(The Wiley Finance Series) Salvatore Carollo Understanding Oil Prices A Guide To What Drives The Pr

User Manual:

Open the PDF directly: View PDF ![]() .

.

Page Count: 188 [warning: Documents this large are best viewed by clicking the View PDF Link!]

Understanding Oil Prices

For other titles in the Wiley Finance series

please see www.wiley.com/finance

Understanding Oil Prices

A Guide to What Drives the Price of Oil

in Today’s Markets

Salvatore Carollo

A John Wiley & Sons, Ltd., Publicatio

n

This edition first published 2012

© 2012 Salvatore Carollo

Registered office

John Wiley & Sons Ltd, The Atrium, Southern Gate, Chichester, West Sussex, PO19 8SQ,

United Kingdom

For details of our global editorial offices, for customer services and for information about how to

apply for permission to reuse the copyright material in this book please see our website at

www.wiley.com.

The right of the author to be identified as the author of this work has been asserted in accordance

with the Copyright, Designs and Patents Act 1988.

All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or

transmitted, in any form or by any means, electronic, mechanical, photocopying, recording or

otherwise, except as permitted by the UK Copyright, Designs and Patents Act 1988, without the

prior permission of the publisher.

Wiley publishes in a variety of print and electronic formats and by print-on-demand. Some

material included with standard print versions of this book may not be included in e-books or in

print-on-demand. If this book refers to media such as a CD or DVD that is not included in the

version you purchased, you may download this material at http://booksupport.wiley.com. For

more information about Wiley products, visit us at www.wiley.com.

Designations used by companies to distinguish their products are often claimed as trademarks.

All brand names and product names used in this book are trade names, service marks, trademarks

or registered trademarks of their respective owners. The publisher is not associated with any

product or vendor mentioned in this book. This publication is designed to provide accurate and

authoritative information in regard to the subject matter covered. It is sold on the understanding

that the publisher is not engaged in rendering professional services. If professional advice or other

expert assistance is required, the services of a competent professional should be sought.

Library of Congress Cataloging-in-Publication Data

Carollo, Salvatore.

Understanding oil prices : a guide to what drives the price of oil in today’s markets / Salvatore

Carollo.

p. cm.—(The wiley finance series)

Includes bibliographical references and index.

ISBN 978-1-119-96272-4 (hardback)

1. Petroleum products—Prices. 2. Petroleum industry and trade—History. I. Title.

HD9560.4.C37 2012

338.23282—dc23

2011039266

A catalogue record for this book is available from the British Library.

ISBN 978-1-119-96272-4 (hardback) ISBN 978-1-119-96289-2 (ebk)

ISBN 978-1-119-96290-8 (ebk) ISBN 978-1-119-96291-5 (ebk)

Set in 11/13pt Times by Aptara Inc., New Delhi, India

Printed in Great Britain by TJ International Ltd, Padstow, Cornwall, UK

A Sofia e Riccardo

Parmi d’aver per lunghe esperienze osservato

tale essere la condizione umana

intorno alle cose intellettuali,

che quanto altri meno ne intende e ne sa,

tanto pi`

u risolutamente voglia discorrerne;

e che, all’incontro, la moltitudine delle cose conosciute ed intese

renda pi`

u lento e irresoluto al sentenziare circa qualche novit`

a.

It seems to me, after long experience

in observing the human condition

as regards intellectual matters,

that some persons, the less they understand and know,

all the more forcibly wish to hold forth;

and that, when we encounter something new,

the myriad things known and understood

make any judgement regarding it slower and less conclusive.

Galileo Galilei

Contents

Foreword xiii

Preface xv

Quick Reference Guide xix

List of Figures xxiii

List of Tables xxvii

List of Boxes xxix

1 The World Crude Oil Paradoxes 1

2 The Market Events from 2008 to 2011 7

World Energy Policy 8

The Financial Crisis and the Oil Market 10

Fundamentals or Financial Speculation? 17

Demand/Supply of Gasoline and Gasoil 21

WTI – Brent Differential 24

3 Evolution of the Price of Crude Oil from the 1960s

up to 1999 29

1960–1980: The Oil Monopoly and the Two Crises

in the 1970s 30

The 1980s: The Gradual Disappearance of OPEC 33

The Price War 35

x Contents

1985–2000: From the Introduction of Brent as an

International Benchmark to the Clean Air Act 37

The Suicide of OPEC 40

The Start of the Free Market 41

The Consequences of the Environmental Turnaround 44

4 Changes in the Market for Automotive Fuels 45

Evolution of Environmental Demand 45

Gasoline and its Components 50

Reforming 51

Cracking 52

Alkylation 53

Isomerization 53

Refiners Walk the Tightrope 53

The Fiscal Policy of the Industrialized Countries

Regarding Fuels 55

5 World Oil Flow 63

Transformations in the Downstream 66

World Supply Structure 70

6 The Classical Model of the International Oil Market 73

7 The Short-term Model of the International

Oil Market 81

8 The Brent Market 89

The Sale and Purchase Contract 90

The Forward Market for Brent (15 day Brent Contract) 94

The IPE Brent Market 100

The Divorce Between Oil Price and Oil 102

9 Principal Uses of the Forward and Futures Markets 105

Tax Spinning 105

Benchmarking 105

Hedging the Price Risks 106

Speculations on Operational Flexibilities at Loading 114

Market Structure: Contango and Backwardation 117

Procedures at the Loading Terminals 119

Contents xi

10 Problems of the Brent Forward Market 123

11 The European Refinery Crisis 131

12 Conclusions: We are Ourselves OPEC 155

Bibliography 163

Index 165

Foreword

This book was conceived after a critical re-reading of the lectures I gave

at the Eni Corporate University (ECU) for the Master MEDEA and for

the Annual Seminar on oil marketing.

It is therefore the result not only of my elaborations and market models

developed over the years to interpret the international oil market, but

also of the discussions in the lecture hall with the students of the Master

MEDEA and with the representatives of those producing countries who

have taken part in the various editions of the Annual Seminar.

My thanks are due above all to these persons.

I also wish to thank Prof. Enzo Di Giulio, president of ECU, who

desired to be present in these lectures and encouraged me to put the

content of my presentations in book form.

Finally, I owe particular thanks to Dr Caterina Marmorato who, apart

from helping me with notable professional commitment in the delivery

of the lectures for the Master course, dedicated a good part of her free

time for several months in preparing the technical annexes and in the

task of editing.

Preface

The title of the book you are holding – Understanding Oil Prices: A

Guide to What Drives Oil Prices in Today’s Markets – brings to mind

the telling of a story. Now, we know that for a story to be a good story

it should meet three conditions: a) there are certain events to relate;

b) these events run in order, that is, their sequence has some sense and,

if possible, succeeds in holding the attention of the reader; c) there

is a voice that narrates the story effectively and clearly. We feel that

Salvatore Carollo’s book satisfies all three of these conditions, and it

tells a story of great interest to all of us.

The world of oil seems to be cloaked by a form of disparity in

comprehension. Without oil, our entire existence – as we know it today –

would not be possible. Despite the countless discussions regarding the

oil peak and the end of the oil era, this fuel still represents, by far, the

primary energy source. According to the last World Energy Outlook

of the IEA, the proportion of oil as a source of energy stands at 34%

against the 26% of coal and 21% of gas. According to the IMF’s World

Economic Outlook (WEO) reference scenario, in 2030 it will still be

the primary source: 30% as against the 29% of coal and 22% of gas.

Oil has, and continues to have, a profound influence on the lives of

westerners and perhaps even more so on that of the peoples of the east.

Certainly, it is a non-renewable source and this means that its days, in

the long term, are numbered. But that is not the point here: the heart of

the matter is that we are dealing with a material that shapes, changes,

models, directs and configures the history of the world. And this is

destined to carry on for a long time – true even when the lusty flames

of oil, ephemeral like all the things in this world, fade away in the great

emptiness of time. Just as the Hellenistic or Roman worlds still influence

xvi Preface

our lives despite their decline – consider for a moment our language –

in the same way, oil has given the world a development and geopolitical

model, which is destined to last for the coming centuries. But this is

the future. Today, rather, we are in the midst of the oil era. And yet,

as we said earlier, there is a depressingly inadequate awareness of the

significance of this essential source. This very book has come to your

hands, reader, thanks to oil. Here we are not talking about a technical

knowledge of the complex work of exploration, or oilfield production,

or of the transport of crude oil across the oceans of the globe. Rather,

we refer to those three words that millions, if not billions, of times

stand out in the media: the ‘price of oil’. This expression, the content

of which has such a powerful influence on our lives, is the synthesis of

immense forces – costs, decisions regarding investments and expenses,

use of reserves, operations to cover risks, speculations, transactions, the

policies of contracting companies, the policies of nations, oil companies

and so on – that interact to form it. At the same time, from the price

itself stem innumerable chains of actions that influence variables of

fundamental importance for the entire economy: the quotations of the

dollar and the euro, the balance of payments, the price of gasoline and

gasoil, the cost of electricity, the rate of inflation, employment and so on.

Thus, the price of oil has a vast and forceful impact on our existence.

And despite all this, the issue is not adequately discussed. Rather, it

is mentioned, hinted at and at times journalists try to explain it; but

beyond the inner circle of specialists no one talks much about it. And

this circle, to tell the truth, is very restricted. This is a destiny that oil

shares, unfortunately, with all the sources of energy. Just reflect on the

scarce availability of courses in energy economics in universities across

the world. A similar reflection applies to books on energy economics

that are a rara avis on this planet, particularly if we compare them

with the plethora of texts on environmental economics. Paradoxically,

energy – which represents perhaps the central axle around which the

entire economy rotates – is almost never an issue to dissect in our degree

courses, in particular those regarding economics. Thus, tethered within

the strict boundaries of a territory for specialists, the price of oil remains

an abstruse, esoteric matter. When an attempt is made to pass from the

esoteric to the exoteric, it is often done in a misguided, amateurish way.

The media advances information that evokes horrific scenarios – until

last year some were predicting a price of around $200 per barrel – they

talk of an oil peak and the end of oil. Alternatively, OPEC is indicted as

Preface xvii

being responsible for the high prices, inflating its role disproportionately.

In this way, public opinion tends to form biased opinions based on

explanations that draw attention to just one main force, as the only one

responsible for what happens.

This book by Salvatore Carollo speaks of all this. It tells a story, as

we said, and it does so starting from the end, namely the crude oil price

collapse of last year from almost $150 to under $40 per barrel. Why did

this happen? To what extent can the fundamentals explain it? Starting

from these questions, the book offers an examination of the phenomenon

that takes us nimbly through the essential phases of the evolution of crude

oil price. The volume deals with relevant aspects – some quite technical –

such as purchase contracts, the structure of world supply, the evolution of

environmental regulations and, naturally, the refining process for crude

oil. But at its core remains the key question of the price and its formation.

The various issues discussed serve as fodder for the exploration of the

primary question, as if they were pieces of a jigsaw to be completed.

Certainly, as regards the role of the various forces that drive prices up

or down, the book offers a very clear explanation. In one sense, it tracks

down some of those guilty. We will not reveal them here, so as not to

deprive the readers of the pleasure of discovering them in due course.

We will only declare that the text materializes from the vast experiences

of the author. As we read, we hear the voice of a professional, namely a

man who works in the oil arena and whose main task is, for his part, to

contribute towards the formation of prices, and not explain them. And

yet, the author belongs to that class of professionals that master, thanks

to their deliberation, whatever they do, in this way succeeding to unify

thought with action. Unfortunately, their class is very rare: it is hard to

say whether it is more or less rare than that of the academic who follows

the inverse route, passing from theory to practice. What is certain is

that the marriage of practice and reflection has produced a stimulating

and enjoyable book. Some readers will appreciate its structure, which

alternates the narration with the technical aspects, others the voice, still

others will find it an interesting and nimble introduction to the world

of oil, and others, finally, may see it as a sort of text book. Some will

agree with its propositions, others not: we can be certain of that. But the

function of a book is precisely this: to stimulate reflection and nurture

knowledge with thought. To quote the celebrated words of a troubled

writer of the 1900s, Franz Kafka – as troubled as the oil market! – ‘a

book must be a pickaxe for the frozen sea that resides within us’. And the

xviii Preface

frozen sea is not only the existential and interior one as navigated by the

writer from Prague. Often, the ice on the sea is created by prejudices, the

knowledge fossilized inside us and never seen again, by the ready-made

explanations, by their nebulosity which is never questioned. This book

has the honour and duty to be a robust pickaxe.

Enzo Di Giulio

President, Scuola Enrico Mattei

Quick Reference Guide

To assist the reader a glossary of the technical terms that have been only

briefly considered in the text has been added. Other terms have been

described in some detail in the pertinent chapters.

rASSESSMENT: this term is used in the text to mean estimate and/or

valuation.

rAUTHOR’S SOURCE: when this reference is indicated, the source

of data and graphs should be intended as a personal elaboration of

data available in the market and from public sources.

rBENCHMARK: in the crude oil sector, a benchmark provides a

reference parameter based on which other crudes are evaluated or

priced. Some benchmarks are localized in specific geographic areas

(e.g. Dubai in the Middle East or Tapis in the Asia-Pacific area) while

others have global application, e.g. Brent Dated.

rBLENDING of GASOLINES: final operations in a refinery for mix-

ing semi-finished products arriving from various plants. Actually, with

very few exceptions, for technical/economic reasons, gasoline as a fin-

ished product is not directly obtained in a refinery from one sole plant,

but usually through mixing various components.

rDOWNSTREAM/UPSTREAM: downstream is the part of the oil

cycle that embraces transport, refining and marketing. The preceding

operations, i.e. exploration and production of crude, represent the

upstream.

rDRIVING SEASON: this term indicates the season for gasoline in

America. Normally this phase starts in late May and continues for the

entire summer season; in other words, as a result of summer travel, it

is the period of greatest gasoline consumption in the USA.

xx Quick Reference Guide

rICE: acronym for the Intercontinental Exchange, previously known

as the International Petroleum Exchange (IPE), one of the major

exchange markets for physical products and their derivates. The con-

tracts dealt with on ICE include the following products: exchange

rates, stocks and shares, crude and refined products, natural gas, cof-

fee, cotton, sugar and so on. When reference is made to ICE futures,

this signifies the futures contract for ICE Brent, dealt with in Europe

on the London Exchange.

rIEA: Acronym for the International Energy Agency, an international

organization founded by the Organization for Economic Cooperation

and Development (OECD) with headquarters in Paris.

rJET-FUEL or JET-KERO: aviation fuel.

rJOINT VENTURE: a contract between organizations for the imple-

mentation of a project that involves notable technical and financial

risks. The obligations and responsibilities of each partner are shared

proportionately on the basis of each partner’s participation quota in

the project. Joint ventures between oil companies occur frequently

in the exploration and exploitation of oilfields (in particular offshore

ones).

rOCTANE NUMBER: the index of resistance to detonation of a fuel.

If the octane number is too low the speed of combustion of the gasoline

is too high and this causes shock waves in the combustion chamber

of the engine (‘pinking’) and dispersion of energy.

rNYMEX: acronym for the New York Mercantile Exchange, one of

the biggest commodity markets. Founded in 1872 for trading eggs,

butter and cheese, it is now the reference bourse for oil. When the text

refers to NYMEX futures this means the WTI futures contract.

rOPEC: acronym for the Organization of the Petroleum Exporting

Countries.

rOPEN INTEREST/OPEN POSITIONS: in the futures market, this

indicates the aggregate of the purchase and sale operations that have

not been closed by operations in the opposite side.

rTERMINAL OPERATOR: the body that manages and administers

a production terminal for crude oil (loading tankers, administration of

production data, allocation of barrels). Normally this body coincides

with the partner that has a majority shareholding in the project.

rOSP: Acronym for Official Selling Price. This provides one of the

many ways for determining crude prices. The OSPs are normally fixed

unilaterally and published by the producing countries.

Quick Reference Guide xxi

rSPARE CAPACITY: in general, this refers to the unused capacity

of a refinery (namely the capacity to produce greater quantities of

refined products as compared with those already in production), or

the unused production capacity of an oilfield (namely the capacity to

produce greater quantities of crude oil as compared with those already

in production).

rSWING PRODUCER: a producing country or association of such

countries likely to adjust its offer of crude to the demand so as to

control price movements.

rARMS-LENGTH TRANSACTIONS: those between related par-

ties but whose contractual terms reflect market conditions between

independent and unrelated parties.

rWTI: acronym for West Texas Intermediate, also called Texas Light

Sweet. This crude is used as a benchmark throughout America. The

WTI derived contract is traded on the NYMEX.

List of Figures

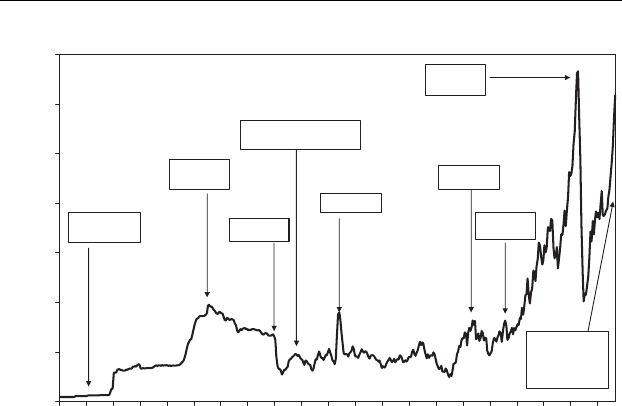

Figure 1.1 Brent Dated 1970–2010 and main historical events 2

Figure 1.2 OPEC production versus Brent 4

Figure 1.3 Complexity and interdependence in the oil market 4

Figure 1.4 World oil demand (average in 2005–2010),

million barrels per day 6

Figure 2.1 World oil demand versus supply 8

Figure 2.2 NYMEX WTI crude oil futures open interest:

non-commercial versus total traders 14

Figure 2.3 Comparison between volumes of NYMEX and

Brent traded in the futures and physical markets 15

Figure 2.4 Futures: daily trades in 2008–2010 18

Figure 2.5 Provisional and final assessments of stock

changes versus Brent prices 21

Figure 2.6 Price movements during the winter months 25

Figure 2.7 WTI NYMEX–ICE Brent differential 26

Figure 2.8 Brent and inter-monthly volatility (1988–2011) 27

Figure 3.1 Crude oil prices (1970–2011) 30

Figure 3.2 The price of crude with reference to the

benchmark 31

Figure 4.1 USA crude demand by sector (2009) 46

Figure 4.2 Evolution of gasoil specifications 47

Figure 4.3 Evolution of oil demand in the USA, Europe and

Asia-Pacific (1985–2020) 49

Figure 4.4 Per capita oil demand in the USA, Europe and

Asia-Pacific (1985–2010) 49

Figure 4.5 Gasoline and refining plants 51

xxiv List of Figures

Figure 4.6 USA imports: gasoline versus blending

components 54

Figure 4.7 Simplified refinery scheme 56

Figure 4.8 Gasoline prices in the world 60

Figure 4.9 Price (excluding taxes) of gasoline in Europe

and the USA 60

Figure 4.10 Tax burden on diesel fuel in 2010 (Europe

and the USA) 61

Figure 5.1 World oil flow 64

Figure 5.2 Number of refineries versus average refining

capacity 68

Figure 5.3 Refining capacity versus rate of

utilization (USA) 69

Figure 5.4 Destinations guaranteed and destinations

dependent on the price 71

Figure 5.5 Destination of crude (%) 71

Figure 6.1 Variation of stocks versus variation in the

Brent price 75

Figure 6.2 The classical model of demand/supply 76

Figure 6.3 The modern supply/demand model 77

Figure 6.4 The vicious circle in the classical

demand/supply model 78

Figure 6.5 Adjustments to the estimate of the yearly

imbalance between demand and supply 79

Figure 7.1 The classical industrial model 82

Figure 7.2 Refining cycle for a heavy crude to produce

1 tonne of gasoline 84

Figure 7.3 The modern oil industrial cycle 85

Figure 7.4 Relative prices of gasoline, gasoil, jet fuel

and fuel oil 86

Figure 7.5 Relative prices of products in 2008 86

Figure 9.1 Example of price-lock hedging 107

Figure 9.2 Example of integrated price-lock hedging 112

Figure 9.3 Example of operational flexibility effects 115

Figure 10.1 Distorted Brent Dated quotations 125

Figure 10.2 Movement of the benchmark before and after

July 2002 127

Figure 10.3 Relationship between demand and supply of

regional crudes 129

List of Figures xxv

Figure 11.1 USA: number of refineries versus average

refining capacity 133

Figure 11.2 Europe: number of refineries versus distillation

and conversion refining capacity 133

Figure 11.3 NWE and MED refinery margins:

cracking plants 134

Figure 11.4 EUROPE: surplus/deficit in capacity, refining

margins and demand 136

Figure 11.5 EUROPE and USA: surplus/deficit in capacity,

refining capacity and demand 137

Figure 11.6 US import: gasoline and blending components

from Europe 138

Figure 11.7 Alkylate premium to gasoline 139

Figure 11.8 Brent and products prices 2004 143

Figure 11.9 Brent and products prices 2010 144

Figure 11.10 Brent and products prices 2004 (base:

1 January =100) 145

Figure 11.11 Brent and products prices 2010 (base:

1 January =100) 145

Figure 11.12 Gasoline/Brent prices ratio 146

Figure 11.13 Gas oil/Brent prices ratio 147

Figure 11.14 Comparison between a financial refinery and a

real refinery (MED, January 2011) 148

Figure 11.15 NWE: refinery margins (cracking plant)

versus crack spread (seasonal 3–2–1) 149

Figure 11.16 MED: refinery margins (cracking plant)

versus crack spread 149

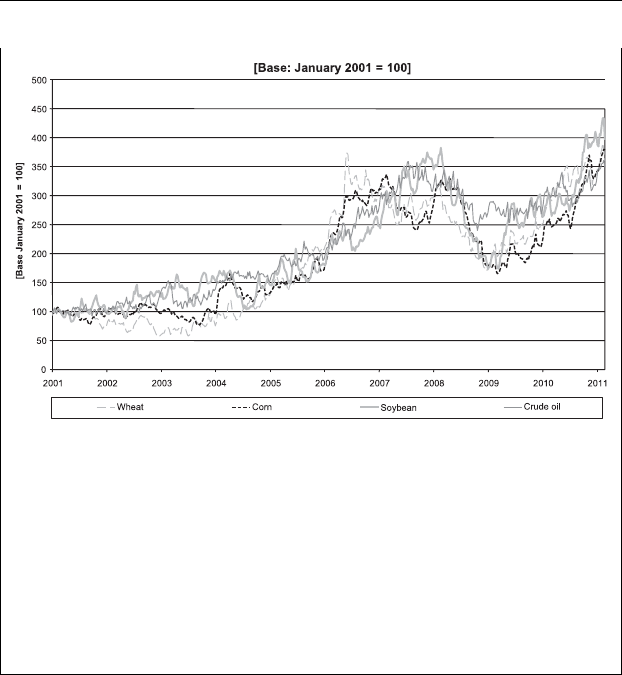

Figure 11.17 Agricultural and oil demand and prices 150

Figure 11.18 GDP per capita and open interest 151

Figure 11.19 Agricultural and oil futures open interest

on NYMEX 153

List of Tables

Table 2.1 Comparative analysis of the value of NYMEX and

Brent in the financial and physical markets 16

Table 2.2 Total production costs by region 19

Table 2.3 Demand of oil products in OECD Europe and

in the USA 22

Table 4.1 Evolution of gasoline specifications 46

Table 4.2 Evolution of gasoil specifications 47

Table 4.3 World crude oil demand 47

Table 4.4 Gasoline in Europe and the USA: list price and price

at the pump 58

Table 4.5 Price of gasoline and diesel fuel in some

European countries 59

Table 5.1 Italian refineries 67

Table 6.1 Global oil demand and supply 74

Table 9.1 Correlation index between Brent and other

international crudes 106

Table 11.1 EUROPE: surplus/deficit in capacity, refining

margins and demand 135

Table 11.2 USA: surplus/deficit in capacity, refining

margins and demand 137

List of Boxes

Box 2.1 Cost of the Marginal Barrel 18

Box 2.2 Jet Fuel and Gasoil Market 24

Box 3.1 The Netback Value System 36

Box 6.1 Variations in Estimated IEA Stocks 79

Box 8.1 The Principal Clauses in a Sale and

Purchase Contract 90

Box 8.2 The Daisy Chain 95

Box 8.3 15 day Brent Contract 96

Box 8.4 The Price Risk in the 15 day Brent Contract 98

Box 9.1 First Example of Hedging 107

Box 9.2 Second Example of Hedging 110

Box 9.3 Example of Synergies Between Operational

Flexibilities and Hedging 114

Box 9.4 Floating Storages 117

Box 10.1 Market Squeeze 124

Box 10.2 Assessment of Brent Dated (Platts’ Methodology) 128

Box 11.1 Trends in Agricultural Products and Oil Prices 150

1

The World Crude Oil Paradoxes

For some years now, the price of oil has been out of control. None of the

great names of the industry, the production cycle or the oil market is able

to intervene to decide its level or guide its progress. The oil companies,

the OPEC producing countries as well as the non-OPEC, the consuming

countries, the consumers: not one of these has this capability.

The price of oil, in the imagination of western consumers, is still

linked to the equilibrium developed during the 1970s and 1980s, with

the emerging of the Persian Gulf countries and the OPEC nations.

It is still a popular belief that the cartel of the largest oil producing

countries in the world is capable of regulating the volume of production

and using this key raw material to achieve political aims.

Even today, when the price of oil rises beyond any level considered

critical, the vast majority of the oil market analysts turn their eyes

towards Vienna, where the oil ministers of the OPEC countries meet,

imagining, hoping for and analysing decisions which either will not be

taken or, if taken, will turn out to be completely ineffective. Lately, in

some market reports, more sophisticated analyses are merely focused

on the availability of OPEC countries’ spare capacity; linking to this

factor the dynamics of the oil price. When we look at the graph of the

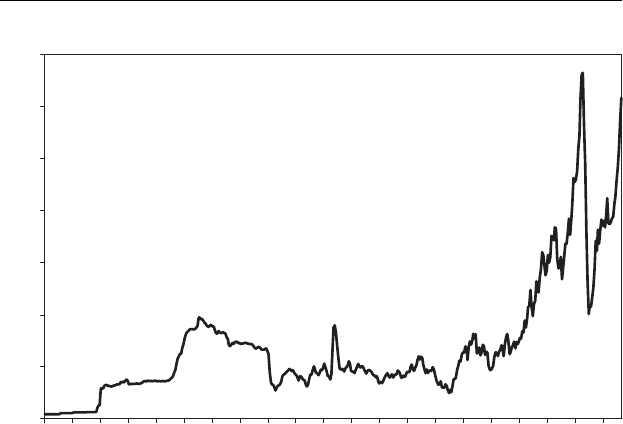

price of crude oil in Figure 1.1 we do not see the result of market forces,

but rather a design traced by the hand of a powerful invisible architect

who, following his own purposes, has established a course along which

the price of oil should travel.

Since the end of 1998 analysts, oil companies and producing countries

have mistaken every forecast of the price of oil, clearly showing not only

that they no longer control the fundamental market mechanisms, but that

they are not even able to comprehend its real dynamics – it is as if the

invisible architect had lost his pencil.

If we take our memory back to December 1998, when the price of

crude oil fell to $9 per barrel, all the respected names of the oil industry,

bar none, forecast that the price would stay for at least one or two decades

under $15 per barrel. It is enough to glance at the investment budgets

of all the oil companies or the financial programmes of the producing

Understanding Oil Prices: A Guide to What Drives the

Price of Oil in Today’s Markets

by Salvatore Carollo

Copyright © 2012, Salvatore Carollo

2 Understanding Oil Prices

0

20

40

60

80

100

120

140

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

$/bbl

Yom Kippur

War

Iraq/Iran

War

Gulf War

Iraq War

Price War

Financial

Crisis

Clean Air

Act

Brent as International

Benchmark

2011 Unrest in

Middle East and

Earthquake in

Japan

Figure 1.1 Brent Dated 1970–2010 and main historical events

countries to confirm that only the most optimistic among them estimated

maximum price levels between $14 and $15 per barrel in the long run.

Some oil companies, based on this view, hedged their production at

this level of prices and went bankrupt. Yet only a few months later,

in the summer of 2000, the price had already reached $35 per barrel,

taking everyone – market analysts, oil companies, producing countries,

economists, politicians and consumers – by surprise. Rivers of ink were

consumed to explain the nature of this event through analysis where the

causes were sought in transient factors; a sudden storm, nervousness

between two OPEC countries, political uncertainties and so on.

The years of the energy crises were far away and deeply buried in

the collective subconscious. The reappearance of such a thorny question

was regarded, before it raised any anxiety, as almost a nuisance. Still

today, after a decade of price hikes for crude from $9 to more than $140

and then down to $37 and once again above $120 per barrel, most people

limit themselves to reciting a series of clich´

es to try to find justifications

for an incomprehensible phenomenon:

rLimited supply from the producing countries, apparently inadequate

to satisfy the growing demand for oil.

rUnexpected growth in the demand for oil by China and India, appar-

ently upsetting the stability of the oil market.

The World Crude Oil Paradoxes 3

rTensions in the Middle East.

rThe prospect of a decrease in the crude reserves/crude production

ratio and therefore the availability of spare capacity.

rThe excessive taxes on petroleum products (gasoline, diesel, LPG

etc.) imposed by European governments.

This type of analysis has the advantage of being simple and easily

presentable to the public at large, without, however, explaining what

has really happened or is happening. Nevertheless, this approach has

enabled some commentators to exaggerate on the contentious issues

regarding the excessive power of the OPEC countries and the ways to

bring them to reason.

The problem which all serious analysts have to face up to is actually

quite simple. The essence is to explain oil price movements by use of

the classic model of economics, which assumes that price is a function

of the relationship between demand and supply:

Price =f (demand, supply)

This principle of economics seems too valid to allow any space

for querying it. Notwithstanding this, the fundamental classic method

applied tout-court to the oil market does not work. Yes, it is correct to

say that the price is linked to the supply and demand balance, but of

which good? We need to find out the merchandise or commodity whose

supply and demand is determining the dynamics of oil price. For sure,

it is not the physical crude oil.

OPEC has programmed and put into effect increases or cuts in pro-

duction on numerous occasions, but always with scarce results. To every

public announcement of increased production by the OPEC countries,

the markets have responded with an increase in the crude oil price by at

least a couple of dollars per barrel – and vice versa, when they announced

cuts (Figure 1.2).

It is therefore reasonable to question whether the economic model

utilized really works or if it is applied in an incorrect way to the oil

market. Or, rather, that the technological complexity of this market does

not allow it to be modelled on the simple relationship between demand

and supply at a global level. The internal dynamics of this particular

market require a much more detailed and complex model, capable of

describing some of the fundamental dynamics of the system.

Unfortunately, the majority of analysts in this field have exclusively

economic backgrounds and tend to apply general or econometric mod-

els to the crude oil, which are suitable for other commodities (coffee,

4 Understanding Oil Prices

25

26

27

28

29

30

31

32

33

34

Jan-05

May-05

Sep-05

Jan-06

May-06

Sep-06

Jan-07

May-07

Sep-07

Jan-08

May-08

Sep-08

Jan-09

May-09

Sep-09

Jan-10

May-10

Sep-10

million bbl/day

30

50

70

90

110

130

$/bbl

Total OPEC production

Brent Quotation

Figure 1.2 OPEC production versus Brent

Source: International Energy Agency

copper, gold etc.), where the production and technological transforma-

tion processes are less complex.

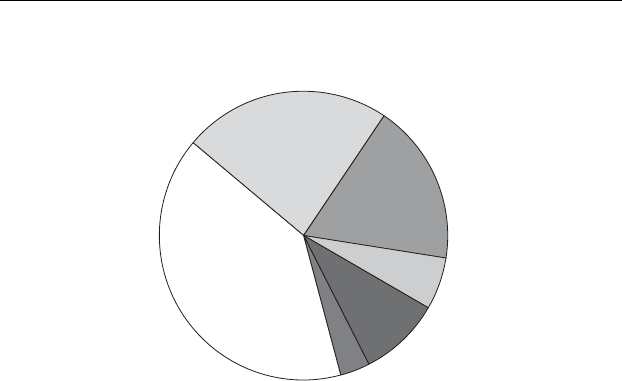

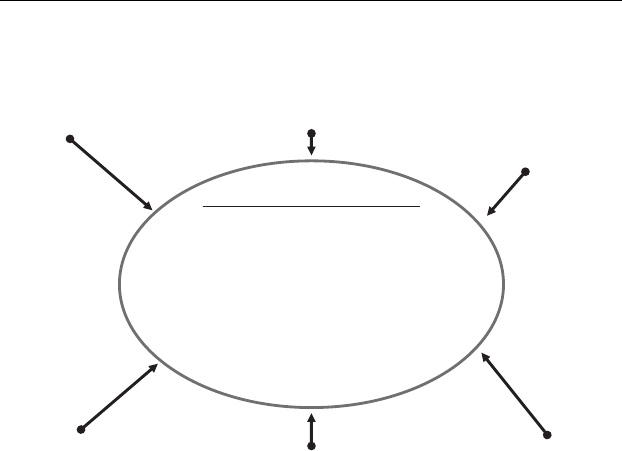

One starting point should be the recognition that what is commonly

called the oil market is actually the conjunction and interaction of

different markets which operate separately and independently but

which are linked by certain complex forms of correlation and dynamics

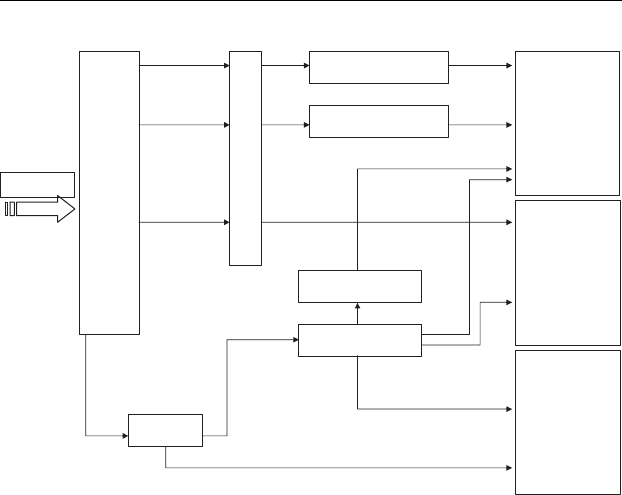

(Figure 1.3).

Producing Countries

and Oil Companies

Crude Oil

Market

Financial

Institutions

Trading

Companies

Refineries Final Product

Market

Consumers

ICE/NYMEX

Brent/WTI

Financial

Market

Physical

Market

Figure 1.3 Complexity and interdependence in the oil market

The World Crude Oil Paradoxes 5

We refer now to the crude oil market (raw material), to the finished

products market (gasoline, diesel, jet fuel, fuel oil, chemical feedstocks,

lubricants) and to the financial market for crude and finished products

(futures). We should always remember that in our cars and in airplanes

we do not use crude oil, but finished products, which are increasingly

difficult to produce. We cannot also neglect the dramatic developments

of the futures market and its predominant role in the world economy.

Each and all these markets respond to different behavioural patterns

and they are operated by bodies with differing interests, culture and

business objectives. A model that does not take into account the inter-

relations between these markets and their individual dynamics is inca-

pable of describing what happens to oil prices.

When the analyst is confronted by the unequivocal event of a price

variation, and having only the classic model of the global demand/

supply, he can only create a scenario of probable events (input to the

model), which, when processed, might generate the variation in price

which actually took place. If the price rises it is clear that there must have

been an increase in demand or a reduction in supply. Therefore, one looks

for all the clues which might prove that something like this has taken

place. In the absence of reliable and prompt information there is more

than enough space for these concoctions. It is thus very easy to reach

the mistaken conclusion that China and India (the distant enemy, the

invisible tartars) are becoming the critical factors for our planet. And that

certainly OPEC (the conflict of civilizations) is yet again, for political

and ideological reasons, not producing enough crude. Unquestionably

there is no need to verify the production data of Venezuela under Chavez,

or Iran under Ahmadinejad. It seems highly likely that both would wish

to create problems for the west by raising prices.

The economic and strategic importance of the themes related to the

price of crude oil would require a far more detailed technical analysis.

In this discussion we shall firstly try to examine the structural changes

in the oil industry in recent decades, to see what has changed to make

these dramatic and uncontrollable variations in price possible. And

above all we shall try to understand why, in the space of a few short

weeks (August–November 2008), without having seen even a small vari-

ation in the physical crude oil demand/supply situation the price tumbled

from $144 to $37 per barrel. Then, in a couple of months it climbed

back to $70–80 per barrel, exceeding again $120 per barrel in 2011.

These events have silenced many analysts, who have not been able to

provide consistent answers to the following questions. First of all, why

did the price drop in 2008? What happened in those few weeks? Did the

6 Understanding Oil Prices

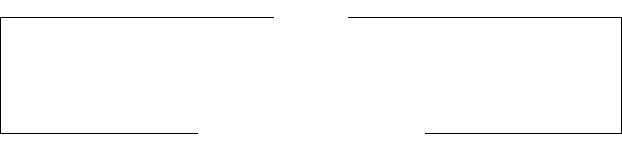

Others

34.4

India

3.0

China

7.8

Japan

5.0

Europe

15.5

USA 50

19.9

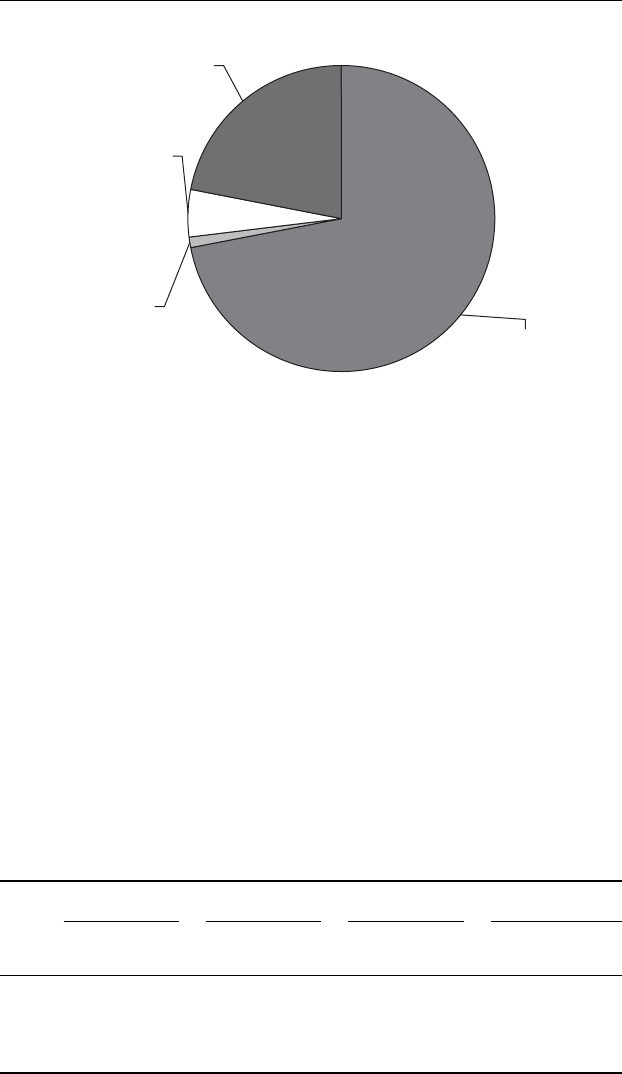

[million barrels per day]

Figure 1.4 World oil demand (average in 2005–2010), million barrels per day

Source: International Energy Agency

demands of China and India dry up or did the tensions in the Middle

East calm down? Was OPEC flooding the markets with crude?

The truth is that OPEC cut production, the data regarding world

demand for oil (see Figure 1.4) showed no reduction in global con-

sumption, and – in the previous weeks – the Middle East lived through

one of the most dramatic crises in recent history. In all this turmoil, the

oil price plunged by almost $110 per barrel.

What is the factor that then pushed the price up again above $120 per

barrel, during a worldwide dramatic economic crisis and stagnation of

oil consumption?

Is there an economic model that can explain these recent events? A

description will be attempted in the following pages.

2

The Market Events from

2008 to 2011

This conversation starts by taking a quick look at what happened in the

international oil market during 2008. Actually, 2008 was the year when

all the contradictions brewing in the previous decade surfaced. Events

as dramatic as the collapse of crude oil to under $40 per barrel after a

surge to more than $140 per barrel had never been seen before in the

history of the oil industry. Not even the impressive crises of 1973 and

1979 were able to cause price swings of this size and speed.

It has already been mentioned that in the last decade, despite the

available supply constantly exceeding the demand, we have witnessed

the continual growth of the crude price.

The upward trend in prices underwent a brisk acceleration in spring

2008 and went on to touch a peak of $144 per barrel in summer (see

Figure 2.1). After this we saw a spectacular nosedive of almost $110 per

barrel. Analysts, economists and commentators have tried in all possi-

ble ways to provide explanations (sometimes far-fetched) for this phe-

nomenon which apparently seemed unexplainable. In fact from the data

available to all, we can safely say that in the passage from the phase of

price increases to the phase of their fall, nothing changed in the physical

oil market. On the contrary, in that very moment there was a seasonal

increase in global demand of around 2 million barrels per day and a

reduction in crude production of about the same amount. These changes

should have worked in the opposite way, that is, an increasing price.

The classic explanations (India, China, Middle East, crude oil reserves

etc.) used by the analysts to explain the upward trend of the market

became obsolete instantaneously and proved insufficient to account for

the subsequent price tumble. The textbook explanations are unable to

pinpoint the real causes behind everything.

Only recently some financial analysts have tried to link the fall of

the price in November 2008 with the lack of financial capacity to open

letters of credit of some traders, when trading their cargoes of oil. It

is true that some banks had problems in issuing a letter of credit for

Understanding Oil Prices: A Guide to What Drives the

Price of Oil in Today’s Markets

by Salvatore Carollo

Copyright © 2012, Salvatore Carollo

8 Understanding Oil Prices

65

70

75

80

85

90

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

million bbl/day

WORLD OIL DEMAND

WORLD OIL SUPPLY

Figure 2.1 World oil demand versus supply

Source: International Energy Agency

some traders, but it was just a very marginal phenomenon relative only

to very few cargoes in the market. The oil kept moving from the loading

terminals to the end users, from the producers to the consumers. No

interruption or excess of supply occurred at all and, therefore, nothing

justified the fall of $110 per barrel.

It is not even comparable with the apparently similar events of 1986

and 1988 when the forward Brent market collapsed to $9 per barrel. At

that time the oversupply of OPEC crude oil was real and the level of

stocks evident.

WORLD ENERGY POLICY

It is important to clarify from the beginning that a short cut is not being

sought by using a simplistic model where the financial speculation

is soley responsible for all the chaos in the oil market. The financial

investments are likely just taking advantage of the existing paradoxes

and bottlenecks in the oil industry and in the energy policy worldwide.

The stability will eventually come only when and if these structural

problems are solved.

For the time being we are just observing further additional elements

of crisis arriving and making the scenario even worse. The North Africa

The Market Events from 2008 to 2011 9

crisis (Libya in particular) and the Fukushima nuclear accident are

referred to.

These two events will amplify the structural crisis of the oil market,

accelerating all the processes already in progress since the Chernobyl

accident.

We have already experienced in all the industrialized countries the

lack of an energy policy that is capable of harmonizing the growing

energy demand with the new respect for the environment. The develop-

ment of environmental regulations in the last two decades has created

burdensome (but unchallengeable) limits for the energy and oil com-

panies in particular, but has not driven the bodies concerned to make

the investments necessary to create ‘compliant’ energy and products.

The result of these divergent processes has been the net reduction of

availability of finished products marketable in the western industrial-

ized countries. There is now a shortage of clean gasoline and gasoil.

In total the shortfall in the USA amounts to about 50 million tonnes

per year of gasoline, and about 40 million tonnes per year of gasoil

in Europe. To bridge these gaps it is necessary to import from other

geographical areas, which obviously deprives local consumers of these

products or forces them to pay the higher prices that consumers in the

strong countries can pay to get their hands on the missing products. It is

a real competition where the winners are always the ones who can pay

more.

A glance at the newspapers is enough to discover the limitations

imposed on motorists in Middle Eastern countries (Iran, Egypt etc.) or

all of West Africa.

The deficit of these high-quality finished products has bolstered the

rise in crude oil prices, particularly the light varieties such as those from

the North Sea or North Africa. Somewhat similar to what would happen

if, for some strange reason, a rule were introduced to allow the sale of

only choice cuts of meat (fillet steak, entrecˆ

ote, silverside): the price of

these would rise but so would the price of the cow.

This potential shortage of finished products has spread the feeling

in the trading market that something is at risk and, on a daily basis,

somebody may not be able to get the product he or she is looking for.

The oil market has become nervous and very transient, with the same

level of volatility experienced during the Gulf wars (when the risk of a

shortage of supply was evident).

The recent dramatic events (Fukushima and Libya) will definitely

amplify the already existing concerns and tensions and will spread the

10 Understanding Oil Prices

sensitivity about the environmental issues worldwide and accelerate the

increase of the demand for clean products.

We cannot forget that the only decision taken at the global political

level in one of the G20 meetings, to reduce the impact on the economy

of the increasing price of oil, was to encourage the construction of new

nuclear plants for producing electricity. This decision was inadequate

already when it was taken (less than 10% of the oil is used to produce

electricity) but today, after Fukushima, it appears to be almost obsolete.

We can say without any doubt that there is a lack of energy policy

worldwide, but especially in the industrialized countries; only China

and India are building what they need, despite the apparent general

market indication.

The world oil market is already in the middle of these tensions, but we

have not yet seen the worst. The forthcoming summers will offer some

anticipation of the future developments we can expect in the near future,

with a shortage of supply of high-quality gasoline and clean gasoil and

a significant increase of the price differential between light and heavy

crude oils.

Later the combined impact of the reduction of the sweet light crude

oils (like the ones produced by Libya) and the shortage of clean products

will be examined with more technical detail and analysis. An under-

standing will be gained as to why Saudi Arabia was ready to increase

the production to compensate the reduction of supply from Libya, but,

after a couple of weeks had to stop producing additional barrels of oil.

The quality (more than the quantity) of the crude oils offered to the

market is today a crucial factor for meeting the demand of products

worldwide. With the existing quality of the raw materials, it takes new

technologies and massive investments in the refinery industry. We are

far away from implementing such solutions worldwide.

It is evident that the structural problems for the oil industry will remain

as they are in the next decade and they will keep providing grounds for

financial speculation and therefore for the increase of prices, as has

happened in the last ten years.

THE FINANCIAL CRISIS AND THE OIL MARKET

In December 1988, OPEC decided to adopt as reference for the price of

crude oil (rather than the value of the Arabian light, the Saudi crude of

light quality) the value of the Brent.

The Market Events from 2008 to 2011 11

At that time, everyone thought that this was the value of the crude

produced in the North Sea, the name of which was indeed Brent. No-one

realized that this was a misunderstanding, a case of a homonym. The

Brent in question was not a crude oil, but a financial commodity.

Let us imagine, for a moment and as a game, which OPEC had decided

to adopt, as a reference for fixing the price of oil, the value of a particular

type of cherry tomato, to which the creator and biggest producer gave

the name of ‘Brent’. The reason for the choice could have been the high

energy consumption needed to produce the new ‘Brent’ cherry tomato.

Once the decision was taken, it would become obvious that the price

of oil would depend, almost exclusively, on the supply and demand of

Brent tomatoes on the international market. A plentiful harvest would

equal low prices and a difficult year, high prices. Cherry tomatoes in

fashion means high prices; and so on.

No-one would dream of looking, to analyse the movements of the

price or to make predictions of the future, at the supply and demand of

the physical crude oil.

We have taken the above example as a joke, but one capable, although

with the differentiation needed and analyses concerned, of giving us a

description that is fairly close to reality. These dynamics of the oil market

are slowly beginning to become clear and understandable to the principal

subjects in the oil market, producing countries and oil companies.

What is in fact the Brent market, the true one that defines the price

of oil?

This is a huge game like the ‘Panini football stickers’, those carrying

the picture of football players. The stickers, once printed and sold, create

an exchange market between the children or fans that look for them, and

their value varies according to the demand. Those of the famous and

popular players will go for more than those of unknown or less well-

known players.

Let us imagine that one day, for some reason, the football teams of the

world, with the agreement of UEFA and FIFA, decide that the market

value of the various players is that of the respective stickers or that they

are indexed to that reference.

A double market would be created, that of the football market where

against real money a club recruits a player in flesh and blood, and the

other where everyone can buy or sell stickers without ever becoming

owners of a player. If the market of the stickers should develop massively,

thanks to the ease with which it is possible to buy and sell (online for

example), it could at a certain point become a form of investment in

12 Understanding Oil Prices

itself, with participants that have never been interested in football and

even less in stickers.

If an international bank, for various reasons, should invest significant

amounts of capital in the stickers of a particular player, this would cause

an increase in value, regardless of the performance of the player and the

policy of the club to which the player belongs.

We would say that the football market has slipped through the hands

of the operators of that sport and has become an instrument of financial

speculation with positive and negative effects also for the world of

football (profits or losses for the bodies that ‘own’ the players whose

stickers are the subject of speculation).

Something similar has taken place in the world of oil. In the eighties

a sticker market was created, that of the futures contracts, which is just

like plastic cards (or stickers) on which a barrel of crude is depicted.

Whoever buys these plastic cards buys the drawing of a barrel, but

does not have any possibility of exchanging a plastic card with a real

barrel. The market of the oil stickers is a market that is almost totally

independent from the real oil market, with bodies operating there and

dominating it (controlling it and manipulating it) that normally have no

relationship with or interest in the oil industry.

In December 1988, the OPEC countries decided that the price of

their crude oils would be fixed on the basis of the value of the ‘oil

stickers’. This was an almost unnoticed change of a geo-political nature

that transferred control and management of the international oil market

out of the hands of the OPEC countries into those of the City of London

and, slightly less so, Wall Street. This was the event that overturned

the balance of the power that had been established since the crisis

of 1973.

For years the constant expansion of this parallel market supported

the real market. The value of the ‘drawing of the barrel’ was almost

always higher than the one the physical market would have guaranteed,

bringing benefits to those who invest in this sector and to the various

producing countries. Yes, it is a crazy game, but with a useful purpose.

In the autumn of 2008, the bankruptcy of the principal banks, which

owned massive quantities of oil stickers, obliged them to sell the oil

stickers and therefore cause a slump in the value of such stickers and

hence in the price of oil, the reference value of which derives from these.

From that moment there began talks about the need to review the

mechanism used to set the price of oil, but quietly and without haste.

The Market Events from 2008 to 2011 13

During 2009, the oil price, thanks to the recovery of what we called

the sticker market (where the banks have placed a significant share of

the money received from the governments), started to increase again.

The attitude of the producing countries became: let us discuss,

examine and wait. Any action will eventually be taken if and when

the banks find more profitable ways to invest their money, not in the

Panini stickers anymore but maybe in the real economy. For now, we

carry on this way.

So we have to resign ourselves to seeing the price of oil go up and

down, avoiding having to pretend to be able to explain the correlations

between these fluctuations and the fundamentals of the oil industry or

the non-existing policies of OPEC.

For most of 2009 and 2010, we saw the price fluctuating, in the range

of $70–80 per barrel. Everybody started to announce the new kind

of ideal range of the price of oil, considered sacred by the main OPEC

official representatives. As usual the market, a few months later, deviated

from all these guidelines given by the gurus and by the authorities. We

can say, then, that since December 1988 the global reference for the

price of crude has lost its direct relationship with the physical market.

Initially, the oil futures market had in common with the oil market,

apart from the name Brent, the historic fact that it was born to support

the trading operations of the oil companies, as a financial instrument to

provide risk hedging against oscillations in crude oil prices.

At the start of the year 2000, the oil futures market detached itself

almost completely from its original nature, becoming a market purely

for financial purposes. International banks entered this business without

having any involment in the oil business, just as an opportunity to make

profit, but some oil companies and almost all the oil trading organizations

also started to consider the futures market as an independent business

beyond the hedging purposes. All those analysts who tried to explain

the movements of the crude oil price on the basis of the evolution of the

relationship between demand and supply of physical crude have failed,

simply because the link between the financial market and the crude oil

market has become increasing ephemeral or even non-existent.

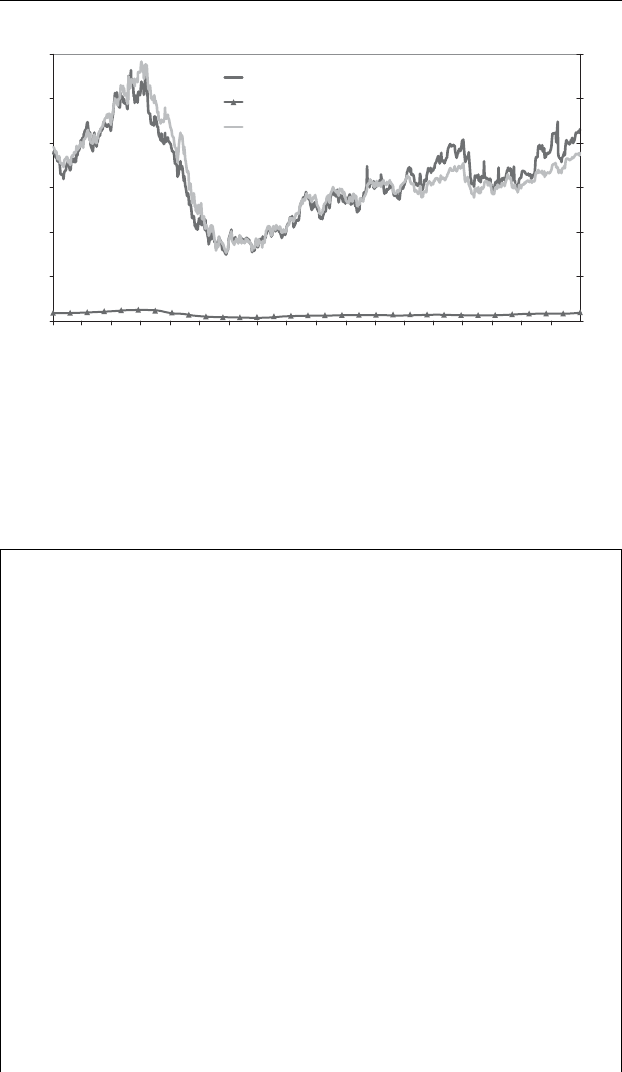

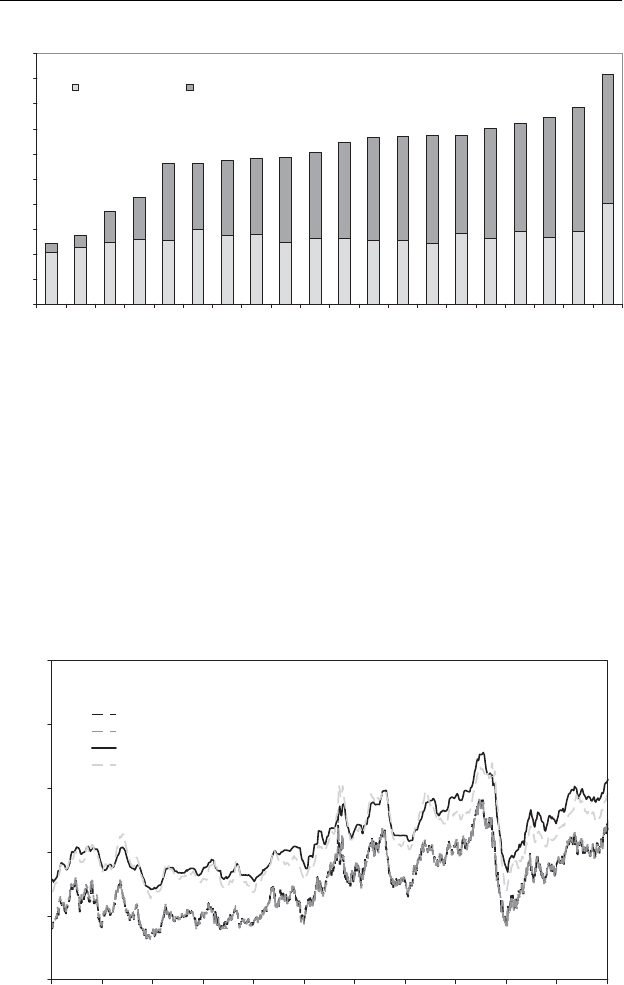

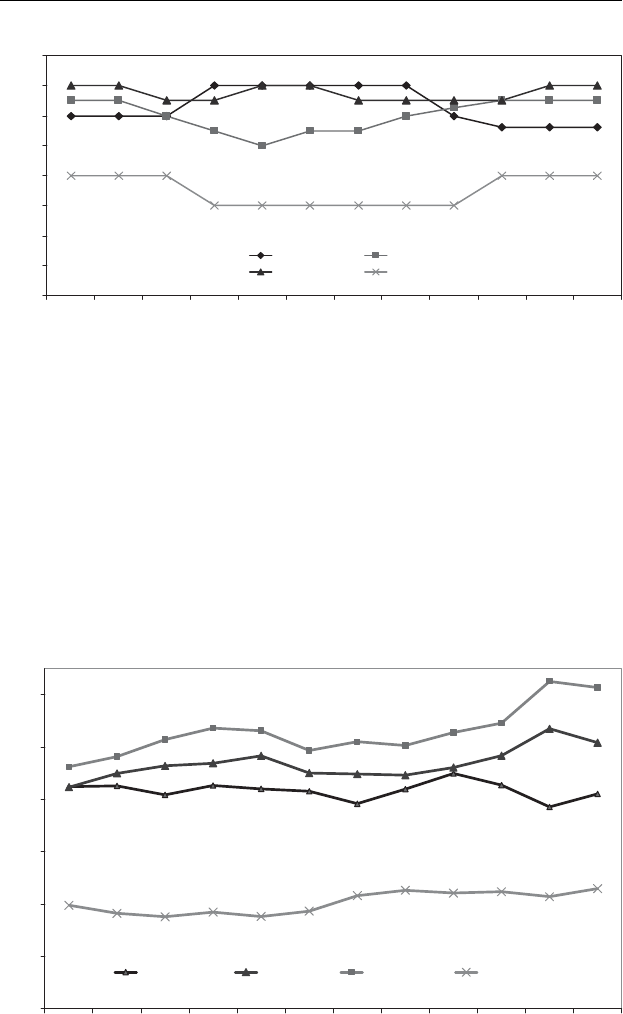

The graph in Figure 2.2 clearly shows how the volume of business on

the crude oil futures market has risen tenfold in the last 10 years, closely

following the entry of the great financial institutions in this field and the

change in the attitude of the traditional oil players. This has caused the

complete disruption of the internal dynamics of the oil market.

14 Understanding Oil Prices

0

200

400

600

800

1000

1200

1400

1600

1800

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

1000 contracts

NonReportables Average positions

Non-commercial Average positions

Commercial Average positions

Figure 2.2 NYMEX WTI crude oil futures open interest: non-commercial versus

total traders

Source: NYMEX

Brent (on paper, financial) is now traded on the market simply for

investment purposes or financial speculation, to protect capital by park-

ing it in a safe place for a certain period of time (even just for a few

minutes), to profit from a momentary wave of speculation, or to manip-

ulate a market which otherwise would be stable.

To understand better the size of the phenomenon, let us glance at the

numbers of this business (see Figure 2.3), which is almost unknown to

those who complain about the price of gasoline.

During 2008–2010, with world crude production around 86 million

barrels per day, only about 20 million barrels per day were marketed.

The remainder, about 65 million barrels per day, was not put on the

international markets because it was consumed directly by the produc-

ing countries.

If we refer to a valuation made in the period January 2008–December

2010, with an average price for Brent of $80 per barrel, we can easily cal-

culate that the value of the mass of money in movement due to purchases

and sales of physical crude as traded amounts to around $1,900 billion.

If we further assume that all the crude produced (86 million barrels per

day) was traded at market price, the mass of money in play, in the same

period from January 2008 to December 2010, would have been around

$7,600 billion. The balance between demand and supply of physical

crude at world level fluctuates within these values.

The Market Events from 2008 to 2011 15

0

5

10

15

20

25

Jan/08

Mar/08

May/08

Jul/08

Sep/08

Nov/08

Jan/09

Mar/09

May/09

Jul/09

Sep/09

Nov/09

Jan/10

Mar/10

May/10

Jul/10

Sep/10

Nov/10

Jan/11

Mar/11

billion barrels/month

0

20

40

60

80

100

120

140

160

$/bbl

ICE + NYMEX Volume of Transactions World Crude Oil Production

Physical Crude Oil Sales Brent ICE price [right axis]

Figure 2.3 Comparison between volumes of NYMEX and Brent traded in the futures

and physical markets

Sources: NYMEX and International Energy Agency

Now we can look at the volumes traded on the Exchange to dis-

cover that we have a totally different picture and with degrees of mag-

nitude enormously higher. During 2008–2010, about $51,000 billion

were traded on the futures market, that is to say, 27 times more than the

value traded on the physical market and about six to seven times more

than the entire world production of crude.

Table 2.1 shows a situation with daily trades of about $46 billion

(about $4 billion per working hour), just as if on the crude market about

580 million barrels per day were traded on the crude market and not the

20 million actually commercialized or the 86 produced. What are these

580 million barrels per day on paper, which have nothing to do with the

oil market and the demand and supply of oil for energy consumption,

and what influence do they have on the pricing system for petroleum

products? What effect do they have on the price of gasoline for the

poor motorist?

In theory the futures market for Brent was created to stabilize crude

prices after the epic oil crises of the 1970s and 1980s. The daily quotation

for Brent was supposed to permit greater transparency in the transactions

and thus a stabilization of prices in the short and medium term. In the

early years this was the case; the volumes of crude traded on the futures

16 Understanding Oil Prices

Table 2.1 Comparative analysis of the value of NYMEX and Brent in the financial

and physical markets

January 2008–December 2010

Production

of Physical

Crude Oil

Transactions

of Physical

Crude Oil

Transaction of

equivalent oil

in the financial

market

Ratio

Futures/

Physical

Ratio

Physical/

Futures

Volume

(billion barrels) 93.7 23.4 623.1 27 3.8%

Value (billion $) 7,594 1,899 50,806 27 3.7%

Sources: NYMEX and International Energy Agency

market never exceeded the physical quantities produced and sold. This

can only mean that the oil companies operated on the paper market to

stabilize the price of their crudes with hedging operations. Today we

see 580 million barrels of oil equivalent arriving on the market – which

strangely enough we continue to call an oil market – and they are behind

the real dynamics that move the quotation for Brent, which is still called,

for no good reason, the price of crude oil.

Let us give an even more concrete example. At the end of June

2008 the price of Brent touched levels above $140 per barrel. Rivers

of ink flowed to try to explain the reasons behind this increase. There

was discussion of the threats from China and India, the fall in world

oil reserves, geopolitical scenarios, stock variances and so on. But a

simple, crude and dramatic truth was overlooked. The level of prices

above the $140 per barrel number, which in June was used to trade the

commodity called oil, does not derive from the market for this particular

commodity and is not the result of the demand and supply balance of this

merchandise. It has nothing to do with oil. Going back to our previous

example, the crisis was in the cherry tomato (called Brent) market, not

in the market of the crude oil (called also Brent).

Thus, to try to explain its dynamics using models related to the market

for consumption and production of energy will be an exercise carried

out in vain.

During the whole month of June, about 700 million barrels of crude

(the physical kind that dirties your hands if you touch it) were traded.

In the same month on the paper market for Brent up to 20,000 million

equivalent barrels were traded, in other words nearly 30 times more than

the physical market.

The Market Events from 2008 to 2011 17

In the course of 2008, just when the wind seemed to be blow-

ing the prices towards $144 per barrel, the long-awaited event took

place, namely the crash of the banks and the main international

financial institutions, which also burst the oil bubble. Following the

bankruptcy of some banks and the much-reduced liquidity of many

financial institutions, transactions in the Petroleum Exchange quickly

nosedived, at the same time bringing down the price of Brent to under

$40 per barrel.

In this context OPEC, aware of a dramatic curtailment in the revenues

of various member countries, tried to keep up appearances and show a

minimum level of action, announcing and trying to implement cuts in

production to bolster up the crude price which was in free-fall (from

the $144 per barrel of July to the $40 per barrel of December). Such

a collapse had never been seen in the history of the oil industry. As

usual, the result of the cuts announced was the continuation of the fall

in prices, confirming the completely insignificant influence of OPEC on

the dynamics of crude oil prices.

From the data we have seen, it follows that OPEC represents 30% of

a segment of 4% of the business that we call the oil market. This being

so, how can it have a significant influence on price trends?

The great financial crisis has, however, highlighted some important

novelties in the international oil market scenario. In the year 2008, we

saw the downturn in the financial activity on the futures market (see

Figure 2.4). Daily trades of oil contracts on the financial markets fell

from levels of almost $282 billion per day in June to around $75 billion

per day at year-end: a nosedive of almost 4 times.

Fundamentals or financial speculation?

During the second part of 2008 the exclusively financial activities of

the banks disappeared progressively from the crude oil futures market,

leaving mainly the oil companies and the physical market professionals

to operate for the sole purpose of covering the risk of price fluctuations:

in other words, we digressed back to a market structure closer to that

of the late 1990s. The players of the oil market, although for a very

limited period of time, were once again the physical producers, oil

producers and oil companies. The price of crude, although still linked to

the movements of the crude markets of London and New York, during

the last quarter of 2008 and the first one of 2009 seemed more closely

correlated to the balance of demand and supply in the physical market,

18 Understanding Oil Prices

0

50

100

150

200

250

300

Jan/08

Mar/08

May/08

Jul/08

Sep/08

Nov/08

Jan/09

Mar/09

May/09

Jul/09

Sep/09

Nov/09

Jan/10

Mar/10

May/10

Jul/10

Sep/10

Nov/10

BILLION $

0

25

50

75

100

125

150

$/bbl

ICE+NYMEX Open Interest [left axis]

Physical Oil Sales [left axis]

ICE Brent Price, 1st position, $/bbl [right axis]

Figure 2.4 Futures: daily trades in 2008–2010

Source: NYMEX

moving in the range of $40–50 per barrel, which, at that time, seemed

to represent a reasonable and long-lasting point of balance.

Box 2.1 Cost of the Marginal Barrel

The crisis of November 2008 confirmed an important indication about

what price level crude oil would have reached if driven exclusively by

physical balances in the demand and supply of gasoline and gasoil.

Everyone remembers that until the 1990s, whenever there was a crisis

of excess supply in the market, the crude price quickly fell below $10

per barrel. This price represented the production cost in the marginal

fields at that time, namely offshore wells in the North Sea or the

Texas Gulf.

Holding the price at those levels removed the production of part

of such crudes from the market and thus contributed to realigning

supply and demand, or at least it triggered actions on the international

market (or international political decisions), which created stability.

Today the marginal fields are the producing wells borderline from

the technological point of view, such as the tar sands of Canada or

Venezuela, or certain offshore fields in ultra deep waters.

Production costs in these fields are over $40 per barrel. This is,

therefore, the new lower limit to the crude price. Below this there

would be a drastic stoppage in the flow of energy to fundamental

The Market Events from 2008 to 2011 19

areas of the industrialized countries, with severe consequences for

the economy.

Table 2.2 Total production costs by region

2003–2005 2004–2006 Delta

Region $/boe $/boe %

USA

Onshore 14.00 19.46 39

Offshore 50.56 69.75 38

Total USA 16.70 23.16 39

Canada 23.84 26.59 12

Europe 16.43 29.79 81

Africa 22.26 32.13 44

Middle East 9.78 14.31 46

Others

Eastern Hemisphere 14.98 18.76 25

Western Hemisphere 31.06 47.63 53

Worldwide 17.45 24.29 39

Source: International Energy Agency

We therefore have always suggested abandoning scenarios which

contemplate further falls in price down to the levels of the past

and to be realistic with regard to the possibility of increases in the

near future.

During 2009, as it is well known, all the major international banks,

which were saved by the governments, re-started to invest the money

received again in the financial market and in particular in the oil

futures (back to the stickers market). The result has been the increase

of the price of oil during the period of lower consumption. Then, at

the end of 2010 the price of crude reached a level of $90 per barrel

with an average of $10 per barrel above the value of 2009, and in

2011 (the time of writing) is already above $120 per barrel. The

imaginary new equilibrium value, established in the range of $70–80

per barrel, does not exist anymore. It has just gone. This increase of

about $50 per barrel in two years, above the ideal range, was once

again beyond any expectations.

The recent events, after 2009, in the oil market have reopened the dis-

cussion about the real reason for the price uptrend. Many analysts have

concluded that the new trend is firmly supported by strong fundamentals

and the financial ‘investments’ are just following suit.

20 Understanding Oil Prices

Despite some positive signs in the evolution of the oil demand, we do

not think that what has happened in the last three years and the recent

increase of the oil price can be explained simply through the evolution

of the fundamentals.

The analysis of the dynamics of the market has currently become

complex and the distinction between the effects due to the pure financial

activity (speculation) or due to the fundamentals is not so clear.

First of all, we should try to take into account the deep change in the

organization and in the attitude of the financial institutions playing in

the oil futures market.

The financial institutions in the last few years have invested in hiring

experts and traders from the physical oil markets. They normally don’t

move a drop of oil, but they plan their financial operations following

closely the evolution of the fundamentals and every single rumour about

the life of the oil industry. They move their money based on these

elements of information. We have already seen the dimension of the

impact of the movement of this amount of money, which is so massive

to overcome the ‘natural’ dynamics of the physical market. There are

always overreactions due to the enormous flow of money and number of

transactions on the futures market. What in the past would have caused

a price fluctuation of a few cents per barrel, nowadays can produce a

price change of many dollars per barrel.

Sometimes the direction of the financial operations are in line with

the fundamentals, but there are moments where the money is moved to

or from the oil futures market because of the evolution of other com-

modities and with no relationship at all to the dynamics of the oil world.

It looks like the new alignments between finance and fundamentals

materialize in the mind of financial traders.

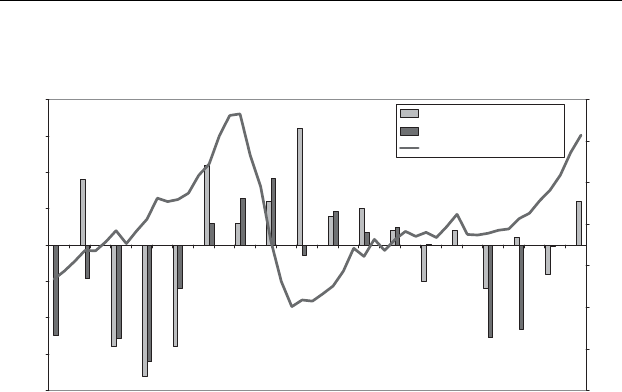

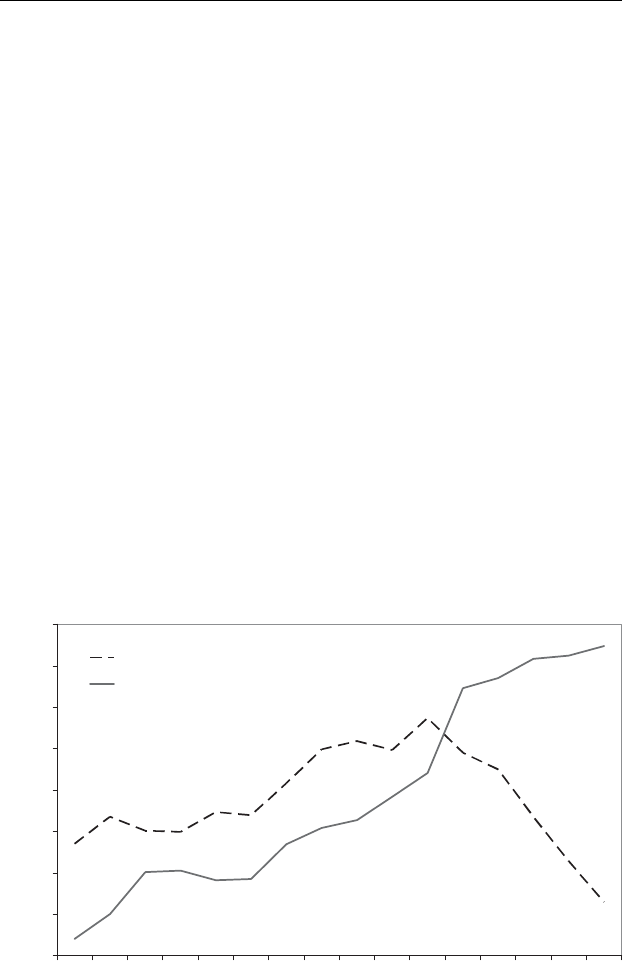

In Figure 2.5 we can see how fragile is the link between the funda-

mentals and the price of oil, taking also into account that the actual data

of the supply and demand become available (and reliable) with delays

of months, when the price is already history.

Of course, the financial analysts are very proud to affirm that all

the financial investments are made only on the basis of the oil market

fundamentals. And the investors seem to trust them.

It seems, however, evident that the real alignment between the funda-

mentals and the financial activity takes place in the minds of the financial

traders.

For this reason it is useful to have a look at the real physical market

since the financial crisis also became an economic crisis. Let’s have a

The Market Events from 2008 to 2011 21

Δ Stock Vs Brent

[provisional and final data]

-2000

-1500

-1000

-500

0

500

1000

1500

2000

Jan-07

Mar-07

May-07

Jul-07

Sep-07

Nov-07

Jan-08

Mar-08

May-08

Jul-08

Sep-08

Nov-08

Jan-09

Mar-09

May-09

Jul-09

Sep-09

Nov-09

Jan-10

Mar-10

May-10

Jul-10

Sep-10

Nov-10

Jan-11

Mar-11

Thousand bbl/day

0

20

40

60

80

100

120

140

$/bbl

Δ Stock (PROVISIONAL)

Δ Stock (FINAL)

Brent Dated

Figure 2.5 Provisional and final assessments of stock changes versus Brent prices

Source: International Energy Agency

look at some relevant phenomena which have affected the evolution of

the prices, and let’s try to understand better the role of the financial

speculation.

DEMAND/SUPPLY OF GASOLINE AND GASOIL

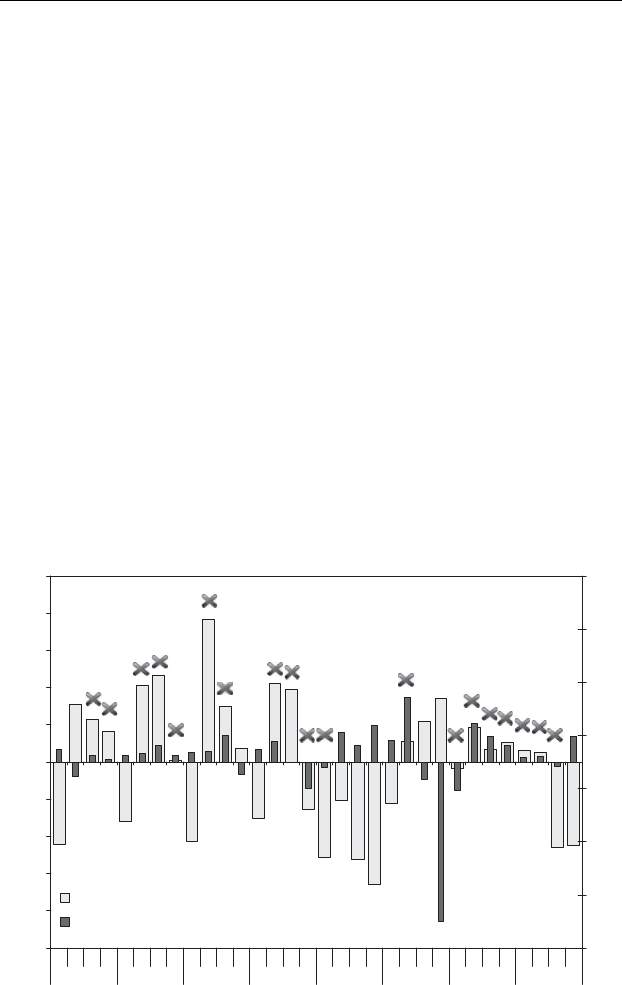

Looking at the actual data, in Table 2.3, about oil consumption in Europe

and the USA, it is evident that we are still facing a downward trend in

oil consumptions in the main western consuming countries, with some

substantial differences between Europe and the USA. During 2010 we

still had a declining trend in Europe, but a quite positive reaction in

the USA.

However, the main element of the analysis is not the direction of the

global consumption in these main market areas, but the evolution of

some critical products.

When the Brent price was at its peak, some signs of the economic

crisis started to show up and all the analysts were looking for a possible

fall in US gasoline demand, a fall considered responsible for triggering

a sort of domino effect inside the world oil market (crash in the demand

Table 2.3 Demand of oil products in OECD Europe and in the USA

OECD Europe [kbbl/day] 2007 2008 2009 2010 2011 2008–2007 2009–2008 2010–2009

LPG and Ethane 993 1,016 924 924 921 23 −92 0

Naphtha 1,283 1,157 1,108 1,208 1,220 −126 −49 100

Motor Gasoline 2,481 2,360 2,287 2,195 2,128 −121 −73 −92

Jet and Kerosene 1,303 1,323 1,267 1,270 1,297 20 −56 3

Gas/Diesel Oil 6,117 6,269 6,021 6,138 6,155 152 −248 117

Diesel 4,273 4,290 4,228 4,334 4,416 17 −62 106

Other Gasoils 1,844 1,979 1,793 1,804 1,739 135 −186 11

Residual Fuels 1,725 1,661 1,434 1,290 1,214 −64 −227 −144

Other Products 1,552 1,572 1,451 1,405 1,451 20 −121 −46

Total Products 15,453 15,357 14,493 14,431 14,387 −96 −864 −62

United States [kbbl/day] 2007 2008 2009 2010 2011 2008–2007 2009–2008 2010–2009

LPG and Ethane 2,091 1,959 2,056 2,113 2,104 −132 97 57

Naphtha 294 248 246 263 241 −46 −217

Motor Gasoline 9,355 9,047 9,055 9,129 9,169 −308 8 74

Jet and Kerosene 1,696 1,587 1,446 1,493 1,526 −109 −141 47

Gas/Diesel Oil 4,277 4,013 3,700 3,852 3,889 −264 −313 152

Diesel 3,520 3,484 3,221 3,345 3,401 −36 −263 124

Other Gasoils 757 529 478 507 489 −228 −51 29

Residual Fuels 818 702 591 642 610 −116 −111 51