TRM Instruments: Processing And Calculations Instrument Guide

User Manual:

Open the PDF directly: View PDF ![]() .

.

Page Count: 930 [warning: Documents this large are best viewed by clicking the View PDF Link!]

- Contents

- Preface

- Chapter 1 Concepts

- Chapter 2 Market standards and calculations

- 2.1 Market standards

- 2.1.1 Date basis

- 2.1.2 Interest types

- 2.1.3 Price types

- 2.1.4 Yield/price conversions

- 2.1.4.1 Price/yield conversion

- 2.1.4.2 Yield/price conversion

- 2.1.4.2.1 *ISMA-30/360-BIMONTHLY (financial/instrument/isma@price)

- 2.1.4.2.2 *ISMA-30E360-ANNUAL (financial/instrument/isma@price)

- 2.1.4.2.3 *ISMA-30E360-SEMI-ANNUAL (financial/instrument/isma@price)

- 2.1.4.2.4 *ISMA-30E360-QUARTERLY (financial/instrument/isma@price)

- 2.1.4.2.5 *ISMA-ACTACT-ANNUAL (financial/instrument/isma@price)

- 2.1.4.2.6 *ISMA-ACTACT-QUARTERLY (financial/instrument/isma@price)

- 2.1.4.2.7 *ISMA-ACTACT-SEMI-ANNUAL (financial/instrument/isma@price)

- 2.1.4.2.8 *ISMA-ACT360-ANNUAL (financial/instrument/isma@price)

- 2.1.4.2.9 *ISMA-ACT365-ANNUAL (financial/instrument/isma@price)

- 2.1.4.2.10 *U.S.STREET-ACT365-SEMIANNUAL (financial/instrument/us-street@price)

- 2.1.4.2.11 *U.S.STREET-ACTACT-SEMIANNUAL (financial/instrument/us-street@price)

- 2.1.4.2.12 *U.S.STREET-ACTACT-ANNUAL (financial/instrument/us-street@price-1)

- 2.1.4.2.13 *U.S. Treasury (financial/instrument/us-treasury@price)

- 2.1.4.2.14 BOND-BR-LFT (financial/instrument/isma@price)

- 2.1.4.2.15 BOND-BR-NBC (financial/instrument/isma@price)

- 2.1.4.2.16 BOND-BR-NTN (financial/instrument/isma@price)

- 2.1.4.2.17 GOVT-AU (financial/instrument/australian@price)

- 2.1.4.2.18 GOVT-CA (financial/instrument/canadian@price)

- 2.1.4.2.19 GOVT-CH (financial/instrument/isma@price)

- 2.1.4.2.20 GOVT-DK-OLD-30E360 (financial/instrument/isma@price)

- 2.1.4.2.21 GOVT-DK (financial/instrument/isma@price)

- 2.1.4.2.22 GOVT-EUROZONE (financial/instrument/isma@price)

- 2.1.4.2.23 GOVT-FR-OAT-OLD-AIR3 (financial/instrument/isma@price)

- 2.1.4.2.24 GOVT-FR-OAT (financial/instrument/isma@price)

- 2.1.4.2.25 GOVT-GR-OLD-30E360 (financial/instrument/isma@price)

- 2.1.4.2.26 GOVT-HU (financial/instrument/isma@price)

- 2.1.4.2.27 GOVT-IT (financial/instrument/isma@price)

- 2.1.4.2.28 GOVT-IT-ZC (financial/instrument/isma@price)

- 2.1.4.2.29 GOVT-JP (financial/instrument/simple-yield@price)

- 2.1.4.2.30 GOVT-MALAYSIA (financial/instrument/isma@price)

- 2.1.4.2.31 GOVT-NO (financial/instrument/norwegian@price)

- 2.1.4.2.32 GOVT-NZ (financial/instrument/isma@price)

- 2.1.4.2.33 GOVT-SE (financial/instrument/isma@price)

- 2.1.4.2.34 GOVT-SG (financial/instrument/us-street@price)

- 2.1.4.2.35 GOVT-UK (financial/instrument/isma@price)

- 2.1.4.2.36 GOVT-US (financial/instrument/us-street@price)

- 2.1.4.2.37 GOVT-USAGENCY (financial/instrument/isma@price)

- 2.1.4.2.38 GOVT-ZA (financial/instrument/south-african@price)

- 2.1.4.2.39 INDEX-UK (function/index-uk@price)

- 2.1.5 Discount Margin

- 2.1.6 Calculation methods

- 2.2 Yield curves

- 2.2.1 Yield curve

- 2.2.2 Basis swaps

- 2.2.3 Yield Curve interpolation

- 2.2.4 FX rate interpolation

- 2.3 Key-figures

- 2.3.1 Valuation

- 2.3.2 Profit and Loss

- 2.3.2.1 Accrued Interest

- 2.3.2.2 Accrued Interest Local

- 2.3.2.3 Accrued Profit

- 2.3.2.4 Accrued Profit Local

- 2.3.2.5 FX Profit

- 2.3.2.6 Accrued Margin Profit

- 2.3.2.7 Accrued Margin Profit Local

- 2.3.2.8 Margin Profit

- 2.3.2.9 Margin Profit Local

- 2.3.2.10 Total Margin Profit

- 2.3.2.11 Total Margin Profit Local

- 2.3.2.12 MtoM Profit

- 2.3.2.13 MtoM Profit Local

- 2.3.2.14 Other Profit

- 2.3.2.15 Other Profit Local

- 2.3.2.16 Total Profit

- 2.3.2.17 Total Profit Local

- 2.3.3 Option figures

- 2.3.4 Risk

- 2.3.5 Dual currency

- 2.4 Performance calculations

- 2.4.1 Actual basis and all cash basis

- 2.4.2 Trade date and value date based performance

- 2.4.3 Time-weighted rate of return (TWR)

- 2.4.4 Money-weighted return

- 2.4.5 Instrument market values for third currency

- 2.4.6 Instrument market values and cashflows

- 2.4.7 Example portfolio

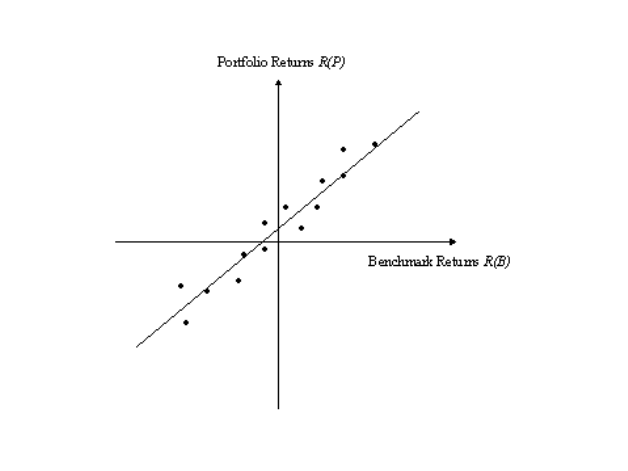

- 2.4.8 Risk-adjusted returns

- 2.4.9 Risk-adjusted return measures

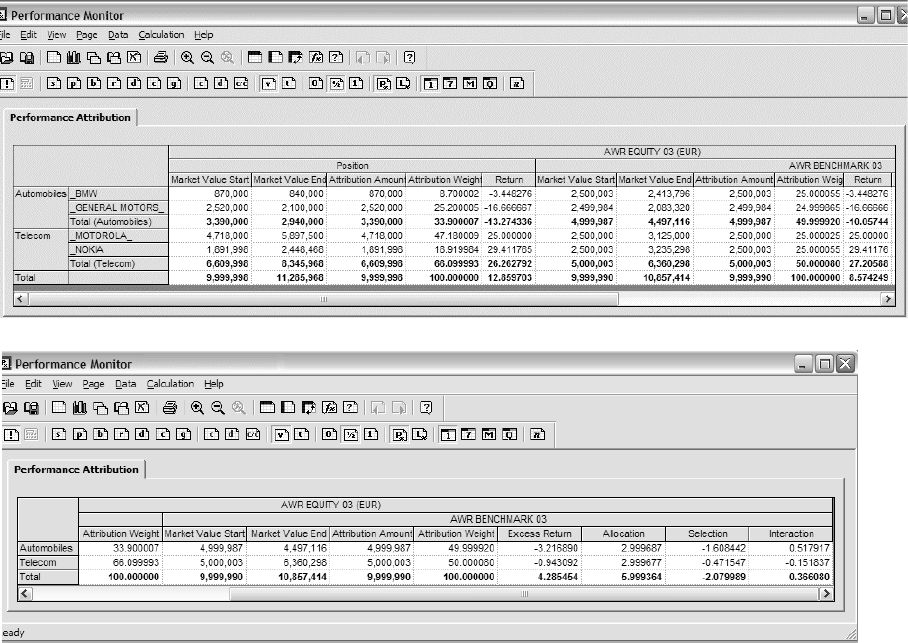

- 2.4.10 Performance attribution

- 2.4.11 Performance measurement key-figures

- 2.5 Value-at-Risk calculations

- 2.1 Market standards

- Chapter 3 Debt instruments

- 3.1 Bond

- 3.2 Structured bonds

- 3.3 Schuldscheindarlehen

- 3.4 Denominated bond

- 3.5 Convertible bond

- 3.6 Index-linked bond

- 3.6.1 Instrument setup

- 3.6.2 Deal capture

- 3.6.3 Processing

- 3.6.4 Australian index-linked annuity bond

- 3.6.5 Australian index-linked bond

- 3.6.6 Brazilian (LFT) selic-linked security

- 3.6.7 Brazilian FX-linked NBC-E/NTN-D

- 3.6.8 Brazilian inflation-linked NTN

- 3.6.9 Canadian real return bond

- 3.6.10 French OATıi

- 3.6.11 Greek index-linked bond

- 3.6.12 Israeli index-linked bond

- 3.6.13 Italian BTP ıi

- 3.6.14 Japanese index-linked bond

- 3.6.15 Swedish index-linked bond

- 3.6.16 UK index-linked gilt

- 3.6.17 US Tips

- 3.7 Asset backed security

- 3.8 Short term loan

- 3.9 Discount paper

- 3.10 Loan

- Chapter 4 Equities

- Chapter 5 Security lending

- Chapter 6 Forex

- Chapter 7 Index

- Chapter 8 Cash

- Chapter 9 Futures

- 9.1 Forward rate agreement

- 9.2 Bond forward

- 9.3 Money market future

- 9.4 Bond future

- 9.5 Equity future

- 9.6 FX future

- 9.7 Index future

- Chapter 10 Options

- 10.1 Cap/floor/collar

- 10.2 Swaption

- 10.3 Option on MM future

- 10.4 Bond option

- 10.5 Bond Future Option

- 10.6 Equity option

- 10.7 Index option

- 10.8 FX option

- 10.9 Exchange traded FX option

- Chapter 11 Swaps

- 11.1 Interest rate swap

- 11.1.1 Single-currency IR swap

- 11.1.2 Asset swap

- 11.1.3 Cross-currency swap

- 11.1.4 Brazilian IDxUSD Swap

- 11.1.5 Overnight index swap

- 11.1.6 Other swap structures

- 11.2 Total return swap

- 11.3 Credit default swap

- 11.1 Interest rate swap

- Chapter 12 Commodities

- Chapter 13 Funds

- Appendix A Features

- A.1 Categories of features

- A.2 List of features

- A.2.1 ABS - Asset Backed Security

- A.2.2 ABS Valuation

- A.2.3 Accrual Yield Setup

- A.2.4 Allow Ad-Hoc Instructions

- A.2.5 Allow Ad-Hoc Clients/Instructions

- A.2.6 Allow Forcing Type to Spot

- A.2.7 Allow FX Currency Pair Shift

- A.2.8 Allow Manual Classification

- A.2.9 Allow Roll Over

- A.2.10 Allow Roll Over (Dual Currency)

- A.2.11 Allow Roll Over (FX)

- A.2.12 Allow Roll Over (FX - Margin Result)

- A.2.13 Allow Roll Over (repo)

- A.2.14 Allow Roll Over (Short Loan)

- A.2.15 Allow Roll Over (Short Loan - Margin Result)

- A.2.16 Allow Roll Over (FX - Swap Style)

- A.2.17 Allow Roll Over (FX - Swap Style - Margin Result)

- A.2.18 Allow Roll Over (Guarantee)

- A.2.19 Allow Security Loan

- A.2.20 Allow Sight Account Transfer

- A.2.21 Allow Signature Date

- A.2.22 Allow Spread Curves

- A.2.23 Allow Swap

- A.2.24 Allow Transaction Transfer

- A.2.25 Allow Weight Difference

- A.2.26 Allow Valuation Curves

- A.2.27 Alternative Repayment Estimates

- A.2.28 Australian Bond Future Option

- A.2.29 Australian CIB

- A.2.30 Australian FRN

- A.2.31 Australian FRN Method

- A.2.32 Australian IAB

- A.2.33 Australian IAB Valuation

- A.2.34 Australian IAB (Round to 3)

- A.2.35 Australian IAB Valuation (Round to 3)

- A.2.36 Australian IAB Par Curve Valuation

- A.2.37 Australian IAB Par Curve Valuation (Round to 3)

- A.2.38 Australian Index-Linked Bond Valuation

- A.2.39 Australian MBS

- A.2.40 Australian MBS Valuation

- A.2.41 Average FX Rate Forward

- A.2.42 Average FX Rate Valuation

- A.2.43 Average FX Rate Option

- A.2.44 Average FX Rate Option Valuation

- A.2.45 Bank Account Balance

- A.2.46 Bank Account Interest

- A.2.47 Bank Account Valuation

- A.2.48 Base IR Exposure Setup

- A.2.49 Base IR Setup

- A.2.50 Base Valuation Setup

- A.2.51 Bond

- A.2.52 Bond - Brazilian LFT

- A.2.53 Bond - Brazilian LFT Valuation

- A.2.54 Bond - Brazilian FX-Linked NBC

- A.2.55 Bond - Brazilian FX-Linked NBC Valuation

- A.2.56 Bond - Brazilian Inflation-Linked NTN

- A.2.57 Bond - Brazilian Inflation-Linked NTN Valuation

- A.2.58 Bond - Canadian RRB

- A.2.59 Bond - Canadian Index-Linked Bond Valuation

- A.2.60 Bond Denominations Setup

- A.2.61 Bond Forward

- A.2.62 Bond Forward (Swedish)

- A.2.63 Bond Forward Dates

- A.2.64 Bond Forward Valuation

- A.2.65 Bond - French OATıi

- A.2.66 Bond - French Index-Linked Bond Valuation

- A.2.67 Bond Future

- A.2.68 Bond Future - Australian

- A.2.69 Bond Future Valuation

- A.2.70 Bond Future Option Valuation

- A.2.71 Bond - Greek Index-Linked Bond

- A.2.72 Bond - Greek Index-linked Bond Valuation

- A.2.73 Bond - Israeli Index-Linked Bond

- A.2.74 Bond - Israeli Index-Linked Bond Valuation

- A.2.75 Bond - Italian BTPıi

- A.2.76 Bond - Italian Index-Linked Bond Valuation

- A.2.77 Bond Option

- A.2.78 Bond Option Valuation

- A.2.79 Bond Pricing

- A.2.80 Branch Codes

- A.2.81 Bootstrap Instrument

- A.2.82 Call Account

- A.2.83 Call Account Valuation

- A.2.84 Call Money

- A.2.85 Call Money Valuation

- A.2.86 Cancel Provisional Settlements

- A.2.87 Cap/Floor/Collar

- A.2.88 Cap/Floor/Collar Valuation

- A.2.89 Cashflow Charges

- A.2.90 Cash Collateral Account

- A.2.91 Cash Payment

- A.2.92 Choose Coupon

- A.2.93 Collateral

- A.2.94 Collateral Delivery

- A.2.95 Collateral Setup

- A.2.96 Collateral Transfer

- A.2.97 Collateral Valuation

- A.2.98 Competitive Premiums

- A.2.99 Competitive Prices

- A.2.100 Competitive Rates

- A.2.101 Competitive Rates (FX Swap)

- A.2.102 Complex Payment (cash)

- A.2.103 Convertible Bond

- A.2.104 Convertible Bond Valuation

- A.2.105 Convertible Bond Setup

- A.2.106 Cost of Carry Balance

- A.2.107 Cost of Carry Interest

- A.2.108 Cost of Carry Valuation

- A.2.109 Credit Client Setup

- A.2.110 Credit Default Swap

- A.2.111 Credit Default Swap Valuation

- A.2.112 CreditManager position template

- A.2.113 Credit Rating

- A.2.114 Credit Default Swap Curve Setup

- A.2.115 Credit-Step-Up

- A.2.116 CTD Future

- A.2.117 Currency Conversion

- A.2.118 Debt Flows Valuation (payment amount extraction)

- A.2.119 Delivery

- A.2.120 Denominated Bond

- A.2.121 Discount Paper

- A.2.122 Discount Paper OTC

- A.2.123 Discount Valuation

- A.2.124 Dividend Estimate

- A.2.125 Dual Currency

- A.2.126 Dual Currency Forecast

- A.2.127 Equity

- A.2.128 Equity Cash Dividend

- A.2.129 Equity Conversion

- A.2.130 Equity Detachment

- A.2.131 Equity Future

- A.2.132 Equity Info

- A.2.133 Equity Option

- A.2.134 Equity Option Pricing

- A.2.135 Equity Option Setup

- A.2.136 Equity Option Valuation

- A.2.137 Equity Return of Capital

- A.2.138 Equity Split

- A.2.139 Estimation Curve Setup

- A.2.140 Exotic Structure (Option)

- A.2.141 Expiry Date Setup

- A.2.142 External Valuation

- A.2.143 Fed Fund Future Chain

- A.2.144 Fed Fund Future Dates

- A.2.145 Fed Fund Future Par Valuation

- A.2.146 Fed Fund Future Valuation

- A.2.147 Filtered Valuation

- A.2.148 Fixed Bond Valuation

- A.2.149 Fixed IR Quote Valuation

- A.2.150 Fixed IR Valuation

- A.2.151 Fixed Quoted Valuation

- A.2.152 Force Trade Date Performance

- A.2.153 Forecast

- A.2.154 Forecast Valuation

- A.2.155 Forward Price Setup

- A.2.156 FRA Dates

- A.2.157 Forward Rate Agreement (Deposit)

- A.2.158 Forward Rate Agreement (Discount)

- A.2.159 Forward Rate Agreement (Swedish)

- A.2.160 FRA Valuation

- A.2.161 FRA Option

- A.2.162 FRA Option Valuation

- A.2.163 FRA Periods

- A.2.164 FRN Valuation

- A.2.165 Fund

- A.2.166 Fund Fee Accrual and Realization

- A.2.167 Fund Fee Valuation

- A.2.168 Future Dates

- A.2.169 Future Valuation

- A.2.170 FX

- A.2.171 FX Cross Method

- A.2.172 FX Estimate (Forward)

- A.2.173 FX Estimate (IR Difference)

- A.2.174 FX Fixing

- A.2.175 FX Forward

- A.2.176 FX Future

- A.2.177 FX Future Netting

- A.2.178 FX Future Valuation

- A.2.179 FX - Lagged FX Function

- A.2.180 FX Margin Result

- A.2.181 FX Valuation

- A.2.182 FX Option

- A.2.183 FX Option Compound

- A.2.184 FX Option Digital

- A.2.185 FX Option Listed

- A.2.186 FX Option Premium

- A.2.187 FX Option Pricing

- A.2.188 FX Option Setup

- A.2.189 FX Option Valuation

- A.2.190 FX Pricer (Forward)

- A.2.191 FX Pricer (Option)

- A.2.192 FX Setup

- A.2.193 FX Swap

- A.2.194 FX Swap Cost-of-Funding

- A.2.195 FX Swap Margin Result

- A.2.196 FX Swap Quote Default

- A.2.197 FX Swap Split

- A.2.198 FX Time Option

- A.2.199 FX Time Option Valuation

- A.2.200 FX Trading Platform

- A.2.201 Generic IR Valuation

- A.2.202 Generic Loan

- A.2.203 Index

- A.2.204 Index Averaging

- A.2.205 Index Composite

- A.2.206 Index Derived

- A.2.207 Index Estimate

- A.2.208 Index Future

- A.2.209 Index - Lagged Index Function

- A.2.210 Index-Linked Bond

- A.2.211 Index Option

- A.2.212 Index Option Setup

- A.2.213 Index Option Valuation

- A.2.214 Index Rebase (Index-Linked Bond)

- A.2.215 Index Totaling

- A.2.216 Index - UK Index Function

- A.2.217 Index Valuation

- A.2.218 Instrument Quote Estimate

- A.2.219 Internal Deal Mirroring

- A.2.220 IR Derivative Valuation

- A.2.221 IR Derivative Valuation Setup

- A.2.222 IR Pricer (Swap)

- A.2.223 IR Pricer (Swaption)

- A.2.224 Issue

- A.2.225 Japanese JGBi

- A.2.226 Japanese Index-Linked Bond Valuation

- A.2.227 Loan Structure

- A.2.228 Manual Charges

- A.2.229 Margin Movement

- A.2.230 Maturity Date Setup

- A.2.231 MM Future

- A.2.232 MM Future - Australian Bank Bill Future

- A.2.233 MM Future - Australian 90-Day Bank Bill Future Chain

- A.2.234 MM Future - Money Market Future Chain

- A.2.235 MM Future - Money Market 1M Future Chain

- A.2.236 MM Future - Money Market 3M Future Chain

- A.2.237 MM Future Method - Australian

- A.2.238 MM Future Dates

- A.2.239 MM Future Option

- A.2.240 MM Future Option - Australian Bank Bill Future Option

- A.2.241 MM Future Option Valuation

- A.2.242 Money Market Future Par Valuation

- A.2.243 Money Market Future Valuation

- A.2.244 Mode Specific Method

- A.2.245 Mode/Transaction Specific Method

- A.2.246 MtoM Instrument Setup

- A.2.247 Netted Instrument

- A.2.248 Non Deliverable Forward FX Instrument

- A.2.249 NumeriX Asset Swap Setup

- A.2.250 NumeriX Setup

- A.2.251 NumeriX Single-Swap Valuation

- A.2.252 NumeriX Swap Valuation

- A.2.253 NumeriX Valuation

- A.2.254 Option Dates

- A.2.255 Option Premium

- A.2.256 Option Template Setup

- A.2.257 Payment Agent

- A.2.258 Performance, Cash In/Out

- A.2.259 Performance, FX Hedge

- A.2.260 Performance, Index

- A.2.261 Per-Leg Cashflow Valuation

- A.2.262 Premium

- A.2.263 Premium Date Setup

- A.2.264 Price Exposure Setup

- A.2.265 Price Valuation

- A.2.266 Quote Default

- A.2.267 Quote Default (Australian FRN)

- A.2.268 Quote Default (Australian MBS)

- A.2.269 Quote Default (Chain)

- A.2.270 Quote Default (Collateral)

- A.2.271 Quote Default (Discount Paper OTC)

- A.2.272 Quote Default (FX)

- A.2.273 Quote Default (Short Loan)

- A.2.274 Quoted

- A.2.275 Quoted Chain

- A.2.276 Range Accrual

- A.2.277 Repo Cash Delivery

- A.2.278 Repo Cash Delivery (Floating)

- A.2.279 Repo Cash Delivery (Substitution)

- A.2.280 Repo Rounding

- A.2.281 Repo Valuation

- A.2.282 Repo Valuation (Floating)

- A.2.283 Repurchase Agreement

- A.2.284 Repurchase Agreement (Floating)

- A.2.285 Result

- A.2.286 Result with Classification

- A.2.287 RiskManager position template

- A.2.288 Risk Setup (BOND)

- A.2.289 Risk Setup (FRN)

- A.2.290 Risk Venture Capital

- A.2.291 Risk Yield

- A.2.292 Schedule Data

- A.2.293 Schedule Template Setup

- A.2.294 Schuldschein

- A.2.295 Security Identifiers

- A.2.296 Security Info

- A.2.297 Security Loan

- A.2.298 Settlement Setup

- A.2.299 Short Term Loan

- A.2.300 Short Term Loan Margin Result

- A.2.301 Short Term Loan Valuation

- A.2.302 Single Swap Valuation

- A.2.303 Special Issue

- A.2.304 Spot Date Setup

- A.2.305 Spread Curve Setup

- A.2.306 Substitution

- A.2.307 Swap

- A.2.308 Swap (Book, FX Rate)

- A.2.309 Swap (Deal, FX Rate)

- A.2.310 Swap Valuation

- A.2.311 Swaption Valuation

- A.2.312 Swaption Pricing

- A.2.313 Swap Per Leg Valuation

- A.2.314 Swap Pricing

- A.2.315 Swaption

- A.2.316 Swap, Upfront

- A.2.317 Swedish Index-Linked Treasury Bond

- A.2.318 Swedish Index-Linked Bond Valuation

- A.2.319 Ticks Netting

- A.2.320 Trading Unit (Derivative)

- A.2.321 Trading Unit (Equity)

- A.2.322 Trading Unit (Index)

- A.2.323 Trading Yield

- A.2.324 Transaction Charges

- A.2.325 Transaction Conversion

- A.2.326 Transfer (cash)

- A.2.327 TRS - Total Return Swap

- A.2.328 TRS Deferred

- A.2.329 UK ILG (3M)

- A.2.330 UK ILG (8M)

- A.2.331 UK Index-Linked Bond (3M) Valuation

- A.2.332 UK Index-Linked Bond (8M) Valuation

- A.2.333 US Index-Linked Bond Valuation

- A.2.334 US TIPS

- A.2.335 US TIPS (with Rounding)

- A.2.336 VaR Mapping Type

- A.2.337 Valuation Curve Setup

- A.2.338 Valuation Setup (Floating)

- A.2.339 Value Date Setup

- A.2.340 Volatility Surface Setup

- A.2.341 XAU Loan

- A.2.342 Yield

- A.2.343 Z-DM/Spread Setup

- Appendix B Schedules

- B.1 Schedule parameters

- B.2 Templates

- B.2.1 System-defined templates

- B.2.1.1 Primary templates

- B.2.1.1.1 ABS-MBS, Fixed Rate

- B.2.1.1.2 ABS-MBS, Floating Rate

- B.2.1.1.3 Australian Capital Indexed Bond

- B.2.1.1.4 Australian Indexed Annuity Bond

- B.2.1.1.5 Brazilian FX-Linked Bond (NBC)

- B.2.1.1.6 Brazilian IDxUSD Swap

- B.2.1.1.7 Brazilian LFT Bond

- B.2.1.1.8 Canadian Real Return Bond

- B.2.1.1.9 Cap

- B.2.1.1.10 Cap and Floor

- B.2.1.1.11 Collar

- B.2.1.1.12 Cost of Carry Compounding, Bullet Repayment

- B.2.1.1.13 Credit Default Swap

- B.2.1.1.14 Credit Default Swap, ISDA Standard

- B.2.1.1.15 Dual Currency, Known FX Rate

- B.2.1.1.16 Dual Currency, Known FX Rate, Floating

- B.2.1.1.17 Dual Currency, Unknown FX Rate

- B.2.1.1.18 Exercise

- B.2.1.1.19 Fixed Expression, Bullet Repayment

- B.2.1.1.20 Fixed, Annuity Repayment

- B.2.1.1.21 Fixed, Bullet Repayment

- B.2.1.1.22 Floating, Bullet Repayment

- B.2.1.1.23 Floor

- B.2.1.1.24 French Index-Linked Bond (OAT)

- B.2.1.1.25 Greek Index-Linked Bond

- B.2.1.1.26 Guarantee, Fixed underlying

- B.2.1.1.27 Guarantee, Floating underlying

- B.2.1.1.28 Israeli Index-Linked Bond

- B.2.1.1.29 Israeli Index-Linked Bond Galil

- B.2.1.1.30 Italian Index-Linked Bond (BTP)

- B.2.1.1.31 Japanese Index-Linked Bond

- B.2.1.1.32 LPI-Linked Annuity Repayment

- B.2.1.1.33 Multi Currency, Bullet Repayment

- B.2.1.1.34 Revisable, Bullet Repayment

- B.2.1.1.35 Revisable, Open-ended, Bullet Repayment

- B.2.1.1.36 RPI-Linked Interest and Capital, Annuity Repayment

- B.2.1.1.37 RPI-Linked Interest and Capital, Bullet Repayment

- B.2.1.1.38 Swedish Index-Linked Bond

- B.2.1.1.39 Swedish Index-Linked ZC Bond

- B.2.1.1.40 Target Redemption

- B.2.1.1.41 Target Redemption, Fixed Then Floating

- B.2.1.1.42 United Kingdom Index-Linked Gilt (3M)

- B.2.1.1.43 United Kingdom Index-Linked Gilt (8M)

- B.2.1.1.44 US Treasury Inflation Protected Security

- B.2.1.1.45 XAU, Unknown FX Rate, Fixed

- B.2.1.1.46 Zero-Coupon

- B.2.1.1.47 Zero-Coupon Swap Leg

- B.2.1.2 Secondary templates

- B.2.1.2.1 Accreting Dates

- B.2.1.2.2 Amortization

- B.2.1.2.3 Amortization, Floating

- B.2.1.2.4 Amortization, To Propagate to Other Legs

- B.2.1.2.5 Call/Put

- B.2.1.2.6 Call/Put, Referenced

- B.2.1.2.7 Capitalizing

- B.2.1.2.8 Capitalizing, with Amortization

- B.2.1.2.9 Compounding

- B.2.1.2.10 Compounding, with special Fixing Offset

- B.2.1.2.11 Convertible Conversion

- B.2.1.2.12 Currency Conversion

- B.2.1.2.13 Delaying

- B.2.1.2.14 Ex Dates

- B.2.1.2.15 Fixing Dates

- B.2.1.2.16 Interest, Fixed

- B.2.1.2.17 Interest, Fixed Annuity

- B.2.1.2.18 Interest, Fixed, In Sequence

- B.2.1.2.19 Interest, Fixed, Referenced

- B.2.1.2.20 Interest, Fixed, Up-Front

- B.2.1.2.21 Interest, Fixed, Up-Front, Referenced

- B.2.1.2.22 Interest, Floating

- B.2.1.2.23 Interest, Floating, In Sequence

- B.2.1.2.24 Interest, Floating, Referenced

- B.2.1.2.25 Interest, LPI-Linked

- B.2.1.2.26 Interest, LPI-Linked Annuity

- B.2.1.2.27 Interest, RPI-Linked

- B.2.1.2.28 Knock-In

- B.2.1.2.29 Knock-In with Rebate

- B.2.1.2.30 Knock-Out

- B.2.1.2.31 Knock-Out with Rebate

- B.2.1.2.32 Margin

- B.2.1.2.33 Payment Dates

- B.2.1.2.34 Principal Increase

- B.2.1.2.35 Principal Increase, Floating

- B.2.1.2.36 Principal Increase, RPI-Linked

- B.2.1.2.37 Principal Increase, with Amortization

- B.2.1.2.38 Redemption Premium

- B.2.1.2.39 Redemption Premium, Floating

- B.2.1.2.40 Referee, Floating

- B.2.1.2.41 Transaction Conversion, to Fixed Interest

- B.2.1.2.42 Transaction Conversion, to Fixed Interest, Referenced

- B.2.1.2.43 Transaction Conversion, to Floating Interest

- B.2.1.2.44 Transaction Conversion, to Floating Interest, Referenced

- B.2.1.2.45 Trigger

- B.2.1.2.46 Up-Front Discounting

- B.2.1.2.47 Value Dates

- B.2.1.1 Primary templates

- B.2.2 User-defined templates

- B.2.1 System-defined templates

- B.3 Schedule template groups

- Appendix C Option schedules

- Appendix D Expressions

- D.1 Expression syntax

- D.2 Market references in expressions

- D.3 Constants in expressions

- D.4 Functions in expressions

- D.4.1 Basic functions

- D.4.2 Referring functions

- D.4.3 Special functions

- D.4.3.1 UK RPI index market reference - ixuk

- D.4.3.2 Index lag

- D.4.3.3 FX lag

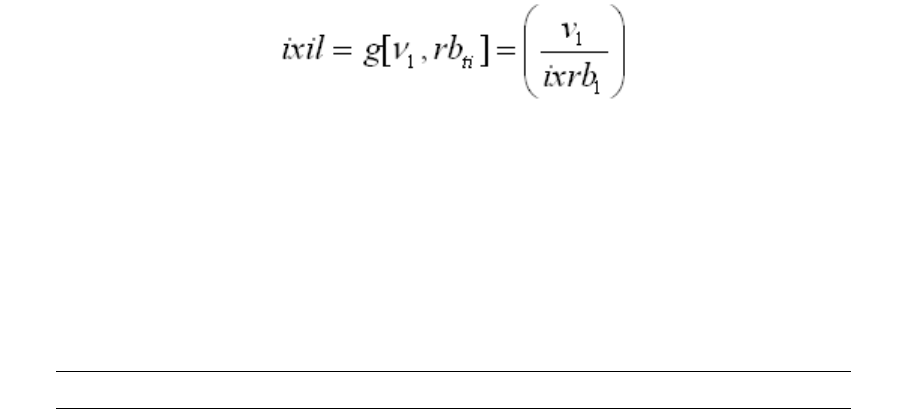

- D.4.3.4 Index Ratio - ixratio

- D.4.3.5 Instrument-specific index - iix

- D.4.3.6 Swedish CPI market reference - ixse

- D.4.3.7 Price - price

- D.4.3.8 Instrument quotes - iq

- D.4.3.9 Range accrual - range

- D.4.3.10 Compound

- D.4.3.11 Average

- D.4.3.12 Dual

- D.4.3.13 ixau

- D.4.4 Special characters

2

Information in this document is subject to change without notice and does not represent a commitment on the part

of Wall Street Systems. The software and documentation, which includes information contained in any databases,

described in this document is furnished under a license agreement or nondisclosure agreement and may only be

used or copied in accordance with the terms of the agreement. It is against the law to copy the software or

documentation except as specially allowed in the license or nondisclosure agreement. No part of this publication

may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical,

photocopying, recording, or otherwise, without the prior written permission of Wall Street Systems.

Although Wall Street Systems has tested the software and reviewed the documentation, Wall Street Systems

makes herein no warranty or representation, either expressed or implied, with respect to software or

documentation, its quality, performance, marketability, or fitness for a particular purpose. As a result, this

software is provided "as is", and in no event will Wall Street Systems be liable for direct, indirect, special,

incidental, or consequential damages from any defect in the software or by virtue of providing this

documentation, even if advised of the possibility of such damages. The documentation may contain technical

inaccuracies and omissions.

The mention of an activity or instrument in this publication does not imply that all matters relating to that activity or

instrument are supported by Wallstreet Suite, nor does it imply that processing of or by that activity or instrument is

carried out in any particular way, even if such processing is customary in some or all parts of the industry.

The windows and screen images shown herein were obtained from prototypes during software development. The

actual windows and screen images in the software may differ.

Wall Street Systems, WSS, WALLSTREET, WALLSTREET SUITE and the Wall Street Systems logos are

trademarks of Wall Street Systems Delaware, Inc.

Finance KIT, Trema and Trema logo are trademarks of Wall Street Systems Sweden AB.

Microsoft and Windows are either registered trademarks or trademarks of Microsoft Corporation in the United States

and/or other countries.

Adobe, Acrobat, and Acrobat Reader are either registered trademarks or trademarks of Adobe Systems

Incorporated in the United States and/or other countries.

All other products mentioned in this book may be trademarks or service marks of their respective companies or

organizations.

Company names, people names, and data used in examples are fictitious unless otherwise noted.

This edition applies to Wallstreet Suite version 7.3.14 and to all later releases and versions until indicated in new

editions or Wall Street Systems communications. Make sure you are using the latest edition for the release level of

the Wall Street Systems product.

© Copyright 2011 Wall Street Systems IPH AB. All rights reserved.

Second Edition (May 2011)

Transaction & Risk Management Module (TRM) Instruments: Processing and Calculations 3

Contents

Preface ...........................................................................................................................19

Intended audience ........................................................................................................................ 19

Associated documents ................................................................................................................ 19

Change history ............................................................................................................................. 20

1 Concepts ....................................................................................................................21

1.1 Instruments ............................................................................................................................ 21

1.2 Classes and types ................................................................................................................. 21

1.2.1 Creating types ................................................................................................................. 22

1.2.2 Customizing types ........................................................................................................... 22

1.3 Instrument templates ............................................................................................................ 23

1.4 Groups ................................................................................................................................... 23

1.5 Features ................................................................................................................................. 24

1.5.1 Primary and trading features ........................................................................................... 25

1.5.2 Action features ................................................................................................................ 25

1.5.3 Valuation approach and valuation setup features ........................................................... 25

1.6 Schedules .............................................................................................................................. 25

1.7 Deal capture ........................................................................................................................... 27

1.7.1 Input data ........................................................................................................................ 27

1.7.2 Generated data ............................................................................................................... 27

1.8 Processing ............................................................................................................................. 28

1.8.1 Setup ............................................................................................................................... 28

1.8.2 Execution ........................................................................................................................ 29

1.8.3 Cancellation .................................................................................................................... 29

1.9 Valuation and results ............................................................................................................ 29

1.9.1 Market value ................................................................................................................... 29

1.9.2 Profits and results ........................................................................................................... 29

1.9.3 Valuation modes ............................................................................................................. 30

2 Market standards and calculations .........................................................................33

2.1 Market standards .................................................................................................................. 33

2.1.1 Date basis ....................................................................................................................... 33

2.1.2 Interest types .................................................................................................................. 37

2.1.3 Price types ...................................................................................................................... 38

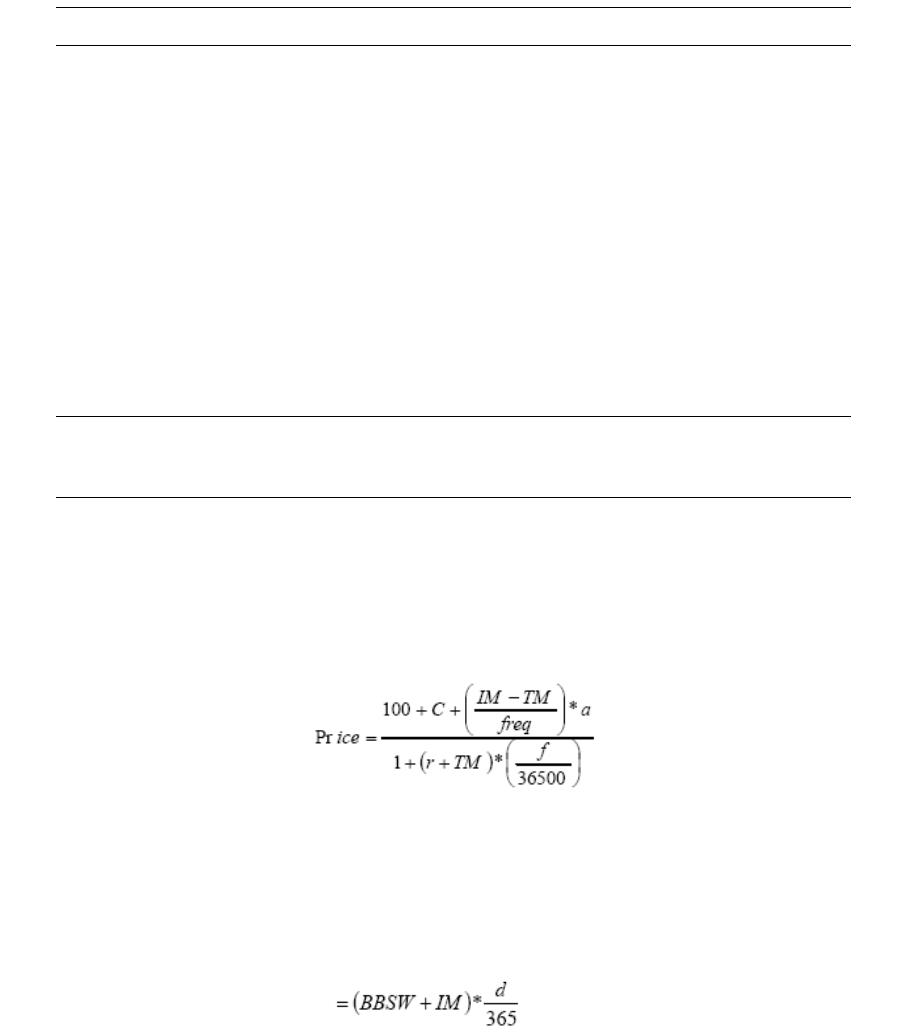

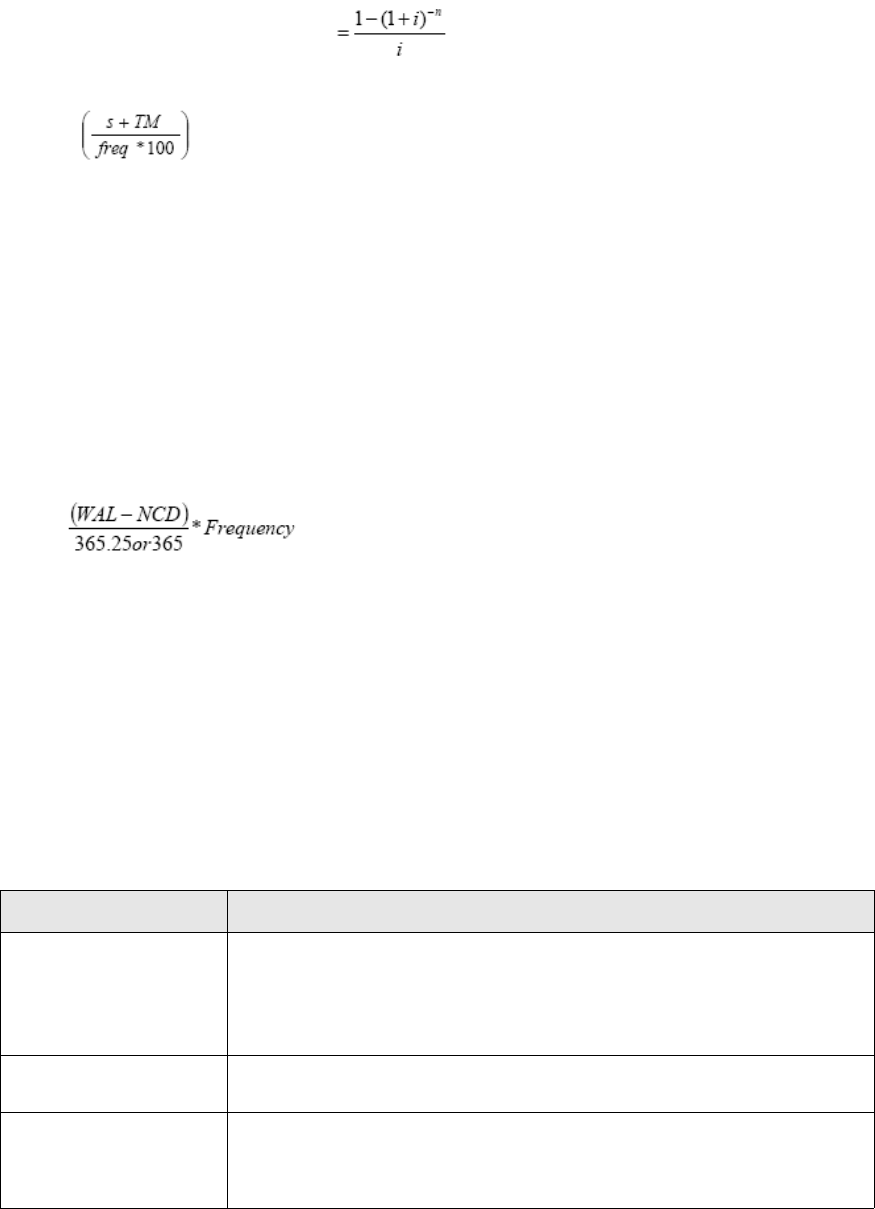

2.1.4 Yield/price conversions ...................................................................................................38

2.1.5 Discount Margin .............................................................................................................. 66

4 © Wall Street Systems IPH AB - Confidential

2.1.6 Calculation methods .......................................................................................................67

2.2 Yield curves ........................................................................................................................... 81

2.2.1 Yield curve ...................................................................................................................... 81

2.2.2 Basis swaps .................................................................................................................... 91

2.2.3 Yield Curve interpolation .................................................................................................98

2.2.4 FX rate interpolation ...................................................................................................... 110

2.3 Key-figures .......................................................................................................................... 112

2.3.1 Valuation ....................................................................................................................... 112

2.3.2 Profit and Loss .............................................................................................................. 113

2.3.3 Option figures ................................................................................................................ 115

2.3.4 Risk ............................................................................................................................... 119

2.3.5 Dual currency ................................................................................................................ 147

2.4 Performance calculations .................................................................................................. 149

2.4.1 Actual basis and all cash basis ..................................................................................... 150

2.4.2 Trade date and value date based performance ............................................................ 150

2.4.3 Time-weighted rate of return (TWR) ............................................................................. 151

2.4.4 Money-weighted return ................................................................................................. 154

2.4.5 Instrument market values for third currency .................................................................. 155

2.4.6 Instrument market values and cashflows ...................................................................... 160

2.4.7 Example portfolio .......................................................................................................... 163

2.4.8 Risk-adjusted returns .................................................................................................... 166

2.4.9 Risk-adjusted return measures ..................................................................................... 175

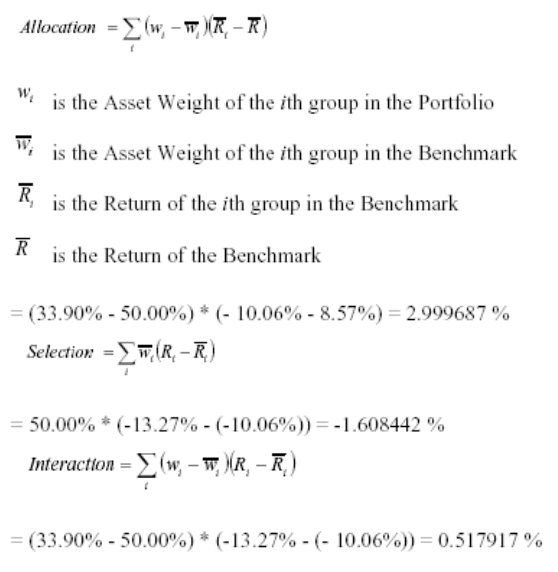

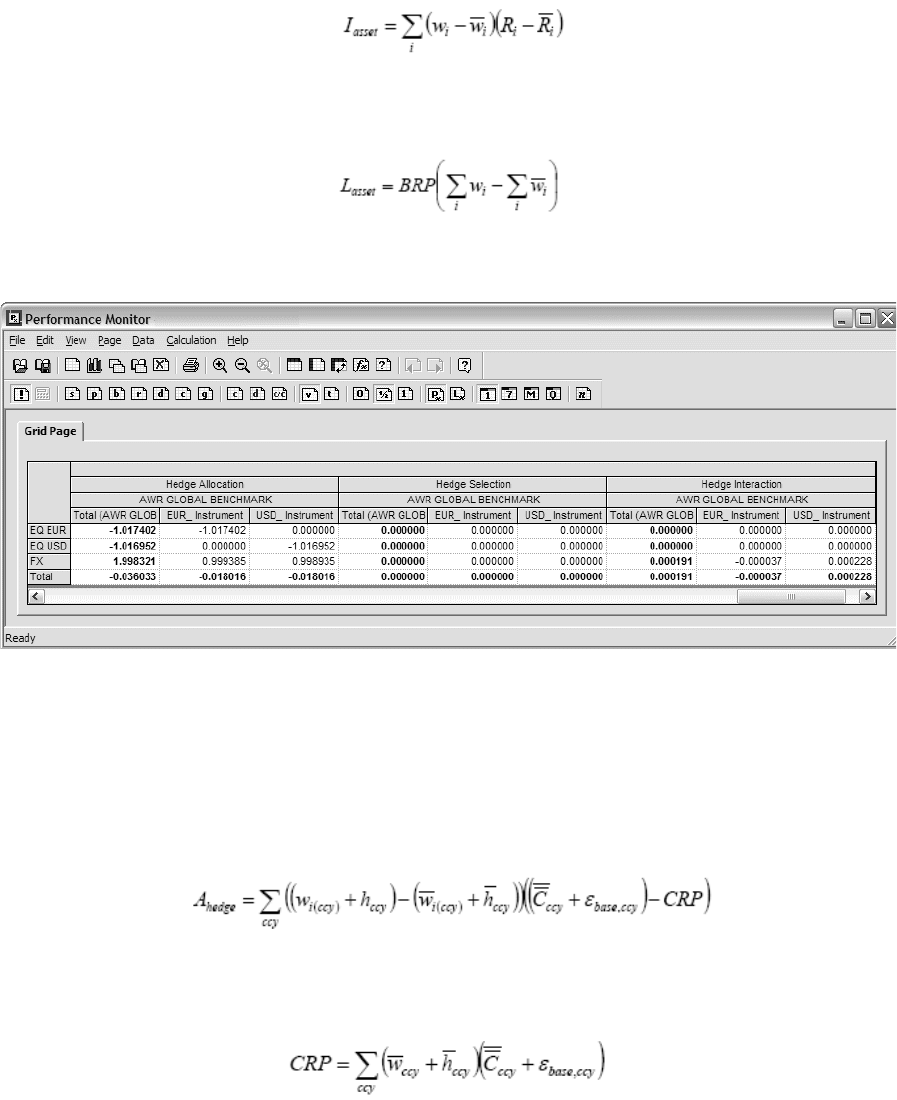

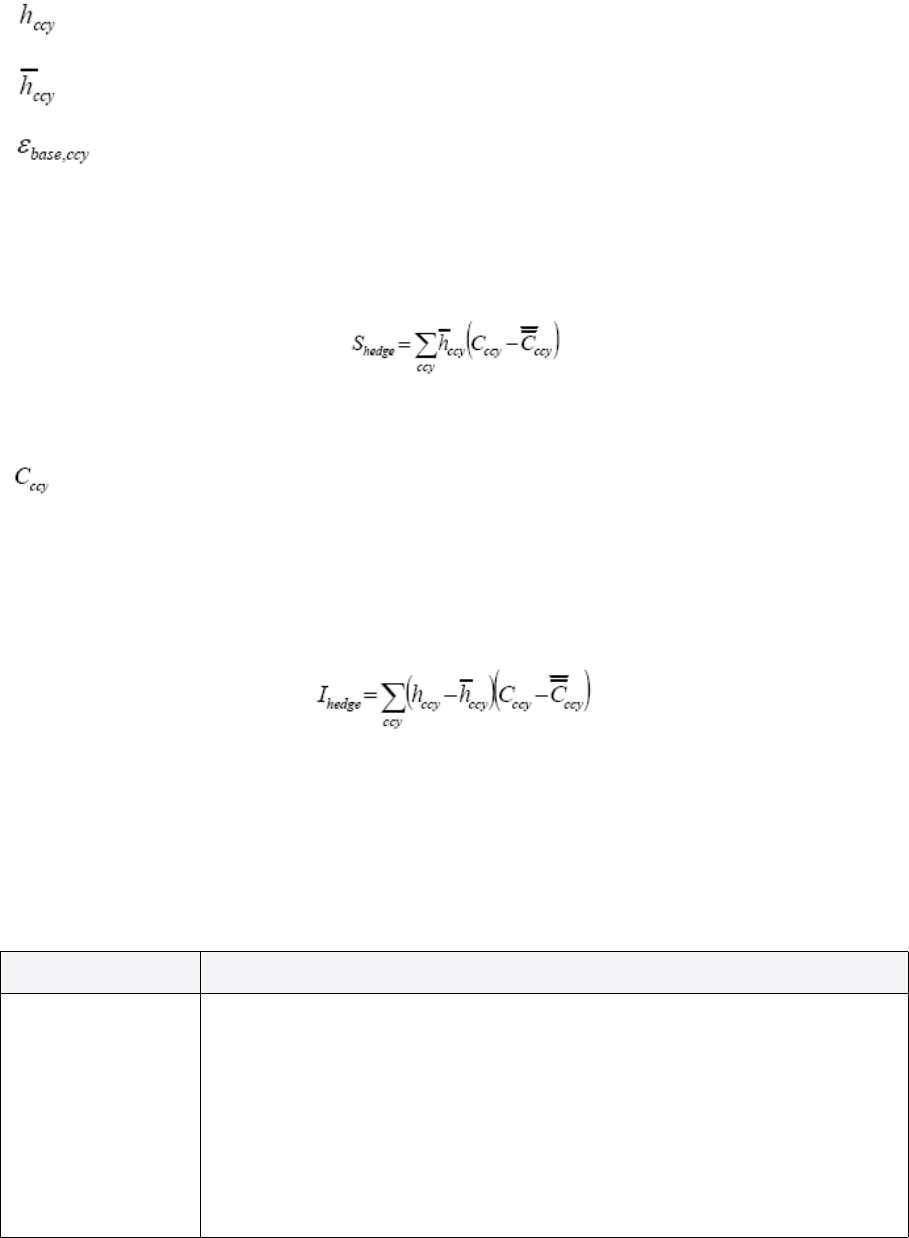

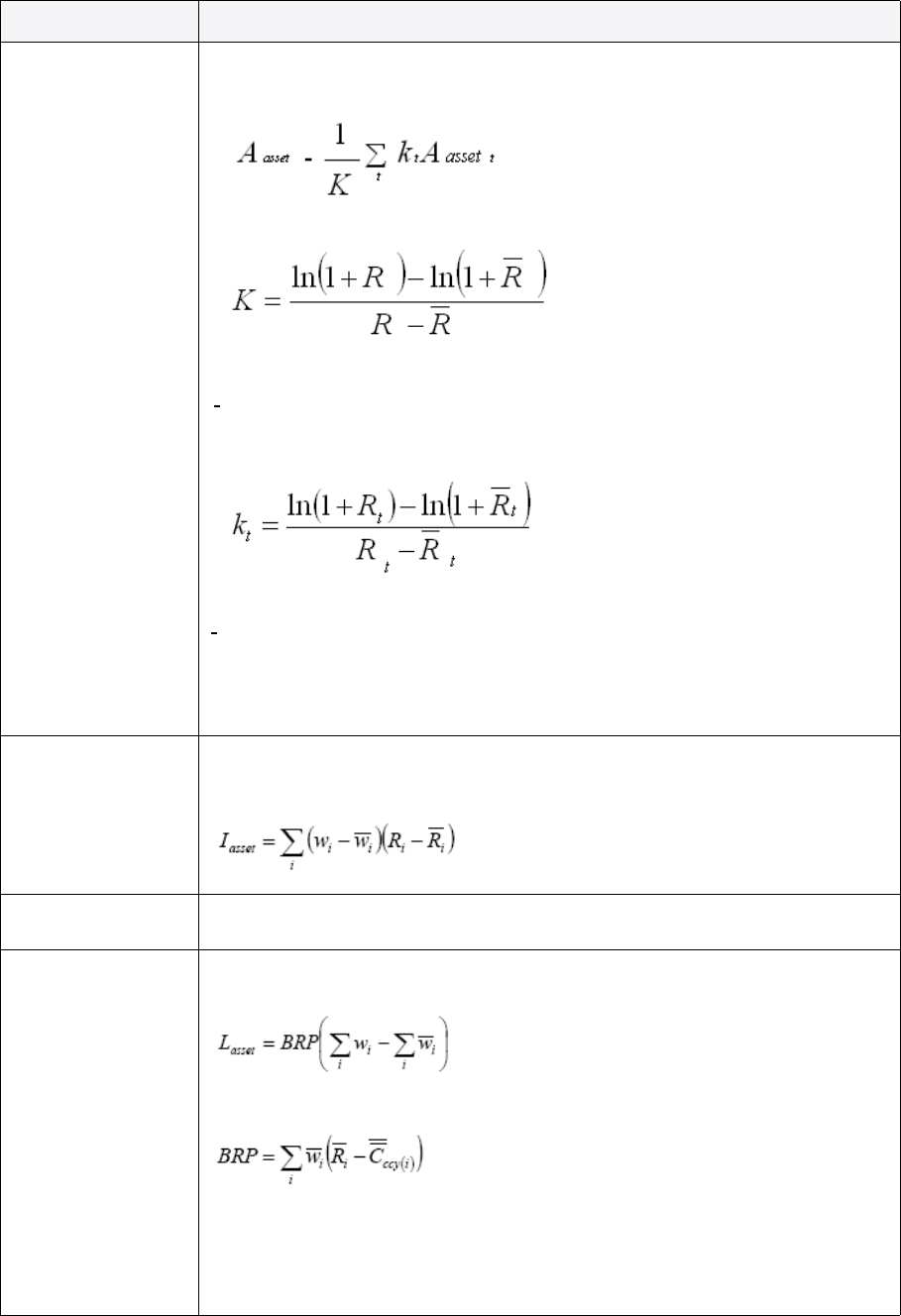

2.4.10 Performance attribution ............................................................................................... 180

2.4.11 Performance measurement key-figures ...................................................................... 189

2.5 Value-at-Risk calculations .................................................................................................. 200

2.5.1 TRM approach to VaR calculations .............................................................................. 201

2.5.2 RiskMetrics data ........................................................................................................... 201

2.5.3 Market variables ............................................................................................................ 202

2.5.4 Transforming RiskMetrics data ..................................................................................... 204

2.5.5 VaR calculations ........................................................................................................... 207

2.5.6 Incremental VaR ........................................................................................................... 212

3 Debt instruments .....................................................................................................215

3.1 Bond ..................................................................................................................................... 215

3.1.1 Fixed-rate bond ............................................................................................................. 215

3.1.2 Floating rate note .......................................................................................................... 228

3.1.3 Australian floating rate note .......................................................................................... 236

3.1.4 Zero-coupon bond ......................................................................................................... 239

3.1.5 Amortizing bond ............................................................................................................ 241

3.1.6 Step-up bond ................................................................................................................ 243

3.2 Structured bonds ................................................................................................................ 244

3.2.1 Callable bond ................................................................................................................ 244

3.2.2 Dual-currency bond ....................................................................................................... 246

3.2.3 Credit step-up bond ...................................................................................................... 249

3.3 Schuldscheindarlehen ........................................................................................................ 250

3.3.1 Instrument setup ........................................................................................................... 250

Transaction & Risk Management Module (TRM) Instruments: Processing and Calculations 5

3.3.2 Deal capture .................................................................................................................. 251

3.3.3 Processing .................................................................................................................... 251

3.3.4 Position monitoring ....................................................................................................... 251

3.4 Denominated bond .............................................................................................................. 254

3.4.1 Instrument setup ........................................................................................................... 254

3.4.2 Deal capture .................................................................................................................. 255

3.4.3 Processing .................................................................................................................... 256

3.4.4 Position monitoring ....................................................................................................... 256

3.5 Convertible bond ................................................................................................................. 258

3.5.1 Instrument setup ........................................................................................................... 258

3.5.2 Deal capture .................................................................................................................. 259

3.5.3 Processing .................................................................................................................... 259

3.6 Index-linked bond ............................................................................................................... 260

3.6.1 Instrument setup ........................................................................................................... 260

3.6.2 Deal capture .................................................................................................................. 262

3.6.3 Processing .................................................................................................................... 262

3.6.4 Australian index-linked annuity bond ............................................................................ 263

3.6.5 Australian index-linked bond ......................................................................................... 267

3.6.6 Brazilian (LFT) selic-linked security .............................................................................. 270

3.6.7 Brazilian FX-linked NBC-E/NTN-D ................................................................................ 271

3.6.8 Brazilian inflation-linked NTN ........................................................................................ 272

3.6.9 Canadian real return bond ............................................................................................ 273

3.6.10 French OAT€i .............................................................................................................. 274

3.6.11 Greek index-linked bond ............................................................................................. 277

3.6.12 Israeli index-linked bond ............................................................................................. 279

3.6.13 Italian BTP €i ............................................................................................................... 281

3.6.14 Japanese index-linked bond ....................................................................................... 282

3.6.15 Swedish index-linked bond ......................................................................................... 283

3.6.16 UK index-linked gilt ..................................................................................................... 287

3.6.17 US Tips ....................................................................................................................... 292

3.7 Asset backed security ........................................................................................................ 297

3.7.1 Instrument setup ........................................................................................................... 297

3.7.2 Deal capture .................................................................................................................. 299

3.7.3 Processing .................................................................................................................... 300

3.7.4 Position monitoring ....................................................................................................... 302

3.7.5 Australian MBS ............................................................................................................. 302

3.8 Short term loan .................................................................................................................... 305

3.8.1 Instrument setup ........................................................................................................... 306

3.8.2 Deal capture .................................................................................................................. 307

3.8.3 Processing .................................................................................................................... 308

3.8.4 Position monitoring ....................................................................................................... 311

3.9 Discount paper .................................................................................................................... 316

3.9.1 Instrument setup ........................................................................................................... 316

3.9.2 Deal capture .................................................................................................................. 317

3.9.3 Processing .................................................................................................................... 319

3.9.4 Position monitoring ....................................................................................................... 320

6 © Wall Street Systems IPH AB - Confidential

3.10 Loan .................................................................................................................................... 326

3.10.1 Fixed-rate loan ............................................................................................................ 326

3.10.2 Floating-rate loan ........................................................................................................ 337

3.10.3 Other loan structures .................................................................................................. 340

4 Equities ....................................................................................................................345

4.1 Equity ................................................................................................................................... 345

4.1.1 Instrument setup ........................................................................................................... 345

4.1.2 Deal capture .................................................................................................................. 346

4.1.3 Processing .................................................................................................................... 347

4.1.4 Position monitoring ....................................................................................................... 352

5 Security lending ......................................................................................................355

5.1 Repurchase agreement ...................................................................................................... 355

5.1.1 Repo (classic) ............................................................................................................... 355

5.1.2 Buy/sell back and sell/buy back .................................................................................... 362

5.1.3 Floating Repo ................................................................................................................ 363

5.1.4 Collateral ....................................................................................................................... 365

5.1.5 Substitution ................................................................................................................... 366

5.1.6 Margin movement ......................................................................................................... 370

5.1.7 Cash Collateral ............................................................................................................. 376

5.2 Security loan ........................................................................................................................ 380

5.2.1 Instrument setup ........................................................................................................... 380

5.2.2 Deal capture .................................................................................................................. 380

5.2.3 Processing .................................................................................................................... 381

6 Forex ........................................................................................................................383

6.1 FX spot and FX forward ...................................................................................................... 383

6.1.1 Instrument setup ........................................................................................................... 383

6.1.2 Market information ........................................................................................................ 384

6.1.3 Deal capture .................................................................................................................. 384

6.1.4 Processing .................................................................................................................... 387

6.1.5 Position monitoring ....................................................................................................... 393

6.2 Average FX rate forward ..................................................................................................... 406

6.2.1 Instrument setup ........................................................................................................... 406

6.2.2 Deal capture .................................................................................................................. 406

6.2.3 Processing .................................................................................................................... 408

6.2.4 Position monitoring ....................................................................................................... 409

6.3 Open Window FX Forward (FX Time Option) ................................................................... 409

6.3.1 Instrument setup ........................................................................................................... 410

6.3.2 Deal capture .................................................................................................................. 410

6.3.3 Processing .................................................................................................................... 411

6.3.4 Position monitoring ....................................................................................................... 411

6.4 FX swap ................................................................................................................................ 416

6.4.1 Instrument setup ........................................................................................................... 416

Transaction & Risk Management Module (TRM) Instruments: Processing and Calculations 7

6.4.2 Market information ........................................................................................................ 418

6.4.3 Deal capture .................................................................................................................. 418

6.4.4 Processing .................................................................................................................... 420

6.4.5 Position monitoring ....................................................................................................... 422

6.5 Cost-of-funding FX swap .................................................................................................... 422

6.5.1 Instrument setup ........................................................................................................... 423

6.5.2 Deal capture .................................................................................................................. 423

6.5.3 Processing .................................................................................................................... 424

6.5.4 Position monitoring ....................................................................................................... 424

7 Index .........................................................................................................................425

7.1 Index types .......................................................................................................................... 425

7.2 Instrument setup ................................................................................................................. 426

7.2.1 Simple Index ................................................................................................................. 426

7.2.2 Composite Index ........................................................................................................... 427

7.2.3 Derived Index ................................................................................................................ 430

7.2.4 Performance averaging index ....................................................................................... 433

7.2.5 Performance totaling index ........................................................................................... 436

7.3 Market information .............................................................................................................. 440

7.4 Processing ........................................................................................................................... 440

7.4.1 Revision ........................................................................................................................ 440

7.4.2 Freezing Index Values .................................................................................................. 440

7.4.3 Updating Factors and Cash .......................................................................................... 441

7.4.4 Rebalancing .................................................................................................................. 441

8 Cash .........................................................................................................................443

8.1 Bank account ....................................................................................................................... 443

8.1.1 Instrument setup ........................................................................................................... 443

8.1.2 Deal capture .................................................................................................................. 444

8.1.3 Processing .................................................................................................................... 445

8.2 Call account ......................................................................................................................... 446

8.2.1 Instrument setup ........................................................................................................... 446

8.2.2 Deal capture .................................................................................................................. 447

8.2.3 Processing .................................................................................................................... 447

8.3 Call money ........................................................................................................................... 450

8.3.1 Instrument setup ........................................................................................................... 450

8.3.2 Deal capture .................................................................................................................. 451

8.3.3 Processing .................................................................................................................... 451

8.3.4 Position monitoring ....................................................................................................... 454

8.4 Cash ..................................................................................................................................... 454

8.4.1 Payment ........................................................................................................................ 454

8.4.2 Transfer ......................................................................................................................... 455

8.4.3 Complex payment ......................................................................................................... 457

8.5 Forecast ............................................................................................................................... 459

8.5.1 Instrument setup ........................................................................................................... 459

8 © Wall Street Systems IPH AB - Confidential

8.5.2 Deal capture .................................................................................................................. 459

8.5.3 Processing .................................................................................................................... 459

8.6 Cost-of-carry ........................................................................................................................ 460

8.6.1 Instrument setup ........................................................................................................... 461

8.6.2 Deal capture .................................................................................................................. 462

8.6.3 Processing .................................................................................................................... 462

9 Futures .....................................................................................................................465

9.1 Forward rate agreement ..................................................................................................... 465

9.1.1 FRA deposit and FRA discount ..................................................................................... 465

9.1.2 Australian FRA .............................................................................................................. 476

9.1.3 Swedish FRA ................................................................................................................ 477

9.2 Bond forward ....................................................................................................................... 479

9.2.1 Bond forward ................................................................................................................. 479

9.2.2 Swedish Bond forward .................................................................................................. 482

9.3 Money market future ........................................................................................................... 485

9.3.1 Money market future (single contract) .......................................................................... 485

9.3.2 Money market future chain ........................................................................................... 503

9.4 Bond future .......................................................................................................................... 506

9.4.1 Bond future ................................................................................................................... 506

9.4.2 CTD future .................................................................................................................... 509

9.4.3 Australian bond future ................................................................................................... 518

9.5 Equity future ........................................................................................................................ 519

9.5.1 Instrument setup ........................................................................................................... 519

9.5.2 Deal capture .................................................................................................................. 521

9.5.3 Processing .................................................................................................................... 521

9.6 FX future .............................................................................................................................. 523

9.6.1 Instrument setup ........................................................................................................... 523

9.6.2 Deal capture .................................................................................................................. 525

9.6.3 Processing .................................................................................................................... 525

9.6.4 Position monitoring ....................................................................................................... 527

9.7 Index future .......................................................................................................................... 529

9.7.1 Instrument setup ........................................................................................................... 530

9.7.2 Deal capture .................................................................................................................. 531

9.7.3 Processing .................................................................................................................... 531

10 Options ...................................................................................................................533

10.1 Cap/floor/collar .................................................................................................................. 533

10.1.1 Vanilla cap/floor/collar ................................................................................................. 533

10.1.2 Exotic cap/floor/collar .................................................................................................. 544

10.2 Swaption ............................................................................................................................ 546

10.2.1 Instrument setup ......................................................................................................... 547

10.2.2 Deal capture ................................................................................................................ 548

10.2.3 Processing .................................................................................................................. 549

10.2.4 Position monitoring ..................................................................................................... 550

Transaction & Risk Management Module (TRM) Instruments: Processing and Calculations 9

10.3 Option on MM future ......................................................................................................... 559

10.3.1 Instrument setup ......................................................................................................... 560

10.3.2 Market information ...................................................................................................... 562

10.3.3 Deal capture ................................................................................................................ 562

10.3.4 Processing .................................................................................................................. 563

10.3.5 Position monitoring ..................................................................................................... 564

10.3.6 Australian MM Future option ....................................................................................... 568

10.4 Bond option ....................................................................................................................... 569

10.4.1 Instrument setup ......................................................................................................... 570

10.4.2 Deal capture ................................................................................................................ 572

10.4.3 Processing .................................................................................................................. 573

10.5 Bond Future Option .......................................................................................................... 574

10.5.1 Instrument setup ......................................................................................................... 574

10.5.2 Australian Bond Future Option .................................................................................... 574

10.6 Equity option ..................................................................................................................... 575

10.6.1 Instrument setup ......................................................................................................... 576

10.6.2 Deal capture ................................................................................................................ 577

10.6.3 Processing .................................................................................................................. 578

10.6.4 Position monitoring ..................................................................................................... 579

10.7 Index option ....................................................................................................................... 582

10.7.1 Instrument setup ......................................................................................................... 582

10.7.2 Deal capture ................................................................................................................ 583

10.7.3 Processing .................................................................................................................. 584

10.8 FX option ............................................................................................................................ 585

10.8.1 Vanilla FX option ......................................................................................................... 585

10.8.2 Digital FX option .......................................................................................................... 593

10.8.3 Barrier FX option ......................................................................................................... 596

10.8.4 Compound FX option .................................................................................................. 601

10.8.5 Average FX rate option ............................................................................................... 605

10.8.6 Position monitoring ..................................................................................................... 610

10.9 Exchange traded FX option .............................................................................................. 628

11 Swaps .....................................................................................................................629

11.1 Interest rate swap .............................................................................................................. 629

11.1.1 Single-currency IR swap ............................................................................................. 629

11.1.2 Asset swap .................................................................................................................. 656

11.1.3 Cross-currency swap .................................................................................................. 656

11.1.4 Brazilian IDxUSD Swap .............................................................................................. 677

11.1.5 Overnight index swap ................................................................................................. 677

11.1.6 Other swap structures ................................................................................................. 682

11.2 Total return swap .............................................................................................................. 682

11.2.1 Instrument setup ......................................................................................................... 683

11.2.2 Deal capture ................................................................................................................ 684

11.2.3 Processing .................................................................................................................. 685

11.3 Credit default swap ........................................................................................................... 688

10 © Wall Street Systems IPH AB - Confidential

11.3.1 Instrument setup ......................................................................................................... 688

11.3.2 Market information ...................................................................................................... 690

11.3.3 Deal capture ................................................................................................................ 690

11.3.4 Processing .................................................................................................................. 692

11.3.5 Position monitoring ..................................................................................................... 694

12 Commodities .........................................................................................................699

12.1 Gold .................................................................................................................................... 699

12.1.1 Gold deposit ................................................................................................................ 699

12.1.2 Gold IR swap .............................................................................................................. 702

12.2 Setting up commodities as currencies ........................................................................... 702

12.3 Commodity futures ........................................................................................................... 703

12.3.1 Setting up instruments ................................................................................................ 703

12.4 Commodity swaps and forwards ..................................................................................... 703

12.4.1 Schedule structure ...................................................................................................... 703

12.4.2 Setting up instruments ................................................................................................ 704

12.4.3 Deal capture ................................................................................................................ 705

13 Funds .....................................................................................................................707

13.1 Fund shares ....................................................................................................................... 707

13.1.1 Instrument setup ......................................................................................................... 707

13.1.2 Deal capture ................................................................................................................ 708

13.2 Fund fees ........................................................................................................................... 708

13.2.1 Instrument setup ......................................................................................................... 708

13.2.2 Deal capture ................................................................................................................ 710

13.2.3 Processing .................................................................................................................. 710

Appendix A: Features ............................................................................................................713

A.1 Categories of features ........................................................................................................ 713

A.2 List of features .................................................................................................................... 713

A.2.1 ABS - Asset Backed Security ....................................................................................... 713

A.2.2 ABS Valuation .............................................................................................................. 714

A.2.3 Accrual Yield Setup ...................................................................................................... 714

A.2.4 Allow Ad-Hoc Instructions ............................................................................................. 715

A.2.5 Allow Ad-Hoc Clients/Instructions ................................................................................. 715

A.2.6 Allow Forcing Type to Spot ........................................................................................... 715

A.2.7 Allow FX Currency Pair Shift ........................................................................................ 716

A.2.8 Allow Manual Classification .......................................................................................... 716

A.2.9 Allow Roll Over ............................................................................................................. 716

A.2.10 Allow Roll Over (Dual Currency) ................................................................................. 717

A.2.11 Allow Roll Over (FX) ................................................................................................... 717

A.2.12 Allow Roll Over (FX - Margin Result) .......................................................................... 718

A.2.13 Allow Roll Over (repo) ................................................................................................ 719

A.2.14 Allow Roll Over (Short Loan) ...................................................................................... 719

A.2.15 Allow Roll Over (Short Loan - Margin Result) ............................................................. 719

Transaction & Risk Management Module (TRM) Instruments: Processing and Calculations 11

A.2.16 Allow Roll Over (FX - Swap Style) .............................................................................. 720

A.2.17 Allow Roll Over (FX - Swap Style - Margin Result) .................................................... 720

A.2.18 Allow Roll Over (Guarantee) ....................................................................................... 720

A.2.19 Allow Security Loan .................................................................................................... 721

A.2.20 Allow Sight Account Transfer ..................................................................................... 721

A.2.21 Allow Signature Date .................................................................................................. 721

A.2.22 Allow Spread Curves .................................................................................................. 721

A.2.23 Allow Swap ................................................................................................................. 722

A.2.24 Allow Transaction Transfer ......................................................................................... 722

A.2.25 Allow Weight Difference ............................................................................................. 722

A.2.26 Allow Valuation Curves ............................................................................................... 723

A.2.27 Alternative Repayment Estimates .............................................................................. 723

A.2.28 Australian Bond Future Option ................................................................................... 724

A.2.29 Australian CIB ............................................................................................................. 724

A.2.30 Australian FRN ........................................................................................................... 724

A.2.31 Australian FRN Method .............................................................................................. 725

A.2.32 Australian IAB ............................................................................................................. 725

A.2.33 Australian IAB Valuation ............................................................................................. 725

A.2.34 Australian IAB (Round to 3) ........................................................................................ 725

A.2.35 Australian IAB Valuation (Round to 3) ........................................................................ 726

A.2.36 Australian IAB Par Curve Valuation ............................................................................ 726

A.2.37 Australian IAB Par Curve Valuation (Round to 3) ....................................................... 727

A.2.38 Australian Index-Linked Bond Valuation ..................................................................... 727

A.2.39 Australian MBS ........................................................................................................... 727