing Services, later.

Home Improvements

See Capital Expenses, earlier.

Hospital Services

You can include in medical expenses amounts you pay for

the cost of inpatient care at a hospital or similar institution

if a principal reason for being there is to receive medical

care. This includes amounts paid for meals and lodging.

Also see Lodging, later.

Insurance Premiums

You can include in medical expenses insurance premiums

you pay for policies that cover medical care. Medical care

policies can provide payment for treatment that includes:

Hospitalization, surgical services, X-rays,

Prescription drugs and insulin,

Dental care,

Replacement of lost or damaged contact lenses, and

Long-term care (subject to additional limitations). See

Qualified LongTerm Care Insurance Contracts under

LongTerm Care, later.

If you have a policy that provides payments for other

than medical care, you can include the premiums for the

medical care part of the policy if the charge for the medi-

cal part is reasonable. The cost of the medical part must

be separately stated in the insurance contract or given to

you in a separate statement.

Health coverage tax credit. If, during 2012, you were

an eligible trade adjustment assistance (TAA) recipient,

alternative TAA (ATAA) recipient, reemployment TAA

(RTAA) recipient, or Pension Benefit Guaranty Corpora-

tion (PBGC) pension recipient, you must complete Form

8885 before completing Schedule A, line 1. When figuring

the amount of insurance premiums you can deduct on

Schedule A, do not include:

Any amounts you included on Form 8885, line 4,

Any qualified health insurance premiums you paid to

“U.S. Treasury–HCTC,” or

Any health coverage tax credit advance payments

shown in box 1 of Form 1099-H.

Employer-Sponsored Health Insurance Plan

Do not include in your medical and dental expenses any

insurance premiums paid by an employer-sponsored

health insurance plan unless the premiums are included in

box 1 of your Form W-2, Wage and Tax Statement. Also,

do not include any other medical and dental expenses

paid by the plan unless the amount paid is included in

box 1 of your Form W-2.

Example. You are a federal employee participating in

the premium conversion plan of the Federal Employee

Health Benefits (FEHB) program. Your share of the FEHB

premium is paid by making a pre-tax reduction in your sal-

ary. Because you are an employee whose insurance pre-

miums are paid with money that is never included in your

gross income, you cannot deduct the premiums paid with

that money.

Long-term care services. Contributions made by your

employer to provide coverage for qualified long-term care

services under a flexible spending or similar arrangement

must be included in your income. This amount will be re-

ported as wages in box 1 of your Form W-2.

Retired public safety officers. If you are a retired pub-

lic safety officer, do not include as medical expenses any

health or long-term care insurance premiums that you

elected to have paid with tax-free distributions from a re-

tirement plan. This applies only to distributions that would

otherwise be included in income.

Health reimbursement arrangement (HRA). If you

have medical expenses that are reimbursed by a health

reimbursement arrangement, you cannot include those

expenses in your medical expenses. This is because an

HRA is funded solely by the employer.

Medicare A

If you are covered under social security (or if you are a

government employee who paid Medicare tax), you are

enrolled in Medicare A. The payroll tax paid for Medicare

A is not a medical expense.

Publication 502 (2012) Page 9

Page 10 of 35 Fileid: Publications/P502/2012/A/XML/Cycle08/source 10:50 - 10-Dec-2012

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

If you are not covered under social security (or were not

a government employee who paid Medicare tax), you can

voluntarily enroll in Medicare A. In this situation you can

include the premiums you paid for Medicare A as a medi-

cal expense.

Medicare B

Medicare B is a supplemental medical insurance. Premi-

ums you pay for Medicare B are a medical expense.

Check the information you received from the Social Se-

curity Administration to find out your premium.

Medicare D

Medicare D is a voluntary prescription drug insurance pro-

gram for persons with Medicare A or B. You can include

as a medical expense premiums you pay for Medicare D.

Prepaid Insurance Premiums

Premiums you pay before you are age 65 for insurance for

medical care for yourself, your spouse, or your depend-

ents after you reach age 65 are medical care expenses in

the year paid if they are:

1. Payable in equal yearly installments or more often,

and

2. Payable for at least 10 years, or until you reach age

65 (but not for less than 5 years).

Unused Sick Leave Used To Pay Premiums

You must include in gross income cash payments you re-

ceive at the time of retirement for unused sick leave. You

also must include in gross income the value of unused

sick leave that, at your option, your employer applies to

the cost of your continuing participation in your employer's

health plan after you retire. You can include this cost of

continuing participation in the health plan as a medical ex-

pense.

If you participate in a health plan where your employer

automatically applies the value of unused sick leave to the

cost of your continuing participation in the health plan

(and you do not have the option to receive cash), do not

include the value of the unused sick leave in gross in-

come. You cannot include this cost of continuing partici-

pation in that health plan as a medical expense.

Insurance Premiums You Cannot Include

You cannot include premiums you pay for:

Life insurance policies,

Policies providing payment for loss of earnings,

Policies for loss of life, limb, sight, etc.,

Policies that pay you a guaranteed amount each week

for a stated number of weeks if you are hospitalized

for sickness or injury,

The part of your car insurance that provides medical

insurance coverage for all persons injured in or by

your car because the part of the premium providing in-

surance for you, your spouse, and your dependents is

not stated separately from the part of the premium

providing insurance for medical care for others, or

Health or long-term care insurance if you elected to

pay these premiums with tax-free distributions from a

retirement plan made directly to the insurance pro-

vider and these distributions would otherwise have

been included in income.

Taxes imposed by any governmental unit, such as Medi-

care taxes, are not insurance premiums.

Coverage for nondependents. Generally, you cannot

deduct any additional premium you pay as the result of in-

cluding on your policy someone who is not your spouse or

dependent, even if that person is your child under age 27.

However, you can deduct the additional premium if that

person is:

Your child whom you do not claim as a dependent be-

cause of the rules for children of divorced or separa-

ted parents,

Any person you could have claimed as a dependent

on your return except that person received $3,800 or

more of gross income or filed a joint return, or

Any person you could have claimed as a dependent

except that you, or your spouse if filing jointly, can be

claimed as a dependent on someone else's 2012 re-

turn.

Also, if you had family coverage when you added this indi-

vidual to your policy and your premiums did not increase,

you can enter on line 1 the full amount of your medical and

dental insurance premiums.

Intellectually and Developmentally

Disabled, Special Home for

You can include in medical expenses the cost of keeping

a person who is intellectually and developmentally disa-

bled in a special home, not the home of a relative, on the

recommendation of a psychiatrist to help the person ad-

just from life in a mental hospital to community living.

Laboratory Fees

You can include in medical expenses the amounts you

pay for laboratory fees that are part of medical care.

Lactation Expenses

See Breast Pumps and Supplies, earlier.

Lead-Based Paint Removal

You can include in medical expenses the cost of removing

lead-based paints from surfaces in your home to prevent a

child who has or had lead poisoning from eating the paint.

Page 10 Publication 502 (2012)

Page 11 of 35 Fileid: Publications/P502/2012/A/XML/Cycle08/source 10:50 - 10-Dec-2012

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

These surfaces must be in poor repair (peeling or crack-

ing) or within the child's reach. The cost of repainting the

scraped area is not a medical expense.

If, instead of removing the paint, you cover the area

with wallboard or paneling, treat these items as capital ex-

penses. See Capital Expenses, earlier. Do not include the

cost of painting the wallboard as a medical expense.

Learning Disability

See Special Education, later.

Legal Fees

You can include in medical expenses legal fees you paid

that are necessary to authorize treatment for mental ill-

ness. However, you cannot include in medical expenses

fees for the management of a guardianship estate, fees

for conducting the affairs of the person being treated, or

other fees that are not necessary for medical care.

Lifetime Care—Advance Payments

You can include in medical expenses a part of a life-care

fee or “founder's fee” you pay either monthly or as a lump

sum under an agreement with a retirement home. The part

of the payment you include is the amount properly alloca-

ble to medical care. The agreement must require that you

pay a specific fee as a condition for the home's promise to

provide lifetime care that includes medical care. You can

use a statement from the retirement home to prove the

amount properly allocable to medical care. The statement

must be based either on the home's prior experience or on

information from a comparable home.

Dependents with disabilities. You can include in medi-

cal expenses advance payments to a private institution for

lifetime care, treatment, and training of your physically or

mentally impaired child upon your death or when you be-

come unable to provide care. The payments must be a

condition for the institution's future acceptance of your

child and must not be refundable.

Payments for future medical care. Generally, you can-

not include in medical expenses current payments for

medical care (including medical insurance) to be provided

substantially beyond the end of the year. This rule does

not apply in situations where the future care is purchased

in connection with obtaining lifetime care of the type de-

scribed earlier.

Lodging

You can include in medical expenses the cost of meals

and lodging at a hospital or similar institution if a principal

reason for being there is to receive medical care. See

Nursing Home, later.

You may be able to include in medical expenses the

cost of lodging not provided in a hospital or similar institu-

tion. You can include the cost of such lodging while away

from home if all of the following requirements are met.

1. The lodging is primarily for and essential to medical

care.

2. The medical care is provided by a doctor in a licensed

hospital or in a medical care facility related to, or the

equivalent of, a licensed hospital.

3. The lodging is not lavish or extravagant under the cir-

cumstances.

4. There is no significant element of personal pleasure,

recreation, or vacation in the travel away from home.

The amount you include in medical expenses for lodg-

ing cannot be more than $50 for each night for each per-

son. You can include lodging for a person traveling with

the person receiving the medical care. For example, if a

parent is traveling with a sick child, up to $100 per night

can be included as a medical expense for lodging. Meals

are not included.

Do not include the cost of lodging while away from

home for medical treatment if that treatment is not re-

ceived from a doctor in a licensed hospital or in a medical

care facility related to, or the equivalent of, a licensed hos-

pital or if that lodging is not primarily for or essential to the

medical care received.

Long-Term Care

You can include in medical expenses amounts paid for

qualified long-term care services and premiums paid for

qualified long-term care insurance contracts.

Qualified Long-Term Care Services

Qualified long-term care services are necessary diagnos-

tic, preventive, therapeutic, curing, treating, mitigating, re-

habilitative services, and maintenance and personal care

services (defined later) that are:

1. Required by a chronically ill individual, and

2. Provided pursuant to a plan of care prescribed by a li-

censed health care practitioner.

Chronically ill individual. An individual is chronically ill

if, within the previous 12 months, a licensed health care

practitioner has certified that the individual meets either of

the following descriptions.

1. He or she is unable to perform at least two activities of

daily living without substantial assistance from an-

other individual for at least 90 days, due to a loss of

functional capacity. Activities of daily living are eating,

toileting, transferring, bathing, dressing, and conti-

nence.

2. He or she requires substantial supervision to be pro-

tected from threats to health and safety due to severe

cognitive impairment.

Publication 502 (2012) Page 11

Page 12 of 35 Fileid: Publications/P502/2012/A/XML/Cycle08/source 10:50 - 10-Dec-2012

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Maintenance and personal care services. Mainte-

nance or personal care services is care which has as its

primary purpose the providing of a chronically ill individual

with needed assistance with his or her disabilities (includ-

ing protection from threats to health and safety due to se-

vere cognitive impairment).

Qualified Long-Term Care Insurance

Contracts

A qualified long-term care insurance contract is an insur-

ance contract that provides only coverage of qualified

long-term care services. The contract must:

1. Be guaranteed renewable,

2. Not provide for a cash surrender value or other money

that can be paid, assigned, pledged, or borrowed,

3. Provide that refunds, other than refunds on the death

of the insured or complete surrender or cancellation

of the contract, and dividends under the contract must

be used only to reduce future premiums or increase

future benefits, and

4. Generally not pay or reimburse expenses incurred for

services or items that would be reimbursed under

Medicare, except where Medicare is a secondary

payer, or the contract makes per diem or other peri-

odic payments without regard to expenses.

The amount of qualified long-term care premiums you

can include is limited. You can include the following as

medical expenses on Schedule A (Form 1040).

1. Qualified long-term care premiums up to the amounts

shown below.

a. Age 40 or under – $350.

b. Age 41 to 50 – $660.

c. Age 51 to 60 – $1,310.

d. Age 61 to 70 – $3,500.

e. Age 71 or over – $4,370.

2. Unreimbursed expenses for qualified long-term care

services.

Note. The limit on premiums is for each person.

Also, if you are an eligible retired public safety officer,

you cannot include premiums for long-term care insurance

if you elected to pay these premiums with tax-free distribu-

tions from a qualified retirement plan made directly to the

insurance provider and these distributions would other-

wise have been included in your income.

Meals

You can include in medical expenses the cost of meals at

a hospital or similar institution if a principal reason for be-

ing there is to get medical care.

You cannot include in medical expenses the cost of

meals that are not part of inpatient care. Also see

WeightLoss Program and Nutritional Supplements, later.

Medical Conferences

You can include in medical expenses amounts paid for

admission and transportation to a medical conference if

the medical conference concerns the chronic illness of

yourself, your spouse, or your dependent. The costs of

the medical conference must be primarily for and neces-

sary to the medical care of you, your spouse, or your de-

pendent. The majority of the time spent at the conference

must be spent attending sessions on medical information.

The cost of meals and lodging while attending the

conference is not deductible as a medical ex

pense.

Medical Information Plan

You can include in medical expenses amounts paid to a

plan that keeps medical information in a computer data

bank and retrieves and furnishes the information upon re-

quest to an attending physician.

Medicines

You can include in medical expenses amounts you pay for

prescribed medicines and drugs. A prescribed drug is one

that requires a prescription by a doctor for its use by an in-

dividual. You can also include amounts you pay for insu-

lin. Except for insulin, you cannot include in medical ex-

penses amounts you pay for a drug that is not prescribed.

Imported medicines and drugs. If you imported medi-

cines or drugs from other countries, see Medicines and

Drugs From Other Countries, under What Expenses Are

Not Includible, later.

Nursing Home

You can include in medical expenses the cost of medical

care in a nursing home, home for the aged, or similar insti-

tution, for yourself, your spouse, or your dependents. This

includes the cost of meals and lodging in the home if a

principal reason for being there is to get medical care.

Do not include the cost of meals and lodging if the rea-

son for being in the home is personal. You can, however,

include in medical expenses the part of the cost that is for

medical or nursing care.

Nursing Services

You can include in medical expenses wages and other

amounts you pay for nursing services. The services need

not be performed by a nurse as long as the services are of

a kind generally performed by a nurse. This includes serv-

ices connected with caring for the patient's condition,

such as giving medication or changing dressings, as well

CAUTION

!

Page 12 Publication 502 (2012)

Page 13 of 35 Fileid: Publications/P502/2012/A/XML/Cycle08/source 10:50 - 10-Dec-2012

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

as bathing and grooming the patient. These services can

be provided in your home or another care facility.

Generally, only the amount spent for nursing services is

a medical expense. If the attendant also provides per-

sonal and household services, amounts paid to the at-

tendant must be divided between the time spent perform-

ing household and personal services and the time spent

for nursing services. For example, because of your medi-

cal condition you pay a visiting nurse $300 per week for

medical and household services. She spends 10% of her

time doing household services such as washing dishes

and laundry. You can include only $270 per week as med-

ical expenses. The $30 (10% × $300) allocated to house-

hold services cannot be included. However, certain main-

tenance or personal care services provided for qualified

long-term care can be included in medical expenses. See

Maintenance and personal care services under

LongTerm Care, earlier. Additionally, certain expenses

for household services or for the care of a qualifying indi-

vidual incurred to allow you to work may qualify for the

child and dependent care credit. See Publication 503,

Child and Dependent Care Expenses.

You can also include in medical expenses part of the

amount you pay for that attendant's meals. Divide the food

expense among the household members to find the cost

of the attendant's food. Then divide that cost in the same

manner as in the preceding paragraph. If you had to pay

additional amounts for household upkeep because of the

attendant, you can include the extra amounts with your

medical expenses. This includes extra rent or utilities you

pay because you moved to a larger apartment to provide

space for the attendant.

Employment taxes. You can include as a medical ex-

pense social security tax, FUTA, Medicare tax, and state

employment taxes you pay for an attendant who provides

medical care. If the attendant also provides personal and

household services, you can include as a medical ex-

pense only the amount of employment taxes paid for med-

ical services as explained earlier. For information on em-

ployment tax responsibilities of household employers, see

Publication 926, Household Employer's Tax Guide.

Operations

You can include in medical expenses amounts you pay for

legal operations that are not for unnecessary cosmetic

surgery. See Cosmetic Surgery under What Expenses

Are Not Includible, later.

Optometrist

See Eyeglasses, earlier.

Organ Donors

See Transplants, later.

Osteopath

You can include in medical expenses amounts you pay to

an osteopath for medical care.

Oxygen

You can include in medical expenses amounts you pay for

oxygen and oxygen equipment to relieve breathing prob-

lems caused by a medical condition.

Physical Examination

You can include in medical expenses the amount you pay

for an annual physical examination and diagnostic tests

by a physician. You do not have to be ill at the time of the

examination.

Example. Beth goes to see Dr. Hayes for her annual

check-up. Dr. Hayes does a physical examination and has

some lab tests done. Beth can include the cost of the

exam and lab tests in her medical expenses, if her insur-

ance does not cover the cost.

Pregnancy Test Kit

You can include in medical expenses the amount you pay

to purchase a pregnancy test kit to determine if you are

pregnant.

Prosthesis

See Artificial Limb and Breast Reconstruction Surgery,

earlier.

Psychiatric Care

You can include in medical expenses amounts you pay for

psychiatric care. This includes the cost of supporting a

mentally ill dependent at a specially equipped medical

center where the dependent receives medical care. See

Psychoanalysis, next, and Transportation, later.

Psychoanalysis

You can include in medical expenses payments for psy-

choanalysis. However, you cannot include payments for

psychoanalysis that is part of required training to be a psy-

choanalyst.

Psychologist

You can include in medical expenses amounts you pay to

a psychologist for medical care.

Special Education

You can include in medical expenses fees you pay on a

doctor's recommendation for a child's tutoring by a

teacher who is specially trained and qualified to work with

Publication 502 (2012) Page 13

Page 14 of 35 Fileid: Publications/P502/2012/A/XML/Cycle08/source 10:50 - 10-Dec-2012

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

children who have learning disabilities caused by mental

or physical impairments, including nervous system disor-

ders.

You can include in medical expenses the cost (tuition,

meals, and lodging) of attending a school that furnishes

special education to help a child to overcome learning dis-

abilities. A doctor must recommend that the child attend

the school. Overcoming the learning disabilities must be a

principal reason for attending the school, and any ordinary

education received must be incidental to the special edu-

cation provided. Special education includes:

Teaching Braille to a visually impaired person,

Teaching lip reading to a hearing disabled person, or

Giving remedial language training to correct a condi-

tion caused by a birth defect.

You cannot include in medical expenses the cost of

sending a problem child to a school where the course of

study and the disciplinary methods have a beneficial ef-

fect on the child's attitude if the availability of medical care

in the school is not a principal reason for sending the stu-

dent there.

Sterilization

You can include in medical expenses the cost of a legal

sterilization (a legally performed operation to make a per-

son unable to have children). Also see Vasectomy, later.

Stop-Smoking Programs

You can include in medical expenses amounts you pay for

a program to stop smoking. However, you cannot include

in medical expenses amounts you pay for drugs that do

not require a prescription, such as nicotine gum or

patches, that are designed to help stop smoking.

Surgery

See Operations, earlier.

Telephone

You can include in medical expenses the cost of special

telephone equipment that lets a person with a hearing or

speech disability communicate over a regular telephone.

This includes teletypewriter (TTY) and telecommunica-

tions device for the deaf (TDD) equipment. You can also

include the cost of repairing the equipment.

Television

You can include in medical expenses the cost of equip-

ment that displays the audio part of television programs as

subtitles for persons with a hearing disability. This may be

the cost of an adapter that attaches to a regular set. It also

may be the part of the cost of a specially equipped televi-

sion that exceeds the cost of the same model regular

television set.

Therapy

You can include in medical expenses amounts you pay for

therapy received as medical treatment.

Transplants

You can include in medical expenses amounts paid for

medical care you receive because you are a donor or a

possible donor of a kidney or other organ. This includes

transportation.

You can include any expenses you pay for the medical

care of a donor in connection with the donating of an or-

gan. This includes transportation.

Transportation

You can include in medical expenses amounts paid for

transportation primarily for, and essential to, medical care.

You can include:

Bus, taxi, train, or plane fares or ambulance service,

Transportation expenses of a parent who must go with

a child who needs medical care,

Transportation expenses of a nurse or other person

who can give injections, medications, or other treat-

ment required by a patient who is traveling to get med-

ical care and is unable to travel alone, and

Transportation expenses for regular visits to see a

mentally ill dependent, if these visits are recommen-

ded as a part of treatment.

Car expenses. You can include out-of-pocket expenses,

such as the cost of gas and oil, when you use a car for

medical reasons. You cannot include depreciation, insur-

ance, general repair, or maintenance expenses.

If you do not want to use your actual expenses for

2012, you can use the standard medical mileage rate of

23 cents a mile.

You can also include parking fees and tolls. You can

add these fees and tolls to your medical expenses

whether you use actual expenses or the standard mileage

rate.

Example. In 2012, Bill Jones drove 2,800 miles for

medical reasons. He spent $500 for gas, $30 for oil, and

$100 for tolls and parking. He wants to figure the amount

he can include in medical expenses both ways to see

which gives him the greater deduction.

He figures the actual expenses first. He adds the $500

for gas, the $30 for oil, and the $100 for tolls and parking

for a total of $630.

He then figures the standard mileage amount. He multi-

plies 2,800 miles by 23 cents a mile for a total of $644. He

then adds the $100 tolls and parking for a total of $744.

Bill includes the $744 of car expenses with his other

medical expenses for the year because the $744 is more

than the $630 he figured using actual expenses.

Page 14 Publication 502 (2012)

Page 15 of 35 Fileid: Publications/P502/2012/A/XML/Cycle08/source 10:50 - 10-Dec-2012

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Transportation expenses you cannot include. You

cannot include in medical expenses the cost of transpor-

tation in the following situations.

Going to and from work, even if your condition re-

quires an unusual means of transportation.

Travel for purely personal reasons to another city for

an operation or other medical care.

Travel that is merely for the general improvement of

one's health.

The costs of operating a specially equipped car for

other than medical reasons.

Trips

You can include in medical expenses amounts you pay for

transportation to another city if the trip is primarily for, and

essential to, receiving medical services. You may be able

to include up to $50 for each night for each person. You

can include lodging for a person traveling with the person

receiving the medical care. For example, if a parent is

traveling with a sick child, up to $100 per night can be in-

cluded as a medical expense for lodging. Meals are not

included. See Lodging, earlier.

You cannot include in medical expenses a trip or vaca-

tion taken merely for a change in environment, improve-

ment of morale, or general improvement of health, even if

the trip is made on the advice of a doctor. However, see

Medical Conferences, earlier.

Tuition

Under special circumstances, you can include charges for

tuition in medical expenses. See Special Education, ear-

lier.

You can include charges for a health plan included in a

lump-sum tuition fee if the charges are separately stated

or can easily be obtained from the school.

Vasectomy

You can include in medical expenses the amount you pay

for a vasectomy.

Vision Correction Surgery

See Eye Surgery, earlier.

Weight-Loss Program

You can include in medical expenses amounts you pay to

lose weight if it is a treatment for a specific disease diag-

nosed by a physician (such as obesity, hypertension, or

heart disease). This includes fees you pay for member-

ship in a weight reduction group as well as fees for attend-

ance at periodic meetings. You cannot include member-

ship dues in a gym, health club, or spa as medical

expenses, but you can include separate fees charged

there for weight loss activities.

You cannot include the cost of diet food or beverages

in medical expenses because the diet food and bever-

ages substitute for what is normally consumed to satisfy

nutritional needs. You can include the cost of special food

in medical expenses only if:

1. The food does not satisfy normal nutritional needs,

2. The food alleviates or treats an illness, and

3. The need for the food is substantiated by a physician.

The amount you can include in medical expenses is limi-

ted to the amount by which the cost of the special food ex-

ceeds the cost of a normal diet. See also WeightLoss

Program under What Expenses Are Not Includible, later.

Wheelchair

You can include in medical expenses amounts you pay for

an autoette or a wheelchair used mainly for the relief of

sickness or disability, and not just to provide transporta-

tion to and from work. The cost of operating and maintain-

ing the autoette or wheelchair is also a medical expense.

Wig

You can include in medical expenses the cost of a wig

purchased upon the advice of a physician for the mental

health of a patient who has lost all of his or her hair from

disease.

X-ray

You can include in medical expenses amounts you pay for

X-rays for medical reasons.

What Expenses Are Not

Includible?

Following is a list of some items that you cannot include in

figuring your medical expense deduction. The items are

listed in alphabetical order.

Baby Sitting, Childcare, and Nursing

Services for a Normal, Healthy Baby

You cannot include in medical expenses amounts you pay

for the care of children, even if the expenses enable you,

your spouse, or your dependent to get medical or dental

treatment. Also, any expense allowed as a childcare credit

cannot be treated as an expense paid for medical care.

Controlled Substances

You cannot include in medical expenses amounts you pay

for controlled substances (such as marijuana, laetrile,

etc.). Such substances may be legalized by state law.

However, they are in violation of federal law and cannot

be included in medical expenses.

Publication 502 (2012) Page 15

Page 16 of 35 Fileid: Publications/P502/2012/A/XML/Cycle08/source 10:50 - 10-Dec-2012

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Cosmetic Surgery

Generally, you cannot include in medical expenses the

amount you pay for unnecessary cosmetic surgery. This

includes any procedure that is directed at improving the

patient's appearance and does not meaningfully promote

the proper function of the body or prevent or treat illness

or disease. You generally cannot include in medical ex-

penses the amount you pay for procedures such as face

lifts, hair transplants, hair removal (electrolysis), and lipo-

suction.

You can include in medical expenses the amount you

pay for cosmetic surgery if it is necessary to improve a de-

formity arising from, or directly related to, a congenital ab-

normality, a personal injury resulting from an accident or

trauma, or a disfiguring disease.

Example. An individual undergoes surgery that re-

moves a breast as part of treatment for cancer. She pays

a surgeon to reconstruct the breast. The surgery to recon-

struct the breast corrects a deformity directly related to the

disease. The cost of the surgery is includible in her medi-

cal expenses.

Dancing Lessons

You cannot include in medical expenses the cost of danc-

ing lessons, swimming lessons, etc., even if they are rec-

ommended by a doctor, if they are only for the improve-

ment of general health.

Diaper Service

You cannot include in medical expenses the amount you

pay for diapers or diaper services, unless they are needed

to relieve the effects of a particular disease.

Electrolysis or Hair Removal

See Cosmetic Surgery, earlier.

Flexible Spending Account

You cannot include in medical expenses amounts for

which you are fully reimbursed by your flexible spending