Web Fraud Prevention, Identity Verification & Authentication Guide 2018 2019 Prevention

Web-Fraud-Prevention-Identity-Verification-Authentication-Guide-2018-2019

User Manual:

Open the PDF directly: View PDF ![]() .

.

Page Count: 251 [warning: Documents this large are best viewed by clicking the View PDF Link!]

- Editor’s letter

- Table of contents

- Fraud Management - Trends and Developments

- Overview on the Innovation Taking Place in the Fraud Management Space – Machine Learning and Artificial Intelligence

- Introduction to ML&AI in Fraud Management | Mirela Ciobanu, The Paypers

- Machine Learning Against Online Fraud: The Advantage of a Risk-Based Approach | Ralf Gladis, Computop

- Why Implement a Fraud Management Solution that Combines Machine Learning with Rules? | Mark W. Hall, CyberSource

- Brick and Mortar Navigates Digital Transformation | Don Bush, Kount

- Why a Machine Learning Based Approach to Mitigate This Risk Is Key in Fraud Prevention | Pavel Gnatenko, Covery

- Best Practices in the Fraud Management Space

- Collaboration Paving the Way for Ecommerce Customer Experience | Keith Briscoe, Ethoca

- Interview with RISK IDENT on the Challenges Merchants Face on Both Sides of the Atlantic | Felix Eckhardt & Piet Mahler, RISK IDENT

- Are You Ready for the New Era of Online Payments? | Amador Testa, Emailage

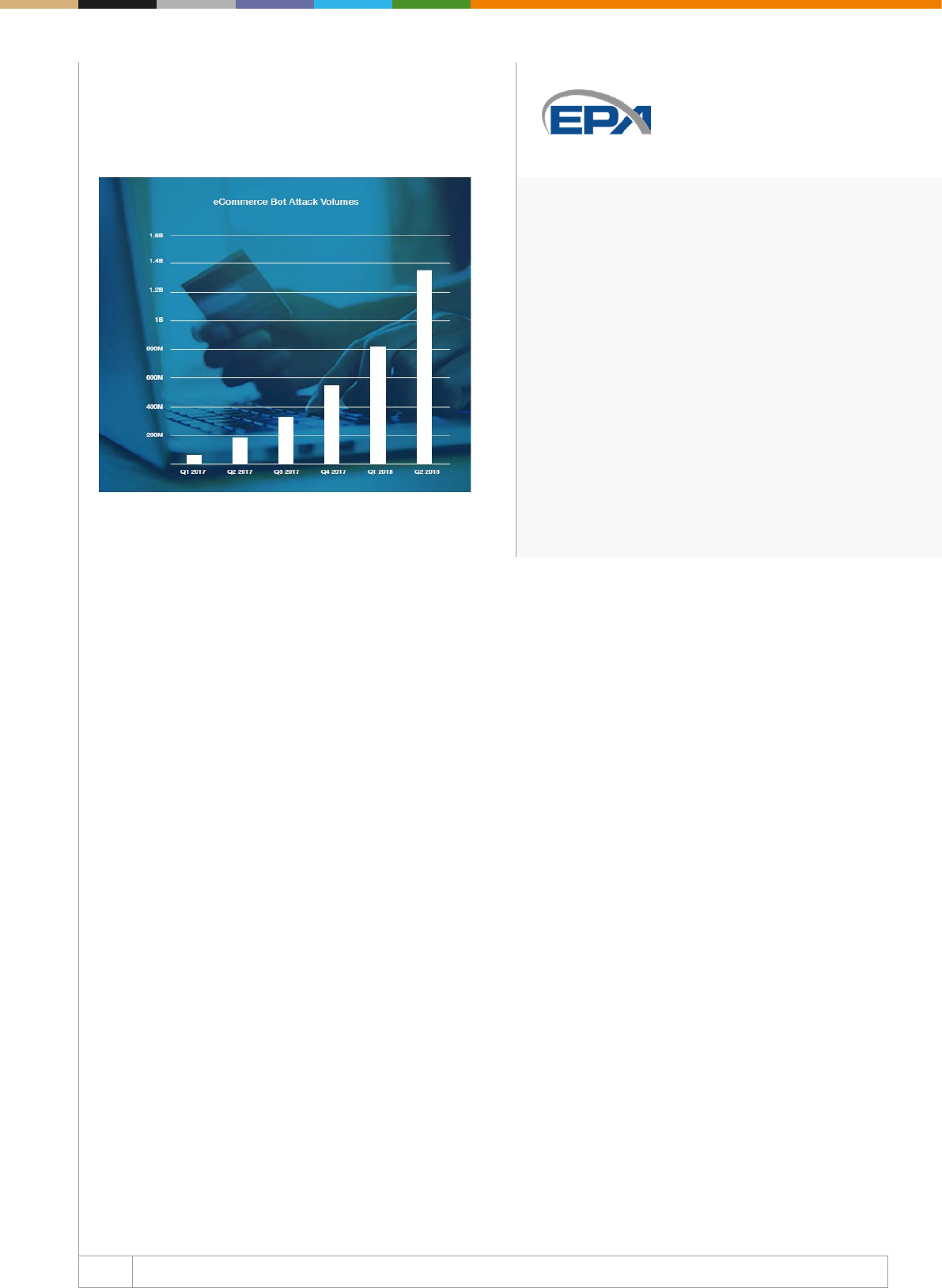

- Account Takeover via Hacking Bots (The Rise of the Bots) | Neira Jones, Emerging Payments Association

- Interview with MRC on the Way This Community Evolved to Support Merchants in Fighting Payments and Commerce Fraud | Paul Kuykendal, Merchant Risk Council

- Best Practices of Mitigating Fraud in Ecommerce - the State of Affairs in Ecommerce Verticals

- Fraud in Ecommerce - Diagnosis and Treatment | Mirela Ciobanu, The Paypers

- Interview with Sift Science on Preventing Loyalty Fraud in Travelling | Kevin Lee, Sift Science

- Fraud in Airline Travel Industry - Airlines Need Better Anti-Fraud Data | Ronald Praetsch, about-fraud.com

- Telecoms Fraud – The Impact of Digitalisation | Jason Lane-Sellers, President and Director, CFCA

- Sim Swap Fraud - an Attack in Multiple Stages | Emma Mohan-Satta, Capital on Tap

- Interview with Ubisoft on the Status of Online Gaming Industry Fraud | Sithy Phoutchanthavongsa, Ubisoft

- With Low Order Volumes, Richemont Faces a Different Fraud Review Challenge | Leon Brown, Richemont

- Best Practices of Mitigating Fraud in Banking

- Fraud Mitigation - Key Challenges for Banks | Mirela Ciobanu, The Paypers

- Machine Learning Innovations for Fighting Financial Crime in an Open Banking Era | Pedro Bizarro, Feedzai

- Accertify and InAuth: Fighting Fraudulent Account Opening | Michael Lynch, InAuth

- Interview with Nordea on Cybercrime Trends and Fraud Management Solutions | Nordea

- Overview on the Innovation Taking Place in the Fraud Management Space – Machine Learning and Artificial Intelligence

- Online Authentication – The Journey from Passwords and Secret Questions to Zero Factor Authentication

- An introduction to Online Authentication and Stronger Authentication | Mirela Ciobanu, The Paypers

- Reimagining Identity in the Post-Data Breach Era | Alisdair Faulkner, ThreatMetrix, a LexisNexis Risk Solutions company

- Adaptive Authentication: Balance Opportunity and Risk in an Omnichannel World | Mathew Long, RSA

- Interview with HID Global on the Role Adaptive Authentication Plays within the Open Banking Ecosystem | Olivier Thirion de Briel, HID Global

- Seamless and Secure Online Authentication: A Solvable Goal? | Robert Holm, Arvato Financial Solutions

- Account Takeover and Step Up Authentication | Andrew Gowasack, Trust Stamp

- Interview with CA Technologies on PSD2, 3DS 2.0, and the New Authentication Landscape | James Rendell, CA Technologies

- Complex Fraud Threats Call for Adaptive Detection Tools | Rahul Pangam, Simility, a PayPal Service

- The Journey towards Zero Factor Authentication | Yinglian Xie, DataVisor

- 2019: The Push for Orchestrated Authentication | Julie Conroy, Aite Group

- Open Banking: Why a New Approach to Authentication Is Key to its Success | Brett McDowell, FIDO Alliance

- Customer Onboarding and Digital Identity Verification

- Customer Onboarding and Identity Verification

- An introduction to Customer Onboarding and Digital Identity Verification | Mirela Ciobanu, The Paypers

- Interview with Melissa on Best Practices in KYC | Barley Laing, Melissa Global Intelligence

- Hard Problems: Identity Verification, Fraud Prevention and the Giant Leap Towards Financial Inclusion | Zac Cohen, Trulioo

- Digitising Complex Onboarding Processes: Who Will Be Leading in Getting It Right? | Josje Fiolet, Manager, INNOPAY

- Interview on Latest Trends in Biometrics Technology | Steve Cook, Independent Biometrics and Fintech Consultant

- Digital Identity at Border: Between Standardisation and Innovation

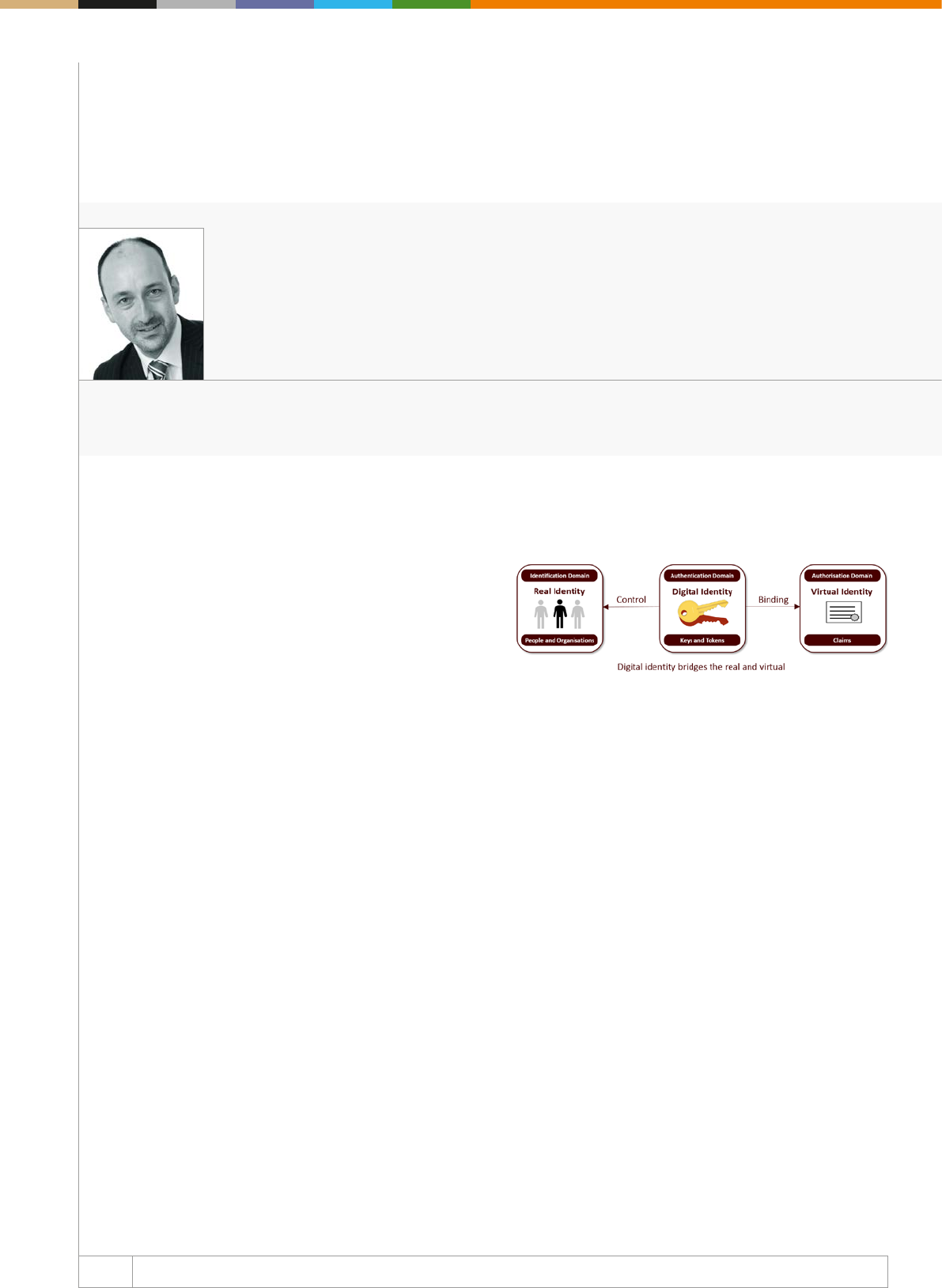

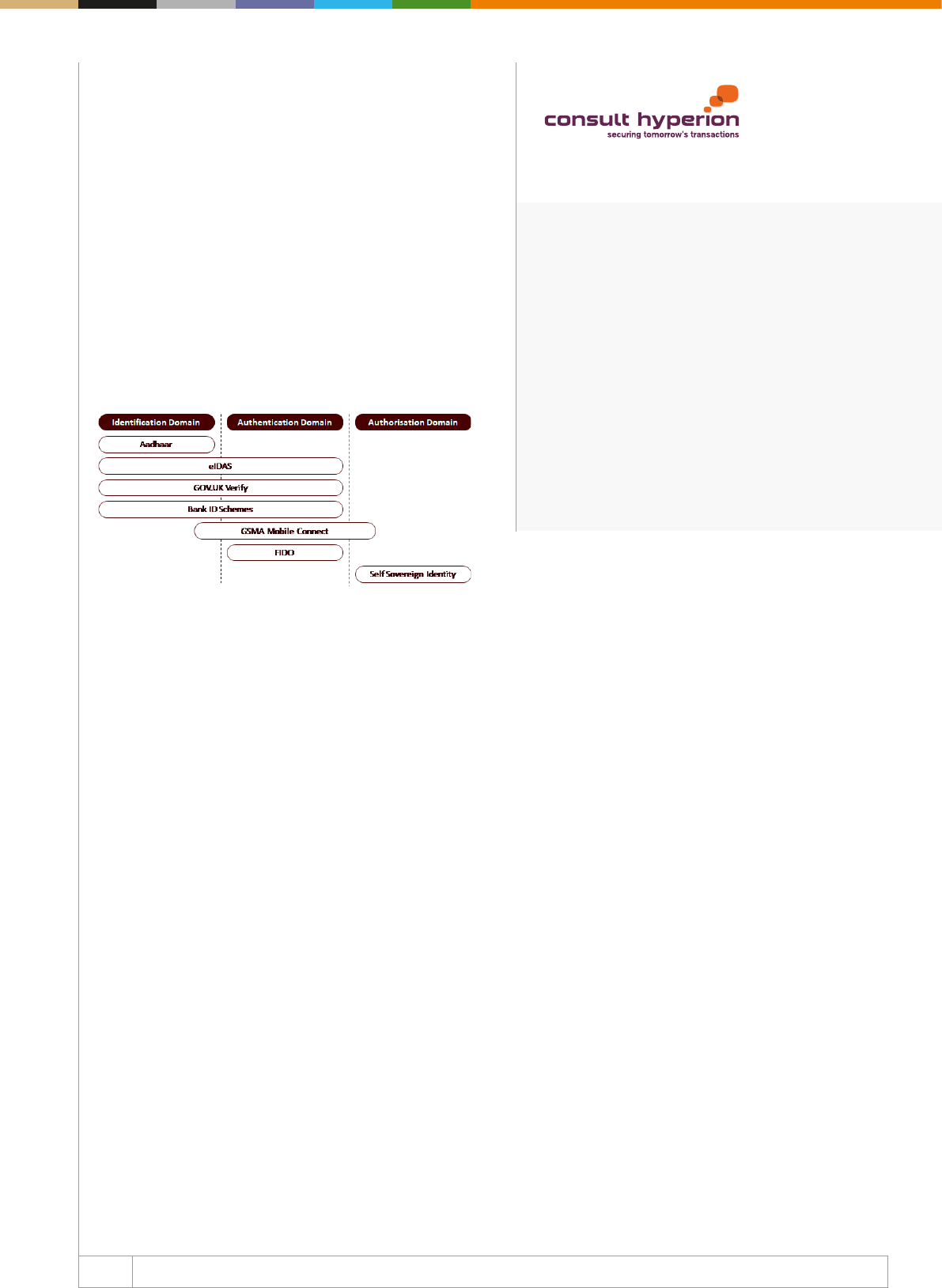

- Making Sense of Digital Identity | Steve Pannifer, Consult Hyperion

- eIDas - Its Role in Our Future | Jon Shamah, Chair, EEMA

- Self-Sovereign Identity and Shared Ledger Technologies. A vanguard of a bright new digital identity world, or an over-hyped innovation? | Ewan Willars, senior associate, Innovate Identity

- An introduction to Customer Onboarding and Digital Identity Verification | Mirela Ciobanu, The Paypers

- Customer Onboarding and Identity Verification

- The Regulatory Space

- Fraud Detection, Identity Verification & Online Authentication – Mapping and Infographic

- Company Profiles

- Glossary

Web Fraud Prevention, Identity Verication

& Authentication Guide 2018 -2019

LATEST INSIGHTS INTO DIGITAL ONBOARDING AND FRAUD MITIGATION FOR

BANKS, MERCHANTS AND PSPS

Key Media Partners Endorsement Partners

Contact us

For inquiries on editorial opportunities please contact:

Email: editor@thepaypers.com

To subscribe to our newsletters, click here

For general advertising information, contact:

Mihaela Mihaila

Email: mihaela@thepaypers.com

RELEASE VERSION 1.0

DECEMBER 2018

COPYRIGHT © THE PAYPERS BV

ALL RIGHTS RESERVED

TEL: +31 20 893 4315

FAX: +31 20 658 0671

MAIL: EDITOR@THEPAYPERS.COM

Web Fraud Prevention, Identity Verication

& Authentication Guide 2018 -2019

LATEST INSIGHTS INTO DIGITAL ONBOARDING AND FRAUD MITIGATION

FOR BANKS, MERCHANTS AND PSPS

3WEB FRAUD PREVENTION, IDENTITY VERIFICATION & AUTHENTICATION GUIDE 2018-2019

Editor’s letter

Customer experience and the conict between oering a fric

tionless customer service to good clients while managing risk

and blocking the bad guys are some themes that are emerging

from acquirers, card schemes, regulators, service providers,

merchants, as well as auditors and journalists alike.

Identifying fraudulent behaviour without rejecting or oending

good customers is key because a blocked good customer will

not return, and as the market is so competitive, they can go every-

where. Moreover, automation technologies based on machine

learning and articial intelligence are gaining prominence in this

conversation. But, as always, some challenges in addressing these

themes, security-wise, still remain.

The Web Fraud Prevention, Identity Verification &

Authentication Guide 2018-2019

To respond to some of these challenges, we have released our

7th edition of the Web Fraud Prevention, Identity Verication

& Authentication Guide to provide payment and fraud and risk

management professionals with a series of insightful perspectives

from industry associations and leading market players on key

aspects of the global digital identity, transactional and web fraud

detection space.

The guide is structured in three parts; the rst part focuses

on presenting the industry, with its most acute problems, but

also shares some best practices from industry leading players on

how to tackle them. With the advent of digitalisation and the use

of smartphones, business and fraud coexist globally, both seen

as profitable activities, involving large masses of customers.

The surge in demand for many goods and services has enabled

not only businesses’ profits to soar but also fraudsters to

capitalize on this growth. Bad actors are tricking retailers/

merchants/banks by hiding beneath large transaction volumes

and exploiting the fact that many products and services providers

are willing to accept a greater degree of risk in order to approve

more orders.

Key challenges for businesses

One of the biggest challenges in the fraud detection space for

retailers/merchants is that for consumers, a transaction needs

to happen in the blink of an eye, and therefore fraud controls

should be invisible for them.

However, fraud attacks are becoming more sophisticated, with

fraudsters having access to the latest technology and sophis ti cated

tools. Therefore, what is really needed? A fraud management

solution can track the customer’s behavioural patterns (beha-

vioural profiling) and instantly detect and report any signs

of fraud, triggering a step up authentication to mitigate the

potential risk (risk-based authentication).

Similarly, when it comes to financial institutions (FIs), FIs

are under intense competitive pressure to make the banking

experience easier and frictionless (while regulators in Europe

appear to be taking the industry in a dierent direction, thanks to

the second Payment Services Directive’s requirement for Strong

Customer Authentication).

The faceless nature of the online and mobile channels makes

authentication hard, however the large amounts of data that have

been breached in recent years combined with fraudsters’ use of

phishing, social engineering, and malware make authentication

much more dicult. As a result, some of the top threats for 2018

in ecommerce and banking are account takeover and new

account applications, according to Aite.

For Europe especially, but also for the US, Canada and Australia,

in 2018, financial discussions revolved around Open Banking

initiatives. The concept of open banking promises users greater

control over their nancial data; however, it is not without risks,

and its success is tied to consumer condence when it comes

to the security and privacy of their information.

At the moment, businesses have become incredibly dependent

on a network of systems to manage, store, and transmit in for

mation such as nancial accounts, personally identiable informa

tion, intellectual property, transaction records etc. Within this web,

authentication, validation and verication have turned out to be

central to the ability of these businesses to effectively secure

access to consumer-facing digital channels and the systems that

underpin their operations. ➔

4WEB FRAUD PREVENTION, IDENTITY VERIFICATION & AUTHENTICATION GUIDE 2018-2019

The right tools for ghting fraud

The second part of our Web Fraud Prevention, Identity Veri

cation & Authentication Guide 20182019 focuses on mapping

the key players in the fraud detection, identity verification

and online authentication space. The chapter aims to create

an accurate picture of what the fraud detection, identity

verication and online authentication oerings looks like, and

it displays the key players of the industry together with their

main capabilities. Depicting the most important features of each

company is part of our goal of helping merchants, banks, ntechs

and payment service providers to grasp the current market

opportunities and to use them according to their own needs.

The whole range of capabilities is designed to address the pain

points that organizations in the payments space are struggling

to remove. To do so, security and risk management leaders

invol ved in online fraud detection have started using machine

lear ning analytics, cloudbased deployment options, articial

intelligence, behavioural analytics, and massive global data

networks.

Such technologies generate real-time insights into the nuanced

patterns of fraud to enable businesses to spot and ght fraud.

These patterns are based on geography, industry, time of day,

time of year, and over 15,000 other signals. Fraud management

specialists/vendors have developed networks that analyse

millions of transactions in real time across billions of devices.

Finally, the third part of our Web Fraud Prevention guide, the

Company Proles section, oers insights into the capabilities

fraud prevention companies offer businesses in order to spot

fraudulent attacks, stop them and prevent them from happening.

Obviously, we would like to express our appreciation to the

Merchant Risk Council and Holland FinTech – our endorsement

partners who have constantly supported us – and also to our

thought leaders, participating organisations and top industry

players that contributed to this edition, enriching it with valuable

insights and, thus, joining us in our constant endeavour to depict

an insightful picture of the industry.

Conclusion

Businesses may think they understand fraud, but the reality

is far more complex, and this lack of insight could lead to

guessing, incorrect conclusions, and bad decisions. Premises

such as the fraudsters as geeky guys, conducting their activi

ties at night in their basements, and living somewhere in

Eastern Europe, or that ATOs are relatively low prole events

could shape businesses’ fraud-fighting operations from top to

bottom. Moreover, these assumptions help determine how ana-

lysts set up rules, how many people the fraud team hires and

stas on a given day, and so on.

Therefore, security and risk management leaders responsible for

fraud prevention and payment security should align with cross

organisational groups (security, identity and access mana ge ment,

credit/underwriting) to detect highrisk or anomalous activity

and identity, and tap into technologies that enable fighting

against these threats. And if we consider the large amounts of

har vested data, the capability of analysing and connecting

data across channels is vital for strong defence.

Enjoy your reading!

Mirela Ciobanu

Senior Editor, The Paypers

5WEB FRAUD PREVENTION, IDENTITY VERIFICATION & AUTHENTICATION GUIDE 2018-2019

Table of contents

4

8

9

10

14

16

18

20

23

24

26

28

30

32

35

36

38

40

42

44

46

48

Editor’s Letter: The Complex Faces of Risk Management and Fraud

1 Fraud Management – Trends and Developments

1.1 Overview on the Innovation Taking Place in the Fraud Management Space – Machine Learning and

Articial Intelligence

The Rise of Machine Learning/Articial intelligence in Fraud Detection – Introduction to ML&AI in Fraud Management |

Mirela Ciobanu, Senior Editor, The Paypers

Machine Learning Against Online Fraud: The Advantage of a Risk-Based Approach | Ralf Gladis, Co-Founder and CEO,

Computop

Why Implement a Fraud Management Solution that Combines Machine Learning with Rules? | Mark W. Hall, Sr. Director

Global Solutions Marketing, Fraud Management, CyberSource

Brick and Mortar Navigates Digital Transformation | Don Bush, Vice President of Marketing, Kount

Why a Machine Learning Based Approach to Mitigate This Risk Is Key in Fraud Prevention | Pavel Gnatenko,

Risk management expert, Covery

1.2 Best Practices in the Fraud Management Space

Collaboration Paving the Way for Ecommerce Customer Experience | Keith Briscoe, Chief Marketing Ocer, Ethoca

Interview with RISK IDENT on the Challenges Merchants Face on Both Sides of the Atlantic | Felix Eckhardt,

Managing Director and CTO, Piet Mahler, COO, RISK IDENT

Are You Ready for the New Era of Online Payments? | Amador Testa, Chief Product Ocer, Emailage

Account Takeover via Hacking Bots (The Rise of the Bots) | Neira Jones, Advisor and Ambassador, Emerging Payments

Association

Interview with MRC on the Way This Community Evolved to Support Merchants in Fighting Payments and Commerce

Fraud | Paul Kuykendal, CEO, Merchant Risk Council

1.3 Best Practices of Mitigating Fraud in Ecommerce - the State of Aairs in Ecommerce Verticals

Fraud in Ecommerce – Diagnosis and Treatment | Mirela Ciobanu, Senior Editor, The Paypers

Interview with Sift Science on Preventing Loyalty Fraud in Travelling | Kevin Lee, Trust and Safety Architect, Sift Science

Fraud in Airline Travel Industry – Airlines Need Better Anti-Fraud Data | Ronald Praetsch, Co-Founder and Managing

Director, about-fraud.com

Telecoms Fraud – The Impact of Digitalisation | Jason Lane-Sellers, President and Director, CFCA

Sim Swap Fraud – an Attack in Multiple Stages | Emma Mohan-Satta, Senior Fraud Manager, Capital on Tap

Interview with Ubisoft on the Status of Online Gaming Industry Fraud, with Insights into the Grey Market |

Sithy Phoutchanthavongsa, Fraud Expert, Ubisoft

With Low Order Volumes, Richemont Faces a Dierent Fraud Review Challenge | Leon Brown, Fraud and Payments

Manager, Richemont

6WEB FRAUD PREVENTION, IDENTITY VERIFICATION & AUTHENTICATION GUIDE 2018-2019

Table of contents

51

52

57

59

61

63

64

68

70

72

74

76

78

80

82

84

86

88

89

90

94

96

98

100

1.4 Best Practices of Mitigating Fraud in Banking

Fraud Mitigation – Key Challenges for Banks | Mirela Ciobanu, Senior Editor, The Paypers

Machine Learning Innovations for Fighting Financial Crime in an Open Banking Era | Pedro Bizarro, Chief Science

Ocer, Feedzai

Accertify and InAuth: Fighting Fraudulent Account Opening | Michael Lynch, Chief Strategy Ocer, InAuth

Interview with Nordea on Cybercrime Trends and Fraud Management Solutions | Fraud Awareness and Communication

team of Nordea

2 Online Authentication – The Journey from Passwords and Secret Questions to

Zero Factor Authentication

An introduction to Online Authentication and Stronger Authentication | Mirela Ciobanu, Senior Editor, The Paypers

Reimagining Identity in the Post-Data Breach Era | Alisdair Faulkner, Chief Identity Officer, Business Services, ThreatMetrix,

a LexisNexis Risk Solutions company

Adaptive Authentication: Balance Opportunity and Risk in an Omnichannel World | Mathew Long, Senior Advisor,

Fraud & Risk Intelligence, RSA

Interview with HID Global on the Role Adaptive Authentication Plays within the Open Banking Ecosystem |

Olivier Thirion de Briel, Global Solution Marketing Director, HID Global

Seamless and Secure Online Authentication: A Solvable Goal? | Robert Holm, Senior Vice President Fraud Management,

Arvato Financial Solutions

Account Takeover and Step Up Authentication – True Customer Satisfaction Means Optimizing Experiences and

Relationships from Start to Finish | Andrew Gowasack, Cofounder and Managing Director, Trust Stamp

Interview with CA Technologies on PSD2, 3DS 2.0, and the New Authentication Landscape | James Rendell, Payment

Security Strategy and Product Management, CA Technologies

Complex Fraud Threats Call for Adaptive Detection Tools | Rahul Pangam, Co-Founder and CEO, Simility, a PayPal

Service

The Journey towards Zero Factor Authentication | Yinglian Xie, CEO and Co-founder, DataVisor

2019: The Push for Orchestrated Authentication | Julie Conroy, Research Director, Aite Group

Open Banking: Why a New Approach to Authentication Is Key to its Success | Brett McDowell, FIDO Alliance

3 Customer Onboarding and Digital Identity Verication

3.1 Customer Onboarding and Identity Verication

An introduction to Customer Onboarding and Digital Identity Verication | Mirela Ciobanu, Senior Editor, The Paypers

Interview with Melissa on Best Practices in KYC | Barley Laing, Managing Director, Melissa Global Intelligence

Hard Problems: Identity Verication, Fraud Prevention and the Giant Leap Towards Financial Inclusion | Zac Cohen,

General Manager, Trulioo

Digitising Complex Onboarding Processes: Who Will Be Leading in Getting It Right? | Josje Fiolet, Manager, Lead Digital

Onboarding, INNOPAY

Interview with Steve Cook on Latest Trends in Biometrics Technology and the Value of Biometric Authentication for

the KYC Process | Steve Cook, Independent Biometrics and Fintech Consultant

7WEB FRAUD PREVENTION, IDENTITY VERIFICATION & AUTHENTICATION GUIDE 2018-2019

103

104

106

108

110

111

113

115

118

119

121

122

144

236

Table of contents

3.2 Digital Identity at Border: Between Standardisation and Innovation

Making Sense of Digital Identity | Steve Pannifer, COO, Consult Hyperion

eIDas – Its Role in Our Future | Jon Shamah, Chair, EEMA

Self-Sovereign Identity and Shared Ledger Technologies. A vanguard of a bright new digital identity world,

or an over-hyped innovation? | Ewan Willars, Senior Associate, Innovate Identity

4 The Regulatory Space

A Brief Summary of EBA Guidelines on Fraud Reporting Under the PSD2 | Irena Dajkovic, Partner of DALIR Law Firm

Reconciling Consent in PSD2 and GDPR | Niels Vandezande, Legal Consultant, Timelex

Bitcoin and AML: Regulating the New Mainstream | Nadja van der Veer, Co-Founder, PaymentCounsel

5 Fraud Detection, Identity Verication & Online Authentication –

Mapping and Infographic

5.1 Introduction

5.2 Fraud Detection, Identity Verication & Online Authentication – Infographic

5.3 Fraud Detection, Identity Verication & Online Authentication – Mapping of Key Players

6 Company Proles

7 Glossary

Fraud Management –

Trends and Developments

Overview on the Innovation Taking Place

in the Fraud Management Space –

Machine Learning and Articial Intelligence

10 WEB FRAUD PREVENTION, IDENTITY VERIFICATION & AUTHENTICATION GUIDE 2018-2019

Mirela Ciobanu | Senior Editor | The Paypers

The lines are blurring between man and machine. As advances in AI, smart tech, and machine learning turn science

ction into fact, a future once fantastical draws near now. How will the payments industry harness these mindblowing

opportunities?

Articial intelligence and machine learning have a wide array of applications, from improving customer experience to ena

bling businesses to ght fraud, from driving the creation of personalised shopping/user experiences by analysing multiple

data points to enabling businesses to stay compliant with the ever changing regulation landscape – KYC, AML. Moreover,

these emerging technologies have also been applied in medicine; popular AI solutions such as IBM’s Watson are actively

used in multiple cancer research hospitals, and they operate as a doctor’s assistant.

However, in this subchapter we will mostly focus on the ways in which these technologies can help ght fraud, manage

and mitigate risk, and enable companies to stay compliant with AML laws and ght transaction laundering.

Articial intelligence

Articial intelligence (AI), sometimes called machine intelligence, is intelligence demonstrated by machines, in contrast

to the natural intelligence displayed by humans and other animals. AI augments human intelligence and should provide

explanations to avoid erroneous interpretations, and its value should be considered in context, as denitive answers do

not exist, according to Pedro Bizarro, Chief Science Ocer, Feedzai.

AI design principles should be transparency, controllability, and automation. Moreover, data provenance is a crucial feature,

as the user needs to keep track of data in order to be able to reconstruct it, and models should learn from real data, and

be able to relearn, while not being inuenced/based on previous models. Most importantly, we must create the means of

developing this tool in order for it to be human-enabled and human-centric.

According to Forbes, AI needs to be ‘Explainable’ and ‘Understandable’. Explainable AI is the domain of data scientists

and AI engineers, the individuals who create and code articial intelligence algorithms. These specialists aim to develop

new algorithms that explain intermediate outcomes or provide reasoning for their solutions.

Understandable AI combines not only the technical expertise of engineers with the design usability knowledge of UI/UX

experts, but also the people-centric design of product developers. Explainable AI is dierent from understandable AI.

Since AIdriven solutions need to be developed with ‘userrst’ principles in mind, understandable AI has become the

domain of UI/UX designers and product developers, in collaboration with AI engineers and data scientists.

Critical to the understandable AI process are the integration of non-data scientists to the development and design of

AI products and enabling people to be a part of the decision-making process in an AI-driven enterprise. ➔

The Rise of Machine Learning/

Articial Intelligence in Fraud Detection

11 WEB FRAUD PREVENTION, IDENTITY VERIFICATION & AUTHENTICATION GUIDE 2018-2019

The Rise of Machine Learning/

Articial Intelligence in Fraud Detection

To begin the journey towards a truly humanmachine collaborative model that creates understandable AI outcomes,

leaders, governance bodies, and companies must:

- develop intuitive user interfaces – by using voice recognition and natural language processing, the technology

industry is currently developing AI user interfaces that enable people to interact with intelligent machines simply by

talking to them. By encouraging the development of these tools, the democratisation of AI technologies is encouraged;

- create ethical principles for AI – all major stakeholders in the future of AI need to work together to build principles that

embed understandability into technology development;

- apply design principles – enterprises should use design-led thinking to examine core ethical questions in context. In

addition, they are advised to build a set of value-driven requirements under which the AI will be deployed – including

where explanations for decisions are expected;

- monitor and audit – the AI solutions used at the enterprise level need to be continually improved through value-driven

metrics such as algorithmic accountability, bias, and cybersecurity.

When it comes to nancial services, articial intelligence can be applied to specic areas such as nancial crime preven

tion, regulatory compliance, and payments. Successful AI projects rely on the deep amounts of research and work that

expertise developers put in, and the application to specic business problems, which can be used in multiple dierent

contexts. A critical element of AI systems is the data on which they are trained – it’s that combination of innovative AI

capabilities and deep domain expertise.

A fundamental concept of AI is machine learning – that is why sometimes these two technologies go intertwined.

Machine learning – an approach to fraud detection and protection

Machine learning, a form of articial intelligence, combines data, context, and feature engineering to allow organisations

evaluate the risk of a particular digital interaction or purchase.

Machine learning is being used at many levels in the online fraud detection market. Some solutions are designed to

run alongside existing capabilities, taking in structured and unstructured data to identify anomalies, while others are

designed to provide a score and information codes that can be used by a real-time policy and decision engine.

A machine learning solution needs access to a big store of historical data to train its models and increase the probability

that it will uncover patterns of new suspicious activity. This technology has the potential to ght cardnotpresent fraud,

chargebacks, account takeover, transaction laundering, and more. Also, machine learning is implemented in solutions

such as device assessment, passive behavioural biometrics, bot detection, phone printing, and voice biometrics. ➔

12 WEB FRAUD PREVENTION, IDENTITY VERIFICATION & AUTHENTICATION GUIDE 2018-2019

The Rise of Machine Learning/

Articial Intelligence in Fraud Detection

With the waves of new and evolving fraud, Gartner has observed the increasing need of financial institutions and

enterprise-scale merchants for rapid and complex risk decisions, and businesses are turning to machine learning to gain

the ability to make rapid and eective risk decisions. However, with the increased number of machinelearning systems,

clients are demanding explanations, as well as decisions, with the aim of:

- controlling the machine – a model that explains its logic empowers security managers to adapt the model to evolving

fraud patterns with more speed and accuracy;

auditing the machine – nancial institutions and large merchants operate in highly regulated environments. These

organisations need to provide trails of explanations for compliance, to demonstrate that the basis for their decisions is

lawful and ethical;

- trusting the machine – a system is only as powerful as the decisions we entrust it to make. How can we trust that the

machine is nding the delicate balance between good risk management and good CX?

To achieve these goals, Gartner suggests that businesses should ensure that each model they develop incorporates

a capability to explain and, moreover, has a loop that provides feedback on the quality of the explanation. The second

method is to develop two systems – one that makes decisions and another that takes the input from the rst system and

generates an explanation.

Here are some types of machine learning that can be deployed:

- Deep Learning – is a class of machine learning algorithms that use a cascade of multiple layers of nonlinear processing

units for feature extraction and transformation. Each successive layer uses the output from the previous layer as

input. These algorithms learn in supervised (eg classication) and/or unsupervised (eg pattern analysis) manners

and understand multiple levels of representations that correspond to dierent levels of abstraction; the levels form a

hierarchy of concepts.

– Ensemble Learning – ensemble methods use multiple learning algorithms to obtain better predictive performance than

could be obtained from any of the constituent learning algorithms alone.

– Unsupervised Learning – does not require outcomes, so it can learn without waiting for the completion of a three-

month chargeback reporting cycle, for example. This type of learning often relies on clustering, peer group analysis,

breakpoint analysis, or a combination of these. This enables fraud prevention solutions to detect patterns and anomalies

rapidly within extremely large sets of data.

- Supervised Learning – uses outcome-labelled training data sets to learn. Models include neural networks, Bayesian

classiers, regression, decision trees, or an ensemble combination. Massive amounts of data run through dened

models to assess risk outcomes.

The power of supervised and unsupervised machine learning

There are two approaches that are used mostly by fraud prevention vendors – supervised and unsupervised learning, the

former approach being the most common and widespread. ➔

13 WEB FRAUD PREVENTION, IDENTITY VERIFICATION & AUTHENTICATION GUIDE 2018-2019

The Rise of Machine Learning/

Articial Intelligence in Fraud Detection

Maxpay explains briey how these systems interact to identify anomalies (outliers). With the supervised approach, in the

beginning, a risk analyst creates a machine learning model based upon historical data. Afterwards, with new transaction

data, the algorithm creates potentially right baskets: fraud and not fraud. After that, the system collects external signals

such as fraud alerts, chargebacks, complaints etc. Based on that information, the algorithm starts looking for new

unrecorded dependencies. Finally, the model starts retraining. Consequently, all the risk analysts are one step behind the

game, thus the cycle continues, and in time new techniques emerge.

Otherwise, unsupervised learning is regarded as an alternative to supervised learning. These algorithms infer patterns

from a dataset without reference to known or labelled outcomes. Unsupervised learning allows risk analysts to approach

problems with no exact idea about what the result will look like. One can derive structure from data where they don’t

necessarily know the eect of the variables. With unsupervised learning, there is no feedback based on the prediction

results. But it can divide data on the basis of anomalous behaviour and, afterwards, risk analysts can apply well-known

supervised approaches to this data.

Therefore, unsupervised machine learning is more applicable to real-world problems and can help solve them when risk

managers are one step behind the fraudsters.

As fraud prevention services use both rule-based and machine learning approaches, including unsupervised techniques,

we should also consider that there is a signicant dierence between fraud detection systems that directly use machine

learning systems and those that are essentially static, rule-based systems. Characteristics of the former type include

exibility in response to new fraud attack patterns. The latter type benets from keeping a human element in the change

control process, which makes it more resistant to skilfully crafted attacks that try to poison the model.

Some banks, merchants, retailers have traditionally relied upon rules-based fraud detection systems in order to counter

threats, such as leveraging weak points through coordinated attacks, but fraud advancements have outpaced the

capabilities of these systems.

According to Feedzai, rules-based systems tend to be either too broad or too narrow in scope to adequately address

fraud attack vectors, requiring nancial institutions to combine multiple solutions into a single system to cover their

bases.

Surely, machine learning does not replace rules completely, but it complements them to expand the capabilities of the risk

management platform. Thus, when applied to large datasets, like those found in account opening analyses, these algo-

rithms can pinpoint surprising and unintuitive fraud signals.

14 WEB FRAUD PREVENTION, IDENTITY VERIFICATION & AUTHENTICATION GUIDE 2018-2019

The increasing popularity of online shopping is creating new

security risks in the transaction process. Data theft and payment

fraud are issues that consumers and merchants alike fear. If

we look at the current status of online fraud, we see that data

breaches still represent a prevalent issue. Moreover, according

to a research by the Identity Theft Resource Center and

CyberScout, 791 data leaks were reported from large companies

in the US from January to June 2017, with criminals stealing

credit card information amongst other things. This represents an

increase of 29% over the rst half of 2016 and exceeded the

781 cases reported for the full year 2015 in just six months.

Other studies conrm the trend: according to information service

provider Experian, the number of data leaks in ecommerce

increased by 56% in 2017 compared to 2016.

Risk-based instead of rule-based

In the ght against fraud, payment service providers (PSPs) must

have better tools at their disposal than ever before. Rule-based

fraud prevention is replaced by risk-based fraud prevention.

The dierence: previous procedures allowed the risk assessment

to be based on certain rules according to which a transaction

was approved or rejected. The criteria were, for example, in

which country the buyer uses a credit card, whether the device

with which he pays online is unknown to the system, whether he

uses the card several times at short intervals, and whether he

exceeds a certain amount of money when paying. In practice,

many other rules apply but, despite their complexity, they do

not protect against fraud as eectively as the machine learning

method does.

The new generation of risk management that has been used

at Computop since the end of October 2018 is not only more

exible than before, but also more secure and ecient. The new

Fraud Score Engine uses machine learning to automatically

optimise fraud prevention and it eliminates the need for manual

intervention. The algorithm behind the risk cost calculation

learns with each transaction and improves the accuracy of the

risk assessment accordingly. If buyer behaviour changes and

new fraud scenarios emerge, it adapts. A concrete example

illustrates this method:

Previously, the retailer made a yes/no decision in which various

factors were queried, for example: ‘If a transaction exceeds the

amount X and is made in country Y, it is rejected.’ On the other

hand, an intelligent fraud scoring engine calculates probabilities:

‘What proportion of all fraud cases recorded to date deal

with amounts greater than EUR 500, and what percentage

of successful, clean payments is greater than EUR 500?’

This results in a data record that the system uses to calculate the

probability of fraud. This method is much more accurate than

the rule-based approach and can be applied to all parameters

(payment location, device used, etc) that also use rule-based

fraud prevention. The accuracy of the calculation improves with

every payment transaction because, based on the empirical

values from past transactions, the precision of the probability

calculation for each individual parameter increases, thus the

quality of the overall statement increases as well. Essentially,

this is the greatest benet of risk-based fraud prevention. ➔

Computop

Machine Learning Against Online Fraud: The Advantage of a Risk-Based Approach

Ralf Gladis | Co-Founder and CEO | Computop

About Ralf Gladis: Ralf Gladis is the Co-Founder and CEO of the international payment service provider

Computop – the payment people. In addition, Ralf acts as non-executive Director at Computop, Inc in

New York. He is also responsible for the international expansion and strategic planning at Computop.

15

Click here for the company profile

WEB FRAUD PREVENTION, IDENTITY VERIFICATION & AUTHENTICATION GUIDE 2018-2019

About Computop: Computop oers local and innovative

omnichannel solutions for payment processing and

fraud prevention around the world. For ecommerce,

at POS and on mobile devices, retailers and service

providers can choose from over 250 payment methods.

Computop, a global player with locations in Germany,

Canada, the UK and the USA processes transactions

for more than 15,000 retailers annually, with a combined

value of USD 31 billion.

www.computop.com

Adaptable, fast and exible

Combined with all the risk factors taken into account – such

as transaction duration, correspondence between invoice and

delivery address, use of an anonymisation service, and many

more –, the engine calculates a score value within fractions of

a second, which represents the basis for the decision, as to

whether the transaction should be submitted to the card-issuing

bank for protection via 3-D Secure.

If the risk factors regarding fraud represent less than a certain

value, the system does not perform an additional query. In the

case of a medium value, the bank either uses its own checking

system to relieve the customer of entering a password or it

requests the password directly. If the 3-D Secure procedure is

used, the bank also takes over the liability risk from the merchant.

If the score is clearly within the red range, the transaction is

rejected directly.

The risk-based method fundamentally changes fraud prevention.

Until now, rule creation was a manual process based on individual

traders. The automation now increases exibility and it is able to

drive double-track. On the one hand, this approach assesses the

riskbased on traderspecic transaction characteristics, and on

the other hand, it uses the entirety of all anonymous transactions

of the PSP for forecasts.

Therefore, each transaction is protected the best possible

way, on the basis of the past, and subsequently contributes to

further optimisation. In principle, PSPs include both successful

transactions and chargebacks from the acquirer’s settlement les

in their risk analysis. Machine learning enables the scoring engine

to move away from the purely manual adaptation to new threats,

that has been adopted, so far, by organisations. This was time-

consuming, inaccurate, and inexible.

With machine learning, the reaction speed to fraudulent actions

increases, as the retailer can rely not only on his own transaction

data but also on risk assessments from Computop’s past payment

transactions – thus, on a signicantly higher overall population.

The combination of machine learning and rule-based risk pre-

vention offers the best possible protection, with experienced

experts monitoring the process and providing the artificial

intelligence with the context it needs, to develop further and

work with the right assumptions.

16 WEB FRAUD PREVENTION, IDENTITY VERIFICATION & AUTHENTICATION GUIDE 2018-2019

According to artificial intelligence (AI) pioneer Arthur Samuel,

machine learning is a ‘eld of study that gives computers the ability

to learn without being explicitly programmed.’ For fraud mana-

ge ment, this means that machine learning can detect subtle

emerging fraud patterns that are impossible to see on a human

level. Virtually, all fraud management systems today use some

form of machine learning, so what sets CyberSource Decision

Manager apart?

Importance of data: Decision Manager has had machine learning

from the beginning. Decision Manager is the only machine learning

fraud solution that draws insights from Visa and CyberSource’s

68B+ annual transactions processed from around the globe.

These transactions come from tens of thousands of merchants

across a wide variety of industries and specialities. With this depth

and breadth of data, it’s like having more high-quality neurons in

the machine learning ‘brain.’ It just makes sense that better data

leads to better fraud detection decisions.

Why rules are needed: Another very important distinction

with Decision Manager is the inclusion of powerful rules, which

adds a level of precision control for Risk Analysts. But why are

rules important? Let’s explore a theoretical example of what can

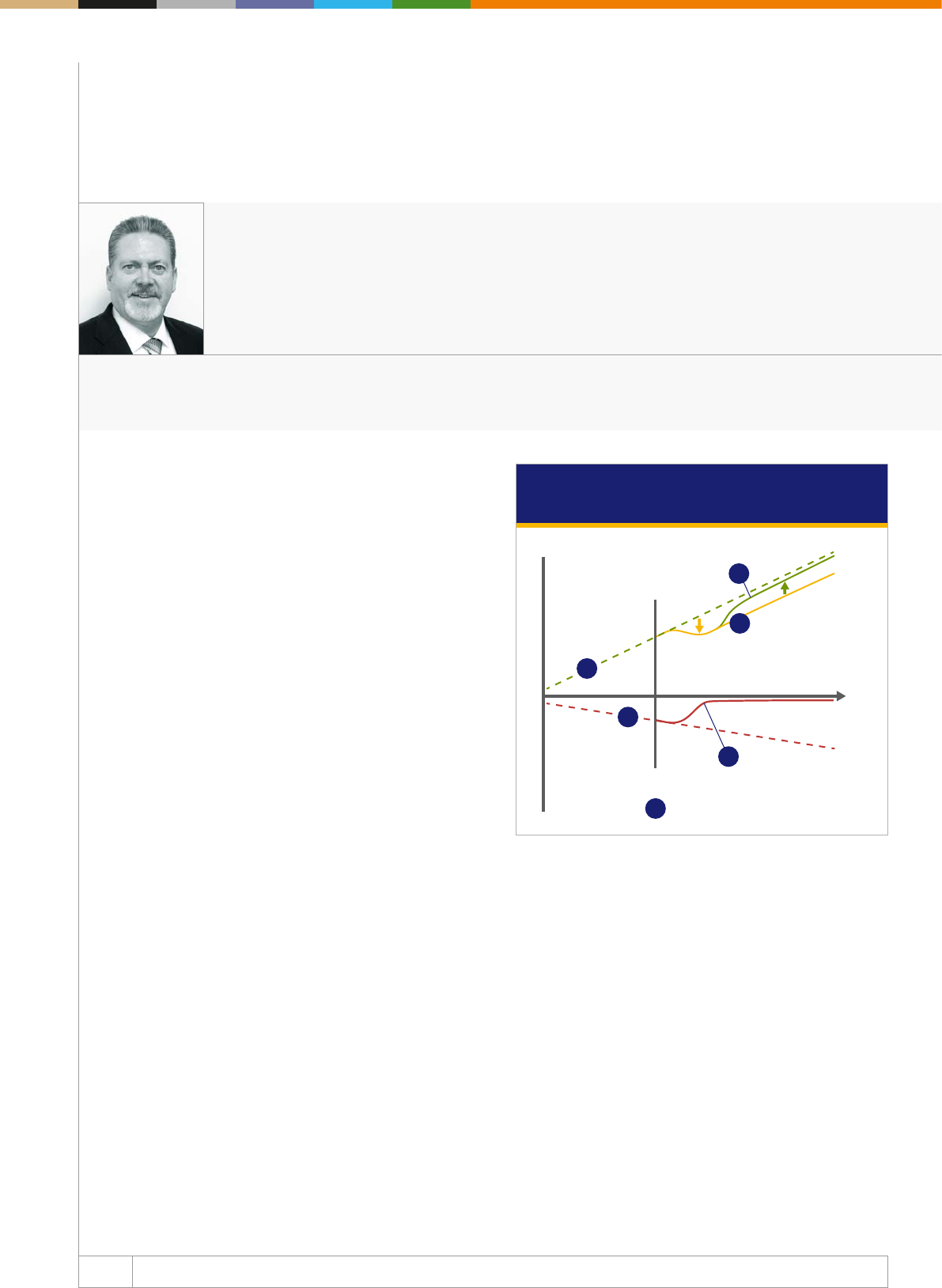

happen without rules in the following diagram.

Line L1 shows revenue growth before applying a fraud pre

vention tool. In the diagram, line L1 represents a theoretical

revenue growth trajectory.

Line L2 shows fraudulent activity as a percentage of revenue.

As revenues grow, if fraud losses are left unchecked, they too

would continue to grow as a percentage of revenues, as shown

on line L2.

Line T0 represents the point in time when an organisation

imple ments a fraud management solution. Once a business

realises they have significant fraud losses, they will institute a

fraud mana ge ment system as shown at time T0.

Line L3 shows the reduced level of fraud by using a fraud

mana ge ment programme. As the fraud management system

starts learning from that business’ transaction data, the fraud

loss level should gradually reduce as shown on the red line L3. ➔

CyberSource

Why Implement a Fraud Management Solution that Combines Machine Learning

with Rules?

Mark W. Hall | Sr. Director Global Solutions Marketing, Fraud Management | CyberSource

About Mark W. Hall: Mark is a seasoned entrepreneurial leader who is passionate about crafting multi-

channel marketing programmes that communicate dierentiation and clarity in the Enterprise B2B

space. At CyberSource, Mark heads global cross-functional marketing, positioning, and messaging for

the company’s fraud solutions.

Why implement a fraud management solution

that combines machine learning with rules?

Gains

Fraud solution

implementation point

© 2018 Visa, Inc. All rights reserved

Theoretical fraud

loss trajectory

without fraud

management

Theoretical

revenue

trajectory

Losses

Revenue

growth

Lost sales

opportunities

Managed fraud is reduced

but never goes to zero

Restored sales

opportunities

Fraud

losses

Time

+

–

L1

L2

L4

T0

L3

L5

17 WEB FRAUD PREVENTION, IDENTITY VERIFICATION & AUTHENTICATION GUIDE 2018-2019

About CyberSource: CyberSource is a global, modular

payment management platform built on secure Visa

infrastructure, with the insights of a USD 427 billion

global processing network. It helps businesses enhance

their customer experience, grow revenue, and mitigate

risk. For more information, visit cybersource.com

www.cybersource.com

It is virtually impossible to prevent all fraud; however, through

active fraud management, the fraud percentage can get very low.

Line L4 represents the reduced level of revenue due to a poor

customer experience while managing fraud. False positives can

lead to lost revenues, as shown on the yellow line L4, not only due

to the loss of the immediate sale, but even more by potentially

losing a customer forever due of the rejected transaction.

This has the impact of reducing revenue growth not only by

interfering with business one transaction at a time, but tarnishing

the expe rience for a legitimate buyer and compromising the

lifetime value of customers.

Line L5 shows what active fraud management can do to

restore revenues closer to the theoretical level. By combining

rules with good manual review practices, many businesses

may actually see an increase in revenue that comes very close

to their theoretical revenue trajectory, as seen in the green line

L5. Decision Manager’s rules can be congured to activate at

a specic time of day or date ranges, which can accommodate

a variety of cyclic, seasonal, and periodic sales promotions –

helping maximize acceptance rates and revenues.

Rules provide customised control: By instituting rules, a risk

analyst can inject human intelligence and set common-sense

para meters for their specic business. For instance, if the item

being sold is a low priced digital good, like a picture or a song,

the risk analyst might have a higher tolerance for the fraud risk

score because there is no cost of goods. This is much dierent

than an online retailer of big-ticket luxury items where the cost

of goods is high – and there’s an open market for fraudsters to

easily turn those goods into cash. Obviously, in the latter case,

the risk analyst will want to send questionable transactions to

manual review prior to shipment.

The best of both worlds: Decision Manager employs machine

learning that operates on insights from 68B+ global Visa and

CyberSource processed transactions, enabling fast detection

of emerging fraud patterns, while at the same time offering

powerful rules that enable the injection of human ingenuity.

Machine learning, combined with rules, provides an excellent

fraud management solution.

Click here for the company profile

18 WEB FRAUD PREVENTION, IDENTITY VERIFICATION & AUTHENTICATION GUIDE 2018-2019

Traditional brick and mortar merchants are expanding beyond their

four walls to engage with customers through mobile apps, kiosks,

desktops, and other digital platforms. At the forefront of this digital

transformation is the introduction and branding of trademarked

native mobile apps supporting rich features for creating and

managing accounts, earning loyalty points, providing reviews,

engaging with customer support, other customers and more.

While mobile apps for retail are nothing new, many of the rst

generation apps are being replaced with apps supporting creative

and elaborate digital interaction use cases. These new apps allow

merchants and retailers, regardless of sector, to engage with

customers in a digital environment, in order to build brand loyalty

and engagement and drive towards greater monetisation with

enhanced ease-of-use and personalisation.

This shift towards digital economy is fueling the growth of the

mobile payments industry and it’s becoming a beacon for fraud-

sters to attack traditional brick and mortar merchants. In fact, The

Mobile Payments and Fraud: 2018 Report stated that detecting

fraudulent orders is one of the top three challenges for merchants

in the mobile channel.

Card Present versus Card Not Present =

Chargebacks

As brick and mortar merchants make this digital transformation

and begin to accept card-not-present and mobile ecommerce,

they become exposed to all types of fraud schemes and charge-

back programmes that can cause disruption and large nancial

and brand loyalty losses.

When brick and mortar merchants experience fraud in their

traditional card-present environment, the liability of loss is

generally on the card issuer if the merchant supports EMV

transactions. In a card-not-present (CNP) environment, however

(online, mobile web, or mobile app), the liability for a fraudulent

transaction now falls to the merchant. This places the merchant

at risk of new fraud tactics, potential chargebacks, and greater

nancial losses.

With a new focus on creating digital accounts for their customers,

traditional brick and mortar merchants are also exposed to all

types of new fraud, including:

• Account takeover: Gaining access to an established digital

account using compromised credentials (username and pass-

word) allows a fraudster to take advantage of the value of that

account. This may include using the saved payment method or

loyalty points to make purchases.

• Loyalty reward points fraud: Because reward points can work

like cash, fraudsters identify weaknesses in the system and steal

reward points to sell them.

• eGift cards fraud: Considered low-hanging fruit, electronic gift

cards are easily converted into cash, a key requirement for fraud-

sters. They sell them at a discount, with the merchant respon sible

for the resulting chargebacks and any merchandise or services

provided for the value of the gift card.

• Promotion fraud: Launching a promotion can often capture the

attention of fraudsters who are skilled at identifying ways to get

around policies or oer limits. ➔

Kount

Brick and Mortar Navigates Digital Transformation

Don Bush | Vice President of Marketing | Kount

About Don Bush: Don is the Vice President of Marketing at Kount. Prior to joining Kount, Don was the Director

of Marketing at Cradlepoint, a leading manufacturer of wireless routing solutions in the mobile broadband

industry. Don has worked in several management roles within the technology segment for over 20 years with

both hardware/software manufacturers and as a partner in two top technology-marketing agencies.

19 WEB FRAUD PREVENTION, IDENTITY VERIFICATION & AUTHENTICATION GUIDE 2018-2019

Approach to fraud protection

Brick and mortar businesses navigating towards a digital

transformation need to deploy a fraud strategy that is multi-

layered and specically accounts for cardnotpresent fraud.

An underpinning technology for stopping CNP fraud is machine

learning. Machine learning combines data, context, and feature

engineering to allow organisations to evaluate the risk of a

particular digital interaction or purchase. Machine Learning, a

form of articial intelligence, allows fraud prevention solutions to

“learn” on their own and continually improve results. In order to

stop a card-not-present payment, there are two critical types of

machine learning that, when combined, provide the best fraud

prevention foundation.

• Unsupervised Machine Learning. Unsupervised learning does

not require outcomes, so it can learn without waiting for the

completion of a three-month chargeback reporting cycle. This

type of learning often relies on clustering, peer group analysis,

breakpoint analysis, or a combination of these. This enables

fraud prevention solutions to detect patterns and anomalies

rapidly within extremely large sets of data.

• Supervised Machine Learning. Supervised learning uses

outcome-labelled training data sets to learn. Models include

neural networks, Bayesian classiers, regression, decision trees,

or an ensemble combination. Massive amounts of data run

through dened models to assess risk outcomes.

Brick and mortar merchants that deploy a mobile app need to

account for a new world of risk through digital fraud attacks. There

are great benets to investing in digital engagement channels,

however, with those opportunities comes risk. By addressing

fraud with a holistic strategy, merchants can authenticate a user,

identify fraudulent behaviour, and stop fraud before it inuences

the bottom line and diminishes the merchant’s brand. By building

a level of fraud prevention in their mobile apps, brick and mortar

merchants are empowering decision makers with data to make

informed decisions and to mitigate fraud before it impacts the

businesses’ bottom line.

Click here for the company profile

About Kount: Kount’s award-winning fraud management,

identity verication and online authentication technology

empowers digital businesses, online merchants and

payment service providers around the world. With Kount,

businesses approve more orders, uncover new revenue

streams, and dramatically improve their bottom line all

while minimizing fraud management cost and losses

and protecting consumers. Through Kount’s global

network and proprietary technologies in AI and machine

learning, combined with policy and rules management,

companies frustrate online criminals and bad actors

driving them away from their site, their marketplace and

o their network.

www.kount.com

20 WEB FRAUD PREVENTION, IDENTITY VERIFICATION & AUTHENTICATION GUIDE 2018-2019

As fraudsters follow the growth of the cashless economy online,

anti-fraud companies are building powerful tools and techniques

that mine various data for fraudulent behaviour patterns.

Fraudulent attacks are getting to be more sophisticated and inven -

tive. Once a new solution against fraud is developed, fraudsters

imme diately nd a new loophole. And it seems that the risk pro

fessio nals are always a step behind.

Machine learning can be used to help solve this problem, but at the

moment it is impossible to completely abandon human interven tion.

Rule-based and machine learning approaches complement each

other because machines can analyse a larger volume of characte-

ristics, based on the context, while risk analysts can create models

that are easily understood by humans, unlike the machine-learning

approach alone. Each industry has its own unique set of features

and each fraud prevention system aims to adapt them to avoid

false positives (good customers identied as fraudsters) and false

negatives (fraudsters identied as good customers). Moreover, the

risk system needs to periodically be examined by risk managers

and afterwards tuned, for example, if online merchants sell new

products or make frequent changes to their billing logic.

The power of supervised and unsupervised machine

learning

A machine learning solution needs access to a big store of histo-

rical data to train its models and increase the probability that it

will uncover patterns of new suspicious activity. The more data,

the better the system becomes at detecting and preventing fraud.

The machine learning process contributes to the learning of non-

linear combinations of latent characteristics and their combi nations

that lead to predictiveness enhancement.

There are two approaches that are used in machine learning:

supervised and unsupervised learning. The rst approach is the

most common and widespread.

With the supervised approach, in the beginning, a risk analyst cre-

ates a machine learning model based on historical data. Then, with

new transaction data, the algorithm creates potentially right

baskets: fraud and not fraud. After that, the system collects exter-

nal signals such as fraud alerts, chargebacks, complaints etc.

Based on that information, the algorithm starts looking for new

unrecorded dependencies. Finally, the model starts retraining.

Consequently, all the risk analysts are one step behind the game,

thus, the cycle continues and with time new techniques emerge.

Unsupervised learning is regarded as an alternative to supervised

learning. These algorithms infer patterns from a dataset without

reference to known or labelled outcomes. Unsupervised learning

allows risk analysts to approach problems with no exact idea

about what the result will look like. One can derive structure from

data where they don’t necessarily know the eect of the variables.

With unsupervised learning, there is no feedback based on the

prediction results. But it can divide data on the basis of anomalous

behaviour and then risk analysts can apply well-known supervised

approaches to this data. ➔

Covery

Next Generation Fraud Prevention Platforms Leverage ML to Secure Payments

Pavel Gnatenko | Risk Management Expert | Covery

About Pavel Gnatenko: Pavel has a master’s degree in intellectual systems for decision-making.

He is a risk management expert with more than seven years of experience in the fintech industry.

Currently, Pavel is focused on developing Covery - next generation of risk management platforms.

21 WEB FRAUD PREVENTION, IDENTITY VERIFICATION & AUTHENTICATION GUIDE 2018-2019

About Covery: Covery is a global risk management

platform helping online companies solve fraud and

minimise risk. We focus on the universality of our

product and its adaptation to any type of business,

based on the individual characteristics and customer

needs using both rule-based and machine learning

approaches.

www.covery.ai

Therefore, unsupervised machine learning is more applicable to

real-world problems and can help to solve them when risk mana-

gers are constantly one step behind the fraudsters.

Why use machine learning in payment fraud

prevention?

When it comes to detecting and ghting online payment fraud,

several advantages become evident:

- it facilitates real-time decision-making and improves the expe-

rience for customers;

it improves accuracy of classication;

- it helps detect new fraudulent behaviour;

- it provides a more rapid response to real-world changes.

What can the best fraud prevention solutions do

The most advanced fraud prevention services use both rule-

based and machine learning approaches, including unsupervised

techniques, with an industry focus and an adaptation for the

business’ individual characteristics and customer needs. The result

is a solution that makes more accurate decisions for each industry

and every customer. One of the companies working in this space

is called Covery. Risk analysts can customise any combination of

data patterns we call ‘features’ that can be applied to a specic

business needs. Covery can also accept any non-payment data

in any user action to supplement the prole with missing details

to analyse by using both rule-based and machine learning models

for more precise decisions.

So what is Covery?

Covery is a global risk management platform helping online com-

panies solve fraud and minimise risk. The company focuses on

the versatility of the product and its adaptability to each type of

business, based on the individual characteristics and customer

needs using both rule-based and machine learning approaches.

Covery works with high-risk as well as with low-risk industries to

nd the right solution for every customer.

What Covery oers to help with fraud prevention:

- wider coverage of user actions for analysis;

exible customisation of data patterns;

- usage of any additional data for analysis;

- rule-based and machine learning approaches;

- functionality to work with loyal users to increase revenue;

- custom machine learning models creation;

- custom functionality upon request;

Conclusions

Fraudsters are always developing new tricks and risk managers

don’t always have the time to adapt to new changes. Machine

learning has long been expected to help solve the problem of

preventing fraud, but the majority of solutions are still on the path

of development. So Covery’s main goal is to solve the problem

when risk managers are constantly one step behind the fraudster.

Click here for the company profile

Best Practices in the Fraud Management Space

24 WEB FRAUD PREVENTION, IDENTITY VERIFICATION & AUTHENTICATION GUIDE 2018-2019

Goodbye fraud, hello customer experience

If the headline to my editorial caught you by surprise, let me

explain. While we’re not kissing ecommerce fraud completely

goodbye anytime soon (courtesy of those increasingly organised

fraudsters, confused customers, and savvy consumers looking for

ways to game the system), the payments industry is continuing to

direct its focus toward the far more lucrative domain of ‘customer

experience’.

If 2018 has shown the payments community one thing, it’s that

we’re at a critical inection point and moment of decision as an

ecosystem. As I’ve talked to payments professionals this year and

closely followed the lightning-fast pace of change, the nature of

this key ‘moment’ is coming into sharp focus.

The pendulum shift from fraud to customer expe-

rience

The CNP fraud conversation continues to shift increasingly to

defining moments of customer experience. While fraud is no

longer the central concern, it’s still very much part of the picture

as the industry continues to cope with a rampant ‘friendly fraud’

(or false claims) problem. Ethoca’s assessment is that the CNP

chargeback problem is estimated at USD 50 billion, comprised

of a combination of blended OPEX for both merchant and card

issuer, and lost value on transactions that are falsely disputed

by cardholders (sometimes unwittingly, but increasingly abusive

in nature). As a blended average across all merchant categories,

friendly fraud is hovering in the 30 to 40% range, but it’s most

acutely felt in digital goods where it can exceed 90%.

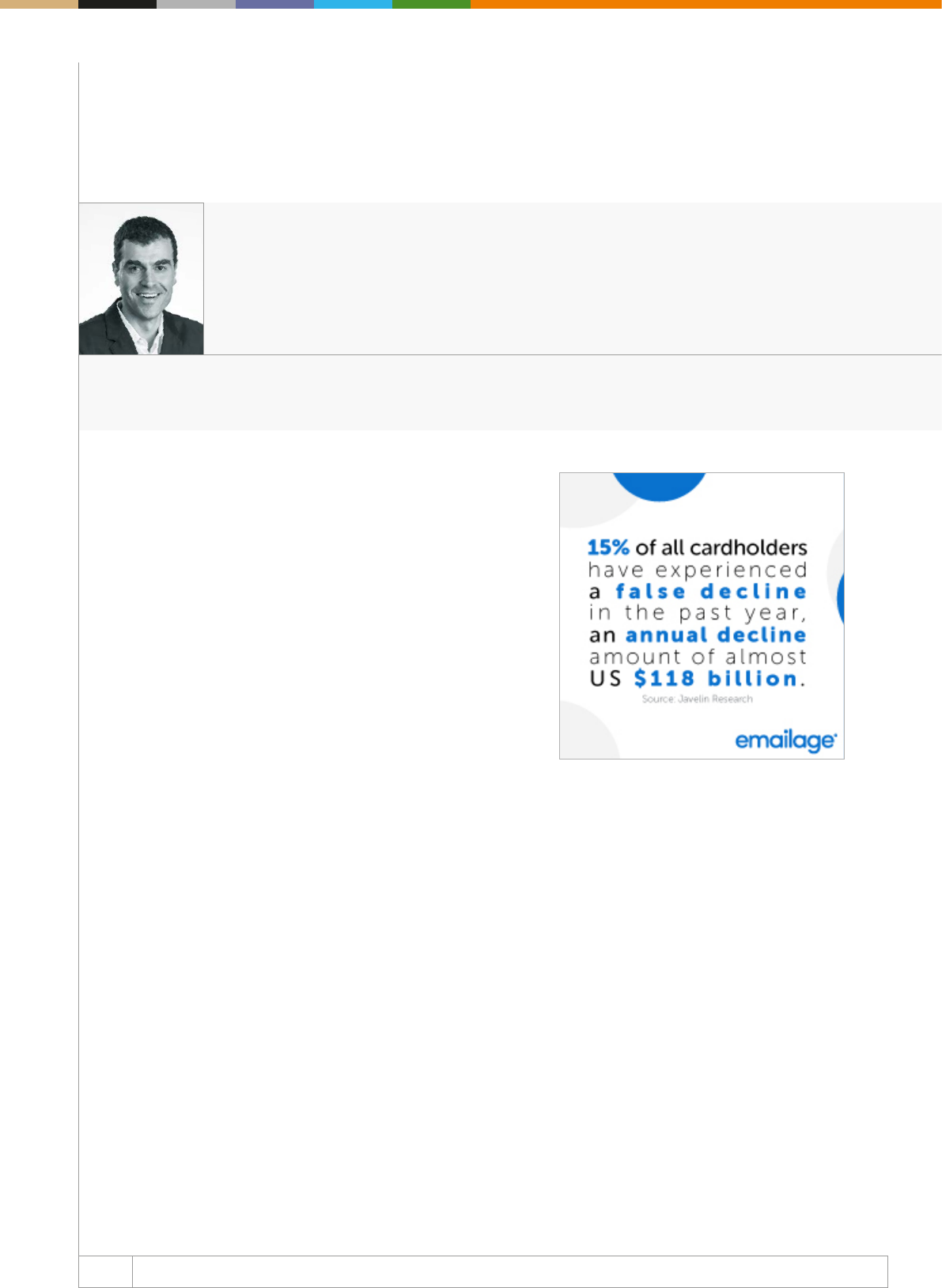

The most staggering fact is that while USD 50 billion is a headline-

grabbing number, it pales next to the lost transaction value and

customer insult factor that comes with false declines – when good

transactions are falsely rejected due to apparent fraud risk. Aite

Group estimates that false declines are costing the industry USD

331 billion annually, and that number is set to rise as the pervasive

inuence of friendly fraud continues to wreak havoc with eective

fraud decisioning.

The compounding regulatory ripple eect

One of the biggest ironies of 2018 is that the rise in customer

experience together with cardholder protection are reaching a

crescendo just as the regulatory environment is about to kick into

motion a series of changes that will potentially make it harder than

ever to create a frictionless customer experience. Enter PSD2 –

particularly the Strong Customer Authentication (SCA) component

of the updated payment directive release by the EBA.

When two-factor authentication becomes mandatory on all trans-

actions over EUR 30, the industry will be waiting with bated breath

to measure the impact of customer conversion and declines.

It’s important to remember that potentially 30% of all customer

declines are never tried again on another card in the cardholder’s

wallet. And while SCA exception scenarios exist when fraud rates

can be held in check at a PSP or acquirer level, it will prove to be

very challenging for ecommerce merchants to realise that benet

with so many false claims in the system. ➔

Keith Briscoe | Chief Marketing Ocer | Ethoca

About Keith Briscoe: Keith Briscoe leads Ethoca’s global product and marketing functions, a role

spanning the development of Ethoca’s suite of collaboration-based fraud/chargeback mitigation and

transaction acceptance solutions, as well as integrated marketing programmes. His mandate includes

product strategy and management, new product innovation, competitive analysis, experiential marketing,

integrated marketing campaigns, public relations, analyst relations, content strategy, and stakeholder

communications.

Collaboration Paving the Way for Ecommerce Customer Experience

Ethoca

25 WEB FRAUD PREVENTION, IDENTITY VERIFICATION & AUTHENTICATION GUIDE 2018-2019

Click here for the company profile

About Ethoca: Ethoca is the leading provider of

collaboration-based technology that closes the

information gap between thousands of card issuers

and ecommerce merchants worldwide – including

the top global brands and banks. Ethoca’s powerful

suite of innovative solutions help stop fraud, eliminate

chargebacks, improve customer experience and

increase card acceptance.

www.ethoca.com

3DS 2.0 holds the promise of delivering higher acceptance rates

as long as merchants can get comfortable with sharing extended

data elds with card issuers to benet from liability shift. However,

in parallel with this key question, there is a lot of chatter about the

‘death of fraud detection’ given that merchants can simply accept

every transaction and let 3DS liability sort out the rest. That would

be a tremendously short-sighted move, ultimately straining the

delicate card issuer – merchant acceptance balance.

For a start, this approach would trigger more step-up authenti-

cation at the card issuer, introducing increased friction – and

abandonment – into the purchase process. In addition, facing

increased losses as a result of liability shift, card issuers’ accept-

ance and fraud detection models would likely decline more.

Once again, we’re seeing all of this potentially set the stage for

anything but a good customer experience. Creating customer

habituation will be key (ease of use, minimal friction and virtual

invisibility). But it must be balanced with responsible and equitable

behaviours from both merchants and card issuers and enabled by

innovative technology that encourages productive, value-based

collaboration.

The case for collaboration

So where is all this heading? During no other period in the history

of payments has the time been more right for industry collabo-

ration to solve the most pressing problems in ecommerce. The rise

of what we at Ethoca call ‘bi-lateral rich data exchange’ is opti-

mally positioned to solve these increasing challenges. Here are

three recommendations for solving the most pressing customer

experience and transaction acceptance challenges heading into

2019:

1. Take the noise out of the system – The tricky thing with

friendly fraud is that it’s virtually impossible to detect with typical

fraud detection tools because it’s largely behavioural in nature.

It simply doesn’t ‘look’ like fraud, because it isn’t. Making

merchants’ deep purchase and account insight available to

card issuers’ mobile applications and to call centre agents –

at the pivotal moment of customer concern – is a critical rst

step in helping customers understand what they bought. The

result: better fraud decisioning (less garbage in means higher-

performing detection systems), fewer false declines, fewer

fraud claims, and improved customer experience.

2. Set the stage for ‘post transaction customer experience’ –

Utilising rich data and intelligence sharing between card issuers

and merchants to solve for dispute challenges is just step one.

Think about where this goes from here: when cardholders

have access to their consolidated digital receipts in the bank’s

mobile app, that’s where customer experience enters ‘next

level’ territory. That digital journey should matter as much to

banks as it does to merchants, laying the foundation for highly

relevant cross-sell opportunities and deeper engagement over

the course of the purchase journey.

3. Build the business case incrementally – One of the biggest

challenges in realising the full potential of bi-lateral rich data

exchange between card issuers and merchants is nding the

‘wedge’ use case(s) that prove the value through an incremental

approach. Ethoca’s view is that by starting with the biggest

pain points – moments of dispute or concern that can be

in stant ly resolved with real-time intelligence ‘in the moment’

– card issuers and merchants alike will become increasingly

comfortable with sharing intelligence that drives the best

possible customer experience.

At Ethoca, we’re welcoming 2019 with open arms and excitement:

the times, it seems, have caught up with collaboration.

26 WEB FRAUD PREVENTION, IDENTITY VERIFICATION & AUTHENTICATION GUIDE 2018-2019

Let’s start with payments. What do European mer-

chants need to be aware of when expanding over-

seas?

In the US, payments reflect consumer behaviour. There are

generally fewer standard payment methods than in Europe, and

the majority of payments are made via credit card rather than

direct debit or money transfer.

These payment types may present some diculties from a fraud

perspective – for example, making it more dicult to claw back

disputed funds.

One economic factor is the interchange fee on credit cards. Unlike

Europe, the US does not have a cap on these charges, which is

why the average interchange fee in the US is 1.73%, compared

to 0.96% in Europe. Interchange fees on debit card transactions

were capped in 2011 by the Durbin Amendment, but this does not

apply to credit cards.

How does Europe compare to the US from a fraud

prevention perspective? How do the strategies for

combatting fraud dier?

In some respects, Europe and the US are similar when it comes

to payment fraud. The majority of merchants on both sides of the

Atlantic review fewer than 10% of transactions and the reject rate

is around 3%.

The overall fraud rate in the US is higher though. One reason

for this is that in Europe fraud patterns are more recognisable,

since they tend to come from specic countries and merchants.

In the US, fraudsters have more opportunity to blend in and nd

sophisti cated ways to get around prevention mechanisms.

It is also easier for fraudsters to build proles for fraud due to the

availability of data in the US, where the focus tends to be on pay-

ment validation rather than identity verication. ➔

Felix Eckhardt | CTO | RISK IDENT Piet Mahler | COO | RISK IDENT

About Felix Eckhardt: Felix Eckhardt was with RISK IDENT at its inception. Initially taking

up the position of senior software engineer, he helped RISK IDENT get on its feet as the

chief architect behind the company’s second fraud prevention product, FRIDA. A year

after the company’s founding, Felix became the CTO and remained in the position until

he moved to Australia in 2016. While abroad, he acted as Senior Software Developer,

developing data-driven solutions for telecoms and marketing industries for two years.

About Piet Mahler: Piet Mahler is the COO at RISK IDENT, leading the strategic direction

of the company alongside the CTO, Felix Eckhardt. He is responsible for the development

of the business side of the company, having previously held the position of VP Operations

& Business Development, helping lead the company’s international growth.

RISK IDENT

Felix Eckhardt, Managing Director (CTO), and Piet Mahler, COO, RISK IDENT consider some of the key payment, fraud prevention,

operational, and regulatory issues for European merchants with aspirations of doing business in the US.

The majority of merchants on

both sides of the Atlantic review

fewer than 10% of transactions

and the reject rate is around 3%.

27 WEB FRAUD PREVENTION, IDENTITY VERIFICATION & AUTHENTICATION GUIDE 2018-2019

Click here for the company profile

Data protection is also a consideration in the US, where individual

states often have their own rules, in addition to national standards.

For example, the FCC is in charge of the rules concerning what

data internet service providers can and can’t sell; health data

is protected under the federal Health Insurance Portability and

Accounta bility Act, and the Federal Trade Commission enforces

the Children’s Online Privacy Protection Act.

Ecommerce in the US is worth almost half a trillion dollars annually,

according to the US Commerce Department. In Europe, it is worth

over half a trillion euros and growing fast.

Cross-border commerce is the Holy Grail for retailers; tune your

fraud prevention today to ensure it doesn’t become the same for

the fraudsters.

European merchants tend to rely on vendors for fraud decisions,

whereas in the US merchants rely on the vendors for the platform

and the merchants figure it out themselves. This seems to be

especially true for larger merchants.

Our research has found that the variety of fraud reporting struc-

tures in the US is quite pronounced. These reports address die

rent corporate priorities and have a general lack of consensus.

This is usually how vulnerabilities that can then be exploited open up.

What operational considerations should merchants

focus on when expanding overseas?

US consumers are demanding. Many will make purchases

during their commute and they expect next day delivery from

all merchants, even those based outside the US. Many of them

will not consider where the merchant is based when making a

purchase online. Having a US fullment house is a consideration.

In Europe, it is critical to oer local payment options to keep con

ver sion rates high. Consumers expect to be able to pay with all

major payment types with national dierences. Missing payment

types lead to abandonment.

GDPR came into eect this year. How does the US

dier from Europe when it comes to regulation?

There has been a great deal of talk about the General Data Protec-

tion Regulation (GDPR), but European data privacy rules and

attitudes have long been far stricter and more discerning than in

North America.

The other big change in online commerce in Europe is the Second

Payment Services Directive (PSD2). Combined with the GDPR, it

provides greater choice for consumers in how they can pay and

control their nances, while also aiming to modernise approaches

to security and privacy.

One dierence is a call for a minimum of twofactor authentication,