Practical Guide To Quantitative Finance Interview

User Manual:

Open the PDF directly: View PDF ![]() .

.

Page Count: 212 [warning: Documents this large are best viewed by clicking the View PDF Link!]

First Edition

Xinfeng Zhou

Edited by Brett Jiu

To

the memory

of

my

sister, Xinli Zhou

©Copyright 2008 by Xinfeng Zhou, http://www.quantfinanceinterviews.com

All right reserved.

No part

of

this book may be reproduced or transmitted in any form or

by

any means,

electronic or mechanical, including photocopying, recording or by any information

storage and retrieval system, without the written permission

of

the Publisher, except

where permitted by law.

Table

of

Contents

Chapter 1 General Principles ......................................................................................... 1

1.

Build a broad knowledge base .................................................

....

.................................................. 1

2.

Practice your interview skills .......................

..

.

..

........................

..

...................................

..

.............. 1

3. Listen carefully .................

..

.........................

..

................................................................

..

..

............ 2

4. Speak your mind .

....

...

..

...

..

.............................

..

.......

..

....

.........

..

................................

..

..................

..

2

5. Make reasonable assumptions ......................

..

................................................................................ 2

Chapter 2 Brain Teasers ................................................................................................. 3

2.1

Problem Simplification ......................................................... ................................... 3

Screwy pirates ...................

..

............................................................

..

..

..

............................................. 3

Tiger

and

sheep ....... ............................................

..

............................................................................. 4

2.2 Logic Reasoning ...................................................................................................... 5

River crossing .................................................................................

..

.

..

..........................

..

.

..

............... 5

Birthday problem .............................................

..

.

..

...........................

..

.

..

..............................

..

..

........... 5

Card

game

.........................................................................................

..

..

........................

..

................... 6

Burning ropes ..................................................

..

.

..

........................................................

..

....

................ 7

Defective ball ......

..

..

............

..

.....

..

.......................

..

.

..

...

..

............

..

..

..

.

..

....................

.. ..

...................

..

... 7

Trailing zeros ...................................................................................

...

............................................... 9

Horse race ...................................................................................................................

..

..

..

................. 9

Infinite sequence ...............................................

.. ..

...........................................................................

10

2.3 Thinking Out

of

the Box ....................................................

..

....................

..

.. ..

........

10

Box packing ....................................................................................

..

...

..

..........................................

10

Calendar cubes .

..

..............................................................................

...

..

.......................

..

..................

11

Door

to

offer ......................................................................................

..

..

........................

..

................

12

Message delivery ...............................................................................

..

..

.........................

..

...............

13

Last ball ...............................

..

..........................

.. ..

.................................................................. ..........

13

Light switches ...................................................

..

..

.............................

..

..

.........................

..

..

.............

14

Quant salary ....................................................................................

..

...

..

..........................................

15

2.4 Application

of

Symmetry ......................

..

.....................................................

..

.......

15

Coin piles .

..

.

..

..

.........................

...

....

..

...

..

.

..

........................................................

..

.......

..

.......

..

...........

15

Mislabeled bags ............................................................................................................................... 16

Wise men ...........................................................................................

..

.

..

......................

...

..

..............

17

2.5 Series Summation ..................................................................................................

17

Clock pieces .........................................................

..

.............................

.. ..

.........................................

18

Missing integers ................................................

..

.

..

.....................

..

...............................

..

..................

18

Counterfeit coins I ..............................

..

.........................................

..

..............................

..

................

19

2.6 The Pigeon Hole Principle .......................................................................

...

........... 20

Matching socks ................................................................................................................................

21

Handshakes ........................

....

..........................................................................................

..

..............

21

Have

we

met before? ...........................................................................

..

...............................

..

.........

21

Ants

on

a square ...........................

..

..

....................................................

..

.......................................... 22

Counterfeit coins II ..........................

..

.................

..

................................

..

.......................

..

................ 22

Contents

2.7 Modular Arithmetic .............................. .

..

...................................................

..

..

........ 23

Prisoner problem ................

..

............................................................

..

............................

..

................

24

Division

by

9 .................................................................................

..

................................................ 25

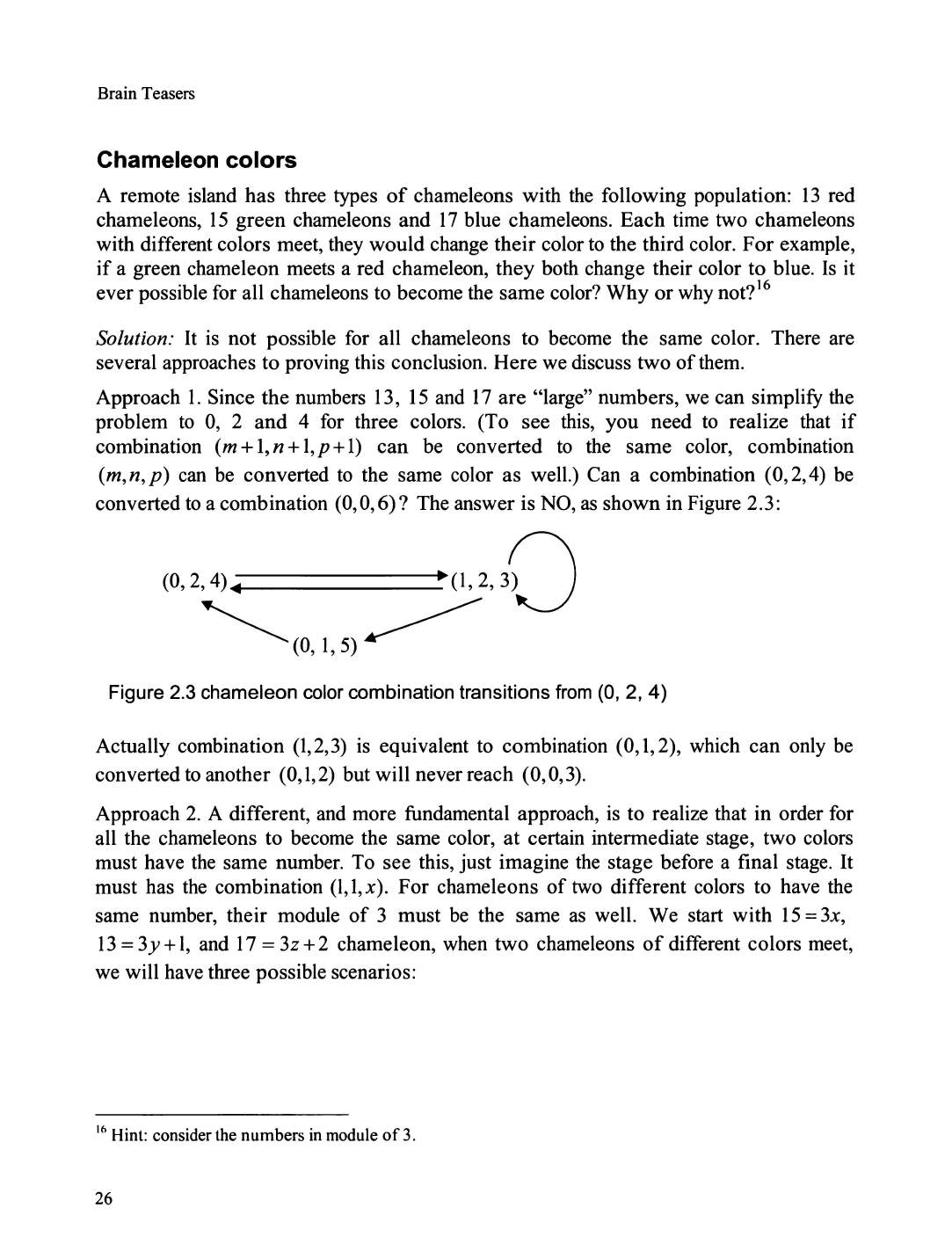

Chameleon colors ............................................................................

..

...............................

..

............. 26

2.8 Math Induction .....................................

..

................................................................ 27

Coin split problem ..........................................................................

..

............................................... 27

Chocolate

bar

problem ....................................................................................................

..

............... 28

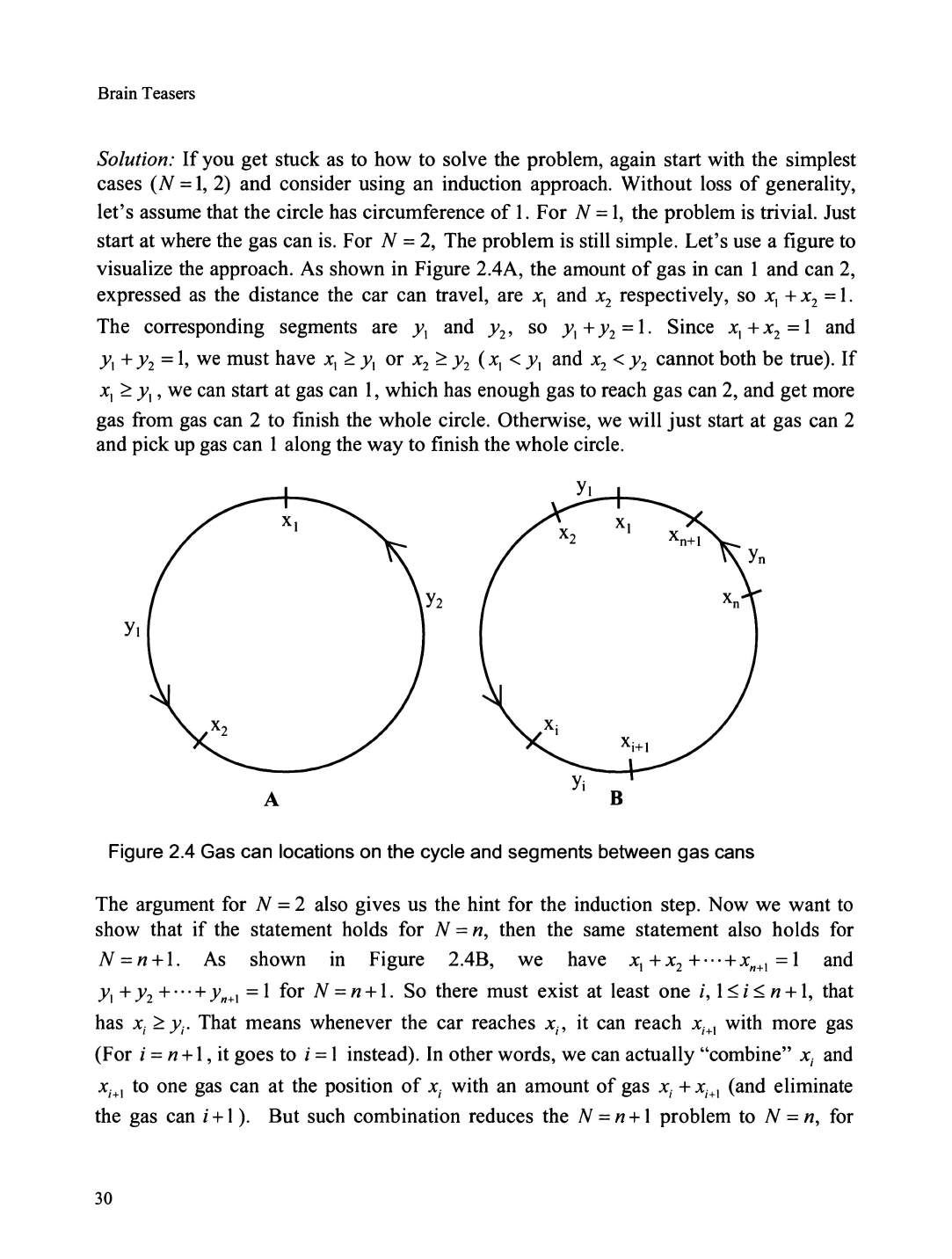

Race track .............................................................................................................................

..

......... 29

2.9 Proof by Contradiction ........................

..

..

........................... ....................................

31

Irrational number

..

..............................................

..

.........................

..

.

..

................... ..

..

....

..

.. ..

............

31

Rainbow hats .....................................................................................................................

..

............

31

Chapter 3 Calculus and Linear Algebra ...................................................................... 33

3.1

Limits and Derivatives

..

......................

..

...

................................................

..

..

..

........ 33

Basics

of

derivatives ........................................................................

..

..............................................

33

Maximum and minimum .... ...............................................................

..

...........................

..

............... 34

L'Hospital's rule .................................................................................................................

..

........... 35

3.2 Integration ............................................

.. ..

......................

...

..........................

..

..

....... 36

Basics

of

integration ........................................................................................................

..

..............

36

Applications

of

integration .................................................................

..

............................

..

............. 38

Expected value using integration ......................................................

..

...............................

..

............

40

3.3 Partial Derivatives and Multiple Integrals ............................................................ .40

3.4 Important Calculus Methods ..................................................................

...

............ .41

Taylor's series ......................................................................................

..

..........................................

41

Newton's method .............................................................................

..

..............................................

44

Lagrange multipliers ........................................................................................................................ 45

3.5 Ordinary Differential Equations ....... ...

..

....

..

.......

..

..........

....

.......

..

.............

..

........... .46

Separable differential equations ..........................

..

...........................................................

..

.............. 4 7

First-order linear differential equations ..........................................................................

..

............... 4 7

Homogeneous linear equations .......................................................

..

............................................... 48

Nonhomogeneous linear equations ..................................................................................................

49

3.6 Linear Algebra ............

..

.......................

..

........................

..

.. ..

...................

..

............. 50

Vectors .................

..

...

.. ..

................................... ..........

..

.

..

...................

..

...............................

..

........... 50

QR

decomposition ......

..

..............................................

..

..... ...............

..

............................................. 52

Determinant, eigenvalue

and

eigenvector .........................................

..

................................

..

........... 53

Positive semidefinite/definite matrix .................................................

..

...............................

..

...........

56

LU decomposition and Cholesky decomposition ...........................................................

..

............... 57

Chapter 4 Probability Theory .......................................................................................

59

4.1

Basic Probability Definitions and Set Operations ..............

..

.......................

..

......... 59

Coin toss game .................................................................................................................................

61

Card game .........................................................

..

...........................................................

..

................

61

Drunk passenger ...............................................................................

..

.

..

.......................................... 62

ii

A Practical Guide

To

Quantitative Finance Interviews

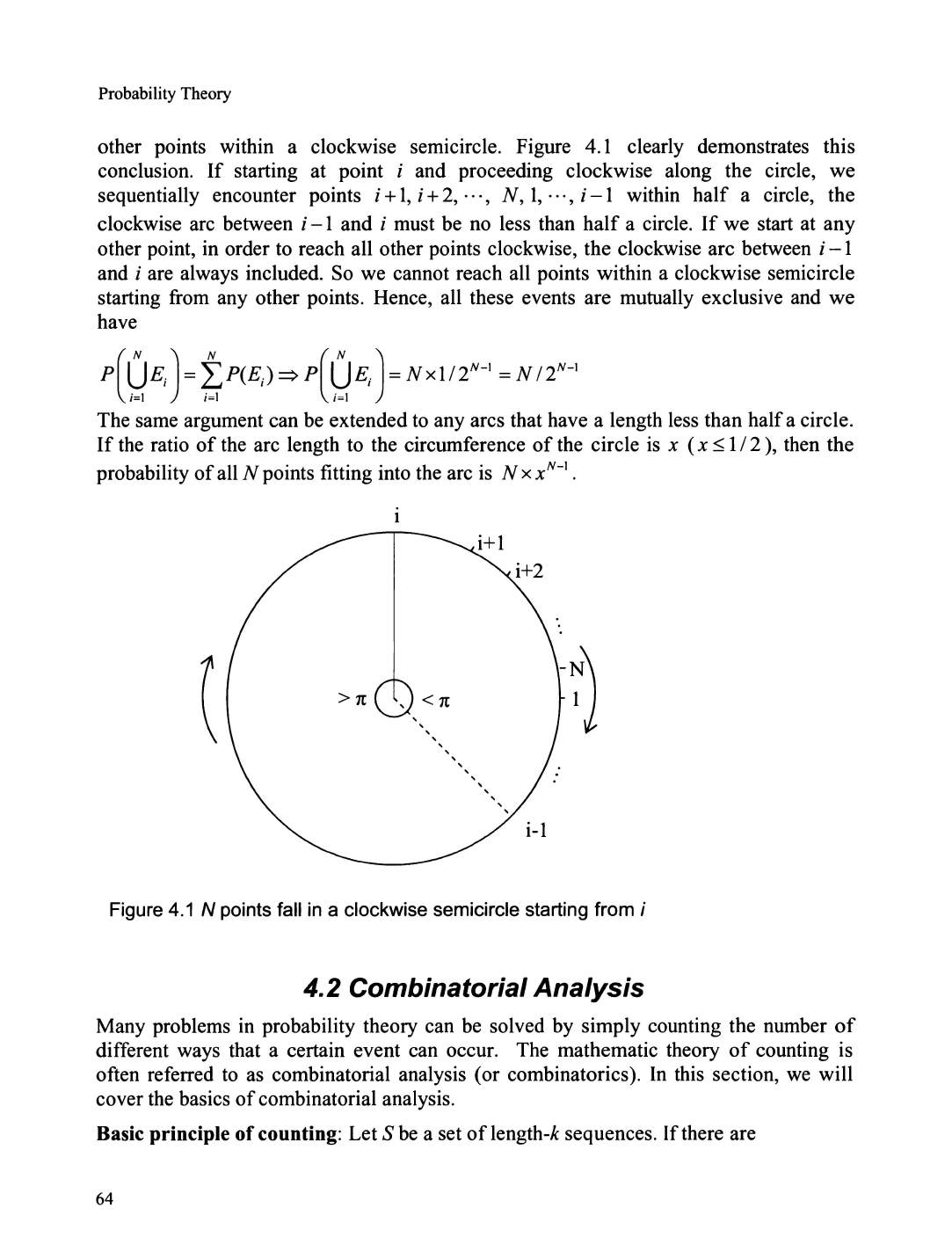

N points on a circle ............

..

............................................................................................................ 63

4.2 Combinatorial Analysis .................................................

..

.........................

..

........... 64

Poker hands ........................

..

............................................................................................................ 65

Hopping rabbit .. .....

..

................ ...........

..

..............................

..

..............................

..

........................... 66

Screwy pirates 2 .............................................................................................................

..

................ 6 7

Chess tournament. ............................................

..

................................... ........................................... 68

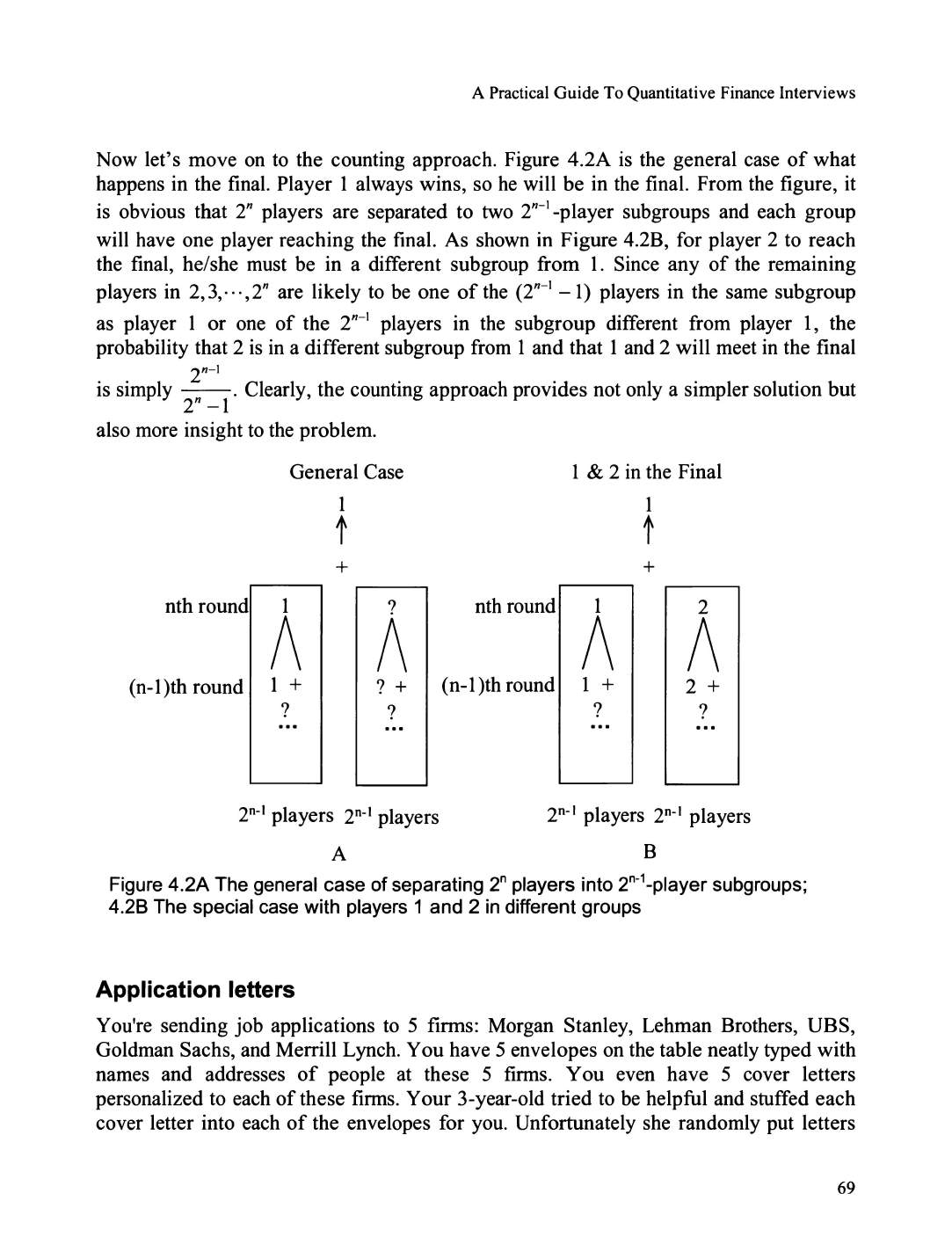

Application letters ..............

..

......................................................................................... ................... 69

Birthday problem .............................................................................................................................

71

I

OOth

digit ...........................

..

........................................................................................ ...................

71

Cubic

of

integer ............................................................................................................................... 72

4.3 Conditional Probability and Bayes' formula .................

..

.......................

..

..

........... 72

Boys and girls ...................................................................................

..

............................................. 73

All-girl world? ................................................................................................................................. 74

Unfair coin .......................................................... ............................................................................. 74

Fair probability from an unfair coin ................................................................................................. 75

Dart game ......................................................................................................................................... 75

Birthday line ....................................................... .........................................................................

..

.. 76

Dice order ........................................................................................................................................ 78

Monty Hall problem ............................................. ............................. ............................................... 78

Amoeba population .............................................. ............................................................................ 79

Candies in a

jar

................................................................................................................................ 79

Coin toss game .................................................... .............................................................. ...............

80

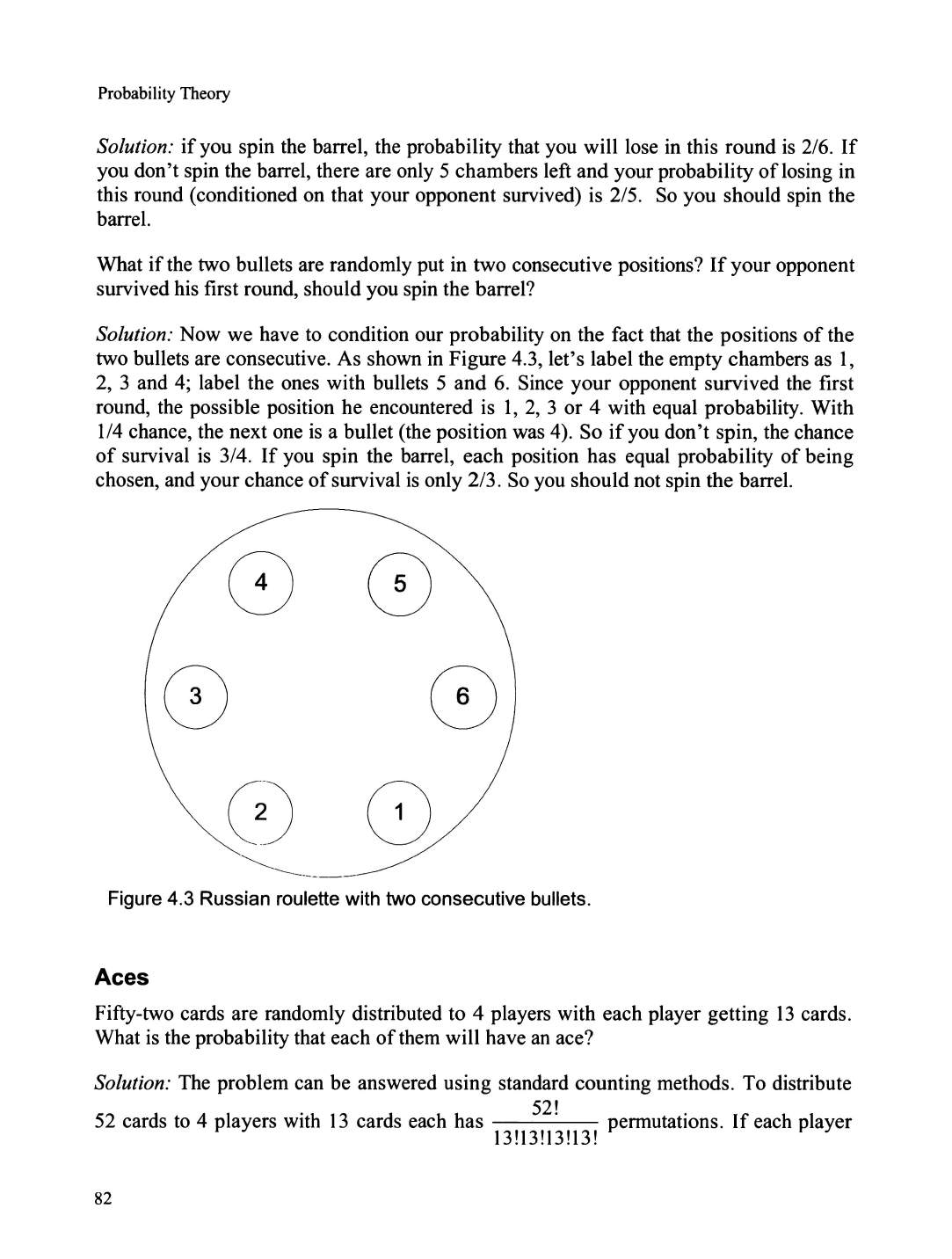

Russian roulette series ......................................... .............................................................. ...............

81

Aces .................................................................... ............................................................................. 82

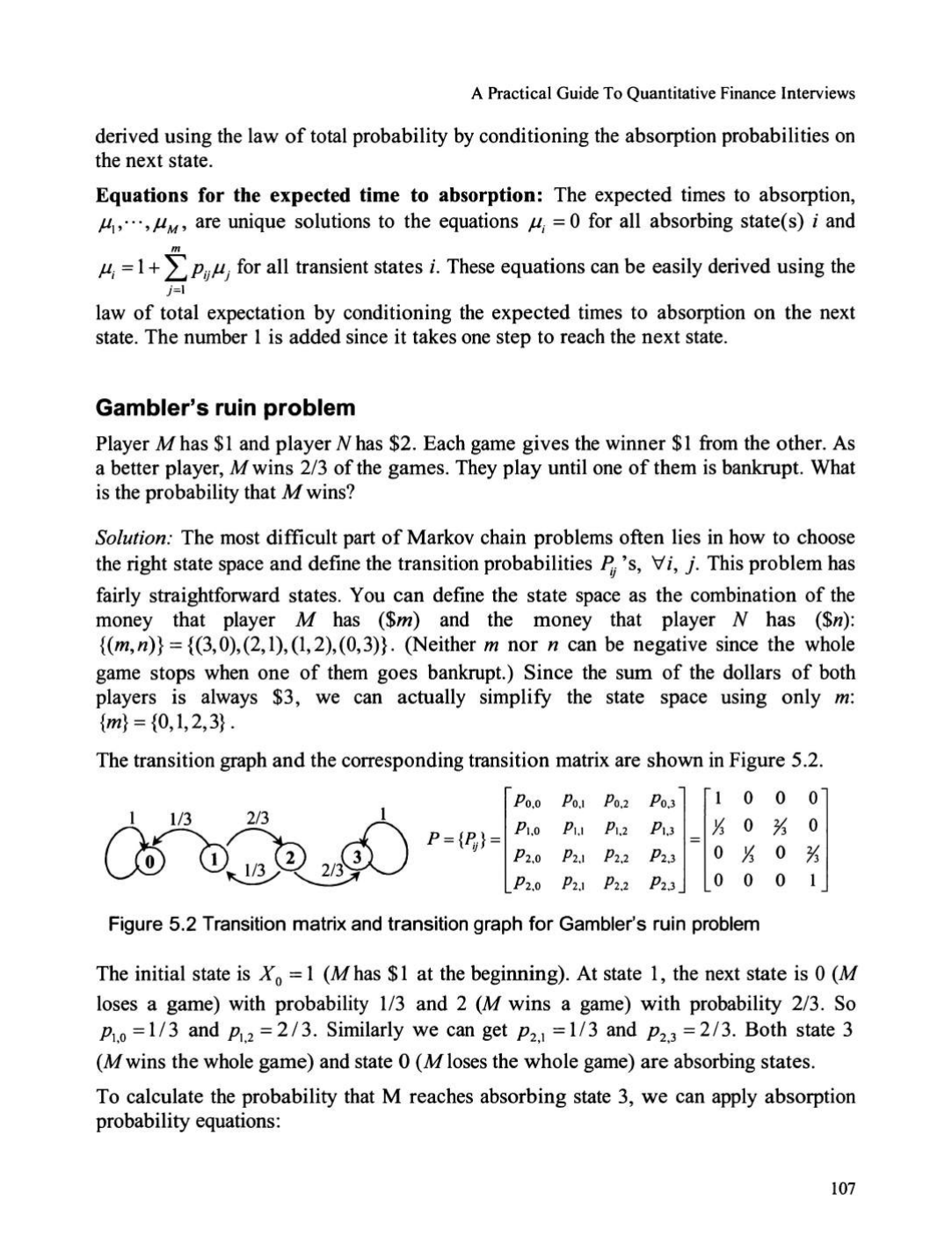

Gambler's ruin problem ....................................... ............................................................................

83

Basketball scores .............................................................................................................................. 84

Cars on road ....................................................................................................................... .............. 85

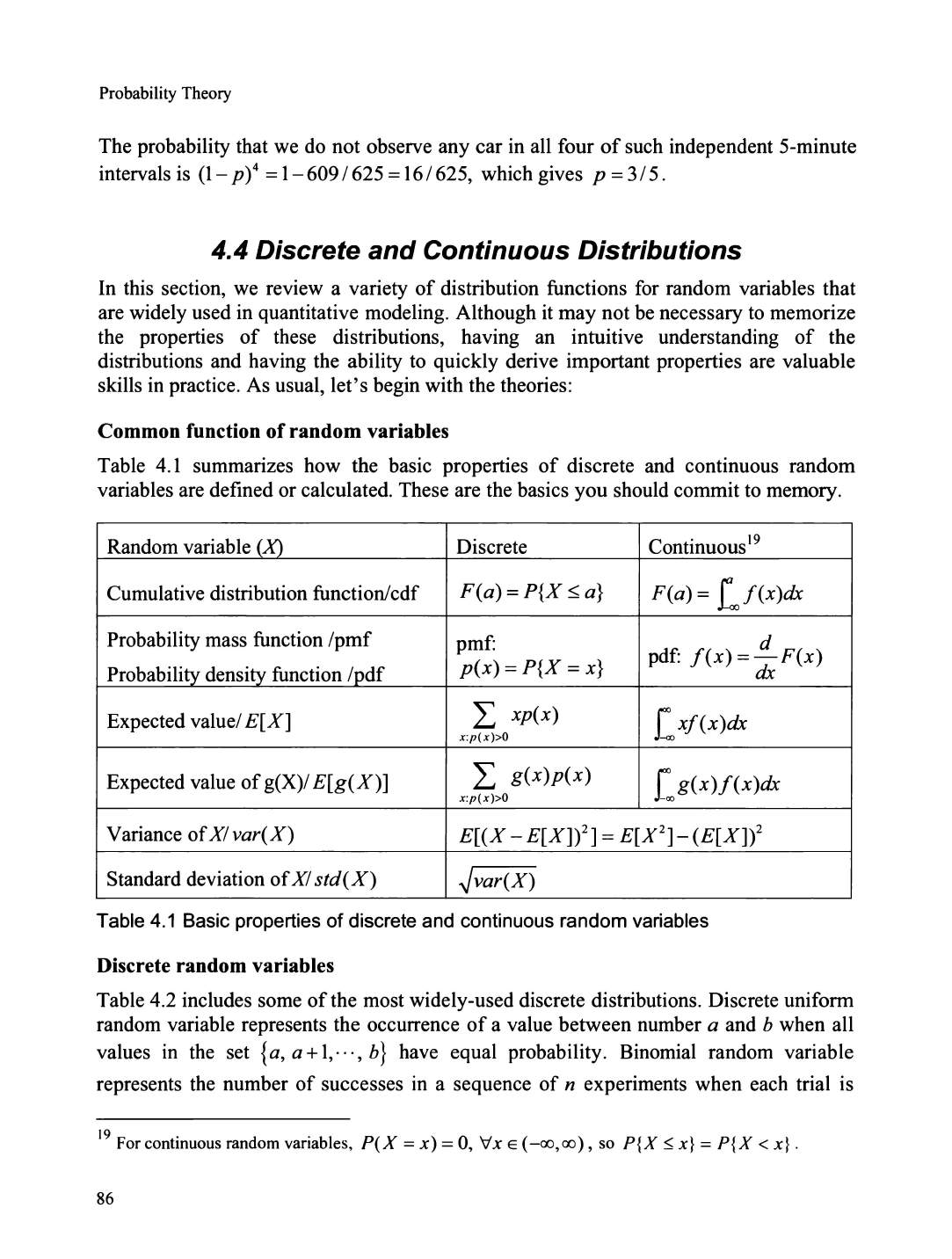

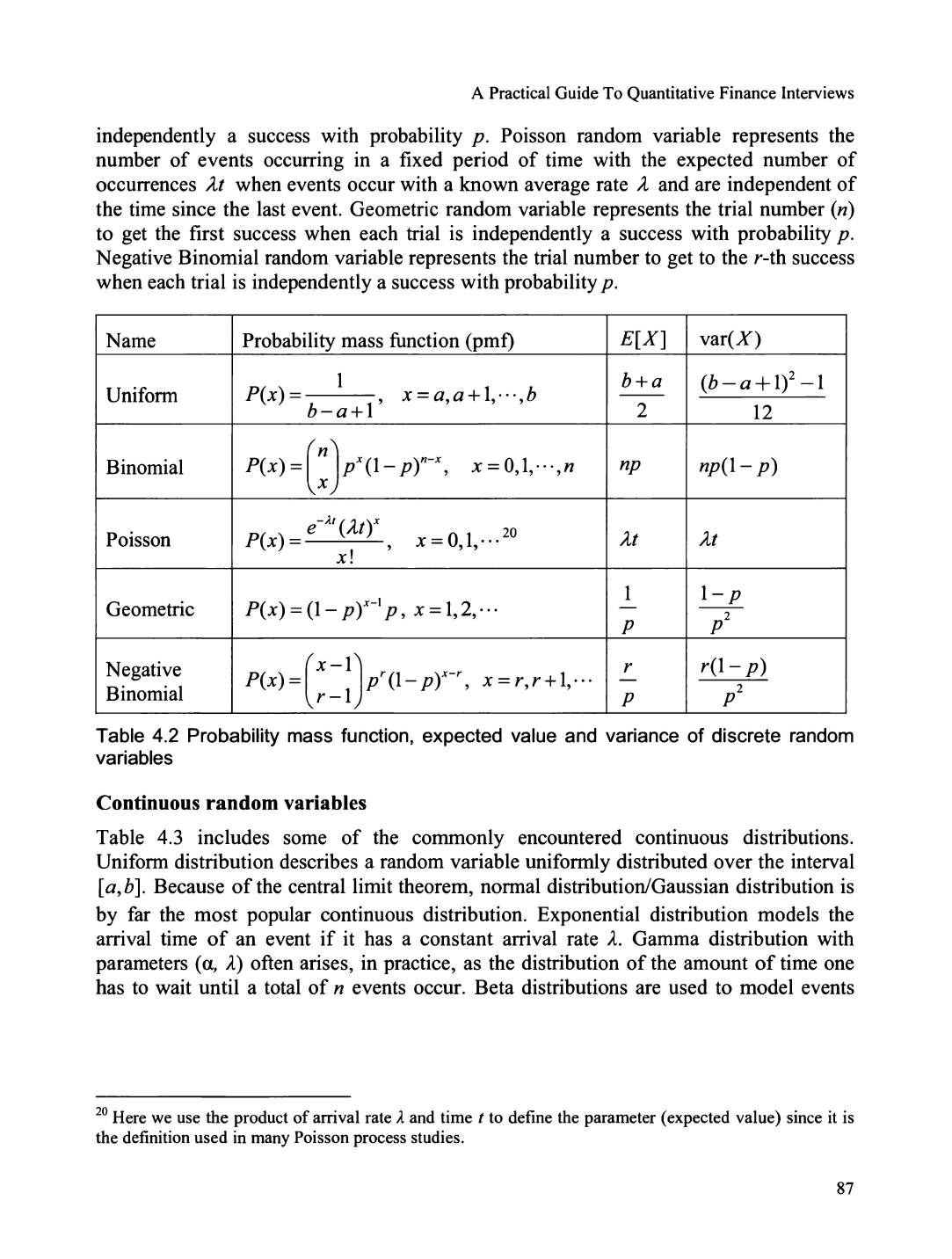

4.4 Discrete and Continuous Distributions .......................................................

..

......... 86

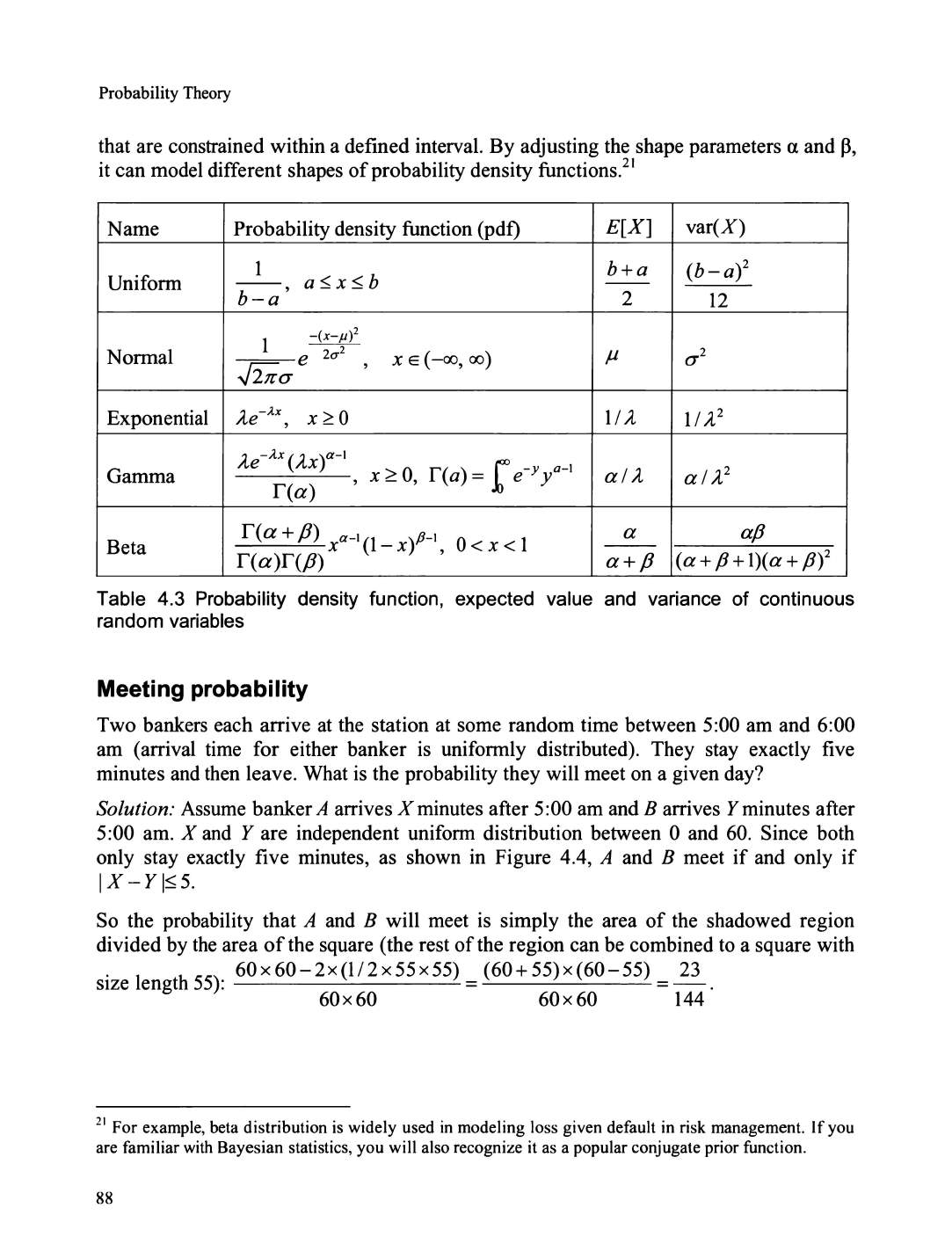

Meeting probability .......................................................................................................................... 88

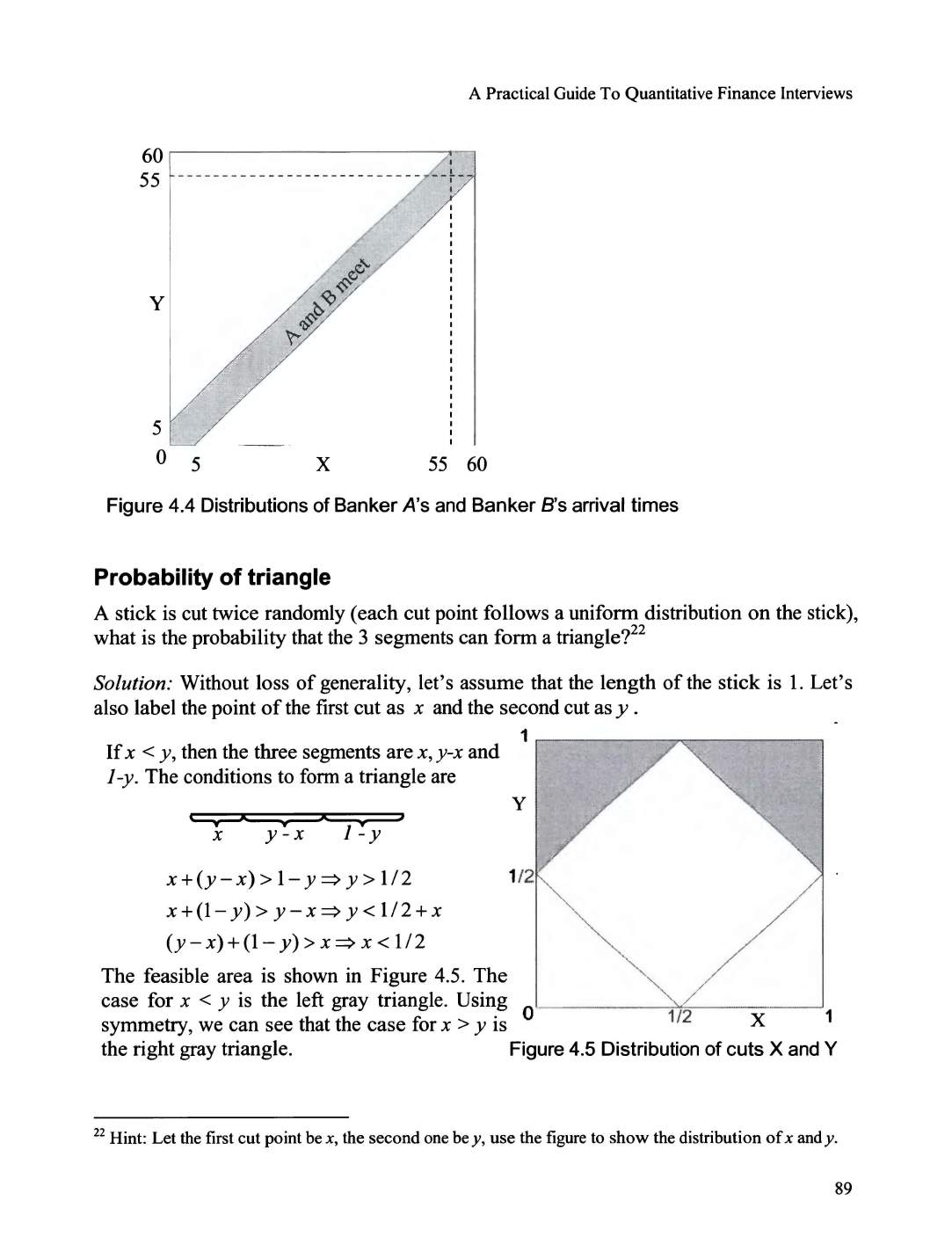

Probability

of

triangle ................................

..

...... .................................................

..

........................... 89

Property

of

Poisson process

..

..............................................................................................

..

........... 90

Moments

of

normal distribution ........................................................ ................................. .............

91

4.5 Expected Value, Variance & Covariance ......................

..

...................................... 92

Connecting noodles .......................................................................................................................... 93

Optimal hedge ratio .............................................. ........................................................................... 94

Dice game ........................................................ .............................. .................................................. 94

Card game ........................................................... ...............

..

............................................................ 95

Sum

of

random variables

..

.................................... ............................

..

......................... .................... 95

Coupon collection .............................................................................. .......................... .................... 97

Joint default probability ....................................... ............................................................................ 98

4.6 Order Statistics ............................................................................................

..

........ 99

Expected value

of

max and min ............................................................................................ ........... 99

Correlation

of

max and min ........................

..

.............. ................................................................... 100

Random ants ...................................................... ............................................................................ l 02

Chapter 5 Stochastic Process and Stochastic Calculus ............................................ 105

iii

Contents

5

.1

Markov Chain ...........

..

..............................................................................

..

.........

105

Gambler's ruin problem ....

..

..........................................................................................

..

........ ....... 107

Dice question ....................

..

..........................................................................................

..

............... 108

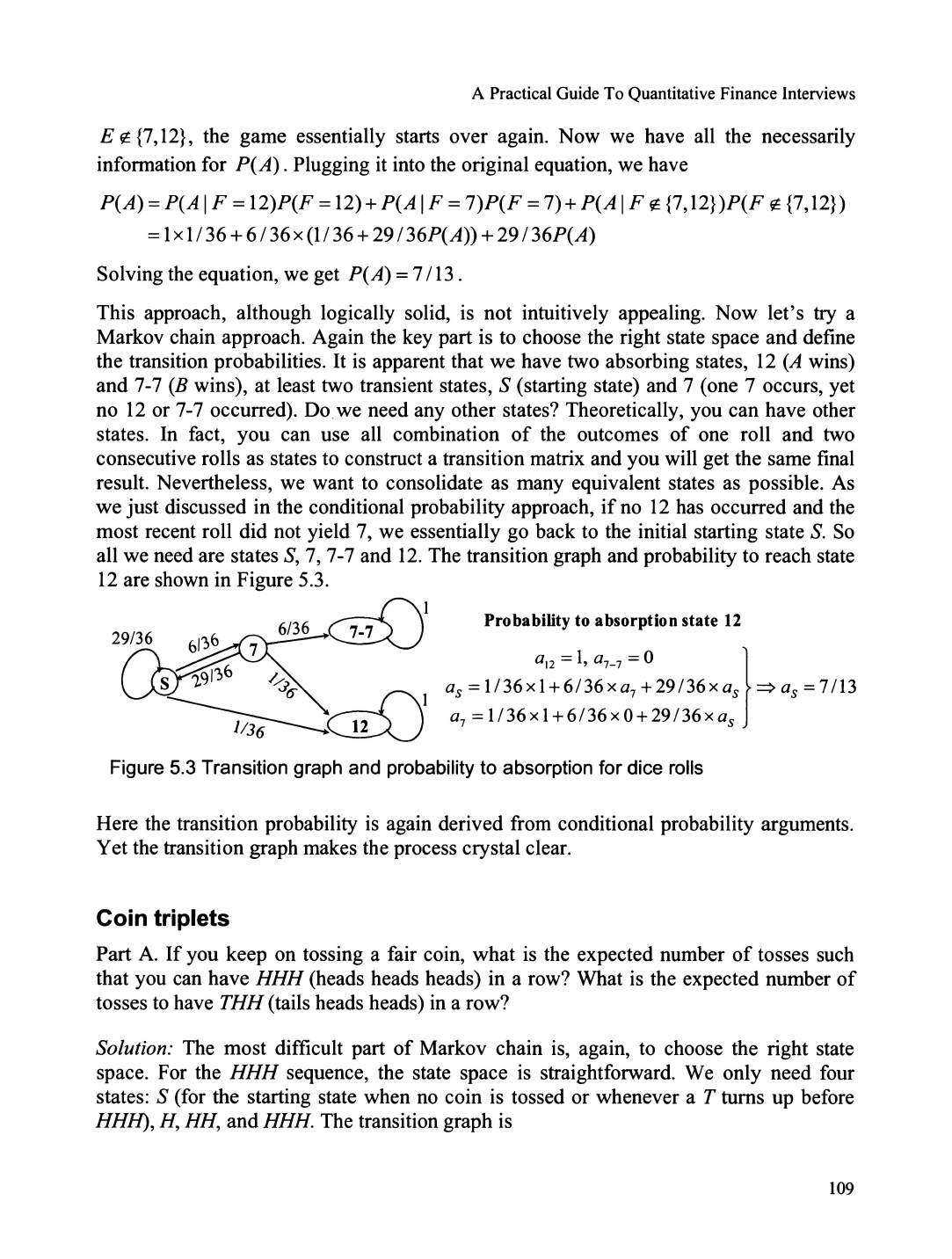

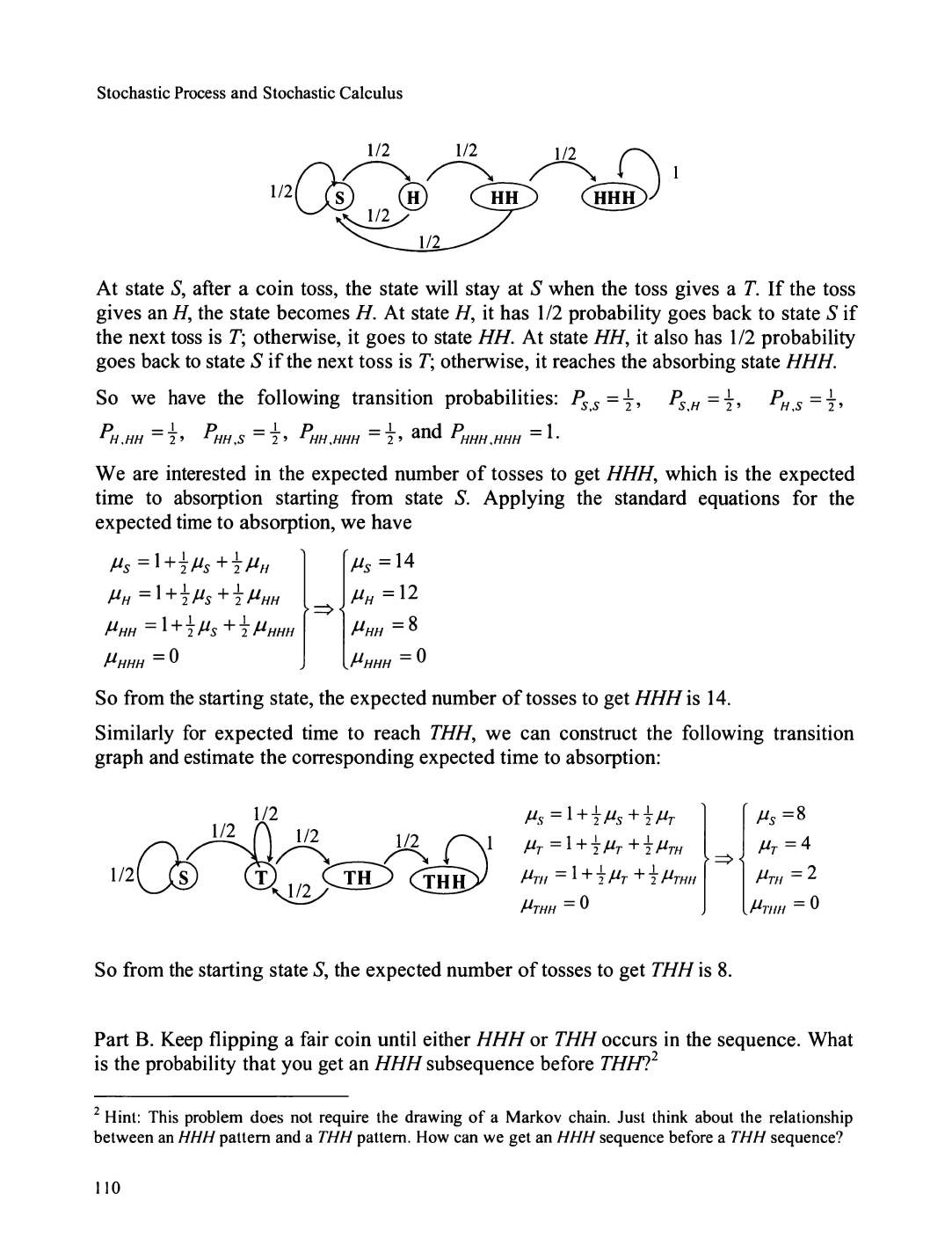

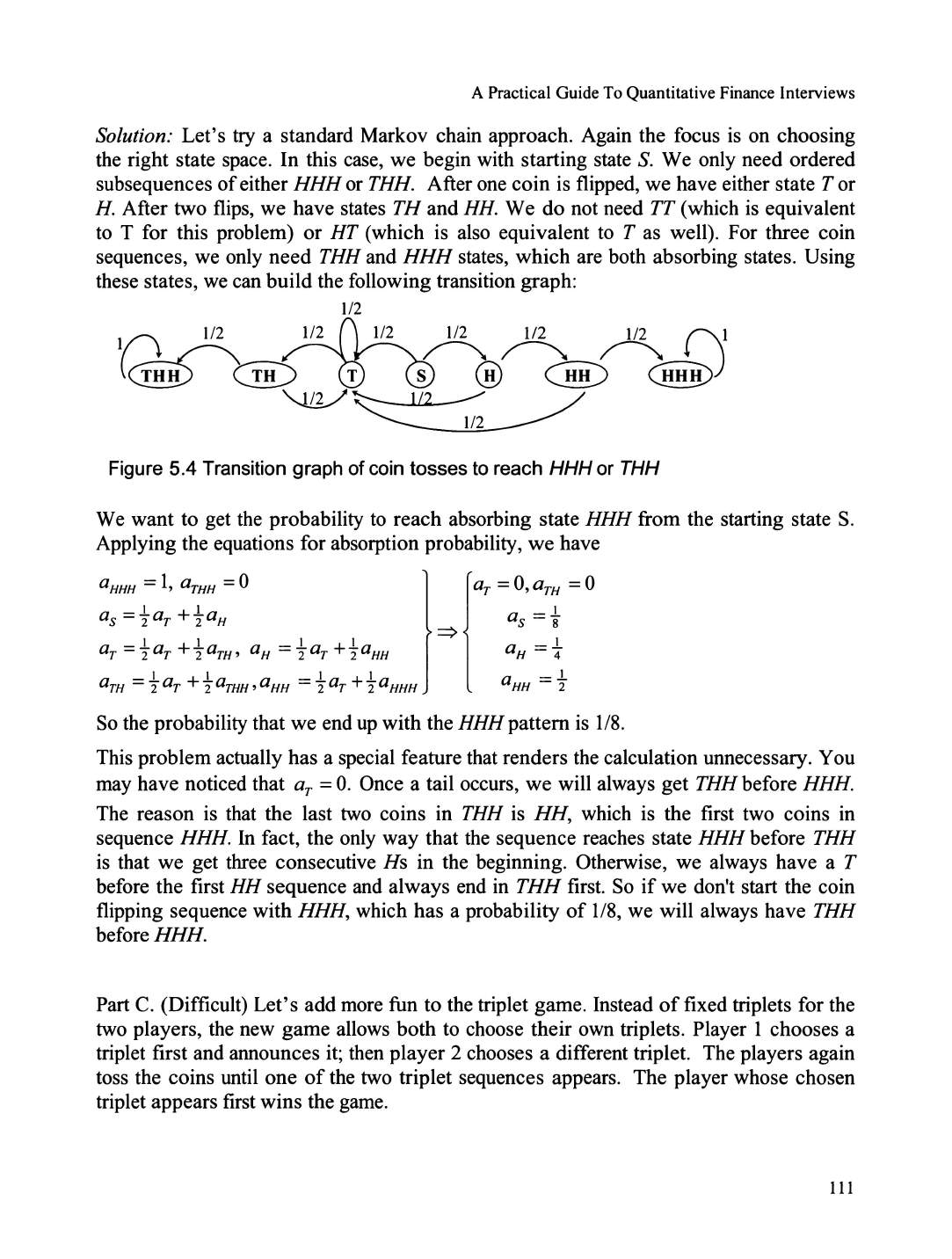

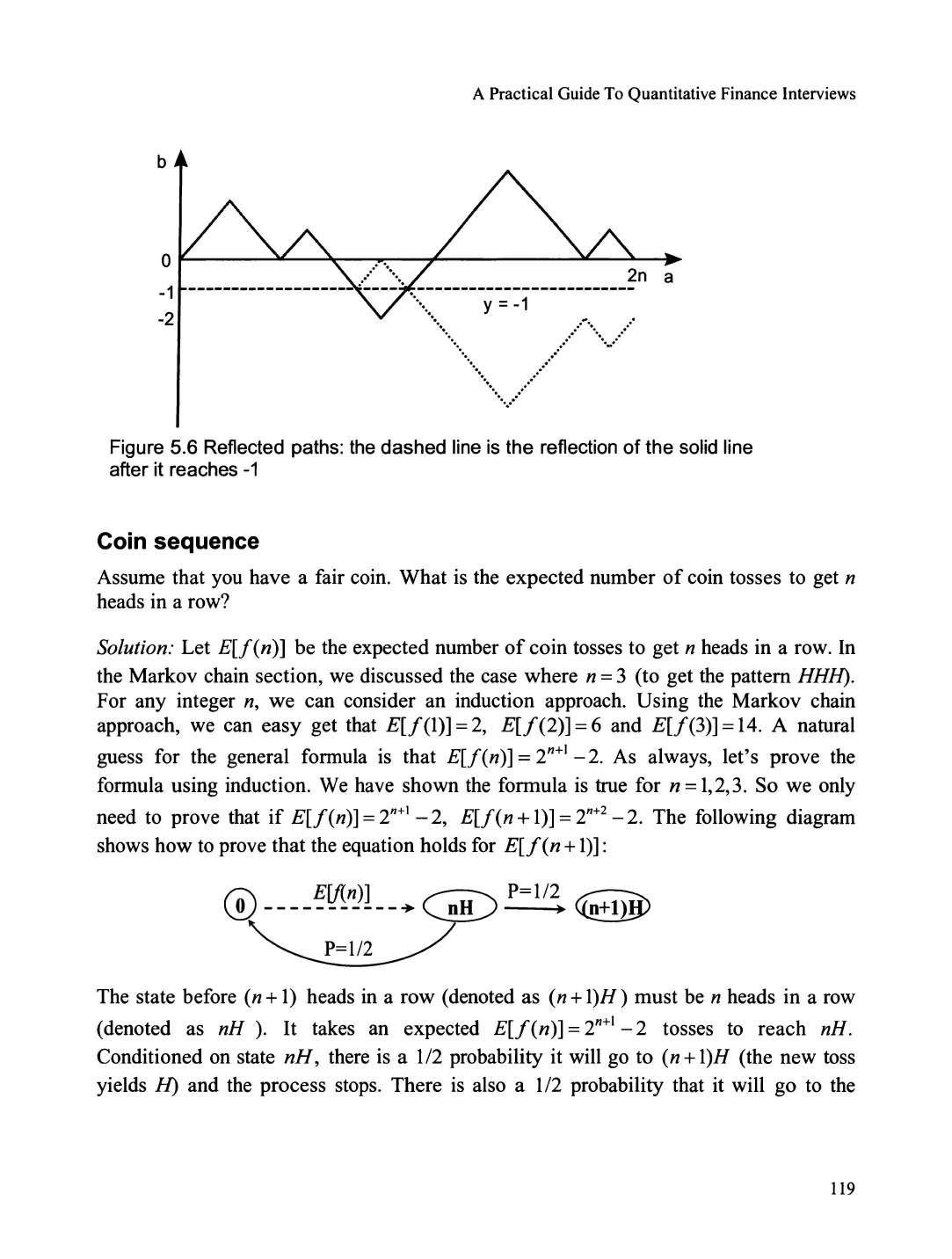

Coin triplets ...................................................................................................................... .. ........... l 09

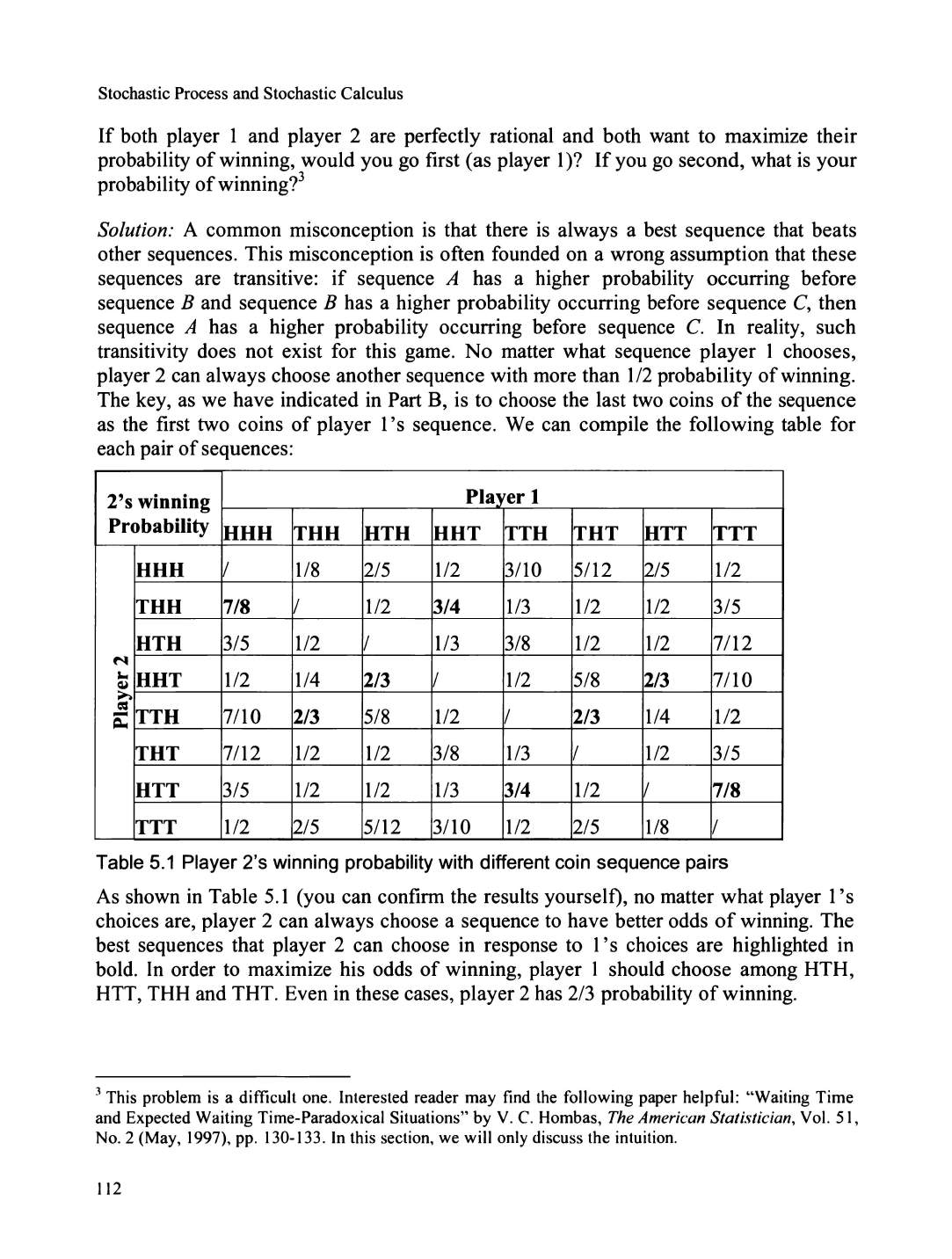

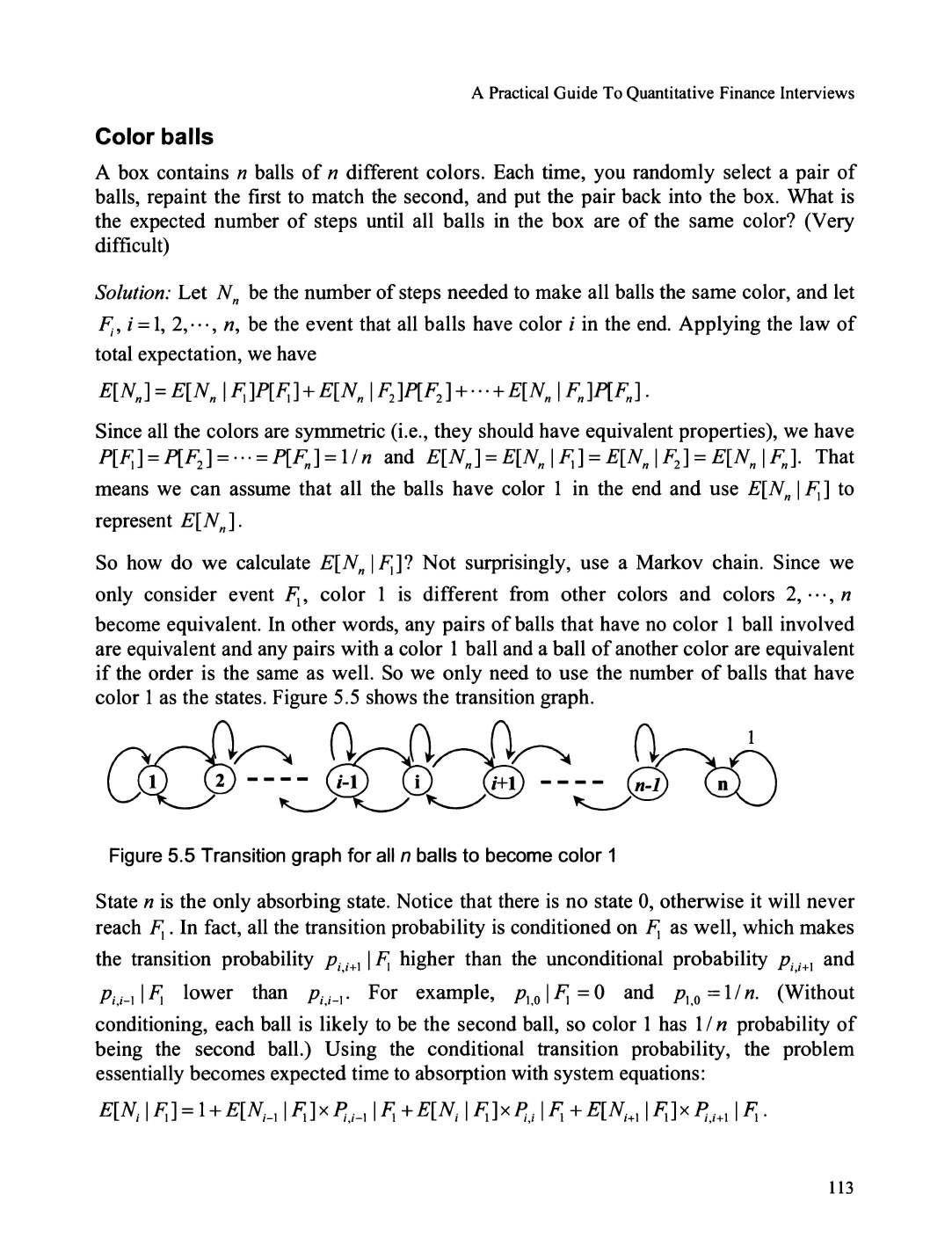

Color balls ........................................................

..

................................

..

..........................................

113

5.2 Martingale

and

Random walk .........................................

..

....................... ............

115

Drunk man ..................................................................................................................................... 116

Dice game ..........................

.. ..

...........................................................

..

............................... ..

..

........ 117

Ticket line .........................................................................................

..

........................................... 117

Coin sequence .........

..

.

..

.................................................................................................................. 119

5.3 Dynamic Programming ........................

..

.........................

..

..........

..

..........

..

..

..

.......

121

Dynamic programming (DP) algorithm ........................................... .................................... .......... 122

Dice game ........................................................................................... ................................ ........... 123

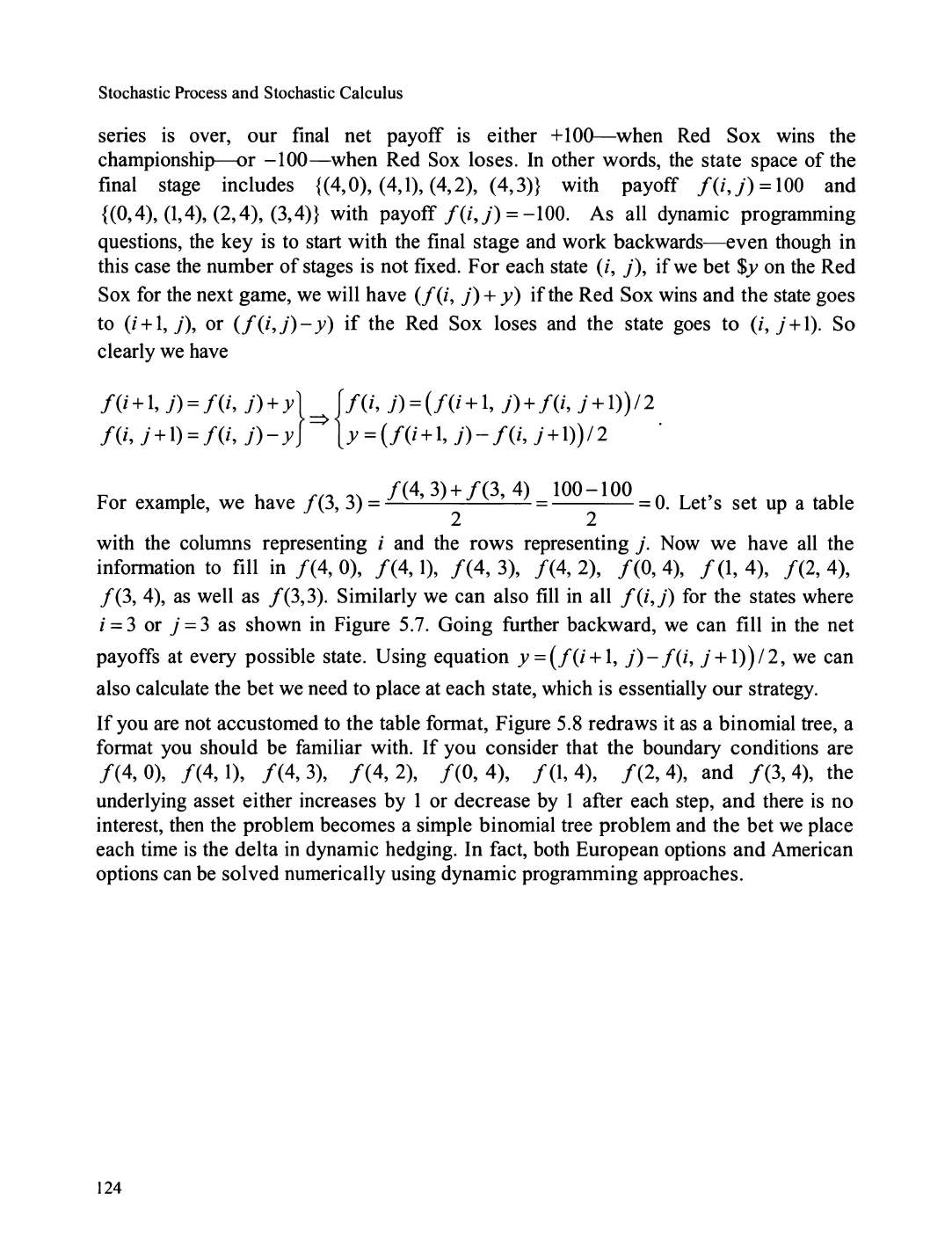

World series ........................................................................................... ........................................ 123

Dynamic dice

game

....................................................................................................................... 126

Dynamic card

game

....................................................................................................................... 127

5.4 Brownian Motion and Stochastic Calculus .........

..

...................................

..

.

..

....... 129

Brownian motion ...............................................................................

..

.......................................... 129

Stopping time/ first passage time .......................................................... .........................................

131

Ito's

lemrna ........................

..

.......................................................................................................... 135

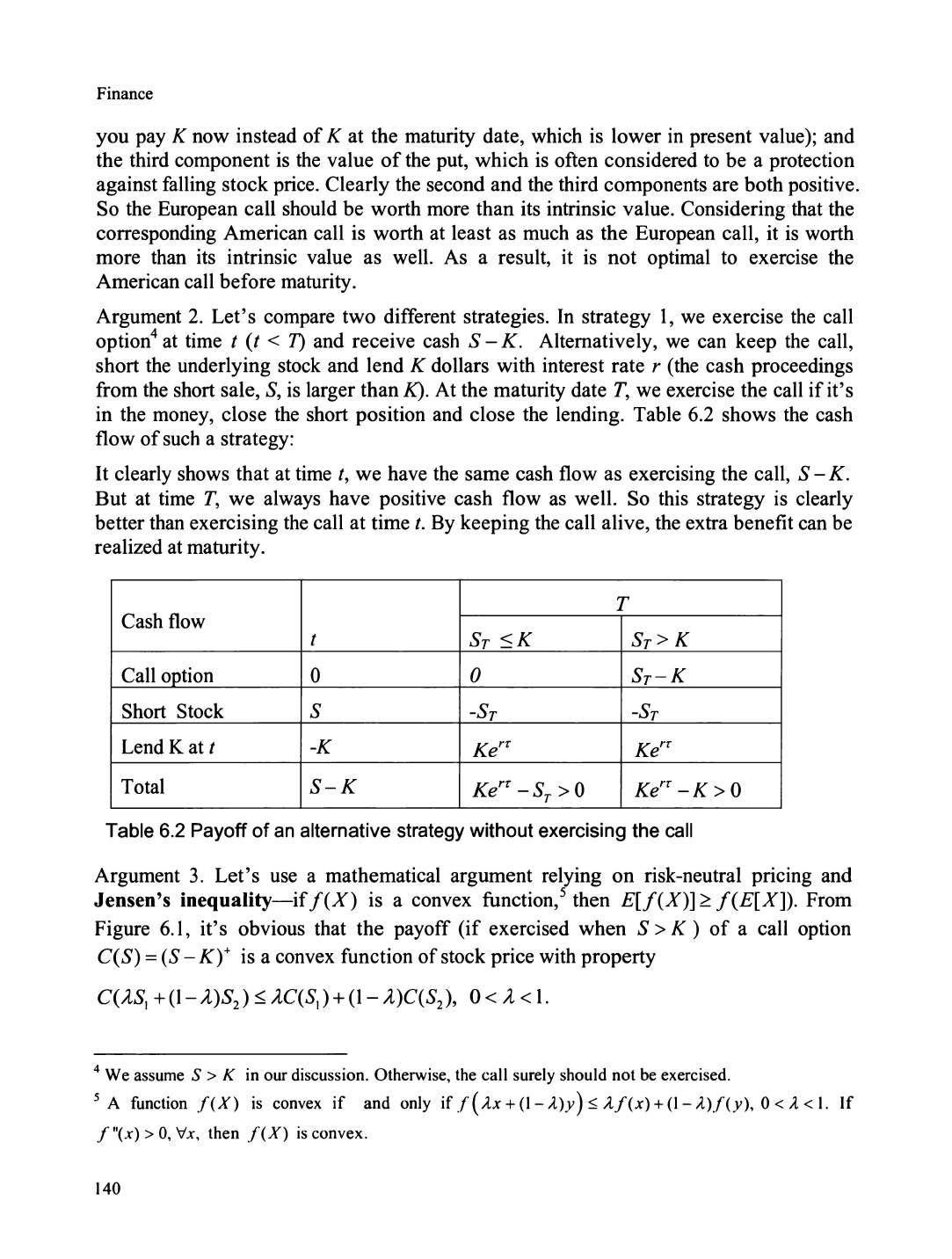

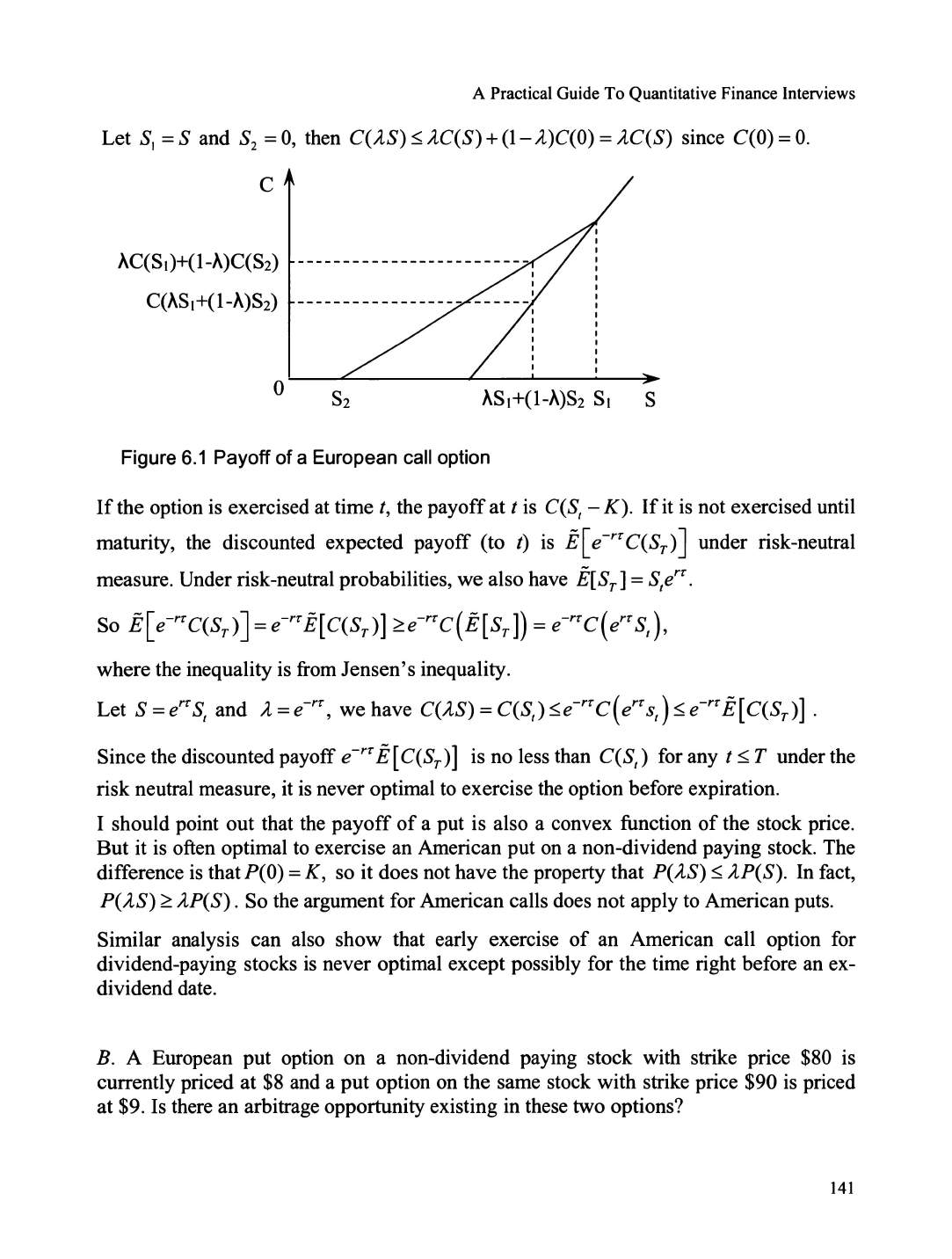

Chapter 6 Finance ........................................................................................................ 137

6.1. Option Pricing .......................................

..

......................

..

.

..

.....................

..

..

..

...... 137

Price direction

of

options ............................................................................................................... 137

Put-call parity ...................

..

.............................

..

................................

..

..........................................

138

American v.s. European options ........................................................

..

.......................................... 139

Black-Scholes-Merton differential equation .......... ........................................................................ 142

Black-Scholes formula ...................................................................................................................

143

6.2. The Greeks ...........................................

..

........................

..

...........................

..

...... 149

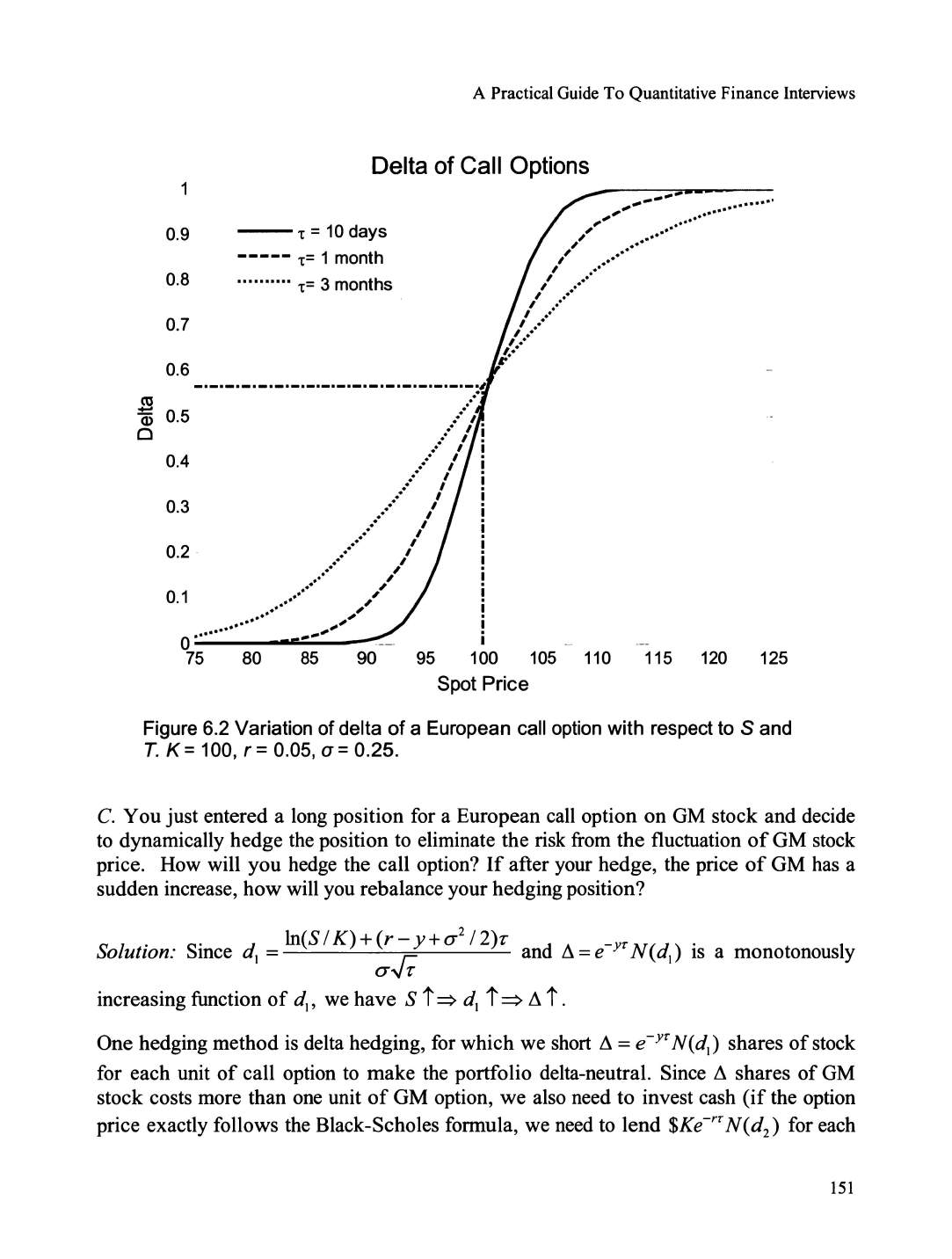

Delta .................................................................................................

..

........................................... 149

Gamma ...............................................................

..

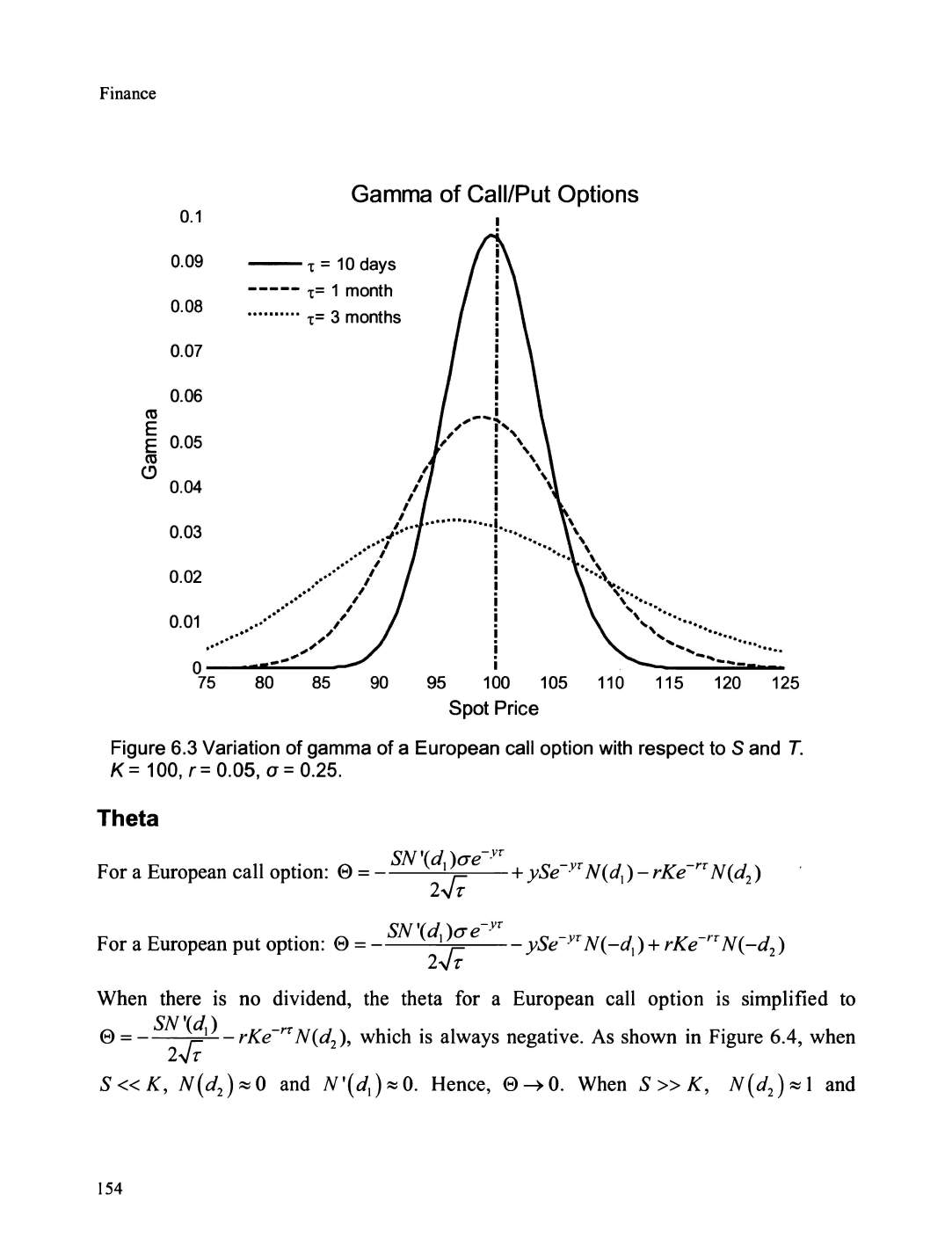

.......................................................................... 152

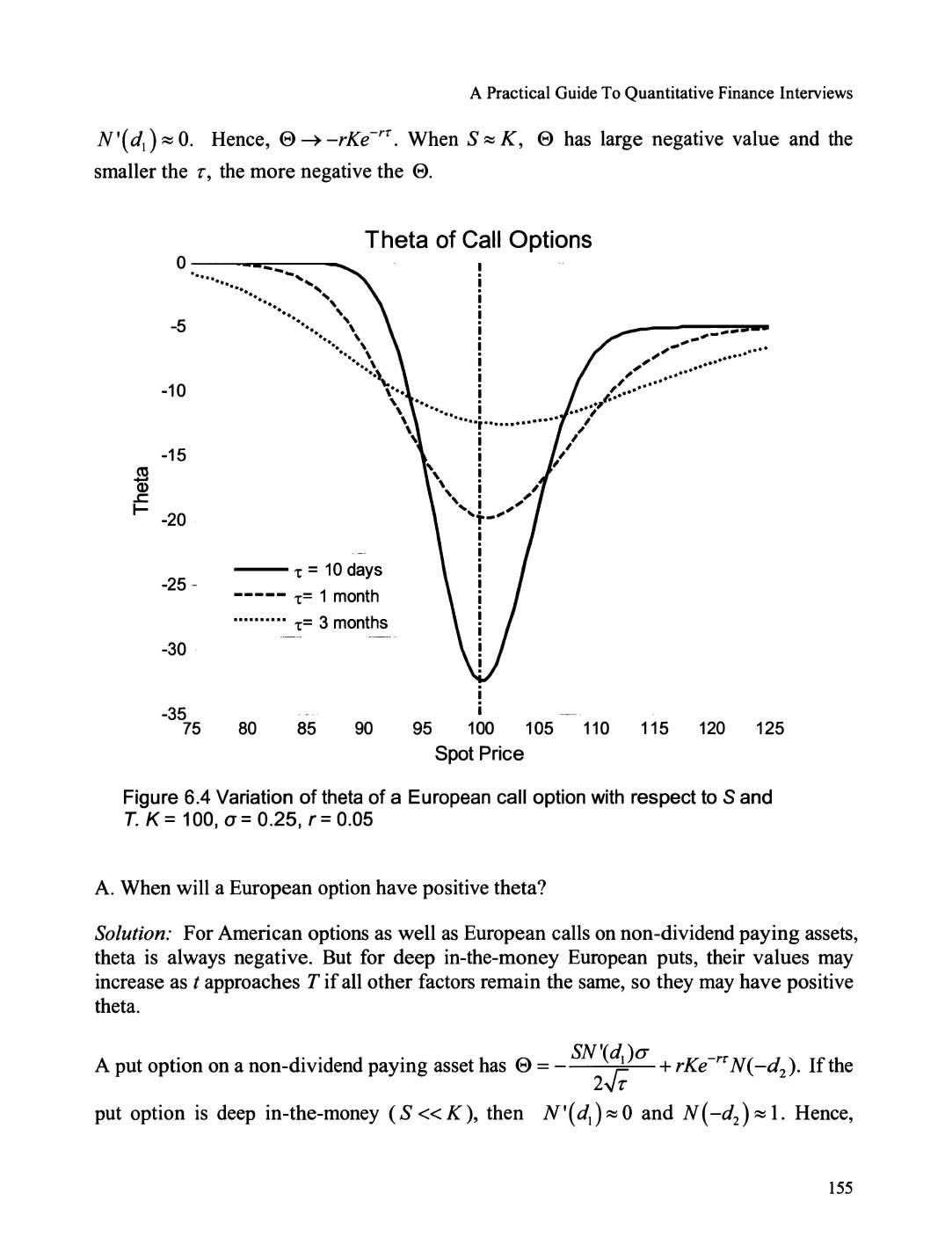

Theta ....

..

............................

..

............................................................................................. ............. 154

Vega ...... ............................................................................................

..

........................................... 156

6.3. Option Portfolios and Exotic Options ....

..

..

....................................

..

........

..

.........

158

Bull spread ..............................................

..

.

..

.....

..

..

..

..........................

..

........................................... 159

Straddle .......................................................................................................................................... 159

Binary options ................................................................................................................................ 160

Exchange options ...........................................................................................................................

161

6.4. Other Finance Questions .....................

..

.

..

......................... ..................................

163

Portfolio optimization .........

..

............ .

..

.......................... ..

.. ..

............................

..

.................... ........

163

Value

at

risk .. .........

..

.............

..

.............................................

..

............... .........................

..

.............. 164

Duration and convexity ..................................................................................................

..

..............

165

Forward and futures ....................................................................................................................... 167

Interest rate models ...........

..

.................................................................. ......................................... 168

IV

A Practical Guide

To

Quantitative Finance Interviews

Chapter 7 Algorithms and Numerical Methods ....................................................... 171

7.1. Algorithms ..................

..

.......................

..

.........................

..

..................................

171

Number swap ................................................................................................................................. 172

Unique elements .................... ............................................................

..

..........................................

173

Homer's algorithm ......................................................................................................................... 174

Moving average ...................................................

..

........................................................................ 174

Sorting algorithm ...............................................

..

.......................................................................... 174

Random permutation ..........................................

..

...............................

..

......................................... 176

Search algorithm ................................................

..

..........................

..

.............................................. 177

Fibonacci numbers ... .............................

..

....................................................................................... 179

Maximum contiguous subarray ..........................

....

.............................

..

......................................... 180

7 .2. The Power

of

Two ..........................................................

..

..................... ............. 182

Power

of

2? .................................................................................................................................... 182

Multiplication by 7 ...........................................

..

..............................................................

..

............ 182

Probability simulation ..........................................................................

..

......................

..

.

..

............. 182

Poisonous wine .............................................................................................................. ................ 183

7.3 Numerical Methods ........................................................

..

................................... 184

Monte Carlo simulation ...................................................................

..

...............................

..

........... 184

Finite difference method .....

..

...............................................................

..

.......................

..

............... 189

v

Preface

This book will prepare you for quantitative finance interviews

by

helping you zero in on

the key concepts that are frequently tested in such interviews. In this book we analyze

solutions to more than 200 real interview problems and provide valuable insights into

how to ace quantitative interviews. The book covers a variety

of

topics that you are

likely to encounter in quantitative interviews: brain teasers, calculus, linear algebra,

probability, stochastic processes and stochastic calculus, finance and programming.

Professionals and students seeking to pursue a career in quantitative finance or related

quantitative fields will benefit most from thoroughly reading this book. In recent years,

we have seen a dramatic surge

in

demand for talents with strong quantitative skills from

investment banks, investment management firms, hedge funds, financial software

vendors and financial consulting companies.

As

a result, quant, an umbrella description

that encompasses quantitative analysts, quantitative researchers, quantitative strategists,

quantitative traders, and quantitative developers, has become an attractive career choice.

Dozens

of

financial engineering or computational finance programs have been

established in the last few years to educate professionals for quantitative finance jobs.

Graduates with backgrounds

in

finance, mathematics, physics, computer sciences, and

various engineering majors are contending for quant jobs as well. Naturally, the

competition is fierce. To be a successful candidate, you have to distinguish yourself

from many other excellent applicants.

In general, a successful candidate for a quantitative finance position is expected to have

a strong mathematics background (in probability, statistics, stochastic calculus, etc.),

solid programming skills and basic to intermediate-level finance knowledge. Most

candidates find quantitative interviews, or at least some interview problems, challenging.

Quantitative interviews cover a broad range

of

mathematics, finance and programming

topics that the candidates may have never used

or

even encountered in their daily work

or study. Moreover, most interview problems require strong problem-solving skills,

beyond reciting formulas or doing simple calculations. A successful candidate needs a

combination

of

knowledge and problem-solving skills in order

to

excel in quantitative

interviews. This is precisely what this book provides!

This book addresses these aspects

by

reviewing the necessary finance and mathematical

concepts that serve as tools to structure and solve interview problems. Since it includes

most

of

the topics used

by

quantitative interviewers, it presupposes some basic

preparation in mathematics, statistics, finance, and programming.

I also strongly recommend that you try to solve each problem on your own first before

reading the answer. Working out solutions on your own will help you improve your

problem-solving skills and help you quickly identify common approaches to tackling

quantitative problems.

Needless to say, you are likely to encounter some problems in interviews that are similar

to or exactly the same as the problems in this book. After all, the book covers many

essential quantitative topics using real interview problems. However, the goal

of

the

book

is

not to teach you how to game the system by remembering the answers!

In

fact,

just memorizing answers may not help much in your interview process. Unless you truly

understand the underlying concepts and can analyze the problems yourself, you will fail

to elaborate on the solutions and will be ill-equipped to answer many other problems

that use similar concepts. (Besides, many experienced quantitative interviewers are good

at

catching those who have simply memorized "canned" answers.)

This

is

exactly the reason why I make significant effort to review essential concepts, to

present solution strategies, and to analyze the solutions in detail instead

of

simply

providing answers to problems. Furthermore, although the building blocks can be

learned, how one analyzes problems and implements these concepts usually makes a big

difference-and

these are the skills you can acquire through practice, practice and

practice.

I realize that there may be better methods to solve some

of

the problems presented in

this book.

It

is entirely possible that despite my best efforts some inadvertent errors may

have crept

in

. Please email me at xinfeng@quantfinanceinterviews.com

if

you have a

better approach to solving some

of

these problems or find errors. I will be grateful for

your feedback and will post corrections and your constructive feedback on the book's

companion website http://www.quantfinanceinterviews.

com

. The website is a joint

venture with my editor, Brett Jiu. You will also find some extra interview problems

with answers that we have gathered.

I sincerely hope that you enjoy solving these problems and are successful in your

interviews.

Xinfeng Zhou

Notations

v

3

s.t.

a

/\b

avb

n

for each/for every/for all

there exists

therefore

whenever A is true, B is also true

such that

the minimum

of

a and b

the maximum

of

a and b

TIX;

X1

XX

2

X··

·

XXn

i=I

n!

x%y

<1>

J

f(x)dx

r

f(x)dx

N(µ,

a2)

cdf

pd/

n

factorial

of

nonnegative integer n, n ! =

f1

i ( 0 ! =

I)

modulo operation

empty set

indefinite integral

of

f(x)

definite integral

of

f(x)

from a to b

max(x, 0)

i=I

normal distribution with mean µ and variance a2

cumulative density function

probability density function

Chapter 1 General Principles

Let us begin this book by exploring five general principles that will be extremely helpful

in

your interview process.

From

my experience on both sides

of

the interview table,

these general guidelines will better prepare you for job interviews and will likely make

you a successful candidate.

1.

Build a broad knowledge base

The length and the style

of

quant interviews differ from firm to firm. Landing a quant

job may mean enduring hours

of

bombardment with brain teaser, calculus, linear algebra,

probability theory, statistics, derivative pricing, or programming problems. To be a

successful candidate, you need to have broad knowledge in mathematics, finance and

programmmg.

Will all these topics be relevant for your future quant job? Probably not. Each specific

quant position often requires only limited knowledge in these domains. General problem

solving skills

may

make more difference than specific knowledge. Then why are

quantitative interviews so comprehensive? There are at least two reasons for this:

The first reason

is

that interviewers often have diverse backgrounds. Each interviewer

has his or her own favorite topics that are often related to his or her own educational

background or work experience. As a result, the topics you will be tested

on

are likely

to

be very broad. The second reason is more fundamental. Your problem solving

skills-a

crucial requirement for any quant

job-is

often positively correlated to the breadth

of

your knowledge. A basic understanding

of

a broad range

of

topics often helps you better

analyze problems, explore alternative approaches, and come

up

with efficient solutions.

Besides, your responsibility

may

not be restricted to your own projects. You will be

expected to contribute as a member

of

a bigger team. Having broad knowledge will help

you contribute to the team's success as well.

The key here

is

"basic understanding." Interviewers do not expect you to be an expert on

a specific

subject-unless

it happens to be your PhD thesis. The knowledge used

in

interviews, although broad, covers mainly essential concepts. This is exactly the reason

why most

of

the books I refer to in the following chapters have the word "introduction"

or "first" in the title.

If

I am allowed to give only one suggestion to a candidate, it will be

know

the

basics very well.

2.

Practice your interview skills

The interview process starts long before you step into an interview room.

In

a sense, the

success or failure

of

your interview is often determined before the first question is asked.

Your solutions to interview problems may fail to reflect your true intelligence and

General Principles

knowledge

if

you are unprepared. Although a complete review

of

quant interview

problems

is

impossible and unnecessary, practice does improve your interview skills.

Furthermore, many

of

the behavioral, technical and resume-related questions can be

anticipated. So prepare yourself for potential questions long before you enter an

interview room.

3. Listen carefully

You should be an active listener in interviews so that you understand the problems well

before you attempt to answer them.

If

any aspect

of

a problem is not clear to you,

politely ask for clarification.

If

the problem is more than a couple

of

sentences,

jot

down

the key words to help you remember all the information. For complex problems,

interviewers often give away some clues when they explain the problem. Even the

assumptions they give may include some information as to how to approach the problem.

So listen carefully and make sure you get the necessary information.

4. Speak your mind

When you analyze a problem and explore different ways to solve it, never do it silently.

Clearly demonstrate your analysis and write down the important steps involved

if

necessary. This conveys your intelligence to the interviewer and shows that you are

methodical and thorough. In case that you

go

astray, the interaction will also give your

interviewer the opportunity to correct the course and provide you with some hints.

Speaking your mind does not mean explaining every tiny detail.

If

some conclusions are

obvious to you, simply state the conclusion without the trivial details. More often than

not, the interviewer uses a problem to test a specific concept/approach. You should focus

on demonstrating your understanding

of

the key concept/approach instead

of

dwelling

on less relevant details.

5. Make reasonable assumptions

In real job settings, you are unlikely to have all the necessary information

or

data

you'd

prefer to have before you build a model and make a decision. In interviews,

interviewers may not give you all the necessary assumptions either. So it is up to you to

make reasonable assumptions. The keyword here is reasonable. Explain your

assumptions to the interviewer so that you will get immediate feedback. To solve

quantitative problems, it is crucial that you can quickly make reasonable assumptions

and design appropriate frameworks to solve problems based on the assumptions.

We are now ready to review basic concepts

in

quantitative finance subject areas and

have

fun

solving real-world interview problems!

2

Chapter 2 Brain Teasers

In

this chapter, we cover problems that only require common sense, logic, reasoning, and

basic-no

more than high school

level-math

knowledge to solve. In a sense, they are

real brain teasers

as

opposed to mathematical problems in disguise. Although these brain

teasers do not require specific math knowledge, they are

no

less difficult than other

quantitative interview problems. Some

of

these problems test your analytical and general

problem-solving skills; some require you to think out

of

the box; while others ask you to

solve the problems using fundamental math techniques in a creative way. In this chapter,

we review some interview problems to explain the general themes

of

brain teasers that

you are likely to encounter in quantitative interviews.

2.

1 Problem Simplification

If

the original problem is so complex that you cannot come up with an immediate

solution, try to identify a simplified version

of

the problem and start with it. Usually you

can start with the simplest sub-problem and gradually increase the complexity. You do

not need to have a defined plan

at

the beginning. Just try to solve the simplest cases and

analyze your reasoning. More often than not, you will find a pattern that will guide you

through the whole problem.

Screwy pirates

Five pirates looted a chest full

of

100 gold coins. Being a bunch

of

democratic pirates,

they agree on the following method to divide the loot:

The most senior pirate will propose a distribution

of

the coins. All pirates, including the

most senior pirate, will then vote.

If

at

least 50%

of

the pirates (3 pirates in this case)

accept the proposal, the gold

is

divided as proposed.

If

not, the most senior pirate will be

fed

to shark and the process starts over with the next most senior pirate

...

The process is

repeated until a plan is approved. You can assume that all pirates are perfectly rational:

they want to stay alive first and to get as much gold as possible second. Finally, being

blood-thirsty pirates, they want to have fewer pirates on the boat

if

given a choice

between otherwise equal outcomes.

How will the gold coins be divided in the end?

Solution:

If

you have not studied game theory or dynamic programming, this strategy

problem

may

appear to be daunting.

If

the problem with 5 pirates seems complex, we

can always start with a simplified version

of

the problem by reducing the number

of

pirates. Since the solution to I-pirate case

is

trivial, let's start with 2 pirates. The senior

Brain Teasers

pirate (labeled as 2) can claim all the gold since he will always get 50%

of

the votes

from himself and pirate 1

is

left with nothing.

Let's add a more senior pirate,

3.

He

knows that

if

his plan

is

voted down, pirate 1 will

get nothing. But

if

he offers private 1 nothing, pirate 1 will be happy to kill him.

So

pirate 3 will offer private 1 one coin and keep the remaining

99

coins, in which strategy

the plan will have 2 votes from pirate 1 and 3.

If

pirate 4 is added, he knows that

if

his plan is voted down, pirate 2 will get nothing. So

pirate 2 will settle for one coin

if

pirate 4 offers one. So pirate 4 should offer pirate 2

one

coin and keep the remaining 99 coins and his plan will be approved with 50%

of

the

votes from pirate 2 and 4.

Now we finally come to the 5-pirate case. He knows that

if

his plan is voted down, both

pirate 3 and pirate 1 will get nothing. So he only needs to offer pirate 1 and pirate 3 one

coin each to get their votes and keep the remaining 98 coins.

If

he divides the coins this

way, he will have three out

of

the five votes: from pirates 1 and 3

as

well as himself.

Once we start with a simplified version and add complexity to it, the answer becomes

obvious. Actually after the case n =

5,

a clear pattern has emerged and we do not need to

stop at 5 pirates. For any

2n

+ 1 pirate case (n should be less than 99 though), the most

senior pirate will offer pirates

1,

3,

· ·

·,

and 2n

-1

each one coin and keep the rest for

himself.

Tiger and sheep

One hundred tigers and one sheep are put on a magic island that only has grass. Tigers

can eat grass, but they would rather eat sheep. Assume: A. Each time only one tiger can

eat one sheep, and that tiger itself will become a sheep after it eats the sheep. B. All

tigers are smart and perfectly rational and they want to survive. So will the sheep

be

eaten?

Solution: 100

is

a large number, so again let's start with a simplified version

of

the

problem.

If

there

is

only 1 tiger ( n = 1 ), surely it will eat the sheep since it does not need

to worry about being eaten. How about 2 tigers? Since both tigers are perfectly rational,

either tiger probably would do some thinking

as

to what will happen

if

it eats the sheep.

Either tiger is probably thinking:

if

I eat the sheep, I will become a sheep; and then I will

be eaten by the other tiger. So to guarantee the highest likelihood

of

survival, neither

tiger will eat the sheep.

If

there are 3 tigers, the sheep will be eaten since each tiger will realize that once it

changes to a sheep, there will be 2 tigers left and it will not

be

eaten. So the first tiger

that thinks this through will eat the sheep.

If

there are 4 tigers, each tiger will understand

4

A Practical Guide

To

Quantitative Finance Interviews

that

if

it eats the sheep, it will tum to a sheep. Since there are 3 other tigers, it will be

eaten. So to guarantee the highest likelihood

of

survival, no tiger will eat the sheep.

Following the same logic,

we

can naturally show that

if

the number

of

tigers

is

even, the

sheep will not be eaten.

If

the number is odd, the sheep will be eaten. For the case

n = l 00, the sheep will not be eaten.

2.2 Logic Reasoning

River crossing

Four people,

A,

B, C and D need to get across a river. The only way to cross the river

is

by

an

old bridge, which holds at most 2 people at a time. Being dark, they can't cross the

bridge without a torch,

of

which they only have one. So each pair can only walk at the

speed

of

the slower person. They need to get all

of

them across to the other side as

quickly as possible. A is the slowest and takes

10

minutes to cross; B takes 5 minutes; C

takes 2 minutes; and D takes 1 minute.

What

is

the minimum time to get all

of

them across to the other side?1

Solution: The key point is to realize that the l 0-minute person should go with the 5-

minute person and this should not happen in the first crossing, otherwise one

of

them

have to go back.

So

C

and

D should go across first (2 min); then send D back (lmin); A

and B go across (

10

min); send C back (2min); C and D go across again (2 min).

It

takes

17

minutes

in

total. Alternatively, we can send C back first and then D back in

the second round, which takes

17

minutes as well.

Birthday problem

You and your colleagues know that your boss

A's

birthday

is

one

of

the following

10

dates:

Mar 4, Mar 5, Mar 8

Jun 4, Jun 7

Sep

1,

Sep 5

Dec

1,

Dec 2, Dec 8

A told you only the month

of

his birthday, and told your colleague

Conly

the day. After

that, you first said: "I

don't

know

A's

birthday; C

doesn't

know it either." After hearing

1 Hint: The key is to realize that A and B should get across the bridge together.

5

Brain Teasers

what you said, C replied: "I didn't know

A's

birthday, but now I know it." You smiled

and said: "Now I know it, too." After looking at the

10

dates and hearing your comments,

your administrative assistant wrote down

A's

birthday without asking any questions. So

what did the assistant write?

Solution: Don't let the "he said, she said" part confuses

you.

Just interpret the logic

behind each individual's comments and try your best to derive useful information from

these comments.

Let D be the day

of

the month

of

A's

birthday, we have

De{l,2,4,5,7,8}

.

If

the

birthday

is

on a unique day, C will know the

A's

birthday immediately. Among possible

Ds, 2 and 7 are unique days. Considering that you are sure that C does not know

A's

birthday, you must infer that the day the C was told

of

is not 2 or 7. Conclusion: the

month is not June or December.

(If

the month had been June, the day C was told

of

may

have been 2;

ifthe

month had been December, the day C was told

of

may have been 7.)

Now C knows that the month must be either March

or

September. He immediately

figures out

A's

birthday, which means the day must be unique in the March and

September list.

It

means

A's

birthday cannot be Mar 5, or Sep 5. Conclusion: the

birthday must be Mar 4, Mar 8 or Sep

1.

Among these three possibilities left, Mar 4 and Mar 8 have the same month. So

if

the

month you have is March, you still cannot figure out

A's

birthday. Since you can figure

out

A's

birthday,

A's

birthday must be Sep

1.

Hence, the assistant must have written Sep

1.

Card game

A casino offers a card game using a normal deck

of

52 cards. The rule is that you

tum

over two cards each time. For each pair,

if

both are black, they go to the dealer's pile;

if

both are red, they go to your pile;

if

one black and one red, they are discarded. The

process is repeated until you two go through all

52

cards.

If

you have more cards in your

pile, you win $100; otherwise (including ties) you get nothing. The casino allows you to

negotiate the price you want to pay for the game. How much would you be willing to

pay to play this game?2

Solution: This surely

is

an insidious casino. No matter how the cards are arranged, you

and the dealer will always have the same number

of

cards in your piles. Why? Because

each pair

of

discarded cards have one black card and one red card, so equal number

of

2 Hint: Try to approach the problem using symmetry. Each discarded pair has one black and one red card.

What does that tell you as to the number

of

black and red cards in the rest two piles?

6

A Practical Guide To Quantitative Finance Interviews

red and black cards are discarded. As a result, the number

of

red cards left for you and

the number

of

black cards left for the dealer are always the same. The dealer always

wins! So we should not pay anything to play the game.

Burning ropes

You have two ropes, each

of

which takes I hour to bum. But either rope has different

densities at different points, so there's no guarantee

of

consistency in the time it takes

different sections within the rope to

bum

. How do you use these two ropes to measure

45

minutes?

Solution: This

is

a classic brain teaser question. For a rope that takes x minutes to bum,

if

you light both ends

of

the rope simultaneously, it takes x I 2 minutes

to

bum. So we

should light both ends

of

the first rope and light one end

of

the second rope. 30 minutes

later, the first rope will get completely burned, while that second rope now becomes a

30-min rope. At that moment,

we

can light the second rope at the other end (with the

first end still burning), and when it is burned out, the total time is exactly

45

minutes.

Defective ball

You have

12

identical balls. One

of

the balls is heavier OR lighter than the rest (you

don't know which). Using just a balance that can only show you which side

of

the tray

is

heavier, how can you determine which ball is the defective one with 3 measurements?3

Solution: This weighing problem is another classic brain teaser and is still being asked

by many interviewers. The total number

of

balls often ranges from 8

to

more than

100.

Here we use n =

12

to show the fundamental approach. The key is to separate the

original group (as well as any intermediate subgroups) into three sets instead

of

two. The

reason is that the comparison

of

the first two groups always gives information about the

third group.

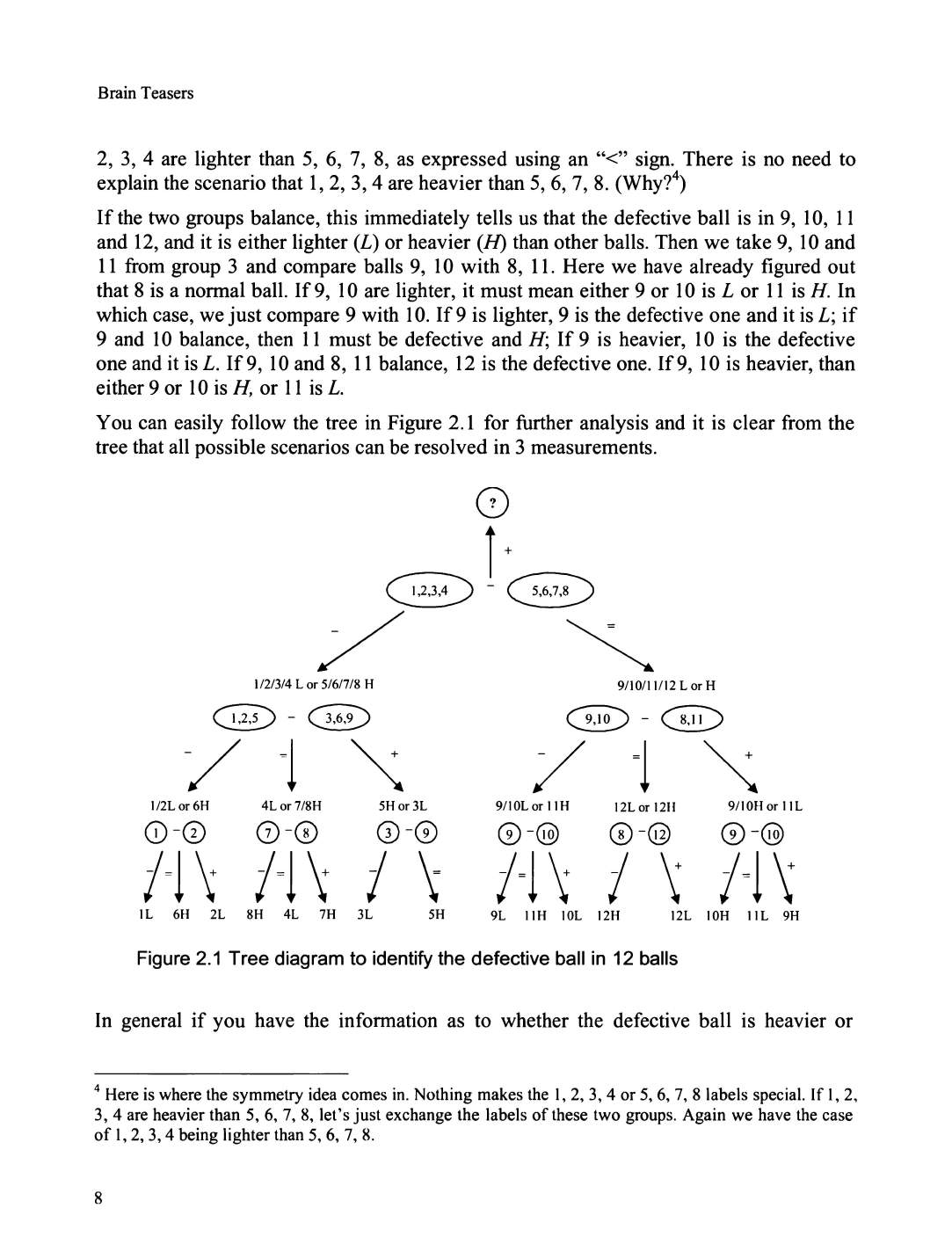

Considering that the solution is wordy to explain, I draw a tree diagram in Figure

2.1

to

show the approach in detail. Label the balls 1 through

12

and separate them to three

groups with 4 balls each. Weigh balls

1,

2, 3, 4 against balls 5, 6, 7,

8.

Then we go on to

explore two possible scenarios: two groups balance, as expressed using an

"="

sign, or

1,

3 Hint: First do it for 9 identical balls and use only 2 measurements, knowing that one is heavier than the

rest.

7

Brain Teasers

2,

3,

4 are lighter than 5, 6, 7,

8,

as expressed using an

"<"

sign. There is no need to

explain the scenario that

1,

2, 3, 4 are heavier than 5, 6, 7,

8.

(Why?4)

If

the two groups balance, this immediately tells us that the defective ball is in

9,

10,

11

and 12, and it is either lighter

(l)

or heavier (H) than other balls. Then we take 9,

10

and

11

from

group 3 and compare balls

9,

10

with 8,

11.

Here we have already figured out

that 8 is a normal ball.

If

9,

IO

are lighter, it must mean either 9 or

10

isl

or

11

is

H.

In

which case, we just compare 9 with

10.

If

9 is lighter, 9 is the defective one and it is

L;

if

9 and

10

balance, then

11

must

be

defective and H;

If

9 is heavier,

10

is the defective

one and it is L.

lf9,

IO

and 8,

11

balance,

12

is the defective one.

lf9

,

10

is heavier, than

either 9 or

10

is

H,

or

11

is

L.

You can easily follow the tree in Figure 2.1 for further analysis and it is clear from the

tree that all possible scenarios can be resolved in 3 measurements.

I /2/3/4 L

or

5/617/8 H 9/ I0/11/

12

Lor

H

l/2L

or

6H

4L

or

7/8H 5H

or

3L

9/IOLor

l

IH

12Lorl211

9/IOfl

or

11

L

IL

6H

2L

8H

4L

7H

3L

5H

9L

l

IH

IOL

12H 12L IOH I

IL

9H

Figure

2.1

Tree diagram to identify the defective ball in 12 balls

In

general

if

you have the information as to whether the defective ball is heavier or

4 Here is where the symmetry idea comes

in.

Nothing makes the I, 2, 3, 4 or 5, 6, 7, 8 labels special.

If

I, 2,

3, 4 are heavier than 5, 6, 7, 8, let's just exchange the labels

of

these two groups. Again

we

have the case

of

I, 2, 3, 4 being lighter than 5, 6, 7,

8.

8

A Practical Guide

To

Quantitative Finance Interviews

lighter, you can identify the defective ball among up to

3n

balls using no more than n

measurements since each weighing reduces the problem size by 2/3.

If

you have no

information as to whether the defective ball is heavier or lighter, you can identify the

defective ball among up

to

(3n

-

3)

I 2 balls using no more than n measurements.

Trailing zeros

How many trailing zeros are there in

100!

(factorial

of

100)?

Solution: This is an easy problem. We know that each pair

of

2 and 5 will give a trailing

zero.

If

we perform prime number decomposition on all the numbers in 100!, it is

obvious that the frequency

of

2 will far outnumber

of

the frequency

of

5.

So

the

frequency

of

5 determines the number

of

trailing zeros. Among numbers

1,

2, · · ·, 99, and

100, 20 numbers are divisible by 5 (

5,

10, · · ·, 100

).

Among these 20 numbers, 4 are

divisible by 52 ( 25, 50,

75,

100

).

So

the total frequency

of

5

is

24 and there are 24

trailing zeros.

Horse race

There are

25

horses, each

of

which runs at a constant speed that

is

different from the

other horses'. Since the track only has 5 lanes, each race can have at most 5 horses.

If

you need to find the 3 fastest horses, what is the minimum number

of

races needed to

identify them?

Solution: This problem tests your basic analytical skills.

To

find the 3 fastest horses,

surely all horses need to be tested. So a natural first step is to divide the horses to 5

groups (with horses 1-5, 6-10, 11-15, 16-20, 21-25

in

each group). After 5 races, we will

have the order within each group, let's assume the order follows the order

of

numbers

(e.g., 6 is the fastest and

IO

is

the slowest

in

the 6-10 group)5. That means 1, 6,

11,

16

and

21

are the fastest within each group.

Surely the last two horses within each group are eliminated. What else can we infer? We

know that within each group,

if

the fastest horse ranks 5th

or

4th among 25 horses, then

all horses in that group cannot be in top 3;

if

it ranks the 3rd, no other horse in that group

can be in the top 3;

if

it ranks the 2nd, then

one

other horse in that group

may

be in top 3;

if

it ranks the first, then two other horses in that group may be in top

3.

5 Such an assumption does not affect the generality

of

the solution.

If

the order is not

as

described,

just

change the labels

of

the horses.

9

Brain Teasers

So

let's

race horses 1, 6,

11,

16

and

21. Again

with

out loss

of

generality,

let's

assume

the order is

1,

6, 11, 16 and 21.

Then

we immediately know that horses 4-5, 8-10, 12-15,

16-20 and 21-25 are eliminated. Since 1

is

fastest among all the horses, 1 is in. We need

to determine which two among horses 2, 3, 6, 7

and

11

are in top 3, which only takes one

extra race.

So all together we

need

7 races (in 3 rounds) to identify the 3 fastest horses.

Infinite sequence

If

x /\ x

/\

x

/\

x

/\

x · · · = 2 , where x /\ y =

xY,

what is x ?

Solution: This

problem

appears to

be

difficult,

but

a simple analysis will give

an

elegant

solution. What do

we

have from the original equation?

limx/\x/\x/\x/\x···=2<=>limx/\x/\x/\x/\x···=2.

In

other words, as

n

terms

n-1

terms

adding

or

minus one x

/\

should

yield

the same result.

so x

/\

x

/\

x

/\

x

/\

x · · · = x

/\

(x

/\

x

/\

x /\ x · · ·) = x

/\

2 = 2 x =

J2.

2.3 Thinking Out

of

the Box

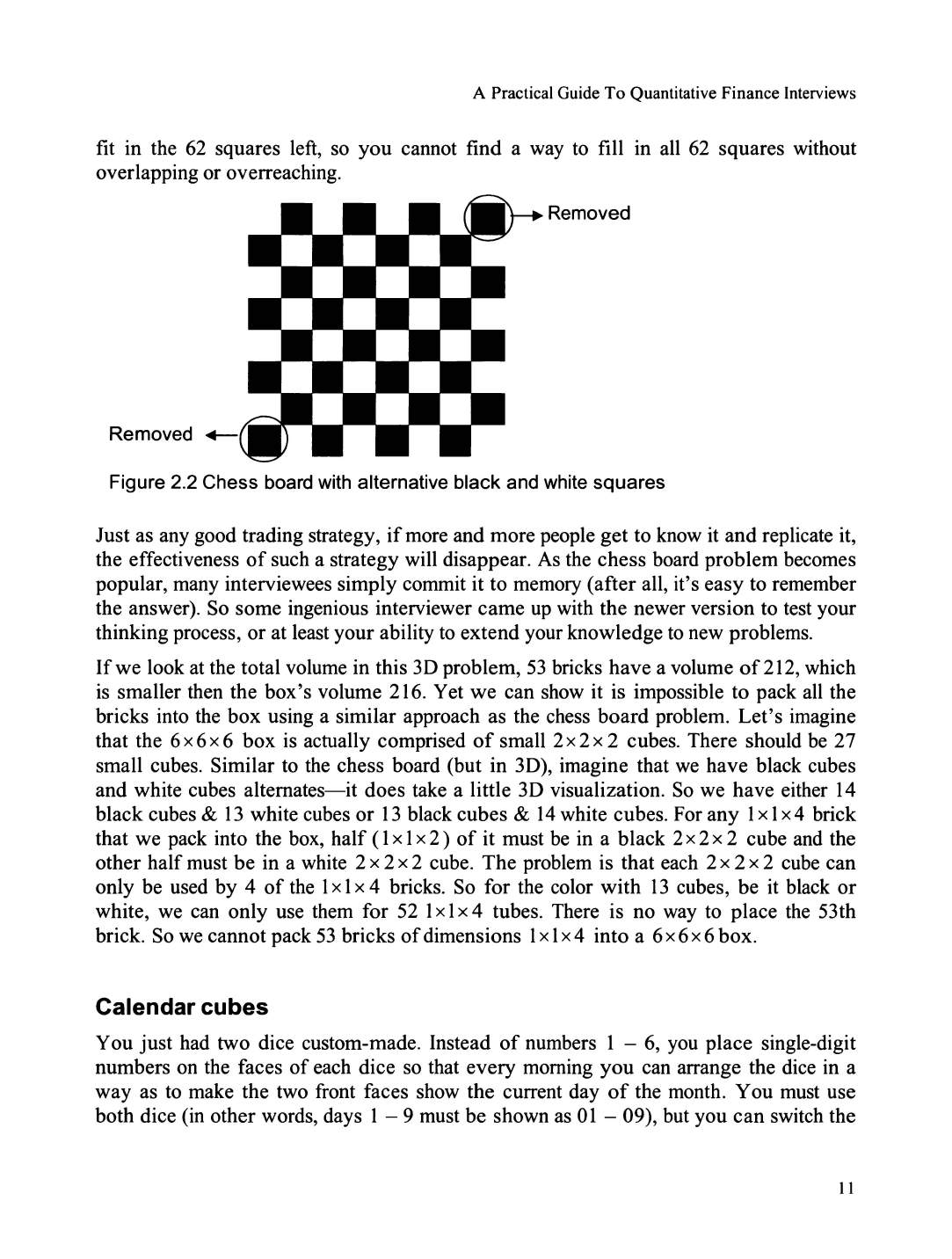

Box packing

Can you pack

53

bricks

of

dimensions

1x1x4

into a 6 x 6 x 6 box?

Solution: This

is

a nice problem extended from a popular chess board problem. In that

problem, you have a 8 x 8 chess

board

with two small squares at the opposite diagonal

comers removed.

You

have many bricks with dimension 1 x

2.

Can

you pack

31

bricks

into the remaining

62

squares?

(An

alternative question is whether you can

cover

all

62

squares using bricks without any bricks overlapping with each other or sticking out

of

the board, which requires a similar analysis.)

A real chess board figure surely helps the visualization. As shown in Figure 2.2, when a

chess board

is

filled with alternative black

and

white squares, both squares at the

opposite diagonal

comers

have the same color.

If

you put a 1 x 2 brick on the board, it

will always cover

one

black square and one white square.

Let's

say it's the

two

black

comer

squares were removed, then the rest

of

the board can fit at most 30 bricks since

we only have 30

black

squares left (and each brick requires one black square). So to

pack

31

bricks is

out

of

the question. To cover all 62 squares without overlapping or

overreaching, we

must

have exactly 3 I bricks. Yet

we

have proved that

31

bricks cannot

10

A Practical Guide

To

Quantitative Finance Interviews

fit in the 62 squares left, so you cannot find a way to fill in all 62 squares without

overlapping or overreaching.

Removed

Removed

+-

Figure 2.2 Chess board with alternative black and white squares

Just as any good trading strategy,

if

more and more people

get

to know it and replicate it,

the effectiveness

of

such a strategy will disappear.

As

the chess board problem becomes

popular, many interviewees simply commit it to memory (after all, it's easy to remember

the answer). So some ingenious interviewer came

up

with the newer version to test your

thinking process, or at least your ability

to

extend your knowledge to new problems.

lfwe

look at the total volume in this

30

problem,

53

bricks have a volume

of

212, which

is

smaller then the box's volume 216. Yet

we

can show it is impossible to pack all the

bricks into the box using a similar approach as the chess board problem. Let's imagine

that the 6 x 6 x 6 box is actually comprised

of

small 2 x 2 x 2 cubes. There should be 27

small cubes. Similar to the chess board (but in

30),

imagine that

we

have black cubes

and white cubes

alternates-it

does take a little

30

visualization.

So

we have either 14

black cubes &

13

white cubes

or

13

black cubes &

14

white cubes. For any

1x1x4

brick

that we pack into the box, half (

1x1x2)

of

it must

be

in a black 2 x 2 x 2 cube and the

other half must be in a white 2 x 2 x 2 cube. The problem is that each 2 x 2 x 2 cube can

only be used

by

4

of

the

1x1

x 4 bricks. So for the color with

13

cubes, be it black

or

white, we can only use them for 52

1x1x4

tubes. There is no way to place the 53th

brick. So we cannot pack

53

bricks

of

dimensions 1x1x4 into a 6 x 6 x 6 box.

Calendar cubes

You just had two dice custom-made. Instead

of

numbers 1 - 6, you place single-digit

numbers on the faces

of

each dice so that every morning

you

can arrange the dice in a

way as to make the two front faces show the current day

of

the month. You must use

both dice (in other words, days 1 - 9 must

be

shown as

01

-09), but you can switch the

11

Brain Teasers

order

of

the dice

if

you

want. What numbers do

you

have to put on the six faces

of

each

of

the two dice to achieve that?

Solution: The days

of

a month include

11

and 22, so both dice must have 1 and

2.

To

express single-digit days,

we

need

to

have at least a 0

in

one dice. Let's put a 0 in dice

one first. Considering that we need to express all single digit days and dice two cannot

have all the digits from 1 - 9, it's necessary to have a 0

in

dice two as well in order to

express all single-digit days.

So far we have assigned the following numbers:

! Dice one

Dice two I : I

If

we can assign all the rest

of

digits 3,

4,

5,

6,

7, 8, and 9 to the rest

of

the faces, the

problem is solved.

But

there are 7 digits left. What can we do?

Here's

where you need to

think out

of

the box.

We

can use a 6 as a 9 since they will never be needed at the same

time! So, simply

put

3, 4, and 5

on

one dice and 6,

7,

and 8

on

the other dice, and the

final numbers on the two dice are:

Dice one 1 2 0 3 4 5

Dice two 1 2 0 6 7 8

Door

to offer

You are facing two doors. One leads to your job offer and the other leads to exit. In front

of

either door

is

a guard. One guard always tells lies and the other always tells the truth.

You can only ask one guard one yes/no question. Assuming you do want to get the job

offer, what question will you ask?

Solution: This is another classic brain teaser (maybe a little out-of-date

in

my opinion).

One popular answer is to ask one gua

rd

: "Would the other guard say that you are

guarding the door to the offer?"

If

he

answers yes, choose the other

door;

if

he answers

no, choose

the

door this guard is standing

in

front of.

There are two possible scenarios:

I . Truth teller guards the door to offer; Liar guards the door to exit.

2. Truth teller guards the door

to

exit; Liar guards the door to offer.

If

we ask a guard a direct question such as "Are you guarding the door to the offer?" For

scenario I, both guards will answer yes; for scenario 2, both guards will answer no. So a

12

A Practical Guide

To

Quantitative Finance Interviews

direct question does not help us solve the problem. The

key

is to involve both guards in

the questions as the popular answer does. For scenario

1,

if

we happen to choose the

truth teller, he will answer no since the liar will say no;

if

we happen to choose the liar

guard,

he

will answer yes since the truth teller will say no. For scenario 2,

if

we happen

to choose the truth teller, he will answer yes since the liar will say yes;

if

we happen to

choose the liar guard,

he

will answer no since the truth teller with say yes. So for both

scenarios,

if

the answer

is

no, we choose that door;

if

the answer

is

yes, we choose the

other door.

Message delivery

You need to communicate with your colleague

in

Greenwich via a messenger service.

Your documents are sent

in

a padlock box. Unfortunately the messenger service

is

not

secure, so anything inside an unlocked box will be lost (including any locks you place

inside the box) during the delivery. The high-security padlocks you and your colleague

each use have only one

key

which the person placing the lock owns. How can you

securely send a document to your colleague?6

Solution:

If

you

have a document to deliver, clearly you cannot deliver it in an unlocked

box. So the first step

is

to deliver it to Greenwich in a locked box. Since you are the

person who has the key to that lock, your colleague cannot open the box to get the

document. Somehow you need to remove the lock before he can get the document,

which means the box should be sent back to you before your colleague can get the

document.

So what can he do before he sends back the box?

He

can place a second lock on the box,

which

he

has the key

to!

Once

the box

is

back to you,

you

remove your own lock and

send the box back to your colleague. He opens his own lock and gets the document.

Last ball

A bag has

20

blue balls and 14 red balls. Each time

you

randomly take two balls out.

(Assume each ball in the bag has equal probability

of

being taken). You do not put these

two balls back. Instead,

if

both balls have the same color, you add a blue ball to the bag;

if

they have different colors, you add a red ball to the bag. Assume that you have an

unlimited supply

of

blue and red balls,

if

you keep on repeating this process, what will

be the color

of

the last ball left in the bag?

7 What

if

the

bag

has 20 blue balls and l 3 red

balls instead?

6 Hint: You

can

have more than

one

lock on the box.

7 Hint: Consider the changes in the number

ofred

and blue balls after each step.

13

Brain Teasers