MMBB_Compensation_Guide_ MMBB0 MMBB Compensation Guide

User Manual: MMBB0

Open the PDF directly: View PDF ![]() .

.

Page Count: 36

Guide to Negotiating

Pastor Compensation

1 | MMBB Financial Services

This publication discusses various forms of compensation and their federal tax implications only. It does

not cover local tax regulations, which dier from state to state.

This guide is not intended as a substitute for legal, accounting, or other professional advice. If legal, tax, or

other expert assistance is required, we recommend that you seek the services of a competent professional.

MMBB Financial Services is pleased to have the collaboration of the American Baptist Churches Ministers

Council Professional Eectiveness Committee in the development of this material.

You can download additional copies of this guide—and other helpful materials—at MMBB.org

Guide to Negotiating Pastor Compensation | 2

Table of Contents

Introduction ...............................................................................3

Components of A Compensation Package .................................................4

Cash Compensation .......................................................................5

Housing/Parsonage Allowance ............................................................7

Benets ....................................................................................9

Flexible Spending Account (FSA) ........................................................11

MMBB Benet Oerings at a Glance .....................................................12

Paid Leave ...............................................................................13

Reimbursement of Job-Related Expenses ...............................................14

Steps for Agreeing on a Compensation Package ........................................16

Determining a “Fair” Wage ...............................................................19

Break a Pattern of Discriminatory Compensation ........................................22

Approaching Negotiations with the Right Frame of Mind ...............................24

Tips for Constructive Negotiations .......................................................27

Bridging the Gap: When Your Church Cannot Aord to Pay a “Fair” Wage ...............29

Additional Resources ....................................................................31

Contact Information .....................................................................33

“Let the elders who rule well be considered worthy of double honor, especially those

who labor in preaching and teaching; for the scripture says, ‘... the laborer deserves

to be paid.’”

1 Timothy 5:17–18

3 | MMBB Financial Services

A Guide for Ministers and

Congregational Leaders

Ministers and congregational leaders routinely collaborate on matters of faith, spiritual health, and the day-to-

day functioning of the congregation. Then—once a year—they address the sensitive issue of the minister’s

compensation.

For 100 years, MMBB Financial Services has counseled churches and faith-based organizations on compensa-

tion and related matters. This guide oers you the benet of that experience. It is intended for both churches

and ministers, as well as for chaplains, pastoral counselors, and those in other forms of ministry.

This guide explains how the tax code treats dierent forms of compensation. It provides suggestions on how

to design a fair compensation package and how churches and ministers can negotiate constructively and

positively to reach a consensus. We believe that both benet from a deliberative process that brings everyone

to agreement on fair compensation.

The goals of a compensation package

You may nd it helpful to begin by considering the goals of a compensation package. A church should provide

its sta with adequate income so that they can fulll their roles without undue concern about current and

future nancial needs. Freedom from nancial anxiety lets a pastor focus on his or her service. It also helps your

church attract and retain qualied pastoral leadership.

A good compensation package is the fair thing to do. It compensates pastoral leaders for their investment in

education, as well as for their talent, experience, and eort. The benets and insurance components protect

both the minister and church from unexpected setbacks. They ensure that pastors receive support, even if they

are unable to fully carry out the church’s ministry.

Finally, a compensation package serves a managerial and motivational function. It can reward sta for meeting

agreed-upon goals.

“Respect those who labor among you and have charge of you in the Lord and

admonish you; esteem them very highly in love because of their work.”

i Thessalonians 5:12–13

Guide to Negotiating Pastor Compensation | 4

Components of a Compensation Package

A compensation package has three components:

• Cash compensation includes the pastor’s cash salary and housing allowance, plus cash equivalents such as

the Social Security oset.

• A benets package often includes a retirement savings plan, life insurance, plus disability and health insurance.

It can also include a paid sabbatical. These contribute to an employee’s feeling of security and well-being.

• Reimbursement of job-related expenses include reimbursement for work-related travel, books, and

education. This helps ministers with the day-to-day costs of performing their responsibilities.

The way you allocate compensation between these three categories has a signicant impact on the taxes your

sta must pay. Read on as we describe each category in detail.

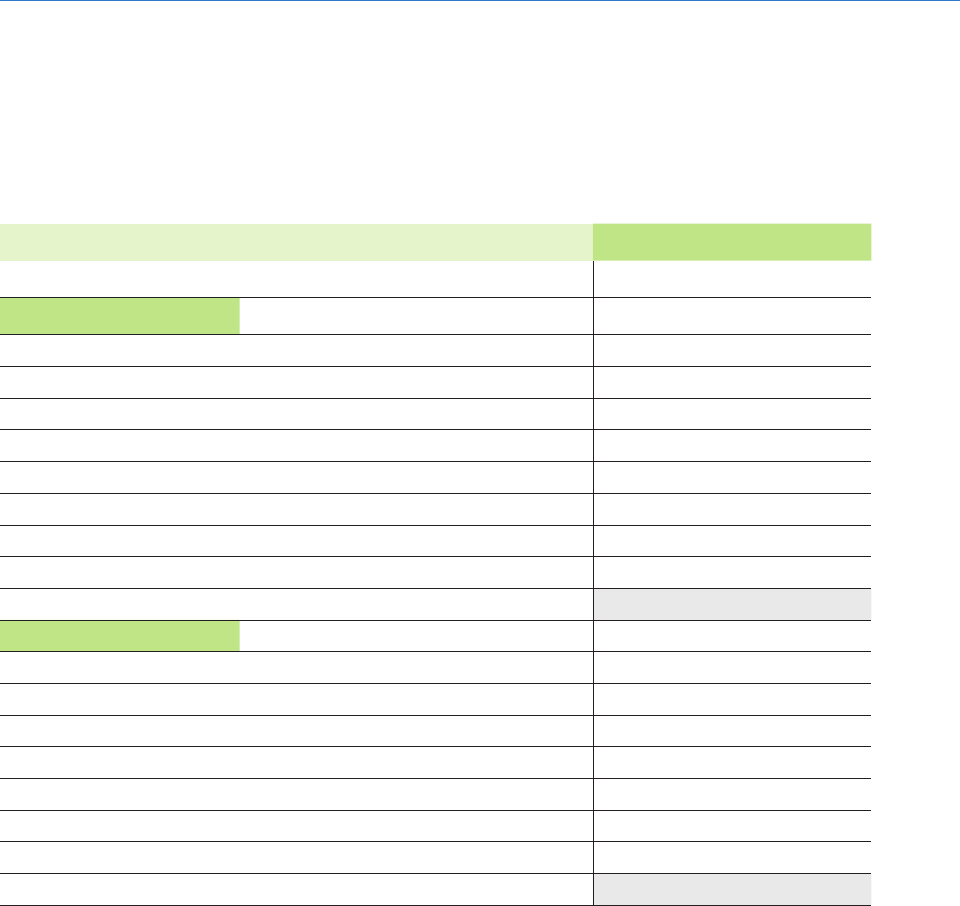

A sample $50,000 compensation package

Cash Compensation

Cash salary $15,000

Housing allowance $10,000

Social Security offset $3,800

Equity allowance $5,000

Benefits

Retirement, plus life and disability insurance $4,400

Health insurance $10,000

Reimbursement for Job-Related Expenses

Auto allowance $650

Conventions $400

Hospitality $250

Subscriptions/books $200

Continuing education $300

Total: $50,000

5 | MMBB Financial Services

Cash Compensation

Cash compensation can include the following four components. Consider the tax implications of each

component as you design this part of the package.

1. Cash salary

A minister’s cash salary can be subject to federal, state, and local income taxes. It also serves as the basis for

calculating allowable retirement plan contributions.

• Increasing the cash portion of a compensation package will obligate the minister to pay more in taxes.

• Because employee-paid retirement plan contributions cannot exceed 100% of includable compensation (plus

any age 50 catch-up contributions), reducing cash salary can potentially limit a minister’s contribution to his or

her retirement plan. Few ministers set aside 100% of their salary for retirement, so this is a lesser concern.

Later in this guide, we explain how to determine a fair cash salary based on national averages and the

minister’s experience and qualications.

2. Housing/parsonage allowance

Section 107 of the Internal Revenue Code allows ordained ministers to exclude from federally taxed income

some or all of the cost of providing their principal residence. For example, a minister receiving a cash salary of

$30,000 might have $5,000 of the cash amount designated as a housing or parsonage allowance. Only $25,000

would be considered taxable for federal income taxes.

This exclusion applies only to a minister’s federal income tax. The implications:

• Designating a larger portion of salary as a housing allowance will reduce a minister’s federal tax liability.

• But overestimating the housing allowance may cause a minister to underreport his or her taxable wages,

which could lead to an underpayment of taxes.

3. Social Security-Medicare tax oset

While ministers are employees for federal income tax reporting purposes, they are self-employed for Social Security

purposes with respect to services they perform in the exercise of their ministry. This “dual status” means they

are not subject to withholding requirements for the employee’s share of Social Security and Medicare taxes.

Instead, they pay a Self-Employment Contributions Act (SECA) tax.

Churches are not permitted to pay the SECA tax for their pastors; however, most churches assist ministers by

providing them with a Social Security/Medicare tax oset of at least 50% of the SECA tax. This provides an

equivalent of Social Security/Medicare taxes that the church would pay on behalf of a lay church worker.

Guide to Negotiating Pastor Compensation | 6

4. Equity allowance for ministers living in a parsonage

Unlike homeowners, ministers living in parsonages do not build equity in their homes. Many churches help

compensate for that by paying an equity allowance that is not subject to federal income tax.

You can read more about the housing, parsonage, and equity allowances on the following pages.

Cash Compensation: Example

ACash salary $15,000

BHousing allowance $10,000

CSocial Security offset $3,800

DEquity allowance $5,000

Amount subject to federal tax: $18,800

(A+C)

Amount subject to state, local, and SECA taxes: $38,800

(A+B+C+D)

7 | MMBB Financial Services

Housing/Parsonage Allowance

Housing allowance

The housing allowance lets ordained sta deduct the cost of housing from income subject to federal taxes.

The amount of the allowance should cover the cost of maintaining a home: mortgage or rent payments, taxes,

repairs, insurance, furnishings, utilities, etc. For federal income tax purposes, the excludable amount of a

housing allowance is limited to the lesser of:

1. The amount designated by the church, or

2. The amount actually spent on housing by the minister for the year, or

3. The fair rental value of a furnished house, plus utilities such as gas, electricity, oil, telephone and water.

A minister cannot exclude more than his or her church designates, so the designated amount must at least be

enough to cover items 2 or 3 above. If the designated amount exceeds the lesser of item 2 or 3, the minister

must report the excess as taxable income.

A church must designate the housing allowance portion of a minister’s salary in advance of when that salary

takes eect. The minister is responsible for documenting actual housing expenses.

Housing Allowance Example

Designated by the church $22,000

Fair rental value of a furnished house, plus utilities $19,000

Actually spent on housing by the minister for the year $17,600

In this example, the church designated $22,000 of its minister’s salary as a housing allowance. A real estate agent’s

estimate of the rental value for a similarly furnished house came to $19,000, so the church’s designation was too high.

But when the minister added up her actual mortgage payments, utility, and maintenance costs for the year, the total

was even lower: $17,600. Since that is the least of the three amounts, the minister can only deduct $17,600 from her

federally taxable income.

Rental value of a parsonage

For a minister living in a parsonage, the church does not report the rental value or any utility costs paid or

reimbursed by the church as income for federal income tax purposes. However, the minister must count the

parsonage rental value, utilities, and parsonage allowance as income when calculating his or her SECA tax.

A church should base the rental value on what the parsonage could be rented for in the community. A local

real estate agent can help you determine this. Alternatively, your church can use 1% of the market value of the

Guide to Negotiating Pastor Compensation | 8

parsonage. For example, if the parsonage market value is $100,000, the monthly rental value would be $1,000.

Consider annual adjustments to the parsonage rental value.

Your church’s accurate report of parsonage value helps MMBB determine death,

disability, and retirement benets

An accurate parsonage rental value does more than help a pastor save on taxes. Your church reports this

value, along with cash salary and utilities, to MMBB for Comprehensive Plan premium purposes.

If the reported rental value is less than the actual value of the parsonage, the minister’s death, disability,

and retirement benets will be lower. That can create considerable hardship if the member’s surviving

family must nd alternative housing.

The impact of underreporting (45-year-old member)

Compensation Death Benefit (4 times reported compensation)

Actual: $50,000 $200,000

Underreported: $45,000 $180,000 ($20,000 less)

Parsonage allowance

In addition to determining the parsonage rental value, your church can also designate a part of a minister’s

cash salary as a parsonage allowance. The parsonage allowance covers anything purchased by the minister to

maintain a home in the parsonage, such as furnishings or renter’s insurance. The amount of this allowance is

excluded from the minister’s taxable income to the extent that it can be justied by actual housing costs.

Equity allowance for ministers living in a parsonage

Unlike homeowners, ministers who live in parsonages usually do not have equity in their homes. This puts them at a

disadvantage when they approach retirement. They must seek housing while not having built up equity over the years.

Churches can help such ministers by providing an equity allowance in addition to the minister’s compensation.

There are several tax-advantaged ways to do this:

• The church can make contributions on behalf of the minister to the Retirement Only Plan, available from MMBB.

Retirement Only Plan contributions and earnings are not taxable to the minister until withdrawn in retirement.

• A minister may choose to supplement the equity allowance by starting or increasing contributions to The An-

nuity Supplement (TAS). Contributions are excluded from Social Security/Medicare taxes for ordained ministers.

9 | MMBB Financial Services

Benets

There are four general categories of benets:

A good benets program is essential for maintaining employee health and morale. There are also tax advantages

for employees. Employers generally oer four categories of benets:

• Retirement savings

• Life insurance

• Disability insurance

• Health insurance

A church should oer all four benets to protect the institution in case the unexpected occurs. You also want to

protect ordained sta so that they can fulll their ministry knowing that they and their family will be cared for.

Retirement savings

By helping your sta build assets for the future, a retirement savings plan gives them condence that helps

them better fulll their ministry. It also assures you that they will not have to work beyond the point where

they —or you—want them to.

To fully appreciate the importance of saving for retirement, consider the following:

• According to data compiled by the Social Security Administration, a man retiring today at age 65 can expect

to live to age 83. A woman can expect to live to age 85. And those are just averages – one in ten 65-year-olds

can expect live past age 95. That means their retirement savings must last 18 to 30 years.

• Financial advisors generally assume that a retiree will need 70-80% of his or her pre-retirement income. So a

pastor earning $50,000 a year at retirement may need $35,000-$40,000 a year … for 18 to 30 years.

• A rough rule of thumb recommends that retirees in their mid-60s should have 20 times their targeted in-

come in savings . The pastor in the above example would need $700,000-$800,000.

A well-structured retirement plan can help build up the necessary savings. The tax advantages of 401(k) plans,

403(b) plans, and traditional IRAs are similar. Amounts contributed today are excluded from current taxable

income. Taxes on the invested amount, along with any investment growth, are deferred until the funds are

withdrawn during retirement years.

1 http://www.ssa.gov/planners/lifeexpectancy.htm

2 http://www.cbsnews.com/8301-505146_162-39940107/how-much-retirement-savings-do-you-need/

Guide To Negotiating Pastor Compensation | 10

Once you have decided to oer a retirement savings plan, usually a 403(b) plan for churches, you must decide

how to structure it. Will your church contribute a percentage of each employee’s salary? Will you have a match-

ing plan to encourage employees to save? A good benet plan provider can help you with these decisions.

Life insurance

The death of a loved one is traumatic enough without the added anguish of not knowing how surviving family

members will meet their expenses. A life insurance plan oers vital protection against economic catastrophe. It

also makes it easier for your church to support the family without undermining the church’s ministry.

Your church can provide up to $50,000 worth of life insurance coverage without tax consequences to the

employee.3 The value of church-paid life insurance over $50,000 does have to be reported as taxable income.

Most employer-provided insurance is oered as group term life. When insurance is purchased through a group

plan, the premium is almost always lower than what an individual would pay for a private policy.

Disability insurance

People often think that only older workers become disabled. But even young and healthy workers are at risk of

becoming disabled from a car accident, sports injury, or other occurrence.

According to the Council for Disability Awareness, a 35 year-old male oce worker with some outdoor physical

responsibilities faces a one-in-ve chance of being disabled for 90 days or longer before he retires. A 35-year-old

woman faces a one-in-four risk. For such workers, the average length of disability is six years and nine months.

A disability insurance policy provides replacement income. It allows your church to continue its ministry by

freeing resources that might otherwise be required to support the disabled minister.

Employer-paid premiums for disability insurance are not taxable for employees. They only pay taxes on income

paid by the policy after they are disabled.4 As with employer-sponsored life insurance, group disability cover-

age is usually less expensive than an individual policy.

Health insurance

Like it or not, our current health insurance system gives signicant preference to employer-provided health

insurance plans. For most employees, group health insurance costs less than a private policy.

Under Internal Revenue Code sections 105 and 106, employer-provided health benets, including claims

reimbursements and insurance, are generally excluded from taxable employee income.

As more provisions of the Aordable Care Act (healthcare reform) take eect, new limits and requirements apply.

You can stay up to date by visiting MMBB.org and searching “healthcare reform.” Or go to www.healthcare.gov.

3 “The Benet of Benets,” NACBA Ledger 31, Summer 2012

4 “The Benet of Benets,” NACBA Ledger 31, Summer 2012

11 | MMBB Financial Services

Flexible Spending Account (FSA)

While technically not a form of compensation, a Flexible Spending Account lets your church oer tax savings

to employees who must pay for health and dependent care expenses.

Each year, employees elect how much to set aside from their paychecks for the coming year, subject to IRS limits.

The withheld funds are not reported as taxable income for federal income tax or Social Security/Medicare tax. In

most states, FSA contributions are not reported for state income tax purposes either. When an employee incurs

an eligible expense, he or she submits documentation to the employer and is reimbursed with tax-free funds.

Your church can set up FSAs for health care, dependent care, or both.

• A health care FSA can be used to pay for eligible medical, dental, vision and hearing expenses.

• A dependent care FSA can be used to pay for care for a dependent child or a dependent adult who is

incapable of self-care.

Under IRS rules, unspent FSA funds cannot be carried over from year to year. Any funds not used to reimburse

claims by the end of the following year’s 2½ month5 grace period are forfeited and returned to the employer.

That said, employees with even a modest level of predictable health care or dependent care spending can

save a signicant percentage by paying for it with pre-tax dollars.

An FSA must be established in writing. Contact MMBB at service@MMBB.org for a free FSA sample kit.

Or call MMBB at 800.986.6222.

5 http://orpebb.asiex.com/graceperiod.htm

Guide to Negotiating Pastor Compensation | 12

MMBB Financial Services Benet Oerings

at a Glance

For more than 100 years, MMBB has specialized in providing retirement and health benets to

faith-based organizations. We work with your church to tailor a exible benets package that ts

your budget. Call 800.986.6222, or send an email to outreach@MMBB.org, to arrange to speak with

one of our Senior Benets Consultants.

MMBB benet oerings and support services

Comprehensive Plan

• Flexible investment options that provide lifetime income in retirement. The housing allowance is

available for clergy in retirement. Based on a 2010 survey, MMBB members receive an average of

86% of pre-retirement when they annuitize, including Social Security.

• Disability insurance coverage includes an annual cost of living adjustment, continued retirement

contributions and a monthly allowance for dependent children under 21.

• Term life insurance includes survivor income for spouses and child allowances for dependent

children under 21.

Retirement Only Plan

• You—the employer—set the contribution rate as a percent of salary or xed dollar amount.

You can even make one-time contributions such as tax-deferred thank you gifts.

• You can create a matching plan to encourage your sta to participate. The plan can be changed

over time.

• In most instances, you can provide dierent benets to dierent classications of employees.

• The housing allowance is available for clergy in retirement.

Employee Contribution Plan

• Employees can contribute on a pre-tax basis through easy payroll deduction.

• Pre-tax saving defers federal income taxes on your contributions until you begin receiving

benets in retirement.

13 | MMBB Financial Services

Paid Leave

Paid leave is an employee benet—but typically not given a dollar value.

Most compensation packages typically specify how much paid leave a minister can take. Since this doesn’t

increase or reduce the pastor’s salary, the dollar value is generally not stated. Still, you can increase or reduce

this part of the compensation package as part of your negotiations.

Paid sick leave—Most churches establish a certain number of days per year for sick leave. Ten days per year is

a common option. Most pastors work more than enough hours to compensate for any days o due to illness.

You may or may not include the option to carry over unused sick days from one year to the next. If you do, we

recommend limiting that to no more than one year’s worth of accumulated sick days.

Paid holidays—The Forth of July, Labor Day, Thanksgiving Day, Christmas, New Year’s Day, etc.. Pastors must

often work on holidays and it is appropriate to allow them days o in lieu of the actual holiday date. It is recom-

mended that unused paid holidays not be carried over from one year to the next. Such “comp” days should be

used within one month of the holiday.

Paid vacations—Generally negotiated by the Pastoral Search Committee or other church board in the hiring

process. A typical starting point would be three weeks in the rst year of service. It is recommended that you

limit the carryover of vacation time by establishing a bank of vacation leave that does not exceed 1½ years of

accumulated vacation days at any time.

Additional paid days—Paid time for working with ministerial organizations, jury duty, military training, bereave-

ment and advanced education are all items to consider. Establish a limit of paid days to limit church liability.

Paid sabbatical—This benet can be tailored to ensure value to the church (e.g., requiring the pastor to

remain with the church for a certain period of time post-sabbatical, or to share learnings from the sabbatical

through special programs).reimbursement of job-related expenses.

Guide to Negotiating Pastor Compensation | 14

Reimbursement of Job-Related Expenses

Church sta are often expected to make home visits, represent your church at conferences, entertain guests, and

develop professionally through continuing education. It is important that you budget for and reimburse these

items separately from compensation. Otherwise, your sta will have to pay taxes on the reimbursed amounts.

The key is to reimburse business expenses through an accountable plan. Under this arrangement, ministry-

related expenses are not reported as taxable income on the employee’s Form W-2 or Form 1040. At the same

time, the employee cannot claim these expenses as tax deductions.

Requirements for an accountable plan

• Expenses must be incurred while performing services as an employee of the organization.

• The employee must provide documentary evidence of the expense. This can be an auto mileage recording

work-related use of a personal car or receipts to verify expense amounts, plus a notation of the time, place,

and professional purpose for each expense.

• Expenses must be reported and substantiated within 60 days of when they occurred.

• An accountable plan cannot be funded through salary reduction. The reimbursements must be over and

above any salary paid to employee, from a spending category that is listed in your church budget.

• Excess reimbursement not spent must be returned. Otherwise, it becomes taxable income.

Your church must pass a resolution establishing an accountable plan

The IRS requires the church board to pass a formal resolution creating an accountable plan. The plan

policy should be in writing and clearly specify which expenses the church will reimburse. State the

documentation and reporting requirements. You may use the following sample wording:

RESOLVED, That, in addition to compensation paid to our (pastor/sta), we will reimburse

(him/her/them) for automobile and other ministry-related expenses considered ordinary and

necessary to carry out (his/her/their) responsibilities. Expenses must be substantiated as to

the date, amount and purpose within 60 days after they are incurred, or they will not be re-

imbursed. Any excess reimbursements must be refunded to the church within 120 days after

expenses are paid or incurred.

15 | MMBB Financial Services

Allowable reimbursable expenses

• Business-related travel and automobile use

• Hospitality

• Conference attendance

• Continuing education

• Subscriptions/books/periodicals

• Fees and dues for professional associations, such as the ABC Ministers Council

• Work-related cellphone use

Guide to Negotiating Pastor Compensation | 16

Steps for Agreeing on a Compensation Package

CHURCH

Begin by forming a Pastoral Relations Committee

A crucial rst step in developing a compensation package is forming a Pastoral Relations Committee (PRC). This

committee provides a channel for your minister or pastoral sta to communicate openly about their needs.

The committee can then conduct the necessary research, work with the minister to design an acceptable

package, and advocate for fair compensation.

Size of the PRC

A PRC should be relatively small, three to seven people. This is large enough to foster group interaction and

small enough to encourage wide participation. Another reason to have a small group is the importance of

maintaining a high trust level and ensuring condentiality.

Selecting PRC members

Given the sensitive nature of the PRC, it is better to select its members by appointment rather than through

formal nominating and election processes. You might ask the minister to provide a suggested list of names to

the chairperson of the board. Then, in mutual consultation between the minister and chairperson of the board,

make your nal selections.

Member qualications

First and foremost, PRC members are people with whom the pastor has a good relationship. Important charac-

teristics include:

• People who are supportive of the minister and sensitive to the feelings and needs of both the congregation

and minister

• Good listeners

• People skilled in human relations and communication

• People who have integrity with regard to maintaining condentiality

• Both men and women of mixed ages

It is best not to have the current chair of the board on the PRC. Nor is it desirable to include members of other

committees or church departments simply because they represent those groups. You are not attempting to

represent the entire church in this small committee. If input is needed from other groups, the PRC can invite

representatives to its meeting and excuse them after a particular topic has been covered.

17 | MMBB Financial Services

Steps for Agreeing on a Compensation Package

MINISTER

As the Pastoral Relations Committee conducts its research, give some thought to your expectations regarding a

fair compensation package. Refer to the Compensation Handbook for Church Sta (described earlier) and other

ndings of the PRC. Make sure the PRC is aware of factors that might justify increases beyond the average salary

for a pastor in your situation:

• Additional experience or degrees acquired since the last salary negotiations

• Performance goals that have been met

• Additional responsibilities that have been assumed

• History of past raises, if those have been limited due to budget constraints

Guide to Negotiating Pastor Compensation | 18

Steps for Agreeing on a Compensation Package

CHURCH AND MINISTER

Once the Pastoral Relations Committee (PRC) has conducted its research, it should work with the minister to

design a fair and viable compensation package. See the previous sections of this guide for tips on optimizing

the mix of taxable and tax-advantaged compensation. Also see the sections that follow on how to approach

negotiations with a constructive frame of mind.

Now is also a good time to agree upon severance compensation. The church and minister can discuss the matter

objectively, free of passions that may arise when actual departure is imminent. Here are two possible formulas:

• One to two weeks of pay for each year of service, up to a maximum of 26 weeks

• Half a month of salary for each year of service (e.g., 5 years of service = 2.5 months of severance pay)

Once a compensation package is agreed upon, present it to the nance committee and/or to the congrega-

tion. Then incorporate it into your church’s annual budget.

19 | MMBB Financial Services

How to Determine a “Fair” Wage

Earlier in this guide, we discussed the components a compensation package should include. How do you

know if the package you’ve designed is reasonable and fair? Compare it with those of thousands of other

church workers nationwide.

Based on a national survey and updated each year, The Compensation Handbook for Church Sta provides

reliable compensation breakdowns for part-time, bi-vocational, and full-time church sta. It presents survey data

from more than 4,600 churches representing nearly 8,000 sta members. It also adjusts for church size, budget,

and geographical setting. Compensation proles are broken down by categories so that you can compare:

• Salary

• Retirement benets

• Health insurance coverage

• Housing/parsonage allowance

• Life insurance benets

• Continuing education

• The proled positions include, but are not limited to:

• Senior Pastor

• Associate Pastor

• Executive/Administrative Pastor

• Youth Pastor

• Adult Ministry Director

• Non-ordained

You’ll nd compensation levels based on personnel characteristics that include years employed, denomination,

region, and education level. This lets you compare your plan to other churches that have similar attributes and

demographics.

The Compensation Handbook for Church Sta is updated annually and can be ordered

at YourChurchResources.com.

Guide to Negotiating Pastor Compensation | 20

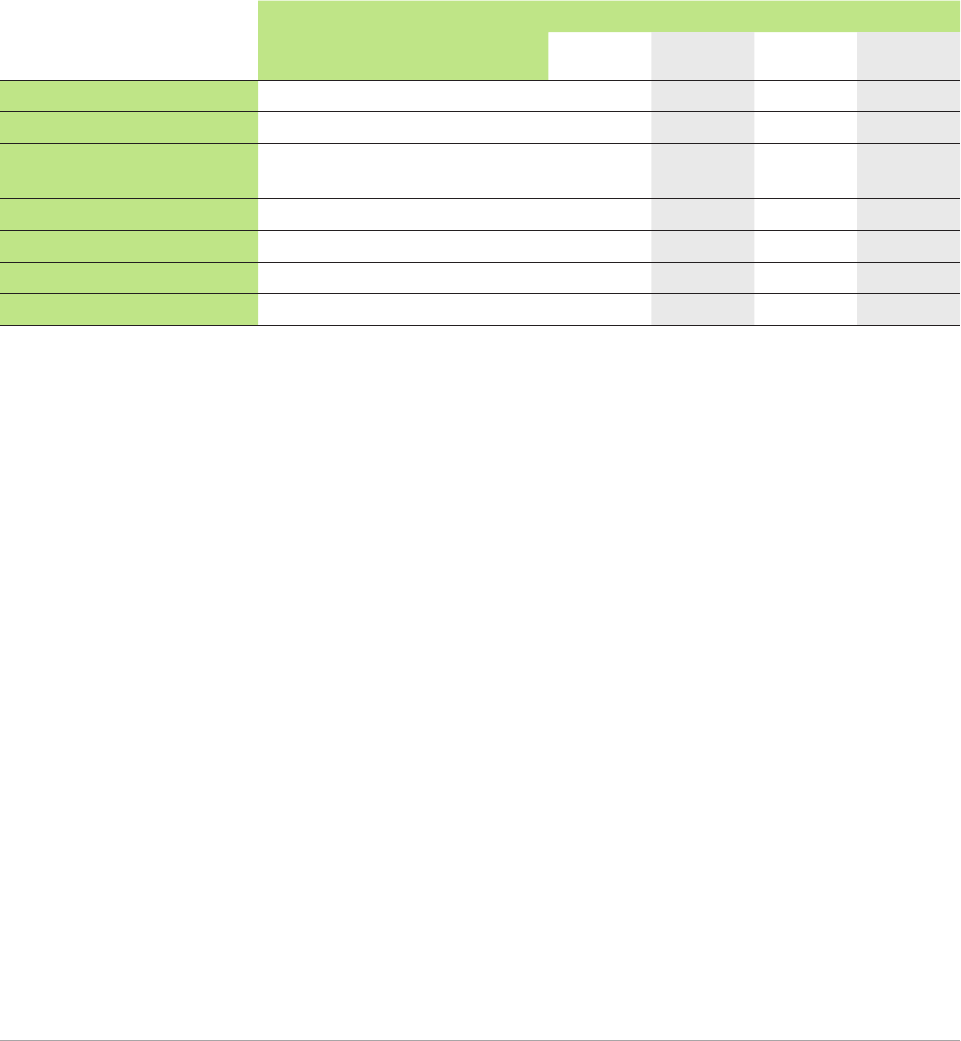

The Compensation Handbook for Church Sta provides a worksheet for each sta position. Enter your church’s data

in the rst column. Then check the reference tables to nd the highest/lowest, median/average compensation for

comparable positions. Your goal is not to come up with a single number, but rather to identify a compensation

range. Once that range is determined, a variety of factors will aect the nal level of compensation.

Example: Senior Pastor Worksheet

Enter Your

Church Data

below

The 2012-2013

Compensation Handbook

for Church Staff

Enter Compensation Handbook Data Below

Highest 25% Median Lowest 25% Average

Church Income $850,000 Table 4-1 Page 34 $114,000 $97,976 $85,225 $100,031

Worship Attendance 475 Table 4-2 Page 35 n/a $89,470 n/a $91,682

Church Settings (metro, suburban,

small town, or farming area)

Suburb of

a large city Table 4-3 Page 36 n/a $89,000 n/a $93,450

Region Pacific Table 4-4 Page 37 n/a n/a $89,428

Person’s Education Master’s Table 4-5 Page 38 n/a $78,631 n/a $82,250

Years Employed 10 years Table 4-6 Page 39 n/a $79,000 n/a $80,077

Denomination (if applicable) n/a Table 4-7 Page 40 n/a $n/a $

1 Worksheets in The Compensation Handbook for Church Sta help you determine a median range of

compensation plus benets.

Determine how your pastor’s compensation should t within the range

After establishing a range for base compensation plus benets, determine where your pastor’s compensation

should t within that range. Refer to the tables and adjust for:

• Church income, worship attendance, and setting (urban/rural)

• Pastor’s years of service, education

Plus additional circumstances such as:

• Cost of living in your area/local economy

• Pastoral performance, workload

• Goodwill

• History of previous raises for the pastor and other sta

1 Pg. 17 of CompHandbook 2012-13_nal_forcd.pdf

21 | MMBB Financial Services

If your church is multi-staed, you may want to set compensation as a percentage of the senior minister’s pay. For example:

• A sta person responsible for planning, developing, and leading ministries across a broad spectrum of

congregational life might receive 75% to 85% of the senior minister’s compensation.

• Someone responsible for one or two aspects of congregational life and requiring minimal supervision might

earn 70% to 80% of that base.

• Someone with entry-level skills requiring substantial supervision might receive 65% to 75% of a senior

minister’s compensation.

After conducting its research and making the appropriate adjustments, the PRC should share its information

with the pastor(s).

MMBB provides additional compensation information for ABC churches

For added perspective on national averages in the Compensation Handbook for Church Sta, MMBB

provides annually updates on average and median compensation for each ABC region, as well as for the

nation as a whole.

Your church can also ask MMBB to conduct a customized compensation study of pastors at churches like

yours within your region. The report will list the high, low, median, and average compensation.

For a copy of the annual update, or a custom compensation analysis request form, call 800.

986.6222 or email service@MMBB.org.

Alternative rules of thumb for determining a fair wage

If you and your pastor want an alternative to basing compensation on national averages, some

churches base their pastor’s salary on the average wage in their community for:

• The CEO of a non-prot organization

• A school principal

Guide to Negotiating Pastor Compensation | 22

Break a Pattern of Discriminatory

Compensation

The average salary for female pastors tends to skew lower because more women than men serve small church-

es. Nevertheless, female pastors earn 19% less then male pastors with similar levels of education and years of

employment. Their annual salary increases are 28% lower, on average.

As a center for teaching fairness and equality, your church should lead by example. Compensate your sta

fairly, regardless of gender.

Gender

Data Distribution* Male Female

Characteristics

Average weekend worship attendance 401 232

Average church income $710,389 $489,019

Average # of years employed 10 9

Average # of paid vacation days 22 25

% College graduate or higher 92% 94%

% Who receive auto reimbursement allowance 63% 56%

% Ordained 100% 100%

% Supervise one or more people 97% 100%

Average % salary increase (for those who had an increase) this year 4.3% 3.1%

Compensation

Base Salary Median $43,567 $39,594

Average $46,877 $41,572

Housing Median $25,000 $17,000

Average $27,025 $22,921

Parsonage Median $12,000 -

Average $14,167 -

Total Compensation Median $67,044 $50,500

Average $71,083 $57,517

Source: The 2012-2013 Compensation Handbook for Church Sta

23 | MMBB Financial Services

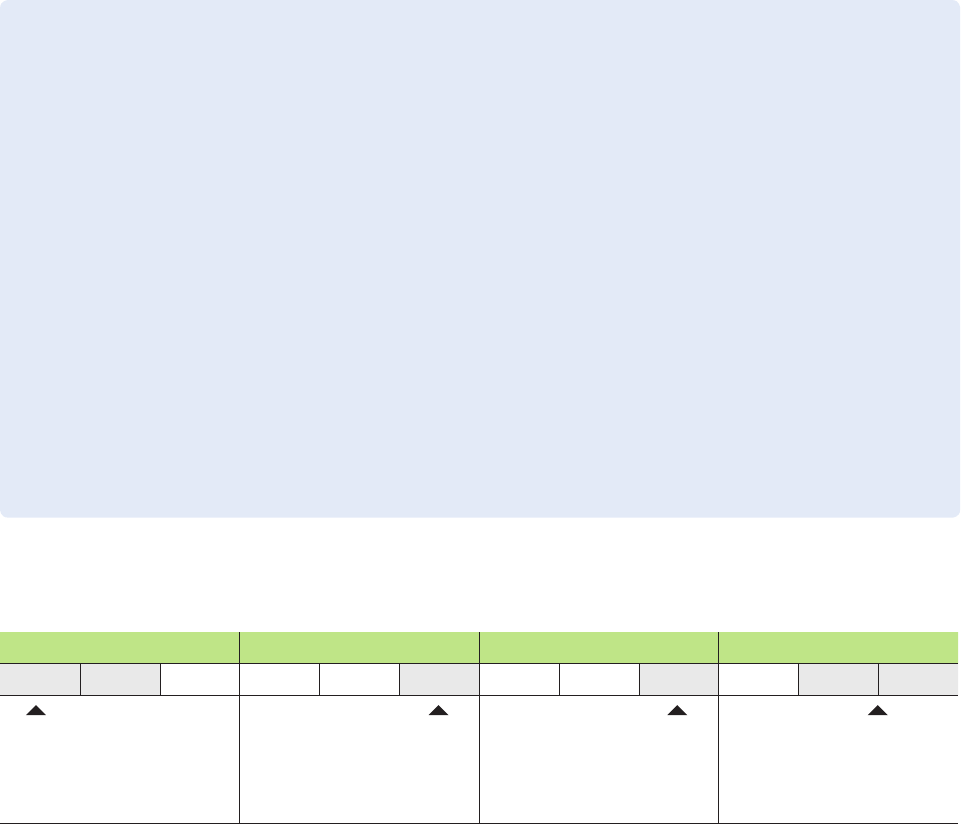

1st Quarter 2nd Quarter 3rd Quarter 4th Quarter

Jan Feb Mar Apr May Jun Jul Aug Sept Oct Nov Dec

Set pastoral goals for the year Give pastor feedback on

progress toward goals

PRC gathers data in

preparation for negotiating

compensation

Agree on compensation,

incorporate into church budget

for coming year, report to MMBB

Report compensation changes to MMBB

Once a compensation change is approved, report the change and its eective date to MMBB within one

month. A member’s retirement income, disability, and death benets are all based on reported compen-

sation. Failure to report changes could result in lower benets to your minister and his or her family.

To report the change, complete MMBB’s Compensation Change Request form, which you can obtain

by calling 800.986.6222. Submit the completed form to:

Attn: Billing Department

MMBB

475 Riverside Drive, Suite 1700

New York, New York 10115

Or fax (Attn: Billing) to 800.986.6782

You can also fax your change notice to 800.986.6782 (Attn: Billing) or email it to billing@MMBB.org

Recommended Timetable for Negotiating Compensation

Guide to Negotiating Pastor Compensation | 24

Approaching Negotiations with the Right Frame

of Mind

Pastors must learn to be their own advocates

While it is hoped that concerned members of the congregation will be committed to providing you with fair

and adequate compensation, you as a pastor must also advocate for yourself. Remember that you have a right

and responsibility to negotiate your own compensation.

Your advocacy need not be combative, hostile, or demanding. Instead, approach negotiation as a positive

activity to be done in a manner that encourages:

• A fair and adequate compensation plan

• A decision based on facts: your goals, achievements, education, and responsibilities, plus a comparison to

national averages

• A healthy and candid pastor and church relationship

• A stronger witness and mission of your church

Don’t leave decisions that aect your compensation to chance. Even well-meaning people need your input.

Don’t feel obligated to leave the room when your compensation is discussed. It is important to negotiate face-

to-face so that everyone knows why the compensation decision is what it is.

“The Lord commanded that those who proclaim the gospel should get their living

by the gospel.”

Corinthians 9:14

25 | MMBB Financial Services

Four common misconceptions when pastors negotiate their salary

“Congregants will dislike me if I request a higher salary.”

People appreciate honesty and would rather know how a pastoral leader is feeling than deal with

unexpressed frustration. Ministers cannot have healthy relationships in a church when they carry a

burden of undisclosed hostile feelings.

When money issues do emerge, they are usually not the root problem, but a symptom of other issues

that should be investigated. People pay more attention to what you do than the salary you request.

“I’m a proclaimer of the gospel, I shouldn’t be preoccupied with such material concerns.”

The scripture acknowledges time and again that church leaders must be cared for and compensated

for their labor. Paying a fair wage is one way your congregation acknowledges that it respects its own

ordained leaders. While being silent and passive is a negotiating option, it can cause your feelings to

emerge in defensive, ways that are counterproductive to doing God’s work.

“My church is poor. It can’t aord to do better.”

To test this theory, check The Compensation Handbook for Church Sta and see what churches like

yours are currently paying. Congregants rarely openly discuss their personal nances. Your perception

may not align with the reality.

“The church’s mission giving will go down if my salary goes up.”

It is better for a church to support its own ministry than to sacrice the pastoral leader’s salary for

wider mission giving. Your church’s rst priority is to appropriately provide for its members and pas-

toral leaders. They are essential for church growth and eective mission giving. You can also test this

theory by checking The Compensation Handbook for Church Sta.

Guide to Negotiating Pastor Compensation | 26

Three common misconceptions when churches negotiate pastors’ salary

“We can pay less because the pastor’s spouse is a high earner.”

Nowhere else in the working world are employee salaries reduced to account for spousal earnings.

Your minister’s eorts are worth no less when his or her spouse earns a good income. A fair wage

should be based on national averages reported in The Compensation Handbook for Church Sta and

adjusted only for your church’s environment and the pastor’s qualications.

“We can pay less because the pastor has modest needs.”

Pastors who live modestly may still need to care for family members. They may have plans for travel or

unpaid service during retirement. A church has no right to pay a less-than-fair wage simply because it

does not know how the pastor will spend the money.

“We’ll just oer a total compensation amount and let the pastor decide how to allocate it.”

A common mistake that distorts the actual amount a pastor will have for living expenses is to propose

a single large gure that covers salary, benets, and expenses. This forces the pastor to choose be-

tween accepting lower take-home pay, waiving essential benets, or paying expenses out of pocket.

As you have seen earlier, the various forms of compensation serve dierent purposes and have dif-

ferent tax implications. It takes considerable thought to develop an optimal mix. It is unfair to make

ministers do this on their own.

Church leadership is responsible for paying a fair wage and retaining

talented leadership

The Word of God is specic when it says that laborers are worthy of their hire. This means churches should give

the maximum amount of support to their pastors, without jeopardizing the overall nancial stability of the

church. That is not always easy during dicult economic times. But the right thing isn’t always the easiest. If

church nances make it dicult to pay what you should, see the section later in this guide on “bridging the gap.”

27 | MMBB Financial Services

Tips for Constructive Negotiations

Your church and minister will need to work together after the salary negotiations. Conduct them in a spirit of

good will that avoids rancor and ensures a positive outcome.

Negotiation tips for a minister

Begin the session with a prayer. But don’t make the prayer an opening statement of your position! Pray that

God’s spirit will lead all present in the discussion (rather than praying that God will open their eyes to the

inadequacy of your previous compensation package).

Know what you want and what you absolutely need, and prioritize your requests. It is important to have

thought through these matters before the negotiation begins. Seeming unprepared diminishes your credibil-

ity. (“How important can this be? He didn’t even know what he wanted.”)

Whenever possible, point out the positive impact your requests will have on you and the church’s ministry. We

are all partners in ministry. Money and ministry are connected.

Three criteria for successful negotiations

• They should be ecient, stay on the subject, and not become sidetracked.

• They should improve, or at very least not damage, the relationship between parties.

• They should lead to a mutually acceptable win-win agreement.

Guide to Negotiating Pastor Compensation | 28

Negotiation tips for all participants

Educate the decision makers on the components of a compensation package and the principle of basing

salaries on national averages. Share your research on compensation comparisons and try to have objective

discussions based on facts.

Be an active listener and try to understand the logic of others’ positions. Many negotiations have broken

down over minor points because people simply didn’t understand what their negotiating partners wanted or

needed. Restate your understanding of your counterpart’s position. It will help you gain added credibility.

Try not to put your negotiating partners on the defensive. (“You might let your family live in a house like that,

but I’d never do it to anyone I loved!”) It prevents people from listening and encourages them to dig in rather

than admit wrongdoing or guilt. Instead, state your position in objective terms. (“The parsonage is lovely in the

summer. But the uninsulated walls and 40-year-old heating system make it hard to keep the temperature in the

winter above 65 degrees.”) Be hard on the problem; be soft on people.

Be realistic in your expectations. You may not be able to achieve all your goals all at once. Expect to give up on

some requests and compromise on others.

Be willing to take a leap of faith. Sometimes the other side needs to see a gesture of good will before they will

soften their position.

You’ll nd additional resources for successful negotiation at the end of this guide.

“Those who are taught the word must share in all good things with their teacher.”

Galatians 6:6

29 | MMBB Financial Services

Bridging the Gap: When Your Church Cannot

Aord to Pay a “Fair” Wage

It may happen that your church determines a fair wage—based on its situation and the minister’s qualications

– but church nances are such that it cannot aord to pay that. Here are some suggestions of creative ways to

“bridge the gap.”

Increase the proportion of tax-advantaged compensation

Without increasing the total compensation amount, your church may be able to increase the minister’s take-

home pay. Consider shifting compensation to such tax-advantaged forms as retirement plan contributions, a

housing allowance, or an increased expense allowance.

Realize that each side has multiple interests

You’ve seen that compensation takes many forms. Take time to understand the other side’s multiple interests

and you may nd other ways to help even the balance. For example, you might say, “Our church cannot aord

the annual increase you requested. But since one of your problems is cash ow early in the year until you’ve

paid your medical insurance deductible, can we restructure your salary schedule so that 60% is paid during

the rst half of the year?” Or, “In lieu of the higher salary increase, how about the lower amount, plus covering

medical deductibles?”

Supplement the minister’s salary with other forms of compensation

Cash is not the only solution. You can enrich your compensation package by adding such non-cash elements as:

• A paid sabbatical

• Church payment of the minister’s continuing education

• More paid leave

The dollar value of the package won’t necessarily be a lot higher. But it may be a better arrangement overall.

Agree on a catch-up schedule

If you’re condent that your church is only experiencing a temporary setback, consider specifying—in writing—

how you will make it up to your pastor with future salary increases. Just be sure that you can follow through on

this promise. Failing to deliver in the future will add feelings of betrayal on top of a salary grievance. (If at any

point the amount paid exceeds what was reported to MMBB, contact MMBB to make up back payments of

Comprehensive Plan premiums.)

Guide to Negotiating Pastor Compensation | 30

Reconsider the pastor’s responsibilities

If your church cannot compensate the minister fairly for all the work he or she is doing, you may want to

consider reducing the minister’s responsibilities. Many smaller churches are able to manage with a part-time or

bi-vocational pastor. Or they reduce the pastor’s workload by providing lay assistance with certain tasks.

Myth: “Part-time pastors aren’t real pastors.”

Churches concerned that they can only aord a part-time pastor should realize that this is a perfectly

viable option. Christian ministry has a long and rich history of implementation by part-time leadership.

The early Christian church grew out of multi-vocational leaders.

While multi-vocational ministry can be fullling and challenging, it is best to begin by setting clear

guidelines:

1. Write a letter of understanding that clearly describes:

• Ministry expectations and the number of days per week for service

• Supplemental pay when circumstances require service beyond the agreed-upon days per week

• Financial arrangements

• Accommodations, if there is no parsonage

2. Do not change the arrangements midstream without mutual agreement.

3. Ensure that there is a clear plan for growth.

No pastor or church should settle for a non-growth environment. Even if the possibility of a full-time

position seems remote, establish a vision and mission for further development. If your church does not

really want to change, then the pastor should be told this before responding to a call.

Additional Resources

Online

• MMBB Church Finances & Administration. Your online guide to church nances and benets administra-

tion, including descriptions of MMBB benets oerings. MMBB.org/Church-Finances-Administration

• ThePastoralRelationsCommittee, prepared and published by the United Church of Christ Parish Life and

Leadership Ministry Team. Suggested policies, principles, and procedures that may enhance the work of the

Pastoral Relations Committee. UCC.org/Ministers/PDFs/prc.pdf

• SuggestedMinisterChurchAgreement. A “covenant making” tool for American Baptist congregations and

ministerial leaders to use during the process of extending a call of ministry to a new leader. Helps establish

and maintain a healthy relationship between the congregation and leader by making clear and specic the

terms and benets of employment. MinistersCouncil.com/ClergyCongregationalRelationships/Sug-

gestedMinisterChurchAgreement.aspx

• FederalReportingRequirementsforChurches, by Richard R. Hammar, J.D., LL.M., CPA. These payroll report-

ing requirements apply, in whole or in part, to almost every church. Yet many churches do not fully comply

with them. Visit MMBB.org and search “reporting requirements.”

• Website of the Program on Negotiation at Harvard Law School. Click on “Browse Topics” for succinct

posts covering various aspects of negotiation and conict resolution. PoN.Harvard.edu

31 | MMBB Financial Services

Print

• TheCompensationHandbookforChurchSta, by Richard R. Hammar, J.D., LL.M., CPA, published by

Christianity Today International (updated annually). Based on survey data from more than 4,600 churches

representing nearly 8,000 sta members, this guide provides reliable compensation breakdowns for part-time

and full-time church sta. Visit the employment section of YourChurchResources.com.

• TheEssentialGuidetoChurchFinances, by Richard J. Vargo and Vonna Laue (2009). How to strategize,

organize, measure, communicate, protect and audit your church nancials. Covers planning and budgeting,

church nancial reports, performance measurements and church audits. Visit the employment section of

YourChurchResources.com.

• GettingtoYes:NegotiatingAgreementWithoutGivingIn, by Roger Fisher and William Ury (2011). Oers a

proven, step-by-step strategy for coming to mutually acceptable agreements in every sort of conict. Based on the

work of the Harvard Negotiation Project, a group that deals with all levels of negotiation and conict resolution.

• DicultConversations:HowtoDiscussWhatMattersMost, by Douglas Stone, Bruce Patton, and Sheila

Heen (2010). From the Harvard Negotiation Project, a step-by-step approach to having tough conversations

with less stress and more success. Learn how to decipher the underlying structure of every dicult conversa-

tion, start a conversation without defensiveness, and move from emotion to productive problem-solving.

Guide to Negotiating Pastor Compensation | 32

Contact Information

MMBB Financial Services

475 Riverside Drive, Suite 1700

New York, NY 10115-0049

MMBB.org

Tel: 800.986.6222 Fax: 800.986.6782

Email: service@MMBB.org

ABCUSA Ministers Council

PO Box 851

Valley Forge, PA 19482-0851

Tel: 610.768.2334

MinistersCouncil.com

Christianity Today

International

465 Gundersen Drive

Carol Stream, IL 60188

Tel: 630.260.6200

ChristianityToday.com

YourChurchResources.com

National Association of Church

Business Administration

100 N. Central Expressway, Suite 914

Richardson, TX 75080-5326

Tel: 800.898.8085

NACBA.net

Source: Edward Koren / The New Yorker Collection

33 | MMBB Financial Services

Guide to Negotiating Pastor Compensation | 34

The Ministers and Missionaries Bene ts Board

475 Riverside Drive, Suite 1700

New York, NY 10115-0049

Tel: 800.986.6222

Fax: 800.986.6782

MMBB.org

Produced in collaboration with the Ministers Council

of the American Baptist Churches, USA.

© 2013 MMBB Financial Services COMP0313