CP 2501 Stephen2501Docs

User Manual: CP-2501

Open the PDF directly: View PDF ![]() .

.

Page Count: 3

Stephen XXXXX

<Date>

Internal Revenue Service

4800 Buford Hwy.

Chamblee, GA 39901-0021 Certified Mail #_____________________________

RE: Notice CP 2501

To: Mr. Kenneth C. Corbin

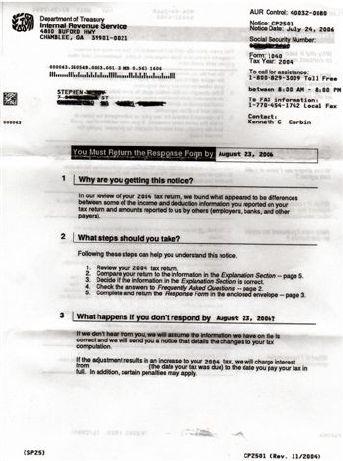

I received an unsigned notice CP2501 dated July 24, 2006, that stated in paragraph 1: “In our

review of your 2004 tax return, we found what appeared to be differences between some of the

income and deduction information you reported on your tax return and amounts reported to us by

others (employers, banks, and other payers).”

The income figures you refer to have been addressed by my filing a correcting Form 1099-MISC

in regards to the misreporting engaged in by XXXXXXXX, Inc. and by the filing of the Form

4852 to correct the misreporting of XXXXXXXXX Company. I DO NOT see a need to supply

you with a copy of information that is already in your possession, namely, my 2004 Form 1040

and the above mentioned attachments to said return. However, if you MUST have them to

satisfy the statement about enclosing documentation under OPTION 3 on page 3 of the CP2501,

then please advise me.

In regards to the Tax Credits section on page 6, the only “credits/deductions” I am claiming are

those for the standard deduction and the personal exemption amounts that everyone claims and

are entitled to. In regards to the Penalty section on the same page, please see below for a

statement that may or may not fulfill any one of the three actions described to reduce or

eliminate the penalty mentioned there.

Statement Regarding Reducing or Eliminating the Accuracy Penalty – IRC § 6662(d)

I have worked in the private-sector for approx. 30 years for XXXXXXXX, Inc. My 2004

private-sector payments that the notice CP2501 erroneously assumes are reportable via a 1099-

MISC are not reportable under Internal Revenue Code (IRC) § 6041(a) regarding Information at

source. Neither are said payments reportable under IRC § 6041A as XXXXXXXX, Inc. is a

private-sector company. As such, they are not described within the definition of “trade or

business” in § 7701(a)(26) and the payments made to me cannot, therefore, be characterized as

“salaries,…wages,…compensations, remunerations,…or other fixed or determinable gains,

profits, and income…” (IRC 6041(a)). Sections 6041(a) and 6041A(a) only apply to a “person”

or “service-recipient” engaged in a “trade or business”. The reporting requirement applies only

to those individuals or entities when the payments described within these two sections are made

to “another person” or “any person”, respectively, in the course of a “trade or business”.

The payments received from XXXXXXXXX Company listed under “Retirement Income Gross”

in the Explanation Section of the CP2501, page 5, are also not reportable under IRC § 6041(a) or

6041A(a) for the same reasons as those noted above for XXXXXXXXX, Inc.

XXXXXXXX, Inc. and XXXXXXXXXXXX Company were not required to report my private-

sector payments on Form 1099-MISC and Form 1099-R, but did anyway, and in so doing

reported to the IRS that my private-sector payments are taxable, which they are not. I corrected

XXXXXXXXX, Inc.’s erroneous Form 1099-MISC by filing a completed and signed rebutting

document correcting the Form 1099-MISC (as XXXXXXXX, Inc. refused to issue me a

corrected form) as part of my 2004 tax return. I also corrected XXXXXXXXX Company’s

1099-R by filing a completed and signed Form 4852 (“Substitute for…Form 1009-R…”). Of

course XXXXXXXX, Inc.’s and XXXXXXXXX Company’s erroneous Form 1099-MISC and

Form 1099-R, respectively, do not match my corrections of them!

I hope this proves to be sufficient information for you to conclude that the information I have

provided via my valid 2004 Form 1040 and attachments is correct. If you require a copy of my

tax return, then let me know.

Sincerely,

Stephen XXXXX

P.S. I am sure that if you will do a little more research, you will find that I was sent a CP49 for

2004 on which was acknowledged an overpayment of tax in the amount of $2,400.00 that was

applied to another year. One would think that 2004 is now closed.