Interim Report January June 2011 TL 2020 TL2020 AR14 ENG 150324 2

User Manual: TL 2020

Open the PDF directly: View PDF ![]() .

.

Page Count: 72

Annual

REPORT

2014

Calendar 2015

Annual General Meeting

2015

Stockholm

May 19

Interim Report

January – March 2014

Financial Reports

Interim Report

January – March

2015

Full year Report

January – December

2014

Interim Report

January – June

2015

Interim Report

January – September

2015

Jan 30

Jul 21 Oct 21

Mar 30 Apr 21

Annual Report

2014

Financial statements – Group Page

Consolidated income statement 25

Consolidated comprehensive income 26

Consolidated balance sheet 27

Consolidated cash flow statement 29

Change in consolidated equity 30

Financial statements – parent company Page

The parent company’s income statement 61

The parent company’s comprehensive income 61

The parent company’s balance sheet 61

The parent company’s cash flow statement 62

Change in the parent company’s equity 62

Notes – Group

Note 1 Accounting principles and other information 31

Note 2 Financial risk management and financial instruments 38

Note 3 Exchange rate effects 39

Note 4 Segment reporting 40

Note 5 Net sales and number of customers 41

Note 6 EBITDA and EBIT as well as depreciation/

amortization and impairment 42

Note 7 Result from shares in joint ventures and associated companies 43

Note 8 Other operating income 43

Note 9 Other operating expenses 43

Note 10 Interest income 44

Note 11 Interest costs 44

Note 12 Other financial items 44

Note 13 Taxes 44

Note 14 Intangible assets 45

Note 15 Tangible assets 47

Note 16 Acquisitions and divestments 48

Note 17 Shares in joint ventures and associated companies 49

Note 18 Other financial assets 49

Note 19 Inventories 49

Note 20 Accounts receivable 49

Note 21 Other current receivables 49

Note 22 Prepaid expenses and accrued income 49

Note 23 Current investments 49

Note 24 Cash and cash equivalents and unutilized overdraft facilities 50

Note 25 Equity, number of shares and earnings per share 50

Note 26 Financial liabilities 51

Note 27 Provisions 53

Note 28 Accrued expenses and deferred income 53

Note 29 Pledged assets 53

Note 30 Contingent liabilities and other commitments 53

Note 31 Leases 54

Note 32 Supplementary cash flow information 54

Note 33 Number of employees 54

Note 34 Personnel costs 55

Note 35 Fees to the appointed auditor 58

Note 36 Discontinued operations 58

Note 37 Joint operations and other related parties 59

Note 38 Corporate Responsibility results 60

Notes – parent company

Note 1 Accounting principles and other information 63

Note 2 Net sales 63

Note 3 Result of shares in group companies 63

Note 4 Other interest revenue and similar income 63

Note 5 Interest expense and similar costs 63

Note 6 Taxes 63

Note 7 Tangible assets 63

Note 8 Shares in group companies 64

Note 9 Receivables from group companies 64

Note 10 Other financial assets 64

Note 11 Cash and cash equivalents and unutilized overdraft facilities 64

Note 12 Financial liabilities 64

Note 13 Accrued expenses and deferred income 64

Note 14 Contingent liabilities and other commitments 65

Note 15 Supplementary cash flow information 65

Note 16 Number of employees 65

Note 17 Personnel costs 65

Note 18 Fees to the appointed auditor 65

Note 19 Legal structure 65

Contents

CEO Word 2

Board of Directors 4

Leadership Team 6

Administration report 8

Financial statements 25

Auditor’s report 67

Definitions 68

Contacts 69

Tele2 – Annual Report 2014 1

In just a few years, the mobile device has become our most

beloved asset, even more dear to us than our wallets. Did

you know that around 80 percent of the smartphone users

check their mobile phones within the first 15 minutes of

when they wake up? Moreover, did you know that we look

at our phones on average 125-150 times per day? And we,

Tele2, make the expensive device you hold in your hand

worth something. Because without the connectivity that

we provide, it is just pieces of glass, metal and plastic.

Hence, I feel confident that our mobile focus is spot on.

The year has been vibrant in many ways. I have had the pleasure of

welcoming several new members to the Leadership Team - new

faces bringing new ideas and perspectives to the table. Also the

Tele2 Group saw some change to the set-up as we sold our Norwe-

gian business. The sale has been completed during 2015 after

approval by regulatory authorities, and is beneficial for both Tele2,

our Norwegian customers and the buyer – although it was a big step

away from the original plan that we had for our Norwegian opera-

tions. Moreover, on the operational side we have seen good devel-

opment in for example Sweden, where we are really hitting it off

when it comes to monetizing data. The prepaid to postpaid migra-

tion has slowed down and instead the voice to data transition is

really picking up speed. And we are only seeing the beginning of

that journey.

Everything starts with a good trend, someone said. I really think

that is true and in our business that trend is data growth. The differ-

ence between winners and losers will be the ability to monetize

data and take good care of the customer, I know that we at Tele2 can

do both.

Hitting change before change hits us

Last year, I said that 2014 would be the year when we were going to

remove uncertainty around Tele2. To a large extent we have man-

aged to do that. We have a clear path forward and now it is just con-

tinued hard work that is needed to get our Rockets in the Nether-

lands, Kazakhstan and Croatia to bear fruit. Adding to the clarity,

wecommunicated our renewed strategy to the Board, our employ-

ees and the market during the year. Our strategic process landed in

four strategic choices, or Way2Win, as we call it; Value Champion,

Focused Technology Choices, Step Change Productivity and

Winning People & Culture. If we manage to excel in each of these

areas, we will be unbeatable. Within Step Change Productivity, we

announced the Challenger Program as an initiative. It is a program

to increase efficiency across the whole Group by doing what we do

even smarter and better. It will lead to productivity improvements

amounting to around SEK 1 billion annually as of 2018.

In Sweden, we fully transitioned to becoming Value Champions

during 2014 when we introduced a new commercial concept which

we refer to as Tele2.0. Putting the customers first and abolishing old

truths like binding periods and expiry dates for top-ups. Instead, we

introduced things like a one-subscription-solution for everyone and

trial periods for both B2C and B2B customers. The purpose of the

concept is to improve customer satisfaction and build the Tele2

brand. It is a bold move but the industry needs to change and in

Sweden we are in a position of strength, giving us the courage to

take these steps. During the year, Sweden maintained its status as

the leader in mobile data for the Group.

In the Netherlands, we are continuing one of the Group’s most

exciting projects at full speed. In the beginning of 2015, some of our

base stations started to radiate and by pushing on with the network

2014 – yet another dynamic and

successful year! Perfect for us at Tele2

who see change as the only constant

Everything starts with a good trend, someone said.

I really think that is true and in our business that trend

is data growth. The difference between winners and

losers will be the ability to monetize data and take good

care of the customer, I know that we at Tele2 can do both.

“

”

2 Tele2 – Annual Report 2014

CEO Word

build-out we expect to have a full coverage by Q1 2016. As far as I

know, it will be the first 4G-only full covering operation in the world.

In the year, we have seen geopolitical developments that affected

our value in Kazakhstan, as it brought monetary instability with it.

Businesswise, on the contrary, we saw more stability in our coun-

tries neighboring Russia. In Kazakhstan, we are back at a strong

positive customer intake. We have increased the number of points of

sales, applied a more regional approach to our business and saw the

revenue sharing retail model continue to yield results. We main-

tained our successful network roll-out and at the end of the year, we

had 30 percent of our revenues coming from data. The voice to data

transition is present everywhere.

I am glad to see that Tele2 Croatia continues its positive trajectory

after last year’s turn-around. Once again I would like to emphasize

the strong management team and employees that are really giving it

all to make that happen. In 2014 we secured 15 MHz in the 1800

MHz spectrum which puts us in a strong position for future data

growth.

Estonia went from a very tough position, to a tough one. A dawn-

ing improvement which I hope will continue. Lithuania continues to

stand out as one of the stars of the Group with a number one position

(no matter how you count) and with impressive EBITDA-margins.

Latvia focused on customer service and managed to reach beyond

world class levels, hitting 86 percent customer satisfaction during

the year.

Germany continued on its present path and in Austria we took the

decision to invest in B2B whilst also launching mobility (through an

MVNO agreement) as a complement to our fixed operations.

2014 was also the year when our M2M business got some traction

in its partnership strategy. That strategy gives us the right tools to

take our M2M business further at a great tempo. The Tele2 M2M

Global Solution organization feels solid and I am hopeful that 2015

will be even more of a springboard year for our M2M activities.

If you are not paranoid,

you do not have enough information

Sustainability and Corporate Responsibility remains a clear focus

for us at Tele2. By providing our customers with great products and

offerings that give access to society’s full range of services and com-

munication, we feel that we are contributing to a better tomorrow at

our very core. However, we are well aware that there are plenty of

challenges along the way in order to get that done in a cautious and

responsible way across our footprint. Our strategy for Corporate Sus-

tainability described in two words would be: transparent action. We

take action when we see wrongdoings within our operational con-

trol. We discuss human rights and ethical dilemmas in our Board.

I,myself, have worked hard to increase transparency around our

business in Kazakhstan towards investors and relevant stakehold-

ers. We try to be as open as we can possibly be about our challenges

(e.g. reporting incidents in our Annual Reports and on our corporate

website, organizing Corporate Responsibility round-tables, drafting

public White Papers etc.) and when things go bad (because they do)

we act upon it. Fulfilling the company’s responsibility to respect

human rights as defined by the United Nations in the best possible

way. This needs to be done to maintain our customers’ trust and

generate maximum shareholder value – and to allow me to sleep

well at night. We follow political and macro-economic trends which

could influence performance and delivery and we are disciplined

when it comes to risk appetite, culture, values and challenger spirit.

We, and our owners, will continue to have tough expectations on

ourselves for the coming years.

The Tele2 Way or the highway

Internally, we have had a continued focus on our unique and price-

less set of values. It is important not to feel satisfied and relaxed

even though employee engagement levels (a combination of clarity

and energy) at Tele2 are world class. In the year, we therefore rolled

out a new Tele2 Way training. Everyone in the Leadership Team are

teachers and all managers have attended the updated training ses-

sions. We have a strong culture and DNA that needs to be taken care

of. Winning People & Culture is one of the Way2Win areas in the

renewed strategy because it is the people at Tele2 that makes us

who we are and defines who we will be.

Just do it

In 2015, we will roll-up our sleeves even further (at Tele2 they are

well above the elbows at any given time) because we have a lot of

work to do. I sometimes say that we are more or less “fully booked”

for 2015. It will be a year of investments and setting up the company

for future continued success. The Netherlands remains a clear focus

and we need to get that right. We are also rolling out networks in

Kazakhstan and Sweden to cater for future needs. Moreover, we

have kick-started the Challenger Program and need to get good

traction from that in 2015.

Mats Granryd

President and CEO

Tele2 – Annual Report 2014 3

CEO Word

Board of Directors

Mike Parton

Chairman of the Board,

elected in 2007

Born: 1954

Nationality: British citizen

Independence: Independent in

relation to the company and

management as well as in

relation to the company’s major

shareholders

Holdings in Tele2: 17,825

Bshares

Committee work: Member of

the Remuneration Committee

Mike Parton is a member of the

Chartered Institute of

Management Accountants.

Furthermore, he is a member of

the Advisory Board of a UK

charity called Youth at Risk.

He was CEO and Chairman of

Damovo Group Ltd, an

international IT company

between 2007 and 2014 and

CEO and Executive member of

Marconi plc between 2001 and

2006.

Trained as Chartered

Management Accountant.

Lorenzo Grabau

Non-Executive Director,

elected in 2014

Born: 1965

Nationality: Italian citizen

Independence: Independent in

relation to the company and

management but not

independent in relation to the

company’s major shareholders

Holdings in Tele2: -

Committee work: Member of the

Audit Committee and the

Remuneration Committee

Lorenzo Grabau is President and

CEO of Investment AB Kinnevik

since 2014. He is also Chairman of

Rocket Internet AG and Avito AB

since 2014 and in Global Fashion

Holding SA since 2015. In addition

he is deputy Chairman of Zalando

SE since 2013, as well as Non-

Executive Director of Millicom

International Cellular S.A., since

2013, Modern Times Group MTG

AB since 2011, Qliro Group AB and

Secure Value EEIG since 2014.

During 2013 and 2014 he was

Non-Executive Director of

Investment AB Kinnevik, CTC

Media, Inc. and Softkinetic BV. He

was a Partner and Managing

Director at Goldman Sachs Inter-

national in London until 2011. He

joined the Investment Banking

division of Goldman Sachs in 1994

and during his 17years at the firm

held various leadership positions

within the Consumer/Retail and

Media/Online industry practices,

and the Financial Sponsors Group.

He began his career in Investment

Banking in 1990 when he joined

Merrill Lynch, where he remained

for five years working in the

Mergers & Acquisitions depart-

ment in London and NewYork.

Dottore in Economia e

Commercio, from Università degli

Studi di Roma, La Sapienza, Italy.

Lars Berg

Non-Executive Director,

elected in 2010

Born: 1947

Nationality: Swedish citizen

Independence: Independent in

relation to the company and

management as well as in

relation to the company’s major

shareholders

Holdings in Tele2: 2,000

Bshares

Committee work: Chairman of

the Remuneration Committee

Lars Berg is the European

venture partner of Constellation

Growth Capital since 2006. He is

non-executive Chairman of Net

Insight AB since 2001 (a Board

member since 2000), a non-

executive Board member of

Ratos AB since 2000 and of

OnePhone Holding since 2009

as well as a non-executive

supervisory Board member of

NORMA Group AG, Frankfurt

since 2011.

He was a member of the

executive Board of Mannesmann

AG as Head of its telecommuni-

cations business from 1999 until

the Vodafone takeover of

Mannesmann in 2000. From

1994 until 1999, he was Chief

Executive Officer of the Telia

Group and President of Telia AB.

Between 1970 and 1994 he held

various executive positions in

the Ericsson Group and was a

member of the Ericsson

Corporate Executive Committee

for ten years, as well as

President of the subsidiaries

Ericsson Cables AB and Ericsson

Business Networks AB.

M.Sc. in Business

Administration and Economics,

Gothenburg School of

Economics.

Mia Brunell Livfors

Non-Executive Director,

elected in 2006

Born: 1965

Nationality: Swedish citizen

Independence: Not

independent in relation to the

company and management (due

to engagement as a Board

member of Transcom Worldwide

AB) and not independent in

relation to the company’s major

shareholders

Holdings in Tele2: 1,000

Bshares

Committee work: -

Mia Brunell Livfors is a member

of the Board of Millicom

International Cellular S.A.,

Modern Times Group MTG AB,

Qliro Group AB, Transcom

Worldwide AB, Stena AB and

Efva Attling Stockholm AB. She

also works as an advisor for Axel

Johnson AB and has been

appointed as a Board member of

Axel Johnson AB from March 25,

2015.

She was President and CEO of

Investment AB Kinnevik

between 2006 and 2014 and

she held several managerial

positions within the Modern

Times Group MTG AB from 1992

to 2001 and was Chief Financial

Officer between 2001 and 2006.

Studies in Economics and

Business Administration,

Stockholm University.

4 Tele2 – Annual Report 2014

Board of Directors

Carla Smits-Nusteling

Non-Executive Director,

elected in 2013

Born: 1966

Nationality: Dutch citizen

Independence: Independent in

relation to the company and

management as well as in

relation to the company’s major

shareholders

Holdings in Tele2: -

Committee work: Chairman of

the Audit Committee and

member of the Remuneration

Committee

Carla Smits-Nusteling is a Non-

Executive Director at ASML. She

is also a member of the

management board of the

Foundation Unilever NV Trust

Office since February 2015.

She has over 10 years’

experience from Koninklijke KPN

N.V., and was KPN’s Chief

Financial Officer between 2009

and 2012. She joined KPN in

2000 and held various financial

positions, whereof three years

as Director of Corporate Control.

During 1990–2000, she worked

at TNT Post Group N.V., an

international express and mail

delivery service, and held

various managerial positions

before her appointment as

Regional Director in 1999.

M.Sc. Business Economics,

Erasmus University, Rotterdam.

Mario Zanotti

Non-Executive Director,

elected in 2013

Born: 1962

Nationality: Italian citizen

Independence: Independent in

relation to the company and

management but not

independent in relation to the

company’s major shareholders

Holdings in Tele2: -

Committee work: -

Mario Zanotti is Senior Executive

VP Operations at Millicom

International Cellular S.A

He has over 20 years of

experience in the Telecom

Service Industry. In 1992 he

founded Telecel in Paraguay and

was also the Managing Director

of the company during 1992–

1998. He was Managing Director

of Tele2 Italy during 1998–2000

and of YXK Systems during

2001–2002. After 2002 he has

held several other managerial

positions within Millicom,

starting as Head of Central

America for Millicom before

becoming Head of Latin America

and later COO of Categories &

Global Sourcing.

M.Sc. in Electrical

Engineering from the Pontificia

Universidade Catolica in Porto

Alegre (Brazil), MBA from INCAE

and the Universidad Catolica de

Asuncion (Paraguay).

Erik Mitteregger

Non-Executive Director,

elected in 2010

Born: 1960

Nationality: Swedish citizen

Independence: Independent in

relation to the company and

management but not

independent in relation to the

company’s major shareholders

Holdings in Tele2: 10,000

Bshares

Committee work: Member of

the Audit Committee

Erik Mitteregger is member of

the Board of Investment AB

Kinnevik since 2004 and of

Rocket Internet AG and Avito AB

since 2014. He is also chairman

of the Boards of Firefly AB and

Wise Group AB.

Previously, he was member of

the Board of Invik & Co. AB

2004–2007 and Metro

International SA 2009–2013. He

was founding partner and Fund

Manager of Brummer & Partners

Kapitalförvaltning AB 1995–

2002. In 1989–1995, he was

Head of Equity Research and

member of the Management

Board at Alfred Berg

Fondkommission.

B.Sc. in Economics and

Business Administration at

Stockholm School of Economics.

Irina Hemmers

Non-Executive Director,

elected in 2014

Born: 1972

Nationality: Austrian citizen

Independence: Independent in

relation to the company and

management as well as in

relation to the company’s major

shareholders

Holdings in Tele2: -

Committee work: Member of

the Audit Committee

Irina Hemmers is Investment

Managing Director at Moonray

Investors, the Principal Investing

Arm of Fidelity International.

She was Non-Executive

Director of Trader Corporation,

Trader Media Group and Top

Right Group until 2013, of Hit

Entertainment until 2012,

Incisive Media/American

Lawyer Media until 2009 and

SULO Group until 2007.

Previously, she was a Partner

with private equity firm Apax

Partners from 2001 to 2013.

During her 12 years with Apax

Partners, she worked in Munich,

Hong Kong and London. She

began her career at McKinsey &

Company in Vienna 1996.

M.Sc. in International

Business and Economic Studies

from University of Innsbruck,

Austria, and an MPA from John F.

Kennedy School of Government,

Harvard University, USA.

Tele2 – Annual Report 2014 5

Board of Directors

Leadership Team

Mats Granryd

President and CEO Tele2 Group

Joined the company in 2010

Born 1962

M.Sc. in Mechanical Engineering,

KTH Royal Institute of Technology

Holdings in Tele21)

57,725 B shares

56,000 share rights (LTI 2012)

56,000 share rights (LTI 2013)

56,000 share rights (LTI 2014)

Joachim Horn

Executive Vice President /

Group CTIO

Joined the company in 2011

Born 1960

M.Sc. in Informatics, Fachhochschule Wedel

Holdings in Tele21)

12,000 B shares

24,000 share rights (LTI 2012)

24,000 share rights (LTI 2013)

24,000 share rights (LTI 2014)

Lars Torstensson

Executive Vice President / Group

Communication & Strategy

Joined the company in 2007

Born 1973

M.Sc. in Business Administration,

Jönköping University

Holdings in Tele21)

16,000 B shares

24,000 share rights (LTI 2012)

24,000 share rights (LTI 2013)

24,000 share rights (LTI 2014)

Allison Kirkby

Executive Vice President /

Group CFO

Joined the company in 2014

Born 1967

FCMA, Fellow of the Chartered Institute

of Management Accountants, SHND in

Accounting, University of Caledonia

Holdings in Tele21)

4,000 B shares

24,000 share rights (LTI 2014)

Anders Olsson

Executive Vice President /

Group CCO

Joined the company in 1997

Born 1969

M.Sc. in Business Administration

and Economics, Uppsala University

Holdings in Tele21)

30,000 B shares

24,000 share rights (LTI 2012)

24,000 share rights (LTI 2013)

24,000 share rights (LTI 2014)

Caroline Fellenius-Omnell

Executive Vice President /

Group General Counsel

Joined the company in 2014

Born 1968

LL.M. College of Europe and LL.M.,

Stockholm University

Holdings in Tele21)

4,000 B shares

24,000 share rights (LTI 2014)

6 Tele2 – Annual Report 2014

Leadership Team

1) Share rights = allocated share rights at grant date, before compensation for dividend

Thomas Ekman

Executive Vice President /

CEO Tele2 Sweden

Joined the company in 2006

Born 1969

M.Sc. in Business administration and

Economics, Stockholm University

Holdings in Tele21)

12,012 B shares

24,000 share rights (LTI 2012)

24,000 share rights (LTI 2013)

24,000 share rights (LTI 2014)

Jeff Dodds

Executive Vice President /

CEO Tele2 Netherlands

Joined the company in 2014

Born 1973

MBA, University of Westminster and M.Sc. in

Marketing Management, Aberdeen Business

School

Holdings in Tele21)

4,000 B shares

24,000 share rights (LTI 2014)

Elinor Skogsfors

Executive Vice President /

Group Human Resources

Joined the company in 2013

Born 1963

B.Sc. in Political Administration major in

HR, Stockholm University

Holdings in Tele21)

3,000 B shares

18,000 share rights (LTI 2014)

Niklas Sonkin

Executive Vice President / Central Europe

and Eurasia

Joined the company in 2009

Born 1967

M.Sc. in Engineering, Helsinki University

of Technology

Holdings in Tele21)

14,500 B shares

24,000 share rights (LTI 2012)

24,000 share rights (LTI 2013)

24,000 share rights (LTI 2014)

In addition, not received 8,307

B shares for LTI 2011

Tele2 – Annual Report 2014 7

Leadership Team

Financial overview

With 14 million customers in nine countries, Tele2 is one of Europe’s

leading telecom operators. We offer mobile services, fixed broad-

band and telephony, data network services and content services.

Ever since Jan Stenbeck founded the company in Sweden in 1993,

Tele2 has been a tough challenger to the former government

monopolies and other established providers.

Our mission is to always offer our customers what they need for

less, and ultimately our vision is to be the champions of customer

value in everything we do.

Mobile services is Tele2’s primary focus and most important

growth segment. In 2014, revenue from mobile operation accounted

for 74 (68) percent of Tele2’s net sales.

In 2014, the Group generated net sales of SEK 26 billion and

reported an operating profit (EBITDA) of SEK 5.9 billion.

Net customer intake

In 2014, the total customer base increased to 13,594,000

(13,582,000) customers. Net customer intake, excluding one-time

adjustments, was 397,000 (253,000) customers. The customer

intake in mobile services amounted to 598,000 (594,000) custom-

ers. The increase was mainly driven by positive customer intake

through Tele2 Kazakhstan, Tele2 Netherlands, Tele2 Germany and

Tele2 Croatia. The fixed broadband base lost –45,000 (–86,000)

customers in 2014, attributable to Tele2’s operation in Sweden,

Austria, Germany and the Netherlands. As expected, the number

offixed telephony customers fell during the year.

Net sales

Tele2’s net sales amounted to SEK 25,955 (25,757) million corre-

sponding to a positive growth of 1 percent including, or –1 percent

decline excluding, exchange rate effects. The net sales development

was mainly a result of strong usage of mobile services increasing 8

percent, however hampered by the negative net sales development

within consumer fixed broadband and fixed telephony.

EBITDA

EBITDA amounted to SEK 5,926 (5,891) million, equivalent to an

EBITDA margin of 22.8 (22.9) percent. This corresponding to an

increase in EBITDA of 1 percent including, or –2 percent excluding,

exchange rate effects. The EBITDA growth was mainly a result of a

strong development in mobile services, and monetising of data.

However, it was also affected by expansion costs in mobile services.

EBIT

Operating profit, EBIT amounted to SEK 3,216 (2,982) million exclud-

ing one-off items. Including one-off items and including the capital

gain from the sale of the Swedish residential cable and fiber opera-

tion, EBIT amounted to SEK 3,490 (2,548) million. The EBIT margin

was 13.4 (9.9) percent.

Profit before tax

Net interest expense and other financial items amounted to SEK 10

(–551) million. Exchange differences of SEK –27 (–28) million were

reported under other financial items. The average interest rate on

outstanding liabilities was 5.0 (5.2) percent. Profit after financial

items, EBT, amounted to SEK 3,500 (1,997) million.

Net profit

Profit after tax amounted to SEK 2,626 (968) million. Earnings per

share amounted to SEK 5.86 (2.15) after dilution. Income tax

expenses for the year amounted to SEK –874 (–1,029) million. Tax

payments for continuing operations affecting cash flow amounted to

SEK –327 (–302) million.

Cash flow

For continuing operations, cash flow from operating activities

amounted to SEK 4,661 (4,983) million and cash flow after paid

CAPEX to SEK 1,162 (799) million.

CAPEX

During 2014, Tele2 made investments of SEK 3,450 (4,399) million

in tangible and intangible assets, driven mainly by further network

expansion in Netherlands, Sweden, Kazakhstan and the Baltics.

Net debt

Net debt amounted to SEK 9,061 (8,007) million on December 31,

2014, or 1.51 times EBITDA in 2014. Tele2’s available liquidity

amounted to SEK 8,224 (9,306) million.

Challenger program

A group-wide program focused on increasing productivity was

launched in the end of 2014. The program will be implemented over

the next 3 years and reap full benefits of SEK 1 billion per annum

starting in 2018. The investment required will be SEK 1 billion,

phased over the next 3 years. In 2014 EBIT was impacted by

SEK–10 million by the program, which was reported as one-off

items (Note 6).

Administration report

The Board of Directors and the CEO herewith present the annual

report and consolidated financial statements for Tele2 AB (publ),

corporate reg. no. 556410-8917 for the financial year 2014.

The figures shown in parentheses correspond to the comparable period last year and continuing operations unless otherwise stated.

8 Tele2 – Annual Report 2014

Administration report

Five-year summary

SEK million 2014 2013 2012 2011 2010

CONTINUING OPERATIONS

Net sales 25,955 25,757 25,993 26,219 27,361

Number of customers (by thousands) 13,594 13,582 14,229 12,392 11,845

EBITDA 5,926 5,891 6,040 6,755 6,880

EBIT 3,490 2,548 2,190 3,613 4,088

EBT 3,500 1,997 1,668 3,074 3,664

Net profit 2,626 968 1,158 2,169 3,986

Key ratios

EBITDA margin, % 22.8 22.9 23.2 25.8 25.7

EBIT margin, % 13.4 9.9 8.4 13.8 14.9

Value per share (SEK)

Net profit 5.89 2.17 2.61 4.88 9.03

Net profit, after dilution 5.86 2.15 2.59 4.85 9.00

TOTAL

Equity 22,682 21,591 20,429 21,452 28,875

Total assets 39,848 39,855 49,189 46,864 42,085

Cash flow from operating activities 4,578 5,813 8,679 9,690 9,966

Cash flow after CAPEX 432 572 4,070 4,118 6,008

Available liquidity 8,224 9,306 12,933 9,986 13,254

Net debt 9,061 8,007 15,745 13,518 3,417

Investments in intangible and tangible assets, CAPEX 3,976 5,534 5,294 6,095 4,094

Investments in shares and other financial assets –439 –17,235 215 1,563 1,424

Average number of employees 5,484 6,143 8,379 7,539 7,402

Key ratios

Equity/assets ratio, % 57 54 42 46 69

Debt/equity ratio, multiple 0.40 0.37 0.77 0.63 0.12

Return on equity, % 10.0 69.5 15.6 18.9 24.0

ROCE, return on capital employed, % 10.1 48.0 15.4 20.5 22.2

Average interest rate, % 5.0 5.2 6.7 6.2 7.3

Value per share (SEK)

Net profit 4.96 32.77 7.34 10.69 15.67

Net profit, after dilution 4.93 32.55 7.30 10.63 15.61

Equity 50.90 48.49 45.95 48.33 65.44

Cash flow from operating activities 10.27 13.06 19.53 21.83 22.59

Dividend, ordinary 4.851) 4.40 7.10 6.50 6.00

Extraordinary dividend 10.001) – – 6.50 21.00

Redemption – 28.00 – – –

Market price at closing day 94.95 72.85 117.10 133.90 139.60

1) Proposed dividend.

Tele2 – Annual Report 2014 9

Administration report

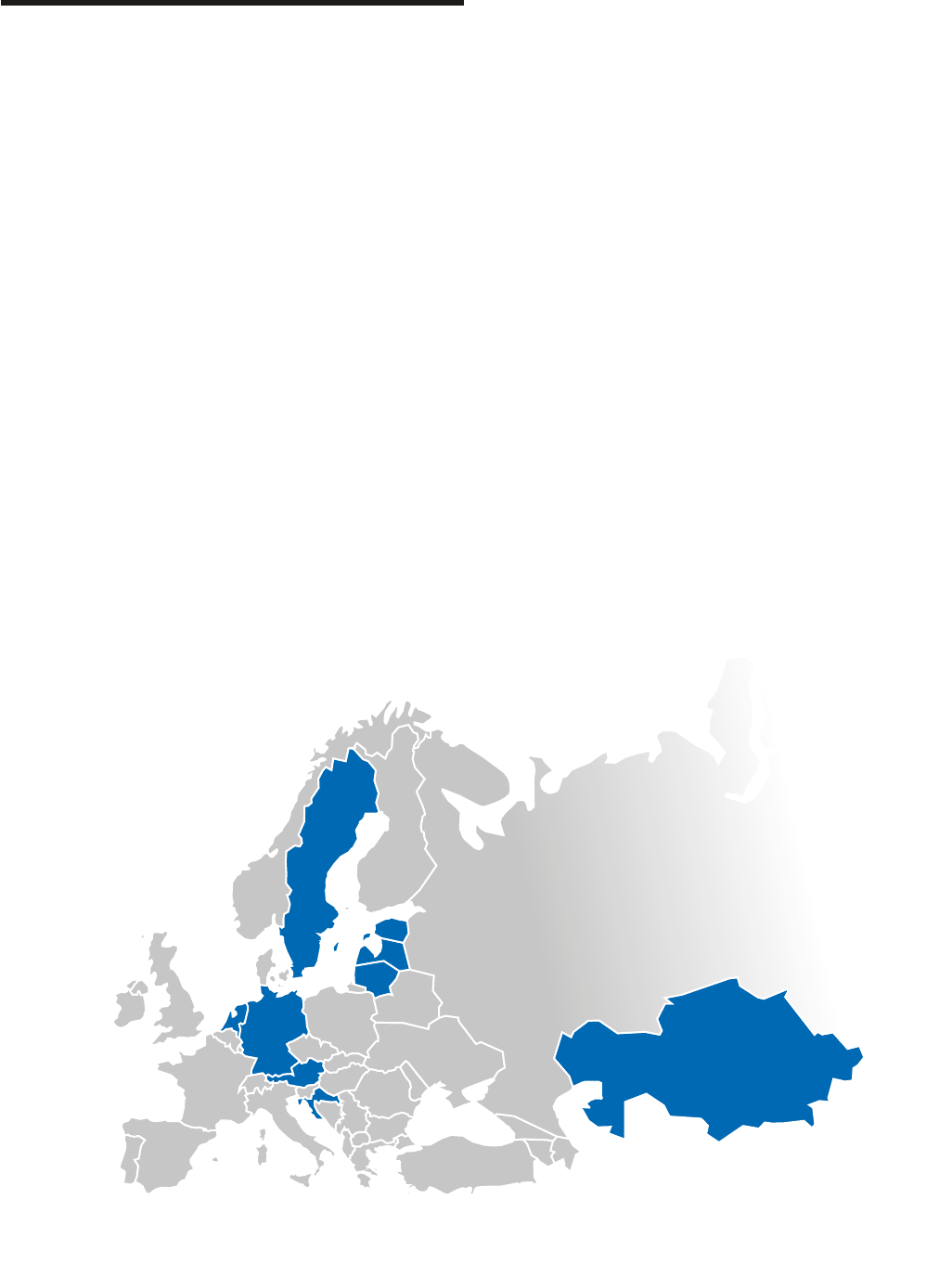

Where we operate

Overview by country

Tele2’s footprint includes both emerging and mature markets,

where cultural, economic and competitive differences are signifi-

cant. However, the trend towards mobility and mobile data is uni-

versal, and is clearly evident in all our countries of operation.

While mobile communication services are fairly standardized

across different countries, the level of maturity differs widely. Tele2

is present in nine countries, of which three are considered larger

markets for Tele2: Sweden, the Netherlands and Kazakhstan. These

three markets comprise 75 percent of the total net sales. Sweden is

the home turf and test bed for new products and services. The Neth-

erlands has its origin in fixed communication services but is now

pursuing a unique mobile opportunity as a 4G only operator.

Kazakhstan is in many ways still virgin territory. However, during

2014 Tele2 Kazakhstan started to deliver positive EBITDA and the

customer intake is accelerating, Tele2 Kazakhstan is the main com-

petitor for other operators in the country, delivering affordable com-

munication services.

Tele2’s position and priorities vary across its footprint. Local

market characteristics differ in many ways, even within the same

country.

Looking forward, Tele2 remains confident in its strategy and ability

to monetize a great customer experience throughout its footprint.

Sweden will maintain its leadership in 4G/LTE, and the company will

take its learning from Sweden to the Baltics and of course the Nether-

lands. 2015 will be another exciting year of investments in the com-

pany’s future ‘Rockets’ of Kazakhstan, Croatia and the Netherlands,

supported by continued strength in Sweden and the Baltics.

While there are important local differences, Tele2 has established

it’s ‘How we win choices’ going into 2015, supporting the overall

objective for the Group. These areas go beyond the local context and

are common to all the regions and countries where Tele2 operates.

How we win choices

• Value Champion – Tele2 aim to be the leader within the transi-

tion from voice to data and go from a discounter to a champion of

value for our customers.

• Focused technology choices – Tele2 shall increase quality

where it matters for the customers, drive down technology costs

continuously in all areas and selectively push for new technolo-

gies and innovations.

• Step change our productivity – Tele2 is in a position of strength

and has therefore invested in a multi-year program to find ways

to become the number one in effectiveness. This will be done by

simplification, discipline, consolidation and transformation.

• Winning people and culture – Tele2 is and will continue to be

an organisation that is driven by our values. We are today also an

organisation with highly engaged employees, something that we

aim to leverage upon.

Objectives

• Happiest customers – Tele2 shall be the operator of choice. By

providing the best value for money we shall be the operator of

choice and grow our market share.

• Engaged employees – We shall be considered a great place to

work. By being a great place to work we shall attract and retain

the best people who can deliver on our vision and mission.

• Profitable growth – We shall have the best Total Shareholder

Return (TSR). By having the happiest customers, engaged employ-

ees and work to become as effective as possible, we shall deliver

profitable growth and the best TSR within our peer group.

These fundamental priorities and objectives will continue to guide

the company’s regional activities moving forward.

10 Tele2 – Annual Report 2014

Administration report

2014 in brief

Despite high level of competition, Tele2 Sweden managed to dem-

onstrate solid results in 2014, driven by strong demand for mobile

data. Mobile end-user service revenue grew by SEK 302 million and

the EBITDA contribution for mobile services was SEK 3,224 (2,971)

million in 2014, representing a growth of 9 percent compared to last

year. Total mobile net intake amounted to –51,000 (38,000) in 2014.

In the end of 2013, Tele2 announced the sale of its Swedish resi-

dential cable and fiber operations to Telenor for SEK 793 million.

The sale was completed on January 2, 2014, after approval by regu-

latory authorities and the capital gain in 2014 amounted to SEK 258

million.

In 2014, Tele2 Sweden prioritised four areas:

• brand repositioning Tele2.0

• upselling of data

• cost efficiency from operating joint-operation networks and

further roll-out of 4G network

• market share gain in the business segment

Brand repositioning Tele2.0

In November 2014, Tele2 Sweden launched its new game changing

commercial concept, Tele2.0, including changes such as no binding

periods, a one-subscription solution, trial periods for both B2C and

B2B customers as well as removed expiry date for all top-ups. This is

expected to improve customer satisfaction, and through this the long

term positioning of Tele2 Sweden’s brands. The reaction from cus-

tomers and media was very positive.

Upselling of data

2014 was characterized by a strong demand for mobile data. Within

the consumer segment the request for mobile data shifted sales

towards higher data buckets. Also, the revenue from data-top ups

increased with about 327 percent compared to 2013, proving that

the consumer behavior has shifted from voice to data services. The

demand for 4G enabled smartphones maintained during the year,

and now stands for 98 percent of total sales.

Further roll-out of 4G network

During the year, Tele2 Sweden continued the rollout of the com-

bined 2G and 4G networks in the joint operation Net4Mobililty, with

aggressive geographic coverage targets. With this rollout, Tele2

Sweden will improve the coverage in all areas of Sweden with the

aim of reaching 90 percent geographic coverage in 2016. Through

this rollout, Tele2 Sweden will cement its position as the operator

offering the best mobile 4G coverage in Sweden while further

future-proofing its network.

Moreover, Tele2 Sweden continued the roll-out of both LTE 800

and LTE 1800, which will further strengthen the network in terms

of 4G capacity and coverage in order to cater for customers’ increas-

ing demand for data.

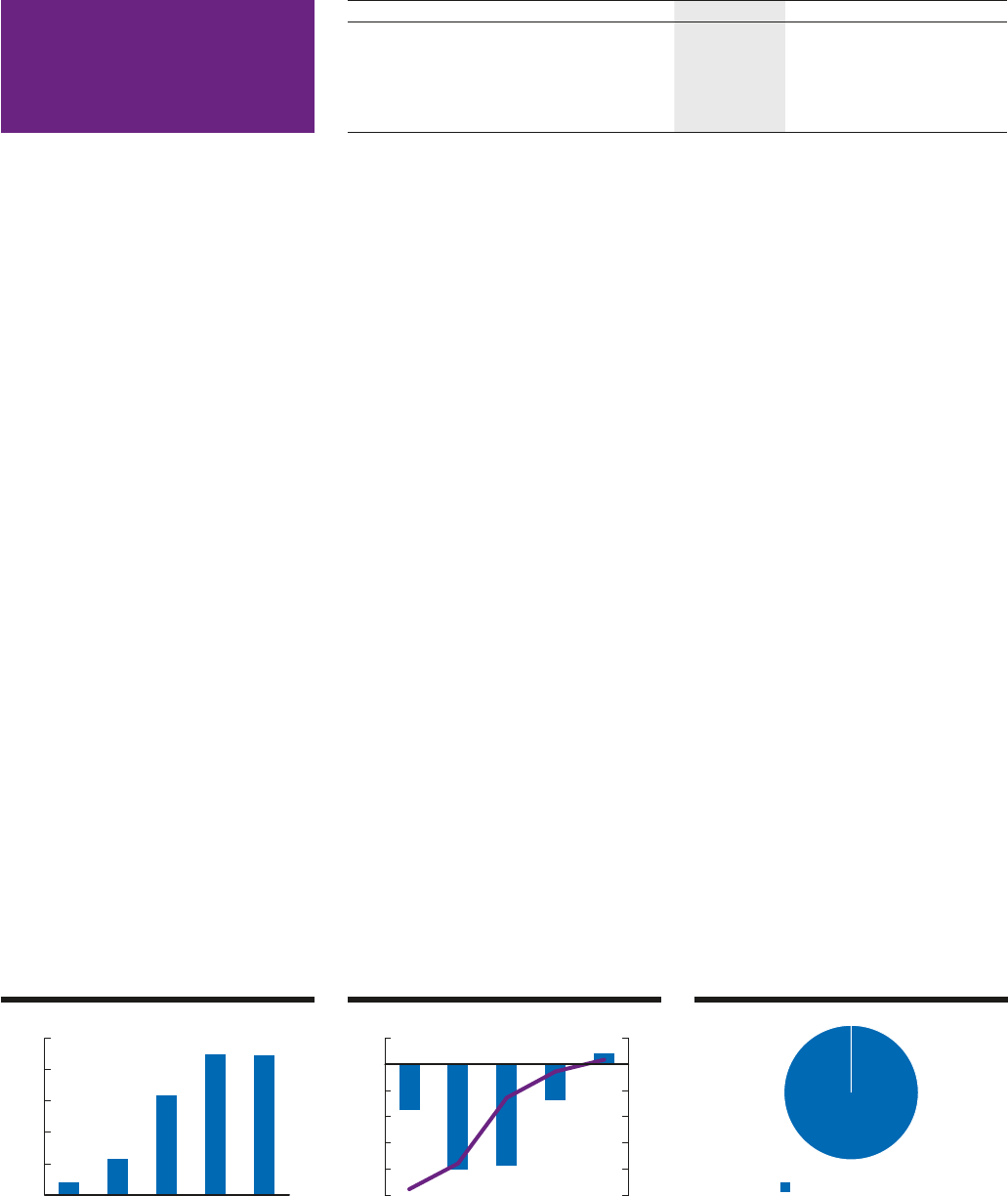

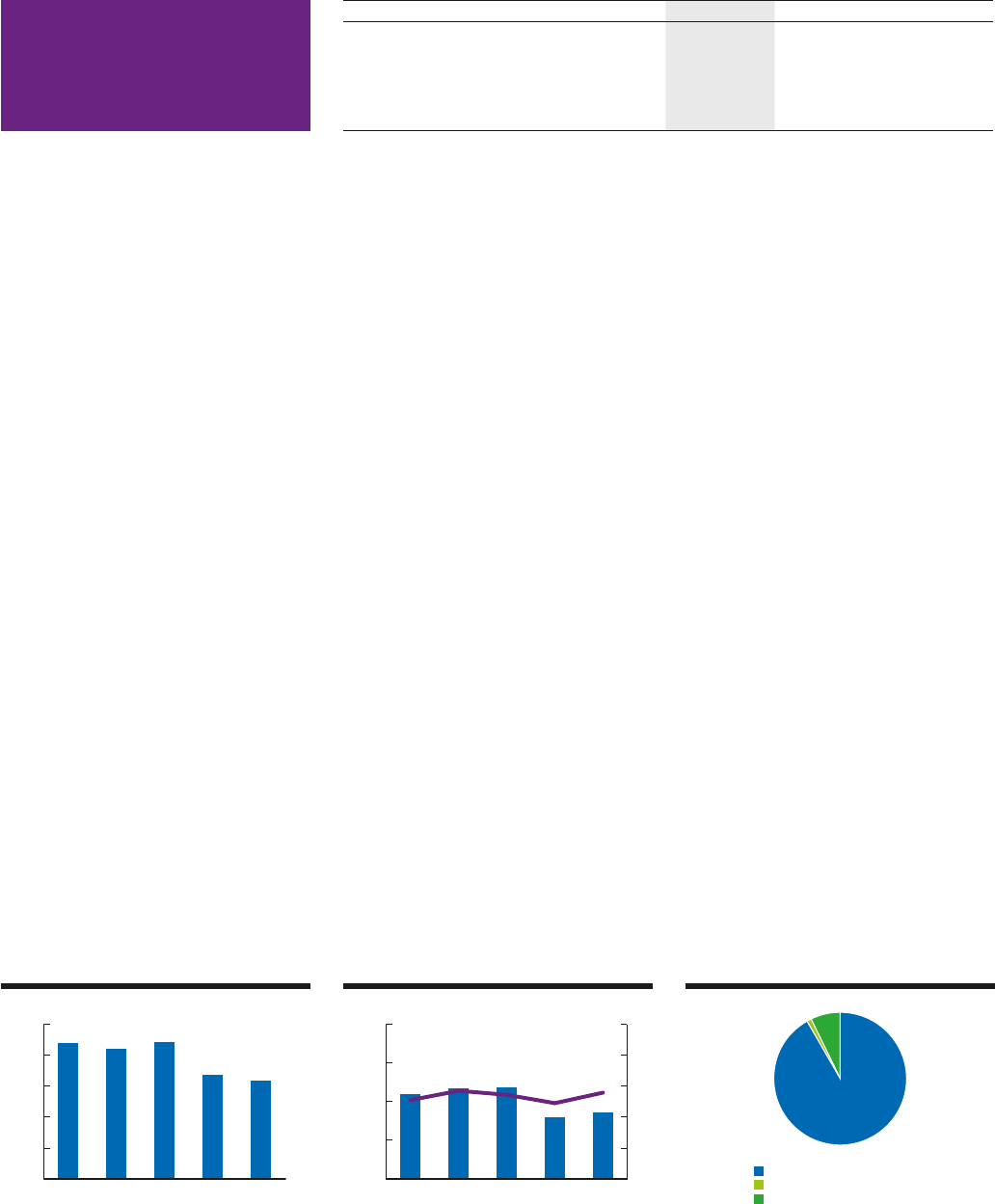

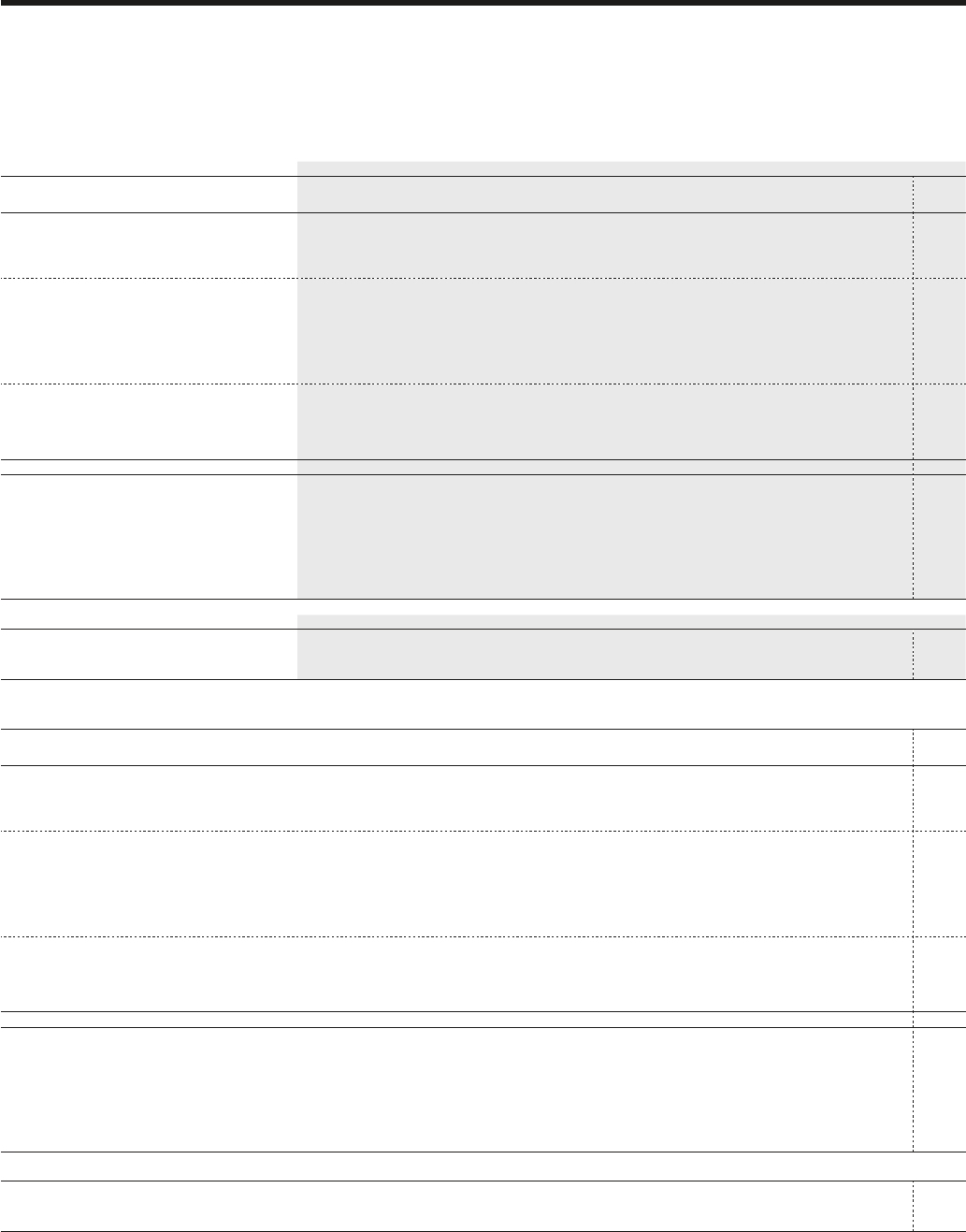

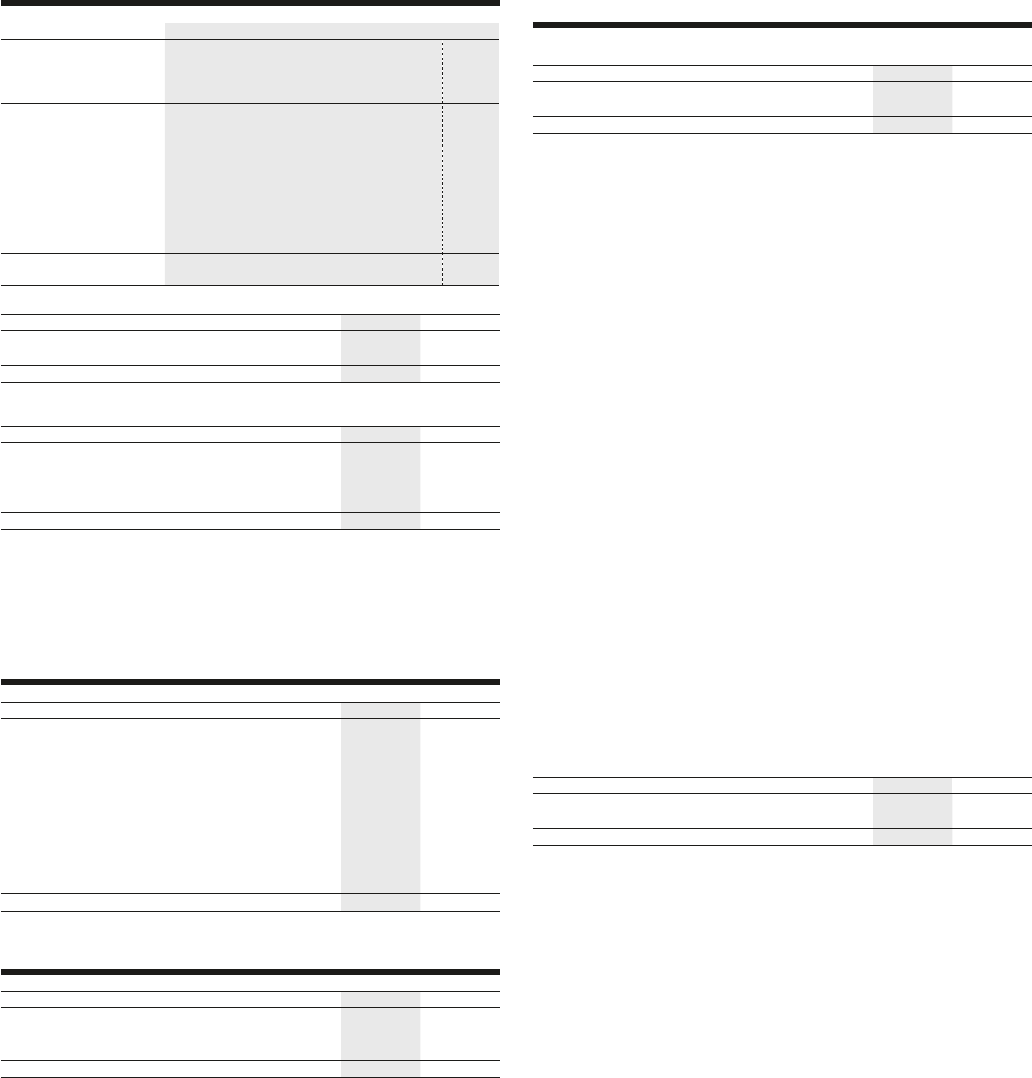

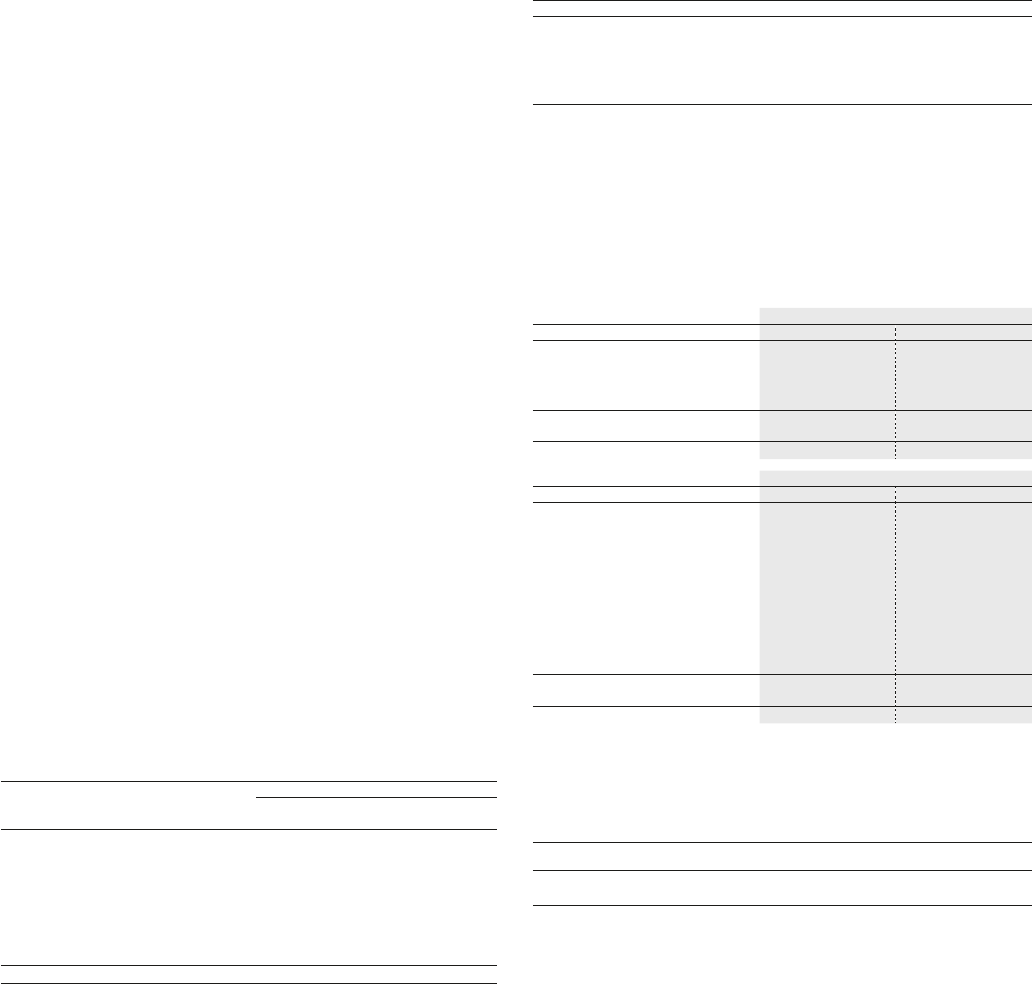

Net sales

0

3,000

6,000

9,000

12,000

15,000

20142013201220112010

SEK million

EBITDA & EBITDA margin

0

1,000

2,000

3,000

4,000

20142013201220112010

0

10

20

30

40

50

SEK million Percent

Net sales per service

Mobile SEK , million

Fixed broadband SEK million

Fixed telephony SEK million

Other operations SEK million

SEK million 2014 2013 Growth

Number of customers (in thousands) 3,976 4,476 –11%

Net sales 12,629 12,453 1%

of which mobile end-user service revenue 7,252 6,950 4%

EBITDA 3,612 3,448 5%

EBIT1) 2,371 2,063

1) excluding one-off items (Note 6)

Sweden

Tele2 – Annual Report 2014 11

Administration report

Market share gain in the business segment

The business segment saw continued strong mobile revenue

growth, driven by an increased customer stock as well as continued

strong intake within cloud PBX. Only 18 months after its launch, the

PBX service was number two in the market. The latest PTS report

(Post- och Telestyrelsen – National Regulatory Authority in Sweden)

showed that Tele2 Business gained most mobile market share dur-

ing the first half of 2014 with an increase of 1 percentage unit, lead-

ing to an estimated total mobile market share of 18 percent. Simi-

larly the Swedish Quality Index for the business market showed that

the customer satisfaction has improved substantially over the year

with Tele2 taking the number one position for broadband and the

number two position for mobile.

The company acquired significant new and extended contracts

such as NCC, Bonnier, Åklagarmyndigheten and Kriminalvården.

Also, the segment continued to see an increased market demand for

communication as a service, driven by the new Kammarkollegiet

frame agreement for the Public sector.

Challenges to address in 2015

Tele2 Sweden will continue its dual brand strategy, positioning

Comviq as the modern mobile price fighter and Tele2 as the full suite

value proposition to meet the different customer needs and follow

the Tele2.0 strategy by continuously aim to see things from the cus-

tomers’ perspective.

The company expects mobile data demand to keep growing as

customers become more and more mobile. Consequently, Tele2

Sweden will increase its focus on the upsell of data, optimizing the

network, and drive sales towards high speed data offerings, thereby

increasing customer value and lowering production cost.

Tele2 Sweden will also keep improving coverage and capacity

throughout the network and continue the roll-out of the 800 MHz

frequency complemented by 1800 MHz in order to enhance its 4G

network.

In summary, Tele2 Sweden aims to continue to deliver good

profitability during 2015 through:

• Leverage increased data consumption among our customers,

mainly driven by upsell of data and transition towards larger

data buckets

• Effective use of distribution channels

• Continue to lever on efficiency in joint operation set-up

• Steering towards online activities and self-service

• Continued cost efficiency in all areas within Tele2 Sweden

operations

Continued Sweden

12 Tele2 – Annual Report 2014

Administration report

2014 in brief

In 2014 Tele2 Netherlands continued to further strengthen its abili-

ties to be able to deliver on the Group’s mission, to offer what our

customers need, for less. This by expanding and improving its

nationwide fiber network, rolling out its LTE-advanced 4G network

and developing products and services for both consumer and B2B

customers.

EBITDA amounted to SEK 903 (1,251) million, reflecting the

investment in the MNO rollout as well as maintained price pressure

in the fixed broadband market.

Mobile

During the year Tele2 noted a positive customer base development.

Since the fourth quarter 2014 Tele2 only offers 4G enabled devices,

to ensure that these customers are able to benefit from the new

4G-network. 2014 ended with the thirteenth consecutive quarter of

customer growth bringing the total mobile customer base to

813,000 (694,000).

Announcing commercial launch of its 4G network

In 2014 Tele2 Netherlands executed successfully on its 4G rollout

and in the end of 2014 the company announced that it would open

its 4G network for commercial services in the beginning of 2015.

This announcement marked an important milestone for the rollout,

which began when Tele2 obtained a frequency license in the

beginning of 2013.

From launch, the network will be LTE-advanced and will cover an

area stretching from Rotterdam to Amsterdam and Utrecht, covering

2,100 square kilometres. Tele2 expects to reach nationwide cover-

age in the beginning of 2016, only three years after the frequency

license was awarded.

Fixed broadband

Tele2 Netherlands has focused on improving its fixed service port-

folio during 2014. This by further improving the quality of its TV

product, adding popular channels like HBO and expanding the

amount of channels that can be watched in high definition. The

upgrade of the TV product in the beginning of 2014 was combined

with a new pricing strategy titled; ‘what you need for less’, shifting

the company’s position from a price fighter to a communications pro-

vider that offers a balance of great price and good quality.

As a result of this focus, Tele2 Netherlands managed to once again

grow its residential customer base after a 36 month period of

decline. On December 31, 2014, the total residential broadband base

was 369,000 (374,000).

Expansion of the business portfolio

The Dutch business sales team managed during the year to add sev-

eral new big clients to its already impressive customer list. Among

these were companies like; Royal Dutch Airlines KLM, the Dutch

Salvation Army and the Vattenfall Group.

Challenges to address in 2015

Tele2 Netherlands will continue during 2015 to expand its 4G net-

work. Throughout the year the rollout will continue to spread across

the entire country at a pace that ensures the best possible user

experience for the customers. Tele2 Netherlands is the first provider

in the world in the process of building and launching a nationwide

4G only network.

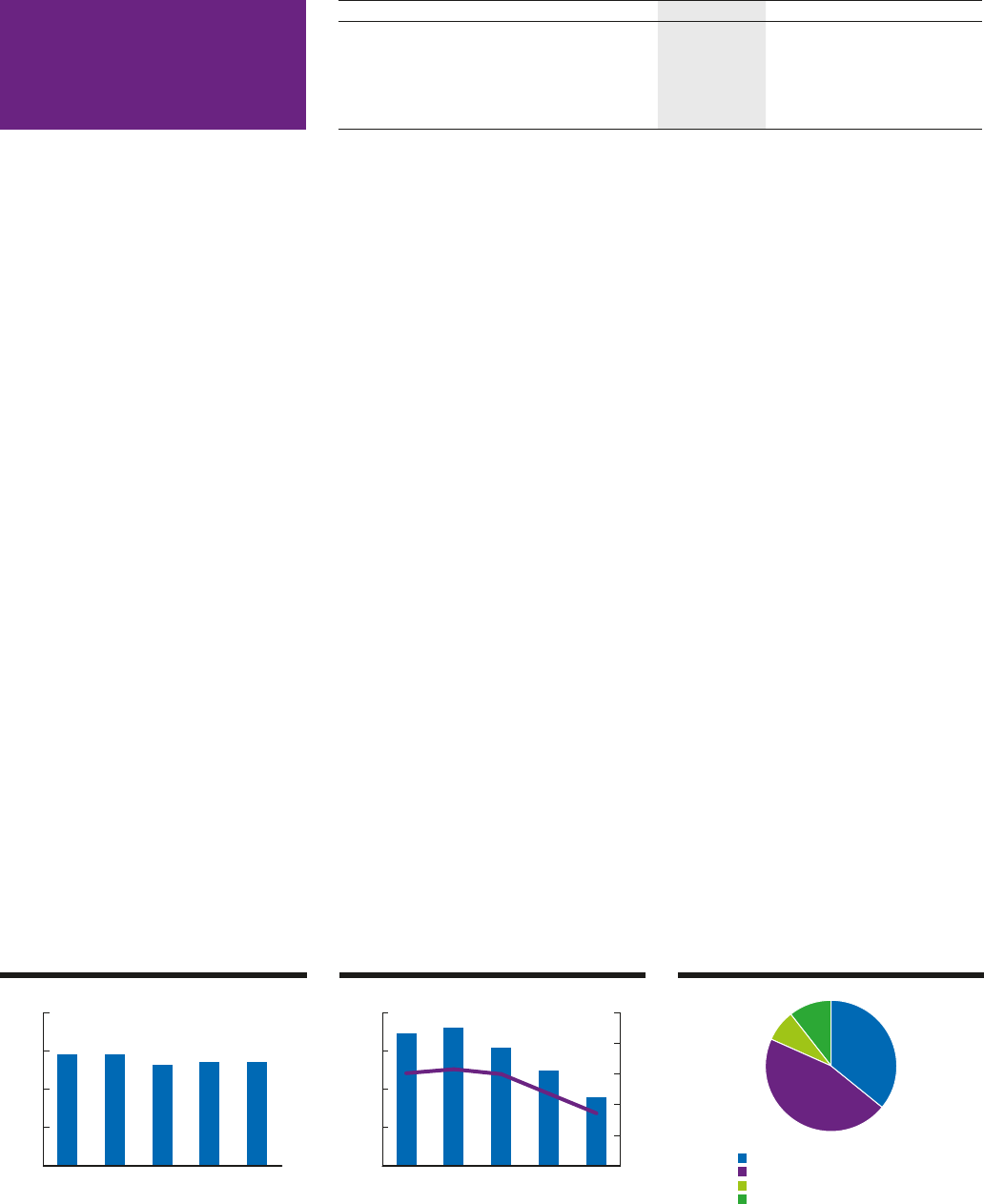

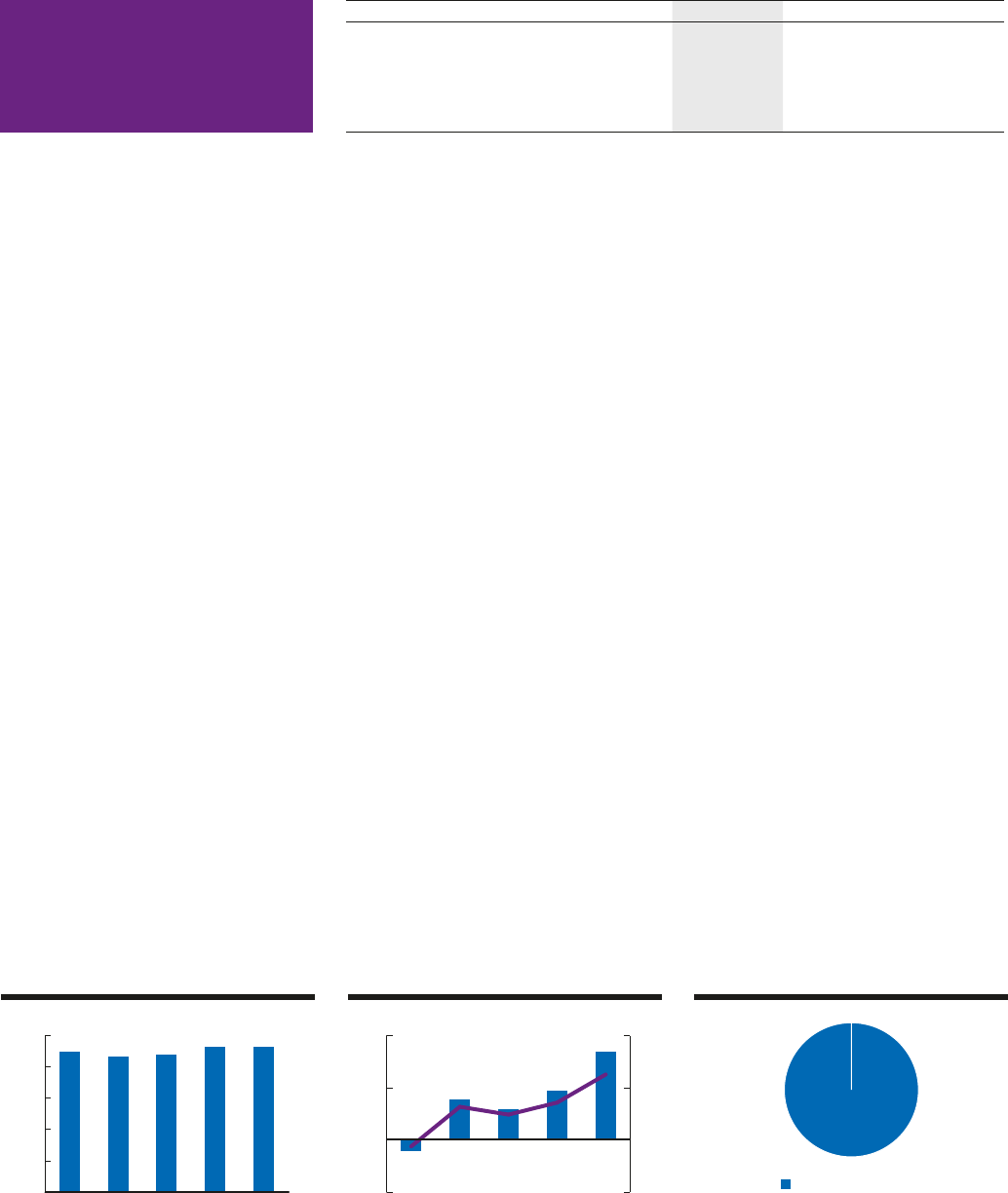

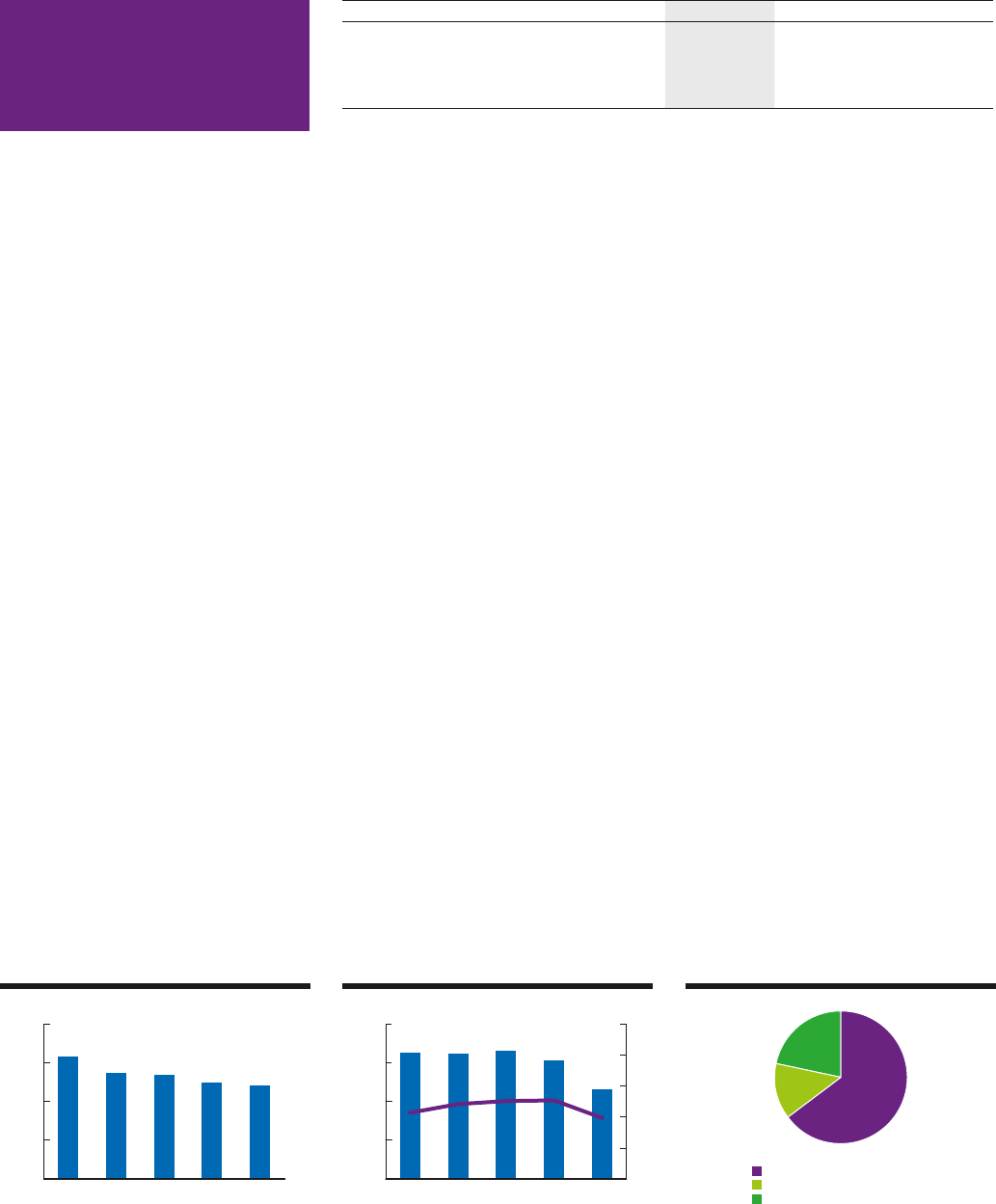

SEK million 2014 2013 Growth1)

Number of customers (in thousands) 1,257 1,175 7%

Net sales 5,439 5,435 –5%

of which mobile end-user service revenue 1,203 944 21%

EBITDA 903 1,251 –32%

EBIT2) 237 650

1) less exchange rate fluctuations

2) excluding one-off items (Note 6)

Netherlands

Net sales

0

2,000

4,000

6,000

8,000

20142013201220112010

SEK million

EBITDA & EBITDA margin

0

500

1,000

1,500

2,000

20142013201220112010

0

10

20

30

40

50

SEK million Percent

Net sales per service

Mobile SEK , million

Fixed broadband SEK , million

Fixed telephony SEK million

Other operations SEK million

Tele2 – Annual Report 2014 13

Administration report

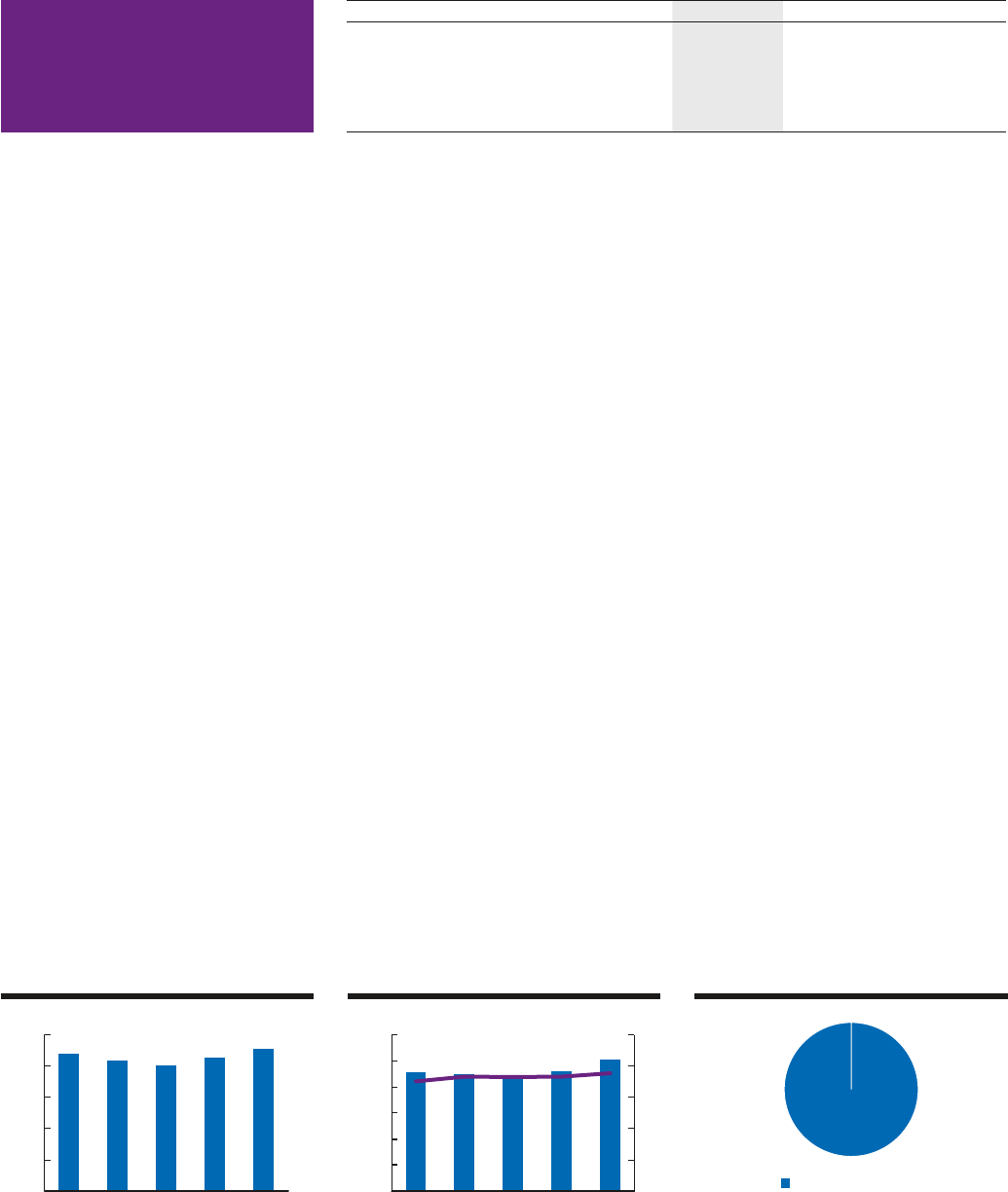

Net sales

0

300

600

900

1,200

1,500

20142013201220112010

SEK million

EBITDA & EBITDA margin

-500

-400

-300

-200

-100

0

100

20142013201220112010 -150

-120

-90

-60

-30

0

30

SEK million Percent

2014 in brief

2014 was a successful year for Tele2 Kazakhstan and the company

delivered its first positive EBITDA results since commercial launch.

Starting from January 1, 2014 the interconnect level in the country

was lowered by 15 percent leading to an improved gross margin for

Tele2 Kazakhstan. This, together with better economies of scale,

were the main reasons for improved operational results in 2014.

Most affordable telecom operator

Increased competition on the telecom market resulted in a move

from pay as you go price plans to bucket price plans. As a result,

Tele2 further increased its price leadership in the market. The new

bucket price plan offers unlimited on-net voice, limited amount of

off-net calls and large amount of data. The plan has attracted a lot of

attention and customers to Tele2.

Earlier in the year Tele2 launched an unlimited on-net tariff plan,

which also attracted new subscribers. Furthermore, the first online

re-registration of a mobile number was launched by Tele2 Kazakh-

stan in June 2014.

The “ComNews Research” agency conducted a comparative

research on all mobile operators’ tariff plans in Kazakhstan (Febru-

ary 2013 - February 2014). The results of this research confirmed

that Tele2 Kazakhstan offers the best value proposition for custom-

ers in the market and Tele2 Kazakhstan was acknowledged to be

the most affordable mobile operator in the country.

Network expansion to improve quality

During the year, Tele2 Kazakhstan continued to invest in the mobile

network to improve the quality perception in the market. Most

efforts were concentrated on expanding the geographical coverage,

increasing capacity and improving quality.

Challenges to address in 2015

The company will continue to work toward increasing customer

market share through improved customer intake quality, leading to

revenue growth and expanding EBITDA level.

The competitive environment is expected to intensify as the mar-

ket has gone from three to four mobile operators. The main chal-

lenge for Tele2 Kazakhstan will be to defend its customer base

through maintained price leadership.

SEK million 2014 2013 Growth1)

Number of customers (in thousands) 3,297 2,751 20%

Net sales 1,334 1,344 11%

of which mobile end-user service revenue 978 909 20%

EBITDA 43 –138

EBIT2) –178 –450

1) less exchange rate fluctuations

2) excluding one-off items (Note 6)

Net sales per service

Mobile SEK , million

Kazakhstan

14 Tele2 – Annual Report 2014

Administration report

2014 in brief

2014 was an important milestone for Tele2 Croatia and the company

made significant operational progress during the year. The

increased profitability was delivered through a combination of solid

subscriber growth and operational cost efficiency. This was man-

aged despite a tough environment with declining market revenues.

Tele2’s subscriber growth came through strong campaigns and

value for money based offers. This was acknowledged by ICERTIAS

(International Certification Association), who awarded Tele2 Croatia

the “Best Buy award 2014” for offering the best value among tele-

communications operators overall. Tele2 also launched a new data

offer within the prepaid segment, which generated great traction in

the market. Another success was the summer tourist season where

Tele2 had highly competitive offers, both for tourist SIMs and visitor

roaming.

In the end of 2014, Tele2 secured 15 MHz of additional spectrum

in the 1800 MHz band in order to continue to improve the network

quality.

Increased prices due to frequency fees

During 2014 the regulatory environment became more uncertain as

the local government unexpectedly announced the increase of radio

frequency fees in the country by three times by December 2014. As

a proactive measure Tele2 Croatia increased its prices from July 1 for

all its customers to cover the increased cost for frequencies.

Challenges to address in 2015

Tele2 Croatia will continue to have a good balance between cus-

tomer intake and improving profitability. The good momentum in

postpaid residential sales is expected to continue and the company

will further develop the business customer segment.

Continuous improvement of Tele2 voice and data network quality

is an imperative, as well as the overall customer experience. How-

ever, to do so the company emphasizes the need for regulatory and

legislative stability in Croatia.

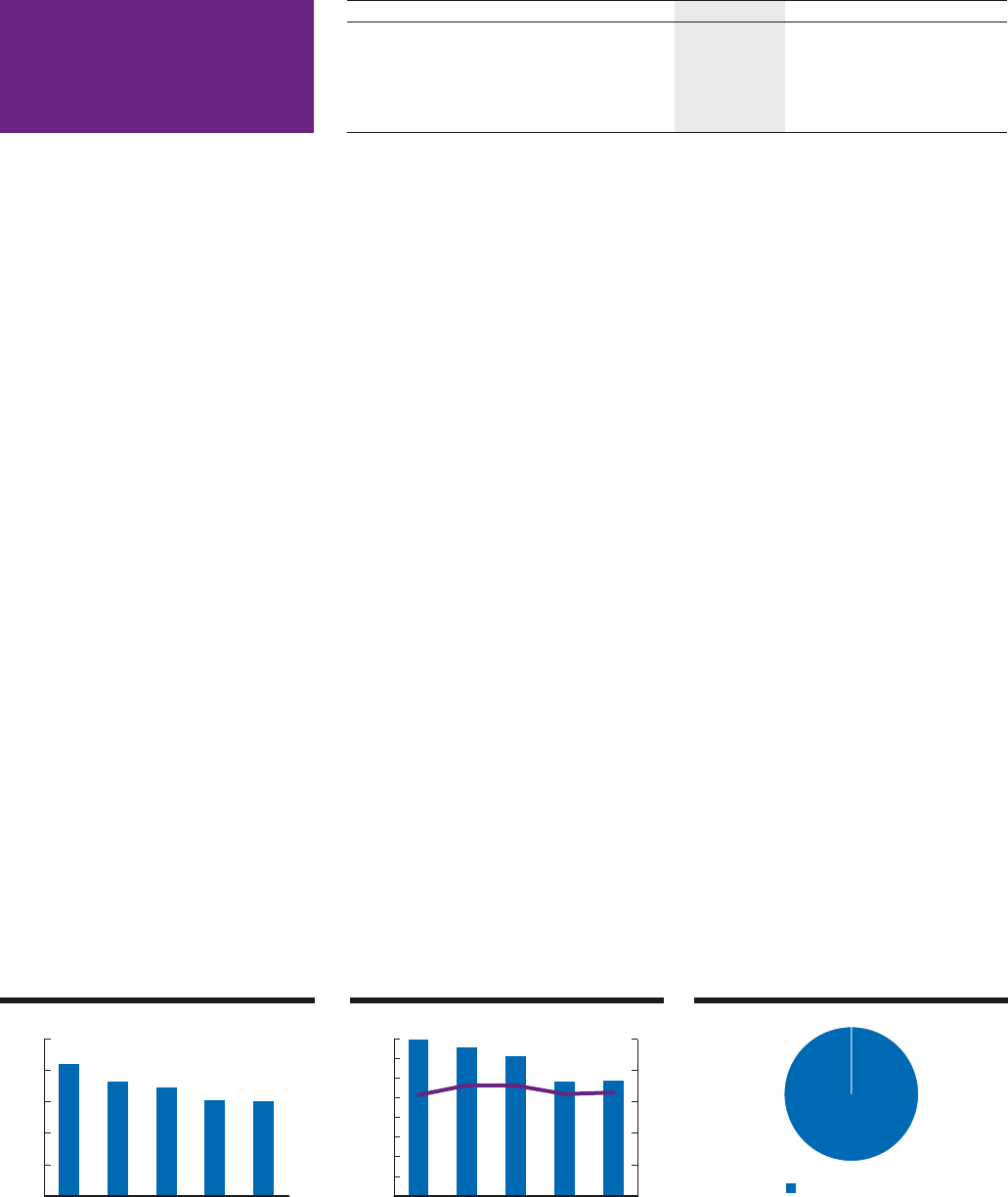

Net sales

0

300

600

900

1,200

1,500

20142013201220112010

SEK million

EBITDA & EBITDA margin

-100

0

100

200

20142013201220112010

-10

0

10

20

SEK million Percent

SEK million 2014 2013 Growth1)

Number of customers (in thousands) 823 793 4%

Net sales 1,390 1,397 –5%

of which mobile end-user service revenue 803 749 3%

EBITDA 169 95 71%

EBIT2) 87 –6

1) less exchange rate fluctuations

2) excluding one-off items (Note 6)

Net sales per service

Mobile SEK , million

Croatia

Tele2 – Annual Report 2014 15

Administration report

2014 in brief

In 2014 the mobile market was increasingly competitive in the Lith-

uanian market. However Tele2 Lithuania managed to maintain a

stable operational performance. In the beginning of the year the

company successfully upgraded its mobile network and the upgrade

enabled Tele2 Lithuania to provide all network services including

2G, 3G and 4G. Throughout the year the company has focused on

the 4G rollout and successfully achieved the plan to cover 47 per-

cent of the population by year end 2014.

Market leading

In 2014, Tele2 Lithuania reported the highest mobile revenue among

all three operators in the country and in Q3 2014 the company’s

mobile revenue market share was at an all-time high at 40 percent.

Challenges to address in 2015

The key priority for Tele2 Lithuania in 2015 is to continue with the

LTE rollout to achieve the target to cover 90 percent of the popula-

tion by the end of the year.

The company will also continue to aggressively grow its market

share in the business segment.

Net sales

0

300

600

900

1,200

1,500

20142013201220112010

SEK million

EBITDA & EBITDA margin

0

100

200

300

400

500

600

20142013201220112010

0

10

20

30

40

50

SEK million Percent

Net sales per service

Mobile SEK , million

SEK million 2014 2013 Growth1)

Number of customers (in thousands) 1,810 1,851 –2%

Net sales 1,364 1,280 1%

of which mobile end-user service revenue 847 843 –5%

EBITDA 506 461 5%

EBIT 430 342

1) less exchange rate fluctuations

Lithuania

16 Tele2 – Annual Report 2014

Administration report

2014 in brief

The mobile market was characterized by price competition, how-

ever Tele2 Latvia was able to keep a robust revenue profile and sta-

ble operational development. This was achieved through successful

customer base management, upselling and data revenue growth.

Successful efforts

In the beginning of 2014, Tele2 Latvia launched several new initia-

tives in the customer service area and deployed market leading bill-

ing and customer care solutions. Furthermore, Tele2 Latvia finalized

its network swap and commercially introduced LTE technology to its

mobile broadband services, combined with a new price plan port-

folio. The company also achieved a significant gain in reputation

and trust as a result of ongoing attention to service excellence and

performance.

During the second half of 2014, Tele2 Latvia also launched roaming

data buckets for EU countries, making it more convenient for cus-

tomers to use mobile data abroad. Also new data tariff plans for

domestic use was introduced during the year.

Challenges to address in 2015

The key focus in 2015 is the aggressive LTE rollout as the LTE 800

MHz license allows the company to deploy LTE 800 network rollout

from mid–2015. The target is to cover 90 percent of the population

by year end 2015.

Tele2 Latvia will also continue to strengthen its market position

through focus on revenue growth, customer satisfaction and inno-

vation.

Net sales

0

300

600

900

1,200

1,500

20142013201220112010

SEK million

EBITDA & EBITDA margin

0

50

100

150

200

250

300

350

400

20142013201220112010

0

10

20

30

40

50

SEK million Percent

SEK million 2014 2013 Growth1)

Number of customers (in thousands) 975 1,031 –5%

Net sales 907 915 –6%

of which mobile end-user service revenue 551 533 –2%

EBITDA 294 292 –4%

EBIT 187 188

1) less exchange rate fluctuations

Net sales per service

Mobile SEK million

Latvia

Tele2 – Annual Report 2014 17

Administration report

2014 in brief

2014 was characterized by high competitive pressure on the Estonia

mobile market and especially through telemarketing initiatives.

However, Tele2 Estonia has, under these circumstances, managed

to obtain a satisfactory financial performance throughout 2014 and

achieved a record high Customer Satisfaction score.

Modernisation

In the beginning of 2014 Tele2 Estonia secured two mobile licenses

in the 800 MHz and 2100 MHz frequency bands. The company also

completed a network modernization through a network swap of old

equipment in order to provide the best voice and data service qual-

ity. The upgrade enabled Tele2 Estonia to provide all network ser-

vices including 2G, 3G and 4G to its customers.

In the second half of 2014, Tele2 Estonia introduced data centric

bundled subscriptions with unlimited voice and SMS, to stimulate

further growth of data usage.

In 2014, the EBITDA for mobile in Estonia was positively impacted

by SEK 20 million as a result of the sales of a mobile license in the

2600 MHz frequency band.

Challenges to address in 2015

The key priorities for Tele2 Estonia in 2015 is to continue with the

LTE rollout, monetize increasing data usage and focus on selling

more carrier services with the infrastructure the company has after

the acquisition of Televõrgu.

SEK million 2014 2013 Growth1)

Number of customers (in thousands) 491 507 –3%

Net sales 634 674 –11%

of which mobile end-user service revenue 382 391 –7%

EBITDA 173 161 2%

EBIT 55 55

1) less exchange rate fluctuations

Estonia

Net sales

0

200

400

600

800

1,000

20142013201220112010

SEK million

EBITDA & EBITDA margin

0

100

200

300

400

20142013201220112010

0

10

20

30

40

50

SEK million Percent

Net sales per service

Mobile SEK million

Fixed telephony SEK million

Other operations SEK million

18 Tele2 – Annual Report 2014

Administration report

2014 in brief

Tele2 Austria’s result were impacted by effective marketing activi-

ties, a steady performance within the business segment and a good

contribution from the wholesale data business.

During the year, Tele2 Austria had its strategic focus on growth

and innovation in the business and residential segments, building

on existing areas of operational excellence. Tele2 Austria also con-

centrated its efforts on retaining high value customers across all

segments. The level of customer satisfaction was as a result very

high.

Challenges to address in 2015

In 2015, Tele2 Austria’s growth focus will concentrate on the launch

of mobile B2B services based on an MVNO setup. With the high-

speed broadband and TV products launched in 2014, the residential

segment will continue the focus on retention and selective growth.

Net sales

0

500

1,000

1,500

2,000

20142013201220112010

SEK million

EBITDA & EBITDA margin

0

100

200

300

400

20142013201220112010

0

10

20

30

40

50

SEK million Percent

Net sales per service

Fixed broadband SEK million

Fixed telephony SEK million

Other operations SEK million

SEK million 2014 2013 Growth1)

Number of customers (in thousands) 256 285 –10%

Net sales 1,209 1,244 –8%

EBITDA 231 308 –28%

EBIT 94 183

1) less exchange rate fluctuations

Austria

Tele2 – Annual Report 2014 19

Administration report

2014 in brief

During 2014 Tele2 Germany saw positive effects of its transforma-

tion from a fixed operator to a fixed and mobile service provider.

Despite the tough competition on the market, Tele2 Germany kept its

good balance between profitability and growth within the mobile

segment, supported by a solid performance in the fixed and broad-

band segments.

Going mobile

The mobile segment had a steady accelerated growth during the

year. The results reflect partly the improved sales channels setup

during Q2 2014 and partly the transformation to a fixed and mobile

provider. Within fixed services both the fixed telephony (CPS: Carrier

Pre-Selection and OCBC: Open Call-by-Call) and the fixed broad-

band followed the general declining market trend. However the

segments generated cash contributions above plan and provided a

source for cross-sale to mobile services - both regular mobile ser-

vices and higher ARPU fixed-via mobile services.

Challenges to address in 2015

In the fixed business, Tele2 Germany will aim to defend its position

in CPS and OCBC and continue to maximize profits from those

declining segments.

SEK million 2014 2013 Growth1)

Number of customers (in thousands) 709 713 –1%

Net sales 916 867 0%

of which mobile end-user service revenue 439 316 32%

EBITDA 131 138 –9%

EBIT 78 99

1) less exchange rate fluctuations

Germany

Net sales

0

500

1,000

1,500

2,000

2,500

20142013201220112010

SEK million

EBITDA & EBITDA margin

0

100

200

300

400

500

20142013201220112010

0

10

20

30

40

50

SEK million Percent

Net sales per service

Mobile SEK million

Fixed broadband SEK million

Fixed telephony SEK million

20 Tele2 – Annual Report 2014

Administration report

Acquisitions and divestments

On February 5, 2015 the Norwegian competition authorities

announced that they have approved Tele2’s divestment of its Nor-

wegian operations to TeliaSonera announced in July 2014. The Nor-

wegian operation was sold for SEK 4.8 billion and resulted in a capi-

tal gain in 2015 of SEK 1.7 billion, including costs for central support

system for the Norwegian operation and other transaction costs. The

capital gain include a positive effect of SEK 143 million related to

exchange rate differences previously reported in other comprehen-

sive income which will be recycled over the income statement but

with no effect on total equity. The divested operations have been

reported separately under discontinued operations in the income

statement, with a retrospective effect on previous periods, and as

assets held for sale in the balance sheet on December 31, 2014. Fur-

ther information can be found in Note 36.

On October 23, 2013 Tele2 announced the sale of its Swedish res-

idential cable and fiber operations to Telenor for SEK 793 million.

The sale was completed on January 2, 2014 after approval by regu-

latory authorities and the capital gain in 2014 amounted to SEK 258

million. Further information can be found in Note 16.

No material operations were acquired during 2014.

Events after the end of the financial year

The sale of the Norwegian operation was completed in February

2015 after approval by regulatory authorities. Further information

can be found in Note 36. As a result of the transaction, the Board of

Tele2 has decided to recommend an extraordinary dividend pay-

ment of SEK 10.00 per ordinary A and B shares to the Annual Gen-

eral Meeting in May 2015, in addition to the proposed dividend pay-

ment of SEK 4.85 per ordinary A and B shares.

In February 2015, Tele2 delivered 26,032 B shares in own cus-

tody as a result of share rights in the incentive program LTI 2011

being exercised.

Risks and uncertainty factors

At Tele2, we believe that every risk also presents an opportunity.

Tele2 works proactively to identify and monitor the most important

risks through an enterprise risk management process for the pur-

pose of minimizing surprises, improved decision making, reduced

losses and increased reward.

Strategic risks

Risks and uncertainties which could threaten Tele2’s ability to

achieve its strategic objectives are assessed by the senior executives

as well as the Board of Directors. Summaries of some of these risks

are presented below.

Availability of frequencies and telecom licences

Tele2’s ability to retain customers may be hampered by not obtain-

ing required licences or frequencies, at all or, at a reasonable price.

Hence, Tele2 has put in place processes to ensure compliance with

licence requirements, increase changes for renewal and extension

of existing licences and for obtaining adjacent and new licences.

Tele2 also works in close contact with regulators and industry asso-

ciations to become aware of upcoming licence distributions or redis-

tributions but the outcome of such distributions is coupled with

uncertainty.

Integration of new business models

Tele2’s business environment is experiencing continuous changes

which may affect our position in the market. These include new

forms of connectivity (e.g. VoIP and SoftSIM), new market segments

(e.g. machine-to-machine) and changed customer behaviour (such

as revenue migration from voice to data). Tele2’s senior executives

closely monitors technological advances and market changes to

adapt its strategies to be able to benefit from their possibilities.

Changes in regulatory legislation

Changes in legislation, regulations and decisions from authorities

for telecommunications services can have a considerable effect on

Tele2’s business operations and the competitive situation in its

operating markets. Price regulation, in the area of access and inter-

connect, have great impact on Tele2, and could also result in a risk

for disputes with other operators. Access regulation, which ensures

access to incumbents copper and fibre networks, must ensure and

protect a well-balanced competition in each market. Tele2 works

actively with telecom regulators and industry associations, in order

to promote sufficient regulation which supports fair competition in

its operating markets.

Data privacy

Another area where European regulation is increasing is data pri-

vacy where breaches of customer’s personal information could

potentially result in major fines and significant reputational damage.

Tele2 works actively to be able to comply with any such require-

ment and continuously works to strengthen its procedures to ensure

that our customer’s personal data is secured and protected.

Dependency on suppliers and business partners

Tele2 is dependent on handset manufacturers such as for example

Apple and Samsung for attracting customers. Tele2 is also depen-

dent on equipment and network suppliers for rolling out networks

and be able to offer good quality access services. In Sweden and the

Netherlands, Tele2 has reached agreements with other telecom

operators to build and operate common network infrastructures. In

some other countries, Tele2 depends on agreements with other net-

work operators to provide mobile services. Any of these third party

agreements impose risks, be it in the form of delays in roll-out, limi-

tations for customised development or limitations on operating prof-

itability. Tele2 continuously evaluates existing agreements and the

form of its co-operations in dialogue with its partners.

Operation in Kazakhstan

The political, economic, regulatory and legal environment as well as

the tax system in Kazakhstan is still developing and is less predict-

able than in countries with more mature institutional structures.

This also applies to prevailing corporate governance codes, busi-

ness practices and the reporting and disclosure standards. The mar-

ket and the operations in Kazakhstan therefore represent a different

risk from those associated with investments in other countries and

can affect Tele2’s abilities to operate and develop its operation in

this market. Tele2 continuously monitors the development in this

market and has contact with relevant authorities. Tele2 also contin-

uously monitors its internal operation in Kazakhstan through inter-

nal audits and other central oversight functions.

Geopolitical risks

Depending on how the situation evolves the changed geopolitical

situation following the Crimea crisis could potentially affect some of

Tele2’s operations, particularly in the countries bordering Russia.

Tele2 – Annual Report 2014 21

Administration report

Tele2 is therefore closely monitoring the development and world

events and is kept informed by local management, government offi-

cials and independent sources.

Financial Risk Management

Through its operations, the Tele2 Group is exposed to various finan-

cial risks such as currency risk, interest risk, liquidity risk and credit

risk. Financial risk management is mainly centralized to the Group

treasury function. The aim is to control and minimize the Group’s

financial risks as well as financial costs, and optimize the relation

between risk and cost. Further information on financial risk man-

agement can be found in Note 2.

Employees

On December 31, 2014, the number of employees in Tele2 was 5,387

(4,945) excluding Norway. Please refer to Note 33 and Note 34 for

additional information regarding Number of employees, split per

gender and age groups, and Personnel costs.

Tele2 is a growth-oriented organization. The aim of Tele2’s

human resources management is to prepare and grow our employ-

ees in order to meet the requirements and future needs of the busi-

ness. Tele2’s employees should be highly engaged and motivated

and experience a great sense of pride and identification with the

corporate values of the company and its overall strategy. To attract

and retain the right people is vital to our growth strategy; being

considered a great place to work is a prioritised goal for Tele2 in the

area of people management.

Focus areas

Our main focus areas are stated below.

Leadership and Tele2 Way

Exemplary leadership behaviours are primarily based on the corpo-

rate values, the Tele2 Way. Managers are meant to be the culture

role models that lead by example and truly “walk the talk”. The

Tele2 Way, along with the Code of Conduct, provides a framework

and guides employees in their professional behaviour and decision

making every day. All managers are trained in the Tele2 Way;

which includes refreshment courses every second year.

Performance and Talent management

Tele2 has a common performance management process for the

whole Group, which provides a consistent way of setting goals and

assessing performance. It also serves as a foundation to deal with

talent management. All employees are assessed in two dimensions:

what and how, i.e. goal completion as well as professional behav-

iour based on Tele2’s corporate values, the Tele2 Way.

When it comes to managing talent, Tele2 strongly supports and

encourages internal promotions, both horizontal and vertical. A

greater emphasis has been put on diversity, the aim being that the

percentage of female managers and leaders reflects the percentage

of female employees within the company.

The mapping of top performers, top talents and key roles are con-

ducted every year via the Talking Talent sessions. The purpose of the

talent management process is to ensure long-term succession to man-

agerial and key roles, develop the company’s existing workforce and

minimise business risk if key position holders leave the company.

Tele2 use Tele2 People, an online tool for managing performance

and talent. The tool provides our managers and the organisation

with more accurate and reliable data and serves as base for sound

decision making.

Learning and Development

Tele2 has a common framework for learning and development

based on 70:20:10 principles. According to these principles 70 per-

cent of learning comes from experience, such as learning by doing,

job rotation, participation in cross-functional projects and challeng-

ing work tasks; 20 percent comes from learning from relationships,

such as mentoring, coaching and networking; and 10 percent comes

from official training programs such as academic courses, e-learn-

ing, books/periodicals and media.

Reward and Recognition

Tele2 offers competitive compensation and benefit packages in

order to attract, retain and motivate employees. Tele2’s packages are

determined by the local market and Tele2 participates in local sal-

ary surveys annually to ensure that its offerings remain competitive

in terms of base salary, short-term incentives, long-term incentives

and benefits. The company believes in pay for performance; high-

performing individuals should be rewarded well.

Engagement

Every year, Tele2 conducts an employee survey called ‘My Voice’.

The survey measures:

• Managers´ leadership capabilities by means of the Leadership

Index (LSI);

• Employee engagement;

• Tele2’s internal attractiveness as an employer by means of the Net

Promoter Score (NPS);

• Tele2 Way Index (TWI), assessing how well we live our corporate

values.

A total of 93 percent of all employees participated in the 2014 sur-

vey. My Voice showed that a total of 47 (43) percent of Tele2’s

employees are fully engaged with high energy and high clarity, a

result which is significantly higher compared to 37 percent for the

benchmarked companies. One reason for such good result is that all

managers and organizational units each year identify engagement-

related goals to work with. Tele2 is very proud of its results and will

continue focusing on engagement as engaged employees perform

well, walk the extra mile and are personally motivated to make

Tele2 an even better place to work.

Employer branding

Tele2 has a common global employer branding standard which con-

sists of employer brand offer, guidance for implementation, career

web page, employer branding movie, image library as well as

LinkedIn account. The implementation of the concept is localized,

i.e. each country defines which channels and activities to use based

on local needs and requirements.

Corporate responsibility (CR)