Presentation SMCI 2018 2019 FULL Benefit Guide With Notices

User Manual:

Open the PDF directly: View PDF ![]() .

.

Page Count: 28

The following descriptions of available benefit

elections options, are purely informational and

have been provided to you for illustrative purposes

only. Payment of benefits will vary from claim to

claim within a particular benefit option and will be

paid at the sole discretion of the applicable

insurance provider for each benefit option. The

terms and conditions of each applicable policy or

certificate of coverage will provide specific details

and will govern in all matters relating to each

particular benefit option described in this

summary. In no case will any information in this

summary amend, modify, expand, enhance,

improve or otherwise change any term, condition

or element of the policies or certificates of

coverage that govern the benefit options described

in this summary.

TABLE OF CONTENTS

Presented by:

Additional Contact:

Tammie J. King, RHU, REBC

TJKing@OneDigital.com

803-227-8639 ext. 102

Carol Iverson

Civerson@OneDigital.com

803-227-8639 ext. 103

Enrollment and Eligibility 03

Medical Plans 04

Dental Plan 06

Vision Plan 08

Life Insurance 10

Disability Insurance 12

Special Benefits –FSA 14

Required Notices 16

Confidentiality Notice 22

2

Offering a comprehensive and competitive benefits package is one way we recognize your

contribution to the success of the organization and our role in helping you and your family

to be healthy, feel secure and maintain work/life balance. This enrollment guide has been

designed to provide you with information about the benefit choices available to you.

Remember, open enrollment is your only opportunity each year to make changes to your

elections, unless you or your family members experience an eligible "change in status."

ENROLLMENT AND ELIGIBILITY

How to Enroll in the Plans

Read your materials and make sure you

understand all of the options available.

•Locate your enrollment/change forms or

log on to your benefit administration

system.

•Fill out any necessary personal

information.

•Make your benefit choices.

•If you have questions or concerns,

please contact your HR department.

Whom Can You Add to Your Plan?

Eligible:

•Legally married spouse

•Natural or adopted children up to age

26, regardless of student and marital

status

•Children under your legal guardianship

•Stepchildren

•Children under a qualified medical child

support order

•Disabled children 19 years or older

•Children placed in your physical custody

for adoption

Ineligible:

•Divorced or legally separated spouse

•Common law spouse, even if recognized

by your state

•Domestic partners, unless your

employer states otherwise

•Foster children

•Sisters, brothers, parents or in-laws,

grandchildren, etc.

Change in Status

Generally, you may enroll in the plan, or make

changes to your benefits, when you are first

eligible. However, you can make changes/enroll

during the plan year if you experience a change in

status. As with a new enrollee, you must submit

your paperwork within 30 days of the change or

you will be considered a late enrollee and you may

not be eligible to enroll.

Examples of changes in status:

•You get married, divorced or legally separated

•You have a baby or adopt a child

•You or your spouse takes an unpaid leave of

absence

•You or your spouse has a change in employment

status

•Your spouse dies

•You become eligible for or lose Medicaid

coverage

•Significant increase or decrease in plan benefits

or cost

Open Enrollment is the only

chance to make changes,

unless you experience a

“change in status.”

3

The benefit plan information shown in this guide is illustrative only. To the extent the benefit plan information summarized herein differs from the

underlying plan details specified in the insurance documents that govern the terms and conditions of the plans of insurance described in this

guide, the underlying insurance documents will govern in all cases.

Medical Plans

4

5

The benefit plan information shown in this guide is illustrative only. To the extent the benefit plan information summarized herein differs from the

underlying plan details specified in the insurance documents that govern the terms and conditions of the plans of insurance described in this

guide, the underlying insurance documents will govern in all cases.

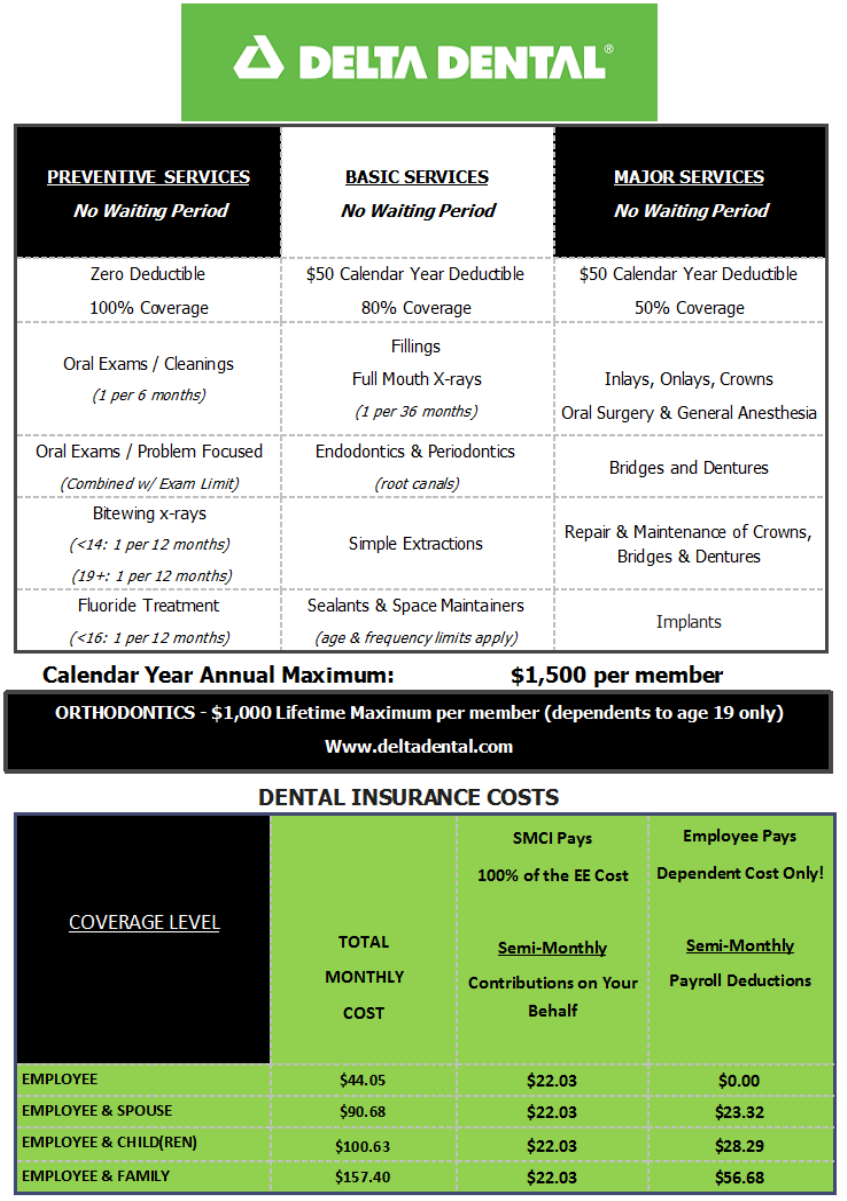

Dental Plan

6

7

The benefit plan information shown in this guide is illustrative only. To the extent the benefit plan information summarized herein differs from the

underlying plan details specified in the insurance documents that govern the terms and conditions of the plans of insurance described in this

guide, the underlying insurance documents will govern in all cases.

Vision Plan

8

9

The benefit plan information shown in this guide is illustrative only. To the extent the benefit plan information summarized herein differs from the

underlying plan details specified in the insurance documents that govern the terms and conditions of the plans of insurance described in this

guide, the underlying insurance documents will govern in all cases.

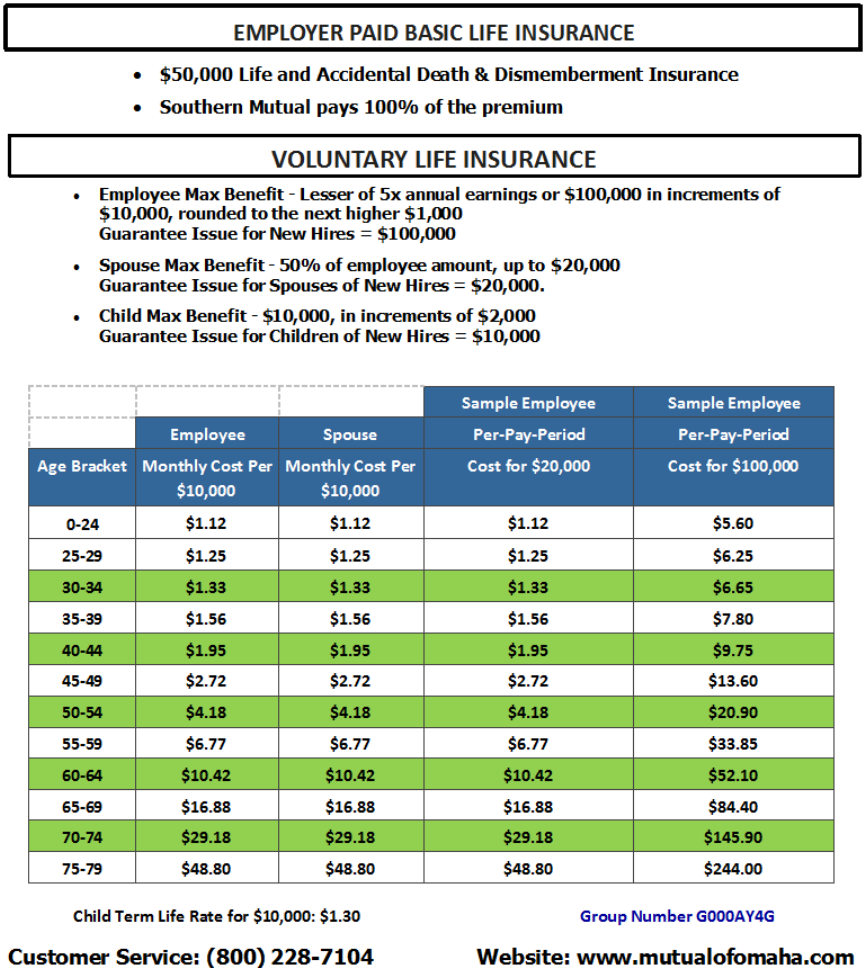

Life / AD&D Plans

10

11

The benefit plan information shown in this guide is illustrative only. To the extent the benefit plan information summarized herein differs from the

underlying plan details specified in the insurance documents that govern the terms and conditions of the plans of insurance described in this

guide, the underlying insurance documents will govern in all cases.

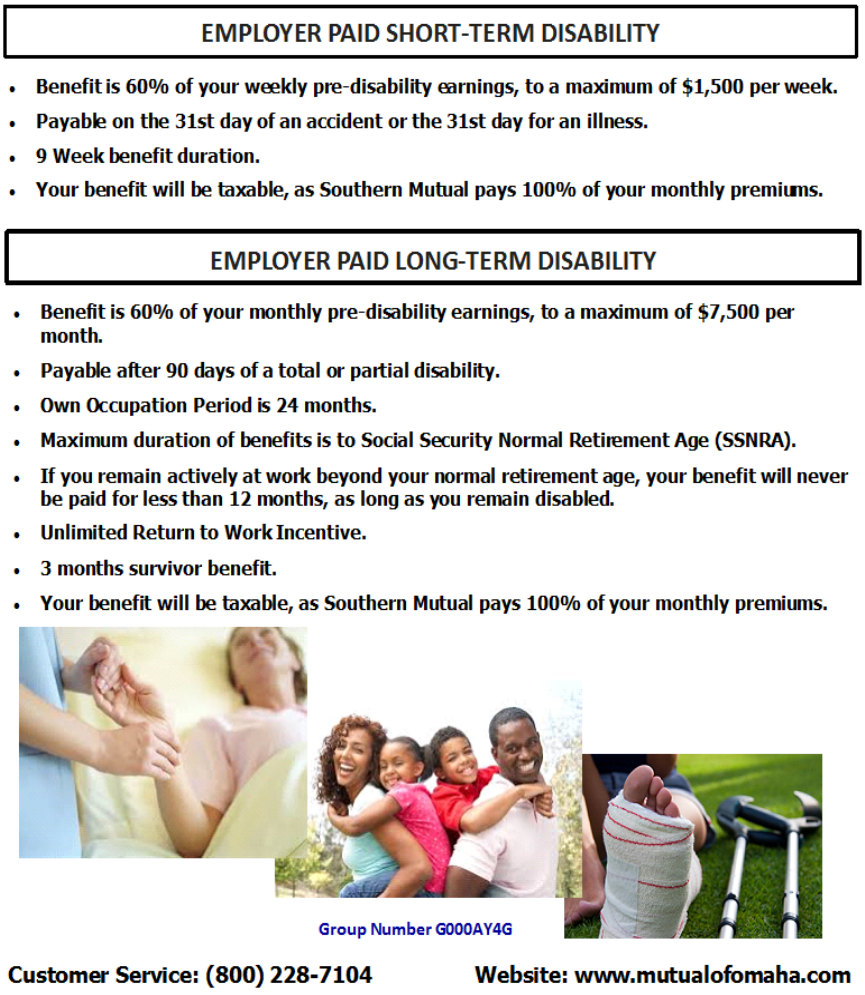

Disability Plans

12

13

The benefit plan information shown in this guide is illustrative only. To the extent the benefit plan information summarized herein differs from the

underlying plan details specified in the insurance documents that govern the terms and conditions of the plans of insurance described in this

guide, the underlying insurance documents will govern in all cases.

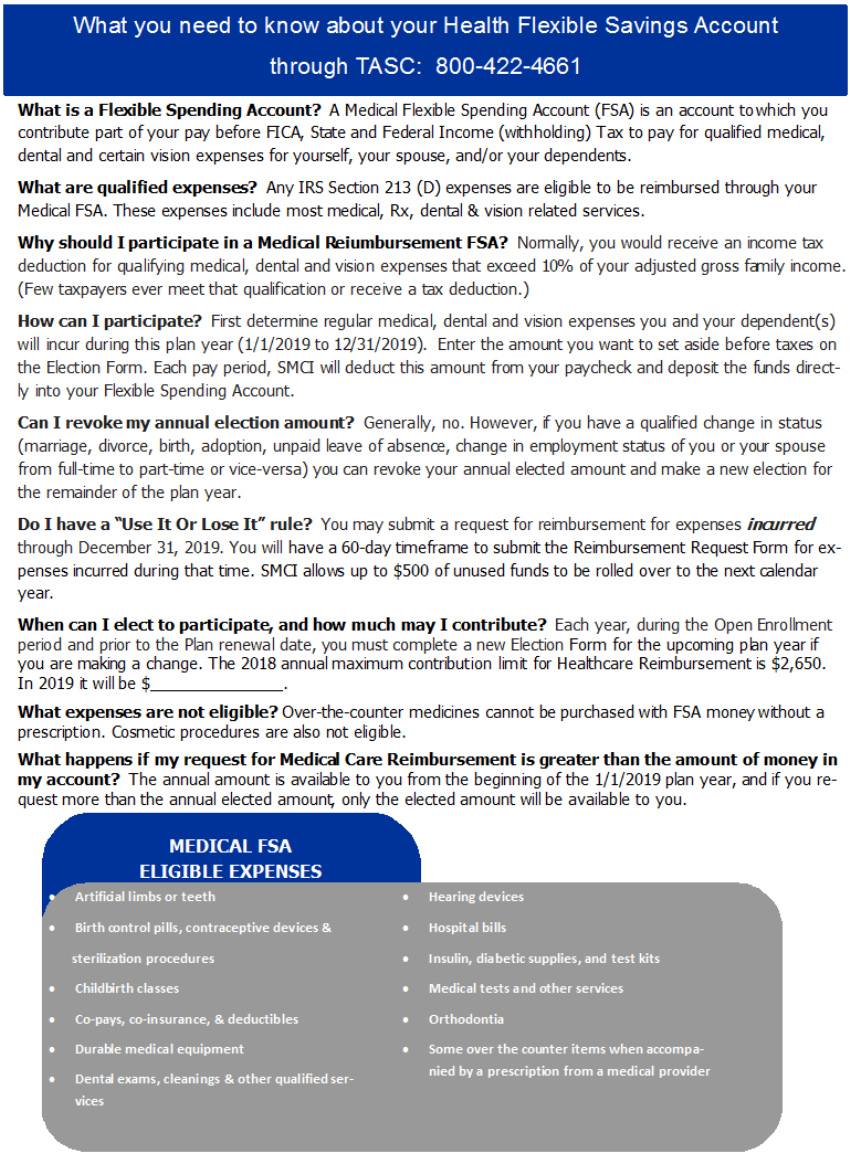

Special Benefits

14

15

REQUIRED NOTICES

Newborn and Mothers’

Health Protection Act

Group health plans and health insurance issuers

generally may not, under federal law restrict

benefits for any hospital length of stay in

connection with childbirth for the mother or

newborn child to less than 48 hours following

vaginal delivery, or less than 96 hours following

a cesarean section. However, federal law

generally does not prohibit the mother’s or

newborn’s attending provider, after consulting

with the mother, from discharging the mother

or newborn earlier than 48 hours (or 96 hours

as applicable). In any case, plans and issuers

may not, under federal law, require that a

provider obtain authorization from the plan or

the issuer for prescribing a length of stay not in

excess of 48 hours (or 96 hours).

Women’s Health and

Cancer Rights Act

In October 1998, Congress enacted the Women’s

Health and Cancer Rights Act of 1998. This notice

explains some important provisions of the Act.

Please review this information carefully. As specified

in the Women’s Health and Cancer Rights Act, a plan

participant or beneficiary who elects breast

reconstruction in connection with a covered

mastectomy is also entitled to the following benefits:

1. All stages of reconstruction of the breast on which

the mastectomy has been performed: 2. Surgery and

reconstruction of the other breast to produce a

symmetrical appearance; and 3. Prostheses and

treatment of physical complications of the

mastectomy , including lymphedemas. Health plans

must provide coverage of mastectomy related

benefits in a manner to determine in consultation

with the attending physician and the patient.

Coverage for breast reconstruction and related

services may be subject to deductibles and insurance

amounts that are consistent with those that apply to

other benefits under the plan.

16

REQUIRED CHIP NOTICE

Alabama –Medicaid Arkansas –Medicaid

Website:

http://myalhipp.com/

Phone: 1

-855-692-5447

Website: http://myarhipp.com/

Phone: 1-855-MyARHIPP (855-692-7447)

Alaska –Medicaid

Colorado –Health First Colorado

(Colorado’s Medicaid Program) & Child Health

Plan Plus (CHP+)

The AK Health Insurance Premium Payment

Program

Website:

http://myakhipp.com/

Phone: 1

-866-251-4861

Email:

CustomerService@MyAKHIPP.com

Medicaid Eligibility:

http://dhss.alaska.gov/dpa/Pages/medicaid/default.aspx

Health First Colorado Website:

https://www.healthfirstcolorado.com/

Health First Colorado Member Contact Center:

1-800-221-3943/ State Relay 711

CHP+: Colorado.gov/HCPF/Child-Health-Plan-Plus

CHP+ Customer Service: 1-800-359-1991/

State Relay 711

Premium Assistance Under Medicaid and the

Children’s Health Insurance Program (CHIP)

If you or your children are eligible for Medicaid or CHIP and you’re eligible for health coverage from your

employer, your state may have a premium assistance program that can help pay for coverage, using funds

from their Medicaid or CHIP programs. If you or your children aren’t eligible for Medicaid or CHIP, you

won’t be eligible for these premium assistance programs but you may be able to buy individual insurance

coverage through the Health Insurance Marketplace. For more information, visit www.healthcare.gov.

If you or your dependents are already enrolled in Medicaid or CHIP and you live in a State listed below,

contact your State Medicaid or CHIP office to find out if premium assistance is available.

If you or your dependents are NOT currently enrolled in Medicaid or CHIP, and you think you or any of your

dependents might be eligible for either of these programs, contact your State Medicaid or CHIP office or

dial 1-877-KIDS NOW or www.insurekidsnow.gov to find out how to apply. If you qualify, ask your state if

it has a program that might help you pay the premiums for an employer-sponsored plan.

If you or your dependents are eligible for premium assistance under Medicaid or CHIP, as well as eligible

under your employer plan, your employer must allow you to enroll in your employer plan if you aren’t

already enrolled. This is called a “special enrollment” opportunity, and you must request coverage within

60 days of being determined eligible for premium assistance. If you have questions about enrolling in your

employer plan, contact the Department of Labor at www.askebsa.dol.gov or call 1-866-444-EBSA (3272).

If you live in one of the following states, you may be eligible for assistance paying your employer health

plan premiums. The following list of states is current as of July 31, 2018. Contact your State for more

information on eligibility –

17

REQUIRED CHIP NOTICE (CONT)

Florida –Medicaid Maine –Medicaid

Website:

http://flmedicaidtplrecovery.com/hipp/

Phone: 1

-877-357-3268

Website:

http://www.maine.gov/dhhs/ofi/public-

assistance/index.html

Phone: 1

-800-442-6003

TTY: Maine relay 711

Georgia –Medicaid Massachusetts –Medicaid and CHIP

Website:

http://dch.georgia.gov/medicaid

-

Click on Health Insurance Premium Payment

(HIPP)

Phone: 404

-656-4507

Website:

http://www.mass.gov/eohhs/gov/departments/ma

sshealth/

Phone: 1

-800-862-4840

Indiana –Medicaid Minnesota –Medicaid

Healthy Indiana Plan for low-income adults 19-64

Website: http://www.in.gov/fssa/hip/

Phone: 1-877-438-4479

All other Medicaid

Website: http://www.indianamedicaid.com

Phone 1-800-403-0864

Website:

http://mn.gov/dhs/people-we-

serve/seniors/health

-care/health-care-

programs/programs

-and-services/medical-

assistance.jsp

Phone: 1

-800-657-3739

Iowa –Medicaid Missouri –Medicaid

Website:

http://dhs.iowa.gov/ime/members/medicaid-a-to-

z/hipp

Phone: 1-888-346-9562

Website:

https://www.dss.mo.gov/mhd/participants/pages/h

ipp.htm

Phone: 573

-751-2005

Kansas –Medicaid Montana –Medicaid

Website: http://www.kdheks.gov/hcf/

Phone: 1-785-296-3512

Website:

http://dphhs.mt.gov/MontanaHealthcarePrograms/

HIPP

Phone: 1

-800-694-3084

Kentucky –Medicaid Nebraska –Medicaid

Website: http://chfs.ky.gov/dms/default.htm

Phone: 1-800-635-2570

Website:

http://www.ACCESSNebraska.ne.gov

Phone: (855) 632

-7633

Lincoln: (402) 473

-7000

Omaha: (402) 595

-1178

Louisiana –Medicaid Nevada –Medicaid

Website:

http://dhh.louisiana.gov/index.cfm/subhome/1/n/331

Phone: 1

-888-695-2447

Medicaid Website: https://dhcfp.nv.gov

Medicaid Phone: 1-800-992-0900

18

REQUIRED CHIP NOTICE (CONT)

New Hampshire –Medicaid Rhode Island –Medicaid

Website: https://www.dhhs.nh.gov/ombp/nhhpp/

Phone: 603-271-5218

Hotline: NH Medicaid Service Center at 1-888-

901-4999

Website:

http://www.eohhs.ri.gov/

Phone: 855

-697-4347

New Jersey –Medicaid and CHIP South Carolina –Medicaid

Medicaid Website:

http://

www.state.nj.us/humanservices/

dmahs

/clients/medicaid/

Medicaid Phone: 609

-631-2392 CHIP Website:

http://www.njfamilycare.org/index.html

CHIP Phone: 1

-800-701-0710

Website:

https://www.scdhhs.gov

Phone: 1

-888-549-0820

New York –Medicaid South Dakota - Medicaid

Website:

https://www.health.ny.gov/health_care/medicaid/

Phone: 1

-800-541-2831

Website:

http://dss.sd.gov

Phone: 1

-888-828-0059

North Carolina –Medicaid Texas –Medicaid

Website:

https://dma.ncdhhs.gov/

Phone: 919

-855-4100

Website:

http://gethipptexas.com/

Phone: 1

-800-440-0493

North Dakota –Medicaid Utah –Medicaid and CHIP

Website:

http://www.nd.gov/dhs/services/medicalserv/medicaid/

Phone: 1

-844-854-4825

Medicaid Website:

https://medicaid.utah.gov/

CHIP Website:

http://health.utah.gov/chip

Phone: 1

-877-543-7669

Oklahoma –Medicaid and CHIP Vermont–Medicaid

Website:

http://www.insureoklahoma.org

Phone: 1

-888-365-3742

Website:

http://www.greenmountaincare.org

Phone: 1

-800-250-8427

Oregon –Medicaid Virginia –Medicaid and CHIP

Website:

http://healthcare.oregon.gov/Pages/index.aspx

http://www.oregonhealthcare.gov/index

-es.html

Phone: 1

-800-699-9075

Medicaid Website:

http://www.coverva.org/programs_premium_assist

ance.cfm

Medicaid Phone: 1

-800-432-5924 CHIP Website:

http://www.coverva.org/programs_premium_assist

ance.cfm

CHIP Phone: 1

-855-242-8282

Pennsylvania –Medicaid Washington –Medicaid

Website:

http://www.dhs.pa.gov/provider/medicalassistance

/healthinsurancepremiumpaymenthippprogram/ind

ex.htm

Phone: 1

-800-692-7462

Website:

http://www.hca.wa.gov/free-or-low-cost-

health

-care/program-administration/premium-

payment

-program

Phone: 1

-800-562-3022 ext. 15473

19

REQUIRED CHIP NOTICE (CONT)

West Virginia –Medicaid Wyoming –Medicaid

Website:

http://mywvhipp.com/

Toll

-free phone: 1-855-MyWVHIPP

(

1-855-699-8447)

Website:

https://wyequalitycare.acs-inc.com/

Phone: 307

-777-7531

Wisconsin –Medicaid and CHIP

Website:

https://www.dhs.wisconsin.gov/publications/p1/p1

0095.pdf

Phone: 1

-800-362-3002

To see if any other states have added a premium assistance program since July 31, 2018, or for more

information on special enrollment rights, contact either:

U.S. Department of Labor

Employee Benefits Security Administration

www.dol.gov/agencies/ebsa

1-866-444-EBSA (3272)

U.S. Department of Health and Human Services

Centers for Medicare & Medicaid Services

www.cms.hhs.gov

1-877-267-2323, Menu Option 4, Ext. 61565

PAPERWORK REDUCTION ACT STATEMENT

According to the Paperwork Reduction Act of 1995 (Pub. L. 104-13) (PRA), no persons are required to

respond to a collection of information unless such collection displays a valid Office of Management and

Budget (OMB) control number. The Department notes that a Federal agency cannot conduct or sponsor a

collection of information unless it is approved by OMB under the PRA, and displays a currently valid OMB

control number, and the public is not required to respond to a collection of information unless it displays a

currently valid OMB control number. See 44 U.S.C. 3507. Also, notwithstanding any other provisions of law,

no person shall be subject to penalty for failing to comply with a collection of information if the collection of

information does not display a currently valid OMB control number. See 44 U.S.C. 3512.

The public reporting burden for this collection of information is estimated to average approximately seven

minutes per respondent. Interested parties are encouraged to send comments regarding the burden

estimate or any other aspect of this collection of information, including suggestions for reducing this

burden, to the U.S. Department of Labor, Employee Benefits Security Administration, Office of Policy and

Research, Attention: PRA Clearance Officer, 200 Constitution Avenue, N.W., Room N-5718, Washington, DC

20210 or email ebsa.opr@dol.gov and reference the OMB Control Number 1210-0137.

(OMB Control Number 1210-0137 (expires 12/31/2019).

20

HIPAA Notice

HIPAA Privacy Notices

HIPAA requires group health plans to provide a notice of current privacy practices regarding protected personal

health information (PHI) to enrolled participants. All employers must distribute HIPAA Privacy Notices if the plan is

self-funded or if the plan is fully- insured and the employer has access to PHI. If the employer maintains a benefits

website, the HIPAA Privacy Notice must be included on the website.

The HIPAA Privacy Notice must be written in plain language and must describe three things: (1) the use and

disclosures of PHI that may be made by the group health plan; (2) plan participants’ privacy rights; and (3) the group

health plan’s legal responsibilities with respect to the PHI.

The Department of Health and Human Services (HHS) has developed three different model Privacy Notices for

health plans to choose from: booklet version, layered version, and full-page version.

More information can be found at: https://www.hhs.gov/hipaa/for-professionals/privacy/guidance/privacy-

practices-for-protected-health-information/index.html

Link to model notice: http://www.hhs.gov/sites/default/files/ocr/privacy/hipaa/nppbooklet_health_plan.pdf

Link to OneDigital’s privacy policy: https://www.onedigital.com/privacy-policy/

Model Special Enrollment Notice

The following is language that group health plans may use as a guide when crafting the special enrollment notice: If

you are declining enrollment for yourself or your dependents (including your spouse) because of other health

insurance or group health plan coverage, you may be able to enroll yourself and your dependents in this plan if you

or your dependents lose eligibility for that other coverage (or if the employer stops contributing toward your or

your dependents’ other coverage). However, you must request enrollment within the appropriate time period that

applies under the plan after you or your dependents’ other coverage ends (or after the employer stops contributing

toward the other coverage). In addition, if you have a new dependent as a result of marriage, birth, adoption, or

placement for adoption, you may be able to enroll yourself and your dependents. However, you must request

enrollment within the appropriate time period that applies under the plan after the marriage, birth, adoption, or

placement for adoption. To request special enrollment or obtain more information, contact the appropriate plan

representative.

More information can be found at: https://www.dol.gov/agencies/ebsa/about-ebsa/our-activities/resource-

center/faqs/hipaa-compliance

Link to model notice: https://www.dol.gov/sites/default/files/ebsa/about-ebsa/our-activities/resource-

center/publications/compliance-assistance-guide-appendix-c.pdf

For additional information on your employer’s privacy policy, please contact your HR department.

21

CONFIDENTIALITY NOTICE

OneDigital Health andBenefits, a division of Digital Insurance,LLCdoes not sell or share any

informationwe learn aboutour clients andunderstands you mayhave to answer sensitive

questions about your medical history, physical condition and personal health habits as

required by our insurance carrier partners.

We collect nonpublic personal information from the followingsources:

•Information from you, including data provided on applications or other forms, such as

name, address, telephone number, date of birth and Social Security number

•Information from your transactions with us and/or our partners such as policy coverage,

premium,claim, and payment history.

OneDigital Health andBenefits recognizes the importance of safeguarding the privacy

of our clients and prospective clients, and we pledge to protect the confidential

nature of your personal information. We understandourability to provide access to

affordable health insurance to businesses and individuals can only succeed with an

environment of complete trust.

In the course of business, we may disclose all or part of your customer information without

your permission to the followingpersons or entities for the following reasons:

•To an insurance carrier, agent or credit reporting agency to detect, prevent or

prosecute actual or potential criminal activity, fraud, misrepresentation,

unauthorized transactions, claims or other liabilities in connection with an

insurance transaction.

•To a medical care institution or medical professional to verify coverage or benefits,

to inform you of a medical problem of which you may or maynot be aware or to

conduct an audit that would enable us to verify treatment.

•To an insurance regulatory authority, law enforcement or other governmental

authorityto protect our interests in detecting, preventing or prosecuting actual

or potential criminal activity, fraud, misrepresentation,unauthorized

transactions, claims or other liabilities in connection with an insurance

transaction.

•To a third party, for any other disclosures requiredor permitted by law. We may disclose

all of the informationthat we collect about you, as described above.

Our practices regarding information confidentiality and security: We restrict access to

your customer informationonly to those individuals who need it to provide you with

products or services, or to otherwise service your account. In addition, we have

security measures in place to protect against the loss, misuse and/or unauthorized

alternation of the customer information underour control, includingphysical, electronic

and procedural safeguardsthat meet or exceed applicable federaland state standards.

22

Glossary of Health Coverage and Medical Terms

This glossary defines many commonly used terms, but isn’t a full list. These glossary terms and definitions are

intended to be educational and may be different from the terms and definitions in your plan or health insurance

policy. Some of these terms also might not have exactly the same meaning when used in your policy or plan, and in

any case, the policy or plan governs. (See your Summary of Benefits and Coverage for information on how to get

a copy of your policy or plan document.)

Underlined text indicates a term defined in this Glossary.

See page 6 for an example showing how deductibles, coinsurance and out-of-pocket limits work together in a real

life situation.

Allowed Amount

This is the maximum payment the plan will pay for a

covered health care service. May also be called "eligible

expense", "payment allowance", or "negotiated rate".

Copayment

Afixed amount (for example, $15) you pay for a covered

health care service, usually when you receive the service.

The amount can vary by the type of covered health care

service.

Balance Billing

When a provider bills you for the balance remaining on

the bill that your plan doesn’t cover. This amount is the

difference between the actual billed amount and the

allowed amount. For example, if the provider’s charge is

$200 and the allowed amount is $110, the provider may

bill you for the remaining $90. This happens most often

when you see an out-of-network provider (non-preferred

provider). A network provider (preferred provider) may

not bill you for covered services.

A request for a benefit (including reimbursement of a

Cost-sharing Reductions

Discounts that reduce the amount you pay for certain

services covered by an individual plan you buy through

the Marketplace. You may get a discount if your income

is below a certain level, and you choose a Silver level

health plan or if you're a member of a federally-

recognized tribe, which includes being a shareholder in an

Alaska Native Claims Settlement Act corporation.

Coinsurance

Your share of the costs

of a covered health care

service, calculated as a

percentage (for

example, 20%) of the

allowed amount for the Jane pays

20%

Her plan pays

80%

service. You generally

pay coinsurance plus (See page 6 for a detailed example.)

any deductibles you owe. (For example, if the health

insurance or plan’s allowed amount for an office visit is

$100 and you’ve met your deductible, your coinsurance

payment of 20% would be $20. The health insurance or

plan pays the rest of the allowed amount.)

OMB Control Numbers 1545-2229, 1210-0147, and 0938-1146

Glossary of Health Coverage and Medical Terms Page 1 of 6

Claim

health care expense) made by you or your health care

provider to your health insurer or plan for items or

services you think are covered.

Cost Sharing

Your share of costs for services that a plan covers that

you must pay out of your own pocket (sometimes called

“out-of-pocket costs”). Some examples of cost sharing

are copayments, deductibles, and coinsurance. Family

cost sharing is the share of cost for deductibles and out-

of-pocket costs you and your spouse and/or child(ren)

must pay out of your own pocket. Other costs, including

your premiums, penalties you may have to pay, or the

cost of care a plan doesn’t cover usually aren’t considered

cost sharing.

Appeal

A request that your health insurer or plan review a

decision that denies a benefit or payment (either in whole

or in part).

Complications of Pregnancy

Conditions due to pregnancy, labor, and delivery that

require medical care to prevent serious harm to the health

of the mother or the fetus. Morning sickness and a non-

emergency caesarean section generally aren’t

complications of pregnancy.

23

Formulary

A list of drugs your plan covers. A formulary may

include how much your share of the cost is for each drug.

Your plan may put drugs in different cost sharing levels

or tiers. For example, a formulary may include generic

drug and brand name drug tiers and different cost sharing

amounts will apply to each tier.

A complaint that you communicate to your health insurer

Habilitation Services

Health care services that help a person keep, learn or

improve skills and functioning for daily living. Examples

include therapy for a child who isn’t walking or talking at

the expected age. These services may include physical

and occupational therapy, speech-language pathology,

and other services for people with disabilities in a variety

of inpatient andor outpatient settings.

Diagnostic Test

Tests to figure out what your health problem is. For

example, an x-ray can be a diagnostic test to seeif you

have a broken bone.

A contract that requires a health insurer to pay some or

Emergency Medical Condition

An illness,injury, symptom (including severe pain), or

condition severe enough to risk serious danger to your

health if you didn’t get medical attention right away. If

you didn’t get immediate medical attention you could

reasonably expect one of the following: 1) Your health

would be put in serious danger; or 2) You would have

serious problems with your bodily functions; or 3) You

would have serious damage to any part or organof your

body.

Home Health Care

Health care services and supplies you get in your home

under your doctor’s orders. Services may be provided by

nurses, therapists, social workers, or other licensed health

care providers.Home health care usually doesn’t include

help with non-medical tasks, such as cooking, cleaning, or

driving.

Services to provide comfort and support for persons in

Hospitalization

Care in a hospital that requires admission as an inpatient

and usually requires an overnight stay. Some plans may

consider an overnight stay for observation as outpatient

care insteadof inpatient care.

Emergency Room Care / Emergency Services

Services to check for an emergency medical condition and

treat you to keep an emergency medical condition from

getting worse. These services may be provided in a

licensed hospital’s emergency room or other place that

provides care for emergency medical conditions.

Glossary of Health Coverage and Medical Terms Page 2 of 6

Hospital Outpatient Care

Care in a hospital that usually doesn’t require an

overnight stay.

Hospice Services

the last stages of a terminal illness and their families.

Emergency Medical Transportation

Ambulance services for an emergency medical

condition. Types of emergency medical transportation

may include transportation by air, land, or sea. Your

plan may not cover all types of emergency medical

transportation, or may pay less for certain types.

Health Insurance

all of your health care costs in exchange for a premium.

A health insurance contract may also be called a “policy”

or “plan”.

Durable Medical Equipment (DME)

Equipment and supplies ordered by a health care provider

for everyday or extended use. DME may include: oxygen

equipment, wheelchairs, and crutches.

Grievance

or plan.

Excluded Services

Health care services that your plan doesn’t pay for or

cover.

Deductible

An amount you could owe

during a coverage period

(usually one year) for

covered health care

services before your plan

begins to pay. An overall

deductible applies to all or

almost all covered items

and services. A plan with

an overall deductible may

Jane pays Her plan pays

100% 0%

(See page 6 for a detailed

example.)

also have separate deductibles that apply to specific

services or groups of services. A plan may also have only

separate deductibles. (For example, if your deductible is

$1000, your plan won’t pay anything until you’ve met

your $1000 deductible for covered health care services

subject to the deductible.)

24

Individual Responsibility Requirement

Sometimes called the “individual mandate”, the duty you

may have to be enrolled in health coverage that provides

minimum essential coverage. If you don’t have minimum

Minimum Essential Coverage

Health coverage that will meet the individual

responsibility requirement. Minimum essential coverage

generally includes plans, health insurance available

essential coverage, you may have to pay a penalty when through the Marketplace or other individual market

policies, Medicare, Medicaid, CHIP, TRICARE, and

certain other coverage.

you file your federal income tax return unless you qualify

for a health coverage exemption.

In-network Coinsurance

Your share (for example, 20%) of the allowed amount

for covered healthcare services. Your share is usually

lower for in-network covered services.

In-network Copayment

A fixed amount (for example, $15) you pay for covered

health care services to providers who contract with your

health insurance or plan.In-network copayments usually Network

The facilities, providers and suppliers your health insurer

or plan has contracted with to provide health care

services.

are less than out-of-network copayments.

A provider who has a contract with your health insurer or

plan. You will pay less if you see a provider in the

“participating provider.”

Orthotics and Prosthetics

Leg, arm, back and neck braces, artificial legs, arms, and

eyes, and external breast prostheses after a mastectomy.

These services include: adjustment, repairs, and

replacements required because of breakage, wear, loss, or

a change in the patient’s physical condition.

Maximum Out-of-pocket Limit

Yearly amount the federal government sets as the most

each individual or family can be required to pay in cost

sharing during the plan year for covered, in-network

services. Applies to most types of health plans and

insurance. This amount may be higher than the out-of-

pocket limits stated for your plan.

Out-of-network Copayment

Afixed amount (for example, $30) you pay for covered

health care services from providers who do not contract

with your health insurance or plan. Out-of-network

copayments usually are more than in-network

copayments.

Glossary of Health Coverage and Medical Terms Page 3 of 6

Medically Necessary

Health care services or supplies needed to prevent,

diagnose, or treat an illness, injury, condition, disease, or

its symptoms, including habilitation, and that meet

accepted standards of medicine.

Out-of-network Coinsurance

Your share (for example, 40%) of the allowed amount

for covered health care services to providers who don’t

contract with your health insurance or plan. Out-of-

network coinsurance usually costs you more than in-

network coinsurance.

Network Provider (Preferred Provider)

plan who has agreed to provide services to members of a

network. Also called “preferred provider” or

Marketplace

A marketplace for health insurance where individuals,

families and small businesses can learn about their plan

options; compare plans based on costs, benefits and other

important features; apply for and receive financial help

with premiums and cost sharing based on income; and

choose a plan and enroll in coverage. Also known as an

“Exchange”. The Marketplace is run by the state in some

states and by the federal government in others. In some

states, the Marketplace also helps eligible consumers

enroll in other programs, including Medicaid and the

Children’s Health Insurance Program (CHIP). Available

online, by phone, and in-person.

Minimum Value Standard

A basic standard to measure the percent of permitted

costs the plan covers. If you’re offered an employer plan

that pays for at least 60% of the total allowed costs of

benefits, the plan offers minimum value and you may not

qualify for premium tax credits and cost sharing

reductions to buy a plan from the Marketplace.

25

Premium

The amount that must be paid for your health insurance

or plan. You andor your employer usually pay it

monthly, quarterly, or yearly.

Financial help that lowers your taxes to help you and

this help if you get health insurance through the

Out-of-pocket Limit

The most you could

pay during a coverage

period (usually one year)

for your share of the

costs of covered

services. After you

meet this limit the

Prescription Drug Coverage

Coverage under a plan that helps pay for prescription

drugs. If the plan’s formulary uses “tiers” (levels),

prescription drugs are grouped together by type or cost.

The amount you'll pay in cost sharing will be different

Jane pays

0%

Her plan pays

100%

plan will usually pay

100% of the

for each "tier" of covered prescription drugs.

(See page 6 for a detailed example.)

allowed amount. This limit helps you plan for health

care costs. This limit never includes your premium,

balance-billed charges or health care your plan doesn’t

cover. Some plans don’t count all of your copayments,

deductibles, coinsurance payments, out-of-network

payments, or other expenses toward this limit.

Preventive Care (Preventive Service)

Routine health care, including screenings, check-ups, and

patient counseling, to prevent or discover illness,disease,

or other health problems.

A physician, including an M.D. (Medical Doctor) or

Plan

Health coverage issued to you directly (individual plan)

or through an employer, union or other group sponsor

(employer group plan) that provides coverage for certain

health care costs. Also called "health insurance plan",

"policy", "health insurance policy" or "health

insurance".

Primary Care Provider

A physician, including an M.D. (Medical Doctor) or

D.O. (Doctor of Osteopathic Medicine), nurse

practitioner, clinical nurse specialist, or physician

assistant, as allowed under state law and the terms of the

plan, who provides, coordinates, or helps you access a

range of health care services.

An individual or facility that provides health care services.

chiropractor, physician assistant, hospital, surgical center,

plan may require the provider to be licensed, certified, or

Glossary of Health Coverage and Medical Terms Page 4 of 6

Provider

Some examples of a provider include a doctor, nurse,

skilled nursing facility, and rehabilitation center. The

accredited as required by state law.

Preauthorization

A decision by your health insurer or plan that a health

care service, treatment plan, prescription drug or durable

medical equipment (DME) is medically necessary.

Sometimes called prior authorization, prior approval or

precertification. Your health insurance or plan may

require preauthorization for certain services before you

receive them, except in an emergency. Preauthorization

isn’t a promise your health insurance or plan will cover

the cost.

Primary Care Physician

D.O. (Doctor of Osteopathic Medicine), who provides

or coordinates a range of health care services for you.

Physician Services

Health care services a licensed medical physician,

including an M.D. (Medical Doctor) or D.O. (Doctor of

Osteopathic Medicine), provides or coordinates.

Prescription Drugs

Drugs and medications that by law require a prescription.

PremiumTax Credits

your family pay for private health insurance. You can get

Marketplace and your income is below a certain level.

Advance payments of the tax credit can be used right

away to lower your monthly premium costs.

Out-of-network Provider (Non-Preferred

Provider)

A provider who doesn’t have a contract with your plan to

provide services. If your plan covers out-of-network

services, you’ll usually pay more to see an out-of-network

provider than a preferred provider. Your policy will

explain what those costs may be. May also be called

“non-preferred” or “non-particiapting” instead of “out-

of-network provider”.

26

Reconstructive Surgery

Surgery and follow-up treatment needed to correct or

improve a part of the body because of birth defects,

accidents, injuries, or medical conditions.

Urgent Care

Care for an illness,injury, or condition serious enough

that a reasonable person would seek care right away, but

not so severe as to require emergency room care.

Rehabilitation Services

Health care services that help a person keep, get back, or

improve skills and functioning for daily living that have

beenlost or impaired because a person was sick, hurt, or

disabled. These services may include physical and

occupational therapy, speech-language pathology, and

psychiatric rehabilitation services in a variety of inpatient

andor outpatient settings.

Skilled Nursing Care

Services performed or supervised by licensed nurses in

your home or in a nursing home. Skilled nursing care is

not the same as “skilled care services”, which are services

performed by therapists or technicians (rather than

licensed nurses) in your home or in a nursing home.

Specialty Drug

A type of prescription drug that, in general, requires

special handling or ongoing monitoring and assessment

by a health care professional, or is relatively difficult to

dispense. Generally, specialty drugs are the most

expensive drugs on a formulary.

Glossary of Health Coverage and Medical Terms Page 5 of 6

Specialist

Aprovider focusing on a specific area of medicine or a

group of patients to diagnose, manage, prevent, or treat

certain types of symptoms and conditions.

Screening

A type of preventive care that includes tests or exams to

detect the presence of something, usually performed

when you have no symptoms, signs, or prevailing medical

history of a disease or condition.

Referral

A written order from your primary care provider for you

to see a specialist or get certain health care services. In

many health maintenance organizations (HMOs), you

needto get a referral before you can get health care

services from anyone except your primary care provider.

If you don’t get a referral first, the plan may not pay for

the services.

UCR (Usual, Customary and Reasonable)

The amount paid for a medical service in a geographic

area based on what providers in the area usually charge

for the same or similar medical service. The UCR

amount sometimes is used to determine the allowed

amount.

27