KE Tax Report__230310 MM900 KPMG Econtech Efficiency Of Taxes Report

User Manual: MM900

Open the PDF directly: View PDF ![]() .

.

Page Count: 178 [warning: Documents this large are best viewed by clicking the View PDF Link!]

KPMG Econtech

CGE Analysis of

the Current

Australian Tax

System

Final Report

26 March 2010

Department of the Treasury

The Excess Burden of Australian Taxes

March 2010

ABCD

i

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

Inherent Limitations

This report has been prepared as outlined in the Engagement Letter from KPMG Econtech to

Commonwealth Treasury dated 6 February 2009. The services provided in connection with this

engagement comprise an advisory engagement which is not subject to Australian Auditing Standards or

Australian Standards on Review or Assurance Engagements, and consequently no opinions or

conclusions intended to convey assurance have been expressed.

No warranty of completeness, accuracy or reliability is given in relation to the statements and

representations made by, and the information and documentation provided by Commonwealth Treasury

as part of the process.

KPMG Econtech have indicated within this report the sources of the information provided. We have not

sought to independently verify those sources unless otherwise noted within the report.

KPMG Econtech is under no obligation in any circumstance to update this report, in either oral or

written form, for events occurring after the report has been issued in final form.

The findings in this report are subject to unavoidable statistical variation. While all care has been taken

to ensure that the statistical variation is kept to a minimum, care should be taken whenever using this

information. This report only takes into account information available to KPMG Econtech up to the date

of this report and so its findings may be affected by new information. Should you require clarification of

any material, please contact us.

The findings in this report have been formed on the above basis.

Third Party Reliance

This report is solely for the purpose set out in contract and is for Commonwealth Treasury’s information.

This report has been prepared at the request of Commonwealth Treasury in accordance with the terms of

KPMG Econtech’s Engagement letter dated 6 February 2009. Other than our responsibility to

Commonwealth Treasury, neither KPMG Econtech nor any member or employee of KPMG Econtech

undertakes responsibility arising in any way from reliance placed by a third party on this report. Any

reliance placed is that party’s sole responsibility.

Forecasting Disclaimer

In the course of our work, projections have been prepared on the basis of assumptions and methodology

which have been described in our report. It is possible that some of the assumptions underlying our

projections may not materialise. Nevertheless, we have applied our professional judgement in making

these assumptions, such that they constitute an understandable basis for estimates and projections.

Beyond this, to the extent that certain assumptions do not materialise, then you will appreciate that our

estimates and projections of achievable results will vary.

ii

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

CONTENTS

Executive Summary 1

1 Introduction 11

1.1 Overview of the Australian Tax System 12

1.2 The Structure of this Report 13

2 Key Literature 14

3 The Cost and Incidence of Taxes 17

3.1 The Excess Burden of Taxation 18

3.2 Using MM900 to Estimate the Excess Burden of Australian Taxes 20

3.3 The Incidence of Taxes 22

3.4 Using MM900 to Estimate the Incidence of Australian Taxes 24

4 The MM900 Model 28

4.1 Over-arching Assumptions 29

4.2 Households 31

4.2.1 Labour Supply versus Leisure 31

4.2.2 Consumption versus Saving 32

4.2.3 Pattern of Consumption 32

4.3 Producers 33

4.3.1 Low and High Skilled Labour 33

4.3.2 Structures and Other Capital 34

4.3.3 Land 35

4.3.4 Natural Resources and Other Generators of Economic Rents 35

4.4 Government Sector 37

4.5 Foreign Sector 38

5 Results 40

5.1 Summary of Excess Burden Results 44

5.2 Summary of Incidence Results 47

5.3 Detailed results 51

5.3.1 Petroleum Resource Rent Tax 51

5.3.2 Land tax and Municipal rates 52

5.3.3 Company Income Tax 54

5.3.4 Resource Royalties and Crude Oil Excise 58

5.3.5 Labour income tax 59

5.3.6 Payroll tax 62

5.3.7 GST 65

5.3.8 Tobacco Excise 68

5.3.9 Alcohol taxes 69

5.3.10 Import duties 71

5.3.11 Luxury Car Tax 72

5.3.12 Fuel excise 73

5.3.13 Motor Vehicle taxes 74

5.3.14 Conveyancing duties 77

5.3.15 Stamp duties other than real property 79

iii

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

5.3.16 Insurance taxes 80

5.3.17 Gambling taxes 81

6 References 83

Appendix A – Detailed Methodology by Individual Tax 85

A.1 Petroleum Resource Rent Tax 85

A.2 Land Taxes and Municipal Rates 87

A.3 Company Income Tax 90

A.4 Crude Oil Excise and Resource Royalties 95

A.5 Labour income tax 97

A.6 Payroll tax 105

A.7 GST 107

A.8 Tobacco Excise 109

A.9 Alcohol Taxes 111

A.10 Import Duties 114

A.11 Luxury Car Tax 115

A.12 Fuel Excise 119

A.13 Motor Vehicle Taxes 121

A.14 Conveyancing Stamp Duties 124

A.15 Stamp Duties Other than on Real Property 127

A.16 Insurance Taxes 129

A.17 Gambling Taxes 131

Appendix B – Modelling Taxes with Partial Coverage 133

Appendix C – Industry Impacts 134

Appendix D – MM900 Parameters 137

Department of the Treasury

The Excess Burden of Australian Taxes

March 2010

ABCD

1

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

Executive Summary

Background

In May 2008, the Treasurer announced an extensive review into Australia’s tax and transfer

system (the Henry Review). Governments aim to raise tax revenue in a way that meets their

funding needs, while paying regard to the three principles of good tax design:

• simplicity (keeping administration and compliance costs low);

• equity (or fairness, which is partly a subjective judgement); and

• economic efficiency.

KPMG Econtech was commissioned to model the existing tax system against the third aim of

economic efficiency, although the modelling also provides some insights into equity. Most

taxes result in losses of economic efficiency by distorting economic behaviour. For example,

most taxes reduce incentives to work or invest, or distort consumption patterns. This leads to

losses in consumer welfare that can be compared to the amount of revenue that is being raised.

An efficient tax system relies on taxes that result in relatively low losses in consumer welfare

per dollar of revenue raised (excess burden).

With this in mind, the Treasury commissioned KPMG Econtech to undertake a rigorous

economic analysis of the economic costs of the Australian tax system. For this, KPMG

Econtech has estimated the economic inefficiencies, or the excess burdens, that arise from

Australia’s major federal, state and local taxes. This report also examines the economic

incidence of each tax, or how the final burden is shared between various sources of real income

(labour, capital, land rents and other economic rents).

The results for each tax have been estimated using KPMG Econtech’s computable general

equilibrium (CGE) model, MM900. MM900 has been constructed by further developing our

existing MM600 model specifically for this study. MM900 goes well beyond previous

Australian modelling in capturing the economic effects of the tax system on the Australian

economy. It distinguishes 19 different major taxes at the Federal, State and Local levels. For

each tax, it identifies the true tax base as closely as possible, and aims to capture the main

behavioural responses to the tax’s imposition. The modelling also allows for certain negative

externalities in consumption that may justify certain specific taxes.

MM900 contains a fine level of detail. For example, in MM900 the economy produces 889

different products, which represents eight times as much product detail as other comparable

models. This allows the model to more accurately capture the application of certain product-

based taxes. For example, MM900 treats beer, wine and spirits as separate substitutable

products within one broad group. Less disaggregated models aggregate all alcohol products

together, and therefore miss the excess burdens that arise from taxing closely substitutable

alcoholic beverages at different rates.

Another example of the fine level of detail in MM900 is that each of the 109 industries uses up

to six different primary factors (or types of labour, capital and fixed factors). The different

fixed factors include land and natural resources, allowing for much more robust modelling of

the effects of taxes based on the value of land or the value of natural resource use.

Department of the Treasury

The Excess Burden of Australian Taxes

March 2010

ABCD

2

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

In addition, in comparison to earlier studies, this analysis incorporates a more comprehensive

analysis of the behavioural responses to each tax. In MM900, taxes can cause households to

change their supply of labour and their levels and patterns of spending. Taxes can cause

businesses to change their choices between the six primary factors of production, affecting

employment, investment and valuations of land and natural resources. Finally, taxes can affect

the propensity to import and export each of the model’s 889 products.

These behavioural responses to taxes, by impairing the functioning of the economy, can reduce

consumer welfare. In MM900, these welfare losses are captured appropriately by using a utility

function in which households derive welfare or utility from leisure, saving and consumption of

products, and then deriving all household behaviour from that same utility function. Other

comparable models include more ad hoc elements in modelling household behaviour.

This modelling approach leads to a more robust analysis of the economic inefficiency of

particular taxes as well as their economic incidence. .

Key Results on Efficiency

This analysis shows that some of Australia’s taxes are much more inefficient than others. This

variation is explained mainly by two economic principles. The mobility principle recognises

that the excess burden of a tax is higher, the higher the mobility of its tax base. When a tax is

applied to a highly mobile tax base, that tax base is likely to shrink, distorting economic activity.

The narrowness principle recognises that the excess burden of a tax is likely to be higher, the

narrower the tax base. A narrow tax base may make it possible to respond to a tax by shifting to

untaxed close substitutes. Such shifts add to economic inefficiency and reduce the revenue

yield. Taxes on goods and services with consumption externalities are exceptions to this. For

example, although the base of the tobacco excise is narrow, shifting consumption away from

tobacco entails a social benefit, so tobacco excise is expected to have a low excess burden.

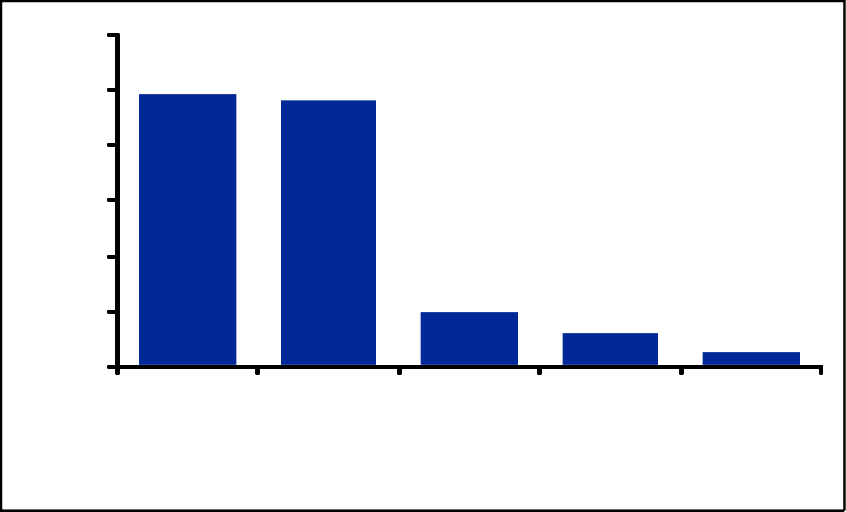

Chart A illustrates the variations in inefficiency between taxes using a selection of six out of the

19 taxes that are modelled. The inefficiency of a tax is measured by its marginal excess burden.

This refers to the effects of a small increase in a tax from its existing level, and is calculated as

the ratio of the loss in consumer welfare relative to the net gain in government revenue. Put

more simply, it is the economic harm expressed in cents per dollar of additional revenue.

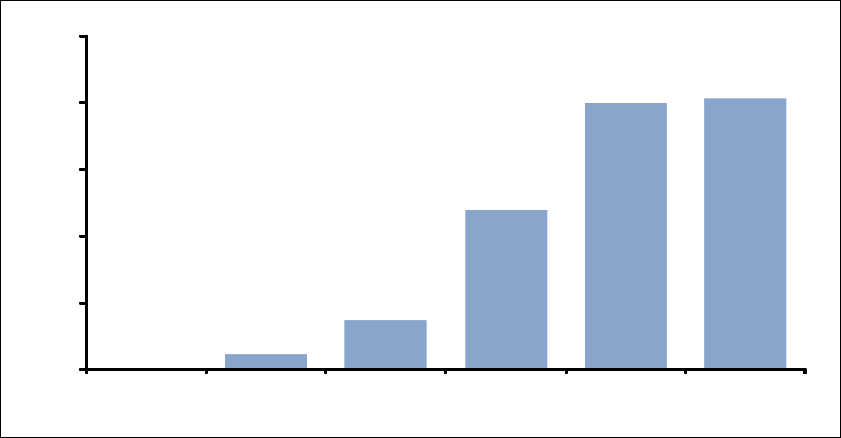

The mobility principle is clearly reflected in the modelling results. Petroleum Resource Rent

Tax (PRRT) is modelled to have a marginal excess burden of zero, because it is applied to a tax

base that is assumed to be completely immobile – oil resources. Similarly, municipal rates have

a marginal excess burden of only two cents of welfare loss per additional dollar of revenue

raised because they are applied to land, which is also completely immobile. Municipal rates

only generate an excess burden to the extent that they are applied non-uniformly to different

land users, distorting the pattern of land use.

At the other extreme, company income tax is modelled to have a high marginal excess burden of

40 cents in the dollar of additional revenue, because it is applied to capital, which is highly

mobile. This high mobility is generated by the international competition for funds.

The economic incidence of the remaining three taxes shown in Chart A falls mainly on labour.

Labour has an intermediate level of mobility, and so under the mobility principle these taxes

Department of the Treasury

The Excess Burden of Australian Taxes

March 2010

ABCD

3

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

would be expected to have medium excess burdens. However, the narrowness principle leads

their excess burdens to vary.

Payroll tax has a relatively narrow base because, under the small business exemption provision,

it applies to only around one-half of labour income. This provision provides an exemption from

payroll tax on the first tranche of labour income for small and large business alike, undermining

revenue raising, while doing little to reduce disincentive effects. This narrowness of the payroll

tax base leads to a high marginal excess burden of 41 cents in the dollar.

Chart A Marginal Excess Burden of Major Australian Taxes

(cents of consumer welfare loss per dollar of additional revenue)

0

2

8

24

40 41

0

10

20

30

40

50

PRRT Municipal rates GST Labour income

tax

Corporate

income tax

Payroll tax

Source: KPMG Econtech estimates from MM900

Personal income tax (as applied to labour income) also narrows the tax base, although to a lesser

degree. The progressive rate structure provides an exemption from tax on income earned up to

the tax-free threshold, and beyond that lower marginal tax rates are applied at lower incomes

than at higher incomes. This narrowing of the tax base (compared with a flat rate tax) leads to a

medium marginal excess burden of 24 cents in the dollar of revenue. Of course there are

compelling equity reasons for the progressive nature of the personal income tax scale, but its

efficiency implications should still be understood.

The GST can also be analysed alongside taxes on labour income. Taxes on labour income and

GST both act as a disincentive to supply labour, by reducing the purchasing power of the

additional pay earned from a given amount of additional labour. Labour income tax does this by

removing tax from the additional pay, while GST does this by reducing the purchasing power of

that pay through raising consumer prices. The GST has a relatively broad base, applying to

close to 70 per cent of consumer spending. This breadth helps keep its marginal excess burden

low, at 8 cents per dollar of additional revenue raised. Also contributing to this favourable

result is the gain in the terms-of-trade associated with applying GST to some expenditures of

international tourists.

Department of the Treasury

The Excess Burden of Australian Taxes

March 2010

ABCD

4

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

These results are closely in line with those found by Johansson et al. in a 2008 study for the

OECD. They used both theory and empirical evidence to conclude that recurrent taxes on

immovable property (particularly residential property) are the “least distortive tax instrument in

terms of reducing long-run GDP per capita” (Johansson et al., 2008, p7). Broad based

consumption taxes, such as the GST, are found to be the second least distortive, followed by

personal income taxes and then corporate income taxes. This is the same as our ranking implicit

in Chart A.

Table A below presents more detail on the relative efficiency of each of Australia’s taxes. It

presents the marginal excess burdens (MEB) and average excess burdens (AEB) for each of the

taxes modelled for this study.

As noted above, the marginal excess burden is the economic harm from a small increase in the

tax, expressed in cents per dollar of additional revenue. The average excess burden is a similar

measure, being the economic harm from introducing the whole tax, expressed in cents per dollar

of additional revenue. The marginal excess burden is useful for considering the impact of small

changes in the tax, while the average excess burden is useful for considering the impact of

abolishing the tax.

Department of the Treasury

The Excess Burden of Australian Taxes

March 2010

ABCD

5

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

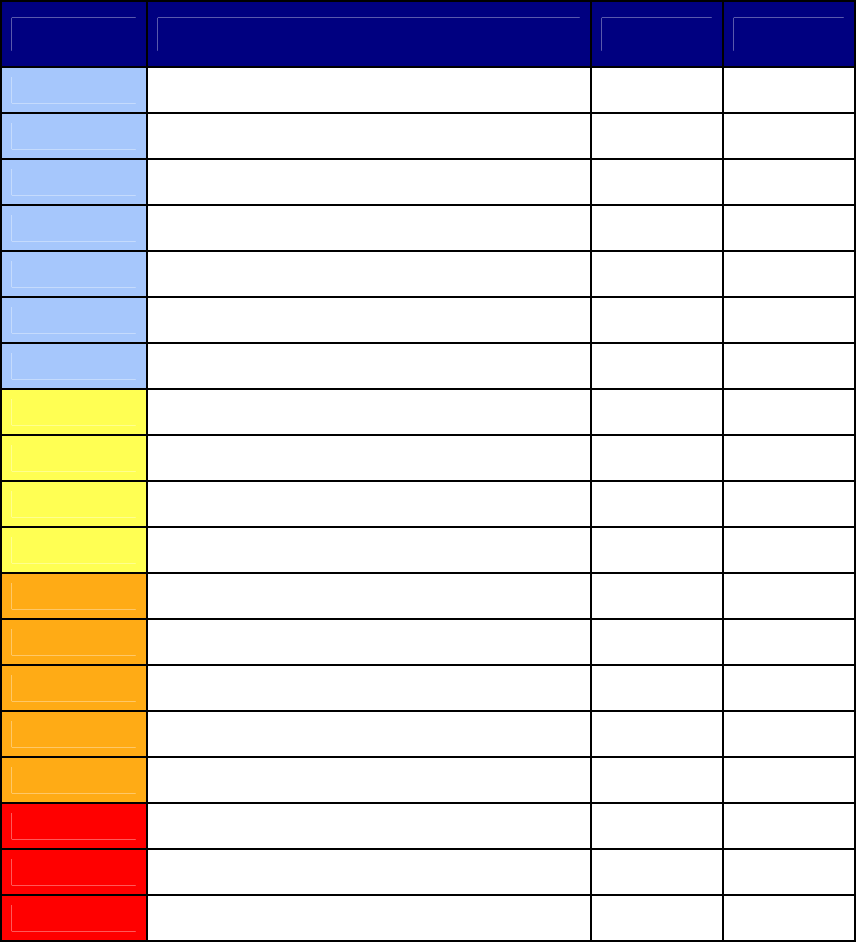

Table A: Marginal and average excess burdens of Australian taxes

(cents of consumer welfare per dollar of revenue)

Rating Tax MEB AEB

Low Tobacco excise

a -8 -23

Low Import duties

b -3 -7

Low Petroleum resource rent tax c 0 0

Low Municipal rates 2 1

Low GST 8 6

Low Land taxes

d 8 6

Low Alcohol excise and WET a 9 7

Medium Fuel taxes 15 10

Medium Stamp duties other than real property e 18 18

Medium Luxury car tax

f 20 9

Medium Labour income tax 24 16

High Conveyancing stamp duties g 34 31

High Motor vehicle registration h 37 32

High Motor vehicle stamp duties h, i 38 38

High Corporate income tax 40 23

High Payroll tax 41 22

Very High Insurance taxes 67 47

Very High Royalties and crude oil excise 70 50

Very High Gambling taxes j 92 54

Source: KPMG Econtech’s MM900 model estimates

Notes to Table 5.1:

a. The excess burden for tobacco excise and alcohol tax will be influenced by the assumptions for externalities

associated with tobacco and alcohol consumption.

b. The low (negative) excess burden estimate for import tariffs is an under-estimate in some contexts. It refers to the

efficiency of import tariffs post the tariff reductions scheduled for 1 January 2010. Those reductions mean that

all import tariffs will be five per cent or less, apart from a tariff of 10 per cent on clothing. These rates are below

a theoretical ‘optimal’ tariff of around 11 per cent (based on average export demand elasticities in MM900 of

around -10), so such low rates of tariff are not distorting. However, Australia has had much higher import tariffs

in the past, which were highly distorting. Further, the notion of an optimal tariff ignores the risk that other

countries will impose tariffs in retaliation, leading to welfare losses for Australia.

Department of the Treasury

The Excess Burden of Australian Taxes

March 2010

ABCD

6

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

c. The zero excess burden for the PRRT rests on the assumption that it is designed so that it only taxes the excess

profits of petroleum extractors, which they derive from access to a natural resource which is in limited supply.

d. The estimate of the excess burden for land tax does not take into account that the rate structure is progressive

because of the exemptions for land holdings under a certain threshold value and an increasing tax rate for higher

valued land holdings. Also, the data for land tax collections by industry was highly aggregated and does not

reflect the full extent of the variability of land tax paid by industry. The excess burden may therefore be an under-

estimate.

e. The excess burden estimates for stamp duties other than on real property are likely to be under-estimates because

there are a number of distortions from these stamp duties that are not readily amenable to CGE modelling. For

example, these stamp duties may reduce the frequency of transactions.

f. The excess burden estimates for luxury car tax are likely to be under-estimates, because the modelling does not

capture the point that the luxury car tax distorts the choice between luxury and non-luxury cars.

g. The excess burden estimates for conveyancing duties have a downward bias because there are a number of

distortions from conveyancing duties that are not readily amenable to CGE modelling, such as the distortion

between renting and buying housing.

h. The excess burdens for motor vehicle registration and motor vehicle stamp duties are only for the proportion of

those taxes paid by businesses. This is because motor vehicle taxes paid by households do not appear in input-

output tables used to construct the model. The impact that this has on the size of the excess burden is ambiguous.

i. The excess burden estimates of motor vehicle stamp duties are likely to be under-estimates because there are a

number of distortions from motor vehicle stamp duties that are not readily amenable to CGE modelling. For

example, motor vehicle stamp duties may lead to less frequent motor vehicle transactions.

j. The excess burden estimates for gambling taxes are likely to be over-estimates if there are negative externalities of

gambling, which have not been taken into account.

k. The excess burden of state taxes (excluding land tax and resource royalties) have a conservative bias, because any

economic cost arising from differences in tax regimes between the states has not been taken account of in the

modelling.

Key Results on Incidence

While excess burdens give information about the size of the overall cost to the economy of

taxation, the question of who actually bears the burden of taxes is also important. In

considering the burden of taxes, it has long been appreciated that there is an important

distinction between who has the liability to government for a tax, and therefore carries its

impact, and who bears its final burden after all economic adjustments, and therefore bears its

incidence. It is the incidence of a tax, not its impact, which matters for economic analysis, and

often they are different.

The concept of mobility of a tax base is important for determining the incidence of a tax, just as

it is important for determining the efficiency of a tax. Highly mobile primary factors of

production are unlikely to bear much of the final incidence of a tax. Rather, they are likely to

partly move to lower taxed alternative uses. This partial withdrawal of supply from the original

use generates a shortage that is likely to push up its price for that use, partly or wholly offsetting

the tax impost on the mobile factor. The incidence of the tax will then be passed on to other

factors of production. In contrast, completely immobile factors of production have no scope for

passing on taxes, so when they carry the impact of a tax, they will also bear its final incidence.

The importance of the mobility principle can be seen in Table B below, which shows the final

incidence for each of the 19 taxes under reference. The results in the table identify where most

of the incidence of each tax falls, based on model simulations. The simulations involved

abolishing a tax, and observing the impacts on consumer prices and different sources of private

Department of the Treasury

The Excess Burden of Australian Taxes

March 2010

ABCD

7

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

income. The full numerical results of the incidence analysis are contained in the main body of

the report.

Each of the columns in Table B corresponds to the different ways that the incidence of a tax can

be borne. For example, a tax may reduce the nominal income from any of the primary factors of

production: labour; land; other fixed factors; or capital. Or it may also be transmitted into

higher prices, reducing real incomes.

Table B reveals that none of the taxes have their main incidence falling on capital. This result

comes about because of the highly internationally mobile nature of capital. The mobility of

capital means that rather than accepting any burden of the tax, capital will move to alternative

uses in which the prevailing global after-tax rate of return can be obtained.

Table B shows that the final incidence of a large number of taxes falls mainly on consumer

prices. These taxes can be divided into two categories. The first is the group of taxes which are

levied on consumption directly. This group includes the GST, excise duties and taxes on fuel,

insurance and gambling. In this case, the party carrying the impact of the tax, consumers, is the

same as the party bearing its final incidence. The second category is taxes that are not levied on

consumption directly, yet have their final incidence on consumer prices. Thus, the party

carrying the impact of the tax is different to the party bearing its final incidence. These taxes

include payroll tax and business motor vehicle taxes.

Department of the Treasury

The Excess Burden of Australian Taxes

March 2010

ABCD

8

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

Table B Final Incidence or Burden of Each Major Tax (Long run)

Tax labour land other rents capital

Tobacco excise X

Import duties X

Petroleum resource rent

tax X

Municipal rates X

GST X

Land taxes X

Alcohol excise and WET X

Fuel taxes X

Stamp duties other than

real property X

Luxury car tax X

Labour income tax X

Conveyancing stamp

duties X

Motor vehicle

registration X

Motor vehicle stamp

duties X

Corporate income tax X X X

Payroll tax X

Insurance taxes X

Royalties and crude oil

excise X X

Gambling taxes X

Source: KPMG Econtech estimates from MM900

Note: The table shows the party that bears the main portion of the final incidence for each tax.

Department of the Treasury

The Excess Burden of Australian Taxes

March 2010

ABCD

9

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

Such taxes that increase consumer prices can be thought of as having their final incidence on

labour. Higher consumer prices decrease the purchasing power of the wage, reducing the return

to work. Similarly, labour income tax (i.e. personal income tax applied to labour income)

reduces the incentive to work, but through the different channel of reducing the after-tax wage.

Therefore, the results from Table B show that labour bears the main incidence for the majority

of Australian taxes – either directly through labour income or indirectly through consumer

prices.

Labour bears much of the final incidence of Australian taxes because, in contrast to capital,

labour is relatively immobile. For example, payroll tax has its impact on employers, but its final

incidence is on labour. Payroll tax increases the cost of employing labour, and since prices are

equal to the marginal cost of production, firms must pass this cost on. This will either be

through decreased nominal wages or increased consumer prices. In MM900, firms pass the cost

of payroll tax on, in the form of higher consumer prices1. This, in turn, reduces the real wage

that labour receives, and in response, labour supply falls. This fall creates a shortage of labour

that will push up the wage that employers must pay. However, households’ supply of labour

has a low responsiveness to the after-tax real wage, and so the fall in labour supply is relatively

small. Thus, the increase in the wage offsets only a small part of the initial increase in

consumer prices, and labour is left to bear the main burden of payroll tax in the form of higher

prices and lower real wages.

Land and other fixed factors also bear the burden of a number of taxes. These factors of

production are on the opposite end of the spectrum to capital, with their supply completely

fixed. When a tax is applied to any of these fixed factors, such as petroleum resource rent tax to

oil resources, municipal rates or land tax to land, the supply does not fall in response to the

lower rate of return. With no change in supply, the pre-tax price of fixed factors will not

change. Instead, the after-tax return that owners of the fixed factors are able to receive falls by

the full amount of the tax.

Company income tax has a more complex incidence. Company income tax is applied to profits,

or return to capital, land and other fixed factors, spreading its impact three ways. The fixed

supply of land and other fixed factors means that they will bear the full incidence of the

company tax that is applied to them, as described above. However, capital will not bear the

incidence of company tax that is applied to it. Instead, the supply of capital will fall until the

increase in its pre-tax return fully offsets the increase in company income tax. This process may

take several years so that returns to capital fall initially, but ultimately the higher cost of capital

will be passed on to consumers in the form of lower real wages. In MM900, this is transmitted

through higher prices2. This means that part of the final incidence of company income tax is

borne by labour. It is not borne by capital because it is highly mobile, at least in the long run.

Resource royalties and crude oil excise are applied to the output of mining industries rather than

to the profits derived from the natural resources used in mining industries. However, these

natural resources, as fixed factors, still bear some of the incidence of these taxes. In the same

way as company tax, the mobility of capital means that it will not bear the incidence of resource

1 The incidence of payroll tax is transmitted through higher prices rather than a lower nominal wage because the

nominal wage is the numeraire in MM900. However, the choice of numeraire does not affect the real outcome of the

model, which is that the real wage falls in response to a payroll tax and so labour bears the final incidence.

2 The incidence of company income tax is transmitted through higher prices rather than a lower nominal wage

because the nominal wage is the numeraire in MM900. However, the choice of numeraire does not affect the real

outcome of the model, which is that the real wage falls in response to a company income tax and so labour bears part

of the final incidence.

Department of the Treasury

The Excess Burden of Australian Taxes

March 2010

ABCD

10

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

royalties and crude oil excise. When some of the capital in mining industries is withdrawn, this

reduces the productivity of natural resources, leading to lower rents for those natural resources.

The higher cost of capital also flows through into consumer prices, lowering the real wage and

implying that labour also bears some of the incidence.

In summary, while the impacts of our taxes are widespread, most of their final incidence falls on

labour through a reduction in the real wage either directly in the case of labour income tax, or

indirectly through higher consumer prices. The remaining incidence falls on the fixed factors of

land and natural resources. However, these fixed factors are ultimately owned by households

either directly, or through the corporate veil as shareholders. So in the end consumers bear most

of the burden of the tax system.

Since consumers bear the final burden of virtually all taxes, an informed approach to tax design

should not focus superficially on who carries the initial impact. Rather it should focus on the

three principles of good tax design – efficiency (choosing taxes that keep excess burdens low –

see Table A); equity (but with judgements based on who bears the final burden of a tax – see

Table B); and simplicity.

Department of the Treasury

The Excess Burden of Australian Taxes

March 2010

ABCD

11

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

1 Introduction

In May 2008, the Treasurer announced an extensive review into Australia’s tax and transfer

system (the Henry Review). Governments aim to raise tax revenue in a way that meets their

funding needs, while paying regard to the three principles of good tax design:

• simplicity (keeping administration and compliance costs low);

• equity (or fairness, which is partly a subjective judgement); and

• economic efficiency.

KPMG Econtech was commissioned to model the existing tax system against the third aim of

economic efficiency, although the modelling also provides some insights into equity. Most

taxes result in losses of economic efficiency by distorting economic behaviour. For example,

certain taxes reduce incentives to work or invest, or distort consumption patterns. This leads to

losses in consumer welfare that can be compared to the amount of revenue that is being raised.

An efficient tax system relies on taxes that result in relatively low losses in consumer welfare

per dollar of revenue raised (excess burden).

With this in mind, the Treasury commissioned KPMG Econtech to undertake a rigorous

economic analysis of the economic costs of the Australian tax system. For this, KPMG

Econtech has estimated the economic inefficiencies, or the excess burdens, that arise from

Australia’s major federal, state and local taxes. This report also examines the economic

incidence of each tax, or where the final burden falls – which may be on consumer prices, or

various types of income (labour, capital, land rents and other economic rents).

The results for each tax have been estimated using KPMG Econtech’s computable general

equilibrium (CGE) model, MM900. MM900 has been constructed by further developing our

existing MM600 model specifically for this study. MM900 goes well beyond previous

Australian modelling in capturing the economic effects of the tax system on the Australian

economy. It does this by distinguishing 19 different major taxes at the Federal, State and Local

levels. Further, for each tax, the model identifies the true tax base as closely as possible, and

aims to capture the main behavioural responses to the tax’s imposition.

Some of the important features of MM900 are listed below.

• MM900 contains 109 industries producing 889 products. This is around eight times as

many products as other models, so that economic impacts of selective taxes on individual

products – such as fuel, alcohol, tobacco and gambling taxes – can be captured more fully.

• MM900 has a more detailed treatment of primary factors. The model recognises not only

capital and labour, but also land and natural resources as primary factors of production in

each industry. This allows for more appropriate modelling of the economic impacts of taxes

on land (land taxes and municipal rates) and taxes on natural resources (the existing

petroleum resource rent tax and other potential resource rent taxes).

• In MM900, particular attention has been paid to the structure of taxes. For example, the

modelling of the application of payroll tax to labour inputs takes into account the economic

impacts of the small business exemption. The modelling also recognises that the

progressive nature of personal income tax adds to work disincentives (while accepting the

compelling equity argument for such progressivity).

Department of the Treasury

The Excess Burden of Australian Taxes

March 2010

ABCD

12

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

• The modelling allows for negative externalities that may justify certain narrowly-based

taxes. These include negative externalities from consumption of alcohol and tobacco.

• The GST is modelled in fine detailed in MM900. That is, MM900 identifies the individual

GST treatment for each of the 889 products - taxable, GST-free or exempt.

1.1 Overview of the Australian Tax System

There are currently around 125 taxes in Australia levied at the national, state and local

government level (Treasury, 2008). These taxes have two broad aims.

• First, taxes are levied to raise government revenues to meet government spending

requirements, which is often referred to as the revenue-raising requirement.

• Second, some taxes are levied to alter the behaviour of firms and households in a welfare-

improving way. Alcohol and tobacco excises are examples of this.

The structure of the Australian tax system affects the operation of businesses, households and

governments. Therefore, Australia’s tax-transfer system forms an integral part of the economic

structure – through its influence on decisions of: saving; consuming; investing; and working.

The combined revenues of federal, state and local governments in Australia was around $350

billion in 2007/08, or more than 30 per cent of the national Gross Domestic Product (GDP).

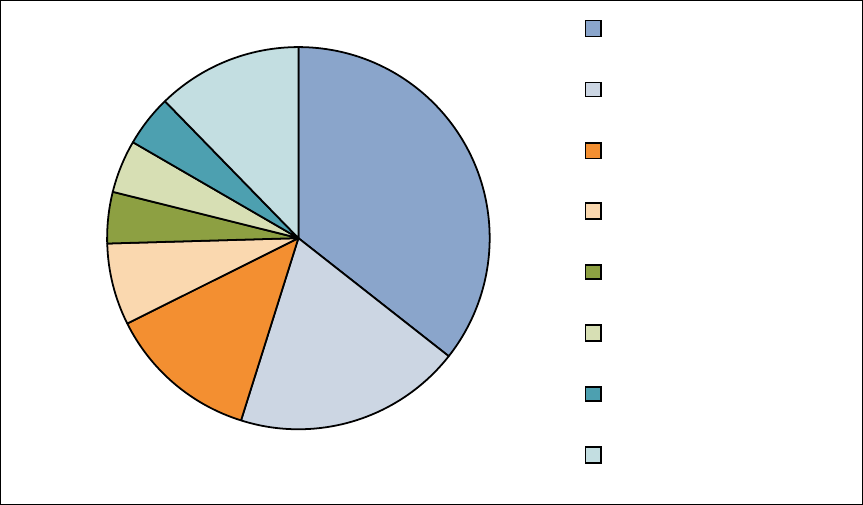

Chart 1.1 shows that Australia’s tax mix is heavily reliant on income tax revenue from both

businesses and individuals, with these taxes making up 55 per cent of total revenue. The next

most important revenue source is GST, accounting for a further 13 per cent. The efficiency of

these taxes will therefore be important for assessing the overall efficiency of our tax system.

Chart 1.1 Government Revenue Composition

36%

19%

13%

7%

5%

4%

4%

12% Personal income tax

Company income tax

GS T

Excises and levies

Payroll tax

Property taxes

Taxes on financial and

capital transactions

Other taxes

Source: ABS Taxation Revenue, Australia, 2007/08, cat. no. 5506.0, Canberra.

Department of the Treasury

The Excess Burden of Australian Taxes

March 2010

ABCD

13

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

1.2 The Structure of this Report

This report is structured as follows.

Section 2 sets the context of this report by comparing its scope and methodology to other

studies into the efficiency and incidence of taxes.

Section 3 describes costs of Australian taxes and who pays them. It explains the concepts of the

excess burden and incidence of taxation, and how they are measured in this report.

Section 4 describes the key features of MM900 that makes it the most appropriate tool to

conduct this comprehensive evaluation.

Section 5 presents the results and a discussion of the excess burdens and incidence of each tax.

Section 6 includes the references used in the report.

Appendix A provides details on the modelling methodology for each tax individually. For each

tax, this section includes:

a description of the tax;

a literature review of previous studies into the impact of this type of tax;

theoretical and modelling issues pertinent to estimating the excess burdens and incidence of

the tax; and

considering these issues, it then describes KPMG Econtech’s modelling approach.

Appendix B includes technical details on modelling taxes with partial coverage.

Appendix C provides tables identifying the industries most impacted by each tax.

Appendix D provides additional detail in relation to the MM900 model.

Department of the Treasury

The Excess Burden of Australian Taxes

March 2010

ABCD

14

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

2 Key Literature

There have been a number of theoretical and applied studies surrounding the excess burden and

incidence of different taxes. This literature analyses a broad range of taxes in a number of

countries, and helps to develop an idea of the likely excess burden of the major Australian taxes.

This study goes further than any previous study done in the Australian context. It analyses 19 of

the major Australian taxes in a consistent framework, allowing policy makers to easily compare

their economic costs. It is also a more detailed modelling than has been undertaken in the past,

with the model identifying the base of each tax to a high level of precision, and a large range of

behavioural responses are taken into account.

In a 2008 study for the OECD, Johansson et al. examine the efficiency of a number of taxes

commonly used among OECD countries. They determined a ranking of taxes that is similar to

the results of this study, although their conclusions are necessarily less specific because of the

cross-country nature of the study. They conclude from theory and empirical evidence that

recurrent taxes on immovable property (particularly residential property) are the “least distortive

tax instrument in terms of reducing long-run GDP per capita” (Johansson et al., 2008, p7).

Broad based consumption taxes, such as the GST, are found to be the second least distortive,

followed by personal income taxes and then corporate income taxes. These findings are

summarised in Table 2.1 below.

Table 2.1 Tax Ratings from OECD study(a)

Rating Tax

Low Immovable property tax

Low Consumption taxes

Medium Personal income taxes

High Corporate income taxes

(a) ratings by KPMG Econtech based on rankings from the OECD study

These rankings give the same qualitative results of the relative efficiency for each tax as the

estimates made with MM900 in this report.

A range of both state and local government level taxes are investigated in a 1998 report by the

Productivity Commission (PC). The PC report includes a partial equilibrium assessment of the

efficiency costs (marginal excess burdens) of a number of state taxes. The partial equilibrium

approach focuses only on the impact of the tax in one market – the market in which the tax is

levied. This means that the effects of a tax in one market on the consumption and tax

collections in other markets will not be taken into account. Therefore, such estimates of

efficiency costs of taxes will be incomplete. For example, as a tax on labour, payroll tax may

reduce employment which in turn will reduce income derived from labour. As consumption

falls in line with incomes, tax collections from consumption-type taxes will also fall. This

second-round loss of tax revenue is an additional cost of payroll tax, which a partial equilibrium

estimation will not capture. Conversely, the computable general equilibrium (CGE) model used

in this study means that all second round effects are taken into account.

Department of the Treasury

The Excess Burden of Australian Taxes

March 2010

ABCD

15

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

The Centre for International Economics (CIE) conducted a qualitative analysis of state taxes,

focusing on those levied on businesses (CIE, 2009). The report identifies state taxes as having

high deadweight losses, partly because of the narrow bases of some state taxes, such as payroll

tax. Rather than assessing each tax individually, as is done in this study, the CIE study

estimates the economic impact of introducing a number of tax reforms concurrently. Using the

MMRF model, they model the impacts of reducing a number of state taxes and replacing the lost

revenue through an increase in the GST. The CIE modelling finds that this tax policy switch

leads to an increase in GDP and consumption. This indicates that the package of state taxes has

a higher economic cost than the GST. However, the results of the CIE study do not allow an

assessment of the relative inefficiencies of each individual tax.

The CIE findings are broadly in line with the results of the current analysis, which finds that

GST has a lower economic cost per unit of revenue raised than many state taxes. However,

features of the MMRF model used by CIE will result in some differences between the results of

the CIE study and this study. For example, the modelling of payroll tax and land tax is more

sophisticated in the MM900 than the MMRF. MM900 treats land as a fixed factor, as explained

in section 4.5.3., including distinguishing between residential, urban and rural land, and has a

detailed modelling of the payroll tax, as explained in Appendix A, section A.2.

Access Economics has also conducted a CGE analysis of states taxes, for the Financial Industry

Council of Australia (2008). Their rankings for the efficiency of these taxes are included in the

table below.

Table 2.2 Tax Ratings from Access Economics study(a)

Rating Tax

Low Municipal rates

Low Land Tax

Low Gambling tax

Medium Payroll tax

Medium Conveyancing Duty

Medium Insurance tax

Medium Motor Vehicle tax

(a) ratings by KPMG Econtech based on rankings from the Access Economics study

Similar to the results in this study, Access Economics find a low excess burden of taxes on land.

The remainder of their excess burden rankings are low compared to this study.

• While the current report does not include the consideration of any potential externalities

from gambling, the Access Economics report does. This means that the Access Economics

ranking for gambling taxes is much lower.

Department of the Treasury

The Excess Burden of Australian Taxes

March 2010

ABCD

16

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

• The more sophisticated treatment of payroll tax in the MM900 model includes the impact of

the small business exemption, which contributes to the excess burden by reducing the

revenue raising ability of the tax, as discussed in section 5.3.

• The lower excess burden ranking for conveyancing duty, insurance tax and motor vehicle

tax reflects the smaller amount of choices that are available in the model used by Access

Economics, the Monash Multi-Regional Forecasting Model. MM900’s more comprehensive

coverage of economic decisions improves the estimates of excess burdens, as discussed in

Section 4.

Baylor and Beauséjour (2004) use a CGE model of the Canadian economy to estimate the

marginal excess burden of a number of different taxes. Their results are broadly in line with

both the literature and this study. They estimate that corporate income tax has a high economic

cost, at 37 cents per dollar of tax revenue. This is followed by personal income tax, at 32 cents

per dollar of tax revenue. Consumption taxes have the smallest economic costs, at 13 cents per

dollar of tax revenue. Baylor and Beauséjour’s estimation of the cost of payroll tax (15 cents

per dollar of tax revenue) is in line with our estimate of the cost of a payroll tax if the small

business exemption were removed, which again is discussed in section 5.3. A further

comparison of Baylor and Beauséjour’s results with the KPMG Econtech estimates is contained

in chapter 5 of this report.

Studies focused on estimating the economic costs of particular taxes are also widely available.

The results of some of these studies are compared with the results in this study in Section 5.

However, estimating the efficiency of all taxes in a consistent framework, rather than using a

series of separate studies, will be the most appropriate way to compare the relative economic

costs of different Australian taxes.

This study therefore builds on the work of the authors mentioned above, and forms the most

extensive study of the efficiency of Australian taxes to date. The contributions of this report to

the literature are summarised briefly below.

• This study uses a computable general equilibrium model, giving quantitative results which

are consistent with qualitative research that has been undertaken by the OECD.

• The general equilibrium nature of the model used takes into account both how all markets

within the economy interact as well as the constraints on the macro-economy.

• The separate analysis of each tax allows policy makers to compare all taxes on a consistent

basis.

• It is the most thorough analysis done to date, in capturing where taxes impact on the

economy, and how it responds.

Department of the Treasury

The Excess Burden of Australian Taxes

March 2010

ABCD

17

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

3 The Cost and Incidence of Taxes

As background to the results on the efficiency and incidence of each tax presented in section 5,

this section explains the importance and meaning of the concepts of tax efficiency and

incidence, the main drivers, and how they have been modelled.

For any tax, it is usually straightforward to assess the amount of revenue that is collected and

from whom. But that only gives a superficial view of the tax system. Most taxes distort

economic incentives giving rise to excess burdens – economic costs over and above the amount

of revenue that is raised. Further, taxes may lead to economic responses such as price increases

that mean that the party who bears the economic incidence or final burden of the tax, is

different from the party who pays the tax. In assessing the merit of any tax, understanding its

economic incidence and excess burden is fundamental. This section explains these concepts and

how they have been modelled.

This study estimates the excess burdens arising from Australian federal, state and local taxes.

Most taxes carry some excess burden. For example, certain taxes reduce incentives to work or

invest, or distort consumption patterns, adversely impacting on economic performance and

ultimately on consumer welfare. This excess burden can be compared to the amount of revenue

that is being raised to assess the degree of economic inefficiency that each tax entails.

The study also identifies the incidence of (or “who really pays”) each tax. The party paying a

tax, and so carrying its impact, is sometimes different from the party who actually bears the

final burden or incidence of a tax, after economic responses. For example, while company tax is

collected from businesses, a business may pass the burden of the tax on to households through

higher prices or lower wages. In that case, while the business would carry the impact of the tax,

households would bear its economic incidence.

Understanding the incidence of a tax is an important step in assessing its implications for equity.

However, further analysis is also required, linking the incidence of a tax to the situations of

different types of households. This distribution analysis is outside of the scope of this study.

Further, good tax design is not only about economic efficiency and equity of taxes, but also their

simplicity. Taxes are considered to be simple when they involve low administration costs for

tax collectors and low compliance costs for taxpayers. An assessment of the simplicity of each

tax is also outside of the scope of this study.

MM900, KPMG Econtech’s CGE model of the Australian economy, was used to estimate the

excess burden and incidence of key Federal, State and Local taxes. The excess burden results

show, for every dollar in tax revenue raised, the additional cost to consumers in excess of that

dollar. The incidence results show how the economic incidence of each tax is spread between

consumer prices and various types of income (labour, capital, land rents and other economic

rents).

The remainder of this section discusses in further detail the excess burden and economic

incidence of taxes and how these have been modelled. Section 3.1 looks more closely at the

excess burden of taxation, section 3.2 discusses how excess burdens have been modelled,

section 3.3 discusses the economic incidence of taxes, and section 3.4 explains how incidence

has been modelled.

Department of the Treasury

The Excess Burden of Australian Taxes

March 2010

ABCD

18

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

3.1 The Excess Burden of Taxation

Most taxes change the behaviour of households, firms and/or the foreign sector. These changes

in behaviour create distortions in economic activity. Taxation may influence behaviours in the

following ways.

• Households may change their level of consumption, their consumption patterns or the

amount that they work.

• Firms may change what they produce or how they produce it.

• The foreign sector may demand less of Australia’s exports or supply Australia with fewer

imports.

The “excess burden of taxation” is a measure of the economic costs associated with these

distortions. More specifically, the excess burden is defined as the reduction in welfare3 from

imposing or raising a tax, after the additional tax revenue has been returned to individuals as a

lump-sum payment. The higher the tax rate, the higher will be the reduction in welfare.

Moreover, if the tax rate increases, the excess burden increases at a greater rate. In fact, the

excess burden of a tax is generally roughly proportional to the square of the tax rate4. Figure 3.1

below illustrates the excess burden of a tax in a market that has variable producer and consumer

prices.

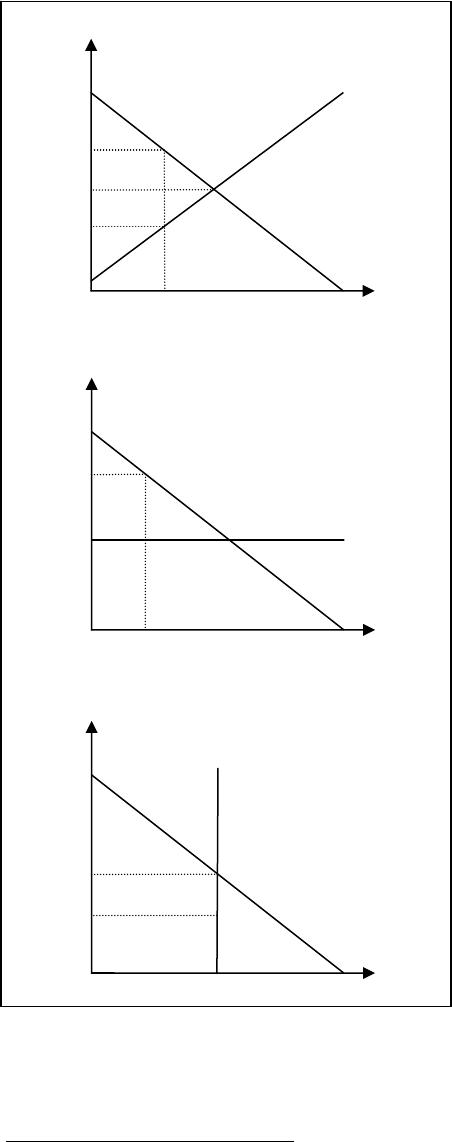

Figure 3.1 Excess Burden of a Distorting Tax

Figure 3.1(a) shows a partial equilibrium model with no taxes. In this case, an equilibrium will

be reached at the point where the demand and supply schedules intersect (at Q*). Here, the

marginal value of the last unit consumed is equal to the marginal cost of the last unit supplied.

3 Technically speaking, welfare is defined as the collective level of utility of Australian households, where the utility

of each household is determined by the commodities and leisure they consume.

4 This is because if, for example, the tax rate is doubled, then it is likely that not only will the loss in economic

activity approximately double, but also the gap between the marginal value and marginal cost of that activity will also

approximately double.

Quantity

Price

Quantity

Q* QT Q*

Demand

Supply

(

a

)

No Tax

(

b

)

Distortin

g

Tax

Supply

Demand

q = p + t

q* = p*

p

DWL

TR

PS

PS

CS

CS

Price

Department of the Treasury

The Excess Burden of Australian Taxes

March 2010

ABCD

19

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

When a tax is imposed, as in Figure 3.1(b), it raises the price paid by consumers and lowers the

price received by producers. This drives a wedge between the marginal value and the marginal

cost and, consequently, reduces market activity. The size of this wedge, the Deadweight loss

(DWL) shown in Figure 3.1(b), is the loss to consumer and producer surplus that is not

recouped as tax revenue. This can be thought of as the welfare loss associated with the tax.

The implication is that, in practice, raising a dollar of tax revenue usually creates a welfare loss

(a positive excess burden). This report expresses the excess burden (EB) per unit of additional

tax revenue, as shown in Box 3.1.

Box 3.1: Definition of Excess Burden

revenuetax

welfare

Δ

Δ

−≡EB

Where:

(a) the change in welfare is defined as the amount of (lump sum) compensation required after

the tax change to restore the consumer’s utility back to its original level.

(b) the change in tax revenue from the tax increase is defined as the amount of the lump sum

transfer back to consumers financed by the tax increase. This is equal to the total change in tax

revenue, including any changes in revenue stemming from changes in other markets.

As indicated above, the change in welfare is the compensation required to restore the

consumer’s utility back to its original level. For this purpose, it is assumed that the revenue

raised by the tax is returned to the consumer as a non-distorting or lump sum transfer, so that the

consumer does not directly lose any income from the change in the tax. This means that the

change in welfare only arises from the distortions to economic behaviour generated by the tax.

This measure of the change in welfare is known as the compensating variation (CV). In the

MM900 model, the CV can be interpreted as the real change in consumption5, saving and leisure

enjoyed by the consumer.

The change in tax revenue from the tax increase is defined as the amount of the lump sum

transfer to consumers that would be financed by the tax increase, while keeping the budget in

balance, and given fixed government expenditures. This will reflect both the additional revenue

from the tax whose rate is increased, as well as any second round effects on tax revenues (due to

impacts on tax bases).

There are two types of excess burden that can be measured.

• The marginal excess burden (MEB) is defined as the additional welfare loss imposed by

increasing a particular tax by a small amount, divided by the change in government revenue.

The MEB is useful for considering small reforms of the current system or ways of raising

additional revenue within the existing tax framework.

5 The model uses a generalised linear expenditure system utility function, in which households derive utility from

consumption of products, saving and leisure. It specifies an essential level of consumption for each product. The

consumer then maximises their utility by choosing how to allocate the remainder of their full income.

Department of the Treasury

The Excess Burden of Australian Taxes

March 2010

ABCD

20

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

• The average excess burden (AEB) is defined as the total welfare loss from imposing a

particular tax, expressed as a proportion of total revenue raised by that tax. These measures

are useful for considering the abolition of a certain tax.

A concept related to the excess burden is the marginal cost of funds, which is one plus the

marginal excess burden. This gives the cost to the economy of raising an additional dollar in tax

revenue, if the revenue were not returned to consumers. The marginal cost of funds exceeds one

dollar because it takes into account that raising a dollar of revenue also entails an excess burden.

To be worthwhile, the value to the community of a public spending program must exceed the

marginal cost of funds.

3.2 Using MM900 to Estimate the Excess Burden of Australian

Taxes

Estimating the Marginal Excess Burden and Average Excess Burden for each Tax

The MM900 model has been constructed so that both the change in welfare and the change in

tax revenue are standard outputs of the model. Thus, MM900 estimates the numerator and

denominator of the excess burden formula. This allows the excess burden of each tax to be

calculated and compared (see section 5 of this report). As noted above, MM900 uses a measure

of the change in welfare known as the compensating variation (CV), while the change in tax

revenue is measured by the transfer payment to consumers that can be financed from the tax

change, while keeping the budget in balance.

For each tax, two versions of the excess burden have been simulated in MM900. Specifically,

the Marginal Excess Burden (MEB) is estimated by simulating in MM900 a small

(five per cent) increase in the tax being considered and performing the excess burden

calculations. The Average Excess Burden (AEB), on the other hand, is estimated by simulating

in MM900 the abolition of the tax being considered, and performing the excess burden

calculation.

When a tax is imposed, it impacts upon behaviour not only in the taxed market, but also in other

related markets. For example, in the case of two goods that are gross substitutes, the imposition

of a tax on one good will cause consumers to reallocate their consumption spending from the

taxed good towards the untaxed good. CGE models like MM900 are designed so as to pick up

these ‘related market effects’. CGE models also identify other second round effects, such as

changes in aggregate consumption due to changes in consumers’ income. Related market

effects impact on the MEB and the AEB when the tax affects activity and tax collections in

other distorted markets. The features of MM900 relevant to modelling the excess burden of

taxes are described in Section 4.

Excess Burden in MM900

Some of Australia’s taxes are thought to be more inefficient than others. This is because of two

economic principles. The mobility principle recognises that the excess burden of a tax is higher,

the higher the mobility of its tax base. When a tax is applied to a highly mobile tax base, that

tax base is likely to shrink, distorting economic activity. The narrowness principle recognises

that the excess burden if a tax is likely to be higher, the narrower is the tax base. A narrow tax

Department of the Treasury

The Excess Burden of Australian Taxes

March 2010

ABCD

21

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The KPMG logo and name are trademarks of KPMG.

Liability limited by a scheme approved under Professional Standards Legislation.

base may make it possible to respond to a tax by shifting to untaxed close substitutes. Such

shifts add to economic inefficiency and reduce the revenue yield.

Under the mobility principle, resource rent taxes and land taxes would be expected to have low

excess burdens. This is because they are assumed to be applied to immobile tax bases – natural

resources and land. MM900 treats both land and natural resources as completely immobile. At

the other extreme, company income tax is expected to have a high marginal excess burden,

because it is applied to capital, which is highly mobile. This high mobility is generated by the

international competition for funds. In fact, in MM900, capital is treated as perfectly mobile.