VSDC And Visa PayWave US Acquirer Implementation Guide V2 Smart Debit Credit Pay Wave U.S. V2.0 Apr 2014

User Manual:

Open the PDF directly: View PDF ![]() .

.

Page Count: 141 [warning: Documents this large are best viewed by clicking the View PDF Link!]

- About This Guide

- 1 Overview

- 2 VSDC Transaction Flow

- 2.1 Initiating a Transaction

- 2.2 Application Selection

- 2.3 Initiating Application Processing

- 2.4 Reading the Application Data

- 2.5 Risk Management Checks

- 2.6 Terminal Action Analysis

- 2.7 Card Risk Management

- 2.8 Online Processing

- 2.9 VisaNet Processes Acquirer Authorization Request

- 2.10 Issuer Receives Authorization Request

- 2.11 VisaNet Processes the Issuer Response

- 2.12 Transaction Conclusion

- 2.13 Clearing and Settlement

- 3 Visa payWave Transaction Flow

- 4 Visa’s Chip Terminal and Reader Requirements

- 4.1 Terminal Types

- 4.2 Application Identifiers (AIDs)

- 4.3 Language

- 4.4 VSDC Requirements

- 4.4.1 Contact EMV Application Selection

- 4.4.2 Cardholder Application Selection/Confirmation

- 4.4.3 Contact Application Selection and Routing Options

- 4.4.4 Processing Restrictions

- 4.4.5 Cardholder Verification

- 4.4.6 Cardholder Verification and Selectable Kernels

- 4.4.7 Terminal Risk Management

- 4.4.8 Terminal Action Analysis

- 4.4.9 Implementation Activities

- 4.4.10 Online Processing

- 4.4.11 Completion

- 4.4.12 Implementation Activities

- 4.5 Visa payWave Reader Requirements

- 4.6 Additional Requirements for VCPS 2.1

- 5 Additional Terminal Considerations

- 5.1 Magnetic Stripe Transaction Terminal Requirements

- 5.2 Card Data in Online Messages

- 5.3 Support for up to 19 Digit PANs

- 5.4 Terminal Display Messages

- 5.5 PIN Length and Character Set

- 5.6 Cardholder Receipt Requirements

- 5.7 Transaction Routing

- 5.8 Acquirer Stand-In

- 5.9 Deferred Authorization

- 5.10 Transaction Type Requirements

- 5.11 EMV Transactions in Specific Industries

- 5.12 Purchase with Cash-back

- 5.13 Terminal PIN Requirements

- 5.14 Terminal Types and Configurations

- 5.15 Terminal Requirements for CVM

- 6 Terminal Selection and Approval

- 6.1 Terminal and Reader Selection Criteria

- 6.2 VSDC Terminal Approvals

- 6.3 Considerations for EMV Approval

- 6.4 Contactless Reader Approvals and Renewals

- 6.5 Payment Card Industry Requirements

- 6.6 Acquirer Device Validation Toolkit

- 6.7 Contactless Device Evaluation Toolkit

- 6.8 qVSDC Device Module

- 6.9 Additional Toolkit Requirements

- 6.10 Visa Chip Vendor Enabled Service (CVES)

- 6.11 Acquirer Host Testing

- 6.12 Implementation Activities

- 7 Terminal Testing and Maintenance

- 8 Terminal Management Systems

- 9 Acquirer System Changes

- 10 Acquirer Host Testing

- 11 Acquirer Back-Office Changes

- 12 Merchant Support

- 12.1 Merchant Agreement

- 12.2 Merchant Registration

- 12.3 Technology Innovation Program

- 12.4 Contactless Reader Migration

- 12.5 Merchant Services

- 12.6 Merchant Systems Changes

- 12.7 Contactless Reader Branding and Placement

- 12.8 Merchant Training

- 12.8.1 Merchant Training Plan

- 12.8.2 Cardholder Application Selection

- 12.8.3 Cardholder Verification

- 12.8.4 Fallback Transactions

- 12.8.5 Other Transactions

- 12.8.6 Care of the Terminal

- 12.8.7 International Transactions

- 12.8.8 Terminated Visa payWave Transactions

- Appendix A Planning Checklist

- Appendix B V.I.P. System Message Requirements

- Appendix C Reference Materials

- Appendix D Standard EMV Terminal Logic

- Appendix E Special Terminal Logic

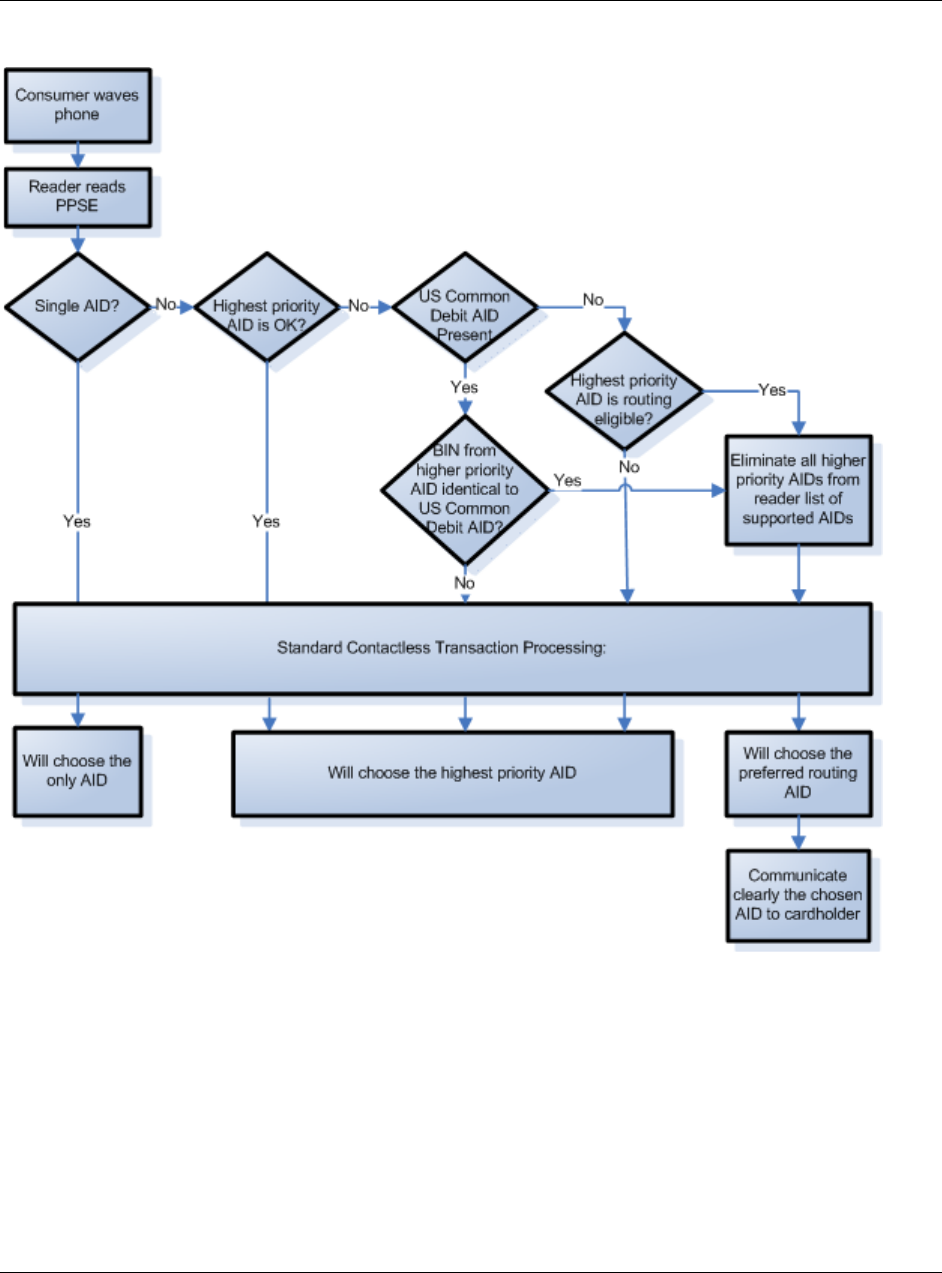

- E.1 Contact Terminal Application Selection/Routing Option Logic

- E.2 Processing

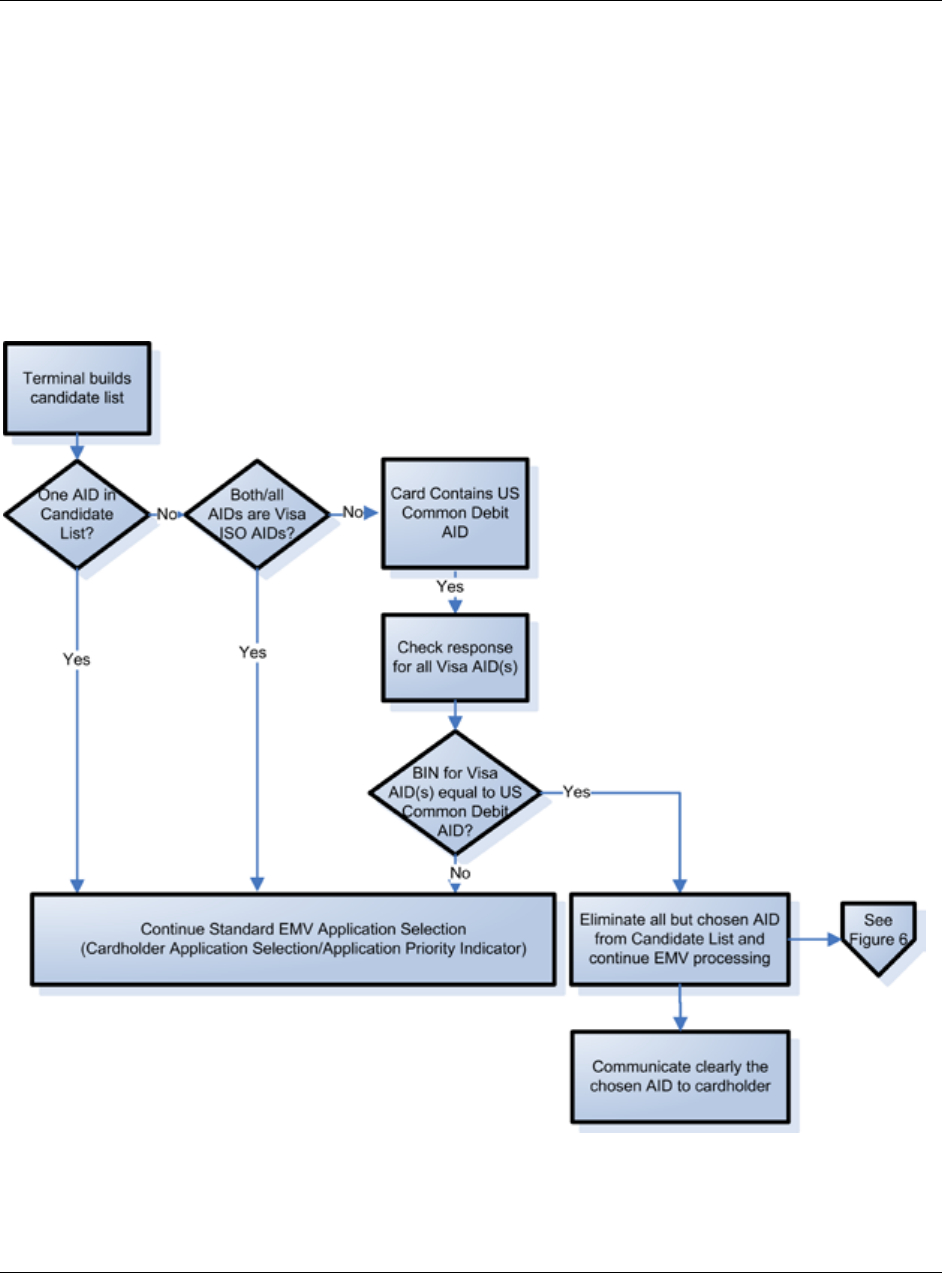

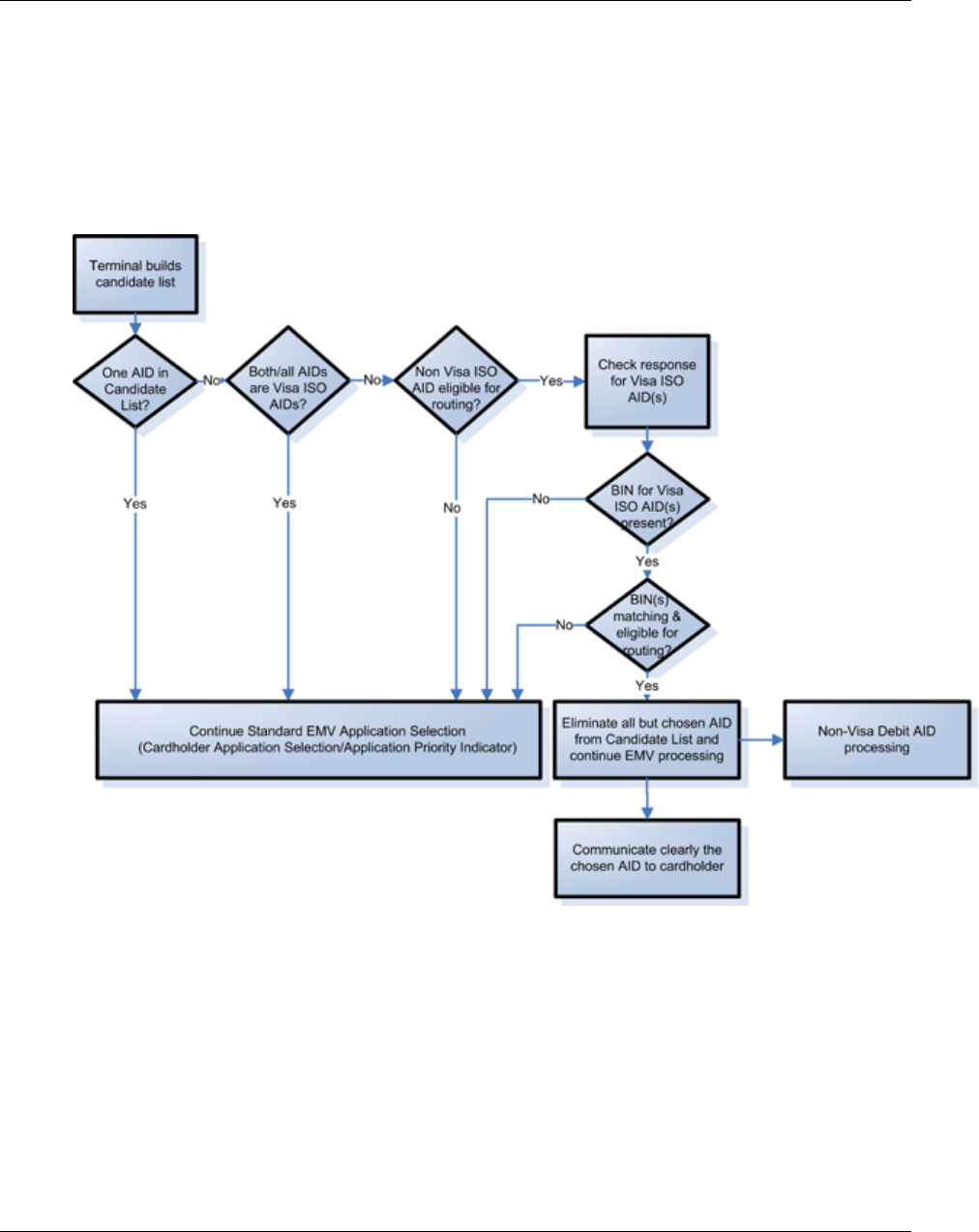

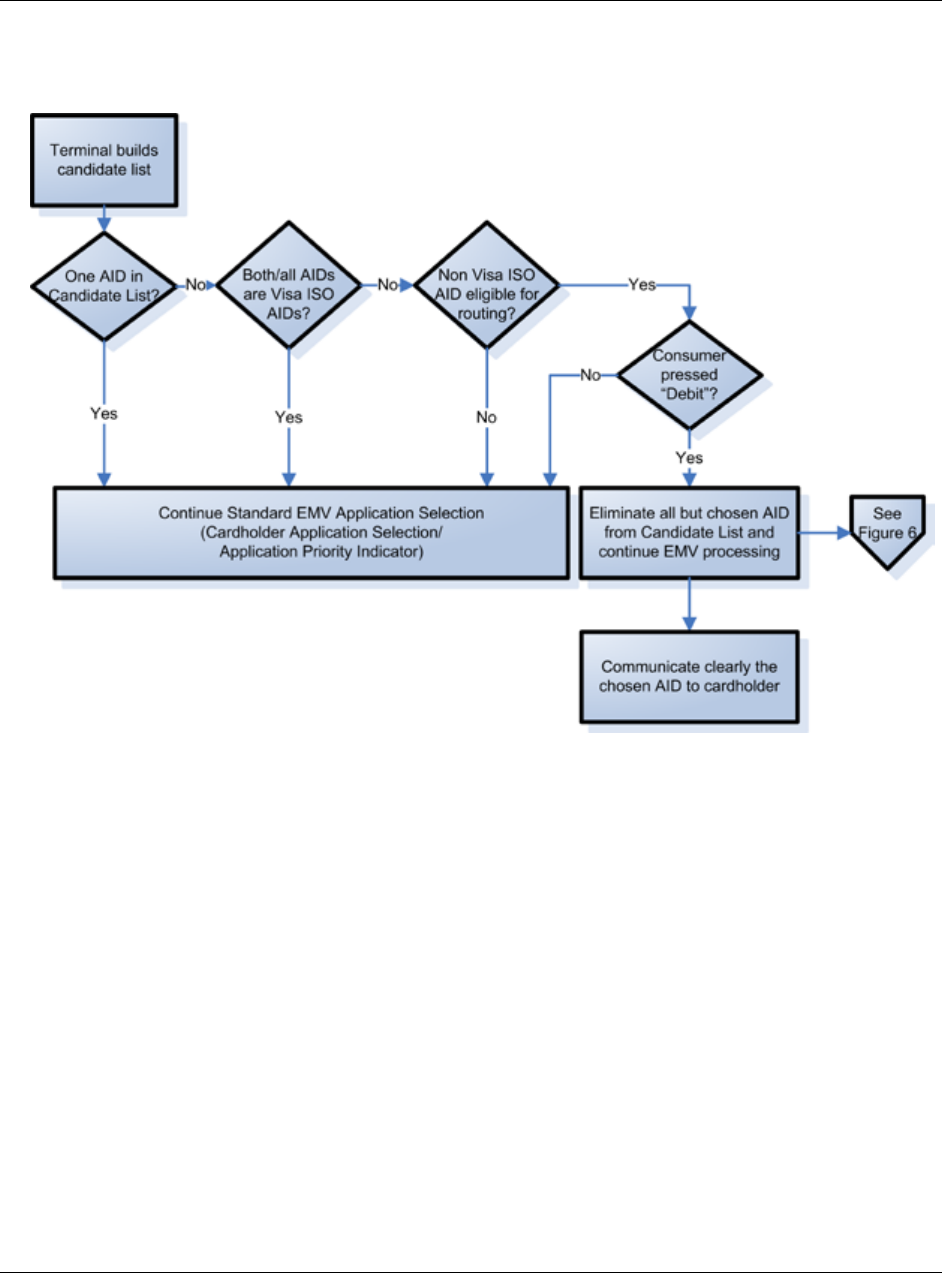

- E.3 Flow Example using Visa US Common Debit AID

- E.4 Flow Example using BIN / IIN Logic

- E.5 Flow Example using Consumer Indication

- E.6 Flow Example for Visa US Common Debit

- E.7 Contactless Reader Application Selection and Routing Option Logic

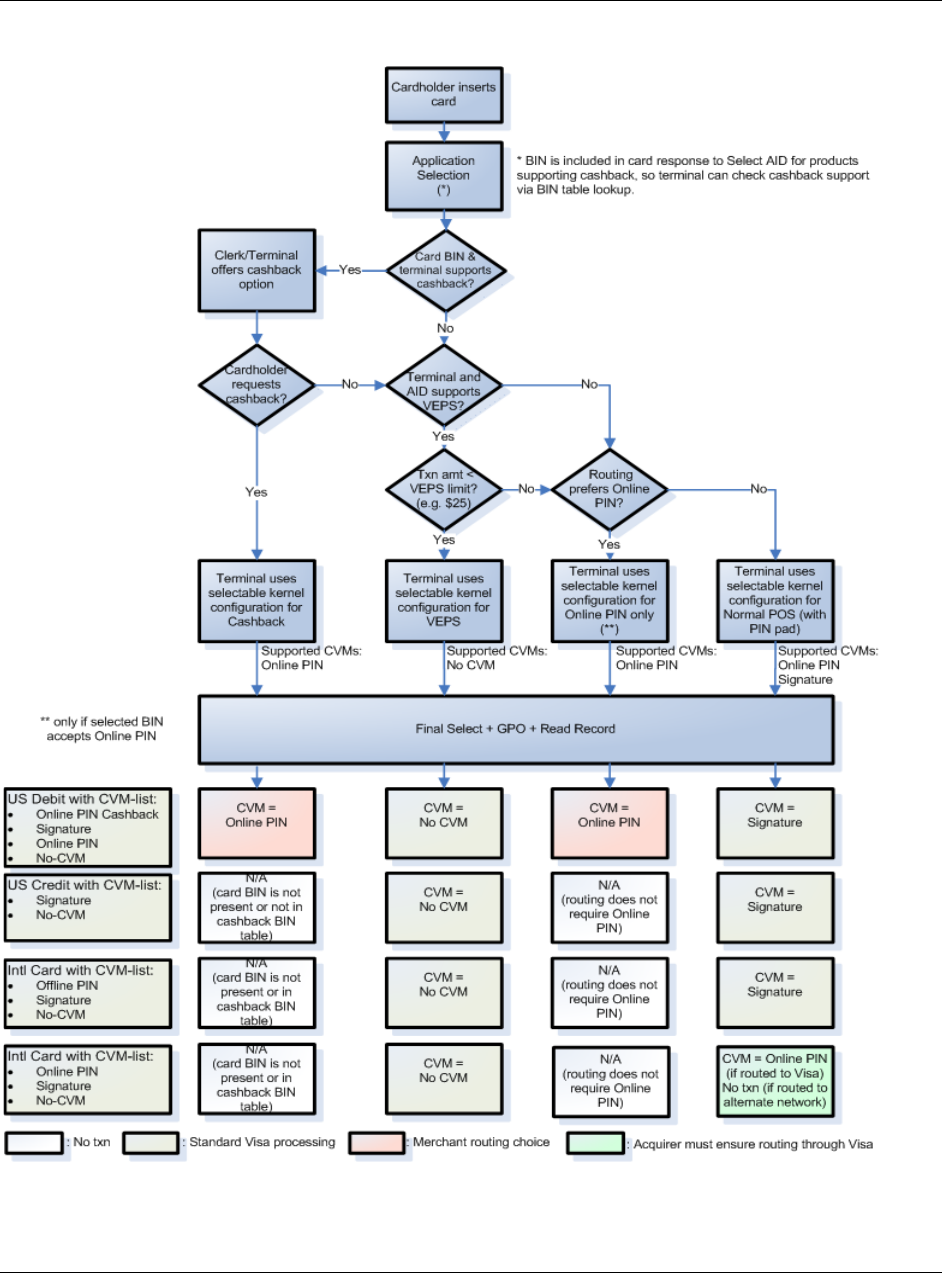

- E.8 Contact CVM Processing and Selectable Kernels Logic

Visa Smart Debit/Credit and Visa payWave

U.S. Acquirer Implementation Guide

Version 2.0

April 2014

Visa Smart Debit/Credit and Visa payWave

U.S. Acquirer Implementation Guide

Version 2.0

Visa International Operating Regulations Extension

April 2014

April 2014 VISA CONFIDENTIAL ii

Notice: This information is proprietary and CONFIDENTIAL to Visa. It is distributed to Visa participants for use

exclusively in managing their Visa programs. It must not be duplicated, published, distributed or disclosed, in whole

or in part, to merchants, cardholders or any other person without prior written permission from Visa. © 2014 Visa.

All Rights Reserved.

THIS PAGE INTENTIONALLY LEFT BLANK.

April 2014 VISA CONFIDENTIAL iii

Notice: This information is proprietary and CONFIDENTIAL to Visa. It is distributed to Visa participants for use

exclusively in managing their Visa programs. It must not be duplicated, published, distributed or disclosed, in whole

or in part, to merchants, cardholders or any other person without prior written permission from Visa. © 2014 Visa.

All Rights Reserved.

Visa Smart Debit/Credit and Visa payWave U.S. Acquirer Implementation Guide

Important Note on Confidentiality and Copyright

The Visa Confidential label signifies that the information in this document is confidential and proprietary to

Visa and is intended for use only by Visa Clients subject to the confidentiality restrictions in Visa's

Operating Regulations, non-Client Third Party Processors that have an executed and current Exhibit K on

file with Visa, and terminal vendors and other third parties that have a current license agreement or

nondisclosure agreement (NDA) with Visa that covers the information contained herein.

This document is protected by copyright restricting its use, copying, distribution, and decompilation. No

part of this document may be reproduced in any form by any means without prior written authorization of

Visa.

Visa and other trademarks are trademarks or registered trademarks of Visa.

All other product names mentioned herein are the trademarks of their respective owners.

THIS PUBLICATION COULD INCLUDE TECHNICAL INACCURACIES OR TYPOGRAPHICAL

ERRORS. CHANGES ARE PERIODICALLY ADDED TO THE INFORMATION HEREIN: THESE

CHANGES WILL BE INCORPORATED IN NEW EDITIONS OF THE PUBLICATION. VISA MAY MAKE

IMPROVEMENTS AND/OR CHANGES IN THE PRODUCT(S) AND/OR THE PROGRAM(S)

DESCRIBED IN THIS PUBLICATION AT ANY TIME.

If you have technical questions or questions regarding a Visa service or capability, contact your Visa

representative.

April 2014 VISA CONFIDENTIAL iv

Notice: This information is proprietary and CONFIDENTIAL to Visa. It is distributed to Visa participants for use

exclusively in managing their Visa programs. It must not be duplicated, published, distributed or disclosed, in whole

or in part, to merchants, cardholders or any other person without prior written permission from Visa. © 2014 Visa.

All Rights Reserved.

Visa Smart Debit/Credit and Visa payWave U.S. Acquirer Implementation Guide

Table of Contents

About This Guide ...........................................................................9

Out of Scope ........................................................................................ 9

Assumptions ....................................................................................... 10

Audience ............................................................................................ 10

Document Organization ..................................................................... 10

Summary of Changes ........................................................................ 11

1 Overview ................................................................................ 12

1.1 Compliance Documents and Reference Documentation .......... 12

1.2 Terminology .............................................................................. 13

2 VSDC Transaction Flow ......................................................... 16

2.1 Initiating a Transaction .............................................................. 16

2.2 Application Selection ................................................................. 16

2.3 Initiating Application Processing ............................................... 17

2.4 Reading the Application Data ................................................... 17

2.5 Risk Management Checks ........................................................ 17

2.6 Terminal Action Analysis ........................................................... 20

2.7 Card Risk Management ............................................................ 20

2.8 Online Processing ..................................................................... 21

2.9 VisaNet Processes Acquirer Authorization Request ................ 21

2.10 Issuer Receives Authorization Request .................................... 21

2.11 VisaNet Processes the Issuer Response ................................. 22

2.12 Transaction Conclusion ............................................................ 22

2.13 Clearing and Settlement ........................................................... 22

3 Visa payWave Transaction Flow ........................................... 23

3.1 Acquirer Approaches ................................................................ 23

3.2 U.S. Contactless Acceptance Requirements ............................ 23

3.3 Contactless Processing Requirements ..................................... 24

3.4 Initiating a Visa payWave Transaction ...................................... 24

3.5 qVSDC Transactions ................................................................ 25

3.6 MSD Transaction Flow .............................................................. 28

3.7 Visa payWave for Mobile .......................................................... 30

4 Visa’s Chip Terminal and Reader Requirements ................. 31

4.1 Terminal Types ......................................................................... 31

4.2 Application Identifiers (AIDs)..................................................... 32

4.3 Language .................................................................................. 34

April 2014 VISA CONFIDENTIAL v

Notice: This information is proprietary and CONFIDENTIAL to Visa. It is distributed to Visa participants for use

exclusively in managing their Visa programs. It must not be duplicated, published, distributed or disclosed, in whole

or in part, to merchants, cardholders or any other person without prior written permission from Visa. © 2014 Visa.

All Rights Reserved.

Visa Smart Debit/Credit and Visa payWave U.S. Acquirer Implementation Guide

4.4 VSDC Requirements ................................................................. 34

4.5 Visa payWave Reader Requirements ....................................... 44

4.6 Additional Requirements for VCPS 2.1 ..................................... 48

5 Additional Terminal Considerations ..................................... 49

5.1 Magnetic Stripe Transaction Terminal Requirements .............. 49

5.2 Card Data in Online Messages ................................................. 51

5.3 Support for up to 19 Digit PANs ................................................ 52

5.4 Terminal Display Messages ...................................................... 52

5.5 PIN Length and Character Set .................................................. 53

5.6 Cardholder Receipt Requirements ........................................... 53

5.7 Transaction Routing .................................................................. 54

5.8 Acquirer Stand-In ...................................................................... 55

5.9 Deferred Authorization .............................................................. 55

5.10 Transaction Type Requirements ............................................... 55

5.11 EMV Transactions in Specific Industries .................................. 59

5.12 Purchase with Cash-back ......................................................... 60

5.13 Terminal PIN Requirements ..................................................... 60

5.14 Terminal Types and Configurations .......................................... 61

5.15 Terminal Requirements for CVM .............................................. 63

6 Terminal Selection and Approval .......................................... 64

6.1 Terminal and Reader Selection Criteria .................................... 64

6.2 VSDC Terminal Approvals ........................................................ 66

6.3 Considerations for EMV Approval ............................................. 67

6.4 Contactless Reader Approvals and Renewals ......................... 68

6.5 Payment Card Industry Requirements ...................................... 69

6.6 Acquirer Device Validation Toolkit ............................................ 70

6.7 Contactless Device Evaluation Toolkit ...................................... 72

6.8 qVSDC Device Module ............................................................. 73

6.9 Additional Toolkit Requirements ............................................... 73

6.10 Visa Chip Vendor Enabled Service (CVES) ............................. 74

6.11 Acquirer Host Testing ............................................................... 74

6.12 Implementation Activities .......................................................... 74

7 Terminal Testing and Maintenance ....................................... 76

7.1 Terminal Testing Process ......................................................... 76

7.2 Interoperability Problems .......................................................... 78

7.3 Chip Interoperability Compliance Program ............................... 80

8 Terminal Management Systems ............................................ 82

8.1 EMV Functions .......................................................................... 82

8.2 Data Elements .......................................................................... 82

April 2014 VISA CONFIDENTIAL vi

Notice: This information is proprietary and CONFIDENTIAL to Visa. It is distributed to Visa participants for use

exclusively in managing their Visa programs. It must not be duplicated, published, distributed or disclosed, in whole

or in part, to merchants, cardholders or any other person without prior written permission from Visa. © 2014 Visa.

All Rights Reserved.

Visa Smart Debit/Credit and Visa payWave U.S. Acquirer Implementation Guide

8.3 Software Updates ..................................................................... 84

8.4 EMV Functionality Considerations ............................................ 84

9 Acquirer System Changes ..................................................... 86

9.1 U.S. Acquirer Processor Mandate ............................................ 86

9.2 Terminal-to-Acquirer Interface .................................................. 86

9.3 Host System Changes .............................................................. 87

9.4 Implementation Activities .......................................................... 89

10 Acquirer Host Testing ............................................................ 90

10.1 Testing Environment ................................................................. 90

10.2 Testing Process ........................................................................ 91

10.3 End-to-End Testing ................................................................... 94

10.4 Pilot Testing .............................................................................. 94

11 Acquirer Back-Office Changes .............................................. 95

11.1 Dispute Resolution Management .............................................. 95

11.2 EMV Liability Shift ..................................................................... 96

11.3 Chargebacks and Representments .......................................... 96

11.4 Reporting................................................................................... 97

11.5 Visa Reporting .......................................................................... 98

11.6 Internal Staff Training ................................................................ 98

11.7 Implementation Activities .......................................................... 99

12 Merchant Support ................................................................. 100

12.1 Merchant Agreement .............................................................. 100

12.2 Merchant Registration ............................................................. 100

12.3 Technology Innovation Program ............................................. 100

12.4 Contactless Reader Migration ................................................ 102

12.5 Merchant Services .................................................................. 102

12.6 Merchant Systems Changes ................................................... 105

12.7 Contactless Reader Branding and Placement ........................ 105

12.8 Merchant Training ................................................................... 106

Appendix A Planning Checklist ................................................ 112

Appendix B V.I.P. System Message Requirements................. 116

Appendix C Reference Materials .............................................. 119

Appendix D Standard EMV Terminal Logic ............................. 123

Appendix E Special Terminal Logic ......................................... 124

April 2014 VISA CONFIDENTIAL vii

Notice: This information is proprietary and CONFIDENTIAL to Visa. It is distributed to Visa participants for use

exclusively in managing their Visa programs. It must not be duplicated, published, distributed or disclosed, in whole

or in part, to merchants, cardholders or any other person without prior written permission from Visa. © 2014 Visa.

All Rights Reserved.

Visa Smart Debit/Credit and Visa payWave U.S. Acquirer Implementation Guide

List of Tables

Table 1: EMV and VSDC Terminal Types ...................................................... 31

Table 2: Application Identifiers (AIDs) for Visa ISO RID................................. 33

Table 3: Application Identifier (AID) for Visa US Common Debit AID ............ 33

Table 4: Types of Cardholder Verification Methods ....................................... 39

Table 5: Acquirer Host Testing Steps ............................................................. 91

Table 6: Policy Related Tasks ...................................................................... 112

Table 7: Operational Related Tasks ............................................................. 113

Table 8: Technical Related Tasks ................................................................ 114

Table 9: V.I.P. System Field 55 Mandated Data Tags ................................. 116

Table 10: V.I.P. System Chip-related Fields ................................................. 118

Table 11: Reference Materials ...................................................................... 119

List of Figures

Figure 1: Card Requests Terminal and Transaction Data .............................. 26

Figure 2: EMV Terminal Logic ...................................................................... 123

Figure 3: Special Application Selection Using Visa US Common Debit AID 127

Figure 4: Special Application Selection Using BIN / IIN Logic ...................... 128

Figure 5: Special Application Selection Using Consumer Indication ............ 129

Figure 6: US Common Debit Application Acceptance Overview .................. 131

Figure 7: Special Contactless Application "Pre-Selection" ........................... 136

Figure 8: Combined CVM Processing and Selectable Kernel ...................... 139

•

April 2014 VISA CONFIDENTIAL viii

Notice: This information is proprietary and CONFIDENTIAL to Visa. It is distributed to Visa participants for use

exclusively in managing their Visa programs. It must not be duplicated, published, distributed or disclosed, in whole

or in part, to merchants, cardholders or any other person without prior written permission from Visa. © 2014 Visa.

All Rights Reserved.

Visa Smart Debit/Credit and Visa payWave U.S. Acquirer Implementation Guide

About This Guide

This guide is referenced in, and has the same authority as, the Visa International Operating

Regulations. The Visa International Operating Regulations governs in the event of any

inconsistency or contradiction, unless Visa specifically grants a variance.

• This guide is designed to help U.S. acquirers prepare the terminal, host and back-office

infrastructure to support a combined Visa Smart Debit/Credit (VSDC) and Visa

payWave program. Because the U.S. is an always online or ‘zero floor limit’

environment, the cost and complexity of a traditional chip implementation is reduced.

This guide includes:

• Best practices, suggestions, considerations and descriptions of step-by-step activities to

assist with the implementation.

• Information to assist acquirers in supporting their merchants as they migrate to chip.

• A Section on implementation activities to highlight the support required in each section.

• Given the nature of the U.S. payment environment, where all transactions are authorized

online, this guide focuses solely on the implementation requirements relating to online-

only terminals and does not discuss offline processing requirements in detail.

• This guide also outlines requirements for supporting VSDC and Visa payWave using the

qVSDC and MSD paths.

• This guide references a number of other Visa and industry documents that are essential

for implementing a chip program. Refer to Appendix C Reference Materials.

Out of Scope

• This guide is not intended to aid acquirers in making the decision to begin deployment of

chip devices but, provide information on benefits and features of the service or provide

in-depth educational background on chip cards, terminals or systems.

• This guide will not address the capability of other networks to carry full chip data if the

transaction is routed over a non-Visa network.

• It does not address requirements relating to:

• Tasks related to implementing a new card acceptance program.

• Offline Processing: Acquirers considering offline processing support should review the

global VSDC Acquirer Implementation Guide and the Visa payWave Acquirer

Implementation Guide.

• Support for Visa Contactless Payment Specification (VCPS )1.4.2 readers.

April 2014 VISA CONFIDENTIAL 9

Notice: This information is proprietary and CONFIDENTIAL to Visa. It is distributed to Visa participants for use

exclusively in managing their Visa programs. It must not be duplicated, published, distributed or disclosed, in whole

or in part, to merchants, cardholders or any other person without prior written permission from Visa. © 2014 Visa.

All Rights Reserved.

Visa Smart Debit/Credit and Visa payWave U.S. Acquirer Implementation Guide

• Chip processing at ATMs

Assumptions

• This document assumes that the:

• Acquirer currently accepts Visa cards at its terminals.

• Acquirer currently accepts Visa Interlink cards at its terminals.

• Acquirer is familiar with V.I.P. processing requirements.

• Acquirer is connected to VisaNet.

• Acquirer has an established mechanism for installing and configuring all devices.

Audience

• The Visa Smart Debit/Credit and Visa payWaveU.S. Acquirer Implementation Guide is

intended for acquirers, acquirer processors, and direct connect merchants in the U.S.

responsible for the implementation, testing and activation of a dual-interface acceptance

program combining support for VSDC and Visa payWave.

Document Organization

• Section 1, Overview – This Section provides an overview of chip technology and the

EMV global foundation for chip-based payment services.

• Section 2, VSDC Transaction Flow – This Section describes the VSDC chip

transaction steps at the terminal/card level and the host level.

• Section 3, Visa payWave Transaction Flow – This Section describes the Visa

payWave steps at the terminal/card level and the host level.

• Section 4, Visa's Chip Terminal and Reader Requirements – This Section describes

the requirements for deploying EMV-compliant VSDC terminals and VCPS compliant

contactless readers.

• Section 5, Additional Terminal Considerations – This Section discusses the

additional consideration for the requirements outlined in Section 2.

• Section 6, Terminal Selection and Approval – This Section is intended to assist

acquirers in creating selection criteria for chip terminals and provides background

information on the terminal approval process before deployment in the field.

• Section 7,Terminal Testing and Maintenance – This Section outlines Visa's

recommendations for acquirers to undertake post deployment testing to address and

resolve acceptance and interoperability problems that may be inadvertently introduced

during rollout.

April 2014 VISA CONFIDENTIAL 10

Notice: This information is proprietary and CONFIDENTIAL to Visa. It is distributed to Visa participants for use

exclusively in managing their Visa programs. It must not be duplicated, published, distributed or disclosed, in whole

or in part, to merchants, cardholders or any other person without prior written permission from Visa. © 2014 Visa.

All Rights Reserved.

Visa Smart Debit/Credit and Visa payWave U.S. Acquirer Implementation Guide

• Section 8, Terminal Management Systems – This Section provides the recommended

functions to be supported by a Terminal Management System (TMS) in a chip

environment.

• Section 9, Acquirer System Changes – This Section outlines acquirer system changes

to support EMV chip.

• Section 10, Acquirer Host Testing – This Section addresses acquirer host testing to

support VSDC and Visa payWave transactions. It assumes the acquirer is already a

VisaNet endpoint.

• Section 11, Acquirer Back-Office Changes – This Section addresses the technical

changes to back-office functions that acquirers will need to support an EMV chip

program.

• Section 12, Merchant Support – This Section reviews the tasks related to supporting

merchants as they make the transition to chip card acceptance. It focuses on the

merchant support needs in areas such as system changes and training.

• Appendix A, Planning Checklist – This appendix is designed to help acquirers plan the

implementation of their chip program and develop a detailed work plan.

• Appendix B, V.I.P. System Message Requirements – This appendix outlines the

mandated tags that must be supported, and the related chip fields.

• Appendix C, Reference Materials – This appendix lists all the key guides referenced

throughout the document.

• Appendix D, Standard EMV Terminal Logic – This appendix provides an overview of

standard EMV terminal logic.

• Appendix E, Special Terminal Logic – This appendix includes the special terminal

logic that is necessary for a merchant to determine the AID to be selected for an eligible

transaction. Also this appendix illustrates the special contact terminal CVM logic that is

necessary for a merchant participating in Visa’s VEPS program or a merchant that

supports cash-back.

Summary of Changes

Since this document was last published in June 2013, Visa has updated and expanded the

appendix that illustrates special terminal logic. Special terminal logic could be necessary when

accepting debit transactions. An appendix was also added to describe Standard EMV

Terminal Logic, providing an overview of standard EMV terminal logic with a specific focus on

the selection process discussed in Section 4 Visa’s Chip Terminal and Reader Requirements.

April 2014 VISA CONFIDENTIAL 11

Notice: This information is proprietary and CONFIDENTIAL to Visa. It is distributed to Visa participants for use

exclusively in managing their Visa programs. It must not be duplicated, published, distributed or disclosed, in whole

or in part, to merchants, cardholders or any other person without prior written permission from Visa. © 2014 Visa.

All Rights Reserved.

Visa Smart Debit/Credit and Visa payWave U.S. Acquirer Implementation Guide

1 Overview

• New technology is presenting Visa with exciting opportunities to provide enhanced

payment services. Chip technology based on EMV can help prevent the compromise of

sensitive cardholder data while providing consumers and merchants with fast and

convenient ways to complete purchases across various form factors including mobile.

• Because EMV provides a global foundation for chip-based payment services, adherence

to its specifications ensures global interoperability and offers enhanced security and

greater functionality to today’s Visa products. Using the EMV foundation layer, Visa has

developed additional specifications, for example, the Visa Integrated Circuit Card

Specification (VIS), the Visa Contactless Payment Specification (VCPS) and payment

service rules and implementation guidelines. Visa Smart Debit/Credit (VSDC) is a

program specifically designed to aid Visa acquirers in migrating magnetic stripe Visa

card programs and acceptance infrastructure to a chip-based payment service.

• Additionally Visa payWave provides a flexible and globally interoperable approach to

contactless transactions. It offers several implementation options – all while ensuring the

Visa payWave cards and other contactless form factors receive the same level of

acceptance whether used at home or abroad.

• To implement acceptance for VSDC and Visa payWave, as part of their migration to

chip, acquirers will need to consider various changes to their existing terminals and host

processing, including:

• New terminal applications and support for selectable EMV kernels

• Compliance with Visa and industry requirements for contact and contactless chip

terminals

• Testing and approval processes for chip terminals

• Changes to terminal and host messaging

• Changes to host systems to process new or additional data

• Back office changes

• Impact to merchants and additional training

NOTE: The term “acquirer,” as used in this Guide, will be defined as the acquirer or acquirer

processor.

1.1 Compliance Documents and Reference Documentation

• To facilitate requirements while ensuring global interoperability, terminals accepting Visa

cards must comply with the following documents:

April 2014 VISA CONFIDENTIAL 12

Notice: This information is proprietary and CONFIDENTIAL to Visa. It is distributed to Visa participants for use

exclusively in managing their Visa programs. It must not be duplicated, published, distributed or disclosed, in whole

or in part, to merchants, cardholders or any other person without prior written permission from Visa. © 2014 Visa.

All Rights Reserved.

Visa Smart Debit/Credit and Visa payWave U.S. Acquirer Implementation Guide

• Visa International Operating Regulations

• Visa Transaction Acceptance Device Requirements

NOTE: Refer to Appendix C Reference Materials for a more complete list of reference

documents and for information on where to obtain the documents listed in this

Section and throughout the Guide.

• Contact chip terminals must comply with the EMV Integrated Circuit Card Specifications

for Payment Systems, available from the EMVCo website (www.emvco.com) including

any specification updates released by EMVCo.

• Visa payWave readers must comply with the EMV Contactless Specifications, including

Book C-3, and the Visa Contactless Payment Specification (VCPS), Version 2.1

including all published updates.

• Devices accepting personal identification numbers (PINs) must comply with the Payment

Card Industry (PCI) PIN Transaction Security (PTS) Point of Interaction (POI) Modular

Security Requirements available from www.pcisecuritystandards.org and with the Visa

PCI PIN Security Requirements.

• A number of best practice documents are also available to assist acquirers in

determining their terminal requirements:

• Best practices relating to the deployment of acceptance terminals that support magnetic

stripe, contact chip and contactless chip can be found in the Visa Transaction

Acceptance Device Guide (TADG).

• Best practices relating to the Visa Easy Payment Service (VEPS) can be found on

www.visa.com in the Visa Easy Payment Service – Merchant Program Guide.

• Best practices relating to payment acceptance for retail petroleum merchants can be

found in the Visa Payment Acceptance Best Practices for Retail Petroleum Merchants.

• Risk management best practices for prepaid programs that will utilize a self-service kiosk

can be found in the Prepaid Product Risk Management Best Practices.

• In addition to complying or following best practices outlined in the above-mentioned

documents, acquirers can customize their programs beyond these minimum

requirements through adoption of optional functionality and proprietary processing.

Proprietary processing, however, must not interfere with global interoperability.

NOTE: Visa acquirers must download Visa chip documentation from the Visa Chip and Contactless

webpage on Visa Online. Please see Appendix C for information on enrolling and gaining

entitlement. Licensed vendors may download licensed Visa materials from the Visa

Technology Partner site (https://technologypartner.visa.com).

1.2 Terminology

• The following terms are used throughout this guide:

April 2014 VISA CONFIDENTIAL 13

Notice: This information is proprietary and CONFIDENTIAL to Visa. It is distributed to Visa participants for use

exclusively in managing their Visa programs. It must not be duplicated, published, distributed or disclosed, in whole

or in part, to merchants, cardholders or any other person without prior written permission from Visa. © 2014 Visa.

All Rights Reserved.

Visa Smart Debit/Credit and Visa payWave U.S. Acquirer Implementation Guide

• Acquirer – A Member that signs a Merchant or disburses currency to a Cardholder in a

Cash Disbursement, and directly or indirectly enters the resulting Transaction Receipt

into Interchange. Visa International Operating Regulations ID#: 010410-010410-

0024219.

• AID – A data element that identifies the application in a card or terminal, such as Visa

Debit/Credit or Visa Electron. It is composed of the Registered Application Provider

Identifier (RID) and the Proprietary Application Identifier Extension (PIX).

• Card (Visa Card) – A Magnetic Stripe and/or a Visa contactless card bearing the Visa

Brand Mark, or a non-Card form Contactless Payment device bearing the Visa Brand

Mark, that enables a Visa Cardholder to obtain goods, services, or cash from a Visa

Merchant or an Acquirer. All Visa Cards must bear the Visa Brand Mark.

• Chip Card – A Card embedded with a Chip that communicates information to a

Transaction Acceptance Device (TAD).

• Dual-interface Terminals – A terminal that supports both contact and contactless chip

cards and complies with the EMV Specifications and VCPS. Support for contactless may

be either as a reader separate from the POS device or via a reader integrated into a

POS device.

• EMV® Specifications – EMV Integrated Circuit Card Specifications for Payment

Systems encompassing all 4 books which make the contact chip specifications and the

EMV Contactless Specifications for Payment Systems encompassing 4 books which

make up the contactless specification plus any updates published in specification

bulletins on the EMVCo website.

• Merchant Routing Option – the option provided to U.S. merchants pursuant to the

Dodd-Frank Act and Federal Reserve Board Regulation II to route covered debit

transactions over one of at least two unaffiliated payment networks enabled on a card.

• Reader, Contactless Reader – The merchant device communicating with the card.

• There are two scenarios in which typically a reader is used for a contactless transaction:

• Either as a reader, also called a dongle or Proximity Coupling Device (PCD), separated

from, but communicating with, a POS device.

• Or as a reader integrated into a POS device.

• The word reader in this guide will cover both scenarios unless explicitly stated otherwise.

It is not intended to imply in which physical component (the reader or the POS device) a

specific action is performed.

• Terminal – A transaction acceptance device.

• US Common Debit AID – See Visa US Common Debit Application Identifier.

April 2014 VISA CONFIDENTIAL 14

Notice: This information is proprietary and CONFIDENTIAL to Visa. It is distributed to Visa participants for use

exclusively in managing their Visa programs. It must not be duplicated, published, distributed or disclosed, in whole

or in part, to merchants, cardholders or any other person without prior written permission from Visa. © 2014 Visa.

All Rights Reserved.

Visa Smart Debit/Credit and Visa payWave U.S. Acquirer Implementation Guide

• US Covered Visa Debit Card – A Visa US debit card as defined in VIOR for debit and

prepaid products covered by the unaffiliated network requirements of the Dodd-Frank

Act and Federal Reserve Board Regulation II.

• Visa Contactless Payment Specification (VCPS) – The Visa Contactless Payment

Specification, which covers versions 2.1 and all published updates.

• Visa Operating Regulations – The Visa International Operating Regulations including

any U.S. specific operating regulations.

• Visa US Common Debit Application Identifier – An EMV-compliant Application

Identifier licensed for use with Visa’s EMV and VIS-based applications for the purpose of

processing a transaction for debit and prepaid products covered by the unaffiliated

network requirements of the Dodd-Frank Act and Federal Reserve Board Regulation II.

In this document referred to as the Visa US Common Debit AID.

April 2014 VISA CONFIDENTIAL 15

Notice: This information is proprietary and CONFIDENTIAL to Visa. It is distributed to Visa participants for use

exclusively in managing their Visa programs. It must not be duplicated, published, distributed or disclosed, in whole

or in part, to merchants, cardholders or any other person without prior written permission from Visa. © 2014 Visa.

All Rights Reserved.

Visa Smart Debit/Credit and Visa payWave U.S. Acquirer Implementation Guide

2 VSDC Transaction Flow

• To better understand the impact of chip on an acquirer’s systems and processes it is

important to understand the various steps in a VSDC chip transaction. This Section

describes the steps at the terminal/card level and the host level.

• All activities, prior to the transaction going online for issuer approval, are transparent to

the acquirer and occur between the card and the terminal. Some of these functions will

not apply to terminals in the U.S. which operate as online-only terminals, and are so

noted.

• These functions are included in this Section to provide acquirers with an overall

understanding of the processing that may occur in an EMV chip transaction. Their

presence does not indicate the need to support them.

2.1 Initiating a Transaction

• The chip card is inserted into the terminal or swiped through a magnetic stripe reader. If

swiped, the terminal checks the service code in the magnetic stripe. If the first digit of the

service code indicates a chip card, the terminal prompts the sales clerk or cardholder to

insert the card into the terminal.

NOTE: To provide a faster transaction, merchants should be trained to insert the card into the

chip reader when presented with a chip card rather than swiping the magnetic stripe.

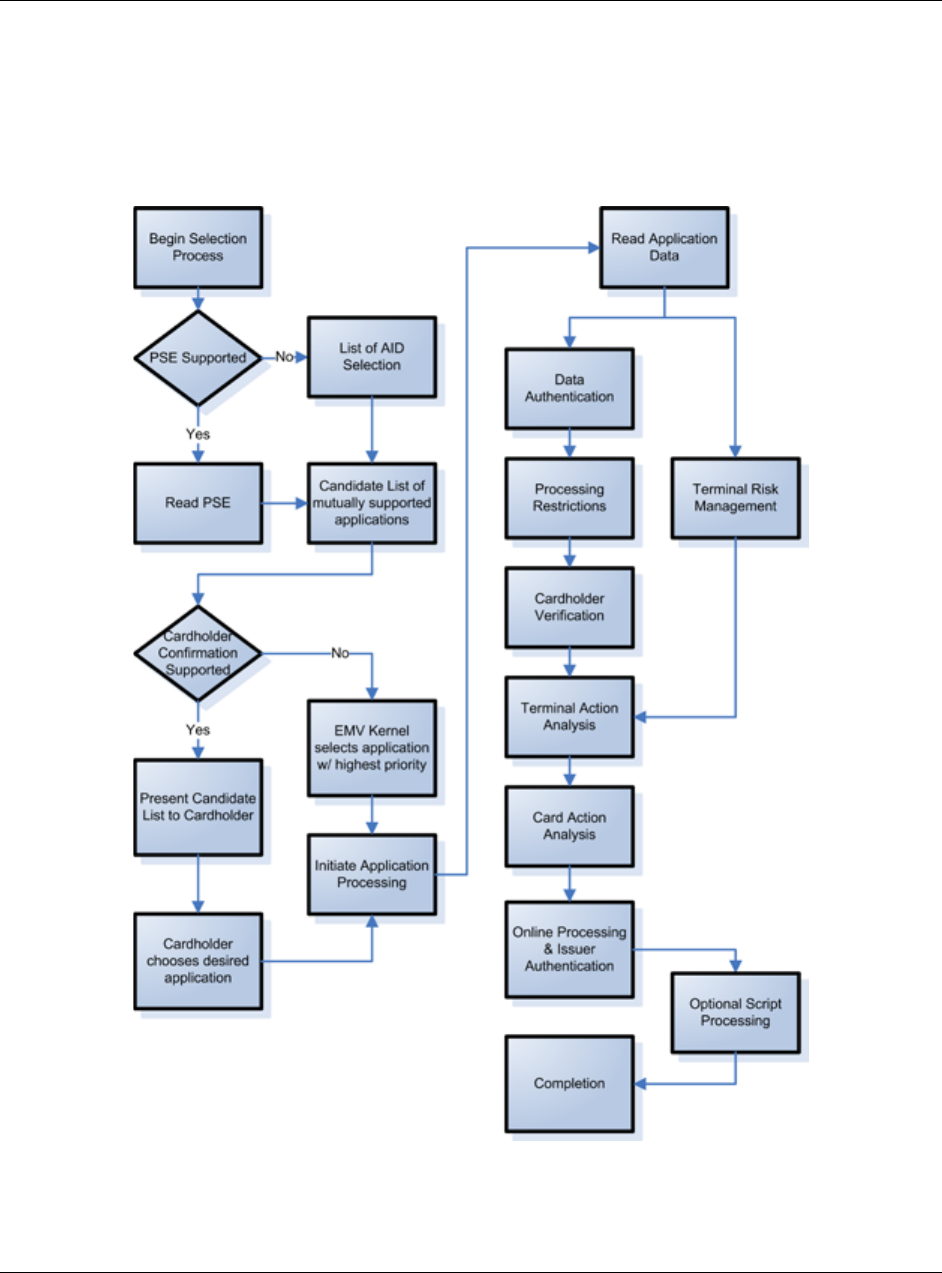

2.2 Application Selection

• The terminal determines the applications supported by the card and compares them to

the applications supported by the terminal. Application Selection is mandatory and

follows these rules:

• If the chip card and terminal have no applications in common and no application can be

selected, the device should display a message noting the card type is not supported and

fall back to magnetic stripe processing.

• If the chip card and terminal have one application in common and cardholder

confirmation is not required, that application is used.

• If the chip card and terminal have more than one application in common or if there is

a single application and cardholder confirmation is required, the terminal should display

a list of applications for cardholder selection.

• The cardholder then selects his or her preferred application from the available options

or the application is selected automatically based on the issuer priority list (including

whether or not cardholder confirmation is required) unless the Visa US Common Debit

AID selection logic described later in this document is used.

April 2014 VISA CONFIDENTIAL 16

Notice: This information is proprietary and CONFIDENTIAL to Visa. It is distributed to Visa participants for use

exclusively in managing their Visa programs. It must not be duplicated, published, distributed or disclosed, in whole

or in part, to merchants, cardholders or any other person without prior written permission from Visa. © 2014 Visa.

All Rights Reserved.

Visa Smart Debit/Credit and Visa payWave U.S. Acquirer Implementation Guide

All transactions initiated with a Visa owned Application Identifier (AID – see Section 4.2)

other than the Visa US Common Debit AID must be routed to VisaNet and be processed

according to Visa or Visa Interlink (as applicable) network operating rules and technical

standards. Some products may be personalized with more than one AID, with the other

AID(s) representing products with their own specific network and routing option(s), for

instance the Visa US Common Debit AID. To initiate a transaction using such a preferred

AID, certain terminal logic must be executed as part of the outlined VSDC transaction flow.

This logic is defined in Section 4.4.3.

2.3 Initiating Application Processing

• The terminal signals to the card that the transaction is about to begin. The card response

to the terminal includes data and risk management information for use during the

transaction. Before responding, the card performs the following steps:

1. Restrictions Check (Optional)

The card may determine if the transaction is taking place in an environment that the card

does not allow. When the transaction is not allowed for this application, the card directs

the terminal to a different application or alternatively terminates the transaction.

2. Card sends the Application Interchange Profile (AIP) and Application File Locator (AFL)

to terminal (mandatory).

The card may send a different AIP or AFL depending on the transaction environment.

For example, the card might send a different AIP and AFL for domestic versus

international transactions.

• AIP specifies the application functions that are supported by the application in the

chip card.

• AFL designates which records the terminal should read from the chip card.

2.4 Reading the Application Data

• The terminal uses the AFL to determine the card data it should read to process the

transaction. Once the terminal reads the data, it uses the AIP to determine what

processing is needed for the transaction.

2.5 Risk Management Checks

• Risk management checks are performed (if present on the card and supported by the

terminal) to determine how the transaction should be processed.

• In the U.S. all transactions require online processing, thus the terminal will send the

transaction online.

April 2014 VISA CONFIDENTIAL 17

Notice: This information is proprietary and CONFIDENTIAL to Visa. It is distributed to Visa participants for use

exclusively in managing their Visa programs. It must not be duplicated, published, distributed or disclosed, in whole

or in part, to merchants, cardholders or any other person without prior written permission from Visa. © 2014 Visa.

All Rights Reserved.

Visa Smart Debit/Credit and Visa payWave U.S. Acquirer Implementation Guide

2.5.1 Offline Data Authentication

• Offline Data Authentication allows the terminal to confirm that the card data has not been

tampered with after the card was issued by the issuer and in the case of Dynamic Data

Authentication (DDA) and Combined DDA/Application Cryptogram Generation (CDA),

protects against the re-use of copied chip data in an offline environment. This process is

important for offline capable devices where there may be a possibility of an offline

approved transaction.

• For online-only devices, Offline Data Authentication is superfluous and devices are

therefore not required to support Offline Data Authentication.

NOTE: Since all transactions in the U.S. will be sent online for issuer approval due to a

zero floor limit, support for Offline Data Authentication is not required and not

recommended. Acquirers or merchants that do not obtain an online approval do so

at their own liability.

• Depending on the card capabilities, one of the following Offline Data Authentication

methods may be performed if the terminal supports Offline Data Authentication:

• Static Data Authentication (SDA)

• Dynamic Data Authentication (DDA)

• Combined DDA/Application Cryptogram Generation (CDA) (optionally supported)

• SDA is performed by the terminal using static data read from the card. DDA and CDA

are performed by the card and the terminal using dynamic data from the card and

terminal. Offline capable devices need to support SDA and DDA.

• U.S. acquirers that consider supporting Offline Data Authentication should review the

global VSDC Acquirer Implementation Guide for further details.

2.5.2 Processing Restrictions

• The processing restrictions function is used to determine the degree of compatibility

between the application in the card and the terminal. These checks include determining

whether there are any geographic or transaction-type limitations or whether the

application on the card has expired.

• The terminal performs the following checks using data read from the card:

• Effective/Expiration Date Checking

• Application Usage Control Checking

• Application Version Number Checking

• Further information regarding Processing Restrictions can be found in the EMV

Specifications and in Section 4.

April 2014 VISA CONFIDENTIAL 18

Notice: This information is proprietary and CONFIDENTIAL to Visa. It is distributed to Visa participants for use

exclusively in managing their Visa programs. It must not be duplicated, published, distributed or disclosed, in whole

or in part, to merchants, cardholders or any other person without prior written permission from Visa. © 2014 Visa.

All Rights Reserved.

Visa Smart Debit/Credit and Visa payWave U.S. Acquirer Implementation Guide

2.5.3 Cardholder Verification

• The terminal reads the Cardholder Verification Method (CVM) List on the card to

determine the CVM to use for the transaction. It selects the CVM based on the CVMs

mutually supported (between card and terminal) and the circumstances of the

transaction.

• CVM is used by the terminal and/or the merchant to verify that the cardholder is

legitimate and that the card is not lost or stolen. The following CVM options are available

in EMV:

• Online PIN

• Signature

• Offline Plaintext PIN

• Offline Enciphered PIN

• No CVM required

• More information regarding support by terminals for each of the CVMs can found in

Section 4.4.5 Cardholder Verification, and in the Visa Operating Regulations and the

Transaction Acceptance Device Requirements.

• Terminal request of specific CVMs for specific transaction types may be supported by

selectable kernels as defined in contact EMV (see Section 4.4.6 and 8.4.2).

2.5.4 Terminal Risk Management

• The terminal performs checks based on the acquirer risk control features and the

capabilities of the terminal. For offline capable terminals, some of the checks are

mandatory whereas others are optional and at the discretion of the acquirer. The checks

include:

• Floor limit check

• Random selection

• Transaction velocity checking

• Exception file check (optional)

• Offline transaction limit check (optional)

• The results of these checks are used to determine how the terminal processes the

transaction. For online-only terminals in the U.S., these checks are not required as all

transactions will be sent online. However any acquirer considering use of offline-capable

terminals needs to ensure that terminals support floor limit checks and the floor limits are

set according to the Visa International Operating Regulations.

April 2014 VISA CONFIDENTIAL 19

Notice: This information is proprietary and CONFIDENTIAL to Visa. It is distributed to Visa participants for use

exclusively in managing their Visa programs. It must not be duplicated, published, distributed or disclosed, in whole

or in part, to merchants, cardholders or any other person without prior written permission from Visa. © 2014 Visa.

All Rights Reserved.

Visa Smart Debit/Credit and Visa payWave U.S. Acquirer Implementation Guide

2.6 Terminal Action Analysis

• The results of the previous steps are used in Terminal Action Analysis to determine the

disposition of the transaction. The results of the previous checks are stored in the

Terminal Verification Results (TVR) data element, which is then compared to specific

rules that are set by the issuer (in the card) and Visa (in the terminal).

• Depending on the results, the terminal will request a cryptogram from the card. A

cryptogram is data element dynamically generated by the card using transaction specific

data and a cryptographic key stored in the card. It allows the issuer to confirm data

integrity and that the transaction was undertaken using a valid card. The result of

Terminal Action Analysis determines which of the following cryptogram is generated:

• Transaction Certificate (TC)

• Application Authentication Cryptogram (AAC)

• Authorization Request Cryptogram (ARQC)

• For online-only terminals in the U.S., other than in some exception situations, the

terminals will always request an ARQC and go online.

• The cryptogram is generated by the card and its generation is transparent to the

terminal. Further information regarding the generation of the cryptograms and Terminal

Action Analysis processing, including exceptions, can be found in the EMV

Specifications and the Visa Integrated Circuit Card Specification (VIS).

2.7 Card Risk Management

• Card Risk Management is transparent to the acquirer, merchant and terminal. However

its outcome confirms the disposition of the transaction. It allows the card to perform

velocity checking and other risk management checks on behalf of the issuer to see if it

agrees with the terminal’s decision. The card may perform the following checks:

• New Card check

• Checking results from previous transactions (such as PIN Tries exceeded, Issuer Script

results and result of Offline Data Authentication)

• Offline spending amounts and transaction counts (Velocity) checking

• Once the card has completed the risk management checks, it responds to the terminal’s

request for a cryptogram with one of three cryptograms listed in Section 2.6 Terminal

Action Analysis.

• In the U.S., where the terminal will request to go online, the card will agree and respond

with an ARQC.

April 2014 VISA CONFIDENTIAL 20

Notice: This information is proprietary and CONFIDENTIAL to Visa. It is distributed to Visa participants for use

exclusively in managing their Visa programs. It must not be duplicated, published, distributed or disclosed, in whole

or in part, to merchants, cardholders or any other person without prior written permission from Visa. © 2014 Visa.

All Rights Reserved.

Visa Smart Debit/Credit and Visa payWave U.S. Acquirer Implementation Guide

2.8 Online Processing

• Once the card generates an ARQC for online processing, the terminal captures the

ARQC, the original data elements used by the chip card to generate the ARQC and

information regarding the selected application and the interface used. This information,

together with standard transaction data and the results of the risk management checks

are forwarded online to the acquirer.

• Acquirers format this data into the authorization message and forward the information to

VisaNet. For authorization and full financial messages, acquirers send the chip data in

Field 55 in TLV (Tag-Length-Value) format. It is critical that acquirers do not alter any of

the data received from the card and terminal as these are used by the issuer, or Visa on

its behalf, when authorizing the transaction. Altering data or data quality issues may

have serious consequences that may result in a decline of the transaction by the issuer.

2.9 VisaNet Processes Acquirer Authorization Request

• VisaNet may perform the following functions after it receives the authorization request:

• If the message format of the acquirer is different from the message format of the Full

Data issuer (Field 55 acquirer to third bit map issuer), VisaNet converts the authorization

to the issuer’s message format.

• VisaNet uses the pre-processing chip indicators to help determine whether to route to

the issuer. If the transaction is processed in Stand-In (STIP), these chip transaction

indicators influence the approve/decline decision.

• VisaNet forwards the authorization request to the issuer if it has not been processed in

STIP. If processed in STIP, the transaction proceeds as outlined in Section 2.11 VisaNet

Processes the Issuer Response.

2.10 Issuer Receives Authorization Request

• When the authorization request is received, the issuer or issuer processor will validate

the cryptogram. In certain cases Visa may validate the cryptogram on the issuer’s

behalf.

• The issuer may additionally review the chip data received in the authorization to

determine whether to authorize or decline the transaction.

• The issuer decides whether to approve or decline the transaction and sends the

authorization response to VisaNet to transmit to the acquirer. The response may

optionally include:

• An Authorization Response Cryptogram (ARPC), which is an equivalent to the ARQC

but generated by the issuer, which the card will validate.

• An Issuer Script that is typically used to reset risk parameters on the card.

April 2014 VISA CONFIDENTIAL 21

Notice: This information is proprietary and CONFIDENTIAL to Visa. It is distributed to Visa participants for use

exclusively in managing their Visa programs. It must not be duplicated, published, distributed or disclosed, in whole

or in part, to merchants, cardholders or any other person without prior written permission from Visa. © 2014 Visa.

All Rights Reserved.

Visa Smart Debit/Credit and Visa payWave U.S. Acquirer Implementation Guide

2.11 VisaNet Processes the Issuer Response

• If the issuer is participating in the Visa Chip Authenticate, VisaNet generates the ARPC

on behalf of the issuer and includes it in the authorization response to the acquirer.

Otherwise VisaNet forwards the issuer response to the acquirer.

2.12 Transaction Conclusion

• The acquirer receives the authorization response and sends it to the terminal. The card

and terminal perform final processing to complete the transaction including:

• If an ARPC is returned in the authorization response, the card validates the ARPC

to ensure that the authorization response came from a valid issuer.

• Card authenticates and executes Issuer Script commands, if present.

• The card generates the final cryptogram, a TC for approval or an AAC for decline. Once

the transaction is completed the terminal prompts the cashier or the customer to remove

the card.

2.13 Clearing and Settlement

• For approved transactions, the card generates a TC as the final cryptogram. The

acquirer then submits the approved transaction to VisaNet for clearing and settlement.

• Acquirers send TCR 0 with POS Terminal Capability Code = 5 and POS Entry Mode =

05 or 95.

• Acquirers send TCR1 if cash-back is supported.

• Acquirers send TCR 5 and TCR 7 with new chip data. Acquirers and merchants in the

U.S. deploying online-only terminals or terminals set with a Zero Floor Limit and that

obtain an online authorization for all transactions are not required to support TCR 7 in

the clearing record.

NOTE: TCR 7 is still required if a transaction is offline approved. If you plan to support

offline approved transactions please refer to the global VSDC Acquirer

Implementation Guide.

April 2014 VISA CONFIDENTIAL 22

Notice: This information is proprietary and CONFIDENTIAL to Visa. It is distributed to Visa participants for use

exclusively in managing their Visa programs. It must not be duplicated, published, distributed or disclosed, in whole

or in part, to merchants, cardholders or any other person without prior written permission from Visa. © 2014 Visa.

All Rights Reserved.

Visa Smart Debit/Credit and Visa payWave U.S. Acquirer Implementation Guide

3 Visa payWave Transaction Flow

• To better understand the impact of Visa payWave on an acquirer’s systems and

processes it is important to understand the various steps in a Visa payWave transaction.

This Section describes the steps at the terminal/card level and the host level.

• All activities, prior to the transaction going online for issuer approval, are transparent to

the acquirer and occur between the card, the reader and terminal.

• Section 4 Visa’s Chip Terminal and Reader Requirements provides further detail on

some of the steps outlined in this Section and their implementation impacts. Section 9

Acquirer System Changes provides further information regarding host processing steps.

3.1 Acquirer Approaches

• Acquirers must support Visa payWave qVSDC and MSD transactions (as per Section

3.1.2). To provide support for the long term development of the contactless platform, and

its dependent propositions such as mobile proximity and transit, Visa introduced new

requirements relating to the support of qVSDC and MSD in the U.S.

• The two approaches and Visa’s requirements are outlined in more detail in the following

sections.

3.1.1 Quick Visa Smart Debit/Credit (qVSDC)

• qVSDC transactions follow an expedited EMV-processing model and chip-processing

rules. These transactions can be sent online and validated using one of three dynamic

authentication methods, Cryptogram Version Number 17 (CVN 17), CVN 10, or CVN 18.

• The issuer decides whether to support CVN 17, CVN 10, or CVN 18, which is

personalized on the card and carried during transaction processing. qVSDC is only

suited for acceptance environments with EMV infrastructure including support for chip

data by the acquirer host.

3.1.2 Magnetic Stripe Data (MSD)

• MSD contactless transactions follow magnetic stripe processing rules. MSD transactions

are sent online and validated using CVN 17 (MSD CVN 17) or dynamic Card Verification

Value (dCVV) (MSD Legacy). MSD is best suited for magnetic stripe acceptance

environments.

3.2 U.S. Contactless Acceptance Requirements

• Effective 1 April 2013, all new Visa payWave accepting contactless readers deployed in

the U.S. must actively support both MSD and the qVSDC transaction path of VCPS 2.1

including all published updates. qVSDC may be supported on an online only basis

(i.e.no support for offline authorizations).

April 2014 VISA CONFIDENTIAL 23

Notice: This information is proprietary and CONFIDENTIAL to Visa. It is distributed to Visa participants for use

exclusively in managing their Visa programs. It must not be duplicated, published, distributed or disclosed, in whole

or in part, to merchants, cardholders or any other person without prior written permission from Visa. © 2014 Visa.

All Rights Reserved.

Visa Smart Debit/Credit and Visa payWave U.S. Acquirer Implementation Guide

NOTE: Existing Visa payWave accepting contactless readers that can only support

transactions as specified in VCPS 1.4.2 may remain in market until their natural

retirement.

• New Visa payWave accepting contactless readers deployed between 1 December 2011

and 1 April 2013 must be configured to either:

• Support only transactions as specified in VCPS 1.4.2, or

• Actively support both the MSD and the qVSDC transaction path of VCPS 2.1 including

all published updates and transmit the resulting chip data to VisaNet.

• Effective 1 January 2015, Visa contactless readers connected to acquirer platforms that

are certified for chip data no longer need to support the MSD transaction path.

• Further details can be found in the Visa Business News article dated December 22,

2011 or from a Visa representative.

3.3 Contactless Processing Requirements

• All transactions initiated with a Visa owned Application Identifier (AID – see Section 4.2)

other than the Visa US Common Debit AID must be routed to VisaNet and be processed

according to Visa or Visa Interlink (as applicable) network operating rules and technical

standards. Some products may be personalized with more than one AID, with other

AID(s) representing products with their own specific network and routing option(s). To

initiate a transaction using an AID that is not the highest priority mutually supported AID

(as specified by the card) certain terminal logic must be executed before the outlined

qVSDC transaction flow. This logic is defined in Section 4.5.1.

• Acquirers are responsible for their merchants’ compliance with Visa rules governing Visa

Contactless transactions, including ensuring proper transaction routing.

3.4 Initiating a Visa payWave Transaction

• During a Visa payWave transaction, consumers briefly hold their Visa payWave card

near the reader when prompted, instead of inserting their card in the reader as with

VSDC transactions or swiping the magnetic stripe. The Visa payWave card is embedded

with an antenna and a chip. The chip, through the antenna, communicates with the

merchant’s contactless reader to enable the transaction.

• Acquirers should be aware that Visa payWave transactions may be initiated not only

from a traditional plastic card but also from other form factors and devices such as Near

Field Communication (NFC) enabled mobile devices and key fobs.

April 2014 VISA CONFIDENTIAL 24

Notice: This information is proprietary and CONFIDENTIAL to Visa. It is distributed to Visa participants for use

exclusively in managing their Visa programs. It must not be duplicated, published, distributed or disclosed, in whole

or in part, to merchants, cardholders or any other person without prior written permission from Visa. © 2014 Visa.

All Rights Reserved.

Visa Smart Debit/Credit and Visa payWave U.S. Acquirer Implementation Guide

3.5 qVSDC Transactions

3.5.1 Preliminary Processing

• Before the card and reader begin their interaction, the transaction amount is typically

received by the reader before it performs its preliminary processing. Preliminary

Processing expedites the transaction by allowing the reader to perform several risk

management steps prior to interacting with the card.

• During Preliminary Processing, the reader may use the transaction amount to perform

the following checks:

• Reader Contactless Transaction Limit: Transactions for amounts above this limit are

terminated and may be processed only by using a different interface.

NOTE: Contactless readers are required to either have the reader contactless transaction

limit disabled or set to its maximum amount. This limit is not used in the U.S. region.

• Reader Cardholder Verification Method (CVM) Limit: Transaction amounts above this

limit require cardholder verification for the contactless transaction.

• Reader Contactless Floor Limit: Transactions above this limit require an online

authorization by the card issuer. For the U.S. region this limit is set to zero or is not

supported to ensure all transactions are sent online to be authorized by the issuer.

• The reader sets the results of these checks in the Terminal Transaction Qualifiers (TTQ),

a reader data element. The TTQ provides the card with the reader’s capabilities and

requirements. For U.S. readers the TTQ must reflect online-only transactions with no

contact transaction limits.

3.5.2 Application Selection

• Once the reader has completed Preliminary Processing, the reader signals to the

consumer that the reader is ready for the contactless card. The cardholder briefly waves

or holds the Visa payWave card close to the contactless reader to initiate the

transaction. The reader determines whether it shares a contactless application with the

card by selecting the card’s list of contactless AIDs (called the Proximity Payment

Systems Environment [PPSE]). If there is an AID in common, that AID is automatically

selected; otherwise the reader terminates the transaction and the transaction may

proceed via another interface such as magnetic stripe or contact chip.

• If there are two or more AIDs in common, the AID with the highest priority is

automatically selected as per EMV Contactless standards. For example, a card may

have both credit and debit AIDs, in which case the issuer or consumer will have defined

one of those AIDs as a higher priority than the other.

NOTE: For qVSDC readers supporting a merchant routing option, a pre-select step as defined

in Section 3.3 may be required to identify the AIDs supported on the card/consumer

device and thereby the possible routing options that are available to the merchant.

Section 4.5.1 provides further information on this issue.

April 2014 VISA CONFIDENTIAL 25

Notice: This information is proprietary and CONFIDENTIAL to Visa. It is distributed to Visa participants for use

exclusively in managing their Visa programs. It must not be duplicated, published, distributed or disclosed, in whole

or in part, to merchants, cardholders or any other person without prior written permission from Visa. © 2014 Visa.

All Rights Reserved.

Visa Smart Debit/Credit and Visa payWave U.S. Acquirer Implementation Guide

3.5.3 Dynamic Reader Limits (Optional)

• Once the application has been selected, readers that support Dynamic Reader Limits

(DRL) examine the Application Program Identifier (Program ID) returned by the

application to determine the applicable reader limits for the transaction.

• When the Program ID returned by the card does not match a reader Program ID (or the

card does not return a Program ID), the reader processes the transaction using the

reader limits and results determined during Preliminary Processing.

3.5.4 Card Request Terminal and Transaction Data

• Once the application is selected, the Visa payWave card responds by requesting

information such as the transaction amount, TTQ, and the reader’s currency code for

use during the transaction. The reader responds with the requested information.

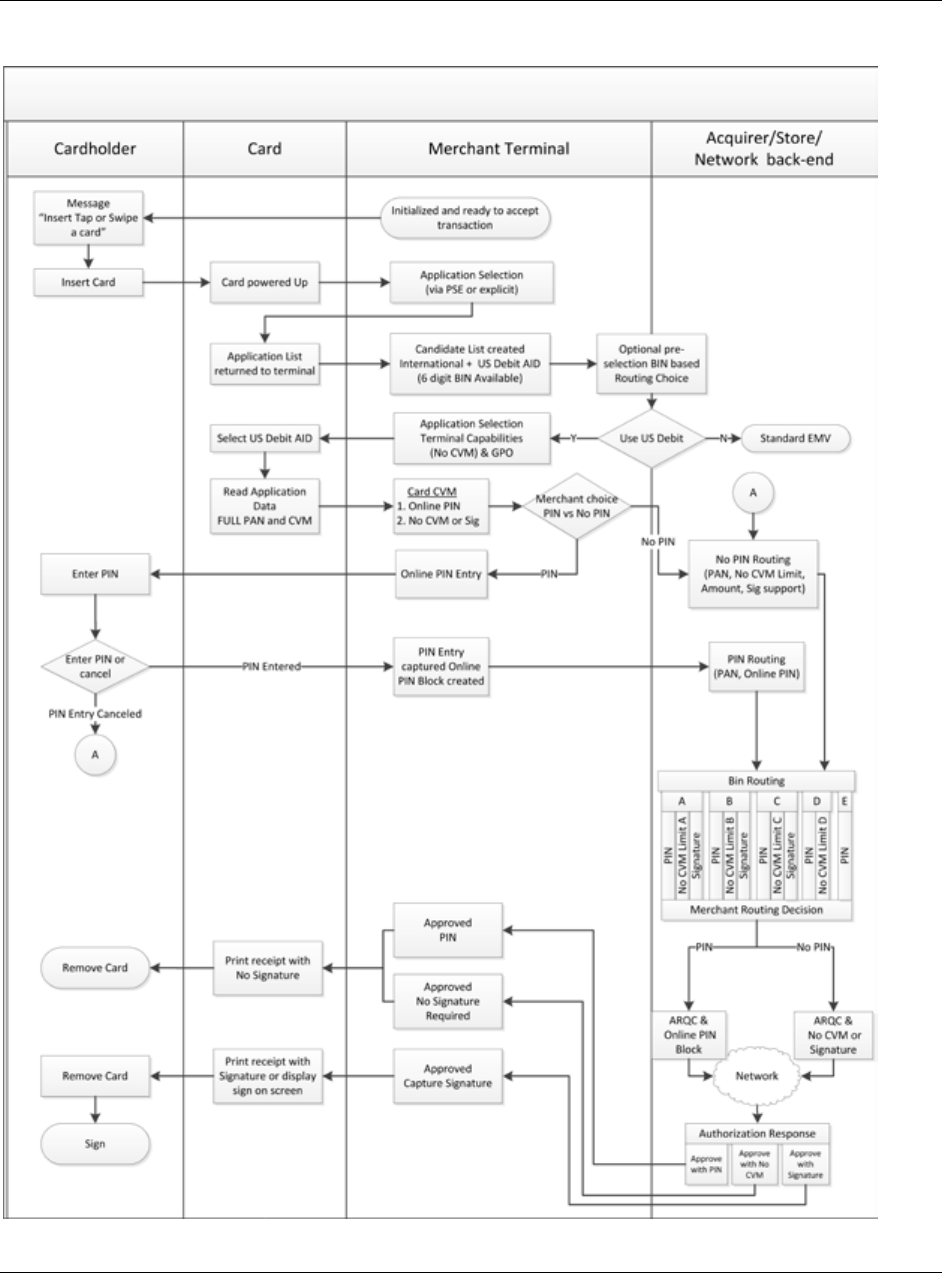

• Figure 1 below provides a processing overview of the card requesting terminal and

transaction data.

Figure 1: Card Requests Terminal and Transaction Data

• The TTQ advises the Visa payWave card of the reader’s requirements and capabilities

for processing the specific transaction as follows:

• Whether it supports qVSDC or MSD as well as whether it supports contact VSDC

• Whether it supports Signature, Online PIN, Offline PIN through the Contact Interface,

and/or Consumer Device CVM

NOTE: A Consumer Device CVM is a CVM that is performed on and validated by the

consumer’s payment device, independent of the reader.

• Whether cardholder verification is required for the transaction

• Whether the reader supports Issuer Update Processing

• In qVSDC transactions, the card uses the information provided in the TTQ to make risk

management decisions before responding to the reader.

April 2014 VISA CONFIDENTIAL 26

Notice: This information is proprietary and CONFIDENTIAL to Visa. It is distributed to Visa participants for use

exclusively in managing their Visa programs. It must not be duplicated, published, distributed or disclosed, in whole

or in part, to merchants, cardholders or any other person without prior written permission from Visa. © 2014 Visa.

All Rights Reserved.

Visa Smart Debit/Credit and Visa payWave U.S. Acquirer Implementation Guide

3.5.5 Transaction Terminated

• Rather than decline a transaction needlessly, if a Visa payWave transaction cannot be

completed as a contactless transaction, the contactless transaction is terminated and

may be processed as a physical contact chip or magnetic stripe transaction. If either the

card or the reader decides to terminate the transaction, the transaction is terminated and

the transaction may be completed using another interface (such as contact chip). In

these instances the reader should power down the contactless interface and direct the

cardholder to use the alternate interface.

• Terminated transactions differ from declined transactions because declined transactions

may not be reinitiated. The acquirer’s merchant environment may have specific best

practices or requirements for situations where it is preferred to terminate the transaction

and proceed with a contact interface.

3.5.6 Online Processing

• The reader indicates to the cardholder that the card can be removed from the reader’s

field. The reader uses the information provided by the card and transmits the transaction

to the acquirer.

• The reader sends the data from the transaction including the cryptogram, information

regarding the selected application and the interface used together with standard

transaction data to the acquirer. The acquirer then formats the corresponding VisaNet

authorization message including the relevant data fields. For qVSDC transactions the

following V.I.P. Field values are included:

• Field 22 – POS Entry Mode with a value of 07

• Field 23 – Card sequence number that uniquely identifies the card used to initiate the

transaction

• Field 55 – Including relevant Tags to support the Cryptogram, Form Factor Indicator

(Tag 9F6E) and if present in the card the Customer Exclusive Data (Tag 9F7C)

• Field 60.2 – Terminal Entry Capability with a value of 5 (contact or contact and

contactless chip capable terminal) or 8 (contactless chip capable terminal)

• VisaNet performs processing on the authorization message to determine if the issuer

participates in Visa Chip Authenticate. If not then authorization is sent directly to the

issuer.

• During a qVSDC transaction, the issuer validates the card using CVN 17, CVN 10, or

CVN 18. Based on the results of online card verification, along with other standard risk

management checks (such as ensuring that the card is not expired, and verifying that

the account is in good standing and has available funds), the issuer either approves or

declines the transaction in the authorization response.

April 2014 VISA CONFIDENTIAL 27

Notice: This information is proprietary and CONFIDENTIAL to Visa. It is distributed to Visa participants for use

exclusively in managing their Visa programs. It must not be duplicated, published, distributed or disclosed, in whole

or in part, to merchants, cardholders or any other person without prior written permission from Visa. © 2014 Visa.

All Rights Reserved.

Visa Smart Debit/Credit and Visa payWave U.S. Acquirer Implementation Guide

• The authorization response is sent to the acquirer which logs the response and forwards

the response to the merchant terminal.

3.5.7 Transaction Outcome

• The reader conveys the issuer’s authorization response by displaying whether the

transaction is approved or declined. If approved, depending on Visa rules, the

transaction may not require a cardholder signature or a receipt.

3.6 MSD Transaction Flow

• During an MSD transaction, the consumer briefly holds their Visa card near the

contactless reader, instead of swiping or inserting it. The Visa payWave card is

embedded with an antenna and a chip. The chip, via the antenna, communicates with

the merchant’s contactless reader to conduct the transaction. The card and reader

exchange information in less than a half of a second and the transaction is processed

and completed.

• The transaction follows magnetic stripe processing and rules except that it includes

enhanced online card authentication using CVN 17 or dCVV. Depending on

requirements and rules, transactions below a certain defined value may not require

cardholder verification (signature or online PIN) or a receipt. Regional rules and

requirements define the Cardholder Verification Method for particular transactions.

Acquirers should contact their Visa representative for specific information. The following

sections outline the steps involved in a MSD transaction.

3.6.1 Application Selection

• Unlike qVSDC, MSD readers do not support preliminary processing but otherwise

Application Selection is identical to qVSDC transaction processing as defined in Section

3.5.2.

3.6.2 Card Request Terminal and Transaction Data

• Once the contactless application is selected, the Visa payWave card requests

information from the reader to use during the transaction by sending the Processing

Options Data Object List (PDOL) to the reader. The reader responds with the requested

information.

• The information includes the transaction amount, the reader’s capabilities and

requirements in the Terminal Transaction Qualifiers and other transaction data. The card

uses the TTQ to ascertain the capabilities of the reader including whether the reader

supports MSD CVN 17. After reviewing the TTQ, the card completes its part of the MSD

transaction by sending data to the reader such as the Track 2 data and a CVN 17

cryptogram. The reader then indicates to the cardholder that the card can be removed

from the reader’s field.

• Acquirers must support qVSDC and MSD CVN 17 and continue to support dCVV (MSD

Legacy) until 1 January 2015.

April 2014 VISA CONFIDENTIAL 28

Notice: This information is proprietary and CONFIDENTIAL to Visa. It is distributed to Visa participants for use

exclusively in managing their Visa programs. It must not be duplicated, published, distributed or disclosed, in whole

or in part, to merchants, cardholders or any other person without prior written permission from Visa. © 2014 Visa.

All Rights Reserved.

Visa Smart Debit/Credit and Visa payWave U.S. Acquirer Implementation Guide