Time Series Guide

User Manual:

Open the PDF directly: View PDF ![]() .

.

Page Count: 273 [warning: Documents this large are best viewed by clicking the View PDF Link!]

Time series

Introduction

Simple time series models

ARIMA

Validating a model

Spectral Analysis

Wavelets

Digital Signal Processing (DSP)

Modeling volatility: GARCH models (Generalized AutoRegressive Conditionnal Heteroscedasticity)

Multivariate time series

State-Space Models and Kalman Filtering

Non-linear time series and chaos

Other times

Discrete-valued time series: Markov chains and beyond

Variants of Markov chains

Untackled subjects

TO SORT

This chapter contrasts with the topics we have seen up to now: we were interested in the study of several independant realizations of a

simple statistical process (e.g., a gaussian random variable, or a mixture of gaussians, or a linear model); we shall now focus on a single

realization of a more complex process.

Here is the structure of this chapter.

After an introduction, motivating the notion of a time series and giving several examples, simulated or real, we shall present the classical

models of time series (AR, MA, ARMA, ARIMA, SARIMA), that provide recipes to build time series with desired properties. We shall

then present spectral methods, that focus on the discovery of periodic elements in time series. The simplicity of those models makes

them amenable, but they cannot describe the properties of some real-world time series: non-linear methods, built upon the classical

models (GARCH) are called for. State-Space Models and the Kalman filter follow the same vein: they assume that the data is build from

linear algebra, but that we do not observe everything -- there are "hidden" (unobserved, latent) variables.

Some of those methods readily generalize to higher dimensions, i.e., to the study of vector-valued time-series, i.e., to the study of several

related time series at the same time -- but some new phenomena appear (e.g., cointegration). Furthermore, if the number of time series to

study becomes too large, the vector models have too many parameters to be useful: we enter the realm of panel data.

We shall then present some less mainstream ideas: instead of linear algebra, time series can be produced by analytical (read: differential

equations) or procedural (read: chaos, fractals) means.

We finally present generalizations of time series: stochastic processes, in which time is continuous; irregular time series, in which time is

discrete but irregular; and discrete-valued time series (with Markov chains and Hidden Markov Models instead of AR and state-space

models).

Introduction

Examples

In probability theory, (you will also hear mention of "stochastic process": in a time series, time is discrete, in a stochastic

process, it is continuous)

. In statistics, it is

: for instance, the price of a stock, that changes every day; the air temperature, measured every month; the heart rate of a patient,

minute after minute, etc.

plot(LakeHuron,

ylab = "",

main = "Level of Lake Huron")

a time series

is a sequence of random

variables a variable that depends on

time

x <- window(sunspots, start=1750, end=1800)

plot(x,

ylab = "",

main = "Sunspot numbers")

plot(x,

type = 'p',

ylab = "",

main = "Sunspot numbers")

k <- 20

lines( filter(x, rep(1/k,k)),

col = 'red',

lwd = 3 )

Sometimes, it is so noisy that you do not see much,

You can then smooth the curve.

You can underline the periodicity, graphically, with vertical bars.

data(UKgas)

plot.band <- function (x, ...) {

plot(x, ...)

a <- time(x)

i1 <- floor(min(a))

i2 <- ceiling(max(a))

y1 <- par('usr')[3]

y2 <- par('usr')[4]

if( par("ylog") ){

y1 <- 10^y1

y2 <- 10^y2

}

for (i in seq(from=i1, to=i2-1, by=2)) {

polygon( c(i,i+1,i+1,i),

c(y1,y1,y2,y2),

col = 'grey',

border = NA )

}

par(new=T)

plot(x, ...)

}

plot.band(UKgas,

log = 'y',

ylab = "",

main = "UK gas consumption")

(someti have both the value and the time: you should then check that the order is the correct one), (histogram or,

better, density estimation), y[i+1] ~ y[i], outliers -- the more data you have, the dirtier: someone may have forgotten the decimal dot

while entering the data, someone may have decided to replace missing values by 0 or -999, etc.)

x <- LakeHuron

op <- par(mfrow = c(1,2),

mar = c(5,4,1,2)+.1,

oma = c(0,0,2,0))

hist(x,

col = "light blue",

xlab = "",

main = "")

qqnorm(x,

main = "")

qqline(x,

col = 'red')

par(op)

mtext("Lake Huron levels",

line = 2.5,

font = 2,

cex = 1.2)

x <- diff(LakeHuron)

op <- par(mfrow = c(1,2),

mar = c(5,4,1,2)+.1,

oma = c(0,0,2,0))

hist(x,

col = "light blue",

xlab = "",

main = "")

qqnorm(x,

main = "")

qqline(x,

col = 'red')

par(op)

mtext("Lake Huron level increments",

line = 2.5,

font = 2,

As always, before analysing the series, we have a look at it

(evolution with time, pattern changes, misordered values

mes, you distribution

font = 2,

cex = 1.2)

boxplot(x,

horizontal = TRUE,

col = "pink",

main = "Lake Huron levels")

plot(x,

ylab = "",

main = "Lake Huron levels")

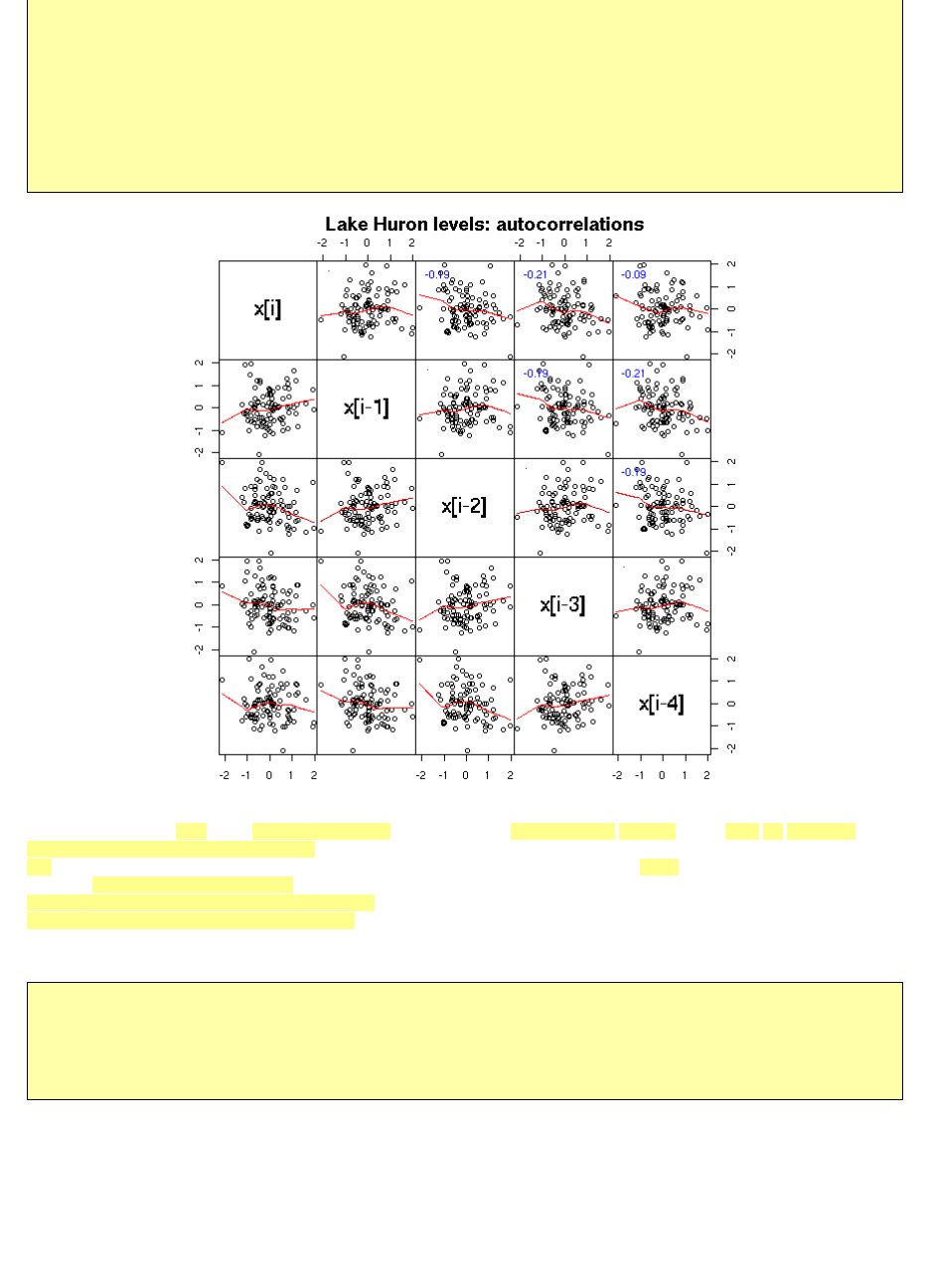

n <- length(x)

k <- 5

m <- matrix(nr=n+k-1, nc=k)

colnames(m) <- c("x[i]", "x[i-1]", "x[i-2]",

"x[i-3]", "x[i-4]")

for (i in 1:k) {

m[,i] <- c(rep(NA,i-1), x, rep(NA, k-i))

}

pairs(m,

gap = 0,

lower.panel = panel.smooth,

upper.panel = function (x,y) {

upper.panel = function (x,y) {

panel.smooth(x,y)

par(usr = c(0, 1, 0, 1))

a <- cor(x,y, use='pairwise.complete.obs')

text(.1,.9,

adj=c(0,1),

round(a, digits=2),

col='blue',

cex=2*a)

})

title("Lake Huron levels: autocorrelations",

line = 3)

We shall also see other , more . The first one, the (ACF)

(these are the numbers that already appeared in the previous pair plot). The second one, the (Partial AutoCorrelation

Function),

(more about this later, when we speak of AR models). The last one, the spectrogram,

tries to find periodic components, of various frequencies, in the signal and displays the importance of the various frequencies (more

about this later).

op <- par(mfrow = c(3,1),

mar = c(2,4,1,2)+.1)

acf(x, xlab = "")

pacf(x, xlab = "")

spectrum(x, xlab = "", main = "")

par(op)

plots specific to time series AutoCorrelation Function gives the correlation

between x[i] and x[i-k], for increasing values

of k PACF

contains the same information,

but gives the correlation between x[i] and x[i-k] that is

not explained by the correlations with a shorter lag

Simulations

ne (or one step)

Here are, in no particular order, a few simulated time series.

The first is just gaussian noise; the second is an integrated noise (a "random walk"). We can then build on those, integrating several

times, adding noise to the result, adding a linear or periodic trend, etc.

op <- par(mfrow = c(3,3),

mar = .1 + c(0,0,0,0))

n <- 100

k <- 5

N <- k*n

x <- (1:N)/n

plot(ts(y1),

xlab="", ylab="", main="", axes=F)

box()

plot(ts(y2),

xlab="", ylab="", main="", axes=F)

box()

)

plot(ts(y3),

xlab="", ylab="", main="", axes=F)

box()

)

plot(ts(y4),

xlab="", ylab="", main="", axes=F)

box()

plot(ts(y5),

xlab="", ylab="", main="", axes=F)

box()

# With a trend

O aim of time series analysis is to find the

"structure" of a time series, i.e., to find how it was

build, i.e., to find a simple algorithm that could produce

similar-looking data.

y1 <- rnorm(N)

y2 <- cumsum(rnorm(N))

y3 <- cumsum(rnorm(N))+rnorm(N

y4 <- cumsum(cumsum(rnorm(N))

y5 <- cumsum(cumsum(rnorm(N))+rnorm(N))+rnorm(N)

# With a trend

y6 <- 1 - x + cumsum(rnorm(N)) + .2 * rnorm(N)

plot(ts(y6),

xlab="", ylab="", main="", axes=F)

box()

y7 <- 1 - x - .2*x^2 + cumsum(rnorm(N)) +

.2 * rnorm(N)

plot(ts(y7),

xlab="", ylab="", main="", axes=F)

box()

# With a seasonnal component

y8 <- .3 + .5*cos(2*pi*x) - 1.2*sin(2*pi*x) +

.6*cos(2*2*pi*x) + .2*sin(2*2*pi*x) +

-.5*cos(3*2*pi*x) + .8*sin(3*2*pi*x)

plot(ts(y8+ .2*rnorm(N)),

xlab="", ylab="", main="", axes=F)

box()

lines(y8, type='l', lty=3, lwd=3, col='red')

y9 <- y8 + cumsum(rnorm(N)) + .2*rnorm(N)

plot(ts(y9),

xlab="", ylab="", main="", axes=F)

box()

par(op)

.

often called "innovations", usually by going in the other direction:

We can present this problem from another point of view: when you study a statistical phenomenon, you usually have several realizations

of it. With time series, you have a single one. Therefore, we replace the study of several realizations at a given point in time by the study

The main problem of time series analysis

In statistics, we like independent data -- the problem is

that time series contain dependent data The aim of a time

series analysis will thus be to extract this structure and

transform the initial time series into a series of

independant values by providing a recipe (a "model")

to build a series similar to the one we have with noise as only

ingredient.

of a single realization at several points in time. Depending on the statistical phenomenon, these two points of view may be equivalent or

not -- this problem is called ergodicity -- more about this later.

As the

(strictly speaking, one can consider the Sample ACF, if it is computed from a sample, or the

theoretical autocorrelation function, if it is not computed from actual data but from a model)

In order to compute it from a sample, you have to assume that it does not depend on n but only on the lag, k.

We could do it by hand

my.acf <- function (

x,

lag.max = ceiling(5*log(length(x)))

) {

m <- matrix(

c( NA,

rep( c(rep(NA, lag.max-1), x),

lag.max ),

rep(NA,, lag.max-1)

),

byrow=T,

nr=lag.max)

x0 <- m[1,]

apply(m,1,cor, x0, use="complete")

}

n <- 200

x <- rnorm(n)

plot(my.acf(x),

xlab = "Lag",

type = 'h')

abline(h=0)

but there is already such a function.

op <- par(mfrow=c(2,1))

acf(x, main="ACF of white noise")

x <- LakeHuron

acf(x, main="ACF of a time series (Lake Huron)")

par(op)

Autocorrelation

observations in a time series are generally not

independant, we can first have a look at their correlation:

the AutoCorrelation Function (ACF)

at lag k

is the correlation between observation number n and

observation number n - k.

The y=0 line traditionnally added to those plots can be misleading: it can suggest that the sign of a coefficient is known, while this

coefficient is not significantly different from zero. The boundaries of the confidence interval are sufficient

op <- par(mfrow=c(2,1))

set.seed(1)

x <- rnorm(100)

# Default plot

acf(x, main = "ACF with a distracting horizontal line")

# Without the axis, with larger bars

r <- acf(x, plot = FALSE)

plot(r$lag, r$acf,

type = "h", lwd = 20, col = "grey",

xlab = "lag", ylab = "autocorrelation",

main = "Autocorrelation without the y=0 line")

ci <- .95

clim <- qnorm( (1+ci) / 2 ) / sqrt(r$n.used)

abline(h = c(-1,1) * clim,

lty = 2, col = "blue", lwd = 2)

Here are the

but the plots have been shuffled: can you put them back in the correct order? Alternatively, can you see

several groups among those time series?

op <- par(mfrow=c(3,3), mar=c(0,0,0,0))

for (y in sample(list(y1,y2,y3,y4,y5,y6,y7,y8,y9))) {

acf(y,

xlab="", ylab="", main="", axes=F)

box(lwd=2)

}

par(op)

autocorrelation functions of the simulated

examples from the introduction,

Personnally, I can see three groups:

;

;

A white noise is

In other words, these are iid (independant, identically distributed) random variables, to the second order. (They may be dependent, but in

non-linear ways, that cannot be seen from the correlation; they may have different distributions, as long as the mean and variance remain

the same; their distribution need not be symetric.)

For instance, a series of iid random variables is a white noise.

my.plot.ts <- function (x, main="") {

op <- par(mar=c(2,2,4,2)+.1)

layout( matrix(c(1,2),nr=1,nc=2), widths=c(3,1) )

plot(x, xlab="", ylab="")

abline(h=0, lty=3)

title(main=main)

hist(x, col="light blue", main='', ylab="", xlab="")

par(op)

}

n <- 100

x <- ts(rnorm(n))

my.plot.ts(x, "Gaussian iid noise")

when the ACF is almost

zero, the data are not correlated when the ACF is sometimes

positive sometimes negative, the data might be periodic in

the other cases, the data are correlated -- but the speed at which

the autocorrelation decreases can vary.

White noise

a series of uncorrelated random variables,

whose expectation is zero, whose variance is constant.

Quite often, we shall try to decompose our time series into

a "trend" (or anything interpretable) plus a noise term,

that should be white noise.

A series of iid random variables of mean zero is also a white noise.

n <- 100

x <- ts(runif(n,-1,1))

my.plot.ts(x, "Non gaussian iid noise")

x <- ts(rnorm(100)^3)

my.plot.ts(x, "Non gaussian iid noise")

But you can also have a series of uncorrelated random variables that are not independant: the definition just asks that they be

"independant to the second order".

n <- 100

x <- rep(0,n)

z <- rnorm(n)

for (i in 2:n) {

x[i] <- z[i] * sqrt( 1 + .5 * x[i-1]^2 )

}

}

my.plot.ts(x, "Non iid noise")

Some deterministic sequences look like white noise.

n <- 100

x <- rep(.7, n)

for (i in 2:n) {

x[i] <- 4 * x[i-1] * ( 1 - x[i-1] )

}

my.plot.ts(x, "A deterministic time series")

n <- 1000

tn <- cumsum(rexp(n))

# A C^infinity function defined as a sum

# of gaussian densities

f <- function (x) {

# If x is a single number: sum(dnorm(x-tn))

apply( dnorm( outer(x,rep(1,length(tn))) -

outer(rep(1,length(x)),tn) ),

1,

sum )

}

op <- par(mfrow=c(2,1))

curve(

f(x),

xlim = c(1,500),

n = 1000,

main = "From far away, it looks random..."

)

curve(

f(x),

xlim = c(1,10),

n = 1000,

main="...but it is not: it is a C^infinity function"

)

par(op)

We have a few tests t

as we said in the introduction.

(exactly as we did with regression).

z <- rnorm(200)

op <- par(mfrow=c(2,1), mar=c(5,4,2,2)+.1)

plot(ts(z))

acf(z, main = "")

par(op)

o check if a given time series actually

is white noise.

Diagnostics: is this white noise?

The analysis of a time series mainly consists in finding out

a recipe to build it (or to build a similar-looking series)

from white noise, But to

find this recipe, we proceed in the other direction: we

start with our time series and we try to transform it into something that looks like white noise. To check if our

analysis is correct, we have to check that the residuals are

indeed white noise To

this end, we can start to have a look at the ACF (on

average, 5% of the values should be beyond the dashed lines

-- if there are much more, there might be a problem).

x <- diff(co2)

y <- diff(x,lag=12)

op <- par(mfrow=c(2,1), mar=c(5,4,2,2)+.1)

plot(ts(y))

acf(y, main="")

par(op)

To have a numerical result (a p-value), we can perform a Box--Pierce or Ljung--Box test (these are also called "portmanteau statistics"):

the idea is to consider the (weighted) sum of the first autocorrelation coefficients -- those sums (asymptotically) follow a chi^2

distribution (the Ljung-Box is a variant of the Box-Pierce one that gives a better Chi^2 approximation for small samples).

> Box.test(z) # Box-Pierce

Box-Pierce test

X-squared = 0.014, df = 1, p-value = 0.9059

> Box.test(z, type="Ljung-Box")

Box-Ljung test

X-squared = 0.0142, df = 1, p-value = 0.9051

> Box.test(y)

Box-Pierce test

X-squared = 41.5007, df = 1, p-value = 1.178e-10

> Box.test(y, type='Ljung')

Box-Ljung test

X-squared = 41.7749, df = 1, p-value = 1.024e-10

op <- par(mfrow=c(2,1))

plot.box.ljung <- function (

z,

k = 15,

main = "p-value of the Ljung-Box test",

ylab = "p-value"

) {

p <- rep(NA, k)

for (i in 1:k) {

p[i] <- Box.test(z, i,

type = "Ljung-Box")$p.value

}

plot(p,

type = 'h',

ylim = c(0,1),

lwd = 3,

main = main,

ylab = ylab)

abline(h = c(0,.05),

lty = 3)

}

plot.box.ljung(z, main="Random data")

plot.box.ljung(y, main="diff(diff(co2),lag=12)")

par(op)

There are other such tests: McLeod-Li, Turning-point, difference-sign, rank test, etc.

We can also use the Durbin--Watson we have already mentionned when we tackled regression.

TODO: check that I actually mention it.

library(car)

?durbin.watson

library(lmtest)

?dwtest

Here (it is the same test, but it is not implemented in the same way: the results may differ):

> dwtest(LakeHuron ~ 1)

Durbin-Watson test

data: LakeHuron ~ 1

DW = 0.3195, p-value = < 2.2e-16

alternative hypothesis: true autocorrelation is greater than 0

> durbin.watson(lm(LakeHuron ~ 1))

lag Autocorrelation D-W Statistic p-value

1 0.8319112 0.3195269 0

Alternative hypothesis: rho != 0

op <- par(mfrow=c(2,1))

library(lmtest)

plot(LakeHuron,

main = "Lake Huron")

acf(

LakeHuron,

main = paste(

"Durbin-Watson: p =",

signif( dwtest( LakeHuron ~ 1 ) $ p.value, 3 )

)

)

par(op)

n <- 200

x <- rnorm(n)

op <- par(mfrow=c(2,1))

x <- ts(x)

plot(x, main="White noise", ylab="")

acf(

x,

main = paste(

"Durbin-Watson: p =",

signif( dwtest( x ~ 1 ) $ p.value, 3)

)

)

par(op)

n <- 200

x <- rnorm(n)

op <- par(mfrow=c(2,1))

y <- filter(x,.8,method="recursive")

plot(y, main="AR(1)", ylab="")

acf(

y,

main = paste(

"p =",

signif( dwtest( y ~ 1 ) $ p.value, 3 )

)

)

par(op)

But beware: the default options tests wether the autocorrelation is positive or zero -- if it is significantly negative, the result will be

misleading...

set.seed(1)

n <- 200

x <- rnorm(n)

y <- filter(x, c(0,1), method="recursive")

op <- par(mfrow=c(3,1), mar=c(2,4,2,2)+.1)

plot(

y,

main = paste(

"one-sided DW test: p =",

signif( dwtest ( y ~ 1 ) $ p.value, 3 )

)

)

acf( y, main="")

pacf(y, main="")

par(op)

op <- par(mfrow=c(3,1), mar=c(2,4,2,2)+.1)

res <- dwtest( y ~ 1, alternative="two.sided")

plot(

y,

main = paste(

"two-sided p =",

signif( res$p.value, 3 )

)

)

acf(y, main="")

pacf(y, main="")

par(op)

There are other tests, such as the runs test (that looks at the number of runs, a run being consecutive observations of the same sign; that

kind of test is mainly used for qualitative time series or for time series that leave you completely clueless).

library(tseries)

?runs.test

or the Cowles-Jones test

TODO

A sequence is a pair of consecutive returns of the same sign; a

reversal is a pair of consecutive returns of opposite signs.

Their ratio, the Cowles-Jones ratio,

number of sequences

CJ = ---------------------

number of reversals

should be around one IF the drift is zero.

tsdiag

Actually, there is already a function, "tsdiag", that performs some tests on a time series (plot, ACF and Ljung-Box test).

data(co2)

r <- arima(

co2,

order = c(0, 1, 1),

seasonal = list(order = c(0, 1, 1), period = 12)

)

tsdiag(r)

he class

d white noise.

In this section, we shall try to model time series from this idea, using classical statistical methods (mainly regression). Some of the

procedures we shall present will be relevant, useful, but others will not work -- they are just ideas that one might think could work but

turn out not to. Keep your eyes open!

TODO: give the structure of this section

We shall first start to model the time series to be studied with regression, as a polynomial plus a sine wave or, more generally, as a

polynomial plus a periodic signal.

We shall then present modelling techniques based on the (exponential) moving average, that assume that the series locally looks like a

constant plus noise or a linear function plus noise -- this is the Holt-Winters filter.

First attempt: regression

data(co2)

plot(co2)

Simple time series models

T ical model

Classically, one tries to decompose a time series into a sum

of three terms: a trend (often, an affine function), a

seasonal component (a perdiodic function) an

Here, we , as when we were playing with regressions. Let us first try to write the data as the sum of

an affine function and a sine function.

y <- as.vector(co2)

x <- as.vector(time(co2))

r <- lm( y ~ poly(x,1) + cos(2*pi*x) + sin(2*pi*x) )

plot(y~x, type='l', xlab="time", ylab="co2")

lines(predict(r)~x, lty=3, col='red', lwd=3)

This is actually insufficient. It might not be that clear on this plot, but if you look at the residuals, it becomes obvious.

plot( y-predict(r),

main = "The residuals are not random yet",

xlab = "Time",

ylab = "Residuals" )

consider time as a predictive variable

Let us complicate the model: a degree 2 polynomial plus a sine function (if it were not sufficient, we would replace the polynomial by

splines) (we could also transform the time series, e.g., with a logarithm -- here, it does not work).

r <- lm( y ~ poly(x,2) + cos(2*pi*x) + sin(2*pi*x) )

plot(y~x, type='l', xlab="Time", ylab="co2")

lines(predict(r)~x, lty=3, col='red', lwd=3)

That is better.

plot( y-predict(r),

main = "Better residuals -- but still not random",

xlab = "Time",

ylab = "Residuals" )

We could try to refine the periodic component, but it would not really improve things.

r <- lm( y ~ poly(x,2) + cos(2*pi*x) + sin(2*pi*x)

+ cos(4*pi*x) + sin(4*pi*x) )

plot(y~x, type='l', xlab="Time", ylab="co2")

lines(predict(r)~x, lty=3, col='red', lwd=3)

plot( y-predict(r),

type = 'l',

xlab = "Time",

ylab = "Residuals",

main = "Are those residuals any better?" )

However, the ACF suggests that those models are not as good as they seemed:

r1 <- lm( y ~ poly(x,2) +

cos(2*pi*x) +

sin(2*pi*x) )

r2 <- lm( y ~ poly(x,2) +

cos(2*pi*x) +

sin(2*pi*x) +

cos(4*pi*x) +

sin(4*pi*x) )

op <- par(mfrow=c(2,1))

acf(y - predict(r1))

acf(y - predict(r2))

par(op)

if the residuals were really white noise, we

would have very few values beyond the dashed lines...

Those plots tell us two things: first, after all, it was useful to refine the periodic component; second, we still have autocorrelation

problems.

Other attempt (apparently a bad idea)

To estimate the periodic component, we could average the january values, then the february values, etc.

m <- tapply(co2, gl(12,1,length(co2)), mean)

m <- rep(m, ceiling(length(co2)/12)) [1:length(co2)]

m <- ts(m, start=start(co2), frequency=frequency(co2))

op <- par(mfrow=c(3,1), mar=c(2,4,2,2))

plot(co2)

plot(m, ylab = "Periodic component")

plot(co2-m, ylab = "Withou the periodic component")

r <- lm(co2-m ~ poly(as.vector(time(m)),2))

lines(predict(r) ~ as.vector(time(m)), col='red')

par(op)

However, a look at the residuals tell us that the periodic component is still there...

op <- par(mfrow=c(4,1), mar=c(2,4,2,2)+.1)

plot(r$res, type = "l")

acf(r$res, main="")

pacf(r$res, main="")

spectrum(r$res, col=par('fg'), main="")

abline(v=1:6, lty=3)

par(op)

Other attempt (better than the previous)

Using the mean as above to estimate the periodic component would only work if the model were of the form

y ~ a + b x + periodic component.

But here, we have a quadratic term: averaging for each month will nt work. However, we can reuse the same idea with a single

regression, to find both the periodic component and the trend. Here, the periodic component can be anything: we have 12 coefficients to

estimate on top of those of the trend.

k <- 12

m <- matrix( as.vector(diag(k)),

nr = length(co2),

nc = k,

byrow = TRUE )

m <- cbind(m, poly(as.vector(time(co2)),2))

r <- lm(co2~m-1)

summary(r)

b <- r$coef

y1 <- m[,1:k] %*% b[1:k]

y1 <- ts(y1,

start=start(co2),

frequency=frequency(co2))

y2 <- m[,k+1:2] %*% b[k+1:2]

y2 <- ts(y2,

start=start(co2),

frequency=frequency(co2))

res <- co2 - y1 - y2

res <- co2 - y1 - y2

op <- par(mfrow=c(3,1), mar=c(2,4,2,2)+.1)

plot(co2)

lines(y2+mean(b[1:k]) ~ as.vector(time(co2)),

col='red')

plot(y1)

plot(res)

par(op)

Here, the analysis is not finished: we still have to study the resulting noise -- but we did get rid of the periodic component.

op <- par(mfrow=c(3,1), mar=c(2,4,2,2)+.1)

acf(res, main="")

pacf(res, main="")

spectrum(res, col=par('fg'), main="")

abline(v=1:10, lty=3)

par(op)

To pursue the example to its end, one is tempted to fit an AR(2) (an ARMA(1,1) would do, as well) to the residuals.

innovations <- arima(res, c(2,0,0))$residuals

op <- par(mfrow=c(4,1), mar=c(3,4,2,2))

plot(innovations)

acf(innovations)

pacf(innovations)

spectrum(innovations)

par(op)

Same idea, with splines

In the last example, if the period was longer, we would use splines to find a smoother periodic component -- and also to have fewer

parameters: 15 was really a lot.

Exercise left to the reader...

Finding the trend (or removing the seasonal component): Moving Average

x <- co2

n <- length(x)

k <- 12

m <- matrix( c(x, rep(NA,k)), nr=n+k-1, nc=k )

y <- apply(m, 1, mean, na.rm=T)

y <- y[1:n + round(k/2)]

y <- ts(y, start=start(x), frequency=frequency(x))

y <- y[round(k/4):(n-round(k/4))]

yt <- time(x)[ round(k/4):(n-round(k/4)) ]

plot(x, ylab="co2")

lines(y~yt, col='red')

To find the trend of a time series, you can simply "smooth"

it, e.g., with a Moving Average (MA).

The Moving average will leave invariant some functions (e.g., polynomials of degree up to three -- choose the coefficients accordingly).

The "filter" function already does this. Do not forget the "side" argument: otherwise, it will use values from the past and the future -- for

time series this is rarely desirable: it would introduce a look-ahead bias.

x <- co2

plot(x, ylab="co2")

k <- 12

lines( filter(x, rep(1/k,k), side=1), col='red')

MA: Filtering and smoothing

Actually, one should distinguish between "smoothing" with a Moving Average (to find the value at a point, one uses the whole sample,

including what happend after that point) and "filtering" with a Moving Average (to find the smoothed value at a point, one only uses the

information up to that point).

When we perform a usual regression, we are interested in the shape of our data in the whole interval. On the contrary, quite often, when

we study time series, we are interested in what happens at the end of the interval -- and try to forecast beyond.

In the first case, we use smoothing: to compute the Moving Average at time t, we average over an interval centered on t. The drawback is

that we cannot do that at the two ends of the interval: there will be missing values at the begining and the end.

In the second case, as we do want values at the end of the interval, we do not average on an interval centered on t, but on the values up to

time t. The drawback is that this introduces a lag: we have the same values as before, but t/2 units later.

The "side" argument of the filter() function lest you choose between smoothing and filtering.

x <- co2

plot(window(x, 1990, max(time(x))), ylab="co2")

k <- 12

lines( filter(x, rep(1/k,k)),

col='red', lwd=3)

lines( filter(x, rep(1/k,k), sides=1),

col='blue', lwd=3)

legend(par('usr')[1], par('usr')[4], xjust=0,

c('smoother', 'filter'),

lwd=3, lty=1,

lwd=3, lty=1,

col=c('red','blue'))

Filters are especially used in real-time systems: we want the best estimation of some quantity using all the data collected so far, and we

want to update this estimate when new data comes in.

Applications of the Moving Average

Here is a classical investment strategy (I do not claim it works): take a price time series, compute a 20-day moving average and a 50-day

one; when the two curves intersect, buy or sell (finance people call the difference between those two moving averages an "oscillator" -- it

is a time series that should wander around zero, that should revert to zero -- you can try to design you own oscillator: the strategy will be

"buy when the oscillator is low, sell when it is high").

library(fBasics) # RMetrics

x <- yahooImport("s=IBM&a=11&b=1&c=1999&d=0&q=31&f=2000&z=IBM&x=.csv")

x <- as.numeric(as.character(x@data$Close))

x20 <- filter(x, rep(1/20,20), sides=1)

x50 <- filter(x, rep(1/50,50), sides=1)

matplot(cbind(x,x20,x50), type="l", lty=1, ylab="price", log="y")

segments(1:length(x), x[-length(x)], 1:length(x), x[-1], lwd=ifelse(x20>x50,1,5)[-1], col=ifelse(x20>x50,"black","blue")[-1])

Exercise: do the same with an exponential moving average.

Exponential Moving average

The moving average has a slight problem: it uses a window with sharp edges; an observation is either in the window or not. As a result,

when large observations enter or leave the window, there is large jump in the moving average.

This is another moving average: instead of taking the N latest values, equally-weighted, we take all the preceding values and give a

higher weight to the latest values.

exponential.moving.average <-

function (x, a) {

m <- x

for (i in 2:n) {

# Definition

# Exercise: use the "filter" function instead,

# with its "recursive" argument (that should be

# much, much faster)

m[i] <- a * x[i] + (1-a)*m[i-1]

}

m <- ts(m, start=start(x), frequency=frequency(x))

m

}

plot.exponential.moving.average <-

function (x, a=.9, ...) {

plot(exponential.moving.average(x,a), ...)

par(usr=c(0,1,0,1))

text(.02,.9, a, adj=c(0,1), cex=3)

}

op <- par(mfrow=c(4,1), mar=c(2,2,2,2)+.1)

plot(x, main="Exponential Moving Averages")

plot.exponential.moving.average(x, main="", ylab="")

plot.exponential.moving.average(x,.1, main="", ylab="")

plot.exponential.moving.average(x,.02, main="", ylab="")

par(op)

r <- x - exponential.moving.average(x,.02)

op <- par(mfrow=c(4,1), mar=c(2,4,2,2)+.1)

plot(r, main="Residuals of an exponential moving average")

acf(r, main="")

pacf(r, main="")

spectrum(r, main="")

abline(v=1:10,lty=3)

par(op)

As with all moving average filters, there is a lag.

Actually, there is already a function to do this (it is a special case of the Holt-Winters filter -- we shall present the general case in a few

moments):

x <- co2

m <- HoltWinters(x, alpha=.1, beta=0, gamma=0)

p <- predict(m, n.ahead=240, prediction.interval=T)

plot(m, predicted.values=p)

y <- x20 > x50

op <- par(mfrow=c(5,1), mar=c(0,0,0,0), oma=.1+c(0,0,0,0))

plot(y, type="l", axes=FALSE); box()

plot(filter(y, 50/100, "recursive", sides=1), axes=FALSE); box()

plot(filter(y, 90/100, "recursive", sides=1), axes=FALSE); box()

plot(filter(y, 95/100, "recursive", sides=1), axes=FALSE); box()

plot(filter(y, 99/100, "recursive", sides=1), axes=FALSE); box()

par(op)

Other moving quantities

The "runing" function in the "gtools" package, the "rollFun" function in the "rollFun" in the "fMultivar" package (in RMetrics) and the

"rollapply" function in the "zoo" package compute a statistic (mean, standard deviation, median, quantiles, etc.) on a moving window.

library(zoo)

op <- par(mfrow=c(3,1), mar=c(0,4,0,0), oma=.1+c(0,0,0,0))

plot(rollapply(zoo(x), 10, median, align="left"),

axes = FALSE, ylab = "median")

lines(zoo(x), col="grey")

box()

plot(rollapply(zoo(x), 50, sd, align="left"),

axes = FALSE, ylab = "sd")

box()

library(robustbase)

plot(sqrt(rollapply(zoo(x), 50, Sn, align="left")),

axes = FALSE, ylab = "Sn")

box()

par(op)

Finding the trend: Fourrier Transform

One can also find the trend of a time series by performing a Fourier transform and removing the high frequencies -- indeed, the moving

averages we considered earlier are low-pass filters.

Exercise left to the reader

Finding the trend: differentiation

If a time series has a trend, if this trend is a polynomial of degree n, then you can transform this series into a trend-less one by

differentiating it (using the discrete derivative) n times.

TODO: an example

To go back to the initial time series, you just have to integrate n times ("discrete integration" is just a complicated word for "cumulated

sums" -- but, of course, you have to worry about the integration constants).

TODO: Explain the relations/confusions between trend, stationarity,

integration, derivation.

TODO: Take a couple of (real-world) time series and apply them all the methods above, in order to compare them

Local regression: loess

The "stl" function performs a "Seasonal Decomposition of a Time Series by Loess".

In case you have forgotten, the "loess" function performs a local regression, i.e., for each value of the predictive variable, we take the

neighbouring observations and perform a linear regression with them; the loess curve is the "envelope" of those regression lines.

op <- par(mfrow=c(3,1), mar=c(3,4,0,1), oma=c(0,0,2,0))

r <- stl(co2, s.window="periodic")$time.series

plot(co2)

lines(r[,2], col='blue')

lines(r[,2]+r[,1], col='red')

plot(r[,3])

acf(r[,3], main="residuals")

par(op)

mtext("STL(co2)", line=3, font=2, cex=1.2)

The "decompose" function has a similar purpose.

r <- decompose(co2)

plot(r)

op <- par(mfrow=c(2,1), mar=c(0,2,0,2), oma=c(2,0,2,0))

acf(r$random, na.action=na.pass, axes=F, ylab="")

box(lwd=3)

mtext("PACF", side=2, line=.5)

pacf(r$random, na.action=na.pass, axes=F, ylab="")

box(lwd=3)

axis(1)

mtext("PACF", side=2, line=.5)

par(op)

mtext("stl(co2): residuals", line=2.5, font=2, cex=1.2)

Holt-Winters filtering

This is a generalization of exponential filtering (which assumes there is no seasonal component). It has the same advantages: it is not

very sensible to (not too drastic) structural changes.

For exponential filtering, we had used

a(t) = alpha * Y(t) + (1-alpha) * a(t-1).

This is a good estimator of the future values of the time series if it is of the form Y(t) = Y_0 + noise, i.e., if the series is "a constant plus

noise" (or even if it is just "locally constant").

This assumed that the series was locallly constant. Here is an example.

data(LakeHuron)

x <- LakeHuron

before <- window(x, end=1935)

after <- window(x, start=1935)

a <- .2

b <- 0

g <- 0

model <- HoltWinters(

before,

alpha=a, beta=b, gamma=g)

forecast <- predict(

model,

n.ahead=37,

prediction.interval=T)

plot(model, predicted.values=forecast,

main="Holt-Winters filtering: constant model")

lines(after)

We can add a trend: we model the data as a line, from the preceding values, giving more weight to the most recent values.

data(LakeHuron)

x <- LakeHuron

before <- window(x, end=1935)

after <- window(x, start=1935)

a <- .2

b <- .2

g <- 0

model <- HoltWinters(

before,

alpha=a, beta=b, gamma=g)

forecast <- predict(

model,

n.ahead=37,

prediction.interval=T)

plot(model, predicted.values=forecast,

main="Holt-Winters filtering: trend model")

lines(after)

Depending on the choice of beta, the forecasts can be very different...

data(LakeHuron)

x <- LakeHuron

op <- par(mfrow=c(2,2),

mar=c(0,0,0,0),

oma=c(1,1,3,1))

before <- window(x, end=1935)

after <- window(x, start=1935)

a <- .2

b <- .5

g <- 0

for (b in c(.02, .04, .1, .5)) {

model <- HoltWinters(

before,

alpha=a, beta=b, gamma=g)

forecast <- predict(

model,

n.ahead=37,

prediction.interval=T)

plot(model,

predicted.values=forecast,

axes=F, xlab='', ylab='', main='')

box()

text( (4*par('usr')[1]+par('usr')[2])/5,

(par('usr')[3]+5*par('usr')[4])/6,

paste("beta =",b),

cex=2, col='blue' )

lines(after)

}

par(op)

mtext("Holt-Winters filtering: different values for beta",

line=-1.5, font=2, cex=1.2)

You can also add a seosonal component (and additive or a multiplicative one).

TODO: Example

TODO: A multiplicative example

Structural models

Before presenting general models whose interpretation may not be that straightforward (ARIMA, SARIMA), let us stop a moment to

consider structural models, that are special cases of AR, MA, ARMA, ARIMA, SARIMA.

A random walk, with noise (a special case of ARIMA(0,1,1)):

X(t) = mu(t) + noise1

mu(t+1) = mu(t) + noise2

n <- 200

plot(ts(cumsum(rnorm(n)) + rnorm(n)),

main="Noisy random walk",

ylab="")

A random walk is simply "integrated noise" (as this is a discrete integration, we use the "cumsum" function). One can add some noise to

a random walk: this is called a local level model.

We can also change the variance of those noises.

op <- par(mfrow=c(2,1),

mar=c(3,4,0,2)+.1,

oma=c(0,0,3,0))

plot(ts(cumsum(rnorm(n, sd=1))+rnorm(n,sd=.1)),

ylab="")

plot(ts(cumsum(rnorm(n, sd=.1))+rnorm(n,sd=1)),

ylab="")

par(op)

mtext("Noisy random walk", line=2, font=2, cex=1.2)

A noisy random walk, integrated, with added noise (ARIMA(0,2,2), aka local trend model):

X(t) = mu(t) + noise1

mu(t+1) = mu(t) + nu(t) + noise2 (level)

nu(t+1) = nu(t) + noise3 (slope)

n <- 200

plot(ts( cumsum( cumsum(rnorm(n))+rnorm(n) ) +

rnorm(n) ),

main = "Local trend model",

ylab="")

Here again, we can play and change the noise variances.

n <- 200

op <- par(mfrow=c(3,1),

mar=c(3,4,2,2)+.1,

oma=c(0,0,2,0))

plot(ts( cumsum( cumsum(rnorm(n,sd=1))+rnorm(n,sd=1) )

+ rnorm(n,sd=.1) ),

ylab="")

plot(ts( cumsum( cumsum(rnorm(n,sd=1))+rnorm(n,sd=.1) )

+ rnorm(n,sd=1) ),

ylab="")

plot(ts( cumsum( cumsum(rnorm(n,sd=.1))+rnorm(n,sd=1) )

+ rnorm(n,sd=1) ),

ylab="")

par(op)

mtext("Local level models", line=2, font=2, cex=1.2)

A noisy random walk, integrated, with added noise, to which we add a variable seasonal component.

X(t) = mu(t) + gamma(t) + noise1

mu(t+1) = mu(t) + nu(t) + noise2 (level)

nu(t+1) = nu(t) + noise2 (slope)

gamma(t+1) = -(gamma(t) + gamma(t-1) + gamma(t-2)) + noise4 (seasonal component)

structural.model <- function (

n=200,

sd1=1, sd2=1, sd3=1, sd4=1, sd5=200

) {

sd1 <- 1

sd2 <- 2

sd3 <- 3

sd4 <- 4

mu <- rep(rnorm(1),n)

nu <- rep(rnorm(1),n)

g <- rep(rnorm(1,sd=sd5),n)

x <- mu + g + rnorm(1,sd=sd1)

for (i in 2:n) {

if (i>3) {

g[i] <- -(g[i-1]+g[i-2]+g[i-3]) + rnorm(1,sd=sd4)

} else {

g[i] <- rnorm(1,sd=sd5)

}

nu[i] <- nu[i-1] + rnorm(1,sd=sd3)

mu[i] <- mu[i-1] + nu[i-1] + rnorm(1,sd=sd2)

x[i] <- mu[i] + g[i] + rnorm(1,sd=sd1)

}

ts(x)

}

n <- 200

op <- par(mfrow=c(3,1),

mar=c(2,2,2,2)+.1,

oma=c(0,0,2,0))

plot(structural.model(n))

plot(structural.model(n))

plot(structural.model(n))

par(op)

mtext("Structural models", line=2.5, font=2, cex=1.2)

Here again, we can change the noise variance. If the seasonal component is not noisy, it is constant (but arbitrary).

n <- 200

op <- par(mfrow=c(3,1),

mar=c(2,2,2,2)+.1,

oma=c(0,0,2,0))

plot(structural.model(n,sd4=0))

plot(structural.model(n,sd4=0))

plot(structural.model(n,sd4=0))

par(op)

mtext("Structural models", line=2.5, font=2, cex=1.2)

You can model a time series along those models with the "StructTS" function.

data(AirPassengers)

plot(AirPassengers)

plot(log(AirPassengers))

x <- log(AirPassengers)

r <- StructTS(x)

plot(x, main="AirPassengers", ylab="")

f <- apply(fitted(r), 1, sum)

f <- ts(f, frequency=frequency(x), start=start(x))

lines(f, col='red', lty=3, lwd=3)

Here, the slope seems constant.

> r

Call:

StructTS(x = x)

Variances:

level slope seas epsilon

0.0007718 0.0000000 0.0013969 0.0000000

> summary(r$fitted[,"slope"])

Min. 1st Qu. Median Mean 3rd Qu. Max.

0.000000 0.009101 0.010210 0.009420 0.010560 0.011040

matplot(

matplot(

(StructTS(x-min(x)))$fitted,

type = 'l',

ylab = "",

main = "Structural model decomposition of a time series"

)

You can also try to forecast future values (but it might not be that reliable).

l <- 1956

x <- log(AirPassengers)

x1 <- window(x, end=l)

x2 <- window(x, start=l)

r <- StructTS(x1)

plot(x)

f <- apply(fitted(r), 1, sum)

f <- ts(f, frequency=frequency(x), start=start(x))

lines(f, col='red')

p <- predict(r, n.ahead=100)

lines(p$pred, col='red')

lines(p$pred + qnorm(.025) * p$se,

col='red', lty=2)

lines(p$pred + qnorm(.975) * p$se,

col='red', lty=2)

title(main="Forecasting with a structural model (StructTS)")

Examples

TODO: put this at the end of the introduction?

# A function to look at a time series

eda.ts <- function (x, bands=FALSE) {

op <- par(no.readonly = TRUE)

par(mar=c(0,0,0,0), oma=c(1,4,2,1))

# Compute the Ljung-Box p-values

# (we only display them if needed, i.e.,

# if we have any reason of

# thinking it is white noise).

p.min <- .05

k <- 15

p <- rep(NA, k)

for (i in 1:k) {

p[i] <- Box.test(

x, i, type = "Ljung-Box"

)$p.value

}

if( max(p)>p.min ) {

par(mfrow=c(5,1))

} else {

par(mfrow=c(4,1))

}

if(!is.ts(x))

x <- ts(x)

plot(x, axes=FALSE);

axis(2); axis(3); box(lwd=2)

if(bands) {

a <- time(x)

i1 <- floor(min(a))

i2 <- ceiling(max(a))

y1 <- par('usr')[3]

y2 <- par('usr')[4]

if( par("ylog") ){

y1 <- 10^y1

y2 <- 10^y2

}

for (i in seq(from=i1, to=i2-1, by=2)) {

polygon( c(i,i+1,i+1,i), c(y1,y1,y2,y2),

col='grey', border=NA )

}

lines(x)

lines(x)

}

acf(x, axes=FALSE)

axis(2, las=2)

box(lwd=2)

mtext("ACF", side=2, line=2.5)

pacf(x, axes=FALSE)

axis(2, las=2)

box(lwd=2)

mtext("ACF", side=2, line=2.5)

spectrum(x, col=par('fg'), log="dB",

main="", axes=FALSE )

axis(2, las=2)

box(lwd=2)

mtext("Spectrum", side=2, line=2.5)

abline(v=1, lty=2, lwd=2)

abline(v=2:10, lty=3)

abline(v=1/2:5, lty=3)

if( max(p)>p.min ) {

main <-

plot(p, type='h', ylim=c(0,1),

lwd=3, main="", axes=F)

axis(2, las=2)

box(lwd=2)

mtext("Ljung-Box p-value", side=2, line=2.5)

abline(h=c(0,.05),lty=3)

}

par(op)

}

data(co2)

eda.ts(co2, bands=T)

Transformations

TODO: Put this section somewhere above

As for the regression, we first transform the data so that ot looks "nicer" (as usual, plot the histogram, density estimation, qqplot, etc., try

a Box-Cox transformation). For instance, if you remark that the larger the value, the larger the variations, and if it is reasonable to think

that the model could be "something deterministic plus noise", you can take the logarithm.

More generally, the aim of time series analysis is actually to transform the data so that it looks gaussian; the inverse of that

transformation is then a model describing how the time series may have been produced from white noise.

Examples

data(AirPassengers)

x <- AirPassengers

plot(x)

plot(x)

abline(lm(x~time(x)), col='red')

The residuals or the first derivative suggest that the amplitude of the variations increase.

plot(lm(x~time(x))$res)

plot(diff(x))

Let us try with the logarithm.

x <- log(x)

plot(x)

abline(lm(x~time(x)),col='red')

plot(lm(x~time(x))$res)

plot(diff(x))

We could also have a look at the next derivatives.

op <- par(mfrow=c(3,1))

plot(diff(x,1,2))

plot(diff(x,1,3))

plot(diff(x,1,4))

par(op)

There seems to be a 12-month seasonal component.

op <- par(mfrow=c(3,1))

plot(x)

abline(h=0, v=1950:1962, lty=3)

y <- diff(x)

plot(y)

abline(h=0, v=1950:1962, lty=3)

plot(diff(y, 12,1))

abline(h=0, v=1950:1962, lty=3)

par(op)

You can also use a regression to get rid of the up-trend.

op <- par(mfrow=c(3,1))

plot(x)

abline(lm(x~time(x)), col='red', lty=2)

abline(h=0, v=1950:1962, lty=3)

y <- x - predict(lm(x~time(x)))

plot(y)

abline(h=0, v=1950:1962, lty=3)

plot(diff(y, 12,1))

abline(h=0, v=1950:1962, lty=3)

par(op)

Let us look at the residuals and differentiate.

z <- diff(y,12,1)

op <- par(mfrow=c(3,1))

plot(z)

abline(h=0,lty=3)

plot(diff(z))

abline(h=0,lty=3)

plot(diff(z,1,2))

abline(h=0,lty=3)

par(op)

How many times should we differentiate?

k <- 3

op <- par(mfrow=c(k,2))

zz <- z

for(i in 1:k) {

acf(zz, main=i-1)

pacf(zz, main=i-1)

zz <- diff(zz)

}

par(op)

TODO: What is this?

data(sunspots)

op <- par(mfrow=c(5,1))

for (i in 10+1:5) {

plot(diff(sunspots,i))

}

par(op)

ARIMA

ACF

The main difference between time series and the series of iid random variables we have been playing with up to now is the lack of

independance. Correlation is one means of measuring that lack of independance (if the variables are gaussian, it is even an accurate

means).

The AutoCorrelation Function (ACF) is the correlation between a term and the i-th preceding term

ACF(i) = Cor( X(t), X(t-i) )

If indeed this does not depend on the position t, the time series is said to be weakly stationary -- it is said to be strongly stationary if for

all t, h, the joint distributions of (X(t),X(t+1),...,X(t+n)) and (X(t+h),X(t+h+1),...,X(t+h+n)) are the same.

In the following plot, most (1/20) of the values of the ACT should be between the dashed lines -- otherwise, there might be something

else than gaussian noise in your data.

Strictly speaking, one should distinguish between the theoretical ACF, computed from a model, without any data and the Sample ACF

(SACF), computed from a sample. Here, we compute the SACF of a realization of a model.

op <- par(mfrow=c(2,1), mar=c(2,4,3,2)+.1)

x <- ts(rnorm(200))

plot(x, main="gaussian iidrv",

xlab="", ylab="")

acf(x, main="")

par(op)

A real example:

op <- par(mfrow=c(2,1), mar=c(2,4,3,2)+.1)

data(BJsales)

plot(BJsales, xlab="", ylab="", main="BJsales")

acf(BJsales, main="")

par(op)

f <- 24

x <- seq(0,10, by=1/f)

y <- sin(2*pi*x)

y <- ts(y, start=0, frequency=f)

op <- par(mfrow=c(4,1), mar=c(2,4,2,2)+.1)

plot(y, xlab="", ylab="")

acf(y, main="")

pacf(y, main="")

spectrum(y, main="", xlab="")

par(op)

f <- 24

x <- seq(0,10, by=1/f)

y <- x + sin(2*pi*x) + rnorm(10*f)

y <- ts(y, start=0, frequency=f)

op <- par(mfrow=c(4,1), mar=c(2,4,2,2)+.1)

plot(y, xlab="", ylab="")

acf(y, main="")

pacf(y, main="")

spectrum(y, main="", xlab="")

par(op)

Correlogram, variogram

The ACF plot is called an "autocorrelogram". In the case where the observations are not evenly spaced, one can plot a variogram instead:

(y(t_i)-y(t_j))^2 as a function of t_i-t_j.

TODO: plot with irregularly-spaced data

TODO: smooth this plot.

Often, these are (regular) time series with missing values, In this case, for a given value of k=t_i-t_j (on the horizontal axis), we have

several values. You can replace them by their mean.

TODO: example

Take a time series, remove some of its values, compare the

correlogram and the variogram.

(There is also an analogue of the variogram for discrete-valued time series: the lorelogram, based on the LOR -- Logarithm of Odds

Ratio.)

MA (Moving Average models)

Here is a simple way of building a time series from a white noise: just perform a Moving Average (MA) of this noise.

n <- 200

x <- rnorm(n)

y <- ( x[2:n] + x[2:n-1] ) / 2

op <- par(mfrow=c(3,1), mar=c(2,4,2,2)+.1)

plot(ts(x), xlab="", ylab="white noise")

plot(ts(y), xlab="", ylab="MA(1)")

acf(y, main="")

par(op)

n <- 200

x <- rnorm(n)

y <- ( x[1:(n-3)] + x[2:(n-2)] + x[3:(n-1)] + x[4:n] )/4

op <- par(mfrow=c(3,1), mar=c(2,4,2,2)+.1)

plot(ts(x), xlab="", ylab="white noise")

plot(ts(y), xlab="", ylab="MA(3)")

acf(y, main="")

par(op)

You can also compute the moving average with different coefficients.

n <- 200

x <- rnorm(n)

y <- x[2:n] - x[1:(n-1)]

op <- par(mfrow=c(3,1), mar=c(2,4,2,2)+.1)

plot(ts(x), xlab="", ylab="white noise")

plot(ts(y), xlab="", ylab="momentum(1)")

acf(y, main="")

par(op)

n <- 200

x <- rnorm(n)

y <- x[3:n] - 2 * x[2:(n-1)] + x[1:(n-2)]

op <- par(mfrow=c(3,1), mar=c(2,4,2,2)+.1)

plot(ts(x), xlab="", ylab="white noise")

plot(ts(y), xlab="", ylab="Momentum(2)")

acf(y, main="")

par(op)

Instead of computing the moving average by hand, you can use the "filter" function.

n <- 200

x <- rnorm(n)

y <- filter(x, c(1,-2,1))

op <- par(mfrow=c(3,1), mar=c(2,4,2,2)+.1)

plot(ts(x), xlab="", ylab="White noise")

plot(ts(y), xlab="", ylab="Momentum(2)")

acf(y, na.action=na.pass, main="")

par(op)

TODO: the "side=1" argument.

AR (Auto-Regressive models)

Another means of building a time series is to compute each term by adding noise to the preceding term: this is called a random walk.

For instance,

n <- 200

x <- rep(0,n)

for (i in 2:n) {

x[i] <- x[i-1] + rnorm(1)

}

This can be written, more simply, with the "cumsum" function.

n <- 200

x <- rnorm(n)

y <- cumsum(x)

op <- par(mfrow=c(3,1), mar=c(2,4,2,2)+.1)

plot(ts(x), xlab="", ylab="")

plot(ts(y), xlab="", ylab="AR(1)")

acf(y, main="")

par(op)

More generally, one can consider

X(n+1) = a X(n) + noise.

This is called an auto-regressive model, or AR(1), because one can estimate the coefficients by performing a regression of x against

lag(x,1).

n <- 200

a <- .7

x <- rep(0,n)

for (i in 2:n) {

x[i] <- a*x[i-1] + rnorm(1)

}

y <- x[-1]

x <- x[-n]

r <- lm( y ~ x -1)

plot(y~x)

abline(r, col='red')

abline(0, .7, lty=2)

More generally, an AR(q) process is a process in which each term is a linear combination of the q preceding terms and a white noise

(with fixed coefficients).

n <- 200

x <- rep(0,n)

for (i in 4:n) {

x[i] <- .3*x[i-1] -.7*x[i-2] + .5*x[i-3] + rnorm(1)

}

op <- par(mfrow=c(3,1), mar=c(2,4,2,2)+.1)

plot(ts(x), xlab="", ylab="AR(3)")

acf(x, main="", xlab="")

pacf(x, main="", xlab="")

par(op)

You can also simulate those models with the "arima.sim" function.

n <- 200

x <- arima.sim(list(ar=c(.3,-.7,.5)), n)

op <- par(mfrow=c(3,1), mar=c(2,4,2,2)+.1)

plot(ts(x), xlab="", ylab="AR(3)")

acf(x, xlab="", main="")

pacf(x, xlab="", main="")

par(op)

PACF

The partial AutoCorrelation Function (PACF) provides an estimation of the coefficients of an AR(infinity) model: we have already seen

it on the previous examples. It can be easily computed from the autocorrelation function with the "Yule-Walker" equations.

Yule-Walker Equations

To compute the auto-correlation function of an AR(p) process whose coefficients are known,

(1 - a1 B - a2 B^2 - ... - ap B^p) Y = Z

we just have to compute the first autocorrelations r1, r2, ..., rp, and then use the Yule-Walker equations:

r(j) = a1 r(j-1) + a2 r(j-2) + ... + ap r(j-p).

You can also use them in the other direction to compute the coefficients of an AR process from its autocorrelations.

Stationarity

A time series is said to be weakly stationary if the expectation of X(t) does not depend on t and if the covariance of X(t) and X(s) only

depends on abs(t-s).

A time series is said to be stationary if all the X(t) have the same distribution and all the joint distribution of (X(t),X(s)) (for a given

value of abs(s-t)) are the same. Thus, "weakly stationary" means "stationary up to the second order.

For instance, if your time series has a trend, i.e., if the expectation of X(t) is not constant, the series is not stationary.

n <- 200

x <- seq(0,2,length=n)

trend <- ts(sin(x))

plot(trend,

ylim=c(-.5,1.5),

lty=2, lwd=3, col='red',

ylab='')

r <- arima.sim(

list(ar = c(0.5,-.3), ma = c(.7,.1)),

n,

n,

sd=.1

)

lines(trend+r)

Other example: a random walk is not stationary, because the variance of X(t) increases with t -- but the expectation of X(t) remains zero.

n <- 200

k <- 10

x <- 1:n

r <- matrix(nr=n,nc=k)

for (i in 1:k) {

r[,i] <- cumsum(rnorm(n))

}

matplot(x, r,

type = 'l',

lty = 1,

col = par('fg'),

main = "A random walk is not stationnary")

abline(h=0,lty=3)

Ergodicity

Ergodicity and stationarity are two close but different notions.

Given a stochastic process X(n), (n integer), to compute the mean of X(1), we can use one of the following methods: either take several

realizations of this process, each providing a value for X(1), and average those values; or take a single realization of this process and

average X(1), X(2), X(3), etc.. The result we want is the first, but if we are lucky (if the process is ergodic), both will coincide.

Intuitively, a process is ergodic if, to get information that would require several realizations of the process, you can instead consider a

single longer realization.

The practical interest of ergodic processes is that usually, when we study time series, we have a single realization of this time series. With

an ergodic hypothesis, we can say something about it -- without it, we are helpless.

TODO: understand and explain the differences.

For instance, a stationnary process need not be ergodic.

AR and stationarity

In an autoregressive (AR) process, it is reasonable to ask that past observations have less influence than more recent ones. That is why

we ask, in the AR(1) model,

Y(t+1) = a * Y(t) + Z(t) (where Z is a white noise)

that abs(a)<1. This can also be written:

Y(t+1) - a Y(t) = Z(t)

or

phi(B) Y = Z (where phi(u) = 1 - a u

and B is the Backwards, operator,

aka shift, delay or lag operator)

and we ask that all the roots of phi have a modulus greater than 1.

More generally, an AR process

phi(B) Y = Z

where phi(u) = 1 - a_1 u - a_2 u^2 - ... - a_p u^p

is stationary if the modulus of all the roots of phi are greater that 1.

You can check that these stationary AR process are MA(infinity) processes (this is another meaning of the Yule--Walker equations).

MA and invertibility

TODO: understand and correct this.

Symetrically, for a Moving Average (MA) process, defined by

Y = psi(B) Z

where psi(u) = 1 + b_1 u + b_2 u^3 + ... + b_q u^q

We shall also ask that modulus of the roots of psi be greater than 1. The process is then said to be invertible. Without this hypothesis, the

autocorrelation function does not uniquely define the coefficients of the Moving Average.

For instance, for an MA(1) process,

Y(t+1) = Z(t+1) + a Z(t),

you can replace a by 1/a without changing the autocorrelation function.

n <- 200

ma <- 2

mai <- 1/ma

op <- par(mfrow=c(4,1), mar=c(2,4,1,2)+.1)

x <- arima.sim(list(ma=ma),n)

plot(x, xlab="", ylab="")

acf(x, xlab="", main="")

lines(0:n,

ARMAacf(ma=ma, lag.max=n),

lty=2, lwd=3, col='red')

x <- arima.sim(list(ma=mai),n)

plot(x, xlab="", ylab="")

acf(x, main="", xlab="")

lines(0:n,

ARMAacf(ma=mai, lag.max=n),

lty=2, lwd=3, col='red')

par(op)

TODO: an example with a higher degree polynomial (I naively thought I would just have to invert the roots of the polynomial, but

apparently it is more complicated...)

sym.poly <- function (z,k) {

# Sum of the products of k

# distinct elements of the vector z

if (k==0) {

r <- 1

} else if (k==1) {

r <- sum(z)

} else {

r <- 0

for (i in 1:length(z)) {

r <- r + z[i]*sym.poly(z[-i],k-1)

}

r <- r/k # Each term appeared k times

}

r

}

sym.poly( c(1,2,3), 1 ) # 6

sym.poly( c(1,2,3), 2 ) # 11

sym.poly( c(1,2,3), 3 ) # 6

roots.to.poly <- function (z) {

n <- length(z)

p <- rep(1,n)

for (k in 1:n) {

p[n-k+1] <- (-1)^k * sym.poly(z,k)

}

p <- c(p,1)

p

}

roots.to.poly(c(1,2)) # 2 -3 1

round(

Re(polyroot( roots.to.poly(c(1,2,3)) )),

digits=1

)

# After this interlude, we can finally

# construct an MA process and one of

# its inverses

n <- 200

k <- 3

ma <- runif(k,-1,1)

ma <- runif(k,-1,1)

# The roots

z <- polyroot(c(1,-ma))

# The inverse of the roots

zi <- 1/z

# The polynomial

p <- roots.to.poly(zi)

# The result should be real, but because

# of rounding errors, it is not.

p <- Re(p)

# We want the constant term to be 1.

p <- p/p[1]

mai <- -p[-1]

op <- par(mfrow=c(4,1), mar=c(2,4,1,2)+.1)

x <- arima.sim(list(ma=ma),n)

plot(x, xlab="")

acf(x, main="", xlab="")

lines(0:n, ARMAacf(ma=ma, lag.max=n),

lty=2, lwd=3, col='red')

x <- arima.sim(list(ma=mai),n)

plot(x, xlab="")

acf(x, main="", xlab="")

lines(0:n, ARMAacf(ma=mai, lag.max=n),

lty=2, lwd=3, col='red')

par(op)

The MA(p) processes have another interesting feature: they are AR(infinity) processes.

TODO: on an example, plot the roots of those polynomials.

Unit root tests

TODO: To check if the series we are studying has unit roots.

library(tseries)

?adf.test

?pp.tests

ARMA

Of course, one can mix up MA and AR models, to get the so-called ARMA models. In the following formulas, z is a white noise and x

the series we are interested in.

MA(p): x(i) = a1 z(i-1) + a2 z(i-2) + ... + ap z(i-p)

AR(q): x(i) - b1 x(i-1) - b2 x(i-2) - ... - bq x(i-q) = z(i)

ARMA(p,q): x(i) - b1 x(i-1) - ... - bq x(i-q) = a1 z(i-1) + ... + ap z(i-p)

Remark: AR(q) processes are also MA(infinity) processes, we could replace ARMA processes by MA(infinity) processes, but we prefer

having fewer coefficients to estimate.

Remark: Wold's theorem states that any stationary process can be written as the sum of an MA(infinity) process and a deterministic one.

TODO: I have not defined what a deterministic process was.

Remark: if we let B be the shift operator, so that the derivation operator be 1-B, an ARMA process can be written as

phi(B) X(t) = theta(B) Z(t)

where theta(B) = 1 + a1 B + a2 B^2 + ... + ap B^p

phi(B) = 1 - b1 B - b2 B^2 - ... - bq B^q

Z is a white noise

ARMA processes give a good approximation to most stationary processes. As a result, you can use the estimated ARMA coefficients as

a statistical summary of a stationary process, exactly as the mean and the quantiles for univariate statistical series. They might be useful

to forecast future values, but they provide little information as the the underlying mechanisms that produced the time series.

Overfitting an ARMA process

An ARMA(p,q) process

phi(B) Y = theta(B) Z

in which phi and theta have a root in common can be written, more simply, as an ARMA(p-1,q-1).

How to get to a stationary process

To model a time series as an ARMA model, it has to be stationnary. To get a stationary series (in short, to get rid of the trend), you can

try to differentiate it.

The fact that the series is not stationary is usually obvious on the plot. You can also see it on the ACF: if the series is stationary, the ACF

should rapidly (usually exponentially) decay to zero.

data(Nile)

op <- par(mfrow=c(2,1), mar=c(2,4,3,2)+.1)

plot(Nile, main="There is no trend", xlab="")

acf(Nile, main="", xlab="")

par(op)

data(BJsales)

op <- par(mfrow=c(3,1), mar=c(2,4,3,2)+.1)

plot(BJsales, xlab="",

main="The trend disappears if we differentiate")

acf(BJsales, xlab="", main="")

acf(diff(BJsales), xlab="", main="",

ylab="ACF(diff(BJsales)")

par(op)

n <- 2000

x <- arima.sim(

model = list(

ar = c(.3,.6),

ma = c(.8,-.5,.2),

order = c(2,1,3)),

n

)

x <- ts(x)

op <- par(mfrow=c(3,1), mar=c(2,4,3,2)+.1)

plot(x, main="It suffices to differentiate once",

xlab="", ylab="")

acf(x, xlab="", main="")

acf(diff(x), xlab="", main="",

ylab="ACF(diff(x))")

par(op)

n <- 10000

x <- arima.sim(

model = list(

ar = c(.3,.6),

ma = c(.8,-.5,.2),

order = c(2,2,3)

),

n

)

x <- ts(x)

op <- par(mfrow=c(4,1), mar=c(2,4,3,2)+.1)

plot(x, main="One has to differentiate twice",

xlab="", ylab="")

acf(x, main="", xlab="")

acf(diff(x), main="", xlab="",

ylab="ACF(diff(x))")

acf(diff(x,differences=2), main="", xlab="",

ylab="ACF(diff(diff(x)))")

par(op)

To check more precisely if the ACF decreases exponentially, one could perform a regression (but it might be overkill).

acf.exp <- function (x, lag.max=NULL, lag.max.reg=lag.max, ...) {

a <- acf(x, lag.max=lag.max.reg, plot=F)

b <- acf(x, lag.max=lag.max, ...)

r <- lm( log(a$acf) ~ a$lag -1)

lines( exp( b$lag * r$coef[1] ) ~ b$lag, lty=2 )

}

data(BJsales)

acf.exp(BJsales,

main="Exponential decay of the ACF")

acf.exp(BJsales,

lag.max=40,

main="Exponential decay of the ACF")

data(Nile)

acf.exp(Nile, lag.max.reg=10, main="Nile")

Differentiating can also help you get rid of the seasonal component, if you differentiate with a lag: e.g., take the difference between the

value today and the same value one year ago.

x <- diff(co2, lag=12)

op <- par(mfrow=c(4,1), mar=c(2,4,3,2)+.1)

plot(x, ylab="", xlab="")

acf(x, xlab="", main="")

pacf(x, xlab="", main="")

spectrum(x, xlab="", main="",

col=par('fg'))

par(op)

y <- diff(x)

op <- par(mfrow=c(4,1), mar=c(2,4,3,2)+.1)

plot(y, xlab="", ylab="")

acf(y, xlab="", main="")

pacf(y, xlab="", main="")

spectrum(y, col=par('fg'),

xlab="", main="")

par(op)

ARIMA

ARIMA processes are just integrated ARMA processes. In other words, a process is ARIMA of order d if its d-th derivative is ARMA.

The model can be written

phi(B) (1-B)^d X(t) = theta(B) Z(t)

where B is the shift operator, Z a white noise, phi the polynomial defining the AR part, theta the polynomial defining the MA part of the

process.

ARIMA processes are not stationary processes. We have already seen it with the random walk, which is an integrated ARMA(0,0)

process, i.e., an ARIMA process of order 1: the variance of X(t) increases with t. This is the very reason why we differentiate: to get a

stationary process.

TODO: Give an example of ARIMA(0,1,0) process, show that

it is not stationary.

Recall the tests to check if it is stationary.

Quick and dirty stationarity test: cut the data into two

parts, compute Cor(X(t),X(t-1)) on each, compare.

To infer the order of an ARIMA process, you can differentiate it until its ACF rapidly decreases.

n <- 200

x <- arima.sim(

list(

list(

order=c(2,1,2),

ar=c(.5,-.8),

ma=c(.9,.6)

),

n

)

op <- par(mfrow=c(3,1), mar=c(2,4,4,2)+.1)

acf(x, main="You will have to defferentiate once")

acf(diff(x), main="First derivative")

acf(diff(x, differences=2), main="Second derivative")

par(op)

n <- 200

x <- arima.sim(

list(

order=c(2,2,2),

ar=c(.5,-.8),

ma=c(.9,.6)

),

n

)

op <- par(mfrow=c(3,1), mar=c(2,4,4,2)+.1)

acf(x, main="You will have to differentiate twice")

acf(diff(x), main="First derivative")

acf(diff(x, differences=2), main="Second derivative")

par(op)

Here is a concrete example.

data(sunspot)

op <- par(mfrow=c(4,1), mar=c(2,4,3,2)+.1)

plot(sunspot.month, xlab="", ylab="sunspot")

acf(sunspot.month, xlab="", main="")

plot(diff(sunspot.month),

xlab="", ylab="diff(sunspot)")

acf(diff(sunspot.month), xlab="", main="")

par(op)

Same here (but actually, the differentiation discards the affine trend).

data(JohnsonJohnson)

x <- log(JohnsonJohnson)

op <- par(mfrow=c(4,1), mar=c(2,4,3,2)+.1)

plot(x, xlab="", ylab="JJ")

acf(x, main="")

plot(diff(x), ylab="diff(JJ)")

acf(diff(x), main="")

par(op)

In the following examples, you might want to differentiate twice. But beware, it might not always be a good idea: if the ACF decreases

exponentially, you can stop differentiating.

data(BJsales)

x <- BJsales

op <- par(mfrow=c(6,1), mar=c(2,4,0,2)+.1)

plot(x)

acf(x)

plot(diff(x))

acf(diff(x))

plot(diff(x, difference=2))

acf(diff(x, difference=2))

par(op)

data(austres)

x <- austres

op <- par(mfrow=c(6,1), mar=c(2,4,0,2)+.1)

plot(x)

acf(x)

plot(diff(x))

acf(diff(x))

plot(diff(x, difference=2))

acf(diff(x, difference=2))

par(op)

# In the preceding example, there was a linear trend:

# let ut remove it.

data(austres)

x <- lm(austres ~ time(austres))$res

op <- par(mfrow=c(6,1), mar=c(2,4,0,2)+.1)

plot(x)

acf(x)

plot(diff(x))

acf(diff(x))

plot(diff(x, difference=2))

acf(diff(x, difference=2))

par(op)

SARIMA

These are Seasonnal ARIMA processes (the integration, the MA or the AR parts can be seasonal). They are often denoted:

(p,d,q) \times (P,D,Q) _s

and they are described by the model:

phi(B) Phi(B^s) (1-B)^d (1-B^s)^D X(t) = theta(B) Theta(B^s) Z(t)

where s is the period

theta(B) = 1 + a1 B + a2 B^2 + ... + ap B^p is the MA polynomial

phi(B) = 1 - b1 B - b2 B^2 - ... - bq B^q is the AR polynomial

Theta(B^s) = 1 + A1 B^s + A2 B^2s + ... + AP B^(P*s) is the seasonal MA polynomial

Phi(B^s) = 1 - B1 B^s - B2 B^2s - ... - BQ B^(Q*s) is the seasonal AR polynomial

Z is a white noise

There is no function to simulate SARIMA processes -- but we can model them.

my.sarima.sim <- function (

n = 20,

period = 12,

model,

seasonal

) {

x <- arima.sim( model, n*period )

x <- x[1:(n*period)]

for (i in 1:period) {

xx <- arima.sim( seasonal, n )

xx <- xx[1:n]

x[i + period * 0:(n-1)] <-

x[i + period * 0:(n-1)] + xx

}

x <- ts(x, frequency=period)

x

}

op <- par(mfrow=c(3,1))

x <- my.sarima.sim(

20,

12,

12,

list(ar=.6, ma=.3, order=c(1,0,1)),

list(ar=c(.5), ma=c(1,2), order=c(1,0,2))

)

eda.ts(x, bands=T)

x <- my.sarima.sim(

20,

12,

list(ar=c(.5,-.3), ma=c(-.8,.5,-.3), order=c(2,1,3)),

list(ar=c(.5), ma=c(1,2), order=c(1,0,2))

)

eda.ts(x, bands=T)

x <- my.sarima.sim(

20,

12,

list(ar=c(.5,-.3), ma=c(-.8,.5,-.3), order=c(2,1,3)),

list(ar=c(.5), ma=c(1,2), order=c(1,1,2))

)

eda.ts(x, bands=T)

The Box and Jenkins method

TODO

The co2 example (somewhere above) could well be modeled as an SARIMA model.

x <- co2

eda.ts(x)

First, we see that there is a trend: we differentiate once to get rid of it.

eda.ts(diff(x))

There is also a periodic component: we differentiate, with a 12-month lag, to get rid of it.

eda.ts(diff(diff(x),lag=12))

But wait! We have differentiated twice. Couldn't we get rid of both the periodic component and the trend by differentiating just once,

with the 12-month lag?

eda.ts(diff(x,lag=12))

Well, perhaps. We hesitate between

SARIMA(?,1,?)(?,1,?)

and

SARIMA(?,0,?)(?,1,?).

If we look at the ACF and the PACF:

SARIMA(1,1,1)(2,1,1)

SARIMA(1,1,2)(2,1,1)

SARIMA(2,0,0)(1,1,0)

SARIMA(2,0,0)(1,1,1)

Let us compute the coefficients of those models:

r1 <- arima(co2,

order=c(1,1,1),

list(order=c(2,1,1), period=12)

)

r2 <- arima(co2,

order=c(1,1,2),

list(order=c(2,1,1), period=12)

)

r3 <- arima(co2,

order=c(2,0,0),

list(order=c(1,1,0), period=12)

)

r4 <- arima(co2,

order=c(2,0,0),

list(order=c(1,1,1), period=12)

)

This yields:

> r1

Call:

arima(x = co2, order = c(1, 1, 1), seasonal = list(order = c(2, 1, 1), period = 12))

Coefficients:

ar1 ma1 sar1 sar2 sma1

0.2595 -0.5902 0.0113 -0.0869 -0.8369

s.e. 0.1390 0.1186 0.0558 0.0539 0.0332

sigma^2 estimated as 0.08163: log likelihood = -83.6, aic = 179.2

> r2

Call:

arima(x = co2, order = c(1, 1, 2), seasonal = list(order = c(2, 1, 1), period = 12))

Coefficients:

ar1 ma1 ma2 sar1 sar2 sma1

0.5935 -0.929 0.1412 0.0141 -0.0870 -0.8398

s.e. 0.2325 0.237 0.1084 0.0557 0.0538 0.0328

sigma^2 estimated as 0.08132: log likelihood = -82.85, aic = 179.7

> r3

Call:

arima(x = co2, order = c(2, 0, 0), seasonal = list(order = c(1, 1, 0), period = 12))

Coefficients:

ar1 ar2 sar1

0.6801 0.3087 -0.4469

s.e. 0.0446 0.0446 0.0432

sigma^2 estimated as 0.1120: log likelihood = -150.65, aic = 309.3

For r4, it was even:

Error in arima(co2, order = c(2, 0, 1), list(order = c(1, 1, 1), period = 12)) :

non-stationary AR part from CSS

The AIC of a3 is appallingly high (we want as low a value as possible): we really need to differentiate twice.

Let us look at the p-values:

> round(pnorm(-abs(r1$coef), sd=sqrt(diag(r1$var.coef))),5)

ar1 ma1 sar1 sar2 sma1

0.03094 0.00000 0.42007 0.05341 0.00000

> round(pnorm(-abs(r1$coef), sd=sqrt(diag(r1$var.coef))),5)

ar1 ma1 ma2 sar1 sar2 sma1

0.00535 0.00004 0.09635 0.39989 0.05275 0.00000

This suggests an SARIMA(1,1,1)(0,1,1) model.

r3 <- arima( co2,

order=c(1,1,1),

list(order=c(0,1,1), period=12)

)

This yields:

> r3

Call:

arima(x = co2, order = c(1, 1, 1), seasonal = list(order = c(0, 1, 1), period = 12))

Coefficients:

ar1 ma1 sma1

0.2399 -0.5710 -0.8516

s.e. 0.1430 0.1237 0.0256

sigma^2 estimated as 0.0822: log likelihood = -85.03, aic = 178.07

> round(pnorm(-abs(r3$coef), sd=sqrt(diag(r3$var.coef))),5)

ar1 ma1 sma1

0.04676 0.00000 0.00000

We now look at the residuals:

r3 <- arima(

co2,

order = c(1, 1, 1),

seasonal = list(

seasonal = list(

order = c(0, 1, 1),

period = 12

)

)

eda.ts(r3$res)

Good, we can now try to use this mode to predict future values. To get an idea of the quality of those forecasts, we can use the first part

of the data to estimate the model coefficients and compute the predictions and the second part to assess the quality of the predictions --

but beware, this is biased, because we chose the model by using all the data, including the data from the test sample.

x1 <- window(co2, end = 1990)

r <- arima(

x1,

order = c(1, 1, 1),

seasonal = list(

order = c(0, 1, 1),

period = 12

)

)

plot(co2)

p <- predict(r, n.ahead=100)

lines(p$pred, col='red')

lines(p$pred+qnorm(.025)*p$se, col='red', lty=3)

lines(p$pred+qnorm(.975)*p$se, col='red', lty=3)

# On the contrary, I do not know what to do with

# this plots (it looks like integrated noise).

eda.ts(co2-p$pred)

It is not that bad. Here are our forecasts.

r <- arima(

co2,

order = c(1, 1, 1),

seasonal = list(

order = c(0, 1, 1),

period = 12

)

)

p <- predict(r, n.ahead=150)

plot(co2,

xlim=c(1959,2010),

ylim=range(c(co2,p$pred)))

lines(p$pred, col='red')

lines(p$pred+qnorm(.025)*p$se, col='red', lty=3)

lines(p$pred+qnorm(.975)*p$se, col='red', lty=3)

What we have done is called the Box and Jenkins method. The general case can be a little more complicated: if the residuals do not look

like white noise, we have to get back to find another model.

0. Differentiate to get a stationary process.

If there is a trend, the process is not stationary.

If the ACF decreases slowly, try to differentiate once more.

1. Identify the model:

ARMA(1,0): ACF: exponential decrease; PACF: one peak

ARMA(2,0): ACF: exponential decrease or waves; PACF: two peaks

ARMA(0,1): ACF: one peak; PACF: exponential decrease

ARMA(0,2): ACF: two peaks; PACF: exponential decrease or waves

ARMA(1,1): ACF&PACF: exponential decrease

2. Compute the coefficients

3. Diagnostics (go to 1 if they do not look like white noise)

Computhe the p-values, remove unneeded coefficients (check on the

residuals that they are indeed unneeded).

4. Forecasts

Sample ARMA processes and their ACF and PACF

Here are a few examples of ARMA processes (in red: the theoretic ACF and PACF).

The ARMA(1,0) is characterized by the exponential decrease of the ACF and the single peak in the PACF.

op <- par(mfrow=c(4,2), mar=c(2,4,4,2))

n <- 200

for (i in 1:4) {

x <- NULL

while(is.null(x)) {

model <- list(ar=rnorm(1))

try( x <- arima.sim(model, n) )

}