Api Reference Guide

api_reference_guide

User Manual:

Open the PDF directly: View PDF ![]() .

.

Page Count: 440 [warning: Documents this large are best viewed by clicking the View PDF Link!]

Trader Workstation API

Reference Guide

Version 973.07

Table of Contents

Chapter 1 Introduction 3

Chapter 2 Initial Setup 7

Chapter 3 Using Third Party API Platforms 11

Chapter 4 Excel APIs 19

Chapter 5 Troubleshooting and Support 55

Chapter 6 Programming the API: Architecture 59

Chapter 7 Connectivity 61

Chapter 8 Financial Instruments (Contracts) 65

Chapter 9 Orders 89

Chapter 10 Streaming Market Data 199

Chapter 11 Historical Market Data 241

Chapter 12 Account & Portfolio Data 255

Chapter 13 Options 273

Chapter 14 Financial Advisors 279

Chapter 15 Fundamental Data 295

Chapter 16 Error Handling 297

Chapter 17 Market Scanners 315

Chapter 18 News 321

Chapter 19 IB Bulletins 327

Chapter 20 Display Groups 329

Chapter 21 Namespace Index 332

Chapter 22 Hierarchical Index 333

Chapter 23 Class Index 337

Chapter 24 Namespace Documentation 339

Chapter 25 Class Documentation 341

Chapter 1

Introduction

http://interactivebrokers.github.io/tws-api/introduction.html

The TWS API is a simple yet powerful interface through which IB clients can automate their trading strategies,

request market data and monitor your account balance and portfolio in real time.

2.1 Audience

Our TWS API components are aimed at experienced professional developers willing to enhance the current TWS

functionality. Regrettably, Interactive Brokers cannot offer any programming consulting. Before contacting our API

support, please always refer to our available documentation, sample applications and Recorded Webinars

2.2 How to use this guide

This guide reflects the very latest version of the TWS API -9.72 and higher- and constantly references the Java,

VB, C#, C++ and Python Testbed sample projects to demonstrate the TWS API functionality. All code snippets are

extracted from these projects and we suggest all those users new to the TWS API to get familiar with them in order

to quickly understand the fundamentals of our programming interface. The Testbed sample projects can be found

within the samples folder of the TWS API's installation directory.

2.3 Requirements

• • The TWS API is an interface to TWS or IB Gateway, and as such requires network connectivity to a running

instance of one of these programs.

•To obtain the TWS API source and sample code, download the API Components.

•To make use of TWS API 9.72+, will require TWS build 952.x or higher.

• A working knowledge of the programming language our Testbed sample projects are developed in.

• • To obtain the TWS API source and sample code, download the API Components.

• To make use of TWS API 9.72+, will require TWS build 952.x or higher.

• A working knowledge of the programming language our Testbed sample projects are developed in.

• Java 8 or higher is required for running the Java API client.

Code samples in this guide are presented in the order:

•C#

•Java

•VB.NET

•C++

•Python

4 Introduction

• • To obtain the TWS API source and sample code, download the API Components.

• To make use of TWS API 9.72+, will require TWS build 952.x or higher.

• A working knowledge of the programming language our Testbed sample projects are developed in.

• Microsoft .Net Framework 4.5 or higher is required for running the VB API client.

• • To obtain the TWS API source and sample code, download the API Components.

• To make use of TWS API 9.72+, will require TWS build 952.x or higher.

• A working knowledge of the programming language our Testbed sample projects are developed in.

• A compiler that supports C++11 is required for running the C++ API client.

• For Windows users who use Visual Studio, a version of 2012 or higher is required.

• • To obtain the TWS API source and sample code, download the API Components (API version 9.73 or

higher is required).

• To make use of TWS API 9.73+, will require TWS build 952.x or higher.

• A working knowledge of the programming language our Testbed sample projects are developed in.

• Python version 3.1 or higher is required to interpret Python API client.

2.4 Limitations

Our programming interface is designed to automate some of the operations a user normally performs manually

within the TWS Software such as placing orders, monitoring your account balance and positions, viewing an instru-

ment's live data... etc. There is no logic within the API other than to ensure the integrity of the exchanged messages.

Most validations and checks occur in the backend of TWS and our servers. Because of this it is highly convenient to

familiarize with the TWS itself, in order to gain a better understanding on how our platform works. Before spending

precious development time troubleshooting on the API side, it is recommended to first experiment with the TWS

directly.

Remember: If a certain feature or operation is not available in the TWS, it will not be available on the API side

either!

2.4.1 Requests

The TWS is designed to accept up to fifty messages per second coming from the client side. Anything coming

from the client application to the TWS counts as a message (i.e. requesting data, placing orders, requesting your

portfolio... etc.). This limitation is applied to all connected clients in the sense were all connected client applications

to the same instance of TWS combined cannot exceed this number. On the other hand, there are no limits on the

amount of messages the TWS can send to the client application.

Generated by Doxygen

2.4 Limitations 5

2.4.2 Paper Trading

If your regular trading account has been approved and funded, you can use your Account Management page to open

aPaper Trading Account which lets you use the full range of trading facilities in a simulated environment

using real market conditions. Using a Paper Trading Account will allow you not only to get familiar with the TWS API

but also to test your trading strategies without risking your capital. Note the paper trading environment has inherent

limitations.

Generated by Doxygen

Chapter 2

Initial Setup

http://interactivebrokers.github.io/tws-api/initial_setup.html

The TWS API is an interface to IB's standalone trading applications, TWS and IB Gateway. These are both

standalone, Java-based trading applications which were designed to require the use of a graphical user interface

for the security of user authentication. For that reason, "headless" operation is not supported.

3.1 The Trader Workstation

Our market maker-designed IB Trader Workstation (TWS) lets traders, investors, and institutions trade stocks, op-

tions, futures, forex, bonds and funds on over 100 markets worldwide from a single account. The TWS API is a

programming interface to TWS and as such, it forcefully requires a TWS to connect to. To use version 9.72+ of the

API, it is necessary to have TWS version 952 or higher.

3.2 The IB Gateway

As an alternative to TWS for API users, IB also offers IB Gateway (IBG). From the perspective of an API application,

IB Gateway and TWS are essentially identical; both represent a server to which an API client application can open

a socket connection once the user has first authenticated a session. In either case (TWS or IBG), the user must

authenticate a session by manually entering credentials into the login window- for security reasons, a headless

session of TWS or IBG without a GUI is not supported. From the user's perspective, IB Gateway is a lighter

application which consumes about 40% fewer resources and has some advantages over using an API connection

to TWS- most noticeably, it does not have the designed limitation that an autologoff time is programmed when it

must shutdown to be restarted. IB Gateway does not update automatically and it is recommended to upgrade to a

current version from the website every few months or less.

•There are however some times in which it will also be necessary to restart IB Gateway, for instance if there is

a change to IB's contract database because of a ticker symbol changed or the introduction of a new contract,

it will be necessary to restart IBG to access the updated contract information.

The advantages of TWS over IBG is that it provides the end user with many tools (Risk Navigator, OptionTrader,

BookTrader, etc) and a graphical user interface which can be used to monitor an account or place orders. For

beginning API users, it is recommended to first become acquainted with TWS before using IBG.

For simplicity, this guide will mostly refer to the TWS although the reader should understand that for the

TWS API's purposes, TWS and IB Gateway are synonymous.

8 Initial Setup

3.3 Enable API connections

Before any client application can connect to the Trader Workstation, the TWS needs to be configured to listen

for incoming API connections on a very specific port. By default when TWS is first installed it will not allow API

connections. IBG by contrast accepts socket-based API connections by default. To enable API access in TWS,

navigate to the TWS' API settings at Edit ->Global Configuration ->API ->Settings and make sure the "Enable

ActiveX and Socket Clients" option is activated as shown below:

Also important to mention is the "Socket port". By default a production account TWS session will be set for socket

port 7496, and a paper account session will listen on socket port 7497. However these are just default values

chosen because they are almost always available on any computer. They can be changed to any open socket port,

as long as the socket ports specified in the API client and TWS settings match. If there are multiple TWS sessions

on one computer, the socket port is used to distinguish the TWS session. Since only one application can listen on

one port at a time you will need to assign different ports to each running TWS.

Important: when running paper and live TWS on the same computer, make sure your client application is

connecting to the right TWS!

3.4 Read Only API

The API Settings dialogue allows you to configure TWS to note accept API orders with the "Read Only" setting. By

default, "Read Only" is enabled as an additional precautionary measure. Information about orders is not available

to the API when read-only mode is enabled.

3.5 Master Client ID

By default the "Master Client ID" field is unset. To specify that a certain client should automatically receive updates

about all open orders, as well as commission reports from orders placed from all clients, the client's ID should be set

as the Master Client ID in TWS or IBG Global Configuration. The clientID is specified from an API client application

in the initial function call to IBApi::EClientSocket::eConnect (p. ??).

3.6 Installing the API source

The API itself can be downloaded and installed from:

http://interactivebrokers.github.io/

Many third party applications already have their own version of the API which is installed in the process of installing

the third party application. If using a third party product, it should first be verified if the API must be separately

installed and what version of the API is needed- many third party products are only compatible with a specific API

version.

The Windows version of the API installer will create a directory "C:\\TWS API\" for the API source code in addition

to automatically copying two files into the Windows directory for the ActiveX/DDE and C++ APIs. It is important

that the API installs to the C: drive, as otherwise API applications may not be able to find the associated files.

The Windows installer also copies compiled dynamic linked libraries (DLL) of the 32 versions of the ActiveX control

TWSLib.dll, C# API CSharpAPI.dll, and C++ API TwsSocketClient.dll. Starting in version 973.03, the Windows

installer also installs a 32 bit version of the RTDServer control. To use a 64 bit application which loads the API as a

dynamic library, it is necessary to compile and install a 64 bit version of the desired control.

Generated by Doxygen

3.7 Changing the installed API version 9

3.7 Changing the installed API version

(On Windows Only)

If a different version of the ActiveX (v9.71 or lower) or C++ API is required than the one currently installed on the

system, there are additional steps required to uninstall the previous API version to manually remove a file called

"TwsSocketClient.dll":

1) Uninstall the API from the "Add/Remove Tool" in the Windows Control Panel as usual

2) Delete the C:\TWS API\ folder if any files are still remaining to prevent a version mismatch.

3) Locate the file "C:\Windows\SysWOW64\TwsSocketClient.dll". Delete this file.

4) Restart the computer before installing a different API version.

Generated by Doxygen

Chapter 3

Using Third Party API Platforms

http://interactivebrokers.github.io/tws-api/third_party.html

Third party software vendors make use of the TWS' programming interface (API) to integrate their platforms with

Interactive Broker's. Thanks to the TWS API, well known platforms such as Ninja Trader or Multicharts can interact

with the TWS to fetch market data, place orders and/or manage account and portfolio information.

•It is important to keep in mind that most third party API platforms are not compatible with all IB

account structures. Always check first with the software vendor before opening a specific account type or

converting an IB account type. For instance, many third party API platforms such as NinjaTrader and Trade←-

Navigator are not compatible with IB linked account structures, so it is highly recommended to first check with

the third party vendor before linking your IB accounts.

A non-exhaustive list of third party platforms implementing our interface can be found in our Investor's

Marketplace. As stated in the marketplace, the vendors' list is in no way a recommendation from Interac-

tive Brokers. If you are interested in a given platform that is not listed, please contact the platform's vendor directly

for further information.

4.1 Frequently Asked Questions

Below is a list of frequently asked questions. All answers are given considering a standard usage of the TWS. Note

that some vendors might provide an additional customisation level to simplify things. If the below description does

not reflect the way you operate your third party software with the TWS, please contact your vendor directly.

•How to connect a 3rd party platform to Interactive Brokers' Trader Workstation

•Where to get support for a third party software connecting to the TWS.

•My program's vendor did not find any issue on its side and asked me to contact Interactive Brokers

directly.

•TWS generates warning messages that block my orders being automatically transmitted

•I cannot see any market data in my third party program

•I do have the Live Data Subscriptions I need but when using my paper trading user name I am still

unable to obtain it.

•I am obtaining a message saying "Historical data request pacing violation"

•I am obtaining a "HMDS query returned no data" message.

12 Using Third Party API Platforms

•I cannot chart CFDs from my third party program yet the TWS shows the data correctly.

•Can I connect simultaneously to my live and paper TWS?

•The charts shown by my charting software differ from the ones shown by the TWS

•Is there a fee involved to receive data from the API?

•Can the TWS API be used with trial accounts?

•What types of APIs are available?

•What are differences between connecting to the TWS API and using a FIX/CTCI connection?

•Can I use another trading application (IBKR mobile, WebTrader, TWS) while an API program is

con-nected?

•Can the TWS API be used with any IB account?

•Why does an order from the API appear as untransmitted in TWS with a 'T' button next to it?

•Is autolaunching of TWS or IB Gateway supported by IB?

•Is it possible to disable the daily auto-logoff requirement of TWS?

•Do you recommend any third party products or programming consultants?

•What are the differences between using an API application with TWS and IB Gateway?

•Is it possible to run TWS or IB Gateway on a headless server?

•Do I ever need to upgrade the TWS API?

•The data indicator in IB Gateway is red. Is something wrong?

•How do I report a problem to the API Support team?

•Are historical account positions or account values available from the TWS API?

•Does IB provide hosting services for custom algorithms?

•Is there an Excel API for MacOS?

4.1.1 How to connect a 3rd party platform to Interactive Brokers' Trader Workstation

Connecting any third party program to the TWS requires you to enable API connectivity on the TWS itself as

explained in Enable API connections section. Your third party program will need to provide means for you to

specify at least a host and a port. In the vast majority of cases the third party program will be running on the exact

same computer as the TWS therefore the host IP can be specified as 127.0.0.1 whereas the port needs to be the

exact same as the one configured in the TWS' API Settings, typically 7496 or 7497. Below is an illustration showing

one of our API sample applications highlighting the typical connectivity fields a program connecting to the TWS

should provide. Note there is an additional field for "clientId". You can set this id to any positive integer including zero

or to whatever your third party application's provider recommends.

Note: for vendor-specific instructions please contact your third party provider directly.

4.1.2 Where to get support for a third party software connecting to the TWS.

Interactive Brokers cannot provide any kind of support or advice for software not developed by IB itself. Depending

on the nature of your inquiry, our support staff's advice might be quite limited since in most of cases it is not realistic

to reverse-engineer a third party program in order to understand how is it using our API. Because of this, the third

party vendor's support team should always be the first contact option.

Generated by Doxygen

4.1 Frequently Asked Questions 13

4.1.3 My program's vendor did not find any issue on its side and asked me to contact Interactive Brokers

directly.

There will be occasions when a given operation will not be fulfilled as expected not because of a malfunction in

either platform but because of the business logic involved. The typical behaviour of the TWS is to either perform the

requested operation or to return an explanatory message which will point you in the right direction. It is the duty of

the third party program to clearly show these TWS' messages within its own user interface. Without a relevant error

message our support team will not be able to give any advice.

In case of a malfunction on Interactive Broker's side, clear and concise technical information needs to be provided

including evidence of the malfunction in the form of TWS or API message log files as detailed in Log Files section of

this guide. Collecting all the needed information is not a trivial process and might require a very detailed knowledge

of our API. To prevent being caught in between support teams, please request your third party vendor to contact us

directly via email to api@interactivebrokers.com with as much information as possible.

4.1.4 TWS generates warning messages that block my orders being automatically transmitted

There are precautionary settings in TWS that are designed to be a order safety check. TWS would usually generate

a pop-up warning dialogue, or sent back an error message via the API, when there is any violation to the pre-define

precautionary settings in TWS Presets.

For users who uses a third party software to place orders but also receives data feed from a different vendor other

than IB, TWS would also generate a default warning "You are trying to submit an order without having market data

for this instrument" on receiving orders from third party. The checked order will not be transmitted automatically

unless user click "Transmit" button of the order in TWS.

TWS precautions can be bypassed by navigating to File/Edit → Global Configuration → API → Precautions, and

check the box "Bypass Order Precautions for API Orders". Once this is done, API orders placed from a third party

software will not be checked by TWS precautions.

4.1.5 I cannot see any market data in my third party program

As explained in our Streaming Market Data page, in order to be able to pull market data from the TWS, you need

to acquire the Live Market Data of the product(s) you are interested in.

4.1.6 I do have the Live Data Subscriptions I need but when using my paper trading user name I am still

unable to obtain it.

Make sure you are Sharing Market Data Subscriptions

4.1.7 I am obtaining a message saying "Historical data request pacing violation"

Please refer to our Historical Data Limitations page

4.1.8 My third party program shows "No data of type EODChart is available" when trying to load a chart

This message is returned when the requested End of Day (EOD) market data is not available in our systems. You

can easily verify this by loading the exact same chart using the TWS to obtain the same result:

Please contact our General Support team's Market Data department for further information.

Generated by Doxygen

14 Using Third Party API Platforms

4.1.9 I am obtaining a "HMDS query returned no data" message.

Sometimes the data prior to the specified requested date is also not available for several reasons. Suppose a

product started quoting (generating data) on 1st January 2016 but your third party program requests data prior to

this date. To prevent this error message adjust your third party program's charting parameters accordingly.

4.1.10 I cannot chart CFDs from my third party program yet the TWS shows the data correctly.

Except for Index CFDs, CFDs do not have any market data of their own. What the TWS displays is the CFD's

underlying contract's data. Whenever you try to fetch non-Index CFD data from the TWS, you will obtain an error

message asking you to pull it's underlying contract's data instead. Some third party programs' user interface only

allow placing orders via their charts. Given that no data can be loaded for these products and the impossibility of

the third party program to apply a similar conversion as the TWS, you might find your third party software not able

to place orders as a consequence!

4.1.11 How can I connect my third party program to my paper trading account?

Connections via the TWS API are not aware of the user name with which you are logged in with in your TWS.

From this point of view the API makes no difference between live or paper trading. Since third party programs only

connect any running TWS on the specified host and port it only takes you to launch the TWS and log into it with your

paper trading credentials, make sure you Enable API connections and connect to it from your third party

application using the same procedure.

4.1.12 Can I connect simultaneously to my live and paper TWS?

From our side, yes. You can launch as many instances of the TWS as you need using different user name/password

combinations. It is crucial though to make sure each TWS is listening on a different port as described in the Enable

API connections section. Note that your might as well need to launch multiple instances of your third party

program and/or have a way of telling when is your program using the paper or the live accounts.

4.1.13 The charts shown by my charting software differ from the ones shown by the TWS

Given that the historical data sent down the TWS API comes from the same source as the one displayed by the

TWS itself it is almost impossible for it to differ.

Some charting platforms circumvent our Historical Data Limitations by combining real time and historical data.

Since our real time market data is not tick-by-tick, bars built from it will hardly match those retrieved from our

historical market data service.

Alternatively, you might as well be comparing different charts without noticing. A chart displaying data from NYSE

will never be the same as another built from the ARCA exchange or from our SMART routing strategy. inadvertently

you might as well be looking at TRADES on one side while having MIDPOINT or BID_ASK on another. Another

common mistake involves having different timezones between the TWS and your client application.

4.1.14 Is there a fee involved to receive data from the API?

Streaming real time data or receiving historical bars from the API requires streaming level 1 market data subscrip-

tions. Subscriptions for instruments other than forex, bonds, and index CFDs incur a monthly fee.

http://interactivebrokers.github.io/tws-api/market_data.html

Generated by Doxygen

4.1 Frequently Asked Questions 15

4.1.15 Can the TWS API be used with trial accounts?

Yes it is possible to connect an API application to a trial account. However it is not possible to receive real time

market data or historical candlesticks for most instruments from the TWS API with a trial account login.

4.1.16 What types of APIs are available?

There is an API for Traders Workstation (TWS API). It is the most full-featured and can be used by all clients with

trading access. There is a WT Web API for white-branded advisors and introducing brokers that provides streaming

and historical data. There is a REST WebAPI for third party companies and institutions. It can be used to place

stock and forex orders, receive market data snapshots, and receive account and portfolio information. https←-

://www.interactivebrokers.com/en/index.php?f=1325

4.1.17 What are differences between connecting to the TWS API and using a FIX/CTCI connection?

The TWS API is an interface to TWS or IB Gateway. It provides many functionalities, such as the ability to receive

market data, place orders, and receive account information. The TWS API requires that the user first login to either

TWS or IB Gateway, both standalone desktop applications. The TWS API has an order rate limitation of 50 orders

per second.

FIX/CTCI connectivity can be configured to connect either with IB Gateway or directly to IB. Unlike the TWS API,

FIX/CTCI is only for order placement and can not be used to receive market data. Also, FIX/CTCI has monthly

minimum commissions involved.

4.1.18 Can I use another trading application (IBKR mobile, WebTrader, TWS) while an API program is con-

nected?

To connect to the same IB account simultaneously with multiple trading applications it is necessary to have multiple

usernames. Additional usernames can be created through Account Management free of charge. Market data

subscriptions however only apply to individual usernames so the fees would be charged separately.

4.1.19 Can the TWS API be used with any IB account?

Most third party API applications do not support all IB account structures, so it is highly recommended to consult

with the third party software vendor before opening or converting to a specific IB account type to use with a third

party application.

4.1.20 Why does an order from the API appear as untransmitted in TWS with a 'T' button next to it?

If an order appears in TWS as untransmitted and is not sent to IB, there are generally three causes: (1) There is

an error in the order preventing transmission (2) There is a TWS precautionary setting preventing transmission to

IB. Precautionary settings can be globally overridden in TWS through the settings in Global Configuration at API ->

Precautions ->Bypass Order Precautions for API Orders (3) The order was sent with the 'transmit' boolean flag in

the API Order class set to False. By default, its value is True.

Generated by Doxygen

16 Using Third Party API Platforms

4.1.21 Is autolaunching of TWS or IB Gateway supported by IB?

Unfortunately for security reasons auto-launching of TWS or IB Gateway is not supported. Both applications are

designed to require the user to manually enter his or her credentials into the UI.

4.1.22 Is it possible to disable the daily auto-logoff requirement of TWS?

It is possible to adjust the time of auto-logoff, but not disable it. However, IB Gateway can be substituted for TWS

for use with an API application and it does not have the daily logoff requirement.

4.1.23 Do you recommend any third party products or programming consultants?

IB does not recommend particular third parties, but a list is maintained on the Investors Marketplace. https←-

://gdcdyn.interactivebrokers.com/Universal/servlet/MarketPlace.MarketPlace←-

Servlet

4.1.24 What are the differences between using an API application with TWS and IB Gateway?

From the point of view of an API application, TWS and IB Gateway are essentially identical. TWS additionally offers

the user the ability to directly view positions, trades, and market data, and provides a number of tools for trading, re-

search, and analysis. IB Gateway has a simple graphical user interface that is only used for modifying settings. The

advantages of IB Gateway is that it consumes 40% fewer resources and can run for longer periods without automat-

ically closing down. http://interactivebrokers.github.io/tws-api/initial_setup.html

4.1.25 Is it possible to run TWS or IB Gateway on a headless server?

Both TWS and IB Gateway are designed to have a user interface for the client to enter their account credentials.

For that reason, headless or GUI-less operation is not supported.

4.1.26 Do I ever need to upgrade the TWS API?

TWS is very backwards compatible with the API so it is not necessary to upgrade the API when upgrading to a new

version of TWS. Generally the only reason it is necessary to upgrade the API is to take advantage of a new feature

introduced in a more recent API version.

4.1.27 The data indicator in IB Gateway is red. Is something wrong?

It is normal for the market data farm connection indicator to stay red until a market data request is made from the

API application. The farms can also turn red after extended inactivity.

4.1.28 How do I report a problem to the API Support team?

Diagnosing specific issues will generally require that API logging is enabled in TWS or IB Gateway when the issue

occurs. In TWS this is done by navigating to Global Configuration ->API ->Settings and checking the box "Create

API Message Log", and setting the logging level to "Detail" In IB Gateway, these settings are found at Configure ->

Settings ->API ->Settings If an issue occurs after logs are enabled, they can be uploaded using the combination

Ctrl-Alt-Q and then clicking Submit. Please let API Support know logs have been uploaded.

Generated by Doxygen

4.1 Frequently Asked Questions 17

4.1.29 Are historical account positions or account values available from the TWS API?

Since the API cannot provide information not available in TWS, historical portfolio information is not available. It is

available from statements and flex queries in Account Management.

4.1.30 Does IB provide hosting services for custom algorithms?

Unfortunately no, web hosting is not provided.

4.1.31 Is there an Excel API for MacOS?

The Excel APIs require a Windows computer with Microsoft Excel.

Generated by Doxygen

Chapter 4

Excel APIs http://interactivebrokers.github.io/tws-api/excel_apis.html

5.1 Available Excel APIs

There are several API technologies available for Microsoft Excel. Since they utilize Windows technologies the Excel

APIs require a Windows OS.

•RTD Server for Excel

•Dynamic Data Exchange

•ActiveX for Excel API

Important: Sample spreadsheet applications are distributed with the API download for each of the API technologies

(RTD Server, ActiveX, DDE). It is important to keep in mind that the sample applications are intended as simple

demonstrations of API functionality for third party programmers. They do not have robust error handling functionality

and are not intended to be used as production level trading tools.

Recorded webinars providing an introduction to Excel API technologies are available from the IB website at←-

:Recorded Excel API Webinars

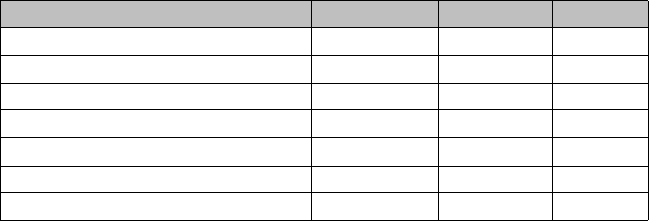

5.2 Excel API comparison

RTDServer DDE ActiveX

Full API functionality Not currently No Yes

Easy to use formulas Yes Sometimes No

Use without VBA Yes Sometimes No

Designed to not overwhelm Excel Yes No No

Open Source Yes No Yes

Market Data Refresh rate 250 ms 250 ms 1 sec

Sample compatible with 64 bit Excel No∗Yes Yes∗∗

∗expected in next API release, to be named 973.07

∗∗API ActiveX installer is compatible with both 32 and 64 bit applications starting with v973.05

20 Excel APIs

5.3 Limitations of Microsoft Excel APIs

By design, Microsoft Excel gives precedence to the user interface over the data connection to other applications.

For that reason, Excel only receives updates when it is in a 'ready' state, and may ignore data sent for instance

when a modal dialogue box is displayed to the user, a cell is being edited, or Excel is busy doing other things. A

new Excel Real Time Data server (RTD) API has been introduced to help address some of these limitations, but

they are inherent to Excel as a trading application and not specific to an API technology.

5.4 RTD Server for Excel

5.4.1 Introduction

TWS RTD Server API is a dynamic link library which allows user to request real-time market data from TWS via API

using Microsoft Excel®. The TWS RTD Server API directly uses the C# API Client source, which connects to TWS

via the socket. It allows displaying streaming live (or 15-minute delayed) market data in Excel by entering formulas

into an Excel cell following a specific syntax.

Note: At the current stage, only top-level market data is supported via TWS RTD Server API. No trading capability

or other data types are supported. Both Delayed and Real-Time data are supported via TWS RTD Server API.

Market Data Subscription is required for requesting live streaming market data.

5.4.2 What You Will Need

5.4.2.1 - Windows Operating System

Since the TWS RTD Server API technology directly refers to the C# API client source functions, it is supported on

Windows Environment only.

5.4.2.2 - API version 9.73.03+

You need to download IB API Windows version 9.73.03 or higher and install on your computer. Once you have

installed the API, you can verify the API Version by checking C:\TWS API\API_VersionNum.txt by default.

5.4.2.3 - TWS (or IB Gateway) Build 963+

By default, market data requests sent via TWS RTD Server will automatically request for all possible Generic Tick

Types (p. ??). There are several generic tick types being requested that are only supported in TWS 963 or higher.

Sending any RTD market data request with default generic tick list to an old build of TWS will trigger a "TwsRtd←-

Server error" indicating incorrect generic tick list is sent. Make sure a TWS builds 963+ is downloaded from IB

website and kept running at the background for TWS RTD Server API to function properly.

Generated by Doxygen

5.4 RTD Server for Excel 21

5.4.2.4 - Enable Socket Client in TWS (or IB Gateway)

Since the TWS RTD Server API directly refers to the C# API source, RTD market data requests will be sent via the

socket layer. Please make sure to Enable ActiveX and Socket Client settings in your TWS.

Please also be mindful of the socket port that you configure in your TWS API settings. The default socket port TWS

will listen on is 7496 for a live session, and 7497 for a paper session. It is further discussed in section Connection

Parameters that TWS RTD Server connects to port 7496 by default, and you are able to customize the port number

to connect by specifying pre-defined Connection Parameters or using rtd_complex_syntax string "port=<port>".

You can use any valid port for connection as you wish, and you just need to make sure that the port you are trying to

connect to via the API is the same port your TWS is listening on.

5.4.2.5 - Microsoft Excel®

After installing the API, the pre-compiled RTD library file (located at C:\TWS API\source\csharpclient\TwsRtd←-

Server\bin\Release\TwsRtdServer.dll by default) registered on your computer will be in 32-bit by default for API

versions from 973.03 to 973.06. If you are using 64-bit Microsoft Excel, you would need to re-compile RTD server dll

file into 64-bit and register the library by re-building the RTD source solution using Visual Studio. Please refer to the

TWS Excel APIs, featuring the RealTimeData Server recorded webinar for more information.

Beginning in API v973.07∗ it is expected that the API installer for RTD Server will be compatible with both 32 bit and

64 bit Excel (∗ expected version number).

5.4.3 TWS RTD Server Formula Syntax

Customer can request market data by entering the following formula with corresponding parameters into an Excel

spreadsheet cell:

=RTD(ProgID, Server, String1, String2, ...)

where

•ProgID = "Tws.TwsRtdServerCtrl"

•Server = "" (empty string)

•String1,String2, ... is a list of strings representing Ticker,Topic,Connection Parameters or other Com-

plex Syntax strings.

Note: TWS RTD Server API formula is not case-sensitive.

There are three ways to compose an RTD Formula:

•Simple Syntax

•Complex Syntax

•Mixed Syntax

Generated by Doxygen

22 Excel APIs

5.4.4 Syntax Samples

A resourceful Syntax Samples page is provided for demonstration of RTD formulas categorized by security type

using different syntaxs.

•Forex Pairs

•Stocks

•Indexes

•CFDs

•Futures

•Options

•Futures Options

•Bonds

•Mutual Funds

•Commodities

•Spreads

Besides reading through the written documentation, you can also watch the TWS Excel APIs, featuring

the RealTimeData Server recorded webinar for a more interactive tutorial video.

5.4.5 Outgoing message rate limit

• It is important to keep in mind the 50 message/second API limit applies to RTD Server in the same way as

other socket-based API technologies. So the Excel spreadsheet can send no more than 50 messages/second

to TWS. Each subscription or cancellation request counts as 1 message (messages in the opposite direction

are not included). So a spreadsheet can have hundreds of streaming tickers, but the subscriptions must be

spread out over time so that no more than 50 new subscriptions are made per second, or the spreadsheet

can become disconnected.

5.4.6 Change Data Refresh Rate

•Change Data Refresh Rate

5.4.7 Troubleshooting Common Errors

•Troubleshooting Common Errors

Generated by Doxygen

5.4 RTD Server for Excel 23

5.4.8 Simple Syntax

Basic components of a Simple Syntax RTD formula are ProgID, Server, Ticker (p. ??), Topic and Connec-tion

Parameters (optional):

=RTD(ProgID, Server, Ticker, Topic, ConnectionParams...)

where

•ProgID = "Tws.TwsRtdServerCtrl"

•Server = "" (empty string)

5.4.8.1 Ticker

Besides ProgID and Server, the first string should represent the Ticker in Simple Syntax.

To define a contract Ticker properly, you would need to find the correct contract attributes first. The easiest way to

find contract attributes is to directly look at the Contract Description page in TWS.

The syntax for Ticker should strictly follow the below squence:

Forex Contract:

"CURRENCY1.CURRENCY2/CASH"

e.g. EUR.USD Forex can be defined as "EUR.USD/CASH"

Other Contract Types:

"SYMBOL@EXCHANGE/PRIMEXCH/SECTYPE/EXPIRATION/RIGHT/STRIKE/CURRENCY"

e.g. The E-mini futures can be defined as "ES@GLOBEX//FUT/201712///USD"

Notes:

1. Not all contract attributes are required to be specified. You can leave the field to be blank to make that field

un-specified. Sequencially, if you only need to specify several contract attributes at the begining part of the

Ticker string, you can leave out the rest of the string entriely as well. For example, instead of specifying

"IBM@SMART//////", "IBM@SMART" would be sufficient to define the contract properly.

2. There are several default contract attributes in the Ticker string. If you leave them un-specified, they will take

the default values as following:

•EXCHANGE = "SMART"

•SECTYPE = "STK"

•CURRENCY = "USD"

For example, Ticker = "IBM" is the same as "IBM@SMART//STK////USD".

See more Syntax examples (p. ??).

Generated by Doxygen

24 Excel APIs

5.4.8.2 Topic

The second (or other strings) can be Topic.Topic string defines the tick type you would like to receive in the formula

cell. Topic can be specified within the Ticker string, or as a separate string.

For exmaple, the two formulas below both request the Bid Size for IBM from ISLAND exchange, where the first

formula includes Topic in Ticker and the second formula specifies Topic as a separate string:

=RTD("Tws.TwsRtdServerCtrl"„"IBM@ISLAND BidSize")

=RTD("Tws.TwsRtdServerCtrl"„"IBM@ISLAND", "BidSize")

If no Topic string is defined, the Topic will be defaulted to "Last".

For example, the below formula will request the last price for IBM from Island exchange:

=RTD("Tws.TwsRtdServerCtrl"„"IBM@ISLAND")

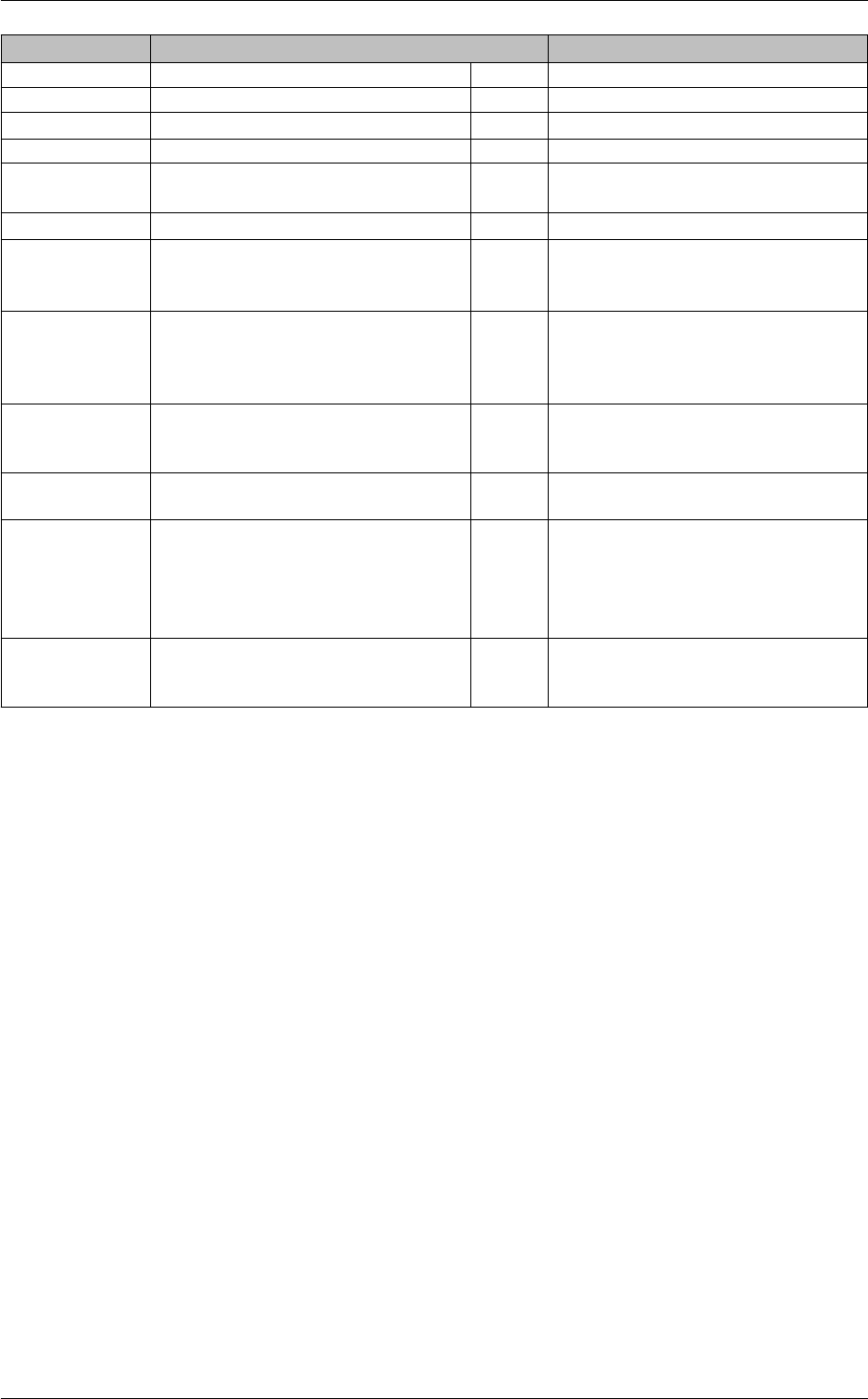

5.4.8.2.1 Basic Tick Types

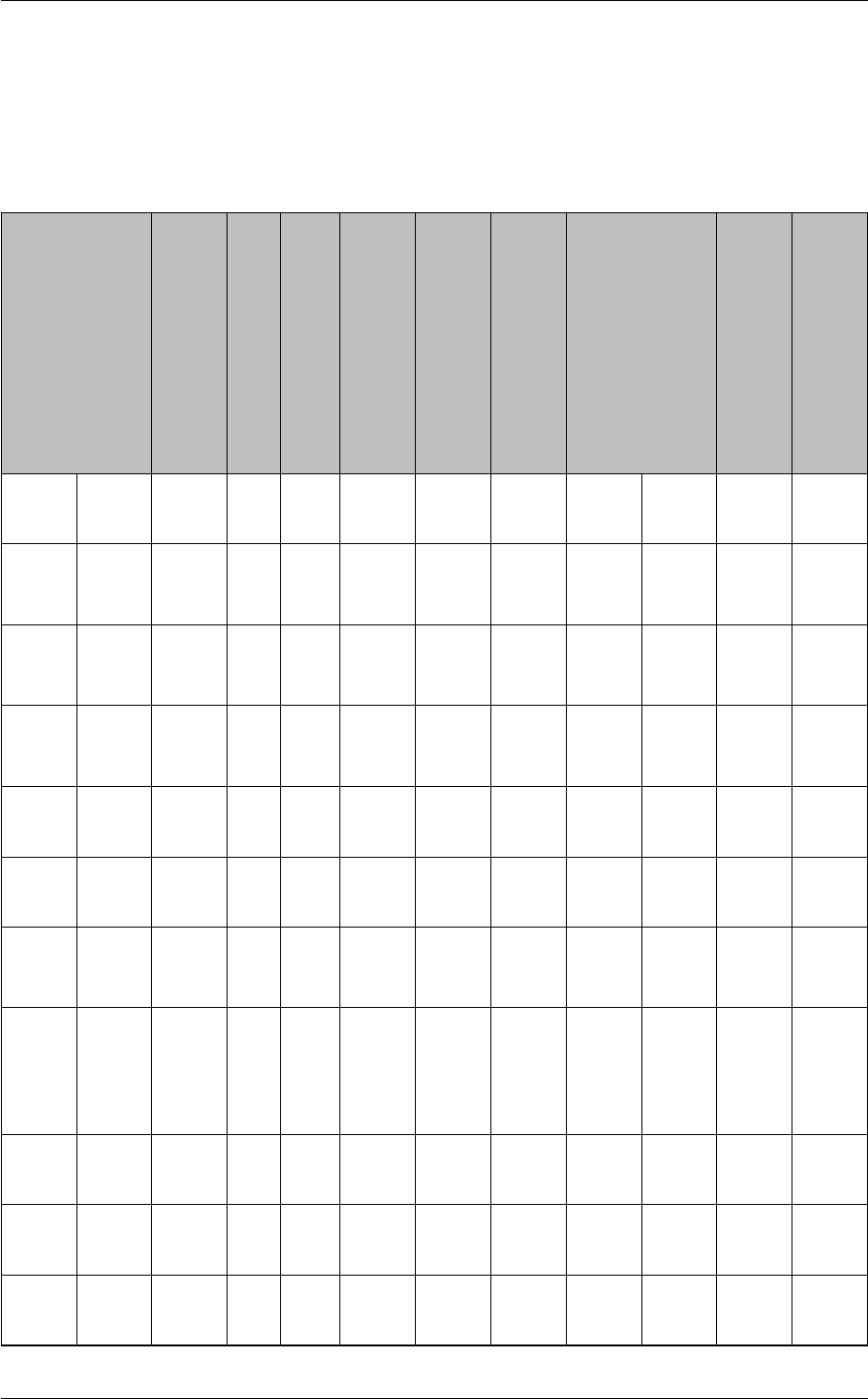

The table below shows a full list of available basic tick types that can be specified for the Topic:

Tick Name Topic String Description

Bid Size "BidSize" Number of contracts (or lots) offered at the bid price.

Bid Price "Bid" Highest bid price for the contract.

Ask Price "Ask" Lowest offer price for the contract.

Ask Size "AskSize" Number of contracts (or lots) offered at the ask price.

Last Price "Last" Last price at which the contract traded.

Last Size "LastSize" Number of contracts or lots traded at the last price.

High "High" High price for the day.

Low "Low" Low price for the day.

Volume "Volume" Trading volume for the day for the selected contract (Vol-

ume for US Stocks are quoted in lots. The actual number

of shares in volume can be calculated by multiplying 100).

Close Price "Close" The last available closing price for the previous day. For US

Equities, we use corporate action processing to get the clos-

ing price, so the close price is adjusted to reflect forward and

reverse splits and cash and stock dividends.

Open Price "Open" Today's opening price. The official opening price requires a

market data subscription to the native exchange of a con-

tract.

Last Exchange "LastExch" The exchange where the Last Price is provided from.

Bid Exchange "BidExch" The exchange where the Bid Price is provided from.

Ask Exchange "AskExch" The exchange where the Ask Price is provided from.

Last Timestamp "LastTime" Time of the last trade (in UNIX time).

Halted "Halted" Indicates if a contract is halted. See Halted

Bid Implied Volatility "BidImpliedVol" Implied volatility calculated from option bid prices.

Bid Delta "BidDelta" Delta calculated from the option bid prices.

Bid Option Price "BidOptPrice" Current bid price for the option contract.

Bid PV Dividend "BidPvDividend" The present value of dividends expected on the option's un-

derlying.

Bid Gamma "BidGamma" The option gamma value calculated from the option bid

prices.

Generated by Doxygen

5.4 RTD Server for Excel 25

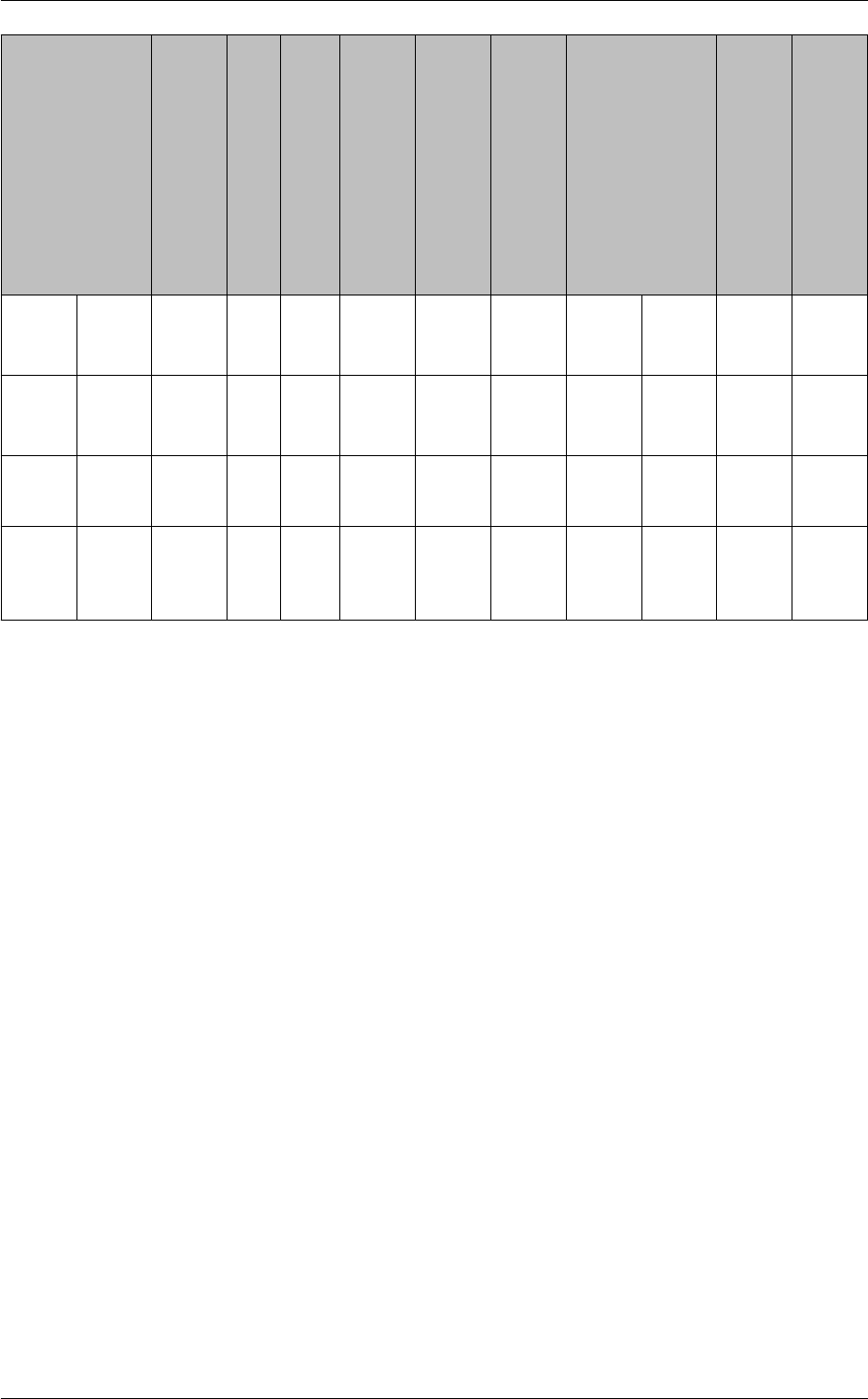

Tick Name Topic String Description

Bid Vega "BidVega" The option vega value calculated from the option bid prices.

Bid Theta "BidTheta" The option theta value calculated from the option bid prices.

Bid Price of Underlying "BidUndPrice" The current bid price of the option underlying.

Ask Implied Volatility "AskImpliedVol" Implied volatility calculated from option ask prices.

Ask Delta "AskDelta" Delta calculated from the option ask prices.

Ask Option Price "AskOptPrice" Current ask price for the option contract.

Ask PV Dividend "AskPvDividend" The present value of dividends expected on the option's un-

derlying.

Ask Gamma "AskGamma" The option gamma value calculated from the option ask

prices.

Ask Vega "AskVega" The option vega value calculated from the option ask prices.

Ask Theta "AskTheta" The option theta value calculated from the option ask prices.

Ask Price of Underlying "AskUndPrice" The current ask price of the option underlying.

Last Implied Volatility "LastImpliedVol" Implied volatility calculated from option last prices.

Last Delta "LastDelta" Delta calculated from the option last prices.

Last Option Price "LastOptPrice" Current last price for the option contract.

Last PV Dividend "LastPvDividend" The present value of dividends expected on the option's un-

derlying.

Last Gamma "LastGamma" The option gamma value calculated from the option last

prices.

Last Vega "LastVega" The option vega value calculated from the option last prices.

Last Theta "LastTheta" The option theta value calculated from the option last prices.

Last Price of Underlying "LastUndPrice" The current last price of the option underlying.

Model Implied Volatility "ModelImpliedVol" Implied volatility calculated from option model prices.

Model Delta "ModelDelta" Delta calculated from the option model prices.

Model Option Price "ModelOptPrice" Current model price for the option contract.

Model PV Dividend "ModelPvDividend" The present value of dividends expected on the option's un-

derlying.

Model Gamma "ModelGamma" The option gamma value calculated from the option model

prices.

Model Vega "ModelVega" The option vega value calculated from the option model

prices.

Model Theta "ModelTheta" The option theta value calculated from the option model

prices.

Model Price of Underlying "ModelUndPrice" The current model price of the option underlying.

Note: If you do not have the corresponding Market Data Subscription ( p. ??), '0' will be displayed if you request

for live tick types above. Please refer to Delayed Tick Types if you are interested.

API version 9.73.05 or higher is required to request option greeks data.

5.4.8.2.2 Generic Tick Types

A selection of Generic Tick Types are also supported in TWS RTD Server API. To request for any Generic Tick

Type, you just need to specify the name of the generic tick type as the Topic string in the RTD formula.

For example, the below formula will request the 52-Week High price for IBM@SMART:

=RTD("Tws.TwsRtdServerCtrl"„"IBM@SMART", "Week52Hi")

See table below for a full list of currently supported Generic Tick Types:

Generated by Doxygen

26 Excel APIs

Generic Tick Type

Name

Topic String Description Generic Tick Required

Auction Volume "AuctionVolume" The number of shares

that would trade if no

new orders were received

and the auction were held

now.

225

Auction Imbalance "AuctionImbalance" The number of un-

matched shares for the

next auction; returns how

many more shares are on

one side of the auction

than the other.

225

Auction Price "AuctionPrice" The price at which the

auction would occur if no

new orders were received

and the auction were held

now. The indicative price

for the auction.

225

Regulatory Imbalance "RegulatoryImbalance" The imbalance that

is used to determine

which at-the-open or

at-the-close orders can

be entered following

the publishing of the

regulatory imbalance.

225

PL Price "PlPrice" The PL Price, also known

as the Mark Price, is the

current theoretical calcu-

lated value of an instru-

ment. Since it is a calcu-

lated value, it will typically

have many digits of preci-

sion.

232

Creditmanager Mark

Price

"CreditmanMarkPrice" Not currently available. 221

Creditmanager Slow

Mark Price

"CreditmanSlowMark←-

Price"

Slow Mark Price update

used in system calcu-

lations (same as Mark

Price update in TWS Ac-

count Window ->Portfo-

lio).

619

Call Option Volume "CallOptionVolume" Call option volume for the

trading day.

100

Put Option Volume "PutOptionVolume" Put option volume for the

trading day.

100

Call Option Open Interest "CallOptionOpenInterest" Call option open interest. 101

Put Option Open Interest "PutOptionOpenInterest" Put option open interest. 101

Option Historical Volatility "OptionHistoricalVol" The 30-day historical

volatility (currently for

stocks).

104

RT Historical Volatility "RTHistoricalVol" 30-day real time historical

volatility (Futures only).

411

Generated by Doxygen

5.4 RTD Server for Excel 27

Generic Tick Type

Name

Topic String Description Generic Tick Required

Option Implied Volatility "OptionImpliedVol" A prediction of how

volatile an underlying will

be in the future. The IB

30-day volatility is the

at-market volatility esti-

mated for a maturity thirty

calendar days forward

of the current trading

day, and is based on

option prices from two

consecutive expiration

months.

106

Index Future Premium "IndexFuturePremium" The number of points that

the index is over the cash

index (Indeses only).

162

Shortable "Shortable" Describes the level of dif-

ficulty with which the con-

tract can be sold short.

See Shortable .

236

Fundamental Ratios "Fundamentals" Provides the available

Reuter's Fundamental

Ratios. See Funda-

mental Ratios .

258

Trade Count "TradeCount" Trade count for the day. 293

Trade Rate "TradeRate" Trade count per minute. 294

Volume Rate "VolumeRate" Volume per minute. 295

Last RTH Trade "LastRthTrade" Last Regular Trading

Hours traded price.

318

IB Dividends "IBDividends" Contract's dividends.

See IB Dividends .

456

Bond Factor Multipler "BondMultiplier" Not currenctly available. 460

Average Volume "AvgVolume" The average daily trad-

ing volume over 90 days

(multiply this value times

100).

165

High 13 Weeks "Week13Hi" Highest price for the last

13 weeks.

165

Low 13 Weeks "Week13Lo" Lowest price for the last

13 weeks.

165

High 26 Weeks "Week26Hi" Highest price for the last

26 weeks.

165

Low 26 Weeks "Week26Lo" Lowest price for the last

26 weeks.

165

High 52 Weeks "Week52Hi" Highest price for the last

52 weeks.

165

Low 52 Weeks "Week52Lo" Lowest price for the last

52 weeks.

165

Short-Term Volume 3

Minutes

"ShortTermVolume3Min" The past three minutes

volume. Interpolation

may be applied.

595

Generated by Doxygen

28 Excel APIs

Generic Tick Type

Name

Topic String Description Generic Tick Required

Short-Term Volume 5

Minutes

"ShortTermVolume5Min" The past five minutes vol-

ume. Interpolation may

be applied.

595

Short-Term Volume 10

Minutes

"ShortTermVolume10←-

Min"

The past ten minutes vol-

ume. Interpolation may

be applied.

595

Futures Open Interest "FuturesOpenInterest" Total number of outstand-

ing futures contracts (T←-

WS Build 965+ is re-

quired)

588

Average Option Volume "AvgOptVolume" Average volume of the

corresponding option

contracts (TWS Build

970+ is required)

105

By default, all Generic Tick Types are automatically requested. User just need to directly specify the Topic as the

name of a generic tick type to populate the data to Excel.

In order to consume less data resource and make your market data request more efficient, you can directly specify

the Generic Tick Type to be requested by defining string "genticks=id1,id2,...".

For example, to request 52-Week High price, only Generic Tick Type = 165 is required. The below formula will only

request Generic Tick Type = 165:

=RTD("Tws.TwsRtdServerCtrl"„"IBM@SMART", "Week52Hi", "genticks=165")

5.4.8.2.3 Delayed Tick Types

When live streaming market data is not availale because of missing Market Data Subscription (p. ??), delayed

data will be automatically relayed back. To request delayed data via RTD, you need to specify delayed tick types for

the Topic. The table below shows a full list of available delayed tick types:

Tick Name Topic String Description

Delayed Bid Size "DelayedBidSize" Number of contracts (or lots) offered at the bid price.

Delayed Bid Price "DelayedBid" Highest bid price for the contract.

Delayed Ask Price "DelayedAsk" Lowest offer price for the contract.

Delayed Ask Size "DelayedAskSize" Number of contracts (or lots) offered at the ask price.

Delayed Last Price "DelayedLast" Last price at which the contract traded.

Delayed Last Size "DelayedLastSize" Number of contracts or lots traded at the last price.

Delayed High "DelayedHigh" High price for the day.

Delayed Low "DelayedLow" Low price for the day.

Delayed Volume "DelayedVolume" Trading volume for the day for the selected contract

(Volume for US Stocks are quoted in lots. The actual

number of shares in volume can be calculated by mul-

tiplying 100).

Delayed Close Price "DelayedClose" The last available closing price for the previous day. For

US Equities, we use corporate action processing to get

the closing price, so the close price is adjusted to re-

flect forward and reverse splits and cash and stock div-

idends.

Delayed Open Price "DelayedOpen" Today's opening price. The official opening price re-

quires a market data subscription to the native ex-

change of a contract.

Delayed Last Timestamp "DelayedLastTimestamp" Delayed time of the last trade (in UNIX time) (TWS Build

970+ is required).

Generated by Doxygen

5.4 RTD Server for Excel 29

For example, the below formula will request the delayed bid price for IBM from Island exchange:

=RTD("Tws.TwsRtdServerCtrl"„"IBM@ISLAND", "DelayedBid")

Note: Delayed tick types are 15-minute delayed. Requesting for live tick types without market data subscription will

result in error message "Requested market data is not subscribed. Displaying delayed market data..."

See more Syntax examples (p. ??).

5.4.8.3 Connection Parameters

Since the TWS RTD Server API directly refers to the C# API Client, so it connects to TWS (or IB Gateway) the

same as C# via the socket. The Host IP Address,Socket Port and Client ID are required parameters for initiating

a socket connection.

• The Host IP Address is the IP address where your TWS is running on. For a local connection, local IP

127.0.0.1 can be used.

• The Socket Port is the port for socket connection. You can setup the host port in TWS API Settings (p. ??),

and you need to have your API connect to the same port as you setup in TWS.

• The Client ID is an identification for each API connection. TWS can maintain up to 32 API Clients connecting

at the same time, and the Client ID is used to distinguish each connection. This was originally designed so

that API users can have multiple API programs (i.e. clients) running at the same using different strategies to

trade separately. Since the TWS RTD Server API is only provided for relaying real-time data, there is no need

to use multiple client IDs.

The above three parameters are defaulted to the following values if not directly specified by the user:

•Host = "127.0.0.1" (i.e. the "localhost")

•Port = "7496"

•ClientID = Integer.MaxValue - 1

Simple Syntax supports several pre-defined Connection Parameters that can be specified as a separate string

(i.e. String2, String3...) in the RTD formula:

•"paper": use port=7497 for connection instead (7497 is the default port for paper TWS essions)

•"gw": use port=4001 for connection instead (4001 is the default port for live IB Gateway sessions)

•"gwpaper": use port=4002 for connection instead (4002 is the default port for paper IB Gateway sessions)

For example, to request High price for IBM@SMART while connecting to a TWS logged with a paper account via

port 7497:

=RTD("Tws.TwsRtdServerCtrl"„"IBM@ISLAND", "High", "paper")

Generated by Doxygen

30 Excel APIs

5.4.8.4 Additional Info

See also:

•Complex Syntax

•Mixed Syntax

5.4.9 Complex Syntax

Complex Syntax provides the most flexibility that it allows users to customize all formula strings individually, where

each string only represent one single parameter. There is no rule for the sequence of the appearance of each

parameter.

=RTD(ProgID,Server,String1,String2,String3...)

where

•ProgID = "Tws.TwsRtdServerCtrl"

•Server = "" (empty string)

For exmaple, the formula below will request the Ask Size for IBM@ISLAND:

=RTD("Tws.TwsRtdServerCtrl"„"sym=IBM", "sec=STK", "exch=ISLAND", "qt=Ask←-

Size")

The formula below will request the Bid price for IBM:

=RTD("Tws.TwsRtdServerCtrl"„"sym=ES", "sec=FUT", "exch=GLOBEX", "cur=USD",

"exp=201712", "qt=Bid")

5.4.9.1 Complex Syntax Strings

See table below for a full list available Complex Syntax strings:

Name String Syntax Description

Contract ID "conid=" The unique contract ID generated by IB. Can be found at

TWS Contract Description .

Symbol "sym=" The contract symbol.

SecurityType "sec=" The type of security, e.g. 'STK', 'FUT' and so on.

LastTradeDateOrContractMonth "exp=" Format 'YYYYMMDD' is used for defining the Last Trade

Date, while format 'YYYYMM' is used for defining the Con-

tract Month.

Strike "strike=" The strike price for an option contract.

Right "right=" 'C' or 'P' for an option contract.

Multiplier "mult=" The contract multiplier.

Generated by Doxygen

5.4 RTD Server for Excel 31

Name String Syntax Description

Exchange "exch=" The exchange where to get market data from. For equities,

'SMART' means top data from all possible exchanges.

PrimaryExchange "prim=" The primary exchange of the contract. It is mostly speci-

fied when an contract ambiguity occurs for equity symbols

that are listed on multiple exchanges.

Currency "cur=" The currency the contract is traded in.

LocalSymbol "loc=" The local symbol of the contract. Note the Local Symbol is

mostly used for futures and options, and is different from

the Symbol.

TradingClass "tc=" The trading class of the contract.

Combo "cmb=" Combo contract has to be defined using Complex Syntax

or Mixed Syntax. The syntax for defining the combo is:

"cmb=<conid1>#<ratio1>#<action1>#<exchange1>;<conid2>#<ratio2>#<action2>#<exchange2>;"

,where combo legs are separated by ';' and individ-

ual leg parameters are separated by '#'. See more

Spread Samples .

DeltaNeutralContract "und=" Delta-Neutral Contract. The syntax for defining the delta-

neutral contract is:

"und=<<conid>#<delta>#<price>"

, where delta-neutral contract parameters are sepa-

rated by '#'.

MktDataOptions "opt=" Currently not supported.

GenericTickList "genticks=" A comma separated Ids of available Generic Tick Types.

Topic "qt=" Topic of market data request.

Host "host=" Host IP address.

Port "port=" Socket port.

ClientId "clientid=" The client ID for socket connection. Note that the client ID

is used for identify multiple simultaneous API connections

to the same TWS. It was originally designed for API users

who would like to manage their strategies separately from

different API programs. Since the TWS RTD Server API is

currently only supported for real-time market data, there is

no need to use multiple client IDs.

5.4.9.2 Additional Info

See also:

•Simple Syntax

•Mixed Syntax

Generated by Doxygen

32 Excel APIs

5.4.10 Mixed Syntax

The Complex Syntax can be mixed with Simple Syntax with only one restriction that Ticker string must be the first

string (i.e. String1) that appears in the RTD formula.

=RTD(ProgID, Server, Ticker, String2, String3...)

where

•ProgID = "Tws.TwsRtdServerCtrl"

•Server = "" (empty string)

For example, the formula below will request the Bid Price for IBM while connecting through a customized Host, Port

and Client ID:

=RTD("Tws.TwsRtdServerCtrl"„"IBM@SMART", "host=1.2.3.4", "port=1234", "client←-

Id=1", "Bid")

See more Syntax Samples (p. ??).

5.4.10.1 Additional Info

See also:

•Simple Syntax

•Complex Syntax

5.4.11 TWS RTD Server Samples

This page is provided as a demonstration of RTD formulas categorized by security type as well as syntax type. Make

sure to get yourself familiar with the various available Syntaxs for RTD formula before looking into the samples.

•Simple Syntax

•Complex Syntax

•Mixed Syntax

5.4.11.1 Forex Pairs

5.4.11.1.1 - Simple Syntax

=RTD("Tws.TwsRtdServerCtrl"„"EUR.USD/CASH", "Bid")

Comment: Forex Ticker is defined in format "CURRENCY1.CURRENCY2/CASH".

Generated by Doxygen

5.4 RTD Server for Excel 33

5.4.11.1.2 - Complex Syntax

=RTD("Tws.TwsRtdServerCtrl"„"sym=EUR","cur=USD", "exch=IDEALPRO", "sec=CAS←-

H", "qt=Bid")

Comment: For Complex Syntax, Forex Symbol is defined as the foreign currency, and the Currency is defined as

the base currency.

5.4.11.1.3 - Mixed Syntax

=RTD("Tws.TwsRtdServerCtrl"„"EUR.USD/CASH", "Bid", "port=1234", "client←-

Id=1")

5.4.11.2 Stocks

5.4.11.2.1 - Simple Syntax

=RTD("Tws.TwsRtdServerCtrl"„"IBM")

Comment: Default values are used: Exchange = "SMART", Currency = "USD", Security Type = "STK", Topic =

"Last".

=RTD("Tws.TwsRtdServerCtrl"„"IBM@ISLAND", "Bid")

Comment: Specifying the Exchange directly means requesting data from that exchange specifically.

=RTD("Tws.TwsRtdServerCtrl"„"BMO@SMART//////CAD", "Bid")

Comment: Currency = "CAD" is needed for BMO listed on TSE, but the rest of the fields can be left out as blank.

=RTD("Tws.TwsRtdServerCtrl"„"ABG.P@SMART//////EUR", "Close")

Comment: Stock symbols that contain a '.' are supported in Simple Syntax as well.

=RTD("Tws.TwsRtdServerCtrl"„"MSFT@SMART/ISLAND", "Ask")

Comment: For certain smart-routed stock contracts that have the same Symbol,Currency and Exchange, you

would also need to specify the PrimaryExchange attribute to uniquely define the contract. This should be defined

as the native exchange of a contract, and is good practice for all stocks.

5.4.11.2.2 - Complex Syntax

=RTD("Tws.TwsRtdServerCtrl"„"sym=IBM", "sec=STK", "exch=SMART", "cur=USD",

"qt=Volume")

Comment: Generally speaking, using the Symbol,SecurityType="STK", Currency and Exchange is sufficient to

define a stock.

=RTD("Tws.TwsRtdServerCtrl"„"sym=MSFT", "sec=STK", "exch=SMART", "cur=USD",

"prim=ISLAND", "qt=Open")

Comment: Specifying the PrimaryExchange as a seprate string to resolve contract ambiguity.

Generated by Doxygen

34 Excel APIs

5.4.11.2.3 - Mixed Syntax

=RTD("Tws.TwsRtdServerCtrl"„"MSFT@SMART", "prim=ISLAND", "qt=High", "paper")

Comment: Use the pre-defined string "paper" to connect to the default port 7497 for paper TWS sessions.

5.4.11.3 Indexes

5.4.11.3.1 - Simple Syntax

=RTD("Tws.TwsRtdServerCtrl"„"SPX@CBOE//IND", "Last")

Comment: Default Currency = "USD" is used.

=RTD("Tws.TwsRtdServerCtrl"„"DAX@DTB//IND////EUR", "Last")

5.4.11.3.2 - Complex Syntax

=RTD("Tws.TwsRtdServerCtrl"„"sym=INDU","cur=USD", "exch=NYSE", "sec=IND",

"qt=Close")

5.4.11.3.3 - Mixed Syntax

=RTD("Tws.TwsRtdServerCtrl"„"DAX@DTB//IND", "cur=EUR", "qt=Last", "host=1.←-

2.3.4")

5.4.11.4 CFDs

5.4.11.4.1 - Simple Syntax

=RTD("Tws.TwsRtdServerCtrl"„"IBDE30@SMART//CFD////EUR", "Bid")

5.4.11.4.2 - Complex Syntax

=RTD("Tws.TwsRtdServerCtrl"„"sym=IBDE30","cur=EUR", "exch=SMART", "sec=CF←-

D", "qt=ASK")

5.4.11.4.3 - Mixed Syntax

=RTD("Tws.TwsRtdServerCtrl"„"IBDE30@SMART//CFD", "cur=EUR", "Bid", "gw")

Comment: Use the pre-defined string "gw" to connect to the default port 4001 for live IB Gateway sessions.

Note: Only Index CFD data can be directly queried via the API, but not equity CFD. Please directly request data for

the underlying equity if you need data for an equity CFD contract.

Generated by Doxygen

5.4 RTD Server for Excel 35

5.4.11.5 Futures

5.4.11.5.1 - Simple Syntax

=RTD("Tws.TwsRtdServerCtrl"„"ES@GLOBEX//FUT/201712///USD", "Bid")

Comment: Use underlying Symbol and LastTradeDateOrContractMonth to define futures contract.

5.4.11.5.2 - Complex Syntax

=RTD("Tws.TwsRtdServerCtrl"„"loc=ESZ7","cur=USD", "exch=GLOBEX", "sec=FUT",

"qt=Ask")

Comment: The LastTradeDateOrContractMonth and underlying Symbol can be replaced with the contract's own

symbol, also known as LocalSymbol (named as Symbol within the TWS' Contract Description dialog). Local

Symbol is not available in Simple Syntax.

5.4.11.5.3 - Mixed Syntax

=RTD("Tws.TwsRtdServerCtrl"„"DAX@DTB//FUT/201706///EUR", "mult=5", "Low")

Comment: For futures that have multipler Multipliers (e.g. DAX has 5 and 25), Simple Syntax is not adequate to

define the contract uniquely. Mixed Syntax can help to add addition specification for the Multiplier.

5.4.11.6 Options

5.4.11.6.1 - Simple Syntax

=RTD("Tws.TwsRtdServerCtrl"„"GOOG@SMART//OPT/20170421/C/835/USD", "Bid")

Comment: Use Symbol,LastTradeDateOrContractMonth,Right and Strike to define options contract.

5.4.11.6.2 - Complex Syntax

=RTD("Tws.TwsRtdServerCtrl"„"loc=C DBK DEC 20 1600", "cur=EUR", "exch=DTB",

"sec=OPT", "qt=Close")

Comment: Use LocalSymbol to define options contract.

5.4.11.6.3 - Mixed Syntax

=RTD("Tws.TwsRtdServerCtrl"„"SANT@MEFFRV//OPT/20190621/C/7.5/EUR", "mult=100",

"tc=SANEU", "Close")

Comment: For options that have multipler Multipliers or TradingClasses, Simple Syntax is not adequate to define

the contract uniquely. Mixed Syntax can help to add addition specifications for Multipler and TradingClass properly.

Generated by Doxygen

36 Excel APIs

5.4.11.7 Futures Options

5.4.11.7.1 - Simple Syntax

=RTD("Tws.TwsRtdServerCtrl"„"ES@GLOBEX//FOP/20180316/C/1000/USD", "Close")

Comment: Futures Options follow the same rule as conventional option contracts.

5.4.11.7.2 - Complex Syntax

=RTD("Tws.TwsRtdServerCtrl"„"loc=ESH8 C1000", "cur=USD", "exch=GLOBEX",

"sec=FOP", "qt=Close")

5.4.11.7.3 - Mixed Syntax

=RTD("Tws.TwsRtdServerCtrl"„"ES@GLOBEX//FOP/20180316/C/1000/USD", "mult=50",

"tc=ES", "Close")

5.4.11.8 Bonds

5.4.11.8.1 - Simple Syntax

=RTD("Tws.TwsRtdServerCtrl"„"912828C57@SMART//BOND", "Bid")

Comment: Bonds can be specified by defining the Symbol as the CUSIP. Currency = "USD" is used as default

here.

5.4.11.8.2 - Complex Syntax

=RTD("Tws.TwsRtdServerCtrl"„"sym=912828C57","cur=USD", "exch=SMART", "sec=←-

BOND", "qt=Bid")

=RTD("Tws.TwsRtdServerCtrl"„"conid=147554578", "exch=SMART", "qt=Ask")

Comment: Bonds can also be defined with the ConId and Exchange as with any security type.

5.4.11.8.3 - Mixed Syntax

=RTD("Tws.TwsRtdServerCtrl"„"912828C57@SMART, "sec=BOND", "Bid", "gwpaper")

Comment: Use the pre-defined string "gwpaper" to connect to the default port 4002 for paper IB Gateway sessions.

Generated by Doxygen

5.4 RTD Server for Excel 37

5.4.11.9 Mutual Funds

5.4.11.9.1 - Simple Syntax

=RTD("Tws.TwsRtdServerCtrl"„"VINIX@FUNDSERV//FUND", "Close")

5.4.11.9.2 - Complex Syntax

=RTD("Tws.TwsRtdServerCtrl"„"sym=VINIX","cur=USD", "exch=FUNDSERV", "sec=F←-

UND", "qt=Close")

5.4.11.9.3 - Mixed Syntax

=RTD("Tws.TwsRtdServerCtrl"„"VINIX@FUNDSERV//FUND", "Bid", "host=1.2.3.4",

"port=1234", "clientId=1")

5.4.11.10 Commodities

5.4.11.10.1 - Simple Syntax

=RTD("Tws.TwsRtdServerCtrl"„"XAUUSD@SMART//CMDTY", "Bid")

5.4.11.10.2 - Complex Syntax

=RTD("Tws.TwsRtdServerCtrl"„"sym=XAUUSD","cur=USD", "exch=SMART", "sec=CMD←-

TY", "qt=Ask")

5.4.11.10.3 - Mixed Syntax

=RTD("Tws.TwsRtdServerCtrl"„"XAUUSD@SMART//CMDTY", "Last", "port=1234",

"clientId=1")

5.4.11.11 Spreads

Spread contracts, also known as combos or combinations, combine two or more instruments. To define a com-

bination contract it is required to know the Contract ID of the combo legs. The ConId can be easily found in the

Contract Description page in TWS.

The spread contract's symbol can be either the symbol of one of the contract legs or, for two-legged combinations

the symbols of both legs separated by a comma as shown in the examples below.

Simple Syntax is not sufficient to define spread contracts. You need to use either Complex Syntax or Mixed

Syntax . As a reminder, here is the string formula for defining the Combo Legs:

"cmb=<conid1>#<ratio1>#<action1>#<exchange1>;<conid2>#<ratio2>#<action2>#<exchange2>;"

Generated by Doxygen

38 Excel APIs

5.4.11.11.1 Stock Spread

Buy 1 IBKR@SMART + Sell 1 MCD@SMART:

5.4.11.11.1.1 - Complex Syntax

=RTD("Tws.TwsRtdServerCtrl"„"sym=IBKR,MCD", "exch=SMART", "cur=USD", "sec=←-

BAG", "cmb=43645865#1#BUY#SMART;9408#1#SELL#SMART;", "Bid")

5.4.11.11.1.2 - Mixed Syntax

=RTD("tws.twsrtdserverctrl"„"IBKR,MCD@SMART//BAG////USD", "cmb=43645865#1#←-

BUY#SMART;9408#1#SELL#SMART;", "Bid")

Note: EFPs are simply defined as a bag contract of stock and corresponding SSF with a ratio of 100:1.

5.4.11.11.2 Futures Spread

Buy 1 VXJ7@CFE + Sell 1 VXK7@CFE:

5.4.11.11.2.1 - Complex Syntax

=RTD("tws.twsrtdserverctrl"„"sym=VIX", "exch=CFE", "cur=USD", "sec=BAG",

"cmb=249139906#1#BUY#CFE;252623425#1#SELL#CFE;", "Bid")

5.4.11.11.2.2 - Mixed Syntax

=RTD("tws.twsrtdserverctrl"„"VIX@CFE//BAG////USD", "cmb=249139906#1#BUY#CF←-

E;252623425#1#SELL#CFE;", "Bid")

5.4.11.11.3 Options Spread

Buy 1 DBK May19'17 15 CALL @DTB + Sell 1 DBK May19'17 16 CALL @DTB:

5.4.11.11.3.1 - Complex Syntax

=RTD("tws.twsrtdserverctrl"„"sym=DBK", "exch=DTB", "cur=EUR", "sec=BAG",

"cmb=270579950#1#BUY#DTB;270579957#1#SELL#DTB;", "Bid")

5.4.11.11.3.2 - Mixed Syntax

=RTD("tws.twsrtdserverctrl"„"DBK@DTB//BAG////EUR", "cmb=270579950#1#BUY#DT←-

B;270579957#1#SELL#DTB;", "Bid")

Generated by Doxygen

5.4 RTD Server for Excel 39

5.4.11.11.4 Inter-Commodity Futures Spread

For Inter-Commodity futures, the 'Local Symbol' field in TWS is used for the 'Symbol' field in the TWS Contract

Description (p. ??).

Buy 1 CL May'17 @NYMEX + Sell 1 BZ Jun'17 @NYMEX:

5.4.11.11.4.1 - Complex Syntax

=RTD("tws.twsrtdserverctrl"„"sym=CL.BZ", "exch=NYMEX", "cur=USD", "sec=BA←-

G", "cmb=55977404#1#BUY#NYMEX;55807026#1#SELL#NYMEX;", "Bid")

5.4.11.11.4.2 - Mixed Syntax

=RTD("tws.twsrtdserverctrl"„"CL.BZ@NYMEX//BAG////USD", "cmb=55977404#1#BU←-

Y#NYMEX;55807026#1#SELL#NYMEX;", "Bid")

Note: Please be mindful of the fact that Inter-commodity Futures contracts are spread contracts offered by the

exchange directly, and the contract definition is different from regular combo contracts. Please make sure all the

contract attributes are specified in accordance with TWS Contract Description page.

5.4.11.12 Sample Spreadsheet

A sample RTD spreadsheet is provided within the API installation directory. By default, you will be able to find it

under C:\TWS API\samples\ExcelTwsRtdServer.xls.

5.4.12 Change Data Refresh Rate

It is important to mention that our real time market data is not tick-by-tick, meaning you will not obtain every single

price movement happening in the market. Instead, real time data is given as snapshots generated at a fixed given

pace:

Product Frequency

Stocks, Futures and others 250 ms

US Options 100 ms

FX pairs 5 ms

Microsoft RTD interface has a ThrottleInterval property that determines the interval between data re-

freshes. By default, the value is set to 2000 milliseconds, which means Excel waits at least 2000 milliseconds

between checks for updates. You are able to manually change the Throttle Interval to a smaller value∗so as to

increase the refresh rate of real time data.

The easiest way to change the ThrottleInterval property is through VBA:

Generated by Doxygen

40 Excel APIs

1. In Excel, go to the Visual Basic Editor window by pressing Alt_F11.

2. On the Visual Basic Editor window, click on View ->Immediate Window or hold Ctrl_G to open the Imme-

diate Window.

3. On the Immediate Window, type in the following code and then click Enter:

Application.RTD.ThrottleInterval=250

4. To verify that it is set correctly, type this line of code on the Immediate Window and click Enter:

? Application.RTD.ThrottleInterval

5. Verify the next line should display 250. If this value is changed, the new value will persist when Microsoft

Excel is restarted.

∗Warning: As the ThrottleInterval is lowered, updates can come in so frequently that Excel is continuously

updating values and doing calculations, Excel might end up in a state where it never gives the user a chance to do

anything, effectively getting in a hung state. If this happens, set the Excel throttle interval higher.

Source: Microsoft Real-Time Data: Frequently Asked Questions How Do I Configure the RTD Throttle Interval in

Excel?.

5.4.13 Troubleshooting Common Errors for RTD

5.4.13.1 Troubleshooting Common Errors

•TwsRtdServer error: Cannot connect to TWS.

•TwsRtdServer error: No security definition has been found for the request.

•TwsRtdServer error: The contract description specified for <SYMBOL> is ambiguous.

•TwsRtdServer error: Requested market data is not subscribed. Displaying delayed market

data...(p. ??)

•TwsRtdServer error: Error validating request:-'zd':cause - Incorrect generic tick list of

•Some data show '0' when requesting data for many securities

5.4.13.1.1 TwsRtdServer error: Cannot connect to TWS.

This error message is most likely triggered because your TWS has not been configured properly for API socket

connection. Please make sure to Enable ActiveX and Socket Client settings in your TWS. Also bear in mind that

TWS Rtd Server connects to socket port 7496 by default. You will see the above error message if the socket port

configured in your TWS API settings does not match what RTD is trying to connect to. See more details in What You

Will Need .

Generated by Doxygen

5.4 RTD Server for Excel 41

5.4.13.1.2 TwsRtdServer error: RTD Server disconnects from TWS such that cells stop updating

This can occur if the API message rate of 50 messages/second is exceeded. No more than 50 messages can be

sent from an API application such as RTD Server to TWS per second (this does not include messages in the oppo-

site direction). Each ticker subscription request and subscription cancellation request corresponds to 1 message. If

the 50 messages/second rate is exceeded, TWS will eventually close the connection. So for constructing an RTD

spreadsheet with more than 50 tickers, it must be built to only make at most 50 new subscriptions or cancellations

per second.

5.4.13.1.3 TwsRtdServer error: No security definition has been found for the request.