Lennox International 2006 2007 (N) LII09AR

User Manual: 2006-2007 (N)

Open the PDF directly: View PDF ![]() .

.

Page Count: 120 [warning: Documents this large are best viewed by clicking the View PDF Link!]

- 300286 financial_.pdf

- PART I

- Item 1. Business

- Item 1A. Risk Factors

- Item 1B. Unresolved Staff Comments

- Item 2. Properties

- Item 3. Legal Proceedings

- Item 4. Submission of Matters to a Vote of Security Holders

- PART II

- Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

- Item 6. Selected Financial Data

- Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

- Item 7A. Quantitative and Qualitative Disclosures About Market Risk

- Item 8. Financial Statements and Supplementary Data

- Item 9. Changes in and Disagreements with Accountants on Accounting and Financial Disclosure

- Item 9A. Controls and Procedures

- Item 9B. Other Information

- PART III

- Item 10. Directors, Executive Officers and Corporate Governance

- Item 11. Executive Compensation

- Item 12. Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters

- Item 13. Certain Relationships and Related Transactions, and Director Independence

- Item 14. Principal Accounting Fees and Services

- PART IV

- Item 15. Exhibits, Financial Statement Schedules

CREATING NEW GROW TH

Innovation:

2 0 0 9 A N N U A L R E P O R T

L E N N O X I N T E R N A T I O N A L I N C .

0

2

4

6

8

10

12

0

200

400

600

800

1000

0

2

4

6

8

10

12

0

100

200

300

400

500

600

700

800

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

0

100

200

300

400

500

600

700

800

20092008200720062005 20092008200720062005 20092008200720062005

20092008200720062005 20092008200720062005

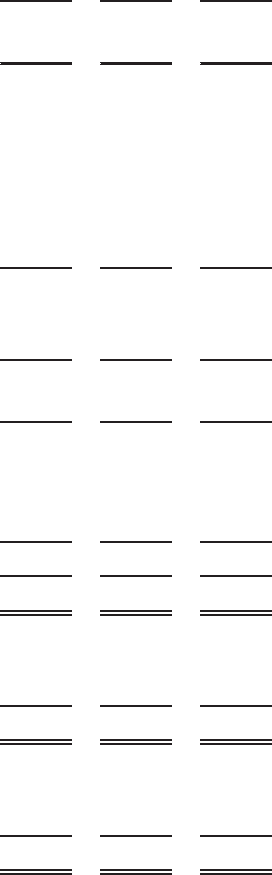

39.04

32.29

41.42

30.61

28.20

Share Price

20092008200720062005 20092008200720062005

Revenue

Segment

Profit Margin

20092008200720062005 20092008200720062005

20092008200720062005 20092008200720062005

$ in millions in dollars

2,848

3,441

3,692

3,662

3,353

Revenue

Segment

Profit Margin

5.8%

7.7%

7.5%

7.0%

6.5%

Segment

Profit Margin

3.1%

3.2%

3.9%

2.9%

2.2%

Segment

Profit Margin

8.6%

9.8%

10.4%

11.4%

12.1%

9.5%

9.7%

10.1%

9.8%

9.4%

Segment

Profit Margin

8.3%

11.2%

11.5%

9.7%

8.3%

595

835

875

751

675

Revenue

535

586

624

601

589

0

1

2

3

4

5

6

7

8

0

500

1000

1500

2000

2500

3000

3500

4000

0

10

20

30

40

50

0

3

6

9

12

15

0

500

1000

1500

2000

Revenue

1,293

1,493

1,670

1,861

1,699

$ in millions

Revenue

513

618

608

530

470

$ in millions

$ in millions

$ in millions

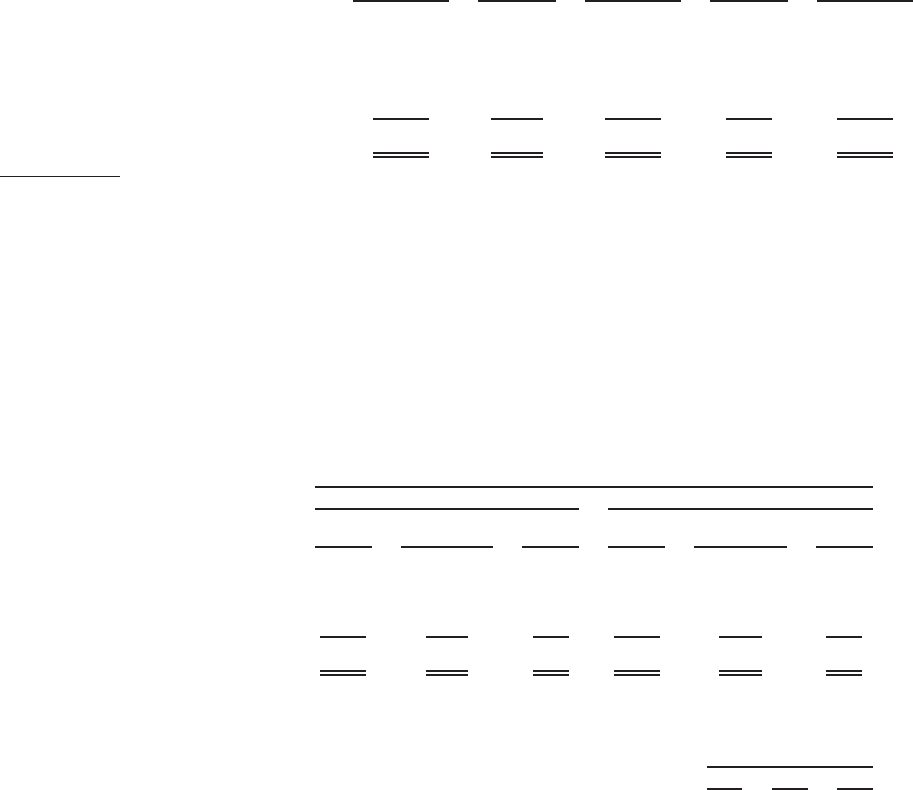

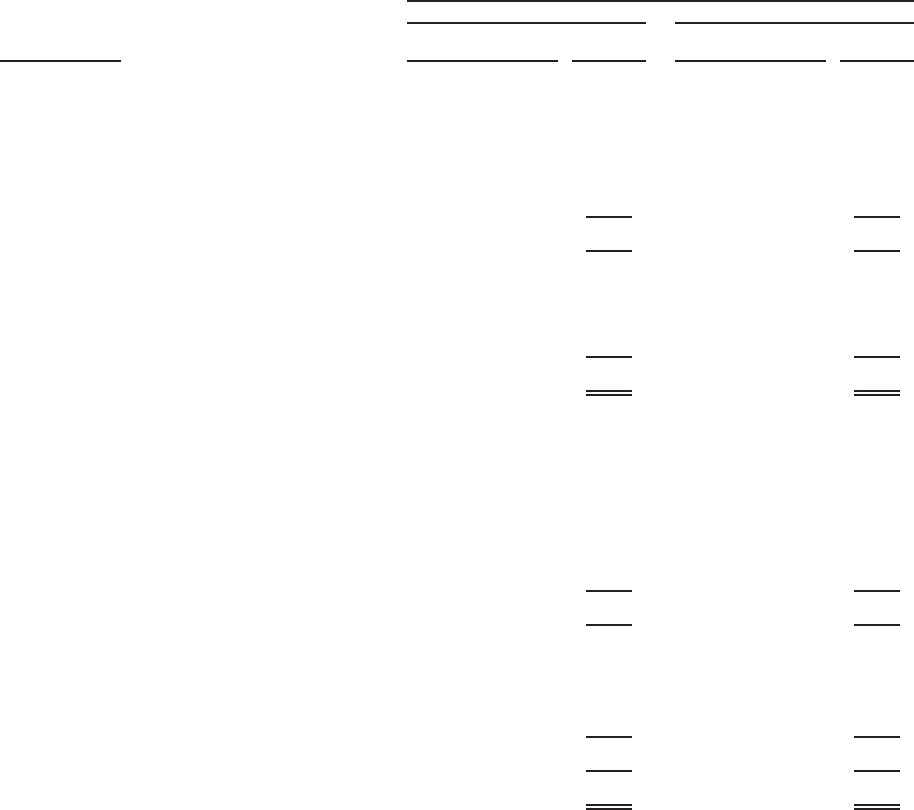

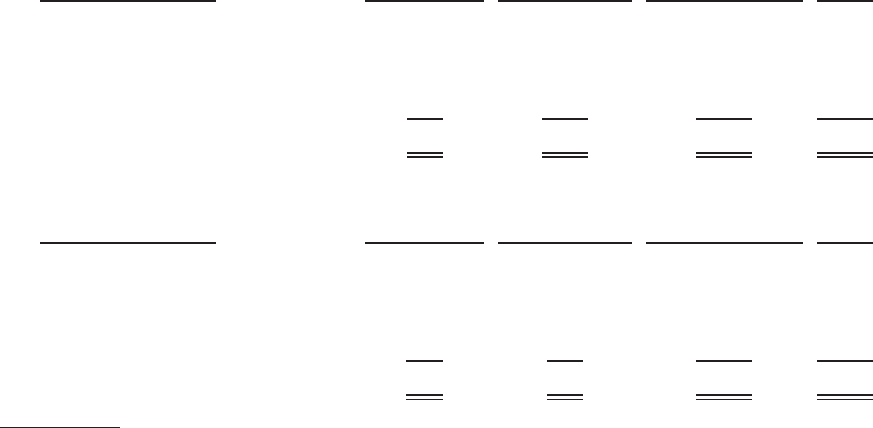

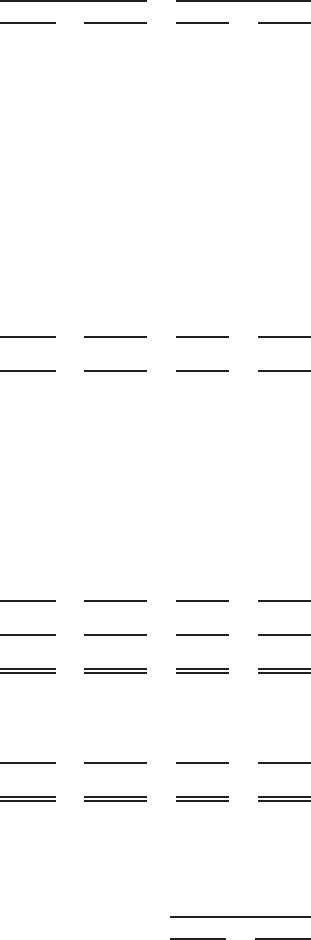

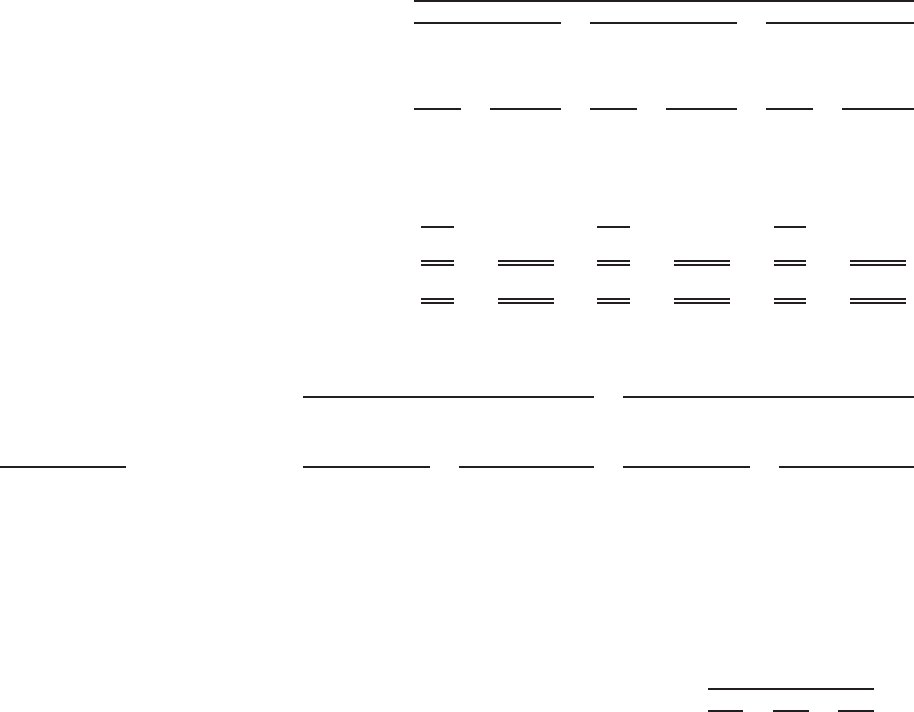

For the Years Ended December 31,

(in millions, except per share data) 2009 2008 2007 2006 2005

Statements of Operations Data

Net Sales $ 2,847.5 $ 3,441.1 $ 3,691.7 $ 3,662.1 $ 3,352.5

Operational Income From Continuing Operations 109.2 218.6 264.9 222.7 248.1

Income From Continuing Operations 61.8 123.8 165.7 167.1 151.7

Net Income 51.1 122.8 169.0 166.0 150.7

Diluted Earnings Per Share From Continuing Operations 1.09 2.12 2.39 2.27 2.12

Dividends Per Share 0.56 0.56 0.53 0.46 0.41

Other Data

Capital Expenditures $ 58.8 $ 62.1 $ 70.2 $ 74.8 $ 63.3

Research and Development Expenses 48.9 46.0 43.6 42.2 40.3

Balance Sheet Data at Period End

Total Assets $ 1,543.9 $ 1,659.5 $ 1,814.6 $ 1,719.8 $ 1,737.6

Total Debt 231.5 420.4 207.9 109.2 120.5

Stockholders’ Equity 604.4 458.6 808.5 804.4 794.4

one

F I N A N C I A L H I G H L I G H T S

Lennox InternatIonaL Inc. (LII),

through our subsidiaries, is a leading provider of climate

control solutions for the heating, air conditioning, and

refrigeration markets around the world. We have

built our business on a heritage of integrity and

innovation dating back to 1895. Today we are focused

on four core businesses: Residential Heating &

Cooling, Commercial Heating & Cooling, Service

Experts, and Refrigeration. Our employees are

dedicated to providing innovative products, trusted

brands, unsurpassed quality, and responsive service.

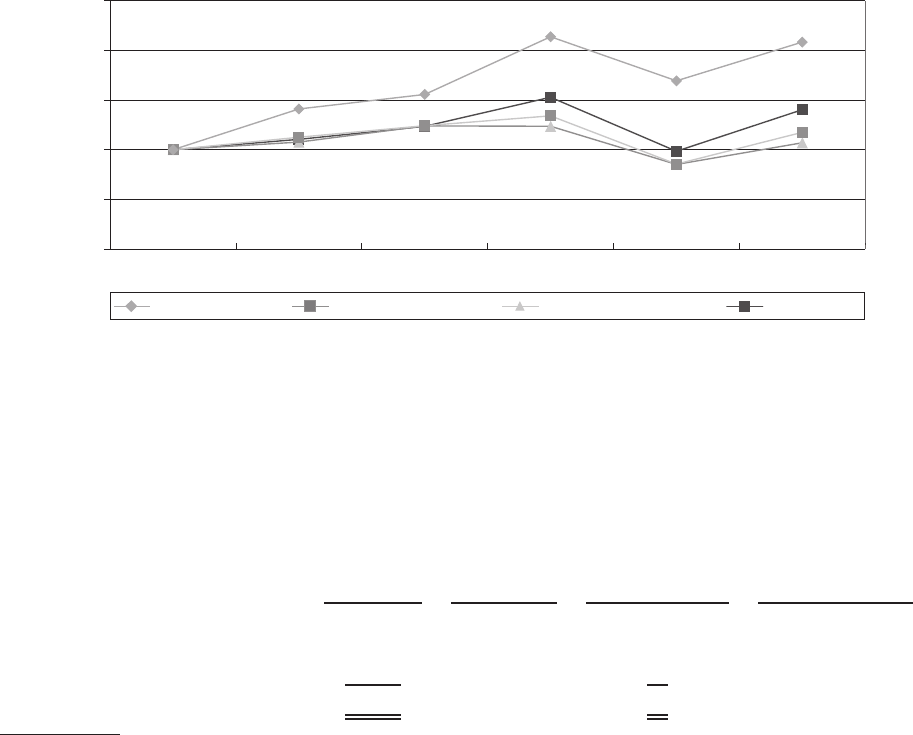

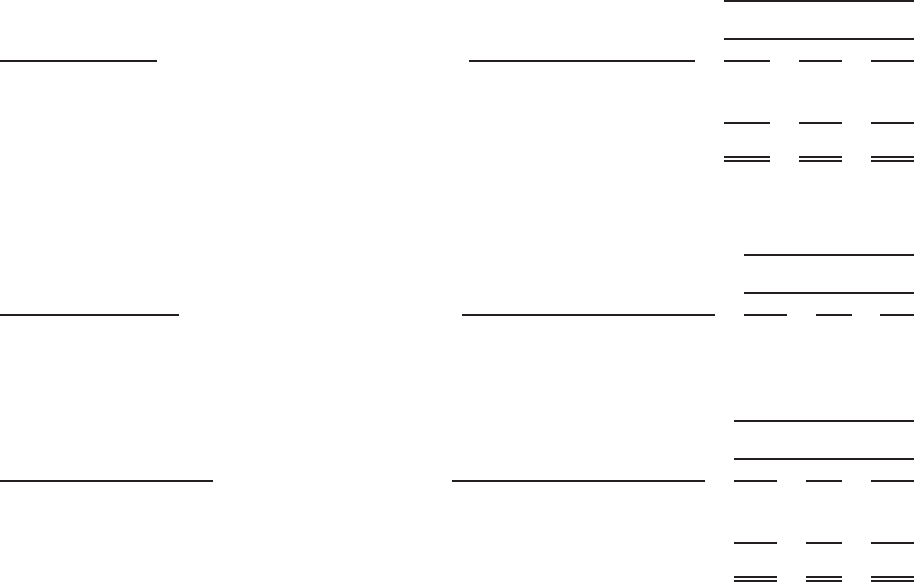

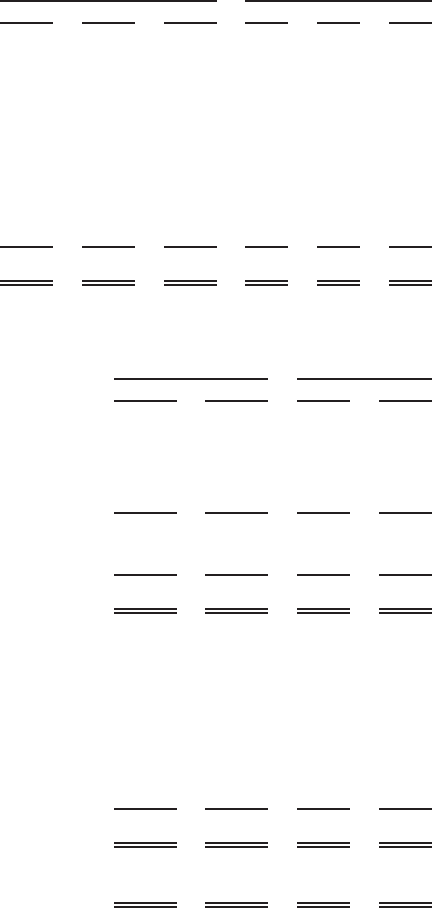

Total company revenue was $2.8 billion, down 17% from the prior year, including a negative one point impact from

foreign exchange. Segment profit margin was down 190 basis points to 5.8%. Diluted earnings per share from

continuing operations was $1.09 compared to $2.12 in the prior year.

Our 2009 cash flow performance was excellent. Cash generated from operations for the year was $225 million.

We invested approximately $58 million in capital assets, resulting in free cash flow of $167 million, up 38% from the

prior year. Total debt as of December 31, 2009 was $232 million, down $189 million from a year ago. Total cash and

cash equivalents were $124 million ending the year.

We expect our end markets to continue their recovery in 2010—and we are ready to take advantage by continued

focus on our strategic priorities, supported by our values and employees worldwide:

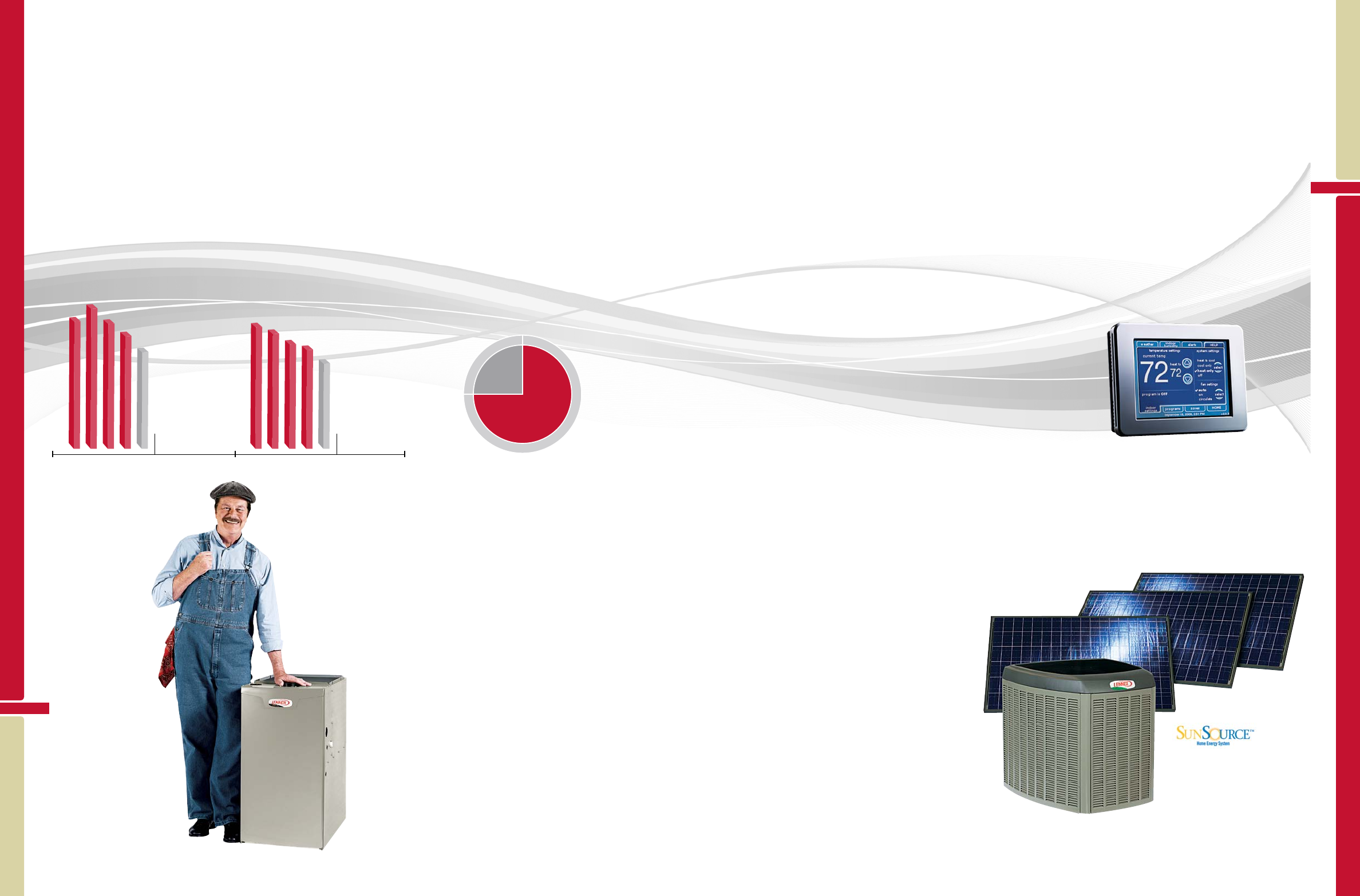

Innovative product and system solutions: From the SunSource™ Home Energy System which harnesses solar power

for heating, cooling and beyond, to our new icomfort Touch™ residential controls system, to our new gas furnace

platform featuring a compact, appliance-like design, we are leading our industry in innovative approaches to home

comfort. Our Energence™ Commercial rooftop line exceeds new efficiency minimums by up to 30%. We are

expanding the uses for our exclusive Hypercore™ microchannel coil technology, which reduces the condenser

refrigerant charge by up to 70%.

Distribution excellence: To drive customer service and market share gains, we made rapid progress in our multi-year

initiative to double our distribution locations across North America, significantly increasing our same day/next day

service levels. Early operational performance is tracking ahead of expectations, with completion on target for 2012.

Effectively leveraging scale to compete locally, Service Experts has implemented an enterprise-wide operating system,

a national call center, consistent standards of excellence, and field automation to enhance productivity.

To Our

Stockholders

Competing in challenging markets, Lennox International delivered

solid earnings and outstanding cash flow performance in 2009.

We continued to reduce our cost structure while making trans-

formational investments in the business. Building on our heritage

of innovation, we introduced an exciting array of industry-leading

new products. We also made excellent progress on expanding

our North American distribution. Armed with a strong balance

sheet, a portfolio of highly innovative new products and a growing

distribution network, we are participating in early cycle markets

with significant pent-up demand—and are well positioned to take

advantage as our markets recover.

Todd M. Bluedorn Richard L. Thompson

Manufacturing and sourcing excellence: Over the past two years, we have reduced the number of our factories

from 28 to 18 and decreased our global manufacturing footprint by 2.7 million sq. ft. We moved more production

to our 325,000 sq. ft. factory in Saltillo, Mexico in 2009, closing our facility in Blackville, South Carolina. Continuing

to extend our global supply chain and qualify the best suppliers, our material spend outside the U.S. and Canada

increased to 25% in 2009, with savings of $20 million.

Geographic expansion: The refrigeration business in China remains our single largest international growth opportunity,

with estimates for the China cold storage market showing threefold growth over the next 10 years. Continuing to

localize our products, we doubled the size of our Wuxi, China manufacturing facility in 2009 to 100,000 sq. ft.,

including a global R&D center. China will not be material to our results in 2010, but we remain very excited about

its growth potential.

Expense reduction: We have decreased our salaried headcount by 20% over the past two years, including a 13%

reduction in 2009. Combined with our factory rationalization initiatives, we have lowered our cost structure more

than $50 million since 2007, with $25 million coming in 2009.

Innovation at every level—from industry-leading new products, to distribution, manufacturing, sourcing, and other

key areas—is driving an exciting future for Lennox International. As the markets recover, we have laid a strong

foundation for success. Through that same spirit of innovation, we will continue to strengthen our balance sheet,

sustain and expand our premium position, and drive new growth and value for our stockholders.

Richard L. Thompson

Chairman of the Board

Todd M. Bluedorn

Chief Executive Officer

L E N N O X I N T E R N A T I O N A L I N C .

three

two

2009

Revenue(1)

2009

Segment Profit(2)

2009

Business Mix

Replacement

RNC*

North America

Europe

Residential

Commercial

Americas

Asia Pacific

Europe

2009

Geographic Revenue Mix

2009

Customer Mix

2009

Geographic Revenue Mix

75%

25%

70%

30%

80%

20%

45%

20%

35%

22%

7% 49%

22%

20%

18% 44%

18%

(1) Excluding eliminations

(2) Excluding eliminations and

unallocated corporate expense

*Residential New Construction

L E N N O X I N T E R N A T I O N A L I N C .

five

four

LENNOX INTERNATIONAL

OPERATES IN 4 KEY BUSINESSES:

REFRIGERATION

We are a leading provider of commercial refrigeration systems in

markets around the world. Our products are primarily used to

preserve food and other perishables in supermarkets, convenience

stores, restaurants, warehouses, and distribution centers, in addition

to other applications such as data center cooling and for

pharmaceutical and industrial processes.

RESIDENTIAL HEATING & COOLING

We offer a wide range of home heating and cooling equipment for

both the residential replacement and new construction markets in the

U.S. and Canada. Our product lines include air conditioners, furnaces,

heat pumps, hearth products, and indoor air quality equipment that

improve indoor comfort.

SERVICE EXPERTS

We are the service company consumers trust for their heating, cool-

ing, and indoor air quality needs. We operate service centers in the

U.S. and Canada that sell, install, maintain, and service heating and

cooling equipment for residential and light commercial applications in

metropolitan areas.

2009

Revenue(1)

2009

Segment Profit(2)

2009

Business Mix

Replacement

RNC*

North America

Europe

Residential

Commercial

Americas

Asia Pacific

Europe

2009

Geographic Revenue Mix

2009

Customer Mix

2009

Geographic Revenue Mix

75%

25%

70%

30%

80%

20%

45%

20%

35%

22%

7% 49%

22%

20%

18% 44%

18%

(1) Excluding eliminations

(2) Excluding eliminations and

unallocated corporate expense

*Residential New Construction

COMMERCIAL HEATING & COOLING

We provide indoor comfort solutions for low-rise office buildings,

schools, restaurants, retail establishments, and other light commercial

applications in North America and Europe. Products include packaged

rooftop units, split systems, commercial controls, indoor air quality

systems, and related equipment.

Our Residential business advanced its heritage of innovation with new

products that transform traditional ideas of home comfort and move

us into new markets.

The SunSource™ Home Energy System uses solar power for heating,

cooling and beyond, while sending any excess power back to the utility

company—which could entitle homeowners to utility bill credits. In the

future, the most efficient Lennox® air conditioners and heat pumps will

come “solar ready.”

Using its large, highly intuitive touchscreen interface, our new icomfort

Touch™ thermostat can be programmed in seconds to

customize a more energy-efficient heating or cooling

environment.

0

2

4

6

8

10

12

0

200

400

600

800

1000

0

2

4

6

8

10

12

0

100

200

300

400

500

600

700

800

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

0

100

200

300

400

500

600

700

800

20092008200720062005 20092008200720062005 20092008200720062005

20092008200720062005 20092008200720062005

39.04

32.29

41.42

30.61

28.20

Share Price

20092008200720062005 20092008200720062005

Revenue

Segment

Profit Margin

20092008200720062005 20092008200720062005

20092008200720062005 20092008200720062005

$ in millions in dollars

2,848

3,441

3,692

3,662

3,353

Revenue

Segment

Profit Margin

5.8%

7.7%

7.5%

7.0%

6.5%

Segment

Profit Margin

3.1%

3.2%

3.9%

2.9%

2.2%

Segment

Profit Margin

8.6%

9.8%

10.4%

11.4%

12.1%

9.5%

9.7%

10.1%

9.8%

9.4%

Segment

Profit Margin

8.3%

11.2%

11.5%

9.7%

8.3%

595

835

875

751

675

Revenue

535

586

624

601

589

0

1

2

3

4

5

6

7

8

0

500

1000

1500

2000

2500

3000

3500

4000

0

10

20

30

40

50

0

3

6

9

12

15

0

500

1000

1500

2000

Revenue

1,293

1,493

1,670

1,861

1,699

$ in millions

Revenue

513

618

608

530

470

$ in millions

$ in millions

$ in millions

L E N N O X I N T E R N A T I O N A L I N C .

seven

six

RESIDENTIAL

HEATING & COOLING:

TRANSFORMING THE TRADITIONS

OF HOME COMFORT

The new Lennox® SLP98V gas furnace

is the quietest and most efficient gas

furnace you can buy.

The compact 33-inch design of our new gas furnace platform can be

used in a wider variety of applications. Used in combination with our

precise comfort technology that automatically adjusts heat and airflow

in increments as small as 1%, homeowners can redefine comfort. The

smaller size also uses fewer parts and raw materials, allowing for up to

50% more furnaces to be shipped at a time and overall improved envi-

ronmental sustainability.

All of our new products are supported by continued progress in imple-

menting our enhanced logistics strategy, eventually doubling our distri-

bution locations throughout North America—a key to success in our

industry, where physical distribution drives market share gains. This

strategy is well underway, performing ahead of expectations, and

remains on target for completion in 2012.

Armed with a broad array of new, highly innova-

tive products and enhanced, customer-focused

distribution for our popular Lennox®, ADP,

Armstrong Air®, AirEase®, Aire-Flo™,

Ducane™, Concord®, and Magic-Pak™ brands,

we have sown the seeds for growth as the

Residential market recovers.

The new icomfort Touch™ helps

create custom home comfort

in seconds.

The Lennox SunSource™ Home

Energy System harnesses solar

power for heating, cooling, and

other home uses.

For more information on individual product claims, refer to Lennox advertisements or visit www.lennox.com.

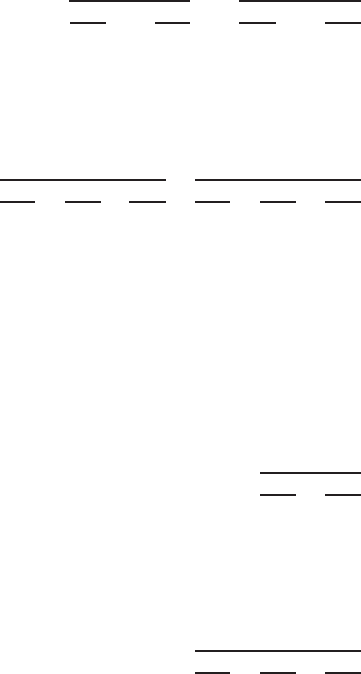

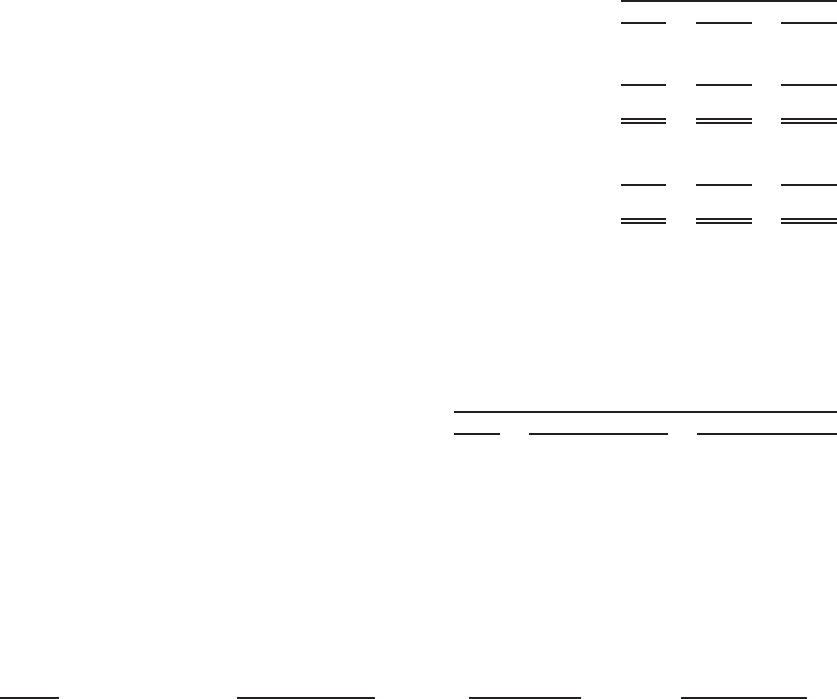

2009

Revenue(1)

2009

Segment Profit(2)

2009

Business Mix

Replacement

RNC*

North America

Europe

Residential

Commercial

Americas

Asia Pacific

Europe

2009

Geographic Revenue Mix

2009

Customer Mix

2009

Geographic Revenue Mix

75%

25%

70%

30%

80%

20%

45%

20%

35%

22%

7% 49%

22%

20%

18% 44%

18%

(1) Excluding eliminations (2) Excluding eliminations and

unallocated corporate expense

*Residential New Construction

Featuring the intuitive Prodigy™

control module, Energence™ roof-

top units exceed 2010 efficiency

minimums by up to 30 percent.

L E N N O X I N T E R N A T I O N A L I N C .

nine

eight

COMMERCIAL

HEATING & COOLING:

LEADING INTO THE NEXT GENERATION

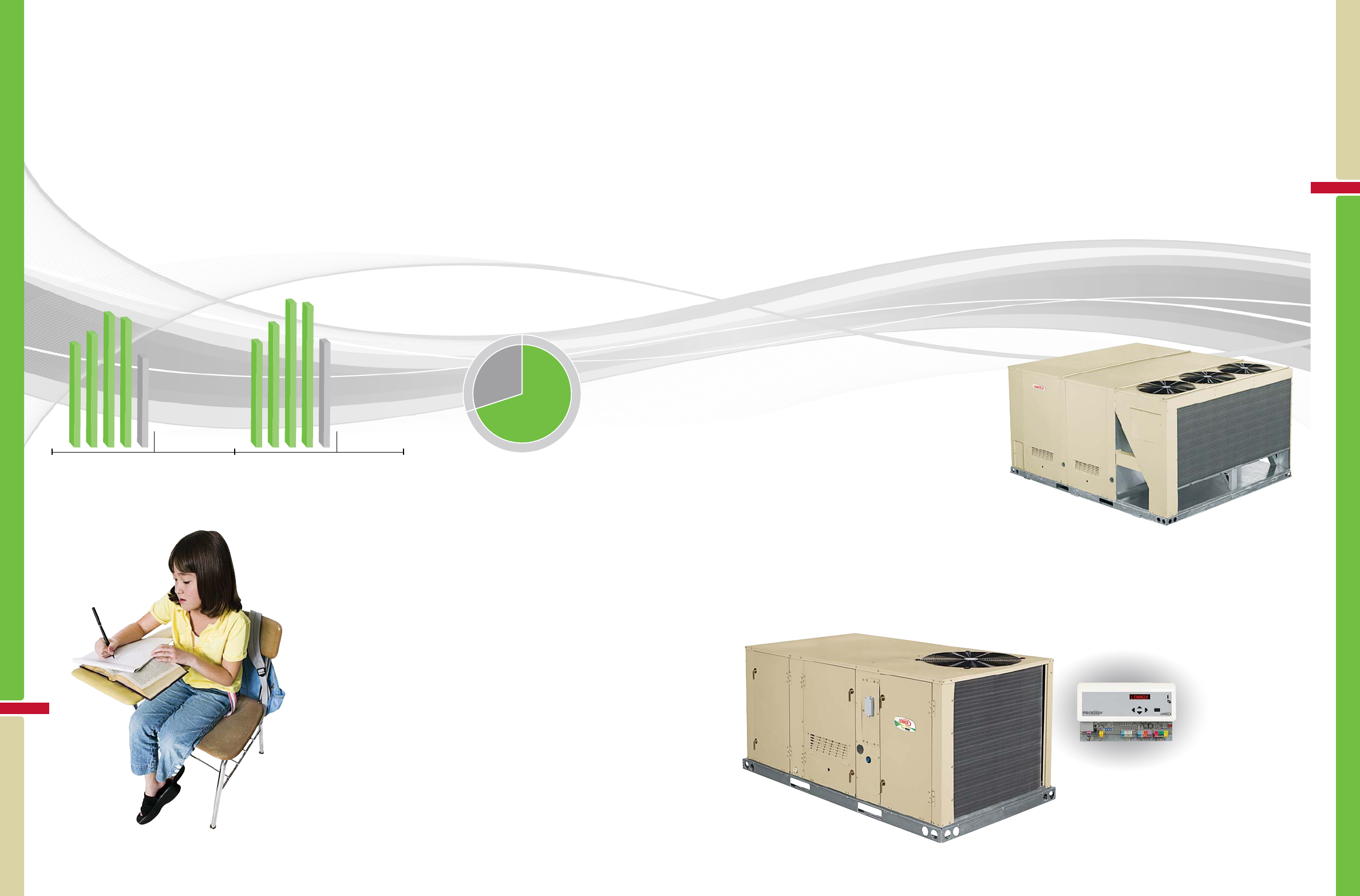

Introduced as the next generation of commercial rooftop design, the

Energence™ 3- to 50-ton rooftop unit product line exceeds new 2010

efficiency minimums by up to 30 percent, with ratings up to 17 SEER

and 12.8 EER—helping buildings qualify for the most LEED® points. Its

advanced Prodigy™ controller provides intelligent real-time unit diagnos-

tics and enhances reliability, while its color-keyed SmartWire™ system

reduces labor installation and service time. The innovative Energence

line will help us to continue growing our industry-leading position in

National Accounts.

Primarily targeting significant growth potential in the emergency replace-

ment market, our new competitive Landmark™ rooftop line is compliant

with new national minimum efficiency standards. Preconfigured Landmark

units are stocked at depots across North America for next-day delivery

in most cases.

In Europe we expanded our Neosys™ line of air-

cooled chillers, which utilize state-of-the-art micro-

channel coil technology to help make them one of

the most energy-efficient, environmentally friendly

products in their class. We also continued to effectively

restructure our European operations by reshaping our

product lineup, streamlining distribution, and selling a

non-core business in the Czech Republic.

Seeking out new business potential in the U.S., we restructured and

refocused our sales operations, developing innovative approaches to

focus on major opportunities in the more specialized school and govern-

ment markets. With a rich lineup of leadership products for all markets

and refocused sales and distribution operations around the world, we

are making the next generation of Commercial HVAC a reality today.

We have developed innovative products and

approaches to focus on major opportunities

in the growing school market.

Our new competitive Landmark™ rooftop line

targets significant growth potential in the

emergency replacement market.

For more information on individual product claims, refer to Lennox advertisements or visit www.lennox.com.

2009

Revenue(1)

2009

Segment Profit(2)

2009

Business Mix

Replacement

RNC*

North America

Europe

Residential

Commercial

Americas

Asia Pacific

Europe

2009

Geographic Revenue Mix

2009

Customer Mix

2009

Geographic Revenue Mix

75%

25%

70%

30%

80%

20%

45%

20%

35%

22%

7% 49%

22%

20%

18% 44%

18%

(1) Excluding eliminations (2) Excluding eliminations and

unallocated corporate expense

*Residential New Construction

0

2

4

6

8

10

12

0

200

400

600

800

1000

0

2

4

6

8

10

12

0

100

200

300

400

500

600

700

800

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

0

100

200

300

400

500

600

700

800

20092008200720062005 20092008200720062005 20092008200720062005

20092008200720062005 20092008200720062005

39.04

32.29

41.42

30.61

28.20

Share Price

20092008200720062005 20092008200720062005

Revenue

Segment

Profit Margin

20092008200720062005 20092008200720062005

20092008200720062005 20092008200720062005

$ in millions in dollars

2,848

3,441

3,692

3,662

3,353

Revenue

Segment

Profit Margin

5.8%

7.7%

7.5%

7.0%

6.5%

Segment

Profit Margin

3.1%

3.2%

3.9%

2.9%

2.2%

Segment

Profit Margin

8.6%

9.8%

10.4%

11.4%

12.1%

9.5%

9.7%

10.1%

9.8%

9.4%

Segment

Profit Margin

8.3%

11.2%

11.5%

9.7%

8.3%

595

835

875

751

675

Revenue

535

586

624

601

589

0

1

2

3

4

5

6

7

8

0

500

1000

1500

2000

2500

3000

3500

4000

0

10

20

30

40

50

0

3

6

9

12

15

0

500

1000

1500

2000

Revenue

1,293

1,493

1,670

1,861

1,699

$ in millions

Revenue

513

618

608

530

470

$ in millions

$ in millions

$ in millions

ten

L E N N O X I N T E R N A T I O N A L I N C .

eleven

SERVICE EXPERTS:

DRIVING LOCAL MARKET SUCCESS

THROUGH NATIONAL EFFICIENCIES

Completing our Project FAST (Field Automation for Service Technicians)

implementation in 2009, all of our residential service technicians now use

a wireless handheld device to improve inventory control and cash flow,

while standardizing and consolidating the closing of work orders. Plans to

further enhance technician productivity through FAST are in progress.

Our national online Customer Satisfaction Program asked for customer

feedback to measure how they perceived our centers. The program

provided performance data that is driving business efficiencies across

our organization, as well as generating new customer referrals.

A new three-tiered selling program, focusing on three levels of sales

experience (new, experienced, and top sellers), resulted in participant

sales closing rates and average sales tickets above our national averages.

We plan to reinforce the program and enhance sales leadership training

for center managers.

As part of our cost reduction and process improvement initiatives, we

consolidated our two regional account centers to a single location and our

three accounts payable functions to one location, while also centralizing

payroll time entry and compliance from each center to one location.

Along with system enhancements to increase processing efficiency, these

projects are expected to result in significant cost savings in 2010.

Investing to expand business opportunities, we formed a strategic alliance

with a national supplier to offer insulation and radiant barriers to our

U.S. customers, with the supplier providing installation through their

national network. We will continue to develop innovative programs and

partnerships to increase national efficiencies and expand potential for

future growth.

2009

Revenue(1)

2009

Segment Profit(2)

2009

Business Mix

Replacement

RNC*

North America

Europe

Residential

Commercial

Americas

Asia Pacific

Europe

2009

Geographic Revenue Mix

2009

Customer Mix

2009

Geographic Revenue Mix

75%

25%

70%

30%

80%

20%

45%

20%

35%

22%

7% 49%

22%

20%

18% 44%

18%

(1) Excluding eliminations (2) Excluding eliminations and

unallocated corporate expense

*Residential New Construction

0

2

4

6

8

10

12

0

200

400

600

800

1000

0

2

4

6

8

10

12

0

100

200

300

400

500

600

700

800

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

0

100

200

300

400

500

600

700

800

20092008200720062005 20092008200720062005 20092008200720062005

20092008200720062005 20092008200720062005

39.04

32.29

41.42

30.61

28.20

Share Price

20092008200720062005 20092008200720062005

Revenue

Segment

Profit Margin

20092008200720062005 20092008200720062005

20092008200720062005 20092008200720062005

$ in millions in dollars

2,848

3,441

3,692

3,662

3,353

Revenue

Segment

Profit Margin

5.8%

7.7%

7.5%

7.0%

6.5%

Segment

Profit Margin

3.1%

3.2%

3.9%

2.9%

2.2%

Segment

Profit Margin

8.6%

9.8%

10.4%

11.4%

12.1%

9.5%

9.7%

10.1%

9.8%

9.4%

Segment

Profit Margin

8.3%

11.2%

11.5%

9.7%

8.3%

595

835

875

751

675

Revenue

535

586

624

601

589

0

1

2

3

4

5

6

7

8

0

500

1000

1500

2000

2500

3000

3500

4000

0

10

20

30

40

50

0

3

6

9

12

15

0

500

1000

1500

2000

Revenue

1,293

1,493

1,670

1,861

1,699

$ in millions

Revenue

513

618

608

530

470

$ in millions

$ in millions

$ in millions

L E N N O X I N T E R N A T I O N A L I N C .

thirteen

twelve

REFRIGERATION:

CREATING SUSTAINABLE SOLUTIONS

FOR GLOBAL NEEDS

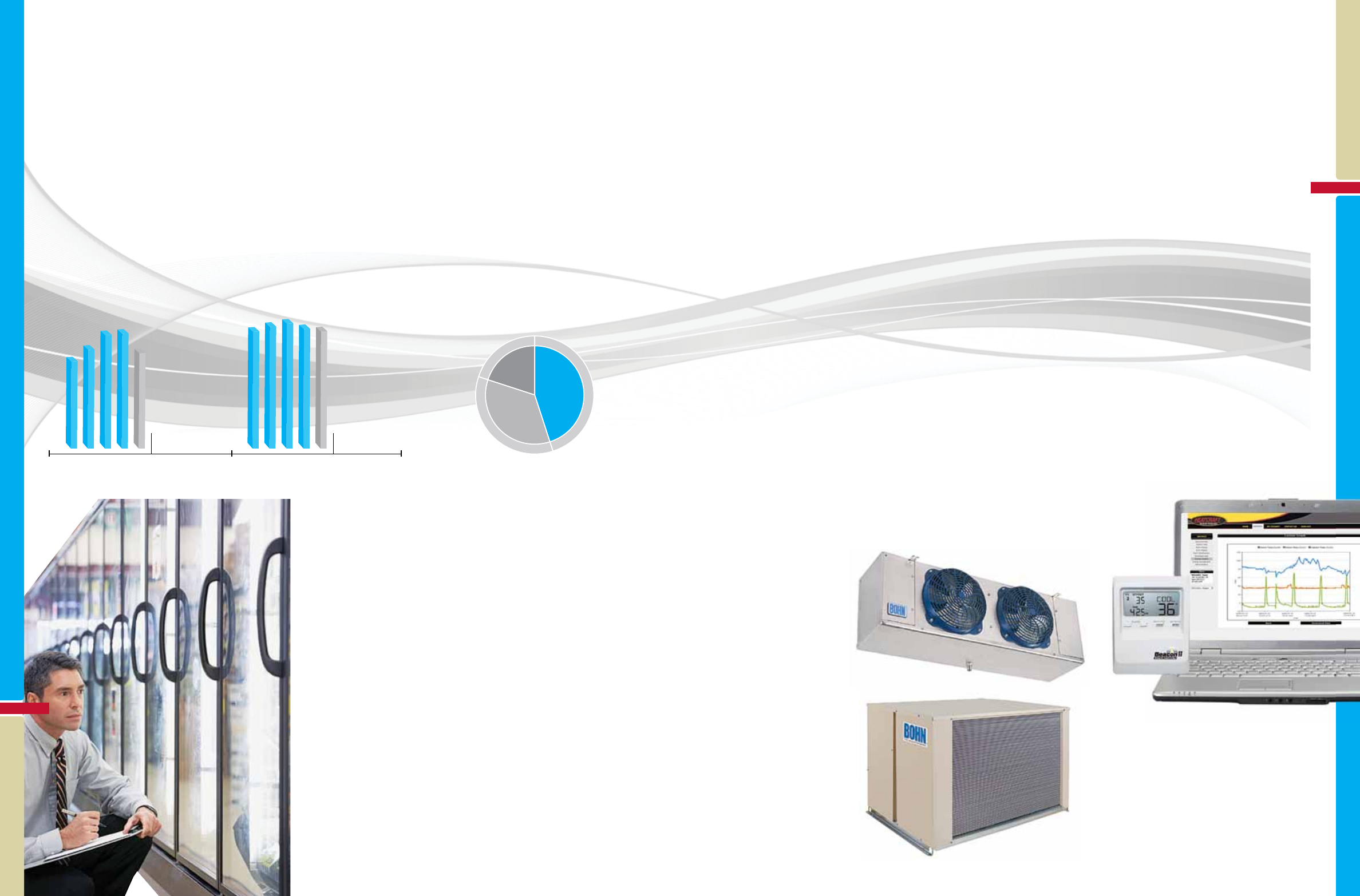

Our product innovations continue to provide unique and sustainable

solutions to our customers. We are expanding the use of Hypercore™

microchannel heat exchanger technology across our global businesses,

resulting in a reduction of over 60 tons of refrigerant to date for our

customers and the environment. When combined with our application

of variable-speed EC motor technologies and proprietary controls, our

optimized systems allow customers to significantly reduce their lifecycle

operational costs, based on energy and refrigerant savings.

We have expanded our innovative product offerings to include monitoring

services for our refrigeration systems. The Heatcraft Vantage™ console

is a web-enabled service helping users track the operating efficiency

of their refrigeration systems, allowing them to remotely monitor and

control multiple refrigeration systems from any geographic location.

We continue to focus on operational excellence through key initiatives

across our global refrigeration businesses. These initiatives include the

further consolidation of our European operations and the completion of

the Australian refrigeration manufacturing operations move to our newly

expanded facility in Wuxi, China. This 100,000 sq. ft. state-of-the-art

operation has nearly doubled in size, allowing us to work more closely

with our Asian customers and support our Australian refrigeration equip-

ment business. Encompassing a new R&D center, our Wuxi expansion

has further positioned our China business for growth by providing a

complete product portfolio to meet this significant market opportunity.

We provide our customers innovative

refrigeration systems that maximize

efficiency, lower environmental impact,

reduce energy costs, and provide real-time

performance data from anywhere via the

Internet.

For more information in individual product claims, refer to Heatcraft Worldwide Refrigeration advertisements or visit www.heatcraftrpd.com.

2009

Revenue(1)

2009

Segment Profit(2)

2009

Business Mix

Replacement

RNC*

North America

Europe

Residential

Commercial

Americas

Asia Pacific

Europe

2009

Geographic Revenue Mix

2009

Customer Mix

2009

Geographic Revenue Mix

75%

25%

70%

30%

80%

20%

45%

20%

35%

22%

7% 49%

22%

20%

18% 44%

18%

(1) Excluding eliminations (2) Excluding eliminations and

unallocated corporate expense

*Residential New Construction

0

2

4

6

8

10

12

0

200

400

600

800

1000

0

2

4

6

8

10

12

0

100

200

300

400

500

600

700

800

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

0

100

200

300

400

500

600

700

800

20092008200720062005 20092008200720062005 20092008200720062005

20092008200720062005 20092008200720062005

39.04

32.29

41.42

30.61

28.20

Share Price

20092008200720062005 20092008200720062005

Revenue

Segment

Profit Margin

20092008200720062005 20092008200720062005

20092008200720062005 20092008200720062005

$ in millions in dollars

2,848

3,441

3,692

3,662

3,353

Revenue

Segment

Profit Margin

5.8%

7.7%

7.5%

7.0%

6.5%

Segment

Profit Margin

3.1%

3.2%

3.9%

2.9%

2.2%

Segment

Profit Margin

8.6%

9.8%

10.4%

11.4%

12.1%

9.5%

9.7%

10.1%

9.8%

9.4%

Segment

Profit Margin

8.3%

11.2%

11.5%

9.7%

8.3%

595

835

875

751

675

Revenue

535

586

624

601

589

0

1

2

3

4

5

6

7

8

0

500

1000

1500

2000

2500

3000

3500

4000

0

10

20

30

40

50

0

3

6

9

12

15

0

500

1000

1500

2000

Revenue

1,293

1,493

1,670

1,861

1,699

$ in millions

Revenue

513

618

608

530

470

$ in millions

$ in millions

$ in millions

Board of Directors Management Team

Richard L. Thompson

Chairman of the Board, Lennox International Inc.

Former Group President, Caterpillar Inc.

Todd M. Bluedorn

CEO, Lennox International Inc.

Steven R. Booth

President and CEO, PolyTech Molding Inc.

Committees: 4

James J. Byrne

Chairman, Byrne Technology Partners, Ltd.

Committees: 3, 4

Janet K. Cooper

Former Senior Vice President and Treasurer

Qwest Communications International Inc.

Committees: 1, 4

C. L. (Jerry) Henry

Former Chairman, President and CEO

Johns Manville Corporation

Committees: 1, 2

John E. Major

President, MTSG

Committees: 1, 3

John W. Norris, III

Chair, Environmental Funders Network

Committees: 2, 4

Paul W. Schmidt

Former Corporate Controller, General Motors Corporation

Committees: 1, 2

Terry D. Stinson

Group Vice President, AAR Corp.

Committees: 2, 3

Jeffrey D. Storey, M.D.

President, Cheyenne Women’s Clinic

Committees: 3, 4

Todd M. Bluedorn

Chief Executive Officer

Prakash Bedapudi

Chief Technology Officer

Harry J. Bizios

President and Chief Operating Officer, Commercial Heating & Cooling

Michael J. Blatz

Executive Vice President, Operations

Scott J. Boxer

President and Chief Operating Officer, Service Experts

Robert W. Hau

Chief Financial Officer

David W. Moon

President and Chief Operating Officer, Worldwide Refrigeration

Daniel M. Sessa

Chief Human Resources Officer

John D. Torres

Chief Legal Officer

Douglas L. Young

President and Chief Operating Officer, Residential Heating & Cooling

Roy A. Rumbough, Jr.

Vice President, Controller, and Chief Accounting Officer

fourteen

BOARD OF DIRECTORS AND

MANAGEMENT TEAM

Committee Legend (bold indicates chairperson)

1: Audit

2: Board Governance

3: Compensation & Human Resources

4: Public Policy

L E N N O X I N T E R N A T I O N A L I N C .

10-K

F O R M 1 0 - K

L E N N O X I N T E R N A T I O N A L I N C .

10-K

F O R M 1 0 - K

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

¥ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2009

OR

nTRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission File Number 001-15149

LENNOX INTERNATIONAL INC.

(Exact name of Registrant as specified in its charter)

Delaware 42-0991521

(State or other jurisdiction of

incorporation or organization)

(I.R.S. Employer

Identification Number)

2140 Lake Park Blvd.

Richardson, Texas 75080

(Address of principal executive offices, including zip code)

(Registrant’s telephone number, including area code): (972) 497-5000

Securities Registered Pursuant to Section 12(b) of the Act:

Title of each class Name of each exchange on which registered

Common Stock, $.01 par value per share New York Stock Exchange

Securities Registered Pursuant to Section 12(g) of the Act: None

Indicate by checkmark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities

Act. Yes ¥No n

Indicate by checkmark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Exchange

Act. Yes nNo ¥

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the

Exchange Act during the preceding 12 months (or for such shorter period that the registrant was required to file such

reports), and (2) has been subject to such filing requirements for the last 90 days. Yes ¥No n

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if

any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T(§232.405 of

this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post

such files). Yes nNo n

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained

herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements

incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. n

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer,

or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting

company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer ¥Accelerated filer nNon-accelerated filer nSmaller reporting company n

(Do not check if a smaller reporting company)

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange

Act). Yes nNo ¥

As of June 30, 2009, the aggregate market value of the common stock held by non-affiliates of the registrant was

approximately $1,345,591,000 based on the closing price of the registrant’s common stock on the New York Stock

Exchange on such date. Common stock held by non-affiliates excludes common stock held by the registrant’s executive

officers, directors and stockholders whose ownership exceeds 5% of the common stock outstanding at June 30, 2009. As

of February 8, 2010, there were 56,300,383 shares of the registrant’s common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s Proxy Statement to be filed with the Securities and Exchange Commission in connection

with the registrant’s 2010 Annual Meeting of Stockholders to be held on May 13, 2010 are incorporated by reference into

Part III of this report.

LENNOX INTERNATIONAL INC.

FORM 10-K

For the Fiscal Year Ended December 31, 2009

INDEX

Page

PART I

ITEM 1. Business ............................................................ 1

ITEM 1A. Risk Factors ......................................................... 10

ITEM 1B. Unresolved Staff Comments .............................................. 14

ITEM 2. Properties ........................................................... 15

ITEM 3. Legal Proceedings ..................................................... 16

ITEM 4. Submission of Matters to a Vote of Security Holders............................ 16

PART II

ITEM 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer

Purchases of Equity Securities ..................................... 16

ITEM 6. Selected Financial Data ................................................. 19

ITEM 7. Management’s Discussion and Analysis of Financial Condition and Results of

Operations ................................................... 19

ITEM 7A. Quantitative and Qualitative Disclosures about Market Risk ...................... 42

ITEM 8. Financial Statements and Supplementary Data ................................ 43

ITEM 9. Changes in and Disagreements With Accountants on Accounting and Financial

Disclosure .................................................... 99

ITEM 9A. Controls and Procedures................................................. 99

ITEM 9B. Other Information ..................................................... 99

PART III

ITEM 10. Directors, Executive Officers and Corporate Governance ......................... 99

ITEM 11. Executive Compensation ................................................ 100

ITEM 12. Security Ownership of Certain Beneficial Owners and Management and Related

Stockholder Matters ............................................ 100

ITEM 13. Certain Relationships and Related Transactions, and Director Independence........... 100

ITEM 14. Principal Accounting Fees and Services ..................................... 100

PART IV

ITEM 15. Exhibits, Financial Statement Schedules ..................................... 100

i

PART I

Item 1. Business

References in this Annual Report on Form 10-K to “we,” “our,” “us,” “LII” or the “Company” refer to Lennox

International Inc. and its subsidiaries, unless the context requires otherwise.

The Company

Through our subsidiaries, we are a leading global provider of climate control solutions. We design, man-

ufacture and market a broad range of products for the heating, ventilation, air conditioning and refrigeration

(“HVACR”) markets. We have leveraged our expertise to become an industry leader known for innovation, quality

and reliability. Our products and services are sold through multiple distribution channels under well-established

brand names including “Lennox,” “Armstrong Air,” “Ducane,” “Bohn,” “Larkin,” “Advanced Distributor Products,”

“Service Experts” and others.

Shown below are our four business segments, the key products and brand names within each segment and

2009 net sales by segment. Segment financial data for 2009, 2008 and 2007, including financial information about

foreign and domestic operations, is included in Note 21 of the Notes to our Consolidated Financial Statements in

“Item 8. Financial Statements and Supplementary Data” and is incorporated herein by reference.

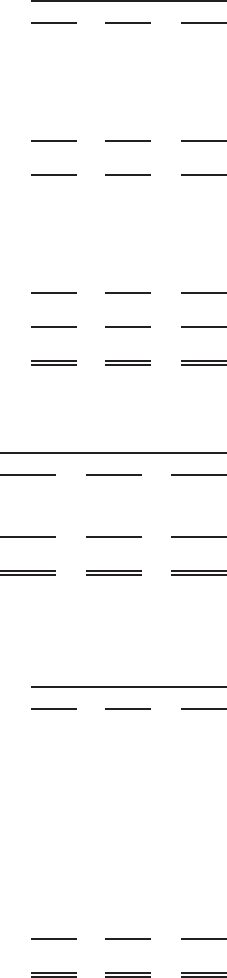

Segment Products/Services Brand Names

2009 Net Sales

(In millions)

Residential Heating &

Cooling

Furnaces, air conditioners,

heat pumps, packaged

heating and cooling systems,

indoor air quality equipment,

pre-fabricated fireplaces,

freestanding stoves

Lennox, Armstrong Air,

Ducane, Aire-Flo, AirEase,

Concord, Magic-Pak,

Advanced Distributor

Products, Superior, Country

Stoves, Security Chimneys

$1,293.5

Commercial Heating &

Cooling

Unitary heating and air

conditioning equipment,

applied systems

Lennox, Allied Commercial 594.6

Service Experts Sales, installation and service

of residential and light

commercial heating and

cooling equipment

Service Experts, various

individual service center

names

535.4

Refrigeration Condensing units, unit

coolers, fluid coolers, air

cooled condensers, air

handlers, process chillers

Heatcraft Worldwide

Refrigeration, Bohn, Larkin,

Climate Control, Chandler

Refrigeration, Friga-Bohn,

HK Refrigeration, Hyfra,

Kirby, Frigus-Bohn

512.7

Eliminations (88.7)

Total $2,847.5

We were founded in 1895 in Marshalltown, Iowa when Dave Lennox, the owner of a machine repair business

for the railroads, successfully developed and patented a riveted steel coal-fired furnace, which was substantially

more durable than the cast iron furnaces used at that time. Manufacturing these furnaces grew into a significant

business and was diverting the Lennox Machine Shop from its core focus. As a result, in 1904, a group of investors

headed by D.W. Norris bought the furnace business and named it the Lennox Furnace Company. We reincorporated

as a Delaware corporation in 1991 and completed our initial public offering in 1999.

1

Products and Services

Residential Heating & Cooling

Heating & Cooling Products. We manufacture and market a broad range of furnaces, air conditioners, heat

pumps, packaged heating and cooling systems, accessories to improve indoor air quality, replacement parts and

related products for both the residential replacement and new construction markets in North America. These

products are available in a variety of designs and efficiency levels and at a range of price points, and are intended to

provide a complete line of home comfort systems. We believe that by maintaining a broad product line marketed

under multiple brand names, we can address different market segments and penetrate multiple distribution

channels.

The “Lennox” and “Aire-Flo” brands are sold directly to a network of approximately 7,000 installing dealers,

making us one of the largest wholesale distributors of residential heating and air conditioning products in

North America. The “Armstrong Air,” “Ducane,” “AirEase,” “Concord,” “Magic-Pak” and “Advanced Distributor

Products” brands are sold through independent distributors.

Our Advanced Distributor Products operation builds evaporator coils and air handlers under the “Advanced

Distributor Products” brand, as well as the “Lennox,” “Armstrong Air,” “AirEase,” “Concord” and “Ducane”

brands. In addition to supplying us with components for our heating and cooling systems, Advanced Distributor

Products produces evaporator coils to be used in connection with competitors’ heating and cooling products as an

alternative to such competitors’ brand name components. We have achieved a significant share of the market for

evaporator coils through the application of technological and manufacturing skills and customer service

capabilities.

Hearth Products. Our hearth products include factory-built gas, wood-burning and electric fireplaces; free

standing wood-burning, pellet and gas stoves; wood-burning, pellet and gas fireplace inserts; gas logs, venting

products and accessories. Many of the fireplaces are built with a blower or fan option and are efficient heat sources

as well as attractive amenities to the home. We currently market our hearth products under the “Lennox,”

“Superior,” “Country Collection” and “Security Chimneys” brand names.

Commercial Heating & Cooling

North America. In North America, we manufacture and sell unitary heating and cooling equipment used in

light commercial applications, such as low-rise office buildings, restaurants, retail centers, churches and schools, as

opposed to larger applied systems. Our product offerings for these applications include rooftop units ranging from

two to 50 tons of cooling capacity and split system/air handler combinations, which range from 1.5 to 20 tons of

cooling capacity. These products are distributed primarily through commercial contractors and directly to national

account customers. We believe the success of our products is attributable to their efficiency, design flexibility, total

cost of ownership, low life-cycle cost, ease of service and advanced control technology.

Europe. In Europe, we manufacture and sell unitary products, which range from two to 70 tons of cooling

capacity, and applied systems with up to 200 tons of cooling capacity. Our European products consist of small

package units, rooftop units, chillers, air handlers and fan coils that serve medium-rise commercial buildings,

shopping malls, other retail and entertainment buildings, institutional applications and other field-engineered

applications. We manufacture heating and cooling products in several locations in Europe and market these

products through both direct and indirect distribution channels in Europe, Russia, Turkey and the Middle East.

Service Experts

Approximately 100 company-owned Service Experts dealer service centers provide installation, preventive

maintenance, emergency repair and replacement of heating and cooling systems directly to residential and light

commercial customers in metropolitan areas in the U.S. and Canada. In connection with these services, we sell a

wide range of our manufactured equipment, parts and supplies, and third-party branded products. We focus

primarily on service and replacement opportunities, which we believe are more stable and profitable than new

construction in our Service Experts segment. We use a portfolio of management procedures and best practices,

including standards of excellence for customer service, a training program for new general managers, common

2

information technology systems and financial controls, regional accounting centers and an inventory management

program designed to enhance the quality, effectiveness and profitability of operations.

Refrigeration

We manufacture and market equipment for the global commercial refrigeration market through subsidiaries

organized under the Heatcraft Worldwide Refrigeration name. These products are sold to distributors, installing

contractors, engineering design firms, original equipment manufacturers and end-users.

North America. Our commercial refrigeration products for the North American market include condensing

units, unit coolers, fluid coolers, air-cooled condensers, compressor racks and air handlers. These products are sold

for refrigeration applications, primarily to preserve food and other perishables, and are used by supermarkets,

convenience stores, restaurants, refrigerated warehouses and distribution centers. As part of the sale of commercial

refrigeration products, we routinely provide application engineering for consulting engineers, contractors and

others. We also sell products for non-food and various industry applications, such as telecommunications,

dehumidification and medical applications.

International. In international markets, we manufacture and market refrigeration products including con-

densing units, unit coolers, air-cooled condensers, fluid coolers, compressor racks and process chillers. We have

manufacturing locations in Europe, Australia, New Zealand, Brazil and China. We also own a 50% common stock

interest in a joint venture in Mexico that produces unit coolers, air-cooled condensers, condensing units and

compressor racks of the same design and quality as those manufactured by our U.S. business. This venture product

line is complemented with imports from the U.S., which are sold through the joint venture’s distribution network.

We also own a 9% common stock interest in a manufacturer in Thailand that produces compressors for use in our

products and for other HVACR customers as well.

Business Strategy

Our business strategy is to sustain and expand our premium market position through organic growth and

acquisitions while maintaining our focus on cost reductions to drive margin expansion and support growth into

target business segments. This strategy is supported by five strategic priorities that are underlined by our values and

our people. The five strategic priorities are:

Innovative Product and System Solutions

In all of our markets, we are continually building on our heritage of innovation by developing residential,

commercial, and refrigeration products that give families and business owners more precise control over more

aspects of their indoor environments, while significantly lowering their energy costs.

Manufacturing and Sourcing Excellence

We maintain our commitment to manufacturing and sourcing excellence by driving low-cost assembly through

rationalization of our facilities and product lines, maximizing factory efficiencies, and leveraging our purchasing

power and sourcing initiatives to expand the use of lower-cost components that meet our high-quality requirements.

Distribution Excellence

By investing resources in expanding our distribution network, we are making products available to our

customers in a timely, cost-efficient manner. Additionally, we provide enhanced dealer support through the use of

technology, training and advertising and merchandising.

Geographic Expansion

We are growing our international presence by extending our successful domestic business model and product

knowledge into developing international markets.

3

Expense Reduction

Through our cost management initiatives, we are focused on areas to reduce operating, manufacturing, and

administrative costs.

Marketing and Distribution

We utilize multiple channels of distribution and offer different brands at various price points in order to better

penetrate the HVACR markets. Our products and services are sold through a combination of distributors,

independent and company-owned dealer service centers, other installing contractors, wholesalers, manufacturers’

representatives and original equipment manufacturers and to national accounts. Dedicated sales forces and

manufacturers’ representatives are deployed across our business segments and brands in a manner designed to

maximize our ability to service a particular distribution channel. To optimize enterprise-wide effectiveness, we have

active cross-functional and cross-organizational teams coordinating approaches to pricing, product design, dis-

tribution and national account customers.

An example of the competitive strength of our marketing and distribution strategy is in the North American

residential heating and cooling market. We use three distinctly different distribution approaches in this market: the

company-owned distribution system, the independent distribution system and sales made directly to end-users. We

distribute our “Lennox” and “Aire-Flo” brands in a company-owned process directly to dealers that install these

heating and cooling products and, in some cases, we sell “Lennox” commercial products directly to national

account customers. We distribute our “Armstrong Air,” “Ducane,” “AirEase,” “Concord,” “Magic-Pak” and

“Advanced Distributor Products” brands through the traditional independent distribution process pursuant to

which we sell our products to distributors who, in turn, sell the products to installing contractors. In addition, we

provide heating and cooling replacement products and services directly to consumers through company-owned

Service Experts dealer service centers.

Over the years, the “Lennox” brand has become synonymous with “Dave Lennox,” a highly recognizable

advertising icon in the heating and cooling industry. We utilize the “Dave Lennox” image in mass media

advertising, as well as in numerous locally produced dealer advertisements, open houses and trade events.

Manufacturing

We operate manufacturing facilities in the U.S. and international locations. We have embraced lean-man-

ufacturing principles, a manufacturing philosophy that reduces waste in manufactured products by shortening the

timeline between the customer order and delivery, accompanied by initiatives designed to achieve high product

quality across our manufacturing operations. In our facilities most impacted by seasonal demand, we manufacture

both heating and cooling products to balance seasonal production demands and maintain a relatively stable labor

force. We are generally able to hire temporary employees to meet changes in demand.

Strategic Sourcing

We rely on various suppliers to furnish the raw materials and components used in the manufacturing of our

products. To maximize our buying effectiveness in the marketplace, our central strategic sourcing group consol-

idates required purchases of materials, components and indirect items across business segments. The goal of the

strategic sourcing group is to develop global strategies for a given component group, concentrate purchases with

three to five suppliers and develop long-term relationships with these vendors. We have several alternative suppliers

for our key raw material and component needs. By developing these strategies and relationships, we leverage our

material needs to reduce costs and improve financial and operating performance. Compressors, motors and controls

constitute our most significant component purchases, while steel, copper and aluminum account for the bulk of our

raw material purchases. We own equity interests in joint ventures that manufacture compressors. These joint

ventures provide us with compressors for our residential, commercial and refrigeration businesses.

Our centrally led supplier development group works with selected suppliers to reduce their costs and improve

their quality and delivery performance. We seek to accomplish this by employing the same business excellence

4

tools utilized by our four business segments to drive improvements in the area of lean manufacturing and six sigma,

a disciplined, data-driven approach and methodology for improving quality.

Research and Development and Technology

An important part of our growth strategy is continued investment in research and product development to both

develop new products and make improvements to existing product lines. As a result, we spent an aggregate of

$48.9 million, $46.0 million and $43.6 million on research and development during 2009, 2008 and 2007,

respectively. We operate a global engineering and technology organization that focuses on new technology

invention, product development, and process improvements.

Intellectual property and innovative designs are leveraged across our businesses. We leverage product

development cycle time improvement and product data management systems to commercialize new products

to market more rapidly. We use advanced, commercially available computer-aided design, computer-aided

manufacturing, computational fluid dynamics and other sophisticated design tools to streamline the design and

manufacturing processes. We use complex computer simulations and analyses in the conceptual design phase

before functional prototypes are created.

We also operate a full line of prototype machine equipment and advanced laboratories certified by applicable

industry associations.

Seasonal Nature of Business

Our sales and related segment profit tend to be seasonally higher in the second and third quarters of the year

because summer is the peak season for sales of air conditioning equipment and services in the U.S. and Canada.

The North American heating, ventilation and air conditioning (“HVAC”) market is driven by seasonal weather

patterns. HVAC products and services are sold year round, but the volume and mix of product sales and service

change significantly by season. The industry ships roughly twice as many units during June as it does in December.

Overall, cooling equipment represents a substantial portion of the annual HVAC market. In between the heating

season (roughly November through February) and cooling season (roughly May through August) are periods

commonly referred to as shoulder seasons when the distribution channel transitions its buying patterns from one

season to the next. These seasonal fluctuations in mix and volume drive our sales and related segment profit,

resulting in somewhat higher sales in the second and third quarters due to the larger cooling season relative to the

heating season.

Patents and Trademarks

We hold numerous patents that relate to the design and use of our products. We consider these patents

important, but no single patent is material to the overall conduct of our business. We proactively obtain patents to

further our strategic intellectual property objectives. We own or license several trademarks and service marks we

consider important in the marketing of our products and services, including LENNOX, ARMSTRONG AIR,

DUCANE, ALLIED COMMERCIAL, AIRE-FLO, CONCORD, ADP ADVANCED DISTRIBUTOR PROD-

UCTS, MAGIC-PAK, HUMIDITROL, PRODIGY, HEATCRAFT WORLDWIDE REFRIGERATION, BOHN,

CHANDLER REFRIGERATION, KIRBY AND LARKIN, among others. We protect our marks through national

registrations and common law rights.

Competition

Substantially all markets in which we participate are highly competitive. The most significant competitive

factors we face are product reliability, product performance, service and price, with the relative importance of these

factors varying among our businesses. Listed below are some of the companies we view as significant competitors

in the three other segments we serve, with relevant brand names, when different from the company name, shown in

parentheses.

• Residential Heating & Cooling — United Technologies Corp. (Carrier, Bryant, Tempstar, Comfortmaker,

Heil, Arcoaire); Goodman Global, Inc. (Goodman, Amana); Ingersoll-Rand plc (Trane, American

5

Standard); Paloma Co., Ltd. (Rheem, Ruud); Johnson Controls, Inc. (York, Weatherking); Nordyne

(Maytag, Westinghouse, Frigidaire, Tappan, Philco, Kelvinator, Gibson); HNI Corporation (Heatilator,

Heat-n-Glo); and Monessen Hearth Company (Majestic).

• Commercial Heating & Cooling — United Technologies Corp. (Carrier); Ingersoll-Rand plc (Trane);

Johnson Controls, Inc. (York); AAON, Inc.; and Daikin Industries, Ltd. (McQuay).

• Service Experts — Local independent dealers; dealers owned by utility companies, including, for example,

Direct Energy; and national HVAC service providers such as Sears and American Residential Services.

• Refrigeration — United Technologies Corp. (Carrier); Ingersoll-Rand plc (Hussmann); Emerson Electric Co.

(Copeland); GEA Group (Kuba, Searle, Goedhart); and Alfa Laval (Alfa Laval, Fincoil, Helpman).

Employees

As of December 31, 2009, we employed approximately 11,600 employees, of whom approximately 4,800

were salaried and 6,800 were hourly. The number of hourly workers we employ may vary in order to match our

labor needs during periods of fluctuating demand. Approximately 2,600 employees are represented by unions. We

believe our relationships with our employees and with the unions representing our employees are good and

currently we do not anticipate any material adverse consequences resulting from negotiations to renew any

collective bargaining agreements.

Environmental Regulation

Our operations are subject to evolving and often increasingly stringent international, federal, state and local

laws and regulations concerning the environment. Environmental laws that affect or could affect our domestic

operations include, among others, the National Appliance Energy Conservation Act of 1987, as amended

(“NAECA”), the Energy Policy Act, the Clean Air Act, the Clean Water Act, the Resource Conservation and

Recovery Act, the Comprehensive Environmental Response, Compensation and Liability Act, the National

Environmental Policy Act, the Toxic Substances Control Act, any regulations promulgated under these acts

and various other international, federal, state and local laws and regulations governing environmental matters. We

believe we are in substantial compliance with such existing environmental laws and regulations.

Energy Efficiency. The U.S. Department of Energy is conducting rule makings to evaluate the current

minimum efficiency standards for residential heating and cooling products. On December 19, 2007, federal

legislation was enacted authorizing the U.S. Department of Energy to study the establishment of regional efficiency

standards for residential furnaces, air conditioners and heat pumps. We anticipate that the U.S. Department of

Energy will establish regional standards for furnaces and air conditioners as part of the rulemakings. We have

established a process that we believe will allow us to offer new products that meet or exceed these new standards in

advance of implementation. Similar new standards are being promulgated for commercial air conditioning and

refrigeration equipment. We are actively involved in U.S. Department of Energy and Congressional activities

related to energy efficiency standards. We are prepared to have compliant product in place in advance of the

implementation of all such regulations being considered by the U.S. Department of Energy or Congress.

Refrigerants. The use of hydrochlorofluorocarbons, “HCFCs,” and hydroflurocarbons “HFCs” as refriger-

ants for air conditioning and refrigeration equipment is common practice in the HVACR industry. Under the

Montreal Protocol and implementing regulations, the use of virgin HCFCs in new pre-charged equipment within the

U.S. was phased out January 1, 2010. We have complied with applicable rules and regulations governing the HCFC

phase out. The United States Congress, Environmental Protection Agency and other international regulatory bodies

are considering steps to phase down the future use of HFCs in HVACR products. We have been an active participant

in the ongoing international and domestic dialogue on this subject and believe we are well positioned to react in a

timely manner to any changes in the regulatory landscape. In addition, we are taking proactive steps to implement

responsible use principles and guidelines with respect to limiting refrigerants from escaping into the atmosphere

throughout the life span of our HVACR equipment.

Remediation Activity. In addition to affecting our ongoing operations, applicable environmental laws can

impose obligations to remediate hazardous substances at our properties, at properties formerly owned or operated

6

by us and at facilities to which we have sent or send waste for treatment or disposal. We are aware of contamination

at some of our facilities; however, based on facts presently known, we do not believe that any future remediation

costs at such facilities will be material to our results of operations. We currently believe that the release of the

hazardous materials occurred over an extended period of time, including a time when we did not own the site.

Extensive investigations have been performed, we have completed remediation pilot-testing and are in the process

of implementing full-scale remediation on-site. For more information, see Note 11 in the Notes to our Consolidated

Financial Statements.

In the past, we have received notices that we are a potentially responsible party along with other potentially

responsible parties in Superfund proceedings under the Comprehensive Environmental Response, Compensation

and Liability Act for cleanup of hazardous substances at certain sites to which the potentially responsible parties are

alleged to have sent waste. Based on the facts presently known, we do not believe environmental cleanup costs

associated with any Superfund sites where we have received notice that we are a potentially responsible party will

be material.

European WEEE and RoHS Compliance. In the European marketplace, electrical and electronic equipment

is required to comply with the Directive on Waste Electrical and Electronic Equipment (“WEEE”) and the Directive

on Restriction of Use of Certain Hazardous Substances (“RoHS”). WEEE aims to prevent waste by encouraging

reuse and recycling and RoHS restricts the use of six hazardous substances in electrical and electronic products. All

HVACR products and certain components of such products “put on the market” in the EU (whether or not

manufactured in the EU) are potentially subject to WEEE and RoHS. Because all HVACR manufacturers selling

within or from the EU are subject to the standards promulgated under WEEE and RoHS, we believe that neither

WEEE nor RoHS uniquely impact us as compared to such other manufacturers. Similar directives are being

introduced in other parts of the world, including the U.S. For example, California, China and Japan have all adopted

unique versions of RoHS possessing similar intent. We are actively monitoring the development of such directives

and believe we are well positioned to comply with such directives in the required time frames.

Available Information

Our web site address is www.lennoxinternational.com. We make available, free of charge through our web

site, our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and

amendments to those reports filed or furnished pursuant to the Securities Exchange Act of 1934, as amended,

as soon as reasonably practicable after such material is electronically filed with, or furnished to, the Securities and

Exchange Commission. The information on our web site is not a part of, or incorporated by reference into, this

annual report on Form 10-K.

Certifications

We submitted the 2009 New York Stock Exchange (the “NYSE”) Annual CEO Certification regarding our

compliance with the NYSE’s corporate governance listing standards to the NYSE on June 12, 2009.

The certifications of our Chief Executive Officer and Chief Financial Officer pursuant to Section 302 and

Section 906 of the Sarbanes-Oxley Act of 2002 are filed and furnished, respectively, as exhibits to this Annual

Report on Form 10-K.

7

Executive Officers of the Company

Our executive officers, their present positions and their ages are as follows:

Name Age Position

Todd M. Bluedorn ................. 46 Chief Executive Officer

Prakash Bedapudi ................. 43 Executive Vice President and Chief Technology

Officer

Harry J. Bizios ................... 60 Executive Vice President and President and Chief

Operating Officer, LII Commercial Heating &

Cooling

Michael J. Blatz .................. 44 Executive Vice President, Operations

Scott J. Boxer .................... 59 Executive Vice President and President and Chief

Operating Officer, Service Experts

Robert W. Hau ................... 44 Executive Vice President and Chief Financial

Officer

DavidW.Moon................... 48 Executive Vice President and President and Chief

Operating Officer, LII Worldwide Refrigeration

Daniel M. Sessa .................. 45 Executive Vice President and Chief Human

Resources Officer

John D. Torres.................... 51 Executive Vice President, Chief Legal Officer and

Secretary

Douglas L. Young ................. 47 Executive Vice President and President and Chief

Operating Officer, LII Residential Heating &

Cooling

Roy A. Rumbough, Jr. . . . .......... 54 VicePresident, Controller and Chief Accounting

Officer

The following biographies describe the business experience of our executive officers:

Todd M. Bluedorn became Chief Executive Officer and was elected to our Board of Directors in April 2007.

Mr. Bluedorn previously served in numerous senior management positions for United Technologies since 1995,

including President, Americas — Otis Elevator Company beginning in 2004; President, North America —

Commercial Heating, Ventilation and Air Conditioning for Carrier Corporation beginning in 2001; and President,

Hamilton Sundstrand Industrial beginning in 2000. He began his professional career with McKinsey & Company in

1992, after receiving an MBA from Harvard University in 1992 and serving in the United States Army as a combat

engineer officer and United States Army Ranger from 1985 to 1990. He also holds a BS in Electrical Engineering

from the United States Military Academy at West Point. Mr. Bluedorn currently serves on the board of directors of

Eaton Corporation, a diversified industrial manufacturer.

Prakash Bedapudi became Executive Vice President and Chief Technology Officer in July 2008. He had

previously served as vice president, global engineering and program management for Trane Inc. Commercial

Systems from 2006 through 2008, and as vice president, engineering and technology for Trane’s Residential

Systems division from 2003 through 2006. Prior to his career at Trane, Mr. Bedapudi served in senior engineering

leadership positions for GE Transportation Systems, a division of General Electric Company, and for Cummins

Engine Company. He holds a BS in Mechanical/Automotive Engineering from Karnataka University, India and an

MS in Mechanical/Aeronautical Engineering from the University of Cincinnati.

Harry J. Bizios was appointed Executive Vice President and President and Chief Operating Officer of LII’s

Commercial Heating & Cooling segment in October 2006. Mr. Bizios had previously served as Vice President and

General Manager, LII Worldwide Commercial Systems since 2005 and as Vice President and General Manager of

Lennox North American Commercial Products from 2003 to 2005. Mr. Bizios began his career with LII in 1976 as

an industrial engineer at LII’s manufacturing facility in Marshalltown, Iowa, subsequently serving in several senior

leadership roles before being appointed Vice President and General Manager of Lennox Industries Commercial

from 1998 to 2003. He holds a BS in Engineering Operations from Iowa State University.

8

Michael J. Blatz was appointed Executive Vice President, Operations in May 2009. Mr. Blatz joined LII in

August 2007 as Vice President, Operations. Mr. Blatz was previously Vice President and General Manager for Tyler

Refrigeration, a division of Carrier Corporation, a United Technologies company. His career at Carrier Corporation

began in 2003 and encompassed senior leadership positions in supply chain, product management, and manu-

facturing operations. He also served as Director of Operations and Director of Worldwide Procurement at

Dell Computer Corporation and held engineering and product development roles at Case Corporation before

joining Carrier Corporation. He holds a BS in mechanical engineering from the United States Military Academy at

West Point and a MS in management and mechanical engineering, both from the Massachusetts Institute of

Technology.

Scott J. Boxer was appointed President and Chief Operating Officer of LII’s Service Experts segment in

July 2003. He served as President of Lennox Industries Inc., an LII subsidiary, from 2000 to 2003. He joined LII in

1998 as Executive Vice President, Lennox Global Ltd. Prior to joining LII, Mr. Boxer spent 26 years with York

International Corporation in various roles, including President, Unitary Products Group Worldwide, where he

directed residential and light commercial heating and air conditioning operations. Mr. Boxer previously served as an

Executive Board Member of the Air-Conditioning & Refrigeration Institute and Chairman of the Board of Trustees

of North American Technical Excellence, Inc. He holds a BS in Industrial Engineering from the University of

Rhode Island.

Robert W. Hau was appointed Executive Vice President and Chief Financial Officer in October 2009. He had

previously served as Vice President and Chief Financial Officer for Honeywell International’s Aerospace Business

Group since 2006. Mr. Hau first joined Honeywell (initially AlliedSignal) in 1987 and served in a variety of senior

financial leadership positions, including Vice President and Chief Financial Officer for the company’s Aerospace

Electronic Systems Unit and for its Specialty Materials Business Group. He holds a BSBA in Finance & Marketing

from Marquette University and an MBA in Finance from the University of Southern California.

David W. Moon was appointed Executive Vice President and President and Chief Operating Officer of LII’s

Worldwide Refrigeration segment in August 2006. Mr. Moon had previously served as Vice President and General

Manager of Worldwide Refrigeration, Americas Operations since 2002. Prior to serving in that position, he served

as Managing Director in Australia beginning in 1999, where his responsibilities included heat transfer manufac-

turing and distribution, refrigeration wholesaling and manufacturing, and HVAC manufacturing and distribution in

Australia and New Zealand. Mr. Moon originally joined LII in 1998 as Operations Director, Asia Pacific. Prior to

that time, Mr. Moon held various management positions at Allied Signal, Inc., Case Corporation, and Tenneco Inc.

in the United States, Hong Kong, Taiwan and Germany. He holds a BS in Civil Engineering and an MBA from Texas

A&M University.

Daniel M. Sessa was appointed Executive Vice President and Chief Human Resources Officer in June 2007.

Mr. Sessa previously served in numerous senior human resources and legal leadership positions for United Tech-

nologies Corporation since 1996, including Vice President, Human Resources for Otis Elevator Company —