TRM CLM User Guide

User Manual:

Open the PDF directly: View PDF ![]() .

.

Page Count: 172 [warning: Documents this large are best viewed by clicking the View PDF Link!]

- Contents

- Preface

- Chapter 1 Overview

- 1.1 CLM

- 1.1.1 Defining contracts in CLM

- 1.1.2 Arranging credit in CLM

- 1.1.3 Structuring of loan products in CLM

- 1.1.4 Capturing and processing drawdowns in CLM

- 1.1.5 Processing loan events in CLM

- 1.1.6 Monitoring credit and debt situations in CLM

- 1.1.7 Receivables management in CLM

- 1.1.8 Managing messages in CLM

- 1.1.9 Information used in CLM

- 1.2 Applications of CLM

- 1.3 Setting up and using CLM

- 1.1 CLM

- Chapter 2 Managing static data

- 2.1 Setting up static data for CLM

- 2.2 Schedule templates

- 2.3 Instrument groups

- 2.4 Instrument types

- 2.5 Instruments

- 2.6 Transaction templates

- 2.7 Facility types

- 2.8 Facility templates

- 2.9 Facilities

- 2.9.1 Defining the main attributes

- 2.9.2 Defining contract details

- 2.9.2.1 Defining credit amount details

- 2.9.2.2 Defining drawdown currency details

- 2.9.2.3 Defining counterparty details

- 2.9.2.4 Defining payback FX rate details

- 2.9.2.5 Defining location details

- 2.9.2.6 Defining owner details

- 2.9.2.7 Defining instrument and event details

- 2.9.2.8 Defining funding type details

- 2.9.2.9 Defining tranche details

- 2.9.2.10 Defining transaction template details

- 2.9.2.11 Defining beneficiary details (optional)

- 2.9.2.12 Defining guarantor details (optional)

- 2.9.2.13 Defining sublimits (optional)

- 2.9.2.14 Defining drawdown condition details (optional)

- 2.9.2.15 Defining collateral agreement details (optional)

- 2.9.2.16 Defining drawdown parameter details (optional)

- 2.9.2.17 Defining mandate details

- 2.9.2.18 Defining switches details

- 2.9.2.19 Defining properties details

- 2.9.2.20 Defining links details

- 2.9.2.21 Defining ad hoc message client details

- 2.9.2.22 Defining contact rule details

- 2.9.3 Approving facilities

- 2.9.4 Modifying facilities

- 2.9.5 Mirroring facilities

- 2.10 Tranches

- 2.11 Approvals (optional)

- 2.12 Funding types (optional)

- 2.13 Mandates (optional)

- 2.14 Cashflow groups (optional)

- Chapter 3 Managing amount events

- Chapter 4 Managing drawdowns

- Chapter 5 Managing loan events

- 5.1 Setting up loan events

- 5.2 Processing loan event actions

- 5.3 Editing loan events

- Chapter 6 Managing equity

- Chapter 7 Managing issued guarantees

- Chapter 8 Monitoring loan activity

- Chapter 9 Managing payment advices

- Chapter 10 Managing payment allocations

- Appendix A Features

- A.1 Categories of features

- A.2 List of features

- A.2.1 Add Facility Guarantees

- A.2.2 Allow Drawdown FX Freeze

- A.2.3 Allow Funding Call

- A.2.4 Allow Guarantee

- A.2.5 Allow Revision

- A.2.6 Allow Subsidy Call

- A.2.7 Cancel Provisional Settlements

- A.2.8 Commercial Loan

- A.2.9 Conditional Remuneration

- A.2.10 Continuation Aggregated Rate Function

- A.2.11 Payment Amount Extraction

- A.2.12 Deferment Commission (Setup)

- A.2.13 Drawdown Amendment

- A.2.14 Drawdown Cancellation

- A.2.15 Drawdown Classification

- A.2.16 Drawdown Fee

- A.2.17 Drawdown Fixing

- A.2.18 Drawdown Prepayment

- A.2.19 Drawdown Rescheduling

- A.2.20 Due Amount Carry Forward

- A.2.21 Edit Commitment Fee

- A.2.22 Guarantee Call

- A.2.23 Guarantee Refund

- A.2.24 Guarantee Valuation

- A.2.25 Insert Default Guarantees

- A.2.26 Late Payment Penalty

- A.2.27 Late Payment Penalty Realization

- A.2.28 Loan Pricing

- A.2.29 Off Balance Sheet Accounting (Facility)

- A.2.30 Risk Venture Capital

- A.2.31 Write Off

- Appendix B Loan event parameters

- B.1 Commitment Fee

- B.2 Conditional Remuneration

- B.3 Deferment Commission

- B.4 Drawdown Amendment

- B.5 Drawdown Cancellation

- B.6 Drawdown Classification

- B.7 Drawdown Fee

- B.8 Due Amount Carry Forward

- B.9 Facility Fee

- B.10 Funding Call

- B.11 Guarantee Call

- B.12 Guarantee Refund

- B.13 Late Payment Penalty

- B.14 Prepayment

- B.15 Rate Condition

- B.16 Write-Off

- Appendix C Activity parameters

2

Information in this document is subject to change without notice and does not represent a commitment on the part

of Wall Street Systems. The software and documentation, which includes information contained in any databases,

described in this document is furnished under a license agreement or nondisclosure agreement and may only be

used or copied in accordance with the terms of the agreement. It is against the law to copy the software or

documentation except as specially allowed in the license or nondisclosure agreement. No part of this publication

may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical,

photocopying, recording, or otherwise, without the prior written permission of Wall Street Systems.

Although Wall Street Systems has tested the software and reviewed the documentation, Wall Street Systems

makes herein no warranty or representation, either expressed or implied, with respect to software or

documentation, its quality, performance, marketability, or fitness for a particular purpose. As a result, this

software is provided "as is", and in no event will Wall Street Systems be liable for direct, indirect, special,

incidental, or consequential damages from any defect in the software or by virtue of providing this

documentation, even if advised of the possibility of such damages. The documentation may contain technical

inaccuracies and omissions.

The mention of an activity or instrument in this publication does not imply that all matters relating to that activity or

instrument are supported by Wallstreet Suite, nor does it imply that processing of or by that activity or instrument is

carried out in any particular way, even if such processing is customary in some or all parts of the industry.

The windows and screen images shown herein were obtained from prototypes during software development. The

actual windows and screen images in the software may differ.

Wall Street Systems, WSS, WALLSTREET, WALLSTREET SUITE and the Wall Street Systems logos are

trademarks of Wall Street Systems Delaware, Inc.

Finance KIT, Trema and Trema logo are trademarks of Wall Street Systems Sweden AB.

Microsoft and Windows are either registered trademarks or trademarks of Microsoft Corporation in the United States

and/or other countries.

Adobe, Acrobat, and Acrobat Reader are either registered trademarks or trademarks of Adobe Systems

Incorporated in the United States and/or other countries.

All other products mentioned in this book may be trademarks or service marks of their respective companies or

organizations.

Company names, people names, and data used in examples are fictitious unless otherwise noted.

This edition applies to Wallstreet Suite version 7.3.14 and to all later releases and versions until indicated in new

editions or Wall Street Systems communications. Make sure you are using the latest edition for the release level of

the Wall Street Systems product.

© Copyright 2011 Wall Street Systems IPH AB. All rights reserved.

First Edition (April 2011)

Commercial Loans Module (CLM) User Guide 3

Contents

Preface ...........................................................................................................................11

Intended audience and prerequisites ......................................................................................... 11

Associated documents ................................................................................................................ 11

Change history: ............................................................................................................................ 11

1 Overview ....................................................................................................................13

1.1 CLM ........................................................................................................................................ 13

1.1.1 Defining contracts in CLM ............................................................................................... 13

1.1.2 Arranging credit in CLM .................................................................................................. 13

1.1.3 Structuring of loan products in CLM ................................................................................ 13

1.1.4 Capturing and processing drawdowns in CLM ............................................................... 14

1.1.5 Processing loan events in CLM ...................................................................................... 14

1.1.6 Monitoring credit and debt situations in CLM .................................................................. 14

1.1.7 Receivables management in CLM .................................................................................. 14

1.1.8 Managing messages in CLM .......................................................................................... 14

1.1.9 Information used in CLM ................................................................................................. 15

1.2 Applications of CLM ............................................................................................................. 15

1.2.1 Editors ............................................................................................................................. 15

1.2.2 Managers and Boards ..................................................................................................... 15

1.2.3 Monitors .......................................................................................................................... 15

1.2.4 Reports ........................................................................................................................... 16

1.2.5 Activities .......................................................................................................................... 16

1.3 Setting up and using CLM ....................................................................................................16

2 Managing static data .................................................................................................19

2.1 Setting up static data for CLM ............................................................................................. 19

2.2 Schedule templates .............................................................................................................. 19

2.3 Instrument groups ................................................................................................................ 20

2.4 Instrument types ................................................................................................................... 21

2.5 Instruments ............................................................................................................................ 21

2.6 Transaction templates .......................................................................................................... 22

2.7 Facility types ......................................................................................................................... 23

2.8 Facility templates .................................................................................................................. 24

2.9 Facilities ................................................................................................................................. 24

2.9.1 Defining the main attributes ............................................................................................ 25

4 © Wall Street Systems IPH AB - Confidential

2.9.2 Defining contract details .................................................................................................. 26

2.9.2.1 Defining credit amount details .............................................................................. 27

2.9.2.2 Defining drawdown currency details ..................................................................... 28

2.9.2.3 Defining counterparty details ................................................................................ 28

2.9.2.4 Defining payback FX rate details .......................................................................... 29

2.9.2.5 Defining location details ........................................................................................ 29

2.9.2.6 Defining owner details .......................................................................................... 29

2.9.2.7 Defining instrument and event details .................................................................. 30

2.9.2.8 Defining funding type details ................................................................................ 30

2.9.2.9 Defining tranche details ........................................................................................ 30

2.9.2.10 Defining transaction template details .................................................................. 31

2.9.2.11 Defining beneficiary details (optional) ................................................................. 32

2.9.2.12 Defining guarantor details (optional) ................................................................... 32

2.9.2.13 Defining sublimits (optional) ............................................................................... 32

2.9.2.14 Defining drawdown condition details (optional) .................................................. 33

2.9.2.15 Defining collateral agreement details (optional) ................................................. 34

2.9.2.16 Defining drawdown parameter details (optional) ................................................ 34

2.9.2.17 Defining mandate details .................................................................................... 35

2.9.2.18 Defining switches details .................................................................................... 35

2.9.2.19 Defining properties details .................................................................................. 35

2.9.2.20 Defining links details ........................................................................................... 36

2.9.2.21 Defining ad hoc message client details .............................................................. 36

2.9.2.22 Defining contact rule details ............................................................................... 36

2.9.3 Approving facilities .......................................................................................................... 36

2.9.4 Modifying facilities ........................................................................................................... 37

2.9.5 Mirroring facilities ............................................................................................................ 37

2.9.5.1 Setting up facility mirroring ................................................................................... 37

2.9.5.2 Approving mirror facilities ..................................................................................... 39

2.9.5.3 Modifying mirror facilities ...................................................................................... 39

2.10 Tranches .............................................................................................................................. 39

2.10.1 Defining the main attributes .......................................................................................... 40

2.10.1.1 Single tranches ................................................................................................... 40

2.10.1.2 Multiple tranches ................................................................................................ 40

2.10.2 Defining the tranche values .......................................................................................... 40

2.11 Approvals (optional) ........................................................................................................... 41

2.12 Funding types (optional) .................................................................................................... 42

2.13 Mandates (optional) ............................................................................................................ 43

2.13.1 Defining the main attributes .......................................................................................... 43

2.13.2 Defining mandate participant details ............................................................................. 44

2.13.3 Defining mandate funding details .................................................................................. 45

2.14 Cashflow groups (optional) ................................................................................................ 46

3 Managing amount events .........................................................................................49

3.1 Amount Event Manager ........................................................................................................49

3.1.1 Amount Event Manager menus ...................................................................................... 49

3.1.1.1 View ...................................................................................................................... 49

Commercial Loans Module (CLM) User Guide 5

3.1.1.2 Command ............................................................................................................. 50

3.1.1.3 New ...................................................................................................................... 50

3.1.2 Start-up parameters ........................................................................................................ 50

3.1.3 Customizing Amount Event Manager ............................................................................. 50

3.2 Processing amount events .................................................................................................. 50

3.2.1 New subsidy estimation .................................................................................................. 50

3.2.2 New credit amendment ................................................................................................... 53

3.2.3 New credit transfer .......................................................................................................... 55

4 Managing drawdowns ...............................................................................................59

4.1 Drawdown Manager .............................................................................................................. 59

4.1.1 Drawdown Manager menus ............................................................................................ 60

4.1.1.1 View ...................................................................................................................... 60

4.1.1.2 New ...................................................................................................................... 60

4.1.2 Start-up parameters ........................................................................................................ 60

4.1.3 Customizing Drawdown Manager ................................................................................... 60

4.2 Processing drawdowns ........................................................................................................61

4.2.1 Entering drawdown transactions ..................................................................................... 61

4.2.2 Approving drawdown transactions .................................................................................. 64

4.2.3 Pricing drawdown transactions ....................................................................................... 65

4.2.3.1 Pricing rate renewal or indexation ........................................................................ 66

4.2.3.2 Loan pricing simulation ......................................................................................... 67

4.2.4 Cancelling drawdown transactions ................................................................................. 67

4.3 Drawdown mirroring ............................................................................................................. 67

4.3.1 Setting up static data for drawdown mirroring ................................................................. 67

4.3.2 Processing drawdown mirroring ...................................................................................... 67

4.3.2.1 Generating drawdown mirroring ........................................................................... 68

4.3.2.2 Executing loan events on mirrored drawdowns .................................................... 68

4.3.2.3 Rejecting mirrored drawdowns ............................................................................. 68

5 Managing loan events ...............................................................................................69

5.1 Setting up loan events .......................................................................................................... 69

5.1.1 Action rule types ............................................................................................................. 70

5.1.1.1 Types of loan events ............................................................................................ 71

5.1.2 Action rules ..................................................................................................................... 72

5.1.2.1 Setting up action rule conditions ........................................................................... 73

5.1.2.2 Defining the action rule actions ............................................................................ 74

5.1.3 Enabling loan events on transactions ............................................................................. 75

5.2 Processing loan event actions ............................................................................................ 75

5.2.1 Commitment fees ............................................................................................................ 76

5.2.1.1 Setup .................................................................................................................... 76

5.2.1.2 Execution .............................................................................................................. 76

5.2.1.3 Generated data ..................................................................................................... 77

5.2.1.4 Updating commitment fees ................................................................................... 77

5.2.2 Conditional remunerations .............................................................................................. 78

5.2.2.1 Setup .................................................................................................................... 78

6 © Wall Street Systems IPH AB - Confidential

5.2.2.2 Execution .............................................................................................................. 78

5.2.2.3 Generated data ..................................................................................................... 79

5.2.3 Deferment commission ................................................................................................... 79

5.2.3.1 Setup .................................................................................................................... 79

5.2.4 Drawdown amendment ................................................................................................... 79

5.2.4.1 Setup .................................................................................................................... 80

5.2.4.2 Execution .............................................................................................................. 80

5.2.4.3 Generated data ..................................................................................................... 86

5.2.5 Drawdown classification .................................................................................................. 87

5.2.5.1 Setup .................................................................................................................... 87

5.2.5.2 Execution .............................................................................................................. 87

5.2.5.3 Generated data ..................................................................................................... 88

5.2.6 Due amount carry forward .............................................................................................. 88

5.2.6.1 Setup .................................................................................................................... 88

5.2.6.2 Execution .............................................................................................................. 88

5.2.6.3 Generated data ..................................................................................................... 89

5.2.7 Facility fees ..................................................................................................................... 89

5.2.7.1 Setup .................................................................................................................... 90

5.2.7.2 Execution .............................................................................................................. 90

5.2.7.3 Generated data ..................................................................................................... 90

5.2.8 Prepayments ................................................................................................................... 91

5.2.8.1 Setup .................................................................................................................... 91

5.2.8.2 Execution .............................................................................................................. 91

5.2.8.3 Generated data ..................................................................................................... 94

5.2.9 Late Payment Penalties .................................................................................................. 95

5.2.9.1 Setup .................................................................................................................... 96

5.2.9.2 Execution .............................................................................................................. 98

5.2.9.3 Generated data ..................................................................................................... 98

5.2.10 Loan pricing .................................................................................................................. 98

5.2.10.1 Setup ..................................................................................................................99

5.2.10.2 Execution ............................................................................................................ 99

5.2.10.3 Generated data ................................................................................................... 99

5.2.11 Write off ......................................................................................................................... 99

5.2.11.1 Setup ..................................................................................................................99

5.2.11.2 Execution ............................................................................................................ 99

5.2.11.3 Generated data ................................................................................................. 100

5.2.12 Rate Renewal ............................................................................................................. 101

5.2.12.1 Setup ................................................................................................................ 101

5.2.12.2 Execution .......................................................................................................... 101

5.2.12.3 Generated data ................................................................................................. 102

5.3 Editing loan events ............................................................................................................. 102

6 Managing equity ......................................................................................................103

6.1 Setting up equity in the facility .......................................................................................... 103

6.2 Processing equity investments ......................................................................................... 104

6.2.1 Entering new equity investments .................................................................................. 104

6.2.2 Entering equity divestments .......................................................................................... 104

Commercial Loans Module (CLM) User Guide 7

6.2.3 Capturing dividend events ............................................................................................ 104

6.2.4 Capturing other corporate actions ................................................................................. 105

7 Managing issued guarantees .................................................................................107

7.1 Setting up issued guarantees ............................................................................................ 109

7.2 Processing issued guarantees .......................................................................................... 110

7.3 Processing guarantee calls ................................................................................................ 110

7.4 Processing guarantee refunds .......................................................................................... 111

7.5 Processing actions on issued guarantees ....................................................................... 113

8 Monitoring loan activity ..........................................................................................115

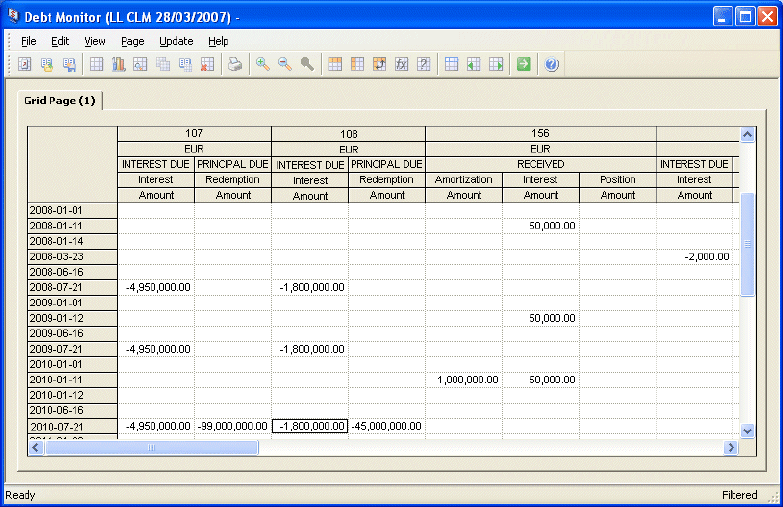

8.1 Monitoring debt positions .................................................................................................. 115

8.1.1 Debt Monitor ................................................................................................................. 115

8.1.1.1 Debt Monitor menus ........................................................................................... 116

8.1.1.2 Start-up parameters ............................................................................................ 116

8.1.2 Monitoring debt flows .................................................................................................... 116

8.1.2.1 Defining position parameters .............................................................................. 117

8.1.2.2 Selecting axis (column and row) groupings ........................................................ 119

8.1.2.3 Configuring axis values ...................................................................................... 120

8.1.2.4 Selecting key-figures in Debt Monitor ................................................................. 120

8.2 Monitoring credit positions ................................................................................................ 121

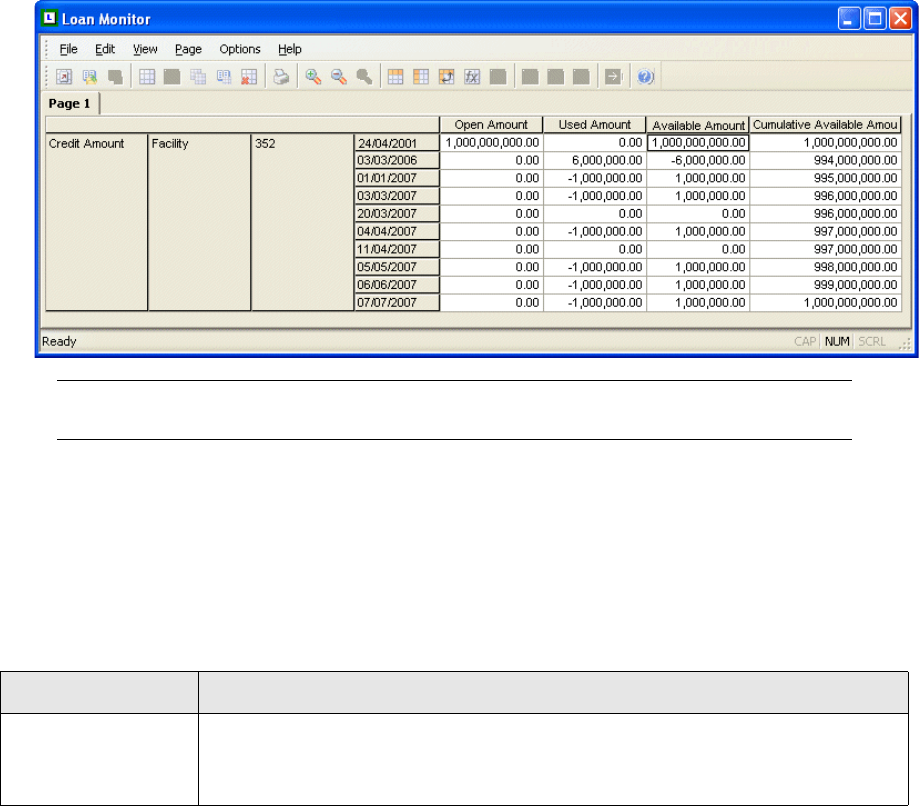

8.2.1 Loan Monitor ................................................................................................................. 121

8.2.1.1 Loan Monitor menus ........................................................................................... 121

8.2.1.2 Start-up parameters ............................................................................................ 122

8.2.2 Monitoring credit flows .................................................................................................. 122

8.2.2.1 Defining query parameters ................................................................................. 122

8.2.2.2 Configuring Loan Monitor ................................................................................... 123

8.3 Querying loan activity ......................................................................................................... 123

8.3.1 Loan Manager ............................................................................................................... 123

8.3.1.1 Loan Manager menus ......................................................................................... 124

8.3.1.2 Start-up parameters ............................................................................................ 124

8.3.1.3 Customizing Loan Manager ................................................................................ 125

8.3.1.4 Configuring default settings ................................................................................ 125

8.3.2 Initiating loan activities from Loan Manager .................................................................. 125

8.4 Managing payment reminders ........................................................................................... 127

8.4.1 Payment Reminder Manager ........................................................................................ 127

8.4.1.1 Payment Reminder Manager menus .................................................................. 127

8.4.2 Processing payment reminders .................................................................................... 128

8.4.2.1 Retrieving payment reminders ............................................................................ 128

9 Managing payment advices ...................................................................................129

9.1 Payment Advice Manager ................................................................................................... 129

9.1.1 Payment Advice Manager menus ................................................................................. 129

9.1.1.1 View .................................................................................................................... 129

8 © Wall Street Systems IPH AB - Confidential

9.1.1.2 Command ........................................................................................................... 130

9.1.1.3 New .................................................................................................................... 130

9.1.2 Start-up parameters ...................................................................................................... 130

9.1.3 Customizing Payment Advice Manager ........................................................................ 130

9.2 Processing payment advices ............................................................................................. 130

9.2.1 Entering payment advices ............................................................................................. 130

9.2.2 Approving payment advices .......................................................................................... 131

9.2.3 Editing imported SWIFT payment advices .................................................................... 131

10 Managing payment allocations ............................................................................133

10.1 Payment Allocation Manager ........................................................................................... 133

10.1.1 Payment Allocation Manager menus .......................................................................... 133

10.1.1.1 View .................................................................................................................. 133

10.1.1.2 Command ......................................................................................................... 134

10.1.1.3 New .................................................................................................................. 134

10.1.1.4 Options ............................................................................................................. 134

10.1.2 Start-up parameters .................................................................................................... 135

10.1.3 Customizing Payment Allocation Manager ................................................................. 135

10.1.4 Configuring payment allocation ................................................................................... 135

10.1.4.1 Auto match criteria ............................................................................................ 136

10.1.4.2 Auto match amount tolerances ......................................................................... 136

10.1.4.3 Auto match tolerances ...................................................................................... 137

10.1.4.4 Cashflow group priorities .................................................................................. 137

10.1.4.5 Default query offsets ......................................................................................... 138

10.2 Processing payment allocations ..................................................................................... 138

10.2.1 Retrieving cashflows and payment advices ................................................................ 139

10.2.2 Grouping cashflows and payment advices ................................................................. 139

10.2.3 Automatic payment allocation ..................................................................................... 139

10.2.4 Approving payment allocations ................................................................................... 140

10.2.5 Manual payment allocation ......................................................................................... 140

10.2.6 Retrieving payment allocations ................................................................................... 141

10.2.7 Unallocating payment allocations ............................................................................... 141

10.3 Processing underpayments and overpayments ............................................................ 141

10.3.1 Processing underpayments ........................................................................................ 142

10.3.1.1 Carry forward .................................................................................................... 142

10.3.1.2 Leave unallocated ............................................................................................ 143

10.3.1.3 Accept as Profit/Loss ........................................................................................ 144

10.3.1.4 Unallocate Cashflows ....................................................................................... 145

10.3.2 Processing overpayments ........................................................................................... 145

10.3.2.1 Offset future cashflows ..................................................................................... 145

10.3.2.2 Leave unallocated ............................................................................................ 146

10.3.2.3 Refund payment ............................................................................................... 147

10.3.2.4 Accept as Profit/Loss ........................................................................................ 147

Appendix A: Features ............................................................................................................149

A.1 Categories of features ........................................................................................................ 149

Commercial Loans Module (CLM) User Guide 9

A.2 List of features .................................................................................................................... 149

A.2.1 Add Facility Guarantees ............................................................................................... 149

A.2.2 Allow Drawdown FX Freeze ......................................................................................... 150

A.2.3 Allow Funding Call ........................................................................................................ 150

A.2.4 Allow Guarantee ........................................................................................................... 150

A.2.5 Allow Revision .............................................................................................................. 150

A.2.6 Allow Subsidy Call ........................................................................................................ 151

A.2.7 Cancel Provisional Settlements .................................................................................... 151

A.2.8 Commercial Loan ......................................................................................................... 151

A.2.9 Conditional Remuneration ............................................................................................ 151

A.2.10 Continuation Aggregated Rate Function .................................................................... 152

A.2.11 Payment Amount Extraction ....................................................................................... 152

A.2.12 Deferment Commission (Setup) ................................................................................. 152

A.2.13 Drawdown Amendment .............................................................................................. 152

A.2.14 Drawdown Cancellation .............................................................................................. 153

A.2.15 Drawdown Classification ............................................................................................ 153

A.2.16 Drawdown Fee ........................................................................................................... 153

A.2.17 Drawdown Fixing ........................................................................................................ 154

A.2.18 Drawdown Prepayment .............................................................................................. 154

A.2.19 Drawdown Rescheduling ............................................................................................ 154

A.2.20 Due Amount Carry Forward ........................................................................................ 154

A.2.21 Edit Commitment Fee ................................................................................................. 155

A.2.22 Guarantee Call ........................................................................................................... 155

A.2.23 Guarantee Refund ...................................................................................................... 155

A.2.24 Guarantee Valuation ................................................................................................... 155

A.2.25 Insert Default Guarantees .......................................................................................... 156

A.2.26 Late Payment Penalty ................................................................................................ 156

A.2.27 Late Payment Penalty Realization .............................................................................. 156

A.2.28 Loan Pricing ................................................................................................................ 156

A.2.29 Off Balance Sheet Accounting (Facility) ..................................................................... 156

A.2.30 Risk Venture Capital ................................................................................................... 157

A.2.31 Write Off ..................................................................................................................... 157

Appendix B: Loan event parameters....................................................................................159

B.1 Commitment Fee ................................................................................................................ 159

B.2 Conditional Remuneration ................................................................................................. 159

B.3 Deferment Commission ..................................................................................................... 160

B.4 Drawdown Amendment ...................................................................................................... 160

B.5 Drawdown Cancellation ..................................................................................................... 161

B.6 Drawdown Classification ................................................................................................... 162

B.7 Drawdown Fee .................................................................................................................... 162

B.8 Due Amount Carry Forward ............................................................................................... 162

B.9 Facility Fee .......................................................................................................................... 163

B.10 Funding Call ...................................................................................................................... 163

B.11 Guarantee Call .................................................................................................................. 163

10 © Wall Street Systems IPH AB - Confidential

B.12 Guarantee Refund ............................................................................................................ 164

B.13 Late Payment Penalty ...................................................................................................... 164

B.14 Prepayment ....................................................................................................................... 164

B.15 Rate Condition .................................................................................................................. 166

B.16 Write-Off ............................................................................................................................ 168

Appendix C: Activity parameters..........................................................................................169

C.1 CLM Bulk Drawdown Amendment .................................................................................... 169

C.2 CLM Fixing Drawdown Cashflow ...................................................................................... 170

C.3 CLM Late Payment Penalty Generation ............................................................................ 170

C.4 CLM Late Payment Penalty Realization ............................................................................ 170

C.5 CLM Late Payment Reminder Generation ........................................................................ 171

C.6 CLM Payment FX Rate Generation ................................................................................... 171

C.7 CLM Payment Reminder Generation ................................................................................ 172

C.8 CLM Subsidy Call Follow-up Generation ......................................................................... 172

Commercial Loans Module (CLM) User Guide 11

Preface

This guide describes how to use the Wallstreet Suite Commercial Loans Module (CLM): it provides

information that applies solely to commercial loans and using CLM.

It explains how to use CLM to set up, manage, and process commercial loans, monitor loan

positions, manage loan events, and so on.

CLM is used in conjunction with the Wallstreet Suite Transaction & Risk Management Module (TRM).

Therefore, this guide does not describe setting up procedures or management processes that are

also found in TRM. For this information, refer to the TRM end-user documentation.

Intended audience and prerequisites

This guide is intended for CLM users responsible for one or more of the following tasks:

•Setting up and managing CLM-related static data

•Capturing and processing drawdowns on commercial loans

•Monitoring credit and debt situations

•Managing and reconciling loan receivables.

Before reading this guide, some prior knowledge and experience of TRM is beneficial.

Associated documents

This guide is supported by the following TRM end-user documentation:

•TRM User Guide

•TRM Instruments: Processing and Calculations.

Other associated documents can be accessed from the Help menu of the Wallstreet Suite’s

applications.

Change history:

Edition Date Changes Updated By

0.1 April 2011 Initial release 7.3.14 TRM Dev Team

12 © Wall Street Systems IPH AB - Confidential

Commercial Loans Module (CLM) User Guide 13

Chapter 1 Overview

This chapter introduces you to CLM and the tasks required to set up and use the module.

1.1 CLM

CLM enables financial institutions and corporate treasuries to manage the whole life cycle of

commercial lending in the same system as their borrowing and treasury activities.

1.1.1 Defining contracts in CLM

In CLM, it is possible to enter the key attributes of a loan contract under a facility agreement.

You can define contractual conditions in the facility. These conditions can then be used to validate a

loan at the time of disbursal, thereby reducing operational risk and making the process more

efficient.

It is also possible to define whether the credit is sanctioned as being of a revolving or non-revolving

nature.

The Loan Officer can also record the decision of the Credit Committee in an approval, and record the

details of any subsidy limits in a mandate. These details can then be checked when entering the

facility agreement.

1.1.2 Arranging credit in CLM

In CLM, it is possible to arrange a credit line under a facility agreement in multiple ways: the credit

line can be disbursed using a combination of tranches and sublimits within each facility. This allows

you to control and monitor the available credit very effectively.

Amendments made to the facility (for example, cancellation of the credit line, a change in the

available credit, a credit transfer, a new borrower, or changes to the type of interest rate), can also

be processed and monitored in CLM.

1.1.3 Structuring of loan products in CLM

CLM caters to a whole range of loan structures – from simple fixed and floating rate loans, to

extremely complex structures, as follows:

•Fixed, floating, annuity, revisable, and structured complex loans

•Collateralized loans and asset-backed loans

•Issued guarantees and subsidized loans

•Private equity

•Parallel and sequential amortization and interest schedules.

The system provides unlimited drawdown structuring to allow sophisticated inter-company and

external lending activity.

1 Overview

1.1 CLM

14 © Wall Street Systems IPH AB - Confidential

1.1.4 Capturing and processing drawdowns in CLM

A drawdown transaction is used to transfer funds between the lender and borrower.

A drawdown has the following characteristics: it is always entered under a facility and a tranche; it

uses a transaction template to default the schedule structure; and it has a process flow (from

contract setup, to the processing of transactions, and finally to payment reconciliation) that allows

the organization to validate the entries through a chain of departments or users.

The predefined transaction and schedule templates are used to automatically enter common

disbursal information at drawdown entry. CLM then retrieves data from the facility or tranche and

completes all of the contractual fields that it can using the predefined information from the

templates. In the simplest case, only a small amount of data, such as the drawdown’s amount,

value date, and maturity date, remains to be entered.

CLM verifies the information and immediately issues an appropriate warning or error message if the

facility’s credit limit, sublimit, or any of its drawdown conditions are violated.

Drawdowns then pass through a user-configurable transaction flow where the data can be checked

by additional users, and other details added (such as, settlement instructions).

1.1.5 Processing loan events in CLM

Facilities and drawdowns can be long term, and CLM helps control and manage events that may

occur during the life-time of the loan contract.

The events managed in the system include such events as the following: the ability to add a variety

of fees (such as commitment, late penalty, or cancellation fees); early repayment of the debt, either

fully or partially; amendments to the drawdown (for example, change in currency, interest rate

type, borrower, or loan structure); automatic pricing of the drawdown; automatic or manual fixing

of rates; and re-classification, or even a total write-off, of the remaining debt.

1.1.6 Monitoring credit and debt situations in CLM

In CLM, the credit situation for a loan agreement can be monitored using a configurable Loan

Monitor application in order to view limit utilizations and cashflows grouped by borrower, facility, or

drawdown.

For example, in this monitor, you can view the following figures: total credit sanctioned under the

agreement; utilized credit under a contract, and the remaining available credit. Additionally, you can

view the use of the sublimits set up under the facility.

The debt situation, for example, the amounts due from a borrower or for a contract, can also be

monitored in CLM in another type of monitor application.

These due amounts may be the result, for example, of the normal repayment of loans, the interest

due on loans, or they may arise from the payment of fees, commissions, and so on, that are due to

various events that occur during the life-cycle of the loan.

In these monitors, the information is updated in real-time and takes into account the other CLM

operations.

1.1.7 Receivables management in CLM

Payment reconciliation in CLM allows you to track, monitor, and reconcile payments against loan

receivables.

Furthermore, the system will automatically generate payment reminders to borrowers before each

payment date: these are both printable and transmissible, for example, by E-mail, Fax, or Telex.

1.1.8 Managing messages in CLM

Commercial lending operations involve extensive communications between lenders and borrowers.

1 Overview

1.2 Applications of CLM

Commercial Loans Module (CLM) User Guide 15

CLM supports the generation of standard loans documents, such as, Billings, Rate Renewals, and

Statements of Commissions. These documents or messages can be produced either as part of the

transaction flow or on a nightly basis.

Note: Managing messages is described in the TRM User Guide.

1.1.9 Information used in CLM

CLM uses the same types of information found in TRM:

•Static data information

•Market data information

•Transaction management information

•Calculated information.

See the TRM User Guide for more information.

1.2 Applications of CLM

This section gives an overview of the different types of CLM applications, and how you use them

depending on your position in the organization.

All types of application are described in detail in the TRM User Guide.

1.2.1 Editors

Editors are used to define the static data information (for example, facility and tranche entities) that

needs to be set up before CLM can be used.

Editors for CLM are defined from a layout based on the Static Data Editor application. Each editor

layout is available as an individual application in CLM.

1.2.2 Managers and Boards

In CLM, there are a number of manager applications (based on the same layout as TRM’s

Transaction Manager) that are used to manage the flow and acceptance process of different types of

information in the system.

Different modes of each manager can be configured to be used for a particular purpose or to display

information in a particular state in its process flow. Each manager mode is available as an individual

application in CLM. Permissions are set up and applied to users to limit their access to different

manager modes according to their responsibilities within the organization.

Drawdown Manager (used to capture and process drawdown transactions) and Drawdown Action

Manager (designed specifically for loan events on drawdown transactions) are examples of these

types of manager applications.

In CLM, there are also several types of Board applications: for example, Enter Board, which is

available in the Drawdown mode of the manager application, offers a simplified alternative for

entering drawdown transactions.

1.2.3 Monitors

Monitors consist of pages, often grouped into books, which display information in grids and charts.

In Loan Monitor, you can view limit utilizations grouped by facility, tranche, or sublimit.

1 Overview

1.3 Setting up and using CLM

16 © Wall Street Systems IPH AB - Confidential

Debt Monitor is a version of TRM’s Treasury Monitor that is designed specifically for monitoring the

debt situation, for example, the amounts due from a counterparty, under a facility or for an

individual drawdown.

1.2.4 Reports

Reports display information which is generated from the information provided by other applications.

You can create different types of reports: such as reports listing your data and position-related

reports.

You can also perform a variety of calculations on the data in a report, such as calculations that are

not available in other applications. You can add, multiply, subtract and divide totals, calculate

averages, produce subtotals at any grouping level, produce running totals, combine the output of

different columns, and create sophisticated “if” conditions for displaying and calculating data.

You can create as many different report layouts as you need (either completely new ones, or ones

based on existing layouts).

Reports are set up and managed in an application called Report Generator.

1.2.5 Activities

Some calculations and batch processes must be run on certain dates or at certain time intervals (for

example, daily or monthly). These calculations and batch processes are called activities and you can

set them up to run automatically.

You can use activities to perform a variety of tasks, such as running batches and generating log

reports, fixing cashflows, creating messages such as payment reminders, updating modified data in

the system automatically, and various other calculations and realizing of key-figures.

Activities are managed and launched from an application called Activity Manager.

1.3 Setting up and using CLM

As a user, you are responsible for one or more of the following tasks:

Task More information

Set up the module:

• Set up loan data.

Chapter 2 Managing static data on page 19

Monitor changes to the credit amount: Chapter 3 Managing amount events on page 49

Capture activity:

• Use the module to process and manage

drawdowns.

• Managing equity in drawdowns

• Managing late payment penalties

Chapter 4 Managing drawdowns on page 59

Chapter 5 Managing loan events on page 69

Chapter 6 Managing equity on page 103

Monitoring activity:

• Monitor debt flows

• Monitor credit positions

• Querying loan activity.

• Managing late payments

Chapter 8 Monitoring loan activity on page 115

Receivables management. Chapter 9 Managing payment advices on page 129

Chapter 10 Managing payment allocations on page 133

1 Overview

1.3 Setting up and using CLM

18 © Wall Street Systems IPH AB - Confidential

Commercial Loans Module (CLM) User Guide 19

Chapter 2 Managing static data

In addition to the static data that is common to other modules (such as, currencies and portfolios),

you also need to set up the static data required for the management of commercial loan

agreements.

This chapter describes the procedures for setting up and managing the static data required for a

loan agreement in CLM.

Note: For more information about setting up and managing both CLM-related and other types of

static data, refer to the associated TRM end-user documentation: see Associated

documents on page 11.

2.1 Setting up static data for CLM

The order for setting up static data for CLM is dependent on the restrictions of assigning one entity

to another and the interdependencies between them. For this reason, the order in which you create

static data is very important: in some cases, you may need to create static data in parallel.

The order in which static data entities are described in this chapter reflects the order you need to set

them up: for example, setting up a transaction template is described before setting up a facility,

since you need to define the transaction template before you can assign it to the facility.

2.2 Schedule templates

A schedule can drive the generation of the cashflow structure of a drawdown (for example, the

interest flows) and also the generation of transaction events (such as fixing rates for dual-currency

structures) which may be required throughout the life of a commercial loan.

Schedules contain a number of values that determine how the cashflows or events of these

instruments are generated.

There are two types of schedule template: Primary and Secondary.

•Primary templates consist of the primary schedules. They define the main cashflow structure of

the drawdown. It is possible to supplement the primary template using secondary templates.

•Secondary templates consist of add-on schedules. They can be attached to one of the primary

schedules and are then dependent on that primary schedule.

CLM is delivered with a set of Primary and Secondary system-defined templates: the available

schedules are listed in the guide TRM Instruments: Processing and Calculations.

Once you have identified the primary schedule you need, you can attach one or more secondary

schedules to the template and store it with its own ID.

Schedules are defined in Schedule Template Editor.

Schedule templates can be organized into groups according to their category or function in Schedule

Template Group Editor.

2 Managing static data

2.3 Instrument groups

20 © Wall Street Systems IPH AB - Confidential

Schedules can be used together with transaction templates (see 2.6 Transaction templates on page

22) to propagate key values into a transaction at drawdown entry. In Drawdown Manager, it is also

possible to dynamically add schedules directly to a drawdown transaction.

To define a schedule template:

1. In Schedule Template Editor, select the system template on which you want to base your own

schedule from the left part of the editor.

2. Define the main attributes of your own schedule template in the upper part of the editor.

3. In the Schedule Template Item page, define the parameters for the schedule.

For information about the parameters that can be entered to define a schedule, see the guide

TRM Instruments: Processing and Calculations.

4. In the Groups page, select and add the schedule template group or groups to which you want this

schedule template to belong.

Schedule template groups are described in the TRM User Guide.

5. Save the whole schedule template using File - Save As New.

2.3 Instrument groups

Each instrument is assigned to an instrument group during the setup process. Groups are used as a

means of identifying instruments and can be used in CLM to restrict the availability of instruments in

drawdown entry using transaction templates.

Instrument groups are arranged into a simple hierarchy, where each group is assigned one parent.

Instruments can only be assigned to a single instrument group in the hierarchy.

The first level of the instrument group hierarchy is predefined in the system, but can be modified at

implementation according to your organization’s requirements. You then create further instrument

groups for the lower levels of the hierarchy to reflect the requirements of your organization.

Instrument groups are defined in Instrument Group Editor: see the TRM User Guide for more

information.

Information Description

ID & Name Unique ID and name for the schedule template.

User / System Identifies the template as system-defined or user-defined.

Note: System-defined templates provide a starting point for creating user-defined

templates.

Primary /

Secondary

Identifies the template as primary or secondary.

Primary user-defined templates can be used in transaction templates and

transactions, while secondary templates can be attached to one or more of the

schedules in either a primary or a secondary template.

Note: Secondary templates cannot be used independently with transaction templates

or transactions.

Payment Adjust

Method

Defines whether the schedule template can be seen and used in the Payment Adjust

Method field in the transaction schedules.

2 Managing static data

2.4 Instrument types

Commercial Loans Module (CLM) User Guide 21

2.4 Instrument types

Instrument classes denote the different categories of instruments which are supported by the

system. They are predefined in the system and cannot be changed by the user.

Classes are used as a basis on which to define instrument types. Once instrument types have been

defined, the instrument classes are no longer used.

An instrument type inherits all the features contained in the instrument class automatically.

Features are system-defined attributes used to give instruments their distinctive functionality and

enable drawdown entry, amount and event processing, and position monitoring.

Commercial loan instruments must be based on an instrument type derived from the class

COMMERCIAL-LOAN.

Instrument types are defined in Instrument Type Editor: see the TRM User Guide for more

information.

2.5 Instruments

All instruments share several main characteristics and are set up in a similar way in Instrument

Editor.

The specific instrument setup required for a particular category of instrument is explained in more

detail in the relevant section of the guide TRM Instruments: Processing and Calculations.

To set up an instrument:

1. In Instrument Editor, define the main characteristics of the instrument in the upper part of the

editor.

2. In the Features page, add or remove the features you need for this instrument.

Note: Some of the features assigned to an instrument need to be configured further, either in the

instrument setup itself, or in the configuration of action rules. For more information, see

Information Description

ID & Name Unique ID and name for the instrument.

Instrument Type Instrument type on which the instrument is based. This is a mandatory field.

Commercial loan instruments must be based on an instrument type derived from the

class COMMERCIAL-LOAN.

Exceptions to this are:

• Funding Call instruments: Instrument Class = CASH

• Facility Collateral instruments: Instrument Class = COLLATERAL TRANSFER.

Instrument Group Instrument group to which the instrument belongs (defined in Instrument Group

Editor).

Active From

Active To

Active period (From/To dates inclusive) to restrict the period in which the instrument

can be traded (optional).

Buy Label

Sell Label

Labeling for Buy/Sell transactions (optional) to override the default settings.

Result Type Result type to use for this instrument (defined in Result Type Editor). This is a

mandatory field.

Domain Domain in which the instrument is available.

2 Managing static data

2.6 Transaction templates

22 © Wall Street Systems IPH AB - Confidential

Appendix A Features on page 149 and Chapter 5 Managing loan events on page 69.

The values you need to enter to define a particular category of instrument are explained in

the guide TRM Instruments: Processing & Calculations.

3. In the Links page, you can add a link to any file stored on your network (for example, a link to a

document which contains information related to trading a specific instrument) or a hyperlink to

an Internet URL (such as, an issuer’s web site).

4. In the Properties page, you can add miscellaneous pieces of information to the instrument

definition for which there is no specific field or switch in the editor.

The properties you will need are added at implementation according to your organization’s

requirements. When you assign a property to an entity, you also need to assign the

corresponding value. Note that it is possible to create more properties using Property Editor.

5. Save the whole instrument definition using File - Save As New.

2.6 Transaction templates

A loan agreement includes financial clauses which specify the drawdown components, along with

data such as interest periods, interest calculation methods, and principal repayment schedules.

A transaction template captures the component values of a particular instrument in which the loan is

to be disbursed and allows you to add the specific clauses of a loan contract into it or to directly

attach the template to a transaction.

Transaction templates allow all the attributes of a transaction and its schedules (principal, interest,

events, and so on) to be predefined and later used to create drawdowns.

The schedules included in a transaction template are defined by the attached schedule template:

therefore, you need to set up at least one schedule template, see 2.2 Schedule templates on page

19.

A transaction template can then be attached to a facility, or it can remain independent so that it is

available for use with all facilities with the relevant instrument.

Transaction templates are defined in Transaction Template Editor.

To define a transaction template:

1. In Transaction Template Editor, enter the main attributes of the template in the upper part of

the editor.

Information Description

ID & Name Unique ID and name for the transaction template.

User ID of the authorized user (or user group) of the template.

Owner User ID of the owner of the template.

Instrument Group Instrument group to which the template belongs.

Instrument Instrument to which the template is applied.

Facility Facility for which the template is defined.

Facilities are defined in Facility Editor: see 2.9 Facilities on page 24 for more

information.

Note: If a facility is specified in this field, the transaction template cannot be used for

any other facility.

Schedule

Templ a te

Schedule template you want to apply to the transaction template.

2 Managing static data

2.7 Facility types

Commercial Loans Module (CLM) User Guide 23

2. Save the transaction template definition using File - Save As New.

3. In Transaction Template Editor’s Transaction Column page, specify the default values for each

transaction column you want to define in the template.

4. In Transaction Template Editor’s Schedule Column page, specify the default values for each

schedule column you want to define in the template.

5. Save the transaction template definition using File - Save.

2.7 Facility types

Facility types can be created as a way of organizing facilities in the system and are assigned to the

facility definitions. For example, a facility created for a standard loan could be divided further into

such types as: Syndicated, Direct, or Global. Facility types are created in Facility Type Editor.

Comment Descriptive text giving further information.

Switches • Fixed Schedule - if this switch is on, only schedules defined in the template are

available in the drawdown transaction using this template. This means that no

other schedules can be added at drawdown entry.

Information Description

Information Description

Column Name of the transaction column for which you want to define a value.

Value Default or fixed value for the specified Column.

Comment Descriptive text giving further information.

Switches • Default - if this switch is on, the corresponding Value is the default for the Column,

but it can be modified at drawdown entry (if Frozen is not set).

• Frozen - if this switch is on, the specified Value cannot be modified.

• Mandatory - if this switch is on, the Column must contain a value before the

transaction can be saved at drawdown entry.

Information Description

ID & Description Part of the schedule for which you want to define a value.

The schedules available for selection are determined by the Schedule Template that you

selected in the upper part of the editor.

Column Name of the schedule column for which you want to define a value.

Value Default or fixed value for the specified Column.

Comment Descriptive text giving further information.

Switches • Default - if this switch is on, the corresponding Value is the default for the Column,

but it can be modified at drawdown entry (if Frozen is not set).

• Frozen - if this switch is on, the specified Value cannot be modified.

• Mandatory - if this switch is on, the Column must contain a value before the

transaction can be saved at drawdown entry.

2 Managing static data

2.8 Facility templates

24 © Wall Street Systems IPH AB - Confidential

To define a facility type:

1. In Facility Type Editor, enter the main attributes of the facility type.

2. Save the facility type definition using File - Save As New.

2.8 Facility templates

You set up Facilities with the aid of a template. In the template, you can define a set of data which

you then use to set up a facility with the same attributes.

A facility template contains all the fields and switches that are available in Facility Editor. In the

template, you can activate or disable the fields and switches and specify which attributes need to be

editable, available, or mandatory in Facility Editor. You can also use the template to restrict the

values displayed in Facility Editor’s selection lists.

When you assign a template in Facility Editor, the template automatically fills in some of the

information, so that you only have to provide a limited set of values when you create the facility

itself.

To define a facility template:

1. In Facility Template Editor, enter an ID and name for the template in the upper part of the

editor.

2. Customize the fields and switches as necessary: the fields and switches are explained in 2.9

Facilities on page 24.

There are three settings which you can apply to fields:

–Mandatory - you must provide values for mandatory attributes.

–Editable - you have access to the field and can provide a value. All mandatory fields are

editable by default.

–Ignore Template List - you will not override a value which was defined before you applied the

template. This means, that if a field is blank in the template, if you apply the template to a

facility for which a value already exists for that field, the existing value is not replaced.

3. Save the facility template using File - Save As New.

2.9 Facilities

When a loan contract has been agreed, the details of the agreement are set up in CLM as a facility.