CHAPTER 1 LAPD VAT G02 404 Guide For Vendors External

User Manual:

Open the PDF directly: View PDF ![]() .

.

Page Count: 139 [warning: Documents this large are best viewed by clicking the View PDF Link!]

- Prepared by

- Legal and Policy Division

- SOUTH AFRICAN REVENUE SERVICE

- 10.1 INTRODUCTION

- This chapter provides a brief overview of the main changes that have been made in respect of penalties under the provisions of Chapters 15 and 16 of the TA Act and a brief introduction to the interest provisions envisaged under Chapter 12 of the TA Act.

- 10.2 PENALTIES

- 10.2.1 Administrative non-compliance penalties

- Fixed-amount penalties

- A fixed amount penalty is imposed when a vendor does not comply with a legally required obligation. Such penalties may only be imposed in respect of the non-compliance listed in a public notice that will be issued by the Commissioner and not every act...

- Percentage-based penalties

- A percentage-based penalty is imposed if SARS is satisfied that an amount of tax was not paid as and when required under the tax Act. In the case of VAT, SARS may impose a penalty equal to the percentage, as prescribed in the VAT Act, of the amount of...

- The circumstances that trigger the imposition of the penalty remains in the VAT Act, for example, when a vendor fails to pay VAT within the period allowed for payment, a 10% penalty is imposed.79F

- 10.2.2 Understatement penalty (USP)

- The previously imposed “additional tax” of up to 200%, has been replaced by the USP. Any USP which is applicable will be included in an assessment issued by SARS and must be paid by the date specified in the notice of assessment.80F USP may only be i...

- defaulted in rendering a return;

- filed a return but omitted an item from that return; or

- filed a return in which an incorrect statement was made.

- For instance, if a vendor did not file a return but conducted an enterprise and should have filed VAT returns and paid VAT of R90 000, the shortfall is the difference between R90 000 and zero. The shortfall is, therefore, an expression of the prejudic...

- USP table

- The TA Act provides for different rates of USP, based on the type of behaviour or the degree of culpability involved, as shown in the table below82F :

- The amount of USP is determined by the amount resulting from applying the highest applicable understatement penalty percentage in accordance with the USP table to the shortfall in each tax period. In other words, if a vendor’s behaviour involves both ...

- The various behaviours will indicate the extent of the penalty that might be imposed. Once the behaviour has been determined, SARS must determine whether –

- the vendor made a voluntary disclosure before or after being notified of an audit,

- the vendor was obstructive when engaging with SARS officials;

- it is a repeat case; or

- the case is not defined by any of the above and is thus a standard case.

- If none of these behaviours can be identified, USP could still be imposed if the prejudice to SARS is the greater of 5% of the tax properly chargeable or R1 million. This is referred to as a “substantial understatement”.

- Refer to the Short Guide to the TA Act, 2011 or more details on the various behaviours.

- 10.3 INTEREST

- Chapter 12 of the TA Act provides that interest due or payable will be calculated on the daily balance owing and will be compounded monthly. This gives effect to the principle that interest is compensation for the loss of the use of money. The compoun...

- Refer to the Short Guide to the TA Act, 2011 and Interpretation Note 68 (Issue 2) dated 7 February 2013 “Provisions of the Tax Administration Act that did not Commence on 1 October 2012 under Proclamation No. 51 in Government Gazette 35687” for more d...

- The current rules provide that interest at the prevailing rate, under section 80 of the Public Finance Management Act (PFMA), will be charged per month or part thereof on late payments of VAT. This is calculated from the first day of the month after t...

- 10.4 REMISSION OF PENALTIES AND INTEREST

- 10.4.1 Remission of non-compliance penalty

- A vendor may apply to SARS to remit both the fixed-amount84F and a percentage-based penalty. The application must be made on the prescribed form and be delivered to SARS before the date the penalty must be paid.85F If a vendor has not filed the remi...

- SARS may remit a percentage-based administrative penalty if satisfied that the –

- amount involved is either less than R2 000, or the non-payment is a first incidence; and

- vendor has reasonable grounds explaining the non-compliance; and

- incidence of non-payment has been remedied.86F

- A “first incidence” means that no other penalty (fixed or percentage-based) must have been imposed in the period of 36 months preceding the one in respect of which the remission is concerned.87F

- A vendor may also qualify for the remission of a percentage-based penalty if exceptional circumstances exist for non-compliance. The exceptional circumstances must have made it impossible for the vendor to have complied with the obligation as prescrib...

- The circumstances are as follows:

- A natural or human-made disaster.

- A civil disturbance or disruption in services.

- The vendor suffers a serious illness or was involved in a serious accident.

- The vendor suffers a serious emotional or mental distress.

- Certain acts by SARS.

- The vendor suffers serious financial hardship.

- Any other circumstances of analogous seriousness.

- Should SARS decide not to remit or reduce the administrative non-compliance penalty, the vendor may object to this decision under the Dispute Resolution provisions of the TA Act (refer to Chapter 16). This is a qualification of the right to object and...

- SARS may remit administrative non-compliance penalties in respect of tax defaults voluntarily disclosed for which relief has been sought and granted under the voluntary disclosure programme (VDP). For the relief to be granted, the vendor must voluntar...

- For more details on the voluntary disclosure programme refer to the following documents which can be accessed on the SARS website:

- 10.4.2 Remission of understatement penalty

- Generally, SARS may not remit USP imposed for an understatement, except when the USP is imposed for a substantial understatement resulting from an “arrangement” referred to in Chapter 34 of the TA Act and SARS is satisfied that the vendor –

- made full disclosure of the “arrangement” that gave rise to the prejudice to SARS or the fiscus by no later than the date that the relevant return was due; and

- was in possession of an opinion by an independent registered tax practitioner which was issued on or before the date that the relevant return was due88F , confirming that the vendor’s position is more likely than not to be upheld if the matter proceed...

- In all other cases, a vendor may object to the USP being imposed and to request a re-classification of the behaviour or for circumstances not previously considered to be taken into account by SARS. If the objection is allowed, this may result in a red...

- 10.4.3 Remission of interest

- Once the interest provisions under the TA Act become operational, a senior SARS official must be satisfied that the interest payable by a vendor was caused by circumstances beyond the vendor’s control in considering an application to remit any interes...

- A natural or human made disaster.

- A civil disturbance or disruption in services.

- A serious illness or accident.

- EXPORTS AND IMPORTS

- Example 26 – Second-hand goods – direct export

- Example 27 – Second-hand goods – indirect export

- Assume the same facts in Example 26, except that Mr M collects the painting in the RSA and exports it himself. (Price advertised: R16 400 including R2 014 VAT). To assist Mr M to obtain his refund from the VRA, at the time of export, the tax invoice s...

- R

- Selling Price excluding VAT 14 386

- VAT @ 14% 2 014

- Selling price including VAT 16 400

- VAT Refund

- Total VAT 2 014

- Less notional input tax deducted (1 400)

- VAT refundable 614

- The tax invoice must contain a full and proper description of the goods supplied (indicating, when applicable, that the goods are second-hand goods). A refund will not be authorised if these details are not clearly indicated on the face of the tax inv...

- 12.2.2 Imports from countries other than Botswana, Lesotho, Namibia or Swaziland (the BLNS countries)

- ATV × 14% = VAT payable

- Example 28 – Importation of goods

- Example 29 – Imported services definition

- Mr A (a VAT vendor), manufactures ball valves and pays a technical license fee to a UK-based company. The service is accordingly supplied by a supplier who is not a resident of the RSA to a resident (Mr A). However, as the services are wholly consumed...

- Example 30 – Imported services (digital products / electronic services)

- Mrs B orders an electronic version of the latest “Harry Potter” novel from XYZ (an internet based business located in Belgium) and downloads the document on her personal computer. She pays €60 for the book by way of a credit card transaction. Therefor...

- VAT payable = R600 × 14% = R84

- From 1 June 2014, a non-resident supplier that provides certain electronic services to a South African resident is required to register for VAT if certain conditions104F are met and the total value of taxable supplies exceeds R50 000. In the event th...

- 12.3.2 When must VAT on imported services be paid?

- Example 31 – Value of imported service

- Notes:

- 1. If A was paid an additional amount to construct a building where the spaza shop enterprise is carried on, no VAT would be payable in this regard as Mrs S would have acquired those services for making taxable supplies.

- Example 32 – Exempt imported services

- VAT is therefore not payable by the recipient (Mrs S or D) on the fees of R120 000 in this case.

- Examples of zero-rated goods:

- Examples of zero-rated services:

- Northern South Africa

- Eastern South Africa

- Vendors residing in KZN and northern parts of the Eastern Cape (up to and including East London).

- Southern South Africa

- Vendors residing in the Eastern Cape, south of East London and the Western Cape.

VAT 404

Guide for Vendors

Value-Added Tax

i

10 IMPORTANT PRINCIPLES

1. All prices charged, advertised or quoted by a vendor must include VAT at the

applicable rate. (Presently 14% for standard-rated supplies).

2. Vendors are charged with the responsibility of levying VAT and paying it over to the

State after deducting permissible VAT inputs and other deductions – please make sure

that you pay it over on time, otherwise penalties and interest will be charged.

3. VAT charged on supplies made (output tax) less VAT paid to your suppliers (input tax)

and other permissible deductions = the amount of VAT payable/refundable.

4. You need a valid tax invoice or a debit note with your VAT number indicated on it as

proof of any input tax deductions which you want to make. You must also keep records

of all your tax invoices and other records of transactions for at least five years.

5. Goods exported to clients in an export country may be charged with VAT at 0%.

However, if delivery takes place in RSA, you must charge VAT at 14% to your client,

unless the goods are supplied under Part Two of the Export Regulations which allows

the zero rate to be applied at the discretion of the supplier when the goods are to be

exported via road or rail or are delivered to a harbour or an airport from where the

goods will be exported. If your client is a vendor, the VAT charged may be deducted as

input tax. If your client is not a vendor, and the goods are subsequently removed from

the country, a claim for a refund of the VAT may be made at the offices of the VAT

Refund Administrator (the VRA). The VRA is only present at the international airports

in the Republic.

6. You may not register for VAT if you only make exempt supplies or if registered, deduct

any input tax on goods or services acquired to make exempt supplies, for private use

or other non-taxable purposes. Also, as a general rule, input tax may not be deducted

where the expense incurred is for the acquisition of a motor car or entertainment, even

if used for making taxable supplies.

7. You are required to advise the South African Revenue Service (SARS) within 21 days

of any changes in your registered particulars, including any change in your authorised

representative, business address, banking details, trading name or if you cease

trading.

8. If you have underpaid VAT as a result of a mistake, report it to SARS as soon as

possible, rather than leaving it for the SARS auditors to detect. You can make a

request for correction on eFiling if registered as a user, otherwise go to your nearest

SARS office.

9. You can pay your VAT by using various electronic methods, including eFiling, internet

banking, and electronic funds transfer (EFT). You may also pay at certain banks.

10. Report fraudulent activities to SARS by calling the Fraud and Anti-

Corruption Hotline on 0800 00 28 70. You may report an incident anonymously if you

wish.

VAT 404 – Guide for Vendors Preface

ii

PREFACE

The VAT 404 is a basic guide where technical and legal terminology has been avoided wherever

possible. Although fairly comprehensive, the guide does not deal with all the legal detail associated

with VAT and is not intended for legal reference.

All references to sections hereinafter are to sections of the Value-Added Tax Act 89 of 1991 (the

VAT Act), unless the context otherwise indicates. The Tax Administration Act 28 of 2011, the Income

Tax Act 58 of 1962 and the Customs and Excise Act 91 of 1964 are referred to as the “TA Act”,

“Income Tax Act” and “Customs and Excise Act” respectively. The terms “Republic”, “South Africa” or

the abbreviation “RSA”, are used interchangeably in this document as a reference to the sovereign

territory of the Republic of South Africa, as set out in the definition of “Republic” in section 1(1). You

will also find a number of specific terms used throughout the guide which are defined in the VAT Act

and the TA Act listed in Chapter 19 in a simplified form for easy reference.

The information in this guide is based on the VAT Act (as amended) and the TA Act (as amended) as

at the time of publishing and includes the amendments contained in the Taxation Laws Amendment

Act 43 of 2014 and the Tax Administration Laws Amendment Act 44 of 2014 which were promulgated

on 20 January 2015 as per GG 38404 and GG 38406, respectively.

Below is a brief synopsis of some of the most important changes affecting the administration of VAT

since the previous issue of this guide:

1. VAT registration of non-resident suppliers of electronic services – The VAT Act was

amended in 2014 to provide that non-resident suppliers of certain electronic services must

register and account for VAT in South Africa if the value of electronic services supplied has

exceeded R50 000 and the supplies are either made to South African residents or payment

originates from a South African bank account. The different types of electronic services to which

these rules apply are set out in a Regulation. The conditions applicable to the registration of a

non-resident supplier of electronic services have now been amended. With effect from

1 April 2015, the non-resident supplier will be liable to register in respect of the supply of

electronic services where at least any two of the following three circumstances apply:

• Electronic services are supplied to South African residents; or

• Payment for such electronic services originates from a South African bank account; or

• The recipient has an address (e.g. residential, business or postal) in South Africa,

and the total value of taxable supplies of electronic services has exceeded R50 000.

Section 11 was also amended with effect from 1 April 2015 to make it clear that electronic

services supplied by non-residents may not qualify to be charged with VAT at the zero rate.

Refer to Chapter 2 for more details.

2. Voluntary VAT registration – The VAT Act was amended by expanding the scope of voluntary

registration by allowing persons who meet certain conditions set out in regulations issued under

section 23(3)(b) and (d) to apply for voluntary registration. At the time of publishing this guide, the

regulations were issued in draft and available on the SARS website. Refer to Chapter 2 for more

details.

VAT 404 – Guide for Vendors Preface

iii

3. Definition of second-hand goods – The definition of second-hand goods, which already

specifically excluded gold coins that are subject to the zero rate, was amended to also exclude

gold and goods containing gold. With effect from 1 April 2015 vendors will not be entitled to

deduct notional input tax on the acquisition of gold and goods containing gold which was

previously owned and used. The compliance issues which the amendment intends to address are

the fraudulent issuing of tax invoices and transactions involving illegally mined gold being

misrepresented as purchases of second-hand jewellery. This amendment is part of a package of

measures introduced by the government to combat illegal mining and the negative effect of such

activities on the economy.

4. Customs legislation alignment – The VAT Act relies on certain provisions of the Customs and

Excise Act with regard to the exportation and importation of goods to ensure that the correct VAT

rate or exemption is applied to exports and imports whilst aligning the rules pertaining to the time

and value of exports and imports. During 2014 the customs and excise legislative framework was

fundamentally restructured by the introduction of the new Customs Control Act, 2014, and the

Customs Duty Act, 2014 which are to replace the existing Customs and Excise Act. These new

Acts will, however, only come into effect from a future date. As a result of this restructuring, a

number of textual amendments had to be made throughout the VAT Act to address alignment

issues, including reference to certain new definitions. The VAT amendments come into effect on

the same date that the new Customs statutes become effective. Refer to Chapter 12 for more

details.

5. Timing of input tax deduction on importation of goods – A vendor is allowed an input tax

deduction under section 16(3)(a)(iii) and (b)(ii) in respect of the VAT charged on the importation of

goods acquired for taxable purposes. The deduction is subject to the vendor or his agent being in

possession of a bill of entry or other document prescribed under the Customs and Excise Act

relating to the importation as well as the receipt for the payment of the VAT to SARS when

making the deduction. In terms of an amendment to section 16(3)(a)(iii) effective 1 April 2014, and

section 16(3)(b)(ii), a vendor is only entitled to the deduction of input tax in the tax period in which

the VAT is actually paid to SARS. A further amendment to section 16(3)(a)(iii) and (b)(ii) with

effect from 1 April 2015, allows a vendor to deduct input tax if the imported goods have been

released to the importer or its agent and the vendor is in possession of the relevant documentary

proof. Refer to Chapter 12 for more details.

6. Importation of equipment for exploration or production of petroleum – Government Notice

No. R288 was published in Government Gazette 37554 on 17 April 2014. The Notice amends

paragraph 8 of Schedule 1 to the VAT Act by the insertion of rebate item 460.23 to provide for an

exemption from the levying of VAT on equipment imported on or after 1 January 2014 which is

used in the exploration for, or production of petroleum. Similar relief is provided in the Customs

and Excise Act in the form of a full rebate of customs duty. The exemption from VAT and the

rebate of duty is subject to the conditions set out in the notes to rebate item 460.23.

7. Farming inputs – Certain changes to the law have been made regarding goods acquired for

agricultural, pastoral or other farming purposes as follows:

• Zero-rating – The zero rating under section 11(1)(g) which applies in respect of

agricultural, pastoral or other goods described in Part A to Schedule 2 which are acquired

for farming purposes will be repealed with effect from a future date to be determined by

the Minister and published by way of notice in the Government Gazette. The notice will

not be published earlier than 20 January 2016. The zero rating remains applicable until

such date of repeal is determined and published.

• Exemption on importation – The exemption in Paragraph 7 to Schedule 1 in respect of the

importation of the goods mentioned in Part A to Schedule 2 will also be repealed from the

future effective date mentioned above. The exemption also remains applicable until such

date of repeal is determined and published.

VAT 404 – Guide for Vendors Preface

iv

8. Elimination of the four monthly tax period for small businesses – With effect from 1 July

2015, the four monthly tax period known as “Category F” will no longer be available. Category F

was introduced from 1 August 2005, but very few vendors registered under this category as a

result of other measures which were introduced to assist small businesses. Vendors registered

under Category F will be absorbed into the bi-monthly categories (that is, either Category A or B).

9. Bargaining councils – The supply of any goods or services by a bargaining council to its

members is exempt from VAT under section 12(ℓ) to the extent that the consideration for such

supplies consists of membership contributions. With effect from 1 April 2015, the extent of the

exemption has been expanded to apply to all goods and services supplied to any of its members

which are within the scope and mandate of the bargaining council under section 27 of the Labour

Relations Act, 1995. The intention of this amendment was to extend the scope of the exemption

to include various administration services supplied by a bargaining council to its members which

are not necessarily covered by membership contributions.

10. Relief period for temporary letting of dwellings by developers – Section 18B provided a relief

period from 10 January 2011 until 31 December 2014 during which there was a suspension of the

liability to declare output tax under section 18(1) for developers that temporarily let dwellings to

tenants whilst still being held for sale. The relief period has now been extended until

31 December 2017.

11. Duties and responsibilities of agents – Section 54 has been amended to clarify, amongst

others, that from 1 April 2015 –

• an agent must issue a tax invoice within a period of 21 days when a supply is made by the

agent on behalf of a principal if it is part of that agent’s duties to issue tax invoices;

• an agent must now also issue a statement envisaged in section 54(3) in respect of the

importation of goods on behalf of the principal. The statement must include certain details in

regard to the goods imported.

The following guides have also been issued and may be referred to for more information relating to

the specific VAT topics:

• Vendors and Employers Trade Classification Guide (VAT/EMP 403);

• Guide for Fixed Property and Construction (VAT 409);

• Guide for Accommodation, Catering and Entertainment (VAT 411);

• Share Block Schemes (VAT 412);

• Guide for Estates (VAT 413);

• Guide for Associations not for Gain and Welfare Organisations (VAT 414);

• Guide for Municipalities (VAT 419);

• Guide for Motor Dealers (VAT 420);

• Guide for Short-Term Insurance (VAT 421).

This guide is not an “official publication” as defined in section 1 of the TA Act and accordingly does

not create a practice generally prevailing under section 5 of that Act. It is also not a binding general

ruling under section 89 of Chapter 7 of the TA Act nor a ruling under section 41B of the VAT Act

unless otherwise indicated.

All previous editions of the Guide for Vendors (VAT 404) are withdrawn with effect from 1 April 2015.

VAT 404 – Guide for Vendors Preface

v

Should there be any aspects relating to VAT which are not clear or not dealt with in this guide, or

should you require further information or a specific ruling on a legal issue, you may –

• contact your local SARS branch;

• visit the SARS website at www.sars.gov.za;

• contact your own tax advisors;

• contact the SARS National Call Centre –

if calling locally, on 0800 00 7277; or

if calling from abroad, on +27 11 602 2093 (only between 8am and 4pm South African

time);

• submit legal interpretative queries on the TA Act by e-mail to TAAInfo@sars.gov.za; or

• submit a ruling application to SARS headed “Application for a VAT Class Ruling” or

“Application for a VAT Ruling” together with the VAT301 form by e-mail to

VATRulings@sars.gov.za or by facsimile on +27 86 540 9390.

Comments regarding this guide may be e-mailed to: policycomments@sars.gov.za.

Prepared by

Legal and Policy Division

SOUTH AFRICAN REVENUE SERVICE

31 March 2015

VAT 404 – Guide for Vendors Contents

vi

CONTENTS

CHAPTER 1 : INTRODUCTION 1

1.1 What is VAT?

1

1.2 How does VAT work?

1.3 Tax Administration

1

4

CHAPTER 2 : REGISTERING YOUR BUSINESS 6

2.1 When do I become liable to register for VAT? 6

2.2 Where must I register?

7

2.3 What documents must I submit with my application? 7

2.4 How do I calculate the value of taxable supplies?

9

2.5 Voluntary registration 10

2.6 Refusal of a voluntary registration application

11

2.7 Separate registration (branches, divisions and separate enterprises)

12

2.8 Cancellation of registration

13

CHAPTER 3 : TAX PERIODS 14

3.1 Which tax periods are available?

14

3.2 Allocation and change of tax periods

16

3.3 The 10-day rule

17

CHAPTER 4 : ACCOUNTING BASIS 18

4.1 Introduction

18

4.2 Invoice basis 18

4.3 Payments basis

19

4.4 Change of accounting basis 20

4.5 Special cases

21

CHAPTER 5 : TIME AND VALUE OF SUPPLY 23

5.1 Introduction

23

5.2 Time of supply 23

5.3 Value of supply

26

VAT 404 – Guide for Vendors Contents

vii

CHAPTER 6 : TAXABLE SUPPLIES 30

6.1 Introduction

30

6.2 Standard rated supplies

30

6.3 Zero-rated supplies

31

6.4 Deemed supplies

35

CHAPTER 7 : EXEMPT SUPPLIES 37

7.1 Introduction

37

7.2 Letting and sub-letting of dwellings 37

7.3 Passenger transport (road and rail)

38

7.4 Fixed property situated outside the Republic

38

7.5 Educational and childcare services

38

7.6 Financial services 39

7.7 Donated goods and services

39

7.8 Public authorities 41

CHAPTER 8 : INPUT TAX AND OTHER DEDUCTIONS 42

8.1 What will qualify as input tax?

42

8.2 When and how do I deduct input tax? 43

8.3 How much input tax can I deduct?

44

8.4 Apportionment 45

8.5 Denial of input tax

52

8.6 Petty cash payments 55

8.7 Pre-incorporation expenses

55

8.8 Adjustments 55

CHAPTER 9 : CALCULATION AND SUBMISSION OF VAT 56

9.1 The VAT201 return

56

9.2 How to calculate your VAT

56

9.3 Submitting your return

58

9.4 How to pay your VAT

59

9.5 Payment limits (EFT/eFiling/debit orders/bank payments)

61

9.6 Managing your payments

61

9.7 Penalties and interest for late payment

9.8 Refunds

62

62

9.9 Change of bank details

63

VAT 404 – Guide for Vendors Contents

viii

CHAPTER 10 : PENALTIES AND INTEREST 64

10.1 Introduction

64

10.2 Penalties

64

10.3 Interest

66

10.4 Remission of penalties and interest

67

CHAPTER 11 : FARMING 70

11.1 Tax periods 70

11.2 Standard rated supplies

70

11.3 Zero-rated supplies 71

11.4 Input tax

72

11.5 Diesel refunds 73

CHAPTER 12 : EXPORTS AND IMPORTS 74

12.1 Exports

74

12.2 Importation of goods

80

12.3 Importation of services

82

CHAPTER 13 : TAX INVOICES 86

13.1 Introduction

86

13.2 What is the difference between an invoice and a tax invoice? 86

13.3 What are the requirements for tax invoices?

86

13.4 Tax invoices prepared by the recipient (recipient-created invoicing) 88

13.5 Tax invoices for mixed supplies

89

13.6 Special cases 90

13.7 Electronic tax invoices and records

92

CHAPTER 14 : DEBIT & CREDIT NOTES 93

14.1 Introduction

93

14.2 When must debit and credit notes be issued?

93

14.3 What details must appear on debit and credit notes?

94

14.4 Adjustments

95

VAT 404 – Guide for Vendors Contents

ix

CHAPTER 15 : ADJUSTMENTS 96

15.1 Introduction 96

15.2 Irrecoverable debts

96

15.3 Debit and credit notes 96

15.4 Prompt settlement discounts

97

15.5 Change in use or application 97

CHAPTER 16 : ASSESSMENTS, OBJECTIONS AND APPEALS 103

16.1 Assessments

16.2 Dispute resolution

103

104

16.3 Alternative dispute resolution (ADR)

107

16.4 The “pay now, argue later” principle

108

CHAPTER 17 : RULINGS 110

17.1 Introduction

110

17.2 Terminology

110

17.3 Who may apply for a ruling? 111

17.4 Different types of rulings

112

CHAPTER 18 :TAX ADMINISTRATION ACT 115

18.1 Introduction

115

18.2 Interpretation

115

18.3 Practice generally prevailing

115

18.4 Registration

116

18.5 Record keeping

116

18.6 Verification and audits

116

18.7 Assessments and dispute resolution

117

18.8 Payments

118

18.9 Penalties and Interest

118

18.10 Refunds 118

GLOSSARY 120

CONTACT DETAILS 128

VAT 404 – Guide for Vendors Chapter 1

1

CHAPTER 1

INTRODUCTION

1.1 WHAT IS VAT?

VAT is an abbreviation for the term value-added tax. It is an indirect tax based on consumption in the

economy. Revenue is raised for the government by requiring certain traders (vendors) to register and

to charge VAT on taxable supplies of goods or services for the benefit of the National Revenue Fund

and to pay it over to the government. SARS is a government agency which administers the VAT Act

and ensures that the tax is collected and that the tax law is properly enforced.

Many countries apply a form of indirect or consumption tax like VAT, and although these tax systems

might be known by different names, for example, GST (Goods and Services Tax), the characteristics

of the tax are normally quite similar. The generally accepted essential characteristics of a VAT-type

tax are as follows:

• The tax applies generally to transactions related to goods and services.

• It is proportional to the price charged for the goods and services.

• It is charged at each stage of the production and distribution process.

• The taxable person (vendor) may deduct the tax paid during the preceding stages on

goods and services acquired (that is, the burden of the tax is on the final consumer).

VAT is only charged on taxable supplies made by a vendor. Taxable supplies include supplies for

which VAT is charged at either the standard rate or zero rate. Taxable supplies do not include:

• Labour services by employees to employers;

• Hobbies or any private recreational pursuits (not conducted in the form of a business);

• Occasional private sale of personal or domestic items;

• Exempt supplies. (Refer to Chapter 7).

1.2 HOW DOES VAT WORK?

The South African VAT is destination based, which means that only the consumption of goods and

services in South Africa is taxed.1 VAT is therefore paid on the supply of goods or services in

South Africa as well as on the importation of goods into South Africa. VAT is currently levied at

the standard rate of 14% on most supplies and importations, but there is a limited range of goods

and services which are either exempt, or which are subject to tax at the zero rate (for example,

exports are taxed at 0% under certain circumstances). The importation of services is only subject to

VAT where the services are imported for private, exempt or other non-taxable purposes. Certain

imports of goods or services are exempt from VAT. Refer to Chapters 6 and 12 for more details.

1 This is known as the invoice-based credit method of the consumption-type VAT.

VAT 404 – Guide for Vendors Chapter 1

2

Persons who make taxable supplies in excess of R1 million in any consecutive 12-month period or

will exceed that amount in terms of a contractual obligation in writing are liable for compulsory

VAT registration.2 A person may also choose to register voluntarily provided the minimum

threshold of R50 0003 has been exceeded in the past 12-month period. There are also certain other

exceptional cases which are to be dealt with in Regulations, which prescribe other conditions which

must be met if the applicant has not met the minimum threshold at the time of applying for voluntary

registration. A vendor is a person who is registered or is required to be registered. Refer to Chapter 2

for more details.

Vendors have to perform certain duties and take on certain responsibilities. For example, vendors are

required to ensure that VAT is collected on taxable transactions, that they submit returns and make

payments on time, that they issue tax invoices where required, that they include VAT in all prices

advertised or quoted etc. Refer to Chapter 2 for more details.

The mechanics of the VAT system are based on a subtractive or credit input method which allows

the vendor to deduct the tax incurred on enterprise inputs (input tax) from the tax collected on

the supplies made by the vendor (output tax). There are, however, some expenses upon which

input tax is specifically denied, such as the acquisition of motor cars and entertainment. Refer to

Chapter 8 for more details.

The vendor reports to SARS at the end of every tax period on a VAT201 return, where the input tax

incurred is offset against the output tax collected for a specific tax period and the resulting net

liability is paid to or net refund claimed from SARS (normally by no later than the 25th day after the

end of the tax period concerned). The VAT charged and collected by vendors is usually paid over to

SARS every two months, but where the value of taxable supplies in a 12-month periods exceeds

R30 million or where the vendor has obtained approval from SARS on written application, the vendor

must account for VAT by paying and submitting returns electronically on a monthly basis. Certain

farming enterprises are allowed to submit returns and pay VAT on a bi-annual basis. Refer to

Chapter 3 for more details.

Late payments of VAT attract a penalty of 10% of the outstanding tax. Interest is also charged at

the prescribed rate on any late payments made after the month in which the payment for the tax

period concerned was due as well as any balance of taxes outstanding for past tax periods. The

TA Act imposes two types of penalties, namely, administrative non-compliance penalties (Chapter 15

of the TA Act) and understatement penalties (Chapter 16 of the TA Act). Refer to Chapter 10 for more

details.

It sometimes occurs that the result of the calculation for the tax period is a refund, instead of an

amount payable to SARS. This happens, for example, where the vendor has incurred more VAT on

expenses than has been collected on any taxable supplies made during the tax period, or where the

vendor has mainly zero-rated supplies (for example, an exporter, or a business which sells only fresh

fruit and vegetables). However, most vendors will not normally be in a refund situation, and should be

paying VAT to SARS at the end of each tax period. Refunds must be paid by SARS within 21

business days of receiving the correctly completed refund return, otherwise interest at the prescribed

rate is payable by SARS to the vendor. However, interest is only paid if certain conditions are met as

a refund may be subject to the finalisation of the verification, inspection or audit of the refund. For

example, no interest is paid where the vendor has outstanding taxes or returns for past tax periods or

where SARS is prevented from gaining access to the vendor’s records to verify the refundable

amount.

2 From 1 June 2014 non-resident suppliers of certain electronic services to South African residents are also

required to register for VAT from the end of any month in which the threshold of R50 000 has been

exceeded.

3 In the case of persons that supply “commercial accommodation” the threshold is R60 000 and not R50 000.

VAT 404 – Guide for Vendors Chapter 1

3

The TA Act allows SARS to authorise the payment of a refund before the finalisation of the

verification, inspection or audit if security in a form acceptable to a senior SARS official is provided by

a vendor.4

The fact that there are often refunds under the VAT system and that it is self-assessed, makes it

tempting for vendors to overstate input tax or to under declare output tax. SARS therefore places

great importance on identifying high risk cases, conducting regular compliance visits and promoting a

high level of visibility of auditors in the field. Refer to Chapters 9, 16 and 18 for more details.

As VAT is an invoice-based tax, vendors are generally required to account for VAT on the

invoice (accrual) basis, but the payments (cash) basis is allowed in some cases. For example,

natural persons with a taxable annual taxable turnover of under R2 500 000, public authorities,

municipalities and non-resident suppliers of certain electronic services that qualify as enterprises are

allowed to account for their VAT on the payments basis. Other legal entities such as companies and

trusts do not qualify for the payments basis of accounting. Refer to Chapters 3 and 4 for more details.

Tax invoices for supplies made (including alternative or requisite documentary proof for zero-

rated supplies), bills of entry for goods imported and the general maintenance of proper

accounting records and documents are all very important aspects of how the whole VAT system

operates. These documents form an audit trail which SARS uses to verify that the vendor has

complied with the law. A tax invoice or bill of entry also serves as the documentary evidence of any

VAT deducted by the vendor as input tax. A tax invoice must contain certain details and must be

issued by the supplier within 21 days of making a taxable supply, regardless of whether the recipient

has requested this or not. A full tax invoice must be issued where the consideration for the supply

exceeds R5 000. Refer to Chapters 13, 14, 15 and 18 for more details.

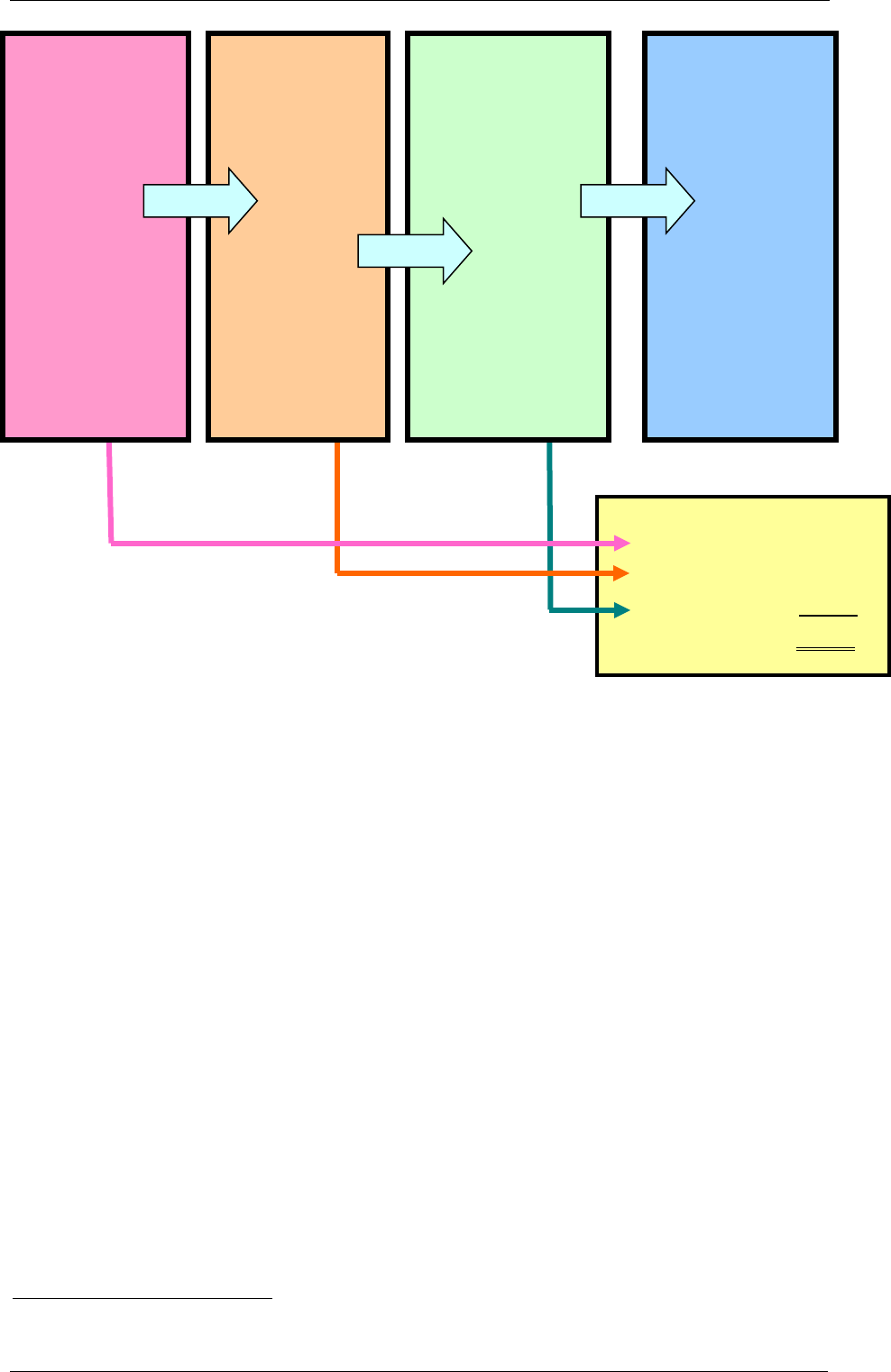

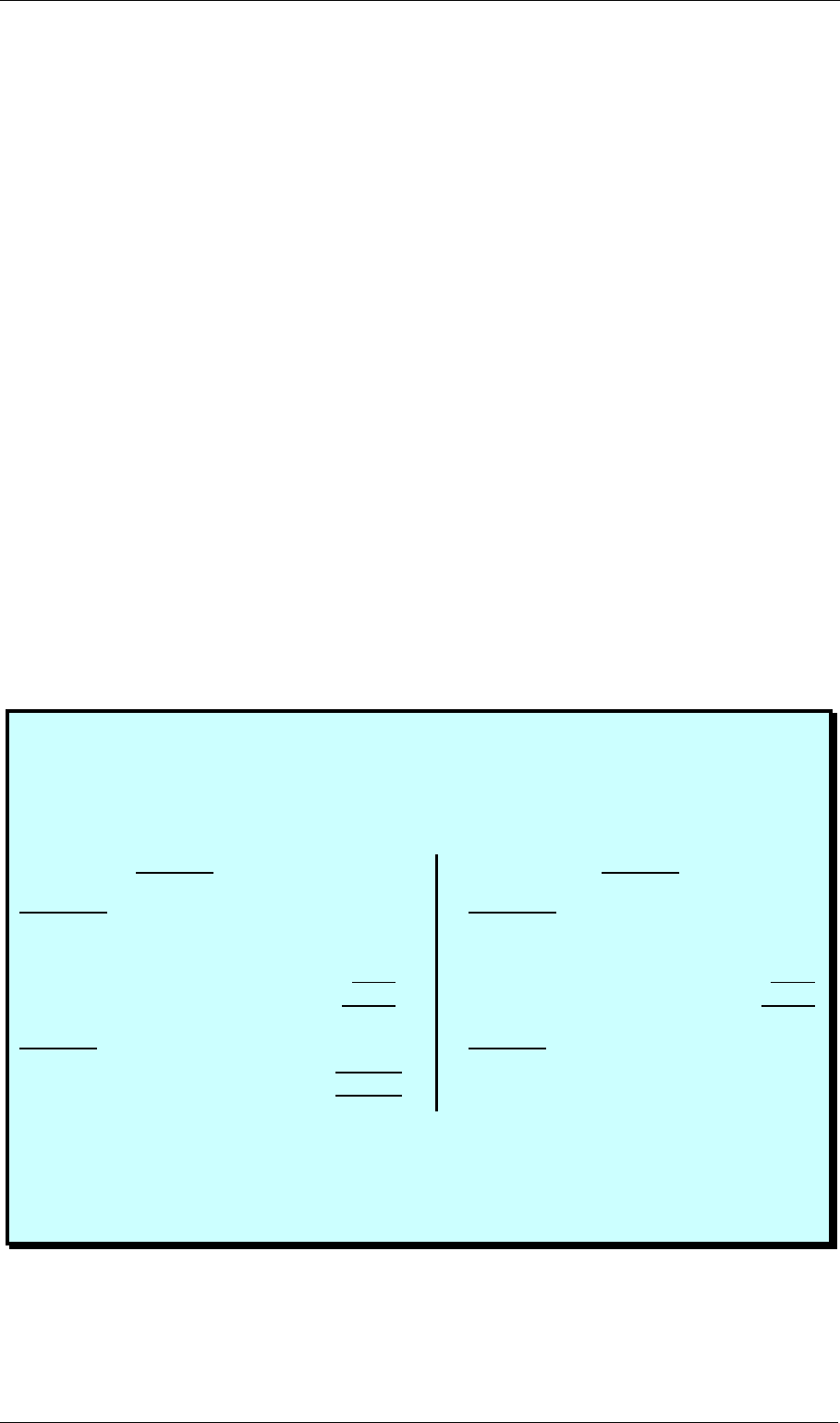

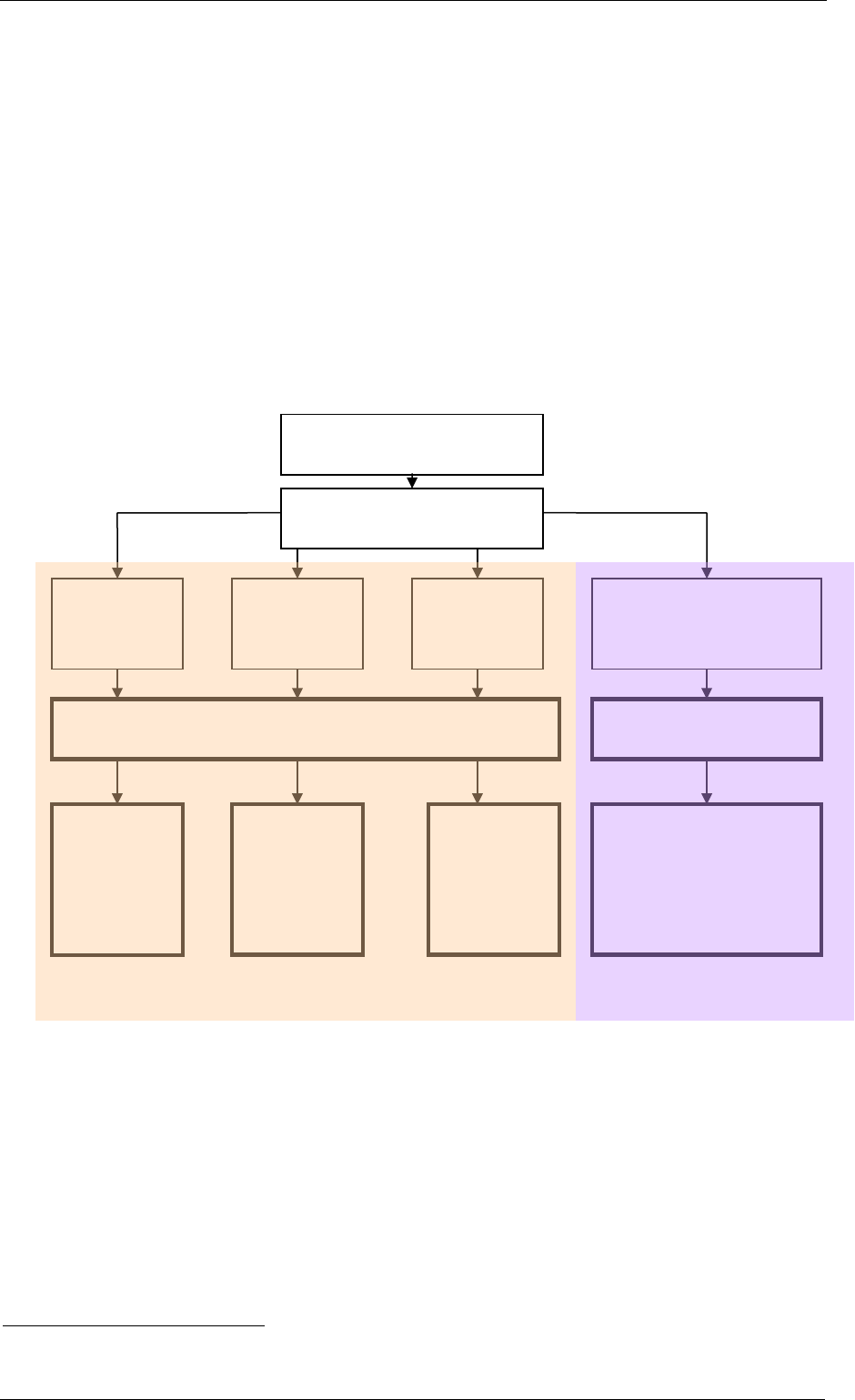

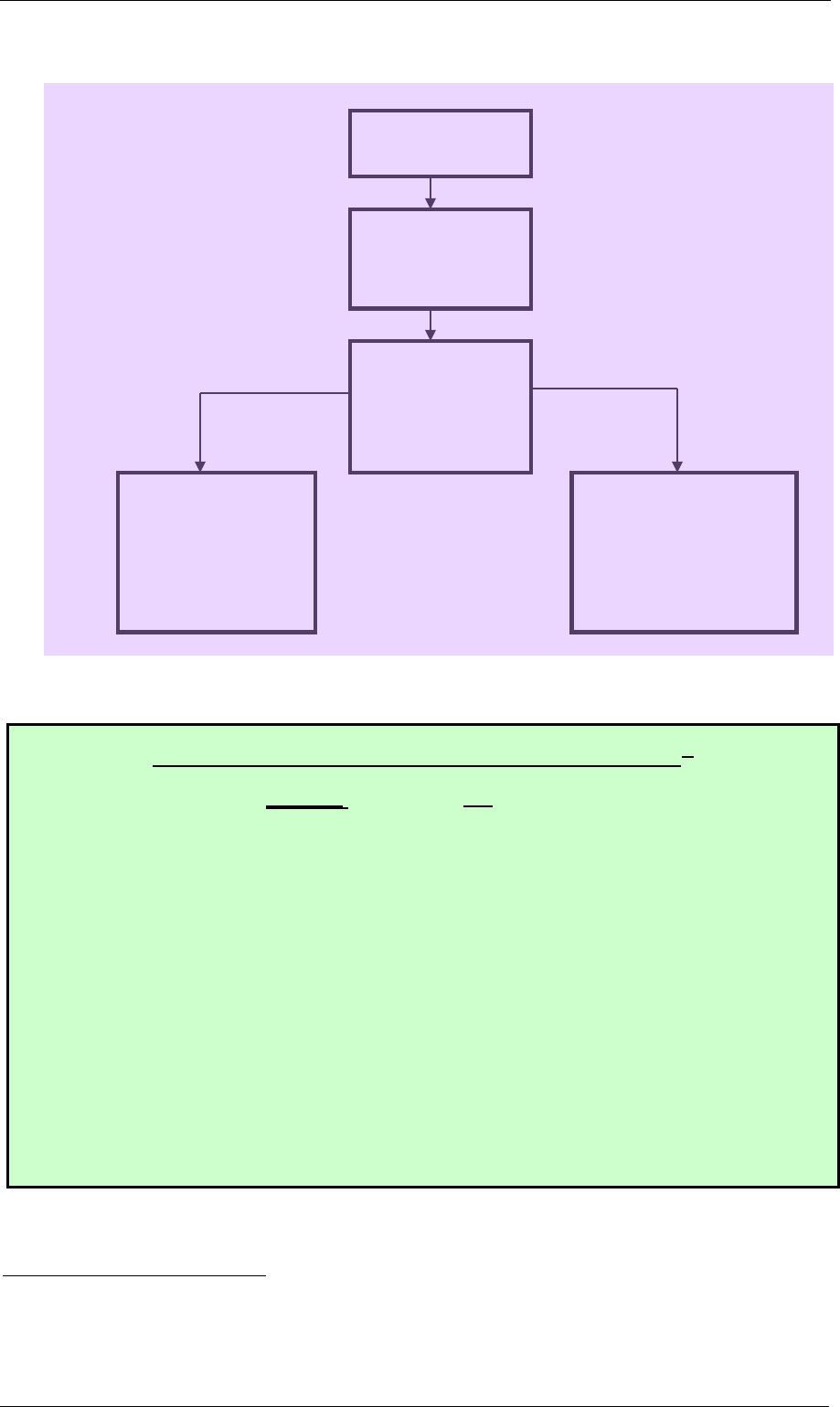

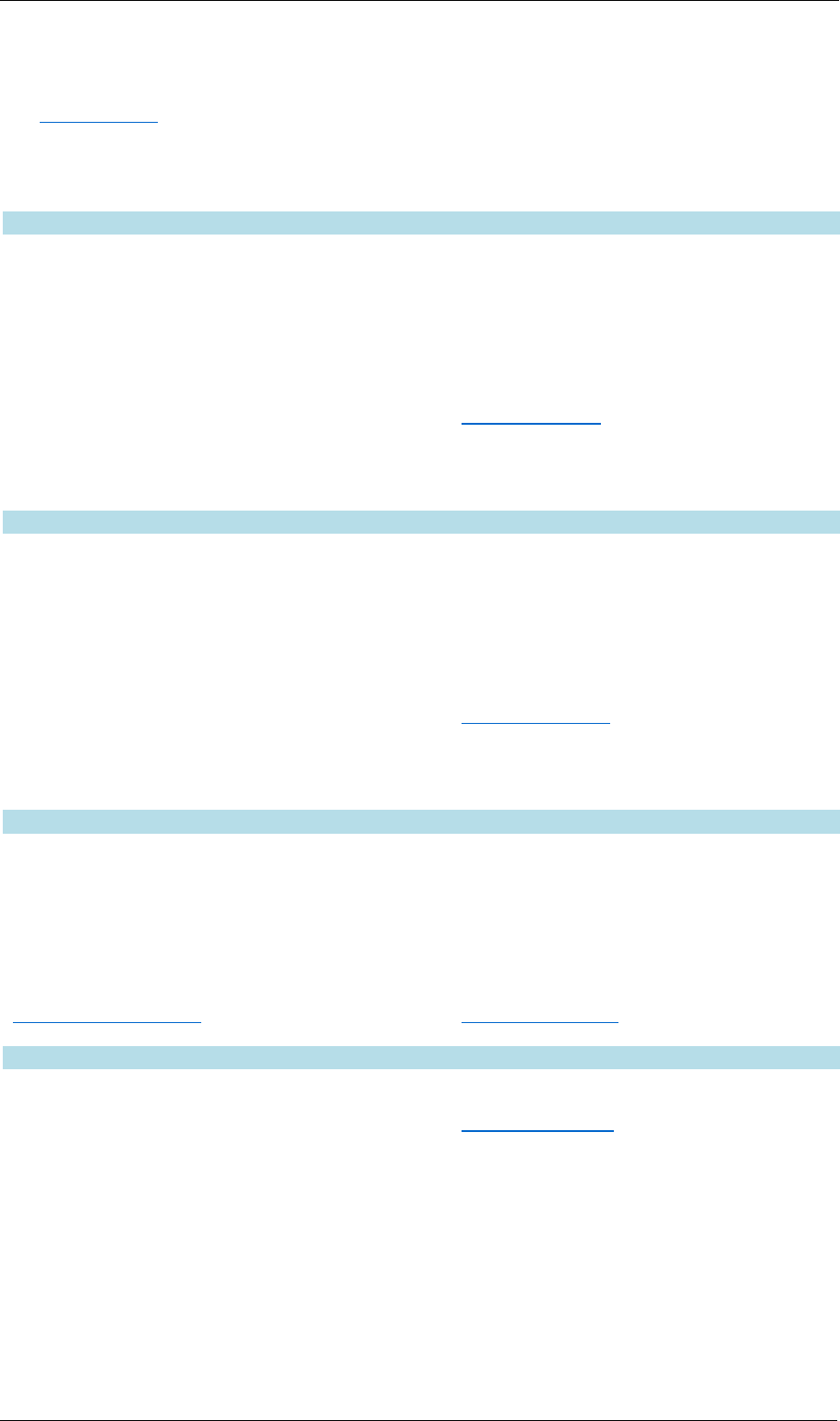

Example 1 – Mechanism of the VAT system

A VAT registered farmer sells 10 pineapples to a VAT registered canning factory for R1 each. No

VAT is charged by the farmer to the factory as the supply of fresh fruit is zero-rated. For purposes

of this example it is assumed that the farmer did not have any input tax to deduct, as all farming

supplies purchased were subject to VAT at the zero rate. (Refer to Chapter 11.)

The canning factory also buys canning metal from another vendor for R22,80 (including 14%

VAT). It manufactures 20 cans of pineapple pieces and sells them to a supermarket for R2,28

each (including 14% VAT). The selling price of each can of pineapples includes 28c VAT. The

factory must therefore pay output tax of 28c on each can sold, which in turn, will be deducted as

input tax by the supermarket.

The supermarket sells 15 of the 20 cans to its customers for R3,42 each (inclusive of 42c VAT).

The supermarket must declare output tax of 42c on each can of pineapple pieces sold. Since the

supermarket’s customers are the final consumers and are not registered for VAT, there is no input

tax deducted on the 42c VAT charged.

The effect in this example is illustrated in the diagram below.

4 Sections 190 and 191 of the TA Act deal with refunds.

VAT 404 – Guide for Vendors Chapter 1

4

Farmer

Selling price = R10

(10 units @ R1)

Output Tax = nil

Input tax = nil

Net VAT = nil

Canning

Factory

Selling price =

R45,60

(20 units @ R2,28)

Output Tax =

R5,60c

Input Tax =

R2,80c

Net VAT = R2,80c

Supermarket

Selling price = R51,30

(15 units @ R3,42)

Output Tax = R6,30c

Input Tax = R5,60c

Net VAT = R0,70c

Customers

Final consumers.

No input tax or

output tax

1.3 TAX ADMINISTRATION ACT

The TA Act was promulgated into law on 4 July 2012 and commenced on 1 October 2012, except for

those provisions relating to interest stipulated in the Schedule to Proclamation No. 51 dated

14 September 2012 (as per GG 35687).

With the implementation of the TA Act, certain administrative provisions previously contained in the

VAT Act were replaced by similar provisions contained in the TA Act but where an administrative

provision applies only to one tax type then the administrative provision is contained in the individual

tax Acts such as the VAT Act. A vendor must therefore adhere to the administrative requirements that

are contained in the TA Act and the VAT Act.

The TA Act covers a broad range of aspects, which will be mentioned briefly throughout the guide

where it concerns the specific content dealt with in a particular chapter. Chapter 18 also deals with

some of the more important aspects of the TA Act which generally apply to all taxes. Some of the

duties of a vendor that are impacted by the TA Act are registration, record-keeping, payments made

to SARS and the obligation to inform SARS of changes in registered particulars to ensure that SARS

has the most current information.5 These duties also apply to persons who have registered voluntarily

as well as persons who should have registered for VAT, but who have not done so.

The administrative provisions mentioned in this guide must therefore be understood within the context

of the TA Act and any public notices under that Act with regard to a tax administration issue.

5 For example, section 23 of the TA Act read with section 25 prescribes that vendors must communicate the

change of an address, representative taxpayer and banking particulars.

Supply

SARS

Farmer nil

Canning Factory R2,80c

Supermarket R0,70c

Total Received R3,50c

Supply

Supply

Each vendor submits a return for each

tax period to SARS, together with any

payment which may be due.

VAT 404 – Guide for Vendors Chapter 1

5

Refer to Chapter 18 and the Tax Administration webpage on the SARS website, where you can find

more information on the TA Act, which includes, amongst others, the following documents:

• The Short Guide to TA Act, 2011; and

• Interpretation Note 68 (Issue 2) dated 7 February 2013 “Provisions of the Tax Administration

Act that did not Commence on 1 October 2012 under Proclamation No. 51 in Government

Gazette 35687”.

VAT 404 – Guide for Vendors Chapter 2

6

CHAPTER 2

REGISTERING YOUR BUSINESS

2.1 WHEN DO I BECOME LIABLE TO REGISTER FOR VAT?

The TA Act, together with the VAT Act regulates the identification and registration of vendors. The

TA Act prescribes the general obligations that a person must comply with when registering for a tax,

while the VAT Act sets out when a person is required to register.

You will be liable for compulsory VAT registration if you are carrying on an enterprise (i.e. activities

are carried on in South Africa or partly in South Africa, resulting in income being earned from selling

goods or services supplied to another person) and make taxable supplies in the course of that

enterprise, exceeding R1 million6 in any consecutive period of 12 months, or will exceed that amount

in terms of a contractual obligation in writing.7 The definition to “enterprise” contains specific

inclusions, for example, the activities of a welfare organisation and a foreign-donor funded project,

and exclusions, for example, activities involving the making of exempt supplies.

Non-resident suppliers of certain electronic services set out in a Regulation8 are also required to

register for VAT in respect of taxable supplies of electronic services if the total value of the taxable

supplies exceeds R50 000.9 With effect from 1 April 2015, electronic services for purposes of VAT

registration include those transactions where at least two of the following circumstances are

present:10

• The recipient of those electronic services is a South African resident;

• Payment to the non-resident supplier in respect of the supply of electronic services originates

from a South African bank account;

• The recipient has an address in South Africa to which the tax invoice for the electronic

services supplied by the non-resident will be delivered.

Persons that are liable to register for VAT must complete a form VAT101 (Application for Registration)

which must be submitted to the local SARS office not later than 21 business days from the date of

liability. For non-resident suppliers of electronic services the completed form must be e-mailed

together with the supporting documents to SARS at eCommerceRegistration@sars.gov.za.

A person who is registered, or who is obliged to register is referred to as a “vendor”. (Note: it is the

legal person and not the trading name of a business which is required to register. Refer to

paragraph 2.7 for more details.)

6 The R1 million compulsory VAT registration threshold applies to the total value of taxable supplies (turnover)

and not the net income (profit) that your business has made for the period.

7 From 1 April 2014, the requirement of a reasonable expectation to exceed R1 million taxable supplies is

replaced with the requirement that the threshold will be exceeded in terms of a contractual obligation in

writing.

8 The regulations were published in Government Gazette No. 37489 of 28 March 2014 as Government Notice

No. R221.

9 Paragraph (b)(vi) of the definition of “enterprise” read with section 23(1A).

10 With effect from 1 April 2015. Before this amendment, non-resident suppliers of electronic services were

liable for VAT registration if the R50 000 threshold was exceeded and supplies were either made to South

African residents or payment in respect of such services originated from a South African bank account.

VAT 404 – Guide for Vendors Chapter 2

7

The term “person” includes the following:

• Individuals.

• Partnerships and bodies of persons.

• Private and public companies, share block companies and close corporations.

• Public authorities11 and municipalities (previously called local authorities).

• Associations not for gain such as clubs and welfare organisations.

• Insolvent and deceased estates.

• Trust funds.

• Foreign donor funded projects.

The following are circumstances where you will not be required or allowed to register:

• Only exempt supplies are made (refer to Chapter 7 for examples).

• Employees who earn a salary or wage from their employers (excluding independent

contractors).

• The supplies are made for example, by a foreign branch located in another tax jurisdiction.

• Hobbies or any private recreational pursuits not conducted in the form of a business.

• Private occasional transactions. For example, the sale of domestic/household goods,

personal effects or a private motor vehicle.

If your sales or fees earned from making taxable supplies are less than R50 000,12 you can register

for VAT voluntarily if you meet certain conditions.13 This type of registration is referred to as a

voluntary registration.14 Refer to paragraph 2.5.

2.2 WHERE MUST I REGISTER?

The VAT101 application for registration must be submitted in person at the SARS office or Large

Business Centre (LBC)15 nearest to the place where your business is situated or carried on. This

means that, in the case of a sole proprietor the individual concerned must submit the application in

person, or in the case of any other person such as a partnership, company or trust fund, the relevant

representative vendor must submit the application in person. Alternatively, a registered tax

practitioner may appear in person on behalf of the applicant. A vendor that has several

enterprises/branches/divisions which will operate under one VAT registration number, should register

in the area where the main enterprise/branch/division is located.

2.3 WHAT DOCUMENTS MUST I SUBMIT WITH MY APPLICATION?

2.3.1 General requirements

It is very important that you submit the correct documents with your application to register; otherwise

there may be a delay in obtaining your VAT registration number. Refer to VAT-REG-02-G01 – Guide

for Completion of VAT Registration Application Forms – External Guide and VAT-REG-01-G02 – VAT

Registration Guide for Foreign Suppliers of Electronic Services on the SARS website for a

comprehensive list of documents that must be submitted.

11 Public authorities are generally not registered as vendors. Refer to paragraph 7.8 for more information on

this topic.

12 Note that where the supplies consist of “commercial accommodation”, the threshold is R60 000 and not

R50 000.

13 The date of registration as a vendor in respect of a compulsory and voluntary registration application may be

determined by the Commissioner. The circumstances applicable when a vendor has not met the R50 000

minimum threshold, will be set out in Regulations on voluntary registration. The Regulations are currently in

draft.

14 Certain types of vendors do not have to meet the R50 000 minimum threshold of taxable supplies for

voluntary registration, for example, certain welfare organisations, foreign donor funded projects and

municipalities.

15 Taxpayers whose administration office is the LBC may submit VAT applications directly to the LBC.

However, a SARS branch office will still process the application if it is submitted at the branch.

VAT 404 – Guide for Vendors Chapter 2

8

The TA Act provides for both a single tax account as well as for a single registration process for all tax

types. The single registration process was implemented by SARS on 12 May 2014 through a legal

entity registration as a first step to register, whereafter an entity can subscribe to the various taxes as

required. Refer to the SARS website for the latest information.

SARS will not accept any faxed or photocopied applications for registration. Please also make sure

that where a certified copy of a specific document is required (for example an ID document), that the

actual certified true copy of the original is submitted with the registration application, and not merely a

photocopy thereof. Posted applications will only be processed if applicants are geographically far from

the branch office or due to any form of disability and the applicant cannot physically present the

application.

Once you have been registered, you will receive a Notice of Registration.16 You can also confirm if

your registration has been processed by entering your details under “VAT vendor search” on the

SARS website. [Go to

www.sars.gov.za

eFiling

select VAT Vendor Search in the drop-

down box on the left hand side of the screen].

Allow at least 21 business days for your application to be processed. The Notice of Registration is

issued to you on eFiling if you are a registered eFiler, or it will be sent to your email address, or

posted to the postal address given on your registration application. Should you need a copy of the

Notice of Registration, you can call the SARS national contact centre or visit a SARS branch office for

assistance.

2.3.2 Foreign donor funded projects

The definition of “person” in section 1(1) includes a “foreign donor funded project” (FDFP). An FDFP

means a project established as a result of an international donor funding agreement to supply goods

or services to beneficiaries, to which the South African government is a party. These international

agreements are referred to as Official Development Agreements (ODAs) and normally provide that

the funds donated should only be used for specific, mutually agreed upon programmes and activities,

and cannot be used to pay for any taxes imposed under South African Law.

Any VAT incurred for the purposes of a project administered in terms of an ODA which is binding on

the Republic under section 231(3) of the Constitution and which also contains a requirement that the

funds may not be used to pay any South African taxes, may be refunded. This includes expenses

such as the acquisition of motor cars17 and entertainment which are usually denied. The refund is

effected by allowing the person who is appointed by the foreign donor as being responsible for

administering the ODA and carrying out the project, to register an FDFP and to obtain a refund of the

VAT incurred on the project deliverables.

An FDFP is a separate person for VAT purposes. Should the FDFP be administered by a public

authority, it is not the public authority but the FDFP that qualifies to register for VAT and the input tax

deductions are limited to the VAT incurred on goods or services acquired which are directly in

connection with the implementation of the FDFP (including entertainment expenses). It does not

entitle the public authority concerned to deduct input tax on its normal VAT inclusive capital and

operating costs.

16 With the implementation of the single registration process the VAT registration certificate (VAT103) was

replaced with the new Notice of Registration which is a standard notice of registration across all tax types

(except Customs and Excise).

17 FDFPs are allowed to deduct input tax on the acquisition of a motor car which is applied in carrying out the

objectives of the FDFP.

VAT 404 – Guide for Vendors Chapter 2

9

The FDFP may apply for VAT registration and forward it to the nearest SARS office, together with the

following documents:

• Original certified copy of latest bank statement or ABSA bank eStamped statement or original

letter from the bank.

• Original certified copy of passport / identity document of the representative person.

• Agreement between International Donor Fund and the RSA Government.

The VAT treatment of FDFPs can therefore be summarised briefly as follows:

(i) The FDFP is allowed to register for VAT on the basis that it is deemed to supply services to

the foreign donor to the extent of the donor funding received to carry out the project;

(ii) The deemed services of the FDFP in (i) above are subject to VAT at the zero rate;18

(iii) VAT must still be charged, where applicable, by suppliers of goods and services actually

acquired by the FDFP using donated funds in carrying out the project deliverables;

(iv) The FDFP will deduct input tax to the extent that the expenses in (iii) above relate to the

project, provided that the relevant tax invoices are held etc.

2.3.3 Diesel refund applicants

Should you consume diesel in carrying on an enterprise involved in primary production activities such

as agriculture, mining, fishing and coastal shipping, you can also register for the Diesel Refund

Scheme which is currently administered through the VAT system. VAT registration is a pre-requisite

for participation in the scheme, but make sure that you actually qualify for the Diesel Refund Scheme

before registering, as any incorrect refunds claimed would have to be paid back to SARS, together

with any interest and forfeiture, which may be applicable. A qualifying diesel user may register for the

scheme at the local SARS office by completing form VAT101D and attaching it to the other

documents required above for your VAT registration. Refer to the SARS website under “Customs and

Excise”

“Excise”

“Fuel Petroleum Products”

“Diesel Refund” for more information.

Due to significant technical problems and administrative challenges experienced with the

implementation of the diesel refund system, the government proposed in its 2015 Budget Review to

delink diesel refunds from the VAT system with effect from 1 April 2016 in order to address these

concerns. The system is currently under comprehensive review and SARS, together with the National

Treasury, will hold consultations with affected industries in the process.

2.4 HOW DO I CALCULATE THE VALUE OF TAXABLE SUPPLIES?

The value of taxable supplies (turnover) is calculated on an ongoing basis. At the time of closing off

your books for the month, you need to keep a running total of your turnover for the past 12 months.

Should this total exceed R1 million in any particular month, you must register from the first day of the

next month.19 You also need to consider the next 12 months, because if you have a contractual

obligation in writing to make supplies in excess of R1 million within that 12-month period, you will be

liable to register at the commencement of any month where the total value of the taxable supplies will

exceed R1 million in the period of 12 months counting from the commencement of the said month.

You must register within 21 business days of so becoming liable to register.20

18 Section 8(5B) read with section 11(2)(q). Note that the zero rate in terms of these provisions does not extend

to any actual supplies of goods or services acquired by the FDFP from local suppliers as contemplated in

point (iii).

19 In the case of non-resident suppliers of certain electronic services to South African residents, the supplier

must register at the end of any month in which the threshold of R50 000 in that case has been exceeded.

20 Section 22 of the TA Act.

VAT 404 – Guide for Vendors Chapter 2

10

Example 2 – Calculating the total value of taxable supplies for registration purposes

Mr Z trades as “ABC Construction”. He tenders for a building contract of R5 million. Presently the

fees earned from construction activities average R10 000 per month (R120 000 per consecutive

12-month period).

If ABC Construction is not awarded the contract, Mr Z has an option to register voluntarily, or

elect not to register. However, if awarded the contract, Mr Z would immediately know that he is

going to exceed the R1 million compulsory VAT registration threshold. In this case, Mr Z would be

required to register and would have 21 business days in which to do this, calculated from the first

day of the month in which the value of taxable supplies will exceed R1 million in a period of 12

months commencing on that month.

The table below gives a general indication of what to include and exclude when calculating the value

of taxable supplies, to determine if you are liable for VAT registration.

Include

Exclude

•

Sales/fees earned from goods and

services supplied in the RSA

• Sales from stock or capital assets when

closing down your business or

substantially reducing (permanently) the

scale of your business

•

Sale of goods exported to an export

country

• Sales from old plant, machinery or other

capital assets when replacing them with

new assets

• Services rendered outside the RSA • Any exempt supplies

•

Sales from all branches and divisions

falling under that person inside the RSA

• Donations received by associations not for

gain and welfare organisations

• Deemed supplies (refer to Chapter 6) • VAT

2.5 VOLUNTARY REGISTRATION

2.5.1 General

As mentioned in paragraph 2.1 above, a person can apply for voluntary registration even though the

total value of taxable supplies is less than R1 million. There is, however, a requirement that the value

of taxable supplies made must have already exceeded the minimum threshold of R50 000 in the past

12-month period.21 There are also certain other exceptional cases which are to be dealt with in

Regulations22, which prescribe other conditions which must be met if the applicant has not met the

minimum threshold at the time of applying for voluntary registration.

Section 23(3)(b)(ii) – Under certain circumstances, a person may apply to register voluntarily even if the

threshold of R50 000 in taxable supplies in a consecutive 12-month period has not yet been attained.

Such registrations are subject to the conditions and exclusions to be dealt with in a Regulation which

provides for a person to register voluntarily if the person –

• has made taxable supplies which do not exceed R50 000, or

• has not made any taxable supplies as yet,

21 Section 23(3)(b)(i).

22 Refers to regulations that may be made by the Minister under section 23(3)(b)(ii) or 23(3)(d), setting out

conditions to be met for voluntary registration when the minimum threshold has not been met.

VAT 404 – Guide for Vendors Chapter 2

11

and the person can satisfy the Commissioner that it can reasonably be expected that taxable supplies

in excess of R50 000 in the following 12-month period commencing from the date of registration will

be made.

Section 23(3)(d) – In cases where the nature of the business activity is such that it is only possible to

make taxable supplies after a certain period of time, the Commissioner must be satisfied that it is

reasonable to conclude that the minimum threshold will be exceeded in a 12-month period. (For

example, plantation farming and mining activities.)

Note that it may be advantageous for a person to register voluntarily where goods or services are

supplied mainly to other vendors and where the customer concerned will be able to deduct the VAT

charged as input tax. It will generally not be advantageous for a person to register voluntarily where –

• the main or only supplies consist of the supply of services and there are very few taxable

expenses on which input tax can be deducted, for example, the enterprise’s main expense is

salaries and wages; or

• most of the supplies are made to final consumers who are not registered for VAT.

Remember that if you choose to register, you will have to carry out all the duties of a vendor. For

example, you will have to charge VAT, submit returns, make VAT payments on time and keep proper

records for at least five years. If you decide to register, remember that you can only charge VAT on

taxable supplies. You may not charge VAT on supplies which are exempt from VAT or supplies which

fall outside the scope of VAT. (These are supplies which are not in the course or furtherance of your

“enterprise”). Refer to Chapter 7 for more details and for examples of exempt supplies.

2.5.2 Turnover Tax for micro businesses

Turnover Tax was initially introduced as a simplified tax system for micro businesses as an alternative

to the current income tax and VAT systems. Micro businesses that made taxable supplies in excess

of the minimum threshold of R50 000 in a 12-month period (or R60 000 in the case of suppliers of

“commercial accommodation”) were previously not allowed to register voluntarily for VAT if registered

for Turnover Tax. However, with effect from 1 March 2012 a qualifying micro business that is

registered for Turnover Tax may also choose to register for VAT provided that all the conditions for

voluntarily registration are met.23

For more information, refer to paragraph 2.8 as well as the SARS website where you can find the

Guide for the Administration of Turnover Tax and the Guide for Micro Businesses.

2.6 REFUSAL OF A VOLUNTARY REGISTRATION APPLICATION24

The Commissioner will not allow any person to register voluntarily for VAT if the applicant –

• has no fixed place of residence or business in RSA; or

• does not keep proper accounting records; or

• has not opened a banking account in the RSA; or

• has previously been registered as a vendor under VAT or General Sales Tax (GST) and failed

to perform the duties of a vendor; or

• has not met the minimum threshold requirement of R50 000 in respect of taxable supplies

made in a preceding period of 12 months.25

23 The new rules for registration will not have any effect on the turnover tax system.

24 Section 23(7). A person cannot register under the Regulation relating to section 23(3) if the registration was

refused in terms of this provision.

25 This requirement will not apply to voluntary registrations approved by the Commissioner in terms of the

Regulations to be issued as referred to in section 23(3)(b) and (d).

VAT 404 – Guide for Vendors Chapter 2

12

2.7 SEPARATE REGISTRATION (BRANCHES, DIVISIONS AND SEPARATE

ENTERPRISES)

A vendor may register separately any enterprises, branches or divisions carried on for VAT purposes.

This means that it is possible for a vendor to have more than one VAT registration number if the

enterprise is carried on in branches or divisions.26 A separate form VAT102e must be completed for

each enterprise/division/branch for which a separate registration is required. It is important to note

that a person who operates several enterprises, or who operates an enterprise in branches or

divisions cannot avoid the liability to register for VAT by considering the turnover of each branch or

division individually. In such cases, the turnover of all the enterprises/divisions/branches must be

added together to determine the total value of the supplies. Only associations not for gain (including

welfare organisations) can apply to be excluded from this rule. There are two conditions under which

separate registration can be granted for any separate enterprise, division or branch, namely:

• An independent system of accounting for each business must be maintained.

• The entity must be capable of being separately identified (that is, either by the nature of

the activities or the geographic location).

The implication of separate registration is that each separately registered enterprise/division/branch is

treated as a vendor in its own right. Each enterprise/division/branch will therefore be required to –

• retain the same tax period as the main branch (except farmers in certain cases);

• submit separate returns and payments;

• retain the same accounting basis as the parent vendor and keep its own accounting

records; and

• remain registered until cancelled by the parent body or until the parent body’s registration is

cancelled.

In addition, any transfers of taxable goods or services between the separately registered

enterprises/divisions or branches must be charged with VAT and accounted for on a VAT201 return

covering that period. As with any other supply, the recipient will require a tax invoice before being able

to deduct input tax.

Example 3 – Separate registrations and the liability to register

Mrs N is a sole proprietor and trades under the following three trading names:

N’s Curry Den G’s Florists B’s Shoe Retailers

Turnover of R510 000 Turnover of R390 000 Turnover of R220 000

The combined turnover of the three businesses is R1 120 000. Since the type of supplies being

made are not exempt (refer to Chapter 7 for examples of exempt supplies), they will constitute

“taxable supplies”.

The “person” carrying on all three businesses is Mrs N, a sole proprietor. Since she is liable for

VAT registration, she is referred to as a “vendor” and must account for VAT at 14% on all the

sales in each business from the date of registration as a vendor. Mrs N will only be issued with

one VAT registration number, but she can apply for three separate VAT numbers if she meets the

two conditions for separate registration, as mentioned in paragraph 2.7 above. If SARS agrees to

allocate separate VAT registration numbers, each separate business is deemed to be a separate

person and VAT must be charged on supplies between the separate businesses, as well as to

any other person.

26 Section 23(5).

VAT 404 – Guide for Vendors Chapter 2

13

2.8 CANCELLATION OF REGISTRATION

A vendor may apply for cancellation of registration if the value of taxable supplies is less than the

compulsory registration threshold of R1 million in any consecutive period of 12 months.

The Commissioner will also deregister27 a vendor if –

• the enterprise closes down and will not commence again within the next 12 months; or

• the enterprise never actually commenced or will not commence within the next 12 months; or

• the person opts out of the VAT system and migrates to the Turnover Tax system.28

Whether you want to voluntarily deregister, or your circumstances have changed so that you are no

longer liable or no longer eligible to be registered as a vendor, you should promptly inform the SARS

office where you are registered in writing of your situation. Cancellation of registration normally takes

effect from the last day of the tax period in which the vendor ceases trading. However, in the case of a

voluntary deregistration, the Commissioner will decide the date of deregistration and the final tax

period. Remember though, that SARS cannot completely deregister you until all outstanding liabilities

or obligations incurred under the VAT Act have been settled or resolved. For example, you cannot be

taken off the VAT register if you still owe SARS returns for past tax periods or if any VAT payments

are outstanding.

The Commissioner may also decide to deregister a person who has successfully applied for voluntary

registration and it subsequently appears that the requirements mentioned under paragraph 2.6 above

have not been met.29

Any of a vendor’s separately registered enterprises/divisions/branches may also be cancelled if –

• the vendor applies in writing;

• the main registration is cancelled; or

• it appears to the Commissioner that the duties under the VAT Act or the TA Act have not

been carried out properly.30

The effect of the cancellation of a branch registration is that all duties revert to the main branch. Refer

to paragraph 6.4: “Deemed Supplies” for the VAT implications of cancelling any VAT registration

number.

Vendors that want to deregister voluntarily have two options. The first option of ordinary deregistration

is where the vendor has no intention to continue as a voluntary VAT registrant. In this case, the

vendor may simply apply to be deregistered on the basis that the value of taxable supplies is less

than R1 million in a 12-month period. In the second option, the vendor can apply to participate in the

Turnover Tax system for micro businesses and may choose to deregister for VAT, as there is no

longer an automatic deregistration from the VAT register.

Refer to the Turnover Tax webpage on the SARS website for more information.

27 From 1 April 2014, the Commissioner has the discretion to deregister any vendor that fails to furnish a VAT

return in respect of a tax period. (Refer to section 24(5)(b).)

28 Note, however, that from 1 March 2012, a person may choose to be registered for VAT as well as Turnover

Tax.

29 From 1 April 2014, the Commissioner has a discretion to cancel the registration of a person that is voluntarily

registered as a vendor under section 23(3)(b) if that person fails to make taxable supplies with a value of R50

000 in the first 12-month period after registration.

30 Refer to Binding General Ruling No.17 (dated 27 March 2013) for more information on the cancellation of

registration of separate enterprises, branches and divisions.

VAT 404 – Guide for Vendors Chapter 3

14

CHAPTER 3

TAX PERIODS

3.1 WHICH TAX PERIODS ARE AVAILABLE?

You are required to submit returns and account for VAT to SARS according to the tax period allocated

to you. Available tax periods cover one, two, four, six or 12 calendar months.31 On acceptance of your

registration by SARS, you will generally be allocated one of these categories. Tax periods end on the

last day of a calendar month. You may, however apply to the SARS branch office in writing for your

tax period to end on another fixed day or date, which is limited to 10 days before or after the end of

the month (the 10-day rule). This must be approved in writing and can only be changed with the

written approval of SARS. Refer to paragraph 3.3 and Binding General Ruling No. 19 (Issue 2) dated

10 March 2014 for more details on tax period cut-off dates.

3.1.1 Two-monthly tax period (Category A or B)

This is the standard tax period, which is generally allocated at the time of registration. Under this

category you are required to submit one return for every two calendar months.

• Category A is a two-month period ending on the last day of January, March, May, July,

September and November.

• Category B is a two-month period ending on the last day of February, April, June, August,

October and December.

3.1.2 Monthly tax period (Category C)

Under this category you are required to submit one return for each calendar month. You will be

registered according to Category C when –

• your turnover exceeds or is likely to exceed R30 million in any consecutive 12-month

period;32

• you have applied in writing for this category; or

• you have repeatedly failed to perform any obligations as a vendor.

You will cease to be registered under Category C if you apply in writing to be allocated to a different

tax period and SARS is satisfied that you meet the requirements of the relevant category. Should your

turnover exceed R30 million subsequent to your registration for VAT, you are required to notify SARS

to amend your registration to a Category C tax period within 21 days of becoming liable to register for

a Category C tax period. Failure to notify SARS may result in interest and penalties being levied. As

from 1 May 2011 all vendors falling within Category C tax period must submit their returns in

electronic format and make payments electronically on eFiling.

31 The TA Act extended the concept of a tax period to include other taxable events (for example, those

envisaged under sections 14, 29, and 30). The TA Act created a simpler and streamlined way of

encapsulating all the filing and payment timeframes (that is, sections 14, 28, 29, 30, and any other “taxable

event”) under the VAT Act. Refer to section 1 of the TA Act, read with section 27.

32 A vendor that operates more than one business, or operates a business with different divisions, branches or

separate enterprise activities must add the sales of all such separate components of the person’s enterprise

together to determine the total turnover. This applies, whether or not permission has been granted to have

separate VAT registration numbers for each component of the enterprise.

VAT 404 – Guide for Vendors Chapter 3

15

3.1.3 Six-monthly tax period (Category D)

Under this category you are required to submit one return for every six calendar months. This is a

category solely for vendors –