The Data Science Design Manual

The%20Data%20Science%20Design%20Manual

User Manual:

Open the PDF directly: View PDF ![]() .

.

Page Count: 453 [warning: Documents this large are best viewed by clicking the View PDF Link!]

Steven S. Skiena

The Data Science Design Manual

Steven S. Skiena

Computer Science Department

Stony Brook University

Stony Brook, NY

USA

ISSN 1868-0941 ISSN 1868-095X (electronic)

Texts in Computer Science

ISBN 978-3-319-55443-3 ISBN 978-3-319-55444-0 (eBook)

DOI 10.1007/978-3-319-55444-0

Library of Congress Control Number: 2017943201

© The Author(s) 2017

This Springer imprint is published by Springer Nature

The registered company is Springer International Publishing AG

The registered company address is: Gewerbestrasse 11, 6330 Cham, Switzerland

Preface

Making sense of the world around us requires obtaining and analyzing data from

our environment. Several technology trends have recently collided, providing

new opportunities to apply our data analysis savvy to greater challenges than

ever before.

Computer storage capacity has increased exponentially; indeed remembering

has become so cheap that it is almost impossible to get computer systems to for-

get. Sensing devices increasingly monitor everything that can be observed: video

streams, social media interactions, and the position of anything that moves.

Cloud computing enables us to harness the power of massive numbers of ma-

chines to manipulate this data. Indeed, hundreds of computers are summoned

each time you do a Google search, scrutinizing all of your previous activity just

to decide which is the best ad to show you next.

The result of all this has been the birth of data science, a new field devoted

to maximizing value from vast collections of information. As a discipline, data

science sits somewhere at the intersection of statistics, computer science, and

machine learning, but it is building a distinct heft and character of its own.

This book serves as an introduction to data science, focusing on the skills and

principles needed to build systems for collecting, analyzing, and interpreting

data.

My professional experience as a researcher and instructor convinces me that

one major challenge of data science is that it is considerably more subtle than it

looks. Any student who has ever computed their grade point average (GPA) can

be said to have done rudimentary statistics, just as drawing a simple scatter plot

lets you add experience in data visualization to your resume. But meaningfully

analyzing and interpreting data requires both technical expertise and wisdom.

That so many people do these basics so badly provides my inspiration for writing

this book.

To the Reader

I have been gratified by the warm reception that my book The Algorithm Design

Manual [Ski08] has received since its initial publication in 1997. It has been

recognized as a unique guide to using algorithmic techniques to solve problems

that often arise in practice. The book you are holding covers very different

material, but with the same motivation.

In particular, here I stress the following basic principles as fundamental to

becoming a good data scientist:

•Valuing doing the simple things right: Data science isn’t rocket science.

Students and practitioners often get lost in technological space, pursuing

the most advanced machine learning methods, the newest open source

software libraries, or the glitziest visualization techniques. However, the

heart of data science lies in doing the simple things right: understanding

the application domain, cleaning and integrating relevant data sources,

and presenting your results clearly to others.

Simple doesn’t mean easy, however. Indeed it takes considerable insight

and experience to ask the right questions, and sense whether you are mov-

ing toward correct answers and actionable insights. I resist the temptation

to drill deeply into clean, technical material here just because it is teach-

able. There are plenty of other books which will cover the intricacies of

machine learning algorithms or statistical hypothesis testing. My mission

here is to lay the groundwork of what really matters in analyzing data.

•Developing mathematical intuition: Data science rests on a foundation of

mathematics, particularly statistics and linear algebra. It is important to

understand this material on an intuitive level: why these concepts were

developed, how they are useful, and when they work best. I illustrate

operations in linear algebra by presenting pictures of what happens to

matrices when you manipulate them, and statistical concepts by exam-

ples and reducto ad absurdum arguments. My goal here is transplanting

intuition into the reader.

But I strive to minimize the amount of formal mathematics used in pre-

senting this material. Indeed, I will present exactly one formal proof in

this book, an incorrect proof where the associated theorem is obviously

false. The moral here is not that mathematical rigor doesn’t matter, be-

cause of course it does, but that genuine rigor is impossible until after

there is comprehension.

•Think like a computer scientist, but act like a statistician: Data science

provides an umbrella linking computer scientists, statisticians, and domain

specialists. But each community has its own distinct styles of thinking and

action, which gets stamped into the souls of its members.

In this book, I emphasize approaches which come most naturally to com-

puter scientists, particularly the algorithmic manipulation of data, the use

of machine learning, and the mastery of scale. But I also seek to transmit

the core values of statistical reasoning: the need to understand the appli-

cation domain, proper appreciation of the small, the quest for significance,

and a hunger for exploration.

No discipline has a monopoly on the truth. The best data scientists incor-

porate tools from multiple areas, and this book strives to be a relatively

neutral ground where rival philosophies can come to reason together.

Equally important is what you will not find in this book. I do not emphasize

any particular language or suite of data analysis tools. Instead, this book pro-

vides a high-level discussion of important design principles. I seek to operate at

a conceptual level more than a technical one. The goal of this manual is to get

you going in the right direction as quickly as possible, with whatever software

tools you find most accessible.

To the Instructor

This book covers enough material for an “Introduction to Data Science” course

at the undergraduate or early graduate student levels. I hope that the reader

has completed the equivalent of at least one programming course and has a bit

of prior exposure to probability and statistics, but more is always better than

less.

I have made a full set of lecture slides for teaching this course available online

at http://www.data-manual.com. Data resources for projects and assignments

are also available there to aid the instructor. Further, I make available online

video lectures using these slides to teach a full-semester data science course. Let

me help teach your class, through the magic of the web!

Pedagogical features of this book include:

•War Stories: To provide a better perspective on how data science tech-

niques apply to the real world, I include a collection of “war stories,” or

tales from our experience with real problems. The moral of these stories is

that these methods are not just theory, but important tools to be pulled

out and used as needed.

•False Starts: Most textbooks present methods as a fait accompli, ob-

scuring the ideas involved in designing them, and the subtle reasons why

other approaches fail. The war stories illustrate my reasoning process on

certain applied problems, but I weave such coverage into the core material

as well.

•Take-Home Lessons: Highlighted “take-home” lesson boxes scattered

through each chapter emphasize the big-picture concepts to learn from

each chapter.

•Homework Problems: I provide a wide range of exercises for home-

work and self-study. Many are traditional exam-style problems, but there

are also larger-scale implementation challenges and smaller-scale inter-

view questions, reflecting the questions students might encounter when

searching for a job. Degree of difficulty ratings have been assigned to all

problems.

In lieu of an answer key, a Solution Wiki has been set up, where solutions to

all even numbered problems will be solicited by crowdsourcing. A similar

system with my Algorithm Design Manual produced coherent solutions,

or so I am told. As a matter of principle I refuse to look at them, so let

the buyer beware.

•Kaggle Challenges: Kaggle (www.kaggle.com) provides a forum for data

scientists to compete in, featuring challenging real-world problems on fas-

cinating data sets, and scoring to test how good your model is relative to

other submissions. The exercises for each chapter include three relevant

Kaggle challenges, to serve as a source of inspiration, self-study, and data

for other projects and investigations.

•Data Science Television: Data science remains mysterious and even

threatening to the broader public. The Quant Shop is an amateur take

on what a data science reality show should be like. Student teams tackle

a diverse array of real-world prediction problems, and try to forecast the

outcome of future events. Check it out at http://www.quant-shop.com.

A series of eight 30-minute episodes has been prepared, each built around

a particular real-world prediction problem. Challenges include pricing art

at an auction, picking the winner of the Miss Universe competition, and

forecasting when celebrities are destined to die. For each, we observe as a

student team comes to grips with the problem, and learn along with them

as they build a forecasting model. They make their predictions, and we

watch along with them to see if they are right or wrong.

In this book, The Quant Shop is used to provide concrete examples of

prediction challenges, to frame discussions of the data science modeling

pipeline from data acquisition to evaluation. I hope you find them fun, and

that they will encourage you to conceive and take on your own modeling

challenges.

•Chapter Notes: Finally, each tutorial chapter concludes with a brief notes

section, pointing readers to primary sources and additional references.

Dedication

My bright and loving daughters Bonnie and Abby are now full-blown teenagers,

meaning that they don’t always process statistical evidence with as much alacrity

as I would I desire. I dedicate this book to them, in the hope that their analysis

skills improve to the point that they always just agree with me.

And I dedicate this book to my beautiful wife Renee, who agrees with me

even when she doesn’t agree with me, and loves me beyond the support of all

creditable evidence.

Acknowledgments

My list of people to thank is large enough that I have probably missed some.

I will try to do enumerate them systematically to minimize omissions, but ask

those I’ve unfairly neglected for absolution.

First, I thank those who made concrete contributions to help me put this

book together. Yeseul Lee served as an apprentice on this project, helping with

figures, exercises, and more during summer 2016 and beyond. You will see

evidence of her handiwork on almost every page, and I greatly appreciate her

help and dedication. Aakriti Mittal and Jack Zheng also contributed to a few

of the figures.

Students in my Fall 2016 Introduction to Data Science course (CSE 519)

helped to debug the manuscript, and they found plenty of things to debug. I

particularly thank Rebecca Siford, who proposed over one hundred corrections

on her own. Several data science friends/sages reviewed specific chapters for

me, and I thank Anshul Gandhi, Yifan Hu, Klaus Mueller, Francesco Orabona,

Andy Schwartz, and Charles Ward for their efforts here.

I thank all the Quant Shop students from Fall 2015 whose video and mod-

eling efforts are so visibly on display. I particularly thank Jan (Dini) Diskin-

Zimmerman, whose editing efforts went so far beyond the call of duty I felt like

a felon for letting her do it.

My editors at Springer, Wayne Wheeler and Simon Rees, were a pleasure to

work with as usual. I also thank all the production and marketing people who

helped get this book to you, including Adrian Pieron and Annette Anlauf.

Several exercises were originated by colleagues or inspired by other sources.

Reconstructing the original sources years later can be challenging, but credits

for each problem (to the best of my recollection) appear on the website.

Much of what I know about data science has been learned through working

with other people. These include my Ph.D. students, particularly Rami al-Rfou,

Mikhail Bautin, Haochen Chen, Yanqing Chen, Vivek Kulkarni, Levon Lloyd,

Andrew Mehler, Bryan Perozzi, Yingtao Tian, Junting Ye, Wenbin Zhang, and

postdoc Charles Ward. I fondly remember all of my Lydia project masters

students over the years, and remind you that my prize offer to the first one who

names their daughter Lydia remains unclaimed. I thank my other collaborators

with stories to tell, including Bruce Futcher, Justin Gardin, Arnout van de Rijt,

and Oleksii Starov.

I remember all members of the General Sentiment/Canrock universe, partic-

ularly Mark Fasciano, with whom I shared the start-up dream and experienced

what happens when data hits the real world. I thank my colleagues at Yahoo

Labs/Research during my 2015–2016 sabbatical year, when much of this book

was conceived. I single out Amanda Stent, who enabled me to be at Yahoo

during that particularly difficult year in the company’s history. I learned valu-

able things from other people who have taught related data science courses,

including Andrew Ng and Hans-Peter Pfister, and thank them all for their help.

If you have a procedure with ten parameters, you probably missed

some.

– Alan Perlis

Caveat

It is traditional for the author to magnanimously accept the blame for whatever

deficiencies remain. I don’t. Any errors, deficiencies, or problems in this book

are somebody else’s fault, but I would appreciate knowing about them so as to

determine who is to blame.

Steven S. Skiena

Department of Computer Science

Stony Brook University

Stony Brook, NY 11794-2424

http://www.cs.stonybrook.edu/~skiena

skiena@data-manual.com

May 2017

Contents

1 What is Data Science? 1

1.1 Computer Science, Data Science, and Real Science . . . . . . . . 2

1.2 Asking Interesting Questions from Data . . . . . . . . . . . . . . 4

1.2.1 The Baseball Encyclopedia . . . . . . . . . . . . . . . . . 5

1.2.2 The Internet Movie Database (IMDb) . . . . . . . . . . . 7

1.2.3 GoogleNgrams........................ 10

1.2.4 New York Taxi Records . . . . . . . . . . . . . . . . . . . 11

1.3 PropertiesofData .......................... 14

1.3.1 Structured vs. Unstructured Data . . . . . . . . . . . . . 14

1.3.2 Quantitative vs. Categorical Data . . . . . . . . . . . . . 15

1.3.3 Big Data vs. Little Data . . . . . . . . . . . . . . . . . . . 15

1.4 Classification and Regression . . . . . . . . . . . . . . . . . . . . 16

1.5 Data Science Television: The Quant Shop . . . . . . . . . . . . . 17

1.5.1 Kaggle Challenges . . . . . . . . . . . . . . . . . . . . . . 19

1.6 About the War Stories . . . . . . . . . . . . . . . . . . . . . . . . 19

1.7 War Story: Answering the Right Question . . . . . . . . . . . . . 21

1.8 ChapterNotes ............................ 22

1.9 Exercises ............................... 23

2 Mathematical Preliminaries 27

2.1 Probability .............................. 27

2.1.1 Probability vs. Statistics . . . . . . . . . . . . . . . . . . . 29

2.1.2 Compound Events and Independence . . . . . . . . . . . . 30

2.1.3 Conditional Probability . . . . . . . . . . . . . . . . . . . 31

2.1.4 Probability Distributions . . . . . . . . . . . . . . . . . . 32

2.2 Descriptive Statistics . . . . . . . . . . . . . . . . . . . . . . . . . 34

2.2.1 Centrality Measures . . . . . . . . . . . . . . . . . . . . . 34

2.2.2 Variability Measures . . . . . . . . . . . . . . . . . . . . . 36

2.2.3 Interpreting Variance . . . . . . . . . . . . . . . . . . . . 37

2.2.4 Characterizing Distributions . . . . . . . . . . . . . . . . 39

2.3 Correlation Analysis . . . . . . . . . . . . . . . . . . . . . . . . . 40

2.3.1 Correlation Coefficients: Pearson and Spearman Rank . . 41

2.3.2 The Power and Significance of Correlation . . . . . . . . . 43

2.3.3 Correlation Does Not Imply Causation! . . . . . . . . . . 45

2.3.4 Detecting Periodicities by Autocorrelation . . . . . . . . . 46

2.4 Logarithms .............................. 47

2.4.1 Logarithms and Multiplying Probabilities . . . . . . . . . 48

2.4.2 Logarithms and Ratios . . . . . . . . . . . . . . . . . . . . 48

2.4.3 Logarithms and Normalizing Skewed Distributions . . . . 49

2.5 War Story: Fitting Designer Genes . . . . . . . . . . . . . . . . . 50

2.6 ChapterNotes ............................ 52

2.7 Exercises ............................... 53

3 Data Munging 57

3.1 Languages for Data Science . . . . . . . . . . . . . . . . . . . . . 57

3.1.1 The Importance of Notebook Environments . . . . . . . . 59

3.1.2 Standard Data Formats . . . . . . . . . . . . . . . . . . . 61

3.2 CollectingData............................ 64

3.2.1 Hunting............................ 64

3.2.2 Scraping............................ 67

3.2.3 Logging ............................ 68

3.3 CleaningData ............................ 69

3.3.1 Errors vs. Artifacts . . . . . . . . . . . . . . . . . . . . . 69

3.3.2 Data Compatibility . . . . . . . . . . . . . . . . . . . . . . 72

3.3.3 Dealing with Missing Values . . . . . . . . . . . . . . . . . 76

3.3.4 Outlier Detection . . . . . . . . . . . . . . . . . . . . . . . 78

3.4 War Story: Beating the Market . . . . . . . . . . . . . . . . . . . 79

3.5 Crowdsourcing ............................ 80

3.5.1 The Penny Demo . . . . . . . . . . . . . . . . . . . . . . . 81

3.5.2 When is the Crowd Wise? . . . . . . . . . . . . . . . . . . 82

3.5.3 Mechanisms for Aggregation . . . . . . . . . . . . . . . . 83

3.5.4 Crowdsourcing Services . . . . . . . . . . . . . . . . . . . 84

3.5.5 Gamification ......................... 88

3.6 ChapterNotes ............................ 90

3.7 Exercises ............................... 90

4 Scores and Rankings 95

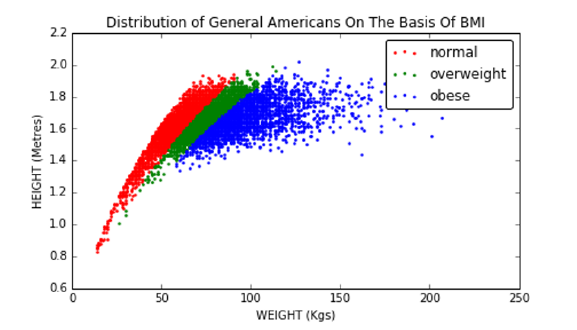

4.1 The Body Mass Index (BMI) . . . . . . . . . . . . . . . . . . . . 96

4.2 Developing Scoring Systems . . . . . . . . . . . . . . . . . . . . . 99

4.2.1 Gold Standards and Proxies . . . . . . . . . . . . . . . . . 99

4.2.2 Scores vs. Rankings . . . . . . . . . . . . . . . . . . . . . 100

4.2.3 Recognizing Good Scoring Functions . . . . . . . . . . . . 101

4.3 Z-scores and Normalization . . . . . . . . . . . . . . . . . . . . . 103

4.4 Advanced Ranking Techniques . . . . . . . . . . . . . . . . . . . 104

4.4.1 EloRankings ......................... 104

4.4.2 Merging Rankings . . . . . . . . . . . . . . . . . . . . . . 108

4.4.3 Digraph-based Rankings . . . . . . . . . . . . . . . . . . . 109

4.4.4 PageRank...........................111

4.5 War Story: Clyde’s Revenge . . . . . . . . . . . . . . . . . . . . . 111

4.6 Arrow’s Impossibility Theorem . . . . . . . . . . . . . . . . . . . 114

4.7 War Story: Who’s Bigger? . . . . . . . . . . . . . . . . . . . . . . 115

4.8 ChapterNotes ............................118

4.9 Exercises ............................... 119

5 Statistical Analysis 121

5.1 Statistical Distributions . . . . . . . . . . . . . . . . . . . . . . . 122

5.1.1 The Binomial Distribution . . . . . . . . . . . . . . . . . . 123

5.1.2 The Normal Distribution . . . . . . . . . . . . . . . . . . 124

5.1.3 Implications of the Normal Distribution . . . . . . . . . . 126

5.1.4 Poisson Distribution . . . . . . . . . . . . . . . . . . . . . 127

5.1.5 Power Law Distributions . . . . . . . . . . . . . . . . . . . 129

5.2 Sampling from Distributions . . . . . . . . . . . . . . . . . . . . . 132

5.2.1 Random Sampling beyond One Dimension . . . . . . . . . 133

5.3 Statistical Significance . . . . . . . . . . . . . . . . . . . . . . . . 135

5.3.1 The Significance of Significance . . . . . . . . . . . . . . . 135

5.3.2 The T-test: Comparing Population Means . . . . . . . . . 137

5.3.3 The Kolmogorov-Smirnov Test . . . . . . . . . . . . . . . 139

5.3.4 The Bonferroni Correction . . . . . . . . . . . . . . . . . . 141

5.3.5 False Discovery Rate . . . . . . . . . . . . . . . . . . . . . 142

5.4 War Story: Discovering the Fountain of Youth? . . . . . . . . . . 143

5.5 Permutation Tests and P-values . . . . . . . . . . . . . . . . . . . 145

5.5.1 Generating Random Permutations . . . . . . . . . . . . . 147

5.5.2 DiMaggio’s Hitting Streak . . . . . . . . . . . . . . . . . . 148

5.6 Bayesian Reasoning . . . . . . . . . . . . . . . . . . . . . . . . . 150

5.7 ChapterNotes ............................151

5.8 Exercises ............................... 151

6 Visualizing Data 155

6.1 Exploratory Data Analysis . . . . . . . . . . . . . . . . . . . . . . 156

6.1.1 Confronting a New Data Set . . . . . . . . . . . . . . . . 156

6.1.2 Summary Statistics and Anscombe’s Quartet . . . . . . . 159

6.1.3 Visualization Tools . . . . . . . . . . . . . . . . . . . . . . 160

6.2 Developing a Visualization Aesthetic . . . . . . . . . . . . . . . . 162

6.2.1 Maximizing Data-Ink Ratio . . . . . . . . . . . . . . . . . 163

6.2.2 Minimizing the Lie Factor . . . . . . . . . . . . . . . . . . 164

6.2.3 Minimizing Chartjunk . . . . . . . . . . . . . . . . . . . . 165

6.2.4 Proper Scaling and Labeling . . . . . . . . . . . . . . . . 167

6.2.5 Effective Use of Color and Shading . . . . . . . . . . . . . 168

6.2.6 The Power of Repetition . . . . . . . . . . . . . . . . . . . 169

6.3 ChartTypes ............................. 170

6.3.1 TabularData.........................170

6.3.2 Dot and Line Plots . . . . . . . . . . . . . . . . . . . . . . 174

6.3.3 ScatterPlots .........................177

6.3.4 Bar Plots and Pie Charts . . . . . . . . . . . . . . . . . . 179

6.3.5 Histograms ..........................183

6.3.6 DataMaps ..........................187

6.4 Great Visualizations . . . . . . . . . . . . . . . . . . . . . . . . . 189

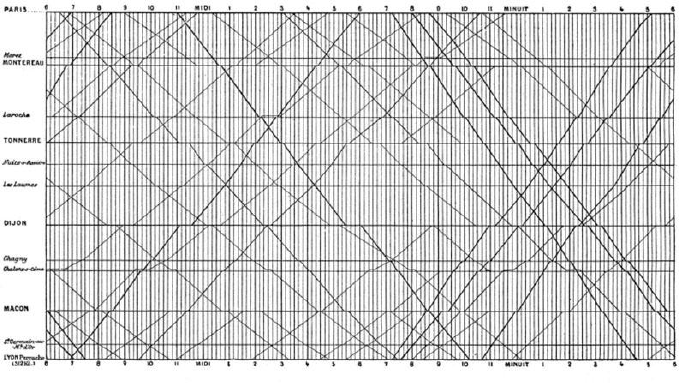

6.4.1 Marey’s Train Schedule . . . . . . . . . . . . . . . . . . . 189

6.4.2 Snow’s Cholera Map . . . . . . . . . . . . . . . . . . . . . 191

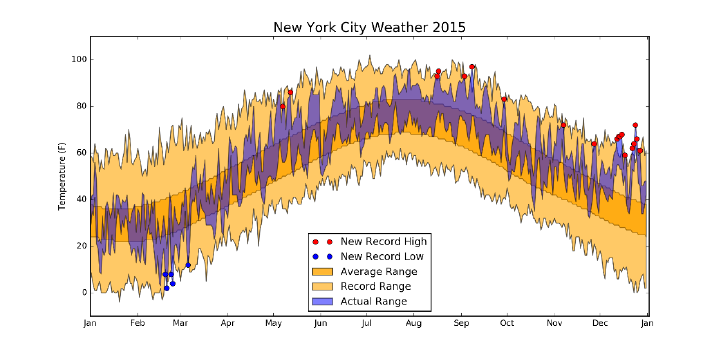

6.4.3 New York’s Weather Year . . . . . . . . . . . . . . . . . . 192

6.5 ReadingGraphs............................192

6.5.1 The Obscured Distribution . . . . . . . . . . . . . . . . . 193

6.5.2 Overinterpreting Variance . . . . . . . . . . . . . . . . . . 193

6.6 Interactive Visualization . . . . . . . . . . . . . . . . . . . . . . . 195

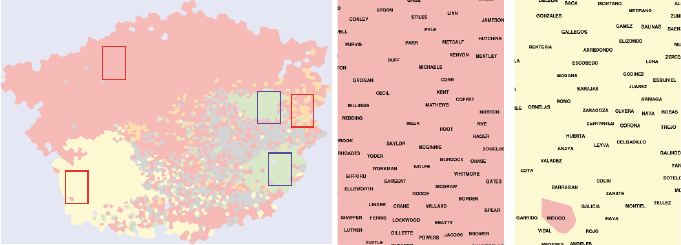

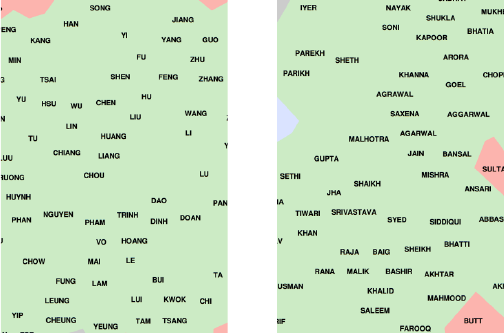

6.7 War Story: TextMapping the World . . . . . . . . . . . . . . . . 196

6.8 ChapterNotes ............................198

6.9 Exercises ............................... 199

7 Mathematical Models 201

7.1 Philosophies of Modeling . . . . . . . . . . . . . . . . . . . . . . . 201

7.1.1 Occam’s Razor . . . . . . . . . . . . . . . . . . . . . . . . 201

7.1.2 Bias–Variance Trade-Offs . . . . . . . . . . . . . . . . . . 202

7.1.3 What Would Nate Silver Do? . . . . . . . . . . . . . . . . 203

7.2 A Taxonomy of Models . . . . . . . . . . . . . . . . . . . . . . . 205

7.2.1 Linear vs. Non-Linear Models . . . . . . . . . . . . . . . . 206

7.2.2 Blackbox vs. Descriptive Models . . . . . . . . . . . . . . 206

7.2.3 First-Principle vs. Data-Driven Models . . . . . . . . . . . 207

7.2.4 Stochastic vs. Deterministic Models . . . . . . . . . . . . 208

7.2.5 Flat vs. Hierarchical Models . . . . . . . . . . . . . . . . . 209

7.3 BaselineModels............................210

7.3.1 Baseline Models for Classification . . . . . . . . . . . . . . 210

7.3.2 Baseline Models for Value Prediction . . . . . . . . . . . . 212

7.4 Evaluating Models . . . . . . . . . . . . . . . . . . . . . . . . . . 212

7.4.1 Evaluating Classifiers . . . . . . . . . . . . . . . . . . . . 213

7.4.2 Receiver-Operator Characteristic (ROC) Curves . . . . . 218

7.4.3 Evaluating Multiclass Systems . . . . . . . . . . . . . . . 219

7.4.4 Evaluating Value Prediction Models . . . . . . . . . . . . 221

7.5 Evaluation Environments . . . . . . . . . . . . . . . . . . . . . . 224

7.5.1 Data Hygiene for Evaluation . . . . . . . . . . . . . . . . 225

7.5.2 Amplifying Small Evaluation Sets . . . . . . . . . . . . . 226

7.6 War Story: 100% Accuracy . . . . . . . . . . . . . . . . . . . . . 228

7.7 Simulation Models . . . . . . . . . . . . . . . . . . . . . . . . . . 229

7.8 War Story: Calculated Bets . . . . . . . . . . . . . . . . . . . . . 230

7.9 ChapterNotes ............................233

7.10Exercises ............................... 234

8 Linear Algebra 237

8.1 The Power of Linear Algebra . . . . . . . . . . . . . . . . . . . . 237

8.1.1 Interpreting Linear Algebraic Formulae . . . . . . . . . . 238

8.1.2 Geometry and Vectors . . . . . . . . . . . . . . . . . . . . 240

8.2 Visualizing Matrix Operations . . . . . . . . . . . . . . . . . . . . 241

8.2.1 Matrix Addition . . . . . . . . . . . . . . . . . . . . . . . 242

8.2.2 Matrix Multiplication . . . . . . . . . . . . . . . . . . . . 243

8.2.3 Applications of Matrix Multiplication . . . . . . . . . . . 244

8.2.4 Identity Matrices and Inversion . . . . . . . . . . . . . . . 248

8.2.5 Matrix Inversion and Linear Systems . . . . . . . . . . . . 250

8.2.6 MatrixRank .........................251

8.3 Factoring Matrices . . . . . . . . . . . . . . . . . . . . . . . . . . 252

8.3.1 Why Factor Feature Matrices? . . . . . . . . . . . . . . . 252

8.3.2 LU Decomposition and Determinants . . . . . . . . . . . 254

8.4 Eigenvalues and Eigenvectors . . . . . . . . . . . . . . . . . . . . 255

8.4.1 Properties of Eigenvalues . . . . . . . . . . . . . . . . . . 255

8.4.2 Computing Eigenvalues . . . . . . . . . . . . . . . . . . . 256

8.5 Eigenvalue Decomposition . . . . . . . . . . . . . . . . . . . . . . 257

8.5.1 Singular Value Decomposition . . . . . . . . . . . . . . . . 258

8.5.2 Principal Components Analysis . . . . . . . . . . . . . . . 260

8.6 War Story: The Human Factors . . . . . . . . . . . . . . . . . . . 262

8.7 ChapterNotes ............................263

8.8 Exercises ............................... 263

9 Linear and Logistic Regression 267

9.1 LinearRegression........................... 268

9.1.1 Linear Regression and Duality . . . . . . . . . . . . . . . 268

9.1.2 Error in Linear Regression . . . . . . . . . . . . . . . . . . 269

9.1.3 Finding the Optimal Fit . . . . . . . . . . . . . . . . . . . 270

9.2 Better Regression Models . . . . . . . . . . . . . . . . . . . . . . 272

9.2.1 Removing Outliers . . . . . . . . . . . . . . . . . . . . . . 272

9.2.2 Fitting Non-Linear Functions . . . . . . . . . . . . . . . . 273

9.2.3 Feature and Target Scaling . . . . . . . . . . . . . . . . . 274

9.2.4 Dealing with Highly-Correlated Features . . . . . . . . . . 277

9.3 War Story: Taxi Deriver . . . . . . . . . . . . . . . . . . . . . . . 277

9.4 Regression as Parameter Fitting . . . . . . . . . . . . . . . . . . 279

9.4.1 Convex Parameter Spaces . . . . . . . . . . . . . . . . . . 280

9.4.2 Gradient Descent Search . . . . . . . . . . . . . . . . . . . 281

9.4.3 What is the Right Learning Rate? . . . . . . . . . . . . . 283

9.4.4 Stochastic Gradient Descent . . . . . . . . . . . . . . . . . 285

9.5 Simplifying Models through Regularization . . . . . . . . . . . . 286

9.5.1 Ridge Regression . . . . . . . . . . . . . . . . . . . . . . . 286

9.5.2 LASSO Regression . . . . . . . . . . . . . . . . . . . . . . 287

9.5.3 Trade-Offs between Fit and Complexity . . . . . . . . . . 288

9.6 Classification and Logistic Regression . . . . . . . . . . . . . . . 289

9.6.1 Regression for Classification . . . . . . . . . . . . . . . . . 290

9.6.2 Decision Boundaries . . . . . . . . . . . . . . . . . . . . . 291

9.6.3 Logistic Regression . . . . . . . . . . . . . . . . . . . . . . 292

9.7 Issues in Logistic Classification . . . . . . . . . . . . . . . . . . . 295

9.7.1 Balanced Training Classes . . . . . . . . . . . . . . . . . . 295

9.7.2 Multi-Class Classification . . . . . . . . . . . . . . . . . . 297

9.7.3 Hierarchical Classification . . . . . . . . . . . . . . . . . . 298

9.7.4 Partition Functions and Multinomial Regression . . . . . 299

9.8 ChapterNotes ............................300

9.9 Exercises ............................... 301

10 Distance and Network Methods 303

10.1 Measuring Distances . . . . . . . . . . . . . . . . . . . . . . . . . 303

10.1.1 Distance Metrics . . . . . . . . . . . . . . . . . . . . . . . 304

10.1.2 The LkDistance Metric . . . . . . . . . . . . . . . . . . . 305

10.1.3 Working in Higher Dimensions . . . . . . . . . . . . . . . 307

10.1.4 Dimensional Egalitarianism . . . . . . . . . . . . . . . . . 308

10.1.5 Points vs. Vectors . . . . . . . . . . . . . . . . . . . . . . 309

10.1.6 Distances between Probability Distributions . . . . . . . . 310

10.2 Nearest Neighbor Classification . . . . . . . . . . . . . . . . . . . 311

10.2.1 Seeking Good Analogies . . . . . . . . . . . . . . . . . . . 312

10.2.2 k-Nearest Neighbors . . . . . . . . . . . . . . . . . . . . . 313

10.2.3 Finding Nearest Neighbors . . . . . . . . . . . . . . . . . 315

10.2.4 Locality Sensitive Hashing . . . . . . . . . . . . . . . . . . 317

10.3 Graphs, Networks, and Distances . . . . . . . . . . . . . . . . . . 319

10.3.1 Weighted Graphs and Induced Networks . . . . . . . . . . 320

10.3.2 Talking About Graphs . . . . . . . . . . . . . . . . . . . . 321

10.3.3 Graph Theory . . . . . . . . . . . . . . . . . . . . . . . . 323

10.4PageRank...............................325

10.5Clustering............................... 327

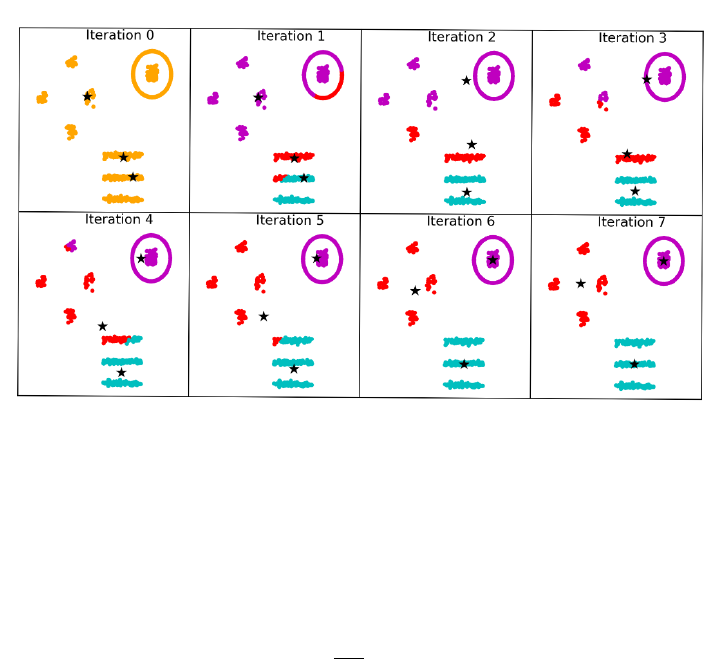

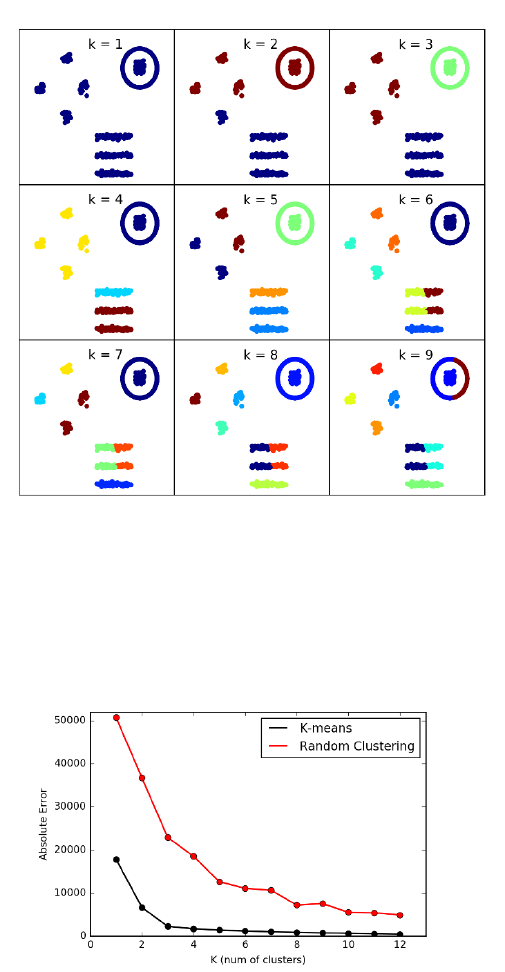

10.5.1 k-means Clustering . . . . . . . . . . . . . . . . . . . . . . 330

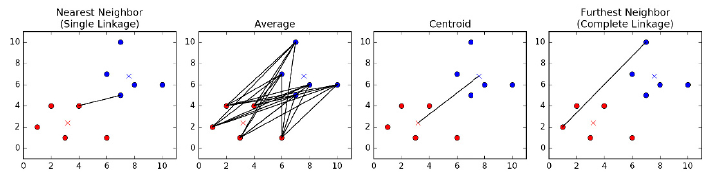

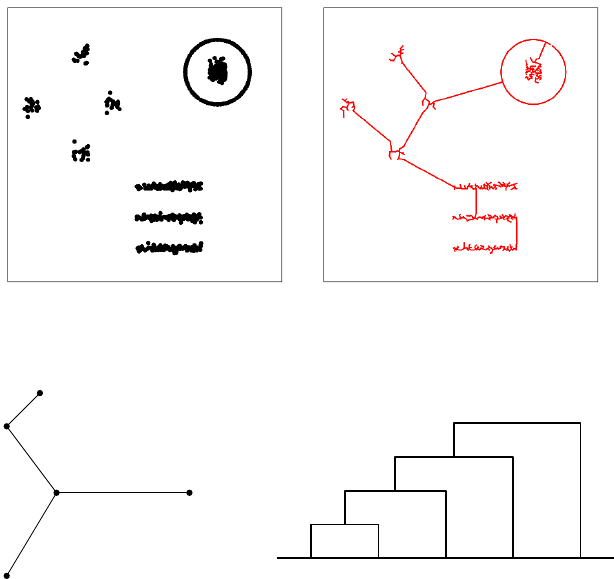

10.5.2 Agglomerative Clustering . . . . . . . . . . . . . . . . . . 336

10.5.3 Comparing Clusterings . . . . . . . . . . . . . . . . . . . . 341

10.5.4 Similarity Graphs and Cut-Based Clustering . . . . . . . 341

10.6 War Story: Cluster Bombing . . . . . . . . . . . . . . . . . . . . 344

10.7ChapterNotes ............................ 345

10.8Exercises ............................... 346

11 Machine Learning 351

11.1NaiveBayes..............................354

11.1.1 Formulation..........................354

11.1.2 Dealing with Zero Counts (Discounting) . . . . . . . . . . 356

11.2 Decision Tree Classifiers . . . . . . . . . . . . . . . . . . . . . . . 357

11.2.1 Constructing Decision Trees . . . . . . . . . . . . . . . . . 359

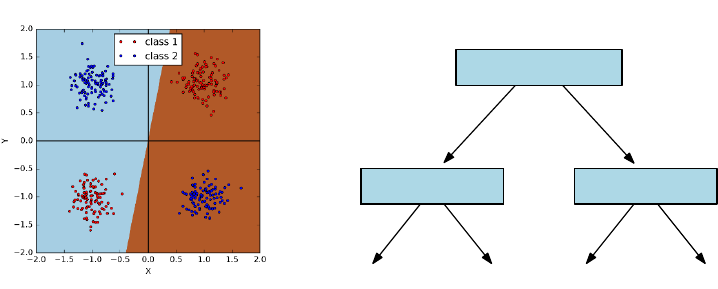

11.2.2 Realizing Exclusive Or . . . . . . . . . . . . . . . . . . . . 361

11.2.3 Ensembles of Decision Trees . . . . . . . . . . . . . . . . . 362

11.3 Boosting and Ensemble Learning . . . . . . . . . . . . . . . . . . 363

11.3.1 Voting with Classifiers . . . . . . . . . . . . . . . . . . . . 363

11.3.2 Boosting Algorithms . . . . . . . . . . . . . . . . . . . . . 364

11.4 Support Vector Machines . . . . . . . . . . . . . . . . . . . . . . 366

11.4.1 LinearSVMs .........................369

11.4.2 Non-linear SVMs . . . . . . . . . . . . . . . . . . . . . . . 369

11.4.3 Kernels ............................371

11.5 Degrees of Supervision . . . . . . . . . . . . . . . . . . . . . . . . 372

11.5.1 Supervised Learning . . . . . . . . . . . . . . . . . . . . . 372

11.5.2 Unsupervised Learning . . . . . . . . . . . . . . . . . . . . 372

11.5.3 Semi-supervised Learning . . . . . . . . . . . . . . . . . . 374

11.5.4 Feature Engineering . . . . . . . . . . . . . . . . . . . . . 375

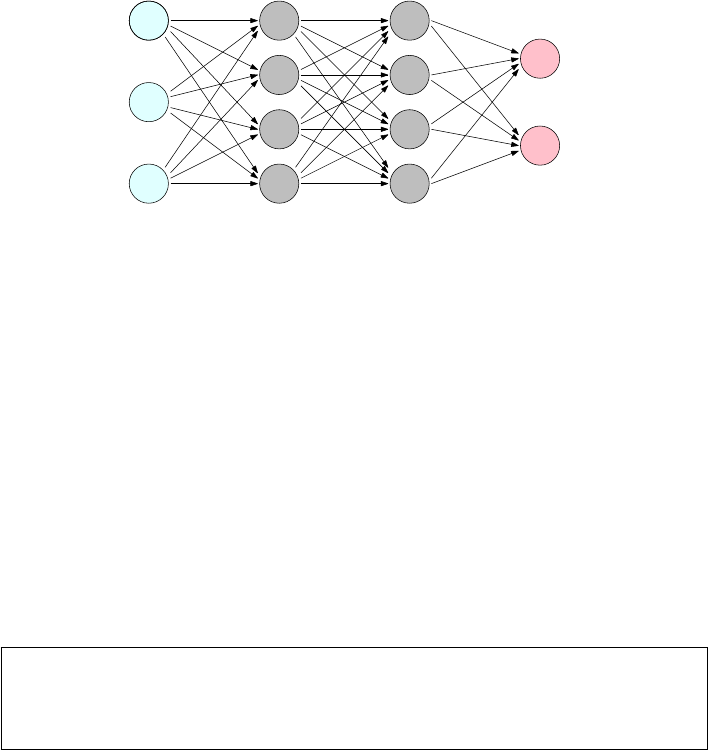

11.6DeepLearning ............................ 377

11.6.1 Networks and Depth . . . . . . . . . . . . . . . . . . . . . 378

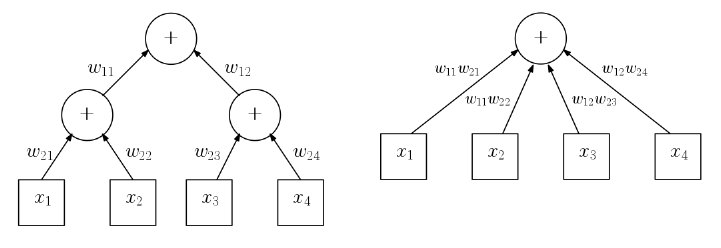

11.6.2 Backpropagation . . . . . . . . . . . . . . . . . . . . . . . 382

11.6.3 Word and Graph Embeddings . . . . . . . . . . . . . . . . 383

11.7 War Story: The Name Game . . . . . . . . . . . . . . . . . . . . 385

11.8ChapterNotes ............................ 387

11.9Exercises ............................... 388

12 Big Data: Achieving Scale 391

12.1WhatisBigData? .......................... 392

12.1.1 Big Data as Bad Data . . . . . . . . . . . . . . . . . . . . 392

12.1.2 TheThreeVs......................... 394

12.2 War Story: Infrastructure Matters . . . . . . . . . . . . . . . . . 395

12.3 Algorithmics for Big Data . . . . . . . . . . . . . . . . . . . . . . 397

12.3.1 Big Oh Analysis . . . . . . . . . . . . . . . . . . . . . . . 397

12.3.2 Hashing............................399

12.3.3 Exploiting the Storage Hierarchy . . . . . . . . . . . . . . 401

12.3.4 Streaming and Single-Pass Algorithms . . . . . . . . . . . 402

12.4 Filtering and Sampling . . . . . . . . . . . . . . . . . . . . . . . . 403

12.4.1 Deterministic Sampling Algorithms . . . . . . . . . . . . . 404

12.4.2 Randomized and Stream Sampling . . . . . . . . . . . . . 406

12.5Parallelism .............................. 406

12.5.1 One, Two, Many . . . . . . . . . . . . . . . . . . . . . . . 407

12.5.2 Data Parallelism . . . . . . . . . . . . . . . . . . . . . . . 409

12.5.3 GridSearch..........................409

12.5.4 Cloud Computing Services . . . . . . . . . . . . . . . . . . 410

12.6MapReduce .............................. 410

12.6.1 Map-Reduce Programming . . . . . . . . . . . . . . . . . 412

12.6.2 MapReduce under the Hood . . . . . . . . . . . . . . . . . 414

12.7 Societal and Ethical Implications . . . . . . . . . . . . . . . . . . 416

12.8ChapterNotes ............................ 419

12.9Exercises ............................... 419

13 Coda 423

13.1GetaJob!...............................423

13.2 Go to Graduate School! . . . . . . . . . . . . . . . . . . . . . . . 424

13.3 Professional Consulting Services . . . . . . . . . . . . . . . . . . 425

14 Bibliography 427

Chapter 1

What is Data Science?

The purpose of computing is insight, not numbers.

– Richard W. Hamming

What is data science? Like any emerging field, it hasn’t been completely defined

yet, but you know enough about it to be interested or else you wouldn’t be

reading this book.

I think of data science as lying at the intersection of computer science, statis-

tics, and substantive application domains. From computer science comes ma-

chine learning and high-performance computing technologies for dealing with

scale. From statistics comes a long tradition of exploratory data analysis, sig-

nificance testing, and visualization. From application domains in business and

the sciences comes challenges worthy of battle, and evaluation standards to

assess when they have been adequately conquered.

But these are all well-established fields. Why data science, and why now? I

see three reasons for this sudden burst of activity:

•New technology makes it possible to capture, annotate, and store vast

amounts of social media, logging, and sensor data. After you have amassed

all this data, you begin to wonder what you can do with it.

•Computing advances make it possible to analyze data in novel ways and at

ever increasing scales. Cloud computing architectures give even the little

guy access to vast power when they need it. New approaches to machine

learning have lead to amazing advances in longstanding problems, like

computer vision and natural language processing.

•Prominent technology companies (like Google and Facebook) and quan-

titative hedge funds (like Renaissance Technologies and TwoSigma) have

proven the power of modern data analytics. Success stories applying data

to such diverse areas as sports management (Moneyball [Lew04]) and elec-

tion forecasting (Nate Silver [Sil12]) have served as role models to bring

data science to a large popular audience.

2CHAPTER 1. WHAT IS DATA SCIENCE?

This introductory chapter has three missions. First, I will try to explain how

good data scientists think, and how this differs from the mindset of traditional

programmers and software developers. Second, we will look at data sets in terms

of the potential for what they can be used for, and learn to ask the broader

questions they are capable of answering. Finally, I introduce a collection of

data analysis challenges that will be used throughout this book as motivating

examples.

1.1 Computer Science, Data Science, and Real

Science

Computer scientists, by nature, don’t respect data. They have traditionally

been taught that the algorithm was the thing, and that data was just meat to

be passed through a sausage grinder.

So to qualify as an effective data scientist, you must first learn to think like

a real scientist. Real scientists strive to understand the natural world, which

is a complicated and messy place. By contrast, computer scientists tend to

build their own clean and organized virtual worlds and live comfortably within

them. Scientists obsess about discovering things, while computer scientists in-

vent rather than discover.

People’s mindsets strongly color how they think and act, causing misunder-

standings when we try to communicate outside our tribes. So fundamental are

these biases that we are often unaware we have them. Examples of the cultural

differences between computer science and real science include:

•Data vs. method centrism: Scientists are data driven, while computer

scientists are algorithm driven. Real scientists spend enormous amounts

of effort collecting data to answer their question of interest. They invent

fancy measuring devices, stay up all night tending to experiments, and

devote most of their thinking to how to get the data they need.

By contrast, computer scientists obsess about methods: which algorithm

is better than which other algorithm, which programming language is best

for a job, which program is better than which other program. The details

of the data set they are working on seem comparably unexciting.

•Concern about results: Real scientists care about answers. They analyze

data to discover something about how the world works. Good scientists

care about whether the results make sense, because they care about what

the answers mean.

By contrast, bad computer scientists worry about producing plausible-

looking numbers. As soon as the numbers stop looking grossly wrong,

they are presumed to be right. This is because they are personally less

invested in what can be learned from a computation, as opposed to getting

it done quickly and efficiently.

1.1. COMPUTER SCIENCE, DATA SCIENCE, AND REAL SCIENCE 3

•Robustness: Real scientists are comfortable with the idea that data has

errors. In general, computer scientists are not. Scientists think a lot about

possible sources of bias or error in their data, and how these possible prob-

lems can effect the conclusions derived from them. Good programmers use

strong data-typing and parsing methodologies to guard against formatting

errors, but the concerns here are different.

Becoming aware that data can have errors is empowering. Computer

scientists chant “garbage in, garbage out” as a defensive mantra to ward

off criticism, a way to say that’s not my job. Real scientists get close

enough to their data to smell it, giving it the sniff test to decide whether

it is likely to be garbage.

•Precision: Nothing is ever completely true or false in science, while every-

thing is either true or false in computer science or mathematics.

Generally speaking, computer scientists are happy printing floating point

numbers to as many digits as possible: 8/13 = 0.61538461538. Real

scientists will use only two significant digits: 8/13 ≈0.62. Computer

scientists care what a number is, while real scientists care what it means.

Aspiring data scientists must learn to think like real scientists. Your job is

going to be to turn numbers into insight. It is important to understand the why

as much as the how.

To be fair, it benefits real scientists to think like data scientists as well. New

experimental technologies enable measuring systems on vastly greater scale than

ever possible before, through technologies like full-genome sequencing in biology

and full-sky telescope surveys in astronomy. With new breadth of view comes

new levels of vision.

Traditional hypothesis-driven science was based on asking specific questions

of the world and then generating the specific data needed to confirm or deny

it. This is now augmented by data-driven science, which instead focuses on

generating data on a previously unheard of scale or resolution, in the belief that

new discoveries will come as soon as one is able to look at it. Both ways of

thinking will be important to us:

•Given a problem, what available data will help us answer it?

•Given a data set, what interesting problems can we apply it to?

There is another way to capture this basic distinction between software en-

gineering and data science. It is that software developers are hired to build

systems, while data scientists are hired to produce insights.

This may be a point of contention for some developers. There exist an

important class of engineers who wrangle the massive distributed infrastructures

necessary to store and analyze, say, financial transaction or social media data

4CHAPTER 1. WHAT IS DATA SCIENCE?

on a full Facebook or Twitter-level of scale. Indeed, I will devote Chapter 12

to the distinctive challenges of big data infrastructures. These engineers are

building tools and systems to support data science, even though they may not

personally mine the data they wrangle. Do they qualify as data scientists?

This is a fair question, one I will finesse a bit so as to maximize the poten-

tial readership of this book. But I do believe that the better such engineers

understand the full data analysis pipeline, the more likely they will be able to

build powerful tools capable of providing important insights. A major goal of

this book is providing big data engineers with the intellectual tools to think like

big data scientists.

1.2 Asking Interesting Questions from Data

Good data scientists develop an inherent curiosity about the world around them,

particularly in the associated domains and applications they are working on.

They enjoy talking shop with the people whose data they work with. They ask

them questions: What is the coolest thing you have learned about this field?

Why did you get interested in it? What do you hope to learn by analyzing your

data set? Data scientists always ask questions.

Good data scientists have wide-ranging interests. They read the newspaper

every day to get a broader perspective on what is exciting. They understand that

the world is an interesting place. Knowing a little something about everything

equips them to play in other people’s backyards. They are brave enough to get

out of their comfort zones a bit, and driven to learn more once they get there.

Software developers are not really encouraged to ask questions, but data

scientists are. We ask questions like:

•What things might you be able to learn from a given data set?

•What do you/your people really want to know about the world?

•What will it mean to you once you find out?

Computer scientists traditionally do not really appreciate data. Think about

the way algorithm performance is experimentally measured. Usually the pro-

gram is run on “random data” to see how long it takes. They rarely even look

at the results of the computation, except to verify that it is correct and efficient.

Since the “data” is meaningless, the results cannot be important. In contrast,

real data sets are a scarce resource, which required hard work and imagination

to obtain.

Becoming a data scientist requires learning to ask questions about data, so

let’s practice. Each of the subsections below will introduce an interesting data

set. After you understand what kind of information is available, try to come

up with, say, five interesting questions you might explore/answer with access to

this data set.

1.2. ASKING INTERESTING QUESTIONS FROM DATA 5

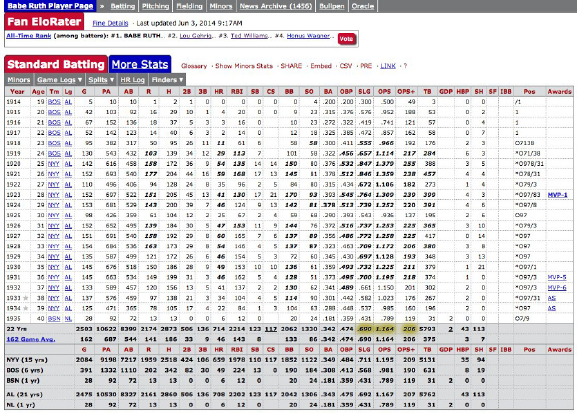

Figure 1.1: Statistical information on the performance of Babe Ruth can be

found at http://www.baseball-reference.com.

The key is thinking broadly: the answers to big, general questions often lie

buried in highly-specific data sets, which were by no means designed to contain

them.

1.2.1 The Baseball Encyclopedia

Baseball has long had an outsized importance in the world of data science. This

sport has been called the national pastime of the United States; indeed, French

historian Jacques Barzun observed that “Whoever wants to know the heart and

mind of America had better learn baseball.” I realize that many readers are not

American, and even those that are might be completely disinterested in sports.

But stick with me for a while.

What makes baseball important to data science is its extensive statistical

record of play, dating back for well over a hundred years. Baseball is a sport of

discrete events: pitchers throw balls and batters try to hit them – that naturally

lends itself to informative statistics. Fans get immersed in these statistics as chil-

dren, building their intuition about the strengths and limitations of quantitative

analysis. Some of these children grow up to become data scientists. Indeed, the

success of Brad Pitt’s statistically-minded baseball team in the movie Moneyball

remains the American public’s most vivid contact with data science.

This historical baseball record is available at http://www.baseball-reference.

com. There you will find complete statistical data on the performance of every

player who even stepped on the field. This includes summary statistics of each

season’s batting, pitching, and fielding record, plus information about teams

6CHAPTER 1. WHAT IS DATA SCIENCE?

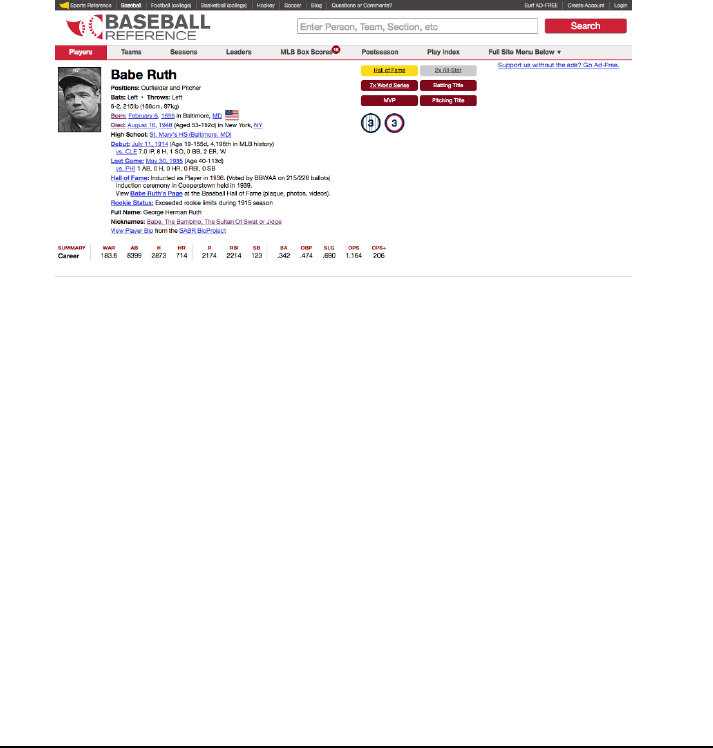

Figure 1.2: Personal information on every major league baseball player is avail-

able at http://www.baseball-reference.com.

and awards as shown in Figure 1.1.

But more than just statistics, there is metadata on the life and careers of all

the people who have ever played major league baseball, as shown in Figure 1.2.

We get the vital statistics of each player (height, weight, handedness) and their

lifespan (when/where they were born and died). We also get salary information

(how much each player got paid every season) and transaction data (how did

they get to be the property of each team they played for).

Now, I realize that many of you do not have the slightest knowledge of or

interest in baseball. This sport is somewhat reminiscent of cricket, if that helps.

But remember that as a data scientist, it is your job to be interested in the

world around you. Think of this as chance to learn something.

So what interesting questions can you answer with this baseball data set?

Try to write down five questions before moving on. Don’t worry, I will wait here

for you to finish.

The most obvious types of questions to answer with this data are directly

related to baseball:

•How can we best measure an individual player’s skill or value?

•How fairly do trades between teams generally work out?

•What is the general trajectory of player’s performance level as they mature

and age?

•To what extent does batting performance correlate with position played?

For example, are outfielders really better hitters than infielders?

These are interesting questions. But even more interesting are questions

about demographic and social issues. Almost 20,000 major league baseball play-

1.2. ASKING INTERESTING QUESTIONS FROM DATA 7

ers have taken the field over the past 150 years, providing a large, extensively-

documented cohort of men who can serve as a proxy for even larger, less well-

documented populations. Indeed, we can use this baseball player data to answer

questions like:

•Do left-handed people have shorter lifespans than right-handers? Handed-

ness is not captured in most demographic data sets, but has been diligently

assembled here. Indeed, analysis of this data set has been used to show

that right-handed people live longer than lefties [HC88]!

•How often do people return to live in the same place where they were

born? Locations of birth and death have been extensively recorded in this

data set. Further, almost all of these people played at least part of their

career far from home, thus exposing them to the wider world at a critical

time in their youth.

•Do player salaries generally reflect past, present, or future performance?

•To what extent have heights and weights been increasing in the population

at large?

There are two particular themes to be aware of here. First, the identifiers

and reference tags (i.e. the metadata) often prove more interesting in a data set

than the stuff we are supposed to care about, here the statistical record of play.

Second is the idea of a statistical proxy, where you use the data set you have

to substitute for the one you really want. The data set of your dreams likely

does not exist, or may be locked away behind a corporate wall even if it does.

A good data scientist is a pragmatist, seeing what they can do with what they

have instead of bemoaning what they cannot get their hands on.

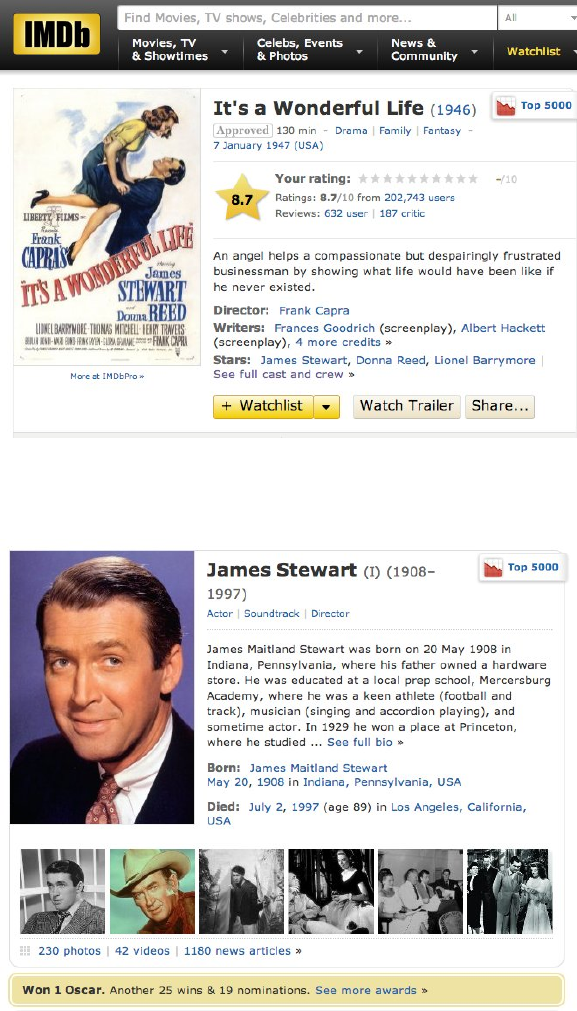

1.2.2 The Internet Movie Database (IMDb)

Everybody loves the movies. The Internet Movie Database (IMDb) provides

crowdsourced and curated data about all aspects of the motion picture industry,

at www.imdb.com. IMDb currently contains data on over 3.3 million movies and

TV programs. For each film, IMDb includes its title, running time, genres, date

of release, and a full list of cast and crew. There is financial data about each

production, including the budget for making the film and how well it did at the

box office.

Finally, there are extensive ratings for each film from viewers and critics.

This rating data consists of scores on a zero to ten stars scale, cross-tabulated

into averages by age and gender. Written reviews are often included, explaining

why a particular critic awarded a given number of stars. There are also links

between films: for example, identifying which other films have been watched

most often by viewers of It’s a Wonderful Life.

Every actor, director, producer, and crew member associated with a film

merits an entry in IMDb, which now contains records on 6.5 million people.

8CHAPTER 1. WHAT IS DATA SCIENCE?

Figure 1.3: Representative film data from the Internet Movie Database.

Figure 1.4: Representative actor data from the Internet Movie Database.

1.2. ASKING INTERESTING QUESTIONS FROM DATA 9

These happen to include my brother, cousin, and sister-in-law. Each actor

is linked to every film they appeared in, with a description of their role and

their ordering in the credits. Available data about each personality includes

birth/death dates, height, awards, and family relations.

So what kind of questions can you answer with this movie data?

Perhaps the most natural questions to ask IMDb involve identifying the

extremes of movies and actors:

•Which actors appeared in the most films? Earned the most money? Ap-

peared in the lowest rated films? Had the longest career or the shortest

lifespan?

•What was the highest rated film each year, or the best in each genre?

Which movies lost the most money, had the highest-powered casts, or got

the least favorable reviews.

Then there are larger-scale questions one can ask about the nature of the

motion picture business itself:

•How well does movie gross correlate with viewer ratings or awards? Do

customers instinctively flock to trash, or is virtue on the part of the cre-

ative team properly rewarded?

•How do Hollywood movies compare to Bollywood movies, in terms of rat-

ings, budget, and gross? Are American movies better received than foreign

films, and how does this differ between U.S. and non-U.S. reviewers?

•What is the age distribution of actors and actresses in films? How much

younger is the actress playing the wife, on average, than the actor playing

the husband? Has this disparity been increasing or decreasing with time?

•Live fast, die young, and leave a good-looking corpse? Do movie stars live

longer or shorter lives than bit players, or compared to the general public?

Assuming that people working together on a film get to know each other,

the cast and crew data can be used to build a social network of the movie

business. What does the social network of actors look like? The Oracle of

Bacon (https://oracleofbacon.org/) posits Kevin Bacon as the center of

the Hollywood universe and generates the shortest path to Bacon from any

other actor. Other actors, like Samuel L. Jackson, prove even more central.

More critically, can we analyze this data to determine the probability that

someone will like a given movie? The technique of collaborative filtering finds

people who liked films that I also liked, and recommends other films that they

liked as good candidates for me. The 2007 Netflix Prize was a $1,000,000 com-

petition to produce a ratings engine 10% better than the proprietary Netflix

system. The ultimate winner of this prize (BellKor) used a variety of data

sources and techniques, including the analysis of links [BK07].

10 CHAPTER 1. WHAT IS DATA SCIENCE?

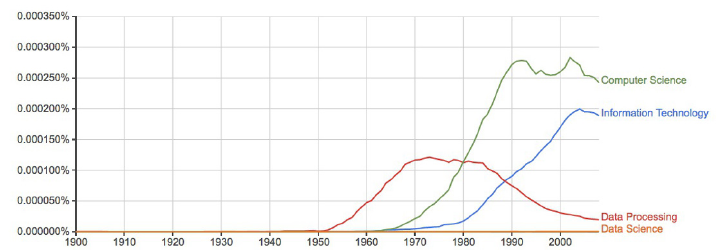

Figure 1.5: The rise and fall of data processing, as witnessed by Google Ngrams.

1.2.3 Google Ngrams

Printed books have been the primary repository of human knowledge since

Gutenberg’s invention of movable type in 1439. Physical objects live somewhat

uneasily in today’s digital world, but technology has a way of reducing every-

thing to data. As part of its mission to organize the world’s information, Google

undertook an effort to scan all of the world’s published books. They haven’t

quite gotten there yet, but the 30 million books thus far digitized represent over

20% of all books ever published.

Google uses this data to improve search results, and provide fresh access

to out-of-print books. But perhaps the coolest product is Google Ngrams, an

amazing resource for monitoring changes in the cultural zeitgeist. It provides

the frequency with which short phrases occur in books published each year.

Each phrase must occur at least forty times in their scanned book corpus. This

eliminates obscure words and phrases, but leaves over two billion time series

available for analysis.

This rich data set shows how language use has changed over the past 200

years, and has been widely applied to cultural trend analysis [MAV+11]. Figure

1.5 uses this data to show how the word data fell out of favor when thinking

about computing. Data processing was the popular term associated with the

computing field during the punched card and spinning magnetic tape era of the

1950s. The Ngrams data shows that the rapid rise of Computer Science did not

eclipse Data Processing until 1980. Even today, Data Science remains almost

invisible on this scale.

Check out Google Ngrams at http://books.google.com/ngrams. I promise

you will enjoy playing with it. Compare hot dog to tofu,science against religion,

freedom to justice, and sex vs. marriage, to better understand this fantastic

telescope for looking into the past.

But once you are done playing, think of bigger things you could do if you

got your hands on this data. Assume you have access to the annual number

of references for all words/phrases published in books over the past 200 years.

1.2. ASKING INTERESTING QUESTIONS FROM DATA 11

Google makes this data freely available. So what are you going to do with it?

Observing the time series associated with particular words using the Ngrams

Viewer is fun. But more sophisticated historical trends can be captured by

aggregating multiple time series together. The following types of questions

seem particularly interesting to me:

•How has the amount of cursing changed over time? Use of the four-

letter words I am most familiar with seem to have exploded since 1960,

although it is perhaps less clear whether this reflects increased cussing or

lower publication standards.

•How often do new words emerge and get popular? Do these words tend

to stay in common usage, or rapidly fade away? Can we detect when

words change meaning over time, like the transition of gay from happy to

homosexual?

•Have standards of spelling been improving or deteriorating with time,

especially now that we have entered the era of automated spell check-

ing? Rarely-occurring words that are only one character removed from a

commonly-used word are likely candidates to be spelling errors (e.g. al-

gorithm vs. algorthm). Aggregated over many different misspellings, are

such errors increasing or decreasing?

You can also use this Ngrams corpus to build a language model that captures

the meaning and usage of the words in a given language. We will discuss word

embeddings in Section 11.6.3, which are powerful tools for building language

models. Frequency counts reveal which words are most popular. The frequency

of word pairs appearing next to each other can be used to improve speech

recognition systems, helping to distinguish whether the speaker said that’s too

bad or that’s to bad. These millions of books provide an ample data set to build

representative models from.

1.2.4 New York Taxi Records

Every financial transaction today leaves a data trail behind it. Following these

paths can lead to interesting insights.

Taxi cabs form an important part of the urban transportation network. They

roam the streets of the city looking for customers, and then drive them to their

destination for a fare proportional to the length of the trip. Each cab contains

a metering device to calculate the cost of the trip as a function of time. This

meter serves as a record keeping device, and a mechanism to ensure that the

driver charges the proper amount for each trip.

The taxi meters currently employed in New York cabs can do many things

beyond calculating fares. They act as credit card terminals, providing a way

12 CHAPTER 1. WHAT IS DATA SCIENCE?

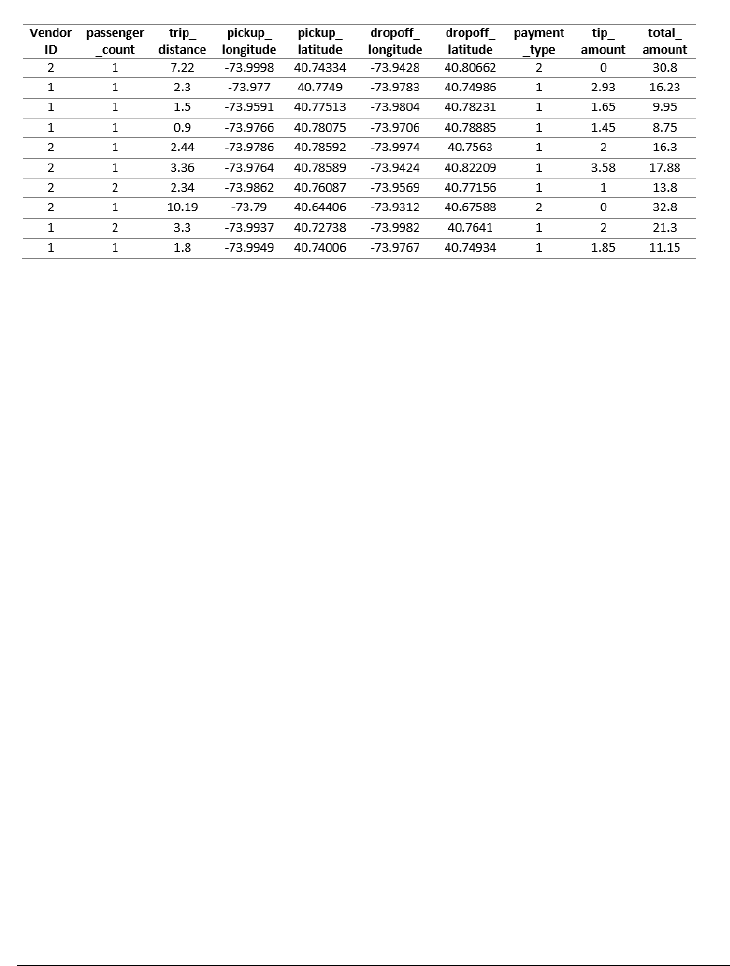

Figure 1.6: Representative fields from the New York city taxi cab data: pick up

and dropoff points, distances, and fares.

for customers to pay for rides without cash. They are integrated with global

positioning systems (GPS), recording the exact location of every pickup and

drop off. And finally, since they are on a wireless network, these boxes can

communicate all of this data back to a central server.

The result is a database documenting every single trip by all taxi cabs in

one of the world’s greatest cities, a small portion of which is shown in Figure

1.6. Because the New York Taxi and Limousine Commission is a public agency,

its non-confidential data is available to all under the Freedom of Information

Act (FOA).

Every ride generates two records: one with data on the trip, the other with

details of the fare. Each trip is keyed to the medallion (license) of each car

coupled with the identifier of each driver. For each trip, we get the time/date

of pickup and drop-off, as well as the GPS coordinates (longitude and latitude)

of the starting location and destination. We do not get GPS data of the route

they traveled between these points, but to some extent that can be inferred by

the shortest path between them.

As for fare data, we get the metered cost of each trip, including tax, surcharge

and tolls. It is traditional to pay the driver a tip for service, the amount of which

is also recorded in the data.

So I’m talking to you. This taxi data is readily available, with records of

over 80 million trips over the past several years. What are you going to do with

it?

Any interesting data set can be used to answer questions on many different

scales. This taxi fare data can help us better understand the transportation

industry, but also how the city works and how we could make it work even

better. Natural questions with respect to the taxi industry include:

1.2. ASKING INTERESTING QUESTIONS FROM DATA 13

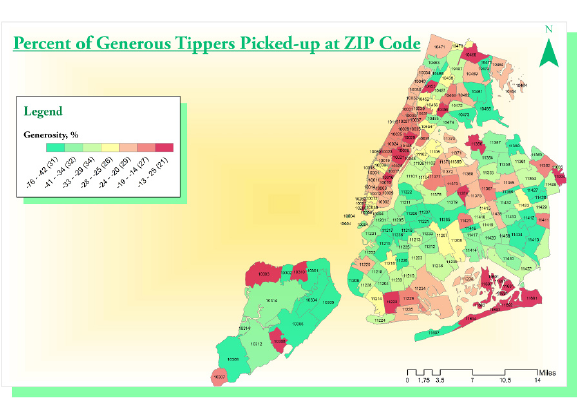

Figure 1.7: Which neighborhoods in New York city tip most generously? The

relatively remote outer boroughs of Brooklyn and Queens, where trips are

longest and supply is relatively scarce.

•How much money do drivers make each night, on average? What is the

distribution? Do drivers make more on sunny days or rainy days?

•Where are the best spots in the city for drivers to cruise, in order to pick

up profitable fares? How does this vary at different times of the day?

•How far do drivers travel over the course of a night’s work? We can’t

answer this exactly using this data set, because it does not provide GPS

data of the route traveled between fares. But we do know the last place

of drop off, the next place of pickup, and how long it took to get between

them. Together, this should provide enough information to make a sound

estimate.

•Which drivers take their unsuspecting out-of-town passengers for a “ride,”

running up the meter on what should be a much shorter, cheaper trip?

•How much are drivers tipped, and why? Do faster drivers get tipped

better? How do tipping rates vary by neighborhood, and is it the rich

neighborhoods or poor neighborhoods which prove more generous?

I will confess we did an analysis of this, which I will further describe in

the war story of Section 9.3. We found a variety of interesting patterns

[SS15]. Figure 1.7 shows that Manhattanites are generally cheapskates

relative to large swaths of Brooklyn, Queens, and Staten Island, where

trips are longer and street cabs a rare but welcome sight.

14 CHAPTER 1. WHAT IS DATA SCIENCE?

But the bigger questions have to do with understanding transportation in

the city. We can use the taxi travel times as a sensor to measure the level of

traffic in the city at a fine level. How much slower is traffic during rush hour

than other times, and where are delays the worst? Identifying problem areas is

the first step to proposing solutions, by changing the timing patterns of traffic

lights, running more buses, or creating high-occupancy only lanes.

Similarly we can use the taxi data to measure transportation flows across

the city. Where are people traveling to, at different times of the day? This tells

us much more than just congestion. By looking at the taxi data, we should

be able to see tourists going from hotels to attractions, executives from fancy

neighborhoods to Wall Street, and drunks returning home from nightclubs after

a bender.

Data like this is essential to designing better transportation systems. It is

wasteful for a single rider to travel from point ato point bwhen there is another

rider at point a+who also wants to get there. Analysis of the taxi data enables

accurate simulation of a ride sharing system, so we can accurately evaluate the

demands and cost reductions of such a service.

1.3 Properties of Data

This book is about techniques for analyzing data. But what is the underlying

stuff that we will be studying? This section provides a brief taxonomy of the

properties of data, so we can better appreciate and understand what we will be

working on.

1.3.1 Structured vs. Unstructured Data

Certain data sets are nicely structured, like the tables in a database or spread-

sheet program. Others record information about the state of the world, but in

a more heterogeneous way. Perhaps it is a large text corpus with images and

links like Wikipedia, or the complicated mix of notes and test results appearing

in personal medical records.

Generally speaking, this book will focus on dealing with structured data.

Data is often represented by a matrix, where the rows of the matrix represent

distinct items or records, and the columns represent distinct properties of these

items. For example, a data set about U.S. cities might contain one row for each

city, with columns representing features like state, population, and area.

When confronted with an unstructured data source, such as a collection of

tweets from Twitter, our first step is generally to build a matrix to structure

it. A bag of words model will construct a matrix with a row for each tweet, and

a column for each frequently used vocabulary word. Matrix entry M[i, j] then

denotes the number of times tweet icontains word j. Such matrix formulations

will motivate our discussion of linear algebra, in Chapter 8.

1.3. PROPERTIES OF DATA 15

1.3.2 Quantitative vs. Categorical Data

Quantitative data consists of numerical values, like height and weight. Such data

can be incorporated directly into algebraic formulas and mathematical models,

or displayed in conventional graphs and charts.

By contrast, categorical data consists of labels describing the properties of

the objects under investigation, like gender, hair color, and occupation. This

descriptive information can be every bit as precise and meaningful as numerical

data, but it cannot be worked with using the same techniques.

Categorical data can usually be coded numerically. For example, gender

might be represented as male = 0 or f emale = 1. But things get more com-

plicated when there are more than two characters per feature, especially when

there is not an implicit order between them. We may be able to encode hair

colors as numbers by assigning each shade a distinct value like gray hair = 0,

red hair = 1, and blond hair = 2. However, we cannot really treat these val-

ues as numbers, for anything other than simple identity testing. Does it make

any sense to talk about the maximum or minimum hair color? What is the

interpretation of my hair color minus your hair color?

Most of what we do in this book will revolve around numerical data. But

keep an eye out for categorical features, and methods that work for them. Clas-

sification and clustering methods can be thought of as generating categorical

labels from numerical data, and will be a primary focus in this book.

1.3.3 Big Data vs. Little Data

Data science has become conflated in the public eye with big data, the analysis of

massive data sets resulting from computer logs and sensor devices. In principle,

having more data is always better than having less, because you can always

throw some of it away by sampling to get a smaller set if necessary.

Big data is an exciting phenomenon, and we will discuss it in Chapter 12. But

in practice, there are difficulties in working with large data sets. Throughout

this book we will look at algorithms and best practices for analyzing data. In

general, things get harder once the volume gets too large. The challenges of big

data include:

•The analysis cycle time slows as data size grows: Computational opera-

tions on data sets take longer as their volume increases. Small spreadsheets

provide instantaneous response, allowing you to experiment and play what

if? But large spreadsheets can be slow and clumsy to work with, and

massive-enough data sets might take hours or days to get answers from.

Clever algorithms can permit amazing things to be done with big data,

but staying small generally leads to faster analysis and exploration.

•Large data sets are complex to visualize: Plots with millions of points on

them are impossible to display on computer screens or printed images, let

alone conceptually understand. How can we ever hope to really understand

something we cannot see?

16 CHAPTER 1. WHAT IS DATA SCIENCE?

•Simple models do not require massive data to fit or evaluate: A typical

data science task might be to make a decision (say, whether I should offer

this fellow life insurance?) on the basis of a small number of variables:

say age, gender, height, weight, and the presence or absence of existing

medical conditions.

If I have this data on 1 million people with their associated life outcomes, I

should be able to build a good general model of coverage risk. It probably

wouldn’t help me build a substantially better model if I had this data

on hundreds of millions of people. The decision criteria on only a few

variables (like age and martial status) cannot be too complex, and should

be robust over a large number of applicants. Any observation that is so

subtle it requires massive data to tease out will prove irrelevant to a large

business which is based on volume.

Big data is sometimes called bad data. It is often gathered as the by-product

of a given system or procedure, instead of being purposefully collected to answer

your question at hand. The result is that we might have to go to heroic efforts

to make sense of something just because we have it.

Consider the problem of getting a pulse on voter preferences among presi-

dential candidates. The big data approach might analyze massive Twitter or

Facebook feeds, interpreting clues to their opinions in the text. The small data

approach might be to conduct a poll, asking a few hundred people this specific

question and tabulating the results. Which procedure do you think will prove

more accurate? The right data set is the one most directly relevant to the tasks

at hand, not necessarily the biggest one.

Take-Home Lesson: Do not blindly aspire to analyze large data sets. Seek the

right data to answer a given question, not necessarily the biggest thing you can

get your hands on.

1.4 Classification and Regression

Two types of problems arise repeatedly in traditional data science and pattern

recognition applications, the challenges of classification and regression. As this

book has developed, I have pushed discussions of the algorithmic approaches

to solving these problems toward the later chapters, so they can benefit from a

solid understanding of core material in data munging, statistics, visualization,

and mathematical modeling.

Still, I will mention issues related to classification and regression as they

arise, so it makes sense to pause here for a quick introduction to these problems,

to help you recognize them when you see them.

•Classification: Often we seek to assign a label to an item from a discrete

set of possibilities. Such problems as predicting the winner of a particular

1.5. DATA SCIENCE TELEVISION: THE QUANT SHOP 17

sporting contest (team Aor team B?) or deciding the genre of a given

movie (comedy, drama, or animation?) are classification problems, since

each entail selecting a label from the possible choices.

•Regression: Another common task is to forecast a given numerical quan-

tity. Predicting a person’s weight or how much snow we will get this year

is a regression problem, where we forecast the future value of a numerical

function in terms of previous values and other relevant features.

Perhaps the best way to see the intended distinction is to look at a variety

of data science problems and label (classify) them as regression or classification.

Different algorithmic methods are used to solve these two types of problems,

although the same questions can often be approached in either way:

•Will the price of a particular stock be higher or lower tomorrow? (classi-

fication)

•What will the price of a particular stock be tomorrow? (regression)

•Is this person a good risk to sell an insurance policy to? (classification)

•How long do we expect this person to live? (regression)

Keep your eyes open for classification and regression problems as you en-

counter them in your life, and in this book.

1.5 Data Science Television: The Quant Shop

I believe that hands-on experience is necessary to internalize basic principles.

Thus when I teach data science, I like to give each student team an interesting

but messy forecasting challenge, and demand that they build and evaluate a

predictive model for the task.

These forecasting challenges are associated with events where the students

must make testable predictions. They start from scratch: finding the relevant

data sets, building their own evaluation environments, and devising their model.

Finally, I make them watch the event as it unfolds, so as to witness the vindi-

cation or collapse of their prediction.

As an experiment, we documented the evolution of each group’s project

on video in Fall 2014. Professionally edited, this became The Quant Shop, a

television-like data science series for a general audience. The eight episodes of

this first season are available at http://www.quant-shop.com, and include:

•Finding Miss Universe – The annual Miss Universe competition aspires

to identify the most beautiful woman in the world. Can computational

models predict who will win a beauty contest? Is beauty just subjective,

or can algorithms tell who is the fairest one of all?

18 CHAPTER 1. WHAT IS DATA SCIENCE?

•Modeling the Movies – The business of movie making involves a lot of

high-stakes data analysis. Can we build models to predict which film will

gross the most on Christmas day? How about identifying which actors

will receive awards for their performance?

•Winning the Baby Pool – Birth weight is an important factor in assessing

the health of a newborn child. But how accurately can we predict junior’s

weight before the actual birth? How can data clarify environmental risks

to developing pregnancies?

•The Art of the Auction – The world’s most valuable artworks sell at auc-

tions to the highest bidder. But can we predict how many millions a

particular J.W. Turner painting will sell for? Can computers develop an

artistic sense of what’s worth buying?

•White Christmas – Weather forecasting is perhaps the most familiar do-

main of predictive modeling. Short-term forecasts are generally accurate,

but what about longer-term prediction? What places will wake up to a

snowy Christmas this year? And can you tell one month in advance?

•Predicting the Playoffs – Sports events have winners and losers, and book-

ies are happy to take your bets on the outcome of any match. How well can

statistics help predict which football team will win the Super Bowl? Can

Google’s PageRank algorithm pick the winners on the field as accurately

as it does on the web?