Guide To Business Analysis Risk Analyst

User Manual:

Open the PDF directly: View PDF ![]() .

.

Page Count: 102 [warning: Documents this large are best viewed by clicking the View PDF Link!]

- 1 INTRODUCTION TO SINGLE BORROWER CREDIT ANALYSIS WITH RISKANALYST

- 2 INTERNAL RATING MODEL METHODOLOGY

- 3 FUNDAMENTAL ANALYSIS METHODOLOGY

- 4 SCORECARD METHODOLOGY

- 5 RATIO ASSESSMENT METHODOLOGY

- 6 RATINGS SUMMARY

- 7 LOSS GIVEN DEFAULT ANALYSIS

- 8 LOSS GIVEN DEFAULT CALCULATIONS

- 8.1 CALCULATING EADS

- 8.2 GUARANTEES

- 8.3 COLLATERAL

- 8.4 ALLOCATING CRMS TO FACILITIES

- 8.5 DERIVATION OF THE LGD FOR THE UNSECURED PORTION OF THE FACILITY

- 8.6 DERIVATION OF THE BORROWER PD

- 9 LOSS GIVEN DEFAULT ALGORITHM

- 9.1 INTRODUCTION TO THE LGD ALGORITHM

- 9.2 LGD ALGORITHM OVERVIEW

- 9.3 CALCULATING EAD

- 9.4 CALCULATE ALLOCATIONS

- 9.5 DERIVE CRM ELIGIBILITY PER SE

- 9.6 CRM SORTING

- 9.7 THE LGD CALCULATION

- 9.8 PERFORM CRM ALLOCATION

- 9.9 ELIGIBILITY PER FACILITY

- 9.10 EXPECTED LOSS

- 9.11 CALCULATE EL AND LGD DATA FOR THE FACILITY

- 9.12 CALCULATE EL AND LGD DATA ACROSS ALL FACILITIES

- 10 FACILITY SUMMARY

- 11 ARCHIVE

- 11.1 ARCHIVE OVERVIEW

- Identify staff

- Training

- Review IRT factors

- Review IRT parameters (scores and weights)

- Mapping the score to your Grading System

- Mapping Grades to PDs

- Overrides

- Consider whether multiple variants of the IRT will be used

- Consider Peer Data

- Implementation Issues

- Select Pilot Users

- Train Pilot Users

- Implementation Issues

- Data Capture and Quality Issues

- Assess and Review IRT Performance

- Peer Database Considerations

- Optimize IRT

- Test Optimized IRT

- Calibrate the IRT to your grading system

- If data is available, determine PD values for grades

- Review Overrides

- Data Capture

- Data Quality and Monitoring

- Assess and Review Internal Rating Model Performance

- Re-optimize

- Validate

- Calibrate

- Considerations for multiple versions

- Factor/ Internal Rating Model Review

- Adding Factors to the IRT

- Amending/Specifying Parameters for Factors

- Peer Database

- Financial Conditions

- Internal Rating Model Validation and Calibration

- Versioning and the Internal Rating Model Author/Tuning Console

- Identify staff

- 11.1 ARCHIVE OVERVIEW

AUGUST 2008

GUIDE TO BUSINESS ANALYSIS

RISKANALYST 5.0

© 2008 Moody’s KMV Company. All rights reserved.

Moody’s KMV, RiskAnalyst, Credit Monitor, Risk Advisor, CreditEdge, LossCalc, RiskCalc, Decisions,

Benchmark, Expected Default Frequency, and EDF are trademarks of MIS Quality Management Corp. used

under license.

All other trademarks are the property of their respective owners.

ACKNOWLEDGEMENTS

We would like to thank everyone at Moody’s KMV who contributed to this document.

Published by:

Moody’s KMV Company

405 Howard Street, Suite 300

San Francisco, CA 94105 USA

Phone: +1.415.874.6000

Toll Free: +1.866.321.6568

Fax: +1.415.874.6799

Author: MKMV

Email: docs@mkmv.com

Website: http://www.moodyskmv.com/

To Learn More

Please contact your Moody’s KMV client representative, visit us online at www.moodyskmv.com, contact

Moody’s KMV via e-mail at info@mkmv.com, or call us at:

NORTH AND SOUTH AMERICA, NEW ZEALAND, AND AUSTRALIA CALL:

+1.866.321.MKMV (6568) or +1.415.874.6000

EUROPE, THE MIDDLE EAST, AFRICA, AND INDIA CALL:

+44.20.7280.8300

ASIA-PACIFIC CALL:

+852.3551.3000

FROM JAPAN CALL:

+81.3.5408.4250

TABLE OF CONTENTS

PREFACE ..............................................................................................................................7

P.1.1 About This Guide......................................................................................7

P.1.2 Audience ..................................................................................................7

P.1.3 Typographic Conventions ........................................................................7

1 INTRODUCTION TO SINGLE BORROWER CREDIT ANALYSIS WITH RISKANALYST ....9

1.1 Borrower module and Internal Rating Models...................................................9

1.2 Facilities module and Loss Given Default...........................................................9

1.3 Archive module ..................................................................................................10

2 INTERNAL RATING MODEL METHODOLOGY ............................................................11

2.1 Fundamental Analysis methodology.................................................................11

2.2 Scorecard methodology.....................................................................................11

2.3 Ratio assessment methodology ........................................................................11

3 FUNDAMENTAL ANALYSIS METHODOLOGY ............................................................13

3.1 Assessments......................................................................................................13

3.2 Assessments with Categorized Components ...................................................13

3.3 Uncertainty.........................................................................................................16

3.4 Range .................................................................................................................17

3.5 Assessment algorithm ......................................................................................18

3.6 Calculating the Assessment..............................................................................18

3.6.1 Scoring of Inputs....................................................................................19

3.6.2 Aggregation of input distributions ........................................................20

3.6.3 Transformation of distribution..............................................................21

3.7 Calculating the Means and Standard Deviations of an Assessment ...............22

3.7.1 Real Mean: .............................................................................................22

4 SCORECARD METHODOLOGY...................................................................................25

4.1 Scorecard overview ...........................................................................................25

4.2 Meters ................................................................................................................26

4.3 Factors ...............................................................................................................26

4.4 Calculation of Scores for Numerical Factors ...................................................27

4.4.1 Scoring Factors Using Values ...............................................................27

4.4.2 Scoring Factors by Banding ..................................................................27

4.4.3 Transformation of Numerical Inputs ....................................................27

4.4.4 Special Numeric Factors.......................................................................30

4.5 Calculation of Scores for Categorized Factors.................................................30

4.6 Weighting ...........................................................................................................30

5 RATIO ASSESSMENT METHODOLOGY......................................................................33

5.1 Financial Ratios .................................................................................................33

5.2 Standard Ratio Assessment Algorithm.............................................................34

5.2.1 Algorithm for numeric factors ..............................................................35

5.2.2 Algorithm for categorized factors.........................................................35

5.3 Absolute assessment ........................................................................................36

5.4 Trend assessment .............................................................................................36

5.4.1 Slope ......................................................................................................37

5.4.2 Volatility .................................................................................................37

5.4.3 Peer Trend .............................................................................................38

5.5 Peer ....................................................................................................................39

5.5.1 Standard Ranking Algorithm ................................................................39

5.5.2 Alternative Ranking Algorithm .............................................................40

5.6 Combining Ratio components ...........................................................................41

5.7 Special Conditions .............................................................................................42

5.7.1 Assess Ratio ..........................................................................................42

5.7.2 Ratio Unacceptable ...............................................................................43

5.7.3 Trend Defaults to Good .........................................................................43

5.8 Debt Coverage Ratio Assessments ...................................................................43

5.8.1 Earnings and Cash Flow Coverage Ratios............................................43

5.8.2 The Cash Flow Management Assessments..........................................44

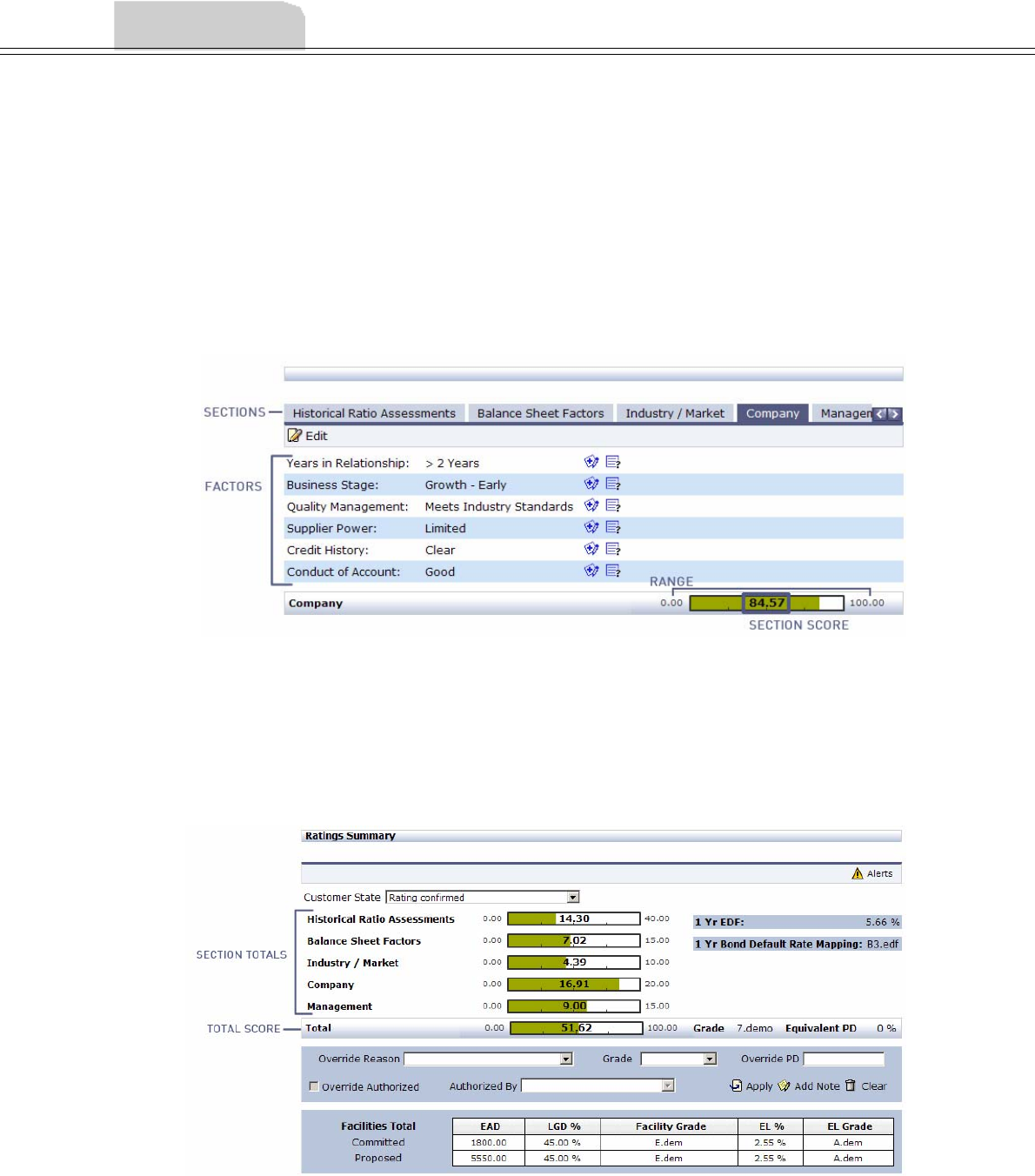

6 RATINGS SUMMARY ................................................................................................47

6.1 Structure of the rating.......................................................................................47

6.2 Ratings Summary screen ..................................................................................48

6.2.1 Customer State......................................................................................48

6.2.2 1-Yr EDF.................................................................................................48

6.2.3 Overrides................................................................................................48

6.2.4 Facilities.................................................................................................48

6.2.5 Constraining ..........................................................................................48

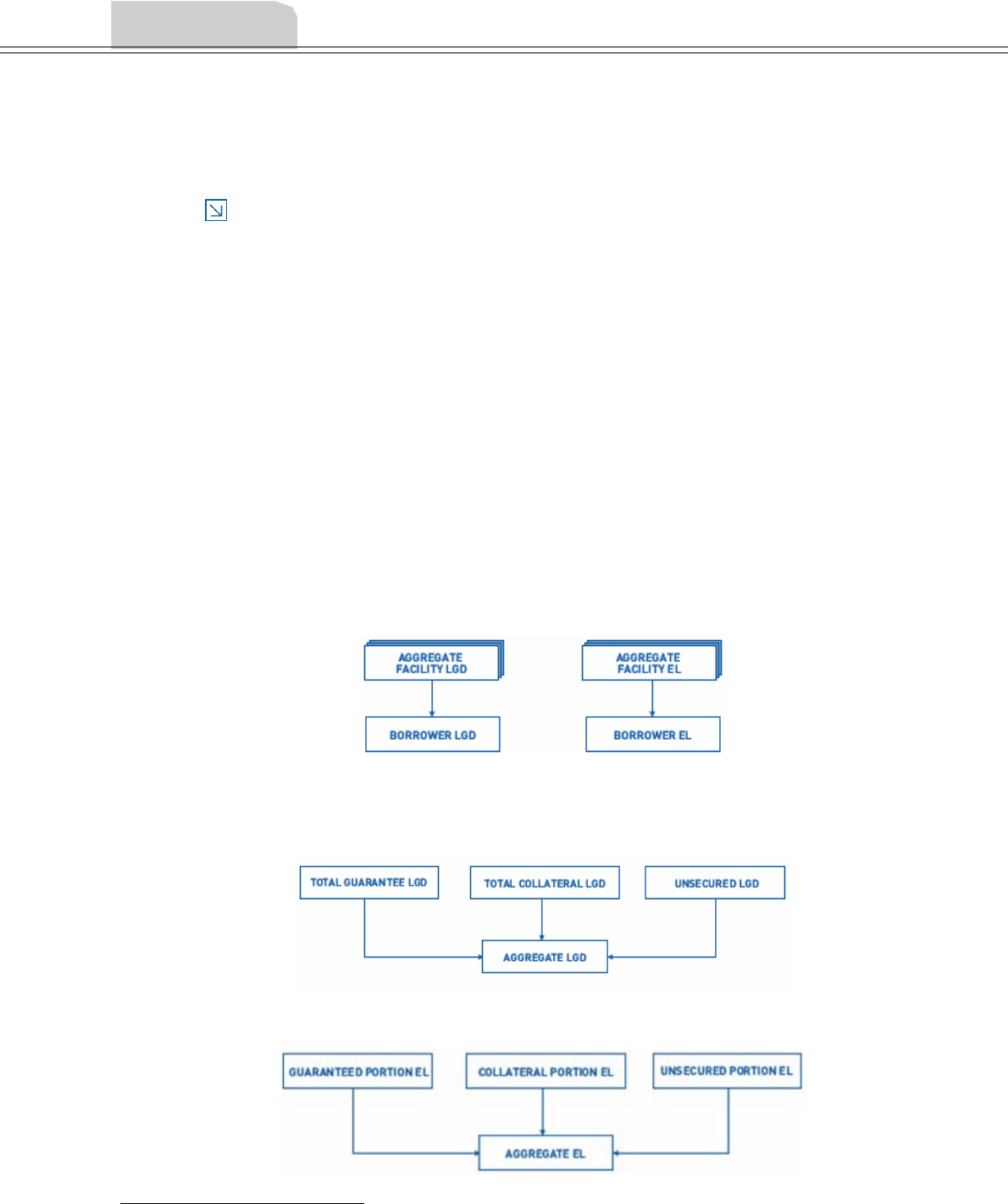

7 LOSS GIVEN DEFAULT ANALYSIS............................................................................49

7.1 Determining LGD and EL Values.......................................................................49

7.2 Facility Status ....................................................................................................51

7.3 Calculating Grades ............................................................................................51

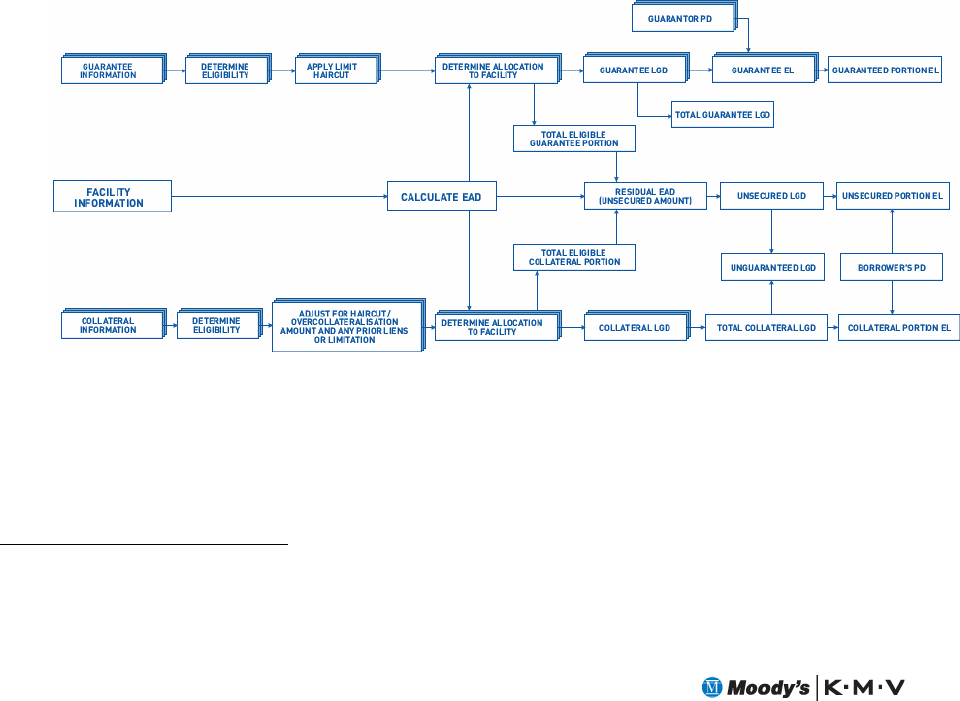

8 LOSS GIVEN DEFAULT CALCULATIONS...................................................................53

8.1 Calculating EADs ...............................................................................................53

8.2 Guarantees.........................................................................................................55

8.2.1 Haircuts Applied to Guarantees............................................................55

8.2.2 Eligibility Criteria for Guarantees .........................................................55

8.3 Collateral ...........................................................................................................56

8.3.1 Mapping RiskAnalyst Collateral Types to Basel II Collateral Types....56

8.3.2 Calculating Haircuts for Financial Collateral.......................................56

8.3.3 Haircuts for Non-Financial Collateral ..................................................57

8.3.4 Prior Liens and Limitations...................................................................58

8.3.5 Eligibility Criteria for Collateral............................................................58

8.3.6 Collateral Minimum LGD% Values .......................................................61

8.4 Allocating CRMs to Facilities.............................................................................63

8.4.1 Automatic Allocation of CRMs using EAD Weighting ...........................63

8.4.2 Manual Allocation of CRMs ...................................................................63

8.5 Derivation of the LGD for the Unsecured portion of the facility.......................64

8.6 Derivation OF the Borrower PD.........................................................................64

GUIDE TO BUSINESS ANALYSIS 5

9 LOSS GIVEN DEFAULT ALGORITHM.........................................................................65

9.1 Introduction to the LGD Algorithm....................................................................65

9.2 LGD Algorithm Overview ...................................................................................66

9.3 Calculating EAD .................................................................................................67

9.4 Calculate Allocations.........................................................................................67

9.5 Derive CRM Eligibility

Per Se

............................................................................68

9.5.1 Deriving CRM Eligibility

Per Se

.............................................................68

9.6 CRM Sorting .......................................................................................................68

9.6.1 Guarantees First....................................................................................69

9.6.2 Guarantees Second ...............................................................................70

9.7 The LGD Calculation ..........................................................................................71

9.7.1 Guarantee First/Second Processing.....................................................71

9.7.2 Guarantee First Processing ..................................................................71

9.7.3 Guarantees Second Processing............................................................71

9.8 Perform CRM Allocation....................................................................................72

9.8.1 Mismatch-Adjusted Eligible Amount ....................................................72

9.8.2 Expected Realization .............................................................................73

9.9 Eligibility

Per Facility

.........................................................................................73

9.9.1 Implementation .....................................................................................73

9.9.2 Determining the Minimum Collateralization Requirement .................75

9.10 Expected Loss ....................................................................................................76

9.11 Calculate EL and LGD Data for the Facility ......................................................76

9.12 Calculate EL and LGD Data Across All Facilities .............................................77

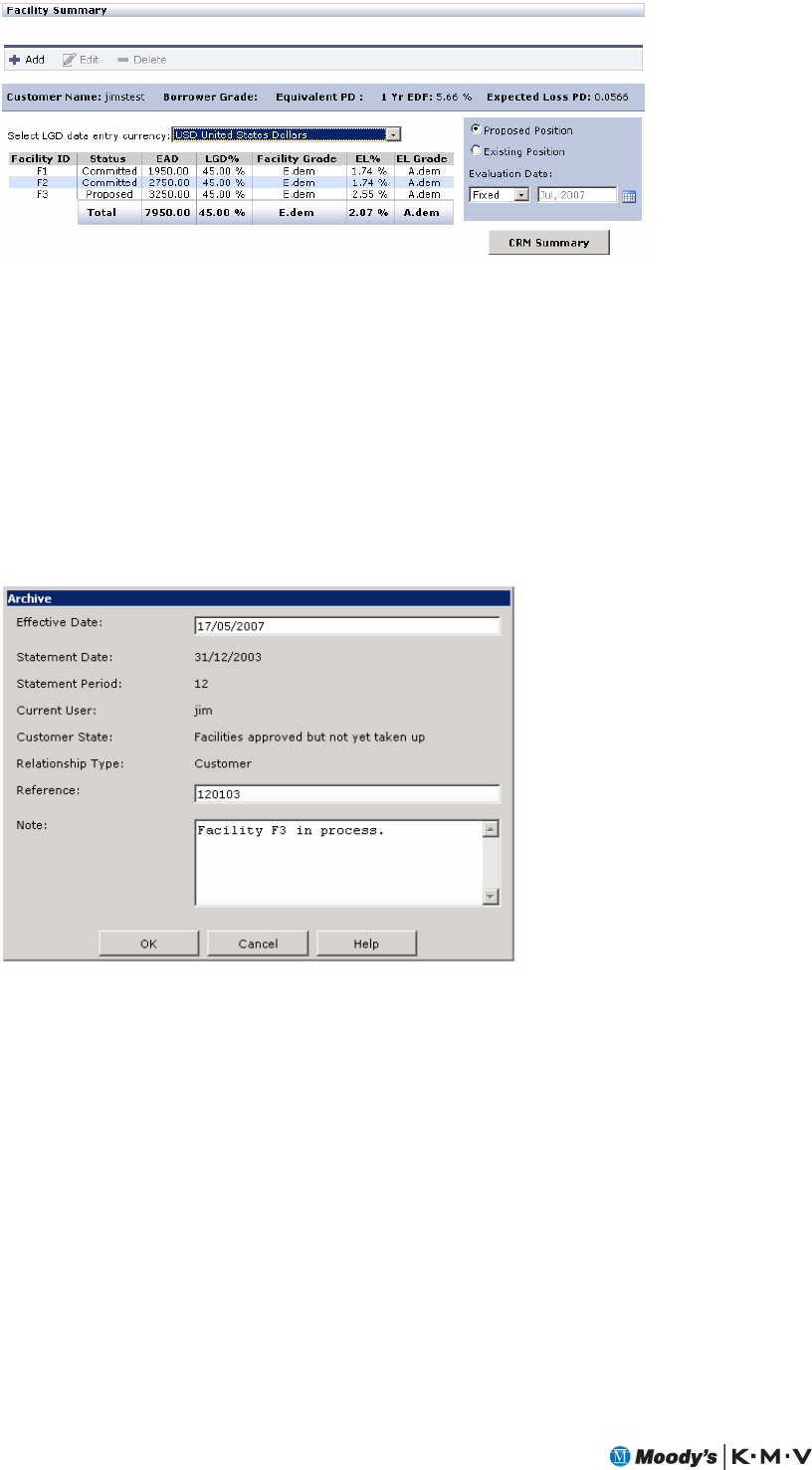

10 FACILITY SUMMARY ................................................................................................79

10.1 Facility Summary ...............................................................................................79

10.1.1 Customer information bar ....................................................................79

10.1.2 Switching between Proposed and Existing Positions ..........................79

10.1.3 Selecting the Evaluation Date ...............................................................79

11 ARCHIVE..................................................................................................................81

11.1 Archive overview ................................................................................................81

A APPENDIX A - INTERNAL RATING TEMPLATES.......................................................83

A.1 The Internal Rating Template Concept .............................................................83

A.2 The Methodology Used to Create Internal Rating Templates..........................84

A.2.1 The Internal Rating Template Creation Process..................................84

A.2.2 Tuning the Internal Rating Template....................................................84

A.2.3 Verification of the Internal Rating Template Performance .................86

A.3 Configuring Internal Rating Templates ............................................................86

A.4 A Typical Internal Rating Template Configuration Life-Cycle .........................87

A.4.1 Model Set-up .........................................................................................89

A.4.2 Pilot Phase.............................................................................................92

A.4.3 Production .............................................................................................94

A.4.4 Some Additional Information on Configuration Tasks .........................95

A.5 Configuration versus Customization.................................................................99

A.6 Making Changes on Your Own...........................................................................99

A.6.1 Configuration Changes..........................................................................99

PREFACE

GUIDE TO BUSINESS ANALYSIS 7

PREFACE

P.1.1 About This Guide

The Guide to Business Analysis is intended for users of the Internal Rating Model Author and

purchasers of internal rating templates. The guide provides detailed information on performing

business analyses using RiskAnalyst. Specifically, it explains the structure and calculations

involved in internal rating models and loss given default. After reading this guide, one should

have a good understanding of how the system arrives at internal rating model grades and loss

given default values.

P.1.2 Audience

This guide is for Moody’s KMV clients and personnel. It assumes a good understanding of

RiskAnalyst.

P.1.3 Typographic Conventions

This guide uses the following typographic conventions—fonts and other stylistic treatments

applied to text—to help you locate and interpret information.

TABLE P.1 Typographic Conventions

Convention Description

Bold Virtual buttons, radio buttons, check boxes, literal key names, menu paths,

and information you type into the system appear in bold type — for

example, “Click Add” or “Press Enter.”

Courier System messages appear in a courier typeface — for example, “The system

displays the following message: Added Amazon.com to your

portfolio.”

Italic Emphasized definitions and words appear in italic type — for example,

“Portfolio Tracker is a portfolio tools page.”

NOTE Information you should note as you work with the system.

WARNING Warning information that prevents you from damaging your system or your

work.

TIP Additional information you can use to improve the performance of the

system.

EXAMPLE Information that illustrates how to use the system.

CHAPTER 1

GUIDE TO BUSINESS ANALYSIS 9

1 INTRODUCTION TO SINGLE BORROWER

CREDIT ANALYSIS WITH RISKANALYST

RiskAnalyst™ optionally includes Borrower, Facilities, and Archive modules. The first two

modules provide the ability to analyze a business and produce risk ratings at both the borrower

and facility level. Once an analysis has been completed, the Archive module is used to create a

record of that analysis.

1.1 BORROWER MODULE AND INTERNAL RATING MODELS

The Borrower module uses internal rating models to analyze industry specific factors and

produce a risk rating grade and PD estimate. Internal rating models can be created or

customized using the RiskAnalyst Internal Rating Model Author (component of RiskAnalyst

Studio). You can also use a Moody’s KMV designed internal rating template (IRT) as a starting

point in producing your own internal rating model.

Internal rating models are assigned to a customer in RiskAnalyst in the Analysis Setup dialog

box. Access the internal rating model using the internal rating model screen.

The methodology behind internal rating models is discussed in detail in Chapters 2-5.

1.2 FACILITIES MODULE AND LOSS GIVEN DEFAULT

When assessing the risk associated with providing credit to borrowers, there are two dimensions

to the risk assessment: the risk that the borrowers will default on their obligations and the risk

associated with any recovery of the obligations from the borrowers if they default. The latter

analysis is often referred to as Loss Given Default (LGD) analysis.

The Facilities module assesses facility risk by calculating LGD and Expected Loss (EL). As

specified by Basel II, LGD and EL are first calculated at the facility level. Each facility's LGD

and EL values are aggregated to provide a total LGD and EL value. Finally, the system produces

a Facility and EL grade based upon the aggregate values.

Access the Facilities module through the Facility Summary screen.

10

Chapters 7, 8, and 9 discuss Facilities and the Loss Given Default calculation in detail.

1.3 ARCHIVE MODULE

The Archive module stores and retrieves records of analyses. When archiving analyses, the

system creates a copy of the customer data contained in the customer database. You can view a

history of the customer’s archives in RiskAnalyst. These archives can later be recovered

individually to support internal audit functions, as well as in batches for model evaluation

purposes.

Access the Archive feature through the Archive dialog box.

Chapter 11 provides an overview of archiving analyses.

CHAPTER 2

GUIDE TO BUSINESS ANALYSIS 11

2 INTERNAL RATING MODEL

METHODOLOGY

RiskAnalyst includes two possible approaches to internal rating models: Fundamental Analysis

and Scorecard. Both approaches support sophisticated analysis of ratios and financial metrics. It

is important to understand that the primary difference between these two approaches is the way

the system calculates and scores the inputs of the model. While the methodologies of these

approaches differ, they are both based on the same technology platform. Additionally, each

internal rating model, no matter the approach used, produces a borrower rating and PD. The

Internal Rating Model Author supports the creation and customization of internal rating

models using both approaches.

This chapter includes a brief description of each of the standard approaches. Subsequent

chapters will explore the methodology behind each approach in detail. Please note that many of

the calculations in both approaches can be overridden by a highly custom designed model. The

following sections and chapters describe the standard calculations and methodologies.

2.1 FUNDAMENTAL ANALYSIS METHODOLOGY

The fundamental analysis approach, like the scorecard approach, supports the analysis of key

financial factors as well as non-financial, subjective factors. Compared to scorecard internal

rating models, however, fundamental analysis internal rating models have a greater degree of

complexity in their scoring mechanism. Assessments are the primary output of the fundamental

analysis approach and the way in which inputs are scored. Assessments are produced by

combining the results of many inputs to produce a number on a scale of 0 to 100. Assessment

results display as this number, called the assessment mean, and also as a graphical meter. The

final assessment in the model is typically mapped to a borrower rating grade and equivalent PD.

Fundamental analysis assessments inherently support uncertainty and can account for missing

information in the model. The methodology behind the fundamental analysis approach, that is,

the way in which inputs are combined to produce assessments, is described in depth in Chapter

3.

2.2 SCORECARD METHODOLOGY

The scorecard approach groups the inputs, or factors, of the internal rating model into sections.

Each factor in a section is scored, and the sum of these scores becomes the total score for that

section. The section scores are summed to produce an overall score, which is then mapped to

the borrower rating grade and equivalent PD. Both the individual factors and the sections can

be weighted. The scoring mechanism is simpler than the fundamental analysis approach since

typically only sums of scores (with any weights) are considered. Inputs are not assessed on a 0 to

100 scale, but rather use the range of possible scores identified when setting up the input.

Because of this, uncertainty and missing information are not supported by scorecard internal

rating models. Scorecard methodology is explored more thoroughly in Chapter 4.

2.3 RATIO ASSESSMENT METHODOLOGY

Ratio assessments are similar to the assessments used in the fundamental analysis approach, but

have unique components and calculations. They can be incorporated in both scorecard and

fundamental analysis internal rating models. Ratio assessments combine a peer, trend, and

absolute assessment to calculate an overall assessment of a ratio or financial metric. The specific

calculations used to produce a ratio assessment can be found in Chapter 5.

CHAPTER 3

GUIDE TO BUSINESS ANALYSIS 13

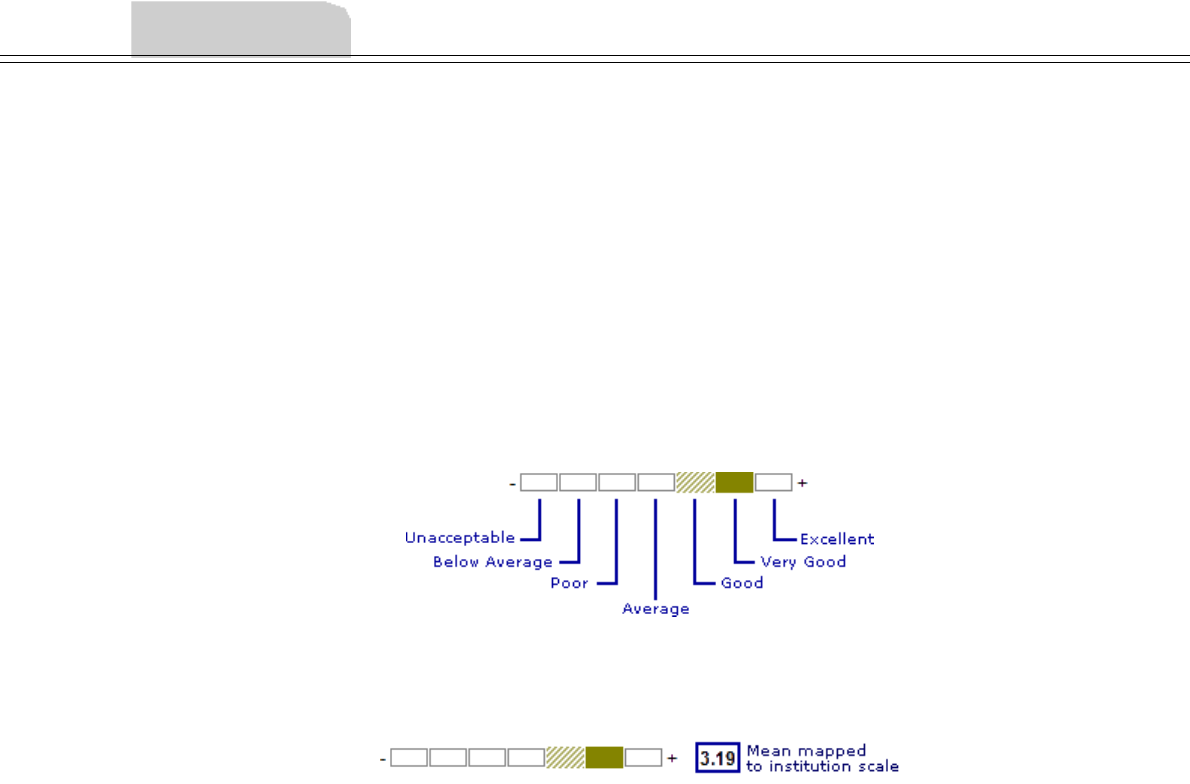

3 FUNDAMENTAL ANALYSIS METHODOLOGY

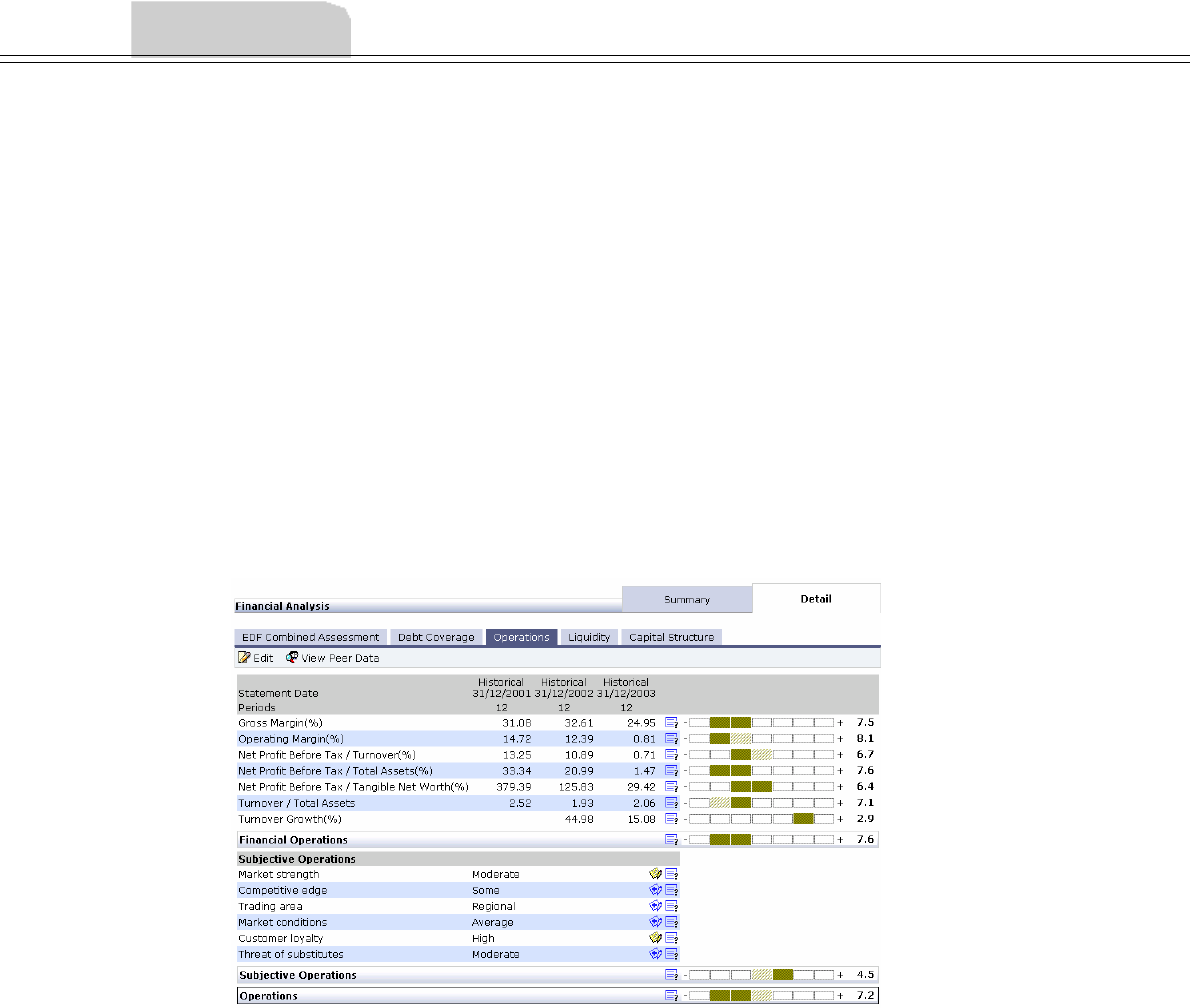

3.1 ASSESSMENTS

Assessments are the primary output of fundamental analysis internal rating models. To create

assessments, an internal rating model combines the results of many inputs to produce a number

on a scale of 0 to 100. Assessment results display as this number, called the assessment mean,

and also as a graphical meter. Meters display the assessment result on a 0 to 100 scale that is

divided into the following seven categories. The certainty of an assessment is also visually

displayed by shaded and solid bands. See section 3.3 for more information about uncertainty.

You can map this scale to your institution's scale using the Configuration Console, Tuning

Console, or the Internal Rating Model Author. If you map this scale, the number on the right

of the meter corresponds to the institution's scale.

The inputs that make up the assessment are called components. For example, an assessment of

Management Character could be made up of two components: one that measures Commitment

and one that measures Integrity. The types of components that make up an assessment

determine how the assessment is calculated:

• Assessments with categorized components (such as subjective factors and aggregated

assessments). The calculation for these assessments is described in the next section.

• Ratio assessments with peer, trend, and absolute components. Ratio assessments are

discussed in Chapter 5.

3.2 ASSESSMENTS WITH CATEGORIZED COMPONENTS

This section discusses how the system produces assessments from components with categorized

inputs. A detailed look at the algorithm behind these calculations can be found in section 3.5.

These components have input values that are predefined categories, such as:

Non-financial factors. Factors with input values that display as drop-down menus and have

categories such as: HIGH, AVERAGE, LOW.

Assessments. Individual assessments have categories (Unacceptable through Excellent) and can

be combined to form an aggregated assessment.

14

To combine categorized inputs into an assessment, the system uses a weight function. The

weight function serves two purposes:

• It allows components with different categories to be combined in the assessment.

• It allows each component category to have more or less importance in the assessment.

The following discussion gives a simplified account of how the system uses weight to create an

assessment. Uncertainty and soft saturation also contribute to the assessment, but to simplify

this discussion they are in a separate section.

Weighting Assessment Components

The weight function assigns a vote to each component category. If the component category

improves the assessment it is assigned a positive vote. If the category worsens the assessment it is

assigned a negative vote. The relative importance of the category is defined by the size of the

vote: the larger the vote, the more influence the component category has on the assessment.

The weight concept in the Tuning Console provides an idea of the importance of individual

components in an assessment (i.e., which components impact the assessment to a greater

degree). It also allows you to adjust, at a very high level, the votes associated with a component

and its categories. It is important to remember that this weight is not explicit in the

fundamental analysis approach; weighting is added to an assessment through the use of votes.

While you can adjust the weights of components in the Tuning Console, what you are really

doing is adjusting the votes.

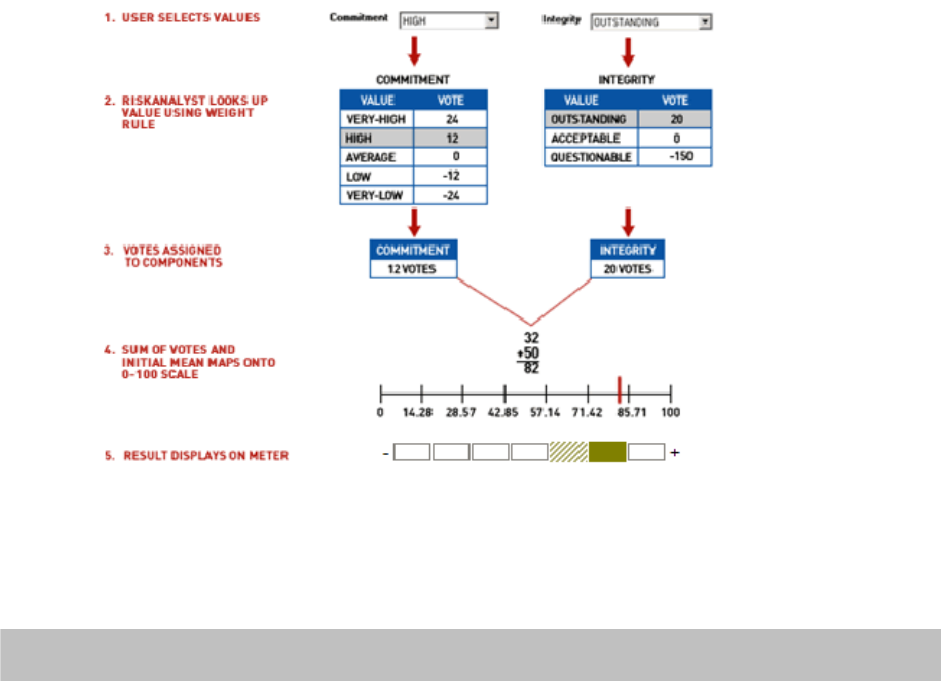

Each component has a list of possible categories and corresponding votes. When a component

receives its value, for example, through user selection, the system looks up the category to assign

the votes. The sum of the votes for all of the assessment’s components contributes to the

assessment value.

Votes, which center on zero, must be mapped onto the assessment scale of 0–100. To do this,

assessments have an initial distribution which is used as a starting point for the assessment. The

initial distribution generally has a mean of 50 (on a 0-100 scale) and a standard deviation of

seven. The sum of the component votes is added to the initial mean to produce the assessment

mean. This value is then mapped onto the seven assessment meter categories to display the

meter.

Consider an assessment of Management Character with two components: Commitment and

Integrity. The votes of the Commitment and Integrity components are summed and the result

is added to the initial mean to produce the assessment mean.

The diagram below demonstrates this process. Note that because uncertainty in the assessment

is taken into account, as discussed in section 3.3, the assessment has a shaded band to the left of

the solid band.

GUIDE TO BUSINESS ANALYSIS 15

The same logic applies when aggregating a group of assessments into an overall assessment.

The example below details an assessment with 266 absolute votes to be distributed among five

components. The components have different numbers of categories (some 4 and some 5). The

266 votes used in this example are based on a Range value of 59.

Category Votes for

Component 1

Votes for

Component 2

Votes for

Component 3

Votes for

Component 4

Votes for

Component 5

1 -5 0 12 10 12

2 20 20 8 5 8

3 -10 -10 0 0 0

4 -20 -30 -15 -8 -10

5 N/A N/A -25 -13 -25

Total

Absolute

Vote

55 60 60 36 55

Average

Absolute

Vote

(55/4) 13.75 (60/4) 15 (60/5) 12 (36/5) 7.2 (55/5) 11

The total of the Average Absolute votes is:

13.75 + 15 + 12 + 7.2 + 11 = 58.95

Average Absolute Vote as a percentage of 58.95:

23.3% 25.4% 20.4% 12.2% 18.7%

Total 100%

Adjusting the weight (through the use of votes) of an individual component affects only that

component. It is necessary, therefore, to adjust other weights in order to achieve a total of 100%

weight across all components.

16

Initial Distribution

Each assessment has an initial distribution which is the mean and standard deviation of the

assessment. Generally, the starting mean is set halfway along the meter at 50, with the standard

deviation of seven. Positive voting moves the meter up, and negative voting moves it down. A

meter mean point of 50 adds no bias to the assessment. A meter starting mean point value of

less than 50 will ensure a built-in conservative bias to the assessment, a value of greater than 50

will ensure an optimistic bias.

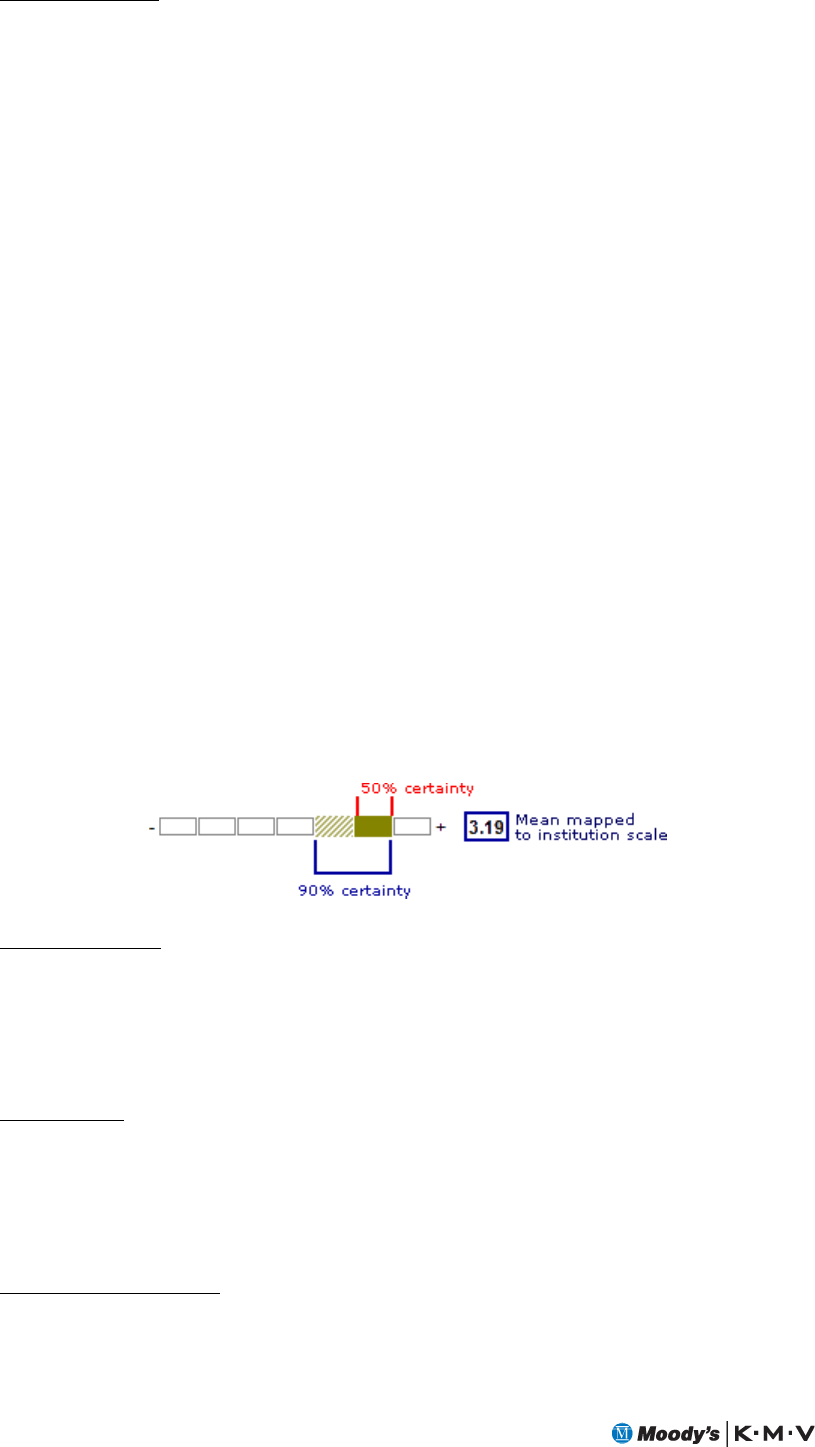

3.3 UNCERTAINTY

As well as the assessment value, meters display RiskAnalyst’s analysis of the certainty or

uncertainty attached to the assessment. Uncertainty can be introduced as a result of:

• Missing data

• Inherent imprecision of the items under assessment, particularly where these are

subjective analyses

Meters use solid and shaded bands to indicate both the assessment value and the level of

certainty attached to the analysis. A meter displays as either a single, solid green band or a

combination of a solid and shaded green bands. The band or bands denote a range with a 90%

degree of certainty.

The system will color in the smallest number of categories it can to cover 50% of the curve, and

then will shade in the smallest number of categories to the left and right to reach 90% of the

curve.

Where a solid band appears without any shaded bands, the range denoted by the solid band has

a 90% degree of certainty. Where a solid band is accompanied by shaded bands, the range

denoted by the solid and shaded bands has a 90% degree of certainty, but the range denoted by

just the solid band is only 50% certain.

Inbuilt Uncertainty

The inbuilt uncertainty of a component is one of the determinants of the width of the

uncertainty band in the component’s meter. A high uncertainty indicates an inherently

uncertain component, and means that, even when all the inputs are given, the meter displays a

wide shaded band.

Soft Saturation

Although meter values theoretically range from 0 to 100, in practice it is usually impossible to

achieve either extreme. This is due to a type of damping mechanism—soft saturation—that

ensures meters stay within range by applying increasing resistance as the value approaches either

extreme. Values lower than about 3 or higher than about 97 would be rare.

Calculation of Uncertainty

The uncertainty for an assessment is the square root of the sum of:

GUIDE TO BUSINESS ANALYSIS 17

The standard deviation squared

The square of the standard deviation associated with each input applied to its weights.

The latter is derived from the difference between the input's mean value (as derived using the

assessment votes) and the votes for each category in the assessment. The resulting differences are

combined by weighting each difference by the probability that the input could take the value

associated with the weight. The differences are also squared and summed. Then the system takes

the square root of the result to eliminate positive and negative differences canceling out each

other.

The spread of votes you enter for an assessment will affect the uncertainty if the input itself has

some uncertainty. This is due to the use of differences between votes and input mean. Using a

greater spread of votes for meters will affect assessments, especially when questions are

unanswered. Note that if the input to the assessment is a specific answer to a question then the

spread of votes has no impact as its value is certain.

3.4 RANGE

The range is the number that controls the boundaries of an assessment and thus its impact – the

greater the range the greater the potential movement of the meter (14 votes is equal to

approximately one category of the meter). Range sets the maximum number of votes for the

components of an assessment, and changing it changes the votes for each component of the

assessment, resetting them to a straight line and overriding the existing distribution. Similar to

weights in the Tuning Console, changing the range is really just another way to change the

votes of the components of an assessment. The range will be changed if tuning (see ‘Range in

the Tuning Console’) changes the total number of votes within the components.

The highest and lowest possible values for an assessment are determined (indirectly) by a factor

using the range. The actual number of votes is determined using the formula explained below.

This calculation produces votes on a straight line through a midpoint of 0. It must be carried

out for each category in each component using the correct formula (determined by whether a

component has an equal or odd number of categories).

Weight (as a percentage) = p

Number of categories in a component = n

Range = r

Category number (ID) = c

Number of votes = v

For each category (c), the vote (v), is given by the following equations:

For even values of n:

v(c) = 2(npr) * (2c - n - 1) / n2

For odd values of n:

v(c) = 2(npr) * (2c - n - 1) / (n2 - 1)

For example, consider the Operations Skill component category ABOVE AVERAGE. When

Operations Skill has a weight of 24.5%, and the range is 39, the number of votes for the ABOVE

AVERAGE category is calculated as follows:

p = 0.245, n= 5, c = 4

18

v4 = 2(5 x 0.245 x 39) x (8-5-1)/25

= 95.55 x 2/25

= 8

Range in the Tuning Console

In the Internal Rating Model Author, you can use the Tuning Console’s Range slider to adjust

the total number of votes that contribute to the assessment. Changing the range overwrites the

distribution of votes in existing assessments by setting them in a straight line that centers on

zero.

When range is set to a low value, the system allocates fewer votes between all component

categories for the assessment and the resultant meter range is narrower.

Conversely, when you set a high value for range the system allocates more votes, the resultant

meter range is broader, and the extremes of the meter can be reached in the assessment. Since

there is a larger potential movement along the meter between best and worst, the meter has a

greater possible impact. The table below displays how the system allocates votes to components

using three different range settings:

Range

Setting

Votes for

Component

1

(50% weight)

Votes for

Component

2

(30% weight)

Votes for

Component

3

(20% weight)

Assessment

Meter

(Worst/Best)

Potential

Meter

Range

(/100)

20 -15 to +15 -9 to +9 -6 to +6 23.1 / 76.9 53.8

40 -30 to +30 -18 to +18 -12 to +12 8.3 / 91.7 83.4

60 -45 to +45 -27 to +27 -18 to +18 2.7 / 97.3 94.6

3.5 ASSESSMENT ALGORITHM

This section describes the main assessment algorithm of the fundamental analysis approach.

This algorithm is used to derive all the assessments except for those that assess ratio values.

However, even these assessments use the main assessment algorithm as a building block.

In order to derive an assessment, each value that an input can take is associated with a vote as

described above. A vote denotes the “score” of an input for a given value of that input. If the

input takes a numeric value, this value is called a fixed point. If the input takes a category (i.e.,

Excellent, Good, Fair) as a value, this value is called a category. A set of fixed point – vote pairs

or category – vote pairs defines a relative function of “goodness” for the various values of an

input and is defined for all inputs. For categorised inputs a vote is typically defined for each

possible category. For numeric inputs it would clearly not be possible to specify a vote for each

possible value and so a number of votes are specified, each corresponding to one possible value

of the input (the fixed point). If the actual value of the input does not match one of the fixed

points, linear interpolation is used to determine the corresponding vote. If the input value is

greater than the largest fixed point the vote corresponding to this is used. Similarly, if the input

value is less than the smallest fixed point the vote corresponding to this is used.

3.6 CALCULATING THE ASSESSMENT

Assessments are created using the following steps:

1. Scoring of inputs: For each input the system calculates the mean and standard deviation

for a Normal distribution from the set of fixed points or categories associated with this

GUIDE TO BUSINESS ANALYSIS 19

input and the value of this input. The fixed point to vote or category to vote mapping

described above is used to determine the score distribution. Fixed points or categories are

defined during the design and tuning of a model, and can later be adjusted using the

Internal Rating Model Author.

2. Aggregation of input distributions: RiskAnalyst assumes the probability of an assessment is

Normally distributed. The total votes of all inputs are aggregated to calculate the mean and

standard deviation of this distribution.

3. Transformation of distribution: The final stage is to transform the Normal distribution

from the continuous domain on an infinite scale to fit our discrete seven-category

assessment on a 0-100 scale. This is done by calculating areas under the standard Normal

distribution that correspond the range of each of the categories on the infinite scale.

3.6.1 Scoring of Inputs

The methods used to score inputs are slightly different depending on whether they are

categorized or numeric. The following sections provide the algorithms for determining the

scores for each input.

Categorized Inputs

Let categorised input

x

have ncategories where 71

≤

≤

n. Let:

• cix denote the i-th category value of

x

.

• pix denote the probability associated with the i-th category value of

x

.

• vix denote the votes associated with the i-th category value of

x

.

•

μ

xdenote the mean of the Normal distribution associated with

x

, where:

∑

≤

=

ni ix

ixx v

p

.

μ

•

σ

xdenote the standard deviation of the Normal distribution associated with

x

,

where:

(

)

∑−

≤

=

ni ix

xx

ix

v

p

μ

σ

2

.

• If the value of

x

is unknown, i.e.

p

ix is undefined, then:

2

)min()max( vv ixix

x

+

=

μ

(

)

)min()max(.2887.0 vv ixixx −=

σ

i.e. the mean and standard deviation of the uniform distribution is assumed.

20

Numeric inputs

Let numeric input

x

have nfixed-points where 71

≤

≤

n. Let:

• uix denote the i-th fixed-point value of

x

.

• vix denote the votes associated with the i-th fixed point value of

x

.

• wxdenote the value of

x

.

•

μ

xdenote the mean of the Normal distribution associated with

x

, where:

()

⎪

⎪

⎪

⎪

⎩

⎪

⎪

⎪

⎪

⎨

⎧

+=≤≤−

⎟

⎟

⎟

⎠

⎞

⎜

⎜

⎜

⎝

⎛

−

+

≤≤=

≤

≥

=−1for if.

1for if

if

if

11

jk

jxx

nj

uwuvv

uu

uw

v

uwv uwv uwv

kxxjxjxkx

jxkx

jx

jxxjx

xxx

nxxnx

x

μ

This is often referred to as linear interpolation.

Note that typically there is no uncertainty associated with numeric inputs ( 0=

σ

x). The

exception is when the input is the slope where it is possible to measure the standard deviation of

the slope. See section 5.4.1 for details. When there is standard deviation associated with the

input then the standard deviation, denoted by

σ

, is calculated by considering the average

difference of the vote around the mean for the standard deviation:

2

xxxx

x

μμμμ σσ

σ

−+−

=−+

Where

σ

μ

+xis calculated as x

μ

with

σ

μ

σ

+=

+x

x

w. Similarly for

σ

μ

−x.

If

x

is unknown the mean and standard deviation are calculated using the same method for

categorised inputs described above. In RiskAnalyst, this is not used in practice since the ratio

assessment algorithm only assesses defined ratios.

3.6.2 Aggregation of input distributions

Let the assessment being constructed be denoted as

y

. Let

p

w denote an initial distribution

associated with y. Let

σ

μ

pw

pw,denote the mean and standard deviation of this initial

distribution. Given minputs, the mean of the Normal distribution associated with

y

is

calculated as:

∑

≤≤

+=

mx xpwy 1

μ

μ

μ

and the standard deviation as:

GUIDE TO BUSINESS ANALYSIS 21

∑

≤≤

+=

mx xpwy 1

22

σσσ

3.6.3 Transformation of distribution

Let cifor 71 ≤≤ idenote the categories of an assessment, where

EXCELLENT BLE UNACCEPTA 71 == cc L. Let cepi denote the class end point of

the i-th assessment category on a 0 to 100 scale, i.e.,

7

100.i

cepi=

Let iepidenote the interval end point of the i-th assessment category on a ∞− to ∞ scale.

The interval end point is calculated from the class end point using the following inverse sigmoid

function:

⎟

⎟

⎠

⎞

⎜

⎜

⎝

⎛

−

+= cep

cep

iep

i

i

i100

ln.2550

Let

Z

iy denote the Z-score for the i-th category of an assessment.

Z

iy is calculated as:

σ

μ

y

yi

iy

iep

Z−

=

Let )(

Z

iy

F denote the probability that the value of

y

is in one of the j categories up to and

including i ( ij ≤

≤

1). Standard lookup tables can be used to determine )(

Z

iy

F. )(

Z

iy

F

corresponds to the area underneath the standard Normal distribution to the left of

Z

iy . These

areas correspond to the probability that the value of the assessment is contained in any of the

first iintervals. For efficiency reasons RiskAnalyst uses an approximation method for finding

the area under the Standard Normal distribution. It uses linear interpolation with the following

values:

Mean Cumulative Integral

-11 0

-10 0

-3.5 0.0002

-3 0.0013

-2.5 0.0062

-2 0.0228

-1.5 0.0668

-1.2 0.1151

-1 0.1587

-0.8 0.2119

-0.5 0.3085

0 0.5

0.5 0.6915

22

0.8 0.7881

1 0.8413

1.2 0.8849

1.5 0.9332

2 0.9772

2.5 0.9938

3 0.9987

3.5 0.9998

10 1

Finally the probability of the i-th category for

y

,

p

iy , can be calculated from the cumulative

probability )(

Z

iy

F:

⎪

⎩

⎪

⎨

⎧

≤<−

=

=

−72for )()(

1for )(

)1( iFF

iF

ZZ

Z

pyiiy

iy

iy

Note that if 0=

σ

y there is no uncertainty and the mean of the distribution fits entirely into

one of the categories. For 0=

σ

y,

p

iy is calculated as:

⎪

⎩

⎪

⎨

⎧<

=Otherwise0

such that of valuesmallest for the1 iep

piy

iy

i

μ

3.7 CALCULATING THE MEANS AND STANDARD DEVIATIONS

OF AN ASSESSMENT

While the assessment meters provide a powerful way of communicating the evaluation of the

assessment, they are limited in that they are complex to describe and are not particularly precise.

Often it is desirable to have a single figure that describes the assessment. To satisfy this

requirement, we use the assessment mean, or Real Mean. The Real Mean is associated with the

mean of the original continuous Normal distribution, and is defined further in section 3.7.1.

When combining assessments, the fundamental analysis approach uses the full information

from the sub-assessments, and doe not simply combine the real means of the sub-assessments.

3.7.1 Real Mean:

Let r

y

mean denote the Real Mean. This is the mean of the continuous Normal distribution

transformed to the 0-100 scale using the RiskAnalyst saturation function and is calculated as:

(

)

()

25

50

25

50

1

.100

−

−

+

=y

y

e

e

meanr

y

μ

μ

GUIDE TO BUSINESS ANALYSIS 23

Let r

y

sd denote the real standard deviation of an assessment. It is calculated as:

(

)

()

50

25

25

1

.100 −

⎟

⎟

⎟

⎟

⎠

⎞

⎜

⎜

⎜

⎜

⎝

⎛

=

+y

y

e

e

sdr

y

σ

σ

CHAPTER 4

GUIDE TO BUSINESS ANALYSIS 25

4 SCORECARD METHODOLOGY

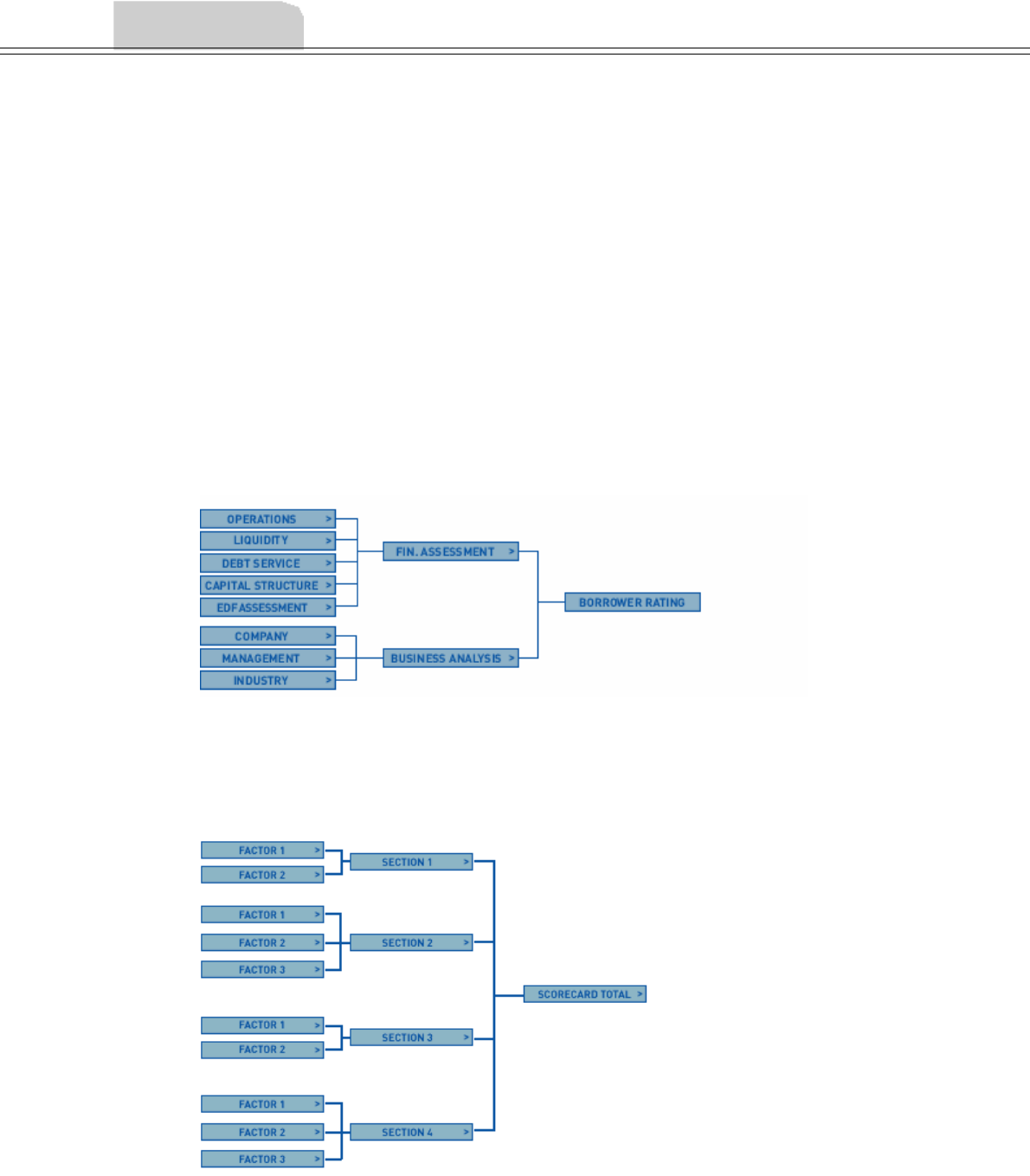

4.1 SCORECARD OVERVIEW

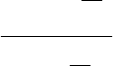

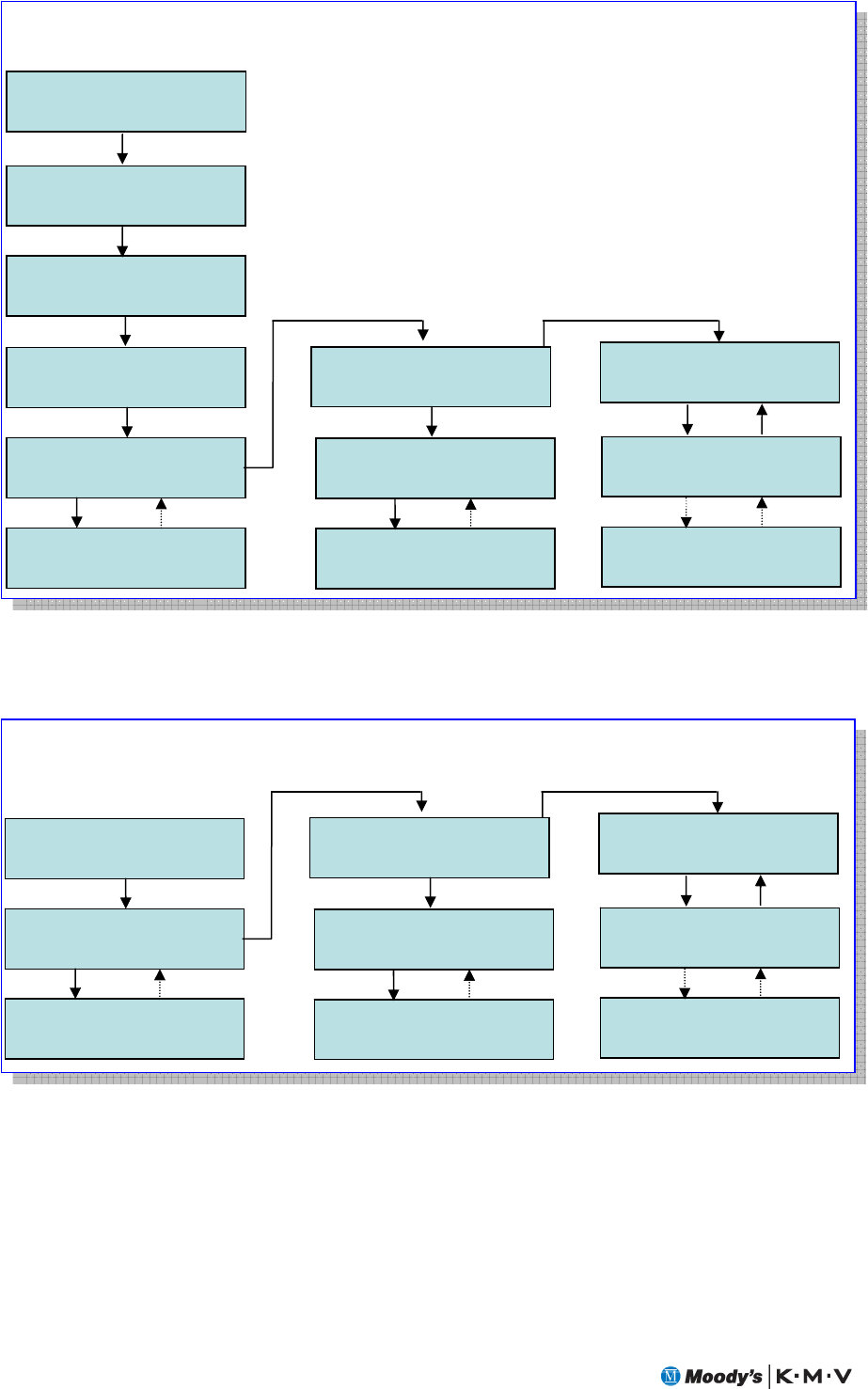

A scorecard internal rating model consists of a set of factors grouped into sections

corresponding to particular areas of analysis. Factors are inputs obtained either from the user or

from values entered in other parts of RiskAnalyst, or from external programs. Each factor within

a section is scored, and the sum of those scores, with any weighting, is the total score for that

section. The sum of each section's total score, with any weighting, is the scorecard's total score.

FIGURE 1.1 Section total

Each factor within a section can be weighted such that it contributes more or less to the section

total than the other factors within that section. Section total scores can also be similarly

weighted to have a greater or lesser influence on the total scorecard score. The Internal Rating

Model screen displays section scores and ranges with factor weighting, but without section

weighting, applied. The Ratings Summary screen shows the section scores and ranges, as well as

the total score, with weighting applied.

FIGURE 1.2 Total score

26

To reiterate, the scoring process is as follows:

• Scorecard factors obtain data from user input or from values entered in other parts of

RiskAnalyst.

• Factors are given a score based on the input value.

• Factor scores are weighted and summed to give a section score.

• The section scores are weighted and summed to give a scorecard total.

• The scorecard total is mapped to a grade and a PD.

4.2 METERS

Once the factors are calculated and the section scores totaled, RiskAnalyst displays a meter to

give a visual representation of the score. The meter includes both the score and the range of

scores possible. The system displays meters for section totals, as well as the total score.

FIGURE 1.3 Scorecard meter

4.3 FACTORS

Scorecard inputs are known as factors and have the following input sources:

• User input. Factors that display in scorecards as drop-down menus or input boxes and

receive their values from user input.

• RiskAnalyst Values. Values entered in other parts of RiskAnalyst. These inputs can be

customer information data, ratios, values, or RiskCalc and Public EDF measures.

• External Program Values. Values obtained from an external program. A module is

necessary to obtain values from an external program and must be configured for use in

the Internal Rating Model Author.

Input values can be:

• Numerical. Values such as ratios or numbers entered by the user.

• Categorized. Predetermined categories, such as drop-down menus, where users select

from a list of possible values.

Each factor is given a score based on its input value. The system calculates numerical factor

scores differently than categorized factor scores. The system can also transform numerical input

values before they are given a score. An explanation of each calculation, and the RiskAnalyst

algorithm for these calculations, follows.

Each factor has a name and belongs to a section. To find out more about the individual factors

associated with a particular section, click the Clarify button on the Internal Rating Model

screen for that section.

GUIDE TO BUSINESS ANALYSIS 27

4.4 CALCULATION OF SCORES FOR NUMERICAL FACTORS

Factors that have numerical inputs, such as ratios and financial statement values, are scored in

one of two ways. Either RiskAnalyst uses the factor’s value as the score, or it calculates the score

using a process called banding.

4.4.1 Scoring Factors Using Values

Using this method, the value of the factor feeds directly into the score. In order to display the

correct score and range for the section on a meter, there must be a minimum and maximum

value for each factor’s input that is scored in this manner. RiskAnalyst uses these values to

determine the lower and upper meter values, and displays the section total on this scale.

4.4.2 Scoring Factors by Banding

Using this method, a number of bands (or numerical ranges) and a score for each of these bands

must be specified:

Band upper point Score

20 0

40 5

60 10

80 20

100 30

RiskAnalyst calculates the factor’s score by determining which band the factor’s input value falls

into. If the value is larger than the highest upper bound, it is scored as if it were within that

band. For example, if the value is 120, a score of 30 is given using the bands shown above. Any

value below 20, including a negative number, is given a score of 0. Band upper points are

inclusive, such that a value of 40 would score 5.

NOTE When banding is set up, it assumes that you are using actual units.

If you are entering currency values, they should be entered in the currency you have

selected for your scorecard.

4.4.3 Transformation of Numerical Inputs

RiskAnalyst can be configured to transform the values of scorecard factors that have numerical

inputs. RiskAnalyst transforms the factor values before calculating their scores.

RiskAnalyst can apply the following three transformation functions to numerical inputs:

• Normalize

• Log (base e)

• LOGIT

Each of these functions is described below.

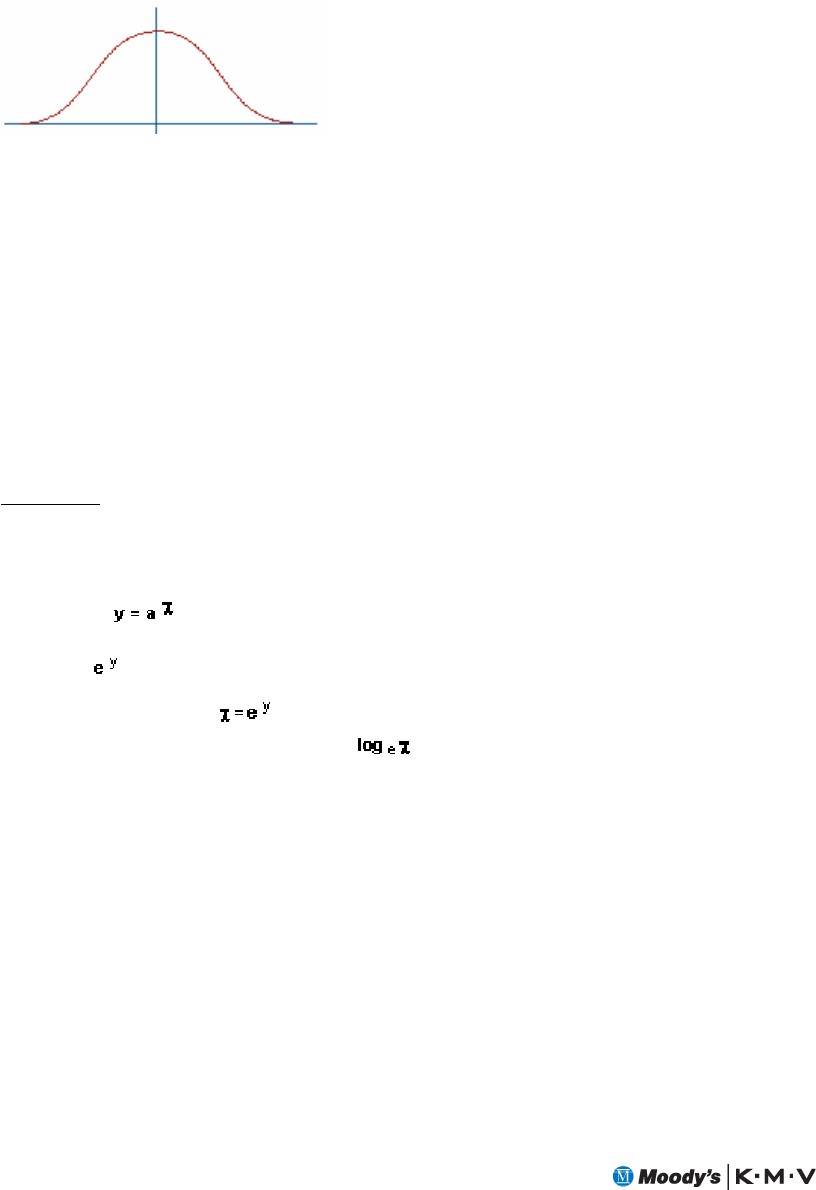

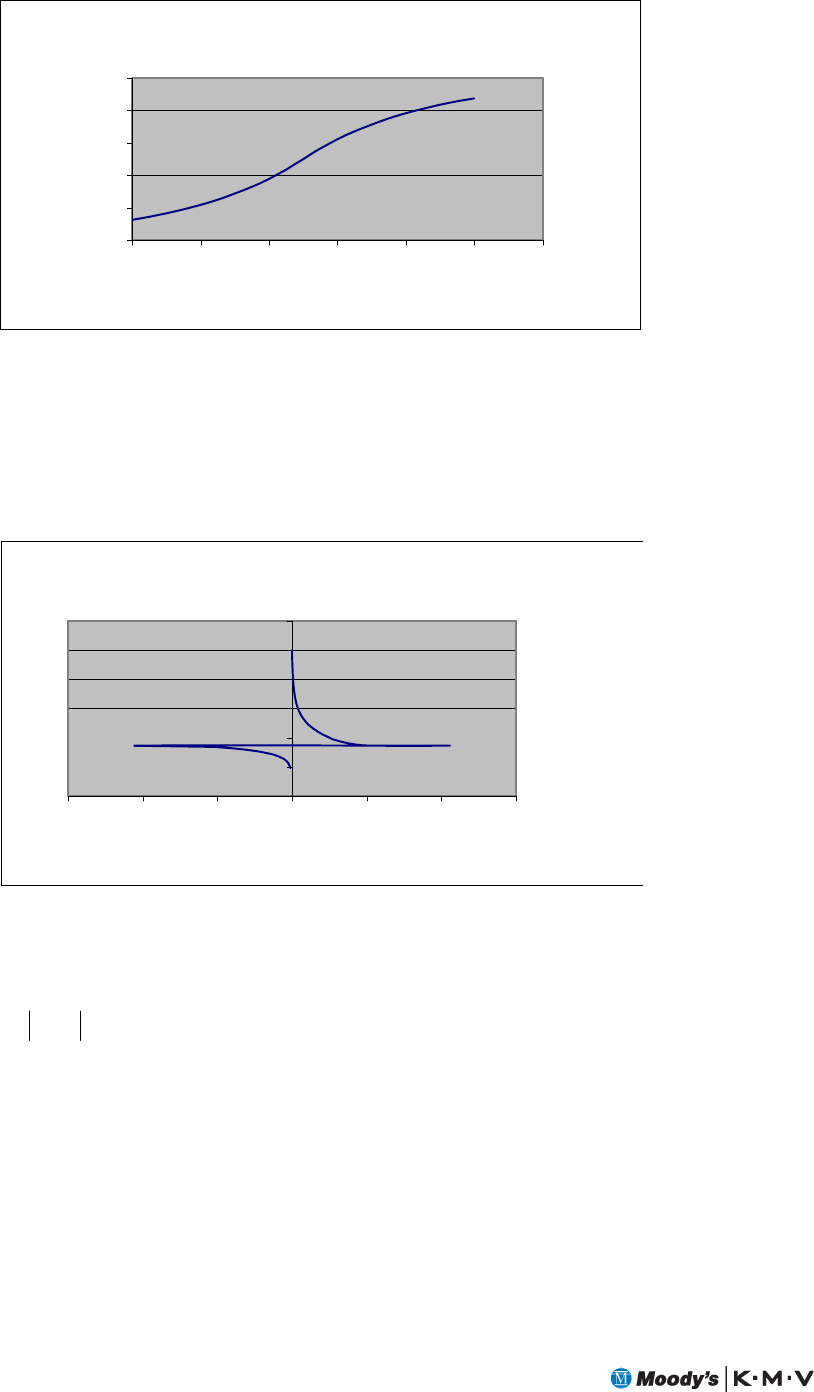

Normalise

Use Normalise to standardize raw data.

28

To standardize raw data χ, subtract mu μ and divide by sigma σ (the parameters of the normal

distribution), where:

μ is the mean or typical value of χ.

σ is the standard deviation. This is a measure of the spread or volatility of the data, and is equal

to the square root of the arithmetic mean of the squares of the deviations from the arithmetic

mean of the data.

The Normalize function gives the data a bell-shaped distribution that is symmetrical about the

mean (or typical value) of the data, as shown below.

Approximately 95% of the data will be within ± two standard deviations from the mean, and

approximately 99.8% of the data will be within ± three standard deviations from the mean.

Example:

A company has reported a Gross Margin of 45%. If the mean industry Gross Margin is 25%

and the standard deviation is 10, then the standardized value of the company’s Gross Margin

figure is:

((45-25)/10) = 2

This tells us that the company’s Gross Margin is two standard deviations above the mean

industry figure.

Log (base e)

The natural logarithm (log in the base e) gears down the importance of higher data values and

reduces the data’s spread.

In the graph , there is a value a (approximately 2.718282) at which the gradient of the

exponential curve at (0,1) is exactly 1. This is an irrational number symbolized by e. In the

expression , e is called the base and y is called the exponent, power, or logarithm.

Therefore, the expression can also be interpreted as meaning y is the logarithm of the

number χ in the base e. This is written as or ln χ.

GUIDE TO BUSINESS ANALYSIS 29

The graph of is shown above. This graph shows that as the value of data χ increases, the

gradient of the curve decreases. Therefore, the impact of higher numbers is disproportionately

reduced, or geared down.

NOTE You cannot enter negative values into logs.

Example:

Take, for example, an internal rating model that has questions resulting in the following scores:

10

50

90

1000

These results give a data spread of 990, and the highest score is 100 times that of the smallest

figure. Transforming the scores with log in the base e results in the following scores:

2.303

3.912

4.499

6.908

Now the spread of data is just 4.6, and the highest score is just 3 times that of the smallest score.

LOGIT

Use LOGIT to estimate the conditional probability of a positive response or the presence of a

characteristic. For example, is a company likely to honor its loan covenants or not? The

function is based on an “S” shaped curve, with the result of the transformation formula:

This gives the probability of a positive response that falls between zero (no chance of a positive

response) and one (100% chance of a positive response).

You need to define the LOGIT coefficients A and B.

30

4.4.4 Special Numeric Factors

The following are two examples of numeric factors that are calculated differently than other

numeric factors.

Ratios

Ratio assessments are a special type of numeric factor, and are calculated by the RiskAnalyst

Ratio Assessment algorithm. The calculations behind this algorithm are described in Chapter 5.

NOTE It is possible to include a Ratio in a scorecard simply as any other financial value. In

this case, the Ratio Assessment algorithm is not used.

EDF measures

EDF measures are another special instance of a numeric factor. RiskAnalyst gathers EDF values

from Moody's KMV RiskCalcTM and CreditEdge®. Whether or not an EDF value is a factor in

the scorecard, the 1-Yr EDF measure will display on the Ratings Summary screen. See Chapter

6 for more information.

4.5 CALCULATION OF SCORES FOR CATEGORIZED FACTORS

For categorized factors such as drop-down menus, RiskAnalyst calculates factor scores from the

categories. Specify a score for each of the categories in the factor value properties, as shown in

the example below:

Categories Scores

INADEQUATE -10

BELOW AVERAGE 0

AVERAGE 10

ABOVE AVERAGE 20

EXCEPTIONAL 30

RiskAnalyst calculates the score when a category is selected, such as when a user makes a menu

selection.

4.6 WEIGHTING

Weighting can be applied to both factors and sections in scorecards. There are various practical

reasons for using weighting in scorecards. The following is an example that uses weighting to

replicate an averaging approach.

GUIDE TO BUSINESS ANALYSIS 31

Suppose you want the total score for each section to be an average of the factors in the section.

You also want the total score to be the average of the section scores.

Section 1 Value

Factor 1 3

Factor 2 4

Factor 3 5

Factor 6 6

Section total Average of (3, 4, 5, 6) = 4.5

Section 2 Value

Factor 1 5

Factor 2 6

Section total: Average of (5, 6) = 5.5

Scorecard total: Average of (4.5, 5.5) = 5.0

To produce the above result in RiskAnalyst, you would set the following factor and section

weights:

Factor Weights

Section 1 Value * Weight = Weighted Score

Factor 1 3 .25 .75

Factor 2 4 .25 1

Factor 3 5 .25 1.25

Factor 4 6 .25 1.5

Section total: 4.5

Section 2 Value * Weight = Weighted Score

Factor 1 5 .5 2.5

Factor 2 6 .5 3

Section total: 5.5

Section Weights

Scorecard Value * Weight = Weighted Score

Section 1 4.5 .5 2.75

Section 2 5.5 .5 2.25

Scorecard total: 5.0

The weights above correspond to 1 / (number of factors) or 1 / (number of sections). This is a

simple example of using weighting to produce averaging. Using the above example as a starting

point, you could also produce a weighted average, such that a particular section has a greater

impact on the total score (i.e., replace Section 2's weight of .5 in the example above with 1.5 to

make Section 2 three times as important).

CHAPTER 5

GUIDE TO BUSINESS ANALYSIS 33

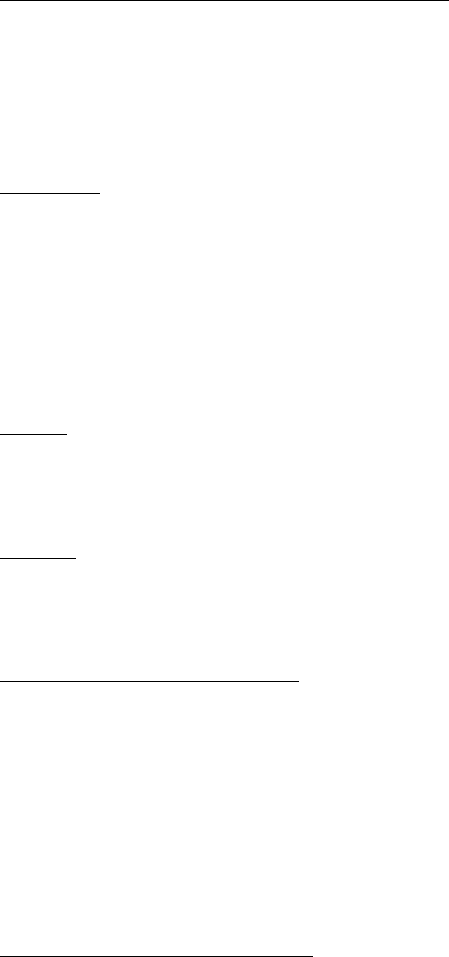

5 RATIO ASSESSMENT METHODOLOGY

5.1 FINANCIAL RATIOS

Both the fundamental analysis and scorecard approaches make use of ratio assessments.

Financial ratios or metrics are used to form ratio assessments. RiskAnalyst performs different

analyses for each ratio. The different analyses take into account a comparison of each ratio to a

peer benchmark, the direction and volatility in the trend of the ratio, and in several ratios, a

comparison to a policy-based absolute benchmark. These analyses are then combined to

produce an overall ratio assessment.

All the information displayed relating to the ratios comes from financial values in RiskAnalyst.

This information consists of the calculated ratios and the peer benchmarks, and is dependant on

the financial periods and the peer group.

Ratio Assessment Analyses

A ratio assessment is the weighted sum of a calculated peer/trend assessment and an absolute

assessment. The trend assessment also includes a volatility analysis component. The absolute

analysis is performed for certain ratios only.

The diagram below gives an overview of the various analysis components that may be involved

in the ratio assessment and how the components are combined together to give the final ratio

assessment.

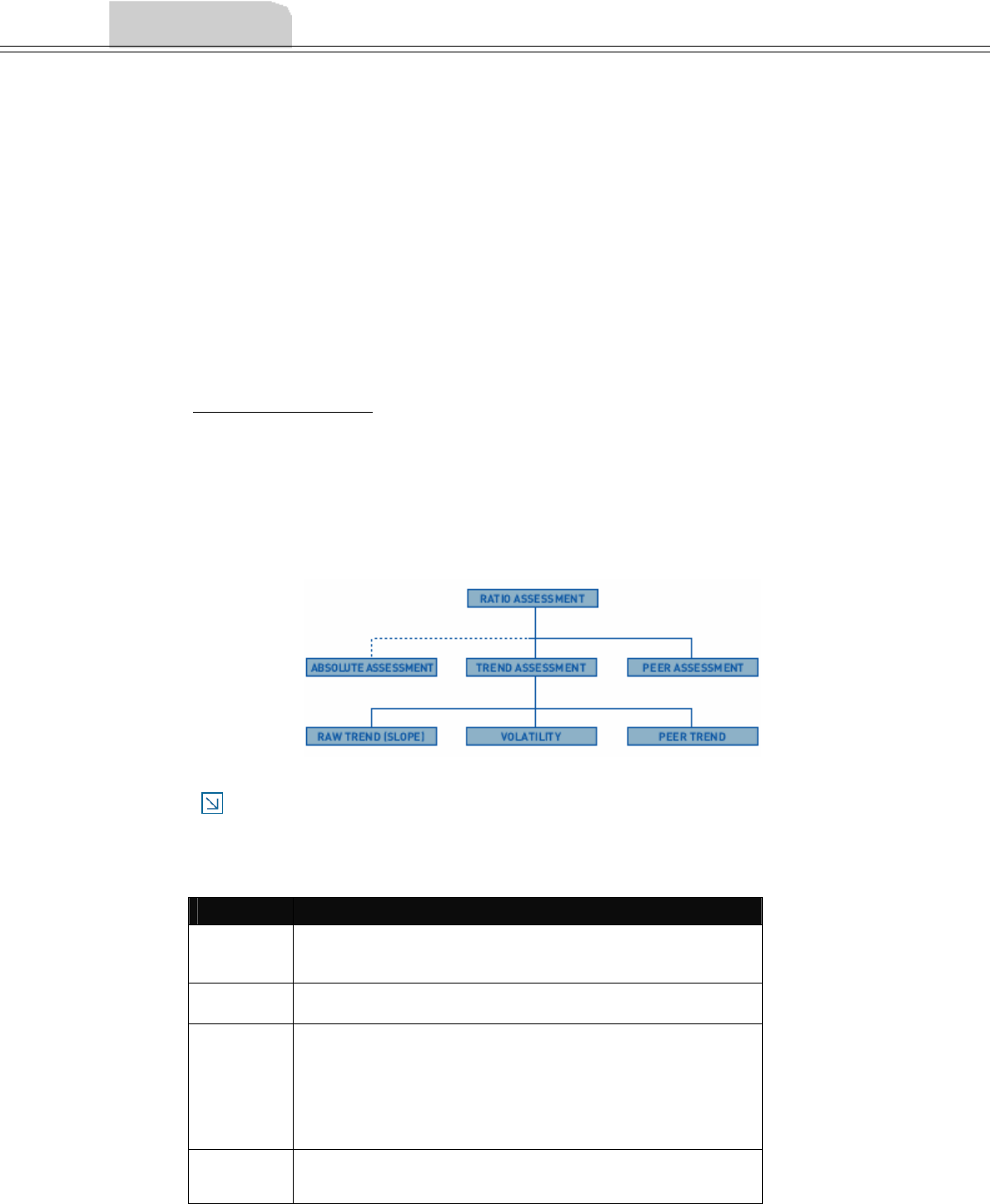

FIGURE 1.4 Structure of ratio assessment

NOTE The Peer Trend assessment is included in the Internal Rating Model Author as a potential

analysis component of ratio assessments. However, the ratio assessments included with the

RiskAnalyst internal rating templates do not include the Peer Trend assessment.

Each of the sub-components of the analysis is described in more detail below.

Component Description

Peer

Assessment

This is an assessment of the ratio’s performance compared to industry values.

The calculated value of the ratio for the current period is compared to the

industry values to derive the company’s ranking.

Trend

Assessment

The overall trend assessment is itself the weighted combination of the trend

analyses and the volatility assessment of this trend.

Absolute

Assessment

For some of the ratios, there are certain standards common in the lending

community above or below which it can safely be said that the company is

performing well or poorly without regard to the rest of the industry. These

standards of ratio performance are used in the ratio assessment to counter the

effects of making ratio comparisons in a very strong or weak industry. The

absolute values used for this analysis may vary depending on the financial

template used to analyze the company.

Raw Trend

Assessment

This assessment considers the trend of the ratio over the periods analyzed.

Remember that trend analysis will only be performed if sufficient historical

statements are available. Typically, a minimum of three historical values are

34

Component Description

required in order to provide a trend analysis. Comparative analyses, like %

Turnover Growth, require a minimum of four historical statements

Volatility

Analysis

The volatility component is an extension of the trend analysis. Generally, a

ratio trend that is either stable or increasing/decreasing at a consistent rate can

be analyzed with greater certainty than ratios that fluctuate from period to

period. If the historical trend of the ratio shows a pattern of wide fluctuation,

the volatility assessment will be unfavorable. Conversely, if the trend of the

ratio shows stability or a relatively even pattern of change, the volatility

assessment will be favorable. However, even an extremely favorable volatility

assessment will have a relatively small impact on the overall trend assessment.

The main function of the volatility analysis is to worsen the overall trend

assessment.

Peer Trend

Assessment

This assessment compares the average rate of change (slope) of the ratio value

for the company over the past three or four years to the average rate of change

(slope) of the median ratio value for the company's peers. To use this

assessment, the average rate of change (slope) for each peer group needs to be

calculated, and this information must be populated in the PEERINFO

reference table.

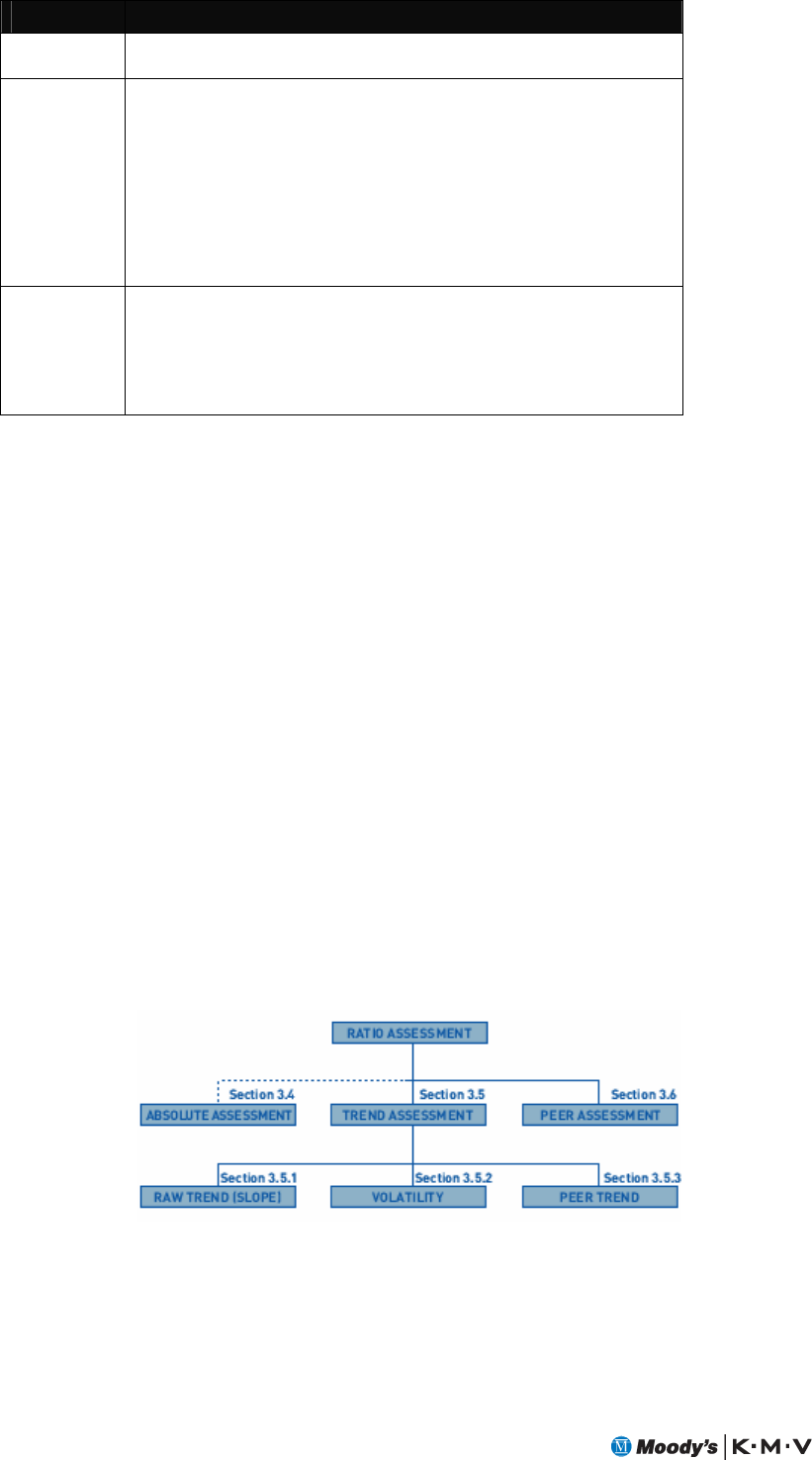

5.2 STANDARD RATIO ASSESSMENT ALGORITHM

This section describes the standard ratio assessment algorithm. It is used for all historical ratio

assessments.

The algorithm has three main components:

1. Absolute: Compares the most recent ratio values to a set of benchmarks.

2. Trend: Looks at how the ratio values for this borrower have changed over time. Derived

from two to three sub-components (see below).

3. Peer: Ranks the ratio values against the borrower’s peer group.

Trend is itself determined from between two and three further sub-components:

• Slope: An assessment of the slope of recent ratio values.

• Volatility: An assessment of the volatility of recent ratio values.

• Peer Trend: Compares the slope of the borrower’s ratio values with those of its peer

group. It is rare for this information to be available and this part of the ratio assessment

is not often used.

FIGURE 1.5 Components of the Standard Ratio Assessment

The three top level ratio assessment components (absolute, trend, and peer) are combined using

a simple weighted sum. This section details each of these components, how they are combined,

and documents a number of special conditions used in the ratio assessment algorithm.

GUIDE TO BUSINESS ANALYSIS 35

By default, RiskAnalyst bases its ratio calculations on statements listed in the Analysis Setup

screen in RiskAnalyst (generally the latest annual, historical statements). Other annual

statements can be selected by hiding statements in the RiskAnalyst grid. Projected statements

can be used in the analysis by selecting the projection to use in the Analysis Setup dialog box.

See the RiskAnalyst Help for more information. For slope and volatility calculations,

RiskAnalyst uses values from prior statements.

The two algorithms below, discussed in 5.2.1 and 5.2.2, are used in the main ratio assessment

algorithm, and will be referenced in the following sections.

5.2.1 Algorithm for numeric factors

Let numeric input

x

have nfixed points where 71

≤

≤

n. Let:

• uix denote the i-th fixed point value of

x

.

• vix denote the votes associated with the i-th fixed point value of

x

.

• wxdenote the value of

x

.

•

μ

xdenote the mean of the Normal distribution associated with

x

, where:

()

⎪

⎪

⎪

⎪

⎩

⎪

⎪

⎪

⎪

⎨

⎧

+=≤≤−

⎟

⎟

⎟

⎠

⎞

⎜

⎜

⎜

⎝

⎛

−

+

≤≤=

≤

≥

=−1for if.

1for if

if

if

11

jk

jxx

nj

uwuvv

uu

uw

v

uwv uwv uwv

kxxjxjxkx

jxkx

jx

jxxjx

xxx

nxxnx

x

μ

This is often referred to as linear interpolation.

Note that typically there is no uncertainty associated with numeric inputs ( 0=

σ

x). The

exception is when the input is the slope where it is possible to measure the standard deviation of

the slope. See section 5.4.1 for details. When there is standard deviation associated with the

input, then the standard deviation, denoted by

σ

, is calculated by considering the average

difference of the vote around the mean for the standard deviation:

2

xxxx

x

μμμμ σσ

σ

−+−

=−+

σ

μ

+xis calculated as x

μ

with

σ

μ

σ

+=

+x

x

w. A similar calculation is used for

σ

μ

−x.

5.2.2 Algorithm for categorized factors

Let categorized input

x

have ncategories where 71

≤

≤

n. Let:

• cix denote the i-th category value of

x

.

36

•

p

ix denote the probability associated with the i-th category value of

x

.

• vix denote the votes associated with the i-th category value of

x

.

•

μ

xdenote the mean of the Normal distribution associated with

x

, where:

∑

≤

=

ni ix

ixx v

p

.

μ

•

σ

xdenote the standard deviation of the Normal distribution associated with

x

,

where:

(

)

∑−

≤

=

ni ix

xx

ix

v

p

μ

σ

2

.

• If the value of

x

is unknown, i.e.

p

ix is undefined, then:

2

)min()max( vv ixix

x

+

=

μ

(

)

)min()max(.2887.0 vv ixixx −=

σ

i.e., the mean and standard deviation of the uniform distribution is assumed.

5.3 ABSOLUTE ASSESSMENT

RiskAnalyst assesses a ratio value against a set of benchmark fixed points. These fixed points are

defined during modelling and are entered in the Internal Rating Model Author. The absolute

assessment is created using the algorithm for numeric factors defined in section 5.2.1. The intial

distribution for the absolute assessment is a mean of 50 and standard deviation of 0.

5.4 TREND ASSESSMENT

RiskAnalyst assesses the trend of the ratio by considering three components. These are

combined using the algorithm for categorized factors described in section 5.2.2. The intial

distribution for the trend assessment is a mean of 50 and standard deviation of 3.

We need to deal with a ratio over a number of data points. For the data points, let idenote an

integer associated with the date of the ratio, where i=1 is the earliest data point. Let t denote a

number specifying the point in time to which the statement date refers. If the statements are all

for twelve month periods, then i=t. For example:

i t Statement date

1 1 12/2000

2 2 12/2001

3 3 12/2002

4 4 12/2003

If statements are for periods other than twelve months, t will be a non-integer for some periods.

For example:

GUIDE TO BUSINESS ANALYSIS 37

i t Statement date

1 1 12/2000

2 2 12/2001

3 2.75 9/2002

4 3.75 9/2003

Let ndenote the number of ratio values and i

xdenotes the ratio value at the i-th data point. For

each ratio, it is possible to choose the maximum and minimum values that n can take.

RiskAnalyst will only consider a maximum of five data points. If the number of data points is

greater than the maximum, only the latest nratio values are used. If the number of data points

is less than the minimum, the trend component is not considered in the assessment of the ratio.

Except where otherwise stated, the summations below all sum over nin

≤

<+

−

)1max_nos( ,

where max_nos is the specified maximum number of periods to be used for the ratio.

5.4.1 Slope

Let ratio

slope denote the fitted slope of the ratio values, where:

()

∑

∑

∑

∑

∑

−

−

=

i

n

t

i

n

slope t

t

x

xt

i

i

i

i

ratio 2

2

As mentioned in the algorithm for numeric factors in section 5.2.1, RiskAnalyst also calculates

the standard deviation of the slope as an input into the slope assessment. This is one-twelfth of

the Residual Standard Deviation calculation. Let slope

ratio

σ

denote the standard deviation of the

slope, where:

()

(

)

()

()

⎟

⎠

⎞

⎜

⎝

⎛∑

−−

∑

−

−

−

⎟

⎠

⎞

⎜

⎝

⎛∑

−

=∑

∑

∑∑∑

∑

i

nn

i

n

t

i

n

i

n

t

t

t

t

x

xt

x

x

i

i

i

i

i

i

slope

ratio 2

2

2

2

2

2

2

)2(

12

1

σ

RiskAnalyst assesses ratio

slope against a set of benchmark fixed points. These fixed points are

defined during modelling and are entered with the tuning tool. The slope assessment is created

using the algorithm for numeric factors defined in section 5.2.1, using both ratio

slope and

slope

ratio

σ

. The intial distribution for the slope assessment is a mean of 50 and standard deviation

of 3.

5.4.2 Volatility

Let i

slope denote the slope between the i-th and i-1 ratio:

nislope tt xx

ii

ii

i≤≤

−

−

=

−

−2,

1

1

Let ratio

ad denote the average difference between consecutive pairs of ratio values, where:

38

(

)

)1(

2

−

=

∑

≤≤

n

slope

ni i

ratio

ad

Let viratio denote the volatility index for a given ratio, where:

n

n

ratio

i

ni i

ni

ratio x

ad

slope

vi ∑

∑−

≤≤

≤≤

−

⎟

⎟

⎠

⎞

⎜

⎜

⎝

⎛⎟

⎠

⎞

⎜

⎝

⎛

=

1

2

2

)1(

RiskAnalyst assesses viratio against a set of benchmark fixed points. There are three fixed points

defined in the system for HIGH, MEDIUM, and LOW volatility groups. The group associated

with a particular ratio is defined during modelling and entered with the Internal Rating Model

Author. The volatility assessment is created using the algorithm for numeric factors defined in

section 5.2.1. The intial distribution for the volatility assessment is a mean of 50 and standard

deviation of 3.

5.4.3 Peer Trend

Let ratio

pt denote the difference between the fitted slope of the ratio values and the peer trend,

where:

peer

ratioratioratio trendslopept −=

peer

ratio

trend is the measured trend of a ratio given a peer group. This value is entered directly into

the RiskAnalyst reference tables. Due to the difficulty in maintaining this data, the peer trend

component has no impact on the trend assessment in the standard models shipped with

RiskAnalyst.

Since there is a standard deviation associated with the slope, this is passed to the peer trend

assessment. It is denoted as pt

ratio

σ

, and it is the same as the standard deviation used in the slope

calculation, i.e.

slope

ratio

pt

ratio

σσ

=

RiskAnalyst assesses ratio

pt against a set of benchmark fixed points. These fixed points are