TRM User Guide

User Manual:

Open the PDF directly: View PDF ![]() .

.

Page Count: 710 [warning: Documents this large are best viewed by clicking the View PDF Link!]

- Contents

- Preface

- Chapter 1 Overview

- Chapter 2 Navigating TRM

- 2.1 Application Manager

- 2.2 Common application features

- 2.2.1 Opening applications

- 2.2.2 Closing applications

- 2.2.3 Generating reports on application activity

- 2.2.4 Using application controls

- 2.2.5 Using keyboard shortcuts

- 2.2.6 Using application menus

- 2.2.7 Customizing the display of applications

- 2.2.8 Sorting data

- 2.2.9 Printing data

- 2.2.10 Using manager applications

- Chapter 3 Managing static data

- 3.1 Static data entities

- 3.2 Static Data Editor

- 3.3 Managing static data in Static Data Editor

- 3.3.1 Creating new static data entities

- 3.3.2 Creating static data from an existing entity

- 3.3.3 Creating static data entities in parallel

- 3.3.4 Modifying static data entities

- 3.3.5 Deleting static data entities

- 3.3.6 Verifying static data entities

- 3.3.7 Finding static data entities

- 3.3.8 Using templates to create static data entities

- 3.3.9 Common Static Data Editor attributes

- 3.4 Managing SDM-enabled static data

- 3.5 Countries

- 3.6 Calendars

- 3.7 Gaps (time intervals)

- 3.8 IR quotes and yield curves

- 3.9 Currencies

- 3.10 Currency priorities

- 3.11 Settlement locations

- 3.12 Client groups

- 3.13 Clients

- 3.13.1 Creating clients

- 3.13.1.1 Assigning clients to groups

- 3.13.1.2 Setting up client contact information

- 3.13.1.3 Defining properties

- 3.13.1.4 Creating groups of clients

- 3.13.1.5 Defining multiple branch SWIFT codes

- 3.13.1.6 Assigning portfolio-owner specific properties

- 3.13.1.7 Setting up internal deal mirroring

- 3.13.1.8 Configuring counterparty-specific limit amounts

- 3.13.1.9 Attaching collateral agreements to portfolio owners

- 3.13.1.10 Applying classification groups to a portfolio owner

- 3.13.1.11 Setting up client accounts

- 3.13.1.12 Linking settlement locations to clients

- 3.13.1.13 Setting up client settlement instructions

- 3.13.1.14 Specifying automatic netting for settlement flows

- 3.13.1.15 Settling in another currency

- 3.13.1.16 Assigning credit ratings to clients

- 3.13.1.17 Assigning credit spread curves to clients

- 3.13.2 Managing clients

- 3.13.1 Creating clients

- 3.14 Portfolios

- 3.14.1 Creating portfolios

- 3.14.1.1 Setting further portfolio attributes

- 3.14.1.2 Assigning allowed users and processes

- 3.14.1.3 Setting up cost-of-carry for portfolios

- 3.14.1.4 Restricting transactions into this portfolio (optional)

- 3.14.1.5 Defining result treatments for a portfolio

- 3.14.1.6 Aggregating result calculations across portfolios

- 3.14.2 Managing portfolios

- 3.14.1 Creating portfolios

- 3.15 Result types and results

- 3.16 Instrument types

- 3.17 Instrument groups

- 3.18 Instrument Templates

- 3.19 Instruments

- 3.20 Classification groups

- 3.21 Classification rules

- 3.22 Comments and comment rules (optional)

- 3.23 Bank Account Type Editor (optional)

- 3.24 Branch codes (optional)

- 3.25 Calendar groups (optional)

- 3.26 Cashflow charges (optional)

- 3.27 Cashflow groups (optional)

- 3.28 Cashflow types (optional)

- 3.29 Cash pools (optional)

- 3.30 Country groups (optional)

- 3.31 Credit ratings (optional)

- 3.32 Currency classes (optional)

- 3.33 Ladder sets (optional)

- 3.34 Ladder rules (optional)

- 3.35 Option schedule templates (optional)

- 3.36 Option schedule template groups (optional)

- 3.37 Package types (optional)

- 3.38 Parameters (optional)

- 3.39 Properties (optional)

- 3.40 Schedule templates (optional)

- 3.41 Schedule template groups (optional)

- 3.42 Security Basket Editor (optional)

- 3.43 Security Criteria Set Editor (optional)

- 3.44 Security identifier types (optional)

- 3.45 Time zones (optional)

- 3.46 Transaction charges (optional)

- 3.47 Volatilities (optional)

- Chapter 4 Managing market data

- 4.1 Defining real-time quotations

- 4.2 Defining scenarios and subscenarios

- 4.3 Freezing rates automatically

- 4.4 Defining simulation scenarios

- 4.5 Rate Monitor

- 4.5.1 Rate Monitor menus

- 4.5.2 Toolbar

- 4.5.3 Start-up parameters

- 4.5.4 Managing market data in Rate Monitor

- 4.5.4.1 Configuring page layouts

- 4.5.4.2 Selecting axes values

- 4.5.4.2.1 Instrument axes

- 4.5.4.2.2 FX Rate axes

- 4.5.4.2.3 FX Volatility axes

- 4.5.4.2.4 FX Fixing Rate axes

- 4.5.4.2.5 IR Quote /Yield Curve axes

- 4.5.4.2.6 Credit Default Swap axes

- 4.5.4.2.7 Bond Option Volatility axes

- 4.5.4.2.8 Cap / Floor Volatility axes

- 4.5.4.2.9 Caplet / Floorlet Volatility axes

- 4.5.4.2.10 Swaption Volatility axes

- 4.5.4.2.11 Composite Index axes

- 4.5.4.2.12 Performance Index axes

- 4.5.4.2.13 Imported Index axes

- 4.5.4.2.14 Example: setting the volatility for EUR/USD

- 4.5.4.3 Configuring period axes

- 4.5.4.4 Selecting figures

- 4.5.4.4.1 Instrument figures

- 4.5.4.4.2 FX Rate figures

- 4.5.4.4.3 FX Volatility figures

- 4.5.4.4.4 FX Fixing Rate figures

- 4.5.4.4.5 IR Quote / Yield Curve figures

- 4.5.4.4.6 Credit Default Swap figures

- 4.5.4.4.7 Bond Option Volatility figures

- 4.5.4.4.8 Cap / Floor Volatility figures

- 4.5.4.4.9 Caplet / Floorlet Volatility figures

- 4.5.4.4.10 Swaption Volatility figures

- 4.5.4.4.11 Composite Index figures

- 4.5.4.4.12 Performance Index figures

- 4.5.4.4.13 Imported Index figures

- 4.5.4.5 Manually adjusting and creating quotations

- 4.5.5 Generating quotation reports

- 4.6 Pricing tools

- 4.7 Pricing complex derivatives

- 4.8 Bloomberg interface

- 4.9 Market Data Status Monitor

- Chapter 5 Managing rules

- Chapter 6 Managing activities

- Chapter 7 Reporting

- Chapter 8 Managing transactions

- 8.1 Transaction Manager

- 8.2 Capturing deals

- 8.2.1 Entering new deals in Transaction Manager

- 8.2.1.1 Calculating key-figures

- 8.2.1.2 Displaying valuation parameters in the Discovery Console

- 8.2.1.3 Using fractional prices

- 8.2.1.4 Defaulting prices

- 8.2.1.5 Changing result mode

- 8.2.1.6 Entering competitive quotes

- 8.2.1.7 Adding charges and fees

- 8.2.1.8 Creating an FX pair shift

- 8.2.1.9 Trade assignment

- 8.2.2 Canceling deals

- 8.2.3 Entering new deals in Enter Board

- 8.2.4 Setting up a pre-trade limit check

- 8.2.5 Enabling limit queries at transaction level

- 8.2.1 Entering new deals in Transaction Manager

- 8.3 Managing settlement instructions

- 8.4 Processing transactions

- 8.4.1 Retrieving transactions

- 8.4.2 Displaying transaction data in a chart

- 8.4.3 Verifying transactions

- 8.4.4 Confirming transactions

- 8.4.5 Correcting transactions

- 8.4.6 Matching and unmatching transactions

- 8.4.7 Performing actions on deals

- 8.4.7.1 Duplicating transactions

- 8.4.7.2 Packaging transactions

- 8.4.7.3 Previewing messages

- 8.4.7.4 Running reports on transactions

- 8.4.7.5 Checking the unavailable actions on a transaction

- 8.4.7.6 Adding information links to deals

- 8.4.7.7 Generating transaction comments

- 8.4.7.8 Setting base FX rates

- 8.4.7.9 Defining the valuation approach at transaction level

- 8.4.7.10 Assigning valuation models at transaction level

- 8.4.7.11 Changing IR exposure calculations at transaction level

- 8.4.7.12 Canceling provisional settlements in Transaction Manager

- 8.4.7.13 Processing special actions or events

- 8.4.8 Generating reports on transactions

- 8.5 Deal mirroring

- 8.6 Managing call transactions

- 8.7 Managing cashflow forecasts

- Chapter 9 Managing orders

- Chapter 10 Managing funds

- Chapter 11 Managing collateral

- 11.1 Setting up master agreements

- 11.2 Monitoring collateral positions

- Chapter 12 Monitoring positions

- 12.1 Treasury Monitor

- 12.1.1 Treasury Monitor menus

- 12.1.2 Start-up parameters

- 12.1.3 Configuring Treasury Monitor

- 12.1.4 Monitoring positions in Treasury Monitor

- 12.1.5 Simulating movements in Treasury Monitor

- 12.1.6 Using Treasury Monitor for risk measurement

- 12.1.7 Monitoring cost-of-carry positions

- 12.1.8 Generating position-related reports

- 12.2 Position Monitor

- 12.3 FX Spot Monitor

- 12.4 FX Position Roll Over activity

- 12.1 Treasury Monitor

- Chapter 13 Monitoring performance

- 13.1 Measuring performance and risk

- 13.2 Setting up performance measurement and risk

- 13.3 Performance Monitor

- Chapter 14 Portfolio modeling

- 14.1 Setting up portfolio modeling

- 14.2 Portfolio Modeling Monitor

- 14.2.1 Portfolio Modeling Monitor menus

- 14.2.2 Start-up parameters

- 14.2.3 Configuring Portfolio Modeling Monitor

- 14.2.4 Analyzing positions in Portfolio Modeling Monitor

- 14.2.5 Rebalancing

- 14.2.6 Generating deals

- Chapter 15 Managing benchmarks

- Chapter 16 Managing limits

- 16.1 Overview

- 16.2 Setting up limits

- 16.3 Limit Monitor

- 16.4 Limit Notifications

- 16.5 Analyzing limit violations

- Chapter 17 Managing transaction conditions

- Chapter 18 Managing cash and settlements

- 18.1 Managing cash and cash position

- 18.1.1 Managing bank account balances and interest

- 18.1.2 Managing cost of carry

- 18.1.3 Managing cash pool leveling

- 18.2 Setting up settlement management

- 18.3 Generating and processing settlements

- 18.3.1 Settlement Processing menus

- 18.3.2 Start-up parameters

- 18.3.3 Settlement processing modes

- 18.3.4 Processing settlements

- 18.3.5 Modifying settlement instructions

- 18.3.6 Generating settlement processing reports

- 18.4 Managing custody movements and balances

- 18.5 Reconciling settlements and custodies

- 18.1 Managing cash and cash position

- Chapter 19 Managing accounting

- 19.1 Parallel accounting

- 19.2 Realizing and processing results

- 19.3 Updating the book value of deals

- 19.4 Using TRM with a General Ledger system

- 19.5 Hedge accounting in Wallstreet Suite

- Chapter 20 Monitoring VaR

- 20.1 Setting up Value-at-Risk

- 20.2 Managing VaR data

- Chapter 21 Managing messages

- Chapter 22 Managing RMI and CMI

- 22.1 Managing RMI

- 22.1.1 Assigning RMI mapping strategies to instruments

- 22.1.2 Grouping by instrument

- 22.1.3 No Pending Cashflows

- 22.1.4 Defining yield curves for RMI

- 22.1.5 Defining equities for RMI

- 22.1.6 Defining instruments for RMI

- 22.1.7 Exporting and importing positions

- 22.2 Managing CMI

- 22.1 Managing RMI

- Chapter 23 Pricing IR and FX trades

- 23.1 Pricing IR trades

- 23.2 Pricing FX trades

- 23.2.1 FX Pricing tool

- 23.2.1.1 Menus

- 23.2.1.2 Sections

- 23.2.1.3 Setting Up FX Pricing instruments

- 23.2.1.4 Capturing transactions and strategies

- 23.2.1.5 Valuating and pricing

- 23.2.1.5.1 Defining the default pricing settings

- 23.2.1.5.2 Overwriting the default pricing settings

- 23.2.1.5.3 Modifying market quotes

- 23.2.1.5.4 Modifying derived market quotes

- 23.2.1.5.5 Monitoring key figures

- 23.2.1.5.6 Changing the preferred premium

- 23.2.1.5.7 Applying new figures to a given target

- 23.2.1.5.8 Charting

- 23.2.1.6 Processing transactions and strategies

- 23.2.1 FX Pricing tool

- Chapter 24 Working with the Dashboard

- Appendix A Activity parameters

- A.1 Bank Account Balances

- A.2 Bank Account Interest Realizing

- A.3 Benchmark Cash Processing

- A.4 Benchmark Rebalancing

- A.5 Book Value Change

- A.6 Call Money Account Update

- A.7 Call Money Roll Over

- A.8 Cash Pool Leveling

- A.9 Cash Settlement Reconciliation

- A.10 Checking Instruments and Transactions Clients

- A.11 Checking Instruments and Transactions Holidays

- A.12 Closing the Books Valuation

- A.13 Copy Market Information

- A.14 Cost of Carry

- A.15 Cost of Carry Interest Realizing

- A.16 Cost of Carry Zero Balancing

- A.17 Custody Balances

- A.18 Dashboard Excel Export

- A.19 Data License Prices

- A.20 Data License Output Processing

- A.21 Delete Instrument

- A.22 Detachment

- A.23 Dividend

- A.24 End of Day Processing

- A.25 End of Period Processing

- A.26 Equity Conversion

- A.27 Fixing ABS Repayment

- A.28 Fixing ABS Repayment (Full Repayment)

- A.29 Fixing Bond Cashflow

- A.30 Fixing Bond Cashflow - Undo

- A.31 Fixing Transaction Cashflow

- A.32 Fixing Transaction Cashflow - Undo

- A.33 Fixing Transaction Trigger

- A.34 Fixing Transaction Trigger - Undo

- A.35 Forecast Exposures from CMM

- A.36 Forward Fixing

- A.37 Fund Data Calculation/Reporting

- A.38 Fund Fee Realizing

- A.39 FX Fixing Transaction Cashflow

- A.40 FX Fixing Transaction Cashflow - Undo

- A.41 FX Option Strategy Exercise

- A.42 FX Position Roll-Over

- A.43 FX Realizing

- A.44 Import Instrument

- A.45 Import Market Information

- A.46 Import Security List

- A.47 Index Freeze

- A.48 Index Rebalance

- A.49 Index Adjustment

- A.50 Netting

- A.51 Netting - Undo

- A.52 NumeriX Calibration

- A.53 NumeriX Valuation

- A.54 FX Option No Exercise

- A.55 Performance Data Calculation

- A.56 Portfolio Modeling Processing

- A.57 Purge Market Quotes

- A.58 Return of Capital

- A.59 Risk Manager Export

- A.60 Save Caplet/Floorlet Volatilities

- A.61 Save Derived IR Quotes and Yield Curves

- A.62 Selling (FIFO and Avg Balances)

- A.63 Selling Values

- A.64 Settlement Generation

- A.65 Security Positions Data

- A.66 Security Settlement Reconciliation

- A.67 Split

- A.68 Undo Book Value Change

- A.69 Update Client

- A.70 Update Corporate Action

- A.71 Update Instrument

- A.72 Update Settlement Instructions

- A.73 CreditManager Exposure Export

- A.74 CreditManager Obligor Export

- Appendix B Report parameters

- B.1 Activity Log Report

- B.2 Balance Report

- B.3 Bank Account Statement Report

- B.4 Book Value Change History Report

- B.5 Call Reports

- B.6 Cashflow Report

- B.7 Cashflow Fixing Report

- B.8 Cashflow Log Report

- B.9 Cheapest to Deliver Report

- B.10 Classification Report

- B.11 Client Update Log

- B.12 Collateral Management Report

- B.13 Collateral Report

- B.14 Competitive Quote Report

- B.15 Corporate Actions Update Log

- B.16 Corporate Actions Update Report

- B.17 Custody Balance Report

- B.18 Custody Reconciliation Report

- B.19 Data License Output Processing Report

- B.20 Data License Prices Log

- B.21 Data License Prices Import Log

- B.22 Delivery Report

- B.23 Drawdown Fixing Report

- B.24 Event Diary Report

- B.25 History Log Report

- B.26 Holidays Checking Report

- B.27 Holidays for Period Report

- B.28 Import Market Information Log Report

- B.29 Instrument Delete Log

- B.30 Instrument Import Log

- B.31 Instrument Import Report

- B.32 Instrument Update Log

- B.33 Instrument Update Report

- B.34 Key Figure Report

- B.35 Limit Log Report

- B.36 Periodic P/L Report

- B.37 Rate Report

- B.38 Rate Comparison Report

- B.39 Rate Log Report

- B.40 Realize Account Interest Report

- B.41 Reconciliation Report

- B.42 Reconciliation Log Report

- B.43 Renaming Client ID Report

- B.44 Security List Import Log

- B.45 Settlement Report

- B.46 Settlement Cashflows Report

- B.47 Settlement Instructions Chain Report

- B.48 Settlement Log Report

- B.49 Transaction Conditions Report

- B.50 Transactions Report

- B.51 Transaction Log Report

- B.52 Transaction Market Rate Report

- Appendix C Start-up parameters

- Appendix D SDM - CMM mapping

- Appendix E TRM - RMI/CMI mapping

- Appendix F Cashflow attributes

2

Information in this document is subject to change without notice and does not represent a commitment on the part

of Wall Street Systems. The software and documentation, which includes information contained in any databases,

described in this document is furnished under a license agreement or nondisclosure agreement and may only be

used or copied in accordance with the terms of the agreement. It is against the law to copy the software or

documentation except as specially allowed in the license or nondisclosure agreement. No part of this publication

may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical,

photocopying, recording, or otherwise, without the prior written permission of Wall Street Systems.

Although Wall Street Systems has tested the software and reviewed the documentation, Wall Street Systems

makes herein no warranty or representation, either expressed or implied, with respect to software or

documentation, its quality, performance, marketability, or fitness for a particular purpose. As a result, this

software is provided "as is", and in no event will Wall Street Systems be liable for direct, indirect, special,

incidental, or consequential damages from any defect in the software or by virtue of providing this

documentation, even if advised of the possibility of such damages. The documentation may contain technical

inaccuracies and omissions.

The mention of an activity or instrument in this publication does not imply that all matters relating to that activity or

instrument are supported by Wallstreet Suite, nor does it imply that processing of or by that activity or instrument is

carried out in any particular way, even if such processing is customary in some or all parts of the industry.

The windows and screen images shown herein were obtained from prototypes during software development. The

actual windows and screen images in the software may differ.

Wall Street Systems, WSS, WALLSTREET, WALLSTREET SUITE and the Wall Street Systems logos are

trademarks of Wall Street Systems Delaware, Inc.

Finance KIT, Trema and Trema logo are trademarks of Wall Street Systems Sweden AB.

Microsoft and Windows are either registered trademarks or trademarks of Microsoft Corporation in the United States

and/or other countries.

Adobe, Acrobat, and Acrobat Reader are either registered trademarks or trademarks of Adobe Systems

Incorporated in the United States and/or other countries.

All other products mentioned in this book may be trademarks or service marks of their respective companies or

organizations.

Company names, people names, and data used in examples are fictitious unless otherwise noted.

This edition applies to Wallstreet Suite version 7.3.16 and to all later releases and versions until indicated in new

editions or Wall Street Systems communications. Make sure you are using the latest edition for the release level of

the Wall Street Systems product.

© Copyright 2011 Wall Street Systems IPH AB. All rights reserved.

Second Edition (September 2011)

Transaction & Risk Management Module (TRM) User Guide 3

Contents

Preface ...........................................................................................................................21

1 Overview ....................................................................................................................23

1.1 TRM ........................................................................................................................................ 23

1.2 Principles of TRM .................................................................................................................. 23

1.2.1 Portfolio hierarchy principle .............................................................................................23

1.2.2 Transaction flow principle ............................................................................................... 24

1.2.3 Cashflow principle ........................................................................................................... 24

1.2.4 Valuation principle ........................................................................................................... 24

1.2.5 Real-time principle .......................................................................................................... 24

1.3 Types of information in TRM ................................................................................................ 25

1.3.1 Static data ....................................................................................................................... 25

1.3.2 Market data ..................................................................................................................... 25

1.3.3 Transaction management information ............................................................................ 25

1.3.4 Calculated information ....................................................................................................25

1.4 Applications of TRM ............................................................................................................. 25

1.4.1 Front, Middle, and Back Office applications .................................................................... 25

1.4.2 Editors ............................................................................................................................. 26

1.4.3 Managers and Boards ..................................................................................................... 26

1.4.4 Monitors .......................................................................................................................... 26

1.4.5 Reports ........................................................................................................................... 27

1.4.6 Activities .......................................................................................................................... 27

1.5 Setting up and using TRM ....................................................................................................27

2 Navigating TRM .........................................................................................................29

2.1 Application Manager ............................................................................................................. 29

2.1.1 Launching Application Manager ...................................................................................... 29

2.1.2 Application Manager menus ........................................................................................... 30

2.1.3 Start-up parameters ........................................................................................................ 31

2.1.4 Customizing Application Manager .................................................................................. 31

2.2 Common application features .............................................................................................. 31

2.2.1 Opening applications ......................................................................................................32

2.2.2 Closing applications ........................................................................................................ 32

2.2.3 Generating reports on application activity ....................................................................... 32

2.2.4 Using application controls ............................................................................................... 32

2.2.5 Using keyboard shortcuts ............................................................................................... 34

2.2.6 Using application menus ................................................................................................. 34

4 © Wall Street Systems IPH AB - Confidential

2.2.7 Customizing the display of applications .......................................................................... 35

2.2.8 Sorting data ..................................................................................................................... 35

2.2.9 Printing data .................................................................................................................... 35

2.2.10 Using manager applications .......................................................................................... 36

3 Managing static data .................................................................................................41

3.1 Static data entities ................................................................................................................ 41

3.2 Static Data Editor .................................................................................................................. 41

3.2.1 Static Data Editor menus and toolbars ........................................................................... 41

3.2.2 Start-up parameters ........................................................................................................ 43

3.2.3 Editor layouts .................................................................................................................. 43

3.2.4 Query and Edit modes .................................................................................................... 44

3.3 Managing static data in Static Data Editor ......................................................................... 45

3.3.1 Creating new static data entities ..................................................................................... 45

3.3.2 Creating static data from an existing entity ..................................................................... 45

3.3.3 Creating static data entities in parallel ............................................................................ 45

3.3.4 Modifying static data entities ........................................................................................... 46

3.3.5 Deleting static data entities .............................................................................................46

3.3.6 Verifying static data entities ............................................................................................46

3.3.7 Finding static data entities ..............................................................................................46

3.3.8 Using templates to create static data entities ................................................................. 48

3.3.9 Common Static Data Editor attributes ............................................................................. 49

3.4 Managing SDM-enabled static data ..................................................................................... 51

3.4.1 SDM-enabled Static Data Editors ................................................................................... 51

3.4.2 Static Data Manager .......................................................................................................54

3.4.3 Processing static data entities ....................................................................................... 57

3.4.4 Sharing SDM-enabled data across Wallstreet Suite modules ........................................ 58

3.5 Countries ............................................................................................................................... 59

3.6 Calendars ............................................................................................................................... 59

3.6.1 Creating calendars .......................................................................................................... 60

3.7 Gaps (time intervals) ............................................................................................................. 62

3.7.1 Order of cashflow sorting to gaps ................................................................................... 63

3.8 IR quotes and yield curves ................................................................................................... 64

3.8.1 Date Conventions ........................................................................................................... 64

3.8.2 Creating IR Quote and Yield Curves ............................................................................... 65

3.8.3 Optional features ............................................................................................................. 78

3.9 Currencies ............................................................................................................................. 80

3.9.1 Creating currencies ......................................................................................................... 80

3.10 Currency priorities .............................................................................................................. 87

3.11 Settlement locations ........................................................................................................... 88

3.12 Client groups ....................................................................................................................... 89

3.13 Clients .................................................................................................................................. 89

3.13.1 Creating clients ............................................................................................................. 90

3.13.2 Managing clients ......................................................................................................... 106

Transaction & Risk Management Module (TRM) User Guide 5

3.14 Portfolios ........................................................................................................................... 107

3.14.1 Creating portfolios ....................................................................................................... 108

3.14.2 Managing portfolios ..................................................................................................... 113

3.15 Result types and results ................................................................................................... 114

3.15.1 Result types ................................................................................................................ 114

3.15.2 Results ........................................................................................................................ 115

3.15.3 Defining result treatments ........................................................................................... 115

3.15.4 Parallel Result Treatment ........................................................................................... 125

3.16 Instrument types ............................................................................................................... 126

3.17 Instrument groups ............................................................................................................ 127

3.18 Instrument Templates ....................................................................................................... 128

3.19 Instruments ........................................................................................................................ 129

3.19.1 Generating reports on instruments ............................................................................. 130

3.20 Classification groups ........................................................................................................ 130

3.21 Classification rules ........................................................................................................... 131

3.22 Comments and comment rules (optional) ...................................................................... 132

3.22.1 Setting up a comment rule .......................................................................................... 132

3.23 Bank Account Type Editor (optional) .............................................................................. 133

3.24 Branch codes (optional) ................................................................................................... 133

3.25 Calendar groups (optional) .............................................................................................. 134

3.25.1 Generating reports on calendar groups ...................................................................... 134

3.26 Cashflow charges (optional) ............................................................................................ 135

3.27 Cashflow groups (optional) .............................................................................................. 138

3.28 Cashflow types (optional) ................................................................................................ 139

3.29 Cash pools (optional) ....................................................................................................... 139

3.30 Country groups (optional) ................................................................................................ 142

3.31 Credit ratings (optional) ................................................................................................... 142

3.32 Currency classes (optional) ............................................................................................. 142

3.33 Ladder sets (optional) ....................................................................................................... 143

3.34 Ladder rules (optional) ..................................................................................................... 145

3.35 Option schedule templates (optional) ............................................................................. 145

3.35.1 Defining simple option schedules ............................................................................... 146

3.35.2 Defining complex option schedules ............................................................................ 146

3.36 Option schedule template groups (optional) .................................................................. 146

3.37 Package types (optional) .................................................................................................. 147

3.38 Parameters (optional) ....................................................................................................... 148

3.39 Properties (optional) ......................................................................................................... 148

3.39.1 Creating properties ..................................................................................................... 149

3.40 Schedule templates (optional) ......................................................................................... 150

3.41 Schedule template groups (optional) .............................................................................. 151

6 © Wall Street Systems IPH AB - Confidential

3.42 Security Basket Editor (optional) .................................................................................... 152

3.43 Security Criteria Set Editor (optional) ............................................................................. 153

3.44 Security identifier types (optional) .................................................................................. 154

3.45 Time zones (optional) ....................................................................................................... 154

3.46 Transaction charges (optional) ........................................................................................ 155

3.47 Volatilities (optional) ......................................................................................................... 158

4 Managing market data ............................................................................................161

4.1 Defining real-time quotations ............................................................................................ 161

4.1.1 Defining the source market quotations ......................................................................... 161

4.1.2 Defining filtering rules for real-time quotations .............................................................. 163

4.1.3 Quoting the rates .......................................................................................................... 165

4.2 Defining scenarios and subscenarios .............................................................................. 165

4.2.1 Defining scenarios ........................................................................................................ 166

4.2.2 Defining subscenarios ................................................................................................... 166

4.3 Freezing rates automatically .............................................................................................. 166

4.4 Defining simulation scenarios ........................................................................................... 167

4.4.1 Defining FX simulation scenarios .................................................................................. 167

4.4.2 Defining IR and volatility simulation scenarios .............................................................. 168

4.5 Rate Monitor ........................................................................................................................ 171

4.5.1 Rate Monitor menus ...................................................................................................... 171

4.5.2 Toolbar .......................................................................................................................... 173

4.5.3 Start-up parameters ...................................................................................................... 173

4.5.4 Managing market data in Rate Monitor ......................................................................... 173

4.5.5 Generating quotation reports ........................................................................................ 186

4.6 Pricing tools ........................................................................................................................ 186

4.6.1 FX Forward Pricing ....................................................................................................... 186

4.7 Pricing complex derivatives ............................................................................................... 190

4.7.1 Defining Calibration Baskets ......................................................................................... 190

4.7.2 Defining a calibration model for a currency ................................................................... 191

4.7.3 Defining cross-currency calibration models .................................................................. 192

4.7.4 Defining BGM calibration models .................................................................................. 193

4.7.5 Calibration Monitor ........................................................................................................ 195

4.7.6 Calibrating pricing models ............................................................................................. 198

4.7.7 Assigning calibration models to instruments ................................................................. 199

4.8 Bloomberg interface ........................................................................................................... 199

4.8.1 Interface configuration and usage overview ................................................................. 199

4.8.2 Generic configuration .................................................................................................... 201

4.8.3 Security import .............................................................................................................. 206

4.8.4 Security list import ......................................................................................................... 210

4.8.5 Instrument update ......................................................................................................... 211

4.8.6 Client update ................................................................................................................. 213

4.8.7 Corporate Actions update ............................................................................................. 216

4.8.8 Prices Import ................................................................................................................. 218

Transaction & Risk Management Module (TRM) User Guide 7

4.9 Market Data Status Monitor ................................................................................................ 218

4.9.1 Market Data Status pane .............................................................................................. 218

4.9.2 Properties pane ............................................................................................................. 218

4.9.3 Other panes .................................................................................................................. 218

4.9.4 Menus ........................................................................................................................... 219

5 Managing rules ........................................................................................................221

5.1 Defining rules ...................................................................................................................... 221

5.1.1 Identifying rule criteria ................................................................................................... 223

5.1.2 Selecting transaction parameter values ........................................................................ 224

5.1.3 Specifying cashflow attributes ....................................................................................... 225

5.1.4 Assigning branch codes to a rule .................................................................................. 225

5.1.5 Capturing transactions according to status ................................................................... 225

6 Managing activities .................................................................................................227

6.1 Activity Manager ................................................................................................................. 227

6.1.1 Activity Manager menus ................................................................................................ 228

6.1.2 Start-up parameters ...................................................................................................... 229

6.1.3 Activity modes ............................................................................................................... 229

6.2 Managing activities ............................................................................................................. 229

6.2.1 Creating activities .......................................................................................................... 229

6.2.2 Running activities immediately ...................................................................................... 232

6.2.3 Adding extra properties to activities .............................................................................. 232

6.2.4 Checking the running of activities ................................................................................. 232

6.2.5 Generating reports on activities .................................................................................... 233

7 Reporting .................................................................................................................235

7.1 Report Generator ................................................................................................................ 235

7.1.1 Report Generator menus .............................................................................................. 235

7.1.2 Start-up parameters ...................................................................................................... 238

7.1.3 Report files .................................................................................................................... 238

7.2 Managing reports ................................................................................................................ 239

7.2.1 Creating new reports ..................................................................................................... 239

7.2.2 Opening entity reports ................................................................................................... 239

7.2.3 Drilling down into reports .............................................................................................. 239

7.2.4 Creating columns for special information or groupings ................................................. 240

7.2.5 Building expressions for reports .................................................................................... 241

7.2.6 Configuring columns ..................................................................................................... 252

7.2.7 List of reports ................................................................................................................ 254

8 Managing transactions ...........................................................................................257

8.1 Transaction Manager .......................................................................................................... 257

8.1.1 Transaction Manager menus ........................................................................................ 258

8.1.2 Start-up parameters ...................................................................................................... 262

8.1.3 Transaction Manager modes ........................................................................................ 262

8 © Wall Street Systems IPH AB - Confidential

8.2 Capturing deals ................................................................................................................... 263

8.2.1 Entering new deals in Transaction Manager ................................................................. 264

8.2.2 Canceling deals ............................................................................................................ 271

8.2.3 Entering new deals in Enter Board ............................................................................... 272

8.2.4 Setting up a pre-trade limit check ................................................................................. 277

8.2.5 Enabling limit queries at transaction level ..................................................................... 280

8.3 Managing settlement instructions ..................................................................................... 280

8.3.1 Modifying settlement instructions .................................................................................. 280

8.3.2 Entering ad-hoc settlement instructions ........................................................................ 281

8.4 Processing transactions .................................................................................................... 283

8.4.1 Retrieving transactions ................................................................................................. 283

8.4.2 Displaying transaction data in a chart ........................................................................... 286

8.4.3 Verifying transactions .................................................................................................... 286

8.4.4 Confirming transactions ................................................................................................ 286

8.4.5 Correcting transactions ................................................................................................. 287

8.4.6 Matching and unmatching transactions ........................................................................ 288

8.4.7 Performing actions on deals ......................................................................................... 289

8.4.8 Generating reports on transactions ............................................................................... 299

8.5 Deal mirroring ...................................................................................................................... 300

8.5.1 Internal deal mirroring ................................................................................................... 300

8.5.2 Deal mirroring using mirror cases ................................................................................. 305

8.6 Managing call transactions ................................................................................................ 315

8.6.1 Call Manager ................................................................................................................. 316

8.6.2 Entering call transactions .............................................................................................. 317

8.6.3 Processing call transactions ......................................................................................... 317

8.6.4 Generating call reports .................................................................................................. 318

8.7 Managing cashflow forecasts ............................................................................................ 318

8.7.1 Setting up forecast instruments .................................................................................... 318

8.7.2 Setting up cashflow forecasting .................................................................................... 318

8.7.3 Forecast Exposure Board ............................................................................................. 321

8.7.4 Processing forecast exposures ..................................................................................... 322

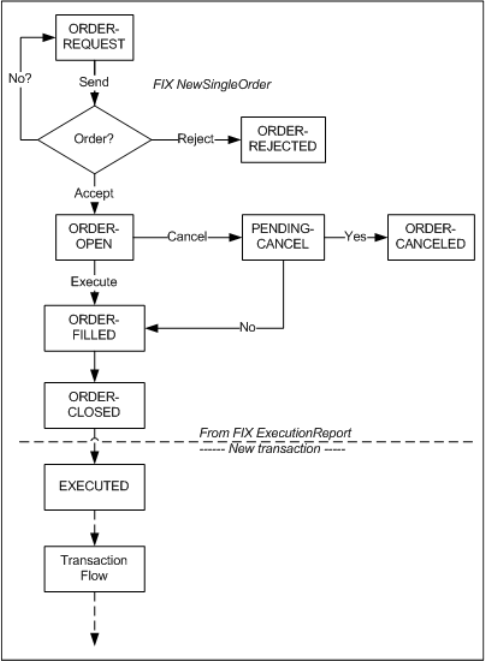

9 Managing orders .....................................................................................................323

9.1 Overview .............................................................................................................................. 323

9.2 Setting up order management ........................................................................................... 324

9.2.1 Defining an order platform ............................................................................................ 325

9.2.2 Defining order routing rule ............................................................................................ 326

9.3 Order Managers ................................................................................................................... 326

9.3.1 Views ............................................................................................................................ 327

9.4 Processing orders ............................................................................................................... 327

9.4.1 Entering orders ............................................................................................................. 328

9.4.2 Manually executing internal orders ............................................................................... 328

9.4.3 Overriding external order execution .............................................................................. 328

9.5 Monitoring orders ............................................................................................................... 329

Transaction & Risk Management Module (TRM) User Guide 9

10 Managing funds .....................................................................................................331

10.1 Setting up fund portfolios ................................................................................................ 331

10.1.1 Creating fund portfolios ............................................................................................... 331

10.2 Fund Managers .................................................................................................................. 333

10.2.1 Managing fund shares ................................................................................................ 333

10.2.2 Managing fund fees .................................................................................................... 333

10.3 Setting up default NAV calculation values ..................................................................... 334

10.4 NAV Monitor ...................................................................................................................... 335

10.4.1 Configuring NAV Monitor ............................................................................................ 335

10.4.2 Monitoring net asset value in NAV Monitor ................................................................. 336

10.4.3 Saving NAV reports .................................................................................................... 341

10.5 NAV Report Manager ........................................................................................................ 341

10.5.1 Managing reports ........................................................................................................ 341

10.5.2 Automating NAV reporting .......................................................................................... 342

11 Managing collateral ...............................................................................................345

11.1 Setting up master agreements ......................................................................................... 345

11.1.1 Defining collateral agreements ................................................................................... 345

11.1.2 Attaching master agreements to portfolio owners ....................................................... 352

11.1.3 Applying master agreements to instruments ............................................................... 352

11.2 Monitoring collateral positions ........................................................................................ 352

11.2.1 Collateral Valuation Board .......................................................................................... 353

11.2.2 Collateral Management Reports ................................................................................. 359

12 Monitoring positions .............................................................................................361

12.1 Treasury Monitor ............................................................................................................... 361

12.1.1 Treasury Monitor menus ............................................................................................. 361

12.1.2 Start-up parameters .................................................................................................... 364

12.1.3 Configuring Treasury Monitor ..................................................................................... 365

12.1.4 Monitoring positions in Treasury Monitor .................................................................... 366

12.1.5 Simulating movements in Treasury Monitor ................................................................ 387

12.1.6 Using Treasury Monitor for risk measurement ............................................................ 390

12.1.7 Monitoring cost-of-carry positions ............................................................................... 390

12.1.8 Generating position-related reports ............................................................................ 391

12.2 Position Monitor ................................................................................................................ 392

12.2.1 Position Monitor menus .............................................................................................. 392

12.2.2 Monitoring positions with Position Monitor .................................................................. 392

12.3 FX Spot Monitor ................................................................................................................ 393

12.3.1 FX Spot Monitor menus .............................................................................................. 393

12.3.2 Start-up parameters .................................................................................................... 393

12.3.3 Monitoring positions in FX Spot Monitor ..................................................................... 393

12.4 FX Position Roll Over activity .......................................................................................... 397

13 Monitoring performance .......................................................................................399

10 © Wall Street Systems IPH AB - Confidential

13.1 Measuring performance and risk ..................................................................................... 399

13.1.1 Performance versus risk ............................................................................................. 399

13.1.2 AIMR-PPS™ standards .............................................................................................. 401

13.2 Setting up performance measurement and risk ............................................................. 401

13.2.1 Setting up entities for performance measurement ...................................................... 401

13.2.2 Generating historical market values for performance measurement .......................... 404

13.2.3 Configuring Treasury Monitor for risk measurement ................................................... 405

13.3 Performance Monitor ........................................................................................................ 405

13.3.1 Performance Monitor menus ....................................................................................... 405

13.3.2 Start-up parameters .................................................................................................... 408

13.3.3 Configuring Performance Monitor ............................................................................... 408

13.3.4 Monitoring performance in Performance Monitor ........................................................ 409

14 Portfolio modeling ................................................................................................413

14.1 Setting up portfolio modeling .......................................................................................... 413

14.1.1 Characteristics of portfolios models ............................................................................ 413

14.1.2 Defining portfolio models ............................................................................................ 415

14.1.3 Defining portfolio model security lists .......................................................................... 416

14.1.4 Applying a portfolio model or benchmark to a portfolio ............................................... 416

14.2 Portfolio Modeling Monitor .............................................................................................. 417

14.2.1 Portfolio Modeling Monitor menus .............................................................................. 418

14.2.2 Start-up parameters .................................................................................................... 420

14.2.3 Configuring Portfolio Modeling Monitor ....................................................................... 421

14.2.4 Analyzing positions in Portfolio Modeling Monitor ....................................................... 423

14.2.5 Rebalancing ................................................................................................................ 424

14.2.6 Generating deals ......................................................................................................... 427

15 Managing benchmarks .........................................................................................429

15.1 About benchmarks ............................................................................................................ 429

15.1.1 Components ................................................................................................................ 429

15.1.2 Definition Methods ...................................................................................................... 430

15.1.3 Re-Investment Methods .............................................................................................. 430

15.1.4 Activities ...................................................................................................................... 430

15.2 Benchmark Manager ......................................................................................................... 431

15.2.1 Benchmark Manager menus ....................................................................................... 431

15.2.2 Actions ........................................................................................................................ 432

15.3 Defining benchmarks ........................................................................................................ 433

15.3.1 Setting up a benchmark portfolio ................................................................................ 433

15.3.2 Setting up a benchmark .............................................................................................. 434

15.4 Processing benchmarks ................................................................................................... 443

15.4.1 Copying a benchmark revision .................................................................................... 444

15.4.2 Rebalancing ................................................................................................................ 444

15.4.3 Cash Processing ......................................................................................................... 445

15.4.4 Performing a manual adjustment ................................................................................ 446

15.4.5 Closing a benchmark .................................................................................................. 446

Transaction & Risk Management Module (TRM) User Guide 11

15.4.6 Deleting a benchmark ................................................................................................. 446

16 Managing limits .....................................................................................................447

16.1 Overview ............................................................................................................................ 447

16.2 Setting up limits ................................................................................................................ 449

16.2.1 Creating limit factor sets ............................................................................................. 450

16.2.2 Creating limit item templates ....................................................................................... 452

16.2.3 Creating sublimit calculation templates ....................................................................... 461

16.2.4 Creating limit client queries ......................................................................................... 467

16.2.5 Creating limit categories ............................................................................................. 467

16.2.6 Creating limits ............................................................................................................. 468

16.2.7 Creating limit templates .............................................................................................. 470

16.3 Limit Monitor ..................................................................................................................... 471

16.3.1 Limit Monitor menus .................................................................................................... 471

16.3.2 Start-up parameters .................................................................................................... 473

16.3.3 Configuring limits ........................................................................................................ 473

16.4 Limit Notifications ............................................................................................................. 482

16.4.1 Limit Notifications menus ............................................................................................ 483

16.4.2 Start-up parameters .................................................................................................... 483

16.5 Analyzing limit violations ................................................................................................. 484

16.5.1 Generating reports on limit violations .......................................................................... 484

17 Managing transaction conditions ........................................................................485

17.1 Overview ............................................................................................................................ 485

17.2 Setting up transaction condition sets ............................................................................. 486

17.3 Processing transaction condition sets ........................................................................... 491

17.3.1 Evaluation ................................................................................................................... 491

17.3.2 Action .......................................................................................................................... 491

17.4 Monitoring transaction conditions .................................................................................. 492

17.4.1 Transaction Manager .................................................................................................. 492

17.4.2 Transaction Condition Violations ................................................................................ 493

17.4.3 Exception Verification ................................................................................................. 493

17.4.4 Transaction Conditions report ..................................................................................... 493

18 Managing cash and settlements ..........................................................................495

18.1 Managing cash and cash position ................................................................................... 495

18.1.1 Managing bank account balances and interest ........................................................... 495

18.1.2 Managing cost of carry ................................................................................................ 499

18.1.3 Managing cash pool leveling ....................................................................................... 502

18.2 Setting up settlement management ................................................................................ 505

18.2.1 Defining settlement parameters .................................................................................. 505

18.3 Generating and processing settlements ......................................................................... 510

18.3.1 Settlement Processing menus .................................................................................... 513

18.3.2 Start-up parameters .................................................................................................... 513

12 © Wall Street Systems IPH AB - Confidential

18.3.3 Settlement processing modes ..................................................................................... 514

18.3.4 Processing settlements ............................................................................................... 514

18.3.5 Modifying settlement instructions ................................................................................ 520

18.3.6 Generating settlement processing reports .................................................................. 520

18.4 Managing custody movements and balances ................................................................ 520

18.4.1 Start-up parameters .................................................................................................... 520

18.4.2 Custody Manager views .............................................................................................. 521

18.4.3 Retrieving custody movements ................................................................................... 521

18.4.4 Generating custody balances ..................................................................................... 521

18.4.5 Retrieving custody balances ....................................................................................... 522

18.4.6 Entering custody statement data ................................................................................ 523

18.4.7 Custody reports ........................................................................................................... 524

18.5 Reconciling settlements and custodies .......................................................................... 524

18.5.1 Start-up parameters .................................................................................................... 525

18.5.2 Reconciliation application views ................................................................................. 525

18.5.3 Defining reconciliation setup ....................................................................................... 526

18.5.4 Entering statements of account .................................................................................. 528

18.5.5 Querying statements of account and settlement information ...................................... 529

18.5.6 Matching settlements .................................................................................................. 529

18.5.7 Processing actions ...................................................................................................... 531

18.5.8 Reconciliation reports ................................................................................................. 532

19 Managing accounting ...........................................................................................533

19.1 Parallel accounting ........................................................................................................... 533

19.1.1 Classification ............................................................................................................... 533

19.1.2 Result treatment methods ........................................................................................... 535

19.1.3 Classification rules ...................................................................................................... 536

19.1.4 Classification of transactions ...................................................................................... 537

19.2 Realizing and processing results .................................................................................... 537

19.2.1 Realizing profit/loss ..................................................................................................... 537

19.2.2 Processing results ....................................................................................................... 538

19.3 Updating the book value of deals .................................................................................... 539

19.3.1 Defining the book value change method ..................................................................... 539

19.3.2 Making book value changes ....................................................................................... 539

19.3.3 Making book value adjustments .................................................................................. 540

19.3.4 Undoing book value changes and adjustments .......................................................... 541

19.3.5 Generating a book value change report ...................................................................... 542

19.3.6 Posting book value changes ....................................................................................... 542

19.4 Using TRM with a General Ledger system ..................................................................... 542

19.4.1 Setting up the portfolio owner for accounting .............................................................. 543

19.4.2 Configuring accounting for the portfolio owner ........................................................... 543

19.4.3 Defining bookkeeping entries ...................................................................................... 545

19.4.4 Calculating bookkeeping entries ................................................................................. 546

19.5 Hedge accounting in Wallstreet Suite ............................................................................. 546

Transaction & Risk Management Module (TRM) User Guide 13

20 Monitoring VaR ......................................................................................................547

20.1 Setting up Value-at-Risk ................................................................................................... 547

20.1.1 Mapping RM volatilities and correlations to TRM market data .................................... 547

20.1.2 Defining VaR scenarios .............................................................................................. 549

20.1.3 Assigning VaR properties to portfolios ........................................................................ 550

20.2 Managing VaR data ........................................................................................................... 550

20.2.1 VaR Data Board .......................................................................................................... 551

21 Managing messages .............................................................................................555

21.1 Setting up message requests .......................................................................................... 555

21.1.1 Setting up message groups ........................................................................................ 555

21.1.2 Setting up message types ........................................................................................... 556

21.1.3 Setting up message rules ........................................................................................... 558

21.1.4 Assigning message details to clients .......................................................................... 559

21.2 Message Manager ............................................................................................................. 560

21.2.1 Message Manager menus .......................................................................................... 560

21.2.2 Start-up parameters .................................................................................................... 560

21.2.3 Message modes .......................................................................................................... 560

21.3 Processing messages ...................................................................................................... 561

21.3.1 Retrieving messages .................................................................................................. 561