(The Wiley Finance Series) Timothy Jury Cash Flow Analysis And Forecasting The Definitive Guide To

(The%20Wiley%20Finance%20Series)%20Timothy%20Jury-Cash%20Flow%20Analysis%20and%20Forecasting_%20The%20Definitive%20Guide%20to%20

User Manual:

Open the PDF directly: View PDF ![]() .

.

Page Count: 323 [warning: Documents this large are best viewed by clicking the View PDF Link!]

Cash Flow Analysis

and Forecasting

For other titles in the Wiley Finance series

please see www.wiley.com/finance

Cash Flow Analysis

and Forecasting

The Definitive Guide to Understanding

and Using Published Cash Flow Data

Timothy D.H. Jury

A John Wiley & Sons, Ltd., Publicatio

n

This edition first published 2012

© 2012 Timothy D.H. Jury

Registered Office

John Wiley & Sons Ltd, The Atrium, Southern Gate, Chichester, West Sussex, PO19 8SQ,

United Kingdom

For details of our global editorial offices, for customer services and for information about how to

apply for permission to reuse the copyright material in this book please see our website at

www.wiley.com.

The right of the author to be identified as the author of this work has been asserted in accordance with

the Copyright, Designs and Patents Act 1988.

All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or

transmitted, in any form or by any means, electronic, mechanical, photocopying, recording or

otherwise, except as permitted by the UK Copyright, Designs and Patents Act 1988, without the prior

permission of the publisher.

Wiley also publishes its books in a variety of electronic formats and by print-on-demand. Some

content that appears in standard print versions of this book may not be available in other formats. For

more information about Wiley products, visit us at www.wiley.com.

Designations used by companies to distinguish their products are often claimed as trademarks. All

brand names and product names used in this book are trade names, service marks, trademarks or

registered trademarks of their respective owners. The publisher is not associated with any product or

vendor mentioned in this book. This publication is designed to provide accurate and authoritative

information in regard to the subject matter covered. It is sold on the understanding that the publisher

is not engaged in rendering professional services. If professional advice or other expert assistance is

required, the services of a competent professional should be sought.

Library of Congress Cataloging-in-Publication Data:

ISBN 978-1-119-96265-6

A catalogue record for this book is available from the British Library.

Set in 10/12pt Times by Aptara Inc., New Delhi, India

Printed in Great Britain by TJ International Ltd, Padstow, Cornwall, UK

To my mother and father,

brother and sisters for always being there

Contents

Introduction ix

SECTION ONE HISTORIC CASH FLOW ANALYSIS

1 Understanding How Cash Flows in a Business 3

2 Understanding Cash Flows Properly 21

3 Start-up, Growth, Mature, Decline 47

4 Restating the Cash Flows of a Real Business 59

5 Restating US GAAP Cash Flows 83

6 Analysing the Cash Flows of Mature Businesses 99

7 Analysing the Cash Flows of Growth Businesses 135

8 Growth and Mature – Further Analysis Issues 153

9 Analysing the Cash Flows of Start-up Businesses 171

10 Analysing the Cash Flows of Decline Businesses 179

11 What to do about Bad Cash Flows 185

12 Cash Versus Profit as a Measure of Performance 191

viii Contents

13 Cash Flow Analysis and Credit Risk 201

14 Cash Flow Analysis and Performance Measurement 215

15 Analysing Direct Cash Flow Statements 223

16 Generating a Cash Flow Summary from Profit and Loss Account

and Balance Sheet Data 231

17 Summarising Historic Free Cash Flow 247

SECTION TWO FORECASTING CASH FLOWS

18 Introduction 255

19 Spreadsheet Risk 263

20 Good Practice Spreadsheet Development 275

21 The Use of Assumptions in Spreadsheet Models 295

Index 305

Introduction

This book is the definitive guide to cash flow analysis. It is designed to be the

definitive first reference on all aspects of historic cash flow analysis. It also provides

an incisive overview of the risks to be managed in preparing cash flow forecasts.

It has been written from a cash flow-centric point of view. Other financial and

analytical information is introduced whenever relevant to support the process of

cash flow analysis.

This book is designed for people trying to understand and analyse cash flows,

probably in a professional context. Whilst it contains some theoretical content, the

primary objective is to offer a practical handbook of cash flow analysis.

Ideally, it should first be read like a novel and then dipped into chapter-by-

chapter as required; a detailed guide to the contents of each chapter follows this

introduction. Much of the information in the book has been laid out to facilitate

direct reference from the index; also allowing it to be used as a pure reference text.

Considerable effort has been expended to make the book as user friendly as

possible. It has been designed to be relevant and useful both to persons who are

coming to cash flows for the first time, and to those who are more experienced

in the perils of financial statement analysis! I have paid particular attention to the

needs of those who are not native English speakers. I have tried to keep the use

of English as clear and concise as possible whilst avoiding the use of unnecessary

complexity.

Whilst the book is written primarily for those employed as financial analysts,

I have identified four other major user groups whose needs are specifically dealt

with in different sections of the book. They are:

•Novices in financial analysis and other persons new to, or relatively unfamiliar

with, cash flows in general and their analysis in particular, in all fields of

endeavour, who wish to improve their understanding of cash flow.

x Introduction

•Bankers, credit analysts and others involved in business lending and the man-

agement of credit exposures and credit risk.

•Investors, fund managers and credit analysts involved in taking investment

decisions.

•Entrepreneurs, managers and business people involved in controlling business

entities.

The guide to the book, which follows this introduction, provides an indication

of the content of each chapter and its relevance to different users. For example,

persons who have no desire to actually perform the analysis of the cash flows of

a business themselves, but who still wish to understand cash flow, will initially

gain little from Chapters 4 and 5 as they are written for persons who are seeking

to practically apply the technique for the restatement of published cash flows.

THE LOGIC OF THE BOOK DESIGN

Years of experience as a financial trainer have taught me that people acquire

technical knowledge in a very random way from a variety of sources as they come

across information relevant to their needs. This sometimes results in a partial,

incomplete and often inaccurate understanding of the particular subject in issue.

As a trainer and author my objective is to organise the information relevant to a

subject or task in a logical and structured way to facilitate and ease the assimilation

process. The metaphor I like to use is that of a jigsaw. My audiences will typically

have many of the pieces of the jigsaw already in their possession; however, until

I facilitate the process of assimilation they have not previously assembled the

pieces into a complete picture. When working as a trainer not only do I assist in

completing the jigsaw, I also provide the missing pieces, which are different for

each participant!

For this reason the book has been organised into specific blocks of knowledge.

It can be read sequentially. It can also be used as a reference to provide answers

to specific queries and problems by dipping into the relevant part of the book.

COMPLEXITY

The word complex is regularly misused to mean difficult, or beyond the users

present comprehension. When things labelled complex are analysed it often be-

comes clear that what is actually meant is there is a lot of information to assimilate

before comprehension of the whole can be gained. The information itself is not

particularly demanding to comprehend; there is, however, a lot of it! Writing com-

puter software or learning a musical instrument or foreign language are typical

examples.

Introduction xi

My strategy for this type of assimilation problem is to chop the information up

into lots of little bits that are sufficiently elemental that they can be adequately

digested by the person seeking to assimilate the whole area of knowledge and then

build the knowledge in a pyramid form by adding blocks and layers in an ordered

way. This is the approach I have taken in writing this book.

THE USE OF CASE STUDIES IN THE BOOK

Once the initial chapters have introduced the concepts upon which the analysis

of cash flows rely, the book includes a number of case studies that illustrate the

use of the technique for cash flow analysis offered. Most of these cases are based

on financial information taken from the accounting statements of real business

entities. I prefer to do this because there is then no challenge as to the reality of

business behaviour. If I create fictional cases for the book there is a risk users will

question my conclusions about them and cash flow analysis in general on the basis

that the examples are fictionalised and therefore do not represent a reasonable

representation of business reality.

However, this inevitably results in problems with dates! The question of how

to deal with dates in the book is one that has vexed me significantly. The problem

for the publisher and I is that the book will soon appear dated if we show the

years from which the case studies were taken in the original. Users may wrongly

assume the message and content of the book is somehow less relevant because the

material used to illustrate the logic of the technique offered is ageing.

The logic of the cash flow analysis technique offered in the book is essentially

timeless, it should work virtually anywhere and anytime financial information is

available to perform the analysis. For this reason I have partially disguised the

original dates of the material used to illustrate the cases. The timeline of most of

the case studies offered is incidental; the examples are there to illustrate the use

and benefits of the cash flow analysis technique that is the basis of this book.

Experienced analysts will know that in performing any business analysis the

economic context in which the company operates is sometimes highly relevant.

Matters such as inflation, interest rates and the state of the economy may affect the

conclusions drawn about the relative performance of a business. For this reason,

in a small number of cases and where the context of the example warrants it, I

have left the dates as they were originally. This allows the reader to put the case

into the context of the economic conditions prevailing at the time.

Considerable effort has been expended to keep the various examples, tables and

other information both numerically and factually correct, however, it is inevitable

in a work of this length that, despite our best efforts, errors may still creep into

print. Please do not hesitate to bring these to my attention, to further improve the

book as it develops.

xii Introduction

I hope this book changes your life. For those whose job is to analyse cash flows

for a living it may actually do so!

Capitalisation

Throughout the book, where you see CAPITALISED WORDS, these refer directly

to key words in tables and figures that are being discussed and explained in the

text.

GUIDE TO THE BOOK

The book is organised into two sections, the first dealing with the analysis of

historic cash flow data, the second dealing with the forecasting of cash flow

information.

Section One – Historic Cash Flow Analysis

Chapter 1 – Understanding How Cash Flows in a Business

Level basic – the chapter is designed as a layperson’s introduction to the whole

subject of cash flow in business. In addition to introducing the cash flow patterns

seen in business, it outlines a number of other fundamental issues and risks that

managers must overcome in order to trade successfully. No prior knowledge of

cash flow is assumed. The material is presented from the ground up through the

use of straightforward examples.

Despite being offered as a basic introduction everyone seeking to utilise the

cash flow analysis technique presented in the book should read this chapter as it

introduces and defines part of the terminology used throughout the book.

Chapter 2 – Understanding Cash Flows Properly

Level intermediate – this chapter explains the knowledge and the steps required

to analyse cash flows properly. It then commences the process by explaining all

the terminology used in a simple cash flow example and introduces the analysis

technique for the first time.

Chapter 3 – Start-up, Growth, Mature, Decline

Level intermediate – this chapter introduces the non-financial information needed

to get the most out of the cash flow analysis technique offered in the book.

Everything offered in this chapter is covered in more detail in Chapters 6 to 10.

Introduction xiii

Chapter 4 – Restating the Cash Flows of a Real Business

Level advanced – readers without some prior knowledge of financial statement

analysis and accounting will find this chapter demanding. Considerable effort has

gone into explaining the accounting and analytical knowledge required to properly

utilise the cash flow analysis technique offered. The example chosen to illustrate

the process being taken from a business preparing its accounts using International

Financial Reporting Standards.

Chapter 5 – Restating US GAAP Cash Flows

Level advanced – this follows on from the previous chapter by taking an example

of the technique based on a business following US financial accounting rules in

the preparation of its financial statements. It is necessary to be familiar with the

content of the previous chapter in order to get most benefit from this one.

Chapter 6 – Analysing the Cash Flows of Mature Businesses

Level advanced – this chapter defines the term ‘mature’ and presents the informa-

tion required to comprehensively analyse the cash flows of a mature business.

Chapter 7 – Analysing the Cash Flows of Growth Businesses

Level advanced – this chapter defines the term ‘growth’ and presents the informa-

tion required to comprehensively analyse the cash flows of a growth business.

Chapter 8 – Growth and Mature – Further Analysis Issues

Level advanced – this chapter presents two important further issues relevant to the

analysis of both growth and mature businesses.

Chapter 9 – Analysing the Cash Flows of Start-up Businesses

Level advanced – this chapter defines the term ‘start-up’ and presents the infor-

mation required to comprehensively analyse the cash flows of a start-up business.

Chapter 10 – Analysing the Cash Flows of Decline Businesses

Level advanced – this chapter defines the term ‘decline’ and presents the informa-

tion required to comprehensively analyse the cash flows of a decline business.

xiv Introduction

Chapter 11 – What to do about Bad Cash Flows

Level advanced – this chapter offers a variety of strategies to make decisions about

cash flows that are bad. It suggests a number of questions that the analyst should

seek to answer, before coming to conclusions about bad cash flows.

Chapter 12 – Cash Versus Profit as a Measure of Performance

Level advanced – this chapter explains in detail the differences between profit and

cash generation as a measure of performance. It points out the pitfalls of using

profit alone as a performance indicator.

Chapter 13 – Cash Flow Analysis and Credit Risk

Level advanced – this chapter explains how to tailor the cash flow analysis tech-

nique offered specifically to the needs of bankers and others who are exposed to

credit risk.

Chapter 14 – Cash Flow Analysis and Performance Measurement

Level advanced – this chapter looks at ways the cash flow analysis technique

offered in the book can be used for business performance measurement.

Chapter 15 – Analysing Direct Cash Flow Statements

Level advanced – this chapter deals with the differences between direct and indirect

cash flow statements and how to deal with them in applying the cash flow analysis

technique. It is necessary to be familiar with the earlier content of the book in

order to get the most out of this chapter.

Chapter 16 – Generating a Cash Flow Summary from Profit and Loss

Account and Balance Sheet Data

Level advanced – this chapter illustrates how to arrive at a summary of the cash

flows of a business entity that does not produce a cash flow statement as part of

their financial information. It is essential to be familiar with all the earlier content

of the book in order to get the most out of this chapter.

Chapter 17 – Summarising Historic Free Cash Flow

Level advanced – this chapter illustrates how to identify the historic free cash flow

of a business entity from the cash flow information derived by using the cash flow

Introduction xv

analysis technique presented earlier in the book. It is necessary to be familiar with

the earlier content of the book in order to get the most out of this chapter.

Section Two – Forecasting Cash Flows

Chapter 18 – Introduction

Level advanced – this chapter discusses the risks and benefits of forecasting when

compared to the analysis of historic information.

Chapter 19 – Spreadsheet Risk

Level advanced – this chapter introduces spreadsheet risk and offers strategies to

minimise the problem.

Chapter 20 – Good Practice Spreadsheet Development

Level advanced – this chapter introduces a number of techniques to reduce spread-

sheet risk through good modelling practice. It illustrates four examples of common

cash flow forecasting models.

Chapter 21 – The Use of Assumptions in Spreadsheet Models

Level advanced – this chapter offers guidance on dealing with assumptions in

spreadsheet forecasting models. It then discusses the use of scenarios for risk

analysis using spreadsheet forecasts.

Section One

Historic Cash Flow Analysis

Cash Flow Analysis and Forecasting: The Definitive Guide to

Understanding and Using Published Cash Flow Data

by Timothy D.H. Jury

Copyright © 2012, Timothy D.H. Jury

1

Understanding How Cash Flows in

a Business

INTRODUCTION

This chapter is designed to enable those with less direct experience of the operation

of businesses to grasp the fundamental financial and economic logic that governs

how successful businesses operate. It represents the starting point for our journey

through the landscape of cash flow analysis. In order to gain benefit from this

chapter no prior knowledge of either cash flow or business is required.

We start our journey by developing a model of how the cash flows in a simple

business work. We then develop our knowledge of cash flows by incrementally

adding complexity to this model.

Whilst developing this model based on the cash flows of a business we also

introduce some fundamental logic about what different types of business must do

in order to be successful.

THERE IS NOTHING NEW ABOUT BUSINESS

Humans have been engaging in trade for thousands of years, initially through

some sort of barter process. Archaeologists have discovered ancient manufactured

goods such as pottery and metal objects that have travelled vast distances from

their point of manufacture. There are numerous examples of early Greek and

Roman shipwrecks being discovered in many different parts of the Mediterranean

dating back 2000 years or more. In the 1960s evidence was finally discovered

that proved that the Vikings were the first Europeans to discover America some

500 years before Columbus. The remains of a Norse settlement at L’Anse aux

Meadows on the northern tip of Newfoundland have been authenticated and dated

to around 1000AD. During the excavation of the site over 100 objects of European

manufacture were unearthed.

A more recent development in human history was the introduction of money

in the form of coinage and, later, notes. Whilst there is much debate about what

should be recognised as the first coin, a good candidate would be a small lump

of electrum (a natural alloy of gold and silver) stamped with a design and minted

around 600BC in Lydia, Asia Minor (now known as Turkey). Paper money seems

to have emerged in China at about the same time.

Cash Flow Analysis and Forecasting: The Definitive Guide to

Understanding and Using Published Cash Flow Data

by Timothy D.H. Jury

Copyright © 2012, Timothy D.H. Jury

4 Cash Flow Analysis and Forecasting

This innovation, together with many others such as agriculture, settlements, the

wheel and writing led to the modern, technologically based world economy we

have today. Trade or business, in one form or another, has probably been part of

the human condition from our earliest origins.

UNDERSTANDING MONEY IN BUSINESS

We are going to start with two simple examples of business activity. The first

one represents one of the simplest forms of business. (More complex business

examples follow over the next few pages.)

The Simplest Form of Business

Newspaper vending, by which I mean the activity of selling newspapers to passers-

by on a street corner, is a good example of a really simple business. The vendor,

or businessman, buys the newspapers from the publisher or a wholesaler and then

retails them to passers-by for a price that gives him a margin over the cost of

purchasing the newspapers.

A second example of a really simple business is an antique dealer, someone

who buys and sells old objects. We will work with this example from now on.

The Debate About the Purpose and Objectives of a Business

The varying cultures around the world place different emphasis on how the benefits

generated by a successful business should be shared amongst its stakeholders.

I do not propose to examine the merits or otherwise of these views. There is

considerable literature on what measures should be used to assess success or

failure in business. Both growth and profit increase look like good candidates but

fail as measures of success if the improvement in growth or profits is achieved by

investing disproportionate amounts of cash. I do not propose to go much further

with this debate other than to say that increasing the value of a business over

time is now considered the most appropriate measure of success. This is achieved

by continually improving the present and future cash flows of a business on an

ongoing basis.

So, at this point in my explanation, I am assuming that the business I am

describing is being run with the objective of wealth maximisation for the owners.

For the purposes of this book I define that as maximising the future cash flows of

the business.

Understanding How Cash Flows in a Business 5

The Objective of Being in Business is to Generate More Cash

It is important to introduce the purpose of a business here because specifying the

objective of the business defines the task of the business person, entrepreneur,

manager or other business controller (which is to get more cash). In both the

business examples introduced so far we have a trader or dealer who buys and sells,

typically without changing or modifying the items traded in any way. This is the

simplest form of business.

The trader’s objective is to generate more cash than they started with. (Note that

I have not used the terms profit or gain as we are developing a model containing

only items that represent the cash flows in a business. What we mean by profit is

actually quite an abstract concept. This is dealt with in more detail in Chapter 12.)

How Does a Trading Business Add Value?

An initial observation might be that these businesses make money by buying things

for less than they can sell them. While this is an accurate observation of what a

successful trading business does, this fails to explain why or how the business is

able to achieve this beneficial outcome.

What is the key skill for an antique dealer? Is it knowledge of the antiques

traded in? Whilst this may help, much of this information is available from books.

Is it renovation skills? Again this may or may not add value to the items being

renovated depending on consumer taste at the time. The key skill is probably,

knowing where to buy cheaply and where to sell expensively. Here is an example

of what I mean.

For many years the typical vehicle of choice for a British antique dealer has

been the Volvo estate, which is used to travel to distant parts of Scotland and Wales

so that the dealer can purchase furniture and other antiques from remote house

sales and auctions where they are often sold cheaply. The goods purchased are

then transported to London where they can be auctioned through the major auction

houses or retailed to wealthy collectors at collectors’ fairs or from retail premises.

What this antique dealer is doing is relocating the goods traded from a place

where they can be bought cheaply to a place where they can be sold more expen-

sively. It’s all about the relocation of the goods. Why is this so important?

Consider what happens when you get up in the morning. Do you travel to Java

for your coffee beans, Florida for your orange juice, Jamaica for your sugar, and

to your local farm for your milk?

This is unlikely. What most of us do is go to the nearest convenience store,

which may be just down the street and buy what we wish to consume for our

breakfast. So, what then is the owner of the convenience store doing to add value?

What he does is relocate a range of goods he knows we are likely to consume for

6 Cash Flow Analysis and Forecasting

breakfast to a place convenient for us to make our purchases as consumers. The

convenience of the location is the most important thing, the goods offered are in

a sense irrelevant, they are whatever we want to consume.

So, the key to most trading, retail and wholesale businesses is location. What

these businesses do is relocate goods from their places of production or, if second-

hand, their present location, to a location convenient for the target consumer to

consume them. It follows that there is little point in locating a business in a

remote part of the world as there are few consumers there! The ideal location for

newspaper vending is directly outside a major railway station in central London

or any other major city in the world, this is where you will have thousands of

potential consumers passing by every hour of the working day. In other words,

you will sell more newspapers. The location is the essence of the business’s ability

to generate cash.

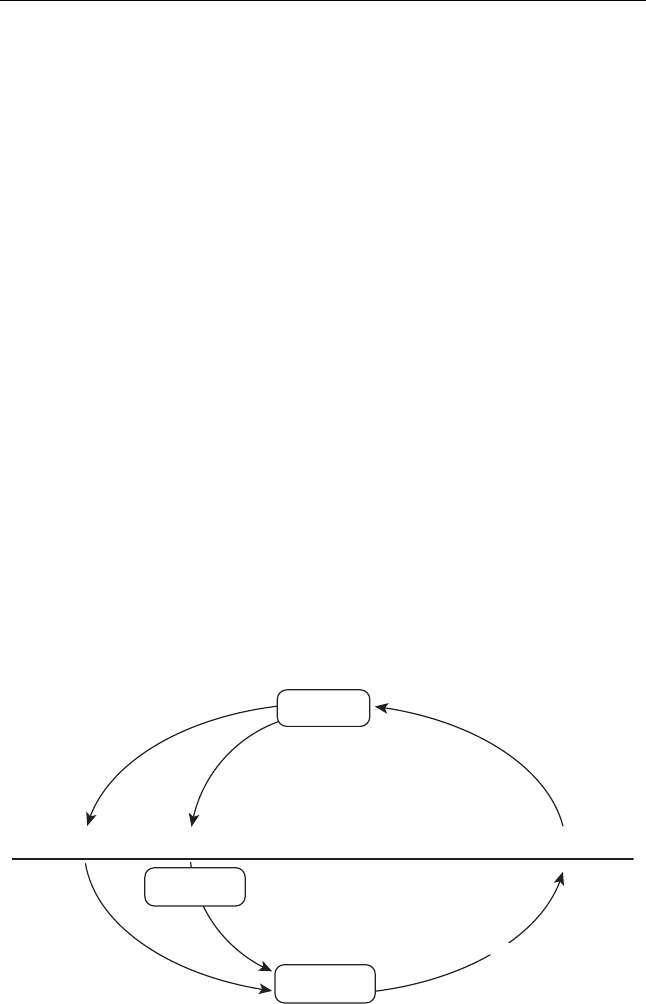

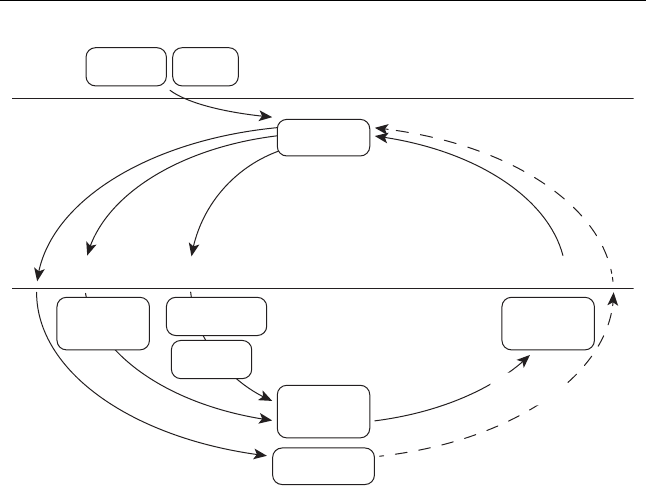

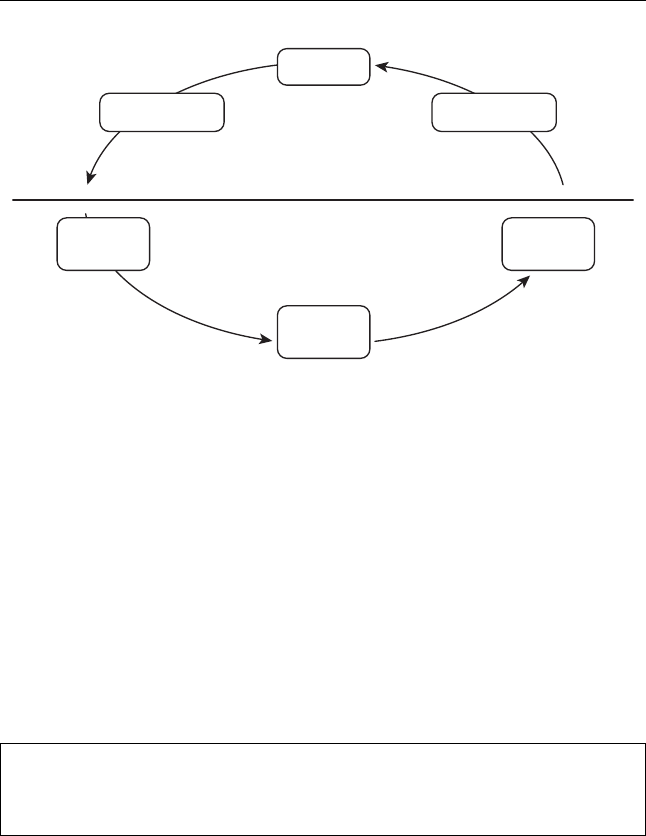

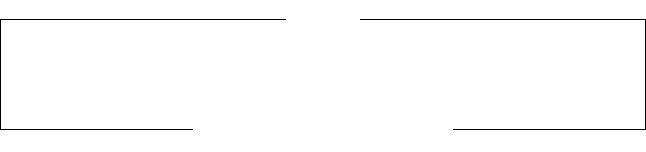

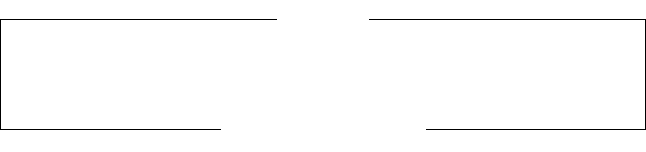

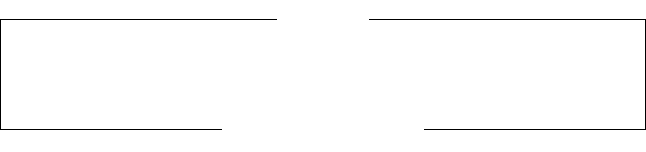

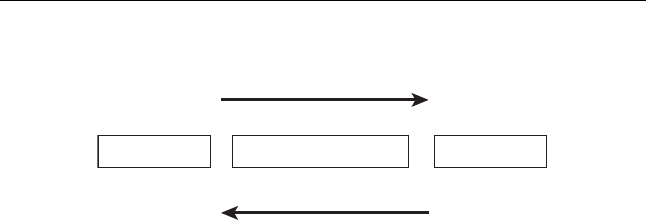

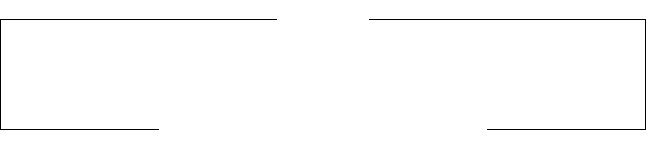

So, the cash flows of our simplest business look like the model shown in

Fig. 1.1. Overheads is the term commonly used in business to refer to all the costs

of trading other than inventory costs.

Using CASH the trader makes purchases of goods, which he holds as INVEN-

TORY. Some time later he resells the goods acquired for more than he paid for

them, receiving cash in exchange for the items. He will typically incur some

OVERHEADS in the process, in our example of the antique dealer these will be

transport, location and communication costs.

This is effectively all a trading, retail or distribution business does, repeating the

journey round the circle many times. Now let us look at a more complex business,

one where work is performed on the purchased inputs of the business.

Cash

Inventory

Overheads

Cash

Non-Cash

Purchase Purchase

Added

value Relocation

knowledge

Sale

Figure 1.1 Diagram of the cash flows of a simple trading business

Understanding How Cash Flows in a Business 7

THE SIMPLE MANUFACTURING BUSINESS

In my other life as a financial trainer I have travelled all over the world offering

training seminars on financial analysis and related subjects. One of the places I

have visited on my travels is Nairobi in Kenya. When travelling from Nairobi

airport to the training location I noticed business people selling beds and other

simple items of furniture outside their workshops by the side of the road. This

then is the next example we will examine; a simple manufacturing business.

How Does a Simple Manufacturing Business Add Value?

What do manufacturers do to create wealth for themselves? They take raw materials

and change them into something more useful; economists talk about adding utility.

For example, I could sleep on a log. However, this would not be particularly

comfortable, the bark would make my back itch and I might roll off! If the log is

cut up into timber and then turned into a bed frame I am likely to be willing to pay

more for it in this form. Now, I could of course do this myself with the aid of a saw

and a few basic woodworking tools, so why do I not normally bother? There are

three reasons: time, quality and cost. I could make the bed, but it would take me

three days whilst the manufacturer does it in half an hour. Secondly, the result I

achieve might not have the quality of the professionally manufactured alternative

and, finally, it would almost certainly be more expensive when the opportunity

cost of my time as well as the cost of the raw materials is taken into account.

So, manufacturers do not just convert things (raw materials) into more useful

things (finished goods), they are experts at the process of doing so. Successful

manufacturers do it very quickly and efficiently to a very high standard. The key

word here is expert. If you are analysing the performance of a manufacturing

business and find that it receives many customer complaints and returned goods

due to manufacturing defects, or is experiencing significant difficulties actually

producing goods, this suggests they are not experts. To use a metaphor: it implies

they are amateurs rather than professionals. Any business being operated in a non-

professional way is at a higher risk of poor financial performance and eventual

failure than its more professional and competent competitors. The extreme levels

of professionalism required just to be competitive in most manufacturing activities

is simply a consequence of competition over long periods of time.

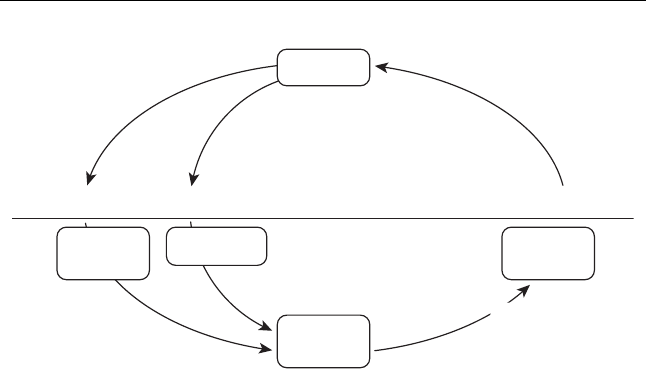

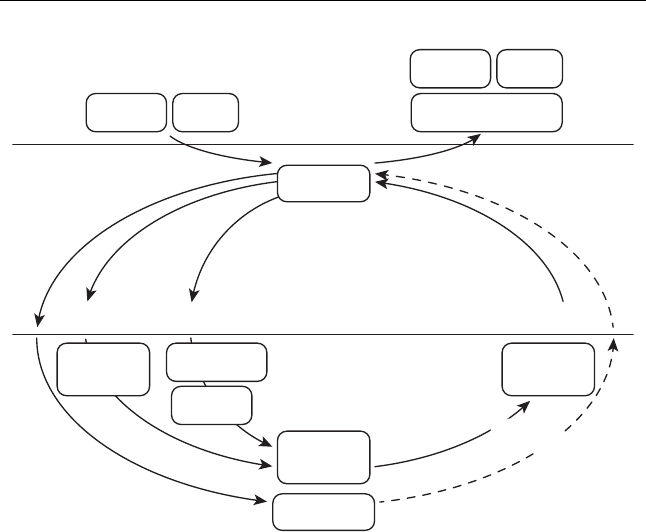

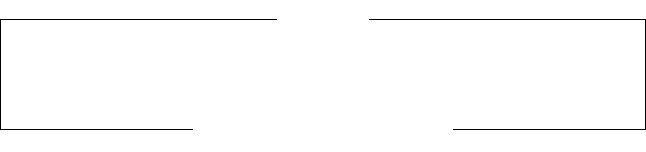

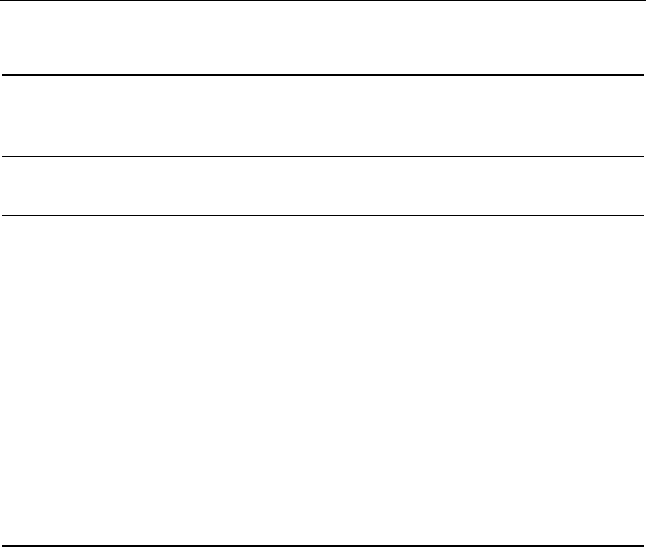

So the cash flows of our simple manufacturing business look like the model

shown in Fig. 1.2.

Using CASH the manufacturer makes a purchase of RAW MATERIALS and

does work on them, so converting them to WORK IN PROGRESS and eventually

FINISHED GOODS. These items being akin to INVENTORY in our previous

model. Some time later he resells the finished goods for more than the cash costs

of producing them, receiving cash in exchange for the items. He will typically

8 Cash Flow Analysis and Forecasting

Cash

Work in

Progress

Raw

Materials

Finished

Goods

Overheads

Cash

Non-Cash

Purchase Purchase

Added

value Conversion

knowledge

Sale

Figure 1.2 Diagram one of the cash flows of a manufacturing business

incur some OVERHEADS in the process of conversion, these being purchasing,

manufacturing, premises, and selling costs in our example.

This is what the cash flows of a new small manufacturing business look like.

Cash is generated by repeating the journey round the circle many times. Now let

us see how this develops as the business evolves over time.

Developing Our Model – the Next Step

Continuing with our example of an African entrepreneur who has recently estab-

lished himself as a manufacturer of furniture, let us assume his new business is

successful. Our entrepreneur is working many hours a day and all the product he

produces sells well. What is likely to be his first major issue in developing his

business?

Given his location his next move is most likely to be adding labour to the

business to increase output and hence cash flow. This is because there is much

labour available and, given the emerging market location of the business, this

labour is available relatively cheaply (Fig. 1.3).

LABOUR now joins overheads as an item purchased and consumed by the

business to add value to raw materials.

If our entrepreneur furniture designer was in Munich in Germany the decision

might be quite different. In this location the economic environment is different

to that in Nairobi in Kenya. In Germany labour costs are significantly higher per

hour and employees are protected in many ways by a mass of social legislation

Understanding How Cash Flows in a Business 9

Cash

Work in

Progress

Raw

Materials

Finished

Goods

Overheads

Labour

Cash

Non-Cash

Purchase Purchase

Added

value Conversion

knowledge

Sale

Figure 1.3 Diagram two of the cash flows of a manufacturing business

giving them extensive rights and obliging employers to compensate employees in

the event of job losses. From an economic point of view the cost of labour is higher

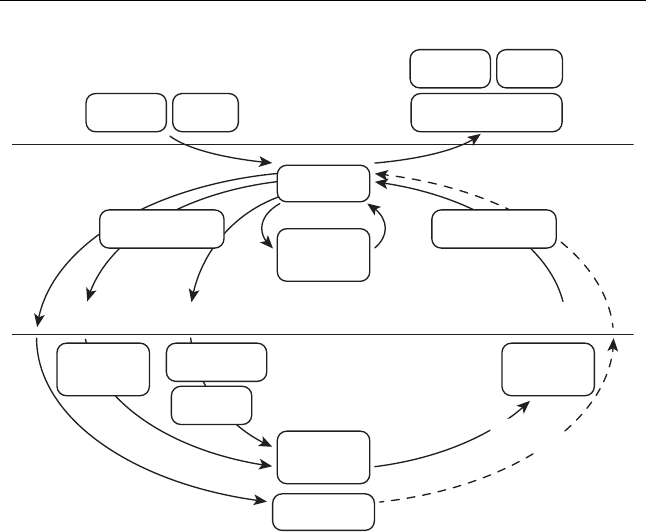

and the cost itself is less variable. In Germany the first major initiative to build our

business is more likely to be the purchase of machinery (i.e. fixed assets) to increase

output and hence cash flow, rather than the addition of more labour (Fig. 1.4).

Why is the decision different depending on the location of the business? This is

because the economic environment is different. Factors that affect the decision of

whether to employ labour or purchase fixed assets would be things like, the law

and regulations affecting the cost and flexibility of labour, the local environment

governing labour and investment in fixed assets, and the availability and quality

of labour.

There are other issues that might inform or determine the decision. Machines

have certain characteristics that could arguably make them superior to labour in

many situations. They do not go on strike; they can, assuming they are properly

maintained, produce a succession of perfect and identical output 24 hours a day

without requiring sleep or food. But, there are also some key negative charac-

teristics of machines. They usually require infrastructure such as electricity, gas,

compressed air and water constantly available without interruption. They are very

good at doing the same thing again and again; they are not so good when the

required output keeps changing. Any change to the product manufactured may

necessitate hours of re-engineering and re-programming of the machine before

productive output recommences.

10 Cash Flow Analysis and Forecasting

Cash

Fixed assets

Work in

Progress

Raw

Materials

Finished

Goods

Overheads

Labour

Cash

Non-Cash

Purchase Purchase

Added

value Conversion

knowledge

Sale

Figure 1.4 Diagram three of the cash flows of a manufacturing business

Labour, despite its imperfections, is very flexible. It can make the tea, collect

the raw materials, deliver finished product and paint the wall, in addition to

being available to produce product as required. It copes well with a succession

of variable tasks. The negatives are that it can go on strike, it requires a safe

and healthy working environment and protection from the risk of injury or death

(known collectively as health and safety). It also needs constant breaks for food

and rest, and it can produce substandard and defective work if not properly trained

and supervised.

So, labour is flexible but inconsistent, machinery is inflexible but consistent. As

our example business grows, whether situated in Kenya or Germany, labour and

fixed assets will be added as required according to their relative utility to cost in

the local environment.

You may have noticed the use of a dotted line to denote the sale of fixed assets.

This is because when we acquire fixed assets we intend to keep them to assist us

in the process of producing or trading our goods and services. We do not intend

to sell them or trade them during their useful lives. Only when they are no longer

of operational use to us do we sell them if we can. The cash flow we get when we

sell them is usually small relative to the cash flow spent on new assets.

The Consequences of Growth and Success

As the business develops it becomes more complex, typically because growth

means an increase in everything. The numbers of labour, machines, products,

Understanding How Cash Flows in a Business 11

customers and suppliers can all increase. With this complexity comes new risks.

When a business is small it can be controlled by one person. As it grows this

becomes more and more difficult because too many things that require control are

happening simultaneously. Delegation of authority to others is required, which

implies the creation of a management structure.

Similarly the cash flows involved in the business all get larger. Turnover, costs,

investment, debtors and creditors all increase. At this point it is sensible to consider

limiting the risk of the owner. How can this be achieved?

The owner can sell the business to a limited company owned by him or herself.

Until this point our example business has been trading as a sole trader. In English

law there are three different ways a person can trade, as a sole trader, as a partner

in a partnership and through the use of some sort of company owned by the

person.

As a sole trader or partner an individual’s risk is unlimited. Should there be any

negative event that results in significant liabilities for the business in which they are

involved, the sole trader and any partner are personally liable for the full amount.

Should a business operating as a limited company suffer an event that leads to

huge liabilities the company itself is the party responsible for the liabilities, not the

owners. The owners are only liable to the extent they have subscribed for shares,

(in other words they may lose the equity they own in the company). As long as

the directors have acted lawfully they cannot be made personally liable for the

liabilities of the company. This means if the company collapses into bankruptcy

the director owner can keep his house, pension fund and other personal assets that

are separate from the limited company in which the business resides.

So, from a risk management viewpoint, are companies a good idea or a bad idea?

For society as a whole they appear to be a good idea, partly because they facilitate

the pooling of investment for new projects. A developed nation has extensive

infrastructure in the form of roads, railways, airports, pipelines, communications,

electricity and oil and gas infrastructure which requires the capital of hundreds of

thousands of individuals to create. By issuing shares to millions of people, each

of which is a part owner of the business, these beneficial assets for society can

be created and maintained. They also encourage risk-taking in the form of new

business creation because entrepreneurs can protect their personal assets by using

a limited company as the vehicle for their new ventures.

The negative aspects of companies arise if you are a creditor of a company.

Banks, suppliers and employees lose money when companies fall into bankruptcy.

In extreme situations a limited company can be used deliberately to acquire the

cash flow of a business, which is then stolen by the owners. This is of course

criminal and fraudulent. This is why it is essential that stakeholders who are

creditors monitor the creditworthiness (or credit risk) of any company they are

involved with as a creditor.

Figure 1.5 introduces equity (and debt) to the model.

12 Cash Flow Analysis and Forecasting

Cash

Fixed assets

Work in

Progress

Raw

Materials

Finished

Goods

Overheads

Labour

DebtEquity

Cash

Non-Cash

Purchase Purchase

Added

value Conversion

knowledge

Sale

Figure 1.5 Diagram four of the cash flows of a manufacturing business

The business is now owned by an independent legal entity (a company) that

is separate from the person or persons who formerly owned it. Their interest is

represented by their shareholding in the EQUITY of the company. The company

may also have raised cash to invest in the company by borrowing, perhaps from a

bank, which is recognised in Fig. 1.5 as DEBT.

Debt, in the form of loans or leases may be used by the company to acquire fixed

assets such as factory premises and machines. Debt may also be used to provide

working capital in the form of an overdraft facility or via the use of factoring or

invoice discounting.

Having introduced these new sources of capital we need to add further items to

the model to keep it consistent with reality. Cash borrowed from banks is not lent

for nothing. Banks charge INTEREST (essentially a rent) for the period that the

money is advanced to the borrower. Similarly, if the company is successful it may

pay DIVIDENDS to its shareholders. Finally, most governments demand that the

company pay TAXATION on any taxable profits from trading or other investment

income generated by the company.

These potential cash outflows do not represent operating costs because they

arise for reasons that differ from the other cash outflows required to operate the

Understanding How Cash Flows in a Business 13

Cash

Fixed assets

Work in

Progress

Raw

Materials

Finished

Goods

Overheads

Labour

DebtEquity Dividends

TaxationInterest

Cash

Non-Cash

Purchase Purchase

Added

value Conversion

knowledge

Sale

Figure 1.6 Diagram five of the cash flows of a manufacturing business

business. DIVIDENDS and INTEREST represent rewards paid to financiers as a

consequence of their investment. TAXATION is a government levy on surpluses

generated by the company. All the other operating costs of the business should be

incurred because they are necessary in order to generate the operating cash flow of

the business. When we add these items our model of the cash flows of the business

looks like Fig. 1.6.

The Implications of Supplier and Customer Credit

So far we have assumed that all transactions in the business take place in cash.

In the real world this is not so. There is often a difference between the time we

take physical delivery of something we have purchased and when we pay for it.

Conversely, it is common to sell something to a customer allowing them a period

of time to pay, the cash due on the sale of the product being received some time

later.

14 Cash Flow Analysis and Forecasting

Let us consider the example of our business of our African entrepreneur some

years on. He is no longer manufacturing furniture outside his home; he now has

a substantial factory full of machinery and labour, owned by a limited company

controlled by him.

When he buys timber he does not collect it on foot with a handcart any more.

He telephones his timber merchant and asks him to deliver three truckloads of

timber. When the timber arrives he does not pay for it, he signs a delivery note.

A CREDITOR (or PAYABLE) is created at this point (being the money due to

the supplier in payment for the goods) which may be settled (paid) one to three

months later.

Similarly when the business sells a bed it is no longer sold for cash on the

side of the road. Instead the beds are now manufactured in the form of flat packs,

stuffed in a container and sent to IKEA, a major global discount furniture retailer.

When IKEA receive the beds they do not pay cash, they sign a delivery note for the

goods and create a DEBTOR (or RECEIVABLE), (being the money due from the

customer for the goods sold to them) which may be settled one to three months later.

So, CREDITORS effectively grant the business a short-term interest-free loan

whilst the liability to them remains unpaid. Conversely, our furniture business

essentially lends its DEBTORS short-term, interest-free funds for the duration of

the period whilst the debt owed to the furniture business remains unpaid.

These time delays have a substantial and important effect on the cash flows of a

business and must therefore be incorporated in our model. Our model now evolves

further (Fig. 1.7).

The model is now essentially complete; it contains all the cash flows relating

to a single business entity. We can see clearly how the cash flows round a busi-

ness. Having constructed this model, we can now work with it to develop our

understanding of cash flow and business practice. What else is important to our

understanding of cash flow?

The Working Capital Cycle

We can now see that cash flows round the business as follows:

1. The business orders goods and services (these being either RAW MATERIALS,

LABOUR or OVERHEADS).

2. The goods and services are delivered, creating a CREDITOR. They enter

production or are consumed in the production process.

3. The RAW MATERIALS are converted into WORK IN PROGRESS and finally

FINISHED GOODS.

4. The FINISHED GOODS are then sold, creating a DEBTOR.

5. The DEBTOR pays the invoice some time later providing CASH to the business.

6. The CASH is used to pay CREDITORS as they fall due.

Understanding How Cash Flows in a Business 15

Cash

Fixed assets

Work in

Progress

Raw

Materials

Finished

Goods

Creditors

Overheads

Labour

Debt

Debtors

Equity Dividends

Ta xInterest

Cash

Non-Cash

Purchase Purchase

Added

value Conversion

knowledge

Sale

Figure 1.7 Diagram six of the cash flows of a manufacturing business

This movement of cash and resources around the business is known as the

WORKING CAPITAL CYCLE. It represents the most active and volatile set

of cash flows through most businesses. It is the most demanding area of cash

management to control. Experienced managers know that managing the working

cash flows is a demanding exercise. Most of the daily tasks of management arise

from problems achieving the timely supply of goods and services at the right level

of quality to the business, and the problems of manufacturing the product right

first time without quality defects. Both tasks have to be satisfactorily completed

before delivery and invoicing can take place in turn resulting in cash flow from

customers to the business.

The investment requirements of a business and the amount of business risk

inherent in a particular business are both affected by the nature and behaviour of

the working capital cycle. Understanding the working capital cycle is therefore

very important. The main problem is recognising the risk implications – of the

impact of time – on the business.

You may be wondering what time has to do with all this. Timing is the essence

of working capital management which, in turn, is the key component of cash flow

management. Let us take two examples:

16 Cash Flow Analysis and Forecasting

On day one Tesco plc (a leading UK supermarket group) orders a truckload

of beans from Heinz plc (a major global food manufacturer). The beans arrive at

Tesco’s distribution depot on day three and arrive in the store on day four. By the

end of day five all the beans are sold to customers for cash or credit card payment

with Tesco in possession of cleared funds by day seven. Tesco then holds the cash

for 53 days before paying Heinz for the beans. Contrast this with Airbus Industrie

(a major civil aircraft manufacturer) who are constructing an Airbus A380 for a

major airline.

Following years of negotiation Airbus receives an order for a number of aircraft,

this in turn initiates the thousands of orders necessary to obtain the various compo-

nents and sub-assemblies required from their respective suppliers. Over a period

of many months raw materials are received and the aircraft is assembled (being

work in progress at this point, which takes about 12 months), then completed and

tested (becoming finished goods at this point). Finally, after further performance

tests by Airbus and the purchasing airline the aircraft is accepted into service

and paid for. The journey round the working capital cycle takes between one and

two years.

What conclusions can we draw from these two deliberately extreme examples?

If Tesco has agreed 60 day settlement terms with Heinz they will be able to sell

the beans and hold the resultant cash for 53 days before settling their liability to

Heinz. In other words Tesco plc generates cash from the working asset cycle as

a consequence of trading. No external finance is required to trade. All the cash

required comes from credit provided by suppliers. The operating creditors of Tesco

exceed the inventory and there are no debtors. Where the operating creditors of

a business exceed the amounts invested in the inventory and operating debtors of

a business we say the business has negative net working asset investment. In this

situation the more turnover increases the more cash is generated from working

assets. Another way of illustrating the benefits of this is that Tesco would have the

benefit of this cash for 53 days and be able to earn interest on it even if Tesco sold

the goods acquired with trade credit at the same price they were purchased from

the supplier.

Airbus Industrie enjoys much less favourable working asset behaviour. They

have to invest many millions of euros in the working capital cycle to manufacture

each Airbus A380. The funding of the working capital requirement for each major

contract is a major undertaking. Each aircraft sells for approximately $US320

million. The more successful Airbus is at selling the Airbus A380 aircraft the

more cash has to be found to invest in working capital. Airbus has to invest vast

sums into the working asset cycle in order to trade. Increased trading requires

more cash to be invested in the working capital cycle. Airbus has positive working

asset investment. No cash is generated from working assets; as the business grows

cash is typically absorbed by working asset investment.

Understanding How Cash Flows in a Business 17

Investing in Fixed Assets

Cash is also required to invest in FIXED ASSETS as required. The need for

investment is determined largely by the nature of competition in the markets

in which the business operates. In a competitive market, changes in consumer

expectations and technology will constantly drive suppliers to design better and

cheaper products to satisfy consumer needs, the fixed asset investment needed to

do this must then be committed before production can take place. Depending on

the nature of the fixed assets acquired, it may be possible to borrow much of the

funds required to finance acquisition or construction.

Timing is also important when investing in fixed assets. Invest too early and you

may not achieve sufficient utilisation to recover your investment, invest too late

and your competitors may have already captured markets and reduced operating

costs ahead of you.

HOW DOES ANY BUSINESS GENERATE CASH?

In order to generate cash the business must go round the WORKING ASSET

CYCLE at least once. Every time the business completes a circuit more cash is

generated. It follows from this that it makes sense to get very good at going round

the working asset cycle very quickly as this will generate more and more surplus

cash! This is what good businesses seek to optimise. Delays in completing a circuit

can wipe out the extra cash simply due to the cost of financing the working asset

investment. If you can regularly make a circuit round the WORKING ASSET

CYCLE faster than your competitors you have a competitive advantage.

What Causes Businesses to Fail?

There is only one answer to this question. It is because they have run out of cash.

In a crisis all the boxes in the model become temporary or short term sources of

cash, fixed assets can be sold, inventory reduced, creditors increased, overheads

reduced, and so on. However, there is a natural limit to this process, there comes

a point where the assets left in the business and overheads remaining are those

without which it cannot continue to trade. As the business is distressed equity

providers and lenders are no longer interested in supporting the business. At this

point the business has run out of sources of cash.

More specifically, businesses fail because two adverse events take place simul-

taneously. A creditor demands payment in respect of a liability and the business

does not have the cash available to pay as is demanded. As a result the creditor

successfully forces the business into bankruptcy.

The rules regarding the actions to take when a business becomes insolvent vary

depending on the location of the business. In countries with Roman law legal

18 Cash Flow Analysis and Forecasting

Cash

Fixed assets

Surplus

Cash

Work in

Progress

Raw

Materials

Finished

Goods

Creditors

Overheads

Labour

Debt

Debtors

Equity Dividends

Ta xInterest

Cash

Non-Cash

Purchase Purchase

Added

value Conversion

knowledge

Sale

Figure 1.8 Diagram seven of the cash flows of a manufacturing business

systems the directors may be obliged to apply for court supervision and direction

when the business becomes insolvent.

In Anglo-Saxon law countries it is usually an offence to trade whilst knowingly

insolvent. However, exactly what constitutes this condition is not tightly speci-

fied. So, if there is no creditor who has any interest in forcing the business into

bankruptcy it is unlikely to happen, irrespective of the state of the balance sheet

or the availability of liquidity.

Remember the only sustainable (and most important) source of cash generation

is the cash generated from operating the business (for which I use the term the

OPERATING CASH MARGIN), which is the extra cash generated each time

the business goes round the inner circle in the model (which I have labelled the

WORKING CAPITAL CYCLE). This is shown in Fig. 1.8.

THE COMPLETE REAL BUSINESS MODEL

Our model is now almost complete. We see the WORKING CAPITAL CYCLE,

we see cash spent on FIXED ASSETS and we see the sources of the cash invested

in the business, these being labelled EQUITY and DEBT in the model.

Understanding How Cash Flows in a Business 19

For the purposes of this model and any further discussion in this book, DEBT

represents all forms of borrowing, such as loans, mortgages, commercial paper,

bonds, lease finance, hire purchase, factoring, invoice discounting and any other

form of external debt financing. Basically, if the company pays interest in some

form or other in exchange for the loan of the cash, the liability that results is a

debt liability.

Any cash surpluses generated that are not paid out are retained in the business as

SURPLUS CASH. When this is added to the model the model is complete. This

represents an accurate and comprehensive representation of all the significant

cash flows of a single business entity. The descriptions on the left-hand side of the

diagram refer to the nature of the items shown in the model. Debtors, creditors

and cash are items generally denominated as cash values. The non-cash items,

inventory, overheads, labour and fixed assets all represent real as opposed to

monetary items.

SUMMARY OF THE CHAPTER

Running a business is all about cash. More specifically it is about generating as

much cash as possible from going round the working capital cycle again and again.

The primary objective is to receive more cash when we sell goods or services than

we paid out in fixed asset investment, overheads, labour and raw materials to make

or create them.

Businesses receive cash from the following sources:

•From successful trading (this being the OPERATING CASH MARGIN)

•From owners in the form of EQUITY

•From lenders and other cash providers in the form of DEBT

•In certain businesses (such a supermarkets) from the WORKING CAPITAL

CYCLE itself

Businesses spend cash in the following ways.

Within the trading cycle of the business to pay for:

•RAW MATERIALS, LABOUR and OVERHEADS

•Investing in the WORKING ASSET CYCLE

•Investing in FIXED ASSETS

They also make payments to external finance providers and the government in

the form of:

•INTEREST

•DIVIDENDS

•TAXATION

20 Cash Flow Analysis and Forecasting

•Debt repayment

•Equity buy backs and redemptions

Any cash held but not invested in the operations of the business is defined as

SURPLUS CASH. This cash may be the accumulation of historic surpluses or be

debt and equity not yet invested in the business itself. It may be retained in order

to display that the business has adequate liquidity to operate in the future and to

reinforce its credibility as a reliable counter-party.

CONCLUSION

Irrespective of the level of your prior knowledge you should now have an under-

standing of the way a business operates from a cash flow centric point of view.

You should also now appreciate some of the fundamental logic that underpins

business operation. The purpose of this chapter is to provide an adequate grasp

of the fundamentals of business, and more specifically cash flow, to assist in the

assimilation of the more advanced material that follows.

2

Understanding Cash Flows

Properly

INTRODUCTION

It is human nature to seek short cuts when engaged in any repetitive process. The

main purpose of these shortcuts being to save time and expense.

In my other life as a trainer I have observed experienced financial analysts adopt

a number of strategies to try to reduce the amount of time they spend evaluating

financial statements in order to come up with the required output. Many use pre-

prepared spreadsheet models and groups of ratios with which they are familiar.

Less experienced analysts generally seek to oversimplify the task, ignoring im-

portant information they do not yet understand and placing too much emphasis

on what they believe are the most important numbers. The tendency is to overem-

phasise and over-analyse what they know about and to underemphasise the source

information that is beyond their current level of comprehension.

However, there comes a point where omitting to gain a proper understanding

of the task and then failing to complete the analysis fully leads to the wrong

conclusions.

I have added the word ‘properly’ to this chapter heading in order to empha-

sise that it is necessary to acquire a solid understanding of cash flow analysis,

accounting theory, business strategy and financial control issues, before drawing

conclusions about a business entities cash flows. Those seeking immediate short

cuts are going to be disappointed! Although I would always encourage users of

this book to read as widely as possible around the subject, this book contains all

the knowledge required in order to complete this task.

There are three discrete steps involved in the process of analysing the reported

cash flows of a business. These are as follows:

1. We need to be able to understand a published cash flow statement.

2. We need to know how restate it into a more user-friendly format.

3. Finally, we need to understand what the restated values and totals signify.

This chapter deals with these tasks.

Cash Flow Analysis and Forecasting: The Definitive Guide to

Understanding and Using Published Cash Flow Data

by Timothy D.H. Jury

Copyright © 2012, Timothy D.H. Jury

22 Cash Flow Analysis and Forecasting

THE NATURE OF THE BEAST

We will start by familiarising ourselves with the basic anatomy of a cash flow

statement. Table 2.1 is a fairly simple cash flow statement. This is in the format of

a typical cash flow statement prepared in accordance with International Accounting

Standard 7 – Cash Flow Statements (IAS 7).

Table 2.1 A typical cash flow statement

Simple Limited

Cash Flow Statement Euros Euros

For the year ended 31st December 20XX ’000 ’000

Cash flows from operating activities

Profit before taxation 5600

Adjustments for:

Depreciation 550

Increase in operating provision 30

Investment income −500

Interest expense 350

6030

Increase in trade and other receivables −600

Decrease in inventories 1100

Decrease in trade payables −1690

Cash generated from operations 4840

Interest paid −310

Income taxes paid −1800

Net cash from operating activities 2730

Cash flows from investing activities

Acquisition of subsidiary X net of cash acquired −650

Purchase of property plant and equipment −460

Proceeds from sale of equipment 30

Interest received 350

Dividends received 320

Net cash used in investing activities −410

Cash flow from financing activities

Proceeds from issue of share capital 400

Proceeds from long term borrowings 360

Payment of finance lease liabilities −110

Dividends paid −1450

Net cash used in financing activities −800

Net increase in cash and cash equivalents 1520

Understanding Cash Flows Properly 23

Looking at the statement in its entirety the first thing that is evident is the cash

flow is split into three main sections. These have the following headings:

•Cash flows from operating activities,

•Cash flows from investing activities, and

•Cash flows from financing activities.

These primary headings have been used since the first standards on cash flows

were introduced in 1987. It appears the choice of these headings was quite arbitrary,

the objective being to make the cash flow statement more logical for the user.

Remember that the cash flow statement is still a relatively new invention when

compared to the balance sheet and profit and loss account. They have been around

for hundreds of years.

Let us see what each section contains.

CASH FLOWS FROM OPERATING ACTIVITIES

This section of a cash flow statement discloses two things:

1. The cash generated by the business, which is derived from generating more

cash from selling goods or services than the cash costs of production.

2. The amount invested or generated from the net working assets of the business.

In this example both these values sub-total to an item headed ‘Cash generated

from operations’. This section also contains the cash interest paid and the cash

taxes paid.

What is the Cash Generated from Operations?

In Chapter 1 Understanding How Cash Flows in a Business I introduced a cash

flow model, which I call the complete real business model. I offered the observation

that modern financial theory implies that the purpose of running a business is to

generate cash flow by selling goods and/or services for more cash than it costs to

produce them. Typically this is achieved in a manufacturing business by purchasing

raw materials and other inputs such as labour and overheads, which are combined

into finished products and then sold.

Notice I am talking solely in terms of cash, not profit. Profit and cash flow are

not the same thing. Over the past few decades the issue of what is profit has

become very complex. This will be discussed in more detail later in the book.

For a single product the cycle begins when we purchase the raw materials and

ends when the debt relating to the sale of the finished goods to the customer is

24 Cash Flow Analysis and Forecasting

paid. In an established business it is usual to enjoy a period of credit from suppliers

when purchasing raw materials and other overheads. To summarise, in order to

generate a cash flow from producing products we typically do the following:

1. Purchase inputs, typically RAW MATERIALS, LABOUR and OVERHEADS,

being granted credit by suppliers (and so creating a CREDITOR) in the

process.

2. Process these inputs through WORK IN PROGRESS into FINISHED GOODS.

3. Sell the FINISHED GOODS to a customer, typically granting them a credit

period as well (so creating a DEBTOR).

4. Collect the cash due from the customer at the appropriate time.

Intuitively it appears obvious that the cash generated from operations is likely to

be the value of the cash value received from customers when they have purchased

finished goods minus the cash costs of purchasing the inputs required to produce

them, such as raw materials, labour and overheads. There is, however, something

else we have to do in order to get this cash flow from customers.

We need to recognise that we have to invest cash in raw materials, work in

progress and finished goods. We also have to invest cash in lending money to our

customers until they pay us. Offsetting this is the fact that we get an interest free

loan from our suppliers for the period that they grant us credit when we purchase

goods from them. The amount invested in the inventory and debtors minus the

amount invested in operating creditors is known as the amount invested in net

working assets.

At the beginning of the reporting period we already have cash invested in these

items. As we proceed through the year it may be necessary to adjust the values

invested making them higher or lower depending on the flow of work through our

business and changes in the price and credit period granted in respect of inputs

to our business and the effects of changing our prices and the credit we give to

customers.

So, the effects of these changes to net working assets are also recognised in

the cash flow statement. They are to be found in the cash flow from operating

activities section of the cash flow statement together with the cash generated from

operations value.

To summarise, the business generates cash by going round the circle (Fig. 2.1)

at least once (and ideally many times) in a given period.

The business also needs to have cash invested in DEBTORS and INVENTORY,

less any contribution from CREDITORS, in order to trade. These three values may

also increase or decrease in any given reporting period.

Let us now go through this section in detail to understand its contents more

thoroughly.

Understanding Cash Flows Properly 25

Cash

Work in

Progress

Raw

Materials

Finished

Goods

Creditors Debtors

Cash

Non-Cash

Figure 2.1 Diagram of the working asset cycle

CASH FLOWS FROM OPERATING

ACTIVITIES – DETAILED REVIEW

Profit Before Taxation

The first item shown is the profit before taxation. You may be wondering what a

profit number is doing in the cash flow. Most published cash flows are prepared

using the indirect method. This means the reported cash flows are identified by

deriving them from data contained in the profit and loss account of the business for

the period and by identifying changes between the values disclosed in the opening

and closing balance sheets for the same period.

There is a second method of preparing a cash flow statement in published

accounts known as the direct method. This method is explained in more detail

in chapter 15 – Analysing direct cash flow statements.

When preparing an indirect cash flow statement the process commences by taking

one of the profit values disclosed in the profit and loss account. This is then

converted into the value of the operating cash flow by adjusting the profit value for

non-cash items that have already been added or deducted. Non-cash expenses are

added back and non-cash income items are removed. In this particular example

the cash flow statement begins with the profit before taxation value from the profit

and loss account of Simple Limited.

26 Cash Flow Analysis and Forecasting

Indirect cash flow statements can start from other profit values in the profit

and loss account. This depends on local GAAP variations and local custom in

preparing cash flow statements. Usually the starting value is either the profit

before interest and tax (also known as earnings before interest and tax ‘EBIT’,

or operating profit) or the profit after tax (also known as net income). These

variations are explained in more detail later in the book

GAAP stands for Generally Accepted Accounting Principles. This acronym

being used to encompass the laws, regulations, standards and customs used in

a particular jurisdiction to arrive at a set of published accounts.

A non-cash item is an income or expense item that appears in the profit and

loss account for which there is no corresponding cash flow. Typically, the most

substantial of these is the amount charged in the period for depreciation (also

known in some regions as amortisation). Depreciation is a non-cash item. You do

not write a cheque to anyone for depreciation!

Depreciation

Depreciation is an accounting adjustment. Its purpose is to charge the original cost

of purchasing an asset to the profit and loss account in a series of instalments over

its estimated useful life. Depreciation was invented by accountants a long time

ago to make the profit and loss account more meaningful as a document seeking

to communicate the annual performance of a business to its owners. If we did

not have depreciation in accounts and capital expenditure was simply a cost, the

business would show losses every time a substantial number of new fixed assets

were acquired and much higher profits in periods when no fixed asset expenditure

took place.

The effect of depreciation is to spread the cost effect of acquiring capital assets

over their estimated useful life. This is a reasonable way of dealing with fixed

assets because we continue to have the use of the fixed assets to assist us in

producing goods for the duration of their useful life. Another way of considering

the nature of depreciation is to think of it as a notional rent for the use of the fixed

assets from the balance sheet to the profit and loss account, which is charged each

year of the life of an asset to the profit and loss account.

The cash flow statement deals solely with cash flows. Depreciation is not a cash

flow. We must therefore adjust for the value of depreciation charged to profits in

identifying the cash flow generated from operations because it is a non-cash item.

When depreciation is deducted in the profit and loss account it is a cost or

expense item. Thus, when we adjust for it in the cash flow statement we are adding

it back to the disclosed profit before taxation value from the profit and loss account

in the process of arriving at the operating cash margin. This is why depreciation

appears as a positive value when disclosed in the cash flow statement.

Understanding Cash Flows Properly 27

Increase in Operating Provision

In a typical indirect cash flow statement there may be a number of further items

listed representing other non-cash items of income or expenditure in the profit and

loss account. In this particular example, in order to arrive at the correct value for

the cash generated from operations we are also adjusting the profit before taxation

value for an increase in operating provision. This label is a little vague. It does

not tell us exactly what operating provision is involved. For example, it might be

a provision relating to warranty claims on the years production, or further costs to

be incurred in respect of a recent product recall.

Vague labels of this type crop up again and again in published cash flow

statements. The fact that the label is vague is merely irritating, it will not affect our

ability to analyse the cash flow statement as long as we know what to do with the

item. As this item appears within the section of the cash flow statement labelled

‘adjustments’ we know it represents another add back to the profit before taxation

value required in order to arrive at the cash generated from operations value. It

is listed as an adjustment because movements in provisions do not represent cash

flows. They represent the recognition in this period’s accounts of the value of

a future expected cost related to activities within the current accounting period,

(an example of this might be the future warranty costs arising on this year’s

production).

The recognition of an expected future cost in the current periods profit and loss

account is not a cash flow. The fundamental accounting concept known as the

prudence concept requires that we recognise this future expected cost as soon as

we are aware of it. However, we do not expend any cash flow in respect of this

item until customers actually claim from the business in respect of warranties. The

cash costs involved therefore arise in future accounting periods and are shown as

such in the cash flow statement at that time.

The value of an increase in operating provision is shown as a positive number

in the cash flow statement. This is because, once again, we are reversing an item

that originally represented an increase in a future expected cost when charged to

the profit and loss account.

Conversely, the value of a decrease in operating provision is shown as a negative

number in the cash flow statement, this is because we are reversing an item that

originally represented a reduction in a future expected cost in the profit and loss

account.

Investment Income

This value represents the amount of investment income recognised in the profit

and loss account in the current period. Once again we are showing it here in the

cash flow statement as a reversing item because we need to remove it in order to

arrive at the correct value for the cash generated from operations.

28 Cash Flow Analysis and Forecasting

As we have mentioned before this cash flow statement commences with the

value profit before taxation. The investment income of the business has already

been recognised in the profit and loss account before arriving at this value. In order